March 231 2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

March 31, 2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD; $1948.60 UP $13.30

SILVER: $24.94 UP $.03

ACCESS MARKET: GOLD $1937.10

SILVER: $24.78

Bitcoin morning price: $47,173 UP 3268 from Monday

Bitcoin: afternoon price: $48,693 up 4788 from Monday

Platinum price: closing UP to $993.40 FROM MONDAY

Palladium price; closing UP 17.45 at $2268.95

END

Today is options expiry for the comex

end

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

comex notices/

March: JPMorgan stopped/total issued 1374/12,491

EXCHANGE: COMEX

CONTRACT: APRIL 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,933.500000000 USD

INTENT DATE: 03/30/2022 DELIVERY DATE: 04/01/2022

FIRM ORG FIRM NAME ISSUED STOPPED

072 C GOLDMAN 434

099 H DB AG 1116

104 C MIZUHO 5

118 C MACQUARIE FUT 100

132 C SG AMERICAS 58

219 C SANTANDER-C 1

285 C NANHUA USA-HK 1

323 C HSBC 1

323 H HSBC 1516

357 C WEDBUSH 1

363 H WELLS FARGO SEC 396

365 C ED&F MAN CAPITA 2

365 H ED&F MAN CAPITA 4

435 H SCOTIA CAPITAL 629

624 H BOFA SECURITIES 1267

657 C MORGAN STANLEY 26 896

657 H MORGAN STANLEY 672

661 C JP MORGAN 6611 1374

685 C RJ OBRIEN 3

686 C STONEX FINANCIA 100 37

700 H UBS 333

709 C BARCLAYS 2893

732 C RBC CAP MARKETS 2

732 H RBC CAP MARKETS 2666

800 C MAREX SPEC 4

880 C CITIGROUP 2070

880 H CITIGROUP 1637

905 C ADM 13 114 TOTAL: 12,491 12,491MONTH TO DATE: 12,491

NUMBER OF NOTICES FILED TODAY FOR APRIL. CONTRACT 12,491 NOTICE(S) FOR 1249100 OZ (32.852 TONNES)

total notices so far: 12,491 contracts for 1,249100 oz (32.852 tonnes)

SILVER NOTICES:

647 NOTICE(S) FILED TODAY FOR 3,235,000 OZ/

total number of notices filed so far this month 647 : for 3,235,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

END

GLD

WITH GOLD UP $13.30

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

A BIG CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.74 TONNES FROM THE GLD//FROM MONDAY

INVENTORY RESTS AT 1091.44 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UIP 3 CENTS

AT THE SLV// A HUGE CHANGE IN SILVER INVENTORY AT THE SLV/ THE SLV//A DEPOSIT OF 2.171 MILLION OZ INTO THE SLV

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 556.338 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A TINY SIZED 60 CONTRACTS TO 147,120 AND CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE STRONG LOSS IN OI WAS ACCOMPLISHED WITH OUR STRONG $0.30 LOSS IN SILVER PRICING AT THE COMEX ON FRIDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.38) AND WERE SUCCESSFUL IN KNOCKING OUT SOME SILVER LONGS AS WE HAD A STRONG GAIN OF 1580 CONTRACTS ON OUR TWO EXCHANGES

WE MUST HAVE HAD:

I) HUGE BANKER SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A GOOD ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A HUGE INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 4.305 MILLION OZ V) STRONG SIZED COMEX OI GAIN/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS : —-768 (the differential in silver is now increasing every day)

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAR. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAR:

TOTAL CONTACTS for 23 days, total contracts: : 41,486 contracts or 207.430 million oz OR 9.01MILLION OZ PER DAY. (1803 CONTRACTS PER DAY)

TOTAL NO OF OZ UNDERGOING EFP TO LONDON 41,486 CONTRACTS X 5,000 PER CONTRACT:

EQUATES TO: 207.43 MILLION OZ WHICH FINALIZES THE RECORD FOR MARCH AND FOR ANY MONTH

.

LAST 11 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

RESULT: WE HAD A STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 828 WITH OUR STRONG $0.38 GAIN IN SILVER PRICING AT THE COMEX// WEDNESDAY THE CME NOTIFIED US THAT WE HAD A GOOD SIZED EFP ISSUANCE OF 640 CONTRACTS( 640 CONTRACTS ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A HUGE INITIAL SILVER OZ STANDING FOR MAR. OF 4.305 MILLION OZ /// .. WE HAD AN STRONG SIZED GAIN OF 1580 OI CONTRACTS ON THE TWO EXCHANGES FOR 7.54 MILLION OZ WITH THE STRONG GAIN IN PRICE.

WE HAD 642 NOTICES FILED TODAY FOR 3,235,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A GOOD SIZED 4647 CONTRACTS TO 579,168 AND CLOSER TO NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: —–58 CONTRACTS. (differentials are lowering in gold)

THE BIS HAS ABANDONED THE GOLD COMEX TRADING!!!

.

THE GOOD SIZED INCREASE IN COMEX OI CAME WITH OUR GAIN IN PRICE OF $21.50//COMEX GOLD TRADING/WEDNESDAY/.AS IN SILVER WE MUST HAD HUGE BANKER/ALGO SHORT COVERING ACCOMPANYING OUR GOOD SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR APRIL AT 78.28 TONNES

YET ALL OF..THIS HAPPENED WITH OUR GAIN IN PRICE OF $21.50 WITH RESPECT TO WEDNESDAY’S TRADING

WE HAD AN STRONG SIZED GAIN OF 5469 OI CONTRACTS (17.01 PAPER TONNES) ON OUR TWO EXCHANGES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A SMALL SIZED 880 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 579,168.

IN ESSENCE WE HAVE AN GOOD SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 5527, WITH 4647 CONTRACTS DECREASED AT THE COMEX AND 880 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 5527 CONTRACTS OR 17.17 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (880) ACCOMPANYING THE GOOD SIZED GAIN IN COMEX OI (4647,): TOTAL GAIN IN THE TWO EXCHANGES 5527 CONTRACTS. WE NO DOUBT HAD 1) HUGE BANKER SHORT COVERING ,2.) HUGE INITIAL STANDING AT THE GOLD COMEX FOR APRIL. AT 78.28 TONNES/// 3) ZERO LONG LIQUIDATION ///. ,4) GOOD SIZED COMEX OI. GAIN 5) SMALL ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

MARCH

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAR :

131,591 CONTRACTS OR 1,315,910 OR 409.30 TONNES 23 TRADING DAY(S) AND THUS AVERAGING: 5965 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 23 TRADING DAY(S) IN TONNES: 409.30TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2020, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 409.30/3550 x 100% TONNES 11.52% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF MAY.WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF APRIL HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF MAY, FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (MAR), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A TINY SIZED 60 CONTRACTS TO 148,198 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 4 1/2 YEARS AGO.

EFP ISSUANCE 680 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 680 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 665 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 680 CONTRACTS AND ADD TO THE 680 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A STRONG SIZED GAIN OF 720 OPEN INTEREST CONTRACT FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 3.6 MILLION OZ,

OCCURRED WITH OUR STRONG GAIN $0.38 IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

5. Other gold commentaries

6. Commodity commentaries/cryptocurrencies

3. ASIAN AFFAIRS

i)THURSDAY MORNING// WEDNESDAY NIGHT

SHANGHAI CLOSED UP 2.26 PTS OR 0.07% //Hang Sang CLOSED UP 280.09 PTS OR 1.31 % /The Nikkei closed DOWN 205.95 PTS OR 0.73% //Australia’s all ordinaires CLOSED DOWN 0.01% /Chinese yuan (ONSHORE) closed DOWN 6.3703 /Oil DOWN TO 107.28 dollars per barrel for WTI and DOWN TO 114.11 for Brent. Stocks in Europe OPENED ALL GREEN // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.3703 OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.3859: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER//

A)NORTH KOREA/

b) REPORT ON JAPAN

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A GOOD SIZED 4589 CONTRACTS TO 579,110 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX INCREASE OCCURRED WITH OUR LOSS OF $14.65 IN GOLD PRICING MONDAY’S COMEX TRADING. WE ALSO HAD A FAIR SIZED EFP (2098 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE ACTIVE DELIVERY MONTH OF APRIL.. THE CME REPORTS THAT THE BANKERS ISSUED A SMALL SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 880 EFP CONTRACTS WERE ISSUED: ;: , . 0 JUNE :880 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 880 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 5469 CONTRACTS IN THAT 880 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED COMEX OI GAIN OF 4589 CONTRACTS..AND THIS FAIR SIZED GAIN OCCURRED DESPITE THE HUGE GAIN IN PRICE OF $21.50.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING FOR APRIL (78.21),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 78.21

THE BANKERS WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $21.50) BUT THEY WERE UNSUCCESSFUL IN FLEECING ANY LONGS AS WE HAVE REGISTERED A FAIR SIZED GAIN OF 7.832 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR APRIL (78.21 TONNES)…

WE HAD –58 CONTRACTS SUBTRACTED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 5527 CONTRACTS OR 552700 OZ OR 17,17 TONNES

Estimated gold volume today: 151,338 ///poor

Confirmed volume yesterday: 162,315 contracts poor

INITIAL STANDINGS FOR APRIL ’22 COMEX GOLD //MARCH 31

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 58,445.949 oz Manfra Delaware |

| Deposit to the Dealer Inventory in oz | 262,520.945 oz Manfra Brinks OZ |

| Deposits to the Customer Inventory, in oz | 54,335.190 oz (1690 kilobars) |

| No of oz served (contracts) today | 12,491 notice(s)1,249,100 OZ 38,852 TONNES |

| No of oz to be served (notices) | 12,655 contracts 1,265,500 oz 39.36 TONNES |

| Total monthly oz gold served (contracts) so far this month | 12491 notices 1,249,100 OZ 38.852 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For today:

dealer deposits 2

i) Into Dealer Brinks: 202.907.000 oz

ii Into dealer Manfra: 59,613.945 oz

total dealer deposit 262m520.945 oz//total dealer deposit 8.165

No dealer withdrawal 0

1 customer deposits

ii) Into HSBC 54,335.190 oz

total customer deposit: 54,335.190 oz //total dealer and customer deposit 9.855 tonnes

2 customer withdrawal

i)out of Delaware: 1671.852 oz

ii) Out of Manfra 56,784.09 oz

total withdrawals: 58,445.949 oz

ADJUSTMENTS: dealer to customer

i) jpmorgan: 27,418.953 oZ

adjustment customer to dealer

Loomis: 26,042.893 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR APRIL.

For the front month of APRIL we have an INITIAL out of 25,157 contracts having LOST ONLY 3601

Thus the initial amount of gold standing for April is as follows;

25,146 x 100 oz per notice: equals: 2,514,600 oz or a huge 78.21 tonnes

Our banker friends have run out of gold metal everywhere.

May saw a GAIN of 203 contracts to stand at 5502

June saw a GAIN of 8652 contracts up to 473,866 contracts

We had 12,491 notice(s) filed today for 1,249,100 oz FOR THE APRIL 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 6611 notices were issued from their client or customer account. The total of all issuance by all participants equates to 12,491 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 1374 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 434 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the APRIL /2021. contract month,

we take the total number of notices filed so far for the month (12,491) x 100 oz , to which we add the difference between the open interest for the front month of (APRIL 25,167: CONTRACTS ) minus the number of notices served upon today 12,491 x 100 oz per contract equals 2,516,700 OZ OR 78.28 TONNES the number of TONNES standing in this active month of APRIL.

thus the INITIAL standings for gold for the APRIL contract month:

No of notices filed so far (12,491) x 100 oz+ (25,167) OI for the front month minus the number of notices served upon today (12,491} x 100 oz} which equals 2,616,700 oz standing OR 78.21 TONNES in this active delivery month of APRIL.

TOTAL COMEX GOLD STANDING: 78.21 TONNES (A WHOPPER FOR A APRIL ( ACTIVE) DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

191,133,764.7, oz NOW PLEDGED /HSBC 5.94 TONNES

99,258.893 PLEDGED MANFRA 3.08 TONNES

54,339.114oz PLEDGED JPMorgan no 1 1.690 tonnes

243,923.704, oz JPM No 2 7.58 TONNES

898,821.330 oz pledged Brinks/27,96 TONNES

International Delaware:: 0

Loomis: 18,615.429 oz

total pledged gold: 1,487,476.805 oz 46.27 tonnes

TOTAL REGISTERED AND ELIG GOLD AT THE COMEX: 35,199.058.447 OZ (1094.81TONNES)

TOTAL ELIGIBLE GOLD: 18,087.308.310OZ (562.57 tonnes)

TOTAL OF ALL REGISTERED GOLD: 17,111,750.780 OZ (532.24 tonnes)

REGISTERED GOLD THAT CAN BE SERVED UPON: 15,624.274.0 OZ (REG GOLD- PLEDGED GOLD) 490.50 tonnes

END

MAR 2022 CONTRACT MONTH//SILVER//MARCH 31

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 861,723.212 oz Brinks CNT Manfra |

| Deposits to the Dealer Inventory | Manfra857,050.230OZ |

| Deposits to the Customer Inventory | 273,623.780 oz Brinks |

| No of oz served today (contracts) | 647CONTRACT(S) 3,285,,000 OZ) |

| No of oz to be served (notices) | 214 contracts (1,070,000 oz) |

| Total monthly oz silver served (contracts) | 647 contracts 3,235,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

we had 1 deposits into the dealer

i)Into Manfra: 857,050.230 oz

total dealer deposits: 857,050.230 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 1 deposits into the customer account

i) Into Brinks 273,623.780 oz

total deposit: 273,623.780 oz

JPMorgan has a total silver weight: 179.710 million oz/340.969 million =52.71% of comex

i) Comex withdrawals: 2

i) Out of HSBC: 100,290.700 oz

v) Out of Manfra: 273,623.780 oz

total withdrawal 373,914.480 oz

0 adjustments:

the silver comex is in stress!

TOTAL REGISTERED SILVER: 85.709 MILLION OZ

TOTAL REG + ELIG. 340.969 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR APRIL

silver open interest data:

FRONT MONTH OF APRIL OI: 861, HAVING GAINED 29 CONTRACTS FROM WEDNESDAY WHICH IS A HUGE SURPRISE.

THUS BY DEFINITION THE INITIAL AMOUNT OF SILVER STANDING IN THIS NON ACTIVE MONTH OF APRIL IS AS FOLLOWS:

861 X 5000 oz per notice = 4,305,000 oz

which is excellent for April

MAY HAD A LOSS OF 1514 CONTRACTS DOWN TO 105,305 contracts

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 647 for 3,325,000 oz

Comex volumes: 39,579// est. volume today//poor/

Comex volume: confirmed yesterday: 43,682 contracts ( poor )

To calculate the number of silver ounces that will stand for delivery in APRIL. we take the total number of notices filed for the month so far at 647 x 5,000 oz = 3,285,000oz

to which we add the difference between the open interest for the front month of APRIL (861) and the number of notices served upon today 647 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the APRIL./2021 contract month: 647 (notices served so far) x 5000 oz + OI for front month of MAR 861) – number of notices served upon today (647) x 5000 oz of silver standing for the APRIL contract month equates 4,305,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

MARCH 31/WITH GOLD UP $13.30 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD FROM MONDAY A WITHDRAWAL OF 1.71 TONNES FROM THE GLD:INVENTORY RESTS AT 1091.44

MARCH 28/WITH GOLD DOWN $14.65: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1093.18 TONNES

MARCH 25/WITH GOLD DOWN $7.60 : A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.52 TONNES INTO THE GLD///INVENTORY RESTS AT 1093.18 TONNES

MARCH 24/WITH GOLD UP $24.95: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.06 TONNES INTO THE GLD..//INVENTORY RESTS AT 1087.66 TONNES

MARCH 23/WITH GOLD UP $15.75//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1083.60 TONNES

MARCH 22/WITH GOLD DOWN $7.75: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.16 TONNES OF GOLD DEPOSITED INTO THE GLD//INVENTORY RESTS AT 1083.60 TONES

MARCH 21//WITH GOLD UP $.25 : A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 9.00 TONNES INTO THE GLD////INVENTORY RESTS AT 1082.44 TONES

MARCH 18/WITH GOLD DOWN $13.55 NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1073.44 TONES

MARCH 17/WITH GOLD UP $33.50: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.61 TONNES INTO THE GLD//INVENTORY RESTS AT 1073.44 TONNES

MARCH 16/WITH GOLD DOWN $18.50//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.33 TONNES FROM THE GLD///INVENTORY RESTS AT 1061.83 TONNES

MARCH 15/WITH GOLD DOWN $30.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1064.16 TONNES

MARCH 14//WITH GOLD DOWN $22.75, HUGE CHANGES IN GOLD INVENTORY AT THE GLD//STRANGE: A DEPOSIT OF 2.62 TONNES INTO THE GLD.//INVENTORY RESTS AT 1064.16 TONNES

MARCH 11/WITH GOLD DOWN $14.60: A BIG CHANGE IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 1061.54 TONNES

MARCH 10//WITH GOLD UP $11.55: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.06 TONNES FORM THE GLD///INVENTORY RESTS AT 1063.28 TONNES

MARCH 9/WITH GOLD DOWN $53.85//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.64 TONNES INTO THE GLD//INVENTORY RESTS AT 1067.34 TONNES

MARCH 8/WITH GOLD UP $46.10: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 8.42 TONNES INTO THE GLD///INVENTORY RESTS AT 1062.70 TONNES

MARCH 7/WITH GOLD UP $28.40 A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.06 TONNES INTO THE GLD..//INVENTORY RESTS AT 1054.28 TONNES

MARCH 4/WITH GOLD UP $28.40//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1050.22 TONNES

MARCH 3/WITH GOLD UP $13.95: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 7.84 TONNES//INVENTORY RESTS AT 1050.22 TONNES

MARCH 2/WITH GOLD DOWN $20.80//A MONSTER CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 13.36 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 1042.38 TONNES

MARCH 1/WITH GOLD UP $42.60: NO CHANGES IN GOLD INVENTORY AT THE GLD: //INVENTORY RESTS AT 1029.32 TONNES

FEB 28/WITH GOLD UP $12.95: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1029.32 TONNES

FEB 25/WITH GOLD DOWN $38.95: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1029.32 TONNES

FEB 24/WITH GOLD UP $17.35//A HUGE CHANGE AT THE GLD: 5.23 TONNES INTO THE GLD// IN GOLD INVENTORY AT THE GLD/INVENTORY REST AT 1029.32 TONNES

FEB 23/WITH GOLD UP $2.00 : NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1024.09 TONNES

CLOSING INVENTORY FOR THE GLD//1091.44 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MARCH 31/WITH SILVER UP 3 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 2.171 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 554.167 MILLION OZ

MARCH 28/WITH SILVER DOWN 30 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.847 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 554.167 MILLION OZ//

MARCH 25/WITH SILVER DOWN 20 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 552.320 MILLION OZ//

MARCH 24/WITH SILVER UP 54 CENTS TODAY; A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.092 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 552.320 MILLION OZ//

MARCH 23/WITH SILVER UP 24 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 550.288 MILLION OZ//

MARCH 22/WITH SILVER DOWN $0.29 TODAY : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 550.288 MILLION OZ//

MARCH 21/WITH SILVER UP 16 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 550.288 MILLION OZ//

MARCH 18/WITH SILVER DOWN 37 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.217 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 550.288 MILLION OZ//

MARCH 17/ WITH SILVER UP 72 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.049 MILLION OZ INTO THE SLVV//INVENTORY RESTS AT 548.071 MILLION OZ

MARCH 16/WITH SILVER DOWN 56 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 462,000 OZ FROM THE SLV//INVENTORY RESTS AT 544.560 MLLION O

MARCH 15/WITH SILVER DOWN 18 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 545.022 MILLION OZ

MARCH 14/WITH SILVER DOWN 64 CENTS TODAY; STRANGE A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.125 MILLION OZ/INVENTORY RESTS AT 545.022 MILLIONOZ

MARCH 11/WITH SILVER DOWN 13 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.897 MILLION OZ

MARCH 10/WITH SILVER UP 39 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.897 MILLION OZ/

MARCH 9/WITH SILVER DOWN 88 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 5.174 MILLION OZ OF FAKE SILVER.//INVENTORY RESTS AT 542.897 MILLION OZ//

MARCH 8/WITH SILVER UP 88 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.217 MILLION OZ INTO THE SLV////INVENTORY RESTS A 548.071 MILLION OZ//

MARCH 7/WITH SILVER UP 40 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 545.854 MILLION OZ//

MARCH 4/WITH SILVER UP 50 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 545.854 MILLION OZ/

MARCH 3/WITH SILVER UP 2 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 545.854 MILLION OZ//

MARCH 2/WITH SILVER DOWN $.32 TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 198,000 OZ FROM THE SLV//INVENTORY RESTS AT 545.854 MILLION OZ//

MARCH 1/WITH SILVER UP $1.13 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 546.052 MILLION OZ//

FEB 28/WITH SILVER UP 31 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT 546.052 MILLION OZ//

FEB 25/WITH SILVER DOWN 64 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 5.510 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 546.052 MILLION OZ/

FEB 24/WITH SILVER UP 15 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 551.597 MILLION OZ

FEB 23/WITH SILVER UP 22 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 551.597 MILLION OZ//

SLV FINAL INVENTORY FOR TODAY: 554.167 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

2.LAWRIE WILLIAM//,//Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, James RICKARDS/

Rickards: I’ve Never Heard So Many Lies

THURSDAY, MAR 31, 2022 – 01:29 PM

Authored by James Rickards via DailyReckoning.com,

All wars are full of lies.

Winston Churchill famously said, “In wartime, truth is so precious that she should always be attended by a bodyguard of lies.”

We accept that idea broadly. Secret invasion plans should be closely held. The identities of spies must be kept under wraps. New weapons and defensive tools should not be revealed because enemies will be alerted to their potential and begin offensive workarounds.

Still, just because the government has legitimate reasons to deceive the public in wartime does not mean that citizens don’t have a duty to find the truth to the extent they can.

The Russian-Ukraine kinetic war and the broader U.S.-Russian economic war are full of more lies than any public events I’ve seen in my lifetime including Vietnam, Watergate and the Iraq War.

That’s how big the lies are.

The Bodyguard of Lies

Here’s the official U.S. narrative as echoed by the mainstream media: Russia’s invasion of Ukraine was unprovoked, Putin’s three-day blitzkrieg of Kyiv has failed, Russian forces are bogged down and valiant Ukrainian troops are putting up a powerful defense and regaining lost ground with the help of weapons from NATO.

In this version, President Zelenskyy is the new Churchill rallying patriots against an evil dictator. All of that is either entirely or mostly false.

Here’s the real story: Russia’s invasion is the end result of 14 years of provocation by the West, including repeated declarations that Ukraine will join NATO and a U.S.-backed coup d’état in 2014 that displaced a pro-Russian president.

Russia never planned a blitzkrieg on Kyiv. That’s a Western invention intended to make Putin look like a failure. In fact, Russia is slowly and methodically taking territory in the south and east of Ukraine in order to control the seacoasts, eliminate pro-fascist elements in Mariupol and establish pro-Russian autonomous zones in Donbas.

Churchill? Really?

A full assault on Kyiv, if it ever comes, is last on the list. Ukraine may reoccupy a village here and there, but they’re losing ground in Kherson, Mykolaiv, Melitopol, Mariupol, Kharkiv, Luhansk, Donetsk and surrounding areas.

Moreover, Zelenskyy is no Churchill.

He’s succeeded in presenting himself as a strong wartime leader, standing up to the big, bad Putin. But in reality, he’s a corrupt oligarch with millions of dollars hidden offshore. His acting skills have enhanced his propaganda efforts, but it doesn’t take much training to see how phony he is.

Innocent civilians, including women and children, are dying under his failed leadership and inability to come to terms with Putin before the invasion began. In a nutshell, Zelenskyy bet on support from Biden and the West and lost.

There is ample evidence from numerous sources to support this analysis. Some of the best sources come from Switzerland, where military experts are infuriated that traditional Swiss neutrality has been cast aside.

Most tellingly, Pentagon leaks say the same thing. The story from inside the Pentagon is that Putin is not acting recklessly but is being patient and methodical. It also says that, despite some civilian casualties, Putin is actually using a restrained approach. Furthermore, there are no signs he is preparing for the use of chemical or biological weapons.

So what about the economic sanctions? Are they working?

The Most Severe Sanctions in History

Payments in and out of Russia have been blocked. The Central Bank of Russia has been banned from the global dollar payments systems. The same is true for the 10 largest Russian banks and a long list of oligarchs and Russian government officials.

Accounts of Russian targets in Western banks have been frozen. Exports of critical technology and high-tech equipment to Russia have been banned. U.S. and European airspace has been closed to Russian airlines.

Secondary sanctions have been imposed so that if another nation like China sells goods to Russia made with U.S. technology or machines, that nation will be punished also. The list goes on.

Economic sanctions of these kinds sound powerful when they’re announced and do have some impact. But in the long run they never work. In the end, the costs are real but the effects of the sanctions are nil. It’s a lose-lose proposition.

Sanctions Against Oligarchs Are Doing Putin a Favor

Some losses are incurred by those whose accounts are frozen or whose businesses are handicapped. A few Russian oligarchs may lose their yachts, but guess what? Putin doesn’t like the oligarchs anyway.

We’re actually doing Putin a favor by clipping the oligarchs’ wings. Putin’s power comes from the military and security services, not the oligarchs.

Tellingly, the strategic goals that justified the sanctions are never achieved. At most, they are slowed down temporarily. It’s just a matter of time before the affected parties devise workarounds to the sanctions.

The bottom line is Russia has not stood still. Russian exports of critical strategic metals such as nickel, titanium, palladium and aluminum have been cut off. Russian (and Ukrainian) wheat and other grains have also been cut off.

This will result in starvation in certain parts of the world and massive food price inflation everywhere. Given the extent of these sanctions and the retaliation, the damage to world trade, supply chains and even the availability of goods will be massive.

But what about the strategic aims of the sanctions?

Sanctions Won’t Stop the Ukrainian War

Here, the sanctions are a complete failure. They have had zero impact on Russian advances on the battlefield and Russian goals in Ukraine. In fact, Putin has proved to be a master chess player as he runs rings around the sanctions.

When the U.S. imposed sanctions on Russian banks, the value of the ruble collapsed. Still, oil and natural gas exports from Russia were allowed because Europe is dependent on them and the world is facing an energy shortage independent of the war in Ukraine.

Oil and natural gas are paid for in dollars. In a masterpiece of judo, Putin is now demanding that Russian oil and natural gas bought by states imposing sanctions be paid for in rubles. This mystified many. If Russia needs dollars (they do), why be paid in rubles?

The answer is that the only way for Europe to get rubles quickly is to buy them from the Central Bank of Russia using dollars. Under Putin’s plan, Russia still gets the dollars, still sells oil and natural gas but he has the added benefit of making rubles stronger because Europe has to buy them to pay for the energy exports.

Cutting off Russian exports of oil and natural gas is pointless because Russia will just sell the same energy to China and India. But the price will go up. It’s a world market, after all.

Putin’s Many Moves Ahead of Biden

This is how judo works. You use your enemy’s power against him by avoiding the main attack and turning the tables. Putin’s a judo expert in real life and he just demonstrated that he can practice it in economic warfare. The West will now be engaged in propping up the ruble after they did so much to destroy it.

Putin thinks many moves ahead on the chessboard while Biden is playing pin the tail on the donkey, blindfolded.

Sanctions ultimately harm everyday citizens and consumers most. Inflation is surging in Russia and the United States because of the sanctions. But the pain on the American people has only begun. It’s about to get much worse.

U.S. consumers and investors will suffer as prices soar, growth lags and stocks collapse.

This is all unpleasant news for Western warmongers. But it’s critical for investors to know what’s actually going on so they don’t lose money in the chaos to come.

The best information is that the war in Ukraine will last longer than most expect, will produce supply chain disruptions and will amplify the inflation that’s already present.

In the end, Putin will prevail in Ukraine, while the Ukrainian people and Western consumers will pay the heaviest price.

-END

–

-END-

LAWRIE WILLIAMS

LAWRIE WILLIAMS: : Swiss Feb gold exports show little change

With Swiss gold imports and exports providing such a reliable window on worldwide gold flows, the latest figures for February will have been viewed with particular interest given the Ukraine war situation. With the Russian invasion only commencing on the 24th of that month, it is too early yet to see the direct consequences of the war, although there will have been some nervousness in the gold markets ahead of that date as Russia’s intentions were then still uncertain. There will also have been some direct impact, though, on flows right at the end of the month. The March figures when they come out in just under a month’s time will perhaps give us a better idea of any impact, if any, on global gold flows.

What the February figures do show is that export volumes had indeed begun to pick up a little. Global geopolitical uncertainty will always likely boost gold take-up in traditional gold demand areas as investors seek to protect their wealth by accessing traditional safe haven investments.

As usual the country-by-country destinations of the Swiss exports continued to see the usual flows from West to East with China plus Hong Kong returning to be the largest recipient, followed by India which continued to import a substantial volume of Swiss re-refined gold.

The Swiss gold refineries are the historic leaders in independent gold refining worldwide taking gold scrap, doré bullion from mines, and large good delivery gold bars and refining them to the marginally higher quality and smaller size gold bars, wafers and coins most in demand in the global marketplace. They refine, between them, around 1,300 tonnes of gold a year – a little over a quarter of the world’s total annual gold output despite the country having no domestic gold production itself

.Chart: February’s Swiss gold exports by principal recipient nation

The destinations of the Swiss gold exports thus provide an excellent destination indicator of global gold flows with the world’s two biggest gold consumers topping the list once again. For February some 80% of the Swiss gold was destined for the Middle and Far East and South Asia where the gold is thought to be held in firmer hands and less likely to be sold on as speculative holdings. With gold flows into the Gold ETF sector back to being positive again as well gold appears to be going through a strong demand phase which is, no doubt, being further enhanced by the Russian invasion of Ukraine – the more so as fighting there continues relatively unabated.

There is some evidence, although this does not seem to be being confirmed on the ground yet that Russia may be changing its tactics. Its purported objectives now seem to be a concentration in taking over those parts of the Donbass region currently not fully under its control, and effectively merging them into the Russian Federation although Ukraine seems unlikely to accede to this without further resistance.

There are some ongoing peace negotiations under way in Istanbul with both sides seemingly willing to make some concessions on previously hugely entrenched positions. There has also been a promise from Russia that the intensity of the assault on the key northern Ukrainian cities of Kyiv, the country’s capital, and Chernihiv will be reduced, although whether this is a realistic promise, or perhaps a tacit admission that the Russian advance has come up against a Ukrainian brick wall, still remains to be clarified.

While the conflict continues, which may be for some time to come, the gold price will probably remain elevated, although in part this will be the indirect consequence of the Russian invasion, rather than its reality. Global inflation is running high, enhanced by the direct and indirect consequences of the sanctions being applied to the Russian economy, and the disruption to international trade caused by the war. In combination Russia and Ukraine are major suppliers to world markets of key energy, metal and foodstuff-related commodities and interruptions to these are already having huge, and growing, inflationary consequences. High inflation, coupled with low central bank-imposed interest rates, tends to be very positive for non interest- generating safe haven assets like gold, so the yellow metal’s price path looks like remaining positive for some time to come.

3. Chris Powell of GATA provides to us very important physical commentaries

Kinross close to selling its Russian mine to Russian interests

(Wall Street Journal)

Kinross Gold nears sale of Russian mine to Russian mining executive

Submitted by admin on Wed, 2022-03-30 23:43Section: Daily Dispatches

By Ben Dummett and Alistair MacDonald

The Wall Street Journal

Wednesday, March 30, 2022

Canadian miner Kinross Gold Corp. is in exclusive talks to sell its giant Arctic Russian mine to Fortiana Holdings Ltd., according to people familiar with the matter, a deal that if consummated could mark the first sale of an asset a Western company is leaving behind in Russia.

Fortiana is a Russian-backed investment firm with interests in gold mining assets.

Companies from oil major BP to brewing giant Carlsberg have said they would exit their Russian businesses after Moscow’s invasion of Ukraine, in some cases warning of large writedowns. A big question has been who might snap up those assets and how much they might pay.

Kinross, the only large Western miner with a presence in Russia, flagged it could leave the country when it announced plans to suspend its operations there this month. On Tuesday the company said it had entered exclusive talks with an unnamed buyer after considering a number of proposals in recent weeks. …

… For the remainder of the report:

END

The associated press finally gets it: the Russian ruble’s rebound raises questions on the sanctions impact

(Associated Press)

Russian ruble’s rebound raises questions of sanctions’ impact

Submitted by admin on Wed, 2022-03-30 23:33Section: Daily Dispatches

By Ken Sweet and Ellen Knickmeyer

Associated Press

via Yahoo News, Sunnyvale, California

Wednesday, May 30, 2022

WASHINGTON — The ruble is no longer rubble.

The Russian ruble by Wednesday had bounced back from the fall it took after the U.S. and European allies moved to bury the Russian economy under thousands of new sanctions over its invasion of Ukraine. Russian President Vladimir Putin has resorted to extreme financial measures to blunt the West’s penalties and inflate his currency.

While the West has imposed unprecedented levels of sanctions against the Russian economy, Russia’s central bank has jacked up interest rates to 20% and the Kremlin has imposed strict capital controls on those wishing to exchange their rubles for dollars or euros.

It’s a monetary defense Putin may not be able to sustain as long-term sanctions weigh down the Russian economy.

But the ruble’s recovery could be a sign that the sanctions in their current form are not working as powerfully as Ukraine’s allies counted on when it comes to pressuring Putin to pull his troops from Ukraine.

It also could be a sign that Russia’s efforts to artificially prop up its currency are working by leveraging its oil and gas sector. …

… For the remainder of the report:

https://www.yahoo.com/news/russias-ruble-rebound-raises-questions-191011961.html

end

Chris Powell…a must read

Chris Powell: Russia conscripts gold into defense of the ruble

Submitted by admin on Wed, 2022-03-30 23:06Section: Daily Dispatches

Gold Market Manipulation Update

Remarks by Chris Powell

Secretary/Treasurer, Gold Anti-Trust Action Committee Inc.

Mining Investment Asia Conference

Intercontinental Hotel, Singapore

Thursday, March 31, 2022

In recent months gold market manipulation particularly and commodity futures market manipulation generally have been ever-more exciting fields of study.

The most dramatic development may have been the default of the London Metals Exchange’s nickel futures contract three weeks ago. The default was relevant to gold and silver futures contracts and all major commodity futures contracts everywhere insofar as the exchange allowed a trader to maintain a huge naked short position — not only a naked short position, but a short position larger than all the nickel supply readily available in the world — and then got crushed for its irresponsibility.

To rescue the nickel shorts, or the biggest nickel short, the LME even reversed many completed trades, causing some traders to ridicule the LME, calling it the “Soviet Metals Exchange”:

https://www.gata.org/node/21786

Not surprisingly, the primary banker for the big nickel short, the bank assembling loans from other banks to help the big short meet its margin calls without having to dump its entire short position, is JPMorganChase & Co. JPMorganChase is one of the banks that in recent years have paid hundreds of millions of dollars in government fines and civil lawsuit settlements for manipulating the monetary metals markets.

Huge short positions similar to the short position in nickel futures long have been maintained on the books of major investment banks in gold futures and especially silver futures. The U.S. Office of the Comptroller of the Currency reported a few days ago that, strangely, the largest derivatives position in any commodity being traded by U.S. banks is in silver.

Because their trading is so large and consistent, it is unlikely that the banks trading so heavily in monetary metals derivatives and other commodity derivatives are trading entirely for their own books. More likely the banks are often acting as brokers for the U.S. government and possibly other governments.

Indeed, the CME Group, operator of the major U.S. futures exchanges, maintains a special system to facilitate surreptitious intervention in the commodity and financial futures markets by governments and central banks. It’s called the Central Bank Incentive Program and provides governments and central banks with volume discounts for trading surreptitiously through exchange-approved brokers.

https://www.gata.org/node/18925

Suspicions of such market intervention by government through the Central Bank Incentive Program have been supported by the refusal of the U.S. Commodity Futures Trading Commission to answer a crucial question posed by GATA and even by a member of Congress, U.S. Rep. Alex Mooney, R-West Virginia. That is: Does the commission have jurisdiction over manipulative futures trading undertaken by or at the behest of the U.S. government, or is such trading legal under the Gold Reserve Act of 1934?

https://www.gata.org/node/20089

As GATA construes the act, it authorizes the U.S. government to intervene secretly in and to manipulate not only any market in the United States but any market in the world. The CFTC refuses to contradict or even discuss this interpretation. Since the CFTC refuses to discuss its jurisdiction, even for a member of Congress, it seems fair to assume that secret trading by the government in the commodity markets in pursuit of a general policy of commodity price suppression is indeed happening and is a highly sensitive issue.

It increasingly seems that the British economist Peter Warburton was correct in 2001 when he wrote that Western central banks were using derivatives to control commodity prices and protect government currencies against the public’s recognition of currency devaluation.

Warburton’s essay, “The Debasement of World Currency: It Is Inflation But Not as We Know It,” is posted at GATA’s internet site:

https://www.gata.org/node/8303

* * *

Today, on account of Russia’s war against Ukraine, a worldwide currency war is raging as well and it is largely a war over gold.

Led by the United States, the West is trying to prohibit most commerce with Russia and is specifically targeting Russia’s gold reserves, trying to prevent the use of Russian gold in trade:

https://www.ft.com/content/76e52790-7d3d-4303-a8c4-441da2aa39a8

This attempt to freeze Russia’s gold is a proclamation by the West that gold remains the most powerful sort of money — money without counterparty risk.

In response Russia is making the same acknowledgment, since Russia is more or less remonetizing gold officially. The Russian central bank has begun buying gold from Russian mines at a fixed price in rubles, establishing a gold standard within Russia.

The Russian government is suggesting that gold can be payment for its oil and gas exports.

And the Russian government has removed the value-added tax from domestic gold sales to the public to encourage Russians to trade their rubles for domestically mined metal instead of foreign currency.

These moves by Russia have strengthened the ruble after its crash when the West’s sanctions were imposed. Indeed, the ruble finished March as the month’s best-performing currency, only 10% lower against the U.S. dollar compared to where the ruble was on February 24 when Russia invaded Ukraine and the West began imposing economic sanctions on Russia:

From a low of 139 rubles to the dollar as of March 7, the ruble was up to 83 to the dollar yesterday.

That is, the West is trying to prevent gold from becoming international money again, while Russia is striving to restore gold as an international reserve currency if not the international reserve currency. For the time being Russia seems to be buying gold, not selling it, as the West thought Russia would do and sought to prevent Russia from doing.

Gold seems to be working well for Russia and the ruble.

* * *

In recent months there have been less dramatic but still substantial indications of surreptitious government intervention against gold.

The Bank for International Settlements, the central bank of the central banks, continues to trade gold surreptitiously for its members. GATA’s consultant about the BIS, Robert Lambourne, studies the monthly reports of the BIS and calculates that the bank’s gold swap and derivatives positions remain on the high side historically:

For whom is the BIS trading and swapping gold and for what purposes? The BIS refuses to say:

https://www.gata.org/node/17793

But a BIS PowerPoint presentation to potential BIS members in 2008 showed that the bank’s services include secret interventions in the gold and currency markets:

http://www.gata.org/node/11012

Last year the U.S. Treasury Department refused to answer most of Representative Mooney’s questions about U.S. gold reserves held at the New York Fed, starting with why the Treasury keeps gold there in the first place if not to trade or exchange it surreptitiously for market manipulation:

In January this year the financial journalists Pam and Russ Martens of Wall Street on Parade reported that the Federal Reserve has a trading floor not only at the Federal Reserve Bank of New York but also in Chicago, near the Chicago Mercantile Exchange, the commodity trading center:

Why does the Fed need a trading floor adjacent to the commodity markets in Chicago if the Fed, through intermediaries, isn’t trading commodities as well as regular financial instruments on behalf of the U.S. government?

And of course in recent months some big investment banks, including JPMorganChase, Barclays, and Societe Generale, as well as the London Gold Market Fixing Ltd., have paid collectively about $200 million in civil lawsuit settlements for rigging the gold market.

What I have cited today are only the latest chapters in longstanding Western government policy of pushing gold out of the world financial system to maintain the dominance of the U.S. dollar through manipulation of the currency and commodity markets and particularly through suppression of the gold price.

The history is summarized and documented in “The Basics” section at the top left side of the home page of GATA’s internet site, GATA.org:

This isn’t mere “conspiracy theory.” It is conspiracy fact, much of it drawn from government’s own archives.

The objective of this longstanding policy, like the objective of modern central banking itself, is to destroy markets and enable government to set prices, to determine the prices of all capital, labor, goods, and services in the world.

Markets today are an illusion.

That is totalitarianism, and it is the most effective kind, because, compared to traditional totalitarianism, it is much more subtle. But it is visible to anyone who wants to see it, and you can see it at GATA’s internet site.

* * *

Documents supporting all the assertions I have made here today are posted at GATA’s internet site and my remarks today will be posted there too and will contain links to the documents.

GATA is a nonprofit educational and charitable corporation recognized as tax-exempt by the U.S. Internal Revenue Service under Section 501-c-3 of the U.S. Internal Revenue Code. We are sustained by financial donations from our supporters. By e-mail we distribute daily dispatches of interest to monetary metals investors and post them at our internet site. I invite you to join our dispatch list, and you can do so in the right column of our home page at GATA.org.

If you’re looking for a document or other information from GATA and can’t find it, please e-mail me at CPowell@GATA.org and I’ll try to help you.

Thanks for your kind attention.

end

Deteriorating conditions inside the uSA is beginning to show in the huge $23 trillion USA government debt market as the Fed starts to tighten

(London’s Financial Times)

Strains in $23 trillion U.S government debt market intensify as Fed tightens

Submitted by admin on Wed, 2022-03-30 11:57Section: Daily Dispatches

By Kate Duguid

Financial Times, London

Wednesday, March 30, 2022

Investors’ ability to trade US government debt has deteriorated to its lowest point since the ructions of March 2020, deepening worries about the world’s most important bond market as the Federal Reserve tightens monetary policy.

Liquidity, or the ease of buying and selling, in U.S. government securities has dropped since the beginning of this year, reaching levels not seen since the first months of the coronavirus crisis, according to an index compiled by Bloomberg.

The deteriorating trading conditions have exacerbated this month’s price swings, with investors increasingly concerned about how well the market will function as the Fed starts reducing the size of its $9 trillion balance sheet.

Treasuries are already on course to post their worst quarter since at least 1973 after the Fed raised interest rates for the first time since 2018 this month in its attempt to battle inflation, which is running at its highest level in 40 years. It has also halted its crisis-era bond-buying programme. …

… Dispatch continues below …

https://www.ft.com/content/3494abc9-0b87-4206-8ad3-9e09b5e11730

end

Japan will now ban the export of gold to Russia…as well as other sanctions

(Reuters)

Japan to ban Russia-bound exports of gold, may adopt more sanctions

Submitted by admin on Wed, 2022-03-30 11:27Section: Daily Dispatches

By Tetsushi Kajimoto and Daniel Leussink

Reuters

Tuesday, March 29, 2022

TOKYO — Japan will ban the shipment to Russia of precious metals, especially gold, in response to its invasion of Ukraine, the Ministry of Finance said on Tuesday.

The ban on Russia-bound precious metal reflects Prime Minister Fumio Kishida’s resolve to impose further sanctions against the country, pledged at last week’s meeting of leaders from the Group of Seven advanced nations.

From April 5 Japan will ban the export of precious metals such as gold as well as other items including luxury cars, jewellery, cosmetics and liquor.

Japan’s move comes after the United States and Britain took steps to curtail transactions in gold with Russia. …

… For the remainder of the report:

https://www.reuters.com/business/japan-ban-russia-bound-exports-gold-april-5-mof-2022-03-29

end

4.OTHER GOLD/SILVER COMMENTARIES

Stefan Gleason..

4 Scenarios for BIG Moves in Precious Metals Markets

March 31, 2022

Stefan Gleason

Money Metals

World events are driving a volatile and potentially pivotal environment ahead for investors. Huge swings in financial markets are likely still to come.

Direction, magnitude, and timing are difficult to predict. But precious metals bulls are eying massive upside potential for gold and silver as war and inflation stoke safe-haven buying.

What follows are four major macro scenarios that could impact metals markets in a big way in the months ahead.

Scenario 1: Recession Incoming

In recent weeks, rising yields have stuck bondholders with big losses. Higher borrowing costs also threaten to hit the housing market and force businesses to scale-down spending.

Economists are paying particularly close attention to the shape of the yield curve.

A flattening yield curve (meaning long-term rates are converging closer to shorter-term rates) suggests a slowing economy. An inverted yield curve (with long-term bond yields falling below shorter duration paper) is a classic indicator of an incoming recession.

On Tuesday, a key zone of the U.S. Treasury yield curve inverted for the first time since September 2019. Yields on the two-year note moved slightly above those on the benchmark 10-year note.

Federal Reserve officials may be afraid to hike their ultra-short benchmark rate much further into this yield curve setup.

If recession warnings continue to build, the Fed may opt to pause on tightening – and possibly even reverse course by next year with rate cuts.

In the event of a recession, though, industrial metals and other economically sensitive commodities could suffer sharp sell-offs – at least until the Fed reinflates the economy.

Gold, being uncorrelated to the economic cycle, is likely to hold up relatively well in a recession scenario.

Scenario 2: Summer of Shortages

Recent spikes in energy and food prices are raising fears of widespread supply shortfalls.

image-20220331142816-1A devastating war in agriculture- rich Ukraine combined with sanctions on Russian fertilizer exports could deliver a massive shock to the global food supply chain. Some are warning of a famine in food-insecure countries.

By the summer, it will be too late to recapture losses from a diminished planting season.

Summer also typically sees peak demand for gasoline. But with global energy markets thrown into chaos by war and sanctions, supply may be insufficient to meet that demand.

Any shortages in food, energy, and other essentials are likely to extend to precious metals markets at the retail bullion level – and possibly the physical delivery mechanism on futures exchanges as well.

Scenario 3: Global Monetary Disorder

The world monetary order based on the U.S. dollar as world reserve currency is becoming unstable.

In waging a currency war on Russia, the U.S. government may have inadvertently accelerated the process of dethroning King Dollar. The U.S. has essentially announced to all countries that wish to trade with Russia that they must seek alternatives to the dollar. (Or if they ever envision themselves being crossways with the U.S. in the future.)

Russia, meanwhile, has declared that those who wish to obtain oil, gas, and other Russian exports should be ready to pay in rubles or in gold.

In a surprising twist, Russia is now seeing an influx of demand for rubles – and the currency is actually strengthening in value.

In part that is because Moscow intends to use surplus rubles to buy gold.

Gold could suddenly become a lot more relevant to other countries, including China, as the ultimate money and a facilitator of international trade.

Even if no new formal gold standard emerges, a large increase in central bank buying of gold around the world would pressure precious metals prices higher in terms of depreciating U.S. currency.

Scenario 4: World War III

The final scenario is the bleakest for investors and for humanity overall: an escalation of U.S.-Russia tensions past the point of no return.

Vladimir Putin’s government has said it won’t use nuclear weapons unless it perceives an “existential threat.” A U.S.-led campaign for regime change would likely constitute such a threat.

President Joe Biden asserted last week in supposedly off- the-cuff remarks that Putin “cannot remain in power.”

Biden’s foreign policy handlers scrambled to issue statements denying that the administration intends to pursue regime change in Russia.

They understand the dangers of such talk even if Biden himself doesn’t.

A single misstatement or diplomatic blunder could start World War III. The nuclear Doomsday Clock is ticking closer toward midnight than at any time since the height of the Cold War.

Among the economic consequences of war are huge spending commitments, a scramble for resources, and ramped up pressure on inflation.

The time to hunker down is before the first bombs are dropped. Hunkering down financially means holding assets outside the banking system and far removed from Wall Street. It means holding the highest-quality, most durable, most universally recognized assets. It means holding gold and silver in physical form.

5.OTHER COMMODITIES/

DIESEL

.

end

LITHIUM

NICKEL/LME

6.CRYPTOCURRENCIES

7. GOLD/ TRADING TODAY

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings THURSDAY morning 7:30 AM

ONSHORE YUAN: CLOSED UP 6.3428

OFFSHORE YUAN: 6.3497

HANG SANG CLOSED DOWN 280.09 PTS OR 1.31%

2. Nikkei closed DOWN 205.95PTS OR 0.73%

3. Europe stocks ALL RED

USA dollar INDEX UP TO 99.20/Euro FALLS TO 1.0966

3b Japan 10 YR bond yield: RISES TO. +.260/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 124.19/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 107,38 and Brent: 114.11

3f Gold DOWN /JAPANESE Yen UP CHINESE YUAN: UP -SHORE CLOSED DOWN// OFF- SHORE UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.0.547%/Italian 10 Yr bond yield FALLS to 2.05% /SPAIN 10 YR BOND YIELD RISES TO 1.47%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 1.51: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield RISES TO : 2.67

3k Gold at $1933.00 silver at: 25.03 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3l USA vs Russian rouble;// Russian rouble UP 1 1/4 in roubles/dollar; ROUBLE AT 82,25

3m oil into the 101 dollar handle for WTI and 105 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 121.67 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning .9252– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0268 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 2.4324 UP 3 BASIS PTS

USA 30 YR BOND YIELD: 2.466 DOWN 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 14.67

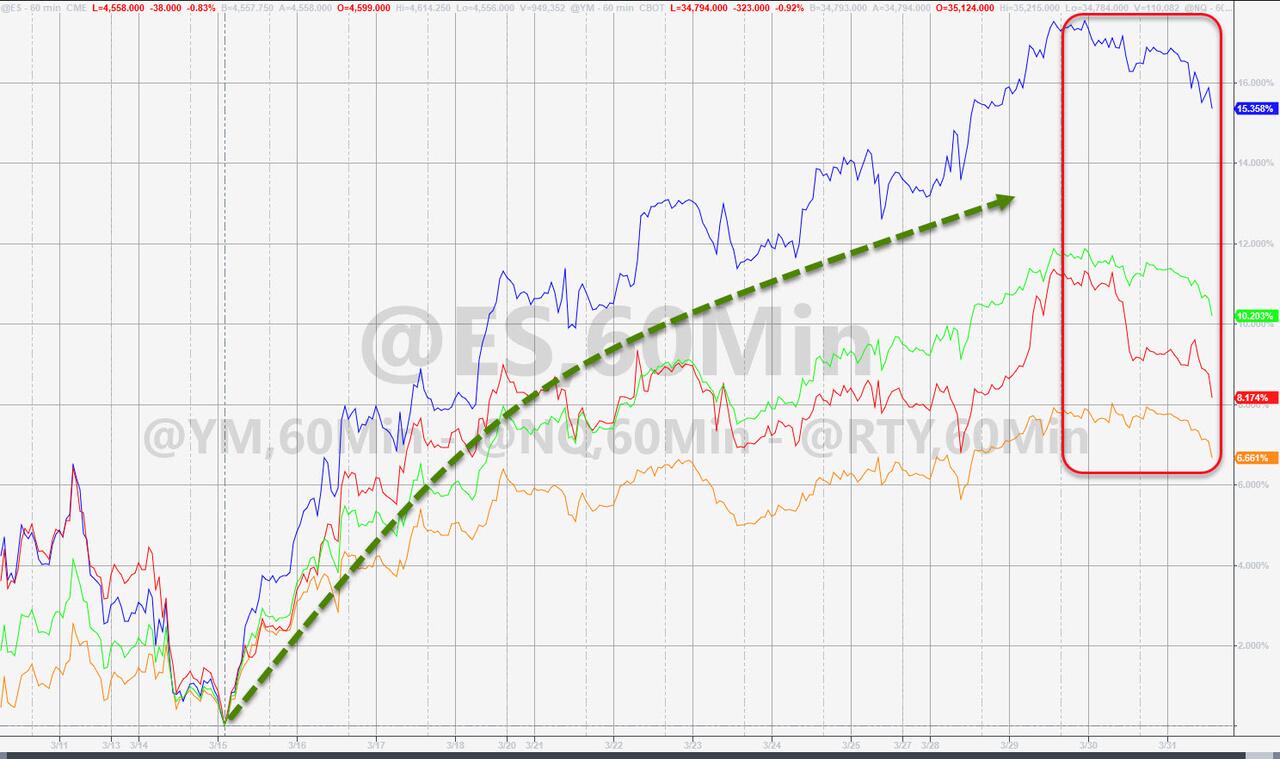

Futures Flat On Last Day Of Dismal Quarter, Oil Tumbles As Biden Preps Massive SPR Release

THURSDAY, MAR 31, 2022 – 07:56 AM

US equity futures were muted and flat on the last trading day of the month and quarter, fading a modest overnight gain as the underlying index headed for its first quarterly decline in two years on worries about surging inflation, hawkish monetary policy and an economic slowdown. Contracts on the S&P 500 were down 0.1% at 730 a.m. ET while Dow futures were little changed and Nasdaq 100 futures rose 0.2%, while European stocks fell, heading for the first quarterly decline since 2020. Asian equities retreated on lackluster Chinese PMI data and regulatory concerns. Treasuries held gains with the 10Y yield dropping to 2.31% (from 2.50% earlier this week when the 2s10s inverted) and the dollar ticked up against almost all G-10 peers. Fed watchers will be focused on the PCE deflator, which may have sped up in February.

The big overnight action was in oil, which plunged following the news late on Wednesday that the White House was (again) mulling a plan to release roughly a million barrels a day from reserves to combat crashing Democrat approval rating ahead of the midterms as a result of soaring gasoline prices coupled with supply shortages in response to US sanctions of Russia. The proposal, which includes 180 million barrels being freed over several months, may help the market rebalance this year but won’t solve a structural deficit, Goldman said.

The reserve release news came just hours ahead of an OPEC+ supply meeting, where the cartel is expected to stick with its strategy of a modest output boost in May.

Equities globally are poised for their worst quarter since the early days of the pandemic on concerns about tightening monetary policy, red-hot inflation and a looming recession. While stocks remained resilient to the historic rout in bond markets this month, some strategists see little room for them to rally this year, partly as high costs threaten corporate profits. French inflation accelerated more than expected to reach another record, following unexpectedly high readings on Wednesday from Germany and Spain.

“Our base case now is for only modest upside for stocks,” said Mark Haefele, chief investment officer at UBS Global Wealth Management, adding that he expects the S&P 500 to end the year at 4,700, about 2% higher than current levels. He also trimmed his estimate for global earnings growth to 8% from 10% for 2022.

“Aside from quarter-end considerations, oil is very much the center of attention,” Simon Ballard, chief economist at First Abu Dhabi Bank, wrote in a note to investors. Still, “all the usual suspects are still in play, keeping the market in check, including the specter of the Fed pursuing an aggressive path of monetary policy normalization over the coming months.”

Elsewhere, officials from Ukraine and Russia are set to resume talks via video conference on Friday, according to a Ukrainian negotiator, though there was no immediate confirmation from Moscow. Friday’s video discussions between Ukraine and Russia would follow in-person talks this week in Turkey that didn’t produce a short-term cease-fire or major progress toward a broader peace deal. Ukraine’s negotiator said the hope was to have enough agreed on paper in another week to be able to move toward a meeting between President Vladimir Putin and President Volodymyr Zelenskiy.

Going back to the US market, shares in big U.S. energy companies slumped in premarket trading along with crude prices drop (Exxon Mobil -1.9% and Chevron -1.5% premarket, Occidental Petroleum -2.6%, Gran Tierra Energy -3.1%, Imperial Petroleum -3.8%, Camber Energy -4.3%). Bank stocks are also lower putting them on track to fall for a second straight day as the U.S. 10-year yield falls to 2.31%. Goldman Sachs warned that stagflation could make bank stocks less profitable. U.S.-listed Chinese stocks slipped in premarket trading as Securities and Exchange Commission Chair Gary Gensler dialed down prospects of an imminent deal to allow Chinese firms to keep trading on American exchanges. Russian equities advanced as the nation partly lifted the short-selling ban on local stocks on Thursday, removing one of the measures that helped limit the declines in the market after a record long shutdown. Other notable premarket movers include:

- Vipshop ADRs (VIPS US) rise 8.4% in premarket trading after the Chinese online retailer announces a $1b share buyback plan.

- Robinhood Markets (HOOD US) shares rise 1.4% in U.S. premarket trading, set to extend the previous day’s 24% gains after the online brokerage announced plans to expand the trading day by four hours, while Morgan Stanley begins coverage of the stock with an equal-weight rating.

- Energy companies decline in premarket trading as crude prices drop. The U.S. is considering tapping its reserves again in a potentially massive release aimed at managing inflation and supply shortages. Exxon Mobil (XOM US) -1.9%, Chevron -1.5% (CVX US).

- U.S.-listed Chinese stocks are heading for a lower open after Securities and Exchange Commission Chair Gary Gensler dialed down prospects of an imminent deal to allow Chinese firms to keep trading on American exchanges. Alibaba (BABA US) fell 1.7% in premarket, while its e-commerce rival JD.com (JD US) lost 2.8%.

- Advanced Micro Devices (AMD US) shares fall 1.3% in U.S. premarket trading, after the semiconductor maker is downgraded to equal- weight from overweight at Barclays, which says that the growth story “needs a pause.”.

- IZEA Worldwide (IZEA US) shares surge 27% in U.S. premarket trading after the influencer marketing company reported fourth-quarter earnings and saw total revenue increase 62% to a record of $10.3m.

In Europe, the Stoxx 600 reversed initial gains and dropped 0.3%, the Euro Stoxx 50 fell 0.2%, and other major indexes trade flat to slightly lower with retailers, telecoms and energy the worst performing sectors. Retail and telecom stocks led declines while utilities and insurance sectors outperformed. Some notable premarket movers:

- Brewin Dolphin shares rise as much as 62% and trade slightly below the agreed bid for the firm from RBC Wealth Management. The transaction, being carried out at a high premium, highlights the attractiveness of the U.K. wealth sector, analysts say.

- Orpea shares climb to their highest level in almost 2 months after Societe Generale says that allegations of mistreatment at its facilities are likely to have “limited” financial impact.

- Fresenius SE shares rise as much as 3.3% on news that the company’s Kabi intravenous drug unit has bought a majority stake in mAbxience SL and acquired Ivenix.

- Pernod Ricard shares rise as much as 2.6% as Citi says 3Q sales are likely to beat expectations, also lifting its which lifts EPS estimates and PT, as well as opening a positive catalyst watch.

- Tate & Lyle shares gain as much as 3.7% after saying it would buy Quantum Hi-Tech, a prebiotic dietary fiber business in China. The deal enhances Tate & Lyle’s portfolio, Goodbody says.

- Pearson shares rise as much as 3.5%, rebounding from Wednesday’s losses after private equity firm Apollo Global Management said it won’t make an offer for the education publisher.

Earlier in the session, Chinese data and regulatory concerns weighed on Asia stocks. China’s NBS manufacturing PMI declined to 49.5 in March from 50.2 in February, missing estimates, likely due to Covid-related restrictions and geopolitical tensions. The output sub-index in the NBS manufacturing PMI survey fell by 0.9 points in March, and the new orders sub-index fell by 1.9 points. The NBS non-manufacturing PMI fell to 48.4 in March from 51.6 in February, also missing expectations, and entirely driven by the decline of services sector due to recent Covid outbreaks in multiple provinces. Separately, Bloomberg reported that Chinese authorities are considering a plan to raise several hundred billion yuan for a new fund to backstop troubled financial firms.

Asian stocks retreated after a two-day advance, as the U.S. securities regulator’s tough stance on a potential delisting of Chinese firms and weak China manufacturing data worried investors. The MSCI Asia Pacific Index declined as much as 0.8%, and was poised to finish its worst quarterly performance in two years, with Taiwan Semiconductor Manufacturing and Tencent among the biggest drags. Benchmarks in Hong Kong and China underperformed regional peers. Japanese equities headed for a second day of declines while Australia stocks retreated after seven straight day of gains in response to a stimulatory federal budget. The U.S. Securities and Exchange Commission’s chief said Chinese firms need to fully comply with audit requirements in order to stay on American exchanges. Meantime, China’s manufacturing contracted in March, underscoring the growing toll of lockdowns. Investors are also watching how a tumble in oil prices can alleviate inflation risks and affect corporate earnings.

“If you look at the PMIs there’s an obvious explanation for why PMIs are weak, which is China pursuing zero-Covid strategy,” Kieran Calder, head of Asia Equity Research at Union Bancaire Privee, said in an interview with Bloomberg Television. “The reality of Covid-19 versus the response in China, the mismatch is too strong right now and I think that’s the biggest worry for us.” For the quarter, Asian stocks were poised for nearly a 7% loss, the worst performance since early 2020 when the emergence of the pandemic shocked investors. Investors had to grapple with a U.S. rate hike, a war in Ukraine and continued regulatory risks out of China, which caused huge volatility

Japanese equities fell for a second day following a rally in the yen. Electronics makers and banks were the biggest drags on the Topix, which fell 1.1%. Recruit and SoftBank were the largest contributors to a 0.7% loss in the Nikkei 225. The yen was little changed after gaining 1.6% against the dollar over the previous two sessions. Both key gauges still capped their first monthly gains of the year. The Nikkei 225 rose 4.9% in March, the most since November 2020, while the Topix climbed 3.2% on the month.