GOLD: $1314.70 DOWN $4.90 (COMEX TO COMEX CLOSING)

Silver: $15.61 DOWN 12 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : 1313.00

silver: $15.60

/

For comex gold and silver:

MARCH

NUMBER OF NOTICES FILED TODAY FOR MAR CONTRACT: 126 NOTICE(S) FOR 15200 OZ (0.3919 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 126 NOTICES FOR 12600 OZ (.3919 TONNES)

SILVER

FOR FEBRUARY

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

3319 NOTICE(S) FILED TODAY FOR 16,950,000 OZ/

total number of notices filed so far this month: 3319 for 16,950,000

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $3838:UP $20

Bitcoin: FINAL EVENING TRADE: $3850 DOWN 1

end

XXXX

JPMorgan or Goldman Sachs are taking a huge issuance (stopping) of gold at the comex.

today 41/116

EXCHANGE: COMEX

CONTRACT: MARCH 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,317.700000000 USD

INTENT DATE: 02/27/2019 DELIVERY DATE: 03/01/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

657 C MORGAN STANLEY 67

661 C JP MORGAN 41

685 C RJ OBRIEN 1

690 C ABN AMRO 22

709 C BARCLAYS 4

737 C ADVANTAGE 33 19

800 C MAREX SPEC 33

878 C PHILLIP CAPITAL 6

905 C ADM 26

____________________________________________________________________________________________

TOTAL: 126 126

MONTH TO DATE: 126

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST FELL BY A HUGE SIZED 7392 CONTRACTS FROM 206447 DOWN TO 199,055 WITH YESTERDAY’S TINY 14 CENTS LOSS IN SILVER PRICING AT THE COMEX. TODAY WE ARRIVED FURTHER FROM AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS. WE ALWAYS WITNESS A CONTRACTION IN TOTAL OI AS WE APPROACH FIRST DAY NOTICE AND IT SEEMS THE CULPRIT IS THE FORCED LIQUIDATION OF SPREADERS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

2843 EFP’S FOR MARCH, 0 FOR APRIL, 0 FOR MAY, 0 FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 2843 CONTRACTS. WITH THE TRANSFER OF 2843 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 2843 EFP CONTRACTS TRANSLATES INTO 22.75 MILLION OZ ACCOMPANYING:

1.THE 14 CENT LOSS IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST NINE MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.

AND NOW: 23.315 MILLION OZ STANDING IN MARCH.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF FEBRUARY: 29,480 CONTRACTS (FOR 19 TRADING DAYS TOTAL 29,480 CONTRACTS) OR 147.400 MILLION OZ: (AVERAGE PER DAY: 1551 CONTRACTS OR 7.757 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF FEB: 147.4 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 21.05% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 352.41 MILLION OZ. (CORRECTED)

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2-19 TOTALS: 147.4 MILLION OZ/

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 7392 WITH THE 14 CENT LOSS IN SILVER PRICING AT THE COMEX /YESTERDAY..THE CME NOTIFIED US THAT WE HAD STRONG SIZED EFP ISSUANCE OF 2843 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE LOST A CONSIDERABLE SIZED: 4549 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 2843 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 7392 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 14 CENT LOSS IN PRICE OF SILVER AND A CLOSING PRICE OF $15.73 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.995 BILLION OZ TO BE EXACT or 157% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT FEBRUARY MONTH/ THEY FILED AT THE COMEX: 3399 NOTICE(S) FOR 16,950,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/AND NOW MARCH: 23.315 MILLION OZ/

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST FELL BY A CONSIDERABLE SIZED 4079 CONTRACTS UP TO 497,189 DESPITE THE FALL IN THE COMEX GOLD PRICE/(A LOSS IN PRICE OF $6.80//YESTERDAY’S TRADING).

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 6469 CONTRACTS:

MARCH HAD AN ISSUANCE OF 0 CONTACTS APRIL 6469 CONTRACTS,JUNE: 0 CONTRACTS DECEMBER: 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 497,189. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A FAIR SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2390 CONTRACTS: 4079 OI CONTRACTS DECREASED AT THE COMEX AND 6469 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN 2390 CONTRACTS OR 239,000 = 7.433 TONNES. AND ALL OF THIS DEMAND OCCURRED WITH A LOSS IN THE PRICE OF GOLD/ YESTERDAY TO THE TUNE OF $6.80.

YESTERDAY, WE HAD 4593 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF FEBRUARY : 107,130 CONTRACTS OR 10,713,000 OZ OR 344.36 TONNES (19 TRADING DAYS AND THUS AVERAGING: 5,638 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 19 TRADING DAYS IN TONNES: 344.36 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 344.36/2550 x 100% TONNES = 13.49% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 852.26 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A CONSIDERABLE SIZED DECREASE IN OI AT THE COMEX OF 4079 WITH THE LOSS IN PRICING ($6.80) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A CONSIDERABLE SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 6469 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 6469 EFP CONTRACTS ISSUED, WE HAD A GOOD GAIN OF 2390 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

6469 CONTRACTS MOVE TO LONDON AND 4079 CONTRACTS DECREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 7.433 TONNES). ..AND ALL OF THIS DEMAND OCCURRED WITH THE LOSS OF $6.80 IN YESTERDAY’S TRADING AT THE COMEX??

we had: 126 notice(s) filed upon for 12600 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $4.90 TODAY

NO CHANGES IN INVENTORY AT THE GLD:

/GLD INVENTORY 788.33 TONNES

Inventory rests tonight: 788.31 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 12 CENTS IN PRICE TODAY:

NO CHANGE IN SILVER INVENTORY AT THE SLV..///

/INVENTORY RESTS AT 309.374 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A HUGE SIZED 7392 CONTRACTS from 206,447 DOWN TO 199,055 AND FURTHER FROM THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

2843 CONTRACTS FOR MARCH. 0 CONTRACTS FOR APRIL., 0 FOR MAY AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 2843 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 7392 CONTRACTS TO THE 2843 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A LOSS OF 4549 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES: 22.75 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY AND NOW 23.315 MILLION OZ FOR MARCH.

RESULT: A HUGE SIZED DECREASE IN SILVER OI AT THE COMEX WITH THE 14 CENT LOSS IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY.BUT WE ALSO HAD A FAIR SIZED 2843 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. THE LOSS IN OPEN INTEREST CONTRACTS IN SILVER WAS CAUSED BY THE FORCED LIQUIDATION OF SPREADERS…IT HAD NO EFFECT ON PRICE..TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED DOWN 12.87 POINTS OR 0.44% //Hang Sang CLOSED DOWN 124.26 POINTS OR 0.43% /The Nikkei closed DOWN 171.35 POINTS OR 0.79%/ Australia’s all ordinaires CLOSED UP 0.31%

/Chinese yuan (ONSHORE) closed UP at 6.6827 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 56.75 dollars per barrel for WTI and 66.31 for Brent. Stocks in Europe OPENED RED//.

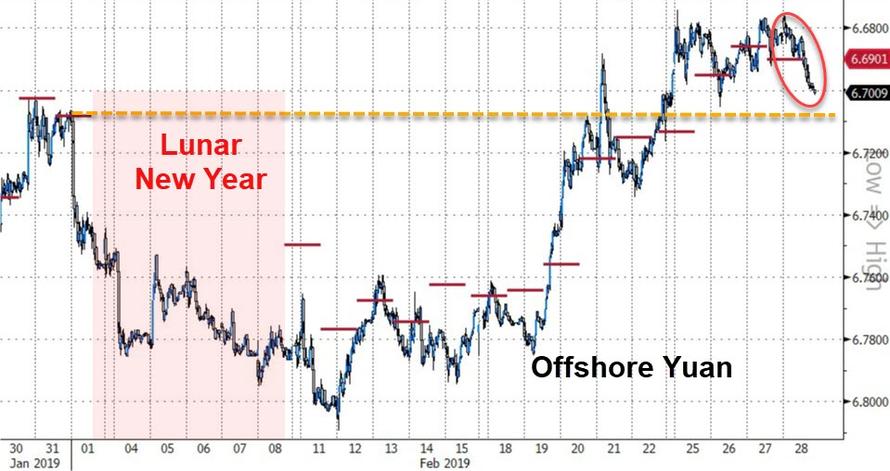

ONSHORE YUAN CLOSED DOWN // LAST AT 6.6827 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.6840: / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A/NORTH KOREA/SOUTH KOREA

i)North Korea//USA

Trump walks as Rocket Man wants sanctions relief prior to his denuclearization. This does not bode well for the Chinese trade talks as obviously China interfered. They need North Korea as a buffer.

(courtesy zerohedge)

b) REPORT ON JAPAN

3 C/ CHINA

i) CHINA/

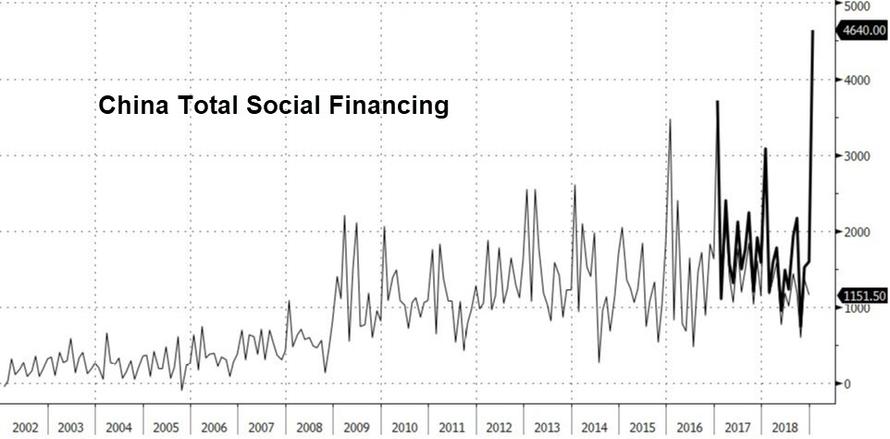

i)This is awful for China as their PMI plunges into contraction yuan. No wonder the PBOC flooded its economy with a huge 4.64 trillion yuan stimulus

( zerohedge)

iii)Huawei in court today as they are accused by T Mobile for stealing trade secrets.( zerohedge)

4/EUROPEAN AFFAIRS

i)UK

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

Israel

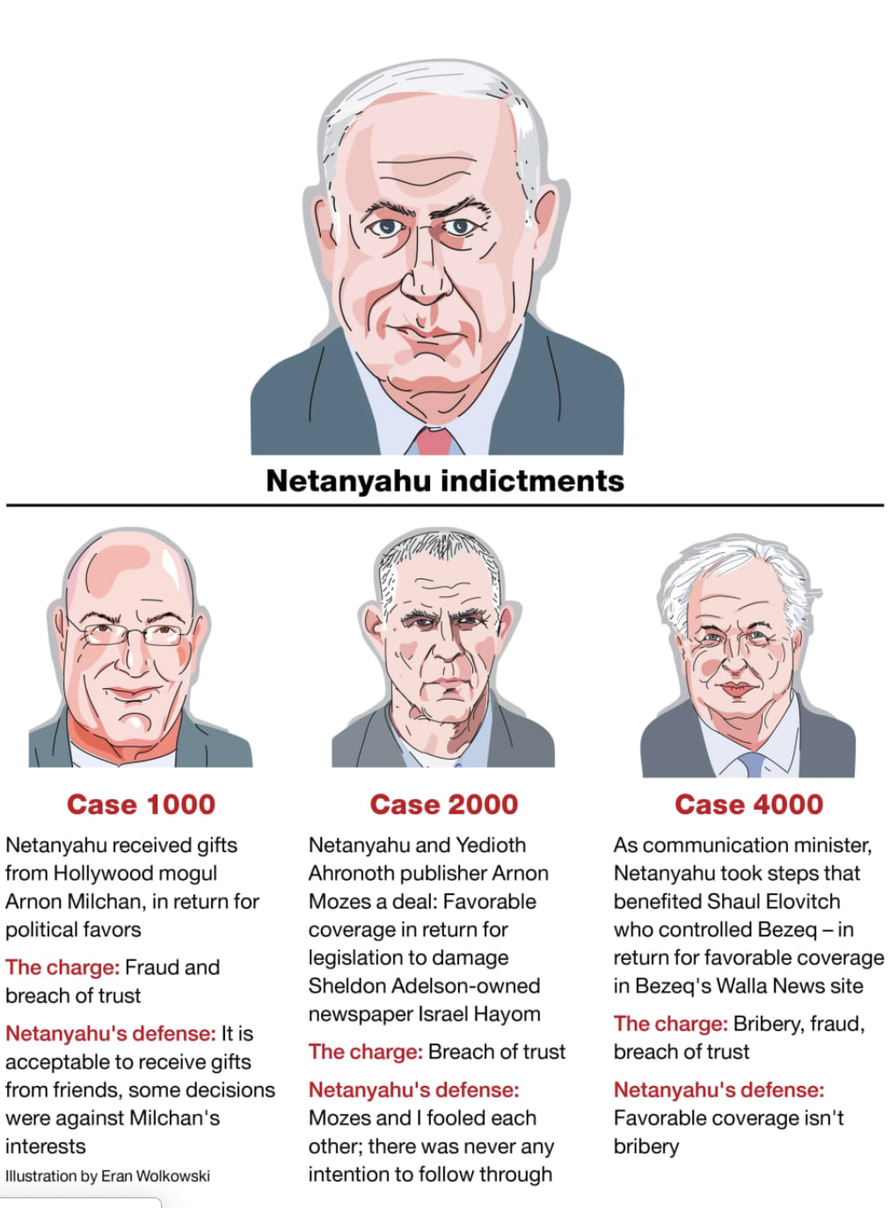

Amazing, Israeli Attorney General indicts Netanyahu on charges of bribery even though no money exchanged..only favourable press and that is not a breach of Trust.

(courtesy zerohedge)

6. GLOBAL ISSUES

i)Yesterday, tanks are massing on the Pakistan border as India is furious with that attack.

( zerohedge)

ii)Pakistan to release the captured Indian pilot as a “goodwill gesture”. However Pakistan needs another bailout from the IMF

(courtesy zerohedge)

7. OIL ISSUES

Oil retreats below 57 dollars after the uSA desires to sell oil from its SPR

(courtesy zerohedge)

8 EMERGING MARKET ISSUES

i)VENEZUELA/

9. PHYSICAL MARKETS

II)We wish the government of Romania all the best as it tries to repatriate its 61 tonnes of gold held at the Bank of England. They were told that they could earn an income on that gold if they leased it out. Now they want it back…we wish them luck!!!!!!!!!!!!!!!!!!!!

10. USA stories which will influence the price of gold/silver)

MARKET TRADING

ii)Market data

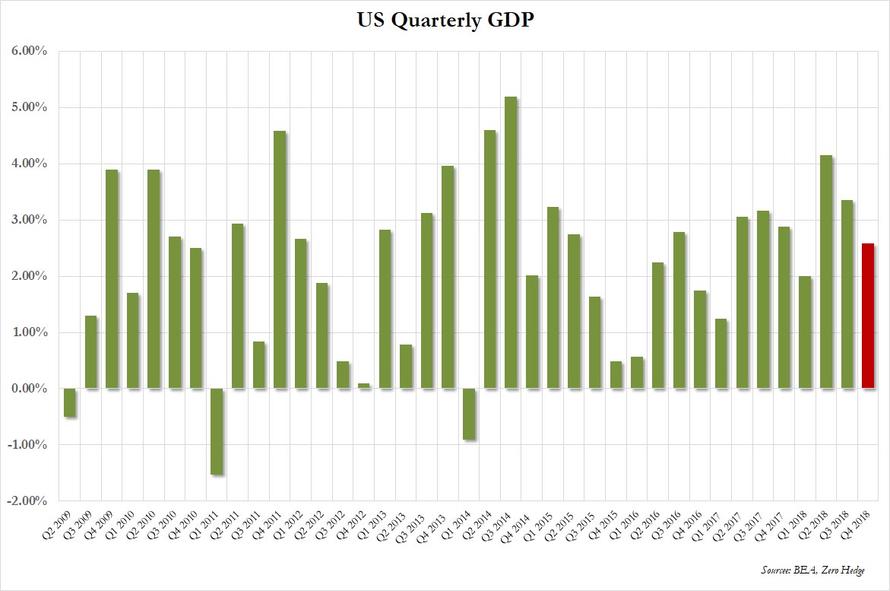

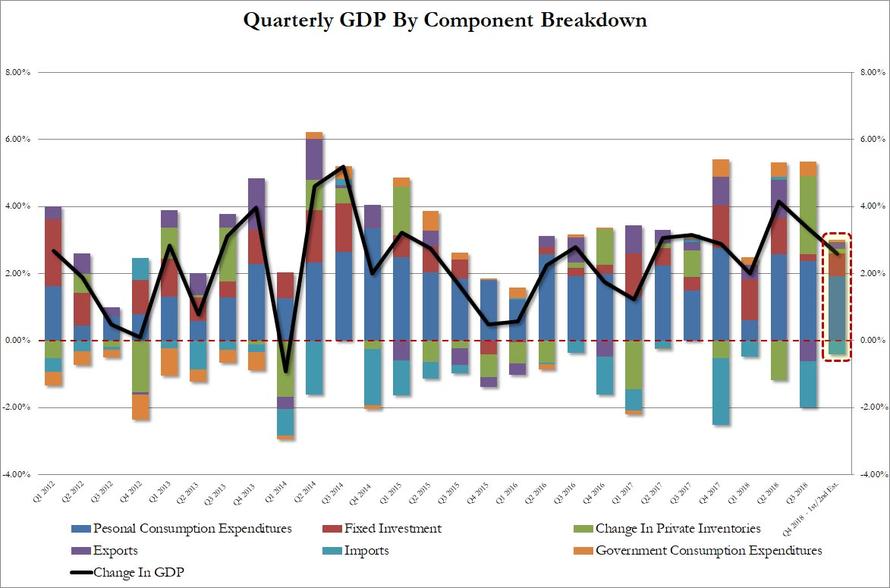

a)The biggest bunch of horse manure..the USA surprisingly grew by 2.6% in the 4th quarter instead of 2.2%. The numbers were fudged.

( zerohedge)

iv)SWAMP STORIES

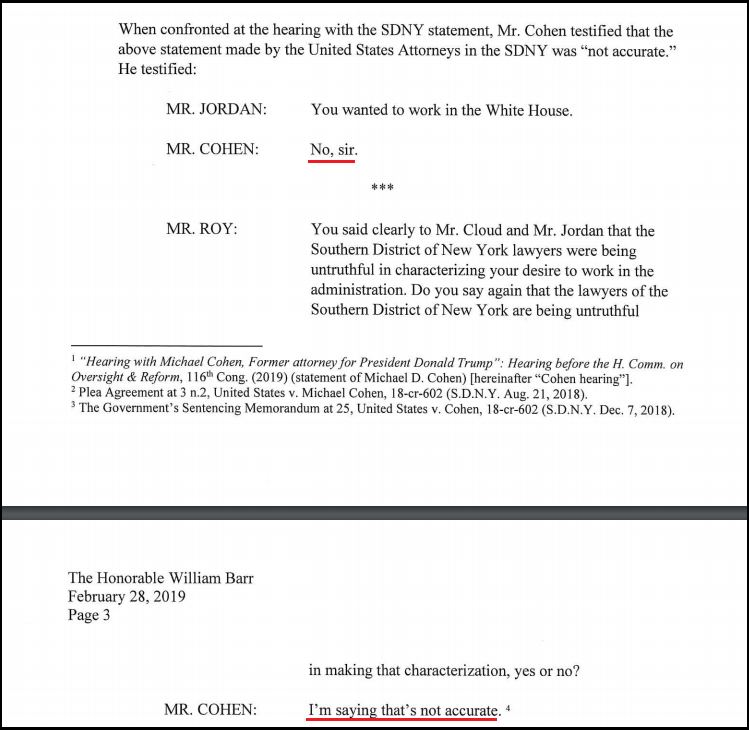

Cohen is accused of perjury and making numerous willfully and intentionally false statements during his testimony

( zerohedge)

end

Let us head over to the comex:

AFTER MARCH, WE HAVE THE NON ACTIVE DELIVERY MONTH OF APRIL. HERE: APRIL ADVANCES TO 784 CONTRACTS FOR A GAIN OF 122 CONTRACTS. AFTER APRIL, THE NEXT BIG ACTIVE DELIVERY MONTH IS MAY AND HERE THE OI ADVANCED BY 2823 CONTRACTS UP TO 146,114 CONTRACTS.

comex gold volumes are getting extremely low as players just do not want to play in this casino.

i

“Gold Is A Global Thermometer Of Risk” – CEO Q+A: Stephen Flood, GoldCore

In Business and Finance, Ireland’s leading business magazine, latest CEO Q+A, speak to Stephen Flood, CEO of GoldCore, about the global economy, debt levels, and making the most of your personal strengths.

Q. What are your main priorities and goals in your role?

To provide a convenient, efficient and most importantly safe way of owning gold bullion for clients who want to hedge financial and economic risks.

We believe that most investors are wholly unprepared for the next recession and any oncoming volatility.

We may well be on the verge of the next financial crisis, with risks building throughout the economy and global markets. And it’s for these reasons that we believe it has never been more important to have a financial insurance in the form of precious metals.

As CEO I share the common goals of the business which are:

- To increase assets held in our GoldCore Secure Storage programme. Last year we grew the total assets by 24%

- To increase awareness of precious metal ownership as part of a diversified portfolio of assets. Numerous studies confirm that gold can reduce investment and pension portfolios volatility and enhance returns in the long term

- To use cutting edge technology to increase the efficiency for clients looking to buy, sell, take delivery and store gold and silver bullion in the safest ways.

Q. What are your biggest challenges as CEO?

Finding enough time in the day!

One bug bear is the manipulation of search engines by other providers in our industry. The public are increasingly being herded by dominant “Disinformation Technology” companies. Often it seems that value and service are not enough to win and hold position, instead investing in search engine technology and online advertising at the expense of product development appears to be the core focus of some organisations.

Increased regulation and transparency is needed to ensure fairness in the market – as it is how 90% of searches can be dominated by one provider using a secret algorithm!

Q. How do you keep your team/staff motivated?

We are a tight team, communicating and interacting throughout the day. The best motivator is simply having respect and being honest. Empowering team members to expand their skills, understanding and backing them to take risks and take on new responsibilities is key.

Employees now see through many of the “perks” offered by larger companies and they ring shallow. I believe that 90% of the time I work for my employees, making sure that they have the skills and tools they need to realise their potential and play their role in our organisation. 10% of the time I set the tone for where we are going as an organisation.

Goals are 360 degrees and multi-faceted: increasing income, reducing risks, continuously improving our offering. I celebrate when an employee takes me to task without fear if I have dropped the ball – this is organisational strength, there are no sacred cows, although I have been called worse, I am sure!

Everyone in our company knows that building gold storage assets is our key commercial goal, but not at any cost. Since our foundation in 2003, our client’s welfare has always come first, and we also believe that our goals and that of our clients can and must be symbiotic.

Q. What are the challenges facing the industry going forward?

Our industry is buffeted by a number of factors. The price of gold, crypto-currencies, government regulation, competitive forces and the changing face of consumer information sources have all served to drive up the demand for gold at various times. We operate in a very tight margin business, managing financial risks is key. It also makes life very interesting and we never have a dull day.

I would like to see more industry regulation as there are a number of cowboy operators who should not be operating at all and they see clients as nothing but fodder. We have seen companies selling what they claim to be pure gold coins which are in fact gold plated coins!

Q. What new trends are emerging in your industry?

Gold is a global thermometer of risk. We believe that debt levels are unsustainable, and the risk of a disorderly default is increasing every day. Economic inequality is increasing, and political systems are facing massive disruption.

All of this occurs because of the corrosive effects of printed money which arguably tempered the worst effects of the Global Financial Crisis but have now been left in place due to political comfort and expediency.

Our global debt is now at 340% of GDP, up from 220% during the last Financial crisis – madness! History tell us this ends badly. The last time our economies were so unequal was in the 1930’s and we all know how that ended.

In terms of trends, we see the biggest test facing the EU is not from Brexit, but a disorderly exit of Italy. I see a new banking crisis emerging and spreading far faster than previously thought. This could come from the corporate debt market or China. Crypto money alternatives are a grass roots movement to take back personal sovereignty from what is perceived as a rigged system.

Opportunities will be considerable as those with expandable balance sheets will be gifted with cut price assets during any fire sale that ensues. The biggest opportunity globally will be the technologies that emerge from blockchain technologies – we are at the beginning of the next industrial and technological revolution. Our current systems and process will look positively antiquated when compared to the sheer enormity of what block-chain and its derivatives will bring.

Q. As an employer are you finding any skill gaps in the market?

I think some students come out of third level education without the practical skills needed in real. Creating apprenticeships within courses would be a great way of aligning the youthful creativity of newcomers, with the deep sector knowledge of industry.

If, as I suspect, every industry vertical will be utterly transformed in the next 10 years as blockchain permeates, it will be those organisations with the most nimble, creative and competent staff that will succeed.

An education system run by professors and lecturers that are not also actively engaged in industry is not fit for purpose. Our teachers must be thought leaders.

Q. How did your strategy develop in the context of the banking crisis and economic crisis?

In 2003 we saw the relentless build-up of credit combined with the fall in lending oversight as having obvious ramifications. Credit has a place, but when capital appreciation and credit availability solely drive purchase decisions trouble ensues. We were vocal in warning that an Irish financial crisis and global financial crisis were coming, and that gold would protect investors. This came to pass.

Q. How will Brexit affect you, or have you started to feel the effects already?

No one can really know the impact as the final arrangement has not yet been agreed. We suspect a cobbled solution will be put in place at the last minute. The real risk though is the precedent it sets and, in my view, it greatly increases the likely hood of an EU crisis and possible demise. It is important to watch Italy.

Currently we are seeing more demand for a Dublin Secure storage location. It is a high security vault that meets the Bank of England vault security standards. We will be able to store gold bullion securely for clients privately, as part of their pensions and also for companies. It will act as a deposit account in a superior currency.

Interestingly, unlike bank accounts, the gold held will not be a liability for the client as it is not held on our balance sheet but rather it is held on the client’s balance sheet. We act merely as a custodian and not a creditor.

We believe with Brexit looming an allocation of least 10 % has never been more important. But bullion must be held in professional vaulted facilities where the gold is continuously monitored, liquid and competitively priced.

Q. How do you define success and what drives you to succeed?

For me success is making the most of your own personal strengths.

Time and health are the most important resources we have. Applying yourself to your environment for the betterment of your community, family and your own development is a worthy goal. I find that many people spend their valuable lives beavering away on singular projects at the cost of everything else.

In my 20’s I worked for Goldman Sachs in New York as a sales trader on one of the most powerful trading desks in the world. I decided that while it was an exciting place to be in my 20’s, and I loved every minute working with some of the most incredibly talented people I had ever met, it was not a life that would allow me to have and enjoy a family and to be a Dad. So I left and returned home, partnering with my friend in our own business in Dublin and have never looked back.

I don’t work evenings, or weekends, I have breakfast with my kids and dinner most days.

For me mental health, productive work and a balanced life is key. The secret to happiness is not to mindlessly seek happiness all the time dwelling on what you need or don’t have, it is enjoying what you have and the relationships with the people all around you.

Q. What’s the best advice you’ve been given, or would give, in business?

All business primarily comes down to one single formula: Taking unique knowledge from where it resides and delivering it to where it is needed. Once you understand this, you can approach any opportunity and decide if it is a worthy activity. Business is about the delivery of services and products, simply. Business needs excellent teams, with people who work well together and get the best from each other.

Knowing your customers, how they think, how they evaluate, where they go for information is also key. Never stop innovating but also don’t lose focus in the core offering. Let data inform decisions, but also trust your gut. Always challenge yourself and your biases and debate with people who you would not normally agree with.

Q. What have been your highlights in business over the past year?

Recently launching Dublin Storage has been great. It is a first in Ireland and we believe it will be instrumental in supporting the financial health of Irish consumers, investors and companies. We also launched the new site which allows new clients to buy up to €50,000 worth of gold in just 3 minutes on their smart phone or computer – a first in the industry and a real win for our User Experience approach.

Q. What’s next for your company?

We are ready for Brexit and related issues. We are currently working on an institutional gold investment offering in the Middle East which is really exciting. It will be the largest consumer bullion storage service in the region and has been designed by GoldCore and our local partners. We are also exploring how to get involved in the block-chain space.

Q. Where do you want your business/brand to be this time next year?

We see ourselves reaching more and more Irish investors, pension owners and company’s clients through referral and word of mouth. Our GoldCore Secure Storage programme in Dublin has turned a lot of heads and many financial and pension advisers are seeking to store their client’s gold in Ireland for the first time.

“All business primarily comes down to one single formula: Taking unique knowledge from where it resides and delivering it to where it is needed.”

Courtesy of Business and Finance

News and Commentary

Gold near 2-week lows as dollar rebounds over trade caution (Reuters.com)

Venezuela removed 8 tons of central bank gold last week (Reuters.com)

Trump says he walked from deal with North Korea’s Kim over sanction demands (Reuters.com)

Dumb bank burglars left gold bars strewn across vault floor (TheGuardian.com)

Consumers, weak exports seen curbing U.S. fourth-quarter growth (Reuters.com)

Gold Market Still Bullish – Ira Epstein (GoldSeek.com)

Will Hedge Funds Ramp Up Their Bullish Gold Bets? (GoldSeek.com)

Make-Believe Gold and Silver Scheme Going to Collapse (Youtube.com)

The Perth Mint Has Recast This Gold Bar More Than 65,000 Times (Bloomberg.com)

City of London Faces New Hurdles to EU Markets After Brexit (Bloomberg.com)

10Y Treasurys Suddenly Tumble Amid Rate-Lock Curve Selloff (ZeroHedge.com)

Listen on iTunes,Blubrry & SoundCloud & watch on YouTube above

Gold Prices (LBMA PM)

27 Feb: USD 1,326.45, GBP 998.02 & EUR 1,164.09 per ounce

26 Feb: USD 1,327.55, GBP 1005.79 & EUR 1,168.11 per ounce

25 Feb: USD 1,329.15, GBP 1016.80 & EUR 1,170.32 per ounce

22 Feb: USD 1,322.25, GBP 1016.15 & EUR 1,166.49 per ounce

21 Feb: USD 1,335.05, GBP 1021.85 & EUR 1,177.78 per ounce

20 Feb: USD 1,345.75, GBP 1032.86 & EUR 1,186.82 per ounce

Silver Prices (LBMA)

27 Feb: USD 15.86, GBP 11.91 & EUR 13.92 per ounce

26 Feb: USD 15.83, GBP 11.98 & EUR 13.93 per ounce

25 Feb: USD 15.95, GBP 12.19 & EUR 14.04 per ounce

22 Feb: USD 15.87, GBP 12.20 & EUR 14.00 per ounce

21 Feb: USD 15.91, GBP 12.19 & EUR 14.02 per ounce

20 Feb: USD 16.03, GBP 12.31 & EUR 14.15 per ounce

Recent Market Updates

– U.S. Mint Suspends Silver Bullion Coin Sales After Sales Double In February

– MMT: Modern Monetary Madness Will Lead To Higher Taxes and Inflation

– Gold Broker Has Good Sense and Prefers Gold To All That Glitters (The Times)

– The Utterly Unbelievable Scale of U.S. Debt Right Now

– The Best Time In History To Buy GOLD

– Jim Willie Interviews Mark O’Byrne – Prepare Now For Global Financial Crisis II

– 7 Major Flaws Of The Global Financial System – Excellent Infographic

– The Case for Gold In 2019 – The Economist

– Invest In Gold As a Hedge In Cashless Society – Ex IMF Rogoff

Venezuelan regime took 8 tons of gold from central bank last week, Reuters says

Submitted by cpowell on Wed, 2019-02-27 21:32. Section: Daily Dispatches

By Corina Pons and Mayela Armas

Reuters

Wednesday, February 27, 2019

CARACAS, Venezuela — At least 8 tons of gold were removed from the Venezuelan central bank’s vaults last week, an opposition legislator and three government sources told Reuters, in the latest sign of President Nicolas Maduro’s desperation to raise hard currency amid tightening sanctions.

The gold was removed in government vehicles between Wednesday and Friday last week when there were no regular security guards present at the bank, Legislator Angel Alvarado and the three government sources said.

…

They plan to sell it abroad illegally,” Alvarado said in an interview.

The central bank did not respond to requests for comment.

Alvarado and the government sources, who spoke on condition of anonymity, did not say where the central bank was sending the gold. They said the operation took place while central bank head Calixto Ortega was abroad on a trip. …

… For the remainder of the report:

https://www.reuters.com/article/us-venezuela-gold-exclusive/exclusive-ve…

* * *

Help keep GATA going

GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at:

To contribute to GATA, please visit:

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

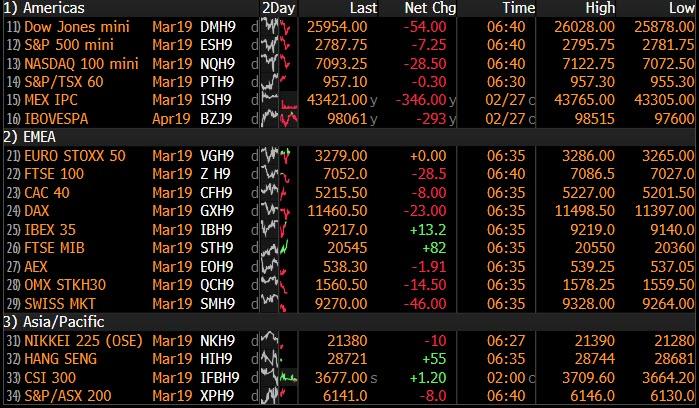

Your early THURSDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED/ LAST AT: 6.6827/

//OFFSHORE YUAN: 6.6840 /shanghai bourse CLOSED DOWN 12.87 POINTS OR 0.44% /

HANG SANG CLOSED DOWN 124.26 POINTS OR 0.43%

2. Nikkei closed DOWN 171.35 POINTS OR 0.79%

3. Europe stocks OPENED RED

/USA dollar index FALLS TO 95.84/Euro RISES TO 1.1414

3b Japan 10 year bond yield: FALLS TO. –.02/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 110.70/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 56.75 and Brent: 66.31

3f Gold UP/JAPANESE Yen UP CHINESE YUAN: ON -SHORE DOWN /OFF- SHORE: DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.16%/Italian 10 yr bond yield UP to 2.77% /SPAIN 10 YR BOND YIELD UP TO 1.16%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.61: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 3.66

3k Gold at $1325.40 silver at:15.81 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 5/100 in roubles/dollar) 65.72

3m oil into the 56 dollar handle for WTI and 66 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 110.76 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9933 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1337 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.16%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.66% early this morning. Thirty year rate at 3.05%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.3162

Futures Fall After Dismal Chinese Data, Korea Summit Ends In Chaos

The recent market weakness continued, and the S&P pulled further back from the 2800 “quadruple-top” overnight, as global stocks dropped for a third day following the latest disappointing PMI data out of China and an unexpected and abrupt collapse to the U.S.-North Korea summit added to investor fears of a rapidly slowing economy, and as the dollar slumped further, safe havens such as the Japanese yen and the Swiss franc, as well as gold, all gained.

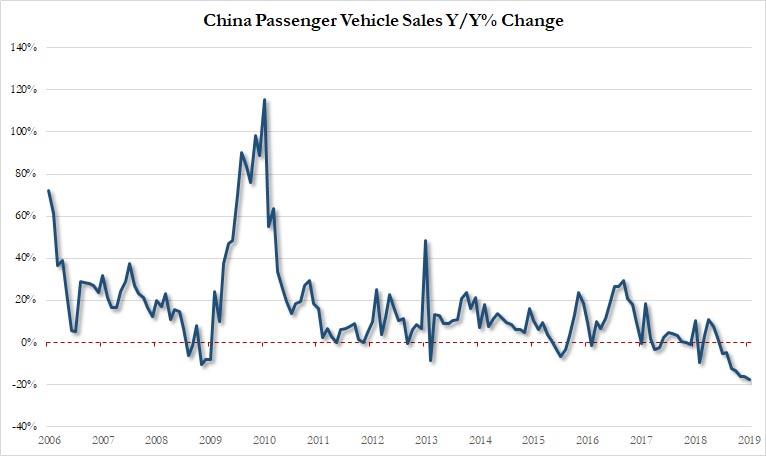

Just two weeks after announcing it had injected more credit into its economy than the GDP of Saudi Arabia, overnight China disappointed again when it reported its February manufacturing PMIs which tumbled deeper into contraction territory even as the Non-mfg PMI also missed expectations: the Mfg PMI dropped to 49.2, below the 49.5 expected as the index of new export orders tumbled to 45.2 from 46.9 – falling at their fastest pace since the global financial crisis – while the non-manufacturing PMI, which reflects activity in the construction and services sectors, also fell, to 54.3 compared with 54.7 in January.

Following the latest slow down in China, European miners led the drop in the Stoxx Europe 600 Index and copper declined amid fresh fears about the global economic slowdown, while Dow, Nasdaq and S&P 500 futures all fell, as the Citi Economic Surprise Index dropped to a fresh 18 month low.

Earlier, South Korean shares were the biggest losers in Asia after President Trump and Kim Jong Un departed the summit venue in Hanoi without a deal, even though expectations for a breakthrough were low. Trump and Kim Jong Un had constructive discussions on denuclearization, the White House said, but news of the summit’s early break-up triggered flight-to-quality bids in safe assets. Riskier assets took a hit, with stocks across the board lower in Europe after the start of trading. The pan-European STOXX 600 index fell more than half a percent.

That followed a retreat in Asian equities, which took a hit on a lack of progress on trade issues between China and the U.S. and data showing factory activity contracting to a three-year low in China. The Shanghai Composite Index fell 0.7 percent following the latest dour comments from U.S. Trade Rep Robert Lighthizer who told U.S. lawmakers on Wednesday that U.S. issues with China are “too serious” to be resolved with promises from Beijing to purchase more U.S. goods, and any deal between the two countries must include a way to ensure commitments are met. The USTR also later clarified in a statement that it was not abandoning the threat of increasing the tariffs to 25 percent from 10 percent.

“This is likely to be the sort of trade deal that comes through: enough of a deal, or delays of further taxes to enable equities to stay supported while still allowing enough room for U.S. President Trump to criticize China on the campaign trail next year,” said Paul Donovan, chief global economist at UBS Wealth Management. “In many ways this indefinite delay in the consequences are reminiscent of the deal agreed between Trump and one of the many EU Presidents Juncker last year.”

“One suspects trade headlines will continue to throw around sentiment for a while yet. The issues are complex, the trade-offs real, and opinions divided,” ANZ strategists said in a note.

As a result of another busy overnight session, the MSCI’s All-Country World Index was 0.2% lower on the day and down for a third day running. Treasuries climbed, most European bond slipped and the dollar held steady.

In overnight central bank news, Bank of Korea maintained its 7-day repo rate at 1.75% as expected, the decision was unanimous. The KRW immediately experienced marginal weakness as policymakers kept in mind the country’s declining exports, rising unemployment and the slowdown in Chinese growth. At the press conference, Governor Lee the central bank is to maintain accommodative rate policy although it is not time to consider easing policy rates.

In currency markets, the Swiss franc and yen led gains among G10 currencies as demand for havens climbed after President Donald Trump’s second summit with Kim Jong Un ended without an agreement, while the dollar index against a basket of six major currencies fell 0.1 percent at 96.041. The index had edged up 0.1 percent on Wednesday, pulling away from a three-week trough as Treasury yields rose ahead of the release of U.S. fourth-quarter GDP data later on Thursday. USD/JPY slid as much as 0.3% after Japan’s factory output posted the biggest decline in a year in January, while USD/CHF slipped 0.4%. Dollar-yen hit session- lows as leveraged funds in Tokyo exited intraday longs in defensive reaction to the Trump-Kim news, according to an Asia- based FX trader.

“Headlines on a shortened Trump-Kim summit lifted the yen as the uncertainty sparked a bit of risk-off moves,” said Jun Kato, chief market analyst at Shinkin Asset Management in Tokyo

The euro jumped 0.4% to $1.1412, a 4 week high, after slipping 0.15 percent on Wednesday. Sweden’s krona rallied by the most in two weeks against the euro and yields on Swedish benchmark bonds surged after stronger-than-forecast growth data.

Oil prices fell on Thursday amid weakening factory output in China and Japan and record U.S. crude output, although markets remained relatively well supported by supply cuts led by producer club OPEC. Brent (-0.8%) and WTI (-0.6%) prices are negative but trading within a very narrow USD 1/oz range as risk sentiment was hampered for the abovementioned reasons.

Expected data include jobless claims, annualized GDP and Chicago Business Barometer. CIBC, Autodesk, Dell Technologies, Marriott, and VMware are among companies due to report earnings.

Market Snapshot

- S&P 500 futures down 0.3% to 2,786.50

- STOXX Europe 600 down 0.4% to 371.22

- MXAP down 0.7% to 159.07

- MXAPJ down 0.6% to 522.82

- Nikkei down 0.8% to 21,385.16

- Topix down 0.8% to 1,607.66

- Hang Seng Index down 0.4% to 28,633.18

- Shanghai Composite down 0.4% to 2,940.95

- Sensex down 0.1% to 35,854.04

- Australia S&P/ASX 200 up 0.3% to 6,168.99

- Kospi down 1.8% to 2,195.44

- German 10Y yield rose 1.3 bps to 0.161%

- Euro up 0.2% to $1.1392

- Italian 10Y yield rose 7.9 bps to 2.425%

- Spanish 10Y yield rose 1.7 bps to 1.176%

- Brent futures down 0.9% to $65.80/bbl

- Gold spot up 0.4% to $1,324.87

- U.S. Dollar Index down 0.2% to 95.98

Top Overnight News

- The U.S. won’t accept a trade deal with China that merely commits the Chinese to buy more American goods, a scenario U.S. Trade Representative Robert Lighthizer dismissed as the “soybean solution,” in reference to promises to buy more American soybeans. “This administration is pressing for significant structural changes that would allow for a more level playing field,” Lighthizer said. “We need new rules.”

- Confidence among U.K. businesses plunged to a seven-year low this month and consumers remained pessimistic about the economic outlook as lawmakers failed to provide further clarity about the nation’s exit from the European Union

- In Wednesday’s Brexit debate, one of the Anti-European Conservatives seemed to have heeded May’s warning that continued obstinacy would jeopardize their entire project. “The choice is no longer perhaps between an imperfect deal and no deal, but between an imperfect deal and no Brexit,” Edward Leigh, a long-standing euroskeptic, told Parliament

- The first official gauge of China’s manufacturing sector in February showed activity contracting further, with a series of domestic holidays, the global slowdown and uncertainty from the trade war all likely playing a part

- Keeping interest rates below zero for too long may hinder the European Central Bank’s policy from trickling down to the economy, according to Francois Villeroy de Galhau. He said normalization of monetary policy is still “desirable” as the current slowdown is mainly due to temporary factors that should fade in the course of the year

- President Donald Trump said he’s in no rush for North Korea to give up its nuclear arms and tamped down expectations for his second summit with Kim Jong Un, saying that over the long term the talks would be a success

- The Bank of Japan made changes to the planned purchase ranges and buying frequencies for the key five-to-10-year segment under its monthly bond operations plan for March, when compared with February

- The Swiss economy returned to growth in the final three months of 2018, dodging the worst of the weakness that hit neighbors to the north and south

- Keeping interest rates below zero for too long may hinder the European Central Bank’s policy from trickling down to the economy, according to Bank of France governor Francois Villeroy de Galhau

- BNP Paribas SA won dismissal of a German lawsuit by a trader seeking 163 million euros ($186 million) for a “fat-finger” mistake in a 2015 transaction

Asian stocks were mixed following a similar lead from Wall Street wherein the Dow and S&P fell for a second consecutive day as investors digested key testimonies from US Trade Representative Lighthizer and Fed Chair Powell. The Dow was also weighed on by shares from UnitedHealth which closed lower by almost 5% whilst the S&P was pressured by the telecom and healthcare sectors. ASX 200 (+0.3%) was kept afloat by its pharma and energy names, while the Nikkei 225 (-0.9%) felt pressure from its heavyweight industrial and machinery sectors. Elsewhere, Shanghai Comp (-0.4%) and Hang Seng (-0.4%) initially traded choppy although the latter recovered from opening losses as pharma and finance stocks led the gains. Finally, South Korea’s KOSPI (-0.6%) slipped after index heavyweights Samsung Electronics (-1.8%) and SK Hynix (-4.2%) succumbed to the semiconductor weakness experienced stateside. BoJ Board Member Suzuki says it is important for the BoJ to maintain powerful monetary easing but there is no need to ease further, BoJ must be mindful of a sustainable framework as inflation may remain subdued for a prolonged period. Suzuki said the BoJ does not intend to raise rates now but will act swiftly through market operations if yield rise sharply, he added that overseas tail risk appear to be heightening.

Top Asian News

- CLO Market’s Japanese Whale Faces Increased Regulatory Scrutiny

- India Refuses to Negotiate Over Fate of Captured Pilot: Official

- BOJ Paves Way to Buy Less Bonds as Yields Drop to 2-Year Low

- Hong Kong Targets Thinly Traded Stock Headache in Strategy Plan

- It’s D-Day for Netanyahu as He Braces for Possible Indictment

Major European equities are currently flat after opening slightly lower [Euro Stoxx 50 U/C] as risk sentiment deteriorated following reports of no agreement being reached between US President Trump and North Korean leader Kim Jong-Un; with US President Trump stating they had some options but decided not to take them. The FTSE 100 (-0.7%) is underperforming its counterparts, weighed on by the pounds recent strength; additional downward pressure is exerted by Rolls Royce (-3.4%) at the bottom of the index in spite of strong earnings as the Co. have withdrawn from Boeing’s engine race. British American Tobacco (-2.5%) are in the red in-spite of good earnings; with some analysts attributing this to a lack of guidance for 2019. Sectors are also in the red with some marginal outperformance in telecom names. Other notable movers include, Zalando (+17.6%) who are leading the Stoxx 600 after their Q4 adj. EBIT came in above expectations; AB InBev (+5.1%) are also higher after a beat on their Q4 revenue. Towards the bottom of the Stoxx 600 are Adecco (-4.7%) after the Co. posted a Q4 net loss of EUR 112mln instead of the expected net profit of EUR 150mln.

Top European News

- Rolls-Royce Shares Drop as Series of Charges Weigh on Business

- AB InBev Report Allays Concern About Ties to Kraft Meltdown

- Scandal Contagion Spreads Past Danske in Bank Funding Rounds

- Sberbank Dividends May Miss Expectations on Denizbank Sale Delay

In FX, super strong Q4 GDP data from Sweden after the surprise contraction in the previous quarter has propelled the Krona through 10.5000 vs the Euro and further above recent lows, but the Franc is also a marked G10 outperformer following sub-forecast Swiss growth in the final 3 months of 2018 and a weaker than expected KoF survey, with Usd/Chf probing below the 100 DMA at 0.9960, while Eur/Chf has slipped under 1.1350. Indeed, the Franc is firmer across the board and clearly benefiting from its premier status as the safest currency destination amidst a storm, with risk sentiment still fragile due to ongoing tensions between India and Pakistan, and in wake of the Trump-Kim summit ending without a nuclear agreement. Back to Eur/Sek, nearest technical support level is seen at 10.4550.

- JPY/EUR – Also firmer into month end, and partly on the aforementioned risk-off or defensive positioning as the Jpy rebounds from 111.00 vs the Dollar yet again (heavy exporter supply touted at the big figure). Eur/Usd has now firmly breached the 1.14 level to the upside, for reference the current high is 1.1418, after surpassing both the 50 and 100 DMA’s, looking ahead is the February 5th high of 1.1441 and prior to this 1.1420. Of note moderate rebalancing sell signals for the Buck are said to be ‘strongest’ against the Euro.

- AUD/GBP/NZD/CAD – All flat to marginally weaker vs the Greenback, with the Aussie and Kiwi undermined by a 3rd consecutive sub-50.0 Chinese manufacturing PMI overnight after mixed independent impulses via a welcome beat in Australian Q4 Capex vs a deterioration in the NBNZ business outlook for the current month. Hence, Aud/Usd is holding up marginally better than Nzd/Usd within 0.7166-28 and 0.6854-35 respective ranges. Meanwhile, the Pound retains a relatively strong Brexit-related bid, albeit off best levels posted on Wednesday, with Cable pivoting 1.3300 vs its new 1.3351 ytd peak and perhaps wary about hefty option expiry interest at 1.3325 (1 bn). Elsewhere, the Loonie has stalled alongside oil prices and is back around the 1.3150 axis vs its US counterpart, as the DXY continues to skirt 96.000.

- EM – Unsurprisingly, the KRW has depreciated in disappointment over no breakthrough on a deal between the US and NK, to a low of almost 1125.00 vs the Usd at one stage.

In commodities, Brent (-0.8%) and WTI (-0.6%) prices are negative but trading within a very narrow USD 1/oz range as risk sentiment is hampered following no agreement being reached between the US and North Korea alongside Chinese Manufacturing PMI printing the third consecutive month of contraction. In terms of recent news flow Libya’s NOC spokesperson stated that there is no technical obstacle to restarting the El Sharara oilfield, but security remains the issue. Elsewhere, UBS highlight that the 8.6mln draw in US crude inventories does not necessarily signal the start of a trend, although the size of the draw indicates that the market is tightening. And just of note Brent futures expire later today. Gold (+0.5%) is firmer and approaching session highs, as the yellow metal is benefitting from the deteriorating risk sentiment after this mornings aforementioned US-North Korea updates. Elsewhere, copper prices were steady in-spite of the poor Chinese manufacturing PMI, with the negative impact of this balanced out by the ongoing supply concerns for the metal; as LME registered warehouse stocks are approaching their lowest level in 10 years.

Looking at the day ahead, the main focus will be on the Q4 GDP reading which is expected to show a +2.2% reading which compares to +3.4% in Q3. In the details of that, core PCE is expected to print at +1.6%. The other data worth watching in the US is the latest weekly initial jobless claims reading and the February Chicago PMI and Kansas City Fed manufacturing survey readings which could give greater insight into the factory sector this month. Away from all that it’s another busy day for Fedspeak with Clarida (1pm GMT), Bostic (1.50pm GMT), Harker (4pm GMT) and Kaplan (6pm GMT) all slated to speak.

US Event Calendar

- 8:30am: BEA Releasing Initial 4Q GDP (Combining Initial/Second)

- 8:30am: Initial Jobless Claims, est. 220,000, prior 216,000; Continuing Claims, est. 1.74m, prior 1.73m

- 8:30am: GDP Annualized QoQ, est. 2.2%, prior 3.4%

- 8:30am: Personal Consumption, est. 2.95%, prior 3.5%

- 8:30am: Core PCE QoQ, est. 1.6%, prior 1.6%

- 9:45am: Chicago Purchasing Manager, est. 57.5, prior 56.7

- 11am: Kansas City Fed Manf. Activity, est. 6, prior 5

Central Banks

- 8am: Fed Vice Chair Clarida Speaks at NABE Conference in Washington

- 8:50am: Fed’s Bostic Speaks on the Economic and Housing Landscape

- 11am: Fed’s Harker Discusses Economic Outlook

- 1pm: Fed’s Kaplan to Speak in Q&A in San Antonio

- 7pm: Fed’s Mester Speaks on Women in Economics

- 8:15pm: Powell speaks on Economic Developments and Longer-Term Challenges

DB’s Jim Reid concludes the overnight wrap

Welcome to the last day of February. You’ll be surprised to learn that I’ve just won the carpet battle I discussed on Tuesday and we’re back to moving into our new place on time. As such after 7 months of renting a place with a 25 year old kitchen and a shower that takes 3 minutes to warm up and trickles out, we are going to hand in our two month notice today. With 3 babies/toddlers, a dog and a husband it will take us this long to fumigate the place. In fact I’m not sure why we even debated the quality of the carpets in the new house as they won’t last very long anyway!! So an exciting countdown nearly two years after first seeing our new place begins. The last day of the month is also the day we say goodbye to 20 degree temperatures as rain is expected with a cooler front. I’m making a market of 45-50 days until we next have a 20-handle temperature in London. Let’s trade!

The temperature rose in bond markets yesterday with the main talking point being to work out why bonds suddenly sold off from lunchtime in Europe and around the US open. Indeed 10y Treasuries finished +4.7bps higher last night (-1.4bps in Asia though) – weakening by the most in four weeks – after similar maturity Bunds had risen +3.0bps – the fifth weakest day since October 19th. In fact Bunds touched their highest level in 3 weeks and are up +5.6bps from last Friday’s intraday yield lows – or +61% if you wanted a more dramatic stat. There were also more multi-week highs for yields in France (+2.6bps) and the Netherlands (+3.0bps), while BTPs (+8.1bps) sold off by the most since February 1st. To be honest we’ve struggled to pinpoint the exact reason for the sell-off.

Gilts (+6.8bps) also underperformed and there was some suggestion that this led the wider move as Brexit news-flow gets incrementally more market positive. However there were other suggestions it was more technically driven by Treasuries hitting the bottom of a recent range, as well as a heavy day for US IG issuance. Further exacerbating the move was a the +2.59% rally in WTI crude prices after official data showed a 8.65 million barrel decline in US inventories. Additionally, US oil imports fell to a two-decade low and refinery utilisation rose.

As for markets overnight, sentiment is on the weaker side after China’s soft PMIs with the Shanghai Comp (-0.43%), Nikkei (-0.38%) and Kospi (-0.47%) all down while the Hang Seng (+0.26%) is up. Elsewhere, futures on the S&P 500 are down -0.12%. China’s February composite PMI came in at 52.4 (vs. 53.2 last month) with the manufacturing PMI continuing to remain in contractionary territory (at 49.2 vs. 49.5 expected; lowest since Feb 2016) – the third month in a row. Services PMI came in at 54.3 (vs. 54.5 expected). The new export orders component of the manufacturing PMI continued to contract with the reading at 45.2 (vs. 46.9 last month), the lowest since February 2009 and marking 9 months below 50 signaling continued weak global demand. The new order component edged up over 50 again (50.6) after spending two months below. By scale large enterprises showed improvement in their manufacturing PMI (at 51.5 vs. 51.3 last month) while medium (46.9 vs. 47.2 last month) and small enterprises (45.3 vs. 47.3 last month) continued their slump despite the PBoC’s continued push to provide easy credit access to SMEs amidst trade talks. In another sign of the global slowdown Japan’s preliminary January industrial output fell -3.7% mom (vs. -2.5% mom expected), marking three months of continued decline.

So equities on the weaker side in Asia which followed a slightly softer day in US and Europe. Equities initially dropped in unison with the higher rates move but subsequently clawed back somewhat, leaving the S&P marginally lower on the session at -0.06%. The DOW and NASDAQ finished -0.28% and +0.07%, respectively. This was after the STOXX 600 had finished -0.28%, as European markets had closed before the rebound took off. There was one bright spot on both sides of the Atlantic however, with bank stocks appreciating the higher rates and rallying +0.57% and +2.04% in the US and Europe. Part of the original softness in equities appeared to be driven by Lighthizer’s comments during his testimony about the US-China trade talks. The US Trade Representative said that “this administration is pressing for significant structural changes that would allow for a more level playing field” and that the issues between the two sides are “too serious to be resolved with promises of additional purchases”. He also added that “much still needs to be done” and that “there’s no agreement on anything until there’s agreement on everything”. This somewhat undermined previous comments from Secretary Mnuchin that a currency agreement had been finalised. We also seem to have a situation where Mr Trump has increasingly been playing good cop of late and siding more and more with Mnuchin, with Lighthizer firmly in the bad cop territory. It’s also worth noting that the ultra-hawk Peter Navarro seems to have been completely shut out of recent discussions. Ultimately it’s Mr Trump who is the most important but Lighthizer continues to talk hawkishly. There’s been increasingly chatter in the media of late about tensions between the two. Their recent public pronouncements perhaps hints at why that might be. Elsewhere, overnight Lighthizer has said on the USMCA that Trump wants him to get some kind of steel agreement if he can with Canada and Mexico, raising fresh concerns on the passage of USMCA. He further added that “If USMCA doesn’t pass, it would be a catastrophe across the country.” Earlier, Canada’s government had warned that they might not ratify the trade deal if the tariffs remain in place, a sentiment shared last week by Mexico’s envoy to the US, Martha Barcena.

Possibly also having an impact on risk yesterday was Cohen’s testimony. He stopped short of directly accusing the President of collusion with Russia, the subject of Special Counsel Mueller’s ongoing investigation, but did say that “I have my suspicions.” He did say that President Trump committed illegal acts, including alleged campaign finance violations and tax fraud, though Justice Department guidelines say that a sitting President cannot be indicted.

India and Pakistan-linked assets have remained relatively calm despite the escalating confrontation between the two nuclear-armed powers. CDS spreads on both countries remain near recent lows and their currencies remain stable. There are signs of de-escalation amidst contrasting claims from both sides, with no new strikes since yesterday morning. Overnight, the US has urged India and Pakistan to refrain from further military action.

On the theme of geopolitics, the second summit between President Trump and North Korea’s Kim Jong Un included the usual pleasantries however was short of anything particularly noteworthy to take away from. A more substantial announcement on talks between the two sides is expected at some point today so it’s worth keeping an eye on that, possibly at a scheduled press conference at 8:40am London time. Overnight, Trump has said that talks with Kim so far have been “very productive”and said “it’s all leaning toward a very big success”. In the meantime, Kim has said that “If I wasn’t working to do denuclearization I wouldn’t be here,” while Trump said before the start of today’s bilateral meeting that “speed’s not important” in denuclearization and he wants to do the right deal. Although as we go to print the press conference has seemingly been brought forward to 7am London time. So there’s intrigue as to why.

Here in Europe there was some interest in a Die Zeit story yesterday suggesting that high ranking members of the German Government were looking at “possible consequences” of Weidmann taking over the ECB Presidency job post the end of Draghi’s tenure. The story suggested that this was due to growing doubts that Manfred Weber would become the President of the European Commission, although it’s not the first time we’ve seen Weidmann’s name thrown in the ring for the ECB job. Expect these sorts of stories to only pick up over the next couple months.

Meanwhile, the good news is that there isn’t a huge amount of new Brexit news to highlight which makes for a nice change. The Evening Standard reported that senior ministers believed that the EU would insist on a Brexit delay of up to two years should PM May fail to secure a deal in the next few weeks. Interestingly the vote to extend Article 50 in two weeks – assuming May’s deal fails again – is amendable. DB’s Oli Harvey thinks this is very important as Parliament will be able to set the length of time the U.K. will request for such an extension. He believes this could scare the ERG group and make them more likely to vote for May’s deal for fear of a lengthy delay and ultimately the possibility of no Brexit. Labour’s amendment was defeated last night and they are now backing a second referendum as flagged earlier in the week.

On the data front, European money supply and credit data indicated a further slowdown. Credit growth slowed to +3.4% in January, while the M3 money supply grew +3.8% year-on-year, below expectations for +4.0%. Our economists’ preferred metric of the credit impulse dipped to -0.8pp of GDP, its weakest level since the summer of 2013, meaning that bank credit has shifted to become a modest headwind for growth, after several years in which it provided a tailwind. Perhaps most worryingly, there are signs of fragmentation within the euro area. The weakening is most visible in Italy and Spain, where lending to corporates has been zero or negative over the last six months, though lending to households has held up a bit better.

On the US data front, wholesale inventories were confirmed at 1.1% mom for December, beating expectations for a negative revision. Core goods orders were revised 0.3pp lower to -1.0% mom for December, which presents some further downside risks for fourth quarter capex estimates ahead of the GDP print later today. Pending home sales rose +4.6% mom, the biggest leap since 2010, which, combined with strong mortgage application data (+5.3% from +3.6%) shows further signs of the housing market bottoming out.

To the day ahead, where this morning in Germany we’ll get the January import price index reading, followed by February house price data in the UK. Later on the focus turns to the preliminary CPI readings for France, Germany and Italy. In the US the main focus will be on the Q4 GDP reading which are economists expect to show a +2.3% reading (in line with the market) which compares to +3.4% in Q3. In the details of that, core PCE is expected to print at +1.6%. The other data worth watching in the US is the latest weekly initial jobless claims reading and the February Chicago PMI and Kansas City Fed manufacturing survey readings which could give greater insight into the factory sector this month. Away from all that it’s another busy day for Fedspeak with Clarida (1pm GMT), Bostic (1.50pm GMT), Harker (4pm GMT) and Kaplan (6pm GMT) all slated to speak.

3. ASIAN AFFAIRS

i)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED DOWN 12.87 POINTS OR 0.44% //Hang Sang CLOSED DOWN 124.26 POINTS OR 0.43% /The Nikkei closed DOWN 171.35 POINTS OR 0.79%/ Australia’s all ordinaires CLOSED UP 0.31%

/Chinese yuan (ONSHORE) closed UP at 6.6827 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 56.75 dollars per barrel for WTI and 66.31 for Brent. Stocks in Europe OPENED RED//.

ONSHORE YUAN CLOSED DOWN // LAST AT 6.6827 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.6840: / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/USA

Trump walks as Rocket Man wants sanctions relief prior to his denuclearization. This does not bode well for the Chinese trade talks as obviously China interfered. They need North Korea as a buffer.

(courtesy zerohedge)

“Sometimes You Have To Walk”: Hanoi Summit Ends In Disarray As Trump Balks At Kim Demands For Sanctions Relief

Even arm chair observers probably understood long before the Hanoi summit had even been scheduled that the gulf between the American and North Korean positions on denuclearization was probably too wide to overcome (after nearly a year of talks, the two sides are no closer to a deal). Yet, President Trump had apparently hoped that the pomp and circumstance of another historic summit would soften Kim Jong Un up. But despite all the talk about North Korea being “ready to denuclearize” and both leaders hyping up the possibility that a deal would be struck, alas, no deal was forthcoming, and Trump is now headed back to Washington empty handed.

Talks between the two world leaders broke down Thursday afternoon as President Trump abruptly walked away from the table and canceled a planned lunch and signing ceremony (it’s still not clear what the two leaders had hoped to sign, though scheduling the ceremony before a deal had been struck did seem risky). With the talks in disarray, Trump moved up a news conference where he and Secretary of State Mike Pompeo took questions from the press.

Trump told reporters that he had asked Kim to commit to full denuclearization before the US agreed to sanctions relief, and that “he was unprepared to do that.”

BBC News (World)

✔@BBCWorld

“There were several options but this time we decided not to do any of the options. Sometimes you have to walk”

US President Donald Trump on the breakdown of talks with North Korean leader Kim Jong-un in Vietnam#Hanoisummit latest: http://bbc.in/2Uc2wUR

Trump told reporters that the talks collapsed after the North refused to yield from its demand that the US completely remove all of the U.S.-led international sanctions – including the sanctions approved by the UN security council – in exchange for the shuttering of the North’s Yongbyon nuclear facility. Trump and Pompeo refused to make a deal without the North committing to giving up its secretive nuclear facilities outside Yongbyon, as well as its missile and warheads.

According to Trump, the talks ended amicably enough, with a commitment to keep the talks alive, and Kim also promised that he would not resume nuclear and missile tests – the basis for the detente between the two countries – and Trump said he would take Kim at his word.

BBC News (World)

✔@BBCWorld

“There will be no more testing of rockets and nuclear. I trust him and take him at his word”

US President Donald Trump following breakdown of talks with North Korean leader Kim Jong-un in Vietnam#Hanoisummit latest: http://bbc.in/2Uc2wUR

Trump added that he’d “much rather do it right than do it fast.”

“It was about the sanctions,” Trump said. “Basically, they wanted the sanctions lifted in their entirety, and we couldn’t do that. They were willing to denuke a large portion of the areas that we wanted, but we couldn’t give up all of the sanctions for that.”

“I’d much rather do it right than do it fast,” Trump added, echoing his remarks from earlier in the day, when he insisted that “speed” was not important. “We’re in position to do something very special.”

In a brief digression, Trump offered his take on Michael Cohen’s marathon testimony before the House Oversight Committee, saying he was surprised Cohen didn’t go “100%” and lie about Trump colluding with the Russians (Cohen said he had no evidence of collusion).

BBC News (World)

✔@BBCWorld

“He lied a lot… but he only went about 95% instead of 100” – US President Donald Trump responds to ex-lawyer Michael Cohen’s testimony saying he was “impressed” he said there was no Russia collusionhttp://bbc.in/2Uc2wUR

Trump insisted that, when it comes to the subject of denuclearization, “you always have to be willing to walk.”

BBC News (World)

✔@BBCWorld

US President Donald Trump says he “walked away from talks” after North Korean leader Kim Jong-un demanded lifting sanctions#Hanoisummit latest: http://bbc.in/2Uc2wUR

In response to a question about Otto Warmbier, the American student who died shortly after being released from a North Korean prison, Trump said he believed Kim didn’t understand what happened to Warmbier until after it had happened.

BBC News (World)

✔@BBCWorld

“I don’t think the top leadership knew about it. Those prisons are rough”

President Donald Trump says Kim Jong-un “felt very badly” about the death of US student Otto Warmbier who was imprisoned in North Korea#Hanoisummit latest: http://bbc.in/2Uc2wUR

finished off the talks by suggesting that it might be “a long time” before another summit.

BBC News (World)

✔@BBCWorld

“The next meeting might not be for a long time”

Donald Trump finishes his press conference in Vietnam after talks with Kim Jong-un broke down

The US refused North Korean demands for sanctions relief#Hanoisummit latest: http://bbc.in/2Uc2wUR