GOLD:$$1954.60 DOWN $0.90 The quote is London spot price

Silver:$27.14 UP 0.47 London spot price ( cash market)

DONATE

Closing access prices: London spot

i)Gold : $1956.80 LONDON SPOT 4:30 pm

ii)SILVER: $27.12//LONDON SPOT 4:30 pm

CLOSING FUTURES PRICES: KEY MONTHS

OCT GOLD: $1955.50 CLOSE 1.30 PM// SPREAD SPOT/FUTURE OCT /: $0.90 BACKWARD

DEC. GOLD $1947.40 CLOSE 1.30 PM SPREAD SPOT/FUTURE DEC $9.80/ CONTANGO ($2.30 ABOVE NORMAL CONTANGO)

CLOSING SILVER FUTURE MONTH

SILVER SEPT COMEX CLOSE; $27.30…1:30 PM.//SPREAD SPOT/FUTURE SEPT// : ( 14 CENT CONTANGO// 14 CENTS ABOVE NORMAL CONTANGO)

SILVER DECEMBER CLOSE: $27.38 1:30 PM SPREAD SPOT/FUTURE DEC. : 22 CENTS PER OZ CONTANGO ( 14 CENTS ABOVE NORMAL CONTANGO)

COMEX DATA

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

receiving today: 8/175

issued: 148

EXCHANGE: COMEX

CONTRACT: SEPTEMBER 2020 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,937.800000000 USD

INTENT DATE: 09/11/2020 DELIVERY DATE: 09/15/2020

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

435 H SCOTIA CAPITAL 1

624 C BOFA SECURITIES 107

657 C MORGAN STANLEY 48

657 H MORGAN STANLEY 24

661 C JP MORGAN 148 8

732 C RBC CAP MARKETS 6

800 C MAREX SPEC 3

905 C ADM 5

____________________________________________________________________________________________

TOTAL: 175 175

MONTH TO DATE: 4,166

NUMBER OF NOTICES FILED TODAY FOR SEPT CONTRACT: 175 NOTICE(S) FOR 17,500 OZ (0.5443 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 4166 NOTICES FOR 416,600 OZ (12.958 tonnes)

SILVER

225 NOTICE(S) FILED TODAY FOR 1,125,000 OZ/

total number of notices filed so far this month: 9332 for 46.660 MILLION oz

BITCOIN MORNING QUOTE $10451 UP 119

BITCOIN AFTERNOON QUOTE.: $10,661 UP 328

GLD AND SLV INVENTORIES:

WITH GOLD DOWN 90 CENTS AND NO PHYSICAL TO BE FOUND ANYWHERE:

WITH ALL REFINERS CLOSED//MEXICO ORDERING ALL MINES SHUT: WHERE ARE THEY GETTING THE “PHYSICAL?

SURPRISINGLY WE LOST (WITHDRAWAL) A HUGE 4.96 TONNES FROM THE GLD//

GLD: 1,248.00 TONNES OF GOLD//

WITH SILVER UP $0.47 TODAY: AND WITH NO SILVER AROUND:

SURPRISINGLY WE HAD TWO MAJOR WITHDRAWALS: i) 1.675 MILLION OZ FROM THE SLV// 4 pm

ii) at 5:22 pm: .931 million oz//

RESTING SLV INVENTORY TONIGHT:

SLV: 555.956 MILLION OZ./

XXXXXXXXXXXXXXXXXXXXXXXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI ROSE BY A TINY 214 CONTRACTS FROM 160,869 UP TO 161,083, AND CLOSER TO OUR NEW RECORD OF 244,710, (FEB 25/2020. THE GAIN IN OI OCCURRED DESPITE OUR $0.39 FALL IN SILVER PRICING AT THE COMEX. IT SEEMS THAT THE LOSS IN COMEX OI IS DUE TO ATTEMPTED BANKER SILVER SHORT COVERING.. COUPLED AGAINST THE WEAKEST EXCHANGE FOR PHYSICAL ISSUANCE EVER RECORDED: 0 EFPs, MINOR LONG LIQUIDATION, A SMALL DECREASE IN SILVER OZ STANDING AT THE COMEX FOR SEPT. WE HAD A SMALL NET GAIN IN OUR TWO EXCHANGES OF 348 CONTRACTS (SEE CALCULATIONS BELOW).

WE WERE NOTIFIED THAT WE HAD THE WEAKEST EVER NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: ZERO, AS WE HAD THE FOLLOWING ISSUANCE: SEP 0; DEC: 0, MARCH 0 FOR ZERO ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 0 CONTRACTS. WITH THE TRANSFER OF 0 CONTRACTS. THE BANKERS ARE NOW BEING BITTEN BY THOSE SERIAL FORWARDS ARE BEING EXERCISED AND COMING BACK TO NEW YORK TO REDEEM METAL. OUR BANKERS CAN NO LONGER AFFORD TO ISSUE THESE VEHICLES. THUS THE AMOUNT TRANSFERRED TO LONDON IS 0 MILLION OZ

HISTORY OF SILVER OZ STANDING AT THE COMEX FOR THE PAST 26 MONTHS.

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

10.025 MILLION OZ INITIAL STANDING IN AUGUST.

43.030 MILLION OZ INITIALLY STANDING IN SEPT. (HUGE)

7.32 MILLION OZ INITIALLY STANDING IN OCT

2.630 MILLION OZ STANDING FOR NOV.

20.970 MILLION OZ FINAL STANDING IN DEC

5.075 MILLION OZ FINAL STANDING IN JAN

1.480 MILLION OZ FINAL STANDING IN FEB

23.005 MILLION OZ FINAL STANDING FOR MAR

4.660 MILLION OZ FINAL STANDING FOR APRIL

45.220 MILLION OZ FINAL STANDING FOR MAY

2.205 MILLION OF FINAL STANDING FOR JUNE

86.470 MILLION OZ FINAL STANDING IN JULY.

6.475 MILLION OZ FINAL STANDING IN AUGUST

52.0150 MILLION OZ INITIALLY STANDING IN SEPT

FRIDAY, AGAIN OUR CROOKS USED COPIOUS PAPER IN ORDER TO LIQUIDATE SILVER’S PRICE…AND THEY WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL $0.39) ).. AND, OUR OFFICIAL SECTOR/BANKERS WERE UNSUCCESSFUL IN THEIR ATTEMPT TO FLEECE ANY SILVER LONGS. THE RAIDS THESE PAST SEVERAL DAYS WERE ORCHESTRATED BY THE BIS WITH MEGA ASSISTANCE FROM OUR CRIMINAL BANKERS. THEIR CHIEF AIM WAS TO REMOVE SPECULATORS FROM THEIR LONG POSITIONS.THEY FAILED AGAIN WITH FRIDAY’S TRADING…. WE ALSO HAD ii) A ZERO ISSUANCE OF EXCHANGE FOR PHYSICALS 2) A SMALL LOSS IN SILVER OZ STANDING FOR SEPTEMBER, 3) SMALL COMEX GAIN AND 4) ZERO LONG LIQUIDATION. YOU CAN BET THE FARM THAT OUR BANKERS ARE DESPERATE TO LIQUIDATE THEIR HUGE SHORT POSITIONS IN SILVER..

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS

SEPT.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY /FOR MONTH OF SEPT:

6767 CONTRACTS (FOR 9 TRADING DAY(S) TOTAL 6767 CONTRACTS) OR 33.84 MILLION OZ: (AVERAGE PER DAY: 751 CONTRACTS OR 3.759 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF SEPT: 33.84 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 4.83% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2020 TO DATE SILVER EFP’S: 1,419.91 MILLION OZ.

JANUARY 2020 EFP TOTALS SO FAR: 181.61 MILLION OZ

FEB 2020 EFP’S TOTAL : …… 259.600 MILLION OZ

MARCH EFP’S ….. 452.280 MILLION OZ //TOTALS//AND A NEW RECORD FOR THE MONTH)

APRIL EFP 95.355 MILLION OZ. (EX. FOR PHYSICALS BECOMING A LOT LESS)

MAY EFP FINAL: 77.27 MILLION OZ

JUNE EFP 71.15 MILLION OZ.

JULY EFP 133.95 MILLION OZ/ (EXCHANGE FOR PHYSICALS STARTING TO RISE EXPONENTIALLY AGAIN)

AUGUST EFP 127.46 MILLION OZ (EXCHANGE FOR PHYSICALS STARTING TO DECREASE AGAIN)

SEPT EFP 33.84 MILLION OZ (EXCHANGE FOR PHYSICALS DRAMATICALLY FALLING OFF A CLIFF)

RESULT: WE HAD A TINY SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 214, DESPITE OUR $0.39 FALL IN SILVER PRICING AT THE COMEX ///FRIDAY.…THE CME NOTIFIED US THAT WE HAD A ZERO SIZED EFP ISSUANCE: YES 0 CONTRACTS EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS.

TODAY WE GAINED A TINY SIZED 214 OI CONTRACTS ON THE TWO EXCHANGES (DESPITE OUR $0.39 FALL IN PRICE)//

THE TALLY//EXCHANGE FOR PHYSICALS

i.e 0 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH A SMALL SIZED INCREASE OF 214 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH OUR 39 CENT FALL IN PRICE OF SILVER/AND A CLOSING PRICE OF $26.67 // FRIDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY.

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.804 BILLION OZ TO BE EXACT or 115% of annual global silver production (ex Russia & ex China).

FOR THE NEW AUGUST DELIVERY MONTH/ THEY FILED AT THE COMEX: 225 NOTICE(S) FOR 1,125,000 OZ OF SILVER.

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.70//TODAY’S RECORD OF 244,705 WAS SET WITH A PRICE OF: 18.91 (FEB 25/2020)

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ; AUGUST 10.025 MILLION OZ/ SEPT 43.030 MILLION OZ//OCT: 7.665 MILLION OZ// NOV: 2.630 MILLION OZ//DEC: 20.970 MILLION OZ; JAN: 5.075 MILLION OZ.//FEB 1.480 MILLION OZ//MAR: 23.005 MILLION OZ/APRIL 4.660 MILLION OZ//MAY 45.220 MILLION OZ//JUNE: 2.205 MILLION OZ// JULY 86.470 million oz//AUGUST 6.475 MILLION OZ//SEPT. 52.015 MILLION OZ//

- THE RECORD PRIOR TO TODAY WAS SET IN FEB 25/2018: 244,710 CONTRACTS, WITH A SILVER PRICE OF $18.90//.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017 RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

GOLD

IN GOLD, THE COMEX OPEN INTEREST FELL BY A SMALL SIZED 1804 CONTRACTS TO 568,244 AND FURTHER FROM OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE SMALL SIZED LOSS IN COMEX OI OCCURRED WITH OUR CONSIDERABLE FALL IN PRICE OF $14.80 /// COMEX GOLD TRADING// FRIDAY//WE HAD SOME BANKER SHORT COVERING AS WE HAD A SMALL LOSS ON OUR TWO EXCHANGES… VERY FEW HAVE LEFT THE GOLD ARENA. WE ALSO HAD A GOOD ADVANCE IN TONNAGE STANDING AT THE GOLD COMEX FOR SEPTEMBER ACCOMPANYING A SMALL EXCHANGE FOR PHYSICAL ISSUANCE. THIS ALL HAPPENED WITH OUR FALL IN PRICE OF $14.80.

WE HAD A VOLUME OF 0 4 -GC CONTRACTS//OPEN INTEREST 127//

WE LOST A SMALL SIZED 996 CONTRACTS (3.097 TONNES) ON OUR TWO EXCHANGES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A SMALL SIZED 808 CONTRACTS:

CONTRACT .; OCT: 0 DEC: 808; FEB: 0 ALL OTHER MONTHS ZERO//TOTAL: 808. The NEW COMEX OI for the gold complex rests at 568,244. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EXCHANGE DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A SMALL SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 996 CONTRACTS: 1804 CONTRACTS DECREASED AT THE COMEX AND 880 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS OF 996 CONTRACTS OR 3.097 TONNES. FRIDAY, WE HAD A LOSS OF $14.80 IN GOLD TRADING..….

AND WITH THAT LOSS IN PRICE, WE HAD A SMALL SIZED LOSS IN TOTAL/TWO EXCHANGES GOLD TONNAGE OF 3.097 TONNES!!!!!! THE BANKERS WERE SUCCESSFUL IN THEIR ATTEMPT TO LOWER GOLD’S PRICE (IT FELL $14.80). WE HAD A SOME BANKER SHORT COVERING OPERATION . WE ALSO HAD SMALL ISSUANCE IN EXCHANGES FOR PHYSICAL. THE BANKERS COULD HARDLY FLEECE ANY OF OUR SPECULATOR LONGS FROM THEIR POSITIONS

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES:

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (880) ACCOMPANYING THE SMALL SIZED LOSS IN COMEX OI (1804 OI): TOTAL LOSS IN THE TWO EXCHANGES: 996 CONTRACTS. WE NO DOUBT HAD 1 ) SOME BANKER SHORT COVERING ,2.)A GOOD ADVANCE IN STANDING AT THE GOLD COMEX FOR THE FRONT SEPT. MONTH, 3) MINOR LONG LIQUIDATION; 4) SMALL COMEX OI LOSS AND 5) SMALL ISSUANCE OF EXCHANGE FOR PHYSICAL AND …ALL OF THIS WAS COUPLED WITH OUR LOSS IN GOLD PRICE TRADING//FRIDAY//$14.80.

WE ARE BEGINNING TO WITNESS A LACK OF EXCHANGE FOR GOLD PHYSICALS UNDERWRITTEN DUE TO PREMIUMS STARTING TO REAPPEAR IN THE FUTURE PRICE OF GOLD VS LONDON SPOT. THE COST TO THE BANKERS IS JUST TOO GREAT TO ENGAGE IN THESE VEHICLES ONCE THIS OCCURS.

THE FACT THAT WE ARE CONTINUALLY SEEING A DROP IN COMEX OPEN INTEREST AND VOLUMES COUPLED WITH LESS EXCHANGE FOR PHYSICALS PROBABLY MEANS THAT OUR LONGS ARE ALREADY DEPARTING NEW YORK FOR THE NEW PHYSICAL PLATFORM AT LONDON’S LME.

EXCHANGE FOR PHYSICALS//OUTLINE

SPREADING OPERATIONS/NOW SWITCHING TO GOLD (WE SWITCH OVER TO SILVER ON OCT 1)

OUR SPREADING OPERATION HAS NOW SWITCHED INTO GOLD…..

SPREADING OPERATION FOR OUR NEWCOMERS:

FOR NEWCOMERS, HERE ARE THE DETAILS:

SPREADING LIQUIDATION HAS NOW COMMENCED IN GOLD AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF OCT.

FOR THOSE OF YOU WHO ARE NEW, HERE IS THE MODUS OPERANDI OF THE SPREADERS AND THE CRIMINAL ELEMENT BEHIND IT:

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR;

THE SPREADING LIQUIDATION OPERATION IS NOW OVER FOR SILVER..AND WE WILL NOW MORPH INTO AN ACCUMULATION PHASE OF SPREADING CONTRACTS FOR GOLD. THEY WILL ACCUMULATE CONSIDERABLE AMOUNT OF THE CONTRACTS AND THEN LIQUIDATE ONE WEEK PRIOR TO FIRST DAY NOTICE

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO GOLD AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF SEPT. HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF OCT FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE IN THIS NON ACTIVE MONTH OF SEPT. BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN GOLD WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2020 INCLUDING TODAY

SEPT.

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 9 TRADING DAY(S) IN TONNES: 42.85 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2019, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 42.85/3550 x 100% TONNES =1.20% OF GLOBAL ANNUAL PRODUCTION

ISSUANCE OF EXCHANGE FOR PHYSICAL GOLD HAS DISSIPATED THIS MONTH…THE COST TO THE BANKERS TO CARRY THESE CONTRACTS IN LONDON IS BECOMING TOO GREAT FOR THEM.

ACCUMULATION OF GOLD EFP’S YEAR 2020 TO DATE: 3,443.01 TONNES

JANUARY 2220 TOTAL EFP ISSUANCE; : 570.19 TONNES

FEB 2020 TOTAL EFP ISSUANCE : 653.78 TONNES

MARCH TOTAL EFP ISSUANCE 1,098.93 TONNES (*AND A NEW ALL TIME RECORD ISSUANCE//22 DAYS)

APRIL TOTAL EFP. ISSUANCE: 243.45 TONNES (EFP ISSUANCE BECOMING A LOT LESS)

MAY TOTAL EFP ISSUANCE: 248.68 TONNES (EFP ISSUANCE STILL LOW// PREMIUM COST TO THE BANKERS IS HUGE..SO ISSUANCE IS LESS)

JUNE TOTAL EFP ISSUANCE: 192.06 TONNES

JULY TOTAL EFP ISSUANCE; 313.09 TONNES ..(EXCHANGE FOR PHYSICALS REVERSE COURSE AND ARE NOW INCREASING!)

AUGUST TOTAL EFP ISSUANCE; 150.78 TONNES FINAL (AGAIN: RETREATING IN NUMBERS)

SEPT TOTAL EFP ISSUANCE: 42.85 TONNES (AGAIN EXCHANGE FOR PHYSICAL NUMBERS IN FULL RETREAT)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A SMALL SIZED 214 CONTRACTS FROM 160,868, UP TO 161,083 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 2 3/4 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.

THE SMALL SIZED GAIN IN OI SILVER COMEX WAS PRIMARILY DUE TO; 1) MINOR BANKER SHORT COVERING (OR MAYBE ZERO) , 2) A STRANGE 0 ISSUANCE OF EXCHANGE FOR PHYSICALS (SEE BELOW), 3) A SMALL LOSS IN OUNCES STANDING FOR SILVER AT THE COMEX FOR SEPT., AND 4) MINOR LONG LIQUIDATION,

EFP ISSUANCE 0 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT: 0 AND DEC. 0 AND MARCH: 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 214 CONTRACTS TO THE 0 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A SMALL SIZED GAIN OF 214 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 1.070 MILLION OZ, OCCURRED WITH OUR 39 CENT LOSS IN PRICE///

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL..THE EVIDENCE IS CLEAR: HUGE AMOUNTS OF PHYSICAL STANDING FOR BOTH SILVER AND GOLD .

(report Harvey)

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)MONDAY MORNING/ SUNDAY NIGHT:

SHANGHAI CLOSED UP 18.47 POINTS OR 0.57% //Hang Sang CLOSED UP 136.81 POINTS OR 0.56% /The Nikkei closed UP 136.97 POINTS OR 0.56%//Australia’s all ordinaires CLOSED UP .66%

/Chinese yuan (ONSHORE) closed UP at 6.8198 /Oil UP TO 37.20 dollars per barrel for WTI and 39.81 for Brent. Stocks in Europe OPENED MIXED// ONSHORE YUAN CLOSED UP // LAST AT 6.8198 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.8197 TRADE TALKS STALL////TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED//CORONAVIRUS/PANDEMIC : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

61,826.370 oz oz

Brinks

1.92 tonnes

|

| Deposits to the Dealer Inventory in oz | NIL oz

|

| Deposits to the Customer Inventory, in oz |

126,768.370 OZ Malca

|

| No of oz served (contracts) today |

175 notice(s)

17,500 OZ

(.5443 TONNES)

|

| No of oz to be served (notices) |

28 contracts

(2800 oz)

0.087709 TONNES

|

| Total monthly oz gold served (contracts) so far this month |

4166 notices

416,600 OZ

12.958 TONNES

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total withdrawals; 61,823.370 oz

We had 0 kilobar transactions +

ADJUSTMENTS: 0 //

The front month of SEPT registered a total of 203 contracts for a LOSS of 161 contracts. We had 187 notices filed on Friday, so we gained a strong 26 contracts or an additional 2,600 oz will stand for delivery in this non active month of Sept. Remember that we have been adding to our gold deliveries despite the raid these past 6 days.

Oct GAINED A CONSIDERABLE 321 contracts UP to 62,140 ( STRANGELY NOBODY HAS LEFT THE ARENA ON OUR FRONT MONTH OF OCTOBER). November gained 0 contracts to stand at 77.

The big December contract LOST 2788 contracts DOWN to 421,732 contracts..

We had 175 notices filed today for 17,500 oz

To calculate the INITIAL total number of gold ounces standing for the SEPT /2020. contract month, we take the total number of notices filed so far for the month (4166) x 100 oz , to which we add the difference between the open interest for the front month of SEPT (203 CONTRACTS ) minus the number of notices served upon today (175 x 100 oz per contract) equals 419,400 OZ OR 13.045 TONNES) the number of ounces standing in this active month of JUNE

thus the INITIAL standings for gold for the SEPT/2020 contract month:

No of notices filed so far (4166, x 100 oz + 203 OI) for the front month minus the number of notices served upon today (175) x 100 oz which equals 419,400 oz standing OR 13.045 TONNES in this active delivery month. This is a HUGE amount for gold standing for a SEPT delivery month (a NON active delivery month).

October, also looks like we are going to have a strong delivery month.

We gained 26 contracts or an additional 2,600 oz will try their luck searching for metal on this side of the pond.

NEW PLEDGED GOLD: BRINKS

144,088.952 oz NOW PLEDGED JAN 21.2020/HSBC 5.4807 TONNES

42,548.308.00 PLEDGED APRIL 3/2020: SCOTIA: 1.3234 tonnes

deleted Int. Delaware pledge July 7 (600 tonnes)

261,958.320 oz (some deleted august 3) JPM 8.14 TONNES

610,238.285 oz pledged June 12/2020 Brinks/ july 2/july 21 19.017 tonnes

51,084.609 oz Pledged August 21/regular account 1.588 tonnes jpm

total pledged gold: 1,109,918.474 oz 34.523 tonnes

total registered, pledged and eligible (customer) gold 36,594,876.651 oz 1,138.25 tonnes (INCLUDES 4 GC GOLD)

total 4 GC gold: 126.34 tonnes

total gold net of 4 GC: 1011,91 tonnes

end

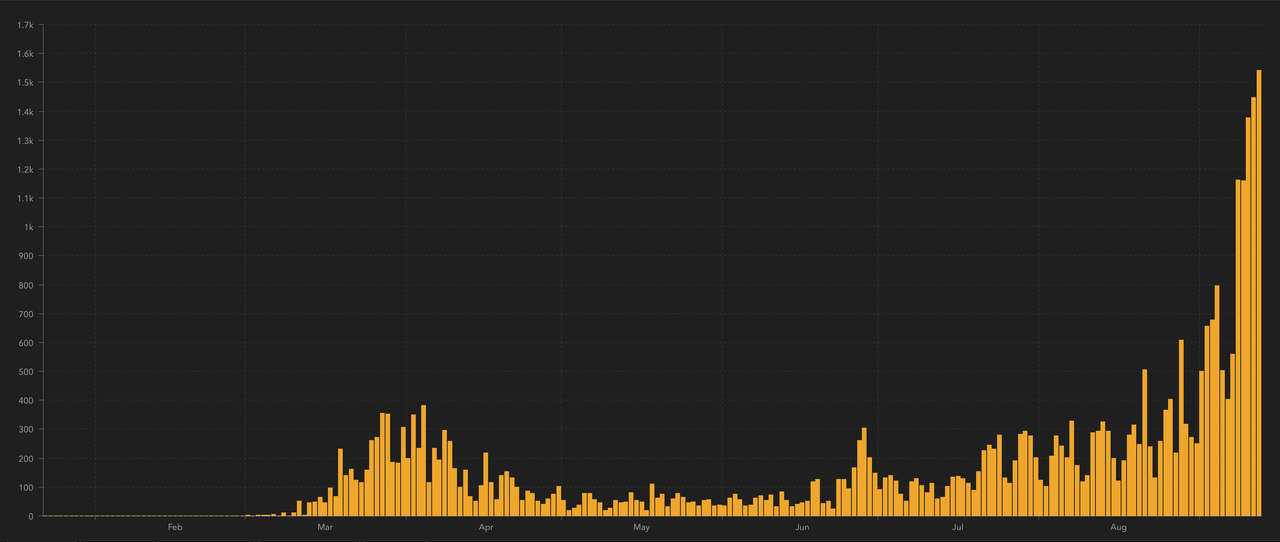

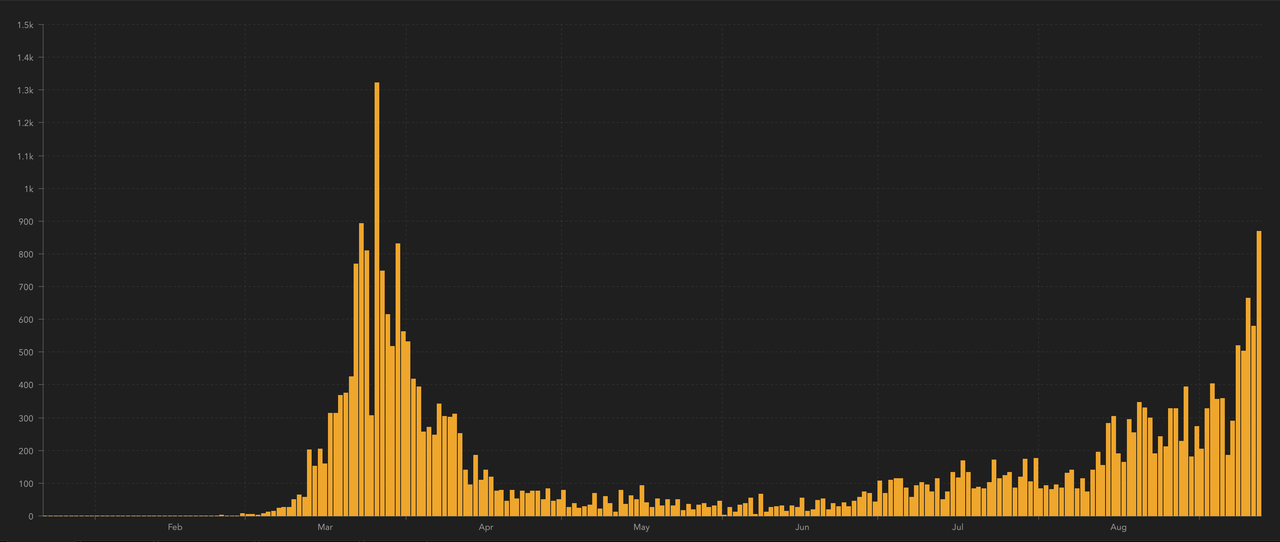

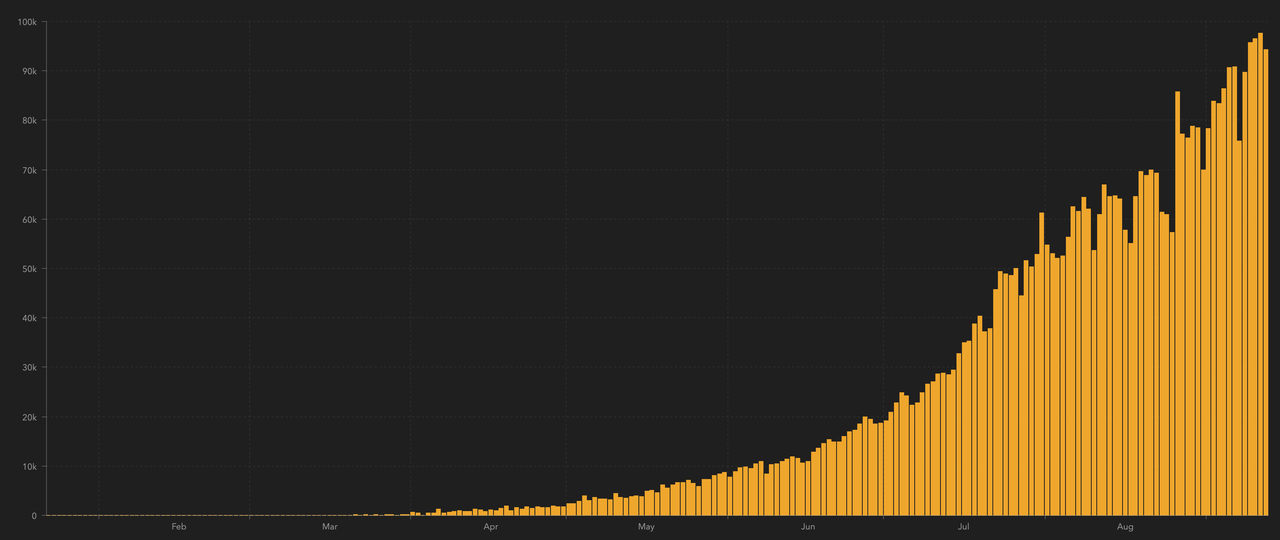

I have compiled data with respect to registered (or dealer) gold taken on first day notice for each of the past 24 months

The data begins on first day notice for the May month taken on the last day of July 2018. and it continues to present day.

I then took, how many deliveries were recorded by the CME for each and every month. I also included for reference the price of gold on first day notice.

The first graph is a logarithmic graph and the second graph, linear.

You can see the huge explosion of registered gold at the comex along with deliveries.

THE GOLD COMEX SEEMS TO BE UNDER SEVERE ASSAULT FOR PHYSICAL

END

And now for the wild silver comex results

And now for the wild silver comex results

INITIAL STANDINGS

SEPT. SILVER COMEX CONTRACT MONTH//INITIAL STANDING

Bill Holter:

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

March 4.2019

Parker City News

JP Morgan faces potential class action lawsuit after guilty pleas by a former metals trader

Traders from across the U.S. are banding together to accuse J. P. Morgan Chase of manipulating precious metals markets for years.

At least six lawsuits, all making similar allegations against the nation‘s largest bank, have been filed in New York federal court in the past month, since federal prosecutors in Connecticut with a former J. P. Morgan Chase metals trader.

The cases could potentially include thousands of people who traded in the precious metals market. The White Plains, N.Y., law firm Lowey Dannenberg is asking the court to combine the cases and name it as the lead.

The law firm‘s commodities group is led by Vincent Briganti, the attorney who filed the first lawsuit on behalf of Dominick Cognata, a New York resident who alleges he suffered losses due to J. P. Morgan‘s trading conduct in the silver and gold futures and options markets.

A combined case, seeking class action status, would include anyone who purchased or sold futures contracts or an option on NYMEX platinum or palladium or COMEX silver or gold between at least Jan. 1, 2009, and Dec. 31, 2015. The lawyers believe that “at least hundreds, if not thousands” of traders would be eligible to join the case.

Named as defendants in all of the lawsuits are John Edmonds, a 36-year old former metals trader at J. P. Morgan, a group of yet-to-be-identified precious metals traders and the bank.

Edmonds, a New York resident, pleaded guilty in October to one count of conspiracy to defraud the market and manipulate prices of precious metals futures contracts and one count of commodities fraud. In the criminal plea, Edmonds admitted that he and other “unnamed co- conspirators” at J. P. Morgan, fraudulently manipulated precious metals markets from 2009 to 2015, the same time frame covered in the class action suits.

Briganti filed the initial class action on Nov. 7, just one day after the Justice Department unsealed Edmonds‘ plea in the U.S. District Court of Connecticut.

Edmonds admitted in his guilty plea that he deployed the illegal trading scheme hundreds of times with the direct knowledge and consent of his immediate supervisors. Plaintiffs say they have suffered economic injury, including monetary losses, as a direct result of actions by Edmonds and the other unnamed J. P. Morgan metals traders in the futures and options contracts.

One of the suits alleges that “the number of unlawful trades that JP Morgan traders executed in precious metals futures markets is at least in the thousands.”

J. P. Morgan declined to comment. Lowey Dannenberg did not respond to a request for comment by CNBC.

The Justice Department‘s criminal investigation is still ongoing and recently caused a separate related civil case to be put on hold for at least six months while the government continues its investigation. That civil lawsuit, which also accuses J. P. Morgan of rigging the precious metals market, was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders.

After reviewing the details of the plea agreement, David Kovel, the attorney for Shak‘s suit, sought to re- interview Edmonds, along with two other current and former senior traders at the bank. However, the government argued that reopening questioning would be detrimental to the ongoing criminal investigation. The federal judge overseeing the proceedings ordered a six-month stay in the civil case.

Kovel declined to comment.

Edmonds was originally scheduled to be sentenced in Hartford, Conn., on Wednesday, Dec. 19, but a court filing on Nov. 27 shows the sentencing has been postponed until June. A spokesman for the U.S. Attorney for Connecticut could not elaborate on why the sentencing was postponed since the court filing is under seal.

-END-

Futures Surge On Monday Merger Mania, Fresh Vaccine Hopes

U.S. stock index futures jumped 1.3% on Monday amid fresh progress in COVID-19 vaccine development and a triumphal return of “Merger Monday” thanks to a flurry of multi-billion dollar deals.

Oracle soared as much as 11% leading gains among the S&P 500 constituents, after emerging as the winner in negotiations to take over the US operations of ByteDance’s TikTok app. As reported last night, the deal specifics are still evolving, with the final option likely to be something closer to a corporate restructuring with Oracle taking a stake in a newly formed U.S. business. While the structure seems to be devised in order to meet recently tightened Chinese oversight rules, Bloomberg notes that it is not clear whether it would pass muster with the Trump administration, which has set tomorrow as the deadline for the sale or shutdown of TikTok’s American operation. For now however, investors are happy, even if it remains unclear just how the two seemingly disparate companies will synergize. A Microsoft-led consortium that included Walmart was also in talks for TikTok’s U.S. business. Their shares fell marginally.

There were more deals to spark market euphoria, key among them the sale of SoftBank’s UK-based chip division Arm to Nvidia for $40 billion in the semiconductor industry’s largest-ever deal. SoftBank will also raise 1.2 trillion yen ($10.4 billion) from selling about a third of its domestic wireless arm. Nvidia added 6.6% on the news, while SoftBank surged 9% boosted also by weekend speculation it was considering a going private deal (which however is very unlikely to happen for the $125 billion company).

Separately, Gilead – whose stock prices has benefited from the recent covid vaccine rally – agreed to acquire Immunomedics, the maker of a promising breast-cancer therapy, for about $21 billion, or $88 a share, more than double Friday’s closing price. Meanwhile, in what could be a groundbreaking development and the biggest merger deal in banking since the financial crisis, the Swiss blog Inside Paradeplatz reported that UBS and Credit Suisse are exploring a potential combination.

Global equities also got a lift on Monday after drugmaker AstraZeneca resumed its British clinical trials of its COVID-19 vaccine, one of the most advanced in development. Pfizer also rose 1.8% after the drugmaker and German biotech firm BioNTech SE proposed expansion of their Phase 3 pivotal COVID-19 vaccine trial to about 44,000 participants. Pfizer CEO Albert Bourla said it’s “likely” the U.S. will deploy a Covid-19 vaccine to the public before year-end.

In European trading, Airline and retail shares advanced in European trading. However, the Stoxx Europe 600 Price Index trimmed and earlier increase of as much as 0.8% to fall 0.1% as energy shares lead losses among sectors, with sub-index down 0.5% and tracking drop for crude. Brent futures slid -1% to $39.45/barrel, while WTI was down -1.1% to $36.94/barrel.

Earlier in the session, Asian stocks also gained, led by materials and IT, after rising in the last session. Most markets in the region were up, with Jakarta Composite gaining 2.9% and South Korea’s Kospi Index rising 1.3%, while Thailand’s SET dropped 0.4%. The Topix gained 0.9%, with Fukushima Bank and Freebit rising the most. SoftBank Group surged after Nvidia agreed to buy the firm’s chip division Arm Ltd. for $40 billion. The Shanghai Composite Index rose 0.6%, with Xi’an Bright Laser and Zhejiang Orient posting the biggest advances.

Global stocks are coming off the back of the first consecutive weeks of declines since March and traders remain on edge given the recent reassessment of valuations and volatility in options markets, however late last week, analysts at Goldman, JPMorgan and Deutsche Bank all suggested the recent pullback in the U.S. is nearing an end. On Wednesday, the Federal Reserve is expected to maintain its dovish stance on policy as investors look for signs the global economy is recovering from the pandemic.

“With such a powerful monetary impulse coursing through the US and European economy, the odds are that the market will be surprised again positively” in the fourth quarter, said Sebastien Galy, senior strategist at Nordea Investment Funds. “The conclusion is that we should remain in a buy on dip market.”

Because, of course.

In rates, Treasuries edged lower in U.S. trading to start week that brings 20-year reopening Tuesday, FOMC decision Wednesday and 10-year TIPS reopening Thursday. Yields remain within 1bp-2bp of Friday’s closing levels, with 10-year yield at 0.67%; 20-year lags ahead of $22b reopening. The US 10Y trails most other developed bond markets led byeuro-zone peripherals, which received favorable strategist calls. Trader focus remains on the FOMC meeting for the possibility of inflation-outcome-based guidance and changes to size or distribution of Fed’s Treasury purchases; however, most strategists expect neither this week.

In FX, the dollar weakened against most G-10 peers again amid the recovery in risk sentiment; the euro advanced a fourth consecutive day against the greenback pushing European stocks lower while the region’s bond curves bull flattened, with the periphery outperforming the core.

Market Snapshot

- S&P 500 futures up 1.2% to 3,362.25

- STOXX Europe 600 up 0.2% to 368.64

- MXAP up 0.9% to 172.61

- MXAPJ up 0.8% to 565.68

- Nikkei up 0.7% to 23,559.30

- Topix up 0.9% to 1,651.10

- Hang Seng Index up 0.6% to 24,640.28

- Shanghai Composite up 0.6% to 3,278.81

- Sensex up 0.04% to 38,870.26

- Australia S&P/ASX 200 up 0.7% to 5,899.52

- Kospi up 1.3% to 2,427.91

- Brent futures down 0.9% to $39.47/bbl

- Gold spot up 0.2% to $1,944.33

- U.S. Dollar Index down 0.3% to 93.06

- German 10Y yield fell 1.4 bps to -0.495%

- Euro up 0.2% to $1.1868

- Italian 10Y yield fell 2.7 bps to 0.856%

- Spanish 10Y yield fell 2.4 bps to 0.285%

Top Overnight News from Bloomberg

- Hedge funds raised their long bets on the pound to the highest in over five months just before talks between the U.K. and European Union took a turn for the worse

- The U.K. is on course for more than twice as many job losses in the coming months than in the recession following the financial crisis, underscoring the bleak outlook for the labor market

- The French government will raise its economic outlook for this year after consumer spending rebounded more strongly than expected once the lockdown aimed at containing the spread of the coronavirus ended

- The European Union’s executive will unveil an ambitious emissions-cut plan this week that’ll leave no sector of the economy untouched, forcing wholesale lifestyle changes and stricter standards for industries

- Japanese Chief Cabinet Secretary Yoshihide Suga was elected leader of the ruling Liberal Democratic Party by an overwhelming majority, ushering in the country’s first change of prime minister in almost eight years

- The chairmen of UBS Group AG and Credit Suisse Group AG are exploring a potential merger to create one of Europe’s largest banks, Inside Paradeplatz reported, citing unidentified people inside the two lenders

Quick stroll across global markets courtesy of RanSquawk

Asian equity markets were positive across the board and US equity futures also began the week on the front foot as sentiment was underpinned by vaccine hopes amid reports that AstraZeneca resumed its vaccine trials and with M&A news also contributing to the constructive risk tone, after SoftBank confirmed it will sell its Arm unit to Nvidia, and ByteDance reportedly picked Oracle as the winning bidder for its TikTok operations in US. ASX 200 (+0.7%) was led higher by strength in commodity names although gains were capped by resistance in the index near around the 5900 level and underperformance seen in tech and financials, with the latter dragged amid losses in Macquarie Group after it flagged a 35% Y/Y decline to H1 2021 results. Nikkei 225 (+0.7%) was also positive ahead of today’s LDP leadership vote in which Abe loyalist and current Chief Cabinet Secretary Suga is widely seen as the front runner to succeed PM Abe with around 70% of LDP’s Diet members expected to support his bid to become the party leader. Furthermore, SoftBank shares surged around 9% after confirmation to sell its Arm Holdings unit for USD 40bln which would be the largest ever semiconductor deal and reports also noted executives revived discussions regarding taking SoftBank private following its recent asset disposals, while KOSPI (+1.3%) was among the biggest gainers as index heavyweight Samsung Electronics benefitted on news it outbid TSMC to win a KRW 1tln order from Qualcomm. Hang Seng (+0.6%) and Shanghai Comp. (+0.6%) also conformed to the broad constructive risk tone amid the TikTok related developments and as participants digested the latest lending data in which both New Yuan Loans and Aggregate Financing topped forecasts. Finally, 10yr JGBs were marginally higher following a recent break above the 152.00 resistance level but with gains limited by the broad positive risk tone and a tepid BoJ Rinban announcement valued at a total JPY 150bln.

Top Asian News

- Philippines Boost Central Bank’s Loans Cap to Government by 50%

- Thai Airways Gets Nod for $11 Billion Debt Rescue Plan

- Alibaba Is Said to Be in Talks to Invest $3 Billion in Grab

- Condo Butler Service Demand in China Sparks 400% Stock Gain

A relatively tame start to the week in terms of fresh fundamental catalysts for Europe, albeit the initial upside seen across cash and futures at the open fizzled out (Euro Stoxx -0.1%) as the region failed to coat-tail on gains seen during APAC hours ahead of a risk-packed week which includes the FOMC policy decision, the US-Sino spat over TikTok’s US assets and Quad witching. Sectors in Europe are now mixed, with Travel & Leisure leading the gains whilst Banks and Health Care resides on the other side of the spectrum, as the former is weighed on by a lower yield environment and the latter shrugged off AstraZeneca’s (-0.3%) COVID-19 vaccine trial resumption with Oxford University, but note US President Trump tweeted that he has signed a new executive order to lower drug prices. The IT sector meanwhile remains underpinned by NVIDIA’s USD 40bln deal to acquire Softbank’s Arms Holdings – touted to be the largest semiconductor deal. In terms of individual movers, LSE (-0.8%) is softer despite a myriad of bids for its Borsa Italiana unit ahead of its Refinitiv takeover, including from the likes of CDP/Euronext (-2.6%), Deutsche Boerse (-0.9%) and SIX, with the latter reportedly making the highest offer. Sticking with M&A, Metro AG (+7%) share are bolstered by reports that EP Global Commerce is launching a takeover offer for shares in Co. with the aim of raising investments to above 30%. EP is expected to offer EUR 8.48/ordinary share and EUR 8.87/preference share – Metro board strongly believes the offer substantially undervalues the Co. Elsewhere, Dassault Aviation (+9.6%) is supported by a deal with Greece for 18 Rafales fighter jets – but the terms of the deal were undisclosed. Finally, H&M (-3.2%) is pressured by a broker downgrade at Morgan Stanley.

Top European News

- U.K. Sets New Cap on Social Gatherings as Virus Cases Spike

- Putin Resolves to Back Belarus Ally, Wary of Protest Spread

- Czech Billionaire Seeks More Control Over Metro AG in Second Try

- Air France’s Survival ‘Guaranteed’ by French After Dutch Warning

In FX, the latest COVID-19 developments have boosted the Kiwi across the board as NZ PM Adern pre-announced a downgrade in nationwide restrictions to Level 1 starting next Monday, while Auckland will remain level 2 for a further week pending another review of the situation. Nzd/Usd is back up near 0.6700 in response, while the Aud/Nzd cross has retreated sharply from around 1.0925 towards 1.0865 as the Aussie remains capped ahead of 0.7300 vs its US counterpart awaiting RBA minutes and Q2 house prices overnight. Note, Aud/Usd appears reluctant to track YUAN gains off a modestly firmer PBoC Cny midpoint fix and in wake of better than expected Chinese new loan and aggregate financing data, perhaps due to ongoing concerns about the fraught relationship between the 2 countries. Elsewhere, some respite for Sterling after last week’s significant underperformance as Cable reclaims 1.2800+ status following a shallower pull-back and Eur/Gbp retreats through 0.9250 awaiting more reverberations from the IMB that is scheduled to be presented to Parliament today. Note, some market observers and a Newsquawk contact are pointing to several key levels in Cable just under last Friday’s base including the 50 DMA, 100 WMA and 200 DMA at 1.2761, 1.2749 and 1.2735 respectively, while rebounds may struggle beyond 1.2900 barring a major U-turn on the Internal Market Bill or breakthrough on Brexit trade talks given the 200 WMA at 1.2932. In Scandinavia, mildly contrasting performances with the Norwegian Crown holding above 10.7000 against the Euro even though oil prices are flagging again, but the Swedish Krona struggling to stay afloat within a 10.4030-10.3750 range amidst deteriorating risk sentiment.

- JPY/EUR/CHF/DXY – All moderately firmer vs the Dollar that has failed to sustain its post-US CPI momentum, albeit in part due to relative strength elsewhere, as the index meanders between 93.328-048 parameters. The Yen has clawed back a bit more lost ground to test 106.00+ levels after the LDP win for Abe advocate Suga, while the Euro has bounced off a firmer base to pivot 1.1850 in advance of more commentary from the ECB and the Franc is hovering just over 0.9100 following the latest rise in weekly Swiss sight deposits.

- CAD/EM – The Loonie is somewhat lethargic and straddling 1.3170 against its US peers against the backdrop of weakness in crude, but holding up better than the Rouble that is trying to contain losses under 75.0000 alongside Brent beneath the psychological Usd 40/brl mark. However, the Lira is arguably showing more resilience just off 7.5000 on the back of Moody’s Turkish ratings downgrade and the stand-off with Greece, but doubtless with help coming via state bank support.

In commodities, WTI and Brent front month futures continue to edge lower in early European trade, despite a lack of fundamental newsflow and against the backdrop of a softer USD. A busy week for the complex with highlights including the OPEC Monthly Oil Market report today (12:40BST/07:40ET), tomorrow IEA report, and the JMMC meeting on the 17th – with prior reports noting that delegates are concerned over the recent slide in energy prices, although Saudi sources reaffirmed the commitment to the pact and downplayed deeper production cuts last week. Meanwhile, desks continued to point to a less-rosier than expected demand outlook reflected by a number of producers cutting their OSPs, “Although this shouldn’t come as too much of a surprise given the weakness that we have seen in refinery margins”, ING writes. On the refinery front, eyes have turned back to the Gulf of Mexico where Tropical Storm Sally is expected to strengthen to a hurricane later today. Participants will be keeping an eye on production shut-ins and refining activity, with the latter particularly vulnerable to flooding, and with the Gulf Coast account for just under 54% of US capacity. Sticking with supply-side, Libya’s National Army (the group that imposed an 8-month blockade), has promised to reopen Libya’s energy shipments after talks with other Libyan group and the US embassy in Tripoli, according to a statement on Saturday. WTI has dipped below the USD 37/bbl level (vs. high 37.68/bbl), while its Brent counterpart surrendered its USD 40/bbl handle to print a base under USD 39.50/bbl. Elsewhere, spot gold and silver eke mild gains, largely as a function of the softer USD and heading into this week’s risk events. The yellow metal meanders sub-1950/oz having had tested the level in APAC trade, whilst spot silver fails to reclaim a USD 27/oz+ status. Over to base metals, Dalian iron ore gained over 2% overnight as a steady rise in iron ore stockpiles added to the firmer demand narrative from China, whilst Shanghai copper held onto gains of some 1% amid the broader gains in Chinese markets.

US Event Calendar

- Nothing major scheduled

DB’s Jim Reid concludes the overnight wrap

I hope you had a good weekend. I hardly stopped. We went Shetland Pony riding ahead of my daughter’s 5th birthday tomorrow, I finished a thoroughly disappointing 48th out of 78th in my golf club’s main Championship event, and I have picked up my first cold since lockdown thanks to our germ carrier children being at school now. I thought there was a good chance that as people have been socially distancing for months that colds and flu would be less prevalent this winter. In fact I think Australia had very low cases of flu in their winter just passed. However the fact that I’m incredibly bunged up suggests otherwise. Thankfully there are no more specific covid symptoms. A loss of taste would have been very annoying given the birthday cake.

A reminder that we published our annual long-term study last week. This year’s is entitled “The Age of Disorder” (link here) and suggests that the 40-year globalisation era is now over and will be replaced with this new one characterised by disorder. The 8 page executive summary contains all you want to know but there is more in-depth analysis if that whets your appetite. We also published our latest credit forecasts last week into year-end ( link here ). After being bullish for Q3 at our half year outlook we’ve decided to reverse that and now expect mild spread widening.

In terms of the weekend news, the main coronavirus development is that the AstraZeneca-Oxford vaccine trials have resumed following last week’s pause as a medical issue from one of the trial recipients was investigated. The pause didn’t have as much of a negative impact on the market as I expected so this probably won’t have too much impact either, but it’s clearly encouraging news given they’re one of the front runners. Elsewhere Pfizer’s CEO said yesterday that he expects the US to deploy a vaccine to the public before year-end, even if the FDA were a bit hawkish last week.

On the coronavirus, there have been increasing signs of a resurgence of cases in Europe, with France reporting 7,183 new coronavirus cases yesterday after more than 10,000 a day earlier, which was the most since a national lockdown ended in May. Meanwhile, Germany’s reproduction rate of the virus has moved up to 1.15, the Robert Koch Institute said yesterday. And here in the UK, over 3,000 cases have been reported over the last 3 days, which is the first time that’s happened since May. In Asia however, South Korea is relaxing its social distancing rules as the second wave shows sign of abating, with distancing requirements for the Seoul metropolitan area being lowered to level 2 from level 2.5 for two weeks.

Asian markets have started the week on the front foot with the vaccine news mentioned above supporting sentiment. The Nikkei (+0.64%). Hang Seng (+0.67%), Shanghai Comp (+0.56%) and Kospi (+1.10%) are all up, while future on the S&P 500 also up +1.20%. In other news, China banned pork imports from Germany on Saturday, which comes just two days before Chinese President Xi is scheduled to discuss trade issues in a video meeting with German Chancellor Merkel, as well as European Commission President Von der Leyen and Council President Michel.

Starting with the FOMC meeting on Wednesday, this is the first monetary policy decision since the virtual Jackson Hole symposium, at which it was announced that the committee’s longer-run goals and monetary policy strategy would be updated. In terms of the major changes, the Fed now “seeks to achieve inflation that averages 2 percent over time”, which would allow inflation to overshoot the target following a period of undershooting. It also changed the wording around its maximum employment objective, now saying that policy will be informed by its “assessments of the shortfalls of employment from its maximum level.” According to our US economists (see their preview here), the release opened the door to adjustments in forward guidance and asset purchases at this meeting, though in a close call, they expect the Fed’s forward guidance on interest rates to remain unchanged and for the Committee to reframe their asset purchases as being focused on providing accommodation, not aiding market functioning. This meeting will also see the release of a new Summary of Economic Projections, which will include the dot plot of where the FOMC think monetary policy should be moving forward.

Here in the UK there are likely to be a number of headlines this week, most notably on Brexit. That follows an escalation in tensions between the UK and the EU last week after the UK government published their Internal Market Bill, which seeks to override parts of the already-signed Withdrawal Agreement with the EU. In response, the EU called on the UK to withdraw these measures from the draft bill by the end of the month, and threatened to use legal remedies if the Withdrawal Agreement were violated. In terms of what happens next, today the bill will receive its first debate in the House of Commons, but the question will be how many Conservative MPs rebel on the matter, with last night seeing the former Conservative Attorney General Geoffrey Cox publish an article in The Times, saying that the bill would do “unconscionable” damage to the country’s international reputation.

Staying with the UK, attention will also be on the Bank of England on Thursday, who’ll be making their latest monetary policy decision. The base case from our UK economist (preview here ) is that there won’t be a further £60bn QE package until December, though there are risks of an earlier announcement at the November meeting. Keep an eye out in case there’s a voting split between the MPC’s 9 members as some might seek additional stimulus.

Turning to Japan, this week sees the election of a new Prime Minister following Shinzo Abe’s decision to stand down for health reasons. In terms of the process, the ruling Liberal Democratic Party will gather today to elect a new Party President, for which the Chief Cabinet Secretary Yoshihide Suga is regarded as the frontrunner. Following the LDP’s election, the Diet will then hold an extraordinary session on Wednesday to elect a new Prime Minister, with the new cabinet expected to be announced on the same day. Against this backdrop, the Bank of Japan will also be holding its latest monetary policy meeting next week, with our economist expecting that the bank will maintain its current policy stance.

Finally on the data front, there are a number of interesting releases. In the US, we’ll get an increasing amount of hard data for August, including industrial production, retail sales, housing starts and building permits. It’ll also be worth keeping an eye on the more topical releases however, especially with last week’s data on initial jobless claims and continuing claims having disappointed. Separately, we’ll also get some major releases from China on Tuesday, including August’s industrial production and retail sales figures.

Reviewing last week now, US equity markets continued sliding led by the large pullback in mega-cap tech stocks. The S&P 500 dropped -2.51% (+0.05% Friday), declining for the second week in a row for the first time since the week ending 1 May. It is also the worst 2-week performance for the index since March, and leaves it down -6.70% from the highs reached less than 2 weeks ago. With tech seeing the largest losses, the NASDAQ again underperformed the broader index, declining -4.06% (-0.60% Friday) and is now down -9.98% from the 2 Sept highs. For context the close on the week has returned us to levels that were first hit in early August and also to levels hit just after the open 10 days ago on the turbulent Friday the day after the sell-off started. So although a bad week, we haven’t sunk through the initial sell-off levels yet.

European equities on the other hand rose last week with the Stoxx 600 ending the week +1.67% higher (+0.13% Friday). The DAX (+2.80%), FTSE 100 (+4.02%), and FTSE MIB (+2.21%) all posted strong weekly equity performances even as worries over increasing Covid-19 caseloads start to permeate. The FTSE was helped by a -3.64% fall in GBPUSD as Brexit risks intensified – the worst week since the pandemic selling peak in March.

The dollar rose (+0.66%) for the second week straight as investors sought havens, it was the first time the dollar index had risen in consecutive weeks since mid-June. Partly on the back of the dollar rise, but also due to weaker risk appetite and worries on global demand WTI (-6.14%) and Brent crude (-6.63%) fell sharply for a second week. With risk assets sliding, core sovereign bonds rose on the week. US 10yr Treasury yields fell -5.2bps (-1.1bps Friday) to finish at 0.666%, while 10yr Bund yields were down -0.9bps (-4.5bps Friday) to -0.48%.

On the data front for Friday, US CPI for August showed inflation quickening primarily driven by the largest spike in used-vehicle costs since 1969. CPI rose by +1.3% y-o-y (+1.2% expected) and +0.4% from last month (+0.3% expected), while on an annual basis, core inflation measured 1.7%. Core CPI rose a similar +0.4%, following last month’s +0.6% rise which was the most in almost 30 years. Elsewhere, the UK’s July GDP reading showed the country continued to bounce back as coronavirus restrictions were eased. GDP rose by +6.6% following June’s +8.7% rise, this was compared to the +6.7% expected.

3A/ASIAN AFFAIRS

i)MONDAY MORNING/ SUNDAY NIGHT:

SHANGHAI CLOSED UP 18.47 POINTS OR 0.57% //Hang Sang CLOSED UP 136.81 POINTS OR 0.56% /The Nikkei closed UP 136.97 POINTS OR 0.56%//Australia’s all ordinaires CLOSED UP .66%

/Chinese yuan (ONSHORE) closed UP at 6.8198 /Oil UP TO 37.20 dollars per barrel for WTI and 39.81 for Brent. Stocks in Europe OPENED MIXED// ONSHORE YUAN CLOSED UP // LAST AT 6.8198 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.8197 TRADE TALKS STALL////TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED//CORONAVIRUS/PANDEMIC : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3 a./NORTH KOREA/ SOUTH KOREA

South Korea

b) REPORT ON JAPAN

Meet Japan’s next Prime Minister: Suga

(zerohedge)

Suga High: Abe’s #2 Becomes Japan’s Next PM After Landslide LDP Victory – What That Means For Japan

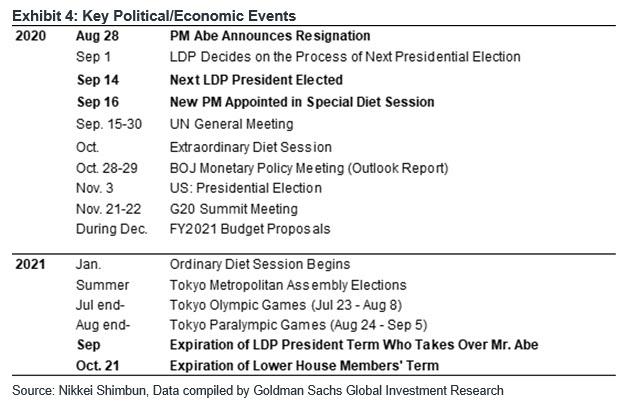

On Monday, two weeks after the (second and final) resignation by Shinzo Abe on Aug 28 who stepped down as Japan’s Prime Minister due to deterioration in a pre-existing health condition (the same condition he cited when he quit for the first time in 2007), Japan’s Liberal Democratic Party (LDP) held its presidential election to appoint a successor to current LDP leader (and Prime Minister) Shinzo Abe.

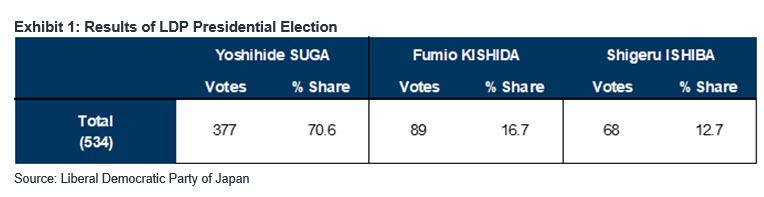

The election results show that Yoshihide Suga (Chief Cabinet Secretary) won a decisive victory over the other two candidates (Fumio Kishida and Shigeru Ishiba), as widely expected, and has been elected the next LDP president. The election will be immediately followed by the wholesale resignation of the current Abe cabinet, the appointment of Suga as the next Prime Minister during a special Diet session on September 16, and Suga forming his own cabinet.

So what does Suga’s election mean for Japan?

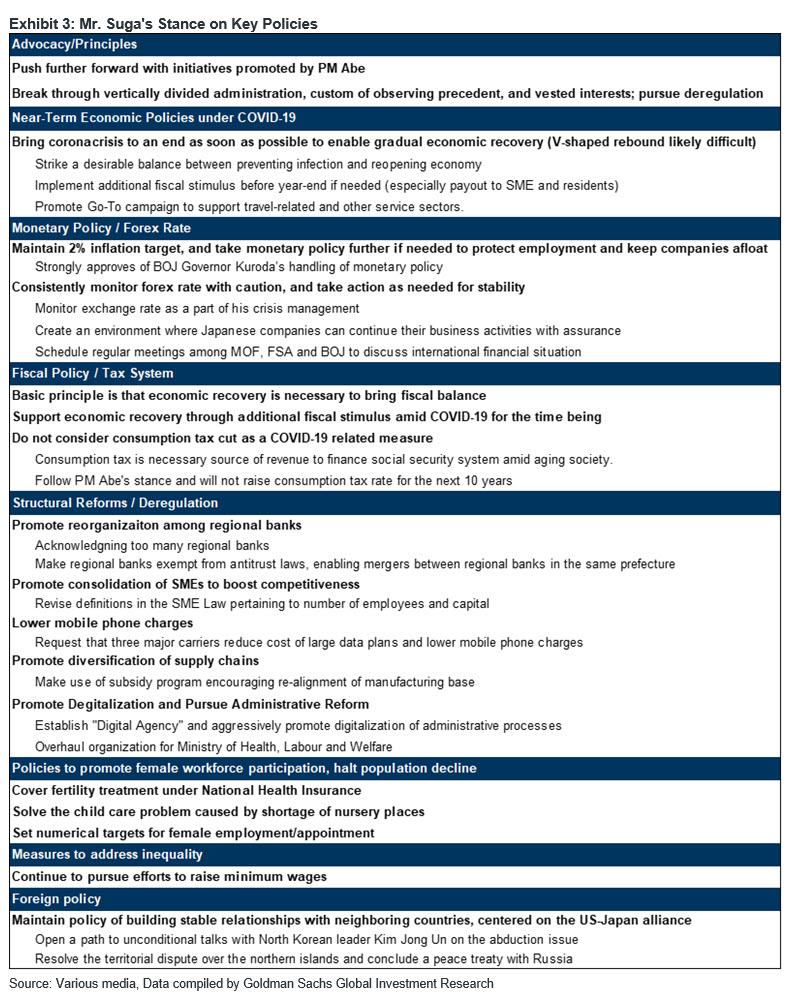

A look at Suga’s stance on key policies, courtesy of Goldman, reveals that he is keen on structural reforms and deregulation, maintaining the status quo. Suga has cited ensuring compatibility between preventing the spread of COVID-19 and reopening social and economic activity as his top priority for the time being.

On the economic policy front, Goldman’s Naohiko Baba writes that Suga’s key focus is to push forward with Abenomics, particularly the combination of the active deployment of fiscal stimulus and the large-scale monetary easing program. In short a continuation of Abenomics.

Although Suga has ruled out the possibility of lowering the consumption tax rate as a short-term stimulus measure, citing the need to generate revenue to fund social security amid population aging, he is open to the possibility of increasing various subsidies if needed.

In addition, Suga has emphasized the importance of maintaining a close relationship with the BOJ, as has been the case under the current Abe administration, and of promoting additional easing measures if deemed necessary to sustain employment and keep companies afloat. In particular, he has identified forex stability as a key area of his crisis management, and as a result, the possibility of the new administration encouraging the BOJ to decide additional easing measures, if the yen appreciates sharply, may garner market attention going forward.

Suga has also indicated a strong desire to tackle structural reforms and deregulation. He already has a robust track record of achievements in these areas, including promoting the furusato nozei (“hometown tax”) program and tourism (by promoting inbound tourism and the Go-To-Travel campaign, for example), expanding the number of foreign workers, lowering mobile telephone charges, promoting agricultural exports, and raising the minimum wage. Aside from continuous efforts to promote the above, Suga additionally expressed his strong willingness to facilitate reorganizing regional banks especially via mergers and digitalizing administrative procedures especially through the establishment of a “Digital Agency,” for example

On the foreign policy front, Suga has emphasized the importance of maintaining the US-Japan alliance, based on which he intends to build stable relationships with neighboring countries.

Suga’s term as LDP president will run through to September 2021, when Abe’s term was originally set to end, and at that point a full LDP presidential election will be held as originally planned. Another key timeline is the expiration of the term for the Lower House Diet members in October 2021. With this in mind, the new Prime Minister will face the option of either waiting until the end of his term to hold an election, or dissolving the Lower House and holding a general election before his term ends.

According to Goldman, the LDP may have a desire to avoid being forced to hold elections when there is little time left before the end of Lower House members’ terms in October 2021. It is also notable that support for a new Prime Minister tends to rise immediately after a change in administration. Given the industrial reforms and deregulation Suga desires to achieve will likely take time to implement, attention will focus on whether the new administration goes to the polls by year’s end in a bid to secure enough time for policy implementations. The key factors here will be how the COVID-19 pandemic pans out, and public opinion regarding a general election. In the event of a snap election, the debate will likely include the possibility of a third supplementary budget.

3 C CHINA

Amazing that we have a Chinese virologist claiming that she has “evidence” that COVID 19 came from a lab and yet nobody is listening to her

(zerohedge)

‘Rogue’ Chinese Virologist Claims She Has “Evidence” COVID-19 Was Created In A Lab

Once again, the claims of a rogue Chinese scientist with a lot to say, and at least some evidence to back up her claims, has been ignored by the mainstream media. Instead, Chinese virologist Dr. Li-Meng Yan, who was among the first to study the virus at a prestigious university in Hong Kong, where she worked before fleeing China, appeared on the British interview show ‘Loose Women’ late last week. During the interview, she answered questions about her claims, and reiterated thatthe CCP didn’t just deliberately cover up COVID-19 in a manner that led to thousands of unnecessary deaths, the party also knew that SARS-CoV-2 was created by Chinese scientists.

Asked about the origins of the virus, the doctor said “it comes from a lab,” again rejecting reports from last year that the virus originated from a Wuhan wet market, claiming they were a “smokescreen”.

Dr. Li also commented on her claims that Beijing deliberately tried to cover up the outbreak when it first learned of the killer virus, effectively allowing it to escape China and infect the world. When she sounded the alarm about human-to-human transmission in December last year, her former supervisors at the Hong Kong School of Public Health, a reference laboratory for the World Health Organization, silenced her. After a while, she “could not keep silent”, and decided to flee.

In April, Yan reportedly fled Hong Kong and escaped to America in an effort to evade persecution and to ‘spread the truth’ about the pandemic.

“From the beginning, I decided to get this message out in the world and it was very scary in the world because I’m a doctor and I knew if I don’t tell the truth to the world I will regret it myself in the future.”

“I never thought this would happen when I did the secret investigation, I [thought] I would speak to my supervisor and they would do the right thing on behalf of the government.”

“But what I saw was nobody responding to that. People are scared of the government but this was something urgent, and Chinese New Year time, [I knew] this was a dangerous virus and all these things meant I could not keep silent, there are human beings and global health [at risk].”

China’s national health commission has denied that the outbreak started in the lab, insisting there is “no evidence” the new coronavirus was created in a laboratory. Beiing has already scapegoated a large group of local party officials for the errors.

But Dr. Li’s testimony remains extremely compelling.

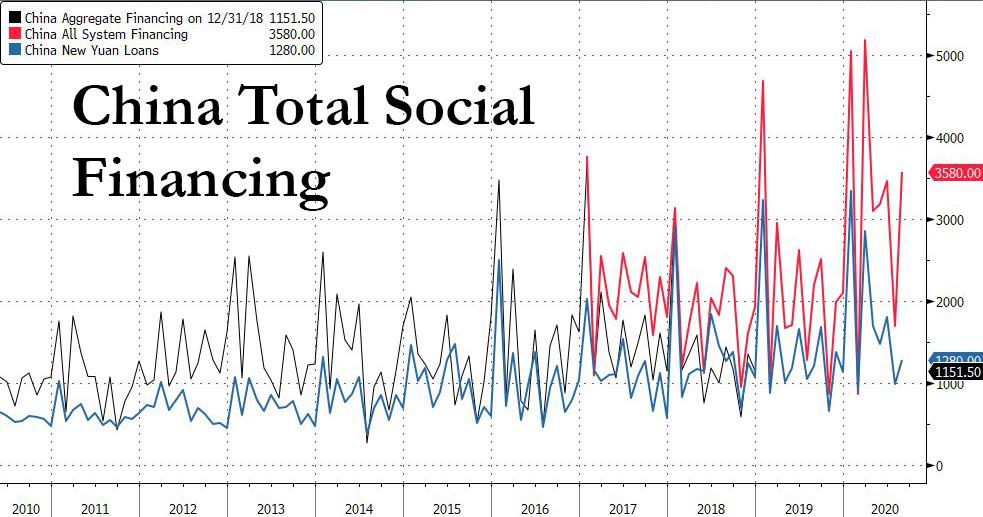

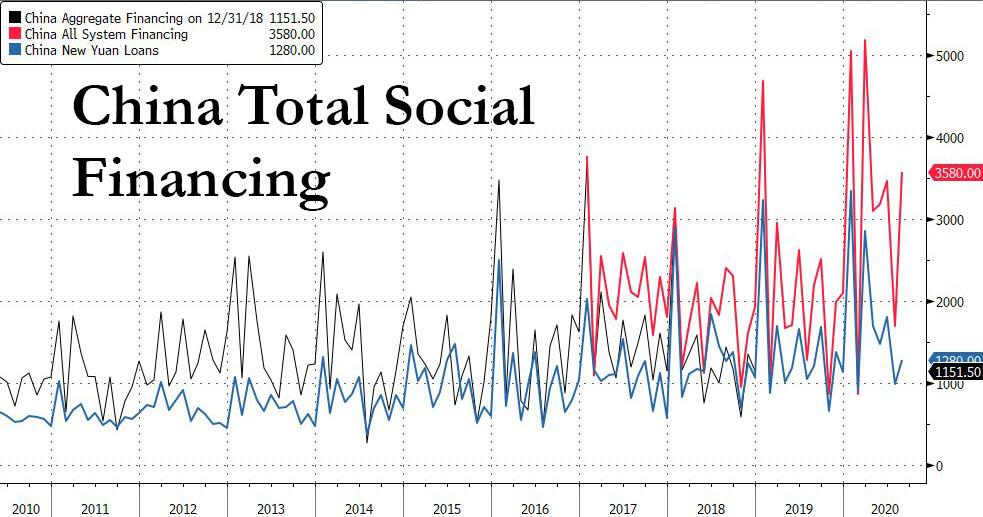

China Injects $500 Billion In New Monthly Credit As Surge In US Real Yields Looms

While the financial punditry is preoccupied with the Fed and its $7 trillion balance sheet, whether Powell is purchasing bond ETFs or has enigmatically stopped doing so (as it did in August), and whether the US central bank has any hope of sparking inflation (with or without the help of Congress), what most are forgetting is that when it comes to any global reflationary spark, China – and its $40 trillion financial system which is double that of the US – has been a far more critical driver than the US ever since the financial crisis.

And so, five months after China injected a record 5.2 trillion yuan ($732 billion) in new total social financing – China’s broadest credit aggregate – in March to offset the catastrophic hit its economy had suffered from the covid pandemic, Beijing once again surprised to the upside when in August China injected a whopping 3.58 trillion yuan into its economy ($520 billion), above the highest Wall Street estimate (1 trillion yuan above the consensus estimate of 2.585 trillion yuan) and the biggest monthly injection since the March record.

Here is a breakdown of the latest August credit data:

- New CNY loans: 1280bn yuan, exp. 1250 billion. Outstanding yuan new loan growth: 13.0% yoy in August, in line with the 13% increase in July 13.0%.

- Total social financing: 3580bn yuan, vs. consensus: RMB 2585bn.

- TSF stock growth: 13.4% yoy in August, higher than 13.0% in July. The implied month-on-month growth of TSF stock accelerated to 14.8% from 12.6% in July.

- M2: 10.4% yoy in August, below the consensus of 10.7% yoy. July, and down from 10.7% yoy in July.

Some observations:

- August credit data surprised the market to the upside, although even though the sequential growth of TSF rose to 14.8% mom annualized from 12.6% in July.

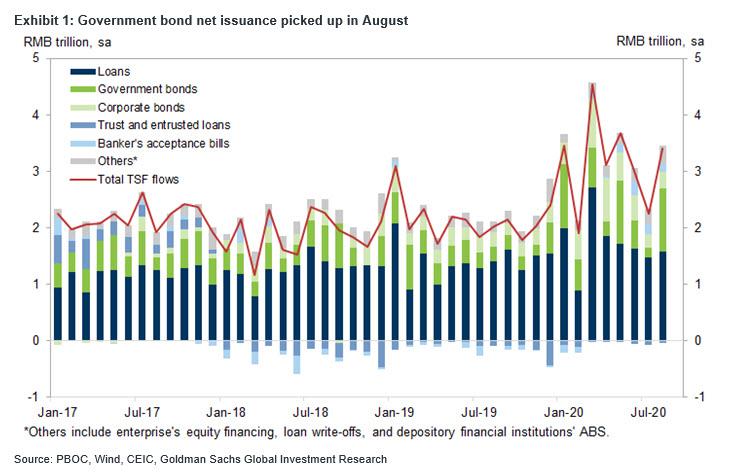

- Among major TSF components, government bonds net issuance contributed the most to the acceleration in August. Corporate bond issuance increased from last month despite higher interbank interest rates, suggesting further growth recovery.

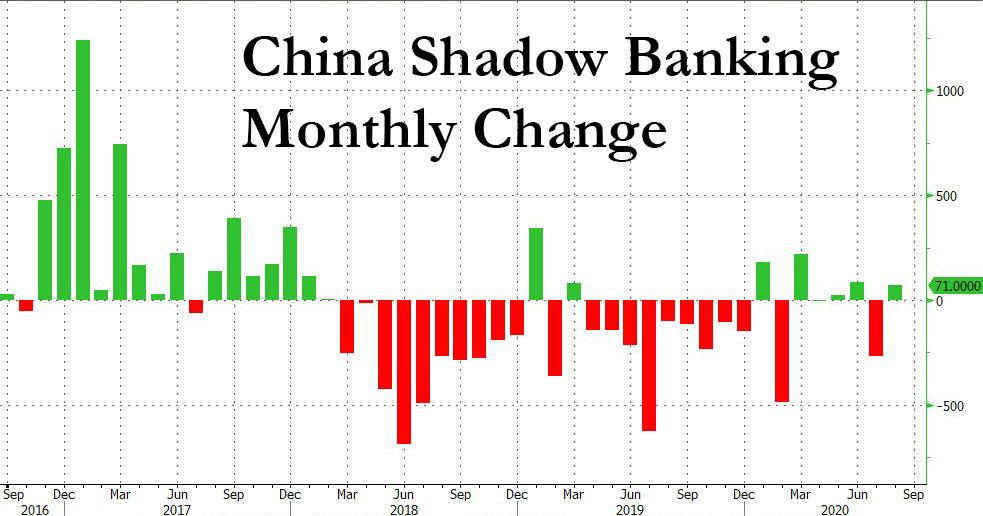

- Shadow banking rose after the steep drop in July, as Beijing appears to be easing its crackdown on sources of shadow funding. Banker’s acceptance bills increased RMB 144bn in non-seasonally adjusted terms, reversing the contraction in July. The decline in trusted and entrusted loans remained modest in August. In total some 71 billion yuan in shadow debt was created.

- On loan extension, the increase in mid-to-long term loans to households remained relatively strong, consistent with the strong property sales suggested by high frequency indicators. The increase in mid-to-long term loans to non-financial enterprises picked up in August in seasonally adjusted terms.

- Finally, in an odd divergence, despite the biggest increase in TSY growth since the start of 2018, M2 growth moderated further to 10.4% yoy in August from 10.7% in July. While it remained well above 2019 levels, it begs the question of just where this newly created credit is ending up if not in the broader monetary aggregate.

Going forward, September TSF is expected to remain “robust” according to Goldman, on continued government bond issuance. Given the recent growth momentum and credit strength, policymakers are likely to stay on hold. That said, a slowdown in credit growth will likely come in Q4 as government bond issuance is likely to slow and monetary authorities are in no rush to loosen.

Why does China’s record credit injection in 2020 matter? Because as we showed recently, China’s notorious credit impulse (which as UBS admitted several years ago is the only thing that matters for global reflation), and which is a function of how much credit Beijing creates leads real 10Y yields with a 12 month lead time. As shown in the chart below, a simple correlation suggests that real yields are set to soar by 150bps from their current -1% to approximately 50bps, and that’s assuming China does nothing to further stimulate its economy over the next 6 months.

In other words, if this relationship holds – and there is no reason to expect why it shouldn’t we are not about 6 months away from the next major spike in real yields, which while probably not as violent as Stanley Druckenmiller expects with his forecast of 5-10% inflation, will be sufficient to cause another crash in both risk assets and Treasurys, and spark some real confusion within the Fed which by then will have firmly cemented the perception that no matter what happens to inflation or real rates it will not tighten financial conditions.

Alas, now that China is once again injecting credit in its economy at a furious pace and has even reactivated the shadow banking spigots, it appears that the next spike higher in real rates is scheduled to hit some time in early 2021.

China’s Global Times Warns: “China Must Be Ready For A Potential War”

By Michael Every of Rabobank

August saw a bumper Chinese total social financing number, up much more than the market had expected at CNY3,580bn. That’s around USD500bn in one month in new borrowing, an annualised pace of USD6 trillion, if far lower in y/y terms due to seasonality. The last time we saw a number like that was March, when Covid was smashing growth, as it has everywhere else too: and this is an economy ostensibly doing far better than everybody else.

While it seems Beijing has gone for a bells and whistles growth approach, the details are less ‘positive’- if that is the right word. (And for market-based Western economies that have long relied on non-market-based Chinese borrowing, it is the right word.) M2 money supply was up just 10.4% y/y in August, down from 10.7%: where is this new borrowing going if it isn’t into the money supply? That should set alarm bells ringing as it’s even worse than the Western/Japanese problem of a flood of new money seeing ever-lower velocity of circulation. It may even suggest rather than the historical correlation between the ‘China credit impulse’ and global real yields meaning the latter will rise due to higher China-driven inflation and then even higher global bond yields, it may instead hold due to low bond yields and even more biting deflation.

That’s already the threat from a US economy with no new stimulus package close to being passed; from a UK economy trying to head for Hard Brexit shortly after its job-protecting furlough scheme is rolled back; and as Israel becomes the first country to enter into a second national lockdown, showing Covid-19 will still be an issue well into 2021. Plus, of course, China itself is openly talking about “internal circulation”, which would reduce the global flow-through from it to the rest of the world – with the exception of the commodities it says it will stockpile so aggressively.

Against that backdrop, there is a virtual summit today between the EU and China to try to agree a bilateral investment treaty. In typically European fashion, this began years ago in an environment where thus was entirely technocratic, and ends in one where it is geopolitical. China is openly stating it wants Europe to align with it more closely –against the US– just ahead of a US presidential election that could potentially prove pivotal for the future of US-EU relations.

The EU will want to show it has options. Rather inauspiciously, however, the talks begin with China having just banned German pork imports; and China’s Global Times has published an editorial which is far louder than the wolf (warrior) whistle blown at India last week titled ’China must be militarily and morally ready for a potential war’. Imagine if the New York Times published a story like that based on White House sources.

The GT argues:

“Chinese people don’t want war, but we have territorial disputes with several neighboring countries instigated by the US to confront China. Some of these countries believe that the US support provides them with a strategic opportunity and try to treat China outrageously. They believe that China, under the US’ strategic pressure, is afraid, unwilling or unable to engage in military conflict with them. Thus they want to pull the chestnuts out of the fire. Considering that there is also the Taiwan question, the risk of the Chinese mainland being forced into a war has risen sharply in recent times.

…