GOLD::$1712.30 UP $0.10 The quote is London spot price

Silver:$17.27 UP 13 CENTS (London spot closing price

OTC/LBMA OPTIONS EXPIRY FRIDAY MAY 29

Expect gold/silver to be subdued in price until after first day notice.

Closing access prices: London spot

i)Gold : $1709.00 LONDON SPOT 4:30 pm

ii)SILVER: $17.09//LONDON SPOT 4:30 pm

CLOSING FUTURES PRICES: KEY MONTHS

MAY COMEX GOLD: XXX

JUNE GOLD: $XXX CLOSE 1.30 PM// SPREAD SPOT (LONDON) VS/FUTURE JUNE: $5.//BACKWARDATION

CLOSING SILVER FUTURE MONTH

JULY: 1:30 PM: $XXX//1:30 PM //SPREAD SPOT LONDON VS FUTURE JULY: 48 CENTS PER OZ//

the gold market continues to be broken as future prices are much higher than spot prices. The comex is desperate to fix things but they have no available gold.

If one is to buy gold and or gold coins, the price is around $2800. usa per oz

and silver; $31.00 per oz//

LADIES AND GENTLEMEN: YOU ARE NOW WITNESSING FIRST HAND THE DIFFERENCE BETWEEN PAPER GOLD/SILVER AND THE REAL PHYSICAL STUFF!!

DO NOT PAY ANY ATTENTION TO WHAT THE CROOKS ARE DOING AT THE COMEX AND LONDON LBMA..PHYSICAL IS THE NAME OF THE GAME AND NOTHING ELSE

COMEX DATA

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING: 0/10

none issued

NUMBER OF NOTICES FILED TODAY FOR MAY CONTRACT: 10 NOTICE(S) FOR 1000 OZ (0.0311 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 10272 NOTICES FOR 1027200 OZ (31.950 TONNES)

SILVER

FOR MAY

124 NOTICE(S) FILED TODAY FOR 620,000 OZ/

total number of notices filed so far this month: 9043 for 45,215,000 oz

BITCOIN MORNING QUOTE $9119 UP $274

BITCOIN AFTERNOON QUOTE.: $9184 DOWN $20

GLD AND SLV INVENTORIES:

WITH GOLD UP $.10 AND NO PHYSICAL TO BE FOUND ANYWHERE:

WITH ALL REFINERS CLOSED//MEXICO ORDERING ALL MINES SHUT: WHERE ARE THEY GETTING THE “PHYSICAL”?

ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.34 TONNES OF GOLD INTO THE GLD

GLD: 1,119.05 TONNES OF GOLD//

WITH SILVER UP 13 CENTS TODAY: AND WITH NO SILVER AROUND

NO CHANGES IN SILVER INVENTORY AT THE SLV///

RESTING SLV INVENTORY TONIGHT:

SLV: 455.817 MILLION OZ./

XXXXXXXXXXXXXXXXXXXXXXXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI ROSE BY A STRONG SIZED 1448 CONTRACTS FROM 156,737 UP TO 158,185 AND CLOSER TO OUR NEW RECORD OF 244,710, (FEB 25/2020. THE STRONG SIZED GAIN IN OI OCCURRED DESPITE OUR VERY SMALL 9 CENT LOSS IN SILVER PRICING AT THE COMEX. IT SEEMS THAT THE GAIN IN COMEX OI IS DUE TO STRONG BANKER SHORT COVERING PLUS A STRONG EXCHANGE FOR PHYSICAL ISSUANCE, ZERO LONG LIQUIDATION, ACCOMPANYING A SMALL DECREASE IN SILVER OZ STANDING AT THE COMEX FOR MAY. WE HAD A NET GAIN IN OUR TWO EXCHANGES OF 2128 CONTRACTS (SEE CALCULATIONS BELOW).

WE HAVE ALSO WITNESSED A HUMONGOUS AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: MAY: 0 AND JULY: 680 AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 680 CONTRACTS. WITH THE TRANSFER OF 680 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 680 EFP CONTRACTS TRANSLATES INTO 3.400 MILLION OZ ACCOMPANYING:

1.THE 9 CENT LOSS IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

10.025 MILLION OZ INITIAL STANDING IN AUGUST.

43.030 MILLION OZ INITIALLY STANDING IN SEPT. (HUGE)

7.32 MILLION OZ INITIALLY STANDING IN OCT

2.630 MILLION OZ STANDING FOR NOV.

20.970 MILLION OZ FINAL STANDING IN DEC

5.075 MILLION OZ FINAL STANDING IN JAN

1.480 MILLION OZ FINAL STANDING IN FEB

23.005 MILLION OZ FINAL STANDING FOR MAR

4.660 MILLION OZ FINAL STANDING FOR APRIL

45.220 MILLION OZ INITIALLY STANDING FOR MAY

TUESDAY, AGAIN OUR CROOKS USED COPIOUS PAPER IN ORDER TO LIQUIDATE SILVER’S PRICE…AND THEY WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL 9 CENTS).. AND, OUR OFFICIAL SECTOR/BANKERS WERE UNSUCCESSFUL IN THEIR ATTEMPT TO FLEECE ANY AMOUNT OF SILVER LONGS FROM THEIR POSITIONS. THE SMALL GAIN AT THE COMEX WAS ACCOMPANIED BY : i) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS 2) A SMALL LOSS IN SILVER OZ STANDING FOR MAY,3) CONSIDERABLE BANKER SHORT COVERING AND 4) ZERO LONG LIQUIDATION AS WE DID HAVE A NET GAIN OF 2128 CONTRACTS OR 10.680 MILLION OZ ON THE TWO EXCHANGES! YOU CAN BET THE FARM THAT OUR BANKER ARE DESPERATE TO LIQUIDATE THEIR HUGE SHORT POSITIONS IN SILVER

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY /FOR MONTH OF MAY:

13,899 CONTRACTS (FOR 18 TRADING DAYS TOTAL 13,899 CONTRACTS) OR 69.0495 MILLION OZ: (AVERAGE PER DAY: 772 CONTRACTS OR 3.887 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF MAY: 69.05 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 9.86% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2020 TO DATE SILVER EFP’S: 1,057.89 MILLION OZ.

JANUARY 2020 EFP TOTALS SO FAR: 181.61 MILLION OZ

FEB 2020 EFP’S TOTAL : …… 259.600 MILLION OZ

MARCH EFP’S ….. 452.280 MILLION OZ //TOTALS//AND A NEW RECORD FOR THE MONTH)

APRIL EFP 95.355 MILLION OZ. (EX. FOR PHYSICALS BECOMING A LOT LESS)

MAY EFP SO FAR: 69.05 MILLION OZ

EXCHANGE FOR PHYSICAL ISSUANCE FOR THE PAST 30 DAYS IS A LOT LESS. NO DOUBT THAT THE COST TO CARRY THESE THINGS HAS EXPLODED AND AS SUCH CANNOT BE DONE AS FREQUENTLY AS BEFORE.

RESULT: WE HAD A STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1448, DESPITE OUR SMALL 9 CENT LOSS IN SILVER PRICING AT THE COMEX ///TUESDAY… THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 680 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER

TODAY WE GAINED A STRONG SIZED OI CONTRACTS ON THE TWO EXCHANGES: 2128 CONTRACTS (DESPITE OUR 9 CENT LOSS IN PRICE)

THE TALLY//EXCHANGE FOR PHYSICALS

i.e 680 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH A STRONG SIZED INCREASE OF 1448 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED DESPITE A SMALL 9 CENT LOSS IN PRICE OF SILVER/AND A CLOSING PRICE OF $17.14 // TUESDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY.

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.7050 BILLION OZ TO BE EXACT or 100.7% of annual global silver production (ex Russia & ex China).

FOR THE NEW MAR DELIVERY MONTH/ THEY FILED AT THE COMEX: 124 NOTICE(S) FOR 620,000 OZ OF SILVER.

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.70//TODAY’S RECORD OF 244,705 IS SET WITH A PRICE OF: 18.91 (FEB 25/2020)

.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ; AUGUST 10.025 MILLION OZ/ SEPT 43.030 MILLION OZ//OCT: 7.665 MILLION OZ// NOV: 2.630 MILLION OZ//DEC: 20.970 MILLION OZ; JAN: 5.075 MILLION OZ.//FEB 1.480 MILLION OZ//MAR: 23.005 MILLION OZ/APRIL 4.660 MILLION OZ//MAY 45.220 MILLION OZ

- THE RECORD PRIOR TO TODAY WAS SET IN FEB 25/2018: 244,710 CONTRACTS, WITH A SILVER PRICE OF $18.90//.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017 RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

GOLD

IN GOLD, THE COMEX OPEN INTEREST FELL BY A CONSIDERABLE SIZED 8349 CONTRACTS TO 519,374 AND FURTHER FORM OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE CONSIDERABLE SIZED LOSS OF COMEX OI OCCURRED WITH OUR HUGE COMEX LOSS IN PRICE OF $23.05 /// COMEX GOLD TRADING// TUESDAY// WE HAD STRONG BANKER SHORT COVERING ,HUGE SPREADER COMEX GOLD LIQUIDATION, A SMALL SIZED INCREASE IN GOLD OZ STANDING AT THE COMEX, ALONG WITH ZERO LONG LIQUIDATION ACCOMPANYING A HUGE EX. FOR PHYSICAL ISSUANCE. THIS ALL HAPPENED WITH OUR LARGE LOSS IN THE PAPER PRICE OF GOLD.

WE HAD A VOLUME OF 0 4 -GC CONTRACTS//OPEN INTEREST 10

WE LOST A GOOD SIZED 3229 CONTRACTS (10.043 TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A HUGE SIZED 11,576 CONTRACTS:

CONTRACT. MAY: 0, AND JUNE 11,576.; AUG 0 AND ALL OTHER MONTHS ZERO//TOTAL: 11,576. The NEW COMEX OI for the gold complex rests at 519,374. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A SMALL SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 3229 CONTRACTS: 8349 CONTRACTS DECREASED AT THE COMEX (MOSTLY FROM SPREADER LIQUIDATION) AND 11,576 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 3229 CONTRACTS OR 10.043 TONNES. TUESDAY, WE HAD A HUGE LOSS OF $23.05 IN GOLD TRADING……

AND WITH THAT LOSS IN PRICE, WE HAD A GOOD SIZED GAIN IN TOTAL/TWO EXCHANGES GOLD TONNAGE OF 10.043 TONNES!!!!!! THE BANKERS/OFFICIAL SECTOR SUPPLIED INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER WITH RECKLESS ABANDON. THE BANKERS WERE SUCCESSFUL IN THEIR ATTEMPT TO LOWER GOLD’S PRICE (IT FELL $23.05).AND IT ALSO SEEMS THAT THEIR ATTEMPT TO FLEECE ANY GOLD LONGS FROM THE GOLD ARENA WAS UNSUCCESSFUL (SEE BELOW).

4 GC VOLUME: 0 // open interest 10

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES:

WE HAD A HUGE SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (11,576) ACCOMPANYING THE SMALL SIZED LOSS IN COMEX OI (8349 OI): TOTAL GAININ THE TWO EXCHANGES: 3229 CONTRACTS. WE NO DOUBT HAD 1 )CONSIDERABLE BANKER SHORT COVERING, 2.)A SMALL INCREASE IN OUNCES STANDING AT THE GOLD COMEX FOR THE FRONT MAY MONTH, 3) ZERO LONG LIQUIDATION; 4) CONSIDERABLE COMEX OI LOSS, 5) HUGE GOLD COMEX SPREADER LIQUIDATION… AND …ALL OF THIS WAS COUPLED WITH OUR STRONG LOSS IN GOLD PRICE TRADING//TUESDAY//$23.05

THE STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS IS DUE TO THE LACK OF PREMIUM IN GOLD (UNLIKE SILVER). IT IS NOW PROFITABLE FOR THE BANKERS TO ENGAGE IN THESE VEHICLES DUE TO THE LACK OF PREMIUM IN GOLD.

SPREADING OPERATIONS

OUR SPREADING OPERATION HAS NOW SWITCHED INTO GOLD…..

SPREADING OPERATION FOR OUR NEWCOMERS:

WE HAVE NOW COMMENCED IN SILVER THE ILLEGAL SPREADING OPERATION \ FOR NEWCOMERS, HERE ARE THE DETAILS:

SPREADING LIQUIDATION HAS NOW STOPPED IN SILVER AS THEY NOW BEGIN TO MORPH INTO GOLD AS WE HEAD TOWARDS THE NEW FRONT MONTH WILL BE JUNE.

FOR THOSE OF YOU WHO ARE NEW, HERE IS THE MODUS OPERANDI OF THE SPREADERS AND THE CRIMINAL ELEMENT BEHIND IT:

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR;

THE SPREADING LIQUIDATION OPERATION IS NOW OVER FOR SILVER..AND WE WILL NOW MORPH INTO AN ACCUMULATION PHASE OF SPREADING CONTRACTS FOR GOLD. THEY WILL ACCUMULATE CONSIDERABLE AMOUNT OF THE CONTRACTS AND THEN LIQUIDATE ONE WEEK PRIOR TO FIRST DAY NOTICE

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO GOLD AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX SILVER OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE IN THIS NON ACTIVE MONTH OF MAY. BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN GOLD WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JUNE), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2020 INCLUDING TODAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 18 TRADING DAY(S) IN TONNES: 220.62 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2019, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 220.62/3550 x 100% TONNES =6.21% OF GLOBAL ANNUAL PRODUCTION

ISSUANCE OF EXCHANGE FOR PHYSICAL GOLD HAS DISSIPATED THIS MONTH…THE COST TO THE BANKERS TO CARRY THESE CONTRACTS IN LONDON IS BECOMING TOO GREAT FOR THEM.

ACCUMULATION OF GOLD EFP’S YEAR 2020 TO DATE: 2781.47 TONNES

JANUARY 2220 TOTAL EFP ISSUANCE; : 570.19 TONNES

FEB 2020 TOTAL EFP ISSUANCE : 653.78 TONNES

MARCH TOTAL EFP ISSUANCE 1,098.93 TONNES (*AND A NEW ALL TIME RECORD ISSUANCE//22 DAYS)

APRIL TOTAL EFP. ISSUANCE: 243.45 TONNES (EFP ISSUANCE BECOMING A LOT LESS)

MAY TOTAL EFP ISSUANCE: 190.84 TONNES (EFP ISSUANCE STILL LOW// PREMIUM COST TO THE BANKERS IS HUGE..SO ISSUANCE IS LESS)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A STRONG SIZED 1448 CONTRACTS FROM 156,737 UP TO 158,185 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 2 3/4 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.

ALL OF THE GAIN IN COMEX OI WAS DUE TO 1) CONSIDERABLE BANKER SHORT COVERING , 2) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS (SEE BELOW), 3) A TINY DECREASE IN SILVER OZ STANDING AT THE COMEX FOR MAY AND 4) ZERO LONG LIQUIDATION

EFP ISSUANCE 680 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

FOR FEB. 0; FOR MAR 0: AND MAY: 0 JULY: 680 CONTRACTS AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 680 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1685 CONTRACTS TO THE 680 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A STRONG GAIN OF 2128 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 10.681 MILLION OZ!!! OCCURRED WITH THE 9 CENT LOSS IN PRICE///

RESULT: A STRONG SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE 9 CENT LOSS IN PRICING THAT SILVER UNDERTOOK IN PRICING// TUESDAY. WE ALSO HAD A STRONG SIZED 680 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED DOWN 9.74 POINTS OR 0.34% //Hang Sang CLOSED DOWN 88.30 POINTS OR 0.36% /The Nikkei closed UP 148.06 POINTS OR 0.30%//Australia’s all ordinaires CLOSED DOWN .09%

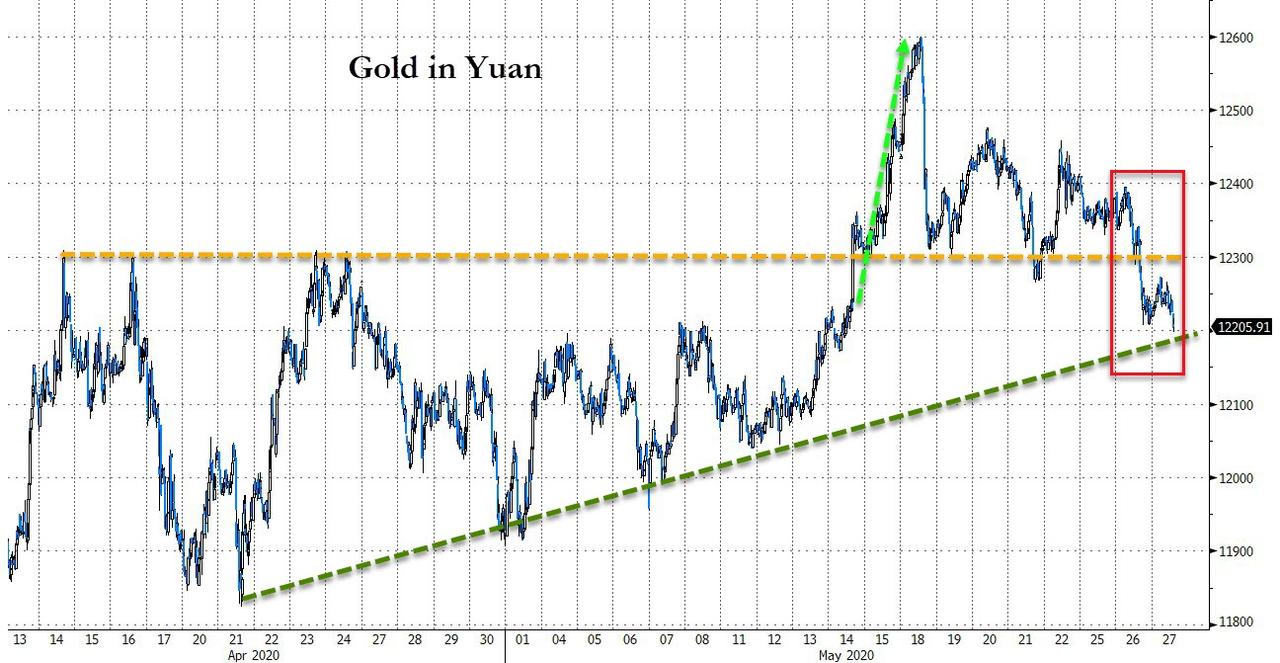

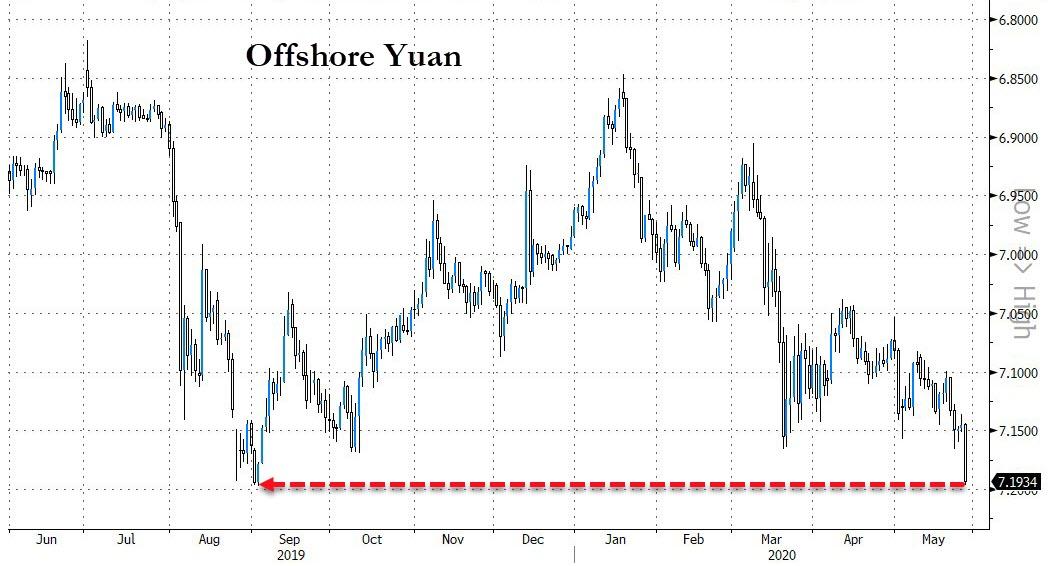

/Chinese yuan (ONSHORE) closed DOWN at 7.1563 /Oil UP TO 33.97 dollars per barrel for WTI and 35.59 for Brent. Stocks in Europe OPENED GREEN// ONSHORE YUAN CLOSED DOWN // LAST AT 7.1563 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 7.1715 TRADE TALKS STALL//YUAN LEVELS GETTING VERY DANGEROUSLY PAST 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

end

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

March 4.2019

Parker City News

JP Morgan faces potential class action lawsuit after guilty pleas by a former metals trader

Traders from across the U.S. are banding together to accuse J. P. Morgan Chase of manipulating precious metals markets for years.

At least six lawsuits, all making similar allegations against the nation‘s largest bank, have been filed in New York federal court in the past month, since federal prosecutors in Connecticut with a former J. P. Morgan Chase metals trader.

The cases could potentially include thousands of people who traded in the precious metals market. The White Plains, N.Y., law firm Lowey Dannenberg is asking the court to combine the cases and name it as the lead.

The law firm‘s commodities group is led by Vincent Briganti, the attorney who filed the first lawsuit on behalf of Dominick Cognata, a New York resident who alleges he suffered losses due to J. P. Morgan‘s trading conduct in the silver and gold futures and options markets.

A combined case, seeking class action status, would include anyone who purchased or sold futures contracts or an option on NYMEX platinum or palladium or COMEX silver or gold between at least Jan. 1, 2009, and Dec. 31, 2015. The lawyers believe that “at least hundreds, if not thousands” of traders would be eligible to join the case.

Named as defendants in all of the lawsuits are John Edmonds, a 36-year old former metals trader at J. P. Morgan, a group of yet-to-be-identified precious metals traders and the bank.

Edmonds, a New York resident, pleaded guilty in October to one count of conspiracy to defraud the market and manipulate prices of precious metals futures contracts and one count of commodities fraud. In the criminal plea, Edmonds admitted that he and other “unnamed co- conspirators” at J. P. Morgan, fraudulently manipulated precious metals markets from 2009 to 2015, the same time frame covered in the class action suits.

Briganti filed the initial class action on Nov. 7, just one day after the Justice Department unsealed Edmonds‘ plea in the U.S. District Court of Connecticut.

Edmonds admitted in his guilty plea that he deployed the illegal trading scheme hundreds of times with the direct knowledge and consent of his immediate supervisors. Plaintiffs say they have suffered economic injury, including monetary losses, as a direct result of actions by Edmonds and the other unnamed J. P. Morgan metals traders in the futures and options contracts.

One of the suits alleges that “the number of unlawful trades that JP Morgan traders executed in precious metals futures markets is at least in the thousands.”

J. P. Morgan declined to comment. Lowey Dannenberg did not respond to a request for comment by CNBC.

The Justice Department‘s criminal investigation is still ongoing and recently caused a separate related civil case to be put on hold for at least six months while the government continues its investigation. That civil lawsuit, which also accuses J. P. Morgan of rigging the precious metals market, was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders.

After reviewing the details of the plea agreement, David Kovel, the attorney for Shak‘s suit, sought to re- interview Edmonds, along with two other current and former senior traders at the bank. However, the government argued that reopening questioning would be detrimental to the ongoing criminal investigation. The federal judge overseeing the proceedings ordered a six-month stay in the civil case.

Kovel declined to comment.

Edmonds was originally scheduled to be sentenced in Hartford, Conn., on Wednesday, Dec. 19, but a court filing on Nov. 27 shows the sentencing has been postponed until June. A spokesman for the U.S. Attorney for Connecticut could not elaborate on why the sentencing was postponed since the court filing is under seal.

-END-

S&P Futures Storm Back Over 3,000 On “Recovery Hopes”, Stimulus Bonanza

A few weeks ago we proposed that what “Phase 1 trade deal hopes” were for 2019, so “Economic Recovery hopes” would be for 2020, and the overnight session was just another indication of that, and after sliding back under 3,000 just before the Tuesday close on renewed concerns about a US escalation over Hong Kong, S&P futures and European stocks stormed higher because, as Reuters put it “investors focused on progress in reopening economies” while an avalanche of fiscal stimulus including 117 trillion yen out of Japan and €750 billion out of Europe, helped spark animal spirits. The Euro jumped above 1.10 for the first time since March, Treasuries slumped further while gold tumbled below 1700.

The pattern is so simple, even an economist can spot it, in this UBS’ global wealth chief economist Paul Donovan:

Today is following the standard pattern—rhetoric between the US and China is ignored, and optimism over economic stimulus is the focus. US President Trump promised unspecified action against China by the end of the week—but markets cannot be expected to pay attention to every comment or Tweet on the Trump Twitter Feed. That would be exhausting.

Despite dismal economic data and corporate earnings, unprecedented monetary and fiscal stimulus, the easing of lockdowns and optimism about an eventual COVID-19 vaccine have powered a rally, helping the S&P 500 end at its highest level since early March on Tuesday. On Tuesday the benchmark index, however, closed just short of 3,000 points, a key psychological level, after President Donald Trump said the United States would announce before the end of the week its response to China’s planned national security legislation for Hong Kong. Those concerns were quickly extinguished overnight as a new wave of buying emerged in the overnight session.

At 8 am ET, S&P 500 e-minis EScv1 were up 1.16% at 3025, after the S&P500 closed up 1.23% at 2,991.77 on Tuesday. Travel-related stocks, which were among the worst hit in the sell-off earlier this year, continued to outperform. United Airlines Holdings, American Airlines Group rose more than 7% in premarket trade. Planemaker Boeing is expected to announce U.S. job cuts this week, people briefed on the plans and a union said. Its shares rose 3.1%. Walt Disney was set to announce its proposal for a phased reopening of its Orlando, Florida, theme parks to a local task force on Wednesday. Disney shares gained 1.9%.

As Bloomberg writes, “Investors have taken daily escalations in US-China friction in stride, including possible sanctions over Beijing’s crackdown in Hong Kong, as they drive global stocks to levels not seen since early March on hopes that economies are beginning to recuperate after a deep downturn.”

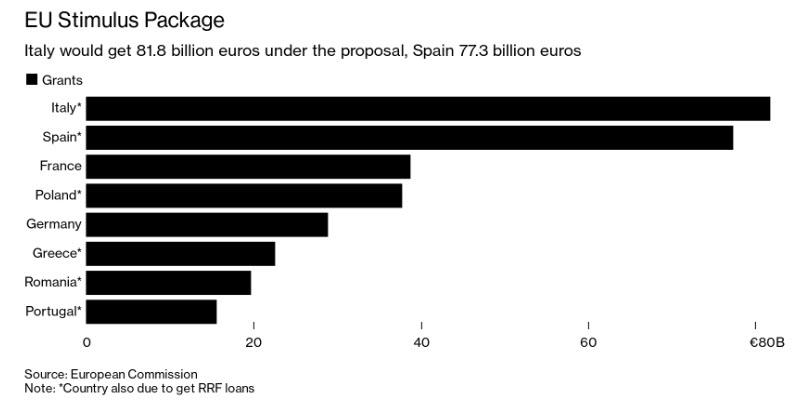

In Europe, the Stoxx 600 Index was headed toward its third daily increase and Italy’s government bonds rose following news the European Commission’s package of grants and loans would total up to 750 billion euros, in an unprecedented push to overcome the region’s deepest recession in living memory.

Earlier in the session, Asian stocks closed mixed in the wake of the latest Sino-American flare-up, and China’s yuan slipped, nearing its weakest level on record against the dollar. India’s S&P BSE Sensex Index and Japan’s Topix Index rose, and Singapore’s Straits Times Index and Hong Kong’s Hang Seng Index fell. The Topix gained 1%, with Torex Semiconductor and J-Lease rising the most after Bloomberg reported that the Abe administration is compiling a new 117 trillion yen ($1.1 trillion) stimulus package. The Shanghai Composite Index retreated 0.3%, with Kingfa Sci & Tech and Zhejiang Jiuzhou posting the biggest slides.

The recent equity rally “is an indication that investors are getting optimistic about the reopening of the economy and the drug-treatment development,” Katerina Simonetti, senior portfolio manager at UBS Private Wealth, said on Bloomberg TV. “We hope that it will eventually lead to a normalization in the market, but we have to keep an eye on the re-emergence of virus cases.”

In rates, Treasuries gave back earlier gains after news that the European Commission aims to mobilize EU750b for European recovery, including EU500b in grants and EU250b in loans. Yields flipped back to cheaper on the day across a slightly flatter curve. Stocks remain elevated, also capping Treasuries, with as S&P 500 futures extend beyond 3000 mark during Asia session. U.S. auctions resume with 5-year note sale for a record size $45b ahead of a 7-year offering Thursday. Yields out to seven years are cheaper by ~1.6bp vs. Tuesday close, while long-end yields up slightly less, flattening 5s30s by 1bp; while 10-year yields hover around 0.71%.

In FX, the dollar gave up earlier gains and many risk-sensitive G-10 currencies swung from declines to advances gains against the greenback as risk appetite picked up in the European session; the Swiss franc was the worst performer as it sold off amid a squeeze versus the euro. The euro rebounded from an early drop, rising a second day; Spanish, Portuguese long-end debt outperformed euro-area peers amid a bid for duration and after Spain didn’t mandate a bond syndication this week. The pound erased most losses, after earlier falling against the dollar as domestic political pressure on Prime Minister Boris Johnson intensified, with the government moving nearer the next round of Brexit talks with the European Union. The Chinese yuan dropped as the Trump administration weighed a range of sanctions against China and protests returned to the streets of Hong Kong.

In commodities, WTI crude oil was steady at about $34 a barrel in New York after declining modestly from the highest settlement in 11 weeks on signs Russia was planning to start easing supply cuts from July, while tensions between the U.S. and China escalated amid the specter of sanctions. Gold briefly dropped below $1,700 before recovering some losses.

U.S. economic data calendar includes May Richmond Fed manufacturing index at 10am ET; GDP, durable goods orders, personal income/spending, PCE deflator, MNI Chicago PMI and University of Michigan sentiment also this week

Market Snapshot

- S&P 500 futures up 0.8% to 3,017.25

- STOXX Europe 600 up 0.5% to 350.63

- MXAP up 0.4% to 149.86

- MXAPJ down 0.08% to 475.04

- Nikkei up 0.7% to 21,419.23

- Topix up 1% to 1,549.47

- Hang Seng Index down 0.4% to 23,301.36

- Shanghai Composite down 0.3% to 2,836.80

- Sensex up 2.9% to 31,496.11

- Australia S&P/ASX 200 down 0.09% to 5,775.01

- Kospi up 0.07% to 2,031.20

- German 10Y yield fell 2.1 bps to -0.45%

- Euro down 0.1% to $1.0967

- Italian 10Y yield fell 2.4 bps to 1.379%

- Spanish 10Y yield rose 3.8 bps to 0.664%

- Brent futures down 1.5% to $35.62/bbl

- Gold spot down 0.1% to $1,708.34

- U.S. Dollar Index up 0.2% to 99.12

Top Overnight News

- The European Union’s executive arm will propose a fiscal stimulus package of 750 billion euros ($823 billion), of which 500 billion euros will be distributed in the form of grants to member states, and 250 billion euros in loans, a person familiar with the matter says, declining to be named, in line with policy. The package will be partly funded via joint debt issuance

- The euro-area economy is faring worse than hoped, facing a recession as bad as the European Central Bank’s more pessimistic forecasts, according to President Christine Lagarde. Output is set to shrink between 8% and 12%, she said, with estimates for a milder slump now “out of date.”

- The House of Representatives is poised to give final passage Wednesday to legislation that would sanction Chinese officials for human rights abuses against Muslim minorities, the latest in a series of moves by Congress and the White House to put pressure on the Beijing government

- The U.S. Treasury Department could impose controls on transactions and freeze assets of Chinese officials and businesses as China pushes a security law for Hong Kong, according to people with knowledge of the matter

- Europe’s push to revive battered economies looks to be on track, as coronavirus infections show no sign of a resurgence during the winding down of restrictions on daily life

- China’s efforts to tighten its grip on Hong Kong pose a threat to the rules-based international order, EU foreign policy chief Josep Borrell said in a letter to the bloc’s 27 foreign ministers, calling on member states to respond with a “robust” message

Asian equity markets traded indecisively for most of the session as the broad global rally stalled following the handover from Wall St, where all major indices finished positive although staggered heading into the close after reports the US is considering sanctions on Chinese officials and firms over Hong Kong, while President Trump later noted we will hear about US actions on China by the end of the week. ASX 200 (U/C) declined heavily at the open with the index pressured by weakness in the metals complex and underperformance in gold miners, although strength in energy and financials provided a cushion to help the index retrace the initial losses. Nikkei 225 (+0.7%) was temperamental with an improvement in the risk appetite seen after initial details of the 2nd extra budget were announced which is valued at JPY 117.1tln and will include direct spending of JPY 72.7tln, while PM Abe suggested they will provide JPY 140tln in financial support to companies. Hang Seng (-0.3%) and Shanghai Comp. (-0.3%) were cautious amid the heightened US-China tensions but with downside stemmed after a firm liquidity injection by the PBoC and as participants digested the latest Chinese Industrial Profits data for April which showed a decline of just 4.3% compared to the 34.9% slump in the prior month. Finally, 10yr JGBs were lower despite the tentativeness in the region with prices subdued amid the lack of BoJ presence in the markets and anticipation of increased supply with Japan’s 2nd extra budget to involve an additional JPY 31.9tln of JGB issuances to push the total issuances for the current fiscal year to JPY 210tln.

Top Asian News

- Hong Kong Police Arrest More Than 240 in Wednesday Protests

European equities have kicked the session off on the front-foot once again (Eurostoxx 50 +1.9%) in a continuation of recent gains with mounting US-China tensions unable to curtail momentum; and further support arising most recently from reports around the EU recovery fund proposal – to be formally unveiled later today. Instead, the composition of today’s movers and shakers across the continents takes a similar form to those yesterday with travel & leisure names continuing to benefit from ongoing reopening optimism with recent easing of lockdown measures not currently triggering any material pick-up in COVID-19 cases/deaths in the region. As such, Tui AG (+20.4%) sit at the top of the leaderboard once again with IAG (+4.2%) shares also extending on yesterday’s gains and the troubled cruise-line sector seeing some reprieve with Carnival shares up over 8%. Elsewhere, banking names are firmer this morning, in-fitting with price action in their transatlantic counterparts yesterday on Wall St. with upside seen for the likes of RBS (+8.6%), BNP Paribas (+8.4%), SocGen (+9.4%), Barclays (+7.8%), Commerzbank (+7.7%), BBVA (+4.6%). Renault (+15.2%) and Peugeot (+8.2%) are benefiting from yesterday’s announcement of a EUR 8bln support package from the French government with the former also reportedly mulling potential cost savings of EUR 2bln by 2024. To the downside, underperformance can be seen in defensive names with health care the laggard in Europe, whilst IT names are also seen lower with Infineon (-2.0%) shares hampered by the Co.’s decision to raise capital.

Top European News

- Virgin Atlantic Suitors Narrow With Clock Ticking on Rescue

- PharmaSGP to Sell Stock in Frankfurt IPO as Markets Heat Up

- New CEO of Norway’s $1 Trillion Fund in Make-Or-Break Moment

- Denmark Told It Can Start Winding Down Coronavirus Aid in July

In FX, consolidation saw the DXY back with a 99.000 handle in APAC trade following yesterday’s heavy selling. The index remains choppy throughout the session as it hit a high of 99.350 before declining on initial details of European Recovery Fund, with losses prompting the DXY to relinquish the round figure to a low of 98.710. Meanwhile, the Yuan continued to decline through late APAC hours after US President Trump said US actions regarding China will be unveiled by the end of the week, whilst sources noted US is mulling sanctions on Chinese officials and firms over Hong Kong. USD/CNY rise to a whisker from 7.1600 (vs. low 7.1350) with the PBOC issued a firmer fix after the dollar decline. USD/CNY sees its 2019 peak at 7.1844 whilst its offshore counterpart resides north of 7.1700 (vs. low 7.1430) ahead of its record high at 7.1965. Focus today will remain on US-Sino developments alongside the unveiling of the EC Recovery Fund proposal.

- EUR, GBP – The Single Currency fought back against the Dollar after reports emerged the European Commission is to propose EUR 750bln for the European Recovery Fund, comprising of EUR 500bln in grants and EUR 250bln in loans. ECB President Lagarde did little to dent the EUR but posited that the ECB’s mild GDP scenario of -5% is outdated – with the metric likely in the range of the medium (-8%) to severe (-12%) scenarios. ECB aside, eyes are on the unveiling of the European Recovery Fund later in the day, with focus on sentiment across EU members, namely the North and South, as the Commission’s proposal is unveiled. EUR/USD took out the 1.1000 handle alongside its 200 DMA (1.1011) having topped its 100 DMA (1.0957) and with EUR 1bln option expiries scattered between 1.0950-60, with a further EUR 1.8bln around 1.0990-1.1000. Meanwhile, Sterling remains lethargic around 1.2300 vs. the USD as overnight weakness emanated from reports UK Chancellor Sunak is set to announce this week that the government will soon stop allowing companies from placing employees on the furlough scheme. Cable trades in the middle of a 1.2290-1.2350 parameter ahead of a potential barrier at 1.2360 (50% Fib from 30 Apr-18 May move).

- AUD, NZD, CAD – High-beta FX largely mirrors USD action, but the Kiwi outperforms as the AUD/NZD cross homes in on the 1.0700 mark to the downside. Meanwhile the Loonie and Aussie initially eke mild gains before the Dollar saw broad losses. NZD/USD reclaimed 0.6200 and topped its 100 DMA around 0.6203 (vs low 0.6175). The Aussie hoverd on either side of 0.6650 before taking out its 200 DMA (0.6658) to the upside and matching yesterday’s high prints at 0.6675. USD/CAD holds onto a bulk of yesterday’s losses and remains sub-1.3800, with the next support point seen at the psychological 1.3750 ahead of 1.3700 mark which coincides with the pair’s 100DMA.

- JPY, CHF – Mixed trade for the traditional safe-haven FX with considerable weakness seen in the Franc relative to the peers amid potential SNB presence. EUR/CHF eyes 1.0650 to the upside whilst USD/CHF trades north of 0.9700 vs. lows of 1.0587 and 0.9650 respectively. The JPY meanwhile remains flat on either side of 107.50 and within a tight 25-pip or so range awaiting fresh fundamental developments and a clear risk tone.

In commodities, WTI and Brent front month futures see a session of modest losses thus far as the July contracts hover around USD 34/bbl and USD 35.75/bbl respectively – both within tight ranges of less that USD 1/bbl, and seemingly deriving support from general sentiment. Eyes now turn to the upcoming OPEC meeting starting June 9th, a day after the proposed JMMC meeting – with focus on the producer’s assessment of the oil market and effectiveness of the current output pact. Participant will also be on the lookout for countries that voice for an extension of current curtailments. Aside from that, US-China developments remain in focus whist the EC Recovery Fund proposal could prove a sentiment risk for complex, whilst the weekly Private Inventory figures will be released later today on account of Monday’s Memorial Day Holiday. Spot gold prices mirrors USD action and threatens a test of USD 1700/oz to the downside (vs high USD 1715/oz). Copper prices tracked Chinese stocks and the yuan as US-China tensions continue to mount.

US Event Calendar

- 7am: MBA Mortgage Applications, prior -2.6%

- 10am: Richmond Fed Manufact. Index, est. -40, prior -53

- 12:30pm: Fed’s Bullard Discusses Economy During the Pandemic

- 2pm: U.S. Federal Reserve Releases Beige Book

- 2pm: U.S. Federal Reserve Releases Beige Book

- 3pm: Fed’s Bostic to Take Part in Virtual Discussion on Economy

DB’s Jim Reid concludes the overnight wrap

While we have stopped the Corona Crisis Daily, we have updated our tables from it and have published them in the pdf of this report today. We may do it every day (or every few days) depending on the demand. Let us know. The latest highlights are that Brazil is now the second most infected country in the world in terms of overall recorded cases with nearly 391k. Until Brazil’s total infections passed New York this past Sunday, the US state has had more total cases than any country in the world since passing Italy in early April. Recently however, case growth and new fatalities in New York State look more akin to Germany and Southern Europe and are now in the 0.1-0.5% range. See the full tables in the pdf for this and more.

Global equities rose yesterday as risk assets surged following the holiday weekend in the UK and US. The positive sentiment was driven by a mix of economic data turning better, more and more economies reopening, the possibility for additional stimulus on both sides of the Atlantic, and hopes over another potential vaccine and treatment from reports out of Merck. Though rising US/China tensions in the last couple of hours of trading took a little shine off the session.

The S&P 500 had rallied roughly +1.8% until the last hour of the day, trading through the 3000 level we first hit in July 2019 but last saw on 5th March, 4 days before Italy locked down on the 9th. The S&P closed at +1.23% and back below 3000 though as headlines materialised suggesting that the Trump administration were considering sanctions over the recent Chinese actions surrounding Hong Kong. Later on Bloomberg reported that amongst the measures the US is considering one is that the Treasury Department could impose controls on transactions and freeze assets of Chinese officials and businesses and added that other measures under consideration include visa restrictions for Chinese Communist Party officials.

Notwithstanding the late dip, the rally saw the virus laggards take the reins, as Banks (+7.86%) and Autos (+4.70%) were the leading industry groups in the US, with Technology and Healthcare the worst performers. Highlighting the lag in healthcare stocks, Merck was only up +1.17% on the news of the antiviral treatment and potential vaccine. J.P. Morgan Chase CEO Jamie Dimon made the headlines at our Deutsche Bank Global Financial Services Conference. He said that “The Fed took out the whole military and applied it. Just announcing these programs reduced spreads in the market. It’s going to save a lot of small businesses” and it’s “helping people avoid stress.” Mr. Dimon also highlighted consumer banking data that he said showed “a healthier consumer. You see that in underlying delinquencies. It’s completely different from a consumer standpoint” than what was seen during 2008. Elsewhere, the Fed’s Bullard said in an interview that although the jobless rate was 14.7% last month, “I think we will be under double digits by the end of the year.”

In Europe, the STOXX 600 was up +1.08% with 17 of 19 sectors higher on the day. Travel and Leisure was the best performing sector, up +6.94%, as news came through that the German government is planning to lift a travel warning on its citizens to 31 European countries on June 15. Chancellor Merkel’s cabinet could approve it later today.

Staying with Europe, spreads of 10yr Italian (-9.0bps), Spanish (-5.1bps), Greek (-7.7ps) and Portuguese (-8.5bps) debt to bunds had all narrowed as 10yr Bund yields rose 6.5bps to -0.429% and US 10yr Treasury yields were up +3.7bps to 0.697%.

This comes ahead of the expectation that today will see the release of proposals from the European Commission over the European recovery fund. Can they release credible proposals given the large void between the Merkel/Macron (MM) proposals and the Frugal Four (FF) counter plan? The recent tightening suggests that the MM proposal was a turning point whatever the bumps are along the way. DB’s Mark Wall suggested in his weekend blog (link here) about the FF counter proposal that the risks of delays to the fund have risen but ultimately he expects agreement on its inception. European Commission President von der Leyen speaks before the European Parliament (EP) later so it’s likely it will coincide with that. From looking at the draft agenda from the EP it looks like the action will be at around 13:30-15:00 CET.

Keeping with the stimulus theme, US Senate Leader Mitch McConnell has been one of the most reticent on the prospect of further stimulus in the US. Though in a public appearance in his home state of Kentucky, where he is up for re-election this autumn, he said, “a lot of Americans have lost their jobs, so we need to make sure we have unemployment insurance properly funded for as long as we need and that could well lead to yet another bill.” Though he continues to believe that it needs to be more targeted than $3 trillion bill that the House passed 2 weeks back.

Stimulus talk is the main theme overnight too with news that the Japanese government looks set to unveil another $1.1tn package helping the Nikkei to gain +0.74%. However it’s more mixed elsewhere with the Kospi and ASX up (+0.13%) and (+0.46%) respectively, while the Hang Seng (-0.39%) and Shanghai Comp (-0.05%) are lagging as renewed protests by pro-democracy groups in Hong Kong and the sanction reports for China weigh on those markets. In FX, the onshore Chinese yuan is down -0.33% to 7.1583, the lowest in 8 months while all G-10 currencies are also trading weak against the greenback. Elsewhere, futures on the S&P 500 are up +0.63% and WTI oil prices are down -0.35% to $34.25.

In other overnight news, ECB Executive Board member Isabel Schnabel said in an interview with the FT that “If we judge that further stimulus is needed, the ECB will be ready to expand any of its tools in order to achieve its price stability objective”. Schnabel also said that “with respect to the Pandemic Emergency Purchase Programme, this concerns the size but also the composition and the duration of the program. We are ready to react to new data coming in.” The euro is trading down -0.20% as we go to print.

Economic data continued to improve from the April and March’s lows yesterday, while still showing the toll the coronavirus has caused across the global economy. The majority of data came from the US yesterday. The Chicago Fed’s National Activity Index fell to -16.74, far exceeding the -3.50 expectations and down from last month’s -4.97 reading. Only 6 of the 85 monthly indicators made a positive contribution to the diffusion index, while all 79 others were negative. Last month was already a record low for the index, but the current reading is over four times worse than the lowest past reading. On the other hand, US consumer confidence, as measured by the Conference Board’s index, rose by 0.9 points to 86.6 (87.0 expected) from last month’s revised 85.7. Interestingly, the present situation component fell further to 71.1 from 73, but was offset by a rise in expectations (96.9 from 94.3). In other somewhat good news, new home sales rose to 623k from 619k in April far exceeding the 480k expectations, though it should be noted that overall sales are down -6.2% y/y. Lastly, Germany’s June GfK consumer confidence survey rose to -18.9 (vs. 18.0 expected) up from -23.1 in May, meanwhile the business expectations improved to -10.4 in May compared to -21.4 in April.

To the day ahead now, and it is a fairly light macroeconomic data day. Though one highlight may be the Fed releasing its Beige Book, which highlights anecdotal information on the current economic conditions and can give insight into the effects of the shutdowns and what to expect as the reopening progress in the US. We will see China’s industrial profits for April and France’s May consumer confidence reading. There is a pair of data readings out of the US, the weekly MBA mortgage applications and the May Richmond Fed manufacturing index. In terms of central bank speakers, the ECB’s President Lagarde and the Fed’s Bullard will both give remarks. While the majority of earnings are behind us, we still have some major names reporting this week – today sees Autodesk and Royal Bank of Canada. Lastly, European Commission President von der Leyen speaks before the European Parliament as discussed above.

3A/ASIAN AFFAIRS

i)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED DOWN 9.74 POINTS OR 0.34% //Hang Sang CLOSED DOWN 88.30 POINTS OR 0.36% /The Nikkei closed UP 148.06 POINTS OR 0.30%//Australia’s all ordinaires CLOSED DOWN .09%

/Chinese yuan (ONSHORE) closed DOWN at 7.1563 /Oil UP TO 33.97 dollars per barrel for WTI and 35.59 for Brent. Stocks in Europe OPENED GREEN// ONSHORE YUAN CLOSED DOWN // LAST AT 7.1563 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 7.1715 TRADE TALKS STALL//YUAN LEVELS GETTING VERY DANGEROUSLY PAST 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3 a./NORTH KOREA/ SOUTH KOREA

South Korea

b) REPORT ON JAPAN

Japan goes bananas: huge QE of 117 trillion stimulus (MMT/helicopter money)

This equates to 1.09 trillion usa dollar QE

(zerohedge)

“Fiscal Firehose”: Japan Approves Record 117 Trillion Stimulus Package

It’s a fiscal firehose.

On the same day as Europe’s “Watershed Moment” saw the European Commission propose a €750BN virus recovery fund, funded by joint debt, and which would offer €500BN in grants to struggling European nations, Japanese Prime Minister Shinzo Abe’s cabinet approved a new $1.1 trillion stimulus package that includes significant direct spending, to counteract the coronavirus pandemic pushing the world’s third-largest economy deeper into recession.

The record stimulus of 117 trillion yen, which as Reuters reported, will be funded partly by a second extra budget, followed another 117 trillion yen package rolled out last month. The new package takes Japan’s total spending to combat the virus fallout to 234 trillion yen ($2.18 trillion), or about 40% of gross domestic product, and will send its already world-record debt load into the stratosphere.

The combined spending ranks among the world’s largest fiscal packages to deal with the coronavirus, approaching the size of the United States’ $2.3 trillion aid programme.

According to the Ministry of Finance, the latest package includes 33 trillion yen in direct spending, and the balance will consists of guarantees and backstops. The new package will include measures such as higher medical spending, aid to firms struggling to pay rent and more subsidies to companies hit by slumping sales.

“We must protect business and employment by any means in the face of the tough road ahead,” Abe told a meeting of ruling party lawmakers. “We must also take all necessary measures to prepare for another wave of epidemic.”

To fund the costs, Japan will issue an additional 31.9 trillion yen in government bonds under the second supplementary budget for the current fiscal year ending in March 2021.

That record double-stimulus will push new JGB issuance this fiscal year to a record 90 trillion yen. Inclusive of issuance to roll over debt maturing during the year, Japan’s total calendar-base annual market issuance would hit a record 212 trillion yen, further straining already tattered finances.

While the Bank of Japan is likely to keep borrowing costs low with aggressive bond buying, the surprise increase in issuance of super-long bonds could trigger some market volatility, analysts quoted by Reuters said.

“The BOJ’s yield curve control should prevent a spike in long-term interest rates,” said Chotaro Morita, the chief bond strategist at SMBC Nikko Security. “Volatility in the JGB market will depend on the BOJ’s ability to control its bond purchases.”

Under Japan’s yield curve control policy, which will soon be adopted by the Fed, the BOJ guides the short-term interest rate at -0.1% and the 10-year bond yield at around 0%.

To prepare for a possible second wave of infections, the government also set aside 10 trillion yen in reserves that can be tapped for emergency spending. To facilitate financing, the government pledged to top up financial assistance to firms hit by the pandemic to 140 trillion yen, from 45 trillion yen in the previous package, by boosting interest-free lending, offering subordinate loans and supply of capital.

* * *

The packages took the size of this fiscal year’s budget to a record 160 trillion yen, with new bond issuance making up 56.3% of annual budget revenue and raising the spectre of more bond issues later to offset falling tax income.

And the punchline: Japan may not be done with helicopter money. “There’s a possibility of a third extra budget,” said Ayako Sera, market strategist at Sumitomo Mitsui Trust Bank.

“Japan may face the risk of credit downgrade in the medium to long run.” Of course it does, the question is not if but when, and that would be the beginning of the end for the world’s foremost experiment in monetary and fiscal stimulus insanity.

3 C CHINA

CHINA

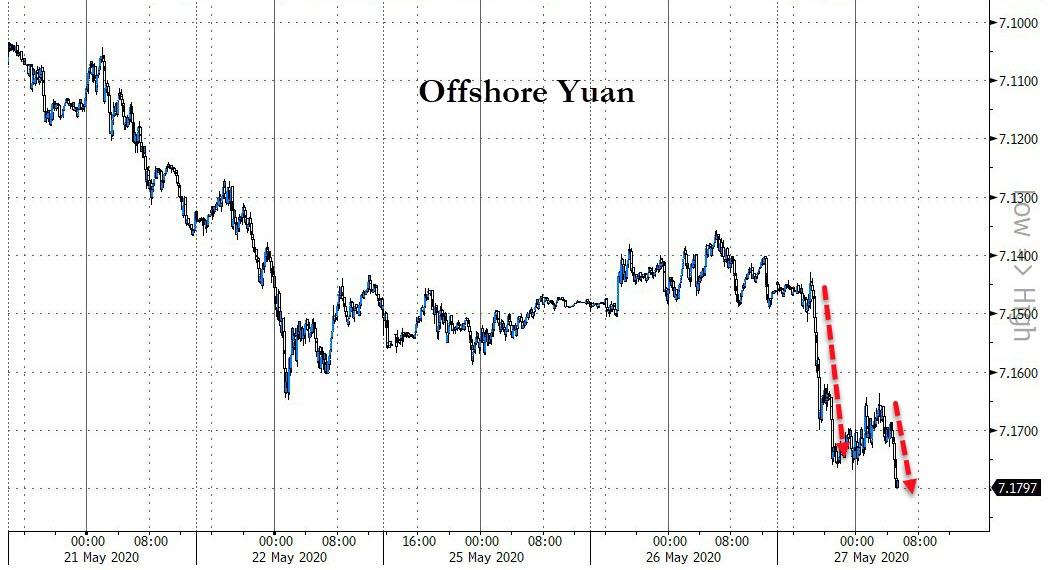

The Yuan suddenly collapses overnight. Now trading at CNY 7.1563 and CNH: 7.1715. This will probably spell trouble for China to obtain badly needed dollars.

(zerohedge)

Chinese Yuan Suddenly Tumbling

Just after 9:45pm ET the offshore yuan – the one which is not subject to the PBOC’s trading band limits – tumbled, plunging 250 pips in minutes.

The move was unexpected, following a stronger than expected setting of the USDCNY by the PBOC, whose midpoint was set at 7.1092, far stronger than the 7.1220 expected and the 12 year low of 7.1293 hit on Tuesday. The drop comes just hours after Bloomberg reported that Trump administration was considering sanctions including transaction controls, and asset freezes, over the implementation of the new national security law in Hong Kong.

While the offshore yuan is not at all time lows yet – it would need to hit around 7.20 for that – there has been no news to justify the move, with the sudden move sparking speculation that Beijing may be using it to telegraph the devaluation that could follow should the US escalate aggressively in response to a Hong Kong crackdown.

Here, once again, is a reminder from Rabobank’s Michael Every why in the current environment of escalating hostility between the US and China, the only thing that matters is the Yuan, and why in the not too distant future, the Chinese currency may have a 10-handle in front of it.

This time last year, when we were all still going abroad regularly (right now just ‘outside’ is becoming a psychological barrier if I am honest) I was traveling with a presentation titled “Clause is Cause”. This argued that from a geostrategic ‘Von Clausewitz’ perspective, not a neoliberal “Let’s assume world peace” version, the US would at some point realise the USD/Eurodollar was a weapon it could wield vs. China, and when it did we would see three key strings cut: trade; tech; and then capital flows. The first was evident during the trade war – which has not been concluded is likely to get far worse soon; the second is also abundantly clear on a variety of fronts, much to Silicon Valley’s chagrin; and potentially, now we see the start of that third step – because if the US does block this first USD50bn going in, other such steps will follow, just as they did on the previously unthinkable idea of US tariffs on China.

CNH is right to be selling off, albeit in a traditionally limited fashion, because if you don’t buy from China and you don’t help China up the value-chain and you don’t invest in China then China is not going to be getting much USD liquidity at all. The US hawks probably don’t get the Eurodollar iron logic there; they are likely just pressing buttons in anger. The outcome would be the same nonetheless.

I can hear the market bulls and technocrats of the world saying “But China has USD3 trillion in reserves!” Perhaps. Most think it’s far lower than that. And not earning USD means you have to dig into that stockpile. And when you do, the PBOC either has to contract the local money supply (because every USD is backed by 7.xx CNY on the other side of the balance sheet) or it just creates new CNY anyway and supply-demand sees CNY move sharply lower – as we have been seeing in all other EM FX. Looking at the drop in BRL, ARS, ZAR, TRY, etc., or even THB,this would be how we would get to the ‘unthinkable’ 8 (9? 10?) handle in CNY. That would also crush those other EM crosses in tandem – and AUD and NZD, as the former tries to navigate its own geopolitical spat with Beijing.

Moves like tonight suggest that either someone knows something, that something big may be coming, or the algos are just doing all they can to trigger another stop loss domino effect.

Is War Next?

Authored by James Rickards via The Daily Reckoning,

Remember the pro-democracy protests in Hong Kong against Chinese authoritarianism?

Well, guess what? They’re about to start again.

And U.S.-Chinese relations could get even worse than they are right now.

Are you prepared for a bumpy ride?

Let’s unpack this…

Last year’s protests came in response to a proposed law that would have allowed the extradition of Hong Kong residents to Beijing for trial on charges that arose in Hong Kong.

That would have deprived Hong Kong residents of legal protections in local law and subjected prisoners to torture and summary execution.

The legislation was proposed by Hong Kong’s Chief Executive Carrie Lam, who many consider a puppet of Beijing.

The demonstrations grew exponentially, ultimately involving hundreds of thousands of protesters.

The list of demands also grew to include more democracy and freedom and adherence to Hong Kong’s rule of law.

Due to social media, these protests were seen around the world.

The proposed bill behind the original protests was scrapped last October, which was a victory for the pro-democracy protesters.

The protests didn’t end altogether, but tensions were at least diffused to a great extent and the world moved on.

Well, here comes round two…

China’s Communist parliament is preparing to roll out legislation that would ban “treason, secession, sedition (and) subversion” in Hong Kong.

This is different from the previous legislation because this bill actually originates in Beijing, not Hong Kong. It’s a direct assault on Hong Kong’s democracy. The Chinese parliament would insert the legislation directly into Hong Kong’s constitution.

It’s scheduled for passage next week.

Pro-democracy activists have called for mass protests this weekend in response to what they rightly consider a Chinese invasion of their autonomy.

We could be in for a fresh round of protests, with as many or more people. China’s reaction will be key.

Will they try to put the protests down by force? That could have major consequences.

Yesterday, news emerged that the U.S. Senate is introducing bipartisan legislation to impose sanctions on officials and business entities that enforce the new law.

And President Trump warned yesterday that the U.S. would react “very strongly” to the Chinese legislation.

In response, China’s foreign ministry warned Beijing would “fight back” against any U.S. interference.

At a time when U.S.-Chinese relations are already at a low ebb due to China’s almost criminal handling of the coronavirus pandemic, it looks like things are about to get even worse.

This situation could become very interesting.

But you shouldn’t be surprised. The current trajectory of U.S.-China relations is following a familiar course. It started with the currency war…

When my first book, Currency Wars, was published in 2011, I made the point that currency wars don’t exist all the time, but when they emerge they can last for 15 or 20 years.

The reason is that the currency devaluations just go back and forth between major trading partners and no one is any further ahead in the long run.

Readers said, “OK, we get that, but what comes next?”

The answer is trade wars. Once currency devaluations fail, countries turn to tariffs to slow down imports and help their own exports.

That’s where the U.S. and China are now, with the ongoing trade war (which could get worse).

But that’s also a dead end from an economic perspective. Again, the question is: What comes next?

Well, with history as a guide, we can see that today’s pattern is a repeat of what the world went through in the 1920s and 1930s.

First came currency wars (1921–1936). Then came trade wars (1930–34) and then finally a shooting war (1939–1945).

Are we heading for another shooting war with China? The signs are not good.

Trade war tariffs can be weaponized to pursue geopolitical goals. Trump is using tariffs to punish China for its criminal negligence (or worse) in connection with the spread of the Wuhan virus to the U.S. and the rest of the world.

This also has historical precedent.

Between June and August 1941, President Franklin Roosevelt placed an oil embargo on Japan and froze Japan’s accounts in U.S. banks.

In December 1941, the Japanese retaliated with the sneak attack on Pearl Harbor. Will China now escalate its retaliation to the point of armed conflict?

We’ll find out soon, possibly in the South China Sea or the Taiwan Strait. The latest reemergence of tensions in Hong Kong only adds kerosene to the fire.

Investors should prepare for U.S.-China geopolitical tension to grow worse. Maybe a lot worse. That’s the lesson of history.

END

Coronavirus “Cover-Up” Is China’s Chernobyl: White House National Security Adviser

Authored by Steve Watson via Summit News,

The White House national security advisor Robert O’Brien has compared China’s response to the coronavirus outbreak to the Soviet Union’s cover-up of the meltdown at the Chernobyl nuclear power plant.

“They unleashed a virus on the world that’s destroyed trillions of dollars in American economic wealth that we’re having to spend to keep our economy alive, to keep Americans afloat during this virus,” O’Brien said in an NBC interview.

“The cover-up that they did of the virus is going to go down in history, along with Chernobyl.” O’Brien added.

“We’ll see an HBO special about it 10 or 15 years from now.” he urged, referring to the recent award winning dramatization of the 1986 disaster.

“This is a real problem and it cost many, many thousands of lives in America and around the world because the real information was not allowed to get out,” O’Brien further proclaimed.

“It was a cover-up. And we’ll get to the bottom of it eventually.” O’Brien asserted.

O’Brien’s comments come as Shi Zhengli, the the deputy director of the Wuhan Institute of Virology, warned that COVID-19 is ‘just the tip of the iceberg’ of unknown deadly viruses, while again denying that her lab had anything to do with the outbreak.

“If we want to prevent human beings from suffering from the next infectious disease outbreak, we must go in advance to learn of these unknown viruses carried by wild animals in nature and give early warnings.” Shi said, adding “If we don’t study them there will possibly be another outbreak.”

As details continue to emerge, China admitted recently that it did order laboratories to destroy samples of the new coronavirus in the early stage of the outbreak.

The destruction of the samples was first noted back in February. It was also noted that the Wuhan Institute of Virology, which was conducting controversial experiments into animal-to-human transmission of bat coronaviruses, altered their database in an apparent attempt to distance the lab from the outbreak.

The alteration was carried out just two days before a gene sequencing lab was ordered by the Health and Medical Commission of Hubei Province to destroy it’s coronavirus samples.

In addition, a scientific study in Austria has found that SARS-CoV-2 was likely created in a lab, barring some “remarkable coincidence” that led to the virus naturally evolving to be optimised to attack human cells.

The authors of the study believe this means that the virus “became specialized for human cell penetration by living previously in human cells, quite possibly in a laboratory.”

end

CORONAVIRUS UPDATE/CHINA/GLOBE//

China Confirms 200 New Cases In Wuhan As India’s Outbreak Passes 150k: Live Updates

Summary:

- India cases top 150k

- France discontinues use of hydroxychloroquine

- Japan, EU push new stimulus

- New Chinese study confirms COVID uses same ‘strategy’ as HIV to cripple immune system

- Wuhan finds 200 ‘asymptomatic’ cases after testing millions

- ECB’s Lagarde said eurozone economy could take 12% hit due to virus

- WHO reiterates warnings about premature reopening

* * *

California Gov. Gavin Newsom’s decision to allow retailers across the state to reopen (along with barbershops and salons in most counties) helped galvanize investors’ hopes for a “V-shaped” rebound in the US, setting US equities on the path to opening with strong gains for a second straight day on Wednesday, even after the death toll in the US surpassed 100k late Tuesday.

A few days ago, authorities in Wuhan claimed that they had tested more than 7 million people, part of an effort to quash a ‘second wave’ of the virus. Overnight, Chinese business news org Caixin reported that roughly 200 patients tested positive for the virus, all of whom were considered “asymptomatic”.

PM Narendra Modi’s heavy-handed response to the coronavirus outbreak has been credited with preventing a destabilizing outbreak in the world’s second-largest country by population. Although many Indians remain leery of the world outside their front door, infection numbers have continued to rise at a steady clip. On Wednesday, Indian public health authorities confirmed another 6,387 new infections and 170 deaths reported in the last 24 hours, bringing India’s total to 151,767 confirmed infections, and 4,337 deaths, according to Nikkei.

France’s health ministry said Wednesday it would discontinue the use of hydroxychloroquine for treating COVID-19 patients, and in all clinical trials, while health officials in India expanded the use of the controversial drug, which was famously touted by President Trump, who also claimed to be taking the medication as a kind of prophylactic. France’s decision is notable because Didier Raoult, a virologist based in Marseille, has repeatedly championed its efficacy if taken alongside zinc or a powerful antibiotic like a Z-Pak.

Across Asia and Europe, new measures to offset the tremendous cost of the outbreak were introduced on Wednesday, with the Japanese cabinet approving another 6% of GDP in stimulus spending, just one month after approving a first supplementary budget. Combined with the prior package, PM Shinzo Abe said that Japan will have pumped the equivalent of 40% of its GDP in stimulus spending into its economy. “With the largest policy package in the world, the Japanese economy will hold fast against this once in a hundred year crisis,” Abe said.

Just when we believed ‘coronabonds’ were as good as dead, the European Commission is reportedly planning to borrow as much as €750 billion to dole out to the hardest-hit countries, according to Commission President Ursula von der Leyen. As was widely reported in March and April, an alliance of wealthy northern states led Germany and the Netherlands seemed to have put the issue to rest, as they insisted that Italy and Spain can always submit to the European Stability Mechanism (and the punishing austerity it would almost certainly prescribe) if they needed emergency financing. Von der Leyen is expected to lay out the details of the new coronavirus relief fund on Wednesday afternoon in Europe.

Watch von der Leyen live:

Regardless of how the EU responds, ECB Chief Christine Lagarde, one of the most vocal advocates for “coronabonds” and a strong fiscal stimulus to revive Europe’s moribund economy, said Wednesday that the eurozone economy could shrink by as much as 12% this year as the “sudden stop” caused by the pandemic is expected to lead to a prolonged recession that’s even deeper than the post-GFC period.

Authorities in Wuhan found more than 200 asymptomatic cases of the new coronavirus since launching an ambitious plan earlier this month to test the city’s entire population, according to municipal health officials.

On May 11, health authorities in the central Chinese metropolis, where the deadly virus was first detected, ordered municipal districts to start conducting nucleic acid tests on all residents. As of Saturday, the city had carried out 6.68 million tests and discovered 206 asymptomatic cases across more than 10 districts, according to notices from the municipal health commission. About 11 million people live in Wuhan.

With the number of confirmed coronavirus cases in Brazil expected to cross the 400k-threshold on Wednesday, prosecutors in President Jair Bolsonaro’s Brazil authorized the arrest of the conservative governor of Rio de Janeiro state on suspicion of corruption, Reuters reports. The arrest follows a falling-out between the governor and Bolsonaro over the latter’s handling of the outbreak.

As the number of newly confirmed cases in the US tumbled to its lowest level since March on Tuesday, the World Health Organization reiterated warnings about the dangers of scaling back coronavirus restrictions too quickly, arguing that a “premature” push to return to normalcy could unleash a brutal ‘second wave’.

“We cannot make assumptions that just because the disease is on the way down now that it’s going to keep going down,” Mike Ryan, head of the WHO’s health emergencies program, told reporters during a briefing.