JAN21/

January 20, 2022 · by harveyorgan · in Uncategorized · Leave a comment ·Edit

January 21, 2022 · by harveyorgan · in Uncategorized · Leave a comment ·Edit

GOLD; DOWN $10.80 to $1831.40

SILVER: $24.25 DOWN 41 CENTS

ACCESS MARKET: GOLD: 1834.60..

SILVER: $24.29

Bitcoin: morning price: 38,220 down 3223

Bitcoin: afternoon price: 37,700 down 3743

Platinum price: closing down $12.35 to $1032.10

Palladium price; closing up $907 at $2103.15

END

end

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

comex notices//JPMorgan notices filed COMEX//NOTICES:

FILED 0/85

EXCHANGE: COMEX

CONTRACT: JANUARY 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,842.500000000 USD

INTENT DATE: 01/20/2022 DELIVERY DATE: 01/24/2022

FIRM ORG FIRM NAME ISSUED STOPPED

435 H SCOTIA CAPITAL 66

624 H BOFA SECURITIES 83

661 C JP MORGAN 3

732 C RBC CAP MARKETS 16

737 C ADVANTAGE 2

TOTAL: 85 85

MONTH TO DATE: 5,649

NUMBER OF NOTICES FILED TODAY FOR JAN. CONTRACT: 85 NOTICE(S) FOR 85000 OZ (0.2643 TONNES)

total notices so far: 5649 contracts for 564,900 oz (17.570 tonnes)

SILVER NOTICES:

72 NOTICE(S) FILED TODAY FOR 360,000 OZ/

total number of notices filed so far this month 2838 : for 14,190,000 oz

GLD

WITH GOLD DOWN $10.80

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):NO CHANGES IN GOLD INVENTORY AT THE GLD:

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

CLOSING INVENTORY: 980.86 TONNES/

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 41 CENTS:/: NO CHANGES IN SILVER INVENTORY AT THE SLV/

AT THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY SLV/ TONIGHT: 527.792 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A STRONG 1687 CONTRACTS TO 152,743 AND RESTS CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THIS GAIN IN OI WAS ACCOMPANIED WITH THE $0.52 GAIN IN SILVER PRICING AT THE COMEX ON THURSDAY. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.52) AND WERE UNSUCCESSFUL IN KNOCKING OUT SOME SILVER LONGS AS WE HAD AN ATMOSPHERIC GAIN OF 5590 CONTRACTS ON OUR TWO EXCHANGES .

WE MUST HAVE HAD:

I) HUGE BANKER SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A GIGANTIC ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A HUGE INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 10.505 MILLION OZ FOLLOWED BY TODAY’S 100,000 OZ QUEUE. JUMP //NEW STANDING 14.435 MILLION OZ V) STRONG SIZED COMEX OI GAIN.

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS -264

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JAN. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JAN:

TOTAL CONTACTS for 14 days, total contracts: : 13,658 contracts or 68.290 million oz OR 4.8778 MILLION OZ PER DAY. (975 CONTRACTS PER DAY)

TOTAL NO OF OZ UNDERGOING EFP TO LONDON 13,658 CONTRACTS X 5,000 PER CONTRACT:

EQUATES TO: 68.290 MILLION OZ

.

LAST 8 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

RESULT: WE HAD A STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1687 WITH OUR 52 CENT GAIN SILVER PRICING AT THE COMEX// THURSDAY THE CME NOTIFIED US THAT WE HAD A HUGE SIZED EFP ISSUANCE OF 3639 CONTRACTS( 3639 CONTRACTS ISSUED FOR MAR AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY:/ AS WELL AS TODAY /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR JAN OF 10.505 MILLION OZ FOLLOWED BY TODAY’S 100,000 OZ QUEUE JUMP //NEW STANDING 14.435, MILLION OZ// .. WE HAD ATMOSPHERIC SIZED GAIN OF 5236 OI CONTRACTS ON THE TWO EXCHANGES FOR 26.30 MILLION OZ//

WE HAD 72 NOTICES FILED TODAY FOR 360,000 OZ

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A STRONG 6,442 TO 559,048 AND CLOSER TO OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: -2691 CONTRACTS

.

THE STRONG SIZED INCREASE IN COMEX OI CAME DESPITE OUR TINY GAIN IN PRICE OF $0.20//COMEX GOLD TRADING/THURSDAY/.AS IN SILVER WE MUST HAVE HAD HUGE BANKER/ALGO SHORT COVERING ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION AS THE TOTAL GAIN ON OUR TWO EXCHANGES TOTALED A VERY STRONG SIZED 12,056 CONTRACTS…

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR JAN AT 3.5614 TONNES FOLLOWED BY TODAY’S 200 OZ QUEUE. JUMP//NEW STANDING: 17.608 TONNES

YET ALL OF..THIS HAPPENED WITH OUR GAIN IN PRICE OF $0.20 WITH RESPECT TO WEDNESDAY’S TRADING

WE HAD A VERY STRONG SIZED GAIN OF 9,345 OI CONTRACTS (29.06 PAPER TONNES) ON OUR TWO EXCHANGES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALLED A FAIR SIZED 2903 CONTRACTS:

FOR FEB 2903 ALL OTHER MONTHS ZERO//TOTAL: 2903

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 561,759.

IN ESSENCE WE HAVE A VERY STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 12,056, WITH 9,153 CONTRACTS INCREASED AT THE COMEX AND 2903 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 12,056 CONTRACTS OR 37.49TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2903) ACCOMPANYING THE STRONG SIZED GAIN IN COMEX OI (6442): TOTAL GAIN IN THE TWO EXCHANGES 9345 CONTRACTS. WE NO DOUBT HAD 1) HUGE BANKER SHORT COVERING ,2.) HUGE INITIAL STANDING AT THE GOLD COMEX FOR JAN. AT 3.7262 TONNES//FOLLOWED BY TODAY’S 200 OZ QUEUE. JUMP.//NEW STANDING 17.608 TONNES 3)ZERO LONG LIQUIDATION,4) STRONG SIZED COMEX OI. GAIN 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF FEB.WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF JAN HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB, FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (FEB), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2021 INCLUDING TODAY

JAN

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JAN : 53,309 CONTRACTS OR 5,330,900 oz OR 165.81 TONNES (14 TRADING DAY(S) AND THUS AVERAGING: 3807 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 14 TRADING DAY(S) IN TONNES: 165.81 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2020, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 165.81/3550 x 100% TONNES 4.67% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO DATE

JANUARY: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 145.12 TONNES//INITIAL ISSUANCE//

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A STRONG SIZED 1687 CONTRACTS TO 150,792 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 4 1/2 YEARS AGO.

EFP ISSUANCE 3639 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 3639 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 3659 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1651 CONTRACTS AND ADD TO THE 3639 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN AN ATMOSPHERIC SIZED GAIN OF 5326 OPEN INTEREST CONTRACT FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 26.630 MILLION OZ,

OCCURRED WITH OUR $0.52 GAIN IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

5. Other gold commentaries

6. Commodity commentaries/cryptocurrencies

3. ASIAN AFFAIRS

i)FRIDAY MORNING// THURSDAY NIGHT

SHANGHAI CLOSED DOWN 32.49 PTS OR 0.91% //Hang Sang CLOSED UP 13.20 PTS OR 0.05% /The Nikkei closed DOWN 250.67 PTS OR 0.90% //Australia’s all ordinaires CLOSED OWN 2.33% /Chinese yuan (ONSHORE) closed UP 6.3399 /Oil DOWN TO 84.45 dollars per barrel for WTI and UP TO 87.05 for Brent. Stocks in Europe OPENED ALL RED // ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.3399. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.3427: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN AND OFF SHORE TRADING STRONGER AGAINST USA DOLLAR

A)NORTH KOREA//USA/OUTLINE

b) REPORT ON JAPAN

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A STRONG SIZED 6442 CONTRACTS AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS STRONG COMEX INCREASE OCCURRED DESPITE OUR TINY GAIN OF $0.20 IN GOLD PRICING THURSDAY’S COMEX TRADING. WE ALSO HAD A FAIR EFP (2903 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. LOOKS LIKE OUR BANKERS ARE FINALLY BAILING OUT

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE NON ACTIVE DELIVERY MONTH OF JAN.. THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2903 EFP CONTRACTS WERE ISSUED: ;: , DEC : 0 & FEB. 2903 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2903 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A VERY STRONG SIZED 9,345 TOTAL CONTRACTS IN THAT 2903 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A VERY STRONG SIZED COMEX OI GAIN OF 6442 CONTRACTS..

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING FOR JAN (17.608),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

THE BANKERS WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $0.20)

AND THEY WERE UNSUCCESSFUL IN FLEECING ANY LONGS AS THE TOTAL GAIN ON THE TWO EXCHANGES REGISTERED A VERY STRONG 29.06 TONNES, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR JAN (17.608 TONNES)…

WE HAD – 2,691 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 9,345 CONTRACTS OR 934,500 OZ OR 29.06 TONNES

Estimated gold volume today: 181,380 /// poor

Confirmed volume yesterday: 325,118 contracts fair

INITIAL STANDINGS FOR JAN ’22 COMEX GOLD

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 148,694.680 ozBrinksHSBCincludes 4000 kilobarsHSBC |

| Deposit to the Dealer Inventory in oz | nilOZ |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 85 notice(s)8500 OZ 0.2643 TONNES |

| No of oz to be served (notices) | 12 contracts 1200 oz 0.0373 TONNES |

| Total monthly oz gold served (contracts) so far this month | 5649 notices 564,900 OZ 17.570 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

| xx oz |

For today:

No dealer deposit 0

No dealer withdrawal 0

0 customer deposit

total deposit: nil oz

2 customer withdrawals

i) Out of BRINKS: 20,090.680 0z (real gold leaving)

ii) Out of HSBC 128,600.000 (4000 kilobars)

ADJUSTMENTS: 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JANUARY.

For the front month of JANUARY we have an oi of 97 stand for JANUARY LOSING 298 contracts. We had 300 notices filed on THURSDAY, so we GAINED 2 contracts or an additional 200 oz will stand for

gold in this very non active delivery month of January.

FEBRUARY LOST 18,232 CONTRACTS TO 165,904

March GAINED 314 contracts to stand at 2721..

We had 85 notice(s) filed today for 85,000 oz FOR THE JAN 2022 CONTRACT MONTH

Today, 3 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 85 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JAN /2021. contract month,

we take the total number of notices filed so far for the month (5649) x 100 oz , to which we add the difference between the open interest for the front month of (JAN: 97 CONTRACTS ) minus the number of notices served upon today 85 x 100 oz per contract equals 566,100 OZ OR 17.608 TONNES the number of TONNES standing in this NON active month of JAN. (numbers corrected from yesterday)

thus the INITIAL standings for gold for the JAN contract month:

No of notices filed so far (5649) x 100 oz+ (97) OI for the front month minus the number of notices served upon today (85} x 100 oz} which equals 565,900 oz standing OR 17.608 TONNES in this NON active delivery month of JAN.

We GAINED 2 contracts or an additional 200 oz of gold will stand for metal on this side of the pond.

TOTAL COMEX GOLD STANDING: 17.608 TONNES (HUGE FOR A JANUARY DELIVERY MONTH

IF THIS HOLDS TO THE END OF THE MONTH, THIS WILL BE THE HIGHEST EVER RECORDED GOLD STANDING FOR A JANUARY, GENERALLY A VERY POOR DELIVERY MONTH.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

206,468.649, oz NOW PLEDGED /HSBC 6.42 TONNES

125,410.592 PLEDGED MANFRA 3.90 TONNES

54,339.114oz PLEDGED JPMorgan no 1 1.690

288,481,604, oz JPM No 2 8.97 TONNES

898,821.330 oz pledged Brinks/27,96 TONNES

12,244.444 oz International Delaware: 0..3808 tonne

Loomis: 18,615.429 oz

total pledged gold: 1,604,386.051oz 49.90 tonnes

TOTAL REGISTERED AND ELIZ GOLD AT THE COMEX: 33,418,839.469 OZ (1039,46 TONNES)

TOTAL ELIGIBLE GOLD: 15,838,298.95 OZ (492.63 tonnes)

TOTAL OF ALL REGISTERED GOLD: 17,580,540.519 OZ (546.82 tonnes)

REGISTERED GOLD THAT CAN BE SERVED UPON: 15,976,154.0 OZ (REG GOLD- PLEDGED GOLD) 496.92 tonnes

END

JANUARY 2022 CONTRACT MONTH//SILVER

INITIAL STANDING FOR SILVER//JAN 21

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 534,568.570 oz Brinks CNT JPMorgan |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 600,722.900 oz CNT |

| No of oz served today (contracts) | 72 CONTRACT(S) 360,000 OZ) |

| No of oz to be served (notices) | 49 contracts (245,000 oz) |

| Total monthly oz silver served (contracts) | 2838 contracts (14,190,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

we had 0 deposits into the dealer

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 3 withdrawals

ii) Into Brinks; 9585.20 oz

iii) Into JPmorgan: 512,926.680 oz

iv) Into CNT; 12,056.60 oz

JPMorgan has a total silver weight: 184.986 million oz/355.993 million =51.95% of comex

ii) Comex withdrawals: 3

a) Out of CNT 925,629.560 oz

b) Out of Delaware; 175,637.090 oz

c) Out of Brinks 101,248.170 oz

d) out of manfra 1183,665.519 oz

total withdrawal 3,186.697.125 oz

we had 1 adjustment

customer to dealer..manfra 1,463,243.149 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 82.616 MILLION OZ

TOTAL REG + ELIG. 355.993 MILLION OZ

TOTAL NO OF CONTRACTS SERVED UPON THIS MONTH: 2838 CONTRACTS FOR 14,190,000 OZ

CALCULATION OF SILVER OZ STANDING FOR JANUARY

NUMBER OF NOTICES FILED TODAY: 72 NOTICES OR 360,000 OZ

silver open interest data:

FRONT MONTH OF JAN//2022 OI: 121 CONTRACTS LOSING 281 contracts on the day

We had 301 notices filed for THURSDAY so we GAINED 20 contracts or 100,000 additional oz will stand for delivery in this non active delivery month of January.

FOR FEB WE HAD A LOSS OF 60 CONTRACTS DOWN TO 596

FOR MARCH WE HAD A GAIN OF 1067 CONTRACTS UP TO 117,818 CONTRACTS.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 72 for 360,000 oz

Comex volumes: 30,145// est. volume today//poor

Comex volume: confirmed YESTERDAY: 79,436 contracts (strong)

To calculate the number of silver ounces that will stand for delivery in JANUARY. we take the total number of notices filed for the month so far at 2838 x 5,000 oz =. 14,190,000 oz

to which we add the difference between the open interest for the front month of JAN (121) and the number of notices served upon today 72 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JAN./2021 contract month: 2838 (notices served so far) x 5000 oz + OI for front month of JAN (121) – number of notices served upon today (72) x 5000 oz of silver standing for the JAN contract month equates 14,435,000 oz. .

We GAINED 20 contracts or an additional 100,000oz will stand for delivery on this side of the pond.

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

GLD

JAN 21/WITH GOLD DOWN $10.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 980.86 TONNNES

JAN 20/WITH GOLD UP $.20 TODAY: A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .58 TONNES FROM THE GLD///INVENTORY RESTS AT 980.86 TONNES

JAN 19/WITH GOLD UP $29.65 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 5.27 TONNES INTO THE GLD/INVENTORY RESTS AT 981.44 TONNES

JAN 18/WITH GOLD DOWN $3.25//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 976.21 TONNES

JAN 14/ WITH GOLD DOWN $5.25/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 976.21 TONNES

JAN 13/WITH GOLD DOWN $5.75: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 976.21 TONNES

JAN 12/WITH GOLD UP $8.65//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 976.21 TONNES

JAN 11/WITH GOLD UP $19.25/A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES FROM THE GLD/INVENTORY RESTS AT 976.21 TONNES

JAN 10/WITH GOLD UP $2.00/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 977.08 TONNES

JAN 7/WITH GOLD UP $8.15//A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWLA OF 1.16 TONNES FROM THE GLD////INVENTORY RESTS AT 978.83 TONNES

JAN 6/WITH GOLD DOWN $35.30//A SMALL CHANGE IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF .32 TONNES/INVENTORY RESTS AT 979.99 TONNES

JAN 5/WITH GOLD UP $10.30: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 980.31 TONNES

Jan 4/WITH GOLD UP $14.00//A HUGE CHANGE OF 4.65 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 980.31 TONNES

JAN 3/WITH GOLD DOWN $26.70: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 975.66 TONNES

DEC 31/WITH GOLD UP $14.05 : NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 975.66 TONNES

DEC 30/WITH GOLD UP $7.75 NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 975.66 TONNES

DEC 29/WITH GOLD DOWN $5.00 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.03 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 975.66 TONNES

DEC 28/WITH GOLD UP $2.00 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 973.63 TONNES

DEC 27/WITH GOLD DOWN $2.05: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.63 TONNES.

DEC 23/WITH GOLD UP $9.85 TODAY//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.94 TONNES FROM THE GLD/// INVENTORY RESTS AT 973.63 TONNES

DEC 22/WITH GOLD UP $12.85 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 978.57 TONNES

DEC 21/WITH GOLD DOWN $7.05 TODAY, NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 978.57 TONNES

DEC 20/WITH GOLD DOWN $9.65 TODAY; A BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.37 TONNES INTO THE GLD///INVENTORY RESTS AT 977.20 TONNES

DEC 17/WITH GOLD UP $7.05 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 977.20 TONNES

DEC 16/WITH GOLD UP $33.05TODAY; A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.4 TONNES FROM THE GLD////INVENTORY REST AT: 977.20 TONNES

DEC15/WITH GOLD DOWN $7.80 TODAY/ A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.04 TONNES FROM THE GLD////INVENTORY RESTS AT 980.60 TONNES.

DEC 14/WITH GOLD DOWN $18.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 982.64 TONNES

DEC 13/WITH GOLD UP $3.20 TODAY/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 982.64 TONNES

DEC 10.WITH GOLD UP $7.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 982.64 TONNES

DEC 9/WITH GOLD DOWN $9.10 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 982.64.

DEC 8/WITH GOLD UP $5.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 984.38 TONNES

DEC 7/WITH GOLD UP $5.15 TODAY; A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 984.38 TONNES

DEC 6/WITH GOLD DOWN $3.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 986.17 TONNES//

CLOSING INVENTORY: 980.86 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

SLV.

JAN 21/WITH SILVER DOWN 41 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 527.792 MILLION OZ

JAN 20/WITH SILVER UP 52 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.998 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 527.792 MILLION OZ

JAN 19/WITH SILVER UP 71 CENTS TODAY: A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.942 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 525.804 MILLION OZ

JAN 18/WITH SILVER UP 51 CENTS TODAY: TWO HUGE CHANGES IN SILVER INVENTORY AT THE SLV: 2 WITHDRAWALS OF 1.11 MILLION OZ AND 1.424 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 527.246 MILLION OZ//

JAN 14/WITH SILVER DOWN 21 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 529.780 MILLION OZ//

JAN 13/WITH SILVER DOWN 2 CENTS: A BIG CHANGE IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 832,000 OZ FROM THE SLV////INVENTORY RESTS AT 529.780 MILLION OZ

JAN 12/WITH SILVER UP 38 CENTS TODAY : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.612 MILLION OZ//

JAN 11/WITH SILVER UP 33 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.612 MILLION OZ/.

JAN 10/WITH SILVER UP 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 530.612 MILLION OZ//.

JAN 7/WITH SILVER UP 17 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.612 MILLION OZ//.

JAN 6/WITH SILVER DOWN 94 CENTS TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL PF 226,000 OZ FROM THE SLV///INVENTORY RESTS AT 530.612 MILLION OZ?/

JAN 5/WITH SILVER UP 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.838 MILLION OZ//

JAN 4/WITH SILVER UP 21 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.838 MILLION OZ//

JAN 3/WITH SILVER DOWN 45 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.219 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 530.838 MILLION OZ//

DEC 31/WITH SILVER UP 29 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 533.057 MILLION OZ//

DEC 31/WITH SILVER UP 29 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 533.057 MILLION OZ//

DEC30/WITH SILVER UP 14 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A HUGE WITHDRAWAL OF 4.624 MILLILON OZ FROM THE SLV.//INVENTORY RESTS AT 533.057 MILLION OZ//

DEC 29/WITH SILVER DOWN 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 537.681 MILLION OZ/

DEC 28/WITH SILVER UP 9 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.682 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 537.681 MILLION OZ//

DEC 27/WITH SILVER UP 6 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 537.681

DEC 23/WITH SILVER UP 19 CENTS TODAY:A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.202 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 537.681 MILLION OZ//

DEC 22/WITH SILVER UP 29 CENTS TODAY; A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.202 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 538.883 MILLION OZ/

DEC 21/WITH SILVER UP 19 CENTS: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.728 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 540.085 MILLION OZ

DEC 20/WITH SILVER DOWN 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 538.282 MILLION OZ

DEC 17/WITH SILVER UP 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 538.282 MILLION OZ//

DEC 16/WITH SILVER UP 91 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 3.33 MILLION OZ FROM THE SLV//INVENTORY REST AT 538.282 MILLION OZ

DEC 15WITH SILVER DOWN 38 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV/: A WITHDRAWAL OF 2.48 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 541.612 MILLION OZ

DEC 14/WITH SILVER DOWN 38 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 543.092 MILLION OZ

DEC 13/WITH SILVER UP 11 CENTS TODAY; A HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 3.561 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 543.092 MILLION OZ//

DEC 10.WITH SILVER UP 19 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 546.653 MILLION OZ..

DEC 9/WITH SILVER DOWN 43 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF 2.96 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 546.653 MILLION OZ/

DEC 8/WITH SILVER DOWN 7 CENTS TODAY; NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 543.693 MILLION OZ///

DEC 7/WITH SILVER UP 24 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 543.693 MILLION OZ..

DEC 6/WITH SILVER DOWN 25 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.110 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 543.693 MILLION OZ//

CLOSING INVENTORY: 527.792 MILLION OZ

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

2.LAWRIE WILLIAM//,//Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,James RICKARDS

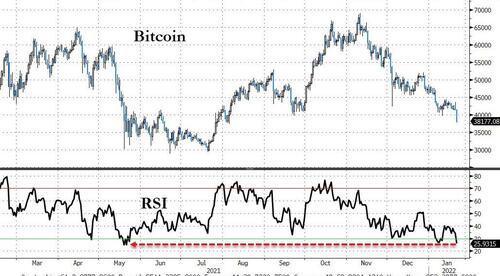

LAWRIE WILLIAMS: Bitcoin and global equities weaken. What now for gold and silver?

Despite numerous recommendations on the web promising huge rises in bitcoin, recent days have seen cryptocurrencies fall quite dramatically, The most visible cryptos – BTC and ETH – have, at the time of writing, fallen below $39,000 and $2,900 respectively after hitting around $67,000 and $4,800 as recently as 5 months ago. Global equities have also been falling, with the Dow Jones Industrial Index, for example, falling around 5% over the past few days. Gold and silver have seen prices surge, though, but have been marked down a little this morning in European trade, although are making something of a partial recovery again as I write. Is this the shape of things to come?

For some time now, many commentators have been predicting an equity market crash. This may already be beginning, although it is almost certainly too early to suggest the kind of prolonged deep downturn these analysts have been suggesting. But perhaps the writing is on the wall! For some time the equity markets and bitcoin had been something of a sure thing in terms of investment growth, blown up by global central bank largesse to try and ward off the potential economic ravages of the Covid-19 pandemic. The U.S., which tends to set the global market tone, has been pre-eminent in this having run up trillions of dollars in debt through its Federal Reserve Bank (Fed) easing programmes. This has, unsurprisingly to most economists, initiated an inflationary surge which may now be getting out of hand.

As a result, the Fed is promising a programme of tightening, involving an end to its bond buying programmes, followed by increasing interest rates to try and stave off future inflationary pressures. Markets are thus beginning to run scared that the gravy train is about to end and that prediction from a number of ‘expert observers’ that we are due for a mega-crash in equity prices may just be beginning to come true. Parallels with the great Wall Street crash of 1929 are beginning to be evident and such generated nervousness could easily develop into a panic – although it is certainly too early to say if this is indeed happening. The trouble facing equity investors is that once such a panic has ensued it is usually too late prices collapse rapidly and it may then be too late to protect built-up wealth accumulated during the good times.

That can lead to an extremely rapid downwards spiral in equity prices unless one can protect one’s gains by switching all, or part, of one’s investments to safe haven assets which may not be adversely affected by an equity market meltdown, or by purchasing power-deterioration due to ongoing inflation. Gold and silver have been among these historical safe haven assets, and moving at least a proportion of one’s investments into these, and maybe into associated stocks, could turn out to be a wealth life-saver. Even if a crash does not happen this would probably be a wise investment choice as gold and silver tend to hold their value regardless, and will also help protect against the threat caused by high inflation levels.

We have continually stressed in past articles the value of holding assets like gold and silver in a negative real interest rate environment and real rates are certainly vey negative at the moment, and look likely to remain so for the foreseeable future. Gold and silver do not generate interest, but even a zero rate is a positive investment parameter when inflationary pressures are driving held wealth downwards in value. Even if the equity and bitcoin crash scenario is not yet forthcoming, it is better to be too early, rather than too late, in taking these kinds of wealth protection measures.

21 Jan 2022

-END-

20 Jan 2022

3.Chris Powell of GATA provides to us very important physical commentaries

Your weekend reading material…. very important

(courtesy Alasdair Macleod/GATA)

Alasdair Macleod..

Alasdair Macleod: Understanding the inflation problem

Submitted by admin on Thu, 2022-01-20 12:56 Section: Daily Dispatches

By Alasdair Macleod

GoldMoney, Toronto

Thursday, January 20, 2022

In recent weeks inflation has become a major economic concern. Nearly all the commentary emanating from monetary policy makers, economists, and the media is misguided, believing inflation is rising prices and must be addressed accordingly.

They are only the symptoms of inflation. The true cause is the expansion of currency and bank credit, which, reflected in the U.S .dollar’s M2 money supply has increased substantially since March 2020, and now stands at nearly three times the level when Lehman failed.

After defining the differences between money, currency, and credit that together make up the media of exchange, this article explains how changes in the quantities of currency and credit translate into prices.

The solution to the inflation problem is not price controls, which are always counterproductive, but to return to a regime of sound money. This article shows what must be done to achieve this outcome and concludes that it is impossible to do so without a sufficiently serious financial and economic crisis to discredit government intervention in markets and to then allow governments to stabilise their currencies and reduce their spending to a bare minimum. …

… For the remainder of the analysis:

END

Fed launches a review of a possible central bank digital currency

I doubt if it is occurs.

(Wall Street Journal/GATA)

Fed launches review of possible central bank digital currency

Submitted by admin on Thu, 2022-01-20 20:01 Section: Daily Dispatches

By Andrew Ackerman

The Wall Street Journal

Thursday, January 20, 2022

WASHINGTON—The Federal Reserve today launched a review of the potential benefits and risks of issuing a U.S. digital currency, as central banks around the world experiment with the potential new form of money to keep pace with private-sector payments innovations.

Fed officials have been divided on the matter, making it unlikely they will decide soon on whether to create a digital dollar. Unlike private cryptocurrencies like bitcoin, a Fed version would be issued by and backed by the U.S. central bank, a government entity, as are U.S. paper dollar bills and coins.

The central bank described today’s long-awaited discussion paper as the first step in a debate of whether and how a U.S. digital dollar could improve the safe and effective domestic payments system. The paper doesn’t favor any policy outcome, and the Fed said the release of the report isn’t meant to signal any imminent decision.

“We look forward to engaging with the public, elected representatives, and a broad range of stakeholders as we examine the positives and negatives of a central bank digital currency in the United States,” Federal Reserve Chairman Jerome Powell said in a statement. …

… For the remainder of the report:

end

same subject as above

(New York Sun//GATA)

New York Sun: The Fed and crypto — back to basics

Submitted by admin on Thu, 2022-01-20 20:28 Section: Daily Dispatches

From The New York Sun

Thursday, January 20, 2022

Could the announcement that the Federal Reserve is weighing “the pros and cons” of issuing a “digital currency” be a chance to move to center stage the question of monetary reform?

That is our optimistic interpretation of the discussion paper issued this afternoon by the central bank. For it will soon be confronted with the question of how a digital dollar might, or might not, be defined — and who defines it.

The way the Federal Reserve Board is retailing the demarche is that the paper itself “does not favor any policy outcome.” Rather, the idea, however novel, is to solicit comment from the public.

The Fed calls the paper “the first step in a discussion of whether and how a central bank digital currency could improve the safe and effective domestic payments system.” We find that less than fully candid. …

… For the remainder of the commentary:

https://www.nysun.com/editorials/the-fed-and-crypto-back-to-basics/91956/

end

Oklahoma is now considering investing its state funds in gold and silver

(Cortez/MMNews)

Oklahoma to consider investing state funds in gold and silver

Submitted by admin on Thu, 2022-01-20 20:36 Section: Daily Dispatches

By JP Cortez

Money Metals News Service, Eagle, Idaho

Thursday, January 20, 2022

An Oklahoma state representative today introduced legislation that would enable the state treasurer to protect Sooner State funds from inflation and financial risk by holding physical gold and silver.

Introduced by Rep. Sean Roberts, HB 3681 would include physical gold and silver, owned directly, to the list of permissible investments the state treasurer can hold.

Currently, Oklahoma government money managers are largely relegated to investing in low-yield, dollar-denominated debt instruments.

Other than Ohio, no state is known to hold any precious metals, even as inflation and financial turmoil accelerate globally. Yet Oklahoma’s own investment guidance prescribes safety of principal as a primary objective for investment of public funds. …

… For the remainder of the report:

end

4.OTHER GOLD COMMENTARIES

Bill Holter….

Crumbling narratives?

At year end I was asked for predictions of what 2022 might see? My #1 prediction was that 2022 would see several narratives collapse. It did not take long to begin! Yesterday, Boris Johnson ended ALL Covid protocols in Britain and was followed by WHO backing off boosters for youngsters. While still trying to discern what prompted BJ to do a 180 (other than trying to retain power?), we will wait to see if others follow suit? We will also wait to see further actuary numbers of deaths from the insurance industry. Raw numbers will be hard to spin … Another area to keep close watch are financial markets. Bluntly, the stock market is also a “narrative”. I have said before and will reiterate now, the ONLY thing holding the social fabric together are stock markets still close to all time highs… but now seriously wobbling. If markets had not been juiced and goosed to ridiculous levels, I believe we would have already had extensive riots and violence. Only “401K” rosy statements have acted as salve on our wounded (mortally?) society. It remains to be seen what happens from here, but it is safe to say, any Fed or central bank tightening will be met with equities severely puking. At close on Thursday we have had another downside equity reversal with option expiration coming tomorrow. Friday will be interesting to watch, a bad OpEx episode could bring Monday and next week into position to break the equity narrative’s back? As for metals, we saw over 100 tons of Dec. COMEX gold contracts stand for delivery, I believe an all time monthly record. 2/3rds of the way through Jan., 18 tons are standing which is also a record for any full January. Actually, 18 tons was about normal for one of the 4 major delivery months just a few years back. It really does look like a stampede for delivery in the making! Silver is even more interesting, and I should say “fraudulent”. Over the last 8 months alone, COMEX claims to have shipped contracts representing over 800 million ounces to London for delivery. The problem is “size”. The entire world only produces slightly less than 800 million silver ounces, are we to believe there were really 800 million ounces laying around London to be delivered? Especially after 2 full years of ridiculously outsized delivery claims? Below are the EFP amounts over the last 8 months courtesy of Harvey Organ.

LAST 8 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZs:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ And speaking of this magic number of 800 million ounces, this is also the amount that Ted Butler claims that Bank of America is now short. I really cannot wrap my head around the reasoning for any bank to be short ANY amount of silver. Especially since we heard from CFTC head Rostin Behnam back last February that “they” had to “tamp” down silver, otherwise there would have been big problems. Yes, they kicked the can down the road about one year, is that can now filled with close to 1 billion short ounces of silver and too heavy to kick any further? To wrap this up, I believe we are at a serious crossroads here and now! We should get many answers to many different markets and narratives in short order. Unfortunately, if the answers include narratives failing left and right as I believe, life as we have known it will be drastically altered by horrid realities. Be careful what you wish for as crumbling equity and real estate pricing, along with higher (drastically?) interest rates and inflation will make for an exploding misery index. Couple this with precious metals and commodity indexes finally trading at true market clearing pricing, and you have almost the perfect storm. Of course, perfection will only arrive with the full breakdown of supply chains, that should about do it for anyone with their heads in the sands of denial!

Standing watch,

Bill Holter

Holter-Sinclair collaboration

END

Special thanks to Doug Cundley for sending this to us:

Central Banks’ Record Gold Stockpiling

January 21, 2022donateFacebookTwitter

According to recently released data by the World Gold Council (WGC), as of September 2021, the total amount of gold held in reserves by central banks globally exceeded 36,000 tons for the first time since 1990. This 31-year record was the result of the world’s central banks adding more that 4,500 tons of the precious metal to their holdings over the last decade and it provides ample support for the investment case for gold, in both directly performance-related terms, but also from a big picture perspective.

This new record went largely underreported in the mainstream financial press and almost entirely unmentioned in official central bank statements and their guidance or policy commentary. Quite to the contrary, policymakers in the US, the Eurozone and in most other major economies, have for over two years now insisted on repeating the exact same talking points and all kinds of arguments and convictions that would in fact nullify the case for holding gold at all.

For example, up until very recently, inflation was largely and decisively dismissed as “transitory”, with leading figures from the Fed and the ECB repeatedly assuring investors and the public at large that consumer prices were under control and that the early hikes we saw last year in official data were nothing but a glitch. Of course, as the pressures continued to build and as it became clear that the CPI figures (that are already a very poorly constructed and misleading gauge of inflation) were not aligned with the version of reality that central bankers publicly espoused, they were forced to perform a policy U-turn, at least in theory if not in practice. However, the most important element to note here, is that if their public statements were actually consistent with their policymaking and strategic outlook, there would be no conceivable reason to ratchet up their gold stockpiling.

Naturally, this is far from the first time we see this kind of dissonance between words and actions by officials and institutional figures of all sorts, not just central bankers. This is why investors need to pay attention to the practical steps that are actually taken, and largely ignore the rhetoric that surrounds, or often even conceals, those steps. As the old saying goes, “do as I do, not as I say”.

And while inflationary risks are very much on top of most conservative investor’s minds, there is also a much larger, long-term shift that the gold buying spree highlights: The reign of the dollar as the world’s reserve currency is slowly but surely coming to an end. The greenback’s value has seen a remarkable decline against gold over the last decade and it’s not just precious metals investors that are keeping a close eye on this trend. Reinforced by solid geopolitical reasons, central bankers in Russia, China and other aligned nations have been pushing for years already to dethrone the USD.

It has certainly been an uphill battle, and the US currency still undoubtedly dominates all others in International trade and in reserves, however, this campaign against it appears to be relentless. In fact, it might have reached an important milestone a few weeks ago: according to a report by the Central Bank of Russia that was analyzed by Bloomberg, last year, the nation’s central bank gold holdings surpassed its dollar reserves for the first time in its history, with gold making up 23% of total reserves as of the end of June and dollar assets dropping to 22%.

Meanwhile, many other nations have also been accelerating their gold buying and shedding their dollar reserves, and that is particularly true of Eastern European and Asian emerging economies. Just within the first nine months of 2021, Thailand added around 90 tons, India 70 tons and Brazil 60 tons. As was highlighted in a recent analysis by Nikkei Asia, “The presence of the dollar in foreign exchange reserves is falling, in contrast with the growth of gold. In 2020, the currency-by-currency ratio of the dollar fell to the lowest level in a quarter of a century.”

All in all, it is essential for investors to pay close attention to this shift. As central bankers themselves also clearly understand, as fiat currency debasement continues and even accelerates in the coming months and years, physical gold is set to provide the only reliable and time-tested haven from the storm that lies ahead.

This article has been published in the Newsroom of pro aurum, the leading precious metals company in Europe with an independent subsidiary in Switzerland.

This work is licensed under a Creative Commons Attribution 4.0 International License. Therefore please feel free to share!endBullion star: Russia starts buyin gold again. This time 3 tonnes//now hold 2302 tonnes. Coming close to Italy and France.

END

Russia adds 3 tonnes to its official reserves. They are now closing in on Italy and France

5.OTHER COMMODITIES/

6.CRYPTOCURRENCIES

end

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings FRIDAY morning 7:30 AM

ONSHORE YUAN: CLOSED UP AT 6.3399

OFFSHORE YUAN: 6.3427

HANG SANG CLOSED UP 13.20 PTS OR 0.05%

2. Nikkei closed DOWN 250.67 PTS OR 0.90%

3. Europe stocks ALL RED

USA dollar INDEX DOWN TO 95.58/Euro RISES TO 1.1349-

3b Japan 10 YR bond yield: FALLS TO. +.137/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 113.77/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 84.45 and Brent: 87.05-

3f Gold DOWN/JAPANESE Yen UP CHINESE YUAN: ON -SHORE CLOSED UP// OFF- SHORE UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO -.0.060%/Italian 10 Yr bond yield FALLS to 1.29% /SPAIN 10 YR BOND YIELD FALLS TO 0.63%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 1.34: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 1.68

3k Gold at $1839.80 silver at: 24.52 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3l USA vs Russian rouble; Russian rouble UP 29/100 in roubles/dollar AT 76.47

3m oil into the 84 dollar handle for WTI and 87 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 113.77 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning .9121– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0350 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

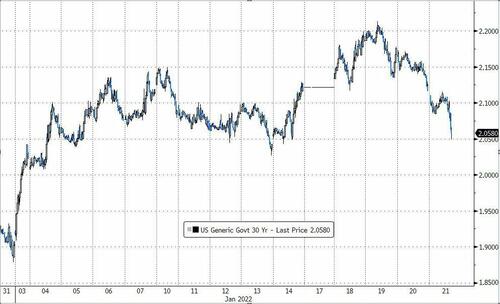

USA 10 YR BOND YIELD: 1.780 DOWN 3 BASIS PTS

USA 30 YR BOND YIELD: 2.100 DOWN 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 13.41

Markets Are “Sea Of Red” Amid “Total Meltdown In Anything Tech And Pandemic Winners”

FRIDAY, JAN 21, 2022 – 08:03 AM

Futures, yields, oil, dollar, cryptos – everything is lower on this $3.1 trillion option expiration day…

… as US traders relocate from their bedroom to their basement on the last day of the week, discovering a sea of red in most assets and a “total meltdown” in others. Emini S&P futures are down 0.5% or 22 points to 4,452 which by the way is well off the session lows which saw the S&P plunge as low as 4,429. Nasdaq futures are down 0.8% or 122 and Dow futures are lower by 95 points or 0.25%, while European stocks touched the lowest level in a month weighed by miners, travel and leisure and automakers. 10Y TSY yields are at 1.778%, rising from 1.76% at the session lows, but down from Thuesday’s close around 1.80%.

Cryptocurrencies crashed with Bitcoin trading below $38,000, the level that Mike Novogratz said is where he would be buying. Presumably he isn’t doing so. Ether, the second largest cryptocurrency by market cap, extends its decline to trade at around $2,750, in its longest daily losing streak since late July. Meanwhile, oil extends declines, with Brent falling 1.7% to below $87, while WTI falls over 2% to below $84 a barrel. Spot gold -0.4% to $1,832/oz, while the dollar also slips 0.1%.

“Risk appetite is widely down, and the cautious trading mood reflects the global uncertainty investors are now facing,” said Pierre Veyret, technical analyst at ActivTrades. “Sentiment is being driven down by monetary policies, uneven corporate results, a bigger Omicron impact on economies as well as rising geopolitical tensions between the USA and Russia over Ukraine.”

Meanwhile, a report that Washington is allowing some Baltic states to send U.S.-made weapons to Ukraine stoked concerns about a standoff with Russia.

“The 2022 outlook for risky assets is likely to be more challenging as central bank accommodation is withdrawn,” said Mohit Kumar, managing director at Jefferies International. “We would wait for more clarity from the Fed before shifting our cautious stance on equities.”

Besides the huge negative gamma overhang (much of which will fade by EOD as trillions in options expire) and the prospect of rising interest rates weighing on investor sentiment, corporate earnings aren’t helping the mood with disappointing earnings from PPG Industry and CSX, while Netflix plunged 21% in premarket trading as analysts cut their ratings and slash price targets after the streaming company’s first-quarter subscriber outlook missed estimates, prompting worries over slowing growth. Alibaba Group dropped in U.S. premarket trading as market participants weigh the stock impact of a report that China’s state broadcaster has implicated Jack Ma’s Ant Group in a corruption scandal. Expected data on Friday include Leading Index, while Huntington Bancshares, IHS Markit, Schlumberger are among companies reporting earnings. Here are all notable premarket movers:

- Peloton (PTON US) shares rise 8.6% in U.S. premarket trading, set to rebound following Thursday’s 24% tumble in the wake of a CNBC report saying the company is temporarily halting production of bikes and treadmills over slow demand, which CEO John Foley later disputed in a memo to staff.

- Apple’s (AAPL US) price target and estimates are raised at Wells Fargo ahead of the tech giant’s results next Thursday. The shares edge 0.1% lower in U.S. premarket trading.

- Alibaba (BABA US) drops as much as 1.5% in U.S. premarket trading as market participants weigh the stock impact of FT report saying China’s state broadcaster has implicated Jack Ma’s Ant Group in a corruption scandal.

- PPG (PPG US) fell 3% postmarket after the chemicals maker forecast adjusted earnings per share for the first quarter that missed the average analyst estimate and cited “significantly higher operating costs.”

- CSX (CSX US) shares dropped over 3.8% in postmarket trading as fourth-quarter profit and revenue beat was overshadowed by a miss in operating ratio, a measure of the railroad’s efficiency.

In Europe, stocks dropped to the lowest level in a month echoing Asia’s slump. Euro Stoxx 600 drops as much as 1.7% with most European cash indexes ~1% in the red. Cyclical sectors such as basic resources, autos and travel led the declines, along with tech, while defensive stocks such as food, personal care and utilities outperformed. European e-commerce stocks fall on Friday, with Markets.com chief market analyst Neil Wilson noting the “total meltdown in anything tech and pandemic winners.” There’s a “huge momentum unwind” and “no one wants to touch them now,” with investors looking for defensive cash flows and value, Wilson writes in emailed comments: Naked Wines -6%, Home24 -5.4%, Global Fashion Group -5.2%, THG -3.5%, Moonpig -3.3%, Asos -3.2%, Made.com -2.9%, Allegro 2.6%, AO World -2.5%, Zalando -2.4%, Westwing -2.1%.

Earlier in the session, Asian equities resumed declines after a one-day reprieve, as global inflation concerns and the impact on borrowing costs weighed on technology stocks. The MSCI Asia Pacific Index fell as much as 1.4%, dragged down by shares of chipmakers TSMC and Samsung, as the global tech selloff deepened. The regional benchmark was headed for a weekly drop of more than 1.7%, its steepest since late November. Read more: A Year’s Worth of Nasdaq Tumult Gets Jammed Into Three Weeks Benchmarks fell across Asia, with Australia’s main gauge sliding more than 2% and Japan’s Topix narrowly missing a technical correction. Elevated energy costs and rising prices of other goods amid supply-chain bottlenecks have added to worries about faster-than-expected monetary-policy tightening. “A world shaped by supply constraints will bring more macro volatility,” BlackRock Investment Institute strategists including Elga Bartsch wrote in a note. “Monetary policy cannot stabilize both inflation and growth: it has to choose between them.” Toyota also ranked among the biggest drags on the regional benchmark after the auto giant announced more production halts on rising Covid-19 cases. Alibaba dropped after a Financial Times report said China’s state broadcaster has implicated Jack Ma’s Ant Group in a corruption scandal

Indian stocks completed their biggest weekly decline since November, as concerns about policy moves by the U.S. Federal Reserve and a rally in crude oil prices dented investors’ appetite for riskier emerging market assets. The S&P BSE Sensex dropped 0.7% to 59,037.18 in Mumbai, extending this week’s losses this to 3.6%. The NSE Nifty 50 Index also fell 0.8% on Friday. Technology stocks were hammered for a fourth consecutive session, with the sector gauge ending with the worst weekly performance since April 2020. Infosys Ltd., down 2.1%, was the biggest drag on the key indexes. All but one of 19 sub-indexes fell, led by a gauge of realty stocks. As the Federal Reserve looks at tackling higher inflation, investors are grappling with the prospect of reduced stimulus that had driven flows into emerging markets and bolstered riskier assets. “The likely Fed action and crude surge have been negative for sentiment after the market had a strong start to the year, and we expect this downward pressure to continue,” said A. K. Prabhakar, head of research at IDBI Capital Ltd. “In earnings, tech results have been strong, but attrition is high, while for others, higher raw material costs are a drag.” Of the 13 Nifty 50 companies that have announced results so far, six have either met or exceeded expectations, six have missed and one can’t be compared. Reliance Industries Ltd., the nation’s most-valuable company, is scheduled to announce results in the day

Australia’s S&P/ASX 200 index slumped 2.3% to close at 7,175.80, its lowest level since June 1, following U.S. shares lower after the tech-heavy Nasdaq 100 slipped into a correction. The Australian benchmark shed 3% this week amid anxiety over interest rates and the outlook for corporate earnings, capping its worst weekly performance since October 2020. Paladin Energy was the worst performer on Friday, plunging 11%, and Whitehaven fell after trimming its full-year managed ROM coal production forecast. In New Zealand, the S&P/NZX 50 index fell 1.2% to 12,348.00. The gauge lost 3.5% this week in its biggest such loss in 11 months

In rates, demand for havens pushed the 10-year U.S. Treasury yield below 1.80%. Treasury futures are off session highs reached during Asia trading hours, hold modest gains from belly to long end, trimming yields by ~1bp vs Thursday’s closing levels. 10-year TSY yield around 1.775% is ~2bp richer on the day after dropping as low as 1.763% during Asia session; German 10- year outperforms by 1.2bp with Estoxx50 down 1.7%. IG dollar issuance slate empty so far; three-deal docket Thursday consisted entirely of banks for combined $5.4bn. Bunds bull flatten, richer by ~3bps at the long end; gilts bull steepen with the belly outperforming.

In FX, Bloomberg Dollar Spot dips 0.2% into the red. SEK and CHF are the best performers in G-10; NZD, AUD and GBP lag, with cable near session low of 1.3562, one tick above the 21-DMA at 1.3561. The Bloomberg dollar index slipped as the greenback traded mixed versus its Group-of-10 peers. The pound lagged most of its Group-of-10 peers, extending declines after data showed U.K. retail sales plummeted in December. BOE’s Mann to speak later. Sweden’s krona is the best G-10 performer as it retraces about half of yesterday’s deep losses that took it to an 18- month low against the greenback in the U.S. session after a triggering stop-losses and options barriers. Australian and New Zealand dollars weakened amid risk-off price action in stocks and commodities. The yen strengthened on haven demand; BOJ minutes of its December meeting showed one board member noting that policy adjustment now would be too early.

In commodities, crude futures are deep in the red, but off worst levels, after a surprise climb in U.S. crude stockpiles. The White House also said it can work to accelerate the release of strategic reserves. WTI regained a $84-handle, Brent trades back above $87. Spot gold drops ~$5 before finding support near $1,830/oz. Base metals are mostly in the green and up on the week. LME lead and tin outperform.

Looking at the day ahead, data releases included UK retail sales for December, which missed badly, and the US Conference Board’s leading index for December. Central bank speakers include ECB President Lagarde and the BoE’s Mann.

Market Snapshot

- S&P 500 futures down 0.2% to 4,467.50

- STOXX Europe 600 down 1.3% to 476.89

- MXAP down 0.9% to 191.91

- MXAPJ down 1.0% to 630.82

- Nikkei down 0.9% to 27,522.26

- Topix down 0.6% to 1,927.18

- Hang Seng Index little changed at 24,965.55

- Shanghai Composite down 0.9% to 3,522.57

- Sensex down 0.8% to 58,998.67

- Australia S&P/ASX 200 down 2.3% to 7,175.81

- Kospi down 1.0% to 2,834.29

- Brent Futures down 1.9% to $86.66/bbl

- Gold spot down 0.3% to $1,832.94

- U.S. Dollar Index down 0.14% to 95.60

- German 10Y yield little changed at -0.05%

- Euro up 0.3% to $1.1344

- Brent Futures down 2.0% to $86.63/bbl

Top Overnight News from Bloomberg

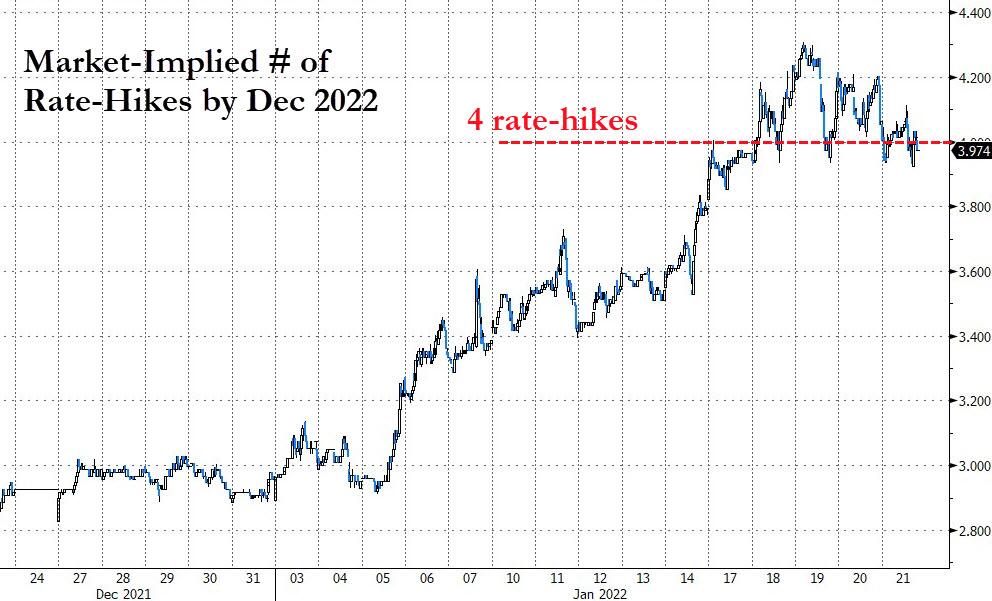

- Federal Reserve officials will signal next week they’ll raise interest rates in March for the first time in more than three years and shrink their balance sheet soon after, economists surveyed by Bloomberg said

- The European Union is ripping up the green investing playbook with plans to allow some gas and nuclear projects to be called sustainable. The bloc is poised to include these kinds of power generation with conditions in its rulebook for sustainable activities, or taxonomy. That’s divided the fund community, as some worry their holdings will no longer be in line with the rules, while others think it’s a necessary compromise.

- China is quietly urging banks to increase lending after a slow start to the year, ramping up efforts to combat the weakest economic expansion since early 2020

- Italy’s papal-style vote for a new president each seven years is the culmination of Rome’s political intrigues and power games. For the first time, the process is attracting international interest as Prime Minister Mario Draghi is touted as a top contender for the job. Voting will start on Jan. 24 at 3 p.m. local time, and it is expected to last a few days

- Iron ore futures climbed to the highest intraday level since October as China made it clear that it will take action to stabilize the economy, bolstering the demand outlook for the raw material

A more detailed look at global markets courtesy of Newsquawk

Asia Pacific

- APAC markets traded lower amid wide-spread risk aversion after late Wall Street selling . ASX 200 (-2.3%) underperformed as miners led the broad downturn.

- Nikkei 225 (-0.9%) dropped more than 500 points intraday on currency strength but finished off lows

- Hang Seng (U/C) and Shanghai Comp. (-0.9%) downside was somewhat cushioned on subsequently confirmed reports of further PBoC action.

- US equity futures traded with losses across the board: NQ underperformed post-Netflix earnings.

Top Asian News

- Rising Cases Spark Covid Superspreader Fears in Hong Kong

- Alibaba Drops in U.S. Premarket on Corruption Report Speculation

- Playtech Sinks as Former F1 Boss Jordan Pulls Possible Offer

- Coal Soars to $300 a Ton as Asia Scrambles for Power Plant Fuel

Europe

- Major European bourses are pressured Euro Stoxx 50 -1.3%; Stoxx 600 -1 5%. as the Wall St rally faded and reverberated through APAC trade . Although, the Stoxx 600 remains -0.5% on the week.

- US futures have been lifting off overnight lows, though the NO continues to lag post-Netflix.

- European sectors are all in the red. but defensives are faring slightly better than cyclicals

Top European News

- U.K. Retail Sales Drop as Omicron Keeps Shoppers Away

- Lotus Explores Electric-Car Battery Tie-Up With Britishvolt

- Amazon’s Alexa Voice Assistant Reportedly Suffers Europe Outages

- Greece Is Great Place to Be in Rough January for Europe Stocks

FX

- Franc finally evades SNB clutches to rally and outshine other safe-haven currencies.

- Pound discounted after dire UK retail sales data and deterioration in consumer sentiment.

- Buck betwixt and between as USTs rebound, but risk aversion gathers momentum.

- Kiwi and Aussie lag due to unfavorable market conditions and their high beta characteristics but Yuan continues to rally as PBoC adds SLFs to the list of official rates being cut to support the Chinese economy Click here for a detailed summary.

Fixed Income

- USTs extend rebound from post-20 year auction highs on amidst more pronounced risk-off positioning.

- Bunds play catch up with Treasuries as demand for safe-havens picks up

- Gilts also correct higher and pay some heed to downbeat UK fundamental

Commodities

- WTI and Brent March contacts remain pressured by the broader risk tone, with focus on geopolitics

- Morgan Stanley has increased its Q3 Brent price forecast to USD 100/bbl vs prev. viev; of around USD 90/bbl.

- Spot gold looks heavy as traders booked some profits from yesterdays rally, while the yellow metal found support around the USD 1 830/oz.

- LME copper re-tested USD 10k/t to the upside but failed to mount the level

DB’s Jim Reid concludes the overnight wrap

Don’t tell anyone but I’m going to betray my first love this weekend. It’s with someone 5 years younger but much less attractive on the eye and with far, far, far less money. I’ll also be introducing them to my kids but will be meeting up in a place that it is far less likely I’ll be seen. Yes as Liverpool fight to keep alive in the Premier League title race I’ll be taking the twins to their first football match at non-league Woking Town who are around 105 places lower in the English football structure. Anfield was just too long a journey to be stuck with them for that length of time! The twins play for Woking Cubs although at this stage persuading them to not pick up the ball and run off with it mid-practise is an achievement.

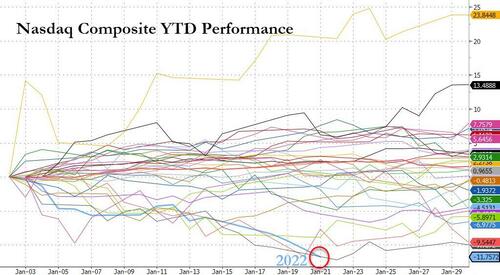

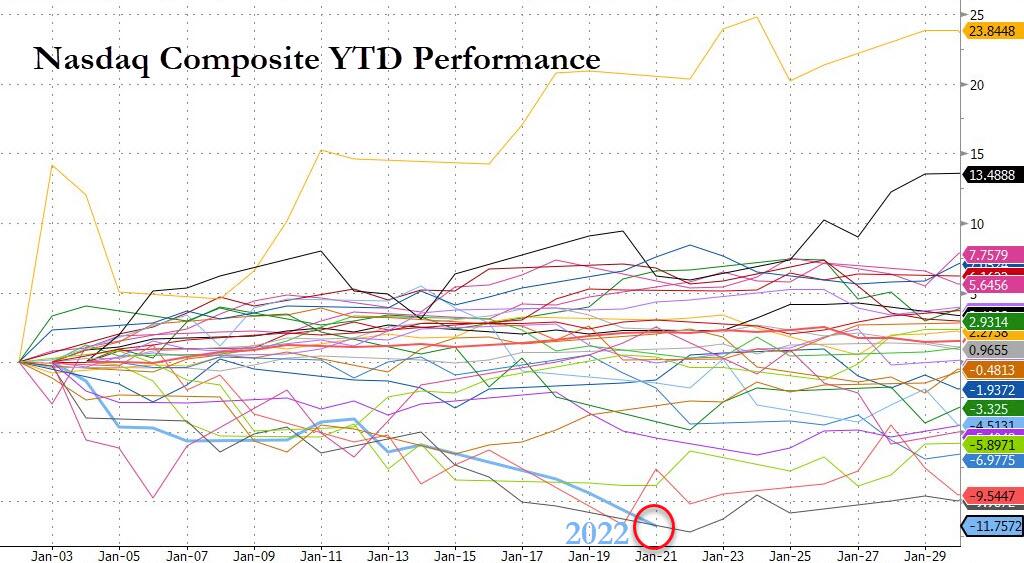

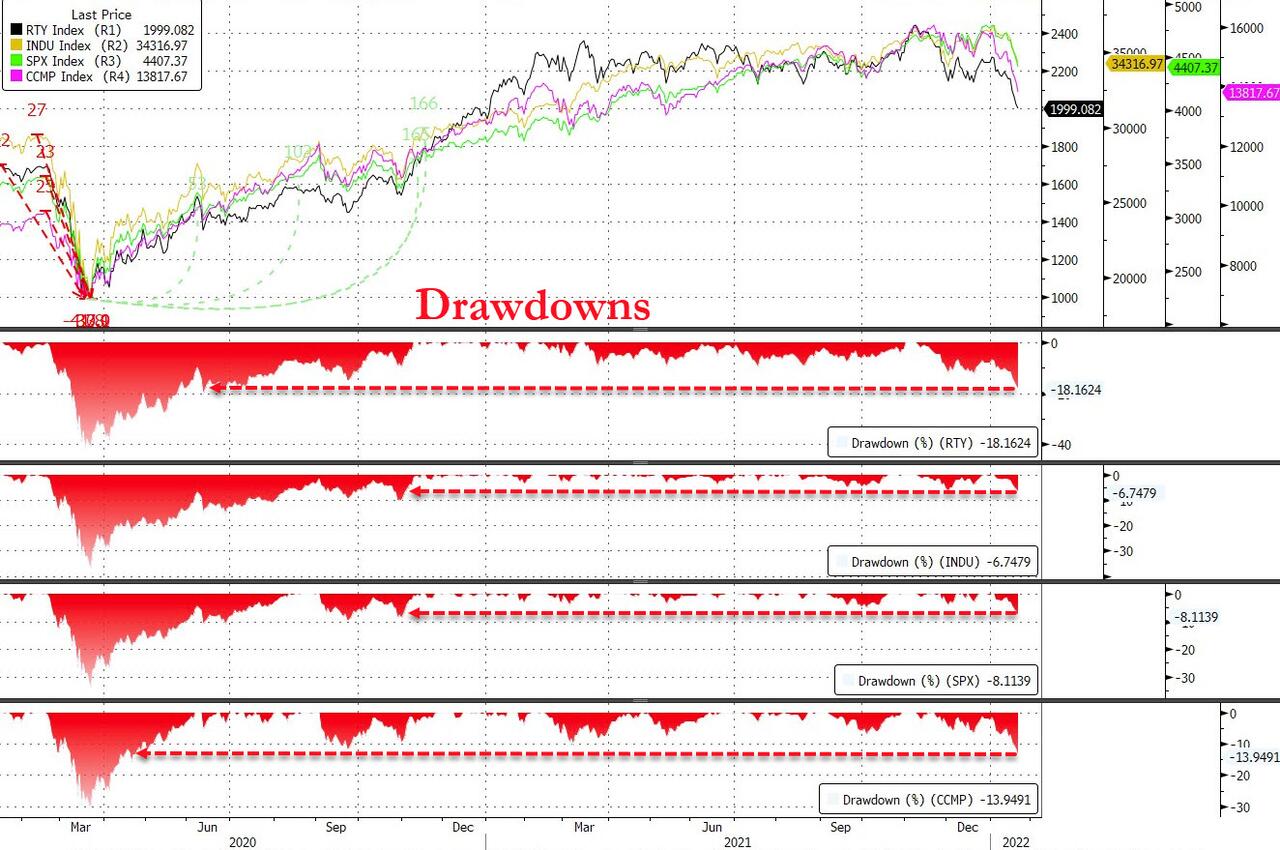

The bears took control of the ball last night as markets followed the recent script whereby equities showed some stability only to take a turn late in the New York session. The S&P 500 was as much as +1% higher intraday, before selling off in the US afternoon, finishing the session down a steep -1.10% and is now -6.48% lower year-to-date. Consumer discretionary (-1.94%) and technology (-1.33%) were again among the biggest decliners, as big tech stocks underperformed. The NASDAQ fell -1.30%, and is down -9.53% YTD, -11.85% from all-time highs and closed below its 200 day average for the first time since the March 2020 Covid-induced volatility.

The S&P declines were broad-based though with 84% of the constituents lower after as much as 90% of the index was in the green intraday. The S&P 500 is on track for a 3rd consecutive weekly decline for the first time since September 2020. The story only got worse for tech stocks after the close, as Netflix posted poor earnings, missing subscriber estimates. The stock declined more than -20% in after hours trading.

Europe saw a stronger performance, but this was before the weak US close with the STOXX 600 ending the day up +0.51%.

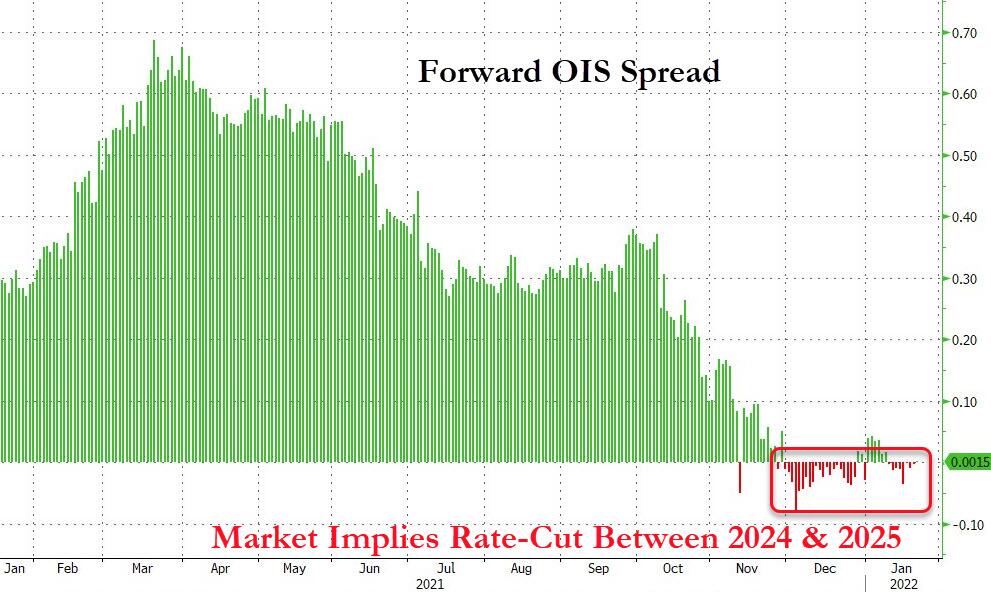

Having experienced the highest levels in yields for many months earlier this week, sovereign bonds also rallied yesterday, with the 10yr Treasury yield down -6.1bps to 1.80%. True to form, most of the declines took place later in the New York session. About half of the declines came from real yields, down -3.4bps. These moves also occurred alongside a further flattening in the yield curve, with the 2s10s slope down -2.8bps to 77.5bps, which is its lowest closing level of the year so far, and not far off the recent low of 73.6bps we saw in late December. As a reminder, whether or not you’re in agreement as to its explanatory power, every US recession in recent times has been preceded by an inversion of the 2s10s curve, and our analysis shows that in the Fed hiking cycles since 1955 you generally see a flattening in the curve of around 80bps in the first year (see our rate hike primer here for more on this). So if the Fed hikes in March and things play out in line with that historic playbook, then that would imply a curve inversion in H1 next year. For the record 10yr yields are currently -3bps in the Asian session and the curve another couple of basis points flatter.

Central bankers will be hopeful they can avoid yield curve inversion, and ECB President Lagarde emphasised yesterday that the ECB had “every reason to not react as quickly and as abruptly as we could imagine the Fed might”. Nevertheless, the minutes from the ECB’s Governing Council meeting in December were released yesterday, which said “it was cautioned that a “higher for longer” inflation scenario could not be ruled out.” The minutes noted that the 2023 and 2024 inflation forecasts were “already relatively close to 2% and, considering the upside risk to the projection, could easily turn out above 2%.” It came as the final reading of December’s Euro Area inflation matched the initial estimate of +5.0%, the highest since the single currency’s formation, whilst sovereign bond yields in Europe followed the US lower, with those on 10yr bunds (-1.3bps), OATs (-1.8bps) and BTPs (-3.7bps) all declining.

Overnight in Asia, all major stock indexes are sharply lower. The Nikkei (-1.49%) is weak, giving up the gains in the previous session as Japan’s headline inflation (+0.8% y/y) in December failed to surpass market expectations of a +0.9% reading and may quell some of the recent policy normalisation stories. The core-CPI remained unchanged at +0.5% y/y in December below the market forecast of +0.6% rise. Elsewhere, the Kospi (-1.48%), Shanghai Composite (-0.82%), CSI (-0.85%) and the Hang Seng (-0.75%) are also down. Looking ahead, stock futures in the DM world continue to paint a weaker picture with S&P 500 (-0.5%), Nasdaq (-1%) and DAX (-1.25%) contracts trading lower again.

After remaining buoyant most of the session yesterday, Oil was also a victim of the late sell-off. Brent crude fell by -1.13% to $87.44/bbl, while WTI was only a smidge lower, declining -0.07% to $86.90/bbl. However the Asian session hasn’t been kind with WTI trading in the low $84s as we type. Other commodities kept the trend going before the late sell-off. Agricultural prices saw fresh gains, with Bloomberg’s agriculture spot index (+0.68%) advancing to a post-2012 high, and both industrial and precious metals generally moved higher on the day as well.

In terms of yesterday’s data, Germany’s PPI inflation accelerated to +24.2% year-on-year in December (vs. +19.3% expected), marking the fastest increase since that statistic was introduced in 1949. Over in the US meanwhile, the weekly initial jobless claims rose to a 3-month high of 286k in the week through January 15. That was some way above the 225k reading expected and potentially reflects the growing impact of the Omicron variant on the labour market. Furthermore, the 4-week rolling average of claims rose to 231k as a result, marking its 3rd consecutive move higher. When it comes to other US data, the Philadelphia Fed’s business outlook survey for January was more promising at 23.2 (vs. 19.0 expected), but the existing home sales for December fell for the first time in 4 months to an annualised rate of 6.18m (vs. 6.42m expected). There were some indications that this was a lack of supply rather than demand issue.

For what it’s worth, after the US close Treasury Chief Janet Yellen lent her support to the Biden administration by expressing confidence in its ability along with the Fed to bring back inflation closer to 2% by the end of 2022.

To the day ahead now, and data releases include UK retail sales for December, the Euro Area’s advance consumer confidence reading for January, and the US Conference Board’s leading index for December. Central bank speakers include ECB President Lagarde and the BoE’s Mann.

3. ASIAN AFFAIRS

i)FRIDAY MORNING// THURSDAY NIGHT

SHANGHAI CLOSED DOWN 32.49 PTS OR 0.91% //Hang Sang CLOSED UP 13.20 PTS OR 0.05% /The Nikkei closed DOWN 250.67 PTS OR 0.90% //Australia’s all ordinaires CLOSED OWN 2.33% /Chinese yuan (ONSHORE) closed UP 6.3399 /Oil DOWN TO 84.45 dollars per barrel for WTI and UP TO 87.05 for Brent. Stocks in Europe OPENED ALL RED // ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.3399. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.3427: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN AND OFF SHORE TRADING STRONGER AGAINST USA DOLLAR

3 a./NORTH KOREA/ SOUTH KOREA

///NORTH KOREA

3B JAPAN

end

3c CHINA

CHINA/

CCP now going after Ant and its founder and Jack Ma

(zerohedge)

Jack Ma’s Ant Group Implicated In Major Corruption Scandal Involving Ex-CCP Official

FRIDAY, JAN 21, 2022 – 02:00 PM

Way back in 2019, long before Alibaba founder Jack Ma’s falling out with the CCP (or, we should say, when the strains in their relationship were far less visible in the business press), we reported the following prediction from Hayman Capital’s Kyle Bass: That Jack Ma would be “jailed, or disappeared” shortly after stepping down as Alibaba’s chairman.

When Ma abruptly disappeared after the CCP sabotaged the (Ma-led) IPO for Ant Group, Alibaba’s financial arm that had become widely used within the Chinese market, we feared the worst.

And even though Ma eventually resurfaced, things have never been the same for a man who was once China’s wealthiest man. What’s worse is that it marked the beginning of a CCP crackdown on China’s burgeoning tech industry that continues to this day.

While shares of Alibaba have staged a modest comeback off their lows, Ma has unfortunately bounced from one troubling allegation to the next. The latest has arrived courtesy of Chinese state broadcaster CCTV, which has published a report implicating Ma’s Ant Group in a wide-ranging corruption scandal – a charge that has been known to carry the death penalty in the PRC.

The documentary didn’t name Ant, but it alluded to the company, which was founded in Hangzhou. But it did further implicate a family member of a high-ranking CCP official, who was arrested back in August. As a result, Ant Group received “discounts” on plots of real-estate and other “government policy” support.

Here’s more from the FT, which published its own report on the CCTV documentary:

A documentary on state-run China Central Television alleged that private companies made “unreasonably high payments” to the brother of the former Chinese Communist party head of Hangzhou, an eastern city that is home to Ant Group’s headquarters, in return for government policy incentives and support with buying real estate.