GOLD:$1839.60 UP $5.70 The quote is London spot price

Silver:$23.98 UP 1 CENT London spot price ( cash market)

ACCESS MARKET

i)Gold : $1839.80 LONDON SPOT 4:30 pm

ii)SILVER: $23.94//LONDON SPOT 4:30 pm

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

c

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED DOWN 26.8 PTS OR .77% //Hang Sang CLOSED UP 95.28 PTS OR .36% /The Nikkei closed DOWN 103.72 POINTS OR 0.39%//Australia’s all ordinaires CLOSED DOWN 0.44%

/Chinese yuan (ONSHORE) closed DOWN AT 6.5463 /Oil UP TO 50.08 dollars per barrel for WTI and 46.71 for Brent. Stocks in Europe OPENED ALL RED// ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.5463. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.5374 TRADE TALKS STALL//YUAN LEVELS //TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED//CORONAVIRUS/PANDEMIC/TRUMP TESTS POSITIVE FOR COVID 19 : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

We had 1 kilobar transactions

ADJUSTMENTS: 1 //

The front month of DEC registered a total of 7704 contracts for a loss of 381. We had 395 notices filed upon yesterday so we GAINED A TINY 14 contacts or 1400 additional oz will stand in this very active delivery month of December as we witness a tiny queue jump by our bankers searching for gold metal to put out fires elsewhere. Our longs remain steadfast in refusing to morph into the paper EFP scheme in London.

January lost 130 contracts to stand at 2066 contracts. FEBRUARY LOST a STRONG 2383 contracts DOWN TO 397,796.

THE BIG STORY AGAIN TODAY IS THE HIGH INITIAL OI STANDING FOR DECEMBER (93.219 tonnes). LONGS STANDING FOR GOLD REFUSE TO TRAVEL TO LONDON

We had 1373 notice(s) filed today for 137300 oz OR 4.2706 TONNES.

To calculate the INITIAL total number of gold ounces standing for the DEC /2020. contract month, we take the total number of notices filed so far for the month (23,639) x 100 oz , to which we add the difference between the open interest for the front month of (DEC 7704 CONTRACTS ) minus the number of notices served upon today (1373 x 100 oz per contract) equals 2,997,000 OZ OR 93.209 TONNES) the number of ounces standing in this active month of DEC

thus the INITIAL standings for gold for the DEC/2020 contract month:

No of notices filed so far (23,639, x 100 oz +7704 OI) for the front month minus the number of notices served upon today (1373) x 100 oz which equals 2,997,000 oz standing OR 93.219 TONNES in this active delivery month of December. This is a HUGE amount for gold standing for DEC delivery month (generally the strongest delivery month of the year). THE COMEX IS UNDER A HUGE FRONTAL ATTACK FROM EUROPEAN BANKS SEEKING PHYSICAL METAL! JUDGING FROM THE INITIAL NOTICES FILED VS THE NUMBER OF NOTICES STANDING, IT WILL BE EXTREMELY DIFFICULT FOR OUR BANKERS TO FIND THE NECESSARY GOLD TO SATISFY OUR EUROPEANS.

NEW PLEDGED GOLD: BRINKS

455,219.430, oz NOW PLEDGED SEPT 15.2020/HSBC

60,784.803 PLEDGED APRIL 3/2020: SCOTIA:

deleted Int. Delaware pledge July 7 (600 tonnes)

292,197.145 oz JPM 8.70 TONNES

819,082.972 oz pledged June 12/2020 Brinks/

88,796.123 oz Pledged August 21/regular account 1.588 tonnes JPMORGAN

178,807.987 oz Pledged Nov 27.2021 MANFRA

total pledged gold: 1,894,888.460. oz 58.93 tonnes

total registered, pledged and eligible (customer) gold 37,562,919.025 oz 1,168.36 tonnes (INCLUDES 4 GC GOLD)

total 4 GC gold: 126.34 tonnes

total gold net of 4 GC: 1042.02 tonnes

end

I have compiled data with respect to registered (or dealer) gold taken on first day notice for each of the past 24 months

The data begins on first day notice for the May month taken on the last day of July 2018. and it continues to present day.

I then took, how many deliveries were recorded by the CME for each and every month. I also included for reference the price of gold on first day notice.

The first graph is a logarithmic graph and the second graph, linear.

You can see the huge explosion of registered gold at the comex along with deliveries.

THE GOLD COMEX SEEMS TO BE UNDER SEVERE ASSAULT FOR PHYSICAL

And now for the wild silver comex results

And now for the wild silver comex results

INITIAL STANDINGS

DEC. SILVER COMEX CONTRACT MONTH//INITIAL STANDING

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

|

Withdrawals from Customer Inventory |

5,909.244 oz

CNT

|

| Deposits to the Dealer Inventory |

579,415.620 oz

Scotia

|

| Deposits to the Customer Inventory |

1,047.860 oz

CNT

|

| No of oz served today (contracts) |

0

CONTRACT(S)

(nil OZ)

|

| No of oz to be served (notices) |

1015 contracts

5,075,000 oz)

|

| Total monthly oz silver served (contracts) | 8172 contracts

40,860,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

total dealer deposits: 579,415.620 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

we had 3 deposits into the customer account (ELIGIBLE ACCOUNT)

JPMorgan now has 192.787 million oz of total silver inventory or 48.95% of all official comex silver. (192.787 million/393.834 million

into

ii) CNT; 178,583.500 oz

iii) Scotia: 20,821.290 oz

total customer deposits today: 1,338,694.313 oz

we had 0 withdrawals:

total withdrawals oz

We had 0 adjustments

Total dealer(registered) silver: 147.785million oz

total registered and eligible silver: 393.834 million oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

December saw a LOSS of 80 contracts DOWN to 1015 contracts. We had 80 notices served upon yesterday so we LOST 0 contracts or nil additional oz will stand in this very active delivery month of December as longs refused to morph into London based forwards.

January saw a gain of 79 contracts up to 1211. FEBRUARY saw another gain of 17 contracts to stand at 152. MARCH gained 172 contracts up to 131,230.

The total number of notices filed today for DEC 2020. contract month is represented by 0 contract(s) FOR nil oz

To calculate the number of silver ounces that will stand for delivery in DEC we take the total number of notices filed for the month so far at 8172 x 5,000 oz = 40,860,000 oz to which we add the difference between the open interest for the front month of DEC ( 1015) and the number of notices served upon today 0x (5000 oz) equals the number of ounces standing.

Thus the DEC standings for silver for the DEC/2019 contract month: 8172 (notices served so far) x 5000 oz + OI for front month of DEC(1015)- number of notices served upon today (0) x 5000 oz of silver standing for the NOV contract month .equals 45,935,000 oz. ..VERY STRONG FOR AN ACTIVE DEC MONTH.

We LOST 0 contracts or nil additional oz will stand as they as they refused to morph into London based forwards.

There is not enough gold or silver over here for our bankers to steal from.

TODAY’S ESTIMATED SILVER VOLUME 51,859 CONTRACTS // volume falling//

FOR YESTERDAY 62,773 ,CONFIRMED VOLUME// falling

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO- 4,28% ((DEC 11/2020)

2. Sprott gold fund (PHYS): premium to NAV RISES TO 2.31% to NAV: (DEC 11/2020 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into NEGATIVE/4,28% (DEC 11)

(courtesy Sprott/GATA

3. SPROTT CEF .A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 18.90 TRADING 18.00///NEGATIVE 4.74

END

And now the Gold inventory at the GLD

DEC 11/WITH GOLD UP $5.70 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1179.78 TONNES

DEC 10/WITH GOLD DOWN $2.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1179.78 TONNES

DEC9/ WITH GOLD DOWN $35.30 TODAY, NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1179.78 TONNES

DEC 8//WITH GOLD UP $9.35 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD/: ANOTHER WITHDRAWAL OF 3.52 TONNES FROM THE GLD/INVENTORY RESTS AT 1179.78 TONNES// THIS IS AN ABSOLUTE FRAUD TO THE HIGHEST DEGREE AND SIMILAR TO THE THEFT OF THE USA ELECTION.!!

DEC 7/WITH GOLD UP $29.55 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//: A WITHDRAWAL OF 7.12 TONES OF GOLD FROM THE GLD///INVENTORY RESTS TONIGHT AT 1182.70 TONNES

DEC4//WITH GOLD DOWN $1.00 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY: A WITHDRAWAL OF 1.46 TONNES FROM THE GLD// RESTS AT 1189.82 TONNES.

DEC 3/WITH GOLD UP $10.60 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS TONIGHT AT 1191.28 TONNES

DEC 2/WITH GOLD UP $12,00 TODAY: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD//: A WITHDRAWAL OF 3.51 TONNES FROM THE GLD//INVENTORY RESTS AT 1191.28 TONNES

DEC 1//WITH GOLD UP $38.55 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLDE//INVENTORY RESTS AT 1194.78 TONNES

NOV 30/WITH GOLD DOWN $11.85 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1194.78 TONNES

NOV 27/WITH GOLD DOWN $18.90 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.96 TONNES OF GOLD FROM THE GLD…//INVENTORY RESTS AT 1194.78 TONNES

NOV 25//WITH GOLD UP $0.05 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE PAPER WITHDRAWAL OF 13.43 TONNES FROM THE GLD..IS THE GLD MAKING GOLD VAPOUR DELIVERIES FOR THE COMEX?//INVENTORY REST AT 1199.74 TONNES

NOV 24/WITH GOLD DOWN $33.00 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.00 TONNES FROM THE GLD//INVENTORY RESTS AT 1213.17 TONNES

NOV 23/WITH GOLD DOWN $33.95 TODAY: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.9 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 1220.17 TONNES

NOV 20/WITH GOLD UP $11.10 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD// A WITHDRAWAL (ROBBERY) OF 1.74 TONNES FROM THE GLD//INVENTORY RESTS AT 1217.26 TONNES

NOV 19/WITH GOLD DOWN $9.80 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.30 TONES FROM THE GLD////INVENTORY REST AT 1219.00 TONNES

NOV 18/WITH GOLD DOWN $13.50 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.10 TONNES FROM THE GLD INVENTORY//INVENTORY RESTS AT 1226.30 TONNES

NOV 17/WITH GOLD DOWN 3 DOLLARS TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.92 TONNES FROM THE GLD////INVENTORY RESTS AT 1231.40 TONNES

NOV 16/WITH GOLD UP $2.20 TODAY/A HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 5.25 TONNES FROM THE GLD////INVENTORY RESTS AT 1234.32 TONNES

NOV 13/WITH GOLD UP $11.90 TODAY//A HUGE CHANGE IN GOLDINVENTORY AT THE GLD; A WITHDRAWAL OF 1.17 TONNES FROM THE GLD////INVENTORY RESTS AT 1239.57 TONNES

Nov 12/WITH GOLD UP $11.00 TODAY: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A PAPERWITHDRAWAL OF 9.02 TONNES FROM THE GLD///INVENTORY RESTS AT 1240.74 TONNES

NOV 11/WITH GOLD DOWN $13.10 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1249.79 TONNES/

NOV 10/WITH GOLD UP $20.10 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 10.51 TONNES/INVENTORY RESTS AT 1249.79 TONNES

NOV 9/WITH GOLD DOWN $88.45 TODAY: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIST OF 7.88 TONNES INTO THE GLD///INVENTORY RESTS AT 1260.30 TONNES

NOV 6/WITH GOLD UP $5.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1252.42 TONNES

NOV 5/WITH GOLD UP $51.45 TODAY: STRANGELY A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.5 TONNES FROM THE GLD////INVENTORY RESTS AT 1252.42 TONNES

NOV 4/WITH GOLD DOWN $9.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1255.92 TONNES

NOV 3//WITH GOLD UP $16.85 TODAY: STRANGE!!! A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER WITHDRAWAL OF 1.75 TONNES FROM THE GLD////INVENTORY RESTS AT 1255.92 TONNES

NOV 2/WITH GOLD UP $13.60 TODAY: A SMALL CHANGE IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF .58 TONNES AND THIS IS GENERALLY TO PAY FOR FEES (STORAGE/INSURANCE)//INVENTORY RESTS AT 1257.67 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Inventory rests tonight at

DEC 11/ GLD INVENTORY 1179.78 tonnes

LAST; 967 TRADING DAYS: +235.71 TONNES HAVE BEEN ADDED THE GLD

LAST 867 TRADING DAYS// +413.20 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY

Now the SLV Inventory

DEC 11/WITH SILVER UP 1 CENT TODAY: TWO CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.859 MILLION OZ IN THE MORNING AND A LATE WITHDRAWAL OF 1.394 MILLION OZ FROM THE SLV ////INVENTORY RESTS AT 547.98- MILLION OZ..

DEC 10./WITH SILVER UP 8 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 551.233 MILLION OZ//

DEC 9/ WITH SILVER DOWN 76 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.974 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 551.233 MILLION OZ.

DEC 8/WITH SILVER UP 1 CENT TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESS AT 548.259 MILLION OZ//

DEC 7/WITH SILVER UP 51 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 548.259 MILLION OZ//

DEC4// WITH SILVER UP 11 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.953 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 548.259 MILLION OZ//

DEC 3//WITH SILVER UP 4 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV/ A WITHDRAWAL OF 236,000 OZ/INVENTORY RESTS AT 546.306 OZ

DEC 2/WITH SILVER UP ONE CENT TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.231 MILLIONOZ INTO THE SLV//INVENTORY RESTS AT 546.542 MILLION OZ//

DEC 1/WITH SILVER UP $1.46 TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.311 MILLION OZ/

NOV 30/WITH SILVER DOWN 15 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.311 MILLION OZ.

NOV 27/WITH SILVER DOWN $0.69 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV/: A WITHDRAWAL OF 1.813 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 544.311 MILLION OZ.

NOV 25/WITH SILVER UP $0.05 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.091 MILLION PAPER OZ FROM THE SLV //// IS THE SLV MAKING SILVER VAPOUR DELIVERIES FOR THE COMEX?//INVENTORY RESTS AT 550.215 MILLION OZ..

NOV 24/WITH SILVER DOWN 33 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 10.322 MILLION OZ FROM THE SLV..//INVENTORY REST AT 550.215 MILLION OZ

AND IF ANYBODY BELIEVES THIS GARBAGE, WE HAVE A GREAT PROPERTY TO SELL YOU (FLORIDA SWAMP LANDS).

NOV 23/WITH SILVER DOWN $.70 TODAY: A HUGE CHANGE IN SILVER AT THE SLV; A WITHDRAWAL OF 2.046 MILLION OZ FROM//INVENTORY RESTS AT 562.583 MILLION OZ

NOV 20//WITH SILVER UP $0.32 TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 52.583 MILLION OZ//

NOV 19/WITH SILVER DOWN 35 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV:2 TRANSACTIONS:1) A WITHDRAWAL OF 1.396 MILLION OZ AND 2). 2.602 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 562.583 MILLION OZ

NOV 18/WITH SILVER DOWN 23 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1581 MILLION OZ FROM THE SLV…//INVENTORY RESTS AT 566.581 MILLION O

NOV 17/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 568.162 MILLION OZ//

NOV 16/WITH SILVER UP $.05 TODAY//A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDDRAWAL OF 1.209 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 568.162 MILLION OZ//

NOV 13/WITH SILVER UP 43 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV” A WITHDRAWAL OF 2.88 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 569.371 MILLION OZ.

NOV 12/WITH SILVER DOWN 2 CENTS TODAY: NO CHANGES IN SILVER INVENTORY FROM THE SLV//INVENTORY RESTS AT 572.254 MILLION OZ

NOV 11/WITH SILVER DOWN 8 CENTS TODAY: A HUGE 3.627 MILLION OZ WITHDRAWAL FROM THE SLV/ INVENTORY RESTS AT 572.254 MILLION OZ

NOV 10/WITH SILVER UP $.65 TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: STRANGE ANOTHER HUGE DEPOSIT OF 4.739 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 575.881 MILLION OZ

NOV 9/WITH SILVER DOWN $1.76 TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 10.324 MILLION OZ ADDED INTO THE SLV INVENTORY////INVENTORY RESTS AT 571.742 MILLION OZ

NOV 6/WITH SILVER UP 47 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 561.418 MILLION OZ//

NOV 5/WITH SILVER UP $1.21 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 561.418 MILLION OZ..

NOV 4/WITH SILVER DOWN 43 CENTS TODAY: TWO HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A) WITHDRAWAL OF 240,000 OZ FROM SLV//// AND THEN B) A DEPOSIT OF 1.83 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 561.418 MILLION OZ

NOV 4/WITH SILVER DOWN 43 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WIHDRAWAL OF 240,000 OZ FROM SLV////INVENTORY RESTS AT 559.558 MILLION OZ

NOV 3/WITH SILVER UP 29 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT 559.798 MILLION OZ///

NOV 2/WITH SILVER UP 40 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 559.798 MILLION OZ//

DEC 11.2020:

SLV INVENTORY RESTS TONIGHT AT 547.980 MILLION OZ/

Great and Wonderful Friday Morning Folks,

February Gold is trading flat to lower with the last price at $1,834.60, down $2.80 after the dip to $1,826.80 with the high to beat at $1,844.40. March Silver is down 16.4 cents with the last price at $23.90, recovering from the low at $23.69 with the high at $24.195. At this second, the US Dollar is virtually flat at 90.82, oops, now it’s up 18.8 at 91.005, as this trade (game) continues to play out with the high at 91.05 and the low at 90.63. Of course, all this happened, while few are watching, before 5 am pst, the Comex open, the London close, and about an hour and fifteen minutes after this currency swap agreement started again before Monday’s Comex Currency rollover.

In Venezuela, Gold is now priced at 18,323.07 Bolivar, providing another 58.92 discount for today’s buyer over yesterday’s trades with Silver’s last swap at 238.701, down only 0.699 of a Bolivar. Argentina’s Peso price for Gold is now at 150,509.38, a loss of 376.07 A-Peso’s overnight with Silver down 4.03 A-Peso’s with the last trade at 1,960.97. Turkey’s Lira price for Gold is now at 14,477.39, down only 6.65 T-Lira with Silver’s last price at 188.602, barely registering a loss of 0.027 of a T-Lira. Since this US Dollar Currency agreement was popped in this past Wednesday, the emerging markets currencies we watch, apparently have had only minor corrections.

December Silver’s Delivery Demands now has a total of 1,015 fully paid for contracts waiting for receipts and with a Volume of 2 up on the board with one price at $23.985, down 4.6 cents while paper pushes the futures prices even lower. Yesterday’s activity inside the delivery’s happened in between a high of $24.31 and the low of $23.945 with the last swap at $24.02, a gain of 9 cents with the Comex Close Calculated at $24.031, registering a gain of 10.1 cents, that had a total of 23 swaps helping to reduce the Demand count by 80 contracts that got their receipts somewhere in the mix between here and London. Silver’s Overall Open Interest gained 432 additional contracts in order to add liquidity bringing this early morning total to 154,316 paper contracts to trade against what’s left of the physicals.

December Gold’s Delivery Demands are still super elevated with the count at 7,704 fully paid for contracts and with a Volume of 16 up on the board with a trading range between $1,838.50 and $1,829.10 with the last agreed upon swap at $1,833.90, up 30-cents so far today. Yesterday’s full Ice/Comex trades happened in between $1,849.10 and $1,828 with the last swap at $1,835.50, a gain of 90 cents, with the Calculated Comex Close at $1,833.60 proving a $1 loss that had a total of 177 contracts swapping hands helping to reduce the demand count by 381 contracts that got receipts or something. Gold’s Overall Open Interest is showing the pump and dump play as they continue to control the prices bringing todays early morning total to 543,159 contracts as 2,550 short trades left the field of play since yesterday morning’s count.

I’ve observed the US Dollar’s activity over the past few days and cannot think of any other way to describe what has happened, except to say, this is organized. This is not the first time these trades have occurred, and I am curious why none of the currency experts have yet to address this anomaly? Maybe there are no more currency experts anymore, since it’s all under the control of a computer Algo.

While this agreed upon trade continues, we see more European bonds go negative, after the ECB pumped in a half a billion Euro’s to keep the system afloat for a little longer. Some of Italy’s, Portugal, (as well as other nations under EU control), debts have already turned, now Spain’s debt-plays, have been added to the list, and have turned negative. We expect the rest to eventually do the same as we move forward into the great reset.

Today is the first day of Hannukah, in which we offer a deep bow of respect, with next week being the Triple Witch Week, where the currencies get rolled out into the next quarter (March), US Treasuries and debts get settled and rolled, and then the stock options, single stock futures, get cleared. In short, a giant central banker’s inventory count. This is also the last TWW of the year, and we still are waiting for the Supreme court to hear the electoral arguments. What can go wrong?

Have a great weekend and keep smiling. Gold and Silver in hand, has made many, comfortable because it’s no longer at risk inside the markets. Keep it close and hold on tight. As always …

Stay Strong!

Jeremiah Johnson

More J.Johnson content is available with purchase of a JSMineset subscription.

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

March 4.2019

Parker City News

JP Morgan faces potential class action lawsuit after guilty pleas by a former metals trader

Traders from across the U.S. are banding together to accuse J. P. Morgan Chase of manipulating precious metals markets for years.

At least six lawsuits, all making similar allegations against the nation‘s largest bank, have been filed in New York federal court in the past month, since federal prosecutors in Connecticut with a former J. P. Morgan Chase metals trader.

The cases could potentially include thousands of people who traded in the precious metals market. The White Plains, N.Y., law firm Lowey Dannenberg is asking the court to combine the cases and name it as the lead.

The law firm‘s commodities group is led by Vincent Briganti, the attorney who filed the first lawsuit on behalf of Dominick Cognata, a New York resident who alleges he suffered losses due to J. P. Morgan‘s trading conduct in the silver and gold futures and options markets.

A combined case, seeking class action status, would include anyone who purchased or sold futures contracts or an option on NYMEX platinum or palladium or COMEX silver or gold between at least Jan. 1, 2009, and Dec. 31, 2015. The lawyers believe that “at least hundreds, if not thousands” of traders would be eligible to join the case.

Named as defendants in all of the lawsuits are John Edmonds, a 36-year old former metals trader at J. P. Morgan, a group of yet-to-be-identified precious metals traders and the bank.

Edmonds, a New York resident, pleaded guilty in October to one count of conspiracy to defraud the market and manipulate prices of precious metals futures contracts and one count of commodities fraud. In the criminal plea, Edmonds admitted that he and other “unnamed co- conspirators” at J. P. Morgan, fraudulently manipulated precious metals markets from 2009 to 2015, the same time frame covered in the class action suits.

Briganti filed the initial class action on Nov. 7, just one day after the Justice Department unsealed Edmonds‘ plea in the U.S. District Court of Connecticut.

Edmonds admitted in his guilty plea that he deployed the illegal trading scheme hundreds of times with the direct knowledge and consent of his immediate supervisors. Plaintiffs say they have suffered economic injury, including monetary losses, as a direct result of actions by Edmonds and the other unnamed J. P. Morgan metals traders in the futures and options contracts.

One of the suits alleges that “the number of unlawful trades that JP Morgan traders executed in precious metals futures markets is at least in the thousands.”

J. P. Morgan declined to comment. Lowey Dannenberg did not respond to a request for comment by CNBC.

The Justice Department‘s criminal investigation is still ongoing and recently caused a separate related civil case to be put on hold for at least six months while the government continues its investigation. That civil lawsuit, which also accuses J. P. Morgan of rigging the precious metals market, was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders.

After reviewing the details of the plea agreement, David Kovel, the attorney for Shak‘s suit, sought to re- interview Edmonds, along with two other current and former senior traders at the bank. However, the government argued that reopening questioning would be detrimental to the ongoing criminal investigation. The federal judge overseeing the proceedings ordered a six-month stay in the civil case.

Kovel declined to comment.

Edmonds was originally scheduled to be sentenced in Hartford, Conn., on Wednesday, Dec. 19, but a court filing on Nov. 27 shows the sentencing has been postponed until June. A spokesman for the U.S. Attorney for Connecticut could not elaborate on why the sentencing was postponed since the court filing is under seal.

-END-

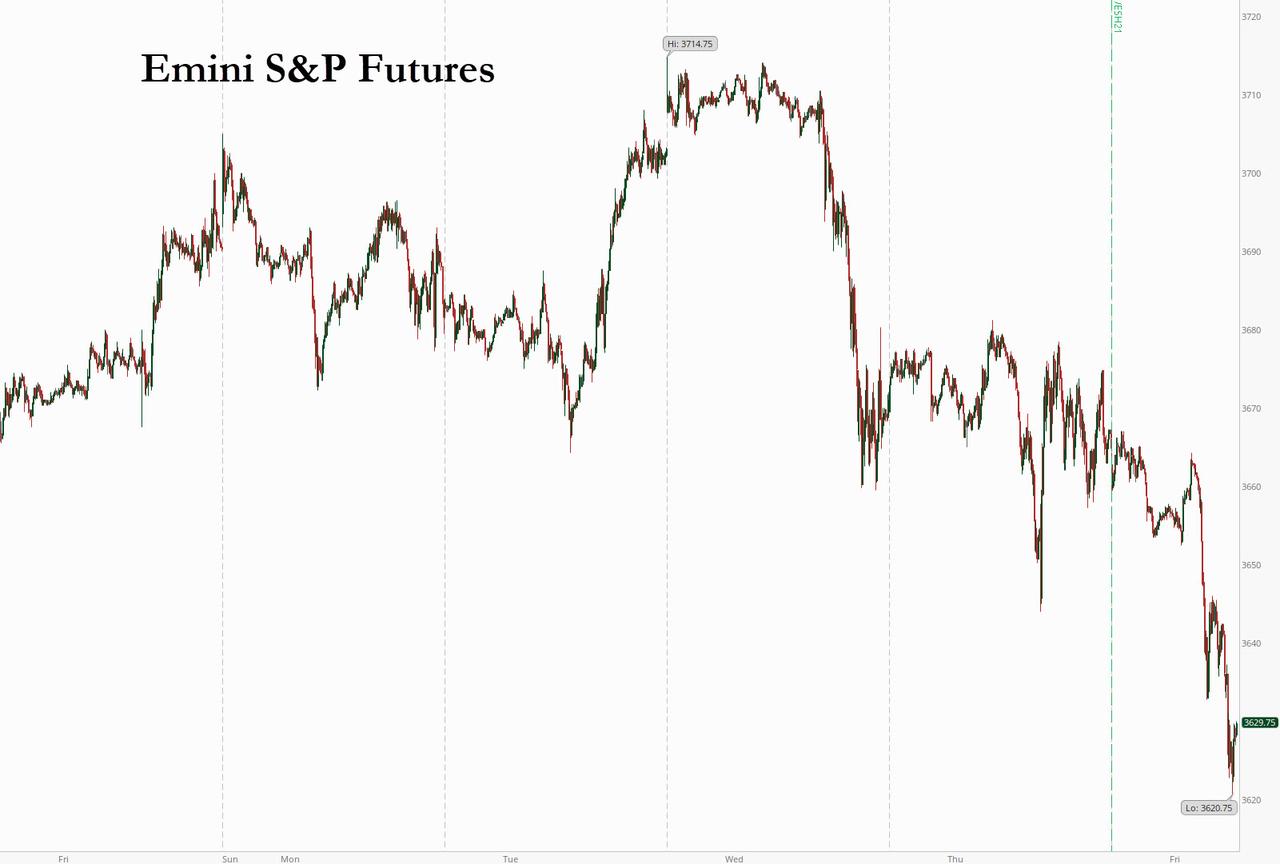

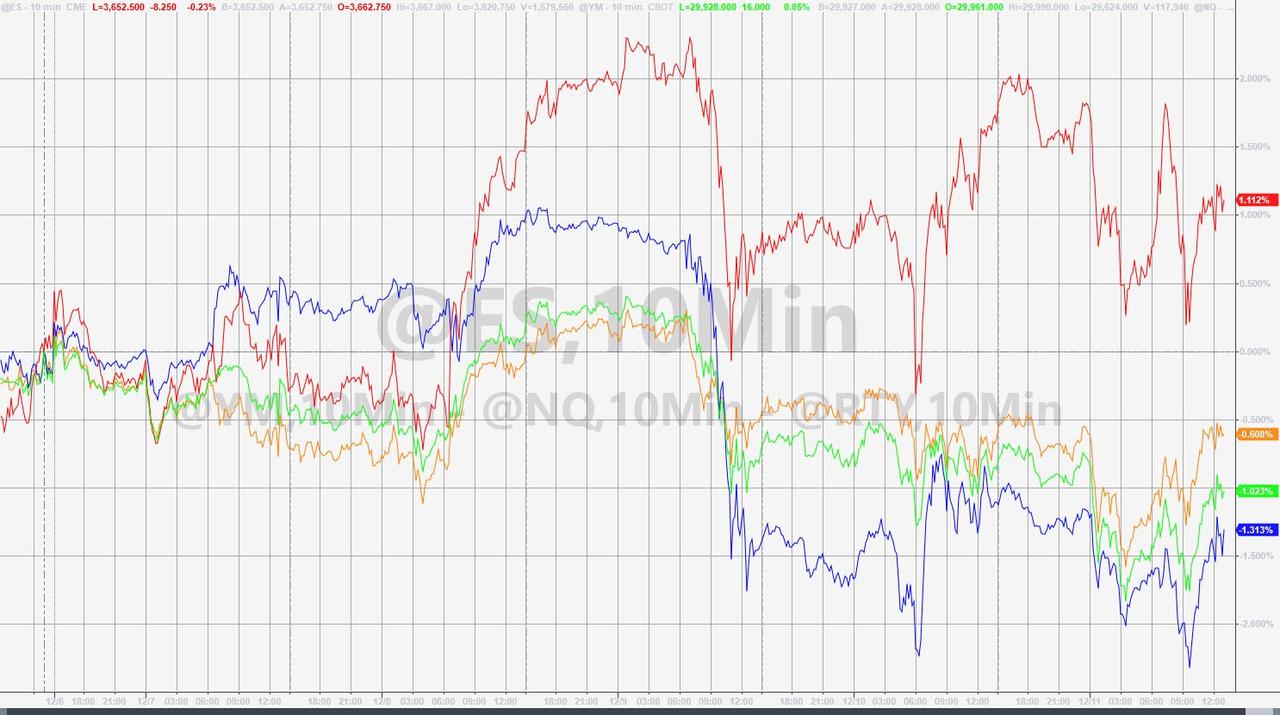

FUTURES TUMBLE ON STALLED STIMULUS TALKS, BREXIT CHAOS

Global markets dropped on Friday as Brexit negotiations appeared on the verge of collapse, while delays over a new fiscal stimulus package and surging coronavirus infections hit risk appetite pushing S&P futures and sterling lower as Treasurys rose and the dollar and the dollar jumped most in two weeks.

At 7am, Dow futures were down 213 points, or 0.7%, S&P 500 E-minis were down 28. points, or 0.8%, and Nasdaq 100 E-minis were down 92.75 points, or 0.7%. Global stock markets were also subdued, with the MSCI world equity index, sliding into the red after scaling record highs earlier this week as the UK became the first country in the world to begin a mass COVID-19 vaccination program. Cyclical stocks led declines in premarket trading on Friday, with energy, industrial and financial sectors all lower. Wells Fargo and JPMorgan slid more than 1%, while industrial bellwethers Boeing and 3M fell 1.6% and 0.9% respectively. Mastercard dropped 1.4% after the UK Supreme Court gave the green light for a $18.5 billion class action against the company for allegedly overcharging more than 46 million people in Britain over a 15-year period.

Global markets slumped after the latest episode in the neverending drama that is Brexit, when Prime Minister Boris Johnson said on Thursday there was “a strong possibility” Britain and the European Union would fail to strike a trade deal. Britain and the EU have set a deadline of Sunday to find an agreement, before Britain’s exit from the bloc on Jan. 1. The odds of a disorderly Brexit rose to 61% on Friday from 53% a day before, according to the Smarkets exchange.

With fresh lockdowns in many states and the US economy rapidly sliding into a double dip, investors are hoping for more fiscal relief to sustain a nascent economic recovery. But an agreement remains elusive after Nancy Pelosi said wrangling over a spending package and coronavirus aid could drag on through Christmas. It wasn’t all bad news: on Thursday, a panel of outside advisers to the FDA voted overwhelmingly to endorse emergency use of Pfizer’s COVID-19 vaccine, sending shares of the drugmaker up 1.9% in premarket trading.

European equities fell, with the broad Euro STOXX 600 down 1.2% and indexes in Paris and London losing 1.2% and 1% respectively on the abovementioned Brexit fears and after Germany said the continent’s biggest economy had record virus cases and deaths. Sanofi dropped on news that its Covid-19 shot failed to produce a strong enough response in older people. The FTSE 250 index underperformed, with Brexit-sensitive stocks declining and travel and leisure names pulled lower by concerns about higher restrictions on London. U.K. Prime Minister Boris Johnson warned businesses and the public to get ready for a no-deal Brexit as negotiations with the European Union falter.

Earlier in the session, Asian shares rose led by energy shares and putting the regional benchmark stock gauge on course for a sixth straight weekly gain. The MSCI Asia Pacific Index was up 0.3%; Hong Kong-listed Cnooc rallied 6.1%, recovering from recent declines following its addition to a U.S. blacklist. China Petroleum & Chemical climbed 4.5% as oil prices headed for a weekly advance, while in India, Oil & Natural Gas Corp. surged as much as 14% after Morgan Stanley upgraded the stock. Meanwhile, investors in China’s stock market are getting uneasy after a stellar year as insiders step up share sales and concerns about liquidity surface. The Shanghai Composite Index’s 2.8% drop this week has made it the second worst-performing major equity benchmark globally. Malaysia’s equity benchmark rallied 1.8% on Friday to be the top performer in Asia, as the ringgit erased virus-fueled losses for the year to climb to the strongest level since July 2018.

As Bloomberg notes, stocks were choppy this week as the fate of an additional relief package in Washington remained unresolved as Democrats and Republicans continue to negotiate. A disappointing jobs report and a strong 30-year auction of Treasuries on Thursday signaled investor caution over whether fresh economic stimulus will come before year-end. On the other hand, stellar demand for recent U.S. initial public offerings suggested investors remain upbeat on equities, even as job data pointed to weakness in the world’s biggest economy. Shares of Airbnb Inc more than doubled in their stock market debut on Thursday, valuing the home rental firm at just over $100 billion in the biggest U.S. initial public offering of 2020. DoorDash stocks doubled in their first day of trading.

In rates, Treasuries followed gilts higher during London session after Bank of England Governor Andrew Bailey said the central bank had a lot in its armory in the event of Brexit disruption. Yields dropped by 1bp-2bp across intermediates; 10-year almost 2bp lower at 0.888%, near low end of 0.88%-0.974% weekly range and ~8bp lower on week. U.K. 10-year ~4bp lower on the day, nearly 20bp on week.

In FX, the dollar rebounded the most in two weeks, rising 0.2% against a basket of six major currencies; the pound lost 0.5%, and was set to end five straight weeks of gains as currency traders weighed an expected hit to the British economy should the sides fail to agree a deal. “Investors are right to be worried,” said Olivier Marciot, a portfolio manager at Unigestion. “If there is no deal, there will be implications. There could be some sort of correction.” Emerging-market currencies were poised for a sixth week of gains, thanks in part to the dollar’s recent weakness. The euro held not far from two-and-a-half-year highs of $1.2140 after the European Central Bank delivered a fresh stimulus package that was broadly in line with market expectations on Thursday.

In commodities, oil prices were flat after Brent hit levels not seen since early March on Thursday, as coronavirus vaccination rollouts fuelled hopes that crude demand would pick up in 2021. Brent crude rose 0.1% to $50.36 per barrel.

Looking at the day ahead, data releases from the US include the November PPI reading and the University of Michigan’s preliminary consumer sentiment index for December, while from Europe there’s Italian industrial production for October. Central bank speakers include the ECB’s Holzmann, Hernandez de Cos and Centeno, along with the Fed’s Quarles and George.

Market Snapshot

- S&P 500 futures down 0.5% to 3,651.25

- STOXX Europe 600 down 0.7% to 390.32

- MXAP up 0.3% to 194.85

- MXAPJ up 0.2% to 644.89

- Nikkei down 0.4% to 26,652.52

- Topix up 0.3% to 1,782.01

- Hang Seng Index up 0.4% to 26,505.87

- Shanghai Composite down 0.8% to 3,347.19

- Sensex up 0.2% to 46,054.37

- Australia S&P/ASX 200 down 0.6% to 6,642.58

- Kospi up 0.9% to 2,770.06

- German 10Y yield fell 2.5 bps to -0.628%

- Euro down 0.08% to $1.2128

- Italian 10Y yield fell 2.0 bps to 0.451%

- Spanish 10Y yield fell 2.0 bps to 0.002%

- Brent futures down 0.6% to $49.97/bbl

- Gold spot little changed at $1,837.04

- U.S. Dollar Index up 0.1% to 90.91

Top Overnight News from Bloomberg

- European Commission President Ursula von der Leyen warned that a no-deal split with the U.K. is the likeliest outcome on Dec. 31 as last-ditch talks to try to reach a deal before Sunday continue in Brussels

- Germany’s daily coronavirus cases and deaths rose the most since the pandemic began, increasing pressure on authorities to impose a hard lockdown over the holiday season

- London Mayor Sadiq Khan beefed up the policing of Covid rules and announced more community testing in the capital in an effort to avoid having the city placed under the U.K.’s toughest virus restrictions

- Sanofi and GlaxoSmithKline Plc, two of the world’s biggest vaccine makers, delayed advanced trials of their experimental Covid-19 shot after it failed to produce a strong enough response in older people, pushing its potential availability to the end of next year

- Wall Street’s biggest banks are predicting the coronavirus-hit world economy will crawl through the early days of 2021 before bouncing back as vaccines and more fiscal stimulus flow into it

- The average forecast from strategists is that the Stoxx Europe 600 Index will climb 6.6% from Wednesday’s close. After a year that’s seen the index plummet 36% in just a few weeks and then claw back most of those losses, it’s an outlook that seems downright undramatic

- A group of 30 asset managers overseeing a combined $9 trillion of assets said they will support efforts to limit global warming by running carbon-neutral investment portfolios by 2050 or sooner

- After wobbling in November, when several European nations imposed fresh lockdowns to combat the spread of Covid-19, demand for gasoline and diesel is accelerating again, according to an index compiled by Bloomberg News tracking dozens of high frequency indicators for road usage, and traffic in countries accounting for more than 70% of global petroleum consumption

Courtesy of Nesquawk, here is a breakdown of the latest developments in global markets:

Asian equity markets traded mixed following a similar subdued performance on Wall Street where sentiment was mired by an increase in jobless claimant numbers and as congressional leaders remained at loggerheads on COVID-19 relief, with rampant infections stateside and no-deal Brexit concerns across the pond also contributing to the cautious tone. ASX 200 (-0.6%) was pressured by underperformance in healthcare after CSL abandoned trials of its COVID-19 vaccine as it generated antibodies that caused false positives on HIV tests, although losses in the index were initially tempered by strength in tech and with mining names buoyed by upside in iron ore and nickel prices. Nikkei 225 (-0.3%) was dragged by currency effects and amid weak same-store sales from convenience store operators Seven & I and Lawson, while KOSPI (+1.0%) was underpinned after preliminary data showed South Korean Exports during the first 10 days in December jumped 26.9% Y/Y. Hang Seng (+0.5%) and Shanghai Comp. (-1.1%) were varied with Hong Kong lifted by notable gains in the energy giants, although the mainland was subdued after the PBoC drained CNY 350bln liquidity for the week and China’s Foreign Ministry announced reciprocal sanctions to target members of US Congress. Finally, 10yr JGBs eked mild gains amid the mostly uninspired risk appetite and with prices spurred by the BoJ rinban operation in which the central bank was in the market for over JPY 1.3tln of JGBs in 1yr-10yr maturities.

Top Asian News

- Sri Lanka Debt Concerns Mount After Downgrade Deeper Into Junk

- China Toymaker Joins Global IPO 1st-Day Pop Party with 79% Jump

- Chinese Authorities Detain Bloomberg News Beijing Staff Member

- Singapore’s Sea Raises $2.6 Billion in Upsized Stock Offering

European equities (Eurostoxx 50 -1.3%) have extended on opening losses as Brexit jitters continue to resonate ahead of Sunday’s self-imposed “deadline”. More specifically, losses after the cash open accelerated after EU Commission President von der Leyen stated that after her meeting with UK PM Johnson on Wednesday, a no deal Brexit is now the most likely option. Although this has echoed comments from other officials in recent days, as Sunday nears and differences remain unresolved, markets will continue to price in the likelihood of an no deal outcome. Accordingly, analysts at Morgan Stanley suggest that a no deal outcome could trigger a 6-10% sell-off in the FTSE 250 and 10-20% decline in banking stocks amid a move into NIRP for the BoE. These fears have subsequently weighed on the likes of Natwest (-6.7%), Lloyds (-4.2%) and Barclays (-3.7%) and overshadowed yesterday’s announcement by the PRA that it judges there is scope for banks to recommence some distributions. Other risks on the horizon, albeit of greater interest stateside is the ongoing logjam on Capitol Hill amid ongoing divisions in stimulus discussions and with the Senate still to vote on the stopgap bill to avert a government shutdown heading into today’s midnight deadline; equity index futures in the US are softer, with the e-mini S&P lower by 0.5%. Sectors in Europe trade lower across the board with telecoms lagging amid losses in Ericsson (-5.5%) after the Co. launched legal action filed against Samsung in the US for non-compliance to FRAND commitments. Sanofi (-2.5%) have acted as a drag on the CAC after the Co. and GSK (+0.6%) announced a delay in their adjuvanted recombinant COVID-19 vaccine programme, in order to improve the immune response in the elderly. Rolls Royce (-6.3%) sit at the foot of the Stoxx 600 after it downgraded its 2020 cashflow forecast and continued to warn over the challenging outlook for the industry.

Top European News

- Italy to Buy Majority Stake in Steel Mill From ArcelorMittal

- Germany Eyes Hard Lockdown After Record Covid Cases, Deaths

- EU Warns No Deal Is Likeliest Outcome of Talks: Brexit Update

- EU Chiefs Back Tough Emission Goal After Last- Minute Scuffle

In FX, sterling sees another session of losses amid compounded Brexit pessimism telegraphed by various sources – whereby EU’s von der Leyen reportedly told leaders she has ‘low expectations’ that they can reach a Brexit deal and that a no deal scenario is the most likely outcome following her dinner with UK PM Johnson and heading into Sunday’s newly set deadline. Further, BoE’s Governor Bailey stated the Central Bank has a lot in its arsenal to tackle disorderly markets, but there are limits to what the BoE can do. Cable has receded from its overnight high at 1.3324 (21 DMA) to a current intraday base at 1.3186 with the next support levels on watch the 50 DMA at 1.3150. The EUR meanwhile experienced a pullback following verbal intervention from ECB GC member Villeroy who highlighted that the central bank is vigilant on the exchange rate and all instruments are available on this if needed, in turn prompting EUR/USD to a current low of 1.2115 from a 1.2162 high – but with losses somewhat cushioned by the EUR/GBP cross extending gains to levels just shy of 0.9200 from its 0.9116 daily low.

- DXY – The index trades firmer but remains contained sub-91.000 within a tight 90.613-989 range as the Sterling’s slip provides support for the Buck, whilst State-side stimulus and government funding remains up in the air. Senate Majority Leader McConnell last night poured cold water on COVID-relief hopes as reports stated the official does not see a path on the two main sticking points but wants a narrow package, although talks are set to continue today behind the scenes. Meanwhile, the Senate ended up not voting on the government funding stopgap bill with the today’s deadline to avert a shutdown nearing.

- JPY, AUD. NZD, CAD – Notwithstanding the firmer Buck, the Yen stands as the G10 gainer amid the deteriorating risk sentiment triggered by a barrage of downbeat Brexit commentary. USD/JPY resides around 104.00 having had briefly dipped below the level to a current low at 103.93 from 104.27 at best. High-beta FX have lost steam and reside towards session lows as the risk environment eroded in early European hours. AUD/USD waned from its overnight peak at 0.7572 to a low at 0.7521, whilst its Kiwi counterpart yielded its 0.7100 handle to print a base at 0.7075 (vs. high 0.7112). USD/CAD meanwhile remains sub-1.2800 but off its 1.2719 low and closer to the 1.2771 intraday high.

- TRY – A double whammy for the Turkish Lira amid two separate geopolitical developments whereby the US is reportedly mulling CAATSA sanctions over Turkey’s purchase of the Russian-made NATO-incompatible S-400, whilst the EU is considering restrictions amid Turkey’s behaviour in the Easter Mediterranean. USD/TRY rose from its 7.8861 base to eclipse 8.000 before waning off highs.

In commodities, WTI and Brent front-month futures trade choppy within tight ranges but with upside limited amid the subdued risk sentiment on the back of pessimistic Brexit updates. Nonetheless, crude futures hold onto a bulk of yesterday’s gains with Brent Feb still north of USD 50/bbl (vs. high 57.74), just off yesterday’s 51.06 best, whilst WTI Jan trades sub-47/bbl after reaching a high of USD 47.72/bbl yesterday. New flow for the complex has remained light throughout the European morning, but note the JMMC will now be meeting on the 16th Dec, a day earlier than scheduled. The upcoming JMMC meeting will see a review secondary source data alongside current market fundamentals before proposing policy recommendations – thus no policy decision will be taken at this meeting. The findings of the gathering are likely to be overlooked as the overall environment is little changed since the start of the month. Elsewhere, spot gold and silver see lacklustre trade once again with the former meandering around USD 1835/oz and spot silver trading sub-24/oz. In terms of base metals, Dalian iron ore futures soared almost 10% spurred by Chinese demand and Sino-Aussie woes, with some traders also citing a cyclone which could affect loadings in Australia. LME copper meanwhile sees losses in tandem with the firmer Buck and deteriorated risk sentiment.

US Event Calendar

- 8:30am: PPI Final Demand MoM, est. 0.1%, prior 0.3%

- 8:30am: PPI Ex Food and Energy MoM, est. 0.2%, prior 0.1%

- 8:30am: PPI Ex Food, Energy, Trade MoM, est. 0.2%, prior 0.2%

- 8:30am: PPI Final Demand YoY, est. 0.7%, prior 0.5%

- 8:30am: PPI Ex Food and Energy YoY, est. 1.5%, prior 1.1%

- 8:30am: PPI Ex Food, Energy, Trade YoY, prior 0.8%

- 10am: U. of Mich. Sentiment, est. 76, prior 76.9

DB’s Jim Reid concludes the overnight wrap

It’s been a pretty strange 24-48 hours in many ways. We’ve had a IPO market in the US that’s partying like its 1999 while US jobless claims spiked higher, Covid-19 restrictions mount, US stimulus talks still appear gridlocked, Brexit trade talks are not looking encouraging, and with a sober reminder of the structural problems Europe faces yesterday as the ECB expanded its stimulus package yet further and seemingly locked in negative rates for longer.

Ahead of the ECB, Spanish 10-year yields were briefly admitted into the “10yr negative yield” club, which is not that exclusive at the moment. On my calculations in Europe they briefly joined Switzerland, Germany, Slovakia, Netherlands, Denmark, Austria, Finland, Belgium, France, Ireland, Slovenia, Sweden and Portugal. See my CoTD yesterday here where we showed the Spanish dip in the context of 230 years of constantly positive yields until yesterday including a peak yield of over 70% in 1819! If you want to be on the daily chart email, please send a message to jim-reid.thematicresearch@db.com.

Sovereign bond yields rose a bit after the ECB though and the euro strengthened as markets were somewhat underwhelmed by the ECB’s latest package of stimulus measures. To be fair, they had been well flagged. To run through the main headlines, the ECB expanded their PEPP programme of bond-buying by a further €500bn to €1.85tn, with the purchases extended by 9 months until March 2022. Furthermore, their TLTRO III programme, which offers cheap loans for banks was extended until June 2022, and four pandemic emergency longer-term refinancing operations (PELTROs) will also be offered next year. However, what markets didn’t like was the fact that President Lagarde said that this additional envelope “need not be used in full”, and sovereign bond yields rose after the decision was announced. By the close, both 10yr bunds (+0.2bps) and OATs (+0.6bps) had reversed their morning gains, though they’d pared back some those losses by the end of the session, and the euro was up +0.47% against the US Dollar.

The fresh stimulus from the ECB came as their latest forecasts revised down their medium-term inflation projections, with the most recent inflation data showing the single currency bloc remained mired in deflationary territory. Though the ECB’s 2021 forecast for HICP remained at +1.0%, the 2022 reading was downgraded two-tenths to 1.1% and the new 2023 reading was still only at 1.4%, so somewhat less than their aim of “below, but close to, 2% over the medium term”. Furthermore, investors’ expectations of future inflation didn’t seem to be helped much either by the latest action, with five-year forward five-year inflation swaps down -2.0bps to 1.23%.

With that backdrop, global equity markets had a mixed performance yesterday. By the close, the S&P 500 had fallen slightly (-0.13%) in spite of a buoyant performance from energy stocks, which came as both Brent Crude (+2.84%) and WTI Oil (+2.77%) rose to post-pandemic highs of $50.25bbl and $46.78/bbl, respectively. Remember when they were negative in the early days of lockdown! Technology stocks, in particular hardware (+0.84%), actually rose on the day. The majority of the underperformance took place in the Autos (-2.59%), Telecoms (-1.80%) and Transportation stocks (-1.37%). 15 of the 24 S&P 500 industry groups moved lower on the day, and the Dow Jones was down -0.23%, as Europe’s STOXX 600 also experienced a -0.44% decline.

Stimulus talks continued with the congressional calendar-end quickly approaching. Yesterday, Treasury Secretary Mnuchin and House Speaker Pelosi both indicated progress was being made toward a new Covid-19 relief deal; however, both sides continue to differ on state and local taxes as well as the liability protections for employers. Democratic Congressional leaders continue to put their weight behind the bipartisan bill that originated in the Senate over Treasury Secretary Mnuchin’s bill. With a new deadline to get a funding deal done by the end of next week, House Minority Leader McCarthy said, “next week will be the week we get it done.” US 10yr Treasuries gained slightly throughout the day with yields down -0.3bps at 0.906%.

In a concerning sign in the face of the lack of stimulus progress, the weekly initial jobless claims in the US rose to 853k (vs. 725k expected) for the week through December 5, which is their highest level since mid-September, and raises the prospect that the labour market progress seen in recent months is slowing significantly. Indeed, the +137k increase in claims from the previous week was the largest one-week jump since the pandemic began back in March.

Overnight Asian markets are mixed with the Hang Seng (+0.46%) and Kospi (+0.84%) up while the Nikkei (-0.34%), Asx (-0.61%) and Shanghai Comp (-0.93%) are down. Futures on the S&P 500 are also down -0.10% and European equivalents are pointing to a weaker open as well. In Fx, the US dollar is down -0.18% overnight after yesterday’s -0.29% move lower.

Here in the UK, the BoE indicated yesterday that it is easing its ban on dividends with the PRA saying that “An extension of the exceptional and precautionary action taken in March is not necessary” and added, “There is scope for banks to recommence some distributions should their boards choose to do so, within an appropriately prudent framework.” The BoE approach is in contrast with developments at the ECB where the central bank is leaning towards extending their own dividend ban well into next year, though with some exceptions for the strongest lenders. European banks were one of the laggards yesterday (-2.09%) on this news and an ECB meeting that reminded investors of the tough yield/rates environment and offered up limited Xmas treats for the sector.

On Brexit, Prime Minister Johnson issued a warning last night – after European markets had closed – that businesses and the public should be prepared for the UK to leave the EU single market without a trade deal in place. While the government is still actively seeking a deal with the European Commission, the Prime Minister continues to see major obstacles. Johnson sees a, “strong possibility we will have a solution that’s much more like an Australian relationship with the EU than a Canadian relationship with the EU.” This would mean that the UK would rely on the rules of the WTO and could face tariffs and quotas when the transition ends on New Year’s Eve.

On the topic of no-deal scenarios, the European Commission put forward some contingency measures on reciprocal air and road connectivity with the UK, as well as fishing access, in the event that a no-deal outcome to the trade talks does indeed come to pass. Regardless of the somewhat negative tone to yesterday’s proceedings, discussions are currently continuing in Brussels ahead of the new Sunday deadline, where President von der Leyen has said a “decision will be taken.” Interestingly, it’s getting more vague about what the specific disagreements are. There is a possibility that politicians from both sides are keen to massively downplay the chances of a deal only to pull one out of the hat by Sunday or at least say one is starting to emerge. We will see.

Through all of this, Sterling ended the session as the worst-performing G10 currency yesterday, falling by -0.78% against the US Dollar and -1.27% against the euro. Furthermore, volatility is being increasingly priced into the exchange rate, with 1 week implied sterling/dollar volatility rising for an 8th consecutive day to its highest level since the start of the pandemic back in March. Paradoxically, however, other UK assets performed relatively strongly, with the multinational-dominated FTSE 100 gaining +0.54% on the back of sterling’s depreciation, while 10yr gilt yields fell -6.0bps as the perceived likelihood of monetary stimulus rose in response to the economic shock of a no-deal outcome.

One European deal did get done yesterday, with EU leaders finally coming together on the massive €1.82 trillion seven-year budget and recovery package to support the region’s economies through the pandemic and beyond. The delegations from Poland and Hungary had been the two dissenting voices after initially agreeing to the budget due to a “rule of law mechanism” they felt might be used to target them for potential breaches of the bloc’s democratic standards. Under the compromise, the European Commission will draw up guidelines for using the new “rule of law” standard and what would trigger it, and no country can be in violation until then.

Elsewhere, the Pfizer/BioNTech vaccine passed a committee of independent vaccine experts with a vote of 17 to 4, with one abstention. They concluded that the benefits of the vaccine outweigh the risks in those 16 and older. The FDA authorization could follow within a few days, after which shots could be immediately distributed across the US. Part of the panel was concerned that there was not enough data on 16 and 17 year olds and some pediatricians were said to be uncomfortable voting for the shot on those grounds. The shots will be distributed to the states, who will make the final decisions about which residents get inoculated first. Advisers to the CDC have recommended health-care workers and elderly care facility residents be prioritized, followed by the elderly. Shares of Pfizer gained +2.46% in after-market trading following the news.

Here in the UK there was rising speculation that London was set for Tier 3 restrictions, following data which showed that it had the highest regional case numbers in England. The measures in England are next being reviewed on December 16, while in Wales it was announced that secondary schools would move online from the start of next week because of the high number of cases. Elsewhere, it was reported that the French PM was set to announce an 8pm curfew from December 15. While in Germany, it was announced that Berlin would close non-essential shops and extend the school break until January 10. Denmark announced that the partial lockdown would be extended to additional municipalities. Meanwhile, in the US, Virginia announced a limited nightly stay-at-home order until January 31 while Pennsylvania announced that it is temporarily suspending indoor dining at bars and restaurants until January 4. Ohio has also extended its night curfew until January 2. Across the other side of world, South Korea has further strengthened social distancing rules and has limited restaurant hours while ordering closure of high-risk facilities such as nightclubs and karaoke bars.

Finally, the US CPI data for November showed month-on-month inflation of +0.2% (vs. +0.1% expected), which meant the year-on-year number remained at +1.2% (vs. +1.1% expected). In the UK, GDP expanded by just +0.4% in October, which was the economy’s slowest monthly growth since the economic rebound from the pandemic began. And in France, industrial production for October was up +1.6% (vs. +0.4% expected), bringing the year-on-year number up to -4.2%.

To the day ahead now, data releases from the US include the November PPI reading and the University of Michigan’s preliminary consumer sentiment index for December, while from Europe there’s Italian industrial production for October. Central bank speakers include the ECB’s Holzmann, Hernandez de Cos and Centeno, along with the Fed’s Quarles and George.

3A/ASIAN AFFAIRS

i)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED DOWN 26.8 PTS OR .77% //Hang Sang CLOSED UP 95.28 PTS OR .36% /The Nikkei closed DOWN 103.72 POINTS OR 0.39%//Australia’s all ordinaires CLOSED DOWN 0.44%

/Chinese yuan (ONSHORE) closed DOWN AT 6.5463 /Oil UP TO 50.08 dollars per barrel for WTI and 46.71 for Brent. Stocks in Europe OPENED ALL RED// ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.5463. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.5374 TRADE TALKS STALL//YUAN LEVELS //TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED//CORONAVIRUS/PANDEMIC/TRUMP TESTS POSITIVE FOR COVID 19 : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3 a./NORTH KOREA/ SOUTH KOREA

South Korea

b) REPORT ON JAPAN

3 C CHINA

CHINA/USA

Bloomberg employee Fan, is detained by the Communists

(zerohedge)

CHINA DETAINS BLOOMBERG NEWS EMPLOYEE

Back in 2014, Bloomberg chairman Peter Grauer effectively admitted that the media titan will go “soft” on its China coverage because it “needs to be there” for one reason: Bloomberg terminal sales.

As the NYT reported then, Grauer said that the company should have reconsidered articles that deviated from its core of coverage of business news, because they jeopardized the huge sales potential for its products in the Chinese market. The comments, as the NYT said “represented the starkest acknowledgment yet by a senior Bloomberg executive that the ambitions of the news division should be assessed in the context of the business operation, which provides the bulk of the company’s revenue. They also signaled which of those considerations might get priority.”

Acknowledging the vast size of the Chinese economy, the world’s second-biggest after that of the United States, Mr. Grauer, said, “We have to be there.”

“We have about 50 journalists in the market, primarily writing stories about the local business and economic environment,” Mr. Grauer said in response to questions after a speech at the Asia Society. “You’re all aware that every once in a while we wander a little bit away from that and write stories that we probably may have kind of rethought — should have rethought.”

Grauer’s comments on Bloomberg’s “journalistic priorities” in China reflected what some Bloomberg employees said was “skepticism from the business side about whether investigative journalism is worth the potential problems it could create for terminal sales.”

“Being in China is very much a part of our long-term strategy and will continue to be so going forward,” Mr. Grauer said. “It occupies a lot of our thinking — Dan Doctoroff, our C.E.O.; me; Mike; and other members of our senior team.”

The reason for that is simple: Michael Bloomberg has built his multi-billion fortune on sales of the company’s terminals, which are ubiquitous on bankers’ desks around the world, and account for over 80% of the company $10 billion in revenue. But sales of those terminals in China declined after the company published an article in June 2012 on the family wealth of “president for life” Xi Jinping, at that time the incoming Communist Party chief. After its publication, officials ordered state enterprises not to subscribe to the service. Mr. Grauer did not specifically mention the article about Mr. Xi or any other articles.

So Bloomberg backed off, effectively refusing to cover the illicit practices of the world’s most corrupt regime.

Which is ironic because fast-forwarding to today, Bloomberg reported that Chinese authorities detained Haze Fan, who works for the Bloomberg News bureau in Beijing, “on suspicion of endangering national security.”

“Chinese citizen Ms. Fan has been detained by the Beijing National Security Bureau according to relevant Chinese law on suspicion of engaging in criminal activities that jeopardize national security. The case is currently under investigation. Ms. Fan’s legitimate rights have been fully ensured and her family has been notified,” the Chinese authorities said.

Fan was last in contact with one of her editors around 11:30 a.m. local time on Monday. Shortly after, she was seen being escorted from her apartment building by plain clothes security officials.

Throughout the four days since her disappearance, Bloomberg has sought information on Fan’s whereabouts from the Chinese government and the Chinese embassy in Washington, DC. Her family was informed within 24 hours. Bloomberg LP, the parent of Bloomberg News, on Thursday received confirmation that Fan is being held on suspicion of participating in activities endangering national security.

“We are very concerned for her, and have been actively speaking to Chinese authorities to better understand the situation. We are continuing to do everything we can to support her while we seek more information,” said a Bloomberg spokesperson.

Fan, a Chinese citizen, began working for Bloomberg in 2017 and was previously with CNBC, CBS News, Al Jazeera and Thomson Reuters. Chinese nationals can only work as news assistants for foreign news bureaus in China and are not allowed to do independent reporting.

One wonders what it was the Bloomberg published – or was about to publish – that sparked this latest retaliation, and does this mean that Bloomberg terminal sales in China are about to slide again…

4/EUROPEAN AFFAIRS

UK/BREXIT

Morgan Stanley warns that if Brexit fails, British banks could drop 20% in price

(zerohedge)

MORGAN STANLEY WARNS BRITISH BANKS COULD DROP 20% AS BREXIT TALKS FAIL

They really mean it this time.

British Prime Minister Boris Johnson is truly living up to his reputation as a tough negotiator as the government in London and its erstwhile partners across the continent are sounding the alarm: negotiations have yielded no progress, and with neither side willing to give ground, Johnson has warned businesses and the public to get ready for the “no deal scenario, which will see the UK plunge out of the EU without a deal as the clock strikes midnight on New Year’s Day.

European Commission President Ursula von der Leyen, Brussels’ bureaucrat-in-chief, has delivered a similar warning to the heads of the 27 remaining European Union member states. Both sides claim to want a comprehensive trade deal cover the roughly $1 trillion in bilateral trade annually, but Britain is unwilling to allow Brussels to dictate rules about climate and labor standards (among other things), while Brussels is anxious about Britain under-cutting European industry once London isn’t beholden to the European Court of Justice.

Yesterday, BoJo warned that the odds of a no-deal outcome were high. On Friday, Reuters quoted an anonymous EU official saying “the probability of a no deal is higher than of a deal”. To be sure, Johnson and von der Leyen have given negotiators until Sunday evening to break the impasse over fishing rights and common rules to ensure a level playing field.

“Situation is difficult. Main obstacles remain,” the EU official said of von der Leyen’s message. “To be seen by Sunday whether a deal is possible.”

Analysts have figured talks would go down to the wire, but the complete and utter lack of progress over the three stumbling blocks, is starting to really bother traders, who sent cable down a full percentage point on Friday morning in Europe. Deadlines have never carried much weight during the negotiations until this point, but if there isn’t a deal by Sunday and the two sides walk away, the market will almost certainly start pricing in the prospect of ‘no deal’. Certainly, it will take some convincing. As analysts at Rabobank said last week, the market has consistently refused to price in ‘no deal’, as investors have always assumed that, since a deal is in the best interest of both sides (at least, economically speaking), an agreement would likely be struck – even if it doesn’t come until the last minute.

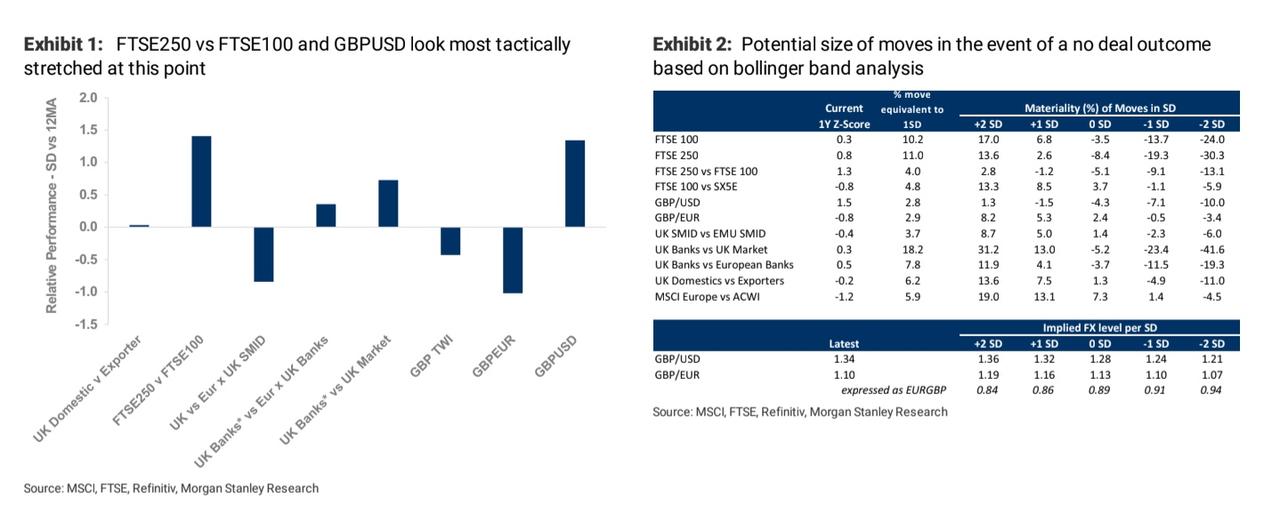

Graham Secker and Matthew Garman at Morgan Stanley see 6%-10% downside for the FTSE 250 in the event of “no-deal”, based on their bollinger band analysis.

Source: Morgan Stanley

Analysts at Citigroup believe British banking stocks could fall between 10% and 20% since no deal would be a serious negative surprise. To be sure, the team at MS still sees an agreement as the most likely outcome, they acknowledge that the odds of ‘no deal’ are rising.

“At this stage we think markets will react with a controlled degree of disappointment rather than distress given that the wider global macro outlook remains healthy, with a strong recovery expected next year,” Morgan Stanley said.

While a “no-deal” Brexit wouldn’t derail the economic recovery in Europe, it could create some uncertainties that might repel investors.

From an equity perspective, there has been “a healthy consensus” that a no-deal Brexit would be “avoided”. The team from Morgan Stanley said that even the prospect of “no deal” “has been absent in almost all of our investor conversations this year”. It’s just another reason to believe that no deal would represent a “genuine and negative ‘surprise'”.

As far as rates are concerned, in the event of the UK and EU reverting to trade on WTO terms (which is what would happen if the two sides can’t agree on a new trade deal), Morgan Stanley’s economists expect a weaker 2021 recovery, accompanied by additional policy easing. A depreciating pound would almost certainly result from ‘no deal’. But that will impact things differently.

Source: Morgan Stanley

Specifically, in the near term, the MS team expects the MPC to cut rates to zero and increase the pace of QE. Looking further down the road, they would expect rates to go negative.

Some insist that BoJo’s recalcitrance is merely a show to placate his most fervently pro-Brexit supporters. However, others have cautioned that Europe’s demands simply aren’t acceptable to London, and that a ‘no deal’ outcome is virtually inevitable. Reuters reminds us that no-deal would damage the economies of northern Europe, send shockwaves through financial markets, cause massive traffic pileups at borders and generally sow chaos through delicate supply chains stretching across Europe.

To be sure, most Wall Street banks still believe a deal will be reached at the 11th hour. But most investment banks also thought that the Brexit referendum would fail. And we all remember how that turned out.

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

Trump is batting 4 for 4

Morocco and Israel enter into a peace deal:

Morocco and Israel in peace

6.Global Issues

CORONAVIRUS UPDATE/POTENTIAL PROBLEMS WITH OUR VACCINES:

Pfizer COVID Vaccine Trial Shows Alarming Evidence of Pathogenic Priming in Older Adults • Children’s Health Defense

While there clear persuasion by government authorities the bigger question is who will pay when people are hurt.

There is talk behind the curtain now that to own and operate a business in Ontario in the future, you will need the jab, by government decree. While in articles like this one, a red flag is raised to suggest the common cold or flu may kill you after the COVID-19 vaccine because your body will not defend itself against a natural wild virus.

Skepticism suggests waiting to see what happens to others first, instead of being first with future regret”.

https://childrenshealthdefense.org/defender/pfizer-covid-vaccine-trial-pathogenic-priming

AUSTRALIA CANCELS COVID VACCINE TRIAL OVER ‘UNEXPECTED’ FALSE POSITIVES FOR HIV

The Australian government has canceled further development of a COVID-19 vaccine after several trial participants had false positive testsfor HIV. The vaccine was being developed by the University of Queensland, while Australian biotech company CSL Limited had been under contract to provide 51 million doses. The vaccine had been on schedule for mid-2021, with phase two and three clinical trials due to commence in December.

On Friday, however, Australian Prime Minister Scott Morrison announced that the “University of Queensland vaccine will not be able to proceed based on the scientific advice, and that will no longer feature as part of Australia’s vaccine plan,” adding “I think the decision we’ve made today should give Australians great assurance that we are proceeding carefully, we are moving swiftly, but not with any undue haste here.”

“Our processes will not be compromised. At the end of the day, the Therapeutic Goods Administration – like with any vaccine in Australia – must give their tick-off. Without the tick, there’s no jab when it comes to vaccines in this country. That is true for the Covid-19 vaccine, as it is true for any other vaccine that is administered here in Australia,” Morrison added.

The vaccine was one of four secured by the Australian government, which will now turn its focus to the AstraZeneca vaccine as well as Pfizer’s.

CSL said in a Friday statement that “following consultation with the Australian government, CSL will not progress the vaccine candidate to phase 2/3 clinical trials.”

According toAustralia’s 10 News, the decision to drop the University of Queensland vaccine was over fears that the false positive results would scare Australians away from the vaccine, despite the fact that patients had not actually contracted the disease.

The now-canceled vaxx focused on the COVID-19 “spike protein” using ‘molecular clamp technology’ to lock the protein into a shape which the human immune system can identify and neutralize. To ensure an immune response, the clamp chosen to trick the immune system into attacking includes two fragments of a protein found in HIV, which by themselves do not pose a threat.

Trial participants were advised of the possibility that vaccine-induced HIV antibodies might be detected as a result, but it was nonetheless unexpected. Subsequent HIV tests provided definitive negative results in the trial participants.

While the HIV tests were false positives and there was no risk to the trial participants, significant changes would need to be made to well-established HIV testing procedures to accommodate rollout of this vaccine, the researchers said. The Phase 1 trial will continue, where further analysis of the data will show how long the antibodies persist. –The Guardian

Professor Paul Young, co-lead researcher on the vaccine, said that it would be possible to re-engineer it to avoid false positives but there wasn’t enough time. “Doing so would set back development by another 12 or so months, and while this is a tough decision to take, the urgent need for a vaccine has to be everyone’s priority,” he said.

Health Minister Greg Hunt said that while the HIV test results were false, “the scientific advice is that the risk to vaccine confidence was the principal issue here.”

Australia, meanwhile, has secured contracts for 140 million doses of vaccine, “one of the highest ratios of vaccine purchases and availability to population in the world” according to Hunt, who added “What we can do is vaccinate our population twice over.”

US TOPS 3K COVID DEATHS FOR 2ND STRAIGHT DAY; GLOBAL CASES NEAR 70MM: LIVE UPDATES