April 20, 2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

april20, 2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD; $1953.20 DOWN 3.05

SILVER: $25.14 DOWN $0.15

ACCESS MARKET: GOLD $1957.65

SILVER: $25.19

Bitcoin morning price: $42,127 UP 645

Bitcoin: afternoon price: $41,053 DOWN 429

Platinum price: closing DOWN $28.10 to $989.65

Palladium price; closing UP 35.70 at $269.85

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

comex notices/

: JPMorgan stopped/total issued 46/135

NUMBER OF NOTICES FILED TODAY FOR APRIL. CONTRACT 135 NOTICE(S) FOR 13,500 OZ (0.4199 TONNES)

total notices so far: 25,345 contracts for 2,534,500 oz (78.833 tonnes)

SILVER NOTICES:

80 NOTICE(S) FILED 400,000 OZ/

total number of notices filed so far this month 1279 : for 6,395,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

END

GLD

WITH GOLD DOWN $3.05

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

A HUGE CHANGE IN GOLD INVENTORY AT THE GLD A HUGE DEPOSIT OF 6.36 TONNES INTO THE GLD//

INVENTORY RESTS AT 1106.74 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 15 CENTS

AT THE SLV// A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WHOPPING DEPOSIT OF 2.955 MILLION OF INTO THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 577.941 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A STRONG SIZED 828 CONTRACTS TO 170,577 AND CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE STRONG GAIN IN OI WAS ACCOMPLISHED DESPITE OUR HUGE $0.62 LOSS IN SILVER PRICING AT THE COMEX ON TUESDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.62) BUT WERE UNSUCCESSFUL IN KNOCKING OUT ANY SILVER LONGS AS WE HAD A STRONG GAIN OF 1678 CONTRACTS ON OUR TWO EXCHANGES

WE MUST HAVE HAD:

I) HUGE BANKER SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A STRONG INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 4.305 MILLION OZ FOLLOWED BY TODAY’S QUEUE. JUMP OF 110,000 OZ//NEW STANDING: 6.410 MILLION OZ// V) HUGE SIZED COMEX OI GAIN/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS : —-662

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS APRIL. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF APRIL:

TOTAL CONTACTS for 13 days, total 10,901 contracts: 54.505 million oz OR 4.19 MILLION OZ PER DAY. (838 CONTRACTS PER DAY)

TOTAL NO OF OZ UNDERGOING EFP TO LONDON 10,901 CONTRACTS X 5,000 PER CONTRACT:

EQUATES TO: 54.505 MILLION OZ

.

LAST 11 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

APRIL: 54.505 MILLION OZ (LOOKS LIKE OUR BANKERS ARE NOW LOATHE TO ISSUE EFP’S)

RESULT: WE HAD A STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 828 DESPITE OUR $0.62 LOSS IN SILVER PRICING AT THE COMEX// TUESDAY THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE CONTRACTS: 850 CONTRACTS ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A HUGE INITIAL SILVER OZ STANDING FOR MAR. OF 4.305 MILLION OZ FOLLOWED BY TODAY’S 110,000 OZ QUEUE JUMP//NEW STANDING: 6.410MILLION OZ/// .. WE HAD A STRONG SIZED GAIN 1678 OI CONTRACTS ON THE TWO EXCHANGES FOR 8.39 MILLION OZ DESPITE THE THE LOSS IN PRICE.

WE HAD 80 NOTICES FILED TODAY FOR 400,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A GOOD SIZED 4410 CONTRACTS TO 575,557 AND FURTHER FROM NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: -355 CONTRACTS.

THE BIS HAS ABANDONED THE GOLD COMEX TRADING!!!

.

THE GOOD SIZED DECREASE IN COMEX OI CAME DESPITE OUR HUGE LOSS IN PRICE OF $26.05//COMEX GOLD TRADING/TUESDAY /.AS IN SILVER WE MUST HAD HUGE BANKER/ALGO SHORT COVERING ACCOMPANYING OUR SMALL SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR APRIL AT 78.33 TONNES ON FIRST DAY NOTICE

YET ALL OF..THIS HAPPENED WITH OUR HUGE LOSS IN PRICE OF $26.05 WITH RESPECT TO TUESDAY’S TRADING

WE HAD A TINY SIZED LOSS OF 700 OI CONTRACTS (2.174 PAPER TONNES) ON OUR TWO EXCHANGES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 3710 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 575,557.

IN ESSENCE WE HAVE A TINY SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 345, WITH 4055 CONTRACTS DECREASED AT THE COMEX AND 3710 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 345 CONTRACTS OR 1/073 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A GOOD SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3710) ACCOMPANYING THE GOOD SIZED LOSS IN COMEX OI (4410,): TOTAL LOSS IN THE TWO EXCHANGES 700 CONTRACTS. WE NO DOUBT HAD 1) HUGE BANKER SHORT COVERING ,2.) HUGE INITIAL STANDING AT THE GOLD COMEX FOR APRIL. AT 78.33 TONNES FOLLOWED BY TODAY’S 1800 OZ QUEUE JUMP //NEW STANDING 82.009 TONNES/// 3) TINY LONG LIQUIDATION IF ANY ///. ,4) GOOD SIZED COMEX OI. LOSS 5) GOOD ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

APRIL

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL :

29,966 CONTRACTS OR 2,996,600 OR 93.206 TONNES 13 TRADING DAY(S) AND THUS AVERAGING: 2305 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 13 TRADING DAY(S) IN TONNES: 93.206TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2020, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 93.206/3550 x 100% TONNES 2.62% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 93.206 TONNES (THIS IS GOING TO BE A LOW ISSUANCE MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF MAY.WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF APRIL HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF MAY, FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (MAR), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A STRONG SIZED 828 CONTRACT OI AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 850 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 850 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 828 CONTRACTS AND ADD TO THE 850 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A VERY STRONG SIZED GAIN OF 1678 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 8.390 MILLION OZ

OCCURRED WITH OUR LOSS IN PRICE OF $0.62 IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

We lost a true patriot..

Financial letter writer, gold advocate James Dines dies

Submitted by admin on Tue, 2022-04-19 21:28Section: Daily Dispatches

From The Dines Letter, Belevedere, Califnrnia

Tuesday, April 19, 2022

https://www.dinesletter.com/index.html

Dear Subscribers:

It is with great sadness that we announce the passing of Mr. Dines at his home in California last week.

Mr. Dines was not only wonderful to work for but gracious and generous with his wisdom. We are grateful that he had a long, productive, and fulfilling life, which he willingly shared with all of us.

As his loyal Dines Letter readers were always his top priority, we wanted to inform you today, and didn’t want to wait for the next issue.

More details will follow in the next The Dines Letter, scheduled for publication on April 29.

Sincerely,

The Dines Letter Team

end

5. Other gold commentaries

Mises…

a must read!

Is There A Case For The Pre-1914 Gold Standard? Yes, If You Believe Inflation Is A Bad Thing

TUESDAY, APR 19, 2022 – 11:25 PM

Authored by Vibhu Vikramaditya via The Mises Institute,

The Russian central bank recently announced that it will stop buying gold at a fixed rate and will instead buy them at the negotiated rate from banks. Following the numerous sanctions which were imposed on Russia. The Ruble had fallen tremendously against the US dollar, to get out of such a situation it had announced that it would buy gold at a fixed price of 5,000 rubles a gram until June 30. Since that announcement, the ruble has strengthened sharply against the dollar for over one month. Five thousand rubles was worth around $52 on March 25 and around $63 on Thursday.

The mechanism which led to the increase was to allow the markets to play themselves out, in order to combat sanctions, they asked the nations to transact in their currency which, due to the extensive and growing array of sanctions by the western front, was becoming devalued by each day. It was here, by demanding payment in rubles, are attempting to increase demand for their currency which led to its increase where being pegged to hard currency allowed the confidence of the markets to increase so ruble wasn’t dumped extensively

But because once you allow for sound money such as gold pegged to your currency which is dictated by the effective allocating mechanism of the market you cannot ignore the market valuation any longer, therefore the bounce-back and effective strengthening of the ruble which took place more and earlier than expected has now forced them to abandon the fixed-rate currency and move towards a more flexible exchange rate mechanism which would allow them to set the rates effectively in line with the motivation of sellers while discounting for factors such as immediacy, global credit standing and the turns of the global economy.

A classical gold standard requires the central bank to exchange by the process of both purchasing and selling gold and the national currency for each other and to do so according to a fixed weight or quantity of gold per unit of currency. Thus, while neither the pegged currency nor the negotiated rates of exchange comprise the classical gold standard, they nonetheless serve as a great case study into the commendatory effects of having hard money serving as the medium of change in the economy.

In the much-celebrated book of his time, Tract on Monetary Reform, economist John Maynard Keynes urged the United States and Great Britain to abandon the gold standard, calling it a “barbarous relic.” In the decades that followed the book’s publication, countries around the globe heeded Keynes’ advice and relegated the gold standard to the dust bin. It is one of the great historical ironies that almost every advice of from Keynes was taken up by the world in the latter half of the 20th century and that none of the supposed benefits of stability, full employment have come to fruition.

The Problem of Gold standard in the Keynesian system

Keynes’s dictum on the gold standard has become the fountainhead of claims against a return back to the gold standard.

Keynes in his analysis found the gold standard to be a barbarous relic of the past that was unscientific and unfit to meet the demands of a modern world.

It is his arguments against the gold standard which have been repeated time and again, thus they serve as an excellent case for demonstration as to why the gold standard is superior based on the very allegations which are leveled against it.

Inflation and Gold standard

He wrote in his tract on monetary reform about the ills of inflation “ Inflation redistributes wealth…. Its most striking consequence is its injustice to those who in good faith have committed their savings to titles to money rather than to things…. Injustice on such a scale has further consequences…. Inflation has… destroyed the atmosphere of confidence which is a condition of the willingness to save….

Reading this one might form the opinion that the author of such lines might be highly unsavory and unscrupulous towards a monetary regime which causes destruction of the price mechanism and people’s stored up wealth through the artificial increase in prices but unfortunately one cannot do so without committing a grave error as both instances in modern history when prices have run amok namely the stagflation of the 70s and the massive rise in prices of around 10% today are both a result of Keynesian economics.

The most widely recognized virtue of the historical gold standard is its low average inflation rate. The rate of inflation was lowest, on average, under the gold standard when compared with the Bretton woods system of a pegged dollar and fluctuating system of fiat dollar reserve. (p. 30).

This was the era of the classical gold standard which lasted from 1880 to 1914, Inflation over this time period, while it fluctuated on a year-to-year basis, was virtually zero, and as a result, prices whose proper role lies in giving signals about market scarcity ensured proper allocation of resources due to which real income per capita in the United States increased by over 60 percent in a generation and a half. This low inflation is not a coincidence but a direct effect that is to be expected when the money supply is bound to the supply of gold. While the central bank can create thousands of dollars out of thin air to increase the money supply with its high stock to flow ratio, gold has the lowest price elasticity of supply, which is calculated as the percentage increase in quantity provided over price rise.

This implies the effects of the increased supply which would be prompted by increases in the price of gold through higher demand would be quite insignificant to cause changes in the absolute price level. For instance, the year 2006 witnessed a 36% rise in the spot price of gold. For any other commodity, this would be expected to increase mining output significantly to flood markets and bring the price down. Instead, annual production in 2006 was 2,370 tons, 100 tons less than in 2005, and it would drop a further 10 tons in 2007. (p. 34).

With changes in money supply being largely unaffected by changes in prices of gold, the general rise in prices which are caused when the supply of money is greater than the demand to hold it doesn’t occur. An economy where price increases are not caused due to an increase in money supply experiences price rise as a function of scarcity based on underlying consumer preferences which lead entrepreneurs to allocate resources properly in line with consumer demand.

Gold Standard and boom-bust cycles

A fiduciary media such as paper currency or bank deposits which are effectively used as the medium of exchange which is redeemable in gold enjoys certain properties which create a mechanism whereby artificial increases in money supply are either discouraged or its effects are reversed.

Suppose if commercial banks were to increase the supply of fiduciary media beyond what its coffers can handle, an increase in supply would first increase the cash balance holdings of its lenders who would when then start spending it on the various inputs of production thereby increasing its price, this increased price would accrue higher profits to the sellers of those inputs who would in-turn increase their output.

The process where sellers of inputs increase their input would lead them to hire more labor and capital goods which in turn would put further inflationary pressures on wages and other consumer goods when the rise in input prices are materialized into higher consumer goods prices.

Due to such an increase in prices, the goods of other economies would gain a competitive advantage over domestic ones which would lead to an increase in demand for gold to trade with other countries, as the demand for gold increases, the over-issued fiduciary media would find themselves back to banks who would then be put in dangers of bank runs and defaulting on their claim. This discipline of defaulting over time would root out banks that would have the habit of overissuing fiduciary media which is the source of an artificial unsustainable boom that eventually bursts and leads the economy towards a recession.

The same restrictions apply to the central banks as well where they can’t run an easy money policy without running the risk of a run on their reserves, given if a central bank lowers its lending rate of interest on its gold reserves to commercial banks in order to create a boom.

It would lead to capital outflows as investors would look to invest in countries where the interest rate is higher, this would mean that the demand for gold by investors to exchange it against foreign currency will increase. This outflow of gold reserves will decrease the quantity of money in the economy which will again lead to an increase in the rate of interest, therefore it not only means that the monetary policy would be rendered ineffective but also lead central banks to lose out on important gold reserves.

The problems of the pseudo gold standard

One of the greatest benefits of the gold standard lies in its ability to restrict and bind the hands of the government. This perhaps becomes most evident when one revisits the episodes of how the gold standard was one by one abandoned by all countries in line for preparation of war efforts of the first world war. Each country in order to build up reserves for arms and ammunition had to increase its defense spending which couldn’t take place under the restraining system which protects individual liberty. Once the war ended there were some attempts at coming back to the gold standard but since they were not based on the underlying dynamic of a market-based gold-currency exchange rate mechanism, it failed to restore the price stability and economic prosperity of the classical gold standard. Each of the countries that participated in the war thus spent huge amounts of money and had massively inflated their currencies, thus economic conditions had changed equilibrium exchange rates between national currencies, and hence gold parities should have been adjusted. If 1914 is taken as the base (= 100), wholesale prices in December 1918 were as follows: USA 202, France 355, UK 246.

After the war in 1918, the USA immediately announced that it would maintain the dollar price of gold at its prewar level. That is, it is willing to export gold at $20.67 per ounce. It was thought that Britain’s national honor was at stake. Failure to restore the prewar parity of the pound would undermine confidence in the pound.

Accordingly, Britain resorted to a deflationary policy and restored the value of the pound to its pre-WW1 levels, this turned out to be a disaster for the British economy and other economies connected to it. Artificially lowering the value of the pound despite the increased money supply during the war period distorted the entire structure of prices whose role is to guide entrepreneurs, it could be compared to a situation wherein amid congestion of traffic, the signals reflect guidance for coordinating yesterday’s traffic.

The USA was able to survive the artificial deflation on the account of its massive gold reserves which had grown during the war and the piling up of debt that countries owned to the United States. This allowed the USA to pursue an easy money policy which first sparked a temporary boom and then characteristically culminated in a bust. This mechanism was explained most adequately by Rothbard in his seminal work America’s Great Depression. Had the currencies been allowed to change as per a fixed weight of gold units per unit of currency, the picture may well have been different.

Conclusion

Keynes began his mission to enunciate his system of economics where the invisible hand of the market will be replaced by the visible hand of policymakers where an increase in government spending through the increase in aggregate demand as a result of the multiplier mechanism will provide full or near full employment. But before such a project could be undertaken, it was important to show why the gold standard fails to provide an order to the society as the foundations of his economic system relies on the fact that a country has independence in monetary and fiscal matters where it is not directly affected by the policies of other economies. There can be no such thing as a Keynesian state on the gold standard, any more than a cocaine addict or compulsive gambler can be on a strict budget.

But now on the backs of substantial evidence and analysis, it becomes quite clear that not only was Keynes incorrect about the question of instability of the value of money and on the gold standard as a monetary system. A stronger case has also been made to show the classical gold standard is superior on every front and a return to the gold standard will cure several economic ills of inflation, improper allocation of resources, and a continuous cycle of booms and busts. This now calls into question a reevaluation of the entire foundation of the fiat money system along with the Keynesian worldview.

end

6. Commodity commentaries/cryptocurrencies

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING// TUESDAY NIGHT

SHANGHAI CLOSED DOWN 42.98 PTS OR 1.35% //Hang Sang CLOSED DOWN 84.09 OR 0.40% /The Nikkei closed UP 232.76 PTS OR 0.86% //Australia’s all ordinaires CLOSED UP .02% /Chinese yuan (ONSHORE) closed DOWN 6.4125 /Oil UP TO 104.11 dollars per barrel for WTI andUP TO 108.65 for Brent. Stocks in Europe OPENED ALL GREEN // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.4125 OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.4431: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER/

a)NORTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A GOOD SIZED 4410 CONTRACTS TO 575,202 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS GOOD COMEX DECREASE OCCURRED WITH OUR VERY STRONG LOSS OF $26.05 IN GOLD PRICING TUESDAY’S COMEX TRADING. WE ALSO HAD A GOOD SIZED EFP (3710 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE ACTIVE DELIVERY MONTH OF APRIL.. THE CME REPORTS THAT THE BANKERS ISSUED A SMALL SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 3710 EFP CONTRACTS WERE ISSUED: ;: , . 0 JUNE :3710 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3710 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A SMALL SIZED TOTAL OF 700 CONTRACTS IN THAT 3710 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A GOOD SIZED COMEX OI LOSS OF 4410 CONTRACTS..AND THIS LOSS OCCURRED WITH OUR STRONG LOSS IN PRICE OF GOLD $26.05.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING FOR APRIL (82.009),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 82.009

THE BANKERS WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $26.05) AND AND WERE BASICALLY UNSUCCESSFUL IN FLEECING ANY LONGS AS WE HAVE REGISTERED A TINY SIZED LOSS OF 2.174 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR APRIL (82.009 TONNES)…

WE HAD — 355 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 700 CONTRACTS OR 70,000 OZ OR 2.174TONNES

Estimated gold volume today: 136,428/// poor

Confirmed volume yesterday: 190,156 contracts poor

INITIAL STANDINGS FOR APRIL ’22 COMEX GOLD //APRIL 20

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 257.210 oz Brinks 8 kilobars |

| Deposit to the Dealer Inventory in oz | nil OZ |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 135 notice(s) 13,500 OZ0. 4199 TONNES |

| No of oz to be served (notices) | 1021 contracts 102,100 oz 3.175 TONNES |

| Total monthly oz gold served (contracts) so far this month | 25,345 notices 2,534,500 OZ 78.833 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For today:

dealer deposits 0

total dealer deposit nil oz//

No dealer withdrawals

0 customer deposit

total customer deposit nil oz

1 customer withdrawals

i) Out of Brinks 257.210 oz

total customer withdrawal: 257.210 oz /

ADJUSTMENTS:

0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR APRIL.

For the front month of APRIL we have an oi of 1156 contracts having GAINED 10 contracts

We had 8 notices filed yesterday so we GAINED 18 contracts or an additional 1800 oz will stand for delivery at the comex

May saw a LOSS of 160 contracts to stand at 3380

June saw a LOSS of 4402 contracts UP to 474,679 contracts

We had 135 notice(s) filed today for 13500 oz FOR THE APRIL 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 135 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 46 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the APRIL /2021. contract month,

we take the total number of notices filed so far for the month (25,345) x 100 oz , to which we add the difference between the open interest for the front month of (APRIL 1156 CONTRACTS ) minus the number of notices served upon today 46 x 100 oz per contract equals 2,636,600 OZ OR 82.009 TONNES the number of TONNES standing in this active month of APRIL.

thus the INITIAL standings for gold for the APRIL contract month:

No of notices filed so far (25,345) x 100 oz+ (1156) OI for the front month minus the number of notices served upon today (135} x 100 oz} which equals 2,636,600 oz standing OR 82.009 TONNES in this active delivery month of APRIL.

We GAINED 1800 additional oz that will stand for delivery on this side of the pond.

TOTAL COMEX GOLD STANDING: 82.009 TONNES (A WHOPPER FOR AN APRIL ( ACTIVE) DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

191,133,764.7, oz NOW PLEDGED /HSBC 5.94 TONNES

99,258.893 PLEDGED MANFRA 3.08 TONNES

54,339.114oz PLEDGED JPMorgan no 1 1.690 tonnes

243,923.704, oz JPM No 2 7.58 TONNES

898,821.330 oz pledged Brinks/27,96 TONNES

International Delaware:: 0

Loomis: 18,615.429 oz

total pledged gold: 1,887,433.936 oz 58.70 tonnes

TOTAL REGISTERED AND ELIG GOLD AT THE COMEX: 35,952,503.296 OZ (1118,27 TONNES)

TOTAL ELIGIBLE GOLD: 18,310,326.079 OZ (569.52 tonnes)

TOTAL OF ALL REGISTERED GOLD: 17,642,177.218 OZ (548.74 tonnes)

REGISTERED GOLD THAT CAN BE SERVED UPON: 15,754,744.0 OZ (REG GOLD- PLEDGED GOLD) 490.03 tonnes

END

APRIL 2022 CONTRACT MONTH//SILVER//APRIL 20

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 765,042.651 oz Manfra CNT Delaware JPMorgan |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 917,859.530 oz Brinks CNT Delaware JPMorgan |

| No of oz served today (contracts) | 80CONTRACT(S)400,000 OZ) |

| No of oz to be served (notices) | 62 contracts (15,000 oz) |

| Total monthly oz silver served (contracts) | 1279 contracts 6,395,,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

we had 0 deposit into the dealer

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 4 deposits into the customer account

i) Into Brinks: 62,255.57 oz

ii) Into CNT: 268,486.180 oz

iii) Into Delaware: 4812.580 oz

iv) Into JPMorgan: 582,305.20

total deposit: 917,859.530 oz

JPMorgan has a total silver weight: 177.007 million oz/334.707 million =52.99% of comex

i) Comex withdrawals: 4

ii) Out of CNT 4954.527 oz

i) Out of Delaware: 10,946.700 oz

iii) Out of JPMorgan 627,881.580 oz

iv) Out of Manfra: 121,259.884 oz

total withdrawal 765,042.651 oz

1 adjustments: dealer to customer//Manfra 177,470.580 oz

and JPMorgan: 5061.880 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 86.207 MILLION OZ

TOTAL REG + ELIG. 334.707 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR APRIL

silver open interest data:

FRONT MONTH OF APRIL OI: 83, HAVING GAINED 22 CONTRACTS FROM MONDAY. We had 0 notices filed yesterday,

so we GAINED 22 contracts or an additional 110,000 oz will stand on this side of the pond

MAY HAD A LOSS OF 4115 CONTRACTS DOWN TO 60,367 contracts

JUNE HAD A GAIN OF 78 TO STAND AT 1226

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 80 for 400,000 oz

Comex volumes: 59,282// est. volume today// fair/

Comex volume: confirmed yesterday: 83,318 contracts ( good )

To calculate the number of silver ounces that will stand for delivery in APRIL. we take the total number of notices filed for the month so far at 1279 x 5,000 oz = 6,395,000 oz

to which we add the difference between the open interest for the front month of APRIL (83) and the number of notices served upon today 80 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the APRIL./2021 contract month: 1279 (notices served so far) x 5000 oz + OI for front month of APRIL (83) – number of notices served upon today (80) x 5000 oz of silver standing for the APRIL contract month equates 6,410,000 oz. .

We GAINED 22 contracts or an additional 110,000 oz will stand on this side of the pond

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

APRIL 20/WITH GOLD DOWN $3.05: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEOISUT IF 6.36 TONNES INTO THE GLD..//INVENTORY RESTS AT 1106.74 TONNES

APRIL 19//WITH GOLD DOWN $26.90//A SMALL CHANGE IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .87 TONNES INTO THE GLD//INVENTORY RESTS AT 1100.36 TONNES

APRIL 18/WITH GOLD UP $11.20: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.93 TONNES FROM THE GLD..//INVENTORY RESTS AT 1099.44 TONNES

APRIL 14/WITH GOLD DOWN $8.90: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.32 TONNES INTO THE GLD..//INVENTORY RESTS AT 1104.42 TONNES

APRIL 13/WITH GOLD UP $8.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1093.10 TONNES

APRIL 12/WITH GOLD UP $26.95: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.61 TONNES INTO THE GLD///INVENTORY REST AT 1093.10 TONNES

APRIL 11/WITH GOLD UP $3.40 //A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD.//INVENTORY RESTS AT 1090.49 TONNES

APRIL 8/WITH GOLD UP $7.70: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES INTO THE GLD//INVENTORY RESTS AT 1088.75 TONNES

APRIL 7/WITH GOLD UP $13.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1087.30 TONNES

APRIL 6/WITH GOLD DOWN $4.10: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.68 TONNES FROM THE GLD..//INVENTORY RESTS AT 1087.30 TONNES

APRIL 5/WITH GOLD DOWN $5.70: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.75 TONNES FROM THE GLD//INVENTORY RESTS AT 1089.98 TONNES

APRIL 4/WITH GOLD UP $.70//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1091.73 TONNES

APRIL 1///WITH GOLD DOWN $19.00 : A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .29 TONNES INTO THE GLD///INVENTORY RESTS AT 1091.73 TONNES

MARCH 31/WITH GOLD UP $13.30 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD FROM MONDAY A WITHDRAWAL OF 1.71 TONNES FROM THE GLD:INVENTORY RESTS AT 1091.44

MARCH 28/WITH GOLD DOWN $14.65: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1093.18 TONNES

MARCH 25/WITH GOLD DOWN $7.60 : A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.52 TONNES INTO THE GLD///INVENTORY RESTS AT 1093.18 TONNES

MARCH 24/WITH GOLD UP $24.95: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.06 TONNES INTO THE GLD..//INVENTORY RESTS AT 1087.66 TONNES

MARCH 23/WITH GOLD UP $15.75//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1083.60 TONNES

MARCH 22/WITH GOLD DOWN $7.75: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.16 TONNES OF GOLD DEPOSITED INTO THE GLD//INVENTORY RESTS AT 1083.60 TONES

MARCH 21//WITH GOLD UP $.25 : A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 9.00 TONNES INTO THE GLD////INVENTORY RESTS AT 1082.44 TONES

MARCH 18/WITH GOLD DOWN $13.55 NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1073.44 TONES

MARCH 17/WITH GOLD UP $33.50: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.61 TONNES INTO THE GLD//INVENTORY RESTS AT 1073.44 TONNES

MARCH 16/WITH GOLD DOWN $18.50//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.33 TONNES FROM THE GLD///INVENTORY RESTS AT 1061.83 TONNES

MARCH 15/WITH GOLD DOWN $30.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1064.16 TONNES

MARCH 14//WITH GOLD DOWN $22.75, HUGE CHANGES IN GOLD INVENTORY AT THE GLD//STRANGE: A DEPOSIT OF 2.62 TONNES INTO THE GLD.//INVENTORY RESTS AT 1064.16 TONNES

MARCH 11/WITH GOLD DOWN $14.60: A BIG CHANGE IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 1061.54 TONNES

MARCH 10//WITH GOLD UP $11.55: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.06 TONNES FORM THE GLD///INVENTORY RESTS AT 1063.28 TONNES

MARCH 9/WITH GOLD DOWN $53.85//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.64 TONNES INTO THE GLD//INVENTORY RESTS AT 1067.34 TONNES

MARCH 8/WITH GOLD UP $46.10: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 8.42 TONNES INTO THE GLD///INVENTORY RESTS AT 1062.70 TONNES

MARCH 7/WITH GOLD UP $28.40 A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.06 TONNES INTO THE GLD..//INVENTORY RESTS AT 1054.28 TONNES

MARCH 4/WITH GOLD UP $28.40//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1050.22 TONNES

CLOSING INVENTORY FOR THE GLD//1106.74 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

APRIL 20/WITH SILVER DOWN 15 CENTS : A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.955 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 577.941 MILLION OZ///

APRIL 19/WITH SILVER DONW 62 CENTS: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .461 MILLION OZ FROM THE SLV INVENTORY…//INVENTORY RESTS AT 574.986 MILLION OZ

APRIL 18/WITH SILVER UP 38 CENTS: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.771 MILLION OZ INTO THE SLV./INVENTORY RESTS AT 575.447 MILLION OZ//

APRIL 14/WITH SILVER DOWN 25 CENTS : A MONSTROUS CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.355 MILLION OZ INTO THE SLV.//INVENTORY RESTS AT 569.676 MILLION OZ//

APRIL 13/WITH SILVER UP 27 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 565.521 MILLION OZ

APRIL 12/WITH SILVER UP 66 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 565.521 MILLION OZ//

APRIL 11/WITH SILVER UP 13 CENTS: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 831,000 OZ FORM THE SLV////INVENTORY RESTS AT 565.521 MILLION OZ

APRIL 8/WITH SILVER UP 11 CENTS :NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 566.352 MILLION OZ//

APRIL 7/WITH SILVER UP 27 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 566.352 MILLION OZ//

APRIL 6/WITH SILVER DOWN 9 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 566.352 MILLION OZ

APRIL 5/WITH SILVER DOWN 16 CENTS : A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.386 MILLION OZ INTO THE SLV..//INVENTORY RESETS AT 566.352 MILLION OZ//

APRIL 4/WITH SILVER DOWN 5 CENTS TO CHANGES IN SILVER INVENTORY AT THE SLV//: A DEPOSIT OF 6.326 MILLION OZ//INVENTORY REST AT 564.966 MILLION OZ//

APRIL 1/WITH SILVER DOWN 39 CENTS A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.302 MILLION OZ INTO THE SLV////INVENTORY REST AT 558.647 MILLION OZ//

MARCH 31/WITH SILVER UP 3 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 2.171 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 556.345 MILLION OZ

MARCH 28/WITH SILVER DOWN 30 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.847 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 554.167 MILLION OZ//

MARCH 25/WITH SILVER DOWN 20 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 552.320 MILLION OZ//

MARCH 24/WITH SILVER UP 54 CENTS TODAY; A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.092 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 552.320 MILLION OZ//

MARCH 23/WITH SILVER UP 24 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 550.288 MILLION OZ//

MARCH 22/WITH SILVER DOWN $0.29 TODAY : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 550.288 MILLION OZ//

MARCH 21/WITH SILVER UP 16 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 550.288 MILLION OZ//

MARCH 18/WITH SILVER DOWN 37 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.217 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 550.288 MILLION OZ//

MARCH 17/ WITH SILVER UP 72 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.049 MILLION OZ INTO THE SLVV//INVENTORY RESTS AT 548.071 MILLION OZ

MARCH 16/WITH SILVER DOWN 56 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 462,000 OZ FROM THE SLV//INVENTORY RESTS AT 544.560 MLLION O

MARCH 15/WITH SILVER DOWN 18 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 545.022 MILLION OZ

MARCH 14/WITH SILVER DOWN 64 CENTS TODAY; STRANGE A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.125 MILLION OZ/INVENTORY RESTS AT 545.022 MILLIONOZ

MARCH 11/WITH SILVER DOWN 13 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.897 MILLION OZ

MARCH 10/WITH SILVER UP 39 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.897 MILLION OZ/

MARCH 9/WITH SILVER DOWN 88 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 5.174 MILLION OZ OF FAKE SILVER.//INVENTORY RESTS AT 542.897 MILLION OZ//

MARCH 8/WITH SILVER UP 88 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.217 MILLION OZ INTO THE SLV////INVENTORY RESTS A 548.071 MILLION OZ//

MARCH 7/WITH SILVER UP 40 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 545.854 MILLION OZ//

MARCH 4/WITH SILVER UP 50 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 545.854 MILLION OZ/

SLV FINAL INVENTORY FOR TODAY: 577.941 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

Peter Schiff: The Risk Of A Market Crash Keeps Growing

WEDNESDAY, APR 20, 2022 – 01:45 PM

Bonds continue to get hammered.

On Tuesday morning, the yield on the 10-year Treasury rose above 2.9%, and the yield on the 30-year is knocking on the door of 3%. Since bond yields rise as bond prices fall, this indicates a serious decline in the bond market. In his podcast, Peter Schiff said that at some point, the market is going to actually crash.

A crash is coming. Because, if the bond market doesn’t crash, the stock market will. And if the bond market does crash, well then, the stock market is going to crash too. So, either way, at some point you’re going to get some kind of crash.”

The last time bond yields were this high was in late 2018. The target Fed funds rate at that time was 2.25% to 2.5%.

So, that was the highest the Fed was able to raise rates, and they had to start cutting them because that 3% yield was doing a lot of damage to the economy, as were the two-and-a-quarter to two-and-a-half Fed funds. Well, the Fed funds rate is still at .25 to .5 now. The Fed has only hiked rates once by 25 basis points. And we’re already almost at 3%. … So, yields are already where they were when the Fed funds rate was 2% higher than it is right now.”

If the Fed actually succeeds in raising short-term rates back to 2.5%, by then, you should see bond yields above 5%.

Does anybody believe that the economy can handle 5%? We couldn’t even handle 3% in 2018 when we had a lot less debt than we have now.”

Peter said the thing that should really scare investors in both the bond and stock markets is just how fast yields rose to 3% even though the Federal Reserve has barely started to move.

We’ve already reached the level where the economy broke down in 2018 because of how much interest rates had already risen.”

Remember, in 2018, when the economy reached this level, the Fed stopped tightening. It began cutting interest rates, and it relaunched quantitative easing. This fact gets lost in the extraordinary monetary policy we got in response to the COVID lockdowns. But the Fed was already loosening before the pandemic.

There is another thing the Fed was doing in 2018 that it’s only just now talking about — balance sheet reduction. In fact, the balance sheet is still growing.

The question is: if the Fed is talking about fighting inflation and they’re serious, why do they continue to create inflation? If the Fed is really going to aggressively shrink its balance sheet, why does it continue to expand its balance sheet? And if the US bond market is this weak when the Federal Reserve is still buying bonds, imagine how much weaker it’s going to get when the Federal Reserve not only stops buying but actually starts selling, which is exactly what they are indicating they are about to do. This is why I’m saying that a crash could be imminent in the stock market when stock investors actually come to terms with the reality of what’s going on in the bond market and what it portends for the economy and corporate earnings.”

In this podcast, Peter also talks about the weakness in the technology and cryptocurrency sectors, strength in gold and silver mining stocks, the high levels of inflation and how far the Fed has fallen behind the curve, and the Musk takeover bid for Twitter.

END

2.LAWRIE WILLIAM//,//Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, James RICKARDS/

3. Chris Powell of GATA provides to us very important physical commentaries

END

4.OTHER GOLD/SILVER COMMENTARIES

It Is “Just A Matter Of Time” Before Gold Rises 5x Or More: Lawrence Lepard

WEDNESDAY, APR 20, 2022 – 10:15 AM

Submitted by QTR’s Fringe Finance

Friend of Fringe Finance Lawrence Lepard released his most recent investor letter a few days ago with his updated take on the seismic changes occurring in monetary policy globally as a result of the Russia/Ukraine conflict.

He takes us through history as to how this landscape has changed in the past, and what could be coming in years ahead.

Larry had joined me for several interviews last year and I believe him to truly be one of the muted voices that the investing community would be better off for considering. He’s the type of voice that gets little coverage in the mainstream media, which, in my opinion, makes him someone worth listening to twice as closely.

Larry was kind enough to allow me to share his most recent thoughts. Part 1 is below, where he lays out his case for massive upside in gold, and Part 2 will be published later this week.

Reviewing the history and structure of the world monetary system is instructive given recent political developments with the kinetic war launched by Russia in the Ukraine. It can help us as we try to determine what happens next (Many of you know this, but allow us to review).

Bretton Woods I: 1944-1960s Period

Toward the end of World War II, in July 19441, the leaders of the free world convened a monetary conference in Bretton Woods, NH to establish the rules for a post war monetary system. This is now referred to as Bretton Woods I.

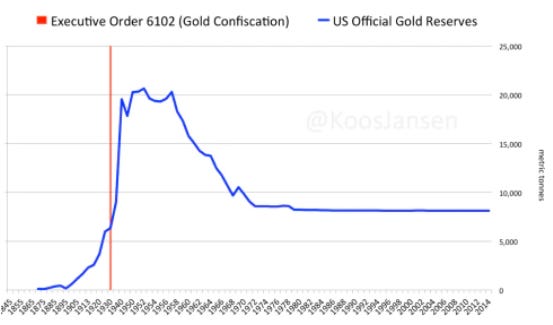

At this conference, the US Dollar was made the international reserve currency for the world financial system. The dollar would be backed by gold and could be exchanged for bullion at the price of $35 per ounce. (US citizens did not have that exchange privilege due to Roosevelt’s 1933 Executive Order 6102, which made it illegal for US citizens to own gold; this was repealed in 1975).

All other foreign currencies would be pegged to the dollar at fixed exchange rates.

The exchangeability of dollars for gold was credible because the US had 650,000 ounces (20.5 metric tonnes) of gold on deposit. In the early post war period, this arrangement worked fairly well, and the dollar was further supported because the US was the leading industrial nation; Japan and Germany’s economies had been devastated by the war.

From 1946-1957, US economic growth was solid, and the US Federal government was generally fiscally responsible and ran budget surpluses in 6 of those 11 years. Deficit years contained small deficits and only the Korean conflict spiked the annual deficit in 1953. Inflation was present in the late 1940’s and 1950’s, but the Fed kept interest rates in check through financial repression (yield curve control). The US dominated the world militarily. US economic growth was robust as returning GI’s started families, bought houses and cars.

The US was a net exporter with a positive balance of trade. There was a high level of trust in the dollar and its exchangeability for gold was a backstop.

1960s: Deficits Drive a “Run on Gold” and the Ultimate Failure of the London Gold Pool

However, the pot started to boil in the 1960’s with the US entering the Vietnam War, along with President Johnson’s “Great Society” social programs (welfare, Medicare, Medicaid). This spending was called “Guns and Butter” at the time and led to significant US Fiscal deficits.

The net result of these deficits, and the monetization (money printing) employed to finance them, was that foreign creditors began to doubt the value of the dollar as measured in gold terms. Thus, many of those creditors began to take the US up on its offer to exchange dollars for gold.

As you can see in the chart below, the trend of foreigners exchanging dollars for US gold bullion began in 1959 when the US ran a fiscal budget deficit of $13 billion (at the time considered very large). Those deficits persisted and grew throughout the 1960’s, and so did the outflow of US Treasury gold.

The leader in the repatriation effort was France, and its President Charles de Gaulle, who was advised by economist Jacques Reuff.

Reuff pointed out that the US Dollar, as the world’s reserve currency, enjoyed an “exorbitant privilege” where foreigners see themselves supporting American living standards. As American economist Barry Eichengreen summarized:

“It costs only a few cents for the Bureau of Engraving and Printing to produce a $100 bill, but other countries had to pony up $100 of actual goods in order to obtain one.”

This was the first instance of the world recognizing that the US Dollar as the world’s reserve currency allowed Americans to live better at the expense of the rest of the world – but it would not be the last.

As the chart above shows, the run on US gold that began in 1959 accelerated throughout the 1960’s. The US deficits from the Vietnam war grew larger, culminating in a US fiscal deficit of $25 billion in 1968 (again – deemed to be a very large deficit at that time), a figure that had not been exceeded since WW II.

(This post is free but if you have the means and would like to support my work, I’d love to have you as a subscriber by clicking here).

In fact, the free market price of gold in London was trading above the official $35 reference price. Investors realized that the US fiscal position was untenable, and foreigners who could legally buy gold were turning their dollars in for gold – well above $35 per ounce for delivery in London. Countries were also taking delivery of gold directly from the US treasury in exchange for the dollars that they had earned in trade.

This was now an accelerating bank run on gold. To mitigate this problem, in the 1960s a group of Central Banks formed the London Gold Pool in an effort to keep the free-market gold price close to the Bretton Woods reference price of $35.

These Central Bankers manipulated the price of gold through strategic selling, and threats of selling of paper gold. However, the run on gold situation in the 1960s ratcheted up in 1967. Overwhelmed by the demand for physical gold, the British were forced to devalue the Pound Sterling by 14% and gold was trading at $50 per ounce.

One by one and led by France, the Central Banks exited the London Gold Pool following 1967 and it failed.

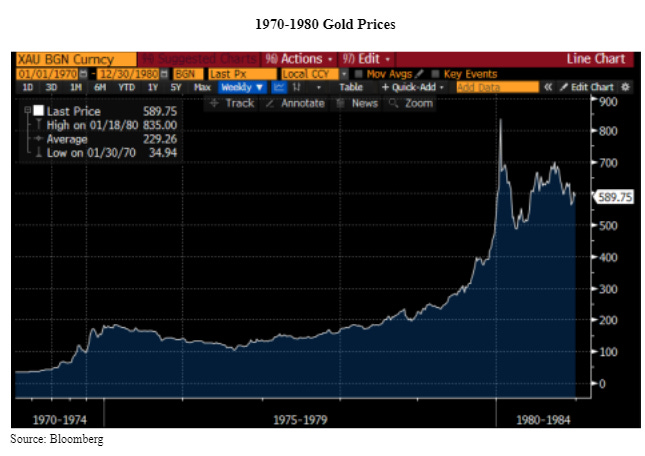

1970s: Nixon Closes Gold Window, Given the Run on Gold

Failure of the London Gold Pool’s manipulation only buoyed physical demand for gold, as all recognized that gold is the ultimate form of scarce and sound money.

The US gold reserves were being drained at a very rapid rate; there was massive pressure on the dollar. On August 15, 1971, President Nixon (who had no interest in, or ability to, contain the war spending) “temporarily” closed the US gold window to thwart the “evil international speculators”.

Consequently, without the promised gold exchangeability, the US government had effectively defaulted on its foreign creditors. We were bankrupt, and confidence in the dollar was fading fast. The impact of the US abandoning the international convertibility of the dollar into gold did not take long to stimulate the price of gold.

The US Treasury Secretary, John Connally, went to the G-10 meetings in Rome in late 1971, after the default, and brazenly said “the dollar is our currency, but it is your problem”.

The sentiment was not lost on the other participants and the gold price responded accordingly:

Paper Gold Suppression

What is instructive about this history of gold price suppression is that the London Gold Pool tried to manipulate the gold price from 1962 to 1968, somewhat successfully, but ultimately physical gold demand overwhelmed the manipulation scheme and it failed.

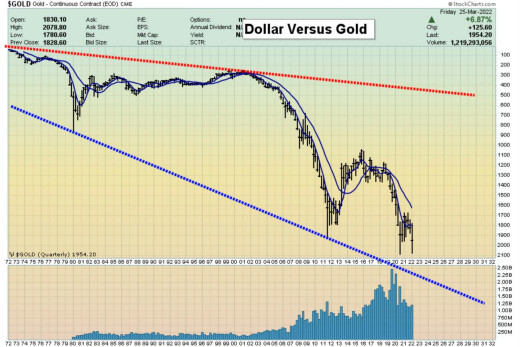

Over the past 20 years, there is substantial evidence that a similar manipulation scheme has been used by Central Banks, the Bank of International Settlements (BIS) and the Fed, whereby they “sell” paper gold contracts to keep gold prices down.

Gold is the only commodity market where there are large, unallocated paper derivatives which many in the Gold community believe have been used to suppress and contain its price. The evidence for this is overwhelming and buried in many places. Suffice it to say, many analysts believe that there are between 20x, 50x and perhaps up to 1,000x paper claims on each physical ounce of gold in the world today.

In effect, the Central Banks, Sovereign Governments and London Bullion Market Association (LBMA) have run a fractional reserve gold market. This scheme will only stay intact if everyone who holds a paper claim on gold does not ask for actual physical delivery (i.e., another run on physical gold like the late 1960s).

Conversely, if all of the claims were presented and asked to provide physical ounces (e.g. think short squeezes in Gamestop in 2021, or more recently nickel) there would either be a Force Majeure (similar to what happened recently in nickel) or the gold price would rise to multiples of its current price to match supply with demand.

We believe that the gold price has been severely suppressed by Western Governments in order to mask the underlying inflation or dilution of value which has taken place in order to support fiat currencies, Keynesian economics, Western government social policies, and credit inflation. Even with this suppression, the price of gold has performed quite well over the long sweep of time since 1971. Note the chart below shows the decline in US Dollars priced in gold terms.

There are some interesting things in this chart above. First, you can see the effect of the raging inflation in the 1970’s (red line above) when gold went from $35 per ounce to $800 per ounce (inverted white line). Note that at $800 an ounce gold in 1980, the US Money Supply (M1) was nearly 55% backed by our gold reserves.

If the price of gold had been $1,459 in 1980, every dollar would have had 100% gold backing. So even though we were not legally on a gold standard the market had effectively taken us more than halfway there by 1983.

It is also interesting to see M1 money supply (green line above) and how much it has skyrocketed since the 2008 crisis and bank bailouts. It is interesting to consider these numbers in today’s terms which show how much the gold price has been artificially suppressed as a measure of monetary inflation. Today, in order to obtain the bare minimum (30% coverage) necessary to have the US Treasury reserves of gold backing the dollar, the price of gold would need to be $23,000 per ounce, and to get to the 1980 peak of 55%% coverage of M1, the price would be $42,000 per ounce vs. gold today at only $1,970 per ounce. Indeed, there has been quite a bit of monetary inflation in terms of gold!

As concerns our portfolio upside, we think it’s just a matter of time until we get that mid-late 1970s 5x+ gold price acceleration. The reason this has not shown up in the gold price is due to the suppression scheme which until recently was perfected by the Western Central banks and the Gold Cartel. Some Bitcoin enthusiasts like to say Bitcoin is going to steal all of gold’s monetary premium. Gold bugs laugh at this because there is not much premium in gold to steal. On average, gold costs about $1,200 per ounce to mine and the sales price of $1,970 barely compensates for the capital costs to build mines and replace reserves.

If gold were to trade at much higher prices, then perhaps there would be a monetary premium to steal.

(This post is free but if you have the means and would like to support my work, I’d love to have you as a subscriber by clicking here).

Part 2 of Larry’s letter, where he discusses Bretton Woods III and the state of monetary policy from 1980 onward will be published this week.

About Larry Lepard

Larry manages the EMA GARP Fund, a Boston based investment management firm. Their strategy is focused on providing “Monetary Debasement Insurance”. He has 38 years experience and an MBA from Harvard Business School. On Twitter he is @LawrenceLepard Managing Partner and, via email, he is llepard@ema2.com

Disclaimer: QTR is long various gold and silver miners and have both long and short exposure to the market through equities and derivatives. I have no position in Larry’s funds. Larry is a subscriber to Fringe Finance and has been on my podcast. The excerpts from Larry’s letter, above, shall not be construed as an offer to sell, or the solicitation of an offer to sell, any securities or services. Any such offering may only be made at the time a qualified investor receives from EMA formal materials describing an offering plus related subscription documentation. There is no guarantee the Fund’s investment strategy will be successful. Investing involves risk, and an investment in the Fund could lose money. The strategy is also subject to the following risks: Currency Risk, Non-US Investment Risks, Issuer Specific Risk

end.

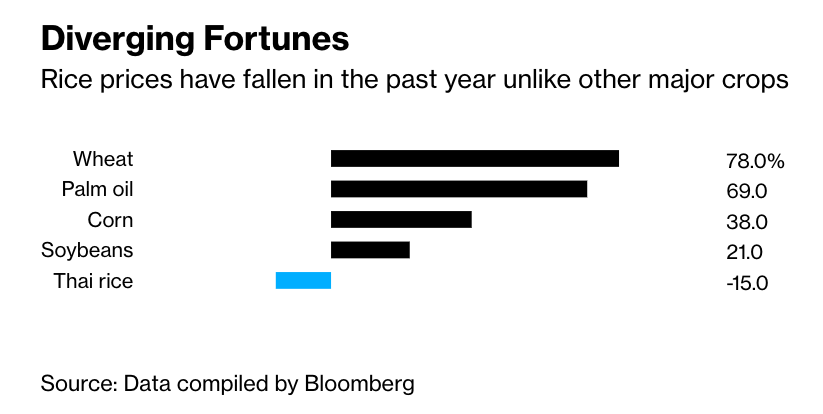

5.OTHER COMMODITIES RICE

Global Rice Production Set To Plunge 10%, Threatening Half Of Humanity

WEDNESDAY, APR 20, 2022 – 04:15 AM

Farmers in China, India, Bangladesh, Indonesia, and Vietnam — the largest rice-producing countries could experience reduced output due to soaring fertilizer prices.

The International Rice Research Institute warns that harvests could plunge as much as 10% in the next season, equating to about 36 million tons of rice, or enough food to feed a half billion people, according to Bloomberg.

Chemical fertilizers, such as nitrogen, phosphorus, and potassium, are the most applied nutrients for high-yielding rice cultivation. Farmers have been particularly vulnerable to soaring fertilizer prices as some have reduced the amount of nutrients to save costs. This threatens future harvests as production declines could stoke food inflation for a crop that feeds half of humanity.

Humnath Bhandari, a senior agricultural economist at the institute, said the 10% drop in global rice production is a “very conservative estimate.” He said if the Ukraine conflict continued and fertilizer prices remained high and supply limited, then the decline of rice output could be even more severe. This may trigger a full-blown global food crisis, similar to the one that the UN has been warning about.

Russia and Belarus are big suppliers of every major type of crop nutrient. Western countries have sanctioned both, which have limited fertilizers shipments to the rest of the world, crimping supply and why prices are soaring. On top of this, Moscow has reduced or halted nutrient exports.

Nguyen Binh Phong, the owner of a fertilizer shop in Vietnam’s Kien Giang province, said nutrient costs have soared three-fold over the past year, forcing farmers in the region to reduce fertilizer use by up to 20% because of rising prices.

“When the farmers cut fertilizer use, they accept that they will get lower profit,” Phong said.

Bloomberg outlines a significant problem: Unlike most crop prices, the price of rice has gone down, not up, which will compress farmers’ margins even more.

Governments across Asia have kept rice prices under control to maintain social order. Some countries offer generous fertilizer subsidies to farmers to keep yields plentiful. For example, India will spend $20 billion this year to shield farmers from soaring nutrient prices, up from the $14 billion budget before the Russian invasion of Ukraine.

Bhandari said it’s “inevitable” that rice prices will go higher; “It has to be reflected somewhere.”

Maybe the world is in the beginning stages of a food crisis and could worsen next year as crops of all sorts could experience harvest declines because farmers are spreading fewer nutrients due to high prices.

Global food prices will remain at record-highs (or at least elevated levels) as forward-looking markets expect tightening supplies in 2023. This will give rise to continued social unrest (see: here & here) as the dominos fall in the weakest countries.

end

COMMODITIES IN GENERAL

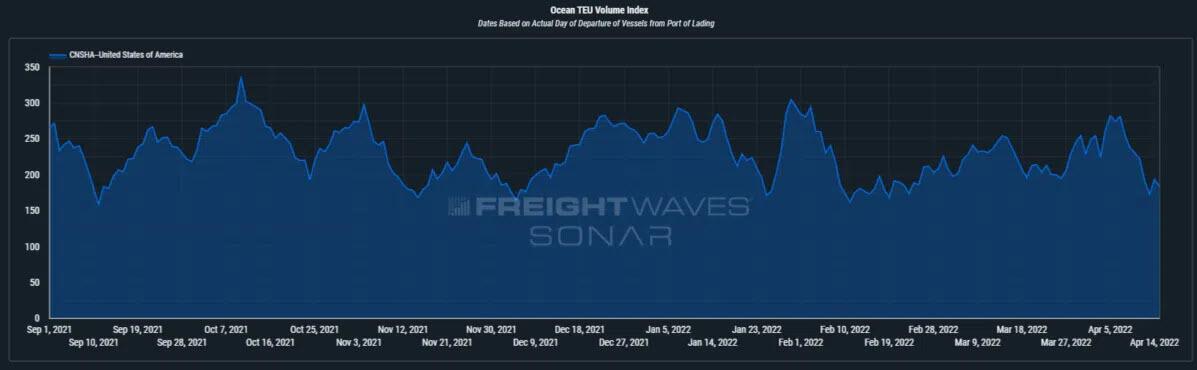

Get Ready For The Next Supply Chain Shockwave

TUESDAY, APR 19, 2022 – 04:50 PM

By Eric Kulisch of FreightWaves

Concern is growing that the spread of COVID cases and city lockdowns in China will have massive downstream effects for global supply chains that could dwarf previous disruptions since the start of the pandemic.

Last May, the huge Yantian container terminal at the Port of Shenzhen throttled down to 30% of normal productivity for a month to stamp out a handful of positive cases there. Hundreds of thousands of shipments that couldn’t enter the port accumulated in factories and warehouses, and many vessels skipped the port to avoid waiting seven days or more at anchor. It took weeks after the port reopened to clear the cargo backlog. The effects cascaded to the U.S. and Europe, resulting in port traffic jams, transit times triple the norm and missed retail deliveries for the holidays.

The difference this time is that an entire metropolis — and highly interconnected global trade center — is essentially shut down. Not since the initial 2020 COVID-19 outbreak in Wuhan have lockdowns been this extensive in China.

“It’s probably worse than Wuhan,” said Jon Monroe, an ocean shipping and supply chain expert who runs a consulting firm. “You’re going to have a lot of pent-up orders. It’s going to be an overwhelming movement of goods” that will drown shipping lines and ports once the lockdowns are lifted.

Freight is piling up

Twenty-five million people in Shanghai have been sequestered for 18 days. Chinese authorities this week slightly eased the restrictions, dividing the city into three categories based on previous screenings and risk levels. People can wander outside their apartment buildings but are encouraged to stay home in neighborhoods with no positive COVID-19 cases in the past two weeks. Those in high-risk areas must still shelter at home.

Spanish financial services firm BBVA predicts Chinese authorities will stick to the “zero-COVID” strategy and lockdowns until at least June. Other China observers say it could take even longer to meet China’s infection standard.

Shanghai is one of the largest manufacturing centers in China, with heavy concentrations of automotive and electronics suppliers. It is home to the largest container port in the world and a major airport that serves inbound and outbound air cargo. Exports produced in Shanghai account for 7.2% of China’s total volume and about 20% of China’s export container throughput moves through the port there, according to the BBVA report.

Most warehouses and plants are closed, nine out of 10 trucks are sidelined, the port and airport have limited function, shipping units are stranded in the wrong places, and freight is piling up.

More and more, the logistics impacts are rippling beyond the contagion epicenter.

Impacts spread beyond Shanghai

Export containers that were already at the Port of Shanghai when the lockdown started are making it onto vessels, but most goods booked on outbound vessels are stranded at warehouses because shuttle trucks can’t make pickups or deliveries.

Truckers require special permits, which are only good for 24 hours, as well as negative COVID tests to get in and out of the city or enter certain zones, according to logistics providers. Checking COVID certificates has led to huge traffic jams at the port.

The French logistics provider Geodis reports that truck drivers in the Shanghai area are being forced to wait up to 40 hours at certain highway entrances. Trucking rates have soared because of the limited supply, and shippers are waiting three to five days for cargo to get picked up, according to San Francisco-based Flexport.

Reduced manufacturing output, along with limited truck access to the port and airport, are causing a significant drop in air and ocean export volumes. Less demand is translating to lower freight rates.

In response to the lack of labor and cargo, air carriers have announced widespread cancellations, and some ocean carriers are skipping Shanghai port calls.

Several shipping lines have also begun offloading refrigerated containers at other ports along their voyage because the storage area with electric plugs is too crowded in Shanghai. Customers face extra port fees and delays routing the cargo to its intended destination. Maersk, the second-largest container vessel operator, said Thursday it has stopped accepting bookings to Shanghai for refrigerated cargo, some types of gas and flammable liquids.

More omissions are expected and liner companies may temporarily idle vessels or cancel some outbound Asia sailings altogether, according to Crane Worldwide Logistics and other service providers.

Asia-U.S. East Coast rates have fallen 7% since the outbreaks in March, said freight booking site Freightos, which also publishes an ocean rate index.

“But even if the lockdown persists and demand drops significantly, ocean carriers will likely reduce capacity which could keep rates from plummeting, just as they were able to do in the first few months of the pandemic when ocean volumes fell significantly but transpacific rates declined by less than 15% and were about level year on year,” it said.

The supply chain is backing up like water behind a dam. When water is released, the landscape gets flooded.

At Shanghai Pudong airport, ground handling companies are operating with skeleton staff.

Shanghai Eastern Airlines Logistics, a cargo terminal operator, ceased bulk loading of containers after a positive COVID case, which will further slow cargo processing, said Dimerco, a Taiwan-based freight forwarder. Airlines report that Pactl, which operates three other cargo terminals, has suspended acceptance of dangerous goods and temperature-controlled cargo because the warehouse is full.

Flexport said in a market update that 80% of commercial freighter services have been canceled and airlines are considering shifting operations to nearby airports. Qatar Airways announced that freighter flights will remain canceled until next Thursday, saying “the latest COVID-19 restrictions announced by local authorities limit our ability to operate flights in and out of Shanghai with sufficient cargo loads.”

Freight forwarders have been rerouting cargo to alternative airports such as Zhengzhou, Xiamen, Shenzhen and Beijing, as well as the Port of Ningbo, but those facilities are beginning to feel congestion effects themselves. Rates to ship from those locations are increasing.

Flights at Zhengzhou Xinzheng International Airport are reduced by 50%, according to Geodis. Most inbound cargo there is transit cargo to other cities, such as Shanghai — which is compounding backlogs because the cargo isn’t allowed to move to the final destination. That means logistics companies can only clear shipments that customers can pick up in Zhengzhou.

Dimerco advises that Zhengzhou airport is not accepting loose cargo – only palletized shipments – because of labor challenges. And it has just implemented a 14-day closed-loop program in which workers live on-site to minimize the potential for virus transmission, forcing the logistics provider to pivot again and reroute shipments to other airports, including back to Shanghai’s second airport – Hongqiao International.

Everstream Analytics, which helps companies manage supply chain risk, predicts U.S. and Canadian automotive assembly plants will quickly face delays and disruptions because the lockdowns will affect shipping of parts such as seats, tires, engines, bodies and brakes.

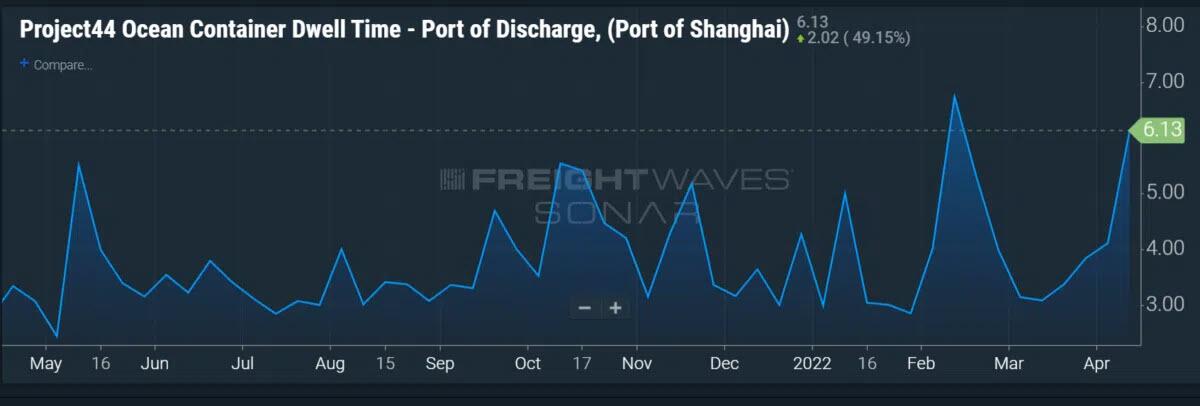

Ships delayed at port of Hong Kong and Yantian

Shipping schedules in South China are being impacted by irregular feeder vessels and large barge services, creating delays for transoceanic vessels at the ports of Hong Kong and Yantian, according to a situational update from supply chain data platform project44. Both ports have been coping with disruptive COVID restrictions for months.

Nearby manufacturing hubs in Vietnam and Cambodia are already suffering from a shortage of Chinese components for their manufacturing industries, project44 reported. And pharmaceutical companies in India, which source 70% of their active ingredients from China, are facing limited supplies.

Ocean shipping delays from the top three Chinese ports to Hamburg, Germany, and Amsterdam had already doubled to more than 12 days during the first quarter, before the Shanghai lockdown fully materialized, according to project44 data.

Ocean freight expert Lars Jensen, CEO of Vespucci Maritime, summed up the situation on his LinkedIn page this way: “Until this situation is resolved — which appears next to impossible when matching the omicron variant with zero-tolerance — we should expect drops in export demand, port omissions and more blank sailings in the near term future as well as Shanghai-bound cargo increasingly being discharged elsewhere.”

COVID lockdowns spread

Meanwhile, COVID infections are spreading beyond Shanghai, according to news reports and logistics companies. The southern manufacturing hub of Guangzhou, for example, has started mass COVID testing, introduced travel restrictions and shifted schools to online learning — steps that often portend a wider lockdown.

The city of Kunshan — an important production center for electronics near Shanghai — is closed down until April 19. Part of Taicang, another manufacturing area in Jiangsu province, is also locked down. A surge of new COVID cases is hitting the coastal cities of Dalian and Tianjin in the north, Ningbo in the east, and Xiamen and Dongguan in the south.

Ningbo officials ordered residents in two downtown districts to sequester at home, but so far the seaport is not affected. Nantong is on a partial lockdown until April 15. Port operations have been severely impacted, with logistics companies diverting shipments to Nanjing. Zhangiagang is also under partial lockdown until April 19, resulting in slower port operations and some factory closures.

Many shippers are exercising contingency plans and using alternative import/export gateways when possible, but road transport is increasingly difficult.

The outbreaks have led to a virtual ban by authorities on truck drivers from high- and medium-risk areas transporting cargo to low-risk areas. That includes transporting cargo from Shanghai and Kunshan to the Port of Ningbo. No cargo will be accepted if drivers have been to medium- or high-risk areas within the last 14 days or the factory is located in medium- or high-risk areas, said UPS Supply Chain Solutions in a customer update.

As of Friday, Dalian, Tianjin, parts of Beijing, Shanghai, and Dongguan are all in high- and medium-risk areas.

Dimerco said in a notice that traffic control for road transportation is getting more strict and it is difficult to secure trucks to bring freight to Shanghai or alternative ports.

Lockdowns ease U.S. supply chain strains before flood of cargo

The slowdown in China exports should provide temporary relief to congestion-plagued U.S. ports on both coasts, as well as in Europe, but logistics experts say the breather is likely to be followed by a tsunami of deferred cargo once the lockdowns are lifted. The cargo volume will far exceed the handling capability of the ports, with containers jamming up terminals faster than they can be transferred to inland transport and pushing vessels into long queues at sea.

Delta Air LInes President Glen Hauenstein said on an earnings call Wednesday that once the Shanghai restrictions are lifted, the airline expects a boom in cargo bookings that more than offsets the current export lag.

A mass quarantine that lasts until June could mean the drawdown of backlogged air and ocean freight pushes into the peak shipping season, as more volume enters the system.

“Even with air and ocean ports open, the length of the shutdown could make this iteration the most significant logistics disruption since the start of the pandemic,” Freightos said in its update.

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings WEDNESDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 6.4131

OFFSHORE YUAN: 6.4431

HANG SANG CLOSED UP DOWN 83.09 PTS OR 0.40%

2. Nikkei closed UP 232.76PTS OR 0.86%

3. Europe stocks ALL GREEN

USA dollar INDEX DOWN TO 100.45/Euro RISES TO 1.0829