GOLD: $1284.00 UP $4.30 (COMEX TO COMEX CLOSING)

Silver: $14.97 UP 5 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : $1283.60

silver: $14.96

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING: 29/50

DLV615-T CME CLEARING

BUSINESS DATE: 04/29/2019 DAILY DELIVERY NOTICES RUN DATE: 04/29/2019

PRODUCT GROUP: METALS RUN TIME: 20:22:06

EXCHANGE: COMEX

CONTRACT: MAY 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,278.600000000 USD

INTENT DATE: 04/29/2019 DELIVERY DATE: 05/01/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

657 C MORGAN STANLEY 48

661 C JP MORGAN 29

690 C ABN AMRO 8

737 C ADVANTAGE 3

800 C MAREX SPEC 10

905 C ADM 2

____________________________________________________________________________________________

TOTAL: 50 50

MONTH TO DATE: 50

NUMBER OF NOTICES FILED TODAY FOR MAY CONTRACT: 50 NOTICE(S) FOR 5,000 OZ (0.1556 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 60 NOTICES FOR 5000 OZ (.1556 TONNES)

SILVER

FOR MAY

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

859 NOTICE(S) FILED TODAY FOR 4,295,000 OZ/

total number of notices filed so far this month: 859 for 4,295,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE :$5260 UP $25

Bitcoin: FINAL EVENING TRADE: $5294 UP 56

end

XXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI FELL BY A LARGE SIZED 3816 CONTRACTS FROM 201,099 DOWN TO 197,286 WITH YESTERDAY’S 13 CENT RISE IN SILVER PRICING AT THE COMEX. , WE DID HAVE CONSIDERABLE LIQUIDATION OF SPREADERS WITH TODAY’S READING AND IT HAD A CONSIDERABLE EFFECT ON PRICE. TODAY WE ARRIVED FURTHER FROM AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A VERY WEAK SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

0 FOR MAY, 0 FOR JUNE, 174 FOR JULY AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 174 CONTRACTS. WITH THE TRANSFER OF 174 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 174 EFP CONTRACTS TRANSLATES INTO 0.87 MILLION OZ ACCOMPANYING:

1.THE 13 CENT FALL IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST NINE MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

AND NOW 16.810 MILLION OZ STANDING FOR SILVER IN MAY.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF APRIL:

36,573 CONTRACTS (FOR 21 TRADING DAYS TOTAL 36,573 CONTRACTS) OR 182.87 MILLION OZ: (AVERAGE PER DAY: 1741 CONTRACTS OR 8.707 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF MAR: 182.87 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 26.12% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 755.56 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

APRIL 2019 TOTAL EFP ISSUANCE: 182.87 MILLION OZ.

RESULT: WE HAD A CONSIDERABLE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 3816 WITH THE 13 CENT FALL IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A TINY SIZED EFP ISSUANCE OF 174 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) . OUR BANKERS RESUMED THEIR LIQUIDATION OF THE SPREAD TRADES TODAY.

TODAY WE LOST A CONSIDERABLE SIZED: 3642 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 174 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 3816 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 13 CENT FALL IN PRICE OF SILVER AND A CLOSING PRICE OF $14.92 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.986 BILLION OZ TO BE EXACT or 141% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 859 NOTICE(S) FOR 4,295,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ AND NOW MAY: 16,810,000 OZ..

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST FELL BY A FAIR SIZED 1962 CONTRACTS, TO 427,589 WITH THE FALL IN THE COMEX GOLD PRICE/(A DROP IN PRICE OF $7.00//YESTERDAY’S TRADING).

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 8232 CONTRACTS:

APRIL 0 CONTRACTS,JUNE: 8232 CONTRACTS DECEMBER: 0 CONTRACTS, JUNE 2020 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 427,589. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A GOOD SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 6270 CONTRACTS: 1962 OI CONTRACTS DECREASED AT THE COMEX AND 8232 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 6270 CONTRACTS OR 627,000 OZ OR 19.50 TONNES. YESTERDAY WE HAD A LOSS IN THE PRICE OF GOLD TO THE TUNE OF $7.00.…AND WITH THAT RISE, WE HAD A STRONG GAIN IN TONNAGE OF 19.50 TONNES!!!!!!.??????????????????????????????????????????

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL : 146,637 CONTRACTS OR 14,443,700 OR 456.10 TONNES (21 TRADING DAYS AND THUS AVERAGING: 6982 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 21 TRADING DAYS IN TONNES: 456.10 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 456.10/3550 x 100% TONNES =12.84% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 1828,82 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

APRIL 2019 TOTAL ISSUANCE: 456.10 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLEDRIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A FAIR SIZED DECREASE IN OI AT THE COMEX OF 1962 WITH THE FALL IN PRICING ($7.00) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 8232 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 8232 EFP CONTRACTS ISSUED, WE HAD A STRONG GAIN OF 6270 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

8232 CONTRACTS MOVE TO LONDON AND 1962 CONTRACTS DECREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 19,50 TONNES). ..AND THIS STRONG DEMAND OCCURRED WITH A FALL IN PRICE OF $7.00 IN YESTERDAY’S TRADING AT THE COMEX.

we had: 50 notice(s) filed upon for 5,000 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $4.30 TODAY

NO CHANGE IN GOLD INVENTORY AT THE GLD

INVENTORY RESTS AT 746.69 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 5 CENTS TODAY:

NO CHANGE IN SILVER INVENTORY AT THE SLV//

/INVENTORY RESTS AT 311.979 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A CONSIDERABLE SIZED 3816 CONTRACTS from 201,099 DOWNTO 197,286 AND FURTHER FROM THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..TODAY,IT LOOKS LIKE OUR SPREADERS SAW CONSIDERABLE ACTION WITH RESPECT TO THEIR USUAL AND CUSTOMARY LIQUIDATION, WITH CONSIDERABLE EFFECT ON THE PRICE OF SILVER

HERE IS HOW THE CROOKS USED SPREADING AS WE ENTER AN ACTIVE DELIVERY MONTH. THUS SILVER HAS THE ACTIVE MONTH OF MAY COMING UP AND THUS SPREADERS DO THE FOLLOWING:

“YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST IS STARTING TO RISE IN THIS NON ACTIVE MONTH OF APRIL BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN SILVER WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (MAY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

0 CONTRACTS FOR APRIL., 0 FOR MAY, FOR JUNE 0 CONTRACTS AND JULY: 174 CONTRACTS AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 174 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 3816 CONTRACTS TO THE 174 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A STRONG LOSS OF 3642 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES: 12.87MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL AND NOW 16.810 MILLION OZ FOR MAY

RESULT: A STRONG SIZED DECREASE IN SILVER OI AT THE COMEX DESPITE THE 13 CENT LOSS IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A SMALL SIZED 174 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

)TUESDAY MORNING/ MONDAY NIGHT:

SHANGHAI CLOSED DOWN 15.84 POINTS OR 0.52% //Hang Sang CLOSED DOWN 193.10 POINTS OR 0.65% /The Nikkei closed/ DOWN 48.85 POINTS OR .22% Australia’s all ordinaires CLOSED DOWN .48%

/Chinese yuan (ONSHORE) closed DOWN at 6.7391 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 64.03 dollars per barrel for WTI and 72.83 for Brent. Stocks in Europe OPENED MIXED// ONSHORE YUAN CLOSED DOWN // LAST AT 6.7391 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7393/ TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A//NORTH KOREA/ SOUTH KOREA

NORTH KOREA

b) REPORT ON JAPAN

3 China/Chinese affairs

i)China/

Stocks dip after China’s all important mfg PMI falters

( zerohedge)

iii)Vodafone finds hidden backdoors in Huawei network equipment and that will anger China to no end. What will Europe do?

(courtesy zerohedge)

iv)China/Canada

Relations between China and Canada are now at an all time low as a second Canadian is sentenced to death on drug trafficking

( zerohedge)

4/EUROPEAN AFFAIRS

i)EU/

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6. GLOBAL ISSUES

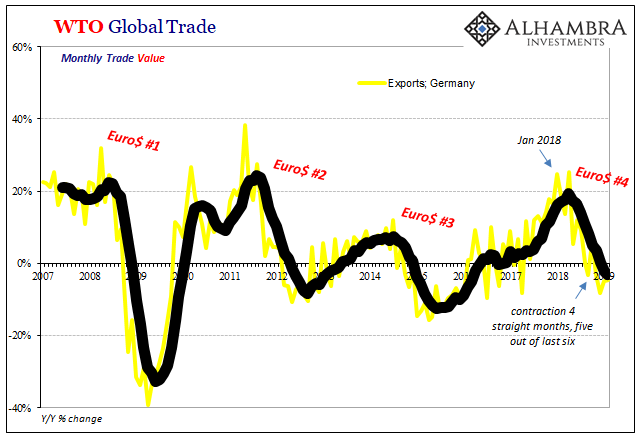

A very important commentary from Jeffrey Snider who looks at the global scene. He states that to him we are entering a huge global slowdown and he references this as Euro dollar no 4 crisis. All previous crises stem from a lack of dollars held outside the USA

( Jeffrey Snider Alhambra)

7. OIL ISSUES

8 EMERGING MARKET ISSUES

VENEZUELA

Looks like a coup is under way in Venezuela.

(courtesy zerohedge)

9. PHYSICAL MARKETS

i)London’s Financial times talks about the life of Bart Chilton and how he stood for the little guy

( London’s Financial Times)

ii)Chilton’s death is attributed to complications of pancreatic cancer

(CNBC/GATA

10. USA stories which will influence the price of gold/silver)

MARKET TRADING//early this morning/TRADING

ii)Market data

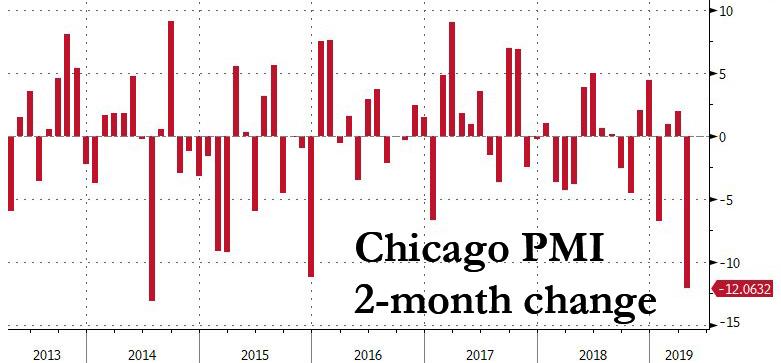

i)Chicago manufacturing and services PMI crashes

( zerohedge)

ii)USA ECONOMIC/GENERAL STORIES

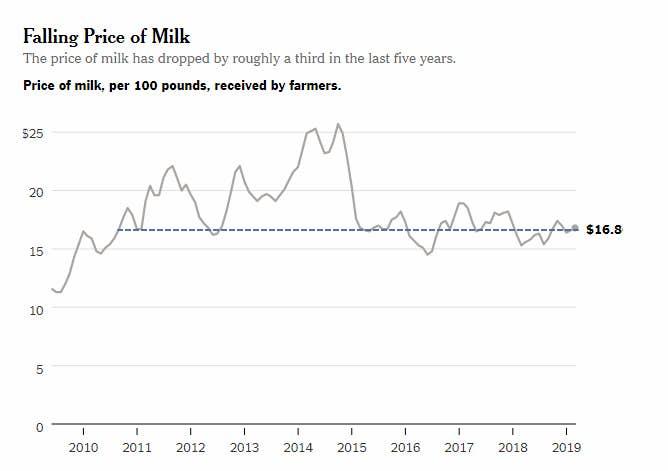

Mish Shedlock provides a great commentary on the plight of Wisconsin dairy farmers who are going bankrupt in record numbers and they all blame the tariffs

( Mish Shedlock/Mishtalk)

iii) TRUMP becoming more vocal as he demands the Fed slash rates by 1% as the FOMC meets

SWAMP STORIES

i)Rosenstein submits his resignation letter to Barr

( zerohedge)

Let us head over to the comex:

3362 NOTICE X 5,000 OZ PER CONTRACT = 16.810 MILL;LION OZ.

(4200 VS 3362 CONTRACTS). i GUESS THEY COULD NOT FIND PHYSICAL SILVER AND THESE BOYS OPTED FOR EFP’S WE SHOULD SEE INCREASING LEVELS IN THE NEXT DAY OR SO.

Gold withdrawals;

i) zero withdrawals.

Gold Investors Taking Possession and Repatriating Gold To Home Country

There is a growing movement by investors and central banks internationally to “repatriate” gold and own it “in country” due to concerns of gold confiscation and financial repression involving capital and exchange controls. A form of gold confiscation has already been seen with Venezuela unable to repatriate their remaining gold from the Bank of England.

Due to persisting uncertainty regarding the outcome of Brexit and other global risks, Irish and some international investors are preferring to store their gold bullion in Dublin rather than London and other locations.

Many investors, institutions and central banks are moving to take possession and ownership of their gold bullion and or opting to own gold in a fully allocated and fully segregated manner in ultra secure vaults.

Gold is flowing from traditional gold storage centres likes of Zurich, Hong Kong, Singapore, Perth and especially London to nations internationally.

Investors are opting to store gold where it is more easily accessible, portable and truly liquid and not dependent on one single counter party.

Never assume that your stored gold or digital gold is easily accessible. It is prudent to test assumptions by selling some and taking delivery of some of your gold and silver. Test how your provider handles this. In our client’s experience there frequently are hidden charges, unexpected terms and conditions and legal impediments to them liquidating their gold for cash or taking delivery.

If you don’t hold it or can’t hold it easily, you don’t own it…

Mark O’Byrne, GoldCore Founder & Research Director joined Bobby Kerr on Newstalk to discuss the new institutional gold vaults in Dublin Ireland and the growing financial risks including the coming global debt crisis.

News & Commentary

Stocks Struggle on Weak Earnings; Dollar Edges Up: Markets Wrap (Bloomberg.com)

Gold futures post first loss in 4 sessions (Marketwatch.com)

Gold slips from more than one-week high as data lifts equities (Reuters.com)

Newmont Goldcorp to suspend Peñasquito operations in Mexico due to blockade (Reuters.com)

Bart Chilton, former CFTC commissioner and high-frequency trading critic, is dead at 58 (CNBC.com)

Fed Is Looking at a New Program that Could Be Another Version of ‘Quantitative Easing’ (CNBC.com)

Decline in world’s monetary reserves signals end to dollar as reserve currency (GATA.com)

Flash Crashes Keep Showing Gold Market Manipulation And The CFTC’s Indifference (SilverDoctors.com)

Near-Record Gold Shorting (SeekingAlpha.com)

Why Warning About A Bubble For A Decade Is Completely Rational (RealInvestmentAdvice)

Gold Prices (LBMA PM)

29 Apr: USD 1,282.15, GBP 991.10 & EUR 1,148.55 per ounce

26 Apr: USD 1,281.50, GBP 992.78 & EUR 1,150.02 per ounce

25 Apr: USD 1,277.85, GBP 991.87 & EUR 1,146.87 per ounce

24 Apr: USD 1,273.80, GBP 984.90 & EUR 1,135.34 per ounce

23 Apr: USD 1,273.45, GBP 979.67 & EUR 1,131.46 per ounce

Silver Prices (LBMA)

29 Apr: USD 14.97, GBP 11.58 & EUR 13.42 per ounce

26 Apr: USD 15.00, GBP 11.62 & EUR 13.47 per ounce

25 Apr: USD 14.86, GBP 11.55 & EUR 13.36 per ounce

24 Apr: USD 14.80, GBP 11.44 & EUR 13.21 per ounce

23 Apr: USD 14.97, GBP 11.51 & EUR 13.31 per ounce

Recent Market Updates

– Australia and Many Property Markets To Crash Like Ireland?

– Death of Inflation and the Death of Equities?

– SWOT Analysis: Venezuela Sells $400 Million Worth Of Gold Bullion

– World’s Central Banks Want More Gold – India May Buy 1.5M Ounces In 2019

– Russia’s 2019 Gold Rush Continues: Buys 600,000 Ounces of Gold In March

– When Should You Sell Your Gold and Silver? (GoldCore Video)

– Understanding Gold: A Step By Step Guide To Gold As An Asset Class

– World Trade Suffers Biggest Collapse Since Financial Crisis

GATA STORIES WITH RESPECT TO GOLD/PRECIOUS METALS.

London’s Financial times talks about the life of Bart Chilton and how he stood for the little guy

(courtesy London’s Financial Times)

Chilton’s support for ‘little guy,’ opposition to silver manipulation, noted by FT

Submitted by cpowell on Mon, 2019-04-29 17:53. Section: Daily Dispatches

Bart Chilton, former CFTC commissioner, 1960-2019

Flamboyant, folksy image signaled his identification with the ‘little man’

By Philip Stafford

Financial Times, London

Monday, April 29, 2019

Bart Chilton, one of the most distinctive and controversial figures in financial-market regulation, has died at the age of 58.

Easily recognised with his shoulder-length white-blond hair, loud enthusiasm, folksy comments and cowboy boots, Chilton was a singular character as a commissioner at the US Commodity Futures Trading Commission.

…

The television channel RT America, for which he hosted its main financial show, “Boom Bust,” announced Chilton’s death on Saturday evening, saying it followed a sudden illness.

Walt Lukken, chief executive of the Futures Industry Association and also a former CFTC commissioner, compared him to a big-haired 1980s rock star, “always colourful, always funny and always passionate … the David Lee Roth of the CFTC.”

A Democrat, Chilton regularly appeared on TV and at industry conferences as a critic of high-frequency traders, calling them “cheetahs.” Although he privately said his flamboyant image in the largely grey world of regulation was partly for show, it also signalled his identification with what he saw as his key constituents: America’s farmers and ranchers. They, he said, were disadvantaged in Washington’s policy making machinations. Powerful and rich interests would try to roll policies back over time, he argued.

Chilton said being the “little man” was a key part of his life, firstly as a worker in a steel mill in Indiana after college and then as a long-serving government official in the agriculture industry. He was also chief of staff at the US National Farmers Union, which represents family farmers and rural communities, from 2006-07.

He was appointed as a commissioner in 2007 by President George W Bush, as technology was beginning to revolutionise trading and the global financial-market meltdown was beginning to simmer.

From 2010, the CFTC, which had previously been a sleepy backwater agency, took on new powers to oversee the US derivatives market, which had been blamed for exacerbating the crisis.

The era of rapid change was further underscored by the flash crash of May 2010, in which US stocks abruptly dived. Although an official government report blamed the poor execution of a trade from Kansas, many of America’s retail investors pointed the finger at high-frequency traders, which dart in and out of bets and execute deals in milliseconds.

From his position, Chilton vividly spoke out against such activity, labelling those market participants as “cyber cowboys” and “high rollers”, and calling out a rampant “Ponzimonium” in financial markets.

His speeches were often peppered with jokes and popular cultural references, from sources such as Lincoln, Shaft and direct-to-DVD Steven Seagal films, but within them were calls for curbs to the size of positions investors could hold in the commodities and metals markets.

He spoke out on behalf of the investors who lost out in the failure of MF Global, the broker-dealer, and schemes of Bernard Madoff. He also tried — unsuccessfully — to prove manipulation in the silver futures market.

Scott O’Malia, a Republican commissioner who served with Chilton at the agency, said Chilton focused intently on the retail aspects of the trade. “He cared passionately for the little guy his entire career in public service,” Mr. O’Malia said.

On leaving the CFTC in 2014, he took a role at DLA Piper, the US law firm, as a senior regulatory adviser. He also controversially took a position as an adviser to the Modern Markets Initiative, a high-frequency traders’ lobby group — a move that left many of his former supporters disappointed, with some labelling him a “sellout.” Chilton defended his actions by saying there was “a significant symmetry between the MMI and what I have called for over the years.”

He joined RT America, the Kremlin-backed network, in 2018, and advocated tighter regulation for bitcoin trading.

Chilton, who lived in Gulf Breeze, Florida, was married to Sherry Daggett Chilton.

* * *

Help keep GATA going:

GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at:

To contribute to GATA, please visit:

END

Chilton’s death is attributed to complications of pancreatic cancer

CNBC/GATA)

‘

Chilton’s death attributed to complications of pancreatic cancer

Submitted by cpowell on Mon, 2019-04-29 21:39. Section: Daily Dispatches

Bart Chilton, Former CFTC Commissioner and High-Frequency Trading Critic, Is Dead at 58

By Yen Nee Lee

CNBC, New York

Monday, April 29, 2019

https://www.cnbc.com/2019/04/29/bart-chilton-former-cftc-commissioner-di…

Bart Chilton, a former commissioner of the U.S. Commodity Futures Trading Commission and advocate for cryptocurrency regulation, has died.

A family member told CNBC the cause of Chilton’s death was complications from pancreatic cancer. He was 58.

Chilton was a frequent guest on CNBC and wrote for CNBC’s website. Most recently, he hosted the show “Boom Bust” for television’s RT America channel.

…

Chilton worked at the CFTC from 2007 to 2014. He was nominated to a position there by President George W. Bush and was renominated by President Barack Obama.There, he headed the Energy and Environmental Advisory Committee and the Global Markets Advisory Committee. His years at the CFTC were remembered for his criticism of high-frequency trading, whose traders he called “cheetahs.”

High-frequency trading refers to the use of computer programs to move in and out of positions very quickly — sometimes in fractions of a second.

In recent months, Chilton wrote for Forbes on topics ranging from cryptocurrencies to financial regulation.

CFTC Chairman Chris Giancarlo, in a Twitter post on Sunday, said Chilton’s death was “sad news for all of us.”

* * *

Help keep GATA going:

GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at:

To contribute to GATA, please visit:

Countries Around The World Are Bringing Gold Home

Authored by Virginia Fidler via GoldTelegraph.com,

European Central Bank’s President Mario Draghi recently announced that the ECB would be required to approve any management of gold reserves within the euro zone countries. The statement was specifically directed at two Italian members.

Why was Italy singled out? According to the Wall Street Journal, Italian citizens are preparing to take control of Italy’s gold reserves. During the past few years, a multitude of small investors lost billions of dollars due to the failure of several Italian banks. The Bank of Italy is seen as an elitist, inefficient entity indifferent to the needs of ordinary people. Deputy Prime Minister Luigi Di Maio is leading the attack against Italy’s central bank, along with the “5 Star Movement” and the nationalist “League,” all of whom blame the countries financial woes on the incompetence of the central bank.

The 5 Star Movement is asking Italy’s Parliament to approve measures that would allow private banks to sell their share in The Bank of Italy at 1930’s prices. Taking it a step further, they are also demanding that ownership of the Bank of Italy’s 2,451.8 tons of gold be taken over by the country’s citizens and spent on populist policies. The current value of these gold reserves is $102 billion.

If these laws are passed, investors would be able to sell gold and greatly deplete the central bank’s reserves. As Giorgia Meloni of the Brothers of Italy states, “The gold belongs to the Italians, not the bankers.”

Italy’s lawmakers hold a different view and are warning against any action that will upend the sovereignty of the central bank’s policies. Such expropriation of government gold would not be tolerated.

But the 5 Star Movement and the League are determined to return ownership of the country’s gold to the public. Approximately 60 percent of lawmakers support the movement, guarantying the law will be enacted. There is also rumbling about nationalizing the Central Bank of Italy entirely.

In the realm of global commerce, gold has become a most potent weapon.

Italy is not the only country embracing gold.

Romania has plans to repatriate gold reserves currently being held by the Bank of England. Romania currently has around 103.7 tons of gold, valued at $3.84 billion. Sixty-five percent of the yellow metal is being kept in storage at the Bank of England. According to a new law, only 5 percent of the country’s gold may be stored abroad. The rest will be repatriated. While the current leadership approves of the repatriation, the National Bank of Romania does not. Mugur Isarescu, director of the central bank, insists that the gold is for economic emergencies and should remain where it is.

Another European country, Germany, has quietly called back 674 tons of gold from France and the U.S. Federal Reserve to its central bank, the Bundesbank. Ninety-eight percent of Germany’s gold was stored abroad during the height of the Cold War to keep it out of the reach of Russia. With the weakening of the Euro, Germany wants the gold closer to home. The Bundesbank now has half of the country’s gold in safe storage.

Following the trend to keep gold close to home, the National Bank of Hungary will be recalling 100,000 ounces of gold from the Bank of England. Hungary has traditionally kept its gold reserves low, with only 50 tons being held in 1989. The global 2008 financial crisis had Hungary rethinking its approach to gold. Now, it wants its gold reserves home for safekeeping in the event of a geopolitical crisis.

Gold is seen by central banks as a way to maintain financial trust during economic upheaval. The move by global central banks to repatriate their gold may be a sign that an economic crisis could be looming in the near future.

end

The rats fleeing a sinking ship?

Societe Generale resigns as London gold market maker

LONDON (Reuters) – The London Bullion Market Association (LBMA) said Societe Generale had resigned as a market maker for gold, as France’s third-largest bank pushes ahead with a downsizing of its commodities business.

SocGen said this month it would cut 1,600 jobs to boost profits after poor performance last year and exit over- the-counter commodities trading.

SocGen declined to comment.

In over-the-counter trading deals are done bilaterally between banks and brokers rather than on a financial exchange. London is the world’s largest over-the-counter gold trading hub, overseen by the LBMA.

Market makers commit to provide liquidity to the market. SocGen’s exit leaves 12 LBMA market-making banks including JPMorgan, HSBC and BNP Paribas.

-END-

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

* * *

Your early TUESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED/ LAST AT: 6.7391/

//OFFSHORE YUAN: 6.7392 /shanghai bourse CLOSED DOWN 15.84 POINTS OR 0.52%

HANG SANG CLOSED DOWN 193.70 points or 0.65%

2. Nikkei closed DOWN 48.85 POINTS OR .22%

3. Europe stocks OPENED MIXED

USA dollar index FALLS TO 97.57/Euro RISES TO 1.1213

3b Japan 10 year bond yield: FALLS TO. –.04/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 111255/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//CARRY TRADERS GETTING KILLED

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 64.35 and Brent: 72.46

3f Gold UP/JAPANESE Yen UP CHINESE YUAN: ON -SHORE DOWN/OFF- SHORE: DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +03%/Italian 10 yr bond yield UP to 2.58% /SPAIN 10 YR BOND YIELD DOWN TO 1.01%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.55: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield RISES TO : 3.38

3k Gold at $1285.80 silver at: 14.99 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 8/100 in roubles/dollar) 64.39

3m oil into the 64 dollar handle for WTI and 72 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 111.25 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 1.0196 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1433 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now NEGATIVE territory with the 10 year RISING to +0.03%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.53% early this morning. Thirty year rate at 2.96%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.9601.. VERY DEADLY

Stocks Slump On Poor Google, Samsung Earnings; China Slowdown Fears Return

US futures were flat, while European equity markets and Asian stocks slipped on Tuesday as weak Chinese business surveys dampened appetite for risk, while a disappointing outlook and earnings at Samsung, the world’s biggest phone maker, and an ad revenue slowdown at Google sent tech stocks lower.

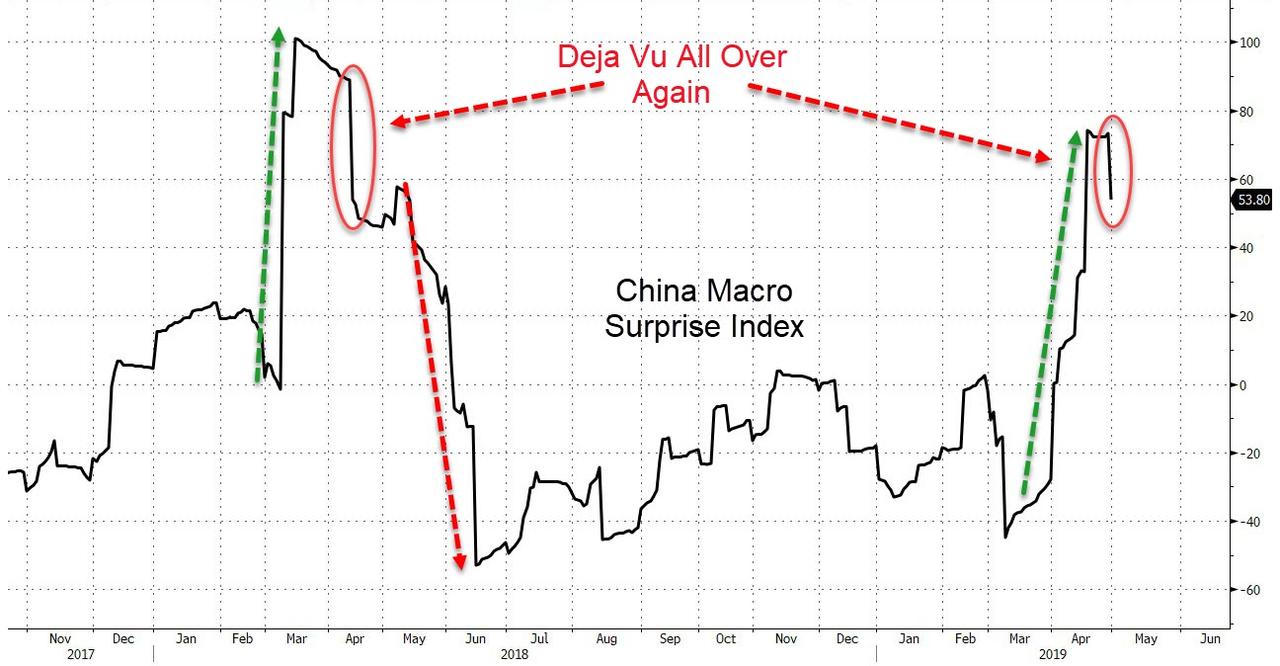

European shares followed Asian peers into the red after surveys on China manufacturing and services missed forecasts – another sign that Beijing’s efforts to spur growth n the world’s second biggest economy had yet to bear fruit, and that the rebound indicated by the spike in China’s PMI print last month was premature. As reported overnight, both official and private business surveys suggested slower Chinese factory growth this month, dashing hopes for a steady reading or even a faster expansion. Data also showed a slower expansion in its services sector. The full details again:

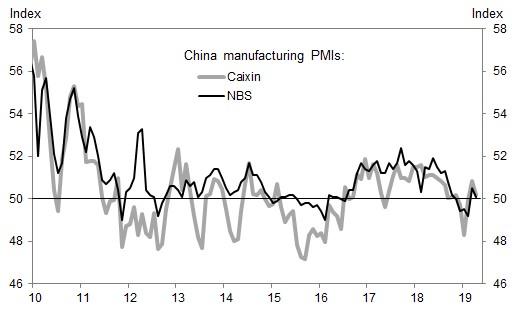

- Chinese Manufacturing PMI (Apr) 50.1 vs. Exp. 50.5 (Prev. 50.5).

- Chinese Non-Manufacturing PMI (Apr) 54.3 vs. Exp. 55.0 (Prev. 54.8)

- Chinese Caixin Manufacturing PMI (Apr) 50.2 vs. Exp. 51.0 (Prev. 50.8)

And visually:

Asian markets fell after the poor Chinese data amid thin trading. MSCI’s index of Asia-Pacific shares outside Japan was off 0.5%. Bourses in South Korea and Hong Kong both fell. apan’s financial markets are closed throughout the week as Japanese Emperor Akihito prepares to abdicate in favor of his elder son, Crown Prince Naruhito.

The latest Chinese data underscored questions over prospects for the Chinese economy despite a record credit injections who impact appears to have fizzled early, while investors across the world are on edge over growing signs of a two-speed global economy where a robust United States outpaces its peers.

Adding to China’s economic disappointment were tech stocks, which slumped following Alphabet’s worse-than-expected results after the Monday close, and after Korean smartphone giant Samsung Electronics’s profit missed analysts’ recently reduced estimates and shared a worse than expected outlook. Equities in Hong Kong, South Korea and Australia all dropped, though trading was quieter than usual thanks to a holiday in Japan. As usual, bad news was good news, and shares rose in Shanghai despite poor Chinese manufacturing data.

The Asian weakness initially spread to Europe, where the Stoxx 600 index was off 0.2%, with British shares down 0.2% and bourses in Germany and France down 0.1 and 0.4% respectively in early trading, while futures on the S&P 500 also pointed to a soft open in New York.

The Stoxx Europe 600 nudged into the red, led by declines in telecommunication and mining shares, as futures on the S&P 500 also pointed to a soft open in New York. France reported steady growth for the first quarter, while Spain’s economy also grew faster than expected. Chipmaker AMS jumped 16% after beating forecasts for first-quarter profit. AMS is a supplier to Apple, which is due to report its results later. Banks dragged heavily on the Stoxx 600. Danske Bank, hit by money-laundering scandals, fell more than 6 percent after lowering its outlook for 2019, while No. 1 euro zone bank Santander also slipped after first-quarter net profit. In contrast, Standard Chartered climbed after unveiling plans for share buybacks of up to $1 billion, its first in at least 20 years. The euro added to gains after regional GDP beat estimates and inflation in some of Germany’s regions accelerated in April.

Tech stocks were hit following Alphabet’s worse-than-expected results after the Monday close, and after Korean giant Samsung Electronics’s profit missed analysts’ recently reduced estimates. Equities in Hong Kong, South Korea and Australia all dropped, though trading was quieter than usual thanks to a holiday in Japan. Shares rose in Shanghai despite poor Chinese manufacturing data.

“It’s not a stellar reporting season — I don’t think anyone expected that,” said Nick Nelson, head of European equity strategy at UBS, on Bloomberg television. “But it’s certainly better than the fourth quarter. And that fits with some of the stabilization in the broader data in the euro zone, in emerging markets and in China.”

Emerging-market stocks and currencies were weaker Tuesday following the disappointing Chinese PMI data and as investors awaited further news on progress in trade talks between the U.S. and China. Still, MSCI’s gauge of developing-nation equities remained on track for a fourth successive monthly gain, the longest streak since January 2018. The currency index, however, is set for a third consecutive drop. Seasonal data complied by Bloomberg suggests both measures may retreat in May, as they have in seven of the past 10 years.

In FX, the euro strengthened for a third day as the euro-area economy expanded more than forecast in the first quarter. The pound shrugged off a report that said U.K. Prime Minister Theresa May faces a challenge from activists within her own party opposing her leadership, and GBPUSD rose above 1.30 for the first time in a week. AUDUSD swung to a loss after an official release showed Chinese manufacturing PMI missed.

Elsewhere, South Korea’s won led currency declines, falling to a two-year low after a weak earnings report from Samsung. The Philippine peso was firmer after the country’s credit score was lifted one step at S&P Global Ratings. Turkey’s lira fluctuated as investors pondered the latest statements by central-bank chief Murat Cetinkaya. The focus now turns to the Federal Reserve policy meeting on Wednesday.

In rates, Treasuries unexpectedly reversed direction around the time Europe opened, and reversed gains that came on the back of weaker-than-forecast China manufacturing growth.

In commodity markets, oil prices reversed losses after Saudi Arabia said a deal between producers to withhold output, in place since January, could be extended beyond June to cover all of 2019. Brent crude futures were last at $71.25 per barrel, down 0.4 percent.

In overnight geopol news, North Korea’s Vice Foreign Minister said that their resolve for denuclearisation is unresolved, adding that denuclearisation will be possible only if the US changes their current calculations. If the US fails to present new positions the US will then see unwanted consequences.

In the latest Brexit news, UK PM May is said to be facing a grassroots vote demanding her resignation with Conservative party local chairman and activists calling for an extraordinary meeting with PM to demand her resignation. May’s office thereafter downplayed the significance of the meeting, suggesting that it would not be legally-binding and the outcome of the meeting wouldn’t necessarily be passed. Furthermore, there will have to be a 28-day wait until such a meeting is held.

Looking ahead, traders will be looking for signals from economic data, a Fed policy meeting on Wednesday and earnings reports from the likes of Apple and McDonald’s. Meanwhile, the next round of trade talks between the U.S. and China will get under way this week with significant issues still unresolved. But enforcement mechanisms are “close to done,” according to Treasury Secretary Steven Mnuchin, although this has been said on countless times before.

Market Snapshot

- S&P 500 futures down 0.07% to 2,941.00

- STOXX Europe 600 down 0.2% to 390.65

- MXAP down 0.1% to 162.36

- MXAPJ down 0.5% to 538.26

- Nikkei down 0.2% to 22,258.73

- Topix down 0.2% to 1,617.93

- Hang Seng Index down 0.7% to 29,699.11

- Shanghai Composite up 0.5% to 3,078.34

- Sensex down 0.6% to 38,840.30

- Australia S&P/ASX 200 down 0.5% to 6,325.47

- Kospi down 0.6% to 2,203.59

- German 10Y yield rose 2.7 bps to 0.03%

- Euro up 0.2% to $1.1203

- Brent Futures up 0.3% to $72.27/bbl

- Italian 10Y yield unchanged at 2.213%

- Spanish 10Y yield rose 2.0 bps to 1.033%

- Brent Futures up 0.3% to $72.27/bbl

- Gold spot up 0.4% to $1,284.33

- U.S. Dollar Index down 0.2% to 97.65

Top Overnight News from Bloomberg

- Yield-starved investors outside the U.S. are abandoning their currency hedges on American assets, and that’s good news for dollar bulls.

- Economic growth in the euro area strengthened more than expected in the first quarter, buoyed by resilience in France and Spain.

- Markets aren’t adequately pricing in the risks from higher oil costs, according to Morgan Stanley Wealth Management. Rallies in stocks and Treasuries that have taken the S&P 500 Index to a record high and 10-year yields down to around 2.5 percent illustrate that investors are complacent about crude prices.

- The first official gauge of China’s manufacturing sector fell in April, signaling that the economic stabilization seen in the first quarter remains fragile

- President Donald Trump sued to block Deutsche Bank AG and Capital One Financial Corp. from complying with congressional subpoenas targeting his bank records, escalating the president’s showdown with Democratic lawmakers investigating his finances

- U.K. Prime Minister Theresa May will face a challenge from activists in her Conservative Party after enough signed a petition opposing her leadership and Brexit strategy to force an emergency vote on her future

- The U.K.’s opposition Labour Party’s ruling council will seek to thrash out a Brexit strategy Tuesday as leader Jeremy Corbyn tries to head off a split that threatens to derail his election plans

- A week after the U.S. flagged tighter sanctions on Iranian crude and spurred oil higher, prices are back down to where they were before the announcement

- U.K. traders are ignoring risk of a hawkish BOE, JPMorgan says

Asian equity markets traded mostly lower following weaker than expected Chinese PMI data and as the region digested a heavy slate of earnings. ASX 200 (-0.5%) was negative in which commodity names led the declines seen across a broad range of sectors due to its high exposure to China and the disappointing factory activity, while KOSPI (-0.6%) suffered amid losses in index heavyweight Samsung Electronics after the Co.’s final Q1 results showed operating profit fell around 60% Y/Y. Elsewhere, Hang Seng (-0.7%) and Shanghai Comp. (+0.5%) diverged with Hong Kong dampened after Chinese Official Manufacturing, Non-Manufacturing and Caixin Manufacturing PMIs all fell short of estimates which overshadowed the earnings releases including the profit growth amongst the Big 4 banks, while the mainland remained afloat on month-end and pre-holiday position squaring as well as the increased hopes for more accommodative policy in the aftermath of the weak Chinese data.

Top Asian News

- Jokowi Wants Indonesians to Have Say Picking New Capital City

- Warning Signs Are Flashing in China Stock Market After Surge

- China Triple Whammy Sees Stocks, Bonds, Yuan All Sink in April

- Breaking Up: Asian Stocks Fall Out of Lockstep With U.S. Market

Major European bourses have drifted marginally lower since the EU open [Eurostoxx 50 -0.3%], following a mostly downbeat Asia-Pac lead and as the region digested a slew of pre-market earnings. Sectors are mixed with Telecom names lagging after France’s Orange (-3.5%) missed revenue forecasts and tumbled to the foot of the CAC 40. On the flip side, the energy sector is faring well amidst price action in the oil complex which aided BP (+0.4%), Shell (+0.2%) and Total (+0.1%) climb back into positive territory. Back to earnings, Standard Chartered (+5.7%) extended on opening gains after optimistic earnings coupled with a USD 1.0bln share buyback programme which is expected to reduce its CET1 ratio by around 35bps in Q2. Elsewhere, DSV (+6.8%), Beiersdorf (+2.3%), MTU Aero Engines (+2.2%), and Caixabank (-3.9%) are amongst the movers post-earnings. Finally, Danske Bank (-8.2%) shares fell to the foot of the Stoxx 600 after FT reported that Brussels vows to pursue a probe into the bank’s money laundering scandal.

Top European NEws

- Greenpeace Norway Says Activists Have Left West Hercules Rig

- Santander’s Bets on Latin America Pay off as Europe Stumbles

- Biggest Nordic Banks Hit by Selloff After Bleak Results

- Tria Says VAT Hike Could Be Inevitable Without Cuts: Il Fatto

In FX, the Dollar is softer across the board after Monday’s soft PCE inflation data and with rebalancing models for the last trading day of April flagging sells signals to varying degrees. Hence, the DXY has slipped back from 98.000+ levels again, and this time the index is probing somewhat deeper blow chart supports that were tested towards the end of last week, but not breached. If 97.544 (50% Fib) and 97.500 fail to hold, 97.460 is next on the radar before a stronger downside target and low from last week looms at 97.258.

- GBP – The Pound is the best G10 performer and biggest beneficiary of month end Greenback weakness with one bank signalling especially strong Cable buying to balance portfolios. Subsequently, the pair has extended recovery gains from the low 1.2900 area to circa 1.2986 and through several DMAs including the 10, 100 and 200 levels (at 1.2940 and 1.2961 coincidentally).

- EUR/JPY – Vying for 2nd place in the major ranks and both impacted by data, albeit diversely, as the single currency draws encouragement from firmer than forecast Eurozone GDP and inflation to reclaim the 1.1200 handle. However, the Jpy has now overcome strong resistance at 111.37 to peer above 111.30 in wake of disappointing Chinese PMIs overnight that spurred some risk-aversion and demand for the safe-haven Yen.

- NZD/CHF/CAD – The next best G10s or gainers due to the more pronounced Usd downturn, with the Kiwi hovering near the top of a 0.6681-56 range and Franc back over 1.0200 within 1.0199-75 trading parameters, while the Loonie is pivoting 1.3350 ahead of Canadian data in the form of monthly GDP and PPI. Note also, BoC Governor Poloz and Wilkins are slated to speak later, and then NZ Q1 jobs and labour costs for Q1 are on tap before attention turns to Wednesday’s FOMC.

- AUD – The Aussie is lagging on the aforementioned PMI misses from China and in particular the official and Caixin manufacturing reads that only just avoided stagnation. Aud/Usd is straddling 0.7050, as the Aud/Nzd cross slips a bit further below recent peaks of 1.0600+ towards 1.0565.

- EM – The Try has been volatile again with further weakness vs the Usd in the run up and during the early part of the CBRT’s inflation presentation, but a partial recovery within a 5.9335-9835 band ultimately as Governor Cetinkaya clarified last week’s post-policy meet statement and guidance to maintain that tightening is still an option if upside inflation risks materialise.

In commodities, energy markets are trending higher, albeit remain relatively choppy in early EU trade following comments from Saudi Energy Minister Al-Falih who (in-fitting with reports) said that the Kingdom is ready to meet shortfalls caused by the expiry of Iranian oil waivers on May 2nd. However, with the upcoming JMMC meeting on May 19th (ahead of the OPEC+ meeting on June 26th) the Saudi Energy Minister also noted that a majority of the cartel’s oil ministers are tilting towards extending the global output deal. Analysts at BNP highlight that there is a “good chance” that OPEC countries and allies will decide to extent the supply curb deal in June, although some changes may be made to the current deal. The energy minister also noted that the nation’s oil output will be significantly lower than 10mln BPD (last recorded around 9.8mln BPD) until May-end, whilst exports will be below 7mln BPD (currently just under 7mln BPD). Meanwhile, IFX reported that Russia’s April oil output stood at 11.23mln BPD, slightly lower than March’s 11.3mln. This, coupled with a receding Dollar aided WTI and Brent futures to climb comfortably above USD 64.00/bbl and USD 72.50/bbl respectively. Elsewhere, precious metals are also benefitting from the weaker Greenback with spot Gold meandering just below its 100 and 200 DMAs at 1293.11 and 1297.40 respectively. Meanwhile, turning to base metals, downside seen from disappointing China Manufacturing data has been offset by the softer Dollar with copper now closer to intraday highs and just a whisker away from its 50 DMA at 2.9054.

US Event Calendar

- 8:30am: Employment Cost Index, est. 0.7%, prior 0.7%;

- 9am: S&P CoreLogic CS 20-City MoM SA, est. 0.2%, prior 0.11%; 20-City YoY NSA, est. 2.95%, prior 3.58%

- 9:45am: MNI Chicago PMI, est. 58.5, prior 58.7

- 10am: Pending Home Sales MoM, est. 1.45%, prior -1.0%

- 10am: Conf. Board Consumer Confidence, est. 126.8, prior 124.1; Pending Home Sales NSA YoY, est. -4.0%, prior -5.0%

- 10am: Conf. Board Present Situation, prior 160.6; Conf. Board Expectations, prior 99.8

DB’s Craig Nicol concludes the overnight wrap

The first couple of days of the week here in the UK have required a strict routine recently. Get through Monday avoiding all social media involving Game of Thrones until the evening when you can then rush home and watch it, and then speculate all day Tuesday with your colleagues about what happens next. As Jim was waiting for his house move to start series 8, we’ve had to remain tight-lipped but the flood gates have now opened since he’s been off, especially after last night’s blockbuster. We’ll politely refrain from saying any more and spoiling the plot for those who haven’t yet watched it.

Markets are stuck in a similarly welcome routine of their own at the moment as US equities continue to nudge higher to fresh record highs. Last night’s +0.11% close for the S&P 500 was the third new closing high for the index in the last week while the NASDAQ (+0.19%) likewise closed at a new high – though it is trading lower overnight after Google’s tepid earnings. The DOW (+0.04%) is still -1.02% off its own all-time high; however, it does feel more like when rather than if it’ll eclipse that level. The VIX ticked +0.38pts higher to 13.11, but remains near the bottom of its year-to-date channel. Remarkably, the VIX has traded in an intraday range of just 3.36pts for all of April. The last time we had a smaller range during a month was February 2017. One key market indicator that has snapped out of its recent range is the US 2s10s yield curve, which rose +1.9bps yesterday to 23.7bps. That’s its steepest level since November, and it was accompanied by a general rise in yields yesterday. Yields on Treasuries and Bunds rose +2.8bps and +2.5bps, respectively. This helped bank stocks, which powered equity gains on both sides of the Atlantic, with bank stock indexes equally gaining +1.32% in both the US and Europe.

Anyway, a soft PCE inflation report in the US yesterday – albeit one which was largely baked in post Friday’s data – got the ball rolling;however, the relatively muted price action likely better reflected what is still an exhausting week ahead of big macro events and earnings.

Indeed, this morning we’ve had China’s PMIs for April where both the official (50.1 vs. 50.5) and Caixin (50.2 vs. 50.9 expected) manufacturing readings have disappointed. They also dropped from 50.5 and 50.8, respectively, last month. The official non-manufacturing reading also declined half a point to 54.3 (vs. 54.9 expected) leaving the composite 0.6pts lower at 53.4. The good news is that the composite reading is still higher than the five months prior to March, while the manufacturing reading is above 50 for a second consecutive month, with underlying components including new orders looking healthy. So, consolidation following a big bounce in March is probably the most appropriate way to describe the data.

Equity markets in China are a little higher post that data with the Shanghai Comp up +0.43% and CSI 300 up +0.19%. Positive trade comments from Mnuchin appear to also be helping. He said on Fox News that the US has “made more progress than ever before” towards a real agreement. A reminder that Mnuchin and Lighthizer travel to Beijing today. Meanwhile, the rest of Asia is a little softer with the Hang Seng (-0.48%) and Kospi (-0.55%) down. The latter seems to be suffering following an earnings miss for Samsung. In FX, Sterling is little changed overnight after the Sun reported that more than 10% of chairmen and women of local parties had signed a petition calling for PM May to resign, thus meeting the threshold for an emergency meeting.

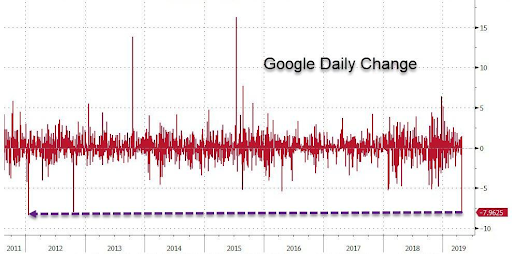

Meanwhile, after the close last night Alphabet’s results came in a bit soft, with revenues surprisingly missing expectations. The company reported overall sales of $29.5 billion, less than the $30.0 billion expected. Profits came in at $6.7 billion, down almost 30% versus the same period last year, but most of that was attributable to a $1.7 billion fine to the European Commission. The stock price, after closing at an all-time high in advance of the earnings report, fell as much as -7% in overnight trading, sending NASDAQ futures -0.25% lower this morning.

Turning back to yesterday, the USD was little changed; however, EM currencies including the Argentinian Peso (+3.50%) had a better day boosted by the announcement from Argentina’s central bank that it would start selling dollars to stabilize the currency. In Europe, the STOXX 600 (+0.08%) recovered from early losses to just about finish onside while the DAX rose +0.10%. Spain’s IBEX (+0.12%) erased losses from earlier in the day to close in line with the rest of Europe after the weekend election result, and 10y Spanish bond yields fell -1.2bps despite the broader bond selloff. Elsewhere WTI oil (+0.32%) rose after declining -4.52% over the preceding three sessions.

Just on the details of that inflation data in the US where the March core PCE deflator was confirmed at 0.0% mom in March compared with expectations for a +0.1% reading. The extra few decimals showed it was a more marginal miss at +0.046%; however, the annual rate, which nudged down from +1.7% to +1.6% yoy was +1.553% with the extra decimal places and so a whisker away from rounding down to an even lower +1.5%. Our US economists noted that the 3-month annualized change is now just +0.7% and the lowest since early 2015 too. Their full thoughts, parsing the various inflation measures and their associated implications for Fed policy, can be found here .

So clearly a soft set of data even if the market had priced much of it in post Friday’s Q1 details. That all being said, our US economists have noted that there are two reasons to expect core PCE to bounce back next month, however. The first is the read-through from the recent bounce in equities for financial services and portfolio management services following a plunge earlier this year, and the second is that core PCE has tended to outperform core CPI in April over recent years.

Other US data didn’t really move the needle. March personal spending rose +0.9% mom versus expectations for a +0.7% rise, but personal incomes rose only +0.1% versus +0.4% expected. Separately, the Richmond Fed manufacturing survey fell -4.9 points to 2.0, a notable decline but still above the negative levels seen in December-January.

Meanwhile, the European Commission’s April confidence indicators were hardly encouraging and underscored the problems facing the manufacturing sector, as the headline economic confidence reading fell -1pt to 104, its lowest level since September 2016. The industrial confidence reading dropped -2.5pts to -4.1, its lowest reading since September 2014. The consumer and services confidence readings were flat and above recent lows, but still a bit off their peaks from last year. Separately, March M1 money supply growth came in better than expected at +7.7%, up from +6.9% in February. Digging into the credit data, however, showed weak corporate loan flows, which pushed the credit impulse to -0.6pp of GDP, its fourth consecutive negative print.

In terms of the rest of the day ahead, all eyes this morning will be on the Q1 GDP reading for the Euro Area where the consensus is for a +0.3% qoq print. We’ll get the data for France prior to that while Italy is due out a little later. Also on the cards today are preliminary CPI data for France, Germany and Italy, while this afternoon we’ve got the Q1 ECI in the US along with the February S&P CoreLogic house price index data, Chicago PMI for April, March pending home sales and April consumer confidence. Away from that we’re due to get comments from the BoE’s Ramsden while Lighthizer and Mnuchin travel to Beijing for more trade talks. The big earnings highlight is Apple after the close tonight, while Pfzier, Merck, McDonalds, Airbus, General Electric and ConocoPhillips are also on the cards. So it should be a busy day.

end

3. ASIAN AFFAIRS

i)TUESDAY MORNING/ MONDAY NIGHT:

SHANGHAI CLOSED DOWN 15.84 POINTS OR 0.52% //Hang Sang CLOSED DOWN 193.10 POINTS OR 0.65% /The Nikkei closed/ DOWN 48.85 POINTS OR .22% Australia’s all ordinaires CLOSED DOWN .48%

/Chinese yuan (ONSHORE) closed DOWN at 6.7391 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 64.03 dollars per barrel for WTI and 72.83 for Brent. Stocks in Europe OPENED MIXED// ONSHORE YUAN CLOSED DOWN // LAST AT 6.7391 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7393/ TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/SOUTH KOREA

3 b JAPAN AFFAIRS

3 C CHINA/CHINESE AFFAIRS

China/

Stocks dip after China’s all important mfg PMI falters

(courtesy zerohedge)

Stocks, Yuan Dip After China PMI ‘Green Shoots’ Dry Up

Nasdaq futures – already hammered by Google’s results – legged lower along with Yuan after China’s PMI prints for April disappointed the green-shoot-believers, slumping back towards contraction.

After all the excitement sparked by the March PMI bounce, China’s April data is big disappointment with China’s official manufacturing and non-manufacturing prints both sliding back (from 50.5 to 50.1 and from 54.8 to 54.3 respectively) with the Caixin China manufacturing PMI tumbling back to 50.2 from 50.8 (and 50.9 expected).

Commenting on the China General Manufacturing PMI™ data, Dr. Zhengsheng Zhong, Director of Macroeconomic Analysis at CEBM Group said:

“The Caixin China General Manufacturing Purchasing Managers’ Index eased to 50.2 in April, down from a recent high of 50.8 in the previous month, indicating a slowing expansion in the manufacturing sector.

1) The subindex for new orders fell slightly despite remaining in expansionary territory. The gauge for new export orders returned to contractionary territory, suggesting cooling overseas demand.

2) The output subindex dropped. The employment subindex returned to negative territory after hitting a 74-month high in March. According to data from the National Bureau of Statistics, the surveyed urban unemployment rate remained at a relatively high level despite edging down in March, suggesting that pressure on the job market remained.

3) While the subindex for stocks of purchased items returned to contractionary territory, the measure for stocks of finished goods fell more markedly. The gauge for future output edged up, pointing to manufacturers’ desire to produce and stable product demand. The subindex for suppliers’ delivery times rose further despite staying in negative territory, implying improvement in manufacturers’ capital turnover.

4) Both gauges for output charges and input costs edged down. There were only small changes in upward pressure on industrial product prices. We predict that April’s producer price index is likely to remain basically unchanged from the previous month.

“In general, China’s economy showed good resilience in April, yet it stabilized on a weak foundation and is not coming to an upward turning point. The Politburo meeting signalled that in the first quarter of this year China had adjusted its countercyclical policy marginally. As pressure on the economy remains in the second quarter, we expect that there will be minor adjustments to the policy but not a turnaround.”

The reaction was a dip in yuan and leg lower in US futures…

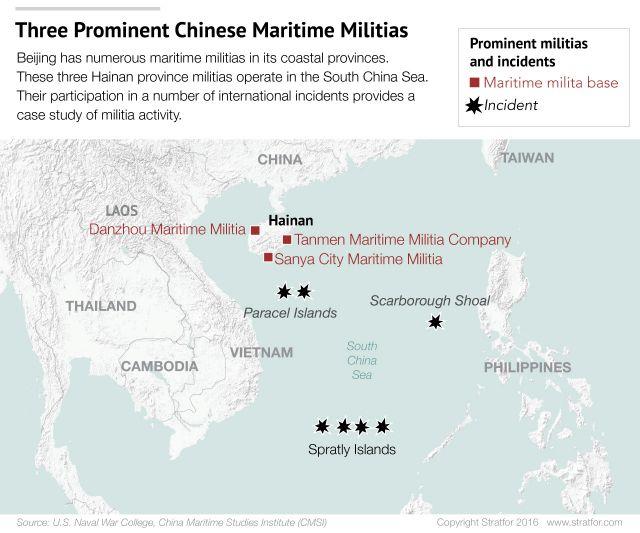

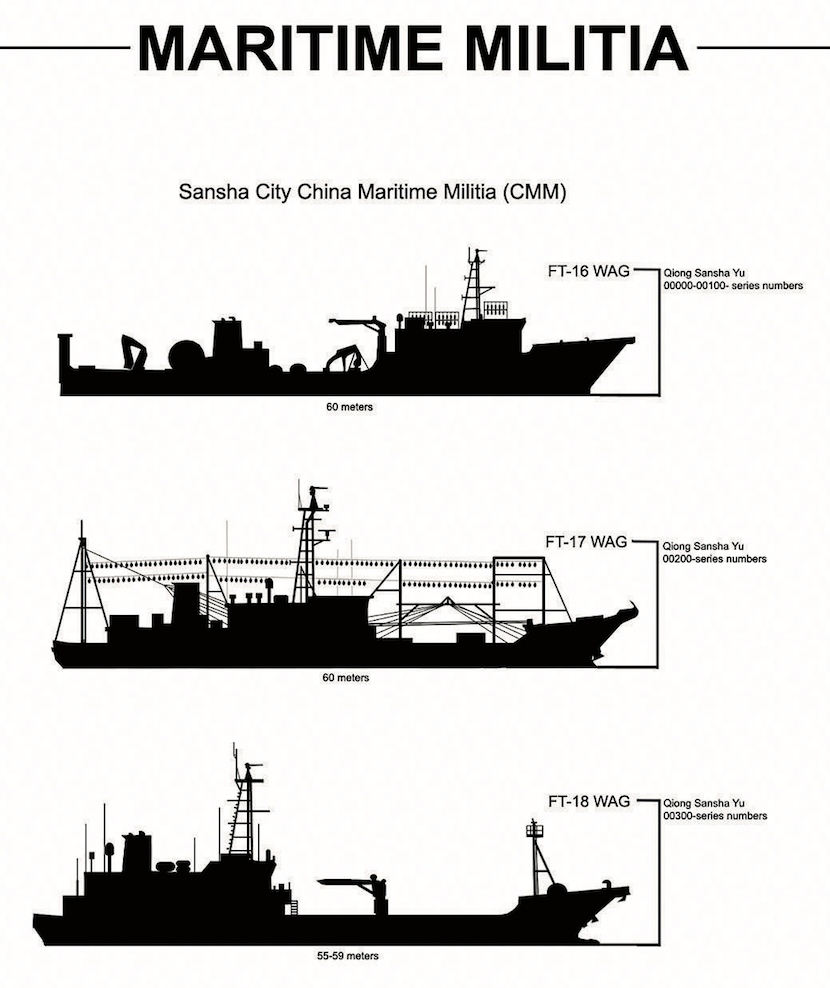

“Warning Shot Across The Bow:” US Warns China On Aggressive Acts By Maritime Militia

Earlier this month, we reported that 275 Chinese fishing militia and Coast Guard vessels surrounded the island of Thitu in the South China Sea, which is currently being occupied by the Philippines. The US recently delivered a stern message to Beijing about its aggression in the highly disputed body of water, announcing that Chinese fishing militia and Coast Guard ships would be treated as military vessels.

Admiral John Richardson, head of the US Navy, described how he told, vice-admiral Shen Jinlon of the Chinese People’s Liberation Army Navy (PLAN), back in January, that the Trump administration would label the Coast Guard and the maritime militia as military vessels.

“I made it very clear that the US navy will not be coerced and will continue to conduct routine and lawful operations around the world, in order to protect the rights, freedoms and lawful uses of sea and airspace guaranteed to all,” Admiral Richardson told the Financial Times.

China’s Coast Guard has more than doubled its feet to over 130 ships in the last decade, making it the largest coast guard in the world. Beijing trains and provides financial subsidies to the maritime militia, an armed reserve force of civilians and fishing boats, has significantly increased in size since 2015.

In its last annual report on the PLAN, the Pentagon said the fleet “plays a major role in coercive activities to achieve China’s political goals without fighting.”

In 2H17 through 1H18, the maritime militia sailed through the East China Sea with commercial grade laser pointers — striking low-flying American warplanes with damaging beams of light.

China has more frequently deployed the maritime militia in the East and South China sea because the US Navy is likely not to respond to aggression from small fishing boats. But that seems to be coming to an end, as the latest warning from Admiral Richardson could provoke a hot conflict.

James Stavridis, a retired US admiral, said Admiral Richardson’s warning is the latest move in the Pentagon to get tough on China.

“It is a warning shot across the bow of China, in effect saying we will not tolerate ‘grey zone’ or ‘hybrid’ operations at sea,” said Stavridis. “A combatant is a combatant is the message, and the CNO (Chief of Naval Operations) is in the right place to warn China early and often.”

Bonnie Glaser, a China specialist at CSIS, a Washington-based think-tank, said: “By injecting greater uncertainty about how the US will respond to China’s grey-zone coercion, the US hopes to deter Chinese destabilizing maritime behavior, including its reliance on coast guard and maritime militia vessels to intimidate its smaller neighbors.”

The warning from Admiral Richardson also affects the Chinese Coast Guard, said Dennis Wilder, a former head of China analysis at the CIA, adding that President Xi Jinping took control of the coast guard in 2018.

“By having both the navy and the coast guard under the Central Military Commission, it improves in wartime the co-ordination and control of maritime forces,” he said. “As China’s coast guard is heavily armed, it is a logical assumption that it would be incorporated into military plans and operations.”

The US Navy has been conducting Freedom of Navigation Operations through the South China Sea, near China’s militarized islands that are considered highly contested areas. Some have warned that labeling the militia and Coast Guard vessels as military vessels would be particularly challenging.

“If the US decides to interpret maritime militia vessels as military, that will lead to increased risk,” said William Choong of the International Institute for Strategic Studies. “With US destroyers in the South China Sea and the continuing Chinese maritime militia operations there, things could go bad very quickly.”

Several weeks ago, China’s Foreign Ministry spokesman Lu Kang said he hopes “non-regional forces don’t stir up troubles in the South China Sea,” after the US Navy amphibious assault ship USS Wasp, carried an unusually large number of Lockheed Martin F-35s, sailed through the South China Sea near the Scarborough Shoal.

China has overlapping economic claims in the South China Sea with Vietnam, Taiwan, Malaysia, the Philippines, and Brunei. While territory disputes remain unsolved, the region remains a flashpoint for the next conflict between the US and China.

END

Vodafone finds hidden backdoors in Huawei network equipment and that will anger China to no end. What will Europe do?

(courtesy zerohedge)

Vodafone Finds Hidden Backdoors In Huawei Network Equipment

As Huawei denies Microsoft’s allegations that it discovered what appears to be a ‘backdoor’ built into the Matebook laptop series, Bloomberg on Tuesday reported on complaints from Vodafone, Europe’s largest wireless provider, about the discovery of what appear to be ‘backdoors’ discovered in Huawei equipment embedded in Vodafone’s Italian wireless network, potentially going back years.