NOV 23/USA ELECTION STORIES//MASSIVE RAID TODAY AS OPTIONS EXPIRY ON THE COMEX IS TOMORROW: GOLD DOWN $33.95 TO $1840.25//SILVER DOWN $.70 TO 23.62//HUGE ADVANCE IN GOLD TONNAGE STANDING AT THE COMEX: UP TO 24.438 TONNES//NO CHANGE IN SILVER OZ STANDING//CORONAVIRUS UPDATES USA AND THE GLOBE//USA VS CHINA//SWAMP STORIES FOR YOU TONIGHT//

GOLD:$1840.25 DOWN $33.95 The quote is London spot price

Silver:$23.62 DOWN $.70 London spot price ( cash market)

Closing access prices: London spot

i)Gold : $1838.50 LONDON SPOT 4:30 pm

ii)SILVER: $23.58//LONDON SPOT 4:30 pm

these people voted for Biden/Harris ticket!

TONIGHT, in the USA section, I have continued to highlight the major stories which happened last night and today. The USA election is one massive fraud.

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

CLOSING FUTURES PRICES: KEY MONTHS

DEC. GOLD $1837.00. CLOSE 1.30 PM SPREAD SPOT/FUTURE DEC $3.25/ BACKWARD // GOOD FOR EFP ISSUANCE//GOOD FOR EUROPEANS TO BUY COMEX GOLD///

FEB GOLD: 1843.00 CLOSE 1:30 PM SPREAD SPOT/FUTURE: $2.75 CONTANGO//$3.25 BELOW NORMAL CONTANGO

CLOSING SILVER FUTURE MONTH

SILVER DECEMBER CLOSE: $23.62 1:30 PM SPREAD SPOT/FUTURE DEC. : 0 CENTS PER OZ CONTANGO ( 0 CENTS ABOVE NORMAL CONTANGO

SILVER MARCH CLOSE: 24.74/SPREAD SPOT/FUTURE: A 12 CENTS

3 CENTS ABOVE NORMAL CONTANGO

XXXXXXXXXXXXXXXXXXXXXXXXX

COMEX DATA

wow!!

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

receiving today: 0/1891

EXCHANGE: COMEX CONTRACT: NOVEMBER 2020 COMEX 100 GOLD FUTURES SETTLEMENT: 1,872.600000000 USD INTENT DATE: 11/20/2020 DELIVERY DATE: 11/24/2020 FIRM ORG FIRM NAME ISSUED STOPPED ____________________________________________________________________________________________ 435 H SCOTIA CAPITAL 2 657 C MORGAN STANLEY 27 657 H MORGAN STANLEY 200 661 C JP MORGAN 95 661 H JP MORGAN 1075 690 C ABN AMRO 450 709 C BARCLAYS 1889 737 C ADVANTAGE 5 800 C MAREX SPEC 31 905 C ADM 8 ____________________________________________________________________________________________

TOTAL: 1,891 1,891 MONTH TO DATE: 7,844

issued:1170

GOLDMAN SACHS STOPPED 0 CONTRACTS.

NUMBER OF NOTICES FILED TODAY FOR NOV. CONTRACT: 1891 NOTICE(S) FOR 189,100 OZ (5.88100 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 7844 NOTICES FOR 784,400 OZ (24.598 tonnes)

SILVER//NOV CONTRACT

0 NOTICE(S) FILED TODAY FOR nil OZ/

total number of notices filed so far this month: 785 for 3,925,000 oz

BITCOIN MORNING QUOTE $18619 UP 195

BITCOIN AFTERNOON QUOTE. :$18,380 DOWN 34 DOLLARS .

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

GLD AND SLV INVENTORIES:

WITH GOLD DOWN $33.95 AND NO PHYSICAL TO BE FOUND ANYWHERE:

WITH ALL REFINERS CLOSED//MEXICO ORDERING ALL MINES SHUT: WHERE ARE THEY GETTING THE “PHYSICAL?

A HUGE CHANGES IN GOLD INVENTORY AT THE GLD

A DEPSOIT OF 2.9 TONNES INTO THE GLD

INVENTORY RESTS AT:

GLD:1,220.17 TONNES OF GOLD//

WITH SILVER DOWN 70 CENTS TODAY: AND WITH NO SILVER AROUND:

IN SILVER THE COMEX OI ROSE BY A HUGE SIZED 4625 CONTRACTS FROM 160,360 UP TO 164,985, AND CLOSER TO OUR NEW RECORD OF 244,710, (FEB 25/2020. THE LOSS IN OI OCCURRED DESPITE OUR RISE OF $0.32 IN SILVER PRICING AT THE COMEX.IT SEEMS THAT THE GAIN IN COMEX OI IS DUE TO CONSIDERABLE BANKER AND ALGO SHORT COVERING,COUPLED AGAINST A TINY EXCHANGE FOR PHYSICAL. WE HAD ZERO LONG LIQUIDATION, AND A ZERO INCREASE IN STANDING AT THE COMEX FOR NOV. WE HAD A STRONG GAIN IN OUR TWO EXCHANGES OF 4966CONTRACTS (SEE CALCULATIONS BELOW).

WE WERE NOTIFIED THAT WE HAD A SMALL NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: 341, AS WE HAD THE FOLLOWING ISSUANCE: DEC: 141, MARCH 200 FOR ZERO ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 341 CONTRACTS. THE BANKERS ARE NOW BEING BITTEN BY THOSE SERIAL FORWARDS (EFP’S CIRCULATING IN LONDON)AS THEY ARE NOW BEING EXERCISED AND COMING BACK TO NEW YORK FOR REDEMPTION OF METAL. THE COST TO SERVICE THESE SERIAL FORWARDS IS HIGH TO OUR BANKERS BUT THEY HAVE NO CHOICE BUT TO ISSUE AS MANY AS THEY CAN!

HISTORY OF SILVER OZ STANDING AT THE COMEX FOR THE PAST 26 MONTHS.

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

10.025 MILLION OZ INITIAL STANDING IN AUGUST.

43.030 MILLION OZ INITIALLY STANDING IN SEPT. (HUGE)

7.32 MILLION OZ INITIALLY STANDING IN OCT

2.630 MILLION OZ STANDING FOR NOV.

20.970 MILLION OZ FINAL STANDING IN DEC

5.075 MILLION OZ FINAL STANDING IN JAN

1.480 MILLION OZ FINAL STANDING IN FEB

23.005 MILLION OZ FINAL STANDING FOR MAR

4.660 MILLION OZ FINAL STANDING FOR APRIL

45.220 MILLION OZ FINAL STANDING FOR MAY

2.205 MILLION OF FINAL STANDING FOR JUNE

86.470 MILLION OZ FINAL STANDING IN JULY.

6.475 MILLION OZ FINAL STANDING IN AUGUST

55.400 MILLION OZ FINAL STANDING IN SEPT

11.400 MILLION OZ FINAL STANDING IN OCT.

3.935 MILLION OZ INITIAL STANDING IN NOV.

FRIDAY, AGAIN OUR CROOKS USED COPIOUS PAPER IN ORDER TO LIQUIDATE SILVER’S PRICE…AND THEY WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE $.32) ).. AND, OUR OFFICIAL SECTOR/BANKERS WERE UNSUCCESSFUL IN THEIR ATTEMPT TO FLEECE ANY SILVER LONGS AS WE HAD A HUGE GAIN IN OUR TWO EXCHANGES (4966 CONTRACTS). NO DOUBT THE STRONG GAIN IN OI ON THE TWO EXCHANGES WAS DUE TO i) STRONG BANKER/ STRONG ALGO SHORT COVERING. WE ALSO HAD ii) A SMALL ISSUANCE OF EXCHANGE FOR PHYSICALS 2) A ZERO GAIN IN SILVER OZ STANDING FOR NOV, iii) HUGE COMEX GAIN AND iv) ZERO LONG LIQUIDATION. YOU CAN BET THE FARM THAT OUR BANKERS ARE DESPERATE TO LIQUIDATE THEIR HUGE SHORT POSITIONS IN SILVER..

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY /FOR MONTH OF NOV:

10,797 CONTRACTS (FOR 16 TRADING DAY(S) TOTAL 10,797 CONTRACTS) OR 53.985 MILLION OZ: (AVERAGE PER DAY: 674 CONTRACTS OR 3.374 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF NOV: 53.985 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 7.46% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)*

ACCUMULATION IN YEAR 2020 TO DATE SILVER EFP’S: 1,583.27 MILLION OZ.

JANUARY 2020 EFP TOTALS SO FAR: 181.61 MILLION OZ

FEB 2020 EFP’S TOTAL : …… 259.600 MILLION OZ

MARCH EFP’S ….. 452.280 MILLION OZ //TOTALS//AND A NEW RECORD FOR THE MONTH)

APRIL EFP 95.355 MILLION OZ. (EX. FOR PHYSICALS BECOMING A LOT LESS)

MAY EFP FINAL: 77.27 MILLION OZ

JUNE EFP 71.15 MILLION OZ.

JULY EFP 133.95 MILLION OZ/ (EXCHANGE FOR PHYSICALS STARTING TO RISE EXPONENTIALLY AGAIN)

AUGUST EFP 127.46 MILLION OZ (EXCHANGE FOR PHYSICALS STARTING TO DECREASE AGAIN)

SEPT EFP 78.360 MILLION OZ (EXCHANGE FOR PHYSICALS DRAMATICALLY FALLING OFF A CLIFF)

OCT EFP 69.73MILLION OZ (STILL FALLING IN NUMBERS)

NOVEMBER EFP 53.985 MILLION OZ (STARTING TO SLOW DOWN AGAIN)

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 4625, WITHOUR $0.32 RISE IN SILVER PRICING AT THE COMEX ///FRIDAY.…THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE OF 341 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS.

TODAY WE GAINED A HUGE SIZED 4966 OI CONTRACTS ON THE TWO EXCHANGES (WITH OUR $0.32 RISE IN PRICE)//

THE TALLY//EXCHANGE FOR PHYSICALS

i.e 341 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH A HUGE SIZED INCREASE OF 4625 OI COMEX CONTRACTS. AND ALL OF THISDEMAND HAPPENED WITH OUR $0.32 FALL IN PRICE OF SILVER/AND A CLOSING PRICE OF $24.32 // FRIDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY.

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.8245 BILLION OZ TO BE EXACT or 118% of annual global silver production (ex Russia & ex China).

FOR THE NEW NOV DELIVERY MONTH/ THEY FILED AT THE COMEX: 0 NOTICE(S) FOR nil OZ OF SILVER.

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.70//TODAY’S RECORD OF 244,705 WAS SET WITH A PRICE OF: 18.91 (FEB 25/2020)

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

GOLD

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A CONSIDERABLE SIZED 4300 CONTRACTS TO 558,792AND CLOSER TO OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE GAIN IN COMEX OI OCCURREDWITH OUR GAIN IN PRICE OF $11.10 /// COMEX GOLD TRADING//FRIDAY.WE HAD SOME BANKER/ALGO SHORT COVERING ACCOMPANYING OUR SMALL SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION AND A POWERFUL GAIN IN GOLD OUNCES STANDING AT THE COMEX….THIS ALL HAPPENED WITH OUR GAIN IN PRICE OF $11.10.

WE HAD A VOLUME OF 0 4 -GC CONTRACTS//OPEN INTEREST 59//

WE HAD A FAIR SIZED GAIN OF 5223 CONTRACTS (18.059 TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A SMALL SIZED 923 CONTRACTS:

CONTRACT .; DEC: 923; FEB: 0 ALL OTHER MONTHS ZERO//TOTAL: 923. The NEW COMEX OI for the gold complex rests at 558,792. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EXCHANGE DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A GOOD SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 5223 CONTRACTS: 4300 CONTRACTS INCREASED AT THE COMEX AND 923 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON.THUS TOTAL OI GAIN OF 5223 CONTRACTS OR 16.245 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES:

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (923) ACCOMPANYING THE CONSIDERABLE SIZED GAIN IN COMEX OI (4300 OI): TOTAL GAIN IN THE TWO EXCHANGES: 5223 CONTRACTS. WE NO DOUBT HAD 1) SOME BANKER SHORT COVERING AND SOME ALGO SHORT COVERING ,2.)ANOTHER POWERFUL INCREASE IN OUNCES STANDING AT THE GOLD COMEX FOR THE FRONT NOV. MONTH TO 24.438 TONNES) 3) ZERO LONG LIQUIDATION ;4) CONSIDERABLE COMEX OI GAIN AND 5) SMALL SIZED ISSUANCE OF EXCHANGE FOR PHYSICAL ...ALL OF THIS OCCURRED WITH OUR GAIN IN GOLD PRICE TRADING/FRIDAY//$11.10.

WE ARE BEGINNING TO WITNESS A LACK OF EXCHANGE FOR GOLD PHYSICALS UNDERWRITTEN DUE TO PREMIUMS STARTING TO REAPPEAR IN THE FUTURE PRICE OF GOLD VS LONDON SPOT. THE COST TO THE BANKERS IS JUST TOO GREAT TO ENGAGE IN THESE VEHICLES ONCE THIS OCCURS.

We have now switched to GOLD for our spreaders!!

FOR DETAILS ON THE SPREADING EXERCISE HERE IS A BRIEF OUTLINE:

SPREADING OPERATIONS/NOW SWITCHING TO GOLD (WE SWITCH OVER TO SILVER ON DEC 1)

SPREADING OPERATION FOR OUR NEWCOMERS:

FOR NEWCOMERS, HERE ARE THE DETAILS:

SPREADING LIQUIDATION HAS NOW COMMENCED IN GOLD AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF DEC.

FOR THOSE OF YOU WHO ARE NEW, HERE IS THE MODUS OPERANDI OF THE SPREADERS AND THE CRIMINAL ELEMENT BEHIND IT:

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR;

THE SPREADING LIQUIDATION OPERATION IS NOW OVER FOR SILVER..AND WE WILL NOW MORPH INTO AN ACCUMULATION PHASE OF SPREADING CONTRACTS FOR GOLD. THEY WILL ACCUMULATE CONSIDERABLE AMOUNT OF THE CONTRACTS AND THEN LIQUIDATE ONE WEEK PRIOR TO FIRST DAY NOTICE

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO GOLD AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF OCT. HEADING TOWARDS THE NON ACTIVE DELIVERY MONTH OF NOV FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE IN THIS NON ACTIVE MONTH OF NOV. BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST INGOLD WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (DEC), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2020 INCLUDING TODAY

Nov.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF NOV : 46,298 CONTRACTS OR 4,629,800 oz OR 144.00TONNES (16 TRADING DAY(S) AND THUS AVERAGING: 2964 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 16 TRADING DAY(S) IN TONNES: 144.00 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2019, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 144.00/3550 x 100% TONNES =4.05% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2020 TO DATE: 3,806.73 TONNES

JANUARY 2220 TOTAL EFP ISSUANCE; : 571.19 TONNES

FEB 2020 TOTAL EFP ISSUANCE : 653.78 TONNES

MARCH TOTAL EFP ISSUANCE 1,098.93 TONNES (*AND A NEW ALL TIME RECORD ISSUANCE//22 DAYS)

APRIL TOTAL EFP. ISSUANCE: 243.45 TONNES (EFP ISSUANCE BECOMING A LOT LESS)

MAY TOTAL EFP ISSUANCE: 248.68 TONNES (EFP ISSUANCE STILL LOW// PREMIUM COST TO THE BANKERS IS HUGE..SO ISSUANCE IS LESS)

JUNE TOTAL EFP ISSUANCE: 192.06 TONNES (EFP ISSUANCE EXTREMELY LOW)

JULY TOTAL EFP ISSUANCE; 313.09 TONNES ..(EXCHANGE FOR PHYSICALS REVERSE COURSE AND ARE NOW INCREASING!)

AUGUST TOTAL EFP ISSUANCE; 150.78 TONNES FINAL (AGAIN: RETREATING IN NUMBERS)

SEPT TOTAL EFP ISSUANCE: 178.49 TONNES (EFP’s AGAIN RISING DUE TO BACKWARDATION/LOWER FUTURE PREMIUMS//THUS LESS COST TO CARRY)

OCT TOTAL EFP ISSUANCE. 158.78TONNES (AGAIN DROPPING)

NOV TOTAL EFP ISSUANCE: 144.00 TONNES (SLIGHTLY INCREASING AGAIN)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A HUGE SIZED 4625 CONTRACTS FROM 160,360 UP TO 164,985 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 2 3/4 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.

THE HUGE SIZED GAIN IN OI SILVER COMEX WAS PRIMARILY DUE TO; 1) CONSIDERABLE BANKER SHORT COVERING//ALGO SHORTCOVERING//// , 2) A SMALL ISSUANCE OF EXCHANGE FOR PHYSICALS (SEE BELOW), 3) A ZERO INCREASE IN STANDING FOR SILVER AT THE COMEX FOR NOV., AND 4) ZEROLONG LIQUIDATION

EFP ISSUANCE 341 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE: DEC. 141 AND MARCH: 200 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 341 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 4625 CONTRACTSTO THE 341 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A HUGE SIZED GAIN OF 4966 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 24.83 MILLION OZ, OCCURRED WITH OUR $0.32 GAIN IN PRICE///

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL..THE EVIDENCE IS CLEAR: HUGE AMOUNTS OF PHYSICAL STANDING FOR BOTH SILVER AND GOLD .

SHANGHAI CLOSED UP 36.76 PTS OR 1.09% //Hang Sang CLOSED UP 34.66 PTS OR .13% /The Nikkei closed DOWN 106.97 POINTS OR 0.42%//Australia’s all ordinaires CLOSED UP 0.48%

/Chinese yuan (ONSHORE) closed /Oil UP TO 42.90 dollars per barrel for WTI and 45.59 for Brent. Stocks in Europe OPENED ALL GREEN// ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.5683. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.5595 TRADE TALKS STALL//YUAN LEVELS //TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED//CORONAVIRUS/PANDEMIC/TRUMP TESTS POSITIVE FOR COVID 19 : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY BY A CONSIDERABLE SIZED 4300 CONTRACTS TO 559,375 MOVING CLOSER TO OUR RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX INCREASE OCCURRED WITH OUR STRONG GAIN OF $11.10 IN GOLD PRICING FRIDAY’S COMEX TRADING/). WE ALSO HAD A SMALL EFP ISSUANCE (923 CONTRACTS). WE ALSO HAD 1) CONSIDERABLE BANKER SHORT COVERING// ALGO SHORT COVERING//, 2) ZEROLONG LIQUIDATION AND 3) ANOTHER MONSTER GAIN IN GOLD STANDING AT THE COMEX ( NOW STANDING AT 24.438 TONNES)//NOV. DELIVERY MONTH (SEE BELOW) … AS WE ENGINEERED A GOOD SIZED GAIN ON OUR TWO EXCHANGES OF 5223 CONTRACTS. WE HAVE LATELY WITNESSED THE EXCHANGE FOR PHYSICALS ISSUED BEING SMALL….. AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. WE CAN NOW VISUALLY SEE THAT SHORTS ARE TRYING TO EXTRICATE THEMSELVES FROM THEIR MESS (“TRYING TO GET OUT OF DODGE”) AS LONGS DEPART THE COMEX FOR THE SAFER CONFINES OF LONDON.

(SEE BELOW)

WE HAD 0 4 -GC VOLUME//open interest REMAINS AT 59

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF NOV.. THE CME REPORTS THAT THE BANKERS ISSUED A SMALL SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS., THAT IS 923 EFP CONTRACTS WERE ISSUED: DEC 923; FEB// ’21 0 AND ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 923 CONTRACTS.

YOU WILL FIND THAT WHEN WE HAVE A GOOD PREMIUM IN THE FUTURES/SPOT, THEN THE NUMBER OF EXCHANGE FOR PHYSICALS DECLINE IN NUMBERS. THE COST IS JUST TOO MUCH FOR THEM TO ISSUE.

IT SEEMS THAT OUR BANKER FRIENDS ARE LOATHE TO ISSUE EFPS DESPITE THE LOW PREMIUM ON FUTURE GOLD CONTRACTS.

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: 5223 TOTAL CONTRACTS IN THAT 923 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE GAINED A CONSIDERABLE SIZED 4300 COMEX CONTRACTS.. THE BIG NEWS IS THE GIGANTIC LEVEL OF NOV 2020 GOLD CONTRACTS STANDING FOR DELIVERY. ((24.438 TONNE) AS NOVEMBER IS A NON ACTIVE AND GENERALLY A VERY POOR DELIVERY MONTH. LADIES AND GENTLEMEN, OUR COMEX IS OFFICALLY UNDER ASSAULT.

THE BANKERS WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $11.10). AND,THEY WERE UNSUCCESSFUL IN FLEECING ANY LONGS. AS MENTIONED ABOVE THE TOTAL GAIN ON THE TWO EXCHANGES REGISTERED 16.245 TONNES,

NET GAIN ON THE TWO EXCHANGES :: 5223 CONTRACTS OR 522300 OZ OR 16.235 TONNES.

COMMODITY LAW SUGGESTS THAT COMMODITY FUTURES OPEN INTEREST SHOULD APPROXIMATE 3% OF TOTAL PRODUCTION. IN GOLD THE WORLD PRODUCES AROUND 3500 TONNES PER YEAR BUT ONLY 2200 TONNES ARE AVAILABLE FROM THE WEST (THUS EXCLUDING RUSSIA, CHINA ETC..WHO KEEP 100% OF THEIR PRODUCTION)

THUS IN GOLD WE HAVE THE FOLLOWING: 558,792 TOTAL OI CONTRACTS X 100 OZ PER CONTRACT = 55.87 MILLION OZ/32,150 OZ PER TONNE = 1738 TONNES

THE COMEX OPEN INTEREST REPRESENTS 1738/2200 OR 78.99% OF ANNUAL GLOBAL PRODUCTION OF GOLD.

Trading Volumes on the COMEX TODAY: 416,088 contracts// volume good but raid and spreader liquidation ////they are bailing out of gold comex faster than fox news viewers.

CONFIRMED COMEX VOL. FOR YESTERDAY: 243,200 contracts// volume: poor

Total monthly oz gold served (contracts) so far this month

7844 notices

784,400 OZ

24.598 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

xxx oz

We had 0 deposit into the dealer

total deposit: NIL oz

total dealer withdrawals: nil oz

we had 2 deposit into the customer account

i) Into JPMorgan: 94,013.169 oz

ii) Into Malca: 128,604.000 oz (4,000 kilobars)

total customer deposit: 222,617.169 oz oz

6.9 tonnes

we had 2 gold withdrawals from the customer account:

i) Out of Delaware: 1907.210 oz

ii) Out of HSBC: 1236.000 oz ???

iii) Out of Malca 643.02 oz (20 kilobars)

total withdrawals: 3786.23 oz

We had 2 kilobar transactions +

ADJUSTMENTS: 1 //

out of JPMorgan 12,387.8 oz//customer to dealer.

The front month of NOV registered a total of 1904 contracts for a GAIN of 1805 contracts. We had 91 notices filed on Friday so we gained 1896 contracts or 189,600 additional oz of gold will stand in this non active month of November. There is now no question that we are experiencing a massive onslaught at the gold comex. This is a new record(gold deliveries) for a November month. If you think that this is high, you can just imagine what will stand in December.

The big December contract lost 20,517 contracts down to 197,009 contracts. We will be watching December closely. We have just 4 more reading days before we reach the huge December delivery month. January LOST 10 contracts to stand at 3661 contracts. FEBRUARY gained a STRONG 19,989 contracts UP TO 253,673. WE ARE STILL WITNESSING THE ALGOS LEAVE THE DECEMBER ARENA. WE NOW AWAIT TO SEE HOW MANY EUROPEAN LONGS REMAIN AS THESE GUYS WILL TAKE DELIVERY AND REMOVE PHYSICAL GOLD FROM NY AND SHIP TO THEIR SHORES.

THE BIG STORY AGAIN TODAY IS THE HIGH INITIAL OI STANDING FOR NOVEMBER (24.438 tonnes). GENERALLY NOVEMBER IS A VERY POOR DELIVERY MONTH AS MOST INVESTORS PREFER TO SKIP THIS MONTH AND MOVE STRAIGHT TO DECEMBER. IT LOOKS LIKE SOME MAJOR ENTITIES( MAJOR EUROPEAN BANKS) JUST CANNOT WAIT FOR DECEMBER AS THEY ALONG WITH OTHERS ARE MAKING THEIR MOVE FOR PHYSICAL METAL. GOLDMAN SACHS ONE OF THE LEADERS OF THE NEW LONDON LME EXCHANGE NEEDS THE GOLD INVENTORY FOR LIQUIDITY AND THEIR INITIAL CONTRIBUTION. OTHER MAJOR PLAYERS ON THAT SIDE OF THE POND ARE ALSO JOINING IN ON THE ASSAULT. AS MENTIONED ABOVE THE GOLD COMEX IS EXPERIENCING A MASSIVE ONSLAUGHT FOR METAL

We had 1891 notice(s) filed today for 189100 oz OR 5.8810 TONNES.

FOR THE NOV 2020 CONTRACT MONTH)Today, 95 notice(s) were issued from

JPMorgan dealer account and 1075 notices were issued from their client or customer account. The total of all issuance by all participants equates to 1891 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notices received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the NOV /2020. contract month, we take the total number of notices filed so far for the month (7844) x 100 oz , to which we add the difference between the open interest for the front month of NOV (1904 CONTRACTS ) minus the number of notices served upon today (1891 x 100 oz per contract) equals 785,700 OZ OR 24.438 TONNES) the number of ounces standing in this active month of NOV

thus the INITIAL standings for gold for the NOV/2020 contract month:

No of notices filed so far (7844, x 100 oz +1904 OI) for the front month minus the number of notices served upon today (1891) x 100 oz which equals 785,700 oz standing OR 24.438TONNES in this active delivery month. This is a GIGANTIC amount for gold standing for a NOV delivery month (a very poor non active delivery month). THE COMEX IS UNDER A HUGE FRONTAL ATTACK FROM EUROPEAN BANKS SEEKING PHYSICAL METAL!

We gained 1896 contracts or an additional 189,600 oz will search out metal on this side of the pond.

NEW PLEDGED GOLD: BRINKS

606,360.007, oz NOW PLEDGED SEPT 15.2020/HSBC 18.860 TONNES ( A HUGE INCREASE FROM 10.6)

60,784.803 PLEDGED APRIL 3/2020: SCOTIA: 1.3234 tonnes

deleted Int. Delaware pledge July 7 (600 tonnes)

267,622.245 oz JPM 8.324 TONNES

602,840.325 oz pledged June 12/2020 Brinks/ july 2/july 21 18.75 tonnes

88,796.123 oz Pledged August 21/regular account 1.588 tonnes jpm

96.453 oz Manfra Nov 23/2020

total pledged gold: 1,626,595.479 oz 50.59 tonnes

SURPRISINGLY WE HAVE BEEN WITNESSING NO REAL PHYSICAL GOLD ENTERING THE COMEX VAULTS FOR THE PAST YEAR!! ..ONLY PHONY KILOBAR ENTRIES…. WE HAVE 489.66 TONNES OF REGISTERED GOLD WHICH CAN SETTLE UPON LONGS i.e. 24.438 tonnes

CALCULATION OF REGISTERED GOLD THAT CAN BE SETTLED UPON:

total registered or dealer 17,360,154.416 oz or 539.99 tonnes

total weight of pledged: 1,626,595.479 oz or 50.59 tonnes

thus:

registered gold that can be used to settle upon: 15,733,559.0 (489,37 tonnes)

total eligible gold: 20,136,600.189 oz (626.33 tonnes)

total registered, pledged and eligible (customer) gold 37,496,754.605 oz 1,166.31 tonnes (INCLUDES 4 GC GOLD)

total 4 GC gold: 126.34 tonnes

total gold net of 4 GC: 1039.97 tonnes

end

I have compiled data with respect to registered (or dealer) gold taken on first day notice for each of the past 24 months

The data begins on first day notice for the May month taken on the last day of July 2018. and it continues to present day.

I then took, how many deliveries were recorded by the CME for each and every month. I also included for reference the price of gold on first day notice.

The first graph is a logarithmic graph and the second graph, linear.

You can see the huge explosion of registered gold at the comex along with deliveries.

THE DATA AND GRAPHS:

THE GOLD COMEX SEEMS TO BE UNDER SEVERE ASSAULT FOR PHYSICAL

November saw a LOSS OF 116 notices FALLING to 2 contracts. We had 116 notices filed on Friday so we gained 0 contracts or NIL additional silver oz will stand in this non active delivery month of November.

December saw a LOSS of 4747 contracts DOWN to 52,073 contracts. January saw a GAIN of 69 contracts UP to 359. MARCH gained 8788 contracts up to 96,695.

We have 4 more reading days before first day notice. It looks like we are going to have a monster delivery for silver as well.

The total number of notices filed today for the NOV 2020. contract month is represented by 0 contract(s) FOR nil oz

To calculate the number of silver ounces that will stand for delivery in NOV we take the total number of notices filed for the month so far at 785 x 5,000 oz = 3,925,000 oz to which we add the difference between the open interest for the front month of NOV(2) and the number of notices served upon today 0x (5000 oz) equals the number of ounces standing.

Thus the NOV standings for silver for the NOV/2019 contract month: 785 (notices served so far) x 5000 oz + OI for front month of NOV( 2)- number of notices served upon today (0) x 5000 oz of silver standing for the NOV contract month .equals 3,935,000 oz. ..VERY STRONG FOR A NON ACTIVE NOV MONTH.

WE GAINED 0 CONTRACTS OR AN ADDITIONAL NIL OZ WILL STAND FOR DELIVERY AT THE COMEX AND FORGO ANY FIAT BONUS AS THEY SEARCH FOR METAL ON THIS SIDE OF THE POND VS LONDON. SEEMS THAT WE HAVE A WHALE COMING AFTER COMEX SILVER

YESTERDAY’S CONFIRMED VOLUME OF 100,009 CONTRACTS EQUATES to 0.500 billion OZ 71.9% OF ANNUAL GLOBAL PRODUCTION OF SILVER..

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO- 4.28% ((Nov 23/2020)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -2.37% to NAV: (NOV23/2020 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into NEGATIVE/4.28% (Nov 23)

(courtesy Sprott/GATA

3. SPROTT CEF .A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 18.79 TRADING 18.01///NEGATIVE 4.16

END

And now the Gold inventory at the GLD

NOV 23/WITH GOLD DOWN $33.95 TODAY: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.9 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 1220.17 TONNES

NOV 20/WITH GOLD UP $11.10 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD// A WITHDRAWAL (ROBBERY) OF 1.74 TONNES FROM THE GLD//INVENTORY RESTS AT 1217.26 TONNES

NOV 19/WITH GOLD DOWN $9.80 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.30 TONES FROM THE GLD////INVENTORY REST AT 1219.00 TONNES

NOV 18/WITH GOLD DOWN $13.50 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.10 TONNES FROM THE GLD INVENTORY//INVENTORY RESTS AT 1226.30 TONNES

NOV 17/WITH GOLD DOWN 3 DOLLARS TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.92 TONNES FROM THE GLD////INVENTORY RESTS AT 1231.40 TONNES

NOV 16/WITH GOLD UP $2.20 TODAY/A HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 5.25 TONNES FROM THE GLD////INVENTORY RESTS AT 1234.32 TONNES

NOV 13/WITH GOLD UP $11.90 TODAY//A HUGE CHANGE IN GOLDINVENTORY AT THE GLD; A WITHDRAWAL OF 1.17 TONNES FROM THE GLD////INVENTORY RESTS AT 1239.57 TONNES

Nov 12/WITH GOLD UP $11.00 TODAY: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A PAPERWITHDRAWAL OF 9.02 TONNES FROM THE GLD///INVENTORY RESTS AT 1240.74 TONNES

NOV 11/WITH GOLD DOWN $13.10 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1249.79 TONNES/

NOV 10/WITH GOLD UP $20.10 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 10.51 TONNES/INVENTORY RESTS AT 1249.79 TONNES

NOV 9/WITH GOLD DOWN $88.45 TODAY: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIST OF 7.88 TONNES INTO THE GLD///INVENTORY RESTS AT 1260.30 TONNES

NOV 6/WITH GOLD UP $5.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1252.42 TONNES

NOV 5/WITH GOLD UP $51.45 TODAY: STRANGELY A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.5 TONNES FROM THE GLD////INVENTORY RESTS AT 1252.42 TONNES

NOV 4/WITH GOLD DOWN $9.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1255.92 TONNES

NOV 3//WITH GOLD UP $16.85 TODAY: STRANGE!!! A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER WITHDRAWAL OF 1.75 TONNES FROM THE GLD////INVENTORY RESTS AT 1255.92 TONNES

NOV 2/WITH GOLD UP $13.60 TODAY: A SMALL CHANGE IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF .58 TONNES AND THIS IS GENERALLY TO PAY FOR FEES (STORAGE/INSURANCE)//INVENTORY RESTS AT 1257.67 TONNES

OCT 30/WITH GOLD UP $11 TODAY: NO CHANGE IN GOLD INVENTORYAT THE GLD//INVENTORY RESTS AT 1258.25 TONNES

OCT 29/WITH GOLD DOWN $11.80 DOLLARS TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER WITHDRAWAL OF 8.47 TONNES FROM THE GLD////INVENTORY RESTS AT 1258.25 TONNES

OCT 28/STRANGE!WITH GOLD DOWN $30.50 TODAY, A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1266.72 TONNES

OCT 27/WITH GOLD UP $6.20 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1263.80 TONNES

OCT 26/WITH GOLD UP $1.50 TODAY; A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.77 TONNES FROM THE GLD//INVENTORY RESTS AT 1263.80 TONNES

OCT 23/WITH GOLD DOWN 80 CENTS TODAY: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWL OF 3.8 TONNES FROM THE GLD////INVENTORY RESTS AT 1265.55 TONNES

OCT 22/WITH GOLD DOWN $22.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1269.35 TONNES

OCT 21//WITH GOLD UP $17.50 DOLLARS TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1269.93 TONNES

OCT 20/WITH GOLD UP $3.30 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: ANOTHER PAPER WITHDRAWAL OF 2.92 TONNES//INVENTORY RESTS AT 1269.93 TONNES

OCT 19WITH GOLD UP $5.15 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.5 TONNES FROM THE GLD///INVENTORY RESTS AT 1272.56 MILLION OZ//

OCT 16//WITH GOLD DOWN 10 CENTS TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.59 TONNES FROM THE GLD//INVENTORY RESTS AT 1276.06 MILLION OZ

OCT 15//WITH GOLD UP $1.10 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1277.65 TONNES

OCT 14/WITH GOLD UP $12.00 : NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1277.65 TONNES

OCT 13/WITH GOLD DOWN $31.70 DOLLARS: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1277.65 TONNES.

OCT 12/WITH GOLD UP $2.00 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 6.13 TONNES INTO THE GLD////INVENTORY RESTS AT 1277.65 TONNES

OCT 12/WITH GOLD UP $2.00 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1271.52 TONNES

OCT 9/WITH GOLD UP $31.10 TODAY/NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1271.52 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Inventory rests tonight at

NOV23/ GLD INVENTORY 1220.17 tonnes

LAST; 953 TRADING DAYS: +276.71 TONNES HAVE BEEN ADDED THE GLD

LAST 853 TRADING DAYS// +454.19 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY

end

Now the SLV Inventory

NOV 23/WITH SILVER DOWN $.70 TODAY: A HUGE CHANGE IN SILVER AT THE SLV; A WITHDRAWAL OF 2.046 MILLION OZ FROM//INVENTORY RESTS AT 560.537 MILLION OZ

NOV 20//WITH SILVER UP $0.32 TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 52.583 MILLION OZ//

NOV 19/WITH SILVER DOWN 35 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV:2 TRANSACTIONS:1) A WITHDRAWAL OF 1.396 MILLION OZ AND 2). 2.602 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 562.583 MILLION OZ

NOV 18/WITH SILVER DOWN 23 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1581 MILLION OZ FROM THE SLV…//INVENTORY RESTS AT 566.581 MILLION O

NOV 17/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 568.162 MILLION OZ//

NOV 16/WITH SILVER UP $.05 TODAY//A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDDRAWAL OF 1.209 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 568.162 MILLION OZ//

NOV 13/WITH SILVER UP 43 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV” A WITHDRAWAL OF 2.88 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 569.371 MILLION OZ.

NOV 12/WITH SILVER DOWN 2 CENTS TODAY: NO CHANGES IN SILVER INVENTORY FROM THE SLV//INVENTORY RESTS AT 572.254 MILLION OZ

NOV 11/WITH SILVER DOWN 8 CENTS TODAY: A HUGE 3.627 MILLION OZ WITHDRAWAL FROM THE SLV/ INVENTORY RESTS AT 572.254 MILLION OZ

NOV 10/WITH SILVER UP $.65 TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: STRANGE ANOTHER HUGE DEPOSIT OF 4.739 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 575.881 MILLION OZ

NOV 9/WITH SILVER DOWN $1.76 TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 10.324 MILLION OZ ADDED INTO THE SLV INVENTORY////INVENTORY RESTS AT 571.742 MILLION OZ

NOV 6/WITH SILVER UP 47 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 561.418 MILLION OZ//

NOV 5/WITH SILVER UP $1.21 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 561.418 MILLION OZ..

NOV 4/WITH SILVER DOWN 43 CENTS TODAY: TWO HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A) WITHDRAWAL OF 240,000 OZ FROM SLV//// AND THEN B) A DEPOSIT OF 1.83 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 561.418 MILLION OZ

NOV 4/WITH SILVER DOWN 43 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WIHDRAWAL OF 240,000 OZ FROM SLV////INVENTORY RESTS AT 559.558 MILLION OZ

NOV 3/WITH SILVER UP 29 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT 559.798 MILLION OZ///

NOV 2/WITH SILVER UP 40 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 559.798 MILLION OZ//

OCT 30/WITH SILVER UP 23 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 931,000 FROM THE SLV////INVENTORY RESTS AT 559.798 MILLION OZ..

OCT 29/WITH SILVER DOWN 4 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 2.326 MILLION OZ//INVENTORY RESTS A 560.729 MILLION OZ..

OCT 28/WITH SILVER DOWN $1.09 TODAY: A HUGE WITHDRAWAL OF 2.791 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 558.403 MILLION OZ..

OCT 27/WITH SILVER UP 18 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 561.194 MILLION OZ//

OCT 26/WITH SILVER DOWN 18 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 561.194 MILLION OZ

OCT 23/WITH SILVER DOWN 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 561.194 MILLION OZ

OCT 22/WITH SILVER DOWN 46 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 561.194 MILLION OZ

OCT 21/WITH SILVER UP 26 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.977 MILLION OZ FROM THE SLV..//INVENTORY RESTS AT 561.194 MILLION OZ.

OCT 20/WITH SILVER UP 31 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 652,000 OZ INTO THE SLV////INVENTORY RESTS AT 564.171 MILLION OZ//

OCT 19/WITH SILVER UP 27 CENTS TODAY: NO CHANGES IN SLV INVENTORY AT THE SLV//INVENTOR RESTS AT 563.519 MILLION OZ/

OCT 16/WITH SILVER UP 15 CENTS TODAY: NO CHANGES IN SLV INVENTORY//INVENTORY RESTS AT 563.519 MILLION OZ.

OCT 15/WITH SILVER DOWN 16 CENTS TODAY:NO CHANGES IN SLV INVENTORY//INVENTORY RESTS AT 563.519 MILLION OZ//

OCT 14/WITH SILVER UP 24 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.652 MILLION OZ//INVENTORY RESTS AT 563.519 MILLION OZ/

OCT 13/WITH SILVER DOWN 105 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 558.867 MILLION OZ..

OCT 12/WITH SILVER UP 28 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV; A WITHDRAWAL 0F 1.396 MILLION OZ//INVENTORY RESTS AT 558.867MILLION OZ/

OCT 9/WITH SILVER UP $1.00 TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 560.263

NOV 23.2020:

SLV INVENTORY RESTS TONIGHT AT 560.537 MILLION OZ//

ii) Important gold commentaries courtesy of GATA/Chris Powell

We brought this story to you on Friday but worth repeating:

Pam and Russ pound the table that the Fed must explain the missing billions and this money must be returned to treasury. Late Saturday night the Fed want to get together with Mnuchin and talk about the return of this money.

Pam and Russ Martens//Wall Street on Parade/GATA

But why should Mnuchin explain missing billions? Mainstream news organizations will never ask

Submitted by cpowell on Fri, 2020-11-20 16:16. Section: Daily Dispatches

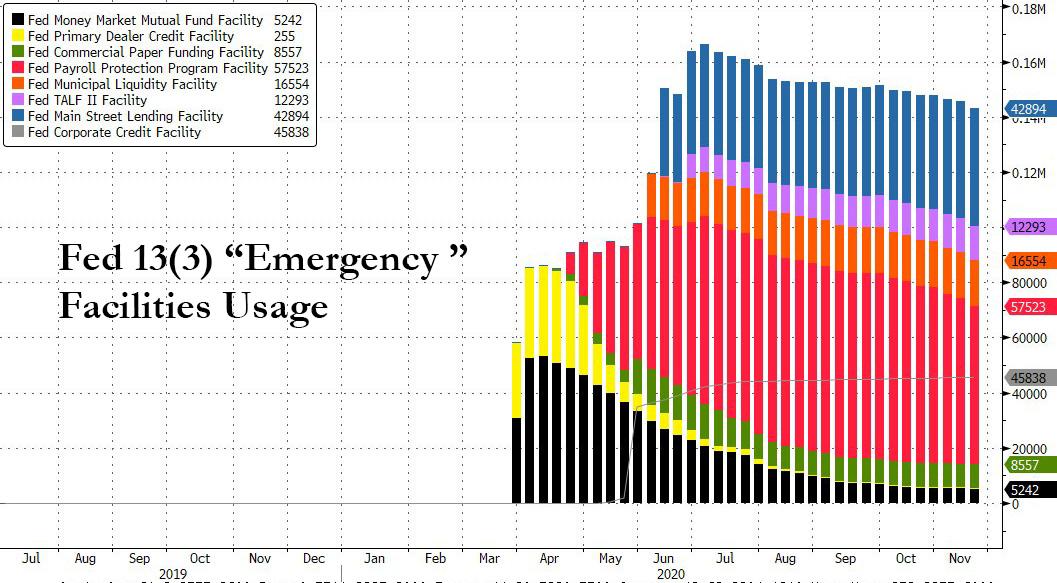

Mnuchin Demands the Return of Emergency Funds from the Fed, without Explaining What He’s Been Doing with a Missing $340 Billion

By Pam and Russ Martens Wall Street on Parade Friday, November 20, 2020

Yesterday U.S. Treasury Secretary Steve Mnuchin stunned markets by demanding in a letter to Federal Reserve Chairman Jerome Powell that the Fed return Treasury funds that are backstopping the bulk of its emergency lending programs and wind down these programs by year’s end. Adding further shock, the Fed rebuked the idea with its own statement, saying this:

“The Federal Reserve would prefer that the full suite of emergency facilities established during the coronavirus pandemic continue to serve their important role as a backstop for our still-strained and vulnerable economy.”

At issue in this newly-emerged war between Treasury and the Fed is $454 billion, $340 billion of which has yet to be accounted for. …

Wall Street On Parade has been repeatedly asking for an explanation as to what has happened to the balance of $340 billion that Congress intended to be used to help American families and businesses during the worst economic downturn since the Great Depression. …

Not only does the American public not know what happened to that $340 billion but as we pointed out previously, “despite regular promises from the Fed chairman that the Fed will be transparent about its lending programs, there are four programs for which the Fed has yet to provide transaction-level data — meaning the names of the borrowers and how much they borrowed.”

Dave is 100% correct: it is not the delivery demands that are important but all of those seeking to remove gold (Europeans) from the comex vaults.

(Dave Kranzler/IRD/GATA)

Dave Kranzler: Delivery demands won’t break Comex but metal removal from vaults will

Submitted by cpowell on Fri, 2020-11-20 23:40. Section: Daily Dispatches

6:43p ET Friday, November 20, 2020

Dear Friend of GATA and Gold:

Dave Kranzler of Investment Research Dynamics in Denver writes today that “the price management team” in gold is striving to shake out gold futures longs before what are shaping up to be huge delivery demands on the December Comex contract.

Kranzler opines that these delivery demands themselves will not break the Comex but delivery demands that also move gold out of Comex vaults will break it.

Kranzler’s analysis is headlined “The Next Move for Silver and Gold,” links to an interview at Chris Marcus’ Arcadia Economics, and can be found at IRD here:

CHRIS POWELL, Secretary/Treasurer Gold Anti-Trust Action Committee Inc. CPowell@GATA.org

END

China’s central bank sees a bigger global role for the yuan as the dollar wanes. The problem is that many see China has the guilty party that brought on the virus and they do not want to do business with them.

South China Morning post/GATA

China’s central bank officials see bigger global role for yuan as dollar wanes

Submitted by cpowell on Sun, 2020-11-22 16:08. Section: Daily Dispatches

By He Huifeng and Guo Rui South China Morning Post, Hong Kong Sunday, November 22, 2020

The Chinese currency is set to play a bigger role in global trade and investment in the wake of the pandemic, with the dominance of the U.S. dollar in the international monetary system expected to decline, two Chinese central bank officials said on the weekend.

Ding Zhijie, head of a research centre at the State Administration of Foreign Exchange, said the yuan had become a sought-after asset for global investors seeking stability and absolute returns as government bonds denominated in the U.S. dollar, yen, and euro offered little or even negative, yields.

Whether you look at interest rates or exchange rates, yuan assets have clear advantages now” against assets denominated in other currencies, Ding said Saturday at the Understanding China Conference in the southern city of Guangzhou, an event hosted by China to promote the country’s global influence.

China’s five-year government bonds still offer an annual yield over 3 percent while U.S. government debt of the same maturity offers only 0.4 percent and the yield on German bonds is a negative rate of about 0.8 percent.

In addition, China’s quick economic recovery from the coronavirus has helped the yuan to appreciate to a two-year high against the U.S. dollar, despite the central bank’s efforts to slow the appreciation.

Ding’s optimistic message reflected Beijing’s fresh confidence that the yuan, despite its inconvertibility under the capital account, will play an increasingly important role on the international stage to indirectly undermine the anchor role of the U.S. dollar. …

A very important read…why this Professor at Tufts University is wrong in disparaging the gold standard

(Chris Powell/GATA)

A professor’s mistaken disparagement of the gold standard

Submitted by cpowell on Sun, 2020-11-22 17:31. Section: Daily Dispatches

12:38p ET Sunday, November 22, 2020

Dear Friend of GATA and Gold:

GATA does not advocate returning currency systems to a gold standard. This organization advocates free and transparent markets for the monetary metals and keeping government out of them.

Of course if governments adopted such a policy, people everywhere probably would remonetize gold as the world reserve currency in less than a week, diminishing the influence of government-issued money and thereby also diminishing government power.

That’s exactly why governments long have striven mightily — sometimes openly, sometimes surreptitiously — to drive gold out of the world financial system and discredit it as money. Gold is the most serious threat to government power and the strongest protector of individual liberty, a point that often has been made through the ages, almost back to the very invention of money, though it is most politically incorrect today.

Defending the monetary status quo this week, Michael Klein, professor of international economic affairs at the Fletcher School at Tufts University in Medford, Massachusetts, published an essay disparaging the gold standard and Federal Reserve Board nominee Judy Shelton for her sympathy to it.

Professor Klein’s essay, “What’s the Gold Standard, and Why Does the U.S. Benefit from a Dollar That Isn’t Tied to the Value of a Glittery Hunk of Metal?,” posted at The Conversation here —

— may express the financial establishment view well enough but it is so misleading and even erroneous as to deserve rebuttal.

Professor Klein notes that the international gold standard that worked well throughout the first century of the industrial age was dropped at the outbreak of World War I. But he doesn’t explain why it was dropped. That is, of course, because monetary gold imposes restraint on government and thereby hampers the waging of war.

Professor Klein writes: “Afterward, some countries such as the United Kingdom and United States continued to rely on gold as a centerpiece of their monetary policies, but lingering geopolitical tensions and the high costs of the war made it much less stable, showing its severe flaws in times of crisis.”

What this really means is that the gold standard kept getting in the way of stupid imperial wars and other governmental extravagance. Would the U.S. have waged so many such wars after disconnecting the dollar from gold in 1971 if the country didn’t also have the advantage of issuing the world reserve currency? That advantage freed the U.S. from monetary restraint and allowed the country to stick the rest of the world with the cost of those wars.

Professor Klein writes: “The onset of the Great Depression finally forced the U.S. and the other countries that still pegged their currencies to gold to abandon the system entirely. Economist Barry Eichengreen has found that efforts to maintain the gold standard at the beginning of the Great Depression ended up worsening the downturn because they limited the ability of central banks like the Fed to respond to deteriorating economic conditions. For example, while central banks today typically cut interest rates to boost a faltering economy, the gold standard required them to focus solely on keeping their currency pegged to gold.”

But this is misleading, since governments that believe they need more money under a gold standard can always devalue their currencies in gold terms. That’s exactly what the U.S. did in 1933 and 1934.

Professor Klein writes that since 1971, when President Nixon terminated the international convertibility of the dollar to a fixed weight of gold, “major currencies like the dollar have traded freely on global exchanges, and their relative value is determined by market forces.”

Free currency markets? Let’s hope that Professor Klein isn’t teaching that fable to his students. Apparently he has never heard about central bank currency market intervention generally or, particularly, about the Bank for International Settlements, which acknowledges that its primary purpose is to give camouflage to central banks in their rigging of the currency markets, including the gold market:

Professor Klein writes: “The dollar in your pocket is backed by nothing more than your belief that you’ll be able to buy a hot dog with it.”

Not so. Quite without formal convertibility to gold or to anything else the U.S. dollar and most government currencies are powerfully backed — by the taxing power of the governments that issue them. Indeed, governments that issue money that is not formally convertible at a fixed rate are free to issue essentially infinite amounts of money, as they lately have been doing, restrained only by the risk of currency devaluation. Governments issuing inconvertible currency impose taxes not to raise money for themselves to spend but to create demand for and give value to their currencies.

Professor Klein writes: “It is particularly odd, however, to advocate for a gold standard at a time when one of the main problems a gold standard would supposedly address — runaway inflation — has been low for decades.”

Apparently Professor Klein believes government data on inflation. But many people who live in the real world — people who, for example, pay taxes, medical insurance premiums, and college tuitions and who buy food — don’t believe it as much as Professor Klein does.

Professor Klein writes: “Clearly, it would be destabilizing if the dollar were pegged to gold when its price swings wildly. Exchange rates between major currencies are typically much more stable.”

But where does the volatility of the gold price come from? Has Professor Klein ever investigated surreptitious intervention in the gold market by governments and central banks, precisely to prevent price stability? He gives no indication of doing so.

Professor Klein writes in defense of the Federal Reserve: “The Federal Reserve is an independent agency that is vital to America’s economic stability and prosperity. Like the courts, it is important that it acts with integrity and free from political considerations.”

But if it is acting with integrity and serving the public interest, why is the Fed so often acting in secret as it bestows its monetary patronage on the favored few, especially investment banks? And since control of money and interest rates is essentially control of the value of all capital, labor, goods, and services in the world — control of nearly everything — how can this control be removed from politics without also removing it from democracy?

Maybe someday one of Professor Klein’s students will challenge him on these issues. That might be an interesting class.

CHRIS POWELL, H.S.G. Secretary/Treasurer Gold Anti-Trust Action Committee Inc. CPowellGATA.org

Central banks became net gold buyers in 2010, three years after the financial crisis. In response to Covid-19, major central banks have doubled down on unconventional policy measures, which have further depressed yields. In this context, do you expect gold to become increasingly attractive for reserve managers?

Gold remains an attractive asset class for reserve managers. Amid the uncertainties created by Covid-19, gold is acting as a ‘safe-haven asset’, which is reflected in higher gold prices. The other important consideration is the opportunity cost. Because of the crisis, central banks eased policies further and fiscal policies followed suit. In this context, the opportunity cost of holding gold has decreased further.

Gold allocations as a share of total reserves have increased substantially over the past decade due to an increase in purchases. Have gold purchases reached their ceiling and will this stem demand?

I do not think we are approaching this ceiling. First, recent surveys have revealed central banks are still willing to increase their gold exposures. Second, the drivers boosting the gold price are very powerful. The low and negative sovereign yield environment is very supportive. Geopolitical and global trade tensions also boost the gold price. For example, growing competition between China and the US is a long-term factor that will not go away after the pandemic or with a new US administration. Third, central banks in different regions look at gold in a different way than before the financial crisis. A very obvious sign of this was the termination of the Washington Agreement on Gold in 2019.

Exchange-traded funds (ETFs) have allowed the creation of a more liquid gold market. This development has been credited with contributing to higher prices over recent years. From a central banking perspective, has this development affected gold’s assessment as a reserve asset?

For reserve managers there is a basic triangle. We need liquid assets, safe assets, and we should avoid losses on them. This is very challenging to achieve in this low and negative environment, and to balance these three goals. In this context, liquidity is extremely important for central banks. Nonetheless, our approach to gold and ETFs is a little different to that of other investors. On the one hand, liquidity in gold markets is welcome and it has improved over recent years. But most central banks usually do not buy ETF products to gain exposure to gold, instead buying through the over-the-counter market. In the case of gold-producing countries, central banks buy gold from the national producers. Another important point separating reserve managers from other gold investors is that we do not normally trade gold on a daily basis. As a result, daily liquidity is less important.

In spite of sustained price increases and higher liquidity, the market has recorded high volatility over the past two years. In fact, since August, it has recorded a significant correction. To what extent can price volatility deter central banks considering a reconfiguration of their portfolios?

First, we should decide the way in which we look at gold through a proper evaluation of costs and benefits of holding gold reserves on a standalone basis. In my view, gold is a strategic asset that has room in foreign exchange reserves. From this perspective, the volatility of the gold price is only one of many factors to consider. The volatility stemming from the gold exposure should also be examined through the share of gold holdings and the correlation gold has with other assets in the reserves portfolio. You should consider the downside risk pressures stemming from other asset classes during periods of stress, when reserve managers need to deploy their reserves. This would usually require a scenario analysis to discover gold’s behaviour compared with that of other asset classes.

Róbert Rékási has been head of foreign exchange reserves management at the Central Bank of Hungary since 2013. Having joined in 2001, he has a 19-year career at the central bank, previously working as a portfolio manager. Rékási has been a chartered financial analyst (CFA) since 2008, and has been president of the CFA Society Hungary since 2016. He graduated with a degree in finance from Corvinus University in Budapest.

Over the past few years, gold has been praised as a source of protection from negative rates. However, its price has tended to move in tandem with other recently adopted reserve assets such as equities. Could this correlation diminish gold’s allure among reserve managers looking for higher diversification?

Looking at the structure of reserves globally, approximately two-thirds of central banks hold gold; only 25% of them invest in equities. Not every central bank considers the relationship between equities and gold. But I believe there are some common drivers between the price movements of gold and equities. But gold is a ‘two-faced’ asset. It’s true that central banks’ asset purchases ultimately boost equity prices during times of stress. We have seen that happening this year. But, in more conventional scenarios, gold tends to rise during crises as a safe-haven asset, offsetting losses you may record on riskier assets. And, more importantly, in contrast to equities, gold’s strength through economic turmoil is not dependent on central banking policies. It’s a much more reliable source of strength in crises.

A relatively small group of central banks – Russia, China and Turkey being the main players – have led gold purchases since the financial crisis. To what extent have their operations been aimed to reduce their exposures to the US dollar, and the effectiveness of US sanctions on their economies?

This goes beyond the traditional reason of holding gold reserves, and portfolio optimisation too. I am certain tensions between the US and China may have contributed to higher gold holdings in China and other countries with difficult bilateral relations with Washington, such as Turkey.

What is especially relevant in this regard is that gold is a very good source of liquidity for US dollars. We live in a dollar-centric global monetary system, and dollar access remains key for every single country. In this regard, reducing US Treasury holdings – while boosting gold – may reduce your immediate exposure to US actions, but still guarantees that, when needed, gold will allow you to raise dollars in the market.

The Central Bank of Hungary sharply increased gold holdings over the last decade to 31.5 tonnes. In June 2020, total reserves stood at €30.2 billion, and the current market value of its gold holdings is in excess of €2.1 billion, more than 5% of the portfolio’s value. What has been the rationale behind these purchases?

It was a long-term national and economic policy strategy decision to increase the size of our gold holdings. The decision was driven by stability objectives; there were no investment considerations behind holding gold reserves. In normal circumstances, gold has a confidence-building feature, so it may play a stabilising role and act as a major line of defence under extreme market conditions, in times of structural changes in the international financial system or during deep geopolitical crises. The central bank also decided to repatriate overseas gold holdings. Holding precious metals within the country is consistent with international trends, enhances financial stability and may strengthen market confidence in the Hungarian economy.

An alternative is to hold part of your holdings in major financial and gold trading centres such as London, New York or Switzerland. This is useful in terms of liquidity as you can lend gold through swap agreements in return for US dollars. It can also enhance returns, but this obviously depends on the specific objectives of central banks.

Poland has also followed a similar approach to boosting gold reserves and repatriating them. Do you think the negative rate environment in the eurozone makes gold more interesting for European Union member states that are not part of the eurozone, but have important exposures to the euro?

As mentioned, it was not the main consideration behind increasing the gold reserves of Hungary. Although, if we consider gold investments from a different angle, this is also a factor to bear in mind. If you don’t buy gold, will you buy more expensive German government Bunds? The negative interest rate environment can play a crucial role in many reserve managers’ minds. Non-eurozone member states, because of their economic ties, must keep some part of their reserves in euro. The question is to what extent: how much loss can these central banks bear year on year?

In August, central banks became net sellers of gold for the first time in 18 months. This was mainly the result of muted purchases, and large sales by one country. Uzbekistan reduced its gold reserves by almost 32 tonnes, thought to be connected to overall difficulties in financing the government’s response to the Covid-19 crisis. To what extent can we expect more countries using their gold portfolios to access hard currency in the months ahead?

I would stress once more that gold is a strategic asset. I do not see central banks starting to reduce their holdings significantly. However, some gold-producing countries can adopt this strategy, and Uzbekistan is an important producer. It is an interesting case; up to a point, you could compare it with Norway. Where the Scandinavians leverage oil resources to accumulate reserves and public assets, Uzbekistan has gold-mining activities it can exploit in a similar fashion. Very likely, the state is involved in the gold-mining industry, and the central bank acquires part of the production, which, in some circumstances, can be sold. If you consider the requirement for higher public spending because of Covid-19, it would make sense for them to engage in these operations. But, as a global trend, I do not see a meaningful number of reserve managers following them.

It is widely accepted that gold would thrive in a scenario of stagflation similar to that experienced in the second half of the 1970s. However, taking into account the current below-target medium-term inflation expectations, this seems unlikely. To what extent would you link the outlook for gold as a reserve asset with the evolution of inflation in the coming years?

I would not put too much emphasis on inflation in the short term. In theory, increasing global debt levels at some point could have an inflationary effect. But, in the current context, it is not an immediate threat. Changes to the market structure are more important than the inflation outlook for gold. In the last decade we saw how central banks became net gold buyers mainly because of the ultra-low-yield environment. The development of the ETFs market has boosted it even further. All of these moves took place in a context of subdued inflation. A bullish gold outlook does not depend on the world economy ending up in stagflation.

In August, the US Federal Reserve unveiled a new policy framework that will allow it to temporarily tolerate inflation above the 2% target. It announced in September that it will maintain the Fed funds rate at 0–0.25% through 2023. What repercussions do you expect this policy change to have on the gold market, and the thinking of reserve managers worldwide?

I think is very supportive for the gold market in the long run. Opportunity cost is an important driver of gold price, and yields do not look like they will be rising any time soon. The Fed is basically saying it will keep interest rates low for longer, at least until 2023. On the one hand, that is good for gold prices. On the other, it says it will allow inflation to temporarily be over the 2% target. Let us see whether that is possible but, if that happened, it would also support gold as a reserve asset. That is why I think the Fed’s new policy approach to average inflation targeting is so positive for gold.

So far during the Covid-19 crisis, emerging market currencies have remained stable as the reserve portfolios of their central banks. Could this indicate – alongside the weaker dollar fostered by a dovish Fed – gold’s role to hedge against currency depreciation has become less relevant for reserve managers?

In the 1980s and early 1990s, global reserves looked very different. Now portfolios are far larger. As a result, most emerging currencies are more stable than they used to be. Nevertheless, beyond the portfolio size, you need to consider asset allocations. In this respect, gold’s allocations remain unchanged or have even increased as portfolios have grown larger. Gold is a good hedge against inflation; it is the ultimate store of value. Even if economic fundamentals evolve, and requirements can vary from advanced to emerging economies, gold’s strengths remain.

This interview was conducted by Central Banking in October 2020

This feature will form part of the Central Banking focus report, Gold for central banking 2020

END

Due to the criminal conviction of trader Edmonds, the USA prosecution is seeking to halt the civil lawsuit. I was misinformed: all discoveries in a civil suit are public and because of that, the prosecution gives the defendants the right to plead the 5th if their testimony incriminates them

(courtesy zerohedge/Chris Powell)

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

A sign of JP Morgan Chase Bank is seen in front of their headquarters tower in New York.

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

A federal judge tells traders that they can combine cases (with the other 6 banks) as they accused JPMorgan of rigging the precious metals market

(courtesy CNBC)

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Spencer Platt | Getty Images

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

March 4.2019

Parker City News

JP Morgan faces potential class action lawsuit after guilty pleas by a former metals trader

Traders from across the U.S. are banding together to accuse J. P. Morgan Chase of manipulating precious metals markets for years.

At least six lawsuits, all making similar allegations against the nation‘s largest bank, have been filed in New York federal court in the past month, since federal prosecutors in Connecticut with a former J. P. Morgan Chase metals trader.

The cases could potentially include thousands of people who traded in the precious metals market. The White Plains, N.Y., law firm Lowey Dannenberg is asking the court to combine the cases and name it as the lead.

The law firm‘s commodities group is led by Vincent Briganti, the attorney who filed the first lawsuit on behalf of Dominick Cognata, a New York resident who alleges he suffered losses due to J. P. Morgan‘s trading conduct in the silver and gold futures and options markets.

A combined case, seeking class action status, would include anyone who purchased or sold futures contracts or an option on NYMEX platinum or palladium or COMEX silver or gold between at least Jan. 1, 2009, and Dec. 31, 2015. The lawyers believe that “at least hundreds, if not thousands” of traders would be eligible to join the case.

Named as defendants in all of the lawsuits are John Edmonds, a 36-year old former metals trader at J. P. Morgan, a group of yet-to-be-identified precious metals traders and the bank.

Edmonds, a New York resident, pleaded guilty in October to one count of conspiracy to defraud the market and manipulate prices of precious metals futures contracts and one count of commodities fraud. In the criminal plea, Edmonds admitted that he and other “unnamed co- conspirators” at J. P. Morgan, fraudulently manipulated precious metals markets from 2009 to 2015, the same time frame covered in the class action suits.

Briganti filed the initial class action on Nov. 7, just one day after the Justice Department unsealed Edmonds‘ plea in the U.S. District Court of Connecticut.

Edmonds admitted in his guilty plea that he deployed the illegal trading scheme hundreds of times with the direct knowledge and consent of his immediate supervisors. Plaintiffs say they have suffered economic injury, including monetary losses, as a direct result of actions by Edmonds and the other unnamed J. P. Morgan metals traders in the futures and options contracts.

One of the suits alleges that “the number of unlawful trades that JP Morgan traders executed in precious metals futures markets is at least in the thousands.”

J. P. Morgan declined to comment. Lowey Dannenberg did not respond to a request for comment by CNBC.

The Justice Department‘s criminal investigation is still ongoing and recently caused a separate related civil case to be put on hold for at least six months while the government continues its investigation. That civil lawsuit, which also accuses J. P. Morgan of rigging the precious metals market, was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders.

After reviewing the details of the plea agreement, David Kovel, the attorney for Shak‘s suit, sought to re- interview Edmonds, along with two other current and former senior traders at the bank. However, the government argued that reopening questioning would be detrimental to the ongoing criminal investigation. The federal judge overseeing the proceedings ordered a six-month stay in the civil case.

Kovel declined to comment.