MARCH22

GOLD; $1921.40 DOWN $7.75

SILVER: $24.82 DOWN $0.29

ACCESS MARKET: GOLD $1921.55

SILVER: $24.78

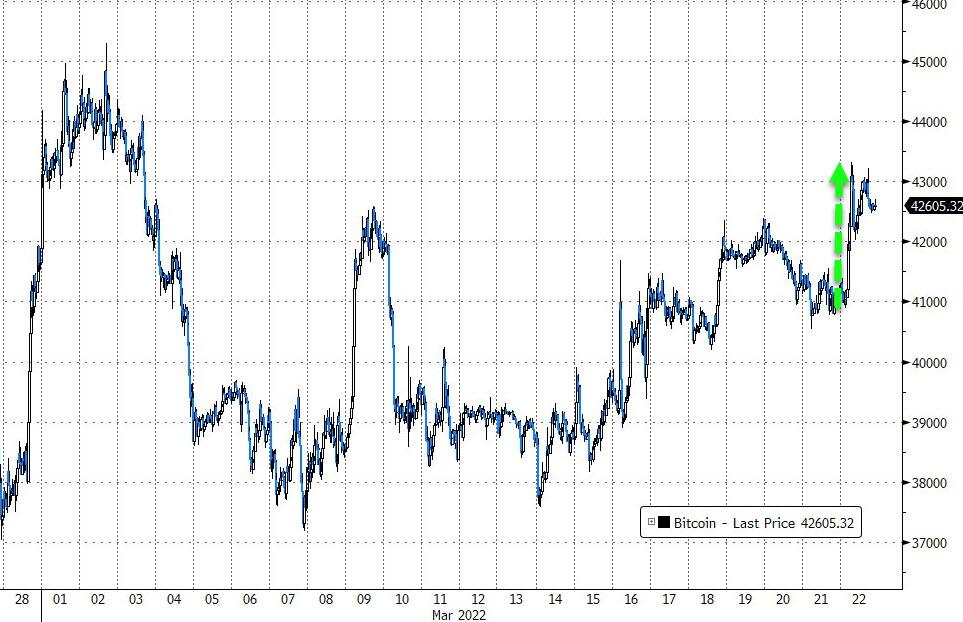

Bitcoin morning price: $42930 UP 1889

Bitcoin: afternoon price: $42,598 UP 1557

Platinum price: closing DOWN $15.55 to $1026.45

Palladium price; closing DOWN $119.45 at $2447.55

END

end

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

comex notices/

March: JPMorgan stopped/total issued 10/21

DLV615-T CME CLEARING

BUSINESS DATE: 03/21/2022 DAILY DELIVERY NOTICES RUN DATE: 03/21/2022

PRODUCT GROUP: METALS RUN TIME: 20:25:46

EXCHANGE: COMEX

CONTRACT: MARCH 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,928.600000000 USD

INTENT DATE: 03/21/2022 DELIVERY DATE: 03/23/2022

FIRM ORG FIRM NAME ISSUED STOPPED

363 H WELLS FARGO SEC 2

435 H SCOTIA CAPITAL 3

624 H BOFA SECURITIES 2

661 C JP MORGAN 19 10

709 C BARCLAYS 2

737 C ADVANTAGE 2

905 C ADM 2

TOTAL: 21 21

MONTH TO DATE: 11,510

NUMBER OF NOTICES FILED TODAY FOR Mar. CONTRACT 21 NOTICE(S) FOR 2100 OZ (0.0653 TONNES)

total notices so far: 11,510 contracts for 1,151,000 oz (35.800 tonnes)

SILVER NOTICES:

5 NOTICE(S) FILED TODAY FOR 25,000 OZ/

total number of notices filed so far this month 10,468 : for 52,340,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

END

GLD

WITH GOLD DOWN $7.75

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 1.16 TONNES INTO THE GLD//

INVENTORY RESTS AT 1083.60 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 29 CENTS

AT THE SLV// NO CHANGES IN SILVER INVENTORY AT THE LV/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 550.288 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A GOOD SIZED 630 CONTRACTS TO 157,972 AND CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE GAIN IN OI WAS ACCOMPLISHED WITH OUR $0.16 GAIN IN SILVER PRICING AT THE COMEX ON MONDAY. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.16) AND WERE UNSUCCESSFUL IN KNOCKING OUT ANY SILVER LONGS AS WE HAD A STRONG GAIN OF 1170 CONTRACTS ON OUR TWO EXCHANGES

WE MUST HAVE HAD:

I) HUGE BANKER SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A FAIR ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A HUGE INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 42.860 MILLION OZ FOLLOWED BY TODAY’S QUEUE JUMP OF NIL OZ //NEW STANDING 52.585 MILLION OZ // V) STRONG SIZED COMEX OI GAIN/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS : -115

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAR. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAR:

TOTAL CONTACTS for 16 days, total contracts: : 29,945 contracts or 149.8 million oz OR 9.36 MILLION OZ PER DAY. (1872 CONTRACTS PER DAY)

TOTAL NO OF OZ UNDERGOING EFP TO LONDON 29,945 CONTRACTS X 5,000 PER CONTRACT:

EQUATES TO: 149.8 MILLION OZ

.

LAST 11 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 149.8 MILLION OZ//THIS IS GOING TO BE A HUGE EFP ISSUANCE MONTH AND MOST LIKELY WILL SET A RECORD FOR ANY MONTH

RESULT: WE HAD A GOOD SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 630 WITH OUR $0.16 GAIN IN SILVER PRICING AT THE COMEX// MONDAY THE CME NOTIFIED US THAT WE HAD A FAIR SIZED EFP ISSUANCE OF 425 CONTRACTS( 425 CONTRACTS ISSUED FOR MAR AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A HUGE INITIAL SILVER OZ STANDING FOR MAR. OF 42.860 MILLION OZ FOLLOWED BY TODAY’S NIL OZ QUEUE JUMP//NEW STANDING 52.585 MILLION OZ// /// .. WE HAD A STRONG SIZED GAIN OF 1055 OI CONTRACTS ON THE TWO EXCHANGES FOR 5.275 MILLION OZ WITH THE SMALL GAIN IN PRICE.

WE HAD 5 NOTICES FILED TODAY FOR 25,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A SMALL SIZED 788 CONTRACTS TO 610,889 AND FURTHER CLOSER TO NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: +871 CONTRACTS.

THE BIS HAS ABANDONED THE GOLD COMEX TRADING!!!

.

THE SMALL SIZED INCREASE IN COMEX OI CAME DESPITE OUR TINY GAIN IN PRICE OF $0.25//COMEX GOLD TRADING/MONDAY/.AS IN SILVER WE MUST HAD HUGE BANKER/ALGO SHORT COVERING ACCOMPANYING OUR HUMONGOUS SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR MARCH AT 14.818 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 200 OZ//NEW STANDING 36.249 TONNES

YET ALL OF..THIS HAPPENED WITH OUR GAIN IN PRICE OF $0.25 WITH RESPECT TO FRIDAY’S TRADING

WE HAD AN FAIR SIZED GAIN OF 3638 OI CONTRACTS (11.315 PAPER TONNES) ON OUR TWO EXCHANGES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2850 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 610,018.

IN ESSENCE WE HAVE AN FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2767, WITH 83 CONTRACTS DECREASED AT THE COMEX AND 2850 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 2767 CONTRACTS OR 8.606 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2850) ACCOMPANYING THE SMALL SIZED GAIN IN COMEX OI (788,): TOTAL GAIN IN THE TWO EXCHANGES 3638 CONTRACTS. WE NO DOUBT HAD 1) HUGE BANKER SHORT COVERING ,2.) HUGE INITIAL STANDING AT THE GOLD COMEX FOR MARCH. AT 14.818 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 200 OZ//NEW STANDING 36.249 TONNES /// 3) ZERO LONG LIQUIDATION ///. ,4) SMALL SIZED COMEX OI GAIN 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

MARCH

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAR :

100,771 CONTRACTS OR 10,077,100 OR 313.44 TONNES 16 TRADING DAY(S) AND THUS AVERAGING: 6298 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 16 TRADING DAY(S) IN TONNES: 313.44TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2020, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 313.44/3550 x 100% TONNES 8.82% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 313.44 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE MONTH.

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL.WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MARCH HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF APRIL, FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (MAR), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A GOOD SIZED 630 CONTRACTS TO 157,972 AND FURTHER FROM OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 4 1/2 YEARS AGO.

EFP ISSUANCE 425 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 425 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 425 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 680 CONTRACTS AND ADD TO THE 425 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A STRONG SIZED GAIN OF 1055 OPEN INTEREST CONTRACT FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 5.275 MILLION OZ,

OCCURRED WITH OUR SMALLISH $0.16 GAIN IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

5. Other gold commentaries

6. Commodity commentaries/cryptocurrencies

3. ASIAN AFFAIRS

i)TUESDAY MORNING// MONDAY NIGHT

SHANGHAI CLOSED UP 6.18 PTS OR 0.19% //Hang Sang CLOSED UP 667.94 PTS OR 3.15 % /The Nikkei closed UP 396.88 PTS OR 1.48% //Australia’s all ordinaires CLOSED UP 0.82% /Chinese yuan (ONSHORE) closed DOWN 6.3643 /Oil UP TO 111.61 dollars per barrel for WTI and UP TO 116.06 for Brent. Stocks in Europe OPENED ALL GREEN // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.3643. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.3660: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

A)NORTH KOREA/

b) REPORT ON JAPAN

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A SMALL SIZED 788 CONTRACTS TO 610,889 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX DECREASE OCCURRED DESPITE OUR TINY GAIN OF $0.25 IN GOLD PRICING MONDAY’S COMEX TRADING. WE ALSO HAD A SMALL SIZED EFP (1364 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE NON ACTIVE DELIVERY MONTH OF MAR.. THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2850 EFP CONTRACTS WERE ISSUED: ;: , & FEB. 0 APRIL:2850 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2850 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 3638- CONTRACTS IN THAT 2850 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A SMALL SIZED COMEX OI GAIN OF 788 CONTRACTS..AND THIS SMALL GAIN OCCURRED WITH THE GAIN IN PRICE OF $0.25.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING FOR MAR (36.249),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.249 TONNES

THE BANKERS WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $0.25) AND THEY WERE UNSUCCESSFUL IN FLEECING ANY LONGS AS WE HAVE REGISTERED A FAIR SIZED GAIN OF 8.606 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR MAR (36.249 TONNES)…

WE HAD +788 CONTRACTS ADDED TO COMEX TRADES???. THESE WERE ADDED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 3658 CONTRACTS OR 365800 OZ OR 11.315 TONNES

Estimated gold volume today: 188,815 ///poor

Confirmed volume yesterday: 203,295 contracts poor

INITIAL STANDINGS FOR MAR ’22 COMEX GOLD //

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 8,102.05 oz Int Delaware 250 kilobars & Brinks: 2 kilobars |

| Deposit to the Dealer Inventory in oz | nil OZ |

| Deposits to the Customer Inventory, in oz | 64,302.000 oz JPMORGAN 2,000 kilobars |

| No of oz served (contracts) today | 21 notice(s) 2100 OZ 0.0155 TONNES |

| No of oz to be served (notices) | 144 contracts 14,400 oz 0.4479 TONNES |

| Total monthly oz gold served (contracts) so far this month | 11,510 notices 1151,000 OZ 35.800 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For today:

dealer deposits 0

total dealer deposit nil oz

No dealer withdrawal 0

2 customer deposits

i) Into JPMORGAN: 64,302.000 oz (2000 kilobars

total customer deposit: 64,302.000 oz

total gold deposits in tonnage: 2.0090 tonnes

2 customer withdrawal

i) Out of Brinks 64.30 oz (2 kilobars)

ii) out of Int. Delaware 8037.75 oz (250 kilobars)

total withdrawals: 32.151 oz

ADJUSTMENTS: 1

manfra..// customer to dealer//1,832.607 oz (57 kilobars)

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MARCH.

For the front month of MARCH we have an oi of 165 contracts having LOST 3

We had 5 notices filed yesterday so we finally gained 2 contracts or 200 oz will stand at the comex as these guys refused to be EFP’d over to London.

Our banker friends have run out of gold metal everywhere.

April saw a loss of 27,441 contracts down to 198,628.

May saw a GAIN of26 contracts to stand at 4349

June saw a GAIN of 27,694 contracts up to 337,297 contracts

We had 5 notice(s) filed today for 500 oz FOR THE MAR 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 19 notices were issued from their client or customer account. The total of all issuance by all participants equates to 21 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 10 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the MAR /2021. contract month,

we take the total number of notices filed so far for the month (11,510) x 100 oz , to which we add the difference between the open interest for the front month of (MAR: 165 CONTRACTS ) minus the number of notices served upon today 21 x 100 oz per contract equals 1,165,400 OZ OR 36.249 TONNES the number of TONNES standing in this active month of mar.

thus the INITIAL standings for gold for the MAR contract month:

No of notices filed so far (11,510) x 100 oz+ (165) OI for the front month minus the number of notices served upon today (21} x 100 oz} which equals 1,165,400 oz standing OR 36.249 TONNES in this NON active delivery month of MAR.

TOTAL COMEX GOLD STANDING: 36.249 TONNES (A WHOPPER FOR A MAR (NON ACTIVE) DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

191,133,764.7, oz NOW PLEDGED /HSBC 5.94 TONNES

99,258.893 PLEDGED MANFRA 3.08 TONNES

54,339.114oz PLEDGED JPMorgan no 1 1.690 tonnes

243,923.704, oz JPM No 2 7.58 TONNES

898,821.330 oz pledged Brinks/27,96 TONNES

12,249,333 oz International Delaware: 0..3810 tonnes

Loomis: 18,615.429 oz

total pledged gold: 1,506,092.234 oz 46.84 tonnes

TOTAL REGISTERED AND ELIG GOLD AT THE COMEX: 34,491,736.522 OZ (1072.83TONNES)

TOTAL ELIGIBLE GOLD: 16,798,210.136 OZ (522.49 tonnes)

TOTAL OF ALL REGISTERED GOLD: 17,693,526.386 OZ (550.34 tonnes)

REGISTERED GOLD THAT CAN BE SERVED UPON: 16,187,434.0 OZ (REG GOLD- PLEDGED GOLD) 503.49 tonnes

END

MAR 2022 CONTRACT MONTH//SILVER//MARCH 22

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1,333,773.399 oz Malca CNT |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | nil oz |

| No of oz served today (contracts) | 5CONTRACT(S)25,000 OZ) |

| No of oz to be served (notices) | 49 contracts (245,000 oz) |

| Total monthly oz silver served (contracts) | 10,468 contracts 52,340,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

we had 0 deposits into the dealer

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 0 deposits into the customer account

total deposit: nil oz

JPMorgan has a total silver weight: 180.228 million oz/341.425 million =52.78% of comex

ii) Comex withdrawals: 2

A) Out of CNT: 1,248,359.339 oz

ii) Out of Malca: 85,414,060 oz

total withdrawal 1,333,773.399 oz

one adjustment:

JPMorgan/dealer to customer 600,079.100 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 92.449 MILLION OZ

TOTAL REG + ELIG. 341,424 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR MARCH

silver open interest data:

FRONT MONTH OF MARCH OI: 54, HAVING LOST 0 CONTRACTS FROM MONDAY.

WE HAD 0 NOTICES SERVED UPON YESTERDAY, SO WE GAINED 0 CONTRACTS OR AN ADDITIONAL NIL OZ WILL STAND

FOR DELIVERY OVER HERE AS THESE GUYS REFUSED TO BE EFP’D TO LONDON.

APRIL HAD A 1 CONTRACT GAIN// CONTRACTS REMAINS AT 611

MAY HAD A GAIN OF 64 CONTRACTS UP TO 119,008 contracts

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 5 for 25,000 oz

Comex volumes: 45,093// est. volume today//poor/

Comex volume: confirmed yesterday: 36,869 contracts ( extremely poor )

To calculate the number of silver ounces that will stand for delivery in MAR. we take the total number of notices filed for the month so far at 10,468 x 5,000 oz = 52,340,000 oz

to which we add the difference between the open interest for the front month of MAR (54) and the number of notices served upon today 5 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MAR./2021 contract month: 10,468 (notices served so far) x 5000 oz + OI for front month of MAR (x54) – number of notices served upon today (5) x 5000 oz of silver standing for the MAR contract month equates 52,585,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

MARCH 22/WITH GOLD DOWN $7.75: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.16 TONNES OF GOLD DEPOSITED INTO THE GLD//INVENTORY RESTS AT 1083.60 TONES

MARCH 21//WITH GOLD UP $.25 : A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 9.00 TONNES INTO THE GLD////INVENTORY RESTS AT 1082.44 TONES

MARCH 18/WITH GOLD DOWN $13.55 NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1073.44 TONES

MARCH 17/WITH GOLD UP $33.50: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.61 TONNES INTO THE GLD//INVENTORY RESTS AT 1073.44 TONNES

MARCH 16/WITH GOLD DOWN $18.50//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.33 TONNES FROM THE GLD///INVENTORY RESTS AT 1061.83 TONNES

MARCH 15/WITH GOLD DOWN $30.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1064.16 TONNES

MARCH 14//WITH GOLD DOWN $22.75, HUGE CHANGES IN GOLD INVENTORY AT THE GLD//STRANGE: A DEPOSIT OF 2.62 TONNES INTO THE GLD.//INVENTORY RESTS AT 1064.16 TONNES

MARCH 11/WITH GOLD DOWN $14.60: A BIG CHANGE IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 1061.54 TONNES

MARCH 10//WITH GOLD UP $11.55: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.06 TONNES FORM THE GLD///INVENTORY RESTS AT 1063.28 TONNES

MARCH 9/WITH GOLD DOWN $53.85//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.64 TONNES INTO THE GLD//INVENTORY RESTS AT 1067.34 TONNES

MARCH 8/WITH GOLD UP $46.10: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 8.42 TONNES INTO THE GLD///INVENTORY RESTS AT 1062.70 TONNES

MARCH 7/WITH GOLD UP $28.40 A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.06 TONNES INTO THE GLD..//INVENTORY RESTS AT 1054.28 TONNES

MARCH 4/WITH GOLD UP $28.40//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1050.22 TONNES

MARCH 3/WITH GOLD UP $13.95: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 7.84 TONNES//INVENTORY RESTS AT 1050.22 TONNES

MARCH 2/WITH GOLD DOWN $20.80//A MONSTER CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 13.36 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 1042.38 TONNES

MARCH 1/WITH GOLD UP $42.60: NO CHANGES IN GOLD INVENTORY AT THE GLD: //INVENTORY RESTS AT 1029.32 TONNES

FEB 28/WITH GOLD UP $12.95: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1029.32 TONNES

FEB 25/WITH GOLD DOWN $38.95: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1029.32 TONNES

FEB 24/WITH GOLD UP $17.35//A HUGE CHANGE AT THE GLD: 5.23 TONNES INTO THE GLD// IN GOLD INVENTORY AT THE GLD/INVENTORY REST AT 1029.32 TONNES

FEB 23/WITH GOLD UP $2.00 : NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1024.09 TONNES

FEB 22/WITH GOLD UP $6.20: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.65 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 1024.09 TONNES

FEB 18/WITH GOLD DOWN $1.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1019.44 TONNES

FEB 17/WITH GOLD UP $29.50: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1019.44 TONNES

FEB 16/WITH GOLD UP 414.60 NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1019.44 TONNES

FEB 15/WITH GOLD DOWN $12.70 NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1019.44 TONNES

FEB 14/WITH GOLD UP $27.20 NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1019.44 TONNES

FEB 11/WITH GOLD UP $4.50 A HUGE CHANGE IN GOLD IVNETORY AT THE GLD// A DEPOSIT OF 3.48 TONNES INTO THE GLD//INVENTORY RESTS AT 1019.44 TONES

CLOSING INVENTORY FOR THE GLD//1083.44 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MARCH 22/WITH SILVER DOWN $0.29 TODAY : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 550.288 MILLION OZ//

MARCH 21/WITH SILVER UP 16 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 550.288 MILLION OZ//

MARCH 18/WITH SILVER DOWN 37 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.217 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 550.288 MILLION OZ//

MARCH 17/ WITH SILVER UP 72 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.049 MILLION OZ INTO THE SLVV//INVENTORY RESTS AT 548.071 MILLION OZ

MARCH 16/WITH SILVER DOWN 56 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 462,000 OZ FROM THE SLV//INVENTORY RESTS AT 544.560 MLLION O

MARCH 15/WITH SILVER DOWN 18 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 545.022 MILLION OZ

MARCH 14/WITH SILVER DOWN 64 CENTS TODAY; STRANGE A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.125 MILLION OZ/INVENTORY RESTS AT 545.022 MILLIONOZ

MARCH 11/WITH SILVER DOWN 13 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.897 MILLION OZ

MARCH 10/WITH SILVER UP 39 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.897 MILLION OZ/

MARCH 9/WITH SILVER DOWN 88 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 5.174 MILLION OZ OF FAKE SILVER.//INVENTORY RESTS AT 542.897 MILLION OZ//

MARCH 8/WITH SILVER UP 88 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.217 MILLION OZ INTO THE SLV////INVENTORY RESTS A 548.071 MILLION OZ//

MARCH 7/WITH SILVER UP 40 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 545.854 MILLION OZ//

MARCH 4/WITH SILVER UP 50 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 545.854 MILLION OZ/

MARCH 3/WITH SILVER UP 2 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 545.854 MILLION OZ//

MARCH 2/WITH SILVER DOWN $.32 TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 198,000 OZ FROM THE SLV//INVENTORY RESTS AT 545.854 MILLION OZ//

MARCH 1/WITH SILVER UP $1.13 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 546.052 MILLION OZ//

FEB 28/WITH SILVER UP 31 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT 546.052 MILLION OZ//

FEB 25/WITH SILVER DOWN 64 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 5.510 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 546.052 MILLION OZ/

FEB 24/WITH SILVER UP 15 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 551.597 MILLION OZ

FEB 23/WITH SILVER UP 22 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 551.597 MILLION OZ//

FEB 22/WITH SILVER UP 30 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 350,000 OZ INTO THE SLV///INVENTORY RESTS AT 551.597 MILLION OZ//

FEB 18/WITH SILVER UP 7 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.017 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 551.227 MILLION OZ

FEB 17/WITH SILVER UP 31 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.402 MILLION OZ//INVENTORY RESTS AT 550.210 MILLION OZ/

FEB 16/WITH SILVER UP 21 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 547.808 MILLIONOZ

FEB 15/WITH SILVER DOWN 46 CENTS TODAY : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 547.808 MILLION OZ//

FEB 14/WITH SILVER UP 49 CENTS TODAY; A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.235 MILLION OZ INTO THES LV////INVENTORY RESTS AT 547.808 MILLION OZ

FEB 11/WITH SILVER DOWN 18 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.573 MILLION OZ///

SLV FINAL INVENTORY FOR TODAY: 550.288 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

Schiff: The Fed Will Raise Rates… Until It Can’t

TUESDAY, MAR 22, 2022 – 08:16 AM

After going from not even thinking about thinking about raising interest rates, to thinking about it, to talking about it, the Fed finally got around to raising rates last week. Peter Schiff called it the most anticipated and probably the least significant rate hike ever. So, what’s next? In his podcast, Peter said the Fed will keep raising rates … until it can’t.

In the past, Peter has said this could be it for hikes. The Fed could be one and done. But the central bank has indicated that it will raise rates six more times this year. In his podcast last week, Peter said there are likely more hikes coming down the pike and the markets haven’t come to terms with how high rates might rise.

So, which is it?

Peter said it will be one-and-done if this first hike causes enough damage to the markets and the economy.

I believe that Powell is very worried about the impact rate hikes might have on the economy and the markets. He may not be forthright about admitting that. But if you read between the lines – and he doesn’t make it that difficult when he talks about raising rates with care and being data-dependent and it’s not on autopilot – if we get a significant reaction between the first rate hike and the second rate hike, there may not be a second rate hike.”

So far, the reaction has been positive. The markets rallied after the hike announcement. If this continues and there is no major economic hiccup, the Fed will almost certainly raise rates again.

The Fed is going to raise rates as many times as it can without hurting the economy, without crashing the markets.”

So, we could have a number of hikes, given that the plan is to only notch interest rates up 25 basis points at a time. But we will eventually get a crash.

At some point, the rate hikes are too many. You get that straw that breaks the camel’s back.”

The Fed is between a rock and a hard place. The central bankers know they need to fight inflation. But they also know that the entire economy is built on accommodative monetary policy. They’re in a corner. They can’t win the inflation fight. And there is no way any of these rate hikes will dent inflation.

So, inflation is going to be here for a long time. And it’s going to keep getting worse. That means the Fed is going to be in a position where it’s forced to continue to raise interest rates until something breaks in the markets and the economy. So, either way, you’re going to lose in the stock market because if it doesn’t crash now, it’s going to crash later.”

The crash is the only thing that will stop rate hikes. Until then, the Fed will keep nudging up rates.

When it happens, the Fed is going to stop hiking. But inflation is not going to go away. Inflation is going to keep getting worse. And then when it stops hiking, it could go from getting worse to getting much worse. We could kick in a whole new gear when it comes to more inflation. Because once we start to really see the negative consequences in the economy and in the markets, I expect not only that Fed will stop hiking rates, but it will start reducing rates.”

Interestingly, while the Fed cut rates, during the week of March 16, it expanded its balance sheet by another $43.6 billion. That pushed the balance sheet up to a new record high of $8.954 trillion.

The Fed hiked rates on Wednesday. But during the week that ended on that same Wednesday, the Fed printed another $43.6 billion and bought more US Treasuries. So in other words, the Fed is supposedly committed to fighting inflation and its hiking rates by 25 basis points in its efforts to fight inflation. Yet during the same week it’s hiking rates, it’s creating more inflation. It’s printing more money. It’s monetizing more government debt. Did it really have to do another 43.6 billion in QE on the very week that it’s hiking rates?”

The fact is the US economy is addicted to low interest rates. Even if interest rates remain relatively low through the hiking process, they won’t be low enough to satisfy that addiction.

The economy is going to start to go into withdrawal. We’re going to start to see the impact of rising interest rates on the economy, of rising bond yields on the economy, on the stock market. And as consumers are struggling with rising prices, now they’re going to be struggling with rising interest rates.”

When you have an economy built on consumers borrowing and spending money, raising borrowing costs takes the juice out of that economy. It will crash. And that’s when the real problems start for the Fed.

In this podcast, Peter also talks about the market reaction to the first hike and comments he made about Ukraine President Zelensky.

END

2.LAWRIE WILLIAM//,//Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, James RICKARDS/

-END-

-END-

LAWRIE WILLIAMS

3. Chris Powell of GATA provides to us very important physical commentaries

Not so sure about this!

(Bloomberg/GATA)

Usurping dollar’s dominance is nearly impossible, analysts say

Submitted by admin on Mon, 2022-03-21 10:38Section: Daily Dispatches

Ruth Carson, Libby Cherry, and Tania Chen

Bloomberg News

via Yahoo Finance, Sunnyvale, California

Monday, March 21, 2022

Dethroning the dollar is easier said than done.

That’s the conclusion of investors after Washington’s freeze of Russia’s dollar holdings created fresh impetus among central bankers to rethink the security of access to foreign-exchange reserves. The move fueled speculation that countries such as China could redouble efforts to unshackle itself from greenback-denominated financial systems and look for alternatives.

While Goldman Sachs Group Inc. and Credit Suisse Group AG have flagged threats to the dollar’s supremacy, finding a valid replacement is going to be extremely challenging, according to funds from Brandywine Global Investment Management to JPMorgan Asset Management.

The size and strength of the world’s largest economy are unparalleled, Treasuries are still one of the safest ways to store money, and the dollar remains a pre-eminent beneficiary of haven flows.

There are simply “no other options at this stage in the game” for currency alternatives to the greenback, said Mark Mobius, a four-decade markets veteran and founder of Mobius Capital Partners. “The dollar is still strong and will probably get stronger if tensions continue to escalate.” …

… For the remainder of the report:

https://finance.yahoo.com/news/usurping-dollar-dominance-impossible-task-215507488.html

end

Here is a case where a farmer could not sell any of his wheat crop on the futures market. Reuters explains what is going on

(zerohedge)

Spike in futures prices crushes buying in grains as markets panic

Submitted by admin on Mon, 2022-03-21 10:55Section: Daily Dispatches

Wheat Prices Soar on Ukraine Fears but U.S. Growers Can’t Cash In

By Julie Ingwersen and P.j. Huffstutter

Reuters

Monday, March 21, 2022

CHICAGO — After Russia’s invasion of Ukraine sent global wheat futures soaring, U.S. farmer Vance Ehmke was eager to sell his grain.

Local prices shot up roughly 30% to nearly $12 a bushel, about the highest Ehmke could recall in 45 years of farming near the western Kansas town of Healy.

Instead of reaping a windfall, Ehmke found a commodities market turned upside down.

He and his wife, Louise, told Reuters they couldn’t sell a nickel of their upcoming summer wheat harvest for future delivery.

Futures prices for corn and wheat had rocketed so abruptly that many along the complex chain of grain handling — local farm cooperatives, grain elevators, flour millers, and exporters — stopped buying for fear they couldn’t resell at a profit.

Others couldn’t afford an industry-wide risk-management strategy known as hedging that keeps global commodities markets moving. Missiles falling in Ukraine had rocked that system, sending middlemen scrambling to shore up positions in the futures market that were costing them millions of dollars per day.

“The market is just in a panic,” Andrew Jackson, a Kentucky grain merchandiser, told Reuters. …

… For the remainder of the report:

END

For your interest….

UK’s Royal Mint to recover gold from circuit boards, mobile phones

Submitted by admin on Mon, 2022-03-21 21:30Section: Daily Dispatches

From the Daily Mail, London

Monday, March 21, 1011

The Royal Mint is building the world’s first recycling factory to turn old laptops and mobile phones into gold.

The state-of-the-art plant will be the first of its kind to recover gold from discarded circuit boards.

High-quality gold taken from the items will then be used by the Royal Mint at its site in Llantrisant, South Wales

Technology created in Canada will recover 99% of precious metals from electronic waste destined for the scrap heap.

Bosses expect to process up to 90 tonnes of British circuit boards every week — making hundreds of kilograms of gold per year. …

… For the remainder of the report:

4.OTHER GOLD/SILVER COMMENTARIES

END

5.OTHER COMMODITIES/EGGS

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING TODAY

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings TUESDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 6.3643

OFFSHORE YUAN: 6.3760

HANG SANG CLOSED UP 667.94 PTS OR 3.15%

2. Nikkei closed UP 396.88 PTS OR 1.48%

3. Europe stocks ALL GREEN

USA dollar INDEX UP TO 98.67/Euro FALLS TO 1.1007

3b Japan 10 YR bond yield: RISES TO. +.219/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 120.76/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//

3c Nikkei now ABOVE 17,000

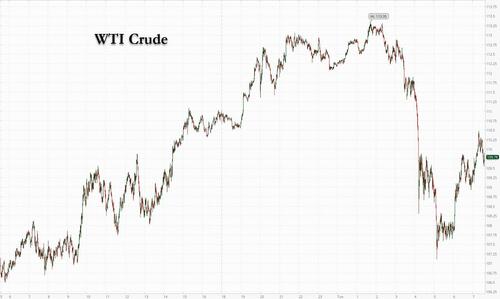

3d USA/Yen rate now well below the important 120 barrier this morning

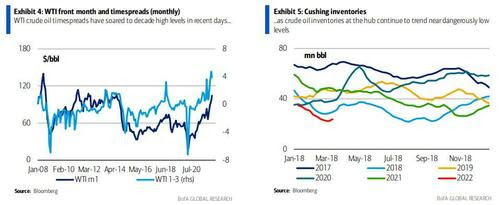

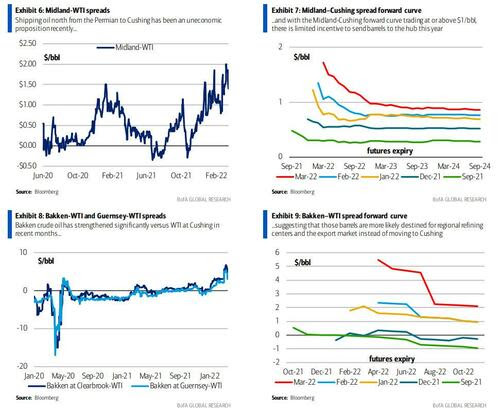

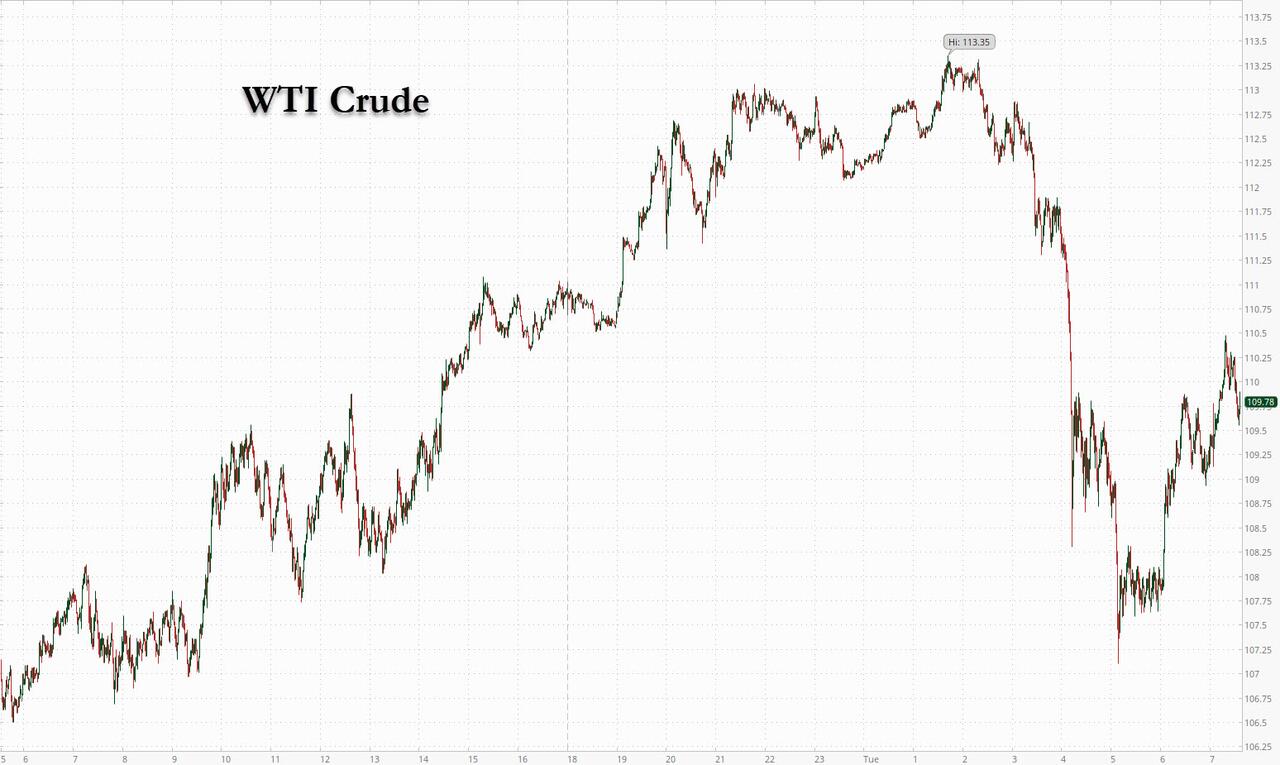

3e WTI:: 111.61 and Brent: 116.06

3f Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: DOWN -SHORE CLOSED DOWN// OFF- SHORE DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.0.506%/Italian 10 Yr bond yield RISES to 2.04% /SPAIN 10 YR BOND YIELD RISES TO 1.43%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 1.534: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield RISES TO : 2.73

3k Gold at $1925.35 silver at: 24.96 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3l USA vs Russian rouble;// Russian rouble UP 2.60/100 in roubles/dollar; ROUBLE AT 104.08

3m oil into the 111 dollar handle for WTI and 116 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 120.76 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning .9334– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0272 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 2.343 UP 5 BASIS PTS

USA 30 YR BOND YIELD: 2.559 UP 4 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 14.82

Futures Rise As Torrid Oil Rally Pauses

TUESDAY, MAR 22, 2022 – 08:03 AM

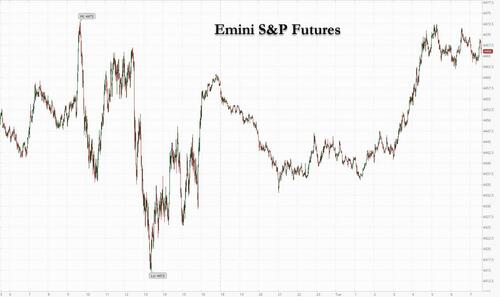

US equity futures reversed earlier losses and European stock markets rose as a sharp rally in crude oil stalled, even as a selloff in bonds deepened Tuesday after Fed Chair Powell signaled a stronger commitment to clamp down on inflation.

Futures on the S&P 500 and Nasdaq 100 flipped to gains from losses, the former trading 0.3% higher or 14 points to 4,466 while the latter was 0.25% in the green. The Stoxx Europe 600 Index marched 0.4% higher, led by banks and cyclical stocks like automakers, while the Hang Seng led gains in Asia, closing up 3.15% after Ali Baba raised its stock buyback by $10 billion. Treasury yields continued their ascent after short-dated rates posted one of the biggest daily climbs of the past decade on Monday.

In a mostly quiet session oil was the outlier, and after climbing 18% in three days, Brent futures initially rose as high as $119 before sliding sharply to $113 a barrel around the time Europe opened with WTI mirroring the move. Bloomberg reported that Germany and Hungary are putting the brakes on a potential embargo by the European Union on Russian oil, deepening differences in the bloc over how to further punish Moscow for its invasion of Ukraine.

“We have quite an unpleasant situation for markets currently in the sense that normally a Fed tightening cycle is at the early stages quite risk-on, and later on you worry about the financial conditions tightening driving a growth slowdown,” Christian Mueller-Glissmann, managing director of portfolio strategy and asset allocation at Goldman Sachs Group Inc., said in an interview with Bloomberg TV. “You now have this incredible urgency to tighten, you have a very steep hiking cycle and that puts the problem much earlier into investors’ minds that you might be facing a growth slowdown.”

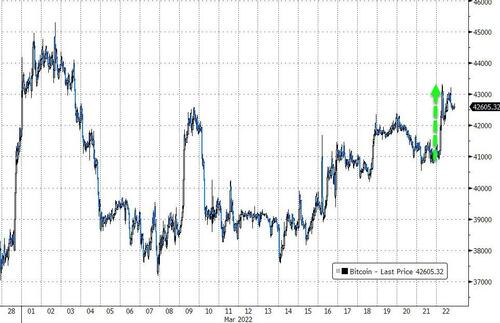

In premarket trading, Nike rose more than 7% after reporting quarterly results that beat analysts’ expectations as the world’s largest athletic-wear retailer overcame struggles with its supply chain and the China market. Cryptocurrency-linked stocks gained in premarket trading as digital tokens from Bitcoin to Ether rise: Bitcoin climbs 3.3% to exceed $42,400 while Ether rises 3.2% to more than $3,000. Names benefiting from the move include Bit Digital +5.6%; Ebang +5.4%; Marathon Digital +5%; Riot Blockchain +4.5%; Coinbase +2.4%. Here are the other notable premarket movers:

- Alibaba (BABA US) shares jump 8.8% in U.S. premarket trading after the e-commerce giant announced an increase in its share buyback program to $25 billion from $15 billion. The move will enhance shareholder value and could be a signal that regulatory scrutiny by authorities is letting up, analysts say.

- Shares in Chinese stocks rally in U.S. premarket trading, boosted after e- commerce giant Alibaba upsized its share buyback to $25b, while tech stocks post broad gains. Baidu (BIDU US) +4.8%, JD.com (JD US) +5.5%.

- Tencent Music’s (TME US) shares rise as much as 6.7% in U.S. premarket trading following results. While the Chinese online music company reported a decline in year-over-year revenue, the figure met the average analyst estimate. The company also announced a plan to pursue a secondary listing in Hong Kong.

- Stocks related to cryptocurrencies gain in premarket trading as digital tokens from Bitcoin to Ether rise. Bit Digital (BTBT US) +5.6%; Ebang (EBON US) +5.4%.

- Okta (OKTA US) shares drop 8.5% in U.S. premarket trading, amid worries over a potential data breach after hacking group Lapsus$ claims it has gained internal access to the tech firm’s system privileges.

- HireRight Holdings Corp. (HRT US) jumped 11% postmarket after the employment background screening company provided a 2022 forecast that beat estimates. 4Q revenue increased 32% from a year ago.

- Dave Inc. (DAVE US) advanced in after-hours trading as the company announced a partnership with West Realm Shires Services and reported fourth-quarter results.

Commodity-market disruptions stemming from the Ukraine war have increased pressure on the Fed and some other key central banks to tighten monetary policy. Powell said the Fed is prepared to raise interest rates by 50 basis points at the next policy meeting if needed. His comments led to a deepening selloff in bond markets. Many investors welcomed the Fed’s strong will to combat inflation, said AcivTrad’s Pierre Veyret. However, “flattening yield curves suggesting rising concerns of an economic slowdown to come in the longer run, associated with the lack of any clear breakthrough in Ukraine-Russia diplomatic talks in the short-term, could be seen as a sign market volatility and large swings in prices may not be over yet,” he said.

The Fed hiked by a quarter-point last week and signaled six more such moves this year. Derivative traders Monday priced in about 7.5 quarter-point rate hikes at the remaining six Fed meetings this year, effectively making provision for more than one half-point rise. Overnight, Goldman Sachs economists said they now expect the Fed to raise interest rates by 50 basis points at both its May and June policy meetings. Economists led by Jan Hatzius said the Fed will likely raise by 25 basis points in the four remaining meetings in the second half of the year, with three quarterly hikes in the first nine months of 2023.

“Our best guess is that the shift in wording from ‘steadily’ in January to ‘expeditiously’ today is a signal that a 50 basis points rate hike is coming,” they wrote adding that “the Russian invasion of Ukraine and the possibility that financial conditions could tighten more aggressively in response to a faster pace of Fed tightening both present downside risks to our new forecast.”

European equities trade well, led by banks, insurance and auto names. Euro Stoxx 50 rises as much as 1% before stalling. FTSE MIB outperforms. Here are some of the biggest European movers today:

- Nemetschek shares gain as much as 13%, the most since October 2020, after the firm delivered 2022 guidance ahead of estimates which should trigger up to high single-digit upgrades to consensus Ebitda numbers, Baader Helvea (add) writes in note.

- Softcat shares rally as much as 12%, the most in a year, after saying full year results will be ahead of expectations. Jefferies boosts its price target, saying first-half results are “strong” and the IT reseller is managing supply chain constraints in a “healthy way.”

- Dermapharm shares rise as much as 7.2%, the most since Feb. 9, with Berenberg (buy) saying the pharmaceutical manufacturer’s margins topped estimates.

- Casino shares rise as much as 3.6% on renewed takeover speculation after a BFM Business report saying CEO Jean-Charles Naouri wants to play a role in French grocer consolidation.

- Trustpilot shares fall as much as 24%, the biggest intraday decline on record, after full-year results that Morgan Stanley says highlights the consumer-review platform’s intention to accelerate investments. Broker estimates the company is guiding to an Ebitda loss of $15m-$20m in 2022.

- Shares in equipment-parts supplier Diploma drop as much as 5.5% after JPMorgan analyst Oscar Val Mas cut the stock to underweight from neutral, citing “unfavourable” risk-reward at current levels.

- CRH share fall as much as 2.1% in Dublin. Valuation looks “undemanding but uncompelling” as higher costs and weaker growth in Europe look set to dent recent margin gains, Redburn analyst Will Jones writes in a note, downgrading the construction materials supplier to neutral from buy. CRH .

Earlier in the session, stocks also rose in the Asia-Pacific region, helped by Alibaba’s increased buyback program and a lift for Japanese exporters from a weaker yen. The MSCI Asia Pacific Index jumped as much as 1%, with Alibaba the biggest contributor to gains in the regional benchmark as well as the Hang Seng Index after the e-commerce giant expanded its share-repurchase program to $25 billion from $15 billion. The Topix advanced for a sixth straight day as the Japanese market reopened after a holiday. The gains came even amid weakness in U.S. equities after Federal Reserve Chair Jerome Powell said he is prepared to raise interest rates by a half percentage-point at the next meeting if needed to fight inflation. Asian financial stocks climbed as bond yields surged on Powell’s comments. Shares in India and South Korea also gained as the rally in oil prices paused. Still, inflation concerns, the Russia-Ukraine war and China’s growth slowdown remain a weight on regional stocks, with the MSCI Asia Pacific Index down more than 7% year-to-date. “Given the sell off we have seen thus far, it is only natural that investors try to identify if the market is at an inflection point,” said Justin Tang, the head of Asian research at United First Partners

A Bloomberg Intelligence gauge of China property shares rose as much 3.2% as market watchers say more cities have rolled out easing policies, such as lowering mortgage rates. Property stocks lead gains on the Shanghai Composite Index; Shanghai Stock Exchange Property Index rises as much as 3.8%. China Fortune Land jumps by the 10% daily limit; Seazen Group rises as much as 9.3%, Country Garden Holdings +7.6%, Greenland Holdings +6.6%, Yuzhou +6.1%. Mortgage rates in major cities have dropped more than 10 basis points in March compared to the previous month, says Geng Xinxin, an analyst at ZhiXin Investing Research Institute.

Japanese equities rose for a sixth-straight day, with electronics and auto makers among the drivers as the yen continued to weaken. The Topix gained 1.3%, with financials and energy-related stocks also gaining. Tokyo Electron and KDDI were the biggest contributors to a 1.5% rise in the Nikkei 225. The yen slid 0.8% against the dollar, pushing its loss to 4.9% since March 4. Yields jumped as hawkish comments from Federal Reserve Chair Jerome Powell caused a slide in Treasuries. Oil surged on signs the European Union may be edging closer to a ban on Russian crude imports. “With the dollar-yen pair approaching the key 120 mark, it’s going to be a tailwind for export-related stocks,” said Norihiro Fujito, chief investment strategist at Mitsubishi UFJ Morgan Stanley Securities. “As crude oil future prices rise, trading companies and other resource-related stocks could be bought.”

Australia’s S&P/ASX 200 index rose 0.9% to 7,341.10, closing at the highest level since Jan. 20. The materials and energy sectors rose the most. Mineral exploration company AVZ Minerals Limited advanced for a fourth day to end at a record high. Mobile payment solution company Block fell, snapping four days of gains. In New Zealand, the S&P/NZX 50 index rose 0.2% to 12,204.69

In Rates, treasuries added to Monday’s steep declines during Asia session and European morning, sending yields across the curve to new YTD highs, with the 10Y TSY briefly rising above 2.30%. Benchmark Treasury yields added four basis points to Monday’s 14-basis point jump after Powell said the central bank is prepared to raise interest rates by a half percentage-point at its next meeting, if needed. Yields remain cheaper by 3bp-5bp, with most curve spreads slightly flatter on the day. 2-year TSY yields top at 2.195%, highest since May 2019, and remain cheaper by ~6bp on the day; 10-year higher by ~5bp at ~2.34%, cheapening by ~1.5bp vs comparable bunds and gilts. Fed-dated OIS price around 43bp of rate hikes — or 72% of a 50bp move — into the May meeting. In Europe, fixed income trades heavy with bund and gilt curves all bear flatter on the session. Peripheral spreads only marginally tighter to core. Focal points for U.S. session include potential for another busy corporate issuance slate; Monday’s caused choppy price action in swap spreads; also, three Fed speakers are scheduled, following hawkish comments from Chair Powell Monday.

In FX, the dollar initially climbed against all its G-10 peers as hawkish rhetoric from Federal Reserve Chair Jerome Powell propelled U.S. yields higher, however it then dipped in early London trade . The yen slid to a six-year low: a surge in dollar demand into the Tokyo fix pushed USD/JPY above 120 for the first time since February 2016, traders said. The greenback’s haven appeal got a boost after U.S. President Joe Biden said Russia had deployed a hypersonic missile against Ukraine and warned about new indications of possible cyberattacks. “The dollar looks to be finding the support from a hawkish Fed outlook that it really should have seen after the FOMC meeting last week,” said Sean Callow, senior currency strategist at Westpac Banking Corp. “It seems markets needed to be told twice by Powell what he planned to do on rates and where the risks lie to the baseline view”

In commodities, Crude futures decline. May WTI futures decline as much as 2.5%, back near $108. Base metals are mixed; LME nickel trades down over 9%, but remains within exchange limit. Spot gold falls roughly $11 to trade near $1,925/oz.

Bitcoin is bid, but off highs, having surpassed last week’s peak of USD 42,392 in a short-lived foray above the USD 43k mark.

Looking to the day ahead now, and data releases include the Richmond Fed’s manufacturing index from the US for March, as well as UK public sector net borrowing for February. Central bank speakers include ECB President Lagarde, Vice President de Guindos and the ECB’s Villeroy, Panetta and Lane, along with the Fed’s Williams, Daly and Mester, and BoE Deputy Governor Cunliffe.

Market Snapshot

- S&P 500 futures up 0.3% to 4,467.75

- STOXX Europe 600 up 0.4% to 456.81

- MXAP up 1.0% to 179.08

- MXAPJ up 1.2% to 585.14

- Nikkei up 1.5% to 27,224.11

- Topix up 1.3% to 1,933.74

- Hang Seng Index up 3.1% to 21,889.28

- Shanghai Composite up 0.2% to 3,259.86

- Sensex up 1.2% to 57,953.59

- Australia S&P/ASX 200 up 0.9% to 7,341.10

- Kospi up 0.9% to 2,710.00

- German 10Y yield little changed at 0.49%

- Euro down 0.2% to $1.0998

- Brent Futures down 0.6% to $114.96/bbl

- Gold spot down 0.4% to $1,927.22

- U.S. Dollar Index up 0.19% to 98.68

Top Overnight News from Bloomberg

- Federal Reserve Chair Jerome Powell said the central bank is prepared to raise interest rates by a half percentage-point at its next meeting if needed, deploying a more aggressive tone toward curbing inflation than he used just a few days earlier.

- The yen fell to a six-year low against the dollar, reflecting expectations of a growing divergence in monetary policy between the U.S. and Japan.

- Fed Chair Jerome Powell on Monday weighed in on a major topic of debate in the bond market: where to look to determine the chances for a U.S. recession.

A more detailed breakdown of global markets from Newsquawk

Asia-Pac stocks were mostly positive with the region shrugging off the higher yields and oil advances. ASX 200 was led higher by strength in the commodity-related sectors including energy after further gains in oil. Nikkei 225 gained as exporters benefitted from a weaker currency and amid stimulus speculation. Hang Seng and traded higher with outperformance among the blue-chip tech stocks including Shanghai Comp. Alibaba after it boosted its share buyback to USD 25bln from USD 15bln and with oil majors underpinned. China is to hold a press conference on Tuesday night regarding the latest updates of the crashed China Eastern Jet, according to State Media.

Top Asian News

- Evergrande Unit Starts Probe as $2.1 Billion of Cash Seized

- Kishida Likely to Respond Before BOJ as Yen Breaches 120

- Tycoon-Led Group Said to Win Approval to Buy Singapore Press

- Japan Rushes to Avoid Tokyo Blackout as Snowfall Hits City

European bourses have been erring higher after a contained open, Euro Stoxx 50 +0.9%, with upside occurring as crude and bonds slipped further. US futures are in-fitting directionally but magnitudes more contained, ES +0.2%, with a slew of Central Bank speakers ahead. Sectors features defensive names as the current underperformers while Consumer Products is bolstered post-Nike earnings. EU leaders could endorse taxing windfall profits of energy firms, according to a draft summit statement

Top European News

- Fortum Exits Oslo Heating Company Valued at $2.3 Billion

- Sunak Given Budget Boost as Borrowing $34 Billion Below Forecast

- U.K. Government Prepares to Take Over Gazprom Retail Arm

- EToro Clients’ Missing Russia Stock Shows Risk in Market Tumult

In FX, the dollar extends gains as Fed chair Powell delivers hawkish speech at NABE, underlining 50bps hikes at one or more meetings, a potentially higher terminal rate and QT kicking off in May perhaps/ DXY gets to within a whisker of 99.000 before waning. Yen extends slump as BoJ Governor Kuroda says any exit from ultra accommodation would be premature, USD /JPY now testing 121.00 after breaching a key Fib just over 119.50 and 120.00 with little resistance. Kiwi and Aussie bounce as risk appetite picks up, former back above 0.6900 and latter on the 0.7400 handle again. Loonie lags as oil prices retreat, USD/CAD over 1.2600. Pound and Euro derive some traction from corrective gains in Gilt and EGB yields; Cable close to 1.3200 and EUR/USD tests 1.1000 where 1.35bln option expiries start and end at 1.1010.

In commodities, WTI and Brent are pressured, but off lows, as the benchmarks are hit amid China’s COVID updates and reports of further support in the EU for an energy price cap. WTI and Brent May contracts have slipped from intraday highs of USD 113.30/bbl and USD 119.48/bbl to current lows of USD 107.10/bbl and USD 112.64/bbl, respectively. France and “several eastern EU countries” reportedly back the idea of energy price caps with Germany and the Netherlands left to be convinced, according to Journalist Keating; Germany/Netherlands argue that refusing to pay market price could mean suppliers go elsewhere. Subsequently, a Senior German official says that Berlin’s opposition to energy sanctions is “unlikely to unless Russia uses “chemical or nuclear weapons”, according to Eurasia Group’s Rahman. Adds, “One change” idea would see a “coalition of the willing” – member states with less Russian energy dependency, move first” – Note, it is unclear if this is the journalists’ view or an official. Japanese government says power supply is tightening in the Tohoku region amid low temperatures. Spot / are pressured, though off lows, amid what appears to be a outflow from “havens” with core-debt gold silver and JPY pressured. LME CEO says price limits should prevent a repeat of the squeeze seen in Nickel, via Bloomberg. At the open, LME Nickel -12%, at USD 27,600/T.

US Event Calendar

- 10am: March Richmond Fed Index, est. 2, prior 1

Central Bank Speakers

- 9:10am: New York Fed’s Wuerffel Discusses a Post-Libor World

- 10:35am: Fed’s Williams Takes Part in BIS Panel Discussion

- 2pm: Fed’s Daly Speaks at Brookings Institution Event

- 5pm: Fed’s Mester Discusses Economic Outlook and Monetary Policy

DB’s Jim Reid concludes the overnight wrap

Whilst Ukraine undoubtedly remains the most important news story right now, central bank comments dominated the market agenda once again yesterday, with a fresh aggressive bond sell-off occurring before and after Fed Chair Powell signalled that the Fed wouldn’t shy away from tightening policy in order to curb inflation. It was especially telling that the Chair indicated nothing would stop the Fed from hiking in 50bp increments if they needed to. Surely they would have gone 50bp last week but for the uncertainty of events in Ukraine. Indeed, it’s increasingly dawning on investors that this is going to be a very different hiking cycle from its predecessor back in 2015, and yesterday Fed Funds futures moved to price in more than 200bps worth of hikes for 2022 for the first time (including the 25bps we saw last week). In turn, that served to turbocharge the losses among sovereign bonds and led the S&P 500 to turn from positive territory before he spoke to close ever so slightly lower (-0.04%) and end a run of 4 consecutive gains. Yields exploded up too with the 10yr yield up +14.0bps to its highest level since 2019, at 2.29%. Around a half of the gains post Powell showing that momentum was moving in that direction anyway. We’ve moved another +4bps this morning in Asia.

Significantly as well, there was a noticeable flattening in the yield curve, with the 2s10s curve closing beneath 20bps (17.0bps) for the first time this cycle after the 2yr yield (+17.9bps) flew past 2% for the first time since 2019 as well, closing the day at 2.12% but now 2.175% in Asia with the curve now at c.15bps as I type.

As mentioned at the top, the speech also triggered a reappraisal in the future path of monetary policy, with Fed funds futures pricing an additional 186bps of hikes this year (on top of the 25bps we saw last week), which would take the total tightening this year beyond 200bps if realised, and implies a +50bp hike at some point this year. Even in Asia trading this morning we’ve seen an additional quarter of a hike added which is a pretty big move for an overnight session. Bear in mind that the last time we saw more than 200bps of hikes in a calendar year was all the way back in 1994 (when rates rose +250bps), so again a pace of tightening that’s potentially faster than anything else in the last 3 decades. Rate hikes were added into money markets beyond this year, which had 5yr Treasuries (+17.8bps) moving in lockstep with the 2yr tenor, inverting the 5s10s yield curve (-3.3bps).

In terms of the headlines, there were a number of hawkish comments made by Powell in his speech, including that “the labor market is extremely tight, significantly tighter than the very strong job market just before the pandemic”, whilst he also acknowledged that “forecasters widely underestimated the severity and persistence of supply-side frictions”. Furthermore, he said that the Fed would “take the necessary steps to ensure a return to price stability”, and that they would be willing to move by more than 25bps per meeting and also shift policy into restrictive territory if necessary. That said, he (unsurprisingly) struck an optimistic tone on the odds of lowering inflation via a soft landing, noting that in 1965, 1984 and 1994 the Fed was able to raise rates without triggering a recession, and pointed out that others (such as the pandemic recession in 2020) were not induced by monetary policy. Powell also downplayed the importance of my favourite cycle indicator, namely 2s10s, preferring to look at the shorter part of the yield curve to get a cleaner read on near-term Fed policy expectations, as ostensibly longer duration assets contain more drivers that confound the read-through to the policy outlook. Those shorter yield curves are still quite steep, indicative of the sharp Fed hiking cycle ahead. Despite near-term steepness, markets are nevertheless pricing in peak policy rates and subsequent cuts as soon as the second half of next year, and it remains the case that every post-war recession has been preceded by a 2s10s inversion.

With Treasury yields climbing to multi-year highs, we saw a similar pattern in Europe yesterday, with 10yr yields on bunds (+9.6bps), OATs (+9.7bps) and gilts (+14.2bps) all seeing significant increases. For bunds, that takes the 10yr yield up to the heady heights of 0.46%, which is a level not seen since late-2018, whilst the 4yr bund yield also closed in positive territory for the first time since 2015. That came as Bundesbank President Nagel said that an end to ECB bond-buying in Q3 “opens up the possibility of raising interest rates this year, if needed”, although unlike for the Fed we didn’t see that echoed in future ECB pricing, with the amount of hikes expected by the December meeting seeing a modest fall of -2.2bps yesterday. This growing divergence between an aggressive Fed and a more cautious ECB has been evident in market pricing elsewhere, with the gap between 2yr yields on US and German debt widening to 240.6bps yesterday, which we haven’t seen since 2019. On top of that, the relative differences in the US 2s10s (at 17.0bps) and the German 2s10s (at 76.4bps) is also the widest gap we’ve seen since 2019 too.

On Ukraine, the headline risk around the stilted negotiation progress continued. Following from the weekend’s news that Ukraine refused to surrender Mariupol and that the battles would continue, yesterday’s tone was more negative, as the Kremlin indicated progress in talks had been less than they would have liked, and no agreements had been reached as of yet. The more negative rhetoric around Ukraine saw oil prices added to their gains at the end of last week, with Brent Crude (+7.12%) closing at $115.62/bbl, whilst WTI saw a similar +7.09% increase to $112.12/bbl. As I type this morning, Brent futures are up a further +2.28% while WTI futures are advancing +1.96%. In contrast, European natural gas futures fell -8.32% yesterday, their lowest in three weeks, and are now -72.52% below the peaks reached during the height of the supply fears from the invasion earlier in the month.

Overnight in Asia, equity markets are mostly trading even as markets aggressively reprice the Fed. The Nikkei (+1.63%) is leading gains across the region after yesterday’s holiday driven by gains in financial stocks, as the yen weakened against the dollar. The Hang Seng (+1.13%) is advancing, reversing earlier session losses after Hong Kong listed shares of Alibaba rose more than +3% after the company ramped up its share buyback size from $15 billion to a record high $25 billion to prop up its beaten-up shares. This is the second time Alibaba has upsized its buyback programme in a year. Mainland Chinese stocks are trading mixed with the Shanghai Composite (+0.14%) higher whilst CSI (-0.08%) trading fractionally lower this morning. Meanwhile, Coronavirus-related developments continues to be monitored, following Hong Kong’s move to gradually lift its Covid-19 restrictions.

Moving ahead, stock futures in the US indicate a negative start with contracts on the S&P 500 (-0.29%) and Nasdaq (-0.43%) lower after rate fears continue to rise. Indeed, yesterday the S&P 500 came off its best week since November 2020. That saw the S&P 500 only lose -0.04% but the more interest-sensitive tech stocks saw bigger declines, with the NASDAQ down -0.40% and the FANG+ index down -0.65%. Europe also put in a subdued performance, with the STOXX 600 up +0.04%. However, that masked divergences at the country level, with the UK’s FTSE 100 (+0.51%) adding to its YTD gains, whereas the CAC 40 (-0.57%) and the DAX (-0.60%) both ended the day in negative territory.

It’s taken a back seat given the other global developments recently, but it’s worth noting that we’re now less than 3 weeks away from the first round of the French presidential election on April 10. Since the Russian invasion of Ukraine, President Macron has seen a notable bounce in the polls, and now stands at 30%, according to Politico’s polling average, up from 25% prior to the invasion. If realised, that would build on the 24% he scored in the first round back in 2017. President Macron’s second-round challenger in 2017, Marine Le Pen of the far-right Rassemblement National, is also currently in second-place this time around at 18%, and behind them are the far-left Jean-Luc Mélenchon (13%), the conservative Valérie Pécresse (11%) and the far-right Eric Zemmour (11%).

There wasn’t much at all on the data front yesterday, although a notable exception was the German PPI reading for February, which rose to +25.9% on a year-on-year basis (vs. +26.2% expected). I looked at this on a historical perspective in my chart of the day yesterday (link here) and it’s the highest producer price inflation since the aftermath of WWII, and on par with the highest peacetime levels on record. Even excluding energy, PPI is now running at +12.4%, which is the highest since the mid-1970s. Let me know if you want to be added to my CoTD.

To the day ahead now, and data releases include the Richmond Fed’s manufacturing index from the US for March, as well as UK public sector net borrowing for February. Central bank speakers include ECB President Lagarde, Vice President de Guindos and the ECB’s Villeroy, Panetta and Lane, along with the Fed’s Williams, Daly and Mester, and BoE Deputy Governor Cunliffe.

END

3. ASIAN AFFAIRS

i)TUESDAY MORNING// MONDAY NIGHT

SHANGHAI CLOSED UP 6.18 PTS OR 0.19% //Hang Sang CLOSED UP 667.94 PTS OR 3.15 % /The Nikkei closed UP 396.88 PTS OR 1.48% //Australia’s all ordinaires CLOSED UP 0.82% /Chinese yuan (ONSHORE) closed DOWN 6.3643 /Oil UP TO 111.61 dollars per barrel for WTI and UP TO 116.06 for Brent. Stocks in Europe OPENED ALL GREEN // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.3643. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.3660: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER//

3 a./NORTH KOREA/ SOUTH KOREA

///NORTH KOREA

END

3B JAPAN

3c CHINA

CHINA

Big news!!Evergrande states that lenders seized $2billion in deposits. Evergrande has not paid foreigners since they defaulted in Dec 2021

(zerohedge)

Evergrande Promises Emergency Debt-Restructuring Proposal After Lenders Seize $2 Billion In Deposits

TUESDAY, MAR 22, 2022 – 11:45 AM

China Evergrande Group has become infamous for its unsustainable debt load, the result of runaway development that saddled the company with unfinished and unsold condos, leading it to stiff foreign creditors to the tune of $20 billion (while employees of the company’s EV unit abruptly stopped paying staff and suppliers late last year) when it defaulted late last year.

And so, after months of failing to repay its foreign creditors, lenders have decided to take back what’s owed by force: to wit, Evergrande’s more financially stable property services subsidiary recently discovered that more than $2 billion of its cash had been seized by foreign lenders.

The company made the revelation Tuesday in a filing to the Hong Kong stock exchange, where it said that unnamed foreign lenders had seized more than RMB13.4 billion ($2.1 billion) of the subsidiary’s deposits that were pledged as security for “third party guarantees”. The company didn’t disclose which lenders had seized the money, or offer any additional details.

It also announced that it would unveil a debt-restructuring proposal by the beginning of July, according to a Reuters report (back in January, the company said it was aiming to have a restructuring proposal in place within six months). Of course, the loss of more than $2 billion in cash from its subsidiary’s balance sheet has only hastened the need for a new plan.

Evergrande, which owns more than 50% of the property services subsidiary, said it considers the seizure a “major incident” that could negatively impact the company. It has formed an independent committee to “investigate the pledge guarantees” and assess the implications of the seizure.

The seizure is bad news for bondholders, as Evergrande’s foreign currency bonds in default were already trading at a fraction of their $20 billion face value.

However, one source familiar with the situation told the FT that they suspected the money had actually been seized by a Chinese bank.

One person familiar with the situation suggested the money was likely to have been claimed by a mainland Chinese bank. “I think a western bank would understand they can’t take that money,” the person added.

The company said said it “is actively looking for solutions and communicating with its creditors” and had hired King & Wood Mallesons, a Hong Kong law firm, as a legal adviser.

Evergrande, Evergrande Property Services and China Evergrande New Energy Vehicle Group (Evergrande’s EV subsidiary) said Tuesday that “a large number of additional audit procedures” and the pandemic meant they couldn’t publish its audited annual report by the March 31 deadline, as required by Hong Kong markets. Trading in the firms’ securities has been halted since Monday.

The disaster also threatens to involve at least one “Big Four” firm: PricewaterhouseCoopers has been facing an inquiry by Hong Kong market regulators tied to its work on Evergrande since late last year. The incident has made auditors nervous about their work for Chinese property developers, as other firms – notably Shimao Group and Ronshine China – also said they wouldn’t have their audited financial statements prepared on time.

The question now is will this be the domino the sets off another debt crisis among China’s deeply indebted developers?

end

CHINA//USA/RUSSIA//UKRAINE

USA unexpectedly sanctions Chinese officials for their failure to condemn Russia for their actions in Ukraine. Also on the list is human rights violations

(zerohedge)

US Unexpectedly Sanctions China Officials Hours After Demanding Beijing Condemn Russia

MONDAY, MAR 21, 2022 – 06:20 PM

Apparently not content with diplomatic war on one front with Russia, the Biden administration appears ready to escalate with China following on the heels of last week’s persistent accusations that Beijing was mulling cooperation with Moscow on weapons resupplies for its Ukraine operation, as well as assistance on Western sanctions evasion.

Monday afternoon Secretary of State Antony Blinken announced more visa restrictions on Chinese officials related to prior charges that state authorities are overseeing the ethnic cleansing of Uighurs. It’s certainly interesting timing in terms of pulling out the the human rights card, given that throughout last week the admin’s China criticisms seemed exclusively focused on its “fence-sitting” over Ukraine.

Blinken called on China to “end its ongoing genocide and crimes against humanity in Xinjiang, repressive policies in Tibet, crackdown on fundamental freedoms in Hong Kong, and human rights violations,” as cited in Bloomberg.

“The United States rejects efforts by (Chinese) officials to harass, intimidate, surveil, and abduct members of ethnic and religious minority groups, including those who seek safety abroad, and U.S. citizens, who speak out on behalf of these vulnerable populations,” Blinken said. “We are committed to defending human rights around the world and will continue to use all diplomatic and economic measures to promote accountability.”

It’s unclear as yet which and how many Chinese state officials will be impacted by the new visa restriction measures, which will effectively ban them from travel into the United States, and it’s an expansion of prior Trump restrictions.

Earlier, the White House issued a statement saying – like UK prime minister Boris Johnson’s words over the weekend – that Beijing must condemn Russia’s invasion of Ukraine and stop downplaying it.

Meanwhile, here’s commentary from Rabobank on the implications of how China figures into the Ukraine crisis…

* * *