GOLD; $1820.35 DOWN $3.05

SILVER: $20.87 DOWN 26 CENTS

ACCESS MARKET: GOLD $1819.70

SILVER: $20.83

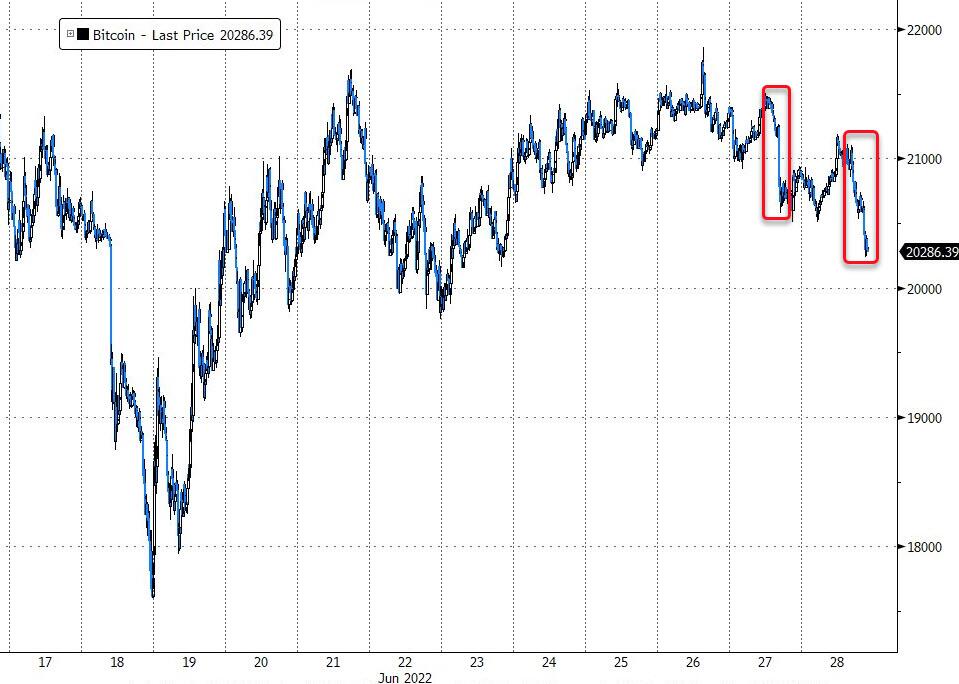

Bitcoin morning price: $20,979 UP 245

Bitcoin: afternoon price: $20,317 DOWN 417

Platinum price: closing UP $4.15 to $913.45

Palladium price; closing UP $4.00 at $1883.45

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX EXCHANGE:EXCHANGE:

EXCHANGE: COMEX

CONTRACT: JUNE 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,820.900000000 USD

INTENT DATE: 06/27/2022 DELIVERY DATE: 06/29/2022

FIRM ORG FIRM NAME ISSUED STOPPED

435 H SCOTIA CAPITAL 5

657 C MORGAN STANLEY 4

686 C STONEX FINANCIA 1

737 C ADVANTAGE 25

991 H CME 25

TOTAL: 30 30

MONTH TO DATE: 23,955

no. of contracts issued by JPMorgan: 0/20

_____________________________________________________________________________________

NUMBER OF NOTICES FILED TODAY FOR JUNE CONTRACT 30 NOTICE(S) FOR 3000 Oz//0.09331 TONNES)

total notices so far: 23,955 contracts for 2,395,500 oz (74.510 tonnes)

SILVER NOTICES:

21 NOTICE(S) FILED 105,000 OZ/

total number of notices filed so far this month 1851 : for 9,255,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD DOWN $3.05

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.64 TONNES FROM THE GLD//

INVENTORY RESTS AT 1056.40 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 26 CENTS

AT THE SLV// ://NO CHANGES IN SILVER INVENTORY AT THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 542.000 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A HUGE SIZED 4419 CONTRACTS TO 137,671 AND FURTHER FROM THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE STRONG GAIN IN OI WAS ACCOMPLISHED WITH OUR $0.04 LOSS IN SILVER PRICING AT THE COMEX ON MONDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.04) BUT WERE UNSUCCESSFUL IN KNOCKING OFF SOME SILVER LONGS//BUT MAINLY WE HAD ADDITIONAL SPECULATOR ADDITIONS. ALL OF THE COMEX LOSSES DUE TO INITIATION OF SPREADER LIQUIDATION

WE MUST HAVE HAD:

I) HUGE SPECULATOR SHORT ADDITIONS /. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A STRONG INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 7.635 MILLION OZ FOLLOWED BY TODAY’S QUEUE JUMP OF 10 CONTRACTS OR 50,000 OZ//NEW STANDING: 9,375,000 / // V) STRONG SIZED COMEX OI LOSS/SPREADER LIQUIDATION

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS : –973

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JUNE. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JUNE:

TOTAL CONTACTS for 19 days, total 15,774, contracts: 78.870 million oz OR 34.151MILLION OZ PER DAY. (830 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 78.870 MILLION OZ

.

LAST 11 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 78.870 MILLION OZ

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 4419 DESPITE OUR TINY $0.04 LOSS IN SILVER PRICING AT THE COMEX// MONDAY.,. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE CONTRACTS: 1504 CONTRACTS ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A HUGE INITIAL SILVER OZ STANDING FOR JUNE. OF 7.635 MILLION OZ FOLLOWED BY TODAY’S 50,000 QUEUE JUMP //NEW STANDING: 9,375,000 OZ // .. WE HAD A VERY STRONG SIZED LOSS OF 2914 OI CONTRACTS ON THE TWO EXCHANGES FOR 14.575 MILLION OZ WITH THE LOSS IN PRICE. ALL OF THE COMEX LOSS WAS DUE TO SPREADER LIQUIDATION.

WE HAD 21 NOTICES FILED TODAY FOR 105,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A SMALL SIZED 1073 CONTRACTS TO 498,078 AND CLOSER TO RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: +47 CONTRACTS.

.

THE SMALL INCREASE IN COMEX OI CAME WITH OUR FALL IN PRICE OF $4.90//COMEX GOLD TRADING/MONDAY / WE MUST HAVE HAD SOME SPECULATOR SHORT COVERING ACCOMPANYING OUR STRONG SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION //AND SOME SPECULATOR SHORT COVERING

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR JUNE AT 69.26 TONNES ON FIRST DAY NOTICE /FOLLOWED BY TODAY’S 3400 OZ E.F.P. JUMP TO LONDON //NEW STANDING: 74.609TONNES

YET ALL OF..THIS HAPPENED WITH OUR LOSS IN PRICE OF $4.90 WITH RESPECT TO MONDAY’S TRADING

WE HAD A GOOD SIZED GAIN OF 4958 OI CONTRACTS 15.421 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 3885 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 498,031

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 4958, WITH 1073 CONTRACTS INCREASED AT THE COMEX AND 3885 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 2812 CONTRACTS OR 8.746TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3885) ACCOMPANYING THE SMALL SIZED GAIN IN COMEX OI (1073,): TOTAL GAIN IN THE TWO EXCHANGES 2812 CONTRACTS. WE NO DOUBT HAD 1) SOME SPECULATOR SHORT COVERING AND SOME ADDITION TO SPECULATOR SHORTS ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR JUNE. AT 69.26 TONNES FOLLOWED BY TODAY’S E.F.P JUMP OF 2500 OZ//NEW STANDING: 74.715 TONNES / 3) ZERO LONG LIQUIDATION//SOME SPECULATOR SHORT COVERING//SOME SPECULATOR SHORT ADDITIONS //.,4) SMALL SIZED COMEX OI LOSS 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

JUNE

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JUNE :

68,527 CONTRACTS OR 6,852,700 OZ OR 213.14 TONNES 19 TRADING DAY(S) AND THUS AVERAGING: 3606 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 19 TRADING DAY(S) IN TONNES: 213.14 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 213.14/3550 x 100% TONNES 6.00% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 213.14 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF APRIL HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF MAY, FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A HUGE SIZED 4419 CONTRACT OI TO 137,671 AND FURTHER FROM OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 1504 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 1504 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 4419 CONTRACTS AND ADD TO THE 1504 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A STRONG SIZED LOSS OF 2915 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES 14.575 MILLION OZ

OCCURRED WITH OUR FALL IN PRICE OF $0.04 .

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)TUESDAY MORNING// MONDAY NIGHT

SHANGHAI CLOSED UP 30.03 PTS OR 0.89% //Hang Sang CLOSED UP 189.45 PTS OR 0.85% /The Nikkei closed UP 178.20 OR 0.66% //Australia’s all ordinaires CLOSED UP 0.87% /Chinese yuan (ONSHORE) closed DOWN 6.6947 /Oil UP TO 101.20 dollars per barrel for WTI and UP TO 117.02 for Brent. Stocks in Europe OPENED ALL GREEN // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.6947 OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.6962: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A SMALL SIZED 1073 CONTRACTS TO 498,031 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX DECREASE OCCURRED WITH OUR LOSS OF $4.90 IN GOLD PRICING MONDAY’S COMEX TRADING. WE ALSO HAD A GOOD SIZED EFP (4052 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO SHORT BIG TIME AND THEY ADDED TO THEIR SHORT POSITIONS

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING PAST THE ACTIVE DELIVERY MONTH OF JUNE.. THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 3885 EFP CONTRACTS WERE ISSUED: ;: , . 0 AUG :3885 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3885 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A GOOD SIZED TOTAL OF 4958 CONTRACTS IN THAT 3885 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A SMALL SIZED COMEX OI GAIN OF 1073 CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR FALL IN PRICE OF GOLD $4.90.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING JUNE (74.609),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.609 TONNES

THE BANKERS WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $4.90) BUT WERE UNSUCCESSFUL IN KNOCKING OFF SPECULATOR LONGS/COMMERCIAL LONGS BUT SPECULATOR SHORTS CONTINUED TO ADD TO THEIR POSITIONS//// WE HAVE REGISTERED A GOOD SIZED GAIN OF 4975 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR JUNE (74.609 TONNES)…

WE HAD +37 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 4958 CONTRACTS OR 495800 OZ OR 15.4 TONNES

Estimated gold volume 59,977/// poor/

final gold volumes/yesterday 156,728 /poor

INITIAL STANDINGS FOR JUNE ’22 COMEX GOLD //JUNE 28

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | NIL oz |

| Deposit to the Dealer Inventory in oz | nilOZ |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 30 notice(s)3000 OZ 0.09331 TONNES |

| No of oz to be served (notices) | 32 contracts 3200 oz 0.0995 TONNES |

| Total monthly oz gold served (contracts) so far this month | 23,955 notices 2,395,500 OZ 74.510 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total dealer deposit 0

No dealer withdrawals

0 customer deposit

total deposits: NIL oz

0 customer withdrawals:

total withdrawal: NIL oz

ADJUSTMENTS:1//dealer to customer

Loomis: 32,215.302 OZ

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JUNE.

For the front month of JUNE we have an oi of 62 contracts having lost 43 contracts

We had 9 notices filed on MONDAY so we LOST 34 contracts or an additional 2500 oz wil NOT stand for gold in this very active month of June as they were EFP’d to London

July has a LOSS OF 139 OI to stand at 1267

August has a LOSS of 1205 contracts DOWN to 405,474 contracts

We had 30 notice(s) filed today for NIL 3000 oz FOR THE JUNE 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 9 contract(s) of which 30 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JUNE /2021. contract month,

we take the total number of notices filed so far for the month (23,955) x 100 oz , to which we add the difference between the open interest for the front month of (JUNE 62 CONTRACTS ) minus the number of notices served upon today 30 x 100 oz per contract equals 2,398,700 OZ OR 74.609 TONNES the number of TONNES standing in this active month of JUNE.

thus the INITIAL standings for gold for the JUNE contract month:

No of notices filed so far (23,955) x 100 oz+ (62) OI for the front month minus the number of notices served upon today (30} x 100 oz} which equals 2,398,700 oz standing OR 74.609 TONNES in this active delivery month of JUNE.

TOTAL COMEX GOLD STANDING: 74.609 TONNES (A STRONG STANDING FOR A JUNE ( ACTIVE) DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,419,784.828 oz 75.26 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 33,183,194,729 OZ

TOTAL ELIGIBLE GOLD: 16,003,775.914 OZ

TOTAL OF ALL REGISTERED GOLD: 17,179,418.815 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 14,792,235.0 OZ (REG GOLD- PLEDGED GOLD)

END

SILVER/COMEX/JUNE 28

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 2,007,650.420 oz Brinks CNT DELAWARE HSBC JPMORGAN |

| Deposits to the Dealer Inventory | nilOZ |

| Deposits to the Customer Inventory | 600,157.100 oz jpm |

| No of oz served today (contracts) | 21CONTRACT(S) 105,000 OZ) |

| No of oz to be served (notices) | 24 contracts (120,000 oz) |

| Total monthly oz silver served (contracts) | 1851 contracts 9,255,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 1 deposit into the customer account

i) Into JPMorgan: 600,157.100 oz

total deposit: 600,157.100 oz

JPMorgan has a total silver weight: 169.097 million oz/333.529 million =50.67% of comex

Comex withdrawals: 5

Brinks 200,020,720 oz

CNT: 599,734.320 oz

Delaware 3661.300 oz

HSBC 600,417.480 oz

JPMorgan: 603,846.600 oz

total withdrawal 2,007,680.420 oz

adjustments: 2

dealer to customer:

JPMorgan 191,912.800 oz

Manfra: 169,898.460 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 69.749 MILLION OZ

TOTAL REG + ELIG. 333.529 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR JUNE

silver open interest data:

FRONT MONTH OF JUNE OI: 45 HAVING GAINED 0 CONTRACTS.

WE HAD 10 NOTICES FILED ON MONDAY SO WE GAINED 10 CONTRACTS OR AN ADDITIONAL 50,000 OZ WILL STAND IN THIS NON ACTIVE

DELIVERY MONTH OF JUNE

JULY HAD A LOSS OF 7775 CONTRACTS DOWN TO 14,210 CONTRACTS.

AUGUST GAINED 60 CONTRACTS TO STAND AT 1386

SEPTEMBER HAD A GAIN OF 3481 CONTRACTS UP TO 103,680 CONTRACTS.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 10 for 50,000 oz

Comex volumes:37,057// est. volume today// weak

Comex volume: confirmed yesterday: 85,571 contracts ( strong )

To calculate the number of silver ounces that will stand for delivery in JUNE we take the total number of notices filed for the month so far at 1851 x 5,000 oz = 9,255,000 oz

to which we add the difference between the open interest for the front month of JUNE(45) and the number of notices served upon today 21 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JUNE./2022 contract month: 1851 (notices served so far) x 5000 oz + OI for front month of JUNE (45) – number of notices served upon today (21) x 5000 oz of silver standing for the JUNE contract month equates 9,375,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

JUNE 28/WITH GOLD DOWN $3.05//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.64 TONNES FROM THE GLD///INVENTORY RESTS AT 1056.40 TONNES

JUNE 27/WITH GOLD DOWN $4.90 CENTS TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD///INVENTORY RESTS AT 1061.04 TONNES

JUNE 24/WITH GOLD UP 45 CENTS TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 8.70 TONNES FROM THE GLD//INVENTORY RESTS AT 1063.07 TONNES

JUNE 23/WITH GOLD DOWN $8.60:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD//INVENTORY RESTS AT 1071.77 TONNES

JUNE 22/WITH GOLD UP 15 CENTS:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 1073.80 TONNES

JUNE 21/WITH GOLD DOWN $2.00: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1075.54 TONES

JUNE 17/WITH GOLD DOWN $11.25: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.60 TONNES INTO THE GLD.///INVENTORY RESTS AT 1075.54 TONNES

JUNE 16/WITH GOLD UP $28.95: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1063.74 TONNES

JUNE 15/WITH GOLD UP $6.50/BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.65 TONNES FROM THE GLD////INVENTORY RESTS AT 1063.74 TONNES

JUNE 14/WITH GOLD DOWN $18.80/NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1065.39 TONNES

JUNE 13/WITH GOLD DOWN $41.55: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1065.39 TONNES

JUNE 10/WITH GOLD UP $21.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1065.39 TONNES

JUNE 9/WITH GOLD DOWN $3.50: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.32 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 1065.39 TONNES

JUNE 8/WITH GOLD UP $4.75: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1063.07 TONNES

JUNE 7/WITH GOLD UP $7.45: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1063.07 TONNES

JUNE 6/WITH GOLD DOWN $5.85: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1066.04 TONNES

JUNE 3/WITH GOLD DOWN $19.75//A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FROM THE GLD//INVENTORY RESTS AT 1066.04 TONNES

JUNE 2/WITH GOLD UP $22.50: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.64 TONNES FROM THE GLD//INVENTORY RESTS AT 1067.20 TONNES

JUNE 1/WITH GOLD UP $1$ HUGE CHANGES IN GOLD INVENTORY AT THE GLD: AWITHDRAWAL OF 1.45 TONNES FROM THE GLD///INVENTORY RESTS AT 1068.36 TONNES

MAY 31/WITH GOLD DOWN $15.10: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1069.81 TONNES

MAY 27/WITH GOLD UP $4.95//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1069.81 TONNES

May 26/WITH GOLD UP $2.10/A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 1069.81 TONNES

MAY 25/WITH GOLD UP @$2.70: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.89./INVENTORY RESTS AT 1068.07 TONNES

MAY 20/WITH GOLD UP $7.75: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 6.97 TONNES INTO THE GLD/INVENTORY RESTS AT 1056.18 TONNES

MAY 19/WITH GOLD UP $24.20; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1049.21 TONNES//

GLD INVENTORY: 1056.40 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JUNE 28/WITH SILVER DOWN 26 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.00 MILLION OZ..

JUNE 27/WITH SILVER DOWN 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.000 MILLION OZ

JUNE 24/WITH SILVER UP 10 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.137 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 542.000 MILLION OZ

JUNE 23/WITH SILVER DOWN 41 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SL: A WITHDRAWAL OF 2.029 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 545.137 MILLION OZ//

JUNE 22/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 547.166 MILLION OZ.

JUNE 21/WITH SILVER UP 9 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.506 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 547.166 MILLION OZ//

JUNE 17/WITH SILVER DOWN 15 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWAL OF 739,000 OZ FROM THE SLV./:INVENTORY RESTS AT 543.660 MILLION OZ/

JUNE 16/WITH SILVER UP 46 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ

JUNE 15/WITH SILVER UP 44 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ

JUNE 14/WITH SILVER DOWN 32 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ//

JUNE 13/WITH SILVER DOWN 62 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ//

JUNE 10.WITH SILVER UP 13 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 830,000 Z FROM THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ//

JUNE 9/WITH SILVER DOWN 27 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 923,000 OZ INTO THE SLV////INVENTORY RESTS AT 545.229 MILLION OZ

JUNE 8/WITH SILVER DOWN 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 544.306 MILLION OZ//

JUNE 7/WITH SILVER UP 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.306 MILLION OZ/

JUNE 6/WITH SILVER UP 20 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 6.459 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 547.167 MILLION OZ//

JUNE 3/WITH SILVER DOWN $.34: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITTHDRAWAL OF 246,000 OZ FORM THE SLV//INVENTORY RESTS AT 553.626 MILLION OZ..

JUNE 2/WITH SILVER UP 57 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.261 MILLION OZ FORM THE SLV.//INVENTORY RESTS T 553.872 MILLION OZ

JUNE 1/WITH SILVER UP 19 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV//: A WITHDRAWAL OF 2.538 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 556.133 MILLION OZ//

MAY 31/WITH SILVER DOWN $.41 TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST S AT 558.071 MILLION OZ//

MAY 27/WITH SILVER UP 10 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 558.071 MILLION OZ///

MAY 26/WITH SILVER UP 8 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.515 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 558.071 MILLION OZ

MAY 25/WITH SILVER UP 20 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .922 MILLION OZ FROM THE SLV/ //INVENTORY RESTS AT 561.486 MILLION OZ//

MAY 20.WITH SILVER DOWN 20 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WIHDRAWAL OF .785 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 565.085 MILLION OZ//

MAY 19/WITH SILVER UP 34 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT 565.085 MILLION OZ//

CLOSING INVENTORY 542.000 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg

LAWRIE WILLIAMS: Will Russian gold import ban have any effect?

Over the past weekend, it was announced that the countries comprising the G7 nations would be imposing a ban on the purchasing of Russian produced gold in a further attempt to limit Russia’s access to money with which to finance its continuing war on Ukraine. The announcement is, apparently, due today, and will be confirmed by U.S. President Joe Biden and UK Prime Minister Boris Johnson.

Russia is the world’s second largest gold producer, after China, according to the latest data from specialist precious metals consultancy Metals Focus (See: World Top 20 Gold Producing Countries 2021 and Gold Outlook), and its gold output last year was said to be worth some US$15.45 billion to the Russian economy, but whether this supposed export ban by the G7 countries will have any significant effect on Russian export income is somewhat less certain.

Gold tends to find buyers regardless of such imposed bans, and it is perhaps notable that the world’s two largest gold consumers, China and India, as well as several other major gold importers, are not members of the G7. India is already known to be building its state gold reserves, while China is thought to be doing so surreptitiously, and Russia itself may also be adding to its gold holdings as it continues its de-dollarisation process, but is currently following in China’s footsteps in being secretive about any volumes involved.

Russia has also gone on record as saying that it, and the other BRICS (Brazil, India, China and South Africa) nations are working together to develop a new reserve currency to rival the U.S. dollar which will probably have gold as a major constituent in parallel with a system to replace SWIFT (Society for Worldwide Interbank Financial Telecommunication) from which Russia has been arbitrarily cut off by the U.S.

The logic behind this is strong and it all may have some appeal globally given apparent U.S. control over the current system and a current reserve currency which is currently mostly declining in value – particularly given inflation levels in the U.S. and elsewhere. If a new reserve currency can offer greater stability in value, and some form of gold, or commodity backing, may offer this, it may find greater worldwide acceptance, although that would undoubtedly take time. Global economic changes of this nature tend to move slowly.

This all creates yet more uncertainty in the gold markets. The yellow metal did advance in price in European trade this morning, but still remains range-bound between $1,820-1,850 with little real sign of breaking out in either direction. It will probably need to take a lead from U.S. activity, which has tended to be largely unsupportive of the gold price of late.

U.S. gold price interest will probably largely depend on the various data releases on inflation, employment, business confidence and GDP growth as and when they are released. All will have an impact on likely Fed policy decisions at the next FOMC meeting due in late July. Our own view is that inflation will remain elevated, employment and the US economy will both show signs of stress and business confidence will turn down. All this suggests a perhaps more aggressive approach by the Fed with higher interest rates than most have been forecasting this year and next unless there is some kind of policy reversal, which some economic analysts have been suggesting.

28 Jun 2022

END

3. Chris Powell of GATA provides to us very important physical commentaries

How foolish can one country get. Bolivia’s central bank plans to put gold produced in their

country by strengthening international reserves. Who thought of this one?

Bolivia’s central bank plans to put gold reserves at risk

Submitted by admin on Mon, 2022-06-27 21:23Section: Daily Dispatches

Bolivia’s Central Bank Will Invest Gold Reserves in International Markets

By Walter Vasquez

El Deber

Santa Cruz de la Sierra, Bolivia

Sunday, May 15, 2022

The Central Bank of Bolivia has as one of its objectives for this year to gain approval of laws that authorize it to buy local gold and carry out financial operations with international gold reserves in international markets, an action that no government has done before and is “a terrible signal for the Bolivian economy,” according to analysts.

The bank’s 2022 Initial Public Rendering of Accounts report realizes that among the tasks the institution has this year is “continuing the procedures for the approval of the proposed regulations that allow the strengthening of international reserves ,” a proposal whose purpose is “to authorize the bank to purchase nationally produced gold and carry out financial operations with international gold reserves in international markets

During the accountability report, the president of the bank, Edwin Rojas, said that this year, in an environment of high volatility and uncertainty caused by the pandemic and the war between Russia and Ukraine, the net international reserves will continue to be invested, taking precautions for the security and liquidity of these investments.

“We are going to continue our efforts so that our bills to strengthen international reserves can be approved. On is the bill we have proposed during the past administration that seeks the purchase of nationally produced gold and allows a more modern management of reserves, strengthening their level as well as the liquidity they must have so that our economy can carry out its international financial operations without any limit,” Rojas said.

The economist Napoleon Pacheco said: “That the central bank is deciding to make use of the gold reserves expresses a much more serious situation than the one we know. The situation must be extremely complicated to reach that level, because no government before the Movement for Socialism in critical situations proposed using the country’s gold reserves. It is a bad sign for the Bolivian economy.”

To “sell the gold or leave it as a guarantee or collateral abroad,” Pacheco added, requires not only a law passed in the Legislative Assembly, where the Movement for Socialism has a majority, but also international certification of the degree of purity of each ingot. “Without that requirement, only clandestine operations can be carried out,” he said.

The reserves as of May 9 last total $4.596 billion, 56.6% of which ($2,602 billion) is in gold .

“In the net international reserves, what counts is cash, and that cash is currently not enough for two months of imports,” Pacheco said.

On March 15, the financial analyst Jaime Dunn indicated that there are three ways to attract more foreign currency to the country (for the payment of foreign debt and for imports): increase exports, which cannot be done due to the recently approved restrictions; borrow more, through bilateral and multilateral credits and bonds, “in which we are doing very badly”; and the attraction of foreign investment, which the country is not achieving either.

“If this gets more complicated, what they are going to have to do is start selling gold . I hope they don’t get to that , because if that’s the case, they would show that they really are in greater trouble,” Dunn said.

The intention to buy local gold to increase reserves is not new. In 2010 the government created the Bolivian Gold Co. to exploit part of the gold wealth. The state company also had the objective of selling the mineral to the central bank, something that was already authorized in 2011, through Law 175 . At the moment there are no known details of the amount of gold that the bank sold in these years.

END

At least this is a start: Zimbabwe is to introduce gold coins to escape soaring inflation. Chris Powell is correct:

why not back your currency with gold produced from the ground. They have enormous reserves but high inflation cannot get it out of the ground

(Herald/Zimbabwe/ChrisPowell)

Zimbabwe to introduce gold coins to offer escape from soaring inflation

Submitted by admin on Mon, 2022-06-27 20:34Section: Daily Dispatches

Good grief, People! You’re sitting on huge gold reserves. Make your paper money convertible to gold at a fixed rate and hold the rate. It won’t be so hard when you can mine your own money. The rest of the world won’t help you, and shouldn’t help you when you so easily can help yourself.

* * *

From The Herald

Harare, Zimbabwe

Monday, June 27, 2022

The Reserve Bank of Zimbabwe says it will be introducing gold coins as part of measures to ensure that investors and the public have alternative means to preserve value, cushioning them from the negative impact of resurgent inflation in the economy.

According to the RBZ, the gold coins will be minted at the Fidelity Gold Refineries and will be available through normal banking channels.

Gold is considered a safe haven against inflation and a gold coin is made mostly or entirely of gold, while most gold bullion coins are pure gold. …

The proposition has the potential to have a stabilizing effect on the economy if conducted properly given the stability and value storage associated with gold.

Zimbabwe’s inflation increased to 191.6% and 30.7% on a year-on-year and month-on-month basis for June 2022, respectively, which is far astride from government projections of achieving a 30% inflation rate by the end of the year. …

… For the remainder of the report:

END

4. OTHER GOLD STORIES

Chinese gold imports via HK surge in May | Kitco News

Inbox

| douglas cundey | 8:28 AM (6 minutes ago) | ||

| to Chris, William, Bill, me |

https://www.kitco.com/news/2022-06-28/Chinese-gold-imports-via-HK-surge-in-May.html

Chinese gold imports via HK surge in May

(Kitco News) – China’s net gold imports via Hong Kong rose 58.3% in May from the previous month, Hong Kong’s official data showed on Monday. This comes as pandemic-related curbs were relaxed in major cities. Net imports stood at 8.281 tonnes, according to the Census and Statistics Department. Imports were, however, down 62% year-on-year.

Total gold imports via Hong Kong rose nearly 47% to 14.13 tonnes from April. The rise in May could reflect some of the restrictions being eased in Shanghai and Beijing, said StoneX analyst Rhona O’Connell. China imports gold also via Shanghai and Beijing, so Hong Kong data may not provide a complete picture of the country’s gold purchases. Shanghai and Beijing began to gradually loosen Covid-curbs by late May.

Swiss customs data, however, showed last week that its shipments of gold to China fell in May. Throughout May, gold changed hands in China and prices ranged from $10 an ounce below global spot prices to on par with the benchmark.

Gold is trading 0.16% higher on Tuesday at $1825/oz. The yellow metal has been in full consolidation mode recently and the current consolidation high stands at $1879.45/oz. This all comes despite the strong USD over the few months.

5.OTHER COMMODITIES

END

COMMODITIES IN GENERAL/

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings TUESDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 6.6947

OFFSHORE YUAN: 6.6962

HANG SANG CLOSED UP 189.45 PTS OR 0.95%

2. Nikkei closed UP 178.20% OR 0.66%

3. Europe stocks ALL CLOSED ALL GREEN

USA dollar INDEX UP TO 103.81/Euro FALLS TO 1.0577

3b Japan 10 YR bond yield: FALLS TO. +.224/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 136.214/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: DOWN -// OFF- SHORE DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +1.665%/Italian 10 Yr bond yield RISES to 3.68% /SPAIN 10 YR BOND YIELD FALLS TO 2.74%…

3i Greek 10 year bond yield RISES TO 3.89//

3j Gold at $1824.90 silver at: 21.24 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 1/2 roubles/dollar; ROUBLE AT 52.82

3m oil into the 111 dollar handle for WTI and 117 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 136.21DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning 0.9556– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0107well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.245 UP 5 BASIS PTS

USA 30 YR BOND YIELD: 3.352 UP 5 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 16.65

Futures, Commodities Jump After China Cuts Quarantine

TUESDAY, JUN 28, 2022 – 08:00 AM

US stock futures rebounded from Monday’s modest losses and traded near session highs after China reduced quarantine times for inbound travelers by half – to seven days of centralized quarantine and three days of health monitoring at home – the biggest shift yet in a Covid-19 policy that has left the world’s second-largest economy isolated as it continues to try and eliminate the virus. The move, which fueled optimism about stronger economic growth and boosted appetite for both commodities and risk assets, sent S&P 500 futures and Nasdaq 100 contracts higher by 0.6% each at 7:15 a.m. in New York, setting up heavyweight technology stocks for a rebound. Mining and energy shares led gains in Europe’s Stoxx 600 and an Asian equity index erased losses to climb for a fourth session. 10Y TSY yields extended their move higher rising to 3.25% or about +5bps on the session, while the dollar and bitcoin were flat, and oil and commodity-linked currencies strengthened.

In premarket trading, the biggest mover was Kezar Life Sciences which soared 85% after reporting positive results for its lupus drug. On the other end, Robinhood shares fell 3.2%, paring a rally yesterday sparked by news that FTX is exploring whether to buy the company. In a statement, FTX head Sam Bankman-Fried said he is excited about the firm’s business prospects, but “there are no active M&A conversations with Robinhood.” Here are some of the other most notable premarket movers”

- Playtika (PLTK US) shares rallied 11% in premarket trading after a report that private equity firm Joffre Capital agreed to acquire a majority stake in the gaming company from a Chinese investment group for $21 a share.

- Nike (NKE US) shares fell 2.3% in US premarket trading, with analysts reducing their price targets after the company gave a downbeat forecast for gross margin and said it was being cautious in its outlook for the China market.

- Spirit Airlines (SAVE US) shares rise as much as 5% in US premarket trading after JetBlue boosted its all-cash bid in response to an increased offer by rival suitor Frontier in the days before a crucial shareholder vote.

- Snowflake (SNOW US) rises 3.3% in US premarket trading after Jefferies upgraded the stock to buy from hold, saying its valuation is now “back to reality” and offers a good entry point given the software firm’s long-term targets.

- Sutro Biopharma (STRO US) shares rise 34% in US premarket trading after the company and Astellas said they will collaborate to advance development of immunostimulatory antibody-drug conjugates, which are a modality for treating tumors and designed to boost anti-cancer activity.

- State Street (STT US) shares could be in focus after Deutsche Bank downgraded the stock to hold, while lowering EPS estimates and price targets across interest rate sensitive coverage of trust banks and online brokers.

- US bank stocks may be volatile during Tuesday’s trading session after the lenders announced a wave of dividend increases following last week’s successful stress test results.

Stock rallies have proved fleeting this year as higher borrowing costs to fight inflation restrain economic activity in a range of nations. European Central Bank President Christine Lagarde affirmed plans for an initial quarter-point increase in interest rates in July, but said policy makers are ready to step up action to tackle record inflation if warranted. Some analysts also argue still-bullish earnings estimates are too optimistic. Earnings revisions are a risk with the US economy set to slow next year, though China emerging from Covid strictures could act as a global buffer, according to Lorraine Tan, Morningstar director of equity research.

“You got a US slowdown in 2023 in terms of growth, but you have China hopefully coming out of its lockdowns,” Tan said on Bloomberg Radio.

In Europe, stocks are well bid with most European indexes up over 1%. Euro Stoxx 50 rose as much as 1.2% before drifting off the highs. Miners, energy and auto names outperform. The Stoxx 600 Basic Resources sub-index rises as much as 3.5% led by heavyweights Rio Tinto and Anglo American, as well as Polish copper producer KGHM and Finnish forestry companies Stora Enso and UPM- Kymmene. Iron ore and copper reversed losses after China eased its quarantine rules for new arrivals, while oil gained for a third session amid risks of supply disruptions. Iron ore in Singapore rose more than 4% after being firmly lower earlier in the session, while copper and other base metals also turned higher. Here are the biggest European movers:

- Luxury stocks climb boosted by an easing of Covid-19 quarantine rules in the key market of China. LVMH shares rise as much as 2.5%, Richemont +3.1%, Kering +3%, Moncler +3%

- Energy and mining stocks are the best-performing groups in the rising Stoxx Europe 600 index amid commodity gains. Shell shares rise as much as 3.8%, TotalEnergies +2.7%, BP +3.4%, Rio Tinto +4.6%, Glencore +3.9%

- Banco Santander shares rise as much as 1.8% after a report that the Spanish bank has hired Credit Suisse and Goldman Sachs for its bid to buy Mexico’s Banamex.

- GN Store Nord shares gain as much as 4.2% after Nordea resumes coverage on the hearing devices company with a buy rating.

- Swedish Match shares rise as much as 4% as Philip Morris International’s offer document regarding its bid for the company has been approved and registered by the Swedish FSA.

- Wise shares decline as much as 15%, erasing earlier gains after the fintech firm reported full- year earnings. Citi said the results were “mixed,” with strong revenue growth being offset by lower profitability.

- UK water stocks decline as JPMorgan says it is turning cautious on the sector on the view that future regulated returns could surprise to the downside, in a note cutting Severn Trent to underweight. Severn Trent shares fall as much as 6%, Pennon -7.7%, United Utilities -2.3%

- Akzo Nobel falls as much as 4.5% in Amsterdam trading after the paint maker announced the appointment of former Sulzer leader Greg Poux-Guillaumeas chief executive officer, succeeding Thierry Vanlancker.

- Danske Bank shares fall as much as 4%, as JPMorgan cut its rating on the stock to underweight, saying in a note that risks related to Swedish property will likely create some “speed bumps” for Nordic banks though should be manageable.

In the Bavarian Alps, limiting Russia’s profits from rising energy prices that fuel its war in Ukraine have been among the main topics of discussion at a Group of Seven summit. G-7 leaders agreed that they want ministers to urgently discuss and evaluate how the prices of Russian oil and gas can be curbed.

Earlier in the session, Asian stocks erased earlier losses as China’s move to ease quarantine rules for inbound travelers bolstered sentiment. The MSCI Asia Pacific Index rose as much as 0.6% after falling by a similar magnitude. The benchmark is set for a fourth day of gains, led by the energy and utilities sectors. BHP and Toyota contributed the most to the gauge’s advance, while China’s technology firms were among the biggest losers as a plan by Tencent’s major backer to further cut its stake fueled concern of more profit-taking following a strong rally. A move by Beijing to cut quarantine times for inbound travelers by half is helping cement gains which have made Chinese shares the world’s best-performing major equity market this month. The nation’s stocks are approaching a bull market even as their recent rise pushes them to overbought levels.

Still, the threat of a sharp slowdown in the world’s largest economy may pose a threat to the outlook. “US recession risk is still there and I think that’ll obviously have impact on global sectors,” Lorraine Tan, director of equity research at Morningstar, said on Bloomberg TV. “Even if we do get some China recovery in 2023, which could be a buffer for this region, it’s not going to offset the US or global recession.” Most stock benchmarks in the region finished higher following China’s move to ease its travel rules. Main equity measures in Japan, Hong Kong, South Korea and Australia rose while those in Taiwan and India fell. Overall, Asian stocks are on course to complete a monthly decline of about 4%.

Meanwhile, the People’s Bank of China pledged to keep monetary policy supportive to help the nation’s economy. It signaled that stimulus would likely focus on boosting credit rather than lowering interest rates.

Japanese stocks gained as investors adjusted positions heading into the end of the quarter. The Topix Index rose 1.1% to 1,907.38 as of the market close in Tokyo, while the Nikkei 225 advanced 0.7% to 27,049.47. Toyota Motor contributed most to the Topix’s gain, increasing 2.2%. Out of 2,170 shares in the index, 1,736 rose and 374 fell, while 60 were unchanged. “As the end of the April-June quarter approaches, there is a tendency for institutional investors to rebalance,” said Norihiro Fujito, chief investment strategist at Mitsubishi UFJ Morgan Stanley. “It will be easier to buy into cheap stocks, which is a factor that will support the market in terms of supply and demand.”

India’s benchmark stock gauge ended flat after trading lower for most of the session as investors booked some profits after a three-day rally. The S&P BSE Sensex closed little changed at 53,177.45 in Mumbai, while the NSE Nifty 50 Index gained 0.1%. Six of the the 19 sector sub-gauges compiled by BSE Ltd. dropped, led by consumer durables companies, while oil & gas firms were top performers. ICICI Bank was among the prominent decliners on the Sensex, falling 1%. Out of 30 shares in the Sensex index, 17 rose and 13 fell.

In rates, fixed income sold off as treasuries remained under pressure with the 10Y yield rising as high as 3.26%, following steeper declines for euro-zone and UK bond markets for second straight day and after two ugly US auctions on Monday. Yields across the curve are higher by 2bp-5bp led by the 7-year ahead of the $40 billion auction. In Europe, several 10-year yields are 10bp higher on the day after comments by an ECB official spurred money markets to price in more policy tightening. WI 7Y yield at around 3.32% exceeds 7-year auction stops since March 2010 and compares with 2.777% last month. Monday’s 5-year auction drew a yield more than 3bp higher than its yield in pre-auction trading just before the bidding deadline, a sign dealers underestimated demand. Traders attributed the poor results to factors including short base eroded by last week’s rally, recently elevated market volatility discouraging market-making, and sub-par participation during what is a popular vacation week in the US. Focal points for US session include 7-year note auction at 1pm ET; a 5-year auction Monday produced notably weak demand metrics.

The belly of the German curve underperformed as markets focus on hawkish comments from ECB officials: 5y bobl yields rose 10 bps near 1.46%, red pack euribors dropped 10-13 ticks and ECB-dated OIS rates priced in 163 basis points of tightening by year end.

In FX, Bloomberg dollar spot index is near flat as the greenback reversed earlier losses versus all of its Group-of-10 peers apart from the yen while commodity currencies were the best performers. The euro rose above $1.06 before paring gains after ECB Governing Council member Martins Kazaks said the central bank should consider a first rate hike of more than a quarter-point if there are signs that high inflation readings are feeding expectations. Money markets ECB raised tightening wagers after his remarks. ECB President Lagarde later affirmed plans for an initial quarter-point increase in interest rates in July but said policy makers are ready to step up action to tackle record inflation if warranted. The ECB is likely to drain cash from the banking system to offset any bond purchases made to restrain borrowing costs for indebted euro-area members, Reuters reported, citing two sources it didn’t identify.

Elsewhere, the pound drifted against the dollar and euro after underperforming Monday, with focus on quarter-end flows, lingering Brexit risks and the UK economic outlook. Scottish First Minister Nicola Sturgeon due to speak later on how she plans to hold a second referendum on Scottish independence by the end of next year. The yen gave up an Asia session gain versus the dollar as US equity futures reversed losses. The Australian dollar rose after China cut its mandatory quarantine period to 10 days from three weeks for inbound visitors in its latest Covid-19 guidance. JPY was the weakest in G-10, drifting below 136 to the USD.

In commodities, oil rose for a third day with global output threats compounding already red-hot markets for physical supplies and as broader financial sentiment improved. Brent crude breached $117 a barrel on Tuesday, but some of the most notable moves in recent days have been in more specialist market gauges. A contract known as the Dated-to-Frontline swap — an indicator of the strength in the key North Sea market underpinning much of the world’s crude pricing — hit a record of more than $5 a barrel. The rally comes amid growing supply outages in Libya and Ecuador, exacerbating ongoing market tightness.

Oil prices also rose Tuesday as broader sentiment was boosted by China’s move to cut in half the time new arrivals must spend in isolation, the biggest shift yet in its pandemic policy. Meanwhile, the G-7 tasked ministers to urgently discuss an oil price cap on Russia.

Finally, the prospect of additional supply from two of OPEC’s key producers also looks limited. On Monday Reuters reported that French President Emmanuel Macron told his US counterpart Joe Biden that the United Arab Emirates and Saudi Arabia are already pumping almost as much as they can.

In the battered metals space, LME nickel rose 2.7%, outperforming peers and leading broad-based gains in the base-metals complex. Spot gold rises roughly $3 to trade near $1,826/oz

Looking to the day ahead now, data releases include the FHFA house price index for April, the advance goods trade balance and preliminary wholesale inventories for May, as well as the Conference Board’s consumer confidence for June and the Richmond Fed’s manufacturing index. From central banks, we’ll hear from ECB President Lagarde, the ECB’s Lane, Elderson and Panetta, the Fed’s Daly, and BoE Deputy Governor Cunliffe. Finally, NATO leaders will be meeting in Madrid.

Market Snapshot

- S&P 500 futures up 0.5% to 3,922.50

- STOXX Europe 600 up 0.6% to 417.65

- MXAP up 0.4% to 162.36

- MXAPJ up 0.4% to 539.85

- Nikkei up 0.7% to 27,049.47

- Topix up 1.1% to 1,907.38

- Hang Seng Index up 0.9% to 22,418.97

- Shanghai Composite up 0.9% to 3,409.21

- Sensex down 0.3% to 52,990.39

- Australia S&P/ASX 200 up 0.9% to 6,763.64

- Kospi up 0.8% to 2,422.09

- German 10Y yield little changed at 1.62%

- Euro little changed at $1.0587

- Brent Futures up 1.4% to $116.65/bbl

- Gold spot up 0.3% to $1,828.78

- U.S. Dollar Index little changed at 103.89

Top Overnight News from Bloomberg

- In Tokyo’s financial circles, the trade is known as the widow- maker. The bet is simple: that the Bank of Japan, under growing pressure to stabilize the yen as it sinks to a 24-year low, will have to abandon its 0.25% cap on benchmark bond yields and let them soar, just as they already have in the US, Canada, Europe and across much of the developing world

- Bank of Italy Governor Ignazio Visco may leave his post in October, paving the way for the appointment of a high profile executive close to Premier Mario Draghi, daily Il Foglio reported

- NATO is set to label China a “systemic challenge” when it outlines its new policy guidelines this week, while also highlighting Beijing’s deepening partnership with Russia, according to people familiar with the matter

- The PBOC pledged to keep monetary policy supportive to aid the economy’s recovery, while signaling that stimulus would likely focus on boosting credit rather than lowering interest rates

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks were mixed with the region partially shrugging off the lacklustre handover from the US. ASX 200 was kept afloat with energy leading the gains amongst the commodity-related sectors. Nikkei 225 swung between gains and losses with upside capped by resistance above the 27K level. Hang Seng and Shanghai Comp. were pressured amid weakness in tech and lingering default concerns as Sunac plans discussions on extending a CNY bond and with Evergrande facing a wind-up petition.

Top Asian News

- China is to cut quarantine time for international travellers, according to state media cited by Reuters.

- Shanghai Disneyland (DIS) will reopen on June 30th, according to Reuters.

- PBoC injected CNY 110bln via 7-day reverse repos with the rate at 2.10% for a CNY 100bln net daily injection.

- China’s state planner official said China faces new challenges in stabilising jobs and prices due to COVID and risks from the Ukraine crisis, while the NDRC added they will not resort to flood-like stimulus but will roll out tools in its policy reserve in a timely way to cope with challenges, according to Reuters.

- China’s state planner NDRC says China is to cut gasoline and diesel retail prices by CNY 320/tonne and CNY 310/tonne respectively from June 29th.

- BoJ may have been saddled with as much as JPY 600bln in unrealised losses on its JGB holdings earlier this month, as a widening gap between domestic and overseas monetary policy pushed yields higher and prices lower, according to Nikkei.

European bourses are firmer as sentiment picked up heading into the cash open amid encouraging Chinese COVID headlines. Sectors are mostly in the green with no clear theme. Base metals and Energy reside as the current winners and commodities feel a boost from China’s COVID updates. Stateside, US equity futures saw a leg higher in tandem with global counterparts, with the RTY narrowly outperforming. Twitter (TWTR) in recent weeks provided Tesla (TSLA) CEO Musk with historical tweet data and access to its so-called fire hose of tweets, according to WSJ sources.

Top European News

- UK lawmakers voted 295-221 to support the Northern Ireland Protocol bill in the first of many parliamentary tests it will face during the months ahead, according to Reuters.

- Scotland’s First Minister Sturgeon will set out a plan today for holding a second Scottish Independence Referendum, according to BBC News.

- ECB’s Kazaks Says Worth Looking at Larger Rate Hike in July

- G-7 Latest: Leaders Want Urgent Evaluation of Energy Price Caps

- Ex- UBS Staffer Wants Payout for Exposing $10 Billion Swiss Stash

- SocGen Blames Clifford Chance in $483 Million Gold Suit

- GSK’s £40 Billion Consumer Arm Picks Citi, UBS as Brokers

- Russian Industry Faces Code Crisis as Critical Software Pulled

ECB

- ECB’s Lagarde said inflation in the euro area is undesirably high and it is projected to stay that way for some time to comeFragmentation tool, via the ECB.

- ECB’s Kazaks said 25bps in July and 50bps in September is the base case, via Bloomberg TV. Kazaks said it is worth looking at a 50bps hike in July and front-loading hikes might be reasonable. Fragmentation risks should not stand in the way of monetary policy normalisation. If necessary, the ECB will come up with tools to address fragmentation.

- ECB’s Wunsch said he is comfortable with a 50bps hike in September; adds that 200bps of hikes are needed relatively fast, and anti-fragmentation tool should have no limits if market moves are unwarranted, via Reuters.

- Bank of Italy said Governor Visco’s resignation is not on the table, according to a spokesperson cited by Reuters.

Fixed Income

- Bond reversal continues amidst buoyant risk sentiment, hawkish ECB commentary and supply.

- Bunds lose two more big figures between 146.80 peak and 144.85 trough, Gilts down to 112.06 from 112.86 at best and 10 year T-note retreats within 117-01/116-14 range

FX

- DXY regroups on spot month end as yields rally and rebalancing factors offer support – index within 103.750-104.020 range vs Monday’s 103.660 low.

- Euro continues to encounter resistance above 1.0600 via 55 DMA (1.0614 today); Yen undermined by latest bond retreat and renewed risk appetite – Usd/Jpy eyes 136.00 from low 135.00 area and close to 134.50 yesterday.

- Aussie breaches technical and psychological resistance with encouragement from China lifting or easing more Covid restrictions – Aud/Usd through 10 DMA at 0.6954.

- Loonie and Norwegian Krona boosted by firm rebound in oil as France fans supply concerns due to limited Saudi and UAE production capacity – Usd/Cad sub-1.2850 and Eur/Nok under 10.3500.

- Yuan receives another PBoC liquidity boost to compliment positive developments on the pandemic front, but Rand hampered by latest power cut warning issued by SA’s Eskom

Commodities

- WTI and Brent futures were bolstered in early European hours amid encouragement seen from China’s loosening of COVID restrictions.

- Spot gold is uneventful, around USD 1,825/oz in what has been a sideways session for the bullion since the reopening overnight.

- Base metals are posting broad gains across the complex – with LME copper back above USD 8,500/t amid China-related optimism.

US Event Calendar

- 08:30: May Advance Goods Trade Balance, est. -$105b, prior -$105.9b, revised -$106.7b

- 08:30: May Wholesale Inventories MoM, est. 2.1%, prior 2.2%

- May Retail Inventories MoM, est. 1.6%, prior 0.7%

- 09:00: April S&P CS Composite-20 YoY, est. 21.15%, prior 21.17%

- 09:00: April S&P/CS 20 City MoM SA, est. 1.95%, prior 2.42%

- 09:00: April FHFA House Price Index MoM, est. 1.4%, prior 1.5%

- 10:00: June Conf. Board Consumer Confidenc, est. 100.0, prior 106.4

- Conf. Board Expectations, prior 77.5; Present Situation, prior 149.6

- 10:00: June Richmond Fed Index, est. -5, prior -9

DB’s Jim Reid concludes the overnight wrap

It’s been a landmark night in our household as last night was the first time the 4-year-old twins slept without night nappies. So my task this morning after I send this to the publishers is to leave for the office before they all wake up so that any accidents are not my responsibility. Its hopefully the end of a near 7-year stretch of nappies being constantly around in their many different guises and states of unpleasantness. Maybe give it another 30-40 years and they’ll be back.

Talking of unpleasantness, as we near the end of what’s generally been an awful H1 for markets, yesterday saw the relief rally from last week stall out, with another bond selloff and an equity performance that fluctuated between gains and losses before the S&P 500 (-0.30%) ended in negative territory.

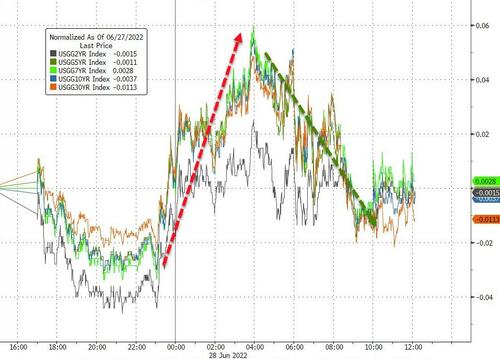

In terms of the specific moves, sovereign bonds lost ground on both sides of the Atlantic, with yields on 10yr Treasuries up by +7.0bps following their -9.6bps decline from the previous week. That advance was led by real rates (+9.6bps), which look to have been supported by some decent second-tier data releases from the US during May yesterday. The preliminary reading for US durable goods orders surprised on the upside with a +0.7% gain (vs. +0.1% expected). Core capital goods orders also surprised on the upside with a +0.8% advance (vs. +0.2% expected). And pending home sales were unexpectedly up by +0.7% (vs. -4.0% expected). Collectively that gave investors a bit more confidence that growth was still in decent shape last month, which is something that will also offer the Fed more space to continue their campaign of rate hikes into H2. This morning 10yr USTs yields have eased -2.45 bps to 3.17% while 2yr yields (-4 bps) have also moved lower to 3.08%, as we go to press.

Staying at the front end, when it comes to those rate hikes, if you look at Fed funds futures they show that investors are still only expecting them to continue for another 9 months, with the peak rate in March or April 2023 before markets are pricing in at least a full 25bps rate cut by end-2023 from that point. I pointed out in my chart of the day yesterday (link here) that the median time historically from the last hike of the cycle to the first cut was only 4 months, and last time it was only 7 months between the final hike in December 2018 and the next cut in July 2019. So it wouldn’t be historically unusual if Fed funds did follow that pattern whether that fits my view or not.

Over in Europe yesterday there was an even more aggressive rise in yields, with those on 10yr bunds (+10.9bps), OATs (+11.0bps) and BTPs (+9.1bps) all rising on the day as they bounced back from their even larger declines over the previous week. That came as investors pared back their bets on a more dovish ECB that they’d made following the more negative tone last week, and the rate priced in by the December ECB meeting rose by +8.5bps on the day.

For equities, the major indices generally fluctuated between gains and losses through the day. The S&P 500 followed that pattern and ultimately fell -0.30%, which follows its best daily performance in over 2 years on Friday Quarter-end rebalancing flows seem set to drive markets back-and-forth price this week. Even with the decline yesterday, the index is +6.36% higher since its closing low less than a couple of weeks ago. And over in Europe, the STOXX 600 (+0.52%) posted a decent advance, although that masked regional divergences, including losses for the CAC 40 (-0.43%) and the FTSE MIB (-0.86%).

Energy stocks strongly outperformed in the index, supported by a further rise in oil prices that left both Brent crude (+1.74%) and WTI (+1.81%) higher on the day. G7 ministers reportedly agreed to explore a cap on Russian gas and oil exports, with the official mandate expected to be announced today, but it would take time for any mechanism to be developed. The impact on global oil supply is not clear: if Russia retaliates supply could go down, if this enables other third parties to import more Russian oil supply could go up. Elsewhere, political unrest in Libya and Ecuador could simultaneously hit oil supply. In early Asian trading, oil prices continue to move higher, with Brent futures up +1.13% at $116.39/bbl and WTI futures gaining +1% to just above the $110/bbl level.

Asian equity markets are struggling a bit this morning. The Hang Seng (-1.00%) is the largest underperformer amid a weakening in Chinese tech stocks whilst the Nikkei (-0.15%), Shanghai Composite (-0.15%) and CSI (-0.19%) are trading in negative territory in early trade. Elsewhere, the Kospi (-0.05%) is just below the flatline. US stock futures are slipping with contracts on the S&P 500 (-0.12%) and NASDAQ 100 (-0.18%) both slightly lower.

In central bank news, the People’s Bank of China (PBOC) Governor Yi Gang pledged to provide additional monetary support to the economy to recover from Covid outbreaks and lockdowns and other stresses. In a rare interview conducted in English, the central bank chief did caution though that the real interest rate is low thereby indicating limited room for large-scale monetary easing.

Turning to geopolitical developments, the G7 summit continued in Germany yesterday, and in a statement it said they would “further intensify our economic measures against Russia”. Separately, NATO announced that it will increase the number of high readiness forces to over 300,000, with the alliance’s leaders set to gather in Madrid from today. And we’re also expecting a new round of nuclear talks with Iran to take place at some point this week, something Henry mentioned in his latest Mapping Markets out yesterday (link here), which if successful could in time pave the way for Iranian oil to return to the global market.

Finally, whilst there were some decent May data releases from the US, the Dallas Fed’s manufacturing activity index for June fell to a 2-year low of -17.7 (vs. -6.5 expected).

To the day ahead now, and data releases include Germany’s GfK consumer confidence for July, French consumer confidence for June, whilst in the US there’s the FHFA house price index for April, the advance goods trade balance and preliminary wholesale inventories for May, as well as the Conference Board’s consumer confidence for June and the Richmond Fed’s manufacturing index. From central banks, we’ll hear from ECB President Lagarde, the ECB’s Lane, Elderson and Panetta, the Fed’s Daly, and BoE Deputy Governor Cunliffe. Finally, NATO leaders will be meeting in Madrid.

TUESDAY /MONDAY NIGHT

SHANGHAI CLOSED UP 30.03 PTS OR 0.89% //Hang Sang CLOSED UP 189.45 PTS OR 0.85% /The Nikkei closed UP 178.20 OR 0.66% //Australia’s all ordinaires CLOSED UP 0.87% /Chinese yuan (ONSHORE) closed DOWN 6.6947 /Oil UP TO 101.20 dollars per barrel for WTI and UP TO 117.02 for Brent. Stocks in Europe OPENED ALL GREEN // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.6947 OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.6962: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

3 a./NORTH KOREA/ SOUTH KOREA

///NORTH KOREA/SOUTH KOREA/

3B JAPAN

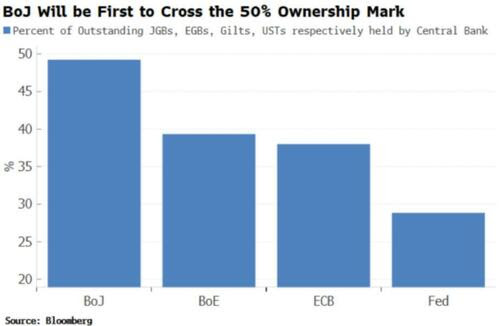

A big story: the Bank of Japan has now crossed the Rubicon and owns more than 50% of all bonds as they defend the yield curve. Something must suffer and that is the value of the yen. Sooner or later, the owners of the other 50% will bail leaving the country in shambles.

(zerohedge)

.

“The Rubicon Has Been Crossed”: The BOJ Now Owns More Than 50% Of All Japanese Bonds

MONDAY, JUN 27, 2022 – 09:35 PM

A little over three years ago, the Bank of Japan crossed a historic milestone when we reported that the central bank had become a top-10 shareholder in 50% of all Japanese companies. Since then, the central bank’s equity stake across Japanese corporations has only grown.

One week ago, we also reported that the BOJ was on the verge of crossing the final “50%” Rubicon, when as consequence of the latest surge in bond buying by Kuroda’s central bank meant to prevent the bank’s Yield Curve Control from collapsing, the BoJ was brought to a place it almost certainly never envisaged when it started QE as a “temporary” measure back in 2001 — owning virtually half of the JGB market.

As Bloomberg’s Simon White said last week, “we are in uncharted territory as no other major central bank has crossed this threshold before.“

He continued:

The BoJ could pass the 50% threshold as early as this week. That would be crossing the Rubicon. However you slice it or dice it, the BoJ will be the JGB market. What this means over the long term we’ll eventually find out. But it’s not a big leap to guess that private JGB holders — both domestic and foreign — will become less comfortable in a market with such lopsided ownership.

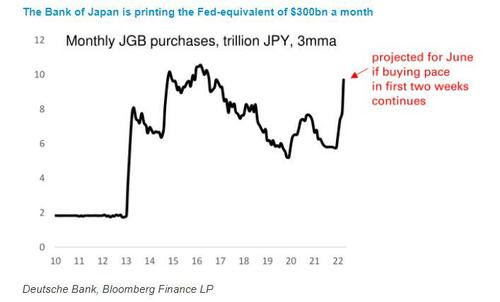

Well, as of today, this final threshold has also been crossed, thanks to the recent burst of YCC-defending debt monetization which reached a mindbogglging 11 trillion in the last week…

BoJ weekly purchases of government bonds. Holy moly pic.twitter.com/pz6e9KRn4z— Duncan Lamont (@DuncanLamont2) June 27, 2022

… and as Japan’s Nikkei reports, the share of Japanese government bonds held by the Bank of Japan just topped 50%, hitting a record Ponzi high.

According to Nikkei calculations, the BOJ purchased JGBs worth 14.8 trillion yen ($110 billion) in June, surpassing the 11.1 trillion yen purchased in November 2002, its largest monthly total. According to the QUICK database, the outstanding value of long-term JGBs as of June 20 totaled 1,021.1 trillion yen, of which the BOJ held 514.9 trillion yen on a face-value basis. That translates to 50.4% of the total amount outstanding, up from 50.0% in February to March 2021.

As we explained a few weeks ago, the BOJ has been buying up the majority of the JGBs on the market, an unusual situation that has caused distortions in the bond market including a deeply inverted yield curve.

Putting the BOJ’s unprecedented bond buying spree in context, the central bank’s JGB holdings were “only” in the 10% range when Gov. Kuroda started the massive monetary easing program in 2013. Its holdings have continued to grow as the ultraloose policy has continued. At this rate, all else equal, the BOJ will own the entire bond market in another decade or so.

Several years ago, the IMF calculated that the BOJ holding around 40% of the bond market would lead to a broken market. Well, it is now 50%+ and there are days when not a single trade crosses – the definition of a broken market.

The problem for the BOJ is that it can’t stop buying now… or ever: According to estimates by the Japan Center for Economic Research, the BOJ will need to increase its JGB holdings by 120 trillion yen from the current level of over 500 trillion yen to keep long-term interest rates at 0.25%. The central bank’s JGB holdings are quickly approaching and are expected to exceed 60% of total.

Until now, the BOJ has concentrated on specific JGBs, holding 87.6% of newly issued 10-year JGBs, a measure of long-term interest rates. However, at this rate it will soon run out of 10Y paper to buy and will be forced to move left and right on the ccurve.

Meanwhile, even though bonds with longer maturities have higher interest rates, as the BOJ has focused on the yield on 10-year JGBs to suppress interest rates, yields on JGBs with seven to nine years to maturity are now higher than those on 10-year JGBs.