april13, 2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD; $1980.75 UP $8.80

SILVER: $25.78 UP $0.27

ACCESS MARKET: GOLD $1977.80

SILVER: $25.74

Bitcoin morning price: $39,863 UP 378

Bitcoin: afternoon price: $41,309 UP 1824

Platinum price: closing UP $16.75 to $989.45

Palladium price; closing DOWN 47.15 at $2319.60

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

comex notices/

: JPMorgan stopped/total issued 48/134

EXCHANGE: COMEX

CONTRACT: APRIL 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,972.100000000 USD

INTENT DATE: 04/12/2022 DELIVERY DATE: 04/14/2022

FIRM ORG FIRM NAME ISSUED STOPPED

072 C GOLDMAN 5

118 C MACQUARIE FUT 8

132 C SG AMERICAS 16

167 C MAREX 1

363 H WELLS FARGO SEC 3

435 H SCOTIA CAPITAL 2

624 H BOFA SECURITIES 10

657 C MORGAN STANLEY 8

661 C JP MORGAN 125 48

709 C BARCLAYS 21

737 C ADVANTAGE 1

880 H CITIGROUP 20

TOTAL: 134 134

MONTH TO DATE: 24,499

NUMBER OF NOTICES FILED TODAY FOR APRIL. CONTRACT134 NOTICE(S) FOR 13400 OZ (0.4167 TONNES)

total notices so far: 24,499 contracts for 2,449,900 oz (76.202 tonnes)

SILVER NOTICES:

10 NOTICE(S) FILED TODAY FOR 50,000 OZ/

total number of notices filed so far this month 1080 : for 5,400,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

END

GLD

WITH GOLD UP $8.80

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

A HUGE CHANGE IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.61 TONNES FROM THE GLD//

INVENTORY RESTS AT 1093.10 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP 27 CENTS

AT THE SLV// NO CHANGES IN SILVER INVENTORY AT THE SLV/ THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 565.521 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A GIGANTIC SIZED 3868 CONTRACTS TO 158,813 AND CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE HUGE GAIN IN OI WAS ACCOMPLISHED WITH OUR STRONG $0.66 GAIN IN SILVER PRICING AT THE COMEX ON MONDAY. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.66) AND WERE UNSUCCESSFUL IN KNOCKING OUT ANY SILVER LONGS AS WE HAD A HUMONGOUS GAIN OF 9765 CONTRACTS ON OUR TWO EXCHANGES

WE MUST HAVE HAD:

I) HUGE BANKER SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A STRONG INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 4.305 MILLION OZ FOLLOWED BY TODAY’S QUEUE. JUMP OF 105,000 OZ//NEW STANDING: 5.560 MILLION OZ// V) HUGE SIZED COMEX OI GAIN/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS : —-859 (which is huge)

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS APRIL. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF APRIL:

TOTAL CONTACTS for 9 days, total 7216 contracts: 36.08 million oz OR 4.00MILLION OZ PER DAY. (801 CONTRACTS PER DAY)

TOTAL NO OF OZ UNDERGOING EFP TO LONDON 7216 CONTRACTS X 5,000 PER CONTRACT:

EQUATES TO: 36.08 MILLION OZ

.

LAST 11 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

APRIL: 36.08 MILLION OZ (LOOKS LIKE OUR BANKERS ARE NOW LOATHE TO ISSUE EFP’S)

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 3868 WITH OUR STRONG $0.66 GAIN IN SILVER PRICING AT THE COMEX// TUESDAY THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE CONTRACTS: 2195 CONTRACTS ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A HUGE INITIAL SILVER OZ STANDING FOR MAR. OF 4.305 MILLION OZ FOLLOWED BY TODAY’S 105,000 OZ QUEUE JUMP//NEW STANDING: 5.5600 MILLION OZ/// .. WE HAD AN HUGE SIZED GAIN 6063 OI CONTRACTS ON THE TWO EXCHANGES FOR 34.61 MILLION OZ WITH THE VERY STRONG GAIN IN PRICE.

WE HAD 10 NOTICES FILED TODAY FOR 50,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A STRONG SIZED 6844 CONTRACTS TO 577,639 AND CLOSER TO NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: -31 CONTRACTS.

THE BIS HAS ABANDONED THE GOLD COMEX TRADING!!!

.

THE STRONG SIZED INCREASE IN COMEX OI CAME WITH OUR VERY STRONG GAIN IN PRICE OF $26.95//COMEX GOLD TRADING/TUESDAY /.AS IN SILVER WE MUST HAD HUGE BANKER/ALGO SHORT COVERING ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR APRIL AT 78.33 TONNES ON FIRST DAY NOTICE

YET ALL OF..THIS HAPPENED WITH OUR GAIN IN PRICE OF $26.95 WITH RESPECT TO MONDAY’S TRADING

WE HAD A STRONG SIZED GAIN OF 9734 OI CONTRACTS (30.273 PAPER TONNES) ON OUR TWO EXCHANGES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2890 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 577,639.

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 9734, WITH 6844 CONTRACTS INCREASED AT THE COMEX AND 2890 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 9765 CONTRACTS OR 30.73 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2890) ACCOMPANYING THE STRONG SIZED GAIN IN COMEX OI (6844,): TOTAL GAIN IN THE TWO EXCHANGES 9734 CONTRACTS. WE NO DOUBT HAD 1) HUGE BANKER SHORT COVERING ,2.) HUGE INITIAL STANDING AT THE GOLD COMEX FOR APRIL. AT 78.33 TONNES FOLLOWED BY TODAY’S 16,800 OZ QUEUE JUMP //NEW STANDING 81.225 TONNES/// 3) ZERO LONG LIQUIDATION ///. ,4) STRONG SIZED COMEX OI. GAIN 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

APRIL

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL :

22,087 CONTRACTS OR 2,208,700 OR 68.69 TONNES 9 TRADING DAY(S) AND THUS AVERAGING: 2454 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 9 TRADING DAY(S) IN TONNES: 68.69TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2020, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 68.69/3550 x 100% TONNES 1.94% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 68.69 TONNES (THIS IS GOING TO BE A LOW ISSUANCE MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF MAY.WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF APRIL HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF MAY, FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (MAR), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A HUGE SIZED 3868 CONTRACTS TO 158,813 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 2195 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 2195 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 3868 CONTRACTS AND ADD TO THE 2195 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUMONGOUS SIZED GAIN OF 6063 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 30.315 MILLION OZ

OCCURRED WITH OUR SMALL GAIN OF $0.66 IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

5. Other gold commentaries

6. Commodity commentaries/cryptocurrencies

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING// TUESDAY NIGHT

SHANGHAI CLOSED DOWN 26.51 PTS OR 0.82% //Hang Sang CLOSED UP 55.24 PTS OR 0.26% /The Nikkei closed UP 508.51 PTS OR 1.83% //Australia’s all ordinaires CLOSED UP .47% /Chinese yuan (ONSHORE) closed UP 6.3665 /Oil UP TO 97.25 dollars per barrel for WTI and DOWN TO 102.75 for Brent. Stocks in Europe OPENED ALL RED EXCEPT SPAIN // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.3665 OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.3772: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER//

A)NORTH KOREA/

b) REPORT ON JAPAN

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A STRONG SIZED 6844 CONTRACTS TO 577,639 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS STRONG COMEX INCREASE OCCURRED WITH OUR VERY STRONG GAIN OF $26.95 IN GOLD PRICING TUESDAY’S COMEX TRADING. WE ALSO HAD A FAIR SIZED EFP (2890 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE ACTIVE DELIVERY MONTH OF APRIL.. THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2890 EFP CONTRACTS WERE ISSUED: ;: , . 0 JUNE :2890 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2890 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 9734 CONTRACTS IN THAT 2890 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A STRONG SIZED COMEX OI GAIN OF 6844 CONTRACTS..AND THIS GAIN OCCURRED WITH OUR VERY STRONG GAIN IN PRICE OF GOLD $26.95.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING FOR APRIL (81.225),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 81.225

THE BANKERS WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $26.95) AND AND WERE UNSUCCESSFUL IN FLEECING ANY LONGS AS WE HAVE REGISTERED A STRONG SIZED GAIN OF 30.273 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR APRIL (81.225 TONNES)…

WE HAD — 31 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 9734 CONTRACTS OR 973400 OZ OR 30.273 TONNES

Estimated gold volume today: 132,741/// extremely poor

Confirmed volume yesterday: 188,023 contracts poor

INITIAL STANDINGS FOR APRIL ’22 COMEX GOLD //APRIL 13

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | nil oz |

| Deposit to the Dealer Inventory in oz | 964.53OZ 30 kilobars |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 134 notice(s) 13400 OZ 0.4167 TONNES |

| No of oz to be served (notices) | 1615 contracts 161500 oz 5.023 TONNES |

| Total monthly oz gold served (contracts) so far this month | 24,499 notices 2,449900 OZ 76.202 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For today:

dealer deposits 1

i)) Into Manfra; 964.53 oz (30 kilobars)

total dealer deposit 964.30 oz//

No dealer withdrawals

0 customer deposits.

total customer deposit nil oz

0 customer withdrawals

total customer withdrawal: nil oz /

ADJUSTMENTS: nil

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR APRIL.

For the front month of APRIL we have an oi of 1749 contracts having LOST 256.

We had 424 notices filed yesterday so we GAINED 168 contracts or an additional 16,800 oz will stand for delivery at the comex

May saw a LOSS of 138 contracts to stand at 3505

June saw a GAIN of 4110 contracts UP to 480,073 contracts

We had 134 notice(s) filed today for 13,400 oz FOR THE APRIL 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 125 notices were issued from their client or customer account. The total of all issuance by all participants equates to 134 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 48 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 5 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the APRIL /2021. contract month,

we take the total number of notices filed so far for the month (24,499) x 100 oz , to which we add the difference between the open interest for the front month of (APRIL 1749 CONTRACTS ) minus the number of notices served upon today 134 x 100 oz per contract equals 2,611,400 OZ OR 81.225 TONNES the number of TONNES standing in this active month of APRIL.

thus the INITIAL standings for gold for the APRIL contract month:

No of notices filed so far (24,499) x 100 oz+ (1749) OI for the front month minus the number of notices served upon today (134} x 100 oz} which equals 2,611,400 oz standing OR 81.225 TONNES in this active delivery month of APRIL.

We GAINED 16,800 oz as a QUEUE. jump as our banker friends scrounge around for some gold

TOTAL COMEX GOLD STANDING: 81.225 TONNES (A WHOPPER FOR AN APRIL ( ACTIVE) DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

191,133,764.7, oz NOW PLEDGED /HSBC 5.94 TONNES

99,258.893 PLEDGED MANFRA 3.08 TONNES

54,339.114oz PLEDGED JPMorgan no 1 1.690 tonnes

243,923.704, oz JPM No 2 7.58 TONNES

898,821.330 oz pledged Brinks/27,96 TONNES

International Delaware:: 0

Loomis: 18,615.429 oz

total pledged gold: 1,884,464.742 oz 58.61 tonnes

TOTAL REGISTERED AND ELIG GOLD AT THE COMEX: 35,908,058.973 OZ (1116,89 TONNES)

TOTAL ELIGIBLE GOLD: 18,255,237.054 OZ (567.81 tonnes)

TOTAL OF ALL REGISTERED GOLD: 17,652,785.389 OZ (549.06 tonnes)

REGISTERED GOLD THAT CAN BE SERVED UPON: 15,768,321.0 OZ (REG GOLD- PLEDGED GOLD) 503.117 tonnes

END

APRIL 2022 CONTRACT MONTH//SILVER//APRIL 13

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 316,384.459 oz JPM CNT |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 607,442.662 oz JPM |

| No of oz served today (contracts) | 10CONTRACT(S) 50,000 OZ) |

| No of oz to be served (notices) | 32 contracts (160,000 oz) |

| Total monthly oz silver served (contracts) | 1080 contracts (5,400,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

we had 0 deposit into the dealer

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 1 deposits into the customer account

i) Into JPMorgan: 607,442.662 oz

total deposit: 607m442,662 oz

JPMorgan has a total silver weight: 176.505 million oz/334.353 million =52.79% of comex

i) Comex withdrawals: 2

i) Out of JPM 295,853.200 oz

ii) Out of CNT 19,530.990 oz

total withdrawal 316,384.459 oz

0 adjustments: dealer to customer

the silver comex is in stress!

TOTAL REGISTERED SILVER: 86.352 MILLION OZ

TOTAL REG + ELIG. 334.353 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR APRIL

silver open interest data:

FRONT MONTH OF APRIL OI: 42, HAVING LOST 50 CONTRACTS FROM MONDAY. We had 71 notices filed yesterday,

so we GAINED 21 contracts or an additional 105,000 oz will stand on this side of the pond

MAY HAD A LOSS OF 5522 CONTRACTS DOWN TO 74,256 contracts

JUNE HAD A GAIN OF 6 TO STAND AT 996

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 10 for 50,000 oz

Comex volumes: 86,425// est. volume today// strong/

Comex volume: confirmed yesterday: 96,151 contracts ( strong )

To calculate the number of silver ounces that will stand for delivery in APRIL. we take the total number of notices filed for the month so far at 1080 x 5,000 oz = 5,400,000oz

to which we add the difference between the open interest for the front month of APRIL (42) and the number of notices served upon today 10 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the APRIL./2021 contract month: 1080 (notices served so far) x 5000 oz + OI for front month of APRIL (42) – number of notices served upon today (10) x 5000 oz of silver standing for the APRIL contract month equates 5,560,000 oz. .

We GAINED 21 contracts or an additional 105,000 oz will stand on this side of the pond

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

APRIL 13/WITH GOLD UP $8.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1093.10 TONNES

APRIL 12/WITH GOLD UP $26.95: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.61 TONNES INTO THE GLD///INVENTORY REST AT 1093.10 TONNES

APRIL 11/WITH GOLD UP $3.40 //A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD.//INVENTORY RESTS AT 1090.49 TONNES

APRIL 8/WITH GOLD UP $7.70: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES INTO THE GLD//INVENTORY RESTS AT 1088.75 TONNES

APRIL 7/WITH GOLD UP $13.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1087.30 TONNES

APRIL 6/WITH GOLD DOWN $4.10: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.68 TONNES FROM THE GLD..//INVENTORY RESTS AT 1087.30 TONNES

APRIL 5/WITH GOLD DOWN $5.70: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.75 TONNES FROM THE GLD//INVENTORY RESTS AT 1089.98 TONNES

APRIL 4/WITH GOLD UP $.70//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1091.73 TONNES

APRIL 1///WITH GOLD DOWN $19.00 : A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .29 TONNES INTO THE GLD///INVENTORY RESTS AT 1091.73 TONNES

MARCH 31/WITH GOLD UP $13.30 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD FROM MONDAY A WITHDRAWAL OF 1.71 TONNES FROM THE GLD:INVENTORY RESTS AT 1091.44

MARCH 28/WITH GOLD DOWN $14.65: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1093.18 TONNES

MARCH 25/WITH GOLD DOWN $7.60 : A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.52 TONNES INTO THE GLD///INVENTORY RESTS AT 1093.18 TONNES

MARCH 24/WITH GOLD UP $24.95: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.06 TONNES INTO THE GLD..//INVENTORY RESTS AT 1087.66 TONNES

MARCH 23/WITH GOLD UP $15.75//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1083.60 TONNES

MARCH 22/WITH GOLD DOWN $7.75: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.16 TONNES OF GOLD DEPOSITED INTO THE GLD//INVENTORY RESTS AT 1083.60 TONES

MARCH 21//WITH GOLD UP $.25 : A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 9.00 TONNES INTO THE GLD////INVENTORY RESTS AT 1082.44 TONES

MARCH 18/WITH GOLD DOWN $13.55 NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1073.44 TONES

MARCH 17/WITH GOLD UP $33.50: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.61 TONNES INTO THE GLD//INVENTORY RESTS AT 1073.44 TONNES

MARCH 16/WITH GOLD DOWN $18.50//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.33 TONNES FROM THE GLD///INVENTORY RESTS AT 1061.83 TONNES

MARCH 15/WITH GOLD DOWN $30.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1064.16 TONNES

MARCH 14//WITH GOLD DOWN $22.75, HUGE CHANGES IN GOLD INVENTORY AT THE GLD//STRANGE: A DEPOSIT OF 2.62 TONNES INTO THE GLD.//INVENTORY RESTS AT 1064.16 TONNES

MARCH 11/WITH GOLD DOWN $14.60: A BIG CHANGE IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 1061.54 TONNES

MARCH 10//WITH GOLD UP $11.55: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.06 TONNES FORM THE GLD///INVENTORY RESTS AT 1063.28 TONNES

MARCH 9/WITH GOLD DOWN $53.85//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.64 TONNES INTO THE GLD//INVENTORY RESTS AT 1067.34 TONNES

MARCH 8/WITH GOLD UP $46.10: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 8.42 TONNES INTO THE GLD///INVENTORY RESTS AT 1062.70 TONNES

MARCH 7/WITH GOLD UP $28.40 A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.06 TONNES INTO THE GLD..//INVENTORY RESTS AT 1054.28 TONNES

MARCH 4/WITH GOLD UP $28.40//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1050.22 TONNES

CLOSING INVENTORY FOR THE GLD//1093.10 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

APRIL 13/WITH SILVER UP 27 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 565.521 MILLION OZ

APRIL 12/WITH SILVER UP 66 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 565.521 MILLION OZ//

APRIL 11/WITH SILVER UP 13 CENTS: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 831,000 OZ FORM THE SLV////INVENTORY RESTS AT 565.521 MILLION OZ

APRIL 8/WITH SILVER UP 11 CENTS :NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 566.352 MILLION OZ//

APRIL 7/WITH SILVER UP 27 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 566.352 MILLION OZ//

APRIL 6/WITH SILVER DOWN 9 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 566.352 MILLION OZ

APRIL 5/WITH SILVER DOWN 16 CENTS : A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.386 MILLION OZ INTO THE SLV..//INVENTORY RESETS AT 566.352 MILLION OZ//

APRIL 4/WITH SILVER DOWN 5 CENTS TO CHANGES IN SILVER INVENTORY AT THE SLV//: A DEPOSIT OF 6.326 MILLION OZ//INVENTORY REST AT 564.966 MILLION OZ//

APRIL 1/WITH SILVER DOWN 39 CENTS A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.302 MILLION OZ INTO THE SLV////INVENTORY REST AT 558.647 MILLION OZ//

MARCH 31/WITH SILVER UP 3 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 2.171 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 556.345 MILLION OZ

MARCH 28/WITH SILVER DOWN 30 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.847 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 554.167 MILLION OZ//

MARCH 25/WITH SILVER DOWN 20 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 552.320 MILLION OZ//

MARCH 24/WITH SILVER UP 54 CENTS TODAY; A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.092 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 552.320 MILLION OZ//

MARCH 23/WITH SILVER UP 24 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 550.288 MILLION OZ//

MARCH 22/WITH SILVER DOWN $0.29 TODAY : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 550.288 MILLION OZ//

MARCH 21/WITH SILVER UP 16 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 550.288 MILLION OZ//

MARCH 18/WITH SILVER DOWN 37 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.217 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 550.288 MILLION OZ//

MARCH 17/ WITH SILVER UP 72 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.049 MILLION OZ INTO THE SLVV//INVENTORY RESTS AT 548.071 MILLION OZ

MARCH 16/WITH SILVER DOWN 56 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 462,000 OZ FROM THE SLV//INVENTORY RESTS AT 544.560 MLLION O

MARCH 15/WITH SILVER DOWN 18 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 545.022 MILLION OZ

MARCH 14/WITH SILVER DOWN 64 CENTS TODAY; STRANGE A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.125 MILLION OZ/INVENTORY RESTS AT 545.022 MILLIONOZ

MARCH 11/WITH SILVER DOWN 13 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.897 MILLION OZ

MARCH 10/WITH SILVER UP 39 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.897 MILLION OZ/

MARCH 9/WITH SILVER DOWN 88 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 5.174 MILLION OZ OF FAKE SILVER.//INVENTORY RESTS AT 542.897 MILLION OZ//

MARCH 8/WITH SILVER UP 88 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.217 MILLION OZ INTO THE SLV////INVENTORY RESTS A 548.071 MILLION OZ//

MARCH 7/WITH SILVER UP 40 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 545.854 MILLION OZ//

MARCH 4/WITH SILVER UP 50 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 545.854 MILLION OZ/

SLV FINAL INVENTORY FOR TODAY: 565.521 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

END

2.LAWRIE WILLIAM//,//Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, James RICKARDS/

LAWRIE WILLIAMS:

LAWRIE WILLIAMS: 8.5% US CPI rise sees gold rise again sharply

The latest US Consumer Price Index (CPI) came in today showing an 8.5% year on year increase – higher than most had expected but still perhaps a little lower than the more pessimistic commentators, ourselves included, might have anticipated. Inflationary pressures are riding particularly high, boosted by the perhaps unintended adverse consequences which have impacted globally and on the U.S. resulting from the stringent sanctions being applied to sectors of the Russian economy over the Ukraine war.

Tomorrow we will get the new Producer Price Index (PPI) data which one suspects will come in comfortably into double digits. The PPI measures the average change over time in the selling prices received by US domestic producers for their output and had already reached 10% year on year in the previous data release of a month ago. The PPI data releases don’t quite seem to have the same impact as the CPI on equities and precious metals prices, but it is certainly an even better indicator of the price rises currently being experienced by the U.S. public. Indeed we suspect the average U.S. consumer may be experiencing higher price rises than these figures might suggest once retail outlets have added their own mark-ups.

As we have pointed out before, the U.S. inflation data were massaged downwards in the early 1980 s and again in the 1990s by the government wishing to present a better economic picture to the public. John Williams’ shadowstats.com service calculates the inflation data as it used to be assessed and this would put annual U.S. inflation as perhaps well above 15% – a figure that would probably be better recognised by the consumer as the current reality.

The U.S. Fed is almost powerless to do much about trying to mitigate the high inflation levels. It takes some comfort in that its preferred inflation data calculation is the Personal Consumption Expenditure (PCE) Index which tends to track a percentage point or so below the CPI, but on current trends the next PCE data release due out on April 29th will probably come out at 7% or more (It was 6.4% year on year at the last data release on March 31st).

This has generated speculation that the Fed may even raise the Federal Funds interest rate by 75 basis points (it normally only looks at 25 basis point increases if it does raise rates) at the next FOMC meeting in early May, or even before. Such an increase would certainly be something of a shock to the U.S. economy and to equity prices and, with further rate increases flagged, could quite possibly drive the U.S. economy into a recessionary phase. And even this well-above –the-norm level of rate rise would probably be insufficient to slay the inflation dragon.

At this unusually high rate level increase, real interest rates would probably still remain in negative territory which, as we have explained before tends to be positive for a non-interest generating safe haven asset like gold. The silver price would probably benefit too as it still tends to ride on gold’s coat tails, but we’re not so sure about platinum and palladium which are very much dependent on industrial activity and motor vehicle sales, which could both turn down sharply in a period of economic weakness.

The gold price, as we had forecast, did rise sharply today on the high CPI figure and was heading up through the upper $1,970s at one time, before being brought back down again quite sharply to the mid 1,960s. Silver too was looking strong but ended at around the $25.30 mark after hitting $25.70. There always seems to be an almost immediate correction when gold and silver seem to begin to show strength. The higher gold price levels, even if only briefly achieved, put the $2,000 psychological level firmly in the sights.

Somewhat surprisingly U.S. equities and bitcoin moved up as well initially before falling back into negative territory, while the dollar index (USDX) regained the 100 mark. The oil price rose too, but managed to maintain its early gains ending up back over the $100 per barrel mark.

So where from here? With the PPI coming out tomorrow and likely to show a significant rise over the reading of a month ago we could well see some further appreciation in gold and silver prices and some more equity weakness too. We seem to be in a positive phase for gold and silver prices and falling general equities, but the markets are always somewht data driven and consequently volatile so some positive data could quickly reverse this trend.

12 Apr 2022

3. Chris Powell of GATA provides to us very important physical commentaries

Craig Hemke: How much will the Fed break the stock market before relenting?

Submitted by admin on Tue, 2022-04-12 22:36Section: Daily Dispatches

10:35p ET Tuesday, April 12, 2022

Dear Friend of GATA and Gold:

Craig Hemke of the TF Metals Report, writing tonight at Sprott Money, speculates on how much the Federal Reserve is prepared to “break” the stock market in the name of fighting inflation before returning with infinite liquidity to drive stock prices up again.

Hemke’s analysis is headlined “Concern for Stonks” and it’s posted at Sprott Money here:

https://www.sprottmoney.com/blog/Concern-For-Stonks-Craig-Hemke-April-12-2022

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

A must read..

Ronan Manly…

Ronan Manly: Sanctions won’t stop Russian-Chinese cooperation on gold

Submitted by admin on Tue, 2022-04-12 23:17Section: Daily Dispatches

11:15p ET Tuesday, April 12, 2022

Dear Friend of GATA and Gold:

Bullion Star’s Ronan Manly writes tonight that cooperation in the gold market between Russia and China is far too serious to be undone by silly talk in political circles in the United States about sanctions to freeze Russian gold out of the world financial system.

Manly’s analysis is headlined “China and Russia in Close Cooperation Aiming for Win-Win in Gold Markets” and it’s posted at Bullion Star here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

4.OTHER GOLD/SILVER COMMENTARIES

5.OTHER COMMODITIES

LITHIUM

With Lithium Prices Up Ninefold, Report Underscores US Dependence On Foreign Minerals

TUESDAY, APR 12, 2022 – 10:45 PM

Authored by Nathan Worcester via The Epoch Times (emphasis ours),

A recent white paper has laid out some of the challenges in supplying minerals for any energy transition from fossil fuels, offering a timely warning for policymakers as the increased demand for electric vehicles (EVs) drives up the costs of materials used in such products.Brine pools from a lithium mine, that belongs to U.S.-based Albemarle Corp, is seen on the Atacama salt flat in the Atacama desert, Chile, on Aug. 16, 2018. (Ivan Alvarado/Reuters)

Notably, the benchmark prices of lithium, lithium carbonate, and lithium hydroxide have rapidly increased in recent months, as detailed at Benchmark Minerals.

Hovering at just $115.80 per ton in September 2020, the benchmark price of lithium has surged to $1045.90 a ton in March 2022. That’s more than a ninefold increase.

Zach Schumacher, a North American metals price expert with Argus Media, told The Epoch Times that the costs of EVs will likely increase as a result. The estimated average transaction price for a new electric vehicle was $56,437 in November 2021, according to Kelley Blue Book.

The prices of other key minerals—including the rare-earth metal neodymium that goes into wind turbines—have also trended sharply upward in recent months and years.

“Lithium is not the only raw material directly correlated to the EV market witnessing higher costs, so parsing out precisely how much of the increased costs for vehicles in the coming months originates from lithium alone could prove fairly difficult. Nickel, stainless steel, semiconductor and labor costs are among other costs that have all also risen compared to levels from recent years,” said Schumacher, who added that the prices of consumer electronics could also rise.

“Increasingly, scholars are questioning the mineral requirements that would be needed to reach either 100 [percent] renewable or clean energy targets,” states the March report, which was authored by Phil Rossetti and George David Banks for the Citizens for Responsible Energy Solutions (CRES) Forum.

The document notes that EVs are six times as mineral intensive as vehicles that use conventional internal combustion engines, citing a report from the International Energy Agency (IEA).

Renewable energy sources are also more mineral intensive than their hydrocarbon-based alternatives. Wind turbines, for example, need roughly nine times as many minerals as natural gas plants, according to the IEA report.

“China is the dominant supplier for multiple critical minerals and is likely to remain so. In the case of minerals it does not supply—such as cobalt—China has near-monopolistic control of refining capacity through its state-owned enterprises,” the CRES Forum’s analysis states.

“Policymakers should also understand the energy security implications of policies that lean heavily on mineral-intensive products for abating greenhouse gas emissions, as scarcity of materials could raise prices as well as create dependency on foreign suppliers that could have an interest in manipulating the market.”

In addition to creating national security risks, the current situation also makes the United States culpable in using forced, or otherwise ethically questionable, labor.

One crucial solar panel input, polysilicon, is largely produced in China’s Xinjiang region, likely through the slave labor of the region’s Uyghur ethnic minority.

Likewise, much of the cobalt in lithium-ion batteries is obtained through child labor from the Democratic Republic of the Congo (DRC).

The CRES Forum report argues that the National Environmental Policy Act (NEPA) impedes domestic mining of minerals for renewable energy, even more than it impedes hydrocarbon production.

“Forty-two percent of DOE NEPA environmental assessments and environmental impact statements [are] for clean energy, transmission, or conservation efforts compared with 15 percent for fossil fuel,” it states, referencing an R Street analysis from one of the report’s co-authors, Phillip Rossetti.

A major proposed project along these lines, the Thacker Pass Lithium Mine in Humboldt County, Nevada, received its Record of Decision under NEPA in January 2021. Nevada’s Division of Environmental Protection issued mining, water, and air permits to it earlier this year.

Yet, the mine has continued to generate controversy, with Shoshone Paiute Gary McKinney writing in the Reno Gazette Journal that “our ancestors’ burial site is no place for a mine.”

The Canadian developer of Thacker Pass, Lithium Americas, has made major deals with the Chinese firm Ganfeng Lithium, including through joint ownership of the Cauchari-Olaroz brine lithium carbonate project in Argentina.

Lithium Americas’ website indicates that Ganfeng owns 46.7 percent of the project while Lithium Americas owns 44.8 percent. The remaining 8.5 percent is owned by Argentina’s state-run Jujuy Energía y Minería Sociedad del Estado (JEMSE).

Even if new domestic mines such as Thacker Pass go online, CRES Forum’s meta-analysis of three studies on the energy transition suggests that demand could outpace proven reserves of multiple key minerals, including cobalt, lithium, nickel, chromium, and zinc.

“In short, the potential mining requirements for a complete clean energy transition with existing technology is so large that it is not clear if it is economically viable to extract enough minerals to meet the needs modeled in those studies,” the report states.

In February, President Joe Biden drew attention to a range of new investments aimed at reducing the United States’ reliance on China for lithium, rare earths, cobalt, and other critical minerals.

This includes $35 million from the Department of Defense for a heavy rare earth element separation facility operated by MP Materials, owner of the country’s only rare-earth mine in Mountain Pass, California.

MP Materials is partly owned by a Chinese firm, Shenghe Resources.

“As proposed by Chinese government, and characteristic in Chinese rare earth industry, Shenghe Resources designed its equity structure on mixed ownership,” the website for the firm states, indicating that the company is partly owned by the state.

The Epoch Times has reached out to Shenghe Resources for comment.

Reuters reported in late March that Sen. Lisa Murkowski (R-Alaska) has described herself as “worried” about the Chinese stake in MP Materials.

The investments announced in February also include a $140 million Department of Energy (DoE) project to obtain critical minerals from mine waste, coal ash, and similar resources.

The CRES Forum report suggests that the challenges it describes could be mitigated by technological breakthroughs, including better approaches to carbon capture and the development of low-carbon fuels for conventional, non-electric vehicles.

It also urges the United States to sanction companies or countries that use unethical labor, arguing that such moves must be made quickly, before the country is too reliant on such minerals.

“As a major consuming market, the United States is best positioned to effect change by refusing market access to unethical suppliers,” it states.

end

COMMODITIES IN GENERAL

6.CRYPTOCURRENCIES

7. GOLD/ TRADING TODAY

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings WEDNESDAY morning 7:30 AM

ONSHORE YUAN: CLOSED UP 6.3665

OFFSHORE YUAN: 6.3772

HANG SANG CLOSED UP 55.24 PTS OR 0.26%

2. Nikkei closed UP 508.51 PTS OR 1.93%

3. Europe stocks ALL MIXED

USA dollar INDEX UP TO 100.33/Euro RISES TO 1.0839

3b Japan 10 YR bond yield: FALLS TO. +.234/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 125.70/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 102.09 and Brent: 106.21

3f Gold UP /JAPANESE Yen DOWN CHINESE YUAN: UP -SHORE CLOSED UP// OFF- SHORE UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.0.800%/Italian 10 Yr bond yield FALLS to 2.40% /SPAIN 10 YR BOND YIELD FALLS TO 1.72%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 1.60: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield RISES TO : 2.81

3k Gold at $1979.70 silver at: 25.70 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3l USA vs Russian rouble;// Russian rouble DOWN 1 /3 roubles/dollar; ROUBLE AT 80.00

3m oil into the 102 dollar handle for WTI and 106 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 125.70 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning .9336– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0119 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 2.725 DOWN 0 BASIS PTS

USA 30 YR BOND YIELD: 2.828 DOWN 10BASIS PTS

USA DOLLAR VS TURKISH LIRA: 14.59

Futures Rise As Earnings Season Begins

WEDNESDAY, APR 13, 2022 – 06:57 AM

US index futures bounced, with Nasdaq 100 contracts halting a three-day drop, as investor attention turned to the start of corporate earnings season, which BofA dubbed the “Last big beat for a while” amid concerns over high inflation and slowing growth. Contracts on the Nasdaq 100 were up 0.4% as of 630 a.m. in New York, signaling a pause in the rout that wiped $1.6 trillion from the market value of technology behemoths in just over a week. S&P 500 futures and Dow futures gained 0.4%, with Asian stocks also rising even as Europe’s Stoxx 600 Index dropped; the selloff in U.S. Treasuries also eased with the 10Y yield flat at 2.72% while the US Dollar resumed its advance and the yen fell to a 20-year low as the growing gap between rising U.S. bond yields and perpetually low ones in Japan continued to pressure the currency. Oil rose after Russia vowed to continue the war in Ukraine and China partially eased Covid curbs. Bitcoin continued to trade on either side of $40K.

A quick look around the world: U.K. inflation surged to a 30-year high, surging 7% above expectations of 6.7%, before the Bank of England’s next decision in May, while New Zealand’s central bank delivered a surprise 50bps rate hike (exp 25bps) its biggest interest-rate increase in 22 years. Meanwhile, markets continued to digest Tuesday’s U.S. inflation data which was viewed by many as a peak in CPI, which prompted traders to pare back expectations on how aggressively the Federal Reserve will raise interest rates. St. Louis Fed President James Bullard said U.S. monetary policy needs to be tightened to a point that it curtails economic growth or policy makers will end up risking their credibility (translation: he wants stocks 30% lower). He supports a half percentage point increase at the Fed’s policy meeting in May and says the rate should move up “sharply” after that.

On the geopolitical front, the presidents of Poland and the three Baltic states are heading to Kyiv in a show of support that follows the visits of other leaders to the Ukrainian capital, including from Boris Johnson and European Union chiefs. The Biden administration is preparing a new military assistance package for Ukraine. Here are some of the latest news out of Ukraine:

- Ukrainian President Zelensky proposed swapping pro-Russian politician Medvedchuk for Ukrainian prisoners of war, according to Reuters.

- Ukrainian Deputy PM says it is not possible to open humanitarian corridors on Wednesday; occupying forces have violated the ceasefire, via Reuters.

- Sweden’s largest party Social Democrats favour applying to NATO at the June meeting in Spain, according to SvD.

- US President Biden said it will be up to lawyers to determine if Russia’s actions in Ukraine qualify as genocide but added it seems like genocide to him and that the evidence is mounting, according to Reuters.

- US President Biden’s administration is expected to announce at least USD 750mln in additional weapons for Ukraine and deliberations continue on a mix of weapons, which could evolve, according to Reuters.

- Ukrainian President Zelensky said it is not possible to draw 100% firm conclusions about whether Russia used chemical weapons in Mariupol and that it is not possible to conduct a full investigation in a besieged city, according to Reuters.

- Chechen leader Kadyrov said over 1,000 Ukrainian marines surrendered in Mariupol, according to Sputnik.

US equities have been roiled again this month by the double whammy of soaring bond yields and concerns around a looming global recession. After data on Tuesday showed a smaller-than-expected increase in core inflation last month, focus this week will be on quarterly earnings starting with the big banks, which generally offer a window on the economy since they touch on everything from mortgages to general consumer behavior.

“Despite the increased price pressure, analysts are still expecting profit margins of the S&P 500 to reach new all-time highs by the second quarter, which seems optimistic in our view,” said Mathieu Racheter, head of equity strategy at Julius Baer. “We see a higher risks of negative earnings revision ahead, driven by the cyclicals sectors. We continue to recommend investors to remain defensively positioned within their equities allocation.”

Among notable pre-market moves in the US, Sierra Oncology shares jumped 37% to $54.30 after GlaxoSmithKline agreed to buy the maker of therapies for rare forms of cancer for $55/shares in cash, or about $1.9 billion. Genius Group shares, on the other hand, tumbled 29% after a whopping 408% gain on their first day of trading yesterday. JPMorgan was little changed ahead of its first-quarter results due later in the morning. Here are some of the biggest U.S. movers today:

- Antares Pharma (ATRS US) surges 48% in premarket trading after Dow Jones reported that Halozyme Therapeutics (HALO US) is close to buying the maker of needle-free systems for $5.60 per share in cash, citing people familiar with the matter.

- The departure of PayPal (PYPL US) finance chief John Rainey to become CFO at Walmart (WMT US) was less concerning to some analysts than the absence of a guidance update with the announcement. PayPal stock falls 1.5% in premarket, Walmart +0.5%.

- Hillman Solutions (HLMN US) fell 8.9% postmarket Tuesday after holders offered 10m shares.

Investors are now turning their attention to the earnings season, while awaiting the European Central Bank’s meeting on Thursday. Money managers are increasingly hedging the risk of stagflation, especially in Europe, amid concerns that high inflation and slowing growth will end up squeezing company profits.

“It appears that the market is swinging quickly to try and price ‘peak inflation,’” Jeffrey Halley, senior market analyst at Oanda, wrote in a note. “Naturally, ‘peak inflation’ should be a reason to pile back into equities. However, it just isn’t that simple. The environment for equities remains challenging.”

“We’re hopeful that this is where it’s going to peak,” Ann Miletti, head of active equity at Allspring Global Investments, said on Bloomberg Television, referring to U.S. inflation. But she added that markets continue to face a wall of worry, ranging from rising rates to the impact of China’s Covid lockdowns.

In Europe, the Stoxx 600 Index was down 0.4%, with travel and leisure sector leading declines as energy, miners and media are the strongest performing sectors. FTSE 100 outperforms, adding 0.3%; DAX lags, dropping 0.3%. LVMH erased early gains as it warned of a negative impact on demand because of lockdowns in China. Here are some of the biggest European movers today:

- Telecom Italia shares rise as much as 4.7% after a local press report that Apax and France’s Iliad are preparing a joint offer for its ConsumerCo business.

- Ted Baker shares rise as much as 5.7% after the high-street retailer said Sycamore will participate in formal sale process.

- Oxford Instruments gains as much as 9.4% after the firm said it expects its financial performance to be marginally ahead of expectations.

- Tesco shares slump as much as 7% after the U.K. grocer said profit may show little change or decline slightly this year amid the U.K.’s cost of living crisis. Analysts noted Tesco’s focus on providing customers with “compelling” value.

- Other U.K. grocery stocks including Ocado, Sainsbury and Marks & Spencer also fell

- Adidas shares declined as much as 4.1% after being downgraded to reduce from add and PT cut to Street-low EU190 at Baader Helvea based on rising headwinds and a “more cloudy” outlook for rest of the year.

- LVMH shares fall as much as 1.3%, reversing earlier gains, as worry over a Covid-19 resurgence in the key market of China remained at the forefront of investors mind even as the luxury conglomerate beat first-quarter expectations.

- Barry Callebaut shares fall as much as 5.4% amid worries the Swiss chocolate maker may be further affected by the war in Ukraine and its far- reaching consequences. The company said it’s taking an impairment for its financial assets in Russia.

Earlier in the session, Asian equities rose for the first time in three days as U.S. Treasury yields retreated from multi-year highs, easing concerns over potential damage to corporate earnings. The MSCI Asia Pacific Index climbed as much as 1.2%, rebounding from its lowest level since March 16. Tech hardware stocks drove gains after the 10-year Treasury yield slipped overnight following a smaller-than-expected jump in a key U.S. inflation gauge. TSMC was among the biggest contributors to gains in Asia ahead of its earnings release Thursday.

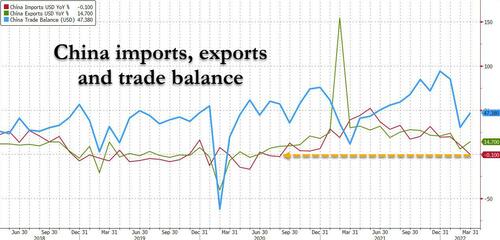

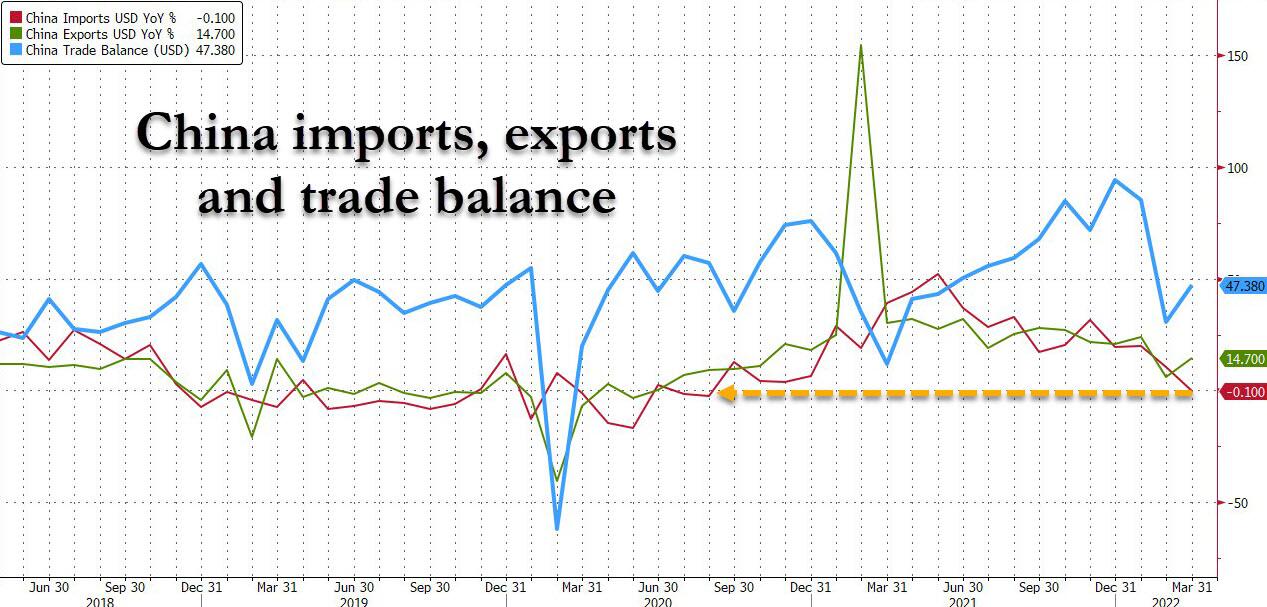

“A pause in the yield rally at the current level may provide a breather for the equities market in the coming days, as attention will be shifted to the upcoming earnings season to drive sentiment,” said Jun Rong Yeap, a strategist at IG Asia. Benchmarks in Taiwan, Japan and South Korea led gains around the region. New Zealand’s main index fell after an unexpectedly large 50-basis-point hike by its central bank –its biggest in 22 years. Chinese stocks declined as a top virus expert stressed the importance of the nation’s dynamic zero strategy and data showed Chinese imports unexpectedly fell. China’s Imports Drop, Export Growth Slows on Covid Lockdowns Amid news of looser quarantines in some Chinese cities, investors are keenly awaiting formal relaxation of Beijing’s strict virus policies as its growth slowdown weighs on the region. Meanwhile, soaring prices in the U.S. and parts of Europe have finally reached Asia, deepening concerns about rising input costs for businesses

Japanese equities gained, rebounding after two days of losses, following a smaller-than-expected rise in U.S. inflation and a drop in Treasury yields. Electronics and auto makers were the biggest boosts to the Topix, which rose 1.4%. Fast Retailing and Tokyo Electron were the biggest contributors to a 1.9% advance in the Nikkei 225. The yen extended losses against the dollar to a ninth day. The U.S. consumer price index increased 8.5% in March compared with a year earlier, less than economists expected. The 10-year Treasury yield slipped six basis points Tuesday following the inflation data. “Markets had been pricing in substantial negative impacts from higher U.S. interest and lockdowns in China, so stocks are rebounding somewhat today,” said Tomo Kinoshita, global market strategist at Invesco Asset Management. “There was a risk that if the U.S. CPI came in higher than market expectations that the Fed would turn more hawkish, but that didn’t happen.”

In FX, the Bloomberg dollar spot index is near flat. CHF and EUR are the strongest performers in G-10 FX, NZD and JPY underperform. Yen drops to a 20-year low against the U.S. dollar, trading now at 126.15.

In fixed income, bonds bounced ahead of Tuesday’s new lows, but recovery remains weak rather than firm as Bunds hover above 155.00, Gilts just under 119.00 and T-note midway between 119-31/120-17 extremes. Lacklustre 10-year Bund auction in keeping with T-note sale last night, and with long bond supply still to come. Italy sees decent demand for multi-tranche offerings after recent heavier concession.

In commodities, crude futures advanced with Brent extending on its torrid Tuesday gains and rising 2% back over $106. The International Energy Agency halved its estimate for a decline in Russian crude oil output for April as the nation has been able to find new customers even with global restrictions and self-sanctioning by traditional buyers. But top oil trader Vitol Group said it intends to completely stop trading Russia-origin crude and products by the end of this year. Most base metals trade in the green; LME zinc rises 2.8%, outperforming peers. LME copper lags, dropping 0.1%. Spot gold rises roughly $9 to trade at $1,976/oz. Spot silver gains 1.2% to ~$26.

Looking at the day ahead now, data releases include US PPI for March, UK CPI for March and Italy’s industrial production for February. From central banks, we’ve got a policy decision from the Bank of Canada, as well as a speech from Bank of Japan Governor Kuroda. Finally, today’s earnings releases include JPMorgan Chase, BlackRock, Tesco and Delta Air Lines.

Market Snapshot

- S&P 500 futures up 0.6% to 4,418.25

- MXAP up 0.7% to 173.79

- MXAPJ up 0.7% to 577.71

- Nikkei up 1.9% to 26,843.49

- Topix up 1.4% to 1,890.06

- Hang Seng Index up 0.3% to 21,374.37

- Shanghai Composite down 0.8% to 3,186.82

- Sensex down 0.3% to 58,425.03

- Australia S&P/ASX 200 up 0.3% to 7,479.02

- Kospi up 1.9% to 2,716.49

- STOXX Europe 600 little changed at 456.72

- German 10Y yield little changed at 0.84%

- Euro little changed at $1.0832

- Brent Futures up 0.2% to $104.89/bbl

- Gold spot up 0.4% to $1,975.13

- U.S. Dollar Index little changed at 100.37

Top Overnight News from Bloomberg

- Federal Reserve Bank of St. Louis President James Bullard said U.S. monetary policy needs to be tightened to a point that it curtails economic growth or policy makers will end up risking their credibility

- The Biden administration is preparing a military assistance package of roughly $750 million for Ukraine in its battles against Russian invaders, people familiar with the matter said Tuesday night

- An immediate interruption in Russian energy supplies over the war in Ukraine could jeopardize 220 billion euros ($240 billion) of German output over the next two years, a report warned

- The yen’s drop to a two-decade low versus the dollar sets the tone in the options space, while overnight volatility in the euro rallies ahead of the ECB decision Thursday

- It’s the next big market call that could enrich traders across Wall Street: The raging global energy crisis and ever-more hawkish central banks knock key economies into 1970s- style stagflation

- French President Emmanuel Macron led his rival Marine Le Pen 53.2% to 46.8% ahead of the run-off presidential election set for April 24, according to a polling average calculated by Bloomberg on April 13. The gap between them has narrowed from the 8 percentage points recorded on April 11

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks mostly shrugged off the weak lead from the US and rebounded from a two-day losing streak. ASX 200 was kept afloat by the commodity-related sectors including energy after WTI crude futures climbed back above USD 100/bbl landmark and with Australia’s government providing funding for domestic refiners. Nikkei 225 outperformed currency weakness and with the index unfazed by disappointing Machinery Orders. Hang Seng and Shanghai Comp lagged on COVID woes despite China testing an easing of quarantine rules in eight cities, as infections continued to spread with a fresh record of daily cases in Shanghai, while Sunac’s missed coupon payment, further inclusions to the US HFCAA list and mixed trade data added to the cautious mood.

Top Asian News

- Yen Falls to 20-Year Low as Policy, Yield Divergence Continues

- Japan Finance Minister Says Sudden FX Moves Problematic: Kyodo

- SMBC Nikko Ex-Deputy President Indicted Over Block Offers

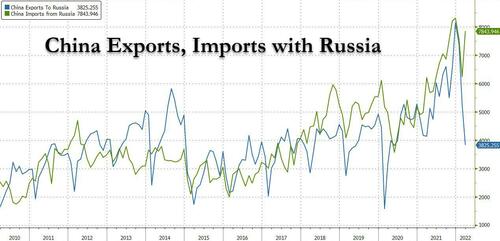

- China’s Exports to Russia Slump After Ukraine Invasion

European bourses are pressured across the board, Euro Stoxx 50 -0.7%, in what has been a somewhat choppy European morning with limited fresh macro drivers emerging. Sectors are similar to their initial cash open performance, as Energy and Basic Resources outperform while Travel, Retail and Personal Goods lag. US futures are firmer across the board, ES +0.3%, and while they have been directionally moving with Europe magnitudes are more limited; support following yesterday’s CPI but ahead of PPI and JPM earnings. BlackRock Inc (BLK) Q1 2022 (USD): EPS 9.52 (exp. 8.95), Revenue 4.699bln (exp. 4.74bln). +0.3% in the premarket.

Top European News

- Deutsche Telekom Edges Closer to T-Mobile Control With New Stake

- U.K. Inflation Jumps More Than Expected to 30-Year High of 7%

- European Gas Rises With Lower Flows Via Ukraine, Norway Outages

- U.K. Homebuilders Commit $2.6 Billion for Fire Safety Repairs

FX:

- Kiwi knee jerks higher after bigger than generally expected 50 bp RBNZ hike before retreating abruptly on reflection of unchanged OCR outlook; NZD/USD sub-0.6800 vs peak just over big figure above.

- Yen flogged yet again as Japanese officials continue to fret about speed rather than size of moves and core machinery orders miss consensus; USD/JPY knocks down barriers at 126.00 to reach 126.31 and breach 2015 peak.

- DXY extends advance above 100.000 before waning ahead of May 2020 peak just over 100.500.

- Aussie retains 0.7400+ status vs Greenback before jobs data, but with assistance from sharp reversal in AUD /NZD cross flows – from circa 1.0833 to 1.0950.

- Euro keeps its head above 2022 low against Dollar, narrowly, and Pound rebounds after minor boost from strong UK inflation prints, EUR/USD down to 1.0811 or so vs 1.0806, Cable revisits 1.3000 vs 1.2972 at worst.

- Loonie immersed in technical levels awaiting BoC and guidance to accompany a widely forecast half point rate rise; USD/CAD near 1.2650 and flanked by 200, 100 and 50 DMAs.

Fixed Income:

- Bonds bounce ahead of Tuesday’s new lows, but recovery remains feline rather than firm as Bunds hover above 155.00, Gilts just under 119.00 and T-note midway between 119-31/120-17 extremes.

- Lacklustre 10-year Bund auction in keeping with T-note sale last night, and with long bond supply still to come. Italy sees decent demand for multi-tranche offerings after recent heavier concession.

Commodities:

- WTI and are firmer in a continuation of the consolidation from the upside seen in yesterday’s session amid Brent geopolitical tensions.

- Most recently, the benchmarks have eclipsed a circa. USD 2/bbl range that had been holding throughout the morning; current bests, USD 102.13/bbl and USD 106.45/bbl respectively.

- US Private Energy Inventory Data (bbls): Crude +7.8mln (exp. +0.9mln), Cushing +0.4mln, Gasoline -5.1mln (exp. -0.4mln), Distillate -5.0mln (exp. -0.5mln).

- IEA OMR: Lowers 2022 global oil demand estimate by 260k BPD on COVID in China and lower OECD demand.

- February global stocks 714mln/bbl below the end-2020 level, OECD accounts for 70% of the decline. Russian oil supply is expected to fall by 1.5mln BPD in April and by around 3mln BPD from May.

- CNOOC (883 HK) is said to be considering exiting operations in Britain, US and Canada amid tensions with the West, according to Reuters sources.

- Spot gold and are bid this morning, though the yellow metal is still shy of yesterday’s USD 1978.21/oz silver peak.

- LME Zinc outperforms piggybacking the performance of its Shanghai peer overnight

US Event Calendar

- 07:00: April MBA Mortgage Applications, prior -6.3%

- 08:30: March PPI Final Demand YoY, est. 10.6%, prior 10.0%; 08:30: PPI Final Demand MoM, est. 1.1%, prior 0.8%

- 08:30: March PPI Ex Food and Energy YoY, est. 8.4%, prior 8.4%; MoM, est. 0.5%, prior 0.2%

- 08:30: March PPI Ex Food, Energy, Trade YoY, est. 6.5%, prior 6.6%; MoM, est. 0.5%, prior 0.2%

DB’s Henry Allen concludes the overnight wrap

After a succession of major bond selloffs this month, yesterday marked the first time so far in April that US Treasuries put in a positive performance. Given the US CPI report showed inflation hitting its highest rate since 1981 in March, with a year-on-year rate of +8.5%, that might seem counter-intuitive. But the monthly print of +1.2% was already expected by the consensus, even if it was the strongest since September 2005, whilst there was also a downside surprise in core inflation, which came in at +0.3% over the month (vs. +0.5% expected). In turn, that saw investors take out some of the expected monetary tightening they’d been pricing over the rest of the year, with the futures-implied policy rate by December’s meeting down by -10bps relative to the previous day.

Looking at some of the details, higher gasoline prices were responsible for more than half of the headline monthly increase in CPI, having gone up by +18.3% in March. That’s their biggest monthly increase since June 2009, and follows the major spike in oil prices following Russia’s invasion of Ukraine. On the other hand, used cars and trucks came down -3.8% over the month, which is their largest monthly decline since May 1969. In terms of housing inflation, rent of primary residence fell back to +0.43% (vs. +0.57% in Feb), though owners’ equivalent rent came in at +0.43%, in line with the narrow band of +0.41-0.45% in which it’s been rising since September.

Against that backdrop, yields on 10yr Treasuries came down -5.9bps to 2.721%, marking their first daily decline so far this month, with trademark intraday volatility, as 10yrs were as much as +5.3bps higher in early morning trading, before trading -10.8bps lower during the New York lunch hour. 2yr yields had a larger on net decline (-9.2bps) that saw the 2s10s curve steepen up to 31.2bps, which is the steepest its been since the March FOMC meeting when the Fed embarked on their new hiking cycle. And although the total number of hikes priced for the year as a whole came down somewhat, the odds of a 50bp move at the next meeting in May actually ticked up to 93.5%, the highest to date. Overnight though, the 10yr yield has pared back some of its declines yesterday, moving up +2.3bps to 2.744%.

While the CPI release may have triggered a bond rally, Fed communications remained just as hawkish, and yesterday we heard more from Governor Brainard, who is awaiting confirmation to her new post as Vice Chair. She expressed a preference to get the policy rate to neutral by the end of this year, echoing similar comments from Fed officials earlier in the week. She still thinks the Fed has room to engineer a soft landing and sustain the current economic expansion due to the historic strength of the labour market. Separately, in an interview released overnight with the FT, St Louis Fed President Bullard (who voted for a 50bps hike in March) said that it was a “fantasy” that the Fed could bring inflation down without going above neutral.

Even as investors priced in a slightly shallower pace of Fed rate hikes over the coming year, US equities still managed to rollover after trading in the green for most of the day, with the S&P 500 down -0.34%. Financials (-1.07%) led the way lower with the decline in yields ahead of financials earnings kicking off today, while energy (+1.72%) was the clear outperformer on rebounding crude prices. Small-cap stocks put in a decent performance, with the Russell 2000 (+0.33%) ending a run of 5 consecutive declines. European equities also traded lower as well, with the STOXX 600 down -0.35%, along with other indices including the DAX (-0.48%), the CAC 40 (-0.28%) and the FTSE 100 (-0.55%).

Turning to commodities, oil prices moved sharply higher yesterday, with Brent Crude (+6.26%) closing above $104/bbl for the first time in over a week. That came as Russian President Putin said that talk with Ukraine were “at a dead end”, and other haven assets including gold (+0.68%) also moved higher on the day. Over in the US meanwhile, President Biden accused Russia of “genocide”, standing by his comments and saying that “it has become clearer and clearer that Putin is just trying to wipe out the idea of being able to be Ukrainian”.

Those further gains in oil prices meant that European inflation expectations rose to fresh highs, with the 10yr German breakeven up to 2.90%, its highest level yet in data going back to 2009, whilst the 10yr Italian breakeven rose to 2.69%, a level not seen since 2008. Importantly, measures of long-run inflation expectations, ostensibly beyond the influence of the current shock, have increased as well, with the 5y5y forward inflation swap for the Euro Area rising to +1.6bps to 2.38% yesterday, marking its highest level since 2013.

In spite of those rises in European inflation expectations, sovereign bond yields in Europe moved lower along with US Treasuries, paring back an initial rise that saw the 10yr bund yield move to its highest intraday level since 2015, at 0.87%. By the close of day however, yields on 10yr bunds (-2.6bps), OATs (-1.9bps) and BTPs (-5.7bps) had all moved lower.

Overnight in Asia, equity markets have bucked the trend seen in the US and Europe, with the Nikkei (+1.60%), the Kospi (+1.40%) and the Hang Seng (+0.29%) all moving higher. However, the Shanghai Composite (-0.44%) and CSI (-0.51%) are both lagging as the Covid-19 outbreak in China continues to weigh on investor sentiment. Looking forward, stock futures in the US are pointing to a decent start today, with contracts on the S&P 500 (+0.51%) and Nasdaq 100 (+0.69%) both higher. On the monetary policy front, we also heard from the Reserve Bank of New Zealand overnight, who hiked their official cash rate by +50bps to 1.50% as they seeks to tame inflation. This is the fourth consecutive interest rate hike by the central bank and its biggest hike since 2000.

Turning to the French election, we’re now just 11 days away from the second round between President Macron and Marine Le Pen, and the polls continued to point to a fairly tight race, albeit with Macron in the lead. In terms of yesterday’s polls, Macron was ahead by 54-46 in Opinionway (down from 55-45 the previous day), whilst Ifop’s 52.5-47.5 margin was unchanged from the previous day. French assets performed basically in line with their European counterparts yesterday, with the spread of French 10yr yields over bunds moving up by just +0.6bps to 50.8bps.

Running through yesterday’s other data, the UK employment report was somewhat softer than expected, with payrolled employees up by just +35k in March (vs. +125k expected). Nevertheless, the unemployment rate did fall back to the pre-pandemic low of 3.8% in the three months to February, in line with expectations. Elsewhere, Germany’s ZEW survey saw further declines in April, with the current situation reading down to an 11-month low of -30.8 (vs. -35.0 expected), and the expectations component fell to a 2-year low of -41.0 (vs. -48.5 expected), even if both were somewhat better than expected. Finally in the US, the NFIB’s small business optimism index fell to a 2-year low of 93.2 in March (vs. 95.0 expected).

To the day ahead now, and data releases include US PPI for March, UK CPI for March and Italy’s industrial production for February. From central banks, we’ve got a policy decision from the Bank of Canada, as well as a speech from Bank of Japan Governor Kuroda. Finally, today’s earnings releases include JPMorgan Chase, BlackRock, Tesco and Delta Air Lines.

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING// TUESDAY NIGHT

SHANGHAI CLOSED DOWN 26.51 PTS OR 0.82% //Hang Sang CLOSED UP 55.24 PTS OR 0.26% /The Nikkei closed UP 508.51 PTS OR 1.83% //Australia’s all ordinaires CLOSED UP .47% /Chinese yuan (ONSHORE) closed UP 6.3665 /Oil UP TO 97.25 dollars per barrel for WTI and DOWN TO 102.75 for Brent. Stocks in Europe OPENED ALL RED EXCEPT SPAIN // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.3665 OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.3772: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER//

3 a./NORTH KOREA/ SOUTH KOREA

///NORTH KOREA

END

3B JAPAN

end

3c CHINA

CHINA/COVID/SHANGHAI LOCKDOWNS//LAST NIGHT

USA pulls its consulate staff from Shanghai with Beijing easing lockdowns at bit

(zerohedge)

US Pulls Consulate Staff From Shanghai As Beijing Eases Lockdown

TUESDAY, APR 12, 2022 – 06:25 PM

Despite continuing to report record numbers of daily cases (more than 25K on Monday and another 22K+ on Tuesday), Shanghai started easing its lockdown on Monday, while the American State Department starting pulling all non-essential personnel from its consulate in the city of more than 25 million – a decision that greatly angered the Chinese government.

City officials announced on Monday that they would be easing the lockdown after a tremendous public backlash. From now on, they would be grouping residential units into three risk categories as a step towards allowing “appropriate activity” for those who live in neighborhoods with no positive cases during a two-week stretch.

Authorities insisted they remained committed to a “dynamic zero” strategy – that is, a modified version of the “zero COVID” policy that has been such a spectacular failure in the country, which is presently struggling with its worst COVID outbreak since Wuhan.

Across Shanghai, anger has risen over food shortages, the inability to access medical care and even the killing of pets by COVID workers. But the pullout of diplomats from Shanghai comes as relations between the US and China have soured as the West has pressured China to do more to restrain Russia in its war in Ukraine.

“Many Americans in Shanghai were dismayed to hear of the previous consulate staff departures given the current situation,” said Josef Gregory Mahoney, a professor of politics and international relations at East China Normal University in Shanghai, referring to an earlier announcement that staff could leave.

“This new order will certainly increase the impression that the situation is worsening despite indications to the contrary, or that this is political posturing on behalf of the U.S., or that consulate staff – who are already rather privileged – are unable to stomach the inconveniences that others are required to endure.”

The latest US State Department order comes days after Washington said all non-emergency employees and their family members from the consulate in Shanghai were allowed to leave. The department also told Americans to reconsider travel to China due to what it calls an “arbitrary enforcement” of virus restrictions.

“Our change in posture reflects our assessment that it is best for our employees and their families to be reduced in number and our operations to be scaled down as we deal with the changing circumstances on the ground,” an Embassy spokesperson said in a statement Tuesday, noting that staffers and their relatives would leave on commercial flights.

“The United States has no higher priority than the safety and security of US citizens overseas, including Mission China’s personnel and their families,” the spokesperson added.

CCP authorities weren’t exactly thrilled about America’s decision to withdraw.

Zhao Lijian, a spokesman for the Foreign Ministry, said they deplored the way the US has politicized the departure of staff from the consulate.