April 8, 2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

april8, 2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD; $1941.660 UP $7.70

SILVER: $24.72 UP $0.11

ACCESS MARKET: GOLD $1947.60

SILVER: $24.78

Bitcoin morning price: $43,383 DOWN 298

Bitcoin: afternoon price: $43,120 DOWN 561

Platinum price: closing UP $11.30 to $977.80

Palladium price; closing UP 223.70 at $2421.30

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

comex notices/

: JPMorgan stopped/total issued 24/64

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: APRIL 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,933.800000000 USD

INTENT DATE: 04/07/2022 DELIVERY DATE: 04/11/2022

FIRM ORG FIRM NAME ISSUED STOPPED

072 C GOLDMAN 4

072 H GOLDMAN 5

363 H WELLS FARGO SEC 1

435 H SCOTIA CAPITAL 1

624 H BOFA SECURITIES 6

657 C MORGAN STANLEY 4

661 C JP MORGAN 59 24

709 C BARCLAYS 12

880 H CITIGROUP 12

TOTAL: 64 64

MONTH TO DATE: 23,879

NUMBER OF NOTICES FILED TODAY FOR APRIL. CONTRACT 64 NOTICE(S) FOR 6400 OZ (0.1990 TONNES)

total notices so far: 23,879 contracts for 2,387,900 oz (74.233 tonnes)

SILVER NOTICES:

132 NOTICE(S) FILED TODAY FOR 660,000 OZ/

total number of notices filed so far this month 988 : for 4,940,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

END

GLD

WITH GOLD UP $7.70

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

A HUGE CHANGE IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 1.45 TONNES FROM THE GLD//

INVENTORY RESTS AT 1088.75 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP 11 CENTS

AT THE SLV// A HUGE CHANGE IN SILVER INVENTORY AT THE SLV/ THE SLV//A DEPOSIT OF 1.386 MILLION OZ INTO THE SLV

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 566.352 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A STRONG SIZED 1477 CONTRACTS TO 149,110 AND CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE STRONG GAIN IN OI WAS ACCOMPLISHED WITH OUR STRONG $0.27 GAIN IN SILVER PRICING AT THE COMEX ON THURSDAY. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.27) AND WERE UNSUCCESSFUL IN KNOCKING OUT ANY SILVER LONGS AS WE HAD A STRONG GAIN OF 1477 CONTRACTS ON OUR TWO EXCHANGES

WE MUST HAVE HAD:

I) HUGE BANKER SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A ZERO ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A STRONG INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 4.305 MILLION OZ FOLLOWED BY TODAY’S QUEUE. JUMP OF 370,000 OZ//NEW STANDING: 5.385 MILLION OZ// V) STRONG SIZED COMEX OI GAIN/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS : —-519

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS APRIL. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF APRIL:

TOTAL CONTACTS for 6 days, total 2771 contracts: 13.855 million oz OR 2.30MILLION OZ PER DAY. (461 CONTRACTS PER DAY)

TOTAL NO OF OZ UNDERGOING EFP TO LONDON 2771 CONTRACTS X 5,000 PER CONTRACT:

EQUATES TO: 13.855 MILLION OZ

.

LAST 11 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

APRIL: 13.855 MILLION OZ

RESULT: WE HAD A STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1477 WITH OUR $0.27 GAIN IN SILVER PRICING AT THE COMEX// THURSDAY THE CME NOTIFIED US THAT WE HAD A ZERO SIZED EFP ISSUANCE CONTRACTS( 0 CONTRACTS ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A HUGE INITIAL SILVER OZ STANDING FOR MAR. OF 4.305 MILLION OZ FOLLOWED BY TODAY’S 370,000 OZ QUEUE JUMP//NEW STANDING: 5.385 MILLION OZ/// .. WE HAD AN STRONG SIZED GAIN 1996 OI CONTRACTS ON THE TWO EXCHANGES FOR 9.80 MILLION OZ DESPITE THE LOSS IN PRICE.

WE HAD 132 NOTICES FILED TODAY FOR 660,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A SMALL SIZED 1414 CONTRACTS TO 563,771 AND CLOSER TO NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: 511 CONTRACTS.

THE BIS HAS ABANDONED THE GOLD COMEX TRADING!!!

.

THE SMALL SIZED INCREASE IN COMEX OI CAME DESPITE OUR STRONG GAIN IN PRICE OF $13.40//COMEX GOLD TRADING/THURSDAY /.AS IN SILVER WE MUST HAD HUGE BANKER/ALGO SHORT COVERING ACCOMPANYING OUR SMALL SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD SOME LONG LIQUIDATION

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR APRIL AT 78.33 TONNES

YET ALL OF..THIS HAPPENED WITH OUR GAIN IN PRICE OF $13.40 WITH RESPECT TO TUESDAY’S TRADING

WE HAD AN FAIR SIZED GAIN OF 3234 OI CONTRACTS (10.05 PAPER TONNES) ON OUR TWO EXCHANGES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A SMALL SIZED 1820 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 564,282.

IN ESSENCE WE HAVE AN GOOD SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 3234, WITH 1414 CONTRACTS INCREASED AT THE COMEX AND 1820 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 3234 CONTRACTS OR 10.05 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1820) ACCOMPANYING THE SMALL SIZED GAIN IN COMEX OI (1414,): TOTAL GAIN IN THE TWO EXCHANGES 3234 CONTRACTS. WE NO DOUBT HAD 1) HUGE BANKER SHORT COVERING ,2.) HUGE INITIAL STANDING AT THE GOLD COMEX FOR APRIL. AT 78.33 TONNES FOLLOWED BY TODAY’S 19,800 OZ QUEUE JUMP //NEW STANDING 80.500 TONNES/// 3) ZERO LONG LIQUIDATION ///. ,4) SMALL SIZED COMEX OI. GAIN 5) SMALL ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

APRIL

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL :

15,312 CONTRACTS OR 1,531,200 OR 47.62 TONNES 6 TRADING DAY(S) AND THUS AVERAGING: 2552 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 6 TRADING DAY(S) IN TONNES: 47.62TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2020, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 47.62/3550 x 100% TONNES 1.35% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 47.62 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF MAY.WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF APRIL HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF MAY, FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (MAR), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A STRONG SIZED 1477 CONTRACTS TO 149,110 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 4 1/2 YEARS AGO.

EFP ISSUANCE 0 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1477 CONTRACTS AND ADD TO THE 0 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A STRONG SIZED GAIN OF 1,477 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 7.355 MILLION OZ,

OCCURRED WITH OUR STRONG LOSS $0.09 IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

5. Other gold commentaries

6. Commodity commentaries/cryptocurrencies

3. ASIAN AFFAIRS

i)FRIDAY MORNING// THURSDAY NIGHT

SHANGHAI CLOSED UP 15.15 PTS OR 0.47% //Hang Sang CLOSED UP 63.03 PTS OR 0.29% /The Nikkei closed UP 97.23 PTS OR 0.36% //Australia’s all ordinaires CLOSED UP 0.48% /Chinese yuan (ONSHORE) closed DOWN 6.3637 /Oil DOWN TO 96.44 dollars per barrel for WTI and DOWN TO 100.58 for Brent. Stocks in Europe OPENED ALL GREEN EXCEPT // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.3637 OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.3682: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

A)NORTH KOREA/

b) REPORT ON JAPAN

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A SMALL SIZED 1414 CONTRACTS TO 563,771 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS SMALL COMEX INCREASE OCCURRED DESPITE OUR STRONG GAIN OF $13.40 IN GOLD PRICING THURSDAY’S COMEX TRADING. WE ALSO HAD A SMALL SIZED EFP (1820 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE ACTIVE DELIVERY MONTH OF APRIL.. THE CME REPORTS THAT THE BANKERS ISSUED A SMALL SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 1820 EFP CONTRACTS WERE ISSUED: ;: , . 0 JUNE :1820 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1109 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A GOOD SIZED TOTAL OF 3234 CONTRACTS IN THAT 1820 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A SMALL SIZED COMEX OI GAIN OF 1925 CONTRACTS..AND THIS GAIN OCCURRED WITH OUR GAIN IN PRICE OF GOLD $13.40.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING FOR APRIL (80.500),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 80.012

THE BANKERS WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $4.10) AND BUT WERE UNSUCCESSFUL IN FLEECING ANY LONGS AS WE HAVE REGISTERED A GOOD SIZED GAIN OF 8.709 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR APRIL (80.500 TONNES)…

WE HAD — 511 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 3234 CONTRACTS OR 323,400 OZ OR 10/05 TONNES

Estimated gold volume today: 144,205 ///poor

Confirmed volume yesterday: 135,121 contracts poor

INITIAL STANDINGS FOR APRIL ’22 COMEX GOLD //APRIL 8

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 6430.209 oz Brinks 200 kilobars 8037.75 oz Int. Delaware 250 kilobars Manfra 482.265 oz15 kilobars total: 14,950.224 oz |

| Deposit to the Dealer Inventory in oz | 5690.27Oz Manfra 177 kilobars |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 64 notice(s)6400 OZ 0.1991 TONNES |

| No of oz to be served (notices) | 2002 contracts 200,200 oz 6.227 TONNES |

| Total monthly oz gold served (contracts) so far this month | 23,879 notices 2,387,900 OZ 74.233 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For today:

dealer deposits 1

i)Into Manfra: 5690.27 oz 177 kilobars

total dealer deposit 5690.27 oz//

No dealer withdrawals

0 customer deposits.

/

3 customer withdrawals

i) out of Brinks 6430.209 oz 200 kilobars

ii) out of Int. Delaware 8037.75oz (250 kilobars)

iii) Out of Manfra: 482.265 oz 15 kilobars

total customer withdrawal: 14,950.224 oz /

ADJUSTMENTS: customer to dealer

ii) Brinks 25,648.004 oz

dealer to customer:

i) Manfra: 192.900 oz (6 kilobars)

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR APRIL.

For the front month of APRIL we have an oi of 2066 contracts having LOST 1822.

We had 2020 notices filed yesterday so we GAINED 198 contracts or 19800 oz will stand for delivery at the comex

May saw a LOSS of 470 contracts to stand at 4,078

June saw a GAIN of 1924 contracts UP to 472,924 contracts

We had 2020 notice(s) filed today for 202,000 oz FOR THE APRIL 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 59 notices were issued from their client or customer account. The total of all issuance by all participants equates to 64 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 59 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 4 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the APRIL /2021. contract month,

we take the total number of notices filed so far for the month (23,879) x 100 oz , to which we add the difference between the open interest for the front month of (APRIL 2066 CONTRACTS ) minus the number of notices served upon today 64 x 100 oz per contract equals 2,572,300 OZ OR 80.009 TONNES the number of TONNES standing in this active month of APRIL.

thus the INITIAL standings for gold for the APRIL contract month:

No of notices filed so far (23,879) x 100 oz+ (2066) OI for the front month minus the number of notices served upon today (64} x 100 oz} which equals 2,572,300 oz standing OR 80.009 TONNES in this active delivery month of APRIL.

We GAINED 19,800 oz as a QUEUE. jump as our banker friends scrounge around for some gold

TOTAL COMEX GOLD STANDING: 80.500 TONNES (A WHOPPER FOR AN APRIL ( ACTIVE) DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

191,133,764.7, oz NOW PLEDGED /HSBC 5.94 TONNES

99,258.893 PLEDGED MANFRA 3.08 TONNES

54,339.114oz PLEDGED JPMorgan no 1 1.690 tonnes

243,923.704, oz JPM No 2 7.58 TONNES

898,821.330 oz pledged Brinks/27,96 TONNES

International Delaware:: 0

Loomis: 18,615.429 oz

total pledged gold: 1,488,458.117 oz 46.29 tonnes

TOTAL REGISTERED AND ELIG GOLD AT THE COMEX: 35,900,924.844 OZ (1116,66 TONNES)

TOTAL ELIGIBLE GOLD: 18,287,671.056 OZ (568.82 tonnes)

TOTAL OF ALL REGISTERED GOLD: 17,613,253.788 OZ (547.84 tonnes)

REGISTERED GOLD THAT CAN BE SERVED UPON: 16,124,795.0 OZ (REG GOLD- PLEDGED GOLD) 502,886 tonnes

END

APRIL 2022 CONTRACT MONTH//SILVER//APRIL 8

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1,176,383.213 oz Brinks CNT Manfra Delaware HSBC JPMorgan |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 542,787.7000 oz JPM |

| No of oz served today (contracts) | 132CONTRACT(S)660,000 OZ) |

| No of oz to be served (notices) | 89 contracts (445,000 oz) |

| Total monthly oz silver served (contracts) | 988 contracts 4,940,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

we had 0 deposits into the dealer

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 1 deposits into the customer account

i) Into JPMorgan: 542,787.700

total deposit: 542,787.70 oz

JPMorgan has a total silver weight: 176.457 million oz/335.775 million =52.54% of comex

i) Comex withdrawals: 6

i) Out of JPM 599,005.800 oz

ii) Out of Delaware: 975.200 oz

iii) Out of Brinks 289,004.770 oz

iv) Out of CNT 75,529.425 oz

v) out of HSBC 177,291.500 oz

vi) out of Manfra: 34,576.518 oz

total withdrawal 1,176,383.213 oz

1 adjustments: dealer to customer

jpmorgan; 313,212.230 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 86.281 MILLION OZ

TOTAL REG + ELIG. 335.755 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR APRIL

silver open interest data:

FRONT MONTH OF APRIL OI: 221, HAVING LOST 58 CONTRACTS FROM THURSDAY. We had 132 notices filed yesterday,

so we GAINED 74 contracts or an additional 370,000 oz will stand on this side of the pond

MAY HAD A LOSS OF 5910 CONTRACTS DOWN TO 91,144 contracts

JUNE HAD A GAIN OF 198 TO STAND AT 832

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 132 for 660,000 oz

Comex volumes: 63,466// est. volume today// poor/

Comex volume: confirmed yesterday: 65,108 contracts ( poor )

To calculate the number of silver ounces that will stand for delivery in APRIL. we take the total number of notices filed for the month so far at 988 x 5,000 oz = 4,940,000oz

to which we add the difference between the open interest for the front month of APRIL (221) and the number of notices served upon today 132 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the APRIL./2021 contract month: 988 (notices served so far) x 5000 oz + OI for front month of APRIL (221) – number of notices served upon today (132) x 5000 oz of silver standing for the APRIL contract month equates 5.385,000 oz. .

We GAINED contracts or 370,000 oz will stand on this side of the pond

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

APRIL 8/WITH GOLD UP $7.70: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES INTO THE GLD//INVENTORY RESTS AT 1088.75 TONNES

APRIL 7/WITH GOLD UP $13.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1087.30 TONNES

APRIL 6/WITH GOLD DOWN $4.10: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.68 TONNES FROM THE GLD..//INVENTORY RESTS AT 1087.30 TONNES

APRIL 5/WITH GOLD DOWN $5.70: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.75 TONNES FROM THE GLD//INVENTORY RESTS AT 1089.98 TONNES

APRIL 4/WITH GOLD UP $.70//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1091.73 TONNES

APRIL 1///WITH GOLD DOWN $19.00 : A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .29 TONNES INTO THE GLD///INVENTORY RESTS AT 1091.73 TONNES

MARCH 31/WITH GOLD UP $13.30 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD FROM MONDAY A WITHDRAWAL OF 1.71 TONNES FROM THE GLD:INVENTORY RESTS AT 1091.44

MARCH 28/WITH GOLD DOWN $14.65: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1093.18 TONNES

MARCH 25/WITH GOLD DOWN $7.60 : A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.52 TONNES INTO THE GLD///INVENTORY RESTS AT 1093.18 TONNES

MARCH 24/WITH GOLD UP $24.95: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.06 TONNES INTO THE GLD..//INVENTORY RESTS AT 1087.66 TONNES

MARCH 23/WITH GOLD UP $15.75//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1083.60 TONNES

MARCH 22/WITH GOLD DOWN $7.75: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.16 TONNES OF GOLD DEPOSITED INTO THE GLD//INVENTORY RESTS AT 1083.60 TONES

MARCH 21//WITH GOLD UP $.25 : A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 9.00 TONNES INTO THE GLD////INVENTORY RESTS AT 1082.44 TONES

MARCH 18/WITH GOLD DOWN $13.55 NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1073.44 TONES

MARCH 17/WITH GOLD UP $33.50: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.61 TONNES INTO THE GLD//INVENTORY RESTS AT 1073.44 TONNES

MARCH 16/WITH GOLD DOWN $18.50//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.33 TONNES FROM THE GLD///INVENTORY RESTS AT 1061.83 TONNES

MARCH 15/WITH GOLD DOWN $30.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1064.16 TONNES

MARCH 14//WITH GOLD DOWN $22.75, HUGE CHANGES IN GOLD INVENTORY AT THE GLD//STRANGE: A DEPOSIT OF 2.62 TONNES INTO THE GLD.//INVENTORY RESTS AT 1064.16 TONNES

MARCH 11/WITH GOLD DOWN $14.60: A BIG CHANGE IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 1061.54 TONNES

MARCH 10//WITH GOLD UP $11.55: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.06 TONNES FORM THE GLD///INVENTORY RESTS AT 1063.28 TONNES

MARCH 9/WITH GOLD DOWN $53.85//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.64 TONNES INTO THE GLD//INVENTORY RESTS AT 1067.34 TONNES

MARCH 8/WITH GOLD UP $46.10: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 8.42 TONNES INTO THE GLD///INVENTORY RESTS AT 1062.70 TONNES

MARCH 7/WITH GOLD UP $28.40 A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.06 TONNES INTO THE GLD..//INVENTORY RESTS AT 1054.28 TONNES

MARCH 4/WITH GOLD UP $28.40//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1050.22 TONNES

MARCH 3/WITH GOLD UP $13.95: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 7.84 TONNES//INVENTORY RESTS AT 1050.22 TONNES

MARCH 2/WITH GOLD DOWN $20.80//A MONSTER CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 13.36 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 1042.38 TONNES

MARCH 1/WITH GOLD UP $42.60: NO CHANGES IN GOLD INVENTORY AT THE GLD: //INVENTORY RESTS AT 1029.32 TONNES

FEB 28/WITH GOLD UP $12.95: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1029.32 TONNES

FEB 25/WITH GOLD DOWN $38.95: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1029.32 TONNES

FEB 24/WITH GOLD UP $17.35//A HUGE CHANGE AT THE GLD: 5.23 TONNES INTO THE GLD// IN GOLD INVENTORY AT THE GLD/INVENTORY REST AT 1029.32 TONNES

FEB 23/WITH GOLD UP $2.00 : NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1024.09 TONNES

CLOSING INVENTORY FOR THE GLD//1088.75 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

APRIL 8/WITH SILVER UP 11 CENTS :NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 566.352 MILLION OZ//

APRIL 7/WITH SILVER UP 27 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 566.352 MILLION OZ//

APRIL 6/WITH SILVER DOWN 9 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 566.352 MILLION OZ

APRIL 5/WITH SILVER DOWN 16 CENTS : A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.386 MILLION OZ INTO THE SLV..//INVENTORY RESETS AT 566.352 MILLION OZ//

APRIL 4/WITH SILVER DOWN 5 CENTS TO CHANGES IN SILVER INVENTORY AT THE SLV//: A DEPOSIT OF 6.326 MILLION OZ//INVENTORY REST AT 564.966 MILLION OZ//

APRIL 1/WITH SILVER DOWN 39 CENTS A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.302 MILLION OZ INTO THE SLV////INVENTORY REST AT 558.647 MILLION OZ//

MARCH 31/WITH SILVER UP 3 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 2.171 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 556.345 MILLION OZ

MARCH 28/WITH SILVER DOWN 30 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.847 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 554.167 MILLION OZ//

MARCH 25/WITH SILVER DOWN 20 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 552.320 MILLION OZ//

MARCH 24/WITH SILVER UP 54 CENTS TODAY; A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.092 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 552.320 MILLION OZ//

MARCH 23/WITH SILVER UP 24 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 550.288 MILLION OZ//

MARCH 22/WITH SILVER DOWN $0.29 TODAY : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 550.288 MILLION OZ//

MARCH 21/WITH SILVER UP 16 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 550.288 MILLION OZ//

MARCH 18/WITH SILVER DOWN 37 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.217 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 550.288 MILLION OZ//

MARCH 17/ WITH SILVER UP 72 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.049 MILLION OZ INTO THE SLVV//INVENTORY RESTS AT 548.071 MILLION OZ

MARCH 16/WITH SILVER DOWN 56 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 462,000 OZ FROM THE SLV//INVENTORY RESTS AT 544.560 MLLION O

MARCH 15/WITH SILVER DOWN 18 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 545.022 MILLION OZ

MARCH 14/WITH SILVER DOWN 64 CENTS TODAY; STRANGE A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.125 MILLION OZ/INVENTORY RESTS AT 545.022 MILLIONOZ

MARCH 11/WITH SILVER DOWN 13 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.897 MILLION OZ

MARCH 10/WITH SILVER UP 39 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.897 MILLION OZ/

MARCH 9/WITH SILVER DOWN 88 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 5.174 MILLION OZ OF FAKE SILVER.//INVENTORY RESTS AT 542.897 MILLION OZ//

MARCH 8/WITH SILVER UP 88 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.217 MILLION OZ INTO THE SLV////INVENTORY RESTS A 548.071 MILLION OZ//

MARCH 7/WITH SILVER UP 40 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 545.854 MILLION OZ//

MARCH 4/WITH SILVER UP 50 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 545.854 MILLION OZ/

MARCH 3/WITH SILVER UP 2 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 545.854 MILLION OZ//

MARCH 2/WITH SILVER DOWN $.32 TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 198,000 OZ FROM THE SLV//INVENTORY RESTS AT 545.854 MILLION OZ//

MARCH 1/WITH SILVER UP $1.13 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 546.052 MILLION OZ//

FEB 28/WITH SILVER UP 31 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT 546.052 MILLION OZ//

FEB 25/WITH SILVER DOWN 64 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 5.510 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 546.052 MILLION OZ/

FEB 24/WITH SILVER UP 15 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 551.597 MILLION OZ

FEB 23/WITH SILVER UP 22 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 551.597 MILLION OZ//

SLV FINAL INVENTORY FOR TODAY: 566.352 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

Why Won’t The Fed Be Able To Shrink Its Balance Sheet?

FRIDAY, APR 08, 2022 – 09:01 AM

Authored by Michael Maharrey via SchiffGold.com,

Earlier this week, Federal Reserve governor and vice-chair nominee Lael Brainard indicated the central bank will shrink its balance sheet at a “considerably” more rapid pace than it did during the previous cycle. I, Peter Schiff and a few others outside the mainstream have said the Fed won’t be able to do this.

Why not?

The Fed first expanded its balance sheet in the wake of the 2008 financial crisis. Through three rounds of quantitative easing (QE), the Fed expanded its balance sheet from under $1 trillion to $4.5 trillion. When the central bank started QE, then-Fed Chair Ben Bernanke swore the central bank wasn’t monetizing federal government debt. He said the balance sheet expansion was an emergency measure and that the Fed would eventually sell the bonds it was buying.

The Fed didn’t get around to balance sheet reduction until 2018, and it did so at a relatively slow pace. By the time it ended tightening in August 2019, the balance sheet was just below $3.8 trillion. In all, the Fed shed about $700 billion from its balance sheet in a little more than 18 months.

Why did the Fed abandon tightening in 2019?

Because in the fall of 2018, the stock market tanked and the economy went wobbly. The markets and the economy couldn’t handle even the modest monetary tightening the Fed managed to implement.

It’s important to remember that the Fed resumed QE months before the pandemic — although it didn’t call it QE. By the time the Fed launched QE 4 in 2020, the balance sheet had already expanded back to just over $4 trillion.

Over the last two years, the Fed has added another $5 trillion to the balance sheet expanding it to nearly $9 trillion.

Brainard indicated that the upcoming balance sheet runoff will be “considerably” faster than last time. She did not say what that actually means, but the Fed minutes from the March meeting shed a little bit of light on the nuts and bolts of the plan.

According to the minutes, the plan is to reduce the balance sheet by about $3 trillion over a three-year period. This would leave the balance sheet at $6 trillion – up by $2 trillion from its pre-pandemic level and more than $5 trillion above the pre-2008 financial crisis level. So much for Bernanke’s promise.

Looking at the big picture, the Fed’s plan is relatively modest. If it sticks to this plan, it will shrink the balance sheet by about $1 trillion per year.

But I don’t even think it can accomplish this.

If the central bank couldn’t run off $700 billion in 2018 without popping the bubbles and shaking up the economy, what makes anybody think it can decrease its balance sheet holdings by $3 trillion this time around with even bigger bubbles and more debt in the economy?

THE MECHANISM

I’m not basing my skepticism purely on speculation. The process of balance sheet reduction makes it extremely unlikely that the Fed can accomplish its goal.

First, you have to understand how and why the Fed expanded its balance sheet to begin with.

Through quantitative easing, the Fed buys US Treasury bonds and mortgage-backed securities with money created out of thin air on the open market. For our purposes, we’ll focus on US Treasuries.

QE accomplishes two important things for the US government. First, it injects currency and liquidity to juice the economy. (By that I mean inflate bubbles.) Second, it reduces the supply of bonds on the market and holds bond prices artificially high. Bond yields are inversely correlated with bond prices. When the price of a bond rises, the yield falls. Propping bond prices up through its artificial demand keeps interest rates low.

So, QE benefits the federal government in two ways. It allows the US Treasury to sell more bonds to finance its deficits because the Fed is absorbing some of the supply and keeping demand higher than it otherwise would be. And it keeps the government’s borrowing costs low by artificially suppressing interest rates.

Balance sheet reduction, or quantitative tightening (QT), reverses this process.

The Fed can shrink its balance sheet in two ways.

- Typically, the Fed rolls over the bonds on its balance sheet as they mature. In other words, it takes the money the government pays for the mature bond and buys a new one to replace it. The Fed can shrink its balance sheet simply by letting the old bonds roll off the books without replacing them. This is a relatively slow way to shrink the balance sheet.

- The Fed can decrease its bond holding more quickly by selling them on the open market.

Either way, it creates a big problem for the federal government. If the Fed sheds $1 trillion in bonds from its balance sheet over the next year, the US Treasury will have to find buyers for $1 trillion in additional bonds, on top of the $1 trillion or so in new bonds it will have to sell to finance the annual deficit. And it will also have to sell new bonds to replace maturing bonds that are currently out there in the market. That’s how the government Ponzi scheme works. It pays off old debt with money borrowed from new lenders.

We’re talking about $3 to $4 trillion in bonds that will need buyers over the next year.

This raises a very important question: who is going to buy all of these bonds?

The Fed ranks as the second-largest holder of US debt behind US individuals and institutions. If the Fed is out of the market, and shedding some of its holdings, who is going to fill that gap? Where will the Fed find buyers for an additional $1 trillion in Treasuries every year for the next three years, on top of all the new bonds it needs to sell to finance its massive deficits? The Fed was in the QE game to prop up the bond market. What happens when it pulls out those props?

Supply and demand dictate that as the Fed dumps bonds onto the market, supply will rise and the price will fall. That means yields will rise.

This creates another big problem for the US government.

Rising interest rates mean Uncle Sam’s borrowing costs rise. It’s the same problem you would have if the bank started rising your mortgage rate, or your credit card company raised your interest rate. The US government will have to pay more to finance its debt. That means it will have to borrow more. And that means even more bonds on the market.

This will ripple through the entire financial system and the broader economy. We saw the impacts of tightening in 2018. There is no reason to think it will be any different this time around.

The Fed can talk about balance sheet reduction all it wants. But talking and doing are two different things.

END

2.LAWRIE WILLIAM//,//Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, James RICKARDS/

LAWRIE WILLIAMS: Ukraine war second phase and impact on gold

Russia’s invasion of Ukraine seems to be taking a new twist, but whether this suggests a de-escalation, or perhaps may presage a renewal of Russia’s efforts to take total control of Ukraine’s Donbass region and its Black Sea coastline remains to be seen. Certainly the latest reports suggest a complete withdrawal of Russian troops from the areas around Kyiv and Chernihiv in the north of the country – perhaps due to ‘significant’ losses at the hands of Ukraine’s defence force, which Russia now seems to be admitting in a new statement from Kremlin spokesman Dmitri Peskov. Ukraine claims its forces have killed over 18,000 Russian soldiers and destroyed or captured a large amount of military equipment. Russia puts casualties far lower in its domestic news, but one suspects the true figure is somewhere between – probably around 10,000 Russian fatalities.

Russia claims the withdrawal is because its objectives have been achieved. However Western military opinion suggests that this was a response to the heavy loss of life and equipment and the total failure of the Russian forces invading from Belarus to quickly take Kyiv and depose the elected government.

It does appear though that Russia will now focus its assault on the Donbass region and the parts of the Black Sea and Sea of Azov coastline it does not yet fully control. It also does not appear to have withdrawn from the area around Ukraine’s second largest city of Kharkiv. It does appear to be concentrating, therefore, on areas directly bordering Russia which do not cause it the logistical and re-supply problems that faced its forces attacking from Belarus. However it will also enable the Ukraine army to redeploy some of its forces into these areas, although it will have to leave sufficient forces in place in the north to protect against a renewed Russian advance and perhaps try to retake areas around Kharkiv.

One thing which is unlikely to change is Western economic pressure on Russia in the form of sanctions, particularly if Europe manages to reduce its dependence on Russian oil and gas thereby further increasing sanctions effectiveness. Given the apparent atrocities which appear to have been inflicted by Russian troops on previously occupied areas and the devastation wreaked on Mariopol, anti-Russian economic moves may well be further increased. Mariopol is in a predominantly Russian speaking area of Ukraine supposedly being ‘liberated’ by the Russian forces. Instead the city has been totally devastated with a slaughter of civilians, Russian speakers included, seemingly unparalleled elsewhere. Western attitudes towards the Russian state will thus likely be hardened and sanctions extended and probably prolonged.

All this, of course, will as we have often noted in previous articles, increase inflationary pressures globally, as well as in Russia itself. There is a price everyone must pay for the support of the Ukrainian nation and this is coming at a time when inflation is already running high as the world tries to extricate itself from the effects of the Covid-19 pandemic. Russia and Ukraine in combination are major global foodstuff exporters and Russia a top exporter of oil, natural gas and many precious and base metals. Sanctions will have an inflationary price impact on all of these as nations imposing the sanctions – i.e. much of the so-called developed world – will have to seek replacements from assumed friendlier areas almost certainly at a higher cost.

Global inflationary trends will drive some nations into recession and/or a period of stagflation – both of which tend to be positive for gold as a reliable wealth protector. While we don’t necessarily anticipate gold price fireworks we do anticipate a slow and steady rise for some time to come – perhaps lasting for several years. In any case we expect gold price strength, with maybe the occasional setback, until the Ukraine war is a distant memory.

08 Apr 2022

-END-

3. Chris Powell of GATA provides to us very important physical commentaries

Russia is not worried at all with this:

Will Russia really care if U.S. actions make it default on its debt?

Submitted by admin on Thu, 2022-04-07 11:31 Section: Daily Dispatches

By Layna Mosley

The Washington Post

Thursday, April 7, 2022

On Tuesday the U.S. Treasury tightened the financial pressure on Vladimir Putin by prohibiting U.S. financial institutions from facilitating dollar-denominated debt payments to investors.

Simply put, this made it much harder for Russia to pay its bondholders, raising the risk that Russia will default on its sovereign debt.

Usually, governments that default on their debts face serious consequences. However, it is possible that Russia may be less worried about this action than other governments would be. …

… For the remainder of the analysis:

END

Pam and Russ Martens: Does the NY Fed’s trading floor near the futures exchange in Chicago cause the gyrations in the stock market?

Submitted by admin on Thu, 2022-04-07 11:51Section: Daily Dispatches

By Pam and Russ Martens

Wall Street on Parade

Thursday, April 7, 2022

The editor of Wall Street On Parade has been watching stock market trading patterns for more than three decades — 21 of those years at two Wall Street firms.

A new pattern is emerging that strongly suggests there is an invisible hand flipping the market on a dime from a plunge in prices to a dramatic spike in prices.

This could happen legitimately if sudden positive news broke, but it is happening regularly with no major news to explain the dramatic shift in sentiment.

On January 31 Wall Street On Parade reported that the New York Fed, which is the only one of the 12 regional Fed banks to have a trading floor — complete with those expensive Bloomberg data terminals and speed dials to Wall Street’s biggest trading houses — had decided for some reason after 100 years of operation that it needed a second trading floor in Chicago.

What does Chicago have that New York does not have that might come in handy to those traders at the New York Fed?

The Chicago office of the New York Fed sits close to the Chicago Mercantile Exchange, where S&P 500 futures are traded, as well as other futures contracts.

The closer one is to the computers that process those S&P 500 trades, the bigger the trading advantage. …

… For the remainder of the analysis:

END

This was yesterday’s big story: Russian coal and oil has been purchased in yuan as these commodities head to China

(Yahoo/GATA)

Russian coal and oil purchased in yuan start heading to China

Submitted by admin on Thu, 2022-04-07 12:40Section: Daily Dispatches

From Bloomberg News

via Yahoo News, Sunnyvale, California

Thursday, April 7, 2022

Russian coal and oil paid for in yuan is about to start flowing into China as the two countries try to maintain their energy trade in the face of growing international outrage over the invasion of Ukraine.

Several Chinese firms used local currency to buy Russian coal in March, and the first cargoes will arrive this month, Chinese consultancy Fenwei Energy Information Service Co. said.

These will be the first commodity shipments paid for in yuan since the U.S. and Europe penalized Russia and cut several of its banks off from the international financial system, according to traders.

Sellers of Russian crude have also offered to give buyers in Asia’s largest economy the flexibility to pay in yuan. The first cargoes of the ESPO grade bought with the Chinese currency will be delivered to independent refiners in May, according to people familiar with the purchases.

China has long bristled at the dollar’s dominance in global trade and the political leverage it gives the U.S. Efforts to chip away at the status quo are now being accelerated by Western steps to punish Russia for its war of aggression. Moscow is offering rupee-ruble payments to Indian oil buyers, while Saudi Arabia is in talks with Beijing to price some of its crude in yuan. …

… For the remainder of the report:

https://www.yahoo.com/finance/news/russian-coal-oil-paid-yuan-043249490.html

END

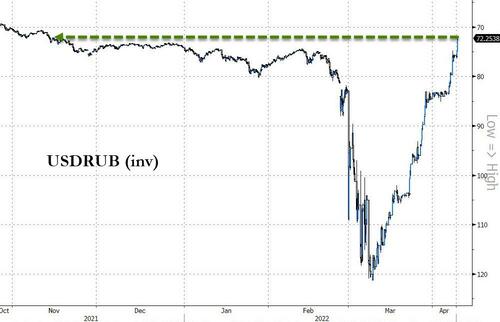

That did not take long: with the Ruble rising extremely fast, Russia now switches to a negotiated price for its gold purchases.

(Reuters/Hobson/GATA)

Russian central bank switches to negotiated price for gold purchases

Submitted by admin on Thu, 2022-04-07 19:47Section: Daily Dispatches

By Peter Hobson

Reuters

Thursday, April 7, 2022

Russia’s central bank said today that due to a “significant change in market conditions” it would buy gold from commercial banks at a negotiated price from April 8.

On March 25, the bank had said it would buy gold at a fixed price of 5,000 roubles a gram until June 30.

Since that announcement, the rouble has strengthened sharply against the dollar. Five thousand roubles was worth around $52 on March 25 and around $63 today.

… For the remainder of the report:

END

A MUST READ…

your weekend reading material

(courtesy Alasdair Macleod/GATA)

Alasdair Macleod: The commodity currency revolution

Submitted by admin on Thu, 2022-04-07 21:50Section: Daily Dispatches

By Alasdair Macleod

GoldMoney, Toronto

Thursday, April 7, 2022

We will look back at current events and realise that they marked the change from a dollar-based global economy underwritten by financial assets to commodity-backed currencies. We face a change from collateral being purely financial in nature to becoming commodity based. It is collateral that underwrites the whole financial system.

The ending of the financially based system is being hastened by geopolitical developments. The West is desperately trying to sanction Russia into economic submission, but is only succeeding in driving up energy, commodity, and food prices against itself. Central banks will have no option but to inflate their currencies to pay for it all. Russia is linking the rouble to commodity prices through a moving gold peg instead, and China has already demonstrated an understanding of the West’s inflationary game by having stockpiled commodities and essential grains for the last two years and allowed her currency to rise against the dollar.

China and Russia are not going down the path of the West’s inflating currencies. Instead, they are moving towards a sounder money strategy with the prospect of stable interest rates and prices while the West accelerates in the opposite direction.

The Credit Suisse analyst, Zoltan Pozsar, calls it Bretton Woods III. This article looks at how it is likely to play out, concluding that the dollar and Western currencies, not the rouble, will have the greatest difficulty dealing with the end of fifty years of economic financialisation. …

… For the remainder of the analysis:

end

4.OTHER GOLD/SILVER COMMENTARIES

5.OTHER COMMODITIES

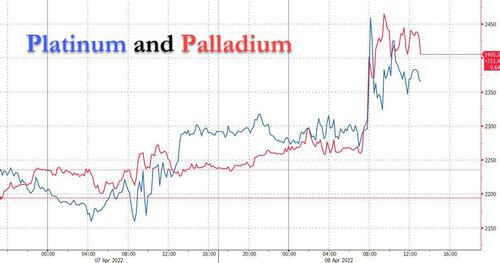

Palladium, Platinum Soar After London Market Blocks Russian Products

FRIDAY, APR 08, 2022 – 03:35 PM

First Russian gold and silver, then diamonds, now platnium and palladium.

On Friday, newly refined Russian platinum and palladium was suspended from trading in London, denying Russia access to the metals’ biggest trade hub in the latest in a growing list of measures against Russian interests because of the conflict in Ukraine. Of course, the Russian physical metal ban also means that commodity traders will now have to buy much more for physical – not paper – metal.

The London Platinum and Palladium Market (LPPM), an industry association, said the situation in Ukraine prompted it to review its list of “good delivery” refiners accredited to deliver metal into the London trading system. The LPPM said it would suspend with immediate effect both Russian refiners on its list, JSC Krastsvetmet and the Prioksky Plant of Non-Ferrous Metals.

The suspension blocks platinum and palladium produced by these refiners after April 8 from trading in London, though products they made while accredited remain eligible to trade, the LPPM said.

The decision comes a month after a similar industry group, the London Bullion Market Association (LBMA), suspended the accreditation of Russian refiners, blocking new Russian gold and silver from London.

Prices of palladium surged as much as 11%, with traders fearing the move could worsen a shortage of the metal automakers use in exhaust pipes to reduce emissions.

Just how reliant is the world on Russian metals? Russia’s Norilsk Nickel produces 25-30% of the world’s palladium supply and about 10% of platinum, which is also used to curb vehicle emissions as well as in other industries and to make jewellery. The company’s website says that it sends metals to Krastsvetmet, Prioksky and another refinery, Uralintech, for refining.

A source close to Nornickel said the LPPM decision would restrict its ability to sell to banks but sales to manufacturers, which form the bulk of its business, would be unaffected. However, speaking to Reuters, industry sources in London said the move increases pressure on manufacturers to reject Russian platinum and palladium similar to what happened with Russian oil, which just means even higher prices.

Indeed, recyclers and miners in South Africa and North America, the other main producers, stand to benefit from any boycott of Russian material.

The European Union on Friday adopted its fifth package of sanctions, including bans on the import of coal, wood, chemicals and other products. EU governments have also frozen about 30 billion euros ($32.6 billion) of assets linked to oligarchs and other sanctioned people with ties to the Kremlin. read more

/FERTILIZER

COMMODITIES IN GENERAL

6.CRYPTOCURRENCIES

7. GOLD/ TRADING TODAY

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings FRIDAY morning 7:30 AM

ONSHORE YUAN: CLOSED UP 6.3637

OFFSHORE YUAN: 6.3682

HANG SANG CLOSED UP 63.03 PTS OR 0.29%

2. Nikkei closed UP 97.23 PTS OR 0.36%

3. Europe stocks ALL GREEN

USA dollar INDEX UP TO 99.93/Euro FALLS TO 1.0862

3b Japan 10 YR bond yield: FALLS TO. +.2310/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 124.19/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 96.44 and Brent: 100.58

3f Gold UP /JAPANESE Yen DOWN CHINESE YUAN: UP -SHORE CLOSED DOWN// OFF- SHORE DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.0.696%/Italian 10 Yr bond yield RISES to 2.38% /SPAIN 10 YR BOND YIELD RISES TO 1.69%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 1.68: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield RISES TO : 2.84

3k Gold at $1935.50 silver at: 24.66 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3l USA vs Russian rouble;// Russian rouble UP 2 roubles/dollar; ROUBLE AT 77.75

3m oil into the 96 dollar handle for WTI and 100 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 124.19 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning .9351– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0154 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 2.680 UP 7 BASIS PTS

USA 30 YR BOND YIELD: 2.700 UP 6 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 14.75

Futures, Yields And Oil All Rise On Last Day Of Turbulent Week

FRIDAY, APR 08, 2022 – 07:51 AM

After several extremely volatile days, US equity futures are ending the week in the green (for now) with European equities snapping two days of declines sparked by the Federal Reserve’s plan for aggressive monetary-policy tightening, and Asian stocks trading higher. S&P 500 and Nasdaq 100 futures trimmed earlier gains to trade 0.3% higher as traders weighed the latest developments about the war in Ukraine. Contracts on U.S. stock benchmarks trim earlier gains as traders weigh developments about the war in Ukraine.Nasdaq 100 futures flat; S&P 500 futures +0.1%; Dow Jones futures +0.2%. The dollar rose for a 7th consecutive week and US Treasuries sold off across the curve; gold and bitcoin were flat. Oil was steady after three days of losses stoked by plans to release millions of barrels of crude from strategic reserves and China’s demand-sapping virus outbreak.

Markets had a subdued session yesterday after sinking more than 4% in the previous two days as hawkish signals from the Federal Reserve sent Treasury yields surging. Among notable premarket moves, Robinhood slid 3% after Goldman Sachs, not too long ago the lead underwriter on the company’s IPO, cut their rating on the stock to sell, saying softening retail engagement levels and profitability concerns will likely limit any outperformance. Some other notable premarket movers:

- Alcoa (AA US) is 1.2% lower as Credit Suisse analyst Curt Woodworth trims his recommendation to neutral as he views LME aluminum prices near peak levels.

- Quidel (QDEL US) gained in extended trading Thursday after it posted preliminary revenue for the first quarter that beat the average analyst estimate.

- CrowdStrike (CRWD US) advanced 4.1%. Analysts responded positively after management set a framework to reach $5 billion in annual recurring revenue (ARR) by 2026, during the cybersecurity company’s investor briefing.

- WD-40 (WDFC US) is poised to gain after producing a “solid” beat in the second quarter, Jefferies said, adding that an increased market share and new product launches would support volume growth of 3% in 2022.

- Kura Sushi (KRUS US) shares rose in postmarket trading after the restaurant chain reported a year-over-year jump in quarterly sales.

- ACM Research (ACMR US) edged lower in extended trading Thursday after saying in a release its first quarter revenue would be “significantly below” expectations, but reiterated full-year revenue guidance for 2022.

U.S. stocks are on course to snap a three-week winning streak with investors shedding risk assets following indications from the Fed of a faster-than-expected pace of tightening in monetary policy. Concerns are also growing about the impact of high inflation and slowing economic growth on corporate earnings. The two-year Treasury yield rose five basis points and the 10-year yield climbed one point, reversing some of the curve steepening seen in the wake of the Fed minutes Wednesday, which outlined plans to pare the central bank’s balance sheet by more than $1 trillion a year alongside interest-rate hikes.

Global equities are nursing losses for the week as markets grapple with the Fed’s campaign against elevated price pressures, Russia’s grinding war in Ukraine and China’s Covid travails. The lockdown in Shanghai — which recorded more than 21,000 new daily virus cases — has become one of President Xi Jinping’s biggest challenges. Expectations are growing that China will take steps to support its economy.

“Stocks have had a little bit of a harder time this week digesting the fact that interest rates are going to be higher” amid a major shift in expectations around monetary policy, Anthony Saglimbene, global market strategist at Ameriprise Financial Inc., said on Bloomberg Television.

Still, U.S. equities saw a second straight week of inflows at $1.5 billion, with large-cap and growth stocks outperforming small-cap and value sectors, according to Bank of America strategists. Marija Veitmane, a senior strategist at State Street Global Markets, also said stocks still appeared to be the safest option.

“Cash gives you nothing with 7% inflation, bonds just had one of the worse quarters in history, and then if you look at stocks, we still have decent earnings outlook, and to me the biggest attraction is really strong balance sheets,” she said on Bloomberg TV.

In the latest news out of Ukraine, dozens were killed Friday morning as Russian troops allegedly bombed civilians waiting at a train station to be evacuated from the Donetsk region. Meanwhile, U.S. officials warned that the war may last for weeks, months or even years, as Kyiv’s foreign minister pleaded for urgent military assistance. Here are the latest Ukraine war developments:

- Ukraine intends to establish up to 10 humanitarian corridors on Friday, those leaving Mariupol will need to use private vehicles.

- Ukrainian advisor Podolyak says negotiations with Russia continue online constantly, but the mood changed after Bucha events, via Reuters.

- Kremlin says it does not understand EU concerns about European countries paying for Russian gas in RUB, adds Commission President von der Leyen probably needs more information. On planned EU ban of Russian coal, says coal is in high demand. Special operation in Ukraine could be completed in the foreseeable future, given aims are being achieved and work is being carried out by peace negotiators and the military.

- EU ready to release EUR 500mln for arms to Ukraine, according to AFP citing EU chief.

- Russia says it has destroyed a training centre for foreign mercenaries within Ukraine, was located north of Odesa, via Tass.

- Japan’s Industry Ministry plans to reduce Russian coal imports gradually while looking for alternative suppliers, according to Reuters.

- Ukraine PM says they have large stocks of grain, cereals and vegetable oil. Are able to provide themselves with food; this year’s harvest will be 20% less YY.

- Ukraine gas grid warns that Russian actions could impact gas flows to Europe, via Reuters.

On Thursday, St Louis Fed president James Bullard said he prefers boosting the policy rate to 3%-3.25% in the second half of 2022. Chicago Fed President Charles Evans and his Atlanta counterpart Raphael Bostic said they favor raising rates to neutral while monitoring the economy’s performance. The steepening in the Treasury yield curve contrasts with the flattening and inversions that have vexed markets this year. The two-year rate topped the 10-year last week for the first time since 2019, a possible warning of recession.

“We’re seeing a tactical re-steepening right now but the curve is going to continue to flatten,” Kelsey Berro, fixed income portfolio manager at JPMorgan Asset Management, said on Bloomberg Television. “That’s because the Fed has told us, we’d like to get to neutral expeditiously. On top of that, they may need to tighten beyond neutral. Front-end yields can still go higher.”

In Europe, Euro Stoxx 50 rallies over 1.8% before stalling while the Stoxx 600 index climbed 1.2% but drifted off best levels as investors took advantage of beaten-down stock valuations with energy, banks and autos the strongest-performing sectors. Banks outperformed as Banco BPM SpA surged after Credit Agricole SA bought a 9.2% stake in the Italian lender. An Asia-Pacific share index eked out a small increase. Here are some of the biggest European movers today:

- Scout24 shares rise as much as 17%, the most intraday since December 2018, after a report that Hellman & Friedman, EQT and Permira have discussed taking the firm private.

- Banco BPM shares rise as much as 17% after Credit Agricole bought a 9.2% stake in the Italian lender, with Bank of America saying the deal is a reminder that real value should be based on fundamentals.

- Sodexo shares jump as much as 7.4%, their biggest single-day gain in a month, after RBC Capital Markets upgrades the French caterer to outperform from sector perform.

- K+S gains as much as 10% after JPMorgan double-upgraded the shares to overweight from underweight, seeing a very positive environment for fertilizers amid supply disruptions and high energy prices.

- Atlantia shares rise as much as 4.5% following a report in a Italian newspaper that the Benetton family and Blackstone may start their takeover offer for Atlantia at more than EU22 per share.

- Saab rise as much as 5% as SEB upgrades the shares to buy from hold on the Swedish defense firm’s sales potential in the coming decade in the wake of Russia’s invasion of Ukraine.

- Moncler shares rise as much as 4.2% after Barclays upgrades the Italian luxury company to overweight, citing an “attractive” defensive profile in the current environment.

- Genmab fall as much as 10%, the most since September 2020, after saying a tribunal decided in favor of Janssen Biotech over two issues surrounding the cancer drug daratumumab (Darzalex).

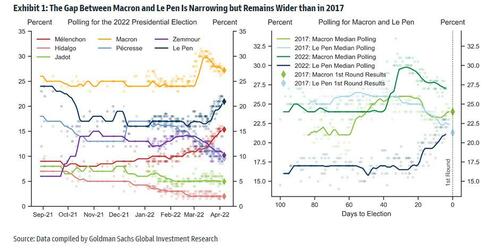

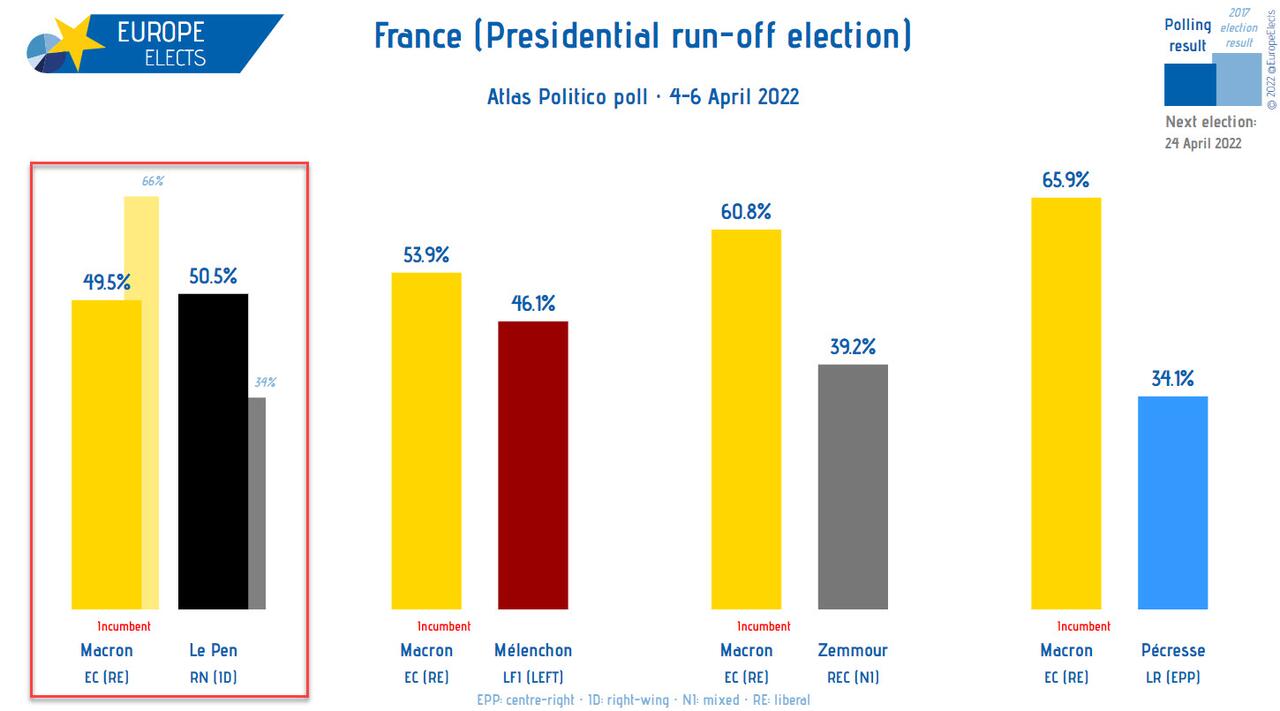

Ahead of this weekend’s French election, Macron’s lead is shrinking: the current President led his rivals in the April 10 election with 26.2% support, down from 27.2% a day earlier, according to a polling average calculated by Bloomberg on April 8. Macron was 3.5 percentage points ahead of second-placed Marine Le Pen, down from 4.1 points.

Asian stocks edged higher on Friday, poised to snap three days of declines as traders assessed the prospect of policy easing by Beijing. The MSCI Asia Pacific Index erased early losses of as much as 0.4% to climb 0.2%. Chinese property and infrastructure-related stocks surged on hopes for fiscal as well as monetary easing as the government seeks to prop up growth. For the week, the Asian benchmark was down 2% as investors turned cautious on risk assets after latest comments from the Federal Reserve suggested aggressive tightening lies ahead. Tech shares were hit hard in particular, with the MSCI Asia-Pacific Information Technology Index losing 4% this week, on track for its worst performance since end-January.

“There appears to be speculation that monetary easing by the PBOC might be imminent,” said Kazutaka Kubo, senior economist at Okasan Securities. There are also expectations that once lockdowns are over, the economy could be supported by pent-up demand, he added. Chinese authorities have repeatedly vowed to support the economy and markets in thet past few weeks, as rising Covid-19 infections and lockdowns darken the outlook for growth. The pledges have spurred bets that some form of monetary easing may come soon. Movements in most national benchmarks in the region were modest on Friday, gaining less than 1%. Stocks in the Philippines and Indonesia outperformed, while Singapore shares fell.

Indian stocks gained after the Reserve Bank of India kept borrowing costs at a record low, even as it raised its inflation forecast on the back of rising commodity prices. The central bank also announced the start of policy normalization as the pandemic’s impact fades. The S&P BSE Sensex climbed 0.7% to 59,447.18 in Mumbai to complete a second week of gains, while the NSE Nifty 50 Index rose 0.8%. Gauges of small- and mid-sized companies gained 1% and 0.9%, respectively. The Reserve Bank of India’s monetary policy panel held the benchmark rate at 4%, in line with predictions of all 36 economists surveyed by Bloomberg. RBI Governor Shaktikanta Das said the central bank will start focusing on withdrawal of banking liquidity accommodation to target inflation but such a move would be “multi-year” and carried out without disrupting the markets.

“Equity markets will like the RBI’s continued focus on growth and its commitment to an accommodative stance,” said Abhay Agarwal, a fund manager at Mumbai-based Piper Serica Advisors Pvt. The RBI’s commentary means adequate flow of liquidity will continue and immediate beneficiaries will be consumers who are borrowing to purchase real estate and autos, he added. All but one of 19 sectoral sub-indexes compiled by BSE Ltd. advanced, led by a gauge of power companies. Reliance Industries Ltd. was a key gainer on the Sensex, which saw 22 of its 30 components advance. The RBI has comforted markets by refraining from being aggressive, unlike its global peers, and by ensuring that the liquidity withdrawal will be gradual, Yesha Shah, head of equity research at Samco Securities wrote in a note. “On the growth front, one can assume that the central bank expects private investment to ramp up now that capacity utilization has improved further,” she said, adding the policy lays the framework for a possible rate increase in coming reviews.

Australian stocks advanced – the S&P/ASX 200 index rose 0.5% to close at 7,478.00 – supported by materials and industrial stocks. GrainCorp shares surged to a record high, after the firm upgraded its FY22 earnings guidance as high levels of rain in Australia lay a path for a bumper crop. Platinum Asset plunged to an all-time low after the company reported net outflows of A$222 million in March. In New Zealand, the S&P/NZX 50 index was little changed at 12,066.27.

In rates, Treasuries fell across the curve, with the front-end of the Treasuries curve pressured lower, flattening 2s10s spread by ~5bp as 2-year yields trade more than 7bp cheaper on the day at ~2.54%. S&P 500 futures near top of Thursday’s range, following bigger advance for European stocks after three straight declines. Yields across long-end of the curve are little changed on the day, as flattening extends out to 5s30s spread which is tighter by ~4bp; 10-year yields around 2.683%, cheaper by 2.5bp vs Thursday close; bunds and gilts outperform by 1bp-2bp in the sector. Bunds reversed opening gains, adding to a three-day run of declines; French debt underperformed bunds ahead of presidential elections beginning Sunday. The German curve bull-flattens, richening 2bps across the back end. Peripheral spreads widen to core with Italy underperforming.

In FX, Bloomberg dollar index advanced a seventh consecutive day and neared the strongest level since July 2020 as the greenback advanced against all of its Group-of-10 peers apart from the Norwegian krone. The euro pared losses after touching a one-month low against the dollar in early London trading. The pound fell to the lowest in more than three weeks as bets for aggressive policy tightening by the Federal Reserve boost the dollar. Gilts rose across the curve as U.S. Treasury yields stabilized following the recent selloff. The Australian and New Zealand dollars were the worst-performing G-10 currencies; Australia’s yield curve steepened following a similar move in Treasuries on Thursday. Most Japanese government bonds rose, thanks to support from the central bank’s regular purchase operations. The yen briefly reversed early an Asia session loss after an ex-BOJ official said there’s likelihood of a policy shift as soon as this summer.

Bitcoin is contained and unable to derive traction either way from the broader risk tone. Strike payment platform launches Shopify (SHOP) integration, which allows merchants to accept Bitcoin (BTC), according to Bloomberg.

In commodities, crude futures trade within Thursday’s range; WTI holds above $96, Brent stalls near $102. Spot gold holds steady near $1,930/oz. Most base metals trade well: LME zinc and lead outperforming, tin lags.

To the day ahead now. Central bank speakers include the ECB’s de Cos, Centeno, Panetta, Stournaras, Makhlouf and Herodotou. Italian retail sales for February and Canadian employment for March round out this week’s data.

Market Snapshot

- S&P 500 futures up 0.5% to 4,517.00

- STOXX Europe 600 up 1.4% to 461.27

- MXAP up 0.2% to 176.33

- MXAPJ up 0.3% to 584.66

- Nikkei up 0.4% to 26,985.80

- Topix up 0.2% to 1,896.79

- Hang Seng Index up 0.3% to 21,872.01

- Shanghai Composite up 0.5% to 3,251.85

- Sensex up 0.9% to 59,558.63

- Australia S&P/ASX 200 up 0.5% to 7,477.99

- Kospi up 0.2% to 2,700.39

- Brent Futures up 1.2% to $101.76/bbl

- Gold spot down 0.0% to $1,931.38

- U.S. Dollar Index up 0.14% to 99.89

- German 10Y yield little changed at 0.68%

- Euro down 0.1% to $1.0865

Top Overnight News from Bloomberg

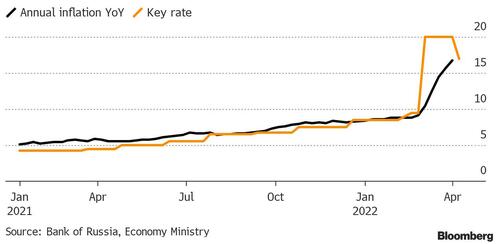

- The Bank of Russia delivered a surprise cut in its key interest rate Friday, reversing some of the steep increase it made after the invasion of Ukraine as the ruble recovered. The central bank lowered the rate to 17% from 20% and said further cuts could be made at upcoming meetings if conditions permit

- EU countries agreed to ban coal imports from Russia, the first time the bloc’s sanctions have targeted Moscow’s crucial energy revenues. Japan is also looking to curb imports, in what could be a shift in policy from one of the world’s largest energy buyers

- The EU is aiming to lock in progress on trade and technology disputes with the U.S. during President Joe Biden’s first term amid concerns that any gains could otherwise be easily reversed

- The relationship between Australia’s equities and currency has become the closest in a decade as commodity prices surge. The 180-day correlation between the country’s stock benchmark and the Australian dollar has climbed to the highest level since late 2011, according to data compiled by Bloomberg. The strengthened ties come as rallies in materials from oil to iron ore have boosted both the nation’s equities and the Aussie

- The ECB will look past threats to economic growth from the war in Ukraine, ending asset purchases in the summer and setting the stage for a first interest-rate increase in more than a decade in December, according to a survey of economists

- Junk bond sales across Europe are experiencing their longest drought in more than 10 years, as the Russian invasion of Ukraine and the prospect of rising interest rates neuter risk appetite

A more detailed look at global markets courtesy of Newsquawk:

Asia-Pacific stocks were choppy and eventually conformed to a mixed picture; some weakness was seen shortly after the Chinese cash open. ASX 200 bucked the trend and was propped up by its energy and gold names. Nikkei 225 was choppy and moved in tandem with action in USD/JPY whilst the KOSPI was weighed on by its chip and telecoms sectors. Hang Seng remained pressured by losses across its large constituents – Alibaba and JD.com. Shanghai Comp swung between gains and losses but overall remained supported by reports from China’s Securities Journal which noted of a potential PBoC RRR in Q2.

Top Asian News

- Hong Kong Tycoons Heed China, Endorse John Lee to lead City

- Chinese Tech Stocks Fall as Tencent Shuts Game Streaming Site

- Abu Dhabi’s IHC Invests $2 Billion in Billionaire Adani’s Empire

- ADDX Rolls Out Private Market Services for Wealth Managers

European bourses are firmer across the board, Euro Stoxx 50 +1.5%, bouncing in a morning of quiet newsflow with the broader tone modestly risk-on. Albeit, benchmarks are still negative on the week and some way from earlier WTD peaks; unsurprisingly, sectors are all in the green with defensive-bias names lagging. Stateside, futures are similarly in the green, ES +0.2%, though magnitudes are more contained ahead of a limited US schedule to round off the week.

Top European News

- U.S. Sanctions Russian Miner Producing 30% of World’s Diamonds

- Atlantia Gains After Reports of Offer Price Above EU22/Share

- Generali CEO Says He Won’t Change Plan Challenged by Investors

- Baader Downgrades Six Chemical Firms, Citing Ukraine War

In FX:

- DXY touches 100.000 as US Treasury yields continue to soar and curve steepen, but unable to break barrier.

- Kiwi underperforms awaiting NZIER Q1 survey, while Aussie holds up better after hawkish warning in RBA FSR; NZD/USD around 0.6950, AUD/USD nearer 0.7460.

- Yen sub-124.00 as Japanese export supply is absorbed, Euro supported by bids circa 1.0850 and Sterling treading water above 1.3000.

- Rouble relatively resilient in the face of 300 bp CBR rate reduction as it remains above pre-conflict highs.

Fixed income:

- Choppy trade in bonds approaching the end of another very bearish week.

- Bunds and Gilts nurse losses mostly above par around 157.00 and 120.00 handles vs fresh cycle lows of 156.40 and 119.83.

- US Treasuries most seeing red, but curve less steep in correction after hawkish FOMC minutes and Fed commentary, via Brainard and Bullard especially

Central Banks:

- RBA Financial Stability Review: important that borrowers are prepared for an increase interest rates; global asset markets are vulnerable to larger-than-expected rate increases, via Reuters.

- RBI leave rates unchanged as expected, retains “accommodative” stance as expected; will focus on withdrawing accommodation going forward. RBI is to restore LAF corridor to 50bps and floor to be constituted by SDF, according to Reuters.

- CBRT April survey sees Turkish End-Year CPI at 46.44% (prev. 40.47%)

- CNB Minutes (March): Dedek and Michl voted in the minority for stable rates. Board assessed risks and uncertainties of winter forecast as being markedly inflationary, particularly in short-term

- CBR cuts its Key Rate to 17.00% (prev. 20.00%) as of April 11th; holds open the prospect of further key rate reduction at its upcoming meetings.

In commodities, WTI and Brent are bolstered amid broader sentiment, though crude/geopolitical specific developments have been limited In-fitting with equities, the benchmarks are negative on the week and some way shy of best levels as such. New York will suspend the state gas tax from June 1st to December 31st, according to Reuters. Barclays raises oil forecasts by USD 7-8/bb assuming no material disruption in Russian supplies beyond Q2 2022, according to Reuters. Spot gold is marginally firmer, but, remains drawn to USD 1930/oz after marginally eclipsing the level overnight; base metals bid in-line with sentiment.

US Event Calendar

- 10:00: Feb. Wholesale Trade Sales MoM, est. 0.8%, prior 4.0%

- 10:00: Feb. Wholesale Inventories MoM, est. 2.1%, prior 2.1%

DB’s Henry Allen concludes the overnight wrap