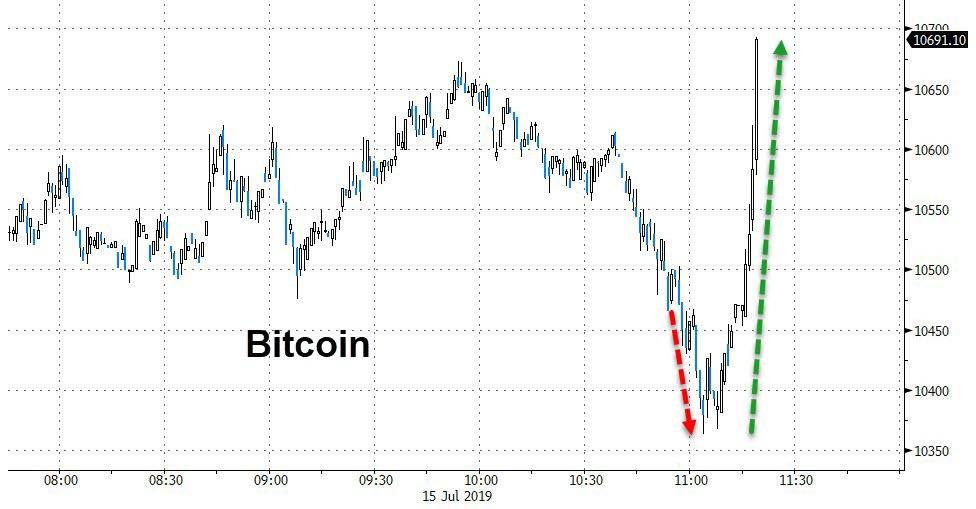

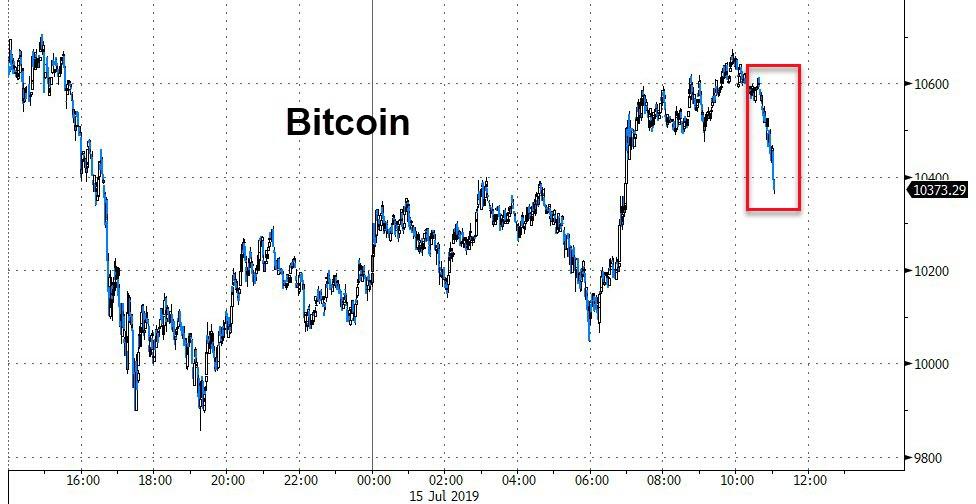

JULY 15/GOLD WITHSTANDS ANOTHER ATTACK BY OUR BANKERS ARE TURNS GREEN AT THE END OF THE COMEX SESSION BY $1.85 TO $1412.15//SILVER HAS A STELLAR DAY UP 11 CENTS TO $15.33//CHINA’S ECONOMIC NUMBERS REALLY BAD!!//TURKEY: ERDOGAN TO LOWER BENCHMARK INTEREST FROM 24% TO SINGLE DIGITS AND TRUMP WILL SANCTION THE COUNTRY FOR BRINGING IN S 400’S: THAT WILL SINK THE LIRA//EPSTEIN PLUS OTHER SWAMP STORIES FOR YOU TONIGHT//

IN SILVER THE COMEX OI FELL A FAIR SIZED 742CONTRACTS FROM 219,160 DOWNTO 218,418 DESPITE THE 10 CENT GAIN IN SILVER PRICING AT THE COMEX.

TODAY WE ARRIVED FURTHER FROM AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGEAMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:,

0 FOR JULY. 0FOR AUGUST, 1259FOR SEPT, AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 1259CONTRACTS. WITH THE TRANSFER OF 1259CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1259 EFP CONTRACTS TRANSLATES INTO 9.08 MILLION OZ ACCOMPANYING:

1.THE 10 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

20.850 MILLION OZ INITIAL STANDING FOR JULY

WE AGAIN HAD CONSIDERABLE SHORT COVERING AT THE SILVER COMEX LAST NIGHT..AND ZERO SPREADING ACCUMULATION.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JULY:

10,321 CONTRACTS (FOR 10 TRADING DAYS TOTAL 10321 CONTRACTS) OR 51.61 MILLION OZ: (AVERAGE PER DAY: 1032 CONTRACTS OR 5.16 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF JULY: 51.61 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 3,37% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 1209.21 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

APRIL 2019 TOTAL EFP ISSUANCE: 182.87 MILLION OZ.

MAY 2019: TOTAL EFP ISSUANCE: 136.55 MILLION OZ

JUNE 2019 , TOTAL EFP ISSUANCE: 265.38 MILLION OZ

RESULT: WE HAD A SMALL SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 742, DESPITE THE 10 CENT GAIN IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A STRONGSIZED EFP ISSUANCE OF 1259 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A GOOD SIZED: 517 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 1259 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 742OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 10 CENT GAIN IN PRICE OF SILVER AND A CLOSING PRICE OF $15.22 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1..094 BILLION OZ TO BE EXACT or 156% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 4NOTICE(S) FOR 20,000OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 20.850 MILLION OZ

HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

IN GOLD, THE OPEN INTEREST ROSE BY A HUGE 7072 CONTRACTS, TO 602,567 ACCOMPANYING THE STRONG $5.20 PRICING GAIN WITHRESPECT TO COMEX GOLD PRICING YESTERDAY// /THE SPREADING ACCUMULATION IS NOW ON GOING FOR GOLD….

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 6165 CONTRACTS:

APRIL 0 CONTRACTS,JUNE: 0 CONTRACTS, AUGUST 2019: 6165CONTRACTS, DEC> 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 602,567. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A HUMONGOUS SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 13,237, CONTRACTS: 7072 CONTRACTS INCREASED AT THE COMEX AND 6165 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 13,237 CONTRACTS OR 1,323,700 OZ OR 41.17 TONNES. FRIDAY WE HAD A STRONG GAIN OF $5.20 IN GOLDTRADING.…AND WITH THAT RISE IN PRICE, WE HAD A HUGE GAIN IN GOLD TONNAGE OF 41.17 TONNES!!!!!! THE BANKERS WERE SUPPLYING INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER.

WITH RESPECT TO SPREADING: WE ARE WITNESSING THE MORPHING OF OUR SPREADERS OUT OF SILVER AND INTO GOLD AS THE JULY MONTH PROCEEDS INTO THE ACTIVE DELIVERY MONTH OF AUGUST.

.

FOR NEWCOMERS, HERE IS THE MODUS OPERANDI OF THE CORRUPT BANKERS WITH RESPECT TO THEIR SPREAD/TRADING.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCHED TO SILVER AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NO INTO THE NON ACTIVE DELIVERY MONTH OF JULY HEADING TOWARDS THE VERY ACTIVE DELIVERY MONTH OF AUGUST.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES, HERE IS THE BANKERS MODUS OPERANDI:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST IS STARTING TO RISE IN THIS NON ACTIVE MONTH OF JULY BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN SILVER WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JULY : 77,989 CONTRACTS OR 7,798,900 oz OR 242.57 TONNES (10 TRADING DAY AND THUS AVERAGING:7790 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 10 TRADING DAYS IN TONNES: 242.57 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3550 TONNES

THUS EFP TRANSFERS OF 242.57 TONNES/3550 x 100% TONNES =6.83% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 3169.41 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

APRIL 2019 TOTAL ISSUANCE: 456.10 TONNES

MAY 2019 TOTAL ISSUANCE: 449.10 TONNES

JUNE 2019 TOTAL ISSUANCE: 642.22 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A HUGE SIZED INCREASE IN OI AT THE COMEX OF 7072 WITH THE GOOD PRICING GAIN THAT GOLD UNDERTOOK ON YESTERDAY($5.20)) WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 6165 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 6165 EFP CONTRACTS ISSUED, WE HAD A HUMONGOUS SIZED GAIN OF 13,237 CONTRACTSIN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

6165 CONTRACTS MOVE TO LONDONAND 7072 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 41.17 TONNES). ..AND THIS STRONG INCREASE OF DEMAND OCCURRED WITH A SMALLISH GAIN IN PRICE OF $5.20 WITH RESPECT TO FRIDAY’S TRADING AT THE COMEX. WE HAVE ALREADY WITNESSED STRONG SPREADING ACCUMULATION IN GOLD AS THE NON ACTIVE DELIVERY MONTH PROCEEDS.

we had: 6 notice(s) filed upon for 600 oz of gold at the comex.

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $1.86 TODAY//

NO CHANGES IN GOLD INVENTORY AT THE GLD//

INVENTORY RESTS AT 800.54 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 11 CENTS TODAY:

NO CHANGES WITH RESPECT TO SILVER INVENTORY AT THE SILVER SLV:

/INVENTORY RESTS AT 332.518 MILLION OZ.

end

OUTLINE OF TOPICS TONIGHT

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A SMALL SIZED 742 CONTRACTS from 219,160 DOWN TO 218,418 AND FURTHER FROM THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..THE SPREADERS HAVE STOPPED THEIR ACCUMULATION OF OPEN INTEREST CONTRACTS IN SILVER AND MORPHED INTO THE ACCUMULATION OF SPREADING CONTRACTS IN GOLD

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

FOR JULY: 0 CONTRACTS FOR AUGUST: 0, FOR SEPT. 1259 AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1259 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 742 CONTRACTS TO THE 1259OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A FAIR SIZED GAIN OF 517 OPENINTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 2.585 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 7.475 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL 18.765 MILLION OZ FOR MAY NOW 2.660 MILLION OZ FOR JUNE WITH JULY AT 20.850 MILLION OZ STANDING SO FAR.

RESULT: A SMALL SIZED DECREASE IN SILVER OI AT THE COMEX DESPITE THE 10 CENT GAIN IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A STRONG SIZED 1259 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

SHANGHAI CLOSED UP 11.64 POINTS OR 0.40% //Hang Sang CLOSED UP 83.26 POINTS OR 0.29% /The Nikkei closed UP 42.37 POINTS OR 0.20%//Australia’s all ordinaires CLOSED DOWN .63%

/Chinese yuan (ONSHORE) closed DOWN at 6.8758 /Oil UP TO 60.50 dollars per barrel for WTI and 66.94 for Brent. Stocks in Europe OPENED GREEN// ONSHORE YUAN CLOSED DOWN // LAST AT 6.8758 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.8752 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3A//NORTH KOREA/ SOUTH KOREA

b) REPORT ON JAPAN

3 China/Chinese affairs

i)China/

The Chinese Military is warning the USA again not to give Taiwan arms

(Two commentaries: courtesy zerohedge)

ii)Trump gloats at the Chinese

(courtesy zerohedge)

iii)The truth behind the real Huawei from expert Gordon Chang

(courtesy Gordon Chang/Gatestone)

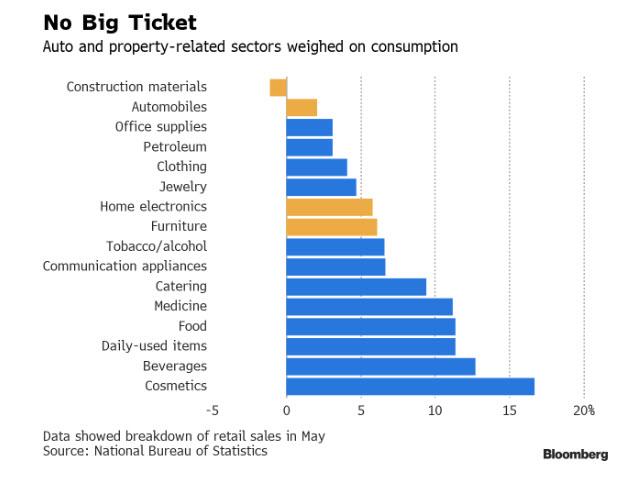

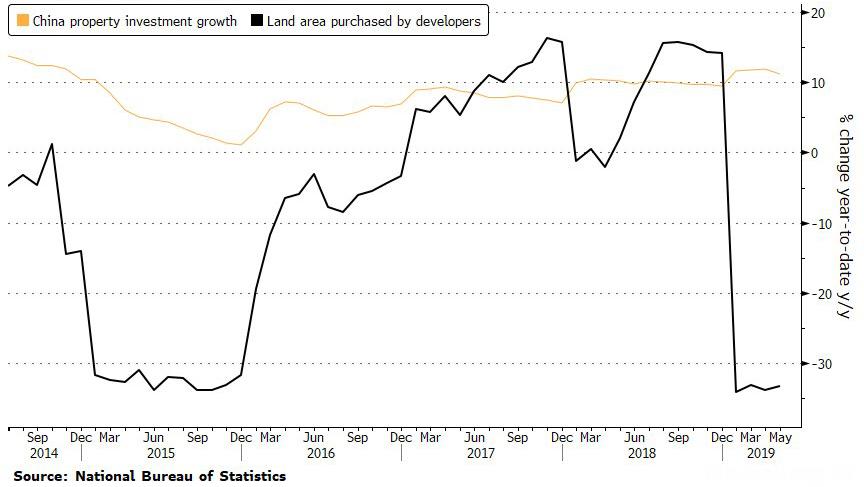

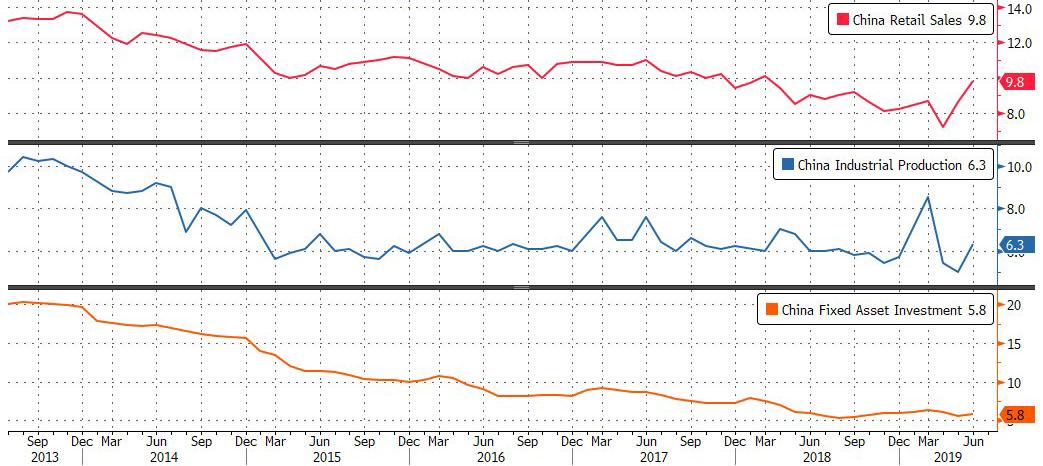

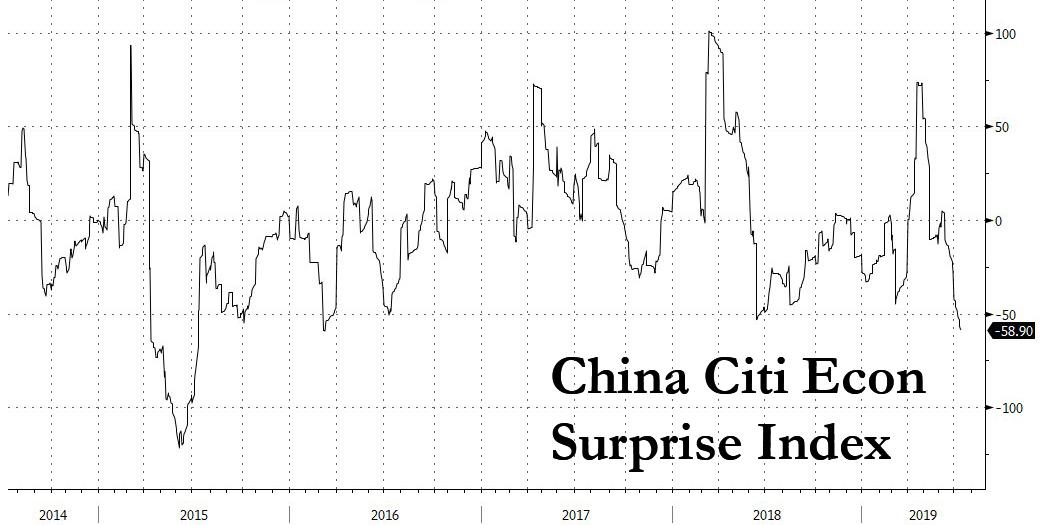

iv)Beijing losing control of its economy. GDP growth only 6.2%..exports falter by 1.2% and imports into the country fall by over 7%. Yet Chin continues to supply debt which will cripple the banks.

( zerohedge)

v)Now Huawei is planning “extensive” USA layoffs(courtesy zerohedge)

4/EUROPEAN AFFAIRS

i)Deutsche bank/Germany

Deutsche bank is lowering the severance payments for workers who were fired last Monday.

( zerohedge)

ii)Saturday: FRANCE/PARIS

Over 700 new migrant protesters: “black vests” occupy the Paris Pantheon. They want citizenship

(zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)TURKEY

Important: Erdogan set to lower interest rates into single digits (from 24%) which will send the Lira tumbling and create a banking crisis in Turkey. Trump is also ready to roll out sanctions on Turkey for the S 400 purchases,

(zero hedge)

ib )TURKEY/CYPRUS/EU/ISRAEL

The following was largely expected: The EU as agreed to sanction Turkey for drilling in Cypriot waters. I have been bringing this to your attention on a daily basis. For newcomers, Israel discovered a huge natural gas find off the coast of Haifa, several years ago and they found it was heading onto Cyprus, Lebanon and Greek waters. They dutifully informed the leaders of these nations of the find. Theproblem is Turkey does not recognize the division of the country by way of an armistice in 1974 with the north government by Cypriot Turks and the southern half which includes the capital Nicosia is controlled by the Greek Cypriots. Now that there is a big discovery Turkey wants it and they have interfered with drilling and intercepting ships.

(zerohedge)

ii)A good commentary from Margolis as Turkey is set to call Trump’s bluff

(courtesy Eric Margolis)

iii)IRAN/UK

Iran tells the UK that they will continue to export oil under any conditions. They released the crew of that detained tanker

(courtesy zerohedge)

6. GLOBAL ISSUES

SWEDEN

A good look at why Sweden is at war and this is all due to the immigration of Muslims into the country

(COURTESY BERGMAN/GATESTONE)

ii)Worldwide semiconductor equipment sales collapse in 2019

(zerohedge)

7. OIL ISSUES

8 EMERGING MARKET ISSUES

9. PHYSICAL MARKETS

I)The following is a must read on the de dollarization of the USA. It is lengthy but a must read.

(courtesy Michael Hudson/GATA)

II)Although slightly up in June, it is down sharply form last year. The BIS is running out of gold to carrry out their nefarious activities

(Robert Labourne/.GATA)

iii)John Hathaway is telling us that gold’s breakout is foretelling and that big changes in the financial order are upon us

(courtesy John Hathaway/GATA)

iv)The hardship for miners due to the low price of gold

(courtesy McGee.Globe and Mail/Toronto/GATA)

v)MMT or Modern Monetary Theory is in fact going on today and as a result market rigging is its chief consequence

(courtesy zerohedge)

10. USA stories which will influence the price of gold/silver)

MARKET TRADING//USA

a)Market trading/LAST NIGHT/USA

II)MARKET TRADING/USA

ii)Market data/USA

Although the NY empire headline number printed better than expected, it still shows that industry continues to struggle..manufacturing employment expectations crash

(zerohedge)

iii)USA ECONOMIC/GENERAL STORIES

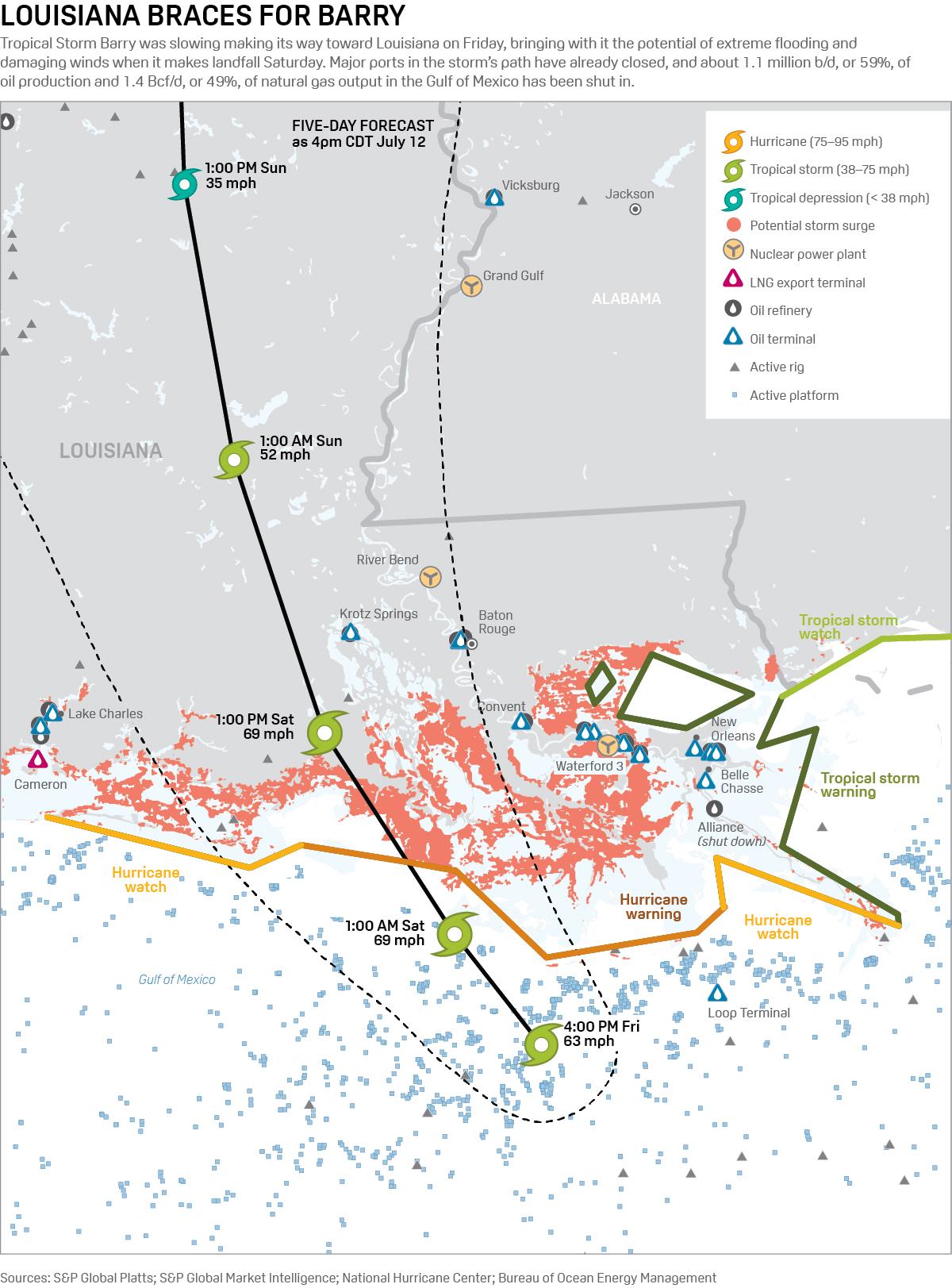

a)FRIDAY NIGHT

Barry missed New Orleans but still flooding is possible

(zerohedge)

b)expect food shortages as Barry rips through central USA

(courtesy Michael Snyder)

c)Bricks and mortar continue to burn and this has been accentuated by the 25% tariffs on many Chinese goods which will put any firms out of business.

(courtesy zerohedge)

SWAMP STORIES

i)Tom Luongo continues with his assessment as to what is going on behind the curtains with respect to Epstein

(courtesy Tom Luongo)

ii)Meet Epstein’s “madame”: she is none other than Robert Maxwell’s daughter, Ghislaine Maxwell.

(zerohedge)

E)SWAMP STORIES/MAJOR STORIES//THE KING REPORT

end

LET US BEGIN:

Let us head over to the comex:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A HUGE SIZED 7072 CONTRACTS TO A LEVEL OF 602,567ACCOMPANYING THE STRONG GAIN OF $5.20 IN GOLD PRICING WITH RESPECT TO FRIDAY’S // COMEX TRADING)

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF JULY.. THE CME REPORTS THAT THE BANKERS ISSUED STRONGSIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS., THAT IS 6165 EFP CONTRACTS WERE ISSUED:

FOR AUGUST; 6165 CONTRACTS: DEC: 0 AND ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 6165 CONTRACTS.

THE OBLIGATION STILL RESTS WITH THE BANKERS ON THESE TRANSFERS. ALSO REMEMBER THAT THERE IS NO DOUBT A HUGE DELAY IN THE ISSUANCE OF EFP’S AND IT PROBABLY TAKES AT LEAST 48 HRS AFTER OUR LONGS GIVE UP THEIR COMEX CONTRACTS FOR THEM TO RECEIVE THEIR EFP’S AS THEY ARE NEGOTIATING THIS CONTRACT WITH THE BANKS FOR A FIAT BONUS PLUS THEIR TRANSFER TO A LONDON BASED FORWARD.

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES:13,237 TOTAL CONTRACTS IN THAT 6165 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE GAINED A STRONG SIZED 7072 COMEX CONTRACTS. THE BANKERS SUPPLIED THE NECESSARY AND INFINITE AMOUNT OF SHORT PAPER IN GOLD TO CONTAIN THE PRICE RISE.

NET GAIN ON THE TWO EXCHANGES :: 13,237 CONTRACTS OR 1,323,700 OZ OR 41.17 TONNES.

We are now in the NON active contract month of JULY and here the open interest stands at 17 CONTRACTS as we LOST 5 contracts. We had 5 notices filed yesterday so we gained 0 contracts or nil additional oz of gold will stand for delivery. The next big active month for deliverable gold is August and here the OI FELL by a strong 9133 contracts DOWN to 330,688. After August we have the non active month of September and here the OI rose by 400 contracts up to 574. The next active delivery month is October and here the OI rose by 589 contracts up to 19,348.

TODAY’S NOTICES FILED:

WE HAD 6 NOTICES FILED TODAY AT THE COMEX FOR 600 OZ. (0.0186 TONNES)

Total COMEX silver OI FELL BY A CONSIDERABLE SIZED 742 CONTRACTS FROM 219,160 DOWN TO 218,888 (AND FURTHER FROM THE NEW RECORD OI FOR SILVER SET ON AUGUST 22.2018. THE PREVIOUS RECORD WAS SET APRIL 9.2018/ 243,411 CONTRACTS) AND TODAY’S OI COMEX LOSS OCCURRED DESPITE A 10 CENT GAIN IN PRICING.//FRIDAY.

WE ARE NOW INTO THE ACTIVE DELIVERY MONTH OF JULY. HERE WE HAVE 533OPEN INTEREST STAND FOR DELIVERY WITH A LOSS OF 17 CONTRACTS. WE HAD 20 NOTICES FILED ON FRIDAY SO WE GAINED 3 CONTRACTS OR AN ADDITIONAL 15,000 OZ OF SILVER WILL ATTEMPT TO STAND AT THE COMEX…. AND THESE GUYS REFUSED TO MORPH INTO A LONDON BASED FORWARD AS WELL AS NEGATING A FIAT BONUS. LET US WAIT AND SEE IF SUCCESSFUL IN OBTAINING PHYSICAL METAL ON THIS SIDE OF THE POND. AFTER JULY WE HAVE THE NON ACTIVE MONTH OF AUGUST AND HERE WE LOST 11 CONTRACTS DOWN TO 1132. THE NEXT BIG ACTIVE DELIVERY MONTH AFTER AUGUST IS SEPT AND HERE THE OI FELL BY 1352 CONTRACTS DOWN TO 150,161 CONTRACTS.

TODAY’S NUMBER OF NOTICES FILED:

We, today, had 4 notice(s) filed for 20,000 OZ for the JULY, 2019 COMEX contract for silver

Trading Volumes on the COMEX TODAY: 230,050 CONTRACTS

CONFIRMED COMEX VOL. FOR YESTERDAY: 334,431 contracts

Total monthly oz gold served (contracts) so far this month

839 notices

83900 OZ

2.6096 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

xxx oz

we had 0 dealer entry:

We had 1 kilobar entry

total dealer deposits: nil oz

total dealer withdrawals: nil oz

we had 0 deposit into the customer account

i) Into JPMorgan: nil oz

ii) Into Everybody else: nil oz

total gold deposits: nil oz

very little gold arrives from outside/ NO amount arrived today

we had 1 gold withdrawal from the customer account:

i ) out of Scotia: 160.75 oz

5 kilobars

total gold withdrawals; 160.75 oz

i) we had 0 adjustment today

FOR THE JULY 2019 CONTRACT MONTH)Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 6 contract(s) of which 3 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account and 0 notices by the squid (Goldman Sachs)

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the JULY /2019. contract month, we take the total number of notices filed so far for the month (839) x 100 oz , to which we add the difference between the open interest for the front month of JULY. (17 contract) minus the number of notices served upon today (6 x 100 oz per contract) equals 85,000 OZ OR 2.6438 TONNES) the number of ounces standing in this NON active month of JULY

Thus the INITIAL standings for gold for the JULY/2019 contract month:

No of notices served (839 x 100 oz) + (17)OI for the front month minus the number of notices served upon today (6 x 100 oz )which equals 85,000 oz standing OR 2.6438 TONNES in this active delivery month of JUNE.

We GAINED 0 contracts or an additional NIL oz will stand as these guys refused to morph into London based forwards as well as negating a fiat bonus.

SURPRISINGLY LITTLE TO NO GOLD HAS BEEN ENTERING THE COMEX VAULTS AND WE HAVE WITNESSED THIS FOR THE PAST YEAR!! WE HAVE ONLY 10.0438 TONNES OFREGISTERED ( GOLD OFFERED FOR SALE) VS 2.6438 TONNES OF GOLD STANDING// THEY SEEM TO BE USING CONSIDERABLE GOLD VAPOUR TO SETTLE UPON UNSUSPECTING LONGS.

total registered or dealer gold: 322,825.827 oz or 10.0412 tonnes

total registered and eligible (customer) gold; 7,696,866.219 oz 239.40 tonnes

IN THE LAST 32 MONTHS 117 NET TONNES HAS LEFT THE COMEX.

THE GOLD COMEX IS NOW IN STRESS AS

1. GOLD IS LEAVING THE COMEX

2. GOLD IS LEAVING THE REGISTERED CATEGORY OF THE COMEX.

end

And now for silver

AND NOW THE DELIVERY MONTH OF JULY

INITIAL standings/SILVER

IN TOTAL CONTRAST TO GOLD, HUGE ACTIVITY IN SILVER TODAY.

JULY 15 2019

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

1047.400 oz

Delaware

Deposits to the Dealer Inventory

NIL oz

Deposits to the Customer Inventory

nil oz

No of oz served today (contracts)

4

CONTRACT(S)

(20,000 OZ)

No of oz to be served (notices)

529 contracts

(2,645,000 oz)

Total monthly oz silver served (contracts)

3641 contracts

18,205,000 oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

**

we had 0 inventory movement at the dealer side of things

total dealer deposits: NIL oz

total dealer withdrawals: nil oz

we had 0 deposits into the customer account

into JPMorgan: nil oz

ii)into everybody else: nil oz

*** JPMorgan for most of 2017 and in 2018 has adding to its inventory almost every single day.

JPMorgan now has 153.4 million oz of total silver inventory or 50.36% of all official comex silver. (153.4 million/304.6 million

total customer deposits today: nil oz

we had 1 withdrawals out of the customer account:

i) out of Delaware: 1047.400 oz

total 1047.400 oz

we had 0 adjustments :

total dealer silver: 91.993 million

total dealer + customer silver: 306.647 million oz

The total number of notices filed today for the JULY 2019. contract month is represented by 4 contract(s) FOR 20,000 oz

To calculate the number of silver ounces that will stand for delivery in JULY, we take the total number of notices filed for the month so far at 3641 x 5,000 oz = 18,205,000 oz to which we add the difference between the open interest for the front month of JULY. (533) and the number of notices served upon today (4 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the JULY/2019 contract month: 3641 (notices served so far) x 5000 oz + OI for front month of JULY (533) number of notices served upon today (4)x 5000 oz equals 20,850,000 oz of silver standing for the JULY contract month.

WE GAINED 3 CONTRACTS OR AN ADDITIONAL 15,000 OZ WILL STAND AT THE COMEX AS THESE GUYS REFUSED TO MORPH INTO A LONDON BASED FORWARDS AND AS WELL THEY ALSO NEGATED A FIAT BONUS. IT SEEMS THAT SOMEBODY WAS BADLY IN NEED OF PHYSICAL SILVER ON THIS SIDE OF THE POND JOINING GOLD!.

TODAY’S NUMBER OF NOTICES FILED:

We, today, had 20 notice(s) filed for 100,000 OZ for the JUNE, 2019 COMEX contract for silver

CONFIRMED VOLUME FOR YESTERDAY: 53,814 CONTRACTS..(we no doubt had considerable spreading activity as they are now starting to accumulate in silver)

YESTERDAY’S CONFIRMED VOLUME OF 53,814 CONTRACTS EQUATES to 26.90 million OZ 38.4% OF ANNUAL GLOBAL PRODUCTION OF SILVER..makes sense!!

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

1. Sprott silver fund (PSLV): NAV FALLS TO -0.94% (JULY 15/2019)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -1.33% to NAV (JULY 15/2019 )

Note: Sprott silver trust back into NEGATIVE territory at -0.94%-/Sprott physical gold trust is back into NEGATIVE/

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 13.82 TRADING 13.28/DISCOUNT 3.93

END

And now the Gold inventory at the GLD/

JULY 15: WITH GOLD UP $1.85 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 800.54 TONNES

JULY 12/WITH GOLD UP $5.20 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 800.54 TONNES

JULY 11.WITH GOLD DOWN $5.25: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 800.54 TONNES

JULY 10//WITH GOLD UP $11.65 A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER GOLD DEPOSIT OF 6.46 TONNES/INVENTORY RESTS AT 800.54 TONNES

JULY 9/WITH GOLD UP 70 CENTS, A HUGE PAPER WITHDRAWAL OF 2.89 TONNES WHICH WAS USED IN THE FUTILE RAID ON GOLD AND SILVER THIS MORNING//INVENTORY RESTS AT 794.08 TONNES

JULY 8/ WITH GOLD DOWN 35 CENTS A HUGE WITHDRAWAL OF 1.47 TONNES FROM THE GLD/INVENTORY FALLS TO 796.97 TONNES

JULY 5TH/WITH GOLD DOWN $19.50/NO CHANGES IN GOLD INVENTORY AT THE GLD//INV RESTS AT 798.44 TONNES

JULY 3// WITH GOLD UP $12.60 TODAY A SURPRISE WITHDRAWAL OF 1.76 TONNES FROM THE GLD//INVENTORY RESTS AT 798.44

JULY 2. WITH GOLD UP $18.90 A HUGE “PAPER” DEPOSIT OF 6.16 TONNES INTO THE GLD/INVENTORY RESTS AT 800.20 TONNES

JULY 1: WITH GOLD DOWN $24.70 A HUGE “PAPER GOLD” WITHDRAWAL OF 1.76 TONNES FROM THE GLD/INVENTORY RESTS TONIGHT AT 794.04 TONNES

JUNE 28/WITH GOLD UP $.90 TODAY: ANOTHER 2.05 TONNES OF PAPER GOLD REMOVED AND THIS GOLD WAS USED IN ATTACKING GOLD AT THE COMEX/INVENTORY RESTS AT 795.80 TONNES

JUNE 27/WITH GOLD DOWN $6.10: ANOTHER HUGE WITHDRAWAL OF 1.76 PAPER TONNES FROM THE GLD INVENTORY/INVENTORY RESTS AT 797.61 TONNES

JUNE 26/WITH GOLD DOWN $3.00: WE HAD A HUGE WITHDRAWAL OF 2.37 TONNES FROM THE GLD/INVENTORY RESTS AT 799.61 TONNES

JUNE 25/WITH GOLD UP $1.30 (AND WAY UP BEFORE THE BANKERS WHACKED) WE WITNESSED ANOTHER 1.95 TONNES OF PAPER GOLD ADDED TO THE GLD INVENTORY//INVENTORY RESTS AT 801.98 TONNES

JUNE 24/WITH GOLD UP $18.00 A MONSTROUS PAPER DEPOSIT OF 34.93 TONNES/INVENTORY RESTS AT 799.03 TONNES

JUNE 21/WITH GOLD UP $ 2.90, NO CHANGE IN GOLD INVENTORY: INVENTORY RESTS AT: 764.10 TONNES

June 20/WITH GOLD UP $47.95, NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 764.10 TONNES

JUNE 19 WITH GOLD DOWN $1.65: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 764.10 TONES

JUNE 18/JUNE 18/WITH GOLD UP $7.60: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 764.10 TONNES

JUNE 17/WITH GOLD DOWN $1.65 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 764.10 TONNES

JUNE 14/ WITH GOLD UP $1.05 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.40 TONNES OF PAPER GOLD INTO THE GLD///INVENTORY RESTS AT 764.10 TONNES

june 13/WITH GOLD UP $6.60 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.52 TONNES INTO THE GLD INVENTORY/INVENTORY RESTS AT 759.70 TONNES

JUNE 12/WITH GOLD UP $7.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 756.18 TONNES

JUNE 11/WITH GOLD UP $1.65 CENTS TODAY: A TINY CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .24 TONNES AND THIS IS TO PAY FOR FEES/INVENTORY RESTS AT 756.18 TONNES

JUNE 10/WITH GOLD DOWN $16.40 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.17 TONNES/INVENTORY RESTS AT 756.42 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

JULY 15/2019/ Inventory rests tonight at 800.54 tonnes

*IN LAST 623 TRADING DAYS: 134.22 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 523 TRADING DAYS: A NET 31.46 TONNESHAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

JULY: 15 WITH SILVER UP 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 332.518 MILLION OZ

JULY 12/WITH SILVER UP 10 CENTS: NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 332.518 MILLION OZ//

JULY 11/NO CHANGE IN SILVER INVENTORY

JULY 10/WITH SILVER UP 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 332.518 MILLION OZ//

JULY 9/WITH SILVER UP A SMALL 7 CENTS A GIGANTIC INVENTORY GAIN OF 4.026 MILLION OZ/ INVENTORY RESTS AT 332.518 MILLION OZ AND NOW IT SHOULD BE QUITE CLEAR THAT THE SLV ( AND GLD ARE FRAUDS)

JULY 8/WITH SILVER UP 7 CENTS: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 328,492 MILLION OZ

JULY 5/WITH SILVER DOWN 32 CENTS WE STRANGELY HAD A HUGE INVENTORY GAIN OF 2,234 MILLION OZ//INVENTORY RESTS AT 328.492 MILLION OZ

JULY 3 WITH SILVER UP 10 CENTS A HUGE INCREASE IN INVENTORY..INVENTORY RESTS AT 326.151 MILLION OZ

JULY 2/WITH SILVER UP 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY/INVENTORY RESTS AT 323.330 MILLION OZ//

JULY 1/ WITH SILVER DOWN 16 CENTS: A SURPRISING DEPOSIT OF 936,000 OZ INTO THE SLV/INVENTORY RESTS TONIGHT AT 323.330 MILLION OZ/

JUNE 28/WITH SILVER UP 6 CENTS: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 322.394 MILLION OZ//

JUNE 27/WITH SILVER DOWN 7 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.575 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 322.394 MILLION OZ//

JUNE 26/WITH SILVER UP 17 CENTS: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.819 MILLION OZ/

JUNE 25/WITH SILVER DOWN 25 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.819 MILLION OZ.

JUNE 24/WITH SILVER UP 11 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.819 MILLION OZ//

JUNE 21/WITH SILVER DOWN 22 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.819 MILLION OZ//

JUNE 20/WITH SILVER UP 53 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.819 MILLION OZ/

JUNE 19/WITH SILVER DOWN 3 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 319.070 MILLION OZ/

JUNE 18 WITH SILVER UP 18 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 319.070 MILLION OZ

JUNE 17/WITH SILVER UP XXX CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.775 MILLION OZ//

JUNE 14/WITH SILVER DOWN 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.775 MILLION OZ/

JUNE 13/WITH SILVER UP 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.775 MILLION OZ/

JUNE 12/WITH SILVER UP 4 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.413 MILLION OZ INTO THE SLV INVENTORY/INVENTORY RESTS AT 316.775 MILLION OZ/

JUNE 11/WITH SILVER UP 10 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 315.652 MILLION OZ//

Inventory 332.518 MILLION OZ

LIBOR SCHEDULE AND GOFO RATES:

YOUR DATA…..

6 Month MM GOFO 2.24/ and libor 6 month duration 2.23

Indicative gold forward offer rate for a 6 month duration/calculation:

G0LD LENDING RATE: – .01

XXXXXXXX

12 Month MM GOFO

+ 2.19%

LIBOR FOR 12 MONTH DURATION: 2.23

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.04

end

end

PHYSICAL GOLD/SILVER STORIES

end

i) GOLDCORE BLOG/Mark O’Byrne

Why Gold Prices Have Climbed to Their Highest Since 2013

Dovish statements from global central banks recently aren’t the only reason for gold’s rise past $1,400 an ounce this week to levels it hasn’t seen in nearly six years.

“Gold is a global market and U.S. monetary policy, while important, is not the only driver of performance,” Juan Carlos Artigas, director of investment research at the World Gold Council, told MarketWatch on Friday.

On the macroeconomic level, there’s “the combination of increase geopolitical tensions and a more accommodative monetary policy stance signaled by central banks, including the [European Central Bank] and the [U.S. Federal Reserve], which have pushed global interest rates lower,” he said.

U.S.-China tensions over trade policy persist as traders await an expected meeting and progress toward a resolution on the trade dispute, between U.S. President Donald Trump and Chinese President Xi Jinping at the Group of 20 leaders summit was June 28-29.

ii) Physical stories courtesy of GATA/Chris Powell

The following is a must read on the de dollarization of the USA. It is lengthy but a must read.

(courtesy Michael Hudson/GATA)

Michael Hudson: Dedollarizing may collapse the U.S. financial empire

Submitted by cpowell on Sat, 2019-07-13 04:14. Section: Daily Dispatches

12:15a ET Saturday, July 13, 2019

Dear Friend of GATA and Gold:

Nobody dissects the mechanisms of U.S. dollar imperialism as well as the economist and historian Michael Hudson, a professor of economics at the University of Missouri at Kansas City.

In an interview with Bonnie Faulkner posted Friday at the Naked Capitalism internet site, Hudson describes how the dollar has managed to control the world financial system with the United States being a massive creditor nation as well as being a massive debtor nation. But, Hudson adds, President Trump’s trade wars and economic sanctions are driving the world away from the dollar and away from using U.S. Treasuries for their savings and back to gold as the means of settling trade.

…

The interview is headlined “Michael Hudson: De-Dollarizing the American Financial Empire” and it’s posted at Naken Capitalism here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc. CPowell@GATA.org

END

Although slightly up in June, it is down sharply form last year. The BIS is running out of gold to carrry out their nefarious activities

Robert Labourne/.GATA)

BIS’ gold swaps rise slightly in June but are down sharply since last year

Submitted by cpowell on Sat, 2019-07-13 04:36. Section: Documentation

By Robert Lambourne

Saturday, July 13, 2019

The Bank for International Settlements’ has just published its statement of account for June and it indicate that the bank is still actively trading gold swaps, which the bank uses to gain access to gold held by commercial banks. But recent activity appears to be much reduced from the second half of 2018.

There is not enough information in the monthly reports to calculate the exact amount of swaps, but based on the information in the BIS’ statement for June, the bank’s gold swaps stand at about 126 tonnes at the end of the month, up 48 tonnes from the approximately 78 tonnes as of May 31.

Swaps stood at 88 tonnes as of April 30, 175 tonnes as of March 31, 303 tonnes as of February 28, 247 tonnes as of January 31, 275 tonnes as of December 2018, 308 tonnes as of November 2018, 372 tonnes as of October 2018, 238 tonnes as of September 2018, and 370 tonnes as of August 2018.

…

In addition the BIS’ annual report for the financial year to March 31 was also published recently. Following the bank’s usual approach, the annual report discloses little about the reasons for the bank’s activity in gold and in particular for gold swaps.

During its financial year just concluded the BIS did not sell any of its own gold, the first year for several years without any sales.

Use of BIS gold sight accounts for central banks increased in the financial year, which is also something of a change, since their use has generally declined in the last decade.

More background on the bank’s medium-term history of using gold swaps is posted here:

On February 3 this year GATA published comments from a former gold industry executive describing the activities of the BIS in gold swaps in previous decades.

The former executive wrote: “Effectively this process created a supply of ‘paper gold’ — sometimes but not always marked to market — that had a depressing effect on the gold price”:

— and mainstream financial news organizations refuse to ask the bank about it.

—–

Robert Lambourne is a retired business executive in the United Kingdom who consults with GATA about the involvement of the Bank for International Settlements in the gold market.

* * *

Join GATA here:

New Orleans Investment Conference

Hilton New Orleans Riverside Hotel

Friday-Monday, November 1-4, 2019

GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at:

John Hathaway is telling us that gold’s breakout is foretelling and that big changes in the financial order are upon us

(courtesy John Hathaway/GATA)

Tocqueville’s John Hathaway: Gold’s breakout foretells big change in financial order

Submitted by cpowell on Sat, 2019-07-13 15:39. Section: Daily Dispatches

11:38a ET Saturday, July 13, 2019

Dear Friend of GATA and Gold:

Tocqueville gold fund manager John Hathaway latest investor letter, published this week, questions five points of what seems to be the convention wisdom about the world financial system and the gold mining industry. He asserts that gold’s recent breakout is “a big deal” and “could be an early warning that the global financial order may be headed for significant change.”

…

Hathaway concludes: “During gold’s six years in the penalty box, the underlying forces that have made the metal a superior strategic investment over centuries have not been idle. The extrapolation of current conditions into unrealistic expectations is a dependable flaw of human nature. The capacity of physical gold and precious metals mining shares to absorb inflows has greatly diminished because of the prolonged attrition of investment interest. Once capital market flows revive, there is real potential in our opinion for parabolic upside in the metal and the shares.”

Hathaway’s letter is posted at Tocqueville’s internet site here:

Junior gold-mining executive Scott Caldwell was in a jovial mood as he sat down for a national television interview in February, 2016.

Even though the price of gold bullion had tumbled by more than a third from its 2011 peak, and many of his competitors were struggling, his company was defying the odds.

Guyana Goldfields Inc. had managed to raise US$700-million from investors and put a high-grade gold mine into production in early 2016.

…

Mr. Caldwell, an avuncular mining engineer with a soothing tone, was happy to promote the company’s Aurora mine, located in a remote Guyanese rainforest, as a cash machine.

Indeed, at the prevailing gold price of US$1,200 an ounce, Guyana looked like a surefire winner.

“A little less than US$800 an ounce [cost], US$400 an ounce margin,” he said during a segment on Business News Network (BNN). “Pretty easy to figure out how we’re going to do.”

The company’s share price soared as it ramped up production, and its market capitalization crested above $1.5-billion.

But last October, seemingly out of nowhere, the wheels came off. Guyana shed half its stock-market value in one trading session after the company raised doubts about the geology at Aurora. A technical report, upon which the mine was built, had vastly overestimated the amount and grade of gold at Aurora. This past March, Guyana cut its reserves by more than 40 per cent, after releasing an updated study on the mine. Guyana’s chairman, René Marion, later admitted in an interview that some 1.5 million ounces of gold assumed by Guyana to be in the ground was “never there.”

Ten months on, Guyana’s share price is down 87 per cent from its peak. Its founder and almost its entire legacy management and board of directors have left. Mr. Caldwell will step down once a replacement is found. Nobody is sure whether the company can weather the crisis.

The meltdown at Guyana’s isn’t a one-off. Over the past few years, several other mining companies have shocked the market with nasty technical surprises.

Vancouver-based Pretium Resources Inc. has seen its share price whipsawed on multiple occasions by geological setbacks at its erratic Brucejack deposit in British Columbia; Toronto-based New Gold Inc. saw the economics of its Rainy River mine in northwest Ontario go up in smoke last year after it fell short on grade; and shareholders in Rubicon Minerals Inc. were almost completely wiped out after its deposit in Ontario’s Red Lake camp turned out to be not mineable at all.

Virtually all of the incidents are occurring at technically demanding ore bodies that require exhaustive study.

While seniors, such as Goldcorp Inc. (now owned by Newmont Mining Corp.), haven’t been immune from technical blunders, this is mostly a small company problem.

Many juniors have little or no experience in building mines and lack the technical talent that might head off calamities in advance.

Small mining companies rely heavily on external consulting firms that prepare resource models. The bigger companies have reams of inhouse talent — geologists, metallurgists and engineers — who vet the work of consultants. But juniors often don’t have the same level of expertise to be able to push back if something seems off.

“[Smaller gold companies] don’t have the human expertise to be able to steer away from those disasters. They don’t have the technical bench strength. They don’t have people that can look at it, and say ‘hey this is wrong.’ ” said Andrew Kaip, mining analyst with BMO Nesbitt Burns Inc. “They’re reliant on external advice and that can be flawed. It can have wildly bad outcomes.”

The industry’s recent flops also raise the issue of accountability when things go wrong. It’s very easy to blame the consultant when the mine plan falls apart, but the management and boards of troubled companies, often responsible for making questionable decisions, are no angels either.

“In order for these things to collapse, half a dozen constituents of people have to not do their jobs,” said John Tumazos, chief executive of New Jersey-based Very Independent Research. “And the reason they don’t do their jobs is that no one wants to kill the golden goose, the gravy train. Even when the project sucks.”

Compared with almost any other mineral, gold is a geological nightmare — harder to find, harder to model and harder to mine. There is no MRI machine for finding gold. Prospectors still have to identify a promising property, drill test holes, send samples to a lab for analysis and cross their fingers.

Even if you find gold, invariably there will be hardly any of it in the ore. The term “high grade” is actually misleading. Eight grams of gold in a tonne of rock is considered high grade. That’s eight parts per million. Low grade is one part per million — a grain of salt in a giant bag of Doritos.

The gold industry is perhaps unrivaled in its wastefulness. A producer has to dig up about 20 tonnes of ore for enough gold to make a wedding ring.

Sometimes gold play nice, occurring as a fine powdery-like substance in rock, with consistent grades throughout the entire ore body — specks of salt uniformly spread across the Doritos. If drill samples confirm that consistency over and over, such deposits can be fairly straightforward to model.

But gold deposits can also be “nuggety” — low grade in most spots, but with the occasional high-grade cluster. And often there is no discernible pattern — like finding a random pretzel in the Doritos.

These ore bodies are among the toughest to model, because geologists can’t be entirely sure whether the high-grade is a statistical fluke, or a pattern across the entire deposit.

Since it’s financially feasible to drill only a tiny proportion of any potential gold deposit, experts have to take sample data and try to figure out what the rest holds.

Correctly modelling a mine, based on a sample that is perhaps only 0.13 per cent of the total mineralized rock, requires immense skill. Such work is typically done by a select group of independent mining consultants. Combining geological field work, and a branch of mathematics called geostatistics, the job is a blend of art, science and luck.

In 2012, SRK Consulting (Canada) Inc. produced a model for Guyana’s Aurora property. Like all gold deposits, Aurora had its charms and its challenges. Early drilling revealed it was a little nuggety.

One way geologists deal with the presence of high-grade gold in what appears to be a mostly lower-grade deposit is to assume it’s an anomaly. In constructing a geological model, consultants will routinely disregard high-grade drill samples above a certain level.

This practice, known as “capping,” is supposed to prevent consultants from overestimating the overall average grade. But here’s the rub. If a deposit is capped too low, that can kill the financial case for building the mine.

In 2012, SRK capped a section of Aurora, called Rory’s Knoll, at 80 grams of gold per tonne. That meant Guyana could expect to find a certain amount of high-grade ore when it mined the area. But last year, as it mined Rory’s Knoll, the high grade simply wasn’t there.

“We weren’t seeing the grade that we thought we would, based on the original 2012 model,” Guyana’s CEO, Mr. Caldwell, told The Globe and Mail earlier this year.

Guyana’s chairman, Mr. Marion, pointed the finger squarely at SRK. The consultant was “very aggressive” in capping the deposit, he said.

Late last year, Guyana asked another consultant, Roscoe Postle Associates (RPA Inc.), to redo the technical report on Aurora from scratch. In its report issued in March, RPA capped Rory’s Knoll at just 35 grams per tonne. Guyana’s current management team maintains that RPA’s capping is much more appropriate.

But SRK isn’t taking any of this on the chin. The consultancy points the finger back at Guyana. After an internal review earlier this year, SRK concluded that its 2012 report on Aurora was technically sound based on data available at the time.

Adam Nott, general counsel with SRK, disputes any notion that the consultancy was aggressive in its modelling. The report was produced when Aurora was at an early stage, and was never meant to be relied upon for the construction of the mine, which came some four years later.

SRK would have had discussions with Guyana about the need to update the model and get lots more data before building Aurora. That would have required more drilling and the outlay of significant amounts of additional capital from Guyana. “For whatever reasons, internal to Guyana Gold, that update wasn’t done until 2018, when new management came in,” Mr. Nott said.

If SRK had access to the same data RPA did in 2018, including three years of actual mining, the consultancy “probably would have come to different results,” he added.

Of course, any allegation that a consultant was too aggressive in its interpretation of the geology of a deposit hits a nerve in the Canadian mining industry.

Consultants are supposed to provide an unbiased and impartial view of an orebody. But the reality is more nuanced.

“Some [consultants] look at deposits and imagine all kinds of good things happening, and others, and we’re among them, try to be more realistic,” said Graham Farquharson, veteran mining consultant with Strathcona Mineral Services Ltd. in Toronto.

(In the late 1990s, when doubts arose about Bre-X Minerals Ltd.’s 70 million ounce gold find, the industry turned to Strathcona to investigate. Mr. Farquharson himself later made what he calls the “six-billion-dollar phone call,” to Bre-x’s board, definitively declaring Busang a hoax.)

There is also an inherent conflict of interest. Because consultants are paid by the mining companies, they face financial pressure to be positive. Having a negative stand on a project, even if it’s spot on, can result in the consultant getting canned.

“It’s a very hard battle telling your client that we think they need to go back to the drawing board,” SRK’s Mr. Nott says. “Especially when the clients know there are other consultants who are willing to use those [data points] and say that’s within a reasonable range.”

Mr. Nott added that SRK has lost work to rival consultants who were willing to provide a more bullish outlook on a deposit.

The technical reports themselves are also heavily influenced by clients. Consultants and management go back and forth on many issues, such as appropriate capping levels, the distance between drill holes and what long-term gold prices to assume in projecting returns.

Sometimes technical reports aren’t as thorough as they could be, either, and that is often because of money. A client may not want to spend more on drilling and will choose to live with the added risk that entails. “SRK, in a lot of ways, is driven by what the client is willing to pay for, and what the client feels its risk-reward balance is,” Mr. Nott said.

Most of the time, these kinds of behind-closed-doors discussions between consultants and mining companies are kept secret. But once in a while they become public. High up in the mountains of northwest British Columbia, Pretium Resource’s Brucejack property was an enigma from the get-go. Early work in 2012 pointed to an extremely high-grade gold deposit. Some drill holes came back with as much as 41,000 grams of gold per tonne.

Despite extensive drilling, Brucejack was incredibly difficult to pin down. “You could come back with one sample that would have spectacular results and then 10 samples all around it that had nothing,” said Mr. Farquharson, whose consultancy did a bulk sample on the deposit.

In 2013, Pretium shares shed half their value within two weeks after it revealed that Strathcona’s analysis didn’t square with a far more optimistic study by an Australian firm, Snowden Mining Industry Consultants. Strathcona insisted that Pretium disclose the discrepancy to its investors, then resigned in the aftermath.

Pretium, in turn, stuck with Snowden and trashed Strathcona’s work as subpar.

Snowden felt Brucejack had similarities with deposits in the South Pacific with similarly eccentric geology. The consultant used a mathematical model called multiple indicator kriging (MIK) to predict the grade and location of the high-grade gold.

MIK is well suited to “mosaic” deposits such as Brucejack, where extremely high-grade gold occurs next to low grade, or even no grade, said international geologist Ashley Brown, who’s now based in Kazakhstan. But MIK is extremely challenging. “The implementation of MIK is very difficult,” he said. “It’s easy to screw up.”

What struck Mr. Brown as odd about Brucejack is that Snowden decided against capping the grade. By forgoing capping, SRK allowed the pockets of high-grade gold samples to strongly influence the average grade for the entire deposit. Brucejack’s reserve grade was pegged at 14.4 grams per tonne, which made it among the highest-grade gold mines in North America.

Snowden’s approach didn’t sit well with Haywood Securities Inc. analyst Kerry Smith, either. A former mining engineer, he’s seen his fair share of geological goofs in his almost 40 years in the business. About four years ago, Mr. Smith attended an information session with Snowden about Brucejack.

“Snowden spent the whole day trying to rationalize why they should model it the way they did, which was basically to model those high-grade numbers and use them to influence the ore around it,” Mr. Smith said. “I came away thinking ‘I wouldn’t do that. That makes no sense,’ because these numbers are not going to have any continuity.”

Mr. Smith was right to be wary. In January of last year, Pretium said Brucejack’s grade was only corresponding 75 per cent to Snowden’s model. The stock lost more than a quarter of its value.

“The high-grade mineralization was in narrower corridors than originally thought,” Pretium CEO Joseph Ovsenek said in an interview.

Earlier this year, after undertaking a review of Brucejack, Pretium cut the mine’s grade to 12.6 grams per tonne, increased its cost projections by 12 per cent and reduced its expected mine life by four years.

Snowden declined an interview request from The Globe. Ivor Jones, who had responsibility for the technical report on Brucejack, also declined to comment beyond saying, “It is easy to criticize other people’s work. Especially something as challenging as Brucejack.”

Pretium’s CEO meantime refuses to play the blame game. Mr. Ovsenek instead points to the baffling geology, calling Brucejack a “beast.”

“I can tell you from talking to a lot of people in the industry and others, there is no orebody like ours out there,” he said. “I challenge anyone to say that they could have done better.”

While Pretium has been wounded, even with a materially lower grade, Brucejack is still plenty profitable. Over the past 18 months, amid a recovery in bullion prices, the company’s share price has regained most of its losses since early 2018.

The trouble for many other juniors is that they don’t have deposits with grades that come anywhere close to Pretium’s Brucejack, or the financial cushion to recover from geological setbacks.

It is possible for a gold producer to make lots of money from a low-grade mine if costs are kept in check and the geology is sound. But it’s crucial that there be a margin for error built in, in case things go wrong. Otherwise, a small slip can spell big trouble.

New Gold Inc.’s Rainy River mine is exhibit A.

Midway through 2018, less than a year into production, New Gold said it was seeing a roughly 11-per-cent shortfall in the grade at Rainy River. With that, the mine’s profit margin vanished.

New Gold also made a basic engineering error in designing the tailings dam at Rainy River and had to build a drastically strengthened structure. The episode blew its capital budget to smithereens.

New Gold now loses hundreds of dollars on every ounce of gold it produces at Rainy River, its debt load is US$780-million and it isn’t expected to produce any free cash flow until 2021.

“Some of these things should just never ever get built. That mine was one of them,” said Rob Cohen, manager of the Dynamic Precious Metals Fund.

If Rainy River’s economics were so dicey, why did it get built? A close reading of the mine’s technical report would have shown thin the margins were. The projected average grade was just 1.12 grams per tonne and the return on mine was forecast at 11 per cent.

But technical reports for the most part are impenetrable, and few investors are skilled enough to understand them. Reports can be penned by as many as a dozen authors, run 700 pages or more and are laced with terms such as “kriging” and “variogram.”

Here’s a passage from New Gold’s 713-page report in 2014, describing Rainy River: “The volcanic rocks have been intruded by a wide variety of plutonic rocks including synvolcanic tonalite-diorite-granodiorite batholiths, younger granodiorite batholiths, sanukitoid monzodiorite intrusions and monzogranite batholiths and plutons.”

The seeds of some mining disasters are buried in technical reports, there for the world to find them before a cent is spent on a mine. But these reports are written by geeks for geeks. The common investor doesn’t stand a chance.

New Gold declined an interview request for this story.

In addition to technical challenges, however, an old chestnut plays a role in some, if not all, of these cautionary tales. The gold industry is renowned for its culture of exaggeration, hype and promotion, and even the smartest among us can fall victim.

Gold mines are almost always built off a feasibility study (FS), which entails extensive drilling to confirm the existence of gold.

But Rubicon Minerals built its Phoenix underground mine in northern Ontario off a preliminary economic assessment — a much more rudimentary early stage study.

Despite the obviously materially higher risk profile, Rubicon raised more than half a billion dollars from investors. It even attracted one of Canada’s most sophisticated institutional money managers: The Canada Pension Plan Investment Board put $50-million into the miner.

In late 2015, mere months after starting production at Phoenix, Rubicon suddenly halted production, citing complications with the geology. Over time, it emerged that Rubicon hadn’t done nearly enough drilling to confirm the gold was actually in the ground. The company, which at one point was worth $1.2-billion, never recovered. Shareholders lost almost everything. In this case, they should have known better.

While most of these catastrophes involve small mining companies, there are a few outliers in the junior and intermediate sector that have demonstrated both geological prowess and sound judgment.

In 2011, junior gold company, Osisko Mining Inc. put what is now Canada’s biggest gold mine into production. While the Canadian Malartic mine in Quebec is low grade, it is very profitable.

The technical team behind Osisko did their homework, including drilling the deposit like crazy. Two of the company’s top three executives were geologists and the other was a mining engineer. (Osisko was acquired by Agnico Eagle Mines Ltd. and Yamana Gold Inc. for $3.9-billion in 2014).

Vancouver-based B2Gold Corp. is another example. Founded in 2007, the company acquired, developed and built Fekola in Mali, now one of the world’s most profitable gold mines. Instead of outsourcing mine construction to external engineering firms, as is industry practice, B2 builds its own mines with a tight-knit staff CEO Clive Johnson has worked with for decades.

But of all of Canada’s gold miners, Toronto-based senior Agnico Eagle Mines probably has the strongest reputation for technical excellence over the long term. Over more than 60 years, the company has never experienced a serious geology mistake, despite dealing with many technically demanding orebodies.

To access ore at its LaRonde mine in Quebec, the company mines three kilometres underground. Agnico built two mines in Nunavut, despite having no access to power, or roads, and operating in a brutally harsh climate. In Finland, the company deals with complex metallurgy.

Agnico is known for its conservative approach. It’s stacked with technical staff, and renowned for its airtight chain of command that starts at the top, with CEO Sean Boyd, and extends through the entire organization.

“Sean Boyd knows how to delegate responsibility. He understands the importance of his technical guys, understands about getting the mine engineers talking to the metallurgist, talking to the electricians. Everyone,” Dynamic’s Mr. Cohen said.

“That’s what brings success to these projects. Having a sharp pencil and being no nonsense.”

A decade ago, Pretium, Guyana Goldfields and New Gold might well have been bought by a bigger miner, well before major problems occurred. Within a technically stronger and better capitalized senior, basic geology mistakes could have been averted or minimized.

But in 2012, the mergers and acquisitions (M&A) market in mining went into a deep freeze. A vicious gold bear market in the first half of this decade, and terribly timed acquisitions during the last bull market, forced the majors onto the sidelines.

Smaller companies have been forced to hang around as standalones longer than before. That has forced many of them into the uncomfortable terrain of building mines by themselves — often for the first time.

The risk of something going wrong was always going to be higher. While M&A has taken off again in a limited way among the seniors, for the most part it’s crickets further down the ladder. If that dynamic doesn’t change, more mines will invariably be built by the tenderfoot, and investors will be left to wonder where the next geological shock lies.

* * *

Join GATA here:

New Orleans Investment Conference

Hilton New Orleans Riverside Hotel

Friday-Monday, November 1-4, 2019

MMT or Modern Monetary Theory is in fact going on today and as a result market rigging is its chief consequence

(courtesy zerohedge)

Modern Monetary Theory is fact and practice, and market rigging is its consequence

Submitted by cpowell on Sun, 2019-07-14 15:21. Section: Daily Dispatches

2:04p ET Sunday, July 14, 2019

Dear Friend of GATA and Gold:

Modern Monetary Theory, which has been getting much attention lately, is so controversial mainly because it is misunderstood.

It is misunderstood first because it is not a theory at all but a truism.

That is, MMT holds essentially that a government issuing a currency without a fixed link to a commodity like gold or silver is constrained in its currency issuance only by inflation and devaluation.

…

This is a very old observation in economics, going back centuries, even to the classical economist Adam Smith, and perhaps first formally acknowledged by the U.S. government with a speech given in 1945 by the president of the Federal Reserve Bank of New York, Beardsley Ruml. The speech was published in 1946:

“The necessity for a government to tax in order to maintain both its independence and its solvency is true for state and local governments, but it is not true for a national government. Two changes of the greatest consequence have occurred in the last 25 years which have substantially altered the position of the national state with respect to the financing of its current requirements.

“The first of these changes is the gaining of vast new experience in the management of central banks.

“The second change is the elimination, for domestic purposes, of the convertibility of the currency into gold.

“Final freedom from the domestic money market exists for every sovereign national state where there exists an institution which functions in the manner of a modern central bank and whose currency is not convertible into gold or into some other commodity.”

Ruml noted that in a fiat currency system such as the United States had adopted by 1945, government did not need to tax to raise revenue but could create as much money as it wanted and deploy it as it thought best, using taxes instead to give value to its currency and implement social and economic policy.

MMT does not claim that the government should create and deploy infinite money. It claims that money can be created and deployed as much as is necessary to improve general living conditions and eliminate unemployment until the currency begins to lose value.

The second big misunderstanding about MMT is that it is not a mere policy proposal but is actually the policy that has been followed by the U.S. government for decades without the candor of Ruml’s 1945 acknowledgment.

The problem with MMT is that, in its unacknowledged practice, it already has produced what its misunderstanding critics fear it for: the creation and deployment of infinite money and credit by central banks as well as vast inflation.

In accordance with MMT, this creation of infinite money and credit has necessitated central banking’s “financial repression” — its suppression of interest rates and commodity prices through both open and surreptitious intervention in bond and futures markets and the issuance of financial derivatives.

That is, since money creation in the current financial system is restrained only by inflation, this restraint can be removed or lessened with certain price controls, which, to be effective, must be disguised, lest people discern that there are no markets anymore, just interventions.

The British economist Peter Warburton perceived this in his 2001 essay, “The Debasement of World Currency — It Is Inflation, But Not As We Know It”:

Warburton wrote: “What we see at present is a battle between the central banks and the collapse of the financial system fought on two fronts. On one front, the central banks preside over the creation of additional liquidity for the financial system to hold back the tide of debt defaults that would otherwise occur. On the other, they incite investment banks and other willing parties to bet against a rise in the prices of gold, oil, base metals, soft commodities, or anything else that might be deemed an indicator of inherent value.

“Their objective is to deprive the independent observer of any reliable benchmark against which to measure the eroding value not only of the U.S. dollar but of all fiat currencies. Equally, they seek to deny the investor the opportunity to hedge against the fragility of the financial system by switching into a freely traded market for non-financial assets. [EMPHASIS ADDED.]

“Central banks have found the battle on the second front much easier to fight than the first. Last November I estimated the size of the gross stock of global debt instruments at $90 trillion for mid-2000. How much capital would it take to control the combined gold, oil, and commodity markets? Probably no more than $200 billion, using derivatives.

“Moreover, it is not necessary for the central banks to fight the battle themselves, although central bank gold sales and gold leasing have certainly contributed to the cause. Most of the world’s large investment banks have overtraded their capital so flagrantly that if the central banks were to lose the fight on the first front, then the stock of the investment banks would be worthless. Because their fate is intertwined with that of the central banks, investment banks are willing participants in the battle against rising gold, oil, and commodity prices.”

This “financial repression” and commodity price suppression have channeled into financial and real estate assets — the assets of property owners — the vast inflation resulting from the policy of infinite money creation, thereby diverting inflation from assets whose prices are measured by government’s consumer price indexes. Meanwhile those indexes are constantly distorted and falsified to avoid giving alarm.

As a result the ownership class is enriched and the working class impoverished.

Of course this is exactly the opposite of what MMT’s advocates intend.

But while the monetary science conceived by MMT people well might develop a formula for operating a perfect monetary system with full employment and prosperity for all, the monetary system always will confer nearly absolute power on its operators, and as long as the operators are human, such power will always corrupt many of them — even MMT’s advocates themselves.

That’s why market rigging is the inevitable consequence of MMT as it is now practiced and why the world is losing its free and competitive markets to monopoly and oligopoly and becoming less democratic and more totalitarian.

So what is the solution?

Maybe some libertarianism would help: Let governments use whatever they want as money, but let individuals do the same and don’t mess with them. Gold, cryptocurrencies, seashells, oxen, whatever — leave them alone.

Most of all, require government to be completely transparent in whatever it does in the markets. If government wants to rig markets, require that it be done in the open and reported contemporaneously.

After all, the world can hardly know where to go when it isn’t permitted to know where it is.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc. CPowell@GATA.org

iii) Other physical stories:

Data from Nicholas to me:

Nicholas Biezanek

Sun, Jul 14, 6:21 AM (1 day ago)

to William, me

Hi Bill/Harvey,

Gold related statistics are frequently quoted in tonnes whilst those relating to silver are in troy ounces.An individual Comex gold contract is 100 troy ounces whilst a silver contract is 5,000 troy ounces. I found it interesting to reduce some headline statistics to tonnes in respect of both metals.

Recent annual global mine supply (ex Russia and China) may vary considerably depending on what data is reviewed and the year of such data.. My computations produce the following.

Silver mine production exceeds gold by about nine times.

‘Criminal’ EFPs silver transfers exceed gold twelve times

SLV silver inventory exceeds GLD gold inventory thirteen times

Net residual LBMA vault silver exceeds gold fourteen times

The COMEX has to work a bit harder to suppress silver paper prices and the

most recent volumes indicate that the silver open interest is eighteen times larger than that for gold.

The gold/silver ratio on Friday evening was ninety three times.(no comment)

Here is my data table:

Tonnes

Tonnes

Ratio

Gold

Silver

Approx Annual Mine Supply

3,150

26,616

Less China

-440

-3,575

Less Russia

-255

-1,350

Net exportable

2,455

21,691

8.84

Comex open int.12/07/2019

1,852

34,084

18.40

EFPs to 13/07/2019

3,150

37,721

11.97

EFPs 2018

7,310

88,554

12.11

Total of above

10,460

126,275

12.07

GLD/SLV at 12/07/2019

800

10,358

12.95

LBMA Total vault at 29/03,2019

7,671

36,196

Less BOE

-5,057

–

Less GLD/SLV at 29/03/2019

-784

-9,642

Net residual LBMA

1,830

26,553

14.51

Regards

Nicholas

end

The way the CME formulates its longs and shorts, it is difficult to disprove or approve Butler.

Here’s an amended excerpt from the weekly review sent to subscribers on Saturday, July 13 –

The 4 big concentrated silver longs, which I have been writing about for nearly a month, further reduced their net long position by 3882 contracts to 62,707 contracts. The only reporting category to have liquidated enough (or any real) number of contracts in the reporting week were managed money traders, proving conclusively that managed money traders held a significant percentage of the very strange concentrated net long position in COMEX silver. How else could I have expected managed money long liquidation by the 4 concentrated longs on Monday?

This is in direct conflict with the new article by Alasdair Macleod, of which many of you asked my opinion. As I think most of you know, it is not my custom to critique others’ work, as that strikes me as unprofessional. Let everyone present what they wish to present. But there is enough factually incorrect in Macleod’s article that it would be a disservice not to address those very serious errors.

Since I’ve been writing about the highly unusual and unprecedented concentrated long position in COMEX silver futures for weeks, I thought at first Alasdair picked it up from me (certainly, I didn’t pick it up from him). Macleod holds, among other things, that the concentrated long position is mostly (or exclusively held) by commercials and not managed money traders. That’s false on its face.

Since May 28 (all COT dates) the concentrated silver long position grew by nearly 18,000 contracts from 49,614 contracts to 67,328 contracts on June 25 (to coincide with Macleod’s article). Over that time the managed money traders bought a total of 59,930 net silver contracts. Over that same period, the commercials SOLD 53,678 net silver contracts. Unless there’s a new math being deployed here, the sharp increase in the concentrated long position was very unlikely to have been caused by commercials.

I have stipulated all along that there might be a commercial trader in the ranks of the concentrated long, but clearly at least two and most likely three of the four big silver longs are managed money traders. Plus this week’s exclusive long liquidation by the managed money traders and the concurrent reduction in the concentrated long position (nearly matching contract for contract) further confirms that Macleod’s basic premise is fundamentally incorrect. In addition, the concentrated long position grew the most when silver penetrated its moving averages to the upside and shrank when the moving averages were penetrated to the downside.