“

GOLD:$1891.50 DOWN $31.70 The quote is London spot price

Silver:$24.06 DOWN $1.05 London spot price ( cash market)

Today’s raid was official sector led by the BIS/Fed and their purpose was to cool the jets of gold/silver pricing.

your data…

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)TUESDAY MORNING/ MONDAY NIGHT:

SHANGHAI CLOSED UP 1.29 PTS OR .04% //Hang Sang CLOSED UP 530.55 PTS OR 2.20% /The Nikkei closed UP 43.09 POINTS OR 0.18%//Australia’s all ordinaires CLOSED UP 0.90%

/Chinese yuan (ONSHORE) closed /Oil UP TO 40.29 dollars per barrel for WTI and 42.54 for Brent. Stocks in Europe OPENED ALL RED// ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.7351. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7340 TRADE TALKS STALL//YUAN LEVELS //TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED//CORONAVIRUS/PANDEMIC/TRUMP TESTS POSITIVE FOR COVID 19 : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

We had 1 kilobar transactions +

ADJUSTMENTS: 1 //

i) Out of Malca: 33,276.285 oz adjusted out of customer account into the dealer account

The front month of OCT registered a total of 4306 contracts for a LOSS of 1535 contracts. We had 1592 notices filed on Monday so we gained 57 contracts or 5,700 additional oz will stand for delivery in this active delivery month of October. In gold we have not seen queue jumping start so early in the month. Thus you can bet the farm that throughout October, the total number of gold oz standing will increase from this level.

November gained 96 contracts to stand at 1733.

The big December contract LOST 650 contracts DOWN to 450,660 contracts..

THE BIG STORY AGAIN TODAY IS THE HIGH OI STANDING FOR OCTOBER (102.354 tonnes). GENERALLY OCTOBER IS A POOR DELIVERY MONTH AS MOST INVESTORS PREFER TO SKIP THIS MONTH AND MOVE STRAIGHT TO DECEMBER. IT LOOKS LIKE SOME MAJOR ENTITY(GOLDMAN SACHS) JUST CANNOT WAIT FOR DECEMBER AS THEY ARE MAKING THEIR MOVE ON OCTOBER FOR PHYSICAL METAL. GOLDMAN SACHS ONE OF THE LEADERS OF THE NEW LONDON LME EXCHANGE NEEDS THE GOLD INVENTORY FOR LIQUIDITY AND INITIAL CONTRIBUTION WITH OTHER MAJOR PLAYERS. THE MAJOR DIFFERENCE BETWEEN THIS MONTH AND OTHER MONTHS IS THAT THIS GOLD STANDING IN OCTOBER WILL LEAVE THE COMEX AND HEAD FOR LONDON.

We had 1517 notices filed today for 151,700 oz OR 4.718 TONNES.

To calculate the INITIAL total number of gold ounces standing for the OCT /2020. contract month, we take the total number of notices filed so far for the month (30,118) x 100 oz , to which we add the difference between the open interest for the front month of OCT (4306 CONTRACTS ) minus the number of notices served upon today (1517 x 100 oz per contract) equals 3,290,700 OZ OR 101.354 TONNES) the number of ounces standing in this active month of Oct

thus the INITIAL standings for gold for the OCT/2020 contract month:

No of notices filed so far (30,118, x 100 oz +4306 OI) for the front month minus the number of notices served upon today (1517) x 100 oz which equals 3,290,700 oz standing OR 102.354 TONNES in this active delivery month. This is a HUGE amount for gold standing for a OCT delivery month (a poor active delivery month).

We gained 57 contracts or an additional 5700 oz will stand on this side of the pond searching for metal.

NEW PLEDGED GOLD: BRINKS

592,648.822 oz NOW PLEDGED SEPT 15.2020/HSBC 18.433 TONNES ( A HUGE INCREASE FROM 10.6)

42,548.308.00 PLEDGED APRIL 3/2020: SCOTIA: 1.3234 tonnes

deleted Int. Delaware pledge July 7 (600 tonnes)

277,934.09 oz (some deleted august 3) JPM 8.644 TONNES

610,238.285 oz pledged June 12/2020 Brinks/ July 2/July 21 19.017 tonnes

67,289.041 oz Pledged August 21/regular account 2.092 tonnes JPM

total pledged gold: 1,590,658.551 oz 49.476 tonnes

total registered, pledged and eligible (customer) gold 37,626,099.708 oz 1,170.32 tonnes (INCLUDES 4 GC GOLD)

total 4 GC gold: 126.34 tonnes

total gold net of 4 GC: 1043.98 tonnes

end

I have compiled data with respect to registered (or dealer) gold taken on first day notice for each of the past 24 months

The data begins on first day notice for the May month taken on the last day of July 2018. and it continues to present day.

I then took, how many deliveries were recorded by the CME for each and every month. I also included for reference the price of gold on first day notice.

The first graph is a logarithmic graph and the second graph, linear.

You can see the huge explosion of registered gold at the comex along with deliveries.

THE GOLD COMEX SEEMS TO BE UNDER SEVERE ASSAULT FOR PHYSICAL

And now for the wild silver comex results

And now for the wild silver comex results

INITIAL STANDINGS

OCT. SILVER COMEX CONTRACT MONTH//INITIAL STANDING

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory |

749,873.334 oz

BRINKS

Delaware

LOOMIS

|

| Deposits to the Dealer Inventory |

546,552.500 oz

Manfra

|

| Deposits to the Customer Inventory |

596,567.615 oz

Int.

Delaware

|

| No of oz served today (contracts) |

24

CONTRACT(S)

(120,000 OZ)

|

| No of oz to be served (notices) |

87 contracts

435,000 oz)

|

| Total monthly oz silver served (contracts) | 1920 contracts

9,600,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

March 4.2019

Parker City News

JP Morgan faces potential class action lawsuit after guilty pleas by a former metals trader

Traders from across the U.S. are banding together to accuse J. P. Morgan Chase of manipulating precious metals markets for years.

At least six lawsuits, all making similar allegations against the nation‘s largest bank, have been filed in New York federal court in the past month, since federal prosecutors in Connecticut with a former J. P. Morgan Chase metals trader.

The cases could potentially include thousands of people who traded in the precious metals market. The White Plains, N.Y., law firm Lowey Dannenberg is asking the court to combine the cases and name it as the lead.

The law firm‘s commodities group is led by Vincent Briganti, the attorney who filed the first lawsuit on behalf of Dominick Cognata, a New York resident who alleges he suffered losses due to J. P. Morgan‘s trading conduct in the silver and gold futures and options markets.

A combined case, seeking class action status, would include anyone who purchased or sold futures contracts or an option on NYMEX platinum or palladium or COMEX silver or gold between at least Jan. 1, 2009, and Dec. 31, 2015. The lawyers believe that “at least hundreds, if not thousands” of traders would be eligible to join the case.

Named as defendants in all of the lawsuits are John Edmonds, a 36-year old former metals trader at J. P. Morgan, a group of yet-to-be-identified precious metals traders and the bank.

Edmonds, a New York resident, pleaded guilty in October to one count of conspiracy to defraud the market and manipulate prices of precious metals futures contracts and one count of commodities fraud. In the criminal plea, Edmonds admitted that he and other “unnamed co- conspirators” at J. P. Morgan, fraudulently manipulated precious metals markets from 2009 to 2015, the same time frame covered in the class action suits.

Briganti filed the initial class action on Nov. 7, just one day after the Justice Department unsealed Edmonds‘ plea in the U.S. District Court of Connecticut.

Edmonds admitted in his guilty plea that he deployed the illegal trading scheme hundreds of times with the direct knowledge and consent of his immediate supervisors. Plaintiffs say they have suffered economic injury, including monetary losses, as a direct result of actions by Edmonds and the other unnamed J. P. Morgan metals traders in the futures and options contracts.

One of the suits alleges that “the number of unlawful trades that JP Morgan traders executed in precious metals futures markets is at least in the thousands.”

J. P. Morgan declined to comment. Lowey Dannenberg did not respond to a request for comment by CNBC.

The Justice Department‘s criminal investigation is still ongoing and recently caused a separate related civil case to be put on hold for at least six months while the government continues its investigation. That civil lawsuit, which also accuses J. P. Morgan of rigging the precious metals market, was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders.

After reviewing the details of the plea agreement, David Kovel, the attorney for Shak‘s suit, sought to re- interview Edmonds, along with two other current and former senior traders at the bank. However, the government argued that reopening questioning would be detrimental to the ongoing criminal investigation. The federal judge overseeing the proceedings ordered a six-month stay in the civil case.

Kovel declined to comment.

Edmonds was originally scheduled to be sentenced in Hartford, Conn., on Wednesday, Dec. 19, but a court filing on Nov. 27 shows the sentencing has been postponed until June. A spokesman for the U.S. Attorney for Connecticut could not elaborate on why the sentencing was postponed since the court filing is under seal.

-END-

3A/ASIAN AFFAIRS

i)TUESDAY MORNING/ MONDAY NIGHT:

SHANGHAI CLOSED UP 1.29 PTS OR .04% //Hang Sang CLOSED UP 530.55 PTS OR 2.20% /The Nikkei closed UP 43.09 POINTS OR 0.18%//Australia’s all ordinaires CLOSED UP 0.90%

/Chinese yuan (ONSHORE) closed /Oil UP TO 40.29 dollars per barrel for WTI and 42.54 for Brent. Stocks in Europe OPENED ALL RED// ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.7351. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7340 TRADE TALKS STALL//YUAN LEVELS //TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED//CORONAVIRUS/PANDEMIC/TRUMP TESTS POSITIVE FOR COVID 19 : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

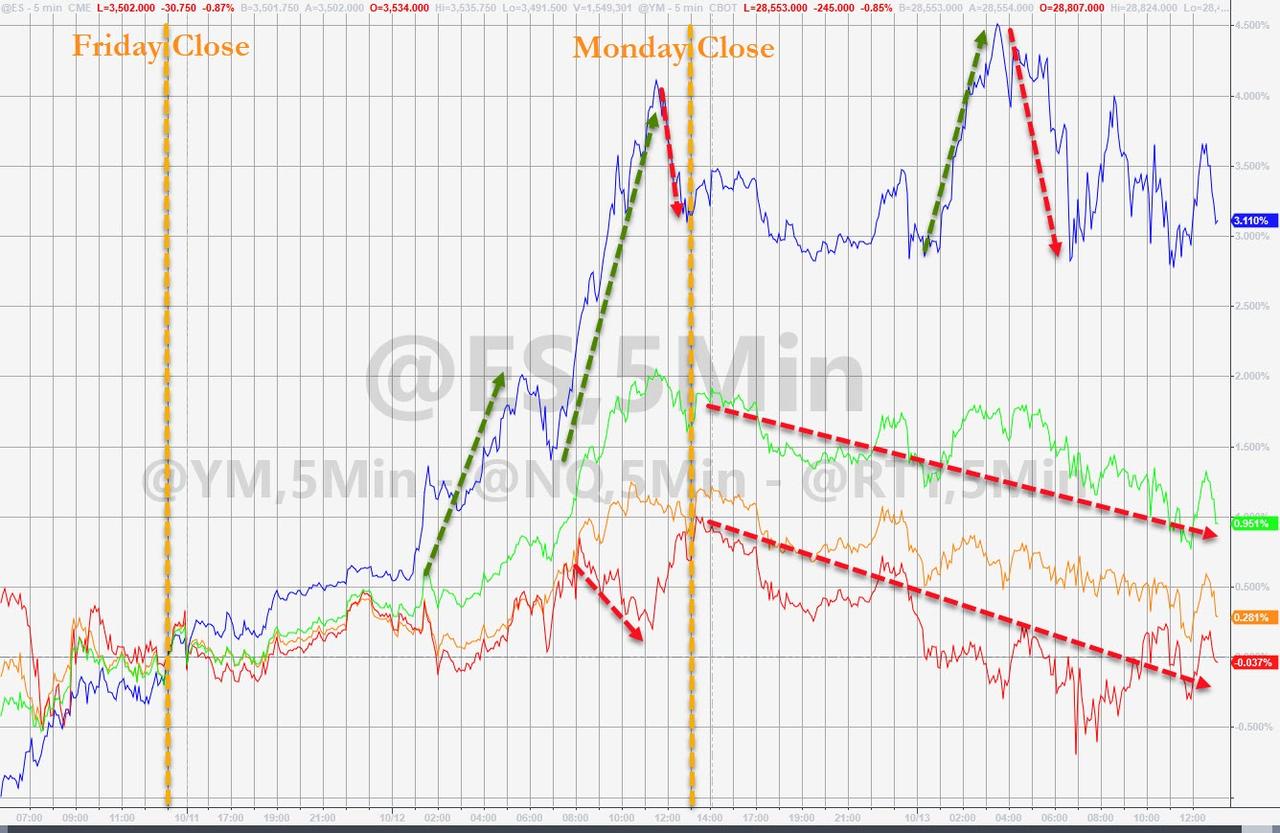

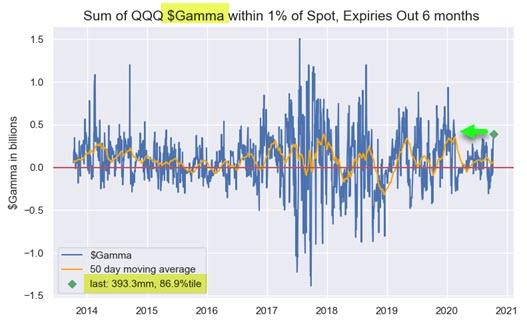

Nasdaq Futures Surge Despite Vaccine Setback As Gamma Squeeze Continues

Global stocks and S&P futures struggled on Tuesday amid concerns over a Johnson & Johnson vaccine setback, which overshadowed Chinese trade data that pointed to a buoyant recovery, while yields dropped and the U.S. dollar edged away from a three-week low.

S&P 500 contracts were modestly in the red after falling as much as 0.6% after a late Monday report that Johnson & Johnson’s Covid-19 vaccine study has been paused due to an unexplained illness in a participant. BlackRock rose in pre-market trading after earnings beat estimates and assets under management surged to a record, while JPMorgan climbed after revenue and EPS topped expectations as a result of a massive reserve release.

However while the S&P was trading with fractional losses, Nasdaq futures were sharply higher again as the European open appears to have triggered a continuation of yesterday’s gamma squeeze which sent the Nasdaq up as much as 4% in what many believe is another attempt by a Nasdaq whale such as SoftBank to squeeze shorts in either options or NQ futures, as we explained yesterday.

The MSCI world equity index, which tracks shares in nearly 50 countries, fell 0.1%. The Euro STOXX 600 fell 0.4% before trimming losses, with markets in Frankfurt, London and Paris mirroring its moves. It was last down 0.2%, on course to end three straight days of gains. The travel and leisure and autos sectors suffered, losing 1% and 0.3% respectively after heavier falls in early trading, after the J&J news spooked traders. Investors had seen the quick introduction of a vaccine as key to helping economies recover. J&J’s move comes after AstraZeneca paused late-stage trials of its experimental vaccine in September, also due to a participant’s unexplained illness.

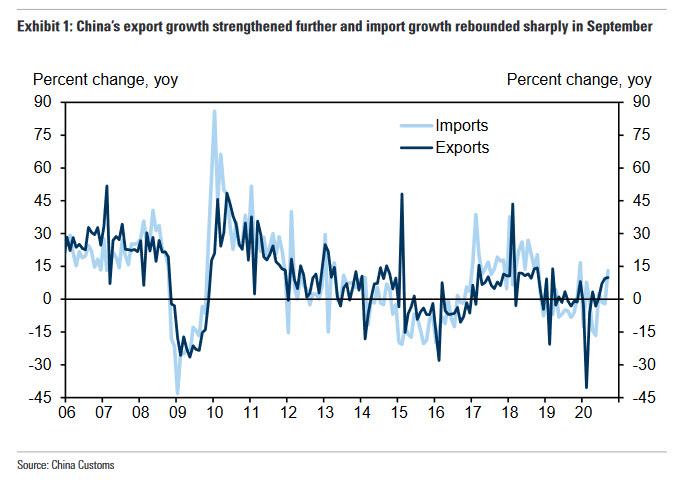

The risk-off mood contrasted with earlier resilience for Asian markets. They recovered losses after Chinese data showed exports rising 9.9% in September, in line with the 10% expected, while imports swung to a 13.2% gain, far higher than expected, versus a 2.1% drop in August.

The data, which suggests Chinese exporters are recovering from the pandemic’s damage to overseas orders, helped MSCI’s broadest index of Asia-Pacific shares outside Japan gain 0.2%. Chinese blue-chip shares added 0.3% after dipping early in the day. Some investors, though, raised questions about how strong consumer demand would prove to be.

“The question is not necessarily how China’s trade is doing per se, but how well will consumers spend on Christmas to give some sense of normalcy amid a period of great stress,” said Nordea Investments’ Sebastien Galy, according to Reuters.

Currency traders were also watching Chinese trade-related issues. Reports that Beijing has stopped taking shipments of Australian coal caused the Australian dollar to drop as much as 0.6% to $0.7165.

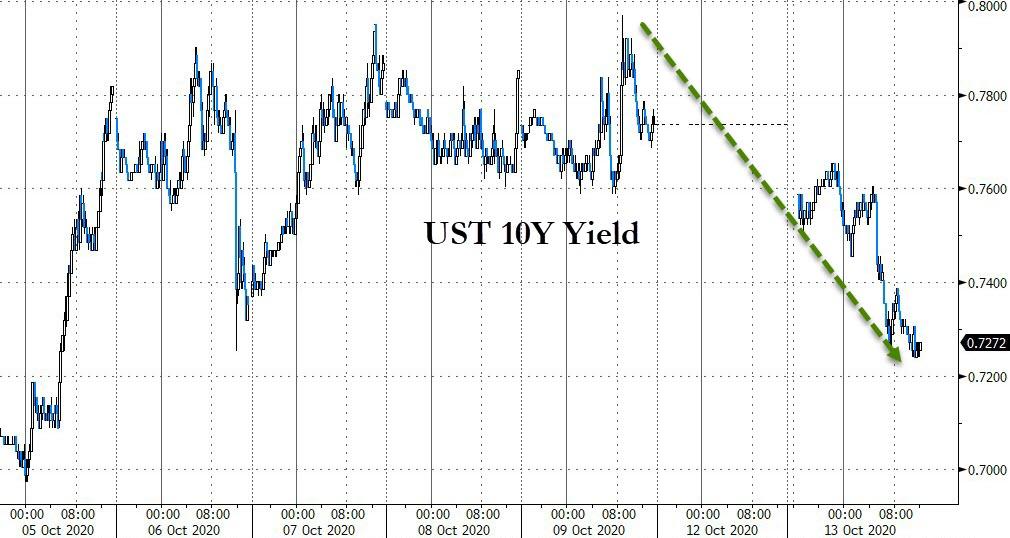

In rates, treasuries flattened as cash trading resumes following Monday’s Fed-observed holiday; long-end yields were richer by ~2bps vs Friday’s close. These long-end-led gains flattened the 2s10s, 5s30s by ~1bp; 10-year yields down 1.7bp at 0.757% vs little-changed bunds and gilts. Government bond yields in the euro zone held near recent troughs, with hefty supply failing to dent a market bolstered by expectations for further central bank easing. Germany’s 10-year Bund yield touched -0.538%, its lowest in just over a week. Italian and Greek benchmark 10-year debt both hit record lows.

Meanwhile, despite a total gridlock on fiscal stimulus, markets are now increasingly bulled up that Joe Biden will win the presidential election next month, which the narrative expects to lead to a big stimulus package to help the coronavirus-battered U.S. economy. “Biden effectively leading in the polls is removing some element of uncertainty,” said Jeremy Gatto, an investment manager at Unigestion in Geneva. “In investors’ minds, it’s not a question of if we get a stimulus, but when.”

“The hurdles at the moment come from the uncertainty around the U.S. election and the uncertainty about the timing and effectiveness of a vaccine,” Chris Iggo, chief investment officer at AXA IM Core Investments.

At the same time, many banks such as Goldman Sachs, expect a Biden win to undermine the U.S. dollar, since he’s pledged to raise corporate tax rates. But the dollar rose 0.2% against a basket of other currencies to 93.214, trying to extend a rebound from Friday’s near-three-week low of 92.997. The Chinese yuan fell 0.1% to 6.7466 per dollar after the central bank set a weaker-than-forecast midpoint, offsetting any boost from the trade data, and followed Monday’s drop when the PBOC made it easier to short the currency.

In commodities, WTI & Brent prices have been choppy but at present are supported as attention moves from the trio of supply-side factors that were impacting benchmarks yesterday and turns towards the sessions events with the OPEC MOMR due for release today (timing TBC); ahead of the IEA equivalent due tomorrow. Spot gold is essentially unchanged on the session and has been relatively steady ~USD 1920/oz for the morning given the USD’s rangebound performance and lack of fundamental catalysts thus far. Silver is up notably after the recent upgrade of the precious metal by Goldman Sachs.

Today, the hearings for the Supreme Court nomination of Judge Amy Coney Barrett continue in the Senate Judiciary Committee as Republicans try to cement a conservative majority on the court before the Nov. 3 election. Expected data include inflation. BlackRock, Citigroup, Delta Air, Fastenal, J&J and JPMorgan are among companies reporting earnings

Market Snapshot

- S&P 500 futures little changed at 3,529.75

- STOXX Europe 600 down 0.1% to 372.56

- MXAP up 0.2% to 177.24

- MXAPJ up 0.2% to 588.52

- Nikkei up 0.2% to 23,601.78

- Topix up 0.4% to 1,649.10

- Hang Seng Index up 2.2% to 24,649.68

- Shanghai Composite up 0.04% to 3,359.75

- Sensex down 0.01% to 40,588.00

- Australia S&P/ASX 200 up 1% to 6,195.75

- Kospi down 0.02% to 2,403.15

- Brent futures up 1.6% to $42.39/bbl

- Gold spot little changed at $1,923.07

- U.S. Dollar Index up 0.1% to 93.15

- German 10Y yield fell 0.5 bps to -0.55%

- Euro down 0.1% to $1.1797

- Italian 10Y yield fell 4.6 bps to 0.475%

- Spanish 10Y yield rose 0.3 bps to 0.148%

Top Overnight News from Bloomberg

- European Union leaders will discuss preparations for the potential collapse of trade talks with the U.K. when they hold a summit later this week after France dug in, questioning whether it could hold Boris Johnson’s government to any agreement

- Boris Johnson clashed with his own government’s scientific advisers who wanted tougher action against the resurgent coronavirus outbreak in the U.K. in September

- China’s exports rose for the fourth straight month in September while imports surged, pointing to further recovery in the month for global trade and a robust domestic rebound

- U.K. job cuts jumped the most on record in the three months through August even as lockdown eased, raising concern that the worst is yet to come. The number of redundancies climbed 114,000 in the June-August period, the most since 1995, the Office for National Statistics said Tuesday

A quick look at global markets courtesy of Newsquawk

Asia-Pac equities traded mixed following the upbeat performance on Wall Street where the Nasdaq posted its best session in around month as the tech-sector led the gains and Apple shares closed higher by over 6% ahead of the Apple Event and the much-anticipated unveiling of the iPhone 12. Sentiment softened following a firm re-opening of cash Treasuries, which could’ve encouraged defensive flows in other assets, whilst the risk-mood further waned following reports that Johnson & Johnson paused its COVID-19 study (ahead of earnings) amid an unexplained illness in a participant – with the company later confirming and caveating that adverse events are an expected part of any clinical study, especially large ones. Nonetheless, ASX 200 (+1.2%) was supported by advances in its heavyweight financials as the broader sector eyes US bank earnings set to kick off with JP Morgan and Citi, meanwhile mining names in the index retrace some of yesterday’s upside. Nikkei 225 (unch) was choppy and gave up opening gains at one point as shares in heavyweight Softbank reversed course following the announcement of its Vision Fund mulling a special purpose acquisition company (SPAC) and is seeking outside investments, albeit it may reportedly put its own capital in the vehicle. Elsewhere, KOSPI (-0.5%) continued grinding lower as South Korea’s new COVID-19 cases rebounded to over 100 a day after the country eased restrictions. Meanwhile, Shanghai Comp (-0.4%) was lacklustre after the PBoC skipped open market operations for a net daily drain of CNY 100bln – with little reaction to September exports and imports hitting record highs in Yuan terms, whilst the Hang Seng session was cancelled due to tropical storm Nangka. Finally, broader defensive flows have kept JGBs supported, with the 5yr outperforming in cash and futures.

Top Asian News

- China’s Exports Gain, Imports Surge in September Amid Reopenings

- Singapore Marks Milestone in Virus Fight with No New Local Cases

- China Evergrande Seeks Up to $1.09 Billion in Share Placement

- HSBC Is Left Off First China Dollar Bond Deal Since 2017

European equities (Eurostoxx 50 -0.2%) have seen a mild scaling back of yesterday’s gains with a decline in US equity index futures alongside the EU cash open dictating the sate-of-play early doors; although, the NQ is the mornings outperform with gains of 0.7%. In terms of the current key themes for the market, little in the way has changed in the Presidential election or stimulus front since yesterday’s close, whilst on the vaccine front, Johnson & Johnson announced that it has paused all dosing in its Janssen COVID-19 vaccine trial due to an unexplained illness. Johnson & Johnson caveated the announcement by noting that such incidents are an expected part of any clinical study, especially of this size. On the vaccine front, even in the event of a more material disruption to the trial process, desks will likely be cognizant of the volume of vaccine candidates in the pipeline and therefore would likely remain confident that a vaccine of some description will materialise at some stage. Across Europe, losses are relatively broad-based across major indices with sectoral performance mixed. To the downside, banking names are notably softer this morning as the sector remains out of favour with investors; Pantheon Macro highlights that the Eurostoxx bank index is down 40% YTD compared to losses of 12% for the broader index. Travel & leisure stocks are also softer with the tenor of updates on the COVID front continuing to come in on the negative side for the sector. To the upside, telecom and utilities names are faring better than peers with the later supported by SSE (+4.0%) after the Co. disposed of its 50% stake in Multifuel Energy Limited for GBP 995mln. Elsewhere, Maersk (+1.9%) have seen mild support after the Co. upgraded its 2020 adj. EBITDA outlook, Airbus (-3.1%) trade softer after signing a labour deal with French unions and being downgraded at JP Morgan, whilst stock-specific newsflow is otherwise relatively light this morning. Looking ahead, increasing focus will likely be placed on US earnings with Johnson & Johnson, BlackRock, JP Morgan, Delta Airlines and Citi all due to report before the opening bell today.

Top European News

- Top U.K. Scientists Clash With Johnson Over Virus Lockdown

- U.K. Job Cuts Jump Most on Record With More Pain on the Way

- Investor Hopes For German Recovery Plunge After Virus Resurgence

- Macron Turns to Former Taxi Driver to Save French Shopkeepers

In FX, ironically, a significantly narrower trade surplus due to imports exceeding consensus by a huge margin in China has not helped the Aussie at all given the fact that the latter is now tightening levels of custom checks for coal and related products from the former after banning other goods. Indeed, Aud/Usd has now lost grip of the 0.7200 handle and the Aud/Nzd cross is testing support/bids at the psychological 1.0800 mark to provide the Kiwi with some relative support above 0.6600 vs its US peer. Ahead, Aussie consumer sentiment before a speech by RBA Governor Lowe on Wednesday and jobs data the day after.

- USD – The Dollar seems to be benefiting at the expense of others rather than in its own right, though a downturn in risk sentiment after Monday’s excesses on Wall Street may also be impacting alongside some consolidation after the DXY held above 93.000 yesterday and subsequently eclipsed the 50 DMA, albeit unconvincingly so far within 93.273-034 parameters as attention turns to US CPI data and the start of Q3 earnings.

- CAD/JPY/CHF/EUR/GBP – All softer against the Greenback, though to varying degrees as the Loonie gleans some encouragement from stabilising oil prices to stay within reach of 1.3100 and the Yen holds above 105.50 amidst reports that new Japanese PM Suga is mulling further economic support measures to be rolled out in November. Meanwhile, the Franc remains anchored around 0.9100, the Euro is striving to keep sight of 1.1800 where even bigger option expiries (2.5 bn) align with the 50 DMA and Sterling has survived another test of 1.3000 in wake of mixed UK labour and retail survey data in the run up to another speech from BoE Governor Bailey and a report on Brexit trade negotiations from EU Ministers. Note, Eur/Usd has slipped a few pips on the back of a pretty downbeat October German ZEW survey.

- SCANDI/EM – Softer than forecast Swedish CPI readings have not hampered the Swedish Crown given the Riskbank’s insistence that inflation undershoots are transitory blips and likelihood that Governor Ingves will stick to that script if he mentions the data later. Elsewhere, the Norwegian Krona is also deriving a degree of traction from the aforementioned recovery in crude awaiting a trio of Norges Bank commentators including chief Olsen, while the SA Rand could receive some independent impetus from Gold and overall mining production as Usd/Zar hovers under 16.5000, Eur/Sek eyes 10.3500 and Eur/Nok probes 10.7800.

In commodities, WTI & Brent prices have been choppy throughout the morning but at present are supported as attention moves from the trio of supply-side factors that were impacting benchmarks yesterday and turns towards the sessions events with the OPEC MOMR due for release today (timing TBC); ahead of the IEA equivalent due tomorrow. Currently, WTI and Brent futures are at the top end of session ranges, USD 40.22/bbl and USD 42.43/bbl respectively, seemingly moving in tandem to the grinding upside seen in US futures; but, as mentioned, have been choppy thus far printing both fresh session highs and lows in the European morning. Elsewhere and ahead of today’s OPEC MOMR, thus far this month the EIA STEO cut both 2020 and 2021 world oil demand growth by 300k and 280k BPD respectively; note, attention from an OPEC perspective is perhaps more on the upcoming JMMC meeting on October 19th for any potential alterations to the output cut schedule given returning Libyan demand among other factors. Separately, updates from the IEA overnight saw them forecast oil demand -8% this year alongside a -5% drop in global energy demand; such commentary comes ahead of the IEA monthly report tomorrow and as a reminder in September the agency cut their demand forecast for both this year and next. Moving to metals, where spot gold is essentially unchanged on the session and has been relatively steady ~USD 1920/oz for the morning given the USD’s rangebound performance and lack of fundamental catalysts thus far.

US Event Calendar

- 8:30am: US CPI MoM, est. 0.2%, prior 0.4%; YoY, est. 1.4%, prior 1.3%

- 8:30am: US CPI Ex Food and Energy MoM, est. 0.2%, prior 0.4%; YoY, est. 1.7%, prior 1.7%

- 8:30am: Real Avg Weekly Earnings YoY, prior 3.9%; Avg Hourly Earning YoY, prior 3.3%

DB’s Jim Reid concludes the overnight wrap

Today is the annual day where resistance is futile. Every year I go into it with good intentions after a conversation with my wife the night before as to how I don’t need to join the crowd. Then by the end of the day I’ve always committed to becoming a stampeding lemming. Yes today I shall agree to buy the new iPhone regardless of what features the product launch tells me it has. I’d imagine they could go all retro and go back to a phone that just allows you to speak to someone and l’d simply ask them to name their price. Oh and as I’ve been typing this I’ve just had an alert telling me it’s Amazon Prime Day. I could be much poorer by the time you read this and then bankrupt by the time the Apple event ends tonight.

Ahead of this big product launch and the start of US earnings season today, global equity markets followed up the last two weeks of gains with yet another strong performance yesterday. Even with the US slow due to the Columbus Day holiday, by the close the S&P 500 was up another +1.64%, as the index closed at its 2nd highest level ever, just over 1% down from its record close. The index’s biggest component, Apple (+6.35%), was the best performing S&P stock in anticipation of today’s news. Overall, megacap tech stocks outperformed the broader index leading the NASDAQ to finish an even stronger +2.56% higher, the best day for the index since early September. The rally was still fairly broad-based with 22 of the 24 S&P industry groups higher with only defensives like consumer durables (-0.44%) giving way. Over in Europe, the STOXX 600 climbed +0.72% to reach its own 3-week high. Energy stocks were among the laggards on both sides of the Atlantic as Brent crude (-2.64%) and WTI (-2.88%) oil prices fell back. The drop was the most in just over a week and comes as news that supply disruptions are easing. Specifically, Royal Dutch Shell, BHP Group and Chevron all said they have resumed operations in the Gulf of Mexico and separately Libya’s National Oil Corp has ramped up production of its largest oil field. The STOXX 600 travel and leisure index was down -0.64% in spite of the broader market rally as the move to tighter restrictions gathered pace.

Attention will now turn to the start of the Q3 earnings season with today’s releases including Johnson & Johnson, JPMorgan Chase, Citigroup and BlackRock, ahead of a number of other financials releasing later in the week. As our asset allocation team wrote in their preview (link here), the bottom-up consensus for Q3 is for a sharp rebound in headline earnings, but the bulk is being driven by reductions in loan loss provisions and energy sector losses. If you exclude these, underlying earnings growth is forecast to barely move up, in spite of rising Q3 GDP growth estimates pointing to a strong macro rebound. According to them, this suggests the consensus is likely again underestimating the bounce in earnings. This is the same as we highlighted in Q2 but the big difference is that US equity positioning is more neutral now and that election uncertainty has increasingly been priced out over the last couple of weeks. So while the Q2 season was set up for a big market rally, it’s going to be much harder in Q3 even if the positive earnings story is similar.

You can bet companies will continue to be asked about ESG on their earnings calls. The ESG themes this year may have been dominated by health and sustainability, but Luke and Karthik from my team have just published a piece that shows the hottest growth topics in the third quarter were new ones as companies looked to start rebuilding from the pandemic. Their piece also reviews Q3 performance and flows for ESG funds. See here for more.

Back to the virus and in terms of the new measures, UK Prime Minister Johnson announced there’d be a new tiered alert system for England, which would see different areas grouped into medium, high and very high. The new measures come as data showed hospitalisations in England rose to 3,665 yesterday, which its highest level since June 12. Areas under a Very High alert will see pubs and bars close, though shops and schools are remaining open. Later today Dutch Prime Minister Rutte is expected to announce stricter measures and Italy’s Prime Minister Conte was also reportedly looking into new restrictions on private parties, amateur sports activities and social gatherings.

Elsewhere in the US, Covid cases are now averaging over 48,000 per day over the last week and to the highest levels since mid-August. The highest impacted states per 10K people are those that missed the initial wave (Northeast and West Coast) and the second wave (Sun Belt). The states most affected now are in the upper Midwest – North and South Dakota as well as Wisconsin. The latter continues to be a big focus of next month’s election and the impact of the virus may make counting votes there take longer than normal with many voters mailing in ballots for the first time.

On the vaccine front, Johnson & Johnson said overnight that its Covid-19 Phase 3 trial has been paused due to an unexplained illness in a participant. Elsewhere, China’s local daily Jiemian reported that Sinopharm has started to administer its two vaccines to residents in Wuhan and Beijing. Residents can now make appointments to get the shot and students who need to go abroad from November to January are being given priority. As a reminder, Sinopharm already has limited approval in China to administer its vaccine.

The above news on J&J is weighing on risk overnight even if most markets have recovered from their respective intraday lows. The Shanghai Comp (-0.28%) and Kospi (-0.36%) are down while the Nikkei (+0.12%) is up. S&P 500 futures also retreated following the news and is now -0.41% as we type. The Hang Seng suspended morning trading on the likelihood of a tropical storm hitting Hong Kong’s shore. In FX, the US dollar index is trading up +0.13%. Elsewhere, spot gold prices are down -0.62%. In terms of overnight data, China’s September exports came in at +9.9% yoy (vs. +10.0% yoy expected) while imports jumped to +13.2% yoy (vs. +0.4% yoy expected). As a result the trade balance for the month stood at $37bn (vs. $60bn expected). In other news, the hearings for the Supreme Court nomination of Judge Amy Coney Barrett have begun in the Senate Judiciary Committee.

Back to the election and investor sentiment was further supported yesterday by the continued poll lead for Joe Biden amidst hopes that a blue wave for the Democrats will set markets up for substantial fiscal stimulus next year. The FiveThirtyEight and the RealClearPolitics polling averages now put Biden +10.4pts and +10.2pts ahead respectively. The FiveTirthyEight Senate model now gives Democrats a 69% chance of winning control of the Senate (given the Vice President is the tiebreaker), the highest probability of this election cycle. The November VIX future, which expires two weeks following the election, fell to its lowest level since August 20 as polls continue to widen. On this today DB are hosting a live video call on “Who is going to win the 2020 US Presidential election?” at 3pm BST/4pm CET/10am ET with US polling experts Amy Walter, National Editor, The Cook Political Report and G. Elliott Morris, Data journalist for The Economist. Register here if you want to get the details.

New records were set over in the fixed income sphere, as yields on 10yr Italian debt hit another record low of 0.67%. In our chart of the day yesterday (link here ), we looked at 700 years of data on this, and show how Italian yields have continued to fall even as the country’s public debt burden looks set to climb to even higher records. The spread of 10yr yields over bunds has also continued to narrow, and yesterday hit a fresh 2-year low of 1.22%. Bunds themselves saw a -1.8bps fall in yields to -0.55%, while US Treasury markets were closed for a bond holiday in the US. Yields on 10y USTs are trading down -1.3bps this morning at 0.763%.

To the day ahead now, and earnings season kicks off with releases from Johnson & Johnson, JPMorgan Chase, Citigroup and BlackRock. From central banks, we’ll hear from Bank of England Governor Bailey, the ECB’s Hernandez de Cos and the Fed’s Barkin. Data releases include the US CPI reading for September, while the IMF will be releasing their latest World Economic Outlook.

3 a./NORTH KOREA/ SOUTH KOREA

South Korea

b) REPORT ON JAPAN

3 C CHINA

CHINA/USA

4/EUROPEAN AFFAIRS

CORONAVIRUS UPDATE/HOLLAND//GLOBE

Dutch Woman Dies After Being Reinfected With COVID-19, Global Cases See Biggest Weekly Jump Yet: Live Updates

Summary:

- Dutch woman dies after being reinfected

- First American confirmed reinfected with COVID-19

- Russia, Hungary report record deaths

- China launches another massive testing campaign

- India new cases lowest in 2 months

- WHO says world saw record jump in COVID-19 cases last week

- 14% of those infected with COVID are health-care workers

- Italy imposes new restrictions

* * *

Speaking to a massive crowd in Florida last night, President Trump declared that he felt “powerful” and that he would “kiss” every person in the crowd if he could. Shortly before the start of Trump’s performance, Press Secretary Kayleigh McEnany posted a memo from President Trump’s doctor, Dr. Sean Conley, telling the public that Trump had tested negative repeatedly over the course of several days.

Trump went ahead with his rally even as Dr. Anthony Fauci slammed the president for holding the rallies despite the chance of spreading COVID-19 (even after he repeatedly refused to weigh in on the potential impact of all those protests) and even accused the president and his campaign of “harassing me” by using clips that Dr. Fauci said were taken out of context.

But perhaps the biggest news on the COVID-19 front from overnight was Johnson & Johnson’s decision to “pause” its 60,000 patient COVID-19 vaccine trial. JNJ’s halt comes a little over a month after the AstraZeneca-Oxford trial was stopped by regulators after a patient was afflicted with a rare spinal condition. Although AZ’s trials have resumed in India, the UK and elsewhere, regulators in the US are still enforcing a hold, and their reasoning isn’t clear. Though JNJ insisted that it voluntarily halted the trial, we await more information from US regulators, who have been convened to investigate what went wrong. According to the STAT News report that broke the story, the trial was halted due to an “unspecified” illness.

Moving on to Tuesday morning, there has been some big news out of Europe. The FT reported, citing a scientific paper published in the journal Clinical Infectious Disease, that an 89-year-old Dutch woman has become the first person reinfected with COVID-19 to succumb to the virus. According to the paper, the patient first arrived at a hospital in the Netherlands complaining of fatigue. She tested positive, and was later discharged. But 59 days later, she returned to the hospital with even more serious conditions, and tested positive for COVID-19 again. She died shortly after.

The news follows last night’s exclusive WSJ report documenting the first case of a patient who was reinfected with COVID-19 in the US. We’ll have more on that later. The report in the Lancet cited by WSJ also shows that the second bout of COVID-19 is often more severe in reinfected patients.

Finally, after announcing a slate of new restrictions last week, the Italian government has on Tuesday set out the tighter restrictions on social gatherings, restaurants and school activities to stop the spread of the virus after the average number of daily cases doubled over the course of a week.

PM Giuseppe Conte signed off on a decree outlining the measures that are expected to come into force from Tuesday and to be in force for the next 30 days. The measures include restaurants and bars needing to close by midnight, or before 2100 local time if they don’t have table service.

Finally, the WHO confirmed yesterday that global COVID-19 cases set a new record last week.

Though it has slowed somewhat since September, India’s outbreak was one of the biggest contributors to this trend, along with Europe, the US and Brazil.

Here’s a rundown of the key COVID-19 news from overnight and Tuesday morning:

Globally, Global cases have reached 37,722,044, according to Johns Hopkins data. The global death toll has hit 1,078,411 (Source: JHU).

India reports fewest new cases in two months, reporting just 55,342 new cases for the past 24 hours, bringing the country total to 7.18 million. That’s well below the numbers from last month, when India was reporting 90k+ new cases on average. The health ministry also reported 706 deaths in the past 24 hours, raising the toll to 109,856. (Source: Nikkei).

South Korea reports 102 cases, marking the first triple-digit increase in six days. Daily infections had mostly fallen into the double digits over the past two weeks, prompting the government to relax social distancing rules this week (Source: Nikkei).

After reporting China’s first domestic outbreak in more than 2 months, the Chinese city of Qingdao said on Monday it will test its entire population of more than 9 million people for coronavirus, after discovering 12 new infections that appeared to be linked to a hospital treating imported infections (Source: Nikkei).

The World Health Organization chief has warned against suggestions by some to just allow COVID-19 to spread in the hope of achieving so-called herd immunity, saying this was “unethical” (Source: Al Jazeera).

Russia reported its highest number of deaths over 24 hours from Covid-19. The total of 244 exceeds the previous high of 232 on May 29, according to data from the country’s anti-coronavirus task force. Overall, 22,966 people have died from the disease, it said. Hungary also registered record coronavirus deaths on Monday, as well as 1,025 new cases, official data show (Source: Bloomberg).

A key member of Hong Kong’s top orchestra has been infected with Covid-19, sending some 100 musicians into quarantine and raising concerns about the risk of exposure to a concert audience that included the city’s leader and home affairs chief (Source: SCMP).

Hong Kong will extend all social distancing rules for another week to Oct. 22, according to a government statement. Rules include a public-gathering limit of four people, compulsory mask-wearing and no dining in restaurants after midnight (Source: Bloomberg).

No, Europe! More Debt Is Not The Answer

In an article published in the Frankfurter Allgemeine Zeitung, Isabel Schnabel, Member of the Executive Board of the ECB states that governments taking more debt now should not be a concern, and would strengthen the central bank independence in the future.

She claims that “the decisive fiscal policy intervention in the coronavirus (COVID-19) crisis strengthens the effectiveness of monetary policy and mitigates the long-term costs of the pandemic. With targeted, forward-looking investment, not least under the umbrella of the EU Recovery Fund, governments can foster sustainable growth, increase long-term competitiveness and facilitate the necessary reduction of the debt ratio once the crisis has been overcome”.

The problem of Ms Schnabel’s article is that it ignores the facts and bets the future of the central bank independence on a rigorous, profitable and successful level of government investment that has never happened and is even more less likely to occur now.

Ms Schnabel should be, in fact, warning about the enormous risk of malinvestment and excessive debt that may arise from the European Recovery Fund implementation and the massive deficit spending arising throughout the Eurozone. Why? Because she has the empirical evidence of the failure to achieve the virtuous growth and debt reduction she expects with the examples of the Growth and Jobs Plan of 2009, the Juncker plan and the enormous rise in deficit spending between 2009 and 2011 among many European nations. Once growth recovered, three things were evident:

- Most Eurozone countries maintained a level of deficit spending that elevated the debt to GDP in growth and recession periods because governments get used to spending more in boom times and even more in recession times. Ms Schnabel expects of the Eurozone governments a level of discipline and fiscal prudence that only Germany and Holland implemented. With the budgets of Spain and Italy soaring without control, the idea that governments will spend money wisely and productively is not just wishful thinking, it is negated by the evidence of the past.

- The debt burden created by the “decisive fiscal policies” in recession times not only stays and grows but leads to rising taxes afterwards to “reduce the deficit” that hinder growth and job creation. The eurozone already suffers from an uncompetitive tax wedge in many countries, and unproductive deficit spending followed by taxes on investment and job creation has become a norm. The eurozone growth has not been slower and with higher unemployment than the United States due to bad luck, but because of the constant crowding out of wealth and productive capacity on the side of many governments.

- Ms Schnabel should know by now, after years of stimuli, that governments do not “foster sustainable growth and increase long-term competitiveness”. In her article she mentions that productivity growth has been stubbornly weak, yet she does not see any connection between low productivity and the increasing role of government spending and monetary policy in incentivising low productivity via negative rates and public intervention. Government investment cannot boost growth and competitiveness enough to cover the massive debt burden that is being built because governments do not have the incentive to be productive and generate investments with real economic returns. The incentive to malinvest and perpetuate overcapacity is enormous because governments do not suffer the consequences of bad investment decisions, taxpayers do.

Ms Schnabel knows that the experience of previous crises shows us that no, in times of weakness governments should not decide to supplant the private sector. Governments do not have better or more information than the private sector on where and how to invest and have all the incentives to malinvest and overspend because the ECB continues to support by buying sovereign bonds and cutting rates. The evidence of rising debt, poor productivity and higher unemployment than its peers of the eurozone should be enough of a warning sign, and the example of Japan should serve as a red flag as well.

Ms Schnable knows that the elevated levels of debt to GDP incurred by most eurozone countries will not be reduced to pre-pandemic levels, even less to sustainable levels, with constant public deficit spending promoted by monetary policy and with calls to questionable “investments”. Ms Schnable may ask herself one question: If all those massive “investments” that some eurozone governments are announcing are profitable, productive and will promote long-term growth and jobs, why none of them had been implemented in the 2014-2019 period despite low rates, high liquidity and the Juncker plan to support? Because the vast majority of what most eurozone countries will include in the “investment” recovery plan are not productive, profitable or growth-oriented projects.

Ms Schnable should know that many eurozone countries like Spain have relied on monetary policy to disguise structural challenges, and that monetary policy has gone from being a tool to buy time to implement structural reforms to a tool to avoid them. Ms Schnable should also know that the euro is not the world reserve currency and that replicating the Federal Reserve’s policy does not make governments spend wisely and productively. The ECB balance sheet is now 57% of GDP and negative rates have been there for years, and the result has been disappointing growth in the good times and a larger crisis in the bad times. The rising role of governments in the economy is not a coincidence. It is one of the leading causes of the eurozone’s weakness, when governments already consume more than 40% of annual GDP.

The evidence of the past shows us that governments do not create jobs, growth or competitiveness. An IMF paper analysing government spending plans concluded that “the effect of government consumption is very small on impact, with estimates clustered close to zero… which raises questions as to the usefulness of discretionary fiscal policy for short-run stabilization purposes” (Ilzetki et al, 2011). The eurozone has showed that negligible positive impact for years.

Unconventional monetary policy was not implemented because governments spent too little, but because governments spent too much, and could not finance themselves without central bank quantitative easing and asset purchases.

The ECB will not strengthen its independence with large deficit spending and massive debt from member states. It will be even more dependent on disguising the insolvency of countries once, when Covid-19 stops being an excuse, debt and government spending will continue to rise.

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

RUSSIA/USA

Trump seeking alast minute pre election nuke deal with Russia

(zerohedge)

Trump Seeking Last Minute Pre-Election Nuke Deal With Putin

The clock is winding down on the last major arms control agreement between Moscow and Washington, after prior late Cold War era treaties like the INF and Open Skies faltered – or rather the US abruptly withdrew from them with Trump complaining he wants “a better deal”. If an extension agreement is not reached on the New Strategic Arms Reduction Treaty (New START) during ongoing talks, the latest of which were hosted in Vienna and Helsinki within past weeks, it will expire in February of next year, or merely in less than four months.

Russia’s unwavering position has been to push for an unconditional five-year extension of the treaty, while Washington said it will only consider a short-term extension if a new agreement that brings all nuclear warheads including those possessed by China into the framework. The Kremlin has called the US plan “absolutely unrealistic,” bringing talks to an impasse.

But now it looks like President Trump wants to rapidly push out a deal ambitiously ahead of the November 3 election, as Axios reports, “President Trump is looking to Vladimir Putin to close the deal on a pre-election nuclear agreement, a timetable that’s an October surprise even for senior Republicans and some in the White House.”

Trump and Putin over the past half-year have engaged in a series of phone calls that have reportedly focused on New START. Axios notes further that it’s being handled at the highest national security levels of the administration, though there are mixed signals of just how it’s actually going.

Axios writes, “On Friday, a source familiar with the discussions said the Trump administration believed it now had an agreement in principle, blessed by Putin and Patrushev, that could be finalized within a week once negotiations resume in earnest.”

However, other signals especially out of Kremlin official statements suggest this is an over optimistic reading of where things actually stand. There’s also the fact that Joe Biden has clearly indicated he’s ready to agree to the unconditional 5-year extension of the nuclear arms reduction treaty.

All of this would make wrapping up the deal in a mere week a huge difficulty. It’s likely the Russians will want to wait and see what the outcome of November is before entering into significant compromises.

Indeed Deputy Foreign Minister Sergei Ryabkov said on Saturday that “there are still huge differences in approaches, including to the central elements of such an agreement.” He also called a one week timetable “unrealistic”.

Complicating matters is the reality that (contrary to years of ‘Russiagate’ and “collusion” narrative claims) the Trump presidency has sunk US-Russian relations to new lows.

Putin underscored this in an interview with a Russian TV broadcaster last week when he said: “the greatest number of various kinds of restrictions and sanctions were introduced [against Russia] during the Trump presidency.”

“Decisions on imposing new sanctions or expanding previous ones were made 46 times. The incumbent’s administration withdrew from the INF treaty. That was a very drastic step. After 2002, when the Bush administration withdrew from the ABM treaty, that was the second major step. And I believe it is a big danger to international stability and security,” Putin explained.

So again, the Russians are more likely to wait things out a mere few weeks to see if Biden comes out on top, then all of this becomes moot.

Azerbaijani Military Destroys Armenian S-300s As Humanitarian Ceasefire Nears Collapse

Submitted by SouthFront,

The Armenian-Azerbaijani war in the Nagorno-Karabakh region does not show signs of nearing its end despite the humanitarian ceasefire launched in the region. The ceasefire started in the Nagorno-Karabakh region at 12:00 local time on October 10. The ceasefire deal was reached by the Azerbaijani and Armenian sides following long talks in Moscow a day ago. Russia played a key role in forcing the sides to make steps towards the de-escalation.

Azerbaijan and Armenia also formally agreed to begin substantive negotiations of a peaceful settlement of a military conflict over the disputed region of Nagorno-Karabakh that erupted on September 27. These talks will be mediated by the Organization for Security and co-operation in Europe’s Minsk Group of international negotiators. Following the ceasefire agreement, Azerbaijani President Ilham Aliyev said that the first phase of the military operation in the Nagorno-Karabakh region is completed. The Russian diplomatic intervention allowed to put an end to the hottest phase of the military confrontation and force the sides to halt active offensive operations on the ground.

Despite this, the situation on the ground remained very tense. Almost immediately after the start of the ceasefire regime, the sides simultaneously accused each other of violating the ceasefire and of shelling civilian and military targets, and repeated these claims on October 11 and October 12.

Meanwhile, Armenia and Azerbaijan released a new batch of fresh and few days old footage showcasing casualties of each other and making loud statements. In particular, pro-Azerbaijani sources claimed that at least two more S-300 systems of Armenia were destroyed in Karabakh. The released videos accompanying these claims include the moments of the alleged destruction of 35D6 (ST-68U) radars and a S-300 missile launcher of the Armenian military with Israeli IAI Harop loitering munitions near the village of Khojaly in the Khojaly District and the village of Qubadlı in the Kashatagh District.

The 35D6 is a vehicle-carried three-dimensional air surveillance radar system. The range of the radar’s primary functions includes the detection of low-flying targets protected with active and or passive jamming screens, and also the performance of air traffic control. It can be operated as a separate installation as well as a part of the S-300 air-defense system. Nonetheless, if it was the S-300 batteries, as Azerbaijani sources insist, it still remains unclear what these long-range air defense systems were doing so close to the frontline.

Meanwhile, the Armenian military reported that its forces repelled large Azerbaijani attacks in the northeastern and southern parts of the region. The hottest area of the frontline is the town of Hardut. Azerbaijani President Aliyev officially announced that his forces captured it a few days ago. Nonetheless, videos from the ground show that in fact most of the town remained in the hands of the Armenians. Another part of it is now a gray zone, which is not controlled by any side. According to Armenian sources, Azerbaijani troops, supported by Turkish special forces and Syrian militants, tried to capture the town just a few hours before the start of the ceasefire. After this failed attack, Azerbaijani combat drones and artillery units delivered powerful strikes on Hardut and nearby villages, but were not able to force Armenian troops to retreat.

The Armenian Defense Ministry insists that the Turkish Air Force is leading the aerial operations of Azerbaijan. “Turkish aerial command centers, flying within the Turkish airspace, are commanding the Turkish UAV’s operating in the Azerbaijani air force. UAVs, accompanied by six F-16 units, are directly attacking the peaceful population and civilian infrastructure of Artsakh,” the defense ministry spokesman said.

In its own turn, the Azerbaijani side says that it’s just taking the necessary steps to respond to Armenian violations of the ceasefire and strikes on Azerbaijani settlements. The most widely covered incident of this kind took place on October 11, when an alleged Armenian ballistic missile hit Ganja city.

END

TURKEY/RUSSIA/ARMENIA/AZERBAIJAN

Belligerent Erdogan notifies Russia and Armenia must withdraw from Azerbaijani lands.

(AlMasdarNews)

Turkey Notifies Russia: Armenia Must Withdraw From ‘Occupied Azerbaijani Lands’

Ankara said that the Turkish Defense Minister, Hulusi Akar, stressed during a telephone conversation he had today with his Russian counterpart, Sergey Shoigu, “the necessity of Armenia’s withdrawal from the occupied Azerbaijani lands.”

The Turkish Ministry of Defense stated, in a statement, that Akar called on Monday with Shoigu, and during the call, “views were exchanged on Armenia’s attacks on Azerbaijan.”

According to the statement, Akar stressed that Armenia, which he claimed “launched an attack on the civilian population and violated the ceasefire regime, must stop its attacks and withdraw from the occupied territories.”

Akar pointed out that “Azerbaijan cannot wait another 30 years,” stressing Turkey’s support for Azerbaijan in its move to “regain control of its lands.”

On September 27, armed clashes erupted on the line of contact between Azerbaijani and Armenian forces in the Karabakh region and adjacent areas, in the most dangerous escalation between the two parties in more than 20 years, amid mutual accusations of starting hostilities and bringing in foreign militants.

Despite Russia and Armenia maintaining a formal mutual defense pact, analysts see little incentive for Russia to weigh too deeply into the long-running territorial dispute:

Turkey is considered a major ally of Azerbaijan, which is involved in the clashes against Armenian forces reportedly by transferring foreign mercenary (especially Syrian Islamists), but also allegedly through air support.

6.Global Issues

7. OIL ISSUES

8 EMERGING MARKET ISSUES

Your early morning currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings TUESDAY morning 7:00 AM….

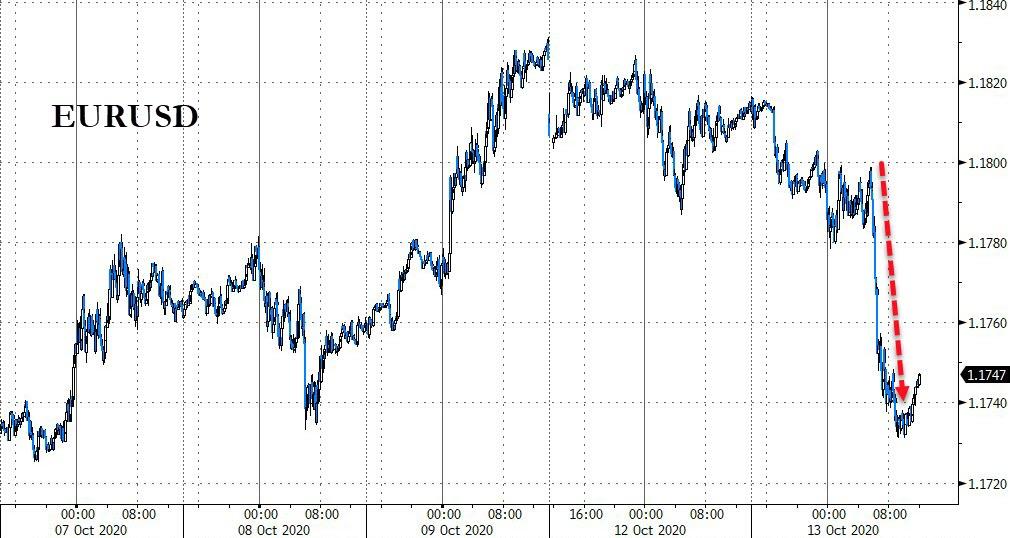

Euro/USA 1.1758 DOWN .0035 REACTING TO MERKEL’S FAILED COALITION/ REACTING TO +GERMAN ELECTION WHERE ALT RIGHT PARTY ENTERS THE BUNDESTAG/ huge Deutsche bank problems ///ITALIAN CHAOS//CORONAVIRUS/PANDEMIC/TRUMP POSITIVE WITH VIRUS /AND NOW ECB TAPERING BOND PURCHASES/JAPAN TAPERING BOND PURCHASES /USA RISING INTEREST RATES /FLOODING/EUROPE BOURSES /RED

USA/JAPAN YEN 105.50 UP 0.165 (Abe’s new negative interest rate (NIRP), a total DISASTER/NOW TARGETS INTEREST RATE AT .11% AS IT WILL BUY UNLIMITED BONDS TO GETS TO THAT LEVEL…

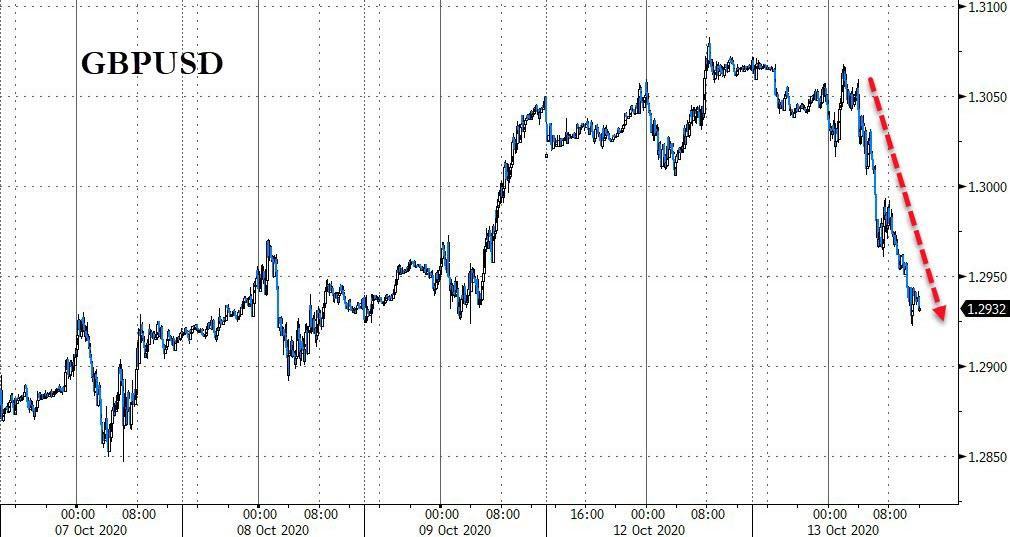

GBP/USA 1.3028 DOWN 0.0036 (Brexit March 29/ 2019/ARTICLE 50 SIGNED/BREXIT FEES WILL BE CAPPED/

USA/CAN 1.3109 DOWN .0003 CANADA WORRIED ABOUT TRADE WITH THE USA WITH TRUMP ELECTION/ITALIAN EXIT AND GREXIT FROM EU/(TRUMP INITIATES LUMBER TARIFFS ON CANADA/CANADA HAS A HUGE HOUSEHOLD DEBT/GDP PROBLEM)

Early THIS TUESDAY morning in Europe, the Euro FELL BY 25 basis points, trading now ABOVE the important 1.08 level FALLING to 1.1758 Last night Shanghai COMPOSITE UP 1.29 POINTS OR .04%

//Hang Sang CLOSED UP 530.55 POINTS OR 2.20%

/AUSTRALIA CLOSED UP 0,90%// EUROPEAN BOURSES ALL RED

Trading from Europe and Asia

EUROPEAN BOURSES ALL RED

2/ CHINESE BOURSES / :Hang Sang CLOSED UP 530.55% OR 2.20%

/SHANGHAI CLOSED UP 1.29 POINTS OR .04%

Australia BOURSE CLOSED DOWN 0.90%

Nikkei (Japan) CLOSED UP 43.09 POINTS OR 0.18%

INDIA’S SENSEX IN THE GREEN

Gold very early morning trading: 1920.40

silver:$24.96-

Early TUESDAY morning USA 10 year bond yield: 0.759% !!! DOWN 2 IN POINTS from MONDAY’S night in basis points and it is trading WELL BELOW resistance at 2.27-2.32%.

The 30 yr bond yield 1.550 DOWN 2 IN BASIS POINTS from MONDAY night.

USA dollar index early TUESDAY morning: 93.19 UP 12 CENT(S) from MONDAY’s close.

This ends early morning numbers TUESDAY MORNING

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx6

And now your closing TUESDAY NUMBERS \1: 00 PM

Portuguese 10 year bond yield: 0.15% DOWN 1 in basis point(s) yield from YESTERDAY/

JAPANESE BOND YIELD: +.03.% DOWN 1 BASIS POINTS from YESTERDAY/JAPAN losing control of its yield curve/

SPANISH 10 YR BOND YIELD: 0.15%//DOWN 0 in basis point yield from yesterday.

ITALIAN 10 YR BOND YIELD:0.67 DOWN 1 points in basis points yield from yesterday./

the Italian 10 yr bond yield is trading 52 points higher than Spain.

GERMAN 10 YR BOND YIELD: FALLS TO –.56% IN BASIS POINTS ON THE DAY//

THE IMPORTANT SPREAD BETWEEN ITALIAN 10 YR BOND AND GERMAN 10 YEAR BOND IS 1.23% AND NOW ABOVE THE THE 3.00% LEVEL WHICH WILL IMPLODE THE ENTIRE ITALIAN BANKING SYSTEM. AT 4% SPREAD THERE WILL BE A HUGE BANK RUN…

END

IMPORTANT CURRENCY CLOSES FOR TUESDAY

Closing currency crosses for TUESDAY night/USA DOLLAR INDEX/USA 10 YR BOND YIELD/1:00 PM

Euro/USA 1.1741 DOWN .0072 or 72 basis points

USA/Japan: 105.53 UP .153 OR YEN DOWN 15 basis points/

Great Britain/USA 1.2974 DOWN .0071 POUND DOWN 71 BASIS POINTS)

Canadian dollar DOWN 27 basis points to 1.3138

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

The USA/Yuan,CNY: closed DOWN 6.7466 ON SHORE (DOWN)..

THE USA/YUAN OFFSHORE: 6.7414 (YUAN DOWN)..

TURKISH LIRA: 7.92 EXTREMELY DANGEROUS LEVEL/DEATH WISH.

the 10 yr Japanese bond yield at +0.03%

Your closing 10 yr US bond yield DOWN 4 IN basis points from MONDAY at 0.736 % //trading well ABOVE the resistance level of 2.27-2.32%) very problematic USA 30 yr bond yield: 1.526 DOWN 4 in basis points on the day

Your closing USA dollar index, 93.53 UP 46 CENT(S) ON THE DAY/1.00 PM/

Your closing bourses for Europe and the Dow along with the USA dollar index closing and interest rates for TUESDAY: 12:00 PM

London: CLOSED DOWN 31.67 0.53%

German Dax : CLOSED DOWN 111.42 POINTS OR .91%

Paris Cac CLOSED DOWN 31.68 POINTS 0.64%

Spain IBEX CLOSED DOWN 75.80 POINTS or 1.09%

Italian MIB: CLOSED DOWN 160.05 POINTS OR 0.81%

WTI Oil price; 40.22 12:00 PM EST

Brent Oil: 42.37 12:00 EST

USA /RUSSIAN / RUBLE FALLS: 77.13 THE CROSS HIGHER BY 0.01 RUBLES/DOLLAR (RUBLE LOWER BY 1 BASIS PTS)

TODAY THE GERMAN YIELD FALLS TO –.56 FOR THE 10 YR BOND 1.00 PM EST EST

END

This ends the stock indices, oil price, currency crosses and interest rate closes for today 4:30 PM

Closing Price for Oil, 4:00 pm/and 10 year USA interest rate:

WTI CRUDE OILPRICE 4:30 PM : 40.22//

BRENT : 42.45

USA 10 YR BOND YIELD: … 0.726..down 5 basis points…

USA 30 YR BOND YIELD: 1.512 down 7 basis points..

EURO/USA 1.1749 ( DOWN 65 BASIS POINTS)

USA/JAPANESE YEN:105.48 UP .142 (YEN DOWN 14 BASIS POINTS/..

USA DOLLAR INDEX: 93.50 UP 44 cent(s)/

The British pound at 4 pm Britain Pound/USA:1.2937 down 127 POINTS

the Turkish lira close: 7.93

the Russian rouble 77.07 DOWN 0.3 Roubles against the uSA dollar. (DOWN 3 BASIS POINTS)

Canadian dollar: 1.3140 DOWN 27 BASIS pts

German 10 yr bond yield at 5 pm: ,-0.56%

The Dow closed DOWN 157.52 POINTS OR 0.55%

NASDAQ closed DOWN 12.36 POINTS OR 0.10%

VOLATILITY INDEX: 25.92 CLOSED UP .85

LIBOR 3 MONTH DURATION: 0.229%//libor dropping like a stone

USA trading today in Graph Form

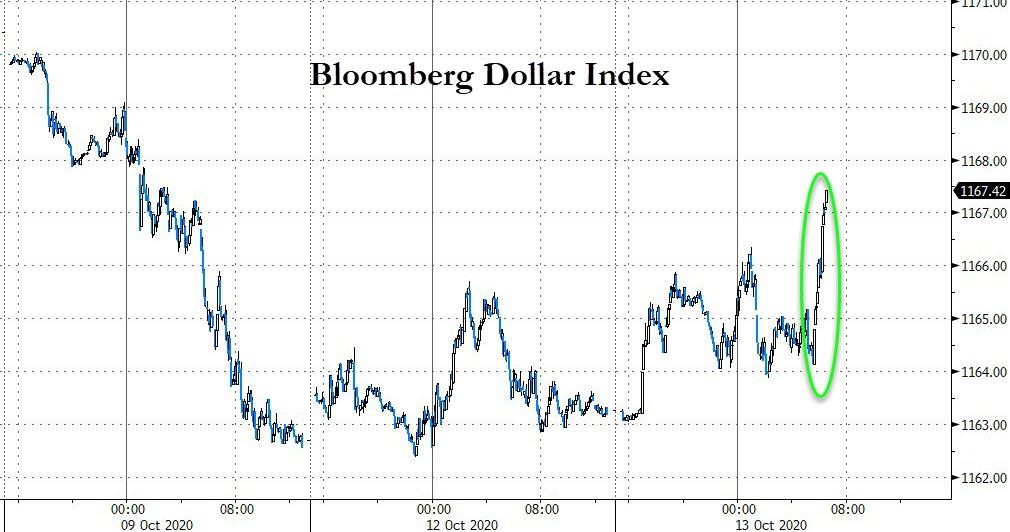

Banks Bust, Bullion Battered, But Big-Tech Bid (Again)

Another day, another Nasdaq-Whale-driven gamma-squeeze in Nasdaq as the rest of the market deteriorated, giving back a lot (if not all) of yesterday’s gains (Small Caps red from Friday)…

While Nasdaq ended very marginally lower on the day, it outperformed significantly as FANG stocks managed gains (despite AAPL losses)

Source: Bloomberg

Nasdaq faces record delta and surging gamma into this Friday’s Op-Ex…

Source: Nomura

And if you don’t know what gamma is – probably better not to play at this point in the farce…

Nasdaq outperformed Small Caps once again, but also gave back a lot of the early day outperformance…

The S&P 500 was unable to take out its recent highs…

Source: Bloomberg

Despite claims by the great and the good that earnings were awesome (thanks to cuts in provisions, despite no optimism on the economy?), bank stocks were battered today…

Source: Bloomberg

With Citi hit hardest…

Source: Bloomberg

AAPL tumbled during its iPhone launch as China killed the livestream…

VIX did not rise with the underlying market today, suggesting the (call-buying) whale is starting to leave the market…

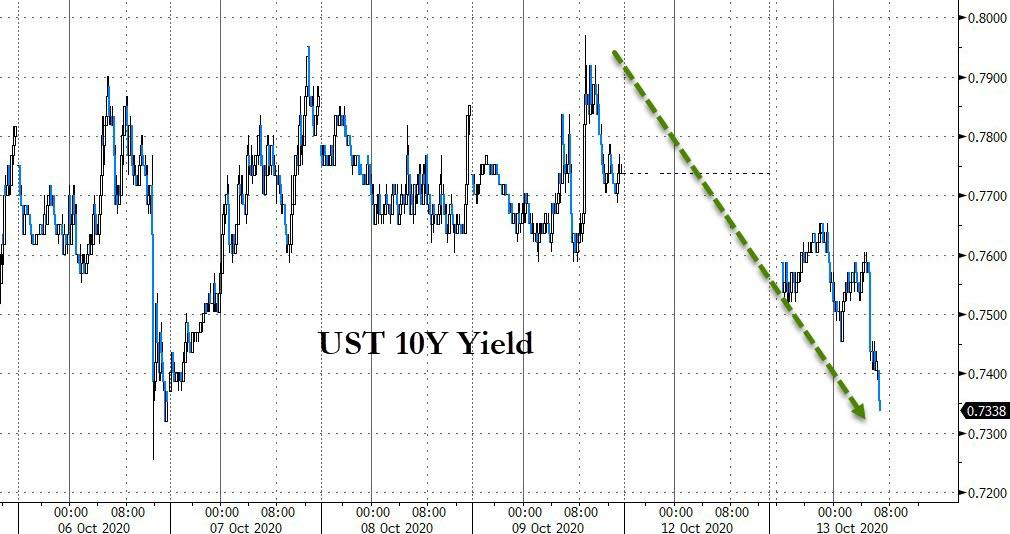

Having been closed yesterday, bond yield tumbled today…

Source: Bloomberg

With 10Y back down to 72bps…

Source: Bloomberg

EUR and GBP dropped as Brexit talks breakdown…

Source: Bloomberg

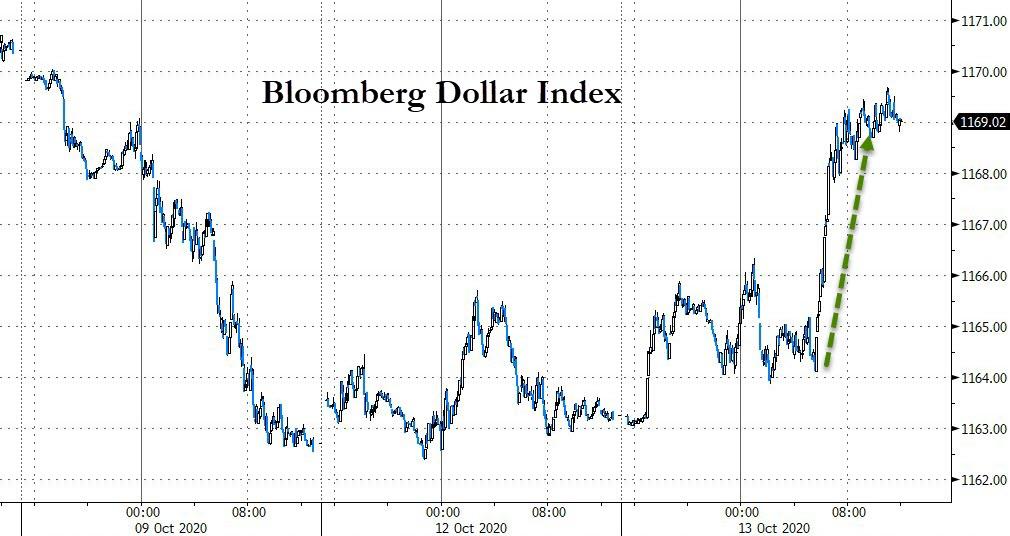

Sending the dollar spiking higher…

Source: Bloomberg

Cryptos slipped lower as the USD rallied…

Source: Bloomberg

The dollar spike sparked a plunge in precious metals.

Gold futs tumbled back below $1900…

Silver tanked below $25…

Oil price rebounded modestly today with WTI back above $40 ahead of tonight’s API inventory data…

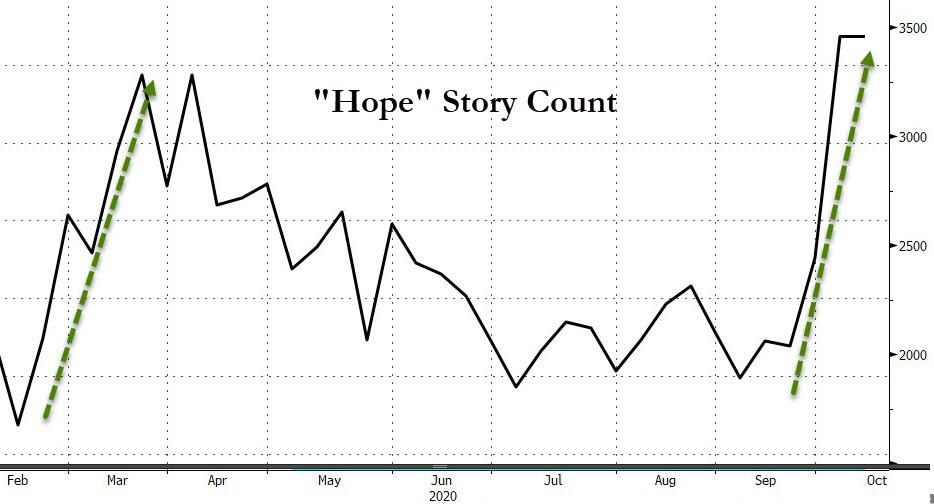

Finally, in case you were wondering what – aside from Softbank’s Whale call-buying malarkey – is driving this meltup… it’s “hope”…

Source: Bloomberg

…and everyone knows “hope is not a strategy!”

a)Market trading/THIS MORNING/USA

PMs Pummeled As Dollar Spikes

The dollar is spiking this morning, helped by a no-deal-brexit bashing for cable and euro…

Source: Bloomberg

And as the dollar spikes, precious metals are getting clubbed like a baby seal.

Gold futures are pushing back down towards $1900…

And Silver futures are back below $25…

And while that ‘safe haven’ is sold, bonds are well bid…

Source: Bloomberg

b)MARKET TRADING/USA//Non farm payrolls

ii)Market data/USA

CONSUMER PRICES

A mixed bag: used car prices rise, but shelter and rent costs lower on latest CPI data

(zerohedge)

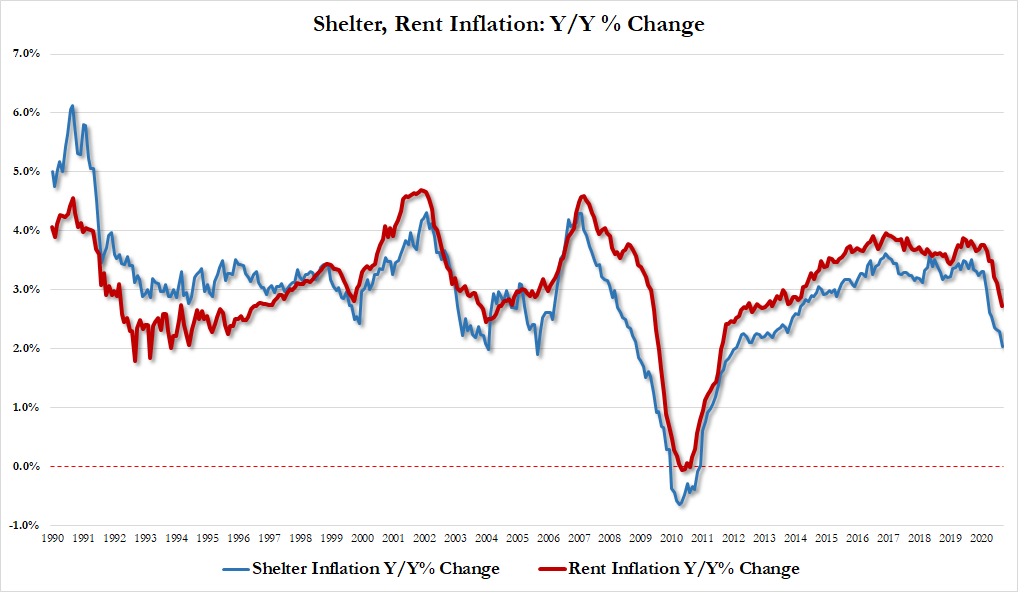

Used-Car Prices Soar As Shelter/Rent Costs Slow In September CPI Data

Consumer prices were very mixed in September with headline CPI accelerating to +1.4% YoY and core CPI decelerating to +1.7% YoY.

Source: Bloomberg

The three most important factors for Americans – food, shelter, and energy costs – were a mixed bag:

The most notable driver on the downside was shelter/rent inflation collapsing:

- Shelter inflation up 2.04% Y/Y, lowest since Feb 2012

- Rent inflation up 2.72% Y/Y, lowest since April 2013

The energy index fell 7.7 percent over the past 12 months with its component indexes mixed. The gasoline index decreased 15.4 percent and the fuel oil index fell 27.2 percent. In contrast, energy service indexes rose, with the index for natural gas increasing 3.8 percent and the index for electricity advancing 0.7 percent.

The food index was unchanged in September after rising 0.1 percent in August. The index for food at home fell 0.4 percent in September as five of the six major grocery store food group indexes declined. The index for nonalcoholic beverages fell 0.8 percent, its largest monthly decline since December 2010. The index for other food at home declined 0.6 percent in September after rising 0.5 percent in August. The index for dairy and related products declined 0.5 percent in September after rising 1.5 percent in August.

Despite the September decline, the food at home index increased 4.1 percent over the last 12 months. All six major grocery store food group indexes rose over that span, with increases ranging from 2.6 percent (cereals and bakery products) to 6.3 percent (meats, poultry, fish, and eggs). The index for food away from home rose 3.8 percent over the last year. The index for limited service meals increased 5.5 percent and the index for full service meals rose 2.8 percent over the last 12 months.

The index for food away from home continued to rise, increasing 0.6 percent in September. The index for limited service meals rose 0.9 percent in September, the largest increase in the history of the index, which dates to 1997. The index for full service meals rose 0.3 percent in September.

Additional drags included motor vehicle insurance, which declined in September, falling 3.5 percent. The index for airline fares fell 2.0 percent in September after rising in each of the previous 3 months. The apparel index also turned down in September, falling 0.5 percent after rising the last 3 months. The education index fell 0.3 percent in September, the same decline as in August. The index for household furnishings and operations fell slightly in September, declining 0.1 percent after rising 0.9 percent in August. The indexes for communication and for alcoholic beverages also declined in September.

* * *

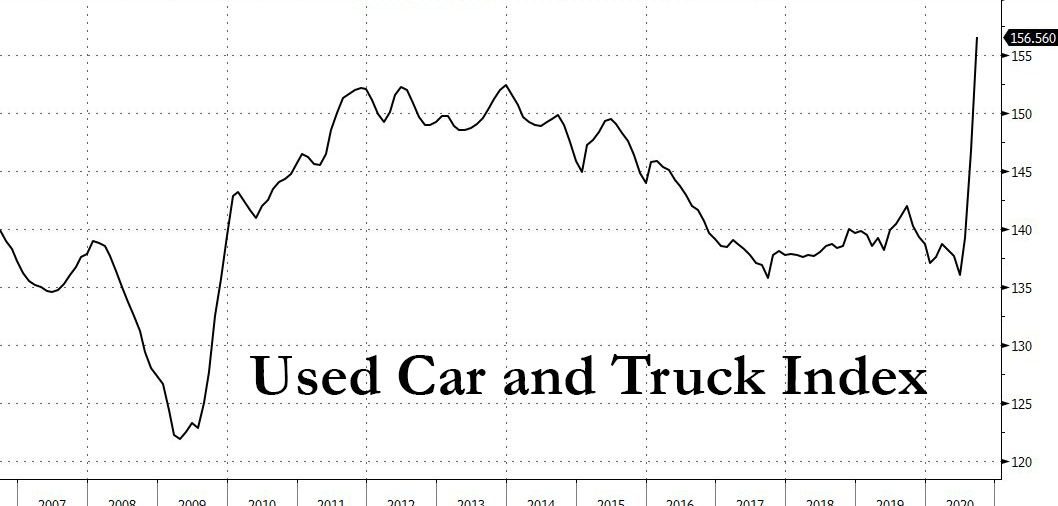

As was the case last month, the index for used cars and trucks was the dominant factor to the upside; it rose 6.7 percent in September following a 5.4-percent increase in August.

The used cars and trucks index accounted for more than 100 percent of the monthly increase in the index for all items less food and energy.

The index for new vehicles increased 0.3 percent in September after being unchanged in August. The recreation index rose 0.2 percent in September after rising 0.7 percent in August. The medical care index was unchanged in September with its components mixed; the hospital services index rose 0.6 percent, while the physicians’ services index declined 0.3 percent and the prescription drugs index fell 0.1 percent.

Crucially, Goods prices are accelerating as Services price growth is slowing rapidly…

Source: Bloomberg

iii) Important USA Economic Stories

White House doctor says Trump has tested negative for two consecutive days

(zerohedge)

White House Doctor Says Trump Tested Negative For Covid On “Consecutive Days”

On of the most frequently asked questions addressed to the White House in recent days, was whether the president had tested negative for covid following his self-diagnosis that he was now cured of the virus.

Moments ago Trump’s physician Dr. Conley answered, and in a statement published by the White House, said that Trump has tested negative for Covid-19 on “consecutive days” using the Abbott BinaxNOW antigen card.

Conley also said that the test was not used in isolation, and was used in context with additional clinical and lab data, including subgenomic RNA and PCR measurements, “all of which indicated a lack of detectable viral replication.”

The Doctor’s conclusion: based on this comprehensive data, and “in concert with the CDC’s guidelines for removal of transmission-based precautions” the medical team has assessed “that the President is not infectious to others.”

![]()

We doubt his announcement will have any impact on the decision by the debate commission to cancel Thursday’s presidential debate, although we wonder just which “alternative science” will now be used to justify the claim that it is in Biden’s interest not to be in Trump’s proximity.

Trump: “I Was Right About Damaging Lockdowns”

Authored by Steve Watson via Summit News,