GOLD:$1797.00 UP 33.05 The quote is London spot price

Silver:$22.45 UP 91 CENTS London spot price ( cash market)

4:30 closing price

Gold $1776.50 silver: $22.07

PLATINUM AND PALLADIUM PRICES BY GOLD-EAGLE (MORE ACCURATE)

PLATINUM $940.30 UP $19.25

PALLADIUM: $1732.05 UP $129.75/OZ

END

Editorial of The New York Sun | February 1, 2021

end

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

COMEX DETAILS//NOTICES FILED

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

receiving today 500/530

Goldman Sachs stopped: 0

NUMBER OF NOTICES FILED TODAY FOR DEC. CONTRACT: 500 NOTICE(S) FOR 50,000 OZ (1.555 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR THIS MONTH: 33,899 FOR 3,382,900 OZ (105.44 TONNES)

SILVER//DEC CONTRACT

60 NOTICE(S) FILED TODAY FOR 3,000,000 OZ/

total number of notices filed so far this month 8510 : for 42,550,000 oz

BITCOIN MORNING QUOTE $48,765 UP 2442

BITCOIN AFTERNOON QUOTE.:48,100 UP 1780

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

GLD AND SLV INVENTORIES:

GLD AND SLV INVENTORIES:

GLD

WITH GOLD UP $33.05 AND NO PHYSICAL TO BE FOUND ANYWHERE:

A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.04 TONNES

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS)

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

THIS IS A MASSIVE FRAUD!!

GLD 977,20 TONNES OF GOLD//

GLD CLOSING PRICE: $168.16. UP $2.01 OR 1.21%

Silver//SLV

AND WITH NO SILVER AROUND TODAY: WITH SILVER UP 91 CENTS

A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3,33 MILLION

OZ FROM THE SLV

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY SLV/ TONIGHT: 538.282 MILLION OZ

SLV closing price NYSE 20.79 up .38 OR 1.86%

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A VERY STRONG 2754 CONTRACTS TO 145,138, AND CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020.. DESPITE THE $0.38 LOSS IN SILVER PRICING AT THE COMEX ON WEDNESDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.38) BUT WERE QUITE UNSUCCESSFUL IN KNOCKING OUT ANY SILVER LONGS AS WE HAD ANOTHER STRONG GAIN OF 3806 CONTRACTS ON OUR TWO EXCHANGES .

WE MUST HAVE HAD:

I) HUGE BANKER SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A HUGE INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 47.535 MILLION OZ FOLLOWED BY TODAY’S 10,000 OZ E.F.P. JUMP TO LONDON V) STRONG SIZED COMEX OI GAIN.

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS –27

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS DEC 16 ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF DEC:

TOTAL CONTACTS for 12 days, total contracts: 13,884 or …average per day: 1157 contracts or 5.785 million oz per day.

TOTAL NO OF OZ UNDERGOING EFP TO LONDON: 69.420 MILLION OZ.

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF

DEC: # OF MILLION PAPER OZ HAVE MORPHED OVER TO LONDON: 69.420 MILLION OZ

LAST 7 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

RESULT:,WE HAD A STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2754 DESPITE OUR 38 CENT LOSS SILVER PRICING AT THE COMEX// WEDNESDAY THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 1025 CONTRACTS( 1025 CONTRACTS ISSUED FOR MAR AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY:/ AS WELL AS TODAY /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR DEC OF 47.535 MILLION OZ FOLLOWED BY TODAY’S 10,000 OZ E.F.P. JUMP TO LONDON .. WE HAD STRONG SIZED GAIN OF 3779 OI CONTRACTS ON THE TWO EXCHANGES

WE HAD 60 NOTICES FILED TODAY FOR 3,000,000 OZ

GOLD//OUTINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A SMALL SIZED 260 CONTRACTS TO 503,969 ,AND CLOSER TO OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY. 1916 CONTRACTS.

THE SMALL SIZED INCREASE IN COMEX OI CAME DESPITE OUR LOSS IN PRICE OF $7.85//COMEX GOLD TRING/WEDNESDAY/.AS IN SILVER WE MUST HAVE HAD HUGE BANKER/ALGO SHORT COVERING ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LIQUIDATION AS THE TOTAL GAIN ON OUR TWO EXCHANGES TOTALLED A GOOD SIZED 3806 CONTRACTS… WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR DEC AT 98.000 TONNES, FOLLOWED BY TODAY’S STRONG QUEUE JUMP OF 22,200OZ//, NEW STANDING 105.726 TONNES

YET ALL OF..THIS HAPPENED WITH OUR LOSS IN PRICE OF $7.80 WITH RESPECT TO WEDNESDAY’S TRADING

WE HAD A FAIR SIZED 2059 OI CONTRACTS (6.404 PAPER TONNES) ON OUR TWO EXCHANGES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALLED A FAIR SIZED 1799 CONTRACTS:

FOR FEB 1799 ALL OTHER MONTHS ZERO//TOTAL: 1799

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 503,969. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EXCHANGE DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2059 CONTRACTS 260 CONTRACTS INCREASED AT THE COMEX AND 1799 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 2059 CONTRACTS OR 6.404 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1799) ACCOMPANYING THE SMALL SIZED GAIN IN COMEX OI (260 OI): TOTAL GAIN IN THE TWO EXCHANGE 2059 CONTRACTS. WE NO DOUBT HAD 1) HUGE BANKER SHORT COVERING ,2.) HUGE INITIAL STANDING AT THE GOLD COMEX FOR DEC. AT 98.000 TONNES/FOLLOWED BY TODAY’S QUEUE JUMP OF 22,200 OZ TO LONDON////NEW STANDING OF 105.726 TONNES//. 3)ZERO LONG LIQUIDATION,4) SMALL SIZED COMEX OI GAIN 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL

SPREADING OPERATIONS(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS:

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF NOV.WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF OCT HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF NOV, FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (DEC), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2021 INCLUDING TODAY

DEC

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF DEC : 33,390, CONTRACTS OR 3,339,0000 oz OR 103.85TONNES (12 TRADING DAY(S) AND THUS AVERAGING: 2782 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 12 TRADING DAY(S) IN TONNES: 103.85 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2020, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 103.85/3550 x 100% TONNES 2.90% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO DATE JANUARY: 265.26 TONNES (RAPIDLY INCREASING AGAIN) FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN).. MARCH:. 276.50 TONNES (STRONG AGAIN///IT SURPASSED JANUARY!!)

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 103,85 TONNES//INITIAL ISSUANCE

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A STRONG SIZED 2754 CONTRACTS TO 145,165 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 4 1/2 YEARS AGO.

EFP ISSUANCE 1025 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 1025 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1025 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 2754CONTRACTS AND ADD TO THE 1025 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A VERY STRONG SIZED GAIN OF 3779 OPEN INTEREST CONTRACT FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 18.895 MILLION OZ, OCCURRED WITH OUR $0.38 LOSS IN PRICE.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL..THE EVIDENCE IS CLEAR: HUGE AMOUNTS OF PHYSICAL STANDING FOR BOTH SILVER AND GOLD .

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe, Gold

(Peter Schiff, Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

3. ASIAN AFFAIRS

THURSDAY MORNING/WEDNESDAY NIGHT:

SHANGHAI CLOSED UP 28.79 PTS OR 0.75% //Hang Sang CLOSED UP 54.74 PTS OR 0.23% /The Nikkei closed UP 606.60 PTS OR 2.13% //Australia’s all ordinaires CLOSED DOWN 0.23%

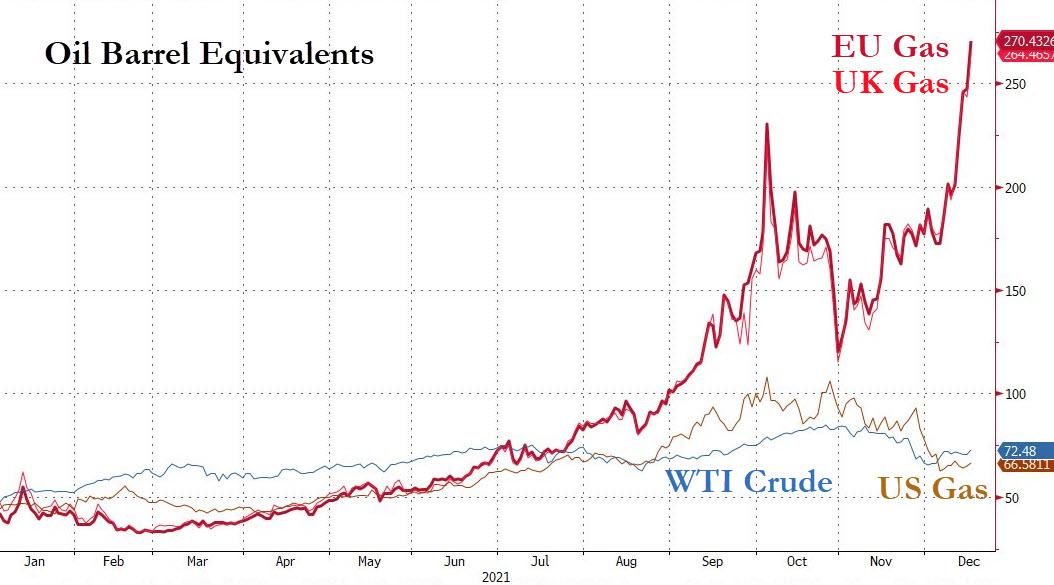

/Chinese yuan (ONSHORE) closed DOWN 6.3678 /Oil UP TO 71.19 dollars per barrel for WTI and UP TO 74.18 for Brent. Stocks in Europe OPENED ALL GREEN // ONSHORE YUAN CLOSED DOWN AT 6.3678 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.3758: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%i) 3 a./NORTH KOREA/ SOUTH KOREA

A)NORTH KOREA//USA/OUTLINE

b) REPORT ON JAPAN

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

OUTLINE

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A SMALL SIZED 260 CONTRACTS AND CLOSER TO TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX INCREASE OCCURRED DESPITE OUR LOSS OF $7.80 IN GOLD PRICING WEDNESDAY’S COMEX TRADING.WE ALSO HAD A FAIR EFP ISSUANCE (1799 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. LOOKS LIKE OUR BANKERS ARE FINALLY BAILING OUT

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE ACTIVE DELIVERY MONTH OF DEC.. THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 1799 EFP CONTRACTS WERE ISSUED: ;: , DEC : 0 & FEB. 1799 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1799 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED 2059 TOTAL CONTRACTS IN THAT 1799 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A SMALL GAIN COMEX OI OF 260 CONTRACTS..

// WE HADEA STRONG AMOUNT OF GOLD TONNAGE STANDING FOR DEC (105.726),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 9 MONTHS OF 2021:

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB. 113.424 TONNES

JAN: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- NOV): 488.996 TONNES

THE BANKERS WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $7.80)

BUT THEY WERE UNSUCCESSFUL IN FLEECING ANY LONGS AS THE TOTAL GAIN ON THE TWO EXCHANGES REGISTERED 6.404 TONNES,ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR DEC (105.726 TONNES)…

I STRONGLY BELIEVE THAT OUR BANKER FRIENDS ARE GETTING QUITE NERVOUS. THEY ARE LOOKING OVER THEIR SHOULDERS AND WITNESSING MASSIVE SILVER/GOLD SHORTAGES THAT CANNOT BE COVERED. THEY ARE TRYING TO FLEE IN HASTE “FROM DODGE”AS BASE III BEGINS JAN 1/2022 FOR EUROPEAN BANKS

WE HAD – 1916 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 2059 CONTRACTS OR 205900 OZ OR 6.404 TONNES

COMMODITY LAW SUGGESTS THAT COMMODITY FUTURES OPEN INTEREST SHOULD APPROXIMATE 3% OF TOTAL PRODUCTION. IN GOLD THE WORLD PRODUCES AROUND 3500 TONNES PER YEAR BUT ONLY 2200 TONNES ARE AVAILABLE FROM THE WEST (THUS EXCLUDING RUSSIA, CHINA ETC..WHO KEEP 100% OF THEIR PRODUCT.THUS IN GOLD WE HAVE THE FOLLOWING: 503,969 TOTAL OI CONTRACTS X 100 OZ PER CONTRACT = 50.39 MILLION OZ/32,150 OZ PER TONNE = 15.67 TONNES

THE COMEX OPEN INTEREST REPRESENTS 15.67/2200 OR 71.24% OF ANNUAL GLOBAL PRODUCTION OF GOLD

Trading Volumes on the COMEX GOLD TODAY 164,664 contracts// ///volume poor////

CONFIRMED COMEX VOL. FOR YESTERDAY: 166,196 contracts// quite poor

// //most of our traders have left for London

DEC 16 COMEX INVENTORY MOVEMENTS//AMOUNTS STANDING

For today:

No dealer deposit

No customer account deposit:

We had two customer withdrawals:

i) Out of Brinks: 33,051.220 oz (1028 kilobars)

ii) Out of Manfra: 9,163.035 oz

total customer withdrawal. 42,214.255 oz

We had 3 kilobar transactions 3 out of 3 transactions)

ADJUSTMENTS 1 DEALER TO CUSTOMER: BRINKS//

32,794.02 OZ (1020 KILOBARS)

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR DECEMBER.

For the front month of DECEMBER we have an oi 692 stand for December. for a GAIN of 221contracts. We had 1 notice filed on WEDNESDAY so we GAINED 222 contracts or an additional. 22,200 oz will stand for delivery in this very active delivery month of December. JANUARY GAINED 408 CONTRACTS TO STAND AT 2732FEBRUARY LOST 952 CONTRACTS TO 389,899

We had 530 notice(s) filed today for 53000 ozFOR THE DEC 2021 CONTRACT MONTH

Today, 1 notice(s) were issued from J.P.Morgan dealer account and 499 notices were issued from their client or customer account. The total of all issuance by all participants equates to 500 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 499 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the DEC /2021. contract month,

we take the total number of notices filed so far for the month (33,830) x 100 oz , to which we add the difference between the open interest for the front month of (DEC: 692 CONTRACTS ) minus the number of notices served upon today 530 x 100 oz per contract equals 3,382,900, OZ OR 105.726 TONNES) the number of ounces standing in this active month of DEC.

thus the INITIAL standings for gold for the DEC contract month:

No of notices filed so far (33,830) x 100 oz+ (692) OI for the front month minus the number of notices served upon today (530} x 100 oz} which equals 3,382,900 oz standing OR 105.726 TONNES in this active delivery month of DEC.

This is a huge delivery for December.

We GAINED 222 contracts or an additional 22,200 oz WILL STAND FOR GOLD OVER HERE

TOTAL COMEX GOLD STANDING: 105.726 TONNES

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

206,468.649, oz NOW PLEDGED /HSBC 6.42 TONNES

174,041.813 PLEDGED MANFRA 5.41 TONNES

500.648 oz PLEDGED JPMorgan no 1 0.0155

288,481,604, oz JPM No 2 8.97 TONNES

698,821.330 oz pledged June 12/2020 Brinks/27,96 TONNES

12,244.444 oz International Delaware: 0..3808 tonnes

total pledged gold: 1,599,178.906oz 49.74 tonnes

CALCULATION OF GOLD THAT CAN SETTLE UPON LONGS:

SURPRISINGLY WE HAVE BEEN WITNESSING NO REAL PHYSICAL GOLD ENTERING THE COMEX VAULTS FOR THE PAST YEAR!! ..ONLY PHONY KILOBAR ENTRIES…. WE HAVE 456.43 TONNES OF REGISTERED GOLD WHICH CAN SETTLE UPON LONGS 105.726 tonnes

TOTAL GOLD COMEX REGISTERED: 17,804.844.987 OZ (553.80 TONNES)

CALCULATION OF TOTAL REGISTERED GOLD THAT CAN BE SERVED UPON

ELIGIBLE GOLD: 16,273.558.691. (506.175 TONNES)

PLEDGED GOLD: 1,599,178.906 OZ. (49.74 TONNES

NET PHYSICAL GOLD THAT CAN SERVED UPON FOR DELIVERY.

(REG.GOLD – PLEDGED GOLD). 14,674,380.000 (456.43 TONNES)

TOTAL ELIGIBLE GOLD+ REGISTERED GOLD 34,078,403.675 OZ (1059.98 TONNES)

end

I have compiled data with respect to registered (or dealer) gold taken on first day notice for each of the past 24 months

The data begins on first day notice for the May month taken on the last day of July 2018. and it continues to present day.

I then took, how many deliveries were recorded by the CME for each and every month. I also included for reference the price of gold on first day notice.

The first graph is a logarithmic graph and the second graph, linear.

You can see the huge explosion of registered gold at the comex along with deliveries. THE DATA AND GRAPHS:

END

SILVER COMEX DEC 16/2021

And now for the wild silver comex results

We had 1 deposit into the dealer

i)Into the dealer Manfra: 290,661.810 oz

total dealer deposits: 290,661.810 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

we had 2 deposits into customer account (ELIGIBLE ACCOUNT)i).

Into Delaware: 30,584.329 oz

Into JPMorgan: 595,288.000 oz

JPMorgan now has 182.933 million oz silver inventory or 51.65% of all official comex silver. (182.933 million/354.121 million

total customer deposits today 625,877.329 oz

we had 3 withdrawals

i) Out ofBrinks: 1954.700 oz

ii) Out of. CNT: 600,485.630 oz

iii) Out of HSBC: 250,262.130 oz

total withdrawal 852,702.460 oz

adjustments: 0

Total dealer(registered) silver: 94.008 million oz

total registered and eligible silver: 354.121million oz leaves the comex silver vaults.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

silver open interest data:

Total oi for the silver complex: 145,165 contracts

FRONT MONTH OF DEC OI: 615 CONTRACTS

TOTAL NO OF CONTRACTS SERVED UPON THIS MONTH: 8510 CONTRACTS FOR 42,550,000 OZ

CALCULATION OF SILVER OZ STANDING FOR DECEMBER

For the front month of DECEMBER we have an amount of silver standing AT 615 CONTRACTS for a LOSS of 2 contracts. We had 0 notices filed on WEDNESDAY, so we LOST 2 contracts or an additional 10,000 oz will NOT stand for delivery in this very active delivery month of December

JANUARY GAINED 176 CONTRACTS TO STAND AT 2211

FEBRUARY LOST 5 CONTRACTS TO STAND AT 42 NO. OF NOTICES FILED: 60 FOR 3,000,000 OZ.

To calculate the number of silver ounces that will stand for delivery in DEC. we take the total number of notices filed for the month so far at 8510 x 5,000 oz =42,550,000 oz

to which we add the difference between the open interest for the front month of DEC (615) and the number of notices served upon today 60 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the DEC./2021 contract month: 8510 (notices served so far) x 5000 oz + OI for front month of DEC (615) – number of notices served upon today (60) x 5000 oz of silver standing for the DEC contract month .equals 45,325,000 oz. .

We LOST 2 contracts or AN ADDITIONAL 10,000 oz will NOT stand for delivery on this side of the pond.

THIS IS STILL A TERRIFIC INITIAL STANDING FOR DELIVERY FOR SILVER IN DECEMBER.

silver comex volumes:

TODAY’S ESTIMATED SILVER VOLUME 53,907 CONTRACTS // volume awful;

FOR YESTERDAY 67,461 contracts ,CONFIRMED VOLUME/ poor/

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SILVER INVENTORY

And now the Gold inventory at the GLD/(this vehicle is a fraud as there is no gold behind them

DEC 16/WITH GOLD UP $33.05TODAY; A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.4 TONNES FROM THE GLD////INVENTORY REST AT: 977.20 TONNES

DEC15/WITH GOLD DOWN $7.80 TODAY/ A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.04 TONNES FROM THE GLD////INVENTORY RESTS AT 980.60 TONNES.

DEC 14/WITH GOLD DOWN $18.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 982.64 TONNES

DEC 13/WITH GOLD UP $3.20 TODAY/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 982.64 TONNES

DEC 10.WITH GOLD UP $7.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 982.64 TONNES

DEC 9/WITH GOLD DOWN $9.10 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 982.64.

DEC 8/WITH GOLD UP $5.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 984.38 TONNES

DEC 7/WITH GOLD UP $5.15 TODAY; A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 984.38 TONNES

DEC 6/WITH GOLD DOWN $3.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 986.17 TONNES//

DEC 3/WITH GOLD UP $20.35 TODAY; A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.85 TONNES FROM THE GLD///INVENTORY RESTS AT 986.17 TONNES

DEC 2/WITH GOLD DOWN $19.80 TODAY; A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.83 TONNES FROM THE GLD///INVENTORY RESTS AT 990.82 TONNES

DEC 1/WITH GOLD UP $7.05 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 992.85 TONNES

NOV 30/WITH GOLD DOWN $8.70 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESS AT 992.85 TONNES.

NOV 29/WITH GOLD DOWN $3.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 992.85 TONNES/

NOV 26/WITH GOLD UP $2.70 TODAY/A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.76 TONES INTO THE GLD////INVENTORY RESTS AT 992.85 TONNES

NOV 24/WITH GOLD UP $.40 TODAY//NO CHANGES IN GOLD INVENTORY AT THE GLD..INVENTORY RESTS AT 991.11 TONNES

NOV 23/WITH GOLD DOWN $21.85 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 6.11 TONNES INTO THE GLD////INVENTORY RESTS AT 991.11 TONNES.

NOV 22/WITH GOLD DOWN 54.10 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 985.00 TONNES

NOV 19/WITH GOLD DOWN $9.40 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 8.13 TONNES INTO THE GLD//INVENTORY RESTS AT 985.00 TONNES.

NOV 18/WITH GOLD DOWN $8.40 TODAY:A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .88 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 976.87 TONNES

NOV 17/WITH GOLD UP $14.10 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 975.99 TONNES

NOV 16/WITH GOLD DOWN $10.30 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 975.99 TONNES

NOV 15/WITH GOLD DOWN $1.55 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY AT 975.99 TONNES//

NOV 12/WITH GOLD UP $4.65 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY AT 975.99 TONNES

NOV 11/WITH GOLD UP $14.45 TODAY: A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .58 TONES OF GOLD INTO THE GLD////INVENTORY RESTS AT 975.99 TONNES

NOV 10/WITH GOLD UP $18.00 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 975.41 TONNES

NOV 9/WITH GOLD UP $1.85 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 975.41 TONNES

NOV 8/WITH GOLD UP $11.75 TODAY;NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 975.41 TONNES

XXXXXXXXXXXXXXXXXXXXXXXXX

Inventory rests tonight at:

DEC 16 / GLD INVENTORY 977.20 tonnes

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

DEC 16/WITH SILVER UP 91 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 3.33 MILLION OZ FROM THE SLV//INVENTORY REST AT 538.282 MILLION OZ

DEC 15WITH SILVER DOWN 38 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV/: A WITHDRAWAL OF 2.48 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 541.612 MILLION OZ

DEC 14/WITH SILVER DOWN 38 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 543.092 MILLION OZ

DEC 13/WITH SILVER UP 11 CENTS TODAY; A HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 3.561 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 543.092 MILLION OZ//

DEC 10.WITH SILVER UP 19 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 546.653 MILLION OZ..

DEC 9/WITH SILVER DOWN 43 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF 2.96 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 546.653 MILLION OZ/

DEC 8/WITH SILVER DOWN 7 CENTS TODAY; NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 543.693 MILLION OZ///

DEC 7/WITH SILVER UP 24 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 543.693 MILLION OZ..

DEC 6/WITH SILVER DOWN 25 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.110 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 543.693 MILLION OZ//

DEC 3/WITH SILVER UP 21 CENTS TODAY; A BIG CHANGE IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 3.199 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 544.803 MILLION OZ//

DEC 2/WITH SILVER DOWN 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 548.002 MILLION OZ.

DECM 1/WITH SILVER DOWN 44 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 740,000 OZ FROM THE SLV////INVENTORY RESTS AT 548.002 MILLION OZ//

NOV 30/WITH SILVER DOWN 3 CENTS TODAY; A SMALL CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF .555 MILLION OZ FORM THE SLV//INVENTORY RESTS AT 548.742 MILLION OZ///

NOV 29/WITH SILVER DOWN 25 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 549.297 MILLION OZ//

NOV 26/WITH SILVER DOWN 36 CENTS TODAY; A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.038 MILLION OZ INTO THE SLV.//INVENTORY RESTS AT 549.297 MILLION OZ///

NOV 24/WITH SILVER UP 5 CENTS //NO CHANGE IN SILVER INVENTORY AT THE SLV..INVENTORY RESTS AT 547.261 MILLION OZ

NOV 23.WITH SILVER DOWN 81 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV/: A WITHDRAWAL OF 2.128 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 547.261 MILLION OZ//

NOV 22/ WITH SILVER DOWN 47 CENTS TODAY; A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A SURPRISE DEPOSIT OF 1.156 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 549.389 MILLION OZ/

NOV 19/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 548.233 MILLION OZ..

NOV 18/WITH SILVER DOWN 27 CENTS TODAY/ NO CHANGES IN SILVER STANDING AT THE SLV.//INVENTORY REST AT 548.233 MILLION OZ//

NOV 17/WITH SILVER UP 24 CENTS TODAY: NO CHANGES IN SILVER STANDING AT THE SLV//INVENTORY RESTS AT 548.233 MILLION OZ//

NOV 16/WITH SILVER DOWN 17 CENTS TODAY: NO CHANGES IN SILVER STANDING AT THE SLV//INVENTORY RESTS AT 548.233 MILLION OZ//

NOV 15/WITH SILVER DOWN 25 CENTS TODAY: NO CHANGES IN SILVER AT THE SLV/ INVENTORY RESTS AT 548.233 MILLION OZ

NOV 12/WITH SILVER UP 8 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 3.933 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 548.233 MILLION OZ//

NOV 11/WITH SILVER UP 51 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.300 MILLION OZ//

NOV 10 WITH SILVER UP 45 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 544.300 MILLION OZ//

NOV 9/WITH SILVER DOWN 21 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.300 MILLION OZ.

NOV 8/WITH SILVER UP 38 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.300 MILLION OZ//

DEC 14/2021 SLV INVENTORY RESTS TONIGHT AT 541.612 MILLION OZ

PHYSICAL GOLD/SILVER STORIES

PETER SCHIFF

A GOOD COMMENTARY AS TO WHAT HAPPENED YESTERDAY WITH RESPECT TO POWELL’S ANNOUNCEMENT

PETER SCHIFF

Peter Schiff: A Dove Doesn’t Change Its Feathers

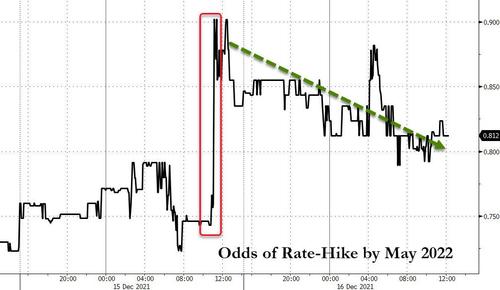

THURSDAY, DEC 16, 2021 – 12:00 PM

The Federal Reserve is set to launch its war on inflation. But it looks like it’s carrying a pea-shooter to a gunfight.

Or as Peter Schiff put it, a dove can’t change its feathers.

The final FOMC meeting of the year wrapped up with rates still set at zero. But the Fed announced it will speed up tapering its asset purchase program. It will double the pace of the taper with the central bank buying $60 billion in bonds beginning in January. That would be down from $120 billion a month in bond purchases at the quantitative easing peak. At that pace, the taper should be complete by March 2022.

Once the Fed wraps up its asset purchase program, it will begin raising interest rates. The FOMC released a new “dot-plot” projecting three rates hikes of 25 basis points next year, three in 2023 and two more in 2024. That would push rates to around 2%.

The Fed bankers expressed concern about sizzling hot inflation. There was no mention of the word “transitory.” But the committee members continue to skirt their own responsibility for rising prices, instead, blaming them on pandemic-related issues.

“Supply and demand imbalances related to the pandemic and the reopening of the economy have contributed to elevated levels of inflation,” the FOMC statement said.

During his post-meeting press conference, Powell said he expects inflation to begin coming down toward the back-end of next year, but conceded that’s not a certainty.

We can’t act as though that’s a certainty, and we’re not going to act as though that’s a certainty. There’s a real risk now, we believe, I believe, that inflation may be more persistent, and that may be putting inflation expectations under pressure, and that the risk of higher inflation becoming entrenched has increased. It’s certainly increased.”

So, what is the Fed going to do about it? It appears, not much.

These moves by the Fed amount to little more than spitting into the wind when it comes to taking on inflation. As Mike Maharrey wrote after the November data came out showing the Producer Price Index rose at the fastest rate ever, this is a runaway inflation freight train that the Fed won’t stop.

In order to truly take on inflation, the central bank needs to push interest rates at least as high as the inflation rate. Even using the government’s cooked CPI numbers that understate inflation, that would mean taking rates to at least 7%.

The plan is to push them to 2% — in three years.

You can do the math.

The Fed also needs to shrink the money supply. It does this by shrinking its balance sheet. The central bank isn’t even talking about this, at least not publicly. When asked about actually shrinking the $8.7 trillion balance sheet, chairman Jerome Powell set a cautious tone saying it’s “best to take a careful, methodical approach,” noting that “markets can be sensitive” about it.

There has been a lot of anticipation of the Fed moving against inflation. But in his podcast, Peter pointed out that if the central bank was really serious about fighting inflation, it would have started the war long ago.

If the Fed was ever going to get serious, they would have already done so. The evidence was overwhelming that we had an inflation problem a year or two ago, and the Fed did nothing.”

Instead, the Fed made an all-or-nothing bet on “transitory.”

First Jerome Powell denied there was any inflation on the horizon. Then he pivoted to “don’t worry, it’s just transitory.” Now, he’s finally admitted that it’s not transitory. But the policy moves announced by the Fed will prove feckless in the face of this inflation wave.

Peter raised an important question.

The Fed has gotten everything wrong when it comes to inflation. So, why does the market still believe the Fed is going to get it right when it comes to fighting inflation? It’s going to be just as wrong in its fight against inflation as it was in its forecast regarding inflation.”

Peter said that if the Fed was really serious about fighting inflation, it would just end quantitative easing immediately instead of tapering it over time.

If you’ve got a fire, just stop pouring gasoline on it. Don’t just gradually pour on less. Just stop.”

In practice, the Fed is barely altering the “tightening” policy it announced when inflation was still supposedly just “transitory. It’s going to wrap up the taper 2 months earlier and raise rates a little quicker.

Now, all of a sudden, inflation is a problem, yet we have the same approach? We’re still going to taper QE instead of going cold turkey? And we’re still going to have these quarter-point rate hikes, maybe just one extra rate hike in 2022? How is that going to do anything about the severity of the inflation problem we have right now? It’s not.”

When you really step back and look at Powell’s posture coming out of this FOMC meeting, you got the same old dove.

Although this dove is still talking about fighting inflation. But if you actually listen to what he’s saying, what is his battle plan for this war against inflation — again, it’s pretty much the same battle plan he had when there was no inflation. So, how can this be serious?”

Listen to Peter’s podcast for more analysis of the Fed meeting, along with the November retail sales numbers, the debt ceiling hike and how history will judge Jerome Powell.

end

LAWRIE WILLIAM//,//Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,James RICKARDS

ii) Important gold commentaries courtesy of GATA/Chris Powell

CRAIG HEMKE …..

Craig Hemke at Sprott Money: After the Fed

Submitted by admin on Wed, 2021-12-15 22:18 Section: Daily Dispatches

By Craig Hemke

Sprott Money, Toronto

Wednesday, December 15, 2021

As I type this on Wednesday morning, there’s really no sense in discussing other news or datapoints today, as everything is meaningless ahead of the Federal Open Market Committee — which should stop you in your tracks when you consider how Fed-dependent EVERYTHING has become.

The news doesn’t matter anymore. All that matters is the anticipated Fed reaction to said news. Could “the markets” be any more broken?

So what is expected today? Anything and nothing. How about these scenarios? …

… For the remainder of the analysis:

https://www.sprottmoney.com/blog/After-the-Fed-Craig-Hemke-December-15-2021

end

Real rates will stay negative, Turk tells King World News

Submitted by admin on Thu, 2021-12-16 13:28 Section: Daily Dispatches

1:25p ET Thursday, December 16, 2021

Dear Friend of GATA and Gold:

In comments to King World News, GoldMoney founder and GATA consultant James Turk ridicules as merely nominal the efforts to curb inflation that are being made by the Federal Reserve, European Central Bank, and Bank of England. These efforts, Turk says, won’t come close to turning negative real interest rates positive.

Turk’s comments at KWN can be found here:»

end

OTHER COMMODITIES/LUMBER

END CRYPTOCURRENCIES/

END

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings THURSDAY morning 7:30 AM….

1.Chinese yuan vs usa dollar/CLOSED DOWN 6.3678

//OFFSHORE YUAN 6.3758 /shanghai bourse CLOSED UP 28.79 PTS OR 0.75%

HANG SANG CLOSED UP 54.74 PTS OR 0.23%

2. Nikkei closed UP 606.60 PTS OR 2.13%

3. Europe stocks ALL GREEN

USA dollar INDEX DOWN TO 96;04/Euro RISES TO 1.1336-

3b Japan 10 YR bond yield: RISES TO. +.045/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 114.17/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//

3c Nikkei now JUST ABOVE 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 71.19 and Brent: 74.18-

3f Gold UP/JAPANESE Yen DOWN CHINESE YUAN: ON -SHORE CLOSED DOWN// OFF- SHORE DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO -.0.324%/Italian 10 Yr bond yield RISES to 0.99% /SPAIN 10 YR BOND YIELD RISES TO 0.39%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 1.31: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 1.24

3k Gold at $1787.30 silver at: 21.81 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3l USA vs Russian rouble; (Russian rouble UP 3/100 in roubles/dollar) 73.72

3m oil into the 69 dollar handle for WTI and 72 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 114.17 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning .9229 as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0459 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now NEGATIVE territory with the 10 year RISING to –0.324%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 1.469% early this morning. Thirty year rate at 1.887%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 15.49.. EXTREMELY DEADLY

“Santa Rally Is Finally Here”: Futures Hit All Time High Day After Powell Goes Full Jean-Claude Trichet

THURSDAY, DEC 16, 2021 – 08:29 AM

One day before what everyone knew would be a hawkish pivot by the Fed, the mood was dour with tech names tumbling and futures hanging one for dear life. One day after, Jerome Powell confirmed he would go full Jean-Claude Trichet as the Fed would not only turbo-taper into a sharply slowing economy, ending its QE program by March but then proceed with hiking rates as many as 3 times in 2022 (more than the 2 hike consensus), with the BOE shocking markets moments ago with a surprise rate hike and even the ECB trimming its turbo QE, and futures are…. at all time highs. That’s right – eminis are higher by 140 points in 24 hours because the Fed was more hawkish than consensus expected. At 8:00 a.m. ET, Dow e-minis were up 215 points, or 0.61%, S&P 500 e-minis were up 27.25 points, or 0.57%, and Nasdaq 100 e-minis were up 100 points, or 0.61%.

Treasury yields jumped alongside European bonds after the BOE became the first major central bank to raise rates since the pandemic, while the dollar fell and the pound jumped. The Euro also hit session highs after the ECB seemed to turn ever so slightly more hawkish as its monthly QE is set to shrink in the coming year.

“The market likes facts it can digest. With the uncertainty now gone, it finds relief,” said Frederik Hildner, a portfolio manager at Salm-Salm & Partner. Gradual rising rates “provides more firepower for the next downturn, as it displays the ability normalize monetary policy.”

On Wednesday, Jerome Powell said the U.S. economy no longer needed increasing amounts of policy support as annual inflation has been running at more than double the central bank’s target in recent months, while the economy nears full employment. Recent readings on surging producer and consumer prices as well as the fast-spreading Omicron variant of the coronavirus have fueled anxiety as the benchmark S&P 500 inches closer to a record high.

“Is the Santa Rally finally here? Markets certainly seem to have a spring in their step… the prospect of three interest rate hikes in 2022 would suggest the central bank has a clear plan to not let inflation get out of control,” Russ Mould, investment director at AJ Bell wrote in a client note.

“Equally, it isn’t being too aggressive to trip up the economy. This sense of balance is exactly what investors want, and an upbeat tone from the Fed certainly seems to have rubbed off on markets” Bell said, clearly goalseeking his narrative to the market’s response as just 24 hours later he would be saying just the opposite when futures were tanking of hawkish Fed fears.

Big tech stocks and banks led gains in premarket trading. Shares in Tesla, Microsoft, Meta and Amazon.com rose between 0.7% and 2.4%, with the lift pushing Apple shares nearer to an historic market value of $3 trillion. Bank stocks including JPMorgan, Morgan Stanley, Bank of America, Wells Fargo and Citigroup all gained between 0.7% and 0.8%. Here are some of the biggest U.S. movers today:

- Apple (APPL) and other big U.S. tech stocks rise after the Federal Reserve said that it would speed up its taper, joining in with a broader relief rally across risk assets. Apple shares are up 0.6%, with the stock drawing nearer to an historic market capitalization of $3 trillion. Also Thursday, Goldman Sachs said lead times for Apple’s iPhone have declined in the latest week.

- Assertio (ASRT US) shares rise 4% after the company announced the $44 million acquisition of the Otrexup device from Antares Pharma.

- Blue Bird (BLBD US) dropped 6% after the school bus-maker provided a weaker-than-expected sales outlook. The company also offered $75m shares at $16/share in a private placement.

- Danimer Scientific (DNMR) falls 10% after announcing that it plans to offer $175 million of convertible senior notes.

- Delta Air Lines (DAL) is up 2% after saying it expects to report a profit for the fourth quarter, citing a strong demand for travel over the winter holiday period and a decline in jet fuel prices. Other airline stocks are also higher.

- DocuSign (DOCU) falls 2% as Morgan Stanley issued a downgrade, saying third-quarter results changed the firm’s view regarding the durability of growth through tough post-pandemic comparables.

- Freyr Battery (FREY) gains 14% after executing its inaugural offtake agreement for at least 31 GWh of low-carbon battery cells.

- IronNet (IRNT US) slumps 25% after the cybersecurity company’s results fell short of expectations, prompting a Street-low target from Jefferies.

- Lennar Corp. (LEN US) declined 6% after it reported a forecast for purchase contracts that was weaker than expected.

- Plug Power (PLUG) gains 5% after signing an agreement with Korean electric-vehicle manufacturer Edison Motors to develop an electric city bus powered by hydrogen fuel cells.

- Syndax Pharmaceuticals (SNDX) falls 8% after pricing 3.2 million shares at $17.50 each.

- Tesla (TSLA) is up 2%, rising with other electric vehicle stocks amid a broader gain in technology stocks and U.S. futures on hopes that the Federal Reserve’s policy tightening will fight high inflation without hampering economic growth.

- Wayfair

falls 2% after BofA downgraded the stock to underperform, citing weak near-term data and difficult comparisons through the first quarter of 2022 for the online furniture retailer.

falls 2% after BofA downgraded the stock to underperform, citing weak near-term data and difficult comparisons through the first quarter of 2022 for the online furniture retailer.

European equities rally with Euro Stoxx 50 up as much as 2.1% before drifting off best levels. The U.K.’s exporter-heavy FTSE 100 Index pared some gains after the BOE decision, while European dipped modestly after the European Central Bank’s meeting. Miners, tech and autos are the best performers, utilities and media names lag.

Equities have whipsawed in recent weeks as investors attempted to price in the prospect of rate hikes, while assessing risks from the spread of the omicron variant. The market’s early response to the Fed signals some relief arising from policy clarity, and optimism that the rebound from pandemic lows can weather the pivot away from ultra-loose monetary settings.

“The market is breathing a sigh of relief that the FOMC meeting suggested that it is taking inflation risks in the United States more seriously,” Ann-Katrin Petersen, an investment strategist at Allianz Global Investors, said in an interview with Bloomberg TV. “The question really will be whether the Fed will dare to do even more in order to taper the inflation risk.”

Asian stocks rose, halting a four-day slide, as confidence in Federal Reserve policy allowed investors to take on riskier assets. The MSCI Asia Pacific Index climbed as much as 0.8%, buoyed by energy and technology shares. Japan was Asia’s top performer, aided by a weaker yen. Hong Kong and China stocks eked out gains amid ongoing concern over U.S. sanctions. Australian equities declined for a third day. Asia’s benchmark advanced for the first time this week on hopes the Fed will effectively combat surging prices without choking off economic growth. The U.S. central bank said it will double the pace of its asset tapering program to $30 billion a month and projected three interest-rate increases in 2022. In the run-up to the Fed’s decision, Asia’s equity gauge slumped almost 2% over the past four days, keeping it below the 50-day moving average. The short-term boost to stock market sentiment is from Fed Chair Jerome Powell’s comments about wage inflation not being the main issue for now, and expectations that there’ll be full employment next year, said Ilya Spivak, head of Greater Asia at DailyFX. However, there’s a “meaningful risk” that the Fed’s latest policy stance will trigger liquidation as Asia stock portfolios are de-risked, Spivak said.

Japan’s stocks rose for a second day after the yen weakened and U.S. stocks rallied amid speculation the Federal Reserve will combat surging prices without choking off economic growth. The Topix index climbed 1.5% to close at 2,013.08 in Tokyo, while the Nikkei 225 Stock Average advanced 2.1% to 29,066.32. Keyence Corp. contributed the most to the Topix’s gain, increasing 2.5%. Out of 2,181 shares in the index, 1,674 rose and 421 fell, while 86 were unchanged. “It wouldn’t be strange to see the discount on Japanese equities narrowing following the FOMC meeting results, with market interest centered around electronics, machinery, automakers and marine transportation stocks,” said Takashi Ito, an equity market strategist at Nomura Securities. Electronics firms and automakers helped lift the Topix as the yen headed for a four-day slump against the dollar, with the currency falling 0.1% to 114.19

Australia’s S&P/ASX 200 index fell 0.4% to close at 7,295.70, extending its losing streak to a third day. CSL was the worst performer after the benchmark’s second-biggest company by weighting completed a placement to fund its Vifor acquisition. Mesoblast was the top performer after saying it plans to conduct an additional U.S. Phase 3 trial of rexlemestrocel-L in patients with chronic low back pain. Investors also digested November jobs data. Australian employment soared last month, smashing expectations and pushing the jobless rate lower as virus restrictions eased on the east coast. In New Zealand, the S&P/NZX 50 index fell 0.7% to 12,777.54

In rates, cash USTs bull steepened, bolstered by a large curve steepener that blocked in early London. Bunds are soft at the back end, peripherals slightly wider ahead of today’s ECB meeting. Gilts bear steepen slightly, white pack sonia futures are lower by 2-3.5 ticks.

In FX, the dollar slipped for a second day and oil rose; cable snapped to best levels of the week after the BOE unexpectedly hiked rates. The Bloomberg Dollar Spot Index fell for a second day as the greenback weakened against all its Group-of-10 peers apart from the yen; Tresury yields fell, led by the belly of the curve. Commodity currencies were the best G-10 performers, led by the krone, which reversed an earlier loss after Norway’s central bank raised its interest rate for the second time this year and flagged another increase in March as officials acted to cool the rebounding economy despite renewed coronavirus concerns. The Australian and New Zealand dollars reversed earlier losses amid upbeat stock markets; the Aussie earlier weakened as RBA Governor Lowe hinted at the prospect of no rate hikes next year. The yen fell as the Federal Reserve’s decision reaffirmed yield differentials ahead of the Bank of Japan’s outcome on Friday. Bonds rose after a solid auction. Elsewhere in FX, NOK outperforms in G-10 after Norges Bank rate action, other commodity currencies are similarly well bid.

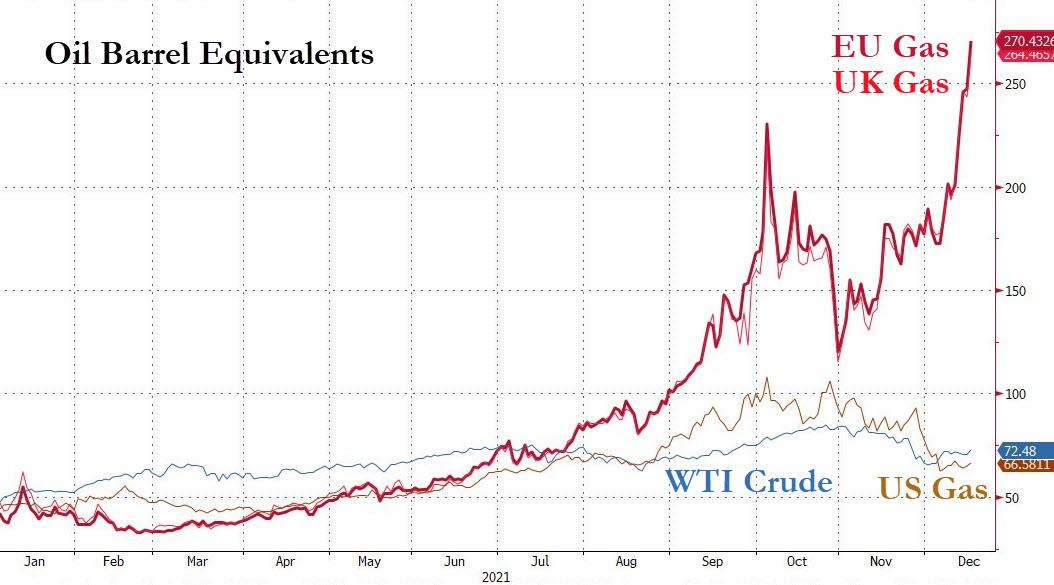

In commodities, Crude futures hold a narrow range around best levels of the session. WTI is up 1.1% near $71.70, Brent near $74.70. Spot gold grinds higher, adding ~$9 near $1,786/oz. LME copper outperforms in a well-bid base metals complex

To the day ahead now, and the main highlights will be the aforementioned policy decisions from the ECB and the BoE. On the data side, we’ll also get the flash PMIs for December from around the world, the Euro Area trade balance for October, and in the US there’s November data on industrial production, housing starts and building permits, as well as the weekly initial jobless claims. Finally, EU leaders will be meeting for a summit in Brussels.

Market Snapshot

- S&P 500 futures up 0.5% to 4,734.25

- STOXX Europe 600 up 1.2% to 476.39

- MXAP up 0.8% to 193.11

- MXAPJ up 0.5% to 623.76

- Nikkei up 2.1% to 29,066.32

- Topix up 1.5% to 2,013.08

- Hang Seng Index up 0.2% to 23,475.50

- Shanghai Composite up 0.8% to 3,675.02

- Sensex up 0.1% to 57,851.57

- Australia S&P/ASX 200 down 0.4% to 7,295.66

- Kospi up 0.6% to 3,006.41

- Brent Futures up 1.0% to $74.59/bbl

- Gold spot up 0.5% to $1,786.03

- U.S. Dollar Index down 0.36% to 96.16

- German 10Y yield little changed at -0.36%

- Euro up 0.2% to $1.1316

Top Overnight News from Bloomberg

- The greenback is set for its biggest annual gain in six years and its rally appears to be far from over, market participants say. The prime mover: a hawkish Federal Reserve that’s drawn a roadmap of interest-rate increases over the next three years, while other central banks look much more reticent to withdraw stimulus

- The ECB is poised to unveil a gradual withdrawal from extraordinary pandemic stimulus in the face of soaring inflation whose path is further clouded by the omicron coronavirus variant

- The “phenomenal pace” at which the new Covid-19 omicron strain is spreading across the U.K. will trigger a surge in hospital admissions over the holiday period, according to Boris Johnson’s top medical adviser

- The Swiss National Bank kept both the deposit and the policy rate at -0.75%, as widely predicted by economists. With the global economic recovery on shaky footing due to the omicron variant, President Thomas Jordan and fellow policy makers also reiterated their pledge to supplement subzero rates with currency interventions as needed

- France will impose tougher rules on people traveling from the U.K., including a ban on non-essential trips and a requirement to self-isolate, as it tries to slow the spread of the omicron variant

- IHS Markit said its index tracking output across the U.K. economy fell to 53.2 this month from 57.6 in November, reflecting weaker-than-expected growth in service industries including hotels, restaurants and travel-related businesses. Business-to-business services stalled

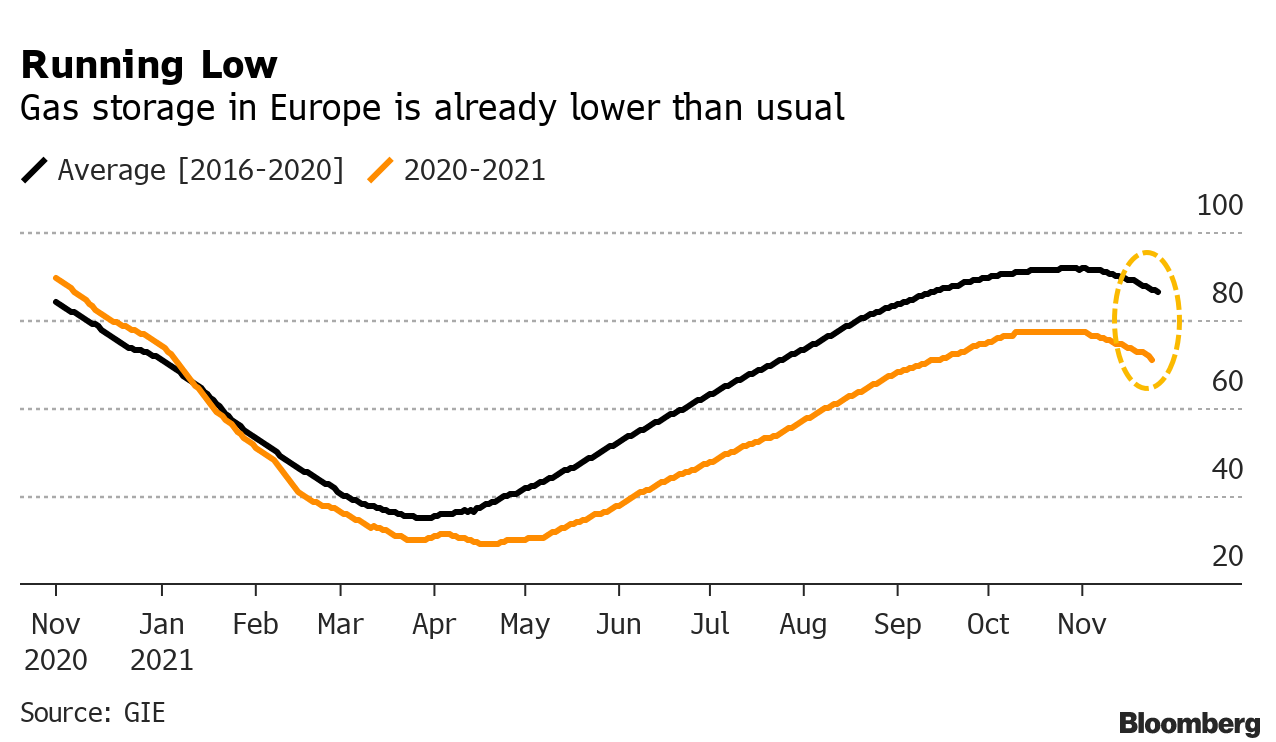

- European power prices soared to records after Electricite de France SA said that two nuclear reactors will stop unexpectedly and two will have prolonged halts — just as the continent heads for a cold snap with already depleted gas inventories

- Hungary’s central bank increased the effective base interest rate for the fifth time in as many weeks to tackle the fastest inflation since 2007 and shore up the battered forint

A more detailed look at global markets courtesy of Newsquawk

Asian equity markets traded mixed as the region digested the FOMC meeting. The ASX 200 (-0.4%) was negative with heavy losses in the healthcare sector and as COVID infections remained rampant. There were also notable comments from RBA Governor Lowe that the board discussed tapering bond purchases in February and ending it in May or could even end purchases in February if economic progress is better than expected, although it is also open to reviewing bond buying again in May if the data disappoints. The Nikkei 225 (+2.1%) outperformed and reclaimed the 29k level after the Lower House recently passed the record extra budget stimulus and with the latest trade data showing double-digit percentage surges in Imports and Exports, despite the latter slightly missing on expectations. The Hang Seng (+0.2%) and Shanghai Comp. (+0.8%) were varied with Hong Kong pressured by losses in the big tech names amid ongoing frictions between the world’s two largest economies and as US lawmakers proposed a bill to allow the US oversight of China audits, although the mainland was kept afloat amid further speculation of a potential LPR cut this month, as well as reports that China will boost financial support for small businesses and offer more longer-term loans to manufacturers. Finally, 10yr JGBs were indecisive despite the constructive mood in Tokyo and with price action stuck near the 152.00 focal point, while demand was also sidelined amid mixed results at the 20yr JGB auction and as the BoJ kickstarts its two-day meeting.

Top Asian News

- Indonesia Reports First Omicron Case in Jakarta Facility

- Asia Stocks Snap Four-Day Drop as Traders Take on Risk After Fed

- Shimao Group Shares Set for Best Day in Month

- Money Manager Vanishes With $313 Million From China Builder

Equities in Europe have taken their cue from the post-FOMC rally seen across Wall Street (Euro Stoxx 50 +1.6%; Stoxx 600 +1.1%) following somewhat mixed APAC trade. As a reminder, markets saw relief with one of the major risk events out of the way, and with Chair Powell refraining from throwing hawkish curveballs. That being said, the forecast does see three rate hikes next year, whilst the Fed Board next year will also be more hawkish – at least within the rotating voters – with George, Mester and Bullard poised to vote from 2022. Nonetheless, US equity future continues grinding higher with all contracts in the green and the RTY (+1.3%) outperforming vs the NQ (+0.7%), ES (+0.6%), and YM (+0.5%). Bourses in Europe also experience broad-based gains with no real outliers, although the upside momentum somewhat waned amid some softer-than-expected PMI metrics ahead of ECB. Sectors in Europe paint a clear pro-cyclical bias. Tech outperforms following a similar sectorial performance seen on Wall Street. Basic Resources and Oil & Gas follow a close second, with Autos and Travel & Leisure also among the biggest gainers. The downside sees Personal & Household Goods, Telecoms and Food & Beverages. Healthcare meanwhile fares better than its defensive peers as Novartis (+4%) is bolstered after commencing a new USD 15bln buyback, highlighting confidence in growth and pipeline. On the flip side, EDF (-12%) shares have slipped after it narrowed FY EBITDA forecasts and highlighted some faults with some nuclear reactors amid corrosion.

Top European News

- Britain’s Covid Resurgence Cuts Growth to Slowest Since Lockdown

- SNB Says Franc Is Highly Valued as Omicron Clouds Outlook

- Norway Delivers Rate Hike That Omicron Had Threatened to Derail

- Erdogan Approves Third Capital Boost for State Banks Since 2019

In FX, not much bang for the Buck fits the bill accurately as it is panning out in the FOMC aftermath even though market expectations were matched and arguably exceeded in terms of dot plots showing three hikes in 2022 vs two anticipated by most and only one previously, while the unwinding of asset purchases will occur in double quick time to end in March next year instead of June. However, there appears to be enough in the overall statement, SEP and Fed chair Powell’s post-meeting press conference to offset the initial knee-jerk spike in the Dollar and index that lifted the latter very close to its current y-t-d peak at 96.914 vs 96.938 from November 24. Indeed, the terminal rate was maintained at 2.5%, no decision has been taken about whether to take a break after tapering before tightening, and the recovery in labour market participation has been disappointing to the point that it will now take longer to return to higher levels. In response, or on further reflection, the DXY has recoiled to 96.141 and through the 21 DMA that comes in at 96.238 today.

- NZD/AUD/CAD/GBP/EUR/CHF – All on the rebound vs their US counterpart, with the Kiwi back on the 0.6800 handle and also encouraged by NZ GDP contracting less than feared in Q3, while the Aussie is hovering around 0.7200 in wake of a stellar jobs report only partly tempered by dovish remarks from RBA Governor Lowe who is still not in the 2022 hike camp and non-committal about ending QE next February or extending until May. Elsewhere, the Loonie has clawed back a chunk of its losses amidst recovering crude prices to regain 1.2800+ status ahead of Canadian wholesale trade that is buried between a raft of US data and survey releases, Sterling is flirting with 1.3300 in advance of the BoE that is likely to hold fire irrespective of significantly hotter than forecast UK inflation, the Euro is pivoting 1.1300 pre-ECB that is eyed for details of life after the PEPP and the Franc is somewhat mixed post-SNB that maintained rates and a highly valued assessment of the Chf with readiness to intervene as required. Note, Usd/Chf is meandering from 0.9256 to 0.9221 vs Eur/Chf more elevated within a 1.0455-30 band.

- JPY – The Yen is underperforming on the eve of the BoJ and looking technically weak to compound its yield and rate disadvantage after Usd/Jpy closed above a key chart level on Wednesday (at 114.03). As such, Fib resistance is now exposed at 114.38 vs the circa 114.25 high, so far, while decent option expiry interest may be influential one way or the other into the NY cut given around 1.3 bn at the 114.25 strike, 1.7 bn at 114.30 and 1.2 bn or so at 114.50.

In commodities, WTI and Brent front-month futures are taking advantage of the risk appetite coupled with the softer Buck. WTI Jan trades on either side of USD 71.50/bbl (vs low USD 71.39/bbl) while Brent Feb sees itself around USD 74.50/bbl (vs low USD 74.28/bbl). Complex-specific news has again been on the quiet end, with prices working off the macro impulses for the time being, and with volumes also light heading into Christmas trade. Elsewhere spot gold and silver ebb higher – in tandem with the Dollar, with the former eyeing a group of DMAs to the upside including the 100 (1,788/oz), 21 (1,789/oz) 200 (1,794/oz) and 50 (1,796/oz). Turning to base metals, LME copper has been catapulted higher amid the risk and weaker Dollar, with prices re-testing USD 9,500/t to the upside. Meanwhile, a Chinese government consultancy has said that China’s steel consumption will dip 0.7% on an annual basis in 2022 amid policies for the real estate market and uncertainties linked to COVID-19 curb demand.

US event calendar

- 8:30am: Dec. Initial Jobless Claims, est. 200,000, prior 184,000; Continuing Claims, est. 1.94m, prior 1.99m

- 8:30am: Nov. Housing Starts MoM, est. 3.1%, prior -0.7%

- 8:30am: Nov. Housing Starts, est. 1.57m, prior 1.52m

- 8:30am: Nov. Building Permits MoM, est. 0.5%, prior 4.0%, revised 4.2%

- 8:30am: Nov. Building Permits, est. 1.66m, prior 1.65m, revised 1.65m

- 8:30am: Dec. Philadelphia Fed Business Outl, est. 29.6, prior 39.0

- 9:15am: Nov. Manufacturing (SIC) Production, est. 0.7%, prior 1.2%; Industrial Production MoM, est. 0.6%, prior 1.6%

- 9:45am: Dec. Markit US Manufacturing PMI, est. 58.5, prior 58.3

- 9:45am: Dec. Markit US Services PMI, est. 58.8, prior 58.0

DB’s Jim Reid concludes the overnight wrap

Yesterday’s biggest story was obviously the Fed. In line with our US economists call (their full recap here), the FOMC doubled the pace of taper to $30bn a month, which would bring an end to QE in mid-March. The new dot plot showed three rate hikes in 2022, up from the Committee being split over one hike in September. Farther out, the median dot had 3 additional hikes in 2023 and 2 hikes in 2024, bringing fed funds just below their estimate of the longer-term rate. Notably, all 18 Committee members have liftoff occurring next year, and 10 have 3 hikes penciled in, suggesting consensus behind the recent hawkish turn was strong. Short-end market pricing increased in line and now has around 2.9 hikes priced for 2022. The first hike is fully priced for the June meeting, but notably, meetings as early as March are priced as live, more on that in a bit.

In the statement, the Committee admitted that inflation had exceeded target for some time (dropping ‘transitory’ completely), and that liftoff would be tied to the economy reaching full employment. By the sounds of the press conference, progress toward full employment has proceeded pretty rapidly. Chair Powell noted that while labour force participation progress has been disappointing, almost every other measure of labour market strength shows a very strong labour market, and could create upside risks to inflation should wage growth start to increase beyond productivity. It is within that context that he framed the decision to taper faster, it will leave the Fed in a position to react as needed, providing optionality. In that vein, he stressed a few times that the lag between the end of taper and liftoff need not be as long as it was in the last cycle, and that the Fed will raise rates after taper is done whenever needed, hence meetings as early as March being live.

Notably on Omicron, the Chair, like the rest of us, recognises we don’t know much about the variant yet, but seemed optimistic about the economy’s ability to withstand subsequent Covid shocks, regardless of Omicron’s specifics. While Covid shocks can tighten supply chains, discourage labour participation, and reduce demand, as more people get vaccinated those impacts should dwindle over time, so his argument went. Hammering the point home, he sounded confident that the economy can handle whatever Omicron brings without any additional QE, justifying the accelerated taper path despite Covid risks.

The hawkish turn had been well forecast through Fed speakers since the last meeting, not least of which the Chair himself during Congressional testimony, which served to dull the market impact. Treasury yields were slightly higher, (2yr Tsys +0.6bps and 10yr Tsys +1.5 bps) but were quite docile for an FOMC afternoon. The dollar initially strengthened on the statement release before reversing course and ending the day -0.24% lower. Stocks were the real outperformers, as the S&P 500 rallied through the FOMC events, gaining +1.63%, the best daily performance in two months, while the Nasdaq increased +2.15%. The Russell 2000 matched the S&P, gaining +1.65%. Obviously the market was anticipating the change in policy, but if doubling taper and adding three rate hikes in the next year isn’t enough to tighten financial conditions, what is? The Chair was asked about that in so many words in the press conference, where he responded by noting financial conditions could change on a dime. Indeed, they will have to tighten from historically easy levels if the Fed is to bring inflation back to target through policy.

The Fed may be out of the way now, but the central bank excitement continues today as both the ECB and the BoE announce their own policy decisions later on. We’ll start with the ECB, who like the Fed have faced much higher than expected inflation lately, with the November flash estimate coming in at +4.9%, which is the highest since the formation of the single currency. Whilst Omicron has cast a shadow of uncertainty, with Commission President von der Leyen saying yesterday that it was likely to become dominant in Europe by mid-January, our European economics team doesn’t think there has been anything concrete enough to alter the ECB from their course (like the Fed). In our European economists’ preview (link here) they write the ECB appears on track to initiate a transition to a monetary policy stance based more on policy rates and rates guidance and less on liquidity provision. The ECB is set to confirm that PEPP net purchases will end in March, but will cushion the blow by working flexibility into the post-PEPP asset purchase arrangement. They are also set to make the policy framework more flexible to better respond to inflation uncertainties.

One thing to keep an eye out for in particular will be the latest inflation projections, with a report from Bloomberg suggesting that they’ll show inflation beneath the 2% target in both 2023 and 2024. So if that’s true, that could offer a route to arguing against a tightening of monetary policy for the time being, since the ECB’s forward guidance has been that it won’t raise rates until it sees inflation at the target “durably for the rest of the projection horizon”.

Today’s other big decision comes from the BoE, where our UK economist is expecting that there’ll be a 15bps increase in Bank Rate, taking it up to 0.25% although they suggest it’s a very close call. See here for the rationale. Ahead of that decision later on, we received a very strong UK inflation print for November, with CPI rising to +5.1% (vs. +4.8% expected), up from +4.2% in October and the fastest pace in a decade. That’s running ahead of the BoE’s own staff forecasts in the November Monetary Policy Report, which had seen inflation at just +4.5% that month, so six-tenths beneath the realised figure. We’ll get their decision at 12:00 London time, 45 minutes ahead of the ECB’s.

In terms of the latest on the Omicron variant, there are continued signs of concern in South Africa, with cases coming in at a record 26,976 yesterday, whilst the number in hospital at 7,339 is up +73% compared to a week ago. Meanwhile the UK recorded their highest number of cases since the pandemic began, at 78,610. England’s Chief Medical Officer, Chris Whitty, said that a lot of Covid records would be broken in the coming weeks, and also that a majority of cases in London were now from the Omicron variant. Separately, the French government is set to hold a meeting tomorrow on Covid measures, and EU leaders will be discussing the pandemic at their summit today.

When it comes to Omicron’s economic impact, we could see some light shed on that today as the December flash PMIs are released from around the world. Overnight we’ve already had the numbers out of Australia and Japan where hints of a slowdown are apparent. Japan’s Manufacturing PMI came out at 54.2 (54.5 previous) and the Composite at 51.8 (53.3 previous) while Australia’s Manufacturing and Composite came in at 57.4 and 54.9 respectively (59.2 and 55.7 previous).

Overnight in Asia stocks are trading mostly higher led by the Nikkei (+1.78%) followed by the Shanghai Composite (+0.28%), and KOSPI (+0.22%). However the CSI (-0.07%) and Hang Seng (-0.81%) are losing ground on concerns of US sanctions on Chinese tech companies. In Australia, the November employment report registered a strong beat by adding 366.1k jobs against 200k consensus. This is being reflected in a +12.75 bps surge in Australia’s 3y bond. Elsewhere, in India wholesale inflation for November rose +14.2% year on year, levels last seen in 2000 against a consensus of +11.98% on the back of higher food and input prices. DM futures are indicating a positive start to markets today with S&P 500 (+0.19%) and DAX (+1.04%) contracts both higher as we type.

Ahead of the Fed, European markets had put in a fairly steady performance yesterday, with the STOXX 600 up +0.26%. That brought an end to a run of 5 successive declines, with technology stocks in particular seeing an outperformance. Sovereign bond markets were also subdued ahead of the ECB and BoE meetings later, with yields on 10yr bunds (+0.9bps), OATs (+0.5bps) and gilts (+1.2bps) only seeing modest moves higher.

In DC, despite optimistic sounding talks earlier in the week, the latest yesterday was President Biden and Senator Manchin remained far apart on the administration’s build back better bill, imperiling its chances of passing before Christmas. Elsewhere, reports suggested the President would have more nominations for the remaining Fed Board vacancies this week.

Looking at yesterday’s other data, US retail sales underwhelmed in November with growth of just +0.3% (vs. +0.8% expected), and measure excluding gas and motor vehicles was also up just +0.2% (vs. +0.8% expected). Also the NAHB’s housing market index for December moved up to a 10-month high of 84, in line with expectations.

To the day ahead now, and the main highlights will be the aforementioned policy decisions from the ECB and the BoE. On the data side, we’ll also get the flash PMIs for December from around the world, the Euro Area trade balance for October, and in the US there’s November data on industrial production, housing starts and building permits, as well as the weekly initial jobless claims. Finally, EU leaders will be meeting for a summit in Brussels.

3A/ASIAN AFFAIRS

) THURSDAY MORNING/WEDNESDAY NIGHT:

SHANGHAI CLOSED UP 28.79 PTS OR 0.75% //Hang Sang CLOSED UP 54.74 PTS OR 0.23% /The Nikkei closed UP 606.60 PTS OR 2.13% //Australia’s all ordinaires CLOSED DOWN 0.23%/Chinese yuan (ONSHORE) closed DOWN 6.3678 /Oil UP TO 71.19 dollars per barrel for WTI and UP TO 74.18 for Brent. Stocks in Europe OPENED ALL GREEN // ONSHORE YUAN CLOSED DOWN AT 6.3678 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.3758: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3 a./NORTH KOREA/ SOUTH KOREA

///SOUTH KOREA/COVID

HONG KONG/COVID/VACCINE MANDATE

3B CHINA

Both China and Russia are closer than ever in their joint cooperation to counter USA interference. You will recall that both of these nations are purchasing and hoarding gold

(zerohedge)

‘Closer Than Allies’: Xi & Putin Hail China-Russia Cooperation To Counter US “Interference”

WEDNESDAY, DEC 15, 2021 – 09:20 PM

Just before Wednesday’s Putin-Xi virtual summit, the Kremlin described that the meeting among allies is essential as at this moment “We see very, very aggressive rhetoric on the NATO and US side, and this requires discussion between us and the Chinese.” China’s Foreign Ministry had said the meeting would “further enhance the high-level mutual trust between the two sides.”

As expected, both leaders emphasized the need to resist “interference” in their countries’ internal affairs from the West and in particular the United States. “A new model of cooperation has been formed between our countries, based among other things on such principles as not interfering in internal affairs [of each other], respect for each other’s interests, determination to turn the shared border into a belt of eternal peace and good neighborliness,” Putin told his Chinese counterpart.

In the discussion which lasted from 4:07 p.m. to 5:21 p.m. Beijing time, Xi responded by affirming that the Russian president “strongly supported China’s efforts to protect key national interests and firmly opposed attempts to drive a wedge between our countries.” Bloomberg characterized the tone of the meeting as between two leaders that are ‘closer than allies’: “Chinese President Xi Jinping hailed relations with Russia as better than an alliance in a video call with President Vladimir Putin, according to the Kremlin, as the two leaders made a show of solidarity amid rising tensions with the West.”Image source: TASS

Calling Putin “an old friend,” Xi described relations with Russia as going beyond that of traditional allies and partners, saying, “Such a figurative expression very accurately reflects the essence of what is happening now in relations between our two countries.” He said the Russian president had “firmly supported China in defending its core interests and opposed attempts to divide China and Russia,” according to state broadcaster CCTV.

The summit comes a week after the Biden-Putin virtual summit, wherein the Russian leader pressed for dialogue to put in place a plan for legal guarantees that NATO would not expand further eastward near Russia’s border. On Wednesday China’s Xi declared formal support for this central security concern of Russia’s:

Putin won support from Xi for his push to obtain binding security guarantees for Russia from the West, a Kremlin official said, according to Reuters.

Russia wants the United States and NATO to guarantee the military alliance will not expand further eastward or deploy weapons systems in Ukraine and other countries on Russia’s border.