GOLD: $1309.75 UP $5.45 (COMEX TO COMEX CLOSING)

Silver: $15.28 UP 4 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : $1308.30

silver: $15.23

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING: 1/12

EXCHANGE: COMEX

CONTRACT: APRIL 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,303.500000000 USD

INTENT DATE: 04/09/2019 DELIVERY DATE: 04/11/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

323 H HSBC 3

357 C WEDBUSH 1

661 C JP MORGAN 1

737 C ADVANTAGE 11 4

880 H CITIGROUP 4

____________________________________________________________________________________________

TOTAL: 12 12

MONTH TO DATE: 4,147

NUMBER OF NOTICES FILED TODAY FOR APRIL CONTRACT: 12 NOTICE(S) FOR 1200 OZ (.0373 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 4147 NOTICES FOR 414700 OZ (12.898 TONNES)

SILVER

FOR APRIL

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1 NOTICE(S) FILED TODAY FOR 5,000 OZ/

total number of notices filed so far this month: 758 for 3,790,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

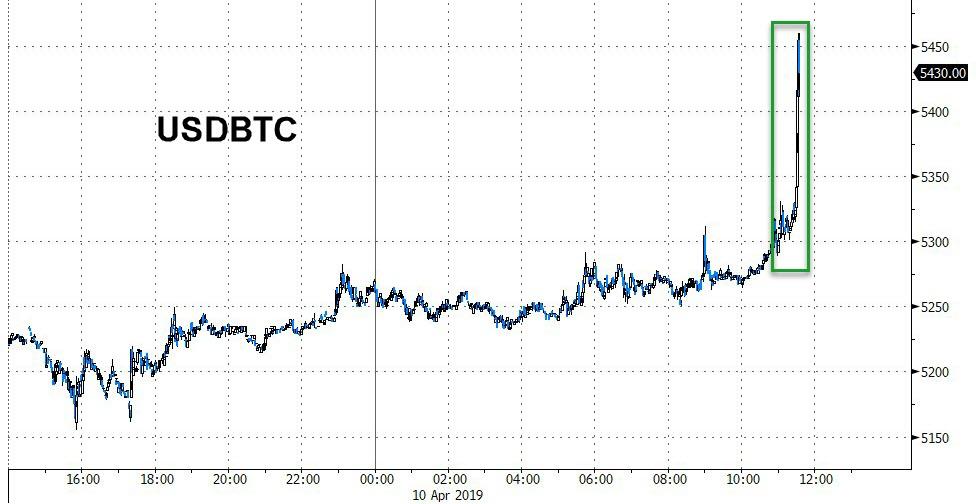

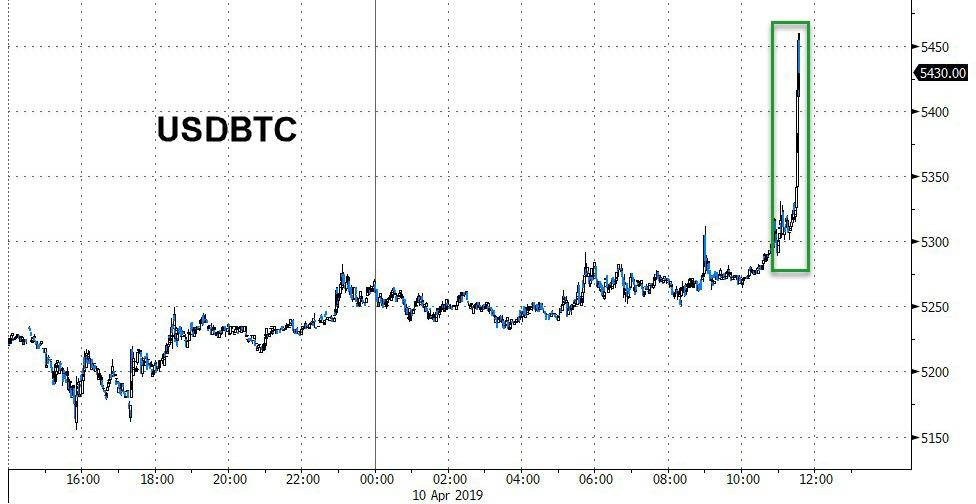

Bitcoin: OPENING MORNING TRADE :$5190 UP $56

Bitcoin: FINAL EVENING TRADE: $5380 UP $230

end

XXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI ROSE BY A STRONG SIZED 2093 CONTRACTS FROM 206,691 UP TO 208,784 DESPITE YESTERDAY’S 1 CENT FALL IN SILVER PRICING AT THE COMEX. TODAY WE ARRIVED CLOSER TO AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS. WE MUST HAVE HAD CONSIDERABLE SHORT COVERING AGAIN TODAY. NO DOUBT THAT THE ENTIRE RISE AT THE COMEX WAS DUE TO THE SPREADERS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A GOOD SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

0 EFP’S FOR MARCH, 0 FOR APRIL, 996 FOR MAY, 397 FOR JULY AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 1383 CONTRACTS. WITH THE TRANSFER OF 1383 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1383 EFP CONTRACTS TRANSLATES INTO 6.915 MILLION OZ ACCOMPANYING:

1.THE 1 CENT FALL IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST NINE MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

AND NOW 3.865 MILLION OZ STANDING FOR SILVER IN APRIL.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF APRIL:

9758 CONTRACTS (FOR 8 TRADING DAYS TOTAL 9758 CONTRACTS) OR 48.79 MILLION OZ: (AVERAGE PER DAY: 1219 CONTRACTS OR 6.098MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF MAR: 48.79 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 6.97% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 621.48 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

RESULT: WE HAD A STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2298 DESPITE DESPITE THE 1 CENT LOSS IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A GOOD SIZED EFP ISSUANCE OF 1383 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A VERY STRONG SIZED: 3681 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 1383 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 2298 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 1 CENT FALL IN PRICE OF SILVER ???? AND A CLOSING PRICE OF $15.24 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAVE A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.997 BILLION OZ TO BE EXACT or 143% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 1 NOTICE(S) FOR 5,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ AND NOW APRIL AT 3.865 MILLION OZ/

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST ROSE AND THIS TIME BY A VERY STRONG SIZED 7884 CONTRACTS, TO 447,539 WITH THE GAIN IN THE COMEX GOLD PRICE/(A RISE IN PRICE OF $6.40//YESTERDAY’S TRADING).

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A SMALL SIZED 2892 CONTRACTS:

APRIL 0 CONTRACTS,JUNE: 2892 CONTRACTS DECEMBER: 0 CONTRACTS, JUNE 2020l 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 447,539. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A VERY STRONG GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 10,776 CONTRACTS: 7884 OI CONTRACTS INCREASED AT THE COMEX AND 2892 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 10,776 CONTRACTS OR 1,077,600 OZ OR 33.52 TONNES. YESTERDAY WE HAD A RISE IN THE PRICE OF GOLD TO THE TUNE OF $6.40….AND YET WITH THAT, WE HAD A HUGE GAIN IN TONNAGE OF 33.52 TONNES!!!!!!.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL : 39,862 CONTRACTS OR 3,986,200 OR 123.96 TONNES (8 TRADING DAYS AND THUS AVERAGING: 4983 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 8 TRADING DAYS IN TONNES: 123.96 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 123.96/3550 x 100% TONNES = 3.49% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 1499.58 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLEDRIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A VERY STRONG SIZED INCREASE IN OI AT THE COMEX OF 7884 WITH THE GAIN IN PRICING ($6.40) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A GOOD SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 2892 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 2892 EFP CONTRACTS ISSUED, WE HAD A STRONG GAIN OF 11210 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

2892 CONTRACTS MOVE TO LONDON AND 7884 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 33.52 TONNES). ..AND ALL OF THIS GOOD DEMAND OCCURRED WITH RISE IN PRICE OF $6.40 IN YESTERDAY’S TRADING AT THE COMEX

we had: 12 notice(s) filed upon for 1200 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $5.45 TODAY

VERY VERY STRANGE AGAIN!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!

ANOTHER BIG CHANGE IN GOLD INVENTORY AT THE GLD

ANOTHER WITHDRAWAL OF GOLD FROM THE GLD: 2.64 TONNES

THE CROOKS NEED THIS GOLD TO PUT OUT DEMAND FIRES HERE AND ABROAD.

WE ARE COMING TO THE BOTTOM OF THE BARREL WITH RESPECT TO PHYSICAL GOLD HELD AT THE GLD.

FOR 4 CONSECUTIVE DAYS WE HAVE HAD GOLD RISE AND ON 4 CONSECUTIVE DAYS GOLD LEFT THE GLD THROUGH WITHDRAWALS.. ACTUALLY GLD HAS HAD 5 CONSECUTIVE WITHDRAWALS AS WE DID HAVE A MINOR WITHDRAWAL WITH GOLD DOWN 90 CENTS ON APRIL 4..

INVENTORY RESTS AT 757.85 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 4 CENTS TODAY:

NO CHANGES IN SILVER INVENTORY AT THE SLV

IT SURE LOOKS LIKE THERE IS NO PHYSICAL SILVER AT THE SLV TO ROB.

/INVENTORY RESTS AT 309.167 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A VERY STRONG SIZED 2093 CONTRACTS from 206,691 UP TO 208,784 AND CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET….. I WROTE THE FOLLOWING ON THURSDAY AND FRIDAY:

“YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST IS STARTING TO RISE IN THIS NON ACTIVE MONTH OF APRIL BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN SILVER WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (MAY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

AND TODAY WAS NO DIFFERENT WITH THE RISE IN OPEN INTEREST AS WE ARE HEADING INTO AN ACTIVE DELIVERY MONTH FOR SILVER..NO DOUBT A CONSIDERABLE AMOUNT OF THE INCREASE WAS DUE TO SPREADERS.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

0 CONTRACTS FOR APRIL., 996 FOR MAY AND JULY: 387 CONTRACTS AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1383 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 2093 CONTRACTS TO THE 1383 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN AN VERY STRONG SIZED GAIN OF 3476 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 17.38 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH. AND NOW 3.865 MILLION OZ FOR APRIL.

RESULT: A STRONG SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE 1 CENT FALL IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A SMALL SIZED 1383 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING/ TUESDAY NIGHT:

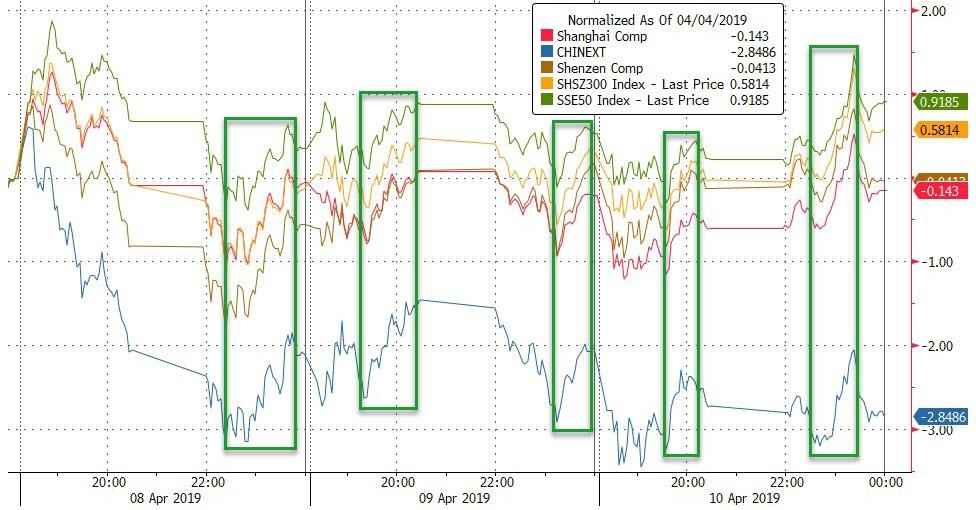

SHANGHAI CLOSED UP 2.27 POINTS OR .07% //Hang Sang CLOSED DOWN 37.93 POINTS OR .13% /The Nikkei closed DOWN 115.02 POINTS OR 0.53%/ Australia’s all ordinaires CLOSED UP .02%

/Chinese yuan (ONSHORE) closed DOWN at 6.7177 AS TRUCE DECLARED FOR 3 MONTHS /Oil UP to 64.43 dollars per barrel for WTI and 70.94 for Brent. Stocks in Europe OPENED GREEN EXCEPT GERMAN DAX

ONSHORE YUAN CLOSED UP // LAST AT 6.7177 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7250 / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A//NORTH KOREA

b) REPORT ON JAPAN

3 China/Chinese affairs

i)China/Greece

Locals are stalling the advancement of the major port at Piraeus, Greece.

( zerohedge)

4/EUROPEAN AFFAIRS

i)/EU/ECB

As expected the ECB is keeping rates unchanged through to the end of 2019.

( zerohedge)

ii)The Euro tumbles after Draghi states again: we will do “whatever it takes”

( zerohedge)

iii) UK

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)Iran/USA

The USA is now targeting Soleimani, leader of Iran’s revolutionary guard as equivalent to an ISIS leader and that means he is an assassination target

( zerohedge)

6. GLOBAL ISSUES

An excellent commentary from Daniel Lacalle. He points out that it is central banks that are driving the world towards a stagnant global zombie economy. It looks like we are repeating what happened in 2008 except one major point:

“The difference with the Asian or the 2008 crisis is that this time the excess risk is hidden under central banks’ balance sheets and will continue to do so.”

a must read…

Daniel Lacalle/DLacalle.com

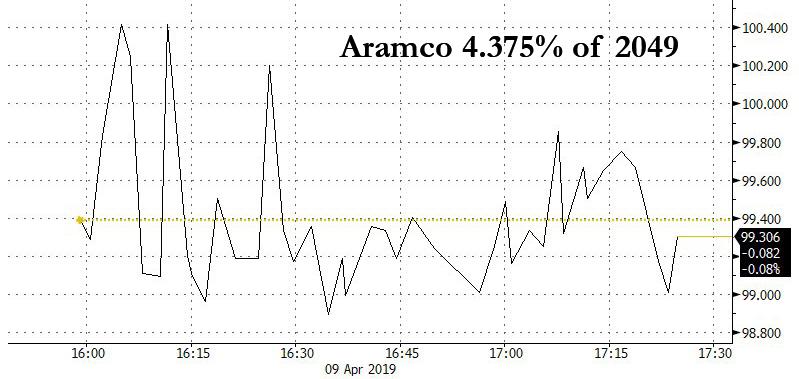

7. OIL ISSUES

Trading in Aramco bonds after initial offering yesterday is a dud. It seems that demand for these bonds were inflated

( zerohedge)

8 EMERGING MARKET ISSUES

i)VENEZUELA

9. PHYSICAL MARKETS

ii))Venezuela removed 8 tonnes of gold and that gold would be sold..most likely to China. Venezuela at the start of the year had about 100 tonnes of gold and at this rate they will be deplete of gold by the end of the year and will have extreme trouble even paying for necessities( Reuters/GATA)

iii)A case of bad money replacing sound money…all the silver coins have disappeared to coin collections and melting.

( Bullionstar/JPKonig/GATA)

10. USA stories which will influence the price of gold/silver)

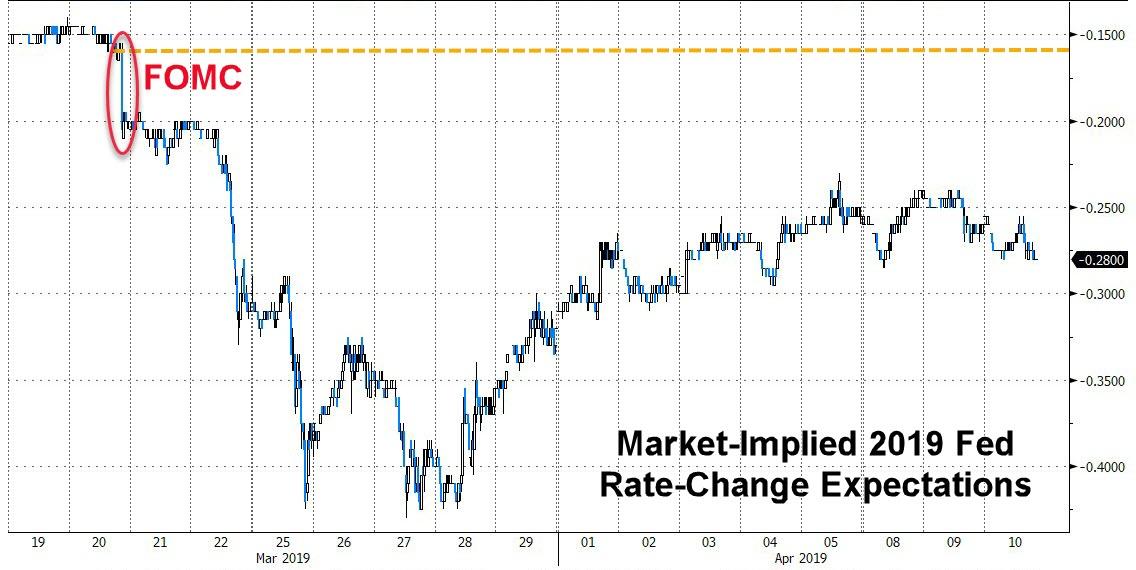

MARKET TRADING//early this morning/FOMC

ii)Market data

ii)USA ECONOMIC/GENERAL STORIES

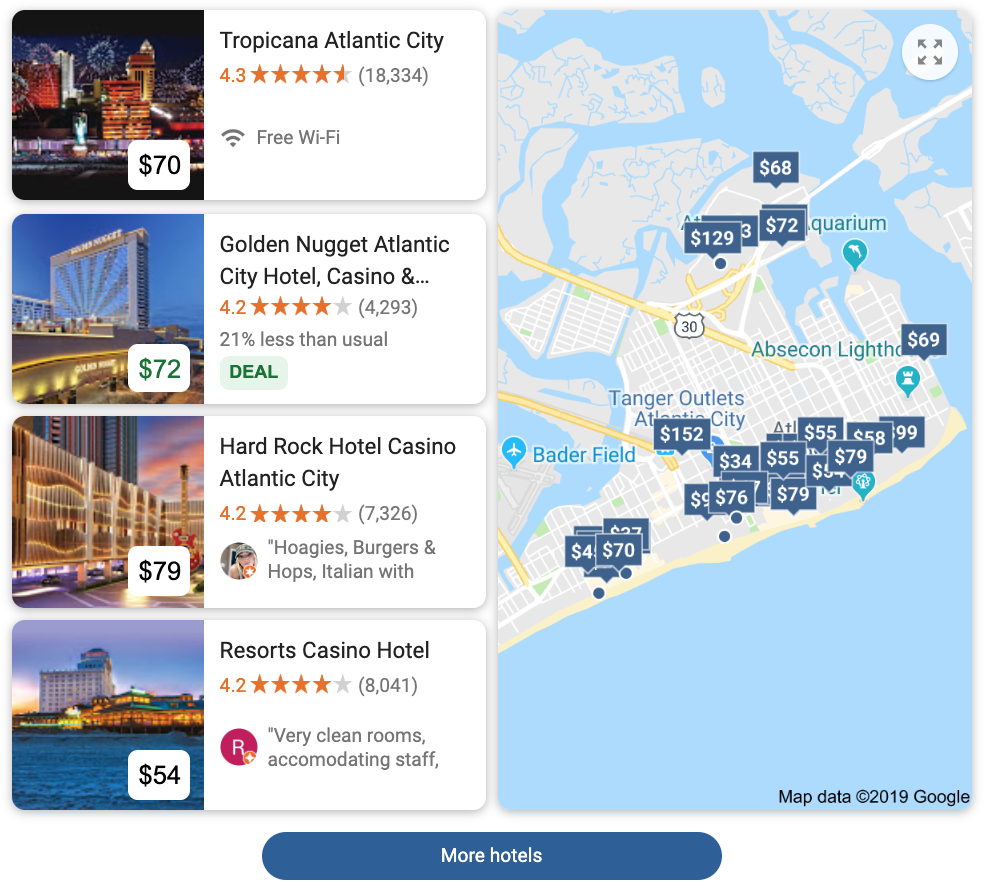

With less discretionary money, one would expect this: casino profits collapse in Atlantic City

( zerohedge)

iv)SWAMP STORIES

a)The beginning to the end of the Democratic crooks as Barr forms an investigate team going after the FBI malfeasance during the 2016 election. Note..the “summer of 2016..he is going after the genesis of the witch hunt

( zerohedge)

end

Let us head over to the comex:

AFTER APRIL, WE HAVE THE ACTIVE DELIVERY MONTH OF MAY AND HERE THE OI FELL BY 4524 CONTRACTS DOWN TO 117,796. CONTRACTS.. THE NEXT MONTH OF JUNE ADDED 16 CONTRACTS TO TOTAL 66. AFTER JUNE, THE VERY BIG DELIVERY MONTH OF JULY HAD A GAIN OF 4856 CONTRACTS UP TO 57,119 CONTRACTS.

i) Out of Scotia: 4,492.847 oz

GATA STORIES WITH RESPECT TO GOLD/PRECIOUS METALS.

Venezuela removed 8 tonnes of gold and that gold would be sold..most likely to China. Venezuela at the start of the year had about 100 tonnes of gold and at this rate they will be deplete of gold by the end of the year and will have extreme trouble even paying for necessities

(courtesy Reuters/GATA)

Gold & Basel 3: A Revolution That Once Again No One Noticed

By Aleksandr Khaldey

Translated by Ollie Richardson and Angelina Siard

cross posted with https://www.stalkerzone.org/basel-3-a-revolution-that-once-again-no-one-noticed/

source: http://www.iarex.ru/articles/65626.html

Real revolutions are taking place not on squares, but in the quiet of offices, and that’s why nobody noticed the world revolution that took place on March 29th 2019. Only a small wave passed across the periphery of the information field, and the momentum faded away because the situation was described in terms unclear to the masses.

No “Freedom, equality, brotherhood”, “Motherland or death”, or “Power to Councils, peace to the people, bread to the hungry, factories to the worker, and land to the farmers” – none of these masterpieces of world populism were used. And that’s why what happened was understood in Russia by only a few people. And they made such comments that the masses either did not fully listen to them or did not read up to the end. Or they did listen to the end, but didn’t understand anything.

But they should’ve, because the world changed so cardinally that it is indeed time for Nathan Rothschild, having crumpled a hat in his hand, to climb onto an armoured Rolls-Royce [a joke referencing what Lenin did – ed], and to shout from on top of it to all the Universe: “Comrades! The world revolution, the need for which revolutionaries spoke about for a long time, came true!” [paraphrasing what Lenin said – ed] And he would be completely right. It’s just that the results of the revolution will be implemented slowly, and that’s why they are imperceptible for the population. But the effects, nevertheless, will be soon seen by absolutely everyone, up to the last cook who even doesn’t seek to learn to govern the state soon.

This revolution is called “Basel III”, and it was made by the Bank for International Settlements (BIS). Its essence is in the following: BIS runs the IMF, and this, in turn, runs the central banks of all countries. The body of such control is called BCBS – the Basel Committee on Banking Supervision. It isn’t just some worthless US State Department or Congress of American senators. It’s not a stupid Pentagon, a little Department of the Treasury, which runs around like the CIA’s servant on standby, or a house of collective farmers with the name “White House”.

This isn’t even the banks of the US Federal Reserve, which govern all of this “wealth”. This is a Government of all of them combined. That real world Government that people in the world try not to speak about aloud.

BCBS is the Politburo of the world, whose Secretary General, according to rumours, is comrade Baruch, and the underground structure of the Central Committee is even more secret. It has many euphemisms, the most adequate of which is “Zurich gnomes”. This is what Swiss bankers are called. Not even owners of commercial banks, but namely those ordinary-looking men sitting in the Swiss city of Basel who Hitler – who tried to attach the whole world to the Third Reich, and who preserved neutrality with Switzerland during all the war – didn’t dare to attack. And, as is known, in Switzerland, besides Swiss rifleman, in reality there isn’t even an army. So who was the frenzied Fuhrer afraid of?

Nevertheless, the “recommendations” that were made by BCBS on March 29th 2019 were immediately, at the snap of the fingers, accepted for execution by all the central banks of the world. And our Russian Central Bank is not an exception. There is even the statement of the press service of the Central Bank of the Russian Federation posted on the official website of the Central Bank. It is called “Concerning the terms of implementation of Basel III”. The planned world revolution was in 2017 (magic of dates and digits or just a coincidence [a reference to 1917 – ed]?), but it has started only now.

Its essence is simple.

In the world the system of exclusive dollar domination established in 1944 in Bretton Woods and reformed in 1976 in Jamaica, where gold’s equivalency to money was cancelled. The dollar became world money and gold became an ordinary exchange good, like metal or sugar traded in London on commodity exchanges. However, this was determined there by only three firms of the “Pool of London” that belong to an even smaller number of owners, but, nevertheless, it’s not gold, but oil that became the dollar filler.

We have lived in such a world ever since. Gold was considered as a reserve of the third category for all banks, from central to commercial ones, where the reserves were, first of all, in dollars and bonds of the US. The norms of Basel III demand an increase, first of all, in monetary reserves. This impeded the volumes of monetary resources of banks that could be used to carry out expansion, but it was a compulsory measure for saving the stability of a world banking system that showed to be insufficient in a crisis.

In Russia pseudo-patriots were very much indignant at this, demanding to reject Basel III, which they called a sign of “a lack of sovereignty”. In reality, this is a quite normal demand to observe international standards of bank security, which were becoming more rigid, but since we [Russians – ed] were not printing dollars, so of course it had an impact on us. And since the alternative is an exit from world financial communications into full isolation, so our authorities, of course, did not want to accept such nonsense that was even designated by pseudo-patriots as a “lack of sovereignty”. To call sovereignty – freedom, to put your head in the noose is, let’s agree, a strange interpretation of the term.

The Basel III decision meant that gold as a reserve of the third category was earlier estimated at 50% of its value on the balance sheets of world banks. At the same time, all owners of world money traded in gold not physically, but on paper, without the movement of real metal, the volume of which in the world wasn’t enough for real transactions. This was done in order to push down the price of gold, to keep it as low as possible. First of all, for the benefit of the dollar. After all, the dollar is tied to oil, which had to cost no less than the price of one gram of gold per barrel.

And now it was decided to place gold not in the third, but “just” in the first category. And it means that now it is possible to evaluate it not at 50, but at 100% of its value. This leads to the revaluation of the balance sheet total. And concerning Russia, it means that now we can quietly, on all legal grounds, pour nearly 3 trillion rubles into the economy. If to be precise, it is 2.95 trillion rubles or $45 billion at the exchange rate in addition to the current balance sheet total. The Central Bank of the Russian Federation can pour this money into our economy on all legal grounds. How it will happen in reality isn’t yet known. Haste here without calculating all the consequences is very dangerous. Although this emission is considered as noninflationary, actually everything is much more complicated.

During the next few months nothing will change in the world. The U-turn will be very slow. In the US the gold reserves officially total 8133.5 tons, but there is such a thing as a financial multiplier: for every gold dollar, the banks print 20-30 digital paper ones. I.e., the US can only officially receive $170 billion in addition, but taking into account the multiplier – $4.5 trillion. This explains why the Federal Reserve System holds back on increasing interests rates and so far maintains the course towards lowering the balance sheet total – they are cautious of a surge in hyperinflation.

But all the largest states and holders of gold will now revalue their gold and foreign exchange reserves: Germany, Italy, France, Russia, China, and Switzerland – countries where the gold reserves exceed 1,000 tons. Notice that there is no mumpish Britain in this list. Its reserves are less than 1000 tons. Experts suspect that it is perhaps not a coincidence that the dates of Brexit and the date of Basel III coincide. The increased financial power of the leaders of Europe – Germany and France – is capable of completely concluding the dismantlement of Britain on the European continent. It was necessary to get out as soon as possible.

Thus, it seems that it is possible to congratulate us – the dollar era lasting from 1944 to 2019 has ended. Now gold is restored in its rights and is not an exchange metal, but world money on an equal basis with the dollar, euro, and British pound. Now gold will start to rise in price, and its price will rise from $1200-1400 per troy ounce up to $1800-2000 by this autumn. Now it is clear why Russia and China during all these years so persistently decanted its export income into the growth of gold reserves. There is now such a situation where nobody in the world will sell gold.

Injections of extra money will suffice for the world economy for 5-6 months. In the US this money can be used to pay off the astronomical debt. Perhaps this wasn’t Zurich’s last motive for making such a decision. But after all, the most important thing is an attempt to slip out from under the Tower of Pisa that is the falling dollar.

Since the dollar and oil are connected, the growth of the price of gold will directly affect the growth of the price of oil. Now a barrel costs as much as 1.627 grams of gold. A price growth will cause the world economy – where 85% of the money dollar supply turns into stock surrogates like shares, bonds, and treasuries – to cave in. The stock exchange will not be able to bundle together such an additional mass of money any more.

It will be good for oil industry workers – even, perhaps, best of all, but not for long. The economical crash because of expensive oil will become a crash for all oil industry workers too. It is precisely this that is the main reason why our rights for additional emissions can remain unused in full volume, although a gift in such a form will not be completely ignored. The May ‘Decrees of Putin’ in the current context are being understood completely differently. Russia runs away from the oil-based economic model in all ways. Including by political reforms and changing the elites.

However, why is the decision of Basel a revolution?

Because from the autumn the financial flood in the world economy will begin. It will entail the acceleration of Russia and China’s isolation from the dollar system and the crash of the economies that completely depend on the dollar – the vassal countries of the US. It will be worst of all for them. And this means that the reasons for increased distancing between the EU and the US will increase in number manyfold.

A redrawing of the map of global unions awaits the world.

And the redrawing of these unions will be carried out not least by military methods. Or with their partial use, but in one way or another, reasoning involving force in the world will increase almost to the level of guaranteed war. “Almost” is our hope for rescue, because the US loses all main instruments of influence on this world. Except force.

But it’s not for this purpose that the “Zurich gnomes” created this world, so that the US is so simply turned into radioactive ashes. The US will be drenched with cold water like a broken down nuclear reactor, while the world has entered the zone of the most global transformations over the past few centuries. The revolution that so many waited for, were afraid of, and spoke so much about has started. Buckle up and don’t smoke, the captain and crew wish you a pleasant flight.

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

* * *

Your early WEDNESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED/ LAST AT: 6.7177/

//OFFSHORE YUAN: 6.7250 /shanghai bourse CLOSED UP 2.27 or .07%

HANG SANG CLOSED DOWN 37.93 points or .13%

2. Nikkei closed DOWN 115.02 POINTS OR 0.53%

3. Europe stocks OPENED GREEN

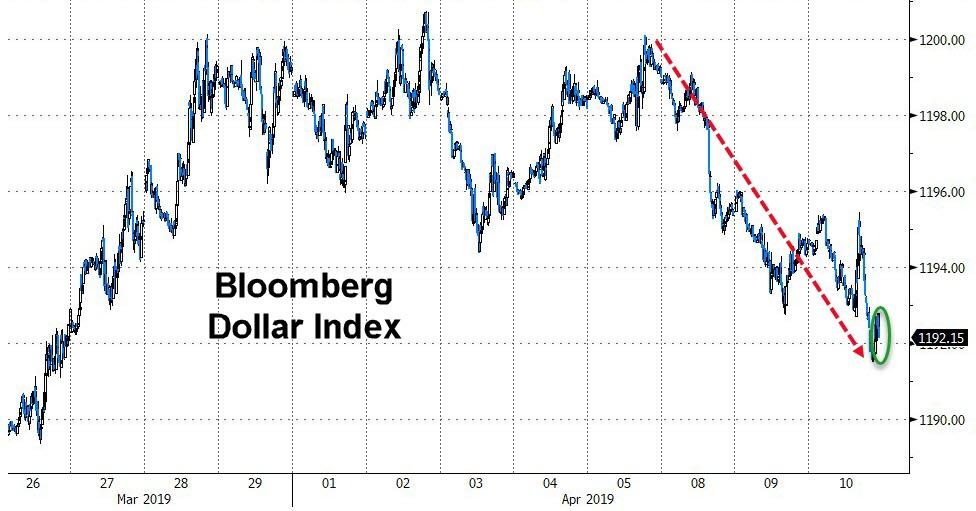

USA dollar index FALLS TO 96.94/Euro RISES TO 1.1275

3b Japan 10 year bond yield: FALLS TO. –.05/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 111.21/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//CARRY TRADERS GETTING KILLED

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 64.43 and Brent: 70.94

3f Gold DOWN/JAPANESE Yen DOWN CHINESE YUAN: ON -SHORE DOWN /OFF- SHORE: DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +00%/Italian 10 yr bond yield DOWN to 2.40% /SPAIN 10 YR BOND YIELD DOWN TO 1.06%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.40: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 3.44

3k Gold at $1303.35 silver at:15.26 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 25/100 in roubles/dollar) 64.69

3m oil into the 64 dollar handle for WTI and 70 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 111.21 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 1.0004 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1281 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now NEGATIVE territory with the 10 year FALLING to +0.00%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.50% early this morning. Thirty year rate at 2.91%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.6911..GETTING DANGEROUS

Stocks Bounce Ahead Of Wednesday’s Data Deluge

One day after the equity rally sputtered following Trump’s threat to impose new tariffs against the EU, global stocks are once again green across the board even as a barrage of critical economic, political and central bank events – including the ECB’s rate decision, the FOMC minutes, the Brexit-related EU Council meeting and US CPI data – is on deck and earnings season is set to begin in two days. Stocks in Europe rose, Asia was mixed, while US equity futures jumped to session highs, while Treasuries were mixed and the dollar dipped.

Europe’s Stoxx 600 index rose for the first time in three days, led by miners and oil companies, while Emini futs edged 8 points higher and just 10 points away from 2,900 as investors ignored the Trump administration’s threat of new tariffs on European goods and the IMF’s worst growth forecasts since the financial crisis. Network International shares surged in London after the payments processor raised 1.1 billion pounds ($1.4 billion) in Europe’s biggest IPO this year.

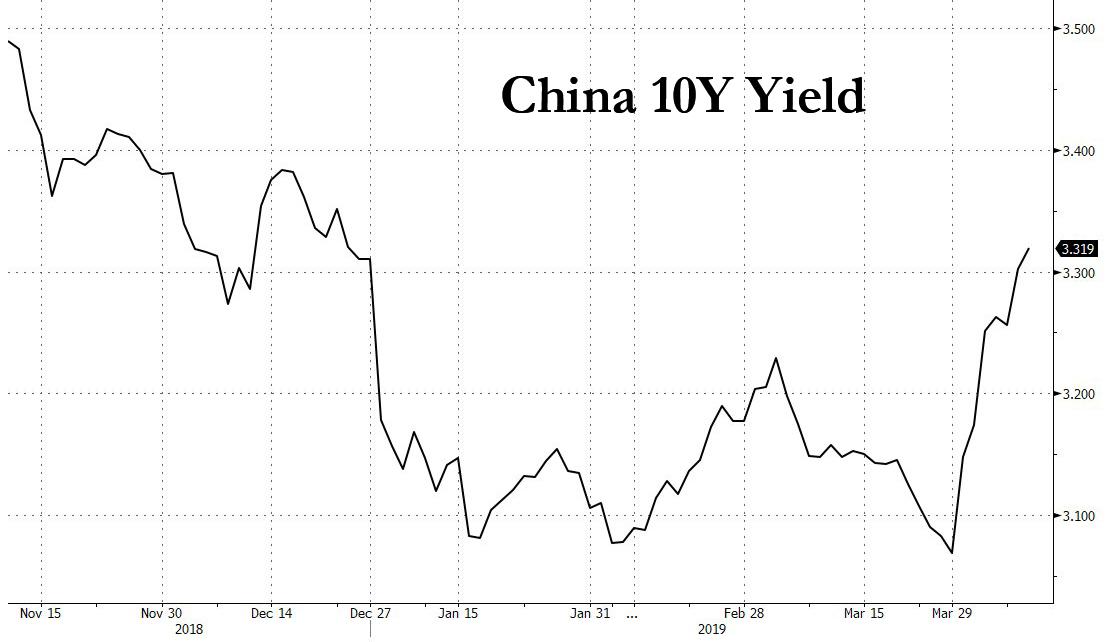

Earlier in the session, MSCI’s index of Asia-Pacific shares ex-Japan dropped 0.1%, a day after rising to its highest since Aug. 1, as shares fell in Japan and Hong Hong Kong earlier, while Chinese and Korean equities rose. Ten-year Treasury yields were stuck at 2.5%, but its yields in China that grabbed attention again, as China’s 10-year sovereign bond yield rose 3bps to 3.33%, the highest level since Dec. 24.

Sentiment rebounded from a Tuesday hit, when the IMF’s somber report on global growth highlighted fears about the outlook for the world economy that have simmered for months, while the U.S. appeared to open another front in its trade dispute with the European Union, and negotiations with China remain unsettled. Federal Reserve minutes, American inflation data and the ECB rates decision Wednesday could add to anxieties or help provide calm, with investors also focusing on the first-quarter earnings season getting under way this week.

With the rally fizzling, analyst commentary turned more sour:

- “Before we preview those, risk assets have been threatening to take their foot off the pedal in recent sessions and yesterday we finally saw that with a delayed reaction to the US/EU tariff headlines from yesterday’s Asian session seemingly doing much of the damage” said Deutsche Bank’s chief market strategist Jim Reid.

- “It’s quite a tricky environment because clearly the economy isn’t in great shape,” Patrik Schowitz, global multi-asset strategist at JPMorgan Asset Management, told Bloomberg TV in Hong Kong. “Central banks going into easing mode, the Fed pivot — that would not be happening if the economy was firing on all cylinders. At the same time, recession risks are overdone.”

Much of today’s attention will be on the ECB which is “going to come out with some more details on the TLTRO,” said Francois Savary, chief investment officer at Prime Partners. “The global picture has been set, now we are waiting for the details about what they do and if they are going to speak maybe about the adjustment of the negative interest rate policy on reserves.”

Israeli stocks and the shekel climbed as Benjamin Netanyahu looks set for a fifth term as prime minister. Turkey’s lira fluctuated as the government announced plans to bolster banks, while emerging-market stocks climbed for a 10th day, extending their longest run since January 2018.

Elsewhere, global debt yields held mostly steady, with the 10-year German Bund yield little changed around the zero percent mark. As a reminder, overnight Saudi Aramco sold $12 billion in debt with its first international bond issue after getting more than $100 billion in orders. It was a record-breaking vote of confidence by investors despite the murder of Saudi journalist Jamal Khashoggi in October.

Ahead of the ECB and US CPI print, major currencies are little changed before a European Union summit and the ECB meeting. The euro edged higher and the pound gained as the EU looks to delay Brexit by as long as a year. The Bloomberg Dollar Spot Index erased its Asia-session advance as the market awaits U.S. inflation data and minutes of the Federal Reserve’s latest review. Norway’s krone reached its strongest level in five months against the euro after the nation’s inflation rate rose at the fastest pace since 2016, boosting the case for interest-rate increases. Australia’s dollar rose against all its Group-of-10 peers except the krone after Deputy Governor Guy Debelle suggested the central bank is in no rush to cut rates despite slowing global growth.

Elsewhere, EU leaders are likely to grant British PM Theresa May a second delay to Brexit, but they could demand a much longer extension as France pushed for conditions to limit Britain’s participation in EU affairs. The British pound rose to session highs, inching close to $1.31 again. The dollar was flat at 111.19 yen, having fallen 0.5 percent so far this week.

In commodities, oil prices remained near Tuesday’s five-month highs as fighting in Libya raised supply disruption concerns. U.S. crude futures stood at $64.32 per barrel, up 0.3 percent after rallying to a five-month high of $64.79 on Tuesday. Brent crude futures were at $70.81 per barrel and in reach of Tuesday’s five-month peak of $71.34.

Expected data include mortgage applications, inflation and Fed minutes. Delta Air Lines and Bed Bath & Beyond are among companies reporting earnings

Market Snapshot

- S&P 500 futures up 0.3% to 2,890.50

- STOXX Europe 600 up 0.2% to 386.51

- MXAP down 0.2% to 163.14

- MXAPJ up 0.1% to 544.21

- Nikkei down 0.5% to 21,687.57

- Topix down 0.7% to 1,607.66

- Hang Seng Index down 0.1% to 30,119.56

- Shanghai Composite up 0.07% to 3,241.93

- Sensex down 0.5% to 38,737.95

- Australia S&P/ASX 200 up 0.03% to

- German 10Y yield rose 0.4 bps to -0.006%

- Euro up 0.04% to $1.1268

- Italian 10Y yield fell 6.0 bps to 2.072%

- Spanish 10Y yield fell 0.9 bps to 1.066%

- Brent futures up 0.4% to $70.91/bbl

- Gold spot little changed at $1,304.50

- U.S. Dollar Index little changed at 96.98

Top Overnight News from Bloomberg

- EU leaders will finalize the length of the Brexit delay at a summit on Wednesday. European Council President Donald Tusk wants them to agree to an extension of up to a year, and diplomats from member states say the debate now is between December and next March for the new departure date.

- ECB policy makers have a lot to ponder over — the U.S. has set off a fresh tariff threat, Italy’s government has almost given up on growth this year, and Brexit remains unresolved. On top of that, the International Monetary Fund on Tuesday cut its global outlook yet again. No policy shift is expected as officials scrutinize the economy to calibrate a new bank lending program announced last month.

- In what could be this year’s largest U.S. IPO, investors could get their first look at hundreds of pages of detailed information about Uber Technologies Inc. as soon as Thursday. As the ride-hailing giant gears up to publicly file for an IPO, with one of the people familiar said the company was looking to raise about $10 billion.

- Brexit anxiety is seeing South Korean borrowers sell Swiss franc bonds at a record pace. They are taking advantage of increased demand from European investors for such notes on expectations that Switzerland will be largely insulated from Brexit-related trouble in the region, according to UBS Group AG.

Asian equity markets were mostly negative amid spill-over selling from Wall St where all majors finished lower and the S&P 500 snapped an 8-day win streak as sentiment was pressured by EU-US trade tensions and downward revisions to IMF’s global growth forecasts. ASX 200 (U/C) was initially subdued with the energy sector pressured by a pullback in oil prices and with heavy losses seen in Crown Resorts after Wynn Resorts abruptly ended takeover talks, although the index has since pared its losses amid strength in gold miners, tech and the largest weighted financials sector. Nikkei 225 (-0.5%) suffered from the recent flows into JPY and disappointing Machine Orders, while Hang Seng (-0.1%) and Shanghai Comp. (U/C) conformed to the global downbeat risk tone amid further PBoC inaction and as participants awaited upcoming central bank activity and any fresh developments in the US-China trade saga. Finally, 10yr JGBs were marginally higher as they tracked gains in T-notes amid the risk averse tone across the region, while the BoJ were also present in the market with today’s Rinban operation heavily focused on the belly.

Top Asian News

- Top China Investor Only Has Eyes for One Mainland Stock

- CLSA Culture Clash Boils Over as More Top Executives Quit

- Singapore Bans Former HSBC, UOB Bankers for Fraud, Dishonesty

- Untouchable in 2018, China Bank Stocks Are Now All the Rage

- Turkey to Bolster State-Owned Banks in Bid to Revive Economy

Major European indices have been drifting higher [Eurostoxx 50 +0.5%] since the open following on from a downbeat Asia-Pac session where equity markets conformed to the negativity seen on Wall Street. European bourses are mostly higher by around 0.2-0.3% whilst the FTSE 100 (Unch) remains the laggard ahead of the crucial Brexit summit set to take place later today. Broad-based gains are seen across most sectors, although some underperformance is experienced in healthcare names. JP Morgan (from today’s note) believe that the consumer sector is currently the most oversold sector in Europe whilst autos “may be seeing tentative signs of recovery”. Furthermore, analysts at JPM think that the banking sector continues to look cheap and “continued underperformance means valuations remain extreme historically, notably on dividend yields where the sector now offers a 2% yield pick-up versus the market”. In terms of notable movers, UK’s Indivior (-72%) wiped out around three-quarters of its market cap (so far) after the US DoJ said the Co. has been charged with having engaged with fraudulent marketing schemes designed to increased opioid-based drug prescriptions. Finally, Tesco (+0.6%) shares rose after the supermarket raised its dividend, despite reporting below-forecast sales figures.

Top European News

- U.K. Economy Set for Strong Quarter as Output Rises in February

- Italy Government Turns on Itself as Forecasts Confirm Stagnation

- Network International Jumps After $1.4 Billion London IPO

- Deutsche Boerse Buys Axioma for $850 Million, Adds Analytics

In FX, NOK and AUD were the major outperformers and outliers, as Norwegian inflation slowed less than expected in March to underpin H2 Norges Bank rate hike guidance after yesterday’s disappointing GDP data raised a few doubts. Meanwhile, RBA deputy Governor Debelle was less dovish than anticipated earlier, with little sign of leaning towards an ease even though he acknowledged conflicting economic trends via strength in jobs vs weakness in consumption and production. Eur/Nok is testing technical support around 9.5900 and Aud/Usd is back up near 0.7150 after retreating to circa 0.7110 at one stage overnight. Note, however, hefty option expiry interest may hamper the Aussie given 1.5 bn sitting between 0.7145-25 and 1 bn from 0.7100 to 0.7090.

- NZD/GBP – The next best of the G10 bunch, as the Kiwi continues to largely track its Antipodean peer on cross consolidation within a 1.0595-43 range and while Aud/Nzd remains capped ahead of 1.0600. Nzd/Usd is back above 0.6750 ahead of US CPI data and the FOMC minutes that together with the ECB meeting and EU Brexit Summit form the key elements of ‘super Wednesday’. On that note, the Pound is underpinned towards the top end of 1.3085-45 trading parameters vs the Greenback after above consensus UK data in the form of GDP, ip, manufacturing and construction output, but will be prone to what evolves from the aforementioned EU gathering and especially the decision whether to grant Britain more breathing space, how much longer and on what terms etc.

- EUR – Also firmer vs the Dollar as the DXY continues to pivot 97.000, but like the index extremely rangebound just shy of Tuesday’s high and above 1.1250. Eur/Usd is still facing pre-1.1300 big figure resistance as 21 and 31 DMAs lie at 1.1280 and 1.1284 respectively, while expiries are also keeping the headline pair relatively contained (1.3 bn at 1.1245-50 and 2 bn at 1.1260-75). As noted, the ECB meeting looms and a full preview is available via the headline feed and Research Suite section.

- CAD/JPY/CHF – All narrowly mixed vs the Usd as the Loonie flits between 1.3320-41 and Yen trades just below 111.00 after a fractional/fleeting breach yesterday fell short of the 100 DMA (110.90). Weak Japanese machine orders and more dovish BoJ commentary courtesy of Governor Kuroda also in the mix along with decent expiry interest just under 111.00 at 110.90-75 (1.7 bn). Meanwhile, the Franc is back on the parity handle awaiting the impending major events.

- EM – The Rand has appreciated further against the Buck and is now testing 13.9700 having cleared the psychological 14.0000 mark, but the Lira continues to struggle amidst the post-regional election results tussle with little support from the eagerly-awaited Turkish Economic plan. Indeed, Usd/Try is still elevated, albeit closer to the base of a 5.7200-6700 band.

In commodities, WTI (+0.7%) and Brent (+0.6%) prices continue climbing despite the wider-than-forecast build in API crude inventories last night (+4.09mln vs. Exp. +2.3mln) where prices saw marginal short-lived downside in the immediate aftermath. Supply woes continue to provide a short-term bullish outlook for the complex with sources stating that Libyan air force undertook airstrikes on military targets for Haftar in the City of Gharyan, in close proximity of the pipeline connecting the El-Feel (340k bpd) oil field to the Zawiya port. Elsewhere, the UAE Energy Minister emerged on the wires, stating that there is a high probability of achieving market balance by the end of this year. It is worth keeping in mind that Russian Energy Minister Novak previously stated that Russia will not extend cuts if the market is expected to be balance in H2 2019. Finally, energy traders will be keeping an eye on the OPEC monthly report which is due to be release at 12:10 BST ahead of the weekly DoE inventory and production data at 15:30 BST. Gold (+0.1%) is essentially flat and trading within a narrow range just above the key USD 1300/oz level, as the yellow metal continues to trade cautiously ahead of today’s ECB decision, FOMC minutes & emergency Brexit summit, whilst copper similarly trades with no firm direction ahead of these key risk events. Separately, sources report that Venezuela removed eight tonnes of gold from its central bank’s vaults, expectations are that Venezuela are to sell the metal in order to generate funds in response to US sanctions.

US Event Calendar

- 7am: MBA Mortgage Applications, prior 18.6%

- 8:30am: US CPI MoM, est. 0.37%, prior 0.2%; CPI Ex Food and Energy MoM, est. 0.2%, prior 0.1%

- US CPI YoY, est. 1.8%, prior 1.5%; CPI Ex Food and Energy YoY, est. 2.1%, prior 2.1%

- Real Avg Hourly Earning YoY, prior 1.9%; Real Avg Weekly Earnings YoY, prior 1.58%

- 2pm: FOMC Meeting Minutes

- 2pm: Monthly Budget Statement, est. $181.0b deficit, prior $208.7b deficit

DB’s Jim Reid concludes the overnight wrap

With less than two weeks until I move house after a 2-year project, yesterday my wife went to the house and learnt that our newly installed front door has been accidentally made 2cm too small. It may not sound a lot but everything now is all out of alignment with the surrounds and there’s a sizeable gap!! A bit like trouser legs that need to be taken down. Unbeknown to me there were numerous stressful meetings on site yesterday with my wife and the builder working out what to do about it. No agreement could be made and like Brexit, talks resume today. Unlike Brexit we can’t extend our membership of the rental accommodation and there will be a hard rentexit in a couple of weeks whether we have doors, windows, toilets, showers or a working kitchen in the new place or not. It’s touch and go on a number of these at the moment.

It’s a busy day to keep my mind off these stresses as today sees the quadruple whammy of an ECB meeting, the Brexit-related EU Council meeting, the US CPI report and FOMC minutes to look forward. Before we preview those, risk assets have been threatening to take their foot off the pedal in recent sessions and yesterday we finally saw that with a delayed reaction to the US/EU tariff headlines from yesterday’s Asian session seemingly doing much of the damage. Bloomberg reported that the EU is preparing retaliatory tariffs which will do little to appease the situation. The EU called the US complaint “greatly exaggerated” and Airbus said the US’s move was “totally unjustified.” Barbara Boettcher published a new note examining the tariff threats (link here ), where she argues that the proposed measures are small, but that risks are elevated moving forward, especially as we await the Section 232 decision on auto tariffs.

The S&P 500 (-0.59%) finally brought to an end an eight-session consecutive winning run with cyclical sectors like energy, industrials and financials really feeling the pinch. The DOW (-0.72%) and NASDAQ (-0.56%) also closed in the red while in Europe there was a fairly heavy fall for the DAX (-0.94%) while the STOXX 600, which in fairness traded higher in the early going, ended down -0.47%. An across the board global growth downgrade from the IMF also hurt sentiment although they were only catching down to more regularly updated street forecasts.

Credit didn’t struggle quite so much with HY spreads just +2bps wider in the US and flat in Europe. Meanwhile rates nudged lower, as Treasuries again flirted with the 2.50% level before ending -2.2bpts lower at 2.501% (down -1.3bps this morning to 2.487%). Bund yields fell back down to -0.01%. Interestingly 10yr BTPs rallied -6.2bps in spite of sharp downgrades to growth from the Government and the IMF and an increase in the forecast deficit from the former (see details later) which could raise tensions with the EC again. However in a way it was good to see Italy trade like a conventional government bond and rallying on weak economic news, rather than a more risky credit as it often does.

EM FX was mostly flat, though the Argentine peso (+0.87%) outperformed sharply. WTI Oil (-0.48%) gave back some of Monday’s gains after Russian President Putin said that he opposes “uncontrollable” increases in oil prices which would negatively impact the non-energy parts of Russia’s economy. He also talked about coordination with Opec, possibly hinting that he would not support a new round of production cuts.

This morning in Asia markets are largely following Wall Street’s lead with the Nikkei (-0.60%), Hang Seng (-0.42%) and Shanghai Comp (-0.39%) all down while the Kospi (+0.12%) is up on the back of news that the South Korean government is planning to draw up a supplementary budget of up to KRW7tn ($6.1bn) to support the slowing economy. Elsewhere, futures on the S&P 500 are trading flat (+0.03%). In terms of overnight data releases, Japan’s March PPI came in at +1.3% yoy (vs. +1.0% yoy expected) while February core machine orders came in at -5.5% yoy (vs. -4.6% yoy expected).

We should mention that yesterday our China Chief Economist Zhiwei Zhang published a short update on the property and land markets in China. He notes that while the land market remained weak in Q1, there are green shoots of signs of stabilisation that are now emerging. He expects more policy easing in the land and property markets in Q2 and a rebound in land sales in H2. This fits in with the narrative of our HouseView that although growth is weak, we’d expect momentum is actually improving. See his full report here .

In terms of the ECB today our economists published their expectations last week in a note you can find here . In summary, following an underwhelming message last month, they see the ECB press conference as an opportunity to inject confidence into the economy and the monetary policy process. They see there being two steps necessary to correcting. The first is for the ECB to talk up the economy and the second is clarification around the reaction function and talking up policy. From the perspective of managing risk, TLTRO3 is not sufficient in our colleague’s view and they now expecting tiering as part of their baseline in the coming months, however it’s unlikely that any new policy will be announced today with June more likely.

As for the FOMC this evening, expect the minutes to shed some light on what sets of conditions compel the Fed to shift from its decidedly neutral policy stance – in either direction. Prior to this we get the March CPI report in the US where the consensus is for a +0.2% mom core reading which would be enough to hold the annual rate steady at +2.1% yoy. Our US economists mirror the consensus.

It’s another crucial day for PM Theresa May with the emergency EU Council meeting deciding the UK’s EU membership extension request. How many more of these crucial days are we going to have before this saga ends? In terms of timing, leaders are due to arrive at 5pm CET (4pm BST) with the working dinner and meeting with PM May not taking place until 6.30pm CET. Tusk and Juncker are then due to host a press conference once the meetings finish however it’s anyone’s guess as to when that might be. We’d imagine there’s a reasonable bid-offer for that market.

There wasn’t a huge amount of new Brexit news to update going into that meeting. The press seems to be suggesting an extension to the end of 2019 (or March 2020) is the most likely take it or leave it offer from the EU, though there may be appetite for a short extension through May 22 if the UK passes the WA over the next two days and maybe the ability to cut short the extension if an alternative agreement can be found further down the line. EU Council President Tusk said in statement that “a rolling series of short extensions” would create “new cliff-edge dates,” seeming to argue in favour of a long extension. He was responding to the desire by some in the EU to insert rolling good behaviour clauses in any long extension.

Staying with the UK, yesterday the IMF cut its growth outlook to 1.2% this year which was a downward revision of -0.3pp from three months ago. The growth rate of the world economy was revised down two tenths to 3.3% which would be the weakest rate of growth since 2009. That is also the third downward revision in the last six months. The US was cut to 2.3% (down two-tenths) and Euro Area to 1.3% (down three-tenths) – but still notably above DB’s forecast of 0.9%. It wasn’t all doom and gloom though with China revised up one-tenth to 6.3%. The biggest downward revisions were reserved for Germany and Italy however, where both were revised down five-fifths to 0.8% and 0.1% respectively. Separately, as discussed earlier it’s worth noting that the Italian government yesterday downgraded growth also to 0.1% for 2019 compared to a previous 1% estimate. The deficit was also set at 2.5%. None of these numbers should have been a surprise yesterday but the headlines didn’t help sentiment.

To quickly recap yesterday’s relatively sparse data releases, the highlight in the US was the JOLTS job report for February, which showed the private quits rate staying at 2.6%, a post-crisis high. That bodes well for wage growth moving forward. In Europe, the only notable release was Italy’s retail sales figure for February, which rose +0.1% mom, beating expectations for -0.2%, with January’s figure revised up 0.1pp to 0.6% as well.

Finally to the day ahead which as mentioned above is headlined by the ECB, the EU Council meeting, FOMC minutes and US CPI report. Away from those we’ll also get the February industrial production report in France and the UK along with trade data in the latter and the February GDP reading. Late this evening in the US we’ll also get the March monthly budget statement. Also worth keeping an eye on today are scheduled comments by the Fed’s Quarles this afternoon and ECB’s Coeure this evening. Former Fed Chair Yellen is also scheduled to take part in a discussion with the Fed’s Kaplan.

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED UP 2.27 POINTS OR .07% //Hang Sang CLOSED DOWN 37.93 POINTS OR .13% /The Nikkei closed DOWN 115.02 POINTS OR 0.53%/ Australia’s all ordinaires CLOSED UP .02%

/Chinese yuan (ONSHORE) closed DOWN at 6.7177 AS TRUCE DECLARED FOR 3 MONTHS /Oil UP to 64.43 dollars per barrel for WTI and 70.94 for Brent. Stocks in Europe OPENED GREEN EXCEPT GERMAN DAX

ONSHORE YUAN CLOSED UP // LAST AT 6.7177 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7250 / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/

3 b JAPAN AFFAIRS

3 C CHINA/CHINESE AFFAIRS

China/Greece

Locals are stalling the advancement of the major port at Piraeus, Greece.

(courtesy zerohedge)

China’s Multi-Billion Dollar Greece Investment Plunged In “Unprecedented Limbo” By Local Bureaucrats

“The challenges for Chinese enterprises to succeed in managing BRI projects is not showering the dollars and yuans, but winning hearts and minds,” a China research fellow at London-based think tank Chatham House told the South China Morning Post in a bombshell full report detailing how Beijing has entered an “unprecedented limbo” on a stalled expansion project on the famous and ancient Port of Piraeus in Greece. It illustrates an emerging trend in other Belt and Road Initiative countries: all the money in the world can’t overcome local and cultural realities, and if Beijing plans to ride roughshod over these in hunger of its broader ambitions, President Xi’s grand initiative is sure to die on the vine.

Cosco Shipping — the China state-owned Shanghai based shipping and logistics services conglomerate — has been operating Piraeus port for the past decade, but local authorities have now banned the company from pursuing a planned expansion of port facilities due to archaeological concerns, halting a €1.5 billion (US$1.7 billion) long term expansion deal with the Greek government which included construction of a sprawling mall next to a new cruise ship terminal, as well as a five-star hotel in port’s southern section. The broader makeover was a planned first step in creating a so-called Athens Riviera — but which now faces endless bureaucratic obstacles amid local fears China is playing an outsized role in Greece.

Last week the Greek Central Archaeological Council unanimously turned down major key aspects to the project, citing potential damage to local heritage and archaeological preservation projects, as well as environmental concerns and “aesthetic” reasons. Crucially, the council effectively declared half the town as an archaeological site, bringing to a halt Cosco’s further plans to construct a new cruise passenger station, a logistics center in nearby Keratsini, four new cruise berths at Pireaus, along with a new berth allocation system, according to the South China Morning Post (SCMP) report.

Ironically, the SCMP observes, “while Greece’s heritage was once an attraction for the Chinese leadership, it may now prove to be a stumbling block for their ambitions.” Though Cosco’s management of Pireaus predates Xi’s BRI plans (Cosco has a 51% stake in the port), China’s success in Greece could convince skeptics concerning Beijing’s role on the European continent.

But it now appears the skeptics are winning, given Cosco will now face much stricter regulations for any expansion due to the extension of the archaeological zone, even as Greece’s leaders lobby for more foreign investors aimed at recovery from a nearly nine-year economic and austerity crisis. It’s further believed that opposition elements within PM Tsipras’ own Syriza party are working against him to block major foreign companies from gaining too much of a stake in Greece.

Citing Cosco company insiders, the SCMP report lends credence to these fears in the following:

Insiders at the company, however, say they are now playing a greater role in Greece than initially expected.

The Chinese brand is seen as a representative of modernity, a provider of jobs in an economically struggling country, a redeveloper of cities – and a constant target for sceptics in the Greek parliament.

Cosco is responsible for the long-term sustainability of the port, given its outsize role in the Piraeus Port Authority, which it took over from the Greek government in 2016 following Tsipras’s privatisation deal.

But now, after last week’s Central Archaeological Council decision, which made Cosco executives “furious” according to some reports, obstacles and red tape are mounting given that “Even projects that had already been approved had to be referred to the Ministry of Culture, the Central Archaeological Council and the Central Council of Modern Monuments for reauthorization,” according to the SCMP.

Moreover, the whole episode underscores Beijing’s overly optimistic approach to BRI-related expansion generally, given the tendency to operate on the assumption that a population’s deep cultural roots combined with local politics can ultimately be overcome with the lure of multi-billion dollar investment.

On the intricacies of the internal long running Greek fight over privatization and the sale of state assets to speed economic recovery, the SCMP reports further:

Speaking to the South China Morning Post, Greece’s Deputy Prime Minister Yanis Dragasakis rejected Greek media reports that the Tsipras administration was employing delaying tactics because it was falling in the polls ahead of elections this year.

“I don’t know there’s a delay here. This is not related to the election. It is related to the complexity of the decision to be made,” Dragasakis said.

“This area is full of antiquities, [a] fact that requires all procedures to be followed properly. In any event, the investment for the port of Piraeus is a very, very important investment.”

The Greek government, he added, “will do our utmost to facilitate [Cosco’s] presence in Greece.”

Sources say the stymied expansion plan will result in at least an eight month delay for implementation of already approved investments, on top of the ongoing two-and-a-half years of delays since the Piraeus Port Authority’s privatization under Cosco.

Initially, Cosco faced very few permits, according to Greece’s Ekathimerini newspaper, and was on its way to surpass Valencia in Spain for becoming the Mediterranean’s busiest container terminal.

Cosco considers the expansion projects and interventions as necessary for Piraeus’ continued operation at such levels, as well as a crucial future link in the so-called new Silk Road linking Europe and Eurasia.

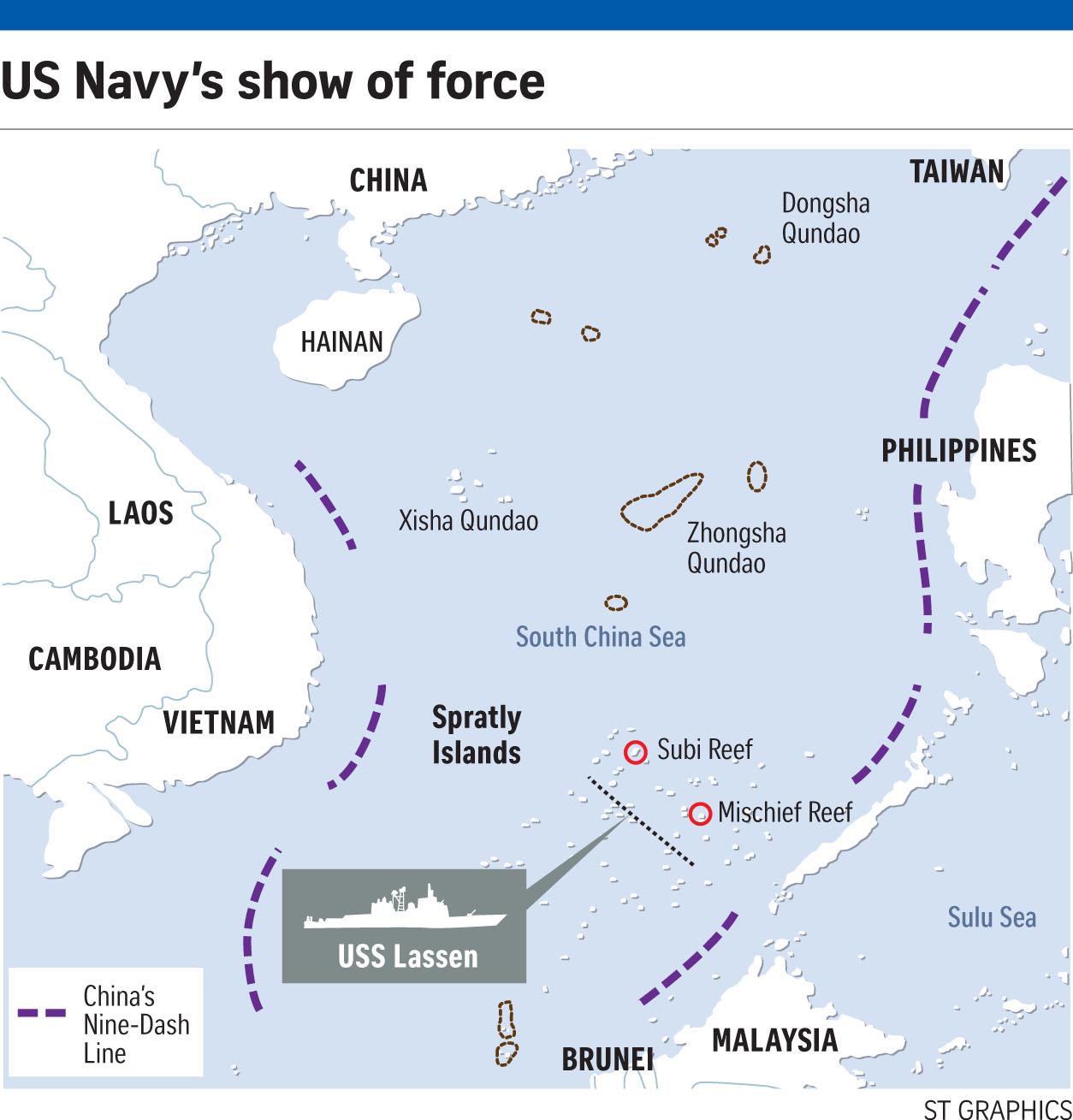

B-52 Bombers Conduct ‘Training ‘Mission’ With Japan Over East China Sea

Two Boeing B-52 long-range, subsonic, jet-powered strategic bombers recently conducted an “integration training” mission with the U.S. Navy and the Japan Air Self Defense Force (JASDF) over the East China Sea.

A statement issued by the U.S. Pacific Air Force (PACAF) last month indicated that two B-52s departed from Andersen Air Force Base in Guam, linked up with McDonnell Douglas F-15 Eagles assigned to the Kadena Air Base in Japan. The mission was conducted on March 20.

“Training missions and patrols of the contested waters are not unheard of, having become a regular exercise by American forces. The US’ use of bombers in the region has been going on for more than 10 years as part of its Continuous Bomber Presence, a mission Washington says is “in support of a free and open Indo-Pacific.”

In response to the U.S. led military exercise, the People’s Liberation Army Air Force (PLAF) conducted an exercise of their own, on March 30, with six Xian H-6 bombers, additional reconnaissance aircraft, and fighter jets, across the Miyako Strait, a waterway which lies between Miyako Island and Okinawa Island.

The U.S. and Japan have routinely carried out air defense training missions in the East China Sea, home to the Japanese-controlled Senkaku Islands.

Last September, we reported that internal documents from China’s People’s Liberation Army (PLA) specified a military crisis was inevitable over sovereignty disputes of the Senkaku Islands.

The U.S. has repeatedly used freedom of navigation (FON) to sail its Arleigh Burke-class destroyers in the South China Sea, near China’s militarized islands. B-52s have made regular flights near some of these highly contested areas. Beijing has blasted these missions as “provocations.”

An estimated $5 trillion worth of global trade passes through the South China Sea annually. Beijing has repeatedly stressed that it’s willing to escalate war drills in the region to defend its territory. The threat has mostly be ignored by American forces, who continue to conduct military exercises in some of the world’s most disputed waters.

Washington and Beijing have frequently unleashed a war of words over the militarization of the South China Sea, where China, Taiwan, Vietnam, Malaysia, Brunei, and the Philippines all have competing economic claims.

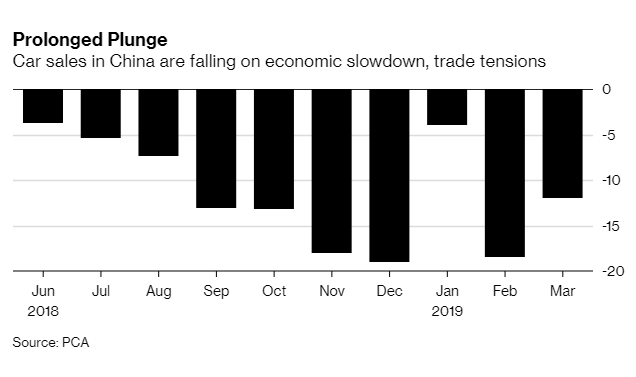

Chinese Car Sales Thrashed In March As Unprecedented Collapse Slump Continues

Car sales in China, the world’s largest vehicle market, continue to tumble, exposing an increasingly ugly picture for the global automotive market. The data marks a dismal and protracted reversal in a market that had done nothing but grow for decades, according to Bloomberg. In March, retail sales of sedans, SUVs, minivans and multipurpose vehicles dropped 12% to 1.78 million units, according to the China Passenger Car Association. This is after an 18.5% drop in February and a 4% drop in January.

The country’s slowing economy and continued trade tensions with the United States are weighing on consumer sentiment among its 1.4 billion people. Additionally, changes in tax policies and import tariffs have also acted as a headwind for car demand. Cars were the only consumer product category in China that shrank the first two months of 2019.

Cui Dongshu, secretary general of the CPCA, is among those calling for more government intervention to spur buying: “There are only 200 million private vehicles in China, leaving huge room for growth. Policies should be put in place to spur vehicle consumption in 2019.” Because as we all know, the government manipulating the market to create demand where there isn’t any could never backfire, right?

Even better, despite the horrifying data, Cui still thinks that car sales “may recover in April”, helped by the country’s planned tax reductions. He stopped short of predicting sales gains, but PCA raised its forecast for 2019 sales of new energy vehicles – battery, hybrid and fuel cell cars – to 1.7 million from 1.6 million.

With China out of the picture, global automakers like Toyota and Ford are left with few places to go for growth in sales. Markets in Europe and North America continue to slow alongside of China as the availability of car sharing services makes buying less necessary. Japan is also slowing down, while gains in smaller markets are unable to offset growth in larger markets.

Chen Hong, chairman of SAIC Motor, China’s biggest automaker, said: “2019 will bring severe challenges.” Trying to rally his employees in an internal worker memo, he called for his company to “accelerate innovation and strive toward higher quality”. SAIC’s sales fell 17% in the first two months of 2019.

Ford reported a 54% sales plunge in China last year and said last week that it’s introducing more than 30 vehicles targeted specifically for Chinese consumers over the next three years to help it hone its focus on the market

4/EUROPEAN AFFAIRS

5.RUSSIAN AND MIDDLE EASTERN AFFAIRS

Iran/USA