GOLD: $1299.00 UP $13.40 (COMEX TO COMEX CLOSING)

Silver: $15.34 UP 30 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : $1298.50

silver: $15.34

For comex gold and silver:

MARCH

NUMBER OF NOTICES FILED TODAY FOR MAR CONTRACT: 9 NOTICE(S) FOR 900 OZ (0.0280 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 310 NOTICES FOR 31000 OZ (.9642 TONNES)

SILVER

FOR MARCH

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

126 NOTICE(S) FILED TODAY FOR 630,000 OZ/

total number of notices filed so far this month: 4848 for 24,240,000

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $3919:UP $23

Bitcoin: FINAL EVENING TRADE: $3928 UP 40

end

XXXX

JPMorgan or Goldman Sachs are taking a huge issuance (stopping) of gold at the comex.

today 4/9

EXCHANGE: COMEX

CONTRACT: MARCH 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,283.800000000 USD

INTENT DATE: 03/07/2019 DELIVERY DATE: 03/11/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

657 C MORGAN STANLEY 1

661 C JP MORGAN 4

737 C ADVANTAGE 9 4

____________________________________________________________________________________________

TOTAL: 9 9

MONTH TO DATE: 319

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST ROSE BY A SMALL SIZED 664 CONTRACTS FROM 191,329 UP TO 191,993 DESPITE YESTERDAY’S 4 CENT LOSS IN SILVER PRICING AT THE COMEX. TODAY WE ARRIVED FURTHER FROM AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS. WE ALWAYS WITNESS A CONTRACTION IN TOTAL OI AS WE APPROACH FIRST DAY NOTICE AND IT SEEMS THE CULPRIT IS THE FORCED LIQUIDATION OF SPREADERS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

0 EFP’S FOR MARCH, 0 FOR APRIL, 3061 FOR MAY, 0 FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 3061 CONTRACTS. WITH THE TRANSFER OF 3061 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 3061 EFP CONTRACTS TRANSLATES INTO 15.31 MILLION OZ ACCOMPANYING:

1.THE 4 CENT LOSS IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST NINE MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.

AND NOW: 25.325 MILLION OZ STANDING IN MARCH.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF MARCH:

17,000 CONTRACTS (FOR 6 TRADING DAYS TOTAL 17,000 CONTRACTS) OR 85.00 MILLION OZ: (AVERAGE PER DAY: 2833 CONTRACTS OR 14.16 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF MAR: 85.00 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 12.14% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 449.89 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

RESULT: WE HAD A GOOD SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 664 DESPITE THE 4 CENT LOSS IN SILVER PRICING AT THE COMEX /YESTERDAY..THE CME NOTIFIED US THAT WE HAD STRONG SIZED EFP ISSUANCE OF 3061 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A HUGE SIZED: 3725 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 3061 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 664 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 4 CENT LOSS IN PRICE OF SILVER AND A CLOSING PRICE OF $15.04 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.975 BILLION OZ TO BE EXACT or 139% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT FEBRUARY MONTH/ THEY FILED AT THE COMEX: 126 NOTICE(S) FOR 630000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/AND NOW MARCH: 25.285 MILLION OZ/

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST ROSE BY A MAKE BELIEVE 21,831 CONTRACTS UP TO 499,967 DESPITE THE FALL IN THE COMEX GOLD PRICE/(A LOSS IN PRICE OF $1.40//YESTERDAY’S TRADING). HOWEVER…….

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 5,000 CONTRACTS:

MARCH HAD AN ISSUANCE OF 0 CONTACTS APRIL 5000 CONTRACTS,JUNE: 0 CONTRACTS DECEMBER: 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 499,967. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A GIGANTIC SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 26,831 CONTRACTS: 21,831 OI CONTRACTS INCREASED AT THE COMEX AND 5,000 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 26,831 CONTRACTS OR 2,683,100= 83.46 TONNES.

YESTERDAY WE HAD A LOSS IN THE PRICE OF GOLD TO THE TUNE OF $1.40.…AND WITH THAT, WE HAD A HUGE GAIN IN TONNAGE OF 83.46 TONNES.

YESTERDAY, WE HAD 4012 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MARCH : 49,564 CONTRACTS OR 4,956,400 OZ OR 154.16 TONNES (6 TRADING DAYS AND THUS AVERAGING: 8260 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 6 TRADING DAYS IN TONNES: 154.16 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 154.16/2550 x 100% TONNES = 6.04% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 1029.5 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A FAIRY TALE SIZED SIZED INCREASE IN OI AT THE COMEX OF 21,831 DESPITE THE LOSS IN PRICING ($1.40) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A GOOD SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 5000 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 5000 EFP CONTRACTS ISSUED, WE HAD A GIGANTIC GAIN OF 28,329 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

5000 CONTRACTS MOVE TO LONDON AND 21,831 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE STRONG GAIN IN TOTAL OI EQUATES TO 83.46 TONNES). ..AND ALL OF THIS DEMAND OCCURRED WITH THE LOSS OF $1.40 IN YESTERDAY’S TRADING AT THE COMEX

we had: 9 notice(s) filed upon for 900 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $13.40 TODAY

NO ADDITIONS OR SUBTRACTIONS TODAY

INVENTORY RESTS AT 766.59 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 30 CENTS IN PRICE TODAY:

WHAT A JOKE!! TWO TRANSACTIONS:

STRANGE: THIS MORNING: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV..

A WITHDRAWAL OF 703,000 OZ DESPITE THE HUGE GAIN IN PRICE.

THEN: A HUGE DEPOSIT OF 1.56 MILLION OZ INTO THE SLV

/INVENTORY RESTS AT 309.160 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A SMALL SIZED 664 CONTRACTS from 191,490 UP TO 191,993 AND CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

0 CONTRACTS FOR MARCH. 0 CONTRACTS FOR APRIL., 3061 FOR MAY AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 3061 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 664 CONTRACTS TO THE 3061 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A STRONG GAIN OF 3868 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 18.62 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY AND NOW 25.285 MILLION OZ FOR MARCH.

RESULT: A SMALL SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE 4 CENT LOSS IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY.BUT WE ALSO HAD A STRONG SIZED 3061 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED DOWN 136..46 POINTS OR 4.40% //Hang Sang CLOSED DOWN 551.03 POINTS OR 1.91% /The Nikkei closed DOWN 430.45 POINTS OR 2.01%/ Australia’s all ordinaires CLOSED DOWN .90%

/Chinese yuan (ONSHORE) closed UP at 6.7221 AS TRUCE DECLARED FOR 3 MONTHS /Oil UP to 56.84 dollars per barrel for WTI and 65.78 for Brent. Stocks in Europe OPENED RED

ONSHORE YUAN CLOSED DOWN // LAST AT 6.7221 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7319: / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A/NORTH KOREA/SOUTH KOREA

i)North Korea/

b) REPORT ON JAPAN

3 C/ CHINA

i)China/last night

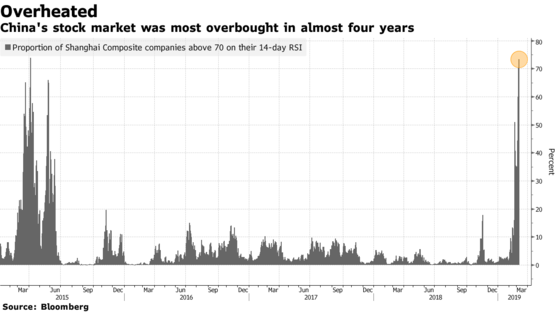

Chinese stocks crash last night as we start to see a rare “sell rating” on many stocks and that shook traders.

( zerohedge)

( zerohedge)

iii)My goodness!~ Despite the massive credit injection exports collapsed by a huge 20.7% in February and the miss is simply stunning

(courtesy zerohedge)

v)As the battle with Huawei heats up, Chinese foreign minister Yi urges Huawei to take up legal weapons against the USA.

vi)NOT GOOD! A Chinese boat rams into a Vietnamese vessel in disputed waters in South CHINESE SEAS

( zero hedge)

4/EUROPEAN AFFAIRS

i)FRANCE

The French city of Grenoble firebombed as we have witnessed the 4th straight night of protests after police were blamed for teenage deaths.

(zerohedge)

Two basket cases are now resuming merger talks. Deutsche bank thinks it can hide its huge derivative exposure

(courtesy zerohedge)

iv)Italy

Strange: Italy’s government is now on the verge of collapse due to the high speed rail linking Italy (Turin) and France (Lyon). The major costs are a huge 36 mile tunnel through the Alps

(courtesy zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6. GLOBAL ISSUES

Canada:

7. OIL ISSUES

8 EMERGING MARKET ISSUES

i)VENEZUELA/

Venezuela now in total darkness for 24 hours as bus-driver Maduro blames the uSA on an “electricity war”

( zerohedge)

9. PHYSICAL MARKETS

i)CME renews its discounts to central banks/governments// engaging in secret trading

(GATA)

ii)In case you missed yesterdays story that China increased its gold reserves by 9.9 tonnes

( Xinhua News Agency/GATA)

iii)Philadelphia is the first USA city to ban cashless stores

(courtesy Calvert/WallStreet Journal/GATA)

iv)The megamerger mania by Barrick to take over Newmont/Goldcorp will see increased interest in this space as some gold miners will eye new partners

( Bloomberg/GATA)

10. USA stories which will influence the price of gold/silver)

MARKET TRADING

/FOMC

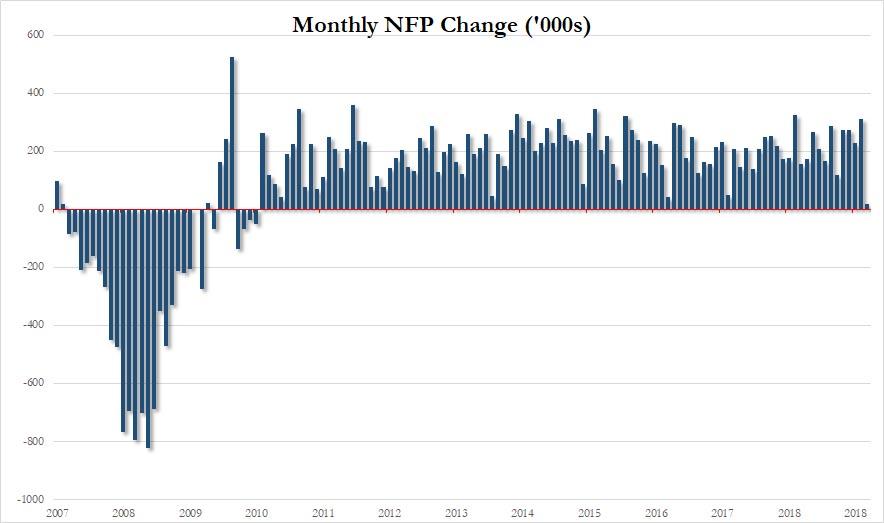

i)the market reacts to a gain of only 20,000 people. Countering that move we witness hourly earnings soar to .4% indicating inflation is lurking. Also strange: in the Household Survey saw a huge loss in unemployed: a big drop of 300,000

( zerohedge)

ii)Market data

a)Bricks and mortar continue to falter: today it is dollar tree closing up to 390 stores

( Mac Slavo/SHTFplan.com)_

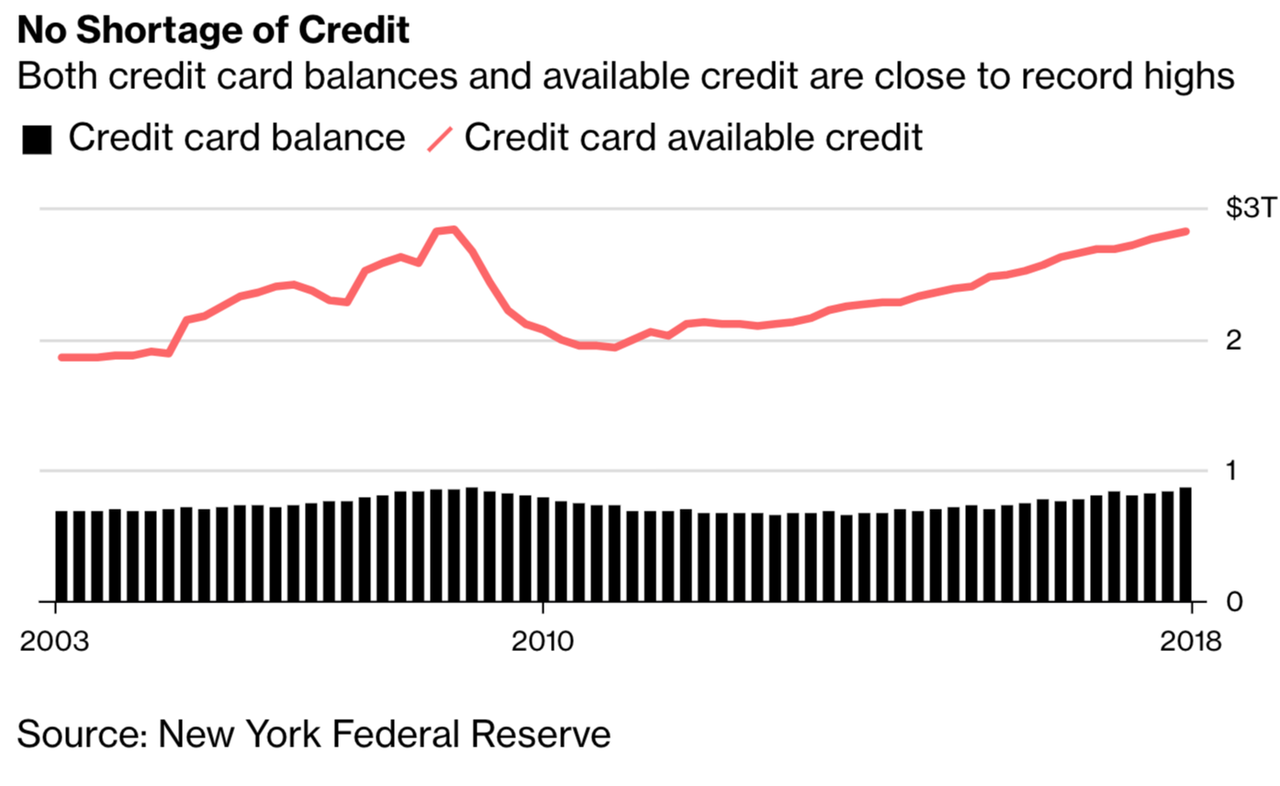

b)A good commentary; a terrific summary on the monthly credit score. We witness 37 million card holders who are 90 days past due and this is something that the Fed is now taking a good look at

iv)SWAMP STORIES

Cohen lies again: he directly asked Trump for a pardon

( zerohedge)

end

Let us head over to the comex:

AFTER MARCH, WE HAVE THE NON ACTIVE DELIVERY MONTH OF APRIL. HERE: APRIL FALLS TO 814 CONTRACTS FOR A LOSS OF 1 CONTRACTS. AFTER APRIL, THE NEXT BIG ACTIVE DELIVERY MONTH IS MAY AND HERE THE OI ROSE BY 444 CONTRACTS UP TO 140,383 CONTRACTS.

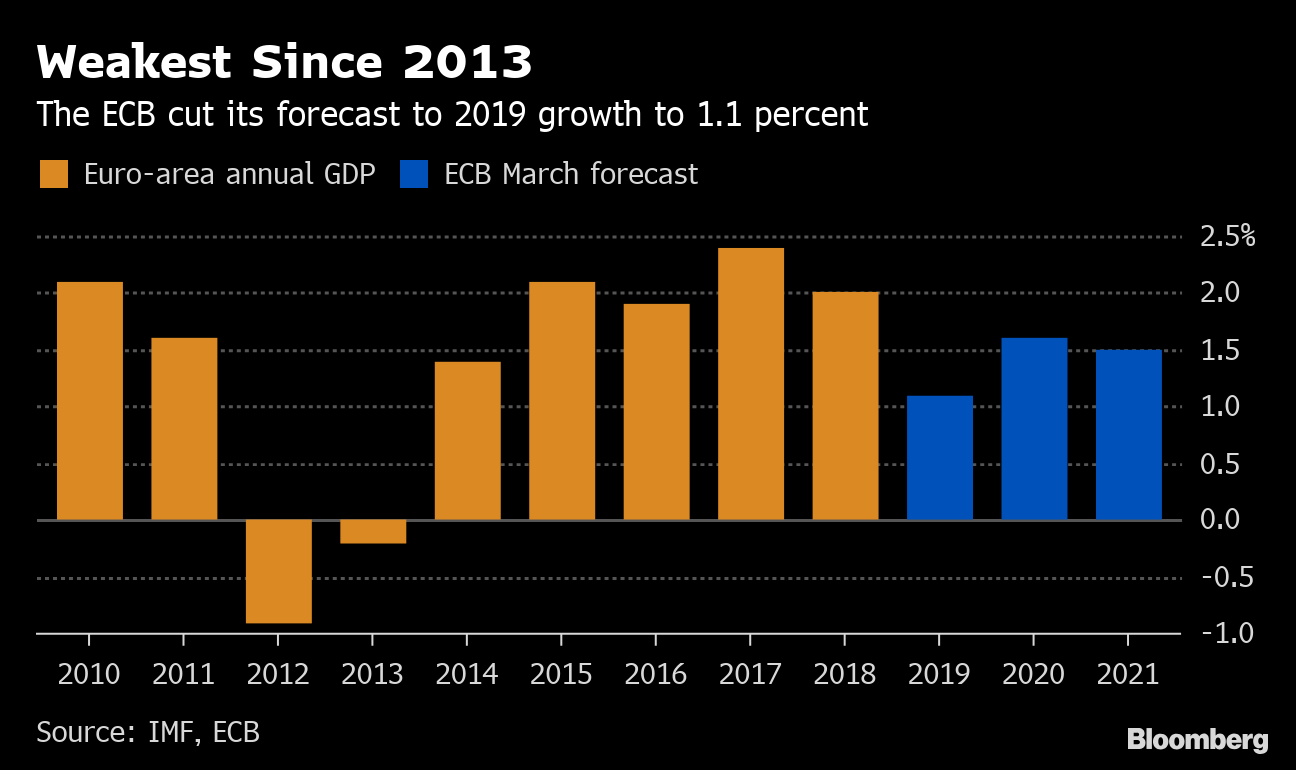

EU Isn’t Ready for the Next Recession

– ECB has just loosened monetary policy. What if that isn’t enough?

– ECB says the risks to Europe’s economies lean to the downside

– Trade wars could get worse and political turbulence could increase

– Brexit, could deliver an especially brutal blow

– Euro set to depreciate against gold (see chart)

The European Central Bank surprised financial markets yesterday with moves to loosen monetary policy.

The prospects for growth in the euro zone have dimmed lately, and policy was going to be tweaked at some point unless things picked up. But a change wasn’t expected so soon. ECB President Mario Draghi and his colleagues are apparently worried.

They have reason to be. Their main problem, however, isn’t the precise timing of monetary adjustments like the ones announced this week. It’s the lack of good options if things get any worse.

The ECB’s new projections show growth in the euro zone slowing this year to just 1.1 percent; in December the central bank had predicted 1.7 percent. That’s roughly in line with other recent downgrades from the International Monetary Fund and the Organization for Economic Cooperation and Development.

Gold in Euros – 10 Year (GoldCore)

The picture varies a lot from country to country within the euro area, and a number of one-off factors have been at work — but across the bloc, slowing international trade and rising political uncertainty have taken a toll. The OECD expects growth of just 0.7 percent this year in Germany, for instance; it thinks Italy’s output will be lower than last year, and will manage only a feeble recovery in 2020.

In response the ECB said its policy rate will stay at zero at least through December, extending its previous guidance by months. And it announced new issues of cheap long-term loans to banks. Yet the actual stimulus provided by these measures will be small at best. In fact, the combination of signaling new concern about the prospects and announcing changes with limited force could turn out to subtract from future demand rather than add to it.

Given its own rules, there’s not much else the ECB can do. The policy rate is zero, and the central bank’s deposit rate is slightly negative. Taking rates farther into negative territory might rattle confidence and destabilize the financial system. Meanwhile the ECB’s enormous bond-buying program, which was paused three months ago, is constrained by rules about the composition of its holdings. These were intended to stop the central bank from disproportionately financing the outlays of high-borrowing countries — such as Italy. They mean the ECB has more or less run out of room.

Monetary policy isn’t enough — and if slow growth in the euro zone should tip into outright recession, Europe will no longer be able to avoid a drastic rethinking of macroeconomic policy. The lack of a sufficiently powerful fiscal instrument is already holding the bloc back. The consequence has been high unemployment, slow growth and less-than-target inflation. If things get any worse, the only effective remedy would be a forceful, coordinated push from tax cuts and/or higher public spending.

Year after year, Europe has dodged this necessary discussion. No further delay should be tolerated. Even after cutting its growth forecasts, the ECB says the risks to Europe’s economies lean to the downside.

Trade-policy frictions could get worse, not better. Political turbulence could increase, not subside.

And Brexit, a big setback for Europe on any plausible projection, could deliver an especially brutal blow if no deal is reached to minimize the disruption.

The ECB says that outright recession is unlikely. If it’s wrong, policy makers will be all but helpless.

Europe can no longer risk being so seriously underequipped. It needs an effective fiscal-policy instrument — at the very least, a bold new approach to fiscal coordination. With the risks mounting, the problem demands immediate attention.

Courtesy of Bloomberg News

News and Commentary

Global Stocks Extend Slide Amid Concerns on Growth: Markets Wrap (Bloomberg.com)

Gold prices finish lower as ECB news pressures the euro, lifting the dollar (MarketWatch.com)

ECB seen taking tentative step to prop up ailing euro zone (Reuters.com)

Wall Street drops for fourth day as ECB stokes growth worries (Reuters.com)

U.S. household wealth posts record loss in fourth-quarter amid stock rout (Reuters.com)

China’s gold reserves continue to grow in February (XinhuaNet.com)

Europe Isn’t Ready for the Next Recession (Bloomberg.com)

BlackRock CEO Larry Fink Says Modern Monetary Theory Is ‘Garbage’ (Bloomberg.com)

Chinese Exports Collapse In February Despite Largest Credit Injection Ever (ZeroHedge.com)

QE – Then, Now, & Why It May Not Work (RealInvestmentAdvice.com)

Philadelphia Is First U.S. City to Ban Cashless Stores (WSJ.com)

07 Mar: USD 1,285.30, GBP 921.20 & EUR 1,144.17 per ounce

06 Mar: USD 1,285.55, GBP 978.82 & EUR 1,136.82 per ounce

05 Mar: USD 1,285.00, GBP 975.19 & EUR 1,134.78 per ounce

04 Mar: USD 1,287.45, GBP 972.93 & EUR 1,135.14 per ounce

01 Mar: USD 1,309.95, GBP 989.27 & EUR 1,152.23 per ounce

28 Feb: USD 1,325.45, GBP 996.21 & EUR 1,162.82 per ounce

Silver Prices (LBMA)

07 Mar: USD 15.07, GBP 11.47 & EUR 13.33 per ounce

06 Mar: USD 15.09, GBP 11.49 & EUR 13.36 per ounce

05 Mar: USD 15.11, GBP 11.47 & EUR 13.33 per ounce

04 Mar: USD 15.16, GBP 11.50 & EUR 13.38 per ounce

01 Mar: USD 15.56, GBP 11.75 & EUR 13.67 per ounce

28 Feb: USD 15.81, GBP 11.89 & EUR 13.85 per ounce

Recent Market Updates

– China Gold Reserves Rise To 60.26 Million Ounces Worth Just $79.5 Billion

– JPMorgan Is Bullish on Gold as a Hedge Against Rising Inflation

– Gold – It Might Be Different This Time

– Euromillions Winners To Invest In Gold In 2019?

– Gold Still on a Long Term Track to Reach $2,000 An Ounce

– “Gold Is A Global Thermometer Of Risk” – CEO Q+A: Stephen Flood, GoldCore

– U.S. Mint Suspends Silver Bullion Coin Sales After Sales Double In February

– MMT: Modern Monetary Madness Will Lead To Higher Taxes and Inflation

CME renews its discounts to central banks/governments// engaging in secret trading

(GATA)

Futures exchange operator renews discounts for secret trading by governments and central banks

Submitted by cpowell on Thu, 2019-03-07 16:37. Section: Daily Dispatches

11:36a ET Thursday, March 7, 2019

Dear Friend of GATA and Gold:

Market manipulation by governments and central banks is right out in the open again, hiding in plain sight in the confidence that mainstream financial news organizations, financial letter writers, and gurus who purport to bring “technical analysis” to bear on markets will avert their gaze.

For as GATA’s friend Jim Anderson of SD Bullion Inc. in Michigan (https://sdbullion.com/) pointed out this week, CME Group, operator of the major U.S. futures exchanges, has just renewed its “Central Bank Incentive Program,” in which governments and central banks receive discounts for surreptitiously trading all major futures contracts on CME Group exchanges — not just financial futures but also monetary metals futures and even agricultural futures.

…

CME Group’s previous discount schedule, called to your attention by GATA a year ago January —

http://www.gata.org/node/17976

— was dated December 2017:

http://www.gata.org/files/CMEGroupCBIP-Q&A-December2017.pdf

Now a new one has been posted, dated last month —

https://www.cmegroup.com/company/membership/files/CBIPFAQ.pdf —

— and has been copied to GATA’s internet site here:

http://www.gata.org/files/CMEGroup-CentralBankIncentiveProgram-Feb2019.p…

It has added bitcoin futures.

Some of the discounts have changed but governments and central banks continue to receive 15 percent discounts on fees for trading gold and silver futures.

Of course CME Group’s trading discount schedule doesn’t prove that any particular government or central bank has been trading any particular contract lately. But on Page 6 of its 2019 10-K form filed with the U.S. Securities and Exchange Commission, CME Group continues to acknowledge that “the customer base of our derivatives exchanges includes professional traders, financial institutions, institutional and individual investors, major corporations, manufacturers, producers, governments, and central banks“:

http://investor.cmegroup.com/node/43571/html

For safety’s sake the form is copied to GATA’s internet site here:

http://www.gata.org/files/CMEGroup-SEC-10-K-2019.pdf

This futures trading is never announced by governments and central banks, so some surreptitious intervention in the U.S. futures markets by governments and central banks is happening, but it continues to escape the curiosity of nearly everyone who would seem obliged to alert investors to it. Perhaps this is because if this surreptitious intervention was exposed, its efficacy would collapse, as government and central bank policy here is based on deception.

GATA will send this new documentation to many major financial news organizations and financial letter writers. Please send it to any monetary metals companies you are invested in, and let us know if you see anyone pick up on it.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

In case you missed yesterdays story that China increased its gold reserves by 9.9 tonnes

(courtesy Xinhua News Agency/GATA)

China’s gold reserves continue to grow in February

Submitted by cpowell on Thu, 2019-03-07 17:17. Section: Daily Dispatches

The news here isn’t the tiny increase in China’s gold reserves but that the People’s Bank of China has announced increases for three months straight after years of reporting no change.

* * *

China’s Gold Reserves Continue to Grow in February

From Xinhua News Agency, Beijing

Thursday, March 7, 2019

BEIJING — China increased its gold reserves for a third straight month in February, data from the central bank showed.

…

The country’s gold reserves amounted to 60.26 million ounces by the end of last month, a slight growth from January, according to the People’s Bank of China.

The gold reserves were equivalent to around $79.5 billion, edging up from 79.3 billion dollars in the previous month, the PBOC said.

The latest gold purchase by the world’s second-largest economy came at a time when global central banks are hoarding the precious metal. …

… For the remainder of the report:

END

Philadelphia is the first USA city to ban cashless stores

(courtesy Calvert/WallStreet Journal/GATA)

Philadelphia is first U.S. city to ban cashless stores

Submitted by cpowell on Thu, 2019-03-07 21:54. Section: Daily Dispatches

By Scott Calvert

The Wall Street Journal

Thursday, March 7, 2019

Philadelphia is the first major U.S. city to ban cashless stores, placing it at the forefront of a debate that pits retail innovation against lawmakers trying to protect all citizens’ access to the marketplace.

Starting in July, Philadelphia’s new law will require most retail stores to accept cash. A New York City councilman is pushing similar legislation there, and New Jersey’s legislature recently passed a bill banning cashless stores statewide. A spokesman for New Jersey Gov. Phil Murphy, a Democrat, declined to comment on whether he would sign it. Massachusetts has gone the farthest on the issue and is the only state that requires retailers to accept cash.

…

The measures seek to blunt a nascent trend that could rapidly accelerate thanks to Amazon.com Inc.’s power to shape nationwide retail trends. They represent an attempt to strike a balance between equity for lower-income consumers and merchants’ eagerness to embrace technological advances.

Businesses that have gone cashless point to greater efficiency for employees, who don’t have to make change or count cash at closing time, and improved safety because workers don’t have to carry large bank deposits.

But backers of measures forcing stores to accept cash say they worry about people who don’t have credit or debit cards. Supporters also say some consumers prefer to pay with currency for privacy reasons. …

… For the remainder of the report:

https://www.wsj.com/articles/philadelphia-is-first-u-s-city-to-ban-cashl…

* * *

Join GATA here:

Mining Investment Asia

Marina Bay Sands Conference and Exhibition Center

Singapore

Tuesday-Thursday, March 26-28

https://www.mininginvestmentasia.com/

Mines and Money Asia

Hong Kong Conference and Exhibition Center

Wan Chai, Hong Kong

Tuesday-Thursday, April 2-4

https://asia.minesandmoney.com/

* * *

Help keep GATA going:

GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at:

To contribute to GATA, please visit:

END

The megamerger mania by Barrick to take over Newmont/Goldcorp will see increased interest in this space as some gold miners will eye new partners

(courtesy Bloomberg/GATA)

Megamerger push has gold miners eyeing new dance partners

Submitted by cpowell on Fri, 2019-03-08 00:01. Section: Daily Dispatches

By Danielle Bochove and Justina Vasquez

Bloomberg News

Thursday, March 7, 2019

A push by the world’s biggest gold miners to get even bigger will likely have a knock-on effect among their competitors, adding new vigor to an industry that failed to inspire investor support in 2018.

The megamerger mania now under way for Newmont Mining Corp., Barrick Gold Corp., and Goldcorp Inc. is likely to result in some of their assets being sold, helping to diversify portfolios for other miners and boosting the interest of investors. More importantly, it could force mid-tier companies to team up in order to successfully compete.

…

This is a competitive marketplace in terms of attracting capital, and you have to make a decision at some point,” Michael Siperco, an analyst at Macquarie Capital Markets, said in a telephone interview. “Yamana, Kinross, Iamgold — what’s the strategy here in terms of not getting absolutely left behind?” …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2019-03-07/-dance-partner-hunt-h…

* * *

END

Chinese demand looks fine averaging around 159 tonnes per month or almost 40 tonnes per week..

LAWRIE WILLIAMS: China’s gold demand looks to be slowing this year so far

Shanghai Gold Exchange (SGE) figures for February’s gold withdrawals are now in and using our assumption (contentious in some analyses) that SGE gold withdrawals equate closely to overall Chinese gold demand it looks as though the nation’s voracious appetite for gold may be slowing. The total of withdrawals for the first two months of the year comes to 318.31 tonnes as against 342.0 tonnes in 2018 and 332.65 tonnes in 2017. Indeed the February 2019 gold withdrawal figure is the first monthly sub 100-tonne total for over 3 years.

Although the fall in the withdrawal figure as total Chinese gold demand would seem to be confirmed by other available data – notably a fall in deliveries of re- refined gold from Switzerland both to Mainland China and to Hong Kong so far this year, perhaps not too much should be read into the decline at this stage of the year. The Chinese (Lunar) New Year, which encompasses a week-long Golden Week holiday commenced on February 5th this year so the whole holiday period – over which time government bodies like the SGE were closed – occurred in February thus reducing total gold withdrawal figures that month. In 2018 the New Year holiday commenced later in the month, but still meant the SGE would have been closed for a full week during February, while in 2017 the New Year holiday commenced on January 28th meaning there will have been a couplke more February trading days in February then.

Table: SGE Monthly Gold Withdrawals 2017-2019 (Tonnes)

Table: SGE Monthly Gold Withdrawals 2017- 2019 (Tonnes)

| Month | 2019 | 2018 | 2017 | % change 2018-2019 | % change 2017-2019 |

| January | 218.54 | 223.58 | 184.41 | -2.30% | 18.51% |

| February* | 99.77 | 118.42 | 148.24 | -15.75% | -32.70% |

| March | 192.61 | 192.25 | |||

| April | 212.64 | 165.78 | |||

| May | 150.58 | 138.08 | |||

| June | 140.59 | 155.51 | |||

| July | 137.41 | 144.71 | |||

| August | 190.59 | 161.41 | |||

| September | 188.12 | 214.24 | |||

| October* | 142.94 | 151.54 | |||

| November | 179.08 | 189.1 | |||

| December | 178.04 | 185.21 | |||

| Year to date | 318.31 | 342.00 | 332.65 | -6.93% | -4.31% |

| Full Year | 2,054.54 | 2,030.48 |

Source: Shanghai Gold Exchange. Lawrieongold.com

* Months include week long New Year and Golden Week holiday periods

So although we say that perhaps not too much sway on overall Chinese demand should be placed on cumulative figures for the first two months of the year because of the week-long February holiday period, the data taken in conjunction with that from other sources does, at this stage, suggest that Chinese demand is indeed turning down along with the slippage in the nation’s GDP growth. Even so China remains the principal driver of global demand for gold bullion, although the gap that has built up between it and India may be slipping.

According to the latest figures from the World Gold Council there has also been a downturn in the Chinese gold ETF Huaan Yifu which shed 3 tonnes in February – a month which saw the giant GLD gold ETF in the USA see withdrawals of 40 tonnes. The big anomaly here though is that the second largest gold ETF in the USA – the iShares Gold Trust – added 7 tonnes of gold that month. European gold ETF withdrawals and additions just about balanced each other out.

(For those who may not have come across my assessments of Chinese gold demand before, we equate SGE withdrawal figures to the nation’s total annual gold absorption as they tend to be far closer to the sums of China’s own gold production plus imports from known sources which publish country-by-country breakdowns of their gold exports plus an allowance for unknown imports plus an allowance for scrap conversion than estimates of Chinese gold consumption by the major Western gold consultancies. China does not publish its own figures, although, in the past, The China Gold Yearbook has equated demand to the SGE withdrawal figures! As the Singapore-based bullionstar.com website put it a couple of years ago: Some high-profile precious metals consultancies such as GFMS and the World Gold Council still publish annual Chinese gold demand figures that are far lower (for example 900 tonnes per annum) than the annual SGE gold withdrawal figures. These discrepancies are so large that they call for rigorous analysis and explanation. Note that other bodies, such as the China Gold Association (CGA) do state that Chinese gold demand equals SGE gold withdrawals.)

08 Mar 2019

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

Your early FRIDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED/ LAST AT: 6.7221/

//OFFSHORE YUAN: 6.7319 /shanghai bourse CLOSED DOWN 136.56 POINTS OR 4.40% /

HANG SANG CLOSED DOWN 551.03 POINTS OR 1.91%

2. Nikkei closed DOWN 430.45 POINTS OR 2.01%

3. Europe stocks OPENED RED

/USA dollar index FALLS TO 96.49/Euro FALLS TO 1.1303

3b Japan 10 year bond yield: FALLS TO. –.03/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 111.15/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 55.71 and Brent: 65.03

3f Gold UP/JAPANESE Yen UP CHINESE YUAN: ON -SHORE DOWN /OFF- SHORE: DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.06%/Italian 10 yr bond yield UP to 2.51% /SPAIN 10 YR BOND YIELD DOWN TO 1.05%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.45: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield RISES TO : 3.83

3k Gold at $1293.40 silver at:15.12 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 19/100 in roubles/dollar) 66.48

3m oil into the 55 dollar handle for WTI and 65 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 111.15 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 1.0092 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1325 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.06%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

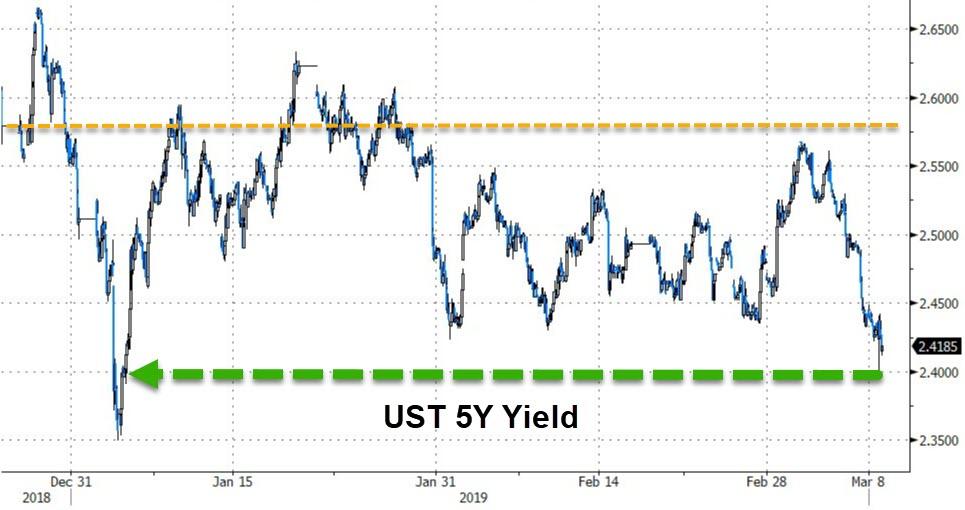

4. USA 10 year treasury bond at 2.64% early this morning. Thirty year rate at 3.02%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.4681

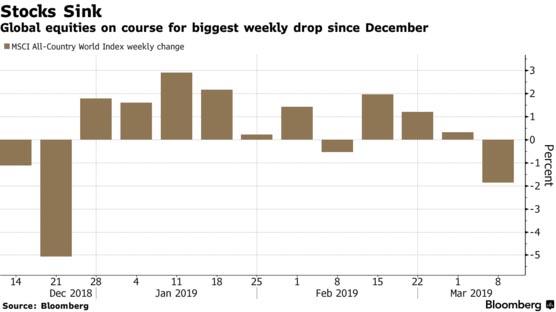

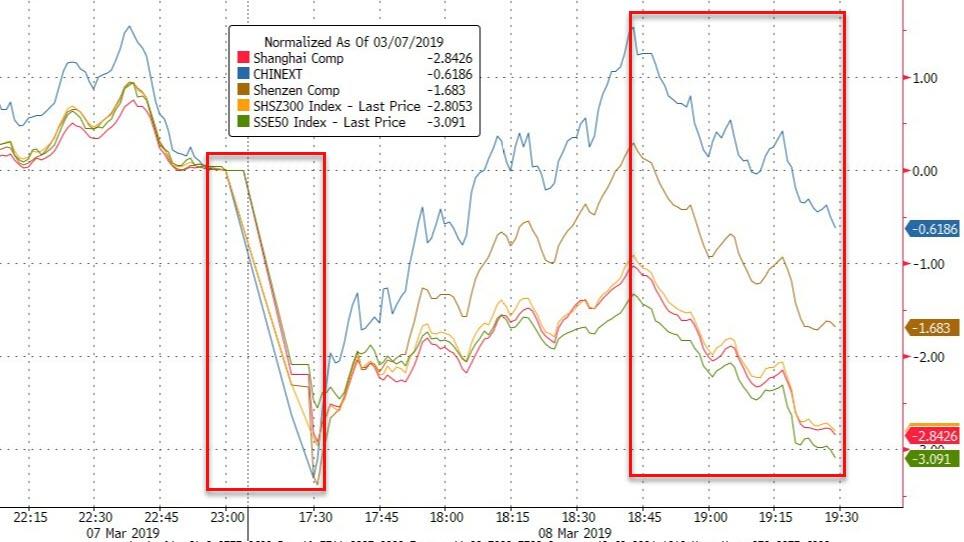

Goldilocks Is Over: Global Stocks Tumble On Fresh Growth Fears, China Crash

Just days after Goldman warned that the Goldilocks rally is over, a selloff swept across world markets with global stocks set for their biggest weekly drop since December, after a plunge in Chinese stocks set the tone for global markets on Friday, with equities in Europe sliding alongside U.S. futures amid growing concerns about the state of US-China trade negotiations and global growth following yesterday’s ECB shocking GDP downgrade. The yen climbed with gold as investors once again scrambled to buy safe havens.

Traders will be closely watching the February U.S. jobs report on Friday (exp. 170K) for more clues on the state of the world’s biggest economy after ECB President Mario Draghi delivered fresh stimulus as he downgraded the outlook for the euro area. The move came during a week that saw China cut its goal for economic expansion, the Bank of Canada dial back its expectations for policy tightening and the Organisation for Economic Co-operation and Development lower its global outlook.

Until then, Europe’s Stoxx 600 Index sank the most in a month, with carmakers and miners leading declines, as global growth concerns continue to dominate market sentiment following yesterday’s ECB TLTRO announcement, pushing back of rate guidance and lowering of growth & inflation forecasts. Sectors are broadly in the red, led by the aforementioned Chinese trade data and fears of another global recession. Significantly underperforming its peers at the bottom of the Stoxx 600 are GVC Holdings (-17.0%) after the company CEO sold 2.1MM worth of shares alongside the Chairman selling 900k shares; with both sales at the price of GBP 6.66/shr. Not helping fears about an imminent European recession, German factory orders fell more than expected in January.

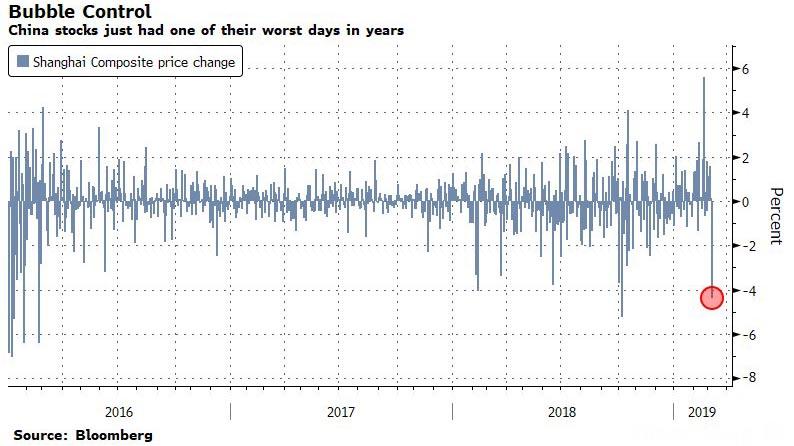

Shares from Sydney to Hong Kong fell, with China’s market slumping the most since October and suffering one of its worst days in years as traders interpreted a rare sell rating from the nation’s largest brokerage as a sign the government wants to curb gains.

Hang Seng (-1.9%) and Shanghai Comp. (-4.4%) slumped with underperformance seen in the mainland in which the CSI 300 slipped by the most so far this year. 10yr JGBs tracked the gains in T-notes amid declining yields in the aftermath of the dovish ECB, while the widespread risk averse tone and BoJ presence in the market in the short-end also contributed to the support for government bonds.

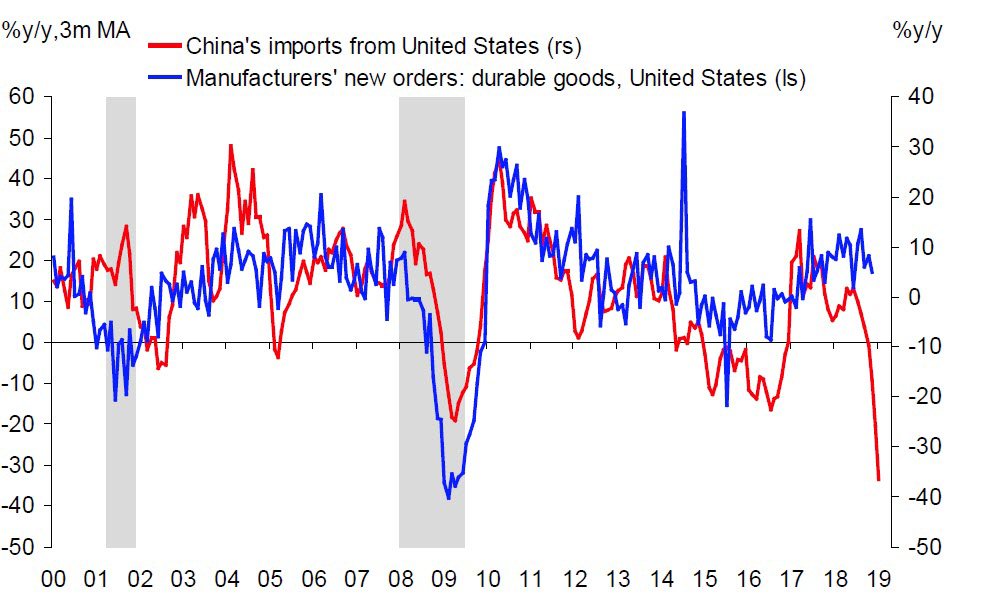

Weak Chinese trade data added to the negativity, with exports plunging over 20%, while imports from the US crashing the most on record.

Stocks in emerging markets dropped the most in almost three months, and their currencies weakened on the back of China’s slump.

“All these different variables are beginning to come together to paint a more dismal outlook for global growth,” Lindsey Piegza, chief economist at Stifel Nicolaus & Co., told Bloomberg TV from Minneapolis. “We saw the ECB wake up to the acknowledgment of a weaker growth and inflation profile in Europe, but this is sending a broad-based signal that contagion may be coming to the U.S.”

In Fx, the dollar weakened modestly after seven days of gains; the euro steadied after tumbling to its lowest level since 2017 on Thursday after the European Central Bank slashed growth forecasts, while the Swedish krona touched its lowest level since 2002 versus the dollar. The yen was among the biggest gainers in the major currencies amid rising concern about global growth and signs that China is trying to slow the country’s equity rally. The pound was steady after the European Union was said to make a new offer to the U.K. in an attempt to break the Brexit impasse.

Treasuries advanced ahead of U.S. payrolls data. Core European bonds continued higher, as volumes in European bonds were more than double recent averages. German 10Y bund yield dropped to just 6bps, and rapidly approaching a negative yield last seen in late 2016.

Elsewhere, Brent (-1.7%) and WTI (-1.6%) prices are extending on their losses, as global growth concerns weigh on risk tone; both WTI and Brent are trading at the bottom of the sessions range, with WTI prices dropping under USD 56.00/bbl to the downside exacerbating the price decline; with session lows of around USD 55.80/bbl. Looking ahead we have the Baker Hughes Rig count, a decline in the crude rig count would be the third consecutive week of oil rigs decline; and as such may provide some reprieve to Brent and WTI prices. Gold (+0.6%) is shining as the yellow metal benefits from the global growth concerns which are dominating markets.

Economic data include housing starts and the February jobs report. Vail Resorts, Allogene Therapeutics and Big Lots are due to report earnings.

Market Snapshot

- S&P 500 futures down 0.5% to 2,742.00

- STOXX Europe 600 down 0.4% to 372.29

- MXAP down 1.4% to 156.20

- MXAPJ down 1.5% to 514.96

- Nikkei down 2% to 21,025.56

- Topix down 1.8% to 1,572.44

- Hang Seng Index down 1.9% to 28,228.42

- Shanghai Composite down 4.4% to 2,969.86

- Sensex down 0.1% to 36,679.26

- Australia S&P/ASX 200 down 1% to 6,203.76

- Kospi down 1.3% to 2,137.44

- German 10Y yield fell 1.4 bps to 0.053%

- Euro up 0.2% to $1.1210

- Brent Futures down 1.1% to $65.56/bbl

- Italian 10Y yield fell 11.9 bps to 2.116%

- Spanish 10Y yield rose 1.6 bps to 1.06%

- Brent Futures down 1.7% to $65.19/bbl

- Gold spot up 0.7% to $1,294.58

- U.S. Dollar Index down 0.2% to 97.45

Top Overnight News from Bloomberg

- Chinese stocks tumbled the most in nearly five months as traders took a rare sell rating from the nation’s largest brokerage as a sign that the government wants to slow down the rally

- The U.S. leaned on German Chancellor Angela Merkel last month to conduct a naval maneuver in Russia’s backyard aimed at provoking President Vladimir Putin, according to three people familiar

- Some European Central Bank policy makers consider the institution’s downgraded growth forecast for 2019 to still be too optimistic, according to people with knowledge of the matter

- China’s exports slumped in February as seasonal factory shutdowns and continued uncertainty from the trade war combined to drag on shipments, adding to concerns over a weakening global economy. Meanwhile, a report showed German factory orders fell more than expected in January

- Italian Deputy Premier Matteo Salvini threatened to pull the plug on the populist coalition as a fight over a proposed high-speed rail line to France risked spiraling out of control

- Finnish Prime Minister Juha Sipila stepped down just weeks before an election after failing to push through parliament plans to overhaul health services and social care in the face of an aging population

Asian equity markets were negative across board on spill-over selling from their global peers after the ECB’s latest policy announcement, while sentiment further deteriorated on disappointing Chinese trade data. ASX 200 (-1.0%) and Nikkei 225 (-2.1%) were lower with the top-weighted financials sector front-running the broad-based declines in Australia, while Japanese sentiment was dragged by a stronger currency with Kawasaki Kisen the worst hit after it widened its FY net loss guidance by fivefold to JPY 100bln. Hang Seng (-1.9%) and Shanghai Comp. (-4.4%) slumped with underperformance seen in the mainland in which the CSI 300 slipped by the most so far this year of more than 3% in early trade, as concern regarding global growth took its toll and with selling exacerbated after Chinese trade data showed the steepest decline in exports for 3 years. Finally, 10yr JGBs tracked the gains in T-notes amid declining yields in the aftermath of the dovish ECB, while the widespread risk averse tone and BoJ presence in the market in the short-end also contributed to the support for government bonds.

Top Asian News

- Foreigners Exit China Stocks at Fastest Pace This Year: Chart

- China’s NPC to Push Forward Property Tax Legislation in 2019

- Alibaba, Ant Are Said to Form Oversight Group to Tighten Control

- China Property Developers Post Sudden Sharp Losses Before Close

Major European indicies are in negative territory [Euro Stoxx 50 -0.6%] as global growth concerns continue to dominate market sentiment; following yesterday’s ECB TLTRO announcement, pushing back of rate guidance and lowering of growth & inflation forecasts. Overnight the Shanghai Composite (-4.4%) was at its worst level in 5 months; also exacerbated by poor Chinese trade data. Sectors are broadly in the red, with the automobile sector lagging on the aforementioned Chinese trade data and growth concerns. Significantly underperforming its peers at the bottom of the Stoxx 600 are GVC Holdings (-17.0%) after the Co’s CEO sold 2.1mln worth of shares alongside the Chairman selling 900k shares; with both sales at the price of GBP 6.66/shr. Elsewhere, and towards the top of the Stoxx 600 are Azimut (+2.1%) benefiting from being upgraded at Kepler Cheuvreux. Elsewhere, following the Norwegian government stating the sovereign wealth fund should cut energy stocks from the investment benchmark, there was an immediate negative reaction in energy names including Total (+0.6%), BP (-1.5%) and Shell (-1.9%).

Top European News

- Hunt Warns EU Could ‘Poison’ Relations for Years: Brexit Update

- Italian Monthly Industrial Output Surges Above Expectations

- GVC Falls Most Since 2010 on CEO, Chairman Share Disposals

- ‘Outright Short’ Iliad, ‘Value Trap’ Vodafone Drop on Exane Cuts

In FX, the dollar index and Greenback overall have succumbed to a bout of broad profit-taking and consolidation along with the aforementioned stronger demand for the Yen, as attention turns towards the looming NFP report and at least partly away from Thursday’s dovish ECB policy moves. The DXY has duly backed off from a new 2019 peak at 97.711 to straddle the 97.500 level as G10 (and EM) counterparts claw back some lost ground.

- JPY – The traditional and enduring safe haven currency is outperforming amidst heightened risk off sentiment, as worrying Chinese trade data and an unexpected decline in German manufacturing orders exacerbate global growth concerns. Usd/Jpy has subsequently retreated further from 112.00+ highs to just under 111.00, and through key technical support in the shape of the 200 DMA at 111.39.

- NZD/AUD – Although risk aversion has been stoked by the factors noted above, short-covering and cross-positioning have protected the Antipodean Dollars from further depreciation and fall-out. In fact, the Kiwi has rebounded firmly enough from recent lows to vie with the Jpy at the top of the major league as its Aussie peer remains depressed following recent worrying data that has prompted yet another bank to predict 2 RBA rate cuts this year. Nzd/Usd is back up over 0.6775 and Aud/Nzd slips below 1.0350, as Aud/Usd languishes between 0.7028-04 with a hefty 1.5 bn option expiry at the 0.7000 strike exerting another gravitational pull.

- EUR/CHF – Some respite for the single currency and Franc, with Eur/Usd pivoting 1.1200 after testing a key chart support at 1.1187 on follow-through selling in wake of the ECB’s decision to offer more TLTROs and delay rate hikes. However, the headline pair looks hemmed in by option expiries at 1.1220-25 (1.6 bn) and 1.1250 (2.6 bn), and with nothing significant on the downside in terms of technical levels until 1.1110-33, aside from another expiry at 1.1150 (1 bn). Meanwhile, Usd/Chf is in a tight band around 1.0100 and now eyeing NFP for the next directional lead.

- GBP/CAD – Marginal underperformers, with Cable looking increasingly bearish after losing grip of 1.3100 and hopes of a Brexit breakthrough appearing more and more forlorn as the latest EU offer on the backstop is not deemed sufficient to appease the majority of UK MPs that rejected the WA at the 1st time of asking. The Loonie has stabilised somewhat after its midweek collapse on a more cautious and uncertain BoC, but remains on the backfoot vs its US rival around 1.3450 ahead of jobs data from both sides of the NA divide.

- SEK/NOK – The Scandi crowns are both weaker vs the Eur and Usd, with the former ruffled by comments from Riskbank’s Floden expressing surprise at the Sek’s recent decline and the fact that the ECB’s policy actions in March will be taken into account when the Swedish Central Bank meet at the end of next month. A rebound in household spending and upward revisions to back data has nudged Eur/Sek off the highs, but the pair remains above 10.6000, while a deeper retreat in oil prices is undermining the Nok, as Norway’s SWF pulls the plug on energy stocks in its benchmark portfolio. Eur/Nok currently around 9.8500.

In commodities, Brent (-1.7%) and WTI (-1.6%) prices are continuing to extend upon their losses, as global growth concerns weigh on risk tone; both WTI and Brent are trading at the bottom of the sessions range, with WTI prices dropping under USD 56.00/bbl to the downside exacerbating the price decline; with session lows of around USD 55.80/bbl. Looking ahead we have the Baker Hughes Rig count, a decline in the crude rig count would be the third consecutive week of oil rigs decline; and as such may provide some reprieve to Brent and WTI prices. Gold (+0.6%) is shining as the yellow metal benefits from the global growth concerns which are dominating markets. With gold at the top of it’s USD 10/oz range, trading around USD 1294.60/oz. Conversely, copper prices are down afflicted by the poor Chinese trade data exacerbating growth concerns in the worlds largest importer of the metals.

Looking at the day ahead, it’s all about the February employment report in the US while January housing starts and building permits is also due out. Away from that the ECB’s Nowotny is speaking at a conference in Prague this morning, and we should also note that the Fed’s Powell is due to speak tonight at 10pm at the Stanford Institute on monetary policy normalization – so that should be worth a watch.

US Event Calendar

- 8:30am: Housing Starts, est. 1.2m, prior 1.08m; Housing Starts MoM, est. 10.86%, prior -11.2%

- Building Permits, est. 1.29m, prior 1.33m; Building Permits MoM, est. -2.94%, prior 0.3%

- 8:30am: Change in Nonfarm Payrolls, est. 180,000, prior 304,000

- Unemployment Rate, est. 3.9%, prior 4.0%

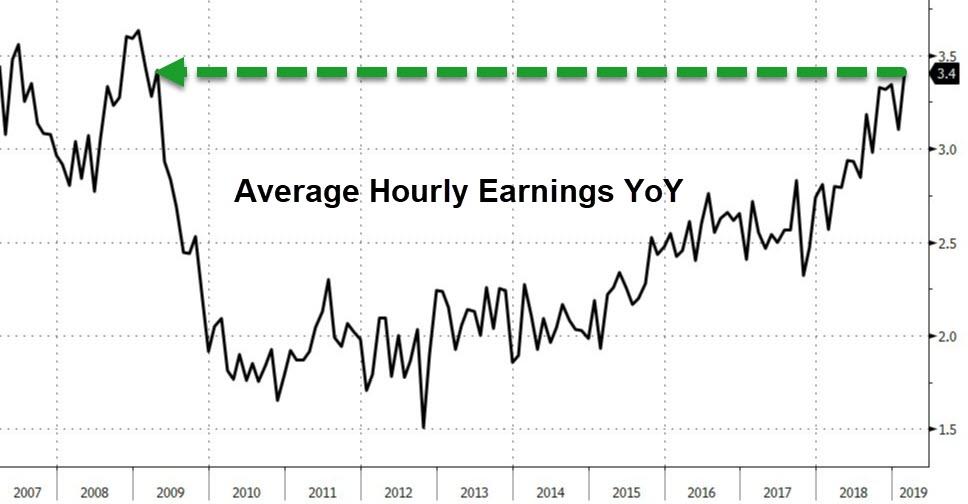

- Average Hourly Earnings MoM, est. 0.3%, prior 0.1%; Average Hourly Earnings YoY, est. 3.3%, prior 3.2%

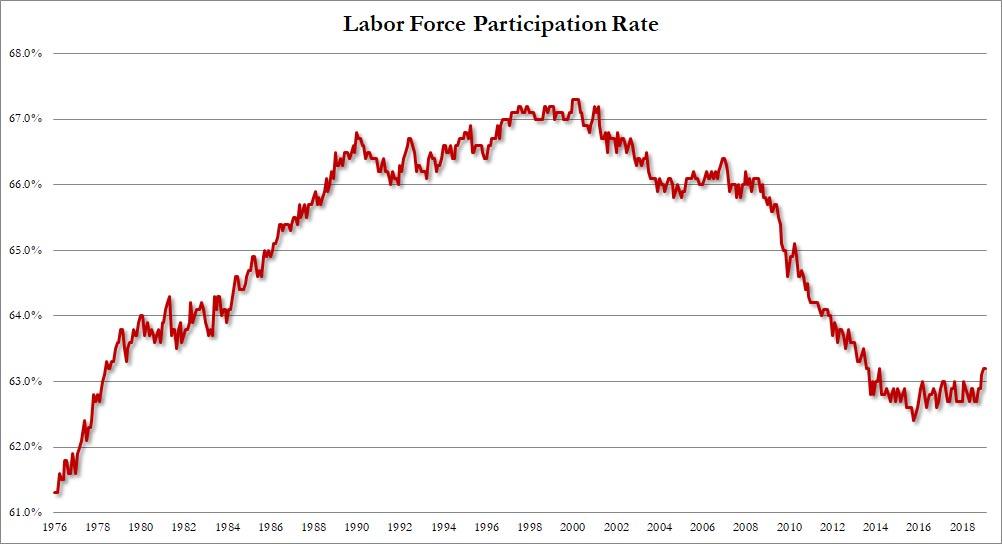

- Labor Force Participation Rate, est. 63.2%, prior 63.2%; Underemployment Rate, prior 8.1%

- 10pm: Powell Discusses Monetary Policy Normalization and Review

DB’s Jim Reid concludes the overnight wrap

The ECB meeting didn’t really impact our spread forecasts as the trade dispute resolution (or the lack of one) will likely be the make or break on those. However what it did do was confuse us greatly and it won’t go down as the most coherent mix of policy and guidance from the ECB. Initially the surprise of an early announcement of TLTRO 3 was greeted positively. However as soon as the ECB provided their revised growth and inflation numbers the market turned to suggesting that the policy response was nowhere near substantial enough if that was there view. So giving with one hand and then taking with two others. To be honest there was lots of other moving parts to the meeting (Draghi’s tone for one) and also with the market reaction but let’s try to decipher it. Warning! We may fail!

So surprisingly we got the TLTRO3 announcement now rather than a strong hint of it however important question marks still remain about the specific details. The guidance on rates was pushed back as well, but it was about as conservative as possible since it only technically extended the earliest potential date for a hike by three months and still way before the market thinks is likely. However the press conference and Q&A was undoubtedly dovish. Inflation forecasts were slashed, growth was revised down albeit not overly significantly, but Draghi did reiterate the maintenance of growth risks to the downside. Finally banks didn’t get any help from the tone on answers about the impact of negative rates. Mark Wall has a full write-up here and we’ll go into a bit more detail after we round up the market reaction.

Indeed it was European Banks and Bunds which really moved on during the day with the former closing down -3.32% for the biggest one-day loss since 20 December. The high-to-low range was also -4.53% which was the biggest since September last year. They initially rallied on the new TLTRO before dropping back on the unfavourable details and the poorer macro forecasts. Bunds closed down -6.3bps at 0.0643% – a level they haven’t closed at since October 2016 – with the bulk of the move coming in the press conference after the inflation forecasts were released. In the morning, they’d flirted with 0.14%, less than a week after breaking through 0.20% for the first time in four weeks. The Bund curve is also now negative out to nine and a half years again. It’s hard to feel this is a healthy development. OATs were down -9.0bps and the most since April 2017. BTPs rallied -12.1bps, which was -18.1bp off their highs. As for other equity markets, the STOXX 600 dropped -0.43% with the FTSE MIB reversing -1.49% from the highs to close down -0.74%. Italian Banks also closed -2.61% and were down -3.82% from the highs.

Credit also suffered however it wasn’t quite as dramatic. The iTraxx Main index closed +1.4bps wider but was as much as -1.4bps tighter during the start of the Q&A and prior to the economic forecasts release. Senior Financials went from -3.1bps tighter to +0.3bps wider. Cash HY spreads were +4bps and +7bps wider in Europe and the US, respectively. Meanwhile in FX the euro followed rates and ended the session down -0.72% at 1.1193, reaching its lowest closing level since October 2016.

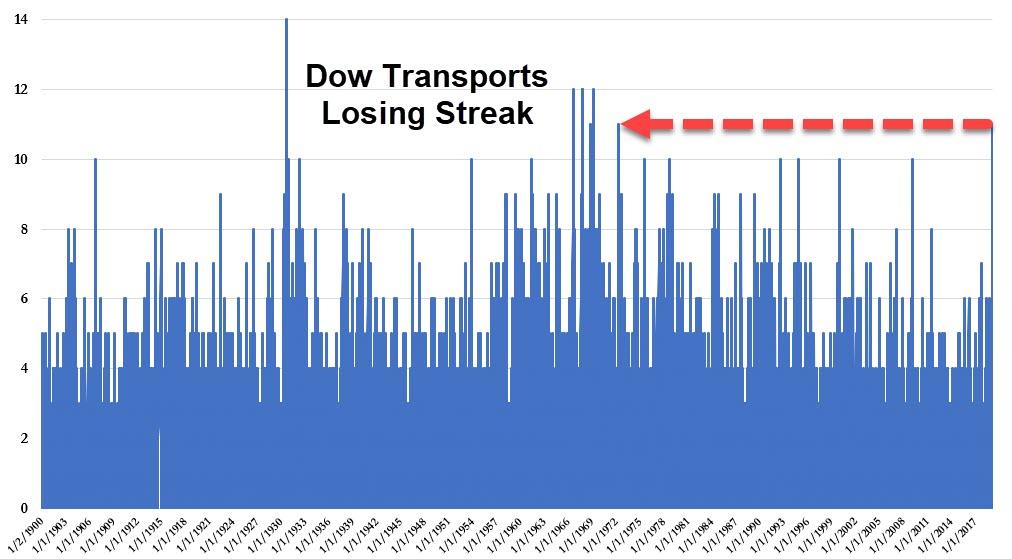

Sentiment didn’t improve on Wall Street with the S&P 500 closing down -0.81% for its worst day in over a month. Banks stocks followed their European cousins to be down -0.95%, and the macro bellwether transports sector fell -0.96% for its tenth consecutive decline. That’s the longest streak for the transport index since February 2009. Seven down days in the last eight for the S&P 500 is something we haven’t seen since mid-late December last year. Meanwhile the DOW closed -0.78% and the NASDAQ -1.13%. Treasuries rallied -5.4bps and are down -11.4bps from the March 1st highs. EM FX felt the pinch with a broad index down -0.79%. The Argentine peso led losses, depreciating -4.07% versus the dollar to its weakest level ever.

Coming back to the ECB, with regards to the TLTRO3, the details of the refinancing operations that we did get appeared broadly in line with what was eventually expected to be implemented. It’s a 2-year maturity quarterly operation (compared to 4-year for TLTRO2) priced off the refi rate and with a cap as to how much banks can borrow (up to 30% of eligible loans) to prevent overreliance. Our economists rightly noted that the uncertainty is how big the first ‘T’ of TLTRO3 will be – the statement does say that it “will feature built-in incentives” but it is not clear yet what those will be, so we’ll have to wait for further details which Draghi suggested would come in “due course”. However, after the meeting, reports circulated that the ECB will favour a rate above the refi rate, which would obviously make the new loans much less attractive, as well as unconfirmed press reports that the final decision could be deferred until later this year instead of the April meeting. Given the lack of clarity from Draghi and the muddled message from anonymous sources after the meeting, it’s apparent that the Governing Council remains divided about how exactly to structure the new loans.

As for the new economic forecasts, markets reacted most to the news that 2019 inflation was being revised down to 1.2% from 1.6%, and 2020 and 2021 forecasts revised down two-tenths to 1.5% and 1.6% respectively. Growth is now expected to be 1.1% in 2019 compared to 1.7% previously (DB already at 0.9% from earlier in the year). The revisions further out were a lot more modest however, with 2020 growth down one-tenth to 1.6% and 2021 unchanged at 1.5%. So the inflation forecasts were notably dovish and Bunds dropped a couple of their collapsing basis points in tow after the forecasts were released. Five-year by five-year inflation swaps dipped -4.0 basis points to 1.47%, its fifth steepest drop since 2016. Headlines came out after the close suggesting some ECB officials were worried they hadn’t cut growth forecasts enough. So another confusing sign.

During the press conference Draghi’s language on growth appeared more dovish, saying that “weakening data points to sizeable moderation in growth” and “we are maintaining our growth assessment to the downside”. He also said that the ECB is “very open to act when needed” on more easing. As for the banks and negative rates question, Draghi avoided directly answering a question on tiering and that “mitigating measures for negative rates were not discussed”. He did suggest that there was a discussion about the need to examine the matter in detail but clearly it wasn’t what the market wanted to hear. Overall it would be hard to suggest that this was one of the most successful pieces of communication/policy responses from the ECB.

Asian markets are heading lower this morning with Chinese bourses leading the declines amidst weak February trade data – the Shanghai Comp (-3.14%), Shenzhen Comp (-1.90%) and CSI (-3.07%) are all down. Sentiment in China is also getting impacted by a rare sell rating from the nation’s largest brokerage which traders are taking as a sign that the government wants to slow down the rally (as per Bloomberg). Citic Securities Co. issued a sell rating on People’s Insurance Company (Group) of China Ltd., and advised clients to sell the shares, saying they are “significantly overvalued” and could decline more than 50% over the next year. The Nikkei (-1.96%), Hang Seng (-1.37%) and Kospi (-1.06%) are also down. Elsewhere, futures on the S&P 500 are down -0.19% and the Japanese yen is up +0.32% this morning. Overnight we saw China’s February trade data with exports falling -20.7% yoy (vs. -5.0% yoy expected) while imports fell -5.2% yoy (vs. -0.6% yoy expected) resulting in trade balance of $4.12bn (vs. $26.20bn expected). February numbers are impacted by Lunar New Year holidays as well as the impact of the trade war. So a fair amount of uncertainty in the data. China’s trade surplus with the US has declined in YtD 2019 in USD terms by -1.97% yoy to $42.02bn.

In other news, Bloomberg reported that the EU Trade Commissioner Cecilia Malmstrom and U.S. Trade Representative Robert Lighthizer had productive meetings on how to address Chinese industrial policies and reform the WTO while adding that the EU chief trade negotiator urged President Donald Trump to stop imposing tariffs on the bloc if he wants a partner to help the US pressure China to abide by rules governing the global economy. She said, “we have a problem: China is dumping the market, China is subsidizing their industry, this creates global distortions. We can agree on that. So what is the solution? Well, we think it is to cooperate on China,” while adding that the EU member states have made resolving the US duties on European steel and aluminium a precondition before any bilateral trade deal can be concluded.

Looking ahead there’s little rest for markets today with the February employment report due in the US this afternoon. Markets are expecting a +0.3% mom earnings reading which would be enough to push the annual rate up to +3.3% yoy and match the post-recession highs from the end of last year. Our US economists also expect a +0.3% mom/+3.3% yoy earnings reading while for payrolls the market is at 180k and our colleagues slightly above that at 195k. A reminder that January was 304k and December 222k so we’ve had two successive strong prints. Indeed our colleagues expect some payback in the data today especially given that it was a few sectors which contributed to January’s outsized gain. Elsewhere the unemployment rate is expected to nudge down to 3.9% and hours hold at 34.5.

Back to yesterday, where the Brexit newsflow continues to remain fairly worrying ahead of next week’s votes with Reuters quoting a UK government source as saying that there is nothing to suggest anything is going to change in talks with the EU this week with the latter not budging from its position. Cox has supposedly been told to rework his backstop proposals and return to Brussels today with talks likely to continue into the weekend again. News yesterday suggested that PM May would not travel to Brussels this weekend so it appears that there is a concerted effort to play down expectations for Tuesday’s vote from the UK government. Overnight Bloomberg reported that Mrs May is likely to say in a speech today that the outcome of the Brexit vote on 12th March is in the hands of the EU and will add that she still hopes to get legally binding changes from the EU ahead of the vote next week. The report also said that the EU has made a new offer in a bid to break the Brexit impasse, though it falls short of what the UK has demanded. Sterling is trading (+0.09%) up this morning. Expect a long and busy weekend of headlines.

On the trade war front, there were no major developments yesterday as the US and China continue to negotiate. There were some noteworthy comments from European Trade Commissioner Cecilia Malmstrom, who spoke at several events in DC. She emphasized that the US and EU need to work together and that the EU would be willing to discuss the automobiles in talks. She also met with USTR Lighthizer, who reportedly did not comment on the recent Commerce Department report on auto imports, which could result in a recommendation to raise tariffs on US imports from Europe. She said that she is “watching carefully” for the report’s conclusions, much like the rest of us.

Fed Governor Brainard spoke yesterday, and her views are often tracked as a bellwether for the center of the committee. She said that “modest downward revisions” to rate hike expectations would be consistent with the slight downward changes to the growth and inflation outlook. Our economists had thought that Brainard’s December rate forecast was for three hikes this year, so she may have moved to one hike but is unlikely to have moved to zero. That’s consistent with our economists’ projections for one more hike this year. That said, she did emphasize the “heightened downside risks” which could yet detail her outlook.

Turning to yesterday’s data, US jobless claims came in at 223,000, down from 226,000 in the prior week. That’s right in the middle of the last 1-2 year range and consistent with a resilient labour market. Continuing claims fell 50k to 1,755,000. Consumer credit grew slightly more than expected at $17.05bn in January, though the December figure was revised down slightly. Elsewhere, China’s FX reserves rose $2.3bn to $3.09trn in February, which is consistent with the view that the PBoC has not been intervening to weaken or strengthen the currency while trade talks are ongoing.

In terms of the day ahead, this morning in Europe we’ve got January factory orders data out of Germany and January industrial production in France and Italy. This afternoon it’s all about the February employment report in the US while January housing starts and building permits is also due out. Away from that the ECB’s Nowotny is speaking at a conference in Prague this morning, and we should also note that the Fed’s Powell is due to speak early tomorrow morning (3am GMT) at the Stanford Institute on monetary policy normalization – so that should be worth a watch.

3. ASIAN AFFAIRS

i)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED DOWN 136..46 POINTS OR 4.40% //Hang Sang CLOSED DOWN 551.03 POINTS OR 1.91% /The Nikkei closed DOWN 430.45 POINTS OR 2.01%/ Australia’s all ordinaires CLOSED DOWN .90%

/Chinese yuan (ONSHORE) closed UP at 6.7221 AS TRUCE DECLARED FOR 3 MONTHS /Oil UP to 56.84 dollars per barrel for WTI and 65.78 for Brent. Stocks in Europe OPENED RED

ONSHORE YUAN CLOSED DOWN // LAST AT 6.7221 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7319: / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/USA

3 b JAPAN AFFAIRS

3 C CHINA

China/last night

Chinese stocks crash last night as we start to see a rare “sell rating” on many stocks and that shook traders.

(courtesy zerohedge)

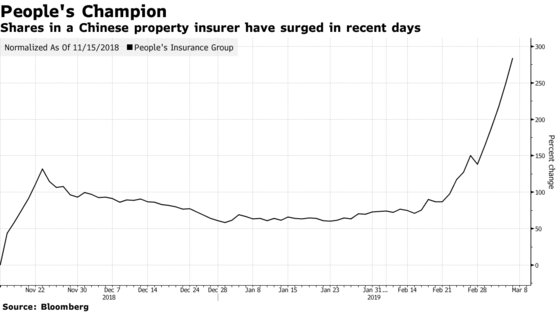

Chinese Stocks Crash As Rare Sell Rating Shocks Traders

The question whether Beijing will tolerate another stock market bubble – one which it appeared to carefully cultivate until now – got an answer on Friday when Chinese stocks crashed, tumbling the most in five months. And it all started with a single sell rating.

The Shanghai Composite tumbled 4.4% to close below the key 3,000 point level, ending an 8 week rally, with the Shenzhen Composite and Chinext all following.

The drop was catalyzed by a limit-down plunge in state-owned insurer People’s Insurance Company of China, which had become a poster child of the ramp-up in equities, and which saw its shares sink by the 10 percent daily limit, after state-owned brokerage Citic Securities advised clients to sell the shares, saying they are “significantly overvalued” and could decline more than 50% over the next year.

The signal was heard loud and clear, and by the time the selling – which accelerated in the last hour of trading – was over as stocks hit lows at the close, the Composite had one of its worst days in years.