April 12, 2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

april12, 2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD; $1971.95 UP $26.95

SILVER: $25.51 UP $0.66

ACCESS MARKET: GOLD $1966.30

SILVER: $25.33

Bitcoin morning price: $40,.328 UP 101

Bitcoin: afternoon price: $39,485 DOWN 742

Platinum price: closing DOWN $5.10 to $972.70

Palladium price; closing DOWN 54.55 at $2366.75

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

comex notices/

: JPMorgan stopped/total issued 155/424

EXCHANGE: COMEX

CONTRACT: APRIL 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,944.300000000 USD

INTENT DATE: 04/11/2022 DELIVERY DATE: 04/13/2022

FIRM ORG FIRM NAME ISSUED STOPPED

072 C GOLDMAN 20

104 C MIZUHO 50

118 C MACQUARIE FUT 262 3

132 C SG AMERICAS 19

167 C MAREX 1

363 H WELLS FARGO SEC 10

435 H SCOTIA CAPITAL 10

624 H BOFA SECURITIES 33

657 C MORGAN STANLEY 1 23

661 C JP MORGAN 110 155

686 C STONEX FINANCIA 1

709 C BARCLAYS 74

732 C RBC CAP MARKETS 1

737 C ADVANTAGE 2

880 H CITIGROUP 71

905 C ADM 1 1

TOTAL: 424 424

MONTH TO DATE: 24,365

NUMBER OF NOTICES FILED TODAY FOR APRIL. CONTRACT424 NOTICE(S) FOR 42,400 OZ (1.3188 TONNES)

total notices so far: 24,365 contracts for 2,436,500 oz (75.705 tonnes)

SILVER NOTICES:

71 NOTICE(S) FILED TODAY FOR 355,000 OZ/

total number of notices filed so far this month 1070 : for 5,350,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

END

GLD

WITH GOLD UP $26.95

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

A HUGE CHANGE IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.61 TONNES FROM THE GLD//

INVENTORY RESTS AT 1093.10 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP 66 CENTS

AT THE SLV// NO CHANGES IN SILVER INVENTORY AT THE SLV/ THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 565.521 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A GIGANTIC SIZED 3275 CONTRACTS TO 14,945 AND CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE HUGE GAIN IN OI WAS ACCOMPLISHED WITH OUR SMALL $0.13 GAIN IN SILVER PRICING AT THE COMEX ON MONDAY. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.13) AND WERE UNSUCCESSFUL IN KNOCKING OUT ANY SILVER LONGS AS WE HAD A HUMONGOUS GAIN OF 6217 CONTRACTS ON OUR TWO EXCHANGES

WE MUST HAVE HAD:

I) HUGE BANKER SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A STRONG INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 4.305 MILLION OZ FOLLOWED BY TODAY’S QUEUE. JUMP OF 5,000 OZ//NEW STANDING: 5.455 MILLION OZ// V) HUGE SIZED COMEX OI GAIN/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS : —-1012 (which is huge)

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS APRIL. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF APRIL:

TOTAL CONTACTS for 8 days, total 5041 contracts: 25.205 million oz OR 3.15MILLION OZ PER DAY. (630 CONTRACTS PER DAY)

TOTAL NO OF OZ UNDERGOING EFP TO LONDON 5041 CONTRACTS X 5,000 PER CONTRACT:

EQUATES TO: 25.205 MILLION OZ

.

LAST 11 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

APRIL: 25.205 MILLION OZ (LOOKS LIKE OUR BANKERS ARE NOW LOATHE TO ISSUE EFP’S)

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 3275 DESPITE OUR SMALL $0.11 GAIN IN SILVER PRICING AT THE COMEX// MONDAY THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE CONTRACTS: 1930 CONTRACTS ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A HUGE INITIAL SILVER OZ STANDING FOR MAR. OF 4.305 MILLION OZ FOLLOWED BY TODAY’S 5,000 OZ QUEUE JUMP//NEW STANDING: 5.455 MILLION OZ/// .. WE HAD AN HUGE SIZED GAIN 5205 OI CONTRACTS ON THE TWO EXCHANGES FOR 26.025 MILLION OZ DESPITE THE SMALL GAIN IN PRICE.

WE HAD 71 NOTICES FILED TODAY FOR 355,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A SMALL SIZED 1643 CONTRACTS TO 570,795 AND CLOSER TO NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: 291 CONTRACTS.

THE BIS HAS ABANDONED THE GOLD COMEX TRADING!!!

.

THE SMALL SIZED INCREASE IN COMEX OI CAME WITH OUR SMALL GAIN IN PRICE OF $3.40//COMEX GOLD TRADING/MONDAY /.AS IN SILVER WE MUST HAD HUGE BANKER/ALGO SHORT COVERING ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR APRIL AT 78.33 TONNES

YET ALL OF..THIS HAPPENED WITH OUR GAIN IN PRICE OF $3.40 WITH RESPECT TO MONDAY’S TRADING

WE HAD AN FAIR SIZED GAIN OF 3678 OI CONTRACTS (11.44 PAPER TONNES) ON OUR TWO EXCHANGES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2326 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 570,795.

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 3678, WITH 1352 CONTRACTS INCREASED AT THE COMEX AND 2326 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 3678 CONTRACTS OR 11.44 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2326) ACCOMPANYING THE SMALL SIZED GAIN IN COMEX OI (1352,): TOTAL GAIN IN THE TWO EXCHANGES 3678 CONTRACTS. WE NO DOUBT HAD 1) HUGE BANKER SHORT COVERING ,2.) HUGE INITIAL STANDING AT THE GOLD COMEX FOR APRIL. AT 78.33 TONNES FOLLOWED BY TODAY’S 1900 OZ QUEUE JUMP //NEW STANDING 80.702 TONNES/// 3) ZERO LONG LIQUIDATION ///. ,4) SMALL SIZED COMEX OI. GAIN 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

APRIL

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL :

19,197 CONTRACTS OR 1,919,700 OR 59.71 TONNES 8 TRADING DAY(S) AND THUS AVERAGING: 2399 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 8 TRADING DAY(S) IN TONNES: 59.71TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2020, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 59.71/3550 x 100% TONNES 1.69% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 59.71 TONNES (THIS IS GOING TO BE A LOW ISSUANCE MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF MAY.WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF APRIL HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF MAY, FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (MAR), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A HUGE SIZED 3275 CONTRACTS TO 155,957 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 340 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 1930 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 3275 CONTRACTS AND ADD TO THE 1930 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUMONGOUS SIZED GAIN OF 5205 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 26.025 MILLION OZ

OCCURRED WITH OUR SMALL GAIN OF $0.13 IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

5. Other gold commentaries

6. Commodity commentaries/cryptocurrencies

3. ASIAN AFFAIRS

i)TUESDAY MORNING// MONDAY NIGHT

SHANGHAI CLOSED UP 46.20 PTS OR 1.46% //Hang Sang CLOSED UP 110.83 PTS OR 0.57% /The Nikkei closed DOWN 486.54 PTS OR 1.81% //Australia’s all ordinaires CLOSED DOWN .48% /Chinese yuan (ONSHORE) closed DOWN 6.3716 /Oil UP TO 97.25 dollars per barrel for WTI and DOWN TO 102.75 for Brent. Stocks in Europe OPENED ALL RED EXCEPT SPAIN // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.3716 OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.3798: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER//

A)NORTH KOREA/

b) REPORT ON JAPAN

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A SMALL SIZED 1352 CONTRACTS TO 570,795 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS SMALL COMEX INCREASE OCCURRED WITH OUR RELATIVELY SMALL GAIN OF $3.40 IN GOLD PRICING MONDAY’S COMEX TRADING. WE ALSO HAD A FAIR SIZED EFP (2326 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE ACTIVE DELIVERY MONTH OF APRIL.. THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2326 EFP CONTRACTS WERE ISSUED: ;: , . 0 JUNE :2326 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2326 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 3678 CONTRACTS IN THAT 2326 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A SMALL SIZED COMEX OI GAIN OF 1352 CONTRACTS..AND THIS GAIN OCCURRED WITH OUR SMALL GAIN IN PRICE OF GOLD $3.40.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING FOR APRIL (80.702),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 80.702

THE BANKERS WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $3.40) AND AND WERE UNSUCCESSFUL IN FLEECING ANY LONGS AS WE HAVE REGISTERED A FAIR SIZED GAIN OF 12.34 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR APRIL (80.702 TONNES)…

WE HAD — 291 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 3969 CONTRACTS OR 396,900 OZ OR 12.34 TONNES

Estimated gold volume today: 171,638 ///poor

Confirmed volume yesterday: 194,489 contracts poor

INITIAL STANDINGS FOR APRIL ’22 COMEX GOLD //APRIL 12

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 36.031.399 oz Manfra BRINKS/REGULAR BRINKS ENHANCED |

| Deposit to the Dealer Inventory in oz | 42,728.679 OZ BRINKS MANFRA 999 KILOBARS AND 330 KILOBARS |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 424 notice(s)42,400 OZ 1.3188 TONNES |

| No of oz to be served (notices) | 1581 contracts 158100 oz 4.917 TONNES |

| Total monthly oz gold served (contracts) so far this month | 24,365 notices 2,436,500 OZ 75.705 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For today:

dealer deposits 2

i) Into the dealer Brinks 32,118.849 oz (999 kilobars)

ii) Into Manfra; 10,609.830 oz (330 kilobars)

total dealer deposit 42,728.679 oz//

No dealer withdrawals

0 customer deposits.

total customer deposit nil oz

3 customer withdrawals

i) out of Brinks 464.30 oz

ii) Out of Brinks enhanced: 2382.628 oz

iii) out of Manfra: 33,184.442 o

total customer withdrawal: 36,031.399 oz /

ADJUSTMENTS: customer to dealer

i) Int Delaware: 771.628 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR APRIL.

For the front month of APRIL we have an oi of 2005 contracts having LOST 43.

We had 62 notices filed yesterday so we GAINED 19 contracts or an additional 1900 oz will stand for delivery at the comex

May saw a LOSS of 41 contracts to stand at 3643

June saw a LOSS of 551 contracts UP to 475,963 contracts

We had 424 notice(s) filed today for 42,400 oz FOR THE APRIL 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 110 notices were issued from their client or customer account. The total of all issuance by all participants equates to 424 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 155 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 20 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the APRIL /2021. contract month,

we take the total number of notices filed so far for the month (24,365) x 100 oz , to which we add the difference between the open interest for the front month of (APRIL 2005 CONTRACTS ) minus the number of notices served upon today 424 x 100 oz per contract equals 2,594,600 OZ OR 80.702 TONNES the number of TONNES standing in this active month of APRIL.

thus the INITIAL standings for gold for the APRIL contract month:

No of notices filed so far (24,365) x 100 oz+ (2005) OI for the front month minus the number of notices served upon today (424} x 100 oz} which equals 2,594,600 oz standing OR 80.702 TONNES in this active delivery month of APRIL.

We GAINED 1900 oz as a QUEUE. jump as our banker friends scrounge around for some gold

TOTAL COMEX GOLD STANDING: 80.702 TONNES (A WHOPPER FOR AN APRIL ( ACTIVE) DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

191,133,764.7, oz NOW PLEDGED /HSBC 5.94 TONNES

99,258.893 PLEDGED MANFRA 3.08 TONNES

54,339.114oz PLEDGED JPMorgan no 1 1.690 tonnes

243,923.704, oz JPM No 2 7.58 TONNES

898,821.330 oz pledged Brinks/27,96 TONNES

International Delaware:: 0

Loomis: 18,615.429 oz

total pledged gold: 1,477,560.869 oz 45.95 tonnes

TOTAL REGISTERED AND ELIG GOLD AT THE COMEX: 35,907,094.054 OZ (1116,86 TONNES)

TOTAL ELIGIBLE GOLD: 18,254,309.054 OZ (567.78 tonnes)

TOTAL OF ALL REGISTERED GOLD: 17,652,785.389 OZ (549.06 tonnes)

REGISTERED GOLD THAT CAN BE SERVED UPON: 16,175,225.0 OZ (REG GOLD- PLEDGED GOLD) 503.117 tonnes

END

APRIL 2022 CONTRACT MONTH//SILVER//APRIL 12

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1,928,509.952 oz Brinks CNT Loomis Delaware JPMorgan |

| Deposits to the Dealer Inventory | 349,685.000 OZ Manfra |

| Deposits to the Customer Inventory | 600,321.710 oz Delaware JPMorgan |

| No of oz served today (contracts) | 71CONTRACT(S) 355,000 OZ) |

| No of oz to be served (notices) | 21 contracts (105,000 oz) |

| Total monthly oz silver served (contracts) | 1070 contracts 5,350,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

we had 1 deposit into the dealer

i) Into Manfra: 349,685.000 oz

total dealer deposits: 349,685.000 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 2 deposits into the customer account

i) Into JPMorgan: 599,359.200 oz

ii) Into Delaware: 962.500 oz

total deposit: 600,321.710 oz

JPMorgan has a total silver weight: 176.194 million oz/334.062 million =52.69% of comex

i) Comex withdrawals: 5

i) Out of JPM 627,962.290 oz

ii) Out of Delaware: 2012.940 oz

iii) Out of CNT 689,503.832 oz

iv) Out of JPMorgan; 627,962.290 oz

v) Out of Loomis: 599,073.420 oz

total withdrawal 1,928,009.952 oz

1 adjustments: dealer to customer

JPMorgan: 278,014.430 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 86.352 MILLION OZ

TOTAL REG + ELIG. 334.062 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR APRIL

silver open interest data:

FRONT MONTH OF APRIL OI: 92, HAVING LOST 10 CONTRACTS FROM FRIDAY. We had 11 notices filed yesterday,

so we GAINED 1 contracts or an additional 5,000 oz will stand on this side of the pond

MAY HAD A LOSS OF 4884 CONTRACTS DOWN TO 79,778 contracts

JUNE HAD A GAIN OF 39 TO STAND AT 990

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 11 for 55,000 oz

Comex volumes: 88,214// est. volume today// strong/

Comex volume: confirmed yesterday: 98,831 contracts ( strong )

To calculate the number of silver ounces that will stand for delivery in APRIL. we take the total number of notices filed for the month so far at 1070 x 5,000 oz = 5,350,000oz

to which we add the difference between the open interest for the front month of APRIL (92) and the number of notices served upon today 71 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the APRIL./2021 contract month: 1070 (notices served so far) x 5000 oz + OI for front month of APRIL (92) – number of notices served upon today (71) x 5000 oz of silver standing for the APRIL contract month equates 5.455,000 oz. .

We GAINED 1 contracts or an additional 5,000 oz will stand on this side of the pond

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

APRIL 12/WITH GOLD UP $26.95: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.61 TONNES INTO THE GLD///INVENTORY REST AT 1093.10 TONNES

APRIL 11/WITH GOLD UP $3.40 //A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD.//INVENTORY RESTS AT 1090.49 TONNES

APRIL 8/WITH GOLD UP $7.70: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES INTO THE GLD//INVENTORY RESTS AT 1088.75 TONNES

APRIL 7/WITH GOLD UP $13.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1087.30 TONNES

APRIL 6/WITH GOLD DOWN $4.10: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.68 TONNES FROM THE GLD..//INVENTORY RESTS AT 1087.30 TONNES

APRIL 5/WITH GOLD DOWN $5.70: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.75 TONNES FROM THE GLD//INVENTORY RESTS AT 1089.98 TONNES

APRIL 4/WITH GOLD UP $.70//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1091.73 TONNES

APRIL 1///WITH GOLD DOWN $19.00 : A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .29 TONNES INTO THE GLD///INVENTORY RESTS AT 1091.73 TONNES

MARCH 31/WITH GOLD UP $13.30 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD FROM MONDAY A WITHDRAWAL OF 1.71 TONNES FROM THE GLD:INVENTORY RESTS AT 1091.44

MARCH 28/WITH GOLD DOWN $14.65: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1093.18 TONNES

MARCH 25/WITH GOLD DOWN $7.60 : A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.52 TONNES INTO THE GLD///INVENTORY RESTS AT 1093.18 TONNES

MARCH 24/WITH GOLD UP $24.95: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.06 TONNES INTO THE GLD..//INVENTORY RESTS AT 1087.66 TONNES

MARCH 23/WITH GOLD UP $15.75//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1083.60 TONNES

MARCH 22/WITH GOLD DOWN $7.75: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.16 TONNES OF GOLD DEPOSITED INTO THE GLD//INVENTORY RESTS AT 1083.60 TONES

MARCH 21//WITH GOLD UP $.25 : A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 9.00 TONNES INTO THE GLD////INVENTORY RESTS AT 1082.44 TONES

MARCH 18/WITH GOLD DOWN $13.55 NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1073.44 TONES

MARCH 17/WITH GOLD UP $33.50: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.61 TONNES INTO THE GLD//INVENTORY RESTS AT 1073.44 TONNES

MARCH 16/WITH GOLD DOWN $18.50//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.33 TONNES FROM THE GLD///INVENTORY RESTS AT 1061.83 TONNES

MARCH 15/WITH GOLD DOWN $30.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1064.16 TONNES

MARCH 14//WITH GOLD DOWN $22.75, HUGE CHANGES IN GOLD INVENTORY AT THE GLD//STRANGE: A DEPOSIT OF 2.62 TONNES INTO THE GLD.//INVENTORY RESTS AT 1064.16 TONNES

MARCH 11/WITH GOLD DOWN $14.60: A BIG CHANGE IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 1061.54 TONNES

MARCH 10//WITH GOLD UP $11.55: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.06 TONNES FORM THE GLD///INVENTORY RESTS AT 1063.28 TONNES

MARCH 9/WITH GOLD DOWN $53.85//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.64 TONNES INTO THE GLD//INVENTORY RESTS AT 1067.34 TONNES

MARCH 8/WITH GOLD UP $46.10: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 8.42 TONNES INTO THE GLD///INVENTORY RESTS AT 1062.70 TONNES

MARCH 7/WITH GOLD UP $28.40 A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.06 TONNES INTO THE GLD..//INVENTORY RESTS AT 1054.28 TONNES

MARCH 4/WITH GOLD UP $28.40//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1050.22 TONNES

CLOSING INVENTORY FOR THE GLD//1093.10 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

APRIL 12/WITH SILVER UP 66 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 565.521 MILLION OZ//

APRIL 11/WITH SILVER UP 13 CENTS: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 831,000 OZ FORM THE SLV////INVENTORY RESTS AT 565.521 MILLION OZ

APRIL 8/WITH SILVER UP 11 CENTS :NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 566.352 MILLION OZ//

APRIL 7/WITH SILVER UP 27 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 566.352 MILLION OZ//

APRIL 6/WITH SILVER DOWN 9 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 566.352 MILLION OZ

APRIL 5/WITH SILVER DOWN 16 CENTS : A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.386 MILLION OZ INTO THE SLV..//INVENTORY RESETS AT 566.352 MILLION OZ//

APRIL 4/WITH SILVER DOWN 5 CENTS TO CHANGES IN SILVER INVENTORY AT THE SLV//: A DEPOSIT OF 6.326 MILLION OZ//INVENTORY REST AT 564.966 MILLION OZ//

APRIL 1/WITH SILVER DOWN 39 CENTS A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.302 MILLION OZ INTO THE SLV////INVENTORY REST AT 558.647 MILLION OZ//

MARCH 31/WITH SILVER UP 3 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 2.171 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 556.345 MILLION OZ

MARCH 28/WITH SILVER DOWN 30 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.847 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 554.167 MILLION OZ//

MARCH 25/WITH SILVER DOWN 20 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 552.320 MILLION OZ//

MARCH 24/WITH SILVER UP 54 CENTS TODAY; A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.092 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 552.320 MILLION OZ//

MARCH 23/WITH SILVER UP 24 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 550.288 MILLION OZ//

MARCH 22/WITH SILVER DOWN $0.29 TODAY : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 550.288 MILLION OZ//

MARCH 21/WITH SILVER UP 16 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 550.288 MILLION OZ//

MARCH 18/WITH SILVER DOWN 37 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.217 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 550.288 MILLION OZ//

MARCH 17/ WITH SILVER UP 72 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.049 MILLION OZ INTO THE SLVV//INVENTORY RESTS AT 548.071 MILLION OZ

MARCH 16/WITH SILVER DOWN 56 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 462,000 OZ FROM THE SLV//INVENTORY RESTS AT 544.560 MLLION O

MARCH 15/WITH SILVER DOWN 18 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 545.022 MILLION OZ

MARCH 14/WITH SILVER DOWN 64 CENTS TODAY; STRANGE A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.125 MILLION OZ/INVENTORY RESTS AT 545.022 MILLIONOZ

MARCH 11/WITH SILVER DOWN 13 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.897 MILLION OZ

MARCH 10/WITH SILVER UP 39 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.897 MILLION OZ/

MARCH 9/WITH SILVER DOWN 88 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 5.174 MILLION OZ OF FAKE SILVER.//INVENTORY RESTS AT 542.897 MILLION OZ//

MARCH 8/WITH SILVER UP 88 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.217 MILLION OZ INTO THE SLV////INVENTORY RESTS A 548.071 MILLION OZ//

MARCH 7/WITH SILVER UP 40 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 545.854 MILLION OZ//

MARCH 4/WITH SILVER UP 50 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 545.854 MILLION OZ/

SLV FINAL INVENTORY FOR TODAY: 565.521 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

END

2.LAWRIE WILLIAM//,//Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, James RICKARDS/

LAWRIE WILLIAMS: On the cusp: Inflation, equities and gold

3. Chris Powell of GATA provides to us very important physical commentaries

Robert Lambourne: stopping QE is going to be extremely difficult for the uSA

(Robert Lambourne/GATA)

Robert Lambourne: Stopping QE is likely to be extremely difficult for U.S.

Submitted by admin on Sun, 2022-04-10 22:45Section: Daily Dispatches

By Robert Lambourne

Monday, April 11, 2022

Cash flow trends at the U.S. Treasury suggest that it will be very challenging to meet the forecasts for government debt.

The major contribution of “quantitative easing” (QE) to federal government funding in recent years is clear from the table below, and reducing QE seems likely to be especially tough in view of inflation and the reluctance to allow interest rates to climb much.

The budget for the fiscal year 2023 was published recently by the Office of Management and Budget:

This document sets out longer-term forecasts on the deficit for the next 10 years, and the more near-term forecasts are for federal government gross debt of $31.292 trillion at 30 September 2022 and $32.593 trillion at 30 September 2023.

The five-year table below has been constructed from the historical records of daily Treasury statements, and the published Federal Reserve balance sheets closest to the end of the month are used to source the QE results. For the avoidance of doubt, the QE numbers quoted below relate entirely to the Federal Reserve holdings of U.S. Treasury bonds. Its holdings of mortgage securities are not included.

This recent history demonstrates that in the five years to 31 March 2022 the net debt of the federal government has increased by $9.855 trillion or 49.5%. In that period quantitative easing by the Federal Reserve contributed $3.296 trillion of the increase in net debt.

Shortly the Federal Reserve is due to commence a program to reduce QE and has committed to a monthly cap of $60 billion to reduce its holdings of U.S. Treasuries. This compares to an average monthly increase in QE over the 12 months to 31 March 2022 of $70 billion. Although not critical in itself, it is worthwhile to recall that debt lent to the federal government via QE is essentially interest-free since the Federal Reserve sends all profits from QE to the federal government.

In the current year this is worth about $100 billion to the government. Eliminating QE would increase the annual government deficit by this $100 billion.

Five-Year Table of U.S. Federal Debt Growth to 31 March 2022 ($ Billions in Debt)

| DATE | CASH | GROSS | NET | QE |

| March 2022 | 652 | 30,401 | 29,749 | 5,760 |

| March 2021 | 1,122 | 28,133 | 27,011 | 4,921 |

| March 2020 | 515 | 23,687 | 23,172 | 2,978 |

| March 2019 | 334 | 22,028 | 22,694 | 2,175 |

| March 2018 | 290 | 21,090 | 20,800 | 2,425 |

| March 2017 | 92 | 19,986 | 19,894 | 2,464 |

In the six months since 30 September 2021 the increase in the net debt of the federal government has been $1.536 trillion and QE has contributed $0.329 trillion. If there is a $60 billion-per-month reduction of QE from April 2022 to meet the Office of Management and Budget forecast is going to require gross funding from outside investors of around $1.9 trillion in the six months to 30 September 2022 versus around $1.2 trillion (excluding QE) in the six months to 31 March 2022. This seems to be challenging as interest rates on Treasury debt are running well below the inflation rate.

Indeed, it seems likely to be a challenge to meet the spending commitments underlying the forecast through to 30 September 2022, since a number of items purchased by the federal government are going to be affected by price increases, such as energy. Similarly the OMB budget for the 12 months to 30 September 2023 looks to be challenging in terms of actual expenditure with a projected deficit of $1.3 trillion. This compares to a projected deficit of around $3 trillion in the 12 months to 30 September 2023.

It will be a challenge to get all the proposed tax increases agreed, and expenditure programs are always easier to start than to stop.

Results published in the daily Treasury statement up to 7 April indicate a cash outflow of $63 billion since the beginning of the month, so there is no evidence that the rate of cash outflow is diminishing. Also, the Federal Reserve balance sheet for 6 April, published last week, actually has a $1 billion increase in its holdings of Treasury bonds. The reduction of QE as it relates to Treasury bonds has yet to start.

So given recent history and the uncertain economic and political outlook with inflation an important risk, it seems likely that the deficit will continue to grow far faster than forecast and that the reversal of QE will prove to be extremely tough.

—–

Robert Lambourne is a retired business executive in the United Kingdom who consults with GATA about the Bank for International Settlements and government finances.

end

Ted Butler….a must read

the real lesson of the LME’s default in nickel and how silver is even worse

(Ted Butler/GATA)

Ted Butler: The real lesson of the London Metals Exchange’s default in nickel

Submitted by admin on Mon, 2022-04-11 21:11Section: Daily Dispatches

9p ET Monday, April 11, 2022

Dear Friend of GATA and Gold:

Silver market analyst Ted Butler notes tonight that the concentrated short position in silver futures and derivatives in the United States is many, many times larger than the short position in nickel that blew up and prompted default of the London Metals Exchange’s nickel contract.

Butler writes that U.S. market regulators should be investigating the grotesque short position in silver.

That there seems to be no regulatory interest in the silver short position suggests that the short position is actually a U.S. government position for which investment banks provide camouflage as brokers.

Such camouflaged intervention is fully authorized by the Gold Reserve Act of 1934, as amended, and presumably is why the U.S. Commodity Futures Trading Commission refuses to answer whether it has jurisdiction over manipulative trading undertaken by or for the government.

Butler’s analysis is headlined “The Real Lesson of LME Nickel” and it’s posted at GoldSeek here:

https://goldseek.com/article/real-lesson-lme-nickel

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

The Real Lesson of LME Nickel

April 11, 2022

Ted Butler

Butler Research

40Shares

The recent debacle in LME nickel led to the London Metals Exchange breaking trades and defaulting on contract terms. Press coverage has been detailed and this offering from CNN is among the most comprehensive.

The culprit who caused this market debacle was “Mr. Big Shot” – head of the Chinese steel and nickel producer Tsingshan Holding Group Co. They held a short position in LME nickel of 30,000 tons on the exchange and an additional 120,000-ton short position off the exchange in OTC derivatives – a combined short position of 150,000 tons. The exchange-listed short position of Tsingshan Holding amounted to 1.2% of world nickel production and, when added to the OTC short position rose to 6% of world production. That was enough to bring the LME to its knees, an institution that has been in existence for 145 years. I can’t help but make comparisons between the concentrated short positions in nickel and silver.

On the listed, or COMEX silver futures short position, the CFTC provides data on the concentrated positions – both long and short. For the 4 largest shorts in COMEX silver, their net short position is around 52,000 contracts (260 million ounces). It can be reasonably projected that the largest COMEX silver short holds 20,000 to 25,000 contracts short. Using the lower number, that means that the largest COMEX short is holding the equivalent of 100 million ounces short or roughly 12% of total annual mine production. This is ten times the equivalent listed net short position held by Mr. Big Shot in LME nickel. Ten times. So, if the listed short position in LME nickel of 1.2% of world nickel production contributed mightily to the effective default in that market, what would a listed short position of ten times that amount imply for COMEX silver?

Moving on to the over-the-counter (OTC) or unlisted short position, the 120,000-ton nickel short position held by Tsingshan amounted to 4.8% of total annual world nickel production (6% when combined with its listed short position) on nickel’s 2.5-million-ton annual production. The latest (as of Dec 31, 2021) OCC derivatives report indicates that Bank of America holds a precious metals derivatives position of $27 billion. It is easy to infer that BofA may be short 800 million ounces of silver or more and if it is, that means that it may be short close to 100% of total annual silver mine production, more than 20 times the 4.8% level of the widely reported Tsingshan OTC nickel short position. So, if an over-the-counter short position of 4.8% of annual world production is at the heart of why the LME is on the ropes in nickel, what potential damage and liability await Bank of America which may be short 100% of the world annual mine production of silver? Does this real-world comparison not rise to the occasion where the regulators – the OCC, the U.S. Treasury Dept, The CFTC and the CME Group – should address and clarify Bank of America’s OTC precious metals position?

Tsingshan was one of the largest, if not the largest processor of nickel in the world, meaning there was a reasonable case of assuming it was legitimately hedged and not speculating wildly. So, the fact that it ran into serious trouble on the run-up in nickel prices proves even a “legitimate” hedger can run into real trouble when too heavily short. If Bank of America is short 100% of annual world silver mine production in the OCC report and can’t possibly be considered a legitimate hedger – is that not a situation the regulators should be all over?

Let’s face it – if a concentrated short position in nickel caused the eventual run-up in prices to the point where they doubled and tripled in a matter of a few days, causing the exchange to bust trades and effectively default, what do you suppose the price reaction will be in silver, with the concentrated short position anywhere from ten times to more than twenty times larger, when the concentrated short position is eventually reckoned with?

Ted Butler

4.OTHER GOLD/SILVER COMMENTARIES

Dysfunctional U.S. Mint Sees Strongest Gold Demand in 23 Years

by: Stefan Gleason

Money Metals News Service

April 12th, 2022

According to recent U.S. Mint production reports, demand for gold coins remains super strong.

Rampant global inflation, the war in Ukraine, stock market volatility, and central bank missteps have fueled retail interest.

US Mint Gold Eagle with Gold Nuggets

Last week, the U.S. Mint reported sales of 426,500 ounces in gold coins during the first quarter of 2022 – up 3.5% from the first quarter of 2021 and the highest in 23 years! In fact, March sales for the U.S. Mint was its best since 1999.

Even as the government-run institution continues to be plagued by its ongoing mismanagement, it sold 155,500 ounces of various denominations of the American Eagle gold coin in March alone, up 73% from the prior month.

With this morning’s 8.5% Consumer Price Inflation (CPI) reading from the Bureau of Labor Statistics, inflation is no longer a topic confined to pundits and economists; its painful bite on Main Street has become widely acknowledged and felt.

Extremely high inflation globally, combined with war in Eastern Europe and a shaky start to the year for equities, should underpin volatility-based demand for bullion throughout the year.

Meanwhile, although the U.S. Mint’s silver coin sales remain strong, high premiums caused by production shortages at the dysfunctional government “enterprise” has put a crimp on sales as compared to early 2021.

The U.S. Mint reported silver sales of roughly 7.5 million ounces in the first quarter, a decline of 37% from the year prior.

Extraordinarily high premiums on silver American Eagles have pushed savvy investors to consider the wide array of more affordable silver options – especially silver bars and rounds along with silver coins produced by other sovereign mints.

5.OTHER COMMODITIES

FERTILIZER

end

/DIAMONDS

END

COMMODITIES IN GENERAL

6.CRYPTOCURRENCIES

7. GOLD/ TRADING TODAY

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings TUESDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 6.3716

OFFSHORE YUAN: 6.3798

HANG SANG CLOSED UP 110.83 PTS OR 0.52%

2. Nikkei closed DOWN 486.54 PTS OR 1.81%

3. Europe stocks ALL RED EXCEPT SPAIN

USA dollar INDEX UP TO 100.18/Euro FALLS TO 1.0857

3b Japan 10 YR bond yield: RISES TO. +.239/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 125.54/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 97.97 and Brent: 102.75

3f Gold UP /JAPANESE Yen DOWN CHINESE YUAN: UP -SHORE CLOSED DOWN// OFF- SHORE DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.0.821%/Italian 10 Yr bond yield RISES to 2.45% /SPAIN 10 YR BOND YIELD RISES TO 1.73%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 1.63: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield RISES TO : 2.88

3k Gold at $1957.90 silver at: 25.01 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3l USA vs Russian rouble;// Russian rouble DOWN 1 /4 roubles/dollar; ROUBLE AT 79.62

3m oil into the 97 dollar handle for WTI and1028 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 125.54 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning .9326– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0125 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 2.771 DOWN 1 BASIS PTS

USA 30 YR BOND YIELD: 2.808 DOWN 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 14.69

US Futures On Edge Ahead Of “Extraordinarily Elevated” CPI Print

TUESDAY, APR 12, 2022 – 08:02 AM

US index futures were flat on Tuesday, rebounding off overnight session lows as investors braced for red hot inflation data which the White House yesterday called “extraordinarily elevated” and which will likely boost the argument for aggressive monetary tightening – perhaps even a 75bps or intermeeting rate hike – despite a looming economic slowdown. Nasdaq futures were 0.2% higher, while S&P futures were flat after dropping as much as 0.5%.

China’s Premier Li Keqiang issued a third warning about economic growth risks in less than a week but Chinese stocks bounced back over bets that policy makers will take measures to support the economy. The rate on 10-year Treasuries rose to the highest since 2018 as the global bond rout continued, rising for an 8th straight day as high as 2.83% before easing. The Bloomberg dollar index was set to extend its longest winning streak since 2020, rising for a ninth day. Both trends reflect expectations that the Fed will implement its fastest monetary tightening since 1994. The euro weakened. Oil staged a partial recovery after a tumble that saw crude erase most of the gains sparked by Russia’s invasion of Ukraine. China’s virus outbreaks and mobility curbs, in pursuit of a controversial Covid-zero strategy, are imperiling demand.

“What we’re faced with this year is stagflation,” Kathryn Rooney Vera, head of global macro research at Bulltick LLC, said on Bloomberg Television. “It’s a very complicated environment that the Fed has found itself in” and the market is pricing in potentially 50 basis points of hikes at each of the next two policy meetings, she added. Meanwhile, the Peterson Institute for International Economics expects a global recession by the end of the year due to Covid-related shutdowns in China and the Russia-Ukraine war

In premarket trading, Apple was flat after Citi said that it was likely to announce an incremental stock buyback of $80b-$90b and raise its dividend by 5-10% when it reports 2Q results later this month, according to Citi. Hewlett Packard Enterprise fell 3.6% after Morgan Stanley downgraded the stock to underweight and lowered its industry view for telecom and networking equipment to cautious from in-line, citing demand data. Other notable premarket movers include:

- Cisco (CSCO US) drop as much as 2.1% in premarket after Citi cuts rating to sell from neutral, citing competition and more difficult year-over-year comparisons for quarters ahead.

- Biodesix (BDSX US) surges 79% premarket after its chairman, board members revealed they had bought shares in the biotechnology firm.

- Coinbase (COIN US) price target cut by Mizuho Securities for a second straight week, this time citing analysis which suggests the cryptocurrency exchange is losing market share to other platforms. Shares up 0.8% premarket.

- Aeglea BioTherapeutics (AGLE US) shared added data from the PEACE Phase 3 study of pegzilarginase for the treatment of arginase 1 deficiency, with shares gaining 31% premarket.

Global growth optimism sank to a fresh all-time low, with recession fears surging in the world’s investment community, according to the latest monthly Bank of America survey of fund managers. The next major test for markets looms later Tuesday, when the U.S. is expected to unveil an inflation print for March of more than 8%, the highest since early 1982 (see our CPI preview here).

One of the more dangerous scenarios for markets “is that we have to raise rates at such a pace that it will clamp down on growth,” Kathryn Kaminski, chief research strategist at AlphaSimplex Group, said on Bloomberg Television. “That’s the scenario that most people are worried about.”

“These concerns over inflation are likely to remain in focus over the next two days,” said Michael Hewson, chief analyst at CMC Markets in London. “Today’s CPI numbers look set to seal the deal on a 50 basis-point rate move at the Federal Reserve’s May meeting, a move that bond markets are already discounting with the prospect of more to come.”

In Europe, stocks pared some losses as energy benefits from oil’s rally, while global yields slightly cool their ascent. Declines in the personal care and healthcare industries outweighed gains for energy and mining companies, with the Stoxx Europe 600 Index down 0.5% and the Euro Stoxx 50 falling 0.9%. IBEX outperformed, dropping 0.3%, DAX lags, dropping 1.1%. Health care, banks and financial services are the worst performing sectors. Energy is the best performing sector of Stoxx 600. Banking stocks were among the biggest decliners in Europe as concern over the impact of war in Ukraine and the possibility of recession started to impact profit estimates. Deutsche Bank AG and Commerzbank AG led the drop after stake sales worth a combined 1.75 billion euros ($1.9 billion) in Germany’s two largest listed banks. Russian stocks fell for a third day. Dubai Electricity & Water Authority jumped in its trading debut after raising $6.1 billion in the world’s second-biggest initial public offering this year. In the U.K., living standards fell at the fastest pace in more than eight years in February as wages lagged further behind the rate of inflation.

Earlier in the session, Asia’s stock benchmark pared much of its early drop on Tuesday, with Chinese shares bouncing back on speculation that policy makers will step in to support the economy. The MSCI Asia Pacific Index was down 0.6% as of 6:00 p.m. in Singapore after falling as much as 1%. The CSI 300 Index advanced by the most this month as traders bet that authorities may step up monetary-policy easing or relax some of the most severe Covid-19 restrictions. The broader risk-off sentiment remained, however, as lockdowns in China and higher U.S. interest rates dim the region’s growth prospects. Industrial firms were among the biggest drags on the MSCI measure, while chipmakers and electronic-hardware stocks followed U.S. tech peers lower as the 10-year Treasury yield climbed above 2.8%. “Investors globally are looking to hold defensive stocks and sell cyclical stocks that may be affected economically, and machinery-related stocks are one of the more economically sensitive ones,” said Shogo Maekawa, a strategist at JPMorgan Asset Management. Key gauges in Japan, the Philippines and South Korea led equity declines. Chinese tech stocks edged higher after a volatile trading day, as investors tipped toward optimism after Beijing’s approval of new video game licenses. China’s Covid-Zero policy remains a concern for international investors and is expected to continue to weigh on Asian shares, with the regional benchmark trading at its lowest since March 16.

Sri Lanka warned of an unprecedented default and halted payments on foreign debt, an extraordinary step taken to preserve its dwindling dollar stockpile for essential food and fuel imports.

Japanese equities dropped, dragged by technology shares for a second day amid ongoing concerns over inflation and Federal Reserve monetary policy. Electronics and machinery makers were the biggest drags on the Topix, which fell 1.4%. Fast Retailing and Tokyo Electron were the largest contributors to a 1.8% loss in the Nikkei 225. The yen slightly extended losses to around 125.5 per dollar after weakening 0.8% Monday. “Earnings will start coming out now, and I think it will still take some time before the uncertainty clears up and people start to buy back,” said said Shogo Maekawa, a strategist at JPMorgan Asset Management. “Investors globally are looking to hold defensive stocks and sell cyclical stocks that may be affected economically, and machinery-related stocks are one of the more economically sensitive ones.”

Australian stocks fell, led by the healthcare sector: the S&P/ASX 200 index fell 0.4% to close at 7,454.00, with the health sector falling most. Imugene was the biggest decliner on the benchmark gauge. Mining company Regis rose for a fourth day to the highest since Oct. 25, leading gains in the materials sector. In New Zealand, the S&P/NZX 50 index fell 0.4% to 11,889.17

In rates, treasuries remained cheaper across the curve after paring declines that were led by bunds as ECB and BOE policy-tightening premium increased further. U.S. yields cheaper by up to 2bp across front-end of the curve which underperforms slightly; 10-year yields around 2.79%, higher by ~1bp, with German 10-year cheaper by an additional 1bp. Focal points for U.S. session include March CPI data — with 5-year TIPS breakeven rate ~25bp off its March peak — and $34b 10-year note reopening. Monday’s 3-year auction was solid; cycle concludes Wednesday with $20b 30-year bond reopening. Gilts and bunds extended their drop as the market set pre-CPI positioning. U.K.’s 10-year debt sale had a bid-to-cover ratio of 2.64. Germany’s 2-year notes sale ahead, while U.S. 10-year sale is due after inflation data later Tuesday.

In FX, the greenback traded mixed against its Group-of-10 peers and the Bloomberg Dollar Spot Index edged up 0.1%, advancing for a ninth consecutive session – its longest winning stretch since 2020 – as traders bet on the Federal Reserve hiking rates to counter heated price growth, with the Australian dollar outperforming while the Swiss franc lagged. Hedge funds faded the euro move below 1.0860, while trimming dollar-yen longs above 125.50, two Europe-based traders say.

- The euro neared $1.0850 before paring losses; the bund curve bear steepens Germany’s ZEW investor expectations fell to to -41.0 (estimate -48.5) in April from -39.3 in March

- The pound fell below 1.30 per dollar, while gilts inched lower, led by the long end of the curve. U.K. jobs data showed a strong labor market, although average earnings excluding bonuses adjusted for prices dropped the most since late 2013 year-on-year. U.K. retailers warned that inflation is curbing demand, recording a sharp slowdown in sales in March.

- The Australian and New Zealand dollars erased an Asia session loss against the U.S. dollar. Australian sovereign bonds followed Treasuries lower and in view of a bounce in crude oil and iron ore, the latter of which arrested a five-day slide. Australian business sentiment surged as firms passed on increasing costs to consumers, reflecting strong underlying demand that highlights both economic momentum and gathering inflationary pressures

- The yen weakened for an eighth day before U.S. CPI numbers that are expected to reinforce the economic and monetary policy divergence between America and Japan. Five-year bonds outperformed after a solid auction. The yen’s implied and historical volatility may not be in the driver’s seat for the Group-of-10, but traders are betting it’s the currency that can move the most over the next month

Bitcoin is firmer and is holding onto the USD 40k mark after pronounced pressure in yesterday’s session saw a breach of the level and a subsequent fall to a USD 39.21k overnight low. Bitcoin has dropped for seven days out of the past eight.

In commodities, crude futures advanced with WTI trading within Monday’s range, adding 3.2% to around $97. Brent rises 3.4% above $101. Spot gold falls roughly $2 to trade around $1,950/oz. Base metals are mixed; LME tin falls 0.6% while LME nickel gains 1.5%.

Looking at the day ahead, today brings the ever-important US CPI release. Consensus expects the monthly gain in headline CPI of +1.2% will push the year-on-year rate to +8.4%, the highest since 1981. However, many economists also think that March is the peak in the year-on-year rates for both headline and core. Elsewhere in the US, there’s the March NFIB small business optimism index. We’ll also get February UK unemployment and the April German ZEW survey. Finally, central bank speakers today include the Fed’s Brainard and Barkin.

Market Snapshot

- S&P 500 futures down 0.2% to 4,402.00

- STOXX Europe 600 down 0.8% to 454.78

- MXAP down 0.5% to 172.46

- MXAPJ little changed at 573.96

- Nikkei down 1.8% to 26,334.98

- Topix down 1.4% to 1,863.63

- Hang Seng Index up 0.5% to 21,319.13

- Shanghai Composite up 1.5% to 3,213.33

- Sensex down 0.7% to 58,579.23

- Australia S&P/ASX 200 down 0.4% to 7,453.98

- Kospi down 1.0% to 2,666.76

- German 10Y yield little changed at 0.86%

- Euro down 0.2% to $1.0862

- Brent Futures up 2.2% to $100.65/bbl

- Gold spot up 0.0% to $1,954.10

- U.S. Dollar Index up 0.24% to 100.17

Top Overnight News from Bloomberg

- Global growth optimism has sunk to an all-time low, with recession fears surging in the world’s investment community, according to the latest Bank of America Corp. fund manager survey

- Some Russian exporters face difficulties selling foreign currency proceeds in the market, newspaper Vedomosti reports, citing unidentified people close to the government, Bank of Russia and some exporters

- Global crude markets have swung from chaos to calm in just a few weeks as frenzied trading and a run- up in prices triggered by Russia’s invasion of Ukraine gives way to a return to more normal conditions

- U.K. living standards fell at the fastest pace in more than eight years in February as wages lagged further behind the rate of inflation. Average earnings excluding bonuses rose 4.1% from a year earlier, the Office for National Statistics said Tuesday. Adjusted for prices over the same period, however, they dropped 1.3%, the most since late 2013

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks followed suit to the losses across global counterparts amid higher yields and inflationary concerns. ASX 200 was dragged lower by weakness across defensives and tech but with losses in the broader market somewhat contained amid the improvement in NAB Business Confidence and Conditions. Nikkei 225 declined despite recent currency depreciation and the ruling LDP seeking to provide cash handouts. Hang Seng and Shanghai Comp were indecisive with early support in the former as gaming and internet stocks were boosted by China’s resumption of videogame approvals following a 9-month suspension. However, the gains for the Hong Kong benchmark were later pared and the mainland bourse was also cautious amid ongoing COVID woes.

Top Asian News

- China Tech Stocks Slide as Risks Outweigh Game Approval Uplift

- Tencent Soars After China Ends Eight-Month Gaming Freeze

- Macau Premium Mass Operators to Outperform Peers: Citi

- Australia Minister To Make Rare Solomon Islands Trip, ABC says

European bourses are subdued, Euro Stoxx 50 -0.7%, but off lows as participants await the US CPI metrics for fresh insight into the inflation narrative and for any read across to ongoing yield upside. The breakdown features relatively broad-based losses as the CAC 40 is in-line after Monday’s election inspired outperformance while Banking names lag initially in a pullback from that session’s strength while Energy & Tech fare better. Stateside, futures are attempting to move into positive territory, ES Unch., but are yet to find a robust foothold.

Top European News

- German Investor Mood Sours Further Amid War-Driven Inflation

- U.K. Workers See Biggest Fall in Living Standards in Eight Years

- U.K. Labor Market Missing Almost 600,000 People Since Covid Hit

- EasyJet Sees Summer Flight Capacity Approaching 2019 Levels

Fixed Income

- Bonds bounce after sliding once more and setting fresh yield highs; 10 year T-note, Bunds and Gilts off new 119-10+, 154.27 and 118.42 cycle lows.

- UK and German debt may be gleaning some comfort from solid covers at Schatz and 2032 DMO auctions.

- Treasuries await US CPI and 10 year supply.

FX:

- Greenback grinds higher before US CPI with White House officials upping the ante for a hot set of inflation data, DXY eclipses last Friday’s peak within a firmer 100.230-99.923 range.

- Aussie resilient after increases in NAB business sentiment and conditions and Kiwi underpinned awaiting 25bp or 50bp from the RBNZ, overnight; AUD/USD bounces off 0.7400 and NZD/USD keeps grip of 0.6800 handle.

- Euro holds above recent low and 2022 trough with some traction from Germany’s ZEW survey showing not as bad as feared economic sentiment and current conditions, EUR/USD above 1.0850 vs 1.0836 last Friday and 1.0806 y-t-d base.

- Sterling treading water around 1.3000 after mixed UK jobs and earnings, Loonie looking for support via decent option expiry interest at 1.2650 or chart levels after dropping through 200 DMA before BoC on Wednesday.

- Yen and Franc yield to divergent dynamics; USD/JPY poised below 2015 peak and USD/CHF rebounds from low 0.9300 zone.

- Japanese Finance Minister Suzuki said FX stability is important but did not comment on FX levels, while he added they are watching closely with vigilance how FX moves could impact Japan’s economy. Suzuki also noted that excess FX volatility and disorderly FX moves could have an adverse effect on Japan’s economy, while they will respond to FX as appropriate while communicating with the US and other countries.

Commodities:

- Crude benchmarks are continuing to regain composure after Monday’s pressure, with WTI and Brent in proximity to highs of USD 97.72/bbl and USD 102.15/bbl respectively.

- European Commission official said the EU repeated its call during a meeting with OPEC for oil producers to look at whether they can increase deliveries, according to Reuters.

- US President Biden will on Tuesday lay out plans to extend the availability of higher biofuels-blended gasoline during the summer in a bit to control fuel costs, according to Reuters sources.

- Spot gold and silver are contained, particularly in the context of yesterday’s price action, ahead of the key US events on the schedule.

US Event Calendar

- 06:00: March SMALL BUSINESS OPTIMISM dropped to 93.2, est. 95.0, prior 95.7

- 08:30: March CPI YoY, est. 8.4%, prior 7.9%; CPI MoM, est. 1.2%, prior 0.8%

- 08:30: March CPI Ex Food and Energy YoY, est. 6.6%, prior 6.4%; CPI Ex Food and Energy MoM, est. 0.5%, prior 0.5%

- 08:30: March Real Avg Hourly Earning YoY, prior -2.6%, revised -2.5%

- 08:30: March Real Avg Weekly Earnings YoY, prior -2.3%, revised -2.2%

- 14:00: March Monthly Budget Statement, est. -$190b, prior -$659.6b

DB’s Tim Wessel concludes the overnight wrap

Yesterday was painted with a panoply of senior-level gatherings. The EU foreign ministers met in Luxembourg, where they weighed whether to sanction Russia’s energy sector. Those closer to Russia’s border were quicker to advocate for a ban on oil imports. The idea was not ruled out, with several EU countries seeking more time to transition energy supplies before signing up for an outright ban. This, as Russia posted its biggest current account surplus in nearly three decades on the back of strong energy export revenues. Germany is also ready to send weapons to Ukraine according to Chancellor Scholz. Austrian Chancellor Nehammer, meanwhile, became the first European head of state to meet with President Putin in person since his invasion. Nehammer expressed pessimism on peace prospects following the discussion.

Farther afield, President Biden met with Indian Prime Minister Modi. Biden pledged to help India diversify its energy sources in an attempt to persuade India from increasing purchases of Russian energy exports.

Finally, as we go to press this morning, the Pentagon is monitoring claims that Russia used a chemical agent in Mariupol. A number of news agencies have reported the accusation, but as of yet, none have been able to verify the original claim. If true, that would mark a much-feared escalation in tactics as Ukraine braces for a renewed assault on its territory in the east. After starting the week off on a weak foot, S&P 500 futures are down another -0.41% this morning.

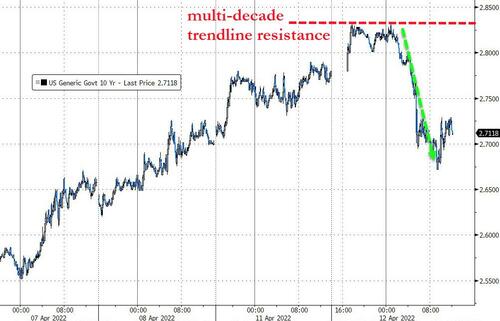

Back to yesterday, Treasury yields continued their blistering selloff and curve re-steepening. Chicago Fed President Evans, owner of an inimitable dovish CV, thought that a +50bp hike in May was not only possible, but likely. He went on to say that policy should get to neutral by December, a range he pegged between 2.25% and 2.5%, which implies at least two +50bp hikes this year. The implied probability of a +50bp hike in May edged to a cycle high of 91.2%, with the amount of anticipated 2022 policy rate tightening hitting its own high at +255bps. 10yr Treasury yields gained another +8.0bps to 2.78%, their highest levels since January 2019, with breakevens (+4.3bps) and real yields (+3.7bps) each contributing. 2s10s steepened another +9.6bps to +27.4bps, its highest level in a month.

Much like how the Fed’s rhetoric has shaded ever more restrictive over the last few months, so too has their recent handicapping of a soft landing turned more pessimistic. Once a widely-accepted base case, yesterday Governor Waller was much more blunt, if not fatalistic, noting that interest rates are a “brute-force tool” and that there will be some “collateral damage” when they are used to slow inflation.

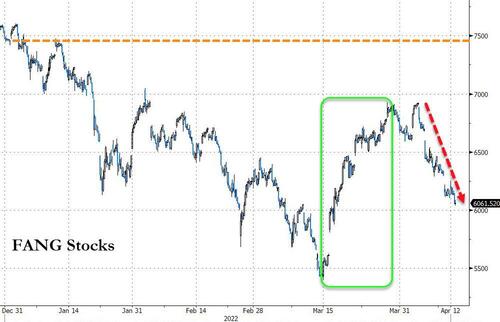

US equities took some collateral damage yesterday, with the S&P 500 down -1.69% to start the week, with every sector in the red, bringing YTD performance down to -7.42%. Energy (-3.11%) led the declines on the fall in oil prices, with brent crude futures down -4.18% to close below $100 for the first time in a month. Mega-cap tech names underperformed, with FANG+ falling -3.03%, given the discount rate hit to valuations, capping off five straight days of declines that has brought the FANG+ -11.73% lower. The index is now down -17.69% on the year.

It was a similar story in Europe, with year-end OIS rates increasing +5.4bps to +67.6bps, a cycle high, suggesting some probability that the deposit rate could end the year in positive territory. 10yr bund yields climbed +10.9bps to 0.82%, the highest level since 2015, while 10yr gilts gained +9.7bps to 1.85%, their highest since 2016. European stocks were a touch more resilient, with the STOXX 600 falling -0.59%.

In Europe, markets were also reacting to the first round of the French election. French assets outperformed as President Macron’s lead over Marine Le Pen was slightly wider than the final polls had implied. In particular, the spread of French 10yr yields over bunds narrowed by -5.2bps, coming down from its 2-year high last Friday. Furthermore, the CAC 40 (+0.12%) outperformed all the other major European equity indices.

The second round is set for later this month, and polls over the last 24 hours were a bit more favorable to Macron than the readings from late last week. Macron leads Le Pen by 55%-45% in Opinionway’s poll, and then 54.5%-45.5% in Odoxa’s. Ifop was somewhat narrower, at 52.5%-47.5%, but even that was wider than the 51%-49% margin they reported Sunday night. Harris had a 53-47% margin, also wider than its previous reading. For those after further information on the election, Marc de-Muizon from DB’s European economics team has published his takeaways following the first round (link here).

The other major thematic story is the continued Covid spread in China, their strict lockdown response, and the downstream impacts on supply chains and markets. Asian equities are broadly in the red to start trading this morning, with tech shares also lagging on the increase in long-dated sovereign yields. The Nikkei (-1.44%) is leading losses, which comes as Japanese PPI rose to +9.5% in March, while the February figure was revised to a four-decade high of +9.7%.

Oil prices have partially retraced yesterday’s big decline, with Brent futures rising +1.33% to $99.79/bbl. 10yr Treasury yields continue to forge a path higher, increasing +4.2bps to a three-year high of 2.82% this morning. The yield curve has shifted higher in parallel, with 2yr yields not far behind at +3.7bps.

There wasn’t a massive amount of data yesterday, but we did get the monthly GDP reading for February from the UK. That showed the economy grew by just +0.1% that month (vs. +0.2% expected). Consumers increased their inflation expectations for the year ahead to +6.6%, while three-year inflation dropped to +3.7%, according to the New York Fed’s survey.

To the day ahead, today brings the ever-important US CPI release. Our US econ and rates team put our their joint-preview, here. They’re expecting the monthly gain in headline CPI of +1.3% will push the year-on-year rate to +8.6%, the highest since 1981. However, they think that March is the peak in the year-on-year rates for both headline and core.

Elsewhere in the US, there’s the March NFIB small business optimism index. We’ll also get February UK unemployment and the April German ZEW survey. Finally, central bank speakers today include the Fed’s Brainard and Barkin.

3. ASIAN AFFAIRS

i)TUESDAY MORNING// MONDAY NIGHT

SHANGHAI CLOSED UP 46.20 PTS OR 1.46% //Hang Sang CLOSED UP 110.83 PTS OR 0.57% /The Nikkei closed DOWN 486.54 PTS OR 1.81% //Australia’s all ordinaires CLOSED DOWN .48% /Chinese yuan (ONSHORE) closed DOWN 6.3716 /Oil UP TO 97.25 dollars per barrel for WTI and DOWN TO 102.75 for Brent. Stocks in Europe OPENED ALL RED EXCEPT SPAIN // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.3716 OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.3798: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER//

3 a./NORTH KOREA/ SOUTH KOREA

///NORTH KOREA

END

3B JAPAN

end

3c CHINA

CHINA/COVID/SHANGHAI LOCKDOWNS

still massive problems with backlogs

(Kulish/Freightwaves)

Another Supply Chain Shock On Deck: Cargo Backlog Ripples Beyond Shanghai As Lockdown Stops Trucks, Containerships

TUESDAY, APR 12, 2022 – 12:45 PM

By Eric Kulish of Freight Waves

Rerouting freight to avoid the extended lockdown in Shanghai, where daily confirmed COVID cases topped a record 17,000 this week, is becoming more difficult and expensive as cargo facilities in other Chinese cities become overcrowded, logistics companies and carriers warn.

The logistics challenges for ocean and airfreight in Shanghai are extreme.

More than 90% of truck capacity is out of service. Trucks are prevented from moving in and out of the city without a special permit, which is only valid for 24 hours and only on specific routes. “Even with this arranged, it is possible for booked trucks to be commandeered by the government to transport aid supplies,” Seko Logistics said in an update for clients.

Most warehouses in the city are closed. Pactl, the large airport cargo terminal operator, only has skeleton operations.

Limited truck access to Shanghai port terminals is causing shipping containers to pile up and slowing ship transfers. Seko said its team in Shanghai has seen an 80% decrease in container pickups from outside the lockdown area because of driver shortages and restrictions, with drivers requiring a special pass and negative COVID test results.

Mediterranean Shipping Co., the world’s largest container vessel operator, on Thursday said it will begin offloading refrigerated containers at other ports because there are no available power plugs to connect to in Shanghai. Unless customers request a specific change in destination within seven days, reefers will be discharged at intermediate or alternate ports of the carrier’s choosing. Additional freight charges for transshipment, storage, equipment rental and electrical connection may apply.

“If the situation does not improve soon it may be necessary to abandon the voyage and advise you from where your container may be collected,” MSC said in a customer notice.

Ocean Network Express also said overcrowding at two Shanghai container terminals might prevent its vessels from discharging reefer boxes.

Several ocean carriers have announced they will skip berthing at Shanghai due to traffic restrictions, which Seko said will intensify congestion at the terminals once restrictions are lifted.

Congestion spreads

Meanwhile, terminals at the Port of Ningbo are filling up and facing equipment shortages as more freight is diverted from Shanghai, freight forwarders report. Freight rates from Ningbo are rising as a result.

AIT Worldwide, based in Itasca, Illinois, notified customers that cargo terminals at other airports are now reporting delays of their own with Shanghai Pudong International Airport effectively out of action.

In Zhengzhou, for example, inbound and outbound air shipments can take up to seven days to get through a queue and another three to four days to be processed. Import operations at the Nanjing airport are suspended. And authorities are requiring all imported cargo in Qingdao to be stored in the terminal for 10 days following disinfection.(Source: AIT Worldwide)

Logistics providers are also redirecting cargo to airports in Wuhan, Hangzhou and Nanchang.

International passenger and cargo airlines have responded by canceling the majority of flights in and out of Shanghai Pudong airport. Delta Air Lines, for example, said this week it won’t process cargo there until at least April 18. Most international cargo flights are now being operated by Chinese airlines, said Itasca-based Seko Logistics, which has moved more than 10 tons of airfreight through alternate airports since the Shanghai restrictions began nearly two weeks ago.

Seko also reported that an outbreak in Quzhou is spreading, with shipments scheduled for departure in the coming weeks needing to be postponed until the government settles on a course of action.

Nick Bartlett, director of CBIP Logistics in Hong Kong, told FreightWaves cases of infection are increasing in Suzhou and all of Jiangsu Province and that Zhejiang is likely to next feel restrictive measures.

“We have cargo stuck on trucks, in warehouses and container freight stations,” in Shanghai and no new containers are able to reach the port there, he said via email.

The lockdown in Kunshan, an important electronics manufacturing hub next to Shanghai, is supposed to end by the end of the week. Truck movements in and out of the city are severely restricted, except for pandemic relief supplies approved by the local government, Seko said. Trucks can only shuttle within the city between warehouses and factories with special approval. The restrictions are impacting the Wuxi Logistics Park and Seko clients with suppliers in the city.

CHINA/AFRICA

A very important read as to China’s love affair with Africa. They seeded them with loans and Africa supplied much needed commodities

They left the uSA behind.

(Bergman/Gatestone)

Africa Is Becoming China’s “Second Continent” As US Lags Behind

TUESDAY, APR 12, 2022 – 02:00 AM

Authored by Judith Bergman via The Gatestone Institute,