GOLD; DOWN $36.15 to $1794.20

SILVER: $22.67 DOWN 113 CENTS

ACCESS MARKET: GOLD: 1796.75..

SILVER: $22.76

Bitcoin: morning price: 35,246 down 1491

Bitcoin: afternoon price: 36,093 down 644

Platinum price: closing down $24.45 to $1023.35

Palladium price; closing up $17.25 at $2357.10

END

end

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

comex notices//JPMorgan notices filed COMEX//NOTICES: 0/56

FILED 56/// EXCHANGE: COMEX

CONTRACT: JANUARY 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,829.900000000 USD

INTENT DATE: 01/26/2022 DELIVERY DATE: 01/28/2022

FIRM ORG FIRM NAME ISSUED STOPPED

118 H MACQUARIE FUT 33

624 H BOFA SECURITIES 56

657 C MORGAN STANLEY 3

880 C CITIGROUP 12

905 C ADM 8

TOTAL: 56 56

MONTH TO DATE: 5,707

NUMBER OF NOTICES FILED TODAY FOR JAN. CONTRACT: 56 NOTICE(S) FOR 5600 OZ (0.1741 TONNES)

total notices so far: 5707 contracts for 570,700 oz (17.7511 tonnes)

SILVER NOTICES:

86 NOTICE(S) FILED TODAY FOR 430,000 OZ/

total number of notices filed so far this month 3022 : for 15,110,000 oz

GLD

WITH GOLD DOWN $36.15

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS): STRANGE ANOTHER STRONG DEPOSIT OF 1.16 TONNES INTO THE GLD.

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

CLOSING INVENTORY: 1014.26 TONNES/

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 113 CENTS:/: NO CHANGE IN SILVER INVENTORY AT THE SLV//

AT THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY SLV/ TONIGHT: 535.003 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A SMALL 92 CONTRACTS TO 151,871 AND RESTS CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THIS SMALL GAIN IN OI WAS ACCOMPANIED WITH OUR SMALL $0.07 LOSS IN SILVER PRICING AT THE COMEX ON THURSDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.07) BUT WERE UNSUCCESSFUL IN KNOCKING OUT ANY SILVER LONGS AS WE HAD A SMALL GAIN OF 362 CONTRACTS ON OUR TWO EXCHANGES .

WE MUST HAVE HAD:

I) HUGE BANKER SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A ZERO ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A HUGE INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 10.505 MILLION OZ FOLLOWED BY TODAY’S 220,000 OZ QUEUE. JUMP //NEW STANDING 15.130 MILLION OZ V) SMALL SIZED COMEX OI GAIN.

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS 120

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JAN. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JAN:

TOTAL CONTACTS for 18 days, total contracts: : 15,083 contracts or 75.415 million oz OR 4.189 MILLION OZ PER DAY. (838 CONTRACTS PER DAY)

TOTAL NO OF OZ UNDERGOING EFP TO LONDON 15,083 CONTRACTS X 5,000 PER CONTRACT:

EQUATES TO: 75.415 MILLION OZ

.

LAST 8 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

RESULT: WE HAD A SMALL SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 92 DESPITE OUR 7 CENT LOSS SILVER PRICING AT THE COMEX// WEDNESDAY THE CME NOTIFIED US THAT WE HAD A TINY SIZED EFP ISSUANCE OF 150 CONTRACTS( 150 CONTRACTS ISSUED FOR MAR AND 150 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR JAN OF 10.505 MILLION OZ FOLLOWED BY TODAY’S 220,000 OZ QUEUE JUMP //NEW STANDING 15.130, MILLION OZ// .. WE HAD A SMALL SIZED GAIN OF 242 OI CONTRACTS ON THE TWO EXCHANGES FOR 1.210 MILLION OZ//

WE HAD 86 NOTICES FILED TODAY FOR 430,000 OZ

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A GIGANTIC SIZED 18,871 TO 553,207 AND FURTHER FROM OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: -1099 CONTRACTS

.

THE GIGANTIC SIZED DECREASE IN COMEX OI CAME WITH OUR STRONG LOSS IN PRICE OF $21.60//COMEX GOLD TRADING/WEDNESDAY/.AS IN SILVER WE MUST HAD INITIAL COMEX SPREADER LIQUIDATION FOLLOWED BY HUGE BANKER/ALGO SHORT COVERING ACCOMPANYING OUR STRONG SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION AS THE TOTAL LOSS ON OUR TWO EXCHANGES TOTALED A HUMONGOUS SIZED 11,744 CONTRACTS…WITH THE ENTIRE COMEX LOSS COMING FROM SPREADER LIQUIDATION.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR JAN AT 3.5614 TONNES FOLLOWED BY TODAY’S 5300 OZ QUEUE. JUMP //NEW STANDING: 17.7912 TONNES

YET ALL OF..THIS HAPPENED WITH OUR LOSS IN PRICE OF $21.60 WITH RESPECT TO TUESDAY’S TRADING

WE HAD A STRONG SIZED LOSS OF 11,744 OI CONTRACTS (36.53 PAPER TONNES) ON OUR TWO EXCHANGES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALLED A STRONG SIZED 7127 CONTRACTS:

FOR FEB 7127 ALL OTHER MONTHS ZERO//TOTAL:7127

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 554,306.

IN ESSENCE WE HAVE A STRONG SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 11,744, WITH 18,871 CONTRACTS DECREASED AT THE COMEX AND 7127 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 11,744 CONTRACTS OR 36.53TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (7127) ACCOMPANYING THE HUGE SIZED LOSS IN COMEX OI (18,871): TOTAL LOSS IN THE TWO EXCHANGES 11,744 CONTRACTS. WE NO DOUBT HAD 1) HUGE BANKER SHORT COVERING ,2.) HUGE INITIAL STANDING AT THE GOLD COMEX FOR JAN. AT 3.7262 TONNES//FOLLOWED BY TODAY’S 100 OZ QUEUE JUMP .//NEW STANDING 17.7912 TONNES 3)ZERO LONG LIQUIDATION AS ENTIRE COMEX LOSS DUE TO INITATION OF SPREADER LIQUIDATION,4) HUGE SIZED COMEX OI. LOSS 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF FEB.WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF JAN HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB, FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (FEB), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2021 INCLUDING TODAY

JAN

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JAN : 68,629 CONTRACTS OR 6,862,900 oz OR 213.47 TONNES 18 TRADING DAY(S) AND THUS AVERAGING: 3829 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 18 TRADING DAY(S) IN TONNES: 213.47 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2020, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 213,47/3550 x 100% TONNES 6.01% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO DATE

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 145.12 TONNES//FINAL ISSUANCE//

JAN:2022 213.46 TONNES //

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A SMALL SIZED 92 CONTRACTS TO 151,871 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 4 1/2 YEARS AGO.

EFP ISSUANCE 150 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 150 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 150 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 92 CONTRACTS AND ADD TO THE 150 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A SMALL SIZED GAIN OF 242 OPEN INTEREST CONTRACT FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 1.210 MILLION OZ,

OCCURRED WITH OUR $0.07 LOSS IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

5. Other gold commentaries

6. Commodity commentaries/cryptocurrencies

3. ASIAN AFFAIRS

i)THURSDAY MORNING// WEDNESDAY NIGHT

SHANGHAI CLOSED DOWN 61.42 PTS OR 1.78% //Hang Sang CLOSED DOWN 482.90 PTS OR 1.99% /The Nikkei closed DOWN 841.03 PTS OR 3.11% //Australia’s all ordinaires CLOSED DOWN 1,84% /Chinese yuan (ONSHORE) closed DOWN 6.3674 /Oil UP TO 88.05 dollars per barrel for WTI and UP TO 90.71 for Brent. Stocks in Europe OPENED ALL MIXED // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.3674. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.3728: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN AND OFF SHORE TRADING WEAKER AGAINST USA DOLLAR

A)NORTH KOREA//USA/OUTLINE

b) REPORT ON JAPAN

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A GIGANTIC SIZED 18,871 CONTRACTS AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX DECREASE OCCURRED WITH OUR LOSS OF $21.60 IN GOLD PRICING WEDNESDAY’S COMEX TRADING. WE ALSO HAD A STRONG SIZED EFP (7127 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. LOOKS LIKE OUR BANKERS ARE FINALLY BAILING OUT

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE NON ACTIVE DELIVERY MONTH OF JAN.. THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 7127 EFP CONTRACTS WERE ISSUED: ;: , DEC : 0 & FEB. 7127 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 7127 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED 11,744 TOTAL CONTRACTS IN THAT 7127 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A GIGANTIC SIZED COMEX OI LOSS OF 18,871 CONTRACTS..THE ENTIRE COMEX LOSS WAS DUE TO THE COMMENCEMENT OF SPREADER LIQUIDATION

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING FOR JAN (17.7912),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

THE BANKERS WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $21.60) BUT THEY WERE UNSUCCESSFUL IN FLEECING ANY LONGS AS, EVEN THOUGH THE TOTAL LOSS ON THE TWO EXCHANGES REGISTERED A HUGE 36.53 TONNES ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR JAN (17.7916 TONNES)…THE ENTIRE LOSS AT THE COMEX WAS DUE TO THE COMMENCEMENT OF SPREADER LIQUIDATION

WE HAD – 1099 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 11,744 CONTRACTS OR 1,174,400 OZ OR 36.53 TONNES

Estimated gold volume today: 392,866 /// good

Confirmed volume yesterday: 441,185 contracts very good (spreaders)

INITIAL STANDINGS FOR JAN ’22 COMEX GOLD //JAN 27

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 7551.324 ozBrinksDelaware 4 kilobars//Brinks |

| Deposit to the Dealer Inventory in oz | nilOZ |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 56 notice(s) 5600 OZ 0.1741 TONNES |

| No of oz to be served (notices) | 13 contracts 1300 oz 0.0404 TONNES |

| Total monthly oz gold served (contracts) so far this month | 5707 notices 570700 OZ 17.7511 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

xxx oz |

For today:

No dealer deposit 0

No dealer withdrawal 0

0 customer deposit

total deposit: nil oz

2 customer withdrawals

i) Out of BRINKS: 128.6 0z (4 KILOBARS)

ii) Out of Delaware 7422.724 oz

total withdrawals: 7551.324 oz oz

ADJUSTMENTS: 1

JPMorgan//dealer to customer account 9163.035 oz (285 kilobars)

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JANUARY.

For the front month of JANUARY we have an oi of 69 stand for JANUARY GAINING 53 contracts. We had 0 notices filed on WEDNESDAY, so we GAINED 53 contracts or an additional 5300 oz will stand for

gold in this very non active delivery month of January.

FEBRUARY LOST 41,557 CONTRACTS TO 56,846 (THE MAJORITY OF THE LOSS WAS SPREADER LIQUIDATION)

March GAINED 323 contracts to stand at 3622..

We had 56 notice(s) filed today for 5600 oz FOR THE JAN 2022 CONTRACT MONTH. WE HAVE TWO MORE READING DAYS BEFORE FIRST DAY NOTICE JAN 31/2022.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 56 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JAN /2021. contract month,

we take the total number of notices filed so far for the month (5707) x 100 oz , to which we add the difference between the open interest for the front month of (JAN: 69 CONTRACTS ) minus the number of notices served upon today 56 x 100 oz per contract equals 572,000 OZ OR 17.7912 TONNES the number of TONNES standing in this NON active month of JAN. (numbers corrected from yesterday)

thus the INITIAL standings for gold for the JAN contract month:

No of notices filed so far (5707) x 100 oz+ (69) OI for the front month minus the number of notices served upon today (56} x 100 oz} which equals 572,000 oz standing OR 17.7912 TONNES in this NON active delivery month of JAN.

We GAINED 53 contracts or an additional 5300 oz of gold will stand for metal on this side of the pond.

TOTAL COMEX GOLD STANDING: 17.7912 TONNES (HUGE FOR A JANUARY DELIVERY MONTH)

IF THIS HOLDS TO THE END OF THE MONTH, THIS WILL BE THE HIGHEST EVER RECORDED GOLD STANDING FOR A JANUARY, GENERALLY A VERY POOR DELIVERY MONTH.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

157,392.690, oz NOW PLEDGED /HSBC 4.89 TONNES

125,410.592 PLEDGED MANFRA 2.90 TONNES

54,339.114oz PLEDGED JPMorgan no 1 1.690

288,481,604, oz JPM No 2 8.97 TONNES

898,821.330 oz pledged Brinks/27,96 TONNES

12,249,333 oz International Delaware: 0..3810 tonne

Loomis: 18,615.429 oz

total pledged gold: 1,555,310.092 oz 48.376 tonnes

TOTAL REGISTERED AND ELIZ GOLD AT THE COMEX: 33,571,281.031 OZ (1044,20 TONNES)

TOTAL ELIGIBLE GOLD: 15,838,520.863 OZ (492.64 tonnes)

TOTAL OF ALL REGISTERED GOLD: 17,571,281.031 OZ (546.54 tonnes)

REGISTERED GOLD THAT CAN BE SERVED UPON: 16,015,971.0 OZ (REG GOLD- PLEDGED GOLD) 498.16 tonnes

END

JANUARY 2022 CONTRACT MONTH//SILVER

INITIAL STANDING FOR SILVER//JAN 27

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 130,110.850 oz Brinks CNT |

| Deposits to the Dealer Inventory | 9891.67OZ Manfra |

| Deposits to the Customer Inventory | nil oz |

| No of oz served today (contracts) | 86 CONTRACT(S) (430,000 OZ) |

| No of oz to be served (notices) | 4 contracts (20,000 oz) |

| Total monthly oz silver served (contracts) | 3022 contracts (15,110,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

we had 1 deposits into the dealer

i) Into Manfra: 9891.67 oz

total dealer deposits: 9891.67 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 0 deposits

JPMorgan has a total silver weight: 185.232 million oz/354.385 million =52.28% of comex

ii) Comex withdrawals: 2

a) BRINKS: 129,069.95 OZ

b) out of CNT: 1,040.900 oz

total withdrawal 130,110,850 oz

we had 3 adjustments:

a) dealer to customer

i) JPMorgan 183,287,000 oz

ii) Loomis: 5241.640 oz

b) customer to dealer

i) Manfra: 172,647.206 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 82.455 MILLION OZ

TOTAL REG + ELIG. 354.385 MILLION OZ

TOTAL NO OF CONTRACTS SERVED UPON THIS MONTH: 2838 CONTRACTS FOR 14,190,000 OZ

CALCULATION OF SILVER OZ STANDING FOR JANUARY

NUMBER OF NOTICES FILED TODAY: 1 NOTICES OR 5,000 OZ

silver open interest data:

FRONT MONTH OF JAN//2022 OI: 90 CONTRACTS LOSING 36 contracts on the day

We had 80 notices filed for WEDNESDAY so we GAINED 44 contracts or 220,000 additional oz will stand for delivery in this non active delivery month of January.

FOR FEB WE HAD A GAIN OF 294 CONTRACTS RISING TO 871

FOR MARCH WE HAD A LOSS OF 1634 CONTRACTS UP TO 113,228 CONTRACTS.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 86 for 430,000 oz

Comex volumes: 82,144// est. volume today//good

Comex volume: confirmed YESTERDAY: 60,909 contracts (FAIR)

To calculate the number of silver ounces that will stand for delivery in JANUARY. we take the total number of notices filed for the month so far at 3022 x 5,000 oz =. 15,110,000 oz

to which we add the difference between the open interest for the front month of JAN (90) and the number of notices served upon today 86 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JAN./2021 contract month: 3022 (notices served so far) x 5000 oz + OI for front month of JAN (90) – number of notices served upon today (86) x 5000 oz of silver standing for the JAN contract month equates 15,130,000 oz. .

We GAINED 44 contracts or an additional 220,000 oz will stand for delivery on this side of the pond.

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

GLD

JAN 27/WITH GOLD DOWN $36.15//ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.16 TONNES INTO THE GLD.//INVENTORY RESTS AT 1014.26 TONNES

JAN 26/WITH GOLD DOWN $21.60 A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.65 TONNES INTO THE GLD///INVENTORY RESTS AT 1013.10 TONNES

JAN 25/WITH GOLD UP $10.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1008.45 TONNES

JAN 24/WITH GOLD UP $10.10 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: AN UNBELIEVABLE DEPOSIT OF 27.59 TONNES INTO THE GLD//INVENTORY RESTS AT 1008.45 TONNES

JAN 21/WITH GOLD DOWN $10.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 980.86 TONNES

JAN 20/WITH GOLD UP $.20 TODAY: A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .58 TONNES FROM THE GLD///INVENTORY RESTS AT 980.86 TONNES

JAN 19/WITH GOLD UP $29.65 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 5.27 TONNES INTO THE GLD/INVENTORY RESTS AT 981.44 TONNES

JAN 18/WITH GOLD DOWN $3.25//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 976.21 TONNES

JAN 14/ WITH GOLD DOWN $5.25/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 976.21 TONNES

JAN 13/WITH GOLD DOWN $5.75: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 976.21 TONNES

JAN 12/WITH GOLD UP $8.65//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 976.21 TONNES

JAN 11/WITH GOLD UP $19.25/A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES FROM THE GLD/INVENTORY RESTS AT 976.21 TONNES

JAN 10/WITH GOLD UP $2.00/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 977.08 TONNES

JAN 7/WITH GOLD UP $8.15//A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWLA OF 1.16 TONNES FROM THE GLD////INVENTORY RESTS AT 978.83 TONNES

JAN 6/WITH GOLD DOWN $35.30//A SMALL CHANGE IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF .32 TONNES/INVENTORY RESTS AT 979.99 TONNES

JAN 5/WITH GOLD UP $10.30: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 980.31 TONNES

Jan 4/WITH GOLD UP $14.00//A HUGE CHANGE OF 4.65 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 980.31 TONNES

JAN 3/WITH GOLD DOWN $26.70: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 975.66 TONNES

DEC 31/WITH GOLD UP $14.05 : NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 975.66 TONNES

DEC 30/WITH GOLD UP $7.75 NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 975.66 TONNES

DEC 29/WITH GOLD DOWN $5.00 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.03 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 975.66 TONNES

DEC 28/WITH GOLD UP $2.00 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 973.63 TONNES

DEC 27/WITH GOLD DOWN $2.05: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.63 TONNES.

DEC 23/WITH GOLD UP $9.85 TODAY//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.94 TONNES FROM THE GLD/// INVENTORY RESTS AT 973.63 TONNES

DEC 22/WITH GOLD UP $12.85 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 978.57 TONNES

DEC 21/WITH GOLD DOWN $7.05 TODAY, NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 978.57 TONNES

DEC 20/WITH GOLD DOWN $9.65 TODAY; A BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.37 TONNES INTO THE GLD///INVENTORY RESTS AT 977.20 TONNES

DEC 17/WITH GOLD UP $7.05 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 977.20 TONNES

CLOSING INVENTORY: 1014.26 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

SLV

JAN 27/WITH SILVER DOWN $1.13 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 535.003 MILLION OZ//

JAN 26/WITH SILVER DOWN 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 535.003 MILLION OZ//

JAN 25/WITH SILVER UP 10 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.311 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 535.003 MILLION OZ/

.JAN 24/WITH SILVER DOWN 48 CENTS TODAY: A MASSIVE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.8 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 532.692 MILLION OZ//.

JAN 21/WITH SILVER DOWN 41 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 527.792 MILLION OZ

JAN 20/WITH SILVER UP 52 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.998 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 527.792 MILLION OZ

JAN 19/WITH SILVER UP 71 CENTS TODAY: A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.942 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 525.804 MILLION OZ

JAN 18/WITH SILVER UP 51 CENTS TODAY: TWO HUGE CHANGES IN SILVER INVENTORY AT THE SLV: 2 WITHDRAWALS OF 1.11 MILLION OZ AND 1.424 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 527.246 MILLION OZ//

JAN 14/WITH SILVER DOWN 21 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 529.780 MILLION OZ//

JAN 13/WITH SILVER DOWN 2 CENTS: A BIG CHANGE IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 832,000 OZ FROM THE SLV////INVENTORY RESTS AT 529.780 MILLION OZ

JAN 12/WITH SILVER UP 38 CENTS TODAY : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.612 MILLION OZ//

JAN 11/WITH SILVER UP 33 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.612 MILLION OZ/.

JAN 10/WITH SILVER UP 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 530.612 MILLION OZ//.

JAN 7/WITH SILVER UP 17 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.612 MILLION OZ//.

JAN 6/WITH SILVER DOWN 94 CENTS TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL PF 226,000 OZ FROM THE SLV///INVENTORY RESTS AT 530.612 MILLION OZ?/

JAN 5/WITH SILVER UP 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.838 MILLION OZ//

JAN 4/WITH SILVER UP 21 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.838 MILLION OZ//

JAN 3/WITH SILVER DOWN 45 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.219 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 530.838 MILLION OZ//

DEC 31/WITH SILVER UP 29 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 533.057 MILLION OZ//

DEC 31/WITH SILVER UP 29 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 533.057 MILLION OZ//

DEC30/WITH SILVER UP 14 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A HUGE WITHDRAWAL OF 4.624 MILLILON OZ FROM THE SLV.//INVENTORY RESTS AT 533.057 MILLION OZ//

DEC 29/WITH SILVER DOWN 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 537.681 MILLION OZ/

DEC 28/WITH SILVER UP 9 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.682 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 537.681 MILLION OZ//

DEC 27/WITH SILVER UP 6 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 537.681

DEC 23/WITH SILVER UP 19 CENTS TODAY:A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.202 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 537.681 MILLION OZ//

DEC 22/WITH SILVER UP 29 CENTS TODAY; A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.202 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 538.883 MILLION OZ/

DEC 21/WITH SILVER UP 19 CENTS: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.728 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 540.085 MILLION OZ

DEC 20/WITH SILVER DOWN 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 538.282 MILLION OZ

DEC 17/WITH SILVER UP 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 538.282 MILLION OZ//

CLOSING INVENTORY: 535.003 MILLION OZ

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

Peter Schiff: This Is Going To Be Stagflation

THURSDAY, JAN 27, 2022 – 08:51 AM

Peter Schiff was a guest on the Wharton Business Daily podcast produced by the Wharton School of Business at the University of Pennsylvania. Peter talked about inflation and how it will impact the US economy moving forward. He said ultimately, we’re heading toward stagflation.

Peter said inflation has been a problem for a long time. A lot of people just weren’t cognizant of it.

A lot of the inflation was in financial assets, so, stock prices were going up because of inflation, bond prices, real estate prices. That didn’t bother people because they thought inflation was making them rich.”

Nevertheless, consumer prices were also going up. But the government was able to keep that hidden with a rigged CPI formula that understates inflation. But in 2021, the price increases got so large, the CPI couldn’t hide them.

Based on CPI, prices were up about 7% last year. But if we still measured prices using the same type of CPI that we had in the 1970s or 1980s, prices rose closer to 15%.

Which is why it’s very disingenuous when the politicians tell us, ‘Hey, you know, it’s not that bad. It was way worse in the 70s.’ It wasn’t worse. Last year was a worse year than any year in the 1970s if we measure it the same way we measured prices in the 70s. So, it’s a big problem. And unfortunately, it’s going to get much worse.”

Peter said he thinks 2022 will be worse than 2021 when it comes to inflation. He said he believes a lot of businesses were reluctant to pass on rising costs to their customers. The fact that producer prices rose much more than consumer prices bears this out.

I think that businesses that were reluctant to raise prices last year are going to raise them this year. They have to repair their margins and make up for lost ground. So, I think you’re going to see catch-up. Plus, the pressure on prices is going to continue because the Federal Reserve continues to create inflation.”

Despite talk of tightening, the Fed continues to run loose monetary policy. It continues to run quantitative easing. Interest rates remain at zero. Meanwhile, the US government is spending a lot of money. The government spent over half-a-trillion dollars in December alone.

But we’re not producing. We have record trade deficits. A lot of Americans have left the workforce.”

And the response to the pandemic was one of the most inflationary policies ever pursued. The government ordered people to stay home and not work, and then handed them thousands of dollars to spend on things they weren’t producing.

We threw gasoline on the inflation fire because we pushed down supply while we were stimulating demand – the worst possible policy mistake. And I was criticizing it in real-time as the government and Fed were making it. And now, we’re paying the price for that with these big increases in consumer prices.”

Peter emphasized that the economy didn’t need to be stimulated.

Unfortunately, we needed to be in a recession. Because, if people are not working and not producing, they have to reduce their consumption. We can’t just keep spending money as if we were still making stuff. So, if we’re going to stay at home, to try to deal with COVID, it meant that people had to spend less. But the government didn’t want that. The government wanted people staying home but continuing to spend money as if they still went to work. And that was the problem. And again, we’re paying for it now.”

The Fed has committed to taking on inflation by raising interest rates three to four times in 2022. Peter said even if they start with a 50 basis-point increase, it’s still inadequate. In order to bend the inflation curve, you have to get out in front of it. The Fed needs to go from easy money to tight money. That means interest rates need to be above the level of inflation.

If the inflation rate is seven, you need eight, nine, ten percent. So, what the Fed is talking about doing – going to 1% or 2% – that’s nothing!”

When Alan Greenspan cut interest rates after the dot-com bubble burst, the lowest they got was 1%.

That was very stimulative monetary policy. That is still stimulative. You can’t fight inflation by throwing gasoline on it. We need tight money. But the problem is we can’t afford tight money now because thanks to the Fed keeping interest rates so low for so long, everybody in America borrowed so much money that if interest rates rise to fight inflation, the whole economy collapses, and we have a much worse financial crisis than 2008, and nobody gets a bailout. So, because of that reality, inflation is here to stay. Americans are going to have to live with it.”

So, how will that impact the economy moving forward? Peter said, “The economy is a mess.”

I think inflation is ultimately going to push the economy into a recession as consumers are forced to spend more and more of what they have on food and energy and insurance and just the basics. They’re not going to have discretionary spending. And when they have to cut back, that means a lot of other people lose their incomes, lose their jobs. This is going to be stagflation.”

Peter said he thinks it will be worse than the 1970s with a weaker economy and even higher inflation. Worst of all, the policymakers won’t be able to do anything about it. Paul Volker finally broke inflation by pushing interest rates to 20%.

We don’t have the ability to do that today. We could afford to pay 20% interest on our debt in 1980 because we hardly had any debt.”

END

2.LAWRIE WILLIAM//,//Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,James RICKARDS

3.Chris Powell of GATA provides to us very important physical commentaries

end

4.OTHER GOLD/SILVER COMMENTARIES

Global Silver Coin Sales Reach All-Time Record High In 2021

831

Investors bought a record amount of silver bullion coins as central banks continued to prop-up the economy and financial system. This looks to continue in 2022 as…

by Steve St Angelo of SRSrocco Report

Investors bought a record amount of silver bullion coins as the Fed, and central banks continued to prop up the global economy and financial system with massive asset purchases in 2021. And, this looks to continue into 2022 as the U.S. Mint Silver Eagle sales have already reached 4.4 million in January.

According to the 2021 World Silver Survey, Silver Coin sales were estimated to be 147.7 million oz in 2021. However, they have revised their total silver bar and coin demand higher for 2021, thus I believe silver coin sales topped 150 million oz (Moz).

Interestingly, the 150 Moz figure is that several countries experienced a significant increase in demand for their official silver coin sales last year due to higher premiums for U.S. Silver Eagles and Canadian Maple Leaf coins. Investors turned to the South African Krugerrands, Austrian Philharmonics, and U.K. Britannia’s, selling for much lower premiums. We won’t know the exact sales totals of these official coins until the 2022 World Silver Survey is released in May.

Breaking News… CoinNews.net just published that the Australian Perth Mint Silver bullion sales for 2021 also reached a record high of 19 Moz. It seems as if the official mints around the world are seeing record demand for silver coins.

Interestingly, Silver Eagle sales were slightly lower in 2021 to 28.2 Moz versus 30 Moz in 2020. For whatever reason, the U.S. Mint sold very few Silver Eagles in November and zero for December. But, I believe we will see continued strong Silver Eagle sales this year if the U.S. Mint can access enough silver blanks to meet demand.

Also, the Royal Canadian Mint reported Q1-Q3 2021 total Silver Maple and Bar sales were 27.8 Moz. So, I would estimate Canadian Silver Maple and coin sales will likely surpass 35-36 Moz in 2021, up from 33.3 Moz in 2020.

Lastly, it seems investors are demanding more Silver Coins over Silver Bars. The World Silver Survey estimated last year 148 Moz of Silver Coin demand versus only 105 Moz for Silver Bar. The advantage of Official Silver Coins is that most of the public would recognize the coins are 1 oz, and because they are smaller, they are easier to trade or sell than the larger 10-100 oz bars.

DISCLAIMER: SRSrocco Report provides intelligent, well-researched information to those with interest in the economy and investing. Neither SRSrocco Report nor any of its owners, officers, directors, employees, subsidiaries, affiliates, licensors, service and content providers, producers or agents provide financial advisement services. Neither do we work miracles. We provide our content and opinions to readers only so that they may make informed investment decisions. Under no circumstances should you interpret opinions which SRSrocco Report or Steve St. Angelo offers on this or any other website as financial advice.

Check back for new articles and updates at the SRSrocco Report.

END

5.OTHER COMMODITIES/

end

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings THURSDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN AT 6.3674

OFFSHORE YUAN: 6.3739

HANG SANG CLOSED DOWN 482.99 PTS OR 1.99%

2. Nikkei closed DOWN 841.03 PTS OR 3.11%

3. Europe stocks ALL MIXED

USA dollar INDEX UP TO 97.07/Euro FALLS TO 1.1162-

3b Japan 10 YR bond yield: RISES TO. +.159/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 115.74/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 88.05 and Brent: 90.71-

3f Gold UP /JAPANESE Yen DOWN CHINESE YUAN: ON -SHORE CLOSED UP// OFF- SHORE UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO -.0.036%/Italian 10 Yr bond yield RISES to 1.32% /SPAIN 10 YR BOND YIELD RISES TO 0.68%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 1.37: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield RISES TO : 1.68

3k Gold at $1807.20 silver at: 23.08 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3l USA vs Russian rouble;// Russian rouble UP 114/100 in roubles/dollar AT 78.01

3m oil into the 88 dollar handle for WTI and 90 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 115.24 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning .9308– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0390 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 1.843 DOWN 3 BASIS PTS

USA 30 YR BOND YIELD: 2.120 DOWN 5 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 13.63

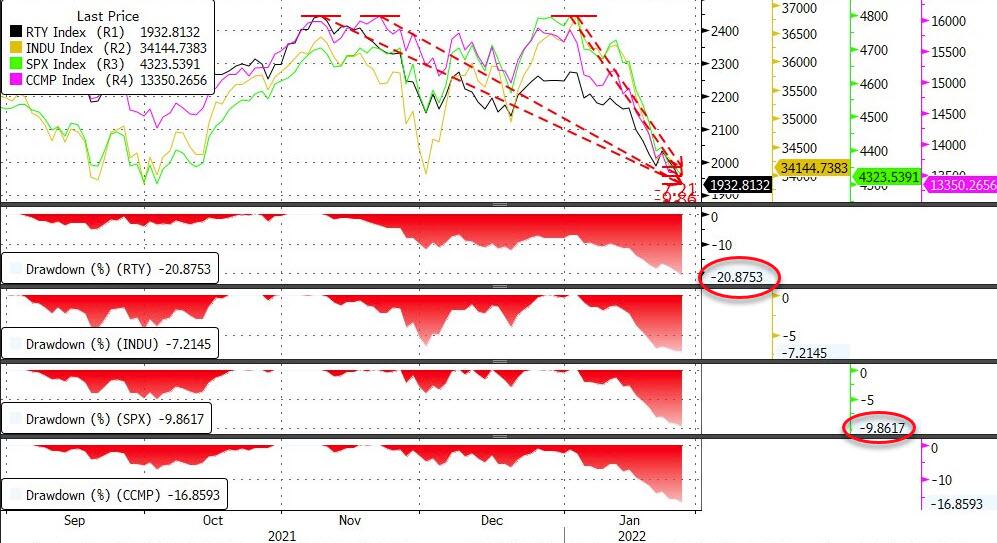

Futures Swing Wildly In Overnight Rollercoaster Session Before Settling Flat

THURSDAY, JAN 27, 2022 – 07:52 AM

After a rollercoaster overnight session, which saw S&P futures tumble as much as 2%, dropping as low as 4,260 following Powell’s hawkish comments, futures have recovered and briefly traded in the green while European stocks are still red though trading near session highs as traders spooked by the Fed’s comments started digging for bargains. At 7:20am ET (incredibly illiquid) emini S&P futures were flat at 4,341, Dow futures were up 0.1% or 36 points and Nasdaq futures swung the most and after dropping as much as 2.2% turned green some 0.5% higher or 75 points after Bill Ackman revealed late on Wednesday he had purchased 3.1 million Netflix shares.

The yield curve shrank to the flattest since 2020 after the meeting. Two-year Treasuries extended declines, though longer-dated ones rebounded. The dollar extended gains. Oil fluctuated as calm reigned for crypto. Expectations of Fed tightening sent the policy-sensitive U.S. two-year yield to 1.208%, levels last reached in February 2020. The benchmark 10-year yield slipped slightly to 1.835% having hit a high of 1.88% on Wednesday. The spread between the 10 and two-year bond yields fell to its narrowest since late 2020 as investors priced in a faster pace of rate rises in the medium-term. This in turn helped the dollar to its highest since June 2020 and sent the euro to its lowest in 19-months. The single currency dropped 0.5% to $1.1182 .

In U.S. premarket trading, Tesla fell after signaling supply chain troubles, while Intel slid as it warned on profit margins. Qualtrics International on the other hand, jumped after posting a better-than-expected revenue forecast. Netflix gained as much as 4.8% after hedge fund founder Bill Ackman said he has acquired more than 3.1 million shares in the online video streaming giant. Meanwhile, Teradyne plunged 18% in premarket after the chip-testing firm’s first-quarter earnings forecast fell short of estimates due to to supply constraints and a drop in demand stemming from a slow transition at one of its customers. Other notable premarket movers:

- DouYu (DOYU US) shares jump 10% in U.S. premarket trading after Reuters reports that Tencent plans to take the live game streaming company private, citing people with knowledge of the matter.

- Teradyne (TER US) shares plunge 18% in U.S. premarket trading after the chip-testing firm’s 1Q earnings forecast fell short of estimates due to to supply constraints and a drop in demand stemming from a slow transition at one of its customers.

- Levi Strauss (LEVI US) shares surge 8.3% in premarket trading after the jeans maker gave an outlook for full-year net revenue that exceeded estimates. Analysts say momentum appears to have carried through to the start of 2022.

- Qualtrics (XM US) shares gain 11% in U.S. premarket trading after the software company gave a revenue forecast for 1Q that beat estimates. Analysts were positive on the company’s organic billings growth and said guidance is strong.

U.S. stocks have swung violently this week as investors worried about the fallout from an increasingly hawkish Federal Reserve on a broader economic recovery and company earnings. Overvalued technology-related stocks have been hit particularly hard since higher interest rates mean a bigger discount for the present value of their future profits, hurting growth stocks with the highest valuations and boosting cheap or so-called value shares.

“The hawkish tone last night from the Fed has led to a renewed rotation into value names but given the magnitude of some of the moves we have now seen in growth stocks year-to-date, we believe the opportunity set is again getting more exciting for growth investors,” said Marcus Morris-Eyton, portfolio manager at Allianz Global Investors. “We expect the market to gradually return to fundamentals now the Fed meeting has passed, and the earnings season moves into full swing.”

Investors expect the speed at which the Fed tightens policy to be the major determinant of risk sentiment in the coming months, although the U.S. central bank has said how quickly it hikes will depend on economic data and especially inflation.

“Powell (is) not committing to the size or the frequency of rate hikes and also the timing of the balance sheet reduction. I think that buys him a bit of wiggle room as to how quickly and with what velocity he wants to normalise monetary policy in the U.S.” said David Chao, global market strategist, Asia Pacific (ex-Japan) at Invesco.

European equities slump at the open but most indexes gradually fade losses. Euro Stoxx 50 is only down 0.6%, having traded off as much as 1.8%. Spain’s IBEX outperforms, turning an initial 1.5% drop into a gain of as much as 0.8%. Banks and autos are the best performers.

Weeks of fretting over the Fed’s plan to combat inflation with higher interest rates is coming to fruition as Asian stock markets tumble into bear markets and technical corrections: Bear Markets Show Pain Across AsiaEquities as Fed Hikes Near; China Stocks Enter Bear Market as Yuan Tumbles Most in 7 Months. Bonds tumbled across Asia after Fed Chair Jerome Powell’s latest hawkish pivot, with Australian and New Zealand benchmark yields spiking to fresh highs: Fed Fallout Sends Sovereign Yields Soaring to Highs Across Asia

China high-yield dollar bonds fell 1-3 cents on the dollar , according to credit traders, after the market notched its longest winning streak since July: China Junk Dollar Bonds Set for First Drop in More Than a Week. Chinese authorities are considering a proposal to dismantle China Evergrande Group by selling the bulk of its assets: China Weighs Dismantling Evergrande to Contain Debt Crisis. The People’s Bank of China’s newfound autonomy may prove to be an unlikely source of support for the recovery: China Rushes to Deliver Stimulus as Fed Pulls Back in New Era.

Investors globally have dumped riskier assets in 2022 and sought safety as they brace for the end of nearly two years of exceptionally cheap and plentiful cash.

“What cheap money has done is provide a safety blanket from bad news,” said Jane Foley, an analyst at Rabobank. “But as this comfort blanket is pulled away, investors will be more exposed and I suspect this will create a more volatile environment for asset prices.”

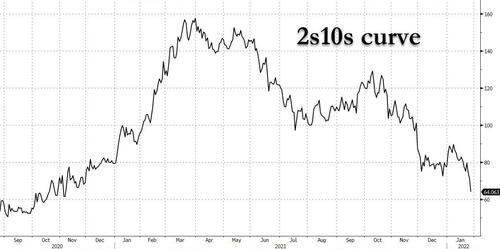

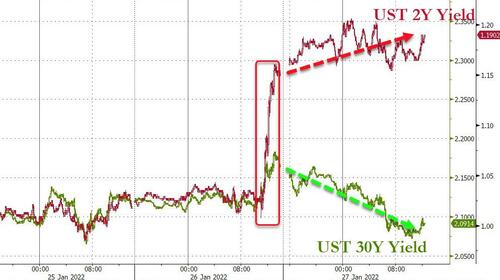

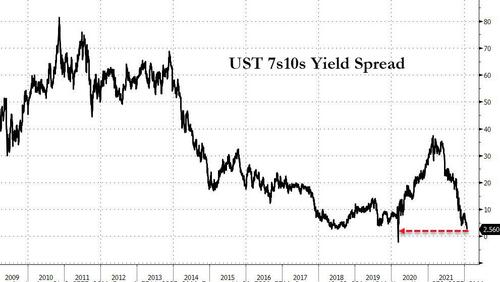

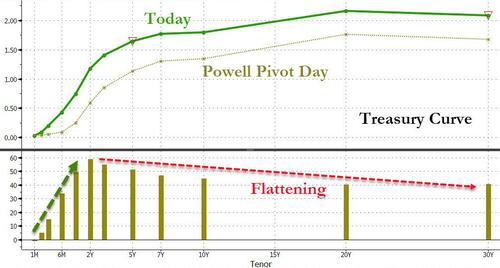

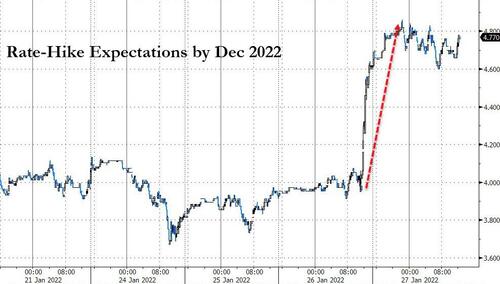

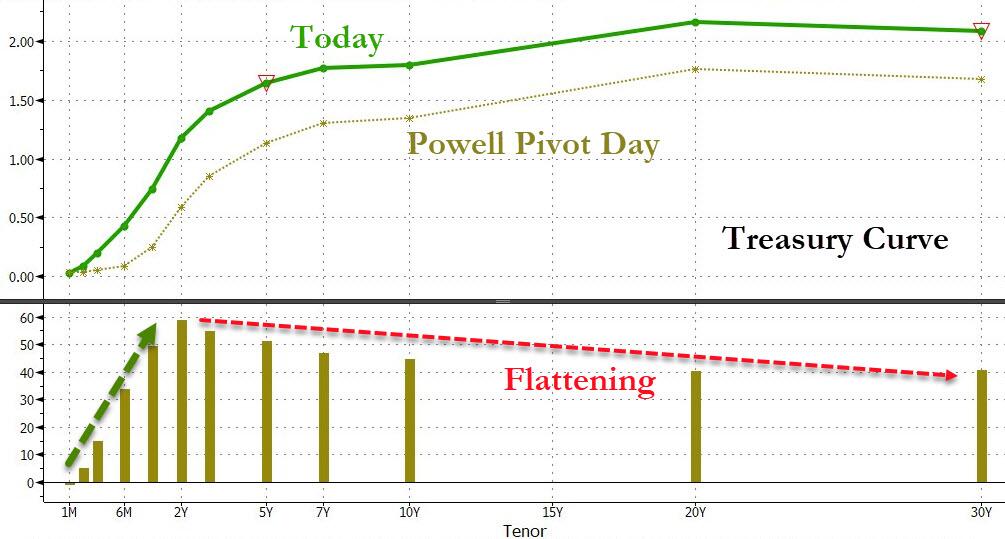

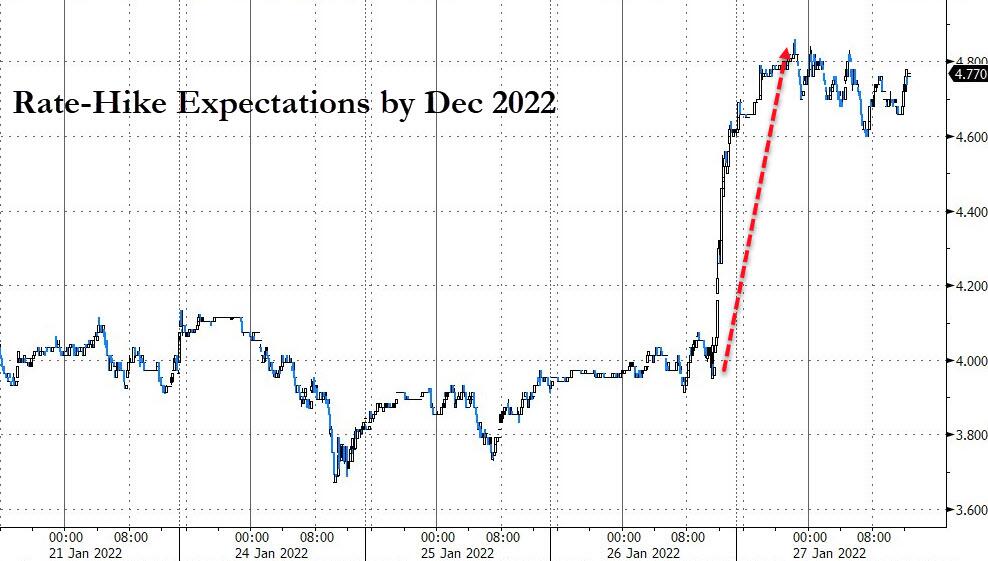

In rates, after extending post-FOMC drop late Wednesday, Treasuries began clawing their way back during Asia session and European morning led by long-end tenors, further flattening the curve. Ten-year Treasury yields slipped three basis points to 1.83% after surging to near a two-year high in the previous session, while the 2-year yield rose by 4bps to 1.19%. Yields are richer by ~5bp across 30-year sector, flattening 5s30s spread by ~3bp to tightest since March 2020; 2s10s spread is flatter by ~6bp and lowest since November 2020; the 10-year yield ~1.83% has retraced about half Wednesday’s surge to 1.876%. The ED market has boosted rate hike expectations to nearly 5 by December.

Treasury auction cycle concludes with $53b 7-year note sale at 1pm ET, following strong demand for 2- and 5-year sales earlier this week. Fed- dated OIS price in ~30bp of rate hikes for March meeting and 117bp by December after Wednesday’s post-FOMC front-end selloff. The hawkish central-bank pricing spills over into Europe: ECB-dated OIS briefly factor in a 20bps move and BOE OIS ~120bps of tightening by year end. Bunds and gilts drop, curves bear-flattening playing catch up to USTs, which bull-flatten away from their post-FOMC extremes. FOMC-dated OIS rates briefly factor in a full five hikes this year. Peripheral spreads tighten, short-end Italy and Spain outperform.

In FX, Bloomberg dollar spot trades close to session highs, adding 0.3%. The Bloomberg Dollar Spot Index rose for a fourth consecutive day as the greenback strengthened against all of its Group-of-10 peers. Hedging costs in major currencies remain relatively low, even as realized steepens and key risk events are captured by the front- end. The euro fell below $1.12 for the first time since November as traders increase bets on higher borrowing costs, with money markets now expecting five Federal Reserve interest-rate increases this year. Bunds extended a decline, sending the German 10-year yield to a one-week high as money markets bet on a faster pace of ECB policy tightening. The Canadian dollar and Norwegian krone held up best against the greenback as oil prices consolidated near a seven-year high and the pound was also among the better-performing G-10 currencies as markets rushed to price in another four interest-rate rises from the Bank of England. Other risk sensitive currencies, led by the New Zealand dollar, were the worst performers. Government bonds dropped in Australia and New Zealand, while the Australian dollar fell to a seven-week low and the New Zealand dollar slid for a sixth consecutive day to touch $0.6596, the lowest since November 2020. New Zealand’s debt auctions drew strong demand even after local data showed inflation quickened to the highest in more than three decades.

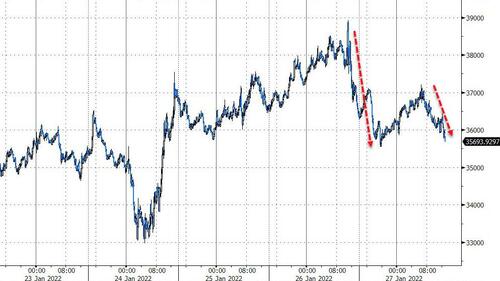

In commodities, crude futures drift back into the green. WTI adds 0.2%, rising back above $87; Brent reclaims $90. U.S. officials say they are in talks with major energy-producing countries and companies worldwide over a possible diversion of supplies to Europe if Russia invades Ukraine, although the White House said it faces challenges finding alternative sources of energy supplies. Spot gold trades off worst levels after finding support near $1,810/oz. Most base metals are in the green with LME tin up over 1%. Crypto markets declined amid broad weakness in risk assets during APAC hours; in-fitting with broader performance, crypto has staged a modest recovery during the European session. Bitcoin was last trading at $36,500.

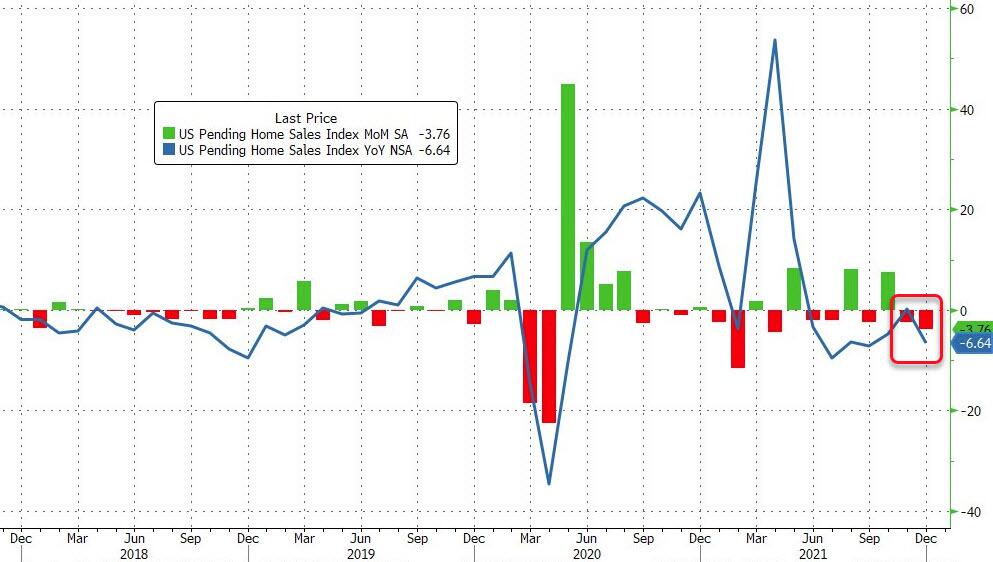

Looking at the day ahead now, data releases include the US GDP reading for Q4, along with the weekly initial jobless claims, December’s pending home sales, durable goods orders, core capital goods orders, and January’s Kansas City Fed manufacturing index. Central bank speakers include the ECB’s Scicluna, whilst earnings releases include Apple, Visa, Mastercard, Comcast, Danaher and McDonald’s.

Market Snapshot

- S&P 500 futures up 0.2% to 4,351.25

- STOXX Europe 600 down 0.4% to 465.34

- MXAP down 2.4% to 182.01

- MXAPJ down 2.1% to 598.93

- Nikkei down 3.1% to 26,170.30

- Topix down 2.6% to 1,842.44

- Hang Seng Index down 2.0% to 23,807.00

- Shanghai Composite down 1.8% to 3,394.25

- Sensex down 1.2% to 57,180.21

- Australia S&P/ASX 200 down 1.8% to 6,838.28

- Kospi down 3.5% to 2,614.49

- German 10Y yield little changed at -0.03%

- Euro down 0.4% to $1.1198

- Brent Futures down 0.3% to $89.72/bbl

- Gold spot down 0.3% to $1,814.46

- U.S. Dollar Index up 0.35% to 96.81

Top Overnight News from Bloomberg

- Spain’s labor market continued to improve in the fourth quarter, with the unemployment rate falling to the lowest since 2008, according to figures released by the nation’s statistics office, INE

- Norway’s $1.3 trillion sovereign wealth fund, the world’s biggest, returned 14.5% in 2021, equivalent to about $176 billion, after stocks rose.

- Turkey’s central bank raised its inflation projections after a collapse in the currency pushed consumer price growth to its highest in President Recep Tayyip Erdogan’s 19-year rule

A more detailed look at global markets courtesy of Newsquawk

In Asia, APAC markets sold off with risk appetite hit as the region digested the hawkish FOMC meeting. Nikkei 225 (-3.1%) suffered losses of more than 3% and with the index down more than 10% from January highs. KOSPI (-3.5%) was mired by another North Korean launch and with Samsung Electronics dwindling post- earnings. Hang Seng (-1.9%) and declined amid a slowdown in Chinese Industrial Profits andShanghai Comp. (-1.7%) with the CSI 300 Index slipping into bear market territory after falling 20% from its February 2021 peak, while developers are hit including Evergrande as investors will have to wait six months for an initial restructuring plan.

Top Asian News

- China Fintech PingPong Is Said to Weigh $1 Billion Hong Kong IPO

- Tencent Plans to Take U.S.-Listed DouYu Private: Reuters

- China Stocks Enter Bear Market as Yuan Tumbles Most in 7 Months

- Japan’s 10-Year Bond Yield Closes at Highest Level Since 2018

In Europe, major bourses in Europe are nursing the post-Fed pressure with the complex now mixed, Stoxx 600 -0.1%. In Europe, with lagging post-Intel (-3.1% pre-market) in-spite of strong numbers givensectors are mixed Tech soft guidance, with European comparables pressured post respective earnings this morning. While Financials outperform post-Fed.

Top European News

- Deutsche Bank Plans to Boost Dividend After Three-Year Drought

- Dutch Government Said to Resume Sale of Majority ABN Amro Stake

- European Gas Fluctuates With Ukraine Tensions and Mild Weather

- U.S., Other ‘Populist’ Nations Mishandled Pandemic, Study Says

In FX, hawkish Fed Powell overshadows official FOMC policy message to give a fresh boost.Greenback Franc, and underperform as Fed gets set to widen the gap between policy stances of SNB, BoJ andYen Euro ECB. Kiwi fails to benefit much from hot NZ CPI and Aussie via a poll predicting RBA tightening in November amidst the Buck’s latest bill run. Rand stands firm awaiting a SARB hike and regains some poise on technical grounds rather than anyRouble real improvement in Russian relations with the US or western nations. CBRT Minutes: the policy stance will be set taking into account the source/permanence of risks, expects the disinflation process to start on the back of measures taken. Will develop tools to support the increase of TRY assets.

In commodities, crude benchmarks have trimmed post-Fed downside in tandem with the equity recovery, as focus remains as Russia receives the US’ written response.very much on geopolitics WTI and have recaptured USD 87.00/bbl and USD 90.00/bbl respectively, and are now holding nearBrent session highs. Spot gold lies near the post-Fed trough and as such the 200- & 50-DMAs are back in view at USD 1805/oz and USD 1803/oz respectively. China Gold Association said 2021 gold consumption increased 36.5% Y/Y to 1,220.9 tons and gold output rose 10.0% Y/Y to 329.0 tons, according to Bloomberg

US Event Calendar

- 8:30am: 4Q GDP Annualized QoQ, est. 5.5%, prior 2.3%

- 8:30am: 4Q GDP Price Index, est. 6.0%, prior 6.0%

- 8:30am: 4Q Personal Consumption, est. 3.4%, prior 2.0%

- 8:30am: 4Q PCE Core QoQ, est. 4.9%, prior 4.6%

- 8:30am: Dec. Durable Goods Orders, est. -0.6%, prior 2.6%

- 8:30am: Dec. -Less Transportation, est. 0.3%, prior 0.9%

- 8:30am: Dec. Cap Goods Ship Nondef Ex Air, est. 0.5%, prior 0.3%

- 8:30am: Dec. Cap Goods Orders Nondef Ex Air, est. 0.4%, prior 0%

- 8:30am: Jan. Initial Jobless Claims, est. 265,000, prior 286,000

- 8:30am: Jan. Continuing Claims, est. 1.65m, prior 1.64m

- 10am: Dec. Pending Home Sales YoY, est. -4.0%, prior 0.2%; MoM est. -0.4%, prior -2.2%

- 11am: Jan. Kansas City Fed Manf. Activity, est. 20, prior 24

DB’s Jim Reid concludes the overnight wrap

I will be doing a Zoom webinar tomorrow at 14:00 London time on my latest chartbook, called “The Road to the next recession”. The link to register to get details of the webinar is here and the link to the chartbook is here.

The chart book also reiterates two big themes we’ve been discussing over the last year. Firstly that the Fed is hugely behind the curve and secondly that this is a totally different cycle to the last one and therefore the trends, especially on inflation, should be totally different. These themes came to a head last night after a hawkish Powell press conference that saw a major negative turnaround in equities and rates.

Upon the statement release, yields were little changed and the NASDAQ rallied around +1.0% bringing it +3.38% higher on the day, as some equity investors were enthused that asset sales appeared to be off the table. However the rhetoric towards tighter rate policy during the press conference undid equity gains immediately. The fact that the NASDAQ then dipped into negative territory before closing just +0.02% higher told the story of the presser. The NASDAQ had a 4.36% intraday range, compared with a 2.75% range Tuesday and a 5.96% range Monday. The S&P 500 closed -0.15% lower, erasing a +2.2% gain, led by real estate (-1.66%), materials (-1.02%), and industrials (-0.82%). The VIX increased for the seventh straight day for the first time since October 2020, climbing +0.8pts to 31.96, its highest level since January 2021.

Treasury yields sold off across the curve, with most of the price action taking place during the press conference: 2yr, 5yr, and 10yr yields increased +13.3bps, +13.0bps, and +9.5bps, respectively. With 2yrs seeing the biggest sell-off since the whipsaw market of March 2020. Real yields did most of the work, with real 5yr and 10yr yields increasing +14.7bps and +10.4bps, respectively. As big as the move in real yields was, there were bigger one-day increases earlier this month, which does a lot to explain how the market has evolved this year. When all was said and done, the market prices a +117% chance of a 25bp March rate hike, so a meaningful probability of a 50bp move, and 4.6 25bp hikes through 2022. In Asia 2-year US Treasury yields are +3.3bps higher with 10yr notes dipping around -1.4bps meaning a notable flattening of the yield curve to c.+65.7bp. See the first few pages of the chartbook for how the historical playbook would suggest inversion by early next year.

So what did the FOMC actually say? Well they did leave policy unchanged as expected, while the statement signalled it would soon be appropriate to raise the federal funds rate, in line with market expectations. The FOMC also released principles for reducing the balance sheet, which were more or less identical to the last round of QT. That is, the Fed will gradually decrease the size of its balance sheet by letting securities mature uninvested, not through sales, in line with our house view.

The press conference proved much more interesting though. Our US econ team has their full review here, where they have added a hike for 2022, with the base case now five. The biggest takeaway was the Chair’s emphasis that this cycle was different from the last round of tightening, in that inflation is well-above target, the labour market is historically tight, and growth projections remain above long-run potential. While the Chair demurred when asked what that specially meant for parameters of monetary policy, he did not rule out a faster pace of rate hikes or larger increments, adding that the Fed had plenty of room to tighten given the state of the labour market. This was the catalyst that sent shorter-dated yields higher, driven by real yields, as markets priced in a higher probability of an earlier and steeper policy path. Underscoring the shift towards tighter policy, he noted the Committee still viewed the balance of risk tilted towards higher inflation, and that the inflation picture had probably gotten worse since the Committee last submitted projections for the dot plot, which only contained three hikes this year. Presumably more hikes will be incorporated in the March dots.

Speaking of March, the Chair confirmed liftoff was likely to take place at the March FOMC, flagging the risks that would prevent that from happening including a worse-than-expected impact from Omicron (which he noted should not be persistent), and intimated geopolitical risks could pose an issue. So March, and every subsequent meeting should be treated as live with a 50bp hike at some point an increasing possibility.

On balance sheet policy, the Chair noted no decisions were made, and that conversations would continue at upcoming meetings (plural), implicitly matching our US econ team’s timeline that QT will begin after multiple rate hikes. He re-emphasized the message laid out in the balance sheet principles document that the Fed will set caps and let securities mature at a predictable pace, adjusting parameters as needed, but the Committee would rely on rate policy to control monetary policy.

Away from the Fed, one of yesterday’s biggest headlines was another surge in oil prices, with Brent crude finishing a shade below $90/bbl in trading for the first time since 2014. That came as the benchmark rose +1.77% in yesterday’s session, whilst WTI was also up +2.04% to its own post-2014 high of $87.35/bbl. In addition to hopes of a return to more normal levels of mobility this year following the pandemic, growing geopolitical tensions have also supported prices lately, not least given Russia is one of the world’s biggest exporters of oil. Bear in mind it was only back in October that Brent crude closed above $80/bbl for the first time since 2018, which in turn led to growing questions that we could be heading back into a period of 1970s-style stagflation. So the $90/bbl milestone won’t be welcomed by central banks looking to get inflation back to target, nor by politicians who face growing public concern about rising petrol prices and the cost of living. This time last year it was around $55 so its going to be tough for YoY CPI around the world to normalise very quickly.

European equities rallied sharply ahead of the Fed, with the STOXX 600 (+1.68%) seeing its strongest performance of 2022 so far as the more cyclical sectors and energy led the advance. The risk-on tone meant that sovereign bonds lost ground too, with yields on 10yr bunds (+0.6bps), OATs (+0.5bps) and BTPs (+3.8bps) all rising on the day. Interestingly, the latest movements also saw another widening in peripheral spreads, with the gap between Italian and German 10yr yields widening to 140.2bps, which is their biggest gap in over a year.

Staying with fixed income, credit continues to hold in ok relative to the year’s equity moves. We did a big note yesterday looking at how in the US the relative concentrations of the S&P 500 and US IG credit indices are at extremes (link here). Indeed the top 6 equity names make up 23.4% of the index. The same names make up 2.6% of the US IG index. Indeed JPM and BoA alone make up around 4.1% so if tech leads any US sell-off, credit will be relatively (if not absolutely) insulated. The note also has all the equivalent European numbers. We covered it also in my CoTD where we showed that the last time the US equity market was this concentrated was during the hubris of the “nifty fifty” bluechip valuation bubble of the late 1960s/early 1970s. Please email jim-reid.thematicresearch@db.com if you want to be added to the CoTD.

Tesla was the latest mega-cap to report earnings, beating analyst revenue and earnings expectations, and reporting annual profits two-years running for the first time in the company’s history. The shares initially dropped -6.45% in after-hours trading on fears that production would remain constrained by continued supply chain issues in 2022, but share prices gradually rebounded traded around +0.3% in extended after-hours.

Asian stock markets are sharply lower this morning post the Fed. The losses are being led by the Kospi (-3.14%) as the index heavyweight Samsung electronics (-2.46%) Q4 operating profit (13.87 trillion won) fell short of average analyst estimates (14.85 trillion won). Further, reports of North Korea firing an “unidentified projectile” in the early hours have also weighed. Separately, the Nikkei (-3.02%) and Hang Seng (-2.57%) are lower. Elsewhere, the Shanghai Composite (-0.88%) and CSI (-0.99%) are going the same way after profits at China’s industrial firms grew at a slower pace in December (+4.2% y/y) from +9.0% in November.

Looking forward, equity futures in the DM world are indicating a weak start with the contracts on the S&P 500 (-1.47%) and DAX (-2.47%) trading lower again.

Staying with Asia, Michael Spencer will today host a Zoom webinar on the Economic Outlook for the region in 2022. The call is at 08:30 EST / 13:30 UK Time / 21:30 Hong Kong Time. Please Register Here to get the joining details.

For those wanting something to listen to, DB Research have released their latest podcast (link here) on Industrials, a sector often said to be an economic bellwether, featuring lead analyst for US multi-industry and machinery research, Nicole DeBlase and Luke Templeman from my team. They discuss how the sector will fair this year as the Fed begins to raise interest rates, as well as how companies are dealing with the rampant input cost inflation they are experiencing. They also discuss how infrastructure bills can influence the sector.

On the Ukraine front, the buzz of headlines continues. Yesterday, the US embassy in Kyiv encouraged its citizens to leave the country, while the State Department responded to Russia’s security demands through a written statement that was not made available to the public, but apparently set out a serious diplomatic path forward.

The other central bank decision yesterday came from the Bank of Canada, who kept rates on hold at 0.25%. That said, they signalled that rate hikes could soon begin, with their statement saying that the Governing Council thought that “overall slack in the economy is absorbed”, and thus they ended their commitment to keeping policy rates at the effective lower bound, saying that they expect “interest rates will need to increase.” Investors are pricing a decent chance of that happening at the next meeting in March, with overnight index swaps pointing to a 94% probability of a hike.

There wasn’t much data of note yesterday, though US new home sales rose to an annualised rate of 811k in December (vs. 760k expected), which is their highest level in 9 months.

To the day ahead now, and data releases include the US GDP reading for Q4, along with the weekly initial jobless claims, December’s pending home sales, durable goods orders, core capital goods orders, and January’s Kansas City Fed manufacturing index. Central bank speakers include the ECB’s Scicluna, whilst earnings releases include Apple, Visa, Mastercard, Comcast, Danaher and McDonald’s.

3. ASIAN AFFAIRS

i)THURSDAY MORNING// WEDNESDAY NIGHT

SHANGHAI CLOSED DOWN 61.42 PTS OR 1.78% //Hang Sang CLOSED DOWN 482.90 PTS OR 1.99% /The Nikkei closed DOWN 841.03 PTS OR 3.11% //Australia’s all ordinaires CLOSED DOWN 1,84% /Chinese yuan (ONSHORE) closed DOWN 6.3674 /Oil UP TO 88.05 dollars per barrel for WTI and UP TO 90.71 for Brent. Stocks in Europe OPENED ALL MIXED // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.3674. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.3728: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN AND OFF SHORE TRADING WEAKER AGAINST USA DOLLAR

3 a./NORTH KOREA/ SOUTH KOREA

///NORTH KOREA

3B JAPAN

end

3c CHINA

CHINA/

China continues its rath against Chinese citizens being too rich and too corrupt. Xi pushes for “common prosperity”. Today is the party secretary for Hangzhou (Zhou), hometown of Alibaba

(zerohedge)

CCP Expels 1st Official For Being Too Rich & Corrupt As Xi Pushes “Common Prosperity” Crackdown

WEDNESDAY, JAN 26, 2022 – 09:05 PM

President Xi’s “Common Prosperity” crackdown has finally ensnared a CCP official who allegedly participated in the “disorderly expansion of capital” by taking bribes, abusing his official power, and other violations of his “official duties” – violations that happen to be not just common, but absolutely essential to the Chinese economy, where connections to the government often leads to economic power.

After cracking down on the country’s biggest tech firms, abolishing the private tutoring industry, limiting minors to just a few hours of video games a week and launching an incipient corruption campaign, many Chinese are still wondering how President Xi’s “Common Prosperity” drive will affect them. The President has taken pains to reassure them that money seized from “monopolists” and other economic abusers will be repurposed for the public good, particularly in China’s underdeveloped rural areas.

And like any of China’s previous “anti-corruption campaigns” (including the anti-corruption drive President Xi used to sideline his enemies early during his first term as China’s paramount leader), it’s inevitable that some heads belonging to senior Communists will roll.

Unfortunately (for the targets), it looks like the latest purge has already started.Zhou Jiangyong

Bloomberg on Wednesday reported that the first CCP apparatchik to be officially expelled from the Party during the current anti-corruption crackdown is none other than Zhou Jiangyong, the former party secretary of Hangzhou, the hometown of Alibaba. Zhou was implicated in a major corruption scandal besides Alibaba and Ant Group, which we reported on late last week.

Reports on the corrupt relationship claimed that bribes were paid by Alibaba to Zhou’s brother, who also appeared to benefit in other ways thanks to his connection to his brother.

China’s Central Commission for Discipline Inspection released a statement about the official’s ouster on Wednesday:

“Zhou Jiangyong has lost his ideals and beliefs,” the Central Commission for Discipline Inspection said. “He covertly opposed central government plans, colluded with capital, supported the disorderly expansion of capital, engaged in superstitious activities and deliberately resisted probes.”

BBG claimed that Zhou’s ouster from the party marked the first citation of “disorderly capital” in a CCDI corruption case, according to a BBG document review. Zhou, who has reportedly been under investigation since August, was also accused of colluding with family members to receive huge bribes, according to the statement.

His case has been referred to prosecutors. Corruption cases are known to occasionally carry the death penalty in China.

Zhou wasn’t the only official expelled from the Party Wednesday over corruption allegations Wednesday: The CCDI also declared that He Xingxiang, a former vice president of China Development Bank, had been expelled from the Party for “serious” violations of the law, including the misuse of financial approval rights, which had created “major risks” and “huge losses” for the country.

The anti-graft authority had reportedly announced last week that it would crack down on “disorderly expansion of capital” when investigating corruption and “monopolistic” enterprises in the country. Efforts will be made to sever “the link between power and capital,” the CCDI said. “Show no mercy to those who engage in political gangs, small circles, and interest groups within the party, and strictly educate, manage and supervise young cadres.”

Hopefully, family members of China’s paramount leaders, many of whom have enjoyed an explosion of wealth thanks to their familial ties, aren’t too worried. After all, the CCP has expelled foreign reporters who have dared to report on the wealth held by members of President Xi’s family.

end

China’s plunge protection team to the rescue…

(zerohedge)

China’s “National Team” Rushes To Save Stocks After Bear Market Signaled

THURSDAY, JAN 27, 2022 – 08:20 AM

China’s equity benchmark tumbled into a bear market while the yuan plunged the most in seven months following the Federal Reserve’s ultra hawkish comments.

On Thursday, the CSI 300 Index sank 2% to the lowest level since September 2020 and officially entered a bear market, which means the main equity index is down more than 20%.

It was only a matter of time before China’s “National Team” (the local plunge protection team) used political pressure on funds and state media outlets to soothe fears. Local media reported seven of China’s ten largest fund-management companies, including E Fund Management Co. and GF Fund Management Co., were putting money to work and buying stocks, according to WSJ.

A day earlier, state-owned Securities Times published a story on the front page that blamed domestic institutional investors for the downdraft in onshore-listed stocks for their short-term investment outlooks. The article called upon the investment community, such as brokerage firms, fund managers, insurers, and other institutions, to “stiffen the spine” and support capital markets amid surging volatility.

Beijing has often used state media outlets to urge big investors to buy the dip. The verbal intervention shows authorities are concerned about capital markets and are increasing support following a round of central bank easing.

The statements this week from China’s National Team were very similar to ones in late July 2021 when Chinese stocks suffered historic losses and Hong Kong’s technology sector imploded. This eventually led to a multi-week rally.

“Even though domestic A-shares are holding up relatively better than others, investors may be offloading them before the long Chinese New Year holiday taking cues from the Fed-driven volatility,” said Marvin Chen, a strategist at Bloomberg Intelligence.

He expected ample liquidity to return after the holidays.

So given China’s National Team is working to recover beaten-down stocks, and the People’s Bank of China is easing, the question foreign investors have: is it time to buy the dip? To answer this question is Asia equity strategist at JPMorgan Chase & Co. Mixo Das, who told Bloomberg this week:

“Within Asia, if you just follow policy, China is definitely the place to be,” Das said, adding the investment bank had upgraded Chinese equities to overweight just weeks ago.

4/EUROPEAN AFFAIRS

//EUROPE/COVID/

end

UK/WALES/VACCINE MANDATE

END

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

UKRAINE/RUSSIA/USA/ EU/UK/NATO

Russia and the UKraine agree to uphold the Donbass ceasefire in talks

(Dave DeCamp/Antiwar.com)

Russia, Ukraine Agree To Uphold Donbas Ceasefire In Normandy Format Talks

THURSDAY, JAN 27, 2022 – 07:25 AM

Authored by Dave DeCamp via AntiWar.com,

Officials from Russia and Ukraine met in Paris on Wednesday and held what Moscow described as “tough” talks. Despite whatever difficulties there were, the two sides agreed that the ceasefire in Ukraine’s eastern Donbas region must be upheld.

German and French officials were also present for the meeting, which lasted eight hours. The four countries started holding talks together after the Donbas war started in 2014 in a forum known as the Normandy format.

Russia and Ukraine signed the Minsk agreements during Normandy format talks in 2014 and 2015 that established a ceasefire in the Donbas. While there have been occasional flare-ups, the war has essentially been at a stalemate since 2015.

Russian envoy Dmitry Kozak said that “despite all the differences in interpretations (of the Minsk agreements), we agreed that the ceasefire must be maintained by all the parties in line with the accords.” He also said the next Normandy format meeting will take place in two weeks in Berlin.

The talks were held at the Elysee, the residence of French President Emmanuel Macron. In a statement, the Elysee said that the envoys “support unconditional respect for the ceasefire and full adherence to the ceasefire strengthening measures of July 22, 2020, regardless of differences on other issues relating to the implementation of the Minsk agreements.”

Prior Normandy four talks which took place on December 9, 2019 in Paris…AFP via Getty Images