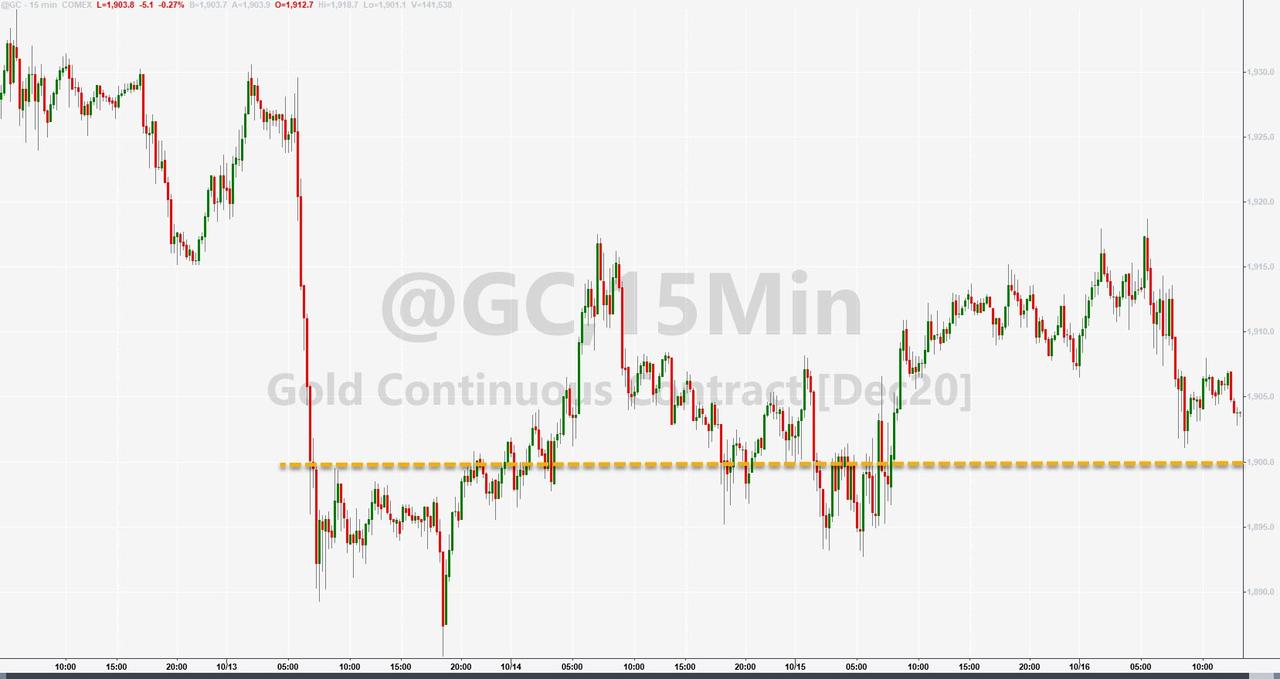

GOLD:$1903.40 DOWN $0.10 The quote is London spot price

Silver:$24.29 DOWN $0.15 London spot price ( cash market)

your data…

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED UP 4.18 PTS OR .13% //Hang Sang CLOSED UP 228.25 PTS OR .94% /The Nikkei closed DOWN 96.60 POINTS OR 0.41%//Australia’s all ordinaires CLOSED DOWN 0.45%

/Chinese yuan (ONSHORE) closed /Oil UP TO 40.60 dollars per barrel for WTI and 42.75 for Brent. Stocks in Europe OPENED ALL GREEN// ONSHORE YUAN CLOSED UP 6.6983 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.6919 TRADE TALKS STALL//YUAN LEVELS //TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED//CORONAVIRUS/PANDEMIC/TRUMP TESTS POSITIVE FOR COVID 19 : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

We had 0 kilobar transactions +

ADJUSTMENTS: 1 //

i) Out of JPMorgan: 12,056.625 oz

adjusted out of customer account into the dealer account

The front month of OCT registered a total of 1736 contracts for a GAIN of 40 contracts. We had 181 notices filed on Thursday so we gained 221 contracts or 22,100 additional oz will stand for delivery in this active delivery month of October. In gold we have not seen queue jumping start so early in the month. Thus you can bet the farm that throughout October, the total number of gold oz standing will increase from this level.

November LOST 38 contracts to stand at 1581.

The big December contract GAINED 5539 contracts UP to 448,481 contracts..

THE BIG STORY AGAIN TODAY IS THE HIGH OI STANDING FOR OCTOBER (103.34 tonnes). GENERALLY OCTOBER IS A POOR DELIVERY MONTH AS MOST INVESTORS PREFER TO SKIP THIS MONTH AND MOVE STRAIGHT TO DECEMBER. IT LOOKS LIKE SOME MAJOR ENTITY(GOLDMAN SACHS) JUST CANNOT WAIT FOR DECEMBER AS THEY ARE MAKING THEIR MOVE ON OCTOBER FOR PHYSICAL METAL. GOLDMAN SACHS ONE OF THE LEADERS OF THE NEW LONDON LME EXCHANGE NEEDS THE GOLD INVENTORY FOR LIQUIDITY AND INITIAL CONTRIBUTION WITH OTHER MAJOR PLAYERS. THE MAJOR DIFFERENCE BETWEEN THIS MONTH AND OTHER MONTHS IS THAT THIS GOLD STANDING IN OCTOBER WILL LEAVE THE COMEX AND HEAD FOR LONDON.

We had 606 notices filed today for 60600 oz OR 1.884 TONNES.

To calculate the INITIAL total number of gold ounces standing for the OCT /2020. contract month, we take the total number of notices filed so far for the month (32,094) x 100 oz , to which we add the difference between the open interest for the front month of OCT (1736 CONTRACTS ) minus the number of notices served upon today (606 x 100 oz per contract) equals 3,322,400 OZ OR 103.340 TONNES) the number of ounces standing in this active month of Oct

thus the INITIAL standings for gold for the OCT/2020 contract month:

No of notices filed so far (32,094, x 100 oz +1736 OI) for the front month minus the number of notices served upon today (606) x 100 oz which equals 3,322,400 oz standing OR 103.340 TONNES in this active delivery month. This is a HUGE amount for gold standing for a OCT delivery month (a poor active delivery month).

We gained 221 contracts or an additional 22,100 oz will stand on this side of the pond searching for metal.

NEW PLEDGED GOLD: BRINKS

592,648.822 oz NOW PLEDGED SEPT 15.2020/HSBC 18.433 TONNES ( A HUGE INCREASE FROM 10.6)

42,548.308.00 PLEDGED APRIL 3/2020: SCOTIA: 1.3234 tonnes

deleted Int. Delaware pledge July 7 (600 tonnes)

277,934.09 oz (some deleted august 3) JPM 8.644 TONNES

610,238.285 oz pledged June 12/2020 Brinks/ July 2/July 21 19.017 tonnes

67,289.041 oz Pledged August 21/regular account 2.092 tonnes JPM

total pledged gold: 1,590,658.551 oz 49.476 tonnes

total registered, pledged and eligible (customer) gold 37,753,932.084 oz 1,174.30 tonnes (INCLUDES 4 GC GOLD)

total 4 GC gold: 126.34 tonnes

total gold net of 4 GC: 1047.96 tonnes

end

I have compiled data with respect to registered (or dealer) gold taken on first day notice for each of the past 24 months

The data begins on first day notice for the May month taken on the last day of July 2018. and it continues to present day.

I then took, how many deliveries were recorded by the CME for each and every month. I also included for reference the price of gold on first day notice.

The first graph is a logarithmic graph and the second graph, linear.

You can see the huge explosion of registered gold at the comex along with deliveries.

THE GOLD COMEX SEEMS TO BE UNDER SEVERE ASSAULT FOR PHYSICAL

And now for the wild silver comex results

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory |

nil oz

|

| Deposits to the Dealer Inventory |

nil oz

|

| Deposits to the Customer Inventory |

nil oz

|

| No of oz served today (contracts) |

49

CONTRACT(S)

(245,000 OZ)

|

| No of oz to be served (notices) |

97 contracts

485,000 oz)

|

| Total monthly oz silver served (contracts) | 1994 contracts9970,,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

Goldman Sachs: Dump Dollars, Buy Silver

Sell dollars and buy silver. That’s Goldman Sachs’ recommendation.

Peter Schiff has been warning about a dollar collapse and now the mainstream is even getting bearish on the dollar.

In response to the economic shutdowns imposed by governments to deal with the coronavirus pandemic, the Federal Reserve is printing money to infinity and beyond. On top of that, it has shifted its inflation targeting to allow inflation to run hot meaning there is no end in sight to the currency debasement. This is bearish for the dollar and an article published by Reuters last month quoted a number of mainstream analysts talking about “dollar woes.”

Goldman Sachs has jumped on that bandwagon, saying in a recent report that “the risks are skewed toward dollar weakness.” Analysts see an increasing likelihood of a Biden victory in the upcoming election.

A ‘blue wave’ US election and favorable news on the vaccine timeline could return the trade-weighted dollar and DXY index to their 2018 lows.”

Goldman sees broad-based dollar weakness and recommended shorting the greenback against the Mexican peso, South African rand and Indian rupee. It is also advised buying the euro, along with both Canadian and Australian dollars against the US dollar.

During his speech at the Money Show in August, Peter Schiff said the government is trying to replace the economy with a money printing press and he warned that a dollar crisis is looming.

The dollar is going to fall through the floor and inflation is going to ravish the United States. What’s about to happen is that the world is going to go off the dollar standard and go back to the gold standard. That is where we are headed.”

Keep in mind, dollar weakness is also bullish for both gold and silver.

In a separate report, Goldman analyst Mikhail Sprogis said recommended buying silver. He said the white metal is “an obvious beneficiary” of the global move toward solar energy.

Silver is a vital component in the solar energy sector and solar power generation is expected to nearly double by 2025. A report by the Silver Institute earlier this year projected that a combination of global efforts to reduce fossil fuel reliance, legislation to lower carbon emissions, and favorable government tax policies, should result in a continued expansion of solar panel installations over the next decade. A recent report from the World Bank forecasts that by 2050, consumption of silver in energy technologies could grow dramatically, reaching a level equivalent to more than 50% of current total silver demand; the largest proportion for any non-battery metal.

“Now, with silver at $24/toz and a few potential upward solar surprises in the coming months, we reopen the trade,” Sprogis wrote.

According to the Goldman report, global solar installations are projected to rise by 50% between 2019 and 2023. But Sprogis said we could see “upward solar surprises” from that base-case scenario, including the US and China extending their solar installations plans. And if Biden wins, he has a plan to proceed with 500 million new solar panels in the US over the next five years. That could lead to a rise of 15% in global solar installations.

Silver is coming off its best quarter since 2010 and the fundamentals indicate there is still plenty of upside.

On the supply side, mine output fell precipitously with the COVID-19 economic lockdown. Many major mines were forced to shut down due to the pandemic. Analysts at the Silver Institute say they expect mine supply to continue its four-year slide. Even with most mines back online, the institute projects a 7% decline in mine output this year. Global mine production fell by 1.3% in 2019.

Looking at the big picture, the biggest driver for precious metals continues to be Federal Reserve monetary policy. In order to turn bearish on gold and silver, you have to believe the Federal Reserve is actually going to tighten monetary policy and the dollar is going to remain strong. Both of these prospects seem pretty implausible. Even the mainstream is starting to see it.

end

https://www.jsmineset.com/2020/10/16/precious-metal-bull-riders-at-the-ready/

Precious Metal Bull Riders At The Ready!

Posted October 16th, 2020 at 8:45 AM (CST) by J. Johnson & filed under General Editorial.

Great and Wonderful Friday Morning Folks,

Gold is up $4.30 with the last trade at $1,913.20, close to the London high at $1,917.90 with the low at $1,906.50. Silver is up a percent with the trade at $24.495, gaining 28.6 cents, it too, close to the high at $24.59 with the low not that far away at $24.25. The US Dollar, refuses to do anything, even when our election news and accusations, gets corralled by Google, Twitter, Facebook, and Youtube, with the trade at 93.67, down 19.4 points and close to the low at 93.635 with the high at 93.885. Yes, all this happened overnight, before the Comex open, the London close, and before the liability clause, used to protect the big tech companies, which is now up for review, by the supreme court, is decided upon. It appears that these big tech companies have “hidden” real news from the American voters, including Hillary’s email’s and the Wiener laptop evidence. Yet somehow, the truth is sought and found.

Precious Metals prices have reversed everywhere! In Venezuela, the noble metal gained 131.84 with the last price at 19,108.09 Bolivar, Silver is up as well with the last trade at 244.644 Bolivar, gaining 4.844 in the early morning. Argentina’s Peso price for Gold is now at 148,220.35, a gain of 1,164.09 A-Peso’s with Silver gaining 39.04 A-Peso’s with the last trade at 1,897.52. Over in Europe, the Turkish Lira’s price for Gold last traded at 15,198.81, proving a gain of 118.33 T-Lira’s overnight with Silver adding 4.015 with the last trade at 194.588 T-Lira.

October Silver’s Delivery Demands now has a total of 146 contracts waiting for receipts and with a Volume of 83 already up on the board, during London’s time, with the trading range between $24.26 and $24.23 with the last swap at $24.255, up 6.2 cents so far today. Yesterday’s physical draw had a total of 16 contracts swapping hands with no price again, yet Comex closed the delivery day out at $24.193, a gain of 6.2 cents. This makes 3 days in a row that there was no trading range, yet we see all these no price swaps totaling 132 contracts, and as the count is reduced by 6 from yesterday’s post. Silver’s Overall Open Interest lost 1,254 shorts against the physicals leaving a total of 156,884 Overnighters to hold the prices in place.

October Gold’s Delivery Demands now has a post of 1,736 fully paid for contracts waiting for receipts and with no Volume so far this morning. Yesterday’s full Comex/ICE trades had a total of 254 contracts swapping hands between $1,906.30 and $1,889.60 with the Comex Calculated Close at $1,903.20, a gain of $1.90. Of note, the last 221 Resolute purchases, happened really close to the ICE close, which increased the demand count by 40 contracts after some FIFO receipts were given out. The fear is right here as Gold’s Overall Open Interest proves 7,050 more short contracts had to be re-added in order to keep Gold up just a little, while the Resolute Buyers stepped in, giving this morning’s paper total at 557,589 short contracts to go against the physicals.

Last night was supposed to be the second presidential debate, which many believe, there would be no way Biden could compete, without the help of an earpiece. The Chris Wallace bias made the last show spectacularly obvious, since then Trump and team got the bug and got cured, then Team Biden gets sick and won’t compete because their science says there’s no cure. At least that’s their story, and they are sticking with it.

The presidential debate deciders had picked Steve Scully to direct the next show. Alas, he used to be a 30-year C(rime)-SPAN veteran until recently, then he got caught lying about how his twitter account got hacked, and proves he is another one of those, “anyone else but Trump” supporters. No bias here at all huh? Now the cherry on top happened yesterday, when the news came out about Facebook and Twitter censoring the Biden Bombshells, just weeks after the executives joined the Biden Transition Team.

Of course, counter-news-Q had posted a quote yesterday, from Chanel Rion, Chief White House Correspondent for One America News Network; “Just saw for myself a behind the scenes look at the #HunterBiden hard drive: Drugs, underage obsessions, power deals…Druggie Hunter makes Anthony Weiner’s down-under selfie addiction look normal. #BidenCrimeFamily has a lot of apologizing to do. So does Big Tech.

With all this going on, the US Dollar, and our Treasuries, ain’t bucking their writer’s. How much political and monetary pressure is being applied to keep our precious metals riders from riding the bull, already staged, and ready to be released, from the bulls shoot and that 8 second ride of a lifetime? Even our friends at SGT Report, got shut down by Youtube, which just recently became part of the Biden Transition Team, owned by Google. Why is all this happening during the last weeks of the election, and why are the markets not reacting to all this? Or is it, and we just can’t see it because of all the obstructions going on right now?

Have a great weekend, and get out there and vote, in person. How much longer the prices stay in place is anyone’s guess. Yet, to have and to hold, will be proven once again, to be the life line in your personal economy, while the world’s economy gets bucked. Get more while you can, enjoy every moment and find the humor in everything. It will keep you sane in an insane world, maybe. As always …

Stay Strong!

Jeremiah Johnson

More J.Johnson content is available with purchase of a JSMineset subscription.

end

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

March 4.2019

Parker City News

JP Morgan faces potential class action lawsuit after guilty pleas by a former metals trader

Traders from across the U.S. are banding together to accuse J. P. Morgan Chase of manipulating precious metals markets for years.

At least six lawsuits, all making similar allegations against the nation‘s largest bank, have been filed in New York federal court in the past month, since federal prosecutors in Connecticut with a former J. P. Morgan Chase metals trader.

The cases could potentially include thousands of people who traded in the precious metals market. The White Plains, N.Y., law firm Lowey Dannenberg is asking the court to combine the cases and name it as the lead.

The law firm‘s commodities group is led by Vincent Briganti, the attorney who filed the first lawsuit on behalf of Dominick Cognata, a New York resident who alleges he suffered losses due to J. P. Morgan‘s trading conduct in the silver and gold futures and options markets.

A combined case, seeking class action status, would include anyone who purchased or sold futures contracts or an option on NYMEX platinum or palladium or COMEX silver or gold between at least Jan. 1, 2009, and Dec. 31, 2015. The lawyers believe that “at least hundreds, if not thousands” of traders would be eligible to join the case.

Named as defendants in all of the lawsuits are John Edmonds, a 36-year old former metals trader at J. P. Morgan, a group of yet-to-be-identified precious metals traders and the bank.

Edmonds, a New York resident, pleaded guilty in October to one count of conspiracy to defraud the market and manipulate prices of precious metals futures contracts and one count of commodities fraud. In the criminal plea, Edmonds admitted that he and other “unnamed co- conspirators” at J. P. Morgan, fraudulently manipulated precious metals markets from 2009 to 2015, the same time frame covered in the class action suits.

Briganti filed the initial class action on Nov. 7, just one day after the Justice Department unsealed Edmonds‘ plea in the U.S. District Court of Connecticut.

Edmonds admitted in his guilty plea that he deployed the illegal trading scheme hundreds of times with the direct knowledge and consent of his immediate supervisors. Plaintiffs say they have suffered economic injury, including monetary losses, as a direct result of actions by Edmonds and the other unnamed J. P. Morgan metals traders in the futures and options contracts.

One of the suits alleges that “the number of unlawful trades that JP Morgan traders executed in precious metals futures markets is at least in the thousands.”

J. P. Morgan declined to comment. Lowey Dannenberg did not respond to a request for comment by CNBC.

The Justice Department‘s criminal investigation is still ongoing and recently caused a separate related civil case to be put on hold for at least six months while the government continues its investigation. That civil lawsuit, which also accuses J. P. Morgan of rigging the precious metals market, was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders.

After reviewing the details of the plea agreement, David Kovel, the attorney for Shak‘s suit, sought to re- interview Edmonds, along with two other current and former senior traders at the bank. However, the government argued that reopening questioning would be detrimental to the ongoing criminal investigation. The federal judge overseeing the proceedings ordered a six-month stay in the civil case.

Kovel declined to comment.

Edmonds was originally scheduled to be sentenced in Hartford, Conn., on Wednesday, Dec. 19, but a court filing on Nov. 27 shows the sentencing has been postponed until June. A spokesman for the U.S. Attorney for Connecticut could not elaborate on why the sentencing was postponed since the court filing is under seal.

-END-

Futures Flat On Stalled Stimulus, Europe Elevated On Earnings

US equity futures were modestly green in a quiet overnight session, as optimism about a fresh stimulus package collapsed, while investors assess the potential return of lockdowns in Europe as the region struggles to contain the virus spread. S&P 500 futures were little changed, while Nasdaq contracts rose 0.2%. Eminis were up 0.2% to 3,482 boosted by Boeing and Pfizer shares (see below) which helped push futures on the S&P 500 and Dow Jones Industrial Average into the green after they drifted most of the day. Treasuries held gains, while the dollar slipped with crude oil.

PFizer shares rose 1% in premarket trading after it said it would file for U.S. emergency approval of its COVID-19 vaccine candidate being developed along with Germany’s BioNTech as soon as a safety milestone is achieved in the third week of November. BioNTech’s U.S.-listed shares jumped 2.4%. There was also a revival of trade war concerns, after the European Union and the U.S. exchanged tariff threats this week regarding illegal state aid for Boeing. Separately, the planemaker’s stock was up in pre-market trading after the company’s 737 Max model was judged safe to fly by Europe’s aviation regulator.

On the stimulus front, Treasury Secretary Steven Mnuchin told House Speaker Nancy Pelosi Thursday that President Donald Trump would personally lobby to get reluctant Senate Republicans behind any stimulus deal they reach. However, Senate Majority Leader Mitch McConnell rejected that, saying he could not sell a much larger package to his members, and that the Senate would vote on a narrow stimulus plan worth about $500 billion next week. In short: no deal until after the election, precisely as we have been saying since August.

“It’s a tug-of-war between risks that are well flagged, the pandemic, the U.S. election, Brexit, and at the same time hope that these same risks can be resolved in matter of weeks or months”, said Emmanuel Cau, head of European equity strategy at Barclays. “In the meantime, it’s hard for investors to take positions on the short term given all the uncertainties,” he said. “Looking forward to 2021, there’s a good probability these risks will be behind us.”

In Europe, the benchmark Stoxx 600 Index rose as much as 1% but was still set for a weekly loss after European stocks lost over 2% on Thursday as new social restrictions in Europe, including a curfew in major French cities and tighter restrictions in London, spooked investors. Positive corporate newsflow outweighed concerns over rising coronavirus cases and the state of progress in Brexit trade talks. Car sales surprised to the upside, while Daimler and LVMH both beat estimates, and Thyssenkrupp surged after Liberty Steel Group said it will make a multibillion-euro bid for the German company’s European steel unit.

Earlier in the session, the MSCI Asia Pacific Index slipped 0.2% led by the industrials and IT sectors. Markets in the region were mixed, with Thailand’s SET and Japan’s Topix falling, while Hong Kong’s Hang Seng Index and India’s S&P BSE Sensex Index increased. The Topix lost 0.9%, with Toyota and Sony contributing the most to the move. The Shanghai Composite Index rose 0.1%, driven by China Life and ICBC.

Brexit was in focus, with U.K. Prime Minister Boris Johnson saying the U.K. will now get ready to leave the European Union’s single market and customs union without a new free trade deal in place, blaming the bloc for refusing to offer good enough terms. He said he would always be willing to hear from the EU if the bloc’s leaders came back to the U.K. with “a fundamental change of approach.” Last month, the British leader set a deadline of Oct. 15 for an agreement to be struck — or clearly within sight — saying there would be no point continuing talks beyond this week without adequate progress. Sterling fluctuated on the news.

Elsewhere in FX, the euro also regained some ground, rising about 0.2% to $1.1731 as investors shifted from perceived safe havens such as the dollar and the yen to riskier currencies.

In rates, Treasuries extended advance in early U.S. session following bigger rally in gilts after U.K. Prime minister Boris Johnson said the country should prepare for Australian-style trade terms with the EU after Brexit negotiations failed to produce an alternative. Gilts spiked to session highs, lifting Treasuries. Treasury yields are richer by 0.5bp to 1.5bp across the curve in bull-flattening move; 10-year yields lower by 1bp at 0.722% with both gilts and bunds outperforming by ~1bp. Germany’s 10-year bond yield was set for its biggest weekly drop since August as doubts grew about the economic recovery in the euro zone.

In commodities, oil prices continued to slide, dragged down by concerns that resurgent COVID-19 cases in Europe and the United States would curtail demand. Brent crude futures for December dropped 0.5% to $42.65 a barrel. WTI crude futures for November delivery dipped 0.4%, to $40.81 a barrel. Spot gold prices were flat at $1,909.05 but looked set for their first weekly drop in three.

Macro-economic data to watch include retail sales, industrial production and University of Michigan Confidence, while Bank of New York Mellon, Citizens Financial, JB Hunt, Kansas City Southern, Schlumberger NV, State Street, VF Corp are among companies reporting earnings

Market Snapshot

- S&P 500 futures up 0.1% to 3,479.50

- STOXX Europe 600 up 0.7% to 365.50

- MXAP down 0.3% to 174.47

- MXAPJ unchanged at 579.29

- Nikkei down 0.4% to 23,410.63

- Topix down 0.9% to 1,617.69

- Hang Seng Index up 0.9% to 24,386.79

- Shanghai Composite up 0.1% to 3,336.36

- Sensex up 0.8% to 40,038.80

- Australia S&P/ASX 200 down 0.5% to 6,176.79

- Kospi down 0.8% to 2,341.53

- Brent futures down 0.6% to $42.92/bbl

- Gold spot little changed at $1,909.72

- U.S. Dollar Index down 0.2% to 93.69

- German 10Y yield fell 1.2 bps to -0.622%

- Euro up 0.05% to $1.1714

- Italian 10Y yield rose 4.0 bps to 0.495%

- Spanish 10Y yield unchanged at 0.148%

Top Overnight News from Bloomberg

- Italy’s government is assessing its environmental funding needs, taking an initial step toward selling its first green bond, according to people familiar with the decision

- Chinese police have launched an investigation linked to cryptocurrency exchange giant OKEx, forcing one of the world’s largest Bitcoin trading platforms to block users globally from withdrawing money

- Treasury Secretary Steven Mnuchin told House Speaker Nancy Pelosi Thursday that President Donald Trump will personally lobby to get reluctant Senate Republicans behind any stimulus deal they reach

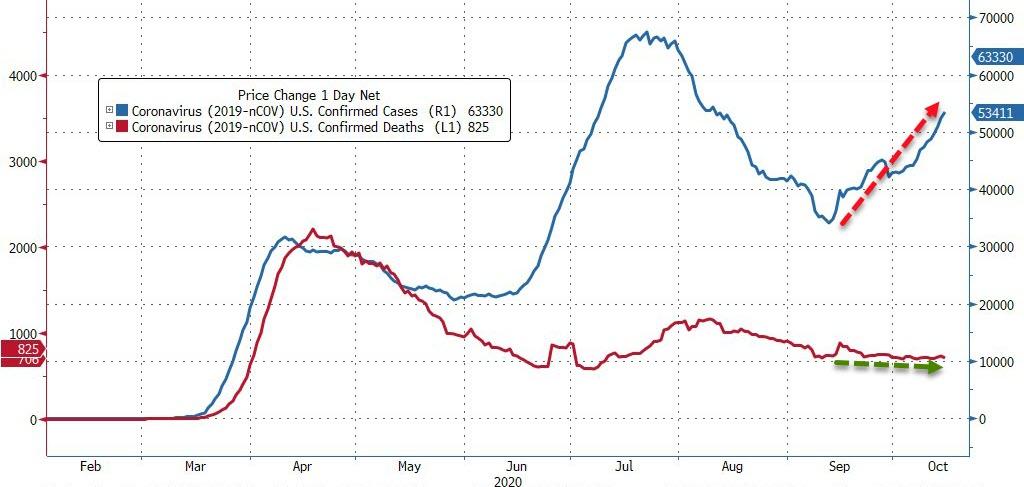

- Covid-19 is hitting the most populous states in the U.S. Midwest, with cases surging in Illinois, Ohio and Michigan. Europe continued to report some of the highest numbers of cases since spring. Remdesivir has no definite effect on a hospitalized patient’s chances of survival, a clinical trial by the World Health Organization found

- In dueling town halls, President Donald Trump embraced controversial conspiracy theories and sparred with the moderator, while Democrat Joe Biden offered policy-focused answers aimed at avoiding anything that could imperil his lead in the polls

- Oil headed lower in Asian trading as the prospect of a resurgent virus forcing more stay-at-home measures in Europe and the U.S. outweighed a bigger-than-expected drop in American stockpiles

- The U.S. will “strike much harder” if the European Union goes ahead with tariffs on $4 billion worth of American products, President Trump said

- New Zealand Prime Minister Jacinda Ardern looks set for a resounding election victory on Saturday as voters applaud her masterful handling of the coronavirus pandemic

A look at global markets courtesy of NewsSquawk

Asia-Pac equities traded mostly lower following a string of lacklustre cash opens, and after another downbeat handover from Wall Street, where the major indices posted a third consecutive down-day as pre-election stimulus hopes fizzle out and with parts of Europe reimposing targeted COVID-19 restrictions amid the resurgence of the virus. European and US equity futures drifted higher throughout most of the night before erasing the bulk of their gains heading into the European open and with no specific news flow driving price action. ASX200 (-0.5%) was flat for a large part of the session as strength in financials were countered by a weak performance across travel and leisure names, whilst concerns mounted over Australia’s deteriorating relationship with China. Nikkei 225 (-0.4%) was caged in a tight band for most of the session and losses accelerated after a downside breach of the 23,500 level, but Fast Retailing shares rose some 4.5% at one point despite revenue and profits declining in the 12-months ending August, as same-store-sales rebounded over 20% in Q4 which drove expectations for a FY21 recovery. KOSPI (-0.8%) remained in negative territory with participants pinning the losses on virus woes. Shanghai Comp. (+0.1%) opened with modest gains as the PBoC underwent another liquidity injection via 7-day reverse repos at a maintained rate, but the index later erased gains with reports also resurfacing that China is set to pass a new law that would restrict sensitive exports vital to national security. Hang Seng (+0.5%) outperformed in a reversal from yesterday’s sub-par performance, and as SMIC shares opened higher by 6% after a guidance upgrade. Finally, 10yr JGB futures firmed overnight before waning off best levels as it tracked USTs.

Top Asian News

- Singapore-Hong Kong Air Fares Jump 40% on Travel Bubble Plan

- Billionaire Lucio Tan’s Bank Expects Bad-Loan Provisions to Drop

- China Drug Stock Jumps After Doctor Endorses Treatment for Covid

- Thai Leaders Have No Easy Options to End Anti-Monarchy Protests

European equities (Eurostoxx 50 +1.0%) trade on a firmer footing in what appears to be more a trimming of yesterday’s heavy losses rather than an outright pick-up in sentiment across the region as incremental macro newsflow remains light. The CAC 40 (+1.3%) has outperformed from the get-go following LVMH’s (+6.4%) Q3 update which saw the Co. exceed revenue expectations citing strong performance in the US and China; Kering (+3.8%), Burberry (+3.0%) and Christian Dior (+7.3%) trade higher in sympathy with the consumer discretionary sector the clear outperformer. Elsewhere, it’s been a session of solid gains thus far for the auto sector with Daimler (+3.4%) leading the charge after its prelim Q3 EBIT exceeded market expectations and the Co. stating that it has seen a faster than expected market recovery and a particularly strong September performance. Furthermore, Renault (+3.8%) have also been supported amid reports the Co. is intending to launch a range of electric vehicles targeting ‘middle class’ consumers, whilst its CEO said the Co. does not have a liquidity problem. Additionally, for the sector, some positivity was garnered from the latest EU27 car registrations which rose 3.1% in September (prev. -18.1%). In terms of stocks specifics, Thyssenkrupp (+15.0%) are a clear standout performer today after Liberty House announced a bid for the Co’s steel operations. Subsequently, the IG Metall Union in the German NRW state rejected Liberty Steel’s bid, suggesting that such a takeover could lead to job losses, however, it is yet to be seen if their objections will be enough to derail the acquisition. To the downside, BT (-1.8%) have hampered the performance of the telecom sector today amid ongoing scepticism suggesting that PM Johnson’s pledge to connect the country to fast broadband by 2025 is considered to be unrealistic.

Top European News

- LVMH Bounces Back on Demand for Louis Vuitton and Dior Bags

- Thyssenkrupp Jumps as Gupta’s Liberty Said to Bid for Steel Unit

- Europe Car Sales Rise 1.1% in Surprise First Gain of the Year

- Daimler, Volvo Post Surprise Profits on Shaky Auto Reprieve

In FX, positive vibes from both sides of the UK-EU divide ahead of the final day of the Summit have given Sterling a lift as chances of clinching a trade deal are kept alive, with Cable back on the 1.2900 handle and Eur/Gbp backing off from the high 0.9000s after Foreign Minister Raab claimed that negotiators are close to agreement and the Irish PM said Barnier has been granted the flexibility to continue discussions. However, PM Johnson still has the final say and there is little sign of compromise on the well documented key issues that stand in the way of an accord so the bar remains high and Pound prone to further disappointment, while Moody’s ratings review after hours also poses a threat to sentiment.

- USD – Brexit aside, the broad risk tone has settled down to dampen some demand for the Dollar and major pairs have reverted to more restrained ranges as a result, as the DXY retreats from highs just shy of Thursday’s 93.910 peak within a 93.883-665 range. The pullback may also be partly psychological and consolidative ahead of primary US data in the form of retail sales and ip before 2 Fed speakers (Williams and Bullard) and preliminary Michigan sentiment, while a firm rebound in the YUAN is also likely to be weighing on the Greenback more generally given the Cny and Cnh both reclaiming 6.7000+ status.

- JPY/NZD – The Yen and Kiwi are benefiting from the waning Buck, with the former back above 105.50 and flanked by decent option expiry interest (3 bn between 105.00-05 and 1.2 bn from 105.35 to 105.40), and the latter pivoting 0.6600 in the run up to NZ elections and getting regional support from favourable Aud/Nzd crosswinds.

- EUR/CAD/CHF/AUD – All narrowly mixed vs their US counterpart as the Euro keeps tabs on 1.1700, just, Loonie paring losses from sub-1.3260 towards 1.3200 in advance of Canadian manufacturing sales and less of a drag via crude prices. Elsewhere, the Franc is straddling 0.9150 again and Aussie underperforming below 0.7100 and the 100 DMA (0.7096) in wake of more worrying reports on the Chinese trade front as cotton exports are said to be added to the embargo list and could be subject to tariffs as big as 40%.

- SCANDI/EM – Further divergence between the Sek and underperforming Nok even though oil is attempting to stabilise and Riksbank’s Ingves may cover exchange rate moves during a speech at the IMF, but the Zar appears content with Gold’s recovery to trade above Usd 1900/oz, albeit by only a few bucks. Conversely, the Brl could be vulnerable following the latest political antics and the resignation of Brazilian President Bolsonaro’s Deputy Senate leader who was caught by police concealing COVID aid funds in his underwear.

In commodities, WTI and Brent front month futures are modestly subdued this morning diverging somewhat from the modestly firmer performance seen in European bourses, with US futures relatively flat; focus for the complex has returned to the supply-side given updates in Libya. Crude production for the country is now said to have hit 500k BPD displaying a significant rise from the October 5th figure of 290k BPD; the increase comes alongside the El Sharara field getting back to around 110k BPD capacity but still someway from the 300k BPD capacity the field is targeting in the near-term. The production increase will likely draw the focus of OPEC’s JMMC gathering on October 19th, among other factors including compliance and plans for the OPEC+ demand schedule, particularly as while the Libyan supply has substantially increased it is still someway off Q4-2019’s figure of circa 1.2mln BPD. Elsewhere, the schedule for crude explicitly is light aside from the usual Baker Hughes rig count. Moving to metals, spot gold is essentially flat on the day residing within comparatively tight ranges of USD 10/oz; given the lack of fundamental newsflow the driver for the metal is once again the USD which is similarly exhibiting lacklustre and range-bound action. Regarding copper, ING highlight that discussions at the Candelaria mine in Chile are still unresolved, regarded as one of the largest copper reserves in the world, and the most recent updates indicate that strike action could still occur next week.

US Event Calendar

- 8:30am: Retail Sales Advance MoM, est. 0.8%, prior 0.6%; Ex Auto MoM, est. 0.4%, prior 0.7%

- 8:30am: Retail Sales Control Group, est. 0.3%, prior -0.1%

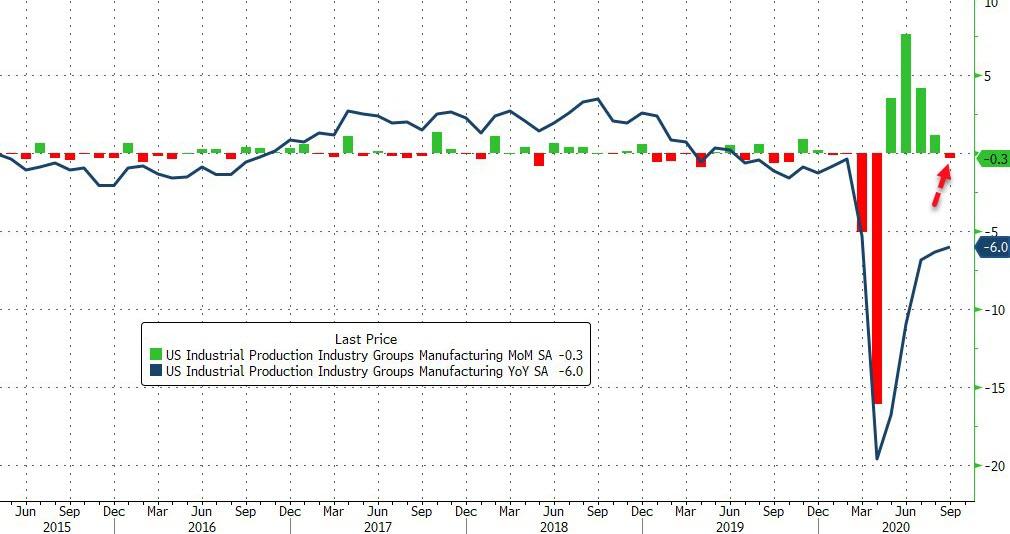

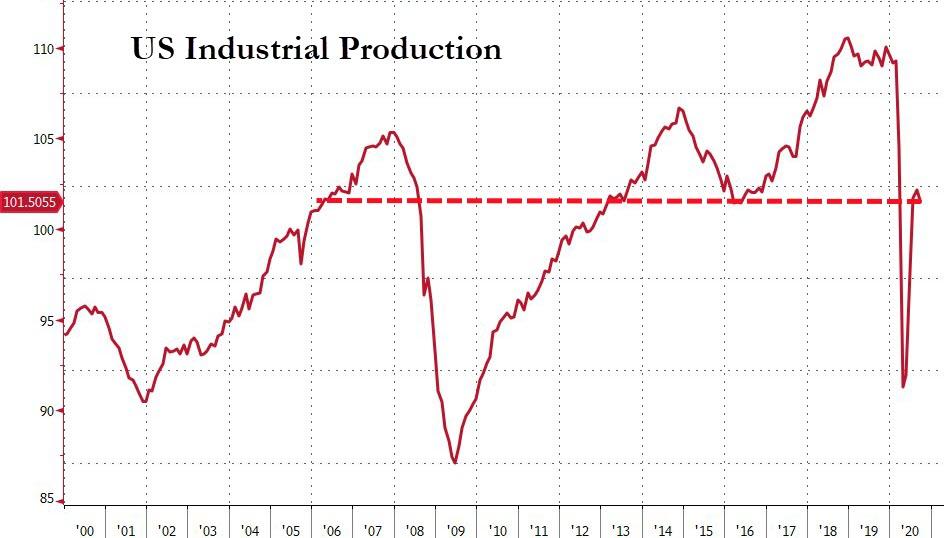

- 9:15am: Industrial Production MoM, est. 0.5%, prior 0.4%; Capacity Utilization, est. 71.8%, prior 71.4%

- 9:15am: Manufacturing (SIC) Production, est. 0.6%, prior 1.0%

- 10am: Business Inventories, est. 0.4%, prior 0.1%

- 10am: U. of Mich. Sentiment, est. 80.5, prior 80.4; Current Conditions, est. 88.5, prior 87.8; Expectations, est. 77, prior 75.6

- 4pm: Net Long-term TIC Flows

DB’s Jim Reid concludes the overnight wrap

It’s the last day of this half term today and the school are allowing the children to come as their favourite book character. As much as my wife has tried to persuade our 5 year old Maisie to go as her own book heroines Lizzy Bennet from Pride and Prejudice or Jane Eyre, Maisie will only go as one thing. Elsa from Frozen. I said to her that Frozen is not a book and she ran to the shelf and showed me a Frozen 2 sticker and colouring in book. So who am I to argue. Hopefully this will pass the school’s no superheroes policy. By the way I wanted her to go as Arya Stark.

Talking of the Starks, winter was coming for a large part of yesterday (virus numbers, weak data, lack of stimulus) before a bit of dragon breath warmed things up late in the session. European equities earlier saw major declines as governments across the continent moved to ramp up restrictions, with the STOXX 600 (-2.08%), the DAX (-2.49%) and the CAC 40 (-2.11%) all moving lower. The US however regained its footing and only closed -0.15% having recovered from being down as much as -1.37% in the early moments of trading yesterday and around -0.75% as Europe went home. Tech (-0.44%) and biotech (-1.69%) stocks were among the largest laggards on the day with the NASDAQ falling -0.47%, although it also rebounded from large early losses (-1.78%). Meanwhile the VIX index of volatility gained +0.57pts to its highest level in a week, having risen every day this week.

The main driver behind the declines was the pandemic, with yesterday seeing a number of further concerning developments for investors to digest. In terms of the numbers, Europe continued to move in the wrong direction, with Italy reporting another record of 8,803 cases, raising fears that the country is moving in a similar direction to France and the UK, while the Netherlands also reported a record 7,857 cases which given its population is just under 30% of Italy’s, is a big number. See the per 10k number in the table below. France saw over 30k new cases, a record that eclipses the previous high of nearly 27k this past Saturday. Germany also saw a record number of infections, with the 7,185 new cases surpassing the previous peak in late March (pre mass testing). This comes as reports indicate that Chancellor Merkel is concerned that the new restrictions agreed to by the regional leaders do not go far enough. In the UK, a further 18,996 cases were confirmed as the government raised the London alert level to high, meaning that residents can no longer mix with other households indoors from tomorrow. Over in Poland, further restrictions were also imposed, while at the summit of EU leaders in Brussels (more on which below), Commission President Ursula von der Leyen went into self-isolation (again) after she was informed that a member of her front office had tested positive that morning.In better news overnight, Reuters has reported that Britain’s National Health Service is in talks with groups including the British Medical Association about mobilising for a potential rollout of a Covid-19 vaccine by December. The report added that there is c. a 50/50 chance that the vaccine can begin to be administered that month.

Over in the US, cases continue to rise throughout the Midwest with Illinois, Ohio and Michigan all approaching new case levels comparable with the height of their first waves – albeit at much higher testing levels. With Ohio, Michigan and Wisconsin all potential swing states the effects on next month’s election will be closely followed. The main Covid news came from the Biden campaign, where VP nominee Kamala Harris cancelled her travel plans until Monday after communications director along with a member of her flight crew tested positive. We’re told that Harris herself tested negative on Wednesday, but that travel was stopped “out of an abundance of caution”. Neither of the positive individuals were in contact with Biden however, and both he and President Trump went ahead with their separately planned town hall events last night in lieu of the debate that was otherwise supposed to have taken place.

Staying on US politics, President Trump said yesterday that he would be open to increasing the $1.8 trillion stimulus bill that he had pushed in the past. It was also reported that House Speaker Pelosi and Secretary Mnuchin continue to discuss potential deals though nothing remains likely to pass in the short term. This is especially true after Senate Majority leader McConnell said that his planned $500 billion bill is “appropriate” and rejected calls for higher levels of funding. Markets took this in its stride, but if Democrats do win the White House but are unable to take back the Senate it may call into question just how much stimulus could be passed in the next 6 months and beyond. Meanwhile, Treasury Secretary Mnuchin has told Pelosi overnight that President Trump will personally lobby to get reluctant Senate Republicans behind any stimulus deal they reach.

Asian markets are largely trading lower this morning outside of the Hang Seng (+0.78%) which is up. The Nikkei (-0.26%), Shanghai Comp (-0.28%), Kospi ( -0.85%) and Asx (-0.41%) are all down. Meanwhile, European futures are pointing to a positive open after the late US rally with those on the Stoxx 50 (+0.60%), FTSE 100 (+0.72%) and Dax (+0.59%) all up. Across the other side of Atlantic, S&P 500 futures are trading broadly flat while those on Nasdaq are down -0.16%. Elsewhere, crude oil prices are down c. -1%.

Brexit was back in the headlines yesterday, as EU leaders agreed at their summit to continue negotiations with the UK over the coming weeks, calling on the UK to “make the necessary moves to make an agreement possible.” The UK’s chief negotiator Frost said he was “surprised by suggestion that to get an agreement all future moves must come from U.K. It’s an unusual approach to conducting a negotiation.” The UK have said they’ll set out their next steps following the Council, so we await to see what’s said and whether they decide to continue negotiating or more likely on what terms. Prime Minister Johnson is planning a statement later today.

Over in sovereign bond markets, southern Europe saw a noticeable selloff yesterday, in line with the broader risk-off move elsewhere. Italian debt saw its remarkable rally come to an end, as 10yr yields came off their record low the previous day to close +4.0bps, while Greek (+5.5bps) and Spanish (+1.4bps) yields also rose. With risk assets rallying back towards flat in the US, core countries diverged with 10yr bund yields down -2.9bps at -0.61%, their lowest level since March, as US Treasuries saw a +0.7bps move to 0.732%. Other safe havens made gains yesterday, with the US dollar index up (+0.51%) for the third day this week, while gold prices were up +0.38% to finish over $1900/oz.

In the US, the latest weekly initial jobless claims for the week through October 10 showed an unexpected uptick to 898k (vs. 825k expected), which was its highest level in 7 weeks. The reading will only add to concerns that the labour market recovery is running out of steam, not least with the lack of further stimulus and fresh rises in the number of Covid cases. Otherwise, the Empire State manufacturing survey fell to 10.5 (vs. 14 expected), while the Philadelphia Fed’s business outlook survey rose to 32.3 (vs. 14.8 expected) – the highest since February.

To the day ahead now, and the data releases out from the US include September’s retail sales, industrial production and capacity utilisation, as well as the preliminary University of Michigan sentiment indicator for October. In the Euro Area, there’ll also be the trade balance for August and the final CPI reading for September. Otherwise, central bank speakers include the Fed’s Williams and Bullard, and earnings releases include Honeywell International and BNY Mellon. Finally, the European Council will conclude.

3A/ASIAN AFFAIRS

i)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED UP 4.18 PTS OR .13% //Hang Sang CLOSED UP 228.25 PTS OR .94% /The Nikkei closed DOWN 96.60 POINTS OR 0.41%//Australia’s all ordinaires CLOSED DOWN 0.45%

/Chinese yuan (ONSHORE) closed /Oil UP TO 40.60 dollars per barrel for WTI and 42.75 for Brent. Stocks in Europe OPENED ALL GREEN// ONSHORE YUAN CLOSED UP 6.6983 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.6919 TRADE TALKS STALL//YUAN LEVELS //TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED//CORONAVIRUS/PANDEMIC/TRUMP TESTS POSITIVE FOR COVID 19 : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3 a./NORTH KOREA/ SOUTH KOREA

South Korea

b) REPORT ON JAPAN

3 C CHINA

CHINA/USA/AUSTRALIA

China tells its local mills to stop using Australian cotton and iron ore

They will wait until the election is over to seee if Biden wins

(zerohedge0

China Tells Local Mills To Stop Using Australian Cotton, Ore

While the rapid deterioration in diplomatic relations between the US and China has been put on hiatus until after the election, at which point Beijing hopes that a Biden administration would promptly restore amicable relations between Beijing and DC, trade relations within the Pacific Rim region are getting worse by the day, with nobody getting more impacted by China’s desire to flex its muscles than Australia: escalating bilateral tensions have resulted in China’s “unofficially” asking cotton and ore traders to stop buying products from Australia.

As Rabobank’s Michael Every writes this morning, the “Australian press claim China is now no longer taking Australian cotton. It’s been all of a few days since we heard the same thing about Aussie coal, and weeks since we heard it about wine and dairy and beef and barley.”

This was confirmed by the SCMP later on Friday, which reported that The Cotton Australia and the Australian Cotton Shippers Association, in a joint statement on Friday, said that China’s National Development Reform Commission has been recently “discouraging” their spinning mills from using Australian cotton. Earlier, Beijing had also reportedly suspended ore imports from Australia.

While Australian Prime Minister Scott Morrison recently said: “It’s not uncommon for China to suspend coal imports,” Canberra is probing the latest moves by Beijing.

Adding some complexity to the passive-aggressive trade war escalation is that there has been no official confirmation from the Chinese side over the issue. Also, the bilateral tensions triggered separate investigations by Beijing into Australia’s wine export and dumping allegations.

China is one of the most important destinations for Australia’s ore and wine, while total two-way trade between China and Australia was worth around A$240 billion (US$170 billion) between July 2019 to June 2020, according to the Australian Bureau of Statistics.

The ongoing tensions were triggered after Canberra started seeking a probe into the ongoing COVID-19 pandemic, caused by the coronavirus which a Chinese whistleblower has now confirmed was created in Wuhan. Similar demands have been made by the US and other western allies of Canberra, frustrating Beijing.

The demand led the Chinese diplomats in Australia hinting at “economic coercion” of Australian goods by Chinese companies.

“The Chinese public is frustrated, dismayed and disappointed with what Australia is doing now,” Chinese Ambassador Jingye Cheng had said early in April, responding to a question on Canberra’s probe push. The Cotton Australia and the Australian Cotton Shippers Association, however, asserted that their relationship with China “is of importance to us”.

“The Australian cotton industry will continue having meaningful conversations with stakeholders to fully understand this situation, and we will continue working with the Australian government to respectfully and meaningfully engage with China to find a resolution,” the statement added.

4/EUROPEAN AFFAIRS

UK/EU

BOJO warns Britons to prepare for a no deal until their is big progress on their talks with the EU

(zerohedge)

BoJo Warns Britons “Prepare For No Deal” Brexit After EU Summit Yields Little Progress

Not even 24 hours after Brussels and London agreed to two more rounds of trade talks – one in London next week, and another in Brussels the week after – UK Prime Minister Boris Johnson told the British people that he would seek a “no-deal” Brexit unless there is a “fundamental change of approach” from the EU.

Sterling sank to a session low against the dollar as Johnson warned Britons to “get ready for no-deal”, though it quickly rebounded off its low of the day and has since been swinging around in volatile trade.

BoJo accused Brussels of failing to negotiate “seriously” as he ratcheted up the pressure for more concessions to come from the Continental side. Since it’s clear that Brussels doesn’t want a more comprehensive “Canada-style” deal, BoJo said his office would instead seek an “Australia”-style deal, a far less “comprehensive” option.

“I have to make a judgement about likely outcome…given [EU] have refused to negotiate seriously for much of the last few months and given this summit appears explicitly to rule out Canada style deal, I’ve concluded we must get ready for arrangements like Australia’s.”

“Unless there’s a fundamental change of approach, we’re going to go to the Australia solution, and we should do it with great confidence,” Johnson said.

He then warned businesses across Briton to prepare for “no deal”.

“Now is the time for our businesses, hauliers and travelers to get ready… and of course we are willing to discuss practicalities”

To be sure, BoJo said that he’d be willing to hear from Brussels if they came back with a “fundamental change of approach”. Otherwise, the UK will leave the single market and customs union without a deal on Jan 1.

Bojo’s remarks follow tweets from his lead negotiator, Lord David Frost, who expressed disappointment in the EU’s negotiating position.”

The pound’s bounce off the daily lows following the speech merely underlines the fact that many traders already expect this thing to go down to the wire, with a last-minute deal still the base case.

UK Downgraded To Aa3 By Moody’s

Three week after Fitch affirmed its long-term debt rating at AA- (and left the outlook negative), Moody’s has just downgraded United Kingdom’s (and The Bank of England’s) credit rating.

Moody’s Investors Service (“Moodys”) has today downgraded the government of the United Kingdom’s long-term issuer and senior unsecured ratings to Aa3 from Aa2. Concurrently, the outlook has changed to stable from negative.

Moody’s has also downgraded the Bank of England‘s long-term issuer and senior unsecured bond ratings to Aa3 (from Aa2) and (P)Aa3 (from (P)Aa2) for the senior unsecured MTN programme. The P-1 short-term issuer rating is affirmed. The outlook on these ratings has also changed to stable from negative.

The three key drivers for this action are closely related and mutually reinforcing…

First, the UK’s economic strength has diminished since we downgraded the rating to Aa2 in September 2017. Growth has been meaningfully weaker than expected and is likely to remain so in the future. Negative long-term structural dynamics have been exacerbated by the decision to leave the EU and by the UK’s subsequent inability to reach a trade deal with the EU that meaningfully replicates the benefits of EU membership. Growth will also be damaged by the scarring that is likely to be the legacy of the coronavirus pandemic, which has severely impacted the UK economy.

Second, the UK’s fiscal strength has eroded. General government debt, already high and sticky prior to the crisis, has risen further as a result of the pandemic. While the UK’s reserve currency status provides a high capacity to carry debt, the material increase in debt poses risks to debt affordability in future years, particularly in the absence of a clear plan to reduce government indebtedness. Notwithstanding recent statements of intent by the government, it is in Moody’s view unlikely that the government will be able meaningfully to rebuild the UK’s fiscal strength in the coming years given the low growth environment and the likely political obstacles to doing so.

The third driver relates to the weakening in the UK’s institutions and governance that Moody’s has observed in recent years, which underlies the previous two drivers. While still high, the quality of the UK’s legislative and executive institutions has diminished in recent years. Policymaking, particularly with respect to fiscal policy, has become less predictable and effective. Looking forward, the self-reinforcing combination of low potential growth and high debt in a fractious policy environment will create additional headwinds to addressing the economic, fiscal and social challenges that the UK faces.

The stable outlook reflects the UK’s intrinsic economic and institutional strengths as well as Moody’s expectations that the debt will stabilise at its current level.

For now, UK’s sovereign credit risk is not showing signs of strain, but as is clear from March, risk happens fast…

end

UK

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

AZERBAIJAN/ARMENIA

Belligerent Erdogan ( Turkey) has summoned 4,000 Syrian and Libyan militants to fight with Azerbaijan against Armenia

(AlMasdarNews)

Nearly 4,000 Syrian & Libyan Militants Are Fighting With Azerbaijan: Armenian Official

An Armenian diplomat said that about 4,000 militants loyal to Turkey from Hay’at Tahrir Al-Sham (formerly Jabhat Al-Nusra, or al-Qaeda in Syria) and the Sultan Murad Brigade arrived in Karabakh from Libya and Syria to fight alongside the Azerbaijani forces.

The former Armenian ambassador to Italy, Sarkis Gazaryan, made the public statements while present with 100 people at the sit-in organized by the Armenian community in front of the House of Representatives’ headquarters in Rome to demand an end to the “Turkish-Azerbaijani aggression”.

“The presence of these anti-Armenian jihadists is dangerous, and even more so if we take into account what the UN Secretary-General called for to stop the fighting to prevent the Covid epidemic,” the former Armenian ambassador confirmed in statements to the Italian AKI news agency.

He asked, “Where is the credibility of the policies of some European countries?”

Turkey has been accused of recruiting Syrian militants to fight against the Armenian forces in Karabakh, following their campaign in Libya.

In rare confirmation, The Wall Street Journal reported this week that “Hundreds of fighters from Syrian militias allied with Turkey have joined the fighting between Azerbaijan and Armenia over the disputed enclave of Nagorno-Karabakh, and hundreds more are preparing to go, according to two Syrians involved in the effort.”

The reported cited “A Syrian rebel involved in deployments said fighters had been traveling there since mid-September—before the latest round of clashes—in groups of up to 100 at a time.”

6.Global Issues

Bill Blain on the major topics of the day..

(Bill Blain)

Blain: Time To Sell Some Tech

Authored by Bill Blain via MorningPorridge.com,

“Tell him I’ve just worked out a completely new strategy. It’s called running away.”

Not a lot to cheer in markets this week as politics and Covid dominate the stage. The slide in European stocks highlights increasing concerns for what look likely to become a double dip Virus hit. Rising US job claims suggest it’s also going to suffer a second pandemic knockback. On the other hand, companies are still making money, the global economy pootles along and investors will see dividends from sectors having a “good pandemic” remain strong. The world is divided into winner and losers: the Occident vs Orient, Tech and Services vs Hospitality, Property and Travel.

Interesting comment from Goldman which says it’s time to buy value stocks and sell some Tech. They say is due to some mumbo-jumbo about three-four month trading patterns they observed back in the last crisis regarding reversals into cyclical shorts, but to be honest life is literally too short to read analyst’s turgid prose. I suspect most bank research is written to please compliance officers, and approved by committees to make sure no one is offended.

But the thing is – I totally agree! Time to sell some Tech.

This is time to get real about fundamental stocks, and that also means its probably time to cull Tech Stocks. Which ones though? Changes are coming. Everyone loves Tech, especially tech that’s disruptive and creates who new markets and revenue streams. But good tech spawns imitators, and as we are about to find out, Regulation. Nothing strangles new revenues as surely as regulation.

Let’s start with the Streaming Wars.

A few weeks ago I triggered another Teams storm with my suggestion Disney will win the Streaming Wars, while Netflix is doomed.. I was told it was a risky call. I stuck to my guns: competition is the critical issue. There already more streaming services than you can point a sharp, pointy stick at..

Netflix is the clear streaming leader with 32% of total streamtime viewing. It produces plenty of its own fantastic content, and has rights on plenty of other stuff that people want to see. Disney’s streaming services get a respectable 16% of streamtime, but has the advantage of a great stable of entertainment classics plus the Marvel, and Star War franchises. Its already spending more on content than Netflix. In less than 1 year Disney+ has attracted 60 million subs.

(Personally, I am mulling over a subscription for Britbox – I still haven’t seen the final episode of Blakes 7 so I still have no idea what the classic UK cheap-as-chips space opera was all about, and apparently every episode of UFO and Space 1999 is on it! Yay! Because I am a registered Apple Addict, I have Apple TV, but there frankly isn’t much to watch..)

Disney has just announced a refocus to spend more on creating new content for its streaming businesses.

It didn’t have much choice. Coronavirus has slaughtered its Parks business (down 83% from 6.6 bln in Q3 2019) and new studio business (down 55% since this time last year). What’s spectacular is that The Mouse corporation has responded fast to the challenge. The virus has shaken Disney awake. Creation, Distribution and Monetisation of content is its future.

It’s using its streaming platform well. Hamilton the Movie, only available on Disney+, was apparently a great success, but I gave up after 20 mins because She-who-is-Mrs-Blain kept asking who was who, who they were, where it was, what it was all about and why were we watching it.. (I told her: A long long time ago in a galaxy far, far away…)

Disney’s decision to launch new films direct into the Stream would probably have got more plaudits if it hadn’t been the live action version of Mulan. A controversial choice.

How many other studios will also monetise direct to the stream? The whole film industry has been pressured by Covid. (Films make a fraction of the revenues of the Home Gaming sector – which is one reason our in-house VC fund, Sure Ventures has been so successful.) Few other studios have the range of marketing opportunities Disney has to sell merchandising tat alongside their content.

As the streaming wars are fought to a bitter end, I suspect Disney will rise. What’s interesting is it will demonstrate that incumbent old businesses can weather, innovate and prosper when new disruptive technologies change the narrative. The risk for the other streamers, including Netflix, is that their tech premium reduces as competition rises and their lack of profitability dooms them to also ran status.

I reckon we will see the same thing in Electric Vehicles.

It’s the hot sector. Just this week we’ve seen a UK electric vehicle start up Arrival raise $118 mm from the private market – to build 10000 commercial vehicles a year on a “flexible skateboard model”. US EV maker Lucid is launching a luxury 480 hp model based at $78k with a 400+ mile range. Volkswagen is “accelerating” a massive capex programme to “automate and digitalise” new EV plants in the US and Germany to build batteries and new car bodies. BMW has just announced its new “5th” generation EV tech, including a home charging “wallbox” that can fill you car full of electric liters in a mere 3.5 hours. Wow… (US readers.. mild sarcasm alert.) Porsche is going a slightly different road – investing in “synthetic fuels”.

You get the drift..

Competition in the EV sector is going to pull down margins.. and probably increase the cost of lithium meaning at least one very large market-capitalisation maker of a very small number of cars is going to struggle not just with competition, but meeting promises to get the cost down and actually make real profits selling cars…. rather than regulatory credits.. Competition is real and will reduce windfall/first mover advantages and profits.

Another major issue is Regulation.

- Amazon, Facebook, Apple and Google are all in the political crosshairs for “anti-competitive, monopolist behaviours” and are likely to suffer new anti-trust regulations.

- Nations around the globe look unable to agree on how to tax the Tech multinationals who charge in one country, bill in another, and deliver to a third.

- And then there is the issue I highlighted yesterday of surveillance capitalism and how certain tech firms have utilised Algorithms to monetise us – which looks, smells, and feels just like subliminal advertising, which was banned in the 1960s.

- There are worries a Biden presidency will accelerate regulation of Tech.

We all know.. the moment government starts to regulate anything… is the moment to sell.

In the case of Google and Facebook – government has to act. But the others? Maybe Amazon has become a monopoly? Would it change much to break it up the same way the oil majors were forced to unravel 120 years ago? If people are stupid enough to pay £1200 for the new iPhone XII then their problem (Me! Me! Me! I am an addict. I need help.)

Meanwhile…

Speaking of cars, lets talk about proper Motors.. the ones that run on dead dinosaurs. Next week my very great mate and market legend, Alex Bridport, a bond market veteran who remembers trading the original South Sea Bubble Bonds, is doing the The Mille Miglia for the fifth time. It’s a race in proper old cars all round Italy. Normally its run in May with nice warm days “this year the delay means it’s going to be a very different kettle of poisons!” He added: “It’s simply an incredible experience in the moist beautiful country in the world!”

Good luck to him!

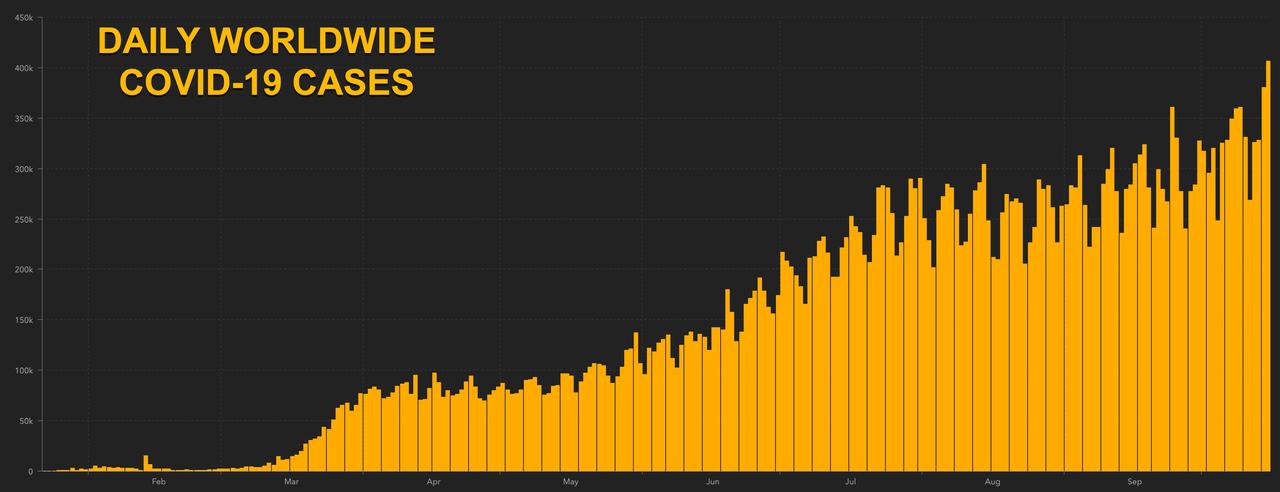

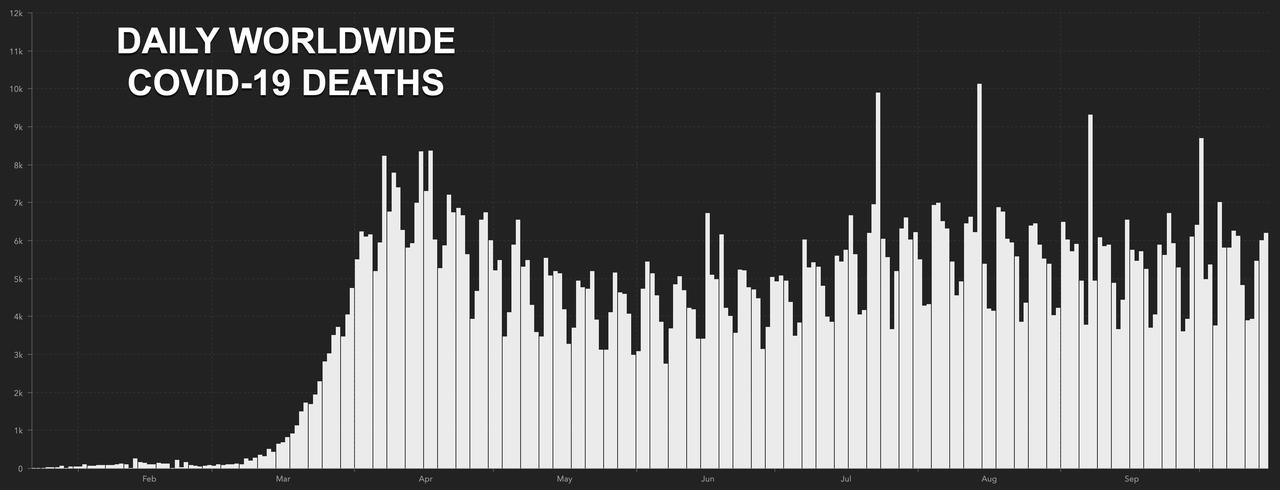

Global COVID-19 Cases Top 400k In 24 Hours For First Time As Outbreaks Flare From Midwest To Europe: Live Updates

Summary:

- Midwestern outbreak hits new records

- Europe tops US in new cases

- Global cases top 400k in a day for first time

- Deaths reported yesterday: 6,189

- North Dakota, South Dakota, Wisconsin lead infections/per 1,000 residents

* * *

A series of new social distancing restrictions have been imposed across Europe this week as the Continent saw its daily number of new COVID-19 cases rocket past the US this week. But on Friday, our attention swings back to the US, where an outbreak in the Midwest has continued to accelerate; fresh daily records for new cases were recorded in Illinois, Wisconsin and North Dakota on Thursday.

The resurgence has brought the number of new cases reported across the world to record highs nine months in a pandemic that has already killed more than 1 million people around the world.

Source: JPM

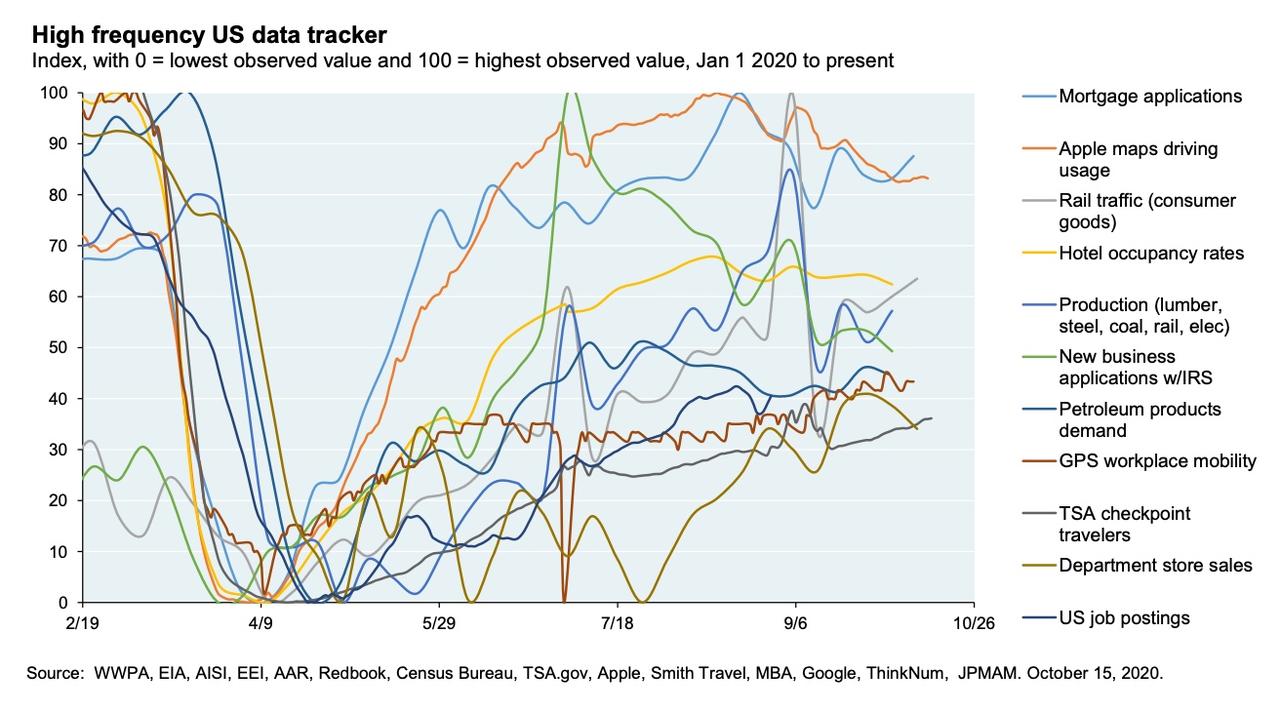

Since the start of the pandemic, investors have increasingly turned to high-frequency indicators to try and measure fluctuations in economic activity in real time. One agglomeration of high-frequency data covering topics, including overall movement, petroleum demand at the pump, new business applications, TSA checkpoint numbers and department-store sales, from JPM shows that activity has generally fallen since a summer peak, when US daily case numbers and deaths were at their lowest, and states across the US were dialing back restrictions on business activity and socializing.

Source: JPM

According to Bloomberg, this latest outbreak in the Midwest started in Wisconsin, and spread to other more populous states nearby.

Source: Bloomberg

Wisconsin Gov. Tony Evers said Thursday he’ll challenge a decision from earlier in the week handed down by a Wisconsin court blocking the governor’s order limiting capacity in bars, restaurants and other public places. WI recorded a record 3,747 cases Thursday.

By 0800ET, the global tally of COVID-19 cases had hit 38,998,580, leaving the world on track to top 39 million cases before Saturday morning. The world reported a second straight daily record on Thursday, topping 400,000 for the first time (the exact total: 406,660.

Deaths, meanwhile, were relatively steady at 6,189.

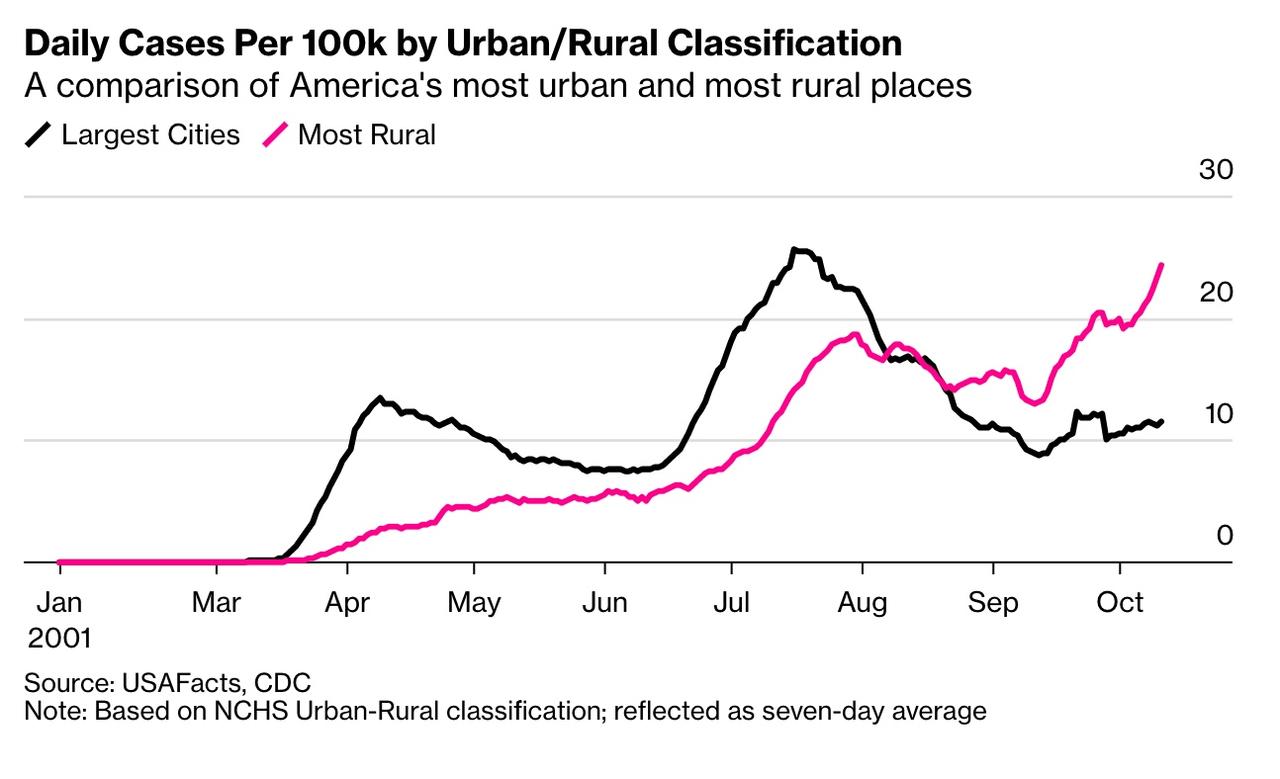

Another interesting trend: as the Midwest becomes the locus of the American COVID-19 outbreak, the divide between rural and urban infections has decidedly tilted toward ‘rural’ for the first time.

Source: Bloomberg

In overall viral prevalence, North Dakota, South Dakota and Wisconsin are currently leading the country. Though while the mainstream media likes to play up this phenomenon, it’s largely a function of the sparsely populated nature of the states, where workers come together in factories and meatpacking plants, often serving as the center of outbreaks.

Source: COVID Tracking Project

Meanwhile, in NYC, Mayor de Blasio is claiming that outbreaks in ‘hot spots’ around the city have been contained.

However, statewide hospitalization numbers have been creeping higher.

Coronavirus: Germany′s confusing patchwork of restrictions | Germany| News and in-depth reporting from Berlin and beyond | DW | 12.10.2020

For a person in their middle years to feel like this is both shocking and a sign of real trouble brewing in France and a collapsing economy. And as I have said before on a number of occasions; forget tourism in Europe for now, which will manifest in mass unemployment across Europe and will show up in devastated real estate prices starting next year.

While in Germany, Merkel seems bent on doing to Germany what East Germans have realized and that is many of them are prisoners of their own mind, being conditioned behind the wall and unable to escape and prosper from the unification. A number of German politicians have come out to say that unification was a mistake in the way it was done because they underestimated the conditioning that people had. And thus East Germans have largely not been able to prosper like west Germans and the divide is still there to this day.

Europe is a mess growing ever larger by the day and week. And these lockdowns will lead to true unrest in coming months and a changed economy. If Britain finds the courage to hard Brexit, it will gain leverage not imagined, if it seizes the opportunity. As the ebb of economic might lessens in Germany, it will impact the rest of Europe in ways not seen in decades, offering opportunities and pitfalls as trade patterns shift and financial realities bare visibility. Astute countries and companies and individuals will take the opportunity to seize the opportunities and while the Davis crowd attempts their “great reset” amongst collapsing economies. The ECB is trapped in a hell of its’ own making and that will become much more apparent next year as debt based existence finds new mud to play in. New banking opportunities will come to be seen as Central Banking loses its’ ability to function which will destroy the power base of of illusional banking as only true assets will count. And in the shadows the long dark shadows are cast of gold hordes in Russia and China ( rumors abound about how much real gold each one has) as they wait for opportunity. And Russia is the only one of the two completely not influenced by USD debt holdings or obligations. And yes, both have digital currencies on the shelf, should this be required. Europe runs the very real risk of implosion, with it being carved up by external forces down the road. It is why I believe current national borders may well change in the future. Europe may well Balkanize itself changing its’ form to deal with changed economic realities. Region within countries may characterize new borders. Italy could split into several entities for example. Bavaria could be quite separate from Germany is another example. Within a 5 year period Europe will not resemble itself today and the socialism being hoisted upon Europe will only hasten its’ splinter.

It would nice to imagine that we can learn from this, but it seems our politicians are just as dense in their approach to lockdowns which are destroying the economy. And while to date we have seen economic damage the true cost will be more acutely visible when the social costs become more evident. People are under stresses not experienced and the impact is rising in divorces and deaths and mental illness impacting families and social interactions. The fallout from this is not a controllable element by government or society as changed behavior produces consequences not forecast. And this will have real economic impact in the future as business and people try to forecast and plan for a future that is in constant flux. From one week to the next, uncertainty grows and it wears on the minds and hearts of all affected. We certainly are living through most strange times where common sense is in less supply than it was several months ago.

https://www.dw.com/en/germany-coronavirus-restrictions/a-55249978

7. OIL ISSUES

8 EMERGING MARKET ISSUES

Your early morning currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings FRIDAY morning 7:00 AM….

Euro/USA 1.1732 UP .0032 REACTING TO MERKEL’S FAILED COALITION/ REACTING TO +GERMAN ELECTION WHERE ALT RIGHT PARTY ENTERS THE BUNDESTAG/ huge Deutsche bank problems ///ITALIAN CHAOS//CORONAVIRUS/PANDEMIC/TRUMP POSITIVE WITH VIRUS /AND NOW ECB TAPERING BOND PURCHASES/JAPAN TAPERING BOND PURCHASES /USA RISING INTEREST RATES /FLOODING/EUROPE BOURSES /GREEN

USA/JAPAN YEN 105.25 DOWN 0.220 (Abe’s new negative interest rate (NIRP), a total DISASTER/NOW TARGETS INTEREST RATE AT .11% AS IT WILL BUY UNLIMITED BONDS TO GETS TO THAT LEVEL…

GBP/USA 1.2909 UP 0.0007 (Brexit March 29/ 2019/ARTICLE 50 SIGNED/BREXIT FEES WILL BE CAPPED/