april1, 2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD; $1929.60 DOWN $19.00

SILVER: $24.55 DOWN $0.39

ACCESS MARKET: GOLD $1924.35

SILVER: $24.64

Bitcoin morning price: $45,814 DOWN 2879

Bitcoin: afternoon price: $46,338 DOWN 2355

Platinum price: closing DOWN 7 to $986.40

Palladium price; closing UP 2.85 at $2271.50

END

Today is options expiry for the comex

end

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

comex notices/

March: JPMorgan stopped/total issued 254/1350

NUMBER OF NOTICES FILED TODAY FOR APRIL. CONTRACT 1350 NOTICE(S) FOR 135,000 OZ (4.199 TONNES)

total notices so far: 13,841 contracts for 1,384100 oz (43.051 tonnes)

SILVER NOTICES:

35 NOTICE(S) FILED TODAY FOR 170,000 OZ/

total number of notices filed so far this month 682 : for 3,410,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

END

GLD

WITH GOLD DOWN $19.00

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

A SMALL CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 0.29 TONNES INTO THE GLD//

INVENTORY RESTS AT 1091.73 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 39 CENTS

AT THE SLV// A HUGE CHANGE IN SILVER INVENTORY AT THE SLV/ THE SLV//A DEPOSIT OF 2.302 MILLION OZ INTO THE SLV

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 558.64 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A STRONG SIZED 1414 CONTRACTS TO 148,844 AND CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE STRONG GAIN IN OI WAS ACCOMPLISHED WITH OUR TINY $0.03 GAIN IN SILVER PRICING AT THE COMEX ON THURSDAY. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.03) AND WERE UNSUCCESSFUL IN KNOCKING OUT ANY SILVER LONGS AS WE HAD A STRONG GAIN OF 2493 CONTRACTS ON OUR TWO EXCHANGES

WE MUST HAVE HAD:

I) HUGE BANKER SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A FAIR ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A STRONG INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 4.305 MILLION OZ FOLLOWED BY TODAY’S QUEUE JUMP OF 75,000 OZ//NEW STANDING: 4,380 MILLION OZ// V) STRONG SIZED COMEX OI GAIN/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS : —-687 (the differential in silver is now increasing every day)

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS APRIL. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAR:

TOTAL CONTACTS for 1 days, total 392 contracts:1.96 million oz OR 1.96MILLION OZ PER DAY. (392 CONTRACTS PER DAY)

TOTAL NO OF OZ UNDERGOING EFP TO LONDON 392 CONTRACTS X 5,000 PER CONTRACT:

EQUATES TO: 1.96 MILLION OZ

.

LAST 11 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

APRIL: 1.96 MILLION OZ

RESULT: WE HAD A STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1414 WITH OUR TINY $0.03 GAIN IN SILVER PRICING AT THE COMEX// THURSDAY THE CME NOTIFIED US THAT WE HAD A FAIR SIZED EFP ISSUANCE OF 392 CONTRACTS( 392 CONTRACTS ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A HUGE INITIAL SILVER OZ STANDING FOR MAR. OF 4.305 MILLION OZ FOLLOWED BY TODAY’S 75,000 OZ QUEUE JUMP//NEW STANDING: 4.380 MILLION OZ/// .. WE HAD AN STRONG SIZED GAIN OF 1806 OI CONTRACTS ON THE TWO EXCHANGES FOR 9.070 MILLION OZ WITH THE TINY GAIN IN PRICE.

WE HAD 35 NOTICES FILED TODAY FOR 175000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A STRONG SIZED 9105 CONTRACTS TO 569,969 AND CLOSER TO NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: —–36 CONTRACTS. (differentials are lowering in gold)

THE BIS HAS ABANDONED THE GOLD COMEX TRADING!!!

.

THE STRONG SIZED DECREASE IN COMEX OI CAME WITH OUR GAIN IN PRICE OF $13.30//COMEX GOLD TRADING/THURSDAY WITH THE LOSS IN COMEX DUE TO THE CONCLUSION OF SPREADER LIQUIDATION/.AS IN SILVER WE MUST HAD HUGE BANKER/ALGO SHORT COVERING ACCOMPANYING OUR GOOD SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR APRIL AT 78.33 TONNES

YET ALL OF..THIS HAPPENED WITH OUR GAIN IN PRICE OF $13.30 WITH RESPECT TO WEDNESDAY’S TRADING

WE HAD AN FAIR SIZED LOSS OF 2172 OI CONTRACTS (6.75 PAPER TONNES) ON OUR TWO EXCHANGES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 6969 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 570,002.

IN ESSENCE WE HAVE AN FAIR SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2139, WITH 9108 CONTRACTS DECREASED AT THE COMEX AND 6969 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 2172 CONTRACTS OR 6.75 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (6969) ACCOMPANYING THE STRONG SIZED LOSS IN COMEX OI (9141,): TOTAL LOSS IN THE TWO EXCHANGES 2172 CONTRACTS. WE NO DOUBT HAD 1) HUGE BANKER SHORT COVERING ,2.) HUGE INITIAL STANDING AT THE GOLD COMEX FOR APRIL. AT 78.33 TONNES/// 3) ZERO LONG LIQUIDATION ///. ,4) STRONG SIZED COMEX OI. LOSS 5) SMALL ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

MARCH

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL :

6969 CONTRACTS OR 696,900 OR 21.676 TONNES 1 TRADING DAY(S) AND THUS AVERAGING: 6969 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 1 TRADING DAY(S) IN TONNES: 21.676TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2020, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 21.76/3550 x 100% TONNES 0.612% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 21.76 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF MAY.WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF APRIL HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF MAY, FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (MAR), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A STRONG SIZED 1414 CONTRACTS TO 148,844 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 4 1/2 YEARS AGO.

EFP ISSUANCE 392 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 392 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 392 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 2101 CONTRACTS AND ADD TO THE 392 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A STRONG SIZED GAIN OF 1806 OPEN INTEREST CONTRACT FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 9.08 MILLION OZ,

OCCURRED WITH OUR tiny GAIN $0.03 IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

5. Other gold commentaries

6. Commodity commentaries/cryptocurrencies

3. ASIAN AFFAIRS

i)FRIDAY MORNING// THURSDAY NIGHT

SHANGHAI CLOSED UP 2.26 PTS OR 0.07% //Hang Sang CLOSED UP 280.09 PTS OR 1.31 % /The Nikkei closed DOWN 205.95 PTS OR 0.73% //Australia’s all ordinaires CLOSED DOWN 0.01% /Chinese yuan (ONSHORE) closed DOWN 6.3703 /Oil DOWN TO 107.28 dollars per barrel for WTI and DOWN TO 114.11 for Brent. Stocks in Europe OPENED ALL GREEN // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.3703 OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.3859: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER//

A)NORTH KOREA/

b) REPORT ON JAPAN

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A STRONG SIZED 9141 CONTRACTS TO 569,969 AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX DECREASE OCCURRED DESPITE OUR STRONG GAIN OF $13.30 IN GOLD PRICING THURSDAY’S COMEX TRADING. WE ALSO HAD A STRONG SIZED EFP (6969 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. A CONSIDERABLE AMOUNT OF THE COMEX LOSS WAS DUE TO THE CONCLUSION OF THE SPREADER/TAS FOLLY/

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE ACTIVE DELIVERY MONTH OF APRIL.. THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 6969 EFP CONTRACTS WERE ISSUED: ;: , . 0 JUNE :6969 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 6969 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 2172 CONTRACTS IN THAT6969 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A STRONG SIZED COMEX OI LOSS OF 9141 CONTRACTS..AND THIS FAIR SIZED GAIN OCCURRED DESPITE THE GAIN IN PRICE OF $13.30.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING FOR APRIL (78.33),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 78.33

THE BANKERS WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $13.30) BUT THEY WERE UNSUCCESSFUL IN FLEECING ANY LONGS AS WE HAVE REGISTERED A FAIR SIZED GAIN OF 7.832 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR APRIL (78.33 TONNES)…

WE HAD –26 CONTRACTS SUBTRACTED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 2172 CONTRACTS OR 217200 OZ OR 6.75 TONNES

Estimated gold volume today: 125,808 ///poor

Confirmed volume yesterday: 171,603 contracts poor

INITIAL STANDINGS FOR APRIL ’22 COMEX GOLD //APRIL 1

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 60,873.077 oz Brinks JPMorgan includes 27 kilobars Brinks |

| Deposit to the Dealer Inventory in oz | 56,358.104OZManfra |

| Deposits to the Customer Inventory, in oz | 321,510.000 jpm 1000 kilobars 60,005.490 oz Malca total: 381,515.490 oz |

| No of oz served (contracts) today | 1350 notice(s)135,000 OZ 4.199 TONNES |

| No of oz to be served (notices) | 11345 contracts 35.28 oz 0.5723 TONNES |

| Total monthly oz gold served (contracts) so far this month | 13841 notices138,4100 OZ 43.05 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For today:

dealer deposits 1

ii Into dealer Manfra: 56,358.104 oz

total dealer deposit 56,358.104 oz//

No dealer withdrawal 0

2 customer deposits

i) Into JPM 321,510.000 oz (10,000 kilobars)

ii) Into Malca: 60,005.490 oz

total customer deposit: 381,515.490 oz //total dealer and customer deposit 13.616 tonnes

2 customer withdrawal

i)out of JPMorgan 60,006.490 oz

ii) Out of Brinks: 868.077 oz (27 kilobars)

total withdrawals: 60,873.567 oz

ADJUSTMENTS: dealer to customer

i) Manfra: 14,0-49.890 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR APRIL.

For the front month of APRIL we have an INITIAL oi of 12,695 contracts having LOST 12,451.

We had 12,491 notices filed yesterday so we gained 40 contracts or 4000 oz will stand for delivery at the comex

May saw a GAIN of 141 contracts to stand at 5361

June saw a GAIN of 2138 contracts up to 476,004 contracts

We had 1350 notice(s) filed today for 135,000 oz FOR THE APRIL 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 1306 notices were issued from their client or customer account. The total of all issuance by all participants equates to 1350 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 254 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 84 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the APRIL /2021. contract month,

we take the total number of notices filed so far for the month (13,841) x 100 oz , to which we add the difference between the open interest for the front month of (APRIL 12,695: CONTRACTS ) minus the number of notices served upon today 1350 x 100 oz per contract equals 2,518,700 OZ OR 78.33 TONNES the number of TONNES standing in this active month of APRIL.

thus the INITIAL standings for gold for the APRIL contract month:

No of notices filed so far (13,841) x 100 oz+ (12,695) OI for the front month minus the number of notices served upon today (1350} x 100 oz} which equals 2,518,600 oz standing OR 78.33 TONNES in this active delivery month of APRIL.

We gained 4000 oz queue jump on day two as our banker friends are desperate for gold.

TOTAL COMEX GOLD STANDING: 78.33 TONNES (A WHOPPER FOR A APRIL ( ACTIVE) DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

191,133,764.7, oz NOW PLEDGED /HSBC 5.94 TONNES

99,258.893 PLEDGED MANFRA 3.08 TONNES

54,339.114oz PLEDGED JPMorgan no 1 1.690 tonnes

243,923.704, oz JPM No 2 7.58 TONNES

898,821.330 oz pledged Brinks/27,96 TONNES

International Delaware:: 0

Loomis: 18,615.429 oz

total pledged gold: 1,487,476.805 oz 46.27 tonnes

TOTAL REGISTERED AND ELIG GOLD AT THE COMEX: 35,576,058.474 OZ (1106.56TONNES)

TOTAL ELIGIBLE GOLD: 18,157,716.04 OZ (564.78 tonnes)

TOTAL OF ALL REGISTERED GOLD: 17,418,342.090 OZ (541.78 tonnes)

REGISTERED GOLD THAT CAN BE SERVED UPON: 15,930.866.0 OZ (REG GOLD- PLEDGED GOLD) 495.52 tonnes

END

APRIL 2022 CONTRACT MONTH//SILVER//APRIL 1

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1,618,866.055 oz Brinks CNT Loomis |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 298,413.348 oz Delaware |

| No of oz served today (contracts) | 35CONTRACT(S) 175,000 OZ) |

| No of oz to be served (notices) | 194 contracts (970,000 oz) |

| Total monthly oz silver served (contracts) | 682 contracts 3,410,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

we had 0 deposits into the dealer

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 1 deposits into the customer account

i) Into Delaware: 298,413.348 oz

total deposit: 298,413.348 oz

JPMorgan has a total silver weight: 179.710 million oz/339.649 million =52.70% of comex

i) Comex withdrawals: 3

i) Out of Brinks 771,293.540 oz

ii) Out of CNT 723,067.988 oz

iii) Out of Loomis: 124,504.530 oz

total withdrawal 1,618,866.055 oz

0 adjustments:

the silver comex is in stress!

TOTAL REGISTERED SILVER: 85.709 MILLION OZ

TOTAL REG + ELIG. 339.649 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR APRIL

silver open interest data:

FRONT MONTH OF APRIL OI: 229, HAVING LOST 632 CONTRACTS FROM THURSDAY. We had 647 notices filed yesterday,

so we gained 15 contracts or an additional 75,000 oz will stand on this side of the pond

MAY HAD A GAIN OF 279 CONTRACTS UP TO 105,584 contracts

JUNE HAD AN INITIAL GAIN OF 13 TO STAND AT 13

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 35 for 175,000 oz

Comex volumes: 46,243// est. volume today//poor/

Comex volume: confirmed yesterday: 42,892 contracts ( poor )

To calculate the number of silver ounces that will stand for delivery in APRIL. we take the total number of notices filed for the month so far at 682x 5,000 oz = 3,410,000oz

to which we add the difference between the open interest for the front month of APRIL (229) and the number of notices served upon today 35 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the APRIL./2021 contract month: 682 (notices served so far) x 5000 oz + OI for front month of MAR (229) – number of notices served upon today (35) x 5000 oz of silver standing for the APRIL contract month equates 4,380,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

APRIL 1///WITH GOLD DOWN $19.00 : A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSITY OF .29 TONNES INTO THE GLD///INVENTORY RESTS AT 1091.73

MARCH 31/WITH GOLD UP $13.30 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD FROM MONDAY A WITHDRAWAL OF 1.71 TONNES FROM THE GLD:INVENTORY RESTS AT 1091.44

MARCH 28/WITH GOLD DOWN $14.65: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1093.18 TONNES

MARCH 25/WITH GOLD DOWN $7.60 : A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.52 TONNES INTO THE GLD///INVENTORY RESTS AT 1093.18 TONNES

MARCH 24/WITH GOLD UP $24.95: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.06 TONNES INTO THE GLD..//INVENTORY RESTS AT 1087.66 TONNES

MARCH 23/WITH GOLD UP $15.75//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1083.60 TONNES

MARCH 22/WITH GOLD DOWN $7.75: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.16 TONNES OF GOLD DEPOSITED INTO THE GLD//INVENTORY RESTS AT 1083.60 TONES

MARCH 21//WITH GOLD UP $.25 : A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 9.00 TONNES INTO THE GLD////INVENTORY RESTS AT 1082.44 TONES

MARCH 18/WITH GOLD DOWN $13.55 NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1073.44 TONES

MARCH 17/WITH GOLD UP $33.50: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.61 TONNES INTO THE GLD//INVENTORY RESTS AT 1073.44 TONNES

MARCH 16/WITH GOLD DOWN $18.50//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.33 TONNES FROM THE GLD///INVENTORY RESTS AT 1061.83 TONNES

MARCH 15/WITH GOLD DOWN $30.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1064.16 TONNES

MARCH 14//WITH GOLD DOWN $22.75, HUGE CHANGES IN GOLD INVENTORY AT THE GLD//STRANGE: A DEPOSIT OF 2.62 TONNES INTO THE GLD.//INVENTORY RESTS AT 1064.16 TONNES

MARCH 11/WITH GOLD DOWN $14.60: A BIG CHANGE IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 1061.54 TONNES

MARCH 10//WITH GOLD UP $11.55: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.06 TONNES FORM THE GLD///INVENTORY RESTS AT 1063.28 TONNES

MARCH 9/WITH GOLD DOWN $53.85//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.64 TONNES INTO THE GLD//INVENTORY RESTS AT 1067.34 TONNES

MARCH 8/WITH GOLD UP $46.10: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 8.42 TONNES INTO THE GLD///INVENTORY RESTS AT 1062.70 TONNES

MARCH 7/WITH GOLD UP $28.40 A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.06 TONNES INTO THE GLD..//INVENTORY RESTS AT 1054.28 TONNES

MARCH 4/WITH GOLD UP $28.40//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1050.22 TONNES

MARCH 3/WITH GOLD UP $13.95: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 7.84 TONNES//INVENTORY RESTS AT 1050.22 TONNES

MARCH 2/WITH GOLD DOWN $20.80//A MONSTER CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 13.36 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 1042.38 TONNES

MARCH 1/WITH GOLD UP $42.60: NO CHANGES IN GOLD INVENTORY AT THE GLD: //INVENTORY RESTS AT 1029.32 TONNES

FEB 28/WITH GOLD UP $12.95: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1029.32 TONNES

FEB 25/WITH GOLD DOWN $38.95: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1029.32 TONNES

FEB 24/WITH GOLD UP $17.35//A HUGE CHANGE AT THE GLD: 5.23 TONNES INTO THE GLD// IN GOLD INVENTORY AT THE GLD/INVENTORY REST AT 1029.32 TONNES

FEB 23/WITH GOLD UP $2.00 : NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1024.09 TONNES

CLOSING INVENTORY FOR THE GLD//1091.73 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

APRIL 1/WITH SILVER DOWN 39 CENTS A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.302 MILLION OZ INTO THE SLV////INVENTORY REST AT 558.647 MILLION OZ//

MARCH 31/WITH SILVER UP 3 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 2.171 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 556.345 MILLION OZ

MARCH 28/WITH SILVER DOWN 30 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.847 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 554.167 MILLION OZ//

MARCH 25/WITH SILVER DOWN 20 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 552.320 MILLION OZ//

MARCH 24/WITH SILVER UP 54 CENTS TODAY; A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.092 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 552.320 MILLION OZ//

MARCH 23/WITH SILVER UP 24 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 550.288 MILLION OZ//

MARCH 22/WITH SILVER DOWN $0.29 TODAY : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 550.288 MILLION OZ//

MARCH 21/WITH SILVER UP 16 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 550.288 MILLION OZ//

MARCH 18/WITH SILVER DOWN 37 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.217 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 550.288 MILLION OZ//

MARCH 17/ WITH SILVER UP 72 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.049 MILLION OZ INTO THE SLVV//INVENTORY RESTS AT 548.071 MILLION OZ

MARCH 16/WITH SILVER DOWN 56 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 462,000 OZ FROM THE SLV//INVENTORY RESTS AT 544.560 MLLION O

MARCH 15/WITH SILVER DOWN 18 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 545.022 MILLION OZ

MARCH 14/WITH SILVER DOWN 64 CENTS TODAY; STRANGE A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.125 MILLION OZ/INVENTORY RESTS AT 545.022 MILLIONOZ

MARCH 11/WITH SILVER DOWN 13 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.897 MILLION OZ

MARCH 10/WITH SILVER UP 39 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.897 MILLION OZ/

MARCH 9/WITH SILVER DOWN 88 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 5.174 MILLION OZ OF FAKE SILVER.//INVENTORY RESTS AT 542.897 MILLION OZ//

MARCH 8/WITH SILVER UP 88 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.217 MILLION OZ INTO THE SLV////INVENTORY RESTS A 548.071 MILLION OZ//

MARCH 7/WITH SILVER UP 40 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 545.854 MILLION OZ//

MARCH 4/WITH SILVER UP 50 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 545.854 MILLION OZ/

MARCH 3/WITH SILVER UP 2 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 545.854 MILLION OZ//

MARCH 2/WITH SILVER DOWN $.32 TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 198,000 OZ FROM THE SLV//INVENTORY RESTS AT 545.854 MILLION OZ//

MARCH 1/WITH SILVER UP $1.13 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 546.052 MILLION OZ//

FEB 28/WITH SILVER UP 31 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT 546.052 MILLION OZ//

FEB 25/WITH SILVER DOWN 64 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 5.510 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 546.052 MILLION OZ/

FEB 24/WITH SILVER UP 15 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 551.597 MILLION OZ

FEB 23/WITH SILVER UP 22 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 551.597 MILLION OZ//

SLV FINAL INVENTORY FOR TODAY: 558.647 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

Peter Schiff: Eurozone Inflation Exposes European Central Bank Lies

FRIDAY, APR 01, 2022 – 06:30 AM

During a recent podcast, Peter Schiff talked about how the Bank of Japan lied about inflation being too low in order to justify its reckless monetary policy and keep interest rates artificially low in order to prop up the country’s massive debt. In a subsequent podcast, Peter talked about similar lies coming out of the European Central Bank.

The United States isn’t the only country with an inflation problem. The month-over-month increase in the CPI in Germany for March came in at 2.5%. Year-over-year, the CPI increase was 7.3%. Meanwhile, in Italy, producer prices were up 41.4% year-over-year in February.

It’s clear there is a significant inflation problem in the eurozone and it will likely get worse.

The ECB has kept interest rates at zero, and sometimes below, for years. The European central bank has also run massive quantitative easing programs. Former ECB president Mario Draghi always justified this extraordinarily loose monetary policy by saying there wasn’t enough inflation in the eurozone.

Peter said he was one of the few people questioning the absurdity of calling low inflation a problem central banks need to solve.

Low inflation is not a problem. In fact, lower inflation is better than higher inflation. The lower the better. In fact, if prices fall, that’s actually better than prices rising by a little bit. It’s better if things get cheaper than more expensive.”

In reality, all of this talk about inflation being too low is really just a smokescreen to allow central banks and governments to continue their reckless monetary policy.

Keep in mind, when these bureaucrats and politicians tell you “there is not enough inflation,” they’re really saying the cost of living isn’t rising fast enough.

If they said it that way, it would illustrate the absurdity. Why does anybody want the cost of living to go up? Doesn’t everybody want their cost of living to go down? Of course, they do! People don’t want higher gas prices. They want lower gas prices. People don’t want to pay more for health insurance. They want to pay less. They want to pay less for everything.”

The original ECB mandate was to keep inflation below 2%. Draghi reinvented the mandate so that the central bank would try to keep inflation as close to 2% as possible, without going over. In effect, Draghi was saying, “We want inflation to be 1.999%.” Peter called it “asinine.” In effect, that means if inflation is 1.8%, the central bank needs to keep rates at zero and continue QE.

It makes no sense to raise an inflation rate of 1.8 to 1.9. when you’re trying to stay below 2%. In fact, it doesn’t make any sense to try to raise an inflation rate of 1.5 to 1.9 and risk overshooting. The whole idea of the mandate being close to but below 2% was complete nonsense.”

At the time, Peter said it was crazy to think a central bank could micromanage the inflation rate to that degree. And he asked the key question: what happens when they overshoot?

Well, now we know.

It’s ignoring the overshoot. It is doing nothing. Because you have a 30-year high in German inflation. You have an inflation problem all over the world. Yet here you have the ECB continuing to hold rates at zero and continuing to do quantitative easing.”

Why?

If the ECB’s real goal was to create higher inflation but keep it below 2%, they’ve succeeded. In fact, they’ve more than tripled 2%.

Why are they pursuing the same monetary policy? They’re pursuing the same monetary policy today when they have too much inflation as they were using in the past when they claimed they had too little inflation.”

Just like with the Bank of Japan, this highlights the big lie Draghi and the current ECB president Christine Lagarde have been telling — that the artificially low interest rates and QE were driven by too little inflation.

Low inflation was never a problem. It was a manufactured problem to cover up the real problem. And now they have another real problem of too high inflation that they can’t solve. But the problem that they were trying to cover up was another insolvency issue. Why was the ECB continuing to print euros to buy government bonds, in particular Greek government bonds, Italian government bonds, Spanish government bonds? And the answer is those governments were profligate. They’re running big deficits. They are not complying with the original premise of the European Union. They are not holding their deficits down in relation to their GDP. And so the reason the ECB is interfering in those bond markets is to keep interest rates in a lot of these southern European countries artificially low. So, in order to justify intervening in the bond markets, to spare Italian or Spanish politicians from the hard choices of cutting government spending or raising taxes, the ECB monetized that debt. But they couldn’t say the reason we’re printing all of this money is so we can bail out the Italians or bail out the Spanish, so they had to come up with another excuse. And their lame excuse was that inflation was too low.”

The situation isn’t much different in the US. The Fed has also used “low” inflation to justify loose monetary policy so that it can continue to monetize the massive US debt.

In this podcast, Peter also talks about how politicians and central bankers are using COVID and Putin as an excuse for inflation, the problem of big government, and the reaction of gold and oil to the peace talks in Ukraine.

2.LAWRIE WILLIAM//,//Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, James RICKARDS/

-END

–

-END-

LAWRIE WILLIAMS

3. Chris Powell of GATA provides to us very important physical commentaries

Amazing, at least two major refiners are refusing to remelt Russian gold bars

(Bloomberg/GATA)

At least two major refiners refuse to remelt Russian gold bars

Submitted by admin on Thu, 2022-03-31 21:49Section: Daily Dispatches

By Eddie Spence

Bloomberg News

Thursday, March 31, 2022

Some gold refineries are refusing to remelt Russian bars even though market rules permit them to do so, in a sign of how toxic the country’s products have become in certain commodity markets.

The London Bullion Market Association, a club of big banks that acts as the overseer of the world’s key gold market, has drawn a distinction between newly produced Russian gold, which it has barred from its market, and metal that was produced before the invasion, which it is still allowing to trade.

However, at least two major gold refiners are refusing to remelt old Russian bullion bars, according to people familiar with the situation who asked not be identified as the matter is private. …

… For the remainder of the report:

END

end

end

4.OTHER GOLD/SILVER COMMENTARIES

Steve Brown…

.

Gold Supports the Ruble

Chris Powell/Steve Brown…

From Chris Powell of GATA:

“The Russian central bank has begun buying gold from Russian mines at a fixed price in rubles, establishing a gold standard within Russia .. (and) the Russian government is suggesting that gold can be payment for its oil and gas exports. And the Russian government has removed VAT tax from domestic gold sales to the public to encourage Russians to trade their rubles for domestically mined metal instead of foreign currency.” Link: https://gata.org/node/21839

It’s a Russian gold standard because the metal is monetized directly by the Russian government and central bank, where the bank will exchange its gold for rubles, at a price fixed by the Russian government. That move has already caused the ruble to strengthen from 139:1 (ru to USD) to 83:1 now, making the ruble the strongest performing currency in March.

Link: Ruble becomes best-performing currency in March https://gata.org/node/21833

The ruble is strengthened via domestic gold trade when the Russian people exchange their rubles-fiat for hard gold. Such exchange looks attractive to the populace, since gold remains stable as a store of value with zero counterparty risk.

The western gold cartel has barred Russia from the LBMA and western gold trading, perhaps not a wise move for the cartel. The LBMA-BIS-CME-LME-Fed-IMF gold cartel can only remain such when others agree to play.* And Western sanctions will have no impact on Russia’s gold trade. Where bilateral gold trades occur between central banks, US-Euro financial sanctions are irrelevant. That applies to the gold carry trade as well, which is private and opaque even for governments.** Note that Venezuela was able to survive weaponization of the dollar US by trading its gold to Deutsche Bank in bilateral exchange not affected by US Treasury sanctions.

Japan has stated that it will not ship or sell gold to Russia; but it’s exceedingly unlikely that Russia cares about that, since Russia has its own very productive mines and gold trade elsewhere in Asia.

Such positioning as above and stronger trade relations among the Asian block, while excluding Japan and South Korea, promises a gradual shift in world trade pattern, with the consequence and long-term result not yet apparent. Perhaps in response, US State sent its ‘economic hitman’ emissary of the NSA to New Delhi, to warn India about what happens when you mess with Empire. Link: https://www.thehindu.com/news/national/us-deputy-nsa-daleep-singh-cautions-india-against-trade-deals-with-russia/article65277933.ece

Foreign Secretary Harsh Shringla met with US Deputy NSA Daleep Singh in New Delhi March 31, 2022

Meanwhile Bloomberg, a western finance media outfit deeply mired in the culture of Fed criminality, is whining that galloping inflation is “destroying demand”. Tough luck, Mike. We’re all crying for you.

Another point is Russia’s ability to quickly reposition itself with regard to crypto, specifically bitcoin. Russia had formerly imposed strict BTC controls to prevent capital flight, but – in a major bit of irony – western exchanges imposed the same control, subsequent to the Russian support of the DPR/LPR and its police action/invasion of the Ukraine.

With reduced prospect for capital flight to the west, Russia can directly challenge the west by using bitcoin for its real intent, as a currency. Until now bitcoin has been more of a speculative asset than a currency, and it will be interesting to see how the western monetary Empire reacts when and if Bitcoin is effectively used as a means to evade US Treasury sanctions and weaponization of the dollar. So far US Treasury sanctions evasion via Bitcoin prima facie appears minor, while Russia apparently intends to make it major. We shall see!

NB: Russian central bank trade of gold for rubles as set by the RCB represents an internal gold standard — and not an international one. The international gold standard existed until August 15th, 1972, when the former United States ended it. But Russia’s move may be a first step in that direction.

*China has the largest gold market in the Shanghai Exchange but it is difficult for westerners to participate in that market due to China’s capital controls. That has allowed the western gold cartel to operate somewhat autonomously. Due to the collective west’s collective hysteria and inability to reason, it’s unlikely that China will relax its capital controls for westerners, and to the contrary is likely to strengthen them.

**Somewhat analogous to peer-to-peer crypto trade where a third-party exchange is not involved

Steve Brown

end

5.OTHER COMMODITIES/

FOOD/IN GENERAL/MIDDLE EAST

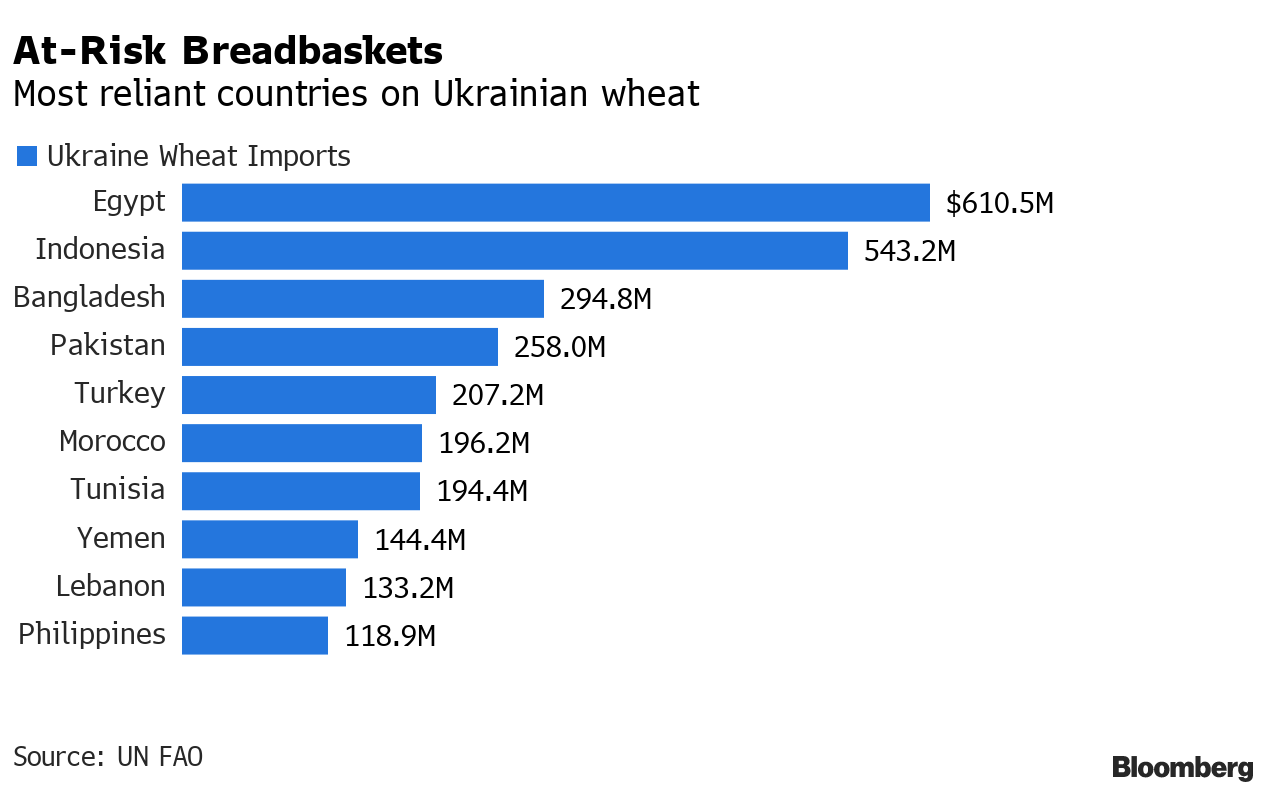

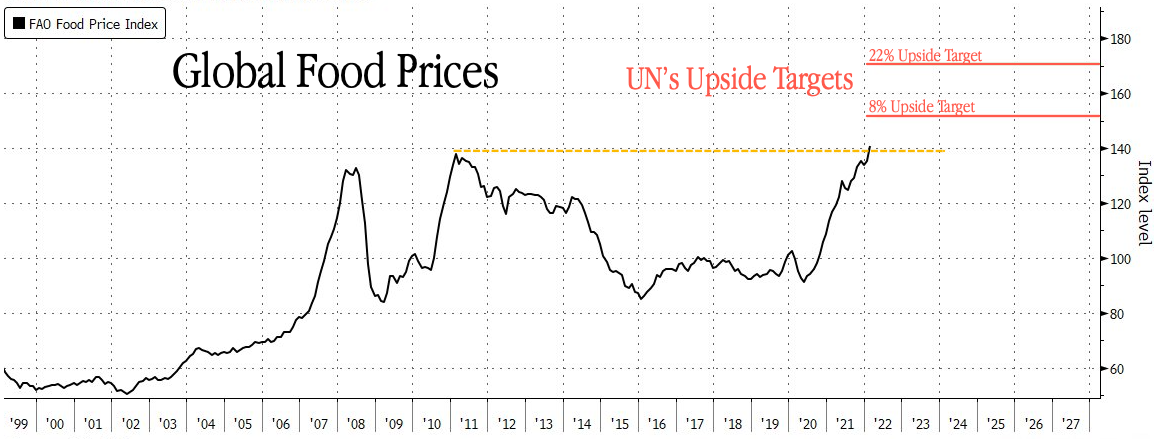

UN warns that the Middle East is at the breaking point as food prices are rising by alarming levels

(zerohedge)

UN Warns Middle East At “Breaking Point” As Food Prices Hit Alarming Highs

FRIDAY, APR 01, 2022 – 04:15 AM

Could it only be a matter of time before food riots erupt across the Middle East?

Even before Russia invaded Ukraine and disrupted the global food supply, menacing food inflation ripped around the world, crushing emerging market households the hardest.

A new report Thursday via the United Nations’ World Food Programme (WFP) warns a toxic combination of the conflict in Ukraine, economic disruptions due to COVID-19, and climate volatility resulting in bad harvests, are driving food prices to record highs as fears of shortages flourish.

WFP said millions of Middle Eastern and North African families struggle to buy even the most basic foods to keep hunger at bay.

“People’s resilience is at a breaking point. This crisis is creating shock waves in the food markets that touch every home in this region. No one is spared,” Corinne Fleischer, WFP Regional Director said.

For example, the cost of basic food for a family in Lebanon registered an annual increase of 351%, the highest in the region, followed by Syria with a near 100% rise, and Yemen at 81%. These three countries are incredibly reliant on food imports and prone to currency depreciation. A devastating drought has reduced Syria’s annual wheat production, while Ukraine’s grain exports have ceased.

WFP’s warning reminds us of everyone’s favorite permabear, SocGen’s Albert Edwards, opined two years ago about future agricultural price shocks and how it could spark another Arab Spring.

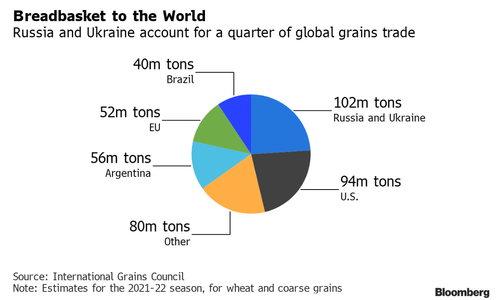

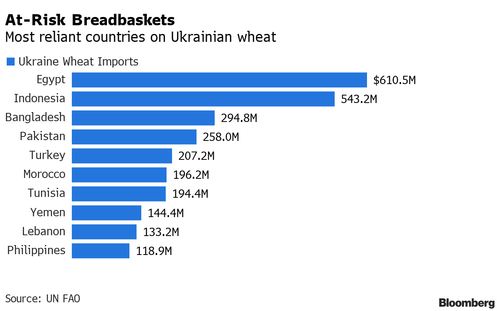

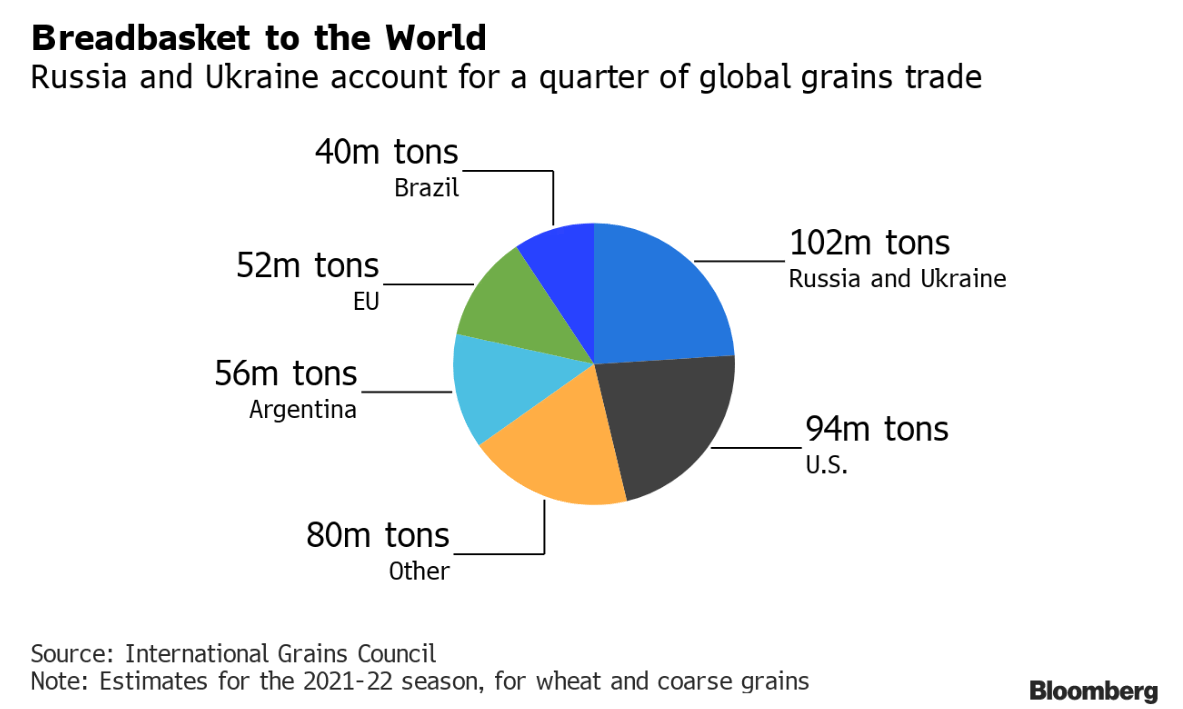

Russia and Ukraine export about a quarter of the global wheat trade, about a fifth of corn, and 12% of all calories traded globally. With trading disrupted in both countries, soaring prices and shortages are beginning to impact Middle Eastern and North African countries.

Bloomberg data shows the most reliant countries on Ukraine wheat are Egypt, Indonesia, Bangladesh, Pakistan, and Turkey. These countries are also the most prone to social unrest.

If the UN’s Food and Agriculture Organization is correct, food prices could jump another 20%, further pressuring emerging market households.

WFP’s warning that millions of families in the countries noted above are at “breaking points” because of rapid food inflation may suggest Edward’s Arab Spring 2.0 could be nearing.

.

end

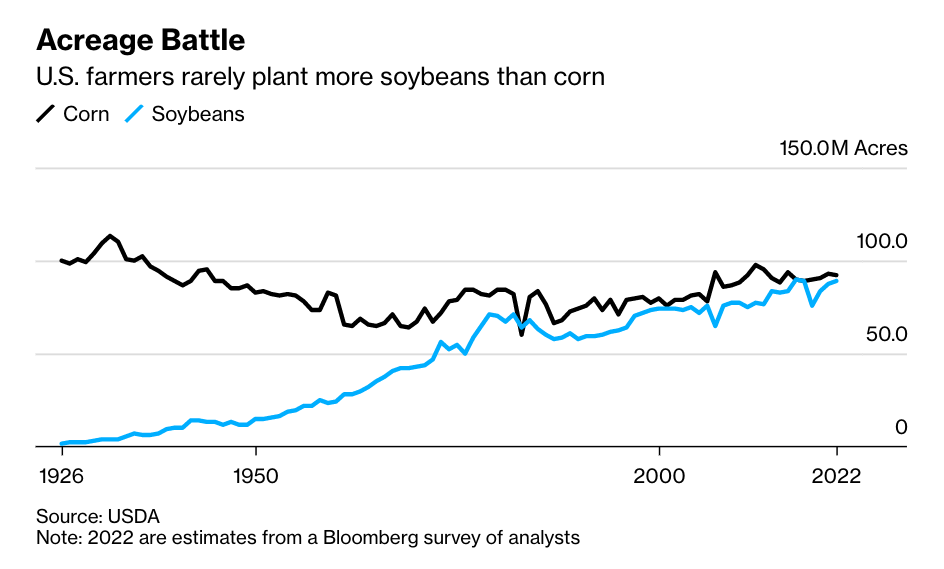

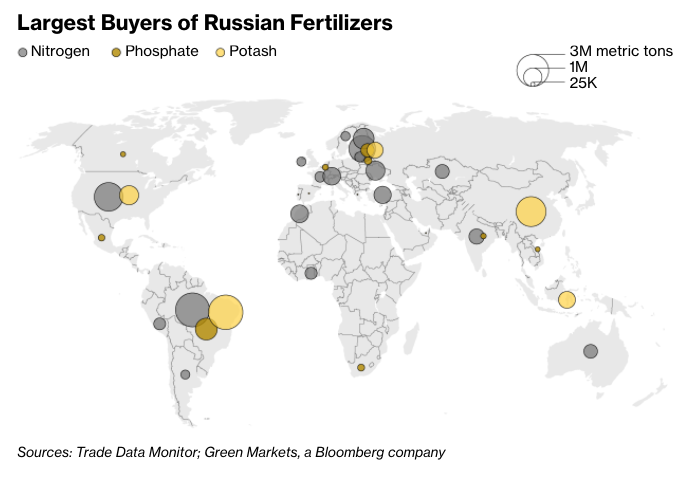

FERTILIZER

Prices out of control. USA farmers are ditching corn for soy to save on costs

(zerohedge)

“Fertilizer Is Out Of Control” – US Farmers Ditch Corn For Soy To Save On Costs

FRIDAY, APR 01, 2022 – 05:45 AM

Fertilizer prices are at record highs following Russia’s invasion of Ukraine puts massive pressure on American farmers to transition to crops that need less fertilizer.

A Bloomberg survey found that farmers will plant 2 million more acres of soybeans and about 2 million fewer of corn. That’s because soybeans require very little fertilizer versus corn.

Farmer Tim Gregerson of Omaha, Nebraska, said he’ll plant more soybeans this year because “fertilizer is out of control.” He said fertilizer prices spiked even before the Russian invasion, and it was then he decided to reduce the corn-to-soy ratio to about 50-50 this upcoming growing season.

On top of soaring fertilizer prices, he told Bloomberg, diesel, tractors, machine parts, feed for livestock, herbicide, and seed costs, and just about everything to do with farming are astronomically higher this year.

Farmer John Gilbert near Iowa Falls, Iowa, said his decision was made in January when fertilizer prices spiked.

A gauge of prices for US Gulf Coast Urea, US Cornbelt Potash, and NOLA Barge DAP, called the Green Markets North American Fertilizer Price Index, is up 43% since the Russian invasion and up 233% to $1,270 per ton since the start of the 2021 growing season.

The rising cost of natural gas, the primary input for most nitrogen fertilizer, has been one reason for rising fertilizer prices. Also, global supplies are expected to tighten as Russia will limit fertilizer exports to ‘unfriendly‘ countries. Russia is one of the biggest exporters globally — the US just so happens to be a large importer of nitrogen and potash from Russia.

Gregerson said due to global disruptions, “getting fertilizer is going to be more and more of a problem for the world in general.” In return, farmers will transition to crops that use less fertilizer — and it will be done globally.

In central Illinois, farmer Kenneth Hartman said he might not get much income off the soybeans but won’t have the expenses of planting corn.

Hartman also said high costs to plant corn is still a gamble because there’s still an environmental factor the crop year could be poor.

Increasing fertilizer prices could convince more farmers to plant more soy and less corn. If so, this would be the first time since 1983.

end

6.CRYPTOCURRENCIES

7. GOLD/ TRADING TODAY

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings FRIDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 6.3619

OFFSHORE YUAN: 6.3657

HANG SANG CLOSED DOWN 42.70 PTS OR 0.19%

2. Nikkei closed DOWN 155.45PTS OR 0.56%

3. Europe stocks ALL GREEN

USA dollar INDEX UP TO 98.49/Euro FALLS TO 1.1049

3b Japan 10 YR bond yield: FALLS TO. +.216/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 122.48/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 98.60 and Brent: 103.40

3f Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: DOWN -SHORE CLOSED DOWN// OFF- SHORE DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.0.573%/Italian 10 Yr bond yield RISES to 2.11% /SPAIN 10 YR BOND YIELD RISES TO 1.49%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 1.54: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 2.66

3k Gold at $1926.30 silver at: 24.51 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3l USA vs Russian rouble;// Russian rouble DOWN 1 3/4 in roubles/dollar; ROUBLE AT 83.52

3m oil into the 98 dollar handle for WTI and 103 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 122.48 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning .9246– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0216 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

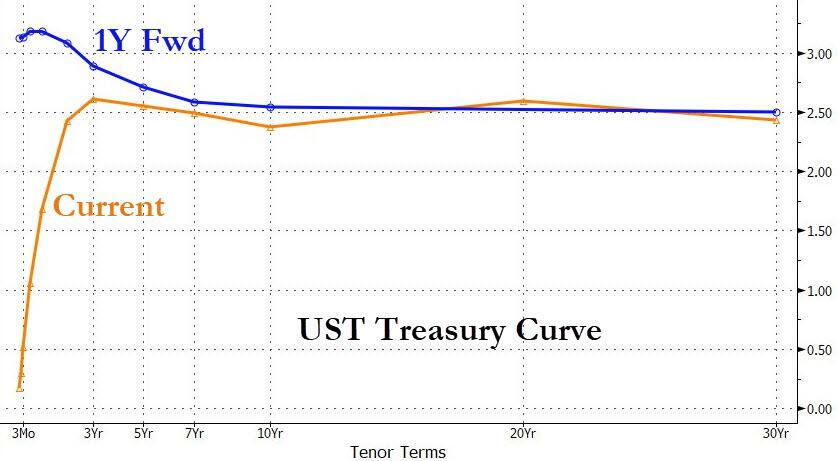

USA 10 YR BOND YIELD: 2.401 UP 6 BASIS PTS

USA 30 YR BOND YIELD: 2.503 UP 5 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 14.69

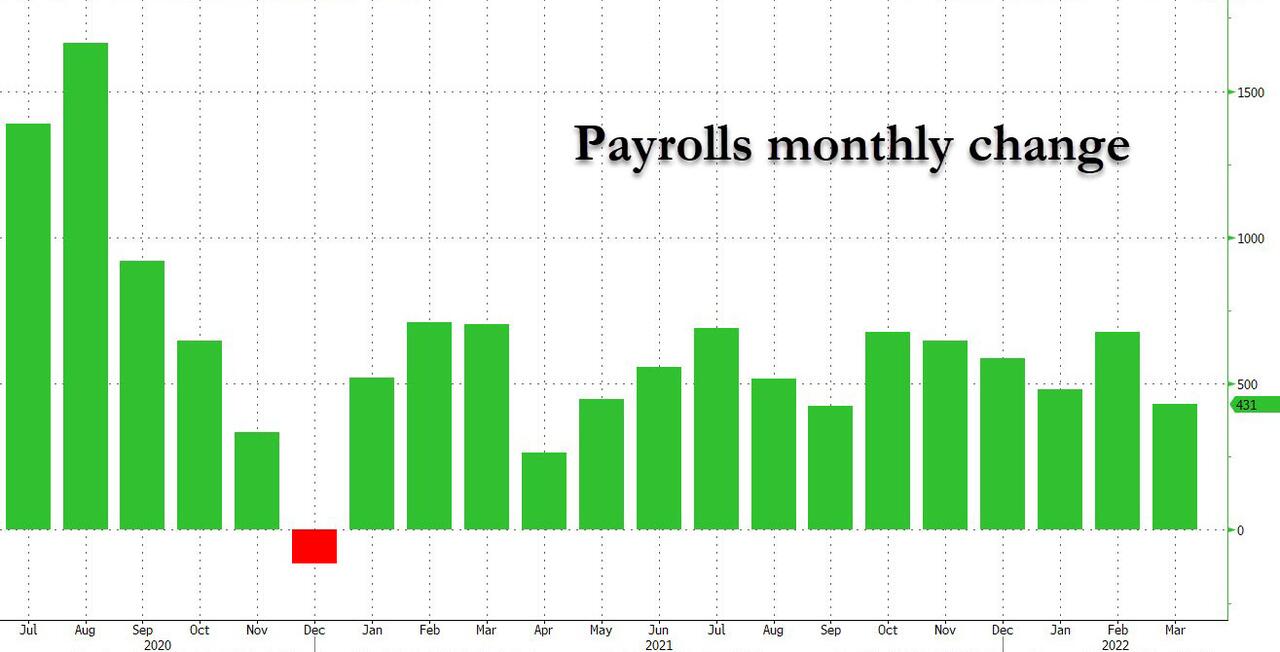

Futures Grind Higher To Start New Quarter With All Eyes On Payrolls

FRIDAY, APR 01, 2022 – 08:06 AM

Following yesterday’s furious quarter-end puke, which saw the S&P tumble 50 points in the last hour of trading as a massive $10 billion Market on Close sell imbalance sparked a liquidation frenzy, U.S. index futures started off the new quarter on the right foot, rising as investors weighed a drop in oil prices sparked by Biden’s unprecedented pre-midterm election draining of the petroleum reserve, ongoing developments in the Ukraine war and tightening monetary policy ahead of ISM and payrolls data. S&P500 and Nasdaq 100 futures gained around 0.5% before March payrolls figures later on Friday, after U.S. stocks ended their worst quarter since the start of the pandemic. Europe’s Stoxx 600 gained after its worst quarter since the pandemic bear market. Oil reversed an earlier decline as euro-area inflation accelerated to another all-time high and Russia’s Gazprom PJSC started telling clients how to pay for gas in rubles. Treasury yields rose and the dollar was steady as traders await the jobs report, which unless it is a total disaster, will strengthen the case for a 50bps rate hike in May. U.S. data on Friday include nonfarm payroll and ISM data while no major company is expected to report earnings.

U.S.-listed Chinese stocks jumped in premarket trading after Bloomberg News reported that Chinese authorities are preparing to give U.S. regulators full access to auditing reports of the majority of the 200-plus companies listed in New York. Alibaba shares rose 5.8% in premarket trading; E-commerce peers JD.com up 4% and Pinduoduo up 7.9%. Didi Global was among the top gainers, rising more than 18%, following a 15% drop Thursday. Meanwhile, shares of Lulu’s Fashion Lounge Holdings Inc. rose 27% in U.S. premarket after better-than-expected fourth-quarter and full-year guidance. Here are some other notable premarket movers:

- Chicken Soup For The Soul Entertainment (CSSE US) shares rise 21% in U.S. premarket, rebounding from yesterday’s losses, after Guggenheim’s Michael Morris (buy) said the company posted a “solid” 4Q performance, with sales modestly below his estimates but adjusted Ebitda slightly better.

- GameStop (GME US) shares rose 15% in premarket trading and were on course to open at the highest level this year after the video-game retailer announced plans for a stock split, fueling a rally in fellow so-called meme stocks.

- Redwire (RDW US) slumps 22% in U.S. premarket trading after the space infrastructure company reported 2021 results, with Jefferies saying that while the firm’s outlook was encouraging, it was disappointing versus prior expectations.

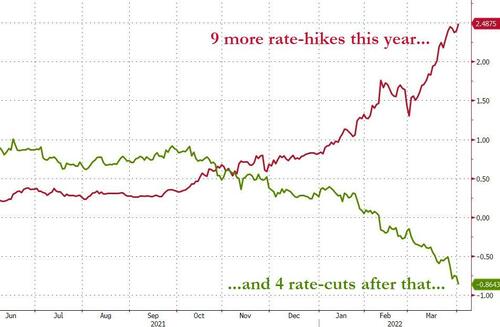

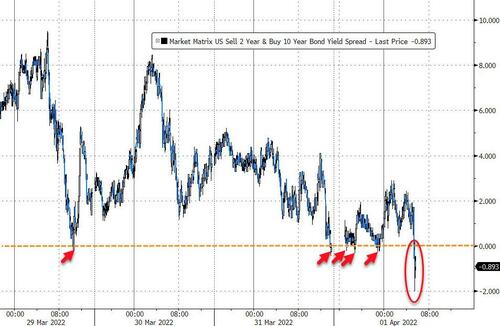

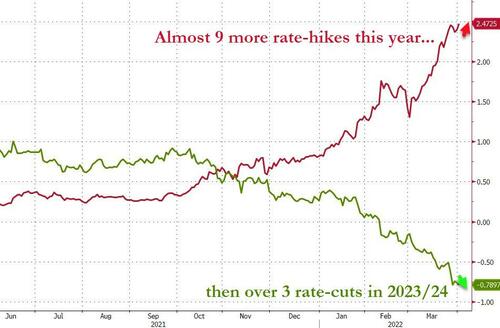

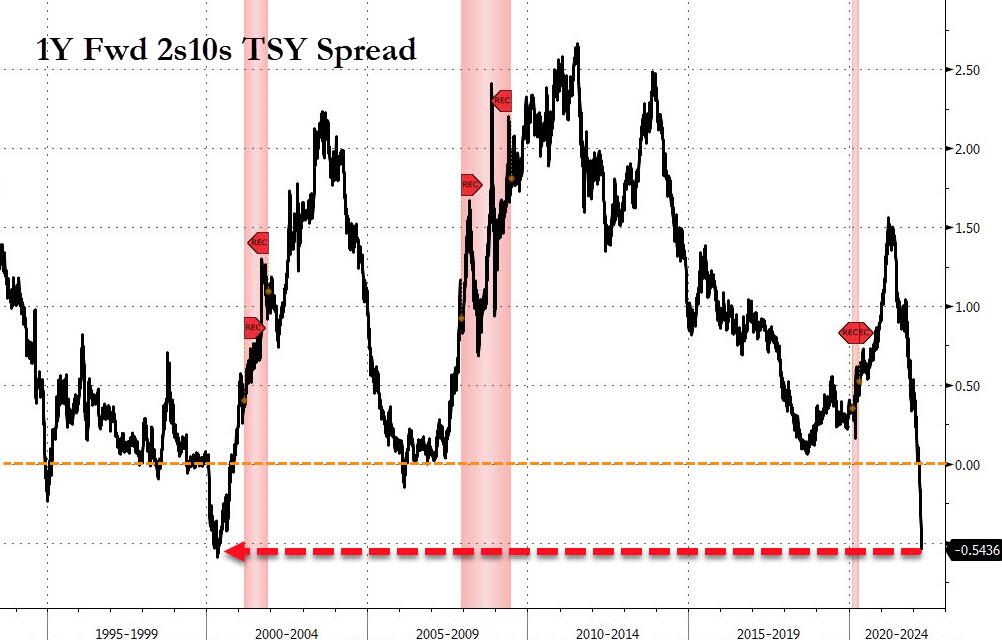

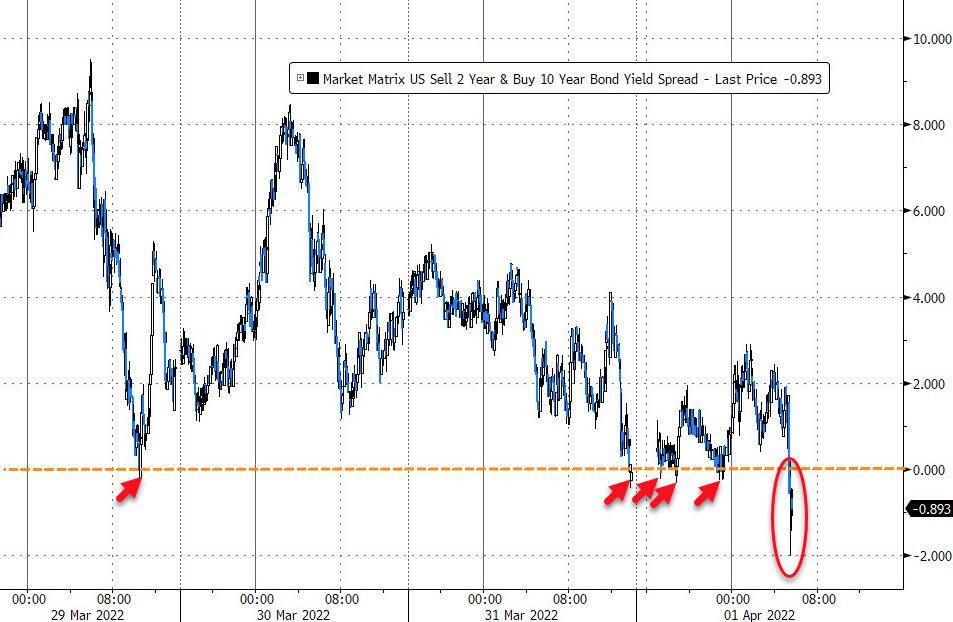

Meanwhile, the curve between two-year and 10-year Treasuries yields is flipping between positive and negative, signaling that the countdown to the next recession has begun (see “The Yield Curve Inverts: What Happens Next“).

“The market, like the Fed, has no idea how much tightening is necessary to stop a wage inflation spiral, but by upping the ante on the market with a series of 50bp rate hikes this year and a higher terminal rate, it can regain the control of the narrative and market expectations,” said Sebastien Galy, senior macro strategist at Nordea.

Investors begin a new quarter wondering if the fighting in Ukraine, the isolation of Russia and the Fed’s increasingly hawkish turn will engender still more volatility and losses for stocks and bonds. Raw materials are the only key asset class to deliver major gains so far in 2022.

Meanwhile, in Ukraine, talks between Ukraine and Russia resumed Friday via video link, following meetings earlier in the week in Turkey. Russia said two Ukrainian military helicopters made a rare strike across the border, hitting an oil tank facility in the city of Belgorod. Russian Foreign Minister Sergei Lavrov said Moscow is preparing a response to Ukraine’s proposals on ending hostilities; Lavrov also said Russia is preparing a response to Ukraine’s proposals, says there has been movement forward; he also added that Russia has seen “much more understanding” of the situation in Crimea and Donbass from the Ukrainian side. Lavrov says peace talks with Ukraine need to continue. UK reportedly urged Ukraine not to back down and is concerned US, France and Germany will push Ukraine to “settle” and make significant concessions to Russia, according to The Times citing a government source. Mayor of Ukraine’s Mariupol says Russian forces are not allowing humanitarian aid in; City is dangerous to try and exit.

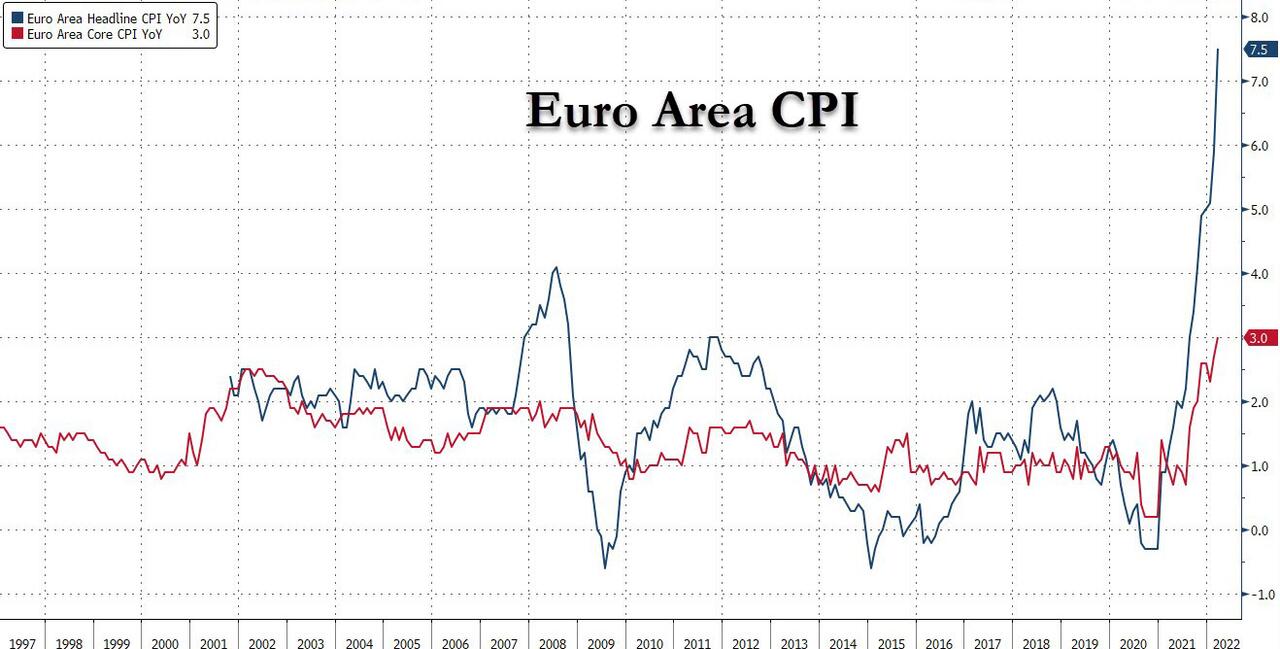

European equities also drifted higher after a slow start. Euro Stoxx 50 rises 0.7%. IBEX outperforms, adding 0.9%, FTSE 100 lags. Retailers, banks and miners are the strongest performing sectors. Euro-zone inflation accelerated to another all-time high as Russia’s invasion roiled global supply chains and provided a fresh driver for already-soaring energy costs. Euro-zone March consumer prices surged 7.5% from a year ago, up from 5.9% in February and far higher than the 6.7% median estimate in a Bloomberg survey.

The Stoxx Europe 600 Index however, was on the rise, led by retail and banking stocks. Here are some of the biggest European movers today:

- Santander shares rise as much as 3.2% after reiterating its financial targets for the year and saying its business remained resilient in the first quarter. The statement provides reassurance of recent trends, Barclays writes.

- Vestas Wind Systems gains as much as 5.4% after announcing orders totaling 2,179 MW in 1Q, with Handelsbanken saying the order intake is “promising” and well-above estimates.

- Bridgepoint Group jumps as much as 7.8% after the private-equity firm was upgraded to buy from neutral at Citi following a drop in the shares since the broker’s initiation in August 2021.

- Assicurazioni Generali rises as much as 3.8%, climbing for a third session, amid speculation the Italian insurer may get involved in industry M&A going forward.

- Greggs gains as much as 2.9% after Berenberg reiterates its buy recommendation, saying there is a “rare opportunity” to invest in the U.K. bakery chain at a “reasonable multiple.”

- Yara climbs as much as 1.8% after the company said it pre-ordered 15 floating bunkering terminals from Azane Fuel Solutions to establish a carbon-free ammonia fuel bunker network in Scandinavia.

- Stratec rises as much as 21% after a Bloomberg report that EQT and KKR are among several private equity firms weighing bids for the German health-care technology provider.

- Energiekontor jumps as much as 6.8%, extending its record high, after Warburg raised its price target to a Street- high, saying there is an “appetite for more” following Thursday’s FY results.

- Sodexo shares fall as much as 10% after the French caterer said the environment “remains uncertain” due to intermittent local outbreaks of Covid-19 and the war in Ukraine.

Russian stocks gained for a third day, the longest winning streak since trading resumed on March 24. Talks between Ukraine and Russia will resume Friday via video link, following meetings earlier in the week in Turkey. Russian Foreign Minister Sergei Lavrov said Moscow is preparing a response to Ukraine’s proposals on ending hostilities.

The manufacturing resurgence in Europe and Asia softened in March as factories saw worsening supply shortages and soaring costs after Russia’s invasion. Friday’s data follow inflation overshoots this week from Spain and Germany that prompted investors to bring forward bets on when the European Central Bank will end almost eight years of negative interest rates.

Earlier in the session, Asian stock retreated for a second day amid concerns about the extent the war in Ukraine will hurt global growth and as Chinese tech shares extended a selloff. The MSCI Asia-Pacific Index slid as much as 1.1% before paring about two-thirds of that loss. The benchmark still remained on pace to finish the week up 0.3%, extending its winning streak to a third week. Tech shares including Taiwan Semiconductor Manufacturing and Alibaba were major drags on Friday as traders assessed economic data and continued to eye possible U.S. delistings of Chinese firms. Equities in Japan underperformed the region while China’s consumer shares boosted the mainland benchmark. Investors are watching the impact of soaring inflation and higher interest rates on global growth as the war in Europe continues. Asia’s manufacturing resurgence softened in March as factories saw worsening supply shortages and surging costs after Russia’s invasion of Ukraine. Data on Friday showed Japan’s business mood weakened while South Korean imports jumped on rising costs. Also on investors’ radars are the trading halts of dozens of firms in Hong Kong from today after they missed a deadline to report annual results, increasing uncertainty in the market. “We are in the middle of a war between two globally vital suppliers of energy and food,” said Justin Tang, the head of Asian research at United First Partners. “The ramifications are plenty and as long as there is no cease fire, we will continue to experience ebbs and flows in volatility.” Asian stocks finished their worst quarter since early 2020 on Thursday with a drop of nearly 7%. Still, the measure has bounced back from the quarter-low touched in mid-March.

Sri Lanka’s stock market stopped trading on Friday and the rupee extended its loss after protests against surging living costs and daily power cuts amid dwindling foreign-exchange reserves. Trading in 33 Hong Kong-listed stocks was halted after a number of firms missed a deadline to report annual results

Japanese stocks fell in Tokyo fell for a third day after U.S. peers declined and the Tankan survey showed a gloomier view of business conditions among Japan’s biggest manufacturers. The yen slipped 0.5% against the dollar during the trading day, helping stocks trim earlier losses. Still, both major gauges capped their first weekly losses in three, shedding more than 1.7% each since March 25. Electronics and auto makers were the biggest drags as the Topix fell 0.1% Friday, paring an earlier slide of as much as 1.3%. Tokyo Electron and Fast Retailing were the largest contributors to a 0.6% loss in the Nikkei 225. The Tankan index of sentiment dropped to 14 from a revised 17 in the previous quarter, the first deterioration since June 2020, according to the central bank’s quarterly report Friday. The business mood among large non-manufacturers slipped to 9 from a revised 10 in the December report

India’s benchmark stocks index completed its third weekly gain in four weeks, as local buying helped steady war-induced volatility in equities. The S&P BSE Sensex rose 1.2% to 59,276.69 in Mumbai, taking it weekly advance to 3.3%. The key gauge completed its best monthly climb since August in the previous session. The NSE Nifty 50 Index rose 1.2% to 17,670.45 on Friday. HDFC Bank Ltd. surged 2.4% to its highest in more than a month and was the biggest boost to the Sensex, which saw 25 of the 30 shares trading higher. All 19 sectoral sub-indexes compiled by BSE Ltd. rose, led by a measure of utilities. Funds in India bought $5.2 billion worth of shares in March, while foreign investors extended their selling to a sixth consecutive month. The new fiscal year and quarter have started with concerns about the war in Ukraine, a hawkish U.S. Federal Reserve and the impact of higher commodity costs on company earnings. “We expect FY23 to witness continued volatility in equity markets, especially in the first half of the year with rising interest rates globally and high inflation, which is expected to persist,” Nishit Master, portfolio manager at Axis Securities Ltd., wrote in a note. The brokerage expects the Nifty index to rise to 20,200 by year-end and is positive on metals, hospitals, oil refining and capital goods.

In FX, the Bloomberg Dollar index inched up as the greenback traded mixed against its Group-of-10 peers; commodity currencies and the Swedish krona led gains while the yen was the worst performer. The euro fell and European bonds came off lows after euro-zone March consumer prices surged 7.5% from a year ago, up from 5.9% in February and more than the 6.7% median estimate in a Bloomberg survey. The pound consolidated against the euro, after rebounding from its weakest level since December on Thursday; the yen slid for the first time in four days. Japanese government bond yield curve resumed its steepening even as the Bank of Japan raised the amounts it plans to buy through regular market operations this quarter. Australia’s yield curve bear flattened, following a similar move in Treasuries. New Zealand dollar weakened; a gauge of consumer confidence dropped to an all-time low last month, according to ANZ data.

In rates, Treasuries dropped across the curve Friday as investors positioned before U.S. jobs data forecast to show average hourly earnings accelerated in March, backing the case for a faster pace of Federal Reserve interest-rate hikes. Treasury futures traded off session lows in early U.S. trading, although yields remain cheaper by 4bp to 7bp across the curve after Thursday’s late month-end selling was extended in early Asia. Fixed income weakness is Treasuries centric, with both bunds and gilts outperforming on the day. 10-year yields trade around 2.40% after peaking at 2.437% in early European session – bunds and gilts outperform by 4bp and 2bp in the sector. Long-end led losses steepens 5s30s spread by 1.4bp and 2s10s by 2bp on the day; March jobs report is due at 8:30am with headline change in payrolls expected at 490k vs. 678k prior — whisper number is higher than estimate at 529k. In Europe, the German curve bear steepened, cheapening up 2-3bps across the back end but broadly brushing off a hot Eurozone inflation print . Peripheral spreads mostly widen to core with long end Spain underperforming. Cash USTs maintain Asia’s bear flatten bias ahead of today’s payrolls release; the belly cheaper by ~6bps.

In commodities, crude futures recoup Asia’s weakness. WTI returns to little changed, regaining a $100-handle after a brief dip in late Asia. Base metals are mixed; LME zinc rises 1.4%, outperforming peers. LME copper lags. Spot gold falls roughly $2 to trade near $1,935/oz.

The US will also have the March ISM manufacturing reading, while global manufacturing PMIs are due. Otherwise, central bank speakers include the ECB’s Centeno, De Cos, Makhlouf, Schnabel and Knot, as well as the Fed’s Evans.

Market Snapshot

- S&P 500 futures up 0.4% to 4,548.50

- STOXX Europe 600 up 0.3% to 457.37

- MXAP down 0.4% to 179.71

- MXAPJ little changed at 590.96

- Nikkei down 0.6% to 27,665.98

- Topix down 0.1% to 1,944.27

- Hang Seng Index up 0.2% to 22,039.55

- Shanghai Composite up 0.9% to 3,282.72

- Sensex up 0.7% to 58,980.92

- Australia S&P/ASX 200 little changed at 7,493.80

- Kospi down 0.6% to 2,739.85

- German 10Y yield little changed at 0.58%

- Euro little changed at $1.1065

- Brent Futures down 1.0% to $103.69/bbl

- Gold spot down 0.3% to $1,931.84

- U.S. Dollar Index up 0.16% to 98.47

Top Overnight News from Bloomberg

- China’s factory activity fell to its worst level since the pandemic’s onset two years ago and a housing slump showed no sign of easing, darkening the outlook for the world’s second- largest economy

- Bundesbank President Joachim Nagel urged the European Central Bank to respond to quickly accelerating price pressures.

- Australia named Michele Bullock as the Reserve Bank’s first female deputy governor, propelling her to the front of the queue to succeed Philip Lowe in the top job

- At the U.S. Commerce Department, Secretary Gina Raimondo’s teams are working on ways to further undermine Putin’s ability to wage war

- For all the hardships visited on consumers at home and the financial chokehold put on the government from abroad, Bloomberg Economics expects Russia will earn nearly $321 billion from energy exports this year, an increase of more than a third from 2021.

- Iron ore futures in Asia gained with investors anticipating a strong recovery following the lifting of virus-related restrictions, even as news of Chinese housing giants missing earnings-report deadlines emerged

- Prime Minister Fumio Kishida’s government signed off on the reappointment of one of the Bank of Japan’s key policy architects in a move that suggests the central bank is looking for policy continuity after Governor Haruhiko Kuroda steps down next April

A more detailed look at global markets courtesy of Newsquawk:

Asia-Pac stocks were cautious following the uninspiring lead from Wall St, where the major indices closed off their worst quarterly performance in two years and as the region digested weak data releases. ASX 200 traded rangebound as pressure from losses in tech, industrials and financials was counterbalanced by resilience in the commodity-related sectors and upgrade to Australian PMI data. Nikkei 225 was subdued after mixed Tankan data in which the headline Large Manufacturing Index topped estimates, but Large Manufacturers and Non-Manufacturers’ sentiment worsened for the first time in 7 quarters. Hang Seng and were mixed with sentiment clouded after the PBoC drained liquidity andShanghai Comp. Chinese Caixin Manufacturing PMI slipped into contraction territory, although the mainland recovered amid the partial lifting of the lockdown in Shanghai and as Chinese press continued to advocate monetary easing

Top Asian News

- Shanghai Shifts Lockdown; Singapore Border: Virus Update

- Quarantine Eased for Hong Kong Flight Crew in Boost for Cathay

- China Chipmaker’s Buyer Said to Miss $9 Billion Payment Deadline

- Kasikornbank Said to Weigh Sale of $2 Billion Asset Manager Unit

European equities (Stoxx 600 +0.6%) opened marginally firmer before extending on gains after positive commentary from Russian Foreign Minister Lavrov. The Stoxx 600 set to close the week out with marginal gains of around 0.6% in what has been a choppy week for indices. Sectors in Europe are higher across the board with Retail, Banks and Autos top of the leaderboard.

Top European News

- London IPO Market Hasn’t Been This Bad in More Than a Decade

- Tiber Crossing Left in Limbo After War Sends Steel Surging

- Global Manufacturing Rebound Falters as War Takes Its Toll

- EU to Warn China It Will Hurt Global Role by Helping Russia

In FX, the Yen has relented as yields rebound and repatriation demand dries up – Usd/Jpy bounced further from recent lows beyond near term resistance through to circa 122.75. Greenback has regrouped in advance of NFP with the DXY straddling 98.500. Aussie outperforms as risk appetite picks up and 0.7500 continues to prove pivotal. Euro finds a base after marked month end reversal as hot inflation offset lukewarm manufacturing PMIs – Eur/USD holding around 1.1050 after soaking up stops on a minor and brief half round number break.Yuan weaker after sub-50 Caixin Chinese manufacturing print, softer PBoC Cny midpoint fix and 7-day liquidity drain – USDCNH above 6.3650.

In commodities, WTI (+0.6%) and Brent (+0.8%) kicked the session off on the backfoot following yesterday’s SPR announcement by the Biden administration with WTI breaching it’s weekly low printed on Tuesday at USD 98.44 with Brent so far unable to take out its weekly low of USD 102.19. Since then, crude benchmarks have attempted to claw back lost ground and sit in minor positive territory. White House Press Secretary Psaki said a gas tax holiday is not off the table, according to Reuters. US House Majority Leader Hoyer said oil companies should either produce on leases and drill wells or pay a fee for unused leases and idled wells, according to EIN News. Russian oil and gas condensate production slipped to 11.01mln BPD in March vs. 11.08mln BPD in February, according to Reuters sources Gazprom says refilling storage ahead of winter will be a challenge for the EU. Gazprom says it has begun sending requests of gas-for-rouble payment switch to clients today; sats it remains a responsible partner and continues to secure gas supplies

US Event Calendar

- 08:30: March Change in Nonfarm Payrolls, est. 490,000, prior 678,000

- Change in Private Payrolls, est. 495,000, prior 654,000

- Change in Manufact. Payrolls, est. 32,000, prior 36,000

- March Unemployment Rate, est. 3.7%, prior 3.8%

- Underemployment Rate, prior 7.2%

- Labor Force Participation Rate, est. 62.4%, prior 62.3%

- Average Hourly Earnings YoY, est. 5.5%, prior 5.1%; MoM, est. 0.4%, prior 0%

- Average Weekly Hours All Emplo, est. 34.7, prior 34.7

- 09:45: March S&P Global US Manufacturing PM, est. 58.5, prior 58.5

- 10:00: March ISM Employment, est. 53.1, prior 52.9

- ISM Prices Paid, est. 80.0, prior 75.6

- ISM New Orders, est. 58.5, prior 61.7

- ISM Manufacturing, est. 59.0, prior 58.6

- 10:00: Feb. Construction Spending MoM, est. 1.0%, prior 1.3%

DB’s Jim Reid concludes the overnight wrap

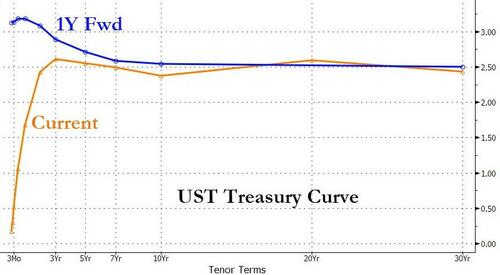

Filling in while Jim is on holiday, my quick scan for sports-related injuries for this introduction yielded nothing. Meanwhile, a scan of quarter end markets showed sovereign bonds again yielding less than nothing, as 2yr bund yields (-7.8bps) fell back below 0 to -0.09% while the 2s10s Treasury curve closed below zero for the first time since 2019. Yields farther out the curve followed oil and transatlantic equity prices lower as well. No rest for the weary, though, as today’s US employment data kickstarts the new quarter.

Before diving into markets, a couple of research plugs.

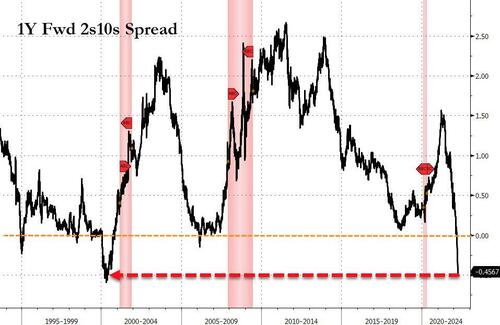

*** Jim’s latest chartbook, “The yield curve inverts … what happens next?”, is out. We looked at all things inversion, including recession risks, asset price performance, the Fed’s viewpoint, our economists’ latest recession models and also how yield curve inversions have been explained away in previous cycles. You can take a look here ***

Staying in advertising mode, with Q2 starting, we will publish our Q1 performance review shortly. Q1 was a dramatic time in financial markets, with Russia’s invasion of Ukraine, accelerating inflation, the Fed hiking rates, and the yield curve closing the quarter inverted. As a result, it was a pretty bad month for most assets, with losses across equities, credit, and sovereign bonds. The big exception were commodities as energy, metals and agricultural goods realized large gains. See the full report out shortly for more.

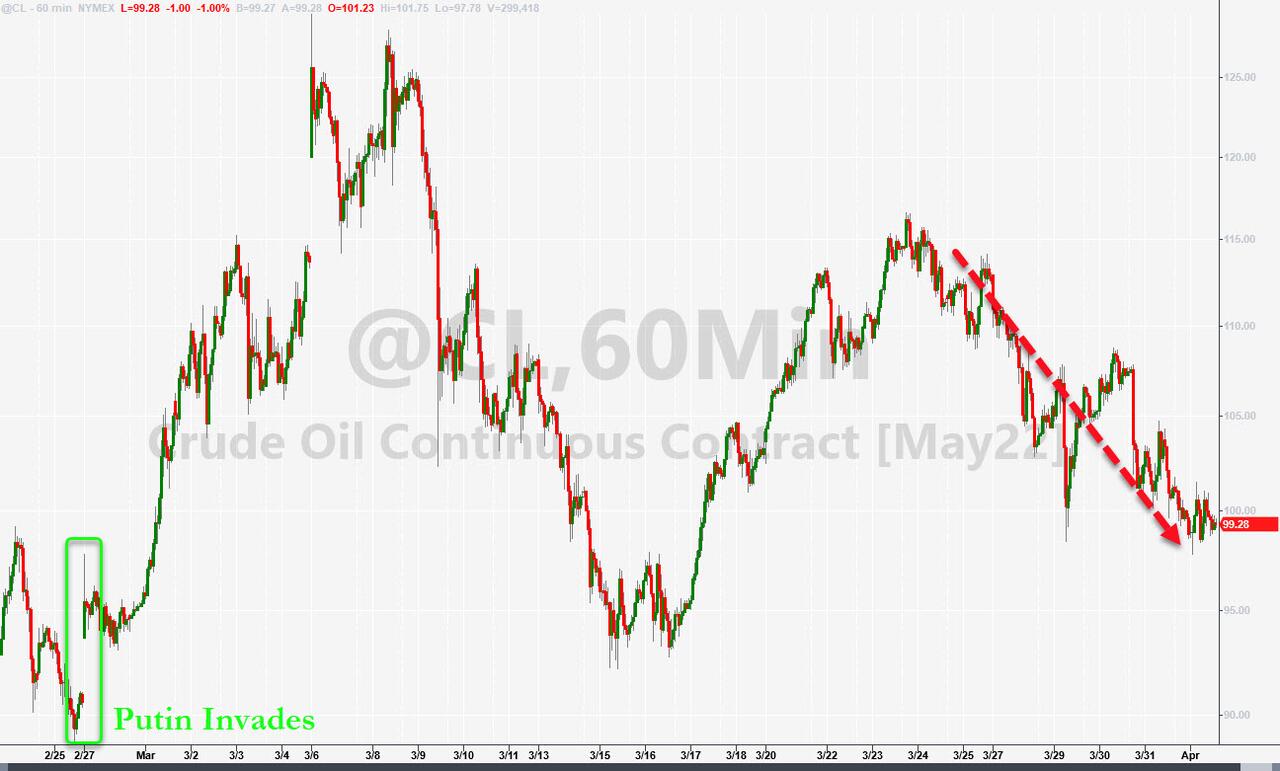

Turning back to yesterday’s markets, Brent and WTI crude futures fell -4.88% and -6.99%, respectively, following the US’s plan to release 1m barrels per day from its Strategic Petroleum Reserve for the next six months to combat eye-watering energy prices, the largest such SPR release on record. In an address to the nation, President Biden also announced measures to pressure domestic producers to increase their supply to the market along with easing regulations that currently restrict oil transport between American ports to American vessels. The President will also invoke the Defense Production Act to compel manufactures to prioritize the production of minerals used for large capacity batteries.

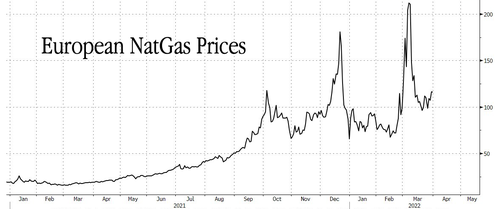

While the UK is considering whether to join the reserve-releasing effort, OPEC+ production will be steady as she goes, with the cartel ratifying the plan to increase production only gradually by 432k barrels a day, in line with expectations. Even without a material increase in OPEC+ production, reports overnight that the US was strategically aligned with allies on Iran inched us closer to a nuclear deal that would open up Iranian supply. Crude oil futures are down a further -3.23% as we go to press this morning. The debate about Russian natural gas invoicing appeared to reach a denouement yesterday; European importers will be able to pay for Russian supply in euros and dollars as contracts specify, with the conversion to rubles happening internally within Russia. Nevertheless, European natural gas gained +5.83%.

On the war, more reports joined the chorus signalling that Russian troops were indeed retreating from certain theatres, including various cities, airports, and the Chernobyl nuclear facility. While positive, the consensus is the locus of the war is moving to the east, rather than ending. Negotiations between Ukraine and Russia are set to resume today.

Foreshadowed in the lede, European sovereign yields staged a large rally to end the quarter. 10yr bunds, OATs, and BTPs all rallied more than -9bps, led by falling inflation compensation on the drawdown in oil prices; 10yr breakevens across Germany, France, and Italy, narrowed -7.0bps, -8.1bps, and -6.5bps, respectively. The rallies weren’t confined to the long-end, as -6.8bps of expected ECB rate hikes through 2022 were priced out as well.

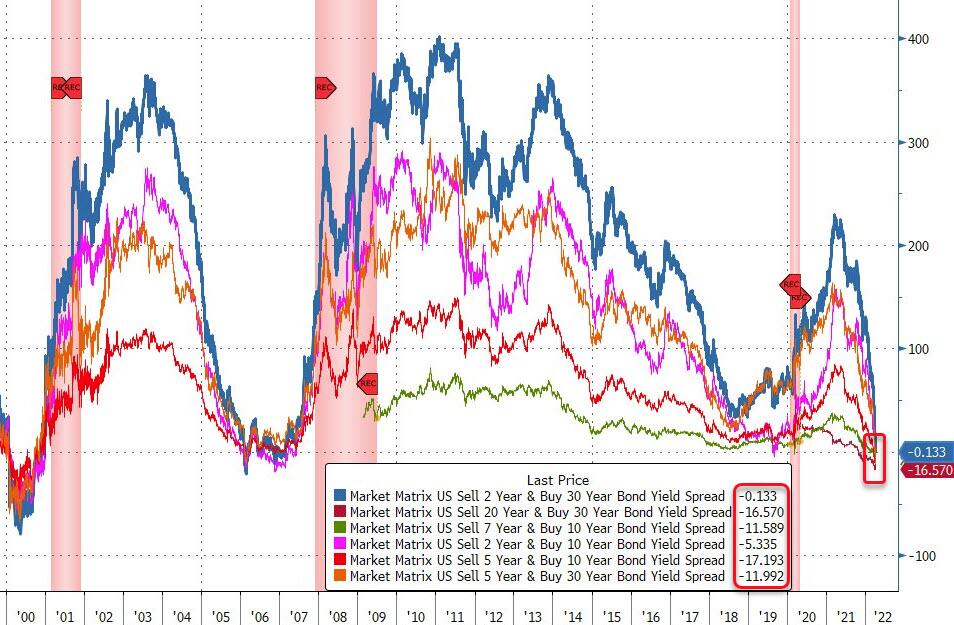

It was smoother sailing for Treasury yields after a stormy quarter, but 2s10s nevertheless managed to dip below zero to close the quarter after briefly testing the waters earlier this week. 2yr yields climbed +2.8bps while 10yr yields dropped anchor, falling -1.1bps, leaving 2s10s at -0.06bps. As was the case earlier this week, the curve re-steepened after the initial inversion plunge, trading at +1.2bps this morning.

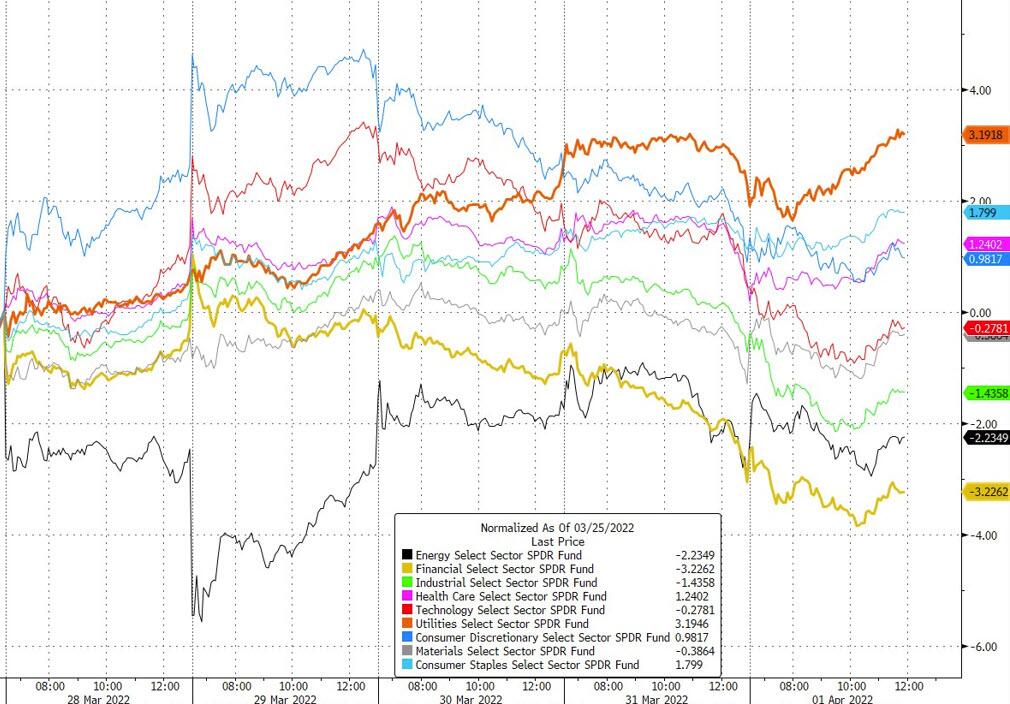

Stocks retreated on both sides of the Atlantic, with the STOXX 600 and S&P 500 falling -0.94% and -1.57%, cementing the first negative quarterly return for both indices since the original Covid onslaught in Q1 2020. STOXX 600 utilities (+0.37%) were the only sector in the green across both indices, with cyclical stocks the largest underperformers. The retreat was likely exacerbated by quarter end, which served to push the VIX (+1.23ppts) back above 20 for the first time this week.

Major Asian bourses are trading on the downbeat with tech stocks among the worst performers. Losses in the region are led by the Hang Seng (-0.72%), extending its previous session losses, with Chinese tech stocks listed in Hong Kong plunging. The Nikkei (-0.42%) is lagging after the BOJ’s quarterly Tankan business sentiment survey revealed that sentiment at Japan’s large manufacturers soured in the first three months of 2022. Chinese Caixin services PMI dropped to 48.1 in March, the steepest rate of contraction since February 2020. The deterioration was mainly triggered by the domestic Covid-19 resurgence. Despite the underwhelming data, Chinese stocks are outperforming the region, with the Shanghai Composite up +0.69%.

Outside of Asia, stock futures in the US are pointing to a positive start, with contracts on the S&P 500 (+0.25%), Nasdaq (+0.26%) and Dow Jones (+0.25%) all trading higher.

In data, US PCE increased 0.4%, month-over-month, in line with expectations, while the year-over-year measure moved to fresh four-decade high of 5.4%. The Chicago PMI printed at 67.9 vs. expectations of 57.0, while weekly initial jobless claims ticked up to a still low 202k vs. expectations of 196k. German unemployment fell by -18k in March (vs. -20k expected), which is the smallest monthly decline since last April. In turn, the unemployment rate remained at 5.0%, in line with expectations.

To the day ahead, Q2 kicks off with the March US employment situation report in the New York morning. Strong January and February data coincided with upside surprises and revisions to payrolls data, lending credence to the Fed’s position that the labor market is ready to withstand much tighter monetary policy, if not beckons it. Our US economists expect nonfarm payrolls to increase by +400k, bringing the unemployment rate to a post-pandemic low of 3.7%.

The Euro Area flash CPI will be the other main data, due at 10 am London, and is expected to show inflation rise to a fresh record since the single currency’s formation. After the massive upside surprises from Germany and Spain’s releases on Wednesday, yesterday brought another above-consensus print from France, where inflation rose to +5.1% on the EU-harmonised measure (vs. +4.9% expected). Meanwhile, Italy was the only one of the 4 biggest Euro Area countries not to see an upside surprise, but the +7.0% print (vs. +7.2% expected) nevertheless marked a gain over February’s +6.2% release.