GOLD:$1938.70 DOWN $34.00 The quote is London spot price

Silver:$27.22 DOWN $1.04 London spot price ( cash market)

DONATE

Closing access prices: London spot

i)Gold : $1942.60 LONDON SPOT 4:30 pm

ii)SILVER: $27.44//LONDON SPOT 4:30 pm

CLOSING FUTURES PRICES: KEY MONTHS

SEPT GOLD: $XXX CLOSE 1::30 PM SPREAD SPOT/FUTURE XXX//) //

OCT GOLD: $1937.50 CLOSE 1.30 PM// SPREAD SPOT/FUTURE OCT /: : $1.20//BACKWARD//

DEC. GOLD $1945.00 CLOSE 1.30 PM SPREAD SPOT/FUTURE DEC $6.30/ CONTANGO ($5.70 BELOW NORMAL CONTANGO)

CLOSING SILVER FUTURE MONTH

SILVER SEPT COMEX CLOSE; $27.25…1:30 PM.//SPREAD SPOT/FUTURE SEPT// : ( 3 cents contango//0 CENTS ABOVE NORMAL contango)

SILVER DECEMBER CLOSE: $27.76 1:30 PM SPREAD SPOT/FUTURE DEC. : 54 CENTS PER OZ CONTANGO ( 40 CENTS ABOVE NORMAL CONTANGO)

COMEX DATA

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

receiving today: 0/18

issued 0

EXCHANGE: COMEX

CONTRACT: SEPTEMBER 2020 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,968.200000000 USD

INTENT DATE: 09/01/2020 DELIVERY DATE: 09/03/2020

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

624 C BOFA SECURITIES 1 2

657 C MORGAN STANLEY 2 2

657 H MORGAN STANLEY 5

709 C BARCLAYS 8

709 H BARCLAYS 1

737 C ADVANTAGE 3

800 C MAREX SPEC 6

905 C ADM 6

____________________________________________________________________________________________

TOTAL: 18 18

MONTH TO DATE: 2,233

NUMBER OF NOTICES FILED TODAY FOR AUGUST CONTRACT: 18 NOTICE(S) FOR 1800 OZ (0.0559 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 2233 NOTICES FOR 223300 OZ (6.9455 tonnes)

SILVER

470 NOTICE(S) FILED TODAY FOR 2,350,000 OZ/

total number of notices filed so far this month: 7723 for 38.615 MILLION oz

BITCOIN MORNING QUOTE $11,328 UP 517

BITCOIN AFTERNOON QUOTE.: $11,351 UP 569

GLD AND SLV INVENTORIES:

WITH GOLD DOWN $34.00 AND NO PHYSICAL TO BE FOUND ANYWHERE:

WITH ALL REFINERS CLOSED//MEXICO ORDERING ALL MINES SHUT: WHERE ARE THEY GETTING THE “PHYSICAL?

GLD: 1,250.04 TONNES OF GOLD//

WITH SILVER DOWN $1.04 TODAY: AND WITH NO SILVER AROUND:

A HUGE CHANGE IN INVENTORY AT THE SLV/// A WITHDRAWAL OF 2.365 MILLION OZ FROM THE SLV

RESTING SLV INVENTORY TONIGHT:

SLV: 571.688 MILLION OZ./

XXXXXXXXXXXXXXXXXXXXXXXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI ROSE BY A STRONG SIZED 906 CONTRACTS FROM 165,543 DOWN TO 166,449, AND CLOSER TO OUR NEW RECORD OF 244,710, (FEB 25/2020. THE GAIN IN OI OCCURRED WITH OUR 9 CENT RISE IN SILVER PRICING AT THE COMEX. IT SEEMS THAT THE GAIN IN COMEX OI IS DUE TO ATTEMPTED BANKER SILVER SHORT COVERING.. COUPLED AGAINST A STRONG EXCHANGE FOR PHYSICAL ISSUANCE, ZERO LONG LIQUIDATION, A GOOD GAIN IN SILVER OZ STANDING AT THE COMEX FOR SEPT.. WE HAD A CONSIDERABLE NET GAIN IN OUR TWO EXCHANGES OF 2571 CONTRACTS (SEE CALCULATIONS BELOW).

WE HAVE ALSO WITNESSED A STRONG AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: SEP 0; DEC: 1665, MARCH 0 FOR ZERO ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 1655 CONTRACTS. WITH THE TRANSFER OF 1655 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1655 EFP CONTRACTS TRANSLATES INTO 8.325 MILLION OZ ACCOMPANYING:

1.THE 9 CENT RISE IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

10.025 MILLION OZ INITIAL STANDING IN AUGUST.

43.030 MILLION OZ INITIALLY STANDING IN SEPT. (HUGE)

7.32 MILLION OZ INITIALLY STANDING IN OCT

2.630 MILLION OZ STANDING FOR NOV.

20.970 MILLION OZ FINAL STANDING IN DEC

5.075 MILLION OZ FINAL STANDING IN JAN

1.480 MILLION OZ FINAL STANDING IN FEB

23.005 MILLION OZ FINAL STANDING FOR MAR

4.660 MILLION OZ FINAL STANDING FOR APRIL

45.220 MILLION OZ FINAL STANDING FOR MAY

2.205 MILLION OF FINAL STANDING FOR JUNE

86.470 MILLION OZ FINAL STANDING IN JULY.

6.475 MILLION OZ FINAL STANDING IN AUGUST

52.6400 MILLION OZ INITIALLY STANDING IN SEPT

TUESDAY, AGAIN OUR CROOKS USED COPIOUS PAPER IN ORDER TO LIQUIDATE SILVER’S PRICE…AND THEY WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE 9 CENTS) ).. AND, OUR OFFICIAL SECTOR/BANKERS WERE BASICALLY UNSUCCESSFUL IN THEIR ATTEMPT TO FLEECE ANY SILVER LONGS FROM THEIR POSITIONS AS FEAR STRUCK AS BANKERS AS THE RATS ARE STARTING TO FLEE A SINKING SHIP. WE ALSO HAD ii) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS 2) A GOOD GAIN IN SILVER OZ STANDING FOR SEPTEMBER, AND 3) ZERO LONG LIQUIDATION. YOU CAN BET THE FARM THAT OUR BANKERS ARE DESPERATE TO LIQUIDATE THEIR HUGE SHORT POSITIONS IN SILVER..

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS

SEPT.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY /FOR MONTH OF SEPT:

2854 CONTRACTS (FOR 2 TRADING DAY(S) TOTAL 2854 CONTRACTS) OR 14.270 MILLION OZ: (AVERAGE PER DAY: 1427 CONTRACTS OR 7.135 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF AUGUST: 14.270 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 0.849% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2020 TO DATE SILVER EFP’S: 1,400.355 MILLION OZ.

JANUARY 2020 EFP TOTALS SO FAR: 181.61 MILLION OZ

FEB 2020 EFP’S TOTAL : …… 259.600 MILLION OZ

MARCH EFP’S ….. 452.280 MILLION OZ //TOTALS//AND A NEW RECORD FOR THE MONTH)

APRIL EFP 95.355 MILLION OZ. (EX. FOR PHYSICALS BECOMING A LOT LESS)

MAY EFP FINAL: 77.27 MILLION OZ

JUNE EFP 71.15 MILLION OZ.

JULY EFP 133.95 MILLION OZ/ (EXCHANGE FOR PHYSICALS STARTING TO RISE EXPONENTIALLY AGAIN)

AUGUST EFP 127.46 MILLION OZ (EXCHANGE FOR PHYSICALS STARTING TO DECREASE AGAIN)

SEPT EFP 14.270 MILLION OZ

RESULT: WE HAD A STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 906, WITH OUR 9 CENT RISE IN SILVER PRICING AT THE COMEX ///TUESDAY AS ONE A NET BASIS, NOBODY REALLY LEFT THE SILVER ARENA.…THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 1655 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER

TODAY WE GAINED A STRONG SIZED 2571 OI CONTRACTS ON THE TWO EXCHANGES (WITH OUR 9 CENT GAIN IN PRICE)//

THE TALLY//EXCHANGE FOR PHYSICALS

i.e 1655 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH A CONSIDERABLE SIZED INCREASE OF 906 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH OUR 9 CENT RISE IN PRICE OF SILVER/AND A CLOSING PRICE OF $28.38 // TUESDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY.

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.843 BILLION OZ TO BE EXACT or 120% of annual global silver production (ex Russia & ex China).

FOR THE NEW AUGUST DELIVERY MONTH/ THEY FILED AT THE COMEX: 470 NOTICE(S) FOR 2,350,000 OZ OF SILVER.

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.70//TODAY’S RECORD OF 244,705 WAS SET WITH A PRICE OF: 18.91 (FEB 25/2020)

.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ; AUGUST 10.025 MILLION OZ/ SEPT 43.030 MILLION OZ//OCT: 7.665 MILLION OZ// NOV: 2.630 MILLION OZ//DEC: 20.970 MILLION OZ; JAN: 5.075 MILLION OZ.//FEB 1.480 MILLION OZ//MAR: 23.005 MILLION OZ/APRIL 4.660 MILLION OZ//MAY 45.220 MILLION OZ//JUNE: 2.205 MILLION OZ// JULY 86.470 million oz//AUGUST 6.475 MILLION OZ//SEPT. 52.640 MILLION OZ//

- THE RECORD PRIOR TO TODAY WAS SET IN FEB 25/2018: 244,710 CONTRACTS, WITH A SILVER PRICE OF $18.90//.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017 RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

GOLD

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A FAIR SIZED 3698 CONTRACTS TO 547,704 AND CLOSER TO OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE FAIR SIZED GAIN IN COMEX OI OCCURRED WITH OUR GOOD RISE IN PRICE OF $7.10 /// COMEX GOLD TRADING// TUESDAY//WE HAD ATTEMPTED BANKER SHORT COVERING, A STRONG ADVANCE IN STANDING AT THE GOLD COMEX FOR SEPT, ALONG WITH ZERO LONG LIQUIDATION ACCOMPANYING A SMALL EXCHANGE FOR PHYSICAL ISSUANCE. THIS ALL HAPPENED WITH OUR GOOD GAIN IN PRICE OF $7.10.

WE HAD A VOLUME OF 0 4 -GC CONTRACTS//OPEN INTEREST 134// (2400 OZ WAS DELIVERED ON FRIDAY FROM THE ENHANCED GOLD INVENTORY)…

WE GAINED A GOOD SIZED 5086 CONTRACTS (15.82 TONNES) ON OUR TWO EXCHANGES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A SMALL SIZED 1388 CONTRACTS:

CONTRACT .; AUG 0 AND OCT: 0 DEC: 1388; JUNE: 0 ALL OTHER MONTHS ZERO//TOTAL: 1388. The NEW COMEX OI for the gold complex rests at 547.704. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EXCHANGE DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 5086 CONTRACTS: 3698 CONTRACTS INCREASED AT THE COMEX AND 1688 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 5086 CONTRACTS OR 15.82 TONNES. TUESDAY, WE HAD A GOOD GAIN OF $7.10 IN GOLD TRADING……

AND WITH THAT GAIN IN PRICE, WE HAD A GOOD SIZED GAIN IN TOTAL/TWO EXCHANGES GOLD TONNAGE OF 15.82 TONNES!!!!!! THE BANKERS WERE UNSUCCESSFUL IN THEIR ATTEMPT TO LOWER GOLD’S PRICE (IT ROSE $7.10). WE HAD ATTEMPTED BANKER SHORT COVERING OPERATION WITH SMALL ISSUANCE IN EXCHANGES FOR PHYSICAL. THEY BANKERS COULD NOT FLEECE ANY OF OUR SPECULATOR LONGS.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES:

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1388) ACCOMPANYING THE FAIR SIZED GAIN IN COMEX OI (3698 OI): TOTAL GAIN IN THE TWO EXCHANGES: 5086 CONTRACTS. WE NO DOUBT HAD 1 )ATTEMPTED BANKER SHORT COVERING ,2.)A STRONG ADVANCE IN STANDING AT THE GOLD COMEX FOR THE FRONT SEPT. MONTH, 3) ZERO NET LONG LIQUIDATION; 4) FAIR COMEX OI GAIN AND 5) SMALL ISSUANCE OF EXCHANGE FOR PHYSICAL AND …ALL OF THIS WAS COUPLED WITH OUR GOOD GAIN IN GOLD PRICE TRADING//TUESDAY//$7.10.

WE ARE BEGINNING TO WITNESS A LACK OF EXCHANGE FOR GOLD PHYSICALS UNDERWRITTEN DUE TO PREMIUMS STARTING TO REAPPEAR IN THE FUTURE PRICE OF GOLD VS LONDON SPOT. THE COST TO THE BANKERS IS JUST TOO GREAT TO ENGAGE IN THESE VEHICLES ONCE THIS OCCURS.

THE FACT THAT WE ARE CONTINUALLY SEEING A DROP IN COMEX OPEN INTEREST AND VOLUMES COUPLED WITH LESS EXCHANGE FOR PHYSICALS PROBABLY MEANS THAT OUR LONGS ARE ALREADY DEPARTING NEW YORK FOR THE NEW PHYSICAL PLATFORM AT LONDON’S LME.

EXCHANGE FOR PHYSICALS//OUTLINE

SPREADING OPERATIONS/NOW SWITCHING TO GOLD (WE SWITCH OVER TO SILVER ON OCT 1)

OUR SPREADING OPERATION HAS NOW SWITCHED INTO GOLD…..

SPREADING OPERATION FOR OUR NEWCOMERS:

FOR NEWCOMERS, HERE ARE THE DETAILS:

SPREADING LIQUIDATION HAS NOW COMMENCED IN GOLD AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF OCT.

FOR THOSE OF YOU WHO ARE NEW, HERE IS THE MODUS OPERANDI OF THE SPREADERS AND THE CRIMINAL ELEMENT BEHIND IT:

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR;

THE SPREADING LIQUIDATION OPERATION IS NOW OVER FOR SILVER..AND WE WILL NOW MORPH INTO AN ACCUMULATION PHASE OF SPREADING CONTRACTS FOR GOLD. THEY WILL ACCUMULATE CONSIDERABLE AMOUNT OF THE CONTRACTS AND THEN LIQUIDATE ONE WEEK PRIOR TO FIRST DAY NOTICE

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO GOLD AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF SEPT. HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF OCT FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE IN THIS NON ACTIVE MONTH OF SEPT. BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN GOLD WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2020 INCLUDING TODAY

SEPT.

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 2 TRADING DAY(S) IN TONNES: 7.054 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2019, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 7.054/3550 x 100% TONNES =0.19% OF GLOBAL ANNUAL PRODUCTION

ISSUANCE OF EXCHANGE FOR PHYSICAL GOLD HAS DISSIPATED THIS MONTH…THE COST TO THE BANKERS TO CARRY THESE CONTRACTS IN LONDON IS BECOMING TOO GREAT FOR THEM.

ACCUMULATION OF GOLD EFP’S YEAR 2020 TO DATE: 3,417.87 TONNES

JANUARY 2220 TOTAL EFP ISSUANCE; : 570.19 TONNES

FEB 2020 TOTAL EFP ISSUANCE : 653.78 TONNES

MARCH TOTAL EFP ISSUANCE 1,098.93 TONNES (*AND A NEW ALL TIME RECORD ISSUANCE//22 DAYS)

APRIL TOTAL EFP. ISSUANCE: 243.45 TONNES (EFP ISSUANCE BECOMING A LOT LESS)

MAY TOTAL EFP ISSUANCE: 248.68 TONNES (EFP ISSUANCE STILL LOW// PREMIUM COST TO THE BANKERS IS HUGE..SO ISSUANCE IS LESS)

JUNE TOTAL EFP ISSUANCE: 192.06 TONNES

JULY TOTAL EFP ISSUANCE; 313.09 TONNES ..(EXCHANGE FOR PHYSICALS REVERSE COURSE AND ARE NOW INCREASING!)

AUGUST TOTAL EFP ISSUANCE; 150.78 TONNES FINAL (AGAIN: RETREATING IN NUMBERS)

SEPT TOTAL EFP ISSUANCE: 7.054 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A STRONG SIZED 906 CONTRACTS FROM 165,543, UP TO 166,449 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 2 3/4 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.

THE CONSIDERABLE SIZED GAIN IN OI SILVER COMEX WAS PRIMARILY DUE TO; 1) ATTEMPTED BANKER SHORT COVERING , 2) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS (SEE BELOW), 3) A GOOD GAIN IN STANDING FOR SILVER AT THE COMEX FOR SEPT., AND 4) ZERO LONG LIQUIDATION,

EFP ISSUANCE 1665 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT: 0 AND DEC. 1655 AND MARCH: 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1655 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 906 CONTRACTS TO THE 1655 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A STRONG SIZED GAIN OF 2612 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 12.860 MILLION OZ, OCCURRED WITH OUR GOOD 9 CENT GAIN IN PRICE///

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL..THE EVIDENCE IS CLEAR: HUGE AMOUNTS OF PHYSICAL STANDING FOR BOTH SILVER AND GOLD .

(report Harvey)

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED DOWN 5.60 POINTS OR 0.17% //Hang Sang CLOSED DOWN 64.76 POINTS OR 0.26% /The Nikkei closed UP 109.08 POINTS OR 0.47%//Australia’s all ordinaires CLOSED UP 1.77%

/Chinese yuan (ONSHORE) closed UP at 6.8260 /Oil UP TO 43.00 dollars per barrel for WTI and 45.91 for Brent. Stocks in Europe OPENED GREEN// ONSHORE YUAN CLOSED UP // LAST AT 6.8260 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.8269 TRADE TALKS STALL////TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED/CORONAVIRUS PANDEMIC : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

total withdrawals; 146,331.745 oz

lots of gold starting to leave the comex (4.5 tonnes)

We had 1 kilobar transactions +

ADJUSTMENTS: 0 //

The front month of SEPT registered a total of 942 contracts for a loss of 240 contracts. We had 287 notices filed on Tuesday, so we gained 37 contracts or an additional 3,700 oz will stand for delivery in this non active month of Sept.

Oct LOST 398 contracts DOWN to 62,438. November gained 2 contracts to stand at 3.

The big December contract GAINED 3428 contracts UP to 406,202 contracts…

We had 18 notices filed today for 1800 oz

To calculate the INITIAL total number of gold ounces standing for the SEPT /2020. contract month, we take the total number of notices filed so far for the month (2233) x 100 oz , to which we add the difference between the open interest for the front month of SEPT (942 CONTRACTS ) minus the number of notices served upon today (18 x 100 oz per contract) equals 315,700 OZ OR 9.819 TONNES) the number of ounces standing in this active month of JUNE

thus the INITIAL standings for gold for the SEPT/2020 contract month:

No of notices filed so far (2233, x 100 oz + (942 OI) for the front month minus the number of notices served upon today (18) x 100 oz which equals 315,700 oz standing OR 9.819TONNES in this active delivery month. This is a HUGE amount for gold standing for a SEPT delivery month (a NON active delivery month).

we gained 37 contracts or an additional 3700 oz will try their luck searching for metal on this side of the pond.

THE NAME OF THE GAME TODAY IS BANKER SHORT COVERING AS FINALLY FEAR BECAME THEIR CENTRAL FOCUS. YOU CAN VISUALIZE THIS LAST NIGHT AND TODAY WITH GOLD’S STRONG ADVANCE IN TUESDAY’S COMEX. TODAY ATTEMPTED BANKER SHORT COVERING WHICH FAILED WITH THE HIGHER PRICES.

NEW PLEDGED GOLD: BRINKS

144,088.952 oz NOW PLEDGED JAN 21.2020/HSBC 5.4807 TONNES

42,548.308.00 PLEDGED APRIL 3/2020: SCOTIA: 1.3234 tonnes

deleted Int. Delaware pledge July 7 (600 tonnes)

261,955.892 oz (some deleted august 3) JPM 8.1479 TONNES

611,401.341 oz pledged June 12/2020 Brinks/ july 2/july 21 19.017 tonnes

51,084.609 oz Pledged August 21/regular account 1.588 tonnes jpm

total pledged gold: 1,109916.036 oz 34.52 tonnes

total registered, pledged and eligible (customer) gold; 37,062,434.425 oz 1,152.79 tonnes (INCLUDES 4 GC GOLD)

total 4 GC gold: 126.34 tonnes

total gold net of 4 GC: 1026,45 tonnes

end

I have compiled data with respect to registered (or dealer) gold taken on first day notice for each of the past 24 months

The data begins on first day notice for the May month taken on the last day of July 2018. and it continues to present day.

I then took, how many deliveries were recorded by the CME for each and every month. I also included for reference the price of gold on first day notice.

The first graph is a logarithmic graph and the second graph, linear.

You can see the huge explosion of registered gold at the comex along with deliveries.

THE GOLD COMEX SEEMS TO BE UNDER SEVERE ASSAULT FOR PHYSICAL

END

And now for the wild silver comex results

INITIAL STANDINGS

SEPT. SILVER COMEX CONTRACT MONTH//INITIAL STANDINGS

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory |

243,510.921 oz

Brinks

Delaware

|

| Deposits to the Dealer Inventory |

295,241.320 oz

Brinks

Scotia

|

| Deposits to the Customer Inventory |

2,308,238.296 oz

CNT

Delaware

JPMorgan

Scotia

|

| No of oz served today (contracts) |

479

CONTRACT(S)

(2,350,000 OZ)

|

| No of oz to be served (notices) |

2806 contracts

14,030,000 oz)

|

| Total monthly oz silver served (contracts) | 7723 contracts

38,615,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

total dealer deposits: 295,241.320 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

we had 4 deposits into the customer account

i)into JPMorgan: nil

ii) Into CNT: 601,004.57 oz

iii) into Delaware: 248,495.326 oz

iv) Into JPMorgan: 1,160,569.900 oz

v) Into Scotia: 2927.320 oz

*** JPMorgan for most of 2017, 2018 and onward, has adding to its inventory almost every single day.

JPMorgan now has 167.320 million oz of total silver inventory or 48.42% of all official comex silver. (167.320 million/345.468 million

total customer deposits today: 2,308,238.296 oz

we had 2 withdrawals:

i) Out of Delaware; 4971.171 oz

ii) Out of Brinks: 238,539.750 oz

total withdrawals; 243,510.921 oz

We had 0 adjustments

Total dealer(registered) silver: 139.890 million oz

total registered and eligible silver: 347.533 million oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

the front month of SEPTEMBER registered an open interest of 3285 contracts thus losing 693 contracts. We had 708 notices filed on Monday so we GAINED A GOOD 15 contracts or an additional 75,000 oz will stand in this active delivery month of September as they morphed into London based forwards and received a fiat bonus for their efforts. However this time our London boys are ready to exercise these EFP’s and they will turn them into real physical metal as we now have a full frontal attack on both of our two precious metals.

Oct saw another GAIN of 1 contract to stand at 695.November gained 12 contract to stand at 14,

The big December contract month saw its OI rise by good 1569 contracts up to 145,603

The total number of notices filed today for the SEPT 2020. contract month is represented by 470 contract(s) FOR 2,350,000, oz

To calculate the number of silver ounces that will stand for delivery in SEPT we take the total number of notices filed for the month so far at 7723 x 5,000 oz = 38,615,000 oz to which we add the difference between the open interest for the front month of SEPT(3261) and the number of notices served upon today 470 x (5000 oz) equals the number of ounces standing.

Thus the INITIAL standings for silver for the SEPT/2019 contract month: 7723 (notices served so far) x 5000 oz + OI for front month of AUGUST (3285)- number of notices served upon today (470) x 5000 oz of silver standing for the SEPT contract month.equals 52,645,000 oz. ..VERY STRONG FOR AN ACTIVE MONTH.

We GAINED 15 contracts or AN ADDITIONAL 75,000 oz. WILL STAND FOR DELIVERY IN THIS ACTIVE DELIVERY MONTH.

TODAY’S ESTIMATED SILVER VOLUME : 126,806 CONTRACTS // volume huge//raid orchestrated by the BIS

FOR YESTERDAY: 121,269. ,CONFIRMED VOLUME//volume huge

YESTERDAY’S CONFIRMED VOLUME OF 121,269 CONTRACTS EQUATES to 0.606 billion OZ 86.6% OF ANNUAL GLOBAL PRODUCTION OF SILVER..

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO- 2.67% ((SEPT 2/2020)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -0.60% to NAV: (SEPT 2/2020 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into NEGATIVE/2.67%

(courtesy Sprott/GATA

3. SPROTT CEF .A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 20.51 TRADING 20.12///NEGATIVE 2.18

END

And now the Gold inventory at the GLD/

SEPT 2/WITH GOLD DOWN $34.00 TODAY, WE HAVE 2 SMALL CHANGES IN GOLD INVENTORY AT THE GLD: 2 WITHDRAWALS OF .87 TONNES AND.59 TONNES FROM THE GLD////INVENTORY RESTS AT 1250.04 TONNES

SEPT 1/WITH GOLD UP $7.10 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1251.50TONNES

AUGUST 31//WITH GOLD UP $5.90 TODAY/WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD..//INVENTORY RESTS AT 1251.50 TONNES/

AUGUST 28/WITH GOLD UP $38.20 TODAY, WE SURPRISINGLY HAD A .59 TONNE WITHDRAWAL//INVENTORY RESTS AT 1251.50 TONNES

AUGUST 27/WITH GOLD DOWN 17.50 TODAY: WE HAD A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 3.24 TONNES INTO THE GLD//INVENTORY REST AT 1252.09 TONNES

AUGUST 26/WITH GOLD UP $26.70 TODAY/ WE HAD A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.53 TONNES FROM THE GLD//RESTS AT 1248.85 TONNES

AUGUST 25/WITH GOLD DOWN $14.60 TODAY, WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD//RESTS AT 1252.38 TONNES

AUGUST 24//WITH GOLD DOWN $7.20 TODAY: WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD: /INVENTORY RESTS AT 1258.38 TONNES

AUGUST 21//WITH GOLD DOWN $.40 TODAY: WE HAD NO CHANGE IN GOLD INVENTORY AT THE GLD: /INVENTORY RESTS AT 1252.38 TONNES

AUGUST 20/WITH GOLD DOWN $23.45 TODAY: WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD: .//INVENTORY REST AT 1252.38 TONNES

AUGUST 19//WITH GOLD DOWN $39.65 TODAY: WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1252.38 TONNES

AUGUST 18/WITH GOLD UP $14.60 TODAY: WE HAD A HUGE CHANGE IN GOLD INVENTORY: A DEPOSIT OF 4.09 TONNES//GLD INVENTORY RESTS TONIGHT AT 1252.38 TONNES

AUGUST 17/WITH GOLD UP $46.30 TODAY: SURPRISINGLY WE HAD A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF 3.8 TONNES//INVENTORY RESTS AT 1248.29 TONNES

AUGUST 14/ WITH GOLD DOWN $19.45 TODAY: SURPRISINGLY, WE HAD A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 1.46 TONNES/INVENTORY RESTS AT 1252.63 TONNES.

AUGUST 13/WITH GOLD UP $23.15 TODAY: WE HAD A HUGE CHANGE IN GOLD INVENTORY: SURPRISINGLY A PAPER WITHDRAWAL OF 7.30 TONNES/INVENTORY RESTS AT 1250.63 TONNES

AUGUST 12/ WITH GOLD UP $1.00 TODAY: WE HAD A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF 4.19 TONNES//INVENTORY RESTS AT 1257.93 TONNES

AUGUST 11//WITH GOLD DOWN $92.40 TODAY, WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1262.12 TONNES.

AUGUST 10/WITH GOLD UP $11.35 TODAY, WE HAD A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.84 TONNES//INVENTORY RESTS AT 1262.12 TONNES

AUGUST 7/WITH GOLD DOWN $38.30 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1267.96 TONNES

AUGUST 6/WITH GOLD UP $20.45 TODAY, WE HAVE ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A PAPER DEPOSIT OF 10.23 TONNES INTO THE GLD/INVENTORY RESTS AT 1267.96 TONNES//

AUGUST 5/WITH GOLD UP $ 33.75 TODAY, WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD/A DEPOSIT OF 9.35 TONNES INTO THE GLD//INVENTORY RESTS AT 1257.73 TONNES

AUGUST 4//WITH GOLD UP $31.75 TODAY, WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 6.48 TONNES/GLD INVENTORY RESTS AT 1248.38 TONNES

AUGUST 3/WITH GOLD UP $2.20 TODAY, WE HAVE NO CHANGES IN THE GOLD INVENTORY AT THE GLD////INVENTORY RESTS AT 1241,96 TONNES

JULY 31/WITH GOLD UP $17.90 TODAY/WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY RESTS AT 1241.96 TONNES.

JULY 30/WITH GOLD DOWN $10.00 TODAY, WE HAVE ANOTHER SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES//INVENTORY RESTS AT 1241.96 TONNES.

JULY 29//WITH GOLD UP $12.45 TODAY, WE HAVE ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A HUGE DEPOSIT OF 8.47 TONNES/INVENTORY RESTS AT 1243.12 TONNES

JULY 28///WITH GOLD UP $13.25 TODAY, WE HAVE ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A HUGE DEPOSIT OF 5.84 TONNES/INVENTORY RESTS AT 1234.65

JULY 27//WITH GOLD UP $35.30 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF XXX TONNES/INVENTORY RESTS AT 1228.81 TONNES

JULY 24/WITH GOLD UP $8.80 TODAY: WE HAVE ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.80 TONNES//INVENTORY RESTS AT 1228.81 TONNES

JULY 23/WITH GOLD UP $24.90 TODAY: WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 7.26 TONNES/INVENTORY RESTS AT 1225.01 TONNES

JULY 22/WITH GOLD UP $22.00 TODAY: WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD/ A DEPOSIT OF 7.89 TONNES/INVENTORY RESTS AT 1219.75 TONNES

JULY 21//WITH GOLD UP $26.00 TODAY, WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.97 TONNES INTO THE GLD// INVENTORY RESTS AT 1211.86 TONNES

JULY 20/WITH GOLD UP $7.70 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1206.89 TONNES

JULY 17/WITH GOLD UP $7.70 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD: /INVENTORY RESTS AT 1206.89 TONNES

JULY 16/WITH GOLD DOWN $9.80 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD: INVENTORY RESTS AT 1206.89 TONNES

JULY 15//WITH GOLD UP $1.55 TODAY/A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 2.96 TONNES INTO THE GLD///INVENTORY RESTS AT 1206.89 TONNES

JULY 14//WITH GOLD DOWN $1.65 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD/A DEPOSIT OF 3.51 TONNES/INVENTORY RESTS AT 1203.97 TONNES

JULY 13//WITH GOLD UP $12.50 TODAY: A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.36 TONNES INTO THE GLD//INVENTORY RESTS AT 1200.46 TONNES

JULY 10/WITH GOLD DOWN $.50 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD//A STRANGE WITHDRAWAL OF 1.75 TONNES FROM THE GLD//INVENTORY RESTS AT 1200.82 TONNES

JULY 9//WITH GOLD DOWN $11.75 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OX 3.21 TONNES INTO THE GLD//INVENTORY RESTS AT 1202.57 TONNES

JULY 8/WITH GOLD UP $13.75 TODAY; A BIG CHANGE IN GOLD INVENTORY AT THE GLD:A DEPOSIT OF 7.89 TONNES INTO THE GLD//INVENTORY RESTS AT 1199.36 TONNES

JULY 7/WITH GOLD UP $12.50 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD: /INVENTORY RESTS AT 1191.47 TONNES

JULY 6/WITH GOLD UP $6.50 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 9.36 TONNES INTO THE GLD//INVENTORY RESTS AT 1191.47 TONNES

JULY 2/WITH GOLD UP $7.00 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.21 TONNES INTO THE GLD////INVENTORY RESTS AT 1182.11 TONNES

JULY 1/WITH GOLD DOWN $12.90//NO CHANGES IN GOLD INVENTORY AT THE GLD: /INVENTORY RESTS AT 1178.90 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Inventory rests tonight at

SEPT 2/ GLD INVENTORY 1250.04 tonnes*

LAST; 894 TRADING DAYS: +310.54 NET TONNES HAVE BEEN ADDED THE GLD

LAST 794 TRADING DAYS://+489.07 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

SEPT 2.WITH SILVER DOWN $1.04 TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.365 MILLION OZ FROM THE SLV///INVENTORY REST AT 571.688 MILLION OZ.

SEPT 1//WITH SILVER UP 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 574.053 MILLION OZ//

AUGUST 31/WITH SILVER UP 80 CENTS TODAY: A HUGE CHANGE IN THE SLV//A DEPOSIT OF 2.982 MILLION OZ ENTERS THE SLV/INVENTORY RESTS AT 574.053 MILLION OZ//

AUGUST 28/WITH SILVER UP 48 CENTS TODAY: A MASSIVE PAPER DEPOSIT OF 4.652 MILLION OZ ENTERS THE SLV//INVENTORY RESTS AT 571.071 MILLION OZ

AUGUST 27/WITH SILVER DOWN 28 CENTS TODAY// NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 566.419 MILLION OZ

AUGUST 26//WITH SILVER UP $1.04 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.65 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 566.419 MILLION OZ..

AUGUST 25/WITH SILVER DOWN 21 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.607 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 571.074 MILLION OZ//

AUGUST 24//WITH SILVER DOWN 18 CENTS TODAY: WE HAD A NO CHANGES//INVENTORY RESTS AT 573.843 MILLION OZ//

AUGUST 21//WITH SILVER DOWN 30 CENTS TODAY: WE HAD A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF.838 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 573.843 MILLION OZ..

AUGUST 20/WITH SILVER DOWN $.26 TODAY: WE HAD A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A WITHDRAWAL OF 3.724 MILLION OZ FROM THE SLV..//INVENTORY REST AT 572.843 MILLION OZ

AUGUST 18/WITH SILVER UP $.44 TODAY: WE HAD A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 2.514 MILLION OZ//THE SLV INVENTORY RESTS TONIGHT AT 576.567 MILLION OZ//

AUGUST 17/WITH SILVER UP $1.27 TODAY: WE HAD NO CHANGES IN SILVER INVENTORY: //INVENTORY RESTS AT 574.053 MILLION OZ//

AUGUST 14/WITH SILVER DOWN $1.31 TODAY, WE HAD A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 6.984 MILLION OZ// //INVENTORY RESTS AT 574.053 MILLION OZ//

AUGUST 13//WITH SILVER UP $1.76 TODAY: WE HAVE TWO HUGE CHANGES IN SILVER INVENTORY AT THE SLV//A PAPER DEPOSIT OF 2.421 MILLION OZ INTO THE SLV AT 2 PM AND ANOTHER DEPOSIT OF 6.984 MILLION OZ AT 5 20 PM/INVENTORY RESTS AT 581.037 MILLION OZ//

AUGUST 12/WITH SILVER DOWN 40 CENTS TODAY: WE HAVE ANOTHER CHANGE IN SILVER INVENTORY AT THE SLV//A WITHDRAWAL OF XX MILLION OZ//INVENTORY RESTS AT XX MILLION OZ/

AUGUST 11/WITH SILVER DOWN $3.25 CENTS, WE HAVE ANOTHER CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 2.41 MILLION OZ//INVENTORY RESTS AT 571.632 MILLION OZ//

AUGUST 10/WITH SILVER UP 1.89 TODAY, WE HAVE ANOTHER HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A WITHDRAWAL OF 3.538 MILLION OZ/INVENTORY RESTS AT 569.491 MILLION OZ//

AUGUST 7/WITH SILVER DOWN 69 CENTS TODAY: WE HAVE ANOTHER HUGE CHANGE IN SILVER INVENTORY: A DEPOSIT OF 0.465 MILLION OZ/INVENTORY RESTS AT 573.029 MILLION OZ.

AUGUST 6/WITH SILVER UP $1.52 TODAY, WE HAVE NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 572.564 MILLION OZ///

AUGUST 5/WITH SILVER UP $1.03 TODAY, WE HAVE A HUGE CHANGE IN SILVER INVENTORY AT THE SLV// A MONSTROUS DEPOSIT OF 5.403 MILLION OZ//INVENTORY RESTS AT 572.564 MILLION OZ//

AUGUST 4/WITH SILVER UP $1.45 TODAY, WE HAVE NO CHANGES IN SILVER INVENTORY: //INVENTORY RESTS AT 367.161 MILLION OZ//

AUGUST 3/WITH SILVER UP 23 CENTS TODAY: WE HAVE A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//SURPRISINGLY ANOTHER WITHDRAWAL OF 0.931 MILLION OZ//INVENTORY RESTS AT 367.161 MILLION OZ//

JULY 31/WITH SILVER UP 82 CENTS TODAY: WE HAVE A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: SURPRISINGLY A HUGE WITHDRAWAL OF 3.26 MILLION OZ//INVENTORY RESTS AT 368.092 MILLION OZ//

JULY 30//WITH SILVER DOWN 97 CENTS TODAY: WE HAVE A SMALL CHANGE IN SILVER INVENTORY: A WITHDRAWAL OF 0.931 MILLION OZ//INVENTORY RESTS AT 571.352 MILLION OZ//

JULY 29/WITH SILVER UP 7 CENTS TODAY, WE HAD A BIG CHANGE IN SILVER INVENTORY//A DEPOSIT OF 5.984 MILLION OZ//INVENTORY RESTS AT 572.283 MILLION OZ//

JULY 28 WITH SILVER DOWN 14 CENTS TODAY, WE HAD A BIG CHANGE IN SILVER INVENTORY: A DEPOSIT OF 7.52 MILLION OZ//INVENTORY RESTS AT 566.299 MILLION OZ//

JULY 27/WITH SILVER UP $2.67 TODAY, WE HAD NO CHANGES IN SILVER INVENTORY: A DEPOSIT OF XX MILLION OZ//INVENTORY RESTS AT 558.779 MILLION OZ//

JULY 24/WITH SILVER DOWN $0.12 TODAY: NO CHANGE IN SILVER INVENTORY//INVENTORY RESTS AT 558.779 MILLION OZ/

JULY 23/WITH SILVER UP $.04 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV// A HUMONGOUS PAPER DEPOSIT OF 9.594 MILLION OZ//INVENTORY RESTS AT 558.779 MILLION OZ///

JULY 22/WITH SILVER UP $1.54 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A HUMONGOUS PAPER DEPOSIT OF 7.218 MILLION OZ//INVENTORY RESTS AT 549.185 MILLION OZ/

JULY 21/WITH SILVER UP $1.38 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A HUMONGOUS PAPER DEPOSIT OF 15.368 MILLION OZ////INVENTORY RESTS AT 541.967 MILLION OZ//

JULY 20/WITH SILVER UP 40 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A MASSIVE PAPER DEPOSIT OF 3.819 MILLION OZ ‘ENTERED” THE SLV..INVENTORY RESTS AT 526.599 MILLION OZ/

JULY 17/WITH SILVER UP 15 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A DEPOSIT OF 1.583 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 522.780 MILLION OZ//

JULY 16//WITH SILVER DOWN 14 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.123 MILLION OZ//INVENTORY RESTS AT 521.197 MILLION OZ..

JULY 15.WITH SILVER UP 21 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.956 MILLION OZ//INVENTORY RESTS AT 516.074 MILLION OZ//

JULY 14/WITH SILVER DOWN 21 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT 514.118 MILLION OZ//

JULY 13//WITH SILVER UP 67 CENTS TODAY: A HUGE CHANGE IN SILVER: A WITHDRAWAL OF 1.677 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 514.118 MILLION OZ//

JULY 10/WITH SILVER UP 7 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 4.844 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 515.795 MILLION OZ

WHAT A FRAUD!!

JULY 9/WITH SILVER DOWN 8 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 8.198 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 510.951 MILLION OZ/

JULY 8/WITH SILVER UP 37 CENTS TODAY//A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.118 MILLION OZ FROM THE SLV//VERY SURPRISING.//INVENTORY RESTS AT 502.753 MILLION OZ//

JULY 7/WITH SILVER UP 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:/INVENTORY RESTS AT 503.871 MILLION OZ///

JULY 6//WITH SILVER UP 24 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.863 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 503.871 MILLION OZ

JULY 2/WITH SILVER UP 4 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//: A DEPOSIT OF 4.01 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 502.008 MILLION OZ

JULY 1/WITH SILVER DOWN 23 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 5.403 MILLION OZ//INVENTORY RESTS AT 498.007 MILLION OZ/

SEPT 2.2020:

SLV INVENTORY RESTS TONIGHT AT

571.688 MILLION OZ

PHYSICAL GOLD/SILVER STORIES

i) GOLDCORE BLOG/Mark O’Byrne

ii) Important gold commentaries courtesy of GATA/Chris Powell

Somewhat better as the B. of E will publish gold holdings with a one month lag instead of 3. It should be one day

(Reuters)

Bank of England to publish gold holdings data with one-month lag, not three

Submitted by cpowell on Wed, 2020-09-02 00:20. Section: Daily Dispatches

By Andy Bruce

Reuters

Tuesday, September 1, 2020

https://www.reuters.com/article/britain-boe-gold/bank-of-england-to-publ…

LONDON — The Bank of England said today it will publish data on gold holdings with a one-month lag to improve transparency.

“Alongside the London Bullion Market Association and other commercial vaults, the Bank of England will now publish gold holding data with a one-month lag,” the central bank said in a statement.

“The reduction from a three-month lag will increase transparency around gold holdings, in line with the Fair and Effective Market Review’s goal to increase transparency in the gold market

END

Our good friends over at Barrick not happy today as they lost a court battle over their big Papula New Guinea gold mine. Buffett also not happy

(Toronto Star)

Barrick reports court loss as battle continues over Papua New Guinea gold mine

Submitted by cpowell on Wed, 2020-09-02 00:28. Section: Essays

From the Canadian Press

via Toronto Star

Tuesday, September 1, 2020

TORONTO — Barrick Gold Corp. says it has suffered further setbacks in its fight with the national government over control of its Porgera Gold Mine in Papua New Guinea.

The operating company that represents the Toronto-based miner and its partners says it lost a court challenge in the country over rights to the gold mine and intends to appeal to the country’s supreme court.

…

It adds it has confirmation from the prime minister that the government has granted a special mining lease for Porgera to Kumul Mineral Holdings Ltd., the national mining company.

… For the remainder of the report:

https://www.thestar.com/business/2020/09/01/barrick-reports-court-loss-a…

* * *

END

Craig Hemke over at Sprott is also catching on that EFP’s are being used less and less

(Craig Hemke/GATA)

Craig Hemke at Sprott Money: Comex (ab)use of gold EFPs has collapsed

Submitted by cpowell on Wed, 2020-09-02 00:42. Section: Daily Dispatches

8:40p ET Tuesday, September 1, 2020

Dear Friend of GATA and Gold:

Use of the strange “exchange for physicals” mechanism to settle gold futures contracts on the New York Commodities Exchange has diminished dramatically this year, the TF Metals Report’s Craig Hemke writes today at Sprott Money.

Hemke writes: “Bank EFP use is down by as much as 75 percent versus years past. This is significant, as it betrays both a lack of physical metal and a lack of counterparty confidence.

…

“This also explains why the spread between spot gold and the front-month futures contract persists. When you lack confidence in your counterparty, what was once perceived as a risk-free arbitrage becomes something quite risky indeed.”

Hemke’s analysis is headlined “Comex EFP (Ab)use Has Collapsed” and it’s posted at Sprott Money here:

https://www.sprottmoney.com/blog/COMEX-EFP-AbUse-Has-Collapsed-Craig-Hem…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.o

END

Stefan Gleason:

Now pension funds are looking to gold to avert disaster

(Stefan Gleason)

Stefan Gleason: Pension funds start looking to gold to avert disaster

Submitted by cpowell on Wed, 2020-09-02 01:38. Section: Daily Dispatches

By Stefan Gleason

Money Metals News Service, Eagle, Idaho

Tuesday, September 1, 2020

Public and private pension plans face a dual crisis.

The first and most obvious threat to pensioners is that defined-benefit vehicles are severely underfunded. By one estimate, pension systems taken as a whole are $638 billion in the red.

…

Some are in better shape financially than others. But all pension plans will have to reckon with a second huge challenge going forward.

Namely, they are already entirely unable to meet their stated return objectives by owning conventional “safe” interest-bearing instruments such as Treasury bonds. …

How can pension funds obtain protection from this threat? They can own gold. …

… For the remainder of the commentary:

https://www.moneymetals.com/news/2020/09/01/pension-funds-look-to-gold-0…

iii) Other physical stories:

We brought this commentary to you yesterday but it is worth repeating

Jan Nieuenhuijs

Former Central Banker: “The World Is Heading Towards A New Monetary System That Incorporates Gold”

Submitted by Jan Nieuwenhuijs of Voima Gold

An interview with Pentti Pikkarainen—former Head of Banking Operations at the central bank of Finland—on the future of the international monetary system.

When it comes to the development of the price of gold, it’s important to know in what direction the international monetary system is evolving. For example, if gold is assigned a greater role in a forthcoming arrangement, not only will the price of gold rise while approaching that arrangement, the price increase will be sustained during that arrangement.

Introduction

According to my analysis the world is heading towards a new monetary system that incorporates gold, although I do not know how that system will be structured. To get a better perspective I decided to interview Pentti Pikkarainen, former Head of Banking Operations at the central bank of Finland, member of the Voima Gold Advisory Board, and Professor of Practice at the University of Oulu in Finland. Pikkarainen thinks we are moving towards a multi-reserve currency system. My interpretation of Pikkarainen’s view is that the dollar will lose its primacy status, and gold, the dollar, euro, yen, pound, renminbi, etc., will be competing each other.

When I thought about this system, I remembered an article I published last January: “Hitting Zero: 700 Years of Declining Global Real Interest Rates.” The article is about an academic study by Paul Schmelzing, who has shown that global real interest rates have been declining for eight centuries, and the trend line was nearly hitting zero in 2018. (Real interest rates are nominal interest rates minus inflation.) The data of the study is displayed in the chart below.

Noteworthy is that since 2018 nominal interest rates in advanced economies have declined, and the Federal Reserve—the most important central bank in the world—disclosed on August 27, 2020, that it will target higher inflation (above 2%). Other central banks will likely follow this policy.

Because of the massive debt overhang, it’s impossible for central banks to raise nominal interest rates. Real interest rates will thus continue to plummet, as the chart above suggests.

A huge factor that drives the gold price is real interest rates. See the chart below. U.S. real rates on 10-year government bonds are shown on the left axis (inversely), and the gold price on the right axis. The lower real rates, the higher the gold price.

Schmelzing was correct in predicting global real rates will continue to fall. He also wrote that real rates “could soon enter permanently negative territory.” In such a scenario gold will be an essential store of value for citizens, and a very popular reserve asset for central banks. Possibly, gold will be sun in a new monetary cosmos.

Having said that, let’s turn to the interview with Pikkarainen.

Heading Towards A Multi-Reserve Currency System

(JN is Jan Nieuwenhuijs, PP is Pentti Pikkarainen.)

JN: Do you think it was a mistake for Europe to launch the euro?

PP: It was a big mistake to start the euro area with a large number of countries. Moreover, the convergence criteria were not strictly applied. The euro was an experiment, and we should have been much more careful. We should have started with a small set of countries, like Germany, France, Austria, Belgium, the Netherlands and Luxembourg. The door should have been closed for other countries for at least 20 years. If the results of the experiment turned out positive, the door could have been opened slowly for new countries. That is, if strict criteria would allow it. The convergence criteria should also include more variables like GDP per capita.

JN: Was the euro launched to break dollar dominance?

PP: That argument is partly true. But, to challenge the dollar the development of the euro had to be a great success, which it is not.

JN: Do you think the current international monetary system is sustainable?

PP: No. I believe that we are moving towards a multi-reserve currency system in which gold, the dollar, the euro and other currencies take part. I am a great fan of the floating exchange rate regime. It usually works well for large and small economies. For many countries a too rigid exchange rate regime is a problem. There are exceptions, like Denmark.

JN: How should central bankers continue monetary policy to get out of the current debt overhang.

PP: The debt overhang is a serious issue. In many countries we need to have debt restructurings both in the private sector and public sector. Elevated inflation is also an option. These considerations are driving the price of gold and will determine gold’s position in a multi-reserve currency system.

Central bankers should take very seriously the risks related to loose monetary policy (like creating bubbles in asset markets, and eliminate incentives to conduct sound economic policies). When we get out of the current situation, we should “start a new regime” in central banking taking into account this aspect. Central banks should keep their main interest rates positive, i.e., higher than zero. Central banks should not go below one per cent. There is no reason to intervene in stock markets. Interventions in bond markets should be very exceptional.

JN: Do you think there is a risk of elevated consumer price inflation like in the 1970s?

PP: During the 1970s the factor behind elevated inflation was the high price of oil, which was translated in goods and services. I do not believe that the price of oil will be the driving factor of inflation during the forthcoming years. Many are concerned about the consequences of very loose monetary policy and the risk of debt monetization. Unfortunately, that risk cannot be excluded.

JN: Do you think it would be sensible or doable that gold would be officially reintroduced in the international monetary system?

PP: I think all “serious” central banks hold gold in their reserves. There is no need to give advice to good central bankers. They know what to do. Other central bankers will follow.

JN: Is the classic gold standard an option in your view?

PP: I do not believe that the classic gold standard is an option. The classic gold standard had many positive features but also some weaknesses.

JN: Do you think the SDR will play a bigger role in international economics going forward? What about international cooperation in general, through for example the IMF?

PP: The SDR reflects the value of a basket of currencies, but it’s not a currency itself. I think currencies of “strong” (large) countries, and gold, will be more successful.

The role of the IMF and the World Bank depend on the role of developing countries in the decision-making bodies of these institutions. We should get rid of the mandates of Europe (IMF) and USA (WB) leading these institutions. Simply, the best candidates should be elected. Europe dominates too much the decision making in the IMF. This is not good even for Europe. The role of developing countries should be enhanced clearly in the decision-making bodies of the IMF and the World Bank.

* * *

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

March 4.2019

Parker City News

JP Morgan faces potential class action lawsuit after guilty pleas by a former metals trader

Traders from across the U.S. are banding together to accuse J. P. Morgan Chase of manipulating precious metals markets for years.

At least six lawsuits, all making similar allegations against the nation‘s largest bank, have been filed in New York federal court in the past month, since federal prosecutors in Connecticut with a former J. P. Morgan Chase metals trader.

The cases could potentially include thousands of people who traded in the precious metals market. The White Plains, N.Y., law firm Lowey Dannenberg is asking the court to combine the cases and name it as the lead.

The law firm‘s commodities group is led by Vincent Briganti, the attorney who filed the first lawsuit on behalf of Dominick Cognata, a New York resident who alleges he suffered losses due to J. P. Morgan‘s trading conduct in the silver and gold futures and options markets.

A combined case, seeking class action status, would include anyone who purchased or sold futures contracts or an option on NYMEX platinum or palladium or COMEX silver or gold between at least Jan. 1, 2009, and Dec. 31, 2015. The lawyers believe that “at least hundreds, if not thousands” of traders would be eligible to join the case.

Named as defendants in all of the lawsuits are John Edmonds, a 36-year old former metals trader at J. P. Morgan, a group of yet-to-be-identified precious metals traders and the bank.

Edmonds, a New York resident, pleaded guilty in October to one count of conspiracy to defraud the market and manipulate prices of precious metals futures contracts and one count of commodities fraud. In the criminal plea, Edmonds admitted that he and other “unnamed co- conspirators” at J. P. Morgan, fraudulently manipulated precious metals markets from 2009 to 2015, the same time frame covered in the class action suits.

Briganti filed the initial class action on Nov. 7, just one day after the Justice Department unsealed Edmonds‘ plea in the U.S. District Court of Connecticut.

Edmonds admitted in his guilty plea that he deployed the illegal trading scheme hundreds of times with the direct knowledge and consent of his immediate supervisors. Plaintiffs say they have suffered economic injury, including monetary losses, as a direct result of actions by Edmonds and the other unnamed J. P. Morgan metals traders in the futures and options contracts.

One of the suits alleges that “the number of unlawful trades that JP Morgan traders executed in precious metals futures markets is at least in the thousands.”

J. P. Morgan declined to comment. Lowey Dannenberg did not respond to a request for comment by CNBC.

The Justice Department‘s criminal investigation is still ongoing and recently caused a separate related civil case to be put on hold for at least six months while the government continues its investigation. That civil lawsuit, which also accuses J. P. Morgan of rigging the precious metals market, was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders.

After reviewing the details of the plea agreement, David Kovel, the attorney for Shak‘s suit, sought to re- interview Edmonds, along with two other current and former senior traders at the bank. However, the government argued that reopening questioning would be detrimental to the ongoing criminal investigation. The federal judge overseeing the proceedings ordered a six-month stay in the civil case.

Kovel declined to comment.

Edmonds was originally scheduled to be sentenced in Hartford, Conn., on Wednesday, Dec. 19, but a court filing on Nov. 27 shows the sentencing has been postponed until June. A spokesman for the U.S. Attorney for Connecticut could not elaborate on why the sentencing was postponed since the court filing is under seal.

-END-

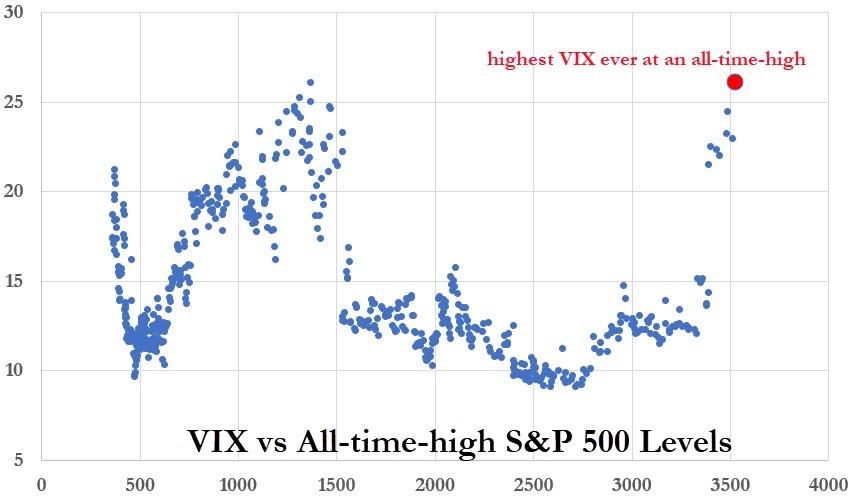

Another Day, Another Record S&P High As Central Banks Fan Biggest Ever Bubble

When rigging and manipulating stocks or markets, one usually allows for the occasional down day to avoid the impression of too much artificiality. But when it comes to the S&P and certainly the Nasdaq, the market (just like its central bank sponsor) is not even thinking about thinking about a dip. And with both Clarida and Brainard repeating this week that no rate hikes are coming any time soon, if ever (see Japan), there is no reason for the party to stop until everything blows and millions of Robinhood Gen-Zers go postal when they lose everything with leverage.

Peter Chatwell, head of multi-asset at Mizuho International, said strong U.S. manufacturers data on Tuesday is combining with dovish commentary from officials including Lael Brainard at the Federal Reserve earlier this week to underpin risk assets. “The central bank easing theme has moved another notch higher,” he said.

But we digress. On Wednesday, S&P futures rose for the ninth time in past ten sessions, hitting a new all time high helped by a seemingly endless rally in tech stocks in general and Apple in particular, as focus turns to economic data that is likely to show a jump in private jobs in August.

The MSCI world equity index rose 0.2%, with Wall Street futures gauges pointed to gains of 0.7%, the ES last seen just around 3,550, up more than 60% from the March lows.

High-flying shares of technology companies, seen as resilient to the hit from the coronavirus outbreak, including Apple, Amazon, Intel, Facebook, AMD, Nvidia and Slack Technologies all rose between 1.3% and 2.4% in high volumes premarket.

While we have extensively discussed the gamma chase in dealer delta as the main reason behind the market meltup (with Bloomberg catching up yesterday), one separate reason why the momentum names keep soaring is because of idiocy like this from Bank of America, which one day after upgrading Apple on multiple expansion, raised its Tesla price target claiming that a higher stock price is bullish, so it expects an even higher stock price (no really, read the note).

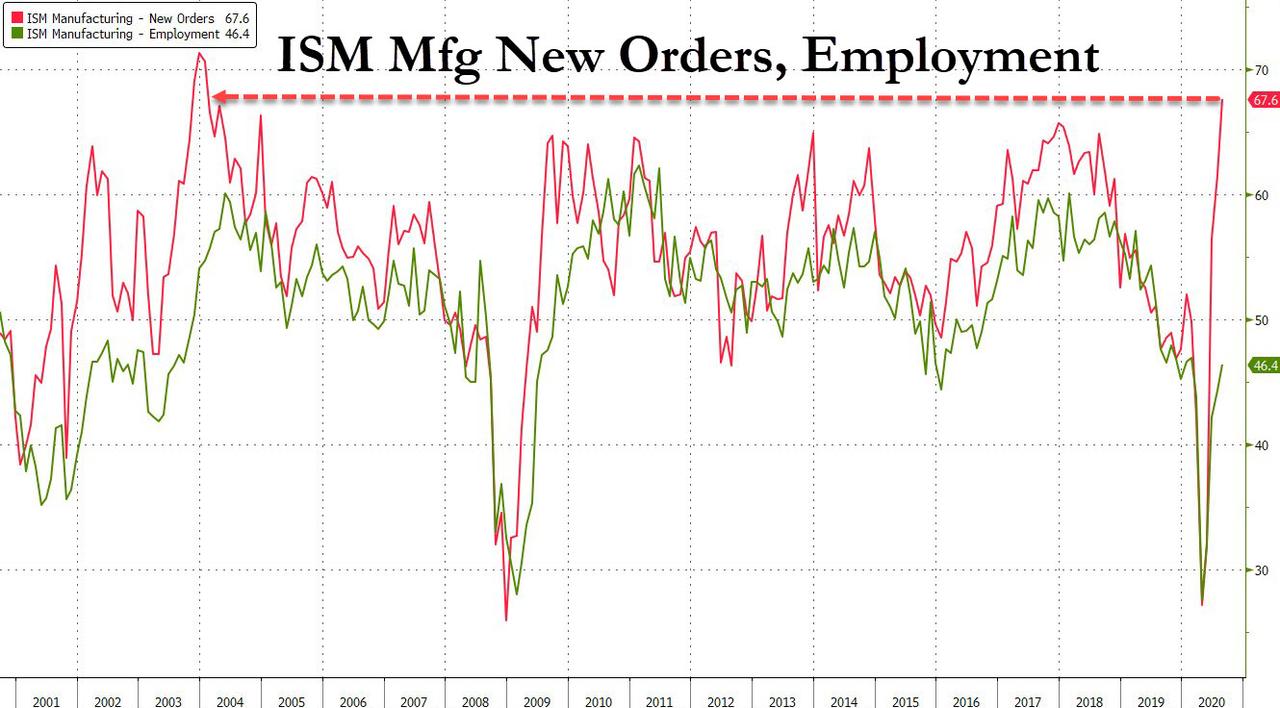

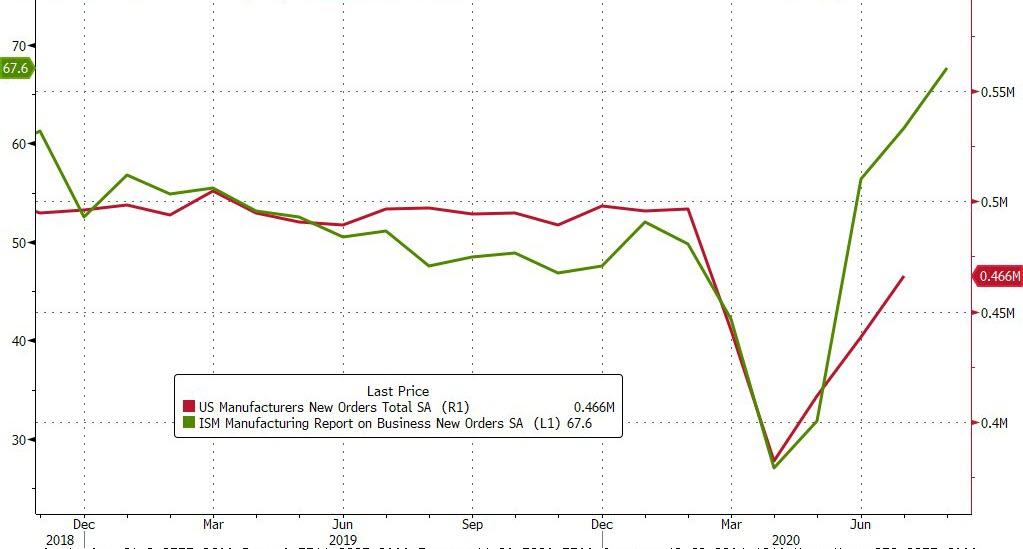

Fuelling the market optimism were also bets that the world’s major economies were recovering from the damage caused by the coronavirus pandemic. Economic survey data over recent days has fuelled such expectations, buoying stocks and helping the dollar rise from two-year lows. On Tuesday, data showed that U.S. manufacturing activity sped to a nearly two-year high in August on a surge in new orders, its highest level since November 2018.

“The data in the U.S. is telling us that the recovery is on track, and this is good news,” said Alessia Berardi, senior economist at Amundi, adding there was a “disconnection” between economic fundamentals and market positioning. “It’s too early to say that we will shift the recovery to a much stronger acceleration, or a V-shaped recovery,” she said.

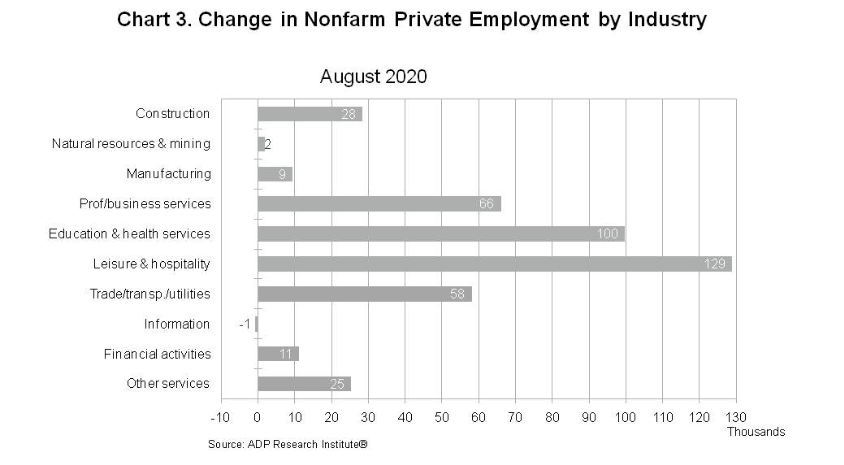

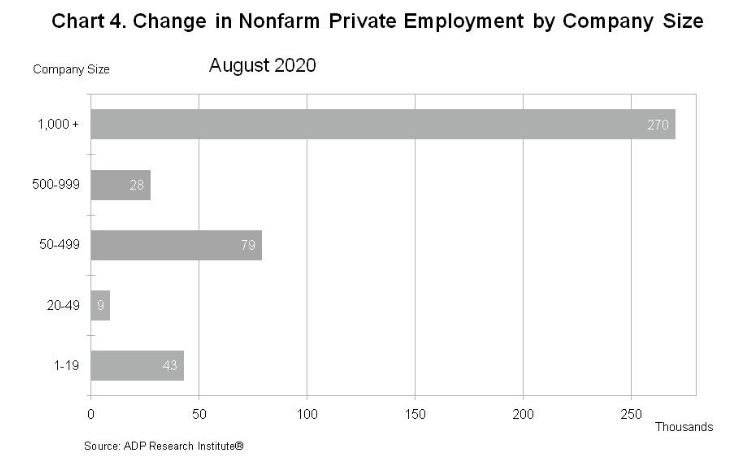

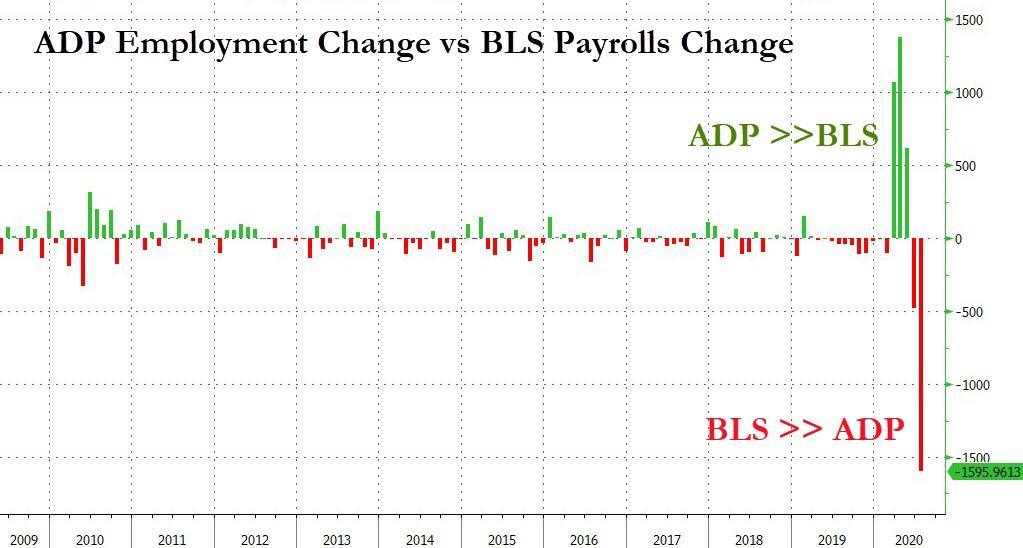

That said, in a melt up economic data is irrelevant, yet at 815am ET, we will get the latest ADP National Employment report which is expected to show private payrolls increased by 950,000 last month after a disappointing 167,000 rise in July. The report follows encouraging manufacturing sector surveys on Tuesday. As the COVID-19 pandemic rages on, signs that the recovery in the labor market was faltering has been a worry for investors. The official monthly jobs report from the BLS is due on Friday.

In Europe, the party was in full blast too, with the Stoxx Europe 600 Index headed for its biggest gain in almost a month, rising as much as 2% to session high, crossing above 200-day moving average. Chemicals, personal and household goods and technology led gains. Still, recovery from the euro zone’s deepest recession on record will take two years or more, according to a Reuters poll of economists last month, although investors spoke of cautious optimism. “We do need to focus on what the numbers are telling us,” said Gregory Perdon, co-chief investment officer at Arbuthnot Latham. “We are trying to cautiously embrace risk, without trying to be foolish about it.”

Earlier in the session, Asian stocks also gained, with MSCI’s broadest index of Asia-Pacific shares outside Japan rising 0.3%, led by communications and IT, after rising in the last session. Markets in the region were mixed, with Australia’s S&P/ASX 200 and South Korea’s Kospi Index rising, and Hong Kong’s Hang Seng Index and Singapore’s Straits Times Index falling. The Topix gained 0.5%, with Nippon Kinzoku and TYK rising the most. The Shanghai Composite Index retreated 0.2%, after the PBOC drained a whopping 180bn yuan in liquidity, with Changzhou Shenli Electrical Machine and JCET Group Co Ltd posting the biggest slides.

Things got a little weird in Australia where shares soared, on track to recoup Tuesday’s losses as investors brushed off a record gross domestic product slump and confirmation of the nation’s first recession in almost 30 years. As we reported last night, GDP for Aoril-June for plunged 7% compared with the first three months of the year, the largest fall in records dating back to 1959, the statistics bureau said in Sydney Wednesday. Once again: there is nothing as quite so good for stocks as bad news.

Also feeding the positive mood were signs that Washington was moving closer to offering some fiscal stimulus support to counter damage from the coronavirus. White House chief of staff Mark Meadows said on Tuesday that Republicans in the Senate were likely to take up a COVID-19 relief bill next week offering $500 billion in additional federal aid. The administration was still weighing help for U.S. airlines, he added. The fact that Pelosi poured cold water all over Meadows’ optimism was completely ignored by traders.

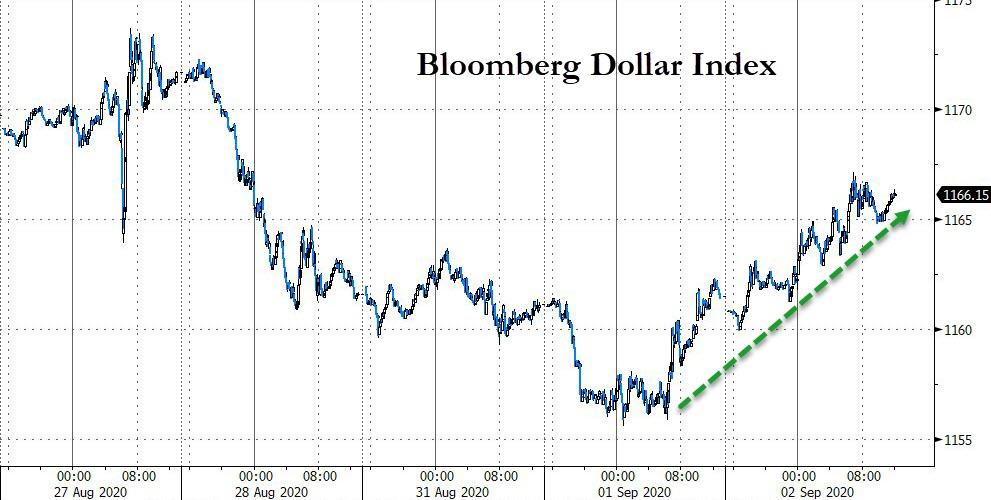

In FX, the dollar index added 0.4% at 92.612, rising on Tuesday from its lowest since April 2018 at 91.737. The euro and the pound both fell against the greenback, in a modest pullback from recent moves. The euro slid further below $1.20, a level it breached for the first time in over two years Tuesday, after the ECB’s Lane made it clear it won’t allow further gains in the currency. Ten-year bunds rose along with most of their sovereign peers, benefiting Germany, which took in 33 billion euros ($39 billion) of orders for its first green bonds. The pound also weakened against the greenback before BOE Governor Bailey addresses a parliamentary committee Wednesday afternoon. The Australian dollar fell after data showed that the nation fell into its first recession in almost three decades, with its GDP down 7% in the three months through June, more than the estimated 6% slump.

In rates, Treasuries fell, shortly before the ADP employment report may signal the pace of private-sector employment is picking up. Yields were cheaper by less than 2bp across the curve with 2s10s, 5s30s spreads steeper by 1.3bp and 0.9bp; 10-year yields around 0.685%, trailing bunds and gilts by more than 4bp. Core European debt outperformed despite Euro Stoxx 50 higher by 2.2% on the day; chemicals and technology shares are among the top gainers.

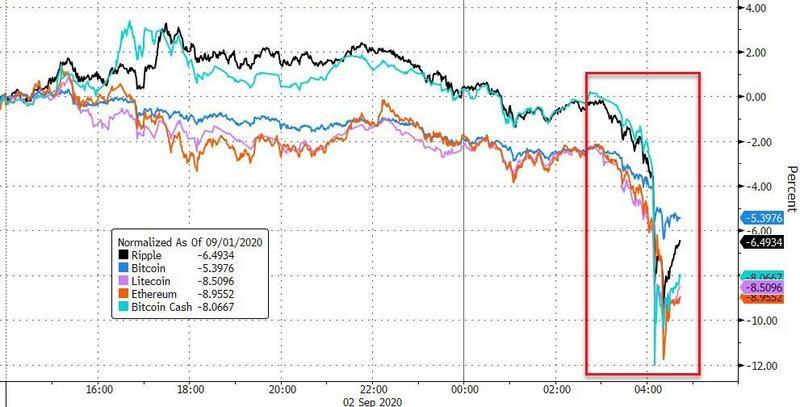

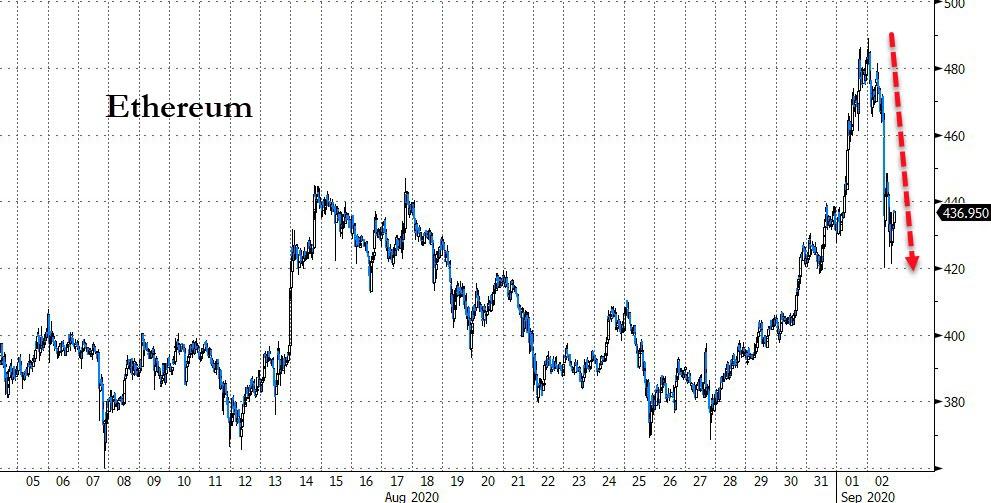

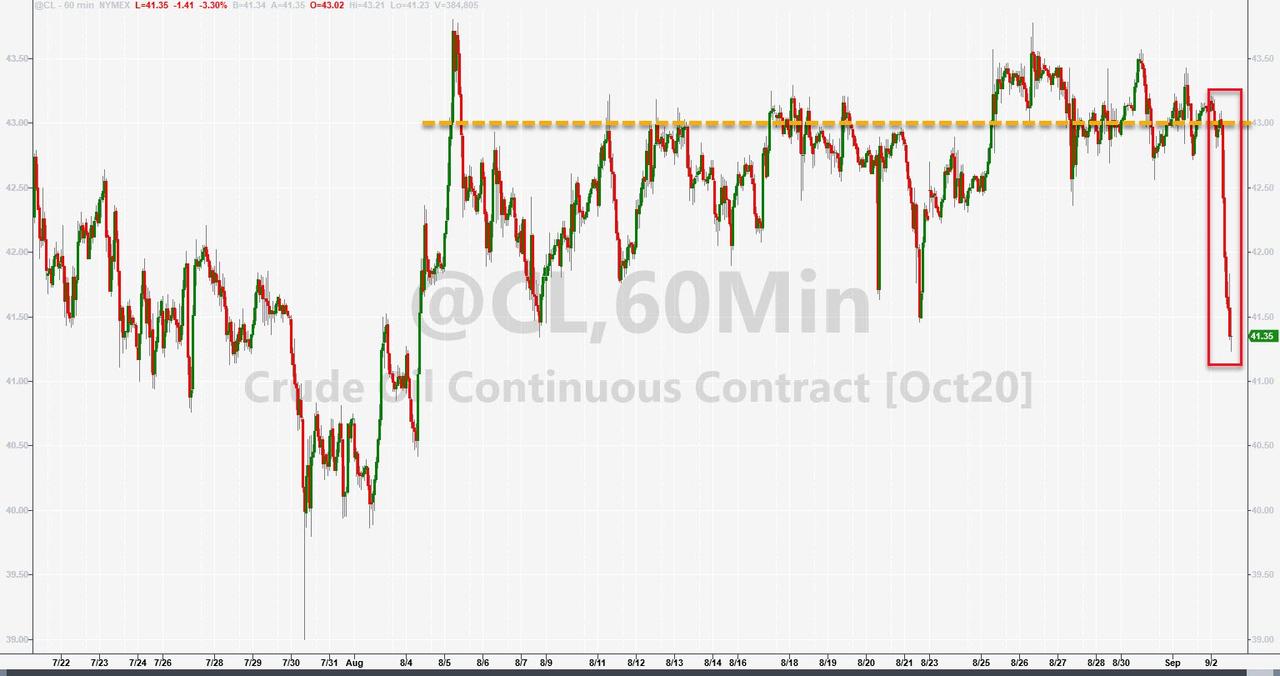

In commodities, oil rose towards $46 a barrel, gaining for a third day. Brent crude, the global benchmark, was up 1 cents at $45.68 a barrel. Crytpos were inexplicably crushed earlier this morning, despite a clear bubble forming in absolutely every asset class.

Expected data include employment change and factory orders. Macy’s and CrowdStrike are among companies reporting earnings

Market Snapshot

- S&P 500 futures up 0.6% to 3,548.50

- STOXX Europe 600 up 1.8% to 371.84

- MXAP up 0.3% to 174.19

- MXAPJ up 0.3% to 578.14

- Nikkei up 0.5% to 23,247.15

- Topix up 0.5% to 1,623.40

- Hang Seng Index down 0.3% to 25,120.09

- Shanghai Composite down 0.2% to 3,404.80

- Sensex up 0.05% to 38,918.98

- Australia S&P/ASX 200 up 1.8% to 6,063.21

- Kospi up 0.6% to 2,364.37

- Brent futures up 0.1% to $45.64/bbl

- Gold spot little changed at $1,969.91

- U.S. Dollar Index up 0.3% to 92.63

- German 10Y yield fell 3.4 bps to -0.454%

- Euro down 0.4% to $1.1862

- Italian 10Y yield fell 5.9 bps to 0.909%

- Spanish 10Y yield fell 5.2 bps to 0.346%

Top Overnight News from Bloomberg

- Germany got 30 billion euros ($36 billion) of orders for its first green bond sale as it aims to dominate the market for such debt by the end of the year

- Coronavirus cases exceeded 25.7 million globally, and the number of deaths was above 857,000. U.S. top virus official Anthony Fauci said that a Covid-19 vaccine could be available earlier than expected if clinical trials produce overwhelmingly positive results

- Switzerland’s financial regulator started enforcement proceedings against Credit Suisse over a spying scandal. The bank said it will continue to fully cooperate with the regulator

A quick look around global markets courtesy of NewsSquawk.com

Asian equity markets were mixed as the region partially sustained the momentum from the fresh record highs on Wall St where risk appetite was spurred once again by strength in big tech names and following better than expected ISM Manufacturing PMI data. ASX 200 (+1.8%) was positive with the advance led by materials as it found inspiration from the similar outperformance stateside and with AMP Capital front-running the largest-weighted financials sector after it announced to conduct a portfolio review amid heightened interest and enquiries regarding its assets and businesses. Nikkei 225 (+0.5%) remained afloat although upside was limited by a mixed currency and with heavy losses seen in Nippon Kayaku on news it will be replaced by SoftBank Corp in the index, while Hang Seng (-0.3%) and Shanghai Comp. (-0.2%) were pressured following another substantial PBoC liquidity drain and with underperformance seen in Hong Kong-listed casinos names which suffered from dismal Macau gaming revenue and with notable weakness in financials. 10yr JGBs were rangebound with price action hampered amid the gains in riskier Japanese assets but with downside also limited by the BoJ’s presence in the market for a total JPY 890bln of JGBs with 1-5yr and 10-25yr JGBs.

Top Asian News

- Japan Premier’s Aide Suga Announces Bid to Replace Outgoing Abe

- Turkey Slams U.S. Decision to Ease Its Arms Embargo on Cyprus

- China’s Vow to Keep Schools ‘Public Good’ Slams Education Stocks

- Singapore Can’t Sustain Emergency Measures Forever, PM Says

European stocks continue grinding higher, with solid gains thus far (Euro Stoxx 50 +2.3%) in spite of a relatively mixed APAC performance, with news flow also on the light side ahead of the US market entrance and a slew of notable Central Bank speakers. Broad-based gains are seen across the bourses with no clear out/underperformers. Sectors reside firmly in the green across the board but lack a clear risk bias; Banks, Insurance and Oil & Gas stand as the laggards, amid a low-yield environment and as energy prices recede. In terms of individual movers and shakers, earnings see the likes of Barratt Developments (+6.9%) underpinned as forwards sales improved alongside a future dividend policy based on a dividend cover of 2.5x. Credit Suisse (+0.9%), although firmer, underperforms the wider markets as Swiss regulators have commenced enforcement proceedings against the Co. Elsewhere ITV (+3.2%) has brushed off its relegation from the FTSE 100, whilst the Euro Stoxx 50 shake-up sees Adyen (+1.8%), Prosus (+1.2%), Vonovia (+2.5%), Pernod Ricard (+3.2%) and Kone (+1.3%) replacing SocGen (-0.2%), Fresenius (+1.8%), Orange (+1.3%), Telefonica (+0.3%) and BBVA (-0.6%). Finally, Novartis (+2.1%) is buoyed after announcing that it is to launch its SARS-CoV-2 rapid antigen test in countries accepting the CE mark.

Top European News

- Euro Surge Is ECB’s Newest Complication for Pandemic Economy

- Sunak Has 60 Billion Problems, But Taxes Aren’t One of Them

- Vallourec Slumps as French Pipe Maker Pursues Debt Restructuring

- Bulgarian Protesters Renew Pressure as Premier Seeks Support