April 19, 2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

april19, 2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD; $1956.95 DOWN 26.05

SILVER: $25.29 DOWN $0.62

ACCESS MARKET: GOLD $1950.00

SILVER: $25.19

Bitcoin morning price: $40,789 UP 204

Bitcoin: afternoon price: $41,482 UP 897

Platinum price: closing UP $21.80 to $1014.75

Palladium price; closing UP 98.45 at $2434/15

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

comex notices/

: JPMorgan stopped/total issued 3/8

EXCHANGE: COMEX

CONTRACT: APRIL 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,982.900000000 USD

INTENT DATE: 04/18/2022 DELIVERY DATE: 04/20/2022

FIRM ORG FIRM NAME ISSUED STOPPED

132 C SG AMERICAS 2

624 H BOFA SECURITIES 1

657 C MORGAN STANLEY 7

661 C JP MORGAN 3

709 C BARCLAYS 1

737 C ADVANTAGE 1

880 H CITIGROUP 1

TOTAL: 8 8

MONTH TO DATE: 25,210

NUMBER OF NOTICES FILED TODAY FOR APRIL. CONTRACT 8 NOTICE(S) FOR 800 OZ (0.02488 TONNES)

total notices so far: 25,210 contracts for 2,521,000 oz (78.413 tonnes)

SILVER NOTICES:

0 NOTICE(S) FILED NIL OZ/

total number of notices filed so far this month 1199 : for 5,885,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

END

GLD

WITH GOLD DOWN $26.05

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

A SMALL CHANGE IN GOLD INVENTORY AT THE GLD A HUGE DEPOSIT OF 0.87 TONNES FROM THE GLD//

INVENTORY RESTS AT 1011.36 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 62 CENTS

AT THE SLV// A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WHOPPING DEPOSIT OF 5.771 MILLION OF INTO THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 575.447 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A HUGE SIZED 3369 CONTRACTS TO 170,125 AND CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE HUGE GAIN IN OI WAS ACCOMPLISHED DESPITE OUR $0.38 GAIN IN SILVER PRICING AT THE COMEX ON MONDAY. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.38) AND WERE UNSUCCESSFUL IN KNOCKING OUT ANY SILVER LONGS AS WE HAD A HUMONGOUS GAIN OF 4770 CONTRACTS ON OUR TWO EXCHANGES

WE MUST HAVE HAD:

I) HUGE BANKER SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A STRONG INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 4.305 MILLION OZ FOLLOWED BY TODAY’S QUEUE. JUMP OF NIL OZ//NEW STANDING: 6.300 MILLION OZ// V) HUGE SIZED COMEX OI GAIN/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS : —-376

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS APRIL. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF APRIL:

TOTAL CONTACTS for 12 days, total 10,051 contracts: 50.255 million oz OR 4.18MILLION OZ PER DAY. (838 CONTRACTS PER DAY)

TOTAL NO OF OZ UNDERGOING EFP TO LONDON 10,051 CONTRACTS X 5,000 PER CONTRACT:

EQUATES TO: 50.255 MILLION OZ

.

LAST 11 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

APRIL: 50.255 MILLION OZ (LOOKS LIKE OUR BANKERS ARE NOW LOATHE TO ISSUE EFP’S)

RESULT: WE HAD A GIGANTIC SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 3369 WITH OUR $0.38 GAIN IN SILVER PRICING AT THE COMEX// MONDAY THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE CONTRACTS: 1125 CONTRACTS ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A HUGE INITIAL SILVER OZ STANDING FOR MAR. OF 4.305 MILLION OZ FOLLOWED BY TODAY’S NIL OZ QUEUE JUMP//NEW STANDING: 6.300MILLION OZ/// .. WE HAD AN HUMONGOUS SIZED GAIN 4494 OI CONTRACTS ON THE TWO EXCHANGES FOR 22.47 MILLION OZ WITH THE GAIN IN PRICE.

WE HAD 0 NOTICES FILED TODAY FOR NIL OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A GOOD SIZED 4316 CONTRACTS TO 579,612 AND CLOSER TO NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: -12 CONTRACTS.

THE BIS HAS ABANDONED THE GOLD COMEX TRADING!!!

.

THE GOOD SIZED INCREASE IN COMEX OI CAME WITH OUR STRONG GAIN IN PRICE OF $11.20//COMEX GOLD TRADING/MONDAY /.AS IN SILVER WE MUST HAD HUGE BANKER/ALGO SHORT COVERING ACCOMPANYING OUR SMALL SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR APRIL AT 78.33 TONNES ON FIRST DAY NOTICE

YET ALL OF..THIS HAPPENED WITH OUR GAIN IN PRICE OF $11.20 WITH RESPECT TO MONDAY’S TRADING

WE HAD A STRONG SIZED GAIN OF 5646 OI CONTRACTS (17.56 PAPER TONNES) ON OUR TWO EXCHANGES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A SMALL SIZED 1330 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 579,612.

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 5646, WITH 4330 CONTRACTS INCREASED AT THE COMEX AND 1125 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 5646 CONTRACTS OR 17.56 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1330) ACCOMPANYING THE GOOD SIZED GAIN IN COMEX OI (4316,): TOTAL GAIN IN THE TWO EXCHANGES 5646 CONTRACTS. WE NO DOUBT HAD 1) HUGE BANKER SHORT COVERING ,2.) HUGE INITIAL STANDING AT THE GOLD COMEX FOR APRIL. AT 78.33 TONNES FOLLOWED BY TODAY’S 4700 OZ QUEUE JUMP //NEW STANDING 81.953 TONNES/// 3) ZERO LONG LIQUIDATION ///. ,4) GOOD SIZED COMEX OI. GAIN 5) SMALL ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

APRIL

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL :

26,256 CONTRACTS OR 2,625,600 OR 81.667 TONNES 12 TRADING DAY(S) AND THUS AVERAGING: 2188 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 12 TRADING DAY(S) IN TONNES: 81.667TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2020, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 81.667/3550 x 100% TONNES 2.30% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 81.667 TONNES (THIS IS GOING TO BE A LOW ISSUANCE MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF MAY.WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF APRIL HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF MAY, FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (MAR), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A GIGANTIC SIZED 3369 CONTRACT OI AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 1125 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 1125 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 3369 CONTRACTS AND ADD TO THE 1125 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUMONGOUS SIZED GAIN OF 4496 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 22.47 MILLION OZ

OCCURRED WITH OUR GAIN IN PRICE OF $0.38 IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

5. Other gold commentaries

6. Commodity commentaries/cryptocurrencies

3. ASIAN AFFAIRS

i)TUESDAY MORNING// MONDAY NIGHT

SHANGHAI CLOSED DOWN 1.49 PTS OR 0.05% //Hang Sang CLOSED DOWN 490.32 OR 2.28% /The Nikkei closed DOWN 16.76 PTS OR 0.68% //Australia’s all ordinaires CLOSED UP .58% /Chinese yuan (ONSHORE) closed DOWN 6.3874 /Oil UP TO 106.95 dollars per barrel for WTI and DOW TO 111.63 for Brent. Stocks in Europe OPENED ALL RED // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.3874 OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.3]4066: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER/

a)NORTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A GOOD SIZED 4316 CONTRACTS TO 579,612 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS GOOD COMEX INCREASE OCCURRED WITH OUR STRONG GAIN OF $11.20 IN GOLD PRICING MONDAY’S COMEX TRADING. WE ALSO HAD A FAIR SIZED EFP (1975 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE ACTIVE DELIVERY MONTH OF APRIL.. THE CME REPORTS THAT THE BANKERS ISSUED A SMALL SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 1330 EFP CONTRACTS WERE ISSUED: ;: , . 0 JUNE :1330 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1330 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 5646 CONTRACTS IN THAT 1330 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A GOOD SIZED COMEX OI GAIN OF 5646 CONTRACTS..AND THIS GAIN OCCURRED WITH OUR STRONG GAIN IN PRICE OF GOLD $11.20.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING FOR APRIL (81.953),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 81.953

THE BANKERS WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $11.20) AND AND WERE UNSUCCESSFUL IN FLEECING ANY LONGS AS WE HAVE REGISTERED A STRONG SIZED GAIN OF 17.604 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR APRIL (81.953 TONNES)…

WE HAD — 14 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 5646- CONTRACTS OR 564,600 OZ OR 17.56TONNES

Estimated gold volume today: 169,969/// poor

Confirmed volume yesterday: 141,265 contracts poor

INITIAL STANDINGS FOR APRIL ’22 COMEX GOLD //APRIL 19

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 2,731.929 oz 79 kilobars |

| Deposit to the Dealer Inventory in oz | 5787.180 OZ MANFRA 180 KILOBARS |

| Deposits to the Customer Inventory, in oz | 511.97 OZ BRINKS |

| No of oz served (contracts) today | 8 notice(s) 800 OZ 0.02488 TONNES |

| No of oz to be served (notices) | 1138 contracts 113800 oz 3.5396 TONNES |

| Total monthly oz gold served (contracts) so far this month | 25,210 notices 2,521,000 OZ 78.413 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For today:

dealer deposits 1

i) Into Manfra 5787.180 oz (180 kilobars)

total dealer deposit 5787.180 oz//

No dealer withdrawals

1 customer deposit

i) Into Brinks: 511.97 oz.

total customer deposit 511.97 oz

2 customer withdrawals

i) Out of Brinks 2539.929 oz

ii) Out of Manfra: 192.00 oz

total customer withdrawal: 2731.929 oz /

ADJUSTMENTS: dealer to customer/Brinks: 12,742.975 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR APRIL.

For the front month of APRIL we have an oi of 1146 contracts having LOST 28 contracts

We had 75 notices filed yesterday so we GAINED 47 contracts or an additional 4700 oz will stand for delivery at the comex

May saw a LOSS of 19 contracts to stand at 3540

June saw a GAIN of 42426 contracts UP to 479,086 contracts

We had 8 notice(s) filed today for 800 oz FOR THE APRIL 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 8 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 3 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the APRIL /2021. contract month,

we take the total number of notices filed so far for the month (25,210) x 100 oz , to which we add the difference between the open interest for the front month of (APRIL 1146 CONTRACTS ) minus the number of notices served upon today 8 x 100 oz per contract equals 2,634,800 OZ OR 81.953 TONNES the number of TONNES standing in this active month of APRIL.

thus the INITIAL standings for gold for the APRIL contract month:

No of notices filed so far (25,210) x 100 oz+ (1146) OI for the front month minus the number of notices served upon today (8} x 100 oz} which equals 2,634,800 oz standing OR 81.953 TONNES in this active delivery month of APRIL.

We GAINED 4700 additional oz that will stand for delivery on this side of the pond.

TOTAL COMEX GOLD STANDING: 81.807 TONNES (A WHOPPER FOR AN APRIL ( ACTIVE) DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

191,133,764.7, oz NOW PLEDGED /HSBC 5.94 TONNES

99,258.893 PLEDGED MANFRA 3.08 TONNES

54,339.114oz PLEDGED JPMorgan no 1 1.690 tonnes

243,923.704, oz JPM No 2 7.58 TONNES

898,821.330 oz pledged Brinks/27,96 TONNES

International Delaware:: 0

Loomis: 18,615.429 oz

total pledged gold: 1,884,464.742 oz 58.61 tonnes

TOTAL REGISTERED AND ELIG GOLD AT THE COMEX: 35,949,194.185 OZ (1118,17 TONNES)

TOTAL ELIGIBLE GOLD: 18,291,795.924 OZ (568.95 tonnes)

TOTAL OF ALL REGISTERED GOLD: 17,653,398.261 OZ (549.09 tonnes)

REGISTERED GOLD THAT CAN BE SERVED UPON: 15,768,934.0 OZ (REG GOLD- PLEDGED GOLD) 490.48 tonnes

END

APRIL 2022 CONTRACT MONTH//SILVER//APRIL 19

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 956,253.709 oz Brinks CNT |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 50,695.600 oz Brinks |

| No of oz served today (contracts) | 0CONTRACT(S )NIL OZ) |

| No of oz to be served (notices) | 61 contracts (305,000 oz) |

| Total monthly oz silver served (contracts) | 1199 contracts 5,995,,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

we had 0 deposit into the dealer

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 1 deposits into the customer account

i) Into Brinks: 50,695.600 oz

total deposit: 50,695.600 oz

JPMorgan has a total silver weight: 177.053 million oz/334.554 million =52.93% of comex

i) Comex withdrawals: 1

ii) Out of Brinks 555,134.681 oz

total withdrawal 555,134.681 oz

1 adjustments: dealer to customer//Manfra 215,997.700 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 86.389 MILLION OZ

TOTAL REG + ELIG. 334.534 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR APRIL

silver open interest data:

FRONT MONTH OF APRIL OI: 61, HAVING LOST 113 CONTRACTS FROM MONDAY. We had 113 notices filed yesterday,

so we GAINED 0 contracts or an additional NIL oz will stand on this side of the pond

MAY HAD A LOSS OF 2031 CONTRACTS DOWN TO 64,477 contracts

JUNE HAD A GAIN OF 63 TO STAND AT 1148

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 113 for 565,000 oz

Comex volumes: 75,650// est. volume today// good/

Comex volume: confirmed yesterday: 65,454 contracts ( fair )

To calculate the number of silver ounces that will stand for delivery in APRIL. we take the total number of notices filed for the month so far at 1199 x 5,000 oz = 5,995,000oz

to which we add the difference between the open interest for the front month of APRIL (61) and the number of notices served upon today 0 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the APRIL./2021 contract month: 1199 (notices served so far) x 5000 oz + OI for front month of APRIL (61) – number of notices served upon today (0) x 5000 oz of silver standing for the APRIL contract month equates 6,300,000 oz. .

We GAINED 0 contracts or an additional NIL oz will stand on this side of the pond

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

APRIL 19//WITH GOLD DOWN $26.90//A SMALL CHANGE IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .87 TONNES INTO THE GLD//INVENTORY RESTS AT 1100.36 TONNES

APRIL 18/WITH GOLD UP $11.20: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.93 TONNES FROM THE GLD..//INVENTORY RESTS AT 1099.44 TONNES

APRIL 14/WITH GOLD DOWN $8.90: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.32 TONNES INTO THE GLD..//INVENTORY RESTS AT 1104.42 TONNES

APRIL 13/WITH GOLD UP $8.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1093.10 TONNES

APRIL 12/WITH GOLD UP $26.95: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.61 TONNES INTO THE GLD///INVENTORY REST AT 1093.10 TONNES

APRIL 11/WITH GOLD UP $3.40 //A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD.//INVENTORY RESTS AT 1090.49 TONNES

APRIL 8/WITH GOLD UP $7.70: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES INTO THE GLD//INVENTORY RESTS AT 1088.75 TONNES

APRIL 7/WITH GOLD UP $13.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1087.30 TONNES

APRIL 6/WITH GOLD DOWN $4.10: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.68 TONNES FROM THE GLD..//INVENTORY RESTS AT 1087.30 TONNES

APRIL 5/WITH GOLD DOWN $5.70: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.75 TONNES FROM THE GLD//INVENTORY RESTS AT 1089.98 TONNES

APRIL 4/WITH GOLD UP $.70//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1091.73 TONNES

APRIL 1///WITH GOLD DOWN $19.00 : A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .29 TONNES INTO THE GLD///INVENTORY RESTS AT 1091.73 TONNES

MARCH 31/WITH GOLD UP $13.30 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD FROM MONDAY A WITHDRAWAL OF 1.71 TONNES FROM THE GLD:INVENTORY RESTS AT 1091.44

MARCH 28/WITH GOLD DOWN $14.65: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1093.18 TONNES

MARCH 25/WITH GOLD DOWN $7.60 : A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.52 TONNES INTO THE GLD///INVENTORY RESTS AT 1093.18 TONNES

MARCH 24/WITH GOLD UP $24.95: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.06 TONNES INTO THE GLD..//INVENTORY RESTS AT 1087.66 TONNES

MARCH 23/WITH GOLD UP $15.75//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1083.60 TONNES

MARCH 22/WITH GOLD DOWN $7.75: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.16 TONNES OF GOLD DEPOSITED INTO THE GLD//INVENTORY RESTS AT 1083.60 TONES

MARCH 21//WITH GOLD UP $.25 : A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 9.00 TONNES INTO THE GLD////INVENTORY RESTS AT 1082.44 TONES

MARCH 18/WITH GOLD DOWN $13.55 NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1073.44 TONES

MARCH 17/WITH GOLD UP $33.50: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.61 TONNES INTO THE GLD//INVENTORY RESTS AT 1073.44 TONNES

MARCH 16/WITH GOLD DOWN $18.50//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.33 TONNES FROM THE GLD///INVENTORY RESTS AT 1061.83 TONNES

MARCH 15/WITH GOLD DOWN $30.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1064.16 TONNES

MARCH 14//WITH GOLD DOWN $22.75, HUGE CHANGES IN GOLD INVENTORY AT THE GLD//STRANGE: A DEPOSIT OF 2.62 TONNES INTO THE GLD.//INVENTORY RESTS AT 1064.16 TONNES

MARCH 11/WITH GOLD DOWN $14.60: A BIG CHANGE IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 1061.54 TONNES

MARCH 10//WITH GOLD UP $11.55: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.06 TONNES FORM THE GLD///INVENTORY RESTS AT 1063.28 TONNES

MARCH 9/WITH GOLD DOWN $53.85//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.64 TONNES INTO THE GLD//INVENTORY RESTS AT 1067.34 TONNES

MARCH 8/WITH GOLD UP $46.10: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 8.42 TONNES INTO THE GLD///INVENTORY RESTS AT 1062.70 TONNES

MARCH 7/WITH GOLD UP $28.40 A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.06 TONNES INTO THE GLD..//INVENTORY RESTS AT 1054.28 TONNES

MARCH 4/WITH GOLD UP $28.40//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1050.22 TONNES

CLOSING INVENTORY FOR THE GLD//1100.36 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

APRIL 19/WITH SILVER DONW 62 CENTS: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .461 MILLION OZ FROM THE SLV INVENTORY…//INVENTORY RESTS AT 574.986 MILLION OZ

APRIL 18/WITH SILVER UP 38 CENTS: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.771 MILLION OZ INTO THE SLV./INVENTORY RESTS AT 575.447 MILLION OZ//

APRIL 14/WITH SILVER DOWN 25 CENTS : A MONSTROUS CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.355 MILLION OZ INTO THE SLV.//INVENTORY RESTS AT 569.676 MILLION OZ//

APRIL 13/WITH SILVER UP 27 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 565.521 MILLION OZ

APRIL 12/WITH SILVER UP 66 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 565.521 MILLION OZ//

APRIL 11/WITH SILVER UP 13 CENTS: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 831,000 OZ FORM THE SLV////INVENTORY RESTS AT 565.521 MILLION OZ

APRIL 8/WITH SILVER UP 11 CENTS :NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 566.352 MILLION OZ//

APRIL 7/WITH SILVER UP 27 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 566.352 MILLION OZ//

APRIL 6/WITH SILVER DOWN 9 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 566.352 MILLION OZ

APRIL 5/WITH SILVER DOWN 16 CENTS : A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.386 MILLION OZ INTO THE SLV..//INVENTORY RESETS AT 566.352 MILLION OZ//

APRIL 4/WITH SILVER DOWN 5 CENTS TO CHANGES IN SILVER INVENTORY AT THE SLV//: A DEPOSIT OF 6.326 MILLION OZ//INVENTORY REST AT 564.966 MILLION OZ//

APRIL 1/WITH SILVER DOWN 39 CENTS A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.302 MILLION OZ INTO THE SLV////INVENTORY REST AT 558.647 MILLION OZ//

MARCH 31/WITH SILVER UP 3 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 2.171 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 556.345 MILLION OZ

MARCH 28/WITH SILVER DOWN 30 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.847 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 554.167 MILLION OZ//

MARCH 25/WITH SILVER DOWN 20 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 552.320 MILLION OZ//

MARCH 24/WITH SILVER UP 54 CENTS TODAY; A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.092 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 552.320 MILLION OZ//

MARCH 23/WITH SILVER UP 24 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 550.288 MILLION OZ//

MARCH 22/WITH SILVER DOWN $0.29 TODAY : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 550.288 MILLION OZ//

MARCH 21/WITH SILVER UP 16 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 550.288 MILLION OZ//

MARCH 18/WITH SILVER DOWN 37 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.217 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 550.288 MILLION OZ//

MARCH 17/ WITH SILVER UP 72 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.049 MILLION OZ INTO THE SLVV//INVENTORY RESTS AT 548.071 MILLION OZ

MARCH 16/WITH SILVER DOWN 56 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 462,000 OZ FROM THE SLV//INVENTORY RESTS AT 544.560 MLLION O

MARCH 15/WITH SILVER DOWN 18 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 545.022 MILLION OZ

MARCH 14/WITH SILVER DOWN 64 CENTS TODAY; STRANGE A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.125 MILLION OZ/INVENTORY RESTS AT 545.022 MILLIONOZ

MARCH 11/WITH SILVER DOWN 13 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.897 MILLION OZ

MARCH 10/WITH SILVER UP 39 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.897 MILLION OZ/

MARCH 9/WITH SILVER DOWN 88 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 5.174 MILLION OZ OF FAKE SILVER.//INVENTORY RESTS AT 542.897 MILLION OZ//

MARCH 8/WITH SILVER UP 88 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.217 MILLION OZ INTO THE SLV////INVENTORY RESTS A 548.071 MILLION OZ//

MARCH 7/WITH SILVER UP 40 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 545.854 MILLION OZ//

MARCH 4/WITH SILVER UP 50 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 545.854 MILLION OZ/

SLV FINAL INVENTORY FOR TODAY: 574.986 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

Oof! That Didn’t Age Well!

TUESDAY, APR 19, 2022 – 03:42 PM

Authored by Michael Maharrey via SchiffGold.com,

On July 23, 2020, CNBC published an article by Elizabeth Schulze headlined: Here’s why economists don’t expect trillions of dollars in economic stimulus to create inflation.

That one didn’t age well, did it?

At the time CNBC published this article, the Federal Reserve had expanded its balance sheet from $4 trillion to roughly $7 trillion. (We’re now knocking on the door of $9 trillion.) That means when this article was published, the central bank had created about $3 trillion out of thin air and injected it into the economy. But as Schulze pointed out, the Fed was still projecting “inflation will stay below the central bank’s 2% target over the next two years.”

Oops.

Before we even get to the poor economic analysis that led “economists” to this wildly wrong conclusion, it’s important to point out that the headline was obviously wrong from the very moment it was published.

Creating $3 trillion out of thin air is — by definition — inflation.

When we talk about “inflation” today, most people immediately think about rising prices. That is indeed one of the effects of inflation. But that isn’t inflation itself. Properly defined, inflation is an increase in the money supply. In fact, that used to be the standard definition of inflation. Over time, the government and media pundits have changed the definition. Today, pretty much everybody defines inflation as rising prices.

Economist Frank Shostak explained why getting the definition of inflation right matters.

Policymakers that focus on increases in prices in order to establish the status of inflation while ignoring increases in money supply are likely to misread the state of the economy. As a result, these policymakers and various economic commentators are likely to be surprised on account of the unexpected economic shocks. It follows, then, that employing an unsound definition of what inflation is all about can produce a disastrous economic outcome. It also implies that a central bank policy of stabilizing prices in order to secure stable inflation is erroneous.”

This is exactly what we see in this CNBC article – a disastrous misreading of the economy.

When we understand the actual definition of inflation, we recognize that this is a dumb headline on its face. It’s basically telling you that economists didn’t expect creating inflation to create inflation. This is obviously nonsensical. At the time Schulze penned this article, the Fed had already created $3 trillion in inflation.

Of course, Schulze was really trying to convince you that the inflation the Fed created wasn’t going to manifest itself in rising consumer prices. In hindsight, we also know this was completely wrong.

So, why didn’t economists think that creating $3 trillion out of thin air and injecting it into the economy wouldn’t cause prices to rise?

It was the typical Keynesian claptrap about aggregate demand.

Most mainstream economists believe it’s OK to pump money into the economy during a recession because demand drops. As unemployment rises and the economy tanks, people spend less. As Schulze put it, “Supply shocks have driven up prices for some goods in recent months. Yet many economists expect consumer prices will stay low despite trillions of dollars in government stimulus.”

She then backed up her statement with a quote from Evercore ISI Vice-Chairman Krishna Guha.

While there certainly is quite a lot of disruption to the supply side of the economy, that’s likely to be dominated by the huge hit to aggregate demand.”

Three months before CNBC published this article, the US government had already sent out the first round of stimulus checks. This is where the entire narrative falls apart. Peter Schiff explained exactly what happened during a recent interview with Megyn Kelly.

We told people not to go to work, not to be productive. Don’t help make stuff. Don’t provide services. But here’s a bunch of money to go out and spend. We want you buying stuff even though you aren’t making stuff. And so we flooded the country with money at the same time the production of goods and services slowed down. And of course, prices went up. It’s not a surprise. It’s exactly what I was saying was going to happen when we first went down this misguided path. So, we’re simply reaping the whirlwind of the wind that we sowed.”

But in July 2020, Peterson Institute for International Economics senior fellow Olivier Blanchard told CNBC that the stimulus wasn’t increasing demand and that while the stimulus checks helped “they didn’t lead to a boom in demand.”

So, what did policymakers do? They tripled down with two more rounds of stimulus.

I guess you could maybe argue that the first stimulus was fine but the third was just too much? Or maybe the extra $2 trillion the Fed created after Schulze penned her tome pushed the Consumer Price Index over the edge.

That could be what happened. But it probably wasn’t.

In fact, creating trillions of dollars out of thin air and handing them out was doomed from the start.

It’s fair to say that Schulze and the economists she interviewed in July 2020 couldn’t have known that there would be more stimulus checks handed out (although there was already talk of round two). But they had to know that once the economy started opening up, demand would quickly return. And they had to know that those trillions of dollars would still be floating around out there. So, they should have anticipated big price increases.

In fact, those price increases began showing up just six months later. At that point, the Fed started spinning the “transitory” inflation narrative — another wildly wrong assumption.

The central bankers and mainstream economists have been wrong about inflation every step of the way, from CNBC’s now clearly ridiculous analysis, to “transitory” inflation, to “Putin’s Price Hike.”

Now they are telling us that everything will be fine. The Fed will raise rates a bit and maybe shrink that balance sheet some and the inflation fire will die out. We’re told the economy is strong enough to handle tighter monetary policy. But at this point, shouldn’t we approach what these people say with at least a little bit of skepticism?

END

2.LAWRIE WILLIAM//,//Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, James RICKARDS/

3. Chris Powell of GATA provides to us very important physical commentaries

Craig Hemke warns about the TAS/spreader liquidation which will arrive around the 23 of april.

Craig Hemke at Sprott Money: Watching the silver futures calendar

Submitted by admin on Mon, 2022-04-18 17:44Section: Daily Dispatches

5:40p ET Monday, April 18, 2022

Dear Friend of GATA and Gold:

Craig Hemke of the TF Metals Report, writing today at Sprott Money, cautions that the “trade at settlement” mechanism for silver futures price suppression will be especially active in the next week.

Hemke writes: “All this incessant manipulation does not preclude prices headed higher. The banks operate this scheme for profit, and they can profit each month just as easily at $35 as they can at $25. You, as the trader/investor/enthusiast, simply need to understand these processes so that you can time your own trading actions for maximum personal impact.”

Hemke’s analysis is headlined “Watching the Calendar” and it’s posted at Sprott Money here:

https://www.sprottmoney.com/blog/Watching-the-Calendar-Craig-Hemke-April-18-2022

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Eric Sprott’s makes his biggest bet yet on New Found gold. He rarely misses

(Friedman/NationalPost/GATA)

Eric Sprott makes his biggest bet yet on what could be ‘the greatest gold discovery in Canada’

Submitted by admin on Mon, 2022-04-18 21:37Section: Daily Dispatches

The billionaire, who was an early backer of what became one of the world’s largest gold miners, says this one is even bigger.

* * *

By Gabriel Friedman

National Post / Financial Post, Toronto

Monday, April 18, 2022

Bay Street legend Eric Sprott, who became a billionaire betting on gold and silver, just made his biggest investment yet in a precious metals exploration company.

Last week Sprott, the founder of asset manager Sprott Inc., announced that he had purchased $125.9 million of shares in New Found Gold Corp., an early-stage exploration company that holds exclusive rights to a project in Newfoundland and Labrador that has yielded promising initial drill results but has no official mineral resource.

“I do believe it is special,” Sprott said in an interview. “It’s going to prove to be maybe the greatest gold discovery in the history of Canada, if not in the world. … So that’s what makes it so easy for me to put that additional money in it.”

Sprott retired from the firm he created in 2017 and now invests his own money. But the 77-year-old still has a great deal of influence, as he remains one of the most deep-pocketed and bullish investors in Canada’s precious-metal mining industry.

Sprott has spent hundreds of millions of dollars to obtain stakes in dozens of tiny, often penny-stock companies. In recent years his reputation was bolstered by his role as an early backer of Kirkland Lake Gold Ltd., which grew from obscurity into one of the largest gold miners in the world, valued at $13.5 billion last year when it merged into Agnico Eagle Mines Ltd. …

… For the remainder of the report:

* * *

4.OTHER GOLD/SILVER COMMENTARIES

5.OTHER COMMODITIES

CORN

Corn exceeds $8 a bushel for the first time in 10 years as shortages continue

(zerohedge)

Corn Exceeds $8 A Bushel For First Time In Decade On Shortage Fears

MONDAY, APR 18, 2022 – 07:25 PM

A combination of factors has sent corn futures in Chicago to the highest level in a decade as investors fret over dwindling supplies.

Corn futures haven’t exceeded $8 a bushel since September 2012, following a devastating drought that damaged crops across the U.S. Midwest. Now supply risks return but for different reasons.

The global outlook for corn supplies has plunged since Russia’s invasion of Ukraine began in late February. The war-torn country supplies a fifth of the world’s corn and could experience a 50% decline in output this year.

Soaring fertilizer costs have forced some farmers in the U.S. to increase plantings of soybeans this growing season versus corn as the crop requires fewer nutrients.

Fertilizer prices are at record highs because of rising natural gas costs and Russia limiting fertilizer exports to ‘unfriendly‘ countries. Russia is one of the biggest exporters globally — the U.S. just so happens to be a large importer of nitrogen and potash from Russia.

And the latest development pushing corn prices to the stratosphere is the Biden administration’s announcement of emergency measures last week to expand biofuel sales to curb soaring gasoline prices. The problem with this move is that the ethanol industry absorbs a larger share of the corn crop, which would curb supplies to the food industry. So ultimately, it would increase prices.

This is happening as global food prices jumped a stunning 12.64% MoM in March – almost double the previous record monthly surge…

Global food prices have exceeded levels only seen during the inflation riots of 2010/11, known as Arab Spring.

Investors appear to be pricing in a corn shortage. It’s never been a better time to start growing your own garden

end

COMMODITIES IN GENERAL

6.CRYPTOCURRENCIES

7. GOLD/ TRADING TODAY

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings TUESDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 6.3874

OFFSHORE YUAN: 6.4066

HANG SANG CLOSED DOWN 490.32 PTS OR 2.28%

2. Nikkei closed DOWN 293.48PTS OR 1.08%

3. Europe stocks ALL RED

USA dollar INDEX UP TO 100.86/Euro RISES TO 1.0783

3b Japan 10 YR bond yield: RISES TO. +.244/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 128.19/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 106.95 and Brent: 111.63

3f Gold UP /JAPANESE Yen DOWN CHINESE YUAN: DOWN -SHORE CLOSED UP// OFF- SHORE DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.0.922%/Italian 10 Yr bond yield RISES to 2.53% /SPAIN 10 YR BOND YIELD FALLS TO 1.84%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 1.61: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield RISES TO : 2.95

3k Gold at $1979.15 silver at: 25.95 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3l USA vs Russian rouble;// Russian rouble UP 0 & 7/8 roubles/dollar; ROUBLE AT 78.86

3m oil into the 106 dollar handle for WTI and 111 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 128.19 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning .9466– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0221 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 2.876 UP 1 BASIS PTS

USA 30 YR BOND YIELD: 2.973 UP 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 14.66

Futures Flat As Yen Discombobulation Extends To Record 13th Day

TUESDAY, APR 19, 2022 – 08:05 AM

After some jerky rollercoaster moves in Monday’s illiquid trading session, which jerked both higher and lower before closing modestly in the green, US futures resumed their volatility and at last check were trading flat after earlier in the session rising and falling; Nasdaq futures retreated 0.1%. as investors weighed the risks to economic growth from hawkish Federal Reserve comments. Stocks in Europe dropped as markets reopened after the Easter holiday, while bonds around the globe slumped as investors weighed the prospect of aggressive policy action to curb inflation. Asian stocks also dropped as did oil, while the dollar extended its gains . Treasuries extended declines, with the 10-year yield hitting a fresh three-year peak north of 2.90%. German and U.K. 10-year yields climbed to the highest since 2015 as bonds across Europe plunged.

The grotesque farce that is MMT came one step closer to total collapse as the yen dropped for a record 13th day, its longest-losing streak in at least half a century with the credibility of the BOJ – that central bank that launched MMT, QE and NIRP – now hanging by a thread. It wasn’t all bad news however, because with the yen losing more of its purchasing power, Japanese stocks gained.

Disruptions to supply chains from China’s lockdowns and to commodity flows from the war are keeping pressure on central banks to rein in runaway prices at a time when global growth is tipped to slow. The World Bank cut its forecast for global economic expansion this year on Russia’s invasion.

Meanwhile, investors – already betting on an almost half-point Federal Reserve rate increase next month – continue monitoring comments from policy makers as prospects of monetary tightening weigh on the sentiment. St Louis Fed President James Bullard said the central bank needs to move quickly to raise interest rates to around 3.5% this year with multiple half-point hikes and that it shouldn’t rule out rate increases of 75 basis points. The last increase of such magnitude was in 1994.

“The Bullard comments really encapsulate the quandary that many of the world’s central banks have found themselves in,” said Jeffrey Halley, a senior markets analyst at Oanda. “Luckily, they have plenty of excuses in the shape of the pandemic and the Ukraine war. Central banks can now play catchup, hike aggressively and run the risk of recessions. Getting the pain over and done may be the least worst option.”

Over in Ukraine, President Volodymyr Zelenskiy said Monday that Russian forces had begun the campaign to conquer the Donbas region in Ukraine’s east. Here are all the latest news and headlines over Ukraine:

- Russia’s Belgorod provincial Governor said a village near the Ukrainian border was struck by Ukraine, according to RIA. However, Sputnik noted that no casualties were reported.

- Russian Foreign Minister Lavrov says another stage of its operation is beginning

- Russian Defence Ministry is calling on Ukrainian and foreign fighters to leave the metallurgical plant in Mauripol without arms and ammunition today, via Reuters; adding, the US and other Western countries do everything to drag out the Ukrainian military operation.

- White House said US President Biden will hold a call with allies and partners on Tuesday to discuss continued support for Ukraine and efforts to hold Russia accountable, according to Reuters.

- French Finance Minister Le Maire says an embargo on Russian oil is being worked on, adds that we have always said with President Macron that we want such an embargo, via Reuters; aims to convince the EU on such an embargo in the coming weeks.

- Russia’s Gazprom has not booked gas transit capacity via Yamal-Europe pipeline for May.

In premarket trading, Zendesk rose 4.1% in premarket trading after a report about the software company hiring a new adviser to explore a potential sale. NXP Semiconductors dropped 2.5% in premarket trading after Citi cut the stock to neutral from buy, saying in note that its thesis on margin expansion has played out. Other notable premarket movers include:

- Amazon (AMZN US) could be active as Barclays analyst Ross Sandler is upbeat on it heading into 1Q results and sees gross merchandise value (GMV) accelerating on a 1-yr basis in 2Q.

- Netgear (NTGR US) dropped 11% in extended trading Monday after reporting preliminary net revenue for the first quarter that trailed the average analyst estimate.

- Super Micro Computer (SMCI US) climbed 15% after the maker of server and storage systems reported fiscal 3Q preliminary profit and sales that beat the average analyst estimate.

- Acadia (ACAD US) shares declined in postmarket after it said Phase 2 clinical trial of the efficacy and safety of ACP-044 for acute pain following bunion removal surgery didn’t meet the primary endpoint.

- WeWork (WE US) advanced in postmarket trading Monday as coverage starts with an overweight rating and $10 price target at Piper Sandler, which highlights that the co-working company is on track to achieve profitability by late 2023 or early 2024.

European stocks slumped with the Stoxx 600 dropping 1.1% led lower by healthcare and media shares as traders returned from a lengthy Easter holiday, with technology stocks also underperforming; the energy sub-index the only sector gaining in Europe in Tuesday trading as investors digest the recent rally in crude prices. Meanwhile in Russia equities fell for a second day with the benchmark MOEX Index dropping as Russia’s military pressed on with its offensive in southern and eastern Ukraine, with President Volodymyr Zelenskiy saying Moscow had launched a new campaign focused on conquering the Donbas region. The MOEX dropped as much as 3.2%, adding to declines of 3.4% on Monday with Lukoil, Sberbank and Gazprom leading losses. Here are some of Europe’s biggest movers:

- TotalEnergies rises as much as 3.6% to the highest level since the end of last month after reporting higher refining margins, as well as better liquids and gas prices

- Spectris gains as much as 6.3% after the firm said it will sell its Omega Engineering business to Arcline Investment Management for $525m, and also announced a GBP300m buyback program

- Carrefour climbs as much as 3% as Berenberg upgrades to buy from hold, saying that higher inflation is making the food retail sector more challenging, but will also reveal outperformers

- Virbac advances as much as 11% after the French maker of veterinary products raised the top end of its sales growth forecast. Oddo upgraded the stock to outperform.

- Food delivery shares lead European tech lower as U.S. Treasury yields touch new highs following a hawkish comment from a Federal Reserve President, Just Eat Takeaway -4.5%; Delivery Hero -2.5%

- European consumer staples and luxury stocks fall as markets reopen after a 4-day break, with higher inflation and looming interest-rate hikes at the forefront of investor worries

- L’Oreal, which reports 1Q sales after the market close today, slumps as much as 4.1%; LVMH decreases as much as 1.9%, Hermes down as much as 4%

- Wizz Air drops as much as 6.1% after being downgraded to reduce at HSBC, with the broker saying the low-cost airline’s decision to not hedge its fuel prior to the outbreak of the Ukraine war could bite

- Adevinta falls as much as 9.8% after Bank of America downgraded to underperform from neutral on Thursday, due to the classifieds business’s large exposure to the automotive sector

- Elior and SSP Group shares retreat after both are downgraded to hold from buy at Deutsche Bank on downside risks; Elior down as much as 3.7%, SSP as much as 6.1%

Earlier in the session, Hong Kong technology names declined on ongoing concerns over regulation. China dropped as investors assessed measures to tackle economic headwinds from Covid-led lockdowns.

Asian stocks declined for a third day, as continued concerns over China’s regulatory crackdowns and the prospect of aggressive monetary-policy tightening by the Federal Reserve weighed on sentiment. The MSCI Asia Pacific Index fell as much as 0.6%, with Chinese technology shares including Tencent and Alibaba the biggest drags after Beijing announced a “clean-up” of the video industry. Hong Kong stocks were the worst performers around the region as trading resumed after Easter holidays, while equities rose in Japan and South Korea. The People’s Bank of China on Monday announced measures to help businesses hit by Covid-19, as the latest economic data started to show the impact of extended lockdowns.

Investors are awaiting further easing with the release of China’s loan prime rates on Wednesday, after the central bank last week announced a smaller-than-expected cut in the reserve requirement for banks. Whether policy support measures will “flow significantly into the economy will be on watch,” and market participants may “want to see signs of recovery before taking on more risks in that aspect,” said Jun Rong Yeap, a strategist at IG Asia Pte. Hawkish Fed member James Bullard raised the possibility of a 75 basis-point hike in interest rates. Concerns of inflation and moves by the Fed and other central banks to fight it have driven the recent global equity selloff, with the Asian benchmark down about 11% this year.

In China, markets are also awaiting the release of banks’ benchmark lending rates on Wednesday after the People’s Bank of China reduced the reserve requirement ratio for most banks Friday but refrained from cutting interest rates. The latest policy measures “have really highlighted easing is required,” Gareth Nicholson, Nomura chief investment officer and head of discretionary portfolio management, said on Bloomberg Television. “The markets don’t believe enough has been done and they’re going to have to step it up.”

Japanese equities gained, rebounding after two days of losses as the continued weakening of the yen bolstered exporters. Electronics and auto makers were the biggest boosts to the Topix, which rose 0.8%. Tokyo Electron and Advantest were the largest contributors to a 0.7% rise in the Nikkei 225. The yen extended declines to a 13th straight day, its longest losing streak on record, falling through 128 per dollar.

Australian stocks also advanced, with the S&P/ASX 200 index rising 0.6% to close at 7,565.20 as trading resumed following Easter holidays. The energy and materials sectors gained the most. Cleanaway was among the biggest gainers, climbing the most since April 2021 after a media report said KKR has been preparing an offer for the Australian waste management company. City Chic Collective was the biggest decliner, falling to its lowest since December 2020. In New Zealand, the S&P/NZX 50 index fell 0.5% to 11,835.88.

In rates, Treasuries slipped, with yields rising by as much as 6bps in the long end of the curv, however they traded off session lows reached during European morning as those markets reopened after a four-day holiday. Yields beyond the 5-year are higher by 3bp-4bp, 10-year by 3.3bp at 2.89% after rising above 2.90% earlier; U.K. and most euro-zone 10-year yields are higher by at least 5bp, correcting spreads vs U.S. created Monday when those markets were closed. The yield curve continues to steepen; 7- to 30-year yields reached new YTD highs, nearly 3% for 30-year. Japanese government bonds were mixed. Focal points for U.S. session are corporate new-issue calendar expected to include more financial offerings and comments by Chicago Fed President Evans.

In FX, the Bloomberg Dollar Spot Index was little changed, after earlier rising to its highest since July 2020, and the dollar fell against almost all of its Group-of-10 peers. Commodity-related currencies and the Swedish krona were the best performers while the Japanese currency fell versus all of its G-10 peers. The yen extended its longest-losing streak in at least half a century, and touched 128.45 per dollar, its weakest level since May 2002, amid concerns over further widening in yield differentials. The euro reversed an Asia session loss even amid another round of bearish option bets in the front-end due to political risks. Bunds extended a slump, underperforming Treasuries, before a five-year debt sale and as money markets increased ECB tightening wagers. The Australian dollar surged against the yen to levels last seen almost seven year ago. RBA minutes said quicker inflation and a pickup in wage growth have moved up the likely timing of the first interest-rate increase since 2010. The New Zealand dollar also advanced; RBNZ Governor Orr reiterated the central bank’s aggressive rate stance. The pound was little changed and gilts slid, sending the U.K. 10-year yield to the highest since 2015 as money markets bet on a faster BOE policy tightening path.

In commodities, crude futures declined. WTI trades within Monday’s range, falling 1.5% to trade around $106. Brent falls 1.5% to ~$111. Most base metals trade in the green; LME copper rises 1.4%, outperforming peers. Spot gold is down 0.1% to $1,977/oz.

Bitcoin was flat and holding steady at the bottom of the sessions USD 40.6-41.2k parameters.

Looking at the day ahead, data is light with US March building permits, housing starts, and Canada March existing home sales. The IMF will also release their 2022 World Economic Outlook.

Market Snapshot

- S&P 500 futures up 0.3% to 4,401.75

- STOXX Europe 600 down 0.8% to 456.07

- MXAP down 0.4% to 171.55

- MXAPJ down 0.3% to 570.60

- Nikkei up 0.7% to 26,985.09

- Topix up 0.8% to 1,895.70

- Hang Seng Index down 2.3% to 21,027.76

- Shanghai Composite little changed at 3,194.03

- Sensex up 0.5% to 57,438.93

- Australia S&P/ASX 200 up 0.6% to 7,565.21

- Kospi up 1.0% to 2,718.89

- German 10Y yield little changed at 0.91%

- Euro up 0.2% to $1.0808

- Brent Futures down 0.7% to $112.40/bbl

- Brent Futures down 0.7% to $112.40/bbl

- Gold spot up 0.1% to $1,979.91

- U.S. Dollar Index little changed at 100.73

Top Overnight News from Bloomberg

- Record numbers of U.K. business leaders expect operating costs to soar this year as inflation proves more sticky than thought, according to a survey by Deloitte

- French President Emmanuel Macron led his rival Marine Le Pen 55.5% to 44.5% ahead of the run-off presidential election set for April 24, according to a polling average calculated by Bloomberg on April 19. The gap between them has widened from the 8.2 percentage points recorded on April 15

- Nationalist leader Marine Le Pen never led in the three campaigns she’s run for France’s top job, but a protectionist stance on economic issues in recent years has allowed her to reach some voters who traditionally backed left- wing candidates

- China’s central bank announced a spate of measures to help an economy which has been hit by lockdowns to control the current Covid outbreak, but the focus on boosting credit likely means the chances for broad-based easing are shrinking

A more detailed breakdown courtesy of Newsquawk

Asia-Pac stocks saw a mixed performance as more markets reopened and trade picked up from the holiday lull. ASX 200 gained on return from the extended weekend, led by strength in commodity-related sectors and top-weighted financials. Nikkei 225 briefly reclaimed the 27k level as continued currency depreciation underscored the Fed and BoJ policy divergence. Hang Seng was pressured as it took its first opportunity to react to the PBoC’s underwhelming policy decisions and with tech hit after Shanghai’s market regulator summoned 12 e-commerce platforms including Meituan on price gouging during COVID outbreaks. Shanghai Comp was choppy as participants mulled over the latest virus-related developments including an increase in Shanghai deaths and the lockdown of five districts in the steel producing hub of Tangshan, although policy support pledges from the PBoC and NDRC ultimately provided a cushion.

Top Asian News

- Japan’s Stepped-Up Warnings Fail to Stem Yen’s Slide Past 128

- China’s Promises to Support Covid-Hit Economy Fail to Impress

- China Tech Stocks Slump on Didi Delisting Plan, Regulation Woes

- Sri Lanka Officially Requests Rapid IMF Funds Amid Crisis

European bourses are negative on the session but were choppy and rangebound for much of the morning before dropping further amid renewed yield upside, Euro Stoxx 50 -1.4%. Stateside, US futures have given up their initial positive performance and are now lower across the board, ES -0.3%, and the NQ -0.4% lags given yield action; session is focused on Fed speak and earnings with NFLX due. Truist Financial Corp (TFC) Q1 2022 (USD): Adj. EPS 1.23 (exp. 1.10), Revenue 5.32bln (exp. 5.47bln)

Top European News

- Stellantis Idles One of Russia’s Last Auto Plants Left Running

- Commodities Trader Gunvor Doubled Profits on Hot Gas Market

- European Gas Falls to Lowest Since Russian Invasion of Ukraine

- Credit Suisse’s Top China Banker Tu Steps Aside for New Role

FX:

- USD/JPY breezes through more option barriers and disregards more chat from Japanese officials about demerits of Yen weakness; pair pulls up just pips shy of 128.50.

- DXY tops 101.000 in response before pulling back as Europeans return from long Easter break.

- Aussie outperforms as RBA minutes highlight more recognition about inflationary environment externally and internally.

- Kiwi next best G10 currency as RBNZ Governor Orr underlines that policy is being weighted towards anchoring inflation expectations; AUD/USD hovers under 0.7400 and NZD/USD around 0.6750

- Euro trying to hold near 1.0800 where 1.3bln option expiry interest rolls off at the NY cut, Pound regains 1.3000 plus status and Loonie pivots 1.2600 on the eve of Canadian CPI.

- Yuan close to 6.4000 ahead of Chinese LPR rate verdict on Wednesday amidst heightened easing expectations.

Fixed income:

- EU bonds correct lower after long Easter holiday weekend then pick up the baton to push US Treasuries even lower; Bunds giving up 154.00 and dropping to a 153.58 trough in short order and USTs lower to the tune of 7 ticks.

- Decent demand for German Bobls, but high price in terms of yield and a larger retention – limited relief seen in the benchmark, given broader action.

- Benchmark 10 year cash rates approaching new psychological marks of 1.0%, 2.0% and 3.0% in Bunds, Gilts and T-notes respectively.

Commodities

- Crude benchmarks are softer after yesterday’s firmer session, which was driven by Libya supply concerns, currently moving in tandem with broader equity performance awaiting fresh geopolitical developments.

- Currently, WTI and Brent are modestly above session lows which reside sub USD 106/bbl and USD 111/bbl respectively.

- OPEC+ produced 1.45mln BPD below targets during March, via Reuters citing a report; compliance 157% (132% in February).

- Spot gold and silver are contained with the yellow metal pivoting USD 1975/oz while copper derives further impetus from Peru protest activity.

- MMG said protesters at the Las Bambas copper mine alleged a failure to comply with social investment commitments, while it rejected the allegations and noted that Las Bambas will be unable to continue copper output as of April 20th.

US Event Calendar

- 08:30: March Building Permits MoM, est. -2.4%, prior -1.9%, revised -1.6%

- 08:30: March Housing Starts MoM, est. -1.6%, prior 6.8%

- 08:30: March Building Permits, est. 1.82m, prior 1.86m, revised 1.87m

- 08:30: March Housing Starts, est. 1.74m, prior 1.77m

Central Bank Speakers

- 12:05: Fed’s Evans Speaks to Economic Club of New York

DB’s Tim Wessel concludes the overnight wrap

Welcome back to another holiday-shortened week for many markets. What it lacks in tier one data releases, it makes up for with heavy hitting central bank speakers and a core European Presidential election. We’re also wading into the thick of earnings season, while the on-running war in Ukraine has the potential to tip markets in any direction at the speed of a headline.

Starting with the central bankers, President Lagarde and Chair Powell will sit on an IMF panel to discuss the global economy in the last Fed communications before their May meeting blackout period. The Fed has primed markets for a +50bp hike in May, and pricing has obliged, with futures placing a 98.1% probability of a +50bp rise, along with +246bps of tightening for the entire year. Governor Bailey won’t miss out on the action and is also delivering an address Thursday. Other Fed regional Presidents will speak throughout the week, with the Fed’s Beige Book due Wednesday. The IMF, meanwhile, will release their global outlook later today. As a reminder, DB Research updated our World Outlook earlier this month, where we are calling for recessions in the US and the euro area within the next two years. Plenty more in the link here.

US earnings season will diversify beyond the financials-heavy slate from last week. Today is a nice microcosm of the change up, showcasing earnings from Johnson & Johnson, Halliburton, Hasbro, Lockheed Martin, Netflix, and IBM.

On data the rest of the week, we’ll receive German PPI and Canadian CPI Wednesday, along with global PMIs Friday. US housing data dot the rest of the week, as we unravel the competing threads of tight inventories, heightened demand, and supply constraints, against higher mortgage rates on housing activity.

Finally, the second round of the French Presidential election is this coming Sunday. Politico’s latest polling aggregates still have incumbent President Macron outpacing Marine Le Pen by around 9% in Sunday’s runoff. Our Europe team has their takeaways from the first round here.

The ECB’s April meeting garnered top billing during the EMR’s long weekend (our Euro econ team’s full review here). Overlaid on an inflationary backdrop, the Governing Council is weighing the downside risk to growth against the upside risk to inflation stemming from the recent conflict. While uncertainty pervades, the latter risks are more pressing, which drove their decision to signal net APP purchases would end in Q3, paving the way for policy rate liftoff later this year. Our economists expect the last APP net purchases will occur in July, with the risk skewed toward June, with a +25bp liftoff in September. Markets have +11.8bps of hikes priced by July, +35.6bps by September, and +64.4bps of hikes through 2022.

There was no new tool to address market fragmentation, though the ECB signaled imperfect policy transmission would not stand in the way of lifting rates and a new tool would be created if need be. 10yr BTP spreads were -5.0bps tighter to bunds over the week, and +3.3bps wider the day of the meeting.

Elsewhere, as mentioned, a suite of US financials reported. Looking through the releases, it seems most FICC trading desks benefitted from the quarter of volatility and higher rates are set to improve margins. However, the prospect of an economic slowdown or potential exposures to war fallout cloud the outlook. S&P 500 financials were -2.65% lower on the week.

Taking a longer view of last week, sovereign yields marched higher on the back of tighter expected monetary policy, and the yield curve’s recent sharp steepening continued. 10yr Treasury and bund yields respectively increased +12.8bps (+12.9bps Thursday, +2.5bps yesterday) and +13.5bps (+7.6bps Thursday) with continued heightened volatility. Real yields drove most of the gains in the US (+10.2bps for the week, +4.6bps Thursday, -1.0bps yesterday), ending the week at -0.09%, the highest level since early 2020. 10yr real yields are now +101.7bps higher this year, having had their climb only briefly interrupted by Russia’s invasion of Ukraine. The 2s10s Treasury curve steepened +19.1bps (+2.5bps Friday, +2.9bps yesterday).

There were not many positives to hang onto in Ukraine last week. Negotiation progress turned sour, President Biden labeled Russia’s invasion a ‘genocide’, and the US upped the provision of heavy weaponry to Ukraine, which was met with a diplomatic warning from Russia. The EU also pledged additional aid, while Finland began the process of applying for NATO membership and Sweden is reportedly considering the same. On the ground, Russian forces continued their eastern offensive, surrounding Ukrainian defenders of the port city Mariupol.

Along with the drag on sentiment, the International Energy Agency warned the full disruption to Russian oil supply had yet to bind, with as much as 3 million barrels of oil per day coming offline starting in May. Brent crude futures therefore climbed +8.7% (+2.68% Thursday, +1.31% yesterday), and closed yesterday at $113.16/bbl, their highest level in three weeks.

The S&P 500 fell -2.13% (-1.21% Thursday, -0.02% yesterday in a very quiet session) while the STOXX 600 managed to lose just -0.2% after a +0.7% rally Thursday into the holiday. In the S&P, energy (+3.53%) outperformed given the oil spike, while large cap stocks underperformed on the valuation hit wrought by rising yields, with FANG+ falling -4.81% (-3.16% Thursday, +0.25% yesterday).

Asian equity markets are ambivalent about returning after a long holiday, with the Hang Seng (-2.80%) leading regional losses. Mainland Chinese stocks are faring better, with the CSI dipping -0.38% while the Shanghai Composite is -0.03% lower. This, following the PBOC announcing yesterday increased financial support for industries, businesses, and people affected by Covid-19. Elsewhere, the Nikkei (+0.12%) and the Kospi (+0.90%) are up. Outside of Asia, S&P 500 (+0.20%) and Nasdaq (+0.28%) futures are both trading higher.

The RBA minutes overnight signaled they are not too far from joining the global tightening cycle, as they expect inflation to further increase above target.

The yen extended its depreciation streak against the US dollar, falling -0.58% to 127.73 per dollar, the weakest level since May 2002, as diverging monetary policy paths take their toll.

Oil prices and 10yr Treasury yields are little changed overnight; brent futures are +0.19% higher, while 10yr Treasury yields are -1.5bps lower.

To the day ahead, data is light on top of the aforementioned earnings, with US March building permits, housing starts, and Canada March existing home sales. The IMF will also release their 2022 World Economic Outlook.

3. ASIAN AFFAIRS

i)TUESDAY MORNING// MONDAY NIGHT

SHANGHAI CLOSED DOWN 1.49 PTS OR 0.05% //Hang Sang CLOSED DOWN 490.32 OR 2.28% /The Nikkei closed DOWN 16.76 PTS OR 0.68% //Australia’s all ordinaires CLOSED UP .58% /Chinese yuan (ONSHORE) closed DOWN 6.3874 /Oil UP TO 106.95 dollars per barrel for WTI and DOW TO 111.63 for Brent. Stocks in Europe OPENED ALL RED // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.3874 OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.3]4066: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER//

3 a./NORTH KOREA/ SOUTH KOREA

///NORTH KOREA

END

3B JAPAN

end

3c CHINA

CHINA/COVID/SHANGHAI LOCKDOWNS/

Something is really going on in China as they confirm their first COVID deaths. As Fringe stated yesterday, it China is trying to wreck its economy and its people on purpose or they know something

on the virus that we do not know. You should know that Chinese are very deficient in Vitamin d and that may cause a lot of problems for them

(zerohedge)

Shanghai Finally Confirms First COVID Deaths Since Start Of Lockdown

MONDAY, APR 18, 2022 – 08:05 PM

After weeks of allegedly covering up COVID-related deaths in senior-living facilities, Shanghai has curiously picked Monday – just hours after releasing stronger-than-expected (and likely goalseeked) Q1 GDP figures – to confirm the first COVID deaths in the city of 26 million, where more than 100K people have been confirmed positive with the virus over the past month alone.

To be sure, the official figures are still pretty small: the city confirmed that people have died as of Sunday, the city said, attributing the deaths to preexisting health conditions. The official announcement noted all three people were elderly and were also not vaccinated.

Shanghai authorities have been doing everything they can to try and force more older Chinese to accept its vaccines, which have been said to be less effective than their western counterparts.

To be sure, about 224.8 million people over the age of 60 have already been vaccinated, which represents about 85% of that age group.

But for those who haven’t yet received the vaccine, local authorities are trying another novel tactic: bribing them.

According to CNBC, at least one neighborhood in the capital city of Beijing has said that anyone over the age of 60 getting their first COVID shot could receive a reward worth the equivalent of about $70 to $80, citing anecdotal reports.

Case numbers have started to cool, per the official data, as authorities hope to be able to start rolling back restrictions in the country’s largest city (which is 3x the size of NYC) by Wednesday: On Sunday, Shanghai reported 19,831 cases with no symptoms, and 2,417 new confirmed COVID cases with symptoms. Meanwhile, outside of Shanghai, another 300 newly confirmed cases with symptoms were reported across the rest of mainland China.

Shanghai’s lockdown has been particularly brutal, as local residents describe running low on food and essential supplies while being effectively sealed inside their homes. Many who took to social media – or their balconies – to protest the lockdown were ordered to cease and desist by the authorities, who haven’t hesitated to crack down on all dissent, even while the CCP’s policies have led to unnecessary and otherwise preventable deaths.

One memorable video, which made the rounds on western social media, depicted Shanghaiers taking to their balconies to chant in protest, as CCP drones ordered them to halt and go back inside.

As we have previously noted, analysts at Nomura estimated last week that 45 cities responsible for about 40% of China’s GDP were under complete or partial lockdowns, and said the country was at “risk of recession.” As a result, prices of commodities both agricultural and industrial, have tumbled in China, leading to some speculation that the CCP is using the lockdowns to manipulate commodity prices and prevent the levels of inflation afflicting western economies from ever being imported to China.

Keep in mind: China is desperately in need of crude oil, LNG, food, basic materials, base metals, and other commodities. Putin’s invasion of Ukraine has created additional energy scarcity, inflation, and skyrocketing food inflation. While China hasn’t had any material problems with the virus from Wuhan in the past, it’s interesting that their draconian lockdowns (in conjunction with telegraphing the purchase of fewer cargoes of LNG and crude) are forcing global economists to ratchet growth expectations lower while concurrently blunting future demand projections.

And as the impact of China’s broken supply chains reverberate across the world (from Europe, to North America, and beyond), we can’t help but wonder if the CCP secretly wants to country’s supply chains to remain broken.

END

4/EUROPEAN AFFAIRS//UK AFFAIRS

//EUROPE/RUSSIA

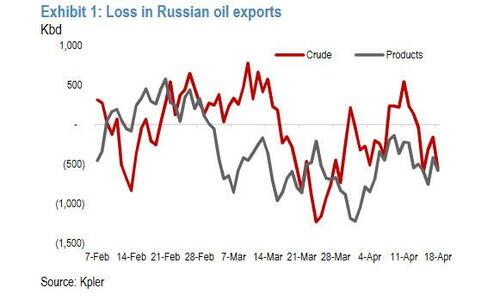

Big news: EU to impose full embargo on Russian oil next week. JPMorgan states that this will send oil above $185

(zerohedge)

EU To Impose Full Embargo On Russian Oil Next Week, Will Send Price Above $185 According To JPMorgan

TUESDAY, APR 19, 2022 – 01:13 PM