GOLD:$: 2,018.45 UP $38.30 The quote is London spot price (cash market)

Silver:$27.57// DOWN $0.69 London spot price ( cash market)

DONATE

Closing access prices: London spot

i)Gold : $2035.00 LONDON SPOT 4:30 pm

ii)SILVER: $28.30//LONDON SPOT 4:30 pm

CLOSING FUTURES PRICES: KEY MONTHS

AUGUST GOLD: $2012.00 CLOSE 1::30 PM SPREAD SPOT/FUTURE AUG (BACKWARD $6.45)

OCT GOLD: $2020.20 CLOSE 1.30 PM// SPREAD SPOT/FUTURE OCT /: : $1.75// BELOW NORMAL CONTANGO

DEC. GOLD $2030.200 CLOSE 1.30 PM SPREAD SPOT/FUTURE DEC $11.75 ($ NORMAL CONTANGO)

CLOSING SILVER FUTURE MONTH

SILVER SEPT COMEX CLOSE; $27.70…1:30 PM.//SPREAD SPOT/FUTURE SEPT// : 13 CENTS PER OZ ( 10 CENTS ABOVE NORMAL CONTANGO)

SILVER DECEMBER CLOSE: $27.97 1:30 PM SPREAD SPOT/FUTURE DEC. : 40 CENTS PER OZ ( 28 CENTS ABOVE NORMAL CONTANGO)

COMEX DATA

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

receiving today: 185/594

issued 21

EXCHANGE: COMEX

CONTRACT: AUGUST 2020 COMEX 100 GOLD FUTURES

SETTLEMENT: 2,051.500000000 USD

INTENT DATE: 08/06/2020 DELIVERY DATE: 08/10/2020

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

072 C GOLDMAN 500 1

072 H GOLDMAN 100

104 C MIZUHO 44

118 H MACQUARIE FUT 6

323 C HSBC 2

332 H STANDARD CHARTE 17

355 C CREDIT SUISSE 3

657 C MORGAN STANLEY 1 8

657 H MORGAN STANLEY 77

661 C JP MORGAN 21 119

661 H JP MORGAN 66

686 C INTL FCSTONE 2

690 C ABN AMRO 55 8

700 C UBS 16

709 C BARCLAYS 48

709 H BARCLAYS 1

732 C RBC CAP MARKETS 1

737 C ADVANTAGE 12 5

800 C MAREX SPEC 3 4

880 C CITIGROUP 1

880 H CITIGROUP 66

905 C ADM 1

____________________________________________________________________________________________

TOTAL: 594 594

MONTH TO DATE: 43,765

NUMBER OF NOTICES FILED TODAY FOR AUGUST CONTRACT: 594 NOTICE(S) FOR 59,400 OZ (1.8475 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 43765 NOTICES FOR 4,376,500 OZ (136.12 TONNES)

SILVER

FOR AUGUST

6 NOTICE(S) FILED TODAY FOR 30,000 OZ/

total number of notices filed so far this month: 1106 for 5.530 MILLION oz

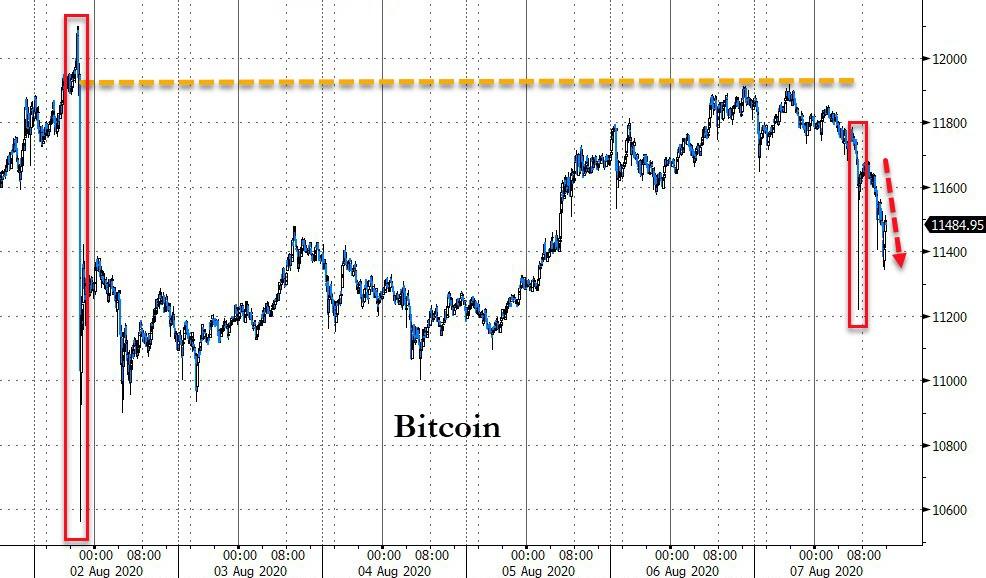

BITCOIN MORNING QUOTE $11,732 DOWN 29

BITCOIN AFTERNOON QUOTE.: $11,525 DOWN 280

GLD AND SLV INVENTORIES:

WITH GOLD DOWN $38.30 AND NO PHYSICAL TO BE FOUND ANYWHERE:

WITH ALL REFINERS CLOSED//MEXICO ORDERING ALL MINES SHUT: WHERE ARE THEY GETTING THE “PHYSICAL?

NO CHANGES IN GOLD INVENTORY AT THE GLD///

GLD: 1,267.96 TONNES OF GOLD//

WITH SILVER DOWN 69 CENTS TODAY: AND WITH NO SILVER AROUND:

A HUGE CHANGE IN SILVER INVENTORY AT THE SLV:

A DEPOSIT OF 465,000 OZ INTO THE SLV

RESTING SLV INVENTORY TONIGHT:

SLV: 573.029 MILLION OZ./

XXXXXXXXXXXXXXXXXXXXXXXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI ROSE BY A STRONG SIZED 1953 CONTRACTS FROM 205,537 UP TO 207,490, AND CLOSER TO OUR NEW RECORD OF 244,710, (FEB 25/2020. THE GAIN IN OI OCCURRED WITH OUR STRONG $1.52 GAIN IN SILVER PRICING AT THE COMEX. IT SEEMS THAT THE GAIN IN COMEX OI IS PRIMARILY DUE TO A MASSIVE BANKER SHORT COVERING PLUS A STRONG EXCHANGE FOR PHYSICAL ISSUANCE, ZERO LONG LIQUIDATION, ACCOMPANYING A VERY TINY DECREASE IN SILVER OZ. STANDING AT THE COMEX FOR AUGUST. WE HAD A STRONG NET GAIN IN OUR TWO EXCHANGES OF 3838 CONTRACTS (SEE CALCULATIONS BELOW).

WE HAVE ALSO WITNESSED A HUGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: SEP 1886 DEC: 0 FOR ZERO ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 1886 CONTRACTS. WITH THE TRANSFER OF 1886 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1886 EFP CONTRACTS TRANSLATES INTO 9.439 MILLION OZ ACCOMPANYING:

1.THE 152 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

10.025 MILLION OZ INITIAL STANDING IN AUGUST.

43.030 MILLION OZ INITIALLY STANDING IN SEPT. (HUGE)

7.32 MILLION OZ INITIALLY STANDING IN OCT

2.630 MILLION OZ STANDING FOR NOV.

20.970 MILLION OZ FINAL STANDING IN DEC

5.075 MILLION OZ FINAL STANDING IN JAN

1.480 MILLION OZ FINAL STANDING IN FEB

23.005 MILLION OZ FINAL STANDING FOR MAR

4.660 MILLION OZ FINAL STANDING FOR APRIL

45.220 MILLION OZ FINAL STANDING FOR MAY

2.205 MILLION OF FINAL STANDING FOR JUNE

86.470 MILLION OZ FINAL STANDING IN JULY.

6.275 MILLION OZ INITIAL STANDING IN AUGUST

THURSDAY, AGAIN OUR CROOKS USED COPIOUS PAPER IN ORDER TO LIQUIDATE SILVER’S PRICE…AND THEY WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE 152 CENTS ).. AND,OUR OFFICIAL SECTOR/BANKERS WERE UNSUCCESSFUL IN THEIR ATTEMPT TO FLEECE ANY SILVER LONGS FROM THEIR POSITIONS. THE STRONG GAIN AT THE COMEX WAS ACCOMPANIED BY : i) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS 2) A TINY DECREASE IN SILVER OZ STANDING FOR AUGUST, MONSTROUS BANKER SHORT COVERING AND 4) ZERO LONG LIQUIDATION AS WE DID HAVE A STRONG NET GAIN OF 3839 CONTRACTS OR 19.19 MILLION OZ ON THE TWO EXCHANGES! YOU CAN BET THE FARM THAT OUR BANKER ARE DESPERATE TO LIQUIDATE THEIR HUGE SHORT POSITIONS IN SILVER

SPREADING OPERATIONS/NOW SWITCHING TO SILVER

OUR SPREADING OPERATION HAS NOW SWITCHED INTO GOLD…..

SPREADING OPERATION FOR OUR NEWCOMERS:

FOR NEWCOMERS, HERE ARE THE DETAILS:

SPREADING LIQUIDATION HAS NOW COMMENCED IN SILVER AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF SEPT.

FOR THOSE OF YOU WHO ARE NEW, HERE IS THE MODUS OPERANDI OF THE SPREADERS AND THE CRIMINAL ELEMENT BEHIND IT:

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR;

THE SPREADING LIQUIDATION OPERATION IS NOW OVER FOR GOLD..AND WE WILL NOW MORPH INTO AN ACCUMULATION PHASE OF SPREADING CONTRACTS FOR SILVER. THEY WILL ACCUMULATE CONSIDERABLE AMOUNT OF THE CONTRACTS AND THEN LIQUIDATE ONE WEEK PRIOR TO FIRST DAY NOTICE

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO SILVER AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF AUGUST HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF SEPT FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE IN THIS NON ACTIVE MONTH OF AUGUST. BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN SILVER WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (SEPT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS

AUGUST

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY /FOR MONTH OF AUGUST:

6053 CONTRACTS (FOR 5 TRADING DAY(S) TOTAL 6053 CONTRACTS) OR 30.265 MILLION OZ: (AVERAGE PER DAY: 1211 CONTRACTS OR 6.053 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF AUGUST: 30.265 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 4.32% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2020 TO DATE SILVER EFP’S: 1,301.65 MILLION OZ.

JANUARY 2020 EFP TOTALS SO FAR: 181.61 MILLION OZ

FEB 2020 EFP’S TOTAL : …… 259.600 MILLION OZ

MARCH EFP’S ….. 452.280 MILLION OZ //TOTALS//AND A NEW RECORD FOR THE MONTH)

APRIL EFP 95.355 MILLION OZ. (EX. FOR PHYSICALS BECOMING A LOT LESS)

MAY EFP FINAL: 77.27 MILLION OZ

JUNE EXP 71.15 MILLION OZ.

JULY EXP 133.95 MILLION OZ/ (EXCHANGE FOR PHYSICALS STARTING TO RISE EXPONENTIALLY AGAIN)

AUGUST EXP 30.265 MILLION OZ (EXCHANGE FOR PHYSICALS INCREASING)

RESULT: WE HAD A CONSIDERABLE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1953, WITH OUR STRONG 152 CENT GAIN IN SILVER PRICING AT THE COMEX ///THURSDAY… THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 1886 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER

TODAY WE GAINED A STRONG SIZED OI CONTRACTS ON THE TWO EXCHANGES: 3839 CONTRACTS (WITH OUR $1.52 GAIN IN PRICE)//

THE TALLY//EXCHANGE FOR PHYSICALS

i.e 1886 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH A STRONG SIZED INCREASE OF 1943 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 152 CENT GAIN IN PRICE OF SILVER/AND A CLOSING PRICE OF $28.26 // THURSDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY.

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.0275 BILLION OZ TO BE EXACT or 146% of annual global silver production (ex Russia & ex China).

FOR THE NEW AUGUST DELIVERY MONTH/ THEY FILED AT THE COMEX: 6 NOTICE(S) FOR 30,000 OZ OF SILVER.

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.70//TODAY’S RECORD OF 244,705 WAS SET WITH A PRICE OF: 18.91 (FEB 25/2020)

.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ; AUGUST 10.025 MILLION OZ/ SEPT 43.030 MILLION OZ//OCT: 7.665 MILLION OZ// NOV: 2.630 MILLION OZ//DEC: 20.970 MILLION OZ; JAN: 5.075 MILLION OZ.//FEB 1.480 MILLION OZ//MAR: 23.005 MILLION OZ/APRIL 4.660 MILLION OZ//MAY 45.220 MILLION OZ//JUNE: 2.205 MILLION OZ// JULY 86.470 million oz//AUGUST 6.275 MILLION OZ//

- THE RECORD PRIOR TO TODAY WAS SET IN FEB 25/2018: 244,710 CONTRACTS, WITH A SILVER PRICE OF $18.90//.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017 RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

GOLD

IN GOLD, THE COMEX OPEN INTEREST FELL BY A SMALL SIZED 1695 CONTRACTS TO 553,130 AND FURTHER FROM OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE LOSS OF COMEX OI OCCURRED DESPITE OUR HUGE RISE IN PRICE OF $20.45 /// COMEX GOLD TRADING// THURSDAY// WE HAD MONSTROUS BANKER SHORT COVERING, A GOOD SIZED INCREASE IN GOLD TONNAGE STANDING AT THE COMEX FOR AUGUST, ALONG WITH ZERO LONG LIQUIDATION ACCOMPANYING A SMALL EXCHANGE FOR PHYSICAL ISSUANCE. THIS ALL HAPPENED WITH OUR HUGE GAIN IN PRICE OF $20.45.

WE HAD A VOLUME OF 5 4 -GC CONTRACTS//OPEN INTEREST 53

WE GAINED A SMALL SIZED 2252 CONTRACTS (7.004 TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A SMALL SIZED 3947 CONTRACTS:

CONTRACT .; AUG 0 AND OCT: 650 DEC: 3297; FEB: 0 ALL OTHER MONTHS ZERO//TOTAL: 3947. The NEW COMEX OI for the gold complex rests at 553,130. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EXCHANGE DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A SMALL SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2252 CONTRACTS: 1695 CONTRACTS DECREASED AT THE COMEX AND 3947 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 2245 CONTRACTS OR 7.004 TONNES. THURSDAY, WE HAD A HUGE GAIN OF $20.45 IN GOLD TRADING……

AND DESPITE THAT GAIN IN PRICE, WE HAD A SMALL SIZED GAIN IN TOTAL/TWO EXCHANGES GOLD TONNAGE OF 7.004 TONNES!!!!!! THE BANKERS/OFFICIAL SECTOR WERE LOATHE TO SUPPLY SHORT GOLD COMEX PAPER. THE BANKERS WERE UNSUCCESSFUL IN THEIR ATTEMPT TO LOWER GOLD’S PRICE (IT ROSE $20.45) AS IT SEEMS THAT THE ENTIRE COMEX LOSS WAS DUE TO A MONSTER BANK SHORT COVERING.!!

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES:

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3947) ACCOMPANYING THE SMALL SIZED LOSS IN COMEX OI (1152 OI): TOTAL GAIN IN THE TWO EXCHANGES: 2252 CONTRACTS. WE NO DOUBT HAD 1 )HUGE BANKER SHORT COVERING, 2.)A GOOD INCREASE IN GOLD TONNAGE STANDING AT THE GOLD COMEX FOR THE FRONT AUGUST MONTH, 3) ZERO LONG LIQUIDATION; 4) SMALL COMEX OI LOSS AND 5) SMALL EXCHANGE FOR PHYSICAL ISSUANCE AND …ALL OF THIS WAS COUPLED WITH OUR VERY STRONG GAIN IN GOLD PRICE TRADING//THURSDAY//$20.45.

WE ARE BEGINNING TO WITNESS A LACK OF EXCHANGE FOR GOLD PHYSICALS UNDERWRITTEN DUE TO PREMIUMS STARTING TO REAPPEAR IN THE FUTURE PRICE OF GOLD VS LONDON SPOT. THE COST TO THE BANKERS IS JUST TOO GREAT TO ENGAGE IN THESE VEHICLES ONCE THIS OCCURS.

THE FACT THAT WE ARE CONTINUALLY SEEING A DROP IN COMEX OPEN INTEREST AND VOLUMES COUPLED WITH LESS EXCHANGE FOR PHYSICALS PROBABLY MEANS THAT OUR LONGS ARE ALREADY DEPARTING NEW YORK FOR THE NEW PHYSICAL PLATFORM AT LONDON’S LME.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2020 INCLUDING TODAY

AUGUST

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 5 TRADING DAY(S) IN TONNES: 37.07 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2019, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 37.07/3550 x 100% TONNES =1.04% OF GLOBAL ANNUAL PRODUCTION

ISSUANCE OF EXCHANGE FOR PHYSICAL GOLD HAS DISSIPATED THIS MONTH…THE COST TO THE BANKERS TO CARRY THESE CONTRACTS IN LONDON IS BECOMING TOO GREAT FOR THEM.

ACCUMULATION OF GOLD EFP’S YEAR 2020 TO DATE: 3,295.57 TONNES

JANUARY 2220 TOTAL EFP ISSUANCE; : 570.19 TONNES

FEB 2020 TOTAL EFP ISSUANCE : 653.78 TONNES

MARCH TOTAL EFP ISSUANCE 1,098.93 TONNES (*AND A NEW ALL TIME RECORD ISSUANCE//22 DAYS)

APRIL TOTAL EFP. ISSUANCE: 243.45 TONNES (EFP ISSUANCE BECOMING A LOT LESS)

MAY TOTAL EFP ISSUANCE: 248.68 TONNES (EFP ISSUANCE STILL LOW// PREMIUM COST TO THE BANKERS IS HUGE..SO ISSUANCE IS LESS)

JUNE TOTAL EFP ISSUANCE: 192.06 TONNES

JULY TOTAL EFP ISSUANCE; 313.09 TONNES ..(EXCHANGE FOR PHYSICALS REVERSE COURSE AND ARE NOW INCREASING!)

AUGUST TOTAL EFP ISSUANCE; 37.07 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A STRONG SIZED 1953 CONTRACTS FROM 205,537 UP TO 207,490 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 2 3/4 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.

THE STRONG SIZED GAIN IN OI SILVER COMEX WAS PRIMARILY DUE TO; 1) A MONSTER BANKER SHORT COVERING , 2) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS (SEE BELOW), 3) A TINY DECREASE IN SILVER OZ STANDING AT THE SILVER COMEX FOR AUGUST, AND 4) ZERO LONG LIQUIDATION

EFP ISSUANCE 1886 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT: 1186 AND DEC. 0 AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1886 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1953 CONTRACTS TO THE 1886 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A STRONG GAIN OF 3838 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 19.19 MILLION OZ, OCCURRED WITH OUR 152 CENT GAIN IN PRICE///

NOBODY IS LEAVING THE SILVER ARENA AND NOBODY IS LEAVING THE GOLD ARENA (EXCEPT OUR BANKERS!!!)

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL..THE EVIDENCE IS CLEAR: HUGE AMOUNTS OF PHYSICAL STANDING FOR BOTH SILVER AND GOLD .

(report Harvey)

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED DOWN 32.43 POINTS OR 0.96% //Hang Sang CLOSED DOWN 398.96 POINTS OR 1.60% /The Nikkei closed DOWN 88.21 POINTS OR 0.39%//Australia’s all ordinaires CLOSED DOWN .57%

/Chinese yuan (ONSHORE) closed DOWN at 6.9586 /Oil UP TO 41.38 dollars per barrel for WTI and 44.59 for Brent. Stocks in Europe OPENED MIXED// ONSHORE YUAN CLOSED DOWN // LAST AT 6.9586 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.9598 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED/CORONAVIRUS/PANDEMIC : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

i) Out of HSBC: 58,339.640 oz

ii) Out of Manfra:: 1060.983 oz

total withdrawals; 59,400.623 oz

We had 2 kilobar transactions +

ADJUSTMENTS: 0 //

The front month of AUGUST registered a total of 5122 CONTRACTS as we lost 1743 contracts. We had 1822 notices served on THURSDAY so we GAINED 79 contracts or an additional 7,900 will stand for delivery on this side of the pond as they refused to morph into London based forwards as well as negating a fiat bonus. The boys are scrambling in search of badly needed physical metal.

After August we have the non active Sept contract month.. Here we saw another gain of 27 contracts to stand at 2990. Oct LOST 723 contracts DOWN to 70,073

The big December contract LOST 443 contracts down to 409,103 contracts.

(December is generally the go to month for longs. To see this number contract with a huge 20 dollar gain in price in gold speaks volumes that we had a wicked short covering today. Also the other active delivery month , October also saw a considerable contraction)

We had 594 notices filed today for 59,400 oz

To calculate the INITIAL total number of gold ounces standing for the AUGUST /2020. contract month, we take the total number of notices filed so far for the month (43,765) x 100 oz , to which we add the difference between the open interest for the front month of AUGUST (5122 CONTRACTS ) minus the number of notices served upon today (594 x 100 oz per contract) equals 4,829,300 OZ OR 150.0211 TONNES) the number of ounces standing in this active month of JUNE

thus the INITIAL standings for gold for the AUGUST/2020 contract month:

No of notices filed so far (43,765, x 100 oz + (5122 OI) for the front month minus the number of notices served upon today (594) x 100 oz which equals 4,829300 oz standing OR 150.0211 TONNES in this active delivery month. This is a HUGE amount for gold standing for a AUGUST delivery month (an active delivery month).

We gained 79 contracts or 7900 oz of gold as these guys refused to morph into London based forwards.

NEW PLEDGED GOLD: BRINKS

144,088.952 oz NOW PLEDGED JAN 21.2020/HSBC 5.4807 TONNES

271,997.477 oz PLEDGED JULY 9// 2020 JPMORGAN: 8.46 TONNES

42,548.308.00 PLEDGED APRIL 3/2020: SCOTIA: 1.3234 tonnes

deleted Int. Delaware pledge July 7 (600 tonnes)

231,924.295 oz (some deleted august 3) JPM

653,730.982 oz pledged June 12/2020 Brinks/ july 2/july 21 20.333 tonnes

total pledged gold: 1,052,918.710 oz 32.75 tonnes

total registered, pledged and eligible (customer) gold; 36,417,930.092 oz 1,132.75 tonnes (INCLUDES 4 GC GOLD)

total 4 GC gold: 126.34 tonnes

total gold net of 4 GC: 1006.41 tonnes

end

I have compiled data with respect to registered (or dealer) gold taken on first day notice for each of the past 24 months

The data begins on first day notice for the May month taken on the last day of July 2018. and it continues to present day.

I then took, how many deliveries were recorded by the CME for each and every month. I also included for reference the price of gold on first day notice.

The first graph is a logarithmic graph and the second graph, linear.

You can see the huge explosion of registered gold at the comex along with deliveries.

THE GOLD COMEX SEEMS TO BE UNDER SEVERE ASSAULT FOR PHYSICAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory |

607,725.748 oz

CNT

Delaware

|

| Deposits to the Dealer Inventory |

nil oz

|

| Deposits to the Customer Inventory |

2,760,018.460 oz

JPMorgan

Scotia

|

| No of oz served today (contracts) |

3

CONTRACT(S)

(15,000 OZ)

|

| No of oz to be served (notices) |

149 contracts

745,000 oz)

|

| Total monthly oz silver served (contracts) | 1106 contracts

5,530,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

we had 2 deposits into the customer account

i)into JPMorgan: 1,195,751.900 oz

ii) Into Scotia: 154,266.560 oz

*** JPMorgan for most of 2017, 2018 and onward, has adding to its inventory almost every single day.

JPMorgan now has 164.3 million oz of total silver inventory or 48,33% of all official comex silver. (164.3 million/337.1 million

total customer deposits today: n2,760,018.460 oz

we had 2 withdrawals:

i) Out of CNT: 604,784.748 oz

ii) Out of Delaware: 2941.000 oz ??

total withdrawals; 607,725.748 oz

We had 0 adjustments

Total dealer(registered) silver: 127.437 million oz

total registered and eligible silver: 337.159 million oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

the front month of August registered an open interest of 155 contracts and thus we lost 8 contracts. We had 3 notices filed on Thursday so we lost 5 contracts or 25,000 oz will not stand for delivery as these guys morphed into London based forwards as well as accepting a fiat bonus for their efforts…. The bankers are now desperate in their search for badly needed silver whether it is on this side of the pond or the European side.

After August we have the big September contract month and here we see a lost 2571 contracts down to 131,868. November saw another gain of 5 contracts to stand at 107.

For September to contract this big on a strong price gain means we also had a massive shortcovering by our bankers.

The big December contract month saw its OI rise by strong 4096 contracts up to 64,898

The total number of notices filed today for the AUGUST 2020. contract month is represented by 6 contract(s) FOR 30,000, oz

To calculate the number of silver ounces that will stand for delivery in AUGUST we take the total number of notices filed for the month so far at 1106 x 5,000 oz = 5,530,000 oz to which we add the difference between the open interest for the front month of AUGUST.(155) and the number of notices served upon today 6 x (5000 oz) equals the number of ounces standing.

Thus the INITIAL standings for silver for the AUGUST/2019 contract month: 1106 (notices served so far) x 5000 oz + OI for front month of AUGUST (155)- number of notices served upon today (6) x 5000 oz of silver standing for the AUGUST contract month.equals 6,275,000 oz. ..VERY STRONG FOR A NON ACTIVE MONTH.(corrected from an error yesterday)

We lost 5 contracts or an additional 25,000 will not stand for delivery.

TODAY’S ESTIMATED SILVER VOLUME : 308,626 CONTRACTS // volume huge++++++++++++++/

FOR YESTERDAY: 265,871. ,CONFIRMED VOLUME//volume huge+++++++/

YESTERDAY’S CONFIRMED VOLUME OF 265,871 CONTRACTS EQUATES to 1.329 billion OZ 189% OF ANNUAL GLOBAL PRODUCTION OF SILVER..

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO- 2.77% ((AUGUST 7/2020)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -1.02% to NAV: (AUGUST 7/2020 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into NEGATIVE/ 2.77%

(courtesy Sprott/GATA

3. SPROTT CEF .A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 21.44 TRADING 20.96///NEGATIVE 2.23

END

And now the Gold inventory at the GLD/

AUGUST 7/WITH GOLD DOWN $38.30 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1267.96 TONNES

AUGUST 6/WITH GOLD UP $20.45 TODAY, WE HAVE ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A PAPER DEPOSIT OF 10.23 TONNES INTO THE GLD/INVENTORY RESTS AT 1267.96 TONNES//

AUGUST 5/WITH GOLD UP $ 33.75 TODAY, WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD/A DEPOSIT OF 9.35 TONNES INTO THE GLD//INVENTORY RESTS AT 1257.73 TONNES

AUGUST 4//WITH GOLD UP $31.75 TODAY, WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 6.48 TONNES/GLD INVENTORY RESTS AT 1248.38 TONNES

AUGUST 3/WITH GOLD UP $2.20 TODAY, WE HAVE NO CHANGES IN THE GOLD INVENTORY AT THE GLD////INVENTORY RESTS AT 1241,96 TONNES

JULY 31/WITH GOLD UP $17.90 TODAY/WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY RESTS AT 1241.96 TONNES.

JULY 30/WITH GOLD DOWN $10.00 TODAY, WE HAVE ANOTHER SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES//INVENTORY RESTS AT 1241.96 TONNES.

JULY 29//WITH GOLD UP $12.45 TODAY, WE HAVE ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A HUGE DEPOSIT OF 8.47 TONNES/INVENTORY RESTS AT 1243.12 TONNES

JULY 28///WITH GOLD UP $13.25 TODAY, WE HAVE ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A HUGE DEPOSIT OF 5.84 TONNES/INVENTORY RESTS AT 1234.65

JULY 27//WITH GOLD UP $35.30 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF XXX TONNES/INVENTORY RESTS AT 1228.81 TONNES

JULY 24/WITH GOLD UP $8.80 TODAY: WE HAVE ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.80 TONNES//INVENTORY RESTS AT 1228.81 TONNES

JULY 23/WITH GOLD UP $24.90 TODAY: WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 7.26 TONNES/INVENTORY RESTS AT 1225.01 TONNES

JULY 22/WITH GOLD UP $22.00 TODAY: WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD/ A DEPOSIT OF 7.89 TONNES/INVENTORY RESTS AT 1219.75 TONNES

JULY 21//WITH GOLD UP $26.00 TODAY, WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.97 TONNES INTO THE GLD// INVENTORY RESTS AT 1211.86 TONNES

JULY 20/WITH GOLD UP $7.70 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1206.89 TONNES

JULY 17/WITH GOLD UP $7.70 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD: /INVENTORY RESTS AT 1206.89 TONNES

JULY 16/WITH GOLD DOWN $9.80 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD: INVENTORY RESTS AT 1206.89 TONNES

JULY 15//WITH GOLD UP $1.55 TODAY/A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 2.96 TONNES INTO THE GLD///INVENTORY RESTS AT 1206.89 TONNES

JULY 14//WITH GOLD DOWN $1.65 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD/A DEPOSIT OF 3.51 TONNES/INVENTORY RESTS AT 1203.97 TONNES

JULY 13//WITH GOLD UP $12.50 TODAY: A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.36 TONNES INTO THE GLD//INVENTORY RESTS AT 1200.46 TONNES

JULY 10/WITH GOLD DOWN $.50 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD//A STRANGE WITHDRAWAL OF 1.75 TONNES FROM THE GLD//INVENTORY RESTS AT 1200.82 TONNES

JULY 9//WITH GOLD DOWN $11.75 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OX 3.21 TONNES INTO THE GLD//INVENTORY RESTS AT 1202.57 TONNES

JULY 8/WITH GOLD UP $13.75 TODAY; A BIG CHANGE IN GOLD INVENTORY AT THE GLD:A DEPOSIT OF 7.89 TONNES INTO THE GLD//INVENTORY RESTS AT 1199.36 TONNES

JULY 7/WITH GOLD UP $12.50 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD: /INVENTORY RESTS AT 1191.47 TONNES

JULY 6/WITH GOLD UP $6.50 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 9.36 TONNES INTO THE GLD//INVENTORY RESTS AT 1191.47 TONNES

JULY 2/WITH GOLD UP $7.00 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.21 TONNES INTO THE GLD////INVENTORY RESTS AT 1182.11 TONNES

JULY 1/WITH GOLD DOWN $12.90//NO CHANGES IN GOLD INVENTORY AT THE GLD: /INVENTORY RESTS AT 1178.90 TONNES

JUNE 30//WITH GOLD UP $16.50 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 1178.90 TONNES

JUNE 29/WITH GOLD UP $2.90 TODAY: A HUGE DEPOSIT OF 3.61 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 1178.90 TONNES

JUNE 26/WITH GOLD UP $5.03 TODAY: VERY STRANGE: A PAPER WITHDRAWAL OF 1.46 TONNES//INVENTORY RESTS AT 1175.39 TONNES

JUNE 25//WITH GOLD DOWN $3.30 TODAY//ANOTHER STRONG PAPER DEPOSIT OF 7.6 TONNES///INVENTORY RESTS AT 1176.85 TONNES

JUNE 24/WITH GOLD DOWN $1.50 TODAY; A STRONG 3.21 TONNES ADDED TO THE GLD//INVENTORY RESTS AT 1169.25 TONNES

JUNE 23/WITH GOLD UP $25.50 TODAY/ANOTHER CRIMINAL PAPER DEPOSIT OF 6.73 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 1166.04 TONNES

JUNE 22/WITH GOLD UP $14.00 A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 23.09 TONNES//INVENTORY RESTS AT 1159.31 TONNES

JUNE 19/WITH GOLD UP$16.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//; INVENTORY RESTS AT 1136.22 TONNES

JUNE 18//WITH GOLD DOWN $2.75 TODAY: NO CHANGES IN GOLD INVENTORY: INVENTORY RESTS AT 1136.22 TONNES

JUNE 17/WITH GOLD DOWN $1.05: NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY RESTS AT 1136.22 TONNES

JUNE 16//WITH GOLD UP $6.70 TODAY: NO CHANGES IN GOLD INVENTORY: /INVENTORY RESTS AT 1136.22 TONNES

JUNE 15/WITH GOLD DOWN ANOTHER $8.80 TODAY, NO CHANGES IN GOLD INVENTORY/INVENTORY RESTS AT 1136.22 TONNES

JUNE 12//WITH GOLD DOWN $1.00 TODAY: A HUGE CHANGE IN GOLD INVENTORY: A DEPOSIT OF 1.17 TONNES AT THE GLD//INVENTORY RESTS AT 1136.22 TONNES

JUNE 11//WITH GOLD UP $16.80 TODAY: A HUGE CHANGE IN GOLD INVENTORY: A DEPOSIT OF 6.55 TONNES AT THE GLD//INVENTORY RESTS AT 1135.05 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Inventory rests tonight at

AUGUST 7/ GLD INVENTORY 1267.96 tonnes*

LAST; 876 TRADING DAYS: +328.52 NET TONNES HAVE BEEN ADDED THE GLD

LAST 776 TRADING DAYS://+506.99 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

AUGUST 7/WITH SILVER DOWN 69 CENTS TODAY: WE HAVE ANOTHER HUGE CHANGE IN SILVER INVENTORY: A DEPOSIT OF 0.465 MILLION OZ/INVENTORY RESTS AT 573.029 MILLION OZ.

AUGUST 6/WITH SILVER UP $1.52 TODAY, WE HAVE NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 572.564 MILLION OZ///

AUGUST 5/WITH SILVER UP $1.03 TODAY, WE HAVE A HUGE CHANGE IN SILVER INVENTORY AT THE SLV// A MONSTROUS DEPOSIT OF 5.403 MILLION OZ//INVENTORY RESTS AT 572.564 MILLION OZ//

AUGUST 4/WITH SILVER UP $1.45 TODAY, WE HAVE NO CHANGES IN SILVER INVENTORY: //INVENTORY RESTS AT 367.161 MILLION OZ//

AUGUST 3/WITH SILVER UP 23 CENTS TODAY: WE HAVE A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//SURPRISINGLY ANOTHER WITHDRAWAL OF 0.931 MILLION OZ//INVENTORY RESTS AT 367.161 MILLION OZ//

JULY 31/WITH SILVER UP 82 CENTS TODAY: WE HAVE A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: SURPRISINGLY A HUGE WITHDRAWAL OF 3.26 MILLION OZ//INVENTORY RESTS AT 368.092 MILLION OZ//

JULY 30//WITH SILVER DOWN 97 CENTS TODAY: WE HAVE A SMALL CHANGE IN SILVER INVENTORY: A WITHDRAWAL OF 0.931 MILLION OZ//INVENTORY RESTS AT 571.352 MILLION OZ//

JULY 29/WITH SILVER UP 7 CENTS TODAY, WE HAD A BIG CHANGE IN SILVER INVENTORY//A DEPOSIT OF 5.984 MILLION OZ//INVENTORY RESTS AT 572.283 MILLION OZ//

JULY 28 WITH SILVER DOWN 14 CENTS TODAY, WE HAD A BIG CHANGE IN SILVER INVENTORY: A DEPOSIT OF 7.52 MILLION OZ//INVENTORY RESTS AT 566.299 MILLION OZ//

JULY 27/WITH SILVER UP $2.67 TODAY, WE HAD NO CHANGES IN SILVER INVENTORY: A DEPOSIT OF XX MILLION OZ//INVENTORY RESTS AT 558.779 MILLION OZ//

JULY 24/WITH SILVER DOWN $0.12 TODAY: NO CHANGE IN SILVER INVENTORY//INVENTORY RESTS AT 558.779 MILLION OZ/

JULY 23/WITH SILVER UP $.04 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV// A HUMONGOUS PAPER DEPOSIT OF 9.594 MILLION OZ//INVENTORY RESTS AT 558.779 MILLION OZ///

JULY 22/WITH SILVER UP $1.54 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A HUMONGOUS PAPER DEPOSIT OF 7.218 MILLION OZ//INVENTORY RESTS AT 549.185 MILLION OZ/

JULY 21/WITH SILVER UP $1.38 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A HUMONGOUS PAPER DEPOSIT OF 15.368 MILLION OZ////INVENTORY RESTS AT 541.967 MILLION OZ//

JULY 20/WITH SILVER UP 40 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A MASSIVE PAPER DEPOSIT OF 3.819 MILLION OZ ‘ENTERED” THE SLV..INVENTORY RESTS AT 526.599 MILLION OZ/

JULY 17/WITH SILVER UP 15 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A DEPOSIT OF 1.583 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 522.780 MILLION OZ//

JULY 16//WITH SILVER DOWN 14 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.123 MILLION OZ//INVENTORY RESTS AT 521.197 MILLION OZ..

JULY 15.WITH SILVER UP 21 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.956 MILLION OZ//INVENTORY RESTS AT 516.074 MILLION OZ//

JULY 14/WITH SILVER DOWN 21 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT 514.118 MILLION OZ//

JULY 13//WITH SILVER UP 67 CENTS TODAY: A HUGE CHANGE IN SILVER: A WITHDRAWAL OF 1.677 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 514.118 MILLION OZ//

JULY 10/WITH SILVER UP 7 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 4.844 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 515.795 MILLION OZ

WHAT A FRAUD!!

JULY 9/WITH SILVER DOWN 8 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 8.198 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 510.951 MILLION OZ/

JULY 8/WITH SILVER UP 37 CENTS TODAY//A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.118 MILLION OZ FROM THE SLV//VERY SURPRISING.//INVENTORY RESTS AT 502.753 MILLION OZ//

JULY 7/WITH SILVER UP 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:/INVENTORY RESTS AT 503.871 MILLION OZ///

JULY 6//WITH SILVER UP 24 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.863 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 503.871 MILLION OZ

JULY 2/WITH SILVER UP 4 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//: A DEPOSIT OF 4.01 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 502.008 MILLION OZ

JULY 1/WITH SILVER DOWN 23 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 5.403 MILLION OZ//INVENTORY RESTS AT 498.007 MILLION OZ/

JUNE 30/WITH SILVER UP 39 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 492.604 MILLION OZ//

JUNE 29/WITH SILVER DOWN ONE CENT TODAY: A TWO CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL WITHDRAWAL OF 466,000 OZ TO PAY FOR STORAGE FEES AND INSURANCE//// AND A LARGE DEPOSIT OF 1.212 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 492.604 MILLION OZ//

JUNE 26/WITH SILVER UP 6 CENTS TODAY: ANOTHER HUGE CHANGE IN SILVER INVENTORY AT THE SLV/ RESTS AT 491.858 MILLION OZ//

JUNE 25/WITH SILVER UP 12 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 931,000 OZ INTO THE SLV////INVENTORY RESTS AT 491.858 MILLION OZ//

JUNE 24///WITH SILVER DOWN 31 CENTS// NO CHANGE IN SILVER INVENTORY//INVENTORY RESTS AT 490.927 MILLION OZ

JUNE 23//WITH SILVER UP 16 CENTS TODAY: A MONSTROUS CHANGE IN INVENTORY: A PAPER DEPOSIT OF 4.473 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 490.927 MILLION OZ//

JUNE 22/WITH SILVER UP 15 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/: INVENTORY/INVENTORY RESTS AT 486/454 MILLION OZ//

JUNE 19//WITH SILVER UP 22 CENTS TODAY: STRANGE!! A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 839,000 OZ FROM THE SLV////INVENTORY RESTS AT 486,454 MILLION OZ..

JUNE 18/WITH SILVER DOWN 16 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 932,000 OZ INTO THE SLV////INVENTORY RESTS AT 487.293 MILLION OZ

JUNE 17/WITH SILVER UP 8 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.261 MILLION OZ INTO THE SLV////INVENTORY REST AT 486.361 MILLION OZ

JUNE 16//WITH SILVER UP 20 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.118 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 483.100 MILLION OZ//

JUNE 15/WITH SILVER DOWN 14 CENTS NO CHANGES IN SILVER INVENTORY: //INVENTORY RESTS AT 481.982 MILLION OZ///

JUNE 12/WITH SILVER DOWN 30 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV/: TWO DEPOSITS OF 7.269 MILLION OZ AND 1.802 MILLION OZ ADDED TO THE SLV///INVENTORY RESTS THIS WEEKEND AT 481.982 MILLION OZ//

JUNE 11//WITH SILVER UP 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY: ///INVENTORY RESTS AT 472.89 MILLION OZ//

AUGUST 7.2020:

SLV INVENTORY RESTS TONIGHT AT

573.029 MILLION OZ.

end

PHYSICAL GOLD/SILVER STORIES

i) GOLDCORE BLOG/Mark O’Byrne

ii) Important gold commentaries courtesy of GATA/Chris Powell

Authers comments on what is the correct price for gold!

(John Authers)

John Authers: Gold is expensive, and may be just warming up

Submitted by cpowell on Thu, 2020-08-06 16:23. Section: Daily Dispatches

By John Authers

Bloomberg News

Thursday, August 6, 2020

As I write, gold has surged to yet another record, topping $2,050 per ounce. Is it overpriced?

The question is impossible to answer. Gold’s value rests in the eye of the beholder, and over recorded human history people have continued to find it beautiful. It pays no income, and its intrinsic value is set by the market. Valuation techniques that work for other assets won’t work for gold.

The fact that we will never scientifically arrive at a “correct” price need not stop us from trying, however. And after going through the various valuation exercises, the rally looks rational. While the current price looks expensive, it could easily rise further. …

… For the remainder of the analysis:

https://www.bloomberg.com/opinion/articles/2020-08-06/gold-is-expensive-…

end

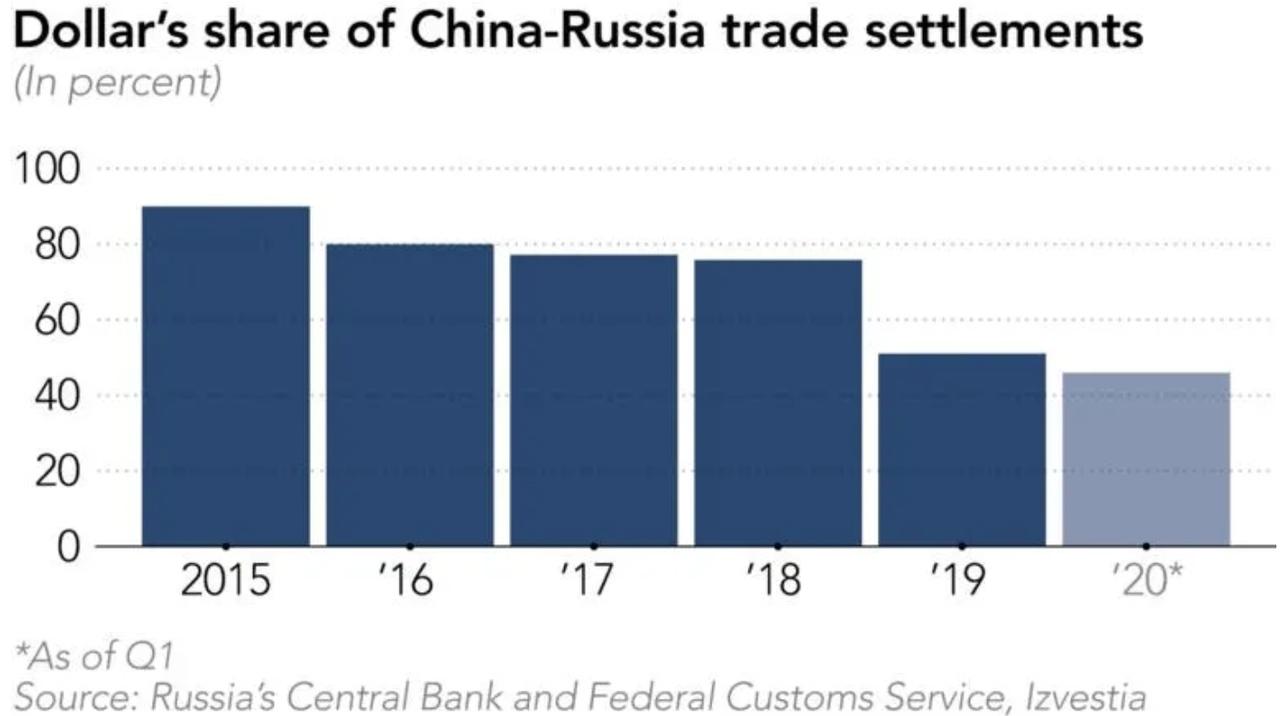

We brought this story to you yesterday but it is worth repeating: China and Russia are ditching the dollar and move to a financial alliance

(Nikkei Asian Review/GATA)

China and Russia ditch dollar in move toward ‘financial alliance’

Submitted by cpowell on Thu, 2020-08-06 16:30. Section: Daily Dispatches

By Dimitri Simes

Nikkei Asian Review, Tokyo

Thursday, August 6, 2020

MOSCOW — Russia and China are partnering to reduce their dependence on the dollar — a development some experts say could lead to a “financial alliance” between them.

In the first quarter of 2020, the dollar’s share of trade between Russia and China fell below 50% for the first time on record, according to recent data from Russia’s Central Bank and Federal Customs Service.

The greenback was used for only 46% of settlements between the two countries. At the same time, the euro made up an all-time high of 30%, while their national currencies accounted for 24%, also a new high.

Russia and China have drastically cut their use of the dollar in bilateral trade over the past several years. As late as 2015, approximately 90% of bilateral transactions were conducted in dollars. Following the outbreak of the U.S.-China trade war and a concerted push by both Moscow and Beijing to move away from the dollar, however, the figure had dropped to 51% by 2019.

Alexey Maslov, director of the Institute of Far Eastern Studies at the Russian Academy of Sciences, told the Nikkei “Asian Review that the Russia-China “de-dollarization” was approaching a “breakthrough moment” that could elevate their relationship to a de-facto alliance. …

… For the remainder of the report:

https://asia.nikkei.com/Politics/International-relations/China-and-Russi.

end

Pam and Russ Martens: Sri Lanka is top user of Fed emergency lending program

Submitted by cpowell on Thu, 2020-08-06 16:58. Section: Daily Dispatches

By Pam and Russ Martens

Wall Street on Parade

Thursday, August 6, 2020

At Fed Chairman Jerome Powell’s press conference on July 29, he persisted in his explanation that all the Fed’s bailout programs are really about helping the American people get back on their feet. Here’s one more, among a growing mountain, of reasons to question that.

Sri Lanka is an island country situated in the Indian Ocean and located about 9,000 miles from the United States. Its population of approximately 21 million ranks it the size of Florida. Despite those statistics, Sri Lanka somehow became the main participant in an emergency lending facility set up by the Fed.

According to an official statement by the Central Bank of Sri Lanka (CBSL), “The CBSL has decided to pledge a sum of US$1 billion worth of U.S. Treasury Bonds held in the CBSL reserve and enter into the above type of repo facility with the Fed. This would permit the CBSL to raise US$1 billion in cash form when required.

“When this repo facility is settled by the CBSL, there will be no change in the CBSL reserve position as the Fed would release the pledged bonds back to the CBSL. The cost to the CBSL would be the applicable repo fee, which is about 0.35 percent per annum.” …

… For the remainder of the report:

https://wallstreetonparade.com/2020/08/the-fed-created-an-emergency-lend…

end

A must view: Andrew Maguire talks about the reset of gold price

(Andrew Maguire/Part ii/Chris Marcus)

In Arcadia Economics interview, Maguire elaborates on expectation of metals price ‘reset’

Submitted by cpowell on Thu, 2020-08-06 18:11. Section: Daily Dispatches

2:10p ET Thursday, August 6, 2020

Dear Friend of GATA and Gold:

In the concluding half hour of his interview with Chris Marcus of Arcadia Economics, London metals trader and Kinesis Money founder Andrew Maguire elaborates on his expectation for a “reset” of monetary metals prices in coming weeks, notes the unprecedented amount of metals deliveries being made on the futures markets, and finds it hard to believe that the New York Commodities Exchange will be able to deliver on all the silver due in its September contracts.

The interview can be viewed at YouTube here:

https://www.youtube.com/watch?v=7SX1Pv6foC8&feature=youtu.be

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

Your weekend reading..

important…

Alasdair Macleod…

Alasdair Macleod: Passing $2,000 is no big deal for gold as it heads to infinity

Submitted by cpowell on Thu, 2020-08-06 21:29. Section: Daily Dispatches

5:29p ET Thursday, August 6, 2020

Dear Friend of GATA and Gold:

GoldMoney research director Alasdair Macleod, writing today, sees little chance of an international currency reset involving gold and silver. Instead, Macleod argues, government currencies are simply going to collapse under infinite issuance and take down with them not only the corrupt fractional-reserve gold banking system but equity markets as well, pushing monetary metals prices to infinity.

Hence, Macleod writes, gold’s passing $2,000 per ounce is no big deal in the unfolding age of infinite fiat money.

Macleod concludes that only restoration of a metallic money system and restraint on government spending can establish a working financial system.

His scary analysis is headlined “Gold at $+2k — So Why the Fuss?” and it’s posted at GoldMoney here:

https://www.goldmoney.com/research/goldmoney-insights/gold-at-2k-so-why-…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

Gold at $2k+. So why the fuss?

There appears to be no way out for the bullion banks deteriorating $53bn short gold futures positions ($38bn net) on Comex. An earlier attempt between January and March to regain control over paper gold markets has backfired on the bullion banks.

Unallocated gold account holders with LBMA member banks will shortly discover that that market is trading on vapour. According to the Bank for International Settlements, at the end of last year LBMA gold positions, the vast majority being unallocated, totalled $512bn — the London Mythical Bullion Market is a more appropriate description for the surprise to come.

An awful lot of gold bulls are going to be disappointed when their unallocated bullion bank holdings turn to dust in the coming months — perhaps it’s a matter of a few weeks, perhaps only days — and synthetic ETFs will also blow up. The systemic demolition of paper gold and silver markets is a predictable catastrophe in the course of the collapse of fiat money’s purchasing power, for which the evidence is mounting. It is set to drive gold and silver much higher, or more correctly put, fiat currencies much lower.

This is only the initial catalysing phase in the rapidly approaching death of fiat currencies.

Sections to this article

-

- Introduction

- The rescue attempt has already failed

- The financial system depends entirely on inflationary fiat

- Forget currency resets

- Transition pains on Comex

- London’s hidden liabilities

- Conclusion

Introduction

Measured in dollars, the current bull market for gold started in December 2015, since when the price in dollars has almost doubled. Other than the odd headline when gold exceeded its previous September 2011 high of $1920, only gold bugs seem to be excited. But in our modern macroeconomic world of government-issued currencies, which has moved on from the days when gold operated as a monetary standard, it is viewed as an anachronism; a pet rock, as Jason Zweig of the Wall Street Journal called it in 2015, only a few months before this bull market commenced.

Despite almost doubling, Zweig’s view of gold is still mainstream. His comment follows the spirit of today’s macroeconomic hero, John Maynard Keynes, who called the gold standard a barbaric relic in his 1924 Tract on Monetary Reform. Keynes went on to invent macroeconomics on the back of his 1936 General Theory, and whether you profess to be Keynesian or not, as an investor you will almost certainly kowtow to macroeconomics. It has been well-nigh impossible to have a successful career in the investment industry unless you subscribed to inflationist Keynesian theories. You are required to substitute the economics of aggregates for those of the human action of individuals, upon which classical economics was based. And with it, you must unquestionably accept the state theory of money.

Well, we are now witnessing the cataclysmic ending of the Keynesian fallacy; the destruction of macroeconomics in a systemic failure centred on paper markets for gold and silver.

The rescue attempt has already failed

You may have missed the establishment’s last-ditch attempt earlier this year to save itself. Figure 1 below shows its failure.

Comex open interest peaked in January, when the gold contract was being overwhelmed by global demand. Never before had open interest been this high: the previous all-time record had been in July 2016, when it hit 658,000 contracts. At that time, the market had recovered strongly from a deeply oversold condition, the price rallying from the December low in our headline chart, from $1049 to $1380. That was successfully crushed with open interest taken down to 392,000 and the gold price to $1120. However, the take-down which commenced in earnest in January this year did not succeed.

There is no question it was a coordinated attempt by the bullion bank establishment to contain a developing crisis. From its peak of 799,541 contracts on 15 January open interest fell to 553,030 on 23 March. Initially, the gold price continued rising to $1680 on 9 March, but by 18March it finally reacted, falling to $1471 in only nine trading sessions. But while open interest went on to fall to 470,000 in early-June, the price exploded higher with unprecedented price premiums developing on Comex from 23 March onwards. The bullion banks’ short exposure net of longs on Comex in a rising market had risen to $35bn and the gross position was $53.5bn before the attempt to drive the market lower. Today, the respective figures are $38.3 and $53bn.

The failure of this well-worn tactic precludes it from being used again. We look at the seriousness of the current position on Comex and the LBMA later in this article.

The financial system depends entirely on inflationary fiat

In the investment industry it is monetary debasement that gives you your living. For the rise in the general level of prices of financial assets, measured by various indices, is little more than a reflection of the loss of purchasing power of your state’s currency. The world has been enjoying the phenomenon particularly from the mid-1970s, four years after the last vestiges of Keynes’s barbarous relic, when President Nixon removed pet rocks from the monetary scene. A continual decline in the dollar’s purchasing power ensued. Apart from the occasional hiccup, from 1982 when the S&P500 Index rose from 291.34 to today’s 3,270 the general public has appeared to make money.

It has not been an easy environment to convincingly challenge, being populated by group-thinkers believing their stock and property gains have been the consequence of their individual financial acumens. But one of those periodic hiccups is now upon us, threatening to be more disruptive than anything seen hitherto in our lifetimes, which the macroeconomists in the central banks and governments tell us will require virtually unlimited inflationary finance to resolve.

The distinction between unlimited fiat currency being issued by the state compared with gold is important, because gold was always the money of the people, disliked by governments because its disciplines are limiting. History has always seen the right to issue money taken away from the failures of kings, emperors and governments and handed back to the people, so the empirical evidence is that it will happen again. But macroeconomists argue that their science is an advance on former economic science, so what went before is irrelevant. Therefore, so is gold.

For these reasons, the investment industry is not attuned to gold. Physical gold is not even a regulated investment, which means that government regulators do not permit the funds they license to hold physical metal beyond, if permitted at all, a small exposure. The uncontentious position, taken by nearly all compliance officers, is for investment managers not to hold any. But besides mining stocks, today there are exchange-traded funds that do offer some investment exposure to gold for fund managers. Assuming, that is, they are willing to contradict the Keynesian views of their colleagues.

But even then, the context is wrong. Gold is not an investment but money, driven out of circulation over the last hundred years by the steady encroachment of gold substitutes evolving into pure unbacked fiat. It is no one’s liability, unlike the dollar, for instance, backed only by the full faith and credit in the Donald — or will it be Joe Biden. In the case of the euro or the yen, with negative interest rates and having banking systems arguably on the point of collapse, their central banks are similarly committed to accelerating debauchment of their currencies.

Even semi-official gold bugs, like the World Gold Council, promote gold as a portfolio investment, with its income arising from the securitisation of gold through the GLD ETF. An audience of professional investment managers, which subsists on an intellectual diet of macroeconomics, does not readily accept that gold is money, and if the World Gold Council argued that it is money and not an investment, they would doubtless fail to attract institutional investors.

But an understanding that gold is money is a vital distinction. When you regard it as an investment, you expect to sell it when its positive trend ends. You assume your government’s currency will always have the objective transactional value and gold is the subjective variable. Accounting conventions force investment managers and advisors to ignore the reality that it is the currency failing and not the price of gold rising. Even the overwhelming majority of gold bugs cheer a rising gold price, instinctively treating it as an investment which rises in value, measured in fiat.

The objective/subjective confusion is the most important concept to understand when it comes to gold. If the wider public begins to understand that measured in goods, the state’s currency is no longer fit for an objective role in day to day transactions, it will be doomed. For that marks the point where fiat money begins to be discarded, and the public then ultimately decides what is its preferred money. That is where all this is going.

Forget currency resets

In recent years, suggestions that a monetary reset, centred on the dollar, is planned by the monetary authorities have been made by a number of observers. Central bank research into blockchain solutions have added to this speculation, but a recent paper by the IMF shows there is no consensus in central banks as to how and for what purpose they would use digital currencies — the central banking version of cryptocurrencies.[i]

In any event, it is likely to take too long for a central bank digital currency to be implemented, given the speed with which monetary events are now unfolding. Empirical evidence suggests that once initiated, a fiat currency collapse happens in a matter of months. Today, the Fed has tightly bonded the future of financial asset values to the dollar — one goes and they both go. The credibility behind financial asset values is already stretched to the limit, and the inevitable collapse, taking fiat money with it, is likely to be sudden.

As a side note, the last time a collapse in financial assets took the currency down in similar circumstances was exactly three hundred years ago — in 1720 when John Law’s Mississippi bubble failed. Interestingly, Richard Cantillon made his second fortune by shorting Law’s currency, the livre, and not his shares. His first fortune was made acting as a banker lending money to wealthy speculators taking in Mississippi shares as collateral, which he then promptly sold, pocketing the proceeds.

An attempt at a currency reset, with or without blockchains, can only be contemplated after the public has begun to abandon existing currencies. But the speed with which events unfurl when fiat currencies die precludes advance planning of currency replacements. Any attempt to produce a new fiat money after the existing one has failed will also fail — rapidly. The idea that the state can take control of the valuation of a new currency in a fiat reset in order to make it durable is the ultimate conceit of macroeconomics, the denial of personal freedom to make choices in favour of the management of the aggregate.

One of the specious arguments that arises time and again is that inflation reduces the true burden of debt. This is true for existing debt, but its advocates as a remedy for government indebtedness fail to understand that it also increases the cost of the government’s future debt. And while it similarly reduces the burden on private sector debtors, by destroying savings inflation leads to capital starvation and hampers any recovery.

It is possible, and desirable, that the ills of fiat currencies will be properly addressed. But that will require an abandonment of inflationism, and a commitment to balanced budgets. It requires governments to rein in their spending, reducing their role in the economies they oversee. Statist interventions, both regulatory and mandated by law have to be axed, and full responsibility for their actions handed back to the people. And only then, sound money, preventing governments from reverting to their inflationary ways, can be successfully introduced.

Assuming all this is possible, the only sound money is one with a track record and where governments have no control over it as a medium of exchange. In other words, metallic money. They will have no alternative to turning their currencies into substitutes fully convertible into gold, with silver in a subsidiary coinage role. Coins in both metals must be freely available on demand from all banks at the fixed rate of exchange for gold, and for silver equating to its monetary value.[ii] The circulation of gold and silver coins ensures the public fully understands their monetary role, thereby deterring future governments from inflationary policies. Bank credit must also be backed by gold, and not expanded by banks out of thin air.

But the pervasive and mistaken beliefs in macroeconomics appear to be an unsurmountable impediment to an orderly change towards sound money. Imposing their fervent denial of economic reality, macroeconomists are in charge of both economic and monetary policy in America, Europe and Japan — and by extension those of almost all other nations. It is not even certain that a currency collapse will dislodge them from their position of power, prolonging the chaos that will ensue.

Talk of a monetary reset only makes any sense if those doing the resetting understand what they are doing. And one thing will become immediately clear: the Americans, who stand to lose power over global affairs, will be the most reluctant of all nations to accept that the days of its hegemonic currency are numbered and that a return to a credible gold standard is the only solution.

Transition pains on Comex

Only through knowledge of why fiat currencies’ days are numbered can one understand what is happening to the gold price. For now, those who do not appreciate the fallacies behind macroeconomics and think of gold as an investment see gold’s move from December 2015 as a bull market which sooner or later will probably come to an end — perhaps when interest rates or bond yields rise. But those who see gold as sound money and no one else’s counterparty risk will understand that a rising price for gold should be regarded as part and parcel of a fall in the purchasing power of their fiat currency. In fact, it is a change of purchasing power for both. As fiat money loses purchasing power, gold gains it disproportionately because of its relative scarcity, while the collapse in fiat money progresses.

In the increasingly likely event that fiat currencies will lose all function as money, measured in them the gold price will trend to infinity. It is now difficult to see how the dollar can avoid this outcome, or something close to it. That being the case, in this context a price move for gold above $2000 per ounce is an insignificant event, except for those trapped with short positions, which brings us to the chaos on the Comex futures market. Figure 2 shows the position in US gold futures markets on 28 July (the last Commitment of Traders information available) with the spread positions removed.

The swaps are bullion bank trading desks, which typically take positions across more than one derivative market, notably London forwards settling unallocated accounts. Together with the Producers and Merchants category, they almost always run net short positions on Comex. Producers, miners and their agents acting for them, hedge against falls in the gold price and make up the bulk of the short positions in their category. Merchants, typically jewellers and buyers for industrial and other purposes, hedge against price rises by holding long contracts.

The concept of futures markets did not originally include banks in the non-speculative category, because futures markets were a means for farmers to unburden themselves from price risk, due to seasonal factors, to speculators willing to take the risk upon themselves. However, banks managed to persuade the CME to be categorised as non-speculators, on the basis they often acted as agents for producers in non-agricultural contracts. And in gold, which is what concerns us, they also ran positions in London which they wished to hedge on Comex. But as has been seen in Figure 2, the bullion banks now account for 70% of the shorts, when in the past they would typically account for significantly less. And as we show later in this article, they have no physical gold in London to hedge. The result is their gross short position of 262,796 contracts is now an uncovered commitment of $53bn spread between 27 traders. Figure 3 puts this in an historical context over the last ten years.

Bullion banks’ shorts net of longs (the blue line) are at record levels, and gross shorts are almost at record highs, only exceeded at the beginning of the year when open interest had risen to an unprecedented level of 799,541 contracts on 15 January.

On the speculator side, the dominant category is nearly always Managed Money, which is predominantly hedge fund traders. They are rarely interested in taking delivery and will close or roll their positions. They are nearly always biased to the buy-side, and over the long term have averaged a net long position of about 112,000 contracts, which we can call the neutral position. But currently, they are an unusual minority 42% of the speculator longs and are only moderately positioned above their neutral net long average.

Far from being the masters of the investment universe, hedge funds have proved to be an easy target for the bullion banks, regularly spooking them out of their long positions. And by acting in the fashion of committed macroeconomists, hedge funds have used the current strength in the gold price to take profits, reducing net longs from the previous week’s COT report by 21,362 contracts. They seem unaware of or disinterested in a bigger picture. Furthermore, at 42,758, the level of their short contracts is above average, which could contribute to the bear squeeze in the coming weeks as they realise their mistake.

The Other Reportable category is for traders that do not fit into the other three categories described above. The longs in this category are close to a previous record level, which was on 24 March at 158,963 contracts. Unusually that was recorded two business days after the market turned higher following the price collapse in early March from $1700 to $1455. We can therefore count the Other Reportable category as smart money, at least in the current climate, less likely to be shaken out of their positions by swap dealers trying to trigger stops.

We can only conclude that swap dealers have not only ended up nearly record short, but the liquidity on Comex provided by hedge funds, which normally enables them to close their shorts, is restricted. Furthermore, mark-to-market losses come at a time when their banks’ wider operations are cutting back on risk exposure to financial commitments where they can. But these near-record losses are likely to increase significantly as central bank money-printing accelerates in an attempt to prevent an economic slump and to maintain financial asset prices. If something else does not break before, a full-scale banking crisis could evolve from the paper gold market.

The authorities can be expected to do everything to avoid a failure on Comex, because the damage to the wider market would be extremely serious. Instead, banking members of the London Bullion Market Association (LBMA) would probably be expected to bid up the gold price in the forward market in an attempt to square their books and for banks to swallow the losses. That cannot happen as will be explained in the next section.

In short, over the coming weeks, we can expect a transition phase as the crisis refocuses on London’s forward settlement market, which is the casino hidden from view.

London’s hidden liabilities

Trading in London for forward settlement is a far larger market than Comex. According to the Bank for International Settlements, at the end of 2019, the notional amount of over the counter (OTC) gold forwards and swaps outstanding stood at $512bn[iii], which compares with Comex open interest of $120bn on the same day, noting that open interest at 786,166 futures contracts at that time was an elevated level.

The London Bullion Market Association makes great play of its liquidity, in its last press release claiming total physical backing for its forward market was 8,424 tonnes in April.[iv] But of that total, 5,464 tonnes are gold vaulted at the Bank of England, of which perhaps 95% is earmarked for central banks and foreign exchequers. We have discovered from the SPDR Gold Trust’s quarterly filing with the SEC (the GLD ETF) that 45.91 tonnes of its gold was held at the Bank of England on 27 April.[v] The fact that GLD’s custodian, HSBC, was forced to use the Bank of England as a sub-custodian suggests a serious lack of available bullion in LBMA member vaults. To explore this issue, Table 1 below shows the notional bullion position in London, confirming the lack of free float.

While admittedly simplistic, these figures show that there is no liquidity in London. According to the World Gold Council, total ETF physical holdings at end-April were 3,364 tonnes, of which, according to Paul Mylchreest’s Hardman report[vi], over 70% is vaulted in London, or 2,390 tonnes in Table 1.[vii] To this figure must be added gold privately vaulted by sovereign wealth funds, institutions, family offices and agglomerating businesses on behalf of retail customers. These bullion stocks are held with the vaulting companies (Brinks, G4S, Loomis and Malca-Amit), and are likely to amount to a further 400-500 tonnes.[viii]

Since April, ETF holdings have increased by a further 387 tonnes, of which we will again assume over 70%, 275 tonnes, is stored in London (24 July – source WGC). While there are some guesses concerning underlying changes in these figures since end-April, they could easily result in a negative figure, as Table 1 suggests. Furthermore, if ETF and private demand for bullion escalate further a crisis in London is bound to emerge.

It is here that the Bank of England might have intervened by leaning on its central bank clients to lease some of their earmarked gold – vide the 45.91 tonnes reported to be held for the GLD ETF in April. But there is a further problem: the notional lease rate has been negative since March, which means that a central bank leasing at the market rate has to pay the lessee for the privilege. This suggests that leasing can only occur if market rates are ignored and a fee is paid instead.

It is important to note that under a lease agreement, ownership remains with the lessor. Gold leased through the agency of the Bank of England is unlikely to leave the Bank’s vaults, merely credited through book-entries to lessees. Therefore, for the lessor there is no counterparty risk because if the lessee defaults, the Bank of England merely reallocates the bullion back to the lessor. But in a wider bullion crisis, the double counting of bullion “ownership” through leasing will be exposed, the liabilities falling entirely on the bullion banks. Holders of the GLD ETF should seek confirmation that none of its gold in the Bank’s vaults is so leased.

The alternative to central banks providing liquidity is unthinkable: that bullion banks obtain their liquidity by illegally using bullion held in their custody. Unfortunately, suspicions are compounded by the LBMA’s secrecy over market operations, only releasing selected information when it is no longer relevant. The LBMA’s press releases are also misleading; headlining total gold vaulted in London creates the impression of physical liquidity, which is patently untrue.

For their wealthier customers, bullion banks offer gold accounts in two forms: allocated and unallocated. They are discouraged from opening an allocated account, through expensive fees, notionally covering the vaulting and insurance of physical metal and administrative costs. The real reason is that banks prefer their customers to open unallocated accounts, encouraging them with minimal fees, because these can be fractionally reserved if they are reserved at all. In other words, a bullion bank can hold enough just enough gold to cover the random demands for withdrawals. But as Table 1 above demonstrates, not even that physical liquidity now exists.

While physical settlement involving allocated gold accounts obviously does occur, it is unallocated accounts settling through the AURUM electronic settlement system which accounts for almost all day to day London trade settlements. AURUM is the means of settlement between members of the LBMA through the London Precious Metal Clearing Limited. Transactions for settlement in unallocated form are funnelled through one of the five members who net them down into a single settlement through AURUM. The five members of LPMCL (JPMorgan, UBS, HSBC, ICBC Standard Bank and Scotiabank) all have unallocated accounts with each other, and the settlements determined by AURUM are for currency on one side and unallocated bullion on the other.[ix]

Therefore, the massive quantities of gold being settled are divorced from physical settlement, and amount to nearly all the BIS derivative estimate quoted above of $512bn in positions outstanding at the end of last year. But depositors with unallocated gold accounts undoubtedly believe they have exposure to the gold price, otherwise they would insist at the least on their accounts being allocated with their bullion bank acting as custodian. As the current crisis in paper markets evolves, loss of faith in the ability of bullion banks to settle unallocated accounts in gold will risk generating a run on these accounts and a rush to secure physical gold before prices rise further.

While the authorities in America will do everything to avoid a gold and silver crisis on Comex, any thought that it can be buried behind closed doors in London is fanciful. The same bullion banks trade both markets. A crisis in the bullion banks threatens to leave at the last count about $500bn of unallocated gold accounts in London plus a further 262,796 Comex contracts ($53bn at $2,030 – see Figure 2 above) swinging in the wind. The expansion of paper gold since the early 1980s which has put a lid on the gold price is coming to its end, and the removal of this obstacle will only serve to push the price significantly higher.

Conclusion

We appear to be witnessing the early stages of a breakdown in the paper gold markets on Comex and in London, brought forward by central banks committed to accelerating their inflationary policies in an act of macroeconomic desperation to save their government finances and their economies. The method employed is a dead ringer for an earlier experiment in France exactly three hundred years ago when John Law’s Mississippi bubble imploded, destroying his currency, the livre.

If you bind the fate of financial assets to that of your fiat currency, as John Law did, and which is now the policy of the Federal Reserve, when the bubble pops the currency goes pop as well. This outcome is so obvious that the smart money is now getting out of fiat and into physical gold and silver, as witnessed through deliveries on Comex active contract expiries and the disappearance of all physical liquidity in London.

This being the case, a gathering stampede out of paper currencies and derivative contracts into physical bullion has just started. Unless it is somehow stopped, it will destroy paper markets and with them the banks that have benefitted from them over the last forty years. The acceleration in the destruction of fiat money will gather pace in the next few months, and anyone who spouts macroeconomic nonsense instead of acting in the face of these developments will end up with nothing.

end

iii) Other physical stories:

Why we must own gold now:

(Von Greyerz)

Von Greyerz: The Nightmare Scenario For The World

Authored by Egon von Greyerz via GoldSwitzerland.com,

“Gold has no role in portfolio of wealthy clients” said the chief investment officer of Goldman Sachs’ private wealth management in the week that gold in US dollars went up by over $100 and made a new high of $1,984.

Many found this statement puzzling as another Goldman department previously has told clients not to sell anything gold.

The CIO went on to say: “Our view is that gold is only appropriate if you have a very strong view that the US dollar is going to be rebased. We don’t have that view.”

THE IMPLODING DOLLAR

So here we have a dollar that has lost 85% against gold in this century and 40% since 2018. How can the CIO of the mighty GS say that the dollar is not being rebased. History certainly tells us that she is not telling the truth. Or does she believe that the dollar won’t go down in coming years. As CIO she can clearly see what everyone is seeing namely that the prospects for the dollar are doomed with what is happening in the US economy causing surging deficits and unlimited money printing.

The truth clearly lies elsewhere. No asset manager is interested in protecting their clients’ assets by investing in the ultimate form of wealth preservation which of course is physical gold. The reason is very simple. Goldman’s private wealth management like all other asset managers are not interested in holding physical gold for their clients for the simple reason that the bank can’t earn sufficient revenue on just holding client gold. Instead they want to put expensive proprietary products and their own managed funds into client portfolios and also buy and sell shares regularly to churn commissions.

No bank, managing client portfolios, tells their clients that in the last 20 years gold has outperformed all major asset classes including stocks. The Dow for example has lost 70% against gold since 1999 (excluding dividends).