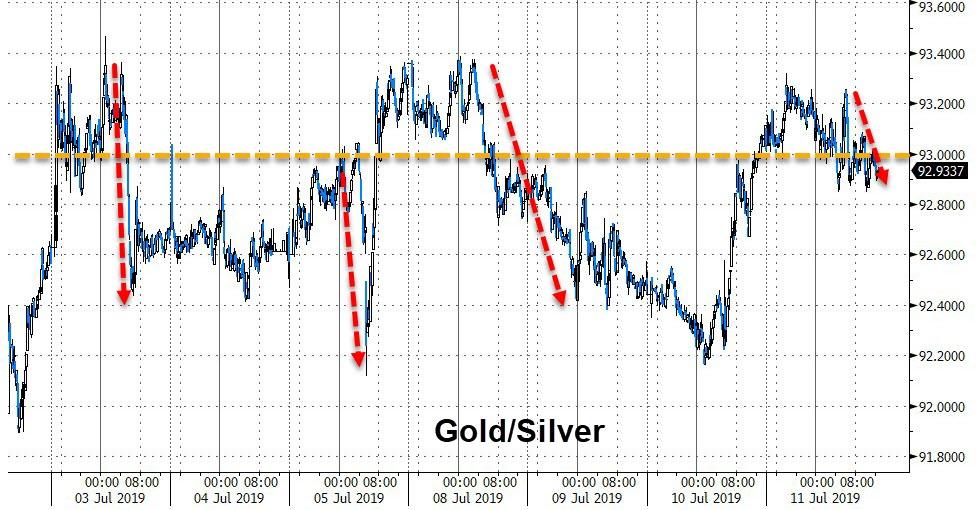

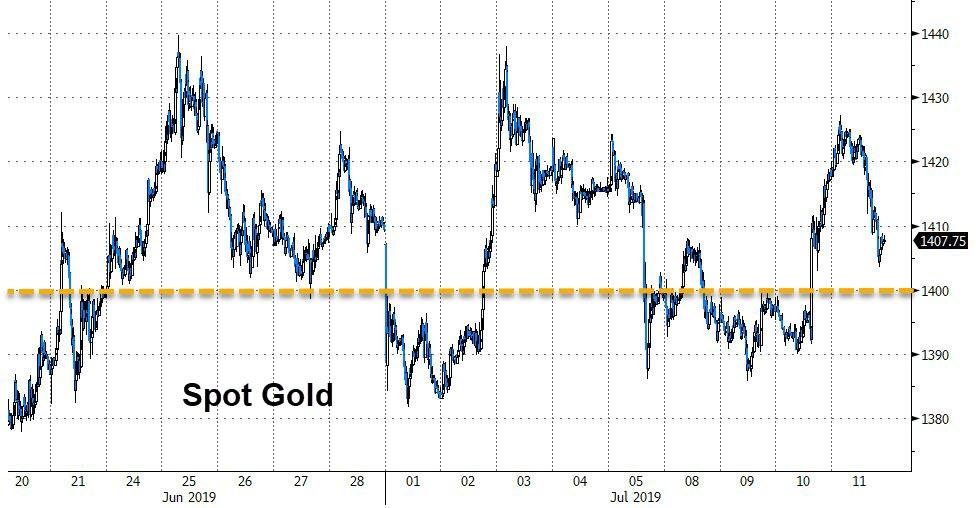

GOLD: $1405.10 DOWN $5.25 (COMEX TO COMEX CLOSING)

Silver: $15.12 DOWN 9 CENTS (COMEX TO COMEX CLOSING)//

Closing access prices:

Gold : $1403.70

silver: $15.12

take a close look at what was read into Hansard UK, on the criminal manipulation of gold and silver.

other than that a small raid on gold and silver as the crooks have a huge derivative obligation especially Deutsche bank. Alasdair Macleod does a good analysis and comes to the conclusion that a sovereign, (and it is China) that is accumulating massive amounts of gold.

YOUR DATA…

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING 33/57

EXCHANGE: COMEX

CONTRACT: JULY 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,410.100000000 USD

INTENT DATE: 07/10/2019 DELIVERY DATE: 07/12/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

657 C MORGAN STANLEY 2

661 C JP MORGAN 33

685 C RJ OBRIEN 1

690 C ABN AMRO 20

737 C ADVANTAGE 30 21

905 C ADM 7

____________________________________________________________________________________________

TOTAL: 57 57

MONTH TO DATE: 828

NUMBER OF NOTICES FILED TODAY FOR JULY CONTRACT: 57 NOTICE(S) FOR 5700 OZ (0.1772 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 828 NOTICES FOR 82800 OZ (2.5754 TONNES)

SILVER

FOR JULY

3 NOTICE(S) FILED TODAY FOR 15,000 OZ/

total number of notices filed so far this month: 3617 for 18,085,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE : $ 11786 DOWN 562

Bitcoin: FINAL EVENING TRADE: $ 11,786 DOWN 1022

end

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI ROSE A CONSIDERABLE SIZED 1047 CONTRACTS FROM 218,493 UP TO 219,540 WITH THE 9 CENT GAIN IN SILVER PRICING AT THE COMEX.

TODAY WE ARRIVED CLOSER TO AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A FAIR SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:,

0 FOR JULY. 0 FOR AUGUST, 551 FOR SEPT, AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 551 CONTRACTS. WITH THE TRANSFER OF 551 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1551 EFP CONTRACTS TRANSLATES INTO 2.755 MILLION OZ ACCOMPANYING:

1.THE 9 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

20.775 MILLION OZ INITIAL STANDING FOR JULY

WE HAD CONSIDERABLE SHORT COVERING AT THE SILVER COMEX LAST NIGHT..AND ZERO SPREADING ACCUMULATION.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JULY:

9613 CONTRACTS (FOR 8 TRADING DAYS TOTAL 9613 CONTRACTS) OR 48.07 MILLION OZ: (AVERAGE PER DAY: 1201 CONTRACTS OR 6.008 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF JULY: 48.07 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 6.86% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION O

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 1206.67 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

APRIL 2019 TOTAL EFP ISSUANCE: 182.87 MILLION OZ.

MAY 2019: TOTAL EFP ISSUANCE: 136.55 MILLION OZ

JUNE 2019 , TOTAL EFP ISSUANCE: 265.38 MILLION OZ

RESULT: WE HAD A CONSIDERABLE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1047, WITH THE 9 CENT GAIN IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A FAIR SIZED EFP ISSUANCE OF 551 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A GOOD SIZED: 1598 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 551 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 1047 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 9 CENT GAIN IN PRICE OF SILVER AND A CLOSING PRICE OF $15.12 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.098 BILLION OZ TO BE EXACT or 156% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 3 NOTICE(S) FOR 15,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 20.775 MILLION OZ

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

.

IN GOLD, THE OPEN INTEREST ROSE BY A CONSIDERABLE 4284 CONTRACTS, TO 603,261 ACCOMPANYING THE STRONG $11.65 PRICING GAIN WITH RESPECT TO COMEX GOLD PRICING YESTERDAY// /THE SPREADING ACCUMULATION WILL NOW IN EARNEST COMMENCE FOR GOLD….

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 5978 CONTRACTS:

APRIL 0 CONTRACTS,JUNE: 0 CONTRACTS, AUGUST 2019: 5940 CONTRACTS, DEC> 38 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 603,261. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A STRONG SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 10,262 CONTRACTS: 4284 CONTRACTS INCREASED AT THE COMEX AND 5978 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 10,262 CONTRACTS OR 1,026,200 OZ OR 31.92 TONNES. YESTERDAY WE HAD A STRONG GAIN OF $11.65 IN GOLD TRADING.…AND WITH THAT STRONG GAIN IN PRICE, WE HAD A HUGE GAIN IN GOLD TONNAGE OF 31.92 TONNES!!!!!! THE BANKERS WERE SUPPLYING INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER.

WITH RESPECT TO SPREADING: WE WILL WITNESS THE MORPHING OF OUR SPREADERS OUT OF SILVER AND INTO GOLD AS THE JULY MONTH PROCEEDS INTO THE ACTIVE DELIVERY MONTH OF AUGUST.

.

FOR NEWCOMERS, HERE IS THE MODUS OPERANDI OF THE CORRUPT BANKERS WITH RESPECT TO THEIR SPREAD/TRADING.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCHED TO SILVER AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NO INTO THE NON ACTIVE DELIVERY MONTH OF JULY HEADING TOWARDS THE VERY ACTIVE DELIVERY MONTH OF AUGUST.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES, HERE IS THE BANKERS MODUS OPERANDI:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST IS STARTING TO RISE IN THIS NON ACTIVE MONTH OF JULY BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN GOLD WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (AUGUST), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JULY : 58 674 CONTRACTS OR 5,867,400 oz OR 184.33 TONNES (8 TRADING DAY AND THUS AVERAGING: 7334 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 8 TRADING DAY IN TONNES: 184.33 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 184.33/3550 x 100% TONNES =5.73% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 3099.33 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

APRIL 2019 TOTAL ISSUANCE: 456.10 TONNES

MAY 2019 TOTAL ISSUANCE: 449.10 TONNES

JUNE 2019 TOTAL ISSUANCE: 642.22 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A STRONG SIZED INCREASE IN OI AT THE COMEX OF 4284 WITH THE STRONG PRICING GAIN THAT GOLD UNDERTOOK YESTERDAY($11.65)) //.WE ALSO HAD A CONSIDERABLE SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 5978 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 5978 EFP CONTRACTS ISSUED, WE HAD A HUMONGOUS AND CRIMINALLY SIZED GAIN OF 10,262 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

5978 CONTRACTS MOVE TO LONDON AND 4284 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 31.92 TONNES). ..AND THIS HUGE INCREASE OF DEMAND OCCURRED ACCOMPANYING THE STRONG GAIN IN PRICE OF $11.65 WITH RESPECT TO YESTERDAY’S TRADING AT THE COMEX. WE HAVE ALREADY COMMENCED WITH SPREADING ACCUMULATION IN GOLD AND IT WILL CONTINUE AS THE MONTH PROCEEDS/

we had: 57 notice(s) filed upon for 5700 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $5.25 TODAY//

NO CHANGES IN GOLD INVENTORY AT THE GLD

INVENTORY RESTS AT 800.54 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 9 CENTS TODAY:

NO CHANGES WITH RESPECT TO SILVER INVENTORY AT THE SILVER SLV:

/INVENTORY RESTS AT 332.518 MILLION OZ.

end

OUTLINE OF TOPICS TONIGHT

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A CONSIDERABLE SIZED 1047 CONTRACTS from 218,493 UP TO 219540 AND CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..THE SPREADERS HAVE COMMENCED THEIR ACCUMULATION OF OPEN INTEREST CONTRACTS IN SILVER AND STOPPED THE LIQUIDATION OF THE SPREADERS IN GOLD

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

FOR JULY: 0 CONTRACTS FOR AUGUST: 0, FOR SEPT. 551 AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 551 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 1047 CONTRACTS TO THE 551 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A STRONG GAIN OF 1598 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 7.99 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 7.475 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL 18.765 MILLION OZ FOR MAY NOW 2.660 MILLION OZ FOR JUNE WITH JULY AT 20.775 MILLION OZ STANDING SO FAR.

RESULT: A CONSIDERABLE SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE 9 CENT GAIN IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A STRONG SIZED 551 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

I)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED UP 2.46 POINTS OR 0.08% //Hang Sang CLOSED UP 227.11 POINTS OR 0.81% /The Nikkei closed UP 110.05 POINTS OR 0.51%//Australia’s all ordinaires CLOSED UP .42%

/Chinese yuan (ONSHORE) closed UP at 6.8659 /Oil UP TO 57.82 dollars per barrel for WTI and 65.36 for Brent. Stocks in Europe OPENED GREEN// ONSHORE YUAN CLOSED UP // LAST AT 6.8659 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.8700 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3A//NORTH KOREA/ SOUTH KOREA

b) REPORT ON JAPAN

3 China/Chinese affairs

i)China/

This does not looks good for China as these Chinese security camera are now banned for spying. They are nearly impossible to identify and remove

( zerohedge)

ii)AN EXCELLENT COMMENTARY ON THE FADING CHINA TRADE DEAL

iii)Is the ceasefire over?: Trump now demands new sanctions on Beijing over its importing of Iranian crude

4/EUROPEAN AFFAIRS

i)DEUTSCHE BANK/GERMANY

When it rains it pours for our good friends over at Deutsche bank. It seems that Tim Leissner is cooperating with the authorities and it ready to throw both Goldman Sachs and Deutsche bank under the bus for money laundering

(courtesy zerohedge)

ii)In a nutshell Snider explains Deutsche banks’ dilemma and why it needs a bad bank. Although it has huge derivative problems it’s real problem occurs if interest rates continue to fall to zero (which I think will happen)> Then their derivative exposure rises exponentially

iii)Your humour story of the day courtesy of Deutsche bank(ZEROHEDGE)

iv)

UK

This is laughable..in order to stop \Brexit some remainers are planning an alternate parliament?

(Mish Shedlock/Mishtalk)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)YEMEN

Cholera is ripping through war torn Yemen; wow! a whopping 500,000 cases in 2019 alone\\

(courtesy zerohedge)

6. GLOBAL ISSUES

This is in continuation of yesterday where Bill Blain discusses the fact that lower rates will not help if there is no growth. He discusses the poor growth prospects coming from China as well as the hardships facing Boeing

(/Bill BLAIN// zerohedge)

7. OIL ISSUES

8 EMERGING MARKET ISSUES

i)VENEZUELA/

9. PHYSICAL MARKETS

10. USA stories which will influence the price of gold/silver)

MARKET TRADING//USA

a)Market trading/LAST NIGHT/USA

II)MARKET TRADING/USA//late morning

ii)Market data/USA

We warned you that China tariffs were hugely inflationary…and this is now becoming a reality as core inflation is very hot and now a huge headache for Jerome Powell

(zerohedge)

iii)USA ECONOMIC/GENERAL STORIES

a)Another huge inflationary signal: big pharma as always are raising drug prices and some of them by 879% on 3400 drugs. They miss Canadian prices.

( Mac Slavo/SHFTPlan.com)

b)My goodness PG and E routinely failed to replace very old lines and that they knew it would fail and eventually cause massive wildfires..Such crooks

( zerohedge)

SWAMP STORIES

a)Re Jeffrey Epstein: Now state attorney Barry Krischer disputes Acosta’s account on the plea deal in 208 where Epstein basically walks out free.

(zerohedge)

b)How Epstein got his wealth

Let us head over to the comex:

we had 0 dealer entry:

We had 0 kilobar entries

total gold withdrawals; 424.184 oz

FOR THE JULY 2019 CONTRACT MONTH)Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 57 contract(s) of which 33 notices were stopped (received) by j.P. Morgan dealer and 10 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account and 0 notices by the squid (Goldman Sachs)

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the JULY /2019. contract month, we take the total number of notices filed so far for the month (828) x 100 oz , to which we add the difference between the open interest for the front month of JULY. (77 contract) minus the number of notices served upon today (57 x 100 oz per contract) equals 84800 OZ OR 2.6376 TONNES) the number of ounces standing in this NON active month of JULY

Thus the INITIAL standings for gold for the JULY/2019 contract month:

No of notices served (828 x 100 oz) + (77)OI for the front month minus the number of notices served upon today (57 x 100 oz )which equals 84,800 oz standing OR 2.6376 TONNES in this active delivery month of JUNE.

We GAINED 49 contracts or an additional 4900 oz will stand as these guys refused to morph into London based forwards as well as negating a fiat bonus. Somebody was in need of physical gold badly on this side of the pond…VERY UNUSUAL TO SEE QUEUE JUMPING THIS EARLY IN THE UP FRONT JULY CONTRACT MONTH.

SURPRISINGLY LITTLE TO NO GOLD HAS BEEN ENTERING THE COMEX VAULTS AND WE HAVE WITNESSED THIS FOR THE PAST YEAR!! WE HAVE ONLY 10.047 TONNES OF REGISTERED ( GOLD OFFERED FOR SALE) VS 2.6376 TONNES OF GOLD STANDING// THEY SEEM TO BE USING CONSIDERABLE GOLD VAPOUR TO SETTLE UPON UNSUSPECTING LONGS.

total dealer silver: 91.993 million

total dealer + customer silver: 306.922 million oz

The total number of notices filed today for the JULY 2019. contract month is represented by 3 contract(s) FOR 15,000 oz

To calculate the number of silver ounces that will stand for delivery in JULY, we take the total number of notices filed for the month so far at 3617 x 5,000 oz = 18,085,000 oz to which we add the difference between the open interest for the front month of JULY. (541) and the number of notices served upon today (3 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the JULY/2019 contract month: 3617(notices served so far)x 5000 oz + OI for front month of JULY( 541) number of notices served upon today (3)x 5000 oz equals 20,775,000 oz of silver standing for the JULY contract month.

WE GAINED 0 CONTRACTS OR AN ADDITIONAL NIL OZ WILL STAND AT THE COMEX AS THESE GUYS REFUSED TO MORPH INTO A LONDON BASED FORWARDS AND AS WELL THEY ALSO NEGATED A FIAT BONUS. IT SEEMS THAT SOMEBODY WAS BADLY IN NEED OF PHYSICAL SILVER ON THIS SIDE OF THE POND JOINING GOLD!.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

TODAY’S ESTIMATED SILVER VOLUME: 60,348 CONTRACTS (we had considerable spreading activity..accumulation

CONFIRMED VOLUME FOR YESTERDAY: 81,495 CONTRACTS..(we no doubt had considerable spreading activity as they are now starting to accumulate in silver)

YESTERDAY’S CONFIRMED VOLUME OF 81,495 CONTRACTS EQUATES to 407 million OZ 58.2% OF ANNUAL GLOBAL PRODUCTION OF SILVER..makes sense!!

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO -0.87% JULY 11/2019)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -0.21% to NAV (JULY 11/2019 )

Note: Sprott silver trust back into NEGATIVE territory at -0.87%-/Sprott physical gold trust is back into NEGATIVE/

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 13.68 TRADING 13.15/DISCOUNT 3.87

END

And now the Gold inventory at the GLD/

JULY 11.WITH GOLD DOWN $5.25: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 800.54 TONNES

JULY 10//WITH GOLD UP $11.65 A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER GOLD DEPOSIT OF 6.46 TONNES/INVENTORY RESTS AT 800.54 TONNES

JULY 9/WITH GOLD UP 70 CENTS, A HUGE PAPER WITHDRAWAL OF 2.89 TONNES WHICH WAS USED IN THE FUTILE RAID ON GOLD AND SILVER THIS MORNING//INVENTORY RESTS AT 794.08 TONNES

JULY 8/ WITH GOLD DOWN 35 CENTS A HUGE WITHDRAWAL OF 1.47 TONNES FROM THE GLD/INVENTORY FALLS TO 796.97 TONNES

JULY 5TH/WITH GOLD DOWN $19.50/NO CHANGES IN GOLD INVENTORY AT THE GLD//INV RESTS AT 798.44 TONNES

JULY 3// WITH GOLD UP $12.60 TODAY A SURPRISE WITHDRAWAL OF 1.76 TONNES FROM THE GLD//INVENTORY RESTS AT 798.44

JULY 2. WITH GOLD UP $18.90 A HUGE “PAPER” DEPOSIT OF 6.16 TONNES INTO THE GLD/INVENTORY RESTS AT 800.20 TONNES

JULY 1: WITH GOLD DOWN $24.70 A HUGE “PAPER GOLD” WITHDRAWAL OF 1.76 TONNES FROM THE GLD/INVENTORY RESTS TONIGHT AT 794.04 TONNES

JUNE 28/WITH GOLD UP $.90 TODAY: ANOTHER 2.05 TONNES OF PAPER GOLD REMOVED AND THIS GOLD WAS USED IN ATTACKING GOLD AT THE COMEX/INVENTORY RESTS AT 795.80 TONNES

JUNE 27/WITH GOLD DOWN $6.10: ANOTHER HUGE WITHDRAWAL OF 1.76 PAPER TONNES FROM THE GLD INVENTORY/INVENTORY RESTS AT 797.61 TONNES

JUNE 26/WITH GOLD DOWN $3.00: WE HAD A HUGE WITHDRAWAL OF 2.37 TONNES FROM THE GLD/INVENTORY RESTS AT 799.61 TONNES

JUNE 25/WITH GOLD UP $1.30 (AND WAY UP BEFORE THE BANKERS WHACKED) WE WITNESSED ANOTHER 1.95 TONNES OF PAPER GOLD ADDED TO THE GLD INVENTORY//INVENTORY RESTS AT 801.98 TONNES

JUNE 24/WITH GOLD UP $18.00 A MONSTROUS PAPER DEPOSIT OF 34.93 TONNES/INVENTORY RESTS AT 799.03 TONNES

JUNE 21/WITH GOLD UP $ 2.90, NO CHANGE IN GOLD INVENTORY: INVENTORY RESTS AT: 764.10 TONNES

June 20/WITH GOLD UP $47.95, NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 764.10 TONNES

JUNE 19 WITH GOLD DOWN $1.65: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 764.10 TONES

JUNE 18/JUNE 18/WITH GOLD UP $7.60: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 764.10 TONNES

JUNE 17/WITH GOLD DOWN $1.65 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 764.10 TONNES

JUNE 14/ WITH GOLD UP $1.05 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.40 TONNES OF PAPER GOLD INTO THE GLD///INVENTORY RESTS AT 764.10 TONNES

june 13/WITH GOLD UP $6.60 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.52 TONNES INTO THE GLD INVENTORY/INVENTORY RESTS AT 759.70 TONNES

JUNE 12/WITH GOLD UP $7.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 756.18 TONNES

JUNE 11/WITH GOLD UP $1.65 CENTS TODAY: A TINY CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .24 TONNES AND THIS IS TO PAY FOR FEES/INVENTORY RESTS AT 756.18 TONNES

JUNE 10/WITH GOLD DOWN $16.40 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.17 TONNES/INVENTORY RESTS AT 756.42 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

JULY 10/2019/ Inventory rests tonight at 800.54 tonnes

*IN LAST 621 TRADING DAYS: 134/22 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 521 TRADING DAYS: A NET 31.46 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

JULY 12/WITH SILVER DOWN 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 332.518 MILLION OZ/

JULY 10/WITH SILVER UP 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 332.518 MILLION OZ//

JULY 9/WITH SILVER UP A SMALL 7 CENTS A GIGANTIC INVENTORY GAIN OF 4.026 MILLION OZ/ INVENTORY RESTS AT 332.518 MILLION OZ AND NOW IT SHOULD BE QUITE CLEAR THAT THE SLV ( AND GLD ARE FRAUDS)

JULY 8/WITH SILVER UP 7 CENTS: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 328,492 MILLION OZ

JULY 5/WITH SILVER DOWN 32 CENTS WE STRANGELY HAD A HUGE INVENTORY GAIN OF 2,234 MILLION OZ//INVENTORY RESTS AT 328.492 MILLION OZ

JULY 3 WITH SILVER UP 10 CENTS A HUGE INCREASE IN INVENTORY..INVENTORY RESTS AT 326.151 MILLION OZ

JULY 2/WITH SILVER UP 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY/INVENTORY RESTS AT 323.330 MILLION OZ//

JULY 1/ WITH SILVER DOWN 16 CENTS: A SURPRISING DEPOSIT OF 936,000 OZ INTO THE SLV/INVENTORY RESTS TONIGHT AT 323.330 MILLION OZ/

JUNE 28/WITH SILVER UP 6 CENTS: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 322.394 MILLION OZ//

JUNE 27/WITH SILVER DOWN 7 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.575 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 322.394 MILLION OZ//

JUNE 26/WITH SILVER UP 17 CENTS: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.819 MILLION OZ/

JUNE 25/WITH SILVER DOWN 25 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.819 MILLION OZ.

JUNE 24/WITH SILVER UP 11 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.819 MILLION OZ//

JUNE 21/WITH SILVER DOWN 22 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.819 MILLION OZ//

JUNE 20/WITH SILVER UP 53 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.819 MILLION OZ/

JUNE 19/WITH SILVER DOWN 3 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 319.070 MILLION OZ/

JUNE 18 WITH SILVER UP 18 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 319.070 MILLION OZ

JUNE 17/WITH SILVER UP XXX CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.775 MILLION OZ//

JUNE 14/WITH SILVER DOWN 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.775 MILLION OZ/

JUNE 13/WITH SILVER UP 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.775 MILLION OZ/

JUNE 12/WITH SILVER UP 4 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.413 MILLION OZ INTO THE SLV INVENTORY/INVENTORY RESTS AT 316.775 MILLION OZ/

JUNE 11/WITH SILVER UP 10 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 315.652 MILLION OZ//

JUNE 10/WITH SILVER DOWN 38 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 315.652 MILLION OZ//

JULY 10/2019:

Inventory 332.518 MILLION OZ

Fed’s Powell explains why a return to the gold standard would be so damaging to the economy

- “If you assigned us [to] stabilize the dollar price of gold, monetary policy could do that, but the other things would fluctuate, and we wouldn’t care,” Powell says.

- Though Powell distanced himself from the Fed nomination process, his comments put him at odds with the writings of Judy Shelton, a current nominee to the central bank.

- Federal Reserve Chairman Jerome Powell told Congress on Wednesday that he doesn’t think a return to the gold standard in the U.S. would be a good idea.

Full article via CNBC here

GOLDNOMICS PODCAST (Episode 12)

Watch Podcast Here or Listen on Apple Podcasts, SoundCloud or Blubrry

News and Commentary

LBMA Gold Prices (AM/ PM Fix – USD, GBP & EUR)

10-Jul-19 1395.45 1408.30, 1117.34 1126.78 & 1243.35 1252.68

09-Jul-19 1387.90 1391.55, 1113.51 1115.61 & 1239.39 1241.54

08-Jul-19 1404.90 1400.10, 1121.11 1119.38 & 1251.20 1248.19

05-Jul-19 1414.40 1388.65, 1126.43 1110.92 & 1255.99 1237.70

04-Jul-19 1415.25 1414.90, 1125.41 1125.55 & 1254.19 1254.59

03-Jul-19 1425.10 1413.50, 1133.52 1123.31 & 1262.78 1251.65

02-Jul-19 1393.10 1391.05, 1105.01 1101.02 & 1233.59 1231.77

01-Jul-19 1390.05 1390.10, 1099.81 1099.99 & 1227.41 1227.74

Receive Our Free Daily or Weekly Updates by Signing Up Here

ii) Physical stories courtesy of GATA/Chris Powell

This is a major development..the entire scam of the bullion banks has been revealed in the UK parliament. UK parliamentary member jeremy Lefroy read into the House of Commons the manipulation of gold and silver and is asking for the FCA and BOE to investigation…the fun begins

(courtesy zerohedge)

Member of Parliament urges investigation of gold-market manipulation in UK

Submitted by cpowell on Thu, 2019-07-11 04:44. Section: Daily Dispatches

12:49a ET Thursday, July 11, 2019

Dear Friend of GATA and Gold:

Citing a confession to gold market manipulation in the United States, a member of Parliament this week urged the British government to investigate possible manipulation of the gold market in London.

The member, Jeremy Lefroy, Conservative for Stafford, prompted a discussion of manipulation during a speech Monday in the House of Commons. Lefroy questioned the economic secretary to the U.K. Treasury, John Glen, Conservative member for Salisbury, as to whether the government was able to prevent gold market manipulation.

Glen responded that the U.K.’s Financial Conduct Authority has “the right tools” and the jurisdiction to “detect and respond” to attempts at market manipulation. But he did not directly respond to Lefroy’s request for an investigation.

…

Lefroy’s statement, much of which is appended, showed detailed knowledge of the gold market and the recent increase in gold reserves by various nations. Lefroy not only cited the conviction for gold market manipulation of a former trader for JPMorganChase in the United States but also expressed concern about the trustworthiness of gold derivatives and paper gold, as well as the possibility that impoverished commodity-producing countries are being cheated by market manipulation.

He also related the complaint of a constituent who accused Deutsche Bank of manipulating the gold and silver markets. Litigation brought by his constituent in Germany and the U.K. was unsuccessful, Lefroy said, but soon afterward Deutsche Bank confessed to such manipulation in regulatory proceedings in the United States.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

* * *

From Hansard, the journal of Parliament, for Monday, July 8, 2019.

https://hansard.parliament.uk/Commons/2019-07-08/debates/A6D6620D-4A27-4…

Statement by Jeremy Lefroy, Conservative member for Stafford:

My first reason for raising the subject is the importance of gold and silver as a store of value internationally.

There are those who say that gold in particular is a relic of the past with little relevance to the modern financial system, but many countries do not seem to agree. Russia is steadily building up its gold reserves, which, 20 years ago, were well below those of the UK; now they are seven times as high. China rapidly increased its gold reserves in 2015. Several European countries, notably Germany and France, hold more than 60% of their reserves in gold.

The United States — the owner of the world’s main reserve currency, which would perhaps have the least reason to hold gold reserves — still believes in gold, which comprises some 73% of its official reserves.

And what of the UK? With just 310 tonnes — pretty much the same quantity for more than 15 years — we hold 8.5% of our official reserves in gold. However, this debate is not about the merits of the UK’s policy on official reserves, although I will refer to that briefly at the end of my speech.

If gold plays such an important role in nations’ reserves, it is vital that the means of trading it and establishing its price on the exchanges be fair and transparent. …

That is what I want to talk about: trust in the markets — and I am asking questions, not giving answers, because I do not have them.

We should note that gold and silver both act as currency crosses, trading as components of the $5-trillion-a-day foreign exchange marketplace. That is an astonishing figure.

Clearly gold and silver are a very small part of the crosses market, but nevertheless they form part of it, and I have to say personally that I get increasingly worried by the huge volumes of daily trades on international markets and the vast amounts of derivatives that are outstanding at any one time. The last report I saw from the United States, I think from the last quarter, showed that something like $200 trillion-worth of derivatives were open at that time.

My second reason for raising the subject is that considerable quantities of gold and silver — and indeed the other precious metals, palladium and platinum — are mined in low- and middle-income countries. As with other commodities — such as coffee and cocoa, with which I worked for many years, and still do a little bit — the price has a major impact on the economies of the producers; it has an impact on those who work in the mining industry, and on the taxation revenues of the countries.

The third reason is that London is at the heart of the global trade in precious metals and has been since the late 17th century. At a time when institutions and businesses are under intense scrutiny, it is vital that we in this country uphold the highest standards, and I am sure my honorable friend the minister entirely agrees with that.

Just last year, a former vice president of a major U.S. bank pleaded guilty in the U.S. to spoofing precious metals markets “hundreds of times with the knowledge and consent of his immediate supervisors.”

Sentencing has been delayed. The implication is that the person is assisting the U.S. Department of Justice’s investigation into others, possibly both within and outside the bank. Spoofing is a technical term, defined in the USA’s Dodd-Frank Act 2010 as “the illegal practice of bidding or offering with intent to cancel before execution,” or, in other words, to deceive the market.

In another case, in January 2018, Deutsche Bank, UBS, and HSBC paid $46.6 million in the U.S. to settle Commodity Futures Trading Commission charges relating to spoofing in the precious metals markets.

I was first alerted to this subject by a constituent who had bought limited quantities of silver as an investment from Deutsche Bank while he was resident in Germany. Over the period in which he purchased the silver, the price peaked at $48 an ounce in 2011 and declined to below $20 by the end of 2014.

It is always very difficult to determine the precise causes of a market’s movement. This was at a time of global uncertainty, financial stress in Europe and North America, and increasing demand for physical silver in electronics and other industrial purposes. My constituent stated in courts in both Germany and Birmingham in the UK that the bank had been manipulating the precious metals market. His cases were dismissed. Nevertheless, shortly afterwards, in 2016, Deutsche Bank and others confirmed that market manipulation had indeed been taking place, and they paid penalties in the U.S.A.

My constituent’s contention, with which I have considerable sympathy, is that it is the small retail investor who pays the price for such illegal behaviour of traders and the banks for which they work. The regulators, and hence the governments, receive the fines, but investors find it almost impossible to prove a loss directly, because a number of factors affect market prices, not simply the illegal activity.

My intention in calling for this debate is not to seek any conclusions at this stage, or to go into the details of precious metals trading — still less of the complexities of derivatives contracts that piggyback on the metals — but rather to ask the minister and the government some questions and to call for action.

My reasoning is that our country depends, more than any other major economy, on the stability of and trust in our financial services sector. The sector provides much well-paid employment, not just in London. Here I should express my regret at the job losses announced today in Deutsche Bank.

At least 2 million people are employed in financial services throughout the UK, not just in London, and the sector contributes up to 10% of government revenue. It also includes our heavy responsibility for and stewardship of the precious metals that we store and trade on behalf of most of the countries in the world.

I wish to ask the minister a number of questions.

First, have the Treasury, the Financial Conduct Authority, or the Bank of England made an assessment of the result of the recent J.P. Morgan case involving the rigging of precious metals markets and its potential impact on the UK? After all, we are talking about financial institutions with a global reach.

Secondly, do the UK authorities believe that any similar activity could take place, or has already taken place, in the UK, or by a bank domiciled here?

Thirdly, if there is evidence that the manipulation of bullion markets by banks over a period has resulted in lower prices than would otherwise have been the case — that is clearly something to be proven — what recourse do producers and retail investors have against banks for that manipulation?

Fourthly, it is estimated that the quantity of so-called paper gold — that is, delivery contracts for gold — is approximately 100 times the quantity of available physical gold. That is not peculiar to the precious metals market; it happens with other commodities as well, but it is nevertheless a noteworthy situation.

I accept that it is unlikely that most such contracts will end up requiring the delivery of physical gold, but what assessment have the authorities made of the risk that if delivery is required, those requirements might not be met? We have to take into account the steady increase in demand for gold — and, indeed, all precious metals — by states as well as by industry.

I suggest that, in addition to answering these questions, the government commission an independent inquiry or review into the bullion market, particularly in the UK.

Gold and silver are not simply commodities like coffee, cocoa, sugar, or copper, vital as those are. They are a bulwark of the global financial system, the importance of which is possibly increasing.

The UK is a relatively minor holder of gold as part of our reserves, but gold constitutes the majority of the reserves of many other countries. We have a significant role in the stewardship of the reserves of others, both physically and in their valuation. The trust that others place in our country and our institutions in this area matters enormously.

An independent inquiry or review at this time would underline the fact that we value that trust greatly, and that we will strengthen controls wherever necessary. Indeed, I believe that some controls have already been strengthened in the recent past. Such a review or inquiry would also flag up risky or illegal activity and ensure that those responsible were brought to book, including by being required to compensate those who have suffered from it.

As I said at the beginning, my aim in this debate is to see whether there has been any activity in these markets in the United Kingdom that we should be taking a closer look at on behalf of investors, particularly the small retail investors who put some of their savings into these commodities. But it is also about the trust in our system in the United Kingdom. There is a huge amount of trust in the UK and its institutions. I believe that that trust is almost always well placed, but it can only continue to be well placed if we constantly scrutinise the system, and check instances where we have an indication that things have not always gone well, or perhaps are not going well now, and take action quickly.

* * *

Join GATA here:

New Orleans Investment Conference

Hilton New Orleans Riverside Hotel

Friday-Monday, November 1-4, 2019

https://neworleansconference.com/

* * *

Help keep GATA going:

GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at:

end

Doorknob Powell explains to the world foolishly by the gold standard is damaging to the economy?

(courtesy CNBC/GATA)

Fed’s Powell explains why gold standard would be damaging to economy

Submitted by cpowell on Wed, 2019-07-10 17:40. Section: Daily Dispatches

By Thomas Franck

CNBC, New York

Wednesday, July 10, 2019

Federal Reserve Chairman Jerome Powell today told Congress he doesn’t think a return to the gold standard in the U.S. would be a good idea.

“You’ve assigned us the job of two direct, real-economy objectives: maximum employment, stable prices. If you assigned us [to] stabilize the dollar price of gold, monetary policy could do that, but the other things would fluctuate and we wouldn’t care,” Powell said from Capitol Hill. “We wouldn’t care if unemployment went up or down. That wouldn’t be our job anymore.”

…

There have been plenty of times in the fairly recently history where the price of gold has sent signals that would be quite negative for either of those goals,” he added. “No other country uses it,” he added. The Fed is tasked and overseen by Congress to maximize employment and keep prices stable.

Though Powell was quick to distance himself from the Fed nomination process, his comments on the gold standard put him at odds with the writings of Judy Shelton, a current Fed nominee and advocate for monetary policy reforms. …

… For the remainder of the report:

https://www.cnbc.com/2019/07/10/feds-powell-explains-why-a-return-to-the…

end

Hugo explains the real money, silver and gold

\(courtesy zerohedge)

Hugo Salinas Price: Bitcoin is just a big distraction from gold

Submitted by cpowell on Thu, 2019-07-11 01:53. Section: Daily Dispatches

9:54p ET Wednesday, July 10, 2019

Dear Friend of GATA and Gold:

Bitcoin, Hugo Salinas Price of the Mexican Civic Association for Silver writes today, protects the U.S. dollar by diverting investment from gold. The cryptocurrency, Salinas Price argues, is a big distraction. His commentary is headlined “About Bitcoin” and it’s posted at the association’s internet site, Plata.com.mx, here:

http://plata.com.mx/enUS/More/380?idioma=2

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

iii) Other physical stories:

The data seems to suggest a huge entity is picking up silver and in Macleod’s opinion it is sovereign China

(Alasdair Macleod)

A Whale Is Accumulating Silver Futures

Authored by Alasdair Macleod via GoldMoney.com,

Silver’s recent price performance has been disappointing. Normally, it is almost twice as volatile as gold, so when the gold price rises 11%, as it has since last December, you would expect silver to rise about 20%. Instead it has fallen marginally.

When we dig into the weekly Commitment of Traders’ Reports covering Comex futures, we see something very odd indeed.

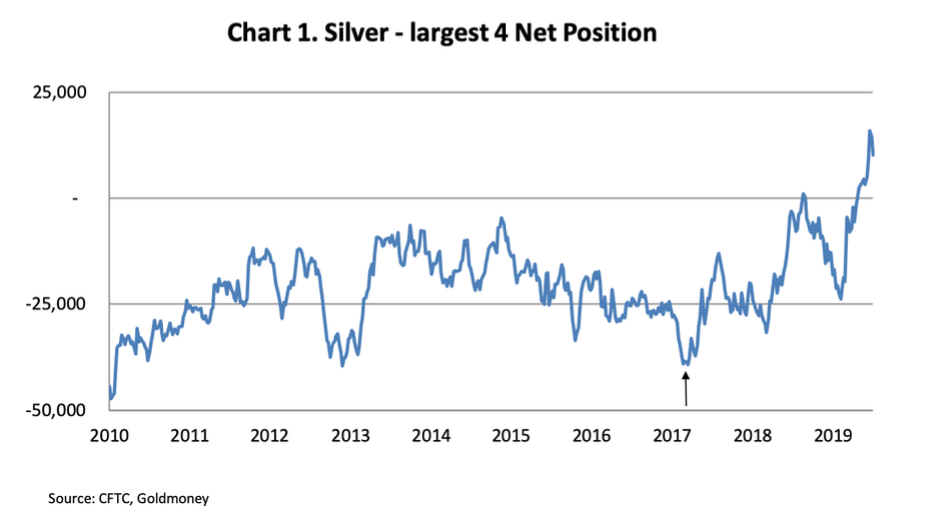

The largest four traders, normally bullion banks or major producers hedging future output, almost always run short positions against speculators’ longs. The more bullish speculators are, the more shorts are carried by the big four to accommodate them. Equally, they only go net long when the speculators are extremely bearish and are collectively marginally long or exceptionally net short. Not now, as the following chart of the Largest Four Traders net positions shows.

The number of contracts either net long or net short are derived from the concentration ratios in the weekly COT releases. The net long position is standing at a record high, a move that started in March 2017, marked by the arrow.

With respect to the concentration ratios, the CFTC’s explanatory notes state the following:

“The report shows the per cents of open interest held by the largest four and eight reportable traders, without regard to whether they are classified as commercial or non-commercial. The concentration ratios are shown with trader positions computed on a gross long and gross short basis and on a net long or net short basis. The “Net Position” ratios are computed after offsetting each trader’s equal long and short positions. A reportable trader with relatively large, balanced long and short positions in a single market, therefore, may be among the four and eight largest traders in both the gross long and gross short categories, but will probably not be included among the four and eight largest traders on a net basis.”

So, anyone can be a large reportable trader. Gross positions include straddles and swaps between different silver futures, and do not concern us. It is the net position ratios that are relevant. Chart 1 above is of the four largest traders net positions in the markets calculated on this basis.

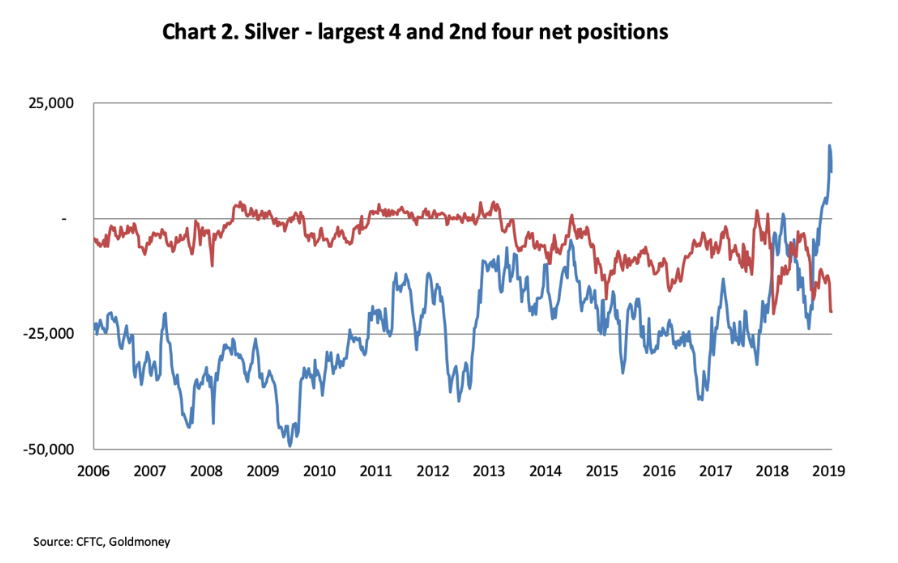

The next largest 4 traders can also be calculated by taking the concentration ratios of the eight largest and subtracting the four largest. It turns out, as one would expect when gold is very overbought, the silver positions of the next largest four at net short 40,305 contracts are close to a record short. The second four see prices have hardly moved, and the speculators in the Managed Money category are only moderately long. Despite their individual short positions, they don’t realise they are in acute danger of being victims of a major bear squeeze.

They appear to be blissfully unaware that they are as a group short to a very larger buyer in their own ranks. It is certainly possible no one has done the analysis covered in this article, because analysts and traders rarely look at the concentration figures. Furthermore, the correlation of the positions between the four largest and next four have not closely followed each other for some time as Chart 2 shows, which perhaps also encourages complacency.

We will return to that point later. However, it is only recently that the second largest four’s net shorts have exceeded those of the first largest four, and now we see the largest four traders are record long while the second largest four are record short.

This is the first time this has happened. It seems unlikely that in normal circumstances any of the largest eight would be running a diametrically opposed trading position to the other seven. Comex doesn’t work like that, consisting of distinct groupings: producers and merchants hedging their future deliveries, bullion banks acting as market-makers, and speculators, who take on the price risk by going long. They all tend to stick within their group motivations.

Given these normally clear distinctions we can probably rule out a collaboration between more than one large trader. If two or more large traders were involved, it would be known by insiders and the other large traders would not risk being short.

Therefore, it is likely to be only one long position, far larger than the charts above indicate, given the largest four traders will include three other large shorts. We can only guesstimate its size. However, if we assume that the other three largest trades are short in tune with the others, our long trader, our whale, is very long indeed. The long position probably began in March 2017, when collectively the large four were net short 39,215 contracts. This is marked by the up arrow in Chart 1, where the trend reversed. If we take that as our starting point, we can see that as of 2 July (the most recent COT figures) the swing is nearly 50,000 contracts. That is an indication of the long position of our large trader, accounting for over 20% of silver’s open interest. Since each contract is for 5,000 ounces, it represents as much as 7,775 tonnes, which is 28% of 2018’s global mine production of 27,550 tonnes.

In the context of the silver futures market it is huge. But it seems unlikely to be an attempt to corner the silver market, because Comex-registered vaults have about 9,500 tonnes of silver bullion and LBMA vaults at the end of March had 36,195 tonnes. In other words, there is 1.66 times annual mine supply in these two vaulting systems alone. Given healthy vaulting supply, someone attempting a repeat of the Bunker-Hunts’ attempt to corner the market in 1979 has a massive hill to climb, particularly when such an attempt might be thwarted by the regulators changing the rules.

Putting cornering the market aside, we can also rule out a large speculator taking a punt on silver. A look at the Managed Money category net position tells us our whale is not there. Nor does a whale this size show up in the Non-Reportable category either.

By a process of elimination, it looks like a commercial entity, which uses silver for manufacturing purposes and is a continuing buyer of the metal. It would make sense that such a buyer would wish to hedge against future price rises by going long of futures. This being the case, it is a behemoth, larger than any individual processor. And that leads to one conclusion: it is probably the Peoples’ Bank of China, the state institution charged with managing all China’s silver distribution. But with a purely circumstantial case, we need more evidence.

Why the trail of evidence leads to China

In 2012, I was speaking at a conference in New York at which a number of silver mining minnows had stands in the hope of attracting investors. I visited all of them to establish the answer to a simple question: how did they ship their silver out, who paid them, and when?

The reason for asking this question was there were allegations going the rounds about the dark deeds of JPMorgan manipulating the silver futures market. That the silver market was open to manipulation by the big banks there was little doubt, and JPMorgan was definitely a major force in the silver market. By not appearing to take credible allegations seriously, Comex and the CFTC as regulator gave the impression they were colluding with JPMorgan, giving the whole story an extra spin.

The assumption that JPMorgan could simply ride roughshod over the CFTC and Comex rulebook was really the weakness in the conspiracy theories. We are all aware of the crony capitalism between banks and regulators, but there are limits. Bending the interpretation of the rules is one thing. Flagrantly breaking them to create false markets is another.

However, there was little doubt JPMorgan dominated trading in Comex silver futures, and my feeling was they were acting for a legitimate client instead of its own trading book. This was confirmed when Blythe Masters, then head of global commodities at JPMorgan and a hate-figure for silver conspiracy theorists, a month earlier than the New York conference gave an interview where she clearly stated that JPMorgan acted only for clients and did not run directional positions as principal.

The outcry from conspiracy theorists was predictable, but I found it impossible to believe that Masters would give an interview, which appeared to be for the main purpose of refuting the rumours, and then tell a barefaced lie. When an interviewee says before answering, “that is a great question” you can be reasonably sure it was pre-agreed, so is an important and considered revelation. The recording of the interview confirms this is what happened.

The question then was what role was JPMorgan playing in the market? They had inherited their silver business from the acquisition of Bear Sterns in 2008 and continued to develop it. And there was no doubt that such a large investment bank had greater clout than Bear Sterns to manage silver positions. Given Blythe Master’s unequivocal denial that JPMorgan was running a trading position on its own book, it must have been acting for one very large client, and that was the evidence I was looking for at the New York conference.

The silver miners all told the same story. When they had enough doré to ship, a specialist from Glencore would assess and certify the value of the silver content and arrange for it to be shipped to a refiner. Glencore was working with JPMorgan, and the silver miner would be paid as soon as the doré was being shipped, enabling the miner to cover its day-to-day costs. Using the doré as collateral, JPMorgan would cover the price risk by selling Comex silver futures or possibly by selling silver on the LBMA for forward delivery. This was why Masters could truthfully say JPMorgan did not take a directional position.

We should bear in mind that Glencore’s assessors would also be assessing the silver content of base metal ores, because more than half of silver mine production is a by-product of base metal processing, and in total involves very large amounts of silver. The sale of large amounts of futures contracts would follow to offset price risk.

This is not the whole story, raising the question as to the doré’s destination. At the New York conference, there was no consensus among the silver miners. But at that time, as it still does today, China had a major position in the global silver market. Furthermore, China had invested in processing and refining facilities when environmental factors led to the closure of rival facilities in western nations, such as Canada. It was therefore almost certain that a big slug of the doré was bound for China, which not only had ample low-cost silver refining capacity, but had also invested heavily in base metal refining for the extraction of silver as well.

All purchases of silver imported into China are the responsibility of the Peoples’ Bank of China, and that would be JPMorgan’s underlying client, not Glencore. Given the standing and resources of the Peoples Bank, and the leading positions of JPMorgan and Glencore in their respective industries, it is easy to envisage the existence of this high-level partnership and the importance of confidentiality.

I could then conclude my own conspiracy theory, which seemed far more likely than the others swirling around: JPMorgan extended the miners credit against the collateral of doré shipments, the price risk being covered by selling futures on Comex and forwards on the LBMA. This was not JPMorgan as a principal, but on behalf of China’s central bank. China had a vested interest in keeping the price as low as possible, which is the natural consequence of this hedging activity.

In their conspiracy theories, frustrated silver bulls were missing the one obvious conclusion confirmed by the Blythe Masters interview, that JPMorgan was, and probably still is, working for the Chinese central bank as their client. China is the whale in the market, which explains why, in Chart 2 above, we see the lack of correlation between the largest four traders and the second four going back over a decade. Bear in mind also that the commitment of trader’s reports covering Comex are not the whole story. Forward trades in London on the LBMA are a significantly larger market and JPMorgan operates its own vaults in London as well.

Switching dealings between OTC forwards and regulated futures makes it very difficult to analyse silver markets. Analysing Comex is like observing the dog’s tail and not seeing the dog. The result is China has managed to import over half her silver needs at suppressed prices. By using both markets it appears that JPMorgan has discharged this role skilfully for the Peoples’ Bank, and it also explains why the regulators were unable to bring them to account, despite evidence that JPMorgan’s actions may have been suppressing the silver price: strictly speaking, there was no wrongdoing within Comex’s rules.

The change from bear to bull

Price management at the behest of the Peoples’ Bank, within certain limits, is a reasonable objective and the bedrock of all large client/broker relationships. In that context, the broker is often given a degree of discretion. Regular liaison between JPMorgan’s dealers and those of the client would be normal, perhaps monthly or quarterly to review both progress and objectives. This allows the broker to act on the clients’ behalf on a semi-discretionary basis within agreed guidelines.

In this case, the client (i.e. the Peoples’ Bank) would be an ongoing buyer of physical silver. In the past, silver prices have been suppressed in the futures market by selling enough futures to cover doré and silver-bearing base metal ore shipments. Doing business this way would have been a significant benefit to China.

None of this explains why a substantial long position appears to have now materialised on Comex. Instead of selling futures to suppress the price, our market whale appears to have turned buyer; buying enough to cover China’s annual silver imports, the equivalent of about 43,000 Comex contracts. Clearly, the new strategy is to hedge against rising prices instead of suppressing the silver price. Given this new development, one would have thought that the other seven large traders would have tried to limit their silver shorts and at least keep an even book. There are several reasons why they may not have not felt the need to do so:

- There are ample quantities of bullion in the vaults in London and Comex depositories, currently totalling 1.66 years’ worth of mine supply, unlike gold where the underlying bullion stock is very small relative to the paper contracts based upon them.

- They appear to be unaware of China’s actions and motives. They may not even be aware of the existence of this long position. If they are aware of it, they may think it is just a technical long, against a short in London’s OTC market.

- With global commercial demand declining due to the economic slow-down, they probably feel relaxed about the price outlook for silver, which they will regard as an industrial metal. Base metals show little sign of entering a bull market.

Therefore, with the Swaps category only moderately oversold (net short 12,735 contracts) and the Managed Money category only average overbought (net long 21,923 contracts), the other seven largest traders are likely to feel individually comfortable with their short positions, unaware of the extent to which their fellow traders are also short. What they fail to realise is that they are the shorts against the one largest trader who is long.

Why is China now buying futures?

If I am correct in thinking the whale in the market is the Peoples Bank of China, then instead of suppressing the silver price, she is now hedging approximately one year’s silver imports against future price rises. Having pinpointed the switch from price suppression to futures accumulation to approximately March 2017, we can now say that courtesy of JPMorgan’s dealing skills, no one was aware of the Peoples Bank’s change in price strategy.

This was shortly after President Trump was elected and assumed office, which could have had a bearing. From China’s point of view, the geopolitical outlook had become very unstable, with its Washington sources reporting the Deep State’s conflict with Trump and its attempts to destabilise his administration. At the same time, the global economic outlook was improving, which would have led to greater global demand for silver, making it difficult for China to continue to suppress the price. These are good enough reasons to change price strategy and lock in silver prices by buying futures to cover future shipments.

More recently, China has begun to declare monthly additions of monetary gold reserves, a trend led by Russia and copied by other Eurasian central banks. Gold has suddenly caught a bid and having risen sharply become dangerously overbought. This is in sharp contrast to silver, which on the surface appears to have been side-lined.

The traders at the Peoples Bank now appear to have protected themselves against an increase in the silver price, which normally rises nearly twice as much as gold. Since the Peoples Bank also controls the nation’s gold, the silver desk could have known about the plans to announce monthly increases in China’s monetary gold reserves in advance. It would have been an added incentive for the desk to buy silver futures from the beginning of this year.

It will be interesting to see if this move, combined with China’s increasing gold reserves, results in a significant jump in the silver price. If the silver whale is China, then it’s a reasonable supposition that China is signalling by its actions that it expects dollar prices for gold, and therefore silver, to continue higher over time. An advantage of taking up a silver position is if things cut up rough in the gold market, China will not be implicated so far as Comex futures are concerned. Unlike large-scale dealings in Comex gold futures (which China appears to have studiously avoided), protecting prices on her silver imports is what the futures market is for and is unlikely to be politically contentious.

The message for silver investors is seven of the eight largest traders appear to have become complacent. If China is the whale in the market, then discovery could be a very painful process for them. Its unfolding could be dramatic, likely to coincide with the next move upwards in the gold price.

end

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

Your early THURSDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/7 AM EST

i) Chinese yuan vs USA dollar/CLOSED / LAST AT: 6.8659/ GETTING VERY DANGEROUSLY CLOSE TO 7:1

//OFFSHORE YUAN: 6.8700 /shanghai bourse CLOSED UP 2.46 POINTS OR 0.08%

HANG SANG CLOSED UP 227.11 POINTS OR 0.81%

2. Nikkei closed UP 110.05 POINTS OR 0.51%

3. Europe stocks OPENED ALL MIXED

USA dollar index UP TO 96.88/Euro RISES TO 1.1272

3b Japan 10 year bond yield: FALLS TO. –.14/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 108.13/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//CARRY TRADERS GETTING KILLED

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 60.59 and Brent: 67.19

3f Gold UP/JAPANESE Yen UP CHINESE YUAN: ON -SHORE UP/OFF- SHORE: UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO -.24%/Italian 10 yr bond yield UP to 1.67% /SPAIN 10 YR BOND YIELD UP TO 0.43%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 1.91: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 2.25

3k Gold at $1419.70 silver at: 14.28 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 17/100 in roubles/dollar) 62.99

3m oil into the 60 dollar handle for WTI and 67 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 108.13 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning .9858 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1112 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now NEGATIVE territory with the 10 year RISING to –0.24%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.07% early this morning. Thirty year rate at 2.59%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.6658..

S&P Futures Above 3,000 After Powell “Gives Traders License To Buy Everything”

There is a Bloomberg headline this morning which best summarizes the market mood on the day after Powell’s 1st day of Congressional testimony: “Traders Take Fed Message as License to Buy Everything“, and it’s pretty much spot on, with S&P futures storming back over 3,000, following Asian stock higher amid certainty that the Fed will cut rates at least by 25-50bps in the immediate future, even as an early European rally fizzled as investors didn’t get the memo, and grew skeptical by the relentless dovish flood. Meanwhile, Treasuries dropped and the dollar edged lower.

The S&P was set to open back over 3,000 as it briefly topped the key psychological level for the first time Wednesday after the Fed Chair made it abundantly clear he is willing to lower rates, citing a slowing global economy and trade issues. In his first day of testimony before Congress on Wednesday, Powell confirmed the U.S. economy was still under threat from disappointing factory activity, tame inflation and a simmering trade war, and said the Fed stood ready to “act as appropriate”.

A strong June U.S. jobs report last Friday heightened expectations the Fed was more likely to cut by 25 basis points than by 50. But Powell’s cautious stance helped fuel bets of two rate cuts at its next policy meeting on July 30-31, and the odds of a 50 bps cut rose to 27.6% from 3.3% on Tuesday, after minutes from the Fed’s last meeting showed many policymakers felt there was not yet a strong case for easing.