GOLD:$1735.70 UP $19.40 The quote is London spot price

Silver:17.88 UP 52 CENTS//LONDON SPOT PRICE

Closing access prices: London spot

i)Gold : $1731.00 LONDON SPOT 4:30 pm

ii)SILVER: $17.86//LONDON SPOT 4:30 pm

CLOSING FUTURES PRICES: KEY MONTHS

JUNE GOLD: $1752 CLOSE 1.30 PM// SPREAD SPOT (LONDON) VS/FUTURE JUNE: $16.80.//

CLOSING SILVER FUTURE MONTH

JULY: 1:30 PM: $1844//1:30 PM //SPREAD SPOT LONDON VS FUTURE JULY: 56 CENTS PER OZ//

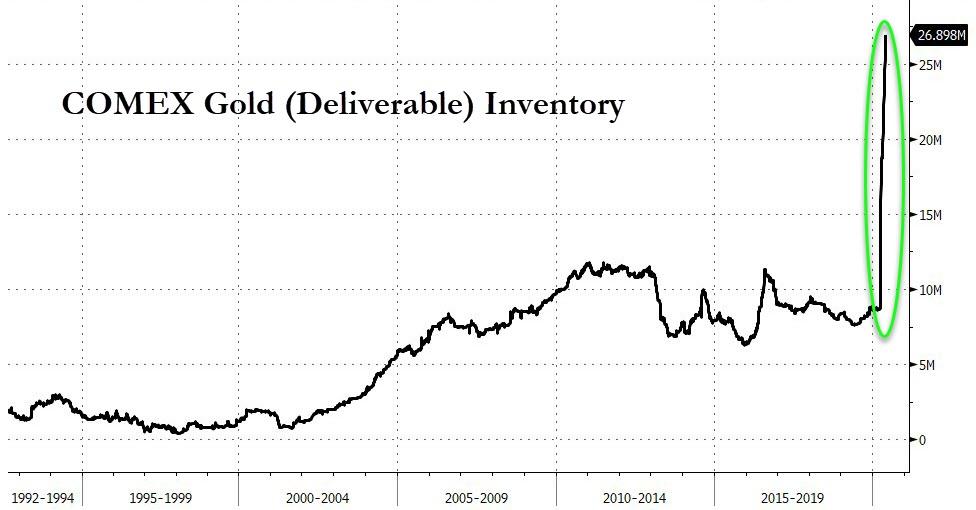

the gold market continues to be broken as future prices are much higher than spot prices. The comex is desperate to fix things but they have no available gold.

If one is to buy gold and or gold coins, the price is around $2800. usa per oz

and silver; $31.00 per oz//

LADIES AND GENTLEMEN: YOU ARE NOW WITNESSING FIRST HAND THE DIFFERENCE BETWEEN PAPER GOLD/SILVER AND THE REAL PHYSICAL STUFF!!

DO NOT PAY ANY ATTENTION TO WHAT THE CROOKS ARE DOING AT THE COMEX AND LONDON LBMA..PHYSICAL IS THE NAME OF THE GAME AND NOTHING ELSE

COMEX DATA

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING: 13,227//28,375// Goldman Sachs receiving: 5538

issued: 1430 JPM

issued: Goldman Sachs: 916

EXCHANGE: COMEX

CONTRACT: JUNE 2020 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,713.300000000 USD

INTENT DATE: 05/28/2020 DELIVERY DATE: 06/01/2020

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

072 C GOLDMAN 916 157

072 H GOLDMAN 5381

099 H DB AG 750

104 C MIZUHO 97

118 H MACQUARIE FUT 1121

132 C SG AMERICAS 153

135 C RAND 1

135 H RAND 18

152 C DORMAN TRADING 39

167 C MAREX 45

190 H BMO CAPITAL 120

323 C HSBC 1697

323 H HSBC 144

355 C CREDIT SUISSE 224 138

357 C WEDBUSH 61

365 C ED&F MAN CAPITA 3

435 H SCOTIA CAPITAL 3724

555 C BNP PARIBAS SEC 90

555 H BNP PARIBAS SEC 2450

624 C BOFA SECURITIES 614

657 C MORGAN STANLEY 11 1149

657 H MORGAN STANLEY 3519

DLV615-T CME CLEARING

BUSINESS DATE: 05/28/2020 DAILY DELIVERY NOTICES RUN DATE: 05/28/2020

PRODUCT GROUP: METALS RUN TIME: 00:21:30

661 C JP MORGAN 14630 12824

661 H JP MORGAN 403

685 C RJ OBRIEN 34 68

686 C INTL FCSTONE 204 179

690 C ABN AMRO 961 879

700 H UBS 50

732 C RBC CAP MARKETS 6 83

732 H RBC CAP MARKETS 3333

737 C ADVANTAGE 9 8

800 C MAREX SPEC 144

845 C GOLDMAN SACHS C 1

878 C PHILLIP CAPITAL 4

880 C CITIGROUP 50 46

905 C ADM 76 136

____________________________________________________________________________________________

TOTAL: 28,375 28,375

MONTH TO DATE: 28,375

NUMBER OF NOTICES FILED TODAY FOR MAY CONTRACT: 28,375 NOTICE(S) FOR 2837500 OZ (88.26 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 28,375 NOTICES FOR 2837500 OZ (88.26 TONNES)

SILVER

FOR JUNE

262 NOTICE(S) FILED TODAY FOR 1,310,000 OZ/

total number of notices filed so far this month: 262 for 1,310,000 oz

BITCOIN MORNING QUOTE $9398 DOWN $176

BITCOIN AFTERNOON QUOTE.: $9451 UP $248

GLD AND SLV INVENTORIES:

WITH GOLD UP $19.40 AND NO PHYSICAL TO BE FOUND ANYWHERE:

WITH ALL REFINERS CLOSED//MEXICO ORDERING ALL MINES SHUT: WHERE ARE THEY GETTING THE “PHYSICAL”?

NO CHANGE IN GOLD INVENTORY AT THE GLD///

REST THIS WEEKEND AT:

GLD: 1,119.05 TONNES OF GOLD//

WITH SILVER UP 52 CENTS TODAY: AND WITH NO SILVER AROUND

A HUGE CHANGE IN SILVER INVENTORY AT THE SLV/// A MASSIVE DEPOSIT OF 2.796 MILLION OZ INTO THE SLV//

RESTING SLV INVENTORY TONIGHT:

SLV: 463.273 MILLION OZ./

XXXXXXXXXXXXXXXXXXXXXXXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI ROSE BY A EXTREMELY STRONG SIZED 4007 CONTRACTS FROM 159,031 UP TO 163,038 AND CLOSER TO OUR NEW RECORD OF 244,710, (FEB 25/2020. THE STRONG SIZED GAIN IN OI OCCURRED WITH OUR GOOD 9 CENT GAIN IN SILVER PRICING AT THE COMEX. IT SEEMS THAT THE GAIN IN COMEX OI IS DUE TO STRONG BANKER SHORT COVERING PLUS A GOOD EXCHANGE FOR PHYSICAL ISSUANCE, ZERO LONG LIQUIDATION, ACCOMPANYING A HUGE INCREASE IN SILVER OZ STANDING AT THE COMEX FOR JUNE. WE HAD A NET GAIN IN OUR TWO EXCHANGES OF 4927 CONTRACTS (SEE CALCULATIONS BELOW).

WE HAVE ALSO WITNESSED A HUMONGOUS AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: MAY: 0 AND JULY: 920 AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 920 CONTRACTS. WITH THE TRANSFER OF 920 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 920 EFP CONTRACTS TRANSLATES INTO 4.600 MILLION OZ ACCOMPANYING:

1.THE 9 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

10.025 MILLION OZ INITIAL STANDING IN AUGUST.

43.030 MILLION OZ INITIALLY STANDING IN SEPT. (HUGE)

7.32 MILLION OZ INITIALLY STANDING IN OCT

2.630 MILLION OZ STANDING FOR NOV.

20.970 MILLION OZ FINAL STANDING IN DEC

5.075 MILLION OZ FINAL STANDING IN JAN

1.480 MILLION OZ FINAL STANDING IN FEB

23.005 MILLION OZ FINAL STANDING FOR MAR

4.660 MILLION OZ FINAL STANDING FOR APRIL

45.220 MILLION OZ FINAL STANDING FOR MAY

1,825 MILLION OF INITIALLY STANDING FOR JUNE

THURSDAY, AGAIN OUR CROOKS USED COPIOUS PAPER IN ORDER TO LIQUIDATE SILVER’S PRICE…AND THEY WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE 9 CENTS).. AND, OUR OFFICIAL SECTOR/BANKERS WERE UNSUCCESSFUL IN THEIR ATTEMPT TO FLEECE ANY AMOUNT OF SILVER LONGS FROM THEIR POSITIONS. THE SMALL GAIN AT THE COMEX WAS ACCOMPANIED BY : i) A GOOD ISSUANCE OF EXCHANGE FOR PHYSICALS 2) A HUGE INITIAL SILVER OZ STANDING FOR JUNE,3) CONSIDERABLE BANKER SHORT COVERING AND 4) ZERO LONG LIQUIDATION AS WE DID HAVE A NET GAIN OF 4927 CONTRACTS OR 24.635 MILLION OZ ON THE TWO EXCHANGES! YOU CAN BET THE FARM THAT OUR BANKER ARE DESPERATE TO LIQUIDATE THEIR HUGE SHORT POSITIONS IN SILVER

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY /FOR MONTH OF MAY:

15,454 CONTRACTS (FOR 20 TRADING DAYS TOTAL 15,454 CONTRACTS) OR 77.27 MILLION OZ: (AVERAGE PER DAY: 773 CONTRACTS OR 3.863 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF MAY: 77.27 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 11.03% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2020 TO DATE SILVER EFP’S: 1,066.12 MILLION OZ.

JANUARY 2020 EFP TOTALS SO FAR: 181.61 MILLION OZ

FEB 2020 EFP’S TOTAL : …… 259.600 MILLION OZ

MARCH EFP’S ….. 452.280 MILLION OZ //TOTALS//AND A NEW RECORD FOR THE MONTH)

APRIL EFP 95.355 MILLION OZ. (EX. FOR PHYSICALS BECOMING A LOT LESS)

MAY EFP SO FAR: 77,27 MILLION OZ

EXCHANGE FOR PHYSICAL ISSUANCE FOR THE PAST 30 DAYS IS A LOT LESS. NO DOUBT THAT THE COST TO CARRY THESE THINGS HAS EXPLODED AND AS SUCH CANNOT BE DONE AS FREQUENTLY AS BEFORE.

RESULT: WE HAD AN EXTREMELY STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 4007, WITH OUR GOOD 9 CENT GAIN IN SILVER PRICING AT THE COMEX ///THURSDAY… THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 960 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER

TODAY WE GAINED A STRONG SIZED OI CONTRACTS ON THE TWO EXCHANGES: 4927 CONTRACTS (WITH OUR 9 CENT GAIN IN PRICE)

THE TALLY//EXCHANGE FOR PHYSICALS

i.e 960 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH A STRONG SIZED INCREASE OF 4007 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED DESPITE A GOOD 9 CENT GAIN IN PRICE OF SILVER/AND A CLOSING PRICE OF $17.36 // THURSDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY.

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.7050 BILLION OZ TO BE EXACT or 100.7% of annual global silver production (ex Russia & ex China).

FOR THE NEW MAR DELIVERY MONTH/ THEY FILED AT THE COMEX: 262 NOTICE(S) FOR 1,310,000 OZ OF SILVER.

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.70//TODAY’S RECORD OF 244,705 IS SET WITH A PRICE OF: 18.91 (FEB 25/2020)

.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ; AUGUST 10.025 MILLION OZ/ SEPT 43.030 MILLION OZ//OCT: 7.665 MILLION OZ// NOV: 2.630 MILLION OZ//DEC: 20.970 MILLION OZ; JAN: 5.075 MILLION OZ.//FEB 1.480 MILLION OZ//MAR: 23.005 MILLION OZ/APRIL 4.660 MILLION OZ//MAY 45.220 MILLION OZ//JUNE: 1.825 MILLION OZ//

- THE RECORD PRIOR TO TODAY WAS SET IN FEB 25/2018: 244,710 CONTRACTS, WITH A SILVER PRICE OF $18.90//.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017 RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

GOLD

IN GOLD, THE COMEX OPEN INTEREST FELL BY A SMALL SIZED 1529 CONTRACTS TO 510,656 AND FURTHER FORM OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE SMALL SIZED LOSS OF COMEX OI OCCURRED DESPITE OUR GAIN IN PRICE OF $4.00 /// COMEX GOLD TRADING// THURSDAY// WE HAD STRONG BANKER SHORT COVERING FINAL SPREADER COMEX GOLD LIQUIDATION, A GIGANTIC SIZE IN INITIAL GOLD OZ STANDING AT THE COMEX, ALONG WITH ZERO LONG LIQUIDATION ACCOMPANYING A STRONG EX. FOR PHYSICAL ISSUANCE. THIS ALL HAPPENED WITH OUR GOOD GAIN IN PRICE OF JUST $4.00 .

WE HAD A VOLUME OF 0 4 -GC CONTRACTS//OPEN INTEREST 11

WE GAINED A SMALL SIZED 1456 CONTRACTS (4.528 TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2985 CONTRACTS:

CONTRACT JUNE 0.; AUG 2985 AND ALL OTHER MONTHS ZERO//TOTAL: 2985. The NEW COMEX OI for the gold complex rests at 510,656. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A SMALL SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1456 CONTRACTS: 1529 CONTRACTS DECREASED AT THE COMEX (MOSTLY FROM FINAL SPREADER LIQUIDATION) AND 2985 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 1456 CONTRACTS OR 4.528 TONNES. THURSDAY, WE HAD A GOOD GAIN OF $4.00 IN GOLD TRADING……

AND WITH THAT GAIN IN PRICE, WE HAD A SMALL SIZED GAIN IN TOTAL/TWO EXCHANGES GOLD TONNAGE OF 4.528 TONNES!!!!!! THE BANKERS/OFFICIAL SECTOR SUPPLIED INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER WITH RECKLESS ABANDON. THE BANKERS WERE UNSUCCESSFUL IN THEIR ATTEMPT TO LOWER GOLD’S PRICE (IT ROSE $4.00).AND IT ALSO SEEMS THAT THEIR ATTEMPT TO FLEECE ANY GOLD LONGS FROM THE GOLD ARENA WAS UNSUCCESSFUL (SEE BELOW).

4 GC VOLUME: 0 // open interest 11

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES:

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2985) ACCOMPANYING THE SMALL SIZED LOSS IN COMEX OI (1529 OI): TOTAL GAIN IN THE TWO EXCHANGES: 1456 CONTRACTS. WE NO DOUBT HAD 1 )CONSIDERABLE BANKER SHORT COVERING, 2.)A HUMONGOUS INITIAL OUNCES STANDING AT THE GOLD COMEX FOR THE FRONT MAY JUNE, 3) ZERO LONG LIQUIDATION; 4) SMALL COMEX OI LOSS, 5) FINAL GOLD COMEX SPREADER LIQUIDATION… AND …ALL OF THIS WAS COUPLED WITH OUR SMALL GAIN IN GOLD PRICE TRADING//THURSDAY//$4.00

WE ARE BEGINNING TO WITNESS A LACK OF EXCHANGE FOR GOLD PHYSICALS UNDERWRITTEN DUE PREMIUMS STARTING TO REAPPEAR. THE COST TO THE BANKERS IS JUST TOO GREAT TO ENGAGE IN THESE VEHICLES ONCE THIS OCCURS.

SPREADING OPERATIONS

OUR SPREADING OPERATION HAS NOW SWITCHED INTO GOLD…..

SPREADING OPERATION FOR OUR NEWCOMERS:

WE HAVE NOW COMMENCED IN SILVER THE ILLEGAL SPREADING OPERATION \ FOR NEWCOMERS, HERE ARE THE DETAILS:

SPREADING LIQUIDATION HAS NOW STOPPED IN SILVER AS THEY NOW BEGIN TO MORPH INTO GOLD AS WE HEAD TOWARDS THE NEW FRONT MONTH WILL BE JUNE.

FOR THOSE OF YOU WHO ARE NEW, HERE IS THE MODUS OPERANDI OF THE SPREADERS AND THE CRIMINAL ELEMENT BEHIND IT:

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR;

THE SPREADING LIQUIDATION OPERATION IS NOW OVER FOR SILVER..AND WE WILL NOW MORPH INTO AN ACCUMULATION PHASE OF SPREADING CONTRACTS FOR GOLD. THEY WILL ACCUMULATE CONSIDERABLE AMOUNT OF THE CONTRACTS AND THEN LIQUIDATE ONE WEEK PRIOR TO FIRST DAY NOTICE

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO GOLD AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX SILVER OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE IN THIS NON ACTIVE MONTH OF MAY. BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN GOLD WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JUNE), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2020 INCLUDING TODAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 20 TRADING DAY(S) IN TONNES: 248.68 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2019, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 248.68/3550 x 100% TONNES =7.00% OF GLOBAL ANNUAL PRODUCTION

ISSUANCE OF EXCHANGE FOR PHYSICAL GOLD HAS DISSIPATED THIS MONTH…THE COST TO THE BANKERS TO CARRY THESE CONTRACTS IN LONDON IS BECOMING TOO GREAT FOR THEM.

ACCUMULATION OF GOLD EFP’S YEAR 2020 TO DATE: 2815.03 TONNES

JANUARY 2220 TOTAL EFP ISSUANCE; : 570.19 TONNES

FEB 2020 TOTAL EFP ISSUANCE : 653.78 TONNES

MARCH TOTAL EFP ISSUANCE 1,098.93 TONNES (*AND A NEW ALL TIME RECORD ISSUANCE//22 DAYS)

APRIL TOTAL EFP. ISSUANCE: 243.45 TONNES (EFP ISSUANCE BECOMING A LOT LESS)

MAY TOTAL EFP ISSUANCE: 248.68 TONNES (EFP ISSUANCE STILL LOW// PREMIUM COST TO THE BANKERS IS HUGE..SO ISSUANCE IS LESS)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A VERY STRONG SIZED 4007 CONTRACTS FROM 159,031 UP TO 163,038 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 2 3/4 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.

THE HUGE GAIN IN OI SILVER COMEX WAS DUE TO; 1) CONSIDERABLE BANKER SHORT COVERING , 2) A GOOD ISSUANCE OF EXCHANGE FOR PHYSICALS (SEE BELOW), 3) A STRONG INITIAL SILVER OZ STANDING AT THE COMEX FOR JUNE AND 4) ZERO LONG LIQUIDATION

EFP ISSUANCE 920 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY: 920 CONTRACTS AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 920 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 4036 CONTRACTS TO THE 920 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A STRONG GAIN OF 4927 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 24.635 MILLION OZ!!! OCCURRED WITH THE 9 CENT GAIN IN PRICE///

RESULT: A STRONG SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE 9 CENT GAIN IN PRICING THAT SILVER UNDERTOOK IN PRICING// THURSDAY. WE ALSO HAD A STRONG SIZED 920 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED DOWN 6.13 POINTS OR 0.22% //Hang Sang CLOSED DOWN 171.29 POINTS OR 0.74% /The Nikkei closed DOWN 38.42 POINTS OR 0.18%//Australia’s all ordinaires CLOSED DOWN 1.44%

/Chinese yuan (ONSHORE) closed UP at 7.1351 /Oil UP TO 57.21 dollars per barrel for WTI and 64.13 for Brent. Stocks in Europe OPENED MIXED// ONSHORE YUAN CLOSED DOWN // LAST AT 7.1351 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 7.1567 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY PAST 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

i)we had 1 deposits into the customer account

into JPMorgan: 0

ii)into CNT: 1,205,369.180 oz

*** JPMorgan for most of 2017, 2018 and onward, has adding to its inventory almost every single day.

JPMorgan now has 160.819 million oz of total silver inventory or 51.22% of all official comex silver. (160.819 million/314.220 million

total customer deposits today: 1,205,369.180 oz

we had 1 withdrawals:

i) Out of Delaware: 1000.00 oz

total withdrawals; 1000.000 oz

We had 1 adjustment

i) Out of CNT: customer to dealer:

1,025,206.77 oz

total dealer silver: 85.801 million

total dealer + customer silver: 311.569 million oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

The total number of notices filed today for the JUNE 2020. contract month is represented by 262 contract(s) FOR1,310,000 oz

To calculate the number of silver ounces that will stand for delivery in JUNE we take the total number of notices filed for the month so far at 262 x 5,000 oz = 1,310,000 oz to which we add the difference between the open interest for the front month of JUNE.(365) and the number of notices served upon today 262 x (5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the JUNE/2019 contract month: 262 (notices served so far) x 5000 oz + OI for front month of JUNE (365)- number of notices served upon today 262) x 5000 oz of silver standing for the JUNE contract month.equals 1,825,000 oz.

TODAY’S ESTIMATED SILVER VOLUME: 62,784 CONTRACTS //volume high

FOR YESTERDAY: 67,272 CONTRACTS..,CONFIRMED VOLUME//

YESTERDAY’S CONFIRMED VOLUME OF 67,272 CONTRACTS EQUATES to 336 million OZ 48.00% OF ANNUAL GLOBAL PRODUCTION OF SILVER..

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV RISES TO- 0.30% ((MAY 29/2020)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -1.23% to NAV: (MAY 29/2020 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into NEGATIVE/ 0.30%

(courtesy Sprott/GATA

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 16.53 TRADING 16.43///NEGATIVE 0.60

END

And now the Gold inventory at the GLD/

MAY 29/WITH GOLD UP $19.40 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD///GLD INVENTORY RESTS THIS WEEKEND AT 1119.05 TONNES

MAY 28//WITH GOLD UP $4.00 TODAY/NO CHANGES IN GOLD INVENTORY TO THE GLD//INVENTORY RESTS AT 1119.05 TONNES

MAY 27/WITH GOLD UP $.10 TODAY: A STRONG 2.34 TONNES OF GOLD ADDED TO THE GLD//INVENTORY RESTS AT 1119.05 TONNES

MAY 26//WITH GOLD DOWN $23.05//NO CHANGES IN GOLD INVENTORY://RESTS TONIGHT AT 1116.71 TONNES

MAY 22//WITH GOLD UP $13.05//A BIG CHANGE IN GOLD INVENTORY:: A PAPER ADDITION OF 3.93 TONNES//INVENTORY RESTS THIS WEEKEND AT: 1116.71 TONNES

MAY 21//WITH GOLD DOWN $26.70//NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1112.32 TONNES

MAY 20/WITH GOLD UP $7.20: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER WITHDRAWAL OF 1.46 TONNES FROM THE GLD////INVENTORY RESTS TONIGHT AT 1112.32 TONNES

MAY 19//WITH GOLD UP $10.60//NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY RESTS AT 1113.78 TONNES

MAY 18/WITH GOLD DOWN $15.40 TODAY: A HUGE CHANGE IN GOLD INVENTORY: A PAPER DEPOSIT OF 9.06 TONNES./INVENTORY RESTS AT 1113.78 TONNES

MAY 15.WITH GOLD UP $16.30 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 12.58 TONNES/ INVENTORY RESTS AT 1104.72 TONNES

MAY 14//WITH GOLD UP $19.25 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY RESTS AT 1092.14 TONNES

MAY 13//WITH GOLD UP $9.05 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 11.07 TONNES/INVENTORY RESTS AT 1092.14 TONNES

MAY 12//WITH GOLD UP $6.60 TODAY; A SMALL CHANGES IN GOLD INVENTORY AT THE GLD/: A WITHDRAWAL OF .58 TONNES FROM THE GLD///INVENTORY RESTS AT 1081.07 TONNES

MAY 11/WITH GOLD DOWN $12.65 TODAY: NO CHANGES IN GOLD INVENTORY: //INVENTORY RESTS AT 1081.65 TONES..

MAY 8/WITH GOLD DOWN $7.00 TODAY; A BIG CHANGE IN GOLD INVENTORY: A PAPER ADDITION OF 5.85 TONNES/INVENTORY RESTS AT 1081.65 TONNES

MAY 7/WITH GOLD UP $29.65 TODAY : A SMALL CHANGE IN GOLD INVENTORY AT THE GLD//A PAPER ADDITION OF .41 TONNES/INVENTORY RESTS AT 1075.80 TONNES

MAY 6//WITH GOLD DOWN $17.00 TODAY/ A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A PAPER ADDITION OF 3.68 TONNES/INVENTORY RESTS AT 1075.39 TONES

MAY 5/WITH GOLD DOWN $1.65 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER ADDITION OF 3.81 TONNES//INVENTORY RESTS AT 1071.71 TONNES

MAY 4//WITH GOLD UP $12.00 TODAY//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A MASSIVE PAPER DEPOSIT OF 11.4 TONNES INTO THE GLD////GOLD INVENTORY RESTS AT 1067.90 TONNES

MAY 1/WITH GOLD UP $8.45 NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1056.50 TONNES

APRIL 30/WITH GOLD DOWN $15.95 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1056.50 TONNES

APRIL 29/WITH GOLD DOWN $7.65/A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 8.19 TONNES OF GOLD INTO THE GLD////INVENTORY REST AT 1056.50 TONNES//

APRIL 28/WITH GOLD DOWN $4.50//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1048.31 TONNES

APRIL 27/WITH GOLD DOWN $12.75//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 5.85 TONNES INTO THE GLD////INVENTORY RESTS TONIGHT AT 1048.31 TONNES

APRIL 24/WITH GOLD DOWN $4.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS TONIGHT AT 1042.46 TONNES

APRIL 23/WITH GOLD UP $10.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS TONIGHT AT 1042.46 TONNES

APRIL 22/WITH GOLD UP $40.75 TODAY:; TWO HUGE CHANGES IN GOLD INVENTORY AT THE GLD//A)A MONSTROUS 3.8 PAPER TONNES WERE ADDED TO THE GLD INVENTORY AND B) ANOTHER HUGE 9.07 TONNES OF PAPER GOLD ADDED LATE IN THE DAY//INVENTORY RESTS AT 1042.46 TONNES

APRIL 21/WITH GOLD DOWN $21.60 TODAY: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MONSTROUS ADDITION OF 7.9 PAPER TONNES TO THE GLD INVENTORY//INVENTORY RESTS AT 1029.59 TONNES

APRIL 20//WITH GOLD UP $10.00 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1021.69 TONNES

APRIL 17/WITH GOLD DOWN $27.80 TODAY: SURPRISINGLY NO CHANGES IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 1021.69 TONNES TONNES..THE STRING OF 12 STRAIGHT STRONG DEPOSITS ENDS..

APRIL 16/WITH GOLD DOWN $4.50 TODAY: ANOTHER HUGE CHANGE IN GOLD INVENTORY: A STRONG DEPOSIT OF 4.10 TONNES WAS ADDED TO THE GLD INVENTORY//INVENTORY RESTS AT 1021.69 TONNES/12TH STRAIGHT STRONG DEPOSIT

APRIL 15//WITH GOLD DOWN $19.10 TODAY; ANOTHER HUGE CHANGE IN GOLD INVENTORY; A STRONG 7.89 TONNES WAS ADDED TO THE GLD INVENTORY//INVENTORY RESTS AT 1117.59 TONNES.//11TH STRAIGHT STRONG DEPOSIT

APRIL 14/WITH GOLD UP $23.55 TODAY: ANOTHER HUGE CHANGE IN GOLD INVENTORY: A STRONG 15.51 TONNES WAS ADDED TO THE GLD INVENTORY/INVENTORY RESTS AT 1009.70 TONNES//THIS IS THE 10TH STRAIGHT STRONG DEPOSIT//THIS IS A FRAUDULENT VEHICLE..THEY HAVE NO PHYSICAL GOLD IN THE TRUST..

APRIL 13//WITH GOLD UP $27.65 TODAY: ANOTHER HUGE CHANGE IN GOLD INVENTORY: A STRONG 5.36 TONNES WAS ADDED TO THE GLD//INVENTORY RESTS AT 994.19 TONNES

APRIL 9 WITH GOLD UP $37.30 TODAY: ANOTHER HUGE CHANGE IN GOLD INVENTORY: A STRONG 2.92 TONNES WAS ADDED TO THE GLD//GOLD INVENTORY RESTS TONIGHT AT..988.63 TONNES

APRIL 8/WITH GOLD DOWN $.60//ANOTHER HUGE CHANGE IN GOLD INVENTORY/;; A STRONG 1.45 TONNES WAS ADDED TO THE GLD/GOLD INVENTORY RESTS AT 985.71 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Inventory rests tonight at

MAY 29/ GLD INVENTORY 1119.05 tonnes*

LAST; 830 TRADING DAYS: +171.99 NET TONNES HAVE BEEN REMOVED FROM THE GLD

LAST 730 TRADING DAYS://+347.14 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

MAY 29//WITH SILVER UP 52 CENTS TODAY: A MASSIVE DEPOSIT OF 2.796 MILLION OZ INTO THE SLV//INVENTORY RESTS THIS WEEKEND AT 463.273 MILLION OZ//

MAY 28//WITH SILVER UP 9 CENTS TODAY: A MASSIVE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.660 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 460.477 MILLION OZ//

MAY 27/WITH SILVER UP 13 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 455.817 MILLION OZ//

MAY 26//WITH SILVER DOWN 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/// INVENTORY RESTS AT 455.817 MILLION OZ//

MAY 22/WITH SILVER UP 22 CENTS TODAY/ A HUGE PAPER WITHDRAWAL OF 1.864 MILLION OZ//INVENTORY RESTS AT 455.817 MILLION OZ/

LAST 5 DAYS: SILVER UP 60 CENTS: INVENTORY UP A WHOOPING 23.767 MILLION OZ///

MAY 21/WITH SILVER DOWN 50 CENTS TODAY: A HUGE PAPER DEPOSIT OF 7.923 MILLION OZ///INVENTORY RESTS AT 457.681 MILLION OZ//

MAY 20//WITH SILVER UP ANOTHER 11 CENTS TODAY: A HUGE CHANGE IN SLV INVENTORY: A HUGE PAPER DEPOSIT OF 9.601 MILLION OZ INTO THE SLV// //INVENTORY RESTS AT 449.758 MILLION OZ

MAY 19/WITH SILVER UP ANOTHER 29 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV////INVENTORY RESTS AT 440.157 MILLION OZ//

MAY 18/WITH SILVER UP ANOTHER 48 CENTS TODAY: TWO BIG CHANGES IN SILVER INVENTORY AT THE SLV I.E. 2 PAPER DEPOSIT OF ( I) 8.39 MILLION OZ AND THEN ( 2) 8.109 MILLION OZ//INVENTORY RESTS AT 432.048 MILLION OZ// (TOTAL DEPOSITS 16.500 MILLION OZ///)

MAY 15/WITH SILVER UP 81 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV: /INVENTORY RESTS AT 423.65 MILLION OZ.

MAY 14//WITH SILVER UP 33 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV.//INVENTORY RESTS AT 423.65 MILLION OZ

MAY 13/WITH SILVER UP 2 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 2.79 MILLION OZ INTO THE SLV..//INVENTORY RESTS AT 423.65 MILLION OZ//

MAY 12/WITH SILVER UP 5 CENTS TODAY: A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.076 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 420.861 MILLION OZ//

MAY 11.WITH SILVER DOWN 5 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 417.785 MILLION OZ//

MAY 8/WITH SILVER UP 11 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A MONSTER DEPOSIT OF 4.661 MILLION OZ OF SILVER INTO THE SLV..///INVENTORY RESTS AT 417.785 MILLION OZ//

MAY 7/WITH SILVER UP 45 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 413.124 MILLION OZ//

MAY 6/WITH SILVER DOWN 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 413.124 MILLION OZ//

MAY 5/WITH SILVER UP 17 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 413.124 MILLION OZ///

MAY 4//WITH SILVER DOWN 5 CENTS TODAY:2 HUGE PAPER CHANGES IN SILVER INVENTORY AT THE SLV.i).A LARGE 1.399 MILLION OZ OF PAPER SILVER REMOVED FROM THE SLV//..//INVENTORY RESTS AT 411.427 MILLION OZ and ii) A LARGE 1.647 MILLION OZ OF PAPER SILVER ADDED TO THE SLV// INVENTORY RESTS AT 413.124 MILLION OZ//

MAY 1/WITH SILVER FLAT IN PRICE: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 412.826 MILLION OZ///

APRIL 30/WITH SILVER DOWN 26 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 412.826 MILLION OZ//

APRIL 29/WITH SILVER DOWN ONE CENT TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 412.826 MILLION OZ//

APRIL 28 /WITH SILVER DOWN 2 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 412.826 MILLION OZ..

APRIL 27/WITH SILVER UP ONE CENT TODAY: TWO SMALL CHANGE IN SILVER INVENTORY AT THE SLV: a) A WITHDRAWAL OF 373,000 OZ FORM THE SLV// b) A SECOND WITHDRAWAL OF 466,000: ////INVENTORY RESTS AT 412.826 MILLION OZ//

APRIL 24//WITH SILVER UP 3 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 413.665 MILLION OZ

APRIL 23/WITH SILVER UP 0 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.891 MILLION OZ INTO THE SLV/////INVENTORY RESTS AT 413.665 MILLION OZ//

APRIL 22/WITH SILVER UP 42 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY: A PAPER WITHDRAWAL OF 1.865 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 410.774 MILLION OZ//

APRIL 21//WITH SILVER DOWN 60 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER ADDITION OF 1.398 MILLION OZ INTO THE SLV INVENTORY//INVENTORY RESTS AT 412.639 MILLION OZ//

APRIL 20//WITH SILVER UP 16 CENTS TODAY: A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.797 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 414.038 MILLION OZ//

APRIL 17/WITH SILVER DOWN 24 CENTS TODAY; A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.3999 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 415.437 MILLION OZ//

APRIL 16/WITH SILVER UP 5 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV////INVENTORY RESTS AT 415.437 MILLION OZ//

APRIL 15//WITH SILVER DOWN 45 CENTS TODAY: TWO HUGE CHANGES IN SILVER INVENTORY AT THE SLV TWO HUGE DEPOSITS: A DEPOSIT OF 1.679 MILLION OZ AND ANOTHER 5.222 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 415.437 MILLION OZ//

APRIL 14./WITH SILVER UP 51 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A MASSIVE PAPER DEPOSIT OF XXX MILLION OZ//INVENTORY RESTS AT 408.536 MILLION OZ//

APRIL 13//WITH SILVER DOWN 29 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A MASSIVE PAPER DEPOSIT OF 6.155 MILLION OZ////INVENTORY RESTS AT 408.536 MILLION OZ//

APRIL 9/WITH SILVER UP 60 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A HUGE DEPOSIT OF 1.84 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 402.381 MILLION OZ.

MAY 29.2020:

SLV INVENTORY RESTS TONIGHT AT

463.273 MILLION OZ.

END

LIBOR SCHEDULE AND GOFO RATES// GOLD LEASE RATES

YOUR DATA…..

6 Month MM GOFO 3.08/ and libor 6 month duration 0.52

Indicative gold forward offer rate for a 6 month duration/calculation:

GOLD LENDING RATE: -2.56%

NEGATIVE GOLD LEASING RATES INCREASING BY A HUGE AMOUNT//GOLD SCARCITY AND CENTRAL BANKS CALLING IN ALL OF THEIR GOLD LEASES

XXXXXXXX

12 Month MM GOFO

+ 2..05%

LIBOR FOR 12 MONTH DURATION: 0.68

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = -1.37%

NEGATIVE GOLD LEASING RATES INCREASING BY A HUGE AMOUNT//GOLD SCARCITY AND CENTRAL BANKS CALLING IN ALL OF THEIR GOLD LEASES

end

PHYSICAL GOLD/SILVER STORIES

i) GOLDCORE BLOG/Mark O’Byrne

ii) Important gold commentaries courtesy of GATA/Chris Powell

We brought you this important story yesterday but it is worth repeating:

bullion banks are preparing to pull away from the Comex and head to the LME

(Peter Hobson/Reuters//GATA)

Bullion banks prepare Comex pullback after virus snarl

Submitted by cpowell on Thu, 2020-05-28 16:24. Section: Daily Dispatches

By Peter Hobson

Reuters

Thursday, May 28, 2020

LONDON — Gold trading banks are preparing to significantly reduce their positions on CME Group’s Comex exchange in New York, nine people familiar with the plans said, shifting more trading to London and raising costs for thousands of investors.

Some bullion banks are no longer willing to hold large positions on Comex, the biggest gold futures market, after the coronavirus snarled the supply of gold bars, sending Comex prices vaulting above London rates in March.

…

The divergence wiped hundreds of millions of dollars off the value of trading books, according to industry sources, with HSBC reporting a $200-million paper loss in a single day.

Many banks have already reduced their day-to-day trading on Comex since the market disruption but they are worried that prices could diverge again and some now intend to reduce their open positions by between 50-75%, sources at six lenders said.

Facing the threat of lost business, CME is considering amending contracts to allow delivery of gold in London as well as in New York, five industry and banking sources said, adding that no decision had yet been taken. …

… For the remainder of the report:

https://www.reuters.com/article/us-health-coronavirus-gold-cme-exclusive…

END

For your interest…

(GATA)

Ronald-Peter Stoferle and Mark Valek: The dawning of a golden decade

Submitted by cpowell on Fri, 2020-05-29 03:57. Section: Daily Dispatches

11:55p ET Thursday, May 29, 2020

Dear Friend of GATA and Gold:

Incrementum’s Ronald-Peter Stoferle and Mark Valek are back with another magisterial “In Gold We Trust” report, painstakingly outlining all the reasons the world should be experiencing what the report’s title calls “The Dawning of a Golden Decade.”

Those reasons begin with infinite money chasing infinite debt, continue with the near-suicide of the world economy as the policy response to the virus epidemic, and conclude with the prospect of a new monetary system for the world.

…

But will the dawn come for gold?

The report seems a little short on central bank policy options, not quite recognizing that for some years now under the leadership of Western central banks the world already had been operating under a system of infinite money, and that the success of a system of infinite money requires infinite commodity price suppression to defend government currencies. After all, do central banks — even those of Russia and China — really want their own currencies displaced by the former world reserve currency, whose revival would tie their hands?

But that is an especially sensitive topic, and regardless of what major central banks want, circumstances certainly are making them more ridiculous every day. Maybe the “In Gold We Trust” report is most valuable for detailing the craziness. It can be found in English and German in both complete and abbreviated versions at the Incrementum internet site here:

https://www.incrementum.li/en/journal/in-gold-we-trust-report-2020-the-d…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

iii) Other physical stories:

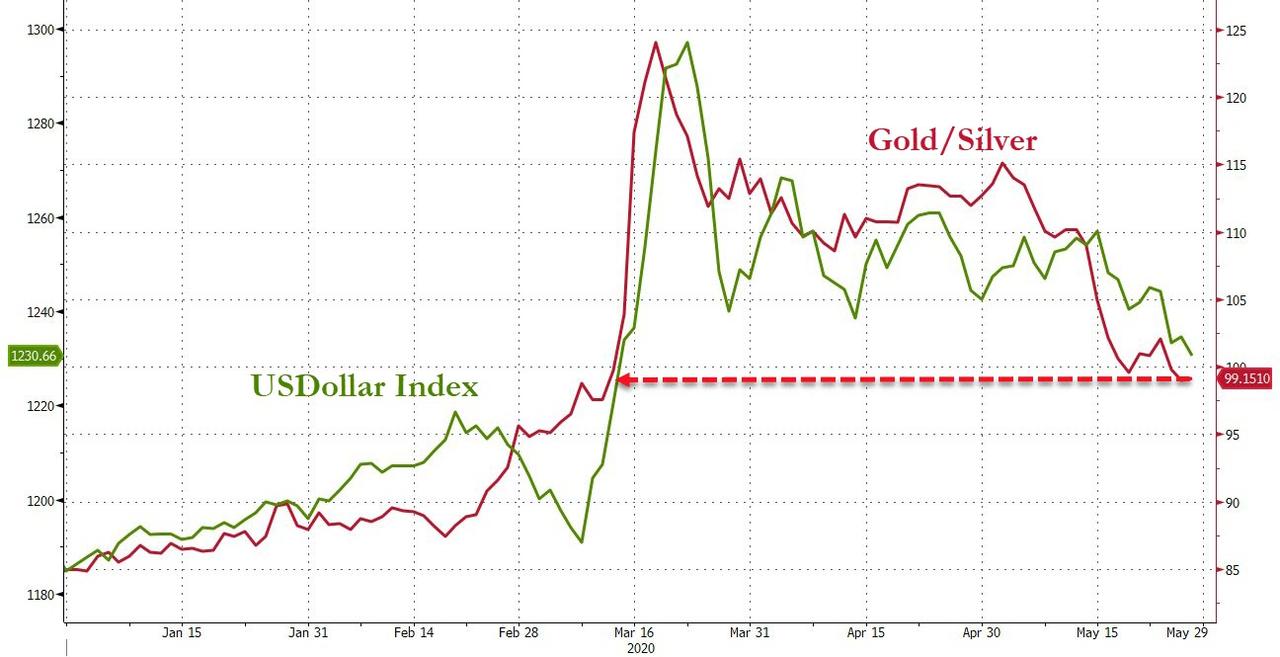

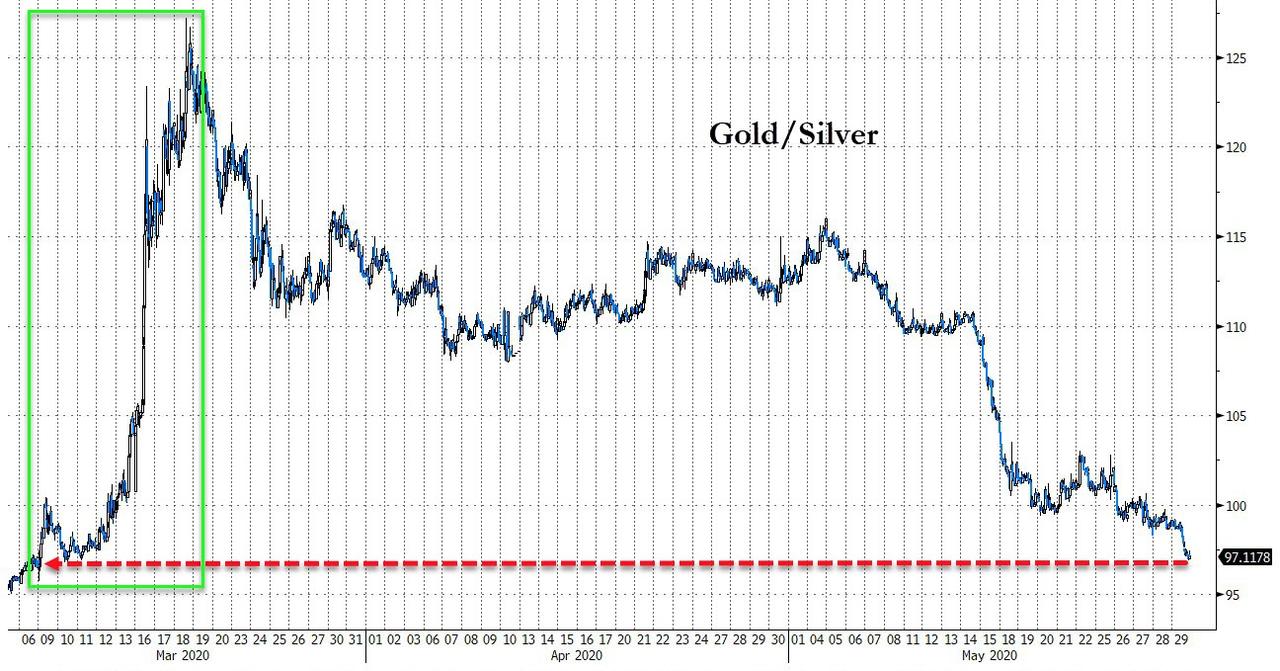

Silver Shines As Gold Glut Weighs On Barbarous Relic

The last two months have seen silver dramatically underperform gold…

…interestingly tracking the dollar index…

…after reaching record ‘lows’ against the yellow metal.

The surge in silver (relative to gold) began around the same time as the gold market “broke” with the COVID crisis causing geographical shortages of physically deliverable gold for futures contracts (decoupling the price of gold futures from the physical price for that liquidity/transportation premium).

But now, as Bloomberg notes (and the chart above shows), the New York gold market has been flipped on its head in just a couple of months, with a scramble for the metal turning into a glut.

June futures sank to more than $20 an ounce below August earlier this week, from a premium in mid-April.

Notices to deliver on June contracts begin to be filed on Thursday. The June contract is also below spot prices, after fetching a $12 premium as recently as mid-May and $60 in March. As Bloomberg points out, the steep discount echoes some of what oil traders saw earlier this year, when crude stockpiles surged after fuel demand plunged.

“It’s a little bit of a game of chicken,” said Tai Wong, head of metals derivatives trading at BMO Capital Markets.

“All of a sudden you get into a similar problem that you had in crude, but slightly different: for crude they literally didn’t have a place to put it — whereas in this case speculative longs don’t want the logistical hassle of holding physical metal, which is why cost to roll has blown out.”

Just as we saw with the June crude expiration, technical pressures are likely to lift as the arb is narrowed:

“It is a seller’s market because of the premium and the buyers are stuck right now,” Peter Thomas, a senior vice president at Chicago-based broker Zaner Group, said in a telephone interview.

“Do you want to deliver now, or do you want to deliver into the back, where the premium is high?”

But, of course, the imbalance in the New York market is a localized phenomenon: gold remains in high demand around the world among investors concerned about the state of the global economy.

And, as Simon Black pointed out recently, EVERY possible scenario is on the table as far as policymakers are concerned, and no one can say for sure what’s going to happen next.

There are very few things that are clear. But in my view, one thing that has become clear is that western governments will print as much money as it takes to bail everyone out.

According to the Congressional Budget Office, the US federal government will post a $3.6 TRILLION deficit this Fiscal Year due to all the bailouts. Plus the Federal Reserve has already printed $2 trillion.

Frankly, they’re just getting started.

With this incomprehensible tsunami of government debt and paper money flooding the system, real assets are a historically great bet.

We’ve talked about this before: real assets are things that cannot be engineered by politicians and central banks– assets like productive land, well-managed businesses, and yes, precious metals.

And they all tend to do very well when central banks print tons of money.

Farmland, for example, was one of the best performing assets during the stagflation of the 1970s.

And financial data over the past several decades shows that whenever they print lots of money, the price of gold tends to increase.

Right now, in fact, the price of gold is relatively cheap compared to the current money supply.

And the price of silver is ridiculously cheap compared to gold. Again, silver has never been cheaper in 5,000 years.

This is why I’d rather just own physical silver. I’m not interested in betting against gold because I expect they’ll continue to print money. In fact I’m happy to buy more gold.

And while we cannot be certain about anything, there’s a strong case to be made that the price of silver could soar alongside gold.

end

A must read..

Egon von Greyerz on gold

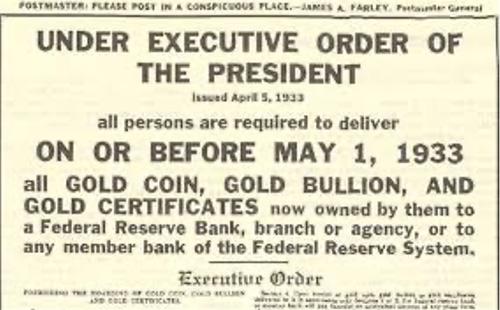

Von Greyerz: US Gold Confiscation Would Be Folly

Authored by Egon von Greyerz via GoldSwitzerland.com,

Will gold be confiscated? Yes, of course, it could be. Desperate governments will take desperate actions. And as the world economy is now slumping into a hyperinflationary depression, unlimited money printing will cause currencies to collapse, leading to a surge in the gold price measured in worthless paper money.

So the first question we must ask is: Why would governments punish prudent savers who have taken protection in gold against the irresponsible mismanagement of the economy and the currency?

GOLD IS 0.5% OF GLOBAL ASSETS

Global financial assets are estimated by Credit Suisse to be $360 trillion. Of that stocks are $85 trillion or 24%. The global bond market is $100 trillion (28%). Investment gold is around 35,000 tonnes or $1.9 trillion. This represents a mere 0.5% of global financial assets.

With investment gold representing only 0.5% of global assets whilst stocks are 24%, you can ask why the US government, are doing all they can do drive up the value of stocks by printing money and at the same time suppressing the price of gold. Why are shareholders supported to become rich whilst gold holders are penalised?

Governments are clearly supporting ever higher stock since this buys votes. But with so few investors holding gold, the government will lose very few votes by manipulating the gold price down.

WILL THE US CONFISCATE GOLD

Since we are now entering a period of major currency debasement and potential hyperinflation, you could ask why governments would stop investors from preserving wealth in the form of gold. So would the US government, instead of encouraging thrift and prudent wealth preservation in the form of gold, confiscate the savings of the Americans? Well, some observers like Jim Sinclair – “Mr. Gold” – thinks this is possible also for US gold mines. He does believe though that coins of the Realm like Eagles would be excluded.

But the confiscation by Roosevelt in 1933 was a totally different situation and not comparable with today. At that time, the US was in a depression and the dollar was tied to gold. The economy was under pressure and the US government decided that the dollar needed to be devalued. A dollar devaluation automatically meant a revaluation of gold since the two were totally interlinked. But FDR decided that the US holders of gold should not get the benefit of a revaluation. Thus gold was confiscated and then revalued from $20.67 per ounce to $35. Gold in bank safe deposit boxes was taken but many Americans hid their gold at home. Gold held outside the US was not confiscated.

AMERICANS HOLD GOLD IN MANY COUNTRIES

Today gold ownership is global. US investors for example are legally storing gold in many countries – Canada, Singapore, Australia, UK, and Switzerland to mention a few. Substantial amounts of gold are stored by US citizens in these countries. Switzerland is a major gold hub where gold is stored in the big banks as well as in many private banks. In addition, there are many private vaults outside the banking system in Switzerland storing considerable amounts of gold.

It would be totally impractical to require Americans to ship the gold back to the US. Also, many countries would not cooperate. I have heard people criticising Switzerland for giving in to the US authorities and revealing the names of Americans who held undeclared accounts in Switzerland at UBS and other banks. As a Swiss I also consider that the Swiss government should not have succumbed as they did this in contravention of the Swiss constitution. Banking secrecy was holy and law in Switzerland at the time. But there was pressure from many European countries also that the Swiss were complicit in tax fraud. In Switzerland, not declaring funds or income was not a criminal event.

TODAY THERE IS AUTOMATIC EXCHANGE OF ALL FINANCIAL INFORMATION

So Switzerland gave in at the time and the banks had to open up their books. And today all banks in the world exchange information based on the OECD Common Reporting Standard. This is an Automatic Exchange Of Information (AEOI) between virtually all countries. Gold held within the financial system is included in this reporting.

The reason Switzerland gave in was the enormous pressure the US authorities put on them, which supposedly included freezing all the assets of the UBS US branch. But also morally the Swiss government had to give in since it was hard to justify actions that were allowed in Switzerland but fraudulent in the US and most other countries.

Gold or other precious metals held in private vaults is at the present not reportable by Americans in their tax returns. The same goes for property. But based on the strict compliance and AML (Anti Money Laundering) regulation, no serious company involved in precious metal storage would accept undeclared funds or metals. Thus no respectable company dealing with gold would accept client funds or gold which are not tax compliant in the country of the client.

So today, gold or other precious metals held in Switzerland by Americans are totally tax compliant. For that reason, I doubt that the Swiss government would cooperate with the US tax authorities if they required the gold to be returned.

GOLD IS A STRATEGIC INDUSTRY IN SWITZERLAND

Gold confiscation in Switzerland is very unlikely. Refining and storing gold in Switzerland is a strategic industry. Switzerland refines 70% of the gold bars in the world. This makes our country a very important party in the global gold industry that could not be replaced elsewhere. In addition, gold is 29% of Swiss exports which is very significant. Also, Switzerland stores a major part of the private gold in the world.

Saving in gold as well as giving gold to children or as a wedding present is a long-standing Swiss tradition. The Swiss will normally buy the Swiss Vreneli coin.

The gold stored in Swiss private vaults is growing significantly every year. The stable political system, rule of law, being a very old democracy and neutrality all contribute to this. Gold confiscation would also be against the constitution. A senior Swiss politician friend of mine told me that if the Swiss government confiscated gold, the people would revolt. For these reasons, I believe that Switzerland will become an even more important gold hub and the best place in the world to store gold.

DOES THE US HOLD 8,000 TONNES OF GOLD?

The US declares holding 8,000 tonnes of gold. This gold has not had an official physical audit since Eisenhower’s days in the mid 1950s. There is clearly a reason for a country not properly auditing their stated $450 billion gold holding. Almost all countries are in the same position. Nobody has an official physical audit of their gold. Since they are all declaring how much gold they hold, they clearly have a responsibility to their people to publicly audit their alleged gold holding.

The answer is simple of course. They don’t have the gold they say that they hold. That can be the only reason why it is never audited. In my view many central banks, including the Fed have covertly reduced their official gold holding. In addition, all central banks are lending or leasing a major part of their gold and most probably also lending the same gold many times over. We know for example that HSBC and JP Morgan hold a major amount of central bank gold. They are also custodian for the biggest gold ETF – GLD. When the gold holdings by GLD increases, there is no gold bought from the Swiss refiners. Instead, the custodians just lend them the central bank gold they hold which has probably been lent many times over.

CENTRAL BANK AND BULLION BANK GOLD IS LOST TO THE EAST

In the past when central banks leased out gold, it would stay with the bullion banks in London or New York. Today, the big buyers are China and India. They buy gold from the bullion banks in London or New York. These 400 oz bars are shipped to Switzerland to be broken down into kilo bars by the Swiss refiners. The kilo bars are the desired size both in India and China. These bars are then shipped on to the East. The bullion banks lease the 400 oz bars from a central bank and then sells them on the buyers in the East.

So instead of staying in London or New York, the central bank has now leased the gold to a bullion bank which has sold it to China or India. The result is that the bullion bank no longer has the physical gold and all the central bank has is an IOU from the bullion bank. This means that the physical gold is permanently lost by both the bullion bank and the central bank. It will never return. The bullion bank will default because they can’t deliver the gold to the central bank which in turn has lost its physical gold forever. This is why central banks don’t have a fraction of the physical gold they declare to have.

JIM SINCLAIR $87,000 GOLD

Jim Sinclair and Bill Holter, two of the most respected individuals in the gold industry, have calculated the real value of the US gold based on 8,000 tonnes allegedly held by the US and balancing the balance sheet of the US. The projected value is $50,000 to $87,000. And as Jim says, that assumes the US holds 8,000 tonnes. Let’s say that the US only holds 4,000t, then the gold price would be double these estimates. And assume that virtually all the US gold has been sold or leased, that would be a gold price going to infinity. But 4,000t or slightly less seems more realistic.

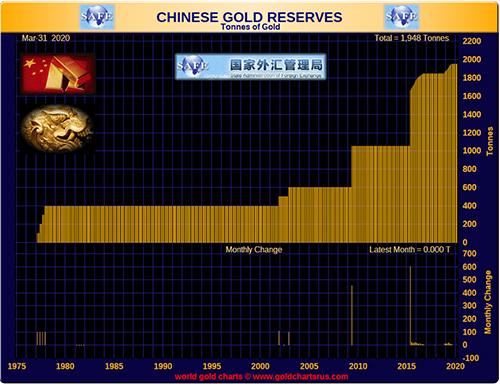

CHINESE GOLD

China has been accumulating gold for decades. Their official holdings are 2,000 tonnes. But it is widely assumed that their real holding is over 10x that. Insiders who have been working with the Chinese confirm that they are likely to hold over 20,000t. All the domestic Chinese gold production, currently 400t p.a. goes to the government.

When China announces a gold-backed yuan, which is not unlikely, they will declare their 20,000+ tonnes and then challenge the US to prove they have the 8,000t. This will lead to some interesting exchanges of aggression, hopefully only verbal.

GOLD CONFISCATION – EVG VIEW

As I said initially, it is possible that some governments attempt to confiscate gold. But in my view, it is an extremely difficult exercise to both legally and logistically conduct. Also, if the gold is held abroad many countries will resist or refuse to ship gold to the US.

Also, the gold market is today global. In China, 1.4 billion people are encouraged by the state to own gold. In India, it is a tradition for most families to hold gold and to give gold as wedding presents. And in Russia, gold reserves have gone from 400 tonnes in 2006 to 2,300 today, a fourfold increase. These countries understand the vital importance of gold.

In today’s global markets, it would be almost impossible to stop companies or individuals to trade gold outside the US or Europe in Shanghai, Singapore or Zurich.

With the epicentre of the gold market moving to China and the East, it is very unlikely for the US and the West to confiscate gold. This would precipitate the fall of the dollar and the Euro and substantially weaken the US and EU positions and their economies.

Remember:

“HE WHO HOLDS THE GOLD MAKES THE RULES”

Thus I believe that confiscation is very unlikely. Governments have a much simpler way of getting at the assets of the wealthy through high taxation. And this is what I believe will happen and not just for gold. As government deficits surge, all assets of the rich will be taxed heavily and not just gold which today represents only 0.5% of global financial assets.

Therefore, tax planning including various jurisdictions is as important as wealth planning.

MARKETS

Stocks

Stock markets are in the course of finishing a correction up. It could take another week or two. Once finished, we will see rapid falls across the globe to new lows.

Metals

The precious metals are in a strong uptrend. The 2011 high for gold in dollars will soon be reached. All other currencies have surpassed the 2011-12 high in gold in the last two years and so will gold in dollars. Remember that corrections are always part of a sound uptrend.

It is totally irrelevant what price gold reaches in worthless paper money whether it is Sinclair’s $58,000 or my 18-year-old prediction of $10,000 in today’s money. Time will tell.

But it is critical to hold physical gold as protection against a currency system and a financial system which are in the process of falling apart.

* * *

ttps://www.jsmineset.com/2020/05/29/we-got-a-lot-of-strange-going-on/

We Got A Lot of Strange Going On!

Posted May 29th, 2020 at 9:02 AM (CST) by J. Johnson & filed under General Editorial.

Great and Wonderful Friday Morning Folks,

Gold is higher again in the early morning with the trade at $1,742.10, up $13.10 and right close to the high at $1,742.90 with the low at $1,725.30. Silver is leading percentage wise with its trade at $18.26, up 29.3 cents with the high at $18.34 and the low at $17.81. The US Dollar seems to be losing its gravitational pull to par with the trade at 98.035, down 33.7 points and right by it’s low at 98.015 with the high at 98.55. Of course, all this was done while we slept, by Algo’s, before 5 am pst, the Comex open, the London close, and after one heck of a great week for precious metals.

We see nothing but gains in the emerging markets this Friday. In Venezuela, Gold is now priced at 17,399.22 Bolivar proving a gain of 32.95 with Silver gaining 3.496 Bolivar with its price at 182.372. Argentina’s currency now has Gold valued at 119,086.58 Peso’s giving the noble metal an additional 346.03 Peso’s gain with Silver gaining 25.10 A-Peso’s with its price at 1,248.25. The Turkish Lira’s price for Gold now rests at 11,901.29 showing a gain of 50.03 Lira’s from yesterday’s price with Silver at 124.738, gaining 2.665 T-Lira.

Today is First Notice Day in June’s precious metals deliveries. This means 100% margins are applied to all trades inside the delivery months (with the exception of spread traders who get a special manipulating discount) with today’s starting count for Silver at 365 and with a Volume of 4 posted up on the board with a single price at $17.865. The Delivery months Open Interest dropped by 9 leaving a request for 1,825,000 ounces standing for delivery. While the prices climb, so does the Open Interest as another 4,018 more short contracts had to be added into the mix or Silver would be substantially higher than it is now, bringing the total to 163,068 positions, against the price and as the deliveries continue.

June Gold’s Delivery Demands now stand at 47,319 contracts proving 13,949 positions jumped the delivery boat from yesterday, with today’s early morning trading range between $1,728.50 and $1,715.10 with the last trade at the high. That’s still a real high number that Comex has to deal with as we watch the world continuing to see the demands for protection gain, as the world’s printer’s fiddle to the flames. We got a lot of strange going on between the 2 precious metals as Gold’s Open Interest continues to decline as another 2,565 left the trade leaving a total of 510,908 Overnighters still in the trade.

Here’s more on “the strange in the game”. Gold’s Overall Open Interest since last Friday fell by 19,235 Contracts. Silver’s OI gained 7,707 within the same time period. It maybe the Resolutes are stretching this inter-commodity-spread between the two to see where the weaknesses really are. Regardless, the buys are solid and the miners maybe starting to refine again (maybe). It will take a long time to see the flow rise up to what it was before the shutdown. Nothing will stop the collapse of the economic system, all we have to do is wait it out as the anger rises, and as the media misdirects once again.

We need to pray for calm, the rush to anger winds up never being a good thing. Rioters do no one any good, but for now they have the stage and it’s all being recorded. All the video cameras and drones, will highlight those that rob, burn, and beat others, who had nothing to do with the event that caused this. In the meantime, make the weekend outstanding! Stay away from the crowds, keep your second Amendment right at arm’s length, and stay calm. We’ll make it through the mess the media is using to inflate the hate. Stay safe, keep calm, and as always

Stay Strong!

Jeremiah Johnson

END

First it was HSBC that lost huge amounts of money on the day that gold went huge future/spot. Now we see Canada’s CIBC also got caught

(Reuters)

Canada’s CIBC lost $64 million in a day on paper in gold market turmoil

LONDON (Reuters) – Canadian Imperial Bank of Commerce (CIBC) took a mark-to-market trading loss of C$88.2 million ($64 million) in one day in March due mainly to volatility in the gold market, the bank said in its second-quarter earnings report on Thursday.

CIBC is not alone in being caught out when the coronavirus outbreak interrupted gold supply routes and gold futures prices in New York shot above London spot prices.

HSBC said earlier this month it suffered paper losses of about $200 million on one day in March.

The losses by both banks are theoretical, reflecting the value of positions they held. They would become real only if the bank exited the positions when their value was low.

CIBC said the loss happened on March 24 and was “mostly attributable to our precious metals trading business”.

It was by far the biggest trading loss of any day since May last year, its report showed. CIBC said it was mostly recouped in April.

Gold trading banks plan to reduce their gold futures positions significantly on CME Group’s Comex exchange in New York because they fear further price volatility, Reuters reported on Thursday.

A reduction of activity by banks on Comex, the world’s largest gold futures market, would increase the relative importance of London as a trading centre and raise costs for thousands of gold investors who use the exchange.

-END-

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

March 4.2019

Parker City News

JP Morgan faces potential class action lawsuit after guilty pleas by a former metals trader

Traders from across the U.S. are banding together to accuse J. P. Morgan Chase of manipulating precious metals markets for years.

At least six lawsuits, all making similar allegations against the nation‘s largest bank, have been filed in New York federal court in the past month, since federal prosecutors in Connecticut with a former J. P. Morgan Chase metals trader.

The cases could potentially include thousands of people who traded in the precious metals market. The White Plains, N.Y., law firm Lowey Dannenberg is asking the court to combine the cases and name it as the lead.

The law firm‘s commodities group is led by Vincent Briganti, the attorney who filed the first lawsuit on behalf of Dominick Cognata, a New York resident who alleges he suffered losses due to J. P. Morgan‘s trading conduct in the silver and gold futures and options markets.

A combined case, seeking class action status, would include anyone who purchased or sold futures contracts or an option on NYMEX platinum or palladium or COMEX silver or gold between at least Jan. 1, 2009, and Dec. 31, 2015. The lawyers believe that “at least hundreds, if not thousands” of traders would be eligible to join the case.

Named as defendants in all of the lawsuits are John Edmonds, a 36-year old former metals trader at J. P. Morgan, a group of yet-to-be-identified precious metals traders and the bank.

Edmonds, a New York resident, pleaded guilty in October to one count of conspiracy to defraud the market and manipulate prices of precious metals futures contracts and one count of commodities fraud. In the criminal plea, Edmonds admitted that he and other “unnamed co- conspirators” at J. P. Morgan, fraudulently manipulated precious metals markets from 2009 to 2015, the same time frame covered in the class action suits.

Briganti filed the initial class action on Nov. 7, just one day after the Justice Department unsealed Edmonds‘ plea in the U.S. District Court of Connecticut.

Edmonds admitted in his guilty plea that he deployed the illegal trading scheme hundreds of times with the direct knowledge and consent of his immediate supervisors. Plaintiffs say they have suffered economic injury, including monetary losses, as a direct result of actions by Edmonds and the other unnamed J. P. Morgan metals traders in the futures and options contracts.

One of the suits alleges that “the number of unlawful trades that JP Morgan traders executed in precious metals futures markets is at least in the thousands.”

J. P. Morgan declined to comment. Lowey Dannenberg did not respond to a request for comment by CNBC.

The Justice Department‘s criminal investigation is still ongoing and recently caused a separate related civil case to be put on hold for at least six months while the government continues its investigation. That civil lawsuit, which also accuses J. P. Morgan of rigging the precious metals market, was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders.

After reviewing the details of the plea agreement, David Kovel, the attorney for Shak‘s suit, sought to re- interview Edmonds, along with two other current and former senior traders at the bank. However, the government argued that reopening questioning would be detrimental to the ongoing criminal investigation. The federal judge overseeing the proceedings ordered a six-month stay in the civil case.

Kovel declined to comment.

Edmonds was originally scheduled to be sentenced in Hartford, Conn., on Wednesday, Dec. 19, but a court filing on Nov. 27 shows the sentencing has been postponed until June. A spokesman for the U.S. Attorney for Connecticut could not elaborate on why the sentencing was postponed since the court filing is under seal.

-END-

Futures Drop As Markets Brace For Trump’s China Response

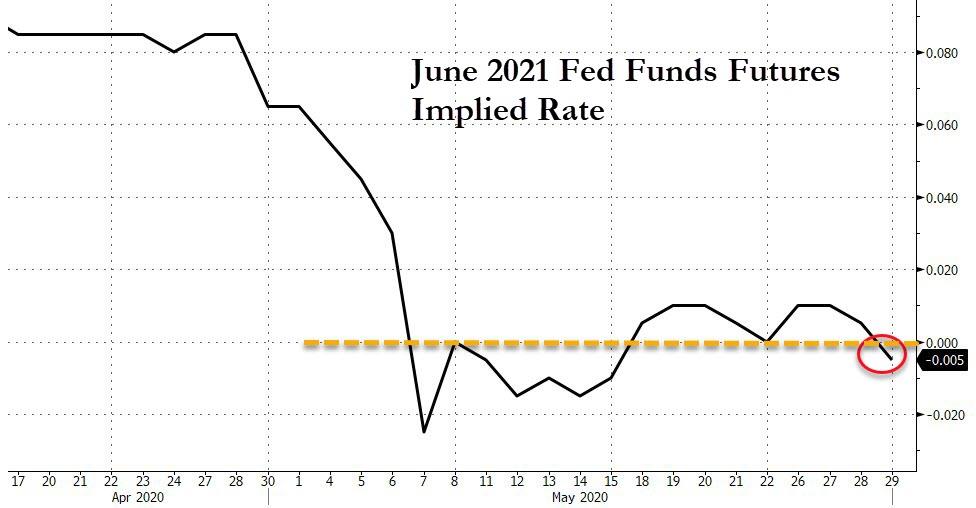

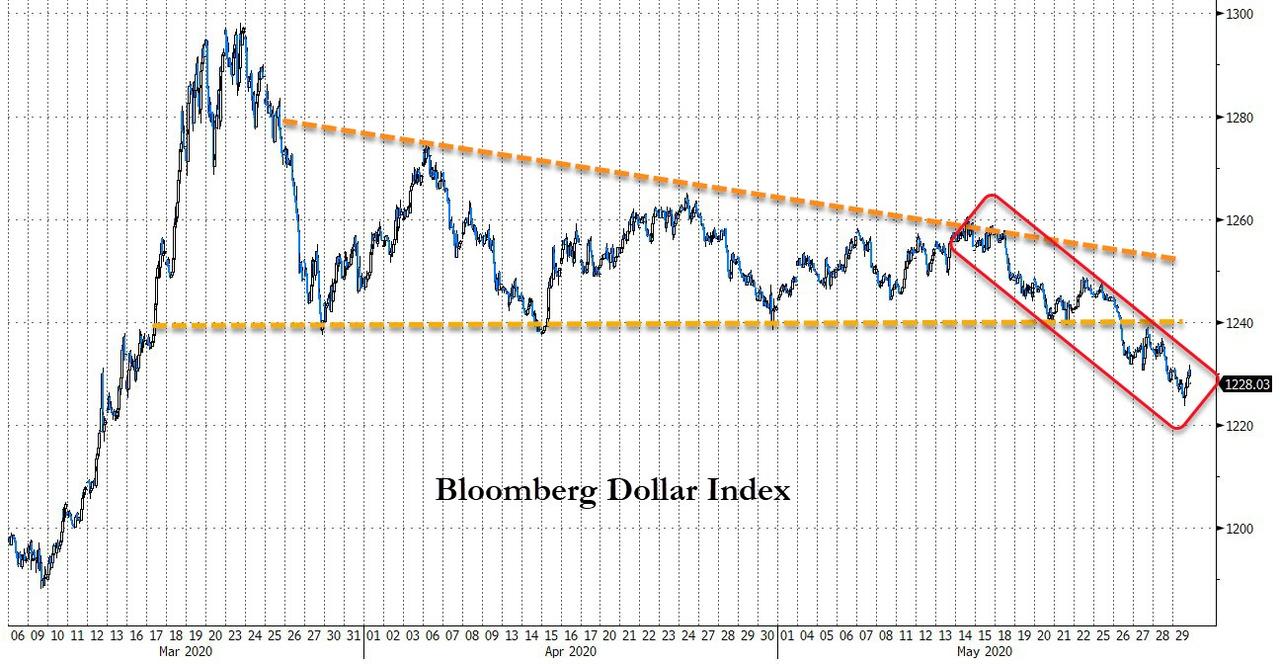

President Donald Trump’s response to China’s national security legislation for Hong Kong, threatening to take the shine off a monster week – and month – for Wall Street, which pushed the S&P above 3,000 and the 200 DMA for the first time since March. Treasuries gained alongside most European bonds, yet the dollar unexpectedly slumped on what many said was month-end FX flows.

U.S. stock indexes sold off late on Thursday’s after algos discovered that Trump was going to make a statement on Friday about China, one which had been scheduled since Monday. Trump has vowed a tough US response to China’s move, which many fear could erode some of the U.S. economic privileges that Hong Kong enjoys.

Amid Sino-US jitters, Europe’s Stoxx 600 fell for the first time in five days, sliding as much as 1.3%, with almost all industry groups in the red. Autos, travel and bank shares slide the most, while telecom is only sector to advance. A rebound laggards resume position at the bottom after rallying hard in recent sessions. As BMO notes, German ex-auto retail sales volumes fell much less-than-expected in April (-5.3% MoM). Multiple data points from a few major economies have been less bad than feared in Q2. Sweden’s merchandise trade surplus increased by 2 billion kronor in April, though exports and imports both collapsed. The Riksbank does not need to worry about an overly strong SEK yet, but Sweden’s export sector is exposed to a weak European economy and global trade decoupling.

Asian stocks fell, led by finance and industrials, after rising in the last session. Markets in the region were mixed, with Jakarta Composite and Shanghai Composite rising, and Australia’s S&P/ASX 200 and Japan’s Topix Index falling. Trading volume for MSCI Asia Pacific Index members was 53% above the monthly average for this time of the day. The Topix declined 0.9%, with IBC and Nissan falling the most. The Shanghai Composite Index rose 0.2%, with Zhongchang Big Data and Shaanxi Broadcast & TV Network Intermediary Group posting the biggest advances

While global stocks have mostly shrugged off escalating tensions between Washington and Beijing until now, confident Trump would not do anything to jeopardize the market’s gains, Trump’s recent actions appear to have spooked investors. They come amid growing good news on the economic front as governments add to stimulus and ease lockdown measures in the wake of the coronavirus. Meanwhile, clues on the next stages for Federal Reserve policy may also come Friday, when Chairman Jerome Powell participates in a virtual discussion.

“I’m very cautious on my medium and even long-term outlook for the markets,” Kate Jaquet, a portfolio manager at Seafarer Capital Partners LLC, said on Bloomberg TV. “I perceive there to be a very large disconnect between stock-market valuations across the globe and underlying company fundamentals.”

Meanwhile, in an escalation in the feud between Trump and Twitter, a day after the president signed the order threatening social media firms with new regulations over free speech, Twitter hid a tweet from the President and accused him of breaking its rules by “glorifying violence.” Twitter shares were down about 0.9% in pre-market trading.

In rates, Treasuries were underpinned on last trading day of the month by pension fund flows, which features a heavy slate of US economic data, a White House news conference on China, comments by Fed Chair Powell and a large Treasury Index duration extension. Yields lower by 0.5bp to 2.5bp across the curve with 2s10s flatter by 1.1bp and 5s30s little changed; 10-year yields around 0.66%, richer by 2bp vs Thursday’s close.Curve is slightly flatter with 20-year bond outperforming. Session low yields were reached during Asia session as USD/JPY slid into the Tokyo fixing. Bunds, gilts cheaper by 0.5bp vs. Treasuries.

In FX, the Bloomberg Dollar Spot Index fell 0.4%, with the greenback falling against most of its major peers. Leveraged funds shorted the greenback ahead of Trump’s conference in view of sliding oil, stock prices and month-end flows, according to Asia-based FX traders. EUR-funded FX carry pairs received some of the biggest lifts (TRY -0.7%, RUB -0.6%). Given the prospect of worsening Sino/US tensions and additional RMB depreciation, broad USD weakness seems all the more peculiar.