FEB 4

FEB4

· by harveyorgan · in Uncategorized · Leave a comment ·Edit

GOLD; UP $3.40 to $1807.20

SILVER: $22.52 UP 16 CENTS

ACCESS MARKET: GOLD: 1807.80..

SILVER: $22.47

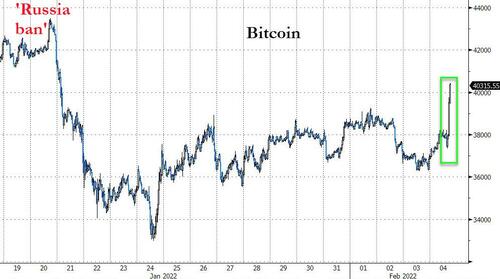

Bitcoin: morning price: 36,813 UP 316

Bitcoin: afternoon price: 40,693 UP 4196

Platinum price: closing down $6.30 to $1028.95

Palladium price; closing down $34.75 at $2298.75

END

end

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

comex notices//JPMorgan notices filed COMEX//NOTICES:EXCHANGE: COMEX FILED: 207/545

EXCHANGE: COMEX

CONTRACT: FEBRUARY 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,803.000000000 USD

INTENT DATE: 02/03/2022 DELIVERY DATE: 02/07/2022

FIRM ORG FIRM NAME ISSUED STOPPED

118 C MACQUARIE FUT 67

332 H STANDARD CHARTE 14

363 H WELLS FARGO SEC 8

435 H SCOTIA CAPITAL 2

624 C BOFA SECURITIES 543

624 H BOFA SECURITIES 213

657 C MORGAN STANLEY 1

661 C JP MORGAN 114

661 H JP MORGAN 93

709 C BARCLAYS 25

732 C RBC CAP MARKETS 3

800 C MAREX SPEC 2 3

905 C ADM 2

TOTAL: 545 545

MONTH TO DATE: 16,243

NUMBER OF NOTICES FILED TODAY FOR FEB. CONTRACT: 545 NOTICE(S) FOR 54,500 OZ (1.6951 TONNES)

total notices so far: 16,243 contracts for 1,624,300 oz (50.522 tonnes)

SILVER NOTICES:

69 NOTICE(S) FILED TODAY FOR 345,000 OZ/

total number of notices filed so far this month 1208 : for 6,040,000 oz

GLD

WITH GOLD UP $3.40

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF 1.75 TONNES FROM THE GLD//

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

CLOSING INVENTORY: 1014.84 TONNES/

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP 16 CENTS:/: NO CHANGES IN SILVER INVENTORY AT THE SLV/

AT THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY SLV/ TONIGHT: 539.212 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A STRONG 2066 CONTRACTS TO 149,733 AND RESTS FURTHER FROM THE NEW RECORD OF 244,710, SET FEB 25/2020 AND DESPITE THIS STRONG GAIN IN OI, IT WAS ACCOMPANIED WITH OUR STRONG $0.35 LOSS IN SILVER PRICING AT THE COMEX ON THURSDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.35) BUT WERE UNSUCCESSFUL IN KNOCKING OUT ANY SILVER LONGS AS WE HAD A VERY STRONG GAIN OF 2916 CONTRACTS ON OUR TWO EXCHANGES .

WE MUST HAVE HAD:

I) HUGE BANKER SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A GOOD ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A HUGE INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 4.110 MILLION OZ FOLLOWED BY TODAY’S 275,000 OZ QUEUE JUMP//NEW STANDING 6.145 MILLION OZ. V) STRONG SIZED COMEX OI GAIN.

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS -107

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS FEB. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF FEB:

TOTAL CONTACTS for 4 days, total contracts: : 2533 contracts or 12.665 million oz OR 3.166 MILLION OZ PER DAY. (633 CONTRACTS PER DAY)

TOTAL NO OF OZ UNDERGOING EFP TO LONDON 2533 CONTRACTS X 5,000 PER CONTRACT:

EQUATES TO: 12.665 MILLION OZ

.

LAST 10 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 12.665 MILLION OZ//

SPREADING OPERATIONS

(/NOW SWITCHING TO SILVER) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF MAR.WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF JAN HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB, FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (MAR), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

RESULT: WE HAD A STRONG SIZED inCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2066 DESPITE OUR $0.35 loss SILVER PRICING AT THE COMEX// THURSDAY THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 850 CONTRACTS( 850 CONTRACTS ISSUED FOR MAR AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR FEB OF 4.1 MILLION OZ FOLLOWED BY TODAY’S 275,000 OZ QUEUE JUMP //NEW STANDING 6.145, MILLION OZ// .. WE HAD A STRONG SIZED GAIN OF 2963 OI CONTRACTS ON THE TWO EXCHANGES FOR 14.815 MILLION OZ//

WE HAD 69 NOTICES FILED TODAY FOR 345,000 OZ

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A FAIR SIZED 2360 TO 510,080 AND FURTHER FROM OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: — 91 CONTRACTS

.

THE FAIR SIZED DECREASE IN COMEX OI CAME WITH OUR LOSS IN PRICE OF $5.55//COMEX GOLD TRADING/THURSDAY/.AS IN SILVER WE MUST HAD HUGE BANKER/ALGO SHORT COVERING ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD SOME LONG LIQUIDATION AS THE TOTAL GAIN ON OUR TWO EXCHANGES TOTALED 65 CONTRACTS…

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR FEB AT 64.3 TONNES FOLLOWED BY TODAY’S 5700 OZ E.F.P. JUMP TO LONDON //NEW STANDING: 59.334 TONNES

YET ALL OF..THIS HAPPENED WITH OUR LOSS IN PRICE OF $5.55 WITH RESPECT TO THURSDAY’S TRADING

WE HAD A SMALL SIZED GAIN OF 65 OI CONTRACTS (0.202 PAPER TONNES) ON OUR TWO EXCHANGES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALLED A FAIR SIZED 2475 CONTRACTS:

FOR APRIL 2475 ALL OTHER MONTHS ZERO//TOTAL:2475

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 510,080.

IN ESSENCE WE HAVE A SMALL SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 65, WITH 2,360 CONTRACTS DECREASED AT THE COMEX AND 2475 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 65 CONTRACTS OR 0.202TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2475) ACCOMPANYING THE FAIR SIZED LOSS IN COMEX OI (2360,): TOTAL GAIN IN THE TWO EXCHANGES 65 CONTRACTS. WE NO DOUBT HAD 1) HUGE BANKER SHORT COVERING ,2.) HUGE INITIAL STANDING AT THE GOLD COMEX FOR FEB. AT 64.30 TONNES WHICH FOLLOWS TODAY’S EFP JUMP TO LONDON OF 5700 OZ//NEW STANDING 59.334 TONNES// 3)ZERO LONG LIQUIDATION ,4) FAIR SIZED COMEX OI. LOSS 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

FEB

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF FEB :

6344 CONTRACTS OR 634,400 oz OR 19.73 TONNES 4 TRADING DAY(S) AND THUS AVERAGING: 1586 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 4 TRADING DAY(S) IN TONNES: 19.93 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2020, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 19.73/3550 x 100% TONNES 0.556% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 145.12 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 19.73 TONNES//INITIAL

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A STRONG SIZED 2066 CONTRACTS TO 149,733 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 4 1/2 YEARS AGO.

EFP ISSUANCE 850 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 850 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 850 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 2066 CONTRACTS AND ADD TO THE 850 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A VERY STRONG SIZED GAIN OF 2916 OPEN INTEREST CONTRACT FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 14.560 MILLION OZ,

OCCURRED WITH OUR $0.35 LOSS IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

5. Other gold commentaries

6. Commodity commentaries/cryptocurrencies

3. ASIAN AFFAIRS

i)FRIDAY MORNING// THURSDAY NIGHT

SHANGHAI CLOSED //Hang Sang CLOSED UP 771.03 PTS OR 3.24% /The Nikkei closed UP 198.68 PTS OR 0.73% //Australia’s all ordinaires CLOSED UP 0.60% /Chinese yuan (ONSHORE) closed HOLIDAY /Oil UP TO 92.16 dollars per barrel for WTI and DOWN TO 92.74 for Brent. Stocks in Europe OPENED ALL RED // ONSHORE YUAN CLOSED XX AGAINST THE DOLLAR AT XXX. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.3588: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN AND OFF SHORE TRADING STRONGER AGAINST USA DOLLAR

A)NORTH KOREA//USA/OUTLINE

b) REPORT ON JAPAN

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 2360 CONTRACTS AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX DECREASE OCCURRED WITH OUR LOSS OF $5.55 IN GOLD PRICING THURSDAY’S COMEX TRADING. WE ALSO HAD A FAIR SIZED EFP (2475 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE ACTIVE DELIVERY MONTH OF FEB.. THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2475 EFP CONTRACTS WERE ISSUED: ;: , & FEB. 0 APRIL: 2475 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2475 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A SMALL SIZED 65 TOTAL CONTRACTS IN THAT 2475 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED COMEX OI LOSS OF 2360 CONTRACTS..

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING FOR FEB (59.318),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

FEB 2022: 59.318 TONNES

THE BANKERS WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $5.55) BUT THEY WERE UNSUCCESSFUL IN FLEECING ANY LONGS AS WE HAVE REGISTERED A GAIN OF 0.6407 TONNES OF TOTAL OI, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR FEB (59.318 TONNES)…

WE HAD –91 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 65 CONTRACTS OR 6500 OZ OR 0.202 TONNES

Estimated gold volume today: 182,636 /// poor

Confirmed volume yesterday: 180,150contracts poor

INITIAL STANDINGS FOR FEB ’22 COMEX GOLD //FEB 4

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 8423.562 oz Manfra Brinks 250 kilobars Brinks12 kilobars Manfra |

| Deposit to the Dealer Inventory in oz | nilOZ |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 545 notice(s) 54500 OZ 1.6951 TONNES |

| No of oz to be served (notices) | 2828 contracts 282,800 oz 8.796 TONNES |

| Total monthly oz gold served (contracts) so far this month | 16,243 notices 1,624,300 OZ 50.522 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For today:

No dealer deposit 0

No dealer withdrawal 0

0 customer deposit

total deposit: nil oz

2 customer withdrawals

i) Out of Brinks: 8037.75 oz 250 kilobars

ii) Out of Manfra: 385.812 oz 12 kilobars

total withdrawals: 8423.562 oz 262 kilobars

ADJUSTMENTS: 1//dealer to customer

i) Out of JPMorgan: 6729.948 oz

2/ customer to dealer: Brinks 192.910 oz 6 kilobars.

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JANUARY.

For the front month of FEBRUARY we have an oi of 3373 stand for LOSING 531 contracts.

We had 469 contracts served upon yesterday, so we lost 62 contracts or an additional 6200 oz will not stand on this side of the pond and

these guys were E.F.P.’d to London where they received a handsome bonus for their effort. Looks like no gold to be found over here.

The month of March saw a loss of 128 contracts and thus the OI standing is 5284.

April saw a loss of 3054 contracts up to 393,477.

We had 545 notice(s) filed today for 54500 oz FOR THE FEB 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 545 contract(s) of which 114 notices were stopped (received) by j.P. Morgan dealer and 93 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the FEB /2021. contract month,

we take the total number of notices filed so far for the month (16,243) x 100 oz , to which we add the difference between the open interest for the front month of (FEB: 3373 CONTRACTS ) minus the number of notices served upon today 545 x 100 oz per contract equals 1,907,100 OZ OR 59.318 TONNES the number of TONNES standing in this active month of FEB.

thus the INITIAL standings for gold for the FEB contract month:

No of notices filed so far (16,243) x 100 oz+ (3373) OI for the front month minus the number of notices served upon today (545} x 100 oz} which equals 1,907,100 oz standing OR 59.318 TONNES in this active delivery month of FEB.

We lost 57 contracts or an additional 5700 oz will not stand over here and were EFP’d. to London

TOTAL COMEX GOLD STANDING: 59.318 TONNES (HUGE FOR A FEBRUARY DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

157,392.690, oz NOW PLEDGED /HSBC 4.89 TONNES

125,410.592 PLEDGED MANFRA 2.90 TONNES

54,339.114oz PLEDGED JPMorgan no 1 1.690

288,481,604, oz JPM No 2 8.97 TONNES

898,821.330 oz pledged Brinks/27,96 TONNES

12,249,333 oz International Delaware: 0..3810 tonne

Loomis: 18,615.429 oz

total pledged gold: 1,553,863.297 oz 48.331 tonnes

TOTAL REGISTERED AND ELIZ GOLD AT THE COMEX: 32,751,574.917 OZ (1018.71 TONNES)

TOTAL ELIGIBLE GOLD: 15,435,400.331 OZ (480.10 tonnes)

TOTAL OF ALL REGISTERED GOLD: 17,316,174.586 OZ (538.60 tonnes)

REGISTERED GOLD THAT CAN BE SERVED UPON: 15,762,311.0 OZ (REG GOLD- PLEDGED GOLD) 490.27 tonnes

END

FEBRUARY 2022 CONTRACT MONTH//SILVER

INITIAL STANDING FOR SILVER//FEB 4

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 173,651.57 oz Brinks CNT |

| Deposits to the Dealer Inventory | nilOZ |

| Deposits to the Customer Inventory | 597,198.120 oz CNT Delaware |

| No of oz served today (contracts) | 69CONTRACT(S) 345,000 OZ) |

| No of oz to be served (notices) | 21 contracts (105,000 oz) |

| Total monthly oz silver served (contracts) | 1208 contracts 6,040,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

we had 0 deposits into the dealer

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 2 deposits

i) Into CNT: 587,264.520 oz

ii) Into Delaware: 9933.600 oz

total deposit: 597,198.120 oz

JPMorgan has a total silver weight: 184.649 million oz/352.225 million =52.42% of comex

ii) Comex withdrawals: 3

a)Brinks: 86,56,500 oz

b) CNT; 163,907.170 oz

c HSBC: 1087.900 oz

total withdrawal 173,651.57 oz

we had 5 adjustments: 4 dealer to customer

Brinks: 161,531.100 oz

ii) Loomis: 126,484.800 oz

iii))JPMorgan: 65,632.500 oz

iv) Manfra 129,489.720 oz

one adjustment customer to dealer; HSBC

i) 5008.75 oz

oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 81.342 MILLION OZ

TOTAL REG + ELIG. 352.225 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR FEBRUARY

silver open interest data:

FRONT MONTH OF FEB//2022 OI: 90 CONTRACTS LOSING 62 contracts on the day. We had 117 contracts served upon yesterday.

So we gained 55 contracts or an additional 275,000 oz will stand for silver on this side of the pond.

FOR MARCH WE HAD A loss OF 935 CONTRACTS UP TO 103,276 CONTRACTS.

APRIL HAD A SMALL GAIN OF 30 CONTRACTS UP TO 51

MAY HAD A GAIN OF 2920 CONTRACTS UP TO 29,809 contracts

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 69 for 345,000 oz

Comex volumes: 51,825// est. volume today//weak

Comex volume: confirmed YESTERDAY: 63,080 contracts (weak)

To calculate the number of silver ounces that will stand for delivery in FEB. we take the total number of notices filed for the month so far at 1203 x 5,000 oz =. 6,040,000 oz

to which we add the difference between the open interest for the front month of FEB (90) and the number of notices served upon today 69 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the FEB./2021 contract month: 1208 (notices served so far) x 5000 oz + OI for front month of FEB (90) – number of notices served upon today (69) x 5000 oz of silver standing for the FEB contract month equates 6,145,000 oz. .

We gained 125 CONTRACTS OR 625,000 ADDITIONAL oz of silver will stand at the comex.

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

GLD

FEB 4/WITH GOLD UP $3.40 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.75 TONNES FROM THE GLD////INVENTORY RESTS AT 1014.84 TONNES

FEB 3/WITH GOLD DOWN $5.55: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD////INVENTORY RESTS AT 1016.59 TONNES

FEB 2/WITH GOLD UP $7.95//A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.78 TONES OF GOLD INTO THE GLD////INVENTORY RESTS AT 1018.04 TONNES

FEB 1/WITH GOLD UP $5.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1014.26 TONNES

JAN 31/WITH GOLD UP $10.10//NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1014.26 TONNES

JAN 28/WITH GOLD DOWN $8.30//NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1014.26 TONNES

JAN 27/WITH GOLD DOWN $36.15//ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.16 TONNES INTO THE GLD.//INVENTORY RESTS AT 1014.26 TONNES

JAN 26/WITH GOLD DOWN $21.60 A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.65 TONNES INTO THE GLD///INVENTORY RESTS AT 1013.10 TONNES

JAN 25/WITH GOLD UP $10.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1008.45 TONNES

JAN 24/WITH GOLD UP $10.10 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: AN UNBELIEVABLE DEPOSIT OF 27.59 TONNES INTO THE GLD//INVENTORY RESTS AT 1008.45 TONNES

JAN 21/WITH GOLD DOWN $10.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 980.86 TONNES

JAN 20/WITH GOLD UP $.20 TODAY: A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .58 TONNES FROM THE GLD///INVENTORY RESTS AT 980.86 TONNES

JAN 19/WITH GOLD UP $29.65 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 5.27 TONNES INTO THE GLD/INVENTORY RESTS AT 981.44 TONNES

JAN 18/WITH GOLD DOWN $3.25//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 976.21 TONNES

JAN 14/ WITH GOLD DOWN $5.25/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 976.21 TONNES

JAN 13/WITH GOLD DOWN $5.75: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 976.21 TONNES

JAN 12/WITH GOLD UP $8.65//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 976.21 TONNES

JAN 11/WITH GOLD UP $19.25/A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES FROM THE GLD/INVENTORY RESTS AT 976.21 TONNES

JAN 10/WITH GOLD UP $2.00/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 977.08 TONNES

JAN 7/WITH GOLD UP $8.15//A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWLA OF 1.16 TONNES FROM THE GLD////INVENTORY RESTS AT 978.83 TONNES

JAN 6/WITH GOLD DOWN $35.30//A SMALL CHANGE IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF .32 TONNES/INVENTORY RESTS AT 979.99 TONNES

JAN 5/WITH GOLD UP $10.30: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 980.31 TONNES

Jan 4/WITH GOLD UP $14.00//A HUGE CHANGE OF 4.65 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 980.31 TONNES

JAN 3/WITH GOLD DOWN $26.70: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 975.66 TONNES

CLOSING INVENTORY: 1014.84 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

SLV

FEB 4/WITH SILVER UP 16 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 539.212 MILION OZ

FEB 3/WITH SILVER DOWN 35 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT539.212 MILLION OZ//

FEB 2/WITH SILVER UP 15 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.411 MILLION OZ INTO THE SLV.//INVENTORY RESTS AT 539.212 MILLION OZ/

FEB 1/WITH SILVER UP 18 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 533.801 MILLION OZ

JAN 31/WITH SILVER UP 7 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.202 MILLION OZ FORM THE SLV.//INVENTORY RESTS AT 533.801 MILLION OZ//

JAN 28/WITH SILVER DOWN 36 CENTS : NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 535.003 MILLION OZ//

JAN 27/WITH SILVER DOWN $1.13 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 535.003 MILLION OZ//

JAN 26/WITH SILVER DOWN 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 535.003 MILLION OZ//

JAN 25/WITH SILVER UP 10 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.311 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 535.003 MILLION OZ/

.JAN 24/WITH SILVER DOWN 48 CENTS TODAY: A MASSIVE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.8 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 532.692 MILLION OZ//.

JAN 21/WITH SILVER DOWN 41 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 527.792 MILLION OZ

JAN 20/WITH SILVER UP 52 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.998 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 527.792 MILLION OZ

JAN 19/WITH SILVER UP 71 CENTS TODAY: A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.942 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 525.804 MILLION OZ

JAN 18/WITH SILVER UP 51 CENTS TODAY: TWO HUGE CHANGES IN SILVER INVENTORY AT THE SLV: 2 WITHDRAWALS OF 1.11 MILLION OZ AND 1.424 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 527.246 MILLION OZ//

JAN 14/WITH SILVER DOWN 21 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 529.780 MILLION OZ//

JAN 13/WITH SILVER DOWN 2 CENTS: A BIG CHANGE IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 832,000 OZ FROM THE SLV////INVENTORY RESTS AT 529.780 MILLION OZ

JAN 12/WITH SILVER UP 38 CENTS TODAY : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.612 MILLION OZ//

JAN 11/WITH SILVER UP 33 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.612 MILLION OZ/.

JAN 10/WITH SILVER UP 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 530.612 MILLION OZ//.

JAN 7/WITH SILVER UP 17 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.612 MILLION OZ//.

JAN 6/WITH SILVER DOWN 94 CENTS TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL PF 226,000 OZ FROM THE SLV///INVENTORY RESTS AT 530.612 MILLION OZ?/

JAN 5/WITH SILVER UP 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.838 MILLION OZ//

JAN 4/WITH SILVER UP 21 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.838 MILLION OZ//

JAN 3/WITH SILVER DOWN 45 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.219 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 530.838 MILLION OZ//

CLOSING INVENTORY: 539.212 MILLION OZ

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

end

2.LAWRIE WILLIAM//,//Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, James RICKARDS

end

end

3. Chris Powell of GATA provides to us very important physical commentaries

For your interest….

No, the ‘soul’ of money is not trust in central banks

Submitted by admin on Thu, 2022-02-03 15:32Section: Daily Dispatches

3:33p ET Thursday, February 3, 2022

Dear Friend of GATA and Gold:

What is the “soul” of money.

In a speech last month to Goethe University’s Institute for Law and Finance in Frankfurt, Germany, the general manager of the Bank for International Settlements, Agustin Carstens, declared that the “soul” of money is trust in central banks:

https://www.bis.org/speeches/sp220118.htm

You know — the institutions that, often in secret, bestow huge amounts of money on their cronies in politically connected financial institutions, rescuing the rich at the expense of the poor; that intervene secretly to manipulate and destroy markets, picking winners and losers; and that, their executives being unelected, generally subvert democracy.This is especially so with the BIS itself, which every day is the broker for the secret interventions in the gold market of its central bank members. Ask the BIS what it does in the gold market, for whom, and for what purpose and you won’t get any talk about the “soul” of money. You’ll get the door slammed in your face. Ask to attend the meetings of the BIS board as it schemes to control the world’s money and you’ll be told to wait for the press release.

As a practical matter the “soul” of money isn’t trust at all. It is just the power of government to levy and collect taxes that must be paid in the government’s own currency. That is, taxation is the primary source of value for any major currency. If there were no taxes, or if payment of taxes was allowed in something other than a government’s own currency, the currency quickly might lose value amid competition with various forms of money.

Any central bank that wants its money to have a “soul” worth trusting should begin by trusting the people using that money to know everything the central bank is doing — to observe closely all its operations.

Of course there are no such central banks.

That central banks and the BIS itself don’t trust the people they purport to serve signifies that they don’t deserve any trust themselves.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

4.OTHER GOLD/SILVER COMMENTARIES

Despite Being Heavily Out of Favor with Fund Managers, India and China Are Quietly Buying Lots of Gold

J. Kim – SK Wealth Academy, February 04, 2022

J. Kim – SK Wealth Academy, February 04, 2022

India and China are quietly buying lots of gold

Yes, India and China are quietly buying lots of gold. For those that believe the Western banking narrative that “gold is dead” and that “bitcoin is the new gold”, just look to the behavior of two nations in which 36 out of every 100 citizens of planet Earth reside. Last year, retail consumers in China increased their gold consumption by more than 33% year over year, despite this significant news failing to make the rounds during bitcoin mania that saw two epic collapses from 2021 highs of about $65,000 and $69,000 respectively in April and November before both price highs collapsed by over 50% in relatively quick time. Due to Western banking media focus on cryptocurrencies, especially BTC, specifically designed to divert money away from physical gold purchases, no one reported on the ravenous gold appetites of the two most heavily populated nations in the world.

Unfortunately, the Chinese still don’t fully understand what form of physical gold will be most beneficial to wealth building in the long run, as displayed by their consumption patterns in which gold jewelry consumption jumped yoy by a whopping 711.29 metric tonnes (45%) while gold bars/coins (the better buy) jumped last year by 312.86 metric tonnes (26.87%). Furthermore, conditions are setting up after another year of unimpressive gold price behavior for the price run we’ve all been waiting for, as production output in China in 2021 fell by 10% to 329 tonnes.

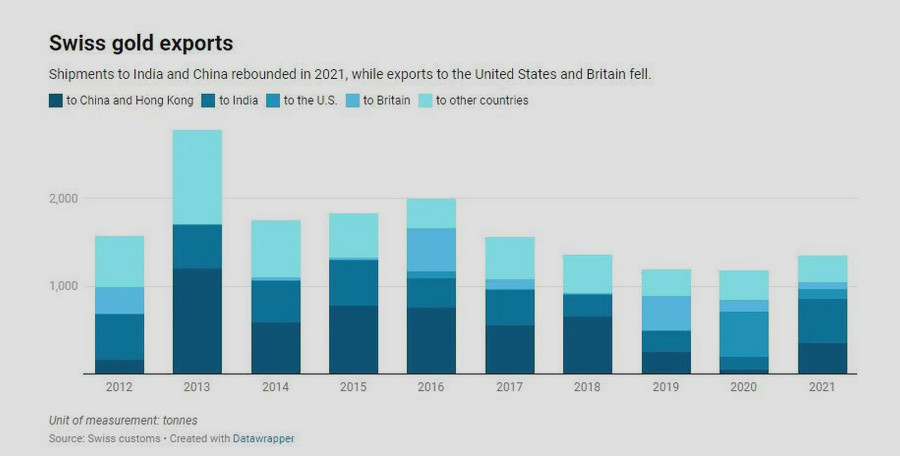

Swiss gold exports, 2021

However, as we can see in the Switzerland gold import chart above, China and India once again ramped up their gold imports last year as opposed to England and the US. India increased their imports yoy last year by 359 tonnes to Exports to 507 tonnes, the most since 2015 and more than their average annual imports of 400 tonnes from 2012 to 2019. China increased their Swiss gold imports by 296.5 tonnes yoy to 354 tonnes last year, the highest figure since 2018 though still well under their 600 tonne average import figure from 2012 to 2019 (all figures are combined Hong Kong and mainland China data). However, what should not be ignored in the fog of banking war is that US gold imports from Switzerland in 2020 actually slightly exceeded India gold imports from Switzerland in 2021 (507.5 to 507.2 metric tonnes) despite the US banking cartel publicly denigrating gold every chance they have to do so in the mainstream financial media. That figure clearly demonstrates that the US banking cartel does not think gold is yet “dead” despite their numerous public declarations to this effect. Of the nations in the Americas, only Canada, led by ignorant politicians that have zero understanding of sound money, was dumb enough to dump all their national gold reserves, while the US is still building them as exposed by Swiss gold export data.

However, for the week of 31 January 2022 to 6 February 2022, despite this bullish data from Asia that has been largely undiscussed in the mainstream financial media, I expect gold prices to decline from gold’s current $1800 mark. If you would like to know the reasons I expect a gold price decline, and by what amount, or if topics such as this interest you, then for greater, in-depth analysis, consider joining my patreon platform here.

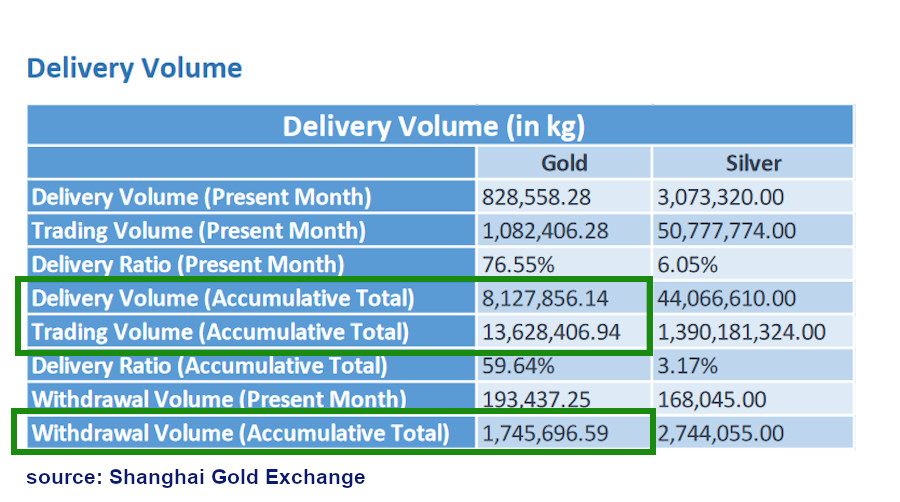

Finally, let’s take a look at the wholesale gold demand in China as reported by the Shanghai Gold Exchange (SGE). Most wholesale gold imported into China and sold in China happens through the SGE (at least the PBOC states this), so if true, SGE data provides good insight into wholesale gold demand annually. Per data provided by the SGE, in 2021, regarding data for physical gold only, 8,127.9 tonnes of gold were delivered, 13,628.4 tonnes were traded, and 1,745.7 tonnes of gold were withdrawn, as compared to the reported (by the WGC) 2021 world gold production of 3,561 tonnes. Furthermore, compare this to the total COMEX registered and pledged inventory of a mere 19.1 tonnes of gold that backs all gold derivatives trading in New York, and it is easy to understand the fraud that is occurring in NY gold futures markets trading

END

5.OTHER COMMODITIES/COTTON

6.CRYPTOCURRENCIES

Steve Brown..

end

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings FRIDAY morning 7:30 AM

ONSHORE YUAN: CLOSED XX

OFFSHORE YUAN: 6.3588

HANG SANG CLOSED UP 771.03 PTS OR 3.24%

2. Nikkei closed UP 198.68 PTS OR 0.73%

3. Europe stocks ALL RED

USA dollar INDEX UP TO 96.15/Euro FALLS TO 1.1295-

3b Japan 10 YR bond yield: RISES TO. +.201/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 114.90/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

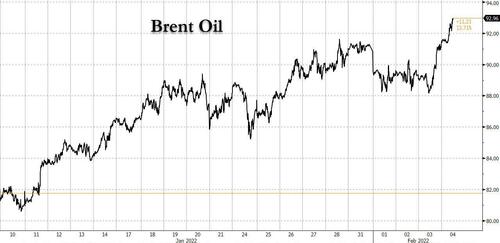

3e WTI:: 92.16 and Brent: 92.74–

3f Gold UP /JAPANESE Yen UP CHINESE YUAN: ON -SHORE CLOSED XX// OFF- SHORE UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

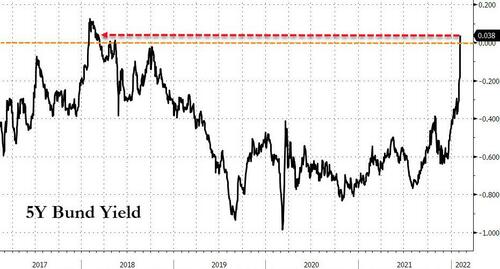

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.0.173%/Italian 10 Yr bond yield RISES to 1.69% /SPAIN 10 YR BOND YIELD RISES TO 1.00%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 1.52: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield RISES TO : 2.24

3k Gold at $1814.55 silver at: 22.60 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3l USA vs Russian rouble;// Russian rouble UP 12/100 in roubles/dollar AT 76.14

3m oil into the 92 dollar handle for WTI and 92 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 114.90 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning .9224– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0511 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

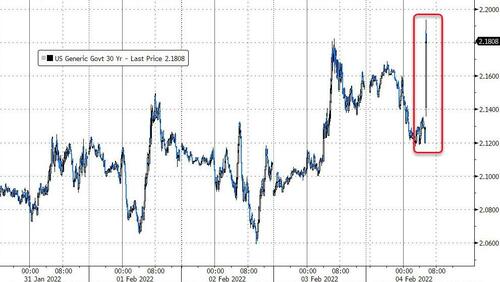

USA 10 YR BOND YIELD: 1.820 DOWN 2 BASIS PTS

USA 30 YR BOND YIELD: 2.132 DOWN 3 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 13.55

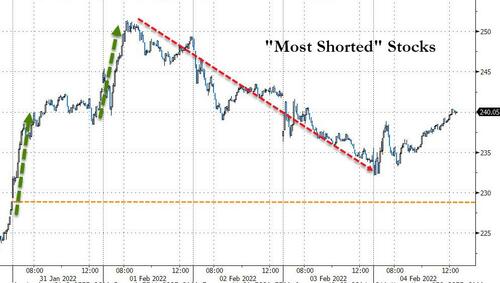

Futures Reverse Overnight Gains As Amazon Euphoria Fizzles

FRIDAY, FEB 04, 2022 – 08:05 AM

We warned last night that the surge in futures following the huge bounce in Amazon stock wouldn’t last (simply because a closer read of the company’s earnings left a lot to be desired) and sure enough, in the overnight (extremely illiquid) session, 500 futures erased gains of as much as 1.3% to trade 0.1% lower, or 10 points, to 4,460 as European stocks extend their decline as inflation and monetary tightening outweighed earnings optimism. Meanwhile, Nasdaq 100 futures pared much of their gains, trading just 0.5% higher after earlier rising more than 2%, one day after the index had the worst day since September 2020. The VIX increased for a third day Friday, hovering just below 26.

The dollar dropped as the EUR surge continued, following yesterday’s unexpectedly hawkish comments from Lagarde…

… while oil was on course for a seventh weekly advance with Brent rising

Relief, as brief as it was, was welcome after a 4.2% crash in the Nasdaq 100 Index on Thursday, its biggest since 2020, fueled by a 26% rout in Meta Platforms following disappointing results. The Nasdaq 100 has plunged 11% this year, and the S&P 500 is down 5%, amid normalization of Fed monetary policy and the prospect of rate hikes.

After soaring as much as 18%, Amazon pared its premarket gains to 11%, still implying an increase of $155 billion in its market capitalization if the stock rises by the same extent during regular trading hours. Amazon’s jump was driven by its price hike for Prime and buoyant sales over Black Friday-Cyber Monday. Snap soared as much as 57%, and Pinterest also jumped. Here are some of the biggest U.S. movers today:

- AC Immune (ACIU) shares rose 1% after the company said preclinical data of its amyloid-beta vaccine were published in peer-reviewed journal Brain Communications.

- Activision Blizzard (ATVI) shares are down 1% after the video-game company, which is being acquired by Microsoft, reported fourth-quarter results that missed expectations.

- Amazon.com (AMZN) shares are up 8% after the e-commerce company reported fourth-quarter results that sailed past expectations, lifted by strong results for its cloud-computing business.

- Bill.com (BILL) shares are up more than 8% after the software company reported second-quarter results that beat expectations and raised its full-year outlook. Analysts are extremely positive on the company and its growth potential.

- Estee Lauder (EL) rises 5% after Citi analyst Wendy Nicholson upgraded the stock to a buy from neutral, citing strong growth with more brands, channels and geographies.

- Gitlab Inc. (GTLB) gains 4% after RBC Capital Markets analyst Matthew Hedberg raised his recommendation to outperform from sector perform after a pullback in its shares.

- Hartford Financial (HIG) shares gained about 1% after the insurance firm reported revenue for the fourth quarter that beat the average analyst estimate.

- Mainz Biomed (MYNZ) gains 9% after announcing that it has started an international clinical study to evaluate the potential to integrate a portfolio of novel mRNA biomarkers into its detection test for colorectal cancer which is being commercialized across Europe.

- Snap Inc. (SNAP) surged 24% in premarket trading, but even that won’t be enough to recoup the social media stock’s year-to-date losses.

- Unity Software (U) shares are up 9% after the 3D game-development company reported fourth-quarter results that beat expectations and gave an outlook that is seen as strong.

While the overall earnings picture in the world’s largest economy remains robust, concerns over Federal Reserve tightening lingers. And fears of stubborn inflation increased after data showed U.S. gasoline surged to the highest in more than seven years.

“Overall, the earnings outlook is still solid, with the global tech sector on track for earnings growth of around 15%,” said Mark Haefele, chief investment officer at UBS Global Wealth Management. “In our base case, we expect valuations to stabilize and for strong mid-teens earnings growth to be reflected in share prices over the next 12 months.”

While Meta’s sluggish numbers dominated the headlines on Thursday, the flurry of earnings releases showed they may be an exception rather than the rule. Of the 272 companies in the S&P 500 that have reported results, 82% have met or beaten estimates. Profits are coming in at 8.8% above projected levels. Still, volatility has become the hallmark of global markets this year. Investors are trying to come to grips with less favorable monetary conditions and a moderating global recovery amid stubborn inflation.

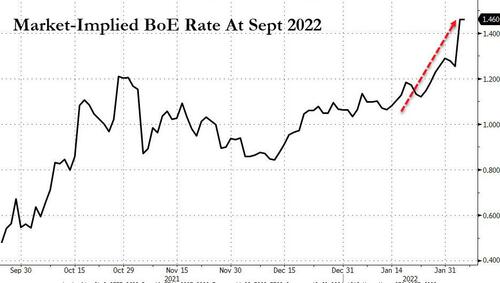

“The first half this year we are now experiencing a rates shock,” Tracy Chen, portfolio manager at Brandywine Global Investment Management, said on Bloomberg Television. “If the Fed and BOE and other emerging-market central banks are too aggressive in hiking interest rates, potentially we are going to face kind of a recession risk in the second half, or at least more slowdown in the economy.”

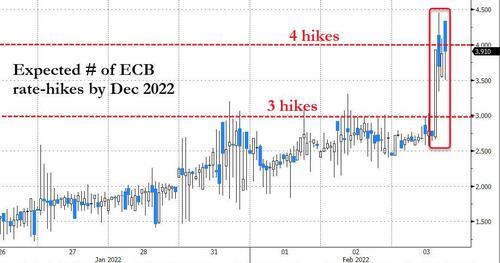

In Europe, the Stoxx 600 is down 1.2%, its biggest drop in a week; Makers of cars and parts were the worst-performing industry group, while gains for technology shares surrendered gains after a surprising hawkish turn from the European Central Bank. Better-than-expected earnings were not enough to offset reduced risk appetite. Expected data on Wednesday include non-farm payrolls, while Air Products, Bristol-Myers, Regeneron and Royal Caribbean are among companies reporting. Hawkish comments from European Central Bank President Christine Lagarde and a Bank of England interest-rate hike underlined risks from inflation. While a selloff in the region’s bonds eased, the mood in the stock market turned sour.

Earlier, an Asia-Pacific equity gauge pushed higher partly on a 3% jump in Hong Kong, which was catching up with global markets after reopening from a holiday. Asia’s equity benchmark headed for its biggest weekly advance since early September, boosted by a rally in Hong Kong stocks as they resumed trading after the Lunar New Year holiday. The MSCI Asia Pacific Index climbed as much as 1%, helped by consumer discretionary and financial stocks. Alibaba and Meituan were among the biggest contributors to the rise, as the Hang Seng Index surged 3.2% to post its biggest post-holiday jump since 2009. Asia’s tech sub-gauge edged higher following Amazon’s earnings release. The MSCI Asia Pacific Index is on track for a 2.8% climb this week, its first advance in three, as concerns ease over the pace of U.S. monetary policy tightening. The measure is set to outperform the S&P 500, which is contending with a plunge in Meta shares overnight — the biggest one-day wipeout in history. As the earnings season continues, traders are awaiting the U.S. payrolls report for January due later Friday for more cues on the health of the world’s-largest economy at a time of China’s growth slowdown. Benchmarks in South Korea, the Philippines and Australia rose, while Japan’s Topix had its best week since October. Markets in mainland China and Taiwan will reopen Monday. “At elevated valuation levels, disappointing earnings growth, higher inflation and interest rates we believe stocks with low valuations, strong balance sheet and safe dividends look more attractive,” Geir Lode, head of global equities at Federated Hermes, wrote in a note. “A larger outbreak of Covid in China would further constrain the global economic growth, limiting the upside in stocks.”

Japanese equities climbed, rebounding from Thursday’s slide to cap their best weekly gain since mid-October. Electronics makers and service providers were the biggest boosts to the Topix, which rose 0.6% for a weekly advance of 2.9%. Fast Retailing and Tokyo Electron were the largest contributors to a 0.7% gain in the Nikkei 225, which increased 2.7% on the week. “The price-to-earnings ratio for local stocks isn’t high when compared with U.S. equities, which makes the case easier for investors to buy here,” said Ayako Sera, a market strategist at Sumitomo Mitsui Trust Bank. “But investors will find it challenging to push equities much higher until there’s more clarity on the pace of U.S. rate hikes.”

India’s benchmark equity index completed its biggest weekly gain since early this year, amid optimism that the government’s plan to ramp up spending will help revive growth in Asia’s third-largest economy. The benchmark S&P BSE Sensex climbed 2.5% this week, the most since the five days ended Jan. 7. The gauge fell 0.2% on Friday to 58,644.82, while the NSE Nifty 50 Index slipped 0.3%, after swinging between gains and losses several times during the session. “Global markets, especially the U.S., have turned extremely volatile during the earnings which are impacting sentiment in our markets as well,” Ajit Mishra, vice president research at Religare Broking Ltd. said. “We recommend maintaining a cautious stance and keeping a check on leveraged positions.” Fourteen of the 19 sub-indexes compiled by BSE Ltd. fell on Friday, led by a gauge of realty stocks. Finance Minister Nirmala Sitharaman earlier this week announced plans to increase capital spending by 35% to 7.5 trillion rupees ($100 billion) in the next financial year, seeking to bolster the economy’s recovery after disruptions from the pandemic. On the earnings front, out of the 34 Nifty 50 companies that have announced results so far, 18 either met or exceeded analyst estimates, 14 missed and two can’t be compared.

Australian stocks advanced, capping the best weekly gain since August. The S&P/ASX 200 index rose 0.6% to close at 7,120.10 in Sydney, lifted by bank and industrial shares. The benchmark added 1.9% since Monday, for its best week since early August. News Corp was among the top performers Friday after its 2Q earnings exceeded analysts’ expectations. Nufarm was among the worst performers, pulling back from Thursday’s 20% surge. Boral also dropped as it traded ex-dividend. In New Zealand, the S&P/NZX 50 index fell 0.5% to 12,279.56.

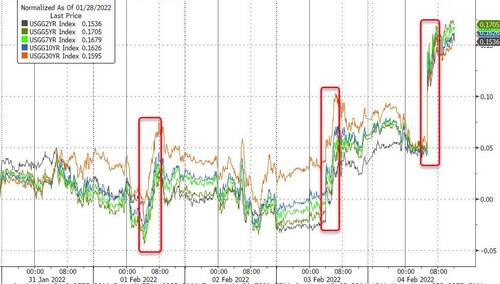

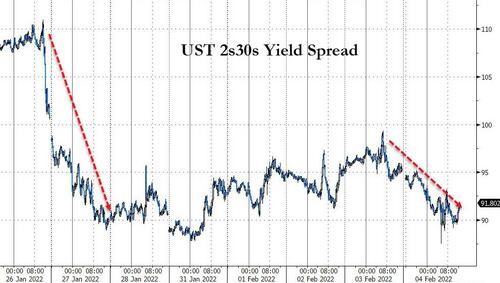

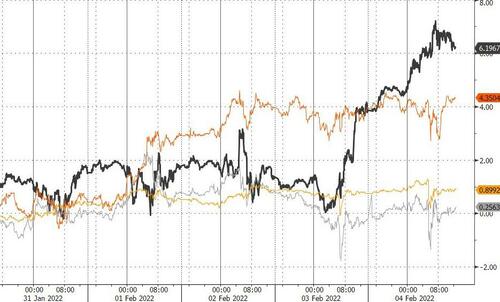

In rates, Treasuries gained from belly out to long-end of the curve as S&P 500 futures give back late-Thursday gains driven by Amazon’s earnings report. Treasuries richer by ~3bp across long-end of the curve with 2s10s, 5s30s spreads flatter by 2bp-3bp; 10-year ~1.815% tightens more than 4bp vs German 10-year to narrowest spread since September; U.S. 2-year is little changed with German 2- year higher by 5bp on day, 33bp on week. Front-end lags, following short-dated German yields higher as EUR swaps reprice for ~50bp of ECB rate hikes this year. January jobs report at 8:30am ET is focal point of U.S. session. German 5y yields turn positive for the first time since 2018. Peripheral spreads widen with 5y Italy underperforming. USTs bull-flatten a touch ahead of today’s payrolls release.

In FX, Bloomberg dollar spot index is near flat. Commodity currencies are the weakest in G-10, EUR outperforms, cable stalls near 1.36.

In commodities, West Texas Intermediate hit a fresh seven-year high and touched $92 a barrel while Brent rose above $93 after surging 19% this year and banks including Goldman Sachs Group Inc. forecast it’ll reach $100. Spot gold rises ~$9 near $1,813/oz. Most base metals trade in the green; LME lead rises 1.2%, outperforming peers

Looking at the day ahead now, and the main highlight will be the aforementioned US jobs report for January. And over in Europe releases include Euro Area retail sales, German factory orders and French industrial production for December, the German and UK construction PMIs for January. From central banks, speakers include the BoE’s Broadbent and Pill, and the ECB’s Villeroy. Finally, earnings releases include Bristol Myers Squibb and Aon.

Market Snapshot

- S&P 500 futures down 0.1% to 4,460

- STOXX Europe 600 down 0.2% to 467.59

- MXAP up 0.8% to 188.00

- MXAPJ up 1.1% to 615.27

- Nikkei up 0.7% to 27,439.99

- Topix up 0.6% to 1,930.56

- Hang Seng Index up 3.2% to 24,573.29

- Shanghai Composite down 1.0% to 3,361.44

- Sensex down 0.2% to 58,660.41

- Australia S&P/ASX 200 up 0.6% to 7,120.21

- Kospi up 1.6% to 2,750.26

- Brent Futures up 1.6% to $92.53/bbl

- Gold spot up 0.3% to $1,809.92

- U.S. Dollar Index little changed at 95.31

- German 10Y yield little changed at 0.16%

- Euro up 0.1% to $1.1457

Top Overnight News from Bloomberg

- The Bloomberg Dollar Spot Index inched lower and was set for its worst falling streak since April even as the greenback advanced versus most of its Group-of-10 peers

- The euro led gains among G-10 currencies, rising above $1.1450 with the currency’s volatility skew shifting higher across tenors compared to a week ago as topside demand gets a fresh boost following the latest ECB policy monetary meeting

- German bonds tumbled on Friday, pushing the yield on five-year notes above zero for the first time in over three years as markets braced for the ECB to scale back its accommodative monetary policy

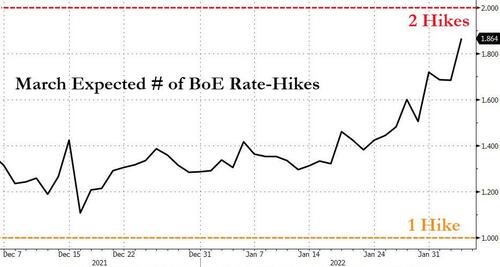

- Money markets have priced in around 50 basis points of ECB tightening for December, which would be enough to end seven years of negative deposit rates. The move builds on wagers from Thursday triggered by ECB President Christine Lagarde’s press conference, where she said policy makers are no longer ruling out an interest-rate hike this year

- The pound fell against both the dollar and euro as the Bank of England’s hike on Thursday failed to quell doubts over the sustainability of a tightening cycle and the possibility of a policy error

- New Zealand dollar rose over its Australian peer on leveraged demand as New Zealand reported a slowdown in omicron cases. Yields of both nations’ bonds advanced with other risk assets

- Japan’s benchmark 10-year and five-year yields rose to a six-year high amid speculation the Bank of Japan will end up joining developed-market peers in normalizing monetary policy. The yen steadied

A more detailed look at global markets courtesy of Newsquawk

Asian stocks eventually traded mostly positive with early indecision seen after the tech-related turbulence in US. ASX 200 (+0.6%) lacked direction for most the session before a late surge lifted the index above 7,100. Nikkei 225 (+0.7) was initially contained by a pullback in USD/JPY, although earnings continued to drive price action. Hang Seng (+3.2%) outperformed on return from a three-day closure with autos underpinned by a jump in deliveries and sports brands bid heading into the official start of the Beijing 2022 Winter Olympics.

Top Asian News

- Lavrov Denies U.S. Video Claims; Putin, Xi Meet: Ukraine Update

- Hong Kong Security Police Arrest 75-Year-Old Democracy Activist

- Carlsberg CEO Downplays Risk of Russia, Ukraine on Business

- Tesla’s Call for Tax Breaks Rejected by India in Fresh Blow

European equities have drifted lower from the mildly positive cash open despite a lack of news flow. European sectors have tilted to a more defensive bias, but Energy outpaces as crude prices remain firm.

Top European News

- Saras Rises; Barclays Double Upgrades on Refining Margins

- Boris Johnson’s Key Aides Quit, Leaving Premier on the Brink

- Ousted Orpea CEO Got 2020 Bonus Even After Missing Growth Target

- Holcim Cut to Sell on Change in Future Strategy: Berenberg

In Fixed Income, core EGB benchmarks came under further pressure in early-European hours on further hawkish repricing. Action that sent the German 5yr yield positive and the 10yr to a test of 0.20%. The Periphery remains hampered with spreads widening further and focus turning to potential looming 30yr syndication via Spain.

In FX, DXY is contained with a negative-bias in pre-NFP trade, while EUR continues to outpace but GBP pullsback on EUR/GBP action. Antipodeans lag following a dovish RBA SOMP, but NZD is somewhat cushioned by AUD/NZD. JPY remains resilient with USD/JPY holding below 115.00. NATO Chief Stoltenberg will be appointed as Governor of the Norges Bank, via Daily VG; Deputy Governor. Bache will be the acting Norges Bank Governor from March 1st until Stoltenberg takes over.

In commodities, WTI and Brent continue to grind higher in a continuation of yesterday’s upward momentum, focus remains very much on geopolitics this morning. Brent-WTI arb continues to contract amid China-Russian deals and the ongoing Texas freeze. Citi recommended selling December 2022 Brent crude futures on expected inventory builds this year and it targets up to 20% downside in Brent December 2022 prices during H2. Spot gold and silver are modestly firmer but remain in recent ranges and near multiple DMAs

US Event Calendar

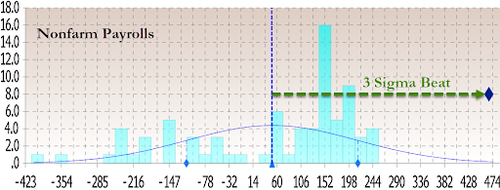

- 8:30am: Jan. Change in Nonfarm Payrolls, est. 125,000, prior 199,000

- 8:30am: Jan. Change in Private Payrolls, est. 32,000, prior 211,000

- 8:30am: Jan. Change in Manufact. Payrolls, est. 20,000, prior 26,000

- 8:30am: Jan. Average Weekly Hours All Emplo, est. 34.7, prior 34.7

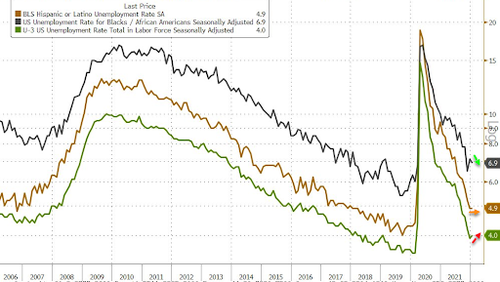

- 8:30am: Jan. Unemployment Rate, est. 3.9%, prior 3.9%

- 8:30am: Jan. Underemployment Rate, prior 7.3%

- 8:30am: Jan. Labor Force Participation Rate, est. 61.9%, prior 61.9%

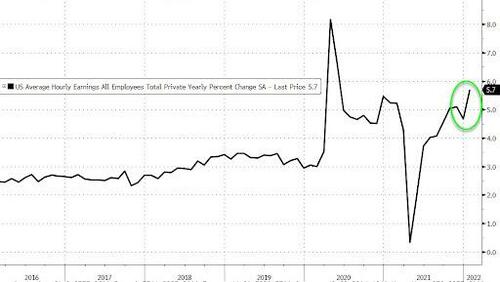

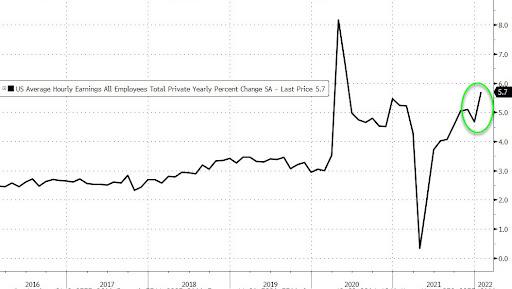

- 8:30am: Jan. Average Hourly Earnings MoM, est. 0.5%, prior 0.6%; YoY, est. 5.2%, prior 4.7%

DB’s Jim Reid concludes the overnight wrap

3. ASIAN AFFAIRS

i)FRIDAY MORNING// THURSDAY NIGHT

SHANGHAI CLOSED //Hang Sang CLOSED UP 771.03 PTS OR 3.24% /The Nikkei closed UP 198.68 PTS OR 0.73% //Australia’s all ordinaires CLOSED UP 0.60% /Chinese yuan (ONSHORE) closed HOLIDAY /Oil UP TO 92.16 dollars per barrel for WTI and DOWN TO 92.74 for Brent. Stocks in Europe OPENED ALL RED // ONSHORE YUAN CLOSED XX AGAINST THE DOLLAR AT XXX. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.3588: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN AND OFF SHORE TRADING STRONGER AGAINST USA DOLLAR

3 a./NORTH KOREA/ SOUTH KOREA

///NORTH KOREA

3B JAPAN

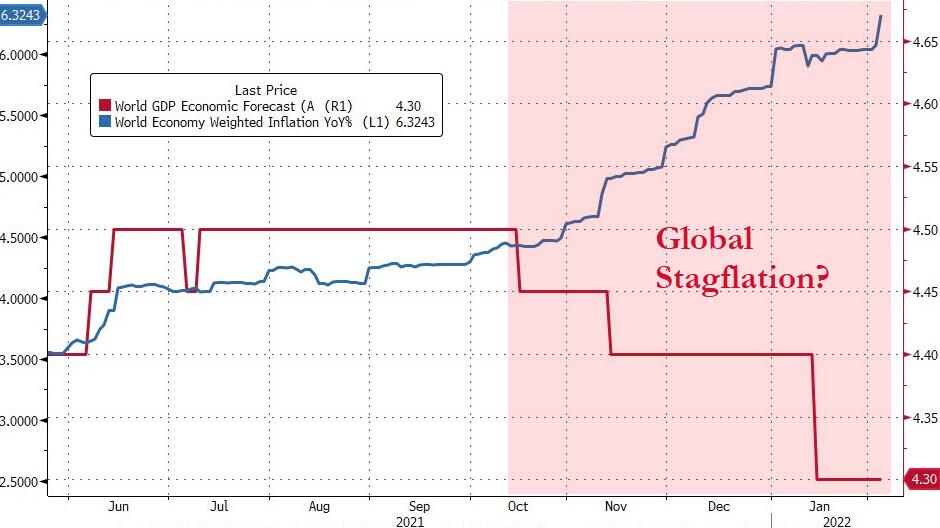

All yields are rising fast and this is panicking our central bankers. What is bugging them? Stagflation. In other words inflation accompanied by no growth.

check out the huge rise in yields on all currencies this morning!!

(zerohedge)

Are Global Central Banks (Ex-China) Suddenly Panicking?

THURSDAY, FEB 03, 2022 – 09:20 PM

The last few weeks or so have seen a chill wind run through the halls of global central planners’ offices.

First (among the majors) it was the Bank of England who surprised investors with a rate-hike in mid-December (after promising they wouldn’t), then this morning ending QE and raising rates again (narrowly avoiding by a 5-4 vote a 50bps hike).

Source: Bloomberg

Then it was The Fed’s various group-thinkers doing an extremely rapid volte-face from forever-dovish to the hawkiest hawks in hawk-land, calling for a halt to QE, imminent and rapidly rising rate-hikes, and the start of QT.

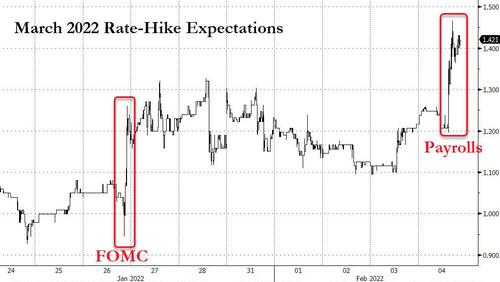

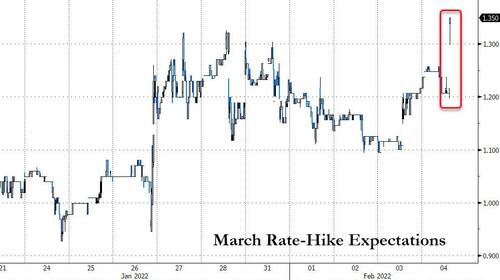

US STIRs are now pricing in 5 rate-hikes by year-end (and a 25% chance of a 50bps hike in March)…

Source: Bloomberg

This morning saw Christine Lagarde change her stripes from uber dove to more fence-sitter (and some would say an actual hawkish bias was overheard with Bloomberg reporting that ECB policymakers “see policy change at the March meeting if inflation doesn’t ease.”

Rate-hike expectations are spiking in European bond markets…

Source: Bloomberg

And rates across the curve are flipping back into positive territory…

Source: Bloomberg

All of which leads us to this evening and the open of Japanese markets.

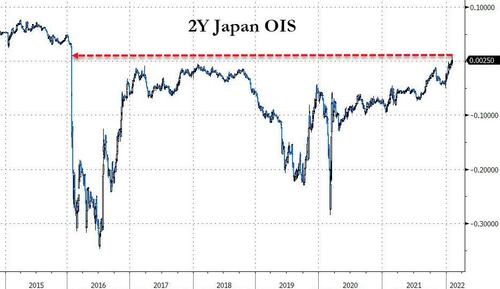

Haruhiko Kuroda has been perhaps the doviest of the dovish central bankers over the years which makes the very recent actions in the Japanese bond markets even more exceptional.

As Bloomberg notes this evening, speculation of monetary policy normalization has reached Japan.

2Y OIS (a proxy for investor expectations of future policy rates) breached zero for the first time since 2016 – the year the Bank of Japan introduced its negative interest rate policy.

Source: Bloomberg

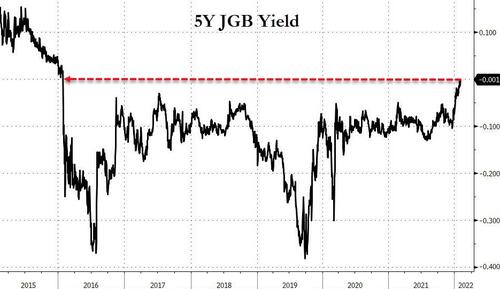

5Y JGB Yields have pushed back above zero for the first time since 2016…

Source: Bloomberg

Of even more note is the fact that the 10Y JGB yield has surged up to the top of its ‘yield curve control’ corridor.

As a reminder, since September 2016, the BoJ has maintained a so-called ‘yield curve control’ policy (allowing 10Y JGB yields to fluctuate within a range regarding of its 0% target – initially +/-10bps but now +/-20bps).

Source: Bloomberg

The last time 10Y yields were at these levels (in Feb 2021), BoJ quickly stepped in, but – for now – this time is different.

“Market participants see an increasing chance that a successor to Kuroda will lift the negative-rate policy,” said Takahide Kiuchi, executive economist at the Nomura Research Institute in Tokyo.

“As the end of his tenure gets closer, the governor’s influence will decrease further.”

Some have argued this pressure is market participants’ desire to test the BOJ’s resolve, and we suspect that if 10-year yields continue to climb well above 0.2% today, BOJ action likely will become a reality.

“The recent rise in the 10-year JGB yield may have gone too far,” Tomonobu Yamashita and Shusuke Yamada, strategists at Bank of America, wrote in a research note.

“Given the BOJ’s dovish stance and leeway for increasing its JGB purchases, this may be an opportunity to buy JGBs cheaply.”

It’s too early to raise interest rates or change the yield curve control program now, Kuroda said last week.

However, once cannot miss the fact that The BoJ has let things get this far without verbal intervention at a minimum. This certainly has the smell of a ‘signal’ that, as Eiichiro Miura, GM of the fixed-income department at Nissay Asset Management notes, the “BOJ may not be seeking to forcibly contain 10-year yield at 0.2% as it may want markets to prepare for a potential change.”

So why are Bailey, Powell, Lagarde, and Kuroda all suddenly shedding their dovish wings?

Is this what has the world’s omnipotent puppet-masters panicking?

Source: Bloomberg

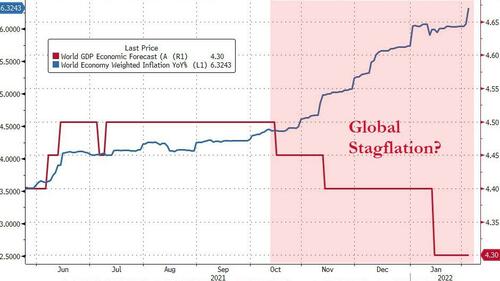

Global economic growth expectations are sliding rapidly and inflation (current and forecast) is accelerating.

The Keynesian boogeyman is back – global stagflation! And with global assets at their bubbliest values ever, is it any wonder those-who-shall-not-be-named are panicking?

So action is needed, but what? Hike and kill growth even more (and the wealth creation that’s been coveted for over a decade); don’t hike and spark fiat-credibility crushing inflationary fires worldwide?

One thing is for sure, the market is expecting some action soon (and The Taylor Rule suggests there’s a long way to go)…

Source: Bloomberg

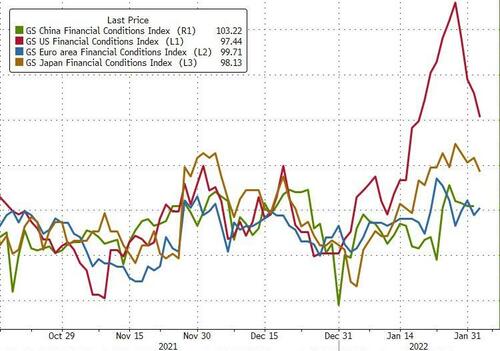

For now, however, only the US appears to be allowing financial conditions to tighten (and perhaps modestly Japan).

Source: Bloomberg

And don’t expect any help from China this time.

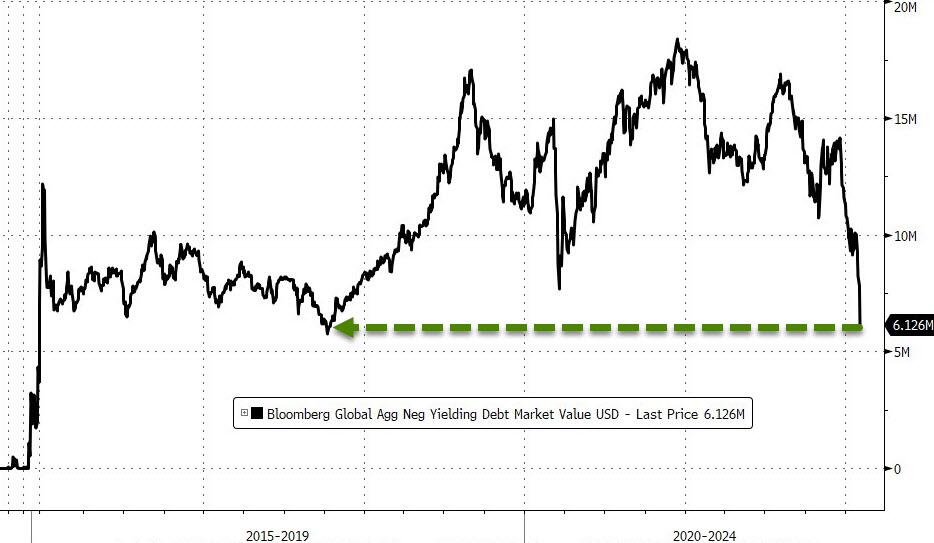

It appears that traders across the world just realized that Central Bankers are serious this time, and as they dump bonds, the global volume of negative-yielding debt has collapsed…

Source: Bloomberg

All of which removes yet another leg from the ‘stool’ of global equity prices. TINA is well and truly dead now.

end

Special thanks to Doug C for sending this to us:

(Wolf Richter/WolfStreet)

Global Tightening amid Raging Inflation: February Update

by Wolf Richter • Feb 3, 2022 • 127 Comments

Brazil and Russia caught up via shock-and-awe rate hikes. But most central banks fell further behind. Then there are the reckless laggards.

By Wolf Richter for WOLF STREET.

The Bank of England today, February 3, started QT (Quantitative Tightening, the opposite of QE) and raised its policy rate by 25 basis points, to 0.50%, the second hike in a row, after having raised by 15 basis points at its December meeting. The hawkish part was how it happened: A bare majority of five members of the Monetary Policy Committee voted for the 25-basis-point hike, while four members voted for a 50-basis-point hike!

The BOE voted unanimously to start QT by reducing its holdings of government bonds by allowing maturing bonds to roll off without replacement, and by selling its corporate bonds outright. In terms of the corporate bonds, the BOE is following in the Fed’s footsteps which sold its corporate bond holdings entirely by November 2021.

The UK is getting hammered by inflation that has surged to 5.4%, the worst in four decades, and is hitting the standard of living of lower-income households particularly hard. The BOE expects inflation to surge to “around 7% in the spring.”

The Czech National Bank, also today, jacked up its policy rate by 75 basis points to 4.5%, the highest since January 2002, and the sixth rate hike in a row since June, totaling 425 basis points, including shock-and-awe hikes of 100 basis points in December and 125 basis points in November, which had been the biggest shock-and-awe rate hike in 24 years.

Unlike certain other central banks – the you-know-which reckless laggards at the bottom of this article – it’s actually battling inflation which spiked to 6.6%.

The Bank of Brazil, on February 2, jacked up its policy rate by another 150 basis points, to 10.75%, the eighth hike in a row since March, totaling 875 basis points.

The central bank said that the next rate hike might be smaller, on hopes that inflation is showing signs of responding to this shock-and-awe treatment. In November, inflation had hit a red-hot 10.7%, and in December it was slightly less red-hot at 10.1%.

With a policy rate of 10.75%, and a December inflation rate of 10.1%, Brazil is one of a few countries were the policy rate is above the rate of inflation, and therefore in real terms no longer negative, and therefore no longer stimulating inflation. By contrast, the Fed is a quadrillion miles behind.

The Central Bank of Armenia, on February 1, hiked its policy rate by 25 basis points, to 8.0%, the eighth hike in a row, including the 50-basis-point hike in December, from liftoff at 4.25%. Inflation backed off to a still red-hot 7.7% in December, from 9.6% in November.

The Bank of the Republic (Colombia), on January 28, jacked up its policy rate by a shock-and-awe 100 basis points, to 4.0%, the fourth hike in a row, totaling 225 basis points since liftoff in September. Inflation spiked to 5.6% in December.

The South Africa Reserve Bank, on January 27, hiked its policy rate by 25 basis points, to 4.0%, the second hike in a row, totaling 50 basis points.

Inflation spiked to 5.9% in December, at the top of the SARB’s target range of 3% to 6%.

The Central Bank of Chile, on January 26, dished out a shock-and-awe rate hike of 150 basis points, to 5.5%, the fifth hike in a row, starting in July, totaling 500 basis points, including two 125-basis-point hikes in December and October.

The central bank is battling inflation that spiked to 7.2% in December, the worst since 2008.

The National Bank of Hungary, on January 25, hiked its policy rate by 50 basis points, to 2.9%, the highest since 2013. The magnitude of the hike surprised economists who’d expected another 30-basis-point hike, as before. It was the eighth hike in a row, from liftoff in June at 0.6%.

Inflation, at 7.4% in November and December, was the worst since 2007. But core inflation spiked to 6.4% in December, the worst since 2002, up from 5.3% in November and 4.0% in September. The central bank pointed at stronger than expected inflationary pressure and sees core inflation increasing further over the coming months.

The State Bank of Pakistan, on January 24, paused with its policy rate at 9.75%, after three rate hikes totaling 275 basis points, including 100 basis points in December, and a shock-and-awe 150 basis points in October. Liftoff was in September from 7.0%.

Inflation spiked to 13% in January.

Norges Bank, the central bank of Norway, on January 20 paused after two rate hikes in December and September of 25 basis points each, to 0.5%. So far, it has raised its rate at every other meeting and is expected to hike by 25 basis points at its next meeting in March.

Inflation jumped to 5.3% in December, the worst since October 2008.

The Bank of Korea, on January 14, raised its policy rate by 25 basis points to 1.25%, the third hike since August, totaling 75 basis points. Inflation in December was 3.7%, following the 3.8% in November, the worst since 2012.

The Central Reserve Bank of Peru, on January 6, hiked its policy rate by another 50 basis points to 3.0%, the sixth hike in a row, since liftoff at 0.25%. Inflation backed off from 6.4% in December to 5.7% in January, same as in November.

The National Bank of Poland, on January 4, hiked its policy rate again by 50 basis points, to 2.25%, after the 50-basis-point hike in December, the fourth hike in a row, totaling 215 basis points, from liftoff at 0.1%.

Inflation spiked to 8.6% in December, the highest since 2000, up from 7.8% in November, from 6.8% in October, and 5.9% in September. Prices soared across many categories, including housing-related costs and utilities, food and beverages, and recreation and cultural activities.

The Bank of Mexico will meet on February 10. At its last meeting on December 16, it surprised by hiking its policy rate by 50 basis points, to 5.5%, the fifth hike in a row, totaling 150 basis points.

Inflation in Mexico has risen to 7.4% in November and December, the worst since January 2001.

The Central Bank of Russia will meet on February 11. At its last meeting on December 17, it hiked its policy rate by another 100 basis points to 8.5%, the seventh rate hike in 2021, totaling 425 basis points.

Inflation in January remained at the same red-hot pace of December, at 8.4%, over double the Bank of Russia’s target of 4%. Food inflation dipped to 10.6%. That inflation has stopped getting worse is raising hopes the shock-and-awe treatments are showing the first of results.

With a policy rate of 8.5% and an inflation rate of 8.4%, the Central Bank of Russia has joined the elite club of central banks whose policy rates have caught up with and surpassed inflation – Brazil being the other major one – thereby no longer stimulating inflation.

The Reserve Bank of New Zealand will meet on February 23. At its last meeting on November 24, it hiked its policy rate by 25 basis points to 0.75%, the second hike in a row. It already ended QE cold-turkey in July.

Inflation spiked to 5.9% in Q4, the highest since the 1980s. And the low interest rates and QE have inflated the worst housing bubble in the world.

The Central Bank of Iceland will meet on February 9. At its last meeting on November 17, it hiked its policy rate by 50 basis points to 2.0%, the fourth hike since liftoff in May from 0.75%.

Inflation has spiked to 5.7% in January, from 5.1% in December, the highest since 2012.

The Biggest Most Reckless Laggards

The Fed, on January 26, announced via Chair Powell at the FOMC press conference that it would hike its policy rate on March 16 and that it would start QT later this year. In November, it began tapering its asset purchases. It has since then accelerated the process of tapering and will end QE entirely in early March, just before liftoff.

But at the moment, the Fed’s target range for the federal funds rate is still 0% to 0.25%, and it is still doing QE even if at a much-reduced pace.

Meanwhile, CPI inflation spiked to 7.04%, the worst since 1982. With the Effective Federal Funds Rate at 0.08%, the “real” EFFR (EFFR minus CPI) is now at -6.96%, the most negative and worst ever.

The ECB, today, under massive pressure from spiking record worst inflation of 5.1% in the Eurozone, performed a policy U-turn and opened the door to a first rate hike in 2022. Lagarde is probably the world’s most dovish central banker, but with inflation eating everyone’s lunch in the Eurozone, she said today, “the situation has indeed changed.”

In December, the ECB announced a sharp reduction of QE from an average of €92 billion a month late last year, to about €40 billion by March, €30 billion a month in Q3, and €20 billion a month in Q4.

The Bank of Japan keeps emphasizing that it is not heading toward “normalization” of monetary policy. Its policy rate is still -0.1%. But it began tapering its ultra-massive QE in the fall of 2020 and since May 2021, its balance sheet has flattened out, regardless of what it said in its announcements.

Inflation has been rising even in Japan, to reach +0.8% in December, the highest since before the pandemic. But this rate of inflation is minuscule compared to the fiascos in the US and elsewhere, giving Japan one of the least negative “real” policy rates of -0.9%, compared to the US “real” EFFR of -6.95%.

The Reserve Bank of Australia, on February 1, announced that it would end QE on February 10. But it kept its policy rate at 0.1% and said that it would be “patient” in raising the rate. Inflation rose to 3.5% in Q4, faster than forecast.

The Bank of Canada ended is massive QE in 2021 and reduced its balance sheet by 13% as it shed its short-term Treasury bills and repos. At its meeting on January 26, it maintained its policy rate at 0.25%, but paved the way for a rate hike at its next meeting on March 2. Inflation has surged to 4.8% in December, the worst since 1991.

The People’s Bank of China has tiptoed back into easing by lowering its policy rates a tiny bit, bringing its Loan Prime Rate down by 10 basis points, to 3.7%. It is struggling with its own universe of problems, including the slow-motion collapse of the highly leveraged real estate development sector, whose activity – construction – was a huge contributor to economic growth. Inflation has eased to 1.5%.

The Central Bank of Turkey has become part of a joke on how to destroy a currency as quickly as possible. Amid raging inflation – it hit 49% in January – the central bank has been cutting its policy rate to 14%, from 19% in mid-2021, after Erdogan fired the head of the central bank. Erdogan is now trying to control this inflation rampage by firing the head of the statistics agency.

Enjoy reading WOLF STREET and want to support it? Using ad blockers – I totally get why – but want to support the site? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

3c CHINA

CHINA/USA

END

4/EUROPEAN AFFAIRS

FRANCE/VACCINE/VACCINE MANDATE

This is very interesting this morning. French protesters gathering around Pfizer’s French headquarters chanting “assassins”

(Watson/SummitNews)

Watch: French Protesters Surround Pfizer HQ Chanting “Assassins”

FRIDAY, FEB 04, 2022 – 02:00 AM

Authored by Steve Watson via Summit News,

Video shot this past weekend in Paris France shows thousands of protesters surrounding the headquarters of Pfizer in the nation’s capitol and chanting “assassins!” in protest of vaccine mandates.

Watch: SEE ZEROHEDGE

Protests have been raging in France for a long time, and have been energised by French President Emmanuel Macron admitting last month that part of his “strategy” on tackling COVID is to “piss off” the unvaccinated as much as possible by limiting their freedoms and coercing them into taking shots.

Macron made the comments in an interview with the Le Parisien newspaper, noting “As for the non-vaccinated, I really want to piss them off. And we will continue to do this, to the end. This is the strategy.”

The French President previously announced that those who don’t have a ‘COVID pass’ will be banned from participating in basic life activities such as visiting shopping malls, restaurants and using public transport. The so called green health pass is now a part of daily life in France.

When the system came into effect, Macron also asserted that showing ‘papers’ to enter cafes is about “freedom”.

In addition, last week the administrative director of the public hospital network of the Paris region, Martin Hirsch argued that unvaccinated citizens should be prohibited from accessing hospital care.

“I don’t want to close the door of the hospital and of care to anyone, but you have to be allied with the responsibility that allows everyone to benefit from it,” Hirsch proclaimed:

END

AUSTRIA

(Paul Craig Roberts)

Austria: A Resurrected Third Reich

February 4, 2022| Categories: Articles & Columns| Tags: |Print This Article

Austria: A Resurrected Third Reich

Paul Craig Roberts

Compulsory Covid vaccination is set to be imposed on Austrians. This is a direct violation of the Nuremberg Laws. Will the Swastika go up all over Europe?

Is there a mere ounce of intelligence and integrity anywhere in the Austrian government? It is an established fact that the Covid vaccine fails to protect. It is an established fact that Covid is deadly only for those with co-morbidities who are not treated with effective means such as HCQ, Ivermectin, or monoclonal antibodies. It is an established fact that the Covid vaccine results in a high rate of health injury and death. It is an established fact that the mass vaccination spawns new variants. It is an established fact that the vaccine is, therefore, counterproductive.

So why has the Austrian government passed a law requiring that every Austrian be injected with a dangerous substance? How much did Big Pharma pay the members of the government? Why when other European governments are ending all mandates has Austria’s government chosen to open itself to the death penalty for violating the Nuremberg Laws?

Why do the Austrian people tolerate their Nazi government coercing them to be injected with a dangerous substance that can injure and kill them? At the least, the Nazi Austrian government should be overthrown, and perhaps more violent methods be used against the government that is legislating mass injury and murder.

https://www.rt.com/news/548263-austria-compulsory-vaccination-vote/

end

UK

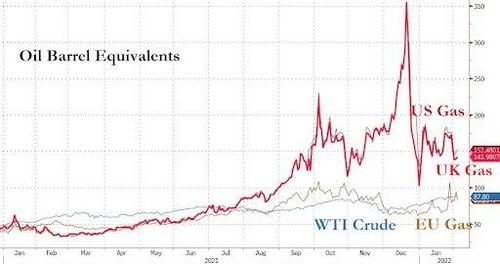

The high cost of energy is causing a huge steep drop in the quality of life for UKer’s. The government scrambles to avert an energy crisis with a subsidy plan

(zerohedge)

Britons Face “Steep Drop In Quality Of Life” As UK Gov’t Scrambles To Avert Energy Crisis With Subsidy Plan

FRIDAY, FEB 04, 2022 – 02:45 AM

Finally, observers of British politics have something else to talk about besides ‘Partygate’.