april14, 2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD; $1971.80 DOWN $8.95

SILVER: $25.53 DOWN $0.25

ACCESS MARKET: GOLD $1972.50

SILVER: $25.60

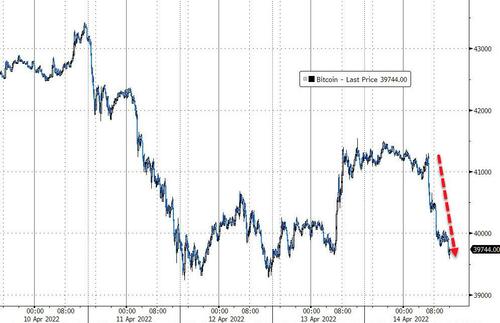

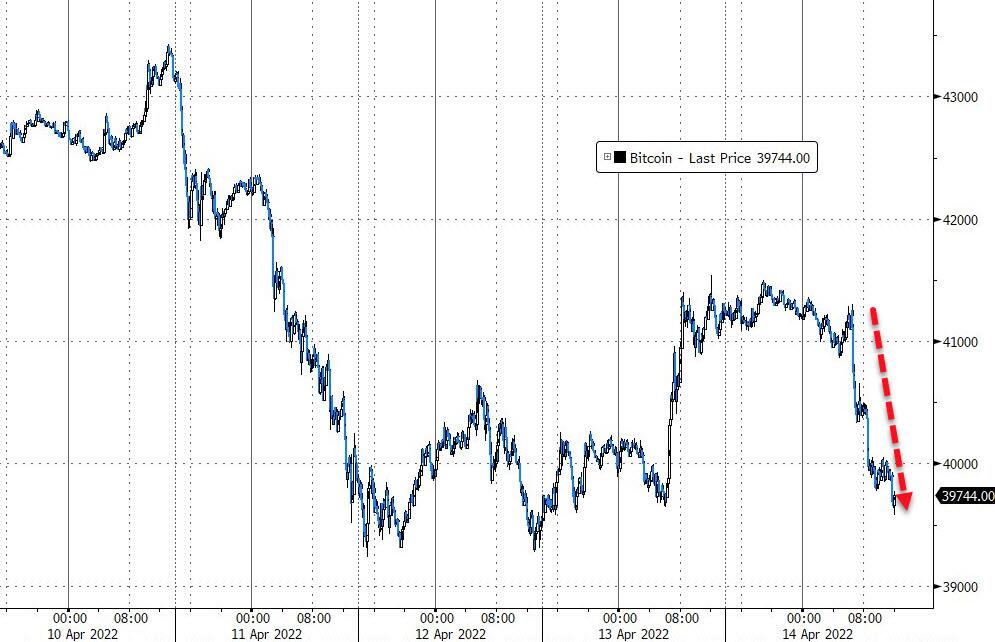

Bitcoin morning price: $41,046 DOWN 263

Bitcoin: afternoon price: $39,743 DOWN 1566

Platinum price: closing UP $3.50 to $992.95

Palladium price; closing UP 31.10 at $2350.70

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

comex notices/

: JPMorgan stopped/total issued 204/628

EXCHANGE: COMEX

CONTRACT: APRIL 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,981.000000000 USD

INTENT DATE: 04/13/2022 DELIVERY DATE: 04/18/2022

FIRM ORG FIRM NAME ISSUED STOPPED

072 C GOLDMAN 333 24

132 C SG AMERICAS 102

363 H WELLS FARGO SEC 14

365 C ED&F MAN CAPITA 2

435 H SCOTIA CAPITAL 12

624 H BOFA SECURITIES 39

657 C MORGAN STANLEY 36

661 C JP MORGAN 292 204

685 C RJ OBRIEN 2

709 C BARCLAYS 87

732 C RBC CAP MARKETS 1

737 C ADVANTAGE 1 9

880 H CITIGROUP 83

905 C ADM 15

TOTAL: 628 628

MONTH TO DATE: 25,127

NUMBER OF NOTICES FILED TODAY FOR APRIL. CONTRACT 628 NOTICE(S) FOR 62,800 OZ (1.9533 TONNES)

total notices so far: 25,127 contracts for 2,512,700 oz (78.155 tonnes)

SILVER NOTICES:

6 NOTICE(S) FILED TODAY FOR 30,000 OZ/

total number of notices filed so far this month 1086 : for 5,430,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

END

GLD

WITH GOLD DOWN $8.95

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

A HUGE CHANGE IN GOLD INVENTORY AT THE GLD A HUGE DEPOSIT OF 11.32 TONNES FROM THE GLD//

INVENTORY RESTS AT 1104.42 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 25 CENTS

AT THE SLV// A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WHOPPING DEPOSIT OF 4.355 MILLION OF INTO THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 569.676 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A GIGANTIC SIZED 6416 CONTRACTS TO 165,229 AND CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE HUGE GAIN IN OI WAS ACCOMPLISHED WITH OUR $0.27 GAIN IN SILVER PRICING AT THE COMEX ON WEDNESDAY. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.27) AND WERE UNSUCCESSFUL IN KNOCKING OUT ANY SILVER LONGS AS WE HAD A HUMONGOUS GAIN OF 8090 CONTRACTS ON OUR TWO EXCHANGES

WE MUST HAVE HAD:

I) HUGE BANKER SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A STRONG INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 4.305 MILLION OZ FOLLOWED BY TODAY’S QUEUE. JUMP OF 450,000 OZ//NEW STANDING: 6.010 MILLION OZ// V) HUGE SIZED COMEX OI GAIN/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS : —-624 (which is huge)

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS APRIL. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF APRIL:

TOTAL CONTACTS for 10 days, total 8266 contracts: 41.330 million oz OR 4.13MILLION OZ PER DAY. (827 CONTRACTS PER DAY)

TOTAL NO OF OZ UNDERGOING EFP TO LONDON 8266 CONTRACTS X 5,000 PER CONTRACT:

EQUATES TO: 41,330 MILLION OZ

.

LAST 11 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

APRIL: 41.330 MILLION OZ (LOOKS LIKE OUR BANKERS ARE NOW LOATHE TO ISSUE EFP’S)

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 6416 WITH OUR $0.27 GAIN IN SILVER PRICING AT THE COMEX// WEDNESDAY THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE CONTRACTS: 1050 CONTRACTS ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A HUGE INITIAL SILVER OZ STANDING FOR MAR. OF 4.305 MILLION OZ FOLLOWED BY TODAY’S 450,000 OZ QUEUE JUMP//NEW STANDING: 6.010MILLION OZ/// .. WE HAD AN HUGE SIZED GAIN 7466 OI CONTRACTS ON THE TWO EXCHANGES FOR 37.33 MILLION OZ WITH THE GAIN IN PRICE.

WE HAD 6 NOTICES FILED TODAY FOR 30,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A SMALL SIZED 1391 CONTRACTS TO 579,030 AND CLOSER TO NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: -191 CONTRACTS.

THE BIS HAS ABANDONED THE GOLD COMEX TRADING!!!

.

THE SMALL SIZED INCREASE IN COMEX OI CAME WITH OUR STRONG GAIN IN PRICE OF $8.80//COMEX GOLD TRADING/WEDNESDAY /.AS IN SILVER WE MUST HAD HUGE BANKER/ALGO SHORT COVERING ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR APRIL AT 78.33 TONNES ON FIRST DAY NOTICE

YET ALL OF..THIS HAPPENED WITH OUR GAIN IN PRICE OF $8.80 WITH RESPECT TO MONDAY’S TRADING

WE HAD A FAIR SIZED GAIN OF 3365 OI CONTRACTS (10.466 PAPER TONNES) ON OUR TWO EXCHANGES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 1975 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 579,030.

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 3365, WITH 1391 CONTRACTS INCREASED AT THE COMEX AND 1975 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 3556 CONTRACTS OR 11.060 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1975) ACCOMPANYING THE SMALL SIZED GAIN IN COMEX OI (1581,): TOTAL GAIN IN THE TWO EXCHANGES 3556 CONTRACTS. WE NO DOUBT HAD 1) HUGE BANKER SHORT COVERING ,2.) HUGE INITIAL STANDING AT THE GOLD COMEX FOR APRIL. AT 78.33 TONNES FOLLOWED BY TODAY’S 12,300 OZ QUEUE JUMP //NEW STANDING 81.608 TONNES/// 3) ZERO LONG LIQUIDATION ///. ,4) SMALL SIZED COMEX OI. GAIN 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

APRIL

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL :

24,062 CONTRACTS OR 2,406,200 OR 74.84 TONNES 10 TRADING DAY(S) AND THUS AVERAGING: 2406 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 10 TRADING DAY(S) IN TONNES: 74.84TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2020, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 74.84/3550 x 100% TONNES 2.11% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 74.84 TONNES (THIS IS GOING TO BE A LOW ISSUANCE MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF MAY.WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF APRIL HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF MAY, FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (MAR), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A HUGE SIZED 6416 CONTRACT OI AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 1050 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 1050 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 6416 CONTRACTS AND ADD TO THE 1050 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUMONGOUS SIZED GAIN OF 7466 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 37.38 MILLION OZ

OCCURRED WITH OUR GAIN OF $0.27 IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

5. Other gold commentaries

6. Commodity commentaries/cryptocurrencies

3. ASIAN AFFAIRS

i)THURSDAY MORNING// WEDNESDAY NIGHT

SHANGHAI CLOSED UP 38.82 PTS OR 1.22% //Hang Sang CLOSED DOWN 143.71 PTS OR 0.67% /The Nikkei closed UP 328.51 PTS OR 1.72% //Australia’s all ordinaires CLOSED UP .65% /Chinese yuan (ONSHORE) closed DOWN 6.3725 /Oil UP TO 102.93 dollars per barrel for WTI and DOWN TO 107.28 for Brent. Stocks in Europe OPENED ALL GREEN // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.3725 OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.3833: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER/

a)NORTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A SMALL SIZED 1391 CONTRACTS TO 5790300 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS SMALL COMEX INCREASE OCCURRED WITH OUR STRONG GAIN OF $8.80 IN GOLD PRICING WEDNESDAY’S COMEX TRADING. WE ALSO HAD A FAIR SIZED EFP (1975 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE ACTIVE DELIVERY MONTH OF APRIL.. THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 1975 EFP CONTRACTS WERE ISSUED: ;: , . 0 JUNE :1975 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1975 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 3365 CONTRACTS IN THAT 1975 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A SMALL SIZED COMEX OI GAIN OF 1391 CONTRACTS..AND THIS GAIN OCCURRED WITH OUR STRONG GAIN IN PRICE OF GOLD $8.80.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING FOR APRIL (81.608),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 81.608

THE BANKERS WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $8.80) AND AND WERE UNSUCCESSFUL IN FLEECING ANY LONGS AS WE HAVE REGISTERED A FAIR SIZED GAIN OF 10.466 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR APRIL (81.608 TONNES)…

WE HAD — 181 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 3365 CONTRACTS OR 336500 OZ OR 10.466 TONNES

Estimated gold volume today: 135,323/// extremely poor

Confirmed volume yesterday: 147,601 contracts poor

INITIAL STANDINGS FOR APRIL ’22 COMEX GOLD //APRIL 14

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 27,306.870 oz Brinks |

| Deposit to the Dealer Inventory in oz | 36,459.234OZBrinks 999 kilobars Manfra 135 kilobars |

| Deposits to the Customer Inventory, in oz | 9507.824 oz Brinks |

| No of oz served (contracts) today | 628 notice(s)62,800 OZ 1.9533 TONNES |

| No of oz to be served (notices) | 1110 contracts 111,000 oz 3.452 TONNES |

| Total monthly oz gold served (contracts) so far this month | 25,127 notices2,512,700 OZ 78.155 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For today:

dealer deposits 2

i)) Into Manfra; 4340.385 (135 kilobars)

ii) Into Brinks 32,118.849 oz (999 kilobars)

total dealer deposit 36,459.234 oz//

No dealer withdrawals

1 customer deposit

i) Into Brinks 9507.824 oz.

total customer deposit 9507.824 oz

1 customer withdrawals

i) Out of Brinks 27,306.870 oz

total customer withdrawal: 27,306.870 oz /

ADJUSTMENTS: customer to dealer/HSBC: 16,107.651 oz

dealer to customer:

a) JPMorgan 96.453 3 kilobars

b) Loomis: 289.359 oz 9 kilobars

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR APRIL.

For the front month of APRIL we have an oi of 1738 contracts having LOST 11 contracts

We had 134 notices filed yesterday so we GAINED 123 contracts or an additional 12,300 oz will stand for delivery at the comex

May saw a GAIN of 9 contracts to stand at 3514

June saw a LOSS of 1627 contracts UP to 478,446 contracts

We had 628 notice(s) filed today for 62,800 oz FOR THE APRIL 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 292 notices were issued from their client or customer account. The total of all issuance by all participants equates to 628 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 204 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 24 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the APRIL /2021. contract month,

we take the total number of notices filed so far for the month (25,127) x 100 oz , to which we add the difference between the open interest for the front month of (APRIL 1738 CONTRACTS ) minus the number of notices served upon today 628 x 100 oz per contract equals 2,623,700 OZ OR 81.608 TONNES the number of TONNES standing in this active month of APRIL.

thus the INITIAL standings for gold for the APRIL contract month:

No of notices filed so far (25,127) x 100 oz+ (1738) OI for the front month minus the number of notices served upon today (628} x 100 oz} which equals 2,623,700 oz standing OR 81.608 TONNES in this active delivery month of APRIL.

We GAINED 12,300 oz as a QUEUE. jump as our banker friends scrounge around for some gold

TOTAL COMEX GOLD STANDING: 81.608 TONNES (A WHOPPER FOR AN APRIL ( ACTIVE) DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

191,133,764.7, oz NOW PLEDGED /HSBC 5.94 TONNES

99,258.893 PLEDGED MANFRA 3.08 TONNES

54,339.114oz PLEDGED JPMorgan no 1 1.690 tonnes

243,923.704, oz JPM No 2 7.58 TONNES

898,821.330 oz pledged Brinks/27,96 TONNES

International Delaware:: 0

Loomis: 18,615.429 oz

total pledged gold: 1,884,464.742 oz 58.61 tonnes

TOTAL REGISTERED AND ELIG GOLD AT THE COMEX: 35,926,719.161 OZ (1117,47 TONNES)

TOTAL ELIGIBLE GOLD: 18,307,454.657 OZ (569.43 tonnes)

TOTAL OF ALL REGISTERED GOLD: 17,619,264.504 OZ (548.03 tonnes)

REGISTERED GOLD THAT CAN BE SERVED UPON: 15,734,800.0 OZ (REG GOLD- PLEDGED GOLD) 489.418 tonnes

END

APRIL 2022 CONTRACT MONTH//SILVER//APRIL 14

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 976,930.873 oz Brinks Delaware JPMorgan |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 1,894,462.082 oz Brinks CNT Delaware JPMorgan |

| No of oz served today (contracts) | 6CONTRACT(S)30,000 OZ) |

| No of oz to be served (notices) | 116 contracts (580,000 oz) |

| Total monthly oz silver served (contracts) | 1086 contracts 5,430,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

we had 0 deposit into the dealer

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 4 deposits into the customer account

i) Into JPMorgan: 548,197.100 oz

ii) Into Brinks: 644,435.770 oz

iii) Into Delaware: 7215.812 oz

iv) Into CNT: 604,614.300 oz

total deposit: 1,804,462.082 oz

JPMorgan has a total silver weight: 176.472 million oz/335.171 million =52.64% of comex

i) Comex withdrawals: 3

i) Out of JPM 581,358.500 oz

ii) Out of Brinks 1394,549.790 oz

iii( Out of Delaware: 1023.583 oz

total withdrawal 976,930.873 oz

1 adjustments: dealer to customer//Manfra 4940.380 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 86.347 MILLION OZ

TOTAL REG + ELIG. 335.181 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR APRIL

silver open interest data:

FRONT MONTH OF APRIL OI: 122, HAVING GAINED 80 CONTRACTS FROM MONDAY. We had 10 notices filed yesterday,

so we GAINED 90 contracts or an additional 450,000 oz will stand on this side of the pond

MAY HAD A LOSS OF 4395 CONTRACTS DOWN TO 69,861 contracts

JUNE HAD A GAIN OF 61 TO STAND AT 1057

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 6 for 30,000 oz

Comex volumes: 61,042// est. volume today// fair/

Comex volume: confirmed yesterday: 86,178 contracts ( strong )

To calculate the number of silver ounces that will stand for delivery in APRIL. we take the total number of notices filed for the month so far at 1086 x 5,000 oz = 5,430,000oz

to which we add the difference between the open interest for the front month of APRIL (122) and the number of notices served upon today 6 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the APRIL./2021 contract month: 1086 (notices served so far) x 5000 oz + OI for front month of APRIL (122) – number of notices served upon today (6) x 5000 oz of silver standing for the APRIL contract month equates 5,560,000 oz. .

We GAINED 90 contracts or an additional 450,000 oz will stand on this side of the pond

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

APRIL 14/WITH GOLD DOWN $8.90: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A ,ASSOVE DEPOSIT OF 11.32 TONNES INTO THE GLD..//INVENTORY RESTS AT 1104.42 TONNES

APRIL 13/WITH GOLD UP $8.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1093.10 TONNES

APRIL 12/WITH GOLD UP $26.95: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.61 TONNES INTO THE GLD///INVENTORY REST AT 1093.10 TONNES

APRIL 11/WITH GOLD UP $3.40 //A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD.//INVENTORY RESTS AT 1090.49 TONNES

APRIL 8/WITH GOLD UP $7.70: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES INTO THE GLD//INVENTORY RESTS AT 1088.75 TONNES

APRIL 7/WITH GOLD UP $13.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1087.30 TONNES

APRIL 6/WITH GOLD DOWN $4.10: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.68 TONNES FROM THE GLD..//INVENTORY RESTS AT 1087.30 TONNES

APRIL 5/WITH GOLD DOWN $5.70: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.75 TONNES FROM THE GLD//INVENTORY RESTS AT 1089.98 TONNES

APRIL 4/WITH GOLD UP $.70//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1091.73 TONNES

APRIL 1///WITH GOLD DOWN $19.00 : A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .29 TONNES INTO THE GLD///INVENTORY RESTS AT 1091.73 TONNES

MARCH 31/WITH GOLD UP $13.30 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD FROM MONDAY A WITHDRAWAL OF 1.71 TONNES FROM THE GLD:INVENTORY RESTS AT 1091.44

MARCH 28/WITH GOLD DOWN $14.65: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1093.18 TONNES

MARCH 25/WITH GOLD DOWN $7.60 : A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.52 TONNES INTO THE GLD///INVENTORY RESTS AT 1093.18 TONNES

MARCH 24/WITH GOLD UP $24.95: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.06 TONNES INTO THE GLD..//INVENTORY RESTS AT 1087.66 TONNES

MARCH 23/WITH GOLD UP $15.75//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1083.60 TONNES

MARCH 22/WITH GOLD DOWN $7.75: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.16 TONNES OF GOLD DEPOSITED INTO THE GLD//INVENTORY RESTS AT 1083.60 TONES

MARCH 21//WITH GOLD UP $.25 : A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 9.00 TONNES INTO THE GLD////INVENTORY RESTS AT 1082.44 TONES

MARCH 18/WITH GOLD DOWN $13.55 NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1073.44 TONES

MARCH 17/WITH GOLD UP $33.50: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.61 TONNES INTO THE GLD//INVENTORY RESTS AT 1073.44 TONNES

MARCH 16/WITH GOLD DOWN $18.50//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.33 TONNES FROM THE GLD///INVENTORY RESTS AT 1061.83 TONNES

MARCH 15/WITH GOLD DOWN $30.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1064.16 TONNES

MARCH 14//WITH GOLD DOWN $22.75, HUGE CHANGES IN GOLD INVENTORY AT THE GLD//STRANGE: A DEPOSIT OF 2.62 TONNES INTO THE GLD.//INVENTORY RESTS AT 1064.16 TONNES

MARCH 11/WITH GOLD DOWN $14.60: A BIG CHANGE IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 1061.54 TONNES

MARCH 10//WITH GOLD UP $11.55: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.06 TONNES FORM THE GLD///INVENTORY RESTS AT 1063.28 TONNES

MARCH 9/WITH GOLD DOWN $53.85//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.64 TONNES INTO THE GLD//INVENTORY RESTS AT 1067.34 TONNES

MARCH 8/WITH GOLD UP $46.10: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 8.42 TONNES INTO THE GLD///INVENTORY RESTS AT 1062.70 TONNES

MARCH 7/WITH GOLD UP $28.40 A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.06 TONNES INTO THE GLD..//INVENTORY RESTS AT 1054.28 TONNES

MARCH 4/WITH GOLD UP $28.40//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1050.22 TONNES

CLOSING INVENTORY FOR THE GLD//1104.42 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

APRIL 14/WITH SILVER DOWN 25 CENTS : A MONSTROUS CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.355 MILLION OZ INTO THE SLV.//INVENTORY RESTS AT 569.676 MILLION OZ//

APRIL 13/WITH SILVER UP 27 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 565.521 MILLION OZ

APRIL 12/WITH SILVER UP 66 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 565.521 MILLION OZ//

APRIL 11/WITH SILVER UP 13 CENTS: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 831,000 OZ FORM THE SLV////INVENTORY RESTS AT 565.521 MILLION OZ

APRIL 8/WITH SILVER UP 11 CENTS :NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 566.352 MILLION OZ//

APRIL 7/WITH SILVER UP 27 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 566.352 MILLION OZ//

APRIL 6/WITH SILVER DOWN 9 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 566.352 MILLION OZ

APRIL 5/WITH SILVER DOWN 16 CENTS : A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.386 MILLION OZ INTO THE SLV..//INVENTORY RESETS AT 566.352 MILLION OZ//

APRIL 4/WITH SILVER DOWN 5 CENTS TO CHANGES IN SILVER INVENTORY AT THE SLV//: A DEPOSIT OF 6.326 MILLION OZ//INVENTORY REST AT 564.966 MILLION OZ//

APRIL 1/WITH SILVER DOWN 39 CENTS A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.302 MILLION OZ INTO THE SLV////INVENTORY REST AT 558.647 MILLION OZ//

MARCH 31/WITH SILVER UP 3 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 2.171 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 556.345 MILLION OZ

MARCH 28/WITH SILVER DOWN 30 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.847 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 554.167 MILLION OZ//

MARCH 25/WITH SILVER DOWN 20 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 552.320 MILLION OZ//

MARCH 24/WITH SILVER UP 54 CENTS TODAY; A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.092 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 552.320 MILLION OZ//

MARCH 23/WITH SILVER UP 24 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 550.288 MILLION OZ//

MARCH 22/WITH SILVER DOWN $0.29 TODAY : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 550.288 MILLION OZ//

MARCH 21/WITH SILVER UP 16 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 550.288 MILLION OZ//

MARCH 18/WITH SILVER DOWN 37 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.217 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 550.288 MILLION OZ//

MARCH 17/ WITH SILVER UP 72 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.049 MILLION OZ INTO THE SLVV//INVENTORY RESTS AT 548.071 MILLION OZ

MARCH 16/WITH SILVER DOWN 56 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 462,000 OZ FROM THE SLV//INVENTORY RESTS AT 544.560 MLLION O

MARCH 15/WITH SILVER DOWN 18 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 545.022 MILLION OZ

MARCH 14/WITH SILVER DOWN 64 CENTS TODAY; STRANGE A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.125 MILLION OZ/INVENTORY RESTS AT 545.022 MILLIONOZ

MARCH 11/WITH SILVER DOWN 13 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.897 MILLION OZ

MARCH 10/WITH SILVER UP 39 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.897 MILLION OZ/

MARCH 9/WITH SILVER DOWN 88 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 5.174 MILLION OZ OF FAKE SILVER.//INVENTORY RESTS AT 542.897 MILLION OZ//

MARCH 8/WITH SILVER UP 88 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.217 MILLION OZ INTO THE SLV////INVENTORY RESTS A 548.071 MILLION OZ//

MARCH 7/WITH SILVER UP 40 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 545.854 MILLION OZ//

MARCH 4/WITH SILVER UP 50 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 545.854 MILLION OZ/

SLV FINAL INVENTORY FOR TODAY: 569.676 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

Peter Schiff: Peak Inflation Is Just Wishful Thinking

THURSDAY, APR 14, 2022 – 02:25 PM

As expected, the March Consumer Price Index was smoking hot with a 1.2% month-on-month increase and an 8.5% annual gain. But the mainstream found a silver lining in the numbers. Core inflation wasn’t quite as high as expected leading many to conclude that we’ve reached “peak inflation.” In his podcast, Peter Schiff said this is just wishful thinking.

The March CPI reflected the first impacts of the Russian invasion of Ukraine and the spiking oil prices that followed. Although the CPI was slightly above the consensus expectation, many thought it would surprise to the upside. Peter said some people were relieved the numbers weren’t even higher.

The annual CPI gain was the biggest since 1981, but Peter reminded us that this is basically comparing apples to oranges.

Forty years ago, we used entirely different CPI than we use today. And as far as I can tell, we are generally missing the mark by about half, meaning that if we use the 1981 CPI to measure the 2022 price increases, we probably would see a year-over-year rise of 17%, which is twice eight-and-a-half.”

Projections for March’s core CPI, excluding more volatile food and energy prices, were 0.5% month-on-month. It came lower, at 0.3%, which was below the range of estimates.

That was a good number as far as the markets were concerned because the core CPI didn’t go up nearly as much as thought.”

And the year-over-year core number came in at 6.5%, a little better than the expected 6.6%.

A little worse on the headline. A little better on the core. But overall, I guess the whisper numbers were that all these numbers would come in hot, and since they didn’t, the market initially was relieved.”

But even though core CPI was lower than expected, 0.3% is still a high number. If you annualize that print, it’s still 3.7% per year, almost double the Fed’s 2% target.

Peter pointed out it doesn’t make any sense to look at year-over-year core inflation if you’re going to take some solace in the fact that inflation is not so bad if we strip out food and energy.

Families can’t strip out food and energy. They can’t survive without food and energy. When food and energy prices are up year-over-year big, that’s not volatility. That’s a trend. And you can’t ignore that trend when you’re trying to calculate inflation and determine whether or not you have a problem. You have a big problem.”

Also, in a normal economy, core prices should drop as energy and food prices should rise. As people spend more on food and energy, they have less to spend on other things.

So, core prices should be falling as the food and energy prices are rising. But the reason that all prices are rising is because everybody has got more money. We’ve got more money to buy food and energy, and we’ve got more money to buy everything else. Where’s all that money coming from to buy all this stuff? It’s coming from the Federal Reserve. The Federal Reserve is creating all the inflation in the core and in the headline. It’s not Putin and it wasn’t COVID.”

We know the markets were anxious about the CPI data because all of the bond yields hit highs the night before the numbers came out. Bond traders were bracing for a hot CPI. When the numbers were relatively benign – at least not as bad as expected – the bond market rallied.

Interestingly, all of the inversions in the yield curve disappeared.

I think the significance of this un-inversion of the yield curve … I think what the bond market is potentially forecasting is that based on this so-called benign number, maybe the Fed won’t have to hike as much as people thought, and so that’s why the shorter end of the curve got an improvement because maybe the Fed won’t have to jack rates up as much.”

There could also be some sense that the Fed will push the economy into a recession sooner, again meaning the Fed won’t have to raise interest rates as high, but the long end of the curve seems to indicate the markets anticipate inflation might hang around longer.

The markets are projecting that interest rates will peak around 3.25% in 2023.

I don’t think that that’s going to be the case because I think before we get to 3.25% the economy will be in recession or will be close enough to a recession that the Fed ultimately backtracks from its rate hikes, and in fact will even return to quantitative easing. So, I don’t think we’ll ever get to that level. Remember, in 2018, the Fed couldn’t get above 2.5% before it had to backtrack and ultimately go back down to zero. And given how much more debt the economy has today than it had then, and how much more leverage there is now, it seems to me if we couldn’t take 2.5% in 2018 we can’t take 2.5% now, let alone 3.25. And so the Fed is not going to be able to get rates that high before something breaks.”

The US government ran another big budget deficit in March. It was almost quadruple expectations.

Back in the day of QE, which was just a few days ago, the Treasury could count on the Fed to buy most of that $192.7 billion. Well obviously, not only can’t the Treasury count on the Fed to buy any of that $192.7 billion, but the Fed is going to be selling billions of dollars worth of Treasuries off of its own balance sheet that has to be financed in addition to that $192.7 billion, which is why I don’t believe the Fed is going to be able to continue with quantitative tightening to the extent that it ever actually begins quantitative tightening, because the US Treasury just has too many bonds to sell and not enough buyers to step up.”

Peter noted that in 1981, the last time CPI was this high, interest rates peaked at 20%. Today, interest rates are at 0.25%. Then, we had real rates of over 6%. Today, real rates are deeply negative.

Is inflation going to peak when interest rates are at -8.25% when it took positive 6.5% to get inflation to peak in 1981? And of course, if we are measuring prices accurately, as I said earlier, we’ve got 17% inflation, which means we have -16.75 real interest rates — inflation is far more likely to accelerate than come down when you have a negative interest rate that high. Instead of being at the end of an inflationary period, we’re just beginning. … All of the people who are saying inflation has peaked they’re just saying that because they hope it’s peaked.

END

2.LAWRIE WILLIAM//,//Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, James RICKARDS/

Gold Vs An Openly Failing/Changing World

THURSDAY, APR 14, 2022 – 06:30 AM

Authored by Matthew Piepenburg via GoldSwitzerland.com,

As central bankers play checkers on a global debt chessboard, we see below how policy hypocrisy, worsening monetary options, failed diplomacy, tanking bonds, rising rates, debt addiction, mismanaged sanctions, de-dollarization and a shift toward a disorderly re-set all spell immense pain for Main Street as well as Wall Street.

In short, the world is in flux, the mess is everywhere and gold is already flexing.

Faces of Hypocrisy

Fed Vice Chair Lael Brainard, a former money-printing dove who helped pour trillions of liquidity into the biggest risk asset bubble and wealth transfer in US history, is suddenly realizing that perhaps she and the FOMC may have gone too far as their open stock market inflation now morphs into just plain everywhere-inflation (and an 8+% CPI).

She is now puffing a Hawkish chest and citing the good ol’ days of Paul Volcker rate-hiking as the kind of tough restraint needed in 2022.

But such a pivot is the equivalent of the Titanic’s captain ordering more lifeboats after the ship has already sunk.

In short, if hypocrisy had a face, and if market comedy a punch-line, surely Brainard (along-side Kashkari, Powell, Yellen, Goldman Sachs and Bridgewater) would qualify for the top-10 list.

The “Greatest Threat to the Economy”? Inflation or the Fed Itself?

In a recent speech, Brainard reminded the audience of Volcker’s warning that runaway inflation “would be the greatest threat to the economy…and ultimately employment.”

Fair enough.

The irony, however, lies in the fact that the Fed (after years of expanding the broad money supply and mouse-click-creating trillions of dollars to buy otherwise unwanted US IOUs) is the very author of this inflation and, by extension, is itself, “the greatest threat to the economy.”

Today, the inflationary hens hatched directly from years of DC’s own spend-and-print policies are now coming home to roost.

As 1) defense and entitlement spending reaches all-time highs of 120% of record-high tax receipts and 2) the Fed balance sheet climbs >10X from a pre-08 number of $800B to a 2022 level of $9T, Fed-driven inflation has emerged not as a surprising or mysterious aberration but as an obvious, predictable and direct consequence of the Fed itself.

In short, former doves like Brainard citing hawks like Volcker to solve their banking policies is akin to Lance Armstrong citing Mother Theresa to defend his biking policies.

Brainless Bravado Rather than Honest Transparency

But in a never-ending effort to signal form over substance and spin over facts, Brainard somehow thinks that the US, with 90T in combined household, corporate and public debt, needs to get “Volcker-tough” on combatting the very inflation she helped create.

But we aren’t in the 1970’s anymore. Things, and debt levels, have changed.

The obvious problem with Brainard’s brainless bravado is that the Federal debt when Volcker raised rates to 20% in 1980 was $908 B; today that national debt figure is over $30 T.

Folks, when saddled by such unprecedented and unpayable debt levels, do you think Uncle Sam can afford to raise rates (i.e., the cost of that debt) without eventually mouse-clicking more debased dollars out of thin air to then pay for it?

Well, the answer we’ll give you is far blunter and more accurate than Brainard’s.

And it boils to this: Nope. It can’t be done—not without ushering a financial recession and market implosion or debasing the dollar with trillions of more fake liquidity.

Period. Full stop.

But if accuracy, candor and intelligent accountability is something you are hoping to find from so-called “experts” like Brainard, we’d remind you again to look elsewhere.

As for Brainard’s expertise (and fork-tongued inaccuracies), it’s worth reminding that: 1) in 2020 she supported inflation “running hot;” 2) in early 2021, she said the Fed’s inflation expectations “were extremely well-anchored,” and then, 3) at the end of that same year, said “I expect inflation to decelerate.”

Wrong every time.

Yet just last week, in 2022, Brainard finally confessed that “inflation is too high”?

Again, so much for trusting the “experts.”

Candor vs. Fantasy

As for us, we warned of the coming and persistent (rather than “transitory”) inflation long before the Fed-Heads would even discuss the inflation reality.

In those same years, we also consistently declared that a cornered Fed can not raise rates and cut money printing to become net sellers (as opposed to former top buyers) of UST without causing formerly – “accommodated’ bonds to tank and hence yields (and thus interest rates) to spike.

And precisely as forecasted, that’s what’s taking place now as rising rates, like rising shark fins, slowly approach the sinking ship that is the bankrupt US economy.

Pivots, Confusion and Insanity

The Fed has pivoted from being the largest buyer of Treasuries to a seller of Treasuries (i.e., Uncle Sam’s IOUs) at the very same time that Uncle Sam is issuing record amounts of those very same IOUs (i.e., borrowing like mad) during the worst inflationary period seen in 40 years.

You literally can’t make this kind of insanity up: One part of DC is borrowing at record levels while across the Street, the Fed is tightening the cash spigot.

Such open confusion, bi-polar policy swings, and exhaustion of any viable/remaining alternatives is going to end very badly for markets and the economy as yields spike and hence the USD, on a relative rather than inherent basis, gets stronger.

By the way, a stronger USD just makes US goods less competitive overseas and worsens US trade deficits—thereby adding more insult to an already injured US GDP.

In short, this perfect and Fed-made disaster is taking place in real time while double-speakers like Brainard stand with a chest puffed yet a back against a wall of their own making.

Given the fatal debt timebombs which the Fed alone unleashed since the Greenspan era, it has cornered itself into a prisoner’s dilemma of either: A) runaway inflation if they don’t raise rates or B) a market implosion if they do.

Sadly, we think the world is about to see both.

The Fed’s Real Mandate Makes Them Easy to Predict

As we have also transparently warned, the Fed’s real mandate is the markets not inflation or the man on the street.

The Fed is already fattening its Standard Repo Facility (SRF) in order to bail out the unloved Treasury market whenever the emergency bell rings in the bond pits.

In short, and despite talking hawkish, the SRF is open proof that the Fed is fully dovish when it comes to cooing over Mr. Market.

In plain-speak, when push comes to shove, the FOMC favors Wall Street over Main Steet—always has, always will.

Why?

The Market is the Thing

The Fed thinks a rising stock market will stimulate consumer spending, which is 70% of its GDP score as well as the core driver of Uncle Sam’s much needed tax receipts.

After all, Net Capital Gains and IRA Distributions are the 200% wind beneath the wings of consumer spending’s annual growth.

Stated even more simply (and mathematically), when markets tank, consumer spending tanks, and when consumer spending tanks, so too does Uncle Sam’s GDP as well as income from US tax receipts.

Given that the US has off-shored its productivity to places like China, the fully bloated and grotesquely distorted stock market is about the only bragging right Uncle Sam has left.

Hence, the Fed’s shadow mandate is to save that market, even at the expense of inflationary suffering on Main Street.

But as we’ve also consistently warned, the Fed’s track record for going too far is long and distinguished, and despite all their twisted (and rigged) efforts, they always fail in preventing market implosions of their own making.

Thus, Wall Street and Main Street can and will suffer together, and the Fed, like our markets, truly are Rigged to Fail.

For now, the Fed is trying to prop the market in secret while simultaneously claiming to fight inflation in public.

This behavior of inflating away debt in practice while publicly claiming to “combat” it is just another classic Fed ruse.

More, rather than less, inflation is ahead—which is why gold (and miners) will rise despite a relatively stronger USD.

Rising Dollar, Rising Gold

But shouldn’t a stronger USD bode poorly for gold?

That is, shouldn’t rapidly rising real yields be bad for gold, which, as we’ve argued for years, favors negative real real yields?

Not necessarily, and not in this totally distorted new-abnormal.

When the dollar is so fully debased, distrusted and set for a fall, and when rising yields bankrupt Uncle Sam, all the old rules change.

The traditional correlations and inverse relationships mean nothing anymore for the simple reason that nothing is normal anymore—thanks to years of central bank folly, political (spending) decadence, record-breaking debt expansion and a global addiction to printed currencies.

More Centralized Controls Are Inevitable

And as for money printing, more is on the way because central banks in general, and the Fed in particular, have no choice but to eventually create more diluted dollars.

Long-term gold investors have always known this.

And the market now knows what double-speakers like Yellen, Powell, Brainard and others won’t confess, namely: That as soon as the economy and markets begin to tank in this raising yield/rate environment, the Fed (and other central banks) will be forced to print (i.e., debase) more inflationary money and impose Yield Curve Controls (YCC) to stem the financial bleeding that always follows a rate hike.

In short, and as forewarned long ago, get ready for far more, rather than less, centralized controls over your money, economy, market and lives.

Such inevitable bond market disasters, yield spikes and subsequent money printing and YCC is why gold is rising and gold miners like Newmont are seeing all-time highs despite a rising USD.

A World in Flux

Meanwhile, as Western central bankers try to manage the optics of their increasingly discredited and disastrous policies (i.e., blaming everything on a politicized pandemic and an avoidable war), the world is rapidly moving in a new direction.

This direction is sailing away from the world reserve currency in general and western financial controls in particular, all of which we’ve warned would happen as the West shot itself in the foot with sanctions otherwise aimed at Russia’s chest.

Poking the Bear

As warned, Putin is moving closer toward the world he and China have otherwise been telegraphing for years—one in which the USD is no longer the only core player.

Squeezed by SWIFT, SDR and FX Reserve sanctions, Russia is now demanding payments for its resources in RUB rather USD from a growing list of states “unfriendly” to Russia.

In short, we poked a bear and now it’s biting us in the tail…

Unlike the post-Nixon West, Putin is also flirting with what wiser economists have hoped other nations would do, namely partially link its currency to gold rather than thin air.

Russia’s central bank has been buying gold at 5000 RUB per gram.

Folks, this flirtation with a gold-currency cover represents a massive shift in history in general and global markets in particular. DO NOT underestimate its implications.

As nations like Russia, China and India slowly move toward and consider a partial-cover of their currencies in gold, the gold price will rise in ways that not even the BIS or its minions in that thoroughly corrupted COMEX market can manipulate downwards.

The West Is Trapped

It seems the West, by failing to find a diplomatic solution in the Ukraine, has fallen straight into a Putin trap, which was so openly foreseeable.

I mean honestly, did the West really think Putin would simply collapse under sanctions he was already prepared to weather and counter-punch?

Unless the US can convince the EU to fully end its reliance on Russian energy (good luck with that), Putin, the chess player we’ve warned of, will have the checker-players in DC and Brussels bouncing off the walls.

In the end, the West has no options going forward (full ban of Russian purchases [?], capital controls with Chinese/Indian consent [?] or admit defeat and end Russian sanctions [?]) that won’t financially cripple western citizens from Austria to Atlanta.

As we’ve argued recently, the sanction genie can’t be put back into the bottle, and the world is now slowly marching toward a commodity-backed rather than “faith” backed currency system, which is running out of faith which each passing day.

Got gold?

You should.

3. Chris Powell of GATA provides to us very important physical commentaries

A must read: James Turk believes that we will have a default in silver similar to what we witnessed in nickel

James Turk/GoldMoney/GATA

GoldMoney’s Turk discusses possible futures market default in silver

Submitted by admin on Wed, 2022-04-13 21:25Section: Daily Dispatches

9:12p ET Wednesday, April 13, 2022

Dear Friend of GATA and Gold:

Last week the German edition of The Epoch Times interviewed GoldMoney founder and GATA consultant James Turk about developments in the currency and futures markets, starting with the London Metals Exchange’s default on its nickel contract and its rescuing the shorts and its expropriation of the longs.

Turk discusses whether a similar default is possible in silver, another market with a huge naked short position.

The German version of the interview is posted at The Epoch Times’ German edition here:

An English translation is posted at Turk’s internet site, the Free Gold Money Report, here:

https://www.fgmr.com/james-turk-interviewed-by-the-epoch-times/

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

END

4.OTHER GOLD/SILVER COMMENTARIES

5.OTHER COMMODITIES

LITHIUM

end

COMMODITIES IN GENERAL

6.CRYPTOCURRENCIES

7. GOLD/ TRADING TODAY

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings THURSDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 6.3725

OFFSHORE YUAN: 6.3833

HANG SANG CLOSED UP 153.71 PTS OR 0.67%

2. Nikkei closed UP 328.51PTS OR 1.22%

3. Europe stocks ALL GREEN

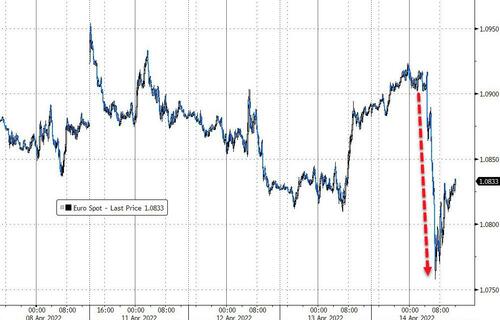

USA dollar INDEX UP TO 99.62/Euro FALLS TO 1.0886

3b Japan 10 YR bond yield: RISES TO. +.242/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 125.22/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 102.93 and Brent: 107.28

3f Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: DOWN -SHORE CLOSED UP// OFF- SHORE DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.0.800%/Italian 10 Yr bond yield FALLS to 2.40% /SPAIN 10 YR BOND YIELD FALLS TO 1.72%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 1.60: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield RISES TO : 2.87

3k Gold at $1979.50 silver at: 25.62 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3l USA vs Russian rouble;// Russian rouble DOWN 1 1 /3 roubles/dollar; ROUBLE AT 81.21

3m oil into the 102 dollar handle for WTI and 107 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 125.22 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning .9363– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0188 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

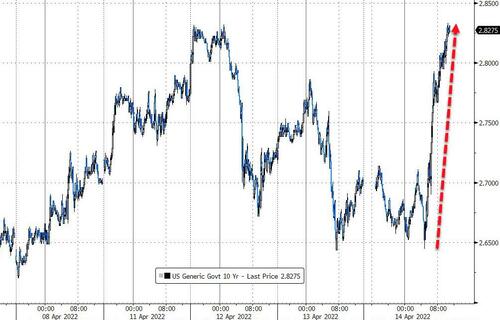

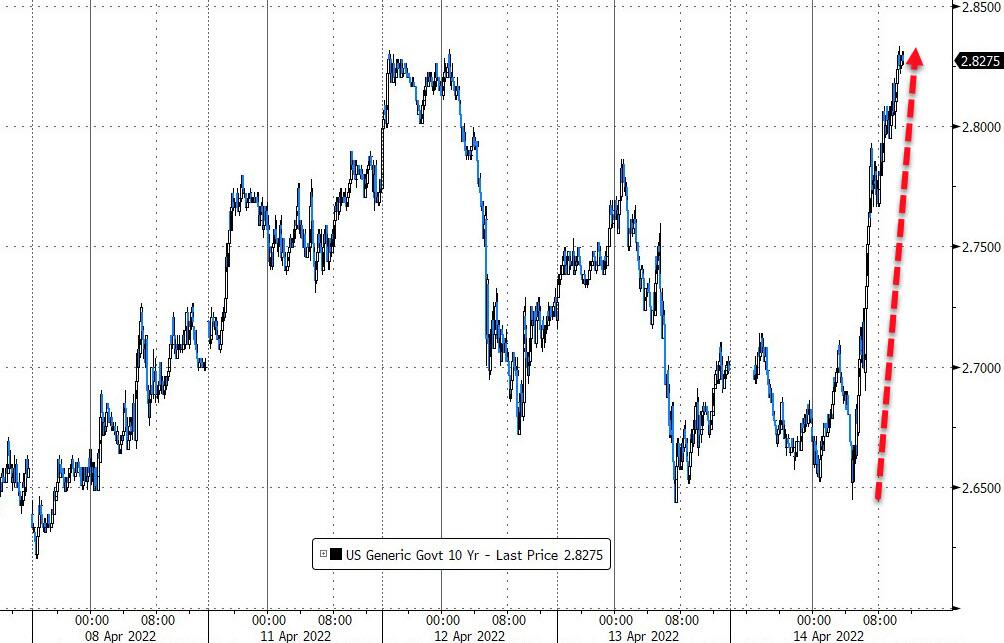

USA 10 YR BOND YIELD: 2.673 DOWN 2 BASIS PTS

USA 30 YR BOND YIELD: 2.793 DOWN 0BASIS PTS

USA DOLLAR VS TURKISH LIRA: 14.62

Futures Flat Ahead Of ECB And Barrage Of Bank Earnings With $2.1 Trillion In Options Expiring

THURSDAY, APR 14, 2022 – 07:25 AM

US index were flat on Thursday, reversing earlier gains sparked by hopes of imminent easing in China, as investors turned their attention to the ECB which is set to maintain its speedier withdrawal of stimulus, data on retail sales and unemployment claims, and a barrage of earnings from Goldman Sachs, Morgan Stanley, Citigroup and Wells Fargo, and all of this happening as $2.1 trillion in options are set to expire (since tomorrow is a holiday).

At 7;00am ET, S&P futures were unchanged at 4440, Nasdaq futures were down 0.1% and Europe’s Stoxx 600 rose 0.2%. Asian stocks rose after China again indicated looser monetary policy is on the way. Treasuries extended gains as investors dialed back aggressive bets on Federal Reserve interest-rate hikes. The yen bounced from a two-decade low against the dollar. The greenback slipped after snapping its longest winning streak since 2020. Oil fell. Twitter shares soared after Elon Musk offered to buy the whole company for $54.20.

Delta Air Lines gained 0.9% in premarket trading, extending this week’s rally after it had its price projection raised at JPMorgan and Barclays. However the biggest mover in the premarket was Twitter which soared as much as 18%, and was last trading at $51 following a hostile offer by Elon Musk; Tesla shares fell.

While elevated and sticky inflation “remains a key risk for investors,” there are signs that price growth will ease in the rest of the year, according to Mark Haefele, chief investment officer at UBS Global Wealth Management. “In our base case, this should allow central banks to slow the pace of monetary tightening and tone down hawkish rhetoric,” he said. “That in turn should lower the threat of an economic hard landing.”

China is expected to cut a key policy interest rate for the second time this year on Friday and reduce the reserve requirement ratio soon. South Korea raised its key interest rate and Singapore further tightened policy, spurring advances in their currencies.

“We have actually turned cautiously optimistic on the Chinese equity market in April already,” Stefanie Holtze-Jen, Asia-Pacific chief investment officer at Deutsche Bank AG in Singapore, said on Bloomberg Television. “We perceived the communication from the government as the line in the sand.”

“We’re still being cautious” about equities, Michael Vogelzang, chief investment officer at CAPTRUST, said on Bloomberg Television. “We think there’s still a lot more that can go wrong than probably can go right.”

The latest developments over the war in Ukraine included a European Union warning for member states that President Vladimir Putin’s demand that “unfriendly countries” effectively pay for Russian gas in rubles would violate sanctions. The U.S. will expand the scope of weapons it’s providing to Ukraine in a new $800 million package of military assistance.

In Europe, gains for travel and consumer companies outweighed declines in the telecommunications and energy industries, leading the Stoxx Europe 600 Index up 0.1% and Stoxx 50 up 0.3%. CAC 40 outperforms, adding 0.4%, FTSE 100 lags, dropping 0.2%. Atlantia jumped 4.9% in Milan after the Benetton family and Blackstone offered to buy out the Italian highway operator for 23 euros per share. Ericsson dropped 5.6% in Stockholm after its earnings missed estimates. Here are some of Europe’s most notable movers:

- Wizz Air shares jump as much as 8.9% after it said it sees its 4Q operating result ahead of guidance provided at 3Q. Concorde says the low-cost carrier’s expectation to fly 30%-40% more compared with 2019 capacity in the next two quarters is “encouraging.”

- Holcim shares rise as much as 4.3%, most since March 29, following a Bloomberg report that the group is considering the sale of assets in India.

- Atlantia shares rise as much as 5.8% after Italy’s Benetton family and Blackstone have made a EU19b bid to buy out the infrastructure group, it follows Bloomberg News last week’s report that the firm was circled by potential suitors.

- Hermes shares advance as much as 4.6% after publishing 1Q sales that one analyst described as “spectacular.” Peers are also up with Richemont rose as much as +3%

- Ericsson shares fall as much as 9.2% after reporting adjusted operating profit that undershot average analyst estimates by 25%. While the first-quarter revenue came ahead of expectations, a “clear miss” on profits together with multiple new headwinds to margins may keep investors on the sidelines, according to Barclays.

- VW shares decline as much as 2.3% after the car-maker reported preliminary figures that Jefferies says are “overall negative.”

- UPM shares decline as much as 5.1% on Friday after the Finnish company said it has not been able to come to new collective labor agreements with the Paperworkers’ Union.

- Ashmore shares sink as much as 9.2%, the most since April 2020, after the emerging markets-focused asset manager reported 3Q net outflows of $3.7b, which analysts say were worse than consensus expectations.

European bonds fell and the euro advanced as attention turns to the ECB, which is set to maintain its speedier withdrawal of stimulus.

Earlier in the session, Asian stocks headed for a two-day gain amid growing expectations that China’s central bank will ease policy to support growth in the region’s biggest economy. The MSCI Asia Pacific Index climbed as much as 0.8% as all sectors rose, with shares in mainland China leading the regionon hopes that the People’s Bank of China will cut its key policy rate soon. A 50-basis point, broad-based reduction in the reserve requirement ratio could also be confirmed as early as Friday, injecting 1.2 trillion yuan ($188 billion) of liquidity into the economy, Citigroup said. While an RRR cut “will help in terms of stabilizing expectations, it could be just an expedient measure as the economy urgently calls for more easing,” wrote Huatai Securities analysts including Yi Huan in a note. Asia’s cyclical and defensive shares climbed with SoftBank Group hauling up the gauge, as Mizuho Securities said the technology giant may sell some of its assets to improve its finances.

Japan’s main gauges were also among the top performers in Asia, rising for a second day, driven by advances in technology shares. Electronics makers were the biggest boost to the Topix, which gained 1%. Fast Retailing and Tokyo Electron were the largest contributors to a 1.2% rise in the Nikkei 225. The Kospi index ended the day little changed after the Bank of Korea raised its seven-day repurchase rate by a quarter percentage point.

China’s growth outlook has been a key pressure point for Asian shares as the country maintains its Covid Zero strategy. The MSCI Asia Pacific Index is down about 10% in 2022, extending last year’s underperformance versus the S&P 500. “China’s dynamic zero-Covid policy could ravage the Chinese economy if lockdowns continue,” Alicia Garcia Herrero, chief economist for Asia Pacific at Natixis, wrote in a note. “Beyond the reduced demand for imports from China, an even more immediate effect is inflation given the world’s dependence on China’s production of intermediate goods.”

In rates, yields are lower by as much as 2bp in 3- to 5-year sector, steepening 5s30s spread by about that much with long-end yields little changed; 10-year, lower by ~1bp at around 2.69%, outperforms bunds and gilts in the sector by 5bp-6bp. Treasuries were slightly richer across front-end and belly of the curve, steepening most curve spreads and outperforming European core rates ahead of ECB policy decision at 7:45am ET and President Christine Lagarde’s press conference. Focal points of U.S. session include retail sales data and three Fed speakers. Sifma has recommended a 2pm close ahead of Friday’s U.S. market holiday. German curve bear-steepens with yields up 2.5-3bps across the back end. Peripheral spreads widen to Germany with 10y BTP/Bund widening 2.9bps to 242.3bps. Cash USTs bull-steepen with the curve seeing ~2bps of riching from the 5y point out. U.K. curve bear-steepens with 30y yields rising over 3bps.

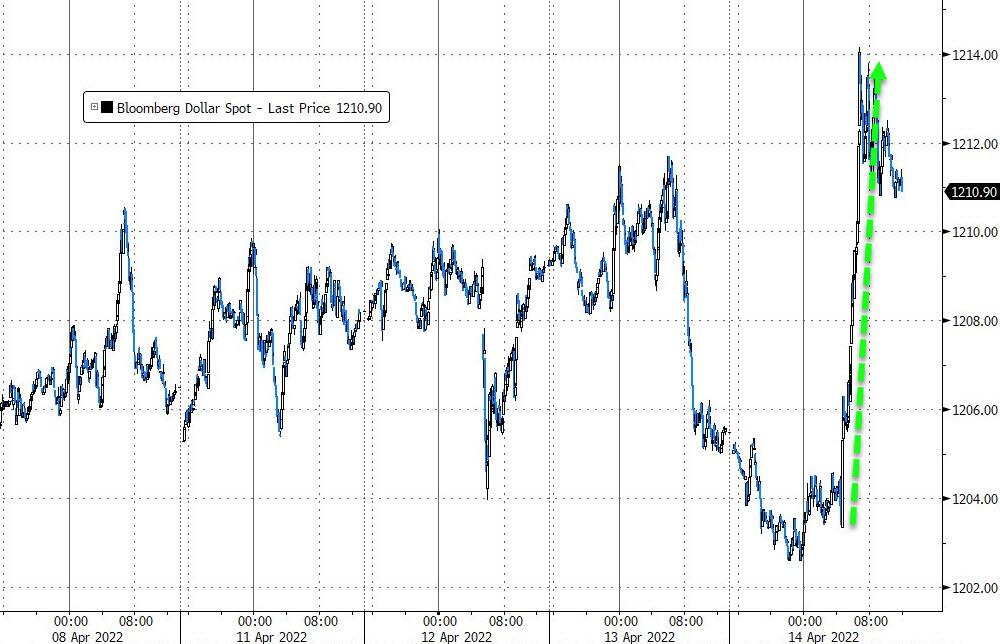

The Bloomberg Dollar Spot Index headed for a second day of losses, falling 0.1%. and the dollar fell against most of its Group-of 10 peers. CHF and AUD are the weakest performers in G-10 FX, SEK and NZD outperform. The euro rose above $1.09 while yields on Bunds and Italian bonds advanced as money markets increased ECB rate hike bets ahead of the monetary policy decision. Sweden’s krona strengthened against all of its G-10 peers and the nation’s sovereign bonds slumped, led by the front-end of the curve. Markets rushed to price in faster Riksbank tightening after its target measure, CPIF, rose to 6.1% on an annual basis in March. Economists surveyed by Bloomberg expected underlying prices to rise by 5.6%. The Australian dollar declined versus its New Zealand counterpart as the economy added fewer jobs than expected last month. Yen snapped a nine-day losing streak as U.S. yields continued to fall and players prepared for the long Easter weekend. Japanese government bonds followed Treasuries higher. BOJ Deputy Governor Masazumi Wakatabe said that it’s desirable for foreign exchange rates to reflect economic fundamentals and move in a stable manner.

In commodities, crude futures decline. WTI trades within Wednesday’s range, falling 0.7% to trade around $103. Brent falls 0.7% to $108. Most base metals trade in the red; LME zinc falls 1.1%, underperforming peers. LME aluminum outperforms, adding 1.1%. Gold weakens to around $1,972.

The commodity-fueled jump in costs exacerbated by Russia’s war in Ukraine continues to ripple across the global economy and color market sentiment. JPMorgan Chase & Co. Chief Executive Officer Jamie Dimon said inflation and the conflict were creating “significant” challenges. The firm was among the first of the big U.S. banks to report earnings.

Looking to the day ahead, the main highlight will be the ECB’s latest policy decision. We’ll also hear from the Fed’s Williams, Mester and Harker. Data releases include US retail sales for March, the weekly initial jobless claims, and the University of Michigan’s preliminary consumer sentiment index for April. Lastly, earnings releases are again financials heavy, with Wells Fargo, Citigroup, Morgan Stanley, Goldman Sachs and UnitedHealth Group showcasing.

Market Snapshot

- S&P 500 futures down 0.1% to 4,437.75

- STOXX Europe 600 little changed at 457.19

- MXAP up 0.6% to 175.12

- MXAPJ up 0.4% to 580.08

- Nikkei up 1.2% to 27,172.00

- Topix up 1.0% to 1,908.05

- Hang Seng Index up 0.7% to 21,518.08

- Shanghai Composite up 1.2% to 3,225.64

- Sensex down 0.4% to 58,338.93

- Australia S&P/ASX 200 up 0.6% to 7,523.43

- Kospi little changed at 2,716.71

- German 10Y yield little changed at 0.78%

- Euro up 0.2% to $1.0906

- Brent Futures down 0.7% to $108.07/bbl

- Gold spot down 0.1% to $1,975.23

- U.S. Dollar Index down 0.17% to 99.71

Top Overnight News from Bloomberg

- Jumbo-sized interest rate hikes from Canada to New Zealand are boosting market confidence that central banks are on track to tame inflation, putting bonds back in investors’ focus

- Russian authorities are considering a step-by-step approach to rolling back the harsh capital controls imposed to stabilize markets after the invasion of Ukraine. Discussions this week focused on options that included extending the deadline for exporters to carry out mandatory conversions of their overseas earnings into rubles and lowering below 80% the share of foreign proceeds that companies are obliged to sell in the market, according to people informed on the matter

- Russia threatened to deploy nuclear weapons in and around the Baltic Sea region if Finland and Sweden join the North Atlantic Treaty Organization as tensions fueled by Vladimir Putin’s invasion of Ukraine spread

- Singapore’s central bank further tightened monetary settings and raised its inflation forecast, sending the currency higher as it seeks to fight cost pressures that threaten the recovery from the pandemic

- Chinese President Xi Jinping says his government will stick to its zero-tolerance approach to Covid even as public anger simmers in Shanghai and economic costs mount

- Copper and aluminum rose on signs China will loosen monetary policy to revive its virus-wracked economy, while zinc dipped but remained near the highest close since 2006 amid a global supply crunch

A More detailed breakdown of global news from Newsquawk

Asia-Pac stocks were mostly positive after the gains on Wall St where risk appetite was supported by lower yields, although some bourses lagged on policy tightening. ASX 200 traded higher but with gains capped by cautiousness in the top-weighted financials sector after Bank of Queensland’s shares failed to benefit post-earnings. Nikkei 225 outperformed and reclaimed the 27,000 level with Japan’s ruling coalition parties unveiling their draft relief proposals. Fast Retailing (9983 JT) 6-month (JPY): Net Profit 146.84bln, +38.7%; Operating Profit 189.3bln, +12.7%; Pretax Profit 212.6bln, +24%; Sees FY net income at 190bln (prev. guidance 175bln). KOSPI and Straits Times Index lagged after the BoK unexpectedly hiked rates by 25bps points and the MAS tightened FX-based policy, respectively. Hang Seng and Shanghai Comp were kept afloat with speculation rife that the PBoC will lower rates tomorrow via an MLF rate cut, while Citi also sees the possibility for a RRR cut on Friday to free up around CNY 1.2tln cash.

Top Asian News

- Chinese Stocks Advance as Key Rate Cut Seen as Soon as Friday

- TSMC Raises Sales Outlook Despite Fears Around Global Demand

- Sri Lanka Seeking Up to $4 Billion as IMF Talks Set to Start

- Uniqlo Owner Gets Serious About Conquering North American Market

European bourses are firmer, Euro Stoxx 50 +0.4%, but off best levels as sentiment was hit on commentary from Russia’s Medvedev and as we await key bank earnings. Sectors in Europe are contained and are not exhibiting any pronounced theme thus far. US futures remain within narrow parameters at this point in time awaiting updates from Goldman Sachs and Morgan Stanley before Retail Sales rounds off the week’s key data; NQ +0.1%. Tesla (TSLA) CEO Musk, on April 13th, offered to purchase all of the outstanding Twitter (TWTR) shares for USD 54.20/shr (vs prior close of USD 45.85); said it was his final offer. TWTR +13% in the pre-market. TSMC (2330 TW) Q1 (TWD): Revenue 491bln (prev. 362bln), Net Profit 202.7bln (exp. 184.7bln), Gross Margin 55.6%. Expects chip demand to continue in the long term, believes capacity will remain tight this year and expects another strong year. Working to address supply chain challenges with tool suppliers.

Top European News

- ArcelorMittal Buys $1 Billion Voestalpine Plant in Texas

- VW Sees Profit Surge on $3.8 Billion Hedging Boost

- Valneva’s Covid Vaccine Gets U.K. Clearance After Rocky Ride

- Macron’s Lead Grows in French Election Polling Average

FX:

- DXY almost full point down from midweek y-t-d peak as US Treasury yields continue to recede ahead of packed pre-Easter agenda index hovering above 95.500 vs 100.520 high.

- Kiwi rebounds after RBNZ letdown with tailwinds from AUD/NZD cross in wake of weaker than forecast Aussie jobs data, NZD/USD back on 0.6800 handle, AUD/USD straddling 0.7450.

- Euro takes advantage of Greenback retreat awaiting words of wisdom from ECB President Lagarde following policy announcement that is not expected to reveal changes; EUR/USD above 1.0900 vs close shave with 2022 low (1.0806) yesterday.

- Swedish Crown aloft as more consensus and Riksbank target topping inflation prints prompt earlier rate hike calls, EUR/SEK pivots 10.3000.

- Korean Won and Singapore Dollar boosted by shock BoK hike and MAS tightening, but Chinese Yuan backs off amidst growing speculation about PBoC easing possibly as soon as tomorrow.

Fixed income:

- Eurozone bonds extend retreat from recovery peaks and underperformance ahead of the ECB.

- Bunds nearer 155.00 after rebound to just shy of 156.00, Gilts sub-119.00 vs 119.65 Liffe high and 10 year T-note closer to 120-19+ overnight bottom than 121-05+ top.

- US Treasuries down in sympathy with Gilts and curve a tad steeper after so-so long bond auction.

- Debt also defensive pre-long Easter weekend and busy line up of US data, including IJC and retail sales.

Commodities:

- WTI and Brent are pressured and in relatively proximity to the session’s troughs of USD 102.50/bbl and USD 107.01/bbl.

- Newsflow remains focused on Ukraine-Russia, particularly Medvedev’s commentary, and the COVID situation in China as other cities are on edge re. Shanghai.

- Libyan National Unity Government adopted a plan to develop the oil sector to raise output to 1.4mln bpd, according to Reuters.

- Chinese refiners are seen cutting April’s crude throughput by 900k BPD, around 6% of the 2021 average, via Reuters citing sources/analysts; expected to export 2mln/T of refined fuel in April, counter to earlier China plan to halt exports.

- Spot gold/silver are pressured and have lost the brief upside derived from earlier geopolitical developments, yellow metal at lows of USD 1967/oz.

US Event Calendar

- 08:30: April Initial Jobless Claims, est. 170,000, prior 166,000

- Continuing Claims, est. 1.5m, prior 1.52m

- 08:30: March Import Price Index YoY, est. 11.9%, prior 10.9%; MoM, est. 2.3%, prior 1.4%

- March Export Price Index YoY, est. 16.2%, prior 16.6%; MoM, est. 2.2%, prior 3.0%

- 08:30: March Retail Sales Advance MoM, est. 0.6%, prior 0.3%

- March Retail Sales Ex Auto MoM, est. 1.0%, prior 0.2%

- March Retail Sales Control Group, est. 0.1%, prior -1.2%

- 10:00: Feb. Business Inventories, est. 1.3%, prior 1.1%

- 10:00: April U. of Mich. Sentiment, est. 59.0, prior 59.4;

- Current Conditions, est. 67.0, prior 67.2

- Expectations, est. 53.6, prior 54.3

- 1 Yr Inflation, est. 5.5%, prior 5.4%; 5-10 Yr Inflation, prior 3.0%

DB concludes the overnight wrap

The EMR will be joining much of the market on holiday and will be back on Tuesday. A happy, restful long weekend to our loyal readers, and cheers to whatever it is you may be celebrating.

Ahead of the holiday, the yield curve rose on the third day straight, with 2s10s having risen +42.5bps since its nadir at the start of the month. Global sovereign yields modestly fell, while US equities outperformed their European counterparts. The ECB meets today, where our economists are not expecting a change in tune.

Starting with Ukraine, the US announced another round of aid, which will include heavy weaponry. Meanwhile, Finland has started the process to obtain NATO membership, and Swedish media report Sweden is considering the same. This, following President Biden labelling Russia’s excursions into Ukraine a genocide, the lack of negotiation progress, and the collective bracing for a renewed assault in the east, has cast a gloomy pall over the conflict. The International Energy Agency elsewhere warned that the disruption to Russian oil supply has yet to bind, with upwards of 3m bbls/day coming offline starting in May. The combined effect was to send Brent crude oil futures higher, which gained +4.14% yesterday to $108.78bbl, their highest level in two weeks following a +10.5% gain over the last two days.

Sovereign yields had a subdued day by the standards of recent volatility, with yields falling across most jurisdictions and tenors. 10yr Treasuries were down -2.3bps, outpaced by the -5.7bp decline in 2yr yields that led to a further steepening of the curve. Most of the declines came in the New York morning, when reports of large block futures trades were relentlessly hitting the tapes.

In Europe, 10yr bund, OAT, and BTP yields were -2.4bps, -3.5bps, and -3.4bps lower ahead of today’s ECB meeting, respectively. Both ECB meetings so far this year have surprised on the hawkish side of expectations, which comes as inflation has continued to accelerate to the fastest since the single currency’s formation, at +7.5% in March. Today, however, our economists preview (link here) that they’re not expecting much change to the ECB’s message. Instead, they believe with the new staff forecasts in June, the ECB will announce that APP purchases will end in July, ahead of liftoff in September.

Equities were mixed in Europe, with the DAX falling -0.34%, while the STOXX 600 and CAC managed marginal gains of +0.03% and +0.07%, respectively. Farther from the conflict, the S&P 500 outperformed, climbing +1.12%, with mega-cap shares leading the way on falling discount rates, as the FANG+ climbed +2.06%. The S&P outperformance came amidst mixed results from some bellwether US financials, with JPM missing analyst earnings expectations while Blackrock sales came below expectations. In their release, JPM noted that they were increasing reserves to account for increased recession probabilities and to account for exposures to the war, two themes likely to suffuse earnings releases this season.

In other central bank news, the Bank of Canada rose rates by +50bps to 1.00%, as was expected, and announced that their bond purchases would stop on April 25, a decision that contained some intrigue. The 50bp hike was the largest since 2000; Canada is no outlier in fighting multi-decade high inflation. The BoC said interest rates would need to rise further, as there was growing risk of higher inflation expectations becoming entrenched, a primal fear for any central banker. How much further? President Macklem suggested rates may need to surpass neutral if inflation doesn’t moderate, and the BoC happened to revise their neutral rate 25bps higher to a range between 2% and 3%. They also revised higher their inflation and GDP forecasts for 2022, revising down their 2023 growth forecast to 3.2%, which is nevertheless still above trend growth.

US producer prices grew at a much faster rate than analysts were expecting, with final demand growing +11.2% year-on-year, versus expectations of +10.6%, while the core measure grew at +9.2%. Interesting enough, the elements of PPI that feed into core PCE were among those that printed to the soft side. Combined with the CPI data from the day before, our economists are expecting core PCE in March to grow at +0.25%