GOLD; $1935.00 UP $13.95

SILVER: $25.14 UP $0.02

ACCESS MARKET: GOLD $1936.60

SILVER: $25.19

Bitcoin morning price: $43,563 DOWN $207

Bitcoin: afternoon price: $42,199 DOWN 1571

Platinum price: closing UP $5.25 to $1081.25

Palladium price; closing UP $114.00 at $2787.45

END

end

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

comex notices/

March: JPMorgan stopped/total issued 0

NUMBER OF NOTICES FILED TODAY FOR Mar. CONTRACT:0 NOTICE(S) FOR nil OZ (0 TONNES)

total notices so far: 3681 contracts for 368,100 oz (11.449 tonnes)

SILVER NOTICES:

268 NOTICE(S) FILED TODAY FOR 1,340,000 OZ/

total number of notices filed so far this month 4456 : for 22,280,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

END

GLD

WITH GOLD UP $13.95

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

A HUGE CHANGE IN GLD INVENTORY//A DEPOSIT OF 7.84 TONNES OF GOLD INTO THE GLD//

INVENTORY RESTS AT 1050.22 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP $0.02

AT THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

NO CHANGES IN SILVER INVENTORY AT THE SLV/

FROM THE SLV.

CLOSING INVENTORY: 545.854 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A STRONG 1402 CONTRACTS TO 159,321 AND CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020 AND WITH THIS STRONG GAIN IN OI, IT WAS ACCOMPANIED WITH OUR $0.32 LOSS IN SILVER PRICING AT THE COMEX ON WEDNESDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.32) BUT WERE UNSUCCESSFUL IN KNOCKING OUT ANY SILVER LONGS AS WE HAD A HUGE GAIN OF 4030 CONTRACTS ON OUR TWO EXCHANGES

WE MUST HAVE HAD:

I) HUGE BANKER SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A HUGE INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 42.860 MILLION OZ FOLLOWED BY TODAY’S EFP OF 1,360,000 OZ //NEW STANDING 40.715 // V) huge SIZED COMEX OI GAIN/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS +528 ???

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAR. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAR:

TOTAL CONTACTS for 3 days, total contracts: : 5824 contracts or 29.120 million oz OR 9.706 MILLION OZ PER DAY. (1941 CONTRACTS PER DAY)

TOTAL NO OF OZ UNDERGOING EFP TO LONDON 5824 CONTRACTS X 5,000 PER CONTRACT:

EQUATES TO: 29.120 MILLION OZ

.

LAST 10 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 29.120 MILLION OZ//

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1930 DESPITE OUR STRONG $0.32 LOSS SILVER PRICING AT THE COMEX// WEDNESDAY THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 2100 CONTRACTS( 2100 CONTRACTS ISSUED FOR MAR AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A HUGE INITIAL SILVER OZ STANDING FOR MAR. OF 42.860 MILLION OZ FOLLOWED BY TODAY’S 1,360,000 OZ EFP TO LONDON /// .. WE HAD A VERY STRONG SIZED GAIN OF 3502 OI CONTRACTS ON THE TWO EXCHANGES FOR 17.510MILLION OZ

WE HAD 268 NOTICES FILED TODAY FOR 1,340,000 OZ

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A FAIR SIZED 2,773 CONTRACTS TO 612,827 AND FURTHER FORM OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: +195 CONTRACTS.

THE BIS HAS ABANDONED THE GOLD COMEX TRADING!!!

.

THE FAIR SIZED DECREASE IN COMEX OI CAME WITH OUR STRONG LOSS IN PRICE OF $20.80//COMEX GOLD TRADING/WEDNESDAY/.AS IN SILVER WE MUST HAD HUGE BANKER/ALGO SHORT COVERING ACCOMPANYING OUR STRONG SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION AS THE TOTAL GAIN ON OUR TWO EXCHANGES TOTALED A TINY 31 CONTRACTS…

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR MARCH AT 14.818 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 4900 OZ//NEW STANDING 17.409 TONNES

YET ALL OF..THIS HAPPENED WITH OUR LOSS IN PRICE OF $20.80 WITH RESPECT TO WEDNESDAY’S TRADING

WE HAD A TINY SIZED GAIN OF 226 OI CONTRACTS (0.7029 PAPER TONNES) ON OUR TWO EXCHANGES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 42999 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 612,827.

IN ESSENCE WE HAVE A TINY SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 226, WITH 2773 CONTRACTS DECREASED AT THE COMEX AND 2999 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 226 CONTRACTS OR 0.7029TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2999) ACCOMPANYING THE FAIR SIZED LOSS IN COMEX OI (2773,): TOTAL GAIN IN THE TWO EXCHANGES 226 CONTRACTS. WE NO DOUBT HAD 1) HUGE BANKER SHORT COVERING ,2.) HUGE INITIAL STANDING AT THE GOLD COMEX FOR MARCH. AT 14.818 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 4900 OZ//NEW STANDING 17.409 TONNES /// 3) ZERO LONG LIQUIDATION/. ,4) FAIR SIZED COMEX OI. LOSS 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

MARCH

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAR :

14,223 CONTRACTS OR 1,422,300 OR 44.23 TONNES 3 TRADING DAY(S) AND THUS AVERAGING: 4743 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 3 TRADING DAY(S) IN TONNES: 44.23 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2020, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 44.23/3550 x 100% TONNES 1.23% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 145.12 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 44.23 TONNES INITIAL

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL.WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MARCH HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF APRIL, FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (MAR), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A STRONG SIZED 1930 CONTRACTS TO 159,321 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 4 1/2 YEARS AGO.

EFP ISSUANCE 2100 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 2100 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 2100 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1402 CONTRACTS AND ADD TO THE 2100 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE SIZED GAIN OF 4020 OPEN INTEREST CONTRACT FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 20.150 MILLION OZ,

OCCURRED WITH OUR $0.32 LOSS IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

5. Other gold commentaries

6. Commodity commentaries/cryptocurrencies

3. ASIAN AFFAIRS

i)THURSDAY MORNING// WEDNESDAY NIGHT

SHANGHAI CLOSED DOWN 3.03 PTS OR 0.09% //Hang Sang CLOSED UP 123.42 PTS OR 0.55% /The Nikkei closed UP 184.24 PTS or 0.70% //Australia’s all ordinaires CLOSED UP 0.55% /Chinese yuan (ONSHORE) closed DOWN 6.3192 /Oil UP TO 113.40 dollars per barrel for WTI and UP TO 116.25 for Brent. Stocks in Europe OPENED ALL RED EXCEPT FRANCE // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.3192. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.3241: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFF SHORE WEAKER//

A)NORTH KOREA/

b) REPORT ON JAPAN

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 2,773 CONTRACTS AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX INCREASE OCCURRED WITH OUR HUGE LOSS OF $20.80 IN GOLD PRICING WEDNESDAY’S COMEX TRADING. WE ALSO HAD A FAIR SIZED EFP (2999 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE NON ACTIVE DELIVERY MONTH OF MAR.. THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2999 EFP CONTRACTS WERE ISSUED: ;: , & FEB. 0 APRIL:2999 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2999 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A TINY SIZED TOTAL OF 31 CONTRACTS IN THAT 2999 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED COMEX OI LOSS OF 2968 CONTRACTS..

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING FOR MAR (17.409),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

FEB 2022: 59.023 TONNES

MARCH: 17.409 TONNES

THE BANKERS WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $20.80) BUT THEY WERE UNSUCCESSFUL IN FLEECING ANY LONGS AS WE HAVE REGISTERED A TINY SIZED GAIN OF 0.7029 TONNES OF TOTAL OI, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR MAR (17.409 TONNES)…

WE HAD + 195 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 226 CONTRACTS OR 2600 OZ OR 0.7029 TONNES

Estimated gold volume today: 225,091 ///FAIR

Confirmed volume yesterday: 236,486 contracts fair to good

INITIAL STANDINGS FOR MAR ’22 COMEX GOLD //

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 3973.377 oz BRINKS |

| Deposit to the Dealer Inventory in oz | nil OZ |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 0 notice(s)0 OZ 0 TONNES |

| No of oz to be served (notices) | 1916 contracts 191,600 oz 5.9595 TONNES |

| Total monthly oz gold served (contracts) so far this month | 3681 notices 3,68,100 OZ 11.449 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

/

For today:

0 dealer deposit

total dealer deposit nil oz

No dealer withdrawal 0

0 customer deposit

total deposit: NIL oz

1 customer withdrawal

i) Brinks: 3973.377 oz

total withdrawals: 3973.377 oz

ADJUSTMENTS: 1//dealer to customer//JPMorgan

15,502.595 oz (dealer to customer/JPM)

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MARCH.

For the front month of MARCH we have an oi of 1916 contracts having gained 19

We had 30 notices filed yesterday so strangely on day 4 we gained a STRONG 49 contracts or 4,900 oz will stand for delivery and these guys refused again to be EFP’d over to London. They must

be after a huge amount of gold on this side of the pond.

April saw a LOSS of 7093 contracts up to 454,553.

May saw a gain of 507 contracts to stand at 545

June saw a GAIN of 2679 contracts up to 97,256 contracts

We had 0 notice(s) filed today for 0 oz FOR THE MAR 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 0 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the FEB /2021. contract month,

we take the total number of notices filed so far for the month (3681) x 100 oz , to which we add the difference between the open interest for the front month of (MAR: 1916 CONTRACTS ) minus the number of notices served upon today 0 x 100 oz per contract equals 559,700 OZ OR 17.409 TONNES the number of TONNES standing in this active month of mar.

thus the INITIAL standings for gold for the MAR contract month:

No of notices filed so far (3681) x 100 oz+ (1916) OI for the front month minus the number of notices served upon today (0} x 100 oz} which equals 559,700 oz standing OR 17.409 TONNES in this NON active delivery month of MAR.

TOTAL COMEX GOLD STANDING: 17.409 TONNES (A WHOPPER FOR A MAR (NON ACTIVE) DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

178,539.763, oz NOW PLEDGED /HSBC 5.55 TONNES

123,963.792 PLEDGED MANFRA 3.86 TONNES

54,339.114oz PLEDGED JPMorgan no 1 1.690 tonnes

262,049.904, oz JPM No 2 8.15 TONNES

898,821.330 oz pledged Brinks/27,96 TONNES

12,249,333 oz International Delaware: 0..3810 tonnes

Loomis: 18,615.429 oz

total pledged gold: 1,548,578.620 oz 48.16 tonnes

TOTAL REGISTERED AND ELIG GOLD AT THE COMEX: 32,593,024.501 OZ (1013.77 TONNES)

TOTAL ELIGIBLE GOLD: 15,207,229.430 OZ (473.00 tonnes)

TOTAL OF ALL REGISTERED GOLD: 17,385,795.131 OZ (540.77 tonnes)

REGISTERED GOLD THAT CAN BE SERVED UPON: 15,837,217.0 OZ (REG GOLD- PLEDGED GOLD) 492.60 tonnes

END

MAR 2022 CONTRACT MONTH//SILVER

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 565,268.800 oz HSBC CNT JPM |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 323,795.840 oz Brinks |

| No of oz served today (contracts) | 268CONTRACT(S)1,340,000 OZ) |

| No of oz to be served (notices) | 3687 contracts (18,435,000 oz) |

| Total monthly oz silver served (contracts) | 4456 contracts 22,280,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

we had 0 deposits into the dealer

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 1 deposits into the customer account

I) Into Brinks: 323,795.840 oz

JPMorgan has a total silver weight: 182.455 million oz/345.121 million =52.85% of comex

ii) Comex withdrawals: 3

a)Out of CNT 201,250.630 oz

b) Out of jpm: 349,065.670 oz

c) Out of HSBC: 14,952.500

total withdrawal 565,268.800 oz

we had 2 adjustments//

customer to dealer:

1. JPMorgan: 1,491,058.600oz

ii) HSBC: 5054.03 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 83.905 MILLION OZ

TOTAL REG + ELIG. 345.121

MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR MARCH

silver open interest data:

FRONT MONTH OF MARCH OI: 3935, HAVING LOST 365 CONTRACTS FROM YESTERDAY.

WE HAD 93 NOTICES SERVED UPON YESTERDAY, SO WE LOST 272 CONTRACTS OR AN ADDITIONAL 1,360,000 OZ WILL NOT STAND

FOR DELIVERY OVER HERE AND THEY WERE EFP’D TO LONDON. THERE IS NO SILVER OVER HERE!!

APRIL HAD A 88 CONTRACT GAIN// CONTRACTS RISING TO 570

MAY HAD A GAIN OF 1514 CONTRACTS UP TO 129,574 contracts

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 268 for 1,340,000 oz

Comex volumes: 67,549// est. volume today//fair/

Comex volume: confirmed yesterday: 74,135 contracts (fair to good)

To calculate the number of silver ounces that will stand for delivery in MAR. we take the total number of notices filed for the month so far at 4456 x 5,000 oz =. 22,280,000 oz

to which we add the difference between the open interest for the front month of MAR (1916) and the number of notices served upon today 268 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MAR./2021 contract month: 4456 (notices served so far) x 5000 oz + OI for front month of MAR (1916) – number of notices served upon today (268) x 5000 oz of silver standing for the MAR contract month equates 40,715,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

MARCH 3/WITH GOLD UP $13.95: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 7.84 TONNES//INVENTORY RESTS AT 1050.22 TONNES

MARCH 2/WITH GOLD DOWN $20.80//A MONSTER CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 13.36 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 1042.38 TONNES

MARCH 1/WITH GOLD UP $42.60: NO CHANGES IN GOLD INVENTORY AT THE GLD: //INVENTORY RESTS AT 1029.32 TONNES

FEB 28/WITH GOLD UP $12.95: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1029.32 TONNES

FEB 25/WITH GOLD DOWN $38.95: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1029.32 TONNES

FEB 24/WITH GOLD UP $17.35//A HUGE CHANGE AT THE GLD: 5.23 TONNES INTO THE GLD// IN GOLD INVENTORY AT THE GLD/INVENTORY REST AT 1029.32 TONNES

FEB 23/WITH GOLD UP $2.00 : NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1024.09 TONNES

FEB 22/WITH GOLD UP $6.20: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.65 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 1024.09 TONNES

FEB 18/WITH GOLD DOWN $1.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1019.44 TONNES

FEB 17/WITH GOLD UP $29.50: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1019.44 TONNES

FEB 16/WITH GOLD UP 414.60 NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1019.44 TONNES

FEB 15/WITH GOLD DOWN $12.70 NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1019.44 TONNES

FEB 14/WITH GOLD UP $27.20 NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1019.44 TONNES

FEB 11/WITH GOLD UP $4.50 A HUGE CHANGE IN GOLD IVNETORY AT THE GLD// A DEPOSIT OF 3.48 TONNES INTO THE GLD//INVENTORY RESTS AT 1019.44 TONES

FEB 10/WITH GOLD UP $1.00: NO CHANGES IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 1015.96 TONNES

FEB 9/WITH GOLD UP $8.05//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1015.96 TONNES

FEB 8/WITH GOLD UP $5.95 TODAY: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.36 TONNES INTO THE GLD//INVENTORY RESTS AT 1015.96 TONNES

FEB 7/WITH GOLD UP $14.00 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.24 TONNES FROM THE GLD/////INVENTORY RESTS AT 1011.60 TONNES//

FEB 4/WITH GOLD UP $3.40 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.75 TONNES FROM THE GLD////INVENTORY RESTS AT 1014.84 TONNES

FEB 3/WITH GOLD DOWN $5.55: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD////INVENTORY RESTS AT 1016.59 TONNES

FEB 2/WITH GOLD UP $7.95//A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.78 TONES OF GOLD INTO THE GLD////INVENTORY RESTS AT 1018.04 TONNES

FEB 1/WITH GOLD UP $5.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1014.26 TONNES

CLOSING INVENTORY FOR THE GLD//1050.22 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MARCH 3/WITH SILVER UP 2 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 545.854 MILLION OZ//

MARCH 2/WITH SILVER DOWN $.32 TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 198,000 OZ FROM THE SLV//INVENTORY RESTS AT 545.854 MILLION OZ//

MARCH 1/WITH SILVER UP $1.13 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 546.052 MILLION OZ//

FEB 28/WITH SILVER UP 31 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT 546.052 MILLION OZ//

FEB 25/WITH SILVER DOWN 64 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 5.510 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 546.052 MILLION OZ/

FEB 24/WITH SILVER UP 15 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 551.597 MILLION OZ

FEB 23/WITH SILVER UP 22 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 551.597 MILLION OZ//

FEB 22/WITH SILVER UP 30 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 350,000 OZ INTO THE SLV///INVENTORY RESTS AT 551.597 MILLION OZ//

FEB 18/WITH SILVER UP 7 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.017 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 551.227 MILLION OZ

FEB 17/WITH SILVER UP 31 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.402 MILLION OZ//INVENTORY RESTS AT 550.210 MILLION OZ/

FEB 16/WITH SILVER UP 21 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 547.808 MILLIONOZ

FEB 15/WITH SILVER DOWN 46 CENTS TODAY : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 547.808 MILLION OZ//

FEB 14/WITH SILVER UP 49 CENTS TODAY; A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.235 MILLION OZ INTO THES LV////INVENTORY RESTS AT 547.808 MILLION OZ

FEB 11/WITH SILVER DOWN 18 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.573 MILLION OZ///

SLV/FEB 10/WITH SILVER UP 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.573 MILLION OZ//

FEB 9/WITH SILVER UP 14 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.573 MILLION OZ//

FEB 8/WITH SILVER UP 15 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.143 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 544.573 MILLION OZ//

FEB 7/WITH SILVER UP 52 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.218 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 541.430 MILLION OZ/

FEB 4/WITH SILVER UP 16 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 539.212 MILION OZ

FEB 3/WITH SILVER DOWN 35 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT539.212 MILLION OZ//

FEB 2/WITH SILVER UP 15 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.411 MILLION OZ INTO THE SLV.//INVENTORY RESTS AT 539.212 MILLION OZ/

FEB 1/WITH SILVER UP 18 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 533.801 MILLION OZ

SLV FINAL INVENTORY FOR TODAY: 545.854 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

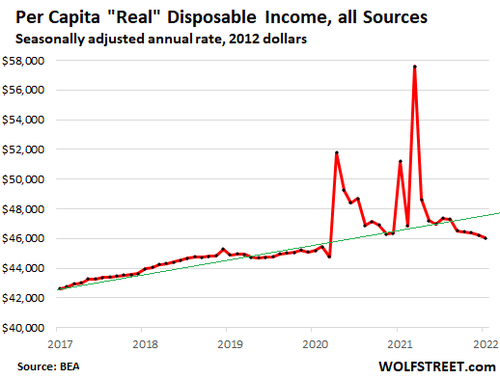

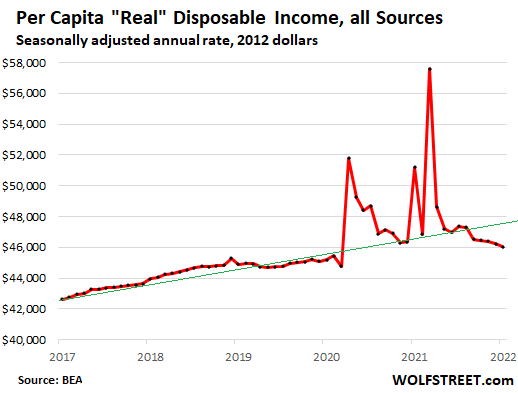

Inflation Continues To Chew Up Your Paycheck

THURSDAY, MAR 03, 2022 – 02:00 PM

Inflation continues to chew up your paycheck.

While consumer prices rose 0.7% in January, income from all sources, including wages, salaries, interest dividends, rental income, unemployment, Social Security, etc. was essentially flat.

And when adjusted for inflation, real personal income fell by 0.5%.

In other words, you didn’t put any more money in your pocket in January. But you’re paying more — for everything.

Looking at the bigger picture, real incomes have fallen 7.5% from stimulus-inflated 2021. Going back to January 2020, real incomes are up a paltry 3.7%.

Keep in mind, this is aggregate data. There are more people in America than there were last year. Adjusted for population growth, the numbers become bleaker. Real personal income fell 10.1% from a year ago and was only up 1.8% from January 2020.

As you can see from the graph, Americans are losing ground fast.

While real income shrinks, Americans are spending more as inflation runs up the price of everything.

Consumer spending rose by 0.8% in January from December (seasonally adjusted), and by 11.6% year-over-year.

When you factor in 7.5% annual CPI, it becomes clear that Americans are spending a lot more, but they getting a whole lot less for it. Most of the increase in spending simply represents rising prices.

And the reality is even worse. These numbers are based on a government-rigged Consumer Price Index. Using an honest CPI of 15%, all of the spending increase is eaten up by inflation — and then some.

Simply put, you’re spending more and getting less. And try as you might, you can’t outrun the inflation dragon.

This obliterates a myth you’ll often hear in mainstream media – the notion that inflation isn’t really that bad for the average American. After all, wages rise too. But as this data shows, wages rarely rise at the same pace as prices. That means inflation puts a significant squeeze on the pocketbook, at least in the short term.

Of course, you don’t need us to tell you that. You’re living it.

Economists and pundits talk about inflation as an academic exercise. They rarely reflect on the fact that rising prices have real impacts on real people. And if you happen to be somebody living on a fixed income or savings, you’re really screwed as inflation is rapidly eating away your purchasing power and your income streams aren’t increasing at all. Inflation always causes the most pain for the poor and elderly.

The focus on rising prices obscures the real villain in all this.

Greedy corporations and mysterious supply chain problems aren’t causing inflation. It’s the Fed. As economist Milton Friedman once said, inflation is always and everywhere a monetary phenomenon. Properly defined, inflation is an increase in the money supply. Rising prices are a symptom.

And the Fed has increased the money supply in spades. Over the last two years, the central bank has printed trillions of dollars out of thin air and injected them into the economy.

The Fed is supposed to make the economy more stable. But it’s clear the real impact is the exact opposite. The Fed causes great harm. And as Ron Paul pointed out in a recent article, it hurts the average American worker the most.

The truth is workers are inflation’s main victims.”

All you have to do is look at the data to see the truth in his words.

end

2.LAWRIE WILLIAM//,//Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, James RICKARDS

-END-

A terrific read!!

LAWRIE WILLIAMS:

02 Mar 2022 |-END-

3. Chris Powell of GATA provides to us very important physical commentaries

end

4.OTHER GOLD/SILVER COMMENTARIES

This is huge news and it is discussed in detail by Tom Luongo

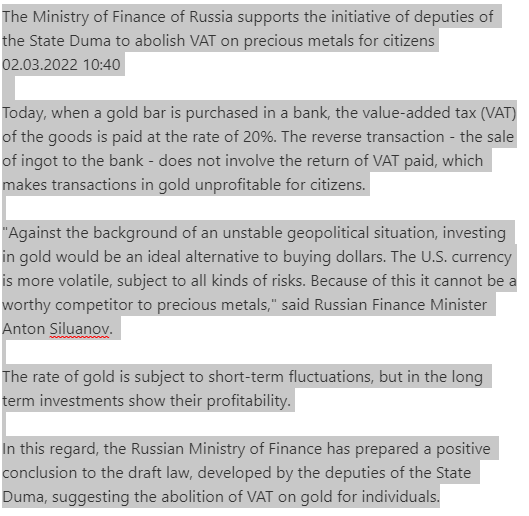

The Ministry of Finance supported the abolition of VAT on gold bullion for individuals

(courtesy Prime Feed)

Brown

March 2, 2022

Gold must become an alternative to foreign currency investment, and to increase demand for the precious metal in Russia, it would make sense to cancel VAT on its purchase from banks. This was stated by Finance Minister Anton Siluanov.

He clarified that the department has already prepared a positive revision of the draft law of the deputies of the State Duma, which implies the abolition of VAT for natural persons in this type of operations.

“Against the background of an unstable geopolitical situation, investing in gold will be an ideal alternative to buying dollars. The US currency is more volatile, subject to various types of risks. Because of this, it cannot compete with precious metals. Siluanov said. in a message on the website of the Ministry of Finance.

The abolition of value added tax when buying gold from banks for investment purposes has been discussed in recent years. The 20% rate is valid at the time of purchase, while the reverse operation – the sale of an ingot to a bank – does not imply a refund of VAT, depreciation of the investment itself. Two years earlier, the Ministry of Finance assumed that they could cancel VAT on bullion after the precious metals marking system (GIIS DMDC) was fully operational.

END

5.OTHER COMMODITIES/COAL (THERMAL)

Aussie coal prices surge almost $100.00 as countries seek alternatives to Russian coal

(Zhu/EpochTimes)

Aussie Coal Prices Surge Almost $100 As Countries Seek Alternatives To Russian Energy

THURSDAY, MAR 03, 2022 – 12:00 PM

Authored by Rebecca Zhu via The Epoch Times,

The price of Australian thermal coal has skyrocketed by US$99, or 33 percent, in one day as countries traditionally reliant on Russian coal scramble to secure alternative sources.

Newcastle coal, the benchmark for thermal coal in the Asia-Pacific region, ended at US$400 (A$549) per tonne on March 2 after peaking at US$446 per tonne during the day.

Resources Minister Keith Pitt confirmed the government was “facilitating access” between interested parties and Australian thermal coal producers.

“Australia’s coal producers have indicated they are willing to help our friends and allies if they can,” Pitt told The Australian.

Poland currently in talks with Australia for coal supply, as the country is pushing for the European Union to stop importing coal from Russia.

“I talked about it today with the prime minister of Australia … to transport coal to Poland from there,” Polish Prime Minister Mateusz Morawiecki said on Wednesday.

Morawiecki said Poland just needed assurance from the European Commission that it would not get penalised for introducing an embargo on Russian coal.

“A blockade on various types of hydrocarbons from Russia —oil, gas, and coal—should be part of the sanctions package,” he said.

“I am calling once again for the European Commission to decide on an embargo on Russian coal.”

Polish Prime Minister Mateusz Morawiecki addresses a press conference in Budapest on April 1, 2021. (Attila Kisbenedek/AFP via Getty Images)

Around 65 percent of Poland’s energy grid in 2021 relied on coal. In the first half of 2021, the country important 6.2 million tonnes of coal of which 4 million of tonnes was from Russia and another 1.2 million tonnes from Australia.

The rest of the European Union similarly relies on Russia for coal, the third biggest exporter of the resource, accounting for over 40 percent of the region’s total coal imports in 2021.

While Australian and Polish authorities are currently in trade talks, other European nations may soon follow.

Current flooding across the east coast of Australia is also causing challenges for ports, with the Port of Brisbane closed.

Coal futures jumped US$161 during the first seven days of the Russian invasion into Ukraine, from $239 on Feb. 24 to $400 on March 2.

It previously surged in late 2021 after the Chinese Communist Party placed a ban on Australian coal as part of its trade war with Australia, which led to rolling blackouts across the nation.

Europe was also facing large energy shortfalls as countries moved towards renewables without a reliable energy grid.

At the time, it reached a peak of US$269 before plummeting back down.

end

6.CRYPTOCURRENCIES

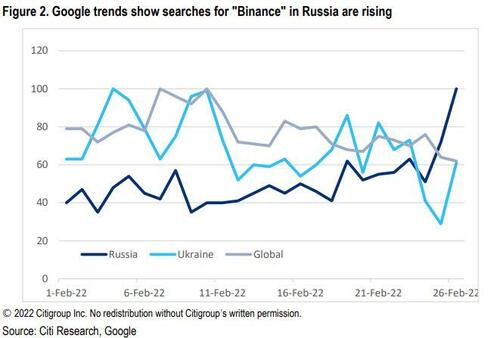

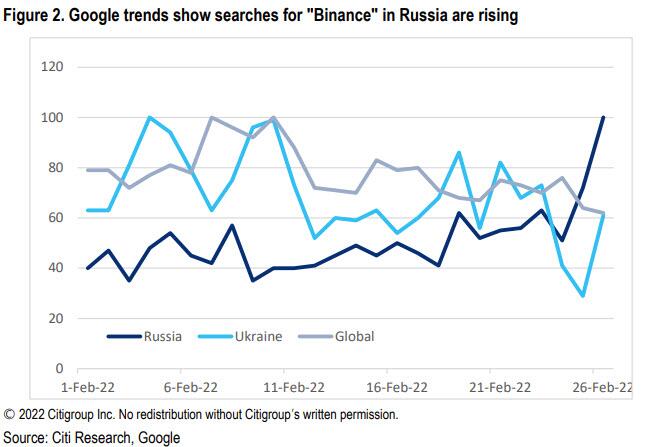

Here’s How Much Bitcoin Russia Has Bought In The Past Week

WEDNESDAY, MAR 02, 2022 – 08:00 PM

In the words of the Washington Post, the battle between Russia and Ukraine is “the world’s first crypto war” as both sides discover the advantages of a borderless, permissionless currency.

Whether it is for enabling donations to Ukrainians (for arms or humanitarian needs) or for Russians evading Putin’s FX transfer bans or escaping western sanctions, both sides appear to see the benefits.

Crypto interest in Russia on the rise; and Google searches do show an uptick in interest in Binance, the world’s largest cryptocurrency exchange, from Russia and, to a lesser extent, from Ukraine.

At this stage 11% of Russians already own crypto; so there is some familiarly with it.

The recent decoupling of bitcoin from tech stocks shows the regime change in demand from some external factor…

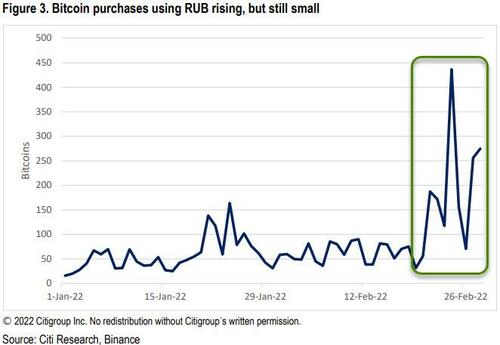

And this could get significantly higher as the potential for capital flight from Russia is large.

In a recent note. Citi details that, net capital outflows from Russia during the 2014 crisis were 151bn (a surge of 90bn from the previous year). In the 2008 crisis, it was 133bn. Of course, that is not the same as capital flight, as it includes debt payments etc. The worst errors and omissions (capital flight proxy) in more recent memory was an outflow of around 5bn USD.

Though this time around the capital flight could be significantly more than that as the crisis is more severe.

Of course, it is an open question just how much crypto would be used for this purpose.

Just for reference, daily bitcoin volume in spot is around 4.8bn according to bitcointradevolume.com, and including derivatives it is around 20-40bn, i.e. it will take meaningful capital flight to move the needle.

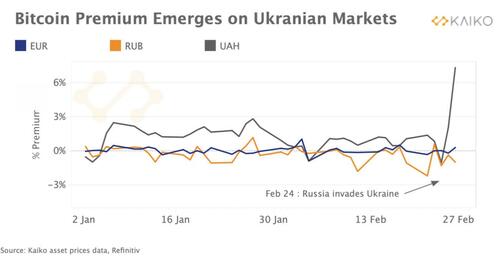

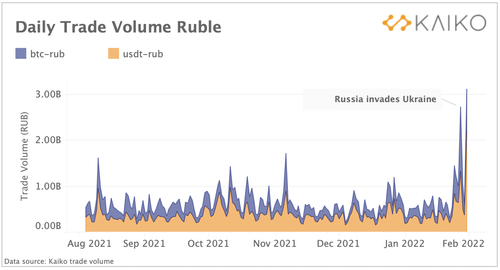

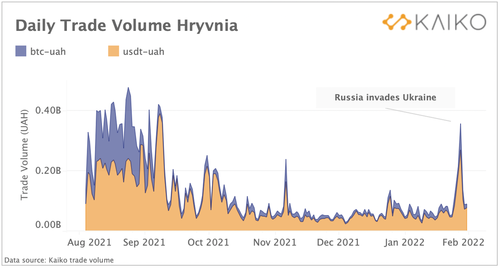

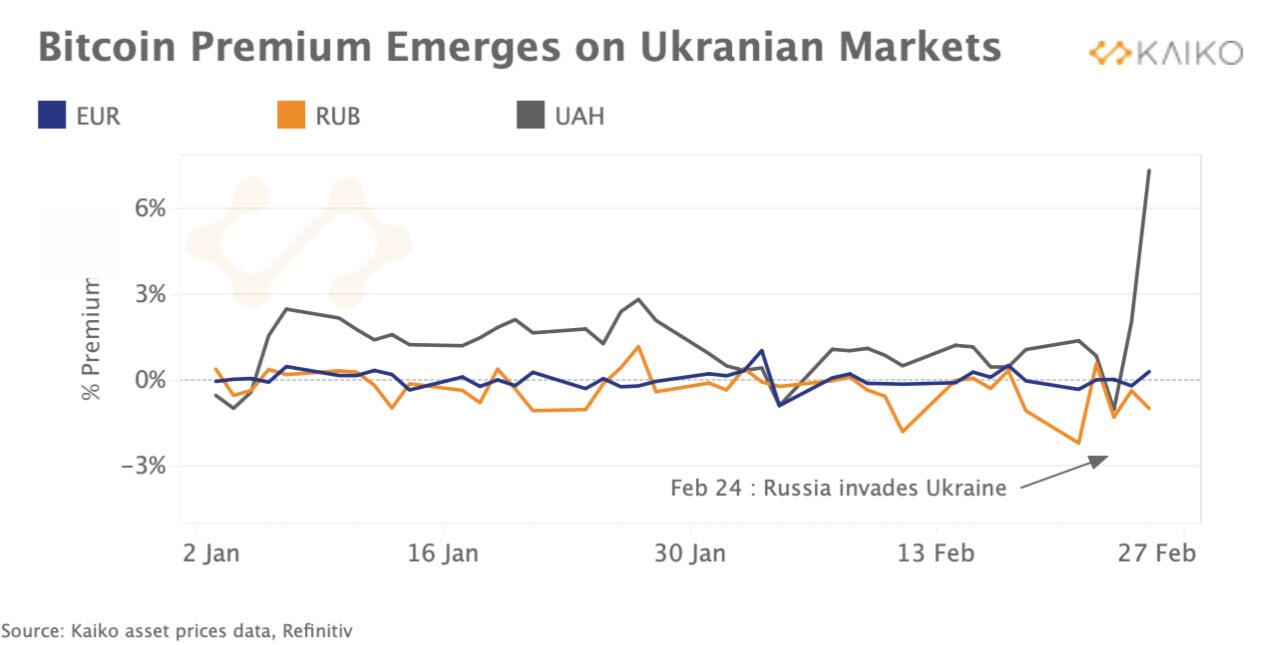

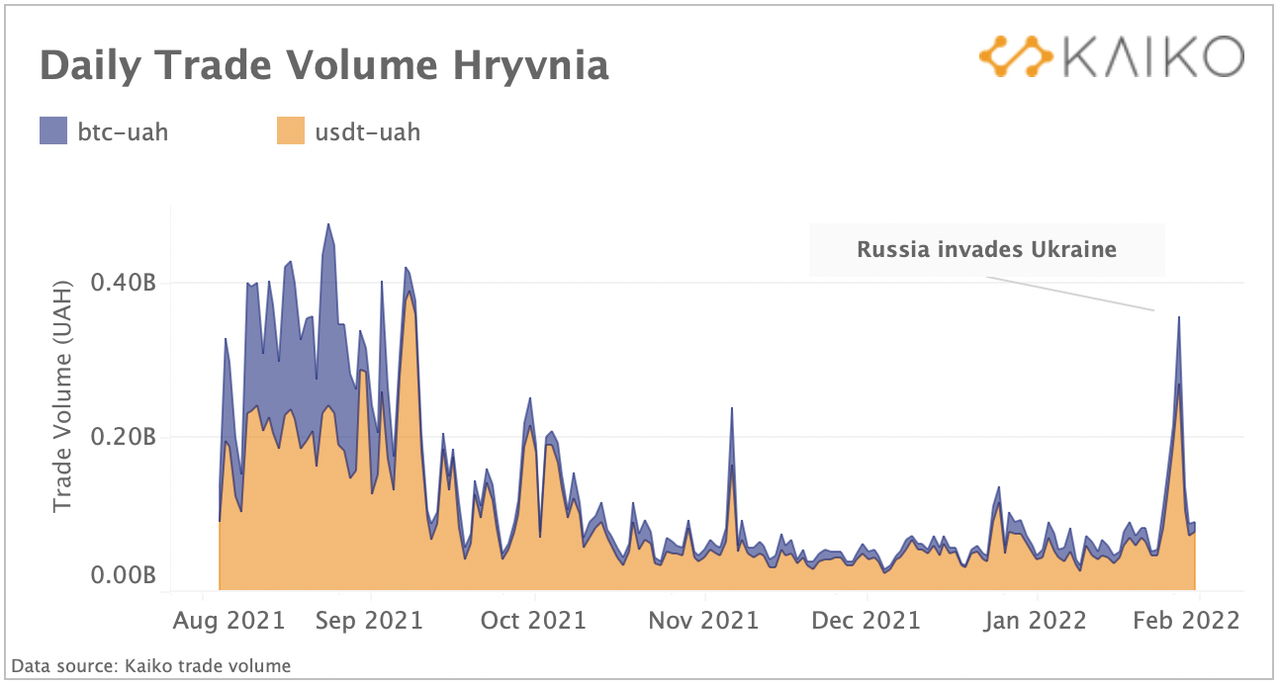

But it is not just Russia, as Kaiko reports that bitcoin traded at a 6% premium on Binance’s Ukrainian hryvnia (UAH) market as demand for cryptocurrencies soared immediately following Russia’s invasion.

Demand surged on Binance as local Ukrainian currency markets faced significant disruptions, with the Ukrainian central bank temporarily halting foreign currency withdrawals and the Ukrainian hryvnia falling to all time lows versus the U.S. Dollar.

Both ruble and hryvnia trade volumes surged to their highest levels in months almost immediately after the Russian invasion, highlighting the complexities of the cryptocurrency industry’s role in the conflict.

While the potential for capital flight is high, as Citi details above, Russian volumes (although impressive-looking on the chart) have been relatively small in absolute terms so far (around 210 bitcoin per day on average), suggesting that the price action is more due to investors positioning for an expected uptick in demand from Russia, rather than Russian demand itself.

This will be important to monitor, as Bitcoin could recouple with technology stocks if the expected Russian buying should not materialize.

Of course, the very fact that volumes of crypto activity have surged from both Russia and Ukraine since the invasion has prompted the establishment to cry ‘no fair!’ with ECB President Christine Lagarde urging regulation to prevent Russia escaping their sanction threats:

“It’s so critically important that MiCA is pushed through as quickly as possible so we have a regulatory framework within which crypto assets can actually be caught.”

And Jay Powell today, with a somewhat mixed message, by discussing the advantages of ‘digital currencies’ – clearly angling towards the use of CBDCs – but hedging his view by placating the regulatory-thirsting politicians by adding that “…to the extent that cryptocurrencies are a means to evade law enforcement and national security that’s not something we should tolerate.”

Finally, Deputy Attorney General Lisa Monaco, while describing the DoJ’s new “Kleptocapture” tak force, said they will freeze the assets of ‘Putin’s cronies” with a “focus on cryptocurrencies,” and Treasury Secretary Yellen warned later that “crypto is a channel to watch for sanctions leakage.”

For now, judging from the Citi data, crypto is not being used for sanctions avoidance on anything but a small scale.

All of which is somewhat humorous since, according to the data above, Russians are ‘laundering’ around $10 million in bitcoin a day, while Credit Suisse helped facilitate $100 billion in laundering over the years and it seemed nobody cared…

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings THURSDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 6.3194

OFFSHORE YUAN: 6.3241

HANG SANG CLOSED UP 123.42 PTS OR 0.55%

2. Nikkei closed UP 184.24 PTS 0.70%

3. Europe stocks ALL RED EXCEPT FRANCE

USA dollar INDEX UP TO 97.54/Euro FALLS TO 1.1081-

3b Japan 10 YR bond yield: RISES TO. +.169/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 115.72/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 113.40 and Brent: 116.25–

3f Gold UP /JAPANESE Yen UP CHINESE YUAN: ON -SHORE CLOSED DOWN// OFF- SHORE DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.0.063%/Italian 10 Yr bond yield riseS to 1.61% /SPAIN 10 YR BOND YIELD RISES TO 1.04%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 1.55: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield RISES TO : 2.39

3k Gold at $1932.40 silver at: 25.40 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

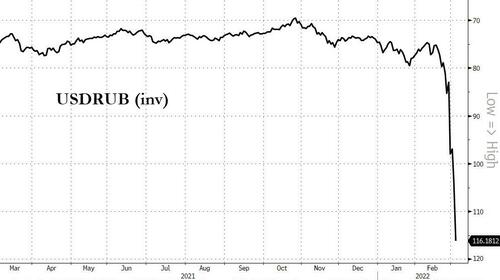

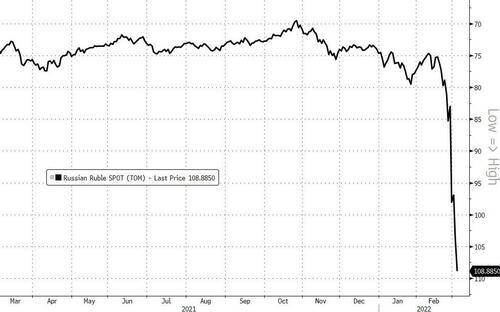

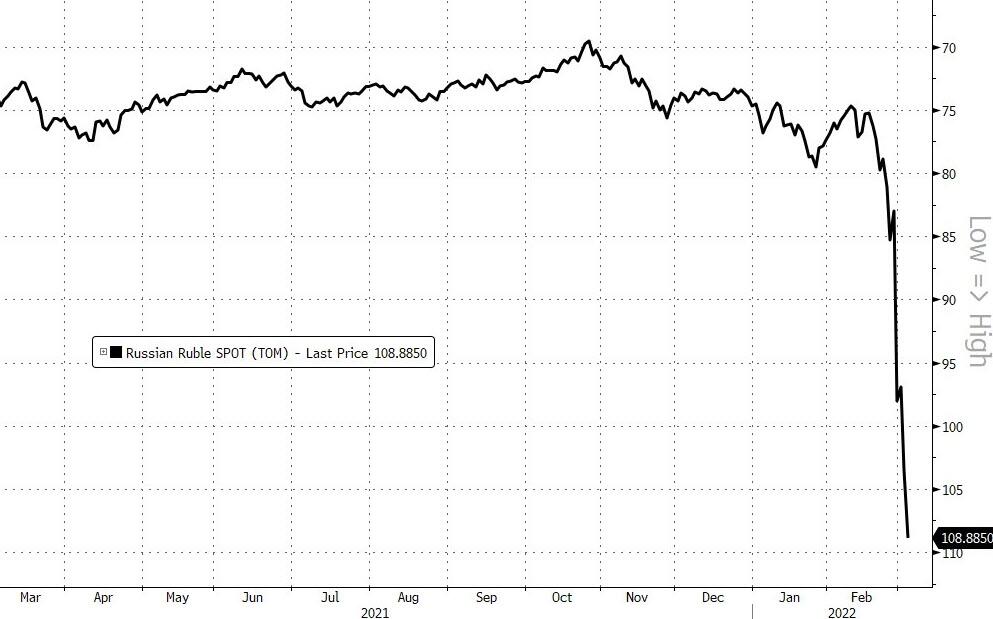

3l USA vs Russian rouble;// Russian rouble DOWN 804/100 in roubles/dollar; ROUBLE AT 110.89

3m oil into the 113 dollar handle for WTI and 116 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 115.72 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning .9202– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0196 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 1.866 DOWN 1 BASIS PTS

USA 30 YR BOND YIELD: 2.247 DOWN 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 14.14

Futures Take Cover As Commodities Go Apeshit

THURSDAY, MAR 03, 2022 – 08:00 AM

US stock index futures were flat on Thursday as investors assessed the impact of a surge in commodity prices on inflation and economic growth while eyeing news that a Ukraine delegation was headed to talks with Russia offering some hope of a ceasefire as the war in Ukraine enters its second week. Contracts on the Nasdaq 100 were down 0.2% by 7:15 a.m. in New York, after the underlying technology-heavy index rallied Wednesday to its highest level in two weeks. S&P 500 futures were flat and Dow futures declined 0.1%.

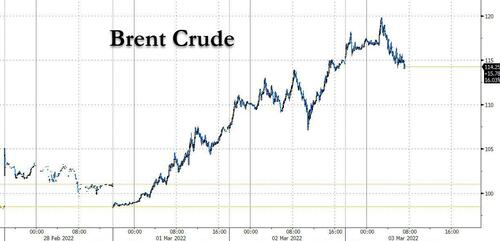

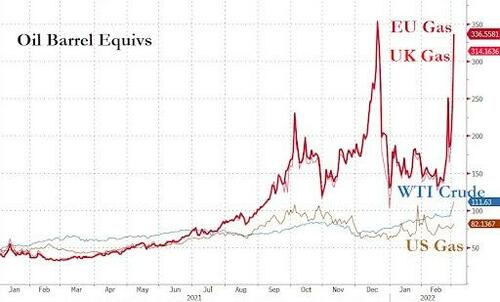

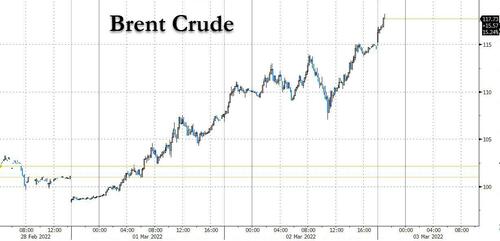

We’ll bring the commodity section up because today that’s where all the action is again: Commodities markets have been upended by the Ukraine crisis as big companies withdraw from Russia, lenders pull back from financing deals and the threat of new sanctions deters buyers. WTI soared to its strongest level since 2008 as the knock-on effect of sanctions starve the world of Russian oil supply, a hole that is over 5mm/d and which can’t reasonably be filled on short notice; Brent neared $120 at one point Thursday before dropping back to $115, while European natural gas whipsawed after rising to a fresh record.

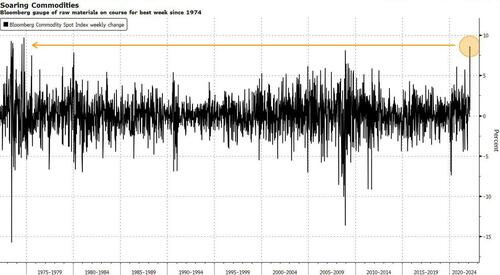

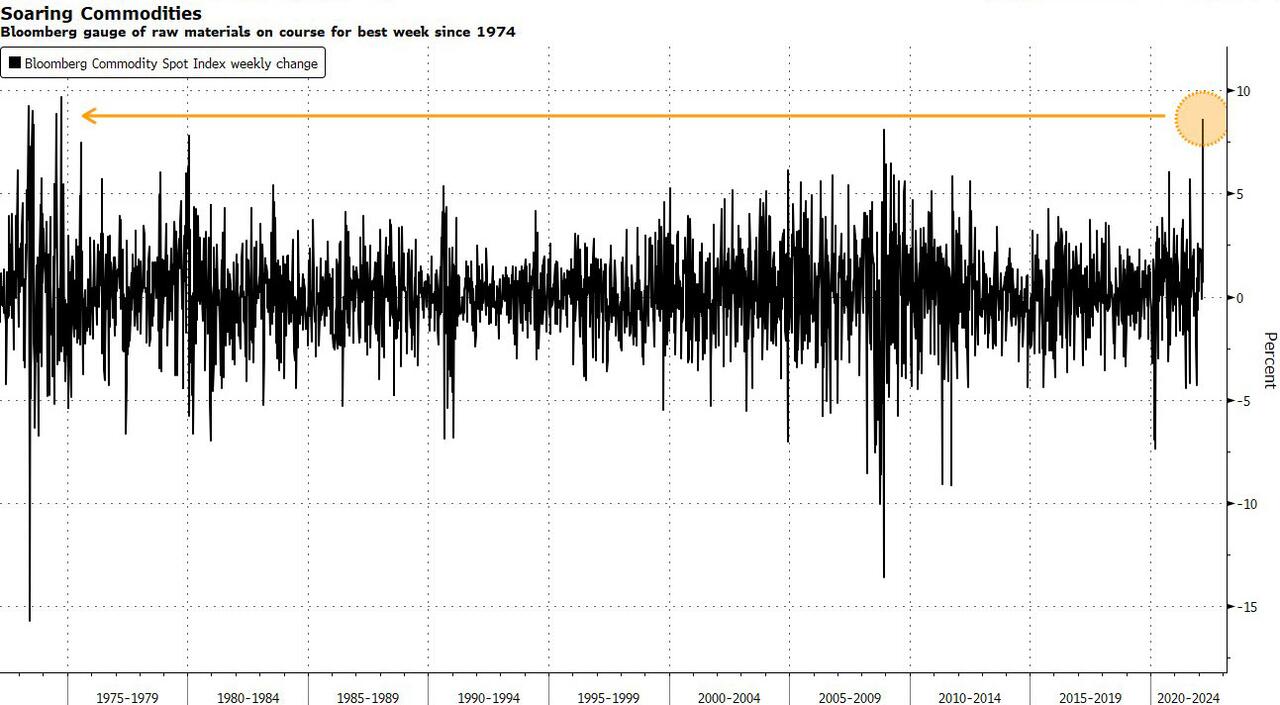

Wheat rocketed past $11 a bushel, zinc hit $4,000 a ton, the highest since 2007, and aluminum hit a new record. The meteoric rallies put the Bloomberg Commodity Spot Index on course for its best week since at least the 1960s. Spot gold rises roughly $3 to trade above $1,930/oz. Most base metals trade in the green; LME nickel outperforms peers. European gas futures pare gains.

Overall, the Bloomberg commodity spot index is having its best week since… the 1973 oil crisis.

Back to stocks, looking at the premarket, Snowflake shares slumped 22% after projecting that product sales growth would slow from its previous triple-digit-percentage pace in the fiscal year, although analysts including at Morgan Stanley remained positive on the software firm. Other notable premarket movers:

- Samsara (IOT US) jumps 15% in Wednesday’s postmarket session after the maker of GPS fleet-tracking devices and other technologies fourth quarter sales beat estimates and set guidance for fiscal 2023 ahead of consensus.

- Several analysts covering Veeva (VEEV US) cut their price targets after the software company forecast adjusted earnings per share for 1Q that missed the average analyst estimate. Shares fell 11% in postmarket trading.

- Anaplan (PLAN US) shares are up 6.6% in postmarket trading after forecasting revenue for the first quarter that topped the average analyst estimate.

- Pure Storage (PSTG US) gains 8.7% in premarket trading after forecasting 2023 revenue, adjusted operating income and adjusted operating margin that beat expectations.

- International Paper (IP US) shares rise 1.1% in premarket after the company tells investors during a presentation that it is “actively reassessing, with all of the stakeholders involved, our options for our investment in Ilim.”

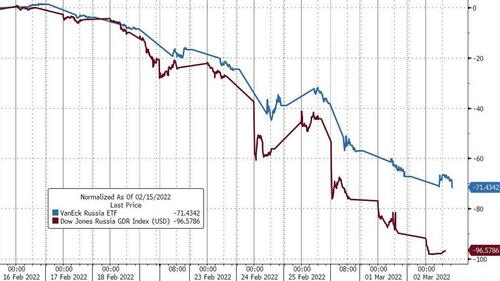

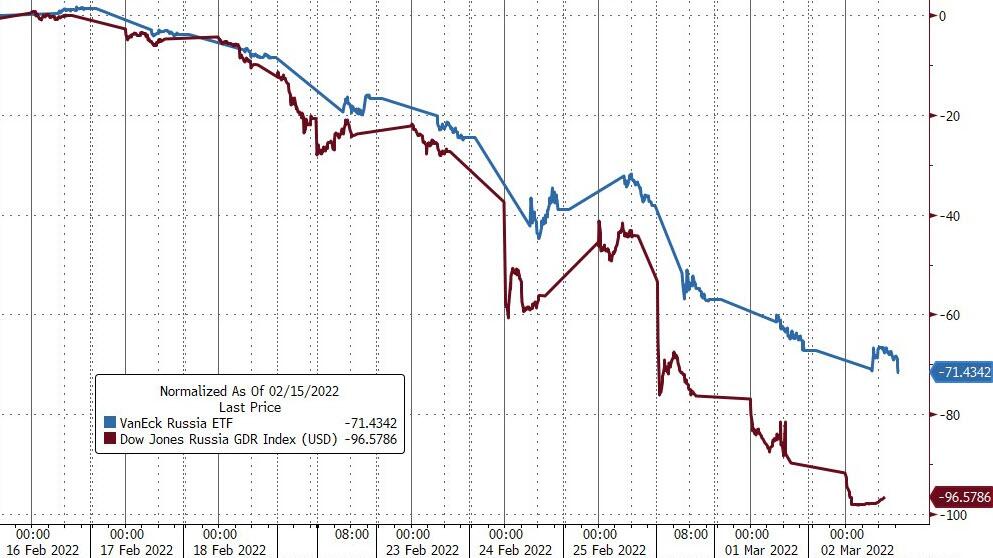

Russia’s ostracism continues: MSCI Inc. and FTSE Russell are cutting Russian equities from widely-tracked indexes, while the London Stock Exchange suspends dozens of Russian depositary receipts from trading, isolating the stocks from a large segment of the investment-fund industry. Russia’s credit rating was cut to junk by Moody’s Investors Service and Fitch Ratings amid doubts about its capability and willingness to service debt. The big question now facing Russian debt owners is whether they ever get their money back. A Russian telecommunications company will be the first test of whether Russian companies continue servicing their foreign-currency bonds. Here is the latest overnight news from Ukraine:

- Next round of Russia-Ukraine discussions could start at 12:00GMT today, according to Belta, citing a Russian Negotiator; with Foreign Minister Lavrov suggesting discussions are to start shortly while the Kremlin remarked that Ukraine is clearly not in a hurry for talks and President Putin’s aide Medinsky says they are still awaiting the arrival of the Ukrainian delegation.

- Most recently, Russian negotiating delegation says “We are waiting for the arrival of the Ukrainian delegation”, according to Sky News Arabia.

- Russian Deputy Foreign Minister believes that talks with Ukraine in Belarus can yield results, via Sky News Arabia.

- Russian Foreign Minister Lavrov says that President Putin and French President Macron are holding phone discussions at the moment. Reported at 10:00GMT/05:00EST

- US President Biden said Russia is responsible for the humanitarian crisis in Ukraine and for devastating human rights abuses.

- US State Department said Russia is engaged in a full assault on the truth regarding the war in Ukraine and that Russia is throttling Twitter, Facebook and Instagram platforms which Russians rely on for independent information.

- Canada imposed sanctions on a total of 10 individuals from Russian energy firms Rosneft and Gazprom.

- FTSE Russell said Russia will be deleted from all FTSE Russell equity indices effective from the open on March 7th, while as portfoliosJapan’s GPIF is looking into announcements by index companies on Russia will need to reflect index changes they track.

- Fitch downgraded Russia’s sovereign rating from BBB to B; Rating Watch Negative and Moody’s also cut .Russia’s sovereign rating from Baa3 to B3; Outlook Negative which put its at junk status

- Germany to deliver 2.7k additional anti-air missiles to Ukraine, via AFP citing gov’t sources.

- Ukraine’s Secretary of the National Security and Defense Council Danilov says that their intelligence is that Russia is set to impose martial law across Russia from March 4th, according to Ukrinform citing the Ukrainian official. Note, this is a report in Ukrainian press and we are yet to see reports on the subject from Russian vendors, as such, proceed with caution. Russian Kremlin subsequently pushed back on such reports.

- Ukraine has requested that the IAEA asks NATO to close the air above Ukrainian power plants to avoid acts of “nuclear terrorism”.

- US President Biden is to hold a call with the Quad leaders Thursday morning re. Ukraine, at 14:00GMT/09:00EST

Besides the chaos unleashed by the Ukraine war, global equity markets have been whipsawed this year as worries around a slowdown in economic growth were compounded by Russia’s invasion of Ukraine, fueling a surge across commodities from oil to grains.

Investors are now watching central banks to see if they are likely to stay the course on aggressively tightening monetary policy, and Fed Chair Jerome Powell managed to “appease risk-markets by ruling out a 50 basis-points hike in March, while simultaneously promising inflation vigilance at following meetings,” Citigroup Inc. strategists William O’Donnell and Edward Acton wrote in a note.

“It’s really time for investors to be prepared for more volatility, especially in the bond markets,” as the Fed has yet to commence balance-sheet reduction, Nancy Davis, chief investment officer at Quadratic Capital Management LLC, said on Bloomberg Television.

“It was quite unusual that Powell was so explicit,” said Stefan Koopman, an economist at Rabobank. “It remains to be seen if the FOMC will be less aggressive in its monetary policy tightening because of the war in Ukraine. It’s also worth emphasizing that this war won’t be settled anytime soon, even as markets derive some optimism on any news of new peace talks. This will continue to keep upwards pressure on (agri-)commodity prices, downward pressure on long-term safe haven yields and some continuously volatile equity markets.”

Bucking the trend in growing pessimism, Citigroup strategists upgraded U.S. stocks and the technology sector to overweight, saying growth trades should benefit from the recent sharp drop in real yields. Of course, this happens one day after Citi closed its oil short at a 11% loss in a month, so maybe this is just the right signal to pile on those shorts.

In Europe, the Stoxx 600 Index fell 0.6% with utilities and travel and leisure stocks among the biggest decliners while shares in firms with exposure to Russia tumbled. Basic resources shares are the best performers in the Stoxx Europe 600 Thursday amid soaring supply concerns across commodities: Glencore, Anglo American and Rio Tinto lead surge for miners; OMV, Repsol and Neste are among the gainers in the energy sector. The Stoxx Europe 600 falls 0.6%; renewables stocks such as Vestas and Siemens Gamesa decline. While all other sectors have declined in Europe this year, the basic resources and energy subgroups have been the sole gainers in the region amid soaring prices. The basic resources sub-index rises as much as 3.9% and trades at the highest since 2008, while the energy segment hit a record high on Thursday before reversing its advance.

Earlier in the session, Asian stocks advanced as comments by Federal Reserve Chair Jerome Powell gave investors some relief amid concerns over the Russia-Ukraine war. The MSCI Asia Pacific Index rose as much as 0.9%, lifted by financial and industrial shares. Japan and South Korea equities were among the best performers, getting boosts from electronics and auto makers. In his testimony to U.S. lawmakers, Powell backed a quarter-point rate increase later this month while vowing to combat inflation in light of global political risks. The modest increase helped ease investor fears of aggressive Fed policies to control the pace of price increases even as oil continued to surge due to the war. “Capital may be flowing back to risk assets for bargain-hunting opportunities after the severe selloff over the last few days,” said Margaret Yang, a strategist at DailyFX. “Still, geopolitical uncertainties may cap the extent of the rally until progress is made between Russia and Ukraine in negotiating a ceasefire agreement.” Asian equities were on track for their first weekly gain in three, as the region remained resilient given its relatively limited exposure to Russia. The Asian stock benchmark has declined less than 6% so far this year, compared with drops of about 8% in European and U.S. counterparts. Chinese stocks fluctuated after the Wall Street Journal reported that the nation is exploring an exit from its zero-tolerance approach to Covid-19. The Indonesia market was closed for a holiday.

Japanese equities climbed, following a rally in U.S. peers after Federal Reserve Chair Jerome Powell said the economy is expanding enough to withstand rate hikes while pledging to be judicious in removing stimulus. Banks and trading houses were the biggest boosts to the Topix, which rose 1.2%. Daikin and M3 Inc. were the largest contributors to a 0.7% rise in the Nikkei 225. The yen slightly extended its 0.5% overnight loss the dollar. “There is still concern about how high rates will go in the medium term,” said Shogo Maekawa, global market strategist at JP Morgan Asset Management. “But for now Powell maintained his outlook of a 0.25 percentage point hike so now we’re past the first point of uncertainty.”

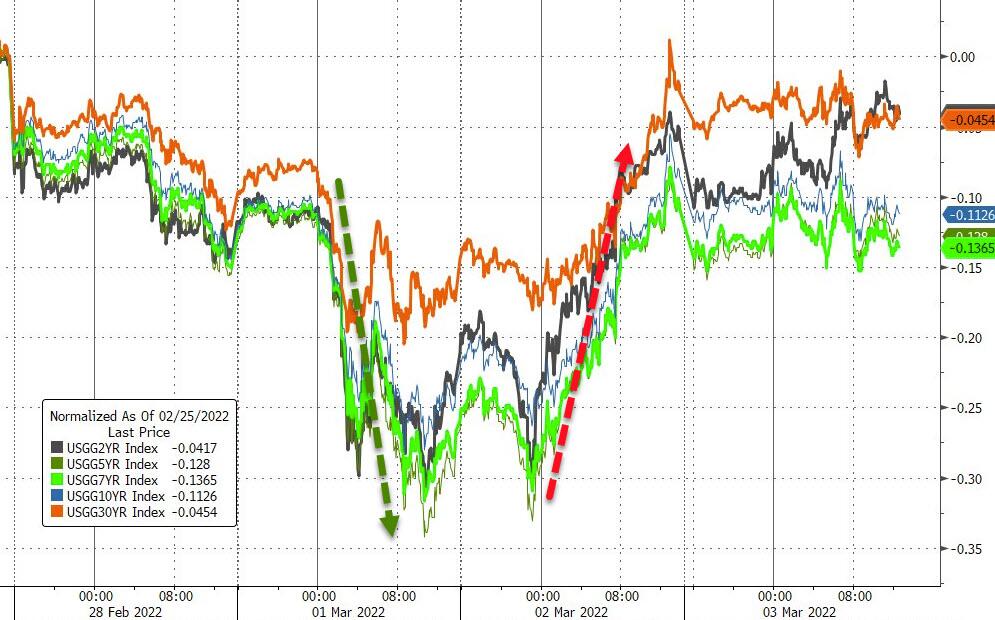

In rates, Treasuries were relatively calm with yields richer by 2bp-3bp across the curve. Curve spreads are broadly within a basis point of Wednesday’s closing levels following extreme volatility in yields and spreads over past two sessions; 10-year yields around 1.86%, ~2bp lower on the day while gilts, bunds are cheaper by 9bp and 6bp in the sector. Gilts lead broad fixed-income selloff, while dollar rallies and stocks fall. Gilts lead a broad selloff in fixed income, bear-flattening with short end about 9bps cheaper. Traders move forward wagers on 125bps of BOE tightening to November from December previously. Bunds also bear-steepen but are ~5bp richer to gilts. IG dollar issuance slate includes CBA 5-part, Sumitomo Mitsui Trust 3Y/5Y and Honda 3Y/5Y/10Y; sixteen issuers priced $18b Wednesday across 28 tranches in busiest day in six months. Focal points of U.S. session include Fed Chair Powell’s second day of congressional testimony and a busy economic data slate. Three-month dollar Libor jumps more than 6bp, biggest increase since Feb. 11.

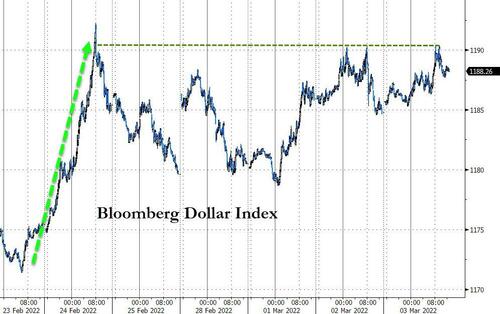

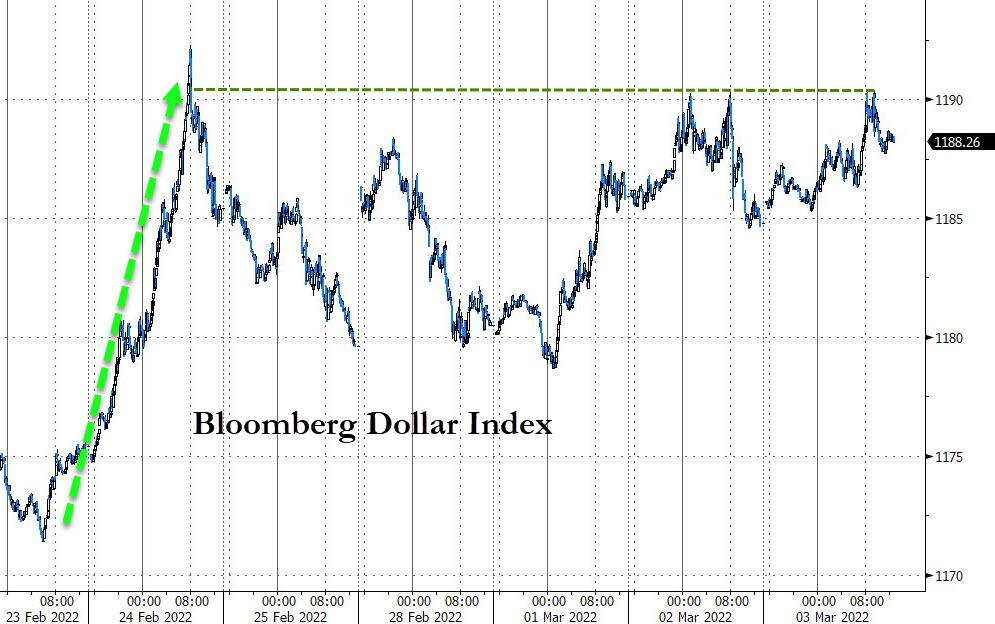

In FX, the Bloomberg Dollar Spot Index climbed 0.2% and the greenback was steady to higher against its Group-of-10 peers; Canadian and Australian dollars were the top performers as commodities powered higher. Treasuries inched up, led by the 2-year tenor. The euro slipped for a fourth day against the greenback, after falling to the lowest since May 2020 on Wednesday. Bunds fell as they caught up with Treasuries, and Italian bonds extended their slide and underperformance against euro-area peers after demand fell at a sale of Spanish debt. The pound weakened against the dollar but rose to its strongest level versus the euro since July 2016 as sterling proved relatively resilient to market shocks from the war in Ukraine. Gilts fell after money markets increased bets on Bank of England rate hikes after the most dovish member of the Monetary Policy Committee, Silvana Tenreyro, said she expects “upside surprises on inflation” on Wednesday. Aussie rose to the highest level since November against the greenback, and neared its 200-DMA, before paring gains. Aussie sovereign bonds extended losses made after Fed Chair Jerome Powell reaffirmed his support for a 25 basis- point rate hike this month. The yen weakened for a second day amid broad strength in the greenback. Japan’s 30-year bond pared an intraday loss after the sale of this tenor confirmed resilient demand. Ruble continues to underperform EMFX peers.

In commodities, the rally faded slightly after assets from gas to oil surged earlier as buyers rushed to stock up on materials due to fears of how the increasing economic isolation of Russia will impact trade. Oil pares some gains. Brent trades at $115 after rising as high as $119 a barrel. WTI falls back to $112 after soaring to the highest since 2008 as buyers shun Russian crude. Investors bet that oil will rise further. Spot gold rises roughly $3 to trade above $1,930/oz. Most base metals trade in the green; LME nickel outperforms peers. European gas futures pare gains.

Bitcoin has been erring lower throughout the session after an initial move higher fizzled out, though, Bitcoin remains towards the top-end of recent levels capped by the USD 45k mark.

Looking at day ahead now, and we’ll hear from Fed Chair Powell again, this time before the Senate Banking Committee. Other central bank speakers include the Fed’s Barkin and Williams, Bank of Canada Governor Macklem and the ECB’s de Cos. On top of that, we’ll also get the minutes from the ECB’s February meeting. On the data side, releases include the global services and composite PMIs for February, as well as the ISM services index for February from the US. Other releases include the Euro Area unemployment rate and PPI for January, while in the US we’ll get the weekly initial jobless claims and January’s factory orders. Finally, earnings releases include Broadcom and Costco.

Market Snapshot

- S&P 500 futures down 0.1% to 4,375.50

- STOXX Europe 600 down 0.3% to 444.91

- MXAP up 0.6% to 181.77

- MXAPJ up 0.4% to 595.82

- Nikkei up 0.7% to 26,577.27

- Topix up 1.2% to 1,881.80

- Hang Seng Index up 0.6% to 22,467.34

- Shanghai Composite little changed at 3,481.11

- Sensex down 0.8% to 55,035.74

- Australia S&P/ASX 200 up 0.5% to 7,151.40

- Kospi up 1.6% to 2,747.08

- German 10Y yield little changed at 0.05%

- Euro down 0.4% to $1.1077

- Brent Futures up 2.8% to $116.11/bbl

- Brent Futures up 2.8% to $116.12/bbl

- Gold spot down 0.1% to $1,926.29

- U.S. Dollar Index up 0.27% to 97.65

Top Overnight News from Bloomberg

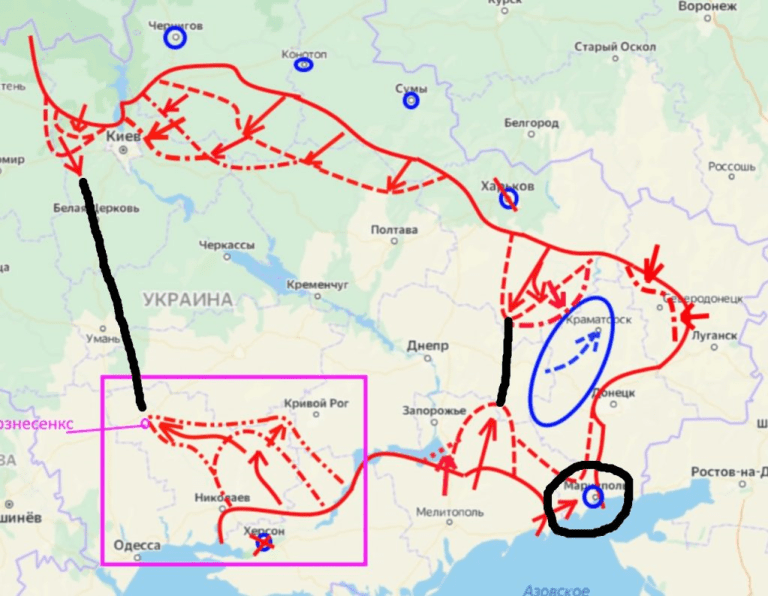

- Russian forces pressed ahead with their offensive in Ukraine as the war entered its second week, firing missiles at Kyiv overnight and stepping up their campaign to take cities in the coastal south

- The sanctions the U.S. and Europe are slapping on Russia’s economy and the billionaires around President Vladimir Putin are unprecedented in scope. Some experts wonder if these powers have made clear what actually needs to happen to get those restrictions lifted

- Bank of Japan board member Junko Nakagawa says there is no need to make a significant change in monetary policy for now in response to events in Ukraine, though the situation warrants close attention

- Commodities are on course for their most stunning weekly surge in records that go back to when Nikita Khrushchev was in the Kremlin

- European natural gas rose to a fresh record near 200 euros a megawatt-hour. The European Commission wants at least 80% of gas storage facilities in the EU to be filled by Sept. 30, accelerating plans to reduce the bloc’s dependence on Russian gas, Der Spiegel reported, citing a draft paper on a new energy security strategy to be presented next week

- As traders try to navigate a global crude market upended by the invasion of Ukraine, an offer of a Russian Far East cargo that drew no bids suggested that spot differentials on the nation’s oil may weaken sharply

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks traded mostly positive after the gains in the US where stocks and yields climbed amid peace talk hopes and hawkish central bank rhetoric, but with upside capped as the region digested a slowdown in Chinese Caixin Services PMI data. ASX 200 was underpinned by a commodity surge, spearheaded by the energy sector as Brent rose to its highest level since 2013. Nikkei 225 benefitted from a weak JPY but with gains capped as Tokyo and neighbours seek an extension of COVID measures. Hang Seng and Shanghai Comp were mixed with the mainland clouded after PBoC’s liquidity drain and soft PMI data

Top Asian News

- Asia Stocks Rise as Powell Comments Boost Investor Mood Amid War

- Indian Agrochemical Firm UPL Said to Draw Takeover Interest

- Developer Shares Gain on Regulator’s Remarks: Evergrande Update

- Hong Kong Reports 56,827 Covid Cases, 144 Deaths Thursday

European bourses, Euro Stoxx 50 -0.5%, are moving in-line with the generally cautious mood as we await the commencement of the Russia-Ukrainian negotiations, which are set for around 12:00GMT/07:00EST; though, we are yet to see the Ukrainian delegation arrive. Within sectors, the picture is mixed after initial relative underperformance in cyclical names. US futures are modestly softer, ES -0.2%, but have been fairly contained amid the geopolitical developments awaiting US data and Chair Powell’s second day of testimony

Top European News

- European Gas Hits Record Near 200 Euros With Sanctions in Focus

- U.K. Feb. Composite PMI 59.9 vs Flash Reading 60.2

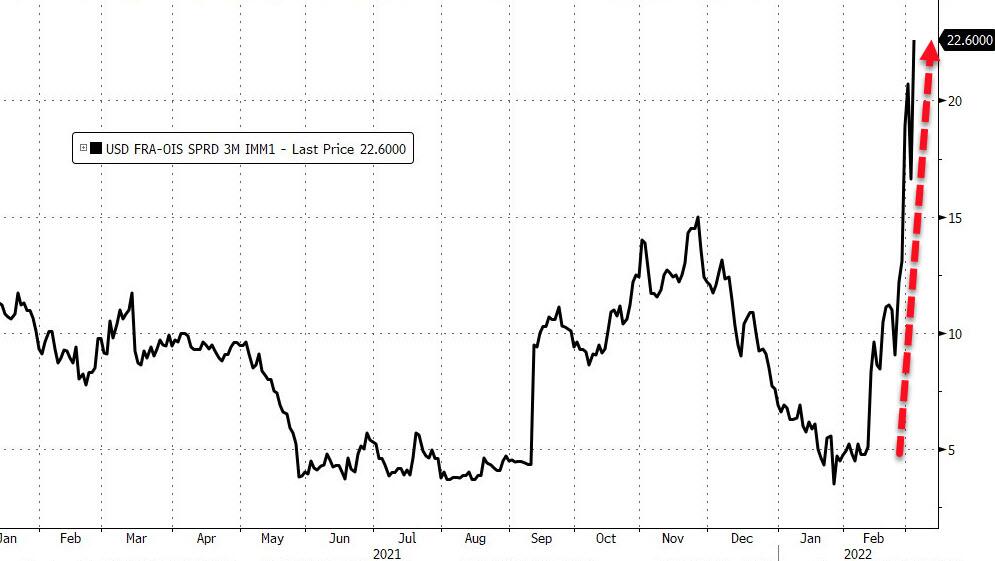

- Traders Stockpiling Bonds Are Causing a Great Collateral Squeeze

- Russia’s Gas Giant Shunned by European Traders and Landlord

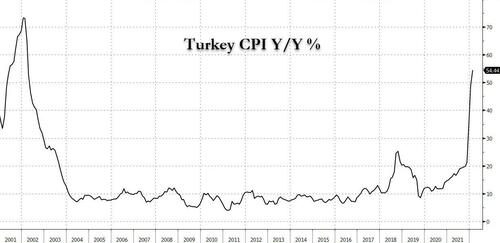

In FX, high stakes and anxiety levels in the FX space as Russia and Ukraine head for ceasefire fire talks from around 12:00GMT/ 07:00EST. DXY firm either side of 97.500 as yields rise again and risk aversion resurfaces. Aussie underpinned near 0.7300 and the 200 DMA as industrial metals remain strong. Franc rebounds following above forecast Swiss CPI in stark contrast to Lira after latest acceleration in headline and pipeline Turkish inflation; USD/CHFf sub-0.9200, EUR/CHF circa 1.0200 and Usd/Try above 14.000. Euro still lagging on conflict contagion and Rouble back down towards all time lows; EUR/USD under 1.1100 and Usd/Rub eyeing 119.00

In commodities, WTI & are off best levels, at USD 116.50/bbl and USD 119.84/bbl for WTI April and Brent May respectively,Brent but remain at elevated levels ahead of negotiations. Japan plans to hold a ministerial meeting on Friday to compile measures to respond to higher oil prices. Gazprom is shipping gas to Europe via Ukraine, in-line with requests; separately, the Yamal-Europe pipeline westbound gas flows to Germany from Poland have stopped, via Reuters citing Gascade data. Iran’s Energy Minister Owji says domestic oil production can hit maximum capacity in one/two months following a nuclear agreement being reached, via Reuters citing a Telegram channel. Spot / are supported but around familiar parameters while base metals experienced noted overnightgold silver upside, particularly nickel and zinc.

US Event Calendar

- 8:30am: U.S. Initial Jobless Claims, Feb. 26, est. 225k, prior 232k

- Continuing Claims, Feb. 19, est. 1420k, prior 1476k

- 9:45am: U.S. Markit US Services PMI, Feb. F, est. 56.7, prior 56.7

- 10am: U.S. Durable Goods Orders, Jan. F, est. 1.6%, prior 1.6%; -Less Transportation, Jan. F, est. 0.7%, prior 0.7%

- Cap Goods Orders Nondef Ex Air, Jan. F, no est., prior 0.9%

- Cap Goods Ship Nondef Ex Air, Jan. F, no est., prior 1.9%

- 10am: U.S. Factory Orders, Jan., est. 0.7%, prior -0.4%

Central bank speakers

- 10am: Fed Chair Powell Testifies Before Senate Panel

- 11:30am: Bank of Canada’s Macklem Gives Economic Progress Report

- 12pm: Fed’s Barkin Speaks on Economy

- 12:45pm: Bank of Canada’s Macklem to Hold Press Conference

- 3:30pm: Bank of Canada Speaks to Lawmakers at Committee Hearing

- 6pm: Fed’s Williams Takes Part in Discussion on the Economy

DB’s Jim Reid concludes the overnight wrap

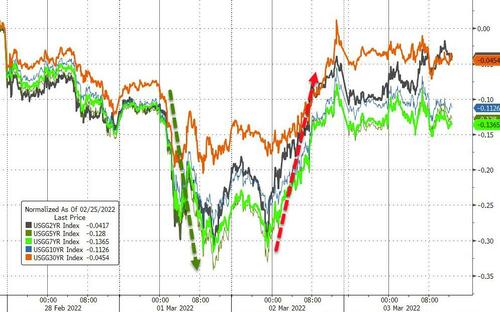

We go to press this morning after another volatile 24 hours in markets, one that saw equities and sovereign bond markets retrace the prior day’s declines (completely so in the case of American assets), while energy prices and inflation breakevens have kept marching higher. Policymakers are facing an unenviable situation over the near-term; inflationary pressures are mounting while the broader outlook grows more uncertain by the day. The latest commodity price spike overnight has now taken Brent Crude oil above $118/bbl, and it’s only slightly retraced that since to $116.75/bbl. Bear in mind that before the US warning of an invasion in mid-February it was trading just above $90/bbl. That spike in oil prices has occured as data yesterday showed Euro Area inflation reached to its highest level since the formation of the single currency. And as our economists have already written, if this commodity shock persists then that’s going to have negative implications for European growth, raising the spectre of a significant slowdown ahead. Indeed yesterday we saw the 2s10s Treasury yield curve hit another low that hasn’t been matched since March 2020 despite the selloff in yields (more below), speaking to the worry that central banks will have to hike in to a deteriorating outlook. Likewise in Europe, after an historic rally the day before that saw 10yr bunds blow through z scores (see my CoTD from yesterday, link here) rates sold right back off yesterday. It’s thus timely that our European rates team will be hosting a call at noon London time today, which you can register for here.

This morning however, Asian markets have followed the rebound in the US and Europe, supported by the comments by Fed Chair Powell that have helped to reduce uncertainty about the Fed’s near-term intentions (more on which below). The Nikkei (+0.76%), Hang Seng (+0.63%) and the Kospi (+1.45%) are all trading higher this morning, with the latter’s advance coming as South Korea reported GDP grew by +1.2% in Q4 (vs. +1.1% expected). Mainland stocks in China have posted a more mixed performance however, with the Shanghai Composite (+0.10%) just about in positive territory whilst the CSI (-0.29%) has lost ground, which has occurred after China’s Caixin services PMI edged down to a 6-month low of 50.2 (vs. 50.7 expected), so just about in expansionary territory still. US equity futures are fairly steady this morning as well, with those on the S&P 500 up +0.11%.

In terms of the latest in Ukraine, there has been continued fighting in the country, although the prospect of talks today between Russia and Ukraine has offered a semblance of hope. Although the ruble strengthened slightly on news of the further peace talks, the broader financial situation hasn’t appeared to improve much for Russia, with Moody’s and Fitch downgrading their sovereign debt to junk status overnight, while MSCI reported it would remove Russia from its equity indices due to issues of market access. The Bank of Russia reported that equity indices would remain closed today, as they have all week so far.

For markets, one of the biggest ways the conflict has manifested itself is this massive spike in commodities, with yesterday bringing yet another round of broad-based increases that will only intensify the inflationary pressures already here. Brent crude ended the day up +7.58% at $112.93/bbl, which was its highest closing level since 2014 and took its YTD gains beyond +40%. Then overnight it surpassed that to reach its highest levels since 2013 and take its YTD gains above +50%. Meanwhile, WTI also saw a similar move higher, rising +6.95% to its highest level since 2013 at $110.60/bbl, and this morning it’s now above $114/bbl. Those increases follow President Biden’s indication that he’d be open to the imposition of sanctions on Russian oil and gas, saying that “nothing is off the table” when he was asked about the potential of the US banning Russian oil imports. Indeed, influential US Senators began drafting a bill that would ban US imports of Russian oil and gas products. When it came to natural gas, we saw some significant price increases there too, with futures in Europe up by a massive +36.05% to €165.54/MWh, which leaves them just shy of their pre-Christmas peak. This pressure could be seen across the board, with aluminium (+2.62%) at a record and wheat prices (+5.67%) reaching levels not seen since 2008, which just shows the extent to which the current conflict is affecting commodity markets right now.

Those commodity price rises came amidst further inflation records, with the Euro Area flash CPI print for February coming in at +5.8% (vs. +5.6% expected), which is its highest level since the formation of the single currency. Core CPI was also up to +2.7% (vs. +2.6% expected), another record since the Euro’s formation. The effects of all this were evident in market-based measures of inflation expectations, with the 10yr German breakeven up by a further +9.0bps to 2.28%, its highest level in a decade, and its Italian counterpart (+4.8bps) also hit a decade high of 2.08%. Interestingly, we heard from ECB Chief Economist Lane later in the European session, who said ahead of the ECB meeting next week, that “the schedule for the March staff projections exercise has been revised in order to take into account the implications of the Russian invasion of Ukraine”, which means that they’ll include the upside inflation release from yesterday as well. He struck a balanced note in his speech, acknowledging that an adverse supply shock means that “the horizon over which inflation returns to the target level could be lengthened in order to avoid pronounced falls in economic activity and employment”. But then he also said that “it is essential to avoid that a spell of temporarily-high inflation pressures – even if arising from a supply shock – becomes entrenched by permanently altering longer-term inflation expectations.”

Staying on that central bank theme, we had some significant headlines from Fed Chair Powell yesterday as he testified before the House Financial Services Committee. First, he said that “I am inclined to propose and support a 25 basis-point rate hike” at the March meeting, so steering away from the more hawkish possibility of a 50bp move that markets had already begun to price out. That said, he noted “we would be prepared to move more aggressively” if inflation remained high, so not ruling out moves larger than 25bps if justified. The Chair also remarked that policy may need to tighten above neutral, which he put as the policy rate between 2%-2.5%, as opposed to simply being less accommodative. Meanwhile on Ukraine, Powell said that the “implications for the US economy are highly uncertain, and we will be monitoring the situation closely.”

That confirmation of likely rate hikes ahead helped Treasury yields fully retrace the previous days’ decline, with the 10yr yield up +14.9bps to 1.88%. As mentioned at the top however, the more policy-sensitive 2yr yield (+17.1bps) saw a larger rise that saw +23.5bps of hikes priced back into money markets through 2022. The curve thus bear flattened, and the 2s10s curve fell to 35.9bps, after falling as low as 31.3bps intraday. The 2s10s curve has now flattened by more than 120bps since its peak at the end of Q1 last year. Those movements in Treasuries echoed what took place in Europe, where yields on 10yr bunds (+9.9bps) moved back into positive territory, and those on 10yr OATs (+11.9bps), gilts (+13.1bps) and BTPs (+15.3bps) all moved higher as well.

For equities, they managed to stage something of a recovery against this backdrop, with the S&P 500 (+1.86%) actually moving back into positive territory for the week. That was part of an incredibly broad-based advance that left 466 companies in the index in the green on the day, which is the second-highest so far this year. In Europe the advances weren’t quite as strong, with the STOXX 600 only up +0.90%, but indices across the continent moved higher including the DAX (+0.69%), the CAC 40 (+1.59%) and the FTSE 100 (+1.36%). When it came to Russian assets, stock trading was closed for a third consecutive day, although depositary receipts in London continued to decline yesterday, with those for Gazprom down -23.50%, whilst Sberbank fell another -78.43%.

Another central bank announcement yesterday came from the Bank of Canada, who became the latest to start hiking rates for the first time since the pandemic. They increased their target for the overnight rate by 25bps to 0.5%, and said in their statement that “the Governing Council expects interest rates will need to rise further.” In reference to the Ukrainian conflict, they said that the invasion was “putting further upward pressure on prices for both energy and food-related commodities”, which along with other factors meant that “inflation is now expected to be higher in the near term than projected in January.” This hawkish-leaning language meant that the Canadian dollar was the strongest performing G10 currency yesterday, gaining +0.88% against the US Dollar, and markets are fully pricing in another hike at their next meeting in April.

Aside from the Euro Area CPI release there wasn’t much in the way other data yesterday. However, we did get the ADP’s report of private payrolls from the US, which rose by +475k in February (vs. 375k expected). That comes ahead of tomorrow’s jobs report, where our US economists are anticipating growth of +300k in nonfarm payrolls.

To the day ahead now, and we’ll hear from Fed Chair Powell again before the Senate Banking Committee. Other central bank speakers include the Fed’s Barkin and Williams, Bank of Canada Governor Macklem and the ECB’s de Cos. On top of that, we’ll also get the minutes from the ECB’s February meeting. On the data side, releases include the global services and composite PMIs for February, as well as the ISM services index for February from the US. Other releases include the Euro Area unemployment rate and PPI for January, while in the US we’ll get the weekly initial jobless claims and January’s factory orders. Finally, earnings releases include Broadcom and Costco.

END

3. ASIAN AFFAIRS

i)THURSDAY MORNING// WEDNESDAY NIGHT

SHANGHAI CLOSED DOWN 3.03 PTS OR 0.09% //Hang Sang CLOSED UP 123.42 PTS OR 0.55% /The Nikkei closed UP 184.24 PTS or 0.70% //Australia’s all ordinaires CLOSED UP 0.55% /Chinese yuan (ONSHORE) closed DOWN 6.3192 /Oil UP TO 113.40 dollars per barrel for WTI and UP TO 116.25 for Brent. Stocks in Europe OPENED ALL RED EXCEPT FRANCE // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.3192. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.3241: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFF SHORE WEAKER//

3 a./NORTH KOREA/ SOUTH KOREA

///NORTH KOREA

3B JAPAN

3c CHINA

CHINA

China considers the possibility of abandoning their zero covid policy with the introduction of Paxlovid. They are developing their own Messenger RNA vaccines which may prove fatal.

A far better choice would be to give all citizens Ivermectin

(zerohedge)

China Considers Possibility Of Abandoning “Zero COVID” Policy

WEDNESDAY, MAR 02, 2022 – 08:40 PM

After more than two years of imposing some of the world’s most restrictive lockdowns on its population, Beijing is finally preparing for a world without its strenuous “ZERO Covid” measures.

WSJ reports that Chinese officials are looking into the use of travel bubbles modeled on what was used during the Winter Olympics.

Collecting data on new antiviral drugs and scouting sites abroad for future production of homegrown Chinese mRNA vaccines, according to people familiar with the matter. However, on the other hand, images of patients in Hong Kong lying on open-air gurneys has intensified the sense of public panic. They now see the former British colony as something of a cross between a science experiment and an actualy community.

Mainland experts now see the former British colony as a “stress test scenario,” as well as a source of data on the effectiveness of various treatments and insight into fighting severe infection surges without resorting to hard lockdowns, according to a person familiar with the discussions.;

While COVID likely won’t ease before next spring, the two sources from within China’s government told WSJ that officials in departments covering transportation, customs and border control have been tasked since January with exploring adjustments to COVID control policies that can eventually be presented to China’s top leadership.

Additionally, officials China’s departments covering transportation, customs and border control have been tasked since January with exploring potential changes to China’s COVID control policies. The hope is that these potential changes – or “adjustments” – will eventually be presented to China’s top leadership, according to a person with knowledge.

In another line of questioning, WSJ added that the approach and timeline for a relaxation of COVID controls isn’t fixed and could change depending damn whether a levee of corporate bankruptcies breaks.

Pfizer’s unleashing of its drug Paxlovid will play a major role in protecting the help of billions as members of the public and lawmakers see the drug as critical in keeping Americans alive in theater.