JAN 28

January 28, 2022 · by harveyorgan · in Uncategorized · Leave a comment ·Edit

GOLD; DOWN $8.30 to $1785.90

SILVER: $22.31 DOWN 36 CENTS

ACCESS MARKET: GOLD: 1792.00..

SILVER: $22.46

Bitcoin: morning price: 36,291 up 198

Bitcoin: afternoon price: 37,343 UP 854

Platinum price: closing down $14.45 to $1008.95

Palladium price; closing up $24.70 at $2381.80

END

end

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

comex notices//JPMorgan notices filed COMEX//NOTICES: 1/13

EXCHANGE: COMEX

CONTRACT: JANUARY 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,793.300000000 USD

INTENT DATE: 01/27/2022 DELIVERY DATE: 01/31/2022

FIRM ORG FIRM NAME ISSUED STOPPED

435 H SCOTIA CAPITAL 10

624 H BOFA SECURITIES 12

661 C JP MORGAN 1

905 C ADM 3 TOTAL: 13 13

MONTH TO DATE: 5,720

NUMBER OF NOTICES FILED TODAY FOR JAN. CONTRACT: 13 NOTICE(S) FOR 1300 OZ (0.0404 TONNES)

total notices so far: 5720 contracts for 572,000 oz (17.7916 tonnes)

SILVER NOTICES:

10 NOTICE(S) FILED TODAY FOR 50,000 OZ/

total number of notices filed so far this month 3032 : for 15,150,000 oz

GLD

WITH GOLD DOWN $8.30

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS): NO CHANGE IN GOLD INVENTORY AT THE GLD..

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

CLOSING INVENTORY: 1014.26 TONNES/

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 36 CENTS:/: NO CHANGE IN SILVER INVENTORY AT THE SLV//

AT THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY SLV/ TONIGHT: 535.003 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A STRONG 2182 CONTRACTS TO 149,689 AND RESTS CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THIS SMALL GAIN IN OI WAS ACCOMPANIED WITH OUR SMALL $0.07 LOSS IN SILVER PRICING AT THE COMEX ON THURSDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $1.13) AND WERE SUCCESSFUL IN KNOCKING OUT A FEW SILVER LONGS AS WE HAD A SMALL LOSS OF 195 CONTRACTS ON OUR TWO EXCHANGES .

WE MUST HAVE HAD:

I) HUGE BANKER SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A HUGE INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 10.505 MILLION OZ FOLLOWED BY TODAY’S 145,000 OZ QUEUE. JUMP //NEW STANDING 15.275 MILLION OZ V) STRONG SIZED COMEX OI LOSS.

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS -103

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JAN. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JAN:

TOTAL CONTACTS for 19 days, total contracts: : 16,967 contracts or 84.835 million oz OR 4.463 MILLION OZ PER DAY. (8393CONTRACTS PER DAY)

TOTAL NO OF OZ UNDERGOING EFP TO LONDON 16,967 CONTRACTS X 5,000 PER CONTRACT:

EQUATES TO: 84.835 MILLION OZ

.

LAST 8 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

RESULT: WE HAD A STRONG SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2182 WITH OUR $1.13 LOSS SILVER PRICING AT THE COMEX// THURSDAY THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 1884 CONTRACTS( 1884 CONTRACTS ISSUED FOR MAR AND 1884 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR JAN OF 10.505 MILLION OZ FOLLOWED BY TODAY’S 145,000 OZ QUEUE JUMP //NEW STANDING 15.275, MILLION OZ// .. WE HAD A SMALL SIZED LOSS OF 298 OI CONTRACTS ON THE TWO EXCHANGES FOR 1.490 MILLION OZ//

WE HAD 10 NOTICES FILED TODAY FOR 50,000 OZ

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A STRONG SIZED 11,481 TO 542,799 AND FURTHER FROM OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: -1073 CONTRACTS

.

THE STRONG SIZED DECREASE IN COMEX OI CAME WITH OUR STRONG LOSS IN PRICE OF $36.15//COMEX GOLD TRADING/THURSDAY/.AS IN SILVER WE MUST HAD SOME COMEX SPREADER LIQUIDATION FOLLOWED BY HUGE BANKER/ALGO SHORT COVERING ACCOMPANYING OUR STRONG SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION AS THE TOTAL LOSS ON OUR TWO EXCHANGES TOTALED A FAIR SIZED 3317 CONTRACTS…WITH THE ENTIRE TOTAL LOSS COMING FROM SPREADER LIQUIDATION.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR JAN AT 3.5614 TONNES FOLLOWED BY TODAY’S 0 OZ QUEUE. JUMP //NEW STANDING: 17.7912 TONNES

YET ALL OF..THIS HAPPENED WITH OUR LOSS IN PRICE OF $36.15 WITH RESPECT TO THURSDAY’S TRADING

WE HAD A FAIR SIZED LOSS OF 4396 OI CONTRACTS (13.673 PAPER TONNES) ON OUR TWO EXCHANGES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALLED A STRONG SIZED 7091 CONTRACTS:

FOR FEB 7091 ALL OTHER MONTHS ZERO//TOTAL:7091

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 542,799.

IN ESSENCE WE HAVE A FAIR SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 4396, WITH 11,487 CONTRACTS DECREASED AT THE COMEX AND 7091 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 3317 CONTRACTS OR 10.307TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (7091) ACCOMPANYING THE STRONG SIZED LOSS IN COMEX OI (10,408): TOTAL LOSS IN THE TWO EXCHANGES 3317 CONTRACTS. WE NO DOUBT HAD 1) HUGE BANKER SHORT COVERING ,2.) HUGE INITIAL STANDING AT THE GOLD COMEX FOR JAN. AT 3.7262 TONNES//FOLLOWED BY TODAY’S NIL OZ QUEUE JUMP .//NEW STANDING 17.7912 TONNES 3)ZERO LONG LIQUIDATION AS ENTIRE TOTAL LOSS WAS DUE TO INITIATION OF SPREADER LIQUIDATION,4) STRONG SIZED COMEX OI. LOSS 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF FEB.WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF JAN HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB, FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (FEB), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2021 INCLUDING TODAY

JAN

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JAN : 75,720 CONTRACTS OR 7,572,000 oz OR 235.52 TONNES 19 TRADING DAY(S) AND THUS AVERAGING: 3985 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 19 TRADING DAY(S) IN TONNES: 235.52 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2020, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 235.32/3550 x 100% TONNES 6.61% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO DATE

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 145.12 TONNES//FINAL ISSUANCE//

JAN:2022 213.46 TONNES //

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A STRONG SIZED 2182 CONTRACTS TO 151,720 AND FURTHER FROM OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 4 1/2 YEARS AGO.

EFP ISSUANCE 1884 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 1884 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1884 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 2182 CONTRACTS AND ADD TO THE 1884 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A SMALL SIZED LOSS OF 298 OPEN INTEREST CONTRACT FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 1.490 MILLION OZ,

OCCURRED WITH OUR $1.13 LOSS IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

5. Other gold commentaries

6. Commodity commentaries/cryptocurrencies

3. ASIAN AFFAIRS

i)FRIDAY MORNING// THURSDAY NIGHT

SHANGHAI CLOSED DOWN 32.81 PTS OR 0.97% //Hang Sang CLOSED DOWN 256.92 PTS OR 1.08% /The Nikkei closed UP 547.04 PTS OR 2.09% //Australia’s all ordinaires CLOSED UP 2.13% /Chinese yuan (ONSHORE) closed UP 6.3620 /Oil DOWN TO 87.22 dollars per barrel for WTI and UP TO 90.56 for Brent. Stocks in Europe OPENED ALL RED // ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.3622. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.3710: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN AND OFF SHORE TRADING STRONGER AGAINST USA DOLLAR

A)NORTH KOREA//USA/OUTLINE

b) REPORT ON JAPAN

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A STRONG SIZED 11,487 CONTRACTS AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX DECREASE OCCURRED WITH OUR STRONG LOSS OF $36.15 IN GOLD PRICING THURSDAY’S COMEX TRADING. WE ALSO HAD A STRONG SIZED EFP (7091 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. LOOKS LIKE OUR BANKERS ARE FINALLY BAILING OUT

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE NON ACTIVE DELIVERY MONTH OF JAN.. THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 7091 EFP CONTRACTS WERE ISSUED: ;: , DEC : 0 & FEB. 7091 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 7091 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED 3317 TOTAL CONTRACTS IN THAT 7091 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A STRONG SIZED COMEX OI LOSS OF 10,408 CONTRACTS..THE ENTIRE TOTAL LOSS WAS DUE TO THE CONTINUING SPREADER LIQUIDATION

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING FOR JAN (17.7912),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

THE BANKERS WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $36.15) BUT THEY WERE UNSUCCESSFUL IN FLEECING ANY LONGS AS, EVEN THOUGH THE TOTAL LOSS ON THE TWO EXCHANGES REGISTERED A STRONG 11.673 TONNES ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR JAN (17.7916 TONNES)…THE ENTIRE LOSS WAS DUE TO THE CONTINUING OF SPREADER LIQUIDATION

WE HAD – 1073 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 4396 CONTRACTS OR 439,600 OZ OR 11.673 TONNES

Estimated gold volume today: 240,021 /// poor

Confirmed volume yesterday: 422,930 contracts very good (spreaders)

INITIAL STANDINGS FOR JAN ’22 COMEX GOLD //JAN 28

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 5079.415 oz Brinks HSBC 133kilobars//Brinks |

| Deposit to the Dealer Inventory in oz | nilOZ |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 13 notice(s)1300 OZ 0.0404 TONNES |

| No of oz to be served (notices) | 0 contracts 0 oz 0.000 TONNES |

| Total monthly oz gold served (contracts) so far this month | 5720 notices 572,000 OZ 17.7916 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For today:

No dealer deposit 0

No dealer withdrawal 0

0 customer deposit

total deposit: nil oz

2 customer withdrawals

i) Out of BRINKS: 4276,09 0z (133 KILOBARS)

ii) Out of HSBC 803.325 oz

total withdrawals: 5079,415 oz

ADJUSTMENTS: 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JANUARY.

For the front month of JANUARY we have an oi of 13 stand for JANUARY LOSING 56 contracts. We had 56 notices filed on THURSDAY, so we GAINED 0 contracts or an additional NIL oz will stand for

gold in this very non active delivery month of January.

FEBRUARY LOST 24,875 CONTRACTS TO 31,971

March GAINED 237 contracts to stand at 3859..

We had 13 notice(s) filed today for 1300 oz FOR THE JAN 2022 CONTRACT MONTH. WE HAVE ONE MORE READING DAY BEFORE FIRST DAY NOTICE JAN 31/2022

We will probably have around 50 tonnes of gold standing for February.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 13 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 1 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JAN /2021. contract month,

we take the total number of notices filed so far for the month (5720) x 100 oz , to which we add the difference between the open interest for the front month of (JAN: 13 CONTRACTS ) minus the number of notices served upon today 13 x 100 oz per contract equals 572,000 OZ OR 17.7912 TONNES the number of TONNES standing in this NON active month of JAN. (numbers corrected from yesterday)

thus the INITIAL standings for gold for the JAN contract month:

No of notices filed so far (5720) x 100 oz+ (13) OI for the front month minus the number of notices served upon today (13} x 100 oz} which equals 572,000 oz standing OR 17.7912 TONNES in this NON active delivery month of JAN.

We GAINED 0 contracts or an additional 5300 oz of gold will stand for metal on this side of the pond.

TOTAL COMEX GOLD STANDING: 17.7912 TONNES (HUGE FOR A JANUARY DELIVERY MONTH)

IF THIS HOLDS TO THE END OF THE MONTH, THIS WILL BE THE HIGHEST EVER RECORDED GOLD STANDING FOR A JANUARY, GENERALLY A VERY POOR DELIVERY MONTH.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

157,392.690, oz NOW PLEDGED /HSBC 4.89 TONNES

125,410.592 PLEDGED MANFRA 2.90 TONNES

54,339.114oz PLEDGED JPMorgan no 1 1.690

288,481,604, oz JPM No 2 8.97 TONNES

898,821.330 oz pledged Brinks/27,96 TONNES

12,249,333 oz International Delaware: 0..3810 tonne

Loomis: 18,615.429 oz

total pledged gold: 1,555,310.092 oz 48.376 tonnes

TOTAL REGISTERED AND ELIZ GOLD AT THE COMEX: 33,404,722.479 OZ (1039,02 TONNES)

TOTAL ELIGIBLE GOLD: 15,833,441.448 OZ (492.48 tonnes)

TOTAL OF ALL REGISTERED GOLD: 17,571,281.031 OZ (546.54 tonnes)

REGISTERED GOLD THAT CAN BE SERVED UPON: 16,015,971.0 OZ (REG GOLD- PLEDGED GOLD) 498.16 tonnes

END

JANUARY 2022 CONTRACT MONTH//SILVER

INITIAL STANDING FOR SILVER//JAN 28

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 40,014.628 oz DelawareCNT |

| Deposits to the Dealer Inventory | nilOZ |

| Deposits to the Customer Inventory | nil oz |

| No of oz served today (contracts) | 10 CONTRACT(S) 50,000 OZ) |

| No of oz to be served (notices) | 23 contracts (115,000 oz) |

| Total monthly oz silver served (contracts) | 3032 contracts 15,160,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

we had 0 deposits into the dealer

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 0 deposits

JPMorgan has a total silver weight: 185.232 million oz/354.345 million =52.27% of comex

ii) Comex withdrawals: 2

a) out of Delaware: 6,974.428 oz

b) out of CNT: 33,040.200 oz

total withdrawal 40,014.628 oz

we had 1 adjustments:

a) dealer to customer

i) Manfra 176,294.550 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 82.278 MILLION OZ

TOTAL REG + ELIG. 354.345 MILLION OZ

TOTAL NO OF CONTRACTS SERVED UPON THIS MONTH: 2838 CONTRACTS FOR 14,190,000 OZ

CALCULATION OF SILVER OZ STANDING FOR JANUARY

NUMBER OF NOTICES FILED TODAY: 10 NOTICES OR 50,000 OZ

silver open interest data:

FRONT MONTH OF JAN//2022 OI: 33 CONTRACTS LOSING 57 contracts on the day

We had 86 notices filed for THURSDAY so we GAINED 29 contracts or 145,000 additional oz will stand for delivery in this non active delivery month of January.

FOR FEB WE HAD A LOSS OF 16 CONTRACTS FALLING TO 855

FOR MARCH WE HAD A LOSS OF 3347 CONTRACTS UP TO 109,881 CONTRACTS.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 10 for 50,000 oz

Comex volumes: 61,936// est. volume today//fair

Comex volume: confirmed YESTERDAY: 88,406 contracts (good)

To calculate the number of silver ounces that will stand for delivery in JANUARY. we take the total number of notices filed for the month so far at 3032 x 5,000 oz =. 15,160,000 oz

to which we add the difference between the open interest for the front month of JAN (33) and the number of notices served upon today 10 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JAN./2021 contract month: 3032 (notices served so far) x 5000 oz + OI for front month of JAN (33) – number of notices served upon today (10) x 5000 oz of silver standing for the JAN contract month equates 15,275,000 oz. .

We GAINED 29 contracts or an additional 145,000 oz will stand for delivery on this side of the pond.

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

GLD

JAN 28/WITH GOLD DOWN $8.30//NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1014.26 TONNES

JAN 27/WITH GOLD DOWN $36.15//ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.16 TONNES INTO THE GLD.//INVENTORY RESTS AT 1014.26 TONNES

JAN 26/WITH GOLD DOWN $21.60 A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.65 TONNES INTO THE GLD///INVENTORY RESTS AT 1013.10 TONNES

JAN 25/WITH GOLD UP $10.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1008.45 TONNES

JAN 24/WITH GOLD UP $10.10 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: AN UNBELIEVABLE DEPOSIT OF 27.59 TONNES INTO THE GLD//INVENTORY RESTS AT 1008.45 TONNES

JAN 21/WITH GOLD DOWN $10.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 980.86 TONNES

JAN 20/WITH GOLD UP $.20 TODAY: A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .58 TONNES FROM THE GLD///INVENTORY RESTS AT 980.86 TONNES

JAN 19/WITH GOLD UP $29.65 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 5.27 TONNES INTO THE GLD/INVENTORY RESTS AT 981.44 TONNES

JAN 18/WITH GOLD DOWN $3.25//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 976.21 TONNES

JAN 14/ WITH GOLD DOWN $5.25/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 976.21 TONNES

JAN 13/WITH GOLD DOWN $5.75: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 976.21 TONNES

JAN 12/WITH GOLD UP $8.65//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 976.21 TONNES

JAN 11/WITH GOLD UP $19.25/A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES FROM THE GLD/INVENTORY RESTS AT 976.21 TONNES

JAN 10/WITH GOLD UP $2.00/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 977.08 TONNES

JAN 7/WITH GOLD UP $8.15//A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWLA OF 1.16 TONNES FROM THE GLD////INVENTORY RESTS AT 978.83 TONNES

JAN 6/WITH GOLD DOWN $35.30//A SMALL CHANGE IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF .32 TONNES/INVENTORY RESTS AT 979.99 TONNES

JAN 5/WITH GOLD UP $10.30: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 980.31 TONNES

Jan 4/WITH GOLD UP $14.00//A HUGE CHANGE OF 4.65 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 980.31 TONNES

JAN 3/WITH GOLD DOWN $26.70: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 975.66 TONNES

DEC 31/WITH GOLD UP $14.05 : NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 975.66 TONNES

DEC 30/WITH GOLD UP $7.75 NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 975.66 TONNES

DEC 29/WITH GOLD DOWN $5.00 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.03 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 975.66 TONNES

DEC 28/WITH GOLD UP $2.00 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 973.63 TONNES

DEC 27/WITH GOLD DOWN $2.05: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.63 TONNES.

DEC 23/WITH GOLD UP $9.85 TODAY//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.94 TONNES FROM THE GLD/// INVENTORY RESTS AT 973.63 TONNES

DEC 22/WITH GOLD UP $12.85 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 978.57 TONNES

DEC 21/WITH GOLD DOWN $7.05 TODAY, NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 978.57 TONNES

DEC 20/WITH GOLD DOWN $9.65 TODAY; A BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.37 TONNES INTO THE GLD///INVENTORY RESTS AT 977.20 TONNES

DEC 17/WITH GOLD UP $7.05 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 977.20 TONNES

CLOSING INVENTORY: 1014.26 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

SLV

JAN 28/WITH SILVER DOWN 36 CENTS : NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 535.003 MILLION OZ//

JAN 27/WITH SILVER DOWN $1.13 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 535.003 MILLION OZ//

JAN 26/WITH SILVER DOWN 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 535.003 MILLION OZ//

JAN 25/WITH SILVER UP 10 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.311 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 535.003 MILLION OZ/

.JAN 24/WITH SILVER DOWN 48 CENTS TODAY: A MASSIVE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.8 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 532.692 MILLION OZ//.

JAN 21/WITH SILVER DOWN 41 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 527.792 MILLION OZ

JAN 20/WITH SILVER UP 52 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.998 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 527.792 MILLION OZ

JAN 19/WITH SILVER UP 71 CENTS TODAY: A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.942 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 525.804 MILLION OZ

JAN 18/WITH SILVER UP 51 CENTS TODAY: TWO HUGE CHANGES IN SILVER INVENTORY AT THE SLV: 2 WITHDRAWALS OF 1.11 MILLION OZ AND 1.424 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 527.246 MILLION OZ//

JAN 14/WITH SILVER DOWN 21 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 529.780 MILLION OZ//

JAN 13/WITH SILVER DOWN 2 CENTS: A BIG CHANGE IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 832,000 OZ FROM THE SLV////INVENTORY RESTS AT 529.780 MILLION OZ

JAN 12/WITH SILVER UP 38 CENTS TODAY : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.612 MILLION OZ//

JAN 11/WITH SILVER UP 33 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.612 MILLION OZ/.

JAN 10/WITH SILVER UP 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 530.612 MILLION OZ//.

JAN 7/WITH SILVER UP 17 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.612 MILLION OZ//.

JAN 6/WITH SILVER DOWN 94 CENTS TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL PF 226,000 OZ FROM THE SLV///INVENTORY RESTS AT 530.612 MILLION OZ?/

JAN 5/WITH SILVER UP 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.838 MILLION OZ//

JAN 4/WITH SILVER UP 21 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.838 MILLION OZ//

JAN 3/WITH SILVER DOWN 45 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.219 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 530.838 MILLION OZ//

DEC 31/WITH SILVER UP 29 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 533.057 MILLION OZ//

DEC 31/WITH SILVER UP 29 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 533.057 MILLION OZ//

DEC30/WITH SILVER UP 14 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A HUGE WITHDRAWAL OF 4.624 MILLILON OZ FROM THE SLV.//INVENTORY RESTS AT 533.057 MILLION OZ//

DEC 29/WITH SILVER DOWN 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 537.681 MILLION OZ/

DEC 28/WITH SILVER UP 9 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.682 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 537.681 MILLION OZ//

DEC 27/WITH SILVER UP 6 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 537.681

DEC 23/WITH SILVER UP 19 CENTS TODAY:A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.202 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 537.681 MILLION OZ//

DEC 22/WITH SILVER UP 29 CENTS TODAY; A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.202 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 538.883 MILLION OZ/

DEC 21/WITH SILVER UP 19 CENTS: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.728 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 540.085 MILLION OZ

DEC 20/WITH SILVER DOWN 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 538.282 MILLION OZ

DEC 17/WITH SILVER UP 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 538.282 MILLION OZ//

CLOSING INVENTORY: 535.003 MILLION OZ

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

Peter Schiff: “We’re Screwed & The Fed Knows It”

FRIDAY, JAN 28, 2022 – 10:40 AM

Authored by Michael Maharrey via SchiffGold.com,

The Federal Reserve wrapped up its first Federal Open Market Committee meeting of the year this week without any real surprises. Despite everybody screaming about an inflation problem, the Fed will keep its loose, inflationary monetary policy in play for at least two more months.

Interest rates remain locked at zero. But the FOMC said it will likely raise rates “soon.”

With inflation well above 2 percent and a strong labor market, the Committee expects it will soon be appropriate to raise the target range for the federal funds rate.”

Most analysts expect “soon” to be at the March meeting.

But Jerome Powell left some wiggle-room in the trajectory of the Fed’s monetary policy, saying, “At this time, we haven’t made any decisions about the path of policy. I stress again that we’ll be humble and nimble.”

Powell also indicated that the Fed would be “data-dependent.” As Peter Schiff said in his podcast, “If the Federal Reserve was depending on the data, they would have raised interest rates a long time ago, and they would now be much higher than zero.”

It’s important to reiterate that despite the inflation freight train, the Fed left interest rates at zero. If the central bank was really ready to go to war with inflation, why wait until March? Why is it still pouring gasoline on the inflation fire?

The FOMC also offered some more details on “significantly reducing” the Fed’s massive balance sheet. The central bankers said the plan was to reduce the balance sheet primarily by limiting how much principal it rolls over from maturing bonds. But the FOMC did not set a specific date for the beginning of quantitative tightening, nor did it offer any hint on how much it would ultimately pair down its nearly $9 trillion balance sheet.

But the FOMC said it was not only going to reduce the size of the balance sheet. It also plans to change the makeup, shifting away from mortgage-backed securities and weighing its holdings more toward US Treasuries. This comes as no surprise given that the federal government needs to Fed to keep its thumb on the Treasury market in order to finance its massive deficits.

During his press conference, Powell said balance sheet reduction would begin at the “appropriate time.” But he then said he didn’t have a specific timeline and that the FOMC hadn’t discussed it.

“Really?” Peter asked in a tweet.

What exactly do they talk about when they meet, sports? We’re screwed and they know it.”

The last time the Fed attempted “double-tightening” – balance sheet reduction and interest rate hikes – was in 2018. The central bank was forced to abandon both when the stock market tanked. By the end of 2019, the Fed had cut rates and had pivoted back to quantitative easing. It seems highly unlikely that the Fed will be able to pull off double-tightening today with an even bigger stock market bubble and an economy even more levered up with debt. Even the mainstream has realized raising rates will exacerbate a global debt crisis.

But Powell claims the economy is much stronger now than it was the last time the Fed tightened. In another tweet, Peter said the economy is not stronger.

It’s just a much bigger bubble. Even a smaller pin would produce a larger financial crisis.”

Quill Intelligence CEO Danielle DiMartino Booth told Kitco News that she thinks this tightening cycle could quickly plunge the economy into a recession.

I think that [a recession] could happen in a very compressed way because we have seen, as opposed to an economic recovery that stretches out over ten or 11 years, we’ve seen a very compressed economic cycle this time and the Fed has shifted from a loosening stance to a tightening stance in what feels like record time, so there’s absolutely no reason to think that the market will not start to anticipate the inversion of the yield curve and even move up expectations for when the economy slides into recession.”

In an interview on the Wharton Business Daily podcast, Peter said he thinks we’re on the path to stagflation.

I think inflation is ultimately going to push the economy into a recession as consumers are forced to spend more and more of what they have on food and energy and insurance and just the basics. They’re not going to have discretionary spending. And when they have to cut back, that means a lot of other people lose their incomes, lose their jobs. This is going to be stagflation.”

END

2.LAWRIE WILLIAM//,//Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,James RICKARDS

3.Chris Powell of GATA provides to us very important physical commentaries

Brought this to your attention but it is worth repeating: Wall Street megabanks sought out non banks to sell crooked derivatives that neither understood but one where the non banks would surely lose

(Pam and Russ Martens/Wall Street on Parade/GATA)

Pam and Russ Martens: Wall Street megabanks have shifted their derivative exposure to corporations

Submitted by admin on Thu, 2022-01-27 11:19 Section: Daily Dispatches

By Pam and Russ Martens

Wall Street on Parade

Thursday, January 27, 2022

The last thing a volatile stock market needs right now is more surprises from the dark corners of Wall Street. Unfortunately, we can guarantee you that more surprises are coming in the way of uncleared derivatives blowing up on the balance sheets of publicly-traded corporations.

How do we know this?

The information comes from a study quietly released last July by the Office of Financial Research. That’s the federal agency that provides research to bank regulators to prevent systemic financial contagion from taking down the Wall Street megabanks and the U.S. economy in another replay of 2008.

What the study actually shows, however, is that neither Congress nor bank regulators have done anything meaningful to prevent derivatives from once again blowing up the world’s largest economy. Instead, the watchdogs have simply allowed a rearrangement of the deck shares on the Titanic. …

… For the remainder of the report:

end

This is a big story: Chinese citizens bought a total of 1120.9 tonnes of gold last year. The country mines around 420 tonnes so the remainder was bought from abroad.

(Reuters/GATA)

China’s 2021 gold consumption jumps by a third in year as economy grows

Submitted by admin on Thu, 2022-01-27 11:53 Section: Daily Dispatches

By Emily Chow

Reuters

Thursday, January 27, 2022

BEIJING — China’s 2021 gold consumption rose by over a third from the previous year, as its economy rebounded from the coronavirus impact, the China Gold Association said today.

Consumption in the world’s largest gold consumer rose 36.53% year-on-year to 1,120.9 tonnes. It was also up 11.78% compared with consumption in 2019, before the pandemic

“In 2021, under the remarkable results of China’s overall economic development and epidemic prevention and control, domestic gold consumption generally maintained a recovery trend and achieved rapid growth compared with the same period” in 2020, the association said in a statement.

… For the remainder of the report:

end

Your weekend reading material and it is very important: why central bank digital currencies may never happen

(Alasdair Macleod)

Alasdair Macleod: Why central bank digital currencies may never happen

Submitted by admin on Thu, 2022-01-27 17:25 Section: Daily Dispatches

By Alasdair Macleod

GoldMoney, Toronto

Thursday, January 27, 2022

The Federal Reserve has just released its first public consultation paper on a dollar-based central bank digital currency. For many, central bank digital currencies (CBDCs) are a means of heading off private-sector cryptos, but coincidentally the prices of bitcoin and others have collapsed, losing half their value since early November.

The CBDC proposition is being sold to us by the central banks as keeping up with the times and taking advantage of the opportunities presented by new technologies to evolve payment system

The Bank for International Settlements has been coordinating research into CBDCs, and this article gives a brief description of how the BIS and its committee members see them evolving. It is early, and there are several important issues yet to be tackled, such as whether CBDCs will pay interest and what will be the likely reaction of commercial banks to seeing central banks muscle in on their territory.

There are also two separate CBDC functions to consider. There is retail, whereby individuals have direct access to their central bank as counterparty, and a wholesale function for financial intermediaries for international settlement.

Whether CBDCs will come into existence is doubtful.

To have credibility, their introduction will have to be coordinated at the G20 level, and they are unlikely to be widely issued before the end of the decade. That will probably be too late to save the world from a developing financial and monetary crisis that threatens to change everything.

Furthermore, the Americans will need to be convinced that their dollar hegemony will not be compromised. And what will almost certainly stop it is the powerful U.S. banking lobby, likely to remind politicians presented with the necessary legislation that a political survivor is one who once bought, stays bought. …

… For the remainder of the analysis:

end

4.OTHER GOLD/SILVER COMMENTARIES

| Live from the Vault: Episode 59. |

| Hi Harvey, In this week’s Live from the Vault, Andrew Maguire reveals the two main reasons behind the current bullish shift in gold and silver and elaborates further on the fragile ETF flywheel, with gold set to rally. The precious metals expert continues to monitor the influence of Basel III on the markets and explains the mechanisms behind futures market backwardation in response to ever-tightening physical supply.Watch the video via the button below, or listen on Apple podcasts or Spotify.WATCH NOW |

Support Contact us Live chat |

|

END

Andy Schectman:

Silver premiums spike as COMEX paper silver crashes & burns

As the pressure on the COVID Deep State banking system mounts, physical silver premiums have spiked, while COMEX paper silver is crashing and burning.

And to offer you a view from the frontlines of the physical silver market, Andy Schectman of Miles Franklin joined me on the show to share what’s happening at this very minute.

So if you want to know what’s really going on with the silver price, click to watch this timely video now!

https://lemetropolecafe.com/pfv.cfm?pfvID=17440

5.OTHER COMMODITIES/

end

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings FRIDAY morning 7:30 AM

ONSHORE YUAN: CLOSED UP AT 6.3622

OFFSHORE YUAN: 6.3710

HANG SANG CLOSED DOWN 256.82 PTS OR 1.08%

2. Nikkei closed UP 547.04 PTS OR 2.08%

3. Europe stocks ALL RED

USA dollar INDEX UP TO 97.44/Euro FALLS TO 1.1131-

3b Japan 10 YR bond yield: RISES TO. +.169/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 115.63/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 87.22 and Brent: 90.56-

3f Gold DOWN /JAPANESE Yen UP CHINESE YUAN: ON -SHORE CLOSED UP// OFF- SHORE UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO -.0.006%/Italian 10 Yr bond yield RISES to 1.36% /SPAIN 10 YR BOND YIELD RISES TO 0.73%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 1.37: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield RISES TO : 1.88

3k Gold at $1788.80 silver at: 22.55 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3l USA vs Russian rouble;// Russian rouble UP 50/100 in roubles/dollar AT 77.47

3m oil into the 87 dollar handle for WTI and 90 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 115.63 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning .9327– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0382 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 1.847 UP 4 BASIS PTS

USA 30 YR BOND YIELD: 2.1420 UP 5 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 13.61

Neurotic Futures Tumble Despite Record Apple Quarter

FRIDAY, JAN 28, 2022 – 08:07 AM

If you thought that yesterday’s blowout, record earnings from Apple would be enough to put in at least a brief bottom to stocks and stop the ongoing collapse in risk assets, we have some bad news for you: after staging a feeble bounce overnight, S&P futures erased earlier gains as traders ignored the solid results from Apple and instead focused on the risk of higher interest rates hurting economic growth. Contracts in S&P 500 dropped as negative sentiment continued to prevail, while Nasdaq 100 futures erased earlier gains after strong Apple earnings. As of 730am, Emini futures were down 48 points or 1.12% to 4,269, Dow futures were down 335 points or 0.99% and Nasdaq futs were down 77 or 0.6%. The dollar was set for a fifth straight day of gains, the longest streak since November, 19Y TSY yields were up 3bps to 1.83%, gold and bitcoin both dropped.

Markets have been whiplashed by volatility this week as the Federal Reserve signaled aggressive tightening, adding to investor concerns about geopolitical tensions and an uneven earnings season. Also sapping sentiment on Friday were weak data on the German economy and euro-area confidence. Meanwhile, geopolitical tensions were still on the agenda with a potential conflict in Ukraine not yet defused.

“Market expectations for four to five rate hikes this year will not derail growth or the equity rally,” said Mark Haefele, chief investment officer at UBS Global Wealth Management. “We expect an eventual relaxation of tensions between Russia and Ukraine,” he added. Expected data on Friday include personal income and spending data, as well as University of Michigan Sentiment, while Caterpillar, Chevron, Colgate-Palmolive, VF Corp and Weyerhaeuser are among companies reporting earnings.

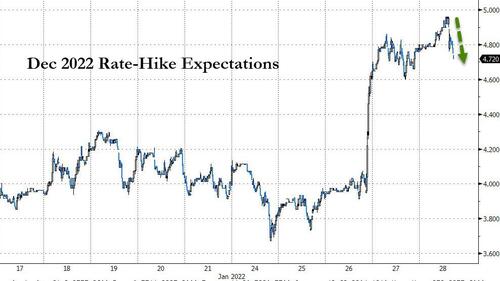

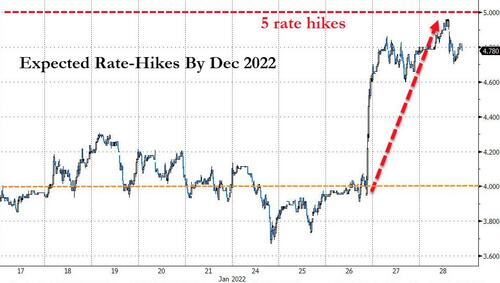

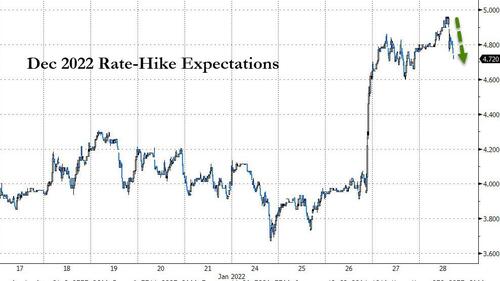

Money markets are now pricing in nearly five Fed hikes this year after a hawkish stance from Chair Jerome Powell. That’s up from three expected as recently as December.

“Tighter liquidity and weaker growth mean higher volatility,” Barclays Plc strategists led by Emmanuel Cau wrote in a note. The “current growth scare looks like a classic mid-cycle phase to us, while a lot of hawkishness is priced in.”

In premarket trading, Apple shares rose 4.5% as analysts rose their targets to some of the most bullish on the Street, after the iPhone maker reported EPS and revenue for the fiscal first quarter that beat the average analyst estimates. Watch Apple’s U.S. suppliers after the iPhone maker posted record quarterly sales that beat analyst estimates, a sign it was able to work through the supply-chain crunch. Peers in Asia rose, while European suppliers are active in early trading. Tesla shares also rise as much as 2% in premarket, set to rebound from yesterday’s 12% slump following a disappointing set of earnings and outlook. Other notable premarket movers:

- Visa (V US) shares gain 5% premarket after company reported adjusted earnings per share for the first quarter that beat the average analyst estimate.

- Cryptocurrency-exposed stocks gain as Bitcoin and other digital tokens rise. Riot Blockchain (RIOT US) +3.7%, Marathon Digital (MARA US) +3.3%, Bit Digital (BTBT US) +1.6%, Coinbase (COIN US) +0.5%.

- Robinhood (HOOD US) shares tumbled 14% in premarket after the online brokerage’s fourth-quarter revenue and first-quarter outlook missed estimates. Some analysts cut their price targets.

- Atlassian (TEAM US) shares jump 10% in extended trading on Thursday, after the software company reported second-quarter results that beat expectations and gave a third-quarter revenue forecast that was ahead of the analyst consensus.

- U.S. Steel (X US) shares fall as much as 2.4% aftermarket following the steelmaker’s earnings release, which showed adjusted earnings per share results missed the average analyst estimate.

The U.S. stock market is priced “quite aggressively” versus other developed nations as well as emerging markets, and valuations in the latter can be a tailwind rather than a headwind as in the U.S., Feifei Li, partner and CIO of equity strategies at Research Affiliates, said on Bloomberg Television.

European equity indexes are again under pressure, rounding off a miserable week, and set for the worst monthly decline since October 2020 as corporate earnings failed to lift the mood except in the retail sector. The Euro Stoxx 50 dropped over 1.5%, DAX underperforming at the margin. Autos, tech and banks are the weakest Stoxx 600 sectors; only retailers are in the green. Hennes & Mauritz shares climbed on a profit beat, while technology stocks continued to underperform. Here are some of the biggest European movers today:

- LVMH shares rise as much as 5.8% after analysts praised the French conglomerate’s full-year results, with several noting improved performance at even minor brands such as Celine.

- Signify gains as much as 15% after saying it expects to grow in 2022 even as the supply chain problems that caused its “worst ever” quarter continue.

- H&M climbs as much as 7.4% after posting a strong margin in 4Q which impressed analysts. Analysts also lauded the Swedish retailer’s buyback announcement and target to double sales by 2030.

- Stora Enso rises as much as 6.2% on 4Q earnings with the CEO noting paper capacity closures have helped boost its pricing power, contributing to a turnaround in the unprofitable business.

- SCA gains as much as 5.5% in Stockholm, the most since May 2020, after reporting better-than-expected Ebitda earnings and announcing a SEK3.25/share dividend — higher than analysts had estimated.

- AutoStore rises as much as 18% after a German court halts Ocado’s case against the company. Ocado drops as much as 8.1%.

- Henkel slides as much as 10% after the company’s forecast for organic revenue growth of 2% to 4% in 2022 was seen as cautious.

- Wartsila falls as much as 9% after posting 4Q earnings that analysts say showed strong order intake overshadowed by lagging margins.

- Alstom drops as much as 7.3% after Exane BNP Paribas downgrades to neutral, citing risk that the company might resort to raising equity financing to forestall a possible credit-rating cut.

Earlier in the session, Asian stocks rose after slumping to their lowest since November 2020, with Japan and Australia leading the rebound as turbulence over the highly anticipated U.S. monetary tightening eased. The MSCI Asia Pacific Index climbed as much as 1% on Friday following a 2.7% slide the day before. Industrials and consumer-discretionary names provided the biggest boosts to the measure. Japan’s Nikkei 225 Stock Average was among the best performers in the region after enduring its worst daily drop in seven months. “It’s undeniable that stock markets last year — as well as the real economy — were supported by continued monetary easing, considering which, more share-price correction could be anticipated,” said Tetsuo Seshimo, a portfolio manager at Saison Asset Management in Tokyo. Even so, “stocks fell too much yesterday.” The Asian benchmark is down almost 5% this week, and set to cap its biggest such drop since February last year. Federal Reserve Chair Jerome Powell said the central bank was ready to raise interest rates in March and didn’t rule out moving at every meeting to tackle inflation, triggering a broad selloff in global equities Thursday. Japan’s Topix and Australia’s S&P/ASX 200 gained after slipping into technical correction earlier this week. South Korea’s Kospi also added almost 2% after sliding into a bear market Thursday. Meanwhile, Chinese shares extended a rout of nearly $1.2 trillion this month.

Japanese equities rose, trimming their worst weekly loss in two months, as some observers saw the selloff on concerns over higher U.S. interest rates as having gone too far. Electronics and auto makers were the biggest boosts to the Topix, which rose 1.9%, paring its weekly decline to 2.6%. Fast Retailing and Shin-Etsu Chemical were the largest contributors to a 2.1% rise in the Nikkei 225. The yen was little changed after weakening 1.3% against the dollar over the previous two sessions. “Looking at the technical indicators like RSI, you can see that Japanese equities have been oversold,” said Nobuhiko Kuramochi, a market strategist at Mizuho Securities. “Shares have fallen too much considering the not-bad corporate earnings and also when compared with U.S. equities.” U.S. futures rallied in Asian trading hours, after a volatile cash session that ended in losses as investors continued to reprice assets on the Fed’s pivot to tighter policy. Apple provided a post-market lift with record quarterly sales that sailed past Wall Street estimates.

In Australia, the S&P/ASX 200 index rose 2.2% to 6,988.10 at the close in Sydney, bouncing back after slipping into a technical correction on Thursday. The benchmark gained for its first session in five as miners and banks rallied, trimming its weekly slide to 2.6%. Champion Iron was a top performer after its 3Q results. Newcrest was one of the worst performers after its 2Q production report, and as gold extended declines. In New Zealand, the S&P/NZX 50 index fell 1.6% to 11,852.15.

India’s benchmark index edged lower on Friday to extend its decline to a second consecutive week as investors grapple with volatility created by the U.S. Federal Reserve’s rate-hike plan. The S&P BSE Sensex fell 0.1% to 57,200.23 in Mumbai on Friday, erasing gains of as much as 1.4% earlier in the session. The NSE Nifty 50 Index ended flat. For the week, the key gauges ended with declines of 3.1% and 2.9%, respectively. All but five of the 19 sector sub-indexes compiled by BSE Ltd. climbed on Friday, led by a measure of health-care companies. BSE’s mid- and small-sized companies’ indexes outperformed the benchmark by rising 1% and 1.1%. “Selling pressure has now cooled off, markets will now focus on local triggers such as expectations from the budget,” said Prashant Tapse, an analyst with Mumbai-based Mehta Equities. Investors will also monitor corporate-earnings reports for the December quarter to gauge demand and inflation outlook. Of the 21 Nifty 50 companies that have announced results so far, 12 either met or exceeded expectations, eight missed, while one can’t be compared. Kotak Mahindra Bank continued the strong earnings run by lenders, reporting fiscal third-quarter profit ahead of the consensus view, while Dr. Reddy’s Laboratories missed the consensus estimate. ICICI Bank contributed the most to the Sensex’s decline, falling 1.6%. Out of 30 shares in the Sensex index, 14 rose and 16 fell.

In rates, bonds trade poorly again with gilts and USTs bear steepening, cheapening 3-3.5bps across the back end. Treasuries are weaker, same as most European bond markets, with stock markets under pressure globally and S&P 500 futures lower but inside weekly range. Treasury yields are cheaper by 4bp-5bp from intermediate to long-end sectors, 10-year around 1.84%, inside weekly range; though front-end outperforms, 2-year yield reaches YTD high 1.22%, steepening 2s10s by ~1bp. Gilts underperformed as traders price in a more aggressive path of rate hikes from the BOE. Treasury curve is steeper for first day in four, lifting spreads from multimonth lows. Globally in 10-year sector, gilts lag Treasuries by 0.5bp while bunds outperform slightly. Bunds bear flatten with 5s30s near 52bps after two block trades but subsequently recover above 54bps. IG dollar issuance slate empty so far; Procter & Gamble priced a $1.85b two-tranche offering Thursday, the first since Wednesday’s Fed meeting.

In FX, Bloomberg Dollar Spot pushes to best levels for the week. Scandies and commodity currencies suffer the most. The Bloomberg Dollar Spot Index was set for a fifth straight day of gains, the longest streak since November, and near its strongest level in 17 months as the greenback was steady or higher against all of its Group-of-10 peers. The euro steadied near a European session low of $1.1121 while risk-sensitive Australian and Scandinavian currencies led the decline. Sweden’s krona sank, despite data showing the Nordic nation’s economy grew more than expected in the final quarter of 2021, fueling speculation that the central bank could soon start to take its foot off the stimulus pedal. Australia’s dollar dropped to the lowest level in 18 months as the Reserve Bank of Australia lags behind many of its peers in signaling monetary tightening. Treasuries sold off, led by the belly; Bunds also traded lower, yet outperformed Treasuries, and Germany’s 5s30s curve flattened to 52bps after two futures blocks traded. Italian government bonds underperformed with the nation’s parliament voting twice on Friday to elect a new president, as the lack of progress after four days of inconclusive ballots adds to pressure to end a process that’s left the country in limbo.

In commodities, Crude futures hold a narrow range, just shy of Asia’s best levels. WTI trades either side of $87, Brent just shy of a $90-handle. Spot gold drops near Thursday’s lows, close to $1,791/oz. Base metals are under pressure; LME copper underperforms peers, dropping over 1.5%.

Crypto markets were rangebound in which Bitcoin traded both sides of the 37,000 level. Russia’s government drafted a roadmap for cryptocurrency regulation, according to RBC.

To the day ahead now, and data releases include Germany’s Q4 GDP, US personal income and personal spending for December, as well as the Q4 employment cost index and the University of Michigan’s final consumer sentiment index for January. Earnings releases include Chevron and Caterpillar.

Market Snapshot

- S&P 500 futures up 0.1% to 4,323.75

- STOXX Europe 600 down 1.0% to 465.51

- MXAP up 0.5% to 182.48

- MXAPJ little changed at 597.31

- Nikkei up 2.1% to 26,717.34

- Topix up 1.9% to 1,876.89

- Hang Seng Index down 1.1% to 23,550.08

- Shanghai Composite down 1.0% to 3,361.44

- Sensex down 0.1% to 57,197.94

- Australia S&P/ASX 200 up 2.2% to 6,988.14

- Kospi up 1.9% to 2,663.34

- Brent Futures up 0.4% to $89.71/bbl

- Gold spot down 0.3% to $1,792.52

- U.S. Dollar Index up 0.13% to 97.38

- German 10Y yield little changed at -0.05%

- Euro down 0.1% to $1.1132

Top Overnight News from Bloomberg

- The euro-area economy kicked off 2022 on a weak footing, with pandemic restrictions taking a toll on confidence and growing fears that Germany may be on the brink of a recession for the second time since the crisis began. A sentiment gauge by the European Commission fell to 112.7 in January, the lowest in nine months, driven by declines in most sectors and among consumers. Employment expectations dropped for a second month

- Germany’s economy shrank 0.7% in the fourth quarter with consumers spooked by another wave of Covid-19 infections and factories reeling from supply-chain problems.

- Russian Foreign Minister Sergei Lavrov said on Friday that the American proposal to defuse tensions with Ukraine contained “rational elements,” even though some key points were ignored

- A U.K. government probe into alleged rule-breaking parties in Boris Johnson’s office during the pandemic could be stripped of key details at the request of police, potentially handing the prime minister a boost as he tries to persuade his Conservatives not to mount a leadership challenge

- Governor Haruhiko Kuroda said the Bank of Japan won’t be switching its bond yield target until inflation rises high enough to warrant exit talks

- Seven straight jumps in the so- called “fear gauge” for the S&P 500 is a signal that it may be time to wager against volatility, if history is any guide. Only 10 times in the past two decades has the Cboe Volatility Index – – better known as the VIX — risen for that many trading sessions in a row

A more detailed look at global markets courtesy of Newsquawk

Asian stocks eventually traded mixed although China lagged ahead of holiday closures next week. ASX 200 (+2.2%) was lifted back up from correction territory. Nikkei 225 (+2.1%) gained on a weaker currency and with corporate results driving the biggest movers. KOSPI (+1.9%) was boosted by earnings including from the world’s second-largest memory chipmaker SK Hynix. Hang Seng (-1.1%%) and Shanghai Comp. (-0.9%) lagged with a non-committal tone in the mainland ahead of the Lunar New Year holiday closures and with Hong Kong pressured by losses in blue chip tech and health care

Top Asian News

- Asia Stocks Rise, Still Head for Worst Week Since February

- Kuroda Hints No Chance of Switching Yield Target Until Exit

- China Fintech PingPong Said to Mull $1 Billion Hong Kong IPO

- Biogen Sells Bioepis Stake for $2.3 Billion to Samsung Biologics

European bourses have conformed to the downbeat APAC handover with losses in the region extending following the cash open, Euro Stoxx 50 -1.7%. Sectors were mixed with Tech and Banking names the laggards while Personal/Household Goods and Retail outperformer following LVMH and H&M respectively; since then, performance has deteriorated though the above skew remains intact. US futures are moving in tandem with European-peers; however, magnitudes are more contained as the ES is only modestly negative and NQ continues to cling onto positive territory following Apple earnings. Apple Inc (AAPL) Q1 2022 (USD): EPS 2.10 (exp. 1.89), Revenue 123.95bln (exp. 118.66bln), iPhone: 71.63 bln (exp. 68.34bln), iPad: 7.25bln (exp. 8.18bln), Mac: 10.85bln (exp. 9.51bln), Services: 19.52bln (exp. 18.61 bln), according to Businesswire. +3.5% in the pre-market, trimming from gains in excess of 5.0% earlier

Top European News

- German Economy Contracted Amid Tighter Virus Curbs, Supply Snags

- H&M CEO Sets Target to Double Retailer’s Sales by 2030

- Telia Sells Tower Stake for $582 Million, Cuts Costs

- U.K. ‘Partygate’ Probe May Be Watered Down at Police Request

In FX, buck bull run continues as DXY takes out another July 2020 high to leave just 97.500 in front of key Fib resistance. Aussie feels the heat of Greenback strength more than others amidst risk-off positioning and caution ahead of next week’s RBA policy meeting. Kiwi also lagging and Loonie losing crude support after the BoC’s hawkish hold midweek. Euro and Yen reliant on some hefty option expiry interest to provide protection from Dollar domination. BoJ Governor Kurdoa if times come to debate the exit of policy, then targeting shorter maturity JGBs could become an option; at this stage its premature to raise yield target or take steps to steepen yield curve.

In commodities, WTI and Brent are consolidating somewhat after yesterday’s choppy price action, but remain towards the lowend

of a circa. USD 1.00/bbl range. Focus remains firmly on geopols as Russia is set to speak with French and German officials on Friday, though rhetoric, remains relatively familiar. Spot gold and silver are pressured as the yellow metal loses the 100-DMA, and drops to circa. USD 1780/oz as the USD rallies, and ahead of inflation data while LME copper follows the equity downside.

In Geopolitics:

- US President Biden reaffirmed in call with Ukraine’s President the readiness of US to respond decisively if Russia further invades Ukraine, according to Reuters.

- Russian Foreign Minister Lavrov says Russia is analysing NATO and US proposals and will decide on how to respond to them, via Reuters; additionally, Lavrov will speaking with German Foreign Minister Baerbock on Friday, via Ifx.

- Russia’s Kremlin says President Putin’s talks with Chinese President Xi will give attention to security in Europe and Russia-US dialoged, according to Reuters; Kremlin does not rule out that Putin will provide some assessments on response to Russian proposals.

- US requested a public UN Security Council meeting for Monday to discuss the build up of Russian forces on Ukraine border, according to Reuters citing diplomats.

- US bipartisan group of Senators have reportedly been meeting to create legislation that would dramatically increase presence of US military aid for Ukraine, according to Reuters sources.

- Lithuania and Germany are in discussions to increase the presence of the German military, given current events, according to Reuters

US Event Calendar

- 8:30am: 4Q Employment Cost Index, est. 1.2%, prior 1.3%

- 8:30am: Dec. Personal Income, est. 0.5%, prior 0.4%

- Dec. PCE Core Deflator YoY, est. 4.8%, prior 4.7%; PCE Core Deflator MoM, est. 0.5%, prior 0.5%

- Dec. PCE Deflator YoY, est. 5.8%, prior 5.7%; PCE Deflator MoM, est. 0.4%, prior 0.6%

- 8:30am: Dec. Personal Spending, est. -0.6%, prior 0.6%; Real Personal Spending, est. -1.1%, prior 0%

- 10am: Jan. U. of Mich. Sentiment, est. 68.8, prior 68.8

- Current Conditions, est. 73.2, prior 73.2; Expectations, est. 65.9, prior 65.9

- 1 Yr Inflation, est. 4.9%, prior 4.9%; U. of Mich. 5-10 Yr Inflation, prior 3.1%

DB’s Jim Reid concludes the overnight wrap

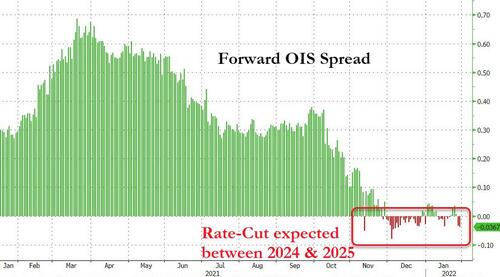

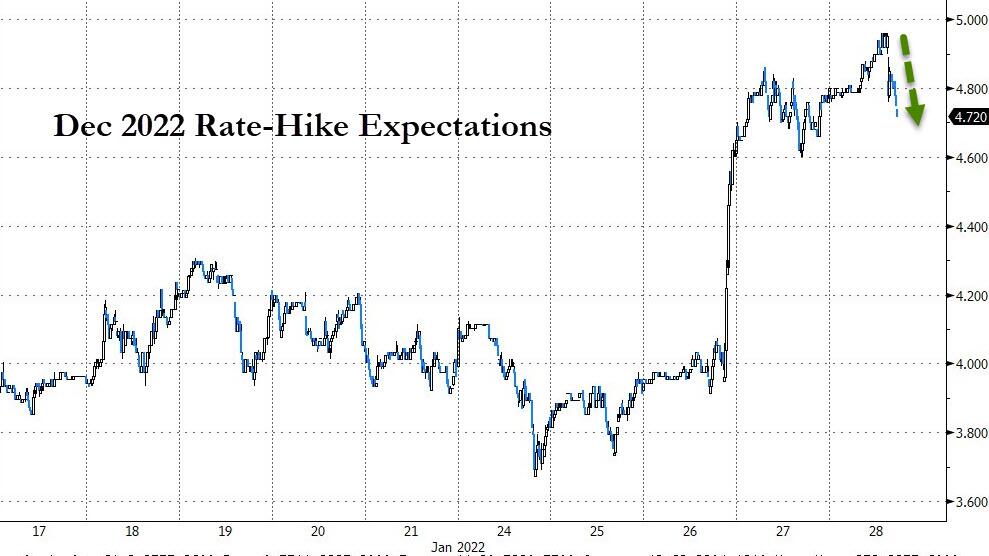

What a week we’ve had. Yesterday saw another market whipsaw as markets continued to try to digest the aftermath of Chair Powell’s press conference. In particular, there was growing speculation that the Fed would embark on back-to-back hikes in order to get inflation under control, with Fed funds futures now pricing 2 full hikes over the next two meetings in March and May, in line with our US econ team’s updated call. Assuming this is realised, then this would be a much faster pace of hikes than anything seen over the last cycle, when the initial hike in December 2015 wasn’t followed by another for an entire year, and the fastest things got was a consistent quarterly pace when the Fed hiked 4 times in 2018. This time, we almost have 4 hikes priced between March and September alone. Of course however, it’s worth noting that today they face a very different set of circumstances, since the last hiking cycle actually began with inflation beneath the Fed’s target, and was a pre-emptive one given their belief that inflation would rise from that point. By contrast, this cycle of rate hikes is set to begin with inflation at levels not seen since the early 1980s, with the Fed seeking to regain credibility after consistently underestimating inflation over the last year. As we’ve highlighted in our work over the last 6-9 months this is a very, very, very different cycle to the last one and we should therefore expect different inflation and Fed outcomes. We repeat a few slides on this in the chart book so feel free to dip in.

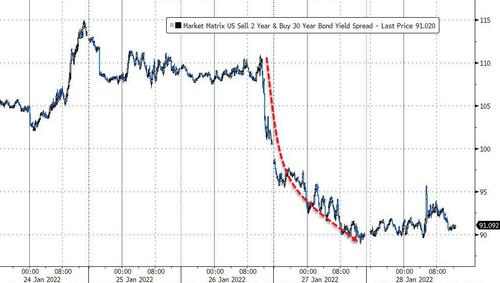

These growing expectations of near-term hikes supported the more policy-sensitive 2yr Treasury yield, which rose a further +3.8bps to a fresh post-pandemic high after the previous day’s massive +13.3bps advance. And the number of hikes priced for 2022 as a whole actually rose to a new high of its own at 4.8 hikes. However, a -6.4bps decline in the 10yr yield to 1.80% meant that there was a further flattening of the yield curve, with the 2s10s down to its flattest level in over a year, at just 60.9bps. This is only adding to the late-cycle signals we’ve been discussing of late, particularly when you consider that the yield curve historically tends to flatten in the year after the Fed begins hiking rates, so an inversion over the next 12 months would be no surprise on a historic basis followed perhaps by a 2024 recession? See the chart book for more on this. Indeed, some parts of the curve are even closer to inverting than the 2s10s, with the 5s10s slope at just 14.1bps yesterday, which is the flattest it’s been since the initial market panic about Covid back in March 2020.

The implications of this hawkish push could also be seen in FX markets, where the dollar index strengthened +0.81% to levels not seen in over 18 months. Conversely though, the Fed’s more aggressive posture on inflation significantly hurt precious metals, with gold (-1.22%) falling by more than -1% for a second consecutive session.

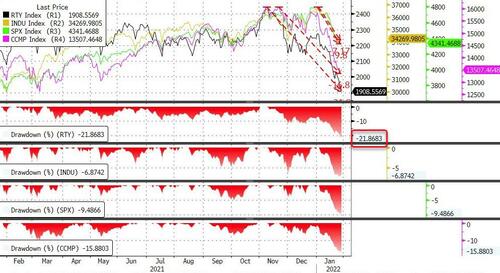

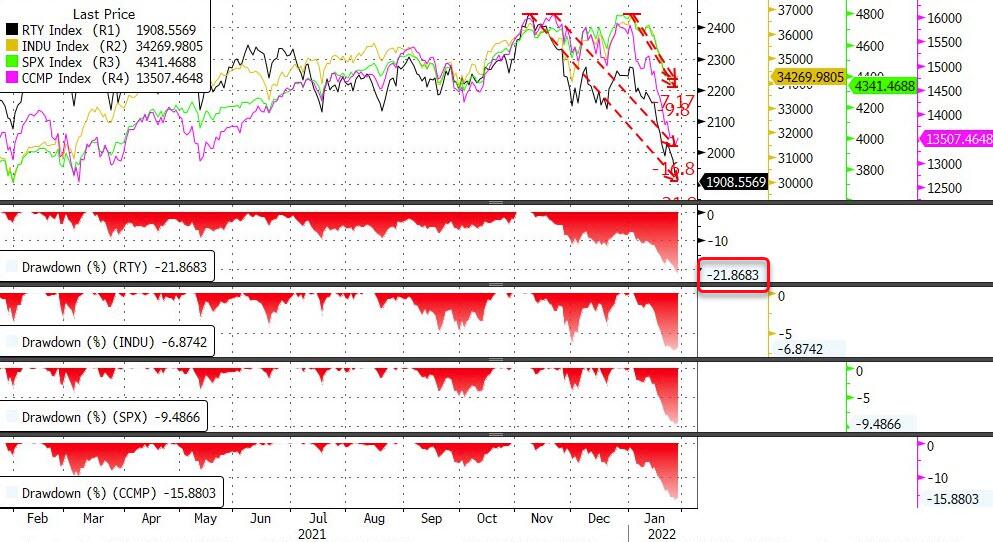

Transatlantic equity performance was a mixed bag yesterday. The STOXX 600 fell -1.47% immediately after the European open, just as US futures were pointing to additional losses on top of the previous day’s. However, sentiment turned into the European afternoon, with the major indices on both sides of the Atlantic moving into positive territory, leaving the STOXX 600 +0.65% higher. True to recent form though, the S&P 500 reversed course after the European optimists called it a day, drifting lower to end the day at -0.54%. Sector performance was fairly split, with five sectors in the red: discretionary (-2.27%) and real estate (-1.75%), industrials (-0.93%), financials (-0.92%), and tech (-0.69%). Energy (+1.24%) was again the outperformer, but didn’t do enough to drag the entire index into the green. Tesla was a big driver of the discretionary drawdown. After bouncing around following its earnings release the evening before, Tesla declined -11.55% yesterday on the back of potential supply chain issues, and to a 3-month low. The NASDAQ underperformed the S&P, declining -1.40%, bringing it -16.84% below its all-time high. The Russell 2000 of small caps (-2.29%) fell into “bear market” territory and is now down -20.94% from its highs in early November. The Vix index of volatility closed modestly lower (-1.37ppts) for the first time in almost two weeks, but remained elevated at 30.59.

Apple reported fourth quarter earnings after the close. Like other goods manufactures, they continued to be besot by supply chain issues, but that did not stop them from beating sales and earnings estimates, posting their best quarter of revenues ever. The stock was more than +5% higher in after-hours trading following the release. Prior to this they were down around -10% YTD. This has helped the S&P 500 (+0.7%) and Nasdaq (+1.1%) futures rebound as we hit the last day of a tough and very volatile week.

Overnight in Asia, equity markets are also recovering some of their recent losses with the Nikkei rebounding (+2.17%), after falling nearly -3% in the previous session, followed by the Kospi (+1.44%). Meanwhile, the Shanghai Composite (+0.05%) and CSI (0.08%) are trading flattish as we type. On the other hand, the Hang Seng (-0.94%) is extending its recent losses this morning ahead of the release of Hong Kong’s Q4 GDP report scheduled in a few hours.

Early morning data showed consumer prices in Tokyo fell to +0.5% y/y in January from +0.8% in December while the core CPI inflation (+0.2% y/y) in January failed to exceed market expectations (+0.3%) after increasing +0.5% last month. Elsewhere, South Korea’s industrial output surprisingly advanced +4.3% m/m in December against economist expectations of -0.3%. It follows November’s upwardly revised +5.3% increase.

Back in Europe, sovereign bond yields rose for the most part, having been closed at the time of Chair Powell’s press conference the previous day. Those on 10yr bunds (+1.6bps), OATs (+0.7bps) and gilts (+3.1bps) all moved higher, and that rise in gilt yields comes ahead of next week’s Bank of England decision, where overnight index swaps are now pricing in a 94% chance of another rate hike, which is also our UK economist’s expectation.

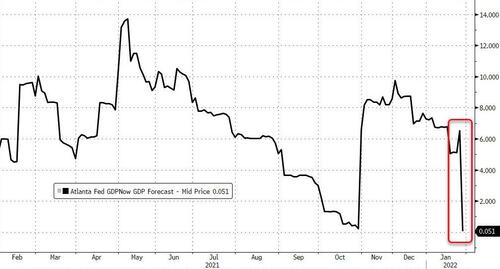

One factor supporting sentiment yesterday was a decent set of economic data, with the US economy growing by an annualised rate of +6.9% in Q4 2021 (vs. +5.5% expected). That’s the fastest quarterly pace since Q3 2020 when the economy rebounded sharply from the various lockdowns, and left growth for the full year 2021 at +5.7%, the fastest since 1984. Meanwhile, the weekly initial jobless claims for the week through January 22 subsided to 260k (vs. 265k expected), ending a run of 3 consecutive weekly increases.

To the day ahead now, and data releases include Germany’s Q4 GDP, US personal income and personal spending for December, as well as the Q4 employment cost index and the University of Michigan’s final consumer sentiment index for January. Earnings releases include Chevron and Caterpillar.

3. ASIAN AFFAIRS

i)FRIDAY MORNING// THURSDAY NIGHT

SHANGHAI CLOSED DOWN 32.81 PTS OR 0.97% //Hang Sang CLOSED DOWN 256.92 PTS OR 1.08% /The Nikkei closed UP 547.04 PTS OR 2.09% //Australia’s all ordinaires CLOSED UP 2.13% /Chinese yuan (ONSHORE) closed UP 6.3620 /Oil DOWN TO 87.22 dollars per barrel for WTI and UP TO 90.56 for Brent. Stocks in Europe OPENED ALL RED // ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.3622. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.3710: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN AND OFF SHORE TRADING STRONGER AGAINST USA DOLLAR

3 a./NORTH KOREA/ SOUTH KOREA

///NORTH KOREA

3B JAPAN

end

3c CHINA

CHINA/COVID

China expands its lockdown in Beijing prior to the Winter Olympics. Cases detected among Olympic personnel

(zerohedge)

CCP Expands Beijing Lockdown As More Cases Detected Among Olympics Personnel

THURSDAY, JAN 27, 2022 – 08:40 PM

The other day, the English-language press picked up on a rumor that President Xi of China had implored his ally, Russian President Vladimir Putin, not to invade Ukraine until after the Winter Games. Anonymously-sourced leaks like these are often propaganda, not truth. But as the Games draw near, the Communist government is tightening the screws on the city of Beijing as COVID continues to spread – albeit, more slowly – despite their draconian measures.

Reuters reports that the CCP has expanded its localized lockdowns in Beijing, restricting movement to those who live within a growing number of neighborhoods and housing complexes, and prohibiting outsiders from entering.

For example, Beijing’s Fengtai district said late on Wednesday residents in a new swath of areas should not leave their residential compounds for unnecessary reasons and must be tested daily for COVID.

Beijing has some reason to target the district: it has produced more local cases than any others, at least going by what the CCP has admitted publicly.

The area had already locked down some compounds that house tens of thousands of people, while several other city districts have restricted the mobility of their residents.

China’s NHC said Beijing saw just five locally transmitted infections confirmed for Wednesday, down from 14 a day earlier.

Locals who spoke with Reuters anonymously indicated that they are all terrified of getting COVID for fear of provoking the government’s wrath.

“I’m anxious everyday because the virus situation is still quite serious,” said a traveler surnamed Wang at Beijing Railway Station. “I don’t want to bring trouble to my hometown. Now I’m tested negative, but what if it changes to positive?”

Beijing has already locked down some compounds that house tens of thousands of people. Several other city districts have imposed mobility restrictions in certain areas. Meanwhile, elsewhere in China, travel has surged during the Lunar New Year holiday. Travel during the first ten days of the holiday season has risen 46% from last year.

Local authorities in charge of the Winter Games said 23 new cases were detected among Games-related personnel on Jan. 26, including eight among those already in the closed-loop Olympics bubble. The rest were discovered upon arrival at the airport.

China isn’t alone. Cases are climbing elsewhere in Asia. For example, in Japan, Tokyo is reportedly facing “an explosive infection situation due to an omicron-fueled wave that’s driving daily case numbers to record highs. Top Japanese health authority Norio Omagari said newly recorded daily infections in Tokyo could exceed 24K in a week if the current trend continues. The capital city reported 16.5K cases on Thursday.

END

China becoming more belligerent as they warn the USA over Ukraine. They also blast the USA for interference in the ongoings of the Beijing Olympics.

(zerohedge)

China Warns US Over Ukraine & Blasts “Interference” In Beijing Olympics

THURSDAY, JAN 27, 2022 – 09:20 PM

China on Thursday blasted the US for continuing to interfere in its affairs, further saying nothing has fundamentally changed, but instead charging there’s been “new shocks” since the Biden-Xi virtual summit of two months ago.

The scathing rebuke came on Thursday as Chinese Foreign Minister Wang Yi held a phone call with his counterpart Secretary of State Antony Blinken. Importantly, Wang took the opportunity to for the first time side with Russia in the direct communication with the US top diplomat, saying Moscow has “reasonable security concerns” over Ukraine that must be “taken seriously”. Chinese state media and Beijing-linked pundits have also become increasingly vocal on the issue, charging NATO with overstepping…

He urged calm on the part of all sides but specifically called on the West to “abandon its Cold War mentality”. It’s been no secret that Washington sanctions and punitive actions against officials in both countries have served to make Russia and China unlikely allies against a common enemy.

“All parties should completely abandon the Cold War mentality and form a balanced, effective and sustainable European security mechanism through negotiation,” Wang spelled out in the call with Blinken, according to AFP.

The tough rhetoric echoed the words of Foreign Ministry spokesperson Zhao Lijian during a Wednesday press briefing. In response to US claims that Russia is likely to invade Ukraine during the Beijing Winter Olympics, Zhao said, “As the world’s largest military alliance, NATO should abandon the outdated Cold War mentality and ideological bias, and do things that are conducive to upholding peace and stability.”