GOLD:$1735.25 UP $13.05 The quote is London spot price

Silver:$17.23 UP 22 CENTS (London spot closing price

COMEX OPTIONS EXPIRY TUESDAY MAY 26

OTC/LBMA OPTIONS EXPIRY FRIDAY MAY 29

The reason for the raid today is the comex expiry this coming Tuesday.

Expect gold/silver to be subdued in price until after first day notice.

Closing access prices: London spot

i)Gold : $1736.50 LONDON SPOT 4:30 pm

ii)SILVER: $17.23//LONDON SPOT 4:30 pm

CLOSING FUTURES PRICES: KEY MONTHS

MAY COMEX GOLD: XXX

JUNE GOLD: $1736.25 CLOSE 1.30 PM// SPREAD SPOT (LONDON) VS/FUTURE JUNE: $0.//PREMIUMS WENT UP AGAIN

CLOSING SILVER FUTURE MONTH

JULY: 1:30 PM: $17.65//1:30 PM //SPREAD SPOT LONDON VS FUTURE JULY: 42 CENTS PER OZ//

the gold market continues to be broken as future prices are much higher than spot prices. The comex is desperate to fix things but they have no available gold.

If one is to buy gold and or gold coins, the price is around $2800. usa per oz

and silver; $31.00 per oz//

LADIES AND GENTLEMEN: YOU ARE NOW WITNESSING FIRST HAND THE DIFFERENCE BETWEEN PAPER GOLD/SILVER AND THE REAL PHYSICAL STUFF!!

DO NOT PAY ANY ATTENTION TO WHAT THE CROOKS ARE DOING AT THE COMEX AND LONDON LBMA..PHYSICAL IS THE NAME OF THE GAME AND NOTHING ELSE

COMEX DATA

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING: 34/440

EXCHANGE: COMEX

CONTRACT: MAY 2020 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,720.500000000 USD

INTENT DATE: 05/21/2020 DELIVERY DATE: 05/26/2020

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

072 C GOLDMAN 2

118 H MACQUARIE FUT 214

132 C SG AMERICAS 2

323 H HSBC 3

355 C CREDIT SUISSE 1

657 C MORGAN STANLEY 12 32

661 C JP MORGAN 34

685 C RJ OBRIEN 2

686 C INTL FCSTONE 6

690 C ABN AMRO 385 127

732 C RBC CAP MARKETS 1

737 C ADVANTAGE 30 13

800 C MAREX SPEC 7

878 C PHILLIP CAPITAL 3

905 C ADM 6

____________________________________________________________________________________________

TOTAL: 440 440

MONTH TO DATE: 10,262

NUMBER OF NOTICES FILED TODAY FOR MAY CONTRACT: 440 NOTICE(S) FOR 44,000 OZ (1.368 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 10262 NOTICES FOR 1026200 OZ (31.912 TONNES)

SILVER

FOR MAY

0 NOTICE(S) FILED TODAY FOR nil OZ/

total number of notices filed so far this month: 8910 for 44,550,000 oz

BITCOIN MORNING QUOTE $9157 UP 91

BITCOIN AFTERNOON QUOTE.: $9169 UP 103

GLD AND SLV INVENTORIES:

WITH GOLD UP $13.05 AND NO PHYSICAL TO BE FOUND ANYWHERE:

WITH ALL REFINERS CLOSED//MEXICO ORDERING ALL MINES SHUT: WHERE ARE THEY GETTING THE “PHYSICAL”?

A HUGE CHANGE IN GOLD INVENTORY AT THE GLD:

A DEPOSIT OF 3.93 TONNES OF GOLD INTO THE GLD///

GLD: 1,116.71 TONNES OF GOLD//

WITH SILVER UP 22 CENTS TODAY: AND WITH NO SILVER AROUND

A HUGE CHANGE IN SILVER INVENTORY AT THE SLV/// A WITHDRAWAL OF 1.864 MILLION OZ FROM THE SLV/

RESTING SLV INVENTORY TONIGHT:

SLV: 455.817 MILLION OZ./

XXXXXXXXXXXXXXXXXXXXXXXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI ROSE BY A SMALL SIZED 231 CONTRACTS FROM 151,890 UP TO 155,485 AND CLOSER TO OUR NEW RECORD OF 244,710, (FEB 25/2020. THE SMALL SIZED GAIN IN OI OCCURRED DESPITE OUR VERY LARGE 50 CENT GAIN IN SILVER PRICING AT THE COMEX. IT SEEMS THAT THE GAIN IN COMEX OI IS DUE TO STRONG BANKER SHORT COVERING PLUS A STRONG EXCHANGE FOR PHYSICAL ISSUANCE, ZERO LONG LIQUIDATION, ACCOMPANYING A SMALL DECREASE IN SILVER OZ STANDING AT THE COMEX FOR MAY. WE HAD A NET GAIN IN OUR TWO EXCHANGES OF 1660 CONTRACTS (SEE CALCULATIONS BELOW).

WE HAVE ALSO WITNESSED A HUMONGOUS AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: MAY: 0 AND JULY: 1120 AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 1120 CONTRACTS. WITH THE TRANSFER OF 1120 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1120 EFP CONTRACTS TRANSLATES INTO 5.60 MILLION OZ ACCOMPANYING:

1.THE 50 CENT LOSS IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

10.025 MILLION OZ INITIAL STANDING IN AUGUST.

43.030 MILLION OZ INITIALLY STANDING IN SEPT. (HUGE)

7.32 MILLION OZ INITIALLY STANDING IN OCT

2.630 MILLION OZ STANDING FOR NOV.

20.970 MILLION OZ FINAL STANDING IN DEC

5.075 MILLION OZ FINAL STANDING IN JAN

1.480 MILLION OZ FINAL STANDING IN FEB

23.005 MILLION OZ FINAL STANDING FOR MAR

4.660 MILLION OZ FINAL STANDING FOR APRIL

45.290 MILLION OZ INITIALLY STANDING FOR MAY

THURSDAY, AGAIN OUR CROOKS USED COPIOUS PAPER IN ORDER TO LIQUIDATE SILVER’S PRICE…AND THEY WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL 50 CENTS).. AND, OUR OFFICIAL SECTOR/BANKERS WERE UNSUCCESSFUL IN THEIR ATTEMPT TO FLEECE ANY AMOUNT OF SILVER LONGS FROM THEIR POSITIONS. THE SMALL GAIN AT THE COMEX WAS ACCOMPANIED BY : i) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS 2) A SMALL LOSS IN SILVER OZ STANDING FOR MAY,3) CONSIDERABLE BANKER SHORT COVERING AND 4) ZERO LONG LIQUIDATION AS WE DID HAVE A NET GAIN OF 1351 CONTRACTS OR 6.755 MILLION OZ ON THE TWO EXCHANGES! YOU CAN BET THE FARM THAT OUR BANKER ARE DESPERATE TO LIQUIDATE THEIR HUGE SHORT POSITIONS IN SILVER

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY /FOR MONTH OF MAY:

12,028 CONTRACTS (FOR 16 TRADING DAYS TOTAL 12,028 CONTRACTS) OR 60.140 MILLION OZ: (AVERAGE PER DAY: 751 CONTRACTS OR 3.758 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF MAY: 60.14 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 8.59% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2020 TO DATE SILVER EFP’S: 1,048.98 MILLION OZ.

JANUARY 2020 EFP TOTALS SO FAR: 181.61 MILLION OZ

FEB 2020 EFP’S TOTAL : …… 259.600 MILLION OZ

MARCH EFP’S ….. 452.280 MILLION OZ //TOTALS//AND A NEW RECORD FOR THE MONTH)

APRIL EFP 95.355 MILLION OZ. (EX. FOR PHYSICALS BECOMING A LOT LESS)

MAY EFP SO FAR: 60.14 MILLION OZ

EXCHANGE FOR PHYSICAL ISSUANCE FOR THE PAST 30 DAYS IS A LOT LESS. NO DOUBT THAT THE COST TO CARRY THESE THINGS HAS EXPLODED AND AS SUCH CANNOT BE DONE AS FREQUENTLY AS BEFORE.

RESULT: WE HAD A TINY SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 231, DESPITE OUR CONSIDERABLE 50 CENT LOSS IN SILVER PRICING AT THE COMEX ///THURSDAY… THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 1120 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER

TODAY WE GAINED A STRONG SIZED OI CONTRACTS ON THE TWO EXCHANGES: 1351 CONTRACTS (DESPITE OUR 50 CENT LOSS IN PRICE)

THE TALLY//EXCHANGE FOR PHYSICALS

i.e 1120 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH A SMALL SIZED INCREASE OF 231 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A HUGE 50 CENT LOSS IN PRICE OF SILVER/AND A CLOSING PRICE OF $17.02 // THURSDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY.

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.7050 BILLION OZ TO BE EXACT or 100.7% of annual global silver production (ex Russia & ex China).

FOR THE NEW MAR DELIVERY MONTH/ THEY FILED AT THE COMEX: 0 NOTICE(S) FOR NIL OZ OF SILVER.

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.70//TODAY’S RECORD OF 244,705 IS SET WITH A PRICE OF: 18.91 (FEB 25/2020)

.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ; AUGUST 10.025 MILLION OZ/ SEPT 43.030 MILLION OZ//OCT: 7.665 MILLION OZ// NOV: 2.630 MILLION OZ//DEC: 20.970 MILLION OZ; JAN: 5.075 MILLION OZ.//FEB 1.480 MILLION OZ//MAR: 23.005 MILLION OZ/APRIL 4.660 MILLION OZ//MAY 45.290 MILLION OZ

- THE RECORD PRIOR TO TODAY WAS SET IN FEB 25/2018: 244,710 CONTRACTS, WITH A SILVER PRICE OF $18.90//.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017 RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

GOLD

IN GOLD, THE COMEX OPEN INTEREST FELL BY A SMALL SIZED 2219 CONTRACTS TO 530,794 AND FURTHER FORM OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE SMALL SIZED LOSS OF COMEX OI OCCURRED DESPITE OUR STRONG COMEX LOSS IN PRICE OF $26.40 /// COMEX GOLD TRADING// THURSDAY// WE HAD STRONG BANKER SHORT COVERING , A SMALL SIZED DECREASE IN GOLD OZ STANDING AT THE COMEX, ALONG WITH ZERO LONG LIQUIDATION ACCOMPANYING A HUGE EX. FOR PHYSICAL ISSUANCE. THIS ALL HAPPENED WITH OUR LARGE LOSS IN THE PAPER PRICE OF GOLD.

WE HAD A VOLUME OF 0 4 -GC CONTRACTS//OPEN INTEREST 10

WE GAINED A STRONG SIZED 7539 CONTRACTS (23.45 TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A HUGE SIZED 9758 CONTRACTS:

CONTRACT. MAY: 0, AND JUNE 9082.; AUG 676 AND ALL OTHER MONTHS ZERO//TOTAL: 9758. The NEW COMEX OI for the gold complex rests at 530,794. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 7539 CONTRACTS: 2219 CONTRACTS DECREASED AT THE COMEX AND 9758 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 7539 CONTRACTS OR 23.45 TONNES. THURSDAY, WE HAD A LOSS OF $26.40 IN GOLD TRADING.…..

AND WITH THAT LOSSIN PRICE, WE HAD A VERY STRONG SIZED GAIN IN TOTAL/TWO EXCHANGES GOLD TONNAGE OF 23.45 TONNES!!!!!! THE BANKERS/OFFICIAL SECTOR WEE SUPPLYING INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER WITH RECKLESS ABANDON. THE BANKERS WERE SUCCESSFUL IN THEIR ATTEMPT TO LOWER GOLD’S PRICE (IT FELL $26.40).AND IT ALSO SEEMS THAT THEIR ATTEMPT TO FLEECE ANY GOLD LONGS FROM THE GOLD ARENA WAS UNSUCCESSFUL (SEE BELOW).

4 GC VOLUME: 0 // open interest 10

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES:

WE HAD A HUGE SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (9758) ACCOMPANYING THE SMALL SIZED LOSS IN COMEX OI (2219 OI): TOTAL GAIN IN THE TWO EXCHANGES: 9112 CONTRACTS. WE NO DOUBT HAD 1 )CONSIDERABLE BANKER SHORT COVERING, 2.)A SMALL DECREASE IN OUNCES STANDING AT THE GOLD COMEX FOR THE FRONT MAY MONTH, 3) ZERO LONG LIQUIDATION; 4) SMALL COMEX OI LOSS, AND …ALL OF THIS WAS COUPLED WITH OUR STRONG LOSS IN GOLD PRICE TRADING//THURSDAY

SPREADING OPERATIONS

OUR SPREADING OPERATION HAS NOW SWITCHED INTO GOLD…..

SPREADING OPERATION FOR OUR NEWCOMERS:

WE HAVE NOW COMMENCED IN SILVER THE ILLEGAL SPREADING OPERATION \ FOR NEWCOMERS, HERE ARE THE DETAILS:

SPREADING LIQUIDATION HAS NOW STOPPED IN SILVER AS THEY NOW BEGIN TO MORPH INTO GOLD AS WE HEAD TOWARDS THE NEW FRONT MONTH WILL BE JUNE.

FOR THOSE OF YOU WHO ARE NEW, HERE IS THE MODUS OPERANDI OF THE SPREADERS AND THE CRIMINAL ELEMENT BEHIND IT:

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR;

THE SPREADING LIQUIDATION OPERATION IS NOW OVER FOR SILVER..AND WE WILL NOW MORPH INTO AN ACCUMULATION PHASE OF SPREADING CONTRACTS FOR GOLD. THEY WILL ACCUMULATE CONSIDERABLE AMOUNT OF THE CONTRACTS AND THEN LIQUIDATE ONE WEEK PRIOR TO FIRST DAY NOTICE

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO GOLD AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX SILVER OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE IN THIS NON ACTIVE MONTH OF MAY. BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN GOLD WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JUNE), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2020 INCLUDING TODAY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY : 53,449 CONTRACTS OR 5,344,900 oz OR 166.24 TONNES (15 TRADING DAYS AND THUS AVERAGING: 3563 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 15 TRADING DAY(S) IN TONNES: 166.24 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2019, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 166.24/3550 x 100% TONNES =4.68% OF GLOBAL ANNUAL PRODUCTION

ISSUANCE OF EXCHANGE FOR PHYSICAL GOLD HAS DISSIPATED THIS MONTH…THE COST TO THE BANKERS TO CARRY THESE CONTRACTS IN LONDON IS BECOMING TOO GREAT FOR THEM.

ACCUMULATION OF GOLD EFP’S YEAR 2020 TO DATE: 2732.259 TONNES

JANUARY 2220 TOTAL EFP ISSUANCE; : 570.19 TONNES

FEB 2020 TOTAL EFP ISSUANCE : 653.78 TONNES

MARCH TOTAL EFP ISSUANCE 1,098.93 TONNES (*AND A NEW ALL TIME RECORD ISSUANCE//22 DAYS)

APRIL TOTAL EFP. ISSUANCE: 243.45 TONNES (EFP ISSUANCE BECOMING A LOT LESS)

MAY TOTAL EFP ISSUANCE: 166.24 TONNES (EFP ISSUANCE STILL LOW// PREMIUM COST TO THE BANKERS IS HUGE..SO ISSUANCE IS LESS)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A SMALL SIZED 231 CONTRACTS FROM 155,794 UP TO 155,485 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 2 3/4 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.

ALL OF THE GAIN IN COMEX OI WAS DUE TO 1) CONSIDERABLE BANKER SHORT COVERING , 2) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS (SEE BELOW), 3) A TINY DECREASE IN SILVER OZ STANDING AT THE COMEX FOR MAY AND 4) ZERO LONG LIQUIDATION

EFP ISSUANCE 1120 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

FOR FEB. 0; FOR MAR 0: AND MAY: 0 JULY: 1120 CONTRACTS AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1120 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 231 CONTRACTS TO THE 1120 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A STRONG GAIN OF 1120 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 6.755 MILLION OZ!!! OCCURRED WITH THE 50 CENT GAIN IN PRICE///

RESULT: A STRONG SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE 50 CENT LOSS IN PRICING THAT SILVER UNDERTOOK IN PRICING// THURSDAY. WE ALSO HAD A STRONG SIZED 1120 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

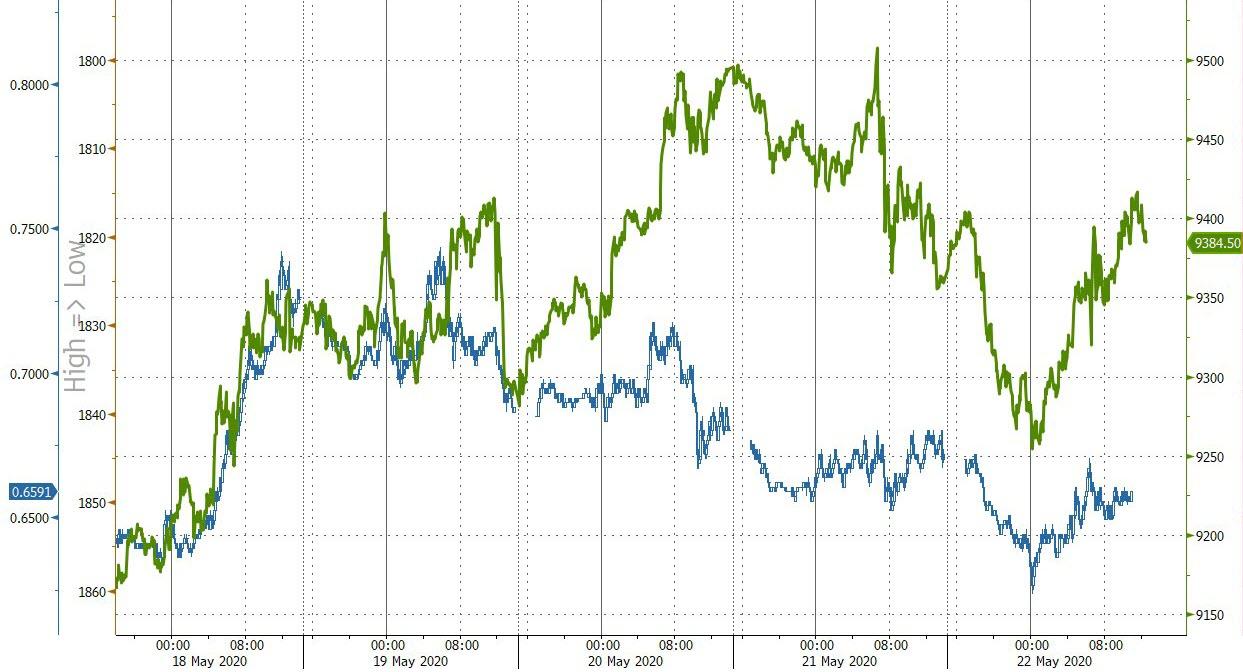

i)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED DOWN 54.16 POINTS OR 1.89% //Hang Sang CLOSED DOWN 1349.89 POINTS OR 5.56% /The Nikkei closed DOWN 164.15 POINTS OR 0.80%//Australia’s all ordinaires CLOSED DOWN .92%

/Chinese yuan (ONSHORE) closed DOWN at 7.1350 /Oil UP TO 32.01 dollars per barrel for WTI and 34.28 for Brent. Stocks in Europe OPENED MIXED// ONSHORE YUAN CLOSED DOWN // LAST AT 7.1350 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 7.1528 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY PAST 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED//CHINA VS HONG KONG// : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

a must must view…

J. Johnson…

https://www.jsmineset.com/2020/05/22/mr-resolute-aint-done-buyn-yet/

Mr. Resolute Ain’t Done Buy’n Yet!

Posted May 22nd, 2020 at 9:04 AM (CST) by J. Johnson & filed under General Editorial.

Great and Wonderful Friday Morning Folks,

They just can’t keep the first currency down like they used to with Gold recovering from yesterday’s dip with the trade at $1,735.50 up $13.60 after reaching $1,742.00 from a low at $1,722.50. Silver is recovering from its usual bigger beating with the trade at $17.47 up 10.6 cents after reaching $17.565 from its low down at $17.19. The US Dollar’s magnet is pulling it towards par with the value pegged at 99.74 up 33.7 points with its high at 99.895 from the low starting point at 99.40. Of course, all this started before 5 am pst, the Comex open, the London close, and after a Philadelphia Judge of Elections was caught stuffing the ballot box, admitting in court he literally was standing in a voting booth and voting over and over, as fast as he could.

The Venezuelan Bolivar now has Gold priced at 17,333.31 showing a loss of 15.98 with Silver losing 2.447 Bolivar with the price at 174.482. Argentina’s price for Gold now sits at 118,094.77 Peso’s as the currencies pull – pushed the price down only 78.39 with Silver at 1,188.19 A-Peso’s showing a drop of 15.38 overnight. The Turkish Lira’s price, close to settling for the week, now sits at 11,811.85 Lira, and increase of 3.21 T-Lira with Silver’s trade at 118.901 down only 1.516 T-Lira.

May Silver Delivery Demands now shows 148 fully paid for contracts waiting for receipts. Reducing yesterday’s count by 10, and with a Volume of 11 up on the board today with a trading range between $17.435 and $17.385 with the last trade at the high, up 10 cents, and with NO way to confirm if any of these 11 “buys” are spread trade entries/exits or “new buys”. Yesterday’s price, for the claimed 8 lot purchase was at $17.335. The daily delivery chart claimed a trade happened at $17.435 yesterday, but it doesn’t show up in their tick chart after I reported yesterday morning’s starting Volume of 2, which went to 4 with no price posted. Silver’s Overall Open Interest gained another round of Call Option Killers as the count reached 155,795 Overnighters proving 434 more shorts stayed in the trade after yesterday’s punch in the gut price drop.

May Gold’s Delivery Demands now total 445 fully paid for contracts waiting for receipts proving a reduction of 83 contracts from yesterday’s trades with today’s starting point trading range between $1,726.70 and $1,726.60 for the 6 Lot Volume already up on the board. Yesterday proves the importance of watching the delivery numbers as Thursday’s Volume reached up to 528 contracts which just so happened to be yesterday’s Open Interest in the delivery month. The Volume Column does not include any of the previous purchases. These are either additional purchases or more entry/exit swaps in deliveries made in a single day. What this may be telling us is Mr. Resolute ain’t done buy’n and soaked up another 52,800 ounces on the dip! That purchase must have puckered up some of the short traders as the Overall Open Interest dropped 342 Obligations leaving the count at 532,367 paper contracts with only 3 days from their Options roll. Maybe it’s nothing to worry about, maybe it is. After all Silver and Gold are very small markets in the eyes of everyone else but the currency manipulators of the world. But when someone steps in and takes away $92,000,000 worth of marbles, they have less marbles (Gold) and more jacks (Debt) to contend with.

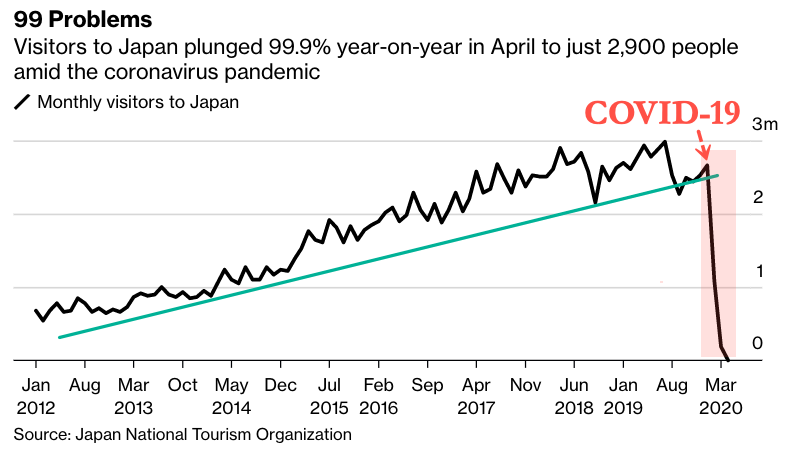

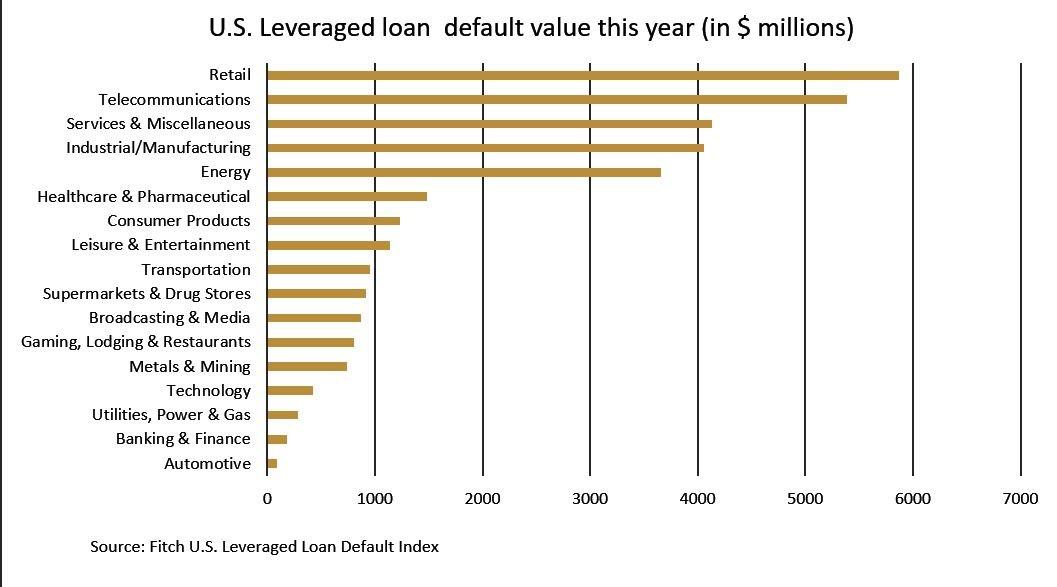

As mentioned here for years, the inability to maintain debt continues to rise and rise (until?) as the virus is now “the blame in the game” as US Commercial Loan defaults, hit a 6 year high. Today’s default news shows a couple of overseas issues with tourism in Japan falling 99.9% in a months’ time with new car sales over in Europe plunging 76% in the same time period, which is also the largest drop ever. These are only a very few examples of the repercussions in the ability to maintain debt payments and staying in business. We expect a sharp increase in these stories, including an epic wave of global bankruptcies, as the world corrects the imbalances in debt, and as the political machine, that seems to have encompassed a few nations politicos, gets fully exposed.

Those that hold the physicals, are not affected by any political news or these highly valued AAA+ rated debt instruments, held by every single central, which are artificially propped up by our ever-so-truthful rating agencies and their positive spin. Back when Jim Sinclair gave the warning, our marbles where placed at Tier 3. Now our marbles are placed as Tier 1 instruments! Since then we simply watch the show, knowing our retirements are in the safety of our own hands and not those that hold more debt than what can be paid. Those that hold debt, are now jacked, with the ratings heading towards Tier 3.

Monday is our Memorial Day. I offer my deepest bow of respect to those that fought, bled, and died before us. If it wasn’t for them, we wouldn’t be here. Have a great and wonderful extended weekend and as always …

Stay Strong!

- Johnson

More J.Johnson content is available with purchase of a JSMineset subscription.

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

March 4.2019

Parker City News

JP Morgan faces potential class action lawsuit after guilty pleas by a former metals trader

Traders from across the U.S. are banding together to accuse J. P. Morgan Chase of manipulating precious metals markets for years.

At least six lawsuits, all making similar allegations against the nation‘s largest bank, have been filed in New York federal court in the past month, since federal prosecutors in Connecticut with a former J. P. Morgan Chase metals trader.

The cases could potentially include thousands of people who traded in the precious metals market. The White Plains, N.Y., law firm Lowey Dannenberg is asking the court to combine the cases and name it as the lead.

The law firm‘s commodities group is led by Vincent Briganti, the attorney who filed the first lawsuit on behalf of Dominick Cognata, a New York resident who alleges he suffered losses due to J. P. Morgan‘s trading conduct in the silver and gold futures and options markets.

A combined case, seeking class action status, would include anyone who purchased or sold futures contracts or an option on NYMEX platinum or palladium or COMEX silver or gold between at least Jan. 1, 2009, and Dec. 31, 2015. The lawyers believe that “at least hundreds, if not thousands” of traders would be eligible to join the case.

Named as defendants in all of the lawsuits are John Edmonds, a 36-year old former metals trader at J. P. Morgan, a group of yet-to-be-identified precious metals traders and the bank.

Edmonds, a New York resident, pleaded guilty in October to one count of conspiracy to defraud the market and manipulate prices of precious metals futures contracts and one count of commodities fraud. In the criminal plea, Edmonds admitted that he and other “unnamed co- conspirators” at J. P. Morgan, fraudulently manipulated precious metals markets from 2009 to 2015, the same time frame covered in the class action suits.

Briganti filed the initial class action on Nov. 7, just one day after the Justice Department unsealed Edmonds‘ plea in the U.S. District Court of Connecticut.

Edmonds admitted in his guilty plea that he deployed the illegal trading scheme hundreds of times with the direct knowledge and consent of his immediate supervisors. Plaintiffs say they have suffered economic injury, including monetary losses, as a direct result of actions by Edmonds and the other unnamed J. P. Morgan metals traders in the futures and options contracts.

One of the suits alleges that “the number of unlawful trades that JP Morgan traders executed in precious metals futures markets is at least in the thousands.”

J. P. Morgan declined to comment. Lowey Dannenberg did not respond to a request for comment by CNBC.

The Justice Department‘s criminal investigation is still ongoing and recently caused a separate related civil case to be put on hold for at least six months while the government continues its investigation. That civil lawsuit, which also accuses J. P. Morgan of rigging the precious metals market, was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders.

After reviewing the details of the plea agreement, David Kovel, the attorney for Shak‘s suit, sought to re- interview Edmonds, along with two other current and former senior traders at the bank. However, the government argued that reopening questioning would be detrimental to the ongoing criminal investigation. The federal judge overseeing the proceedings ordered a six-month stay in the civil case.

Kovel declined to comment.

Edmonds was originally scheduled to be sentenced in Hartford, Conn., on Wednesday, Dec. 19, but a court filing on Nov. 27 shows the sentencing has been postponed until June. A spokesman for the U.S. Attorney for Connecticut could not elaborate on why the sentencing was postponed since the court filing is under seal.

-END-

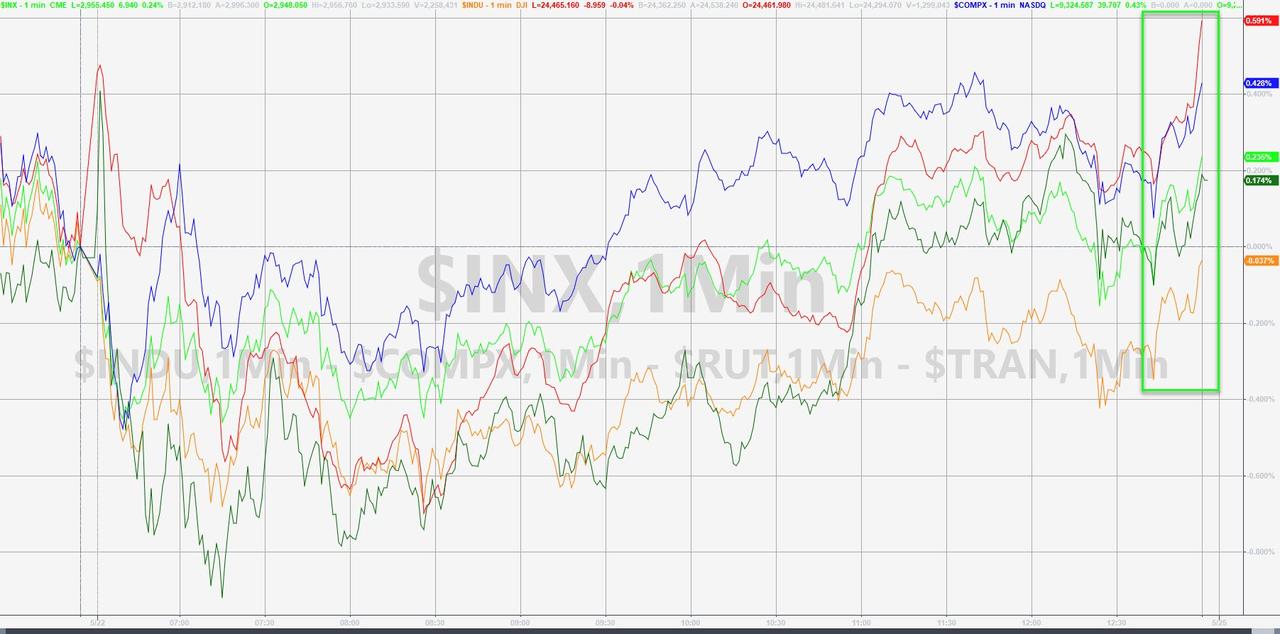

Futures Slide, Yuan Tumbles, Hang Seng Plunges Most In 5 Years On Hong Kong Crackdown

S&P futures dropped alongside European and Asian stocks on Friday, while the Hang Seng index crashed 5.6%, the most in five years, as markets braced for an escalation in tensions between Washington and Beijing after China announced plans to impose a national security law on Hong Kong during its National People’s Congress. Treasuries climbed with the dollar while oil snapped a six-day winning steak.

Still, Wall Street’s main indexes were set to end Friday with weekly gains on the back of stimulus hopes and optimism over a pickup in business activity with a nationwide easing in lockdowns. Hewlett Packard Enterprise fell 7.1% in premarket trade after missing second-quarter revenue and profit estimates, hit by global lockdowns since February.

China moved on Friday to impose a national-security law in Hong Kong that could see Mainland intelligence agencies set up bases in the global financial hub, raising fears of more pro-democracy protests. The move could also ratchet up U.S.-China tensions as President Donald Trump on Thursday warned Washington would react “very strongly” if Beijing went ahead with the law.

After rising above the key resistance level of 2,950 in the Thursday cash session, ES once again slumped below it dropping as low as 2905 before rebounding following the European open, if still holding on to losses while food and mining companies led the Stoxx Europe 600 Index lower. The risk-off tone took hold earlier in Asia, where Hong Kong’s benchmark stock index plunged more than 5%, its biggest drop since July 2015.

Also at the NPC, Chinese Premier Li announced the Government Work Report did not contain a GDP target for 2020 citing global pandemic and uncertainties for global economy and trade, but stated that China will make policy more flexible and will use policy tools such as open market operations, interest rate cut, RRR cut, re-lending and re-discount to keep liquidity reasonably ample. Furthermore, Li stated China is to issue CNY 1tln in special bonds this year and will cut tax and fee burdens for companies by CNY 2.5tln this year although noted China faces unprecedented risks and challenges. China also reiterated its intent to implement phase one of the trade deal with the US despite recent tensions between the two nations.

European stocks drifted lower, led by commodity-related equities such as miners and energy companies after China announced plans to impose a national security law on Hong Kong, while for the first time ever scrapping a GDP target, disappointed investors. Stoxx 600 basic resources dropped as much as 3.1%, dragged lower by miners: Rio Tinto -2%, BHP -2.3%, Glencore -3%, Anglo American -3%; Steelmakers also declined ArcelorMittal -3%, Evraz -2.5%, despite ArcelorMittal raising prices in U.S. Gold miners outperform: Polymetal +0.4%.

Asian stocks fell, led by finance and energy, after falling in the last session. All markets in the region were down, with Hong Kong’s Hang Seng Index dropping 5.6% and Singapore’s Straits Times Index falling 2.2%. Trading volume for MSCI Asia Pacific Index members was 14% above the monthly average for this time of the day. The Topix declined 0.9%, with I’rom Group and Fields falling the most. The Shanghai Composite Index retreated 1.9%, with Wuxi Hongsheng Heat Exchanger Manufacturing and Yangyuan Zhihui posting the biggest slides.

In rates, yields dropped, richer by 0.5bp to 4bp across the curve into early New York trading, holding most of their bull-flattening move during Asia session. Advance was spurred by the prospect of renewed political turmoil in Hong Kong after China introduced sweeping national security legislation, setting up a collision course with the U.S. 10-year TSY yields are lower by more than 2bp at ~0.645% while new 20-year bond continues to outperform; curve flatter with 2s10s, 5s30s spreads tighter by ~2bp. Gilts also in focus, outperforming bunds over European session after BOE policy maker Ramsden said more QE is possible at the June meeting, has an open mind on negative rates.

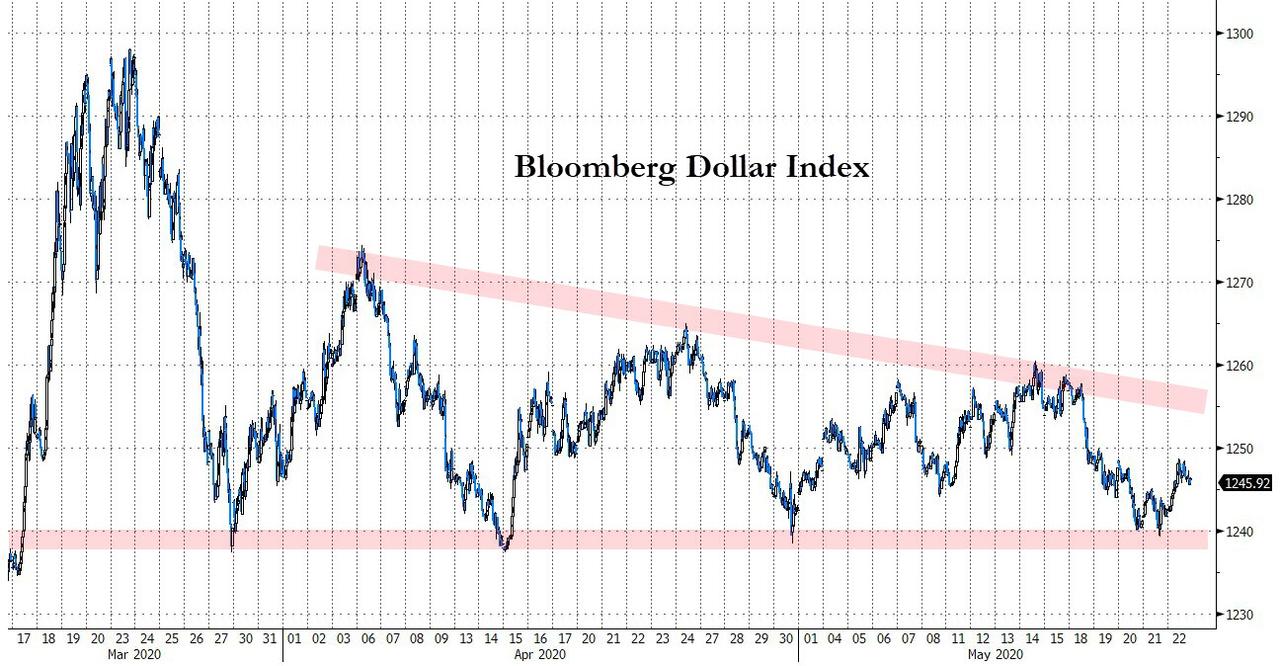

In FX, the Bloomberg Dollar Spot Index headed for its biggest rise in two weeks and Treasuries gained as investors braced for rising tensions between Washington and Beijing. The Australian weakened against most G-10 peers as sentiment was damped by China-Hong Kong tensions; the Norwegian krone led losses, tracking the drop in oil.

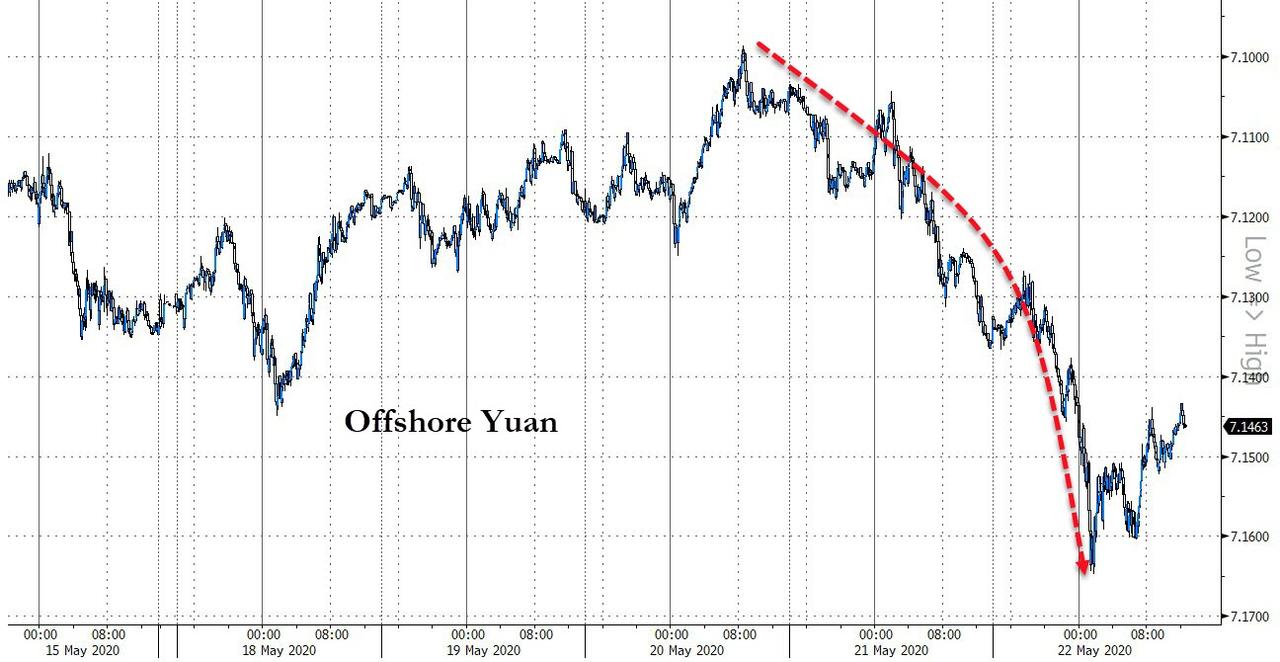

The yuan plunged to a 2 month low as China’s National People’s Congress abandoned its decades-long practice of setting an annual target for economic growth amid uncertainty unleashed by the coronavirus pandemic. The pound weakened for a third day as data showed retail sales in the U.K. dropped by almost a fifth in April.

Many are asking what happens next, with the emerging consensus that China will allow the Yuan to drift lower to 7.20 in response to any moves by the US.

“China’s move on legislation about Hong Kong and the risk of further deterioration in U.S.-China relations is worrying for market players,” said Masafumi Yamamoto, chief currency strategist at Mizuho Securities Co. in Tokyo. “They’re are keen to see how big an economic stimulus China may provide, which would affect risk-sensitive currencies such as the Aussie.”

In commodities, oil plunged, with Brent tumbling as much as $3 from Thursday’s high of $37, before settling around $34.50. West Texas oil plunged as much as 9.4% before trimming its losses to trade around $32 a barrel in New York. Base metals slumped in London on China fears: copper -2%, aluminum -1%, nickel -5%, zinc -1%; iron ore -0.7% in Singapore; gold +0.7%. Citi sees lower copper prices in the near term, as global surplus meets lower Chinese physical and speculative activity, but expect $5,800/t on a 6-12 month view as the market rebalances driving prices up the rising cost curve

Looking to the day ahead now and there are less data highlights. The UK and Canada will release retail sales data, which are likely to continue to show the deterioration caused by the pandemic. From central banks, the ECB will be publishing the account of their most recent monetary policy meeting and will grab some attention. Finally, as usual there are fewer earnings releases on Friday, but two important ones for the macro-environment include Deere & Company and Alibaba.

Market Snapshot

- S&P 500 futures down 0.7% to 2,917.00

- STOXX Europe 600 down 1.1% to 336.50

- MXAP down 2% to 145.25

- MXAPJ down 2.7% to 465.00

- Nikkei down 0.8% to 20,388.16

- Topix down 0.9% to 1,477.80

- Hang Seng Index down 5.6% to 22,930.14

- Shanghai Composite down 1.9% to 2,813.77

- Sensex down 0.9% to 30,649.13

- Australia S&P/ASX 200 down 1% to 5,497.03

- Kospi down 1.4% to 1,970.13

- Euro down 0.4% to $1.0910

- Brent Futures down 5.2% to $34.17/bbl

- Italian 10Y yield fell 1.9 bps to 1.441%

- Spanish 10Y yield rose 1.0 bps to 0.643%

- Brent Futures down 5.3% to $34.16/bbl

- Gold spot up 0.6% to $1,736.71

- U.S. Dollar Index up 0.4% to 99.73

Top Overnight News from Bloomberg

- Asian, European shares slid and futures retreated in the U.S. as China announced plans to impose a national security law on Hong Kong, which threatened to further escalate tensions between Washington and Beijing

- The Chinese government abandoned its decades-long practice of setting an annual target for economic growth amid the storm of uncertainty unleashed by the coronavirus pandemic, and said it would continue to increase stimulus

- Britain posted a record budget deficit in April as the government unleashed an unprecedented package to prevent the collapse of the virus-stricken economy

- Oil retreated from the highest level in more than two months as doubts over the strength of China’s economic recovery and geopolitical tensions ate away at its weekly advance

- Bank of England Deputy Governor Dave Ramsden added his voice to the chorus of policy makers refusing to rule out negative interest rates in the U.K.

Asian indices weakened as markets digested today’s key events including the BoJ off-schedule meeting and start of China’s NPC where it omitted setting a GDP growth target for this year due to the coronavirus pandemic, as well as uncertainties surrounding economy and trade. ASX 200 (-1.0%) declined with energy names pressured by an aggressive pullback in oil prices and with sentiment subdued after Fitch revised its outlook on Australia’s sovereign rating to negative from stable, while Nikkei 225 (-0.8%) suffered the ill-effects of a firmer currency despite the BoJ’s announcement of a new measure to boost lending to small and mid-sized businesses impacted by the coronavirus in which it set aside JPY 75tln for its new loan programme but which was widely anticipated. Hang Seng (-5.6%) and Shanghai Comp. (-1.4%) were lower amid the start of China’s Two Sessions conclave where the Government Work Report refrained from setting an economic growth target but pledged to reduce tax and fee burdens for companies by CNY 2.5tln this year and use several tools to keep liquidity ample. Furthermore, the losses in Hong Kong were exacerbated after China’s attempts to tighten its grip on the Special Administrative Region through a new national security law, and is likely to stoke further unrest for the region which had already been mired by months of protests since the middle of last year. Finally, 10yr JGBs were relatively uninspired with only mild upside seen despite the downbeat risk tone and upside in T-notes, while the conclusion of the BoJ’s emergency meeting and announcement of a new lending scheme also failed to spur any meaningful price action.

Top Asian News

- China Will Improve Hong Kong’s Security Laws, Premier Li Says

- Hong Kong Stocks Haven’t Suffered This Much Since 2008

European majors trade mostly negative (Euro Stoxx 50 -0.3%) but have drifted off lows following a dismal APAC handover in which the Hang Seng was pummelled by the prospect of a resurgence in violent pro-democracy protests, whilst Chinese markets were dragged lower in sympathy as the nation is on course for further escalation with the US and as the NPC did not provide a GDP growth target for the year. Back to Europe, peripheries fare better than the core markets, whilst the FTSE 100 (-0.9%) and SMI (-1.4%) lag European peers, albeit the former weighed on by energy, materials and financials and the latter more-so on catch-up play. Sectors are red across the board but do not reflect a clear risk tone as specific sectors take hits on Hong Kong woes – with Financials and Energy underperforming, the latter amid price action in the complex and the former dragged by a lower yield environment alongside Hong Kong-exposed banks plumbing the depths; HSBC (-5.4%) and Standard Chartered (-4.0%). The wide US-China implication and downbeat sentiment prompts materials sector to trade on a poor footing. Fears of protests also see luxury names on the backfoot; LVMH (-1.2%), Kering (-1.2%), Richemont (-3.1%), Swatch (-1.1%) hold onto losses. In terms of other individual movers: Burberry (+1.8%) holds onto gains after the Co. said it can weather the pandemic with a strong balance sheet and protected liquidity. Renault (-2.0%) opened weaker amid little progress with the French gov’t on state aid; Co. are due to meet with Finance Minister Le Maire today.

Top European News

- U.K. Budget Deficit Largest Since Modern Records Began in 1993

- Putin Presses Plan to Extend Rule Amid Crisis Hurting Russians

- Credit Suisse Targets Luckin Ex-Billionaire’s Family Assets

In FX, USDCNH was not the biggest move in percentage terms, but pertinent in the context of gauging the rising level of US-China angst as the pair climbs to highs not seen since March above 7.1600, and closer to record peaks in early September last year when trade wars were raging. Moreover, confirmation that Beijing is not setting an official 2020 growth target and the NPC drafting legislation on national security for Hong Kong have ruffled the Yuan, with the latter also adding yet another point of dispute to the increasingly long list jeopardising already strained relations between the 2 nations. In terms of the wider repercussions, risk sentiment has deteriorated further to the benefit of the Greenback above all rivals bar the Yen, as the DXY extends its rebound from recent lows and at least 2 close scrapes with the 99.000 level to a 99.838 high, and still seemingly on the up.

- AUD/CAD/EUR/GBP/NZD – No surprise to see the Aussie bearing the brunt of the latest Washington-Beijing spat, especially as the Hong Kong Dollar is pegged, but Aud/Usd and Aud/Nzd have also retreated in response to Fitch downgrading the sovereign’s triple A ratings outlook to negative from stable. The former is now hovering nearer 0.6500 from 0.6600+ yesterday and the latter is down through 1.0700 compared to a 1.0830 apex earlier in the week, as the Kiwi manages to stay within sight of 0.6100 against its US counterpart following comments from NZ Finance Minister Robertson about formative discussions on the topic of helicopter money. Meanwhile, the Euro has handed back more gains vs the Buck after its fleeting or false break over the 1.1000 mark on Thursday and has been back under the round number below, but not quite far enough to stir hefty option expiry interest between 1.0885-75 in 2.8 bn. Elsewhere, the Loonie has lost its oil prop and trying to contain declines through 1.400 ahead of Canadian retail sales data, and on that very note Cable is straddling 1.2200 and the Eur/Gbp cross 0.8950 after weaker than expected UK consumption rattled Sterling somewhat more than equally bad public sector finances and tripped some stops in the former at 1.2180. However, underlying bids said to be sitting from 1.2160 to 1.2150 have not been troubled so far.

- JPY/CHF – As noted above, the Yen is marginally outperforming vs the Greenback, albeit still rangebound either side of 107.50 and only retaining an element of safe-haven premium after no shocks from the inter-schedule BoJ meeting or more recent joint statement from Governor Kuroda and Japanese Finance Minister Aso expanding on the rationale behind new bank lending provisions. Conversely, Usd/Chf remains elevated on the 0.9700 handle, but the Franc is still unwinding losses relative to the Euro and probing 1.0600 ahead of the ECB minutes (full preview available via the headline feed) and next Monday’s Swiss bank sight deposit balance update.

- EM – Aside from broad depreciation on risk aversion, the Indian Rupiah got an unexpected 40 bp RBI rate cut to contend with, though Usd/Idr has reversed after a knee-jerk jump to trade lower on the day.

In commodities, WTI and Brent front month futures experience substantial intraday losses as sentiment takes a hit from developments regarding the Hong Kong legislations as well as wider implications such as escalating trade tensions with the US and souring sentiment with the UK. As such, clear risk aversion is seen – with WTI and Brent July around USD 31.50/bbl and 34/bbl, down around 7% and 5% respectively and with current bases at USD 30.70/bbl and USD 33.50/bbl respectively. Spot gold sees haven demand, residing towards the top-end of its USD 1725-38/oz current range. Copper prices gapped lower below USD 2.4/lb and holds onto sentiment-driven losses, with some also attributing the downside to China refraining from assigning a GDP target.

US Event Calendar

- Nothing major scheduled

DB’s Jim Reid concludes the overnight wrap

Today is the last Corona Crisis Daily unless we see a resurgence of case numbers. Let’s hope not. In our last edition we part with some stats comparing US fatalities between February 1st and May 16th this year for flu and covid-19. Interestingly in all age buckets up to at least 24yrs old, flu has killed more people (141 total) than covid-19 has (27). In the 25-34 year bucket the numbers pivot and are 138 versus 463. By the time we get to the over 55 year olds the divergence is stark with 5,184 dying of flu against 63,923 for covid-19. Across all ages more people have died of pneumonia though than covid-19 in the US over this period. Hopefully we’ve been balanced in our reporting on covid-19. One of the key themes we’ve tried to highlight over the last couple of months or so is how savagely discriminant covid-19 is, especially by age. It’s staggering given that flu is seemingly more deadly for under 24 year olds and is also staggering how susceptible the elderly and those with underlying conditions are relative to the young. Why the young are so spared is a welcome mystery. However as we increasingly understand this about the virus it surely gives the global politicians more options going forward as to how to protect economies from a second wave. Good luck to them.

Moving on to markets now and for a second day in row, US President Trump escalated the rhetoric war with China, specifically criticizing the country’s leadership. Then later in the day Trump posted a letter to Congress on the “Strategic Approach” to China, saying that the US, “has adopted a competitive approach to the People’s Republic of China, based on a clear-eyed assessment of the Chinese Communist Party’s intentions and actions, a reappraisal of the United States’ many strategic advantages and shortfalls, and a tolerance of greater bilateral friction.” Lastly on China, the country is proposing a new security law in Hong Kong that could ban sedition, secession and treason. This will likely draw a large amount of opposition given the pro-democracy protests in the country over the past year. This could be another wedge between China and the US, given how many US politicians on both sides of the aisle supported HK’s efforts last year. The China-US headlines were accompanied by news that the Trump administration is moving to withdraw from the Open Skies treaty, a nearly 30 year old accord meant to reduce tensions between Russia and the West, citing a lack of adherence by the Russians.

Risk markets reacted negatively to the political uncertainty as economic data continued to show that recovery from the virus-induced lockdowns may not be as sharp as markets are pricing. The S&P 500 fell -0.78% although it was off the session lows of -1.11% just as Europe went home. Or at least left the home office and went to the kitchen if they weren’t already there on holiday. For the activity that was there in Europe, stocks fell on the further agitation with the Stoxx 600 down -0.75% on lower volumes (down -17% from the 30-day average) with much of Scandinavia and the Swiss markets closed and France and Germany observing the public holiday albeit with markets thinly trading. Oil continued to rally though, albeit at a slower pace, with WTI futures up +1.28% and Brent crude rallying +0.87%.

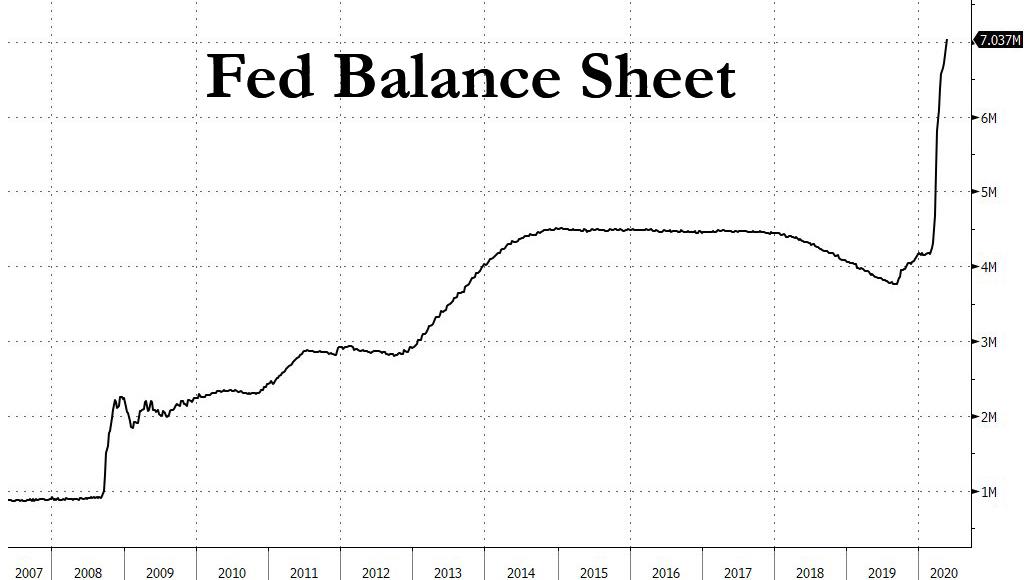

Overall it’s fascinating to see that markets are shaking off the very bad news on the future US/China relationship much more now in the face of a global pandemic than it did last year when the tensions were fraught but most likely still pointing towards a trade deal at some point. The relationship feels more in terminal decline now than it did 6-12 months ago. Maybe the answer to this puzzle lays in the central bank liquidity surge. DB’s Alan Ruskin yesterday updated his aggregated key country central bank liquidity charts (link here) where he showed that rolling 12 month central bank liquidity is already running double the peak it reached at any point during the GFC. It took more than three and a half years (September 2008 thru and into 2012) to ‘achieve’ the $4.5 trillion cumulative expansion in G10 central bank balance sheet assets that we have seen over the last 12 weeks. Worth having a look at the graphs. All fairly remarkable.

Staying with stimulus, DB’s Peter Sidorov updated his latest excellent G-20 policy response document yesterday ( link here ) which actually shows that G-10 central bank balance sheets have now gone well above $20 trillion from over $16 trillion before the crisis. When you include total G-20 central bank measures already injected or promised so far it amounts to around $9 trillion. The piece also includes details of fiscal commitments from every one of these countries. Italy and Germany are the top of the list for combined fiscal above and below the line (guarantees etc.) commitments.

One of the main beneficiaries of this liquidity has been bonds as they’ve stayed firm during the strong risk on over the last two months. In the small risk off seen yesterday they rallied again. US 10yr yields were -0.8bps lower at 0.672%, while German bunds fell -2.7bps to -0.50% and Gilts fell -5.8bps to 0.17%. Both Gilts and US Treasuries are now roughly back to around 11bps from all-time lows. Peripheral spreads widened slightly (1-2bps) during a week of increased tightening. Safe havens were not uniformly higher, as gold had its worst day since 30 April falling -1.21%.

Overnight, the text of China’s Premier Li Keqiang’s annual policy address has confirmed that the country is indeed abandoning its GDP growth target for this year. The text specifically states that, “I would like to point out that we have not set a specific target for economic growth this year” and “this is because our country will face some factors that are difficult to predict in its development due to the great uncertainty regarding the Covid-19 pandemic and the world economic and trade environment.” The text of speech also contained announcement of plans to impose a national security law in Hong Kong which as we noted above will only add to tensions between the US and China. The Hang Seng is trading down -4.61% on the back of this and as you’ll see below, appears to be dragging other markets lower too.

China has also set the target for the urban surveyed unemployment rate of around 6%, higher than 2019’s goal and proposed a wider budget deficit at 3.6% of GDP (vs. 2.8% of GDP in 2019). In terms of policy, fiscal was smaller than what our economists expected while there were strong signals on monetary, “specifically higher than last year”. Finally, the government said explicitly that it will “mutually enforce the phase on trade deal with the US”. More support has also been granted to SMEs. See the full summary from our economists here.

The Shanghai Comp and CSI 300 are down -1.31% and -1.59% respectively in the wake of that and the Kospi -1.46%, while there are more modest losses for the Nikkei (-0.76%). Meanwhile, futures on the S&P 500 are down -0.60% while yields on 10y USTs are down -2.5bps. Elsewhere, WTI oil prices are down -6.93% this morning while iron ore is up +1.34% continuing its winning run since April 29th.

In a busy overnight session, the BoJ’s unscheduled monetary policy meeting has ended with key interest rates and asset purchases unchanged. The central bank instead launched a new lending program worth JPY 30tn to support small businesses struggling amid the coronavirus in order to prevent bankruptcies. The program is due to run through March next year and will channel money to companies via commercial banks and other financial institutions. Also, like the other BoJ facilities, the facility will encourage lending to companies by providing free loans to financial institutions and then paying them 0.1% interest on the amount they in turn lend out. In other overnight news, Fitch revised the outlook for Australia’s credit rating to ‘negative’ from ‘stable’ citing that “Government spending in response to the health and economic crisis will cause large fiscal deficits and a sharp increase in government debt/GDP.”

In a busy week for the Fed Chair, Jerome Powell spoke with Fed Governor Brainard at a live-streamed “Fed Listens session” to get feedback from small-business, labour, and non-profit organization leaders over their policy stances. In remarks that could be used by lawmakers to push for further stimulus, Powell said, “While the burden is widespread, it is not evenly spread…Those taking the brunt of the fallout are those least able to bear it.” Fed Vice Chair Clarida also spoke yesterday, and echoed recent calls for further fiscal stimulus, but thought that the economy would show signs of growth sometime after June.

Looking at the economic data yesterday, US initial jobs claims registered another 2.44m people for the week ending May 16, down from last week’s 2.69m. This was slightly above the consensus forecast of 2.4m. Continuing claims are now at a record 25.1m through the week ending 9 May – this in turn takes the insured unemployment rate to 17.2%. The good news is that initial jobless claims have now fallen for 7 straight weeks, but they are still at least triple the previous highs.

The other big data of the day was the flash PMIs for May. This month, metrics rebounded slightly but remained in deep contraction territory. The Eurozone composite PMI registered 30.5, up appreciably from the 13.6 reading in April and above consensus at 27.0. On the country level, France had one of the bigger recoveries with composite PMIs rising from 11.1 in April to 30.5 in May, still slightly under consensus at 32.4 though. Germany’s flash composite PMI for May was 31.4, up from 17.4 in April but below the consensus estimate of 33.1. The UK’s composite PMI was at 28.9, well above consensus at 25.7 and April’s 13.8 reading.

On the other side of the Atlantic, the US composite PMI was 36.4, up from 27.0. The country did not register as large a fall in April, and so the rebound was not as sharp. Remember again that PMIs are diffusion indices, where respondents simply say whether things are better or worse than last month, and so during extreme events they don’t necessarily give the most accurate picture on the scale of the declines or rebounds when they happen, though direction still matters.

Looking to the day ahead now and there are less data highlights. The UK and Canada will release retail sales data, which are likely to continue to show the deterioration caused by the pandemic. From central banks, the ECB will be publishing the account of their most recent monetary policy meeting and will grab some attention. Finally, as usual there are fewer earnings releases on Friday, but two important ones for the macro-environment include Deere & Company and Alibaba.

3A/ASIAN AFFAIRS

i)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED DOWN 54.16 POINTS OR 1.89% //Hang Sang CLOSED DOWN 1349.89 POINTS OR 5.56% /The Nikkei closed DOWN 164.15 POINTS OR 0.80%//Australia’s all ordinaires CLOSED DOWN .92%

/Chinese yuan (ONSHORE) closed DOWN at 7.1350 /Oil UP TO 32.01 dollars per barrel for WTI and 34.28 for Brent. Stocks in Europe OPENED MIXED// ONSHORE YUAN CLOSED DOWN // LAST AT 7.1350 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 7.1528 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY PAST 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED//CHINA VS HONG KONG// : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3 a./NORTH KOREA/ SOUTH KOREA

South Korea

b) REPORT ON JAPAN

JAPAN

As expected, Japan’s tourism tumbles a huge 99.9% in April

(zerohedge)

Japanic! Tokyo Tourism Tumbles 99.9% In April

Japan saw an estimated 2,900 foreign travelers in April, down 99.9% from a year earlier, as COVID-19 travel restrictions and lockdowns left the once-booming tourism sector in a state of paralysis.

The drop in foreign visitors was the most significant percentage decline on record dating back to 1964, the Japan National Tourism Organization (JNTO) reported. It was the first time the monthly figure fell sub 10,000. The previous low for monthly foreign visitors was 17,543 set back in February 1964.

The reason for the sharp decline stems from the government’s restrictions on international travel following a surge in domestic virus cases and deaths. On April 3, entry restrictions for international travelers were applied to 100 countries, including China, the US, and Europe, resulting in a collapse of inbound travel that severely impacted the country’s tourism industry.

Before the pandemic, tourism in the country was increasing at healthy growth rates. Around 31.8 million people visited Japan in 2019, up 2.2% over the previous year. Japan had high aspirations to boost tourism to a record 40 million this year, but those estimates were crushed due to the now-postponed Tokyo Olympics that have been rescheduled for 2021.

Travel restrictions and shutdowns have found success in mitigating the spread of the virus, Prime Minister Shinzo Abe said on Thursday, adding that Japan could lift the state of emergency in Tokyo as early as next week, that is if virus infections can remain low. Emergencies were recently lifted in Osaka, Kyoto, and Hyogo because of a drop in confirmed cases.

Japan’s tourism industry is expected to remain in a slump throughout the year. The world’s third-largest economy dove into recession for the first time since 2015:

“The economy entered the coronavirus shock in a very weak position,” said Izumi Devalier, chief Japan economist at BofA, but “the real big ugly stuff is going to happen in the April, June print. It’s going to be three-quarters of very negative growth.”

Read: “Japan Exports Worst Since Financial Crisis; Korea Early May Export Data Just As Dire”

Abe, like other world leaders, is quickly trying to reopen his crashed economy and simultaneously contain the pathogen’s spread. This difficult task could ignite into a second virus wave later this year.

Japan’s low rate of testing for the virus suggests the scope of the outbreak is still yet to be known.

end

3 C CHINA

CHINA/LAST NIGHT

What is going on here? China hoarding PPE as it braces for another wave?

(zerohedge)

China Is Hoarding PPE Again As It Braces For COVID-19’s “Second Wave”

A while back, we reported on one notable US Intel leak claiming Beijing deliberately waited until Jan. 22 to warn the world about the possibility of a widespread outbreak (before that, Beijing insisted there was no evidence of human to human transmission, implying that this would likely be an isolated incident) so the CCP would have time to grab up all the PPE and other vital supplies.

That was why, when the tidal wave of infections finally hit in the US, a sudden and inexplicable shortage of PPE forced nurses and doctors in some of the most notorious hotspots – including NYC – to work without masks and gowns. Many used garbage bags, or used one disposable mask for a week or more.

Now, Fox News reports that the CCP appears to be gobbling up all the capacity once again as businessmen complain about suppliers warning about being unable to process new orders.

China’s Communist Party is again seizing factory lines churning out the world’s supply of medical safety gear — sparking fears the country is preparing for a second wave of the coronavirus, American traders in China told The Post.

New Yorker Moshe Malamud, who has done business in China for over two decades, was moving tens of millions of pieces of protective gear to the U.S. at the height of the crisis but said suppliers in recent weeks had been overwhelmed with orders from the Chinese government.

“I was placing a larger order with one of the bigger distributors and he tells me, ‘I can complete this order but after this we’ve been contracted by the Chinese government to produce 250 million gowns,’” said Malamud, who lived in China for a decade before founding aviation company M2Jets.

Thermometer makers have also been inundated with government orders.

He said he heard a similar story about another manufacturer making thermometers.

“We hear how China is up and running and the virus is past them, so I asked, ‘What are they ordering 250 million gowns for?’ and of course no one is talking.”

“I’ve been hearing this a lot from other manufacturing institutions that say, ‘We can give you a little bit, but basically we’re concentrated between now and the end of the summer manufacturing stuff for the Chinese government in anticipation of a second wave,'” he continued.

Last month, leading U.S. manufacturers of medical safety gear told the White House that China had prohibited them from exporting goods as the crisis mounted, a Post report revealed.

Beijing has already forced some 108 million Chinese in northeastern Jilin Province back under “partial lockdown” following another outbreak. They’re also carrying out a mass-testing campaign in Wuhan.

Although Dr. Anthony Fauci has repeatedly warned that the US should brace for a second wave of the virus, a second wave isn’t a foregone conclusion. As NYT opinion columnist Nicolas Kristof wrote in his column published in Thursday’s paper, “epidemiology is full of puzzles.” In 2003, the WHO feared a deadly resurgence of SARS that fall. But instead, the virus petered out. As Dr. Fauci explained once several months ago, we know little for certain about the virus, and because of this, it’s important to be prepared for the worst-case scenario.

And if the outbreak in Brazil continues to rage out of control, the possibility that Brazilians could reinfect the entire Western Hemisphere is looking increasingly plausible.

Sen. Hawley Lays Out Super-Nationalist, Anti-China Vision

Sen. Josh Hawley (R-MO) delivered a well-practiced speech on Wednesday blasting China for its virus response, and warning of the threat posed by Beijing’s economic ambitions.

If Trump’s China rhetoric is a 7, Hawley’s is a solid 11.

“The international order as we have known it for thirty years is breaking. Now imperialist China seeks to remake the world in its own image, and to bend the global economy to its own will,” Hawley warned, adding “Are we in this nation willing to witness the slow destruction of the free world? Are we willing to watch our own way of life, our own liberties and livelihoods, grow dependent on the policy of Beijing?”

Hawley also argued that China’s “failures and lies” unleashed the COVID-19 pandemic onto the world, according to Axios.

He’s also calling for the US to withdraw from the World Trade Organization, which he sees as an obstacle to American sovereignty.

His charge sheet against the WTO reflects White House talking points: US negotiators paid too much in past negotiations and got too little in return; competitive traders like China unfairly exploit rules to help poor developing countries; and the system for settling disputes is flawed with rulings that impinge on US rights and expand US obligations beyond what was agreed at the negotiating table. –Piie

Hawley accused China in a NYT Op-Ed of maintaining “protectionist workarounds” while stealing American intellectual property – which the US cannot contest due to restrictive WTO obligations, according to the Peterson Institute for International Economics.

In his Wednesday speech, Hawley said that Americans cannot be both prosperous and secure in a world where China’s influence and economic power have dwarfed America’s due to unfair trade relations.

Watch:

HONG KONG/CHINA/USA

This is it: China’s Congress announces a huge crackdown on Hong Kong with its new ‘National Security” Law. For the first time it abandons its GDP targets.

(zerohedge)

“This Is The End Of Hong Kong”: China Congress Announces Crackdown On Hong Kong With New “National Security” Law; Abandons GDP Target

With China’s ambitions toward Hong Kong having emerged as the top political fault line in recent days, the market was closely following the start of Friday’s National People’s Congress (NPC) where in addition to disclosures on Chinese political strategy, Beijing announces decisions on targets on GDP, CPI and fiscal deficit.

Which is why many were surprised when in the text of Premier Li Keqiang’s annual address, for the first time China abandoned its usual practice of setting a numerical target for economic growth this year due to the turmoil caused by the coronavirus pandemic.

“I would like to point out that we have not set a specific target for economic growth this year,” the report said, according to Bloomberg which saw a leaked version. “This is because our country will face some factors that are difficult to predict in its development due to the great uncertainty regarding the Covid-19 pandemic and the world economic and trade environment.”

As Bloomberg adds, the shift away from a hard target for output growth not only breaks with decades of Communist Party planning habits, but is an admission of the deep rupture that the disease has caused in the world’s second-largest economy. With the growth outlook depending also on the efforts of trading partners to rein in the pandemic, the government is shifting its focus to employment and maintaining stability.

Among the various other economic goals disclosed by China, are:

- The addition of 9 million urban jobs; surveyed jobless rate around 6% (as we reported recently, the People’s Liberation Army is aggressively hiring all those who lost their jobs due to the pandemic, so at least China’s army will soon be absolutely massive)

- Plans 3.75 trillion Yuan of Special Local Govt Bonds in 2020 (a relatively modest number)

- Sell 1t yuan of anti-virus sovereign bonds in 2020 (even more modest)

- Deficit-to-GDP ratio this year is projected at more than 3.6% and the deficit increase is projected at 1 trillion yuan (about $141.6 billion) over last year (remember when China actually ran a budget deficit)

- China to work with U.S. to implement phase 1 trade deal (a noble goal, also one which will never happen)

- China sets 2020 CPI target at about 3.5% (China may have to launch another “pig ebola” virus to boost food inflation)

- China to use innovative monetary policy tools to finance real economy (so China will do QE as well?)

- China’s monetary stance unchanged; to make prudent monetary policy more flexible, appropriate

- China to use RRR cuts and interest rate cuts, relending

- China to guide money supply ‘significantly’ higher than 2019

- China targets more stable, high-quality imports, exports

- China to keep yuan at reasonable and equilibrium level

- China targets basic equilibrium in balance of payments

- China to cut taxes, fees by about 500b yuan this year

- China to asks large banks to boost lending to small firms by 40% (the US doesn’t hold a trademark on a debt bubble after all)

- China sees defense spending up 6.6% to 1.268 trillion yuan (see “China’s Military Seeks Bigger Budget Amid “Growing Threat Of US Conflict”“)

While none of the above was especially remarkable (with the exception of the hint at QE), the reason why stocks gave the report a thumbs down is because as Premier Li also said, China will safeguard national security in Hong Kong, i.e., China plans on expanding its crackdown on Hong Kong sovereignty, a step that comes one day after China announced dramatic plans to rein in dissent by writing a new law into the city’s charter, and just hours after the Senate passed a bill that will retaliate against China should it do precisely that, effectively ensuring an even further deterioration in US-Sino relations.

Specifically, the National People’s Congress confirmed plans to pass a bill establishing “an enforcement mechanism for ensuring national security” for Hong Kong, with Reuters adding that China’s draft Hong Kong legislation says Hong Kong “should finish enacting as soon as possible the regulations in basic law regarding national security” and that Hong Kong government and legal bodies should effectively prevent, stop and punish activities that endanger national security.

Chinese lawmakers were preparing to soon pass measures that would curb secession, sedition, foreign interference and terrorism in the former British colony, local media including the South China Morning Post reported Thursday, citing unidentified people.

“We will establish sound legal systems and enforcement mechanisms for safeguarding national security in the two special administrative regions, and see that the governments of the two regions fulfill their constitutional responsibilities,” Li said according to prepared remarks on Friday.

As Bloomberg adds, any attempt to impose security laws now could reignite the unrest that hammered the city’s economy last year and serve as a flash point amid broader U.S.-China tensions. Protesters urged democracy advocates to hold rallies across the city Thursday night, with one poster describing the moment as a “battle of life and death,” but mass demonstrations didn’t immediately materialize.