April 25, 2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

april25, 2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

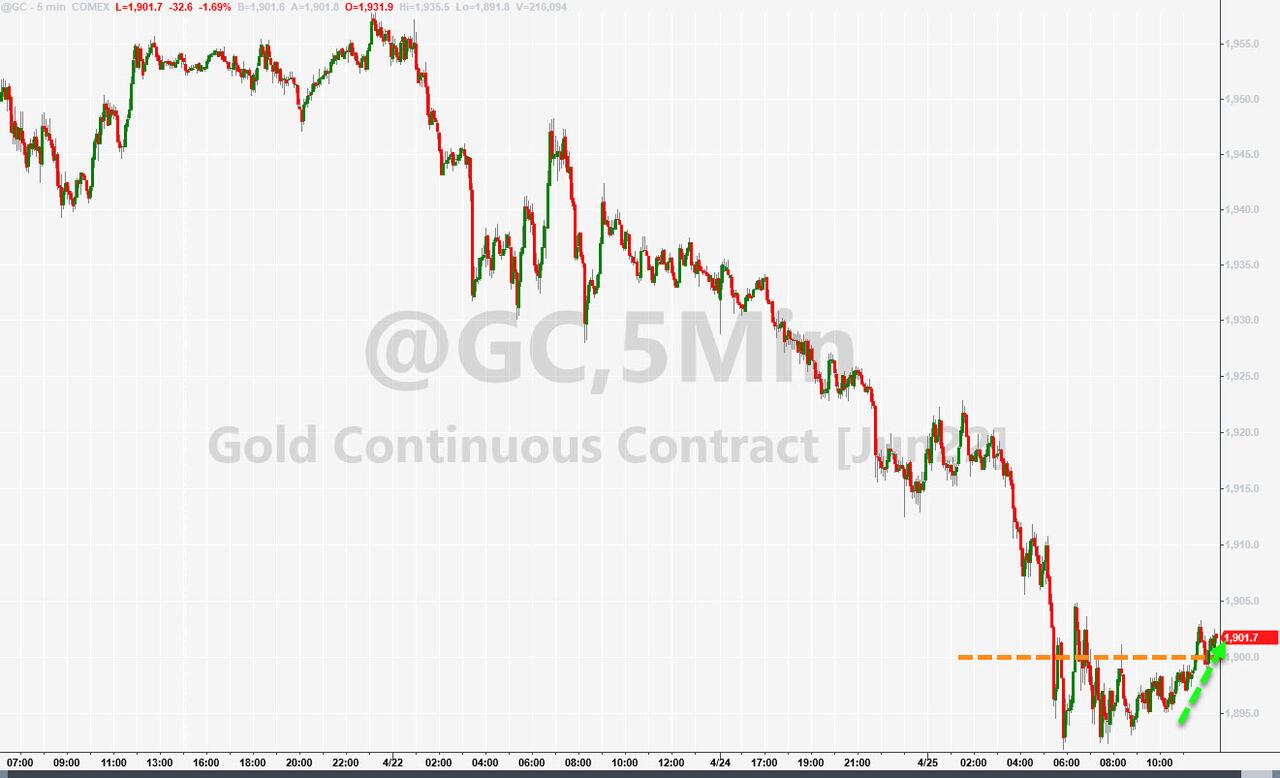

GOLD; $1896.10 DOWN $36.80

SILVER: $23.64 DOWN $0.69

ACCESS MARKET: GOLD $1898.35

SILVER: $23.62

Bitcoin morning price: $38713 DOWN 897

Bitcoin: afternoon price: $40,088 UP 398

Platinum price: closing DOWN $12.50 to $918.76

Palladium price; closing DOWN 44.00 at $2146.30

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

comex notices/

: JPMorgan stopped/total issued 13/37

EXCHANGE: COMEX

CONTRACT: APRIL 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,931.000000000 USD

INTENT DATE: 04/22/2022 DELIVERY DATE: 04/26/2022

FIRM ORG FIRM NAME ISSUED STOPPED

072 C GOLDMAN 1

132 C SG AMERICAS 8

435 H SCOTIA CAPITAL 1

624 H BOFA SECURITIES 2

657 C MORGAN STANLEY 3

661 C JP MORGAN 34 13

709 C BARCLAYS 5

737 C ADVANTAGE 3

880 H CITIGROUP 4

TOTAL: 37 37

MONTH TO DATE: 25,768

NUMBER OF NOTICES FILED TODAY FOR APRIL. CONTRACT 13 NOTICE(S) FOR 1300 OZ (0.1150 TONNES)

total notices so far: 25,768 contracts for 2,576,800 oz (80.149 tonnes)

SILVER NOTICES:

21 NOTICE(S) FILED 105,000 OZ/

total number of notices filed so far this month 1343 : for 6,715,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

END

GLD

WITH GOLD DOWN $36.80

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

NO CHANGES IN GOLD INVENTORY AT THE GLD

INVENTORY RESTS AT 1104.13 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 69 CENTS

AT THE SLV// A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A HUGE WITHDRAWAL OF 2.031 MILLION OZ FROM THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 579.418 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A GIGANTIC SIZED 8245 CONTRACTS TO 155,474 AND FURTHER FROM THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE STRONG LOSS IN OI WAS ACCOMPLISHED WITH OUR STRONG $0.57 LOSS IN SILVER PRICING AT THE COMEX ON FRIDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.57) AND WERE UNSUCCESSFUL IN KNOCKING OUT ANY SILVER LONGS AS EVEN THOUGH WE HAD A STRONG LOSS OF 5590 CONTRACTS ON OUR TWO EXCHANGES. ALL OF THE LOSS WAS DUE TO CONTINUAL SPREADER LIQUIDATION//TAS IN SILVER TODAY.

WE MUST HAVE HAD:

I) HUGE BANKER SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A HUGE ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A STRONG INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 4.305 MILLION OZ FOLLOWED BY TODAY’S QUEUE. JUMP OF 65,000 OZ//NEW STANDING: 6.745,000 MILLION OZ// V) STRONG SIZED COMEX OI LOSS/(ALL THE LOSS DUE TO SPREADERS)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS : —-4109

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS APRIL. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF APRIL:

TOTAL CONTACTS for 16 days, total 16,931 contracts: 84.655 million oz OR 5.28 MILLION OZ PER DAY. (1058 CONTRACTS PER DAY)

TOTAL NO OF OZ UNDERGOING EFP TO LONDON 16,931 CONTRACTS X 5,000 PER CONTRACT:

EQUATES TO: 84.655 MILLION OZ

.

LAST 11 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

APRIL: 84.655 MILLION OZ (LOOKS LIKE OUR BANKERS ARE NOW LOATHE TO ISSUE EFP’S)

RESULT: WE HAD A GIGANTIC SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 8245 WITH OUR STRONG $0.57 LOSS IN SILVER PRICING AT THE COMEX// FRIDAY. WITH ALL OF THE LOSS DUE TO SILVER SPREADER LIQUIDATION TODAY. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE CONTRACTS: 2655 CONTRACTS ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A HUGE INITIAL SILVER OZ STANDING FOR MAR. OF 4.305 MILLION OZ FOLLOWED BY TODAY’S 65,000 OZ QUEUE JUMP//NEW STANDING: 6.745MILLION OZ/// .. WE HAD A STRONG SIZED LOSS OF 5590 OI CONTRACTS ON THE TWO EXCHANGES FOR 27.950 MILLION OZ WITHTHE STRONG LOSS IN PRICE.

WE HAD 21 NOTICES FILED TODAY FOR 105,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A SMALL SIZED 1791 CONTRACTS TO 568,150 AND FURTHER FROM NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: -3134 CONTRACTS.

THE BIS HAS ABANDONED THE GOLD COMEX TRADING!!!

.

THE SMALL SIZED DECREASE IN COMEX OI CAME WITH OUR LOSS IN PRICE OF $13.40//COMEX GOLD TRADING/FRIDAY /.AS IN SILVER WE MUST HAD HUGE BANKER/ALGO SHORT COVERING ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR APRIL AT 78.33 TONNES ON FIRST DAY NOTICE //FOLLOWED BY TODAY’S EFP JUMP TO LONDON OF 1600 OZ//NEW STANDING 81.989 TONNES

YET ALL OF..THIS HAPPENED WITH OUR LOSS IN PRICE OF $13.40 WITH RESPECT TO FRIDAY’S TRADING

WE HAD A SMALL SIZED GAIN OF 1053 OI CONTRACTS (3.275 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2844 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 568,150.

IN ESSENCE WE HAVE A SMALL SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1053, WITH 1343 CONTRACTS INCREASED AT THE COMEX AND 2844 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 1053 CONTRACTS OR 3.275 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2844) ACCOMPANYING THE SMALL SIZED LOSS IN COMEX OI (1771,): TOTAL GAIN IN THE TWO EXCHANGES 1053 CONTRACTS. WE NO DOUBT HAD 1) HUGE BANKER SHORT COVERING ,2.) HUGE INITIAL STANDING AT THE GOLD COMEX FOR APRIL. AT 78.33 TONNES FOLLOWED BY TODAY’S 1,600 OZ EFP JUMP TO LONDON //NEW STANDING 81.987 TONNES/// 3) ZERO LONG LIQUIDATION //.,4) SMALL SIZED COMEX OI. LOSS 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

APRIL

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL :

36,548 CONTRACTS OR 3,654,800 OR 113.67 TONNES 16 TRADING DAY(S) AND THUS AVERAGING: 2284 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 16 TRADING DAY(S) IN TONNES: 113.67 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2020, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 113.67/3550 x 100% TONNES 3.21% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 113.67 TONNES (THIS IS GOING TO BE A LOW ISSUANCE MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF MAY.WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF APRIL HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF MAY, FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (MAR), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A GIGANTIC SIZED 8245 CONTRACT OI AND FURTHER FROM OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 2655 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 2655 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 4136 CONTRACTS AND ADD TO THE 2655 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUMONGOUS SIZED LOSS OF 5590 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES 27.955 MILLION OZ

OCCURRED WITH OUR LOSS IN PRICE OF $0.57 IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

.

end

6. Commodity commentaries/cryptocurrencies

3. ASIAN AFFAIRS

i)MONDAY MORNING// SUNDAY NIGHT

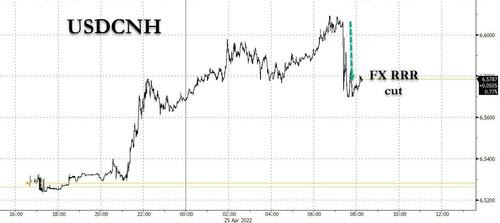

SHANGHAI CLOSED DOWN 158.41 PTS OR 5.13% //Hang Sang CLOSED DOWN 769.18 OR 3.73% /The Nikkei closed DOWN 514.48 PTS OR 1.90% //Australia’s all ordinaires CLOSED DOWN 1.51% /Chinese yuan (ONSHORE) closed DOWN 6.5740 /Oil DOWN TO 97.18 dollars per barrel for WTI andDOWN TO 101.23 for Brent. Stocks in Europe OPENED ALL RED // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.5510 OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.5320: /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER//

a)NORTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A SMALL SIZED 1771 CONTRACTS TO 568,150 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX INCREASE OCCURRED DESPITE OUR STRONG LOSS OF $13.40 IN GOLD PRICING FRIDAY’S COMEX TRADING. WE ALSO HAD A FAIR SIZED EFP (2844 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE ACTIVE DELIVERY MONTH OF APRIL.. THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2844 EFP CONTRACTS WERE ISSUED: ;: , . 0 JUNE :2844 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2844 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A SMALL SIZED TOTAL OF 1791 CONTRACTS IN THAT 2844 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A SMALL SIZED COMEX OI LOSS OF 1053 CONTRACTS..AND THIS GAIN OCCURRED DESPITE OUR LOSS IN PRICE OF GOLD $13.40.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING FOR APRIL (81.984),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 81.984

THE BANKERS WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $6.80) AND BUT WERE UNSUCCESSFUL IN FLEECING ANY LONGS AS WE HAVE REGISTERED A GOOD SIZED GAIN OF 13.023 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR APRIL (81.984 TONNES)…

WE HAD —3134 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 1053 CONTRACTS OR 105,300 OZ OR 3.275TONNES

Estimated gold volume today: 232,173/// fair/raid

Confirmed volume yesterday: 192,043contracts poor/raid

INITIAL STANDINGS FOR APRIL ’22 COMEX GOLD //APRIL 25

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 237,407.504 oz Manfra Brinks Delaware Loomis includes10 kilobars and 9 kilobars Delaware and Loomis |

| Deposit to the Dealer Inventory in oz | 12,995.592OZ Delaware |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 37 notice(s) 3,700 OZ 0.1550 TONNES |

| No of oz to be served (notices) | 590 contracts 59,000 oz 1.835 TONNES |

| Total monthly oz gold served (contracts) so far this month | 25,768 notices 2,576,800 OZ 80.149 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For today:

dealer deposits 1

i)Into dealer Manfra: 12,995.592 oz

total dealer deposit 12,995.592 oz//

No dealer withdrawals

4 customer withdrawals

i) out of Brinks 195,934.390 oz

ii) out of Delaware: 96.453 oz 3 kilobars

iii)Out of Loomis: 289.359 oz (9 kilobars)

iv) Out of Manfra: 76,862.805 oz

total customer withdrawals 233,407.504 oz

0 customer deposits

total customer withdrawal: 237,407.564 oz /

ADJUSTMENTS: one//dealer to customer

i) Out of Brinks: 289.359 oz (9 kilobars)

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR APRIL.

For the front month of APRIL we have an oi of 627 contracts having LOST 67 contracts

We had 50 notices filed yesterday so we LOST 17 contracts or an additional 1700 oz will NOT stand for delivery at the comex , as they were EFP’d to London. No gold over here for the crooks

May saw a LOSS of 151 contracts to stand at 3143

June saw a LOSS of 6258 contracts DOWN to 459,075 contracts

We had 37 notice(s) filed today for 3700 oz FOR THE APRIL 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 34 notices were issued from their client or customer account. The total of all issuance by all participants equates to 37 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 13 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 1 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the APRIL /2021. contract month,

we take the total number of notices filed so far for the month (25,768) x 100 oz , to which we add the difference between the open interest for the front month of (APRIL 627 CONTRACTS ) minus the number of notices served upon today 37 x 100 oz per contract equals 2,635,800 OZ OR 81.984 TONNES the number of TONNES standing in this active month of APRIL.

thus the INITIAL standings for gold for the APRIL contract month:

No of notices filed so far (25,768) x 100 oz+ (627) OI for the front month minus the number of notices served upon today (37} x 100 oz} which equals 2,635,800 oz standing OR 81.984 TONNES in this active delivery month of APRIL.

We LOST 1600 additional oz that will NOT stand for delivery on this side of the pond AS THESE GUYS WERE EFP’D TO LONDON.

TOTAL COMEX GOLD STANDING: 81.987 TONNES (A WHOPPER FOR AN APRIL ( ACTIVE) DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

191,133,764.7, oz NOW PLEDGED /HSBC 5.94 TONNES

99,258.893 PLEDGED MANFRA 3.08 TONNES

54,339.114oz PLEDGED JPMorgan no 1 1.690 tonnes

243,923.704, oz JPM No 2 7.58 TONNES

898,821.330 oz pledged Brinks/27,96 TONNES

International Delaware:: 0

Loomis: 18,615.429 oz

total pledged gold: 1,887,433.936 oz 58.70 tonnes

TOTAL REGISTERED AND ELIG GOLD AT THE COMEX: 35,950,353.100 OZ (1118,20 TONNES)

TOTAL ELIGIBLE GOLD: 18,387,366.763 OZ (571.92 tonnes)

TOTAL OF ALL REGISTERED GOLD: 17,366,986.637 OZ (540.18 tonnes)

REGISTERED GOLD THAT CAN BE SERVED UPON: 15,469,553.0 OZ (REG GOLD- PLEDGED GOLD) 481.47tonnes

END

APRIL 2022 CONTRACT MONTH//SILVER//APRIL 25

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1,240,878.172 oz Brinks CNT Delaware JPMorgan Loomis |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 150,292.900 oz CNT |

| No of oz served today (contracts) | 39CONTRACT(S) 195,000 OZ) |

| No of oz to be served (notices) | 6 contracts (30,000 oz) |

| Total monthly oz silver served (contracts) | 1343 contracts 6,715,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

we had 0 deposit into the dealer

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 1 deposits into the customer account

i) Into CNT: 150,292.900 oz

total deposit: 150,292.900 oz

JPMorgan has a total silver weight: 173.825 million oz/333.749 million =52.06% of comex

Comex withdrawals: 5

i) Out of CNT 93,275.002 oz

ii) Out of JPMorgan 600,350.500 oz

iii) Out of Brinks 25,166.30 oz

iv) Out of Delaware 3953.00 oz

v) Out of Loomis: 518,093.320 oz

total withdrawal 1,240,878.172 oz

0 adjustments:

the silver comex is in stress!

TOTAL REGISTERED SILVER: 85.811 MILLION OZ

TOTAL REG + ELIG. 333.789 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR APRIL

silver open interest data:

FRONT MONTH OF APRIL OI: 27, HAVING LOST 26 CONTRACTS FROM THURSDAY. We had 39 notices filed yesterday,

so we GAINED 13 contracts or an additional 65,000 oz will stand on this side of the pond

MAY HAD A LOSS OF 9914 CONTRACTS DOWN TO 32,266 contracts

JUNE HAD A GAIN OF 31 TO STAND AT 1353

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 21 for 105,000 oz

Comex volumes: 90,979// est. volume today// strong//good indicator of spreader liquidation/

Comex volume: confirmed yesterday: 99,250 contracts ( strong/spreader liquidation )

To calculate the number of silver ounces that will stand for delivery in APRIL. we take the total number of notices filed for the month so far at 1343 x 5,000 oz = 6,715,000 oz

to which we add the difference between the open interest for the front month of APRIL (27) and the number of notices served upon today 21 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the APRIL./2021 contract month: 1343 (notices served so far) x 5000 oz + OI for front month of APRIL (27) – number of notices served upon today (21) x 5000 oz of silver standing for the APRIL contract month equates 6,745,000 oz. .

We GAINED 13 contracts or an additional 65,000 oz will stand on this side of the pond

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

APRIL 25/WITH GOLD DOWN $36.80//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1104.13 TONNES

APRIL 22/WITH GOLD DOWN $13.50: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD.//INVENTORY RESTS AT 1104.13 TONNES

APRIL 21/WITH GOLD DOWN $6.80//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1106.74 TONNES

APRIL 20/WITH GOLD DOWN $3.05: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT IF 6.36 TONNES INTO THE GLD..//INVENTORY RESTS AT 1106.74 TONNES

APRIL 19//WITH GOLD DOWN $26.90//A SMALL CHANGE IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .87 TONNES INTO THE GLD//INVENTORY RESTS AT 1100.36 TONNES

APRIL 18/WITH GOLD UP $11.20: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.93 TONNES FROM THE GLD..//INVENTORY RESTS AT 1099.44 TONNES

APRIL 14/WITH GOLD DOWN $8.90: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.32 TONNES INTO THE GLD..//INVENTORY RESTS AT 1104.42 TONNES

APRIL 13/WITH GOLD UP $8.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1093.10 TONNES

APRIL 12/WITH GOLD UP $26.95: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.61 TONNES INTO THE GLD///INVENTORY REST AT 1093.10 TONNES

APRIL 11/WITH GOLD UP $3.40 //A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD.//INVENTORY RESTS AT 1090.49 TONNES

APRIL 8/WITH GOLD UP $7.70: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES INTO THE GLD//INVENTORY RESTS AT 1088.75 TONNES

APRIL 7/WITH GOLD UP $13.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1087.30 TONNES

APRIL 6/WITH GOLD DOWN $4.10: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.68 TONNES FROM THE GLD..//INVENTORY RESTS AT 1087.30 TONNES

APRIL 5/WITH GOLD DOWN $5.70: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.75 TONNES FROM THE GLD//INVENTORY RESTS AT 1089.98 TONNES

APRIL 4/WITH GOLD UP $.70//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1091.73 TONNES

APRIL 1///WITH GOLD DOWN $19.00 : A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .29 TONNES INTO THE GLD///INVENTORY RESTS AT 1091.73 TONNES

MARCH 31/WITH GOLD UP $13.30 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD FROM MONDAY A WITHDRAWAL OF 1.71 TONNES FROM THE GLD:INVENTORY RESTS AT 1091.44

MARCH 28/WITH GOLD DOWN $14.65: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1093.18 TONNES

MARCH 25/WITH GOLD DOWN $7.60 : A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.52 TONNES INTO THE GLD///INVENTORY RESTS AT 1093.18 TONNES

MARCH 24/WITH GOLD UP $24.95: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.06 TONNES INTO THE GLD..//INVENTORY RESTS AT 1087.66 TONNES

MARCH 23/WITH GOLD UP $15.75//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1083.60 TONNES

MARCH 22/WITH GOLD DOWN $7.75: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.16 TONNES OF GOLD DEPOSITED INTO THE GLD//INVENTORY RESTS AT 1083.60 TONES

CLOSING INVENTORY FOR THE GLD//1104.13 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

APRIL 25/WITH SILVER DOWN 69 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.031 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 579.418 MILLION OZ//

APRIL 22/WITH SILVER DOWN 34 CENTS : STRANGE!! A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WHOPPING DEPOSIT OF 3.508 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 581.449 MILLION OZ//

APRIL 21/WITH SILVER UP 57 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 577.941 MILLION OZ

APRIL 20/WITH SILVER DOWN 15 CENTS : A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.955 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 577.941 MILLION OZ///

APRIL 19/WITH SILVER DOWN 62 CENTS: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .461 MILLION OZ FROM THE SLV INVENTORY…//INVENTORY RESTS AT 574.986 MILLION OZ

APRIL 18/WITH SILVER UP 38 CENTS: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.771 MILLION OZ INTO THE SLV./INVENTORY RESTS AT 575.447 MILLION OZ//

APRIL 14/WITH SILVER DOWN 25 CENTS : A MONSTROUS CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.355 MILLION OZ INTO THE SLV.//INVENTORY RESTS AT 569.676 MILLION OZ//

APRIL 13/WITH SILVER UP 27 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 565.521 MILLION OZ

APRIL 12/WITH SILVER UP 66 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 565.521 MILLION OZ//

APRIL 11/WITH SILVER UP 13 CENTS: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 831,000 OZ FORM THE SLV////INVENTORY RESTS AT 565.521 MILLION OZ

APRIL 8/WITH SILVER UP 11 CENTS :NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 566.352 MILLION OZ//

APRIL 7/WITH SILVER UP 27 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 566.352 MILLION OZ//

APRIL 6/WITH SILVER DOWN 9 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 566.352 MILLION OZ

APRIL 5/WITH SILVER DOWN 16 CENTS : A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.386 MILLION OZ INTO THE SLV..//INVENTORY RESETS AT 566.352 MILLION OZ//

APRIL 4/WITH SILVER DOWN 5 CENTS TO CHANGES IN SILVER INVENTORY AT THE SLV//: A DEPOSIT OF 6.326 MILLION OZ//INVENTORY REST AT 564.966 MILLION OZ//

APRIL 1/WITH SILVER DOWN 39 CENTS A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.302 MILLION OZ INTO THE SLV////INVENTORY REST AT 558.647 MILLION OZ//

MARCH 31/WITH SILVER UP 3 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 2.171 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 556.345 MILLION OZ

MARCH 28/WITH SILVER DOWN 30 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.847 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 554.167 MILLION OZ//

MARCH 25/WITH SILVER DOWN 20 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 552.320 MILLION OZ//

MARCH 24/WITH SILVER UP 54 CENTS TODAY; A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.092 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 552.320 MILLION OZ//

MARCH 23/WITH SILVER UP 24 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 550.288 MILLION OZ//

MARCH 22/WITH SILVER DOWN $0.29 TODAY : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 550.288 MILLION OZ//

SLV FINAL INVENTORY FOR TODAY: 579.418 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

The Quick And Dirty On Inflation

MONDAY, APR 25, 2022 – 11:00 AM

The inflation freight train continues to barrel ahead. Not only are consumer prices at historically high levels; producer prices continue to run ahead of CPI, casting some doubt on the “peak inflation” narrative in the mainstream.

Despite the fact that inflation has been running hot for over a year, the mainstream pundits, government officials and central bankers can’t seem to nail down what’s going on. First, they said printing trillions wouldn’t cause inflation. Then they called inflation transitory. They said it was the pandemic. They pointed their fingers at supply chains and “excess demand.” Now they’re blaming Putin.

The problem is the mainstream won’t come to terms with the real underlying cause of rising prices. Mises Institute President Jeff Deist gives a quick and dirty breakdown of the inflation problem.

The following article was originally published by the Mises Institute. The views expressed are the author’s and don’t necessarily reflect those of Peter Schiff or SchiffGold.

All of a sudden everyone is an expert on inflation. Your brother-in-law, your local paper, and even dilettantes at dubious outlets like the Washington Post or The Atlantic feel compelled to explain our current predicament. With the admitted rate of consumer inflation running somewhere around 8 percent, and the real rate much higher, even central bankers can’t hide the reality from us. So the commentariat has to explain to us why this is happening and make sure we blame the mysterious workings of capitalism for our troubles.

In other words, economics is back. Covid was a nice diversion, and Ukraine took up all the media’s oxygen for a few months. But now we must deal with the economic devastation caused both by lockdowns and two years of crazed fiscal and monetary policy. Every day Americans, stubborn as they are, care more about rising gas and food prices than the political class would like. So they trot out Nancy Pelosi to explain how government spending actually reduces inflation and push pseudoeconomic ideas like modern monetary theory to explain why more federal spending is always the cure.

But what is really happening?

- First, consider the two covid stimulus bills passed by Congress in 2020 and 2021. These pumped more than $5 trillion directly into the economy in the form of payments to government, payments to households, unemployment benefits, employer payroll loans, cash subsides to airlines and countless other industries, and a host of grab-bag earmarks which had nothing to do with covid. This new money injected itself straight into the veins of the daily economy.

- Second, supply chains remain degraded because politicians around the world didn’t think through their lockdown policies. The deeply interconnected global economy does not have an ON/OFF switch. Idle resources and idle workers don’t simply spring to life and produce goods and services on command. But our policy makers have no conception of a structure of production, its temporal elements, or the ravages of malinvestment created by their political decision to shutter businesses.

- Third, covid allowed the Fed to justify yet another spasm of “extraordinary” monetary policies beginning in March 2020. This gave central bankers an easy out, in a sense, because real trouble was already on the horizon back in September 2019. The repo market, which commercial banks use for short-term (overnight) financing of their operations, suddenly seized up and sent rates spiking. These paroxysms embarrassingly forced the Fed to inject billions of dollars into its “standing” (i.e., permanent) repurchase facility and to consider yet another round of QE (asset buying) even after it had promised to shrink its balance sheet, still bloated with the detritus of the 2007 crisis.

All of this happened before any of us had heard of covid. But the obvious question last fall, screaming to be asked, was this: How on earth, after more than a decade of aggressive asset purchases by the Fed (swelling the central bank’s balance sheet from less than $1 trillion in 2007 to more than $4 trillion by 2019), did commercial banks still experience a liquidity crunch? What the hell was the point of all that money?

But covid washed away any question about repo and silenced any critics of the Fed’s largesse. Covid had to be defeated, by God, and monetary policy would lead the way. So the Fed went into hyperdrive, buying trillions in additional assets to send its balance sheet soaring to nearly $9 trillion today—adding nearly 20 percent of all dollars ever created to the M2 money supply measure in 2020 alone.

That same year, with lockdowns firmly in place and a crisis mindset whipped up by both parties, Congress managed to spend almost twice what the Treasury collected in taxes ($3.4 trillion in revenue versus $6.5 trillion in outlays). How is such an arrangement possible? Given historically low rates of return on Treasury debt—well below real inflation—and given the almost unbelievable and irreversible profligacy of the spendthrift US government, why would any sentient being continue to loan money to Uncle Sam? Why would anyone help Congress continue its debt-financed orgy? Why lend America money?

The answer is complex, ranging from the dollar’s status as the world’s reserve currency to pension and sovereign wealth funds around the globe that hold US Treasurys by charter and even the relative strength of America’s military forces. The question is thus as much geopolitical as economic. But in short, the world knows the Fed will always be there as a ready backstop, to buy US debt when appetites for such debt waver. Propping up congressional deficit spending, juicing equity markets, and constantly recapitalizing commercial banks are the Fed’s true mandates.

How does inflation end? Only with pain in the form of a necessary corrective recession or depression. Congress must slash spending, the Fed must stop buying assets and stop tampering with interest rates, and existing US debt must be allowed to mature and roll off the Fed’s balance sheet. We should force the US federal government to sell assets, especially land, to pay off Treasury obligations and fund future Social Security and Medicare entitlements. And if necessary, the federal government should be forced to default or apply a haircut to Treasury investors, who, after all, took a risk like any investor.

If all of this sounds politically impossible, you understand the deep unseriousness of today’s politics.

END

2.LAWRIE WILLIAMS//,//Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, James RICKARDS/

LAWRIE WILLIAMS: All fall down – except the dollar.

The past week certainly ended in disappointment for investors in precious metals, equities and bitcoin, all of which saw big falls in price as the week drew to a close and opened weaker still in Asia and Europe this morning. The downturn appeared to be precipitated by market fears in the U.S. that the Fed might be about to ‘overtighten’ at the early May Federal Open Market Committee (FOMC) meeting due to take place on May 3rd and 4th, potentially leading to at best a mini-recession.

Quite why precious metals prices were so badly affected puzzles us – we might have speculated that this kind of negative equity price movement could even have seen them rise. However the likely above average interest rate rise scenario so envisaged did see an increase in the U.S. dollar index (USDX) = which values the dollar against other world currencies – and there is always a tendency for gold, in particular, to fall when the dollar rises, and vice versa, with the other precious metals following suit.

It is the inflation ‘big bad wolf’ which is causing the price mayhem. The Consumer Price Index (CPI) came in at a massive 8.5% increase year on year earlier in the month and the Producer Price Index (PPI) which perhaps even better reflects the prices actually being received by suppliers at an even more worrying 11.2% year on year. There are worries that these figures may still be rising so the April data releases are being awaited with some degree of trepidation.

The next significant inflation data release is due out on Friday this week and is the Personal Consumption Expenditure Index (PCE) which is the Fed’s preferred inflation measure, and tends to come in a couple of percentage points lower than the CPI. The last PCE data announcement showed this measure of inflation rising at 6.4% year on year, but this, like the other inflation data was at its highest level for more than 40 years. Indeed if the data was still being calculated in the manner it was 40 years ago, all these inflation figures would actually be far higher. John Williams’s ShadowStats service which calculates U.S. government data the way it was in the past before it was manipulated lower in order to justify reducing social security payments among other things, puts the current CPI at approaching 20% – a level that would perhaps be more attuned to the experience of the person in the street.

What has to be particularly worrying for the Powell Fed is that when the inflation rate strayed into double digits just over 40 years ago, the remedy from then Fed chair Paul Volcker was to implement moves taking U.S. interest rates to around 20% and thereby precipitate a very severe recession. This ultimately had the effect of defeating inflation and setting the U.S. economy on an upwards path that has run now for decades. There’s no way Powell can do this, given the enormous cost of servicing the nation’s enormous debt level (estimated at over $30.4 trillion or around 125% of the nation’s GDP) built up over the past several years, at higher interest rate levels!

The kind of interest rate rises available to the Fed without disturbing the U.S.’s continuing economic growth are thus extremely limited, and if the Fed’s judgment on this is wrong it could precipitate either a recession if its inevitable rate increases are seen as being too high by the markets, or continuing runaway inflation if rises are too low. This is a very fine balancing act and we would rate the Fed’s chances of getting it right at probably 50:50 or less. And even if it can raise rates slow enough so as not to spook the markets, any inflation reduction will likely take an inordinate amount of time – maybe a couple of years or more to come back to the Fed’s target 2% rate. A marginal miscalculation either way could put the whole process in jeopardy, and let’s face it the Fed does not have a great record on economic forecasting to date.

25 Apr 2022

A very important read! Pam and Russ Martens

Fed Chair Powell Telegraphs the Perfect Storm for Wall Street’s Megabanks: Rapid Rate Hikes Hitting $234 Trillion in Derivatives

By Pam Martens and Russ Martens: April 25, 2022

The Federal Reserve (the Fed) is the central bank of the United States. It sets monetary policy, including control of the benchmark short-term interest rate known as the Federal Funds rate, or in Wall Street jargon, the “Fed Funds” rate. This is a key rate because it signals the rate at which overnight loans are made between financial institutions and the direction of interest rates in general.

Unfortunately, over time, the Fed has also been granted a supervisory role by Congress over Wall Street’s megabanks alongside its ability to bail them out when its crony brand of supervision fails. There was an epic failure in the Fed’s supervision of the Wall Street megabanks in the leadup to the 2008 financial crash and the September 2019 repo blowup. In both cases, the Fed made trillions of dollars in cumulative loans at below-market interest rates to the trading units of these megabanks in order to resuscitate them and cover up its own failure to properly supervise the banks.

The convulsions the stock market experienced last Thursday and Friday, that investors will continue to witness in the days ahead, are inextricably tied to the failure of Congress to strip the Fed of a supervisory role over these global megabanks.

There is no better snapshot of the Fed’s failure as a banking supervisor than this one fact that is called out every quarter in the Office of the Comptroller of the Currency’s Report on Bank Trading and Derivative Activities. Table 14 of this report (see page 19) shows that the 25 largest bank holding companies in the U.S. are sitting on $234 trillion notional (face amount) in derivatives but just five bank holding companies are responsible for $200.18 trillion of that exposure or 86 percent of the total. Those mega bank holding companies are: JPMorgan Chase (ticker JPM), Citigroup (C), Goldman Sachs (GS), Morgan Stanley (MS) and Bank of America (BAC).

The table also clearly shows that the most dangerous form of these derivatives – the same credit derivatives that blew up Wall Street in 2008 – are also concentrated at those same five bank holding companies.

But here’s what this quarterly report – or any other federal supervisory report – does not tell the public. It does not provide the names of the financial institutions that are on the other side of those derivative bets. To ferret out those names, one has to do independent research and watch stock market action. (More on that in a moment.)

Last Thursday, the delicate dance that Fed Chair Jerome Powell has been doing with Wall Street’s ticking derivatives time bombs, out-of-control inflation, and the Fed’s tardiness in raising rates spilled out during a panel discussion moderated by CNBC news anchor Sara Eisen. Present on the panel were the following: European Central Bank President Christine Lagarde; International Monetary Fund Managing Director Kristalina Georgieva; Federal Reserve Chair (Pro Tempore) Jerome Powell; the Finance Minister of Indonesia, Sri Mulyani Indrawati; and (virtually) the Prime Minister of Barbados, Mia Mottley. (Powell is serving as Chair Pro Tempore because he has yet to be confirmed for his second term as Fed Chair by the full Senate.)

The exchange that sent the stock market plunging went as follows between Eisen and Powell:

Eisen: “The market has three 50 basis point hikes coming at the next three meetings as of this morning. Is that reasonable?”

Powell: “So, I try not to comment on specific market pricing for things, but I will just say this: at our last meeting – and this was in the minutes of the meeting – many on the committee thought it would be appropriate for there to be one or more 50 basis point hikes.”

Eisen: “Were you one of those people?”

Powell: “I don’t disclose my own path. I try to lead the Committee. So, I think markets are processing what we’re saying; they’re reacting appropriately – generally. But I wouldn’t want to bless any particular market pricing. The thing I want to say, though, is we really are committed to using our tools to get 2 percent inflation back and I think, for example, if you look at the last tightening cycle, which was a two-year string of 25 basis point hikes from 2004 to 2006, inflation was a little over 3 percent. So inflation’s much higher now and our policy rate is still more accommodative than it was then. So it is appropriate in my view to be moving more quickly.

“And I also think there’s something in the idea of front-end loading whatever accommodation one thinks is appropriate. So that points in the direction of 50 basis points being on the table certainly.

“We make these decisions at the meeting and we’ll make them meeting by meeting but I would say that 50 basis points will be on the table for the May meeting.”

You can watch the full exchange at this link. The above back and forth between Eisen and Powell begins at 9:33 on the video.

By the closing bell on Thursday, April 21, the Dow Jones Industrial Average had fallen 368 points on Powell’s remarks. The market reflected further on those remarks and plunged by another 981 points on Friday, April 22, for a total two-day wipeout of 1,349 points in the Dow.

The mega banks that are known to have the bulk of the derivative exposure were hit hard in the selloff on Friday, as was the German global bank, Deutsche Bank, which is known to be a counterparty to derivatives on Wall Street. Also reported to have derivative exposure to Wall Street are insurance companies AIG, Metropolitan Life (MET), Prudential Financial (PRU), Ameriprise Financial (AMP) and Lincoln National (LNC). The chart above shows how the stocks of these financial institutions performed in Friday’s selloff.

3. Chris Powell of GATA provides to us very important physical commentaries

LME abandons its attempt to crack the gold/silver market

Bloomberg/Spence/GATA

London Metal Exchange abandons attempt to crack gold market

Submitted by admin on Fri, 2022-04-22 13:26Section: Daily Dispatches

By Eddie Spence

Bloomberg News

Friday, April 22, 2022

The London Metal Exchange will abandon its attempt to break into precious-metal trading after just five years, citing low trading volumes in its gold and silver contracts.

The LME — the world’s biggest exchange for industrial metals — partnered with banks including Goldman Sachs Group and Morgan Stanley in 2017 to launch the contracts. London is one of the two major centers of precious-metals trading, where trillions of dollars in gold, silver, and associated derivatives change hands each year. It’s an almost entirely over-the-counter business, dominated by top bullion banks like JPMorgan Chase & Co. and HSBC Holdings.

The LME’s project sought to move the trade onto an exchange comparable to the Comex in New York, providing more transparency over pricing. Initially it met with some success, but volumes dropped steeply after Societe Generale — one of the LME’s original partners — closed most of its commodity trading business in 2019.

The LMEprecious service is expected to be withdrawn on or about July 11, the exchange said in a notice to members. It took the decision “following discussions with market participants, and in light of the low levels of trading activity within the LMEprecious market.” …

… For the remainder of the report:

END

EU admits rouble payments for Russia’s gas might not breach sanctions

(London Telegraph/GATA)

EU admits rouble payments for Russia’s gas might not breach sanctions

Submitted by admin on Fri, 2022-04-22 20:55Section: Daily Dispatches

By James Warrington and Giulia Bottaro

The Telegraph, London

Friday, April 22, 2022

By James Warrington and Giulia Bottaro

The Telegraph, London

Friday, April 22, 2022

The European Union admitted that countries may be able to comply with Russian President Vladimir Putin’s demand for gas payments in roubles without breaching sanctions against Russia.

Putin has demanded that so-called “unfriendly” nations open accounts at sanctioned lender Gazprombank, where payments in euros or dollars would be converted into roubles.

The European Commission has refused to comply with the order and initially said doing so would fall foul of sanctions. It has now backed down on this claim, although the bloc said it wasn’t clear how such a procedure would work.

It came as the UK issued a temporary licence allowing payments to Gazprombank for gas used in the EU until the end of May.

end

Payment in gold earns big discounts on Russian oil. This is a must view

(GATA/Andrew Maguire/Kinesis)

Payment in gold earns big discount on Russian oil in London trading, Maguire says

Submitted by admin on Sat, 2022-04-23 21:20 Section: Daily Dispatches

Dear Friend of GATA and Gold:

In this week’s “Live from the Vault” program from Kinesis Money, London metals trader Andrew Maguire tells host Shane Morand that, through intermediaries — presumably Chinese — Russian oil is available at a big discount via trading in London when purchased with gold. This arbitrage is increasing demand for real metal in London, Maguire says, and he expects it to put great strain on the “paper” gold trade there.

The program is 36 minutes long and can be seen at YouTube here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

The Fed is losing control over the inflation narrative as bond traders whack long term bonds driving up yields as the betting continues that the Fed cannot get rates down to 2%

(Ambramowicz/Bloomberg)

Lisa Abramowicz: The Fed is losing control over the inflation narrative

Submitted by admin on Sun, 2022-04-24 11:49Section: Daily Dispatches

By Lisa Abramowicz

Bloomberg News

via The Washington Post

Sunday, April 24, 2022

The Federal Reserve is poised to raise interest rates at the fastest pace in 40 years after policy makers’ hawkish rhetoric turned more aggressive last week. The problem, though, is that bond traders keep boosting their longer-term inflation expectations in a very concerning development for the central bank, the economy and financial markets

Traders are betting that even with the Fed boosting its target for the federal funds rate by 2.5 percentage points this year to 3%, it won’t be enough to get the inflation rate back down to 2% over the next decade from around 8.5% currently. This week, 2-year Treasury note yields surged to the highest levels since 2018 as Fed Chair Jerome Powell endorsed the idea of a half-percentage-point increase when policy makers meet in two weeks and saying many officials view “one or more” such moves as appropriate.

Even so, longer-term inflation expectations kept climbing. The market-implied inflation rate over the next five to 10 years rose to the highest since 2014, jumping to almost 2.6%, and 10-year breakeven rates climbed to the highest since at least 1998, surpassing 3%. The long-time bond bulls at Hoisington Investment Management Co. expressed concern in their first-quarter letter to investors, saying an economic downturn would favor buying long-term Treasuries, but “investors should be wary” of the Fed failing to sufficiently tamp down inflation.

All this suggests one of two things: either the world’s most important central bank has lost control over inflation, or it isn’t going to even try to get it back down to their 2% target.

“If the Fed wants to get back to 2% inflation, I find it hard to believe that a soft landing is possible,” Columbia University finance and economics professor Glenn Hubbard said Friday on Bloomberg Surveillance. Traders agree, with breakeven rates suggesting they think policy makers will avoid torpedoing the economy and err on the side of doing less, not more, when it comes to tightening monetary policy. …

… For the remainder of the analysis:

end

4.OTHER GOLD/SILVER COMMENTARIES

5.OTHER COMMODITIES RICE

end

COMMODITIES IN GENERAL//DIAMONDS

Russian Diamond Flow To India Stops As US Sanctions Cause Gem Chaos

FRIDAY, APR 22, 2022 – 09:20 PM

Do you own diamonds? It could be time to call up the local jeweler and reassess them. Here’s why:

Earlier this month, the U.S. Department of the Treasury’s Office of Foreign Assets Control (OFAC) sanctioned Russian diamond miner Alrosa PJSC, removing a third of the global supply of rough stones.

Bloomberg reports rough stones have stopped flowing from Russian mines to Surat, India, the mecca of diamond cutting and polishing.

Industry experts say traders and manufacturers are searching for workarounds as Indian banks are unwilling or unable to process payments with Alrosa due to OFAC’s sanctions.

Alrosa sent top officials earlier this week to Surat to speak with customers and trade groups about future sales.

For some context, Alrosa accounts for 33% of the global supply of rough stones, about the same as De Beers. OFAC’s sanctions against Russia have been seismic for the worldwide diamond industry as supply tightens, sending prices of the rock sky-high.

The Diamond Index via International Diamond Exchange (IDEX) surged 36% in the last two years.

Those experts also said Alrosa’s upcoming sale of rough stones was canceled because banks could not process payments. The Russian miner holds only ten sales each year.

Meanwhile, discontent is growing among G-20 members that not all will stop buying Russian stones. Retailers in China, India, and the Middle East plan to continue buying despite OFAC’s sanctions.

We noted earlier this week that not all BRICs have bowed to U.S. pressure to stop purchasing Russian goods. It lends credibility to an emerging multi-polar world.

Industry experts said Alrosa’s meeting could result in a bilateral (rupees for rubles) payment structure for the uncut gems. Again, this could be another example of the birth of the emerging Bretton Woods III system, recently popularized by Credit Suisse strategist Zoltan Pozsar.

The disruptions around Russian diamonds will persist as supply tightens, only making the prices of the stone even more unaffordable. Then there are lab-grown diamonds, a cheaper alternative to the real thing.

end

Palm Oils

Indonesia Bans Edible Oil Exports, Sparks “Mayhem” As Global Food Crisis Ahead

FRIDAY, APR 22, 2022 – 07:20 PM

The rise of food protectionism by countries could exacerbate a massive hunger crisis that could take the world by storm later this year (well, that’s at least what the Rockefeller Foundation believes).

The world’s biggest palm oil producer, Indonesia, is the latest country to embrace protectionist measures to mitigate domestic food shortages, according to Bloomberg.

President Joko Widodo on Friday announced the export ban of all cooking oil and palm oil products would begin on April 28.

Widodo said during a television broadcast that the measures aimed to ensure domestic markets had ample cooking oil supplies following a dramatic increase in prices.

“I will monitor and evaluate the implementation of this policy so availability of cooking oil in the domestic market becomes abundant and affordable,” he said.

Following the news, traders are placing bullish bets that world supplies of cooking oil and palm oil products will tighten even more. U.S. soyoil futures jumped more than 3% to a record high of 84 cents per pound.

“The news will certainly create a mayhem,” said Paramalingam Supramaniam, director at Selangor-based broker Pelindung Bestari.

“We have the largest producer banning the exports of palm products which will add more uncertainty to the already tight availability of vegetable oil worldwide,” Supramaniam said.

The Ukraine conflict has roiled the global edible oil market. The Black Sea region accounts for 76% of world sunoil exports. Commercial shipments in the region have been disrupted due mainly by insurers for vessels charging very high war premiums that make cargo nearly impossible in insure.

Indonesia’s move adds to the growing food protectionism as several other countries, including Argentina, have raised export taxes on edible oils. Meanwhile, Moldova, Hungary, and Serbia have banned some grain exports.

Increasing food protectionism is another worry for importers dependent on other countries (such as ones in the Middle East and Africa) that may lead to shortages and trigger unrest.

As we noted initially, the Rockefeller Foundation has given a timeframe on when the food crisis begins.

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Gold Tumbles Below $1900 – Erases All Post-Putin Risk-Premia

MONDAY, APR 25, 2022 – 08:28 AM

…as if it never happened.

Judging by the ‘safe haven’ derisking in the barbarous relic, Putin’s invasion of Ukraine and the subsequent chaos in global markets is a nothingburger. For the third time since the Russian President invaded Ukraine, Gold has broken back below $1900…

Will the third time be the charm for a test of $1900?

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings MONDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 6.5510

OFFSHORE YUAN: 6.5740

HANG SANG CLOSED UP DOWN 769.18 PTS OR 3.73%

2. Nikkei closed DOWN 514.48PTS OR 1.90%

3. Europe stocks ALL RED

USA dollar INDEX DOWN TO 101.23/Euro FALLS TO 1.07510

3b Japan 10 YR bond yield: FALLS TO. +.251/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 128.24/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: DOWN -SHORE CLOSED DOWN// OFF- SHORE DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

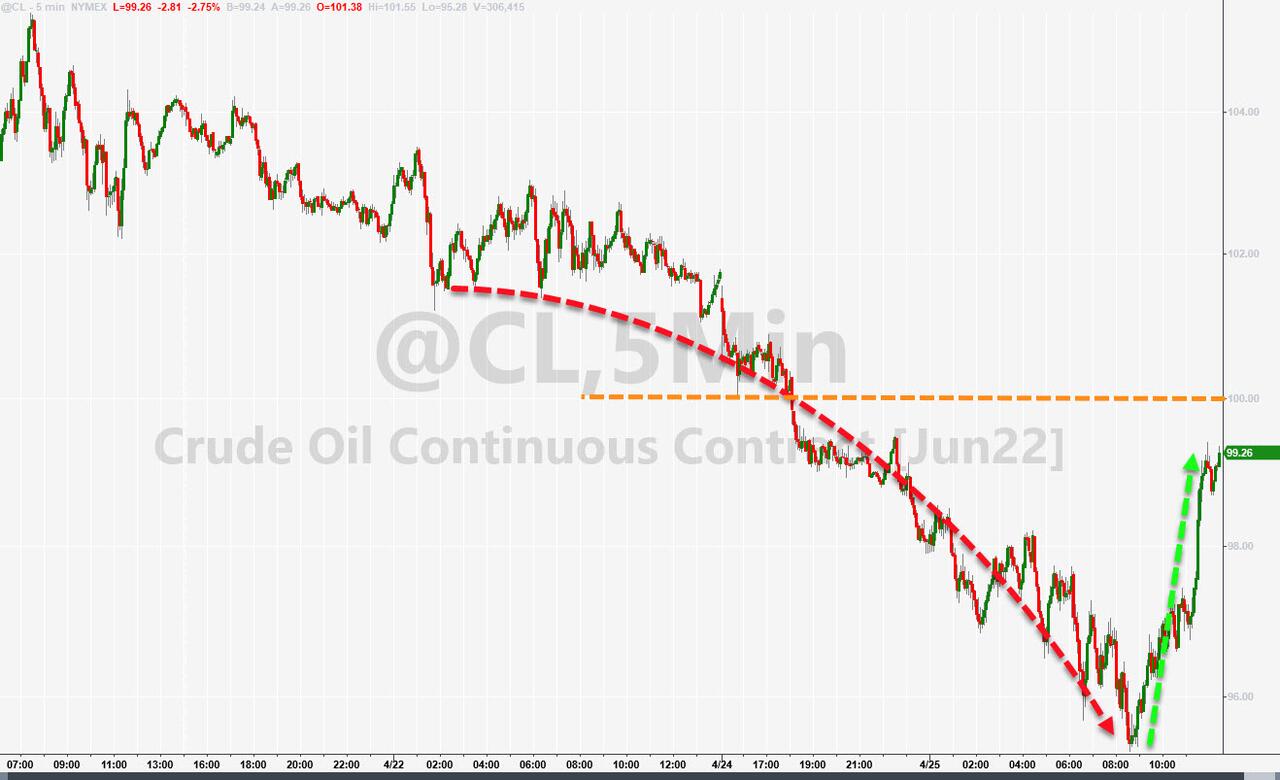

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.0.894%/Italian 10 Yr bond yield FALLS to 2.62% /SPAIN 10 YR BOND YIELDFALLS TO 1.88%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 1.73: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3i Greek 10 year bond yield FALLS TO : 2.97

3j Gold at $1904.95 silver at: 23.55 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 1/3 roubles/dollar; ROUBLE AT 73.16

3m oil into the 97 dollar handle for WTI and 101 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 128.24 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning .9565– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0283well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 2.835 DOWN 7 BASIS PTS

USA 30 YR BOND YIELD: 2.901 DOWN 4 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 14.76

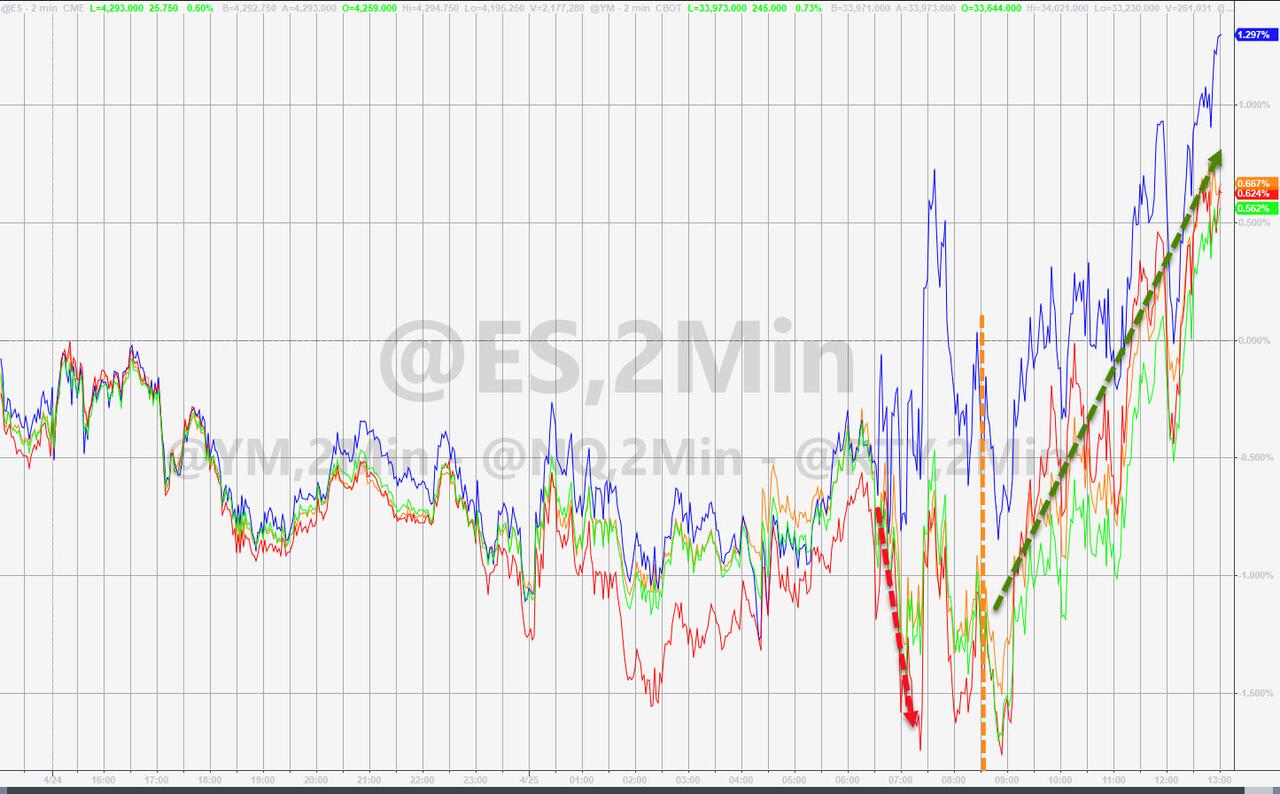

Global Markets Tumble On Hawkish Central Bank Anguish, China Lockdown Fears

MONDAY, APR 25, 2022 – 07:48 AM

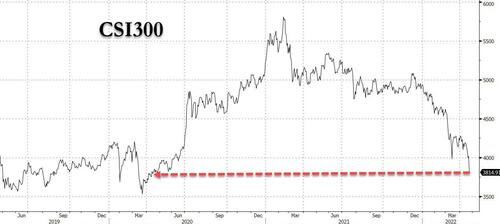

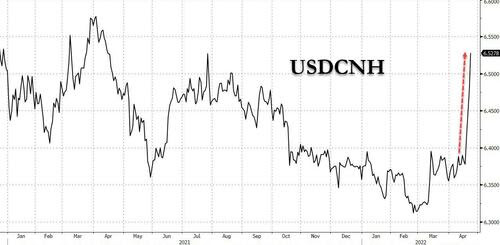

The global selloff that started in Asia, sending China’s CSI300 plunging to the lowest level since May 2020, slamming the offshore yuan below 6.60 and sparking a liquidation in oil and cryptos amid fears that the Shanghai lockdown will spread to the capital Beijing and lead to an even greater slowdown in the global economy…

… has quickly spread around the globe, slamming not just European markets but US equity futures which slid as much as 1% as traders fretted over the prospects of aggressive tightening by the Federal Reserve, Chinese lockdowns and disappointing earnings. S&P 500 futures were down 0.9% as of 7:00am EDT after plunging 2.8% on Friday, while Nasdaq futures retreated 0.8%, with the rout hammering tech stocks especially hard. Some context: the Nasdaq 100 Index has erased about $1 trillion in market value since Netflix released disappointing earnings and is closing in on oversold levels; the tech-heavy FANGMAN basket has lost $2.4 trillion in market cap from 2021 ATH as Netflix and Facebook Meta, have lost most of their gains from past 5yrs. Remember when Facebook hit the $1tn market cap club in 2021? Now it’s worth exactly half that.

But now the tech bear market is finally spreading all US stocks which closed at their lowest levels in more than a month on Friday as fears over a more aggressive Federal Reserve tightening cycle led to broad-based selling. Investors are entering another busy week for big technology companies’ earnings, with Alphabet, Microsoft, Meta Platforms, Paypal and Apple all reporting results although don’t expect some miraculous surge.

Investor mood was already morose after Fed chair erome Powell’s hawkish comments last week hurt sentiment already sapped by the war in Ukraine, a slowdown in China and the risks inflation poses to company earnings, according to Michael Hewson, chief analyst at CMC Markets in London. “The final straw appears to be a concern about the prospect of a policy mistake by central banks, and a possible recession by the end of the year,” he said.

One sole glimmer of green, Twitter shares, rose 0.6% in premarket trading after a WSJ report that Elon Musk met with the social media platform’s executives on Sunday as the company turns more receptive toward the billionaire’s $43 billion takeover offer. As discussed earlier, U.S.-listed Chinese stocks fell in premarket trading as expanded Covid lockdown measures in major Chinese cities spark concerns over the country’s growth outlook. Pinduoduo led a decline in American depositary receipts, down 4.7% in premarket trade. E-commerce peers Alibaba Group fell 3.9% and JD.com lost 2.5%. Electric carmakers including Nio and Li Auto also fell. The weakness tracks a 4.9% slump in China’s CSI 300 Index, which closed at its lowest level in two years. Here are some other notable premarket movers:

- U.S.-listed Chinese stocks look set to open lower on Monday as expanded Covid lockdown measures in major cities sparked concerns over the country’s economic growth outlook.

- Pinduoduo (PDD US) led a decline in American depositary receipts, down 4.7% in premarket trade. E-commerce peers Alibaba (BABA US) fell 3.9% and JD.com (JD US) lost 2.5%. Electric carmakers including Nio (NIO US) and Li Auto (LI US) also fell.

- AT&T (T US) reinstated with a buy rating at Goldman Sachs with the focus turning to the telecom giant’s core business, while the broker cuts its rating on Verizon (VZ US) on valuation grounds. AT&T up 0.6% in premarket, Verizon -1.4%.

- Cenntro Electric (CENN US) rises as much as 22% premarket ahead of the electric-vehicle company’s quarterly update due after the close on Monday.

- Kellogg (K US) was downgraded to hold from buy at Deutsche Bank, which stays cautious and below consensus ahead of 1Q22 results because of headwinds including worsening inflation and supply chain disruptions. Shares down 1.4% in premarket.

- Morgan Stanley says DoorDash (DASH US) is the “best executor around” among food delivery companies, but awaits a better entry point as initiates at equal-weight with Street- low $100 target. Shares down 1.1% in premarket on low volume.

- GoDaddy (GDDY US) upgraded to overweight at Piper Sandler on strong free cash flow potential, with the broker cutting its ratings on Wix.com (WIX US) and Squarespace (SQSP US) in a rejig of its digital presence coverage. GoDaddy little changed in premarket, Wix.com and Squarespace not traded.

Coca-Cola and Activision Blizzard are among companies reporting earnings today.

In Europe, markets are under heavy pressure: Euro Stoxx 50 drops as much as 2.6% with several other core indexes down over 2%. Spain’s IBEX outperforms. Miners are the weakest performers with the Stoxx 600 sector down over 5%. Energy and consumer products and services similarly lag. Europe’s Basic Resources Index crashed 6%, and was set for the worst daily drop since March 2020. Here are some of the biggest European movers today:

- Ubisoft shares rise as much as 12% after Bloomberg reported the video-game publisher is attracting takeover interest from private equity firms including Blackstone and KKR.

- Garanti stock rallies as much as 5.6% after parent BBVA sweetened its voluntary offer for the Turkish lender and the unit said 1Q net income tripled.

- Biogaia shares rise as much as 9.6% after the Swedish food-additives and supplements maker published preliminary 1Q sales figures, which included a large beat on operating profit and net sales.

- Barco shares rise as much as 4.2% after the projector maker’s Cinionic JV won a contract to install laser projectors in 3,500 U.S. auditoriums of cinema chain operator AMC.

- The Stoxx 600 Basic Resources and Energy sub- indexes both slumped on Monday amid broad declines for commodities prices on concerns that a growing Covid-19 outbreak in China will hit demand.

- Shell -4.5%, TotalEnergies SE -3.1%, Glencore -6.0%, Anglo American -6.5%

- Philips stock falls as much as 11% after publishing its latest earnings, where higher provisions related to its recall of Dreamstation breathing machines overshadowed better-than-expected 1Q sales.

- Roche shares fell as much as 3.6% after the Swiss pharma company reported mixed first quarter results. Sales beat expectations due to a boost to the diagnostics division, while the pharmaceutical unit missed.

As we reported on Sunday, the big news out of France is that Macron won the second round of the Presidential Election with 58.6% of the vote vs Le Pen at 41.4%, while Le Pen conceded defeat after the initial projections, according to Reuters and Sky News. Elsewhere, ECB President Lagarde commented that interest rate hikes will not lower energy prices, according to Barron’s. ECB policymakers are said to be keen to finish bond purchases as soon as possible and possibly hike rates in July but no later than August, while they are leaning towards two rate moves this year with three also a possibility, according to Reuters sources. However, an ECB spokesperson declined to comment on the timing of ending bond purchases and potential interest rate increases. The EU is said to prepare the creation of a new trade and tech council with India, according to FT sources. The new forum could be unveiled on Monday during the European Commission President’s visit to India.

Earlier in the session, Asian stocks slumped the most since March 11 as China’s worsening Covid-19 outbreak and a looming rate hike by the Federal Reserve hurt risk sentiment. The MSCI Asia Pacific Index fell as much as 2.2% Monday, setting off a grim start to the region’s busiest week for earnings. The biggest drags were technology stocks sensitive to higher interest rates, including Taiwan Semiconductor Manufacturing, Alibaba and Tencent. Equities in mainland China and Hong Kong were among the region’s worst performers. Chinese stocks slid to a two year low amid fears that rising infections in Beijing may spur an unprecedented city-wide lockdown of the capital. The Chinese regulator also ordered platform companies to better handle online violence, dragging tech stocks lower. READ: China Lockdown Angst Rips Through Markets as Stocks, Yuan Plunge The lockdowns that have now expanded to parts of Beijing will “cause a logistical problem that’s going to affect not just China but also the rest of the world,” Jeffrey Halley, Asia Pacific senior market analyst at Oanda, said in an interview with Bloomberg TV. With no signs of change in Covid zero policy and very little in terms of actual stimulus, “that all points to lower China stocks and we are going to see a weaker yuan going forward,” he added. Investors are also on guard for corporate earnings. Stock-market heavyweights including Kweichow Moutai in China and Samsung Electronics in South Korea are expected to release first-quarter results this week. With a number of Fed speakers recently showing support for 50-basis-point hikes, tech shares led declines of major gauges in the region. Taiwan’s Taiex dropped 10% from its January high.

Japanese equities dropped, extending a global selloff amid prospects for aggressive U.S. interest-rate hikes and a worsening Covid outbreak in China. Electronics and machinery makers were the biggest drags on the Topix, which fell 1.5%, with 32 of 33 industry groups in the red. Fast Retailing and SoftBank Group were the largest contributors to a 1.9% loss in the Nikkei 225.

Indian stocks also fell, joining their peers across Asia, as appetite for risk waned amid renewed concerns over Covid infections and its possible impact on business growth. The S&P BSE Sensex dropped 1.1% to 56,579.89, while the NSE Nifty 50 Index slipped 1.3% to 16,953.95. Reliance Industries Ltd. lost 2.3%, the most in seven weeks. It was the biggest drag on the Sensex, which saw 23 of its 30 stocks trading lower. All but one of 19 sectoral sub-indexes compiled by BSE Ltd. declined, led by a gauge of metal stocks. The continued war in Ukraine and fears of a wider lockdown in Beijing are weighing on sentiment, already impacted by the risk of a global slowdown as the U.S. Fed raises rates to tame inflation. Of the six Nifty 50 firms that have announced results so far, four have missed, while two have beaten analyst estimates. Bajaj Finance, Hindustan Unilever, Axis Bank are among the companies releasing Jan-March earnings this week.

With risk off, safe havens were mostly bid: Treasuries advanced across the curve, with yields on the belly falling about 10bps and 10Y yields sliding 8bps to 2.833%. The belly of the UST curve outperforms by 1-2bps. Peripheral spreads widen to core with 10y Italy lagging peers on the rally. European bonds advanced, yet underperformed Treasuries; the spread between French 10-year bond yields and German equivalents tightened at the open after President Emmanuel Macron was re-elected as French president, only to widen as haven demand supported bunds. IG dollar issuance slate empty so far; preliminary estimates are for around $25 billion this week. • Three-month dollar Libor +1.11bp to 1.22486%.

In FX, the Bloomberg Dollar Spot Index rose a third day to the highest level since May 2020; the greenback advanced against all of its Group-of-10 peers apart from the yen and the Swiss franc; AUD and NZD lag G-10 peers. USD/JPY holds above 128. The euro fell to its lowest level versus the dollar since March 2020, erasing earlier gains amid broader greenback strength. The pound slumped to the lowest versus the dollar since September 2020 and gilts advanced. The Aussie was the worst G-10 performer amid fears over the outlook for China’s demand for iron ore and with the selloff boosted by options-related selling. The yen rose, as concerns about the economic impact of accelerating U.S. rate increases put a pause on the recent aggressive selling of the currency. Japan’s government bonds tracked Treasuries higher with support from purchases by the Bank of Japan.

Perhaps most importantly, the yuan – which until now had resisted any weakness – plunged again, dropping to the lowest level in 17 months as the offshore yuan dropped below 6.60 the lowest level since Nov 2020, spurring a selloff in emerging-market currencies.

In commodities, crude futures sold ell off with WTI down over 4% and back on a $97-handle. Base metals are similarly deep in the red. Spot gold drops ~$14 to trade near $1,916/oz. Monday’s pullback in the soaring price of commodities since Russia’s invasion of Ukraine has done little to assuage concerns about runaway inflation. Fed Jerome Powell had outlined his most bold approach yet to reining in surging prices and the European Central Bank signaled stronger tightening.

Bitcoin continued to tumble alongside the broader crypto market, even though the harder the stocks fall and the more the Fed tightens, the more it will eventually have to ease, unleashing the next surge higher in cryptos which we expect to push bitcoin over $100,000 and Ether over $10,000.

Looking at the calendar, the economic data slate includes March Chicago Fed national activity (8:30am) and April Dallas Fed manufacturing activity(10:30am); consumer confidence, GDP, PCE deflator and University of Michigan sentiment are ahead this week. Today we will earnings from Coca-Cola, Activision Blizzard, Vivendi.

Market Snapshot

- S&P 500 futures down 0.7% to 4,235.25

- STOXX Europe 600 down 1.8% to 445.31

- MXAP down 2.0% to 166.02

- MXAPJ down 2.4% to 546.02

- Nikkei down 1.9% to 26,590.78

- Topix down 1.5% to 1,876.52

- Hang Seng Index down 3.7% to 19,869.34

- Shanghai Composite down 5.1% to 2,928.51

- Sensex down 1.0% to 56,637.35

- Australia S&P/ASX 200 down 1.6% to 7,473.28

- Kospi down 1.8% to 2,657.13

- German 10Y yield little changed at 0.89%

- Euro down 0.4% to $1.0751

- Brent Futures down 4.4% to $101.96/bbl

- Gold spot down 0.6% to $1,920.54

- U.S. Dollar Index up 0.20% to 101.43

Top Overnight News from Bloomberg

- China’s coronavirus outbreak worsened as rising cases in Beijing sparked jitters about an unprecedented lockdown of the capital, with policy makers racing to avert a Shanghai-style crisis that’s already wrought havoc on the financial hub

- China must take stronger action to boost growth above 5% in the second quarter, said a central bank adviser who warned the country needs to lay a foundation for achieving its full-year target in the face of rising economic risks

- A sustained and substantial increase in U.S. real yields would be bad news for developing nations as it typically boosts the dollar and sucks capital out of riskier assets, like in 2008 and 2013

- The U.S. announced it would start sending diplomats back to Ukraine and provide more military aid as Secretary of State Antony Blinken and Secretary of Defense Lloyd Austin visited Kyiv late on Sunday night, in the highest- level U.S. visit to the war-torn country since Russia invaded

- China’s central bank stepped up its support for several distressed developers by allowing banks and bad-debt managers to loosen restrictions on some loans to ease a cash crunch, according to people familiar with the matter

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded negatively after last Friday’s stock rout on Wall Street with risk sentiment hampered by holiday closures, China’s COVID-19 woes and as participants brace for a busy week of key earnings releases. Nikkei 225 shed around 500 points with sentiment not helped by several earnings guidance downgrades and with Nissan shares were hit as alliance partner Renault mulls selling a partial stake in the Japanese automaker. Hang Seng and Shanghai Comp underperformed on the COVID situation after daily deaths in Shanghai rose again and with the city to conduct another round of mass testing, while Beijing also scrambles to contain an outbreak with its Chaoyang district to require residents and workers to undergo three COVID-19 tests this week.

Top Asian News

- Asia Stocks Fall Most in Six Weeks as China Outbreak Worsens

- China Woes Stoking Inflation Angst Set to Weigh on the Euro

- Shimao Unit Proposes to Pay Down Puttable Bond Faster: REDD

- Loan Curbs Eased for Distressed Developers: Evergrande Update

European cash markets kicked off the week lower across the board with a relatively broad-based performance seen across the majors. Sectors are lower across the board with a clear defensive tilt: Energy and Basic Resources sit at the bottom of the bunch amid hefty downside in underlying commodities. Stateside futures are lower in tandem with the broader market sentiment, whilst the NQ is slightly more cushioned by the earlier decline in yields. Twitter is reportedly re-examining Elon Musk’s bid and be more receptive to a deal with the sides meeting on Sunday to discuss the proposal. It was separately reported that Twitter is facing increasing shareholder pressure to negotiate with Elon Musk in his takeover bid and that the Co. is in talks with Elon Musk in which a potential deal could be made as early as this week, according to WSJ.

Top European News

- Macron Gets Second Chance to Show France His Vision Can Work