GOLD:$:1891.50 UP $24.90 The quote is London spot price (cash market)

This is an all time high compared to London gold fix: Sept 5/2011: $1891.30

Silver:$22.76// UP $0.04 London spot price ( cash market)

There is now no question that our bankers’ precious metals derivatives have blown up. The Fed is loaning these crooks mega dollars as they are hugely offside on their shorts of gold and silver.

your data:

Closing access prices: London spot

i)Gold : $1886.35 LONDON SPOT 4:30 pm

ii)SILVER: $22.54//LONDON SPOT 4:30 pm

CLOSING FUTURES PRICES: KEY MONTHS

OCT GOLD: $1869.30 CLOSE 1.30 PM// SPREAD SPOT/FUTURE OCT /: $7.50 ($1.50 ABOVE NORMAL CONTANGO)

DEC. GOLD $1914.00 CLOSE 1.30 PM SPREAD SPOT/FUTURE DEC $22.50 ($10.00 ABOVE NORMAL CONTANGO)

CLOSING SILVER FUTURE MONTH

SILVER SEPT COMEX CLOSE; $22.93…1:30 PM.//SPREAD SPOT/FUTURE SEPT// : 17 CENTS PER OZ

COMEX DATA

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

receiving today:0/108

issued 94

EXCHANGE: COMEX

CONTRACT: JULY 2020 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,864.100000000 USD

INTENT DATE: 07/22/2020 DELIVERY DATE: 07/24/2020

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

226 C DIRECT ACCESS 1

624 C BOFA SECURITIES 1

657 C MORGAN STANLEY 15

657 H MORGAN STANLEY 69

661 C JP MORGAN 94

686 C INTL FCSTONE 3

690 C ABN AMRO 10

737 C ADVANTAGE 5 3

800 C MAREX SPEC 9

905 C ADM 6

____________________________________________________________________________________________

TOTAL: 108 108

MONTH TO DATE: 7,876

NUMBER OF NOTICES FILED TODAY FOR JULY CONTRACT: 108 NOTICE(S) FOR 10800 OZ (.3359 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 7876 NOTICES FOR 787600 OZ (24.497 TONNES)

SILVER

FOR JULY

144 NOTICE(S) FILED TODAY FOR 720,000 OZ/

total number of notices filed so far this month: 15,360 for 76.800 MILLION oz

BITCOIN MORNING QUOTE $9504 DOWN 13

BITCOIN AFTERNOON QUOTE.: $9593 UP $75

GLD AND SLV INVENTORIES:

WITH GOLD UP $24.90 AND NO PHYSICAL TO BE FOUND ANYWHERE:

WITH ALL REFINERS CLOSED//MEXICO ORDERING ALL MINES SHUT: WHERE ARE THEY GETTING THE “PHYSICAL?

A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A MASSIVE PAPER DEPOSIT OF 7.26 TONNES INTO THE GLD

WHAT A MASSIVE FRAUD!

GLD: 1,225.01 TONNES OF GOLD//

WITH SILVER UP $0.04 TODAY: AND WITH NO SILVER AROUND:

A HUGE CHANGE IN SILVER INVENTORY AT THE SLV:

A MASSIVE PAPER DEPOSIT OF 9.594 MILLION OZ INTO THE SLV

WHAT A FRAUD!!

RESTING SLV INVENTORY TONIGHT:

SLV: 558.779 MILLION OZ./

XXXXXXXXXXXXXXXXXXXXXXXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI FELL BY A TINY SIZED 802 CONTRACTS FROM 185,745 DOWN TO 184,943, AND FURTHER FROM OUR NEW RECORD OF 244,710, (FEB 25/2020. THE TINY SIZED LOSS IN OI OCCURRED WITH OUR VERY STRONG $1.54 GAIN IN SILVER PRICING AT THE COMEX. IT SEEMS THAT THE LOSS IN COMEX OI IS PRIMARILY DUE TO HUGE BANKER SHORT COVERING PLUS A STRONG EXCHANGE FOR PHYSICAL ISSUANCE, ZERO LONG LIQUIDATION, ACCOMPANYING A STRONG INCREASE IN SILVER STANDING AT THE COMEX FOR JULY. WE HAD A NET GAIN IN OUR TWO EXCHANGES OF 1061 CONTRACTS (SEE CALCULATIONS BELOW).

WE HAVE ALSO WITNESSED A HUGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: JULY: 0 AND SEP 1863 FOR ZERO ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 1863 CONTRACTS. WITH THE TRANSFER OF 1863 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1863 EFP CONTRACTS TRANSLATES INTO 9.315 MILLION OZ ACCOMPANYING:

1.THE $1.54 GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

10.025 MILLION OZ INITIAL STANDING IN AUGUST.

43.030 MILLION OZ INITIALLY STANDING IN SEPT. (HUGE)

7.32 MILLION OZ INITIALLY STANDING IN OCT

2.630 MILLION OZ STANDING FOR NOV.

20.970 MILLION OZ FINAL STANDING IN DEC

5.075 MILLION OZ FINAL STANDING IN JAN

1.480 MILLION OZ FINAL STANDING IN FEB

23.005 MILLION OZ FINAL STANDING FOR MAR

4.660 MILLION OZ FINAL STANDING FOR APRIL

45.220 MILLION OZ FINAL STANDING FOR MAY

2.205 MILLION OF FINAL STANDING FOR JUNE

82.935 MILLION OZ INITIALLY IN JULY.

WEDNESDAY, AGAIN OUR CROOKS USED COPIOUS PAPER IN ORDER TO LIQUIDATE SILVER’S PRICE…AND THEY WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE $1.54 ).. AND,OUR OFFICIAL SECTOR/BANKERS WERE UNSUCCESSFUL IN THEIR ATTEMPT TO FLEECE ANY SILVER LONGS FROM THEIR POSITIONS. THE TINY LOSS AT THE COMEX WAS ACCOMPANIED BY : i) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS 2) A STRONG INCREASE IN STANDING OF SILVER OZ STANDING FOR JULY, HUGE BANKER SHORT COVERING AND 4) ZERO LONG LIQUIDATION AS WE DID HAVE A NET GAIN OF 1061 CONTRACTS OR 5.305 MILLION OZ ON THE TWO EXCHANGES! YOU CAN BET THE FARM THAT OUR BANKER ARE DESPERATE TO LIQUIDATE THEIR HUGE SHORT POSITIONS IN SILVER

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS

JULY

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY /FOR MONTH OF JULY:

18,023 CONTRACTS (FOR 16 TRADING DAY(S) TOTAL 18,023 CONTRACTS) OR 90.12 MILLION OZ: (AVERAGE PER DAY: 1126 CONTRACTS OR 5.632 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF JULY: 90.12 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 12.87% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2020 TO DATE SILVER EFP’S: 1,227.53 MILLION OZ.

JANUARY 2020 EFP TOTALS SO FAR: 181.61 MILLION OZ

FEB 2020 EFP’S TOTAL : …… 259.600 MILLION OZ

MARCH EFP’S ….. 452.280 MILLION OZ //TOTALS//AND A NEW RECORD FOR THE MONTH)

APRIL EFP 95.355 MILLION OZ. (EX. FOR PHYSICALS BECOMING A LOT LESS)

MAY EFP FINAL: 77.27 MILLION OZ

JUNE EXP 71.15 MILLION OZ.

JULY EXP 90.12 MILLION OZ/

EXCHANGE FOR PHYSICAL ISSUANCE FOR THE PAST 60 DAYS IS A LOT LESS. NO DOUBT THAT THE COST TO CARRY THESE THINGS HAS EXPLODED AND AS SUCH CANNOT BE DONE AS FREQUENTLY AS BEFORE.

RESULT: WE HAD A TINY SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 802, DESPITE OUR 154 CENT GAIN IN SILVER PRICING AT THE COMEX ///WEDNESDAY… THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 1863 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER

TODAY WE GAINED A STRONG SIZED OI CONTRACTS ON THE TWO EXCHANGES: 1061 CONTRACTS (WITH OUR 154 CENT GAIN IN PRICE)//

THE TALLY//EXCHANGE FOR PHYSICALS

i.e 1863 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH A TINY SIZED DECREASE OF 802 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED DESPITE A 154 CENT GAIN IN PRICE OF SILVER/AND A CLOSING PRICE OF $22.72 // WEDNESDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY.

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.892 BILLION OZ TO BE EXACT or 127% of annual global silver production (ex Russia & ex China).

FOR THE NEW JULY DELIVERY MONTH/ THEY FILED AT THE COMEX: 144 NOTICE(S) FOR 720,000 OZ OF SILVER.

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.70//TODAY’S RECORD OF 244,705 IS SET WITH A PRICE OF: 18.91 (FEB 25/2020)

.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ; AUGUST 10.025 MILLION OZ/ SEPT 43.030 MILLION OZ//OCT: 7.665 MILLION OZ// NOV: 2.630 MILLION OZ//DEC: 20.970 MILLION OZ; JAN: 5.075 MILLION OZ.//FEB 1.480 MILLION OZ//MAR: 23.005 MILLION OZ/APRIL 4.660 MILLION OZ//MAY 45.220 MILLION OZ//JUNE: 2.205 MILLION OZ// JULY 82.935 million oz

- THE RECORD PRIOR TO TODAY WAS SET IN FEB 25/2018: 244,710 CONTRACTS, WITH A SILVER PRICE OF $18.90//.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017 RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

GOLD

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A GOOD SIZED 6599 CONTRACTS TO 609,737 AND CLOSER TO OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE GAIN OF COMEX OI OCCURRED WITH OUR RISE IN PRICE OF $22.00 /// COMEX GOLD TRADING// WEDNESDAY// WE HAD HUGE BANKER SHORT COVERING, ANOTHER GOOD SIZED INCREASE IN GOLD OZ STANDING AT THE COMEX FOR JULY, ALONG WITH ZERO LONG LIQUIDATION ACCOMPANYING A SMALL EXCHANGE FOR PHYSICAL ISSUANCE AND THE START OF GOLD SPREADER LIQUIDATION. THIS ALL HAPPENED WITH OUR STRONG GAIN IN PRICE OF $22.00 .

WE HAD A VOLUME OF 0 4 -GC CONTRACTS//OPEN INTEREST 64

WE GAINED A VERY GOOD SIZED 10,844 CONTRACTS (33.73 TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A SMALL SIZED 4245 CONTRACTS:

CONTRACT .; AUG 23845 AND OCT: 0 DEC: 400; FEB: 0 ALL OTHER MONTHS ZERO//TOTAL: 4285. The NEW COMEX OI for the gold complex rests at 609,737. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A GOOD SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 10,844 CONTRACTS: 6599 CONTRACTS INCREASED AT THE COMEX AND 4245 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 10,844 CONTRACTS OR 33.73 TONNES. WEDNESDAY, WE HAD A GAIN OF $22.00 IN GOLD TRADING……

AND WITH THAT GAIN IN PRICE, WE HAD A STRONG SIZED GAIN IN TOTAL/TWO EXCHANGES GOLD TONNAGE OF 33.73 TONNES!!!!!! THE BANKERS/OFFICIAL SECTOR SUPPLIED INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER WITH RECKLESS ABANDON. THE BANKERS WERE UNSUCCESSFUL IN THEIR ATTEMPT TO LOWER GOLD’S PRICE (IT ROSE $22.00).AND IT ALSO SEEMS THAT THEIR ATTEMPT TO FLEECE ANY GOLD LONGS FROM THE GOLD ARENA WAS ALSO UNSUCCESSFUL (SEE BELOW).

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES:

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (4245) ACCOMPANYING THE GOOD SIZED GAIN IN COMEX OI (6599 OI): TOTAL GAIN IN THE TWO EXCHANGES: 16,057 CONTRACTS. WE NO DOUBT HAD 1 )HUGE BANKER SHORT COVERING, 2.)ANOTHER INCREASE IN GOLD STANDING AT THE GOLD COMEX FOR THE FRONT JULY MONTH, 3) ZERO LONG LIQUIDATION; 4) HUGE COMEX OI GAIN AND .5) SMALL EXCHANGE FOR PHYSICAL ISSUANCE 6) THE COMMENCEMENT OF GOLD SPREADER LIQUIDATION… AND …ALL OF THIS WAS COUPLED WITH OUR STRONG GAIN IN GOLD PRICE TRADING//WEDNESDAY//$22.00.

WE ARE BEGINNING TO WITNESS A LACK OF EXCHANGE FOR GOLD PHYSICALS UNDERWRITTEN DUE TO PREMIUMS STARTING TO REAPPEAR IN THE FUTURE PRICE OF GOLD VS LONDON SPOT. THE COST TO THE BANKERS IS JUST TOO GREAT TO ENGAGE IN THESE VEHICLES ONCE THIS OCCURS.

THE FACT THAT WE ARE CONTINUALLY SEEING A DROP IN COMEX OPEN INTEREST AND VOLUMES COUPLED WITH LESS EXCHANGE FOR PHYSICALS PROBABLY MEANS THAT OUR LONGS ARE ALREADY DEPARTING NEW YORK FOR THE NEW PHYSICAL PLATFORM AT LONDON’S LME.

SPREADING OPERATIONS/NOW SWITCHING TO GOLD

OUR SPREADING OPERATION HAS NOW SWITCHED INTO GOLD…..

SPREADING OPERATION FOR OUR NEWCOMERS:

FOR NEWCOMERS, HERE ARE THE DETAILS:

SPREADING LIQUIDATION HAS NOW COMMENCED IN GOLD AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF AUGUST.

FOR THOSE OF YOU WHO ARE NEW, HERE IS THE MODUS OPERANDI OF THE SPREADERS AND THE CRIMINAL ELEMENT BEHIND IT:

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR;

THE SPREADING LIQUIDATION OPERATION IS NOW OVER FOR SILVER..AND WE WILL NOW MORPH INTO AN ACCUMULATION PHASE OF SPREADING CONTRACTS FOR GOLD. THEY WILL ACCUMULATE CONSIDERABLE AMOUNT OF THE CONTRACTS AND THEN LIQUIDATE ONE WEEK PRIOR TO FIRST DAY NOTICE

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO GOLD AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF JULY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF AUGUST FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE IN THIS NON ACTIVE MONTH OF JULY. BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN GOLD WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (AUGUST), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2020 INCLUDING TODAY

JULY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 16 TRADING DAY(S) IN TONNES: 185.62 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2019, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 185.62/3550 x 100% TONNES =5.22% OF GLOBAL ANNUAL PRODUCTION

ISSUANCE OF EXCHANGE FOR PHYSICAL GOLD HAS DISSIPATED THIS MONTH…THE COST TO THE BANKERS TO CARRY THESE CONTRACTS IN LONDON IS BECOMING TOO GREAT FOR THEM.

ACCUMULATION OF GOLD EFP’S YEAR 2020 TO DATE: 3203.82 TONNES

JANUARY 2220 TOTAL EFP ISSUANCE; : 570.19 TONNES

FEB 2020 TOTAL EFP ISSUANCE : 653.78 TONNES

MARCH TOTAL EFP ISSUANCE 1,098.93 TONNES (*AND A NEW ALL TIME RECORD ISSUANCE//22 DAYS)

APRIL TOTAL EFP. ISSUANCE: 243.45 TONNES (EFP ISSUANCE BECOMING A LOT LESS)

MAY TOTAL EFP ISSUANCE: 248.68 TONNES (EFP ISSUANCE STILL LOW// PREMIUM COST TO THE BANKERS IS HUGE..SO ISSUANCE IS LESS)

JUNE TOTAL EFP ISSUANCE: 192.06 TONNES

JULY TOTAL EFP ISSUANCE; 185.62 TONNES SO FAR..

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A TINY SIZED 802 CONTRACTS FROM 185,745 DOWN TO 184,943 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 2 3/4 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.

THE TINY LOSS IN OI SILVER COMEX WAS PRIMARILY DUE TO; 1) HUGE BANKER SHORT COVERING , 2) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS (SEE BELOW), 3) A CONSIDERABLE INCREASE STANDING AT THE SILVER COMEX FOR JULY AND 4) ZERO LONG LIQUIDATION

EFP ISSUANCE 1863 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY: 0 CONTRACTS AND SEPT: 1863 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1863 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 802 CONTRACTS TO THE 1863 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A STRONG GAIN OF 1061 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 5.305 MILLION OZ, OCCURRED WITH OUR 154 CENT GAIN IN PRICE///

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL..THE EVIDENCE IS CLEAR: HUGE AMOUNTS OF PHYSICAL STANDING FOR BOTH SILVER AND GOLD .

(report Harvey)

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED DOWN 8.05 POINTS OR 0.24% //Hang Sang CLOSED UP 208.06 POINTS OR 0.82% /The Nikkei closed DOWN 132.11 POINTS OR 0.58%//Australia’s all ordinaires CLOSED UP .34%

/Chinese yuan (ONSHORE) closed DOWN at 7.0018 /Oil UP TO 41.76 dollars per barrel for WTI and 44.08 for Brent. Stocks in Europe OPENED MOSTLY GREEN// ONSHORE YUAN CLOSED DOWN // LAST AT 7.00018 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 7.0083 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED//CORONAVIRUS/PANDEMIC : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

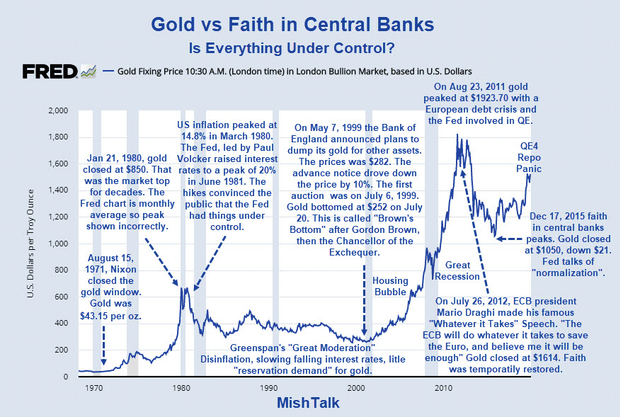

Gold Has Only One Resistance Point Left: The All-Time High

Authored by Mike Shedlock via MishTalk,

On a monthly chart, the last resistance point for gold is the $1923 peak in 2011.

Why Gold?

Tensions of all sorts are on the rise in the US , EU, and globally: Covid, employment, fiscal stimulus China (military and economic), and massive increases in money supply by the central banks, especially the Fed.

Cup and Handle

The Cup and Handle is a technical formation. A handle is formed on a pullback before the pattern blasts higher.

Of course, there may be no handle. Gold may just blast higher (or collapse) but fundamentals suggest higher, perhaps after some consolidation.

Gold vs Faith in Central Banks

Gold does worst when faith in central banks is the highest. Greenspan’s great moderation is the best example. Greenspan was considered the great “Maestro” who could do no wrong.

That theory crashed to earth in the DotCom bust. We have now had 3 major economic bubbles in 20 years.

If you currently have any faith that Central Banks have things under control, then please explain where you got that notion.

In short, the Fed is blowing bubbles, many believe on purpose, and gold has responded to the stress.

I do not see a reversal in Fed policy. Do you?

END

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

March 4.2019

Parker City News

JP Morgan faces potential class action lawsuit after guilty pleas by a former metals trader

Traders from across the U.S. are banding together to accuse J. P. Morgan Chase of manipulating precious metals markets for years.

At least six lawsuits, all making similar allegations against the nation‘s largest bank, have been filed in New York federal court in the past month, since federal prosecutors in Connecticut with a former J. P. Morgan Chase metals trader.

The cases could potentially include thousands of people who traded in the precious metals market. The White Plains, N.Y., law firm Lowey Dannenberg is asking the court to combine the cases and name it as the lead.

The law firm‘s commodities group is led by Vincent Briganti, the attorney who filed the first lawsuit on behalf of Dominick Cognata, a New York resident who alleges he suffered losses due to J. P. Morgan‘s trading conduct in the silver and gold futures and options markets.

A combined case, seeking class action status, would include anyone who purchased or sold futures contracts or an option on NYMEX platinum or palladium or COMEX silver or gold between at least Jan. 1, 2009, and Dec. 31, 2015. The lawyers believe that “at least hundreds, if not thousands” of traders would be eligible to join the case.

Named as defendants in all of the lawsuits are John Edmonds, a 36-year old former metals trader at J. P. Morgan, a group of yet-to-be-identified precious metals traders and the bank.

Edmonds, a New York resident, pleaded guilty in October to one count of conspiracy to defraud the market and manipulate prices of precious metals futures contracts and one count of commodities fraud. In the criminal plea, Edmonds admitted that he and other “unnamed co- conspirators” at J. P. Morgan, fraudulently manipulated precious metals markets from 2009 to 2015, the same time frame covered in the class action suits.

Briganti filed the initial class action on Nov. 7, just one day after the Justice Department unsealed Edmonds‘ plea in the U.S. District Court of Connecticut.

Edmonds admitted in his guilty plea that he deployed the illegal trading scheme hundreds of times with the direct knowledge and consent of his immediate supervisors. Plaintiffs say they have suffered economic injury, including monetary losses, as a direct result of actions by Edmonds and the other unnamed J. P. Morgan metals traders in the futures and options contracts.

One of the suits alleges that “the number of unlawful trades that JP Morgan traders executed in precious metals futures markets is at least in the thousands.”

J. P. Morgan declined to comment. Lowey Dannenberg did not respond to a request for comment by CNBC.

The Justice Department‘s criminal investigation is still ongoing and recently caused a separate related civil case to be put on hold for at least six months while the government continues its investigation. That civil lawsuit, which also accuses J. P. Morgan of rigging the precious metals market, was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders.

After reviewing the details of the plea agreement, David Kovel, the attorney for Shak‘s suit, sought to re- interview Edmonds, along with two other current and former senior traders at the bank. However, the government argued that reopening questioning would be detrimental to the ongoing criminal investigation. The federal judge overseeing the proceedings ordered a six-month stay in the civil case.

Kovel declined to comment.

Edmonds was originally scheduled to be sentenced in Hartford, Conn., on Wednesday, Dec. 19, but a court filing on Nov. 27 shows the sentencing has been postponed until June. A spokesman for the U.S. Attorney for Connecticut could not elaborate on why the sentencing was postponed since the court filing is under seal.

-END-

Global Stocks Rise To Pre-Covid Highs As Earnings Optimism Eclipses US-China Row

S&P futures hit 3,284 overnight, the highest level since February and before the covid crisis unleashed tens of millions of layoffs, while Nasdaq futures rose 1% after solid Tesla earnings levitating along with European stocks as better-than-expected corporate earnings offset worries about a sharp escalation in tensions between the United States and China and a continuing rise in COVID-19 cases. US futures are now up 300 points in the past month in an almost diagonal line; the dollar slipped for a fifth session, gold soared and bond yields were unchanged.

Global stock have rallied to their strongest levels since February this week, in many countries erasing their entire slump in March when the coronavirus pandemic sent markets into freefall, as investors bet that the record stimulus will continue to propel stocks higher, even if its impact on economies is questionable. The MSCI world equity index rose 0.2%, close to Tuesday’s level, which was its highest since late February.

Notable overnight earnings:

- Microsoft (MSFT) Q4 2020 (USD): EPS 1.46 (exp. 1.34); Revenue 38bln (exp. 36.5bln). Intelligent cloud: 13.37bln (exp. 13.09bln). More personal computing: 12.91bln (exp. 11.46bln). Productivity and business processes (which includes Team): 11.75bln (exp. 11.89bln). Search was negatively impacted by reduction in advertising spend in Quarter. Fell 2.3% in after-market trade; -1.9% in the pre-market

- Tesla (TSLA) Q2 2020 (USD): EPS 0.50 (exp. -0.11/-1.09 reported); Revenue 6.04bln (exp. 5.37bln). Q2 production: 82,272 (in line with prior guidance). Q2 deliveries: 90,891 (prev. guided at 90,650). Continues to see over 500k deliveries in FY20. Notes the next Gigafactory site has been selected and preparations are underway. Initially rose 5.5% before paring back to ~+2% in the after-market; +5.5% in the pre-market

“We expect the rally to broaden out, and we do see upside for stocks in the second half of the year,” Mark Haefele, chief investment officer of global wealth management at UBS AG in Zurich, said on Bloomberg TV. “As large asset allocators, when we look across, there are very few alternatives to equities right now.”

The gains came despite Washington’s order to Beijing to close its consulate in Houston, Texas amid accusations against China of spying. These had weighed on risk sentiment earlier in Asia, initially pulling shares lower before Asian stocks rebounded. China said the order was an “unprecedented escalation” by Washington, and a source said Beijing was considering shutting the U.S. consulate in Wuhan in retaliation. U.S. President Donald Trump said that other consulate closures were “always possible”.

“The forces of liquidity are just unparalleled … we’re seeing what happened post the GFC (global financial crisis), but we’re seeing it on steroids,” said Kay Van-Petersen, global macro strategist at Saxo Capital Markets in Singapore. “It’s rare that you see both monetary and fiscal policy turned on, and then when they are they only turn on for a little bit.”

European equities drifted higher, brushing off simmering tensions between China and U.S. in an otherwise quiet morning. The pan-region Euro Stoxx 50 climbed 0.42% while the German DAX gained 0.43% and the FTSE 100 by a similar margin; the Stoxx 600 rose on gains in carmakers and consumer products, led by Unilever NV’s jump of as much as 8.7% after its sales fell less than expected. The auto sector was the best performer, and utilities lagged; Italy’s FTSE MIB index underperformed peers. Positive corporate earnings surprises in Europe helped the mood, including from Unilever, French-Italian chipmaker STMicroelectronics and automaker Daimler.

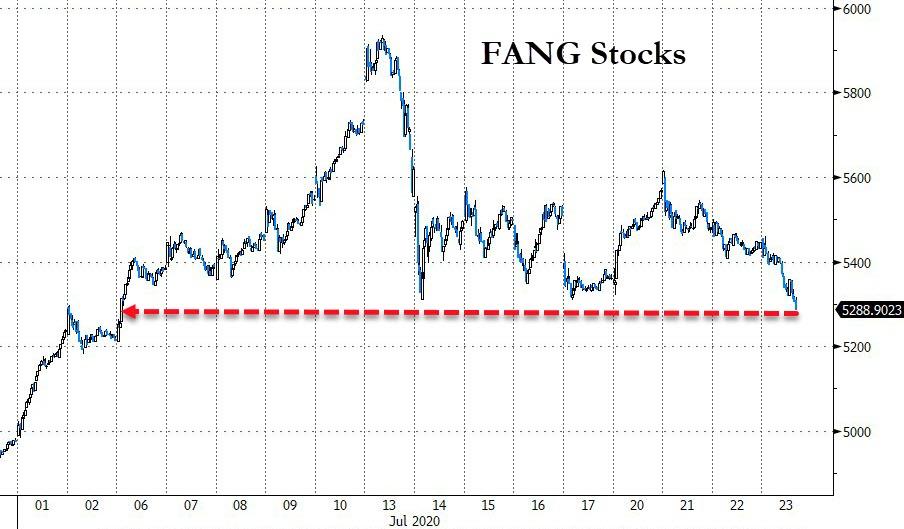

Earlier in the session, Asian stocks traded mostly lower, but finished mixed, as the region failed to derive support from Wall Street’s firm performance, in which the SPX reached five-month highs and the Dow Jones posted its third straight session of gains. After-market earnings State-side saw Tesla soar some 7% after reporting a surprise EPS, whilst Microsoft retreated 3% as quarterly revenue guidance disappointed, and as investors took chips off the table following the stock’s recent rally.

“You almost have a tug of war in markets between positives and negatives and its finally balanced. It looks like markets are pricing a V-shaped recovery so you can expect small negatives to have an outsize impact on markets,” said Justin Onuekwusi, portfolio manager at Legal & General Investment Management. “But the pullback is likely to be shortlived as there are people waiting for a dip.”

In rates, Treasuries were little changed after edging higher led by long end. Volumes were depressed with cash markets closed in Asia for Japan holiday. Yields across the curve are back to within 1bp of Wednesday’s closing levels, 10-year around 0.595%; earlier advance flattened 5s30s to within ~2bp of its 100-DMA, support since March 12. US session includes $14BN in 10-year TIPS new-issue auction and size announcement for next week’s 2-, 5- and 7-year sales.

In commodities, the euro was up 0.1%, close to the 21-month high of $1.1601 it touched on Wednesday as agreement between European Union members on a large economic recovery fund continued to provide lift. The dollar was down marginally against a basket of currencies and unchanged versus the Japanese yen.

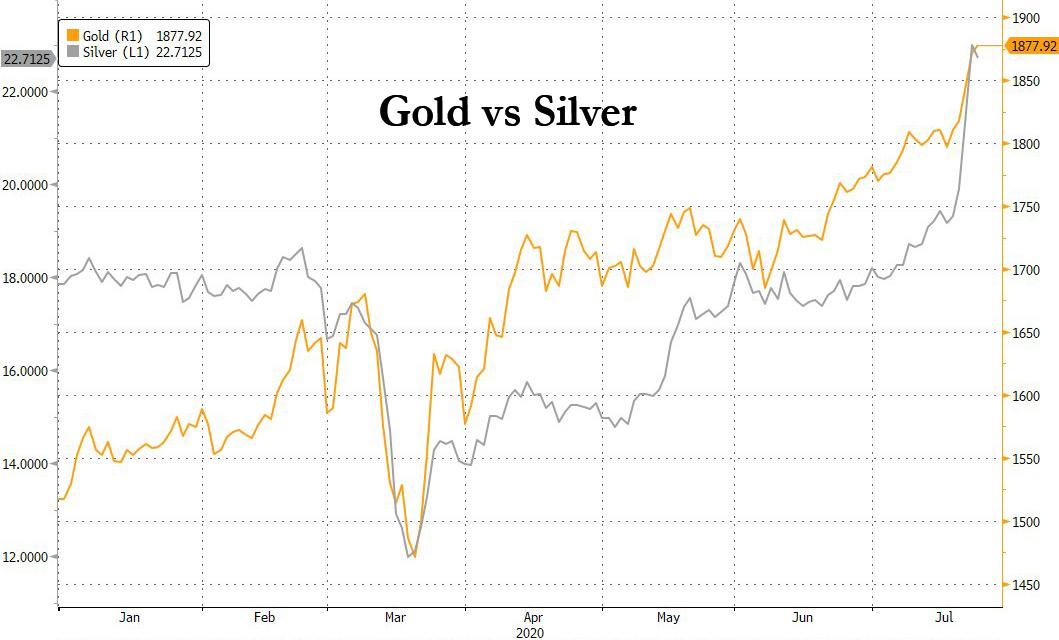

In commodities, gold advanced for a fifth day rising just shy of $1,890 and its September 2011 all time highs just above $1,900. Gold was last trading at $1,878 per ounce, a new nine-year peak, with prices up more than 23% on the year; Investors have flocked to the safe-haven metal as they seek shelter from a potential reversal in pumped-up stock prices and a possible rise in inflation following so much monetary and fiscal stimulus.

Oil prices initially edged up, with U.S. crude adding 14 cents to $42.04 a barrel and global benchmark Brent crude up 12 cents to $44.41 per barrel, before paring sharply sliding just after 6am ET.

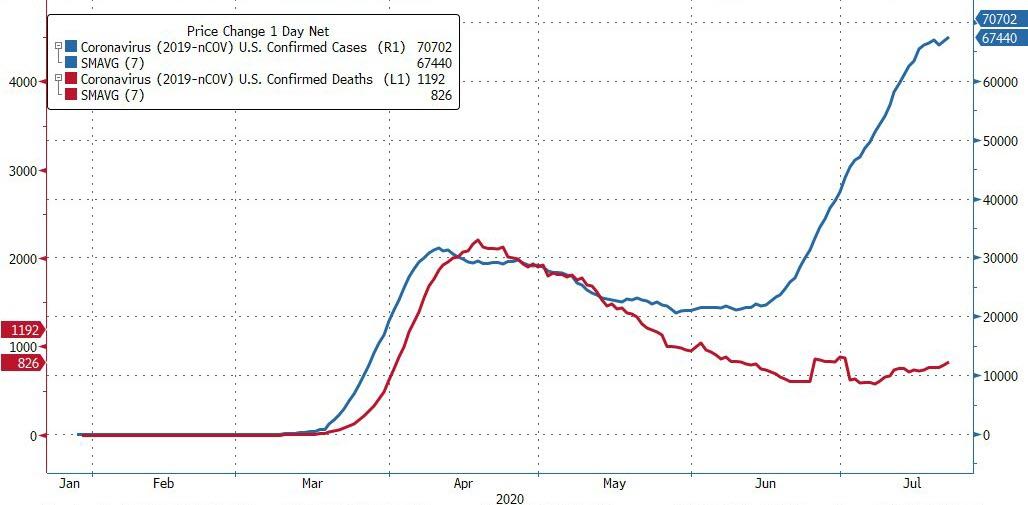

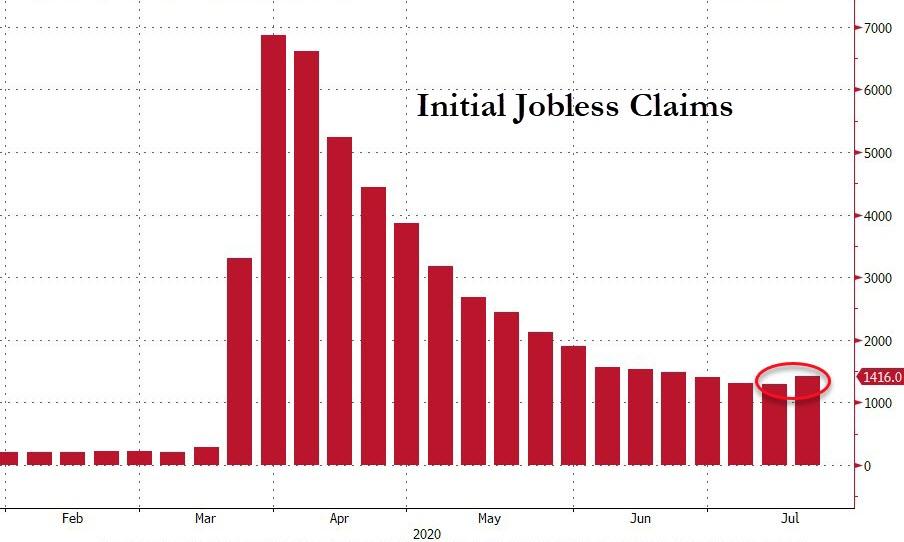

Investors will be keeping a close watch on U.S. weekly jobless claims figures due at 830am for the latest indications of how the novel coronavirus pandemic has affected the American economy. The U.S. recorded more than 1,100 new coronavirus deaths for a second straight day on Wednesday. Despite the virus being far from under control, analysts say unprecedented stimulus measures to boost battered economies continue to provide structural support for riskier assets.

On today’s calendar we have weekly initial jobless claims, June’s US leading index, July Kansas City Fed manufacturing index, and the Euro Area advance July consumer confidence. There will be monetary policy decisions from central banks in Turkey and South Africa, while we will hear from the BoE’s Haskel. Finally we are in the thick of earnings season now and will see results from Roche, Intel, AT&T, Unilever, Union Pacific, Daimler, Twitter and Hyundai.

Market Snapshot

- S&P 500 futures up 0.5% to 3,282.50

- STOXX Europe 600 up 0.7% to 376.22

- MXAP up 0.3% to 166.87

- MXAPJ up 0.4% to 553.10

- Nikkei down 0.6% to 22,751.61

- Topix down 0.6% to 1,572.96

- Hang Seng Index up 0.8% to 25,263.00

- Shanghai Composite down 0.2% to 3,325.11

- Sensex up 0.7% to 38,152.40

- Australia S&P/ASX 200 up 0.3% to 6,094.50

- Kospi down 0.6% to 2,216.19

- Brent futures up 0.8% to $44.63/bbl

- Gold spot up 0.7% to $1,884.14

- U.S. Dollar Index down 0.2% to 94.83

- German 10Y yield rose 0.3 bps to -0.487%

- Euro up 0.09% to $1.1580

- Italian 10Y yield fell 5.8 bps to 0.91%

- Spanish 10Y yield fell 1.1 bps to 0.323%

Top Overnight News

- Italy approved a 25 billion euros ($29 billion) proposal for extra spending as it battles to resuscitate its economy from the Covid-19 pandemic

- Saudi Arabia is accelerating plans to sell off state assets and may introduce income tax to reverse the economic toll of the slump in oil prices

- The U.K. government’s lack of economic planning for the fallout of the virus was an “astonishing” failure of governance, lawmakers say

- Investors who have mopped up 12% returns from Russian government debt in the past three months are waiting to find out if an expected reduction this week will be the last

APAC stocks traded mostly lower, but finished mixed, as the region failed to derive support from Wall Street’s firm performance, in which the SPX reached five-month highs and the Dow Jones posted its third straight session of gains. After-market earnings State-side saw Tesla soar some 7% after reporting a surprise EPS, whilst Microsoft retreated 3% as quarterly revenue guidance disappointed, and as investors took chips off the table following the stock’s recent rally. ASX 200 (+0.3%) opened softer as traders remained cautious over the outbreak in Australia’s Victoria State, but the index later nursed losses as the Australian Treasurer unveiled the biggest budget deficit since World Word II, providing a barrage of support to firms and citizens. Japanese participants were away as the country observes Marine Day Holiday. KOSPI (–0.6%) underperformed for a bulk of the session as South Korea entered a technical recession, prominent chip-maker SK Hynix traded in the green throughout most of session after a stellar earnings report, whilst the group expects chip prices to bottom out H2 and sees smartphone shipments growing by a double-digit percentage in 2021 – however Co. shares succumbed to downside in South Korea in the latter part of trade. Elsewhere, Shanghai Comp (-0.2%) opened lower by almost 1% before initially extending on losses amid Beijing’s rising tensions with the US, and as participants await Beijing’s response to the Chinese consulate shutting in Houston with possibly more on the way. Hang Seng (+0.8%) is propped up by its largest weighted financial and energy stocks ahead of the launch of its tech index on Monday.

Top Asian News

- Malaysia Clamps Down on Film-Making With TikTok in The Fray

- Cellnex Says Four Shareholders to Subscribe 18.7% New Shares

- Hyundai Motor Earnings Top Estimates on Resilient SUV Demand

- Indonesia’s Palm Oil Reserves Seen Slumping to 16-Month Low

European have kicked the session off on the front foot (Eurostoxx 50 +0.6%) in a retracement of some of yesterday’s losses in what has been a busy/upbeat morning of earnings for the region thus far. Furthermore, some positivity could also be gleaned from a lack of additional retaliatory measures between the US and China, albeit rhetoric from either side remains particularly hostile. From an earnings perspective, Unilever (+7.8%) have propelled the Personal & Household Goods sector towards the top of the leaderboard after the Co. reported a beat on expectations for sales amid increased demand for hygiene products amid COVID-19. Autos are also a key gainer in Europe following earnings from Daimler (+4.8%) with the Co. targeting making a profit in 2020; BMW (+3.5%), Continental (+2.4%) and Volkswagen (+2.0%) are all firmer in sympathy. Elsewhere, Publicis (+12.7%) is the clear outperformer in the Stoxx 600 today after its latest earnings report saw the Co.’s sales decline at a slower rate than forecast by analysts. Of note for the tech sector, STMicroelectronics (+2.1%) are another post-earnings gainer in the region after posting a beat on EPS and revenues and raising FY20 revenue guidance. To the downside, Swiss heavyweight Roche (-2.2%) is acting as a drag on the healthcare sector after reporting a 10% decline in sales with the Co. citing a firmer CHF and the fallout from some patients opting to stay away from hospitals for non-COVID treatments amid fears of catching the virus.

Top European News

- ECB, Hungarian Central Bank Set Up Repo Line for Euro Liquidity

- Italy Eyes $29 Billion in Extra Spending to Rescue Economy

- Boris Johnson Makes Scottish Pitch as Separatist Mood Rises

- CEZ Has Almost 50% Upside for J&T as Nuclear-Project Risks Abate

In FX, there was a faint respite for the Greenback and consolidation, but the overriding bearish theme/trend remains intact as the DXY teeters off another low closer to the 94.650 ytd base within a 94.781-95.015 range. Indeed, only the Brexit plagued Pound is actually softer vs the Buck in major circles as others hold close to recent highs and broad risk sentiment is propped by stimulus alongside COVID-19 vaccine progression over concerns about the virus itself and simmering geopolitical, trade and diplomatic tensions. Ahead, the latest look at weekly initial claims could or should provide a distraction, especially as the jobless tally feeds into July NFP and the FOMC looms next week.

- NZD/CAD/AUD/NOK/SEK – The best G10 performers, with the Kiwi hovering just below 0.6700 ahead of NZ trade and clawing back some losses relative to the Aussie amidst the ongoing rise of virus cases in Victoria. Aud/Nzd has slipped back to pivot 1.0700 as Aud/Usd straddles 0.7150 in wake of the Treasury’s fiscal and economic update pegging the budget deficit at Aud 184.5 bn, with S&P noting that the projections are in line with Australia’s triple A rating and negative outlook given that risks remain skewed to a downgrade. Meanwhile, the Loonie has extended post-Canadian inflation data gains through 1.3400 and the Scandinavian Crowns have recovered from midweek retreats with a degree of traction from oil and an improvement in Norwegian Industrial Sentiment rather than higher than expected jobless rates.

- EUR/CHF/JPY/GBP – 1.1600 is proving elusive for the Euro, and perhaps due to apprehension awaiting the EP judgement on the EU’s MFF, but the Franc continues to grind higher after breaching 0.9300 and Yen has recoiled into an even tighter band just under 107.00 amidst holiday-thinned volumes on Japanese Marine Day. Conversely, Sterling has lost momentum on the 1.2700 handle again in advance of an update from chief EU Brexit negotiator Barnier as the post-transition trade deal stalemate rumbles on and the UK is said to be open to holding emerency talks next week. More immediately, CBI trends and business confidence are due before a speech by BoE’s Haskel.

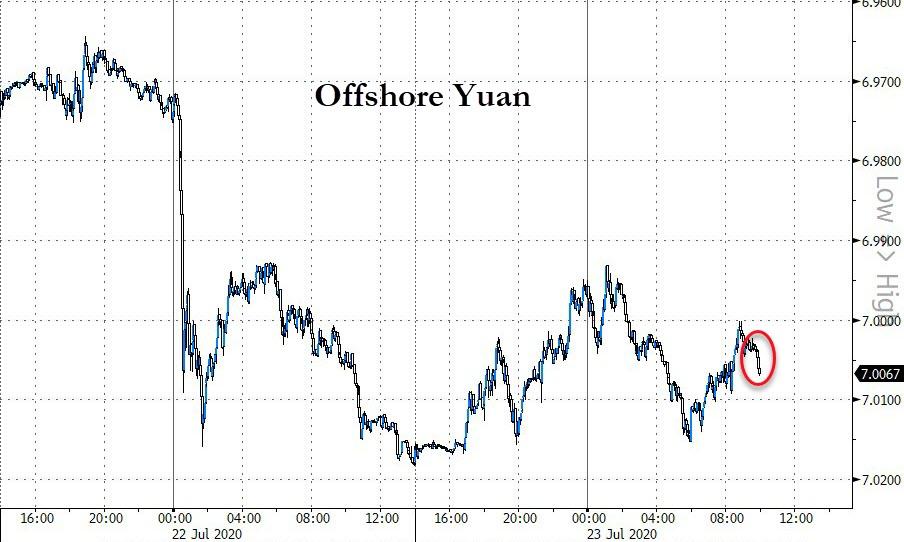

- EM – The Cnh is poised around the 7.0000 mark awaiting further repercussions between the US and China on the consulate spat, while the Try has shrugged off a decline in Turkish consumer sentiment in the run up to the CBRT and Zar is braced for another SARB rate cut, but unsure about the likely size.

- Mexican Finance Ministry’s Pension System Chief said there will be a 2yr grace period after pension reforms before employers are required to make additional contributions, expects reform to become law by early next year. (Newswires)

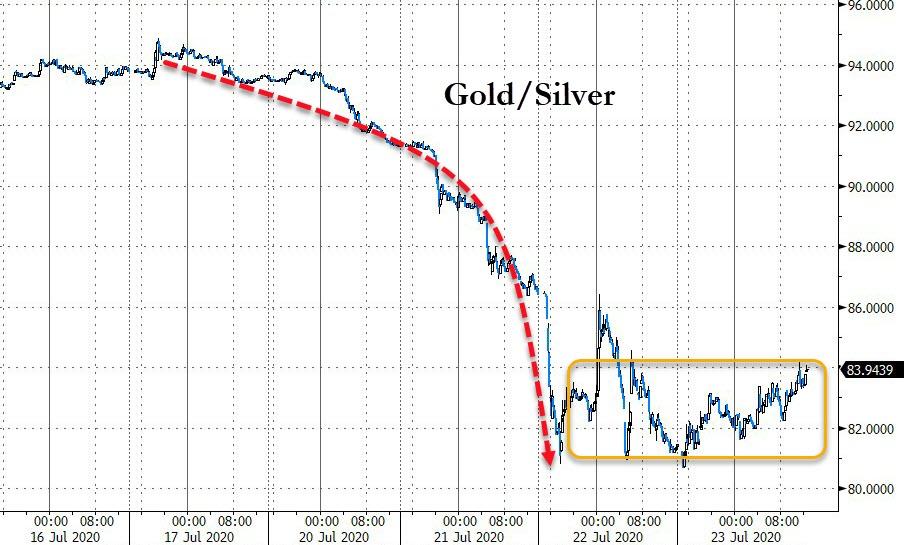

In commodities, WTI and Brent are firmer this morning and once again tracking the generally positive sentiment as we are yet to see a firm retaliation from China regarding the US’ Houston consulate announcement yesterday, alongside a predominantly positive morning for European earnings. As has been the playbook for the week fundamentally new crude newsflow has been sparse and there is nothing scheduled for either today or tomorrow. Most recently, reports note that Russia’s Putin has ordered a study into hedging oil prices, but no decision has been taken on the matter yet. Next week, aside from the usual weekly reports, the schedule for oil is again light but performance/commentary via the earnings releases from a number of European heavyweight oil names will draw attention and provide an insight into the broader complex’s outlook; Co’s scheduled to report include Shell and Total while BP is on the docket for the week after. Turning to metals, where spot gold remains elevated this morning and has printed yet another multi-year high at USD 1888.65/oz eclipsing levels at the USD 1885/oz mark and leaving, aside from the evident psychological figure, just the all time high of USD 1921.75/oz left. Focus has also been on silver which in contrast is modestly subdued today in an easing of the recent rally. On the precious metals, Citi highlight that the gold/silver price ratio is approaching a test of the 80x level which has, for the most part, held since 2018; a level they suggest is likely to be breached imminently.

US Event Calendar

- 8:30am: Initial Jobless Claims, est. 1.3m, prior 1.3m; Continuing Claims, est. 17.1m, prior 17.3m

- 10am: Leading Index, est. 2.1%, prior 2.8%

- 11am: Kansas City Fed Manf. Activity, est. 5, prior 1

DB’s Jim Reid concludes the overnight wrap

There’s been a decent markets tug of war develop over the last 36 hours. On one hand we’ve had continued rising tensions between the US and China, the worry over when additional US stimulus will arrive and also the still rising covid caseloads across many different areas around the world. On the other hand we’ve seen more clarity on the pathway for Europe plus positive vaccine news still bubbling in the background. The easiest way the market has found to deal with all this seems to have been to buy the Euro which was +0.37% yesterday and +1.24% this week and also to buy precious metals. Silver and Gold rallied +7.94% and +1.60% yesterday (near 7 and 9 year highs respectively) and are now up +20.08% and +4.14% since last Thursday’s close. Having said that the S&P 500 survived a few attacks to be up +0.57% and higher for the 4th successive day.

Back to the previous metal rally, yesterday we published a CoTD that showed that commodities struggle to outpace inflation over the long run. Gold is an exception but only really since we abandoned precious metal currency systems for the last time in 1971 and moved to a fiat one. Since then it is up 7 times in real terms. Although I’m a Gold bug I would acknowledge that the S&P 500 is up 22 times in real total return terms since. Since 1860 on this same measure Gold has only doubled in real terms whereas US equities are up 40,000 times. I wish my great, great, great, great grandfather had set up a trust fund for me… oh and been American. Anyway, Gold is definitely a fiat money hedge but on a total return basis equities have tended to do much much better in the long run. If you didn’t see the note it is here and email Jim-Reid.ThematicResearch@db.com if you want to be added to the CoTD.

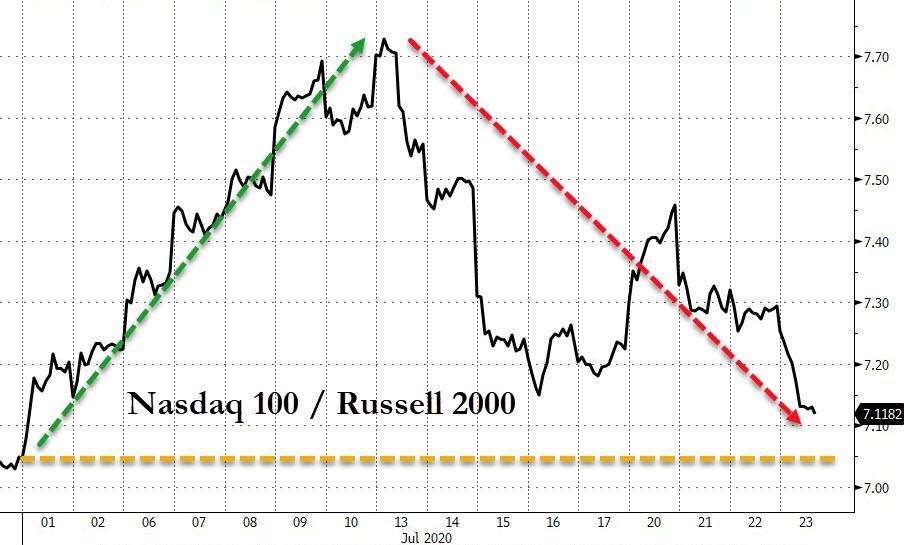

On earnings, Microsoft reported slower growth in their cloud-computing business, with revenues rising 47% and below analysts’ estimates of 49% and far below last quarter’s 59% rise. Overall EPS was $1.46 a share, compared with estimates of $1.36 a share. The stock was down just over -2% after the close. Tesla was the other big tech name announcing after the close, and the automaker reported a $104mn net profit for the second quarter. This compares to a $408mn loss a year ago, with Tesla’s shares up as much as +7.8% in after-hours trading. Meanwhile, this also makes Tesla eligible to become part of the S&P 500 as it has now posted profits in 4 consecutive quarters, thereby meeting a key inclusion criteria and thus could attract index based fund flows. Last week we highlighted the rise of Tesla vs the rest of the auto industry in a CoTD (see here ) and out of c.1200 responses to our flash poll 91% said Tesla was overvalued, while 6% said not and 3% were not sure.

Asian markets are trading mixed overnight with the Hang Seng (+0.37%) and Asx (+0.18%) up while the Kospi (-0.91%), and notably, the Shanghai Comp (-1.19%) is down amidst renewed US-China tension over the closure of Chinese Embassy in Houston, Texas (more below). As we go to print, the SCMP is reporting that China is considering asking the US to close its consulate in Chengdu, the capital of Sichuan province in retaliation. So watch this space. Elsewhere Japan’s markets are closed today and tomorrow for holidays. Futures on the S&P 500 are trading flat with silver (-2%) and gold (-0.13%) reversing some of their recent gains.

Covid-19 news outside of the US, particularly in Asia, continues to worsen. India now has more official covid-19 related deaths than Spain (just under 29,000), as the country now has the seventh most fatalities and the third most overall cases. Given the population size this shouldn’t be too much of a surprise but the outbreak continues to be ongoing in the second largest country on the planet by population. Indonesia saw a record high of 139 fatalities in the last day taking the total to 4,459 while cases rose by 1,882 to 91,751. Tokyo Governor Koike told residents to avoid going outdoors as much as possible during the upcoming four-day weekend after the city’s cumulative cases rose above 10,000 and new cases across Japan hit a new daily record. In Australia, Victoria state saw 403 new cases in the past 24 hours vs. a record 484 the day before.

The US had some marginally good news with Florida reporting that the positivity rate of first time testing fell to 10.6% on Tuesday, from 13.6% the day prior. Texas registered a record 240 fatalities in the past 24 hours though with a growth of 5.7% vs. the 7 day average of 3.2% and recorded 12,544 new cases with a growth of 3.6% vs. the 7 day average of 3.3% In terms of mitigation, the Governors of Ohio and Minnesota have now asked residents to compulsorily wear masks in public starting today, while Ohio also instituted a travel advisory for those coming from high risk areas.

The still high caseload across the US means that the need for additional stimulus is still fairly acute, however optimism surrounding a bill being enacted in the next 2-3 weeks is fading. Congressional Democrats and Republicans remain nearly $2tr apart in funding. Senate Minority Leader Schumer said late yesterday that it would not make sense for Democrats to start talking to their Senate counterparts until Republican leadership had a bill to work off. Overnight, Bloomberg has reported that McConnell may introduce the GOP stimulus plan today with a series of bills that would serve as an opening to negotiations with Democrats. This comes after Republicans and the White House reached agreement overnight on the spending portion of their stimulus plan.

Back to the US/China tensions, yesterday morning it was announced that the US would be giving China 72 hours to close the Chinese consulate in Houston, Texas. The reason the US State Department provided was that it sought “to protect American intellectual property and Americans’ private information.” This comes just a day after the Justice Department in the US accused Chinese hackers of trying to steal vaccine IP from private companies on behalf of the country’s intelligence services. According to China’s Foreign Ministry spokesman Wang Wenbin, the US’s actions are an “unprecedented escalation,” and that China would “react with firm countermeasures” if the orders were not revoked. Meanwhile, US Secretary of State Mike Pompeo is scheduled to make a speech today at 4:40pm EDT at the Richard Nixon Presidential Library in California on ‘Communist China and the future of the free world’. So this could be one to watch in the light of recent events. Interestingly, he was quoted by the Washington Times making a rather hawkish statement on China, saying “We put together a series of remarks aimed at making sure the American people understood the ongoing, serious threat posed by the Chinese Communist Party to our fundamental way of life here in the United States of America”.

In other US-China news, today there will be a hearing in the US Senate on the potential need for the US to create its own cryptocurrency to challenge and keep up with China’s recent action in the field. In a sign of tensions elsewhere Bloomberg is reporting that the Chinese state TV has now taken English football off the airwaves after China/U.K. tensions have climbed in recent weeks.

Back to markets yesterday and outside of precious metals, commodities struggled a bit. Oil dropped over -1.5% early on with the move lower in risk sentiment and also EIA data showing a rise in production and modest decline in demand. However it recovered to nearly flat with Brent Crude at -0.07% and WTI at -0.14%. The recovery in oil may have been partly to do with the dollar’s drop. Copper prices pulled back -1.11%, the metal’s second biggest drop since mid-June when risk assets globally pulled back on news of a potential second wave of covid-19 cases in the US.

Elsewhere, core sovereign bonds rallied slightly yesterday as safe haven assets generally outperformed, with 10yr Treasury yields falling -0.3bps to close at 0.597%, their lowest level since 21 April, while the dollar weakened by -0.14% to its March lows helping the earlier Euro move we discussed. This move in Treasuries could portend the need for the Fed to do more in coming months if the US fiscal stimulus is indeed delayed as outlined above. Bund yields fell by -3.0bps, while in the UK 10yr gilt yields fell by -1.6bps to a fresh record low of 0.12% as negotiations between the UK and EU are set to run into and through Prime Minister Johnson’s July deadline for an outline agreement.

ECB President Lagarde commented on the recent fiscal stimulus agreed to by the European Council, saying that it “is clearly a demonstration of solidarity, of transfer to those that need it most.” She added that “It could have been better, but it’s a very ambitious project actually,” in reference to the allocation of loans and grants in the package.

The data from yesterday was fairly light. We saw US existing home sales for June, which came in 4.72m (vs. 4.75m expected) up from 3.91m last month. The US FHFA house price index for May fell -0.3% (vs. +0.3% expected), while last month’s reading was revised one tenth of a per cent lower to +0.1%. Meanwhile north of their border, Canada’s June CPI month-over-month reading was higher than expected at +0.8% (vs. +0.4% expected) compared to last month’s +0.3%.

Today we will see Germany August GfK consumer confidence, France July business confidence, US weekly initial jobless claims, June’s US leading index, July Kansas City Fed manufacturing index, and the Euro Area advance July consumer confidence. There will be monetary policy decisions from central banks in Turkey and South Africa, while we will hear from the BoE’s Haskel. Finally we are in the thick of earnings season now and will see results from Roche, Intel, AT&T, Unilever, Union Pacific, Daimler, Twitter and Hyundai.

3A/ASIAN AFFAIRS

i)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED DOWN 8.05 POINTS OR 0.24% //Hang Sang CLOSED UP 208.06 POINTS OR 0.82% /The Nikkei closed DOWN 132.11 POINTS OR 0.58%//Australia’s all ordinaires CLOSED UP .34%

/Chinese yuan (ONSHORE) closed DOWN at 7.0018 /Oil UP TO 41.76 dollars per barrel for WTI and 44.08 for Brent. Stocks in Europe OPENED MOSTLY GREEN// ONSHORE YUAN CLOSED DOWN // LAST AT 7.00018 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 7.0083 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED//CORONAVIRUS/PANDEMIC : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3 a./NORTH KOREA/ SOUTH KOREA

South Korea

b) REPORT ON JAPAN

3 C CHINA

Beijing Plans To Shutter US Consulate In China In Retaliation For Houston Mission Closure

China is preparing to unveil its promised retaliation against the US over the Trump Administration’s decision to close China’s Houston consulate, a diplomatic mission that Sen. Marco Rubio once described as “a nest of spies”.

In keeping with the promise, first published in the Global Times, that Beijing would inflict “real pain” on the US in its response to the closure of the Houston consulate, Editor Hu Xijin warned that China’s decision – which would involve the closure of at least one US diplomatic mission (though likely not the one in Wuhan, as Hu dismissed that idea yesterday).

Stocks slid on the news…

….while yuan traded offshore also weakened.

Hu also warned about “serious consequences” for the US. And this was before WSJ published leaked prepared remarks from a speech by Secretary of State Mike Pompeo that he’s set to give later today.

Pompeo To Essentially Call For ‘A People’s Uprising’ In Communist China

Secretary of State Mike Pompeo is about to apply the Syria-Iran-Venezuela model to China.

But unlike these countries, which in recent years have seen US-backed covert proxy war operations attempt to foment ‘mass uprisings’ leading to regime change, it’s likely to produce little effect on the ground, other than further enraging Beijing.

The WSJ, which has seen a copy of the State Department speech to be delivered Thursday afternoon, describes that it more or less calls for a people’s uprising in Communist-run China:

Mr. Pompeo says Chinese leader Xi Jinping is a “true believer in a bankrupt totalitarian ideology.” Mr. Pompeo stops shy of explicitly calling for regime change, urging allied countries and the people of China to work with the U.S. to change the Communist Party’s behavior.

And more:

The Communist Party “fears the Chinese people’s honest opinions more than any foreign foe,” Mr. Pompeo plans to say in the speech at the Richard Nixon Presidential Library and Museum. The U.S. “must also engage and empower the Chinese people,” Mr. Pompeo says, according to the draft.

The speech is entitled “Communist China and the Free World’s Future” and promises to be the most fiery yet, after a series of top officials as well as senators like Marco Rubio, have lambasted China’s theft of trade secrets and coronavirus research.

Pompeo also recently vowed in an interview, “Look, the American people are not going to allow our economic work, our talent to be stolen by the Chinese Communist Party.”

After this week the FBI said the Chinese government is acting like “an organized criminal syndicate” for widespread cyber theft and hacking of American trade secrets as well as coronavirus research, State Department spokesperson Morgan Ortagus said earlier in the day Thursday it’s estimated that China stole at least $1 billion total in research from the United States.

Amazingly, stocks have thus far ignored the growing all-out diplomatic war between Washington and Beijing, but that could change by the day’s end, depending perhaps on just what is layed out in the Secretary of State’s impeding address.

END

4/EUROPEAN AFFAIRS

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

TURKEY/GREECE

Greece braces for war as Turkey sends in her oil drilling team into Greek waters. The oil/gas find EEZ belongs to Greece and Turkey has no right to grab something that is not theirs.

Turkey does not recognize Cyprus and thus the discovery which enters their waters. The original discovery came from Israel who informed Cyprus and Greece of this massive oil gas find.

(zerohedge)

“War” Top Trend On Greek Twitter As Military On ‘High Alert’ Over Turkish Drilling Incursion

Greek news sources are reporting that Greece’s military is on “high alert” after on Tuesday Turkish survey ships entered East Mediterranean waters between Cyprus and Greece.

And Reuters reports that “Greece accused Turkey on Tuesday of attempting to encroach on its continental shelf in a serious escalation of tensions between the two NATO allies at odds over a range of issues.”

For much of the past year European Union leaders have condemned Turkey’s expansive claims to broad swathes of Mediterranean waters around Cyprus and reaching into Greece’s Exclusive Economic Zone (EEZ). The US State Department is also backing Greece’s condemnation of Turkish encroachment. Meanwhile, the number one trending hashtag in Greek Twitter right now happens to be war.

On Tuesday a US State Department statement demanded that Turkey back down from its drilling plans which are sure to immediately escalation already soaring tensions.

“We urge Turkish authorities to halt any plans for operations and to avoid steps that raise tensions in the region,” the statement said. And Greece’s foreign ministry said it clearly violates the country’s sovereignty and that it stands ready to defend its territory.

This as not for the first time a pair of Turkish F-16s reportedly flew over Greece’s easternmost territory, including the islands of Strongyli and Megisti. Greece’s prime minister also said this week that EU sanctions await Turkey if it moves forward with illegal drilling.

Reuters: “An advisory known as a Navtex was issued by Turkey’s navy on Tuesday for seismic surveys in an area of sea between Cyprus and Crete. The advisory is in effect until Aug. 20.”

A number of very recent issues have already significantly built-up tensions. To review:

- Turkey’s provocative move to turn the historic Byzantine Hagia Sophia church into a mosque.

- Continued historic animosity over ethnically-partitioned Cyprus.

- Turkish claims to all waters surrounding Cyprus.

- Recent border tensions involving Erdogan sending thousands of Syrians refugees to Greece’s border.

- Greece’s militarized response along migrant crossing points at the Turkish border.

- Turkey’s involvement in Libya, which has seen its navy patrols expand into the Mediterranean off the north African coast.

To underscore where things stand, see this message being widely shared in Greek on social media and via Greek news sources: Greek social media users are urging people to not post photos, videos or information about Greek military movements.

Meanwhile Greek stocks saw their biggest daily drop in a month on Tuesday amid the renewed Turkey tensions, while the Turkish lira also felt the pressure, falling further against the dollar, for a total 13% decline so far this year.

Turkey Will Send More Troops To Libya If Egyptian Forces Breach Border

The Turkey-based Zaman newspaper quoted informed sources in the Turkish government as saying that a military and diplomatic plan has been prepared to deal with the Egyptian parliament’s decision to send troops to Libya.

According to their sources, the Turkish newspaper said that Ankara “is closely watching the consequences of the Egyptian parliament’s decision.”

Their sources stressed that if “Egypt sends military forces to Libya, Turkey has a plan to increase its forces and military equipment in Libya to stand up to the Egyptian forces.”

It also quoted Turkish sources as saying that Ankara “is ready to respond to any attack on its forces present in Libya, whatever the party that carried out the attack.”

Turkish presidential spokesman Ibrahim Kalin had recently confirmed that his country “does not want to escalate tensions and confront Egypt in Libya,” but at the same time he stressed support for the Government of National Accord (GNA) in Tripoli.

He said in this regard: “When looking at this general scene, it becomes clear that we have no intention of confronting Egypt, France, or any other country there (in Libya).”

Currently, Turkey is the only foreign country that has national troops present inside of Libya.

Early this week Egypt’s parliament approved sending its national forces to assist Gen. Khalifa Haftar in Libya, however, it doesn’t appear Sisi has moved on the authorization yet. Turkey has long backed Tripoli with ground and air forces, including drones.

If Cairo does send troops, which would be the first such foreign deployment since 1992 during the Gulf War, Turkey has promised to surge its own national forces there, in what could hold the potential for direct confrontation in Libya.

6.Global Issues

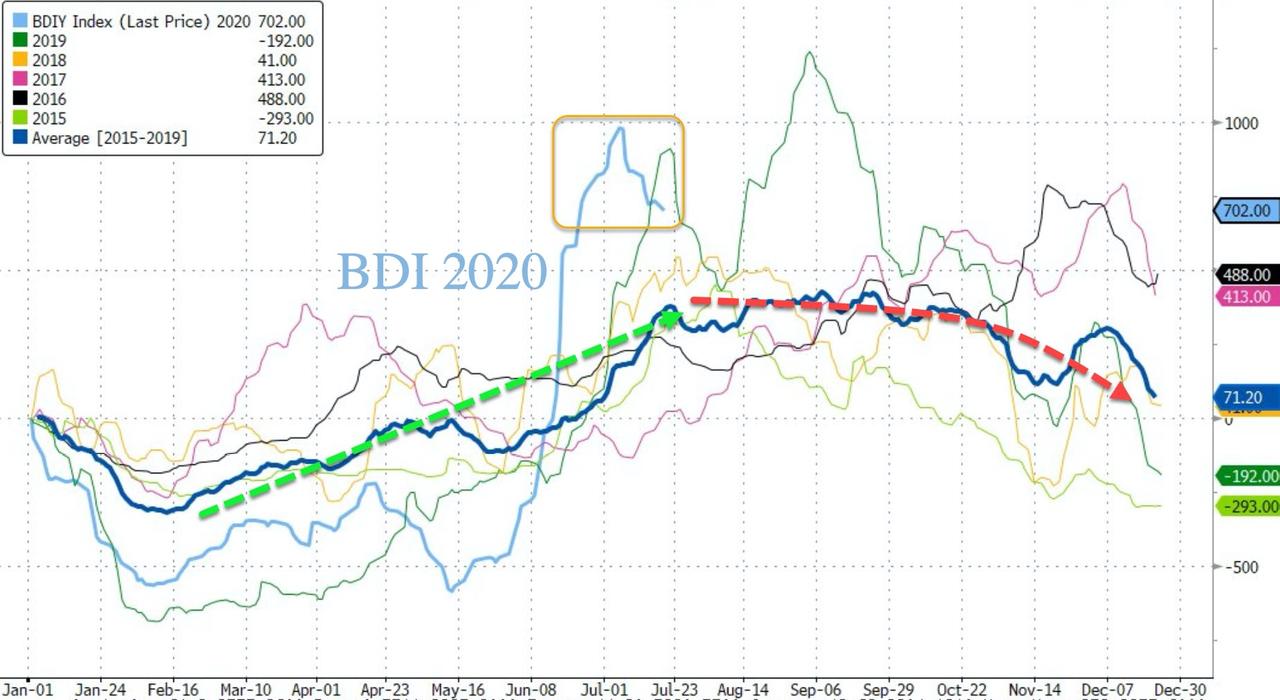

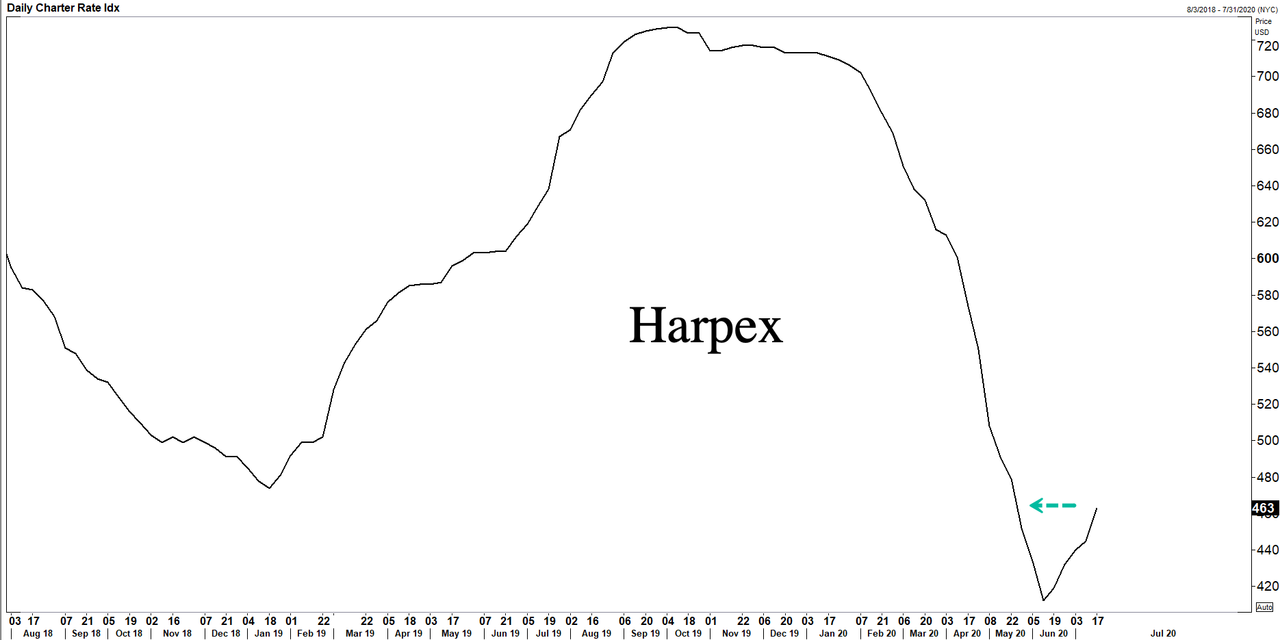

BALTIC DRY INDEX

Looks like no V shaped recovery!

(zerohedge)

Baltic Index Sinks To 1-Month Low As Global Rebound Hopes Fade

The Baltic Dry Index (BDI) is losing steam following an impressive upswing from May’s lows. The BDI began tumbling in August 2019, with an extension to the downside following the virus pandemic.

The BDI is an index of the Capesize, Panamax and Supramax Timecharter Averages, used by investors as a proxy for shipping conditions, and or world trade.

According to Reuters, BDI touched one month lows on Tuesday, weighed down by declining rates for Capesize and Panamax vessels:

- The Baltic dry index, which tracks rates for ships ferrying dry bulk commodities and reflects rates for Capesize, Panamax, and supramax vessels, fell 84 points, or about 5%, to 1,594, its lowest in nearly a month.

- The Baltic Capesize index dropped 221 points, or 7.5%, to 2,729, registering its lowest level since June 17.

- Average daily earnings for Capesizes, which typically transport cargoes of 170,000 tonnes to 180,000 tonnes, including iron ore and coal, was down by $1,834 at $22,635.

- However, rising demand for iron ore from China has helped the Capesize segment to gain nearly 40% this year.

- The Panamax index was down 50 points, or 3.4%, at 1,415, its lowest in more than two weeks.

- Average daily earnings for Panamaxes, which usually carry coal or grain cargoes of about 60,000 tonnes to 70,000 tonnes, fell by $452 to $12,736.

- However, the supramax index rose 9 points, or 1%, to 929.

The index peaked on July 6, now sinking to a one month low, indicating shipping demand in the future is subsiding. BDI and its subcomponents are shown below:

In terms of seasonality, shipping rates tend to peak in summer months and waterfall through the second half.

If seasonality is not a major factory in peaking BDI, then it could be seen as a warning sign for the global recovery, produced by central bank money printing and fiscal stimulus by governments, is beginning to stall.

On Tuesday morning, we noted how the resurgence of the virus pandemic is at risk of derailing the global economic recovery.

Christopher Dembik, head of macroeconomic research at Saxo Bank, recently said the sharp rebound in BDI “cannot suggest a V-shaped recovery.” He said bankruptcies, coronavirus, and Sino-US tensions are weighing on the upswing in economic growth.

With BDI peaking, and no significant rebound in Harpex (HARPER PETERSEN Charter Rates Index for containerships), it appears the robust global rebound pitched by government officials and central bankers is nothing more than fiction.

The next big concern, especially in the US, the world’s largest economy, is a double-dip recession as more than 80% of the population is in areas where state governments have paused or reversed reopenings.

7. OIL ISSUES

8 EMERGING MARKET ISSUES

CORONAVIRUS UPDATE/INDIA/THE GLOBE/

India Suffers New COVID-19 Record As Outbreak Worsens In Asia, Europe: Live Updates

Yesterday, as California and Texas set new records for daily COVID-19 cases and deaths, Brazil reported more than 60k cases in a day. There hasn’t been much in the way of major COVID-19 headlines this morning, but there have been a few notable reports from around the world, particularly in Asia.

Australia, for example, reported its highest daily number of coronavirus-related deaths in three months as new infections continued to climb in Australia’s second-most-populous state. Victoria state said it had confirmed another 403 infections, while five people had died from the virus in the last 24 hours. The daily death toll was Australia’s biggest since April. Tokyo also reported 366 new cases on Thursday, its latest record-breaking number.

In Iran, officials confirmed 221 new deaths from the virus, bringing the nationwide death toll to 15,074, according to the Health Ministry. Another 2,621 people tested positive for COVID-19 in the last 24 hours, raising the overall count to 284,034, according to a spokesperson for Iran’s health ministry.

As its outbreak continues to worsen, India just reported an all-time high of nearly 45,600 new infections over the last day, as the spread of the virus accelerates in the world’s second most populous country. India’s confirmed coronavirus caseload has now risen to 1.2 million, 28,890 of whom have died. The country also reported a record high of 1,120 deaths in the same period. However, the tally also included the addition of more than 444 earlier coronavirus deaths in the southern State of Tamil Nadu that were not previously attributed to the virus.

Northeastern Spain’s Catalonia region reported 721 new cases on Wednesday, with 3/4ths of these found in the Greater Barcelona Area.

Russia reported 5,848 new cases, pushing its national tally to 795,038, still the fourth-largest in the world. More than 12,700 deaths have been recorded to date and more than 570,000 have recovered. SA has roughly half of total cases in South Africa.

South Africa’s confirmed coronavirus cases are rapidly closing in on 400,000 as the country suffers a new daily high of 572 deaths. In terms of reported cases, SA is now the world’s fifth worst-hit county.

South Africa is now one of the world’s top five countries in terms of reported virus cases, and it makes up more than half of the cases on the African continent with 394,948. Deaths are at 5,940.

Public hospitals are struggling as patient numbers climb, and more than 5,000 health workers have been infected.

Finally, China’s National Health Commission has reported 22 new cases of the virus on the mainland on Thursday, with most of them discovered in the far western region of Xinjiang where mass testing, and a strict lockdown, is under way.

Your early morning currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings TUESDAY morning 7:00 AM….

Euro/USA 1.1576 UP .0011 REACTING TO MERKEL’S FAILED COALITION/ REACTING TO +GERMAN ELECTION WHERE ALT RIGHT PARTY ENTERS THE BUNDESTAG/ huge Deutsche bank problems ///ITALIAN CHAOS/CORONAVIRUS/PANDEMIC /AND NOW ECB TAPERING BOND PURCHASES/JAPAN TAPERING BOND PURCHASES /USA RISING INTEREST RATES /FLOODING/EUROPE BOURSES /MOSTLY GREEN EXCEPT ITALY

USA/JAPAN YEN 107.18 UP 0.007 (Abe’s new negative interest rate (NIRP), a total DISASTER/NOW TARGETS INTEREST RATE AT .11% AS IT WILL BUY UNLIMITED BONDS TO GETS TO THAT LEVEL…

GBP/USA 1.2692 DOWN 0.0036 (Brexit March 29/ 2019/ARTICLE 50 SIGNED/BREXIT FEES WILL BE CAPPED/

USA/CAN 1.3392 DOWN .0027 CANADA WORRIED ABOUT TRADE WITH THE USA WITH TRUMP ELECTION/ITALIAN EXIT AND GREXIT FROM EU/(TRUMP INITIATES LUMBER TARIFFS ON CANADA/CANADA HAS A HUGE HOUSEHOLD DEBT/GDP PROBLEM)

Early THIS THURSDAY morning in Europe, the Euro ROSE BY 11 basis points, trading now ABOVE the important 1.08 level RISING to 1.1219 Last night Shanghai COMPOSITE CLOSED DOWN 8.05 POINTS OR 0.24%

//Hang Sang CLOSED UP 208.06 POINTS OR 0.42%

/AUSTRALIA CLOSED UP 0,34%// EUROPEAN BOURSES MOSTLY GREEN EXCEPT ITALY

Trading from Europe and Asia

EUROPEAN BOURSES MOSTLY GREEN EXCEPT ITALY

2/ CHINESE BOURSES / :Hang Sang CLOSED UP 208.06 POINTS OR 0.42%

/SHANGHAI CLOSED DOWN 8.05 POINTS OR 0.24%

Australia BOURSE CLOSED UP .34%

Nikkei (Japan) CLOSED DOWN 132.11 POINTS OR 0.58%

INDIA’S SENSEX IN THE GREEN

Gold very early morning trading: 1878.20

silver:$22.73-

Early THURSDAY morning USA 10 year bond yield: 0.60% !!! UP 0 IN POINTS from WEDNESDAY’S night in basis points and it is trading WELL BELOW resistance at 2.27-2.32%.

The 30 yr bond yield 1.29 DOWN 1 IN BASIS POINTS from WEDNESDAY night.

USA dollar index early THURSDAY morning: 94.92 DOWN 7 CENT(S) from WEDNESDAY’s close.

This ends early morning numbers THURSDAY MORNING

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx6

And now your closing THURSDAY NUMBERS \1: 00 PM

Portuguese 10 year bond yield: 0.32% DOWN 2 in basis point(s) yield from YESTERDAY/

JAPANESE BOND YIELD: +02% UP 1/3 BASIS POINTS from YESTERDAY/JAPAN losing control of its yield curve/56

SPANISH 10 YR BOND YIELD: 0.32%//DOWN 1 in basis point yield from yesterday.

ITALIAN 10 YR BOND YIELD:0.99 DOWN 5 points in basis points yield from yesterday./

the Italian 10 yr bond yield is trading 67 points higher than Spain.

GERMAN 10 YR BOND YIELD: FALLS TO –.48% IN BASIS POINTS ON THE DAY//

THE IMPORTANT SPREAD BETWEEN ITALIAN 10 YR BOND AND GERMAN 10 YEAR BOND IS 1.47% AND NOW ABOVE THE THE 3.00% LEVEL WHICH WILL IMPLODE THE ENTIRE ITALIAN BANKING SYSTEM. AT 4% SPREAD THERE WILL BE A HUGE BANK RUN…

END

IMPORTANT CURRENCY CLOSES FOR THURSDAY

Closing currency crosses for THURSDAY night/USA DOLLAR INDEX/USA 10 YR BOND YIELD/1:00 PM

Euro/USA 1.1610 UP .0046 or 46 basis points

USA/Japan: 106.88 DOWN .296 OR YEN UP 30 basis points/

Great Britain/USA 1.2753 UP .0026 POUND UP 26 BASIS POINTS)

Canadian dollar UP 45 basis points to 1.3373

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

The USA/Yuan,CNY: AT 7.0041 ON SHORE (DOWN)..GETTING DANGEROUS