March 17, 2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

MARCH17

GOLD; $1942.45 UP $33.50

SILVER: $25.32 UP $0.72

ACCESS MARKET: GOLD $1942.60

SILVER: $25.38

Bitcoin morning price: $40,698 DOWN 4

Bitcoin: afternoon price: $40,857 UP 155

Platinum price: closing UP $15.15 to $1024.55

Palladium price; closing UP $98.65 at $2496.40

END

end

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

comex notices/

March: JPMorgan stopped/total issued 2/3

EXCHANGE: COMEX

CONTRACT: MARCH 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,908.000000000 USD

INTENT DATE: 03/16/2022 DELIVERY DATE: 03/18/2022

FIRM ORG FIRM NAME ISSUED STOPPED

435 H SCOTIA CAPITAL 1

661 C JP MORGAN 2

737 C ADVANTAGE 3

TOTAL: 3 3

MONTH TO DATE: 10,657

NUMBER OF NOTICES FILED TODAY FOR Mar. CONTRACT 3 NOTICE(S) FOR 300 OZ (0.00933 TONNES)

total notices so far: 10,657 contracts for 1,065,700 oz (33.148 tonnes)

SILVER NOTICES:

64 NOTICE(S) FILED TODAY FOR 320,000 OZ/

total number of notices filed so far this month 10,437 : for 52,185,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

END

GLD

WITH GOLD UP $33.50

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 11.61 TONNES FROM THE GLD

INVENTORY RESTS AT 1073.44 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP $0.72

AT THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 3.049 MILLION OZ

INTO THE SLV.

CLOSING INVENTORY: 548.071 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A GIGANTIC SIZED 2515 CONTRACTS TO 157,056 ON DAY 6 OF OUR CONTINUAL RAID,(AND LAST) AND FURTHER FROM THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE STRONG LOSS IN OI WAS ACCOMPLISHED WITH OUR STRONG $0.56 LOSS IN SILVER PRICING AT THE COMEX ON WEDNESDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.56) AND WERE SUCCESSFUL IN KNOCKING OUT SOME SILVER LONGS AS WE HAD A STRONG LOSS OF 920 CONTRACTS ON OUR TWO EXCHANGES

WE MUST HAVE HAD:

I) HUGE BANKER SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A HUGE INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 42.860 MILLION OZ FOLLOWED BY TODAY’S QUEUE JUMP OF 220,000 OZ //NEW STANDING 52.480 MILLION OZ // V) GIGANTIC SIZED COMEX OI LOSS/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS : —155

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAR. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAR:

TOTAL CONTACTS for 13 days, total contracts: : 27,228 contracts or 136.140 million oz OR 10.469 MILLION OZ PER DAY. (2094 CONTRACTS PER DAY)

TOTAL NO OF OZ UNDERGOING EFP TO LONDON 27,288 CONTRACTS X 5,000 PER CONTRACT:

EQUATES TO: 136.14 MILLION OZ

.

LAST 11 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 136.140 MILLION OZ//THIS IS GOING TO BE A HUGE EFP ISSUANCE MONTH AND MOST LIKELY WILL SET A RECORD FOR ANY MONTH

RESULT: WE HAD A GIGANTIC SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2360 WITH OUR $0.56 LOSS SILVER PRICING AT THE COMEX// WEDNESDAY THE CME NOTIFIED US THAT WE HAD A HUGE SIZED EFP ISSUANCE OF 1440 CONTRACTS( 1440 CONTRACTS ISSUED FOR MAR AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A HUGE INITIAL SILVER OZ STANDING FOR MAR. OF 42.860 MILLION OZ FOLLOWED BY TODAY’S 220,000 OZ QUEUE JUMP//NEW STANDING 52.255 MILLION OZ// /// .. WE HAD A SMALL SIZED LOSS OF 64 OI CONTRACTS ON THE TWO EXCHANGES FOR 0.320 MILLION OZ DESPITE THE LOSS IN PRICE.

WE HAD 64 NOTICES FILED TODAY FOR 320,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A GOOD SIZED 3715 CONTRACTS TO 613,890 AND FURTHER FROM OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: –155 CONTRACTS.

THE BIS HAS ABANDONED THE GOLD COMEX TRADING!!!

.

THE GOOD SIZED DECREASE IN COMEX OI CAME WITH OUR HUGE LOSS IN PRICE OF $18.50//COMEX GOLD TRADING/WEDNESDAY/.AS IN SILVER WE MUST HAD HUGE BANKER/ALGO SHORT COVERING ACCOMPANYING OUR HUMONGOUS SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR MARCH AT 14.818 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 2400 OZ//NEW STANDING 36.189 TONNES

YET ALL OF..THIS HAPPENED WITH OUR LOSS IN PRICE OF $18.50 WITH RESPECT TO TUESDAY’S TRADING

WE HAD AN SMALL GAIN OF 1685 OI CONTRACTS (5.241 PAPER TONNES) ON OUR TWO EXCHANGES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 5400 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 613,890.

IN ESSENCE WE HAVE AN SMALL SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1685, WITH 3715 CONTRACTS DECREASED AT THE COMEX AND 5400 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 1840 CONTRACTS OR 5.723 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (5,400) ACCOMPANYING THE GOOD SIZED LOSS IN COMEX OI (3715,): TOTAL GAIN IN THE TWO EXCHANGES 1685 CONTRACTS. WE NO DOUBT HAD 1) HUGE BANKER SHORT COVERING ,2.) HUGE INITIAL STANDING AT THE GOLD COMEX FOR MARCH. AT 14.818 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 2400 OZ//NEW STANDING 36.189 TONNES /// 3) ZERO LONG LIQUIDATION ///. ,4) GOOD SIZED COMEX OI LOSS 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL/

LADIES AND GENTLEMEN: THE GOLD COMEX IS ALSO BEING ATTACKED FOR GOLD METAL FROM LONDON ET AL.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

MARCH

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAR :

93,312 CONTRACTS OR 9,331,200 OR 290.23 TONNES 13 TRADING DAY(S) AND THUS AVERAGING: 718 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 13 TRADING DAY(S) IN TONNES: 290.23TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2020, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 290.23/3550 x 100% TONNES 8.17% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 290.23 TONNES INITIAL( THIS WILL PROBABLY BE A RECORD EFP ISSUANCE MONTH. LATER THIS MONTH WE WILL SURPASS NOV 21, THE ALL TIME RECORD MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL.WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MARCH HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF APRIL, FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (MAR), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A GIGANTIC SIZED 2515 CONTRACTS TO 157,211 AND FURTHER FROM OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 4 1/2 YEARS AGO.

EFP ISSUANCE 1440 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 1440 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1440 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 2515 CONTRACTS AND ADD TO THE 1440 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A STRONG SIZED LOSS OF 1075 OPEN INTEREST CONTRACT FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES 5/375 MILLION OZ,

OCCURRED DESPITE OUR $0.56 LOSS IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

5. Other gold commentaries

6. Commodity commentaries/cryptocurrencies

3. ASIAN AFFAIRS

i)THURSDAY MORNING// WEDNESDAY NIGHT

SHANGHAI CLOSED UP 44.33 PTS OR 1.40% //Hang Sang CLOSED UP 1413.73 PTS OR 7.04 % /The Nikkei closed UP 890.88 PTS or 3.46% //Australia’s all ordinaires CLOSED UP 1.15% /Chinese yuan (ONSHORE) closed UP 6.3498 /Oil UP TO 100.56 dollars per barrel for WTI and UP TO 103.76 for Brent. Stocks in Europe OPENED ALL RED EXCEPT LONDON // ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.3498. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.3641: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER/

A)NORTH KOREA/

b) REPORT ON JAPAN

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A GOOD SIZED 3715 CONTRACTS TO 613,890 AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX DECREASE OCCURRED WITH OUR STRONG LOSS OF $18.50 IN GOLD PRICING WEDNESDAY’S COMEX TRADING. WE ALSO HAD A STRONG SIZED EFP (5400 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE NON ACTIVE DELIVERY MONTH OF MAR.. THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 5400 EFP CONTRACTS WERE ISSUED: ;: , & FEB. 0 APRIL:5400 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 5400 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A SMALL SIZED TOTAL OF 1685 CONTRACTS IN THAT 5400 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A GOOD SIZED COMEX OI LOSS OF 3715 CONTRACTS..AND THIS SMALL GAIN OCCURRED DESPITE A HUGE LOSS IN PRICE OF $18.50.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING FOR MAR (36.189),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.189 TONNES

THE BANKERS WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $18.50) BUT THEY WERE UNSUCCESSFUL IN FLEECING ANY LONGS AS WE HAVE REGISTERED A SMALL SIZED GAIN OF 5.241 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR MAR (36.189 TONNES)…

WE HAD –155 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 1685 CONTRACTS OR 168,500 OZ OR 5.241 TONNES

Estimated gold volume today: 171,692 ///poor

Confirmed volume yesterday: 242,225 contracts fair

INITIAL STANDINGS FOR MAR ’22 COMEX GOLD //MARCH 17

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 619.850 oz Int Delaware (10 kilobars)and HSBC |

| Deposit to the Dealer Inventory in oz | 16,101.610OZ Brinks dealer |

| Deposits to the Customer Inventory, in oz | 178,502.352 oz JPMorgan 5000 kilobars and Loomis 552 kilobars |

| No of oz served (contracts) today | 3 notice(s)300 OZ 0.00933 TONNES |

| No of oz to be served (notices) | 978 contracts 97,800 oz 3.0419 TONNES |

| Total monthly oz gold served (contracts) so far this month | 10,657 notices 1,065,700 OZ 33.147 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For today:

1)dealer deposit

i) Into Brinks: 16,101.610 oz

total dealer deposit 16101.610 oz

No dealer withdrawal 0

2 customer deposits

i) Into JPMORGAN: 160,755.000 OZ (5,000 KILOBARS= 5 TONNES)

ii) Into Loomis: 17,747.352 oz (552 kilobars)

total deposit: 178,502.352 oz

2 customer withdrawal

i) Out of Int Delaware: 321.510 oz 10 kilobars

ii) out of HSBC: 298.340 oz

total withdrawals: 619.850 oz

ADJUSTMENTS: 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MARCH.

For the front month of MARCH we have an oi of 1981 contracts having LOST 313

We had 337 notices filed yesterday so strangely again on day 13 we gained another queue jump i.e. 24 contracts or an additional 2400 oz will stand for delivery and these guys refused again to be EFP’d over to London. They must

be after large amounts of gold on this side of the pond after Russia cannot//will not supply any precious metals to London. The 2400 oz is represented by 0.0746 tonnes,

April saw a loss of 19,427 contracts down to 254,908.

May saw a LOSS of 14 contracts to stand at 4238

June saw a GAIN of 14,669 contracts up to 286,364 contracts

We had 3 notice(s) filed today for 300 oz FOR THE MAR 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 33 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 2 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 5 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the MAR /2021. contract month,

we take the total number of notices filed so far for the month (10,657) x 100 oz , to which we add the difference between the open interest for the front month of (MAR: 981 CONTRACTS ) minus the number of notices served upon today 3 x 100 oz per contract equals 1,163,500 OZ OR 36.189 TONNES the number of TONNES standing in this active month of mar.

thus the INITIAL standings for gold for the MAR contract month:

No of notices filed so far (10,657) x 100 oz+ (981) OI for the front month minus the number of notices served upon today (3} x 100 oz} which equals 1,163,500 oz standing OR 36.189 TONNES in this NON active delivery month of MAR.

TOTAL COMEX GOLD STANDING: 36.189 TONNES (A WHOPPER FOR A MAR (NON ACTIVE) DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

191,133,764.7, oz NOW PLEDGED /HSBC 5.94 TONNES

123,963.792 PLEDGED MANFRA 3.86 TONNES

54,339.114oz PLEDGED JPMorgan no 1 1.690 tonnes

243,923.704, oz JPM No 2 7.58 TONNES

898,821.330 oz pledged Brinks/27,96 TONNES

12,249,333 oz International Delaware: 0..3810 tonnes

Loomis: 18,615.429 oz

total pledged gold: 1,543,044.471 oz 47.99 tonnes

TOTAL REGISTERED AND ELIG GOLD AT THE COMEX: 33,805,436.886 OZ (1051.91TONNES)

TOTAL ELIGIBLE GOLD: 16,219,622.847 OZ (504.48 tonnes)

TOTAL OF ALL REGISTERED GOLD: 17,585,814.039 OZ (546.97 tonnes)

REGISTERED GOLD THAT CAN BE SERVED UPON: 16,042,770.0 OZ (REG GOLD- PLEDGED GOLD) 498.99 tonnes

END

MAR 2022 CONTRACT MONTH//SILVER//MARCH 17

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1022,980.136 oz Delaware HSBC Int.Delaware JPMorgan |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 600,576.304 oz CNT |

| No of oz served today (contracts) | 64CONTRACT(S) 320,000 OZ) |

| No of oz to be served (notices) | 59 contracts (295,000 oz) |

| Total monthly oz silver served (contracts) | 10,437 contracts 52, 185,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

we had 0 deposits into the dealer

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 1 deposits into the customer account

i)Into CNT: 600,576.304 oz

total deposit: 600,576.304 oz

JPMorgan has a total silver weight: 180.228 million oz/342.981 million =52.54% of comex

ii) Comex withdrawals: 4

A) Out of JPMorgan 897,579.920 oz

B) Out of HSBC: 35,116.75 oz

C) out of Int Delaware 43,753.800 oz

d) Out of Delaware: 46,529.658 oz

total withdrawal 1022,980.136 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 93.406 MILLION OZ

TOTAL REG + ELIG. 342.981 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR MARCH

silver open interest data:

FRONT MONTH OF MARCH OI: 123, HAVING GAINED 38 CONTRACTS FROM MONDAY.

WE HAD 6 NOTICES SERVED UPON YESTERDAY, SO WE GAINED 44 CONTRACTS OR AN ADDITIONAL 220,000 OZ WILL STAND

FOR DELIVERY OVER HERE AS THESE GUYS REFUSED TO BE EFP’D TO LONDON.

APRIL HAD A 1 CONTRACT GAIN// CONTRACTS RISING TO 616

MAY HAD A LOSS OF 2754 CONTRACTS DOWN TO 119,189 contracts

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 64 for 320,000 oz

Comex volumes: 37,479// est. volume today//weak/

Comex volume: confirmed yesterday: 49,749 contracts (FAIR )

To calculate the number of silver ounces that will stand for delivery in MAR. we take the total number of notices filed for the month so far at 10,437 x 5,000 oz = 52,185,000 oz

to which we add the difference between the open interest for the front month of MAR (123) and the number of notices served upon today 64 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MAR./2021 contract month: 10,437 (notices served so far) x 5000 oz + OI for front month of MAR (123) – number of notices served upon today (64) x 5000 oz of silver standing for the MAR contract month equates 52,255,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

MARCH 17/WITH GOLD UP $33.50: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.61 TONNES INTO THE GLD//INVENTORY RESTS AT 1073.44 TONNES

MARCH 16/WITH GOLD DOWN $18.50//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWALL OF 2.33 TONNES FROM THE GLD///INVENTORY RESTS AT 1061.83 TONNES

MARCH 15/WITH GOLD DOWN $30.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1064.16 TONNES

MARCH 14//WITH GOLD DOWN $22.75, HUGE CHANGES IN GOLD INVENTORY AT THE GLD//STRANGE: A DEPOSIT OF 2.62 TONNES INTO THE GLD.//INVENTORY RESTS AT 1064.16 TONNES

MARCH 11/WITH GOLD DOWN $14.60: A BIG CHANGE IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 1061.54 TONNES

MARCH 10//WITH GOLD UP $11.55: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.06 TONNES FORM THE GLD///INVENTORY RESTS AT 1063.28 TONNES

MARCH 9/WITH GOLD DOWN $53.85//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.64 TONNES INTO THE GLD//INVENTORY RESTS AT 1067.34 TONNES

MARCH 8/WITH GOLD UP $46.10: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 8.42 TONNES INTO THE GLD///INVENTORY RESTS AT 1062.70 TONNES

MARCH 7/WITH GOLD UP $28.40 A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.06 TONNES INTO THE GLD..//INVENTORY RESTS AT 1054.28 TONNES

MARCH 4/WITH GOLD UP $28.40//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1050.22 TONNES

MARCH 3/WITH GOLD UP $13.95: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 7.84 TONNES//INVENTORY RESTS AT 1050.22 TONNES

MARCH 2/WITH GOLD DOWN $20.80//A MONSTER CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 13.36 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 1042.38 TONNES

MARCH 1/WITH GOLD UP $42.60: NO CHANGES IN GOLD INVENTORY AT THE GLD: //INVENTORY RESTS AT 1029.32 TONNES

FEB 28/WITH GOLD UP $12.95: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1029.32 TONNES

FEB 25/WITH GOLD DOWN $38.95: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1029.32 TONNES

FEB 24/WITH GOLD UP $17.35//A HUGE CHANGE AT THE GLD: 5.23 TONNES INTO THE GLD// IN GOLD INVENTORY AT THE GLD/INVENTORY REST AT 1029.32 TONNES

FEB 23/WITH GOLD UP $2.00 : NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1024.09 TONNES

FEB 22/WITH GOLD UP $6.20: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.65 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 1024.09 TONNES

FEB 18/WITH GOLD DOWN $1.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1019.44 TONNES

FEB 17/WITH GOLD UP $29.50: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1019.44 TONNES

FEB 16/WITH GOLD UP 414.60 NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1019.44 TONNES

FEB 15/WITH GOLD DOWN $12.70 NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1019.44 TONNES

FEB 14/WITH GOLD UP $27.20 NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1019.44 TONNES

FEB 11/WITH GOLD UP $4.50 A HUGE CHANGE IN GOLD IVNETORY AT THE GLD// A DEPOSIT OF 3.48 TONNES INTO THE GLD//INVENTORY RESTS AT 1019.44 TONES

CLOSING INVENTORY FOR THE GLD//1074.44 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MARCH 17/ WITH SILVER UP 72 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.049 MILLION OZ INTO THE SLVV//INVENTORY RESTS AT 548.071 MILLION OZ

MARCH 16/WITH SILVER DOWN 56 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 462,000 OZ FROM THE SLV//INVENTORY RESTS AT 544.560 MLLION O

MARCH 15/WITH SILVER DOWN 18 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 545.022 MILLION OZ

MARCH 14/WITH SILVER DOWN 64 CENTS TODAY; STRANGE A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.125 MILLION OZ/INVENTORY RESTS AT 545.022 MILLIONOZ

MARCH 11/WITH SILVER DOWN 13 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.897 MILLION OZ

MARCH 10/WITH SILVER UP 39 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.897 MILLION OZ/

MARCH 9/WITH SILVER DOWN 88 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 5.174 MILLION OZ OF FAKE SILVER.//INVENTORY RESTS AT 542.897 MILLION OZ//

MARCH 8/WITH SILVER UP 88 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.217 MILLION OZ INTO THE SLV////INVENTORY RESTS A 548.071 MILLION OZ//

MARCH 7/WITH SILVER UP 40 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 545.854 MILLION OZ//

MARCH 4/WITH SILVER UP 50 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 545.854 MILLION OZ/

MARCH 3/WITH SILVER UP 2 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 545.854 MILLION OZ//

MARCH 2/WITH SILVER DOWN $.32 TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 198,000 OZ FROM THE SLV//INVENTORY RESTS AT 545.854 MILLION OZ//

MARCH 1/WITH SILVER UP $1.13 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 546.052 MILLION OZ//

FEB 28/WITH SILVER UP 31 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT 546.052 MILLION OZ//

FEB 25/WITH SILVER DOWN 64 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 5.510 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 546.052 MILLION OZ/

FEB 24/WITH SILVER UP 15 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 551.597 MILLION OZ

FEB 23/WITH SILVER UP 22 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 551.597 MILLION OZ//

FEB 22/WITH SILVER UP 30 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 350,000 OZ INTO THE SLV///INVENTORY RESTS AT 551.597 MILLION OZ//

FEB 18/WITH SILVER UP 7 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.017 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 551.227 MILLION OZ

FEB 17/WITH SILVER UP 31 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.402 MILLION OZ//INVENTORY RESTS AT 550.210 MILLION OZ/

FEB 16/WITH SILVER UP 21 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 547.808 MILLIONOZ

FEB 15/WITH SILVER DOWN 46 CENTS TODAY : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 547.808 MILLION OZ//

FEB 14/WITH SILVER UP 49 CENTS TODAY; A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.235 MILLION OZ INTO THES LV////INVENTORY RESTS AT 547.808 MILLION OZ

FEB 11/WITH SILVER DOWN 18 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.573 MILLION OZ///

SLV FINAL INVENTORY FOR TODAY: 548.071 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

Peter Schiff: The Most-Anticipated And Least-Significant Rate-Hike Ever

THURSDAY, MAR 17, 2022 – 11:52 AM

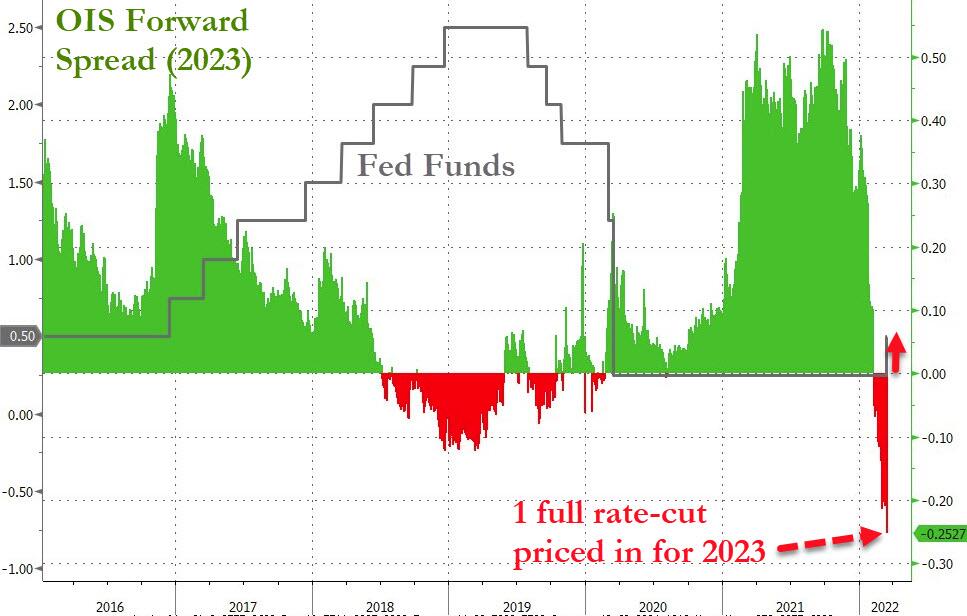

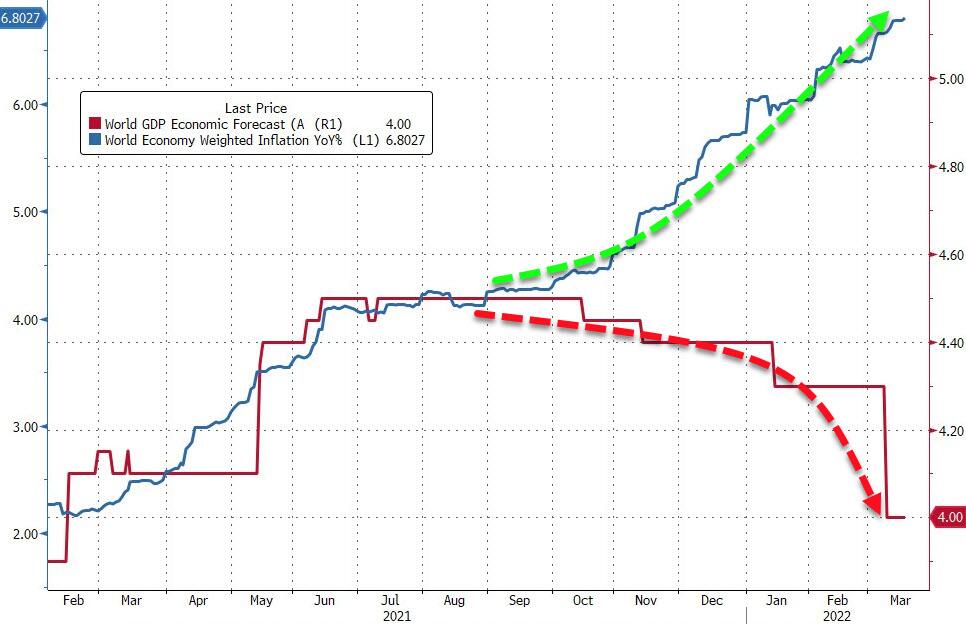

The Federal Reserve wrapped up its March meeting, delivering a 25 basis-point interest rate hike in the face of a 7.9% CPI. Peter Schiff called it the most anticipated and probably the most meaningless rate hike in history.

There was some speculation that the central bank would lift off with a 50 basis-point hike before Russia invaded Ukraine. But Peter said even that would have been too little, too late to derail this juggernaut of inflation.

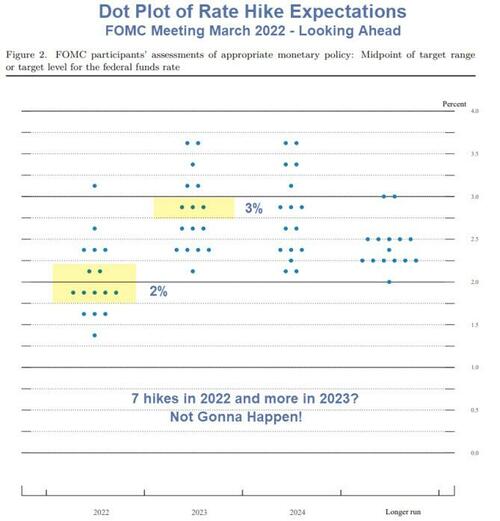

Nevertheless, the Fed’s move was the first salvo in its war on inflation. And while it looks to be a feckless inflation fight, Peter said he thinks the rate hikes that are coming will do more damage to the economy than most people realize. The Fed projects up to six more hikes this year, taking interest rates to just below 2%. (Still not terribly significant in light of historically high inflation.)

The bond market appears to be correctly pricing in a recession. But Peter said bond buyers are still missing the boat.

I agree that bond investors are correct; a recession is coming. But where bond investors are missing the mark is to believe that the arrival of recession means a departure of inflation.”

Peter said he thinks recession is going to exacerbate the inflation problem. That puts the Federal Reserve in a difficult position.

As the US economy weakens, that’s going to put more upward pressure on the budget deficit. The government is going to collect less in the way of taxes. It’s going to be spending more as these stabilizers kick in as the economy weakens. So, the deficits are going to be getting bigger, which so going to be putting more pressure on the US dollar to go down. And as the US dollar really starts to fall, that’s going to be putting more upward pressure on prices.”

If you consider the massive increase in the money supply compared to the rise in prices so far, there’s a long way for prices to run upward.

And there is nothing that the Fed did during its March meeting to alter that trajectory.

Just because the Fed is hiking rates because of inflation doesn’t mean these rate hikes are actually going to work at putting out the inflation fire. They’re not. The Fed is simply doing the minimum that it can get away with and try to save face.”

The Fed’s messaging was widely regarded as “hawkish” with Fed chair Jerome Powell projected firm resolve to stick to the rate hike path. But Peter picked up on something in the Fed minutes most people didn’t seem to notice. The FOMC took out language relating to the start of balance sheet reduction. It now just says it will happen sometime in the future.

The most important thing to me is quantitative tightening is happening later than the Fed initially postured. And it may never happen. That’s kind of my thought. They can raise interest rates slightly, because, on the margin, the first few rate hikes won’t have much of an impact. But I think given the enormity of the federal government deficits, I don’t see how the Federal Reserve is able to shrink its balance sheet. In fact, I think the Fed is going to have to continue to increase the size of its balance sheet even as it notches up interest rates.”

During the post-meeting press conference, Powell took several questions relating to the possibility that monetary tightening will cause a recession. Powell insisted the economy is strong enough to handle the rate hikes coming down the pike.

Maybe it can. Maybe it can’t. The Fed’s been wrong about a lot of stuff in the past. Most recently, it was wrong about inflation being transitory. So, maybe it’s wrong about the ability of the economy to withstand these rate hikes.”

Keep in mind, the US economy is a credit bubble. It hinges on the ability of over-leveraged consumers, businesses and governments to keep on spending borrowed money.

So, obviously, there is a breaking point there when it comes to interest rates. You live by low interest rates; you die by high interest rates. The only question is when are low interest rates no longer low enough and then they become high? We’re only going to find out when get there.”

This isn’t uncharted territory. In the last tightening cycle, we got there at 2.5%. Peter said he thinks the breaking point is much lower than that today given the increase in debt in the economy.

The Fed clearly doesn’t even understand that the economy is a bubble. Or if it does, it sure as hell is not going to admit that to anybody.”

In this podcast, Peter also talks about Elizabeth Warren’s refusal to take the blame for inflation, the gold market’s reaction to rate hikes, a pay raise for congressional staffers, and more on Powell’s post-meeting Q&A.

END

A must read..

Michael Maharrey/SchiffGold

A Petroyuan Would Be A Kick In The Gut For The Dollar

THURSDAY, MAR 17, 2022 – 01:20 PM

Authored by Michael Maharrey via SchiffGold.com,

Last week, I asked the question: is the US undermining the dollar’s credibility?

It appears the answer is — yes.

In another blow for dollar dominance, Saudi Arabia is reportedly considering pricing at least some of its Chinese oil sales in yuan.

According to the Wall Street Journal, the move would “dent the US dollar’s dominance of the global petroleum market and mark another shift by the world’s top crude exporter toward Asia.”

The “petrodollar” serves as a crucial support for the US dollar.

The majority of global oil sales are priced in dollars. This ensures a constant demand for the greenback. Every country needs dollars to buy oil. This helps support the US government’s borrow and spend policy with its massive deficits. As long as the world needs dollars for oil, the Federal Reserve can keep printing dollars to monetize the debt.

ZeroHedge explained how the process works.

One of the core staples of the past 40 years, and an anchor propping up the dollar’s reserve status, was a global financial system based on the petrodollar – this was a world in which oil producers would sell their product to the US (and the rest of the world) for dollars, which they would then recycle the proceeds in dollar-denominated assets and while investing in dollar-denominated markets, explicitly prop up the USD as the world reserve currency, and in the process backstop the standing of the US as the world’s undisputed financial superpower.”

Saudi Arabia has sold oil exclusively for dollars since 1974 under a deal with the Nixon administration. If the Saudis shift away from the dollar and sell oil for yuan, it would be bad news for dollar dominance. And good news for the Chinese currency.

According to the WSJ, China buys more than 25% of Saudi oil exports.

If priced in yuan, those sales would boost the standing of China’s currency. The Saudis are also considering including yuan-denominated futures contracts, known as the petroyuan, in the pricing model of Saudi Arabian Oil Co., known as Aramco.”

China and Saudi Arabia have been talking about yuan-based oil contracts for six years. But Saudi Arabia’s frustration with the US has apparently accelerated those talks. According to the WSJ, the Saudi government is increasingly unhappy with decades-old US security commitments to defend the kingdom along with the Biden administration’s attempt to reinstitute the Iran nuclear deal.

The Chinese rolled out yuan-based oil contracts in 2018. They have been modestly successful, but haven’t dented the dollar’s dominance. If Saudi Arabia begins doing business in yuan, it would be a kick in the gut for the dollar.

And it would be a boon for China. The Chinese would love to limit their exposure to the dollar.

Needless to say, US officials are not pleased with this development. A senior US official called the idea of the Saudis selling oil to China in yuan “highly volatile and aggressive” and “not very likely.”

Calling the move “aggressive” is ironic given how the US has used the dollar as a weapon for decades.

But this could be nothing but talk. Selling oil in yuan would come with some risks to the Saudi economy. The Saudi riyal is pegged to the dollar. Prince Mohammed’s aides have reportedly warned him of unpredictable economic damage should the country hastily start selling millions of barrels of oil for yuan.

Regardless, it’s no surprise that the Chinese and Saudis have ramped up talks in recent weeks. The weaponization of the dollar has been on full display.

After Russia invaded Ukraine, the US cut some Russian banks, including the central bank, off from the SWIFT payment system.

SWIFT stands for the Society for Worldwide Interbank Financial Telecommunication. The system enables financial institutions to send and receive information about financial transactions in a secure, standardized environment. Since the dollar serves as the world reserve currency, SWIFT facilitates the international dollar system.

SWIFT and dollar dominance gives the US a great deal of leverage over other countries.

But that leverage depends on the dollar’s role as the reserve currency. It shouldn’t shock us that we’re seeing blowback from the US using greenbacks as a foreign policy carrot and stick.

A drop in the demand for dollars would be bad news for a US government that depends on dollar demand to fund its out-of-control spending. Imagine a world in which the Chinese didn’t need dollars.

China ranks as the biggest foreign holder of US debt. If it continues to divest itself of dollars, who will pick up the slack? The Federal Reserve has been buying Treasuries hand over fist for the last two years, keeping its big fat thumb on the bond market. But it’s tapering purchases and supposedly planning on shrinking its balance sheet. If global demand for Treasuries drop precipitously — and it would in a world without the petrodollar — the US government would either have to drastically cut spending or the Fed would have to continue printing money to monetize the debt.

Even if this is nothing but talk, it underscores the fact that the dollar is on shaky ground. US policymakers would be wise to consider future dollar weaponization carefully.

2.LAWRIE WILLIAM//,//Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, James RICKARDS/

-END-

LAWRIE WILLIAMS:

-END-

3. Chris Powell of GATA provides to us very important physical commentaries

LME shoots itself in the foot again as they halt trading in nickel within seconds of opening after a one week layoff.

Shanghai now becomes the de facto centre for price discovery.

(London’s Financial Times/GATA)

LME failure with nickel puts Shanghai in charge of price discovery, trader says

Submitted by admin on Wed, 2022-03-16 12:44Section: Daily Dispatches

London Metal Exchange Suffers Fresh Glitch as It Attempts to Restart Nickel Trading

Neil Hume and Philip Stafford

Financial Times, London

Wednesday, March 16, 2022

The London Metal Exchange suspended electronic trading in nickel on Wednesday, just moments after the world’s main market for the metal reopened for business following a week-long shutdown.

Wednesday’s fresh trading halt came after the price of nickel tumbled when the market opened. Newly installed curbs to support the resumption were meant to prevent the price from declining by more than 5%, but some trades appeared to have breached the limit of $45,590 a tonne, according to Refinitiv data.

The LME said it would halt electronic trading to “investigate” the issue, but that it would still allow in-person dealings later in the day around the famous red sofas on its Ring venue, and also through an inter-office telephone exchange between members.

“The scale of sell orders illustrative of the mood in the market — longs just want to get out of a market that has become and is likely to remain dysfunctional,” said traders at Marex. …

Ole Hansen, head of commodities strategy at Saxo Bank, said Wednesday’s trading halt was a “desperately sad situation” for the LME, which prides itself on being the leading global marketplace for metals trading.

“The limit was too small,” he said. “Shanghai is the de-facto centre for price discovery right now.” …

… For the remainder of the report:

https://www.ft.com/content/6a640cd5-3d9b-421d-bc71-8e4d0f2f9522

END

USA mint gives up production in 1922 for silver Morgan and peace dollars

(USA Mint/GATA)

U.S. Mint suspends production of two silver coins, claims blanks aren’t available

Submitted by admin on Wed, 2022-03-16 23:45Section: Daily Dispatches

The virus epidemic supposedly is responsible. But the Comex claims to have plenty of metal, so why not just pay up to get it?

* * *

United States Mint Announces Pause in Production and Sales of Morgan and Peace Dollars for 2022

From the United States Mint, Washington

Monday, March 14, 2022

The United States Mint today announced it will forgo the production and sales of Morgan and Peace Silver Dollars in 2022. This calculated pause is directly related to the global pandemic’s impact upon the availability of silver blanks from the Mint’s suppliers.

The suspension will give the Mint time to evaluate the best way to allocate our limited supply of silver to ensure the best customer experience we can

“We’ll be required to make business decisions like this until the supply chain for silver blanks recovers from the disruptions caused by COVID-19,” said Mint Deputy Director Ventris C. Gibson.

“I want to ensure that our customers know,” she said, “that the modern renditions of the historic Morgan and Peace Silver Dollars will continue next year. Our goal is straightforward: to give our loyal customers the products they want and the service they deserve.”

* * *

END

4.OTHER GOLD/SILVER COMMENTARIES

Gold at $10,000? Death of the 40-year bull market in bonds? What’s next for the global financial system after Russia’s central bank gets cancelled

March 17, 2022 at 6:24 a.m. ET

MarketWatch

Critical information for the U.S. trading day

The shockwaves are still being felt by the incredible Western sanctions that have rendered the $630 billion in reserves the Russian central bank accumulated virtually unusable. Can the current dollar-centered global financial system last if money can be summarily cancelled?

Arthur Hayes, a former emerging markets trader and co- founder of the BitMEX trading platform, argues central banks will choose, instead of dollars, to load up on either gold, storable grains like wheat, or storable commodities like oil and copper. “In essence, the largest surplus countries’ fiat currencies will implicitly grow their gold or commodity backing,” he writes, saying gold could rise beyond $10,000 per ounce.

Luke Gromen, publisher of Forest For The Trees and a long-time dollar bear, said that shift had been happening even before the sanctions. In a podcast with Grant Williams, Gromen said that over the last eight years, global central banks have bought about $260 billion worth of gold, compared to $60 billion in Treasurys. “So there’s been this very slow, but steady and recently accelerating move toward the away from this dollar system that broke in 2005, through 2008 to this system that looks a lot like what was proposed by [John Maynard] Keynes 80 years ago,” he says.

The dollar-centered system has some disadvantages for the U.S. “The issue with this is the American version of this deal that we’re printing dollars for oil as we have since ‘73 is, and this is the downside of the deal, is you got to run the deficits to supply the dollars to the world,” he said. “Which means you got to offshore all the manufacturing. You got to offshore all the manufacturing jobs. You got to run a bunch of deficits at the government level. You got to do all these things that are really, really good for GDP growth and the economy in the short and medium term. And in the long run, they bankrupt you.”

Gromen, like Hayes, expects more gold accumulation. “So every central bank in the world is now looking at this thinking, okay, we need to not be in a position where that can happen to us. Because who knows what might happen in the future and what might get us deemed a bad actor. So presumably they are going to be looking to accumulate a lot more gold,” he said.

(It should be noted that gold has its perils for foreign central banks. In Russia’s case in particular, the central bank won’t be able to sell to any western entity directly, and bipartisan legislation introduced in the U.S. Senate would impose secondary sanctions to any American entities knowingly transacting with or transporting gold from Russia.)

Gromen expects the end of the 40-year bull market in bonds. And he sees the potential for re-industrialization. “When you see Ohio getting an Intel INTC, -0.83% fab and the CEO of Intel saying, ‘We’re going to make Ohio one of the biggest Intel manufacturing regions in the world.’ What? Ohio was ground zero of the people who took it in the shorts from 1973 to present under this deal. Another semi fab in Arizona, another semi fab in Texas,” says Gromen. “It’s not even the first inning in this reindustrialization of America, but reindustrialization was never going to happen until you changed this dollar system and removed treasuries as the primary reserve asset, replaced it with a neutral one. And here we are. We’re two weeks into it. It’s incredibly exciting.”

The buzz

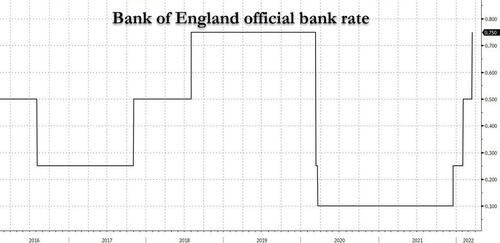

Initial jobless claims fell to 214,000, the latest data show, as both housing starts and the latest Philly Fed manufacturing index improved. The Bank of England made its third rate since December, a day after the Federal Reserve made a quarter-point increase and pencilled in 11 increases over two years.

There weren’t any major developments in the Russia- Ukraine situation as of Thursday morning. Ukrainian President Volodymyr Zelenskyy spoke to Germany’s parliament and criticized its support for the now-halted Nord Stream 2 pipeline project.

Special thanks to Doug C for sending this to us;

U.S. Mint announces silver shortage… – CITIZEN FREE PRESS

Inbox

| douglas cundey | 10:01 PM (1 hour ago) | ||

| to Chris, William, Bill, rkirby, me |

U.S. Mint announces silver shortage…

The United States Mint will not strike 2022 Morgan or Peace dollars, with Mint officials identifying silver planchet shortages as the reason for the cancellation of the planned coins.

WASHINGTON – The United States Mint today announced it will forgo the production and sales of Morgan and Peace Silver Dollars in 2022. This calculated pause is directly related to the global pandemic’s impact upon the availability of silver blanks from the Mint’s suppliers. The suspension will give the Mint time to evaluate the best way to allocate our limited supply of silver to ensure the best customer experience we can.

“We’ll be required to make business decisions like this until the supply chain for silver blanks recovers from the disruptions caused by COVID,” said Mint Deputy Director Ventris C. Gibson.

“I want to be ensure that our customers know,” she said, “that the modern renditions of the historic Morgan and Peace Silver Dollars will continue next year. Our goal is straightforward: to give our loyal customers the products they want and the service they deserve.”

END

5.OTHER COMMODITIES/

end

NICKEL UPDATE

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING TODAY

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings THURSDAY morning 7:30 AM

ONSHORE YUAN: CLOSED UP 6.3498

OFFSHORE YUAN: 6.3641

HANG SANG CLOSED UP 1413.73 PTS OR 7.04%

2. Nikkei closed UP 890.88 PTS 3.46%

3. Europe stocks ALL RED EXCEPT LONDON

USA dollar INDEX DOWN TO 98.21/Euro RISES TO 1.1052

3b Japan 10 YR bond yield: FALLS TO. +.204/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 118.61/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 100.56 and Brent: 103.76

3f Gold UP /JAPANESE Yen UP CHINESE YUAN: ON -SHORE CLOSED UP// OFF- SHORE UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.0.389%/Italian 10 Yr bond yield RISES to 1.92% /SPAIN 10 YR BOND YIELD RISES TO 1.35%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 1.63: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 2.64

3k Gold at $1941.80 silver at: 25.24 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

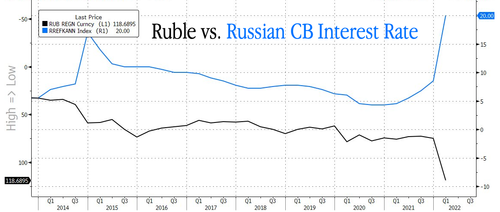

3l USA vs Russian rouble;// Russian rouble DOWN 4.00/100 in roubles/dollar; ROUBLE AT 104.00

3m oil into the 100 dollar handle for WTI and 103 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 118.61 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning .9389– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0387 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 2.143 DOWN 5 BASIS PTS

USA 30 YR BOND YIELD: 2.400 DOWN 6 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 14.80

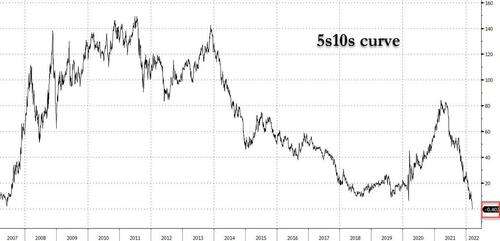

Futures Drift Lower After Kremlin Dashes Ukraine Peace Hopes; Curve Inversion Persists

THURSDAY, MAR 17, 2022 – 07:58 AM

After yesterday’s explosive session, which saw stocks trade in violent kneejerk response to conflicting headlines out of Ukraine at first, only to post the biggest ever post FOMC reversal, as markets realized that the Fed’s overly hawkish ambitions are too great and doom the rapidly slowing economy to an accelerated recession, overnight trading has been positively subdued with emini S&P futs trading in a tight 20 point range between 4,340 and 4,360 until 6 am ET, when European stocks turned negative and US equity futures suddenly dropped as much as 0.5%, after the Kremlin said reports of major progress in Ukraine talks are “wrong” and Kremlin spokesman Dmitry Peskov dismissed reports that the warring parties are moving toward a settlement, blaming Kyiv for slowing the negotiations, crippling any hope for a quick ceasefire deal and adding to worries about the outlook for economic growth as the Federal Reserve’s campaign against inflation gets underway. Futures were already wavering as the bond market flagged a growing risk that the Fed’s efforts to rein in prices could trigger an economic downturn with the 5s10s curve inverting. Ominously, Brent jumped more than $5/bbl after tumbling below $100 yesterday.

Contracts on the Nasdaq 100 dipped 0.4% by 7:30 a.m. in New York, while S&P 500 futures were 0.34% lower. The benchmark S&P 500 on Wednesday posted its best two-day rally since April 2020 as the Fed hiked interest rates by a quarter point and Chair Jerome Powell signaled the economy could weather tighter monetary policy. Gold and 10Y yields dropped to session lows, and bitcoin was modestly lower on the session. Europe was slightly green while Asia stocks closed higher, led by the Hang Seng which rose 7%

On Wednesday, the Fed raised borrowing costs by a quarter percentage point and signaled hikes at all six remaining meetings in 2022, while projecting an “above-normal” policy rate at 2.8% by the end of 2023. Chair Jerome Powell said the U.S. economy is “very strong” and can handle monetary tightening. Treasuries advanced, while a portion of the bond curve – the gap between 5- and 10-year yields – inverted for the first time since March 2020, a sign investors expect recession.

The Fed also said it would begin shrinking its $8.9 trillion balance sheet at a “coming meeting,” without elaborating as Biden breathes down Powell’s neck to get inflation under control. Meanwhile, the commodity shock from Russia’s war in Ukraine is continuing to aggravate price pressures and economic risks, portending more market volatility.

“It won’t be easy — rarely has the Fed safely landed the U.S. economy from such inflation heights without triggering an economic crash,” Seema Shah, chief strategist at Principal Global Investors, said in emailed comments. “Furthermore, the Russia-Ukraine conflict, of course, has the potential to disrupt the Fed’s path. But for now, the Fed’s priority has to be price stability.”

“This type of normalization policy does not always end well,” said Nicolas Forest, global head of fixed income at Candriam Belgium SA. “While the Fed began its tightening cycle later than usual, at a time when inflation has never been so high, financial conditions could also harden, making the 2.80% target ambitious in our view. In this context, it is easy to understand why the U.S. curve has flattened.”

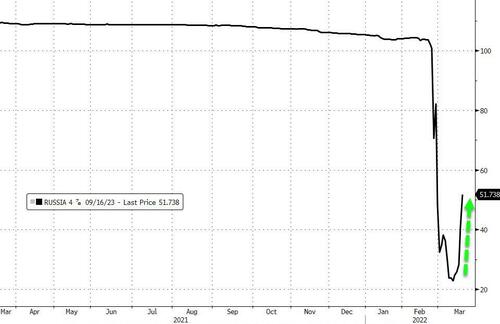

In the latest Ukraine war developments, Russia continued to “hammer” cities like Kharkiv and Cherniyiv with bombardments and rocket systems and isn’t acting like it wants to settle, Pentagon spokesman John Kirby said in an interview with Bloomberg TV. Meanwhile, Russia’s Finance Ministry said a $117 million interest payment due on two dollar bonds had been made to Citibank in London amid mounting speculation that the country is heading for a default. Russia had until the end of business Wednesday to honor the coupons on the two notes. The ruble gained for a sixth day in Moscow trading, while the country’s stock market remains shut. Here are some more headlines courtesy of Newsquawk:

- Ukrainian President Zelensky said talks with Russia are challenging but are still ongoing. He added that Russia has the advantage in the air and already crossed all red lines, while he hopes for assistance from allies.

- Russian Foreign Minister says that discussions with Ukraine are continuing via video link with the sides discussing humanitarian and political issues.

- Ukrainian Defense Minister says so far there is nothing to satisfy us in negotiations with Russia; a peaceful solution can be reached with Russia, but “on our terms”.

- Russian Kremlin says their delegation is putting colossal energy into Ukraine peace talks, conditions are absolutely clear. Agreement with Ukraine with clear parameters could very fast stop what is going on; on the recent FT report re. peace talk progress said this is not right, elements are correct but the entire peace is not true.

A rebound in China stocks listed on U.S. exchanges also cooled a day after they soared the most since at least 2001 on a pledge from Beijing to keep its stock market stable. American depository receipts of Alibaba were down 2% in premarket trading following their biggest gain since their trading debut in September 2014, while Baidu dropped 5.7%. Here are some other notable premarket movers:

- Shares in Marrone Bio (MBII US) jumped 20% premarket after announcing a merger pact with Bioceres Crop Solutions (BIOX US), which falls 5.9%.

- Williams-Sonoma (WSM US) gained 6.2% in extended trading Wednesday after the home-goods retailer reported adjusted fourth-quarter earnings that beat the average analyst estimate. The company also raised its dividend and announced a share buyback authorization.

In Europe, the Stoxx 600 index gained, nearly erasing losses that were sparked by Russia’s invasion of Ukraine. The index then dipped on the abovementioned news out of the Kremlin which said reports of major progress in Ukraine talks are “wrong”, only to bounce back into the green. DAX and FTSE MIB lag, slipping ~1%. Banks, autos and personal care are the worst performing sectors. Energy, real estate and tech outperform. Here are some of the biggest European movers today:

- Deliveroo shares rise as much as 9.8% after reporting full-year results, with Barclays (equal-weight) saying the food-delivery company’s mid-term margin commentary was “helpful.”

- Grenke shares jump 16%, the most since May, after the company reported dividend per share that beat the average analyst estimate.

- EQT shares rise as much as 9.5%, extending Wednesday’s 12% gain following the acquisition of Baring Private Equity Asia for $7.5 billion in what is the biggest takeover of a private equity firm by another in the sector.

- Atos shares jump as much as 7.4% after BFM Business reported that Airbus has been mulling a possible takeover of the French IT firm’s cybersecurity unit. Atos reiterated that its BDS cybersecurity business is not for sale.

- DiaSorin shares soar as much as 9.7%, their best day in nearly one year as analysts upgraded the Italian diagnostics company following results, with the firm reporting net income for the full year that beat the average analyst estimate.

- Verbund shares rise as much as 7.7% after 2021 profit beats estimates and Austria’s biggest utility forecasts higher profit next year.

- Thyssenkrupp shares fall as much as 11% after the company suspended its full-year forecast for free cash flow. The move is a disappointment, given the FCF focus in the steel company’s equity story after years of cash burn, Deutsche Bank says.

Asian stocks extended their rebound through a second day after Chinese shares rallied again on a vow of state support and the Federal Reserve expressed confidence in the U.S. economy. The MSCI Asia Pacific Index rallied as much as 3.6%, lifted by technology and consumer-discretionary shares. Japan and Hong Kong benchmarks led the way, with the Hang Seng Index surging 17% over two days, its biggest back-to-back advance since the Asian financial crisis in 1998, and the Topix jumping 2.5%. A combination of China’s pledge to stabilize markets, Fed comments on the U.S. economy’s strength after the expected quarter-point interest rate hike by the central bank, and hopes for progress on Russia-Ukraine talks have put Asian stocks on track to end four consecutive weekly losses. “Following recent corrections, markets have reached a point that prices in, or presumes, a fair amount of rate hikes and economic stress,” said Ellen Gaske, lead economist for G-10 economies at PGIM Fixed Income. “It would not be surprising to see investors begin to inch back into the market in search of yield.”

Japanese equities rose for a fourth day, as investors were cheered by comments from the Federal Reserve on U.S. economic growth and China’s moves to support its market. Electronics and machinery makers were the biggest boosts to the Topix, which rose 2.5%, to the highest level since Feb. 21. All 33 industry groups advanced. Fast Retailing and Tokyo Electron were the biggest contributors to a 3.5% rise in the Nikkei 225. The yen extended its losses against the dollar after weakening 3.4% over the previous eight sessions. The Fed raised interest rates by a quarter percentage point and signaled hikes at all six remaining meetings this year, while saying “the American economy is very strong” and able to handle tighter policy. Global stocks got a lift Wednesday after Beijing vowed to keep its stock market stable. “The FOMC dot plot clearly shows that the number of interest rate hikes will be reasonable, and the stock market is pleased that the risk of accelerating long-term interest rates rising due to monetary policy following has decreased,” said Kazuharu Konishi, head of equities at Mitsubishi UFJ Kokusai Asset Management. In domestic news, a magnitude-7.3 earthquake struck near Fukushima prefecture late Wednesday, killing four and injuring dozens of people, as well as derailing a bullet train and disrupting power

India’s benchmark stocks index rose, tracking regional peers, as lenders drove gains. The S&P BSE Sensex climbed 1.8% to 57,863.93, in Mumbai. The measure added 4.2% this week, and with local markets closed for a holiday Friday, it is the biggest weekly advance for the index since February 2021. With today’s gains, it completely recovered all losses that followed Russia’s invasion of Ukraine. Mortgage lender Housing Development Finance Corp. rose 5.4%, its biggest jump in over a year and was the best performer on the Sensex, which saw all but two of 30 shares advance. Seventeen of 19 sectoral sub-indexes compiled by BSE Ltd. gained, led by a gauge of realty companies. The NSE Nifty 50 Index added 1.8% to 17,287.05 on Thursday. China’s pledge to support its markets, the prospect of progress on Russia-Ukraine cease-fire talks and the U.S. Federal Reserve’s comments on America’s economic strength boosted sentiment. Brent crude, a major import for India, down to $100 a barrel from $127.98 last week, also eased concerns. The Fed announcement was on expected lines for the market and they rallied in relief, Nishit Master, portfolio manager at Axis Securities wrote in a note. “Despite the recent rally, the markets will continue to remain volatile in the near future on the back of tightening of liquidity conditions globally. One should use this volatility to increase equity allocation for the long term.”

In rates, the post-Fed flattening move has extended as investors continue to digest expectations on latest policy path, with some strategists calling for a top in yields. 10-year yields around 2.12%, richer by ~6bp on the day and outperforming bunds and gilts by 4.5bp and 3bp; 2s10s spread is flatter by ~4bp on the day. US TSY yields are richer by as much as 7bp across long-end of the curve, flattening 5s30s by a further 2.4bp with the spread dropping as low as 24.2bp; the 5s10s was again inverted, trading fractionally in the red after first inverting yesterday during Powell’s FOMC presser.

In FX, the Bloomberg Dollar Spot Index pared a loss and the greenback traded mixed after earlier sliding against all of its Group- of-10 peers apart from the Swedish krona, as risk aversion gave rise to a haven bid. The euro snapped a three- day advance after the news out of Kremlin dampened sentiment; short-dated European benchmark bond yields were little changed while they contracted longer out on the curve. The pound advanced and gilts rose, led by the long end before the Bank of England looks all but certain to take interest rates back to their pre- Covid level. The Australian dollar still outperformed G-10 peers after the nation’s February unemployment rate falls to the lowest since 2008, boosting bets of earlier interest-rate hikes. The yen inched up amid risk aversion, but still held near its lowest level in six years as Bank of Japan Governor Haruhiko Kuroda vowed to continue with monetary stimulus even after the Federal Reserve kicked of its rate hike cycle Wednesday.

In commodities, WTI crude futures climb near $99.50 while Brent rallies through $102; spot gold adds ~$16 to trade around $1,944. Base metals are mixed; LME nickel falls 8% to maximum limit while LME aluminum gains 1.8%. Bitcoin is modestly softer but remains well within yesterday’s parameters and retains a USD 40k handle.

Looking at the day ahead now and housing starts, building permits, initial jobless claims and industrial production are due. We will also hear from ECB’s Lagarde, Lane, Knot, Schnabel and Visco. Earnings releases include Accenture, Enel, FedEx, Dollar General and Verbund.

Market Snapshot

- S&P 500 futures down 0.3% at 4,337.00

- STOXX Europe 600 up 0.4% to 450.44

- MXAP up 3.5% to 178.08

- MXAPJ up 4.0% to 582.21

- Nikkei up 3.5% to 26,652.89

- Topix up 2.5% to 1,899.01

- Hang Seng Index up 7.0% to 21,501.23

- Shanghai Composite up 1.4% to 3,215.04

- Sensex up 2.1% to 58,014.18

- Australia S&P/ASX 200 up 1.1% to 7,250.80

- Kospi up 1.3% to 2,694.51

- German 10Y yield little changed at 0.38%

- Euro up 0.2% to $1.1057

- Brent Futures up 3.0% to $100.97/bbl

- Gold spot up 0.7% to $1,940.77

- U.S. Dollar Index down 0.42% to 98.21

Top Overnight News

- Russia’s Finance Ministry said a $117 million interest payment due on two dollar bonds had been made to Citibank in London amid mounting speculation that the country is heading for a default

- Rates and currency markets are skeptical of the Bank of England’s ability to tame inflation without triggering an economic slowdown. Policymakers may undo tightening as soon as next year, swaps contracts suggest

- After the Federal Reserve raised interest rates and signaled hikes at all six remaining meetings this year, a section of the Treasury curve — the gap between five- and 10-year yields — inverted for the first time since March 2020. Meanwhile the flattening trend between two- and 10-year yields continued

- Hungary’s central bank kept the effective interest rate unchanged after a rally in the forint eased pressure on policy makers to further hike the European Union’s highest key rate

- Commodities trader Pierre Andurand sees a path for crude oil to get to $200 by the end of the year as historically tight markets struggle to ramp up production and replace lost supply from Russia

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks gained post-FOMC while Chinese tech remained euphoric on support pledges. ASX 200 was led higher again by outperformance in tech and following strong jobs data. Nikkei 225 rallied after recent currency weakness and despite the deadly earthquake in Fukushima. Hang Seng and Shanghai Comp. continued to benefit from China’s recent policy support pledges which lifted the NASDAQ Golden Dragon China Index by 33% and with the PBoC boosting its liquidity efforts. Significant gains were also seen amongst developers after reports that China is not planning to expand its pilot property tax reform this year.

Top Asian News

- China Affirms Friendship With Ukraine, Promise to ‘Never Attack’

- Indonesia Holds Rates While Monitoring Inflation, War Risks

- War in Ukraine Triggers Slew of Shelved IPOs in Japan: ECM Watch

- Strong Quake Hits Japan, Killing Two and Halting Factories

European bourses are predominantly negative, Euro Stoxx 50 -0.4%, after a relatively constructive open post Wall St./APAC handover. Initial upside faded as updates on Russia/Ukraine are downbeat overall and push back further on some of Wednesday’s more constructive updates. US futures are lower across the board, ES -0.4%, after yesterday’s upbeat close post a hawkish-FOMC.

Top European News

- Raiffeisen CEO Says Bank is Considering Exit From Russia

- UBS, Mitsubishi Sell Japan Realty Unit to KKR for $2 Billion

- Russia’s Ruined Gameplan for Ukraine Is Visible in the South

- Diageo Rises; JPMorgan Lifts to Overweight on U.S. Position

In FX, the dollar flips after hawkish Fed hike and more aggressive dot plot before unwinding all and more upside in buy rumor, sell fact reaction; DXY almost 100 ticks down from pre-FOMC peak and just off 98.000. Aussie outperforms following upbeat labour data and Kiwi lags on the back of sub-forecast GDP, AUD/USD eyeing Fib ahead of 0.7350, AUD/NZD back up over 1.0700 and NZD/USD capped into 0.6850. Sterling firm awaiting confirmation of 25 bp hike from the BoE and vote split plus MPC minutes for further guidance; Cable close to 1.3200 at best and EUR/GBP sub-0.8400. Euro clears 1.1000 again, while Yen extends decline to cross 119.00 line. Lira looks ahead to CBRT with high bar for any direct support in contrast to Real that got a full point hike from BCB and signal of more to come. Brazilian Central Bank raised the Selic rate by 100bps to 11.75%, as expected, while the decision was unanimous and it considered it appropriate to advance monetary tightening significantly into even more restrictive territory.

In commodities, crude futures continue to nurse recent wounds, with Brent May back around USD 102.50/bbl while WTI April inches toward USD 100/bbl. Upside occurred, picking up from initial choppy action, amid the most recent geopolitical developments from the Kremlin and Ukrainian Defence Ministry. India may purchase up to 15mln bbls of oil from Russia with state-run oil firms preparing to purchase heavy volumes of Russian crude that’s going at a deep discount to help ease the margin pressure oil refiners. China is to increase gasoline prices by CNY 750/ton and diesel by CNY 7220/ton as of March 18th, according to the NDRC via CCTV. Italy is considering blocking the export of raw materials, according to the Deputy Industry Minister. Spot gold/silver are firmer given geopolitical-premia., while LME Nickle hit the new adj. limit down of 8% after the reopen.

In fixed income, debt derives impetus from downturn in risk sentiment as Russia and Ukraine deny major strides towards ceasefire deal. Bond curves remain flatter following Fed’s hawkish dot plots. Bonos and OATs soak up Spanish and French supply.

US Event Calendar

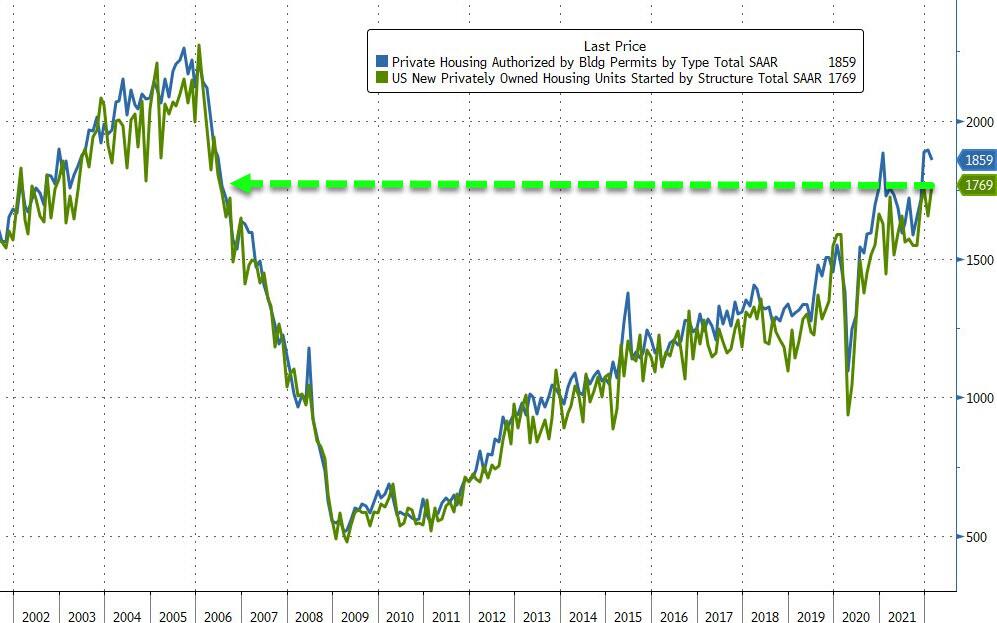

- 8:30am: March Initial Jobless Claims, est. 220,000, prior 227,000; March Continuing Claims, est. 1.48m, prior 1.49m

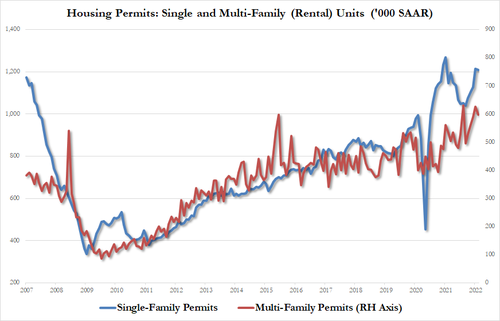

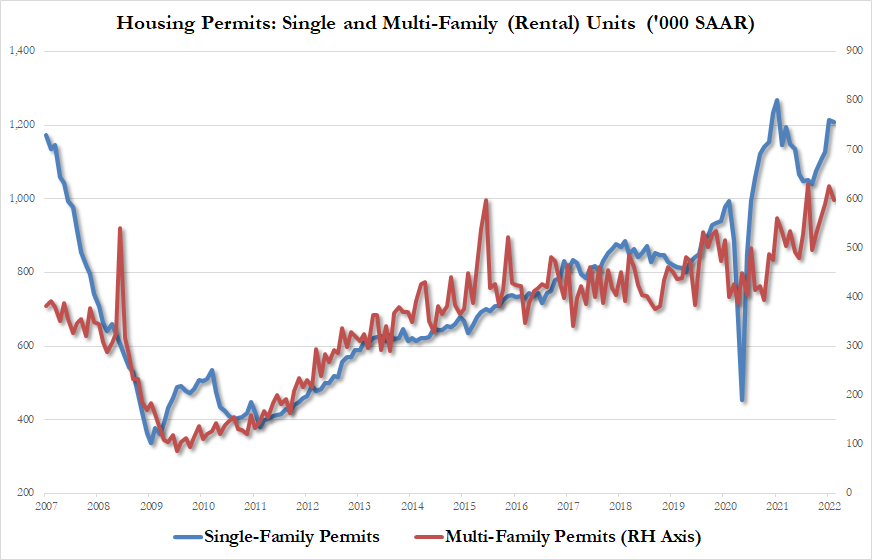

- 8:30am: Feb. Building Permits, est. 1.85m, prior 1.9m; Building Permits MoM, est. -2.4%, prior 0.7%, revised 0.5%

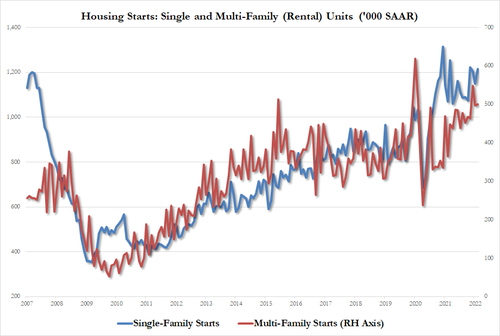

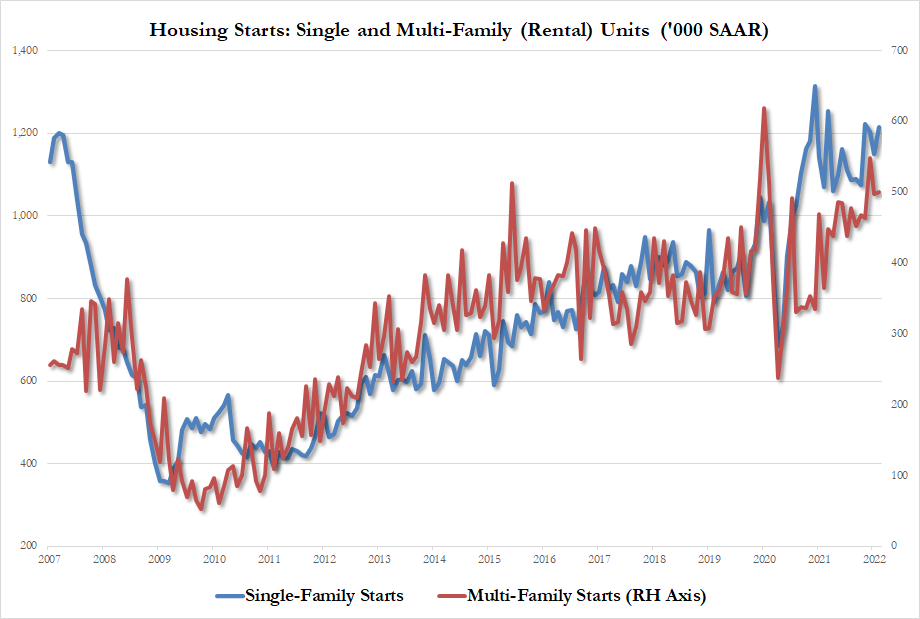

- 8:30am: Feb. Housing Starts, est. 1.7m, prior 1.64m; Housing Starts MoM, est. 3.8%, prior -4.1%

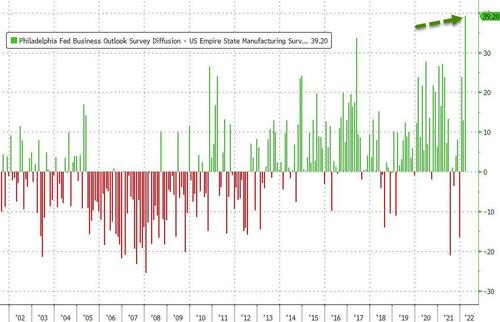

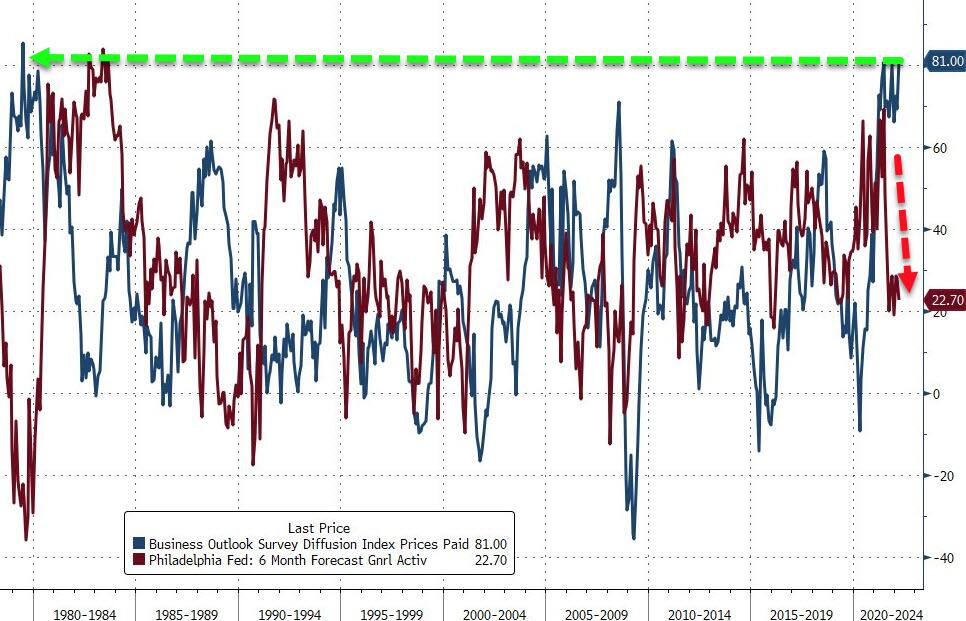

- 8:30am: March Philadelphia Fed Business Outl, est. 14.8, prior 16.0

- 9:15am: Feb. Industrial Production MoM, est. 0.5%, prior 1.4%

- Capacity Utilization, est. 77.9%, prior 77.6%

- Manufacturing (SIC) Production, est. 1.0%, prior 0.2%

DB’s Jim Reid concludes the overnight wrap

After I press send today I’ll be venturing back on a plane for the first time in two years this morning. I’m off to give a speech at a conference in Cannes just at the time when all the tabloid papers here say that London is going to be hotter than Greece and the Costa Brava in a rare March warm spell here in the UK.

Rarer than a warm spell in the UK in March, we now have the start of only the fourth Fed hiking cycle in 27 years. We saw a wild ride in markets after the decision as initially the hawkish dot plot led to a big sell off in rates, and an S&P 500 that fell nearly -1.5% from pre announcement levels and into negative territory for the session. However markets completely turned on Powell’s comments in the press conference that the probability of recession was “not particularly elevated” and that the “economy is very strong” and can handle tighter policy. The S&P closed +2.24%, completing its biggest 2-day move in 23 months, while the Nasdaq climbed +3.77%. The big winners were mega cap tech stocks, with the FANG+ index putting in its best day on record, climbing +10.19%. The latter were almost certainly helped by earlier news that China would “actively introduce policies that benefit markets” and take steps to ease the most spartan lockdown measures. The FANG index includes Baidu and Alibaba that were up nearly +40% yesterday.

To be fair the Fed meeting and the surrounding price action makes sense. Although I think the risks of a US recession by late 2023 / early 2024 are increasingly elevated I’m not convinced that the risks are particularly high in 2022. The start of the hiking cycle isn’t historically the problem point for the economy or for that matter equities.

Further to this, in my CoTD yesterday (link here) I showed that on average it takes around three years from the first Fed hike to recession. However the bad news is that all but one of the recessions inside 37 months (essentially three years) occurred when the 2s10s curve inverted before the hiking cycle ended. With all the recessions that started later than that, none of them had an inverted curve when the hiking cycle ended. In fact, hiking cycles that ended with the curve still in positive territory saw the next recession hit 53 months on average after the first rate hike, whereas the next recession for hiking cycles that ended with an inverted curve started on average in 23 months, so just under two years. As a reminder, none of the US recessions in the last 70 years have occurred until the 2s10s has inverted. On average it takes 12-18 months from inversion to recession. The problem is that all but one of the hiking cycles in the last 70 years have seen a flatter 2s10s curve in the first year of hikes. The exception saw a very small steepening. So these are the risks.

Indeed the yield curve flattened after the Fed with 2s10s moving from just under +31bps to +21bps an hour later. It closed at +23bps. 10yr yields rose 6bps after the announcement but reversed most of this into the close and ended +4.1bps on the day at 2.18%. We are at 2.137% this morning. The rise in 2 years was more durable at +8.9bps on the day with a -2.4bps reversal this morning to 1.912%. At one point yesterday this was +15bps on the day and at a hair’s breadth below 2%. The tighter policy path meant that breakevens declined and real rates increased; 10yr Treasury breakevens fell -5.5bps to 2.80%.

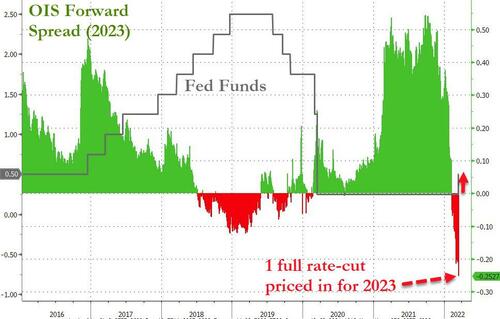

Digging into the meeting itself. Two years to the day after cutting rates to the zero lower bound, the Fed raised rates by 25 basis points yesterday, and communicated a much tighter path of policy to come (our US econ team’s full recap here). Yesterday’s meeting came with an updated Summary of Economic Projections, and the dots were much more hawkish. The median dot showed expectations for 7 hikes in 2022, including yesterday and in line with what our US economics team is expecting, and which would represent a hike at every meeting for the rest of the year. The median dot reaches 2.75% next year, above the Fed’s long-run estimate for the fed funds rate, signaling policy will need to get to a restrictive stance. Indeed, the dots actually showed the long-run neutral fed funds rate fell, so a restrictive stance will come even sooner. These were just the medians. There was considerable variance in the dots, and Chair Powell noted the risks to inflation were to the upside, suggesting rates could be even higher than what the hawkish medians are suggesting.

On the balance sheet, the Fed noted that QT would start at a coming meeting. Chair Powell signaled it could start as early as May, noting the Committee made excellent progress on the parameters of balance sheet runoff, even if they did not provide more details yesterday. Chair Powell noted the minutes from this meeting would have more details around runoff parameters.

Elsewhere in the press conference, the Chair noted that every meeting was live, and that the Fed would move more quickly if appropriate, which ostensibly means +50bp hikes are on the table, but also said the Fed’s expected QT program will equate to approximately one more hike, which is in line with our team’s expectations for QT this year. Indeed, each of the next few meetings is pricing a meaningful chance of a +50bp hike. He noted the Fed would be evaluating month-over-month inflation readings when determining the pace of policy tightening and that financial conditions needed to be tighter. In all, a hawkish meeting, which was expected, with little for doves to cling to.