April 22, 2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

april22, 2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD; $1932.90 DOWN $13.40

SILVER: $24.23 DOWN $0.57

ACCESS MARKET: GOLD $1932.50

SILVER: $24.18

Bitcoin morning price: $40566 DOWN 765

Bitcoin: afternoon price: $39,610 DOWN 1721

Platinum price: closing DOWN $41.79 to $931.16

Palladium price; closing DOWN 3.45 at $2380.30

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

comex notices/

: JPMorgan stopped/total issued 19/50

EXCHANGE: COMEX

CONTRACT: APRIL 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,944.900000000 USD

INTENT DATE: 04/21/2022 DELIVERY DATE: 04/25/2022

FIRM ORG FIRM NAME ISSUED STOPPED

072 C GOLDMAN 1

118 C MACQUARIE FUT 50

132 C SG AMERICAS 11

435 H SCOTIA CAPITAL 1

624 H BOFA SECURITIES 3

657 C MORGAN STANLEY 1

661 C JP MORGAN 19

709 C BARCLAYS 6

880 H CITIGROUP 6

905 C ADM 2

TOTAL: 50 50

MONTH TO DATE: 25,731

NUMBER OF NOTICES FILED TODAY FOR APRIL. CONTRACT 50 NOTICE(S) FOR 5000 OZ (0.1555 TONNES)

total notices so far: 25,731 contracts for 2,573.100 oz (80.03 tonnes)

SILVER NOTICES:

39 NOTICE(S) FILED 195,000 OZ/

total number of notices filed so far this month 1322 : for 6,610,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

END

GLD

WITH GOLD DOWN $13.50

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

A HUGE CHANGE IN GOLD INVENTORY AT THE GLD A HUGE WITHDRAWAL OF 2.61 TONNES FROM THE GLD//

INVENTORY RESTS AT 1104.13 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 34 CENTS

AT THE SLV// A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WHOPPING DEPOSIT OF 3.508 MILLION OF INTO THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 581.449 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A GIGANTIC SIZED 3647 CONTRACTS TO 164,456 AND FURTHER FROM THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE STRONG LOSS IN OI WAS ACCOMPLISHED DESPITE OUR STRONG $0.57 LOSS IN SILVER PRICING AT THE COMEX ON THURSDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.57) AND WERE SOMEWHAT UNSUCCESSFUL IN KNOCKING OUT SOME SILVER LONGS AS WE HAD A STRONG LOSS OF 997 CONTRACTS ON OUR TWO EXCHANGES. SOME EVIDENCE OF SPREADER LIQUIDATION IN SILVER TODAY.

WE MUST HAVE HAD:

I) HUGE BANKER SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A STRONG INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 4.305 MILLION OZ FOLLOWED BY TODAY’S QUEUE. JUMP OF 255,000 OZ//NEW STANDING: 6.680 MILLION OZ// V) STRONG SIZED COMEX OI LOSS/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS : —-737

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS APRIL. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF APRIL:

TOTAL CONTACTS for 15 days, total 14,276 contracts: 71.380 million oz OR 4.73 MILLION OZ PER DAY. (951 CONTRACTS PER DAY)

TOTAL NO OF OZ UNDERGOING EFP TO LONDON 14,276 CONTRACTS X 5,000 PER CONTRACT:

EQUATES TO: 71.38 MILLION OZ

.

LAST 11 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

APRIL: 71.38 MILLION OZ (LOOKS LIKE OUR BANKERS ARE NOW LOATHE TO ISSUE EFP’S)

RESULT: WE HAD A GIGANTIC SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 3647 WITH OUR STRONG $0.57 LOSS IN SILVER PRICING AT THE COMEX// THURSDAY. SOME EVIDENCE OF SILVER SPREADER LIQUIDATION TODAY. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE CONTRACTS: 2650 CONTRACTS ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A HUGE INITIAL SILVER OZ STANDING FOR MAR. OF 4.305 MILLION OZ FOLLOWED BY TODAY’S 255,000 OZ QUEUE JUMP//NEW STANDING: 6.680MILLION OZ/// .. WE HAD A STRONG SIZED LOSS OF 997 OI CONTRACTS ON THE TWO EXCHANGES FOR 4.985 MILLION OZ DESPITE THE STRONG LOSS IN PRICE.

WE HAD 39 NOTICES FILED TODAY FOR 195,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A FAIR SIZED 2385 CONTRACTS TO 569,941 AND FURTHER FROM NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: -206 CONTRACTS.

THE BIS HAS ABANDONED THE GOLD COMEX TRADING!!!

.

THE FAIR SIZED DECREASE IN COMEX OI CAME WITH OUR LOSS IN PRICE OF $6.80//COMEX GOLD TRADING/THURSDAY /.AS IN SILVER WE MUST HAD HUGE BANKER/ALGO SHORT COVERING ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD MINOR LONG LIQUIDATION

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR APRIL AT 78.33 TONNES ON FIRST DAY NOTICE

YET ALL OF..THIS HAPPENED WITH OUR LOSS IN PRICE OF $6.80 WITH RESPECT TO THURSDAY’S TRADING

WE HAD A SMALL SIZED LOSS OF 131 OI CONTRACTS (0.4074 PAPER TONNES) ON OUR TWO EXCHANGES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2516 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 569,941.

IN ESSENCE WE HAVE A TINY SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 131, WITH 2385 CONTRACTS DECREASED AT THE COMEX AND 2516 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 131 CONTRACTS OR 0.4074 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2516) ACCOMPANYING THE FAIR SIZED LOSS IN COMEX OI (2385,): TOTAL GAIN IN THE TWO EXCHANGES 131 CONTRACTS. WE NO DOUBT HAD 1) HUGE BANKER SHORT COVERING ,2.) HUGE INITIAL STANDING AT THE GOLD COMEX FOR APRIL. AT 78.33 TONNES FOLLOWED BY TODAY’S 1,000 OZ EFP JUMP TO LONDON //NEW STANDING 82.0637 TONNES/// 3) ZERO LONG LIQUIDATION //.,4) FAIR SIZED COMEX OI. LOSS 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

APRIL

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL :

33,704 CONTRACTS OR 3,370,400 OR 104.83 TONNES 15 TRADING DAY(S) AND THUS AVERAGING: 2246 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 15 TRADING DAY(S) IN TONNES: 104.83 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2020, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 104.83/3550 x 100% TONNES 3.26% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 104.83 TONNES (THIS IS GOING TO BE A LOW ISSUANCE MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF MAY.WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF APRIL HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF MAY, FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (MAR), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A GIGANTIC SIZED 3647 CONTRACT OI AND FURTHER FROM OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 2650 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 2650 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 3647 CONTRACTS AND ADD TO THE 2650 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A STRONG SIZED LOSS OF 997 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES 4.985 MILLION OZ

OCCURRED WITH OUR LOSS IN PRICE OF $0.57 IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

.

end

6. Commodity commentaries/cryptocurrencies

3. ASIAN AFFAIRS

i)FRIDAY MORNING// THURSDAY NIGHT

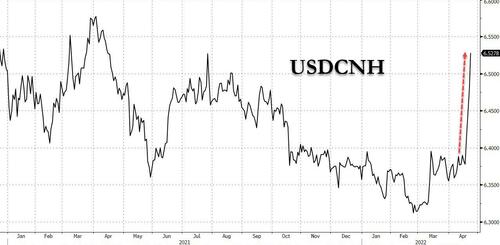

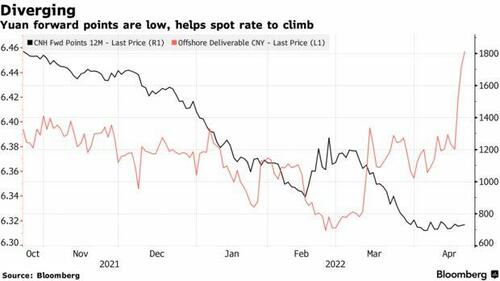

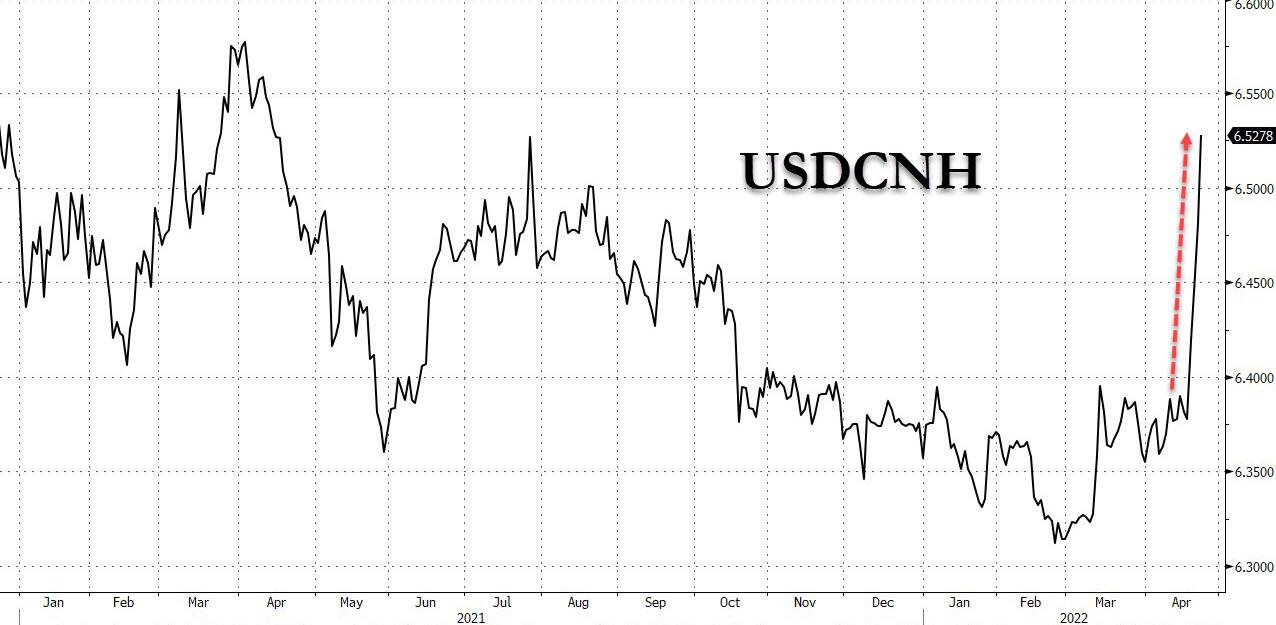

SHANGHAI CLOSED UP 7.11 PTS OR 0.23% //Hang Sang CLOSED 43.70 OR 0.21% /The Nikkei closed DOWN 447.80 PTS OR 1.63% //Australia’s all ordinaires CLOSED DOWN 1.51% /Chinese yuan (ONSHORE) closed DOWN 6.5010 /Oil UP TO 103.09 dollars per barrel for WTI and DOWN TO 107.10 for Brent. Stocks in Europe OPENED ALL GREEN // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.5010 OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.5320: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER//

a)NORTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 2385 CONTRACTS TO 569.941 AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS GOOD COMEX DECREASE OCCURRED WITH OUR LOSS OF $6.80 IN GOLD PRICING THURSDAY’S COMEX TRADING. WE ALSO HAD A fair SIZED EFP (1211 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE ACTIVE DELIVERY MONTH OF APRIL.. THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2516 EFP CONTRACTS WERE ISSUED: ;: , . 0 JUNE :2516 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2516 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A SMALL SIZED TOTAL OF 131 CONTRACTS IN THAT 2516 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED COMEX OI LOSS OF 2385 CONTRACTS..AND THIS GAIN OCCURRED WITH OUR LOSS IN PRICE OF GOLD $6.80.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING FOR APRIL (82.037),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 82.037

THE BANKERS WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $6.80) AND AND WERE UNSUCCESSFUL IN FLEECING ANY LONGS AS WE HAVE REGISTERED A TINY SIZED GAIN OF 0.3076 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR APRIL (82.037 TONNES)…

WE HAD —206 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 131 CONTRACTS OR 13100 OZ OR 0.4074TONNES

Estimated gold volume today: 176,924/// poor

Confirmed volume yesterday: 170,001 contracts poor

INITIAL STANDINGS FOR APRIL ’22 COMEX GOLD //APRIL 22

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 5562.120 OZ Brinks 173 kilobars 96.43 oz JPMorgan 3 kilobars |

| Deposit to the Dealer Inventory in oz | nil OZ |

| Deposits to the Customer Inventory, in oz | |

| No of oz served (contracts) today | 50 notice(s)5000 OZ 0.1555 TONNES |

| No of oz to be served (notices) | 644 contracts 64400 oz 2.003 TONNES |

| Total monthly oz gold served (contracts) so far this month | 25,731 notices 2,573,100 OZ 80.03TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For today:

dealer deposits 0

total dealer deposit nil oz//

No dealer withdrawals

2 customer withdrawals

i) out of Brinks 5562.120 oz (173 kilobars)

ii) out of JPMorgan 96.453 oz (3 kilobars)

total customer withdrawals 5658.573 oz oz

0 customer deposits

total customer withdrawal: nil oz /

ADJUSTMENTS: one//dealer to customer

i) Out of JPMorgan: 32,215.302 oz (1002 kilobars)

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR APRIL.

For the front month of APRIL we have an oi of 694 contracts having LOST 346 contracts

We had 336 notices filed yesterday so we LOST 10 contracts or an additional 1000 oz will NOT stand for delivery at the comex , as they were EFP’d to London.

May saw a LOSS of 50 contracts to stand at 3294

June saw a LOSS of 4353 contracts UP to 465,332 contracts

We had 50 notice(s) filed today for 5000 oz FOR THE APRIL 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 50 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 19 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 1 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the APRIL /2021. contract month,

we take the total number of notices filed so far for the month (25,731) x 100 oz , to which we add the difference between the open interest for the front month of (APRIL 694 CONTRACTS ) minus the number of notices served upon today 50 x 100 oz per contract equals 2,637,500 OZ OR 82.037 TONNES the number of TONNES standing in this active month of APRIL.

thus the INITIAL standings for gold for the APRIL contract month:

No of notices filed so far (25,731) x 100 oz+ (694) OI for the front month minus the number of notices served upon today (50} x 100 oz} which equals 2,637,500 oz standing OR 82.037 TONNES in this active delivery month of APRIL.

We GAINED 1900 additional oz that will stand for delivery on this side of the pond.

TOTAL COMEX GOLD STANDING: 82.037 TONNES (A WHOPPER FOR AN APRIL ( ACTIVE) DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

191,133,764.7, oz NOW PLEDGED /HSBC 5.94 TONNES

99,258.893 PLEDGED MANFRA 3.08 TONNES

54,339.114oz PLEDGED JPMorgan no 1 1.690 tonnes

243,923.704, oz JPM No 2 7.58 TONNES

898,821.330 oz pledged Brinks/27,96 TONNES

International Delaware:: 0

Loomis: 18,615.429 oz

total pledged gold: 1,887,433.936 oz 58.70 tonnes

TOTAL REGISTERED AND ELIG GOLD AT THE COMEX: 35,970,765.02 OZ (1119,01 TONNES)

TOTAL ELIGIBLE GOLD: 18,374,660.230 OZ (571.52 tonnes)

TOTAL OF ALL REGISTERED GOLD: 17,596,104.842 OZ (547.31 tonnes)

REGISTERED GOLD THAT CAN BE SERVED UPON: 15,708,671.0 OZ (REG GOLD- PLEDGED GOLD) 488.60tonnes

END

APRIL 2022 CONTRACT MONTH//SILVER//APRIL 22

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1,227,104.704 oz Brinks CNT Delaware Manfra |

| Deposits to the Dealer Inventory | nilOZ |

| Deposits to the Customer Inventory | 2,027,474.150 oz CNT Delaware HSBC |

| No of oz served today (contracts) | 39CONTRACT(S) 195,000 OZ) |

| No of oz to be served (notices) | 14 contracts (70,000 oz) |

| Total monthly oz silver served (contracts) | 1322 contracts 6,610,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

we had 0 deposit into the dealer

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 3 deposits into the customer account

i) Into CNT: 627,881.580 oz

ii) Into Delaware: 501,599.540 oz

iii) Into HSBC: 898,013.030oz

total deposit: 2,027,494.150 oz

JPMorgan has a total silver weight: 174.426 million oz/334.879 million =52.57% of comex

Comex withdrawals: 4

i) Out of CNT 2886.33 oz

ii) Out of JPMorgan 1,211,063.600 oz

iii) Out of Brinks 953.800 oz

iv) Out of Delaware 12,200.972 oz

total withdrawal 1,227,108.704 oz

1 adjustments: dealer to customer//JPM: 99102.200 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 85.811 MILLION OZ

TOTAL REG + ELIG. 334.879 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR APRIL

silver open interest data:

FRONT MONTH OF APRIL OI: 53, HAVING GAINED 47 CONTRACTS FROM WEDNESDAY. We had 4 notices filed yesterday,

so we GAINED 51 contracts or an additional 255,000 oz will stand on this side of the pond

MAY HAD A LOSS OF 10,077 CONTRACTS DOWN TO 42,180 contracts

JUNE HAD A GAIN OF 78 TO STAND AT 1322

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 80 for 400,000 oz

Comex volumes: 91,986// est. volume today// strong//good indicator of spreader liquidation/

Comex volume: confirmed yesterday: 101,233 contracts ( strong/spreader liquidation )

To calculate the number of silver ounces that will stand for delivery in APRIL. we take the total number of notices filed for the month so far at 1322 x 5,000 oz = 6,610,000 oz

to which we add the difference between the open interest for the front month of APRIL (53) and the number of notices served upon today 39 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the APRIL./2021 contract month: 1322 (notices served so far) x 5000 oz + OI for front month of APRIL (53) – number of notices served upon today (39) x 5000 oz of silver standing for the APRIL contract month equates 6,680,000 oz. .

We GAINED 51 contracts or an additional 255,000 oz will stand on this side of the pond

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

APRIL 22/WITH GOLD DOWN $13.50: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD.//INVENTORY RESTS AT 1104.13 TONNES

APRIL 21/WITH GOLD DOWN $6.80//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1106.74 TONNES

APRIL 20/WITH GOLD DOWN $3.05: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT IF 6.36 TONNES INTO THE GLD..//INVENTORY RESTS AT 1106.74 TONNES

APRIL 19//WITH GOLD DOWN $26.90//A SMALL CHANGE IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .87 TONNES INTO THE GLD//INVENTORY RESTS AT 1100.36 TONNES

APRIL 18/WITH GOLD UP $11.20: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.93 TONNES FROM THE GLD..//INVENTORY RESTS AT 1099.44 TONNES

APRIL 14/WITH GOLD DOWN $8.90: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.32 TONNES INTO THE GLD..//INVENTORY RESTS AT 1104.42 TONNES

APRIL 13/WITH GOLD UP $8.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1093.10 TONNES

APRIL 12/WITH GOLD UP $26.95: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.61 TONNES INTO THE GLD///INVENTORY REST AT 1093.10 TONNES

APRIL 11/WITH GOLD UP $3.40 //A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD.//INVENTORY RESTS AT 1090.49 TONNES

APRIL 8/WITH GOLD UP $7.70: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES INTO THE GLD//INVENTORY RESTS AT 1088.75 TONNES

APRIL 7/WITH GOLD UP $13.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1087.30 TONNES

APRIL 6/WITH GOLD DOWN $4.10: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.68 TONNES FROM THE GLD..//INVENTORY RESTS AT 1087.30 TONNES

APRIL 5/WITH GOLD DOWN $5.70: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.75 TONNES FROM THE GLD//INVENTORY RESTS AT 1089.98 TONNES

APRIL 4/WITH GOLD UP $.70//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1091.73 TONNES

APRIL 1///WITH GOLD DOWN $19.00 : A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .29 TONNES INTO THE GLD///INVENTORY RESTS AT 1091.73 TONNES

MARCH 31/WITH GOLD UP $13.30 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD FROM MONDAY A WITHDRAWAL OF 1.71 TONNES FROM THE GLD:INVENTORY RESTS AT 1091.44

MARCH 28/WITH GOLD DOWN $14.65: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1093.18 TONNES

MARCH 25/WITH GOLD DOWN $7.60 : A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.52 TONNES INTO THE GLD///INVENTORY RESTS AT 1093.18 TONNES

MARCH 24/WITH GOLD UP $24.95: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.06 TONNES INTO THE GLD..//INVENTORY RESTS AT 1087.66 TONNES

MARCH 23/WITH GOLD UP $15.75//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1083.60 TONNES

MARCH 22/WITH GOLD DOWN $7.75: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.16 TONNES OF GOLD DEPOSITED INTO THE GLD//INVENTORY RESTS AT 1083.60 TONES

CLOSING INVENTORY FOR THE GLD//1104.13 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

APRIL 22/WITH SILVER DOWN 34 CENTS : STRANGE!! A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WHOPPING DEPOSIT OF 3.508 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 581.449 MILLION OZ//

APRIL 21/WITH SILVER UP 57 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 577.941 MILLION OZ

APRIL 20/WITH SILVER DOWN 15 CENTS : A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.955 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 577.941 MILLION OZ///

APRIL 19/WITH SILVER DOWN 62 CENTS: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .461 MILLION OZ FROM THE SLV INVENTORY…//INVENTORY RESTS AT 574.986 MILLION OZ

APRIL 18/WITH SILVER UP 38 CENTS: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.771 MILLION OZ INTO THE SLV./INVENTORY RESTS AT 575.447 MILLION OZ//

APRIL 14/WITH SILVER DOWN 25 CENTS : A MONSTROUS CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.355 MILLION OZ INTO THE SLV.//INVENTORY RESTS AT 569.676 MILLION OZ//

APRIL 13/WITH SILVER UP 27 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 565.521 MILLION OZ

APRIL 12/WITH SILVER UP 66 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 565.521 MILLION OZ//

APRIL 11/WITH SILVER UP 13 CENTS: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 831,000 OZ FORM THE SLV////INVENTORY RESTS AT 565.521 MILLION OZ

APRIL 8/WITH SILVER UP 11 CENTS :NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 566.352 MILLION OZ//

APRIL 7/WITH SILVER UP 27 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 566.352 MILLION OZ//

APRIL 6/WITH SILVER DOWN 9 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 566.352 MILLION OZ

APRIL 5/WITH SILVER DOWN 16 CENTS : A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.386 MILLION OZ INTO THE SLV..//INVENTORY RESETS AT 566.352 MILLION OZ//

APRIL 4/WITH SILVER DOWN 5 CENTS TO CHANGES IN SILVER INVENTORY AT THE SLV//: A DEPOSIT OF 6.326 MILLION OZ//INVENTORY REST AT 564.966 MILLION OZ//

APRIL 1/WITH SILVER DOWN 39 CENTS A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.302 MILLION OZ INTO THE SLV////INVENTORY REST AT 558.647 MILLION OZ//

MARCH 31/WITH SILVER UP 3 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 2.171 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 556.345 MILLION OZ

MARCH 28/WITH SILVER DOWN 30 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.847 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 554.167 MILLION OZ//

MARCH 25/WITH SILVER DOWN 20 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 552.320 MILLION OZ//

MARCH 24/WITH SILVER UP 54 CENTS TODAY; A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.092 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 552.320 MILLION OZ//

MARCH 23/WITH SILVER UP 24 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 550.288 MILLION OZ//

MARCH 22/WITH SILVER DOWN $0.29 TODAY : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 550.288 MILLION OZ//

SLV FINAL INVENTORY FOR TODAY: 581.449 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

END

2.LAWRIE WILLIAM//,//Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, James RICKARDS/

LAWRIE WILLIAMS: Russia still mute on gold reserve increases

Gold is perhaps the one foreign exchange asset which will ultimately enable Russia to mitigate the effects of the economic sanctions being imposed on it by many other countries. But the country is playing its cards close to its chest with regard to informing the rest of the world of any change in its central bank’s gold reserve position. It has previously announced that it is resuming gold purchases after an almost two year hiatus, and as the world’s second, or possibly third, largest gold producer with its mines producing over 300 tonnes a year, it is certainly able to increase its reserves – the world’s fifth largest national gold reserve as reported to the IMF – without publicising any actual amounts added. The monthly date has now passed when the Russian central bank has always announced changes in its gold reserve totals, but no such announcement has been forthcoming so far this month.

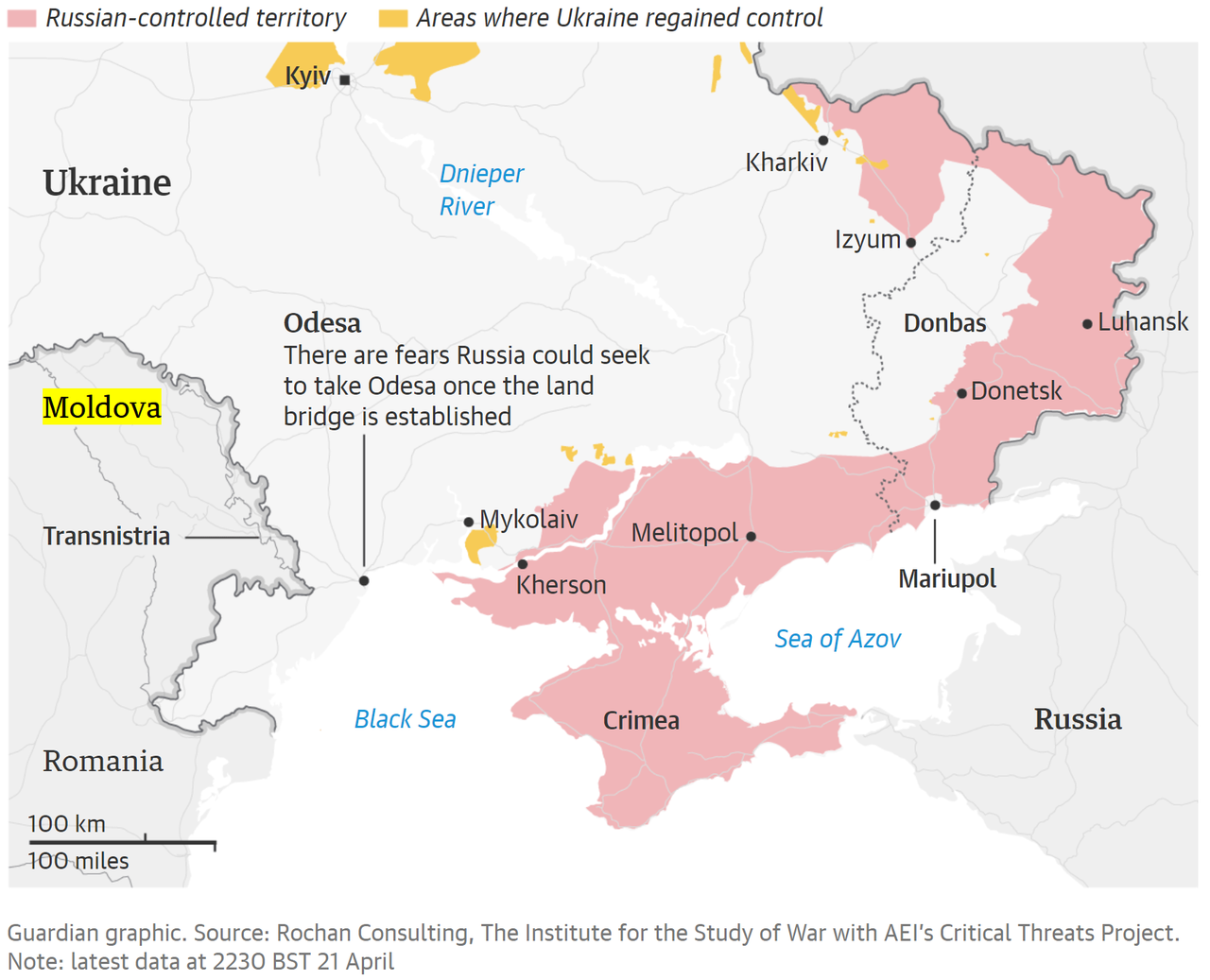

Certainly, if Ukrainian claims of losses so far inflicted on Russian military equipment and personnel are to be believed, and they are probably far more accurate than the remarkably low figures coming out of Russia itself, then the costs of replacing lost equipment alone will be massive. The loss of the Black Sea Fleet’s flagship for example, whether by accident (unlikely) or by Ukrainian missile strike (more probable), will alone have been enormously costly in both monetary and prestige terms.

But back to Russia’s gold reserves. President Putin had issued a decree that the country’s exports of oil and gas to ‘hostile’ nations would need to be paid for in rubles – a move designed to boost the parity of the ruble against other currencies. This has been strongly resisted by some of the key players involved, but inasmuch as they are still importing these key resources from Russia they may well be paying for them in gold given that Russia is currently effectively excluded from the dollar world and is probably rejecting payments in euros. If this is the case then Russia may well be financing its continuing war on Ukraine with gold – which is thus acting as a universal currency, perhaps one of its greatest strengths.

Russia has thus been able to counter some of the Western sanctions through the reliance of so many countries on continuing purchases of Russian energy and other commodities. Even the U.S. is believed to be still sourcing a good proportion of its uranium for its nuclear power industry from Russia and, if it is, may well be paying for these supplies with gold. President Putin is, of course, threatening to cut off these strategic supplies altogether. Russian supply dominance in some sectors is such that Putin is able to play the balance of weaponisation by supply cessation against incoming revenue necessity. Industry cannot function if raw material and energy supplies are suddenly cut completely.

Many countries have just become so reliant on imports of key commodities and materials from Russia that that nation’s apparent stranglehold on their economies will have played a huge part in President Putin’s decision to invade Ukraine. He had presumably gambled that once the invasion was quickly accomplished, through Russian military superiority, and Ukraine subdued, economic factors would quickly return to normal. Wrong on all counts. Ukraine has, against all the odds, proved far more resilient than anticipated and the strength of global anti-Russian feeling will likely be such that as soon as is practicable most of Russia’s key markets for its oil, gas and other strategic commodities will be sourced from elsewhere as importers seek to diversify supply sources, or cut Russia out of the equation altogether.

Russian gold, though, will help the nation through such difficult economic times and there may well be a national push to expand gold output which may well propel Russia to become the world’s No.1 gold producer in a few years. It has, after all, one of the world’s biggest undeveloped gold deposits in Sukhoi Log, although reduced access to Western mining equipment and technology because of continuing sanctions may set it back temporarily. The Russia/Ukraine War has certainly been an economic game changer for both nations, but one from which Russia in particular may find it difficult from which to recover quickly in terms of global trust.

22 Apr 2022

3. Chris Powell of GATA provides to us very important physical commentaries

Russia stores its gold mostly on its soil. Here is where the reserves are stored

Ronan Manly/GATA

Ronan Manly: Where are Russia’s gold reserves stored?

Submitted by admin on Thu, 2022-04-21 12:31Section: Daily Dispatches

12:39p ET Thursday, April 21, 2022

Dear Friend of GATA and Gold:

Bullion Star researcher Ronan Manly today delves into Russia’s gold reserves to determine their locations and the amounts at each location and concludes that not much more can be established than that they are vaulted in Moscow, St. Petersberg, Yakaterinburg in the Urals — and maybe elsewhere in the country.

Manly adds that Russia also may be holding gold outside the country, though probably not with traditionally unfriendly countries.

As with the gold reserves of other countries, the true amounts, location, and disposition of Russia’s gold reserves, Manly concludes, are not permitted to be known, for a reason your secretary/treasurer long has spelled out, which he cites.

Manly’s analysis is headlined “Where Is the Russian Federation’s Gold Stored?” and it’s posted at Bullion Star here:

https://www.bullionstar.com/blogs/ronan-manly/where-is-the-russian-federations-gold-stored/

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Your weekend reading material

Alasdair Macleod…

Alasdair Macleod: Value destruction as the financial bubble collapses

Submitted by admin on Thu, 2022-04-21 12:57Section: Daily Dispatches

By Alasdair Macleod

GoldMoney, Toronto

Thursday, April 21, 2022

In recent articles I have argued that the era of a financialised fiat dollar standard is ending. This article takes my hypothesis further and explains that it is not just the emergence of new commodity backed currencies in Asia that will threaten the dominance of Western currencies, but the Federal Reserve’s failing monetary policies and those of the other major central banks.

An unstoppable rise in interest rates will in large part be responsible for their demise.

Financial markets in thrall to the state underestimate the forces collapsing the financial bubble. Even the existence of the bubble is disputed by those within its envelope. But financial assets represent most of the collateral securing the banking system, and their collapse triggered by higher interest rates will take out businesses, banks, and even central banks and make financing of soaring government deficits impossible without accelerated currency debasement.

Will central banks try to preserve financial asset values to stop the West’s financial system from imploding? Keynesian theory demands increased deficit spending to counteract the contraction of bank credit.

As long as this is the case, the planners will destroy their currencies — confirmed by the John Law episode in 1715-1720 France.

It is from this fate that China, Russia, and the architects planning a new central Asian trade currency are planning their escape. …

… For the remainder of the analysis:

https://www.goldmoney.com/research/goldmoney-insights/value-destruction?gmrefcode=gata

end

4.OTHER GOLD/SILVER COMMENTARIES

| Harvey Organ <harveyorgan@gmail.com> | 11:44 AM (28 minutes ago) | ||

PLEASE LISTEN

———- Forwarded message ———

From: Steve Organ<stephen.organ@gmail.com>

Date: Fri, Apr 22, 2022 at 11:32 AM

Subject: lfv

To: Harvey Organ <harveyorgan@gmail.com>

end.

SILVER…

It’s Time To Talk About Silver–adam baratta

There is an idea in philosophy called Occam’s Razor. It’s also known as the principle of parsimony, which tells us that when an event has two possible explanations, the explanation that requires the fewest assumptions is usually the correct one. So what other explanation can there be for why silver prices are down 50% from 11 years ago?

There is a famous saying, “just because you’re paranoid doesn’t mean they are not out to get you.” It’s why we must ask the question. Perhaps the price of silver is manipulated and rigged?

This is the most simple explanation. It’s also an explanation that is evident in multiple anecdotal and experiential ways.

Silver, it has recently been revealed, has long been suppressed by the bullion banks. In September of 2020, JP Morgan agreed to pay $920 million in fines and admitted wrongdoing for manipulating and ‘spoofing” metals futures markets. They are not alone. Last year Deutsche bank, led by two former Merrill Lynch metals traders, also paid fines for manipulating the silver market.

According to Swissbullion: “Recently a veteran litigator living in Washington DC, J. Scott Nicholson, filed a lawsuit against the banks responsible for regulating the price of silver. The suit was filed for illegally manipulating the silver price for financial benefit. This case soon became a class-action suit. This is significant because it is the first court case filed over silver market manipulation.”

We at Brentwood Research are not much for conspiracy theories and have never resorted to sensationalism and fear- based content to make our case for why we believe in precious metals. At the same time, we cannot continue to sit idly back and watch what we are witnessing without comment. We have been a first-hand witness to the rise in retail investment demand for silver.

In fact, “ending the manipulation in the silver markets” is what has accounted for much of the driving force for the recent surge in retail demand.

According to Reddit, a social media platform that has brought together millions of retail investors, there is a silver squeeze taking place right now. The theory is that the silver market is the “most manipulated of any market on earth.” They argue that mine supply is depleted, physical demand is surging, and the bullion banks have been manipulating silver prices via naked shorts. Reddit argues that J.P Morgan and Bank of America have colluded to control the price of silver and that the way to “squeeze” these banks is for retail investors to take physical possession of silver, forcing the bullion banks who manipulate the market to ultimately be forced “cover” their shorts when the supply mismatch at the comex becomes impossible to maintain.

This supply and demand mismatch is playing out in two key areas that we have direct insight into. In February of 2022, we received word that the U.S Mint was struggling finding supplies of silver. Soon after, on March 14th, the U.S. Mint announced to the world that they would “forgo the production and sales of Morgan and Peace Silver Dollars in 2022. This calculated pause is directly related to the global pandemic’s impact on the availability of silver blanks from the Mint’s suppliers.”

Since the pandemic began, sourcing silver has been a challenge. It’s one that has not gone away. The silver shortage is playing out in a second way that investors may want to pay attention to.

Remember that government mints are “for profit” businesses. They sell their manufactured coins at a price above their costs. In a world where thousands of brokers and dealers are bidding for silver, and due to the lack of supply, the premiums on silver products have risen significantly.

While the spot price for silver has remained in the $25 range for much of the past year, the premiums for silver coinage have gone through the roof. On the wholesale level, premiums on silver bars, the cheapest type of silver, have risen from about 3% in 2019 to what is now roughly 11% today. The premiums on silver coins, like the Canadian Silver Maple and the American Silver Eagle, have risen even more, ranging from roughly 6% to 9% in 2019, to a range as high as 30% to 50% today.

This mismatch between supply and demand and the dramatic increase in premium was a key driver of our successful silver trade in 2020. We see a similar trend happening today and why we have recently added a large portion of physical silver to our portfolio in recent months.

Lastly, there are also technical reasons for our bullish position.

Silver has long had a ratio to gold of 16 to 1. This goes all the way back to the Roman Empire, where 16 silver coins were the equivalent of one gold coin. As recently as April of 2011, this ratio was about 30 to 1. Today, the ratio between the price of gold and silver is 79 to 1.

Clearly, on a ratio alone basis, if you like the price of gold to rise higher in value in the coming years, you may love how silver performs relatively. The ratio is one investors may want to pay attention to.

There is a strong theory today that anything below a ratio of 80 signifies a bullish environment for silver prices. Additionally, we might add that silver has traditionally outpaced gold in precious metal bull markets.

For these reasons, we are very bullish on silver right now.

We believe that the risk versus reward has rarely been this lopsided, and why as you consider how to prepare for a return to real you may want to consider adding physical silver to your portfolio now while supply lasts.

5.OTHER COMMODITIES RICE

end

COMMODITIES IN GENERAL//FOOD

World Bank Chief Warns Of Food Crisis Due To Russia-Ukraine Conflict

FRIDAY, APR 22, 2022 – 02:00 PM

Authored by Katabella Roberts via The Epoch Times (emphasis ours),

The World Bank has warned of a “human catastrophe” from a food crisis that could see millions forced into poverty due to the full-scale invasion launched by Russian forces in Ukraine.

World Bank president David Malpass told the BBC at the IMF-World Bank spring meetings in Washington that record food prices could see hundreds of millions of people forced into poverty if the conflict in Ukraine does not come to an end.

“It’s a human catastrophe, meaning nutrition goes down. But then it also becomes a political challenge for governments who can’t do anything about it, they didn’t cause it and they see the prices going up,” Malpass said.

The World Bank calculates there could be a “huge” 37 percent jump in food prices which will hit the poor the hardest and see them “eat less and have less money for anything else such as schooling,” Malpass continued. “And so that means that it’s really an unfair kind of crisis. It hits the poorest the hardest. That was true also of COVID.”

Regarding the “broad and deep” price hikes, the World Bank chief said it was “affecting food of all different kinds of oils, grains, and then it gets into other crops, corn crops because they go up when wheat goes up.”

Both Russia and Ukraine are key exporters of grain and supply nearly 30 percent of wheat and nearly 20 percent of corn in the global market.

Food prices were up nearly 13 percent in March, the highest on record since 1990, according to the United Nations’ FAO Food Price Index.

Meanwhile, the U.N. has previously warned that Ukraine’s food supply chain is “falling apart” due to Russia’s invasion.

While Malpass noted that there is enough food globally to feed everyone, and stockpiles throughout the world continue to remain large by historical standards, the World Bank president said there would need to be a sharing or sales process to ensure that the food goes where it is needed.

He also said there needs to be more of a focus on boosting supplies of fertilizers and food across the world and assisting the poorest of people while discouraging countries from subsidizing production or capping prices.

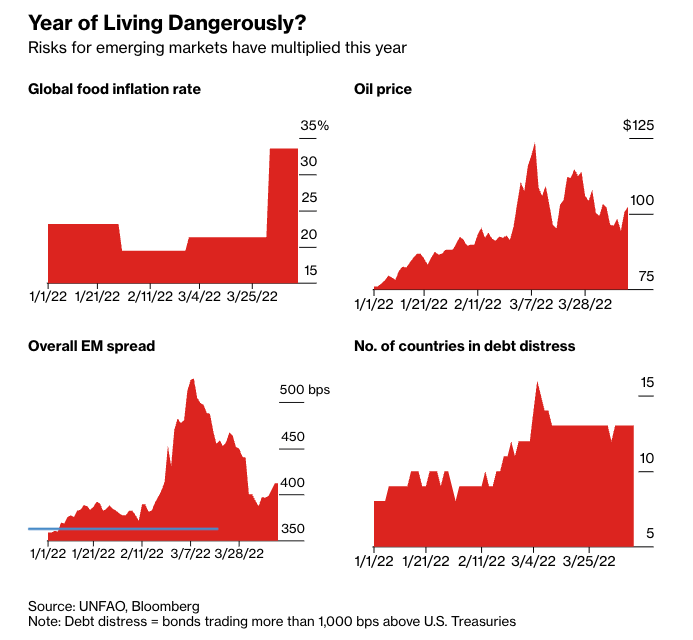

The World Bank chief also warned of a knock-on “crisis within a crisis” that could occur due to developing countries being unable to service their large debts from the COVID-19 pandemic as they struggle with rising food and energy costs.

The International Monetary Fund said on April 19 that 60 percent of low-income countries are at or near “debt distress” adding that it is open to providing financial assistance to these countries via traditional programs or emergency financing.

“This is a very real prospect. It’s happening for some countries, we don’t know how far it’ll go. As many as 60% of the poorest countries right now are either in debt distress or at high risk of being in debt distress,” Malpass said.

“We have to be worried about a debt crisis, the best thing to do is to start early to act early on finding ways to reduce the debt burden for countries that … have unsustainable debt, the longer you put it off, the worse it is,” he added.

Malpass’s comments come after the White House said last month that it anticipates a global food shortage due to the ongoing conflict in Ukraine which could see energy, fertilizer, wheat, and corn prices pushed even higher at a time when inflation levels in the United States have reached their highest in 40 years.

However, Biden administration officials have said the United States is not likely to be impacted by a food shortage.

Meanwhile, David Beasley, the executive director of the United Nations World Food Programme, has warned that the war in Ukraine and subsequent global food crisis could see an influx of illegal immigrants attempting to enter the United States.

Beasley told CBS News’ “Face the Nation” on April 17 that Russian President Vladimir Putin is using starvation as a “weapon” in various ways, and that the U.N. has heard of large numbers of people in central America considering migrating to America as inflation levels in their countries continue to soar, further exacerbated by the situation in Ukraine.

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings FRIDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 6.5010

OFFSHORE YUAN: 6.5320

HANG SANG CLOSED UP DOWN 43.70 PTS OR 0.21%

2. Nikkei closed DOWN 447.80PTS OR 1.63%

3. Europe stocks ALL RED

USA dollar INDEX DOWN TO 100.87/Euro FALLS TO 1.0822

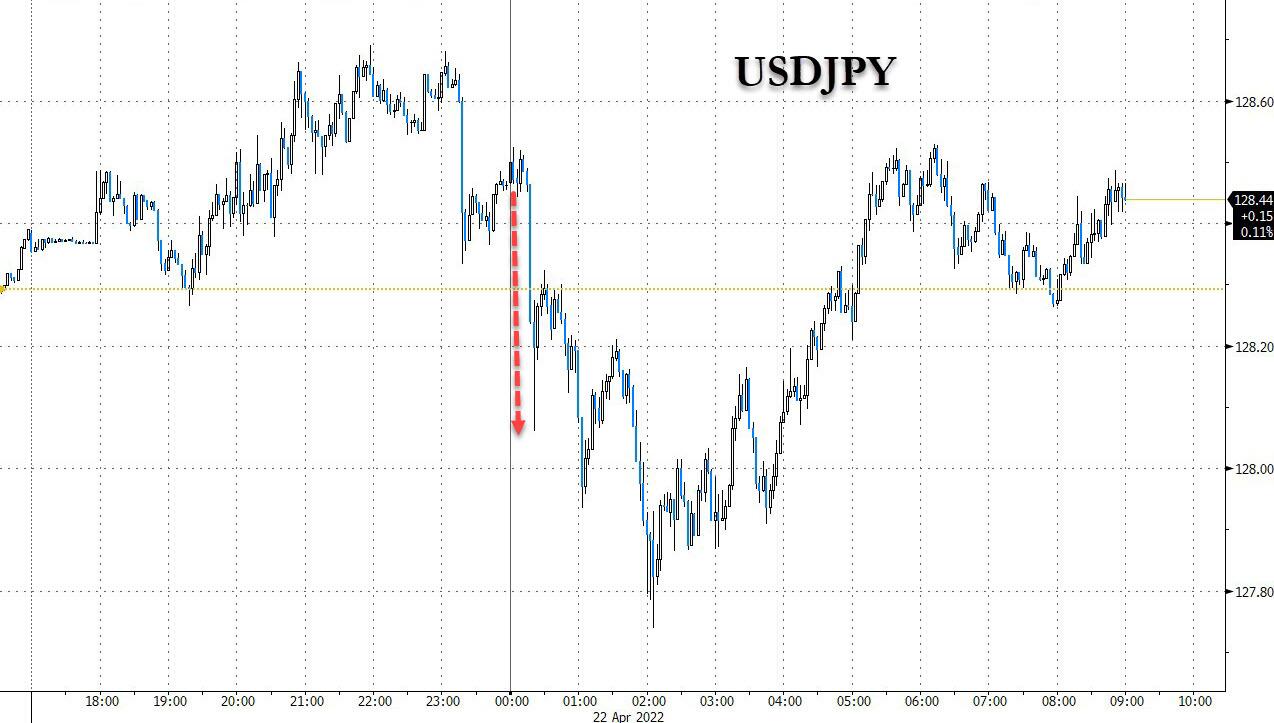

3b Japan 10 YR bond yield: FALLS TO. +.250/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 128.34/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE YUAN: DOWN -SHORE CLOSED DOWN// OFF- SHORE DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.0.939%/Italian 10 Yr bond yield RISES to 2.64% /SPAIN 10 YR BOND YIELD RISES TO 1.90%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 1.70: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3i Greek 10 year bond yield RISES TO : 2.99

3j Gold at $1935.95 silver at: 24.30 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 1 & 4/5 roubles/dollar; ROUBLE AT 72.97

3m oil into the 102 dollar handle for WTI and 107 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 128.34 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning .9595– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0332well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 2.921 UP 1 BASIS PTS

USA 30 YR BOND YIELD: 2.939 UP 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 14.74

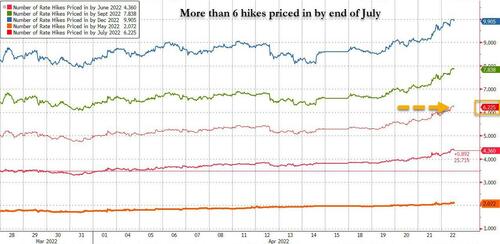

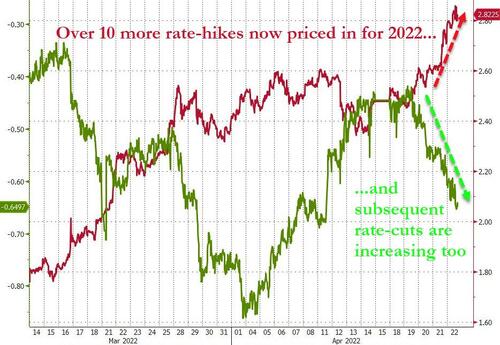

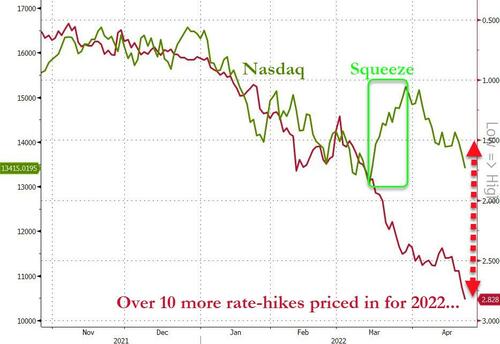

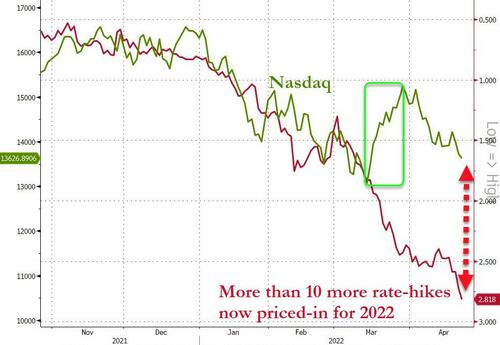

Futures Drop With Traders On Edge Over Hawkish Central Banks

FRIDAY, APR 22, 2022 – 07:49 AM

US equity futures extended their Thursday losses, and were slightly lower on Friday morning as investors fretted over the latest hawkish remarks from Jerome “Crash Stonks” Powell. Nasdaq 100 futs were down 0.1% by at 7:15a.m. EDT after the underlying gauge slumped 2% on Thursday after Powell outlined his most aggressive approach yet to taming inflation, potentially endorsing two or more half percentage-point interest-rate increases, which prompted the market to price in more than six 25bps rate hike by the end of July and 10 hikes by the end of 2022. Shorter-dated Treasury yields surged. The dollar rose to the highest level since July 2020 amid losses for the British pound with data showing the U.K.’s cost-of-living crisis is hampering consumer spending.

The overnight weakness pushed both S&P 500 futures lower by about 0.2% after cash closed down 1.5% Thursday, although trade was muted and range-bound.

The fears over rising rates have been particularly damaging for frothy growth and technology parts of the market amid concerns about the squeeze on their future earnings.

“The problem for the equity market and particularly those rate sensitive long duration stocks is they are simply not valued appropriately for that new regime,” said Roger Lee, head of U.K. equity strategy at Investec. “Investors have been so heavily concentrated in those ‘growth’ parts of the market that the unwind and repositioning as this new rate environment sinks in could take months, if not years.”

“Equities are really torn between these two forces right now and the first one is that earnings are actually pretty good,” Anastasia Amoroso, chief investment strategist at iCapital Securities LLC, said on Bloomberg Television. But “anytime equities rally it seems like the Fed officials are coming in with more and more hawkish talk,” she said.

Powell on Thursday cited minutes from last month’s policy meeting that said many officials had noted “one or more” 50 basis-point hikes could be appropriate to curb the hottest inflation in four decades. Investors are now betting on half-point increases in May, June and possibly July.

“The unknown is Powell’s ability to deliver the needed finesse without completely derailing the recovery, while not falling short of the required magnitude to anchor inflation,” Ian Lyngen, head of interest rate strategy at BMO Capital Markets, wrote in a note.

In premarket trading, Gap sank 13% after lowering its quarterly sales growth guidance and saying Old Navy President and CEO Nancy Green will leave the business this week. Snap shares dipped 3% following mixed results from the social-media company; Q1 revenue missed while adjusted Ebitda beat expectations amid strong user growth. Chindata shares, on the other hand, surged 12% after Bloomberg reported that the Chinese data center company backed by private equity firm Bain Capital had received preliminary takeover interest from other firms in the industry. Here are some other notable premarket movers:

- SVB Financial (SIVB US) rallied 9% in postmarket trading after reporting earnings per share for the first quarter that beat the average analyst estimate. Its net interest margin also topped analyst expectations for the three months ended March 31.

- Spire Global (SPIR US) gained 5.7% in postmarket as coverage starts with an outperform rating and $4 price target at Raymond James, which touts the the satellite-imaging and data company’s potential for “rapid” annual recurring revenue growth.

- Boston Beer (SAM US) fell 3% postmarket after first- quarter results missed estimates, hurt by shipment volume decreases in Truly Hard Seltzer, Twisted Tea, Angry Orchard, and Dogfish Head brands, partially offset by increases in its Samuel Adams brand.

- Globus Medical (GMED US) tumbled 11% in postmarket trading after the company reported preliminary net sales for the first quarter of about $230.5 million, compared to consensus estimates of $236.1 million, and said CEO Dave Demski resigns.

- Qualtrics (XM US) shares gained 4.4% in extended trading on Thursday after the software company reported first-quarter revenue that beat expectations. It also gave a second-quarter revenue forecast that beat the average analyst estimate.

U.S. equities were hammered this week as the first-quarter earnings season began with some high profile misses, including from Netflix. Earnings-per-share growth is tracking down 11% in U.S., according to Barclays strategist Emmanuel Cau, but overall beats are above average so far. That said, U.S. equities have remained rather resilient in the face of increasingly hawkish signals from the Fed and ECB, thanks to hopes for another solid earnings season but those are becoming increasingly frayed. At the same time, traders are mindful of the inevitable risk repricing, especially after Powell outlined his most aggressive approach yet to taming inflation, potentially endorsing two or more half percentage-point rate increases.

In Europe, the Stoxx 50 slumped 1.5% while the Stoxx 600 Index was down 1.2%, pressured by disappointing quarterly earnings from Gucci-owner Kering and SAP. FTSE 100 outperformed, dropping 0.5%. Energy, travel and retailers are the worst-performing sectors. Here are the biggest European premarket movers:

- Essity rises as much as 15%, the most since its 2017 IPO and the biggest gainer on the Stoxx 600, on earnings analysts say show Essity’s pricing efforts to offset cost inflation are proving effective.

- Renault jumps as much as 8.3% after a Bloomberg News report that the company is considering selling part of its Nissan Motor stake. The auto maker also published “solid” 1Q numbers.

- HomeServe jumps as much as 13% after disclosing it has received a number of proposals from Brookfield. Analysts note the increased probability of a bid, while not ruling out counteroffers.

- Holcim shares gain as much as 6.2% after the cement maker reported what Jefferies called a “massive beat” on first-quarter earnings, helped by strong volumes in North America.

- Bureau Veritas shares rise as much as 5.9%. The testing and inspection firm’s 1Q update looks strong, with organic growth well ahead of expectations, RBC says.

- European technology stocks slide as much as 2.4%, underperforming declines for the broader index, with rate-hike fears and an earnings miss by index heavyweight SAP weighing

- Logitech down as much as 6.4%; SAP as much as 4.5% on “disappointing” earnings

- Kering shares slump as much as 7% as investors focused on the 1Q sales miss of the fashion conglomerate’s crucial Gucci brand in spite of beats elsewhere across the business.

- Anglo American falls as much as 3.6%, as the stock was cut to sector perform at RBC, with the broker saying that the miner’s “poor” 1Q and guidance will impact the investment case.

- Ferrari drops as much as 3.3% in Milan after the sports-car maker issued a recall for 2,222 of its vehicles in China as there may be some problem with the brakes.

Earlier in the session, Asian stocks declined after Federal Reserve Chair Jerome Powell outlined an aggressive approach to monetary tightening, weighing on market sentiment. The MSCI Asia Pacific Index fell as much as 1.6% Friday to the lowest level in a month. Technology shares were the biggest drags as Treasury yields resumed their ascent, hurting costlier growth stocks. Japanese equities led losses in the region following the Fed’s hawkish comments. A 50 basis-point interest rate increase “will be on the table” for next month’s policy meeting, Powell said Thursday. He also backed a series of half-point hikes ahead and said the Fed is committed to raising rates “expeditiously” to tame inflation. Powell Hardens Hawkish Pivot Toward Half-Point Fed Rate Hikes Chinese stocks stabilized, with the CSI 300 Index snapping a five-day losing streak, after regulators urged funds to boost their equity investments. Technology shares, however, took a hit from ongoing U.S. delisting concerns. The Hang Seng Tech Index eked out a small gain after falling the previous three sessions. Asian markets have been jittery this week amid the prospect of global monetary tightening, as well as growth risks in China stemming from stringent Covid lockdowns and supply chain disruptions. The Asian stock benchmark has slid more than 2% this week, poised for a third weekly decline. Asian central banks “will be raising rates at a more gradual pace compared with the Fed,” said Tai Hui, chief Asia market strategist at JPMorgan Asset Management in a Bloomberg TV interview. “Cash return across Asia is still going to be pretty low. That will continue to fuel demand for income investments.”

In FX, euro extends decline as traders price in 50 bps of ECB rate hikes by September. Curves have a flattening bias. Bunds and USTs bear-flatten, U.S. short end cheapens 6-8 bps, underperforming bunds by ~2bps. Gilts bull-flatten but ranges are relatively narrow. Peripheral spreads tighten, led by short-end Portugal.

In FX, the Bloomberg Dollar Spot Index rose and the greenback advanced against all of its Group-of-10 peers apart from the yen. The pound was the worst performer and approached $1.29, the lowest in 17 months against the dollar and underperforming all of its G-10 peers, after data showed U.K. retail sales plunged more than forecast in March. Gilts outperformed with Bank of England Governor Andrew Bailey due to speak later. The volume of goods sold in stores and online dropped 1.4% after falling 0.5% in February. Economists had expected a decline of 0.3%. U.K. PMI for both services and the whole economy fell to a three-month low in April, while consumer confidence sank to its lowest since the recession in 2008. The euro fell to trade around $1.08 and European bonds outperformed Treasuries. The Kiwi and Aussie fell under weight of leveraged selling to underperform major peers, according to Asia-based FX traders. The yen gained on a report that Japanese Finance Minister Shunichi Suzuki discussed the possibility of coordinated currency intervention with U.S. Treasury Secretary Janet Yellen. Japanese government bonds edged lower. Japan’s key consumer prices advanced in March at the fastest pace in more than two years, complicating the central bank’s communication of its easy policy stance given a further acceleration is expected in April.

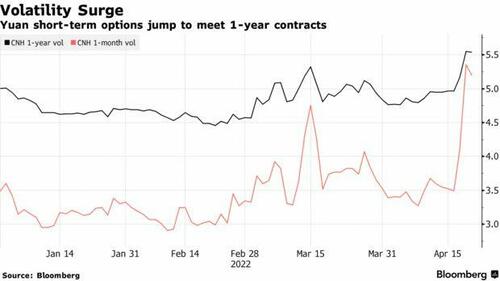

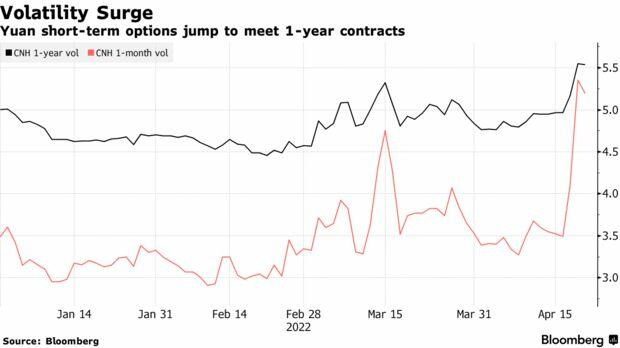

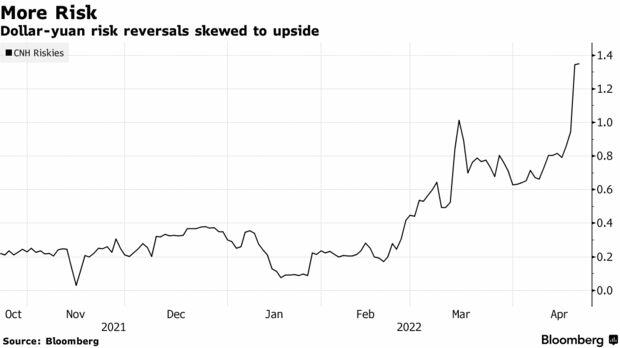

Perhaps most importantly, the Chinese Yuan has its worst week since the August 2015 devaluation.

In rates, the Treasury curve bear flattened as 2-year yields rose by 7bps while long-end yields by around 1bp. Futures are off the lows however, with bunds and gilts outperforming over the London session. 10-year TSY yields trade around 2.92%, cheaper by 2bp on the day and lagging bunds by 2bp, gilts by 4bp; extension of bear-flattening move tightens 2s10s, 5s30s spreads by ~4bp and ~1bp. Weakness during Asia session was led by Aussie bonds, where 10-year yield reached highest level since 2014.

In commodities, WTI drifts 2.1% lower to trade around the $101 level. Spot gold falls roughly $10 to trade around $1,942/oz. Most base metals trade in the red.

Looking to the day ahead now, data releases include the global flash PMIs for April and UK retail sales for March. Central bank speakers include ECB President Lagarde and BoE Governor Bailey. Finally, earnings releases include Verizon Communications and American Express.

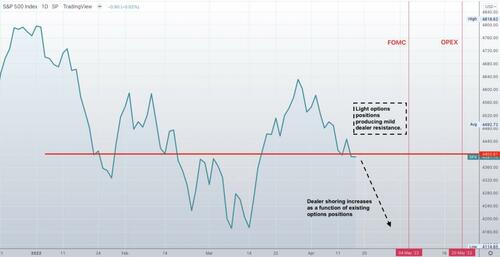

Market Snapshot

- S&P 500 futures down 0.1% to 4,386.00

- STOXX Europe 600 down 0.8% to 457.90

- MXAP down 1.0% to 169.68

- MXAPJ down 1.1% to 559.97

- Nikkei down 1.6% to 27,105.26

- Topix down 1.2% to 1,905.15

- Hang Seng Index down 0.2% to 20,638.52

- Shanghai Composite up 0.2% to 3,086.92

- Sensex down 1.1% to 57,289.28

- Australia S&P/ASX 200 down 1.6% to 7,473.28

- Kospi down 0.9% to 2,704.71

- German 10Y yield little changed at 0.95%

- Euro down 0.4% to $1.0794

- Brent Futures down 1.8% to $106.35/bbl

- Gold spot down 0.3% to $1,946.54

- U.S. Dollar Index up 0.41% to 100.99

Top Overnight News from Bloomberg

- ECB Governing Council member Robert Holzmann says it’s crucial that asset purchases come to an end as soon as possible in order to start “visible” interest rate increases, according to comments made to Die Presse newspaper

- Economic momentum in the euro area unexpectedly picked up in April, with a rebound in services following the end of Covid restrictions making up for stalling manufacturing. A composite gauge for both sectors jumped to a seventh-month high, according to a PMI survey. The increase to 55.8 from 54.9 in March compares to an estimate of 53.9

- Global bonds added to this year’s epic rout as traders brace for the most aggressive Federal Reserve interest-rate hikes in 40 years and the likelihood most global central banks will also tighten.

- India is expected to raise policy rates by the most among major central banks in the region as it seeks to tackle a surge in inflation, according to swaps pricing. The Reserve Bank of India is seen raising its policy rate by around 275 basis points by end 2023 based on front-end swaps, according to a BofA Securities note

- China’s central bank governor stressed the importance of keeping inflation under control in two separate speeches released Friday and pledged more targeted support for small businesses, reinforcing policy makers’ cautious approach to monetary stimulus

- French President Emmanuel Macron led his rival Marine Le Pen 55.5% to 44.5% ahead of the run-off presidential election set for April 24, according to a polling average calculated by Bloomberg on April 22. The gap between them has narrowed from the 12.0 percentage points recorded on April 20

- Applying the sustainable debt format to governments is raising thorny challenges, from just how ambitious to make the targets to the democratic quandary of committing to goals a future administration might disagree with

A more detailed look at global markets courtesy of newsquawk

Asia Pac stocks were negative on spillover selling from Wall St with risk sentiment sapped amid higher yields and hawkish central bank commentary. ASX 200 declined as tech suffered from higher yields and with miners subdued by OZ Mineral’s weak output. Nikkei 225 underperformed as the optimism from incoming relief faded on the hawkish central bank views. Hang Seng and Shanghai Comp weakened amid large losses in Hong Kong’s tech stocks and with sentiment not helped by the US adding another 17 firms to its SEC list for possible delisting.

Top Asian News

- China’s Oil Demand Is Tumbling the Most Since Wuhan Lockdown

- China’s Plunging Markets Trigger Capital Flight, State Support

- Japan Deems Russia’s Occupation of Disputed Islands ‘Illegal’

- A $26 Billion Bond Trade Loved by Banks Faces India Scrutiny

- Mainland China Investors Buy Net HK$3.28B Via Stock Connect

European bourses are pressured across the board, Euro Stoxx 50 -1.8%, following APAC/Wall St. pressure amid hawkish Central Bank rhetoric. The FTSE 100 is the relative outperformer, but still negative, given favourable currency dynamics given broad USD strength and weak Retail Sales. Stateside, futures are modestly softer after spending much of the APAC session near the unchanged mark, ES -0.4%, moving in sympathy with EZ action and pre-PMIs. Note, today is the last day of potential Fed speak before the blackout period for May’s gathering commences; no Fed officials scheduled.

Top European News

- Credit Suisse, SocGen May See Trading Drop as War Upends Markets

- Ferrari Recalls Over 2,000 Cars in China on Brake Risk

- Ghosn Faces Arrest Warrant in French Probe

- French Football Club Olympique Lyonnais Said to Get Six Bids

- U.K. Economic Outlook Dims as Confidence and Sales Falter

FX

- Sterling slides to bottom of G10 pile as UK retail sales data misses consensus by a distance and two out of three preliminary PMIs fall short of expectations, Cable hits new 2022 low circa 1.2865, EUR/GBP approaches 0.8400.

- Non-US Dollars decline amidst general risk aversion and other bearish factors; AUD/USD hovering just above 0.7300, NZD/USD sube-0.6700 and USD/CAD over 1.2675 ahead of Canadian consumption and producer price data.

- Euro fades irrespective of mostly stronger than forecast flash Eurozone PMIs as ECB President Lagarde tones down hawkish vibes, EUR/USD probes 1.0800.

- Yen holds up better than other majors after more concerted effort by Japan’s Finance Minister to curb rapid moves via confirmation that he is in close contact with US Treasury Secretary about currency developments, USD/JPY capped below 129.00.

- Yuan set for weakest week since devaluation seven years ago with PBoC Governor Li pledging policy stimulus for the real economy that is suffering from Covid contagion; USD/CNH through 6.5250.

- ECB President Lagarde told policymakers to refrain from airing dissenting views on decisions for several days, according to Reuters sources.

- Japanese Finance Minister Suzuki said he confirmed with US Treasury Secretary Yellen that US and Japan will communicate closely on FX and discussed with Yellen the recent market developments, in particular, USD/JPY moves, while he explained to Yellen recent JPY declines are rapid, according to Reuters.

- Japanese Finance Minister Suzuki and US Treasury Secretary Yellen likely discussed coordinated currency intervention during bilateral talks, according to TBS News citing a Japanese government source which noted the US side sounded as if it will consider the idea of joint FX intervention positively.

Fixed Income

- Bonds on track to rack up more weekly losses with Bunds down to 153.10 at worst, Gilts hitting 117.22 and 10 year T-note 118-08.

- Benchmark yields still targeting or touching psychological levels, like 1.0% in Germany, 2.0% and 3.0% in the UK and US respectively.

- Curves retain flatter bias and debt could yet derive traction from pre-weekend position squaring plus asset reallocation as equities dump.

Commodities

- WTI and Brent are pressured in tandem with broader price action, USD strength and sources pointing to a China demand shock.

- China is said to face the biggest oil demand shock since early 2020, according to Bloomberg sources.

- Currently, WTI and Brent have recovered marginally from session lows of USD 101.22/bbl and USD 105.80/bbl, respectively.

- Spot gold and silver are also hindered on the USD move, yellow metal continues to fall away from the USD 1950/oz mark (low, USD 1941/oz; high USD 1955.60/oz).

US Event Calendar

- 09:45: April S&P Global US Composite PMI, est. 57.9, prior 57.7

- 09:45: April S&P Global US Services PMI, est. 58.0, prior 58.0

- 09:45: April S&P Global US Manufacturing PM, est. 58.0, prior 58.8

DB’s Jim Reid concludes the overnight wrap

Happy Friday. I’m already longingly looking forward to Monday as my wife is having her first weekend away without any of us since we had children. I’ve been left a full handwritten list of things I need to do to successfully solo look after 3 rowdy kids and a wayward dog. I genuinely don’t think she believes I can do it without incident. If I were to allow unlimited TV, and an endless supply of tomato ketchup and mayonnaise then it would be an absolute doddle. I’ll start off with good intentions tonight and then see how quickly I resort to the easy route at the weekend.

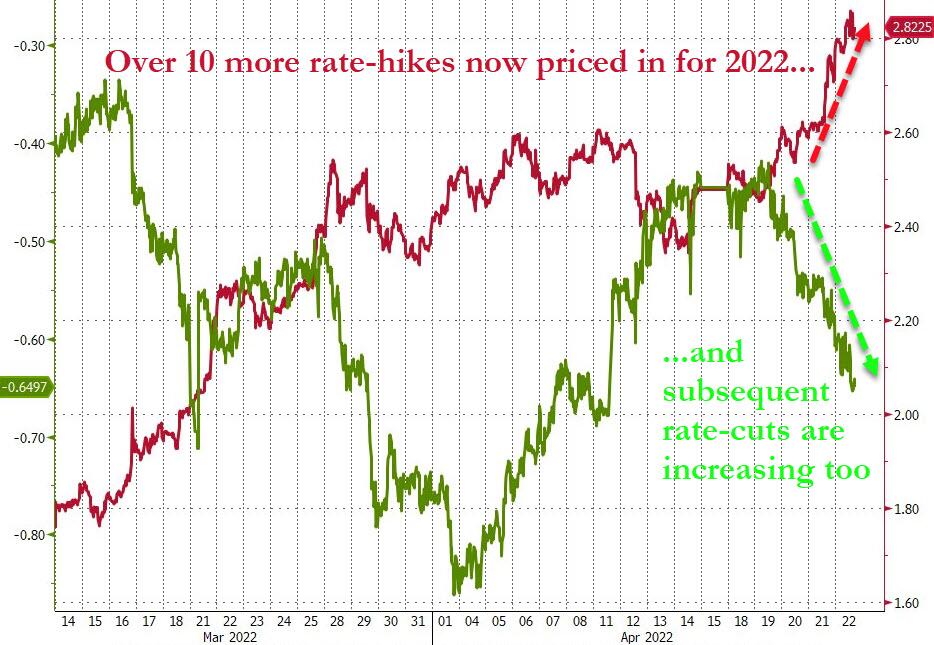

Central bankers are finding there is no easy route at the moment and yesterday was another day of rising hike expectations. There was a full lineup of central bank speakers with most of the heavy hitters coming in after Europe went home. Having said that, the damage in global rates markets was done long before Chair Powell joined President Lagarde on an IMF panel.

With the Fed’s May FOMC communications blackout set to start tomorrow, Powell stayed true to the recent Fed line, saying many FOMC participants favoured one or more +50bp moves, noting that it would be appropriate to move relatively quickly, and that he wanted to get policy rates to neutral. In that vein, he said there was some merit in front-loading the policy tightening given the historically tight labour market and upside risks to already runaway inflation.

President Lagarde drew a distinction between the different economic realities of Europe and the US, but she did not rule out an increase to the ECB’s policy rate as early as the July meeting. Recall, our European econ team’s base case is the ECB will lift rates by +25bps in September, after finishing net APP purchases in the third quarter. Lagarde also noted that the ECB doesn’t target any specific level of the euro, but are watching FX dynamics.

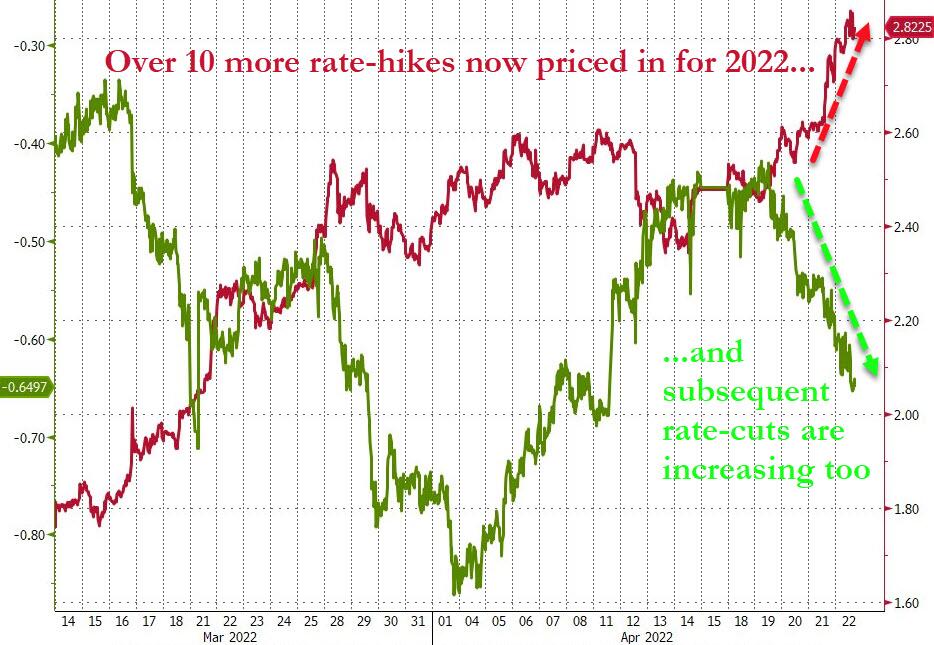

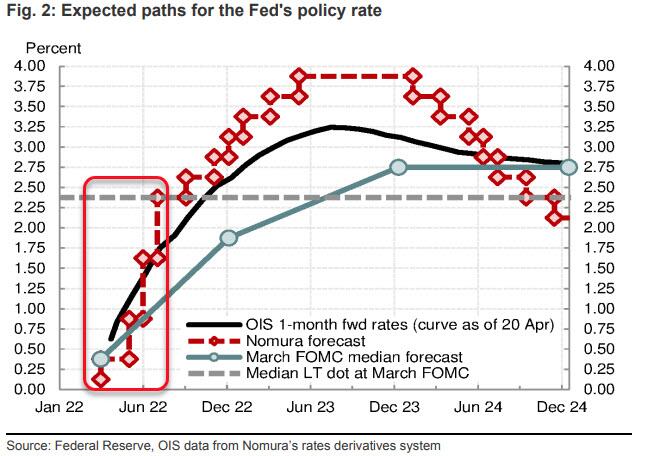

Even before Powell and Lagarde had started speaking, the sizeable bond sell-off came as other central bank speakers endorsed hawkish policies. President Daly, who skews dovish, remarked earlier in the day that a couple of +50bp hikes were likely, while President Bullard, speaking at the same time as Powell, wouldn’t rule out a +75bp hike. The market kept a +50bp hike for May fully priced, and this morning is pricing +151bps of tightening over the next three meetings, so equivalent to just over three consecutive +50bp hikes. When all was said and done, Fed funds futures moved to price in an additional +14.3bps worth of tightening over 2022 yesterday, thus bringing the total amount of hikes priced for the rest of the year to 240bps, which is the highest to date, and this morning they’ve added a further 6bps. Given the 25bp hike we saw last month, if realised that would imply 271bps over the year as a whole, so beating out the 250bps of tightening back in 1994. Futures also became more aggressive on the 2023 profile as well, as they moved to price in a 3% Fed Funds rate as early as March 2023, which is the first time they’ve closed at that level.

The prospect of more aggressive rate hikes led to a significant selloff in Treasuries, with the 10yr yield up by +7.8bps to 2.91%, after trading as high as 2.95% intraday, with a further +3.3bps move this morning back up to 2.94%. Those moves were seen across the curve, though the front end saw the biggest moves higher as further rate hikes were priced in, meaning that the 2s10s flattened -2.7bps on the day to 22.3bps. Real yields led the bulk of the move earlier in the day, but breakevens took the mantle after an exceptionally strong 5yr TIPS auction showed there is strong latent demand for investor protection against inflation, driving 5yr breakevens to +3.64% and 10yr breakevens to 3.04%, the highest levels on record for each.

It was much the same story in Europe, where the chatter around an ECB rate hike as soon as July stepped up a gear, echoing what we saw from the Fed six months ago where the timing of an initial rate hike was increasingly brought forward. First, we heard from Vice President de Guindos, who was asked if a July liftoff was possible, and said that “It will depend on the data we see in June. From today’s perspective, July is possible and September, or later, is also possible.” In addition, Belgian central bank governor Wunsch said that policy rates could even move into positive territory this year, saying that market pricing “to me is on the low side of what might be required to get inflation under control”. Overnight index swaps reacted accordingly, and the amount of tightening priced in by overnight index swaps for December’s meeting closed above 75bps for the first time, so implying at least 3 full 25bp moves. Looking at the July meeting specifically, +21.5bps of tightening were priced in by the close yesterday, an increase of +7.1bps on the day, with +47.4bps priced in by September, a +12.6bp increase. So we’re close to two +25bp hikes being priced in for each of July and September.

That shift in expectations meant that the European bond selloff echoed the US, with yields on 10yr bunds (+9.1bps), OATs (+6.8bps) and BTPs (+9.8bps) all moving higher on the day. The most significant moves were seen in the UK however, where 2yr gilt yields surged by +16.9bps after Catherine Mann of the MPC suggested that rates could move by more than 25bps. That saw overnight index swaps increase the implied probability of a 50bp move at the May meeting up to 58.7%, with 167bps worth of further tightening priced for the rest of the year, on top of the 50bps we’ve already had so far.

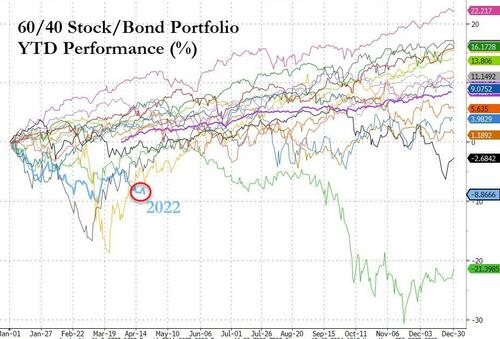

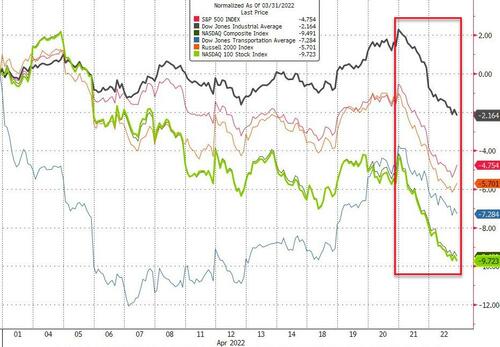

European stocks largely advanced before the magnitude of tighter central bank comms weighed on the market, with the STOXX 600 increasing +0.32%. The DAX (+0.98%) and CAC 40 (+1.36%) outperformed broader European equities. In the US, meanwhile, stocks took a turn for the worse in the New York afternoon following the day’s central bank speak. The S&P 500 fell -1.48% as every sector was lower. Indeed, only stalwart defensive sectors staples (-0.11%) and real estate (-0.63%) avoided declines of greater than 1%. Tech stocks intuitively underperformed on the tighter policy path; the Nasdaq fell -2.07% and FANG+ shares were -2.79% lower.

Those themes have been echoed overnight in Asia, where equities are mostly lower this morning. The Nikkei (-1.89%) is leading losses across the region, with the Hang Seng (-0.70%) and the Kospi (-1.06%) also falling. Mainland Chinese stocks are experiencing a more mixed performance however, with the Shanghai Composite (-0.07%) fractionally lower while the CSI (+0.12%) is up after China’s securities regulator urged institutional investors to buy more domestic stocks. Looking forward, US equity futures are pointing to further losses, with contracts on the S&P 500 (-0.27%) and Nasdaq 100 (-0.18%) both lower.

We’ve also started to see the flash PMIs for April come in overnight, with the numbers from Australia and Japan mostly seeing an improvement on March’s performance. Japan’s composite PMI rose to 50.9 (vs. 50.4 in March), whilst Australia’s composite PMI was up to 56.2 (vs. 55.1 in March), so it’ll be interesting to see if that’s replicated in Europe and the US too. Staying on that data theme, Japan’s CPI rose to +1.2% year-on-year in March as expected, marking its fastest pace since October 2018.

Elsewhere, we’re just 2 days away from the French presidential election run-off on Sunday, which is set to be closely watched by investors. That said, the perceived chances of a surprise victory for Marine Le Pen have fallen in recent days given the polls have moved in President Macron’s favour, with the most recent numbers all putting his margin of victory outside the standard margin of error, with Politico’s average giving him a 10-point lead. The prospect of another Macron victory has made investors increasingly relaxed about the outcome, and the spread of French 10yr yields over bunds narrowed by -2.2bps yesterday to 45.7bps, which is their tightest level so far this month. Furthermore, the CAC 40 (+1.36%) outperformed the other European equity indices as highlighted above. In terms of yesterday’s polls, they had Macron up by 57.5-42.5 (Ipsos), 56-44 (Opinionway), 55.5-44.5 (Ifop) and 53-47 (Odoxa).

On the data side, the weekly initial jobless claims from the US came in at 184k in the week through April 16 (vs. 180k expected). And over in Europe, the final March CPI reading for the Euro Area was revised down to +7.4% (vs. flash +7.5%), albeit still a record since the single currency’s formation, whilst the European Commission’s advance consumer confidence reading for April unexpectedly rose to -16.9 (vs. -20.0 expected), recovering somewhat from its recent low in March.