by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD; $1738.25 DOWN $26.70

SILVER: $19.20 UP 1 CENT

ACCESS MARKET: GOLD $1739.50

SILVER: $19.22

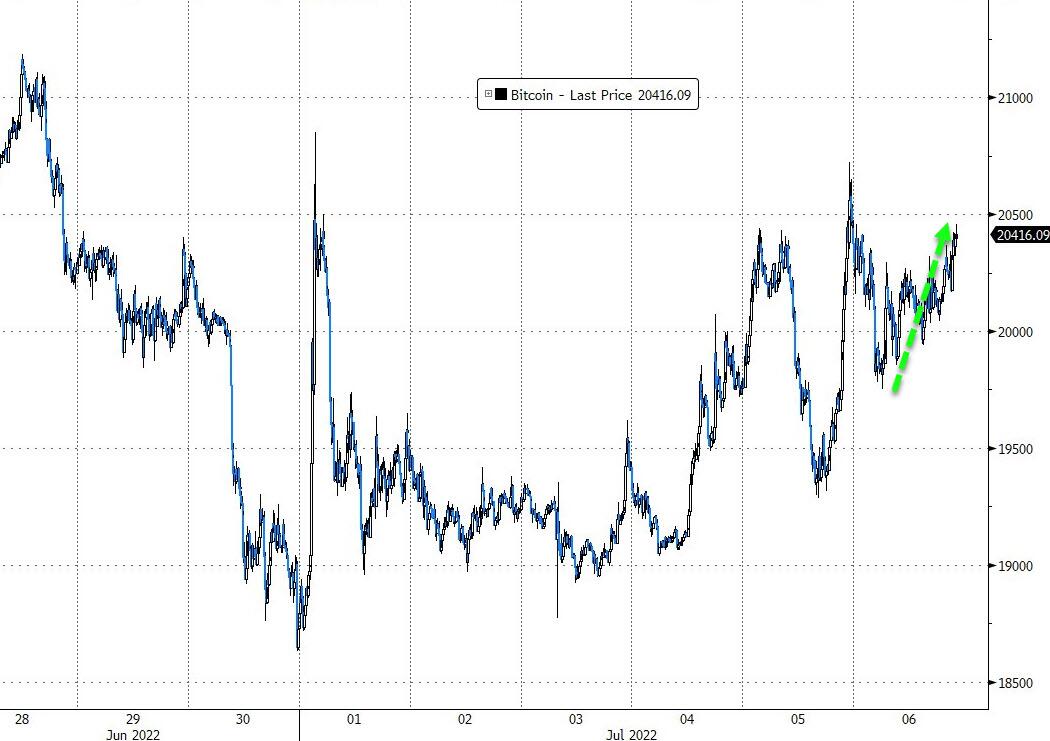

Bitcoin morning price: $20,061 DOWN 142

Bitcoin: afternoon price: $20,381. UP 178

Platinum price: closing DOWN $16.00 to $857.96

Palladium price; closing DOWN $13.00 at $1916.60

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: JULY 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,761.800000000 USD

INTENT DATE: 07/05/2022 DELIVERY DATE: 07/07/2022

FIRM ORG FIRM NAME ISSUED STOPPED

661 C JP MORGAN 33

737 C ADVANTAGE 27 1

800 C MAREX SPEC 9 2

TOTAL: 36 36

MONTH TO DATE: 1,013

no. of contracts issued by JPMorgan: 33/36

_____________________________________________________________________________________

NUMBER OF NOTICES FILED TODAY FOR JULY CONTRACT 36 NOTICE(S) FOR 3600 Oz//0.1119 TONNES)

total notices so far: 1013 contracts for 101,300 oz (3.1580 tonnes)

SILVER NOTICES:

621 NOTICE(S) FILED 3,109,000 OZ/

total number of notices filed so far this month 2513 : for 12,565,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD DOWN $26.70

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

BIG CHANGES IN GOLD INVENTORY AT THE GLD: A HUGE WITHDRAWAL OF 28.27 TONNES FROM THE GLD//

INVENTORY RESTS AT 1032.04 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP 1 CENT

AT THE SLV// ://HUGE CHANGES IN SILVER INVENTORY AT THE SLV//: A WITHDRAWAL OF 12.558 MILLION OZ FROM THE LV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 528.151 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A SMALL SIZED 294 CONTRACTS TO 140,462 AND CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE GAIN IN OI WAS ACCOMPLISHED DESPITE OUR $0.55 LOSS IN SILVER PRICING AT THE COMEX ON TUESDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.55) BUT WERE UNSUCCESSFUL IN KNOCKING OFF SOME SILVER LONGS//BUT MAINLY WE HAD ADDITIONAL SPECULATOR ADDITIONS.

WE MUST HAVE HAD:

I) HUGE SPECULATOR SHORT ADDITIONS /. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A POOR INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 15.220 MILLION OZ FOLLOWED BY TODAY’S 105,000 OZ QUEUE JUMP / // V) SMALL SIZED COMEX OI GAIN

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS : -61

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JULY. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JULY:

TOTAL CONTACTS for 3 days, total 5162 contracts: 25.810 million oz OR 8.6MILLION OZ PER DAY. (1720 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 8.6 MILLION OZ

.

LAST 11 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 8.6 MILLION OZ

RESULT: WE HAD A SMALL SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 294 DESPITE OUR $0.55 LOSS IN SILVER PRICING AT THE COMEX// TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE CONTRACTS: 2402 CONTRACTS ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A HUGE INITIAL SILVER OZ STANDING FOR JUNE. OF 15.22 MILLION OZ FOLLOWED BY TODAY’S QUEUE JUMP OF 105,000 OZ // .. WE HAD A VERY STRONG SIZED GAIN OF 2757 OI CONTRACTS ON THE TWO EXCHANGES FOR 13.785 MILLION OZ DESPITE THE STRONG LOSS IN PRICE..

WE HAD 621 NOTICES FILED TODAY FOR 3,109,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A GOOD SIZED 3546 CONTRACTS TO 498,210 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: —765 CONTRACTS.

.

THE GOOD SIZED INCREASE IN COMEX OI CAME DESPITE OUR FALL IN PRICE OF $36.55//COMEX GOLD TRADING/TUESDAY / WE MUST HAVE HAD SOME SPECULATOR SHORT COVERING ACCOMPANYING OUR GOOD SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION //AND SOME SPECULATOR SHORT COVERING

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR JULY AT 2.914 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 10,100 OZ

YET ALL OF..THIS HAPPENED DESPITE OUR LOSS IN PRICE OF $36.55 WITH RESPECT TO MONDAY’S TRADING

WE HAD A STRONG SIZED GAIN OF 12,806 OI CONTRACTS 42.211 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 9260 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 498,210

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 12,806, WITH 3546 CONTRACTS INCREASED AT THE COMEX AND 9260 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 12,806 CONTRACTS OR 39.83TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (9260) ACCOMPANYING THE GOOD SIZED GAIN IN COMEX OI (3546,): TOTAL GAIN IN THE TWO EXCHANGES 12,806 CONTRACTS. WE NO DOUBT HAD 1) SOME SPECULATOR SHORT COVERING AND SOME ADDITION TO SPECULATOR SHORTS ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR JULY. AT 2.914 TONNES FOLLOWED BY TODAY’S 1300 OZ QUEUE JUMP 3) ZERO LONG LIQUIDATION//SOME SPECULATOR SHORT COVERING//SOME SPECULATOR SHORT ADDITIONS //.,4) GOOD SIZED COMEX OPEN INTEREST GAIN 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

JULY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JULY :

21381 CONTRACTS OR 2,138,100 OZ OR 65.50 TONNES 3 TRADING DAY(S) AND THUS AVERAGING: 7127 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 3 TRADING DAY(S) IN TONNES: 65.50 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 65.50/3550 x 100% TONNES 1.84% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 2238.13 TONNES FINAL

JULY: 65.50 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF JUNE HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JULY, FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A SMALL SIZED 294 CONTRACT OI TO 140,463 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 2402 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 2402 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE:2402 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 294 CONTRACTS AND ADD TO THE 2402 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A GIGANTIC SIZED GAIN OF 2696 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 13.480 MILLION OZ

OCCURRED DESPITE OUR FALL IN PRICE OF $0.55 .

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING// TUESDAY NIGHT

XXX

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A GOOD SIZED 3546 CONTRACTS TO 498,210 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS GOOD COMEX INCREASE OCCURRED DESPITE OUR LOSS OF $36.55 IN GOLD PRICING TUESDAY’S COMEX TRADING. WE ALSO HAD A VERY STRONG SIZED EFP (9260 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO SHORT BIG TIME AND THEY ADDED TO THEIR SHORT POSITIONS

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF JULY.. THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 9260 EFP CONTRACTS WERE ISSUED: ;: , . 0 AUG :9260 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 9260 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A HUGE SIZED TOTAL OF 12,806 CONTRACTS IN THAT 9260 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A GOOD SIZED COMEX OI GAIN OF 3546 CONTRACTS..AND THIS STRONG GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR FALL IN PRICE OF GOLD $36.55.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING JULY (3.3748),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 3.3748 TONNES

THE BANKERS WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $36.55) BUT WERE UNSUCCESSFUL IN KNOCKING OFF SPECULATOR LONGS/COMMERCIAL LONGS BUT SPECULATOR SHORTS CONTINUED TO ADD TO THEIR POSITIONS//// WE HAVE REGISTERED A STRONG SIZED GAIN OF 39.83 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR JULY (3.3748 TONNES)…

WE HAD -765 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 13,571 CONTRACTS OR 1,357,100 OZ OR 42,211 TONNES

Estimated gold volume 308,003/// VERY GOOD/RAID/

final gold volumes/yesterday 369,301 /STRONG/RAID

INITIAL STANDINGS FOR JULY ’22 COMEX GOLD //JULY 6

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 797,322 oz Int. Delaware 22 kilobars |

| Deposit to the Dealer Inventory in oz | nil OZ |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 36 notice(s) 3600 OZ 0.1119 TONNES |

| No of oz to be served (notices) | 72 contracts 7200 oz 0..2239 TONNES |

| Total monthly oz gold served (contracts) so far this month | 1013 notices101,300 OZ 3.1508 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

| Gold | Ounces |

total dealer deposit 0

No dealer withdrawals

0 customer deposits

total deposits: nil oz

1 customer withdrawals:

i) Int. Delaware: 707.322 oz (22 kilobars)

total withdrawal: 707.322 oz

ADJUSTMENTS:3 all dealer to customer

Brinks 38,015.350 oz

JPMorgan 20,249.810 oz

Manfra: 27,498.765 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JULY.

For the front month of JULY we have an oi of 108 contracts losing 138 contracts . We had

209 notices filed on Tuesday so we gained 101 contracts or an additional 10,100 oz will stand in this non active

delivery month of July.

August has a LOSS OF 5761 contracts down to 381,936 contracts

Sept. gained 891 contracts to 1003.

We had 621 notice(s) filed today for 3,109,000 oz FOR THE July 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 36 contract(s) of which 33 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JULY /2022. contract month,

we take the total number of notices filed so far for the month (1013) x 100 oz , to which we add the difference between the open interest for the front month of (JULY 108 CONTRACTS ) minus the number of notices served upon today 36 x 100 oz per contract equals 103,400 OZ OR 3.3748 TONNES the number of TONNES standing in this active month of July.

thus the INITIAL standings for gold for the JULY contract month:

No of notices filed so far (1013) x 100 oz+ (108) OI for the front month minus the number of notices served upon today (36} x 100 oz} which equals 103,400 oz standing OR 3.3748 TONNES in this active delivery month of JULY.

TOTAL COMEX GOLD STANDING: 3.3748 TONNES (A FAIR STANDING FOR A JULY ( NON ACTIVE) DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,419,784.828 oz 75.26 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 32,987.557.415 OZ

TOTAL ELIGIBLE GOLD: 16,123,043.630 OZ

TOTAL OF ALL REGISTERED GOLD: 16,864,513.815 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 14,444,729.0 OZ (REG GOLD- PLEDGED GOLD)

END

SILVER/COMEX/JULY 6

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 766,272.150 oz Brinks CNT Manfra |

| Deposits to the Dealer Inventory | 589,976.7OZ JPMorgan |

| Deposits to the Customer Inventory | nil oz |

| No of oz served today (contracts) | 621CONTRACT(S) 3,105,000 OZ) |

| No of oz to be served (notices) | 369 contracts (1,845,000 oz) |

| Total monthly oz silver served (contracts) | 2513 contracts 12,565,000 oz |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

i) 0 dealer deposit

total dealer deposits: 0 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: x oz

We have 1 deposit into the customer account

i) Into JPMorgan: 589,976.700 oz

total deposit: 589,976.700 oz

JPMorgan has a total silver weight: 172.918 million oz/337.108 million =51.29% of comex

Comex withdrawals: 3

i) Out of Brinks: 614,277.050 oz

ii) out of Int. Delaware 76,995.380 oz

iii) Out of CNT 74,999.720 oz

total withdrawal 766,272.150 oz

adjustments: 1//dealer to customer

JPMorgan: 599,008.500 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 68.732 MILLION OZ

TOTAL REG + ELIG. 337.108 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR JUNE

silver open interest data:

FRONT MONTH OF JULY OI: 990 CONTRACTS HAVING LOST 233. WE HAD 254 NOTICES FILED

ON TUESDAY, SO WE GAINED 21 CONTRACTS OR AN ADDITIONAL 105,000 OZ WILL STAND FOR METAL AT THE COMEX.

AUGUST LOST 65 CONTRACTS TO STAND AT 1463

SEPTEMBER HAD A GAIN OF 21 CONTRACTS UP TO 117,527 CONTRACTS.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 621 for 3,109,000 oz

Comex volumes:64,957// est. volume today// fair

Comex volume: confirmed yesterday: 89,072 contracts ( GOOD )

To calculate the number of silver ounces that will stand for delivery in JULY we take the total number of notices filed for the month so far at 2513 x 5,000 oz = 12,565,000 oz

to which we add the difference between the open interest for the front month of JULY(990) and the number of notices served upon today 621 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JULY./2022 contract month: 2513 (notices served so far) x 5000 oz + OI for front month of JULY (990) – number of notices served upon today (621) x 5000 oz of silver standing for the JULY contract month equates 14,415,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

JULY 6/WITH GOLD DOWN $26.70: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REST AT 1041.90 TONNES

JULY 5/WITH GOLD DOWN $36.55//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 8.41 TONNES FROM THE GLD///INVENTORY RESTS AT 1041.90 TONNES

JULY 1/WITH GOLD DOWN $5.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.32 TONNES//INVENTORY RESTS AT 1050.31 TONNES

JUNE 30/WITH GOLD DOWN $9.20: big CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 1052.63 TONNES//

JUNE 28/WITH GOLD DOWN $3.05//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.64 TONNES FROM THE GLD///INVENTORY RESTS AT 1056.40 TONNES

JUNE 27/WITH GOLD DOWN $4.90 CENTS TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD///INVENTORY RESTS AT 1061.04 TONNES

JUNE 24/WITH GOLD UP 45 CENTS TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 8.70 TONNES FROM THE GLD//INVENTORY RESTS AT 1063.07 TONNES

JUNE 23/WITH GOLD DOWN $8.60:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD//INVENTORY RESTS AT 1071.77 TONNES

JUNE 22/WITH GOLD UP 15 CENTS:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 1073.80 TONNES

JUNE 21/WITH GOLD DOWN $2.00: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1075.54 TONES

JUNE 17/WITH GOLD DOWN $11.25: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.60 TONNES INTO THE GLD.///INVENTORY RESTS AT 1075.54 TONNES

JUNE 16/WITH GOLD UP $28.95: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1063.74 TONNES

JUNE 15/WITH GOLD UP $6.50/BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.65 TONNES FROM THE GLD////INVENTORY RESTS AT 1063.74 TONNES

JUNE 14/WITH GOLD DOWN $18.80/NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1065.39 TONNES

JUNE 13/WITH GOLD DOWN $41.55: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1065.39 TONNES

JUNE 10/WITH GOLD UP $21.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1065.39 TONNES

JUNE 9/WITH GOLD DOWN $3.50: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.32 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 1065.39 TONNES

JUNE 8/WITH GOLD UP $4.75: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1063.07 TONNES

JUNE 7/WITH GOLD UP $7.45: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1063.07 TONNES

JUNE 6/WITH GOLD DOWN $5.85: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1066.04 TONNES

JUNE 3/WITH GOLD DOWN $19.75//A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FROM THE GLD//INVENTORY RESTS AT 1066.04 TONNES

JUNE 2/WITH GOLD UP $22.50: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.64 TONNES FROM THE GLD//INVENTORY RESTS AT 1067.20 TONNES

JUNE 1/WITH GOLD UP $1$ HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD///INVENTORY RESTS AT 1068.36 TONNES

GLD INVENTORY: 1032.31 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JULY 6/WITH SILVER UP ONE CENT: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 12.558 MILLION OZ FORM THE SLV///INVENTORY RESTS AT 528.151 MILLION OZ

JULY 5/WITH SILVER DOWN 55 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 540.709MILLION OZ//

JULY 1/WITH SILVER DOWN 61 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 553,000 OZ//INVENTORY RESTS AT 540.709 MILLION OZ//

JUNE 30/WITH SILVER DOWN 41 CENTS : SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 738,000 OZ FROM THE SLV//INVENTORY RESTS AT 541.262 MILLION OZ//

JUNE 28/WITH SILVER DOWN 26 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.00 MILLION OZ..

JUNE 27/WITH SILVER DOWN 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.000 MILLION OZ

JUNE 24/WITH SILVER UP 10 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.137 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 542.000 MILLION OZ

JUNE 23/WITH SILVER DOWN 41 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SL: A WITHDRAWAL OF 2.029 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 545.137 MILLION OZ//

JUNE 22/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 547.166 MILLION OZ.

JUNE 21/WITH SILVER UP 9 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.506 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 547.166 MILLION OZ//

JUNE 17/WITH SILVER DOWN 15 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWAL OF 739,000 OZ FROM THE SLV./:INVENTORY RESTS AT 543.660 MILLION OZ/

JUNE 16/WITH SILVER UP 46 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ

JUNE 15/WITH SILVER UP 44 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ

JUNE 14/WITH SILVER DOWN 32 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ//

JUNE 13/WITH SILVER DOWN 62 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ//

JUNE 10.WITH SILVER UP 13 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 830,000 Z FROM THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ//

JUNE 9/WITH SILVER DOWN 27 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 923,000 OZ INTO THE SLV////INVENTORY RESTS AT 545.229 MILLION OZ

JUNE 8/WITH SILVER DOWN 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 544.306 MILLION OZ//

JUNE 7/WITH SILVER UP 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.306 MILLION OZ/

JUNE 6/WITH SILVER UP 20 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 6.459 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 547.167 MILLION OZ//

JUNE 3/WITH SILVER DOWN $.34: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITTHDRAWAL OF 246,000 OZ FORM THE SLV//INVENTORY RESTS AT 553.626 MILLION OZ..

JUNE 2/WITH SILVER UP 57 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.261 MILLION OZ FORM THE SLV.//INVENTORY RESTS T 553.872 MILLION OZ

JUNE 1/WITH SILVER UP 19 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV//: A WITHDRAWAL OF 2.538 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 556.133 MILLION OZ//

CLOSING INVENTORY 528.151 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

END

3. Chris Powell of GATA provides to us very important physical commentaries

Craig Hemke at Sprott Money: Looking ahead 90 days for gold and silver

Submitted by admin on Tue, 2022-07-05 22:36Section: Daily Dispatches

By Craig Hemke

Sprott Money, Toronto

Tuesday, July 5, 2022

As Q3 begins, the narrative of higher U.S. interest rates and a soaring dollar continues. But what will the narrative be by the end of Q3?

Answer that question and you’ll know where Comex precious metals prices are headed.

This year has certainly not been much fun for us precious metals enthusiasts. However, as the year began, we all knew that the Federal Reserve was embarking on a schedule of higher interest rates and lessening quantitative easing, so really none of the price action thus far should come as a surprise.

In fact, it has played out pretty closely to what we wrote in our annual forecast back in January. …

… For the remainder of the analysis:

https://www.sprottmoney.com/blog/Looking-Forward-90-Days-Craig-Hemke-July-05-2022

END

Prices don’t drop when inflation eases

Submitted by admin on Tue, 2022-07-05 22:47Section: Daily Dispatches

By Medora Lee

USA Today, McLean, Virginia

via Yahoo News, Sunnyvale, California

Tuesday, July 5, 2022

When it comes to prices during inflation what goes up doesn’t always come down.

When talking about inflation, it’s important to remember that inflation is a rate that measures how fast prices are rising. If the consumer inflation rate drops from its 40-year high of 8.6% in May, prices are still rising — just not as fast.

Consumers won’t feel immediate relief even as the inflation rate slows because many of those elevated prices are likely here to stay, said Michael Ashton, managing principal at Enduring Investments in Morristown, New Jersey.

“The price level has permanently changed,” Ashton said. “Until your wages catch up, it will continue to hurt.”

And wages have a long way to climb to catch up.

In May inflation-adjusted average hourly earnings decreased a seasonally adjusted 3% from a year ago. When combined with a decrease in weekly hours worked, that resulted in a 3.9% decrease in real wages, the Bureau of Labor Statistics says. …

… For the remainder of the report:

https://www.yahoo.com/finance/news/prices-dont-drop-inflation-eases-090014063.html

4. OTHER GOLD COMMENTARIES/COAL

Coal Emerges Victorious As Sanctions And Green Policies Backfire Spectacularly

WEDNESDAY, JUL 06, 2022 – 06:45 AM

When historians look back on this chaotic and turbulent period, they will find that few individuals inflicted as much damage on the environment and promoted the interests of the “dirty fossil fuel” lobby as Greta Tunberg, who by shaming and forcing “serious” politicians to pivot toward green energy at a time when there was nowhere near enough green capacity to replace existing sources of energy, sparked what may be the most spectacular self-own in history. And today, the WSJ, Bloomberg and Reuters all wrote about it.

We start with the WSJ which concedes what was obvious to most long ago (see “Will ESG Trigger Energy Hyperinflation” from last June), namely that “an energy-starved world is turning to coal as natural-gas and oil shortages exacerbated by Russia’s war against Ukraine lead countries back to the dirtiest fossil fuel.”

Yes, contrary to the intentions of Green fanatics everywhere, their push to accelerate away from “dirty” fossil fuel has not only backfired spectacularly, but also exposed the hypocrisy and empty promises of so many virtue-signalers, as “from the U.S. to Europe to China, many of the world’s largest economies are increasing short-term coal purchases to ensure sufficient supplies of electricity, despite prior pledges by many countries to reduce their coal consumption to combat climate change.”

Adding insult to injury, the global competition for coal which is now also in short supply after years of declining investment in new mines and resources, has driven benchmark prices to new records this year. Spot coal prices at Australia’s Newcastle port, a key supplier to Asia, topped $400 a ton for the first time last month.

Hilariously, the push for coal is being led by Europe, ground zero of the “green movement” which finally realized that one can’t burn fake virtue or melt posing in front of camera in the winter to keep warm, and is boosting coal purchases to ensure it can keep power flowing to homes and factories after Russia cut gas supplies to the continent. Germany, which not long ago promised to eliminate coal as a power source by 2030, is among the nations now importing more. Economy Minister Robert Habeck called the increased reliance on coal bitter but necessary. Spoiler alert: Germany will not eliminate coal as a power source by 2030, if anything it will be more reliant on it than ever unless it also restarts its nuclear power plants which it, idiotically, shut down not long ago.

Never one to admit it was dead wrong, however, Europe has a response to everything: “Right now the sentiment is that more coal is better than more Russia,” said Alex Msimang, a London-based partner at law firm Vinson & Elkins LLP specializing in the energy sector.

Whatever dude.

Propaganda bullshit aside, coal is enjoying a renaissance the likes of which it has not seen since the industrial revolution. In addition to soaring coal power use in the US (after the sector was left nearly for dead under Obama), China, the world’s biggest coal consumer, is expanding production of the fuel and its use in power generation, spooked by shortages last year that caused electricity cuts and outages throughout the country, energy experts say.

India is also leaning hard on coal as energy demand increases. The nation’s coal-power generation hit a record in April, said Rahul Tongia, a senior fellow at New Delhi-based think tank the Centre for Social and Economic Progress.

Domestic coal production in China and India helped drive a 10% increase in global investment in 2021, the International Energy Agency reported last month. The IEA projects another 10% increase this year as China and India try to stave off shortages.

Coal miners such as Anglo-Swiss giant Glencore are cashing in. Glencore, one of the last major miners still big in coal, said last month that it now expected $3.2 billion in trading profit in the first half of this year, compared with $3.7 billion for all of 2021.

“We expect elevated coal prices to make Glencore one of the leading shareholder-return companies in the market,” Deutsche Bank AG analysts wrote. The company’s already wealthy shareholders can thank idiots like Greta for becoming even richer.

The best part: the global green lobby is about to be silenced forever.

The resurgence of coal, which emits around double the carbon dioxide as burning natural gas, further threatens to set back international efforts to keep global temperatures under 2 degrees Celsius from preindustrial levels, and preferably close to 1.5 degrees, by the end of the century.

That is the goal that more than 190 nations agreed to pursue under the 2015 Paris Agreement to avoid the most dangerous potential consequences of global warming. The United Nations Intergovernmental Panel on Climate Change says that emissions, which continue to rise, would need to be drastically reduced by the end of the decade to meet the goal.

Then again, with the west especially skilled at deluding itself, who’s to say the lies won’t continue. Indeed, as the WSJ notes, climate activists and forecasters say they are concerned about a rise in coal use, but see it as a short-term phenomenon in the West and are more worried that the Ukraine war and other geopolitical events are spurring new natural-gas investments that could operate for decades.

“It can be justified but not for long,” said Bill Hare, chief executive of the Berlin-based group Climate Analytics, of the coal surge.

Oh ok, we are confident that Putin will end his military campaign in Ukraine just to keep a bunch of Scandianvian teenagers happy so they can continue spouting nonsense into masked microphones.

Joking aside, what Putin will do is continue selling Russian coal to Europe – yes, the same Europe that pretends to have imposed sanctions on Moscow – because as Reuters writes, “much of the focus on sanctions on Russia’s commodity exports is on crude oil and natural gas, but coal is perhaps the best example of the challenges facing those seeking to punish Moscow for its invasion of Ukraine.”

Russia is the world’s fourth-largest coal exporter behind Australia, Indonesia and South Africa, and has the ability to supply both the Atlantic and Pacific basins.

And yes, while Europe – the main buyer of Russian coal – has proposed a ban on imports it has yet to be even partially implemented, while Japan also plans to end purchases from Russia. Likewise, South Korea has yet to formally sanction imports of Russian energy but is said to be planning for an end to the trade, while China and India, the world’s two biggest coal importers, have no sanctions on Russia and are stepping up imports in order to benefit from steep price discounts, similar to what is taking place in the oil market.

And also similar to oil, where Russian exports have increased since before the war…

… an analysis of Russia’s seaborne exports of coal since the invasion of Ukraine show that it has not only managed to maintain volumes but has actually increased them: while there has been some switching of buyers, the loss of some markets in Europe and Japan has been more than offset by increased buying, especially by India and Turkey.

According to data from Kpler, Russia exported 16.45 million tonnes of coal by sea in June, virtually unchanged from May’s 16.56 million. This level of seaborne exports is an acceleration from the same months in 2021, with June shipments up 3.5% and May up 3.8%. It is also a sharp increase on the three months up to the Feb. 24 attack on Ukraine, when Russia’s seaborne coal exports were 13.43 million tonnes in December, 12.28 million in January and 13.08 million in February.

That said, while Europe has been spouting mostly hot air, Europe’s top buyers of Russian seaborne coal – Germany, the Netherlands and Italy – have started to cut back, with June arrivals at a combined 1.47 million tonnes, down from 2.59 million in May. Yet all that Europe is doing is buying coal from resellers of Russian coal, effectively paying more from the same product. One beneficiary is Turkey. The country which has been supplying Ukraine with military drones, has also ramped up imports of Russian coal, with June arrivals at 1.81 million tonnes, which is the most in any month in Kpler’s records going back to 2017.

Turkey’s imports from Russia were 1.06 million tonnes in May and they have risen every month since February. Much of the excess coal is then resold to Europe at a steep mark up.

Overall, what the coal data shows is that Russia has been able to maintain export volumes, even if it has done so by offering discounts. It also shows that it is difficult to both ramp up imports significantly, even if you want to, with both India and China likely to have hit constraints on securing vessels to buy more Russian coal.

And speaking of supply side constraints, we next go to Blooomberg which writes that the hunt by Europe’s coal consumers to replace Russian cargoes with shipments from across the globe has boosted imports to a key hub by more than a third, helping to fill severely depleted stockpiles.

Coal poured into the Antwerp-Rotterdam-Amsterdam region — a huge transport hub for energy and commodities — in the first half of this year, with imports surging 35% to 26.9 million tons compared with the same period last year, according to Kpler. That has helped ARA coal inventories double to almost 6.6 million tons from more than a five-year low in the first quarter. Stockpiles are now close to record levels seen in 2019, according to Kpler. On the downside, the flood of imports is contributing to major congestion at the ports.

Shipments are soaring as the region scrambles to replace missing Russian product amid fears of continued declines in Russian nat gas exports – and a freezing winter- said Matthew Boyle, lead analyst for dry bulks, gas and LNG at Kpler Insight. Helping to fill the gap is more coal from the US, Colombia and Australia — countries that tend to produce better-quality or so-called high-calorific value material that releases more heat and energy when burned. Of course, the high quality product is also priced accordingly, and as shown in the chart above, Australian coal just hit a record high price, something which has led to Europe’s record 29.1% PPI.

Australian exporters including Sydney-based Whitehaven Coal have had supply requests from European nations, including Poland, and the firm previously offered 70,000 tons of coal in a government aid package sent to Ukraine. Soaring differentials between European and Australian prices have made it viable for traders to send cargoes from the Asia-Pacific region, even after taking into account the high shipping cost for the longer journey. Some low-quality Indonesian coal has also made its way into Europe, although Kpler said they were likely blended with US material with higher calorific value.

Meanwhile, in the latest slap on the face of environmentalists and petulant Scandinavian teenagers everywhere, the competition for a fuel many want to consign to history is escalating as power generators across Asia and Europe seek to secure additional shipments amid an energy crunch. Germany and Austria are reviving idled coal power plants in response to Russian gas supply curbs, while Japan and South Korea are stockpiling the fuel ahead of hotter summer weather.

And in the latest example of chaos theory butterflies and unintended side-effects, the heavy inflow of coal shipments is exacerbating gridlock at the ports.

“We are seeing very high congestion for the main European ports,” said Abhinav Gupta, a drybulk shipping analyst at Braemar. There were 71 drybulk ships waiting at anchor at the area off Antwerp, Rotterdam and Amsterdam as of June 29, triple the five-year average of 24 ships for this time of the year.

Current waiting time for coal vessels amounts to about 10 days, according to Kpler, who said low river levels on the Rhine also contributed to delays. It expects that will improve to about eight days by mid-July.

Coal terminals are currently at full storage capacity, and transporting large volumes of the fuel inland “has become a challenge over the past few weeks,” the Rotterdam port said. The situation has been complicated by a shortage of barges, it said, as many vessels are tied up with Ukrainian iron ore and grain exports.

In short: total chaos, courtesy of years of catastrophic policies at the behest of the green lobby.

As for the discredited ideologue Greta, fear not: she still has a podium where more than 5 million followers lap up each of her carefully scripted and produced tweets:

It almost makes one wonder: just how much is Putin paying her? Either that, or as Adam Taggart put it…

END

.

5.OTHER COMMODITIES:

END

COMMODITIES IN GENERAL/

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings WEDNESDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 6.7089

OFFSHORE YUAN: 6.7172

HANG SANG CLOSED DOWN AT 266.41 PTS OR 1.22%

2. Nikkei closed DOWN 315.82 OR 1.20%

3. Europe stocks CLOSED ALL GREEN

USA dollar INDEX UP TO 106.80/Euro FALLS TO 1.0190

3b Japan 10 YR bond yield: RISES TO. +.242/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 135.26/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: UP -// OFF- SHORE DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +1.271%/Italian 10 Yr bond yield RISES to 3.35% /SPAIN 10 YR BOND YIELD RISES TO 2.38%…

3i Greek 10 year bond yield FALLS TO 3.29//

3j Gold at $1762.30 silver at: 19.26 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 1 AND 1/4 roubles/dollar; ROUBLE AT 62.44

3m oil into the 100 dollar handle for WTI and 107 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 135.26DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning 0.9716– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.98983well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

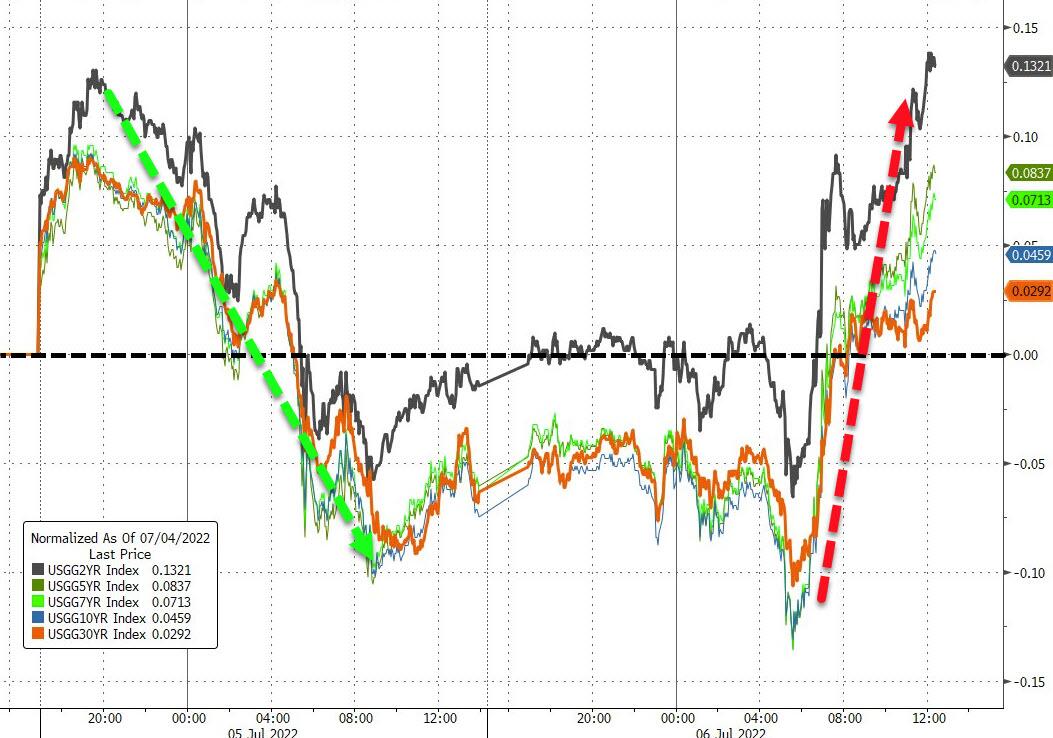

USA 10 YR BOND YIELD: 2.807 DOWN 1 BASIS PTS

USA 30 YR BOND YIELD: 3.051 UP 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 17.23

Futures Flat As Traders Brace For Latest FOMC Minutes

WEDNESDAY, JUL 06, 2022 – 07:55 AM

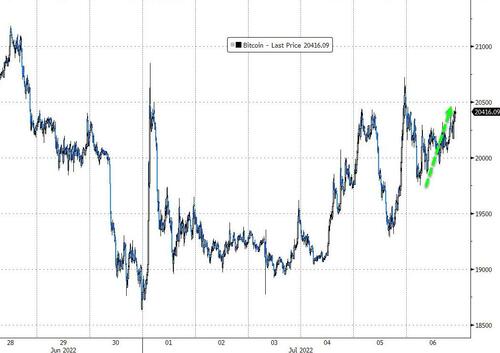

After yesterday’s remarkable U-turn in US stocks which tumbled at the open only to recover all losses by EOD (except the energy sector which suffered a furious rout), overnight futures traded subdued, fluctuating between gains and losses ahead of today’s FOMC minutes as traders debate whether the coming recession is good news (more stimulus from the Fed) or bad news (stagflationary, tying the Fed’s hands). S&P futures were down 0.1% last, having traded on both sides of the unchanged line for much of the past 12 hours while Europe’s Stoxx 600 was much more excited and climbed the most since June 24. The two- and 10-year US yield curve remained inverted as investors awaited the minutes of the Federal Reserve’s last meeting; the 10-year Treasury yield held steady around 2.81%. The dollar rose for a fourth day as the Euro tumbled while bitcoin traded at $20,000.

In China, Shanghai launched mass testing for Covid in nine districts after detecting cases the past two days, fueling concerns that the financial hub may once again find itself locked down in pursuit of Covid Zero. The Shanghai Composite Index slid the most since May 24.

In thin premarket trading, bank stocks were lower as investors await the release of the Federal Reserve’s meeting minutes. In corporate news, crypto broker Voyager Digital filed for Chapter 11 bankruptcy protection. Meanwhile, HSBC is in talks to sell its Russia unit to local lender Expobank, according to people familiar with the matter. Stocks related to cryptocurrencies fell in US premarket trading as Bitcoin fell amid mounting concerns of a global recession. Here are some of the most notable premarket movers:

- Kornit (KRNT US) shares plunged 23% in US premarket trading after the inkjet printer manufacturer issued disappointing preliminary second-quarter results. Stifel cut its recommendation to hold from buy.

- Chip and chip equipment stocks could be active on Wednesday after Bloomberg reported that the US is pushing the Netherlands to ban ASML from selling some chipmaking tools to China. Watch shares including Applied Materials (AMAT US), Lam Research (LRCX US) and KLA (KLAC US), as well as Nvidia (NVDA US), Qualcomm (QCOM US), Intel (INTC US), Advanced Micro Devices (AMD US)

- Stocks related to cryptocurrencies decline as Bitcoin drop amid mounting concerns of a global recession. Riot Blockchain (RIOT US) -4.2%, Coinbase (COIN US) -3.3%, Ebang (EBON US) -5.5%, Marathon Digital (MARA US) -1.8%, BitNile -5.2% (NILE US)

- Shopify (SHOP US) shares slide 0.9% as The Globe and Mail reports, citing people familiar, that the company is delaying a compensation overhaul that would give its employees flexibility on how their salary is paid in stock and cash.

- Cazoo (CZOO US) and Carvana (CVNA US) fall as Davy cuts earnings estimates and price targets for online auto stocks, citing inflation, higher interest rates and weakening consumer sentiment as threats to operational execution.

- RADA Electronic Industries (RADA US) sinks 11%, after the Israeli defense firm said that it’s withdrawing its full-year 2022 revenue guidance in light of its pending merger with Leonardo DRS.

- Watch cybersecurity companies like Palo Alto Networks (PANW US), CrowdStrike Holdings (CRWD US) and Okta (OKTA US) as Morgan Stanley analysts said they expect durable security spending environment in the second half of 2022 against an uncertain macro backdrop.

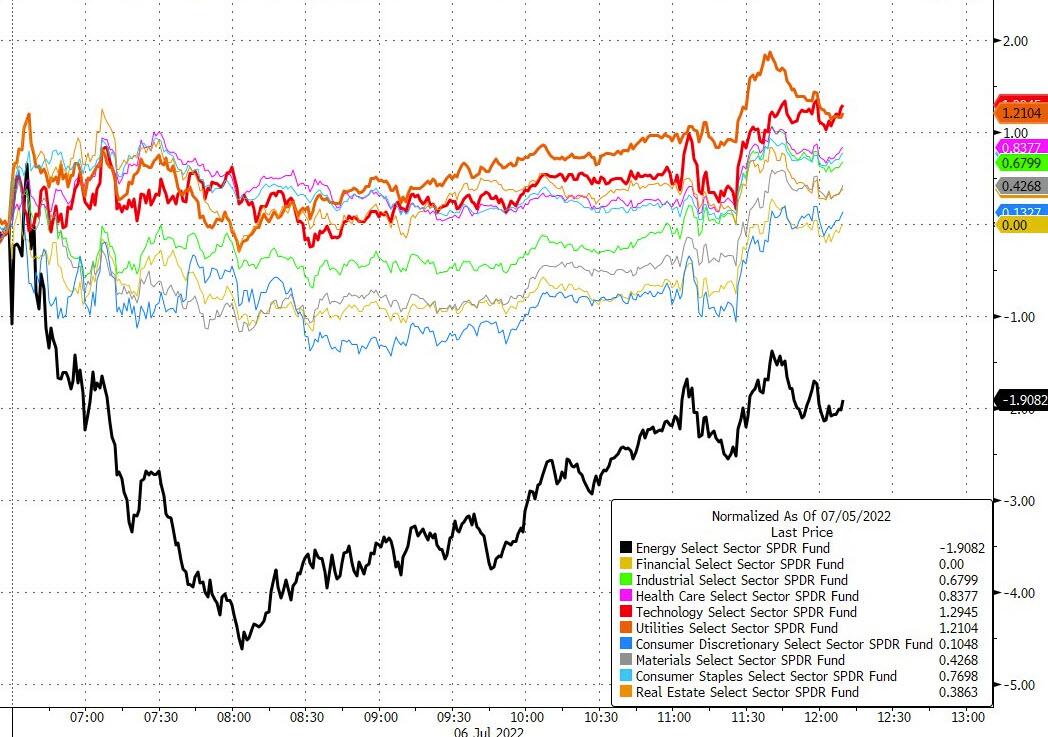

With energy names plunging on expectations of a recession, bargain hunters chased technology stocks boosting US equity indexes on Tuesday, helping mask a deepening slump in stocks linked to economic activity, such as energy, commodity and industrial names. A renewed spike in China’s Covid cases and a worsening gas crisis in Europe signaled that a worldwide slowdown is coming even as central banks tighten monetary policy to contain consumer prices.

“Markets are caught between two opposing forces and that’s the place we are going to be in for the next few months,” Diana Amoa, chief investment officer for long-biased strategies at Kirkoswald Asset Management, said on Bloomberg Television. “We go from trading lower growth to trading high inflation.”

Today’s 2 p.m. release of the June FOMC minutes will provide one of the session highlights.

European stocks gave back over half of their opening gains with the Euro Stoxx 50 up 1.25% as of 7:30 a.m. ET having added as much as 2.3% in early trade, clawing back roughly half of Tuesday’s sharp losses. CAC 40 and FTSE 100 outperform. Retail, tech and media names are the best performers among broad-based sectoral gains within the Stoxx 600. European semiconductor stocks bounced back on Wednesday, following heavy selling in the past three sessions spurred by concerns over cooling chip demand. ASML shares rise 3.2% as of 9:39am CET, halting a seven-day losing streak, despite news that the US is pushing the Netherlands to stop the chip tool maker from selling deep ultraviolet lithography systems to China. Banks remain the only European industry group in the red on Wednesday, with the Stoxx 600 Bank Index. Here are the most notable European movers:

- Just Eat Takeaway shares surge over 20% after the meal delivery firm struck a deal with Amazon for the e-commerce giant to take up to a 15% stake in its US unit Grubhub.

- Abrdn shares jump as much as 8.8% after the UK asset management firm said it will commence a return of £300m through the repurchase of its shares, with a first phase of up to £150m being undertaken by Goldman Sachs, according to a filing.

- Atos shares climb as much as 8.1% after a filing shows Bank of America holding a 7.77% stake in the French tech services company. Meanwhile, governance remains in focus amid a fresh news report of shareholder unrest.

- Airlines rise on Wednesday amid a rebound in the broader European market. Ryanair shares rally as much as 5.1%, EasyJet +4.2%, Wizz Air +4.5%.

- Shop Apotheke shares gain as much as 13% after jumping 12% yesterday when the online pharmacy reported preliminary 2Q results. Baader notes that e-scripts will be mandatory in all German states by January 2023, further pushing the company’s sales prospects in the country.

- Trainline stock surges as much as 24% as its new FY23 guidance implies a 27% upgrade to consensus, Morgan Stanley writes in note following trading update.

- Fresnillo stocks fall as much as 4.2%, while Endeavour rises as much as 4% after Credit Suisse starts coverage of the former with an underperform recommendation and initiates UK-listed shares of the latter at outperform.

- TotalEnergies and Engie fall in Paris, underperforming peers, as President Emmanuel Macron comes under increasing pressure to introduce a windfall tax on energy and transport giants to fund his bill aimed at protecting consumer purchasing power.

- Adidas shares fall as much as 5.4% after Hauck & Aufhaeuser double downgrades to sell from buy, also setting a Street low price target for the sports-apparel maker, whose FY22 targets are likely at risk due to a 2Q margin squeeze.

Earlier in the session, Asian stocks slipped as fears of a global economic recession and fresh Covid-19 outbreaks in China weighed on sentiment. The MSCI Asia Pacific Index fell as much as 1.3%, led by energy-related shares as oil traded below $100 per barrel, while investors snapped up defensive shares. Stocks in China declined as Shanghai ramped up mass testing in nine districts after detecting cases the past two days, fueling concerns that the financial hub may once again find itself locked down in pursuit of Covid Zero. The Shanghai Composite Index slid the most since May 24. Benchmarks in the tech-heavy markets of Taiwan and South Korea also dropped. In China, Shanghai launched mass testing for Covid

The fall in Asia shares came despite US stocks recouping most of their losses in a volatile session overnight. Traders are turning their attention to the minutes of the most-recent Federal Reserve meeting, which will be released later today, for a sense of policy makers’ debate about the near-term path for interest rates. Asian equities have been stuck in range-bound trading in recent months as investors weigh higher interest rates and the prospect of an economic downturn driven by elevated inflation. Still, narratives of peak inflation are building up as the Fed ramps up its policy-tightening campaign. It’s “much too early, in our view, to think that inflation trades are over,” Frank Benzimra, head of Asia equity strategy at Societe Generale, said in a Bloomberg TV interview. For emerging-market assets, “you also have some valuation buffer, some levels of yields which are becoming interesting. So this is where we are seeing that we may be close to the peak of pain.” Equity measures in the Philippines and New Zealand bucked the regional trend to each rise more than 1.6%.

Japanese stocks declined as oil tumbled and concerns of a global economic downturn damped sentiment. The Topix Index fell 1.2% to 1,855.97 at the market close in Tokyo, while the Nikkei 225 declined 1.2% to 26,107.65. Toyota Motor Corp. contributed the most to the Topix’s loss, decreasing 2.8%. Out of 2,170 shares in the index, 572 rose and 1,520 fell, while 78 were unchanged. “Japanese stocks are seen as representative of the global cyclical economy, so when concerns about recession appear, not only in the US but globally as well, stocks overall are likely to be sold off,” said Yasuhiko Hirakawa, head of an investment department at Rakuten Investment Management. Oil Steadies Above $100 After Plunging on Recession Concerns

Key equity gauges in India rallied as commodity prices eased while a recovery in monsoon rainfall buoyed sentiment. The S&P BSE Sensex Index rose 1.2% to 53,750.97 in Mumbai, while the NSE Nifty 50 Index advanced 1.1%. Hindustan Unilever was the biggest boost to the Sensex, increasing 4%. Out of 30 shares in the index, 25 rose and five fell. Seventeen of the 19 sectoral indexes compiled by BSE Ltd. gained, led by automobile and consumer goods companies. Asia’s biggest software exporter Tata Consultancy Services will kickoff the April-June earnings season for companies on Friday.

Australia’s S&P/ASX 200 index fell 0.5% to close at 6,594.50, as fears of a global economic recession as well as tumbling commodity prices hit market sentiment. The benchmark was dragged by a group of mining shares that fell to the lowest level since Nov. 2, and energy stocks that fell the most in over two years. In New Zealand, the S&P/NZX 50 index rose 1.6% to 11,141.07

Fixed income was comparatively quiet. Bunds and USTs bear-steepened as 2y Bunds outperformed. Treasuries are flat in early US trading Wednesday with front end underperforming, pushing 2s10s yield curve into deeper inversion. Yields are mostly lower led by 2-year, at 2.82%; the 10Y yield was trading just south of 2.80% last; 5- to 30-year yields hold increases of less than 2bp after touching lowest levels since late May on Tuesday amid a slump in commodity prices led by oil. 2s10s curve inverted as much as 3.6bp; maximum inversion this year was 9.5bp on April 4, reached as futures markets began to price in bigger Fed rate increases in response to persistently high inflation readings, pushing 2- year yields higher. Latest inversion, by contrast, occurred as 10- year yield declined more than 2-year, with expectations for Fed rate path in broad decline on economic-slowdown concerns. UK Gilts bear-flattened, erasing an initial decline after comments from BOE’s Pill. Peripheral spreads are marginally wider to Germany.

In FX, Bloomberg dollar spot index rises 0.2%. JPY is the strongest in G-10, trading near 135.30/USD. EUR sits at the bottom of the scoreboard with EUR/USD trading through Tuesday’s lows.

In commodities, crude futures drift off Asia’s best levels. WTI slips below $100, Brent trades on a $104 handle, with Goldman Sachs arguing that a plunge driven by fears a recession will hurt demand was overdone. Today’s gains were small compared to Brent’s decline of more than $10 on Tuesday, its third largest ever in dollar terms. Investors have been pricing in the consequences of a slowdown even as physical crude markets continue to show signs of vigor and the war in Ukraine drags on. Copper dropped as fears of a global economic slowdown piled pressure on industrial metals.. Spot gold holds a narrow range near $1,765/oz. Base metals are mixed; LME tin falls 1.5% while LME lead gains 1.7%.

Looking to the day ahead now, today’s 2 p.m. release of the June FOMC minutes will provide one of the session highlights. Prior to that, economic data will include the weekly MBA Mortgage Applications release at 7 a.m., the final June Services PMI data at 9:45 a.m. and June’s ISM Services Index and the May JOLTS Job Openings at 10 a.m. Elsewhere on the central bank front, the Riksbank’s Cecilia Skingsley and BOE’s Jon Cunliffe will speak on central bank digital currencies. Fed’s John Williams is scheduled to deliver comments at a virtual event on banking culture at 9 a.m. Otherwise from central banks, we’ll get the minutes from the June FOMC meeting, and also hear from the Fed’s Williams, the ECB’s Rehn and the BoE’s Cunliffe and Pill.

Market Snapshot

- S&P 500 futures down 0.2% to 3,825.75

- MXAP down 0.8% to 156.29

- MXAPJ down 0.9% to 516.65

- Nikkei down 1.2% to 26,107.65

- Topix down 1.2% to 1,855.97

- Hang Seng Index down 1.2% to 21,586.66

- Shanghai Composite down 1.4% to 3,355.35

- Sensex up 0.8% to 53,570.29

- Australia S&P/ASX 200 down 0.5% to 6,594.48

- Kospi down 2.1% to 2,292.01

- STOXX Europe 600 up 1.4% to 406.26

- German 10Y yield little changed at 1.24%

- Euro little changed at $1.0259

- Brent Futures up 1.3% to $104.15/bbl

- Gold spot up 0.2% to $1,769.16

- U.S. Dollar Index little changed at 106.46

Top Overnight News from Bloomberg

- With the European economy lurching toward a recession, traders are growing more convinced that the euro breaking parity with the dollar is imminent

- “If the fragmentation in bond markets is unwarranted then we should be as unlimited as possible,” European Central Bank Governing Council member Pierre Wunsch tells the Financial Times. “The case to act is strong when faced with unwarranted fragmentation”

- German factory orders unexpectedly rose in May, even as global momentum was affected by rampant inflation and uncertainty stoked by Russia’s war in Ukraine. Demand increased 0.1% compared to the previous month, compared to an economist estimate of -0.5%

- Britain’s new Chancellor of the Exchequer, Nadhim Zahawi, signaled he wants to cut taxes faster than his predecessor Rishi Sunak, as he set out plans to boost the UK’s struggling economy

- British Prime Minister Boris Johnson is on red alert for signs of a coordinated plot from his ministers to bring him down, according to a senior government official

- China’s central bank looks set to withdraw cash from its financial system in a sign that it’s moving toward normalizing monetary policy as major global peers are forcefully raising interest rates

- A combination of the recent bond rebound and the spiraling cost to hedge the volatile yen has wiped out the yield premium a Japanese investor once enjoyed from US debt. The yen-hedged yield on 10-year Treasuries collapsed to 0.24% Tuesday from almost 1.7% in April, just above the 0.22% yield on comparable Japanese debt

- Emerging-market currencies are tumbling as the twin threats of rising US interest rates and a global recession send traders scurrying to the safety of the dollar. The MSCI Emerging Markets Currency Index dropped for a second day, extending this year’s slide to 4.4%, heading for the steepest annual drop since 2015

A more detailed look at global markets courtesy of Newsquawk

Asia-Pacific stocks were mostly negative with risk appetite sapped by headwinds from the global growth concerns and US recession fears. ASX 200 was marginally lower with energy leading the descent in the commodity-related sectors, although the downside in the index was stemmed by tech strength following the duration-sensitive bias stateside and lower yield environment. Nikkei 225 weakened alongside a firmer currency and with Japan said to delay the call on the start of the nationwide travel support.Hang Seng and Shanghai Comp. conformed to the downbeat mood after the PBoC continued to drain liquidity and with reports noting that US President Biden could lift tariffs on just USD 10bln of Chinese goods, while the US was also said to pressure ASML to stop selling key chipmaking equipment to China. In addition, COVID-19 concerns persisted after China’s Xi’an city entered a 7-day period of ‘temporary control measures’ and with Macau officials locking down the Grand Lisboa hotel and casino due to a cluster of infections.

Top Asian News

- PBoC injected CNY 3bln via 7-day reverse repos with the rate at 2.10% for a CNY 97bln net drain.

- Shanghai suspended the operation of KTV venues due to COVID-19 but other entertainment venues can remain open, while the gradual reopening of cinemas and concert venues will go ahead from July 8th, according to Reuters.

- US top diplomat for East Asia Kritenbrink said the top priority for US Secretary of State Blinken’s meeting with Chinese Foreign Minister Wang is to underscore US commitment to diplomacy and maintaining open lines of communication, while he expects Blinken to raise human rights in the meeting with China’s Foreign Minister, according to Reuters.

- Two US senators called for the FTC to investigate TikTok after the disclosure about Chinese access to US data, according to Reuters.

- Chinese Capital Beijing will resume direct international flights in an orderly way, via Reuters.

- ‘Bad for EM’: Why Funds Are Furiously Selling Risky Currencies

- SenseTime Plunge Raises Stakes for Slew of China Lockups Lifts

- Goldman Sachs Sees Kotak Mahindra Bank to Double Market Value

- Singapore’s Price for Right to Buy a Car Hits All- Time High

European bourses are firmer across the board, Euro Stoxx 50 +1.3%, continuing to take impetus from the NDX-led rebound in US hours on Tuesday and shrugging off negative APAC trade. Stateside, futures are mixed/flat at present, but like their European peers have been choppy in overnight ranges awaiting US data and Fed speak; ES -0.1%. Back to Europe, sectors exhibit a pro-cyclical bias that features Tech as the clear outperformer. China’s CPCA says prelim figures show China sold 1.926mln cars in June, +22% Y/Y. Prelim. figures indicate Tesla (TSLA) sold 78k (prev. 32.1k MM) China-made vehicles in June, via Reuters.

Top European News

- Latest British Political Drama Proves ‘Sideshow’ for Investors

- French Rail Strike Adds to European Summer Travel Havoc

- Russia Slams Macron for Breaching Diplomatic Confidentiality

- Bulgaria’s Gerb Holds Narrow Lead Over Ruling PP Party: Poll

- BOE Chief Economist Says Fighting UK Inflation Is Priority

- Italy Five Star Party is leaning on keeping support for PM Draghi, according to ANSA.

Central Banks

- ECB’s Wunsch said If the fragmentation in bond markets is unwarranted then we should be as unlimited as possible, via the FT.

- BoE’s Cunliffe said we will act to ensure the inflation shock does not become imbedded.

- BoE’s Pill says the (BoE) statement re. acting forcefully if necessary reflects both my willingness to adopt a faster pace of tightening than implemented thus far in this tightening cycle & emphasis conditionality on data; Pill will be data-dependant. Much remains to be resolved before we vote on our August policy decision. Adds, that there is a case of steady-handed approach; one-off bold moves can be disturbing to markets.

FX

- Dollar dips, but retains firm underlying bid ahead of FOMC minutes, Fed’s Williams and services ISM, DXY holds around 106.500 within 106.760-340 range.

- Yen outperforms on technical grounds and with JPY crosses maintaining downward momentum; USD/JPY closer to 135.00 than 136.00, but faces stiff support if breached via recent lows .

- Euro remains pressured after largely weak Eurozone construction PMIs and no real compensation from mixed retail sales data, EUR/USD slips to new 20 year low nearer 1.0200.

- Pound precarious as more UK Tory Party MPs quit to pile pressure on PM Johnson, Cable back under 1.1950 after brief rebound from low 1.1900 area.

- Yuan bucks downbeat mood in EM currencies even though China suffers more outbreaks of Covid-19 as it adopts regional safe haven status; USD/CNH and USD/CNY straddle 6.7100.

- Lira lurches again and Forint falls to fresh all time low; USD/TRY tops 17.2550 and EUR/HUF touches 410.50.

Fixed Income

- Bulls keep debt afloat after retreat from Tuesday peaks.

- Bunds subsequently breach prior session best by a lone tick, at 151.66 before running into supply issues, as new 10 year German benchmark technically uncovered.

- Gilts back on 116.00 handle from 115.47 Liffe low and T-note hovers nearer top end of 120-03/119-21 overnight range ahead of Fed’s Williams, US services ISM and FOMC minutes.

- UK debt unruffled by more UK Government resignations and BoE rhetoric awaiting PMQs that will put spotlight on under fire Conservative Party leader Johnson.

Commodities

- Crude benchmarks are firmer and having been moving with the equity space after yesterday’s significant crude selloff; however, the ‘recovery’ is limited with WTI pivoting USD 100/bbl.

- Goldman Sachs said oil has overshot as the global deficit is unresolved and it is premature for oil to drop on recession concerns

- OPEC Secretary General Barkindo has passed away, according to Arab News. Note, from an OPEC personnel perspective, Barkindo’s term as the OPEC SecGen was due to end on July 31st, after which the Kuwaiti oil executive Haitham Al Ghais was due to replace him as the new secretary-general

- Tengiz field in Kazakhstan continues operations following a blast, according to a source cited by Reuters.

- Spot gold is lacklustre after Tuesday’s USD-driven downside; notably, the yellow metal has been fairly resilient to fresh advances in the DXY. While base metals continue to falter, LME copper below 7.5k/T at worst.

US Event Calendar

- 07:00: July MBA Mortgage Applications -5.4%, prior 0.7%

- 09:45: June S&P Global US Services PMI, est. 51.6, prior 51.6

- 10:00: May JOLTs Job Openings, est. 10.9m, prior 11.4m

- 10:00: June ISM Services Index, est. 54.0, prior 55.9

- 14:00: June FOMC Meeting Minutes

Central Banks

- 09:00: Fed’s Williams Makes Remarks at Event on Bank Culture

- 14:00: June FOMC Meeting Minutes

DB’s Jim Reid concludes the overnight wrap

It’s sports day at school today and I’m going to pop in for an hour to watch. However given that my 4yr old twins are the youngest in their year and my daughter is still in a wheelchair I suspect I won’t be building a new trophy cabinet. For those that have asked about Maisie (thanks by the way) she continues to be in great spirits and is exceptional at swimming for her age (6) so she would likely win that if there was such an event. Fingers crossed she’ll be able to get out of the wheelchair in a few months after 8 months so far. The next scan is in 3 weeks and we’ll know if the hip ball has finished collapsing and if it is showing any early sign of regrowing.

As my kids are unlikely to win a prize they’ve asked me to ensure I win some for them to make their tears go away. So if you value our research I would appreciate it if you would vote in the Global Institutional Investor FI survey that opened yesterday. You can see the categories I am up for in this (link here) pdf. There are a number but I’ve listed the priorities. If you could let us know if you voted that would be appreciated unless it is to tell me you voted for one of our competitors!

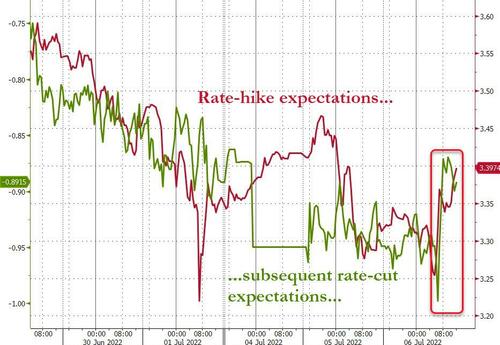

It’s been another tumultuous 24 hours in markets, with a massive risk-off move reversing late in the US session as the S&P (+0.16%) climbed over 2% after Europe closed. We’ll run through the various headlines in a moment, but there was so much going on here’s a quick highlights reel. We’ve seen the euro decline to a 20-year low against the US Dollar, another round of inversions across the Treasury curve, a mammoth rally in bonds, the tightest financial conditions since the initial wave of the Covid pandemic, a market now pricing in at least two full rate cuts by the Fed in 2023, the German government starting work on bailing out the gas sector, near double-digit percentage drops in oil, and a UK Prime Minister who is getting hit with very high profile cabinet resignations.

Running through the day, investor fears were evident from the get-go, with European markets swiftly giving up their gains after the open to move progressively lower through the day. An important catalyst for that was the latest bad news on the energy side, where an escalation in the Norwegian gas strike we mentioned yesterday means that nearly 60% of the country’s gas exports could have been affected from Saturday according to the Norwegian Oil and Gas Association. However, there were some optimistic signs overnight, as it appears the Norway labour minister intervened to put an end to the strike by summoning both sides to the table, saying “When the conflict can have such great social consequences for the whole of Europe, I have no choice but to intervene in the conflict”.

It goes without saying that this strike would have been coming at a particularly bad time for the European economy, not least with the scheduled maintenance on Nord Stream that’s occurring from July 11-21 and the uncertainty over what happens next. Germany yesterday accelerated legislation that will allow it to rescue energy companies if the need arises with Uniper looking set to be the first to receive state support. Economy Minister Habeck has talked about gas as potentially being a Lehman Brothers moment so the stakes are high.

Indeed this is a heavy cloud hanging over European assets at the moment and they were among the worst global performers yesterday as the prospect of a chaotic gas situation and recession came closer into view. Indeed, the euro itself weakened by a massive -1.50% against the US Dollar yesterday, which was its largest daily decline since March 2020, and left the single currency at its lowest level against the dollar since 2002, closing at just $1.0266. It’s dipped another -0.2% overnight.

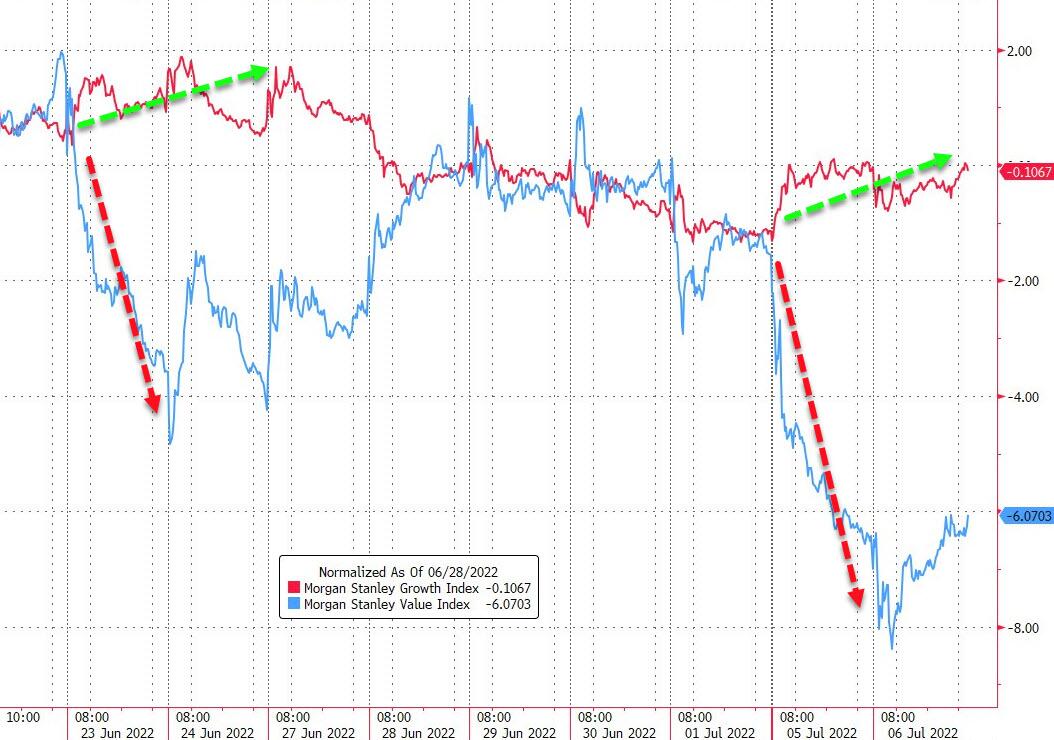

Another factor behind the euro’s weakness were growing doubts that the ECB could embark on as aggressive a hiking cycle as initially thought. That expectation of more dovish central banks was present across the world yesterday in light of the recession fears, but it was particularly prevalent in Europe, where the rate priced in by the June 2023 meeting came down by -11.4bps by the close of trade. It was a similar story in the US where the rate priced in by June 2023 came down by -11.4bps, but what’s becoming increasingly apparent is that investors are now expecting that the Fed will shift towards easing policy by mid-2023, with at least a full 25bp cut now priced in between the February and July meetings in 2023, as well as a further one by year-end.

Those fears of a recession were manifesting themselves in other asset classes too, with commodities more broadly (European natural gas excepted) having an awful day as the resiliency of global demand was brought into question. For instance, Brent crude oil prices (-9.45%) witnessed their largest daily move lower since March, taking prices down to their lowest level since early May at $102.77/bbl while WTI (-8.24%) broke beneath $100/bbl for the first time since April. The traditional industrial bellwether of copper was another victim of this trend, plummeting by another -5.36% yesterday to a 19-month low of its own, whilst wheat futures (-4.61%) are now trading beneath their levels prior to Russia’s invasion of Ukraine. In Asia, oil futures have pared bigger bounce back gains but are still trading slightly higher with Brent futures +1.05% and WTI futures (+0.72%) just above the $100/bbl level again.

Given the rising doubts about future rate hikes and the weakening inflationary pressures from key commodities, sovereign bonds put in a strong performance as they also benefited from their usual appeal as a haven asset. Yields on 10yr Treasuries came down by -7.5bps to 2.81%, and the 10yr breakeven fell -6.2bps to 2.30%, which takes it to a level unseen since September 2021, back before the Fed had even begun to taper their asset purchases. The declines in yields were concentrated at longer maturities, with the 2s10s curve flattening by -6.2bps to -1.9bps, closing inverted for the first time in nearly a month. And speaking of inversions, another milestone was reached yesterday as the 2s5s curve inverted for the first time this cycle in trading, closing -5.0bps lower at -0.9bps. That picture was echoed over in Europe as well, where yields on 10yr bunds (-15.6bps), OATs (-13.8bps) and BTPs (-9.1bps) all moved lower on the day. This morning yields on 10yr USTs (+2.37 bps) are edging higher as I type.

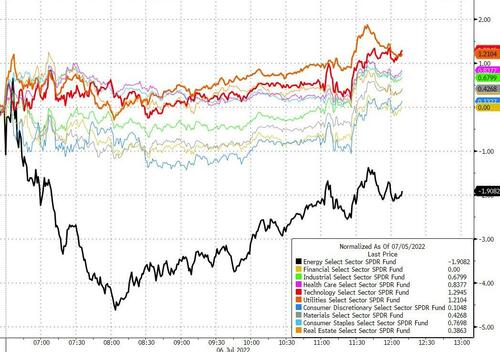

For equities, the layer upon layer of bad news resulted in another significant selloff until the Euro close, with the STOXX 600 shedding -2.11%. However the rate rally supported a steady tech-led march higher in the US after opening very weak and trading more than -2% lower. The S&P 500 finished +0.16% higher and the NASDAQ was up +1.75% on the day. Energy stocks led the moves lower on both sides of the Atlantic, and the index-level gains in the US were supported by a narrow subset of large cap stocks sensitive to lower rates, with only 3 S&P sectors – tech, discretionary, communications – in the green, and a massive 667bps differential between the best performing sector (communications +2.66%) and worst (energy -4.01%). Indeed, the even more concentrated mega-cap FANG+ outperformed the rest of the complex, gaining +3.01%. In line with the late US divergence, it was a tale of two credit markets, with HY credit spreads widening in Europe with the iTraxx crossover +27.4bps to 616bps, a level not seen since early April 2020 at the height of the initial lockdowns, while US HY CDX spreads tightened -11.8bps to 565bps after trading as high as 592bps intra-day.