/GOLD:$1419.50 UP $4.50(COMEX TO COMEX CLOSING)

Silver: $ 16.38 DOWN 2 CENTS (COMEX TO COMEX CLOSING)//

Closing access prices:

Gold : $1419.00

silver: $16.38

YOUR DATA…

we are coming very close to a commercial failure!!

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING 1/4

EXCHANGE: COMEX

CONTRACT: JULY 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,413.900000000 USD

INTENT DATE: 07/25/2019 DELIVERY DATE: 07/29/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

661 C JP MORGAN 1

737 C ADVANTAGE 3

905 C ADM 4

____________________________________________________________________________________________

TOTAL: 4 4

MONTH TO DATE: 958

NUMBER OF NOTICES FILED TODAY FOR JULY CONTRACT: 4 NOTICE(S) FOR 400 OZ (0.0164 tonnes

TOTAL NUMBER OF NOTICES FILED SO FAR: 954 NOTICES FOR 95400 OZ (2.9673 TONNES)

SILVER

FOR JULY

56 NOTICE(S) FILED TODAY FOR 280,000 OZ/

total number of notices filed so far this month: 4499 for 22,495,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE : $ 9276 DOWN 92

Bitcoin: FINAL EVENING TRADE: $ 9834 UP 44

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

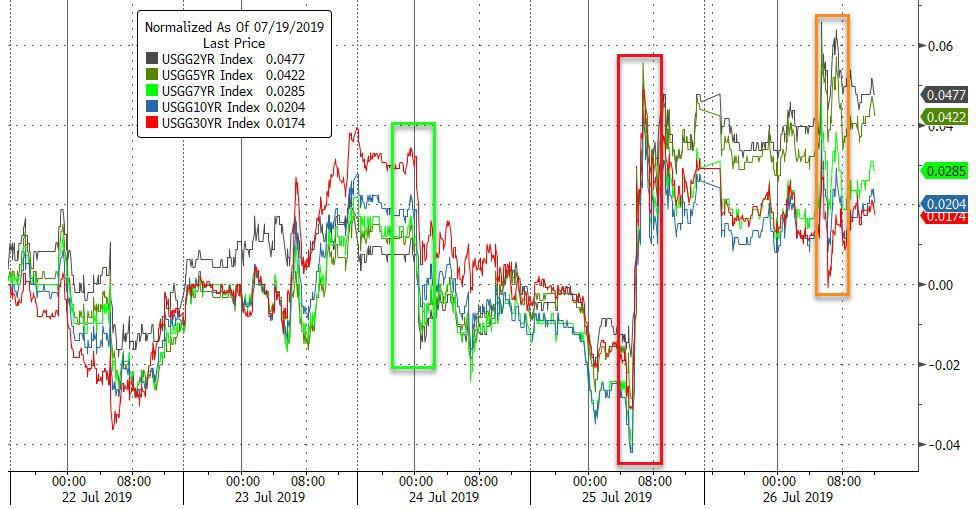

IN SILVER THE COMEX OI FELL BY A STRONG SIZED 2668 CONTRACTS FROM 236,257 DOWN TO 233,589 WITH THE 19 CENT LOSS IN SILVER PRICING AT THE COMEX.

TODAY WE ARRIVED CLOSER TO AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A HUGE SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:,

0 FOR JULY. 0 FOR AUGUST, 0 FOR SEPT 1041, AND SEPT 2020: 75 AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 1146 CONTRACTS. WITH THE TRANSFER OF 3342 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1146 EFP CONTRACTS TRANSLATES INTO 5.73 MILLION OZ ACCOMPANYING:

1.THE 19 CENT LOSS IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.600 MILLION OZ INITIAL STANDING FOR JULY

WE HAD ATTEMPTED COVERING OF SHORTS AT THE SILVER COMEX LAST NIGHT WITH ZERO SUCCESS..AND ZERO SPREADING ACCUMULATION.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JULY:

31,971 CONTRACTS (FOR 18 TRADING DAYS TOTAL 31,971 CONTRACTS) OR 159.86 MILLION OZ: (AVERAGE PER DAY: 1776 CONTRACTS OR 8.880 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF JULY: 159.86 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 22.82% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 1316.05 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

APRIL 2019 TOTAL EFP ISSUANCE: 182.87 MILLION OZ.

MAY 2019: TOTAL EFP ISSUANCE: 136.55 MILLION OZ

JUNE 2019 , TOTAL EFP ISSUANCE: 265.38 MILLION OZ

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2668, WITH THE 19 CENT LOSS IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 1146 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE LOST A STRONG SIZED: 1522 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 1146 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 2668 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 19 CENT LOSS IN PRICE OF SILVER AND A CLOSING PRICE OF $16.40 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.1615 BILLION OZ TO BE EXACT or 167% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 56 NOTICE(S) FOR 450,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.600 MILLION OZ

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

.

IN GOLD, THE COMEX OPEN INTEREST FELL BY AN ATMOSPHERIC AND CRIMINALLY SIZED 20,409 CONTRACTS, TO 593,878 ACCOMPANYING THE FAIR $8.40 PRICING LOSS WITH RESPECT TO COMEX GOLD PRICING YESTERDAY// /THE SPREADING LIQUIDATION HAS NOW COMMENCED IN FULL FORCE FOR GOLD….

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 11,474 CONTRACTS:

APRIL 0 CONTRACTS,JUNE: 0 CONTRACTS, AUGUST 2019: 11,474 CONTRACTS, DEC> 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 593,878,. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE AN ATMOSPHERIC AND CRIMINALLY SIZED LOSS IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 8927 CONTRACTS: 20,409 CONTRACTS DECREASED AT THE COMEX AND 11,474 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS OF 8927 CONTRACTS OR 892,700 OZ OR 27.76 TONNES. YESTERDAY WE HAD A LOSS OF $8.40 IN GOLD TRADING….AND WITH THAT LOSS IN PRICE, WE STILL HAD A GOOD LOSS IN GOLD TONNAGE OF 27.26 TONNES!!!!!! THE BANKERS WERE SUPPLYING INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER. THE MAJORITY OF THE CONTRACT LOSS WAS DUE TO SPREADERS LIQUIDATION..

WITH RESPECT TO SPREADING: WE WILL WITNESS THE MORPHING OF OUR SPREADERS OUT OF SILVER AND INTO GOLD AS THE JULY MONTH PROCEEDS INTO THE ACTIVE DELIVERY MONTH OF AUGUST.

.

FOR NEWCOMERS, HERE IS THE MODUS OPERANDI OF THE CORRUPT BANKERS WITH RESPECT TO THEIR SPREAD/TRADING.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCHED TO GOLD AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NO INTO THE NON ACTIVE DELIVERY MONTH OF JULY HEADING TOWARDS THE VERY ACTIVE DELIVERY MONTH OF AUGUST.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES, HERE IS THE BANKERS MODUS OPERANDI:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST IS STARTING TO RISE IN THIS NON ACTIVE MONTH OF JULY BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN SILVER WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (AUGUST), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JULY : 157,507 CONTRACTS OR 15,750,700 oz OR 489.98 TONNES (18 TRADING DAY AND THUS AVERAGING: 8750 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 17 TRADING DAY IN TONNES: 489.98 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 489.98/3550 x 100% TONNES =13,8% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 3527.71 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

APRIL 2019 TOTAL ISSUANCE: 456.10 TONNES

MAY 2019 TOTAL ISSUANCE: 449.10 TONNES

JUNE 2019 TOTAL ISSUANCE: 642.22 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A HUMONGOUS SIZED DECREASE IN OI AT THE COMEX OF 20,409 WITH THE STRONG PRICING LOSS THAT GOLD UNDERTOOK YESTERDAY($8.40)) //.WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 11474 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 11,474 EFP CONTRACTS ISSUED, WE HAD AN ATMOSPHERIC AND CRIMINALLY SIZED LOSS OF 8927 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

11474 CONTRACTS MOVE TO LONDON AND 20,490 CONTRACTS DECREASED AT THE COMEX. (IN TONNES, THE LOSS IN TOTAL OI EQUATES TO 27.76 TONNES). ..AND THIS HUGE DECREASE OF DEMAND OCCURRED ACCOMPANYING THE LOSS IN PRICE OF $8.40 WITH RESPECT TO YESTERDAY’S TRADING AT THE COMEX. WE ARE NOW IN THE SPREADING LIQUIDATION PHASE IN GOLD AND IT IS IN FULL FORCE AS THE MONTH PROCEEDS TO ITS CONCLUSION..

we had: 4 notice(s) filed upon for 400 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $4.50 TODAY//

A HUGE CHANGE IN GOLD INVENTORY: A WITHDRAWAL OF 4.09 TONNES

INVENTORY RESTS AT 818.14 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 2 CENTS TODAY:

ANOTHER BIG CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER WITHDRAWAL OF 1.01 MILLION OZ REMOVED FROM THE SLV

Z

/INVENTORY RESTS AT 357.183 MILLION OZ.

end

OUTLINE OF TOPICS TONIGHT

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A CONSIDERABLE SIZED 2668 CONTRACTS from 236,257 DOWN TO 233,589 AND FURTHER FROM THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..THE SPREADERS HAVE COMMENCED THEIR LIQUIDATION OF OPEN INTEREST CONTRACTS IN GOLD

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

FOR JULY: 0 CONTRACTS FOR AUGUST: 0, FOR SEPT. 1047 AND SEPT 2020:: 75 AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1146 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 2668 CONTRACTS TO THE 1146 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN AN ATMOSPHERIC AND CRIMINALLY SIZED LOSS OF 1522 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES: 7.61 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 7.475 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL 18.765 MILLION OZ FOR MAY NOW 2.660 MILLION OZ FOR JUNE WITH JULY AT 22.600 MILLION OZ STANDING SO FAR.

RESULT: A STRONG SIZED DECREASE IN SILVER OI AT THE COMEX WITH THE 19 CENT GAIN IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A STRONG SIZED 1142 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED UP 7.18 POINTS OR 0.24% //Hang Sang CLOSED DOWN 196.56 POINTS OR 0.69% /The Nikkei closed DOWN 98.40 POINTS OR 0.45%//Australia’s all ordinaires CLOSED DOWN .36%

/Chinese yuan (ONSHORE) closed UP at 6.8786 /Oil UP TO 57.21 dollars per barrel for WTI and 64.13 for Brent. Stocks in Europe OPENED MIXED// ONSHORE YUAN CLOSED UP // LAST AT 6.8786 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.8775 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3A//NORTH KOREA/ SOUTH KOREA

3b) REPORT ON JAPAN

4/EUROPEAN AFFAIRS

7. OIL ISSUES

8 EMERGING MARKET ISSUES

9. PHYSICAL MARKETS

10. important USA stories which will influence the price of gold/silver

MARKET TRADING//USA

a)Market trading/LAST NIGHT/USA

b)MARKET TRADING/USA/AFTERNOON

ii)Market data/USA

iii) Important USA Economic Stories

iv) Swamp commentaries)

v) King report/Courtesy of Chris Powell of GATA which includes the major swamp stories.

LET US BEGIN:

Let us head over to the comex:

we had 0 dealer entry:

We had 0 kilobar entries

total gold withdrawals; XX oz

FOR THE JULY 2019 CONTRACT MONTH)Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 4 contract(s) of which 1 notices were stopped (received) by j.P. Morgan dealer and 1 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account and 0 notices by the squid (Goldman Sachs)

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the JULY /2019. contract month, we take the total number of notices filed so far for the month (958) x 100 oz , to which we add the difference between the open interest for the front month of JULY. (9 contract) minus the number of notices served upon today (4 x 100 oz per contract) equals 96,300 OZ OR 2.9953 TONNES) the number of ounces standing in this NON active month of JULY

Thus the INITIAL standings for gold for the JULY/2019 contract month:

No of notices served (958 x 100 oz) + (9)OI for the front month minus the number of notices served upon today (4 x 100 oz )which equals 96,300 oz standing OR 2.9953 TONNES in this active delivery month of JULY.

We GAINED 4 contracts or an additional 400 oz will stand as these guys refused to morph into London based forwards as well as negating a fiat bonus.

SURPRISINGLY LITTLE TO NO GOLD HAS BEEN ENTERING THE COMEX VAULTS AND WE HAVE WITNESSED THIS FOR THE PAST YEAR!! WE HAVE ONLY 10.0412 TONNES OF REGISTERED ( GOLD OFFERED FOR SALE) VS 2.9517 TONNES OF GOLD STANDING// THEY SEEM TO BE USING CONSIDERABLE GOLD VAPOUR TO SETTLE UPON UNSUSPECTING LONGS.

oz

total dealer silver: 93.110 million

total dealer + customer silver: 307.430 million oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

TODAY’S ESTIMATED SILVER VOLUME: 134,555 CONTRACTS (we had considerable spreading activity..accumulation

CONFIRMED VOLUME FOR YESTERDAY: 118,180 CONTRACTS..

YESTERDAY’S CONFIRMED VOLUME OF 118180 CONTRACTS EQUATES to 590 million OZ 84.4% OF ANNUAL GLOBAL PRODUCTION OF SILVER..makes sense!!

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO -1.62.% ((JULY 24/2019)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -1.23% to NAV (JULY 18/2019 )

Note: Sprott silver trust back into NEGATIVE territory at -1.59%-/Sprott physical gold trust is back into NEGATIVE/

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 14.14 TRADING 13.66/DISCOUNT 3.43

END

And now the Gold inventory at the GLD/

JULY 26/WITH GOLD UP $4.50: A HUGE INVENTORY WITHDRAWAL OF 4.09 TONNES OF PAPER GOLD LEAVES THE GLD/INVENTORY RESTS AT 818.14 TONNES

JULY 25/ WITH GOLD DOWN$8.40//NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 822.25 TONNES

JULY 24.2019: WITH GOLD UP $2.05 TO DAY: A PAPER WITHDRAWAL OF 2.93 TONNES OF GOLD FROM THE GLD

JULY 23// WITH GOLD DOWN $5.25 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 825.18 TONNES

JULY 22/WITH GOLD UP 0.80 CENTS: TWO MASSIVE PAPER GOLD DEPOSIT OF 5.87 TONNES AND 4.69 TONNES ADDED TO THE GLD..THIS IS A MASSIVE FRAUD!!/INVENTORY RESTS AT 825.18 TONNES

JULY 19/WITH GOLD DOWN $1.00: A MASSIVE DEPOSIT OF 11.44 TONNES OF PAPER GOLD INTO THE GLD/INVENTORY RESTS AT 814.62

JULY 18/WITH GOLD UP $5.55 TODAY: A BIG PAPER DEPOSIT OF 3.81 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 803.18 TONNES

JULY 17/WITH GOLD UP $11.35 TODAY: A BIG WITHDRAWAL OF 1.17 TONNES FROM THE GLD//INVENTORY RESTS AT 799.37 TONNES

JULY 16: WITH GOLD DOWN $2.15 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 800.54 TONNES

JULY 15: WITH GOLD UP $1.85 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 800.54 TONNES

JULY 12/WITH GOLD UP $5.20 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 800.54 TONNES

JULY 11.WITH GOLD DOWN $5.25: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 800.54 TONNES

JULY 10//WITH GOLD UP $11.65 A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER GOLD DEPOSIT OF 6.46 TONNES/INVENTORY RESTS AT 800.54 TONNES

JULY 9/WITH GOLD UP 70 CENTS, A HUGE PAPER WITHDRAWAL OF 2.89 TONNES WHICH WAS USED IN THE FUTILE RAID ON GOLD AND SILVER THIS MORNING//INVENTORY RESTS AT 794.08 TONNES

JULY 8/ WITH GOLD DOWN 35 CENTS A HUGE WITHDRAWAL OF 1.47 TONNES FROM THE GLD/INVENTORY FALLS TO 796.97 TONNES

JULY 5TH/WITH GOLD DOWN $19.50/NO CHANGES IN GOLD INVENTORY AT THE GLD//INV RESTS AT 798.44 TONNES

JULY 3// WITH GOLD UP $12.60 TODAY A SURPRISE WITHDRAWAL OF 1.76 TONNES FROM THE GLD//INVENTORY RESTS AT 798.44

JULY 2. WITH GOLD UP $18.90 A HUGE “PAPER” DEPOSIT OF 6.16 TONNES INTO THE GLD/INVENTORY RESTS AT 800.20 TONNES

JULY 1: WITH GOLD DOWN $24.70 A HUGE “PAPER GOLD” WITHDRAWAL OF 1.76 TONNES FROM THE GLD/INVENTORY RESTS TONIGHT AT 794.04 TONNES

JUNE 28/WITH GOLD UP $.90 TODAY: ANOTHER 2.05 TONNES OF PAPER GOLD REMOVED AND THIS GOLD WAS USED IN ATTACKING GOLD AT THE COMEX/INVENTORY RESTS AT 795.80 TONNES

JUNE 27/WITH GOLD DOWN $6.10: ANOTHER HUGE WITHDRAWAL OF 1.76 PAPER TONNES FROM THE GLD INVENTORY/INVENTORY RESTS AT 797.61 TONNES

JUNE 26/WITH GOLD DOWN $3.00: WE HAD A HUGE WITHDRAWAL OF 2.37 TONNES FROM THE GLD/INVENTORY RESTS AT 799.61 TONNES

JUNE 25/WITH GOLD UP $1.30 (AND WAY UP BEFORE THE BANKERS WHACKED) WE WITNESSED ANOTHER 1.95 TONNES OF PAPER GOLD ADDED TO THE GLD INVENTORY//INVENTORY RESTS AT 801.98 TONNES

JUNE 24/WITH GOLD UP $18.00 A MONSTROUS PAPER DEPOSIT OF 34.93 TONNES/INVENTORY RESTS AT 799.03 TONNES

JUNE 21/WITH GOLD UP $ 2.90, NO CHANGE IN GOLD INVENTORY: INVENTORY RESTS AT: 764.10 TONNES

June 20/WITH GOLD UP $47.95, NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 764.10 TONNES

JUNE 19 WITH GOLD DOWN $1.65: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 764.10 TONES

JUNE 18/JUNE 18/WITH GOLD UP $7.60: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 764.10 TONNES

JUNE 17/WITH GOLD DOWN $1.65 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 764.10 TONNES

JUNE 14/ WITH GOLD UP $1.05 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.40 TONNES OF PAPER GOLD INTO THE GLD///INVENTORY RESTS AT 764.10 TONNES

JUNE 13/WITH GOLD UP $6.60 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.52 TONNES INTO THE GLD INVENTORY/INVENTORY RESTS AT 759.70 TONNES

JUNE 12/WITH GOLD UP $7.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 756.18 TONNES

JUNE 11/WITH GOLD UP $1.65 CENTS TODAY: A TINY CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .24 TONNES AND THIS IS TO PAY FOR FEES/INVENTORY RESTS AT 756.18 TONNES

JUNE 10/WITH GOLD DOWN $16.40 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.17 TONNES/INVENTORY RESTS AT 756.42 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

JULY 25/2019/ Inventory rests tonight at 818.14 tonnes

*IN LAST 629 TRADING DAYS: 116.60 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 529 TRADING DAYS: A NET 49,08 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

*

end

Now the SLV Inventory/

JULY 25.2019: WITH SILVER DOWN 19 CENTS: ANOTHER PAPER WITHDRAWAL OF 1.17 MILLION OZ/INVENTORY REST AT 358.213 MILLION OZ

JULY 24…A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A GAIN OF 1.685 MILLION OZ/INVENTORY RESTS AT 359.383 MILLION OZ

JULY 23/2019: WITH SILVER UP 5 CENTS TODAY: ANOTHER BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.221 MILLION PAPER OZ ADDED INTO THE GLD INVENTORY//INVENTORY RESTS AT 357.698 MILLION OZ////

JULY 22.2019/WITH SILVER UP 21 CENTS TODAY: A MASSIVE CHANGES IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 8.939 MILLION OZ ADDED TO THE SLV INVENTORY/INVENTORY RESTS AT 355.919 MILLION OZ//

JULY 19/WITH SILVER FLAT TODAY: ANOTHER MONSTROUS PAPER DEPOSIT OF 3.276 MILLION OZ ENTERS THE SLV//WHAT A MASSIVE FRAUD//INVENTORY RESTS AT 346.980 MILLION OZ

JULY 18/WITH SILVER UP 24 CENTS TODAY: A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 2.668 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 343.704 MILLION OZ//

JULY 17: WITH SILVER UP ANOTHER 29 CENTS: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 8.518 MILLION OZ/INTO THE SLV INVENTORY///INVENTORY RESTS AT 341.036 MILLION OZ//

JULY 16: WITH SILVER UP 31 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 332.518 MILLION OZ

JULY: 15 WITH SILVER UP 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 332.518 MILLION OZ

JULY 12/WITH SILVER UP 10 CENTS: NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 332.518 MILLION OZ//

JULY 11/NO CHANGE IN SILVER INVENTORY

JULY 10/WITH SILVER UP 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 332.518 MILLION OZ//

JULY 9/WITH SILVER UP A SMALL 7 CENTS A GIGANTIC INVENTORY GAIN OF 4.026 MILLION OZ/ INVENTORY RESTS AT 332.518 MILLION OZ AND NOW IT SHOULD BE QUITE CLEAR THAT THE SLV ( AND GLD ARE FRAUDS)

JULY 8/WITH SILVER UP 7 CENTS: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 328,492 MILLION OZ

JULY 5/WITH SILVER DOWN 32 CENTS WE STRANGELY HAD A HUGE INVENTORY GAIN OF 2,234 MILLION OZ//INVENTORY RESTS AT 328.492 MILLION OZ

JULY 3 WITH SILVER UP 10 CENTS A HUGE INCREASE IN INVENTORY..INVENTORY RESTS AT 326.151 MILLION OZ

JULY 2/WITH SILVER UP 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY/INVENTORY RESTS AT 323.330 MILLION OZ//

JULY 1/ WITH SILVER DOWN 16 CENTS: A SURPRISING DEPOSIT OF 936,000 OZ INTO THE SLV/INVENTORY RESTS TONIGHT AT 323.330 MILLION OZ/

JUNE 28/WITH SILVER UP 6 CENTS: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 322.394 MILLION OZ//

JUNE 27/WITH SILVER DOWN 7 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.575 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 322.394 MILLION OZ//

JUNE 26/WITH SILVER UP 17 CENTS: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.819 MILLION OZ/

JUNE 25/WITH SILVER DOWN 25 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.819 MILLION OZ.

JUNE 24/WITH SILVER UP 11 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.819 MILLION OZ//

JUNE 21/WITH SILVER DOWN 22 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.819 MILLION OZ//

JUNE 20/WITH SILVER UP 53 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.819 MILLION OZ/

JUNE 19/WITH SILVER DOWN 3 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 319.070 MILLION OZ/

JUNE 18 WITH SILVER UP 18 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 319.070 MILLION OZ

JUNE 17/WITH SILVER UP XXX CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.775 MILLION OZ//

JUNE 14/WITH SILVER DOWN 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.775 MILLION OZ/

JUNE 13/WITH SILVER UP 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.775 MILLION OZ/

JUNE 12/WITH SILVER UP 4 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.413 MILLION OZ INTO THE SLV INVENTORY/INVENTORY RESTS AT 316.775 MILLION OZ/

JUNE 11/WITH SILVER UP 10 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 315.652 MILLION OZ//

JUNE 10/WITH SILVER DOWN 38 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 315.652 MILLION OZ//

JULY 25/2019:

Inventory 358.213 MILLION OZ

LIBOR SCHEDULE AND GOFO RATES:

YOUR DATA…..

6 Month MM GOFO 2.23/ and libor 6 month duration 2.18

Indicative gold forward offer rate for a 6 month duration/calculation:

G0LD LENDING RATE: – .05

XXXXXXXX

12 Month MM GOFO

+ 2.14%

LIBOR FOR 12 MONTH DURATION: 2.18

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = -.04

end

end

PHYSICAL GOLD/SILVER STORIES

i) GOLDCORE BLOG/Mark O’Byrne

Gold At 6 Year High In Euros At €1,288 as ECB Says Outlook Is “Worse and Worse”

Gold rose to a six and a half year high in euros at €1,288/oz yesterday prior to giving up the gains as it succumbed to profit taking in volatile trading during and after the ECB meeting.

Gold spiked to its highest level since 2013 in response to the more dovish ECB policy statement. It then quickly changed course following the release of upbeat US durable goods orders data for June which saw it give up gains in all currencies. Stock markets rose before giving up gains as did gold.

Today, gold prices have edged higher and recovered a part of yesterday’s intra-day sell off. Gold is currently set for a small weekly gains in most currencies including euros and pounds with stronger gains for the week seen in the embattled Australian dollar.

The euro hits two-year lows against the dollar and six year lows against gold after the ECB signaled ‘stimulus’ which will involve interest rate cuts and the likely return to digital euro creation in order to support Eurozone bond markets and economies.

Mario Draghi’s ECB announcement was in line with the consensus as he signaled interest rate cuts in the near future as the economic outlook is “getting worse and worse”.

Silver soared to a more than one-year high on increasing expectations that the ECB, the US Federal Reserve and other major central banks will have to adopt a ultra loose monetary policies again to prevent a global recession.

Uncertainty in the Middle East and tensions between the Iran and the UK and the U.S. should support gold and may lead to increased safe haven demand.

Britain has sent a warship to accompany all British-flagged vessels through the Strait of Hormuz, a change in policy announced by new PM Johnson’s government yesterday. The UK government had previously said that it did not have the resources to do so.

U.S. Secretary of State Mike Pompeo said in a television interview yesterday that he would go to Iran and talk to the Iranian people, amid rising tensions between Tehran and Washington.

Gold Prices via LBMA (AM/ PM Fix – USD, GBP & EUR)

25-Jul-19 1426.35 1416.10, 1143.08 1132.88 & 1281.86 1265.85

24-Jul-19 1425.55 1426.95, 1142.29 1142.70 & 1279.86 1279.69

23-Jul-19 1417.55 1425.55, 1140.42 1145.29 & 1268.14 1277.01

22-Jul-19 1424.45 1427.75, 1142.69 1143.63 & 1270.04 1272.13

19-Jul-19 1437.05 1439.70, 1148.06 1148.88 & 1278.11 1281.48

18-Jul-19 1420.90 1417.45, 1139.70 1135.94 & 1264.74 1263.51

17-Jul-19 1400.80 1410.35, 1129.61 1135.61 & 1249.09 1256.90

16-Jul-19 1416.10 1409.85, 1136.85 1134.79 & 1260.05 1256.88

15-Jul-19 1416.25 1412.40, 1127.76 1127.24 & 1255.93 1253.79

News

Gold Falls 1% Despite ECB Poor Outlook

Euro Hits a 2-year Low as ECB Signals More Easing is on the Way

Wall Street Recedes From Record High Following Weak Results, Draghi

Fed to Cut Rates for First Time in a Decade This Month: Poll

Newmont Goldcorp Profit Drops More Than Expected on Cost of Deals, Idle Mines

Former Trader for Scotia Capital, Bear Stearns Confesses to ‘Spoofing’ Monetary Metals

Commentary

Gold Isn’t Necessarily an Investment — It’s Life Insurance

The $6 Trillion Pension Bailout is Coming

$1.6 Trillion Fund Spots a New, Ticking Time Bomb in the Market

Chinese Bank With $100 Billion in Assets is About to Collapse

CFTC Settles Charges Against Former JPM Metals Market Manipulator Edmonds

Today’s Climate Change is Worse Than Anything Earth Has Experienced in the Past 2,000 Years

Click Here to Listen to the latest GoldCore Podcast

Receive our free Daily or Weekly Updates by signing up here and click here to subscribe to GoldCore’s You Tube Channel

end

ii) Important gold commentaries courtesy of GATA/Chris Powell

Alasdair Macleod: The reasoning behind gold’s breakout

Submitted by cpowell on Fri, 2019-07-26 03:14. Section: Daily Dispatches

11:12p ET Thursday, July 25, 2019

Dear Friend of GATA and Gold:

In his new essay, “The Reasoning Behind Gold’s Breakout,” GoldMoney research director Alasdair Macleod delightfully explodes eight of the common myths about gold, myths tightly held by investment fund managers:

— Gold is no longer money.

— Gold doesn’t pay interest.

— Gold is expensive to store and insure.

…

.Gold has no intrinsic value.

— Gold has no use beyond looking pretty.

— Gold is volatile.

— Gold is a “greater fool” investment.

— Gold’s value was higher 40 years ago in real terms.

Macleod concludes: “With governments everywhere itching to increase spending without raising taxes and as the global economy sinks into a trade and credit-cycle-induced recession, budget deficits will fuel monetary inflation at a faster pace than seen before. Relearning that gold is sound money is now the most urgent priority for all those charged with responsibility for other people’s investments.”

Macleod’s analysis is posted at GoldMoney here:

https://www.goldmoney.com/research/goldmoney-insights/the-reasoning-behi…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

* * *

Join GATA here:

New Orleans Investment Conference

Hilton New Orleans Riverside Hotel

Friday-Monday, November 1-4, 2019

https://neworleansconference.com/noic-promo/powellgata/

* * *

Help keep GATA going:

GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at:

To contribute to GATA, please visit:

END

Former trader for Scotia Capital, Bear Stearns confesses to ‘spoofing’ monetary metals

Submitted by cpowell on Fri, 2019-07-26 03:31. Section: Daily Dispatches

Ex-Scotia Capital, Bear Stearns Precious Metals Trader Pleads Guilty, Will Cooperate with Feds in ‘Spoofing’ Probe

By Dave Mangan

CNBC, New York

Thursday, July 25, 2019

https://www.cnbc.com/2019/07/25/ex-scotia-capital-bear-stears-metals-tra…

A former trader at Scotia Capital and Bear Stearns pleaded guilty today to a federal crime and admitted manipulating precious metals markets for nine years — the latest in a series of crackdowns in the commodities markets by the Justice Department.

The trader, Corey Flaum, 41, of Mount Kisco, New York, is cooperating with an ongoing federal criminal investigation, officials said as they announced his guilty plea to one count of attempted commodities price manipulation in U.S. District Court in Brooklyn.

Flaum during his guilty plea admitted that from approximately June 2007 and July 2016 he “placed thousands of orders to manipulate the prices of gold, silver, platinum, and palladium futures contracts,” according to the Justice Department.

Flaum worked at Scotia Capital from 2010 to 2016 and the defunct investment bank Bear Stearns from 2006 to 2008, according to FINRA’s BrokerCheck system. He is scheduled to be sentenced Oct. 29.

Scotia Capital declined to comment when contacted by CNBC. Flaum did not immediately respond to a request for comment.

Flaum was one of two former precious metals traders who separately Thursday agreed to settle regulatory charges filed by the Commodities Futures Trading Commission for a banned market manipulation strategy known as spoofing.

That strategy involves placing trade orders with the intent to cancel them before they can be executed. The goal of spoofing is to affect the price of the commodity and thus benefit a pre-existing trading position.

The CFTC order notes that Flaum and others at the banks where he had worked “engaged in manipulative and deceptive conduct by engaging in the practice of ‘spoofing.'”

The other trader who settled with the CFTC today, former J.P. Morgan employee John Edmonds, pleaded guilty in federal court in Connecticut in October to crimes related to manipulating metals markets.

Edmonds, who has yet to be sentenced in his criminal case, and several other traders who likewise have pleaded guilty to spoofing-related crimes are also cooperating with federal prosecutors in ongoing probes of major banks.

In the past five years federal prosecutors have lodged 11 spoofing cases against 15 defendants.

Both Flaum and Edmonds, the CFTC said, learned spoofing from more senior traders at their respective banks.

In Edmonds; case, that was while he was at J.P. Morgan, according to the CFTC’s charging document.

In Flaum’s case, he learned spoofing by watching a more senior trader at Bear Stearns, and then witnessed similar conduct at Scotia Capital, a CFTC filing says.

The agency did not explicitly name J.P. Morgan, Bear Stearns, and Scotia Capital in documents. But those filings described Edmonds’ and Flaum’s conduct during years they worked at those institutions.

Civil sanctions have yet to be decided against both men by the CFTC.

James McDonald, the CFTC’s director of enforcement, in a prepared statement, said, “Today’s enforcement actions send a clear message that spoofing and manipulation in our markets will not be tolerated and that the CFTC will use all of the tools in its arsenal to aggressively pursue individuals and entities who engage in this misconduct.”

McDonald added, “These cases also show that, where an individual has demonstrated a commitment to cooperate and has cooperated, the CFTC may elect to postpone the assessment of the cooperator’s sanctions until the cooperation is substantially complete.”

Two civil lawsuits alleging market manipulation by J.P. Morgan are on hold in federal court in New York City after prosecutors warned that the cases could interfere with their ongoing criminal probe.

END

Chinese largest miner opens an office in Toronto

(Friedman/National Post/GATA)

Shrugging off rising tensions, China’s largest gold miner opens office in Toronto

Submitted by cpowell on Fri, 2019-07-26 03:44. Section: Daily Dispatches

By Gabriel Friedman

National Post, Toronto

Thursday, July 25, 2019

At a time when Sino-Canadian diplomatic tensions run high, China’s largest gold miner, Shandong Gold Group Co., Ltd. gathered several dozen bankers, lawyers, local mining executives and media at a downtown Toronto hotel to celebrate the company’s new Bay Street office.

Board chairman Chen Yumin, who travelled from China to attend the event, said Toronto remains a capital of talent and finance for the mining industry. By opening an office in the city, he said Shandong hopes to build relationships with Canada’s mining community to help it grow into one of the top ten largest gold miners in the world by 2020.

…

“The reason that we opened a Toronto office is not just (about) the relationship between Canada and China,” Yumin said through a translator during a press conference following the event. “What we are looking at is global reach.”

Its office, which opened in January and will be staffed by a geologist, is located in the Royal Bank Plaza, a shimmering gold skyscraper in the heart of downtown Toronto.

Shandong does not currently have any mines in Canada, but said it operates four of the ten largest gold mines in China.

Yumin pointed to Toronto-based Barrick Gold Corp., currently the largest gold miner in the world by market capitalization, which has mines in the U.S., South America, Africa and all over the world, but derives only a tiny portion of its gold from Canada, and said Shandong has similar ambitions.

The two companies have been working together since 2017 when Barrick sold Shandong a 50 per cent stake in its Veladero mine, the largest gold mine in Argentina, expected to produce as much as 500,000 ounces of gold this year.

Since then, the two have forged agreements to work together on additional mines and exploration in South America, and today Barrick currently owns around 18 per cent of Shandong, which is listed on exchanges in Hong Kong and China. …

… For the remainder of the report:

https://business.financialpost.com/commodities/mining/shrugging-off-risi…

end

iii) Other physical stories:

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

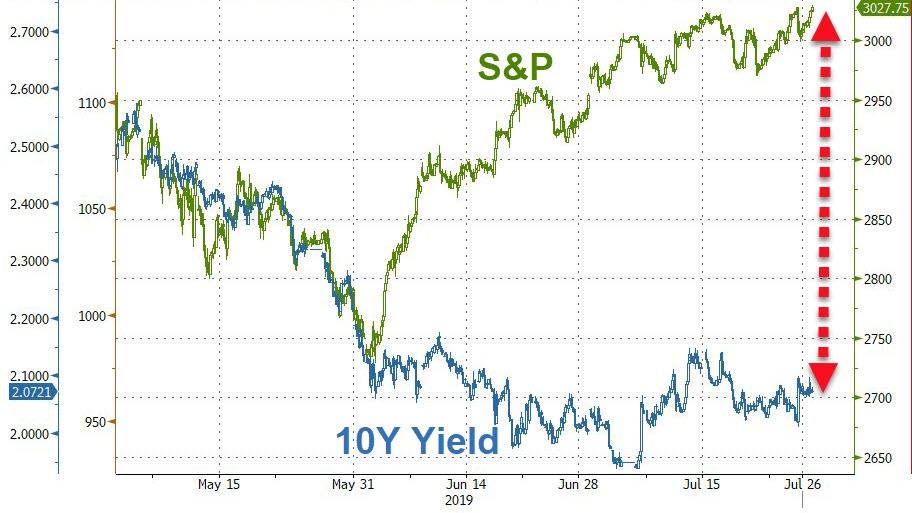

Global Markets Rebound On Back Of Strong Corporate Profits

Global markets were set to end the week mostly in a sea of green, reversing yesterday’s losses, with S&P futures pointing to a higher open as investors greeted the latest batch of corporate earnings, while ignoring Amazon’s downcast outlook and bracing for next week’s Federal Reserve meeting. In the “buy everything” euphoria, the dollar also climbed as did US Treasuries.

S&P Emini futures rose 0.3%, pointing to a turnaround after Wall Street shares fell from record highs on Thursday. Corporate results were mixed as Amazon missed estimates, its profits unexpectedly dropped and the company guided to a weaker than expected operating income, pushing its stock lower, while Google Alphabet rallied after exceeding revenue estimates.

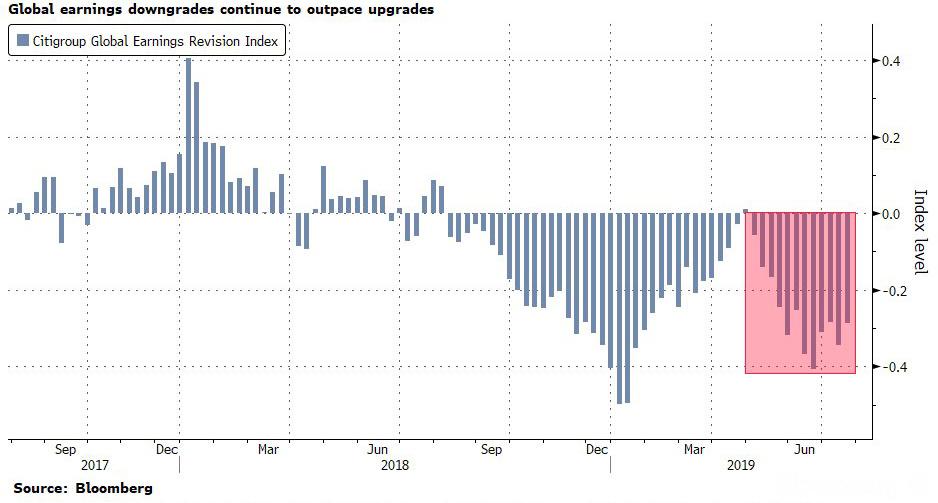

Separately, decent earnings from Intel and Starbucks helped offset worries from weaker Amazon numbers. While corporate results have largely propped up stocks this earnings season, investors continue to watch for any hints of a slowdown in companies’ bottom lines. As a reminder, corporate earnings downgrades continue to sharply outpace upgrades.

“A stream of earnings from the United States has shown people have to pay attention to the corporate cycle as well as the interest rate cycle, and focus is also shifting to the U.S.’s latest GDP numbers this afternoon, which may go some way to influencing what the Federal Reserve decides to do,” said Andrew Milligan, head of global strategy at Aberdeen Standard Investments.

A day after its worst session in three weeks, the European Stoxx 600 index added 0.4%, led by media and telecom shares after positive earnings. Nestle’s higher revenue forecast also lifted the food sector. Among laggards, the retail sector was dragged by disappointing results from luxury giant Kering, while miners slid on metals weakness and after Anglo American’s largest shareholder liquidated its stake. London’s FTSE 100 also revived, helped by Vodafone’s plans to create a separate European tower company and education firm Pearson’s gains from an upbeat trading update.

Meanwhile, it was another bad day for European banks, with the Stoxx 600 Bank Index falling as much as 0.7% as earnings from Spanish banks disappointed. CaixaBank and Sabadell were the worst performers on the gauge, both falling more than 6% after their income from lending missed analysts’ expectations and both banks cut the outlook for core lending. Bankia, which reports on Monday, fell 4.5% and Bankinter also dropped 2.7%.

ECB President Mario Draghi on Thursday all but pledged to ease policy further and even hinted at a reinterpretation of the ECB’s inflation target. But many investors had hoped for an immediate reduction of interest rates.

“After the ECB yesterday opened the door to a looser monetary policy, the Fed is likely to cut interest rates next week,” Joerg Kraemer, chief economist at Commerzbank AG, wrote in a note. “The turnaround in global monetary policy is cementing the low interest rate environment on bond markets.”

Earlier in the session, Asian stocks retreated, led by technology and consumer staples firms, as uncertainties over whether Washington and Beijing will be able to settle gaping differences over trade, technology and even geopolitical ambitions, kept many investors on guard. Negotiators from the two countries will meet in Shanghai next week. MSCI’s broadest index of Asia-Pacific shares outside Japan dropped 0.6, with Indonesia and Singapore leading declines. The Topix fell 0.4%, driven by Keyence Corp. and Toyota Motor Corp. Nissan Motor dropped 3.2% after announcing its plan to cut 12,500 jobs and reduce production capacity amid a global slump in car demand. The Shanghai Composite Index reversed earlier losses and closed 0.2% higher, bringing its weekly gain to 0.7%. China is allowing several domestic companies to buy U.S. cotton, corn, sorghum and pork free of retaliatory tariffs. India’s Sensex rose 0.2%, with Bajaj Finance Ltd. and Kotak Mahindra Bank Ltd. among the biggest boosts, as investors weighed earnings against bad-debt risk. Most Nifty companies that have reported earnings this season have either met or beat estimates

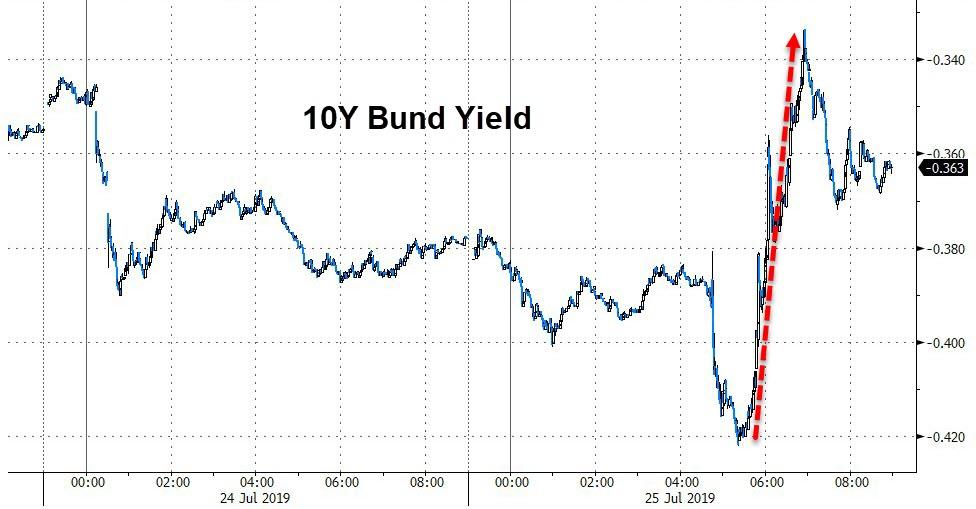

A rally in global bonds ran out of steam after Draghi cautioned about pulling the trigger too quickly on policy easing. Euro zone government bond yields began to reverse some of the rises seen after the ECB meeting. German 10-year bond yields were around one basis points lower at -0.373%, heading back down towards the record low of -0.422%, recorded on Thursday. Other 10-year yields in the euro zone were also around two basis points lower

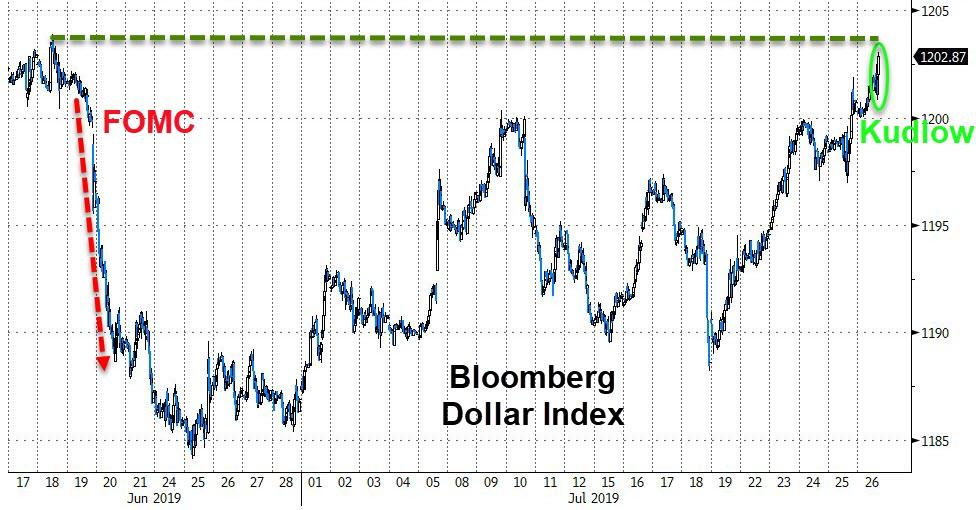

In FX, the Bloomberg Dollar Spot Index rose for a second day, headed for its biggest gain since July 5 as traders trimmed bets on the size of expected Federal Reserve interest-rate cuts and helped by a whisper number for U.S. GDP data that was better than economists’ median forecast. The euro traded at $1.1136, a mild recovery from a two-month low of $1.1102 hit after the ECB decision on Thursday but down 0.1% on the day. For the week, the single currency is down 0.7%. Sterling edged down to $1.2428, and was on course for a 0.6% weekly loss. Cable has stabilised since Boris Johnson became Britain’s new prime minister, but uncertainty remains about Britain’s negotiations to leave the European Union.

In geopolitics, North Korea confirmed it tested a new type of short-range ballistic missile yesterday and its leader Kim stated South Korea has been bringing in weapons for attack, while he added that North Korea must keep developing weapons to eliminate national security threats and that the missile firing was a warning to South Korea’s warmongers. Additionally, officials confirmed Iran tested a medium-range ballistic missile yesterday.

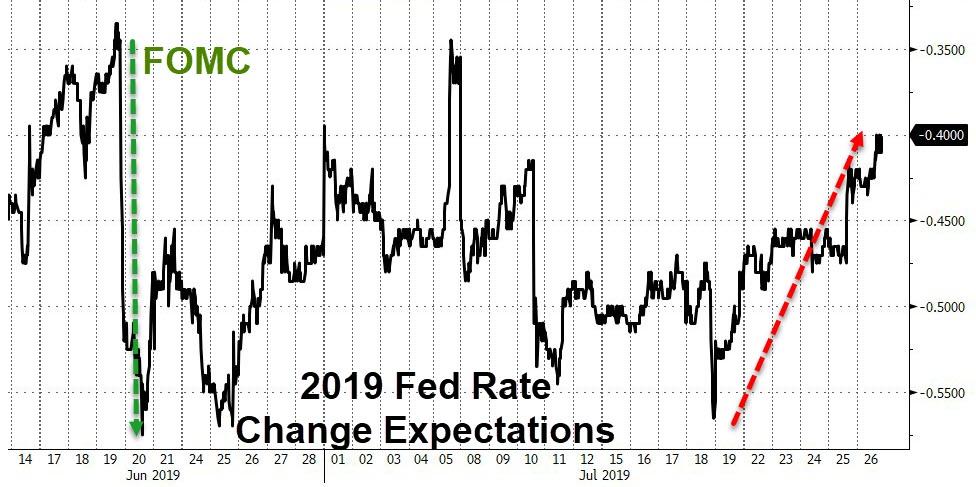

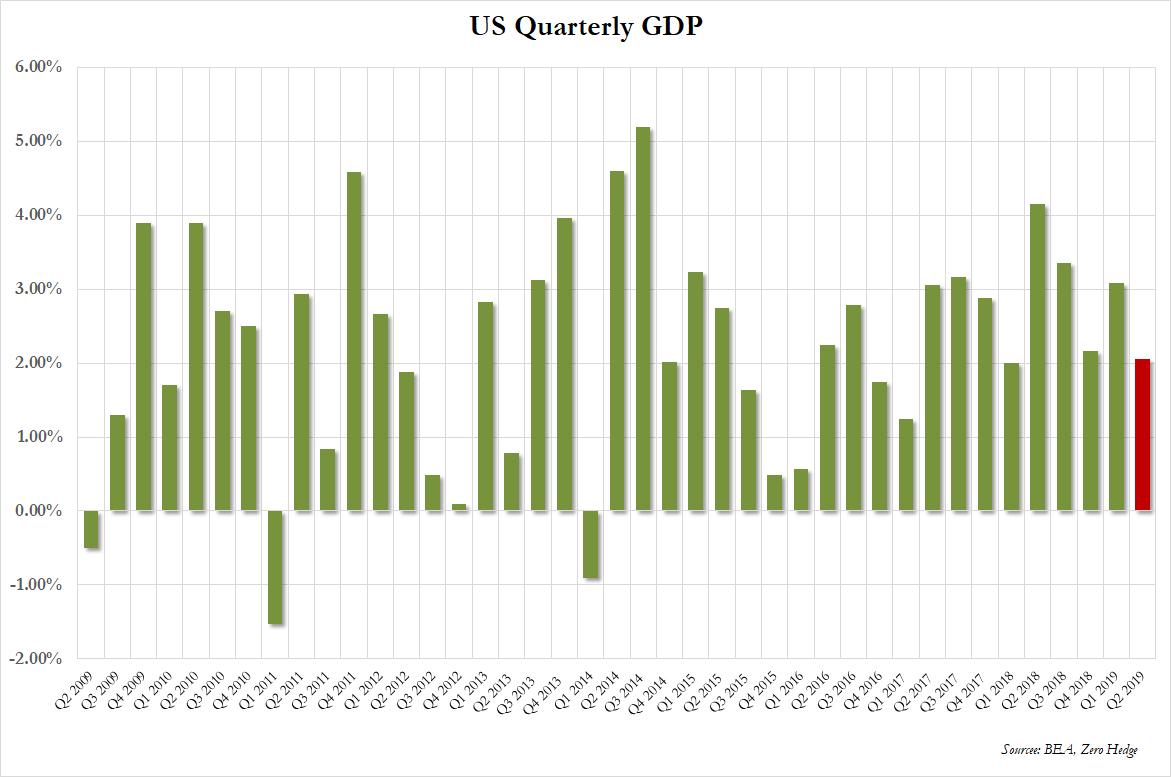

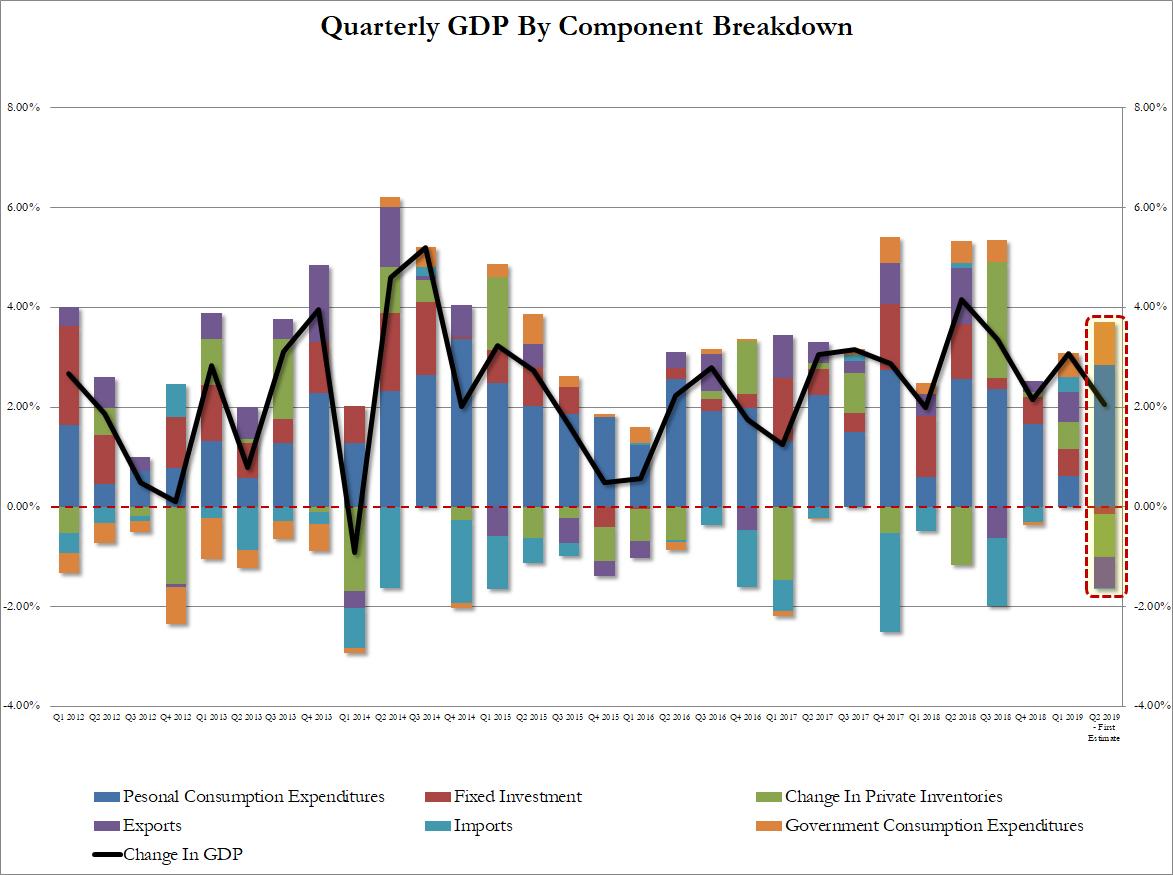

Traders will also be scrutinizing today’s GDP figures, which will probably show growth cooled in the second quarter to 1.8% from the 3.1% annualized pace set in the prior period. Central banks remain at the top of the agenda, with policy makers expected to boost stimulus at next week’s Fed meeting.

Macro economic data to watch include second-quarter GDP and personal consumption figures. Aon, Twitter, AbbVie, McDonald’s, Colgate-Palmolive are among companies reporting earnings.

Market Snapshot

- S&P 500 futures up 0.3% to 3,015.00

- STOXX Europe 600 up 0.2% to 390.18

- MXAP down 0.6% to 160.03

- MXAPJ down 0.7% to 526.29

- Nikkei down 0.5% to 21,658.15

- Topix down 0.4% to 1,571.52

- Hang Seng Index down 0.7% to 28,397.74

- Shanghai Composite up 0.2% to 2,944.54

- Sensex up 0.05% to 37,849.14

- Australia S&P/ASX 200 down 0.4% to 6,793.39

- Kospi down 0.4% to 2,066.26

- German 10Y yield fell 0.5 bps to -0.368%

- Euro down 0.1% to $1.1136

- Brent Futures up 0.1% to $63.47/bbl

- Italian 10Y yield rose 2.3 bps to 1.166%

- Spanish 10Y yield fell 0.8 bps to 0.349%

- Gold spot up 0.2% to $1,418.03

- U.S. Dollar Index up 0.08% to 97.89

Top Overnight News from Bloomberg

- Negative interest rates from central banks come with costs. They’re blamed for squeezing banks, punishing savers, keeping dying companies on life support, and fueling a potentially unsustainable surge in asset prices. This isn’t lost on policymakers at the ECB, who pushed a key rate below zero in 2014. But consider their position: Making money cheaper is the main tool they have to boost stubbornly slow growth. And they aren’t getting a lot of help from governments.

- The enormity of the challenge facing Boris Johnson to break Britain’s political deadlock was laid bare in his first days as prime minister, as the EU rejected his demands for a better Brexit deal

- When Christine Lagarde chairs her first meeting as European Central Bank president in November, she might wonder which of her colleagues don’t really want her there.

- Iran earlier this week test fired a medium-range ballistic missile that traveled 1,000 kilometers, CNN reported citing an unnamed U.S. official,move escalating tensions around one of the world’s most important shipping corridors

- U.S. House passed a two-year debt ceiling extension and budget bill Thursday in a bipartisan deal backed by President Trump that will lessen the chance of a shutdown this fall

- Some Bank of Japan officials see little to be gained from strengthening its interest-rate pledge next week, according to people familiar

- Secretary of State Michael Pompeo said he would be willing to travel to Tehran to address the Iranian people about U.S. foreign policy as the Trump administration applies maximum pressure to renegotiate a nuclear accord

- Mario Draghi is shouting louder than ever for help with the euro-area economy, and still no one is listening.

- As more Chinese companies stumble on their debt, one fund manager is turning wary of riskier bonds from the nation, in another sign that the asset class’s strong performance this year may be nearing an end.

Asian equity markets traded negatively as the region conformed to the downbeat global risk tone post-ECB, while disappointing earnings also added to the glum. ASX 200 (-0.4%) and Nikkei 225 (-0.5%) were lower with tech and financials leading the declines in Australia, while sentiment in Tokyo was dampened by disappointing results including Nissan. Elsewhere, Hang Seng (-0.7%) and Shanghai Comp. (+0.2%) were subdued after further PBoC inaction resulted to a net weekly liquidity drain of CNY 410bln with underperformance in Hong Kong after poor trade data for June in which Exports slipped 9.0% Y/Y and as protesters planned to take their rally to the Hong Kong International Airport. Finally, 10yr JGBs were subdued as they mirrored the lacklustre tone in USTs and European counterparts after a less dovish than hoped ECB, although downside was also stemmed amid weakness in stocks and the BoJ’s presence in the market today.

Top Asian News

- Some at BOJ Are Said to Doubt Effectiveness of Stronger Guidance

- Singapore Home Prices on the Rise Again One Year After Curbs

- Tokyo Electron 1Q Profit Beats Estimate Despite Capex Adjustment

- Singapore Opposition Says ‘Fake News’ Law May Be Used as Muzzle

European stocks are relatively directionless amid another earnings-driven morning for the region [Eurostoxx 50 +0.4%] following on from a mostly negatively Asia-Pac handover post-ECB. Sectors are mixed with clear outperformance seen in telecom names as the sector is bolstered by FTSE-giant Vodafone (+9.5%) after the Co. announced a potential IPO of its Towerco unit alongside its numbers. On the flipside, material names lag, heavily weighted on by Anglo American (-5.0%) after metals tycoon Agarwal sold his stake in the mining name. Elsewhere, gains in the consumer discretionary sector is capped by Kering (-6.2%) after the fashion name open lower in excess of 9% amid disappointing Gucci sales. Meanwhile, optimistic numbers from Intel (+4.8% pre-market) buoyed the European chip names ASM (+3.8%) and STMicroelectonics (+2.6%) and Infineon (+0.8%). Finally, Bayer (+1.4%) shares have received further reprieve after a US judge lowered the verdict against the Co. in the Roundup case to USD 86.7mln from USD 2.2bln. State-side, after-hours yesterday, Amazon (-1.5% pre-market) earnings missed on top and bottom line, whilst Alphabet (+8.5% pre-market) beat on both top and bottom line and advertising revenues topped expectations.

Top European News

- Pearson Jumps After Raising Earnings Outlook in Digital Push

- Money Managers Turn to Turkish Exporters After Surge in Banks

- Europcar Drops to Record Low as Analysts Cite 2Q Report Weakness

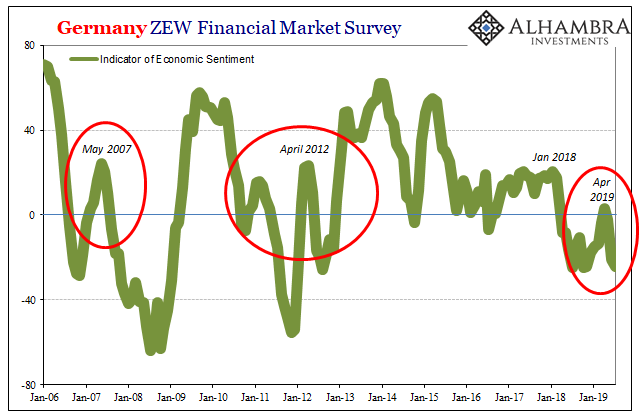

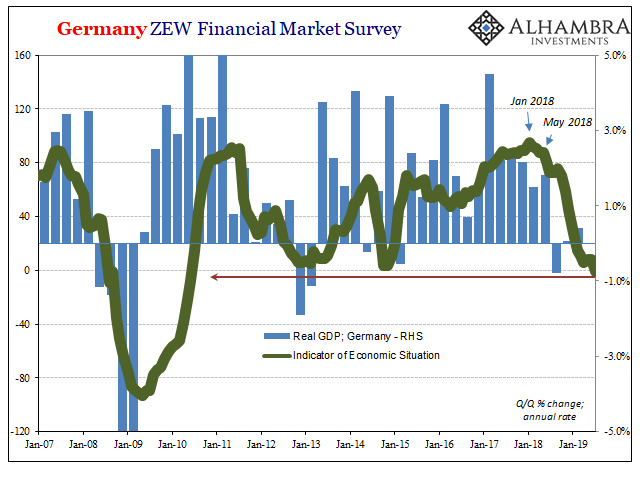

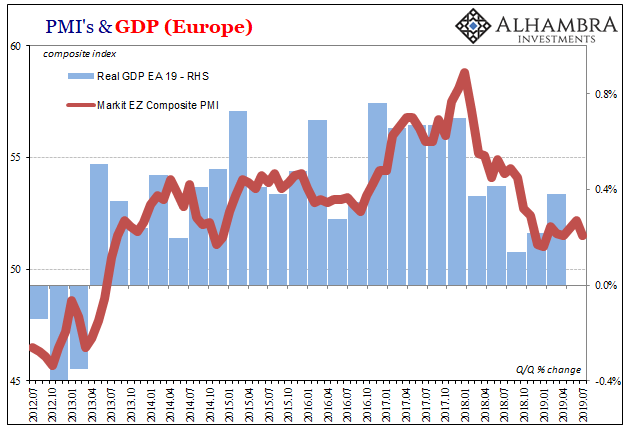

- Three Charts For Those Who Aren’t Worried About German Growth

In FX, the Antipodean Dollars are extending losses and underperformance on the back of increasingly dovish RBA and RBNZ policy outlooks, with expectations building for another 50 bp easing from both Central Banks on top of the rate cuts already administered in the current cycle. In contrast, consensus for the Fed has narrowed to ¼ point for starters and seems unlikely to change materially barring a major development between now and next week’s FOMC. Hence, Aud/Usd has slipped further below 0.6950 towards 0.6925 and July 10’s 0.6911 base beckons before 0.6900, while Nzd/Usd is looking vulnerable under 0.6650 given no real support ahead of 0.6600 and the mtd trough way down at 0.6568.

- ZAR – The Rand continues to reel after its brief post-SARB rebound on the threat of a SA rating downgrade and bearish technical impulses following the break of 14.0000 against the Buck, with key Fib resistance also breached at 14.1360 on the way to 14.1780 and the next chart target looming just shy of 14.2000 in the form of the 200 DMA (14.1920).

- DXY – Amidst broad Greenback gains vs G10 and other counterparts, the index has finally cleared a key technical hurdle of its own at 97.767 and is now nudging 98.000 ahead of US GDP data that could provide more impetus or hamper further advances.

- JPY/GBP/EUR/CHF/CAD – All on the backfoot, as the Yen fails to glean any traction from mixed Japanese inflation data ahead of the BoJ meeting and meanders between 105.57-73 parameters, while Cable has topped out around 1.2520 yet again and saw stops tripped through trend-line support circa 1.2445 to 1.2425 low. Elsewhere, the single currency has drifted back down from post-ECB rebound highs not far from 1.1200, but holding above the minor new pre-Draghi presser 2019 low and the Franc remains off recent highs in 0.9900-20 and 1.050-38 respective bands vs the Dollar and Euro respectively, with perhaps some acknowledgement of a 25 bp SNB rate cut call from UBS. Similarly, the Loonie is softer within a 1.3157-83 range and prone to the aforementioned US data ahead of Canada’s May budget balance.

- EM – Unlike the depreciating Zar, the Try is still unwinding initial post-CBRT losses as Turkish President Erdogan applauds the bold 425 bp move and concurs with the more cautious approach towards further easing between now and the end of the year. The Lira is holding ‘comfortably’ above 5.7000 vs the Buck and the Rouble seems almost as content or prepared for the CBR to cut rates again, with Usd/Rub around 63.1000 and at the lower end of 63.2500-0695 parameters.

In commodities, there was little to report on the energy front as WTI and Brent futures are relatively flat following the decline in the complex heading into yesterday’s settlement. The former currently hovers just above the 56/bbl ahead of its 50 and 200 DMAs at 56.73/bbl and 57.03/bbl respectively, whilst the latter resides around the 63.50/bbl mark. Looking at this week’s performance so far, both benchmarks are currently poised to post gains, albeit off highs. WTI and Brent kicked the week off around 55.70/bbl and 62.60/bbl and have reached highs of 57.62/bbl and 64.64/bbl respectively, bolstered by geopolitical woes. Next up, traders will be eyeing the US Q2 GDP release as the next potential catalyst, with headline expectations of 1.8% annualized growth (Prev. 3.1% in Q1) which would mark the lowest quarterly growth rate since early 2016. Elsewhere, gold is flat despite a firmer Buck as the yellow metal eyes the US tier 1 data release at 1330BST. The precious metal looks set to end the week on the backfoot (weekly range: 1411-33/oz) as the gains seen from rising geopolitical tensions earlier in the week was erased during the ECB press conference yesterday. Meanwhile, copper is lackluster and has dipped below the 2.70/lb amid the cautious risk tone and is currently at the bottom of the weekly 2.68-76/lb range thus far. Finally, Dalian iron ore prices climbed over 3% overnight with traders citing a rise in demand as smaller steel mills take advantage of the production curb on larger competitors amid pollution.

US Event Calendar

- 8:30am: Revisions: National Income and Accounts (GDP)

- 8:30am: GDP Annualized QoQ, est. 1.8%, prior 3.1%

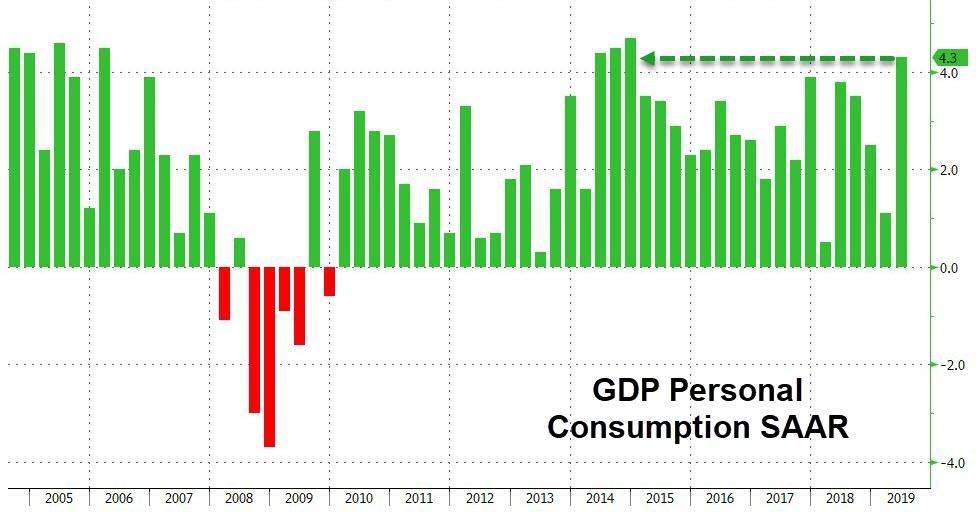

- 8:30am: Personal Consumption, est. 4.0%, prior 0.9%

- 8:30am: GDP Price Index, est. 2.0%, prior 0.9%

- 8:30am: Core PCE QoQ, est. 2.0%, prior 1.2%

DB’s Jim Reid concludes the overnight wrap

For those of you reading across large parts of Europe I hope you haven’t melted in light of what for many has been both the hottest day and hottest night in history. Having been in an air-conditioned office all morning yesterday, stepping out at lunch was like nothing I’d experienced before apart from times where I have been in Singapore! Not only was it hot, it was incredibly humid. Very unlike London. It seems that the surprise cloud mid-afternoon left London a few decimal points away from its hottest day in history and instead we saw the second hottest day on record. The trains home were relatively chaotic last night as fears that the tracks would melt led to multiple cancellations and speed restrictions. There was also a dog on the track and an owner that decided to chase him across the line. This led to a major multi-hour shut down of the network and all power. This left those stranded on trains without air-con. If there’s one job I never want to have it’s the owner of the Twitter account of the help desk of my railway line operator. Never have I read so many angry tweets to them about cancellations, slow trains, dogs on the track, and a lack of aircon. After all the abuse, I think had it have been me I would have cracked and sent back a series of “stop (expletive) moaning” type responses. Remind me never to get into PR.

Mr Draghi has been the master at absorbing all the criticism markets have thrown at him over the years and then come out fighting. Indeed, given what happened yesterday its rather apt that seven years ago today, Mr Draghi made his seminal “whatever it takes” speech which was the main turning point in terms of reversing a then rolling European sovereign crisis. In terms of saving the Euro project, this speech was a great success. Indeed Italian yields which were trading above 6.5% when he stood up to speak are now 1.52%. However the subsequent policies associated with this speech have seen much collateral damage with negative policy rates, €2.6 trillion of QE, 50% of the €11.8 trillion European bond market now trading at a negative yield, mixed growth performance and with lower and lower expectations of inflation. Indeed, 5y5yr forward inflation swaps have fallen from 2.2% back on this day in 2012 to 1.13% before Sintra last month and 1.315% last night. The ECB have succeeded in keeping the Euro together to date, but have failed by a large margin on their inflation mandate.

One day ahead of this anniversary, Mr Draghi pulled out yet another bazooka from his arsenal with the aim of getting inflation higher. However, for markets it was a case of buy the story, sell the delivery as it became clear in the press conference that the written words in the statement were more powerful than the verbal message. Nevertheless yesterday’s meeting lays the groundwork for another big set of policy easing going forward. In more detail, perhaps the key change was strengthening the commitment to price stability by elevating the symmetry of the inflation target, saying that interest rates would be held “for as long as necessary to ensure the continued sustained convergence of inflation to its aim”, whereas previously that had been the convergence of inflation “to levels that are below, but close to, 2%”. Later in the statement, they also referred to the Governing Council’s “commitment to symmetry in the inflation aim” and reintroduced the phrase “or lower” to the rates guidance. The problem is whether monetary policy alone is enough to help. We’ll likely need fiscal policy to get consistent inflation around 2%.

As Mark Wall discussed in his review note, Draghi now has seven weeks to convince the Council to keep with him and deliver a strong enough easing package. Our team have slightly updated their baseline expectation for what the ECB will announce in the coming months. They continue to expect a 10bp deposit rate cut and tiering in September and a further 10bp cut in December. In light of both the breadth of the Policy Decision statement – a sign of Draghi’s powers of persuasion – and the worrying signals on the external side of the economy from the latest PMI and Ifo data and the ECB’s sensitivity to this, they are now including new net asset purchases in their baseline view for September. They expect EUR30bn per month for a minimum 9-12 months split evenly between public and private assets. This move to new QE is still a close call. If data and events surprise to the upside in the meantime, the ECB could stall on this element of the easing package. For more detail on the ECB and our economists’ thoughts see the piece here ( link ).

Markets were all over the place as they digested the ECB statement and press conference. Initially, risk assets rallied strongly, the euro weakened, and rates fell, but the moves completely reversed during the press conference. For example, the Stoxx was +0.86% higher after the statement but dipped to -1.04% lower after the presser ended. It eventually closed -0.56%. In terms of bunds, a -4.4bps rally immediately after the statement (and a fresh all-time low) led to a +8.8bps sell-off into the end of the Q&A before rallying back -2.9bps into the close to end the session +1.5bps higher. Other sovereign markets mirrored the erratic bund moves, with BTPs and OATs ending up +2.4bps and +0.8bps higher, after roundtrip moves of c.20bps and c.11bps, respectively. Swiss 10-year yields fell -1.8bps, and their ultra-long 2064 bond dipped to yield as low as -0.05%, taking the entire universe of Swiss government debt into negative territory. In equities, the Dax (-1.28%), CAC 40 (-0.50%) and the FTSE MIB (-0.80%) all closed lower.

A few of Draghi’s unscripted comments were noteworthy. He said that though there was “broad agreement” on the economic outlook, the council was not unanimous on other topics, thus admitting that there is some pushback against easing in September. He also declined, despite repeated questions, to comment on the size of future cuts, or the scale or composition of QE. Finally, he said that no one argued for immediate action and he did not mention a formal review of the inflation target. These were all hawkish compared to expectations, and drove the reversal in price action. Markets did react positively to Draghi’s attempts to raise inflation, with five-year forward five-year inflation swaps rising by 2.4 bps to a two-month high of 1.315%, although this was below the intra-day peak of 1.3598%. The euro hit its lowest intraday level against the dollar in over two years of 1.1102, before strengthening back to 1.1146 as it was also a victim of the intra-day swing. After European markets closed, anonymously-sourced articles circulated from Reuters and Bloomberg, saying that a September rate cut “appears certain” but that “some ECB policymakers still need to be convinced about tiering.”

In a further sign of the Eurozone slowdown and the perceived need to act, the Ifo business climate index from Germany fell to 95.7 in July (vs. 97.2 expected), the lowest reading since April 2013 and the fourth consecutive monthly decline. There wasn’t much consolation in the other readings either, with the current assessment falling to a 3-year low of 99.4 (vs. 100.4 expected) while the expectations reading fell to a ten-year low of 92.2 (vs. 94.0 expected). Echoing the PMIs from Wednesday, where the German manufacturing reading was at a seven-year low, the Ifo statement said that for manufacturing, “the business climate indicator is in freefall”.

As for US markets, they mostly took their cue from Europe, opening lower and unable to rebound throughout the session. The S&P 500 and DOW retreated -0.51% and -0.47%, with all sector groups retreating. The NASDAQ (-1.00%) and NYFANG (-2.46%) underperformed, with a notable selloff for Tesla (-13.61%) after poorly-received earnings Wednesday evening. The chemicals sector also lagged, shedding -0.75%, as Dow Inc. (-3.83%) reported below-average revenues with management saying that “buying patterns remain cautious due to ongoing trade and geopolitical uncertainties.” There were some positive results from Raytheon (+4.58%) and Bristol-Myers Squibb (+5.02%), who beat expectations and raised guidance.

After markets closed, Google (+7.93% afterhours) announced strong revenue growth of +21% yoy, beating even the most optimistic forecasts. That overnight gain is worth over $60bn in market cap. Intel (+5.10%) said that the second quarter was “much stronger than expected,” with revenues falling only 3% to $16.5bn, compared to expectations for a drop of around 8%. Both companies seem to be adjusting relatively smoothly to tariff-related disruptions. In contrast, Amazon (-1.66%) reported disappointing profit figures of $5.22 per share compared to consensus expectations for $5.57, which outweighed positive revenue growth of +20% yoy. In aggregate, these moves helped NASDAQ futures to gain +0.47% overnight.

Amidst the dovish emphasis from the ECB, the data from the US was more positive. Durable goods orders rose by 2.0% mom in June (vs. 0.7% expected), while the ex-transportation measure rose 1.2% mom (vs. 0.2% expected). Initial jobless claims fell to 206k last week (vs. 218k expected), which brings the 4-week average down to 213k, the lowest since April. Elsewhere, wholesale inventories rose by 0.2% mom in June, (vs. 0.5% expected), and the Kansas City Fed’s Manufacturing index fell to -1 (vs. 3 expected), the first negative reading since August 2016. The June trade deficit was also wider than expected at $74.2bn from a downwardly-revised -$75.0bn. Overall, the data pushed the Atlanta Fed’s estimate of second quarter GDP down -0.3pp to 1.3%, mostly as a function of a wider trade deficit and weaker inventories.

This morning in Asia markets are following Wall Street’s lead with the Nikkei (-0.46%), Hang Seng (-0.45%), Shanghai Comp (-0.16%) and Kospi (-0.54%) all lower. Elsewhere, futures on the S&P 500 are up +0.26%.

In other overnight news, ahead of next week’s BoJ monetary policy meeting ( on July 30th), Bloomberg has reported that some of the BoJ officials see little to be gained from strengthening the bank’s interest rate pledge while adding that the officials would accept a change if pressed at the meeting, but they are concerned that just bolstering the pledge would simply highlight the BOJ’s limited firepower or even backfire, especially with the Fed widely expected to cut US interest rates the following day. As a reminder, the BoJ had changed its guidance just three months back, pledging to keep its interest rates extremely low “at least through around spring 2020,” versus “an extended period of time” previously. Elsewhere, Xinhua reported that China has rejected FedEx claims that it rerouted some Huawei shipments to the US by mistake thereby raising the risks that the delivery giant will be blacklisted in the world’s second-largest economy. The report further added that FedEx’s previous statements are inconsistent with the facts and the company is suspected of holding up more than 100 inbound deliveries involving Huawei.