FEB3

FEB3

· by harveyorgan · in Uncategorized · Leave a comment ·Edit

GOLD; DOWN $5.55 to $1803.80

SILVER: $22.36 DOWN 35 CENTS

ACCESS MARKET: GOLD: 1807.00..

SILVER: $22.65

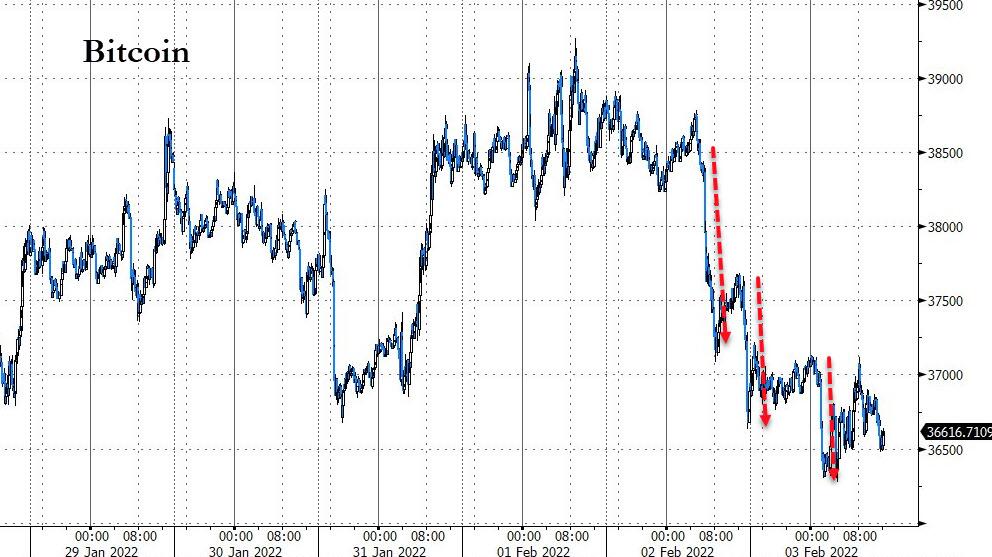

Bitcoin: morning price: 36,220 DOWN 1319

Bitcoin: afternoon price: 36,497 DOWN 1042

Platinum price: closing down $4.35 to $1035.25

Palladium price; closing down $4.10 at $2333.50

END

end

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

comex notices//JPMorgan notices filed COMEX//NOTICES:EXCHANGE: COMEX FILED: 158/469

EXCHANGE: COMEX

CONTRACT: FEBRUARY 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,809.200000000 USD

INTENT DATE: 02/02/2022 DELIVERY DATE: 02/04/2022

FIRM ORG FIRM NAME ISSUED STOPPED

118 C MACQUARIE FUT 57

132 C SG AMERICAS 1

332 H STANDARD CHARTE 11

363 H WELLS FARGO SEC 6

435 H SCOTIA CAPITAL 1

624 H BOFA SECURITIES 182

657 C MORGAN STANLEY 2

661 C JP MORGAN 79

661 H JP MORGAN 79

709 C BARCLAYS 46

732 C RBC CAP MARKETS 2

800 C MAREX SPEC 14 2

880 H CITIGROUP 450

905 C ADM 4 2

TOTAL: 469 469

MONTH TO DATE: 15,698

NUMBER OF NOTICES FILED TODAY FOR FEB. CONTRACT: 469 NOTICE(S) FOR 46,900 OZ (1.4587 TONNES)

total notices so far: 15,698 contracts for 1,569,800 oz (48.827 tonnes)

SILVER NOTICES:

117 NOTICE(S) FILED TODAY FOR 585,000 OZ/

total number of notices filed so far this month 1139 : for 5,695,000 oz

GLD

WITH GOLD DOWN $5.55

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

A HUGE CHANGE IN GOLD INVENTORY AT THE GLD// A WITHDRAWAL OF 1.45 TONNES FROM THE GLD//

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

CLOSING INVENTORY: 1016.59 TONNES/

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 35 CENTS:/: NO CHANGES IN SILVER INVENTORY AT THE SLV/

AT THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY SLV/ TONIGHT: 539.212 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A STRONG 1469 CONTRACTS TO 147,671 AND RESTS FURTHER FROM THE NEW RECORD OF 244,710, SET FEB 25/2020 AND DESPITE THIS STRONG LOSS IN OI, IT WAS ACCOMPANIED WITH OUR GOOD $0.15 GAIN IN SILVER PRICING AT THE COMEX ON WEDNESDAY. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.15) BUT WERE SUCCESSFUL IN KNOCKING OUT A FEW SILVER LONGS AS WE HAD A STRONG LOSS OF 1185 CONTRACTS ON OUR TWO EXCHANGES .

WE MUST HAVE HAD:

I) HUGE BANKER SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A SMALL ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A HUGE INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 4.110 MILLION OZ FOLLOWED BY TODAY’S 625,000 OZ QUEUE JUMP//NEW STANDING 5.870 MILLION OZ. V) STRONG SIZED COMEX OI LOSS.

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS -34

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS FEB. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF FEB:

TOTAL CONTACTS for 3 days, total contracts: : 1683 contracts or 8.415 million oz OR2.804 MILLION OZ PER DAY. (561 CONTRACTS PER DAY)

TOTAL NO OF OZ UNDERGOING EFP TO LONDON 1683 CONTRACTS X 5,000 PER CONTRACT:

EQUATES TO: 8.415 MILLION OZ

.

LAST 10 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 8.415 MILLION OZ//

SPREADING OPERATIONS

(/NOW SWITCHING TO SILVER) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF MAR.WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF JAN HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB, FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (MAR), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

RESULT: WE HAD A STRONG SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1469 DESPITE OUR $0.15 GAIN SILVER PRICING AT THE COMEX// WEDNESDAY THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE OF 250 CONTRACTS( 250 CONTRACTS ISSUED FOR MAR AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR FEB OF 4.1 MILLION OZ FOLLOWED BY TODAY’S 625,000 OZ QUEUE JUMP //NEW STANDING 5.870, MILLION OZ// .. WE HAD A STRONG SIZED LOSS OF 1219 OI CONTRACTS ON THE TWO EXCHANGES FOR 6.095 MILLION OZ//

WE HAD 117 NOTICES FILED TODAY FOR 585,000 OZ

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A FAIR SIZED 2982 TO 512,349 AND FURTHER FROM OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: — 55 CONTRACTS

.

THE FAIR SIZED DECREASE IN COMEX OI CAME DESPITE OUR GAIN IN PRICE OF $7.95//COMEX GOLD TRADING/WEDNESDAY/.AS IN SILVER WE MUST HAD HUGE BANKER/ALGO SHORT COVERING ACCOMPANYING OUR SMALL SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD SOME LONG LIQUIDATION AS THE TOTAL LOSS ON OUR TWO EXCHANGES TOTALED 2214 CONTRACTS…

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR FEB AT 64.3 TONNES FOLLOWED BY TODAY’S 98,400 OZ E.F.P. JUMP TO LONDON //NEW STANDING: 59.511 TONNES

YET ALL OF..THIS HAPPENED WITH OUR GAIN IN PRICE OF $7.95 WITH RESPECT TO TUESDAY’S TRADING

WE HAD A SMALL SIZED LOSS OF 2214 OI CONTRACTS (6.886 PAPER TONNES) ON OUR TWO EXCHANGES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALLED A SMALL SIZED 768 CONTRACTS:

FOR APRIL 768 ALL OTHER MONTHS ZERO//TOTAL:768

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 512,349.

IN ESSENCE WE HAVE A SMALL SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2214, WITH 2,982 CONTRACTS DECREASED AT THE COMEX AND 768 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 2159 CONTRACTS OR 6.715TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (768) ACCOMPANYING THE FAIR SIZED LOSS IN COMEX OI (2927,): TOTAL LOSS IN THE TWO EXCHANGES 2159 CONTRACTS. WE NO DOUBT HAD 1) HUGE BANKER SHORT COVERING ,2.) HUGE INITIAL STANDING AT THE GOLD COMEX FOR FEB. AT 64.30 TONNES WHICH FOLLOWS TODAY’S HUGE EFP JUMP TO LONDON OF 98,400 OZ//NEW STANDING 59.511 TONNES// 3)SOME LONG LIQUIDATION ,4) FAIR SIZED COMEX OI. LOSS 5) SMALL ISSUANCE OF EXCHANGE FOR PHYSICAL

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

FEB

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF FEB :

3859 CONTRACTS OR 385,900 oz OR 12.00 TONNES 3 TRADING DAY(S) AND THUS AVERAGING: 1286 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 3 TRADING DAY(S) IN TONNES: 12.00 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2020, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 12.00/3550 x 100% TONNES 0.330% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 145.12 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 12.000 TONNES//INITIAL

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A STRONG SIZED 1469 CONTRACTS TO 147,701 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 4 1/2 YEARS AGO.

EFP ISSUANCE 250 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 250 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 250 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 1435 CONTRACTS AND ADD TO THE 250 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A STRONG SIZED LOSS OF 1219 OPEN INTEREST CONTRACT FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES 6.095 MILLION OZ,

OCCURRED WITH OUR $0.15 GAIN IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

5. Other gold commentaries

6. Commodity commentaries/cryptocurrencies

3. ASIAN AFFAIRS

i)THURSDAY MORNING// WEDNESDAY NIGHT

SHANGHAI CLOSED //Hang Sang CLOSED /The Nikkei closed DOWN 299.29 PTS OR 1.06% //Australia’s all ordinaires CLOSED DOWN 0.34% /Chinese yuan (ONSHORE) closed HOLIDAY /Oil DOWN TO 87.01 dollars per barrel for WTI and DOWN TO 88.58 for Brent. Stocks in Europe OPENED MOSTLY RED EXCEPT SPAIN // ONSHORE YUAN CLOSED XX AGAINST THE DOLLAR AT XXX. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.3637: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN AND OFF SHORE TRADING WEAKER AGAINST USA DOLLAR

A)NORTH KOREA//USA/OUTLINE

b) REPORT ON JAPAN

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 2982 CONTRACTS AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX DECREASE OCCURRED DESPITE OUR GAIN OF $7.95 IN GOLD PRICING WEDNESDAY’S COMEX TRADING. WE ALSO HAD A SMALL SIZED EFP (768 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE ACTIVE DELIVERY MONTH OF FEB.. THE CME REPORTS THAT THE BANKERS ISSUED A SMALL SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 768 EFP CONTRACTS WERE ISSUED: ;: , & FEB. 0 APRIL: 768 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 768 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A SMALL SIZED 2214 TOTAL CONTRACTS IN THAT 768 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED COMEX OI LOSS OF 2982 CONTRACTS..

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING FOR FEB (59.511),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

FEB 2022: 59.511 TONNES

THE BANKERS WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $7.95) BUT THEY WERE SUCCESSFUL IN FLEECING SOME LONGS AS WE HAVE REGISTERED A LOSS OF 6.876 TONNES OF TOTAL OI, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR FEB (59.511 TONNES)…

WE HAD –55 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 2214 CONTRACTS OR 221,400 OZ OR 6.886 TONNES

Estimated gold volume today: 168,787 /// poor

Confirmed volume yesterday: 130,391contracts poor

INITIAL STANDINGS FOR FEB ’22 COMEX GOLD //FEB 3

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 32,247.450 oz Brinks1003 kilobars |

| Deposit to the Dealer Inventory in oz | nilOZ |

| Deposits to the Customer Inventory, in oz | 96.453 oz Manfra 3 kilobars |

| No of oz served (contracts) today | 469 notice(s )46,900 OZ 1.4587 TONNES |

| No of oz to be served (notices) | 3435 contracts 343,500 oz 10.684 TONNES |

| Total monthly oz gold served (contracts) so far this month | 15,698 notices 1,569,800 OZ 48.827 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For today:

No dealer deposit 0

No dealer withdrawal 0

1 customer deposit

i) Into Manfra: 96.453 oz (3 kilobars)

total deposit: 96.453 oz oz

1 customer withdrawals

i) Out of Brinks: 32,247.450 oz

total withdrawals: 32,247.450 oz

ADJUSTMENTS: 1//dealer to customer

i) Out of JPMorgan: 25,665.733 oz oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JANUARY.

For the front month of FEBRUARY we have an oi of 3904 stand for LOSING 3676 contracts.

We had 2692 contracts served upon yesterday, so we lost 984 contracts or an additional 98,400 oz will not stand on this side of the pond and

these guys were E.F.P.’d to London where they received a handsome bonus for their effort. Looks like no gold to be found over here.

The month of March saw a loss of 68 contracts and thus the OI standing is 5382.

April saw a loss of 699 contracts up to 396,531.

We had 469 notice(s) filed today for 46900 oz FOR THE FEB 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 158 contract(s) of which 79 notices were stopped (received) by j.P. Morgan dealer and 79 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 5900 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the FEB /2021. contract month,

we take the total number of notices filed so far for the month (15,698) x 100 oz , to which we add the difference between the open interest for the front month of (FEB: 3904 CONTRACTS ) minus the number of notices served upon today 469 x 100 oz per contract equals 2,011,700 OZ OR 62.572 TONNES the number of TONNES standing in this active month of FEB.

thus the INITIAL standings for gold for the JAN contract month:

No of notices filed so far (15,698) x 100 oz+ (3904) OI for the front month minus the number of notices served upon today (469} x 100 oz} which equals 2,014,800 oz standing OR 59.511 TONNES in this active delivery month of FEB.

We lost 984 contracts or an additional 98,400 oz will not stand over here and were EFP’d. to London

TOTAL COMEX GOLD STANDING: 59.511 TONNES (HUGE FOR A FEBRUARY DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

157,392.690, oz NOW PLEDGED /HSBC 4.89 TONNES

125,410.592 PLEDGED MANFRA 2.90 TONNES

54,339.114oz PLEDGED JPMorgan no 1 1.690

288,481,604, oz JPM No 2 8.97 TONNES

898,821.330 oz pledged Brinks/27,96 TONNES

12,249,333 oz International Delaware: 0..3810 tonne

Loomis: 18,615.429 oz

total pledged gold: 1,553,863.297 oz 48.331 tonnes

TOTAL REGISTERED AND ELIZ GOLD AT THE COMEX: 32,759,998.479 OZ (1018.97 TONNES)

TOTAL ELIGIBLE GOLD: 15,437,286.855 OZ (480.16 tonnes)

TOTAL OF ALL REGISTERED GOLD: 17,322,711.624 OZ (538.81 tonnes)

REGISTERED GOLD THAT CAN BE SERVED UPON: 15,768,848.0 OZ (REG GOLD- PLEDGED GOLD) 490.48 tonnes

END

FEBRUARY 2022 CONTRACT MONTH//SILVER

INITIAL STANDING FOR SILVER//FEB 3

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1,911,188.931 oz Brinks CNT Manfra Delaware JPMorgan |

| Deposits to the Dealer Inventory | nilOZ |

| Deposits to the Customer Inventory | 603,729.030 oz CNT Delaware |

| No of oz served today (contracts) | 117CONTRACT(S) 585,000 OZ) |

| No of oz to be served (notices) | 35 contracts (175,000 oz) |

| Total monthly oz silver served (contracts) | 1139 contracts 5,695,000, oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

we had 0 deposits into the dealer

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 2 deposits

i) Into CNT: 599,836.880 oz

ii) Into Delaware: 3892.5 oz

JPMorgan has a total silver weight: 184.65 million oz/351.801 million =52.47% of comex

ii) Comex withdrawals: 5

a)Brinks: 639,180.946 oz

b) CNT; 205,350.025 oz

c)Manfra: 481,359.190 oz

d) Delaware: 2025.87 oz

e)JPMorgan: 583,272.920 oz

total withdrawal 1,911,188.931 oz

we had 4 adjustments: all dealer to customer

Brinks: 14,906.06 oz

ii) CNT: 5029.34 oz

iii))JPMorgan: 45,174.830 oz

iv) Manfra 14,740.470 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 81.864 MILLION OZ

TOTAL REG + ELIG. 351.801 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR FEBRUARY

silver open interest data:

FRONT MONTH OF FEB//2022 OI: 152 CONTRACTS LOSING 283 contracts on the day. We had 408 contracts served upon yesterday.

So we gained 125 contracts or an additional 625,000 oz will stand for silver on this side of the pond.

FOR MARCH WE HAD A loss OF 2203 CONTRACTS UP TO 104,211 CONTRACTS.

APRIL HAD A SMALL GAIN OF 6 CONTRACTS UP TO 21

MAY HAD A GAIN OF 910 CONTRACTS UP TO 26,889 contracts

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 117 for 585,000 oz

Comex volumes: 59,336// est. volume today//weak

Comex volume: confirmed YESTERDAY: 42,300 contracts (weak)

To calculate the number of silver ounces that will stand for delivery in FEB. we take the total number of notices filed for the month so far at 1139 x 5,000 oz =. 5,695,000 oz

to which we add the difference between the open interest for the front month of FEB (152) and the number of notices served upon today 117 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the FEB./2021 contract month: 1139 (notices served so far) x 5000 oz + OI for front month of FEB (152) – number of notices served upon today (117) x 5000 oz of silver standing for the FEB contract month equates 5,870,000 oz. .

We gained 125 CONTRACTS OR 625,000 ADDITIONAL oz of silver will stand at the comex.

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

GLD

FEB 3/WITH GOLD DOWN $5.55: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD////INVENTORY RESTS AT 1016.59 TONNES

FEB 2/WITH GOLD UP $7.95//A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.78 TONES OF GOLD INTO THE GLD////INVENTORY RESTS AT 1018.04 TONNES

FEB 1/WITH GOLD UP $5.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1014.26 TONNES

JAN 31/WITH GOLD UP $10.10//NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1014.26 TONNES

JAN 28/WITH GOLD DOWN $8.30//NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1014.26 TONNES

JAN 27/WITH GOLD DOWN $36.15//ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.16 TONNES INTO THE GLD.//INVENTORY RESTS AT 1014.26 TONNES

JAN 26/WITH GOLD DOWN $21.60 A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.65 TONNES INTO THE GLD///INVENTORY RESTS AT 1013.10 TONNES

JAN 25/WITH GOLD UP $10.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1008.45 TONNES

JAN 24/WITH GOLD UP $10.10 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: AN UNBELIEVABLE DEPOSIT OF 27.59 TONNES INTO THE GLD//INVENTORY RESTS AT 1008.45 TONNES

JAN 21/WITH GOLD DOWN $10.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 980.86 TONNES

JAN 20/WITH GOLD UP $.20 TODAY: A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .58 TONNES FROM THE GLD///INVENTORY RESTS AT 980.86 TONNES

JAN 19/WITH GOLD UP $29.65 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 5.27 TONNES INTO THE GLD/INVENTORY RESTS AT 981.44 TONNES

JAN 18/WITH GOLD DOWN $3.25//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 976.21 TONNES

JAN 14/ WITH GOLD DOWN $5.25/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 976.21 TONNES

JAN 13/WITH GOLD DOWN $5.75: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 976.21 TONNES

JAN 12/WITH GOLD UP $8.65//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 976.21 TONNES

JAN 11/WITH GOLD UP $19.25/A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES FROM THE GLD/INVENTORY RESTS AT 976.21 TONNES

JAN 10/WITH GOLD UP $2.00/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 977.08 TONNES

JAN 7/WITH GOLD UP $8.15//A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWLA OF 1.16 TONNES FROM THE GLD////INVENTORY RESTS AT 978.83 TONNES

JAN 6/WITH GOLD DOWN $35.30//A SMALL CHANGE IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF .32 TONNES/INVENTORY RESTS AT 979.99 TONNES

JAN 5/WITH GOLD UP $10.30: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 980.31 TONNES

Jan 4/WITH GOLD UP $14.00//A HUGE CHANGE OF 4.65 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 980.31 TONNES

JAN 3/WITH GOLD DOWN $26.70: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 975.66 TONNES

CLOSING INVENTORY: 1016.59 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

SLV

FEB 3/WITH SILVER DOWN 35 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT539.212 MILLION OZ//

FEB 2/WITH SILVER UP 15 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.411 MILLION OZ INTO THE SLV.//INVENTORY RESTS AT 539.212 MILLION OZ/

FEB 1/WITH SILVER UP 18 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 533.801 MILLION OZ

JAN 31/WITH SILVER UP 7 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.202 MILLION OZ FORM THE SLV.//INVENTORY RESTS AT 533.801 MILLION OZ//

JAN 28/WITH SILVER DOWN 36 CENTS : NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 535.003 MILLION OZ//

JAN 27/WITH SILVER DOWN $1.13 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 535.003 MILLION OZ//

JAN 26/WITH SILVER DOWN 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 535.003 MILLION OZ//

JAN 25/WITH SILVER UP 10 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.311 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 535.003 MILLION OZ/

.JAN 24/WITH SILVER DOWN 48 CENTS TODAY: A MASSIVE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.8 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 532.692 MILLION OZ//.

JAN 21/WITH SILVER DOWN 41 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 527.792 MILLION OZ

JAN 20/WITH SILVER UP 52 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.998 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 527.792 MILLION OZ

JAN 19/WITH SILVER UP 71 CENTS TODAY: A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.942 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 525.804 MILLION OZ

JAN 18/WITH SILVER UP 51 CENTS TODAY: TWO HUGE CHANGES IN SILVER INVENTORY AT THE SLV: 2 WITHDRAWALS OF 1.11 MILLION OZ AND 1.424 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 527.246 MILLION OZ//

JAN 14/WITH SILVER DOWN 21 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 529.780 MILLION OZ//

JAN 13/WITH SILVER DOWN 2 CENTS: A BIG CHANGE IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 832,000 OZ FROM THE SLV////INVENTORY RESTS AT 529.780 MILLION OZ

JAN 12/WITH SILVER UP 38 CENTS TODAY : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.612 MILLION OZ//

JAN 11/WITH SILVER UP 33 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.612 MILLION OZ/.

JAN 10/WITH SILVER UP 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 530.612 MILLION OZ//.

JAN 7/WITH SILVER UP 17 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.612 MILLION OZ//.

JAN 6/WITH SILVER DOWN 94 CENTS TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL PF 226,000 OZ FROM THE SLV///INVENTORY RESTS AT 530.612 MILLION OZ?/

JAN 5/WITH SILVER UP 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.838 MILLION OZ//

JAN 4/WITH SILVER UP 21 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.838 MILLION OZ//

JAN 3/WITH SILVER DOWN 45 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.219 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 530.838 MILLION OZ//

CLOSING INVENTORY: 539.212 MILLION OZ

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

Peter Schiff: The Dollar Is Monopoly Money Supported By A Ponzi Scheme

THURSDAY, FEB 03, 2022 – 11:20 AM

The national debt quietly pushed past $30 trillion on Jan. 31. But that is only the tip of the debt iceberg. The American taxpayer is on the hook for a lot more than that. In his podcast, Peter Schiff said US government borrowing and spending has turned the dollar into monopoly money propped up by a massive Ponzi Scheme.

On top of the federal government’s $30 trillion of debt, you have to add state and local government debt totaling about another $3.2 trillion. That brings the total debt to GDP ratio in the US to 142 percent. Peter called this a “shockingly high number.”

Especially when the GDP is a bunch of fluff like ours. So much of our GDP is service sector. I think only 10%, if that, is from manufacturing. So, we have a very small portion of our GDP related to producing real wealth.”

But that still doesn’t reveal the entire debt story. To really understand the country’s financial health, you also have to include unfunded liabilities. These are payments the government has promised to make in the future, including Social Security and Medicare. That adds another $160 trillion in liabilities to Uncle Sam’s balance sheet.

If you take the unfunded liabilities and add them to the funded debt, you’re at nearly $200 trillion.

As Peter said, this is completely unplayable.

It’s not going to be paid. And so what’s going to happen? Well, it’s going to be defaulted, either honestly or dishonestly.”

The honest way to default is to admit you’re broke and simply not pay.

Of course, it’s not going to do that. No one in Washington is willing to be honest with creditors. So, the other way is through inflation. And that’s what’s going to happen. We are going to inflate the debt away.”

That creates a whole new set of problems. Peter said the realization the US government is simply going to keep inflating will cause a run on the US dollar and US Treasuries.

A lot of people, including proponents of MMT, believe that we don’t really have to worry about credit quality. The US government will never default. Since the US borrows in its own currency, it can print virtually as much money as it needs to. Creditors won’t really be concerned, no matter how much debt the US government runs up.

But they will be concerned because they realize that we can’t repay the debt honestly through taxation because there’s just not enough money available from the taxpayer. When you’ve got the federal government, and the state and local governments, all looking for the same taxpayer, and that guy is broke, how are you going to repay this debt? You can’t. It’s going to be repudiated through inflation.”

Peter said there’s a big difference between getting repaid honestly out of taxation and getting paid dishonestly through inflation.

And if you think it’s going to be the latter, then you want to get out of Dodge.”

Imagine a simple society with one taxpayer, a creditor and the government. The government borrows $100 from the creditor. Now the taxpayer is on the hook for $100. If the government goes ahead and taxes the taxpayer, the creditor gets $100 and everybody is happy. (Except perhaps the taxpayer who is out $100.) Now, the government could decide it doesn’t want to tax the taxpayer. The government needs his vote. So instead, the government prints $100 out of thin air and hands it to the lender. In that case, the taxpayer has $100 and so does the creditor.

But now there’s another problem. The amount of goods and services in the economy hasn’t changed. Prices will double because the government has doubled the money supply.

Now the taxpayer, when he goes to spend his $100, well, he only gets $50 worth of stuff. So, he’s taken a loss. He doesn’t lose as much as if the government had taken his entire $100 and given it to the creditor. But he lost half his money, even though the government took nothing. But now the creditor, when he gets paid $100, he didn’t really get his money back. Because now prices have doubled. He can only buy $50 worth of stuff. Now, he got more money than he would have gotten had the government just defaulted and given him nothing. But because the government didn’t do that, they inflated — he still gets something. But he’s lost half of his purchasing power. That is a real loss. And that loss is going to be factored into the willingness of US creditors to continue to hold US Treasuries.”

Peter said he’s always gotten a big kick out of people who say we don’t have to pay the massive government debt back and claim the government can just keep borrowing indefinitely.

How can that be? If we don’t have to repay it, it’s really not debt. We’re really not borrowing if we don’t have to pay it back. And the thing is — if it’s true that we can borrow money and never pay it back, what kind of idiot is loaning us the money if we’re never going to pay it back? Because the important part about making a loan is getting paid back. That’s what it really boils down to. … The key is to get your money back.”

So, who is going to continue to loan the US money if we tell them right off the bat, “You’re never getting paid back.”?

Apparently, the plan is to pay the current lenders back by borrowing money from new people.

In other words, the reason we can keep on doing this is because it’s a giant Ponzi scheme. But again, if it’s a giant Ponzi scheme, why do people willingly participate? It’s because they don’t realize it’s a Ponzi scheme. They think they’re going to get paid back. When they realize they’re going to be paid back in monopoly money, they’re not going to want to lend. In fact, they’re not going to want to hold on to these Treasuries and the only buyer is going to be the Federal Reserve. And that’s when the printing press is going to overdrive and the dollar is going to fall through the floor.”

In this podcast, Peter also says the stock market is rotating, not crashing, weak economic data will make it harder for the Fed to tighten, the Fed may start blaming rising oil prices on a slowing economy, and 6 more weeks of winter is nothing compared to the crypto winter ahead.

end

2.LAWRIE WILLIAM//,//Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, James RICKARDS

end

end

3. Chris Powell of GATA provides to us very important physical commentaries

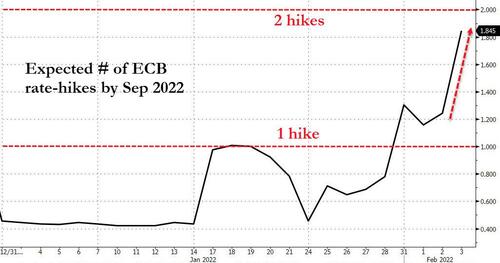

You will recall that Europe had lots of trouble trying to reach an inflation level of 2%. Now they have overshot their target.

Inflation hits a record 5.1% in January

(London’s Financial Times/GATA)

Eurozone inflation hits record 5.1% in January

Submitted by admin on Wed, 2022-02-02 11:00Section: Daily Dispatches

By Martin Arnold

Financial Times, London

Wednesday, February 2, 2022

Consumer prices in the eurozone rose by a record 5.1% in January from a year earlier, keeping inflation higher than expected and increasing the pressure on the European Central Bank to respond with tighter monetary policy.

Steeper increases in the price of energy and food were only partly offset by slower growth in prices of manufactured goods, which meant annual inflation rose from its previous eurozone record of 5% in December, Eurostat said today.

That clashed with widespread expectations of a fall in eurozone inflation. Economists polled by Reuters had on average forecast a eurozone inflation rate of 4.4% in January. …

… For the remainder of the report:

https://www.ft.com/content/ef5ce3b5-f8a6-43ca-9a4d-3a507d12dda

end

Bloomberg reports that a huge whale is picking up gold as soon as it falls below $1800.00 and they hide the purchases well

It could only get governments.

(Bloomberg/GATA)

A whale is snapping up gold below $1,800, likely a government

Submitted by admin on Wed, 2022-02-02 21:01Section: Daily Dispatches

By Eddie van der Walt

Bloomberg News

via Yahoo Finance, Sunnyvale, California

https://finance.yahoo.com/news/looks-whale-snapping-gold-bullion-124225535.html

Spot gold is again bobbing along near $1,800 an ounce, as it has been since mid-2020. The stickiness of that level, particularly as fundamentals turned more bearish, suggests there’s a big buyer somewhere in these waters.

Since breaking above the round number in July 2020, the gold price dipped below it 19 times on a closing basis, only to regain its footing. In the past year, the modeled value of gold, based on a regression study that includes the dollar, real rates, and exchanged-traded fund holdings, dropped nearly 10%. Yet the metal’s price only fell around 2%. Clearly, there is a big buyer who considers the metal a long-term hold.

Such whale activity, which shows up neither in ETF holdings nor in futures positioning, would require a substantial buyer, accumulating in size in the London over-the-counter market. Yet vault holdings reported by the London Bullion Market Association, which include both ETF and some central bank-owned metal, show only a fractional increase in the year through December, from 307 million to 309 million troy ounces.

That would suggest that whoever is buying is able to buy in scale, leave little footprint in the market, and then take delivery and store the metal in secure, invisible vaults.

And that points strongly toward a sovereign buyer.

Central banks normally declare to the International Monetary Fund the amounts of metal they have on their books. But there are precedents where this has been done with some delay. Between 2009 and 2015, China reported no change in holdings, only to reveal that it had bought 53 million ounces of metal over the period.

END

4.OTHER GOLD/SILVER COMMENTARIES

SPECIAL THANKS TO DOUG c FOR SENDING THIS TO US:

There Is An Urgent Need To Revalue The Price Of Silver

February 3, 2022 866

Even if the price of silver were to increase tenfold, it would not be enough to…

by Cyrille Jubert of CyrilleJubert.com

Open Letter to the Glasgow Financial Alliance for Net Zero (GFANZ).

Gentlemen,

First, rest assured that citizens of our planet are grateful to the United Nations and to each one of the members of your assembly for having decided to do everything possible to advance our society towards green energy. As your Financial Alliance for Net Zero brings together the most powerful financial companies in the G7, you can only succeed in this endeavour, as nothing could resist the combination of the will and energy of today’s brightest decision makers, under the leadership of President Mark Carney.

After the creation of the Alliance in April 2021 and the first working meetings late spring and during summer 2021, you must have noticed that there were bottlenecks, which should make it extremely difficult to achieve your objectives and which could only delay their implementation. Despite this, you have set a schedule with very close deadlines. Under the current market conditions, this objectives seems unrealistic. Even by changing some of the factors in the equation, you will remain in an emergency with time constraints that are difficult to compress..

Weeks and months have passed and we have been waiting for you to break these locks, which still limit your actions and your agenda

To achieve the Net Zero objectives, solar energy is brought to an increasing development by 2040, as IEA already predicted at the end of 2019.

Industrial demand, particularly for photovoltaics, has already increased sharply in 2021, bringing global silver demand to 1 029 Moz for a mining production of only 829 Moz. The World Bank anticipates a doubling of the annual demand for silver for solar PV, which should reach 3 200 tons in 2050, while mining production in 2020 was only 25 000 tons (source: USGS). Depending on the scenarios chosen, the demand for silver for green energies will have to increase by 15 000 tons (Page 96 and chart page 103 of the “Minerals for Climate Action: The Mineral Intensity of the Clean Energy Transition” Report).

The mining company South32 estimates that this new demand will require 30 Moz each year for the next 20 years, an increase of 55% but probably even 95% to reach the goal of 1.5 degrees Celsius. (Source: stockhead)

Today, silver reserves in the ground are estimated by the USGS at 500 000 tons, i.e. 20 years of production at the current rate, but less if production is accelerated.

The chart below relates very generally to the geological research budgets for non-ferrous metals, i.e. gold, silver, copper, nickel, platinum, aluminium, tin, lead and zinc. Budgets have barely increased in 2021, despite the very strong increases in some of these metals in the last quarter.

With the continued decline in the silver content of the ores, the former pure silver mines had to diversify, because the silver was no longer profitable enough. As a result, the share of world production of silver from copper, zinc, lead and tin mines is steadily increasing.

The new presidents elected in 2021 in Peru and Chile are making mining companies suffer by questioning previous policies. There will be a sharp increase in royalties paid to the states. The project for a new copper mine is blocked to stop destroying the environment. That seems to be the logic of the times. It simply means that metals will always be more expensive to produce and that their prices must go up.

Whether your name is BlackRock or StateStreet, JPM or Bank of America, to justify to your shareholders an investment in geological research and in Junior Explorers, the game must be worth the candle. However, for the moment, few silver mines are able to make a profit, simply because the price of silver is kept too low. In the Financial Alliance for Net Zero, everyone knows it.

Even if the price of silver were to increase tenfold, it would not be enough to bring it back to a normal price, given the monetary creation of recent years and the loss of purchasing power induced in the main currencies. Even at $200, few investors, who hoard to protect themselves from inflation, would agree to contribute their metal to accelerate the World photovoltaic production.

Between the time when geological research is activated, new veins are identified and the mine goes into production, it takes between 10 and 20 years. If you want to meet your 2030 and 2040 objectives, there is an urgent need to massively revalue the price of silver.

While waiting to see the Financial Alliance at work in this direction, please believe, Gentlemen, in the expression of our respectful consideration.

END

5.OTHER COMMODITIES/COTTON

6.CRYPTOCURRENCIES

Steve Brown..

end

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings THURSDAY morning 7:30 AM

ONSHORE YUAN: CLOSED XX

OFFSHORE YUAN: 6.3637

HANG SANG CLOSED

2. Nikkei closed DOWN 299.29 PTS OR 1.06%

3. Europe stocks MOSTLY RED

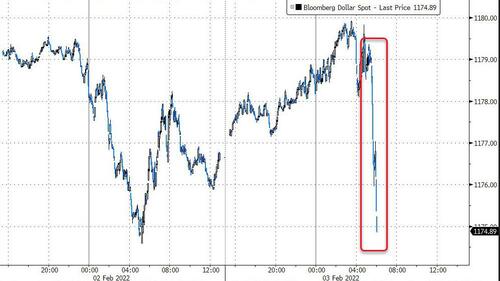

USA dollar INDEX UP TO 96.15/Euro FALLS TO 1.1295-

3b Japan 10 YR bond yield: RISES TO. +.180/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 114.87/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 87.01 and Brent: 88.58–

3f Gold DOWN /JAPANESE Yen UP CHINESE YUAN: ON -SHORE CLOSED XX// OFF- SHORE DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.0.064%/Italian 10 Yr bond yield RISES to 1.49% /SPAIN 10 YR BOND YIELD RISES TO 0.84%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 1.43: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield RISES TO : 1.95

3k Gold at $1801.95 silver at: 22.35 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3l USA vs Russian rouble;// Russian rouble DOWN 14/100 in roubles/dollar AT 76.35

3m oil into the 87 dollar handle for WTI and 88 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 114.87 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning .9221– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0418 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

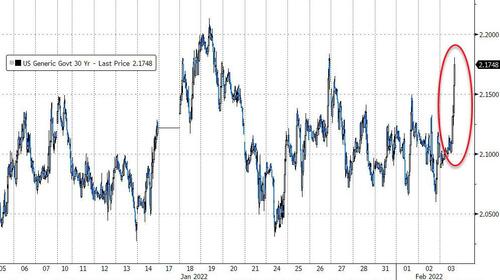

USA 10 YR BOND YIELD: 1.796 UP 2 BASIS PTS

USA 30 YR BOND YIELD: 2.132 UP 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 13.57

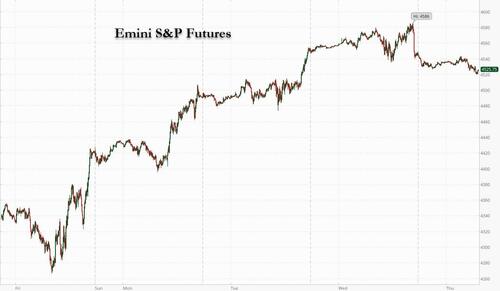

US Equity Futures Tumble After Tech Rout

THURSDAY, FEB 03, 2022 – 07:43 AM

If Google’s earnings on Tuesday sent futures sharply higher yesterday, then Facebook’s disastrous earnings report late on Wednesday has reversed almost all of the gains – US index futures are sharply lower today led by a plunge in technology stocks after a bout of disappointing earnings reports from Meta, Qualcomm and Spotify boosted concern about the market impact of the Fed tightening. Nasdaq futures tumbled 2.2%, emini S&P futs were down 50 points or 1.1% to 4527 and Dow futures were 0.4% lower. The dollar strengthened before rate decisions in Europe and the U.K.

Facebook parent Meta Platforms was on pace for its biggest drop ever and slashing its valuation by about $200 billion- the biggest in market history – after its sales forecast missed estimates amid stagnating user growth and increasing competition from TikTok. Meta shares, which had plunged 22% in late New York trading, continued its losses in Thursday’s premarket session. NVidia Corp. and Qualcomm lost more than 3.8%. Amazon.com Inc., which will post its financial results after U.S. market hours, slid 3.7%. Twitter, Spotify, Snap and Pinterest also fell, while T-Mobile US gained 7.7%.

Investors will now focus on upcoming earnings from Amazon, the last remaining tech giant, while looking past signs of a temporary soft patch in the U.S. job market, according to Ipek Ozkardeskaya, senior analyst at Swissquote.

“There are millions of jobs available in the market, and there is nothing the Fed could do to get people to work,” she wrote in a note. “What people care about is the earnings, and inflation.”

The poorly received earnings reports from the U.S. tech giants are a challenge for dip buyers hoping that corporate performance will ease worries about central bank interest-rate hikes. Markets have swung sharply and stocks are nursing losses this year as officials pare stimulus to curb inflation.

“Volatility is here to stay,” Anna Han, equity strategist at Wells Fargo Securities, said on Bloomberg Television. “Our outlook for 2022 was that we’d see more spikes in volatility. With that choppiness, with that unpredictability, investors are going to express that by compressing multiples.”

Electric vehicle stocks are sliding in premarket trading Thursday amid a broader selloff in tech and growth firms with U.S. stock index futures sinking. Lordstown Motors slides 5.2%, Workhorse falls 3.8%, Rivian slides 3.8%, Nio is 3.6% lower, Tesla drops 3%, Li Auto declines 3%, XPeng loses 2.8% and Nikola slips 1.9%. These stocks have all posted double-digit declines so far this year amid concerns of rising interest rates. Here are some of the biggest U.S. movers today:

- Meta Platforms (FB US) plunges as much as 22% in premarket trading after the Facebook- and Instagram- owner gave a revenue forecast for 1Q that missed estimates amid stagnating user growth. Other social media stocks declining premarket include: Snap (SNAP US) -16%; Pinterest (PINS US) -8.5%; Twitter (TWTR US) -8.1%

- Spotify (SPOT US) falls 9% in premarket trading after the subscription music service’s update, with quarterly growth and margin forecasts slightly missing estimates. However, analysts remain largely positive.

- Semiconductor stocks fall in premarket trading as Qualcomm (QCOM US) slides 3.2% after chip shortages hit results. Areas outside of the company’s phone sales were underwhelming. Advanced Micro Devices -2% (AMD US), Nvidia -3.2% (NVDA US), Micron -2.1% (MU US)

- T-Mobile (TMUS US) shares rise 8% in extended trading after the mobile phone service company gave a full-year outlook for postpaid customer additions that at the midpoint of the range exceeded analysts’ projections.

- Align Technology (ALGN US) falls 2.5% in premarket trading Wednesday after the company’s Invisalign case shipments for the fourth quarter missed analyst estimates.

- Cognizant Technology Solutions (CTSH US) fell 2% in extended trading on Wednesday after the IT services company reported its fourth-quarter results and outlook.

In Europe, tech and industrial companies led declines in the Stoxx Europe 600 Index, which slid as much as 0.9% to just a few points shy of Monday’s opening levels and was close to its 100-day moving average. Tech, industrials and media are the worst-performing sectors; FTSE 100 outperforms, with miners trading well following robust numbers from Shell. Compass Group jumped 8.1% to pre-pandemic levels in London after the catering-services provider reported first-quarter sales that beat estimates. Roche dropped 2.8% after the Swiss drugmaker issued a conservative forecast, saying sales of Covid-19 tests and therapies will likely wane.

The BOE hiked interest rates for the second successive meeting, taking the key rate up 25 basis points to 0.5%. Officials also signaled they would start running down their bond holdings, halting reinvestments on their gilt pile and offloading their corporate-bond portfolio.

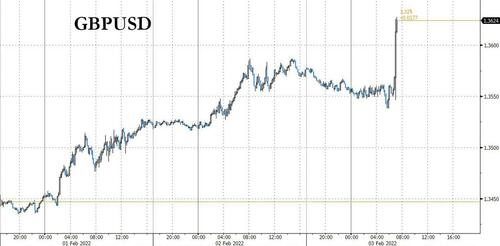

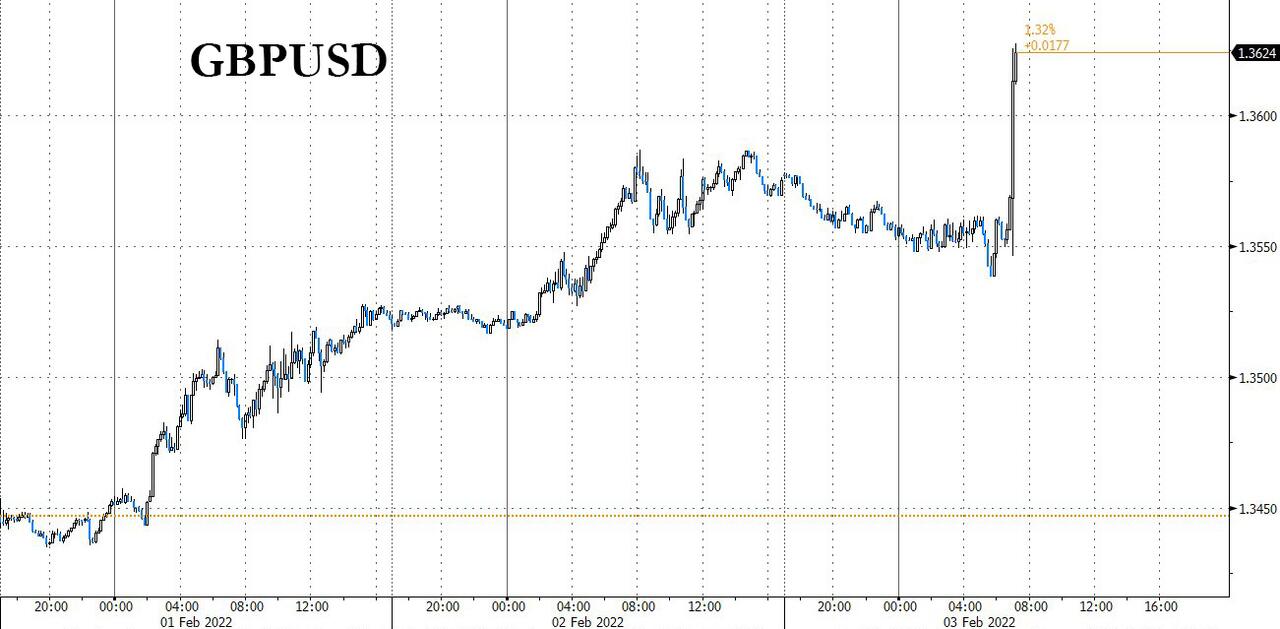

The focus in Europe shifted to the European Central Bank’s rate decision. A record regional inflation print is adding pressure on policy makers to act amid concerns they may be too slow in fighting inflation. The pound advanced for a fifth day and traded at $1.3620.

Asian equities snapped a four-day rally after Meta Platforms and Sony posted subdued earnings and prospects, weighing on the region’s technology sector. The MSCI Asia Pacific Index eased 0.3% after gaining as much as 0.1%. Sony and Panasonic were among the biggest drags on the gauge amid concerns over their future earnings. Regional tech shares also took a hit from disappointing forecasts from Facebook’s parent and Spotify, while materials and utilities climbed. Panasonic Falls Most in 3 Months After 3Q Results Disappoint Sony Drops After Disappointing PlayStation Sales and Outlook Spotify Craters After Forecasting Slower Start to New Year *T Nasdaq 100 futures dropped more than 2% intraday while Japan’s benchmarks fell, offsetting gains in South Korean and Singapore gauges, which staged a catch-up rally after reopening from the Lunar New Year holiday. Asia’s stock gauge yesterday advanced for a fourth day as fears of Fed tightening receded. The earnings season has taken center stage, with investors trawling through management commentary for the outlook for supply chains and corporate profits. Bank of England and European Central Bank rate decisions are due later Thursday. “The downside on Wall Street could create headwinds for the Asian tech sector,” and potential hawkish rhetoric from the central banks in Europe may play a critical role in markets, Anderson Alves, a trader at brokerage ActivTrades, wrote in a note. Hong Kong’s stock market is set to reopen on Friday, followed by mainland China and Taiwan on Monday.

Japanese stocks dropped, ending a four-day rally, as a weak forecast from Facebook’s parent sparked a selloff in technology shares. Electronics and machinery makers were the biggest drags on the Topix, which fell 0.9%. Fast Retailing and Tokyo Electron were the largest contributors to a 1.1% loss in the Nikkei 225. The Topix had gained 5.1% over the previous four sessions, its best four-day gain since May 2021. “We’re seeing a clear divide between firms that are able to continue to grow earnings and those that aren’t,” said Tetsuo Seshimo, a portfolio manager at Saison Asset Management Co. “People are going to be more selective in their stock picks, which means you’ll see some names being sold off.”

Indian stocks also fell, halting the biggest three-day gain in almost a year, dragged by Infosys Ltd. The benchmark S&P BSE Sensex slipped 1.3% to 58,788.02 in Mumbai, while the NSE Nifty 50 Index dropped 1.2%. All but two of the 19 sub-indexes compiled by BSE Ltd. declined, with a measure of tech stocks snapping a four-day winning streak to fall 2%. Shares climbed more than 4% in the last three sessions as the government’s annual budget earmarked higher spending to restart the investment cycle and support a recovery in businesses disrupted by the pandemic.

Australia’s S&P/ASX 200 index fell 0.1% to 7,078.00, dragged lower by tech shares after disappointing earnings from sector bellwethers in the U.S. Regional tech stocks and futures contracts on the Nasdaq 100 dropped after Facebook parent Meta and streaming service Spotify plunged in late trading on soft outlooks. Read: Australia Braces for Tough Earnings Season as Risks Pile Up In Australia, payments firm Block was among the benchmark’s biggest laggards. Nufarm was the top performer after a 1Q update. In New Zealand, the S&P/NZX 50 index rose 0.4% to 12,335.32.

In rates, Treasury yields jjmped following wider losses in gilts after Bank of England raised rates by 25bp in a 5-4 vote, with four MPC members favoring a 50bp hike. BOE Governor Bailey press conference is ahead at 7:30am ET, and European Central Bank rate decision is expected at 7:45am, followed by President Lagarde press conference at 8:30am. Treasury yields are cheaper by 1bp-2bp across the curve, 10-year by 2bp near 1.795% vs 6.5bp increase for U.K. 10-year yield; 2- year gilt yield rose as much as 10bp to 1.129% IG dollar issuance slate empty so far; $7.55b of new debt was priced Wednesday, taking weekly total to $19.5b vs $15b-$20b projected. Peripheral spreads widen with short-end Italy lagging. Japanese government bonds yield edged lower after a 30-year debt sale fetched a higher-than-estimated price.

In FX, Bloomberg dollar spot index drifts higher, rallying as the greenback advanced against all of its Group-of-10 peers, with CHF and NOK underperforming, GBP outperforms in G-10. The euro fell below $1.13 as it snapped a four-day advance; the Bund yield curve steepened slightly into the ECB. Gilt yields rise up to 2bps, led by the long end, while the pound inched lower, trimming its gains on the week, amid broad dollar gains and with traders turning their focus to the BOE. The BOE is expected to raise its policy rate as well as take the initial steps toward unwinding some of its 895 billion-pound ($1.2 trillion) stimulus program. The yen dipped amid broad dollar strength; two-year overnight-indexed yen swaps this week breached zero for the first time since 2016 — the year the Bank of Japan introduced its negative interest rate policy. The sometime proxy for investor expectations of future policy rates has risen three basis points this year. Bank of Japan Deputy Governor Masazumi Wakatabe says it’s a mistake if bond yields are rising on speculation that the BOJ might make adjustments to its monetary policy. Australian dollar declined as falling stock indexes spurred risk-off price action. Bonds rose ahead of the Reserve Bank’s quarterly Statement on Monetary Policy Friday. Turkish lira is the weakest in EMFX after Jan. inflation came in at the highest in 20 years.

In commodities, crude futures decline. WTI trades at the bottom of Wednesday’s range, falling 1% near $87.40. Base metals are mixed; LME copper falls 0.7% while LME aluminum gains 0.9%. Spot gold drops ~$4 near $1,803/oz. Spot silver loses 0.9% near $22

Looking at the day ahead now, and the main highlights will be the aforementioned monetary policy decisions from the ECB and the BoE, with press conferences afterwards from President Lagarde and Governor Bailey. Otherwise on the central bank front, there’s also the confirmation hearings at the Senate Banking Committee for the three new nominees for Fed governor. On the data side, there’s the January services and composite PMIs from around the world, and in the US there’s the ISM services index for January, December’s factory orders and the weekly initial jobless claims. Finally, earnings releases today include Amazon, Eli Lilly, Merck & Co., Honeywell and Ford.

Market Snapshot

- S&P 500 futures down 0.9% to 4,535.75

- MXAP down 0.3% to 186.61

- MXAPJ little changed at 609.19

- Nikkei down 1.1% to 27,241.31

- Topix down 0.9% to 1,919.92

- Hang Seng Index up 1.1% to 23,802.26

- Shanghai Composite down 1.0% to 3,361.44

- Sensex down 1.1% to 58,886.60

- Australia S&P/ASX 200 down 0.1% to 7,078.01

- Kospi up 1.7% to 2,707.82

- STOXX Europe 600 down 0.5% to 474.50

- German 10Y yield little changed at 0.04%

- Euro down 0.2% to $1.1288

- Brent Futures down 0.9% to $88.68/bbl

- Gold spot down 0.1% to $1,805.27

- U.S. Dollar Index up 0.23% to 96.16

Top Overnight News from Bloomberg

- Facebook parent Meta Platforms Inc. is set to shed about $200 billion in market value, in what would be one of the biggest one-day market capitalization wipeouts for any company on record

- The fastest inflation in decades is ending the low-rate era, but governments in the euro area have already locked in 461.85 billion euros ($522.5 billion) of funding in a pandemic- driven debt splurge. On top of that, the economic growth rate in Europe has never been this much higher than the average coupon on European sovereign bonds, suggesting the income nations generate from a growing economy will keep the debt burden manageable

- The world’s well of debt with yields below zero has shrunk to the lowest in more than three years as the prospect of imminent interest-rate hikes drives a selloff in bonds

- The U.K.’s cost of living crisis is set to escalate dramatically on Thursday, with millions facing a record increase in energy bills, forcing the government to roll out a multi-billion pound package to ease the burden

A more detailed look at global markets courtesy of Newsquawk

Asian stocks were mostly negative and took their cues from the selling pressure in US equity futures and Meta slump. ASX 200 (-0.1%) was subdued by losses in tech but with downside stemmed by mining stocks and mixed-to-firm data. Nikkei 225 (-1.1%) weakened as Japan mulls a quasi-emergency extension for Tokyo and with earnings in focus. KOSPI (+1.7%) outperformed and played catch up to this week’s gains on return from the Lunar New Year holiday. US equity futures were mostly pressured after almost USD 200bln was wiped off from Meta’s value which weighed on other social media stocks; E-mini S&P -0.9%, E-mini Nasdaq 100 -2.1%.

Top Asian News

- StanChart Zimbabwe Starts Probe After Reports CEO Suspended

- UAE Wealth Funds Behind $10 Billion Israel Plans Scout for Deals

- UAE Intercepts Hostile Drones After Wave of Attacks

- Tokyo Sets New Guidelines for Seeking Virus Emergency

European bourses are pressured, Stoxx 600 -0.7% given the US after-market read across, followed by numerous earnings releases in the pre-market dictating individual movers/sectors. European sectors are predominantly in the red as Tech lags post-Meta, -20.3% in the pre-market, while Healthcare is hit following Roche’s soft guidance.

Top European News

- StanChart Zimbabwe Starts Probe After Reports CEO Suspended

- U.K. Jan. Composite PMI 54.2 vs Flash Reading 53.4

- ABB Expects Minimum $750 Million From E-Mobility IPO: CEO

- Infineon Shares Decline Despite Raised Revenue Guidance

US Event Calendar

- 7:30am: Jan. Challenger Job Cuts YoY, prior -75.3%

- 8:30am: 4Q Unit Labor Costs, est. 1.0%, prior 9.6%; Nonfarm Productivity, est. 3.8%, prior -5.2%

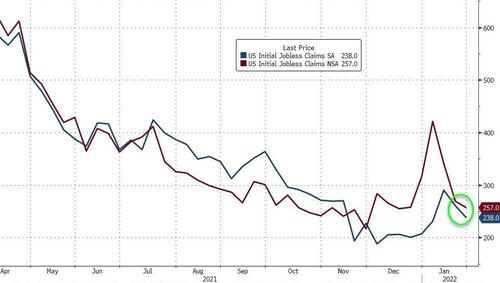

- 8:30am: Jan. Initial Jobless Claims, est. 245,000, prior 260,000; Continuing Claims, est. 1.62m, prior 1.68m

- 9:45am: Jan. Markit US Services PMI, est. 50.9, prior 50.9

- Jan. Markit US Composite PMI, est. 50.8, prior 50.8

- 10am: Dec. Factory Orders, est. -0.4%, prior 1.6%; Factory Orders Ex Trans, est. 0.4%, prior 0.8%

- 10am: Dec. Durable Goods Orders, est. -0.9%, prior -0.9%; -Less Transportation, prior 0.4%

- Cap Goods Orders Nondef Ex Air, prior 0%

- Cap Goods Ship Nondef Ex Air, prior 1.3%

- 10am: Jan. ISM Services Index, est. 59.5, prior 62.0, revised 62.3

DB’s Jim Reid concludes the overnight wrap

With all my injuries of late I can’t help thinking that my future sporting prowess might be more suited to, and also safer, in the metaverse. However even the metaverse isn’t a smooth ride as we found out last night. Indeed it’s rare that I’ll lead on one after hours earnings result but Meta’s (formerly Facebook) earnings miss sent shares down as much as -23.85% in the early hours. For a company that had around $890bn of market cap at yesterday’s close, that would equate to around $200bn of market cap losses, and wiping out the last year of gains. The market cap loss is also bigger than the market cap of Netflix ($202.9bn) at yesterday’s closing prices. This gives a scale of a damage done. The shares were hit hard by a combination of extraordinary expenses associated with building the metaverse, along with what appears to be stagnating growth in the user base. Those were common themes in other earnings releases overnight. Spotify was almost -30% lower in after-hours trading after revealing subscriber growth below analyst expectations, while Qualcomm was nearly -10% lower after hitting snags trying to expand their business. As a result, Nasdaq futures are trading (-2.17%) lower in Asia and the S&P 500 contract is following in sympathy (-0.90%).

Prior to the Meta news things were looking up for equities after a sensational four days. Indeed the S&P 500’s (+0.94% yesterday) advance over the last 4 sessions is +6.07%, which is the biggest 4-day gain since the relief rally following the November 2020 presidential election. For reference, at its recent intraday low at the start of last week, the S&P was down by -11.40% on a YTD basis, but it’s now recovered the bulk of that to only be down -3.71%. Today may put us back into reverse gear for a period of time at least with Amazon the big US earnings release to look forward to.

The S&P 500 climb up to the close was led by communications (+3.09%) following Alphabet’s (+6.43%) strong earnings and stock-split announced after the previous session’s close. The NASDAQ (+0.50%) managed to also advance for the fourth straight day, but by a smaller margin, while the small-cap Russell 2000 underperformed, falling -1.03%. European equities also gained, but lagged behind US indices, with the STOXX 600 advancing +0.45%.

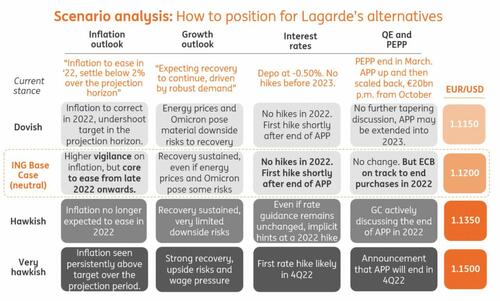

Looking forward and it’s all about central banks today with a likely 25bps rate hike by the Bank of England potentially being overshadowed more by what the ECB doesn’t say today when they also meet. The ECB will be in a slightly difficult spot as it’s a non-forecast meeting so they won’t have any new numbers to present to allow them to methodically adjust their tone (if they indeed wanted to). However the rather large inflation beats seen this week across Europe will make for a difficult press conference if the tone doesn’t somehow become more hawkish. Our chief European economist Mark Wall wrote in a blog post yesterday (link here) that President Lagarde will be under pressure to explain why the ECB continues to expect inflation will fall below target in the medium term. Remember that our economists recently updated their call on ECB liftoff to an initial 25bp hike in December 2022, and in their preview for this meeting (link here) they outline their view that they expect the slow, step-by-step pivot to exit will continue. Will this appease an impatient market though? Expect Lagarde’s press conference to be a box office affair. Could the ECB at some point see a similar kind of attack we saw on front-end pricing in Australia in Q4 last year? There has to be some risk of this. As a minimum remember that in June last year the Fed and market weren’t pricing in a hike until 2024. Now we are debating 3-7 hikes and QT for 2022. So things can change very quickly once momentum builds.

We are entering an interesting week ahead with the central banks meetings today, US payrolls tomorrow and US CPI next Wednesday. Ahead of next Wednesday, the flash CPI estimate for the Euro Area unexpectedly rose to +5.1% in January (vs. +4.4% expected). That’s the highest inflation since the single currency’s formation, and was an unexpected increase from last month’s record as well. Furthermore, core inflation at +2.3% was also stronger than the +1.9% expected, albeit that did come down from the +2.6% reading last month.

Sovereign bond yields reversed an early rally as the inflation numbers came out and edged higher for the most part in Europe yesterday, with those on 10yr bunds (+0.4bps) inching higher to hit their highest level since April 2019. In part that was spurred by the view that the strong inflation data would force an earlier tightening of monetary policy from the ECB over the year ahead, and the euro also strengthened +0.29% in its 4th consecutive move higher. That made a contrast with the US, where diminishing bets that the Fed would hike rates by 50bps at the next meeting helped yields on 10yr Treasuries down -1.2bps to 1.78%. The number of hikes in 2022 got down to 4.625 in early US trading from 5.05 near the US open on Monday before closing at 4.71 (-0.07 hikes on the day), its lowest level in a week.

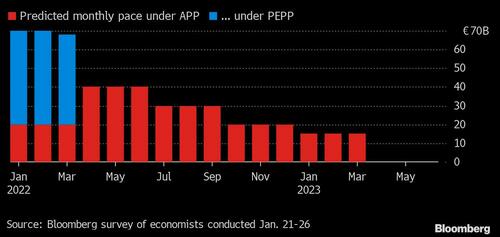

Onto the BoE. They are set to announce their latest decision at 12:00 London time, and we’ll also get the release of their quarterly Monetary Policy Report. In his preview (link here), our UK economist Sanjay Raja writes that he expects the BoE to follow up their December rate hike with another 25bps increase, taking the Bank Rate to 0.5%. Furthermore, he expects that the MPC should confirm that any APF reinvestments will cease from here on out, resulting in around £38bn falling out of the Bank’s balance sheet this year. That view expecting a rate hike is widely shared, with overnight index swaps just about pricing in a 25bp move at the meeting today, and that’s also the consensus view amongst economists on Bloomberg too.

Asian markets are reacting to the after hours US losses in thin holiday trade this morning. The Nikkei (-1.11%) is trading down, after four consecutive sessions of gains while the Kospi (+2.07%) is in positive territory after trading resumed following a three-day holiday break. Elsewhere, markets in China and Hong Kong remain closed for the Lunar New Year holiday. Meanwhile, Iron ore extended its rally for the third day with futures in Singapore up +2.80% at $143.70 ton on hopes that China’s stepped-up monetary easing will boost demand.

Earlier today, IHS Markit showed that South Korea’s January PMI rose to +52.8 from +51.9 in December as new orders picked up despite persistent supply chain woes. Separately, Japan’s services sector shrank at the fastest pace in five months after the Markit’s final estimate showed that the PMI slumped to 47.1 in January from 52.1 in the previous month.

In other news from the last 24 hours, the OPEC+ group agreed to a further output increase of +400k barrels per day in March, although recently the issue has been that suppliers are struggling to meet their quotas for a number of reasons, which has helped oil prices reach post-2014 highs lately. Oil itself was fairly subdued overall on the day, with Brent crude only up +0.35%, but the strength we’ve been mentioning in other commodities continued apace yesterday, with Bloomberg’s Commodity Spot Index (+1.56%) hitting a fresh all-time high thanks in part to a surge in US natural gas futures (+15.79%) amidst signs of further cold weather ahead. See my CoTD (link here) yesterday that showed that this is the strongest cycle for commodities on record at this stage of a US economic recovery.

Aside from the Euro Area inflation release, there wasn’t much in the way of other data yesterday. That said, we did get the ADP’s report of private payrolls for January, which unexpectedly showed a -301k decline as the Omicron variant took hold (vs. +180k expected). We’ll see tomorrow if that has any read through to what is already expected to be a bad headline payroll print. Current expectations are at +150k but I suspect the whisper number might be lower.

Elsewhere, geopolitical tensions in Eastern Europe remained on the edge after the Pentagon indicated to move some of its Europe-based forces further towards east and deploy additional US based troops to Europe.

To the day ahead now, and the main highlights will be the aforementioned monetary policy decisions from the ECB and the BoE, with press conferences afterwards from President Lagarde and Governor Bailey. Otherwise on the central bank front, there’s also the confirmation hearings at the Senate Banking Committee for the three new nominees for Fed governor. On the data side, there’s the January services and composite PMIs from around the world, and in the US there’s the ISM services index for January, December’s factory orders and the weekly initial jobless claims. Finally, earnings releases today include Amazon, Eli Lilly, Merck & Co., Honeywell and Ford.

3. ASIAN AFFAIRS

i)THURSDAY MORNING// WEDNESDAY NIGHT

SHANGHAI CLOSED //Hang Sang CLOSED /The Nikkei closed DOWN 299.29 PTS OR 1.06% //Australia’s all ordinaires CLOSED DOWN 0.34% /Chinese yuan (ONSHORE) closed HOLIDAY /Oil DOWN TO 87.01 dollars per barrel for WTI and DOWN TO 88.58 for Brent. Stocks in Europe OPENED MOSTLY RED EXCEPT SPAIN // ONSHORE YUAN CLOSED XX AGAINST THE DOLLAR AT XXX. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.3637: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN AND OFF SHORE TRADING WEAKER AGAINST USA DOLLAR

3 a./NORTH KOREA/ SOUTH KOREA

///NORTH KOREA

3B JAPAN

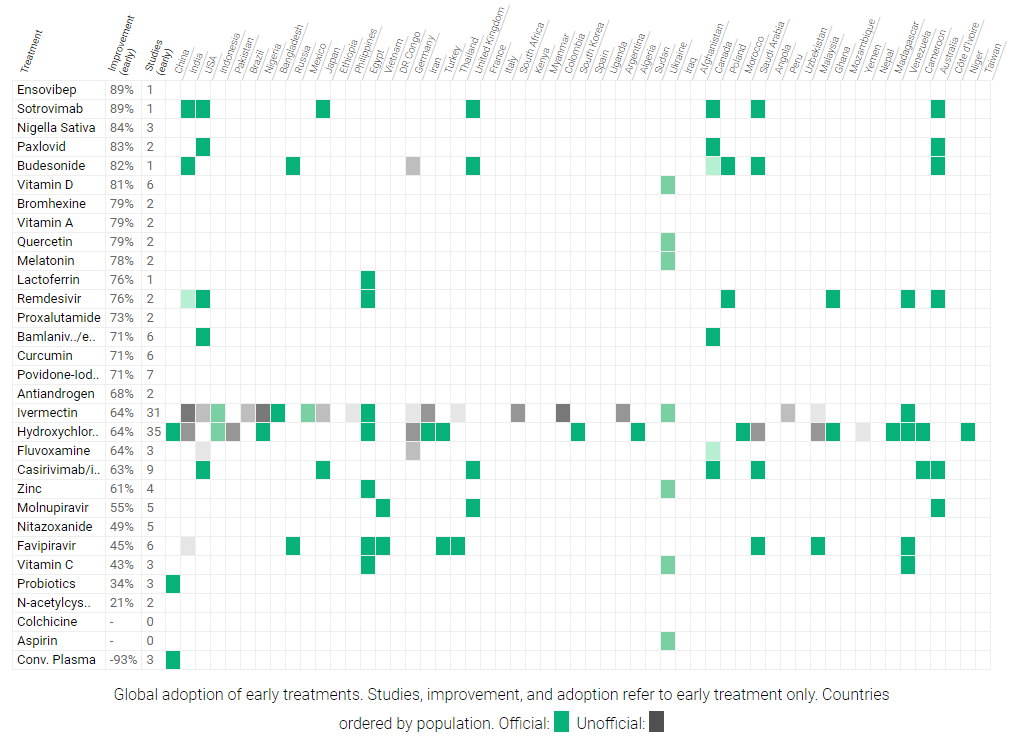

The true story behind ivermectin and what this drug can do as revealed by pharmaceutical Japanese company Kowa

(QTR Fringe Finance)

Has The Red Carpet Been Rolled Out For A Mainstream Pivot On Ivermectin?

WEDNESDAY, FEB 02, 2022 – 11:10 PM

Submitted by QTR’s Fringe Finance

Just yesterday even more ivermectin controversy started: this time around joint nonclinical research being done with the drug by Japanese company Kowa Co Ltd.

Except, instead of the “normal” ivermectin controversy – which consists of arguing over whether or not the drug is “horse paste” despite its discovery being nominated for a Nobel Prize for use in humans, it being including on the World Health Organization’s list of essential medicines and being dosed hundreds of millions of times to human beings by doctors – this week’s controversy was about how Kowa’s research was reported on Tuesday.

Reuters initially ran the headline:

“Japan’s Kowa says ivermectin effective against Omicron in phase III trial”.

That headline was incorrect, and Reuters was forced to retract it. They re-ran the story with a title congruent with the facts:

Ivermectin shows ‘antiviral effect’ against COVID, Japanese company says

Both ivermectin advocates and detractors claimed victory on the day.

Advocates claimed victory because it was yet another study – despite being a nonclinical joint study – that showed antiviral effects from the medicine in vitro. Ivermectin is already a well-known antiviral.

Ivermectin skeptics like the Washington Post claimed the article was “botched”, but still were forced to admit the truth: the “actual news” was that ivermectin was found to carry an “antiviral effect” against Omicron and other coronavirus variants in joint non-clinical research.

The facts as put forth in the corrected version of the Reuters article still seemed to be a net positive:

Japanese trading and pharmaceuticals company Kowa Co Ltd on Monday said that anti-parasite drug ivermectin showed an “antiviral effect” against Omicron and other coronavirus variants in joint non-clinical research.

The company, which has been working with Tokyo’s Kitasato University on testing the drug as a potential treatment for COVID-19, did not provide further details

Kowa and Kitasato University appear to be in the midst of a clinical trial studying whether or not ivermectin is effective, though it was difficult to confirm the details due to a language barrier at the source of the information.

A translated version of Kowa’s Japanese PR seems to confirm that ivermectin is in the midst of a clinical trial for Covid. Included in the translated PR were the following lines:

It is expected to be applied as a therapeutic drug (tablet) for all new coronavirus infectious diseases.

In this clinical trial, the dosage and administration already approved as a therapeutic agent for parasitic infections

Although it is different, we are confirming its efficacy and safety in clinical trials.

Kowa confirmed the clinical effect of ivermectin on SARS-CoV-2 and was one of the first to the public.

But, let’s put aside the Kowa study for a second.

What most people don’t know is that this Japanese trial, whether successful or not – whether clinical or nonclinical – would only serve to supplement robust data already available about ivermectin’s effectiveness on Covid-19.

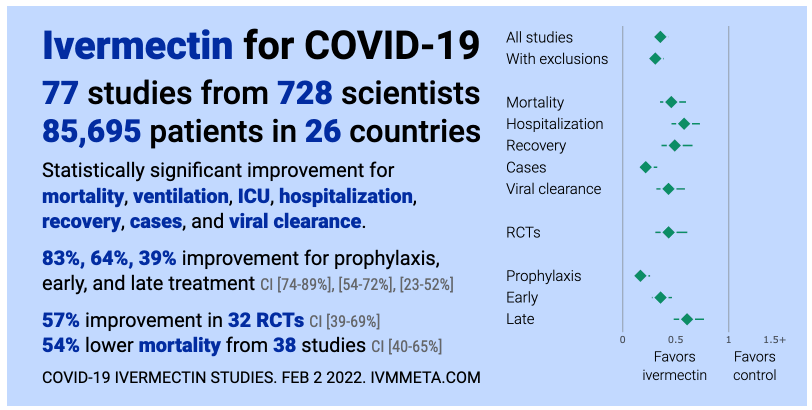

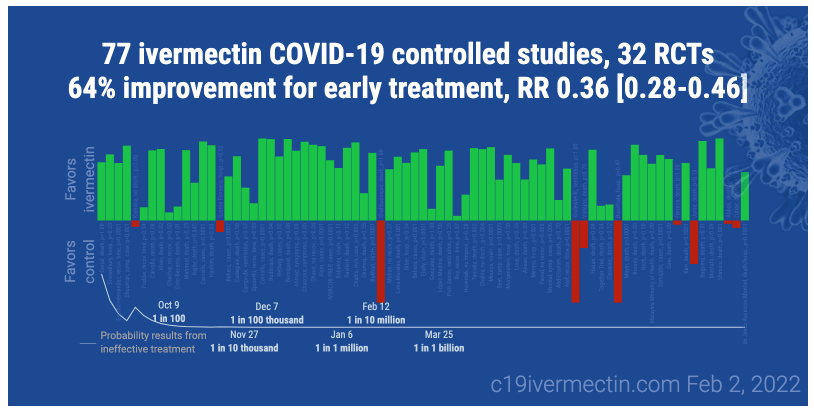

The website c19ivermectin.com keeps a running tally of such studies, and aggregates the data as it comes in.

The website keeps a chronological log of studies, news, theories, of all types of information available about ivermectin that can be aggregated, including meta analyses, dating back to April of 2020. At most recent update, it includes 147 studies, 96 peer reviewed, 77 with results comparing treatment and control groups. (It currently includes the Kowa writeup, but has yet to correct the Reuters headline as of the time of this writing.)

The website also notes that Ivermectin has been officially adopted for early treatment in all or part of 22 countries (39 including non-government medical organizations).

And when the left undoubtedly writes this collection of data off as “anti-vaxx” (a label that is being tossed around with less care for its meaning than ‘white supremacy’ nowadays), remind them that the site also encourages the use of vaccines, stating:

“Vaccines and treatments are both valuable and complementary. All practical, effective, and safe means should be used. Elimination of COVID-19 is a race against viral evolution. No treatment, vaccine, or intervention is 100% available and effective for all current and future variants. Denying the efficacy of any method increases mortality, morbidity, collateral damage, and the risk of endemic status.”

Today’s blog post has been published without a paywall because I believe the content to be far too important to deny to anyone. However, if you have the means and would like to support my work by subscribing, I’d be happy to offer you 22% off for 2022:

I don’t want to rehash the geographic locations that have had success using ivermectin against Covid – with Uttar Pradesh probably being the most obvious – but I do want to point out that it isn’t just this collection of data suggesting there may be efficacy.

People are more than welcome to make up their own minds on what they think about ivermectin. Personally, regardless of whether or not the Japanese study was presented accurately or inaccurately at first by Reuters, it’s still my belief that it’s not going to matter in the future, because history will eventually side with the truth.

And the truth, I believe, is that ivermectin very likely works to treat early stage Covid, as was suggested in Uttar Pradesh and as has been claimed by doctors like Pierre Kory. It may not be a “cure” or “work like magic”, but I believe through rigorous clinical studies in the years to come, it will be found to have had efficacy in early stage Covid.