GOLD:$1741.00 UP $16.50 The quote is London spot price

Silver:$17.64 UP 22 CENTS//LONDON SPOT PRICE

Closing access prices: London spot

i)Gold : $1742.50 LONDON SPOT 4:30 pm

ii)SILVER: $17.60//LONDON SPOT 4:30 pm

CLOSING FUTURES PRICES: KEY MONTHS

AUG GOLD: $1752.80 CLOSE 1.30 PM// SPREAD SPOT (LONDON) VS/FUTURE AUGUST: $ +11.80

CLOSING SILVER FUTURE MONTH

JULY: 1:30 PM: $17.95//1:30 PM //SPREAD SPOT LONDON VS FUTURE JULY: 31 CENTS PER OZ//

the gold market continues to be broken as future prices are much higher than spot prices. The comex is desperate to fix things but they have no available gold.

If one is to buy gold and or gold coins, the price is around $2800. usa per oz

and silver; $31.00 per oz//

LADIES AND GENTLEMEN: YOU ARE NOW WITNESSING FIRST HAND THE DIFFERENCE BETWEEN PAPER GOLD/SILVER AND THE REAL PHYSICAL STUFF!!

DO NOT PAY ANY ATTENTION TO WHAT THE CROOKS ARE DOING AT THE COMEX AND LONDON LBMA..PHYSICAL IS THE NAME OF THE GAME AND NOTHING ELSE

COMEX DATA

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING: 7/12

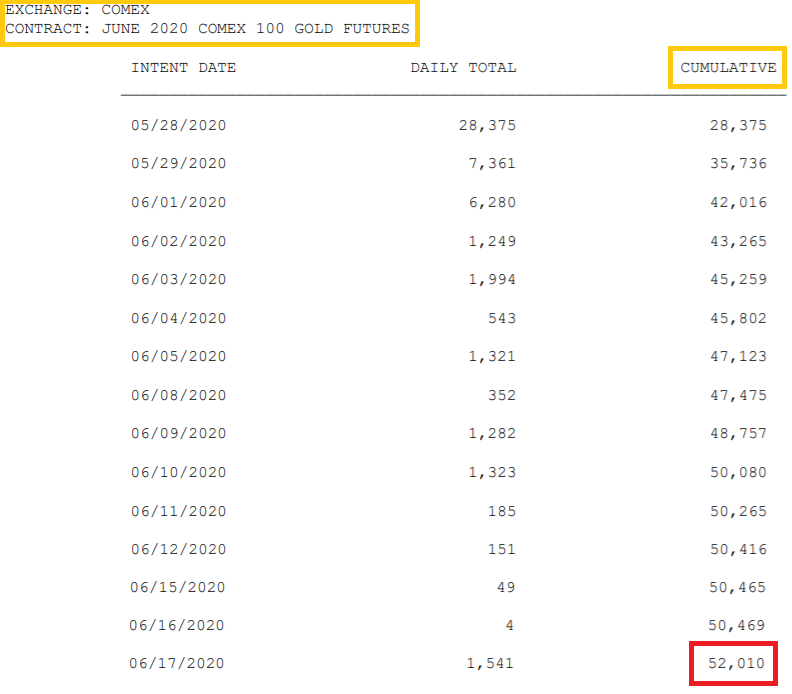

EXCHANGE: COMEX

CONTRACT: JUNE 2020 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,724.800000000 USD

INTENT DATE: 06/18/2020 DELIVERY DATE: 06/22/2020

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

657 C MORGAN STANLEY 2

657 H MORGAN STANLEY 4

661 C JP MORGAN 7

800 C MAREX SPEC 6

905 C ADM 4 1

____________________________________________________________________________________________

TOTAL: 12 12

MONTH TO DATE: 52,022

NUMBER OF NOTICES FILED TODAY FOR JUNE CONTRACT: 12 NOTICE(S) FOR 1200 OZ ( 0.037 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 52022 NOTICES FOR 5,202,200 OZ (161.810 TONNES)

SILVER

FOR JUNE

1 NOTICE(S) FILED TODAY FOR 5,000 OZ/

total number of notices filed so far this month: 428 for 2,140,000 oz

BITCOIN MORNING QUOTE $9415 UP $29

BITCOIN AFTERNOON QUOTE.: $9303 DOWN 83

GLD AND SLV INVENTORIES:

WITH GOLD UP $11.80 AND NO PHYSICAL TO BE FOUND ANYWHERE:

WITH ALL REFINERS CLOSED//MEXICO ORDERING ALL MINES SHUT: WHERE ARE THEY GETTING THE “PHYSICAL”?

NO CHANGES IN GOLD INVENTORY AT THE GLD//

RESTS TONIGHT AT 1136.22 TONNES

GLD: 1,136.22 TONNES OF GOLD//

WITH SILVER UP A STRONG 22 CENTS TODAY: AND WITH NO SILVER AROUND

A HUGE CHANGE IN SILVER INVENTORY AT THE SLV..STRANGE?????

A STRONG WITHDRAWAL OF 0.839 MILLION OZ/

RESTING SLV INVENTORY TONIGHT:

SLV: 486.454 MILLION OZ./

XXXXXXXXXXXXXXXXXXXXXXXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI FELL BY A TINY SIZED 391 CONTRACTS FROM 177,480 DOWN TO 177,122 AND FURTHER FROM OUR NEW RECORD OF 244,710, (FEB 25/2020. THE TINY SIZED LOSS IN OI OCCURRED WITH OUR 16 CENT LOSS IN SILVER PRICING AT THE COMEX. IT SEEMS THAT THE LOSS IN COMEX OI IS DUE TO SOME BANKER SHORT COVERING PLUS A SMALL EXCHANGE FOR PHYSICAL ISSUANCE, MINIMAL LONG LIQUIDATION, ACCOMPANYING A SMALL INCREASE IN SILVER OZ STANDING AT THE COMEX FOR JUNE. WE HAD A NET LOSS IN OUR TWO EXCHANGES OF 251 CONTRACTS (SEE CALCULATIONS BELOW).

WE HAVE ALSO WITNESSED A HUMONGOUS AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A SMALL SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: JULY: 140 AND SEPT 0 FOR ZERO ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 140 CONTRACTS. WITH THE TRANSFER OF 140 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 140 EFP CONTRACTS TRANSLATES INTO 0.700 MILLION OZ ACCOMPANYING:

1.THE 16 CENT FALL IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

10.025 MILLION OZ INITIAL STANDING IN AUGUST.

43.030 MILLION OZ INITIALLY STANDING IN SEPT. (HUGE)

7.32 MILLION OZ INITIALLY STANDING IN OCT

2.630 MILLION OZ STANDING FOR NOV.

20.970 MILLION OZ FINAL STANDING IN DEC

5.075 MILLION OZ FINAL STANDING IN JAN

1.480 MILLION OZ FINAL STANDING IN FEB

23.005 MILLION OZ FINAL STANDING FOR MAR

4.660 MILLION OZ FINAL STANDING FOR APRIL

45.220 MILLION OZ FINAL STANDING FOR MAY

2.175 MILLION OF INITIALLY STANDING FOR JUNE

THURSDAY, AGAIN OUR CROOKS USED COPIOUS PAPER IN ORDER TO LIQUIDATE SILVER’S PRICE…AND THEY WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL 16 CENTS).. AND,OUR OFFICIAL SECTOR/BANKERS WERE SOMEWHAT SUCCESSFUL IN THEIR ATTEMPT TO FLEECE SOME SILVER LONGS FROM THEIR POSITIONS. THE TINY LOSS AT THE COMEX WAS ACCOMPANIED BY : i) A FAIR ISSUANCE OF EXCHANGE FOR PHYSICALS 2) A SMALL INCREASE IN SILVER OZ STANDING SOME BANKER SHORT COVERING AND 4) MINIMAL LONG LIQUIDATION AS WE DID HAVE A STRONG NET LOSS OF 251 CONTRACTS OR 1.050 MILLION OZ ON THE TWO EXCHANGES! YOU CAN BET THE FARM THAT OUR BANKER ARE DESPERATE TO LIQUIDATE THEIR HUGE SHORT POSITIONS IN SILVER

SPREADING OPERATIONS

OUR SPREADING OPERATION HAS NOW SWITCHED INTO SILVER…..

SPREADING OPERATION FOR OUR NEWCOMERS:

FOR NEWCOMERS, HERE ARE THE DETAILS:

SPREADING LIQUIDATION HAS NOW COMMENCED IN SILVER AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JULY.

FOR THOSE OF YOU WHO ARE NEW, HERE IS THE MODUS OPERANDI OF THE SPREADERS AND THE CRIMINAL ELEMENT BEHIND IT:

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR;

THE SPREADING LIQUIDATION OPERATION IS NOW OVER FOR GOLD..AND WE WILL NOW MORPH INTO AN ACCUMULATION PHASE OF SPREADING CONTRACTS FOR SILVER. THEY WILL ACCUMULATE CONSIDERABLE AMOUNT OF THE CONTRACTS AND THEN LIQUIDATE ONE WEEK PRIOR TO FIRST DAY NOTICE

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO SILVER AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX SILVER OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF JUNE HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JULY FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE IN THIS NON ACTIVE MONTH OF JUNE. BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN SILVER WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS

JUNE

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY /FOR MONTH OF JUNE:

7982 CONTRACTS (FOR 16 TRADING DAY(S) TOTAL 7982 CONTRACTS) OR 39.910 MILLION OZ: (AVERAGE PER DAY: 498 CONTRACTS OR 2.494 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF MAY: 39.910 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 5.70% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2020 TO DATE SILVER EFP’S: 1,105.945 MILLION OZ.

JANUARY 2020 EFP TOTALS SO FAR: 181.61 MILLION OZ

FEB 2020 EFP’S TOTAL : …… 259.600 MILLION OZ

MARCH EFP’S ….. 452.280 MILLION OZ //TOTALS//AND A NEW RECORD FOR THE MONTH)

APRIL EFP 95.355 MILLION OZ. (EX. FOR PHYSICALS BECOMING A LOT LESS)

MAY EFP FINAL: 77.27 MILLION OZ

JUNE EXP SO FAR 39.91 MILLION OZ.

EXCHANGE FOR PHYSICAL ISSUANCE FOR THE PAST 60 DAYS IS A LOT LESS. NO DOUBT THAT THE COST TO CARRY THESE THINGS HAS EXPLODED AND AS SUCH CANNOT BE DONE AS FREQUENTLY AS BEFORE.

RESULT: WE HAD A TINY SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 358, WITH OUR 16 CENT LOSS IN SILVER PRICING AT THE COMEX ///THURSDAY… THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE OF 140 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER

TODAY WE GAINED A TINY SIZED OI CONTRACTS ON THE TWO EXCHANGES: 218 CONTRACTS (WITH OUR 16 CENT LOSS IN PRICE)

THE TALLY//EXCHANGE FOR PHYSICALS

i.e 140 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH A TINY SIZED DECREASE OF 358 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED DESPITE A 16 CENT LOSS IN PRICE OF SILVER/AND A CLOSING PRICE OF $17.42 // THURSDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY.

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.846 BILLION OZ TO BE EXACT or 121% of annual global silver production (ex Russia & ex China).

FOR THE NEW JUNE DELIVERY MONTH/ THEY FILED AT THE COMEX: 1 NOTICE(S) FOR 5,000 OZ OF SILVER.

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.70//TODAY’S RECORD OF 244,705 IS SET WITH A PRICE OF: 18.91 (FEB 25/2020)

.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ; AUGUST 10.025 MILLION OZ/ SEPT 43.030 MILLION OZ//OCT: 7.665 MILLION OZ// NOV: 2.630 MILLION OZ//DEC: 20.970 MILLION OZ; JAN: 5.075 MILLION OZ.//FEB 1.480 MILLION OZ//MAR: 23.005 MILLION OZ/APRIL 4.660 MILLION OZ//MAY 45.220 MILLION OZ//JUNE: 2.175 MILLION OZ//

- THE RECORD PRIOR TO TODAY WAS SET IN FEB 25/2018: 244,710 CONTRACTS, WITH A SILVER PRICE OF $18.90//.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017 RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

GOLD

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A SMALL 1117 CONTRACTS TO 493,367 AND CLOSER TO OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE SMALL SIZED GAIN OF COMEX OI OCCURRED WITH OUR LOSS IN PRICE OF $2.75 /// COMEX GOLD TRADING// THURSDAY// WE HAD GOOD BANKER SHORT COVERING, A SMALL SIZED INCREASE IN GOLD OZ STANDING AT THE COMEX, ALONG WITH ZERO LONG LIQUIDATION ACCOMPANYING A SMALL EX. FOR PHYSICAL ISSUANCE. THIS ALL HAPPENED WITH OUR LOSS IN PRICE OF $2.75 .

WE HAD A VOLUME OF 0 4 -GC CONTRACTS//OPEN INTEREST 25

WE GAINED A SMALL SIZED 3717 CONTRACTS (11.56 TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A SMALL SIZED 2600 CONTRACTS:

CONTRACT JUNE 0.; AUG 2600 AND DEC: 100 ALL OTHER MONTHS ZERO//TOTAL: 2600. The NEW COMEX OI for the gold complex rests at 493,240. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A SMALL SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 3717 CONTRACTS: 1117 CONTRACTS INCREASED AT THE COMEX AND 2600 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 3717 CONTRACTS OR 11.56 TONNES. THURSDAY, WE HAD A LOSS OF $2.75 IN GOLD TRADING……

AND WITH THAT LOSS IN PRICE, WE HAD A SMALL SIZED GAIN IN TOTAL/TWO EXCHANGES GOLD TONNAGE OF 11.56 TONNES!!!!!! THE BANKERS/OFFICIAL SECTOR SUPPLIED INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER WITH RECKLESS ABANDON. THE BANKERS WERE SUCCESSFUL IN THEIR ATTEMPT TO LOWER GOLD’S PRICE (IT FELL $2.75).AND IT ALSO SEEMS THAT THEIR ATTEMPT TO FLEECE ANY GOLD LONGS FROM THE GOLD ARENA WAS UNSUCCESSFUL (SEE BELOW).

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES:

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2600) ACCOMPANYING THE SMALL SIZED GAIN IN COMEX OI (1117 OI): TOTAL GAIN IN THE TWO EXCHANGES: 3844 CONTRACTS. WE NO DOUBT HAD 1 )SOME BANKER SHORT COVERING, 2.)A SMALL INCREASE IN GOLD OUNCES STANDING AT THE GOLD COMEX FOR THE FRONT JUNE MONTH, 3) ZERO LONG LIQUIDATION; 4) SMALL COMEX OI GAIN.. AND …ALL OF THIS WAS COUPLED WITH OUR LOSS IN GOLD PRICE TRADING//WEDNESDAY//$2.75.

WE ARE BEGINNING TO WITNESS A LACK OF EXCHANGE FOR GOLD PHYSICALS UNDERWRITTEN DUE TO PREMIUMS STARTING TO REAPPEAR IN THE FUTURE PRICE OF GOLD VS LONDON SPOT. THE COST TO THE BANKERS IS JUST TOO GREAT TO ENGAGE IN THESE VEHICLES ONCE THIS OCCURS.

THE FACT THAT WE ARE CONTINUALLY SEEING A DROP IN COMEX OPEN INTEREST AND VOLUMES COUPLED WITH LESS EXCHANGE FOR PHYSICALS PROBABLY MEANS THAT OUR LONGS ARE ALREADY DEPARTING NEW YORK FOR THE NEW PHYSICAL PLATFORM AT LONDON’S LME.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2020 INCLUDING TODAY

JUNE

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 16 TRADING DAY(S) IN TONNES: 122.03 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2019, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 122.03/3550 x 100% TONNES =3.43% OF GLOBAL ANNUAL PRODUCTION

ISSUANCE OF EXCHANGE FOR PHYSICAL GOLD HAS DISSIPATED THIS MONTH…THE COST TO THE BANKERS TO CARRY THESE CONTRACTS IN LONDON IS BECOMING TOO GREAT FOR THEM.

ACCUMULATION OF GOLD EFP’S YEAR 2020 TO DATE: 2936.17 TONNES

JANUARY 2220 TOTAL EFP ISSUANCE; : 570.19 TONNES

FEB 2020 TOTAL EFP ISSUANCE : 653.78 TONNES

MARCH TOTAL EFP ISSUANCE 1,098.93 TONNES (*AND A NEW ALL TIME RECORD ISSUANCE//22 DAYS)

APRIL TOTAL EFP. ISSUANCE: 243.45 TONNES (EFP ISSUANCE BECOMING A LOT LESS)

MAY TOTAL EFP ISSUANCE: 248.68 TONNES (EFP ISSUANCE STILL LOW// PREMIUM COST TO THE BANKERS IS HUGE..SO ISSUANCE IS LESS)

JUNE TOTAL EFP ISSUANCE: 122.03 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A TINY SIZED 391 CONTRACTS FROM 177,480 UP TO 177,480 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 2 3/4 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.

THE TINY LOSS IN OI SILVER COMEX WAS DUE TO; 1) SOME BANKER SHORT COVERING , 2) A SMALL ISSUANCE OF EXCHANGE FOR PHYSICALS (SEE BELOW), 3) A SMALL INCREASE IN SILVER OZ STANDING AT THE COMEX FOR JUNE AND 4) MINIMAL LONG LIQUIDATION

EFP ISSUANCE 140 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY: 150 CONTRACTS AND SEPT: 100 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 140 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 358 CONTRACTS TO THE 140 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A TINY LOSS OF 251 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES. THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES 1.090 MILLION OZ!!! OCCURRED WITH THE 16 CENT GAIN IN PRICE///

RESULT: A TINY SIZED DECREASE IN SILVER OI AT THE COMEX WITH THE 16 CENT GAIN IN PRICING THAT SILVER UNDERTOOK IN PRICING// THURSDAY. WE ALSO HAD A SMALL SIZED 140 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED UP 28.32 POINTS OR 0.96% //Hang Sang CLOSED UP 178.95 POINTS OR 0.73% /The Nikkei closed UP 123.33 POINTS OR 0.55%//Australia’s all ordinaires CLOSED UP .16%

/Chinese yuan (ONSHORE) closed UP at 7.0733 /Oil UP TO 40.03 dollars per barrel for WTI and 42.54 for Brent. Stocks in Europe OPENED GREEN// ONSHORE YUAN CLOSED UP // LAST AT 7.0733 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 7.0669 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

i)we had 1 deposits into the customer account

into JPMorgan: 0

ii) Into Loomis: 1,115,594.46 oz

*** JPMorgan for most of 2017, 2018 and onward, has adding to its inventory almost every single day.

JPMorgan now has 160.819 million oz of total silver inventory or 50.67% of all official comex silver. (160.819 million/317.323 million

total customer deposits today: 1,151,594.46 oz

we had 1 withdrawals:

i) Out of CNT

231,828.800 oz withdrawn from CNT

total withdrawals; 231,828.800 oz

We had 0 adjustments

total dealer silver: 85.643 million

total dealer + customer silver: 317,323 million oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

The total number of notices filed today for the JUNE 2020. contract month is represented by 1 contract(s) FOR 5,000, oz

To calculate the number of silver ounces that will stand for delivery in JUNE we take the total number of notices filed for the month so far at 428 x 5,000 oz = 2,140,,000 oz to which we add the difference between the open interest for the front month of JUNE.(9) and the number of notices served upon today 1 x (5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the JUNE/2019 contract month: 428 (notices served so far) x 5000 oz + OI for front month of JUNE (9)- number of notices served upon today (1) x 5000 oz of silver standing for the JUNE contract month.equals 2,175,000 oz.

We GAINED 1 contracts or an additional 5,000 oz will stand for delivery as they refused to morphed into London based forwards as well as negating a fiat bonus

TODAY’S ESTIMATED SILVER VOLUME: 76,583 CONTRACTS // volume good/

FOR YESTERDAY: 61,149..,CONFIRMED VOLUME//volume fair/

YESTERDAY’S CONFIRMED VOLUME OF 61,149 CONTRACTS EQUATES to 305 million OZ 43.6% OF ANNUAL GLOBAL PRODUCTION OF SILVER..

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO- 1.18% ((JUNE 19/2020)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -0.68% to NAV: (JUNE 19/2020 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into NEGATIVE/ 1.18%

(courtesy Sprott/GATA

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 16.54 TRADING 16.40///NEGATIVE 0.87

END

And now the Gold inventory at the GLD/

JUNE 19/WITH GOLD UP$16.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//; INVENTORY RESTS AT 1136.22 TONNES

JUNE 18//WITH GOLD DOWN $2.75 TODAY: NO CHANGES IN GOLD INVENTORY: INVENTORY RESTS AT 1136.22 TONNES

JUNE 17/WITH GOLD DOWN $1.05: NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY RESTS AT 1136.22 TONNES

JUNE 16//WITH GOLD UP $6.70 TODAY: NO CHANGES IN GOLD INVENTORY: /INVENTORY RESTS AT 1136.22 TONNES

JUNE 15/WITH GOLD DOWN ANOTHER $8.80 TODAY, NO CHANGES IN GOLD INVENTORY/INVENTORY RESTS AT 1136.22 TONNES

JUNE 12//WITH GOLD DOWN $1.00 TODAY: A HUGE CHANGE IN GOLD INVENTORY: A DEPOSIT OF 1.17 TONNES AT THE GLD//INVENTORY RESTS AT 1136.22 TONNES

JUNE 11//WITH GOLD UP $16.80 TODAY: A HUGE CHANGE IN GOLD INVENTORY: A DEPOSIT OF 6.55 TONNES AT THE GLD//INVENTORY RESTS AT 1135.05 TONNES

JUNE 10/WITH GOLD DOWN $.30 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 4.02 TONNES AT THE GLD/INVENTORY RESTS AT 1129.50 TONNES

JUNE 9//WITH GOLD UP $16.00 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF 2.63 TONNES OF GOLD AT THE GLD//INVENTORY RESTS AT 1125.48 TONNES

JUNE 8//WITH GOLD UP $18.70 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF 4.10 TONNES AT THE GLD//INVENTORY RESTS AT 1128.11 TONNES

JUNE 5//WITH GOLD DOWN $40.40 TODAY: A HUGE CHANGE IN GOLD INVENTORY: A PAPER WITHDRAWAL OF 1.16 TONNES OUT OF THE GLD//INVENTORY RESTS AT 1132.21 TONNES

JUNE 4//WITH GOLD UP $20.60: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD…A DEPOSIT OF 4.09 TONNES INTO THE GLD//INVENTORY RESTS AT 1133.37 TONNES

JUNE 3//WITH GOLD DOWN $26.15//A SMALL CHANGE IN GOLD INVENTORY//A DEPOSIT OF 0.78 TONNES OF GLD INTO THE GLD//INVENTORY RESTS AT 1129.28 TONNES

JUNE 2//WITH GOLD DOWN $11.20 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.26 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 1128.40 TONNES

JUNE 1//WITH GOLD UP $1.30//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.06 TONNES OF GOLD//GLD INVENTORY RESTS TONIGHT AT 1123.14 TONNES

MAY 29/WITH GOLD UP $19.40 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD///GLD INVENTORY RESTS THIS WEEKEND AT 1119.05 TONNES

MAY 28//WITH GOLD UP $4.00 TODAY/NO CHANGES IN GOLD INVENTORY TO THE GLD//INVENTORY RESTS AT 1119.05 TONNES

MAY 27/WITH GOLD UP $.10 TODAY: A STRONG 2.34 TONNES OF GOLD ADDED TO THE GLD//INVENTORY RESTS AT 1119.05 TONNES

MAY 26//WITH GOLD DOWN $23.05//NO CHANGES IN GOLD INVENTORY://RESTS TONIGHT AT 1116.71 TONNES

MAY 22//WITH GOLD UP $13.05//A BIG CHANGE IN GOLD INVENTORY:: A PAPER ADDITION OF 3.93 TONNES//INVENTORY RESTS THIS WEEKEND AT: 1116.71 TONNES

MAY 21//WITH GOLD DOWN $26.70//NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1112.32 TONNES

MAY 20/WITH GOLD UP $7.20: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER WITHDRAWAL OF 1.46 TONNES FROM THE GLD////INVENTORY RESTS TONIGHT AT 1112.32 TONNES

MAY 19//WITH GOLD UP $10.60//NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY RESTS AT 1113.78 TONNES

MAY 18/WITH GOLD DOWN $15.40 TODAY: A HUGE CHANGE IN GOLD INVENTORY: A PAPER DEPOSIT OF 9.06 TONNES./INVENTORY RESTS AT 1113.78 TONNES

MAY 15.WITH GOLD UP $16.30 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 12.58 TONNES/ INVENTORY RESTS AT 1104.72 TONNES

MAY 14//WITH GOLD UP $19.25 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY RESTS AT 1092.14 TONNES

MAY 13//WITH GOLD UP $9.05 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 11.07 TONNES/INVENTORY RESTS AT 1092.14 TONNES

MAY 12//WITH GOLD UP $6.60 TODAY; A SMALL CHANGES IN GOLD INVENTORY AT THE GLD/: A WITHDRAWAL OF .58 TONNES FROM THE GLD///INVENTORY RESTS AT 1081.07 TONNES

MAY 11/WITH GOLD DOWN $12.65 TODAY: NO CHANGES IN GOLD INVENTORY: //INVENTORY RESTS AT 1081.65 TONES..

MAY 8/WITH GOLD DOWN $7.00 TODAY; A BIG CHANGE IN GOLD INVENTORY: A PAPER ADDITION OF 5.85 TONNES/INVENTORY RESTS AT 1081.65 TONNES

MAY 7/WITH GOLD UP $29.65 TODAY : A SMALL CHANGE IN GOLD INVENTORY AT THE GLD//A PAPER ADDITION OF .41 TONNES/INVENTORY RESTS AT 1075.80 TONNES

MAY 6//WITH GOLD DOWN $17.00 TODAY/ A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A PAPER ADDITION OF 3.68 TONNES/INVENTORY RESTS AT 1075.39 TONES

MAY 5/WITH GOLD DOWN $1.65 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER ADDITION OF 3.81 TONNES//INVENTORY RESTS AT 1071.71 TONNES

MAY 4//WITH GOLD UP $12.00 TODAY//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A MASSIVE PAPER DEPOSIT OF 11.4 TONNES INTO THE GLD////GOLD INVENTORY RESTS AT 1067.90 TONNES

MAY 1/WITH GOLD UP $8.45 NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1056.50 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Inventory rests tonight at

JUNE 19/ GLD INVENTORY 1136.22 tonnes*

LAST; 845 TRADING DAYS: +192.22 NET TONNES HAVE BEEN REMOVED FROM THE GLD

LAST 745 TRADING DAYS://+367.52 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

JUNE 19//WITH SILVER UP 22 CENTS TODAY: STRANGE!! A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 839,000 OZ FROM THE SLV////INVENTORY RESTS AT 486,454 MILLION OZ..

JUNE 18/WITH SILVER DOWN 16 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 932,000 OZ INTO THE SLV////INVENTORY RESTS AT 487.293 MILLION OZ

JUNE 17/WITH SILVER UP 8 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.261 MILLION OZ INTO THE SLV////INVENTORY REST AT 486.361 MILLION OZ

JUNE 16//WITH SILVER UP 20 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.118 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 483.100 MILLION OZ//

JUNE 15/WITH SILVER DOWN 14 CENTS NO CHANGES IN SILVER INVENTORY: //INVENTORY RESTS AT 481.982 MILLION OZ///

JUNE 12/WITH SILVER DOWN 30 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV/: TWO DEPOSITS OF 7.269 MILLION OZ AND 1.802 MILLION OZ ADDED TO THE SLV///INVENTORY RESTS THIS WEEKEND AT 481.982 MILLION OZ//

JUNE 11//WITH SILVER UP 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY: ///INVENTORY RESTS AT 472.89 MILLION OZ//

JUNE 10/WITH SILVER UP 3 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 472.849 MILLION OZ//

JUNE 9/WITH SILVER DOWN 6 CENTS TODAY//A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.605 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 422.849 MILLION OZ//

JUNE 8/WITH SILVER UP 36 CENTS TODAY: TWO HUGE WITHDRAWALS OF 932,000 MILLION OZ AND 1.491 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 470.240 MILLION OZ//

JUNE 5/WITH SILVER DOWN 46 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER WITHDRAWAL OF 648,000 OZ FROM THE SLV////INVENTORY RESTS AT 472.663 MILLION OZ

JUNE 4//WITH SILVER UP 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV.//INVENTORY RESTS AT 473.315 MILLION OZ//

JUNE 3//WITH SILVER DOWN 23 CENTS TODAY//NO CHANGES IN SILVER INVENTORY AT THE SLV//

INVENTORY RESTS AT 473.315 MILLION OZ//

JUNE 2//WITH SILVER DOWN 31 CENTS TODAY; A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A HUMONGOUS 6.686 MILLION OZ ADDED TO THE SLV////INVENTORY RESTS TONIGHT AT 473.315 MILLION OZ//

JUNE 1//WITH SILVER UP 38 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.56 MILLION OZ INTO THE SLV////INVENTORY RESTS TONIGHT AT 466.629 MILLION OZ//

MAY 29//WITH SILVER UP 52 CENTS TODAY: A MASSIVE DEPOSIT OF 2.796 MILLION OZ INTO THE SLV//INVENTORY RESTS THIS WEEKEND AT 463.273 MILLION OZ//

MAY 28//WITH SILVER UP 9 CENTS TODAY: A MASSIVE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.660 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 460.477 MILLION OZ//

MAY 27/WITH SILVER UP 13 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 455.817 MILLION OZ//

MAY 26//WITH SILVER DOWN 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/// INVENTORY RESTS AT 455.817 MILLION OZ//

MAY 22/WITH SILVER UP 22 CENTS TODAY/ A HUGE PAPER WITHDRAWAL OF 1.864 MILLION OZ//INVENTORY RESTS AT 455.817 MILLION OZ/

LAST 5 DAYS: SILVER UP 60 CENTS: INVENTORY UP A WHOOPING 23.767 MILLION OZ///

MAY 21/WITH SILVER DOWN 50 CENTS TODAY: A HUGE PAPER DEPOSIT OF 7.923 MILLION OZ///INVENTORY RESTS AT 457.681 MILLION OZ//

MAY 20//WITH SILVER UP ANOTHER 11 CENTS TODAY: A HUGE CHANGE IN SLV INVENTORY: A HUGE PAPER DEPOSIT OF 9.601 MILLION OZ INTO THE SLV// //INVENTORY RESTS AT 449.758 MILLION OZ

MAY 19/WITH SILVER UP ANOTHER 29 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV////INVENTORY RESTS AT 440.157 MILLION OZ//

MAY 18/WITH SILVER UP ANOTHER 48 CENTS TODAY: TWO BIG CHANGES IN SILVER INVENTORY AT THE SLV I.E. 2 PAPER DEPOSIT OF ( I) 8.39 MILLION OZ AND THEN ( 2) 8.109 MILLION OZ//INVENTORY RESTS AT 432.048 MILLION OZ// (TOTAL DEPOSITS 16.500 MILLION OZ///)

MAY 15/WITH SILVER UP 81 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV: /INVENTORY RESTS AT 423.65 MILLION OZ.

MAY 14//WITH SILVER UP 33 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV.//INVENTORY RESTS AT 423.65 MILLION OZ

MAY 13/WITH SILVER UP 2 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 2.79 MILLION OZ INTO THE SLV..//INVENTORY RESTS AT 423.65 MILLION OZ//

MAY 12/WITH SILVER UP 5 CENTS TODAY: A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.076 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 420.861 MILLION OZ//

MAY 11.WITH SILVER DOWN 5 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 417.785 MILLION OZ//

MAY 8/WITH SILVER UP 11 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A MONSTER DEPOSIT OF 4.661 MILLION OZ OF SILVER INTO THE SLV..///INVENTORY RESTS AT 417.785 MILLION OZ//

MAY 7/WITH SILVER UP 45 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 413.124 MILLION OZ//

MAY 6/WITH SILVER DOWN 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 413.124 MILLION OZ//

MAY 5/WITH SILVER UP 17 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 413.124 MILLION OZ///

MAY 4//WITH SILVER DOWN 5 CENTS TODAY:2 HUGE PAPER CHANGES IN SILVER INVENTORY AT THE SLV.i).A LARGE 1.399 MILLION OZ OF PAPER SILVER REMOVED FROM THE SLV//..//INVENTORY RESTS AT 411.427 MILLION OZ and ii) A LARGE 1.647 MILLION OZ OF PAPER SILVER ADDED TO THE SLV// INVENTORY RESTS AT 413.124 MILLION OZ//

MAY 1/WITH SILVER FLAT IN PRICE: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 412.826 MILLION OZ///

JUNE 19.2020:

SLV INVENTORY RESTS TONIGHT AT

486.454 MILLION OZ.

END

LIBOR SCHEDULE AND GOFO RATES// GOLD LEASE RATES

YOUR DATA…..

6 Month MM GOFO 2.55/ and libor 6 month duration 0.42

Indicative gold forward offer rate for a 6 month duration/calculation:

GOLD LENDING RATE: -2.13%

NEGATIVE GOLD LEASING RATES INCREASING BY A HUGE AMOUNT//GOLD SCARCITY AND CENTRAL BANKS CALLING IN ALL OF THEIR GOLD LEASES

XXXXXXXX

12 Month MM GOFO

+ 2.11%

LIBOR FOR 12 MONTH DURATION: 0.58

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = -1.53%

end

PHYSICAL GOLD/SILVER STORIES

i) GOLDCORE BLOG/Mark O’Byrne

ii) Important gold commentaries courtesy of GATA/Chris Powell

A very important discussion between Chris Powell and Andrew Maguire. Maguire states categorically that Scotia’s withdrawal from the precious metals arena is a forced regulatory decision and thus puts in doubt the resolution of the bank’s gold/silver positions as well as creates massive risks for Scotia’s counterparties. Lawsuits will follow forthwith.

(ChrisPowell/Andrew Maguire/Kinesis)

Regulators are kicking Scotiabank out of gold, London trader Maguire says

Submitted by cpowell on Thu, 2020-06-18 16:52. Section: Daily Dispatches

12:51p ET Thursday, June 18, 2020

Dear Friend of GATA and Gold:

In a discussion with your secretary/treasurer this week, London metals trader and Kinesis Money founder Andrew Maguire says longtime metals bank Scotiabank is not only closing its metals trading desk but getting out of the vaulting business and all involvement with gold. Maguire says Scotiabank’s withdrawal is a “forced regulatory decision,” puts in doubt the resolution of the bank’s gold positions, creates risks for the bank’s counterparties, and raises the prospect of lawsuits.

The discussion also covers GATA’s documentation of gold market manipulation at the behest of Western central banks, GATA’s disclosure this month that gold market intervention by the Bank for International Settlements has reached its highest level in three years, the crumbling of the fractional-reserve gold banking system, and the prospect of an international currency revaluation that would peg the price of gold much higher.

The discussion is 37 minutes long and can be viewed at the Kinesis Money channel at You Tube here:

https://www.youtube.com/watch?time_continue=110&v=jeYiJ3kywz0&feature=em…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

This will not end well. European central banks will pay banks to loan money as they borrow a record 1.31 trillion euros

(Reuters/GATA)

European Central Bank will pay banks not to shrink loan books

Submitted by cpowell on Thu, 2020-06-18 14:36. Section: Daily Dispatches

Banks Borrow Record 1.31 Trillion Euros from ECB

By Balazs Koranyi

Reuters

Thursday, June 18, 2020

FRANKFURT, Germany — Euro zone banks borrowed a record 1.31 trillion euros ($1.47 trillion) from the European Central Bank today, taking advantage of negative interest rates to meet growing demand for credit from companies hit by the deepest recession in living memory.

Launched six years ago, the ECB’s targeted-longer term refinancing operations were redesigned earlier this year to help the economy cope with the coronavirus crisis and banks will get the cash for a rate as low as minus 1%.

…

At 1.31 trillion euros, take up is above expectations with most analysts predicting a figure just over 1 trillion euros for the three-year loans. Forecasts were generally in the 900 billion to 1.4 trillion euro range.

Although borrowing was more than twice as big as in any previous ECB facility, the net take is smaller as banks likely rolled over around 750 billion euros worth of earlier ECB funding to take advantage of record low rates.

The negative interest rate means banks that tapped the auction will earn 0.50% for one year with no strings attached and 1% if they simply refrain from shrinking their loan book. …

… For the remainder of the report:

https://uk.reuters.com/article/us-ecb-policy-loans/banks-borrow-record-1…

END

The wealthy are now seeking gold

Reuters/GATA)

World’s ultra-wealthy go for gold amid stimulus bonanza

Submitted by cpowell on Fri, 2020-06-19 02:20. Section: Daily Dispatches

By Brenna Hughes Neghaiwi and Simon Jessup

Reuters

Thursday, June 18, 2020

As stock markets roar back from the coronavirus-led rout, advisers to the world’s wealthy are urging them to hold more gold, questioning the strength of the rally and the long-term impact of global central banks’ cash splurge.

Before the COVID-19 pandemic, most private banks recommended their clients hold none or just a tiny amount of gold

Now some are channelling up to 10% of their clients’ portfolios into the yellow metal as the massive central bank stimulus reduces bond yields — making non-yielding gold more attractive — and raises the risk of inflation that would devalue other assets and currencies.

While gold prices have already risen 14% since the start of the year to $1,730 an ounce, many private bankers bet that gold — a hedge for both inflation and deflation — has more to run.

“Our view is that the weight of monetary supply, expansion, is going to ultimately be debasing to the dollar, and the Fed commitments, which are anchoring real rates, make the case for gold pretty sturdy,” said Lisa Shalett, Chief Investment Officer, Wealth Management at Morgan Stanley.

Nine private banks spoken to by Reuters, which collectively oversee around $6 trillion in assets for the world’s ultra-rich, said they had advised clients to increase their allocation to gold. Of them, four provided forecasts and all saw prices ending the year higher than they are now. …

… For the remainder of the report:

https://www.reuters.com/article/us-health-coronavirus-gold-wealth-analys…

END

Alasdair Macleod explains the crisis initiated on March 23 and how this crisis escalates.

Your weekend reading

(Alasdair Macleod)

Alasdair Macleod: The crisis goes up a gear

Submitted by cpowell on Fri, 2020-06-19 03:32. Section: Daily Dispatches

By Alasdair Macleod

GoldMoney, St. Helier, Jersey, Channel Islands

Thursday, June 18, 2020

Dollar-denominated financial markets appeared to suffer a dramatic change on or about the 23 March. This article examines the possibility that it marks the beginning of the end for the Fed’s dollar.

At this stage of an evolving economic and financial crisis, such thoughts are necessarily speculative. But an imminent banking crisis is now a near certainty, with most global systemically important banks in a weaker position than at the time of the Lehman crisis. US markets appear oblivious to this risk, though the ratings of G-SIBs in other jurisdictions do reflect specific banking risks rather than a systemic one at this stage.

…

A banking collapse will be a game-changer for financial markets, and we should then worry that the Fed has bound the dollar’s future to their fortunes.

The dollar could fail completely by the end of this year. Against that possibility a reset might be implemented, perhaps by reintroducing the greenback, which is not the same as the Fed’s dollar. Any reset is likely to fail unless the US Government desists from inflationary financing, which requires a radically changed mindset, even harder to imagine in a presidential election year. …

… For the remainder of the analysis:

https://www.goldmoney.com/research/goldmoney-insights/the-crisis-goes-up…

The crisis goes up a gear

Dollar-denominated financial markets appeared to suffer a dramatic change on or about the 23 March. This article examines the possibility that it marks the beginning of the end for the Fed’s dollar.

At this stage of an evolving economic and financial crisis, such thoughts are necessarily speculative. But an imminent banking crisis is now a near certainty, with most global systemically important banks in a weaker position than at the time of the Lehman crisis. US markets appear oblivious to this risk, though the ratings of G-SIBs in other jurisdictions do reflect specific banking risks rather than a systemic one at this stage.

A banking collapse will be a game-changer for financial markets, and we should then worry that the Fed has bound the dollar’s future to their fortunes.

The dollar could fail completely by the end of this year. Against that possibility a reset might be implemented, perhaps by reintroducing the greenback, which is not the same as the Fed’s dollar. Any reset is likely to fail unless the US Government desists from inflationary financing, which requires a radically changed mindset, even harder to imagine in a presidential election year.

Introduction

The most important mistake economists and financial watchers make is to assume events and prices tomorrow are simply projections of those of today. It is the basis of all economic and financial modelling. Yet despite the hard lessons of experience economic forecasters persist with their misleading models.

Nowhere is the failure of linear projection from the past more important than in the lifeblood common to everything. While knowing that state-issued currencies change in their utility over time, almost no one expects their demise, other perhaps at some point in the far distant future. But what if this generally linear expectation is as wrong as all other forecasting models? What if the response to the current economic crisis is a more rapid depreciation of currencies? And what happens if they die altogether? And what are the consequences for the ordinary person?

This article explores these what-ifs. It examines the conditions that could lead to this outcome. History gives us a guide, not through extrapolation, but by telling us that every recorded currency collapse has occurred to fiat currencies unbacked by gold or silver. So, we know it will happen — eventually. Less understood is that the pattern is always the same: a prolonged period of falling purchasing power, followed by a sudden collapse when a currency’s users finally reject it. In terms of time the latter phase usually lasts approximately six months.

Assessing the turning point

The early morning of Monday, 23 March was a significant time, marking the top of the dollar’s trade-weighted index. At the same time, gold, silver and copper prices, having fallen in the weeks before turned sharply higher. And while oil initially followed, it was a month before it resumed its uptrend — delayed by the delivery hiatus in the futures markets which briefly drove the price negative. The S&P 500 rallied the following day, ending a near 30% decline before recovering all of it, and then some.

Something had changed. Either markets decided that economic growth, both in the US and the rest of the world was going to continue following lockdowns, and growing demand for key commodities was going to be resumed. Or, as the decline in the dollar’s TWI indicated, the purchasing power of the dollar was going to decline, and commodity prices were reflecting an accelerating downtrend for the dollar’s purchasing power.

The performance of the S&P 500 since 23 March, being unhinged from any business conditions, gives us a clue: the flood of money emanating from the Fed is fuelling stock prices. It is also fuelling prices of all other financial assets.

The turnaround in silver is a more subtle story, shown in the chart as the reciprocal of the more usual gold/silver ratio. Silver had been ignored, classed solely as an industrial metal. Gold was seen by the financial community as the only metallic hedge against uncertainty in the financial system. That changed on 23 March when the gold/silver ratio peaked at 125 on the previous business day. It is now beginning to outperform gold with the gold/silver ratio currently down to 98. We might look back and pinpoint this time as marking the beginning of a return to some moneyness in silver.

The weeks before had seen the Fed ease monetary policy. On 3 March, the Fed cut its funds rate from 1 ½% to 1%. In the accompanying announcement the Fed said that the fundamentals of the economy remained strong, but the coronavirus posed evolving risks to the economy.

On 15 March, the Fed cut its funds rate again, this time to zero, but the statement now said the coronavirus had harmed communities and disrupted economic activity in many countries, including the US. On a twelve-month basis, overall price inflation and price increases for other than food and energy were running at below 2%. The Fed announced renewed quantitative easing of at least $500bn of Treasury purchases and $200bn of mortgage-backed securities “in the coming months”. It was “prepared to use its full range of tools to support the flow of credit to households and businesses and thereby promote its maximum employment and price stability goals.”

That day the Fed made two other announcements. The first detailed arrangements for the encouragement of credit expansion to support both consumers and businesses, including the reduction of reserve ratios for all banks to zero. The second concerned the reduction of costs in drawing down USD swap lines at the other major central banks. They were followed over the course of the week by a series of announcements facilitating the availability of credit.

Clearly, the Fed was engaging the ultimate in aggressive monetary policies. And taking a phrase from the last head of the ECB, the Fed had signalled it was prepared to do whatever it takes without limitation. But the response in the markets took a week to develop into an inflection point, a normal pause before a new direction is found.

Central bank inflation and bank credit difficulties

Since the Fed is one step removed from the non-financial economy it relies on commercial banks to implement its monetary policy. But commercial banks will only act as the Fed’s agents if they are confident the rewards are greater than the risks involved. If the current crisis is simply a matter of the coronavirus being contained before everything returns to normal, then bankers might be prepared to take a punt on an increase of bank lending.

But as time passes, the losses mount. Business and consumer defaults are increasing, and the prospects for a rapid recovery appear to be receding. Furthermore, liquidity strains in the banking system are resurfacing, despite the massive injections of QE by the Fed. After subsiding from the panicky days of last September, overnight repos are on the increase again totalling anything between $20—$100bn daily.

It has been generally forgotten that the global economy was already facing a recession before the virus lockdowns. Trade wars between America and China and bank credit expansion having run for a decade were a repeat of the conditions that led to the Wall Street Crash in 1929, when the Smoot-Hawley Tariff Act following the roaring twenties was enacted, bank credit imploded, and the 1930s depression followed. Similarly, banks are now highly leveraged on their balance sheets and fear of bad debts has taken over from lending greed. The global banking cohort is increasingly desperate to reduce balance sheet commitments at the same time as the Fed and other central banks are frantic to see them expanded.

It is no wonder that the Fed’s expansion has remained bottled up in financial markets, driving financial assets even further into dangerous overvaluation territory. Consequently, without liquidity flowing more freely into the non-financial economy, bad debts can only deteriorate further, with loan risk rapidly increasing for commercial banks.

Systemic issues are being ignored

When the coronavirus first became an economic issue, there were mounting concerns over payment failures in supply chains. In the US, these payments are effectively the equivalent of gross output, which at the end of last year was running at $38 trillion. While we regard gross output as the value of products as they flow through their production stages, the payments flow the other way, back down the chains. Therefore, the $38 trillion figure can be taken as proxy for the sum of all supply chain payments in the US, to which must be added the dollar equivalents of supply chain payments outside the US for semi-manufactured imports.

Not all supply chains have been completely disrupted, so the good news is payment disruptions onshore should be significantly less than $38 trillion but could easily be half that. But there is likely to be additional disruption from abroad, a point addressed by the Fed when it increased the number of central banks (but not China) having access to its swap lines.

The risks to commercial banks are not so much from the largest corporations, likely to be bailed out if in trouble, but from lower tiers of borrowers. This affects banks with exposure to collateralised loan obligations, which are bundled loans to companies often unable to raise funds any other way — today’s version of the collateralised debt obligations that blew up the banking system in 2008. Additionally, banks have direct loans and revolving capital exposure on their balance sheets with all businesses in the $38 trillion of onshore supply chains.

The market capitalisation of the US’s G-SIBs — global systemically important banks — is less than a trillion dollars. Yet the supply chain failures that they are expected to backstop are many trillions — multiple times their market capitalisation, and even of their balance sheet equity.

It seems hardly possible that the US banking system will survive the current supply chain disruption without help. The added bad news is that the US G-SIBs are rated much more highly in stock markets than their Chinese, Japanese, Eurozone, Swiss and UK competitors, shown in Figure 1 above.[i] It indicates that a systemic failure in dollar-denominated financial markets is not widely expected, given the generally higher market ratings afforded to US G-SIBs than for those in other jurisdictions. This probably explains why this topic is not yet a significant issue for dollar investors, though individual bank failures are more obviously an issue in other jurisdictions, where some G-SIB price to book ratios are below 30% while those of US G-SIBs average 93%.

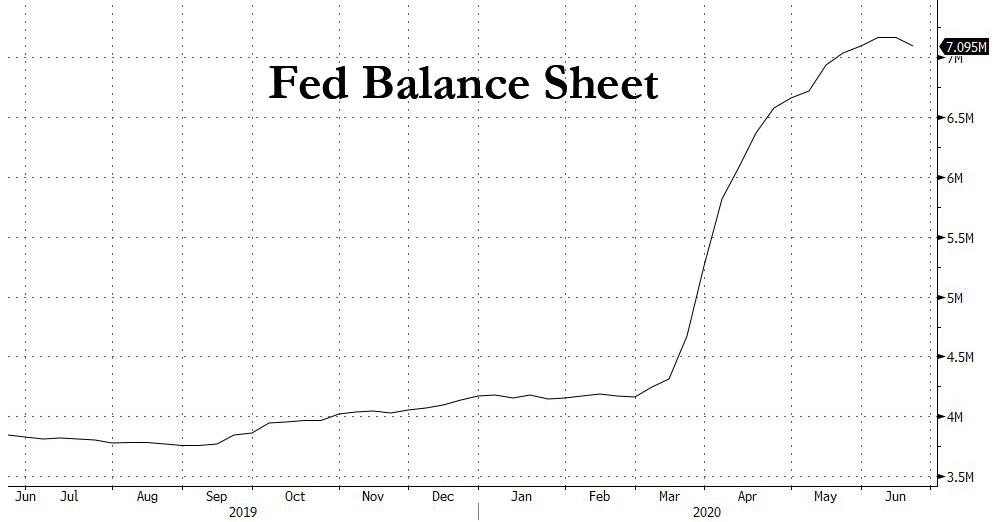

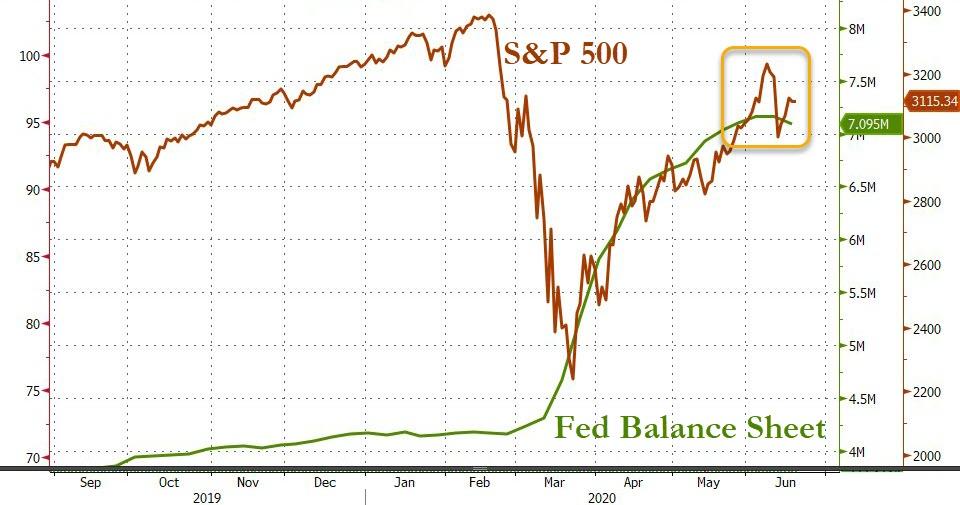

The next significant event therefore will almost certainly be the failure of a G-SIB, if not in America, then elsewhere. Given the sheer scale of the problems in supply chains in all currencies and the accumulating bad debts attributable to lockdowns it could happen in a matter of weeks. Presumably, failing banks will be taken into public ownership with the Fed backstopping it with yet more inflationary finance. The impact on the Fed’s balance sheet, which has already grown to over $7 trillion will probably be several times its current size. But that, on its own, may not be enough to destroy the dollar.

A more direct danger is posed from monetary policies aimed at supporting financial asset values. In common with other major central banks the Fed has become reliant on a policy of ultra-low interest rates to fund its government’s deficit. At the same time, there has been a longstanding belief, particularly in America, that rising prices for financial assets, chiefly stocks, have been vital to generate a wealth effect and therefore maintain public confidence in the economic outlook. In current markets, this overvaluation policy has been taken to extremes with even teenagers reportedly buying fractionalised stocks through aggregating platforms, such as Robinhood, as if it is a just another computer game.

The dollar’s inevitable descent

In more normal times the excessive speculation in the markets seen today would encourage the Fed to inject some caution into monetary policy; but the Fed cannot backtrack for fear of triggering a catastrophic collapse. Consequently, the future of the dollar has become firmly tied to that of confidence in financial markets.

With a rapidly escalating budget deficit the US Government has a growing funding requirement, the cost of which already absorbs $400bn in interest charges annually. The Trump administration had increased its deficit to record levels in the good times when tax revenue was buoyant. And now the crisis has hit, higher interest rates will expose the US Government to a debt trap. This is a weapon the Fed cannot use.

As noted above, the next market shock is likely to be a systemic failure in the banking system. It matters not where that occurs, but when it does it makes bank depositors autarkic. Not only do they withdraw funds from banks they deem to be at risk thereby increasing their problems, but they also reduce cross-border currency exposure. The dollar is most exposed of all currencies to the latter risk: on last known figures foreigners owned about $25 trillion in securities, short-term paper and bank deposits, while Americans held roughly half that invested mainly in illiquid production facilities abroad, limited portfolio exposure to listed securities and with very little liquid foreign currency exposure.

In our headline chart we noted that the dollar’s turning point was 23 March and its subsequent downturn was part of a bigger commodity picture with gold, silver, copper and — belatedly — oil prices rising. In March, US TIC data showed that foreigners reduced their dollar exposure by $227.9bn, only offset by US residents’ net sales of foreign securities of $133.3bn.[ii] Here is the evidence that in troubled times money heads for home. Additionally, that month saw a trade deficit of $44.4bn suggesting total foreign-related dollar selling amounted to $177.7bn. This is only part of a bigger dollar picture, but it does appear foreigners were reducing their dollar exposure at the time that the dollar’s TWI peaked on 23 March.

This is important, because there are two market factors that have always led to a fiat currency collapse. The first is selling by foreigners, which appears to have commenced, and in this respect the dollar is particularly exposed. With some $25 trillion invested in US securities etc., the potential destruction to the dollar’s purchasing power from this source is significant. As global trade shrinks further, not only will foreigners be driven by the need to redeploy dollars into their currencies of origin, but they will stop funding the US Government, choosing to sell down their US Treasury holdings, a process which has already started. If the Fed is to successfully fund the growing budget deficit it must absorb foreign sales of US Treasuries as well as maintain sufficient levels of QE to fund a rapidly increasing budget deficit.

Just imagine the consequences of a systemic failure. The spell cast over financial assets will be broken. First, investors and speculators are likely to turn their attention to equities, being obviously the most overvalued financial assets at a time of intensifying crisis. Foreign investors will join, selling down their portfolio exposure, repatriating some, if not all of the proceeds by selling dollars as well. Next, with a falling dollar and a growing sensitivity to the political aspect of the crisis, market participants will reassess the US Government’s funding requirements and question the yield suppression policy of the Fed. Dollar selling seems bound to intensify.

It will then become obvious to everyone that the Fed is sacrificing the dollar in order to fund the government, keep the banking system going and to support the economy by attempting to provide the liquidity to defray supply chain failures. It will already be demonstrably failing to support financial asset prices, which has become the visible manifestation of a successful monetary policy. It would be a miracle if this failure, in Trump’s election year with a socialistic president being lined up by the Democrats, does not lead to a full-blown financial and dollar crisis.

Unless the Fed can raise interest rates to the point where it is too expensive for speculators to short the dollar (which we can rule out), it will enter the second phase of its collapse, driven by US residents realising the dollar is losing purchasing power, rather than prices rising. The purchasing power of any money depends on the balance between money and goods maintained by its users. If they collectively reject the money in favour of goods, then money’s purchasing power declines, potentially to zero. Following foreign selling, this is the second phase of the destruction of a fiat currency, which in past examples have taken roughly six months for it to become worthless.

There are three factors that could shorten this timescale even further: the replacement of cash and cheques by digital payments, modern communications leading to the rapid spread of information, and as a consequence of the development of cryptocurrencies, wider public foreknowledge of the weaknesses of unbacked fiat currencies.

The case for fiat currency survival beyond 2020

The circumstantial evidence that the dollar will collapse before the year-end is mounting. Cassandra opened her casket, the evils escaped, and only hope remains trapped.

Or so it seems. We cannot divine the future. We can only sift the evidence, be aware of common fallacies and avoid the temptation to wrongly extrapolate from yesterday into the future. While our method may be better than the macroeconomic forecasting beloved of the establishment, a predicted outcome is never reality. And it is possible the US Treasury might attempt a reset, perhaps using Treasury dollars, otherwise known as greenbacks, which were last issued in 1971. But without axing government welfare commitments to the American public, returning to balanced budgets and abandoning Fed dollar denominated debt this sort of legerdemain is unconvincing. Furthermore, the dollar’s reserve role for other currencies would have to be abandoned because of the monetary inflation involved in Triffin’s dilemma. And other currencies tied to the Fed’s dollar held in their reserves would still face their own collapse.

A reset abandoning the Fed’s dollar in favour of greenbacks is possible. But history has shown that the introduction of a replacement currency for one that has collapsed fails unless government financing by monetary expansion is demonstrably abandoned. Only time will tell whether in a presidential election year the US Government musters the clarity of purpose to implement a new lasting dollar regime.

The US Treasury says it still has over 8,000 tonnes of gold. If it is willing to drop its neo-Keynesian economics and its long-standing denial of gold’s monetary function, America could reintroduce gold convertibility for the greenbacks. This would probably be a last resort. It reneges on the Fed’s balance sheet note — which in these conditions would be its only significant asset, involves the abandonment of the welfare state and America’s longstanding geopolitical aims, and it allows China to gain potential advantage by displacing the dollar with a more convincing gold convertibility of its own.

China has deliberately cornered the gold bullion market in plans that go back to the time of Deng. Almost certainly, following the introduction of its Regulations on the Control of Gold and Silver (1983), the Chinese state accumulated sufficient gold for its strategic purposes by the time it then permitted its citizens to buy gold with the opening of the Shanghai Gold Exchange in 2002. The gold acquired by the state at that time is not declared as monetary gold and the quantity is unknown, but after examining inward investment flows net of trade deficits in the 1980s and growing export surpluses subsequently, a ten per cent allocation of foreign exchange gained into gold at contemporary prices suggests a position of some 20,000 tonnes of bullion was likely to have been accumulated by 2002.

There is no way of establishing the facts, and therefore statements about the Chinese state’s ownership of bullion are necessarily speculative. But additional evidence is compelling:

• China is now the largest gold mining nation by far, extracting an estimated 4,200 tonnes since 2010, more than any other nation. This has been driven by government policy.

• The state controls all Chinese gold and silver refining, taking in doré from abroad to add to Chinese stocks. At the same time, virtually no Chinese refined gold kilo bars are permitted to leave the country.

• In 2002, when the Shanghai Gold Exchange was set up by the Peoples’ Bank of China the Chinese government encouraged its nationals to acquire physical gold, even advertising its attractions in state media. Since 2010 alone, 17,200 tonnes have been delivered into public hands by the SGE. These figures were achieved by importing bullion from the West in enormous quantities.

• Its allies in Asia, principally members of the Shanghai Cooperation Organisation, have also been acquiring gold. Russia has been particularly aggressive in dumping dollars for gold.

• China now dominates physical gold markets and can be said to control them.

Given all these verifiable facts, it seems unlikely that a state which centrally plans would not have acquired for its own use substantial quantities of bullion ahead of the establishment of the SGE. America knows it and continues to resist gold having a monetary role. If America’s anti-gold policy changed, it would restrict the dollar’s circulation abroad. It would mark the end of dollar hegemony and a gold-backed yuan would become the foreign currency of choice throughout Asia, eastern Europe, the Middle East and Africa.

Conclusions and consequences

A banking crisis in the coming weeks is an increasingly likely event, given the scale of disruption to supply chains. The escalation of bankruptcies and of non-performing loans worldwide will almost certainly take the banking system down. It will be a watershed, a wake-up call to all those who expect a return to normality after the coronavirus passes.

For the moment, central banks are throwing money at the problem; money which remains stuck in financial assets, inflating them even further, and not being transmitted to the non-financial economy by banks already over-leveraged to failing borrowers.

We can be certain central bankers and government treasury departments are only now grasping the enormity of these problems, but they are still behaving as if chucking money at them is a viable solution. They will only destroy their unbacked fiat currencies, and that destruction, starting with the dollar, is already in progress. The clock is ticking from 23 March. While there may be attempts at a fiat money reset, without clear legal commitments from central banks and treasury departments to end inflationary financing, any reset will only delay currency destruction by a matter of months.

The consequences of such an outcome are always devastating, the more so because all major westernised central banks are committed to the same inflationary policies at the same time. The political consequences do not bear thinking about.

At some stage, hopefully sooner rather than later, metallic money will regain circulation. And when prices are set in gold or silver, perhaps through fully backed substitutes, the stability they bring will end the trappings of fiat currencies. All this destruction is measured in current terms, nearly all from statistics collected by the Bank for International Settlements.

Gone will be worldwide fiat currency debt, amounting to some $250—$300 trillion. Gone will be all OTC derivatives which settle in fiat, amounting to a further $560 trillion. Gone will be listed derivatives, a further $33 trillion. Gone will be options, a further $65 trillion. All these, totalling over $900 trillion, are only part of the destruction.

Global deposits held as bank balances totalling $60 trillion will evaporate. Worldwide equity markets denominated in fiat are a further $70 trillion; anything that does not migrate from fiat pricing disappears, including most, if not all ETFs. Goodbye to hedge funds. Goodbye to offshore financial centres. Goodbye to onshore financial centres. Goodbye to $100 trillion of fiat money.

Life will be very different, and those not prepared for it, principally by retaining a store of non-fiat, sound money, which can only be physical gold and silver until credible substitutes arise, will face impoverishment. Measured in real money, the value of non-financial physical assets will collapse due to the preponderance of desperate sellers to whom survival is most important, even though priced in worthless fiat their prices will have risen. The experience of inflationary collapses in Germany and Austria in the early 1920s showed the way, when country estates went for almost nothing in gold-back dollars and $100 would buy a mansion in Berlin.

None of this is expected. It may not happen, but the chances of it happening appear to have increased significantly from 23 March.

iii) Other physical stories:

A must read on why you should buy silver

(courtesy Steve St Angelo)

MAJOR FACTOR TO INVEST IN SILVER: Five Billion Ounces Of Mine Supply Economically Lost In Past Decade

Silver will likely turn out to be one heck of a better investment than gold due to the rarity of the metal and lack of available supply in the future. While gold has stolen the show recently, I’ll bet my bottom Silver Dollar that silver will outperform gold during the next financial-currency crisis.

But, before I provide my analysis, I wanted to make a few comments about the analysts who say that “SILVER ISN’T A REAL INVESTMENT” like gold. I follow many websites and newsletters, and there seems to be this notion that silver is just an industrial metal, and its lousy price performance so far this year, versus gold, proves it isn’t worth of investing.

Yes, it’s true that silver has underperformed gold and may likely experience a paper price selloff once the broader stock markets begin to crash once again. However, at that time, I imagine acquiring silver retail bullion products will even more difficult than it was during March-April.

Regardless, the reason I believe silver will be one of the few KEY INVESTMENTS to own going forward has to do with the dire energy predicament we face… which I label as the ENERGY CLIFF. Unfortunately, most analysts that look at silver as more of an industrial metal do not understand the Falling EROI – Energy Returned On Investment and how it’s impacting the global economy and financial system.

So, they continue to criticize the “Silver Pumpers” or “Silver Hypers” as mere charlatans. I find this simply hilarious when the Federal Reserve just purchased $3 trillion worth of assets in just the past three months. Furthermore, total U.S. public debt increased $25 billion per day in 2020, more than five times the average daily rate over the past decade.

While all this fancy FED FINANCIAL WIZARD OF OZ propping hasn’t destroyed the U.S. Dollar or the faith in the U.S. Treasury Market, it will in time. Just be patient. At that point, those few who own physical precious metals, especially silver, will be glad that they understood that you couldn’t erase 2,000+ years of SILVER MONETARY HISTORY.

THAT’S CORRECT… Over The Past Decade, 5 Billion Ounces Of Silver Mine Supply Likely Lost Forever

The irony of being an ANTI-SILVER analyst will actually be the reason to invest in silver. Again, most analysts look at silver as more an industrial metal. They say the real monetary metal is gold, not silver. However, what seems to be seriously overlooked by these analysts is that silver is still by far the most acquired investment metal, IN TROY OUNCES. From 2010 to 2019, total global physical silver investment demand was 2.3 billion oz versus 345 million oz for gold. Sure, the Dollar amount of investment gold was much higher, but ounce for ounce, silver is the largest physical metal investment market in the world.

With that being said, silver investors should be happy to know that 5 billion ounces of world mine supply over the past decade is likely lost forever. The term I use for this lost silver supply is “ECONOMICALLY LOST” metal.

Some precious metals analysts, such as Jan Nieuwenhuijs of Voima Gold, stated that there was a lot more above-ground silver in the world than what the Silver Institute discloses as “Identifiable above-ground stocks.” Jan argues that there are 1.6 million tons or 51 billion oz of above-ground stocks in the world, 20 times higher than the quoted 2.5 billion oz of physical investment silver stocks by GFMS in the 2019 World Silver Survey.

What Jan seems to ignore conveniently is that a large percentage of that silver is “Economically Lost” forever. How realistic is it to include most of the silver used for industrial purposes that are still in old homes, appliances, electronics, or in landfills across the world?? We can’t include this “Economically Lost” silver as above-ground inventories in some silly “Stock to Flow” calculation. It’s pure RUBBISH.

If we look at the silver market over the past decade, my calculations suggest that at least 5 billion oz of silver mine supply were Economically lost. I derived this figure by determining how much silver was recycled in each category annually and then estimated the total amount lost. First, I started with the total silver mine supply from 2010 to 2019 and then subtracted the estimated Economically Lost amount:

Approximately 60% or 5 billion oz of the total 8.35 billion oz of silver mine supply from 2010-2019 was economically lost. Now, compare that to the estimated 123 million ounces or only 12% of the gold mine supply lost over the past decade. Thus, 88+% of the 1+ billion oz of gold mined over the same period can still be counted as Above-Ground stocks. Most of the gold that was economically lost 2010-2019 was in the technology sector. According to the World Gold Council, over those ten years, gold consumption in the technology sector was 116 million oz. While some of this high-tech gold is recycled, 90% of global gold recycling comes from scrap gold jewelry (Source: World Gold Council).

Unfortunately, most people who buy silver jewelry end up throwing it away rather than selling it for scrap recycling. It’s just not worth the effort and time to drive to the pawnshop to sell $10-$25 worth of silver jewelry. Thus, the majority of silver jewelry that was fabricated over the past 50 years is likely never to be recycled. Sure, if the silver price goes up to $100, we may see more silver jewelry recycling, but I doubt we will see billions of ounces come back in the market.

For example, over the past decade, of the 1.86 billion ounces of total world silver recycling, jewelry scrap supply only accounted for 12% of that total. Thus, of the total 1.87 billion oz of silver jewelry demand 2010-2019, I determined that at a conservative 15%, only 281 million oz may be recycled. No, it’s not a typo. Total silver recycling from that ten-year period was 1.86 billion oz versus 1.87 billion oz of silver jewelry demand. Source for both silver recycling and mine supply comes from the Silver Institute’s World Silver Surveys.

Now, if we add the total world silver mine supply from 2010 to 2019, it equals 8.35 billion oz:

Here is why silver will be a much better-performing investment asset in the future than gold.

Silver vs. Gold: Mine Supply & Recycling (2010-2019)

- Global Silver Mine Supply = 8.35 billion oz

- Global Silver Recycling = 1.86 billion oz

- Silver Recycling-Mine Supply Ratio = 22%

- Global Gold Mine Supply = 1.03 billion oz

- Global Gold Recycling = 424 million oz

- Gold Recycling-Mine Supply Ratio = 42%

Because only 8% of world gold demand is in the technology sector (2010-2019) versus approximately 50% for silver industrial consumption, most silver mined is economically lost forever. During the ten-year period, 4.8 billion oz of silver was consumed in the industrial sector. On average, only 20% of the annual industrial silver demand is recycled. Thus, less than 1 billion oz of that total 4.8 billion consumed in the industrial sector will likely be recovered.

Thus, adding up the possible recycling from that 8.35 billion of silver mine supply in the Industrial, Jewelry and Silverware sectors, and adding it to the physical silver investment demand (assumed at 100% recycled), I arrived at approximately 3.3 billion oz of silver NOT ECONOMICALLY LOST. By subtracting the two, I came up with the 5 billion oz of Economically Lost silver supply.

Again, this is just a simple calculation. Now, some might say, “If silver price shoots back up to $50, wouldn’t that bring on a lot more silver scrap recycling?” It may. However, in 2011 when the silver price reached $50, the total amount recycled was 230 million oz. Even if we say 250 million oz per year over a decade, that would only be 2.5 billion oz of recycling. That is still far below the 8.35 billion oz of total global silver mine supply over that period.

Silver investors are sitting on an excellent investment that few understand the powerful fundamental dynamics. I say, let the Federal Reserve and U.S. Government continue to print trillions to prop up the markets. The more money they print and the more debt is added to the system, the better the fundamentals to own precious metals, especially silver.

THANK YOU ALL FOR THE SUPPORT: I just wanted to thank all the individuals who continue to support the SRSrocco Report website and youtube channel. I know some of you have canceled memberships as times are tough. I understand. If you are new to the site and find the information valuable, please consider supporting the website, if you have the means to do so, at Paypal or Patreon below.

If you are new to the SRSrocco Report, please consider subscribing to my: SRSrocco Report Youtube Channel.

HOW TO SUPPORT THE SRSROCCO REPORT SITE:

I would also like to thank those foundation supporters, who have chosen to become a member by making donations through PayPal to further the research and publishing work at the SRSrocco Report.

So please consider supporting my work on Patron by clicking the image below:

Or you can go to my new Membership page by clicking the image below:

Check back for new articles and updates at the SRSrocco Report. You can also follow us on Twitter, Facebook, and Youtube

END

This is interesting: Goldman who is now the leader of the pack for the new physical gold contract at the LME states gold will rise to 2,000.00 in the next 12 months.

(Reuters)

Goldman hikes 12-month gold price forecast to $2,000/oz

June 19 (Reuters) – Goldman Sachs raised its gold price forecast on Friday as it expects a rally in bullion to continue due to currency debasement fears and economic uncertainty caused by the coronavirus crisis.

The bank raised its three, six and 12-month gold price estimates to $1,800, $1,900 and $2,000 per ounce from $1,600, $1,650 and 1,800 per ounce, respectively.

“Policy uncertainty aside, we believe that debasement fears remain the key driver of gold prices in a post-crisis environment such as this,” analysts at Goldman Sachs wrote in a note.

A weaker dollar will boost the purchasing power of major gold consumers across emerging markets along with easing of lockdowns, the bank added.

Faced with both an unprecedented shock and policy response, it remains unclear how inflationary the economic recovery will be, Goldman said.

“For gold prices to go materially above $2,000, we believe inflation will need to move above the Federal Reserve’s 2% target and this move to be met with a muted policy response.”

The U.S. bank warned that prices are likely to correct in a similar manner to 2013 if inflation doesn’t return as the global economy recovers.

It added the correction could come when investors start to believe that the Fed will withdraw its monetary policy support.

Lower interest rates and widespread stimulus measures tend to boost demand for bullion, which is often seen as a hedge against inflation and currency debasement.