GOLD; DOWN $5.75 to $1821.90

SILVER: $23.13 DOWN 2 CENTS

ACCESS MARKET: GOLD: 1822.55..

SILVER: $23.09

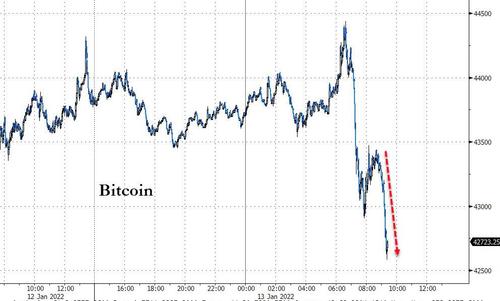

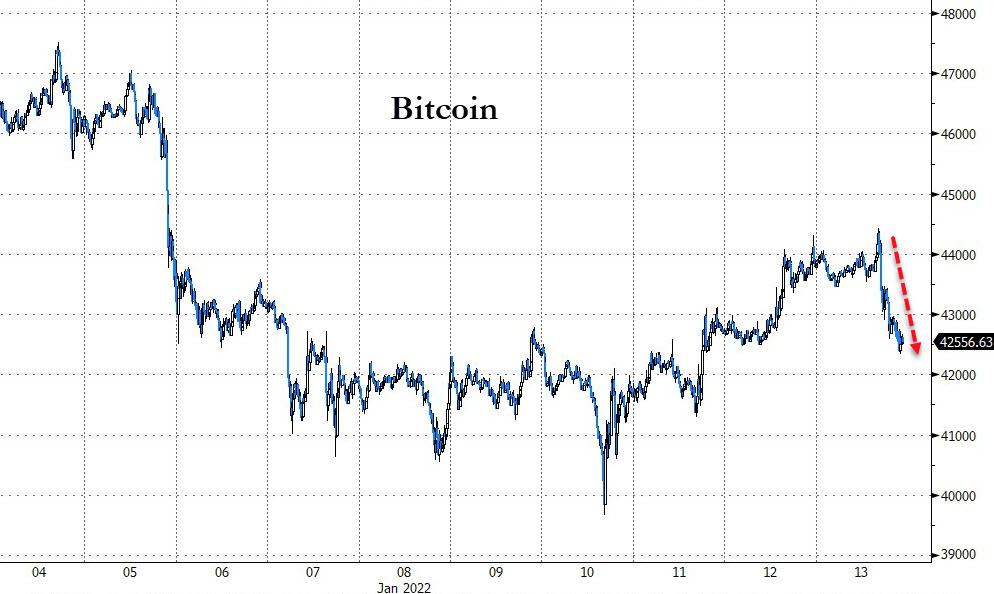

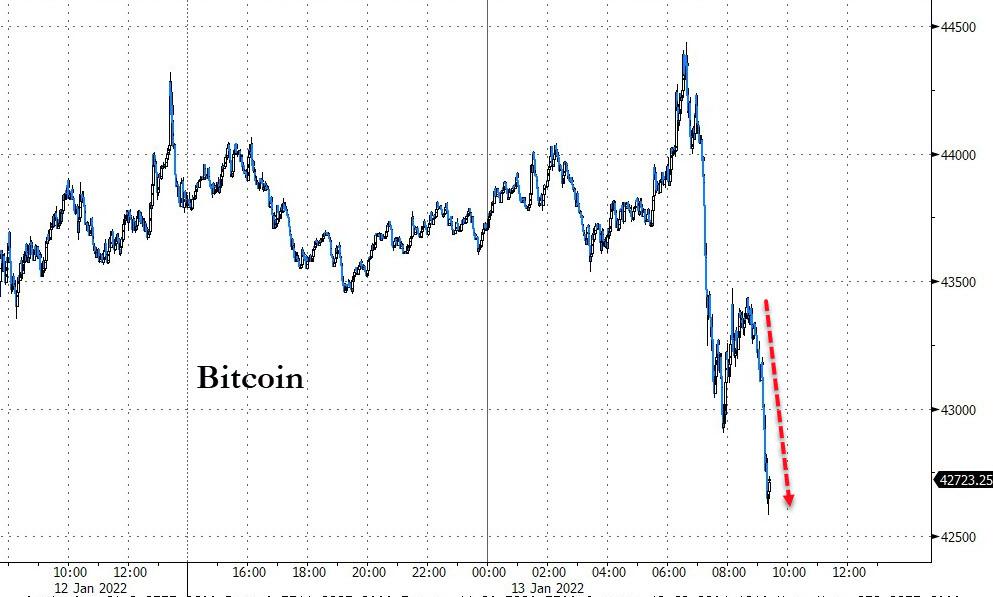

Bitcoin: morning price: 43,807 up 86

Bitcoin: afternoon price: 42,000 down 1721

Platinum price: closing down $8.75 to $974.15

Palladium price; closing down $22.60 at $1892.95

END

end

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

comex notices//JPMorgan notices filed COMEX//NOTICES FILED

EXCHANGE: COMEX

CONTRACT: JANUARY 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,827.200000000 USD

INTENT DATE: 01/12/2022 DELIVERY DATE: 01/14/2022

FIRM ORG FIRM NAME ISSUED STOPPED

323 H HSBC 1001

624 H BOFA SECURITIES 1528

661 C JP MORGAN 534 7

TOTAL: 1,535 1,535

MONTH TO DATE: 3,919

NUMBER OF NOTICES FILED TODAY FOR JAN. CONTRACT: 1535 NOTICE(S) FOR 153,500 OZ (4.774 TONNES)

total notices so far: 3919 contracts for 391,900 oz (12.189 tonnes)

SILVER NOTICES:

0 NOTICE(S) FILED TODAY FOR nil OZ/

total number of notices filed so far this month 2336 : for 11,680,000 oz

GLD

WITH GOLD DOWN $5.75

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS): NO CHANGES IN GOLD INVENTORY AT THE GLD

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

CLOSING INVENTORY: 976.21 TONNES/

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 2 CENTS:/:

A BIG CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 832,000 OZ FROM THE SLV//

AT THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY SLV/ TONIGHT: 529.780 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A VERY STRONG 1702 CONTRACTS TO 144,144 AND RESTS CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020…... WITH THE $0.38 GAIN IN SILVER PRICING AT THE COMEX ON TUESDAY. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.38) AND WERE UNSUCCESSFUL IN KNOCKING OUT ANY SILVER LONGS AS WE HAD A HUGE GAIN OF 2503 CONTRACTS ON OUR TWO EXCHANGES .

WE MUST HAVE HAD:

I) HUGE BANKER SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A HUGE INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 10.505 MILLION OZ FOLLOWED BY TODAY’S 5,000 OZ E.F.P. JUMP TO LONDON V) VERY STRONG SIZED COMEX OI GAIN.

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS -56

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JAN. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JAN:

TOTAL CONTACTS for 9 days, total contracts: : 5364 contracts or 26.820 million oz OR 2.98 MILLION OZ PER DAY. (596 CONTRACTS PER DAY)

TOTAL NO OF OZ UNDERGOING EFP TO LONDON 5364 CONTRACTS X 5,000 PER CONTRACT:

EQUATES TO: 26.820 MILLION OZ

.

LAST 8 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

RESULT: WE HAD A VERY STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1702 WITH OUR 38 CENT GAIN SILVER PRICING AT THE COMEX// WEDNESDAY THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 745 CONTRACTS( 745 CONTRACTS ISSUED FOR MAR AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY:/ AS WELL AS TODAY /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR JAN OF 10.505 MILLION OZ FOLLOWED BY TODAY’S 5,000 E.F.P JUMP TO LONDON//NEW STANDING 13.615, MILLION OZ// .. WE HAD A HUGE SIZED GAIN OF 2447 OI CONTRACTS ON THE TWO EXCHANGES FOR 12.235 MILLION OZ//

WE HAD 0 NOTICES FILED TODAY FOR nil OZ

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A SMALL 595 TO 547,111, AND CLOSER TO OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: -3300 CONTRACTS

.

THE FAIR SIZED INCREASE IN COMEX OI CAME DESPITE OUR STRONG GAIN IN PRICE OF $8.65//COMEX GOLD TRADING/WEDNESDAY/.AS IN SILVER WE MUST HAVE HAD HUGE BANKER/ALGO SHORT COVERING ACCOMPANYING OUR SMALL SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION AS THE TOTAL GAIN ON OUR TWO EXCHANGES TOTALLED A GOOD SIZED 5093 CONTRACTS…

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR JAN AT 3.5614 TONNES FOLLOWED BY TODAY’S MONSTROUS 153,200 OZ QUEUE. JUMP//NEW STANDING: 12.37 TONNES

YET ALL OF..THIS HAPPENED WITH OUR GAIN IN PRICE OF $8.65 WITH RESPECT TO TUESDAY’S TRADING

WE HAD A SMALL SIZED GAIN OF 1793 OI CONTRACTS (5.576 PAPER TONNES) ON OUR TWO EXCHANGES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALLED A SMALL SIZED 1198 CONTRACTS:

FOR FEB 1198 ALL OTHER MONTHS ZERO//TOTAL: 1198

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 550,411.

IN ESSENCE WE HAVE A SMALL SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1793, WITH 595 CONTRACTS INCREASED AT THE COMEX AND 1198 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 1793 CONTRACTS OR 5.576TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1198) ACCOMPANYING THE SMALL SIZED GAIN IN COMEX OI (595): TOTAL GAIN IN THE TWO EXCHANGES 1793 CONTRACTS. WE NO DOUBT HAD 1) HUGE BANKER SHORT COVERING ,2.) HUGE INITIAL STANDING AT THE GOLD COMEX FOR JAN. AT 3.7262 TONNES//FOLLOWED BY TODAY’S 153,200 OZ QUEUE. JUMP.//NEW STANDING 12.370 TONNES 3)ZERO LONG LIQUIDATION,4) SMALL SIZED COMEX OI. GAIN 5) SMALL ISSUANCE OF EXCHANGE FOR PHYSICAL

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF FEB.WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF JAN HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB, FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (FEB), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2021 INCLUDING TODAY

JAN

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JAN : 24,224 CONTRACTS OR 2,422,400 oz OR 75.34 TONNES (9 TRADING DAY(S) AND THUS AVERAGING: 2691 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 9 TRADING DAY(S) IN TONNES: 75.34 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2020, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 75.34/3550 x 100% TONNES 2.12% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO DATE

JANUARY: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 145.12 TONNES//INITIAL ISSUANCE//

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A VERY STRONG SIZED 1702 CONTRACTS TO 146,144 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 4 1/2 YEARS AGO.

EFP ISSUANCE 745 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 745 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 745 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1702 CONTRACTS AND ADD TO THE 745 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE SIZED GAIN OF 2447 OPEN INTEREST CONTRACT FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 12.235 MILLION OZ,

OCCURRED WITH OUR $0.38 GAIN IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

3. ASIAN AFFAIRS

i)THURSDAY MORNING WEDNESDAY NIGHT

SHANGHAI CLOSED DOWN 42.17 PTS OR 1.17% //Hang Sang CLOSED UP 27.60 PTS OR 0.11% /The Nikkei closed DOWN 276.53 PTS OR 0.96% //Australia’s all ordinaires CLOSED UP .45% /Chinese yuan (ONSHORE) closed DOWN 6.3608 /Oil UP TO 82.22 dollars per barrel for WTI and UP TO 84.38 for Brent. Stocks in Europe OPENED MOSTLY GREEN // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.3608. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.3633: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN AND OFF SHORE TRADING WEAKER AGAINST USA DOLLAR

A)NORTH KOREA//USA/OUTLINE

b) REPORT ON JAPAN

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A SMALL SIZED 595 CONTRACTS AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS SMALL COMEX INCREASE OCCURRED WITH OUR STRONG GAIN OF $8.65 IN GOLD PRICING WEDNESDAY’S COMEX TRADING. WE ALSO HAD A SMALL EFP (1198 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. LOOKS LIKE OUR BANKERS ARE FINALLY BAILING OUT

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE NON ACTIVE DELIVERY MONTH OF JAN.. THE CME REPORTS THAT THE BANKERS ISSUED A SMALL SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 1198 EFP CONTRACTS WERE ISSUED: ;: , DEC : 0 & FEB. 1198 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1198 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A SMALL SIZED 1793 TOTAL CONTRACTS IN THAT 1198 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A SMALL SIZED COMEX OI GAIN OF 595 CONTRACTS..

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING FOR JAN (12.370),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

THE BANKERS WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $8.65)

AND THEY WERE UNSUCCESSFUL IN FLEECING ANY LONGS AS THE TOTAL GAIN ON THE TWO EXCHANGES REGISTERED 5.576 TONNES, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR JAN (12.370 TONNES)…

WE HAD – 3300 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 1793 CONTRACTS OR 179,300 OZ OR 5.576 TONNES

Estimated gold volume today: 301,169 better///

Confirmed volume yesterday: 252,095 contracts poor

INITIAL STANDINGS FOR JAN ’22 COMEX GOLD

JAN 13

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 9645.300 ozJPM 30 kilobars and includes 9236.55 oz london enhanced bars total: 19,005.454 |

| Deposit to the Dealer Inventory in oz | nilOZ |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 1535 notice(s)153,500 OZ4.774 TONNES |

| No of oz to be served (notices) | 58 contracts 5800 oz 0.1804TONNES |

| Total monthly oz gold served (contracts) so far this month | 3919 notices 391,900 OZ12.189 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For today:

No dealer deposit 0

No dealer withdrawal 0

0 customer deposit

2 customer withdrawals

i) Out of JPMorgan: 9645.300 oz (30 kilobars)

ii) JPMorgan phony

enhanced accct 9236.55 oz (from London/London 400 oz bars

ADJUSTMENTS: 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JANUARY.

For the front month of JANUARY we have an oi of 1593 stand for JANUARY GAINING 669 contracts. We had 863 notices filed on WEDNESDAY, so we GAINED A WHOPPING 1532 contracts or an additional 153,200 oz will stand for

gold in this very non active delivery month of January. The resulting queue jump equates to 4.76 tonnes, the greatest recorded queue jump in comex history.

FEBRUARY LOST 19,588 CONTRACTS TO 279,039

March lost 59 contracts to stand at 2299..

We had 1593 notice(s) filed today for 159,300 oz FOR THE JAN 2022 CONTRACT MONTH

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 534 notices were issued from their client or customer account. The total of all issuance by all participants equates to 1535 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 7 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JAN /2021. contract month,

we take the total number of notices filed so far for the month (3919) x 100 oz , to which we add the difference between the open interest for the front month of (JAN: 1593 CONTRACTS ) minus the number of notices served upon today 1535 x 100 oz per contract equals 402,357.25 OZ OR 12.515 TONNES the number of TONNES standing in this NON active month of JAN. (numbers corrected from yesterday)

thus the INITIAL standings for gold for the JAN contract month:

No of notices filed so far (3919) x 100 oz+ (1593) OI for the front month minus the number of notices served upon today (1535} x 100 oz} which equals 244,500 oz standing OR 7.605 TONNES in this NON active delivery month of JAN.

We GAINED 1532 contracts or an additional 153,200 oz of gold(4.765 tonnes queue jump) will stand for metal on this side of the pond.

TOTAL COMEX GOLD STANDING: 12.370 TONNES (HUGE FOR A JANUARY DELIVERY MONTH

IF THIS HOLDS TO THE END OF THE MONTH, THIS WILL BE THE HIGHEST EVER RECORDED GOLD STANDING FOR A JANUARY, GENERALLY A VERY POOR DELIVERY MONTH.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

206,468.649, oz NOW PLEDGED /HSBC 6.42 TONNES

174,041.813 PLEDGED MANFRA 5.41 TONNES

54,339.114oz PLEDGED JPMorgan no 1 1.690

288,481,604, oz JPM No 2 8.97 TONNES

698,821.330 oz pledged June 12/2020 Brinks/27,96 TONNES

12,244.444 oz International Delaware: 0..3808 tonne

Loomis: 18,615.429 oz

total pledged gold: 1,653,017.372oz 51.42 tonnes

TOTAL REGISTERED AND ELIZ GOLD AT THE COMEX: 33,617,243.347 OZ (1045.63 TONNES)

TOTAL ELIGIBLE GOLD: 16,005,349.806 OZ (497.83 tonnes)

TOTAL OF ALL REGISTERED GOLD: 17,608,893.542 OZ (547.71 tonnes)

REGISTERED GOLD THAT CAN BE SERVED UPON: 15,955,876.0 OZ (REG GOLD- PLEDGED GOLD) 496.29 tonnes

END

JANUARY 2022 CONTRACT MONTH//SILVER

INITIAL STANDING FOR SILVER//JAN 13

And now for the wild silver comex results

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 885,722.405 oz BrinksCNTManfraJPM |

| Deposits to the Dealer Inventory | nilOZ |

| Deposits to the Customer Inventory | 1194,824.139 ozJPmorganCNT |

| No of oz served today (contracts) | 0 CONTRACT(S)nil OZ) |

| No of oz to be served (notices) | 387 contracts (1,935,000 oz) |

| Total monthly oz silver served (contracts) | 2336 contracts 11,680,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

we had 0 deposits into the dealer

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We had 2 deposits

i)Into JPMorgan: 581,231.800 oz

ii) Into CNT: 613,592.339 oz

total: 1,194,824.139 oz

JPMorgan has a total silver weight: 184.937 million oz/353.378 million =52.32% of comex

ii) Comex withdrawals: 4

a) out of Brinks: 175,998.168 oz

b) out of Manfra: 69,181.107 oz

c) out of Brinks 175,998.168oz

d) Out of CNT 360,965.500 oz

total withdrawal 885,722.405 oz

we had 1 adjustment

i) Out of Brinks: 168,164.510 oz leaves the dealer account and lands into the customer account

the silver comex is in stress!

TOTAL REGISTERED SILVER: 81.331 MILLION OZ

TOTAL REG + ELIG. 353.068 MILLION OZ

TOTAL NO OF CONTRACTS SERVED UPON THIS MONTH: 1980 CONTRACTS FOR 45,095,000 OZ

CALCULATION OF SILVER OZ STANDING FOR DECEMBER

NUMBER OF NOTICES FILED TODAY: 185 NOTICES OR 925,000 OZ

silver open interest data:

FRONT MONTH OF JAN//2022 OI: 387 CONTRACTS LOSING 186 contracts on the day

We had 185 notices filed for WEDNESDAY so we lost 1 contracts or 5,000 additional oz will not stand for delivery in this non active delivery month of January.

FOR FEB WE HAD A LOSS OF 14 CONTRACTS UP TO 711

FOR MARCH WE HAD A GAIN OF 118 CONTRACTS UP TO 114,496 CONTRACTS.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 0 for NIL oz

Comex volumes: 54,233 poor// est. volume today

Comex volume: confirmed YESTERDAY: 61,228 contracts (poor)

To calculate the number of silver ounces that will stand for delivery in JANUARY. we take the total number of notices filed for the month so far at 2336 x 5,000 oz =. 11,680,000 oz

to which we add the difference between the open interest for the front month of JAN (387) and the number of notices served upon today 0 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JAN./2021 contract month: 2336 (notices served so far) x 5000 oz + OI for front month of JAN (387) – number of notices served upon today (0) x 5000 oz of silver standing for the JAN contract month equates 13,615,000 oz. .

We LOST 1 contracts or an additional 5,000 oz will stand for delivery on this side of the pond.

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

GLD

JAN 13/WITH GOLD DOWN $5.75: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 976.21 TONNES

JAN 12/WITH GOLD UP $8.65//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 976.21 TONNES

JAN 11/WITH GOLD UP $19.25/A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES FROM THE GLD/INVENTORY RESTS AT 976.21 TONNES

JAN 10/WITH GOLD UP $2.00/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 977.08 TONNES

JAN 7/WITH GOLD UP $8.15//A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWLA OF 1.16 TONNES FROM THE GLD////INVENTORY RESTS AT 978.83 TONNES

JAN 6/WITH GOLD DOWN $35.30//A SMALL CHANGE IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF .32 TONNES/INVENTORY RESTS AT 979.99 TONNES

JAN 5/WITH GOLD UP $10.30: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 980.31 TONNES

Jan 4/WITH GOLD UP $14.00//A HUGE CHANGE OF 4.65 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 980.31 TONNES

JAN 3/WITH GOLD DOWN $26.70: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 975.66 TONNES

DEC 31/WITH GOLD UP $14.05 : NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 975.66 TONNES

DEC 30/WITH GOLD UP $7.75 NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 975.66 TONNES

DEC 29/WITH GOLD DOWN $5.00 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.03 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 975.66 TONNES

DEC 28/WITH GOLD UP $2.00 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 973.63 TONNES

DEC 27/WITH GOLD DOWN $2.05: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.63 TONNES.

DEC 23/WITH GOLD UP $9.85 TODAY//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.94 TONNES FROM THE GLD/// INVENTORY RESTS AT 973.63 TONNES

DEC 22/WITH GOLD UP $12.85 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 978.57 TONNES

DEC 21/WITH GOLD DOWN $7.05 TODAY, NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 978.57 TONNES

DEC 20/WITH GOLD DOWN $9.65 TODAY; A BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.37 TONNES INTO THE GLD///INVENTORY RESTS AT 977.20 TONNES

DEC 17/WITH GOLD UP $7.05 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 977.20 TONNES

DEC 16/WITH GOLD UP $33.05TODAY; A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.4 TONNES FROM THE GLD////INVENTORY REST AT: 977.20 TONNES

DEC15/WITH GOLD DOWN $7.80 TODAY/ A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.04 TONNES FROM THE GLD////INVENTORY RESTS AT 980.60 TONNES.

DEC 14/WITH GOLD DOWN $18.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 982.64 TONNES

DEC 13/WITH GOLD UP $3.20 TODAY/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 982.64 TONNES

DEC 10.WITH GOLD UP $7.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 982.64 TONNES

DEC 9/WITH GOLD DOWN $9.10 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 982.64.

DEC 8/WITH GOLD UP $5.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 984.38 TONNES

DEC 7/WITH GOLD UP $5.15 TODAY; A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 984.38 TONNES

DEC 6/WITH GOLD DOWN $3.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 986.17 TONNES//

CLOSING INVENTORY: 976.21 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

SLV.

JAN 13/WITH SILVER DOWN 2 CENTS: A BIG CHANGE IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 832,000 OZ FROM THE SLV////INVENTORY RESTS AT 529.780 MILLION OZ

JAN 12/WITH SILVER UP 38 CENTS TODAY : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.612 MILLION OZ//

JAN 11/WITH SILVER UP 33 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.612 MILLION OZ/.

JAN 10/WITH SILVER UP 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 530.612 MILLION OZ//.

JAN 7/WITH SILVER UP 17 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.612 MILLION OZ//.

JAN 6/WITH SILVER DOWN 94 CENTS TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL PF 226,000 OZ FROM THE SLV///INVENTORY RESTS AT 530.612 MILLION OZ?/

JAN 5/WITH SILVER UP 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.838 MILLION OZ//

JAN 4/WITH SILVER UP 21 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.838 MILLION OZ//

JAN 3/WITH SILVER DOWN 45 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.219 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 530.838 MILLION OZ//

DEC 31/WITH SILVER UP 29 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 533.057 MILLION OZ//

DEC 31/WITH SILVER UP 29 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 533.057 MILLION OZ//

DEC30/WITH SILVER UP 14 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A HUGE WITHDRAWAL OF 4.624 MILLILON OZ FROM THE SLV.//INVENTORY RESTS AT 533.057 MILLION OZ//

DEC 29/WITH SILVER DOWN 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 537.681 MILLION OZ/

DEC 28/WITH SILVER UP 9 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.682 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 537.681 MILLION OZ//

DEC 27/WITH SILVER UP 6 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 537.681

DEC 23/WITH SILVER UP 19 CENTS TODAY:A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.202 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 537.681 MILLION OZ//

DEC 22/WITH SILVER UP 29 CENTS TODAY; A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.202 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 538.883 MILLION OZ/

DEC 21/WITH SILVER UP 19 CENTS: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.728 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 540.085 MILLION OZ

DEC 20/WITH SILVER DOWN 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 538.282 MILLION OZ

DEC 17/WITH SILVER UP 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 538.282 MILLION OZ//

DEC 16/WITH SILVER UP 91 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 3.33 MILLION OZ FROM THE SLV//INVENTORY REST AT 538.282 MILLION OZ

DEC 15WITH SILVER DOWN 38 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV/: A WITHDRAWAL OF 2.48 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 541.612 MILLION OZ

DEC 14/WITH SILVER DOWN 38 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 543.092 MILLION OZ

DEC 13/WITH SILVER UP 11 CENTS TODAY; A HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 3.561 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 543.092 MILLION OZ//

DEC 10.WITH SILVER UP 19 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 546.653 MILLION OZ..

DEC 9/WITH SILVER DOWN 43 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF 2.96 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 546.653 MILLION OZ/

DEC 8/WITH SILVER DOWN 7 CENTS TODAY; NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 543.693 MILLION OZ///

DEC 7/WITH SILVER UP 24 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 543.693 MILLION OZ..

DEC 6/WITH SILVER DOWN 25 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.110 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 543.693 MILLION OZ//

CLOSING INVENTORY: 529.780 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

PETER SCHIFF

end

LAWRIE WILLIAM//,//Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,James RICKARDS

Von Greyerz: Coming Market Madness Could Take 70 Years To Recover From

THURSDAY, JAN 13, 2022 – 06:30 AM

Authored by Egon von Greyerz via GoldSwitzerland.com,

Cervantes famous classic novel Don Quixote can in simple terms be described as a fight for liberty and freedom against oppression and against the state. This book is from 1605 and considered to be one of the best books ever written.

In the midst of market madness, risk doesn’t exist because lunatics neither see, nor worry about risk. And still, 2022 will be more about risk and survival than anything else. So I will obviously talk more about “The Triumph of Survival” which I discussed in a recent piece.

“When life itself seems lunatic, who knows where madness lies.” – Don Quixote

The year 2022 will most likely be the culmination of risk. An epic risk moment in history that very few investors will see until it is too late as they expect to be saved yet another time by the Fed and other central banks.

And why should anyone believe that 2022 will be different from any year since 2009 when this bull market started? Few investors are superstitious and therefore won’t see that 13 spectacular years in stocks and other asset markets might signify an end to the epic super bubble.

The Great Financial Crisis (GFC) in 2006-9 was never repaired. Central bankers and governments patched Humpty up with glue and tape in the form of printed trillions of dollars, euro, yen etc. But poor Humpty Dumpty was fatally injured and the intensive care he received would only give him a temporary reprieve.

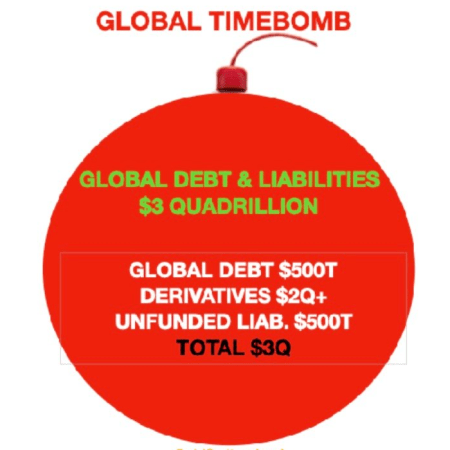

When the GFC started in 2006, global debt was $120 trillion. Today we are at $300t, rising to potentially $3 quadrillion when the debt and derivative bubble finally first explodes and then implodes as I explained in my previous article.

It is amazing what fake money made of just air can achieve. Even better of course is that the central banks have manipulated interest rates to ZERO or below which means the debt is issued at zero or even negative cost.

INVESTORS HAVE FOUND SHANGRI-LA

Investors now believe they are in Shangri-La where markets can only go up and they can live in eternal bliss. Few understand that the increase in global debt since 2006 of $180t is what has fuelled investment markets.

Just look at these increases in the stock indices since 2008:

Nasdaq up 16X

S&P up 7x

Dow up 6X

And there are of course even more spectacular gains in stocks like:

Tesla up 352X or Apple up 62X.

These type of gains have very little to do with skilful investment, but mainly with a herd that has more money than sense fuelled by paper money printed at zero cost.

To call the end of a secular bull market is a mug’s game. And there is nothing that stops this bubble from growing bigger. But we must remember that the bigger it grows, the greater the risk is of it totally wiping out gains not just since 2009 but also since the early 1980s when the current bull market started.

The problem is also that it will be impossible for the majority of investors to get out. Initially they will believe that it is just another correction like in 2020, 2007, 2000, 1987 etc. So greed will stop them from getting out.

But then as the fall continues and fear sets in, investors will set a limit higher up where they intend to get out. And when the market never gets there, the scared investor will continue to set limits that are never reached until the market reaches the bottom at 80-95% from the top.

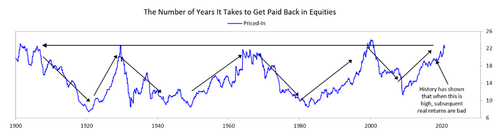

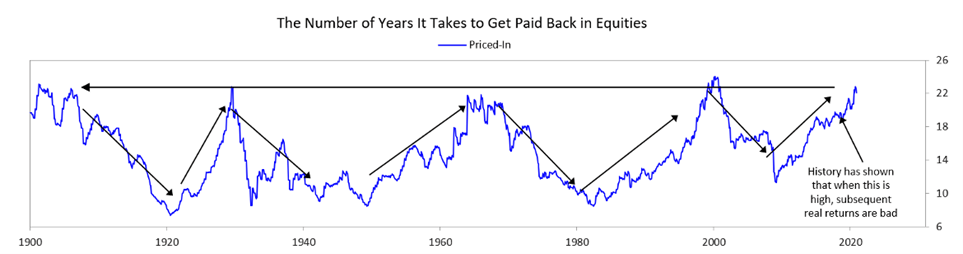

And thus paper fortunes will be wiped out. We must also remember that it can take a painstakingly long time before the market recovers to the high in real terms.

As Ray Dalio shows in the chart below, the 1929 high in the Dow was not even recovered in real terms by the mid 1960s. Finally it was surpassed in 2000.

This means that it took 70 years to recover in real terms! So investors might have to wait until 2090 to recover the current highs after the coming fall.

So looking at the chart, the market is now at a similar overvalued level it was in 1929, 1972 and 2000.

Thus the risk is as great as at some historical tops in the last 100 years.

THE EPIC BUBBLE MIGHT NOT RECOVER UNTIL 2090

The chart below shows that the 1929 top in the Dow was not reached in real terms until 2000.

How many investors are prepared to take the risk of a say 90% fall like in 1929-32 and not recover in real terms until by 2090!

Again, I repeat that this is not a forecast. But it is an epic warning that risk in investment markets are now at a level that investors should avoid.

I fear that sadly very few investors will heed this risk warning.

DON QUIXOTE WOULD HAVE FOUGHT WOKENESS

As the world is being ever more oppressed and controlled by the state, Cervantes’ message in Don Quixote could not be more appropriate.

I am quite convinced that Don Quixote would also have fought against the wokeness that today has become the guideline not onlyfor human behaviour but also for justice.

In the UK last week, a court acquitted four people accused of pulling down a statue of a historical figure who had been a major benefactor of the city of Bristol. Yes, he had made money on the slave trade in the late 1600s but where do we stop rewriting history?

With today’s woke interpretation of history, virtually every historical king, emperor, government leader, general or businessman, to mention a few, should be put on trial even if they are all dead.

For example, Great Britain, France, Spain were all part of invading North America killing a major part of the Indian population and taking their land. So if we rewrite history, shouldn’t all these Europeans as well as the Africans be pulled out of North America and the land handed bank to the Indians.

The same goes for South America of course. The Spanish and the Portuguese must all return and give the land back.

And where do we stop? We should really go back to the Han Dynasty, the Roman, the Mongol, the Ottoman, Spanish, Russian or British Empires.

Why just deal with the slave trade in Africa when all these empires ransacked and conquered major land areas, took slaves and stole the riches of the countries they invaded. In a woke and fair world, all these actions must be reversed too.

If the world decides to rewrite history, it must be done properly with major restitutions. There must of course be a UN Commission, and EU Commission and many more to deal with this properly.

As Don Quixote said: “Who knows where madness lies”.

EASY MONEY MADNESS

But it is most probably the total market Madness in the financial world which will have the biggest effect on the world economy in 2022 and onwards.

As I have pointed out many times, the US has not had a budget surplus since 1930 with the exception of a couple of years in the 1940s and 50s. The Clinton surpluses were fake as debt still increased.

But the money and market Madness started in the 1970s after Nixon couldn’t make ends meet and closed the gold window. The US federal debt in 1971 was $400 billion. Since then the US debt has grown by an average of 9% per year. This means that the US debt has doubled every 8 years since 1971. We can actually go back 90 years to 1931 and find that US debt since then has doubled every 8.3 years.

What a remarkable record of total mismanagement of the US economy for a century!

The US has not had to build an empire in the conventional way by conquering other countries. Instead the combination of a reserve currency, money printing and a strong military power has given the US global power and a global financial empire.

Even worse, since the sinister smart coup by private bankers in 1913 to take control of the creation of money, the US Federal debt has gone from $1 billion to almost $30 trillion.

As Mayer Amschel Rothschild poignantly stated in 1838:

“Permit me to issue and control the money of a nation and I care not who makes its laws”.

And that is exactly what some powerful bankers and a senator decided on Jekyll Island in 1910 when they conspired to take over the US money system through the creation of the Fed which was founded in 1913.

Ever since that time the bankers have helped themselves from the self-filling honeypot.

Controlling the Fed has given the bankers an unlimited supply of money and credit to finance their activities. They have used this to acquire assets around the world as well as power. As is the general rule today, debt is never repaid since new debt always makes the old debt insignificant as the currency is constantly debased with all the new money issued.

The debt issued was not only used for the direct financial gain of the bankers. No debt buys enormous power and by creating money to finance profligate governments, the bankers are also buying power and controlling the politicians.

What a wonderful position as Rothschild made clear almost 200 years ago.

I COME IN A WORLD OF IRON TO MAKE A WORLD OF GOLD – Don Quixote

This was the ambitious goal of Don Quixote.

But he didn’t succeed and today’s bankers have a totally different goal which is to make a world of fiat money. And they have been spectacularly successful at it.

But the investors who wish to survive the coming global economic debacle must heed Don Quixote’s words and turn their paper assets into physical gold.

Stocks, bonds and property in coming years will lose at least 90% in real terms against gold.

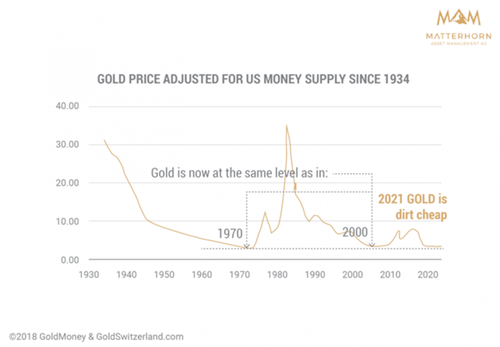

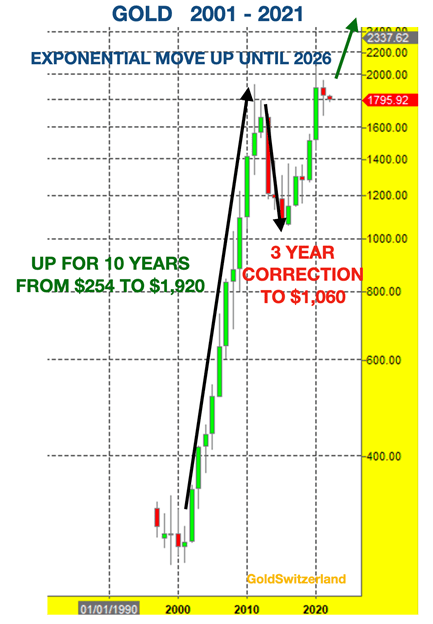

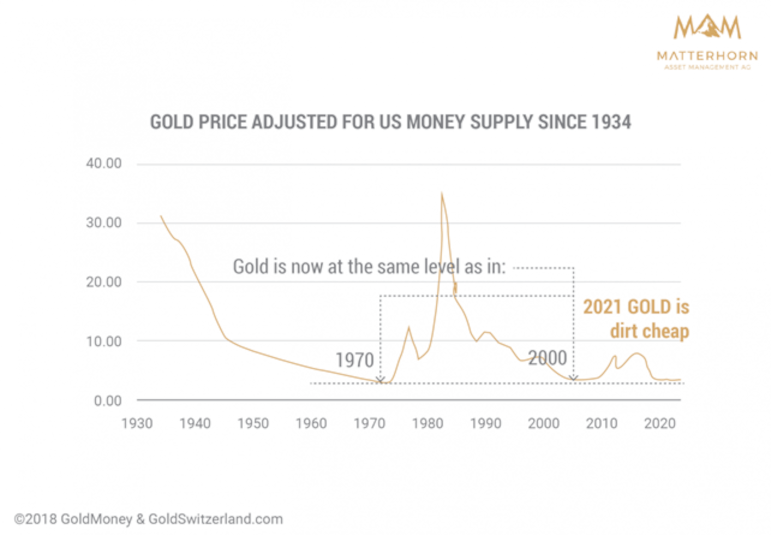

Gold in US dollars started a bull market in 2001 as the chart below shows. Since then, gold is up every year (sideways 2018) until 2021 when we saw a small correction. Gold’s up cycles normally last at least 10 years. This means that the current leg of the bull market in gold should last at least until 2026 and potentially extend beyond that.

As I regularly point out, gold is extremely cheap in relation to the growth in US money supply.

Gold is today as cheap as it was in 1970 at $35 and as cheap as in 2000 at $290.

Thus the upside potential for gold is multiples of the current price, especially since the currency debasement will accelerate due to accelerated money printing.

Gold is the king of wealth preservation and should be held in physical form outside the banking system.

Silver is likely to go up 2-3 times as fast as gold and is therefore a fantastic speculative investment as long as it is held in physical form. The risk of holding paper silver is massive since there is virtually no physical silver available. But due to the volatility of silver, investors should hold a much smaller percentage of their financial assets in silver than in gold.

In summary, 2022 could be the year when investors’ wealth turns into ashes, or for the prudent investor, turns into solid gains in gold and silver.

END

OTHER GOLD STORIES

END

OTHER COMMODITIES/

CRYPTOCURRENCIES

Steve Brown on Bitcoin!

Bitcoin: Vanguard’s Great FinTech Reset

According to the WTO, in 2020 global trade volume decreased by 9%. Of course that global trade decline is attributed to the economic effect of the contagion; however US trade wars and weaponization of the US dollar, along with the US boxing itself into a trade-restrained corner by politically motivated sanctions, must count, too.

Any potential for a reversal in globalization alarms the Vanguard Group to such an extent however, they produced a paper intended to soothe Elite nerves on the matter: Link: https://corporate.vanguard.com/content/dam/corp/research/pdf/Megatrends-The-deglobalization-myths-ISG052021%20(1).pdf and characterize the reversal in global trade as “slowbilization” instead of de-globalization.

The Vanguard “Deglobalization Myth” paper was produced by ivory tower monetary kleptocrats and their serfs, and the paper is full of acronyms like “GFC” (Global Financial Crisis) which is all the reader needs to know about its substance, or lack of it.

Vanguard Group is the wealthiest investment group on earth, and owns a big share of the next largest investment group too, BlackRock. But Elites have desire to avoid the slings and arrows of a potentially torch-bearing public, and notoriety to those who may have, in an earlier era, had their heads. Vanguard Group is particularly sinister in that regard, where participation in the Group is opaque by structure, and Vanguard Group’s major shareholders are effectively impossible to identify.

Filmmaker Tim Gielen, author of “Monopoly Who Owns the World” Link : https://www.bitchute.com/video/EHrd2p3HkTEj/ has researched Vanguard’s ownership in depth, only to determine what we must already suspect, “This means that Vanguard is in the hands of the richest families on earth.” Link: https://www.organicconsumers.org/news/who-owns-world-blackrock-and-vanguard A leading light of Vanguard is of course John Brennan of Rockefeller Capital Management, with deep ties to the Saudi monarchy and to the Evil Empire in general. Link: https://rcm.rockco.com/leadership_items/john-j-brennan/

We can internalize, externalize, or ignore the foregoing facts altogether, but in the west, Vanguard controls and owns what we eat, what we drink, and even our health. In a sense, Vanguard Group determines where we live, how we live, and the materials used to build our homes. Vanguard Group is a monopolistic cartel and also a parasitic entity feeding on ubiquitous cronyism, greed, and a lust for power never known in western history before, to such an extent. Vanguard is where the giant moving parts of an extant sinister regime work together to reinforce one another. And oh, by the way.. Vanguard Group is a substantial owner of Bitcoin, too.

One example is Michael Saylor’s Microstrategy (MSTR) Wall Street bitcoin stock which has a US $6B market capitalization.

With 66%+ institutional ownership, Vanguard Group and BlackRock (in part owned by Vanguard) is the second largest holder of this bitcoin offering, Microstrategy (MSTR):

The Wall Street bitcoin shill is also played out by the Grayscale Bitcoin Trust (GBTC) largely owned by Cathie Wood’s ARK Innovation:

Cathie Wood’s ETF and the Vanguard ETF supposedly compete, but these funds and groups are totally incestuous, meaning they all own parts of each other. Vanguard, BlackRock, Ark etc are simply the moving parts of a massive monopolistic cabal… not truly “investments”. Vanguard and associated whales by market implication own most (Wall Street) bitcoin, but recall that that the Pax Americana’s Fed is heavily invested too, where the Federal Reserve via its Primary Dealers and ESF leverages bitcoin to launder billions in inflationary fiat currency. Link: https://novusconfidential.wordpress.com/2021/02/27/180-billion-just-got-lost/

F U money apes, Link: https://youtu.be/_uJwvlimnNs and FinTech may chant a $100K bitcoin laser eyes mantra, but it’s Vanguard Group’s infinitely corrupt mainstream media, CNBC, MSNBC, Bloomberg etc that chant the BTC bullshit at a fever pitch; as feverish as any Bohemian Grove blood beast. As we examined in Bitcoin Rinse and Repeat, Christine LeGarde and Central Bank cut-outs might whine about bitcoin, but the BTC scam is essential to their DNA of fiat sterilization, the Vanguard Group, and its related financial cabal.

Vanguard’s vanguard are the debauched bitcoin messiahs link: https://www.youtube.com/watch?v=nZyvjJX8RLc who bray about the freedom and liberty that bitcoin supposedly provides to the downtrodden, while Vanguard essentially plans for its financial version of the Great Reset link: https://moneyandmarkets.com/fedcoin-federal-reserve-studying-digital-currency/ for which Bitcoin is the test case. The FinTech messiah’s mantra chant about “decentralization” of Bitcoin is an irrelevance too when any government in the world can prevent its banking system from interacting with any bitcoin exchange in the world, at any time. And, any bitcoin exchange can prevent bitcoin transactions for political reasons.

Crypto.com, coinbase.com, and bitfinex.com prohibit transactions for political reasons, where the SouthFront bitcoin transaction ban by those exchanges provides a concise example. Link: https://southfront.org/the-safest-way-to-donate-cryptocurrency/ I’d written before that avoidance of illegal US Treasury sanctions and weaponization of a deeply corrupt warfare state Federal Reserve dollar provides the only positive use case for bitcoin.** Now, with the SouthFront example, that’s no longer true. And precisely the opposite of what bitcoiners T Maxwell Keiser, Brock Pierce, and Mr Mike “The Burger Guy” Saylor tell their bitcoin converts regarding the purity of “decentralized bitcoin” .

Essentially crypto.com, coinbase.com, bitfinex.com serve Vanguard’s Masters of War; they are serfs of Empire. Which questions the original premise of bitcoin itself, that somehow bitcoin will “screw the man” and liberate oppressed people all over the world from monetary tyranny. It’s a crytpo propaganda crusade endorsed by Vanguard, where we are told that the downtrodden and politically oppressed everywhere will be saved by a Kahzakh hashrater’s hash. Bullshit. It’s a lie like every other lie the Vanguard Group’s “investment” Empire perpetrates, with such emphasis and influence that the alt-media brays the same lying tune as the MSM.

Despite the bitcoin anointed mantra about “decentralization”, factually the OCC may shutdown nearly all bitcoin transactions in the US by preventing any US accredited bank from transacting with any crypto exchange, anywhere. Of course the OCC won’t do that as we examined in Why the Fed Loves Bitcoin Pt 3, because the “open ledger” provides a dark pool for the Fed’s criminal dealers to disappear billions in Federal Reserve-created near-garbage US dollars. Link: Sterilzation of capital Also see: Link: https://novusconfidential.wordpress.com/2021/03/05/why-the-fed-loves-bitcoin-pt-3/

As such, let’s take a deeper dive into the Deep Financial States (of America) suspicious shenanigans. The Fed’s reverse repo gaming* chart shows a big dip from December 31st to January 11th at the far right side of the chart:

https://fred.stlouisfed.org/series/RRPONTSYD

The Fed began tapering some time before, so the dip at the right of the chart does not fully represent that. What does it represent? Coinciding with the first protests in Khazakstan (likely engineered by the same cabal that the Vanguard Group represents Link: https://www.moonofalabama.org/2022/01/mysteries-of-the-failed-rebellion-in-kazakhstan.html and see: https://www.strategeast.org/rothschild-considering-expanding-activities-kazakhstan-uzbekistan/ and see: 1999: US Silk Road Act ) we received a report that the bitcoin hashrate fell by nearly 20%, resolving a mystery regarding where most China bitcoin “miners” had gone. (Beside Texas of course!)

Now let’s examine Bitcoin’s chart to date, which reflects trading in all of the many thousands of other crypto on the blockchain:

Note the dip down from December 31st until now. The performance is identical. This implies that Fed’s dealers are far more implicated in the bitcoin scam than ever imagined. Recall too that the repo market is essentially a Fed insider operation to bankroll its crooked dealers. Link: https://wallstreetonparade.com/2021/12/the-fed-gets-its-ducks-in-a-row-for-the-next-wall-street-bailout-quietly-adds-goldman-sachs-bank-citibank-to-its-new-500-billion-standing-repo-facility/ And see: https://gsiexchange.com/jpmorgan-chase-has-racked-up-5-criminal-felony-counts/

Because the Federal Reserve has somewhat reduced its cash injections to its highly criminalized dealers (QE tapering) that may account, in part, for the chart dip. But the similarity to recent declines in a scam derivative (ie bitcoin – a scam only outdone by the scam of the Fed dollar itself) is uncanny.

Meanwhile another intensely criminal financial house that promoted liar loans while short-selling securities based on those very same liar loans, gloats about the potential for bitcoin to reach $100K US! Link: https://www.forbes.com/sites/korihale/2022/01/11/goldman-sachs-100k-bitcoin-endorsement-buoys-digital-gold/ Of course Goldman Sachs expects the poor and downtrodden who so benefit from bitcoin (crying all the way from their bank) to believe that. And for one reason. Because GS is convinced that you, the reader, are into this ponzi just as much as Goldman Sachs is…. Or perhaps a second …Goldman Sachs simply takes the public for being the perpetual marks they frequently are?

In who or whom do we trust? Perhaps the God in which the USA trusts is the Vanguard Group god of mammon. It certainly seems so. And many F U money young people have gone along with that. After all, ‘Jailers are most happy when their prisoners either cooperatively or unknowingly build their own prison..’

Bitcoin. Wall Street and Fed dealer banks… have never seen a scam they didn’t like!

*called Open Market Operations which involves the world’s most criminal banks)

** “use case” as a currency is minimal; bitcoin may only transact at seven times per second, maximum.

NB: Here Shanti Phula describes the western financial cabal’s incestuous relationships: https://ronaldwederfoort.wordpress.com/2016/04/02/vanguard-group-us-2080-trillion-rothschild-major-shareholder/

NB: Also see: CIA’s Bitcoin Heist (Afghanistan) Link: https://strategika51.org/2021/09/05/cias-bitcoin-heist/

Steve Brown

end

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings THURSDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN AT 6.3608

OFFSHORE YUAN: 6.3636

HANG SANG CLOSED UP 27.60 PTS OR 0.11%

2. Nikkei closed DOWN 276.53 PTS OR 0.96%

3. Europe stocks ALL MOSTLY GREEN

USA dollar INDEX DOWN TO 94.82/Euro RISES TO 1.1462-

3b Japan 10 YR bond yield: RISES TO. +.131/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 114.32/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 82.22 and Brent: 84.38-

3f Gold DON/JAPANESE Yen DOWN CHINESE YUAN: ON -SHORE CLOSED DOWN// OFF- SHORE DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO -.0.064%/Italian 10 Yr bond yield FALLS to 1.23% /SPAIN 10 YR BOND YIELD FALLS TO 0.61%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 1.29: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 1.52

3k Gold at $1821.25 silver at: 23.16 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3l USA vs Russian rouble; Russian rouble UP 100/100 in roubles/dollar AT 75.58

3m oil into the 82 dollar handle for WTI and 84 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 114.32 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning .9120– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0454 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 1.743 UP 0 BASIS PTS

USA 30 YR BOND YIELD: 2.083 DOWN 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 13.59

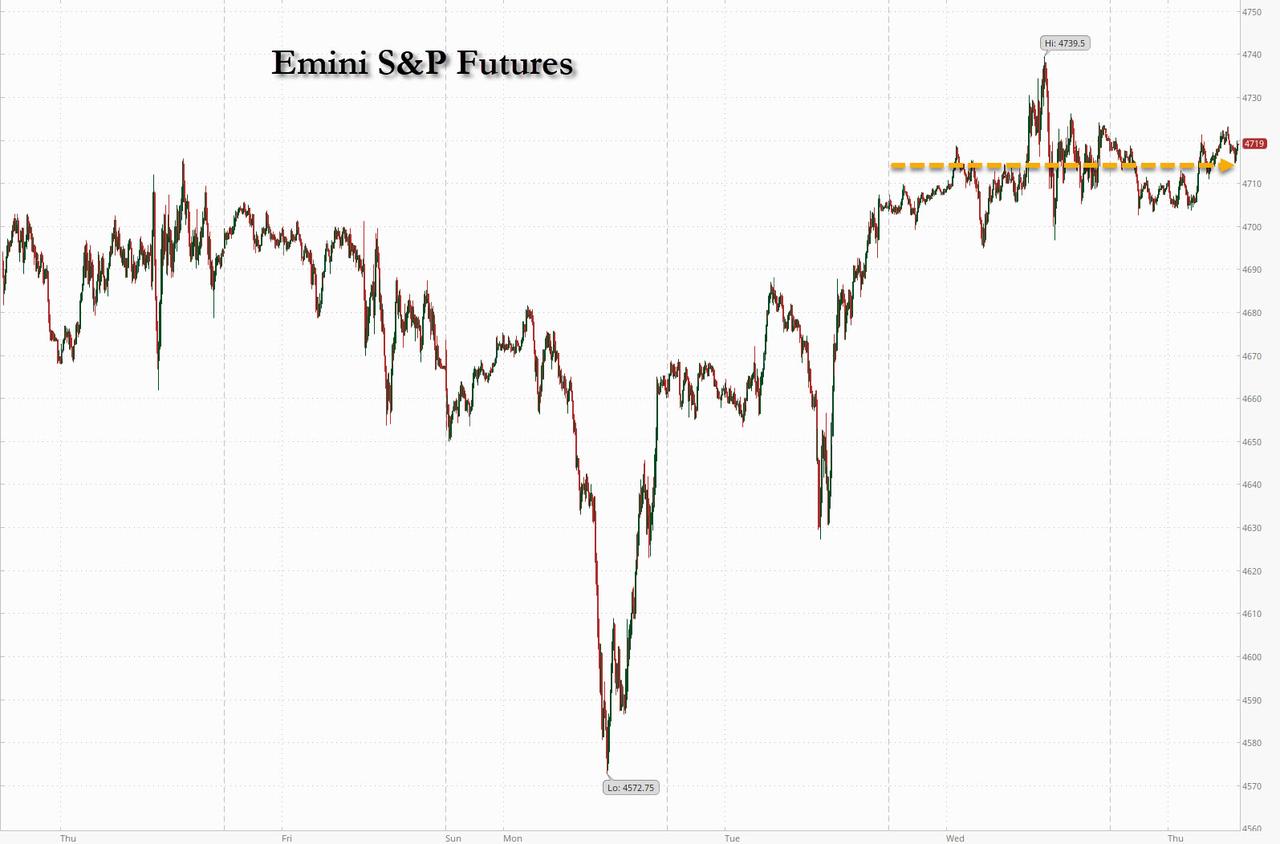

Futures Flat Ahead Of Another Scorching PPI Print

THURSDAY, JAN 13, 2022 – 08:00 AM

US futures were little changed on Thursday one day after the highest CPI print since 1982 and just minutes before another red hot PPI print is expected (9.8%, up from 9.6%), as investors tried to gauge the timing and pace of monetary tightening. S&P 500, Dow and Nasdaq 100 futures were up 0.1% as investors waited for the next trading signal. 10Y yields were flat around 1.74%, and the dollar edged lower as a growing tide of investors bet the world’s reserve currency has reached a peak with rate hikes largely priced-in to the market with Fed tightening likely to lead to an economic slowdown.

“Markets in 2022 have been volatile as the reality of inflation set in, and this reaction mainly reflects relief that the print did not exceed already lofty expectations,” Geir Lode, head of global equities at the international business of Federated Hermes, said in an email.

Inflation hitting 7% could force a quicker move by the Federal Reserve, with the market now pricing four rate hikes this year starting no later than March, according to technical analyst Pierre Veyret at ActivTrades in London. “Investors still struggle with one crucial question: how will the Fed manage to tackle rising price pressure without derailing the fragile post-pandemic economic recovery?”

Sure enough, San Francisco Fed President Mary Daly and her Philadelphia peer Patrick Harker added their voices to the chorus in interviews published yesterday evening and this morning, calling for a rate hike as soon as March when odds of a rate hike have hit a new high of 90%. Attention today will be on the confirmation hearing of Lael Brainard in the Senate. The vice-chair nominee, who last publicly commented on the economic outlook in September, said in prepared remarks that tackling inflation is the bank’s “most important task.”

In premarket trading, shares in Delta Air Lines rose more than 2% even though the carrier missed revenue and EPS expectations, after the company said the omicron variant won’t derail its expectation to remain profitable for the rest of the year, as it released fourth-quarter financial results. Here are some of the biggest U.S. movers today:

- U.S. chip stocks are mixed in premarket trading after sector bellwether TSMC gave a 1Q sales outlook that beat estimates and raised its projected annual capex versus last year. Equipment stock Applied Materials (AMAT US) +2% premarket, while TSMC customers are mixed with Apple (AAPL US) -0.1%, Nvidia (NVDA US) +0.7% and AMD (AMD US) +0.6%.

- Puma Biotechnology (PBYI US) shares surge 13% in U.S. premarket trading, after the company said that its Nerlynx treatment was included in the National Comprehensive Cancer Network’s (NCCN) clinical practice guidelines in oncology for the treatment of breast cancer.

- KB Home (KBH US) shares rise 6.2% in premarket trading after the homebuilder’s 4Q EPS beat estimates, with Wells Fargo calling the results and guidance “solid.”

- Planet Labs (PL US) shares rise 1.6% in U.S. premarket trading, after the satellite data provider said that it plans to launch 44 SuperDove satellites on Thursday on SpaceX’s Falcon 9 rocket.

- Adagio Therapeutics (ADGI US) said ADG20 has neutralization activity against omicron and cites recent findings from three publications on ADG20. Shares jumped 30% in post-market trading.

Discussing yesterday’s scorching CPI print, DB’s Jim Reid writes that “if you did an MRI scan of US inflation yesterday you’d find things to support both sides of the debate which is surprising when it hit 7% YoY and the highest since 1982 when Fed Funds were more than 13% rather than close to zero as they are today. So a slightly different real rate to back then. In fact the real rate is through any level seen in the 1970s and is only comparable to WWII levels. Back to CPI and the YoY number was in line with expectations, but core and MoM figures were all a bit firmer than expected. However, the beats were small enough that the data didn’t significantly change the outlook for monetary policy, with Fed funds futures still pricing in an 89% chance of a March hike, which is roughly around where it’d been over the preceding days.”

In Europe, the Stoxx Europe 600 Index paused after a two-day advance, erasing early declines of as much as 0.3% to trade little changed, with technology and automotive shares offsetting losses in consumer products and health care. CAC 40 underperforms, dropping as much as 0.6%. The Stoxx Europe 600 Technology sub-index is up 1.1%, getting a boost from chip stocks which gained after sector bellwether TSMC gave a 1Q sales outlook that beat estimates and raised its projected annual capex versus last year. Geberit dropped as much as 4.5% to a seven-month low after the Swiss producer of sanitary installations reported fourth-quarter sales.

Bloomberg Dollar Spot dips into the red pushing most majors to best levels of the session. NZD, AUD and GBP are the best G-10 performers. Crude futures maintain a relatively narrow range. WTI is flat near $82.70, Brent stalls near $84.84. Spot gold dips before finding support near $1,820/oz. Most base metals are in the red with LME zinc lagging peers.

Asian stocks were little changed after capping their biggest rally in a year, with health-care and software-technology names retreating while financials advanced. The MSCI Asia Pacific Index fluctuated between a drop of 0.3% and a gain of 0.2% on Thursday. Hong Kong’s Hang Seng Tech Index lost 1.8% after rising the most in three months in the previous session. Benchmarks in China and Japan were the day’s worst performers, while the Philippines and Australia outperformed. “The market rose a bit too much yesterday,” said Mamoru Shimode, chief strategist at Resona Asset Management in Tokyo. “Investors keep shifting back and forth from value stocks to growth names and vise versa. It’s because we don’t know yet where U.S. long-term yields will end up settling around.” The Asian stock measure jumped 1.9% Wednesday on views that the Federal Reserve’s anticipated rate hikes will help curb inflation and allow the global recovery to chug along. U.S. inflation readings overnight, at an almost four-decade high, were in line with expectations and helped investors keep previous bets

Japanese stocks fell after Tokyo raised its Covid-19 alert to the second-highest level on a four-tier system. The Topix dropped 0.7% to 2,005.58 at the 3 p.m. close in Tokyo, while the Nikkei 225 declined 1% to 28,489.13. Recruit Holdings Co. contributed the most to the Topix’s decline, decreasing 4%. Out of 2,181 shares in the index, 500 rose and 1,604 fell, while 77 were unchanged. HIS, Japan Airlines and other travel shares fell. Tokyo’s daily cases jumped more than fivefold on Wednesday to 2,198 compared with 390 a week earlier.

India’s benchmark equity index eeked out gains to complete its longest string of advances since mid-October, buoyed by the nation’s top two IT firms after their earnings reports. The S&P BSE Sensex rose for a fifth day, adding 0.1% to close at 61,235.30 in Mumbai, while the NSE Nifty 50 Index climbed 0.3%. Infosys and Tata Consultancy Services were among the biggest boosts to both measures. Of the 30 shares in the Sensex index, 19 rose and 11 fell. Thirteen of the 19 sector sub-indexes compiled by BSE Ltd. advanced, led by a gauge of metal companies. Infosys’ quarterly earnings beat and bellwether Tata Consultancy Services’s better-than-expected sales offer some hope that the rally in India’s technology sector has further room to run, according to analysts. Still, Wipro sank the most in a year after its profit missed estimates

Fixed income is relatively quiet, with changes across major curves limited to less than a basis point so far. The 10-year yield stalled around 1.75%, slightly cheaper on the day, and broadly in line with bunds and gilts. Eurodollar futures bear steepen a touch after a round of hawkish Fedspeak during Asian hours. Treasuries were steady with yields broadly within a basis point of Wednesday’s close. Eurodollars are slightly lower across green- and blue-pack contracts after Fed’s Daly and Harker sounded hawkish tones during Asia hours. Across front-end, eurodollar strip steepens out to blue-pack contracts (Mar25-Dec25), which are lower by up to 4bp. 30-year bond reopening at 1pm ET concludes this week’s coupon auction cycle.$22b 30-year reopening at 1pm ET follows 0.3bp tail in Wednesday’s 10-year auction, and large tails in last two 30-year sales. The WI 30-year yield at ~2.095% is above auction stops since June and ~20bp cheaper than last month’s, which tailed the WI by 3.2bp.

In FX, the pound advanced to its highest level since Oct. 29 amid calls for U.K. Prime Minister Boris Johnson to resign over a “bring your own bottle” party at the height of a lockdown meant to stem the first wave of coronavirus infections in 2020. The Bloomberg Dollar Spot Index held a two-month low as the greenback weakened against all of its Group-of-10 peers, and the euro rallied a third day as it approached the $1.15 handle. Implied volatility in the major currencies over the two- week tenor, that now captures the next Fed meeting, comes in line with the roll yet investors are choosing sides. The Australian dollar extended its overnight gain as the greenback declined following as-expected U.S. inflation. Iron ore supply concern also supported the currency. The yen hovered near a two-week high as long dollar positions were unwound. Japanese government bonds traded in narrow ranges.

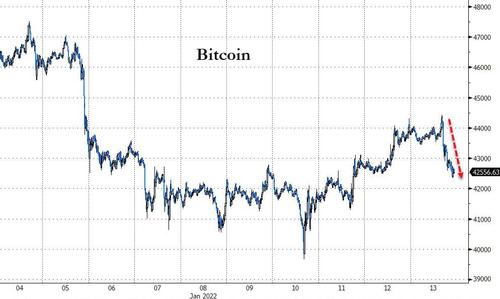

In commodities, cude futures maintain a relatively narrow range. WTI is flat near $82.70, Brent stalls near $84.50. Spot gold dips before finding support near $1,820/oz. Most base metals are in the red with LME zinc lagging peers. Bitcoin traded around $44,000 as the inflation numbers rekindled the debate about whether the cryptocurrency is a hedge against rising consumer prices.

Expected data on Thursday include producer prices, an early indicator of inflationary trends, and unemployment claims.

Market Snapshot

- S&P 500 futures little changed at 4,715.50

- STOXX Europe 600 down 0.1% to 485.67

- MXAP little changed at 196.79

- MXAPJ up 0.1% to 643.93

- Nikkei down 1.0% to 28,489.13

- Topix down 0.7% to 2,005.58

- Hang Seng Index up 0.1% to 24,429.77

- Shanghai Composite down 1.2% to 3,555.26

- Sensex up 0.1% to 61,220.38

- Australia S&P/ASX 200 up 0.5% to 7,474.36

- Kospi down 0.3% to 2,962.09

- German 10Y yield little changed at -0.04%

- Euro up 0.2% to $1.1465

- Brent Futures down 0.1% to $84.58/bbl

- Gold spot down 0.3% to $1,820.68

- U.S. Dollar Index little changed at 94.83

Top Overnight News from Bloomberg

- Federal Reserve Bank of San Francisco President Mary Daly and her Philadelphia Fed peer Patrick Harker joined the ranks of officials publicly discussing an interest-rate increase as early as March as the central bank seeks to combat the hottest inflation in a generation

- Global central banks will diverge on the way they respond to inflation this year, creating risks to economies everywhere, Bank of England policy maker Catherine Mann said

- Norway’s race to appoint a new central bank governor is reaching a finale mired in controversy at the prospect of a political ally and friend of Prime Minister Jonas Gahr Store getting the job

- Italy’s government is working on a spending package that won’t require revising its budget to expand the deficit, people familiar with the matter said

- Several of China’s largest banks have become more selective about funding real estate projects by local government financing vehicles, concerned that some are taking on too much risk after they replaced private developers as key buyers of land, people familiar with the matter said

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks traded mixed following the choppy session in the US where major indices eked mild gains as markets digested CPI data in which headline annual inflation printed at 7.0%. ASX 200 (+0.5%) was underpinned as the energy and mining related sectors continued to benefit from the recent upside in underlying commodity prices, while Crown Resorts shares outperformed after Blackstone raised its cash proposal for Crown Resorts following due diligence inquiries. Nikkei 225 (-1.0%) declined with the index hampered by unfavourable currency flows and with Tokyo raising its COVID-19 alert to the second-highest level. Hang Seng (+0.1%) and Shanghai Comp. (-1.1%) were initially subdued, but did diverge later, after the slight miss on loans and aggregate financing data, while there is a slew of upcoming key releases from China in the days ahead including trade figures tomorrow, as well as GDP and activity data on Monday. In addition, the biggest movers were headline driven including developer Sunac China which dropped by a double-digit percentage after it priced a 452mln-share sale at a 15% discount to repay loans and cruise operator Genting Hong Kong wiped out around half its value on resumption of trade after it warned of defaults due to insolvency of its German shipbuilding business. Finally, 10yr JGBs traded rangebound and were stuck near the 151.00 level following the indecisive mood in T-notes which was not helped by an uninspiring 10yr auction stateside, while the lack of BoJ purchases in the market also added to the humdrum tone.

Top Asian News

- Asia Stocks Steady After Best Rally in a Year; Financials Gain

- Country Garden Selloff Shows Chinese Developer Worries Spreading

- China Banks Curb Property Loans to Local Government Firms

- China’s True Unemployment Pain Masked by Official Data

Bourses in Europe now see a mixed picture with the breadth of the price action also narrow (Euro Stoxx 50 Unch; Stoxx 600 -0.10%). The region initially opened with a modest downside bias following on from a mostly negative APAC handover after Wall Street eked mild gains. US equity futures have since been choppy within a tight range and exhibit a relatively broad-based performance with no real standout performers. Back in Europe, sectors are mixed and lack an overarching theme. Tech remains the outperformer since the morning with some follow-through seen from contract-chip manufacturer TSMC (ADR +4.3% pre-market), who beat on net and revenue whilst upping its 2022 Capex to USD 40bln-44bln from around USD 30bln the prior year, whilst the CEO expects capacity to remain tight throughout 2022. Tech is closely followed by Autos and Parts and Travel & Leisure, whilst the other end of the spectrum sees Healthcare, Oil & Gas, Retail and Personal & Household goods among the straddlers – with Tesco (-1.5%) and Marks & Spencer (-5.3%) weighing on the latter two following trading updates. In terms of other individual movers, BT (+0.5%) trades in the green amid reports DAZN is nearing a deal to buy BT Sport for around USD 800mln, a could be reached as soon as this month but has not been finalized. Turning to analyst commentary: Morgan Stanley’s clients have aligned themselves to the view that European equities will likely perform better than US counterparts. 45% of respondents see Financials as the top-performing sector this year, 14% preferred Tech which would be the lowest score in over six years.

Top European News

- Johnson Buys Time With Apology But U.K. Tory Rage Simmers

- U.K. Retailers Slide as Updates Show Lingering Impact of Virus

- Wood Group Plans Sale of Built Environment Unit Next Quarter

- Just Eat Advisers Pitching Grubhub Sale or Take-Private: Sources

In FX, the Dollar has weakened further in wake of Wednesday’s US inflation data as ‘buy rumour sell fact’ dynamics are compounded by more position paring and increasingly bearish technical impulses to outweigh fundamental factors that seem supportive, on paper or in theory. Indeed, the index only mustered enough recovery momentum to reach 95.022 on the back of hawkish Fed commentary and some short covering before retreating through the psychological level, then yesterday’s 94.903 low and another trough from late 2021 at 94.824 (November 11 base) to 94.710, thus far and leaving little bar the 100 DMA, at 94.675 today, in terms of support ahead of 94.500. However, the flagging Greenback could get a fillip via PPI and/or IJC, if not the next round of Fed speakers and final leg of this week’s auction remit in the form of Usd 22 bn long bonds.

- NZD/AUD – A change in the running order down under where the Kiwi has overtaken the Aussie irrespective of bullish calls on the Aud/Nzd cross from MS, with Nzd/Usd breaching the 50 DMA around 0.6860 on the way to 0.6884 and Aud/Usd scaling the 100 DMA at 0.7288 then 0.7300 before fading at 0.7314.

- GBP/EUR/CHF/CAD/JPY – Also extracting more impetus at the expense of the Buck, but to varying degrees as Sterling continues to shrug aside ongoing Tory party turmoil to attain 1.3700+ status and surpass the 200 DMA that stands at 1.3737, while the Euro has overcome Fib resistance around 1.1440, plus any semi-psychological reticence at 1.1450 to reach 1.1478 and the Franc is now closer to 0.9100 than 0.9150. Elsewhere, crude is still providing the Loonie with an incentive to climb and Usd/Cad has recoiled even further from early 2022 peaks beneath 1.2500 as a result, and the Yen is around 114.50 with scope for a stronger retracement to test the 55 DMA, at 114.22.

- SCANDI/EM – Some signs of fatigue as the Nok stalls on the edge of 9.9000 against the Eur in tandem with Brent just a few cents over Usd 85/brl, but the Czk has recorded fresh decade-plus highs vs the single currency following remarks from CNB chief Rusnok on the need to keep tightening and acknowledging that this may culminate in Koruna appreciation. The Cnh and Cny are firmer vs the Usd pre-Chinese trade and GDP data either side of the weekend, but the Rub is lagging again as the Kremlin concludes that there was no progress in talks between Russia and the West, but the Try is underperforming again with headwinds from elevated oil prices and regardless of a marked pick up in Turkish ip.

In commodities, WTI and Brent front-month contracts have conformed to the indecisive mood across the markets, although the benchmarks received a mild uplift as the Dollar receded in early European hours. As it stands, the WTI Feb and Brent Mar contract both reside within USD 0.80/bbl ranges near USD 82.50/bbl and USD 84.50/bbl respectively. News flow for the complex has been quiet and participants are on the lookout for the next catalyst, potentially in the form of US jobless claims/PPI amid multiple speakers, although the rise in APAC COVID cases remains a continuous headwind on demand for now – particularly in China. On the geopolitical front, Russian-backed troops have reportedly begun pulling out of the 1.6mln BPD Kazakh territory, but Moscow’s tensions with the West do not seem to abate. Russia’s Kremlin suggested talks with the West were “unsuccessful” – which comes after NATO’s Secretary-General yesterday suggested there is a real risk of a new armed conflict in Europe. Elsewhere, spot gold has drifted off best levels as the DXY found a floor, for now – with the closest support yesterday’s USD 1,813/oz low ahead of the 50 and 21 DMAs at USD 1,807/oz and USD 1,806.50/oz respectively. LME copper has also pulled back from yesterday’s best levels to levels under USD 10,000/t as the mood remains cautious, although, copper prices in Shanghai rose to over a two-month high as it played catch-up to LME yesterday.

US Event Calendar

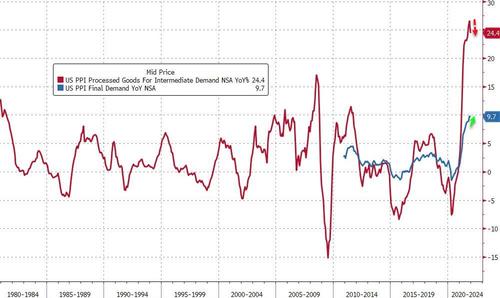

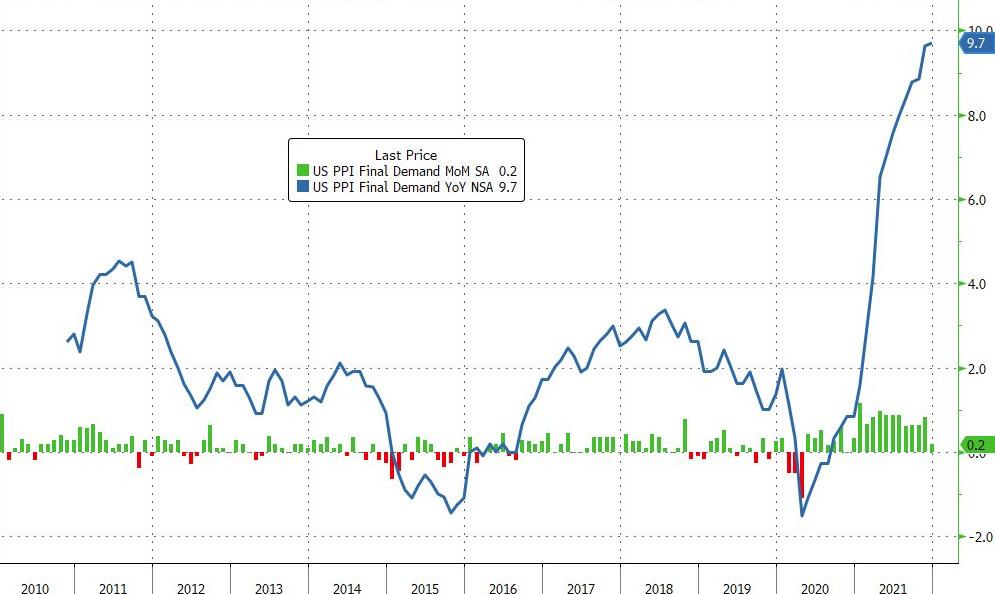

- 8:30am: Dec. PPI Final Demand YoY, est. 9.8%, prior 9.6%; MoM, est. 0.4%, prior 0.8%

- 8:30am: Dec. PPI Ex Food and Energy YoY, est. 8.0%, prior 7.7%; MoM, est. 0.5%, prior 0.7%

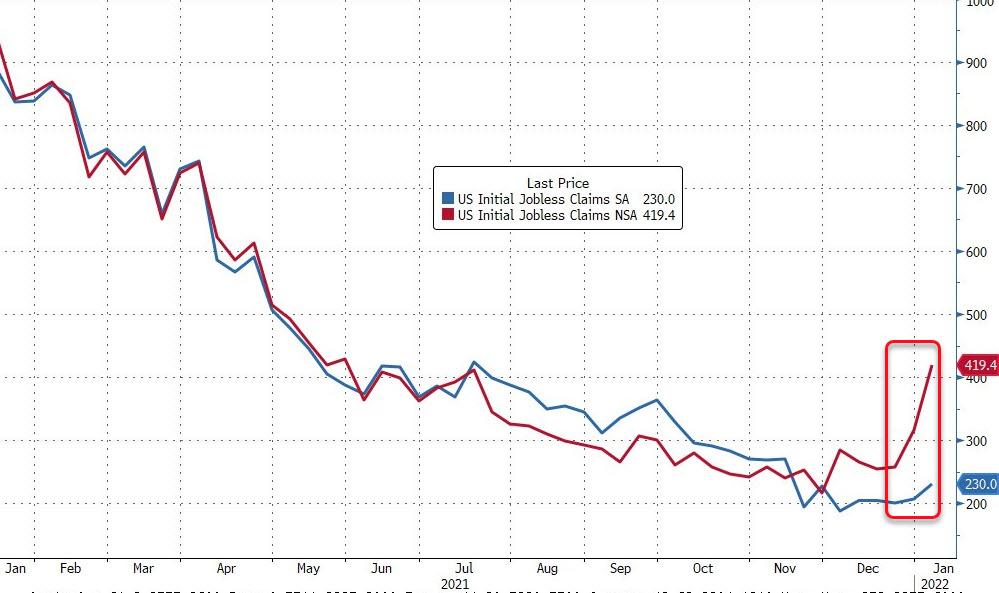

- 8:30am: Jan. Continuing Claims, est. 1.73m, prior 1.75m

- 8:30am: Jan. Initial Jobless Claims, est. 200,000, prior 207,000

DB’s Jim Reid concludes the overnight wrap

Today I have a first. I have two MRI scans. A fresh one on my back and one on my right knee which gave way as I was rehabbing (squats and lunges) the left knee after recent surgery. In my fifth decade of playing sport averagely, but vigorously, it’s all catching up with me very quickly. I’ve exhausted all strengthening exercise routines and injections on my back and the pain gets worse. My surgeon does not want to operate but we will see if he changes his mind after today. If he says play less golf I will walk out mid-meeting even if he may be medically correct. In contrast my knee surgeon is an avid skier and he keeps on doing things to prolong my skiing career even though I’ve said to him that I just really care about golf. So I’ll soon be looking for an avid golfer who just happens to be a back surgeon.

Talking of confirmation bias, if you did an MRI scan of US inflation yesterday you’d find things to support both sides of the debate which is surprising when it hit 7% YoY and the highest since 1982 when Fed Funds were more than 13% rather than close to zero as they are today. So a slightly different real rate to back then. In fact the real rate is through any level seen in the 1970s and is only comparable to WWII levels. Back to CPI and the YoY number was in line with expectations, but core and MoM figures were all a bit firmer than expected. However, the beats were small enough that the data didn’t significantly change the outlook for monetary policy, with Fed funds futures still pricing in an 89% chance of a March hike, which is roughly around where it’d been over the preceding days.

Looking at the details of the release, (our US econ team’s full wrap here) headline month-on-month number came in at +0.5% in December (vs. +0.4% expected), which is the 8thtime in the last 10 months that the print has come in above the consensus expectations on Bloomberg. However, that does still mark a deceleration from the +0.9% and +0.8% monthly growth in October and November respectively. The core CPI reading was also a touch stronger than anticipated, with the monthly print at +0.6% (vs. +0.5% expected), thus sending the annual core CPI measure up to +5.5% (vs. +5.4% expected) and its highest since 1991. Diving into some of the key sub-components, Covid-era favorite used cars and trucks grew +3.5% MoM. More concerning for policymakers, is the continued growth in persistent measures such as shelter, with primary and owners’ equivalent rent both increasing +0.4% MoM. If you were expecting Omicron to slow down American holiday travel, think again, lodging away from home and airfares both posted large increases, +1.2% and +2.7%, respectively. Most forecasters think the peak for inflation is sometime soon, but the pace of the glide path is open to debate. This is a topic we covered in yesterday’s CoTD, found here.

Even though Treasuries had rallied strongly in the immediate aftermath of the report, with the 10yr yield falling back to 1.709% at the intraday low, yields pared back those losses to end the session basically unchanged at 1.74% (+0.7bps). CPI was expected to be bad and therefore the ability to shock was relatively low.