FEB 23

FEB23

· by harveyorgan · in Uncategorized · Leave a comment ·Edit

GOLD; $1907.90 UP $2.40

SILVER: $24.49 UP 22 CENTS

ACCESS MARKET: GOLD $1898.70

SILVER: $24.08

Bitcoin: morning price: $38,975 UP 1101

Bitcoin: afternoon price: $37,656 DOWN 218

Platinum price: closing UP $14.35 to $1091.65

Palladium price; closing UP $101.50 at $2451.00

END

end

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

comex notices//JPMorgan notices filed//comex notices//JPMorgan notices filed 76/261

EXCHANGE: COMEX

CONTRACT: FEBRUARY 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,906.100000000 USD

INTENT DATE: 02/22/2022 DELIVERY DATE: 02/24/2022

FIRM ORG FIRM NAME ISSUED STOPPED

118 C MACQUARIE FUT 10

332 H STANDARD CHARTE 10

363 H WELLS FARGO SEC 28

435 H SCOTIA CAPITAL 11

624 H BOFA SECURITIES 94

657 C MORGAN STANLEY 5

661 C JP MORGAN 261 35

661 H JP MORGAN 41

732 C RBC CAP MARKETS 1

905 C ADM 26

TOTAL: 261 261

MONTH TO DATE: 18,221

NUMBER OF NOTICES FILED TODAY FOR FEB. CONTRACT: 261 NOTICE(S) FOR 26,100 OZ (0.8118 TONNES)

total notices so far: 18,9221 contracts for 1,822,100 oz (56.674 tonnes)

SILVER NOTICES:

150 NOTICE(S) FILED TODAY FOR 750,000 OZ/

total number of notices filed so far this month 1985 : for 9,925,000 oz

GLD

WITH GOLD UP $2.40

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

NO CHANGES AT THE GLD:

CLOSING INVENTORY :1024.09 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP 22 CENTS:/:

AT THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

NO CHANGES IN SILVER INVENTORY AT THE SLV//

CLOSING INVENTORY: 551.597 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A VERY STRONG 1030 CONTRACTS TO 163,745 AND RESTS CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020 AND WITH THIS STRONG GAIN IN OI, IT WAS ACCOMPANIED WITH OUR STRONG $0.30 GAIN IN SILVER PRICING AT THE COMEX ON TUESDAY. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.30) AND WERE UNSUCCESSFUL IN KNOCKING OUT ANY SILVER LONGS AS WE HAD A VERY STRONG GAIN OF 2122 CONTRACTS ON OUR TWO EXCHANGES .

WE MUST HAVE HAD:

I) HUGE BANKER SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A HUGE INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 4.110 MILLION OZ FOLLOWED BY TODAY’S 999,000 OZ QUEUE JUMP//NEW STANDING 10.020 MILLION OZ. V) STRONG SIZED COMEX OI GAIN.

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS -363

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS FEB. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF FEB:

TOTAL CONTACTS for 16 days, total contracts: : 9556 contracts or 47.780 million oz OR 2.986 MILLION OZ PER DAY. (5897CONTRACTS PER DAY)

TOTAL NO OF OZ UNDERGOING EFP TO LONDON 9556 CONTRACTS X 5,000 PER CONTRACT:

EQUATES TO: 47.780 MILLION OZ

.

LAST 10 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 47.780 MILLION OZ//

SPREADING OPERATIONS

(/NOW SWITCHING TO SILVER) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF MAR.WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF JAN HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB, FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (MAR), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

RESULT: WE HAD A VERY STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1393 WITH OUR STRONG $0.30 GAIN SILVER PRICING AT THE COMEX// TUESDAY THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 729 CONTRACTS( 729 CONTRACTS ISSUED FOR MAR AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR FEB OF 4.1 MILLION OZ FOLLOWED BY TODAY’S 999,000 OZ QUEUE JUMP //NEW STANDING 10.020, MILLION OZ// .. WE HAD A VERY STRONG SIZED GAIN OF 1759 OI CONTRACTS ON THE TWO EXCHANGES FOR 8.795 MILLION OZ//

WE HAD 150 NOTICES FILED TODAY FOR 750,000 OZ

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A STRONG 9260 TO 611.488 AND CLOSER TO OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: —704 CONTRACTS.

THE BIS HAS ABANDONED THE GOLD COMEX TRADING!!!

.

THE STRONG SIZED INCREASE IN COMEX OI CAME WITH OUR GAIN IN PRICE OF $6.20//COMEX GOLD TRADING/TUESDAY/.AS IN SILVER WE MUST HAD HUGE BANKER/ALGO SHORT COVERING ACCOMPANYING OUR STRONG SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION AS THE TOTAL GAIN ON OUR TWO EXCHANGES TOTALED 16,001 CONTRACTS…

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR FEB AT 64.3 TONNES FOLLOWED BY TODAY’S 2400 OZ QUEUE. JUMP //NEW STANDING: 58.973 TONNES

YET ALL OF..THIS HAPPENED WITH OUR GAIN IN PRICE OF ONLY $6.20 WITH RESPECT TO TUESDAY’S TRADING

WE HAD A VERY STRONG SIZED GAIN OF 15,297 OI CONTRACTS (47.580 PAPER TONNES) ON OUR TWO EXCHANGES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 6037 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 611,458.

IN ESSENCE WE HAVE A VERY STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 16,001, WITH 9964 CONTRACTS INCREASED AT THE COMEX AND 6037 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 16,001 CONTRACTS OR 49.769TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (6037) ACCOMPANYING THE STRONG SIZED GAIN IN COMEX OI (9260,): TOTAL GAIN IN THE TWO EXCHANGES 15,297 CONTRACTS. WE NO DOUBT HAD 1) HUGE BANKER SHORT COVERING ,2.) HUGE INITIAL STANDING AT THE GOLD COMEX FOR FEB. AT 64.30 TONNES WHICH FOLLOWS TODAY’S 4200 OZ QUEUE JUMP //NEW STANDING 58.973 TONNES// 3) ZERO LONG LIQUIDATION ,4) STRONG SIZED COMEX OI. GAIN 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

FEB

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF FEB :

52,271 CONTRACTS OR 5,227,100 OR 162.58 TONNES 16 TRADING DAY(S) AND THUS AVERAGING: 3266 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 16 TRADING DAY(S) IN TONNES: 162.58 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2020, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 162.58/3550 x 100% TONNES 4.54% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 145.12 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 162.58 TONNES//INITIAL

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A VERY STRONG SIZED 1030 CONTRACTS TO 163,745 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 4 1/2 YEARS AGO.

EFP ISSUANCE 729 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 729 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 729 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1030 CONTRACTS AND ADD TO THE 729 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A VERY STRONG SIZED GAIN OF 1759 OPEN INTEREST CONTRACT FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 8.795 MILLION OZ,

OCCURRED WITH OUR $0.30 GAIN IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

5. Other gold commentaries

6. Commodity commentaries/cryptocurrencies

3. ASIAN AFFAIRS

)WEDNESDAY MORNING// TUESDAY NIGHT

SHANGHAI CLOSED UP 32.00 PTS OR 0.93% //Hang Sang CLOSED UP 140.28 PTS OR 0.60% /The Nikkei closed DOWN 461.26 or 1.71% //Australia’s all ordinaires CLOSED UP 0.70% /Chinese yuan (ONSHORE) closed UP 6.3279 /Oil DOWN TO 91.56 dollars per barrel for WTI and UP TO 96.65 for Brent. Stocks in Europe OPENED ALL GREEN // ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.3179. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.3148: /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFF SHORE STRONGER/

A)NORTH KOREA//USA/OUTLINE

b) REPORT ON JAPAN

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A STRONG SIZED 9260 CONTRACTS AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS STRONG COMEX INCREASE OCCURRED WITH OUR GAIN OF $6.20 IN GOLD PRICING TUESDAY’S COMEX TRADING. WE ALSO HAD A STRONG SIZED EFP (6037 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE ACTIVE DELIVERY MONTH OF FEB.. THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 6037 EFP CONTRACTS WERE ISSUED: ;: , & FEB. 0 APRIL: 6037 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 6037 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A VERY STRONG 16,001 TOTAL CONTRACTS IN THAT 6037 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A STRONG COMEX OI GAIN OF 9260 CONTRACTS..

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING FOR FEB (58.973),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

FEB 2022: 58.973 TONNES

THE BANKERS WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $6.20) AND THEY WERE UNSUCCESSFUL IN FLEECING ANY LONGS AS WE HAVE REGISTERED A STRONG GAIN OF 49.769 TONNES OF TOTAL OI, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR FEB (58.973 TONNES)…

WE HAD –704 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 15,297 CONTRACTS OR 1,529,700 OZ OR 47.580 TONNES

Estimated gold volume today: 150,861 ///POOR

Confirmed volume yesterday: 358,372 contracts GOOD

INITIAL STANDINGS FOR FEB ’22 COMEX GOLD //FEB 23

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 32151.000 oz JPMorgan 1000 kilobars |

| Deposit to the Dealer Inventory in oz | nilOZ |

| Deposits to the Customer Inventory, in oz32 | 3215.100 oz 100 kilobars Manfra |

| No of oz served (contracts) today | 261 notice(s) 26,100 OZ 0.8118 TONNES |

| No of oz to be served (notices) | 739 contracts 73,900 oz 2.298 TONNES |

| Total monthly oz gold served (contracts) so far this month | 18,221 notices 1,822,100 OZ 56.674 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For today:

one dealer deposit

Into Manfra: 15,683.230 oz

No dealer withdrawal 0

1 customer deposit

i) Into Manfra: 3215.000 oz (100 kilobars)

total deposit: 3215.000 oz

1 customer withdrawals

i) Out of JPMorgan: 32151.000 oz (1000 kilobars)

total withdrawals: 32151.000 oz

ADJUSTMENTS: 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR FEBRUARY.

For the front month of FEBRUARY we have an oi of 1000 stand LOSING 408 contracts.

We had 450 contracts served upon yesterday, so we GAINED 42 contracts or an additional 4,200 oz will stand on this side of the pond looking for gold metal.

The month of March saw a GAIN OF 71 contracts and thus the OI standing is 4623.

April saw a GAIN of 15 contracts UP to 470,996.

June saw a gain of 7232 contracts up to 80,536 contracts

We had 261 notice(s) filed today for 26,100 oz FOR THE FEB 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 261 notices were issued from their client or customer account. The total of all issuance by all participants equates to 261 contract(s) of which 35 notices were stopped (received) by j.P. Morgan dealer and 41 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the FEB /2021. contract month,

we take the total number of notices filed so far for the month (18,221) x 100 oz , to which we add the difference between the open interest for the front month of (FEB: 1000 CONTRACTS ) minus the number of notices served upon today 261 x 100 oz per contract equals 1,896,000 OZ OR 58.973 TONNES the number of TONNES standing in this active month of FEB.

thus the INITIAL standings for gold for the FEB contract month:

No of notices filed so far (18,221) x 100 oz+ (1000) OI for the front month minus the number of notices served upon today (261} x 100 oz} which equals 1,896,000 oz standing OR 58.973 TONNES in this active delivery month of FEB.

We GAINE 42 contracts or an additional 4200 oz will stand for gold over here

TOTAL COMEX GOLD STANDING: 58.842 TONNES (HUGE FOR A FEBRUARY DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

157,392.690, oz NOW PLEDGED /HSBC 4.89 TONNES

125,410.592 PLEDGED MANFRA 2.90 TONNES

54,339.114oz PLEDGED JPMorgan no 1 1.690

278,349.354, oz JPM No 2 8.65 TONNES

898,821.330 oz pledged Brinks/27,96 TONNES

12,249,333 oz International Delaware: 0..3810 tonnes

Loomis: 18,615.429 oz

total pledged gold: 1,543,731.047 oz 48.01 tonnes

TOTAL REGISTERED AND ELIZ GOLD AT THE COMEX: 32,635,739,899 OZ (1015.07 TONNES)

TOTAL ELIGIBLE GOLD: 15,360,116.721 OZ (477.76 tonnes)

TOTAL OF ALL REGISTERED GOLD: 17,275,623.178 OZ (537.33 tonnes)

REGISTERED GOLD THAT CAN BE SERVED UPON: 15,731,892.0 OZ (REG GOLD- PLEDGED GOLD) 489.33 tonnes

END

FEBRUARY 2022 CONTRACT MONTH//SILVER

INITIAL STANDING FOR SILVER//FEB 23

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1,771,443.664 oz Brinks CNT |

| Deposits to the Dealer Inventory | nilOZ |

| Deposits to the Customer Inventory | nil oz |

| No of oz served today (contracts) | 150CONTRACT(S) 750,000 OZ) |

| No of oz to be served (notices) | 19 contracts (95,000 oz) |

| Total monthly oz silver served (contracts) | 1985 contracts 9,925,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

we had 0 deposits into the dealer

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 0 deposits into the customer account

JPMorgan has a total silver weight: 183.476 million oz/349.906 million =52.43% of comex

ii) Comex withdrawals: 2

a)Out of CNT 1,326,375,054 oz

b) Out of Brinks: 445,068.000 oz

total withdrawal 1,771,553.666 oz

we had 1 adjustments//all dealer to customer account

i) JPMorgan 313,881.170 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 81.334 MILLION OZ

TOTAL REG + ELIG. 349.906 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR FEBRUARY

silver open interest data:

FRONT MONTH OF FEB//2022 OI: 169 CONTRACTS LOSING 348 contracts on the day. We had 150 contracts served upon yesterday.

So we gained 198 contracts or an additional 990,000 oz will stand for silver on this side of the pond.

FOR MARCH WE HAD A LOSS OF 8318 CONTRACTS DOWN TO 39,458 CONTRACTS.

APRIL HAD A 88 GAIN// CONTRACTS RISING TO 389

MAY HAD A GAIN OF 9208 CONTRACTS UP TO 101,892 contracts

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 150 for 750,000 oz

Comex volumes: 89,325// est. volume today//strong/

Comex volume: confirmed TUESDAY: 143,018 contracts (STRONG)

To calculate the number of silver ounces that will stand for delivery in FEB. we take the total number of notices filed for the month so far at 1985 x 5,000 oz =. 9,925,000 oz

to which we add the difference between the open interest for the front month of FEB (169) and the number of notices served upon today 150 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the FEB./2021 contract month: 1985 (notices served so far) x 5000 oz + OI for front month of FEB (169) – number of notices served upon today (150) x 5000 oz of silver standing for the FEB contract month equates 10,020,000 oz. .

We gained 198 CONTRACTS OR 990,000 ADDITIONAL oz of silver will stand at the comex.

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

GLD

FEB 23/WITH GOLD UP $2.00 : NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1024.09 TONNES

FEB 22/WITH GOLD UP $6.20: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.65 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 1024.09 TONNES

FEB 18/WITH GOLD DOWN $1.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1019.44 TONNES

FEB 17/WITH GOLD UP $29.50: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1019.44 TONNES

FEB 16/WITH GOLD UP 414.60 NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1019.44 TONNES

FEB 15/WITH GOLD DOWN $12.70 NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1019.44 TONNES

FEB 14/WITH GOLD UP $27.20 NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1019.44 TONNES

FEB 11/WITH GOLD UP $4.50 A HUGE CHANGE IN GOLD IVNETORY AT THE GLD// A DEPOSIT OF 3.48 TONNES INTO THE GLD//INVENTORY RESTS AT 1019.44 TONES

FEB 10/WITH GOLD UP $1.00: NO CHANGES IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 1015.96 TONNES

FEB 9/WITH GOLD UP $8.05//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1015.96 TONNES

FEB 8/WITH GOLD UP $5.95 TODAY: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.36 TONNES INTO THE GLD//INVENTORY RESTS AT 1015.96 TONNES

FEB 7/WITH GOLD UP $14.00 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.24 TONNES FROM THE GLD/////INVENTORY RESTS AT 1011.60 TONNES//

FEB 4/WITH GOLD UP $3.40 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.75 TONNES FROM THE GLD////INVENTORY RESTS AT 1014.84 TONNES

FEB 3/WITH GOLD DOWN $5.55: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD////INVENTORY RESTS AT 1016.59 TONNES

FEB 2/WITH GOLD UP $7.95//A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.78 TONES OF GOLD INTO THE GLD////INVENTORY RESTS AT 1018.04 TONNES

FEB 1/WITH GOLD UP $5.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1014.26 TONNES

JAN 31/WITH GOLD UP $10.10//NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1014.26 TONNES

JAN 28/WITH GOLD DOWN $8.30//NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1014.26 TONNES

JAN 27/WITH GOLD DOWN $36.15//ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.16 TONNES INTO THE GLD.//INVENTORY RESTS AT 1014.26 TONNES

JAN 26/WITH GOLD DOWN $21.60 A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.65 TONNES INTO THE GLD///INVENTORY RESTS AT 1013.10 TONNES

JAN 25/WITH GOLD UP $10.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1008.45 TONNES

JAN 24/WITH GOLD UP $10.10 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: AN UNBELIEVABLE DEPOSIT OF 27.59 TONNES INTO THE GLD//INVENTORY RESTS AT 1008.45 TONNES

CLOSING INVENTORY FOR THE GLD//1024.09 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

FEB 23/WITH SILVER UP 22 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 551.597 MILLION OZ//

FEB 22/WITH SILVER UP 30 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 350,000 OZ INTO THE SLV///INVENTORY RESTS AT 551.597 MILLION OZ//

FEB 18/WITH SILVER UP 7 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.017 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 551.227 MILLION OZ

FEB 17/WITH SILVER UP 31 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.402 MILLION OZ//INVENTORY RESTS AT 550.210 MILLION OZ/

FEB 16/WITH SILVER UP 21 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 547.808 MILLIONOZ

FEB 15/WITH SILVER DOWN 46 CENTS TODAY : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 547.808 MILLION OZ//

FEB 14/WITH SILVER UP 49 CENTS TODAY; A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.235 MILLION OZ INTO THES LV////INVENTORY RESTS AT 547.808 MILLION OZ

FEB 11/WITH SILVER DOWN 18 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.573 MILLION OZ///

SLV/FEB 10/WITH SILVER UP 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.573 MILLION OZ//

FEB 9/WITH SILVER UP 14 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.573 MILLION OZ//

FEB 8/WITH SILVER UP 15 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.143 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 544.573 MILLION OZ//

FEB 7/WITH SILVER UP 52 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.218 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 541.430 MILLION OZ/

FEB 4/WITH SILVER UP 16 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 539.212 MILION OZ

FEB 3/WITH SILVER DOWN 35 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT539.212 MILLION OZ//

FEB 2/WITH SILVER UP 15 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.411 MILLION OZ INTO THE SLV.//INVENTORY RESTS AT 539.212 MILLION OZ/

FEB 1/WITH SILVER UP 18 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 533.801 MILLION OZ

JAN 31/WITH SILVER UP 7 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.202 MILLION OZ FORM THE SLV.//INVENTORY RESTS AT 533.801 MILLION OZ//

JAN 28/WITH SILVER DOWN 36 CENTS : NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 535.003 MILLION OZ//

JAN 27/WITH SILVER DOWN $1.13 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 535.003 MILLION OZ//

JAN 26/WITH SILVER DOWN 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 535.003 MILLION OZ//

JAN 25/WITH SILVER UP 10 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.311 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 535.003 MILLION OZ/

.JAN 24/WITH SILVER DOWN 48 CENTS TODAY: A MASSIVE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.8 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 532.692 MILLION OZ//.

SLV FINAL INVENTORY FOR TODAY: 551.597 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

Peter Schiff: The Fed Inflation Fight Will Cause A Recession… And More Inflation

WEDNESDAY, FEB 23, 2022 – 02:16 PM

The markets seem to be anticipating a Fed inflation fight. They also seem to be realizing that this is going to cause a recession. But they still haven’t come to grips with the fact that this is not going to fix the inflation problem. In his podcast, Peter Schiff argues that the recession will actually end up making inflation worse.

The stock market finished up last week with more selling as investors begin to price in more Federal Reserve rate hikes. Some analysts now expect as many as 10 hikes by the end of 2022. Peter said that is scaring the markets.

And in fact, if you look at the yield curve, the yield curve is actually flattening because investors are actually starting to price in the recession that this hawkish Fed is going to cause by jacking up interest rates.”

Peter said the 10-year Treasury yield is factoring in a drop in rates that will follow all of the hikes because they will cause a recession.

This has barely begun to set in on Wall Street. When more and more traders grasp this reality, there’s a lot more downside in stocks. But more importantly, if the Fed acts to stop the carnage on Wall Street, there is way more downside in the US dollar, way more upside in gold.”

But in the big scheme of things, 10 rate hikes are nothing. If each hike is 25 basis points, the interest rate will only be at 2.5% after 10.

Big deal. Inflation is 7.5%. And of course, it’s actually 15%.”

We don’t even have to use the real inflation rate to make the point. We can accept the government’s cooked CPI data. Even if the Fed raises rates to 2.5%, you’ve got -5% real interest rates. The reality is that a 2.5% interest rate in the face of 7.5% inflation is like taking a pea shooter to a bazooka fight. In order to truly tame inflation, the Federal Reserve needs to push interest rates above the level of inflation. Nobody is talking about rate hikes up to 7.5%.

You’re not going to fight inflation with 5% negative rates. There is no history that shows this. It’s impossible. It contradicts any type of economic school of thought you want to put forth.”

And even if the Fed manages to hike 10 times, the CPI will likely be even higher by the time rates get to 2.5%.

So, the Fed will actually be further behind the curve when it gets to 2.5% than it is right now at zero. It’s because moving so slowly allows inflation to accelerate. Because the entire time the Fed is hiking rates, it is still pursuing an expansionary monetary policy.”

St. Louis Fed president James Bullard even conceded this in an interview last week.

But while they are not sufficient to fight inflation, these rate hikes will probably push the US economy into a recession. The markets seem to be starting to grasp this reality. But they still think that the recession will do the job for the Fed and push inflation down.

In other words, the Fed won’t fight inflation with tight money, but simply making money less loose will be enough to tip the economy into recession, and the recession will fight inflation. Because the conventional wisdom is if we have a recession, that is going to reduce demand, and that is going to bring down the rate of inflation. So, that’s what the markets are counting on. It’s not the Fed that’s going to fight inflation. It’s going to be the recession.”

A lot of analysts are calling this a “policy mistake.” They’re worried that the Fed will “hike too much” and cause an economic downturn. But Peter said a recession wouldn’t be a mistake.

The recession is the cure for the mistake. The mistakes were made a long time ago. The Fed continues to make mistakes in raising rates too slowly, not because faster rate hikes will cause a recession, but because they’re trying to delay the recession because the recession is the cure. But the problem is the economy is so sick, we can’t survive the cure.”

We survived the cure in 1980 when Paul Volker pushed rates to 20%. And we had some relative prosperity on the back end. But we can’t do that now. There is too much debt in the system. The underlying economy is much weaker now than it was then.

I mean, we could, in theory, in the long run. But given the political realities that will intervene in the short run, there is no way it’s going to happen.”

So, what will happen when the economy tips into recession? Peter said inflation is going to get even worse — not better. That genie is already out of the bottle.

When the economy tips, inflation will still be high. And the Fed will do what it always does — it will pivot right back to extraordinary loose monetary policy. It will cut rates. It will resume quantitative easing.

When the Fed has to start taking back whatever rate hikes it managed to get in, when the Fed has to go back to QE, the bottom is going to drop out of the dollar.”

Also in this podcast, Peter goes on to talk about how the tanking dollar will constrict domestic supply, further exacerbating inflation. He also discusses Democrats trying to bribe Americans with a gas tax holiday, bitcoin, the situation in Ukraine, and the Cathie Wood ETF.

end

2.LAWRIE WILLIAM//,//Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, James RICKARD

-END-

3. Chris Powell of GATA provides to us very important physical commentaries

He is back!! Ambrose Evans Pritchard claims that Putin will not stop with his two puppet regions, but go after all of the Ukraine! Who will stop him. Europe desperately needs his gas as Russia cannot be strangled because it is systemically central to the world economy.

(Ambrose Pritchard Evans/London Telegraph)

Ambrose Evans-Pritchard: Putin controls supply chain of Western tech, so who is bluffing?

Submitted by admin on Tue, 2022-02-22 11:52Section: Daily Dispatches

By Ambrose Evans-Pritchard

The Telegraph, London

Tuesday, February 22, 2022

The wishful thinking has begun. Core Europe is already persuading itself that Vladimir Putin will be sated with Donetsk and Luhansk, allowing European companies to keep selling Gucci bags and BMWs to Russia in exchange for commodities — after a stern lecture on international law, of course.

The US, UK, and Poland have reached the opposite conclusion, strongly suspecting that the military occupation of the Donbas is the springboard for a full invasion of Ukraine.

Bear in mind what Putin has lost by this action: he has killed the Minsk accord and therefore ended the possibility of controlling Kyiv’s foreign and security policy through the veto power of these two puppet regions.

If he left it there, he would emerge from this crisis in a weaker strategic position.

This stretches credulity, since two-thirds of the Russian army is coiled for a strike on the border, with little to stop them except Ukraine’s valiant but ill-armed reservists. …

It is already well understood that Europe is a captive of Russian gas, and dares not eject Russia from the SWIFT system of international payments because it would suffer a more immediate crisis than fortress Russia itself. …

Russia cannot be strangled because it is systemically central to the world economy. …

... For the remainder of the commentary:

end

Craig Hemke on today’s big events concerning Russia, the Ukraine and the USA

(Craig Hemke/gata)

Craig Hemke at Sprott Money: Russia, Ukraine crisis, and de-dollarization

Submitted by admin on Tue, 2022-02-22 21:03Section: Daily Dispatches

9p ET Tuesday, February 22, 2022

Dear Friend of GATA and Gold:

Craig Hemke of the TF Metals Report, writing tonight at Sprott Money, notes that U.S. economic sanctions against Russia, including explusion of Russia from the SWIFT international payments system, are likely to accelerate the world economy’s move away from the dollar.

Hemke’s analysis is headlined “Russia, Ukraine Crisis, and De-Dollarization” and it’s posted at Sprott Money here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

Stefan outlines the mess that Canadians are now enduring i.e. our financial freedom is under attack

a good read

(Stefan Gleason/GATA)

Stefan Gleason: A warning from Canada — financial freedom is under attack

Submitted by admin on Tue, 2022-02-22 22:40Section: Daily Dispatches

By Stefan Gleason

Money Metals Exchange, Eagle, Idaho

Monday, February 21, 2022

As the world nervously awaits the next development in nuclear-armed Russia’s standoff with Ukraine, a different headline-grabbing standoff may be even more consequential for investors.

Canada’s trucker-led Freedom Convoy has been protesting draconian government mandates and restrictions. In response, Canadian Prime Minister Justin Trudeau’s government has decided to get even more draconian

Last week Trudeau invoked emergency powers to target the finances of the truckers and their backers.

In an unprecedented move sidestepping normal due process guarantees, Trudeau ordered banks, insurance companies, and even cryptocurrency exchanges to close the accounts of anyone deemed to be involved in the Freedom Convoy.

Similar trucker-led protests are scheduled to begin this week in Washington ahead of President Joe Biden’s March 1 State of the Union address. In response, the administration has ordered security fencing to be installed around the Capitol building.

Will Canadian-style assaults on financial freedom soon follow? …

… For the remainder of the commentary:

end

4.OTHER GOLD/SILVER COMMENTARIES

END

5.OTHER COMMODITIES/

6.CRYPTOCURRENCIES

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings WEDNESDAY morning 7:30 AM

ONSHORE YUAN: CLOSED UP 6.3179

OFFSHORE YUAN: 6.3148

HANG SANG CLOSED DOWN 140.28 PTS OR 0.60%

2. Nikkei closed

3. Europe stocks ALL GREEN

USA dollar INDEX DOWN TO 95.92/Euro RISES TO 1.1339-

3b Japan 10 YR bond yield: RISES TO. +.198/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 115.11/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 91,56 and Brent: 96.56–

3f Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: ON -SHORE CLOSED UP// OFF- SHORE UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.0.250%/Italian 10 Yr bond yield RISES to 1.93% /SPAIN 10 YR BOND YIELD RISES TO 1.27%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 1.63: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield RISES TO : 2.61

3k Gold at $1897.35 silver at: 24.16 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

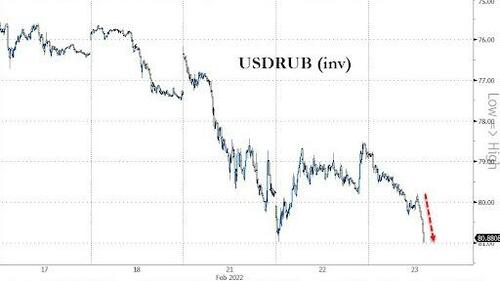

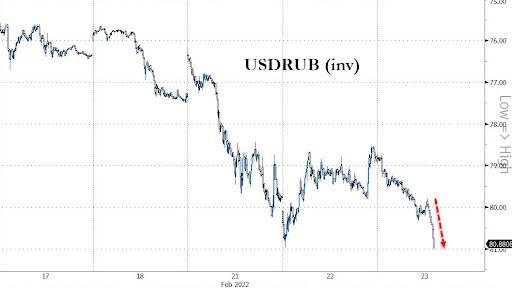

3l USA vs Russian rouble;// Russian rouble DOWN 143/100 in roubles/dollar AT 80.26

3m oil into the 91 dollar handle for WTI and 96 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 115.11 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning .9195– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0427 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 1.978 UP 3 BASIS PTS

USA 30 YR BOND YIELD: 2.257 UP 3 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 13.83

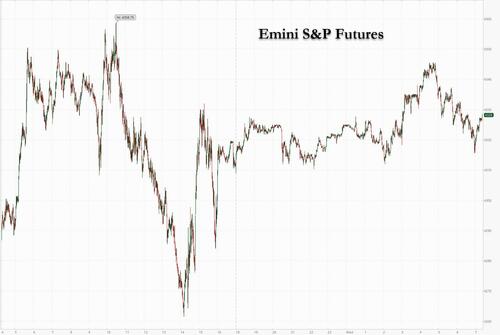

Nervous Markets Rebound As Ukraine Tensions Fade

WEDNESDAY, FEB 23, 2022 – 08:01 AM

US equity futures – which on Tuesday tumbled into a technical correction, down 10% from January’s all time highs – rebounded led by tech companies as investor fears over the standoff in Ukraine eased following the limited initial Western sanctions against Russia. As of 7:15am, eminis pared some gains but were still up 0.7% or 28 points on the day; Nasdaq futures were up 0.9% and Dow futures were up 0.54%. The VIX remained elevated, last seen around 28 after trading above 30 yesterday. Treasuries extended declines after the yield curve flattened in the Wall Street session, with the 10Y yield rising to 1.97% after tumbling as low as 1.85% on Tuesday. Crude oil fluctuated, while gold dipped as haven demand eased. The dollar slipped and cryptos reversed some of their recent losses.

Susannah Streeter, senior analyst at Hargreaves Lansdown, said there were “signs of bargain hunting among traders, keen to snap up shares sensitive to the situation.” But she warned the geopolitical tension could still escalate, while elevated oil and gas prices were boosting inflationary risks. “The volatility which has hit stocks is set to remain as traders assess this latest attempt to slow down the march toward a full invasion,” said Streeter. And while it has been a generally quiet session for once, here are some of the biggest premarket movers today:

- Palo Alto (PANW US) shares rise 7.3% in U.S. premarket trading after 2Q results impressed analysts, with the cybersecurity company beating most expectations and consensus. Stock has been raised to neutral at JPMorgan.

- Stellantis (STLA US) jumps 6.6% in premarket after the carmaker reported FY21 results and said it is targeting double-digit adj. operating income margin and positive industrial free cash flow this year. Oddo BHF said the results were “much above” expectations, “even the most bullish ones like us.”

- Rackspace Technology (RXT US) shares decline 22% in U.S. premarket as analysts highlight weaker-than-expected 1Q guidance and the absence of FY22 outlook. At least 2 analysts cut their price targets, while Deutsche Bank and BMO Capital Markets downgrade the stock.

- Marinus Pharmaceuticals (MRNS US) slumped 12% in postmarket trading after reporting a delay in the phase 3 trial of Raise, a placebo-controlled trial for the treatment of status epilepticus.

- Cadence Design (CDNS US) climbed 5.8% in postmarket trading after forecasting adjusted earnings per share and revenue for 2022 that beat the average analyst estimates. Fourth-quarter adjusted EPS and revenue also beat expectations.

- Piper Sandler upgrades Marathon Oil (MRO US) to overweight in note on exploration and production sector, while reiterating overweight ratings on “favorite ideas” Devon Energy and Pioneer Natural.

U.S. President Joe Biden said Russia had started to invade Ukraine and announced steps targeting Russia’s sale of sovereign debt abroad, its elites and a pair of banks. The sanctions, as well as others by U.S. allies, however stopped short of actually being seen as painful – as Reuters put it, they only “scratch surface of Fortress Russia” – and led to a surge in Russian assets.

“The softer-than-feared sanctions somewhat help lifting the mood,” Ipek Ozkardeskaya, senior analyst at Swissquote, wrote in a note. “The risk appetite is limited, of course, except in some key assets including oil and commodities.”

Meanwhile, Vladimir Putin has denied Russia intends to invade Ukraine, but lawmakers have given him the green light to deploy troops to separatist-held regions. Top U.S. diplomat Antony Blinken later announced that a summit due this week with Russian Foreign Minister Sergei Lavrov had been canceled.

And while there were no draconian sanctions imposed in response to Putin’s decision, German officials did halt certification of the Nord Stream 2 pipeline, an $11 billion project that would have solidified Russia’s grip on Europe’s energy sector. Fears that the Ukraine tension could snarl commodity supplies has bolstered everything from energy to wheat and nickel. Oil paused a blistering rally after the measures against Russia were announced, with Brent crude trading at $96 a barrel after a jump on Tuesday that saw it climb to a 15-year high, just shy of $100.

A key question now is whether the jump in raw material costs stirred by the standoff will spur more aggressive central bank policy. Bets on the number of rate increases by the Federal Reserve in 2022 have settled at about six 25-basis-point hikes, down from seven on Feb. 11. For the European Central Bank, swaps suggest the first quarter-point move will take place by October, compared with September earlier in the month.

“Inflationary pressures will mechanically intensify with higher commodity prices, increasing the risk of stagflation and challenging ECB actions,” according to Amundi SA money managers including Chief Investment Officer Vincent Mortier. “Europe is clearly more vulnerable regarding this geopolitical clash.”

In Europe, the Stoxx 50 rallies 1.2%. CAC 40 outperforms, adding 1.3%, FTSE 100 lags, adding 0.4%. Carmakers and chemical companies led gains in the Stoxx Europe 600 Index, which advanced 0.8%. Stellantis, Danone and Iberdrola all jumped after posting better-than-expected earnings and outlook. Here are some of the other prominent European movers today:

- JDE Peet’s shares surge as much as 13% after the company reported full-year revenue that beat estimates. The results showed the business model is “stronger than feared,” according to Citi.

- Stellantis gains as much as 6.2% in Milan after the carmaker reported FY21 results. Oddo BHF said the results were “much above” expectations, even for the most bullish analysts.

- Danone climbs as much as 4.9% after the yogurt maker reported 4Q figures that beat expectations while reassuring on measures taken to mitigate risk from Russia/Ukraine tensions.

- Henkel jumps as much as 5% after the German consumer- goods group reported 4Q results that indicate “significant” demand recovery in most of its business units, Raiffeisen says.

- Unite Group jumps as much as 9.3%, the most since Nov. 2020, after reporting full-year results, with Liberum noting the student accommodation developer’s return to growth.

- Iberdrola rises after the Spanish power company reported its latest earnings. Jefferies says reaffirmed net income guidance for FY22 was a positive.

- Storskogen drops as much as 18% after the Swedish investment company reported earnings which Kepler says missed consensus expectations. The shares are now down 55% this year.

- Samhallsbyggnadsbolaget i Norden (SBB) falls as much as 9.4% after a two-day rally. Pareto Securities says the company’s earnings show it’s “outperforming all expectations.”

- Campari slumps as much as 7.3% after the Aperol maker reported FY results, with CEO Bob Kunze-Concewitz flagging that input-cost pressure will intensify further, postponing gross margin accretion.

- Uniper falls as much as 5.3% to a five-month low after the German utility warned of a potential impairment to its stake in Nord Stream 2, which is was put on hold amid escalating tensions over Ukraine.

- Tomra Systems declines as much as 6.4% after the Norwegian recycling firm reported profitability that was “a bit shy of consensus,” Handelsbanken says.

- CNH Industrial falls as much as 4.8% in Milan and is the worst-performer on the FTSE MIB benchmark after the company presented its updated 2024 strategic business plan.

Earlier in the session, Asian stocks were poised to snap a three-day decline, as the U.S. unveiled sanctions against Russia that avoided the harshest restrictions and China’s tech shares posted modest gains. The MSCI Asia Pacific Index climbed as much as 0.4%, with consumer discretionary and tech shares driving gains. Meituan and JD.com were among the biggest contributors to the Asian gauge’s advance, as some traders eyed cheaper valuations following a brutal three-day slide in Chinese tech stocks amid regulatory concerns. “It’s just a breather as markets absorb the ongoing flow of news from Ukraine,” said Gary Dugan, chief executive officer at the Global CIO Office. “Asian equities are a defensive play given limited direct exposure to Ukraine and the ongoing positives of still easy monetary conditions and reopening of economies.” Shares in mainland China and Indonesia were among the top performers regionally on Wednesday, while U.S. futures signaled a positive open on Wall Street. Asia stocks have remained resilient this month due to the limited impact from Russia-Ukraine tensions, although concerns around fresh regulatory scrutiny of China’s tech industry — and the exposure of state-owned firms to the likes of Alibaba — is denting sentiment. The MSCI Asia Pacific Index is up about 0.5% in February compared with a 3% decline in its global counterpart

In rates, treasuries sold off, with yields rising by up to 4 basis points, led by the front end of the curve as the market assesses the impact of Western sanctions on Russia as well as Ukraine seeks to declare a nationwide state of emergency. Yields were cheaper by 2bp-3bp across the curve, with switch to new 2-year helping flatten 2s10s spread by more than 2bp to lowest level since March 2020; 10-year yield at about 1.97% is cheaper by 2.8bp vs Tuesday’s close, with comparable gilts and bunds little changed. Gilts curve bull flatten while BOE’s Bailey and other policymakers speak. Bund and Treasuries curves bear flatten. Cash USTs cheapen ~7bps across the short end. Meanwhile the dollar, oil and gold slip.

In FX, the Bloomberg Dollar Spot Index slumped as the greenback weakened or was steady against all of its Group-of-10 peers while JPY, CHF and GBP are the weakest performers in G-10 FX; NZD, NOK and AUD outperform. Risk-sensitive currencies, led by the New Zealand dollar, were the best G-10 performers. The Kiwi advanced as much as 1% to $0.6799, while 2-year sovereign bonds underperformed their Aussie peers as the RBNZ said it now expects the policy rate to rise to at least 2.5% by early next year, versus a forecast in November for it to reach that level by the third quarter of 2023; it also lifted the official cash rate by 25 basis points to 1%, in line with estimates. The Australian dollar reached its highest level in a month even as weak Australian wage and construction data backed the case for the RBA to be patient in tightening policy. Russian ruble lags EMFX, down 0.7% against the dollar.

The euro advanced a second day, but failed to rise above $1.1350; European sovereign bond yield curves bear flattened and money markets rose tightening wagers after ECB’s Holzmann said the ECB should decide on a first rate increase in the summer, before the end of asset purchases, followed by a second move at the end of the year. The pound held modest gains against the dollar and drifted versus the euro as BOE’s Andrew Bailey, Ben Broadbent, Jonathan Haskel and Silvana Tenreyro testified to parliament’s Treasury Committee. Options pricing suggests there’s a 50% chance the ruble will sink to a record low against the dollar within the next two months — dipping below levels from 2016 when the economy was mired in a recession. Technical analysts are also eyeing the same move, with a trendline of the currency pair on the verge of giving way.

In commodities, crude futures declined. WTI drifts 0.9% lower to trade near $91. Brent falls 0.7% to around $96. Spot gold falls roughly $5 to trade around $1,894/oz. Most base metals trade in the red; LME aluminum falls 0.9%, underperforming peers. LME copper outperforms.

Looking to the day ahead now, and central bank speakers include BoE Governor Bailey, Deputy Governor Broadbent, and the BoE’s Haskel and Tenreyro, in addition to ECB Vice President de Guindos, and the ECB’s de Cos, and San Francisco Fed President Daly. Otherwise, earnings releases include Lowe’s, Booking Holdings and TJX.

Market Snapshot

- S&P 500 futures up 1.0% to 4,344.25

- STOXX Europe 600 up 1.1% to 459.96

- MXAP up 0.3% to 185.63

- MXAPJ up 0.4% to 612.54

- Nikkei down 1.7% to 26,449.61

- Topix down 1.5% to 1,881.08

- Hang Seng Index up 0.6% to 23,660.28

- Shanghai Composite up 0.9% to 3,489.15

- Sensex little changed at 57,343.24

- Australia S&P/ASX 200 up 0.6% to 7,205.69

- Kospi up 0.5% to 2,719.53

- German 10Y yield little changed at 0.25%

- Euro up 0.2% to $1.1343

- Brent Futures down 0.5% to $96.34/bbl

- Gold spot down 0.4% to $1,891.03

- U.S. Dollar Index little changed at 95.94

Top Overnight News from Bloomberg

- President Vladimir Putin said he remains ready to pursue “diplomatic solutions” as long as Russia’s interests and security are guaranteed, after the U.S. and its allies agreed on a “first tranche” of sanctions against Moscow for its actions over separatist-held Ukrainian territory

- Ukrainians should leave Russia immediately and not travel there due to the “increasing Russian aggression,” Ukraine’s Foreign Ministry says in statement

- Ukraine’s worsening crisis means the ECB will put even greater emphasis on its flexibility and options as it exits stimulus measures and shifts toward raising rates, Governing Council member Francois Villeroy de Galhau said

- U.S. President Joe Biden’s debut set of sanctions on Russia for its actions over disputed Ukrainian territory hit markets with a whimper and were quickly criticized as limited in scope

- Prices for natural gas and electricity in Europe advanced after President Joe Biden said Russia had begun to invade neighboring Ukraine and imposed a range of sanctions on Moscow

- Traders expect machines and mobile apps to take over even more of the action in financial markets in 2022. More than 60% of traders predicted an increase in algorithmic trading in the next two years, according to JPMorgan Chase & Co.’s annual FICC e-Trading Survey. That’s expected to lead to an additional 19% of their currency trading being done by algorithmic orders

- The Reserve Bank of New Zealand’s Monetary Policy Committee increased the official cash rate by 25 basis points to 1% Wednesday. New forecasts published by the RBNZ show the cash rate climbing to 2.5% over the next 12 months and peaking at about 3.25% at the end of 2023. In November, it had forecast a peak of about 2.5%

- President Joe Biden said the U.S. would impose a first wave of sanctions on Russia and is shifting American forces already based in Europe, and a meeting between the top U.S. and Russian diplomats was canceled. Biden’s announcement followed earlier sanctions after the European Union and the U.K. set out an initial set of limited penalties targeting Moscow

- Australia’s annual wages growth edged higher last quarter, while remaining short of levels needed to bring forward an interest-rate hike

- Oil stabilized after U.S. President Joe Biden unveiled sanctions against Russia that avoided the harshest penalties, while progress on the Iran nuclear talks offered to bring some relief to a tightening market

A more detailed look at global markets courtesy of Nesquawk

Asia-Pac stocks were positive but with upside capped after the S&P 500 closed in correction territory for the first time in two years and as participants digested the sanctions response to Russia’s actions on Ukraine which targeted individuals and banks although the largest Russian banks Sberbank and VTB Bank avoided sanctions. ASX 200 was led higher by outperformance in tech and with focus also on a slew or earnings results. Nikkei 225 remained closed for the Emperor’s Birthday holiday. KOSPI gained but was restricted after daily COVID-19 cases surpassed 150k for the first time on Tuesday. Hang Seng and Shanghai Comp. rebounded from the prior day’s losses after the PBoC boosted its liquidity efforts heading into month-end and with tech stocks finding reprieve from yesterday’s crackdown fears, while Hong Kong’s budget included counter cyclical measures of over HKD 170bln and HKD 54bln of anti-epidemic measures.

Top Asian News

- Hong Kong’s CLP Said to Mull Sale of $2 Billion EnergyAustralia

- Rio Tinto to Pay $7.7 Billion Dividend as Profit Hits Record

- Asian Stocks Advance as Traders Eye Russia Sanctions, China Tech

- Chinese Tech Stocks Rebound as Traders Weigh Crackdown Risks

European bourses are firmer, Euro Stoxx 50 +1.0%, with gains relatively broad based though the oil-exposed FTSE 100 lags given benchmark pricing. US futures, ES +0.6%, are also firmer as newsflow is comparably slower and as participants also take impetus from sanctions being less-stringent than some feared. European sectors are predominantly in the green, though Energy lags given benchmark pricing while Autos and Food, Beverage & Tobacco outperforms on earnings.

Top European News

- Germany Says It Can Do Without Russian Gas. That’s a Tall Order

- Telecom Italia Weighs $1.5 Billion Tower Unit Stake Sale

- Barclays Hits Record Annual Profit as Dealmakers Outperform

- HSBC Bankers Grounded as Pandemic Cut Business Travel by 96%

In FX, the DXY is still hugging 96.000, as firmer US Treasury yields compensate for loss of safe haven premium. Kiwi outperforms following hawkish guidance from RBNZ in wake of latest OCR hike that was finely balanced between the 25 bp delivered and 50 bp deliberated – Nzd/Usd eyes 0.6800. Aussie up due to ongoing improvement in risk appetite evident in commodities and Loonie also benefiting from similar factors, as Aud/Usd clears 0.7250 and Usd/Cad approaches 1.2700. Pound ponders BoE testimony implying more tightening but less hawkish dissent, with Cable cresting 1.3600. Euro holds firmly on the 1.130O handle and well flanked by decent option expiry interest either side of circa 1.1350+ to 1.1280 recent range. Rand awaits SA Budget around the 15.0000 mark and watches Gold attempting to stay within striking distance of Usd 1900/oz

In commodities, crude benchmarks are experiencing a pull-back this morning as newsflow is comparably slower than at this point yesterday and in the context of yesterday’s notable upside. Thus far, Brent has moved to a test of yesterday’s low at USD 95.80/bbl, though WTI remains someway from the comparable mark given the lack of settlement earlier in the week. US State Department official said US actions on Russia will not likely disrupt global energy markets and said officials did not discuss increasing oil output during the US trip to Saudi Arabia last week. US is coordinating with oil consuming countries to make sure all are able to respond if necessary and OPEC countries understand US concerns about importance of stability of global oil markets, while the official added that nothing currently happening on the ground in Ukraine risks oil flows. Spot gold remains in relative proximity to USD 1900/oz but with a negative bias while LME Copper retain an underlying bid but remains below the 10k handle

In fixed income, UK bonds and STIR futures regain poise as BoE members signal a tempered tightening pace going forward. Bunds encouraged by a very strong 2036 German debt sale. US Treasuries lag awaiting USD 53bln 5 year issuance.

Geopolitical news:

- EU Ambassadors have approved sanctions on Russia, according to a EU diplomat via Reuters. *Reminder, there is a 14:00GMT/09:0EST deadline for the EU Foreign Affairs Ministers to give their final approval to the full legal text of such sanctions.

- EU to sanction Russian Defense Minister Shoigu, and Russia’s internet research agency, as part of first-wave restrictions, via WSJ.

- The UK is finalizing a stronger sanctions package to impose on Russia in the coming days, according to sources via Politico.

- Ukraine Foreign Minister Kuleba said sanctions from the US are specific and painful, while he added that pressure on Russia should be stepped up. Kuleba also stated that President Biden’s sanctions announcement looks strong as a first move and they received a promise of more assistance from the US, while they are not seeking US troops on the ground, according to a Fox interview

- Canadian PM Trudeau announced sanctions on Russia in coordination with allies in which Canadians were banned from all dealing with the so-called independent states of Luhansk and Donetsk, while Canadians are also banned from engaging in purchases of Russian sovereign debt. Furthermore, they will apply additional sanctions on two state-backed Russian banks and will sanction Russian parliament members who voted to recognise the so-called republics.

- Australian PM Morrison announced he is to impose sanctions on some Russian individuals, travel bans and targeted financial sanctions, while PM Morrison said expect subsequent tranches of sanctions and that this is only the start of the process.

- Japanese PM Kishida announced a ban of Russian issue of bonds in Japan and said he doesn’t see a big impact on energy supply in the short-term from current situation, while he announced a freeze of assets of certain Russian individuals.

- Russia Finance Ministry closely monitoring financial markets after US placed restrictions on Russian debt; OFZ auction to depend on market conditions; could issue with papers carrying lower level of interest rate risk, via Reuters

Central banks:

- RBNZ hiked the OCR by 25bps to 1.00% as expected and said the OCR is expected to peak at a higher level than assumed in the November statement, while the committee affirmed it was willing to move the OCR in larger increments if required over the coming quarters. RBNZ said many members saw this as a finely balanced decision whether to move OCR up by 25bps or 50bps and it noted more tightening is needed, as well as agreed to commence a gradual reduction of holdings under the LSAP programme in which it intends to commence bond sales in July. Furthermore, it said headline CPI is well above RBNZ target range but will return towards 2% mid-point in coming years. and sees the OCR at 2.84% in June 2023 (prev. 2.40%).

- RBNZ Governor Orr said cannot rule out 50bps hikes in the future and that rates do need to rise significantly but they will take their time step by step, while he added the amount of tightening through bond sales is very small and that it is all about the OCR.

- Fed’s Bostic (2024 voter, hawk) said the economy is still quite strong as officials try to figure out the economy in real time, while companies and output remain restrained by inability to find workers. Fed’s Bostic (2024 voter) says businesses are feeling need to adjust wages but it is not clear how long it will persist, adds have not seen worrisome changes yet in long-term inflation expectations

- ECB’s Holzmann said the council should consider two rate hikes this year and sees neutral rate at 1.50% as realistic by 2024.

- ECB’s Villeroy says, re. Ukraine, we will assess in March the more indirect consequences on inflation/growth and will be facts driven.

- BoE Governor Bailey says there are two-sided risks to the inflation forecast, important not to suggest there is a difference in the view on the MPC about the level that rates need to reach, as opposed to the pace.

- Second-round effects present an upside risk to inflation. If second-round effects materialise, will need to react with higher interest rates.

US Event Calendar

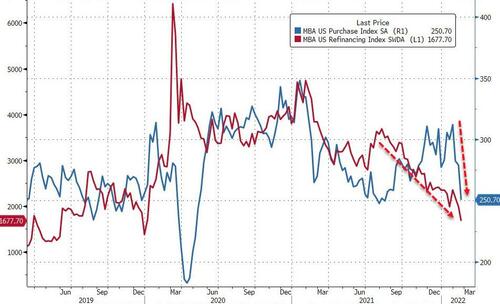

- 7 a.m.: Feb. MBA Mortgage Applications -13.1%, prior -5.4%

- 3:30 p.m.: Fed’s Daly Speaks At Los Angeles World Affairs Council

DB’s Jim Reid concludes the overnight wrap

As we go to press, geopolitical tensions continue to remain the dominant theme in markets, although a number of assets have now begun to stabilise after heavy losses on Monday and early Tuesday. This morning futures on the S&P 500 are up +0.56%, whilst oil has steadied at $97.17/bbl, having come down from a peak of $99.50/bbl over the last 24 hours. Asian equities have also regained ground overnight as risk appetite has recovered, with the Hang Seng (+0.85%), the CSI 300 (+0.88%) and the Shanghai Composite (+0.77%) all posting a decent advance, whilst Japanese markets are closed for a holiday. The coming day could well be pivotal, with Australian Prime Minister Morrison saying overnight that Russia was “at peak readiness to now complete a full-scale invasion of Ukraine, and that is likely to occur within the next 24 hours.”

Those moves follow President Biden’s address last night where he labelled Russia’s moves against Ukraine an invasion and announced a first tranche of sanctions on the country. The sanctions were coordinated with European allies and thus very similar to what European leaders announced. The US will sanction banks connected with the Russian defence industry, certain Russian elites, prevent Russia from issuing debt to western investors, and prevent Russian sovereign debt issued after March 1 from trading on secondary markets in the US. These were not the harshest sanctions the US could impose, and it was noted the sanctions will escalate in severity along with any escalation in Ukraine. Diplomatically, Secretary of State Blinken noted President Putin’s remarks were deeply disturbing and cancelled his upcoming meeting with his Russian counterpart Foreign Minister Lavrov. Blinken described the rationale for cancelling the meeting, “Now that we see the invasion is beginning and Russia has made clear its wholesale rejection of diplomacy, it does not make sense to go forward with that meeting at this time.” While President Biden assured the public that the US had no intention of fighting Russia, they will increase the amount of troops and materiel deployed in eastern Europe.

Meanwhile, the upper house of Russia’s parliament approved the use of troop deployments to the self-proclaimed republics.

Earlier in the day, the EU similarly said that member states had given political agreement for sanctions against Russia, and Commission President von der Leyen said in a statement that they “target banks that finance the Russian military apparatus and contribute to the destabilisation of Ukraine”, and that they were also “limiting the Russian government´s ability to raise capital on the EU’s financial markets.” Separately the UK unveiled some measures, including freezes on 5 banks and 3 individuals, along with sanctions on members of the Russian Duma and Federation Council who voted to recognise the independence of the two breakaway provinces.

There was also a notable development from Germany, as it was announced that they’d be putting the Nord Stream 2 certification process on hold in light of President Putin’s move to send troops into eastern Ukraine. The move was welcomed by the White House, although European natural gas futures ended the day up +9.96% at €79.79 per megawatt hour, with a noticeable spike occurring after Chancellor Scholz’s announcement on the issue. President von der Leyen also welcomed this, saying that “Nord Stream 2 has to be assessed in light of the security of energy supply for the whole of Europe. Because this crisis shows that Europe is still too dependent on Russian gas.”

For markets all this meant it was a fairly mixed day yesterday. The S&P 500 fell -1.01% as it caught up following the previous day’s holiday, although the STOXX 600 in Europe actually eked out a +0.07% gain after recovering from its early losses. For a sense of this big turnaround, you only had to look at Russian assets themselves, where the MOEX equity index initially fell -9.23% shortly after we went to press yesterday, before paring back its losses through the day to actually close up +1.42%, so a recovery of almost 12% by the close compared to those initial losses.

The tensions led to further rises in commodity prices, with Brent crude oil closing at a post-2014 high of $96.84/bbl, albeit that was actually more than a couple of dollars beneath its intraday peak of $99.50/bbl in the European morning. Separately, Nickel prices on the London metal exchange rose above $25,000/ton for the first time in over a decade at one point on an intraday basis, and corn futures (+3.03%) hit a 7-month high of their own. These broad-based rises in commodities sent the Bloomberg Commodity Spot Index (+1.71%) up to a fresh record, which won’t be welcome news for central banks who are grappling with how to avoid supply shocks leading to more generalised inflation.

For sovereign bonds, those fears of inflation outweighed the flight to haven assets yesterday, with yields rising across different countries and maturities. Yields on 10yr Treasuries ended the day up +1.0bps at 1.94%, though just before the European open they’d been beneath 1.85%, so again a big turnaround on the day. That rise was entirely driven by higher breakevens, with the 10yr real yield actually down -2.4bps yesterday to -0.54%. And yesterday also saw the 2s10s yield curve flatten by another -7.3bps, bringing it back to 38.4bps, which is the flattest it has been since the initial Covid outbreak in April 2020. Europe saw a similar movement in yields, with those on 10yr bunds (+3.6bps), OATs (+1.7bps) and BTPs (+1.3bps) all moving higher on the day, whilst those on Russian 10yr debt were up a further +30.0bps.

In light of the Ukraine crisis, the main market theme from a couple of weeks back of the potential for more aggressive central bank hiking cycles has moved off the agenda somewhat. Indeed, the amount of ECB hikes priced in by the December meeting fell back to 35bps yesterday, the lowest since their meeting earlier this month. Meanwhile for the BoE, overnight index swaps were only pricing in a 31% chance of a 50bps move in March by the close yesterday, which followed a speech by Deputy Governor Ramsden, who voted for a larger 50bp move in February. Whilst Ramsden said that “some further modest tightening in monetary policy is likely to be appropriate in the coming months”, he emphasised that “The word “modest” is significant here though”.

Staying on central banks, the Reserve Bank of New Zealand hiked its official policy rate by 25bps overnight, taking the Official Cash Rate to 1%. With inflation remaining a threat, the central bank signalled that more tightening is needed going forward, and they didn’t rule out the possibility of hikes in larger increments if the need arose. Following the policy announcement, which signposted a more aggressive pace of tightening relative to November, the New Zealand dollar has strengthened by +0.44% against the US dollar this morning.

On the data front, the US Conference Board’s consumer confidence indicator fell to a 5-month low in February at 110.5 (vs. 110.0 expected), with the expectations measure falling to 87.5. That said, the flash PMIs came in above expectations, echoing what we saw the previous day in Europe, with the composite PMI up to 56.0 (vs. 52.5 expected). And on top of that, house prices continued to show further strength into the end of last year, with the FHFA house price index for December up +1.2% (vs. +1.0% expected), which is its fastest monthly growth since July. Separately in Germany, the Ifo’s business climate indicator for February rose to a 5-month high of 98.9 (vs. 96.5 expected).

To the day ahead now, and central bank speakers include BoE Governor Bailey, Deputy Governor Broadbent, and the BoE’s Haskel and Tenreyro, in addition to ECB Vice President de Guindos, and the ECB’s de Cos, and San Francisco Fed President Daly. Otherwise, earnings releases include Lowe’s, Booking Holdings and TJX.

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING// TUESDAY NIGHT

SHANGHAI CLOSED UP 32.00 PTS OR 0.93% //Hang Sang CLOSED UP 140.28 PTS OR 0.60% /The Nikkei closed DOWN 461.26 or 1.71% //Australia’s all ordinaires CLOSED UP 0.70% /Chinese yuan (ONSHORE) closed UP 6.3279 /Oil DOWN TO 91.56 dollars per barrel for WTI and UP TO 96.65 for Brent. Stocks in Europe OPENED ALL GREEN // ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.3179. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.3148: /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFF SHORE STRONGER//

3 a./NORTH KOREA/ SOUTH KOREA

///NORTH KOREA

3B JAPAN

3c CHINA

/CHINA

end

CHINA/USA/RUSSIA

4/EUROPEAN AFFAIRS//UK AFFFAIRS

High energy costs to UK households (($2700 //2000 pounds per year) is causing struggles as inflation hits a 30 yr high and yet ne taxes kick in further aggravating the situation

(zerohedge)

UK Households Struggle As Inflation Hits 30-Year High, New Taxes Kick In

WEDNESDAY, FEB 23, 2022 – 04:15 AM

Millions of Britons who previously found themselves financially ‘comfortable’ are feeling the heat over accelerating inflation, record energy bills, and tax increases which kick in this year.

According to the Bank of England, scorching inflation will result in the largest drop in disposable income in 30 years when adjusted for inflation.

In April, UK energy bills are due to jump 54% to around 2,000 pounds ($2,723) a year per household. While some of it will be offset by emergency government support – and social security will also increase, it will be against the backdrop of rising interest rates according to Reuters.

“There’s just too much going up at once,” said 38-yaer-old care worker Nicola Frape, who huddles under blankets with her 14-year-old daughter to conserve heat, and have limited roadtrips due to the price of gas. “The pressure is just going to be even worse in April,” she added.

With economies around the world rebounding from coronavirus lockdowns, prices for everything from food and clothes to haircuts and rent, as well as energy are going up, fuelled by resurgent demand and shortages due to supply chain disruptions.

Accurate national comparisons of changes in living standards are hard to make but concerns about inflation are emerging as a big factor in elections including France’s presidential race in April and U.S. midterm elections in November. -Reuters

A February survey found that the number of people experiencing food insecurity was 20% higher in January than the previous six months, according to FT.

The decline in living standards for much of the UK population prompted chancellor Rishi Sunak last week to announce a £9bn package to help struggling households.

On the same day energy regulator Ofgem announced a 54 per cent rise in energy bills and the Bank of England increased interest rates from 0.25 per cent to 0.5 per cent. It warned inflation could hit 7.25 per cent by April, threatening to limit people’s spending power as a planned increase in National Insurance contributions reduces their take-home pay.

In January, Britain’s consumer price inflation hit 5.5% y/y, the highest since 1992. It’s set to top 7% in April, at which point the BoE thinks they may begin to slow. That said, they also expect it will be above 5% in a year’s time.

In the US, ‘official’ inflation is north of 7% – the highest since the early 1980s.

According to the National Institute of Economic and Social Research think tank, the combination of April’s payroll tax increase plus inflation could result in a 30% rise in destitution across the UK.

The rampant inflation in the UK has sent government interest rates soaring – hitting £6.1bn last month, the highest amount for a January since records began in April 1997 and up from £4.5bn last year, the BBC reports.

The payments are pegged to the Retail Prices Index (RPI) measure of inflation – which reached 7.8% in January.

January’s interest payments were, however, below the all-time high of £9bn in June last year.

Paul Johnson, director of the Institute for Fiscal Studies, told the BBC it was worth noting that “overall interest payments by the government are still at remarkably low levels” despite UK debt levels at the highest for 60 years. -BBC

Meanwhile between April and September of 2021, food bank deliveries rose 11% vs. the same period in 2019, hitting one of its highest levels ever in December. At one West London food bank, Dad’s House, some of the former donors to the charity are now recipients of support.

“I have to pay my bills,” said Jackie Gordon, 52. “I’m behind with my rent and I don’t want to get evicted.”

Rebecca McDonald, a senior economist at the Joseph Rowntree Foundation, said this year will likely leave a lasting mark on poorer households regardless of whatever inflation does.

“It’s going to feel like a much more longer-term issue because this year is going to be incredibly difficult,” she said, adding that many formerly financially sound families will likely go into debt this year.

END

UK/COVID/AUSTRALIA/IVERMECTIN

What a right: an Australiannews program “the Current Affair” has now apologized for “accidentally implying Queen Elzabeth ii could benefit from her COVID 19 illness using ivemectin.

The answer is yes even though she took the shots+ booster

(Teng/EpochTimes)

Aussie News Show Apologises For Implying Queen Could Benefit From Ivermectin

WEDNESDAY, FEB 23, 2022 – 03:30 AM