GOLD: $1285.60 DOWN $1.40 (COMEX TO COMEX CLOSING)

Silver: $15.04 DOWN 4 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : $1285.40

silver: $15.02

For comex gold and silver:

MARCH

NUMBER OF NOTICES FILED TODAY FOR MAR CONTRACT: 8 NOTICE(S) FOR 800 OZ (0.0240 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 310 NOTICES FOR 31000 OZ (.9642 TONNES)

SILVER

FOR MARCH

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

22 NOTICE(S) FILED TODAY FOR 110,000 OZ/

total number of notices filed so far this month: 4722 for 23,610,000

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $3892:UP $2

Bitcoin: FINAL EVENING TRADE: $3887 UP 26

end

XXXX

JPMorgan or Goldman Sachs are taking a huge issuance (stopping) of gold at the comex.

today 4/8

EXCHANGE: COMEX

CONTRACT: MARCH 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,284.900000000 USD

INTENT DATE: 03/06/2019 DELIVERY DATE: 03/08/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

657 C MORGAN STANLEY 1

661 C JP MORGAN 4

686 C INTL FCSTONE 3

737 C ADVANTAGE 1 3

905 C ADM 4

____________________________________________________________________________________________

TOTAL: 8 8

MONTH TO DATE: 310

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST ROSE BY A CONSIDERABLE SIZED 1114 CONTRACTS FROM 190,024 UP TO 191,329 WITH YESTERDAY’S 2 CENT LOSS IN SILVER PRICING AT THE COMEX. TODAY WE ARRIVED FURTHER FROM AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS. WE ALWAYS WITNESS A CONTRACTION IN TOTAL OI AS WE APPROACH FIRST DAY NOTICE AND IT SEEMS THE CULPRIT IS THE FORCED LIQUIDATION OF SPREADERS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A GOOD SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

0 EFP’S FOR MARCH, 0 FOR APRIL, 1141 FOR MAY, 0 FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 1141 CONTRACTS. WITH THE TRANSFER OF 1141 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1141 EFP CONTRACTS TRANSLATES INTO 10.96 MILLION OZ ACCOMPANYING:

1.THE 2 CENT LOSS IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST NINE MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.

AND NOW: 25.325 MILLION OZ STANDING IN MARCH.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF MARCH:

13,939 CONTRACTS (FOR 5 TRADING DAYS TOTAL 13,939 CONTRACTS) OR 69.70 MILLION OZ: (AVERAGE PER DAY: 2787 CONTRACTS OR 13.939 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF MAR: 69.70 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 9.96% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 434.58 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

RESULT: WE HAD A GOOD SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1305 WITH THE 2 CENT LOSS IN SILVER PRICING AT THE COMEX /YESTERDAY..THE CME NOTIFIED US THAT WE HAD GOOD SIZED EFP ISSUANCE OF 1466 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A CONSIDERABLE SIZED: 2446 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 1141 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 1305 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 2 CENT LOSS IN PRICE OF SILVER AND A CLOSING PRICE OF $15.08 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.975 BILLION OZ TO BE EXACT or 139% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT FEBRUARY MONTH/ THEY FILED AT THE COMEX: 22 NOTICE(S) FOR 110,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/AND NOW MARCH: 25.325 MILLION OZ/

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST ROSE BY A HUGE SIZED 6825 CONTRACTS UP TO 478,136 DESPITE THE FALL IN THE COMEX GOLD PRICE/(A GAIN IN PRICE OF $3.30//YESTERDAY’S TRADING). HOWEVER…….

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 4012 CONTRACTS:

MARCH HAD AN ISSUANCE OF 0 CONTACTS APRIL 4012 CONTRACTS,JUNE: 0 CONTRACTS DECEMBER: 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 478,136. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A GIGANTIC SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 10,837 CONTRACTS: 6825 OI CONTRACTS INCREASED AT THE COMEX AND 4012 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 10,837 CONTRACTS OR 1,08,700= 33.70 TONNES.

YESTERDAY WE HAD A GAIN IN THE PRICE OF GOLD TO THE TUNE OF $3.30.…AND WITH THAT WE HAD A HUGE GAIN IN TONNAGE OF 33.70 TONNES.

YESTERDAY, WE HAD 7293 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MARCH : 44,564 CONTRACTS OR 4,456,400 OZ OR 138.612 TONNES (5 TRADING DAYS AND THUS AVERAGING: 8913 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 5 TRADING DAYS IN TONNES: 138.612 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 138.612/2550 x 100% TONNES = 5.43% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 1014.15 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A HUGE SIZED INCREASE IN OI AT THE COMEX OF 6825 WITH THE GAIN IN PRICING ($3.30) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A GOOD SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 4012 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 4012 EFP CONTRACTS ISSUED, WE HAD A GIGANTIC GAIN OF 12,776 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

4012 CONTRACTS MOVE TO LONDON AND 6825 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE STRONG GAIN IN TOTAL OI EQUATES TO 33.70 TONNES). ..AND ALL OF THIS DEMAND OCCURRED WITH THE GAIN OF $3.30 IN YESTERDAY’S TRADING AT THE COMEX

we had: 8 notice(s) filed upon for 800 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $1.40 TODAY

NO ADDITIONS OR SUBTRACTIONS TODAY

INVENTORY RESTS AT 766.59 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 4 CENTS IN PRICE TODAY:

NO CHANGES IN SILVER INVENTORY AT THE SLV..///

/INVENTORY RESTS AT 308,503 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A GOOD SIZED 1305 CONTRACTS from 190,024 UP TO 191,490 AND FURTHER FROM THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

0 CONTRACTS FOR MARCH. 0 CONTRACTS FOR APRIL., 1141 FOR MAY AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1141 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 1305 CONTRACTS TO THE 1141 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A STRONG GAIN OF 2426 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 12.23 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY AND NOW 25.325 MILLION OZ FOR MARCH.

RESULT: A GOOD SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE 2 CENT LOSS IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY.BUT WE ALSO HAD A STRONG SIZED 1141 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED UP 4.32 POINTS OR 0.14% //Hang Sang CLOSED DOWN 258.15 POINTS OR 0.89% /The Nikkei closed DOWN 140.80 POINTS OR 0.65%/ Australia’s all ordinaries CLOSED UP .28%

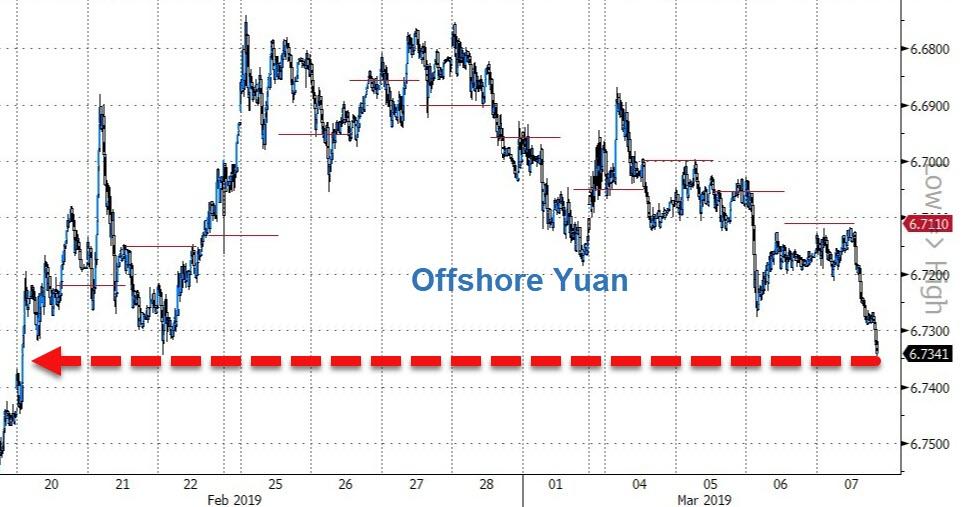

/Chinese yuan (ONSHORE) closed UP at 6.7072 AS TRUCE DECLARED FOR 3 MONTHS /Oil UP to 56.84 dollars per barrel for WTI and 65.78 for Brent. Stocks in Europe OPENED RED

ONSHORE YUAN CLOSED UP // LAST AT 6.7072 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7170: / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A/NORTH KOREA/SOUTH KOREA

i)North Korea/

This does not look good at all: an artificial 2.1 earthquake detected in North Korea and it was due to artificial seismic activity as a result of an explosion inside a mine

( zerohedge)

b) REPORT ON JAPAN

3 C/ CHINA

i)China/the globe

A good indicator of the deterioration in the global economy: semiconductor orders from China plunges the greatest since 2008

( zerohedge)

4/EUROPEAN AFFAIRS

i)ECB

Draghi surprisingly very dovish as he guides rates. The big news is that he is re introducing his key QE vehicle the LTRO or TLTRO. This will no doubt save Italy for the time being..this is great for gold.

( zerohedge)-

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6. GLOBAL ISSUES

Canada:

Vancouver home sales crashed by 33% last month as fewer and fewer can afford a home in this very pricing city

( zerohedge)

7. OIL ISSUES

this should cripple PDVSA and venezuela

( Irina Slav//OilPrice.com//)

8 EMERGING MARKET ISSUES

i)VENEZUELA/

Venezuela expels the German ambassador over his support for Guaido

(courtesy zerohedge)

9. PHYSICAL MARKETS

(McCormick/Bloomberg/GATA)

ii)far left article admonishes German gold bugs and the repatriation of gold to Mother Germany( GATA/)

iii)Van Eck International, the largest shareholder of Barrick is urging a joint venture and not a merger.

( Reuters/GATA)

10. USA stories which will influence the price of gold/silver)

MARKET TRADING

ii)Market data

g)Well that did not last long: Amazon subsidiary slashes worker hours just 4 months after proceeding to the 15 dollar minimum wage level

( zerohedge)

h)this is interesting: the Fed released in its latest flow of funds report that households net worth has dropped by a huge 3.7 trillion dollars, its first drop in 4 years

( zerohedge)

iv)SWAMP STORIES

House democrats erupt into turmoil as they cannot even get a resolution on an antisemitism rebuke from the far left

(courtesy zerohedge)

end

Let us head over to the comex:

AFTER MARCH, WE HAVE THE NON ACTIVE DELIVERY MONTH OF APRIL. HERE: APRIL RISES TO 815 CONTRACTS FOR A GAIN OF 17 CONTRACTS. AFTER APRIL, THE NEXT BIG ACTIVE DELIVERY MONTH IS MAY AND HERE THE OI ROSE BY 842 CONTRACTS UP TO 139,939 CONTRACTS.

i) out of Brinks: 55,955.375 oz..and this landed into JPMorgan

ii) out of HSBC: 63,202.737 oz

China Gold Reserves Rise To 60.26 Million Ounces Worth Just $79.5 Billion

China increased its gold reserves for a third straight month in February, data from the People’s Bank of China (PBOC) showed this morning.

The value of China’s gold reserves rose slightly to $79.498 billion in February from $79.319 billion at the end of January, as the central bank increased the total amount of gold reserves to 60.260 million fine troy ounces from 59.940 million troy ounces. (Harvey; 9.95 tonnes)

The People’s Bank of China (PBOC) did not explain why it bought more gold. It is almost certainly in large part due to concerns about the Chinese, U.S. and global economic outlook and the outlook for the dollar in the coming months and years.

China’s foreign exchange (fx) reserves rose to their highest in six months in February. There are growing concerns over U.S.-China trade talks and the potential for trade wars and the impact of this on their respective economies.

Chinese foreign exchange (fx) reserves, the world’s largest, rose by $2.26 billion in February to $3.090 trillion, central bank data showed on Thursday, marking the highest level since August 2018. The U.S. trade deficit hit its highest in a decade in 2018, in a resounding failure for President Donald Trump’s global trade offensive, U.S. government data showed yesterday.

It is important to realise that the PBoC still have a very meager 2.4% of its foreign exchange reserves in gold, so their gold diversification is likely in it’s infancy. John Reade of the World Gold Council notes on Twitter that the last time the PBoC reported regular monthly increases in gold holdings, it continued for 24 months.

We have long pointed out two other entities, besides the PBOC, have also been buying gold – the State Administration of Foreign Exchange (SAFE) and the China Investment Corporation (CIC).

These potentially sizeable sources of demand are not included in the PBOC figures.

It is important to note this lack of transparency regarding total aggregate Chinese central bank and sovereign fund demand. Therefore, it is likely that we are underestimating Chinese and thus global gold demand.

China may be adopting the Russian strategy of being very public in announcing their increasing gold reserves as they attempt to position the yuan as an alternative reserve currency to the world’s current reserve currency the dollar.

News and Commentary

Gold steady on firmer dollar ahead of ECB policy meeting (Reuters.com)

ECB Readies Response Amid Euro-Area Slowdown (Bloomberg.com)

Asia shares sluggish as global growth concerns return; ECB meeting eyed (Reuters.com)

U.S. senators say Saudi crown prince has gone ‘full gangster’ (Reuters.com)

Sweden’s central bank trims forex reserve after Nordea moves to Finland (Reuters.com)

U.S. Trade Gap Surged to $621 Billion in 2018, 10-Year High (Bloomberg.com)

Trump’s Big Tax Cuts Did Little to Boost Economic Growth (Bloomberg.com)

Global Economy Is Sinking Fast, And It Will Take The US With It (ZeroHedge.com)

Chinese Hackers Stole Maritime Military Secrets From Group Of Universities (ZeroHedge.com)

Gold advocates support free and fair trade with stable, international gold-backed money (Gata.org)

U.S. Trade Gap Surged to $621 Billion in 2018, 10-Year High (Bloomberg.com)

06 Mar: USD 1,285.55, GBP 978.82 & EUR 1,136.82 per ounce

05 Mar: USD 1,285.00, GBP 975.19 & EUR 1,134.78 per ounce

04 Mar: USD 1,287.45, GBP 972.93 & EUR 1,135.14 per ounce

01 Mar: USD 1,309.95, GBP 989.27 & EUR 1,152.23 per ounce

28 Feb: USD 1,325.45, GBP 996.21 & EUR 1,162.82 per ounce

27 Feb: USD 1,326.45, GBP 998.02 & EUR 1,164.09 per ounce

Silver Prices (LBMA)

06 Mar: USD 15.09, GBP 11.49 & EUR 13.36 per ounce

05 Mar: USD 15.11, GBP 11.47 & EUR 13.33 per ounce

04 Mar: USD 15.16, GBP 11.50 & EUR 13.38 per ounce

01 Mar: USD 15.56, GBP 11.75 & EUR 13.67 per ounce

28 Feb: USD 15.81, GBP 11.89 & EUR 13.85 per ounce

27 Feb: USD 15.86, GBP 11.91 & EUR 13.92 per ounce

Recent Market Updates

– JPMorgan Is Bullish on Gold as a Hedge Against Rising Inflation

– Gold – It Might Be Different This Time

– Euromillions Winners To Invest In Gold In 2019?

– Gold Still on a Long Term Track to Reach $2,000 An Ounce

– “Gold Is A Global Thermometer Of Risk” – CEO Q+A: Stephen Flood, GoldCore

– U.S. Mint Suspends Silver Bullion Coin Sales After Sales Double In February

– MMT: Modern Monetary Madness Will Lead To Higher Taxes and Inflation

– Gold Broker Has Good Sense and Prefers Gold To All That Glitters (The Times)

(McCormick/Bloomberg/GATA)

Higher U.S. rates creating carry trade supporting dollar

Submitted by cpowell on Wed, 2019-03-06 15:37. Section: Daily Dispatches

Watching Global Flows Explains Why the Dollar Won’t Be Kept Down

By Liz McCormick

Bloomberg News

Wednesday, March 6, 2019

The dollar’s resilience after what some have categorized as the most dovish Federal Reserve turnaround in history comes as little surprise to Exante Data’s Jens Nordvig.

U.S. President Donald Trump may be looking to jawbone the greenback. But for Exante, it’s still all about the grab for yield, with rates on dollar-denominated assets remaining more attractive relative to the painfully low or negative ones found in Europe and Asia. The firm’s analysis of the holdings of global asset managers suggests that isn’t going to change any time soon.

…

Exante’s flagship global flow analytics product aggregates fund managers positioning in fixed income and currencies to pinpoint extremes. It’s readings — which have helped snag Exante clients willing to pay $60,000 a year for its insights — include gauges of activity tied to carry trades.

Inflows into this strategy, a bet in which an investor borrows in a lower-yielding currency and invests in one with higher rates, using purchases of dollar-denominated assets surged this quarter to multiyear highs. That’s come even as Fed Chairman Jerome Powell and his colleagues have indicated a resolve to stand pat on policy normalization for now. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2019-03-06/watching-the-global-f…

END

far left article admonishes German gold bugs and the repatriation of gold to Mother Germany

(courtesy GATA/)

Leftist New Statesman attacks gold advocates and Germany’s gold repatriation leader

Submitted by cpowell on Wed, 2019-03-06 16:30. Section: Daily Dispatches

11:30a ET Wednesday, March 6, 2019

Dear Friend of GATA and Gold:

The venerable British left-wing magazine The New Statesman today published an article disparaging “gold bugs” as “far right” and nationalist and particularly disparaging GATA’s friend Peter Boehringer, the founder of the movement in Germany to repatriate the country’s gold reserves who is now a member of the country’s parliament, chairman of its budget committee, and a leader of the Alternative for Germany party.

Predictably enough the New Statesman’s article failed to acknowledge surreptitious suppression of the gold price and indeed the rigging of nearly all markets by central banks, since, after all, leftists generally oppose free markets.

…

Your secretary/treasurer forwarded the article to Boehringer, whose quick reply made the article worth calling to your attention. That reply is appended, on top of the article itself.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

* * *

Interesting read. Thank you.

That professor did quite some research on me, Alternative for Germany, and gold in general. Some parts of the article are correct — especially the thesis that gold is globally functioning, real money, as we have been writing for 20 years now. It is therefore absurd that the author accuses us goldbugs of being nationalist, anti-liberal, closed-border lunatics.

We are exactly the opposite. We support free and fair trade with stable, international money, potentially partly gold-backed as was the case for centuries.

I guess the author knows that his article is purely leftist propaganda. The money socialists cry “wolf” to distract from their own socialist and supranationalist plans against humanity. They fear the power of uncontrollable and unbribable gold.

I will continue to uphold the flags of sound money, monetary truth, and gold in the Deutsche Bundestag. We will see what will prevail in the end: monetary truth, soundness, and gold or lies, inflation, and paper deception. History gives us many hints as to the answer.

Peter Boehringer, Chairman

Budget Committee

Deutsche Bundestag

Berlin, Germany

* * *

Why Is the Far Right Obsessed with Gold?

By Quinn Slobodian

The New Statesman, London

Wednesday, March 6, 2019

https://www.newstatesman.com/politics/economy/2019/03/why-far-right-obse…

In 2010 a precious metals blogger called Peter Boehringer posted an image of Karl Marx’s head floating over Frankfurt, the home of the European Central Bank. Like many online “gold bugs,” his message reflected the belief that currencies without the backing of gold amount to “monetary socialism” and pave the way to government overreach and eventual economic collapse. Boehringer now sits in the German Bundestag for the Alternative for Germany Party (AfD), and chairs the parliament’s budget committee.

A few years later, the far-right leader Marine Le Pen launched a campaign to return French gold deposits kept in New York. The gold bars “do not belong to the state, nor the Bank of France, but to the French people,” she announced. Last month, Italy’s Deputy Prime Minister Matteo Salvini called gold the “property of the Italian people” and threatened to plug a gap in the budget by selling off Italy’s gold deposits. Gold has also caught the attention of far-right politicians further eastwards. In 2018 Poland began stockpiling gold; Hungary, under the leadership of Viktor Orban, has multiplied its gold reserves tenfold.

Why is the far right fixated on gold? Politicians like Le Pen and Orban are typically cast as advocates of a “closed society” pitted against globalisation and free movement. Gold doesn’t fit this mold; historically, it has been a symbol of connection, not isolation. The gold standard was the bedrock of the first age of globalisation that enabled exchange across continents and lasted from the 1870s to the outbreak of the First World War. To classical liberals, gold was the metal that bound the world economy together.

But the far right has long understood the power of symbols. Gold is the natural vessel of value that harks back to an era where finance and commerce were unburdened by supranational institutions like the European Central Bank and the U.S. Fed. It evokes morality grounded in traditional ideas of economic value — to stand for gold is to stand against states printing “fiat money” that isn’t backed by precious metal. Think of it as the opposite of left-leaning economists’ recent interest in Modern Monetary Theory, which sees currency as a creation of the state. To understand the right’s political vision, follow the money.

Gold has had a wild ride in the new millennium. Its value more than sextupled from 2000 to a high point in 2011, driven mainly by the Global Financial Crisis of 2007-8 and the subsequent Eurozone crisis. German savers, in particular, fled to gold as a safe haven in times of uncertainty and zero interest rates.

The far right saw the rising price of gold as an index of anti-establishment anxiety. In the United States, Tea Party cheerleaders Glenn Beck and Rush Limbaugh pitched gold on their respective shows, with Beck’s favored company eventually charged with fraud. Gold played an especially visible role in the rise of the far-right AfD, currently the official opposition in Germany’s parliament.

The AfD was formed by a clutch of economists in 2013 to tackle the German government’s perceived mismanagement of the European financial crisis. Germany’s electoral system matches individual political donations with state funds. After garnering little support in 2014 elections, the AfD opened an online gold shop selling the defunct Deutsche Mark alongside four denominations of the South African Krugerrand. It was a canny move: by counting the purchases as donations, the AfD could increase their share of state funding.

In 2014, an AfD spokesperson proudly told a reporter “we are the only party whose headquarters is also a profit centre.” The AfD’s gold shop was a significant boon for a party with a small donor base — it made 2 million euros across 2014 and 2015, before the law was changed.

But the AfD wasn’t just growing its funding base: It was prophesying the downfall of the Euro. By selling gold, the party promoted suspicion of the German state’s ability to manage its own currency, and sold an exit from the state-managed monetary system. At the same time, the AfD profited from the state’s electoral funding law, designed to encourage party competition within Germany’s democracy.

For AfD thinkers, gold was more than just a reliable store of value. It was a filament of cultural and social order. Long-time member of the AfD federal board Dirk Driesang wrote in 2014 that “the fatal effects of fundamentally fake money (“falschgeld”) on our society and politics, our family and our values, are destructive and undermine the fundamentals of our civilisation as well as our western culture.”

To hazard a coinage, we could call the AfD’s approach to gold a type of “auripatriotism” — a national feeling whose reference point is not a territory, ethnicity or language, but whichever monetary system backs its currency with the precious metal that is perceived the natural currency of modern humanity. Although the AfD rejects the slogan of “open borders,” they imagine open borders for gold. Far from eschewing globalisation, the AfD’s vision subjects the actions of the state to the continual audit of those who have the gold.

It was Peter Boehringer himself that launched the “bring our gold home” campaign that was later imitated by Le Pen in France and among copycat organisations in Switzerland, Austria, and Holland, all led by far-right parties. With monetary policy, as with other political matters, the far right isn’t a throwback to a supposedly autarkic past, but a creature of our contemporary moment. Even their demands for sovereignty and autonomy are uttered with one eye on the global picture. The far right is not blind to how the world works. Rather, they are turning its weaknesses into their strengths.

—–

Quinn Slobodian is an associate professor of history at Wellesley College and the author of “Globalists: The End of Empire and the Birth of Neoliberalism.”

* * *

END

Van Eck International, the largest shareholder of Barrick is urging a joint venture and not a merger.

(courtesy Reuters/GATA)

Top Barrick shareholder urges joint venture in Nevada with Newmont, not full merger

Submitted by cpowell on Wed, 2019-03-06 18:33. Section: Daily Dispatches

By Ernest Scheyder and Liana B. Baker

Reuters

Tuesday, March 5, 2019

Barrick Gold Corp.’s top shareholder said Tuesday the miner should focus on striking a joint venture deal in Nevada with rival Newmont Mining Corp. before considering a full-blown merger.

“My preference is a joint venture,” Joe Foster of the Van Eck International Investors Gold Fund said in a phone interview. “I don’t flat-out oppose a merger. If a merger is the only way to unify Nevada, then maybe, just maybe, that’s something we might consider. But as it stands the best path right now is to form a joint venture in Nevada.”

…

.Last month Barrick launched an $18 billion takeover offer for Newmont, which Newmont rejected. Both sides have said they agree that their neighboring Nevada assets should be combined to cut costs, but they disagree on how this should be done. …

… For the remainder of the report:

https://www.reuters.com/article/us-newmont-mining-m-a-barrick-gold/top-b…

* * *

Join GATA here:

Mining Investment Asia

Marina Bay Sands Conference and Exhibition Center

Singapore

Tuesday-Thursday, March 26-28

https://www.mininginvestmentasia.com/

Mines and Money Asia

Hong Kong Conference and Exhibition Center

Wan Chai, Hong Kong

Tuesday-Thursday, April 2-4

https://asia.minesandmoney.com/

* * *

Help keep GATA going

GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at:

To contribute to GATA, please visit:

END

Our good friend and GATA Sec is speaking at conferences in Singapore and Hong kong

(courtesy GATA)

GATA secretary to speak at conferences in Singapore and Hong Kong

Submitted by cpowell on Wed, 2019-03-06 19:24. Section: Daily Dispatches

2:24p ET Wednesday, March 6, 2019

Dear Friend of GATA and Gold:

Your secretary/treasurer will speak at the annual Mining Investment Asia conference in Singapore from March 26-28and the annual Mines and Money Asia conference in Hong Kong from April 2-4.

The Mining Investment Asia conference will be held at the Marina Bay Sands Conference and Exhibition center. The conference’s internet site is here:

https://www.mininginvestmentasia.com/

The Mines and Money Asia conference will be held at the Hong Kong Conference and Exhibition Center. The conference’s internet site is here:

https://asia.minesandmoney.com/

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

Gold swaps continue at the BIS and this is what is underpinning gold

(courtesy Robert Lambourne)

(GATA) Gold swaps by BIS rose by 56 tonnes in February

Submitted by cpowell on 02:55PM ET Thursday, March 7, 2019. Section: Daily Dispatches

By Robert Lambourne

Thursday, March 7, 2019

The recent monthly statements of account published by the Bank for International Settlements indicate that the bank is still actively trading gold swaps, which the bank uses to gain access to gold held by commercial banks.

There is not enough information in the monthly reports to calculate the exact amount of swaps, but based on the information in the BIS’ just-published statement of account for February 2019 —

https://www.bis.org/banking/balsheet/statofacc190228.pd f

— the bank’s gold swaps are estimated to be 303 tonnes compared to 247 tonnes at January 31, 2019, an increase of 56 tonnes. This compares to an estimated holding of 275 tonnes at December 31, 2018, and estimates of 308 tonnes in November, 372 tonnes in October, 238 tonnes in September and 370 tonnes in August 2018.

More background on the bank’s medium-term history of using gold swaps is available here:

http://www.gata.org/node/18825

On February 3 GATA published comments from a former gold industry executive describing the activities of the BIS in gold swaps in earlier decades:

http://www.gata.org/node/18828

The former executive wrote: “Effectively this process created a supply of ‘paper gold’ — sometimes but not always marked to market — that had a depressing effect on the gold price.”

It is interesting that there were swaps that did not mark to market. This appears to have happened at least once in more recent times. At March 31, 2017, the BIS annual report confirmed 438 tonnes of gold swaps, valued at 14,086.9 million in the Special Drawing Rights of the International Monetary Fund. Converting the SDRs into U.S. dollars, this is equivalent to a gold price per troy ounce of approximately $1,355. But the published market price of gold as of that date was approximately $1,245, so the swaps did not mark to market.

Indeed, a perusal of the gold price in the 12 months to March 31, 2017, indicates that the effective price of the gold swaps is equal to the highest market gold price during that 12 months, reached in the summer of 2016.

On the face of it this seems an odd coincidence. But if the gold swaps were undertaken with the intent of trying to suppress the price of gold, then perhaps this coincidence is not so strange. Perhaps the BIS’ counterparty to the swap was willing to undertake it if it was not only entitled to the return of its gold swapped with the BIS but also protected from a fall in the price of gold for the duration of the swaps.

In itself this unusual transaction does not prove gold price suppression but it would be consistent with price suppression as the reason for the swap.

—–

Robert Lambourne is a retired business executive in the United Kingdom who consults with GATA about the involvement of the Bank for International Settlements in the gold market.

* * *

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

Your early WEDNESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED/ LAST AT: 6.7072/

//OFFSHORE YUAN: 6.7170 /shanghai bourse CLOSED UP 4.32 POINTS OR 0.14% /

HANG SANG CLOSED DOWN 258.15 POINTS OR 0.89%

2. Nikkei closed DOWN 140.80 POINTS OR 0.65%

3. Europe stocks OPENED RED

/USA dollar index RISES TO 96.72/Euro FALLS TO 1.1303

3b Japan 10 year bond yield: FALLS TO. +.01/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 111.72/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 56.84 and Brent: 66.88

3f Gold DOWN/JAPANESE Yen DOWN CHINESE YUAN: ON -SHORE UP /OFF- SHORE: UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

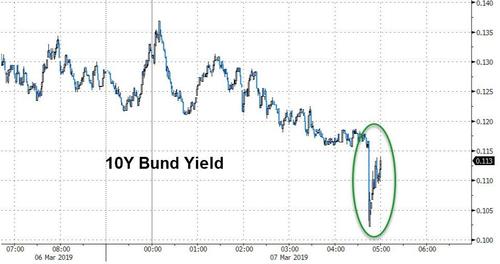

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.13%/Italian 10 yr bond yield UP to 2.62% /SPAIN 10 YR BOND YIELD UP TO 1.13%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.49: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield RISES TO : 3.77

3k Gold at $1286.00 silver at:15.07 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 5/100 in roubles/dollar) 65.97

3m oil into the 56 dollar handle for WTI and 66 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 111.72 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 1.0049 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1365 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.13%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.68% early this morning. Thirty year rate at 3.06%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.4365

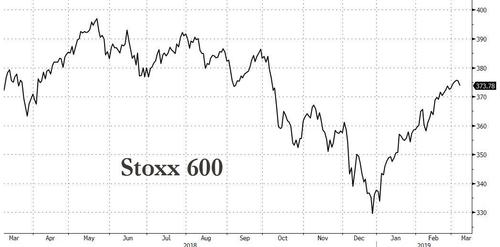

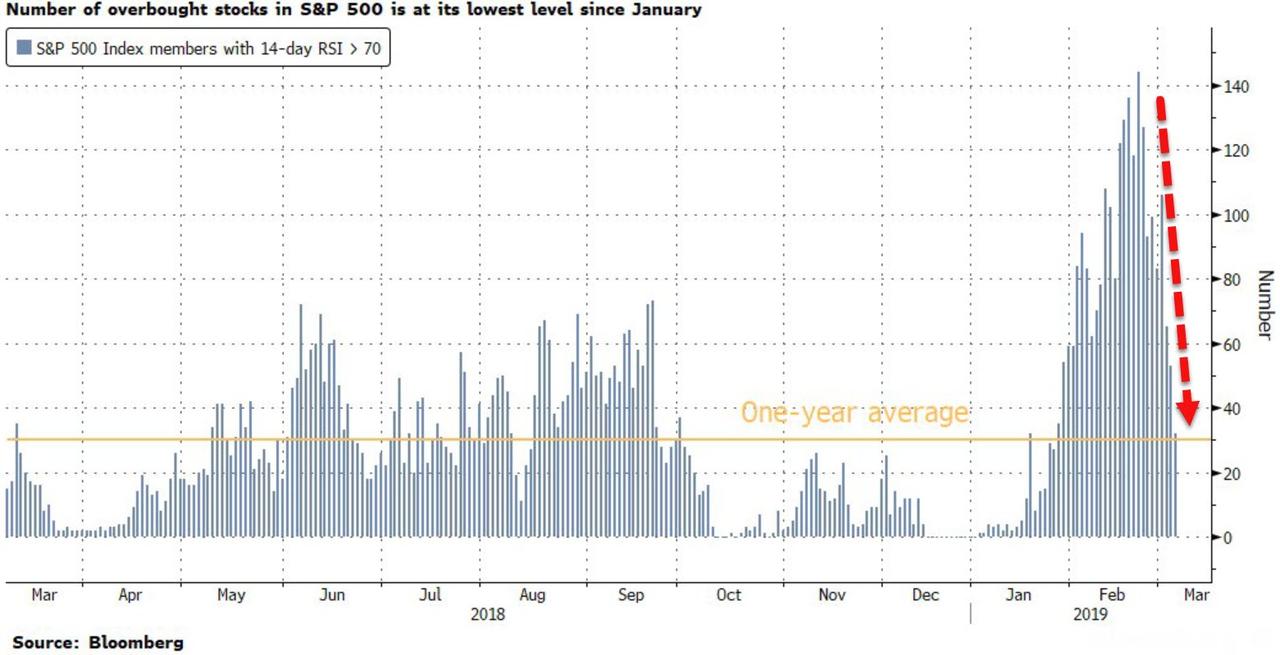

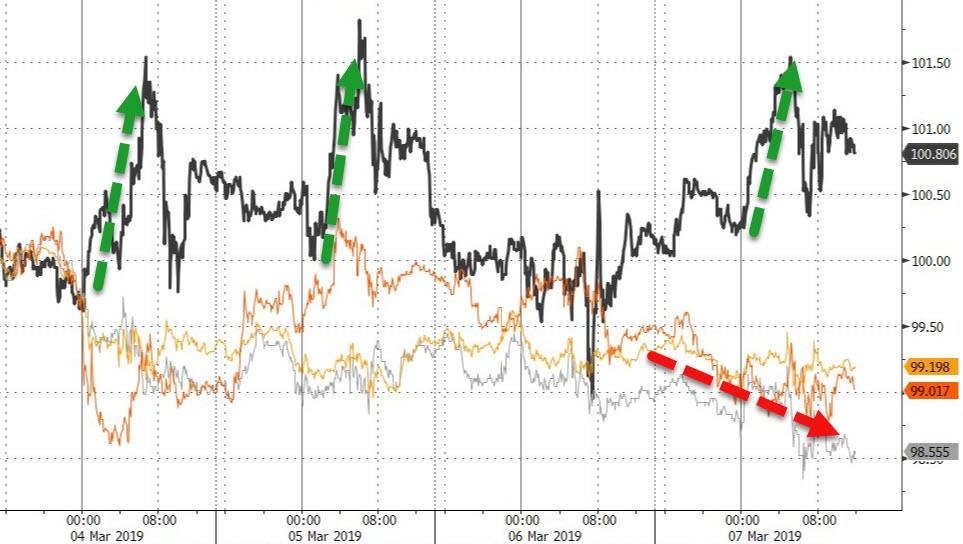

Markets Slide On Worsening Global Growth Outlook, All Eyes On Draghi

World stocks were stuck in their worst run of 2019, declining for a fourth straight day their longest losing streak since December’s rout, as global markets dropped and US equity futures slumped with the EMini pulling further away from the “quad resistance” at 2,800 amid renewed concerns about global growth after the OECD downgraded almost every growth outlook for G-20 nations, as investors waited for confirmation that, as Reuters diplomatically put it, “the ECB will start shoveling cheap cash at the euro zone again” when it cuts its growth and inflation forecasts again.

“We’re seeing a slowdown in the economy, we’re seeing a slowdown in corporate earnings,” Oliver Pursche, chief market strategist at Bruderman Asset Management, told Bloomberg TV in New York. “The market is waiting to see if things are going to turn out better or worse than they expect, and we just don’t know.”

European shares retreated further from five-month highs after the Stoxx Europe 600 Index slid ahead of what is widely expected to be a rather dour ECB meeting where the highlight may be the announcement of further stimulus to the economy through a new round of bank funding, the so-called TLTRO program. The Stoxx 600 was dragged lower by the trade-proxy mining and auto sectors, although the move was exaggerated by several stocks trading ex-dividend, such as Rio Tinto, BHP Group and Roche Holding. The defensive telecoms, utilities and food sectors once again outperformed.

A return to what was once its flagship crisis-fighting tool would be a wrenching change of direction for the ECB just months after it wound down its 2.6 trillion euro QE program, but Head of investments at UK fund manager Hermes, Eoin Murray, said he wondered how much impact such measures, or even more U.S. Fed stimulus, would have, considering the potency has tended to wane with every new round in recent years.

“I just don’t think it will have the power to get the economy to the point of takeoff,” Murray said.

Italy’s government bonds rallied to a 7-month high while its banks, which used the biggest share of the previous round of cheap central bank loans, rose 0.1% but remained below the highs hit in the previous session.

Earlier in Asia, shares fell in Japan and Hong Kong, with China again bucking the trend. MSCI’s broadest index of Asia-Pacific shares outside Japan edged 0.3% lower on Thursday, yet hovering not far from its five-month high marked last week, and was up 10% year-to-date. Japan’s Nikkei average fell 0.7 percent, while Hong Kong’s Hang Seng shed 0.7 percent and Chinese blue-chips snapped a four-day winning streak as the boost from new stimulus plans there ran into the sand.

Contracts on the S&P 500 hit a three-week low failing to break out decisively above the 2,800 “quadruple top” and may extend a three-day drop stocks after the US trade deficit widened to a 10-year high and private companies added fewer employees than expected.

Earlier this week, the S&P 500 posted its biggest one-day decline in a month, as investors sought reasons to buy after a near 20 percent rally since the start the year: “For some time, markets had been pricing in good news, namely that the talks between the U.S. and China will likely go well,” said Tatsushi Maeno, senior strategist at Okasan Asset Management. “Now markets are having a pause.”

Adding to concerns about the talks was data that showed the U.S. goods trade deficit surged to a record high in 2018 as strong domestic demand pulled in imports, despite the Trump administration’s “America First” policies aimed at shrinking the gap. Ahead of tomorrow’s payrolls report, ADP showed private payrolls increased by 183,000 in February after surging 300,000 in January, also missing expectations.

In Rates, treasuries ticked higher while European bonds were mixed.

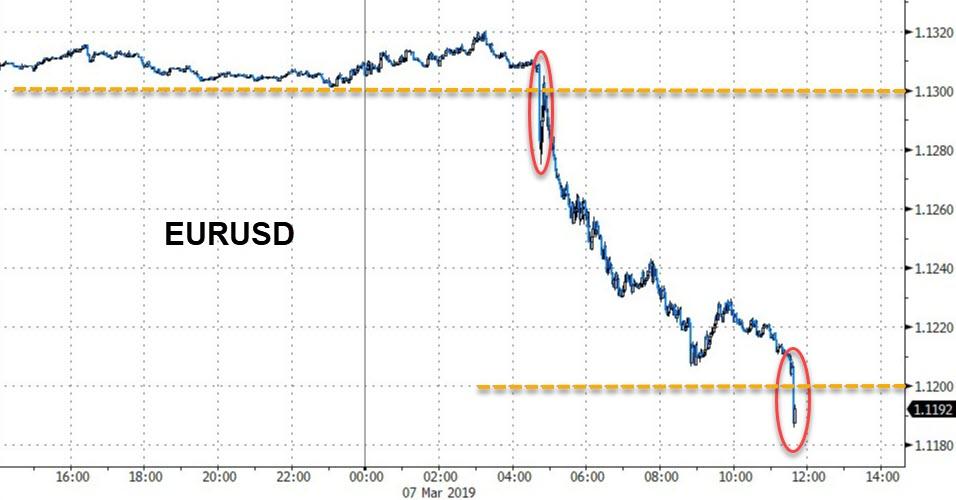

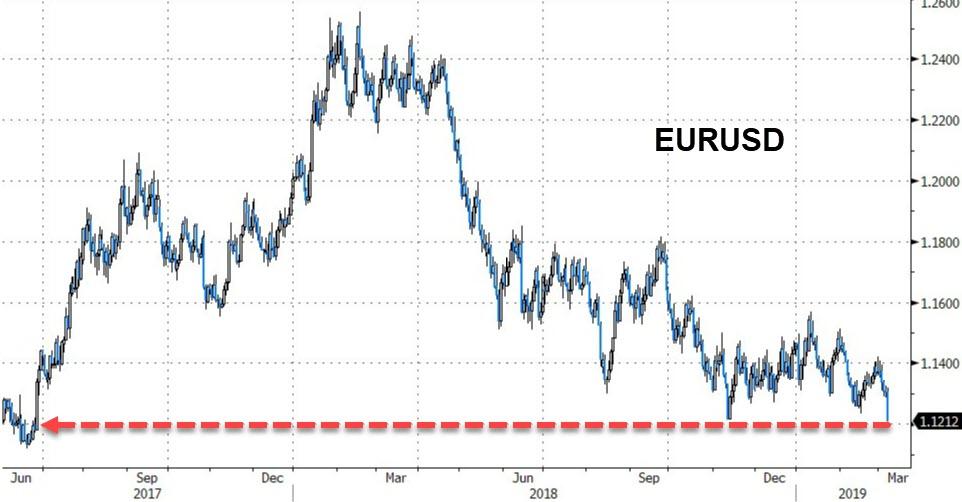

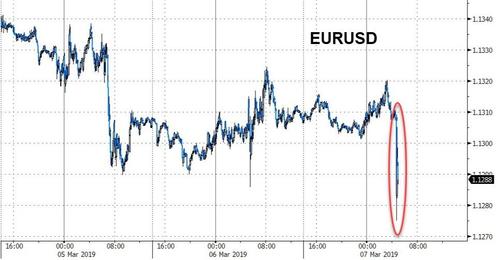

In FX, the euro traded at $1.1304, hovering near a two-week low ahead of the ECB and its expected news on its cheap long-term loans for banks, known as Targeted Long-Term Refinancing Operations (TLTROs). Volumes were low during the London session across the major currencies as the Bloomberg Dollar Spot Index headed for a seventh day of gains, its longest winning streak in more than three weeks, and Treasuries edged higher. The DXY dollar index barely moved at 96.887.

The Canadian and Australian dollar sank to two-month lows on Wednesday as traders scaled back holdings on expectations policy-makers would leave interest rates alone in the foreseeable future or even lower them to counter their softening economies. Adding to the Aussie’s woes on Thursday was data showing local retailers suffered another bleak month in January, in a sign overall economic momentum was slowing.

Brexit uncertainty kept the pound below an eight-month high hit last week as investors waited for some clarity to emerge out of negotiations between Britain and the European Union. Diplomats said talks in Brussels on Tuesday led by British Prime Minister Theresa May’s chief lawyer, Geoffrey Cox, failed to find common ground, with three weeks to go before Britain’s scheduled departure on March 29.

“Markets are getting conflicting signals from lawmakers in Britain and the negative news flow from Brussels on the negotiation process, and that is keeping the pound in a tight range,” said Nikolay Markov, a senior economist at Pictet Asset Management.

In the latest brexit news, EU officials are reportedly pessimistic about reaching a Brexit breakthrough. Negotiators suspect that whatever they offer will not be enough to get Parliament to back PM May’s Brexit deal; according to sources. Furthermore, Brussels believes that unrealistic expectations have build up in London. EU officials have urged the UK to table fresh proposals within the next 48 hours and said they will work non-stop over the weekend if “acceptable” ideas are received to break the Irish backstop impasse.

In central bank news, Riksbank’s Ingves said the need for a highly expansionary monetary policy has decreased slightly; as inflation has become established close to the target and confidence in the target has increase. Adding that the rate path is a forecast not a guarantee. Separately, BoE’s Tenreyro says a disorderly Brexit is more likely to require loosening of monetary policy than tightening, adding that it is easy to envisage other scenarios which would require a opposing response. Sterling is likely to appreciate after a smooth Brexit, which would limit inflation pressure. Going on to say that a small amount of tightening will be needed over the next 3 years assuming a smooth Brexit.

Elsewhere, oil edged up amid ongoing OPEC-led supply cuts and U.S. sanctions against exporters Venezuela and Iran, although prices were prevented from rising further by record U.S. crude output and rising commercial fuel inventories. U.S. crude futures rose 0.1 percent to $56.29 per barrel, moving closer to its 3-1/2-month high of $57.88 touched Friday, while international benchmark Brent futures gained 0.3 percent to $66.20 per barrel.

Expected data include jobless claims. Costco and Kroger are among companies reporting earnings

Market Snapshot

- S&P 500 futures down 0.2% to 2,765.25

- STOXX Europe 600 down 0.3% to 374.30

- MXAP down 0.6% to 158.66

- MXAPJ down 0.4% to 524.53

- Nikkei down 0.7% to 21,456.01

- Topix down 0.8% to 1,601.66

- Hang Seng Index down 0.9% to 28,779.45

- Shanghai Composite up 0.1% to 3,106.42

- Sensex up 0.3% to 36,747.39

- Australia S&P/ASX 200 up 0.3% to 6,263.89

- Kospi down 0.5% to 2,165.79

- German 10Y yield unchanged at 0.128%

- Euro up 0.02% to $1.1309

- Italian 10Y yield fell 11.4 bps to 2.235%

- Spanish 10Y yield rose 1.5 bps to 1.128%

- Brent futures up 0.9% to $66.55/bbl

- Gold spot little changed at $1,286.50

- U.S. Dollar Index little changed at 96.88

Top Overnight News from Bloomberg

- European Central Bank officials are poised to cut their economic forecasts by enough to justify another round of loans for banks, according to people with knowledge of the matter

- European officials are pessimistic about the chances of a breakthrough in Brexit talks this week, as negotiators suspect that whatever they offer won’t be enough to get Parliament to back Theresa May’s deal

- U.K. Prime Minister Theresa May’s government outlined steps to develop technology to keep the Irish border open after Brexit even if Britain is unable to negotiate a trade deal with the European Union

- The Bank of England doesn’t need to rush to raise interest rates until the uncertainty of Brexit lifts, according to policy maker Michael Saunders. In a speech in London Wednesday, Saunders, considered one of the most hawkish members of the Monetary Policy Committee, said that tame inflation and a slowdown in growth meant officials could adopt a wait-and-see approach as Brexit plays out

- President Donald Trump is pushing for U.S. negotiators to close a trade deal with China soon, as he is concerned that he needs a big win on the international stage — and the stock market bump that would come with it — in advance of his re-election campaign

- Trump said he’d be very disappointed in Kim Jong Un if reports are accurate that North Korea has begun rebuilding a missile test site it dismantled last year

- China has drafted tougher rules for its 12.7 trillion yuan ($1.9 trillion) private fund industry, tightening scrutiny as the government reins in financial risks, according to people familiar with the matter

- Bill Browder has filed a criminal complaint alleging that Swedbank AB handled $176 million connected to the death of Russian lawyer Sergei Magnitsky. The allegations follow separate claims that tie Swedbank to almost $6 billion in suspicious transactions

- A smooth Brexit outcome won’t be enough by itself to justify higher interest rates, according to Bank of England policy maker Silvana Tenreyro, who said she’d wait to see stronger domestic price pressure

Asian stocks were mostly lower following a three-day losing streak on Wall Street where the Dow and S&P fell to a three-week low. ASX 200 (+0.3%) was kept afloat by its telecom and utilities sectors, although upside was capped by the underperformance of its heavyweight metal and mining names. Meanwhile, Nikkei 225 (-0.6%) gave up the 21,500 level as the domestic currency gains weighed on the Japanese index. Semi-conductor name Renesas fell over 15% after Nikkei reported the company is to temporarily halt operations at 13 of its 14 production facilities amid uncertainty in China, thus Japanese chipmakers were hit in sympathy. Elsewhere Hang Seng (-0.9%) and Shanghai Comp. (+0.1%) conformed to the overall risk tone with the former pressured by Geely shares after the company fell over 3.5% amid dismal February sales, moreover the Chinese stocks wobbled after Huawei filed a law suit against the US government, but the indices ultimately came off worst levels.

Top Asian News

- MSCI Urges China to Ease Ownership Limits After Dropping Stock

- China’s Record Tax Cuts Spell ‘Tightest Year’ for Local Regions

- China Said to Mull Tougher Rules on Private Equity, Hedge Funds

- Emerging-Debt Rally Raises Concern as Frontier Borrowers Rush In

- Thai Court Disbands Thaksin-Linked Party That Chose Princess

Major European indices are in the red [Euro Stoxx 50 -0.4%] little changed from opening losses, with no standout under/out-performing index as markets take the lead from a subdued overnight session ahead of upcoming key risk events. Sectors are mixed, with some underperformance seen in material names, with the sector likely weighed on by growth concerns; interestingly, there was a report from a Washington think tank which stated that China’s economy is around 12% smaller than the official figure. Notable movers this morning include, Rio Tinto (-7.3%) who are at the bottom of the Stoxx 600 after being downgraded to sell at Societe Generale. Dialog Semiconductor (-0.8%) are also in the red weighed on by the poor performance of Japanese listed Renesas who fell by 15% following Nikkei reports that the Co. are temporarily halting 13/14 of their production facilities amidst uncertainty in China. Elsewhere, and towards the top of the Stoxx 600 are Melrose (+3.4%) after their FY revenue came in significantly above the prior at GBP 8.605bln vs. Prev. GBP 2.092bln.

Top European News

- BAE Production Surge for $8 Billion in Howitzers Delayed by Army

- Merck KGaA Sees First Growth in Annual Profit Since 2016

- Aviva Drops Most in Three Months; Shore Sees Tough Task for CEO

- U.K. House Prices Rebound With Near 6% Surge in February

In FX, NZD/AUD are marginal G10 outperformers, but largely due to a degree of consolidation, profit taking and short covering following heavy losses. Moreover, extremely rangebound trade overall/elsewhere somewhat flatter the actual extent of the recoveries that only equate to between 0.15-0.2% vs the Usd. Nevertheless, the Kiwi and Aussie have clambered off recent lows to sit a bit more comfortably above 0.6750 and 0.7000 respectively as the Aud/Nzd cross rebounds towards 1.0400.

- CAD – The other main non-US Dollar has also gleaned some much needed traction after yesterday’s post-BoC slide, but remains precarious within a 1.3425-50 range vs the Greenback as attention turns to the upcoming EPR presented by Deputy Governor Patterson that could underscore the more dovish or uncertain outlook in terms of the timing of policy normalisation.

- CHF/EUR/JPY/GBP – All narrowly mixed vs the Greenback, and as noted above all broadly stuck in tight confines with the Franc meandering between 1.0040-55 and single currency rooted to 1.1300, albeit hovering just above the big figure following recent breaches below that threatened a steeper decline. Of course, a dovish ECB later may yet see the Euro buckle completely, but technically it remains resilient vs the Dollar having held above Fib support around 1.1305. Note also, big option expiries could limit moves post-ECB, at least into the NY cut, as 2 bn sits at 1.1250 and a mega 3.7 bn from 1.1360-80, if the ECB disappoints – for a full preview of the March policy meeting check out the Research Suite. Meanwhile, Usd/Jpy looks increasingly capped around 112.00 after several attempted breakouts, but again hefty expiries may keep the headline pair contained given a series of 1 bn options stacked all the way down to 111.25-35 (just above the 200 DMA at 111.39) and 1.5 bn from 112.00-05. Turning to Cable, 1.3200-1.3100 essentially covers the recent range with moves towards the top or bottom correlating closely with the tone regarding ongoing Brexit negotiations.

- SEK/NOK – The Swedish Krona has retreated from circa 10.5000 vs the Eur to a low just shy of 10.5600 in wake of comments from Riksbank Governor Ingves that could arguably be perceived as more ambiguous with regard to guidance for another 25 bp repo rate hike in H1 this year. Conversely, the Nok has not been unduly upset by a significant miss in Norwegian manufacturing output and remains around 9.8000 vs the Eur, perhaps with some support from firmer oil prices.

In commodities, Brent (+0.9%) and WTI (+0.9%) prices are firmer, with the complex likely retracing some of the recent losses from the API and EIA crude builds this week coming in above expectations at 7.4mln and 7.1mln respectively; although both Brent and WTI prices are trading within a tight range of around USD 1/bbl on the lack of fundamentals. In terms of recent news flow Saudi Energy Minister Al Falih has reported crude exports of around 7-8mln BPD. Separately, US State Department official has stated that talks are ongoing with the 8 countries who received a waiver in November, as Washington seeks to lower Iranian oil purchases to zero; alongside, India wanting to continue Iranian oil purchases at around 300k BPD in any waiver extension. Elsewhere, China’s customs union have confirmed that it has suspended canola imports from Canada’s Richardson International. Gold (U/C) is unchanged in a similar vain to the dollar, ahead of key events this week including the ECB rate decision later today. Elsewhere, China’s Hebei province is to reduce steel capacity by 14mln tonnes annually this year and next, in an attempt to improve air quality.

Looking at the day ahead, the data this morning includes February Halifax house price index stats for the UK and the final Q4 GDP revisions for the Euro Area (no change from the +0.2% qoq advanced reading expected). The ECB meeting follows that while in the US we’ve got the latest weekly initial jobless claims reading, final Q4 nonfarm productivity and unit labour costs data and the January consumer credit print. Away from that we’re due to hear from the BoE’s Tenreyro this morning and the Fed’s Brainard this afternoon.

US Event Calendar

- 7:30am: Challenger Job Cuts YoY, prior 18.7%

- 8:30am: Initial Jobless Claims, est. 225,000, prior 225,000; Continuing Claims, est. 1.77m, prior 1.81m

- 8:30am: Nonfarm Productivity, est. 1.5%, prior 2.3%; Unit Labor Costs, est. 1.7%, prior 0.9%

- 9:45am: Bloomberg Consumer Comfort, prior 61

- 12pm: Household Change in Net Worth, prior $2.07t

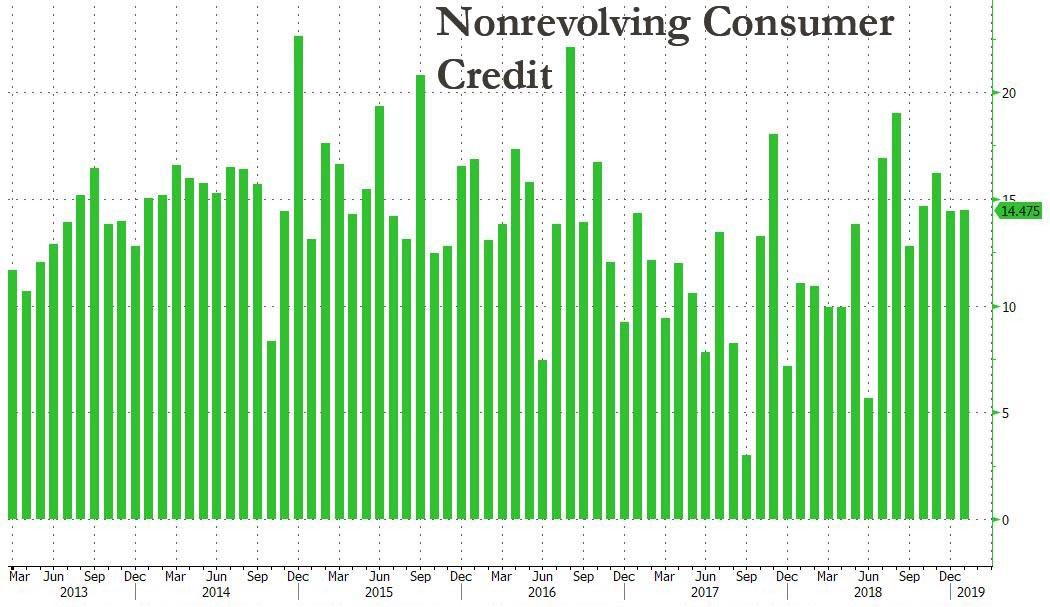

- 3pm: Consumer Credit, est. $17.0b, prior $16.6b

DB’s Jim Reid concludes the overnight wrap

How time flies. As of 8.22pm GMT last night it was officially ten years to the minute that the S&P 500 had hit its famous 2009 intraday low of 666.79. I remember being transfixed by the CNBC stream of unfolding events at home. I remember less as to whether I rung my broker and screamed “buy” at him. The fact that I’m currently worrying about carpets breaking my house renovation budget to a terminal degree suggests I didn’t. Anyway, at that point it was the lowest the index had been since the mid-90s. On a closing basis the low actually came on March 9th 2009 when it hit 676.53. Since that all-time low the S&P is up ‘a mere’ 401% in total return terms although it doesn’t lead the way with the NASDAQ up an even more impressive 557%. Compare that to Europe where the STOXX 600 is up ‘just’ 233%. For credit guys US HY has returned 171% while Treasuries and Bunds have returned just 27% and 40% respectively. There is one market which is negative over the last 10 years and that goes to the Greek Equity market, which is down 41%.

This week hasn’t been quite so interesting, but it should step up a gear into the weekend when we can all enjoy the rest before the upcoming Brexit storm. So we have an ECB meeting to look forward to today, which although will likely be short of any policy changes, should be made all the more interesting by what is or isn’t said on TLTRO. That was certainly given an added focus post Bloomberg headlines yesterday and we’ll touch on those shortly, but just in terms of what our economists expect today, Mark Wall feels like any policy announcement would be a positive surprise. He notes that the latest comments from Council members imply that even the hawks have turned less optimistic. The “patience” mantra is consistent with extending the time commitment to unchanged policy rates for six months. However, the uncertain duration of the economic weakness has the centre of the committee signalling a wait and see approach, in particular with the TLTRO decision. Mark believes that one option for the Council would be to extend forward guidance as a down-payment to buy market goodwill while the ECB examines what it can do and needs to do on TLTROs. More in Mark’s preview here .

Back to the ECB story that hit the wires just after European lunch yesterday on Bloomberg. The main crux of it was that the Council is likely to cut economic forecasts by enough “to justify another bout of loans for banks” but that “a full announcement on new loans may not come” today. Instead, the article suggests that officials are preparing the ground for a new TLTRO but are not yet ready to announce on it. So, similar to Mark’s view.

The talk amongst the floor was that there wasn’t much in the way of new information in the story, both with regards to likely downgraded forecasts and the lack of a TLTRO announcement (it certainly fits with the view of our economists). Indeed, the reaction for equity markets suggested that there is already a reasonable element of this priced in with indices quickly spiking but then reversing just as quickly to end the day broadly lower. That was the case for the STOXX 600, which finished -0.04% and -0.36% off the highs. The DAX (-0.28%) and CAC (-0.16%) also closed in the red although the FTSE MIB (+0.65%) and European Banks (+0.24%) – despite adopting a similar course of travel – did manage to stay onside by the close as markets welcomed a bit more clarity for the two areas that would most directly benefit from further long-term lending.

US markets were on the soft side as Europe closed but got progressively weaker with the S&P 500, DOW and NASDAQ down -0.65%, -0.52% and -0.93% respectively. That’s now 6 down days out of the last 7 for the S&P. That’s the first such stretch of the year, and through three sessions, the S&P 500 is also on track for its worst week of the year. Energy and healthcare did much of the damage in the US, with the former not helped by WTI falling -0.60%. Official US data showed a 7.1 million barrel build in inventories last week, smashing estimates and sparking some worries about fuel demand.

There were positive headlines on the trade front, but they failed to support equities. Bloomberg reported that President Trump is pressuring his trade team to reach a final deal with China soon, in order to support equities. Separately, the South China Morning Post suggested that China will institute new rules to protect foreign investors from forced technology transfers to their Chinese partners, a key area of contention between the US and China in the past. Such a move could help President Trump sell a negotiated deal as a “win.” The same news outlet also reported Trump as saying yesterday that trade talks with China are going well and that either there would be a good deal or it’s not going to be a deal, but I think they’re moving along very nicely.

As equities slid, rates rallied which included some second guessing as to what sort of tone the ECB will deliver today. Bunds rallied -4.2bps, although in fairness, were already a couple of basis points lower prior to the ECB headlines hitting, while yields in Italy, Spain and Portugal were -11.7bps, -4.2bps and -3.6bps lower respectively, positively benefiting from TLTRO hopes. At 2.586%, BTPs are back to testing the January yield lows again, which were then the lowest since July last year. The BTP-Bund spread is also now down to 246bps and within 6bps of the January low. Those moves in Europe, in addition to the oil move and some of the data, also appeared to drag down Treasuries with yields ending -2.4bps lower.

Markets in Asia this morning are following Wall Street’s lead with the Nikkei (-0.88%), Hang Seng (-0.60%), Shanghai Comp (-0.21%) and Kospi (-0.52%) all in the red. Futures on the S&P 500 are also down -0.18%. There hasn’t been much in the way of new newsflow overnight, however, China’s Finance Minister Liu Kun has said that the tax cuts announced this week for 2019 could exceed the proposed plan of CNY 2tn ($298 billion) as the ministry will put tax reduction at the top of its agenda this year. He further added that the government will work to ensure reduction across all the sectors, with a focus on manufactures and small firms.

Back to yesterday, where Brexit talks appear to be heading nowhere very fast again, with officials describing the talks as “difficult.” Prime Minister May has committed to bringing her deal to a parliamentary vote next Tuesday, meaning the UK negotiators have a deadline of Sunday night or Monday morning to seal new details on the deal. Bloomberg reported that if the vote fails next week, May will not re-engage with Brussels for new concessions, meaning the vote on Tuesday is likely the last chance before policymakers turn to an extension of Article 50 request and a scratching of heads as to what comes next. These timelines always seem to shift, but it certainly looks like by this time next week, we’ll know if the March 21-22 EU Summit will be used to finalise the withdrawal agreement or to approve an extension to article 50.

In other news, the highlight of the US data releases yesterday was the ADP employment change reading for February, which came in at a moderately below market 183k (vs. 190k expected), albeit one that is unlikely to move the payrolls expectations dial tomorrow. Also out yesterday was the December trade balance in the US, which confirmed a wider-than-expected deficit of $59.3bn during the month – and notably the widest of the current economic expansion. The widening reflects strong US economic growth and associated demand for imports, as well as more tepid demand abroad, limiting scope for US export growth.

New York Fed President Williams spoke publicly yesterday and provided further confirmation that the Fed is on hold for now. He suggested that the current fed funds rate is right at its neutral level, though he also said that he expects economic growth to be around 2% this year. That suggests that if we get full-year growth of around 2.3% – as DB economists and the FOMC median forecast project – it would likely be enough for him to go back to supporting a rate hike later this year.

Also generating a few headlines yesterday but ultimately not really impacting markets was the OECD’s latest economic forecasts. The biggest downgrades were unsurprisingly made in Europe where 2019 growth for Germany is now expected to be 0.7% compared to previous expectations for 1.6%, and Italy to -0.2% from 1.3%. The latter clearly therefore predicting a recession, which to be fair, it’s already in on a technical definition. World growth this year is expected to be 3.3% compared to the 3.5% forecast made in November.

To the day ahead now, where the data this morning includes February Halifax house price index stats for the UK and the final Q4 GDP revisions for the Euro Area (no change from the +0.2% qoq advanced reading expected). The ECB meeting follows that while in the US we’ve got the latest weekly initial jobless claims reading, final Q4 nonfarm productivity and unit labour costs data and the January consumer credit print. Away from that we’re due to hear from the BoE’s Tenreyro this morning and the Fed’s Brainard this afternoon.

3. ASIAN AFFAIRS

i)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED UP 4.32 POINTS OR 0.14% //Hang Sang CLOSED DOWN 258.15 POINTS OR 0.89% /The Nikkei closed DOWN 140.80 POINTS OR 0.65%/ Australia’s all ordinaires CLOSED UP .28%

/Chinese yuan (ONSHORE) closed UP at 6.7072 AS TRUCE DECLARED FOR 3 MONTHS /Oil UP to 56.84 dollars per barrel for WTI and 65.78 for Brent. Stocks in Europe OPENED RED

ONSHORE YUAN CLOSED UP // LAST AT 6.7072 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7170: / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/USA

3 b JAPAN AFFAIRS

3 C CHINA

China/the globe

A good indicator of the deterioration in the global economy: semiconductor orders from China plunges the greatest since 2008

(courtesy zerohedge)

Beige Book Shocker: “Semiconductor Orders From China Plunged The Most Since The Collapse Of Lehman”

While the latest Beige Book released earlier today carried the usual boring mix of self-serving observations by Fed officials (“slight to moderate” growth in a quarter in which the Atlanta Fed sees GDP plunging to 0.5%) and a handful of enlightening anecdotes, all of which confirmed that the US economy was rapidly slowing as expected with the word “strong” appearing 37 times, compared to 58x in the January and 83x in October while the word “weak-” rose to 34x, up from 13x seven weeks ago and 19x in October, there was one stunner contained in today’s release which may spell serious pain for stocks.

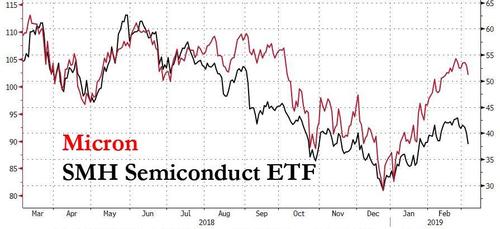

But first we bring your attention to chip and semiconductor bellwether Micron which tumbled as much as 6.2%, its biggest decline in a month, as Wall Street grows increasingly bearish on memory-chip pricing. According to analysis by DRAMeXchange, PC DRAM contract prices will be down a whopping 30% in the first quarter, and since inventory levels are still high, there is little hope of a reversal anytime soon. The Q1 price drop would be the worst since 2011, while a shortage of low-end CPUs is exacerbating the problem, eliminating an avenue for demand growth. “The overall market has thus entered freefall, meaning that large reductions in prices aren’t going to be effective in driving sales,” according to DRAMeXchange.

As a result, Cleveland Research cut its 2019 revenue estimate to $24 billion from $25.5 billion, citing those same DRAM price headwinds.