GOLD::$1927.40 DOWN $3.80 The quote is London spot price

Silver:$26.57 DOWN $.15 London spot price ( cash market)

Yesterday I wrote the following to you:

“We are now in the middle of the 3 or 4 day whacking of our precious metals. Tomorrow is the jobs report and they generally whack around this announcement. Also Labour day is Monday and the day following is another day that they whack. No doubt the bankers are worried about the new physical exchange being developed in London through the auspices of the LME. The bankers need to be onside and they will do anything to get the speculators off their backs so that they can cover””

I guess I was right. You could see the set up as the crooks whacked Wednesday and Thursday hoping for a climax day on Friday with a phony jobs report. The stock market plunge got in the way of the crooks as well as our Londoners who asked for delivery on exercised EFP’s.

In my report, you will see that the crooks could not cover anything as the demand for gold is just too great. The OI on both exchanges (EFP + comex) rose despite the whack. Actually for the two raids, the OI’s on both rose and thus this is a failure for our banks

In silver, we got a small OI loss

I would be willing to bet that the preliminary no. released at midnight tonight will also show a gain in oi in gold. Our banker friends are looking into an abyss!

H

DONATE

Closing access prices: London spot

i)Gold : $1933.00 LONDON SPOT 4:30 pm

ii)SILVER: $26.86//LONDON SPOT 4:30 pm

CLOSING FUTURES PRICES: KEY MONTHS

OCT GOLD: $1926.90 CLOSE 1.30 PM// SPREAD SPOT/FUTURE OCT /: : $0.50//BACKWARD//

DEC. GOLD $1935.90 CLOSE 1.30 PM SPREAD SPOT/FUTURE DEC $4.60/ CONTANGO ($7.40 BELOW NORMAL CONTANGO)

CLOSING SILVER FUTURE MONTH

SILVER SEPT COMEX CLOSE; $26.58…1:30 PM.//SPREAD SPOT/FUTURE SEPT// : ( 1 cent contango//2 CENTS BELOW NORMAL contango)

SILVER DECEMBER CLOSE: $26.77 1:30 PM SPREAD SPOT/FUTURE DEC. : 20 CENTS PER OZ CONTANGO ( 8 CENTS ABOVE NORMAL CONTANGO)

COMEX DATA

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

receiving today: 0/59

issued: 0

EXCHANGE: COMEX

CONTRACT: SEPTEMBER 2020 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,927.600000000 USD

INTENT DATE: 09/03/2020 DELIVERY DATE: 09/08/2020

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

135 H RAND 1

226 C DIRECT ACCESS 1

435 H SCOTIA CAPITAL 6

624 C BOFA SECURITIES 2

657 C MORGAN STANLEY 22

657 H MORGAN STANLEY 6

686 C INTL FCSTONE 1

709 C BARCLAYS 11

737 C ADVANTAGE 35 2

800 C MAREX SPEC 22 3

905 C ADM 6

____________________________________________________________________________________________

TOTAL: 59 59

MONTH TO DATE: 3,183

NUMBER OF NOTICES FILED TODAY FOR AUGUST CONTRACT: 59 NOTICE(S) FOR 5900 OZ (0.1835 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 3183 NOTICES FOR 318,300 OZ (9.900 tonnes)

SILVER

440 NOTICE(S) FILED TODAY FOR 2,200,000 OZ/

total number of notices filed so far this month: 8455 for 42.275 MILLION oz

BITCOIN MORNING QUOTE $10424 UP 276

BITCOIN AFTERNOON QUOTE.: $10,531 UP 427

GLD AND SLV INVENTORIES:

WITH GOLD DOWN $3.80 AND NO PHYSICAL TO BE FOUND ANYWHERE:

WITH ALL REFINERS CLOSED//MEXICO ORDERING ALL MINES SHUT: WHERE ARE THEY GETTING THE “PHYSICAL?

NO CHANGES IN GOLD INVENTORY AT THE GLD…

GLD: 1,250.04 TONNES OF GOLD//

WITH SILVER DOWN $0.15 TODAY: AND WITH NO SILVER AROUND:

WE HAD ANOTHER CRIMINAL PAPER WITHDRAWAL OF 3.631 MILLION OZ//

RESTING SLV INVENTORY TONIGHT:

SLV: 564.799 MILLION OZ./

XXXXXXXXXXXXXXXXXXXXXXXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI FELL BY A SMALLER THAN EXPECTED 2606 CONTRACTS FROM 163,745 DOWN TO 161,139, AND FURTHER FROM OUR NEW RECORD OF 244,710, (FEB 25/2020. THE LOSS IN OI OCCURRED WITH OUR VERY STRONG $0.50 FALL IN SILVER PRICING AT THE COMEX. IT SEEMS THAT THE LOSS IN COMEX OI IS DUE TO SOME BANKER SILVER SHORT COVERING.. COUPLED AGAINST A STRONG EXCHANGE FOR PHYSICAL ISSUANCE, SOME MINOR LONG LIQUIDATION, A HUGE INCREASE IN SILVER OZ STANDING AT THE COMEX FOR SEPT.. WE HAD A SMALL NET LOSS IN OUR TWO EXCHANGES OF 1162 CONTRACTS (SEE CALCULATIONS BELOW).

WE HAVE ALSO WITNESSED A STRONG AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: SEP 0; DEC: 1444, MARCH 0 FOR ZERO ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 1444 CONTRACTS. WITH THE TRANSFER OF 1444 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1444 EFP CONTRACTS TRANSLATES INTO 7.220 MILLION OZ ACCOMPANYING:

1.THE $0.50 CENT FALL IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

10.025 MILLION OZ INITIAL STANDING IN AUGUST.

43.030 MILLION OZ INITIALLY STANDING IN SEPT. (HUGE)

7.32 MILLION OZ INITIALLY STANDING IN OCT

2.630 MILLION OZ STANDING FOR NOV.

20.970 MILLION OZ FINAL STANDING IN DEC

5.075 MILLION OZ FINAL STANDING IN JAN

1.480 MILLION OZ FINAL STANDING IN FEB

23.005 MILLION OZ FINAL STANDING FOR MAR

4.660 MILLION OZ FINAL STANDING FOR APRIL

45.220 MILLION OZ FINAL STANDING FOR MAY

2.205 MILLION OF FINAL STANDING FOR JUNE

86.470 MILLION OZ FINAL STANDING IN JULY.

6.475 MILLION OZ FINAL STANDING IN AUGUST

52.710 MILLION OZ INITIALLY STANDING IN SEPT

THURSDAY, AGAIN OUR CROOKS USED COPIOUS PAPER IN ORDER TO LIQUIDATE SILVER’S PRICE…AND THEY WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL $0.50) ).. AND, OUR OFFICIAL SECTOR/BANKERS WERE SOMEWHAT SUCCESSFUL IN THEIR ATTEMPT TO FLEECE SOME SILVER LONGS. THE RAID YESTERDAY WAS ORCHESTRATED TO REMOVE SPECULATORS FROM THEIR LONG POSITIONS. WE ALSO HAD ii) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS 2) A STRONG GAIN IN SILVER OZ STANDING FOR SEPTEMBER, AND 3) SOME LONG LIQUIDATION. YOU CAN BET THE FARM THAT OUR BANKERS ARE DESPERATE TO LIQUIDATE THEIR HUGE SHORT POSITIONS IN SILVER..

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS

SEPT.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY /FOR MONTH OF SEPT:

4991 CONTRACTS (FOR 4 TRADING DAY(S) TOTAL 4991 CONTRACTS) OR 24.955 MILLION OZ: (AVERAGE PER DAY: 1247 CONTRACTS OR 6.238 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF SEPT: 24.955 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 3.557% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2020 TO DATE SILVER EFP’S: 1,411.04 MILLION OZ.

JANUARY 2020 EFP TOTALS SO FAR: 181.61 MILLION OZ

FEB 2020 EFP’S TOTAL : …… 259.600 MILLION OZ

MARCH EFP’S ….. 452.280 MILLION OZ //TOTALS//AND A NEW RECORD FOR THE MONTH)

APRIL EFP 95.355 MILLION OZ. (EX. FOR PHYSICALS BECOMING A LOT LESS)

MAY EFP FINAL: 77.27 MILLION OZ

JUNE EFP 71.15 MILLION OZ.

JULY EFP 133.95 MILLION OZ/ (EXCHANGE FOR PHYSICALS STARTING TO RISE EXPONENTIALLY AGAIN)

AUGUST EFP 127.46 MILLION OZ (EXCHANGE FOR PHYSICALS STARTING TO DECREASE AGAIN)

SEPT EFP 24.955 MILLION OZ

RESULT: WE HAD A STRONG SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2606, WITH OUR HUGE $0.50 FALL IN SILVER PRICING AT THE COMEX ///THURSDAY AS ONE A NET BASIS, FEW LONGS LEFT THE SILVER ARENA.…THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 1444 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER

TODAY WE LOST A SMALL SIZED 1162 OI CONTRACTS ON THE TWO EXCHANGES (WITH OUR $0.50 LOSS IN PRICE)//

THE TALLY//EXCHANGE FOR PHYSICALS

i.e 1444 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH A CONSIDERABLE SIZED DECREASE OF 2606 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH OUR $0.50 CENT FALL IN PRICE OF SILVER/AND A CLOSING PRICE OF $26.84 // THURSDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY.

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.821 BILLION OZ TO BE EXACT or 117% of annual global silver production (ex Russia & ex China).

FOR THE NEW AUGUST DELIVERY MONTH/ THEY FILED AT THE COMEX: 440 NOTICE(S) FOR 2,220,000 OZ OF SILVER.

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.70//TODAY’S RECORD OF 244,705 WAS SET WITH A PRICE OF: 18.91 (FEB 25/2020)

.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ; AUGUST 10.025 MILLION OZ/ SEPT 43.030 MILLION OZ//OCT: 7.665 MILLION OZ// NOV: 2.630 MILLION OZ//DEC: 20.970 MILLION OZ; JAN: 5.075 MILLION OZ.//FEB 1.480 MILLION OZ//MAR: 23.005 MILLION OZ/APRIL 4.660 MILLION OZ//MAY 45.220 MILLION OZ//JUNE: 2.205 MILLION OZ// JULY 86.470 million oz//AUGUST 6.475 MILLION OZ//SEPT. 52.710 MILLION OZ//

- THE RECORD PRIOR TO TODAY WAS SET IN FEB 25/2018: 244,710 CONTRACTS, WITH A SILVER PRICE OF $18.90//.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017 RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

GOLD

IN GOLD, THE COMEX OPEN INTEREST SURPRISINGLY FELL BY A TINY SIZED 481 CONTRACTS TO 548,934 AND FURTHER FROM OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE SMALL SIZED LOSS IN COMEX OI OCCURRED DESPITE OUR CONSIDERABLE FALL IN PRICE OF $7.50 /// COMEX GOLD TRADING// THURSDAY//WE HAD ATTEMPTED BUT FAILED BANKER SHORT COVERING AS WE HAD A STRONG GAIN ON OUR TWO EXCHANGES… NOBODY LEFT THE GOLD ARENA. WE ALSO HAD A STRONG ADVANCE IN TONNAGE STANDING AT THE GOLD COMEX FOR SEPTEMBER ACCOMPANYING A SMALL EXCHANGE FOR PHYSICAL ISSUANCE. THIS ALL HAPPENED WITH OUR FALL IN PRICE OF $7.50.

WE HAD A VOLUME OF 2 4 -GC CONTRACTS//OPEN INTEREST 136// (2400 OZ WAS DELIVERED ON FRIDAY FROM THE ENHANCED GOLD INVENTORY)…

WE GAINED A SMALL SIZED 1504 CONTRACTS (4.678 TONNES) ON OUR TWO EXCHANGES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A SMALL SIZED 1985 CONTRACTS:

CONTRACT .; AUG 0 AND OCT: 210 DEC: 1775; JUNE: 0 ALL OTHER MONTHS ZERO//TOTAL: 1985. The NEW COMEX OI for the gold complex rests at 548,934. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EXCHANGE DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A SMALL SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1504 CONTRACTS: 481 CONTRACTS DECREASED AT THE COMEX AND 1985 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 1504 CONTRACTS OR 4.678 TONNES. THURSDAY, WE HAD A LOSS OF $7.50 IN GOLD TRADING……

AND WITH THAT LOSS IN PRICE, WE HAD A SMALL SIZED GAIN IN TOTAL/TWO EXCHANGES GOLD TONNAGE OF 4.678 TONNES!!!!!! THE BANKERS WERE SUCCESSFUL IN THEIR ATTEMPT TO LOWER GOLD’S PRICE (IT FELL $7.50). WE HAD ATTEMPTED BUT FAILED BANKER SHORT COVERING OPERATION WITH SMALL ISSUANCE IN EXCHANGES FOR PHYSICAL. THE BANKERS COULD NOT FLEECE ANY OF OUR SPECULATOR LONGS DESPITE THE SECOND RAID IN A ROW .

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES:

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1985) ACCOMPANYING THE SMALL SIZED LOSS IN COMEX OI (481 OI): TOTAL GAIN IN THE TWO EXCHANGES: 1504 CONTRACTS. WE NO DOUBT HAD 1 )ATTEMPTED AND FAILED BANKER SHORT COVERING ,2.)A STRONG ADVANCE IN STANDING AT THE GOLD COMEX FOR THE FRONT SEPT. MONTH, 3) NO LONG LIQUIDATION; 4) SMALL COMEX OI LOSS AND 5) SMALL ISSUANCE OF EXCHANGE FOR PHYSICAL AND …ALL OF THIS WAS COUPLED WITH OUR LOSS IN GOLD PRICE TRADING//THURSDAY//$7.50.

WE ARE BEGINNING TO WITNESS A LACK OF EXCHANGE FOR GOLD PHYSICALS UNDERWRITTEN DUE TO PREMIUMS STARTING TO REAPPEAR IN THE FUTURE PRICE OF GOLD VS LONDON SPOT. THE COST TO THE BANKERS IS JUST TOO GREAT TO ENGAGE IN THESE VEHICLES ONCE THIS OCCURS.

THE FACT THAT WE ARE CONTINUALLY SEEING A DROP IN COMEX OPEN INTEREST AND VOLUMES COUPLED WITH LESS EXCHANGE FOR PHYSICALS PROBABLY MEANS THAT OUR LONGS ARE ALREADY DEPARTING NEW YORK FOR THE NEW PHYSICAL PLATFORM AT LONDON’S LME.

EXCHANGE FOR PHYSICALS//OUTLINE

SPREADING OPERATIONS/NOW SWITCHING TO GOLD (WE SWITCH OVER TO SILVER ON OCT 1)

OUR SPREADING OPERATION HAS NOW SWITCHED INTO GOLD…..

SPREADING OPERATION FOR OUR NEWCOMERS:

FOR NEWCOMERS, HERE ARE THE DETAILS:

SPREADING LIQUIDATION HAS NOW COMMENCED IN GOLD AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF OCT.

FOR THOSE OF YOU WHO ARE NEW, HERE IS THE MODUS OPERANDI OF THE SPREADERS AND THE CRIMINAL ELEMENT BEHIND IT:

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR;

THE SPREADING LIQUIDATION OPERATION IS NOW OVER FOR SILVER..AND WE WILL NOW MORPH INTO AN ACCUMULATION PHASE OF SPREADING CONTRACTS FOR GOLD. THEY WILL ACCUMULATE CONSIDERABLE AMOUNT OF THE CONTRACTS AND THEN LIQUIDATE ONE WEEK PRIOR TO FIRST DAY NOTICE

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO GOLD AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF SEPT. HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF OCT FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE IN THIS NON ACTIVE MONTH OF SEPT. BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN GOLD WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2020 INCLUDING TODAY

SEPT.

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 4 TRADING DAY(S) IN TONNES: 17.51 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2019, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 17.51/3550 x 100% TONNES =0.493% OF GLOBAL ANNUAL PRODUCTION

ISSUANCE OF EXCHANGE FOR PHYSICAL GOLD HAS DISSIPATED THIS MONTH…THE COST TO THE BANKERS TO CARRY THESE CONTRACTS IN LONDON IS BECOMING TOO GREAT FOR THEM.

ACCUMULATION OF GOLD EFP’S YEAR 2020 TO DATE: 3,422.28 TONNES

JANUARY 2220 TOTAL EFP ISSUANCE; : 570.19 TONNES

FEB 2020 TOTAL EFP ISSUANCE : 653.78 TONNES

MARCH TOTAL EFP ISSUANCE 1,098.93 TONNES (*AND A NEW ALL TIME RECORD ISSUANCE//22 DAYS)

APRIL TOTAL EFP. ISSUANCE: 243.45 TONNES (EFP ISSUANCE BECOMING A LOT LESS)

MAY TOTAL EFP ISSUANCE: 248.68 TONNES (EFP ISSUANCE STILL LOW// PREMIUM COST TO THE BANKERS IS HUGE..SO ISSUANCE IS LESS)

JUNE TOTAL EFP ISSUANCE: 192.06 TONNES

JULY TOTAL EFP ISSUANCE; 313.09 TONNES ..(EXCHANGE FOR PHYSICALS REVERSE COURSE AND ARE NOW INCREASING!)

AUGUST TOTAL EFP ISSUANCE; 150.78 TONNES FINAL (AGAIN: RETREATING IN NUMBERS)

SEPT TOTAL EFP ISSUANCE: 17.51 TONNES (AGAIN EXCHANGE FOR PHYSICAL NUMBERS IN RETREAT)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A STRONG SIZED 2606 CONTRACTS FROM 163,745, DOWN TO 161,139 AND FURTHER FROM OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 2 3/4 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.

THE CONSIDERABLE SIZED LOSS IN OI SILVER COMEX WAS PRIMARILY DUE TO; 1) SOME BANKER SHORT COVERING , 2) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS (SEE BELOW), 3) A STRONG GAIN IN OUNCES STANDING FOR SILVER AT THE COMEX FOR SEPT., AND 4) SOME LONG LIQUIDATION,

EFP ISSUANCE 1444 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT: 0 AND DEC. 1444 AND MARCH: 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1444 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 2606 CONTRACTS TO THE 1444 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A SMALL SIZED LOSS OF 1162 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES. THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES 5.810 MILLION OZ, OCCURRED WITH OUR 50 CENT LOSS IN PRICE///

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL..THE EVIDENCE IS CLEAR: HUGE AMOUNTS OF PHYSICAL STANDING FOR BOTH SILVER AND GOLD .

(report Harvey)

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED DOWN 29.61 POINTS OR 0.87% //Hang Sang CLOSED DOWN 312.15 POINTS OR 1.25% /The Nikkei closed DOWN 260.10 POINTS OR 1.11%//Australia’s all ordinaires CLOSED DOWN 3.65%

/Chinese yuan (ONSHORE) closed DOWN at 6.8408 /Oil UP TO 4173 dollars per barrel for WTI and 44.30 for Brent. Stocks in Europe OPENED MIXED// ONSHORE YUAN CLOSED DOWN // LAST AT 6.8408 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.8443 TRADE TALKS STALL//CORONAVIRUS//PANDEMIC//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

total withdrawals; 739.470 oz

We had 1 kilobar transactions +

ADJUSTMENTS: 0 //

The front month of SEPT registered a total of 124 contracts for a loss of 818 contracts. We had 891 notices filed on Thursday, so we gained a strong 73 contracts or an additional 7300 oz will stand for delivery in this non active month of Sept.

Oct LOST 121`9 contracts DOWN to 61,649 (HARDLY ANYBODY LEFT THE ARENA WITH OUR FRONT MONTH). November gained 11 contracts to stand at 14.

The big December contract GAINED 384 contracts UP to 406,220 contracts…(NOBODY LEFT HERE AS WELL)

We had 59 notices filed today for 5900 oz

To calculate the INITIAL total number of gold ounces standing for the SEPT /2020. contract month, we take the total number of notices filed so far for the month (3183) x 100 oz , to which we add the difference between the open interest for the front month of SEPT (124 CONTRACTS ) minus the number of notices served upon today (59 x 100 oz per contract) equals 324,800 OZ OR 10.1026 TONNES) the number of ounces standing in this active month of JUNE

thus the INITIAL standings for gold for the SEPT/2020 contract month:

No of notices filed so far (3183, x 100 oz + (124 OI) for the front month minus the number of notices served upon today (59) x 100 oz which equals 324,800 oz standing OR 10.1026 TONNES in this active delivery month. This is a HUGE amount for gold standing for a SEPT delivery month (a NON active delivery month).

we gained 73 contracts or an additional 7300 oz will try their luck searching for metal on this side of the pond.

THE NAME OF THE GAME TODAY IS BANKER SHORT COVERING AS FINALLY FEAR BECAME THEIR CENTRAL FOCUS. YOU CAN VISUALIZE THIS LAST NIGHT AND TODAY WITH GOLD’S STRONG ADVANCE IN TUESDAY’S COMEX. TODAY ATTEMPTED BANKER SHORT COVERING WHICH FAILED WITH THE HIGHER PRICES.

NEW PLEDGED GOLD: BRINKS

144,088.952 oz NOW PLEDGED JAN 21.2020/HSBC 5.4807 TONNES

42,548.308.00 PLEDGED APRIL 3/2020: SCOTIA: 1.3234 tonnes

deleted Int. Delaware pledge July 7 (600 tonnes)

261,955.892 oz (some deleted august 3) JPM 8.1479 TONNES

610,238.285 oz pledged June 12/2020 Brinks/ july 2/july 21 19.017 tonnes

63,187.561 oz Pledged August 21/regular account 1.965 tonnes jpm

total pledged gold: 1,122,018.988 oz 34.89 tonnes

total registered, pledged and eligible (customer) gold 36,905,839.514 oz 1,147.92 tonnes (INCLUDES 4 GC GOLD)

total 4 GC gold: 126.34 tonnes

total gold net of 4 GC: 1021,58 tonnes

end

I have compiled data with respect to registered (or dealer) gold taken on first day notice for each of the past 24 months

The data begins on first day notice for the May month taken on the last day of July 2018. and it continues to present day.

I then took, how many deliveries were recorded by the CME for each and every month. I also included for reference the price of gold on first day notice.

The first graph is a logarithmic graph and the second graph, linear.

You can see the huge explosion of registered gold at the comex along with deliveries.

THE GOLD COMEX SEEMS TO BE UNDER SEVERE ASSAULT FOR PHYSICAL

END

And now for the wild silver comex results

And now for the wild silver comex results

INITIAL STANDINGS

SEPT. SILVER COMEX CONTRACT MONTH//INITIAL STANDINGS

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory |

627,957.761 oz

CNT

Loomis

Delaware

manfra

|

| Deposits to the Dealer Inventory |

779,636.720 oz

Scotia

|

| Deposits to the Customer Inventory |

2,296,397.620 oz

Brinks

JPMorgan

Scotia

|

| No of oz served today (contracts) |

440

CONTRACT(S)

(2,200,,000 OZ)

|

| No of oz to be served (notices) |

2087 contracts

10,435,000 oz)

|

| Total monthly oz silver served (contracts) | 8455 contracts

42,275,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

total dealer deposits: 779,636.720 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

we had 3 deposits into the customer account

i)into JPMorgan: 1,485,900.200 oz

ii) Into Brinks: 605,567.040 oz

iii) Into Scotia: 204,930.380 oz

*** JPMorgan for most of 2017, 2018 and onward, has adding to its inventory almost every single day.

JPMorgan now has 171.097 million oz of total silver inventory or 48.64% of all official comex silver. (171.097 million/351.67 million

total customer deposits today: 2,296,397.620 oz

we had 4 withdrawals:

i) Out of CNT: 16,423.300 oz

ii) Out of Delaware: 2938.420 oz

iii) Out of Loomis: 5029.000 oz

iv) Out of Manfra: 605,562.04

total withdrawals; 627,957.761 oz

We had 2 adjustments//both customer to dealer

i) CNT: 4904.95

ii)JPMorgan: 492,697.100

Total dealer(registered) silver: 140.358 million oz

total registered and eligible silver: 351.67 million oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

the front month of SEPTEMBER registered an open interest of 2527 contracts thus losing 187 contracts. We had 292 notices filed on THURSDAY so we GAINED BACK A GOOD 105 contracts or an additional 525,000 oz will stand in this active delivery month of September as they refused to morph into London based forwards and negate a fiat bonus. Our London boys are ready to exercise these EFP’s and they will turn them into real physical metal as we now have a full frontal attack on both of our two precious metals.

Oct saw another GAIN of 21 contract to stand at 775.November gained 0 contract to stand at 14,

The big December contract month saw its OI FALL by 2926 contracts DOWN to 140,1498

The total number of notices filed today for the SEPT 2020. contract month is represented by 440 contract(s) FOR 2,220,000, oz

To calculate the number of silver ounces that will stand for delivery in SEPT we take the total number of notices filed for the month so far at 8455 x 5,000 oz = 42,275,000 oz to which we add the difference between the open interest for the front month of SEPT(2527) and the number of notices served upon today 440 x (5000 oz) equals the number of ounces standing.

Thus the INITIAL standings for silver for the SEPT/2019 contract month: 8455 (notices served so far) x 5000 oz + OI for front month of SEPT (2527)- number of notices served upon today (440) x 5000 oz of silver standing for the SEPT contract month.equals 52,710,000 oz. ..VERY STRONG FOR AN ACTIVE MONTH.

We gained a strong 105 contracts or AN ADDITIONAL 525,000 oz. WILL STAND FOR DELIVERY IN THIS ACTIVE DELIVERY MONTH, AS THEY LOOK FOR METAL ON THis SIDE OF THE POND!

TODAY’S ESTIMATED SILVER VOLUME : 110,439 CONTRACTS // volume huge//raid orchestrated by the BIS

FOR YESTERDAY: 132,600. ,CONFIRMED VOLUME//volume huge

YESTERDAY’S CONFIRMED VOLUME OF 132,600 CONTRACTS EQUATES to 0.663 billion OZ 94.7% OF ANNUAL GLOBAL PRODUCTION OF SILVER..

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV RISES TO- 2.98% ((SEPT 4/2020)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -0.59% to NAV: (SEPT 4/2020 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into NEGATIVE/2.98%

(courtesy Sprott/GATA

3. SPROTT CEF .A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 20.36 TRADING 19.86///NEGATIVE 2.46

END

And now the Gold inventory at the GLD/

SEPT 4//WITH GOLD DOWN $3.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1250.04 TONNES

SEPT 3/WITH GOLD DOWN $7.50 ON THIS 2ND DAY OF A 3 DAY RAID: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1250.04 TONNES

SEPT 2/WITH GOLD DOWN $34.00 TODAY, WE HAVE 2 SMALL CHANGES IN GOLD INVENTORY AT THE GLD: 2 WITHDRAWALS OF .87 TONNES AND.59 TONNES FROM THE GLD////INVENTORY RESTS AT 1250.04 TONNES

SEPT 1/WITH GOLD UP $7.10 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1251.50 TONNES

AUGUST 31//WITH GOLD UP $5.90 TODAY/WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD..//INVENTORY RESTS AT 1251.50 TONNES/

AUGUST 28/WITH GOLD UP $38.20 TODAY, WE SURPRISINGLY HAD A .59 TONNE WITHDRAWAL//INVENTORY RESTS AT 1251.50 TONNES

AUGUST 27/WITH GOLD DOWN 17.50 TODAY: WE HAD A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 3.24 TONNES INTO THE GLD//INVENTORY REST AT 1252.09 TONNES

AUGUST 26/WITH GOLD UP $26.70 TODAY/ WE HAD A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.53 TONNES FROM THE GLD//RESTS AT 1248.85 TONNES

AUGUST 25/WITH GOLD DOWN $14.60 TODAY, WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD//RESTS AT 1252.38 TONNES

AUGUST 24//WITH GOLD DOWN $7.20 TODAY: WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD: /INVENTORY RESTS AT 1258.38 TONNES

AUGUST 21//WITH GOLD DOWN $.40 TODAY: WE HAD NO CHANGE IN GOLD INVENTORY AT THE GLD: /INVENTORY RESTS AT 1252.38 TONNES

AUGUST 20/WITH GOLD DOWN $23.45 TODAY: WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD: .//INVENTORY REST AT 1252.38 TONNES

AUGUST 19//WITH GOLD DOWN $39.65 TODAY: WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1252.38 TONNES

AUGUST 18/WITH GOLD UP $14.60 TODAY: WE HAD A HUGE CHANGE IN GOLD INVENTORY: A DEPOSIT OF 4.09 TONNES//GLD INVENTORY RESTS TONIGHT AT 1252.38 TONNES

AUGUST 17/WITH GOLD UP $46.30 TODAY: SURPRISINGLY WE HAD A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF 3.8 TONNES//INVENTORY RESTS AT 1248.29 TONNES

AUGUST 14/ WITH GOLD DOWN $19.45 TODAY: SURPRISINGLY, WE HAD A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 1.46 TONNES/INVENTORY RESTS AT 1252.63 TONNES.

AUGUST 13/WITH GOLD UP $23.15 TODAY: WE HAD A HUGE CHANGE IN GOLD INVENTORY: SURPRISINGLY A PAPER WITHDRAWAL OF 7.30 TONNES/INVENTORY RESTS AT 1250.63 TONNES

AUGUST 12/ WITH GOLD UP $1.00 TODAY: WE HAD A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF 4.19 TONNES//INVENTORY RESTS AT 1257.93 TONNES

AUGUST 11//WITH GOLD DOWN $92.40 TODAY, WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1262.12 TONNES.

AUGUST 10/WITH GOLD UP $11.35 TODAY, WE HAD A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.84 TONNES//INVENTORY RESTS AT 1262.12 TONNES

AUGUST 7/WITH GOLD DOWN $38.30 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1267.96 TONNES

AUGUST 6/WITH GOLD UP $20.45 TODAY, WE HAVE ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A PAPER DEPOSIT OF 10.23 TONNES INTO THE GLD/INVENTORY RESTS AT 1267.96 TONNES//

AUGUST 5/WITH GOLD UP $ 33.75 TODAY, WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD/A DEPOSIT OF 9.35 TONNES INTO THE GLD//INVENTORY RESTS AT 1257.73 TONNES

AUGUST 4//WITH GOLD UP $31.75 TODAY, WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 6.48 TONNES/GLD INVENTORY RESTS AT 1248.38 TONNES

AUGUST 3/WITH GOLD UP $2.20 TODAY, WE HAVE NO CHANGES IN THE GOLD INVENTORY AT THE GLD////INVENTORY RESTS AT 1241,96 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Inventory rests tonight at

SEPT 4/ GLD INVENTORY 1250.04 tonnes*

LAST; 895 TRADING DAYS: +310.54 NET TONNES HAVE BEEN ADDED THE GLD

LAST 795 TRADING DAYS://+489.07 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

SEPT 4//WITH SILVER DOWN 15 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A PAPER WITHDRAWAL OF 3.631 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 564.799 MILLION OZ//

SEPT 3//WITH SILVER DOWN 50 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.258 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 568.430 MILLION OZ/./

SEPT 2.WITH SILVER DOWN $1.04 TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.365 MILLION OZ FROM THE SLV///INVENTORY REST AT 571.688 MILLION OZ.

SEPT 1//WITH SILVER UP 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 574.053 MILLION OZ//

AUGUST 31/WITH SILVER UP 80 CENTS TODAY: A HUGE CHANGE IN THE SLV//A DEPOSIT OF 2.982 MILLION OZ ENTERS THE SLV/INVENTORY RESTS AT 574.053 MILLION OZ//

AUGUST 28/WITH SILVER UP 48 CENTS TODAY: A MASSIVE PAPER DEPOSIT OF 4.652 MILLION OZ ENTERS THE SLV//INVENTORY RESTS AT 571.071 MILLION OZ

AUGUST 27/WITH SILVER DOWN 28 CENTS TODAY// NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 566.419 MILLION OZ

AUGUST 26//WITH SILVER UP $1.04 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.65 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 566.419 MILLION OZ..

AUGUST 25/WITH SILVER DOWN 21 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.607 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 571.074 MILLION OZ//

AUGUST 24//WITH SILVER DOWN 18 CENTS TODAY: WE HAD A NO CHANGES//INVENTORY RESTS AT 573.843 MILLION OZ//

AUGUST 21//WITH SILVER DOWN 30 CENTS TODAY: WE HAD A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF.838 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 573.843 MILLION OZ..

AUGUST 20/WITH SILVER DOWN $.26 TODAY: WE HAD A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A WITHDRAWAL OF 3.724 MILLION OZ FROM THE SLV..//INVENTORY REST AT 572.843 MILLION OZ

AUGUST 18/WITH SILVER UP $.44 TODAY: WE HAD A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 2.514 MILLION OZ//THE SLV INVENTORY RESTS TONIGHT AT 576.567 MILLION OZ//

AUGUST 17/WITH SILVER UP $1.27 TODAY: WE HAD NO CHANGES IN SILVER INVENTORY: //INVENTORY RESTS AT 574.053 MILLION OZ//

AUGUST 14/WITH SILVER DOWN $1.31 TODAY, WE HAD A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 6.984 MILLION OZ// //INVENTORY RESTS AT 574.053 MILLION OZ//

AUGUST 13//WITH SILVER UP $1.76 TODAY: WE HAVE TWO HUGE CHANGES IN SILVER INVENTORY AT THE SLV//A PAPER DEPOSIT OF 2.421 MILLION OZ INTO THE SLV AT 2 PM AND ANOTHER DEPOSIT OF 6.984 MILLION OZ AT 5 20 PM/INVENTORY RESTS AT 581.037 MILLION OZ//

AUGUST 12/WITH SILVER DOWN 40 CENTS TODAY: WE HAVE ANOTHER CHANGE IN SILVER INVENTORY AT THE SLV//A WITHDRAWAL OF XX MILLION OZ//INVENTORY RESTS AT XX MILLION OZ/

AUGUST 11/WITH SILVER DOWN $3.25 CENTS, WE HAVE ANOTHER CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 2.41 MILLION OZ//INVENTORY RESTS AT 571.632 MILLION OZ//

AUGUST 10/WITH SILVER UP 1.89 TODAY, WE HAVE ANOTHER HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A WITHDRAWAL OF 3.538 MILLION OZ/INVENTORY RESTS AT 569.491 MILLION OZ//

AUGUST 7/WITH SILVER DOWN 69 CENTS TODAY: WE HAVE ANOTHER HUGE CHANGE IN SILVER INVENTORY: A DEPOSIT OF 0.465 MILLION OZ/INVENTORY RESTS AT 573.029 MILLION OZ.

AUGUST 6/WITH SILVER UP $1.52 TODAY, WE HAVE NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 572.564 MILLION OZ///

AUGUST 5/WITH SILVER UP $1.03 TODAY, WE HAVE A HUGE CHANGE IN SILVER INVENTORY AT THE SLV// A MONSTROUS DEPOSIT OF 5.403 MILLION OZ//INVENTORY RESTS AT 572.564 MILLION OZ//

AUGUST 4/WITH SILVER UP $1.45 TODAY, WE HAVE NO CHANGES IN SILVER INVENTORY: //INVENTORY RESTS AT 367.161 MILLION OZ//

AUGUST 3/WITH SILVER UP 23 CENTS TODAY: WE HAVE A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//SURPRISINGLY ANOTHER WITHDRAWAL OF 0.931 MILLION OZ//INVENTORY RESTS AT 367.161 MILLION OZ//

SEPT 4.2020:

SLV INVENTORY RESTS TONIGHT AT

564.799 MILLION OZ

PHYSICAL GOLD/SILVER STORIES

i) GOLDCORE BLOG/Mark O’Byrne

ii) Important gold commentaries courtesy of GATA/Chris Powell

Jan Nieuwenhuijus: Gold is the most stable currency

Submitted by cpowell on Thu, 2020-09-03 16:09. Section: Daily Dispatches

12:10p ET Thursday, September 3, 2020

Dear Friend of GATA and Gold:

Voima Gold researcher Jan Nieuwenhuijs today disputes a recent video produced by metals consultancy CPM Group that asserts that gold’s value declines over time just as the value of government currencies does.

Nieuwenhuijs writes: “If gold didn’t retain its purchasing power, why would long-term investors and central banks store it in their vaults for decades?

…

“Hardly is gold used for industrial applications, so, again, why hold large stocks of gold if it would lose its value over time?

“The truth is that gold retains its value, and the stability of gold’s purchasing power in the long term is the main reason to own it.”

Nieuwenhuijus’ commentary is headlined “Gold Is the Most Stable Currency” and it’s posted at Voima Gold here:

https://www.voimagold.com/insight/gold-is-the-most-stable-currency

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

No doubt about it: the LBMA’s new transparency rules will likely help the Comex fudge its gold inventory levels. However the continue raiding by Londoners of Comex gold will create huge nightmares for the CME

Ronan Manly: New ‘transparency’ at Bank of England and LBMA likely means to help Comex obfuscate

Submitted by cpowell on Fri, 2020-09-04 00:43. Section: Daily Dispatches

8:42p ET Thursday, September 3, 2020

Dear Friend of GATA and Gold:

By starting to report their gold and silver vault holdings on a one-month instead of a three-month basis, Bullion Star gold researcher Ronan Manly writes today, the Bank of England and London Bullion Market Association are probably not doing any favors for the “transparency” they tout.

…

Rather, Manly speculates, the Bank of England and LBMA are preparing to help the New York Commodities Exchange fudge its own daily vault holdings report as the Comex begins accepting a much broader range of gold bars and facilitates more vaulting and delivery in London.

Manly’s analysis is headlined “London Gold Vault Bait-and-Switch as LBMA Prepares Bigger Changes” and it’s posted at Bullion Star here:

https://www.bullionstar.com/blogs/ronan-manly/london-gold-vaults-bait-an…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

London Gold Vault Bait-And-Switch As LBMA Prepares Bigger Changes

Submitted by Ronan Manly, BullionStar.com

In a coordinated development which signals more than meets the eye, the Bank of England and London Bullion Market Association (LBMA) have together moved to begin reporting gold and silver vault holdings data on a 1 month lagged basis instead of the 3 month lagged basis under which they had been previously reporting vault stocks since 2017.

London Vault Reporting – As Clear as Mud

In addition to the Bank of England’s gold vaults in London, LBMA vault reporting applies to commercial precious metals vaults in London operated by the LBMA bullion banks HSBC, JP Morgan and ICBC Standard Bank, and vaults operated by the LBMA security providers Brinks, Malca-Amit, Loomis and G4S.

Under these new vault reporting changes, it for example now means that as of the end of August, the Bank of England and LBMA have reported claimed gold bar holdings in the London vaults for month-end July (a 1-month lag) instead of for month-end May (a 3-month lag).

The LBMA has also made the same reporting change (from a 3-month to a 1-month lag) for Good Delivery silver bar inventories claimed to be in the LBMA London vaults. Note that while the Bank of England London vaults hold gold bars in custody storage for central bank and bullion bank clients, the Bank of England does not store silver, so the silver data reported by the LBMA applies to just the other seven vault operators listed above.

Putting aside for a moment as to why gold and silver vault stocks in London are not already reported at the end of each and every business day as happens in the COMEX precious metals vaults in New York, this London vault reporting change is suspicious in that the reason stated from both the LBMA and Bank of England is that its an altruistic move to improve gold market transparency. Furthermore, both parties claim that they are following a recommendation (for improved transparency) set out in the UK regulators’ Fair and Effective Market Review (FEMR).

The trouble with this claim is that the FEMR’s final report (of which the Bank of England was one of the authors) was published over 5 years ago in June 2015, so the explanation now being pitched by the LBMA and Bank of England is both hard to fathom as difficult to swallow. That card had already been played by the LBMA in 2017 so the real motive is something else.

Convincing the world that the London gold and silver vault inventories are healthy may be part of the strategy, but not in the way you might think. The real agenda in my opinion is to prepare the London vaults for COMEX gold and silver contract delivery by giving a more recent glimpse into vault stocks but without giving COMEX like visibility. How could a one month lag meet COMEX vault approval requirements you might ask? By bending the rules would be the answer. Whether this plays out the way I think it will, we will have to wait and see.

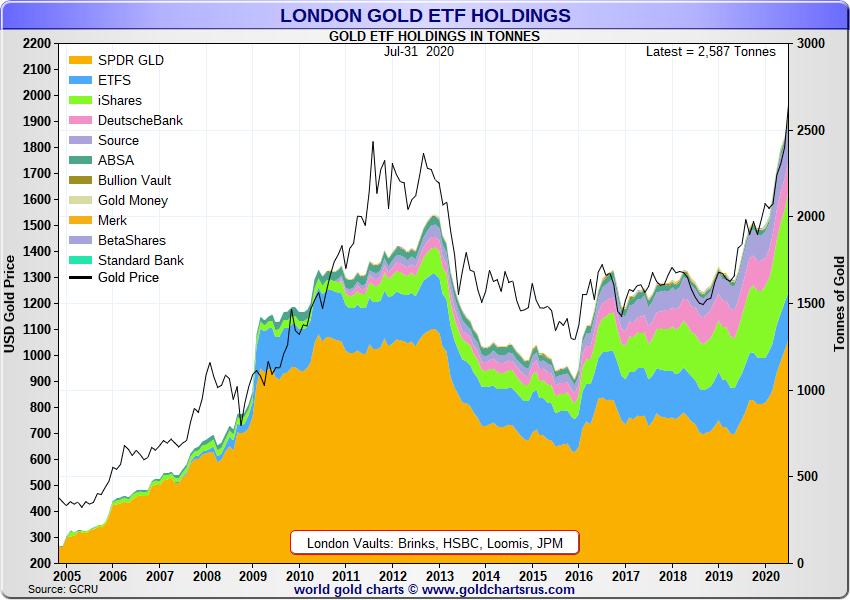

Gold in the Vaults but already Owned

The London gold stocks as of July month-end now total a claimed 8,790 tonnes. Of this total, 5,342 tonnes is claimed to be stored at the Bank of England, meaning that 3,448 tonnes are claimed to be stored in the LBMA London commercial vaults. Subtracting the 2,588 tonnes of ETF gold held in the LBMA London commercial vaults at the end of July, this leaves just 861 tonnes of gold not at the Bank of England and not in ETFs. This 861 tonnes represents gold held by other allocated holders such as institutions, sovereign wealth funds, family offices and ultra high net worth individuals. The bullion banks gold and silver floats then have to compete with these entities to get their fill as well as by raiding GLD and by borrowing gold from central bank clients at the Bank of England.

Singing from the same Song Sheet

According to the Bank of England’s 1 September press release titled “Increased transparency of London gold holdings”:

“The Bank of England will now publish gold holding data with a one-month lag. The reduction from a three-month lag will increase transparency around gold holdings, in line with the Fair and Effective Market Review’s goal to increase transparency in the gold market.”

Likewise, in one of its press releases on the matter dated 1 September and identically titled “Increased Transparency of London Gold Holdings”, the LBMA states that:

“In a move towards greater transparency, LBMA, the Bank of England and the commercial vaults announced earlier today that they will now publish the gold and silver holdings of the vaults in London with just a one month lag (instead of the earlier three-month delay)”

Logically, the LBMA can’t shift its reporting lag from 3 months to 1 month without the Bank following suit and vice-versa, as the two entities and their vault reporting are embedded into each other. So when one moves the other has to also.

Bizarrely, in a second press release on the same day, this one titled “Latest LBMA Data – Clearing and Vault data”, the LBMA self-referentially welcomes its own move, stating that “we welcome the announcement to reduce the time lag for publication of London vault holdings”. Since it was the LBMA itself which actually made both the announcement and the data publication change, you can see that corporate spin is alive and well in London.

As well as trying to justify the change based on the FEMR report which was published more than 5 years ago by three of the tentacles of the City of London financial octopus (Bank of England, HM Treasury and Financial Conduct Authority), this sudden ‘Road to Damascus’ impulse by the Bank of England and LBMA to ‘improve transparency’ around London precious metals vault inventories doesn’t cut the mustard because both parties said the exact same thing back in 2017 when first reporting London precious metals vault holdings.

Additionally, as one of the very authors of the FEMR report in 2015, its rich of the Bank of England, five years later, to now claim its reporting change is based on a recommendation it made to itself five years ago.

As a reminder, the Bank of England first published its gold vault holdings data with a 3-month lag at the end of April 2017, at which time the World Gold Council (WGC) praised the Bank as follows:

“Enhanced transparency from the Bank of England

As a leading custodian of gold, with one of the largest vaults in the world, the Bank of England’s decision is highly significant. Not only will it enhance the transparency of the Bank’s own gold operations; it will also support the drive towards greater transparency across the gold market.

The LBMA then followed suit at the end of July 2017, putting out its press release on 31 July 2017 which was humourly titled “Demystifying London’s Gold and Silver Vault Holdings” and in which it stated that:

“These figures provide an important insight into London’s durability and reinforce the underlying strength of the physical OTC Market.”

“LBMA is therefore very pleased to be able to offer this information on a more timely basis”

At that time, the LBMA also quoted FEMR’s recommendation as follows:

“Transparency

According to the Fair and Effective Markets Review …in markets where OTC trading remains the preferred model, authorities and market participants should continue to explore the scope for improving transparency, in ways that also enhance effectiveness.”

Some questions for the Media

Fast forward to today, more than 3 years later, and its déjà vu all over again with the LBMA and Bank of England now going through the same motions, with the exact same language about transparency, and with the exact same claims. This throws up a number of interesting questions such as:

- With the LBMA now trying to claim that the current move to reporting 1 month lagged vault data is in the interests of transparency, this begs the question as to what exactly was the 3 month lagged data, a mere partial demystifying of London’s gold and silver vault holdings?

- Why does the LBMA now feel the need to again “reinforce the underlying strength of the physical OTC Market” by moving to a 1 month reporting lag? Could it be that the underlying strength of the physical OTC market is not so strong?

- Why was this precious metals vault data not provided on a more timely basis over 3 years ago when the LBMA began vault reporting in 2017?

- Why did the FEMR committee not pull up the LBMA and the Bank of England back in 2017 to direct them to report vault data on a 1 month basis instead of on a 3 month lag?

- Why is this move now happening more than 3 years after the initial reporting, and more than 5 years after the FEMR’s final report was published in June 2015?

- Why are the mainstream financial media not asking these simple questions to the Bank of England and the LBMA?

- Why are the mainstream financial media not covering the recent move by COMEX to ‘mass approve’ for COMEX contract delivery, all LBMA gold and silver refiner bar brands, both on the current and former London Good Delivery Lists?

Fair and Effective Markets? Pull the other one

Nor is it wise for the LBMA and the Bank to have raised the word FEMR, for as in the old adage, they should have let sleeping dogs lie. When it was launched in June 2014, the remit of the Fair and Effective Markets Review (FEMR) was to investigate the Fixed Income, Currency and Commodities (FICC) markets in the wake of massive benchmark manipulation scandals that had taken place in LIBOR, in the London Gold Fix, and in Foreign Exchange indexes. Its final report (the FEMR report) published in June 2015 was a summary of these investigations as well as recommendations (recommended with a straight face) to improve market trading standards and to crack down on market abuse.

Hilariously, while one of the outcomes of the FEMR recommendations was the 2017 implementation of the LBMA Global Precious Metals Code, a Code of Conduct which all LBMA members had to sign and commit to, manipulation in the precious metals markets continued apace for years after the FEMR report was published, with LBMA heavy weights such as JP Morgan and Scotia being progressively involved in bigger and bigger gold and silver price manipulations since then. See Scotia misconduct here in 2020 and JP Morgan here in 2019.

The LBMA also had to contend with the embarrassment that one of the LBMA Board members, Michael Nowak of JP Morgan fame, was charged in 2019 by the US Department of Justice (DoJ)for engaging in a racketeering conspiracy under the “Racketeer Influenced and Corrupt Organizations Act, or RICO, as well as other federal crimes in connection with manipulating precious metals futures markets.”

A further outcome of the FEMR report was that the LBMA Gold Price auction (i.e. the re-disguised former London Gold Fix auction launched in March 2015 by the LBMA bullion banks) became a Regulated Benchmark under which manipulation is now a criminal offence. However, this too turns out to have been nothing more than a sham because for example, as recently as last week on 27 August 2020, as the COMEX gold price was being slammed, the afternoon LBMA Gold Price auction took 33 rounds to settle over 21 minutes, while the 12 direct participants (all LBMA members and mainly LBMA bullion banks) collectively first held the bid volume unchanged for 16 rounds, then after round 17 when the price had fallen by $28, then held the ask volume unchanged until round 33. More on that auction in due course.

The Recent London Vault Data

Turning to the most recent vault data now available following the LBMA – Bank reporting change, there is also nothing obvious in the data that would explain a rationale for the Bank and LBMA making move at this time. Granted, the LBMA claims the London gold vault stocks are at an all time high.

However, with most of that gold held by long term holders and at least some of it claimed by multiple parties, a record gold vault stock in itself doesn’t mean much. Changing from a 3-month to a 1-month reporting window for a one hit wonder record claim would be like firing all your ammo for little or no effect. While the new data itself doesn’t justify the change, its worth highlighting all the same.

Before this week’s change, the LBMA and Bank of England would have, at the end of August, been reporting vault holdings as of May month end. With the move to a 1-month reporting lag, the LBMA and Bank of England have now reported three month end vault holdings totals at the same time, up until July month end. from next month they will just report one month’s data with a 1 month lag.

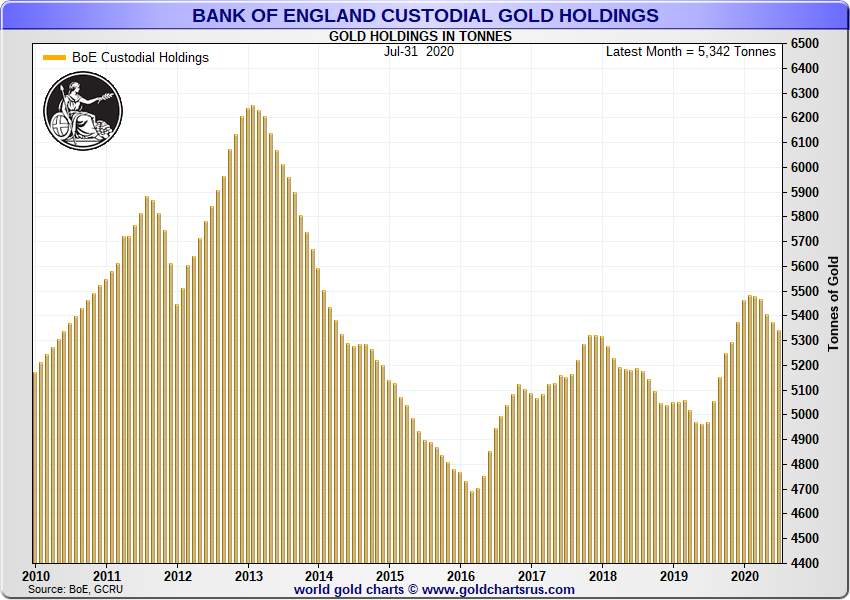

Note that the Bank of England reports its gold vault data separately, while the LBMA vault data figures include all the London vaults, both commercial vaults and the Bank of England vaults. As such the Bank of England data is a subset of the overall totals. Looking first at the Bank of England (BoE) gold vault data, the BoE vaults lost a net 59.9 tonnes in May, lost a net 29.4 tonnes in June, and lost another net 33.1 tonnes in July. In total over the three months from April month-end to July month-end the BoE vaults saw a net outflow of 122.4 tonnes of gold from 5464.4 tonnes at the end of April to 5342 tonnes of gold at the end of July.

Could this be central bank gold sales or withdrawals from the Bank of England vaults? Possibly. However, the more intriguing possibility is that these outflows are SPDR Gold Trust (GLD) gold bar holdings that had been allocated to the GLD over April to June using the Bank of England as gold sub-custodian, and that over May to July were being transferred out of the Bank of England vaults to the HSBC vault in London. This possibility was covered in the BullionStar article a few weeks ago titled “GLD continues to source gold at the Bank of England, at an escalating rate“.

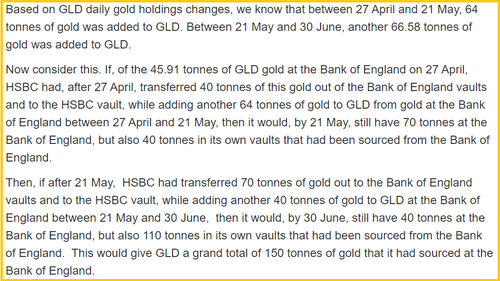

The reason that this is possible is that using GLD SEC filings and GLD daily gold holdings changes, the SPDR Gold Trust could have transferred out up to 110 tonnes of gold over May and June. GLD was also was also still holding 40 tonnes of gold in the Bank of England at month end. The majority of this too could have been transferred out of the Bank of England vaults in July. For more details see the screenshot below.

Looking at the overall London vault data for gold (including the Bank of England vaults) the overall figure claims a net addition of 308 tonnes of gold between the end of April and the end of July, comprising a net 2.3 tonnes in May, a 184 tonnes net inflow in June, and a 121.7 tonnes net inflow in July.

Given the 122.4 tonnes outflows from the Bank of England vaults over that time, this means that the other vaults (excluding the BoE) together saw a net 430.4 tonnes increase over the May to July period, which comprised 62.2 tonnes in May, 213.3 tonnes in June, and 154.9 tonnes in July.

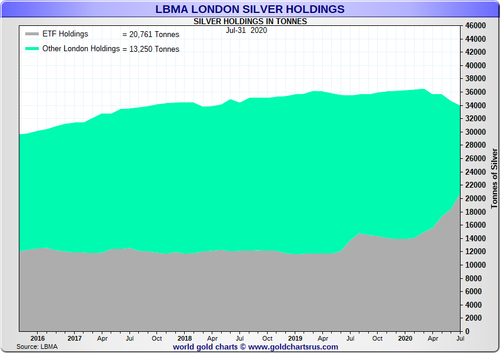

Turning to silver, which is not held at the Bank of England vaults, the LBMA vaults claim that between the end of April and the end of July, the amount of silver held in the London commercial vaults fell from 35,667.8 tonnes to 34,011.9 tonnes, for a net outflow of 1,655.9 tonnes. The bulk of those net silver outflows were in June and July, with the vaults recording a net withdrawal of 915 tonnes of silver in June and 690 tonnes in July, with a residual 51 tonne net outflow in May. With 1600 tonnes of silver leaving the London vaults over June and July, that may be a story for Bloomberg to follow up on.

Conclusion – A More Compelling Reason

On first principles, the LBMA and Bank of England want their vault holdings a) to appear more transparent and b) to create a perception that total metal stocks are deep, and healthy.

But the new claims about transparency and the FEMR report are risible. There is nothing transparent about the London gold and silver markets. Unlike the equity and bond markets, there is no reporting of transactions and trades in the OTC London gold and silver markets. There is no data whatsoever about positions and transactions in the London gold lending market, no data on which commercial banks hold gold accounts at the Bank of England, no data on the identities of central bank gold custody customers of the Bank of England, no data on the size of the enormous unallocated gold and silver liabilities of the bullion banks, no published data on the location of the London commercial vaults, and no published audits of the claimed gold and silver inventories in the LBMA and Bank of England vaults. And that’s just a flavour.

In short, the LBMA bullion banks and Bank of England couldn’t care less gold and silver market transparency. What they do care about though is projecting the illusion of transparency. No more so than when COMEX soon moves to allow gold and silver in the LBMA London vaults to be delivered against the COMEX GC 100 and SI 5000 gold and silver futures contracts.

Last week here I covered the recent move by the COMEX to mass approve all of the gold and silver refiner bar brands of the LBMA (both those on the current and on the former London Good Delivery lists for gold and silver), which is a prelude to facilitating London gold and silver inventories delivery against the COMEX flagship GC 100 oz gold and Si 5000 oz silver futures contarcts . See “LBMA-COMEX collusion intensifies as CME approves 267 LBMA gold and silver bar brands” for details.

As the CME rule wording for the GC 100 contract will probably be when its made: “The depository for gold deliverable against the Gold futures (GC) contract must qualify and be designated a weighmaster and must be located within a 150-mile radius of the City of New York or in London, UK.”

Anyone familiar with the approved COMEX vaults in New York and environs will knows that these vaults publish daily end of day inventory totals of the amount of gold and silver held in each of the vaults, e.g. the New York vaults of HSBC, JP Morgan and Brinks.

In early July when highlighting the recently launched COMEX (Enhanced Delivery) 400 oz contract (4GC), which was a trail balloon for London vault delivery, a Bloomberg article spelled out these requirements:

“Exchange rules require vaults to report daily inventory levels even when metal isn’t marked for delivery. “When London vault applications are submitted and approved, they will follow the same guidelines as those of all exchange-approved facilities for metals,” a CME spokesperson said.

…The same rules will apply to storage facilities in London, potentially bringing more transparency if vaults apply to hold inventory backing the contract.”

My contention however, is that it’s a bridge too far for the secretive and sensitive LBMA vaults in London (HSBC, JP Morgan, Brinks Radius Park, Malca-Amit etc) to allow daily publications of the amount of gold and silver in these commercial vaults. Powerful holders would not want the veil lifted. Hence, to railroad through the London vault delivery into COMEX contracts, a compromise has been reached between the bullion banks and regulators via upcoming CME and CFTC rule changes. After all, as a Scotia or JP Morgan bullion bank trader might say “Rules are made to be broken”.

Thus with this new shift from a 3 month to a 1 month vault reporting lag, the COMEX-LBMA gold pool tag team can, with a bit of spin, hold up a copy of the FEMR report and claim that the London vaults have made a Herculean transparency effort, indeed one that has the blessing of regulators, and successfully ‘lobby’ for a COMEX rule change to allow the London vaults a derogation to only report to COMEX on a 1 month lagged basis instead of the daily end of day requirement of their New York brethren.

* * *

This article was originally published on the BullionStar.com website under the same title “London gold vault Bait-and-Switch as LBMA prepares bigger changes“.

END

Alasdair Macleod: Central banks are running out of road with inflation

Submitted by cpowell on Fri, 2020-09-04 02:26. Section: Daily Dispatches

By Alasdair Macleod

GoldMoney, St. Helier, Jersey, Channel Islands

Thursday, September 3, 2020

If you think that price inflation runs at about 1.6 percent you have fallen for the Consumer Price Index myth of the U.S. Bureau of Labor Statistics.

Two independent analysts using different methods — the Chapwood Index and Shadowstats.com –prove that prices are rising at a far faster rate, more like 10 percent annually and have been doing so since 2010.

…

This article discusses the consequences of price inflation suppression, particularly in the light of Federal Reserve Chairman Jerome Powell’s Jackson Hole speech, in which he downgraded the importance of price inflation in the Fed’s policy objectives in favor of targeting employment.

It concludes that the reconciliation between the BLS CPI figure and the true rate of price inflation is inevitable and will be catastrophic for the Fed’s policy of suppressing interest rates, its maximization of the “wealth effect” of inflated financial asset prices, and for the dollar itself. …

… For the remainder of the analysis:

https://www.goldmoney.com/research/goldmoney-insights/inflation-runnin

Your weekend reading material:

Inflation — running out of road

If you think that price inflation runs at about 1.6% you have fallen for the BLS’s CPI myth. Two independent analysts using different methods — the Chapwood Index and Shadowstats.com — prove that prices are rising at a far faster rate, more like 10% annually and have been doing so since 2010.

This article discusses the consequences of price inflation suppression, particularly in the light of Jerome Powell’s Jackson Hole speech when he downgraded the importance of price inflation in the Fed’s policy objectives in favour of targeting employment.

It concludes that the reconciliation between the BLS CPI figure and the true rate of price inflation is inevitable and will be catastrophic for the Fed’s policy of suppressing interest rates, its maximisation of the “wealth effect” of inflated financial asset prices, and for the dollar itself.

Monetary inflation takes off

Last week saw a virtual Jackson Hole conference, where Jerome Powell downgraded inflation targeting in favour of the other Fed mandate, employment. And Andrew Bailey, Governor of the Bank of England, claimed “We are not out of firepower by any means…. to be honest it looks from today’s vantage point that we were too cautious about our remaining firepower pre-Covid”.

Both men were tearing up earlier scripts. Since they will likely tear up these as well there is little point in examining them further. For the fact is that all the major central banks are trapped in problems of their own making, and some time ago they lost control of their destinies. Figure 1 below encapsulates the problem.

M1 is the US narrow money indicator. Over 28 years from 1980, it grew at a simple average annual rate of 8.8% per annum. From 2008 to last February, following the Lehman crisis it grew at an average annual rate of 16.6%, From 24 February in six months it has grown by 34%, which is an average annual rate of 68%. What Powell effectively admitted at Jackson Hole was that M1 annualised growth of 68% was not enough to ensure the US economy would recover. He would have had to downplay the effect on prices to create leeway for further increases in the rate of monetary growth.

The Fed is evidently trapped by its inflationary policies. And the US Bureau of Labour Statistics, which calculates US consumer price indices, will have to work even harder to suppress the evidence of price inflation. Over the last ten years they have recorded an average annual rate of price inflation of 1.69% measured for US cities (CPI-U), and for the first half of 2020 they say it was 0.83%, or 1.66% annualised. To maintain this fiction has been a remarkable feat of statistical management, when compared with the unadulterated fifty city figures collected by the Chapwood Index.[i] Figure 2 shows the gap between the BLS’s CPI and Chapwood’s unadulterated estimates.

It is not our purpose to imply that the Chapwood Index of prices is an accurate representation of price inflation. We can talk about the general level of prices in a theoretical sense, but in practice it cannot be measured because each consumer has a different price experience. It is only when one subscribes to the macroeconomics version of economics and talk of unworldly aggregates that a figure is calculated. But if you remove the changes in the BLS’s calculation methods since 1980, you end up with a similar rate of price inflation to that of the Chapwood index, which is confirmed by John Williams at Shadowstats.com.

Now let us reconsider Jay Powell’s and Andrew Bailey’s Jackson Hole speeches in this light. Instead of an average rate of annual price inflation over the last ten years of 1.69%, Chapwood tells us that that average is 10.1%, varying between 13.4% in Sacramento and 7.1% in Albuquerque. It is against this background that Powell proposes to downgrade the Fed’s inflation mandate. Given M1 monetary inflation averaged 16% between the Lehman crisis and last February (see Figure 1) the price effect recorded by Chapwood is not surprising. But it gets worse for Powell. If we accept Chapwood’s numbers as being realistic and use them to deflate nominal GDP, we can see that the US economy has been in a slump for the last ten years: adjusted GDP has contracted by 65% since 2010. This is illustrated in Figure 3.

The only offset is the Fed’s much vaunted wealth effect that comes from speculating in financial assets. But that relief is only available to American investors and those employed in financial and related services, disadvantaging the poor and unemployed who inhabit Main Street, the non-financial economy. It is in this context, perhaps, that we should view the current civil unrest and racial strife in America.

Waking up to reality

Nobody in the investment and media mainstreams, let alone at the Fed, appears to understand the extent of statistical distortions and the consequences. We can count them all, including economics professors and senior figures in the investment game, among the 999,999 out of the proverbial million who don’t understand money and the consequences of its debasement.

The other side of the slump in real GDP illustrated in Figure 3 is the transfer of wealth from producers and consumers in the non-financial economy. If, as implied by a Chapwood GDP deflator, GDP has declined by 65% in real terms since the Lehman crisis, then we can say that gives us an approximation of the net wealth transfer through monetary inflation from producers and consumers to the state, the Fed, the commercial banks and their favoured customers.

If macroeconomists think that inflation stimulates demand, apart from initial artificial and final catastrophic effects perhaps, they are wrong: it kills it. The element of monetary debasement that ends up in government hands, taken from the productive non-financial sector along with all taxes, is wasted because a government produces little more than interference with an otherwise working economy. The true purpose of monetary inflation is not to improve our lives but to finance government deficits.

The element of bank credit inflation which ends up with the banking system’s favoured customers, comprised mainly of the large lumbering zombie corporations of yesteryear, disadvantages the more dynamic entrepreneurial businesses among the small and medium size sectors to the extent they are denied similar credit terms. The element of monetary inflation that ends up fuelling speculation in the financial economy is robbed from the liquidity balances and earnings of producers and consumers without their knowledge or consent. Monetary inflation is virtually impossible for the robbed to detect, not being revealed by accounting methods.

Despite M1 money supply accelerating, deflation remains a common fear, prompted doubtless by commercial banks being reluctant to extend credit at a time of increasing loan risk. But the Fed is already concerned that the commercial banks will not pass on its monetary policies, which is why it is bypassing them by buying corporate bonds and commercial mortgage backed securities through BlackRock. Other similar schemes are sure to follow. But it always amounts to supporting yesterday’s businesses, which the markets would otherwise likely judge to be today’s failures.

Clearly, any tendency for bank credit to contract will be countered by the Fed through further and appropriately aggressive expansion of narrow money, for which Powell was clearing the decks at Jackson Hole. It could lead to an even faster rate of M1 growth than the annualised 68% since February. Those who worry about the deflation of bank credit are therefore premature in their analysis and obviously believe in monetary inflation as an economic cure-all. But in real terms the US economy is already contracting because monetary inflation is leading to far faster price rises than is generally realised. Monetary inflation as a policy was only going to make things worse.

It is also a myth that monetary inflation is helpful to businesses. While an artificial and temporary cheapening of domestic manufacturing costs is lauded by neo-Keynesians, businesses need monetary stability in order to calculate the value of future payments: a healthy economy depends on business calculation which relies on the certainty of price stability. It is not good enough to say that suppressing interest rates benefit businesses: it is only true for over-indebted zombie businesses which with state aid can survive a little longer. But that is an artificial boost in their fortunes at the expense of a hidden inflation tax on everyone else. Not only does inflation coupled with the suppression of interest rates promote and sustain these commercial failures, but by doing so it also restricts the redistribution of all forms of capital into more productive use.

If the effects of monetary inflation become apparent to actors in the non-financial economy, they begin a process of reducing their monetary liquidity, knowing that money will buy less in the future than at the present. Until now, economic actors appear to place greater credence in the BLS’s inflation figures than from their own experience; but that cannot last. When the effect on prices of an annualised expansion of narrow M1 money of 68% becomes apparent it is likely to undermine widespread complacency. And when people realise that the general level of prices is rising despite the slump in economic activity, they will begin to dump all forms of dollar liquidity they possess in return for goods, driving price inflation even higher than increased money quantities would suggest. The transition from the false stability of prices as measured by government statistics into a final crack-up boom when money is dumped as worthless need not take long: all it needs is a trigger.

Shutting our eyes to this reality is nonsensical. The BLS’s CPI figures will prove to be defined by a vulgarity suggested by its own acronym. And when markets rumble it, the Fed will be unable to contain US Treasury yields at anything like current low levels. If we take the Chapwood price inflation figures for this year, then the current yield on the 10-year US Treasury bond is minus 9.45%, which must be close to a record in the annals of US monetary history.

Let us assume, for a moment, that financial markets adjust to price inflation rates closer to the Chapwood figures, which have already accelerated from an annual average of 9.6% for 2019 to 10.1% in the first half of 2020. US Treasury yields would initially rise at the short end of the curve to reflect that figure, perhaps with a margin over it. With the government’s budget deficit sure to exceed $3 trillion in the current fiscal year (to October) and perhaps double that next, the 2019 interest bill of $383bn on existing debt and the higher rate for US Treasury bond roll-overs plus the interest on new debt, total annual funding costs are likely to rapidly approach a trillion dollars . It is a debt trap sprung firmly shut and investors will take that into account.

An out of control budget deficit will continue to be funded through quantitative easing — there’s no other way. But a rise in bond yields will also have a catastrophic effect on equities, on their valuations as financial assets, on the cost of new and rolled-over corporate debt, and on valuations for loan collateral. The much-vaunted wealth effect, which has concealed the collapse in real GDP since the Lehman crisis, will quickly evaporate. Because the Fed has gone all in on using monetary inflation to sustain a financial bubble, it has also tied the dollar’s future to it, so its bursting is bound to have a profoundly negative effect on the dollar’s purchasing power.

The inflation problem is about to get worse

We have now established that the Fed is committed to accelerating the increase in the money quantity. We have also established that its monetary policies combined with statistical price manipulation has had the opposite effect of that intended, so much so that since the Lehman crisis the US economy has contracted in real terms by more than half, which any competent sociologist will tell you leads to civil unrest — plainly evidenced today. We have reached a high point in macroeconomic madness.

It’s about to get worse.

Despite the post-Lehman acceleration of money supply, last September the repo market blew up on the day when Deutsche Bank sold its prime brokerage to BNP, the French global systemically important bank — a G-SIB. It may or may not have been the trigger for ongoing problems in the repo market, but clearly, there were liquidity issues in the US’s financial and banking system at that time.

It came on top of last year’s contraction in international trade, due in large measure to trade tensions between America and China with knock-on effects for China’s trading partners, such as Germany. Non-banks, principally insurance companies, pension funds and hedge funds acting directly or through agencies had accumulated large positions in fx swaps, ripping out interest differentials between euros and yen on one side, and a rising dollar on the other. The G-SIBs, particularly JPMorgan, had no excess reserves available to finance further non-bank speculation in this market. The turn of the cycle of bank credit expansion was upon us due to these liquidity issues, instead of the normal end of cycle problem of over-geared bank balance sheets facing escalating lending risk. However, thanks to covid-19 lending risk is now rising rapidly.

The S&P500 index crashed by fully one-third between mid-February and 23 March, as institutional investors suddenly realised the deflationary consequences of liquidity shortages in the banking system. It took the Fed’s cut in its funds rate from 1% to 0% on 16 March and its statement on 23 March, when it promised new QE and infinite monetary support for businesses and households, to relieve the liquidity problem.[ii]

At the same time came the covid-19 lockdowns. China had imposed lockdowns in Hubei Province in January, but from early March the rest of the world started to go into lockdown, with the UK going into lockdown on 23 March. In the US a number of states announced lockdowns from 17 March, with New York locking down on 22 March. The Fed’s actions, cutting its funds rate on 16 March and announcing infinite QE on 23 March were both timely and a financial watershed.

In all the mayhem of lockdowns it is easy to forget that the collapse of overnight liquidity was already a six-month old evolving crisis, marking a cyclical turning point in the expansion of bank credit. Unlike Lehman, which reflected a cycle of excessive property speculation, this one has its roots in a downturn in global and now domestic trade, as well as a global currency imbalance in favour of the dollar. According to US Treasury TIC figures, at end-June 2019, which are the most recent available estimates, foreigners owned $20,534 bn of US securities.[iii] To this must be added bills and cash, which on the most recent TIC report (June 2020) totalled a further $6,227 bn.[iv] Therefore, putting to one side the different dates of record and higher equity valuations today, foreign ownership of dollars is roughly $27 trillion, which equates to 125% of US GDP in 2019.

Foreign ownership amounts to such a large figure relative to GDP due to the dollar’s reserve status, foreign participation in funding US budget deficits and anticipation of an expansion of future trade. But as we have seen, global trade began to contract in 2019, which if continued, reduces the need to hold dollars. And we can be certain that if foreign holders take the view that the US economy is in a slump, beyond their requirements for marginal liquidity there is no reason for them to hold dollars at all because they can always buy them when actually needed.