GOLD:GOLD:$1921.20 UP $31.10 The quote is London spot price

Silver:$24.83 UP $1.00 London spot price ( cash market)

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED UP 54.02 PTS OR 1.68% //Hang Sang CLOSED DOWN 74.22 OR .31% /The Nikkei closed DOWN 155.22 POINTS OR 0.61%//Australia’s all ordinaires CLOSED UP 0.11%

/Chinese yuan (ONSHORE) closed /Oil UP TO 40.78 dollars per barrel for WTI and 43.01 for Brent. Stocks in Europe OPENED ALL MIXED// ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.7018. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.6906 TRADE TALKS STALL//YUAN LEVELS //TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED//CORONAVIRUS/PANDEMIC/TRUMP TESTS POSITIVE FOR COVID 19 : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

total withdrawals; 50,123.409 oz oz

We had 3 kilobar transactions +

ADJUSTMENTS: 3 //

Customer to deaer:

i) Malca: 76,390.776 oz

ii) Scotia: 385.800 oz (12 kilobars)

dealer to customer:

Brinks 160,787.151 oz

The front month of OCT registered a total of 7,423 contracts for a LOSS of 2939 contracts. We had 3105 notices filed yesterday so we gained 166 contracts or 16,600 additional oz will stand for delivery in this active delivery month of October. In gold we have not seen queue jumping start so early in the month. Thus you can bet the farm that throughout October, the total number of gold oz standing will increase from this level.

November gained 44 contracts to stand at 1391.

The big December contract LOST 2547 contracts DOWN to 441,642 contracts..

THE BIG STORY AGAIN TODAY IS THE HIGH OI STANDING FOR OCTOBER (101.362 tonnes). GENERALLY OCTOBER IS A POOR DELIVERY MONTH AS MOST INVESTORS PREFER TO SKIP THIS MONTH AND MOVE STRAIGHT TO DECEMBER. IT LOOKS LIKE SOME MAJOR ENTITY(GOLDMAN SACHS) JUST CANNOT WAIT FOR DECEMBER AS THEY ARE MAKING THEIR MOVE ON OCTOBER FOR PHYSICAL METAL. GOLDMAN SACHS ONE OF THE LEADERS OF THE NEW LONDON LME EXCHANGE NEEDS THE GOLD INVENTORY FOR LIQUIDITY AND INITIAL CONTRIBUTION WITH OTHER MAJOR PLAYERS. THE MAJOR DIFFERENCE BETWEEN THIS MONTH AND OTHER MONTHS IS THAT THIS GOLD STANDING IN OCTOBER WILL LEAVE THE COMEX AND HEAD FOR LONDON.

We had 1844 notices filed today for 184,400 oz OR 5.735 TONNES.

To calculate the INITIAL total number of gold ounces standing for the OCT /2020. contract month, we take the total number of notices filed so far for the month (27,009) x 100 oz , to which we add the difference between the open interest for the front month of OCT (7423 CONTRACTS ) minus the number of notices served upon today (1844 x 100 oz per contract) equals 3,258,800 OZ OR 101.362 TONNES) the number of ounces standing in this active month of Oct

thus the INITIAL standings for gold for the OCT/2020 contract month:

No of notices filed so far (27009, x 100 oz +7423 OI) for the front month minus the number of notices served upon today (1844) x 100 oz which equals 3,258,800 oz standing OR 101.362 TONNES in this active delivery month. This is a HUGE amount for gold standing for a OCT delivery month (a poor active delivery month).

We gained 166 contracts or an additional 16,600 oz will stand on this side of the pond searching for metal.

NEW PLEDGED GOLD: BRINKS

592,648.822 oz NOW PLEDGED SEPT 15.2020/HSBC 18.433 TONNES ( A HUGE INCREASE FROM 10.6)

42,548.308.00 PLEDGED APRIL 3/2020: SCOTIA: 1.3234 tonnes

deleted Int. Delaware pledge July 7 (600 tonnes)

277,934.09 oz (some deleted august 3) JPM 8.644 TONNES

610,238.285 oz pledged June 12/2020 Brinks/ July 2/July 21 19.017 tonnes

67,289.041 oz Pledged August 21/regular account 2.092 tonnes JPM

total pledged gold: 1,590,658.551 oz 49.476 tonnes

total registered, pledged and eligible (customer) gold 37,375,177.646 oz 1,162.52 tonnes (INCLUDES 4 GC GOLD)

total 4 GC gold: 126.34 tonnes

total gold net of 4 GC: 1036.18 tonnes

end

I have compiled data with respect to registered (or dealer) gold taken on first day notice for each of the past 24 months

The data begins on first day notice for the May month taken on the last day of July 2018. and it continues to present day.

I then took, how many deliveries were recorded by the CME for each and every month. I also included for reference the price of gold on first day notice.

The first graph is a logarithmic graph and the second graph, linear.

You can see the huge explosion of registered gold at the comex along with deliveries.

THE GOLD COMEX SEEMS TO BE UNDER SEVERE ASSAULT FOR PHYSICAL

END

And now for the wild silver comex results

And now for the wild silver comex results

INITIAL STANDINGS

OCT. SILVER COMEX CONTRACT MONTH//INITIAL STANDING

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory |

1,247,922.830 oz

CNT

Delaware

HSBC

|

| Deposits to the Dealer Inventory |

nil oz

|

| Deposits to the Customer Inventory |

2,334,999.550 oz

JPMorgan

Loomis

CNT

|

| No of oz served today (contracts) |

16

CONTRACT(S)

(80,000 OZ)

|

| No of oz to be served (notices) |

170 contracts

850,000 oz)

|

| Total monthly oz silver served (contracts) | 1735 contracts

8,675,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

ANDREW EXPLAINS WHY GOLD WILL RISE!!

Gold Soars Above $1900 As USDollar Plunges

After spiking on Tuesday after Trump’s “no deal” tweet, the USDollar has been in free-fall, tumbling to three-week lows this morning…

Source: Bloomberg

That USD weakness has sparked a bid under precious metals, pushing gold futures back above $1900…

And silver futures are breaking out…

As Peter Schiff recently noted,

“The problem is once you accept the false premise that government stimulus actually helps the economy – that it really is a stimulus – then you’ve kind of lost the argument. Because if borrowing and printing $1.6 trillion, if that’s a good thing, why isn’t borrowing and printing $2.4 trillion a better thing? Because you put the Republicans in the position of arguing that 2.4 trillion is too much of a good thing — that somehow, if we just create 1.6 trillion out of thin air and spend it, that’s really going to help. But if we push it to 2.4, it’s actually going to hurt. Why? I mean, when does something good suddenly become something bad? “

Is this the start of a herd-panic at the prospect of $7 trillion in Biden/Harris/AOC stimulus/MMT?

end

https://www.jsmineset.com/2020/10/09/silver-and-gold-shines/

https://www.jsmineset.com/2020/10/09/silver-and-gold-shines/

Silver And Gold Shines!

Posted October 9th, 2020 at 9:22 AM (CST) by J. Johnson & filed under General Editorial.

Great and Wonderful Friday Morning Folks,

Gold is up $27.30 with the trade at $1,922.20 and close to the high at $1,923.80 with the low at $1,898. It might be time for Silver to shine with its trade at $24.54, up 65.9 cents with the nearby high at $24.59 and the low, not so nearby at $23.965. Those currencies inside the US Dollar Index is now valuing our fiat at 93.36, down 28.8 points with its low right here at 93.305 with a high at 93.62. Of course, all this happened before 5 am pst, the Comex open, the London close, and after Q lists a few “Everything has meaning” posts.

Venezuela’s current price for Gold is now posting 19,197.97 Bolivar, as the currency popped in another 260.67 in value with Silver gaining 4.553 Bolivar with its last price at 245.093. Argentina’s Peso has given Gold a 2,067.78 A-Peso gain with the last trade at 148,258.14 with Silver’s latest price at 1,892.69 A-Peso’s proving a gain of 35.81 overnight. Gold’s price under the Turkish Lira is trading at 15,248.13, gaining 212.70 T-Lira’s with Silver’s gains adding 3.68 T-Lira’s with the last price set at 194.666. Let us observe the future moves and what happens now that the primary currency is revaluing the prices of precious metals, this could be a quarter to remember!

October Silver’s Delivery Demands now shows a total of 186 fully paid for contracts waiting for receipts with a Volume of 56 already up on the board with a trading range between $24.40 and $24.32 with the last swap at the high, up 60.3 cents, so far today. Thursday’s full day of trading occurred in between $24.175 and $23.925 with the last swap at the low, a gain of 7.7 cents yet the papers pulled the close down to $23.837, where no trade was made, with a total of 19 contracts swapping hands and reducing the delivery count by 20. Things must be really tight in the markets as the Overall Open Interest in Silver gained 254 more shorts in order to keep Silver’s price at yesterday’s close with today’s early morning count at 156,841 sellers against the physicals and as Ag jumped 66 cents.

October Gold’s Delivery Demands now shows a post of 7,423 fully paid for contracts still waiting, and with a Volume of 149 up on the board with a trading range between $1,915.30 and $1,905.10 with the last buy at the high, a gain of $26.70 so far this morning. Thursday’s full day of delivery activity happened in between $1,893 and $1,882.70 with the last buy at $1,890.80, a gain of $7.20 yet the paper controlled close was settled out at $1,888.60, a $5 gain. The pressure is on, and the shorts are stained, as 2,826 paper contracts jumped ship, leaving a total Open Interest of 548,096 to go against the deliveries and against today’s little rally.

American Politics continues as one side, claims that Trump is losing against Biden/Harris, and is so certain they’ve won that they are attempting to use a panel of Trump haters in order to Coup again. The Debate Commission (what are the odds they are all Trump haters?) refuses to allow in-person debate, so President Trump will hold a rally instead. Just look at the crowd gatherings, over the years, between Joe Biden and Trump. I know it’s going to be close, but I do think one will understand who is least popular and who is going to win, even the popular vote, maybe not the late mailed in votes by the dead or illegal. If one Q’s, at the same time the news hits, you would see another viewpoint, which is clearer and more concise, and imo, is the reason why Q came to be.

Here are last night’s 17 (q in numbers) posts; Nothing is random. Everything has meaning. Now that Russia Collusion is a proven lie, when do the trials for treason begin? … We need Justice!!!! We are ready!!!! Let’s go!!!! WWG1WGA. Could it be, all this obstruction was planned ahead of time and the deep state controllers still don’t realize we have the servers? Q, only gives research clues and news posts, for those who wish to look. With that in mind; Was the 25th amendment ‘arrow in the quiver’ planned?

How long ago?

Was it expected POTUS would be in a critical [health] state re: C19?

Recovery unexpected?

Impossible to unwind?

Next: ‘mentally incapacitated’ re: C19 language [“people are dying”] _safety and security to the well being ……….

Combat tactics, Mr. Ryan. (Btw, that’s Republican Paul Ryan)

Did you notice the missile within the drop re: 25th amendment?

Just in, Q posted again with a twitter from John Brennan dated May 8 2018.

Why did Brennan endorse?

Why did POTUS select as Dir?

Buckle up.

It’s a nice day already, Q’s last statement here; Buckle Up, seems to be apropos to end the weekend, don’t you think? With all this American Style politicking, DOJ investigations, and the ever-printing Federal Reserve, we see more reasons for getting physicals in Silver, Gold, Grub, and Guns/Ammo. Have a great weekend, make every day count, and as always …

Stay Strong!

Jeremiah Johnson

More J.Johnson content is available with purchase of a JSMineset subscription.

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

March 4.2019

Parker City News

JP Morgan faces potential class action lawsuit after guilty pleas by a former metals trader

Traders from across the U.S. are banding together to accuse J. P. Morgan Chase of manipulating precious metals markets for years.

At least six lawsuits, all making similar allegations against the nation‘s largest bank, have been filed in New York federal court in the past month, since federal prosecutors in Connecticut with a former J. P. Morgan Chase metals trader.

The cases could potentially include thousands of people who traded in the precious metals market. The White Plains, N.Y., law firm Lowey Dannenberg is asking the court to combine the cases and name it as the lead.

The law firm‘s commodities group is led by Vincent Briganti, the attorney who filed the first lawsuit on behalf of Dominick Cognata, a New York resident who alleges he suffered losses due to J. P. Morgan‘s trading conduct in the silver and gold futures and options markets.

A combined case, seeking class action status, would include anyone who purchased or sold futures contracts or an option on NYMEX platinum or palladium or COMEX silver or gold between at least Jan. 1, 2009, and Dec. 31, 2015. The lawyers believe that “at least hundreds, if not thousands” of traders would be eligible to join the case.

Named as defendants in all of the lawsuits are John Edmonds, a 36-year old former metals trader at J. P. Morgan, a group of yet-to-be-identified precious metals traders and the bank.

Edmonds, a New York resident, pleaded guilty in October to one count of conspiracy to defraud the market and manipulate prices of precious metals futures contracts and one count of commodities fraud. In the criminal plea, Edmonds admitted that he and other “unnamed co- conspirators” at J. P. Morgan, fraudulently manipulated precious metals markets from 2009 to 2015, the same time frame covered in the class action suits.

Briganti filed the initial class action on Nov. 7, just one day after the Justice Department unsealed Edmonds‘ plea in the U.S. District Court of Connecticut.

Edmonds admitted in his guilty plea that he deployed the illegal trading scheme hundreds of times with the direct knowledge and consent of his immediate supervisors. Plaintiffs say they have suffered economic injury, including monetary losses, as a direct result of actions by Edmonds and the other unnamed J. P. Morgan metals traders in the futures and options contracts.

One of the suits alleges that “the number of unlawful trades that JP Morgan traders executed in precious metals futures markets is at least in the thousands.”

J. P. Morgan declined to comment. Lowey Dannenberg did not respond to a request for comment by CNBC.

The Justice Department‘s criminal investigation is still ongoing and recently caused a separate related civil case to be put on hold for at least six months while the government continues its investigation. That civil lawsuit, which also accuses J. P. Morgan of rigging the precious metals market, was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders.

After reviewing the details of the plea agreement, David Kovel, the attorney for Shak‘s suit, sought to re- interview Edmonds, along with two other current and former senior traders at the bank. However, the government argued that reopening questioning would be detrimental to the ongoing criminal investigation. The federal judge overseeing the proceedings ordered a six-month stay in the civil case.

Kovel declined to comment.

Edmonds was originally scheduled to be sentenced in Hartford, Conn., on Wednesday, Dec. 19, but a court filing on Nov. 27 shows the sentencing has been postponed until June. A spokesman for the U.S. Attorney for Connecticut could not elaborate on why the sentencing was postponed since the court filing is under seal.

-END-

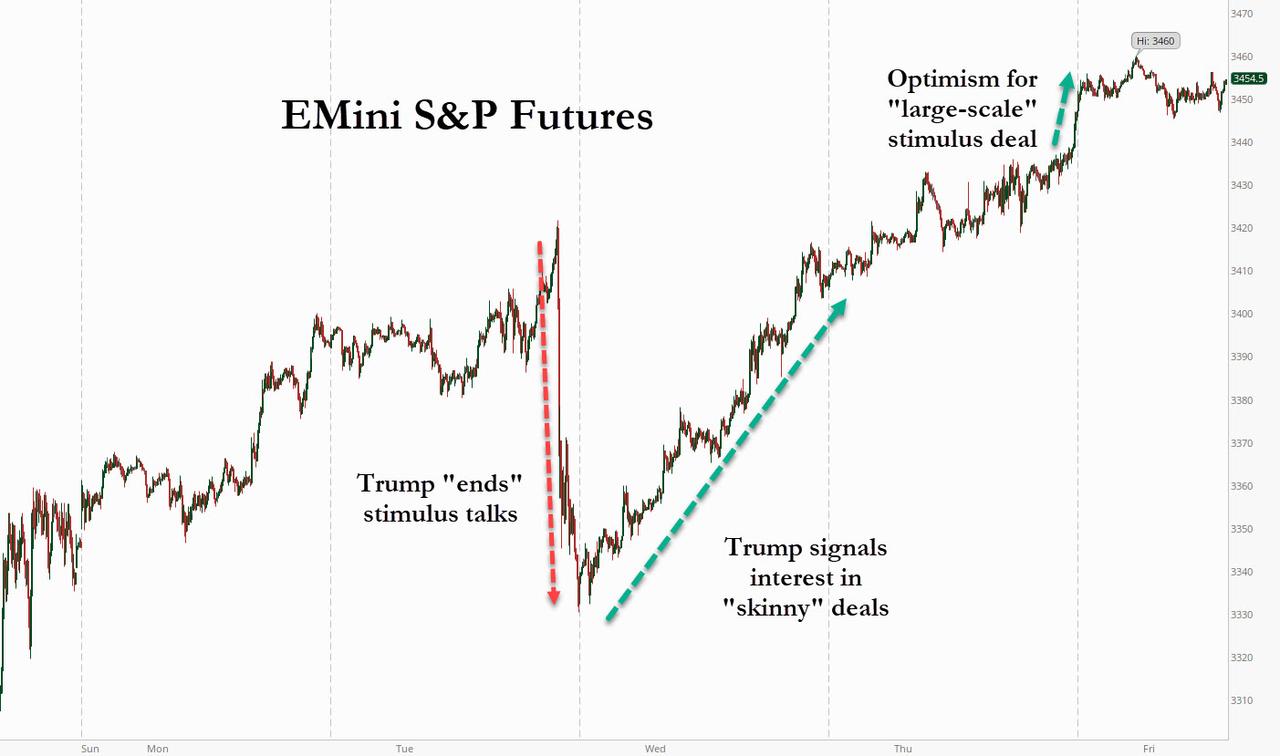

Futures Jump On “Large-Scale” Deal Optimism

Just two days after a Trump tweet “crushed” hopes for any more fiscal stimulus talks, optimism for not just a stimulus deal but for a “large-scale” deal is back front and center, after the White House reversed again late on Thursday after media reports that Trump was concerned by the market reaction to him walking away from stimulus discussions, and signaled that the administration is again leaning toward a large-scale stimulus bill after House Speaker Nancy Pelosi pushed back on the idea of individual measures for parts of the economy hit by the Covid-19 crisis. According to a Pelosi spokesman, Mnuchin told Pelosi in a 40-minute call that President Donald Trump wants agreement on a comprehensive stimulus package, which was enough to send futures blasting higher, and hitting 3460 overnight, a level last seen on Sept 4 just after the market slumped from its all-time highs. The MSCI world equity index was up 0.1% at a more than one month high; yields and the dollar dropped, while the Chinese yuan and gold surged.

However, opposition remains among Senate republicans for a large deal with some saying that enough stimulus has already been injected, and so time is very tight for any legislation to reach the president’s desk before the end of October. As Politico notes, to “get a deal, the White House needs to empower MNUCHIN to get something done — something they haven’t done yet; TRUMP needs to expend serious political capital to get a big vote in House as a signal to the Senate that it has cover voting yes.”

Meanwhile as Bloomberg notes, another obstacle to a successful outcome remains as both Trump and Pelosi are publicly questioning each other’s mental stability.

Democrats are set to announce a bill today that would set up a commission to evaluate using the 25th amendment which can remove a sitting president from office.

With recent trading on Wall Street – particularly in shares of U.S. airlines, which began mass furloughs after a previous payroll support package expired – dictated by negotiations between the White House and Democrats on more fiscal aid, the S&P airlines subindex jumped in the past two sessions and is on track for one of its best months this year after sinking 3% on Tuesday as Trump broke off aid talks. In company news, Xilinxsurged more than 17% after the WSJ reported that AMD was in talks to buy the chipmaker in a deal that could be valued at more than $30 billion. Shares of AMD fell 5.8%. Also overnight Citadel announced it would acquire IMC’s designated market-making unit, firming up its position as the largest floor broker on the NYSE.

Gains in U.S. stocks this week have been concentrated in small- and mid-cap firms, which stand to benefit more from a Biden victory than the large-cap companies that had so far fueled Wall Street’s recovery from the coronavirus lows hit in March, fund managers said. In a sign markets are pricing in a Biden victory, clean energy-related shares have outperformed in recent weeks. The iShares Global Clean Energy ETF has gained 14% so far this month, compared with 4% gains in the S&P 500 energy index. The November VIX contract dropped to 30.25, its lowest level in three weeks, another sign of reduced worries about a contested election.

“Biden seems to have a clear lead following the TV debate and a coronavirus cluster in the White House, which has raised questions about Trump’s crisis management capabilities,” said Mutsumi Kagawa, chief global strategist at Rakuten Securities.

Optimism also prevailed in Europe, where equities rose on Friday, and were set for a second consecutive weekly gain as investors were encouraged by stimulus prospects in the U.S. and positive guidance updates. The Stoxx Europe 600 index was up 0.3% at 730 a.m. ET led by miners and energy shares, while autos underperformed. European stocks also gained as a host of companies raised outlooks, from Denmark’s drugmaker Novo Nordisk to German online clothing retailer Zalando. Stocks fell in Spain, where the government declared a state of emergency for Madrid to control Covid-19. Italy’s 10-year bond yield fell a record low.

“The lower level of uncertainty with regards to the U.S. election combined with the prospect of additional stimulus measures is probably behind the latest positive inflection in equity markets,” says Sylvain Goyon, strategist at Oddo BHF. That’s because Democratic contender Joe Biden’s “increasing lead in the polls gives credence either to a ‘blue wave’ scenario and more stimulus, or more political pressure for President Trump to offer something prior to the vote.”

Earlier in the session, MSCI’s broadest index of Asia-Pacific shares outside Japan rose 0.3%, inching closer to its Aug. 31 peak, which was its highest level since March 2018. China’s CSI300 index gained 2% after the Golden Week holidays. The Shanghai Composite Index rose 1.7%, with Ningbo Ronbay New Energy and Shandong Jinjing posting the biggest advances. In Japan, the Nikkei dipped 0.1% after reaching a seven-and-a-half-month high; while the Topix declined 0.5%, with Danto and Creek & River falling the most.

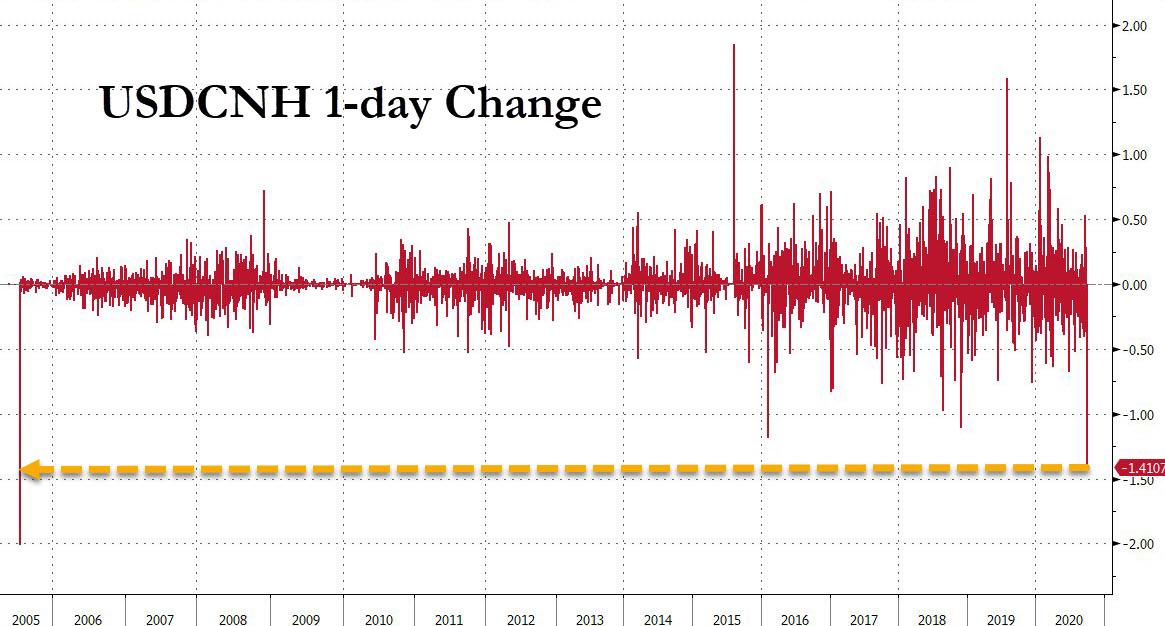

In FX, the dollar weakened, heading for its second weekly loss, as the White House signaled it was open to large-scale U.S. stimulus, while the Chinese yuan was the biggest beneficiary of the rising hopes of a Biden win, posting its biggest daily rise in more than four years after the holidays. The greenback declined against most Group-of-10 peers and hits lowest level since Sept. 21, as measured by the Bloomberg Dollar Spot Index which fell 0.3% Friday, set for its third straight day of declines; it came under pressure during Asia hours as emerging-market currencies advanced with the yuan better bid following an eight-day holiday in China. NZ’s kiwi led gains as the Swiss franc follows suit. The euro rose 0.1% to $1.1776.

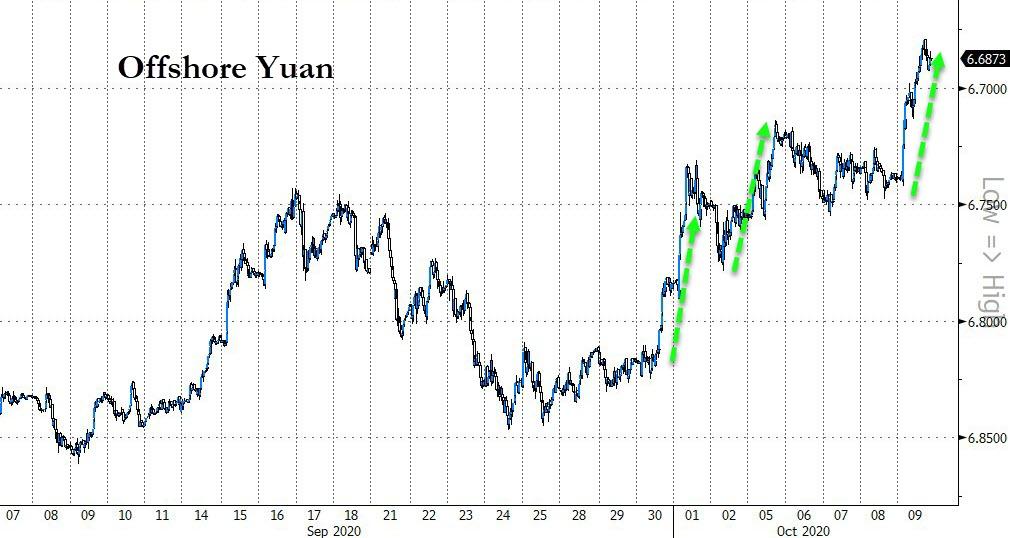

Another notable mover was China’s yuan which rose sharply in onshore trading, catching up with gains seen in offshore trading the past week, as mainland markets reopened after the Golden Week holiday. The yuan climbed as much as 1.4% on Friday while in offshore markets the currency strengthened 0.6%, with both reaching their strongest since April 2019.

The People’s Bank of China put the daily fixing at a stronger-than-expected level. Amid the risk-on mood, the 10-year yield on Chinese sovereign debt reached its highest level since December. Friday’s currency and equity gains “have staying power. Chinese markets will still be supported next week,” said Moh Siong Sim, foreign exchange strategist from Bank of Singapore. He added both asset classes will also be supported by recovering Chinese consumer spending while Joe Biden’s widened poll lead in the U.S. “is also good for Chinese assets as his policy would be less confrontational” than President Donald Trump’s.

In another sign that investors look for a Brexit trade deal to be reached in the end, leveraged funds stepped in to fade a sharp drop in cable following a report that there has been insufficient progress in the talks, a Europe-based trader says. GBP/USD rose earlier 0.3% to 1.2973 high amid broad greenback weakness, only to erase the advance and stabilize around 1.2940.

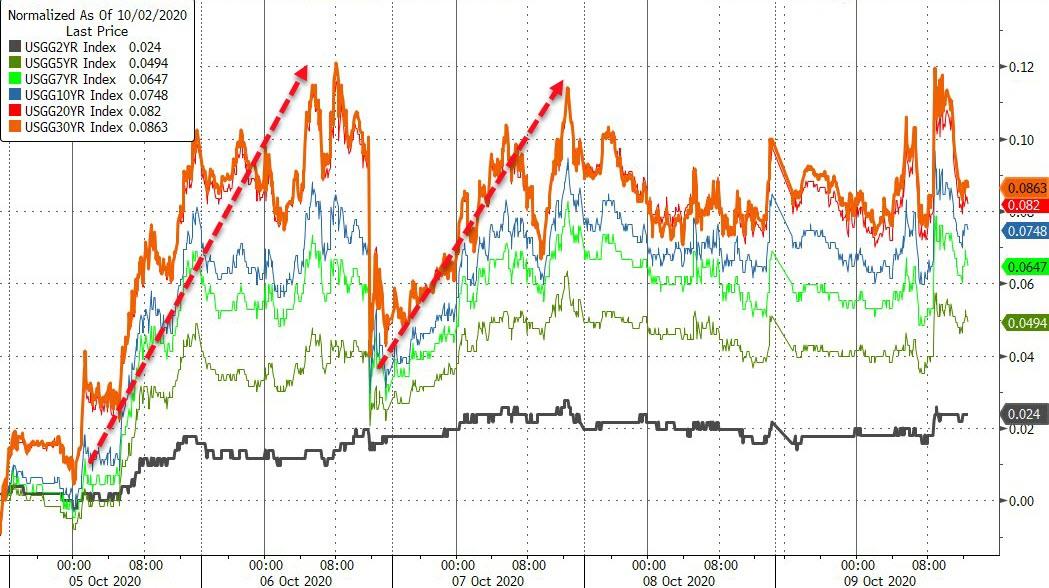

In rates, Treasuries inched higher after advancing during Asia session and European morning. Treasury yields lower by 0.5bp to 2.2bp across the curve, flattening 2s10s, 5s30s by 1.8bp and 0.9bp; 10-year yields around 0.764%, slightly outperforming bunds while lagging behind gilts. Yields remain higher on week in which prospects for a stimulus agreement helped drive steep gains for stocks on Monday and Wednesday; The 10-year is up by more than 6bp, with 50-DMA on cusp of crossing above 100-DMA. Gilts outperformed following weak August U.K. GDP while in Asia session gains for Aussie bonds supported Treasuries. The 10-year German bond yield was unchanged at -0.525%. Other core yields were a touch lower.

“The rise in U.S. yields, particularly at the long end, suggests increased expectations of a blue wave in the election,” said Koichi Fujishiro, economist at Dai-ichi Life Research Institute.

In commodities, oil prices edged up, propelled by supply outages caused by a storm in the Gulf of Mexico and a strike of offshore workers in Norway. Both benchmark contracts were on course for their biggest weekly gains since early June. Brent was up 16 cents at $43.50 a barrel. WTI crude rose 14 cents to $41.33. A weaker dollar boosted gold which gained 1.1% to $1,914.28 per ounce.

Starting next week, attention turns to corporate America’s third-quarter earnings season, kicked off by JPMorgan Chase & Co, Citigroup Inc and drugmaker Johnson and Johnson. Looking at the day ahead, we get final August reading for wholesale inventories in the US. From central banks, the Reserve Bank of India will be deciding on monetary policy, while the Fed’s Barkin and the BoE’s Haldane will also be speaking.

Market Snapshot

- S&P 500 futures up 0.4% to 3,450.25

- STOXX Europe 600 up 0.2% to 369.09

- MXAP up 0.05% to 175.13

- MXAPJ up 0.3% to 579.54

- Nikkei down 0.1% to 23,619.69

- Topix down 0.5% to 1,647.38

- Hang Seng Index down 0.3% to 24,119.13

- Shanghai Composite up 1.7% to 3,272.08

- Sensex up 0.5% to 40,387.55

- Australia S&P/ASX 200 unchanged at 6,102.17

- Kospi up 0.2% to 2,391.96

- Brent futures down 0.4% to $43.19/bbl

- Gold spot up 1.1% to $1,915.04

- U.S. Dollar Index down 0.2% to 93.38

- German 10Y yield fell 1.8 bps to -0.541%

- Euro up 0.3% to $1.1792

- Italian 10Y yield fell 2.7 bps to 0.555%

- Spanish 10Y yield fell 2.7 bps to 0.174%

Top Overnight News from Bloomberg

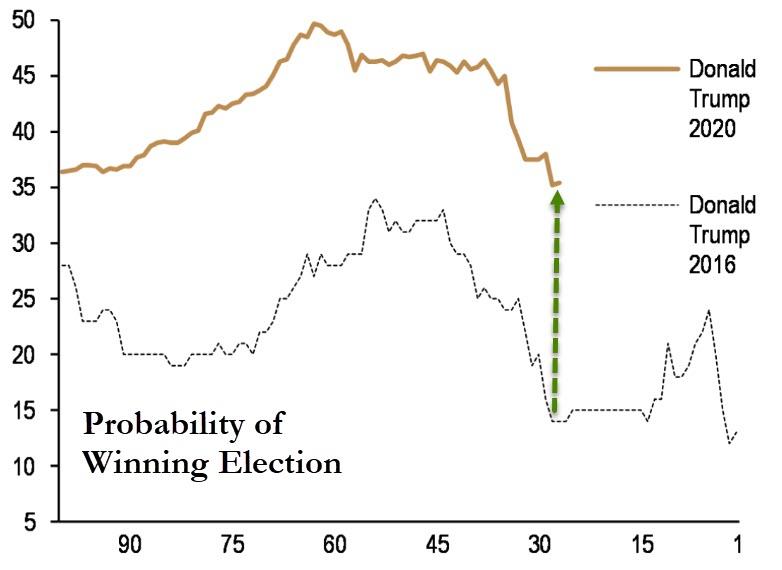

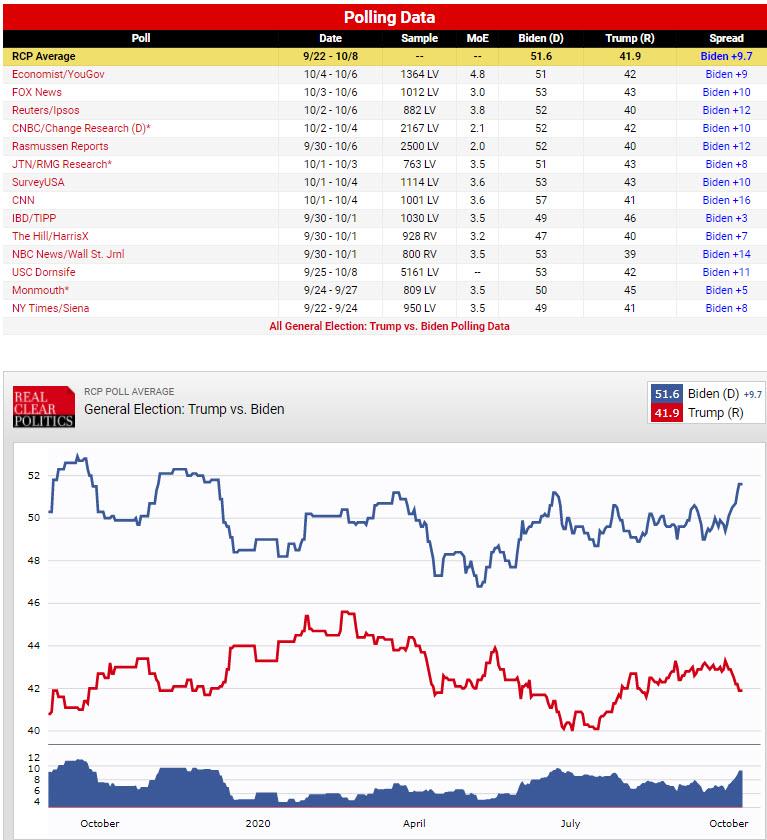

- While the lesson of the 2016 campaign was never to count out Donald Trump, his path to re-election is narrowing dramatically as Democrat Joe Biden’s lead continues to grow and voters sour on the president’s handling of the coronavirus pandemic

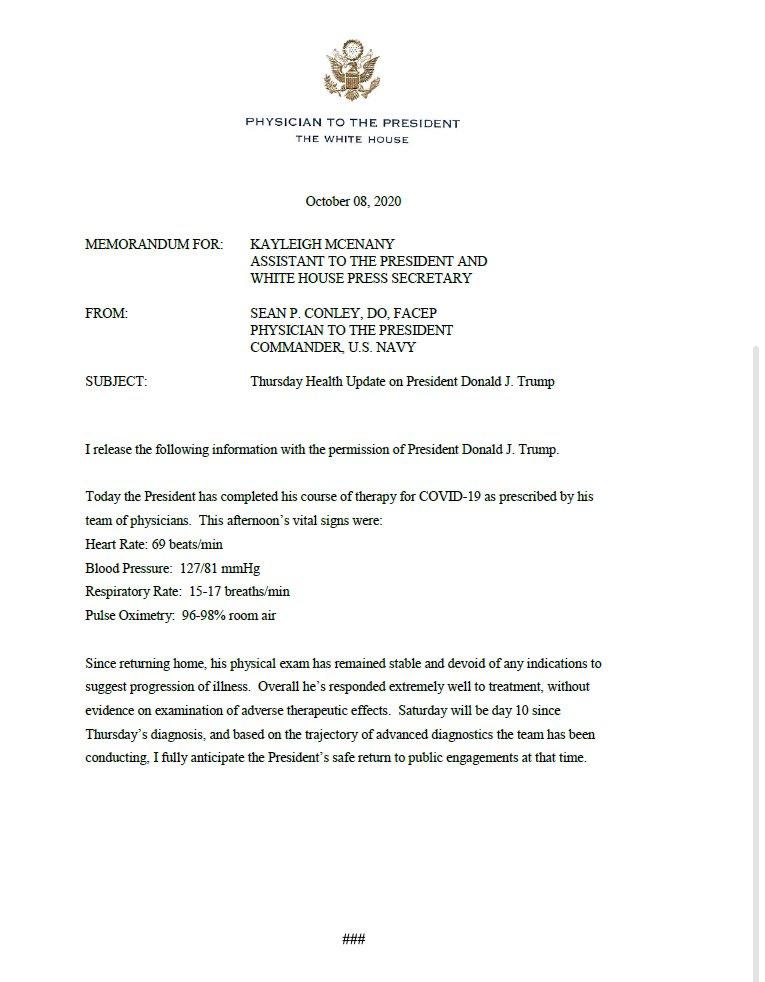

- President Trump’s Dr. Sean Conley said in a statement that “since returning home, his physical exam has remained stable and devoid of any indications to suggest progression of illness; said he expects Trump to safely return to public engagements by Saturday, 10 days after his diagnosis

- Pound traders who have grown used to Brexit brinkmanship between London and Brussels are making two assumptions: there’ll probably be a trade deal, and U.S. elections matter more right now

- In 2016 investors were buying the Russian ruble and selling the Mexican peso in expectation the Republican candidate would mend relations with Russian President Vladimir Putin and cut trade ties with Mexico after winning the election. This time around, the trade has reversed as Joe Biden gains in the polls

- Spanish Prime Minister Pedro Sanchez has called an extraordinary cabinet meeting on Friday to discuss a possible state of emergency for the region of Madrid, while German Chancellor Angela Merkel will speak with mayors of the country’s biggest cities about efforts to contain a recent surge in Europe’s largest economy

A quick look at global markets courtesy of NewsSquawk

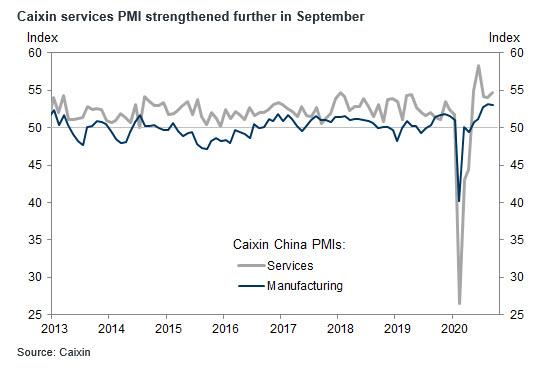

Asian equity markets traded mixed as US equity futures extended on the prior day’s gains amid stimulus hopes after House Speaker Pelosi and US Treasury Secretary Mnuchin continued their relief discussions, while President Trump also suggested optimism that talks are beginning to work and was said to be open to something larger than a skinny bill. Nonetheless, ASX 200 (U/C) was rangebound and took a breather following the outperformance seen for most the week and after the RBA Financial Stability Review noted that domestic banks were well placed to continue lending and supporting the economic recovery, as well as the financial system but added that business failures will increase substantially as loan repayment deferrals and income support end. Nikkei 225 (-0.1%) initially began on the front-foot but then stalled in tandem with a mild pullback in USD/JPY which gave up the 106.00 status and after weaker than expected Household Spending. Hang Seng (-0.3%) and Shanghai Comp. (+1.6%) were varied with outperformance in the mainland as participants returned from the holidays where spending rose by 6.3% Y/Y amid a bout of ‘revenge travel’ which saw Golden Week air passenger numbers recover to 91% of last year’s volume. Participants also welcomed private sector PMI data in which Caixin Services PMI topped estimates at 54.8 vs. Exp. 54.3 and Caixin Composite PMI was lower than previous at 54.5 (Prev. 55.1) but remained at a firm expansion. Finally, 10yr JGBs were steady amid the indecisive risk sentiment seen in Tokyo and as prices continued to eye the psychological 152.00 level, while the BoJ’s presence in the market for nearly JPY 1tln of JGBs has also provided a floor for government bonds.

Top Asian News

- Hong Kong Small Cap Sinks 90% Amid Margin Call Speculation

- India’s RBI Uses Unconventional Tools to Check Borrowing Costs

- China’s Yuan Climbs, Stocks Gain in Upbeat Return for Traders

- Foreigners Buy Most Turkish Assets Since 2018 After Rate Hike

Mixed trade in Europe as regional bourses diverged after opening with mild broad-based gains (Euro Stoxx 50 +0.2%) following on from a similar lead from the APAC region after Mainland China returned to the market following its Golden Week holiday. Meanwhile, US equity futures eke mild gains as hopes for resolution on some stimulus keeps State-side sentiment supported. Back to Europe, varying performance seen across the indices, with UK’s FTSE (+0.7%) outpacing peers on a favourable Sterling action, whilst the peripheries see underperformance after EU Budget talks between the European Parliament and EU ambassadors have been suspended after just an hour, after a German attempt to get a breakthrough failed, with the issue threatening a delay to the swift implementation of the Recovery Fund. Sectors are mostly firmer with Energy outperforming amid yesterday’s rise in the complex, with no risk profiled to be derived from the broader sectors. The breakdown sees Autos and Construction towards the bottom of the pile, whilst Basic Resources coat-tail on the broader gains across base metal markets. In terms of individual movers, Danish-listed Pandora (+14%) resides near the top of the Stoxx 600 after raising its guidance, with Novo Nordisk (+4.0%) also higher amid a forecast upgrade. British Land (+4.0%) is higher on the back of dividend resumption. LSE (+0.5%) is firmer after it announced the sale of Borsa Italian to Euronext (-3.7%) for EUR 4.325bln vs. Exp. ~EUR 4bln.

Top European News

- Russian Covid-19 Cases Hit Record as Moscow Resists Lockdown

- Europe Holds Crisis Talks as Spain Pushes for Emergency Powers

- Italy’s Unflagging Bond Rally Drives Key Yield to Record Low

- LSE Agrees $5 Billion Borsa Sale to Euronext, Italian Banks

In FX, no obvious catalyst, but the Kiwi has derived more than fellow G10 currencies from the Greenback’s deeper pull-back from 93.500+ levels in DXY terms to fresh w-t-d lows of 93.309, as Nzd/Usd breaches resistance at the psychological 0.6600 level that has been capping rebounds since the headline pair retreated from early October highs.

- CHF/EUR/AUD/CAD/JPY – Also taking advantage of their US counterpart’s demise, with the Franc above 0.9150, Euro probing 1.1800 and Aussie eyeing 0.7200 again having cleared the 20 DMA (0.7176) following an encouraging FSR from the RBA. Meanwhile, the Loonie has extended recovery gains from midweek lows around 1.3340 towards 1.3160 ahead of Canadian jobs data and the Yen has rebounded from sub-106.00 levels after mixed Japanese household spending metrics, but may run into option expiry related offers given decent interest at 105.90-80 (1 bn) and then from 105.50 to 105.40 (1.2 bn). On that note, Eur/Usd expiries are well spread either side of 1.1800 and full details are available via the headline feed at 7.08BST.

- GBP – Sterling was relatively resilient in the face of weaker than forecast UK data, and a particularly big miss in monthly GDP, but unable to weather the latest Brexit headlines suggesting insufficient progress in latest talks on trade before EU chief negotiator Barnier returns to Brussels. Cable has reversed through 1.2950 and Eur/Gbp is back over 0.9100 as the Pound awaits further fiscal support for the labour market from Chancellor Sunak and a speech by BoE’s Haldane.

- SCANDI/EM – Only a modest loss of momentum for the Nok beyond 10.9000 vs the Eur in wake of softer than expected Norwegian CPI, while the Sek seems content between 10.4500-10.4100 parameters and unusually large option expiries in the Eur cross either side, especially at the 10.3000 strike where 4.1 bn rolls off vs 1.2 bn at 10.7500. Elsewhere, the Yuan has returned from China’s Golden Week break refreshed and raring to go as Usd/Cnh scales 6.7000 with the aid of a strong PBoC Cny midpoint fix (at 6.7796 vs 6.7905 projected and 6.8101 pre-market closure). Conversely, Lira losses accelerated to 7.9550+ before the CBRT stepped in with another aggressive move to arrest the slide via a 150 bp hike in Try swap rates, but 7.9000 as contained comeback efforts thus far. Ahead, Brazil’s Real in focus given inflation updates and services sector growth.

- RBA Financial Stability Review stated that Australian banks are well placed to continue lending and supporting the economic recovery, as well as the financial system but added that although the financial system is in a strong position, risks are elevated. Furthermore, it stated that overall household income has increased during H1 2020 but the number of households experiencing financial stress has increased and will increase further, while it noted that business failures will increase substantially as loan repayment deferrals and income support end. (Newswires)

In commodities, WTI and Brent front-month futures ebb lower after the holding pattern seen overnight following yesterday’s gains which were fueled by some supply side developments. 1) Hurricane Delta is poised to make landfall along the Gulf Coast later today as a major hurricane, with BSEE’s latest estimate showing 91.5% of oil production and 61.8% of natgas production shuttered ahead of the hurricane. 2) Reports yesterday, citing a senior Saudi oil adviser, noted that the Kingdom is mulling cancelling an output hike next year amidst the rising cases coupled by Libyan oil output slowly coming back online. JP Morgan analysts see potential for Saudi to drive incremental oil cuts at the upcoming November 30th meeting, with the upside scenario a deeper cut whereby the Kingdom reduces output below quota against the backdrop of weakening demand. Meanwhile more recently on the geopolitical front, Armenia and Azerbaijan are in Moscow in a bid to ease tensions – the French Presidency expects a truce to be declared in the Nagorno-Karabakh region by this evening or tomorrow, according to Sky News Arabia. WTI Nov and Brent Dec reside around session lows within a tight range after declining from USD 41.47/bbl and ~43.50/bbl respectively. Elsewhere, spot gold continues to grind higher above USD 1900/oz (vs. low USD 1893/oz) on Dollar-dynamics, with similar action seen in spot silver which remains north of USD 24/oz. In terms of base metals, Shanghai Copper futures ended the day with gains of some 1% with LME copper also trading with gains amid expected strikes at Chile’s mines. Meanwhile, Chinese steel and raw material prices rose after the Golden Week holiday amid touted supply woes alongside forecasts for higher demand in Q4.

US Event Calendar

- 9am: Bloomberg Oct. United States Economic Survey

- 10am: Wholesale Inventories MoM, est. 0.5%, prior 0.5%

- 10am: Wholesale Trade Sales MoM, prior 4.6%

DB’s Jim Reid concludes the overnight wrap

Back to the secondary poll going on at the moment and markets had another strong performance yesterday as optimism remained that a stimulus deal might still be achieved pre-election and also as investors increasingly bet on the likelihood of a Biden presidency (and hence further stimulus) from January. After President Trump’s Tuesday tweet that he was pulling out of the talks, he continued to soften his stance in a Fox Business interview yesterday, and said “I think we have a really good chance of doing something”, as a Politico reporter also tweeted that Secretary Mnuchin had floated restarting talks with Speaker Pelosi. Pelosi noted that any passage of a skinny deal would require an agreement on a larger follow-on bill. One voice that has remained constant throughout the recent talks has been Senate Majority Leader McConnell, who again said Pelosi was insisting on “an outrageous” sum of money and acknowledged that the election timing makes agreeing on a deal “challenging.”

Whether or not we’re actually likely to see further stimulus by Election Day (and it still looks less likely than not), risk assets climbed higher in response to this news flow, and by the end of the session the S&P 500 had risen a further +0.80% to its highest level in over a month, and the VIX index of volatility fell back -1.7pts to a one-week low. It was another broad-based rally as 23 of 24 industries in the S&P 500 rose on the day. Cyclicals outperformed large-cap tech yesterday with the NASDAQ ‘only’ rising +0.50%. Energy stocks led the way on both sides of the Atlantic (+3.73% in the US and +1.63% in Europe) as Brent crude oil prices closed above $43/bbl for the first time in nearly 3 weeks. European equities overall saw similar gains to those in the US, with the STOXX 600 (+0.78%) and the DAX (+0.88%) powering forward.

Updating our screens overnight, US equity futures have continued to be supported by the positive stimulus news, with S&P 500 futures up +0.57%. Meanwhile in Asia, there’s been a more mixed performance, with the Nikkei (-0.20%) losing ground and the Hang Seng (+0.10%) seeing a modest gain. Chinese markets have seen a stronger performance, however, as they reopened after a week-long holiday, and the Shanghai Comp is up +1.89%. Furthermore, the September Caixin PMI from China showed the composite reading at 54.5 (vs. 55.1 last month) and the services reading increase to 54.8 (vs. 54.3 expected).

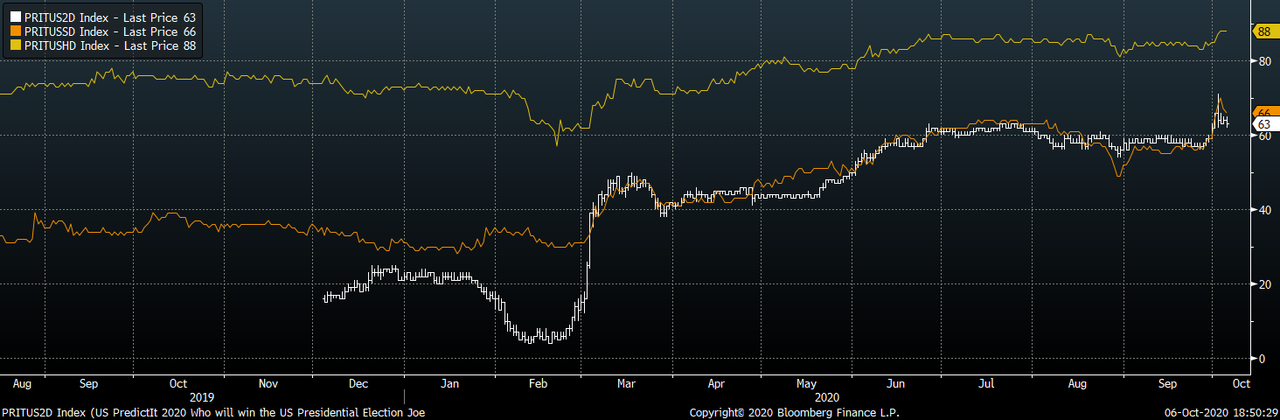

Back to the election, and the main political news from yesterday was President Trump’s announcement that he wouldn’t take part in the second debate next week following the decision that it would be held virtually, as well as the news overnight from his doctor that the President would be able to safely return to public engagements by Saturday. On the debate, Trump campaign manager Bill Stepien said that “We’ll pass on this sad excuse to bail out Joe Biden and do a rally instead.” Meanwhile, the Biden campaign said that he would take voters’ questions instead. With President Trump trailing by nearly 10pts now in both FiveThirtyEight and RealClearPolitics’ polling averages, skipping on the debate means that the president is missing out on any late attempt to reset the trajectory of the race. But in terms of markets, what was noticeable was the increasing focus on a potential Biden presidency and a possible blue wave. His chances on FiveThirtyEight’s model ticked up further to 84%, and the Democratic Party’s chances of winning the Senate are up to 68%, raising the prospect of significant further stimulus in Q1. Along with the House of Representatives, which is heavily expected to remain with the Democrats, this would bring an end to the divided government that we’ve seen these last two years.

On the coronavirus, Europe saw some further troubling news yesterday, which came as the executive director of the European medicines Agency, Guido Rasi, said that a vaccine was “unlikely” to be ready by the end of the year. In terms of the numbers, the UK saw another 17,550 cases reported, while the number of patients in hospital in England rose above the 3,000 mark for the first time since June. Over in France, another 18,129 were reported, and the number of Covid-19 patients in intensive care rose to its highest since May, at 1,427. In response, the government has placed Lyon, Lille and Grenoble on maximum alert, with restrictions similar to those in Paris and Marseille. In Poland, it will be compulsory to wear masks in public from Saturday, while further restrictions were imposed in the Czech Republic, where all cultural events and indoor sporting activities have been banned. There has been some pushback amid the rise in restrictions across the continent with the most recent from a court in Madrid blocking the regional government’s new measures to reduce mobility. This comes as Spain has continued to register nearly 70,000 new infections per week over the last month.

Over in the US, New York Mayor de Blasio announced the closure of a further 61 schools, bringing the total to 169. There were further concerning signs from some first wave northeastern hotspots, as Massachusetts, New York and New Jersey all saw the highest number of new cases since May. Overall, the 7-day rolling sum of cases in the US rose over 316,000 for the first time since mid-August.

In other news, we got the ECB’s account of its September monetary policy meeting, where there were a number of mentions on the exchange rate. Furthermore, it noted that “the recent appreciation of the euro exchange rate had had a material impact on the inflation outlook in the September ECB staff projections.” The euro saw a modest weakening against the US dollar yesterday, and was down -0.03% by the close.

Over in the fixed income sphere, sovereign bonds rose yesterday, with yields on 10yr Treasuries (-0.2bps) and bunds (-3.0bps) both falling. There were also a number of records set in southern Europe, as yields on 10yr Greek debt fell -4.5bps to an all-time low of 0.89%, and yields on 10yr Italian debt fell -2.6bps to an all-time closing low, though they had been lower on an intraday basis back in September 2019.

In terms of yesterday’s data, the initial jobless claims in the US for the week through October 3 fell to 840k (vs. 820k expected though), down from an upwardly revised 849k in the week prior. That said the continuing claims reading for the week through September 26 fell to a post-pandemic low of 10.976m (vs. 11.4m expected), with the insured unemployment rate falling to 7.5%.

To the day ahead now, and the data highlights include UK GDP for August, along with French and Italian industrial production for that month. We’ll also get the Canadian employment report for September, and the final August reading for wholesale inventories in the US. From central banks, the Reserve Bank of India will be deciding on monetary policy, while the Fed’s Barkin and the BoE’s Haldane will also be speaking.

3A/ASIAN AFFAIRS

i)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED UP 54.02 PTS OR 1.68% //Hang Sang CLOSED DOWN 74.22 OR .31% /The Nikkei closed DOWN 155.22 POINTS OR 0.61%//Australia’s all ordinaires CLOSED UP 0.11%

/Chinese yuan (ONSHORE) closed /Oil UP TO 40.78 dollars per barrel for WTI and 43.01 for Brent. Stocks in Europe OPENED ALL MIXED// ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.7018. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.6906 TRADE TALKS STALL//YUAN LEVELS //TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED//CORONAVIRUS/PANDEMIC/TRUMP TESTS POSITIVE FOR COVID 19 : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3 a./NORTH KOREA/ SOUTH KOREA

South Korea

b) REPORT ON JAPAN

3 C CHINA

CHINA/USA//TAIWAN

Not good: USA security adviser O”Brien warns that China will attack Taiwan and the uSA will not intercede

(zerohedge)

US Security Adviser O’Brien Warns China Against Attack On Taiwan

We detailed Wednesday that China’s state-run Global Times issued a major threat, saying China should “fully prepare itself for war” with Taiwan in the event it restores diplomatic relations with the United States. The tabloid’s chief editor Hu Xijin wrote in his latest English language op-ed that “We must no longer hold any more illusions. The only way forward is for the mainland to fully prepare itself for war and to give Taiwan secessionist forces a decisive punishment at any time.”

On the same day National Security Advisor Robert O’Brien addressed just such a scenario at an event hosted at the University of Nevada in Las Vegas, describing as summarized by Al Jazeera that China is “engaged in a significant naval build-up probably not seen since Germany’s attempt to compete with Britain’s Royal Navy prior to WWI.”

“Part of that is to give them the ability to push us back out of the Western Pacific, and allow them to engage in an amphibious landing in Taiwan,” O’Brien said. “The problem with that is that amphibious landings are notoriously difficult.”

As he specified this includes the fact of about a 100-mile distance between the mainland and Taiwan, adding to difficulties of a well-organized amphibious landing.

“It’s not an easy task, and there’s also a lot of ambiguity about what the United States would do in response to an attack by China on Taiwan,” he said, referencing also that China hawks in Congressed have introduced the Taiwan Invasion Prevention Act bill. More directly he was referencing the US longtime posture of ‘strategic ambiguity’ regards defending Taiwan.

“You can’t just spend 1 percent of your GDP [gross domestic product], which the Taiwanese have been doing – 1.2 percent – on defense, and hope to deter a China that’s been engaged in the most massive military build up in 70 years,” he said, during a week where Taiwan’s defense spending was up for question at the US-Taiwan Defense Industry Conference.

O’Brien proffered a strategy that militarily Taiwan needs to “turn themselves into a porcupine” because ultimately “Lions generally don’t like to eat porcupines.”

It didn’t take long for Chinese state media to respond in what it called out as Taiwan’s “weakness”:

Meanwhile, after much of a year which has witnessed Taiwan’s Air Force scramble its jets dozens of times, and conduct deterrence exercises and aerial patrol missions, Taiwan’s Minister of National Defense Yen Teh-fa on Wednesday announced the island has spent nearly $900 million scrambling its jets in response to PLA warplane incursions and provocations

In the end it appears that the message from Washington continues to be that Taiwan should dramatically boost defense spending, because it’s anything but clear that the Pentagon will be there when the Chinese military machine comes calling.

Yuan Surges Most In 15 Years On Expectations Of Pro-China Pivot By “President Biden”

China’s onshore yuan, which was closed for trading during China’s week-long Golden Week holiday, soared 1.4% today as China returned to work and as the onshore yuan (CNY) caught up to the recent surge in the offshore yuan (CNH), driven by the recent plunge in the dollar and the rising expectations that Joe Biden will win the presidency and renormalize US-China relations by pivoting to a pro-China stance.

The onshore rate for the yuan, which had not traded since September 30 due to holiday, soared as much as 1.41% on Friday to 6.6950, the strongest since April 2019.

That was the biggest one-day change in the CNY since July 2005, when China broke the yuan-peg to the dollar and revalued its currency.

The more-loosely regulated offshore renminbi, which traded throughout the holiday, climbed 0.8% to 6.6818 against the dollar.

What prompted the surge? According to strategist cited by the FT, traders in China on Friday were emboldened by the imminent possibility of a US administration that was more friendly towards Beijing.

According to Daniel Been, head of FX strategy at ANZ, the increasing probability of a win for Democratic candidate Joe Biden in next month’s US presidential election had helped to lift the Chinese currency: “The view in the market is that the way a Biden administration approaches [US-China relations] is probably going to be less confrontational and certainly using trade less as a tool or weapon against China.”

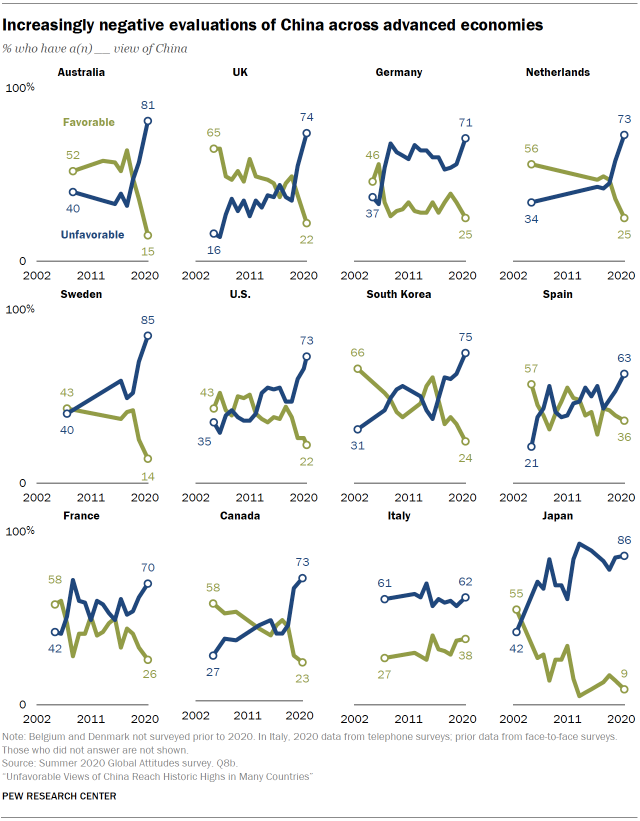

In short, China views Biden a distinctly pro-China president, which is concerning at a time when anti-China sentiment across virtually the entire world has reached record levels, as Pew found this week.

In addition to sentiment about Biden’s pro-China agenda, the Chinese currency was also boosted by fresh signs the economy is improving after authorities controlled Covid-19 in the country. Overnight, the Caixin China Service PMI showed activity climbed to its highest level in three months in September.

At the same time, Macquarie China economist Larry Hu, pointed to rising retail sales and a “significant” 17% year-on-year jump in domestic passenger traffic at Shanghai’s airport during the long holiday. “It’s clear that consumption, especially service consumption, is on the mend.”

Nomura analyst said that while overall passenger trips on public transportation were down about 30% y/y in the first few days of the holiday, transport ministry data showed that average highway traffic volume fell only 5.5%. A snapshot of China’s high frequency economic indicators from Goldman showed continued economic mending.

China’s improving economy stands in contrast to the US, where activity appears to be slowing, and is set to slow further amid continued Congressional gridlock over a new fiscal stimulus package.

Quoted by the FT, Christy Tan, head of Asia markets strategy and research at National Australia Bank, said there was also growing confidence that Chinese authorities would not intervene to stymie the renminbi’s rally.

“The prospect of renminbi appreciation is getting more structural — it’s no longer just cyclical,” Ms Tan said, pointing to greater trading offshore and inflows from global investors into China’s markets. “There’s a sense of confidence that the renminbi is getting more internationalised.” To be sure, the latest IMF data confirmed a record allocation toward CNY by reserve managers.The surge in the yuan was reflected in broad asset optimism, with China’s benchmark CSI 300 index closing 2% higher after onshore markets opened for the first time in six trading days. The tech-focused ChiNext index rose 3.8%.

As the FT notes, flows into China’s onshore equities market have topped Rmb90bn ($13.4bn) this year, taking foreign holdings to more than Rmb1tn on the back of the country’s relatively strong economic recovery. “We expect foreign capital inflows and foreign holdings in the A-share market to continue to rise,” said Bruce Pang, head of macro and strategy research at investment bank China Renaissance, referring to the country’s onshore stock market.

4/EUROPEAN AFFAIRS

CORONAVIRUS//UPDATE/THE GLOBE/LONDON

London Mayor Says Another Lockdown “Inevitable” As Global COVID-19 Cases Near Record Daily Highs: Live Updates

Summary:

- London mayor says lockdown “inevitable”

- Netherland reports latest record jump

- Spain declares “public health emergency” in Madrid

- France places more cities on lockdown

- Confirmed COVID-19 cases neared daily record yesterday

- Russia reports new record

- Takeda enrolls first patients for new drug trial

- China joins WHO vaccine initiative

- Iran bars hospitals from taking non-urgent cases as COVID hammers country

* * *

France reported more than 18,000 new cases yesterday, and now its third-largest city, Lyon, is joining Paris and Marseille in closing bars and other non-essential businesses in the coming days as COVID-19 infection rates surge in the countries hot spots. As the French government continues to insist that national lockdowns will only be a measure of last resort, public health officials are doubling down on the targeted approach as COVID-19 patients fill the country’s hospital beds.

Yesterday, French Health Minister Olivier Veran said Lyon, Lille, Grenoble and Saint-Etienne would go on maximum coronavirus alert level from Saturday. This means they will have to close their bars for two weeks in coming days, as Paris did on Tuesday and Marseille, France’s second-biggest city, did earlier this month.

And more localized measures could be implemented in Toulouse and Montpellier; those cities could see their alert level raised to the maximum s of Monday. Dijon and Clermont-Ferrand would also see their alert levels rise on Saturday. “Unfortunately, the health situation in France continues to deteriorate,” Veran said at his weekly COVID-19 briefing, per Reuters.

Minutes ago, London Mayor Sadiq Kahn told the LBC that new London lockdown restrictions are “inevitable” as officials have tightened restrictions in and around Manchester in the north of England. Meanwhile, Spain declared a public health emergency in Madrid, as expected.

Additionally, the Netherlands just reported another 5,983 new cases, a new daily record, while 69 new patients were reported in the country’s hospitals, bringing that total to 1,139, while deaths climbed by 14 and ICU cases climbed by 11 to 239.

As of earlier this morning, global cases had reached 36,435,290, according to Johns Hopkins data, while the global death toll had climbed to 1,060,869. New cases were just shy of the record set on Sept. 24, with 359,337 new cases confirmed yesterday, along with 6,234 deaths. The surge in new cases is being driven by Europe, Russia, the US, India, Brazil and Southeast Asia. The Czech Republic, which, along with Poland, yesterday announced new restrictions to try and slow the raging outbreak. The Czech Republic reported 5,394 new infections on Friday, its highest daily total yet. The country has now recorded 15% of its entire COVID-19 outbreak tally in the past 3 days. Poland, meanwhile, just reported 4,739 new cases Friday, the third-straight record day.

Russia shot passed its peak from May on Friday as it recorded another 12,126 new infections and 201 virus-linked deaths in the 24-hour period leading up to Friday.

In a lengthy report published in Friday’s FT, the paper examines how a resurgence in the Brazilian city of Manaus, which was hit hard in the spring, only for the virus to slink away over the summer, is raising serious questions about the prospects for herd immunity. The trend “poses fresh challenges…and difficult questions for the scientists and policymakers worldwide who have been edging towards herd immunity policies as an alternative to economy-crushing lockdowns.

This comes after a group of scientists in the US and UK published the Great Barrington Declaration earlier this week. The document calls for public policymakers to examine a strategy of “focused protection” to try and build up herd immunity as safely as possible. The virus, they argued, should be allowed to circulate among the young and healthy, while the elderly and the sick should be shielded. In Western Europe, antibody surveys have determined that roughly 8% of the population has already been infected, and the WHO recently declared that it believes 11% of the global population has already had the virus.

However, it seems, many of the same ‘hot spots’ from the spring are suffering again in the fall. This could also be a factor of population density, however.

As Eli Lilly and Regeneron apply for EUAs from the FDA for their antibody therapeutics, CNBC had Gilead CEO Dan O’Day on Friday morning to talk about the latest remdesivir trial results.

At any rate, here’s some more COVID-19 news from Friday morning, as well as overnight.

Japan’s Takeda Pharmaceutical says an alliance of drugmakers it spearheads has enrolled its first patient in a global clinical trial of a blood plasma treatment for COVID-19 after months of regulatory delays. The Phase 3 trial by the group, known as the CoVIg Plasma Alliance, aims to enroll 500 adult patients from the United States, Mexico and 16 other countries. Patients will be treated with Gilead Sciences’ remdesivir alongside the plasma treatment, which will be provided by CSL Behring, Takeda and two other companies (Source: Nikkei).

China will join a World Health Organization initiative aimed at ensuring fair distribution of Covid-19 vaccines when they become available, the country’s foreign ministry announced on Friday (Source: FT).

India reports 70,496 cases of COVID-19 in the last 24 hours, down from 78,524 the previous day, bringing the country’s total to over 6.9 million. The death toll jumped by 964 to 106,490 (Source: Nikkei).

Australian states and territories report 16 cases in the past 24 hours, down from 28 a day earlier. They also report no deaths for two days — the first time Australia has gone 48 hours without a COVID-19 death since July 11 (Source: Nikkei)

END

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

ARMENIA,AZERBAIJAN/TURKEY/USA

Erdogan who has ambitions of creating another Ottoman empire is creating another Syria in the Caucuses according to Armenian President

(zerohedge)

Armenian President Says Turkey’s Erdogan Creating “Another Syria In The Caucuses”

President Armen Sarkissian has charged that Turkey is creating “another Syria in the Caucasus” through its military and diplomatic support for Azerbaijan in the war for the autonomous ethnic Armenian breakaway region of Nagorno-Karabakh.

“If we don’t act now internationally, stopping Turkey . . . with the perspective of making this region a new Syria . . . then everyone will be hit,” he said to the Financial Times in a new interview.

He further urged an international effort to stop the aggression which he said was fueled by Turkey, which he called “the bully of the region”.

“We need more effort to stop this,” Presdient Sarkissian said. “And the focus of the efforts should be Turkey. The moment Turkey is taken out of the equation, we will be closer to a ceasefire and returning to the negotiation table.”

“What is a Nato member state doing in Azerbaijan helping to fight Nagorno-Karabakh? Explain to me,” he questioned. “That completely redefines the role of Nato.”

Turkish President Erodgan has been vocal in supporting Azerbaijan as Turkey’s “brother country” since hostilities started late last month, and which has since taken hundreds of lives on both sides, military and civilian. But it’s also widely believed Turkey is sending limited airpower in the form of F-16 jets and drones, for use against the Armenian military.

There’s also the issue of Turkey transferring hundreds of Syrian militants from Islamist factions who had previously been warring against Assad, which has been covered widely in Western press, such as in The Guardian, since the start of the latest fighting.

Sarkissian addressed this hugely controversial issue in the interview with FT:

“When the fighting stops, will the [militants] stay,” asked Mr Sarkissian. “It is a threat not only to Armenia but the whole Caucasus, and it is a threat to Russia . . . they can have a dramatic impact on the countries of Central Asia and dramatic impact on the north of Iran.”

As for the still disputed Turkish F-16 question, Armenia last week accused Turkey of shooting down an Armenian jet over its airspace, something both Ankara and Azerbaijan vehemently denied.

However, satellite imagery showed a par of Turkish F-16 jets parked at an airbase in Baku, after which Azerbaijani President Ilham Aliyev was forced to admit the presence. He merely claimed they were there for routine “training” exercises and not to engage in any hostilities.

Interestingly, Syria’s President Bashar Assad weighed in on the issue of Turkish intervention in Nagorno-Karabakh, saying Erdogan was supporting terrorists from Libya to Syria to the Caucuses.

Assad blamed Turkish intervention for heightening the conflict in a series of statements this week, some of which were featured in televised interviews:

Given that Russia and Turkey find themselves on opposite sides of the Caucuses conflict, paralleling the wars in Syria and Libya, the potential for this to explode into a broader regional war remains significant.

end

6.Global Issues

Michael Every ..

on the major stories of the day..

(Michael Every)

“Confusion Reigns”

By Michael Every of Rabobank

Earlier in the week I warned of a lot more US election wackiness to come.

Well, Exhibit A: The debate commission decided the upcoming presidential debate on 15 October will be virtual rather than in person, logical given President Trump has Covid-19; and Trump refused to attend a virtual debate….perhaps understandable given the experiences many of us have had recently: “I can’t use Teams, do you have Skype? No? Can I use Zoom? It’s banned? Oh.” And can you imagine a debate which was all “Hello? Hello? Can you hear me?“ Not that live debates are seeing any answers to the key questions though. Even the Vice Presidential debate was actually akin to the 1970’s Two Ronnies’ Mastermind sketch:

Q: Your chosen subject last time was answering questions before you are asked. This time, you`ve chosen to answer the question before last, each time, is that correct?

A: Charlie Smithers.

Q: And your time starts now. What is palaeontology?

A: Yes, absolutely correct.

Q: What is the name of the directory that lists members of the British peerage?

A: A study of old fossils.

Q: Correct. Who are Len Murray and Sir Geoffrey Howe?

A: Burkes.

Q: Correct. What is the difference between a donkey and an ass?

A: One is a Trade Union leader, the other one is a member of the cabinet.

Q: Correct. Complete the quotation “To be or not to be…”

A: They are both the same.

Q: Correct. What is Bernard Manning famous for?

A: That is the question.

Q: Correct. Who is the current Archbishop of Canterbury?

A: He is a fat man who tells blue jokes.

Trump has now been given a clean medical bill of health to start public events again from Saturday, and is holding a rally…so is the rescheduled debate date of 22 October still virtual? Joe Biden is doing an ABC Town Hall on 15 October now; will Trump do one too? Might it be with Joe Rogan, as Twitter is urging? Confusion reigns. Clear and substantive debate does not.

Exhibit B: Nancy Pelosi will today push a bill to give the House, not the Cabinet, power to remove a president from office for medical reasons under the 25th amendment. A few quick comments:

1) Is this needed by a party up 14-16 points in the polls and three weeks away from a sweep of the White House, House, and Senate?;

2) It will not remove Trump from office. Even if passed in the Democrat-majority House, the bill requires passage in the Republican-majority Senate and a presidential signature – which won’t happen;

3) If it did, it would just put Mike Pence into office for a few days, after which Trump could self-certify himself fit to take over again, and over-ruling that would require a two thirds majority in both the House and the Senate;

4) The move is likely to fire up the base – but possibly the Republicans more as Trump is selling it as an “attempted coup”; and

5) That should be relative risk off for markets, if they can read the political tea leaves – but I am not sure they cocoa, as said in the UK in the era of the Two Ronnies.

Exhibit C: The shocking news of the arrest of anarchist/”extremist libertarians” who had planned to kidnap Michigan governor Whitmer and hold a “treason trial” over her virus-related restrictions. This should underline just how worrying downside scenarios are in this present crisis.

Exhibit D: We are apparently closer to a comprehensive fiscal stimulus after all(?), after the Democrats had rejected offers for a series of clean bills for airlines and households. Perhaps Mnuchin and Pelosi can find a window today to continue their push-me-pull-you as the Fed sits in the background with its head in its hands. Rosengren yesterday called this all “tragic”, and for once it’s hard to disagree with the Fed. “The Fed can ease financial conditions. We can’t replace lose income, though. That’s uniquely suited to fiscal policy.”

On which (lost income), more pubs are closing in the UK, as people old enough to remember the Two Ronnies sadly start to fill the hospitals again. The UK looks set to go back to shielding the vulnerable indoors again for months. Spain is also following suite with a 15-day emergency lockdown in Madrid, while a Spanish virologist warns of up to two years of mask-wearing ahead.

Meanwhile, also very important at the margin is that last night the US imposed sweeping sanctions on another 18 Iranian banks, which now effectively cuts Iran off from the global financial system completely. The US may be a house divided at home, but abroad it is still capable of major action: critics say this US masterplan will backfire, but the campaign of maximum pressure continues. Markets must not forget that there are other countries potentially heading for similar treatment for a variety of different reasons – some of their currencies are recognising it, while one is merrily going on its way as if that kind of thing can’t happen to it. Quite the Masterminds at work there answering the previous question of financial inflows rather than the current one of (more) potential sanctions.

7. OIL ISSUES

8 EMERGING MARKET ISSUES

Your early morning currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings FRIDAY morning 7:00 AM….

Euro/USA 1.1801 UP .0034 REACTING TO MERKEL’S FAILED COALITION/ REACTING TO +GERMAN ELECTION WHERE ALT RIGHT PARTY ENTERS THE BUNDESTAG/ huge Deutsche bank problems ///ITALIAN CHAOS//CORONAVIRUS/PANDEMIC/TRUMP POSITIVE WITH VIRUS /AND NOW ECB TAPERING BOND PURCHASES/JAPAN TAPERING BOND PURCHASES /USA RISING INTEREST RATES /FLOODING/EUROPE BOURSES /MIXED

USA/JAPAN YEN 105.87 DOWN 0.150 (Abe’s new negative interest rate (NIRP), a total DISASTER/NOW TARGETS INTEREST RATE AT .11% AS IT WILL BUY UNLIMITED BONDS TO GETS TO THAT LEVEL…

GBP/USA 1.2946 UP 0.006 (Brexit March 29/ 2019/ARTICLE 50 SIGNED/BREXIT FEES WILL BE CAPPED/

USA/CAN 1.317610 DOWN .0018 CANADA WORRIED ABOUT TRADE WITH THE USA WITH TRUMP ELECTION/ITALIAN EXIT AND GREXIT FROM EU/(TRUMP INITIATES LUMBER TARIFFS ON CANADA/CANADA HAS A HUGE HOUSEHOLD DEBT/GDP PROBLEM)

Early THIS FRIDAY morning in Europe, the Euro ROSE BY 34 basis points, trading now ABOVE the important 1.08 level RISING to 1.1801 Last night Shanghai COMPOSITE CLOSED UP 54.02 POINTS OR 1.08%

//Hang Sang CLOSED DOWN 27.38 POINTS OR .12%

/AUSTRALIA CLOSED UP 0,11%// EUROPEAN BOURSES ALL MIXED

Trading from Europe and Asia

EUROPEAN BOURSES ALL MIXED

2/ CHINESE BOURSES / :Hang Sang CLOSED DOWN 27.38 POINTS OR .12%

/SHANGHAI CLOSED UP 54.02 POINTS OR 1.68%

Australia BOURSE CLOSED UP 0.11%

Nikkei (Japan) CLOSED DOWN 27,38 POINTS OR 0.12%

INDIA’S SENSEX IN THE GREEN

Gold very early morning trading: 1913.80

silver:$24.36-

Early FRIDAY morning USA 10 year bond yield: 0.770% !!! DOWN 1 IN POINTS from THURSDAY’S night in basis points and it is trading WELL BELOW resistance at 2.27-2.32%.

The 30 yr bond yield 1.578 DOWN 1 IN BASIS POINTS from THURSDAY night.

USA dollar index early FRIDAY morning: 93.33 DOWN 28 CENT(S) from THURSDAY’s close.

This ends early morning numbers FRIDAY MORNING

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx6

And now your closing FRIDAY NUMBERS \1: 00 PM

Portuguese 10 year bond yield: 0.18% DOWN 5 in basis point(s) yield from YESTERDAY/

JAPANESE BOND YIELD: +.04.% UP 0 BASIS POINTS from YESTERDAY/JAPAN losing control of its yield curve/56

SPANISH 10 YR BOND YIELD: 0.17%//DOWN 2 in basis point yield from yesterday.

ITALIAN 10 YR BOND YIELD:0.72 DOWN 3 points in basis points yield from yesterday./

the Italian 10 yr bond yield is trading 55 points higher than Spain.

GERMAN 10 YR BOND YIELD: FALLS TO –.53% IN BASIS POINTS ON THE DAY//

THE IMPORTANT SPREAD BETWEEN ITALIAN 10 YR BOND AND GERMAN 10 YEAR BOND IS 1.25% AND NOW ABOVE THE THE 3.00% LEVEL WHICH WILL IMPLODE THE ENTIRE ITALIAN BANKING SYSTEM. AT 4% SPREAD THERE WILL BE A HUGE BANK RUN…

END

IMPORTANT CURRENCY CLOSES FOR FRIDAY

Closing currency crosses for FRIDAY night/USA DOLLAR INDEX/USA 10 YR BOND YIELD/1:00 PM

Euro/USA 1.1819 UP .0051 or 51 basis points

USA/Japan: 105.62 DOWN .385 OR YEN UP 39 basis points/

Great Britain/USA 1.3005 UP .0065 POUND UP 65 BASIS POINTS)

Canadian dollar UP 69 basis points to 1.3005

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

The USA/Yuan,CNY: closed UP 6.6947 ON SHORE (UP)..

THE USA/YUAN OFFSHORE: 6.6846 (YUAN up)..

TURKISH LIRA: 7.848 EXTREMELY DANGEROUS LEVEL/DEATH WISH.

the 10 yr Japanese bond yield at +0.04%

Your closing 10 yr US bond yield DOWN 1 IN basis points from THURSDAY at 0.773 % //trading well ABOVE the resistance level of 2.27-2.32%) very problematic USA 30 yr bond yield: 1.585 DOWN 1 in basis points on the day

Your closing USA dollar index, 93.09 down 52 CENT(S) ON THE DAY/1.00 PM/

Your closing bourses for Europe and the Dow along with the USA dollar index closing and interest rates for FRIDAY: 12:00 PM

London: CLOSED UP 39.53 0.66%

German Dax : CLOSED DOWN 43.58 POINTS OR .03%

Paris Cac CLOSED UP 30.82 POINTS 0.63%

Spain IBEX CLOSED DOWN 40.80 POINTS or 0.58%

Italian MIB: CLOSED UP 5.58 POINTS OR 0.03%

WTI Oil price; 41.08 12:00 PM EST

Brent Oil: 43.23 12:00 EST

USA /RUSSIAN / RUBLE RISES: 76.77 THE CROSS LOWER BY 0.58 RUBLES/DOLLAR (RUBLE HIGHER BY 58 BASIS PTS)

TODAY THE GERMAN YIELD FALLS TO –.53 FOR THE 10 YR BOND 1.00 PM EST EST

END

This ends the stock indices, oil price, currency crosses and interest rate closes for today 4:30 PM

Closing Price f0r Oil, 4:00 pm/and 10 year USA interest rate:

WTI CRUDE OILPRICE 4:30 PM : 40.53//

BRENT : 42.78

USA 10 YR BOND YIELD: … 0.771..down 1 basis points…

USA 30 YR BOND YIELD: 1.569 down 2 basis points..

EURO/USA 1.1823 ( UP 57 BASIS POINTS)

USA/JAPANESE YEN:105.62 DOWN .408 (YEN UP 41 BASIS POINTS/..

USA DOLLAR INDEX: 93.06 UP 54 cent(s)/

The British pound at 4 pm Britain Pound/USA:1.3041 UP 102 POINTS

the Turkish lira close: 7.86

the Russian rouble 76.79 UP 0.56 Roubles against the uSA dollar. (UP 56 BASIS POINTS)

Canadian dollar: 1.3121 UP 71 BASIS pts

German 10 yr bond yield at 5 pm: ,-0.54%

The Dow closed UP 161.39 POINTS OR 0.57%

NASDAQ closed UP 158.97 POINTS OR 1.56%

VOLATILITY INDEX: 24.80 CLOSED DOWN 1.56

LIBOR 3 MONTH DURATION: 0.220%//libor dropping like a stone