GOLD:$1747.20 UP $16.30 The quote is London spot price

Silver:$16.64 UP 81 CENTS (London spot closing price)

Closing access prices: London spot

i)Gold : $1744.00 LONDON SPOT 4:30 pm

ii)SILVER: $16.65//LONDON SPOT 4:30 pm

CLOSING FUTURES PRICES: KEY MONTHS

MAY COMEX GOLD: XXX

JUNE GOLD: $1756.20 CLOSE 1.30 PM// SPREAD SPOT (LONDON) VS/FUTURE JUNE: $9.00.//PREMIUMS WENT UP AGAIN

CLOSING SILVER FUTURE MONTH

SILVER JUNE COMEX CLOSE; $17.04…1:30 PM.//SPREAD SPOT/(LONDON) VS FUTURE JUNE: 40 CENTS PER OZ//PREMIUMS UP AGAIN//HUGE DIFFERENCE

the gold market continues to be broken as future prices are much higher than spot prices. The comex is desperate to fix things but they have no available gold.

If one is to buy gold and or gold coins, the price is around $2800. usa per oz

and silver; $31.00 per oz//

LADIES AND GENTLEMEN: YOU ARE NOW WITNESSING FIRST HAND THE DIFFERENCE BETWEEN PAPER GOLD/SILVER AND THE REAL PHYSICAL STUFF!!

DO NOT PAY ANY ATTENTION TO WHAT THE CROOKS ARE DOING AT THE COMEX AND LONDON LBMA..PHYSICAL IS THE NAME OF THE GAME AND NOTHING ELSE

COMEX DATA

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING: 133/920

issued: 864

EXCHANGE: COMEX

CONTRACT: MAY 2020 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,738.100000000 USD

INTENT DATE: 05/14/2020 DELIVERY DATE: 05/18/2020

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

072 C GOLDMAN 5

118 H MACQUARIE FUT 153

132 C SG AMERICAS 8

167 C MAREX 33

323 H HSBC 8

355 C CREDIT SUISSE 1

624 C BOFA SECURITIES 1

657 C MORGAN STANLEY 22

661 C JP MORGAN 864 133

685 C RJ OBRIEN 1

686 C INTL FCSTONE 46

690 C ABN AMRO 10 432

732 C RBC CAP MARKETS 1

737 C ADVANTAGE 8 56

800 C MAREX SPEC 4 26

905 C ADM 1 27

____________________________________________________________________________________________

TOTAL: 920 920

MONTH TO DATE: 8,820

NUMBER OF NOTICES FILED TODAY FOR MAY CONTRACT: 920 NOTICE(S) FOR 92,000 OZ (2.8615 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 8820 NOTICES FOR 882000 OZ (27.433 TONNES)

SILVER

FOR MAY

29 NOTICE(S) FILED TODAY FOR 145,000 OZ/

total number of notices filed so far this month: 8738 for 43,690,000 oz

BITCOIN MORNING QUOTE $9623 DOWN 172

BITCOIN AFTERNOON QUOTE.: $9396 DOWN 401

GLD AND SLV INVENTORIES:

WITH GOLD UP $16.30 AND NO PHYSICAL TO BE FOUND ANYWHERE:

WITH ALL REFINERS CLOSED//MEXICO ORDERING ALL MINES SHUT: WHERE ARE THEY GETTING THE “PHYSICAL”?

A HUGE CHANGE IN GOLD INVENTORY AT THE GLD// A PAPER DEPOSIT OF 12.58 TONNES INTO THE GLD//

GLD: 1,104.72 TONNES OF GOLD//

WITH SILVER UP 81 CENTS TODAY: AND WITH NO SILVER AROUND

NO CHANGES IN SILVER INVENTORY AT THE SLV//

RESTING SLV INVENTORY TONIGHT:

SLV: 423.658 MILLION OZ./

XXXXXXXXXXXXXXXXXXXXXXXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI ROSE BY A HUGE SIZED 4716 CONTRACTS FROM 136,495 UP TO 141,211 AND CLOSER TO OUR NEW RECORD OF 244,710, (FEB 25/2020. THE FAIR SIZED GAIN IN OI OCCURRED WITH OUR 33 CENT GAIN IN SILVER PRICING AT THE COMEX. IT SEEMS THAT THE GAIN IN COMEX OI IS DUE TO STRONG BANKER SHORT COVERING PLUS A SMALL EXCHANGE FOR PHYSICAL ISSUANCE, ZERO LONG LIQUIDATION, ACCOMPANYING A GOOD INCREASE IN SILVER OZ STANDING AT THE COMEX FOR MAY. WE HAD A NET GAIN IN OUR TWO EXCHANGES OF 5486 CONTRACTS (SEE CALCULATIONS BELOW).

WE HAVE ALSO WITNESSED A HUMONGOUS AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A SMALL SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: MARCH: 00 AND MAY: 0 AND JULY: 680 AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 110 CONTRACTS. WITH THE TRANSFER OF 680 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 680 EFP CONTRACTS TRANSLATES INTO 3.40 MILLION OZ ACCOMPANYING:

1.THE 33 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

10.025 MILLION OZ INITIAL STANDING IN AUGUST.

43.030 MILLION OZ INITIALLY STANDING IN SEPT. (HUGE)

7.32 MILLION OZ INITIALLY STANDING IN OCT

2.630 MILLION OZ STANDING FOR NOV.

20.970 MILLION OZ FINAL STANDING IN DEC

5.075 MILLION OZ FINAL STANDING IN JAN

1.480 MILLION OZ FINAL STANDING IN FEB

23.005 MILLION OZ FINAL STANDING FOR MAR

4.660 MILLION OZ FINAL STANDING FOR APRIL

45.435 MILLION OZ INITIALLY STANDING FOR MAY

THURSDAY, AGAIN OUR CROOKS USED COPIOUS PAPER IN ORDER TO LIQUIDATE SILVER’S PRICE…AND THEY WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE 33 CENTS).. AND, OUR OFFICIAL SECTOR/BANKERS WERE UNSUCCESSFUL IN THEIR ATTEMPT TO FLEECE ANY AMOUNT OF SILVER LONGS FROM THEIR POSITIONS. THE GOOD GAIN AT THE COMEX WAS ACCOMPANIED BY : i) A SMALL ISSUANCE OF EXCHANGE FOR PHYSICALS 2) A GOOD GAIN IN SILVER OZ STANDING FOR MAY,3) CONSIDERABLE BANKER SHORT COVERING AND 4) ZERO LONG LIQUIDATION AS WE DID HAVE A NET GAIN OF 5396 CONTRACTS OR 26.480 MILLION OZ ON THE TWO EXCHANGES! YOU CAN BET THE FARM THAT OUR BANKER ARE DESPERATE TO LIQUIDATE THEIR HUGE SHORT POSITIONS IN SILVER

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY /FOR MONTH OF MAY:

8322 CONTRACTS (FOR 11 TRADING DAYS TOTAL 8322 CONTRACTS) OR 41.61 MILLION OZ: (AVERAGE PER DAY: 756 CONTRACTS OR 3.783 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF MAY: 41.61 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 5.48% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2020 TO DATE SILVER EFP’S: 1,030.45 MILLION OZ.

JANUARY 2020 EFP TOTALS SO FAR: 181.61 MILLION OZ

FEB 2020 EFP’S TOTAL : …… 259.600 MILLION OZ

MARCH EFP’S ….. 452.280 MILLION OZ //TOTALS//AND A NEW RECORD FOR THE MONTH)

APRIL EFP 95.355 MILLION OZ. (EX. FOR PHYSICALS BECOMING A LOT LESS)

MAY EFP SO FAR: 41.61 MILLION OZ

EXCHANGE FOR PHYSICAL ISSUANCE FOR THE PAST 30 DAYS IS A LOT LESS. NO DOUBT THAT THE COST TO CARRY THESE THINGS HAS EXPLODED AND AS SUCH CANNOT BE DONE AS FREQUENTLY AS BEFORE.

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 4716, WITH OUR 33 CENT GAIN IN SILVER PRICING AT THE COMEX ///THURSDAY… THE CME NOTIFIED US THAT WE HAD A GOOD SIZED EFP ISSUANCE OF 680 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER

TODAY WE GAINED A GOOD SIZED OI CONTRACTS ON THE TWO EXCHANGES: 5396 CONTRACTS (WITH OUR 33 CENT GAIN IN PRICE)

THE TALLY//EXCHANGE FOR PHYSICALS

i.e 680 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH A HUGE SIZED INCREASE OF 4716 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 33 CENT GAIN IN PRICE OF SILVER/AND A CLOSING PRICE OF $15.83 // THURSDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY.

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.7050 BILLION OZ TO BE EXACT or 100.7% of annual global silver production (ex Russia & ex China).

FOR THE NEW MAR DELIVERY MONTH/ THEY FILED AT THE COMEX: 29 NOTICE(S) FOR 145,000 OZ OF SILVER.

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.70//TODAY’S RECORD OF 244,705 IS SET WITH A PRICE OF: 18.91 (FEB 25/2020)

.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ; AUGUST 10.025 MILLION OZ/ SEPT 43.030 MILLION OZ//OCT: 7.665 MILLION OZ// NOV: 2.630 MILLION OZ//DEC: 20.970 MILLION OZ; JAN: 5.075 MILLION OZ.//FEB 1.480 MILLION OZ//MAR: 23.005 MILLION OZ/APRIL 4.660 MILLION OZ//MAY 45.380 MILLION OZ

- THE RECORD PRIOR TO TODAY WAS SET IN FEB 25/2018: 244,710 CONTRACTS, WITH A SILVER PRICE OF $18.90//.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017 RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

GOLD

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A STRONG SIZED 10,433 CONTRACTS TO 521,493 AND CLOSER TO OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE HUGE SIZED GAIN OF COMEX OI OCCURRED WITH OUR CONSIDERABLE COMEX GAIN IN PRICE OF $19.25 /// COMEX GOLD TRADING// THURSDAY// WE HAD STRONG BANKER SHORT COVERING , A HUGE SIZED INCREASE IN GOLD OZ STANDING AT THE COMEX, ALONG WITH ZERO LONG LIQUIDATION ACCOMPANYING A GOOD EX. FOR PHYSICAL ISSUANCE. THIS ALL HAPPENED WITH OUR LARGE GAIN IN THE PAPER PRICE OF GOLD.

WE HAD A VOLUME OF 8 4 -GC CONTRACTS//OPEN INTEREST 7

WE GAINED A STRONG SIZED 13,208 CONTRACTS (41.082 TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2775 CONTRACTS:

CONTRACTS, FEB> 0 CONTRACTS; MARCH 00 APRIL: 0. MAY: 0, AND JUNE 2325.; AUG 450 AND ALL OTHER MONTHS ZERO//TOTAL: 2775. The NEW COMEX OI for the gold complex rests at 521.493. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A VERY GOOD SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 13,208 CONTRACTS: 10,433 CONTRACTS INCREASED AT THE COMEX AND 2775 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 13,208 CONTRACTS OR 41.082 TONNES. THURSDAY, WE HAD A GAIN OF $19.25 IN GOLD TRADING……

AND WITH THAT GAIN IN PRICE, WE HAD A VERY STRONG SIZED GAIN IN TOTAL/TWO EXCHANGES GOLD TONNAGE OF 41.082 TONNES!!!!!! THE BANKERS/OFFICIAL SECTOR WERE SUPPLYING INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER WITH RECKLESS ABANDON. THE BANKERS WERE UNSUCCESSFUL IN THEIR ATTEMPT TO LOWER GOLD’S PRICE (IT ROSE $19.25).AND IT ALSO SEEMS THAT THEIR ATTEMPT TO FLEECE ANY GOLD LONGS FROM THE GOLD ARENA WAS UNSUCCESSFUL (SEE BELOW).

4 GC VOLUME: 8 // open interest 7

END

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES:

WE HAD A GOOD SIZED INCREASE IN EXCHANGE FOR PHYSICALS (2775) ACCOMPANYING THE HUGE SIZED GAIN IN COMEX OI (10,433 OI): TOTAL GAIN IN THE TWO EXCHANGES: 13,208 CONTRACTS. WE NO DOUBT HAD 1 )CONSIDERABLE BANKER SHORT COVERING, 2.)A STRONG INCREASE IN OUNCES STANDING AT THE GOLD COMEX FOR THE FRONT MAY MONTH, 3) ZERO LONG LIQUIDATION; 4) HUGE COMEX OI GAIN, AND …ALL OF THIS WAS COUPLED WITH OUR GAIN IN GOLD PRICE TRADING//THURSDAY

SPREADING OPERATIONS

OUR SPREADING OPERATION HAS NOW SWITCHED INTO GOLD…..

SPREADING OPERATION FOR OUR NEWCOMERS:

WE HAVE NOW COMMENCED IN SILVER THE ILLEGAL SPREADING OPERATION \ FOR NEWCOMERS, HERE ARE THE DETAILS:

SPREADING LIQUIDATION HAS NOW STOPPED IN SILVER AS THEY NOW BEGIN TO MORPH INTO GOLD AS WE HEAD TOWARDS THE NEW FRONT MONTH WILL BE JUNE.

FOR THOSE OF YOU WHO ARE NEW, HERE IS THE MODUS OPERANDI OF THE SPREADERS AND THE CRIMINAL ELEMENT BEHIND IT:

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR;

THE SPREADING LIQUIDATION OPERATION IS NOW OVER FOR SILVER..AND WE WILL NOW MORPH INTO AN ACCUMULATION PHASE OF SPREADING CONTRACTS FOR GOLD. THEY WILL ACCUMULATE CONSIDERABLE AMOUNT OF THE CONTRACTS AND THEN LIQUIDATE ONE WEEK PRIOR TO FIRST DAY NOTICE

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO GOLD AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX SILVER OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE IN THIS NON ACTIVE MONTH OF MAY. BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN GOLD WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JUNE), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2020 INCLUDING TODAY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY : 31917 CONTRACTS OR 3,191,700 oz OR 99.27 TONNES (11 TRADING DAYS AND THUS AVERAGING: 2901 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 11 TRADING DAY(S) IN TONNES: 99.27 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2019, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 99.27/3550 x 100% TONNES =2.80% OF GLOBAL ANNUAL PRODUCTION

ISSUANCE OF EXCHANGE FOR PHYSICAL GOLD HAS DISSIPATED THIS MONTH…THE COST TO THE BANKERS TO CARRY THESE CONTRACTS IN LONDON IS BECOMING TOO GREAT FOR THEM.

ACCUMULATION OF GOLD EFP’S YEAR 2020 TO DATE: 2665.52 TONNES

JANUARY 2220 TOTAL EFP ISSUANCE; : 570.19 TONNES

FEB 2020 TOTAL EFP ISSUANCE : 653.78 TONNES

MARCH TOTAL EFP ISSUANCE 1,098.93 TONNES (*AND A NEW ALL TIME RECORD ISSUANCE//22 DAYS)

APRIL TOTAL EFP. ISSUANCE: 243.45 TONNES (EFP ISSUANCE BECOMING A LOT LESS)

MAY TOTAL EFP ISSUANCE: 99.27 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A HUGE SIZED 4716 CONTRACTS FROM 136.495 UP TO 141,211 AND FURTHER FROM OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 2 3/4 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.

ALL OF THE GAIN IN COMEX OI WAS DUE TO 1) CONSIDERABLE BANKER SHORT COVERING , 2) A GOOD ISSUANCE OF EXCHANGE FOR PHYSICALS (SEE BELOW), 3) A GOOD INCREASE IN SILVER OZ STANDING AT THE COMEX FOR MAY AND 4) ZERO LONG LIQUIDATION

EFP ISSUANCE 680 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

FOR FEB. 0; FOR MAR 0: AND MAY: 0 JULY: 680 CONTRACTS AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 110 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 4716 CONTRACTS TO THE 680 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A HUGE GAIN OF 5396 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 26.48 MILLION OZ!!! OCCURRED WITH THE 33 CENT GAIN IN PRICE///

RESULT: A GOOD SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE 33 CENT GAIN IN PRICING THAT SILVER UNDERTOOK IN PRICING// THURSDAY. WE ALSO HAD A GOOD SIZED 680 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED DOWN 1.88 POINTS OR 0.07% //Hang Sang CLOSED DOWN 32.27 POINTS OR 0.14% /The Nikkei closed UP 122.69 POINTS OR 0.62%//Australia’s all ordinaires CLOSED UP 1.38%

/Chinese yuan (ONSHORE) closed DOWN at 7.1067 /Oil UP TO 28,16 dollars per barrel for WTI and 31.72 for Brent. Stocks in Europe OPENED MOSTLY GREEN// ONSHORE YUAN CLOSED DOWN // LAST AT 7.1067 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 7.1314 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

i)we had 1 deposits into the customer account

into JPMorgan: 0

ii)into Delaware: 5859.000 oz

*** JPMorgan for most of 2017, 2018 and onward, has adding to its inventory almost every single day.

JPMorgan now has 160.819 million oz of total silver inventory or 51.22% of all official comex silver. (160.819 million/314.220 million

total customer deposits today: 5859.000 oz

we had 2 withdrawals:

i) Out of Delaware: 3036.100 oz

ii) Out of CNT: 2003.000 oz

total withdrawals; 5039.1000 oz

We had 0 adjustments

total dealer silver: 90.608 million

total dealer + customer silver: 314.221 million oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

The total number of notices filed today for the MAY 2020. contract month is represented by 29 contract(s) FOR 145,000 oz

To calculate the number of silver ounces that will stand for delivery in MAY we take the total number of notices filed for the month so far at 8820 x 5,000 oz = 43,690,000 oz to which we add the difference between the open interest for the front month of MAY.(378) and the number of notices served upon today 29 x (5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the MAY/2019 contract month: 8820 (notices served so far) x 5000 oz + OI for front month of MAY (378)- number of notices served upon today (29) x 5000 oz of silver standing for the MAY contract month.equals 45,435,000 oz.

We GAINED 11 or an additional 55,000 oz will seek out metal on the London side of the pond as they ACCEPTED a London based forward contract..

TODAY’S ESTIMATED SILVER VOLUME: 39,998 CONTRACTS //volume very low

FOR YESTERDAY: 55,019 CONTRACTS..,CONFIRMED VOLUME//extremely low volume

YESTERDAY’S CONFIRMED VOLUME OF 55,019 CONTRACTS EQUATES to 275 million OZ 39.2% OF ANNUAL GLOBAL PRODUCTION OF SILVER..

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO- 1.12% ((MAY 15/2020)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -0.05% to NAV: (MAY 15/2020 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into NEGATIVE/ 1.12%

(courtesy Sprott/GATA

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 15.95 TRADING 15.87///NEGATIVE 0.52

END

And now the Gold inventory at the GLD/

MAY 15.WITH GOLD UP $16.30 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 12.58 TONNES/ INVENTORY RESTS AT 1104.72 TONNES

MAY 14//WITH GOLD UP $19.25 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY RESTS AT 1092.14 TONNES

MAY 13//WITH GOLD UP $9.05 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 11.07 TONNES/INVENTORY RESTS AT 1092.14 TONNES

MAY 12//WITH GOLD UP $6.60 TODAY; A SMALL CHANGES IN GOLD INVENTORY AT THE GLD/: A WITHDRAWAL OF .58 TONNES FROM THE GLD///INVENTORY RESTS AT 1081.07 TONNES

MAY 11/WITH GOLD DOWN $12.65 TODAY: NO CHANGES IN GOLD INVENTORY: //INVENTORY RESTS AT 1081.65 TONES..

MAY 8/WITH GOLD DOWN $7.00 TODAY; A BIG CHANGE IN GOLD INVENTORY: A PAPER ADDITION OF 5.85 TONNES/INVENTORY RESTS AT 1081.65 TONNES

MAY 7/WITH GOLD UP $29.65 TODAY : A SMALL CHANGE IN GOLD INVENTORY AT THE GLD//A PAPER ADDITION OF .41 TONNES/INVENTORY RESTS AT 1075.80 TONNES

MAY 6//WITH GOLD DOWN $17.00 TODAY/ A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A PAPER ADDITION OF 3.68 TONNES/INVENTORY RESTS AT 1075.39 TONES

MAY 5/WITH GOLD DOWN $1.65 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER ADDITION OF 3.81 TONNES//INVENTORY RESTS AT 1071.71 TONNES

MAY 4//WITH GOLD UP $12.00 TODAY//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A MASSIVE PAPER DEPOSIT OF 11.4 TONNES INTO THE GLD////GOLD INVENTORY RESTS AT 1067.90 TONNES

MAY 1/WITH GOLD UP $8.45 NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1056.50 TONNES

APRIL 30/WITH GOLD DOWN $15.95 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1056.50 TONNES

APRIL 29/WITH GOLD DOWN $7.65/A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 8.19 TONNES OF GOLD INTO THE GLD////INVENTORY REST AT 1056.50 TONNES//

APRIL 28/WITH GOLD DOWN $4.50//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1048.31 TONNES

APRIL 27/WITH GOLD DOWN $12.75//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 5.85 TONNES INTO THE GLD////INVENTORY RESTS TONIGHT AT 1048.31 TONNES

APRIL 24/WITH GOLD DOWN $4.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS TONIGHT AT 1042.46 TONNES

APRIL 23/WITH GOLD UP $10.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS TONIGHT AT 1042.46 TONNES

APRIL 22/WITH GOLD UP $40.75 TODAY:; TWO HUGE CHANGES IN GOLD INVENTORY AT THE GLD//A)A MONSTROUS 3.8 PAPER TONNES WERE ADDED TO THE GLD INVENTORY AND B) ANOTHER HUGE 9.07 TONNES OF PAPER GOLD ADDED LATE IN THE DAY//INVENTORY RESTS AT 1042.46 TONNES

APRIL 21/WITH GOLD DOWN $21.60 TODAY: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MONSTROUS ADDITION OF 7.9 PAPER TONNES TO THE GLD INVENTORY//INVENTORY RESTS AT 1029.59 TONNES

APRIL 20//WITH GOLD UP $10.00 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1021.69 TONNES

APRIL 17/WITH GOLD DOWN $27.80 TODAY: SURPRISINGLY NO CHANGES IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 1021.69 TONNES TONNES..THE STRING OF 12 STRAIGHT STRONG DEPOSITS ENDS..

APRIL 16/WITH GOLD DOWN $4.50 TODAY: ANOTHER HUGE CHANGE IN GOLD INVENTORY: A STRONG DEPOSIT OF 4.10 TONNES WAS ADDED TO THE GLD INVENTORY//INVENTORY RESTS AT 1021.69 TONNES/12TH STRAIGHT STRONG DEPOSIT

APRIL 15//WITH GOLD DOWN $19.10 TODAY; ANOTHER HUGE CHANGE IN GOLD INVENTORY; A STRONG 7.89 TONNES WAS ADDED TO THE GLD INVENTORY//INVENTORY RESTS AT 1117.59 TONNES.//11TH STRAIGHT STRONG DEPOSIT

APRIL 14/WITH GOLD UP $23.55 TODAY: ANOTHER HUGE CHANGE IN GOLD INVENTORY: A STRONG 15.51 TONNES WAS ADDED TO THE GLD INVENTORY/INVENTORY RESTS AT 1009.70 TONNES//THIS IS THE 10TH STRAIGHT STRONG DEPOSIT//THIS IS A FRAUDULENT VEHICLE..THEY HAVE NO PHYSICAL GOLD IN THE TRUST..

APRIL 13//WITH GOLD UP $27.65 TODAY: ANOTHER HUGE CHANGE IN GOLD INVENTORY: A STRONG 5.36 TONNES WAS ADDED TO THE GLD//INVENTORY RESTS AT 994.19 TONNES

APRIL 9 WITH GOLD UP $37.30 TODAY: ANOTHER HUGE CHANGE IN GOLD INVENTORY: A STRONG 2.92 TONNES WAS ADDED TO THE GLD//GOLD INVENTORY RESTS TONIGHT AT..988.63 TONNES

APRIL 8/WITH GOLD DOWN $.60//ANOTHER HUGE CHANGE IN GOLD INVENTORY/;; A STRONG 1.45 TONNES WAS ADDED TO THE GLD/GOLD INVENTORY RESTS AT 985.71 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Inventory rests tonight at

MAY 15/ GLD INVENTORY 1104.72 tonnes*

LAST; 821 TRADING DAYS: +158.42 NET TONNES HAVE BEEN REMOVED FROM THE GLD

LAST 721 TRADING DAYS://+333.56 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

MAY 15/WITH SILVER UP 81 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV: /INVENTORY RESTS AT 423.65 MILLION OZ.

MAY 14//WITH SILVER UP 33 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV.//INVENTORY RESTS AT 423.65 MILLION OZ

MAY 13/WITH SILVER UP 2 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 2.79 MILLION OZ INTO THE SLV..//INVENTORY RESTS AT 423.65 MILLION OZ//

MAY 12/WITH SILVER UP 5 CENTS TODAY: A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.076 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 420.861 MILLION OZ//

MAY 11.WITH SILVER DOWN 5 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 417.785 MILLION OZ//

MAY 8/WITH SILVER UP 11 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A MONSTER DEPOSIT OF 4.661 MILLION OZ OF SILVER INTO THE SLV..///INVENTORY RESTS AT 417.785 MILLION OZ//

MAY 7/WITH SILVER UP 45 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 413.124 MILLION OZ//

MAY 6/WITH SILVER DOWN 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 413.124 MILLION OZ//

MAY 5/WITH SILVER UP 17 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 413.124 MILLION OZ///

MAY 4//WITH SILVER DOWN 5 CENTS TODAY:2 HUGE PAPER CHANGES IN SILVER INVENTORY AT THE SLV.i).A LARGE 1.399 MILLION OZ OF PAPER SILVER REMOVED FROM THE SLV//..//INVENTORY RESTS AT 411.427 MILLION OZ and ii) A LARGE 1.647 MILLION OZ OF PAPER SILVER ADDED TO THE SLV// INVENTORY RESTS AT 413.124 MILLION OZ//

MAY 1/WITH SILVER FLAT IN PRICE: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 412.826 MILLION OZ///

APRIL 30/WITH SILVER DOWN 26 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 412.826 MILLION OZ//

APRIL 29/WITH SILVER DOWN ONE CENT TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 412.826 MILLION OZ//

APRIL 28 /WITH SILVER DOWN 2 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 412.826 MILLION OZ..

APRIL 27/WITH SILVER UP ONE CENT TODAY: TWO SMALL CHANGE IN SILVER INVENTORY AT THE SLV: a) A WITHDRAWAL OF 373,000 OZ FORM THE SLV// b) A SECOND WITHDRAWAL OF 466,000: ////INVENTORY RESTS AT 412.826 MILLION OZ//

APRIL 24//WITH SILVER UP 3 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 413.665 MILLION OZ

APRIL 23/WITH SILVER UP 0 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.891 MILLION OZ INTO THE SLV/////INVENTORY RESTS AT 413.665 MILLION OZ//

APRIL 22/WITH SILVER UP 42 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY: A PAPER WITHDRAWAL OF 1.865 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 410.774 MILLION OZ//

APRIL 21//WITH SILVER DOWN 60 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER ADDITION OF 1.398 MILLION OZ INTO THE SLV INVENTORY//INVENTORY RESTS AT 412.639 MILLION OZ//

APRIL 20//WITH SILVER UP 16 CENTS TODAY: A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.797 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 414.038 MILLION OZ//

APRIL 17/WITH SILVER DOWN 24 CENTS TODAY; A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.3999 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 415.437 MILLION OZ//

APRIL 16/WITH SILVER UP 5 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV////INVENTORY RESTS AT 415.437 MILLION OZ//

APRIL 15//WITH SILVER DOWN 45 CENTS TODAY: TWO HUGE CHANGES IN SILVER INVENTORY AT THE SLV TWO HUGE DEPOSITS: A DEPOSIT OF 1.679 MILLION OZ AND ANOTHER 5.222 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 415.437 MILLION OZ//

APRIL 14./WITH SILVER UP 51 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A MASSIVE PAPER DEPOSIT OF XXX MILLION OZ//INVENTORY RESTS AT 408.536 MILLION OZ//

APRIL 13//WITH SILVER DOWN 29 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A MASSIVE PAPER DEPOSIT OF 6.155 MILLION OZ////INVENTORY RESTS AT 408.536 MILLION OZ//

APRIL 9/WITH SILVER UP 60 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A HUGE DEPOSIT OF 1.84 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 402.381 MILLION OZ.

MAY 15.2020:

SLV INVENTORY RESTS TONIGHT AT

423.65 MILLION OZ.

END

LIBOR SCHEDULE AND GOFO RATES// GOLD LEASE RATES

YOUR DATA…..

6 Month MM GOFO 2.39/ and libor 6 month duration 0.68

Indicative gold forward offer rate for a 6 month duration/calculation:

G0LD LENDING RATE: -1.71%

NEGATIVE GOLD LEASING RATES//GOLD SCARCITY AND CENTRAL BANKS CALLING IN ALL OF THEIR GOLD LEASES

XXXXXXXX

12 Month MM GOFO

+ 1.92%

LIBOR FOR 12 MONTH DURATION: 0.77

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = -1.15

NEGATIVE GOLD LEASING RATES//GOLD SCARCITY AND CENTRAL BANKS CALLING IN ALL OF THEIR GOLD LEASES

end

PHYSICAL GOLD/SILVER STORIES

i) GOLDCORE BLOG/Mark O’Byrne

Mark O’Byrne of GoldCore this morning:

Gold Hits New Record Highs On Currency Debasement, Brexit and U.S. China Risks

* Gold has surged to new record highs in British pounds at £1,422/oz, is touching near record highs in euros at €1,607/oz and is 1.8% higher this week in dollars to $1,738/oz, near a new 8 year high.

* Gold’s gains on all currencies are due to concerns about the outlook for global economies and global currencies in an era of currency debasement on a scale never before seen in world history.

* Other risks have not gone away and are set to rear their ugly heads again. These include major geopolitical, monetary and systemic risks from the pandemic and attendant global lockdown, from Brexit and risks to the viability of the Eurozone itself and of course U.S. China tensions are bubbling over once again.

* Gold is consolidating near record highs in euros and is the second best performing asset (only the 30 year US bond has done better) in the world in 2020 year to date in all currencies.

* It is again acting as a hedge and a safe haven exactly when investors need one and most analysts including Goldman Sachs believe it will continue to do so in the coming years with Goldman advising that the case for diversifying into gold is ‘as strong as ever.’

* Gold is 14% higher in dollars,18% higher in euros and 22% higher in embattled sterling year to date…

-END-

ii) Important gold commentaries courtesy of GATA/Chris Powell

Alasdair Macleod states that hedge funds have now overpowered the bullion banks with gold.

(Courtesy Kingworldnews/Alasdair Macleod)

Hedge funds have beaten bullion banks with gold, Macleod tells KWN

Submitted by cpowell on Thu, 2020-05-14 16:12. Section: Daily Dispatches

12:14p ET Thursday, May 14, 2020

Dear Friend of GATA and Gold:

Hedge funds appear to have defeated the bullion banks in the gold market, GoldMoney research director Alasdair Macleod tells King World News today.

Presenting a price chart showing gold breaking out of a “pennant formation,” Macleod says: “Pennants are not infallible, but given that the bullion banks were short before the coronavirus shutdowns in the United States and Europe and all central banks’ subsequent promises to accelerate money printing, the fundamentals appear to back a far higher gold price as well.”

Macleod’s comments are posted at KWN here:

https://kingworldnews.com/alasdair-macleod-gold-breaks-out-set-to-attack…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

iii) Other physical stories:

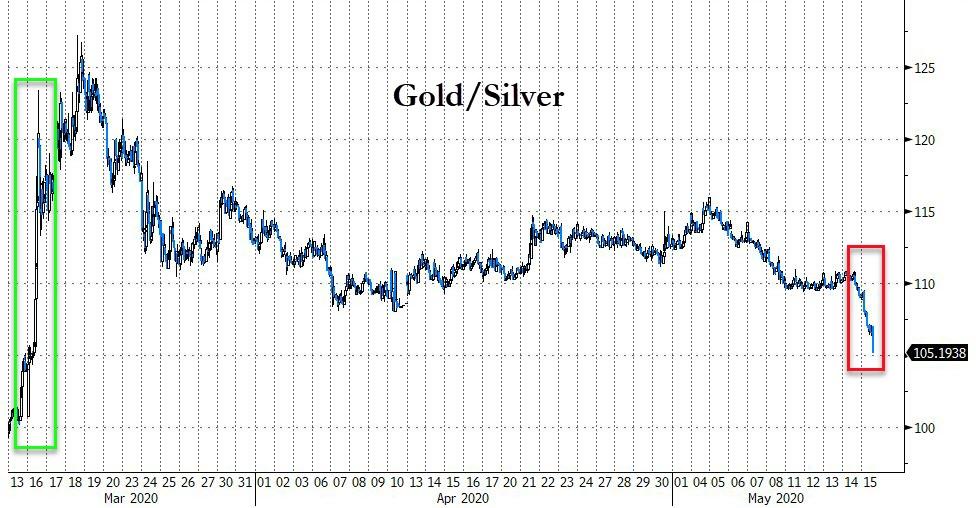

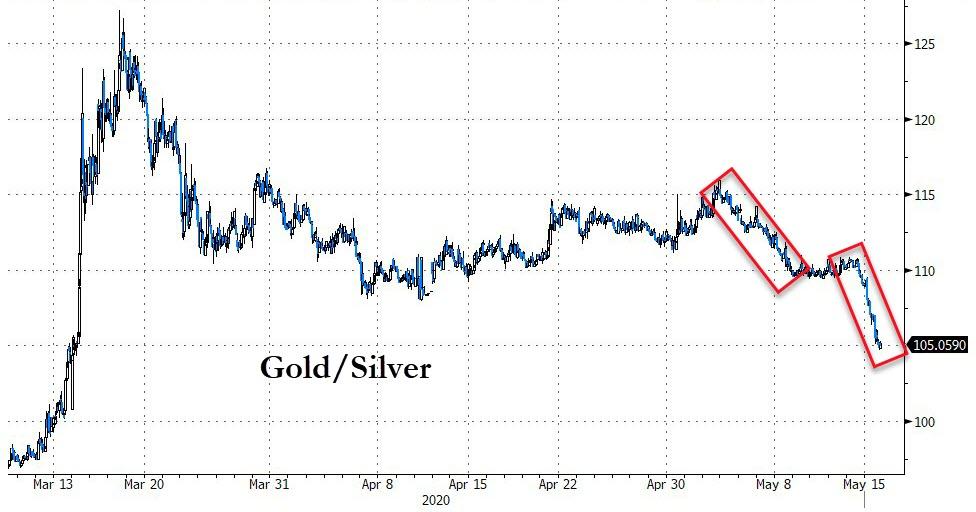

Silver Is Soaring, Gold-Ratio Plunges To 2-Month Lows

Gold and Silver are surging this morning but it is the latter that is dramatically outperforming…

Gold futures are back above $1750…

Gold is at a record high against the yuan this morning (after yuan weakness on trade tensions)…

Silver futures tagged $17…

The gold/silver ratio is tanking dramatically, back at 2-month lows

But has a long way to go…

As Simon Black recently noted, this ratio may stay elevated for a while, or even go higher, but in the past, the ratio has always returned to more traditional levels. Always. Even when the world was facing Adolf Hitler or the Great Depression.

So it stands to reason that, if they keep printing money (which they already are), and the ratio eventually returns to its historical range, the price of silver could really skyrocket.

end

https://www.jsmineset.com/2020/05/15/mr-resolute-keeps-mucking-up-comexs-au-ag-stalls/

Mr. Resolute Keeps Mucking Up Comex’s Au/Ag Stalls

Posted May 15th, 2020 at 9:37 AM (CST) by J. Johnson & filed under General Editorial.

Great and Wonderful Friday Morning Folks,

We start our early morning report with Gold and its confusions, with the June contract down 40 cents at $1,740.50 after reaching up to $1,748.90 with the low at $1,736.80. Today, finally, Silver is leading with the trade up 40.9 cents at $16.565 after hitting $16.705 with the low at $16.155. Par still surrounds the US Dollar, no matter how much is printed. How long this will last, is up to some Algo with the trade at 100.39, down 11.7 points after hitting a low at 100.195 with the high nearby at 100.420. Of course, all this happened already, after 2.2 trillion was created out of thin air, before 5 am pst, the Comex open, the London close, and after China’s bank HSBC taps the BOE for its GLD Bars.

Gold under the Venezuelan Bolivar is now valued at 17,383.24 showing an increase of 193.75 Bolivar with Silver gaining 8.24 with the price now at 165.443 Bolivar. Argentina’s Currency has Gold’s value pegged at 117,608.46 giving our noble metal a 1,436.10 A-Peso gain with Silver showing a 57.33 A-Peso pop with the trade now at 1,119.44. Gold’s value under the Turkish Lira is now at 12,038.72 showing an increase of 49.74 Lira’s with Silver proving a gain of 4.926 T-Lira’s with its price at 114.556.

May Silver Deliveries now has a Demand Count of 378 up on the board with a Volume of 23 so far today inside a trading range between $16.59 and $16.505 with the last trade at the low (what else is new for London?) up 36.9 cents. This proves an increase of 3 – 5,000-ounce contracts above yesterday’s tally which had a total Volume of 49 “swapping” contracts within a trading range between $16.12 and $16.005 with the last trade at the high with the adjusted close above that at $16.135 proving the demand had more action than the centrals could handle. The fear is showing up in the numbers behind the price again with Silver’s Overall Open Interest at 141,302 Overnighters. An increase of 4,718 paper shorts in order to keep Silver from doing more damage to the short traders’ accounts. Also, of note is the closing prices for the 2 front months in Silver suggesting a shortage of product in the eyes of us “old school traders” with May’s close at $16.136, with June’s close at $16.115, giving the delivery month a 2.1 penny premium in an Algo Controlled world. Let’s see how this unfolds.

May Gold’s Demand Count now sits at 1,573 fully paid for contracts with an early morning trading range between $1,745.10 and $1,739.70 with the last trade at $1,742.30 and with a Volume of 591 already up on the board today. Yesterday’s final trading range inside the delivery month was between $1,743.10 and $1,720.50 with the last trade at $1,736.50 with the adjusted close at $1,738.10 ending with a Volume of 672. The Demand Count from yesterday to today increase by 478 – 100-ounce contracts for that barbarous relic that the centrals kept telling everyone is worthless. Gold’s Overall Open Interest is now at 520,235 Overnighters, proving an increase of 4,779 short contracts being added or else the price would have gone much higher.

Whoever Mr. Resolute is (or how many there are), he keeps coming in and mucking up the Comex Stalls in both metals at a time when many mining facilities remain shuttered and for over 1 ½ months’ time. Our southern neighbor’s central bank, BOM cut rates ½% yesterday, as they too are having financial issues and are suffering from the CCP19 virus as this article claims 30 crematoriums across Mexico City are at full capacity. The truth about this airborne topic still needs honest vetting yet the media continues to be everyone’s enemy no matter where one turns. Who are they supporting after all?

The events of the week have been supportive for the precious metals. Gold is still, not that far away from making new life of contract highs and Silver seems to be ready to catch up. Reminder; Silver has yet to reach the 1980 high which Gold blew thru like a hot knife thru a bar of butter way back in 2011. So, we wait, with physicals in our hands and positive thoughts in the head, with a smile on our faces because, the controllers seem to be losing it. Have a great weekend, and keep the faith. With that we will always …

Stay Strong!

Jeremiah Johnson

end

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

March 4.2019

Parker City News

JP Morgan faces potential class action lawsuit after guilty pleas by a former metals trader

Traders from across the U.S. are banding together to accuse J. P. Morgan Chase of manipulating precious metals markets for years.

At least six lawsuits, all making similar allegations against the nation‘s largest bank, have been filed in New York federal court in the past month, since federal prosecutors in Connecticut with a former J. P. Morgan Chase metals trader.

The cases could potentially include thousands of people who traded in the precious metals market. The White Plains, N.Y., law firm Lowey Dannenberg is asking the court to combine the cases and name it as the lead.

The law firm‘s commodities group is led by Vincent Briganti, the attorney who filed the first lawsuit on behalf of Dominick Cognata, a New York resident who alleges he suffered losses due to J. P. Morgan‘s trading conduct in the silver and gold futures and options markets.

A combined case, seeking class action status, would include anyone who purchased or sold futures contracts or an option on NYMEX platinum or palladium or COMEX silver or gold between at least Jan. 1, 2009, and Dec. 31, 2015. The lawyers believe that “at least hundreds, if not thousands” of traders would be eligible to join the case.

Named as defendants in all of the lawsuits are John Edmonds, a 36-year old former metals trader at J. P. Morgan, a group of yet-to-be-identified precious metals traders and the bank.

Edmonds, a New York resident, pleaded guilty in October to one count of conspiracy to defraud the market and manipulate prices of precious metals futures contracts and one count of commodities fraud. In the criminal plea, Edmonds admitted that he and other “unnamed co- conspirators” at J. P. Morgan, fraudulently manipulated precious metals markets from 2009 to 2015, the same time frame covered in the class action suits.

Briganti filed the initial class action on Nov. 7, just one day after the Justice Department unsealed Edmonds‘ plea in the U.S. District Court of Connecticut.

Edmonds admitted in his guilty plea that he deployed the illegal trading scheme hundreds of times with the direct knowledge and consent of his immediate supervisors. Plaintiffs say they have suffered economic injury, including monetary losses, as a direct result of actions by Edmonds and the other unnamed J. P. Morgan metals traders in the futures and options contracts.

One of the suits alleges that “the number of unlawful trades that JP Morgan traders executed in precious metals futures markets is at least in the thousands.”

J. P. Morgan declined to comment. Lowey Dannenberg did not respond to a request for comment by CNBC.

The Justice Department‘s criminal investigation is still ongoing and recently caused a separate related civil case to be put on hold for at least six months while the government continues its investigation. That civil lawsuit, which also accuses J. P. Morgan of rigging the precious metals market, was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders.

After reviewing the details of the plea agreement, David Kovel, the attorney for Shak‘s suit, sought to re- interview Edmonds, along with two other current and former senior traders at the bank. However, the government argued that reopening questioning would be detrimental to the ongoing criminal investigation. The federal judge overseeing the proceedings ordered a six-month stay in the civil case.

Kovel declined to comment.

Edmonds was originally scheduled to be sentenced in Hartford, Conn., on Wednesday, Dec. 19, but a court filing on Nov. 27 shows the sentencing has been postponed until June. A spokesman for the U.S. Attorney for Connecticut could not elaborate on why the sentencing was postponed since the court filing is under seal.

-END-

Futures Tumble After US Restarts Trade War With China, Locks Out Huawei; China Vows Retaliation

Well, we did warn you just two days ago that “US-China Relations Are About To Fall Off A Cliff.” Sure enough…

It was shaping up as a nice, quiet rampy end a tumultuous week, when at 630am ET all hell broke loose after Reuters reported that the Commerce Department moved to block shipments of semiconductors to Huawei Technologies from global chipmakers, by amending a foreign direct product rule to “strategically target Huawei’s acquisition of semiconductors that are the direct product of certain U.S. software and technology” in the process “cutting off Huawei’s efforts to undermine U.S. export controls.”

And while the commerce department did extend the temporary general license for Huawei by another 90 days, the US now “anticipates” this will be the final 90-day extension, effectively giving Huawei – and Beijing – a 3 month ultimatum, one which expires just 2 months before the presidential election.

The report, which culminated a week of increasingly acerbic and belligerent war of words, sent the e-mini S&P future sharply lower into negative territory from modestly positive while triggering a flight to safety…

… as countless US chip suppliers suddenly find themselves scrambling to find a new key client, as well as Huawei which will need an army of new suppliers of semiconductors. Today’s news also confirms what we wrote all the way back in Dec 2018, when we explained that in the escalating trade war with China, Beijing has one giant weakness and that the US has all the leverage – if it wants to use it – with its near monopoly on advanced semiconductor production, the lack of which can stop Huawei dead in its tracks.

The rule change is a blow to Huawei, the world’s no. 2 smartphone maker, as well as to Taiwan’s TSMC, a major producer of chips for Huawei’s HiSilicon unit as well as mobile phone rivals Apple and Qualcomm.

Flaring U.S.-China tensions have hung over markets all week, and President Donald Trump said in remarks broadcast Thursday that he doesn’t want to talk to his Chinese counterpart Xi Jinping right now. Stress between the nations is an extra headache for investors as they grapple with the ongoing fallout of the coronavirus.

As if prepared for just this eventuality, mere minutes later China’s Twitter mouthpiece, Global Times Editor in Chief Hu Xijing tweeted that “China will activate the “unreliable entity list”, restrict or investigate US companies such as Qualcomm, Cisco and Apple, and suspend the purchase of Boeing airplanes.”

Hu Xijin 胡锡进

✔@HuXijin_GT

Based on what I know, if the US further blocks key technology supply to Huawei, China will activate the “unreliable entity list”, restrict or investigate US companies such as Qualcomm, Cisco and Apple, and suspend the purchase of Boeing airplanes.

This back and forth, which indicates that a fresh trade war has now broken out, sent futures from comfortably in the green to down almost 1% on the day. It also shook the Yuan out of its recent hypnosis, with the currency tumbling almost 200 pips to 7.13, the lowest level in over a week.

The good news: now we can rally on “hopes” for progress in the trade war as we did every single day of 2019, in addition to “hopes” for a quick reopening from a global pandemic that has cost 40 million US jobs. In short, the world may be in a depression, and one false flag away from trade war turning into kinetic war, but stocks will keep rallying on “optimism.”

Because in this centrally-planned market for idiots, hope is the only strategy.

There was little hope in Europe, where the Stoxx Europe 600 also trimmed its advance on the news, though it remained higher as Italy edged toward allowing free movement and Germany reported a drop in new infections.

Earlier in the session, Asian stocks gained, led by materials and energy, after falling on Thursday and closed well before the latest news rocked the global economy. Markets in the region were mixed, with Australia’s S&P/ASX 200 and Japan’s Topix Index rising, and India’s S&P BSE Sensex Index and Jakarta Composite falling. The Topix gained 0.5%, with Nomura System Corp and LIFULL rising the most. The Shanghai Composite Index was little changed, with Inesa Intelligent Tech advancing and Jingjin Environmental Protection declining the most.

Then there is the coronavirus pandemic: while the likes of Germany are showing some success at containing the virus, other countries that had quelled the pandemic such as South Korea and China are seeing a rise in cases, underscoring the tough choices policy makers face as they try to resuscitate their economies. Hopes over the rate of infection and a potential compromise on a European recovery fund had helped investors look past data that showed the German economy shrank 2.2% in the first quarter, the most in more than a decade.

In FX, the Bloomberg Dollar Spot index and Treasuries traded in tight ranges Friday, with the former heading for this month’s first weekly gain. The greenback traded mixed versus Group-of-10 peers, before bursting higher following the Huawei news. The euro was steady, after briefly slipping below 1.08 per dollar; Australia’s dollar recovered from a loss that followed after a raft of mixed Chinese data highlighted the challenges confronting the world’s second-largest economy as it seeks to recover from the pandemic.

In commodities, Crude headed for a third weekly gain amid signs the oil market is slowly rebalancing.

Market Snapshot

- S&P 500 futures down 0.9% to 2,819

- STOXX Europe 600 up 1% to 330.06

- MXAP up 0.3% to 144.97

- MXAPJ up 0.2% to 466.60

- Nikkei up 0.6% to 20,037.47

- Topix up 0.5% to 1,453.77

- Hang Seng Index down 0.1% to 23,797.47

- Shanghai Composite down 0.07% to 2,868.46

- Sensex down 0.5% to 30,967.95

- Australia S&P/ASX 200 up 1.4% to 5,404.81

- Kospi up 0.1% to 1,927.28

- German 10Y yield unchanged at -0.543%

- Euro up 0.09% to $1.0815

- Italian 10Y yield rose 1.5 bps to 1.643%

- Spanish 10Y yield fell 0.7 bps to 0.74%

- Brent futures up 2.4% to $31.87/bbl

- Gold spot up 0.4% to $1,736.66

- U.S. Dollar Index down 0.2% to 100.22

Top Overnight News from Bloomberg

- Sweden’s central bank just hired consultants from BlackRock to help it buy the corporate bonds at the center of a legal dispute with the country’s parliament

- The German economy shrank 2.2% in the first quarter, the most in more than a decade, offering an early flavor of the damage from the coronavirus outbreak

- Italy will allow citizens to move freely between its 20 regions starting June 3, according to a draft decree seen by Bloomberg, as Prime Minister Giuseppe Conte’s government opens up the country after more than two months of a stringent lockdown

- China said it did not know until Jan. 19 how infectious the new coronavirus is, pushing back against accusations that it intentionally withheld

- China’s industrial output increased in April for the first time since the virus outbreak, while retail sales slid more than projected information about the severity of the outbreak in Wuhan from the world

- China has a total of five possible vaccines for the coronavirus already in human trials and more will be approved next month, signaling the Asian nation’s rapid progress in the race for immunization

- Bank of America sold a $1 billion bond to fund Covid-19 relief efforts, marking the first issuance from a U.S. financial institution that explicitly earmarks all proceeds to tackle the pandemic

- Britain and the European Union’s talks about their future relationship are stumbling toward the brink, with few signs of progress being made ahead of a key deadline next month

- French Finance Minister Bruno Le Maire pledged government- support measures for the car and aviation industries by the end of June, including incentives to buy electric vehicles

Asian equity markets initially traded indecisively before moving into broadly positive territory; Wall St saw a financial-led session of gains. The APAC session saw mixed Chinese data in which Industrial Production topped estimates but Retail Sales disappointed with a larger than expected contraction. ASX 200 (+1.4%) was buoyed by strength in mining names and with financials cheering the outperformance of their Wall St peers, while Nikkei 225 (+0.6%) initially outperformed due to confirmation the government will lift the State of Emergency in 39 prefectures although the gains were briefly wiped out considering that Tokyo was not included in those areas and with the index oscillating around the 20K level. Hang Seng (-0.1%) and Shanghai Comp. (U/C) were choppy due to the mixed data releases and following the PBoC’s tepid actions whereby it announced a CNY 100bln Medium-term Lending Facility which was half of what had expired yesterday and kept the rate unchanged at 2.95%, but noted that the second phase of its previously announced RRR cuts took effect from today and would release about CNY 200bln of long-term liquidity. Finally, 10yr JGBs were higher but with the gains only marginal amid the indecisive overnight risk tone and with the BoJ also present in the market for relatively reserved JPY 80bln in up to 1yr JGBs, as well as JPY 370bln in the belly.

Top Asian News

- China’s Industrial Economy Improves While Consumers Remain Wary

- MUFG Sees Smaller-Than-Expected Profit Growth on Bad-Loan Costs

- SoftBank Has Spent $2.3 Billion to Buy Own Shares Since March

- Bidders Are Lining Up to Buy Virgin Australia After Collapse

European stocks initially held onto gains [Euro Stoxx 50 +0.6%], having missed out yesterday’s post-Europe rally. However, reports that the US is moving to block Huawei from acquiring US integrated semiconductors and chip sets pressured sentiment and stock markets. Spain’s IBEX (-0.5%) is the region’s underperformer amid steep losses in its Financial names – broad-based upside is seen across the rest of the region. Sectors are all in the green with Energy relinquishing its top spot to later underperform; sector breakdown sees Basic Resources and Autos outperforming while Banks reside alongside Construction & Materials. In terms of individual movers, BT (+4.9%) rose as much as 10% at the open amid source reports via the FT that the Co. is in talks to sell a “multibillion-pound stake” in its GBP 20bln Openreach unit to infrastructure investors, adding that talks were reportedly held with Macquarie. However, an internal memo pushed back against this speculator, thus shares trimmed some gains. Elsewhere, Richemont (-2.6%) shares lag the market amid a slew of downbeat YY metrics in which FY20 adj net, operating profit, diluted EPS and net cash position eroded. William Hill (+6.6%) trades higher after announcing that cash burn reduced to around GBP 15mln per month and liquidity in excess of EUR 700mln. The group also said revolving credit facility covenants waived for 2020 and reset for 2021.

Top European News

- Germany Enters Historic Recession With Biggest Slump in a Decade

- Riksbank Hires BlackRock to Help Pave Way for Corporate Bond QE

- BT Insider Buying Brings Skepticism to Deal Talks, Say Analysts

- Pandora Gains After Carnegie Increases Price Target by 42%

In FX, notwithstanding an element of Friday fatigue and cautious trade ahead of potentially market-moving US data in the form of retail sales and ip ahead of preliminary Michigan sentiment, the Yen and Dollar look tightly bound above 107.00 amidst a recovery in broad sentiment and particularly large expiries rolling off at the NY cut, with over 2 bn at the figure and 107.50 keeping Usd/Jpy contained. Moreover, the remaining Greenback/G10 pairings are also sticking to relatively tight lines awaiting more decisive direction following choppy and erratic price action so far this week, as the DXY consolidates just off yesterday’s new mtd high (100.56) within a 100.390-160 range.

- EUR/AUD/CAD/CHF – As noted above, not much deviation or adverse reaction to Eurozone GDP data that was remarkably close to consensus and largely ignored on the basis that the current quarter will be more telling in terms of gauging COVID-19 contagion. Indeed, after Germany’s 2.2% q/q contraction the Economy Ministry noted no improvement in April vs tangible evidence of recovery from this month, but still predicts a 10% fall overall in Q2. However, the single currency is clinging to 1.0800 vs the Buck following Thursday’s foray below the round number that almost tripped stops at 1.0775. Meanwhile, the Aussie, Loonie and Franc are all meandering between narrow bands against their US counterpart around 0.6460, 1.4045 and 0.9725 respectively, with the former not gleaning much from mixed Chinese data overnight, but the Cad cushioned by firm crude prices and the Chf still wary about ongoing official intervention given further retracement from recent peaks against the Eur to fresh multi-year highs less than 10 pips from 1.0500.

- GBP/SEK/NOK/NZD – Cable remains on the cusp of steeper declines unless 1.2200 continues to provide psychological support or the Pound survives another test of 1.2166 from a technical perspective awaiting updates on this week’s last session of UK-EU trade negotiations. Conversely, the Swedish and Norwegian Kronas appear to have run in to some resistance in Euro cross terms ahead of 10.5800 and 10.9500 respectively, but both retain upward thrust towards the upper bounds of 10.7100-10.5600 and 11.1855-10.9250 extremes on the week so far, in contrast to the Kiwi that is languishing under 0.6000 vs its US peer and not far from 1.0800 against the Aussie in wake of clear NIRP inferences from the RBNZ.

- EM – Most regional currencies are going through the motions, but the Lira has now touched 6.9000 as its resurgence gathers more steam and the Mexican Peso is taking the Banxico’s latest 50 bp ease in stride. However, the Czech Koruna has been hit by comments from CNB Governor Runok playing down the prospect of implementing an FX regime and resorting to negative rates following mixed Q1 GDP reads vs forecasts, albeit q/q and y/y contractions vs better than expected Hungarian, Polish and Romanian prints.

In commodities, WTI and Brent front-month continue to grind higher amid rosier demand and storage prospects alongside a more bullish supply backdrop. Furthermore, the IEA’s more optimistic comments regarding the demand slump not being as steep as feared underpin the complex. That being said, desks note that despite the above, the market remains in surplus, but the magnitude of inventory builds has declined vs. April levels – resulting in strengthening time spreads and narrower contango – suggesting that market improving fundamentals. “we still believe that in the near-term, the upside is limited given that we are still in a surplus environment and as there is plenty of inventory for the market to digest.” ING writes. WTI June hovers around USD 28.00/bbl having printed a base at USD 27.24/bbl, whilst Brent July dipped just below 32/bbl in a USD 30.84-32.50/bbl intraday band. For reference, OPEC Secretary General Barkindo will be appearing on Bloomberg TV at 1500BST. Meanwhile, spot gold tracks Dollar action and gains further ground above 1700/oz – eyeing potential resistance at USD 1738.50/oz (April 23rd high), having traded in a USD 1729-38/oz band thus far. Copper prices move higher in tandem with the broader risk sentiment, but prices remain contained within recent ranges.

US Event Calendar

- 8:30am: Retail Sales Advance MoM, est. -12.0%, prior -8.7%

- Retail Sales Control Group, est. -4.95%, prior 1.7%

- Retail Sales Ex Auto MoM, est. -8.5%, prior -4.5%

- 8:30am: Empire Manufacturing, est. -60, prior -78.2

- 9:15am: Industrial Production MoM, est. -12.0%, prior -5.4%

- 9:45am: Bloomberg May United States Economic Survey

- 10am: Business Inventories, est. -0.2%, prior -0.4%

- 10am: JOLTS Job Openings, est. 5,800, prior 6,882

- 10am: U. of Mich. Sentiment, est. 68, prior 71.8; Current Conditions, est. 62.8, prior 74.3; Expectations, est. 60.2, prior 70.1

- 4pm: Net Long-term TIC Flows, prior $49.4b

DB’s Jim Reid concludes the overnight wrap

If you promise not to tell anyone I’ll let you into a little secret. I logged off the earliest I have done in 8 weeks last night and went to play golf in what was a beautifully sunny evening. My first game since early March after courses reopened Wednesday. Right from the outset I ensured I was social distancing by driving it onto the third green instead of the first fairway. Thankfully it got better but I’m a bit surprised how shattered I am after a couple of months of not walking round with my clubs.

It’s also amazing how sentiment can turn after a few hours on the golf course. When the S&P 500 continued a tough week by being down -1.9%, 30 minutes into the US session, it was hard not to wonder whether the market was finally having its Wile E. Coyote moment and responding to gravity after successfully running off the edge of the cliff a few weeks back and somehow staying airborne. However the market’s weightlessness returned and an impressive snap back materialised with the S&P 500 closing +1.15% – over 3% up from the lows with Banks (4.10%) leading the charge.

For the majority of the day Technology stocks were down, but the late rally lifted all boats and 21 out of 24 S&P 500 industry groups finished in the green. Since the first historic spike of initial jobs claims on 19 March, 7 out of the 9 Thursdays have seen the S&P rally in the face of massive unemployment numbers. Energy stocks – one of the other laggards YTD with Banks – rallied as well on the back of a large rise in oil prices, with the sector up +0.94% – still lagging the overall index.

As mentioned above, oil had a strong day, with WTI (+8.98%) and Brent (+6.65%) both moving consistently higher throughout the day. The moves came as the International Energy Agency said in their monthly Oil Market Report that they were increasing their estimate of global oil demand in Q2 by +3.2m b/d, though this remained well below last year’s number by 19.9m b/d. Furthermore, they said that global oil supply would fall to a 9-year low in May, thanks to the OPEC+ agreement and other production declines. Saudi Aramco also cut sales to US and Europe by roughly 50%, more than they have cut to Asia already, in an effort to further reduce the overall global oversupply. DB’s Michael Hsueh’s turned bullish on oil yesterday as demand is recovering quicker than anticipated and supply cuts are holding better too. See his brief note here for more.

Overnight, China has released a mixed bag of April activity data. Industrial production surprised to the upside, printing at +3.9% yoy (vs. +1.5% yoy expected and -1.1% yoy last month) however retail sales were -7.5% yoy (vs. -6.0% yoy expected and -15.8% yoy last month). Fixed asset investment data was closer to expectations at -10.3% yoy (vs. -10% yoy expected and -16.1% yoy in YtD March) while the surveyed urban jobless rate came in at 6.0% (vs. 5.9% last month). The NBS noted that the Chinese economy “hasn’t returned to normal level,” and that there are “pent-up demand effects” in the data improvement.

Following that, markets in Asia have eked out small gains this morning with the Nikkei (+0.11%), Hang Seng (+0.40%), Shanghai Comp (+0.18%) and Kospi (+0.14%) all up. Meanwhile, futures on the S&P 500 are down -0.08% while WTI oil prices are up +0.76% to $27.77 as we type.

In other overnight news, Mexico’s central bank lowered rates by 50bps to 5.5% as expected. The central bank board stated in the communique that accompanies its decision that it saw an economic slump deepening in the second quarter, along with a significant contraction in employment.

Back to yesterday where the late US rally was in the face of more worrying news flow yesterday. Starting with the politics, concerns over another escalation in the China-US trade war were sparked by a Fox Business Network interview with President Trump, who said in reference to Chinese president Xi that “right now, I don’t want to speak to him. I don’t want to speak to him.” Furthermore, he added that “we could cut off the whole relationship. If we did, what would happen? You’d save $500 billion”. So certainly not comments that bode well for the prospects of global trade once the coronavirus has passed. And when it came to the coronavirus, Trump described himself as “very disappointed” in Beijing’s failure to prevent the virus at the start. Meanwhile, the US Senate passed a legislation yesterday that would pave the way for targeted sanctions against government officials in China over alleged human rights abuses against Muslim ethnic minority groups in the country’s northwest. The legislation directs the White House to submit a report to Congress within 180 days identifying those deemed responsible for torture, extrajudicial detention, forced disappearance and other “flagrant denial(s)” of human rights in China’s Xinjiang Uygur Autonomous Region.

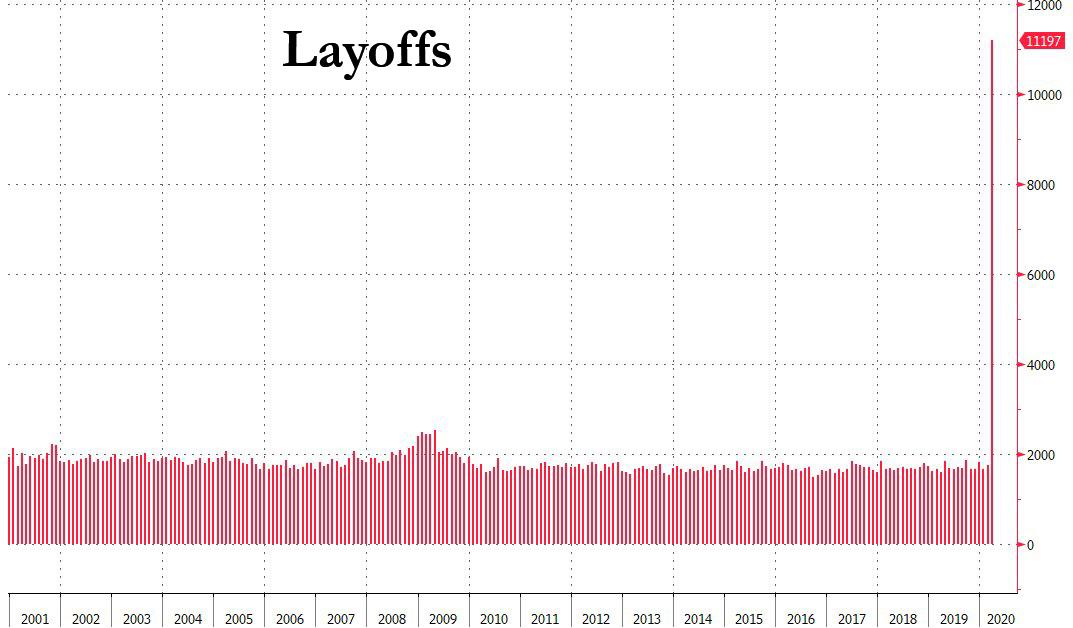

The jitters were then further exacerbated after the weekly US initial jobless claims were released. They showed that 2.981m made claims in the week through May 9. That was well above the 2.5m reading expected, and was the smallest weekly decline (-195k) since the peak back in late March, raising fears that the scale of the ongoing job losses aren’t easing as fast as investors had been hoping for, particularly given the equity rally we’ve seen in recent weeks. However, Connecticut said later in the day that it incorrectly reported unemployment claims at 298,680, about 10 times higher than the correct number of 29,846 due to a “data entry reporting error” which likely inflated the initial claims number. Any revisions will be reflected in the next release on May 21. The one consolation with yesterday’s data was that continuing claims, which covered the previous week up to May 2, came in at 22.833m (vs. 25.120m expected), with the insured unemployment rate up “just” 0.3 percentage points to 15.7%.

Before the late US rally these negative stories set the tone and Europe closed weak with the Stoxx 600 falling -2.17%. Even with the eventual rally in US stocks and oil, investors still sought out safe havens, with gold climbing +0.82% to reach a new 7-year high. Indeed, the turmoil this year has meant that gold is one of the top-performing global assets, with a YTD return of +14.04%. US Treasuries also rallied, with 10yr yields down -3.1bps to 0.622%. In Europe, peripheral spreads over bunds widened however, with those on both Italian (+2.8bps) and Spanish (+2.5bps) ten-year debt paring back yesterday’s moves tighter.

The global negative rates chatter continued yesterday, though once again it was generally denied. Bank of England Governor Bailey said that negative rates were “not something we are currently planning or contemplating”, though he did also add that it’s “always wise not to rule anything out forever”. Meanwhile St. Louis Fed Bullard added to Chair Powell’s remarks the previous day, saying that the Fed wasn’t considering negative interest rates. And over in Japan, Governor Kuroda said that he didn’t think it was necessary for the BoJ to cut the policy rate further.

Finally, the latest round of Brexit negotiations between the UK and the EU on their future relationship will wrap up today. That leaves just one more round at the start of June before a key high level meeting takes place later next month. Yesterday, we heard from Prime Minister Johnson’s spokesman that the UK’s chief negotiator, David Frost, told the cabinet that the EU had “asked far more from the UK than they have from other sovereign countries with whom they have reached free trade agreements”. One of the key points of contention between the two sides have been EU demands that the UK sign up to a so-called level-playing field, where the UK will commit not to undercut the EU on areas such as workers’ rights or environmental standards. We should hear more on the latest round from the EU’s chief negotiator, Michel Barnier, in a press conference later today.

To the day ahead now, and the data highlights from Europe include the first look at German GDP in Q1, as well as the second estimate of Q1’s Euro Area GDP. Alongside that, from the US we’ll get retail sales, industrial production and capacity utilisation for April, along with May’s Empire State manufacturing survey and the preliminary University of Michigan sentiment indicator.

3A/ASIAN AFFAIRS

i)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED DOWN 1.88 POINTS OR 0.07% //Hang Sang CLOSED DOWN 32.27 POINTS OR 0.14% /The Nikkei closed UP 122.69 POINTS OR 0.62%//Australia’s all ordinaires CLOSED UP 1.38%

/Chinese yuan (ONSHORE) closed DOWN at 7.1067 /Oil UP TO 28,16 dollars per barrel for WTI and 31.72 for Brent. Stocks in Europe OPENED MOSTLY GREEN// ONSHORE YUAN CLOSED DOWN // LAST AT 7.1067 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 7.1314 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3 a./NORTH KOREA/ SOUTH KOREA

South Korea

b) REPORT ON JAPAN

CORONAVIRUS UPDATE/JAPAN/AUSTRALIA/USA..

Japan Lifts Emergency Order, Australia Reopens Pubs & Georgia, Texas Vindicated As China Suppresses 2nd Wave: Live Updates

Summary:

- Surge in new cases, deaths fails to materialize in Georgia

- Australia reopens pubs this weekend

- Spain imposes 14 day quarantine order on foreigners

- China reports no new deaths for a month

- Japan lifts ‘state of emergency’ for most prefectures

- NY’s “unPAUSE” begins

*. *. *