y harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD PRICE CLOSE: UP $3.85 to $16453.55

SILVER PRICE CLOSE: UP $0.17 to $19.37

Access prices: closes : 4: 15 PM

Gold ACCESS CLOSE 1653.20

Silver ACCESS CLOSE: 19.36

New: early yesterday morning//

Bitcoin morning price: $19,287 DOWN 132

Bitcoin: afternoon price: $20,240 UP 821

Platinum price closing DOWN $0.85 AT $921.45

Palladium price; closing DOWN $37.25 at $1932.50

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD $2248.90 CDN DOLLARS PER OZ DOWN $13.61 CDN DOLLARS

BRITISH GOLD IN POUNDS: 1441,04 POUNDS PER OZ DOWN 19.72 BRITISH POUNDS PER OZ/

EURO GOLD: 1658.69EUROS PER OZ// DOWN 12.30 EUROS PER OZ///

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: OCTOBER 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,648.700000000 USD

INTENT DATE: 10/24/2022 DELIVERY DATE: 10/26/2022

FIRM ORG FIRM NAME ISSUED STOPPED

132 C SG AMERICAS 2

435 H SCOTIA CAPITAL 4

880 C CITIGROUP 2

TOTAL: 4 4

MONTH TO DATE: 23,307

JPMORGAN STOPPED 0/4

GOLD: NUMBER OF NOTICES FILED FOR OCT CONTRACT: 4 NOTICES FOR 400 OZ or 0.01264 TONNES

total notices so far: 23,307 contracts for 2,330,700 oz (72.494 tonnes)

SILVER NOTICES: 2 NOTICE(S) FILED FOR 10,000 OZ/

total number of notices filed so far this month 452 : for 2,260,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD UP $3.85

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//BIG CHANGES IN GOLD INVENTORY AT THE GLD: /////A SMALL DEPOSIT OF .29 TONNES INTO THE GLD//

INVENTORY RESTS AT 928.39 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP 17 CENTS

AT THE SLV// :/BIG CHANGES IN SILVER INVENTORY AT THE SLV//: A HUGE DEPOSIT OF 2.073 MILLION OZ INTO THE SLV

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 487.683 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A SMALL SIZED 237 CONTRACTS TO 137,971 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THE STRONG GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR $0.06 GAIN IN SILVER PRICING AT THE COMEX ON MONDAY. OUR BANKERS/HFT WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.06)., AND UNSUCCESSFUL IN KNOCKING OFF ANY SPEC LONGS, AS WE HAD A SMALL GAIN IN OUR TWO EXCHANGE OF 159 CONTRACTS. SOME SPECS CONTINUE TO ADD TO THEIR SHORTFALLS FROM WHICH OUR BANKERS CONTINUE TO BE PURCHASERS OF NET COMEX LONGS. SOME SPEC LONGS ADDED TO THEIR POSITIONS

WE MUST HAVE HAD:

I) ZERO SPECULATOR SHORT COVERINGS BUT SOME SHORT ADDITIONS ////CONTINUED BANKER OI COMEX ADDITIONS /// SOME NEWBIE SPEC LONG ADDITIONS. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A SMALL ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 1.580 MILLION OZ FOLLOWING AN 10,000 OZ QUEUE. JUMP / // V) SMALL SIZED COMEX OI LOSS/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: –21

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS OCT. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF OCT:

TOTAL CONTRACTS for 19days, total 56,255 contracts: 28.113. million oz OR 1.479MILLION OZ PER DAY. (295 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 28.113 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 27.940 MILLION OZ INITIAL

RESULT: WE HAD A SMALL SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 237 WITH OUR $0.06 GAIN IN SILVER PRICING AT THE COMEX// MONDAY.,. THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE CONTRACTS: 375 CONTRACTS ISSUED FOR DEC AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR OCT. OF 1.580 MILLION OZ FOLLOWED BY TODAY’S 10,000 QUEUE JUMP .. WE HAD A SMALL SIZED GAIN OF 138 OI CONTRACTS ON THE TWO EXCHANGES FOR 0.690 MILLION OZ..

WE HAD 2 NOTICE(S) FILED TODAY FOR 10,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A SMALL SIZED 3259 CONTRACTS TO 444,410 AND CLOSER TO FROM TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. WE WILL PROBABLY SEE THE COMEX OI FALL TO AROUND 380,000 AS OUR SPECS GET ANNIHILATED.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED -880 CONTRACTS.

.

THE FAIR SIZED INCREASE IN COMEX OI CAME DESPITE OUR SMALL LOSS IN PRICE OF $1.80//COMEX GOLD TRADING/MONDAY // MINOR SPECULATOR SHORT COVERINGS ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE./. WE HAD ZERO LONG LIQUIDATION AND CONSIDERABLE SPEC SHORT ADDITIONS BUT MAJOR SPEC SHORT COVERINGS. // CONTINUED ADDITIONS TO OUR BANKER LONGS!! THE COMEX WILL BLOW UP AS THE SPECS CANNOT DELIVER GOLD TO OUR BANKER LONGS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR OCT. AT 66.099 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE. JUMP OF 8200 OZ//NEW STANDING 73.679TONNES (QUEUE JUMPING = EXERCISING LONDON BASED EFP’S WILL CONTINUE UNTIL MONTH’S END)

YET ALL OF..THIS HAPPENED WITH OUR LOSS IN PRICE OF $1.80 WITH RESPECT TO MONDAY’S TRADING

WE HAD A GOOD SIZED GAIN OF 5450 OI CONTRACTS 16.95 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2191 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 444,410

IN ESSENCE WE HAVE A GOOD SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 5450 CONTRACTS WITH 3259 CONTRACTS DECREASED AT THE COMEX AND 2191 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 4570 CONTRACTS OR 14.214 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2191) ACCOMPANYING THE FAIR SIZED GAIN IN COMEX OI (3259): TOTAL GAIN IN THE TWO EXCHANGES 5450 CONTRACTS. WE NO DOUBT HAD 1) STRONG SPECULATOR SHORT ADDITIONS// CONTINUED GOOD BANKER ADDITIONS/// SOME SPEC SHORT COVERINGS// STRONG NEWBIE SPEC ADDITIONS ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR OCT. AT 66.099 TONNES FOLLOWED BY TODAY’S 8200 OZ QUEUE. JUMP ///NEW STANDING 73.736 TONNES//. 3) ZERO LONG LIQUIDATION //// //.,4) FAIR SIZED COMEX OPEN INTEREST GAIN 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

OCT

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF OCT. :

45,735 CONTRACTS OR 4,573,500 OZ OR 142.26 TONNES 19 TRADING DAY(S) AND THUS AVERAGING: 2407 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 19 TRADING DAY(S) IN TONNES: 142.26 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 142.25/3550 x 100% TONNES 4.00% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 142.25 TONNES INITIAL ( MUCH SMALLER THAN LAST MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW NON ACTIVE FRONT MONTH OF NOV. WE ARE NOW INTO THE SPREADING OPERATION OF BOTH SILVER AND GOLD (WILL BE SMALL AS SPREADERS DO NOT PAY ATTENTION TO NOVEMBER)

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF OCT HEADING TOWARDS THE NON ACTIVE DELIVERY MONTH OF NOV., FOR BOTH GOLD AND SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A SMALL SIZED 237 CONTRACT OI TO 137,971 AND FURTHER FROM OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 375 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 375 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 375 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 237 CONTRACTS AND ADD TO THE 375 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A SMALL SIZED GAIN OF 138 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 0.795 MILLION OZ//

OCCURRED DESPITE OUR GAIN IN PRICE OF $0.06

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)TUESDAY MORNING// MONDAY NIGHT

SHANGHAI CLOSED DOWN 1.27 PTS OR 0.04% //Hang Seng CLOSED DOWN 15.10 OR 0.10% /The Nikkei closed UP 275.38PTS OR 1.02% //Australia’s all ordinaires CLOSED UP 0.22% /Chinese yuan (ONSHORE) closed DOWN TO 7.3087 //OFFSHORE CHINESE YUAN DOWN 7.3632// /Oil DOWN TO 83.38 dollars per barrel for WTI and BRENT AT 92.03 / Stocks in Europe OPENED ALL MIXED. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A FAIR SIZED 3259 CONTRACTS TO 443,530 AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS SMALL COMEX INCREASE OCCURRED WITH OUR FALL IN PRICE OF $1.80 IN GOLD PRICING MONDAY’S COMEX TRADING. WE ALSO HAD A FAIR SIZED EFP (2191 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO MASSIVELY SHORT AND NOW THEY ARE DESPERATELY TRYING TO COVER THEIR FOLLY.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF OCT.. THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2191 EFP CONTRACTS WERE ISSUED: ;: , . 0 DEC : 2191 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2191 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A GOOD SIZED TOTAL OF 5450 CONTRACTS IN THAT 2191 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED COMEX OI GAIN OF 3259 CONTRACTS..AND THIS GOOD SIZED GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR SMALL LOSS IN PRICE OF GOLD $1.80//WE HAD SOME SPEC SHORTS ADDITIONS, WITH BANKERS AS BUYERS OF COMEX GOLD CONTRACTS. WE ALSO HAD SOME ADDITIONAL NEWBIE SPECS GOING LONG

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING OCT (73.736),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 73.736 TONNES

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $1.80) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS// SPEC SHORTS ADDED TO THEIR POSITIONS AS WE HAD A GOOD SIZED TOTAL GAIN ON OUR TWO EXCHANGES OF 2379 CONTRACTS // WE HAVE REGISTERED A FAIR GAIN OF 14.214 PAPER TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR OCT. (73.736 TONNES)…THIS WAS ACCOMPLISHED WITH OUR FALL IN PRICE OF $1.80

WE HAD +880 CONTRACTS COMEX TRADES ADDED. THESE WERE ADDED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 5450 CONTRACTS OR 545000 OZ OR 16.95 TONNES

Estimated gold volume 144,535// poor//

final gold volumes/yesterday 180,624/ poor

INITIAL STANDINGS FOR OCT ’22 COMEX GOLD //OCT 25

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 51,114.890oz Brinks Manfra Malca HSBC |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | nil oz |

| No of oz served (contracts) today | 4 notice(s) 400 OZ 0.01244 TONNES |

| No of oz to be served (notices) | 399 contracts 39900 oz 1.24105 TONNES |

| Total monthly oz gold served (contracts) so far this month | 23,307 notices 2,330,700 72.494 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total dealer deposit 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits nil oz

customer withdrawals:4

i) Out of Manfra: 7,233.975 oz 223 kilobars

ii) Out of Brinks 64.302 OZ (2 kilobars)

iii) Out of Malca 10,706.283 oz (333 kilobars)

iv) Out of HSBC: 33,110.330 oz

total: 51,114.890 oz

total in tonnes: 1.58 tonnes

Adjustments: 4// dealer to customer//huge activity

i)Delaware: 9477.273 oz

ii) Out of Brinks 64,719.963 oz

iii) Out of JPMorgan: 153m955.837 oz

iv) Out of Malca: 5,362.999 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR OCT.

For the front month of OCT we have an oi of 403 contracts having LOST 127 contracts . We had 145 contracts

filed on MONDAY, so we GAINED A STRONG 82 contracts or an additional 8200 oz will stand in this active delivery month of Oct. From this point

we should gain in total gold standing through to the end of Oct.( This is queue jumping and in reality it is the exercising of London based EFP;s for gold at the comex)

November LOST ONLY 7 contracts to stand at 3623 (WE ARE GOING TO HAVE AN EXTRAORDINARILY LARGE NOV.GOLD DELIVERY)

December LOST 2239 contracts DOWN to 356,241

We had 145 notice(s) filed today for 14,500 oz FOR THE OCT. 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 4 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the OCT /2022. contract month,

we take the total number of notices filed so far for the month (23,307) x 100 oz , to which we add the difference between the open interest for the front month of (OCT 403 CONTRACTS) minus the number of notices served upon today 4 x 100 oz per contract equals 2,370,600 OZ OR 73.736 TONNES the number of TONNES standing in this active month of OCT.

thus the INITIAL standings for gold for the OCT contract month:

No of notices filed so far (23,307) x 100 oz+ (403) OI for the front month minus the number of notices served upon today (4} x 100 oz} which equals 2,368,800 oz standing OR 73.736 TONNES in this NON active delivery month of OCTOBER.

TOTAL COMEX GOLD STANDING: 73.736 TONNES (A HUMONGOUS STANDING FOR OCT (GENERALLY THE POOREST DELIVERY MONTHS FOR AN ACTIVE MONTH)

WE WILL INCREASE IN GOLD TONNAGE STANDING FROM THIS DAY FORTH UNTIL THE END OF THE MONTH.

SOMEBODY IS AFTER A HUGE AMOUNT OF GOLD. THE EFPS ARE NOW BEING USED TO TAKE GOLD FROM THE COMEX. THUS THE AMOUNT OF GOLD STANDING FOR SEPT. WILL RISE EXPONENTIALLY.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 1,988,249.858 OZ 61.84 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 25,421,186.689 OZ

TOTAL REGISTERED GOLD: 11,631,353.307 OZ (361.78tonnes)..dropping fast

TOTAL OF ALL ELIGIBLE GOLD: 13,789,833,882 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 9,643,105 OZ (REG GOLD- PLEDGED GOLD) 299.94 tonnes//rapidly declining

END

SILVER/COMEX

OCT 25//INITIAL OCT SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1,552,996,026 oz Brinks Delaware CNT JPMorgan Loomis |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 1,843,443.096 oz Delaware HSBC Loomis |

| No of oz served today (contracts) | 2 CONTRACT(S) (10,000 OZ) |

| No of oz to be served (notices) | 233 contracts (1,165,000 oz) |

| Total monthly oz silver served (contracts) | 452 contracts 2,260,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 5 withdrawals out of the customer account

i) Out of CNT: 117,652.336 oz

ii) out of Brinks 184,973.400 oz

iii) Out of jPMorgan: 1,1162,015.900 oz

iv) Out of Delaware 8,152.950 oz

vi) Out of Loomis: 89,201.440 oz

Total withdrawals: 1,552,996.026 oz

JPMorgan has a total silver weight: 157.073million oz/303.0621million =51.81% of comex

Comex deposits: 3

i) Into Delaware 36,607.746 oz

ii)Into HSBC: 624,793.500 oz

iii) Into Loomis: 1,182,041.85 oz

total: 1,843k443.096 oz

adjustments: 2

Manfra: dealer to customer: 133,739.462 oz

Delaware customer to dealer 9,445.310 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 35.917 MILLION OZ (declining rapidly)

TOTAL REG + ELIG. 303.062 MILLION OZ (also declining)

CALCULATION OF SILVER OZ STANDING FOR SEPT

silver open interest data:

FRONT MONTH OF OCT OI: 235 CONTRACTS HAVING LOST4 CONTRACT(S.)

WE HAD 6 NOTICES FILED ON MONDAY SO WE GAINED 2

SILVER CONTRACTS OR AN ADDITIONAL 10,000 OZ WILL STAND FOR OCT.

NOVEMBER LOST 34 CONTRACTS TO STAND AT 258

DECEMBER SAW A LOSS OF 1587 CONTRACTS DOWN TO 109,050

.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 2 for 10,000 oz

Comex volumes:61,672// est. volume today// fair

Comex volume: confirmed yesterday: 88,347 contracts ( good)

To calculate the number of silver ounces that will stand for delivery in OCT we take the total number of notices filed for the month so far at 452 x 5,000 oz = 2,260,000 oz

to which we add the difference between the open interest for the front month of OCT(235) and the number of notices served upon today 2 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the OCT./2022 contract month: 452 (notices served so far) x 5000 oz + OI for front month of OCT (235) – number of notices served upon today (2) x 5000 oz of silver standing for the OCT contract month equates 3,425,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

Comex volumes:55,335// est. volume today// poor

Comex volume: confirmed yesterday: 64,723 contracts ( fair)

END

GLD AND SLV INVENTORY LEVELS

OCT 25/WITH GOLD UP $3.85: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 928.39 TONNES

OCT 24/WITH GOLD DOWN $1.80 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.89 TONNES FROM THE GLD////INVENTORY RESTS AT 928.10 TONNES

OCT 21/WITH GOLD UP $19.10: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 930.99 TONNES

OCT 20/WITH GOLD UP $2.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 6.08 TONNES FROM THE GLD///INVENTORY RESTS AT 932.73 TONNES

OCT 19/WITH GOLD DOWN $20.65:: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD////INVENTORY RESTS AT 938.81 TONNES

OCT 18/WITH GOLD DOWN $7.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 939.10 TONNES

OCT 17/WITH GOLD UP $14.55: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.28 TONNES FROM THE GLD///INVENTORY RESTS AT 941.13 TONNES

OCT 14/WITH GOLD DOWN $26.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FROM THE GLD///INVENTORY RESTS AT 944.31 TONNES

OCT 13/WITH GOLD DOWN $0.40 TODAY: A DEPOSIT OF 1.16 TONNES INTO THE GLD// CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 945.47 TONNES

OCT 12/WITH GOLD UP $4.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 944.31 TONNES

OCT 11/WITH GOLD UP $10.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 944.31 TONNES

OCT 10//WITH GOLD DOWN $33.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 944.31 TONNES

OCT 7/WITH GOLD DOWN $10.70: NO CHANGES IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 946.34 TONNES

OCT 6/WITH GOLD UP $.70 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.45 TONNES INTO THE GLD//INVENTORY RESTS AT 946.34 TONNES

OCT 4/WITH GOLD UP $28.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.19 TONNES INTO THE GLD//INVENTORY RESTS AT 942.89 TONNES

OCT 3.WITH GOLD UP $29.30 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD AND A BIG SURPRISE: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD////INVENTORY RESTS AT 939.70 TONNES

SEPT 30 WITH GOLD UP $3.75 TODAY : BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.01 TONNES FROM THE GLD////INVENTORY RESTS AT 941.15 TONNES

SEPT 29/WITH GOLD DOWN $.85 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.3 TONNES INTO THE GLD//INVENTORY RESTS AT 943.16 TONNES

SEPT 28/WITH GOLD UP $32.30: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FORM THE GLD////INVENTORY RESTS AT 940.549 TONNES

SEPT 27/WITH GOLD UP $1.75: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.76 TONNES FROM THE GLD////INVENTORY RESTS AT 943.47 TONNES

SEPT 26/WITH GOLD DOWN $17.15: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD////INVENTORY RESTS AT 947.23 TONNES

SEPT 23/WITH GOLD DOWN $24.60: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWALOF 2.03 TONNES FORM THE GLD//INVENTORY RESTS AT 950.13 TONNES

SEPT 22/WITH GOLD UP $5.20; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 952.16 TONNES

TONNES

GLD INVENTORY: 928.39 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

OCT 25/WITH SILVER UP 17 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.083 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 487.683 MILLION OZ/

OCT 24/WITH SILVER UP 6 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .553 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 485.610 MILLION OZ//

OCT 21/WITH SILVER UP 43 CENTS: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .46 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 486.163MILLION OZ//

OCT 20/WITH SILVER UP 33 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .921 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 485.703 MILLION OZ//

OCT 19/WITH SILVER DOWN 27 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: AWITHDRAWAL OF 1.105 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 486.624 MILLION OZ///

OCT 18/WITH SILVER DOWN 5 CENTS:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.658 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 487.729 MILLION OZ///

OCT 17/WITH SILVER UP 53 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.151 MILLION OZ INTO THE SLV////INVENTORY REST AT 486.071 MILLION OZ//

OCT 14/WITH SILVER DOWN 77 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.211 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 484.920 MILLION OZ//

OCT 13/WITH SILVER DOWN 2 CENTS TODAY: BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.513 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 482.709 MILLION OZ//

Oct 12/WITH SILVER DOWN 18 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.196 MILLION OZ

OCT 11/WITH SILVER DOWN 11 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.066 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 478.196 MILLION OZ

OCT 10//WITH SILVER DOWN 65 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 473.130 MILLION OZ/

OCT 7/WITH SILVER DOWN 37 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.447 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 473.130 MILLION OZ/

OCT 6/WITH SILVER UP 11 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY: A WITHDRAWAL OF 5.3 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 475.617 MILLION OZ//

OCT 4WITH SILVER UP $.51 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ

OCT 3/WITH SILVER UP $1.46 : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ//

SEPT 30/WITH SILVER UP 31 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.013 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ//

SEPT 29/WITH SILVER DOWN 15 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV//A WITHDRAWAL OF 645,000 OZ FROM THE SLV//INVENTORY RESTS AT 479.904 MILLION OZ//

SEPT 28/WITH SILVER UP $.52 TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 645,000 OZ FROM THE SLV.//INVENTORY RESTS AT 480.549 MILLION OZ//

SEPT 27/WITH SILVER DOWN 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 481.194 MILLION OZ

SEPT 26/WITH SILVER DOWN 43 CENTS : BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 737.000 OZ FROM THE SLV////INVENTORY RESTS AT 481.194 MILLION OZ//

SEPT 23/WITH SILVER DOWN 68 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .507 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 481.931 MILLION

SEPT 22/WITH SILVER UP 10 CENTS TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .691 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 481.424 MILLION OZ/

CLOSING INVENTORY 487.683 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

Peter Schiff: When The Sucker’s Rally Ends, The Dollar Will Crash

TUESDAY, OCT 25, 2022 – 03:34 PM

The world loves dollars. Whenever there is a problem, people flock to the dollar as a safe haven. But the US has problems of its own. In a podcast, Peter Schiff said America’s problems will eventually catch up to the dollar and at that point, the greenback will crash.

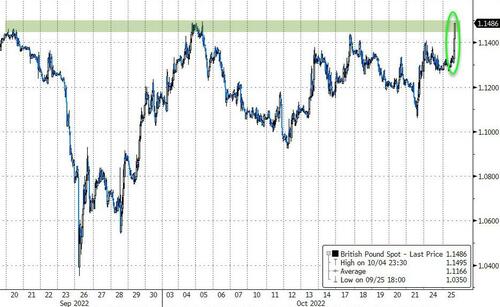

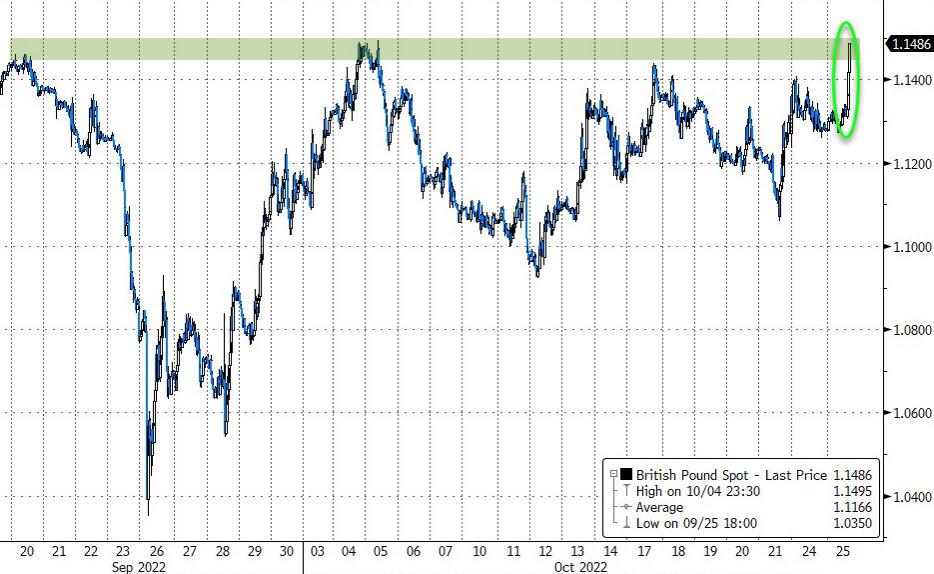

Former British Prime Minister Liz Truss blew into office promising tax cuts in the face of historically high inflation. On the one hand, the Bank of England has been raising interest rates – a contractionary monetary policy. But tax cuts with no corresponding spending cuts increase budget deficits – an inflationary fiscal policy. The British markets recognized this contradiction. The British pound tanked and plunged to a record low.

The government quickly backtracked on the tax cuts and Truss ended up stepping down.

This raises a question that US policymakers need to wrestle with. Why exactly were the British markets concerned about tax cuts?

As Peter pointed out, they were concerned about increasing debts. The debt to GDP ratio in Great Britain is already around 85%.

Now, that is a big number. It is a number that should cause concern. I think, really, anything above 50% of GDP is too big a number. So, because these tax cuts threatened to send British debt to GDP even higher, investors rightly dumped the pound.”

But what did they do?

They bought dollars.

They sold pounds for dollars. But they were selling pounds because Britain has a debt problem. The irony is they were buying dollars despite the fact that the United States has an even bigger debt problem.”

The US national debt pushed above $31 trillion in early October. And the US government continues to pile onto that number. Uncle Sam ran a $1.3 trillion deficit in fiscal 2022. The debt to GDP ratio in the US is already 125%.

And as Peter pointed out, it is actually higher than 125% when you factor in state and local debt. When you include state and municipal debt, the ratio balloons to 140%.

We’re in a much bigger fiscal mess than Great Britain. So, selling pounds and buying dollars because you’re worried that Britain has too much debt is jumping from the frying pan into the fire.”

Why are people doing this? Because there is a perception that US debt doesn’t matter because the dollar serves as the global reserve currency. Therefore, the US dollar is the go-to when there is a problem, even if the problem is bigger in the US. Peter recalled that when S&P downgraded US Treasuries, people bought US Treasuries because they were worried about the downgrade.

People bought US Treasuries as a safe haven from US Treasuries. That shows you how ridiculous it is.”

In the same way, it’s absurd to sell a country’s currency because you’re worried about debt and buy dollars when the US has even more debt.

It’s important to factor state and municipal debt into the equation in the US because all of these governments are funding themselves from the same tax base.

These governments are trying to get blood from the same turnips. Because Americans are broke. We have no savings. So, can we possibly repay this debt? Of course not. Repaying the debt is impossible. So, what’s going to happen? We’re going to default.”

Peter said there are two possible ways the US can default — the honest way or the dishonest way.

But either is a disaster if you own US Treasuries. The honest way is just to admit that we can’t pay and we default. We restructure the debt and we tell our creditors, ‘You are not going to get your money.’ But I don’t think politicians have the integrity to do that. They’re going to take the coward’s way out. They’re going to print. They’re going to inflate the debt away. That’s the only way out of this problem — monetize that debt and repudiate it through inflation, which is why it’s crazy for anyone to believe that the Fed is going succeed in reducing inflation back down to 2%. It can’t succeed.”

The government can’t inflate the debt away at 2% per year. They actually need higher inflation to handle the debt.

There’s another problem. The only reason the US government has been able to push the debt down the road for this long is that interest rates have been low. As rates go up, the problem gets bigger.

This is why Peter calls this a sucker’s rally. And when it ends, the dollar will crash.

END

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

END

3.Chris Powell of GATA provides to us very important physical commentaries

The huge stockpiles of copper is now gone as our two major traders , JPmorgan and ICBC Standard Bank have abandoned ship. Copper supplies nowhere to be find, exactly like zinc and identical to nickel

what a mess

(Bloomberg/Cang Farchy)

With Shanghai stockpile gone, copper market ‘like a room full of gunpowder’

Submitted by admin on Mon, 2022-10-24 09:35Section: Daily Dispatches

China’s Billion-Dollar Cash-for-Copper Trade Grinds to a Halt

Alfred Cang and Jack Farchy

Bloomberg News

via Yahoo News, Sunnyvale, California

Sunday, October 23, 2022

For the past 15 years the center of gravity of the global copper market has been a row of warehouses in Shanghai’s free-trade zone where the Yangtze River meets the Pacific.

Traders from London to Lima would obsess over the flows in and out of Shanghai’s huge bonded copper stockpile. It was the focal point for a multi-billion-dollar cash-for-copper trade, whereby Chinese companies would use metal as collateral for cheap financing. A cottage industry of analysts sprang up to estimate the size of what became the world’s largest cache of copper metal.

But now China’s bonded warehouses are all but empty. The once-frenetic flow of metal into the stockpile has come to a juddering halt as two dominant financiers of Chinese metals, JPMorgan Chase & Co. and ICBC Standard Bank, have halted new business there. Numerous traders and bankers interviewed by Bloomberg said they believe the trade is dead for now, and some predicted the bonded stocks could drop to zero, or close to it.

The implications are being felt across the market as the world’s largest copper consumer becomes more reliant on imports to meet its near-term needs at a time when global stocks are already at historically low levels. The Chinese copper market is at its tightest in more than a decade as traders pay massive premiums for immediate supplies.

For now, the miners, traders and financiers arriving in London this weekend for the annual LME Week jamboree are largely cautious on the near-term prospects for copper, given concerns about the global economy. But many in the market say they are braced for price spikes when the macroeconomic news eventually improves. And without its buffer of bonded stocks, any pickup in Chinese demand could have an explosive effect on the market.

“The physical market is so tight, it’s like a room full of gunpowder — any spark and the whole thing could blow,” said David Lilley, chief executive of hedge fund Drakewood Capital Management Ltd. Without the Shanghai bonded inventory, “we are living without a safety net.” …

… For the remainder of the report:

https://www.yahoo.com/now/china-billion-dollar-cash-copper-003010810.html

end

Ronan Manly is reporting what I have been seeing: the Comex is running out of silver fast. And Manly reports the same for the LBMA silver

(zerohedge)

Ronan Manly: LBMA and Comex running out of silver fast

Submitted by admin on Mon, 2022-10-24 19:51Section: Daily Dispatches

7:50p ET Monday, October 24, 2022

Dear Friend of GATA and Gold:

Bullion Star monetary metals analyst Ronan Manly writes today that silver inventories in the London Bullion Market Association system are at a record low, having fallen for 10 months straight, and that silver inventories at the New York Commodities Exchange are at a five-year low.

His analysis is headlined “Comex Deliverable Silver Far Less than Imagined as 50% of ‘Eligible’ Is Not Available” and it’s posted at Bullion Star here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Biden is now targeting Nicaragua’s gold

(Reuters)

U.S. mining sanctions take aim at Nicaragua’s gold

Submitted by admin on Mon, 2022-10-24 21:17Section: Daily Dispatches

By Tyler Clifford and Susan Heavey

Reuters

Monday, October 24, 2022

U.S. President Joe Biden’s administration today ratcheted up economic pressure on Nicaraguan President Daniel Ortega’s government through a series of steps targeting the country’s mining, gold, and other sectors.

Biden signed an executive order that includes the authority to ban U.S. companies from doing business in Nicaragua’s gold industry, while the U.S. Treasury Department imposed sanctions on Nicaragua’s mining authority, along with another top government official, the department said in a statement. …

… For the remainder of the report:

END

4. OTHER PHYSICAL SILVER/GOLD COMMENTARIES

END

5.OTHER COMMODITIES: DIESEL

COMMODITIES IN GENERAL/

END

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings TUESDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 7.3087

OFFSHORE YUAN: 7.3632

SHANGHAI CLOSED DOWN 1.27 PTS OR .04%

HANG SENG CLOSED DOWN 15.10 OR 0.10%

2. Nikkei closed UP 275.38 PTS OR 1.02%

3. Europe stocks SO FAR: ALL MIXED

USA dollar INDEX DOWN TO 111.93/Euro FALLS TO 0.98630

3b Japan 10 YR bond yield: RISES TO. +.250/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 148.89/JAPANESE YEN COLLAPSING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: DOWN -// OFF- SHORE: DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.2315%***/Italian 10 Yr bond yield FALLS to 4.454%*** /SPAIN 10 YR BOND YIELD FALLS TO 3.31%…** DANGEROUS//

3i Greek 10 year bond yield FALLS TO 4.73//

3j Gold at $1644.35//silver at: 18.93 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 22/100 roubles/dollar; ROUBLE AT 61.40//

3m oil into the 84 dollar handle for WTI and 92 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 148.89DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 1.0023– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9886well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.1670% DOWN 7 BASIS PTS…GETTING DANGEROUS

USA 30 YR BOND YIELD: 4.338% DOWN 2 BASIS PTS//

USA DOLLAR VS TURKISH LIRA: 18,61…GETTTING DANGEROUS

GREAT BRITAIN/10 YEAR YIELD: 3.7140%

end

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE

Futures Trade In Narrow Range Ahead Of Tech Giant Earnings

TUESDAY, OCT 25, 2022 – 08:10 AM

US equity futures erased modest earlier gains and traded modestly in the red, after rebounding from session lows as they struggled for direction while investors awaited major earnings reports and weighed last week’s conflicting comments from central bankers who are now in a blackout period. As of 7:30am, contracts on the S&P 500 dropped 0.1% to 3,803 after positive corporate results boosted the underlying index on Monday; on Tuesday, Coca-Cola, General Motors and United Parcel Service all beat analysts’ earnings estimates, while 3M and General Electric fell short. Alphabet Inc. and Microsoft Corp. are among major companies still reporting after the close. Nasdaq 100 futures were flat, with traders awaiting earnings after market hours from tech giants including Microsoft, Texas Instruments and Alphabet. Treasury yields tumbled for a second day and the dollar was steady even as the Yuan plunged to the lowest on record after the weakest PBOC fix since 2008.

“While the earnings season could still produce many surprises, the outcome so far is consistent with our advice to favor more defensive parts of the market, such as healthcare and consumer staples,” said Mark Haefele, chief investment officer at UBS Global Wealth Management.

In pre-market trading, US-listed Chinese stocks staged a limited rebound after losing almost $80 billion of market value in a record selloff that pushed the shares to their lowest level in over nine years. Major internet companies including Alibaba, JD.com and Pinduoduo gained at least 2% each. Facebook Meta Platforms was slightly weak after a global outage on its WhatsApp messaging service, while broker KeyBanc cut price targets on the stock, as well as on Alphabet, citing skepticism of revenue growth amid mounting concerns of a downturn in 2023. Here are some other notable premarket movers:

- Weber stock surged 22% in US premarket trading as BDT Capital Partners has proposed to buy the shares it doesn’t already own for $6.25 per share in cash.

- Mullen Automotive rose as much as 20% in US premarket trading, set to extend its four-day rising streak. Shares closed up by about a third on Monday after the firm secured exclusive sales rights for the I-GO electric vehicle, in select European markets.

- Taysha Gene Therapies shares surge as much as 60% in US premarket trading, putting the stock on track for a record gain, after Japanese pharmaceutical company Astellas Pharma said it will take a 15% stake in the US gene therapy developer for $50m.

- US-listed Chinese stocks rose in US premarket trading on Tuesday, following a rebound across Hong Kong peers which bounced back from Monday’s historic selloff. Alibaba (BABA US) +2.5%, Baidu (BIDU US) +2.9%, JD.com (JD US) +3.3%, Nio (NIO US) +2%, Li Auto (LI US) +3%, XPeng (XPEV US) +2.7%

- Linde shares dropped 1.9% in US premarket trading after the company said holders will vote on delisting shares from the Frankfurt Stock Exchange. The move would force Europe-only investors to sell their stakes, according to analysts.

- Packaging Corp shares fell 1.7% in US postmarket trading on Tuesday as the company’s 4Q guidance was lighter than expected, analysts said, pointing to weaker demand as the containerboard maker grapples with the impact of cost inflation, overshadowing a beat in 3Q adjusted earnings per share.

- Crown Holdings shares fell 9.4% in US after-hours trading on Monday with analysts pointing to a slowdown in demand as the main reason for the packaging products maker’s lowered guidance for both the 4Q and year, alongside a strong US dollar, higher European energy costs and increased interest expense.

- Keep an eye on Alphabet and Meta (META US) as their price targets were cut at KeyBanc, with the brokerage noting that investors are increasingly skeptical of revenue growth amid mounting concerns of a downturn in 2023.

- Watch Arista Networks stock as it was cut to neutral from outperform and PT slashed to a street-low $110 from $185 at Credit Suisse, with the broker seeing more challenging dynamics for the cloud networking group into 2023.

According to Bloomberg data, about a fifth of S&P 500 companies had posted third-quarter earnings before today, with more than half outperforming estimates. Still, investors are concerned the effects of a slowing economy will be felt further down the line, with the Fed set to raise interest rates next week even as the economy shows signs of flagging.

“What we’ve seen throughout the year is that equity risk premia have really compressed,” Christian Mueller-Glissmann, Goldman Sachs managing director for portfolio strategy, said on Bloomberg TV. “That makes you more vulnerable if you disappoint on growth, cash flows, et cetera. For now that hasn’t happened really, but all the lead indicators are pointing to risks in this direction.”

Manufacturing and services data for the US underwhelmed on Monday, indicating Federal Reserve rate hikes are beginning to slow activity. Fed officials have entered a blackout period ahead of the central bank’s meeting next week, where it’s expected to raise rates 75 basis points. Investors are starting to speculate that the central bank may be approaching the end of its aggressive tightening campaign.

“Investors are getting more confident that inflation will soften as the consumer rethinks massive purchases,” said Edward Moya, a senior markets analyst at OANDA Corp. “Fed rate-hike expectations will remain volatile, but expectations are growing that a weaker economy will let the Fed pause their tightening after the February policy meeting.”

“Even if optimism remains alive, investors are likely to need concrete evidence of monetary and economic improvements before driving stock indexes higher,” said Pierre Veyret, a technical analyst at ActivTrades. “Until then, it’s only investors buying rumours.”

In Europe, the Stoxx Europe 600 Index erased an early advance, with chemicals the worst-performing sector as Linde Plc dropped after proposing to de-list from the Frankfurt exchange. Spain’s IBEX outperforms peers, adding 0.5%, FTSE 100 lags, dropping 0.4%. Banks underperformed as the ECB considers curbing windfall profits from rising interest rates, while HSBC Holdings Plc plunged more than 7% after reporting higher-than-expected charges for possible loan losses. The most notable mover was Adidas, which slumps as much as 3.9%, sinking to lowest since March 2016 after the German sportswear company announced plans to end a partnership with Kanye West, while the firm also received a downgrade from Morgan Stanley. On the plus side, UBS Group AG buoyed financial services after it exceeded earnings estimates, while technology stocks climbed after software developer SAP SE’s third-quarter revenue beat. Here are all the notable European movers:

- SAP shares gained as much as 4.7% after the software firm reported 3Q revenue and operating profit ahead of estimates, helped by strong growth in its cloud business, with gross margin and backlog strong despite macro uncertainties.

- Air Liquide climbs as much as 4.7%, the most since March, after company delivered “strong set of results,” Stifel says in note as 3Q revenue beat estimates.

- UBS Group shares extend gains to as much as 6.0%, the most since June, after it reported net income for the third quarter that beat the average analyst estimate, driven by the investment bank and global wealth management divisions, which benefited from higher rates.

- Universal Music Group rises as much as 9.8%, the most since IPO in 2021, after Citi wrote that Apple’s price increase would “give comfort to UMG bulls.”

- Novartis shares shake off early losses to trade steady after the company released 3Q results that were broadly in line with expectations, with a small increase to the outlook for generics unit Sandoz a positive surprise, analysts say.

- Linde shares drop as much as 7.9%, the most intraday since February, after saying holders will vote on delisting shares from the Frankfurt Stock Exchange.

- HSBC shares drop as much as 8.2% in London, the most in six months, after the lender announced a change of chief financial officer and reported higher-than- expected loan loss charges in its third-quarter results.

- Alfa Laval drops as much as 11.3%, the most since May, as 3Q showed a “big margin miss,” impacted by weak trading in the Marine and Food & Water divisions, Citi writes.

- Viaplay shares drop as much as 31%, the most on record, after Nordic streaming company cut its guidance on slower growth in its Nordic business.

Earlier in the session, Asian stocks climbed, helped by a rebound in Chinese technology shares that followed Monday’s steep losses in the wake of the Communist Party congress. The MSCI Asia Pacific Index rose as much as 0.9% before paring the advance to 0.3%, boosted by gains in internet giants Alibaba and JD.com. A gauge of Chinese tech stocks erased an early loss of almost 3% to jump by a similar magnitude, as Alibaba Health and JD Health climbed. Tech and materials shares in the broader region fell. Benchmarks in Hong Kong and on the mainland whipsawed in volatile trading, closing marginally lower. Sentiment remains fragile after the dramatic selloff Monday following Xi Jinping’s move to secure his grip on power and amid ongoing concern over the nation’s Covid-zero policy.

“Without reopening, visibility on China’s economy and corporate earnings will remain very low, and risk-off trade in the stock market may continue,” BofA Securities strategists, including Winnie Wu, wrote in a note. Value stocks will likely outperform growth stocks, and the onshore market may outperform offshore, they added. China Budget Gap Widens to 7.16t Yuan as Covid, Property Weigh Vietnamese equities fell before reversing losses after the central bank unexpectedly raised interest rates by another one percentage point. Shares in Japan climbed for a second day amid optimism over corporate earnings and hopes for an eventual slowdown in Federal Reserve interest rate hikes.

“We’re certainly staying away from the Chinese market right now because the political scene is not favorable,” Laila Pence, president of Pence Wealth Management, said in an interview on Bloomberg TV. “There’s a lot less risk in the US and just as much upside.”

Japanese stocks climbed, following an extended rally in US peers, as investors assessed the potential for good corporate earnings amid continued monetary tightening by the Fed. The Topix rose 1.1% to close at 1,907.14, while the Nikkei advanced 1% to 27,250.28. Keyence Corp. contributed the most to the Topix Index gain, rising 2.9%. Out of 2,166 stocks in the index, 1,584 rose and 477 fell, while 105 were unchanged. Stocks are getting a boost from the potential slowdown of Fed interest rate hikes, and US earnings “are not that bad,” said Naoki Fujiwara, chief fund manager at Shinkin Asset Management. “Japanese earnings are not that bad as well, with the weak yen, and price pass-throughs have shown up this quarter so domestic-oriented companies are expected to perform better.”

Australia’s S&P/ASX 200 index rose 0.3% to close at 6,798.60, extending gains for a second day, as property and financial sectors supported the benchmark. Traders are also awaiting the unveiling of Australia’s budget later on Tuesday. The nation’s budget deficit in fiscal 2023 is forecast to be less than half the level anticipated by the previous administration in March, bolstered by windfall revenue from surging commodity prices. Read: Australia Budget Expected to Rock Stocks From Housing to Mining In New Zealand, the S&P/NZX 50 index rose 1.1% to 10,902.31.

In rates, treasuries traded at the best levels of the day into early US session, following wider gains across bunds where long-end of the curve is richer by up to 10bp. Treasuries rally led by intermediates, stretching 5s30s spread past 4bp and onto steepest levels since Sept. 13. Focal points of US session include start of auction cycle with 2-year at 1pm New York time. US yields richer by as much as 7bp across 5- to 7-year sector with 2s5s30s fly dropping 5bp as belly outperforms; 10-year yields around 4.1585% with bunds outperforming by 2.5bp and gilts underperforming by 2.5bp anticipating new Prime Minister Rishi Sunak’s fiscal plans over the coming days. German bonds rally ahead of the ECB rate decision this week, led by the long-end. Bunds 10-year yield down ~6.5bps to 2.26%. Peripheral spreads tighten to Germany with 10y BTP/Bund narrowing 5.2bps to 219.8bps. The US auction cycle includes $42b 2-year note followed by $43b 5-year Wednesday and $35b 7- year Thursday. WI 2-year around 4.455% is above auction stops since 2007 and ~16.5bp cheaper than last month’s, which tailed by 1.6bp.

In FX, the Bloomberg Dollar Spot Index steadied and the greenback traded mixed versus its Group-of-10 peers. Here’s how all other majors did:

- The pound led gains and UK government bonds advanced, led by the long end, as investors awaited more details on economic and fiscal policy from the incoming prime minister, who takes office later in the day.

- The euro erased gains, after rising toward $0.99 in Asian trading. Bunds extended yesterday’s advance, while Italian bonds stretched gains to a fourth session, the longest run since November 2021, as money markets pared ECB tightening bets ahead of Thursday’s policy outcome. Germany Oct. IFO business confidence index came in at 84.3 versus estimate 83.5.

- The yen was little changed as traders remained wary of further intervention by authorities, while a drop in US yields weighed on the greenback. Super-long government bonds rallied. Front-end volatility in dollar-yen retreats sharply as the latest round of Japanese intervention makes the case for tighter ranges.

- The Australian dollar inched up. Gains were tempered by elevated Covid case numbers in China and iron ore falling to its lowest level since November. The New Zealand dollar swung to a loss in European trading; the government said it’s made no decision yet on raising the minimum wage for the next year.

- The onshore yuan fell by the most among Asian peers to its lowest level since 2007 after the PBOC’s weaker fixing was interpreted by traders as a sign for a weaker currency. One-month implied volatility of USD/CNH rose to 10.46%, the highest on record in data back to 2011. China’s foreign exchange regulator is consulting some banks on positioning in the currency market as the yuan declines to the lowest levels since 2008, Reuters reports, citing unidentified people familiar with the matter. PBOC adjusted rules to allow companies to borrow more from overseas, enabling more foreign capital inflows at a time when the currency is plunging to fresh 2008 lows against the dollar.

In commodities, WTI trades within Monday’s range, falling 0.6% to near $84 with crude benchmarks pressured amid the general risk tone with sentiment slipping throughout the morning amid a resilient USD and Ifo pointing to a German recession. Currently, WTI and Brent Dec contracts are lower by just over 1% or USD 1/bbl and reside at session lows of USD 83.50/bbl and USD 92/bbl respectively. IEA’s Birol said the OPEC+ decision to cut output by 2mln BPD is a risky one especially as several economies are on the brink of recession; the Global LNG market to tighten further next year as European imports increase and China’s appetite may rebound, via Reuters.

Bitcoin is pressured but within a narrow USD 200 range that is itself a similar magnitude above the USD 19k mark.

Looking to the day ahead now and economic indicators in store will feature the Conference Board consumer confidence index for October, Richmond Fed manufacturing index and August FHFA house price index for the US. In Europe, we will get October Ifo survey for Germany and the Eurozone bank lending survey will also be published. The earnings line-up for today will be key, featuring most prominently Microsoft and Alphabet after the US market close. Earlier in the day, we will hear from Coca-Cola, General Electric, General Motors and UPS. Other notable names reporting will feature Visa, Novartis, Texas Instruments, Raytheon Technologies, HSBC, SAP, 3M, UBS, ADM, Valero Energy, Chipotle, Biogen, Halliburton, Spotify and Norsk Hydro.

Market Snapshot

- S&P 500 futures down 0.2% at 3,800.00

- STOXX Europe 600 up 0.2% to 402.68

- MXAP up 0.4% to 134.79

- MXAPJ little changed at 430.13

- Nikkei up 1.0% to 27,250.28

- Topix up 1.1% to 1,907.14

- Hang Seng Index little changed at 15,165.59

- Shanghai Composite little changed at 2,976.28

- Sensex down 0.1% to 59,750.45

- Australia S&P/ASX 200 up 0.3% to 6,798.62

- Kospi little changed at 2,235.07

- German 10Y yield down 2.6% at 2.27%

- Euro down 0.1% at $0.9863

- Brent Futures down 1.2% to $92.13/bbl

- Gold spot down 0.4% to $1,642.86

- U.S. Dollar Index little changed at 112.031

Top Overnight News from Bloomberg

- Two younger officials promoted to the Communist Party’s ranks are standing out as the most likely candidates to be tasked with steering the People’s Bank of China through challenging economic times

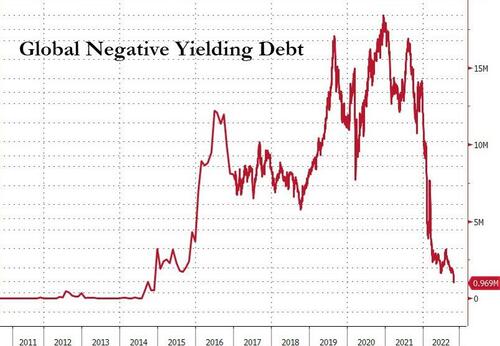

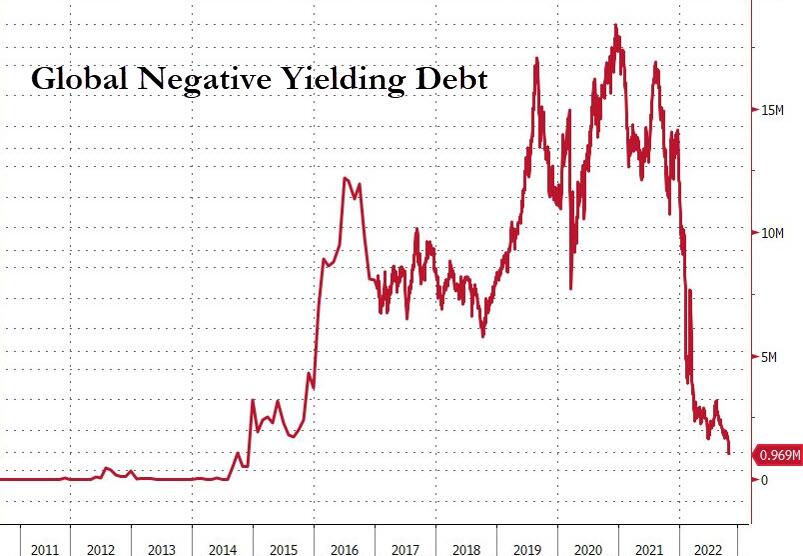

- The era of negative-yielding global bonds looks tantalizingly close to an end, with Japan’s two-year yield on the cusp of breaking above zero for the first time since 2015

- New Zealand’s central bank is “hopeful” that inflation has peaked, even though it was higher than anyone expected in the third quarter, Chief Economist Paul Conway said

- China’s central bank adjusted rules to allow companies to borrow more from overseas, enabling more foreign capital inflows at a time when the currency is plunging to fresh 2008 lows against the dollar

- The offshore yuan fell to a fresh record low after the People’s Bank of China loosened its grip on the tightly controlled fixing by setting the rate at the weakest level in 14 years

- New Zealand’s central bank is “hopeful” that inflation has peaked, even though it was higher than anyone expected in the third quarter, chief economist Paul Conway said

- Australia’s budget deficit in fiscal 2023 is set to be less than half the level anticipated by the previous administration in March, bolstered by windfall revenue from surging commodity prices

- Oil steadied as traders assessed near-term supply tightness in the crude market and broad appetite for risk assets including commodities

- WhatsApp Appears to Have Outage, With Thousands Reporting Issues

- US Stays China Course, Works on Biden Meeting as Xi Cements Grip

- Carney Addresses ‘Tension’ After Bankers Balked at CO2 Proposal

- Oil Steadies as Market Tightness Vies With Slowdown Concerns

- Fed Is Losing Billions, Wiping Out Profits That Funded Spending

- China Rout Puts Focus on Stocks With Foreign Holdings, BofA Says

- Carnival Unit Halts Asia Cruises as China Covid Zero Bites

- Xi Rewards Combat-Ready China Generals Amid Taiwan Tensions

- Warner Bros. Discovery Expects Billions in Restructuring Charges

- Barrack Testifies Trump Presidency Was ‘Disastrous’ for Him

- Sunak Expected to Keep Hunt as He Readies New UK Cabinet

- Tesla Options Hint at Trouble Ahead With Bets Around $200

- State Street’s CEO Says Private Credit Can Lower Risk for Banks

- VIX’s Tandem Swings With S&P 500 Show Options Obsession Persists

- What the Alzheimer’s Drug Breakthrough Means for Other Diseases

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks eventually traded higher following a firm lead from Wall Street, with the Chinese market experiencing a choppy session overnight. ASX 200 held onto gains as the clock ticks down for the unveiling of the Australian Federal Budget, with gains in the index led by financials, telecoms and healthcare. Nikkei 225 remained above the 27,000 mark as its manufacturing stocks kept the index buoyed. KOSPI was supported by the chip sector but gains were capped as South Korean President Yoon said North Korea has completed preparations for a seventh nuclear test, whilst South Korean consumer inflation expectations also ticked up from the prior month. Hang Seng and Shanghai Comp were volatile throughout the session and both indices swung between gains and losses with the former dipping under the 15,000 mark at one point – desks pointed to continued angst following the CCP National Congress. The indices later surged whilst there were unconfirmed reports of Chinese intervention in the stock market.

Top Asian News

- US Treasury Secretary Yellen is unaware of Japan’s FX intervention and Tokyo hasn’t informed them.

- PBoC relaxed cross-border funding by raising the macroprudential parameter to 1.25 from 1.

- PBoC injected CNY 230bln via 7-day reverse repos at a maintained rate of 2.00% for a daily injection of CNY 228bln

- China State Planner said China is to promote the expansion of foreign investments focusing on the manufacturing industry.

- Japan kept its overall economic view unchanged that the economy is picking up moderately, and added that “full attention” must be paid to market volatility. Govt raised Capex view for the first time in eight months; downgrades view on imports.

- Japanese Finance Minister Suzuki does not comment on daily forex moves, ready to take appropriate action on FX movements if necessary; watching FX with a high sense of urgency. Suzuki said they are in constant communication with US authorities and he is aware of US Treasury Secretary Yellen’s comments that she did not know about Japan’s intervention.

- Japanese government official citing BoJ Governor Kuroda said sharp one-sided JPY weakening is not desirable for the economy; BoJ will work closely with govt to monitor financial and currency market moves and their impact on Japan’s economy and prices

- Japanese PM Kishida is to appoint former Health Minister Goto as the new economy minister to replace Yamagiwa, via NHK.

- Japan FX intervention on October 24th has been estimated at JPY 700-900bln, according to calculation provided by a market source to Reuters.

- South Korean Oct 12-month consumer median inflation expectation 4.3% (prev. 4.2% in Sep), according to the BoK.

- RBNZ Chief Economist said the RBNZ anticipates that inflationary pressures will ease and notes that falling house prices are expected to slow consumption.

- Australian Federal Budget: 2022/23 budget deficit seen at 1.5% of GDP, 2023/24 seen at 1.8% of GDP, 2024/25 seen at 2.0% of GDP. Click here for full details.

European bourses are on the backfoot despite a firmer open as participants digest numerous heavyweight earnings and the latest Ifo ahead of key US prints; Euro Stoxx 50 -0.3%. Sectors post outperformance in Media and Tech following Apple’s pricing update and SAP +4.0%, respectively, while Chemicals are pressured as heavyweight Linde considers a Frankfurt delisting. Stateside, futures are pressured and having been moving in-tandem with European bourses as we look to heavyweight US names; ES -0.4%. United Parcel Service Inc (UPS) Q3 2022 (USD): EPS 2.96 (exp. 2.84), Revenue 24.2bln (exp. 24.32bln).

Top European News

- Sky News sources suggest Jeremy Hunt is to remain UK Chancellor, while Penny Mordaunt wants the Foreign Secretary job.

- BoE Chief Economist Pill says might have benefitted if “other institutions” had respected UK institutional framework in recent weeks.

- EU has warned that a price cap on natural gas will need the involvement of the UK and Switzerland for it to be effective, according to Bloomberg citing sources.

- German gov’t increases tax revenue forecast for 2022-2026 by EUR 110bln, via Handelsblatt.

FX

- DXY rangy around the 112.000 handle and Dollar mixed against major peers, Pound reclaims 1.1300+ status as new PM Sunak prepares to take the reins from Truss.

- Loonie lagging ahead of BoC policy meeting on Wednesday as WTI retreats further.

- Aussie hovers above 0.6300 vs the Buck post-as anticipated Budget.

- Euro remains confined between tight 0.9899-52 lines against the Greenback with little reaction to mixed Ifo and ECB lending surveys.

- PBoC set USD/CNY mid-point at 7.1668 vs exp. 7.1348 (prev. 7.1230); weakest since 2008

- China’s FX regulator surveyed banks regarding Yuan positioning as the currency tumbles, via Reuters citing sources.

- Turkish Finance Minister held a meeting with the bank association and senior executives on Monday, via Reuters citing sources; subsequently confirmed.

Fixed Income

- Bonds resume recovery rally as Bunds breach 137.00 and Bobls scale 119.00 irrespective of a weak 5 year auction.

- Gilts establish firmer foothold above 100.00 as new UK PM takes over the helm and US Treasuries flip from bear-steepening to bull-flattening ahead of 2 year note supply.

- German Finance Agency Diemer says volatility is making it harder for primary dealers to take risk in bidding within German auctions, via Reuters.

Commodities

- Crude benchmarks are pressured amid the general risk tone with sentiment slipping throughout the morning amid a resilient USD and Ifo pointing to a German recession.

- Currently, WTI and Brent Dec contracts are lower by just over 1% or USD 1/bbl and reside at session lows of USD 83.50/bbl and USD 92/bbl respectively.

- IEA’s Birol said the OPEC+ decision to cut output by 2mln BPD is a risky one especially as several economies are on the brink of recession; the Global LNG market to tighten further next year as European imports increase and China’s appetite may rebound, via Reuters.

- The European Commission is to discuss a proposal today for a permanent fix to decouple gas from electricity prices, according to Politico.

- Spot gold is tarnished by ongoing USD strength with the DXY remaining resilient around the 112.00 mark after a brief move below. As such, the yellow metal remains below the 10-DMA.

- Aluminium is faring better than the likes of copper at present and perhaps deriving some support from Norsk Hydro announcing it is to commence a partial curtailment of its Norwegian aluminium smelters

Geopolitical

- Russia will regard the use of a “dirty bomb” by Kyiv as an act of nuclear terrorism; Russia said it has not intended nor intends to use nuclear weapons in Ukraine, according to a letter cited by Reuters.

- US DoJ said four Chinese nationals, including three intelligence officials, have been charged in a spy recruitment campaign, according to Reuters.

- South Korean President Yoon said North Korea has completed preparations for a seventh nuclear test, via Yonhap.

US Event Calendar

- 09:00: Aug. S&P CS Composite-20 YoY, est. 14.05%, prior 16.06%

- S&P/CS 20 City MoM SA, est. -0.80%, prior -0.44%

- FHFA House Price Index MoM, est. -0.6%, prior -0.6%

- 10:00: Oct. Conf. Board Expectations, prior 80.3

- Conf. Board Present Situation, prior 149.6

- Conf. Board Consumer Confidenc, est. 106.0, prior 108.0

- 10:00: Oct. Richmond Fed Index, est. -5, prior 0

DB’s Jim Reid concludes the overnight wrap

I’m off to New York this morning as soon as I press send on this. I’ve been told that the kids are queueing up to replace me and sleep on my side of the bed when I’m gone. So much so that I’m not sure I’ll get my old slot back! It’ll be my first visit to NY since just prior to the pandemic. That’s a lot of missing products from the Apple store to make up for. However Sterling’s fall, and inflation since then will likely temper my enthusiasm for the new iPad out on Thursday!

Talking of inflation, this morning we’ve just put out a note looking at what normally happens next when inflation hits 8% through history using 50 DM and EM countries, around 320 unique observations and covering up to a 100 years of data. With consensus being so bad at predicting inflation in this cycle we thought we’d look at what history says. Without too many spoilers, it would be unusual to see inflation now fall back as quickly as consensus believes over the next 2 years. In fact using data from the last 50 years (the fiat money era) current consensus forecasts would be in the most optimistic decile of observations over this period. Whether consensus or the median observation through history is correct will have profound implications for assets over the next few months and years. See the short report here for more.

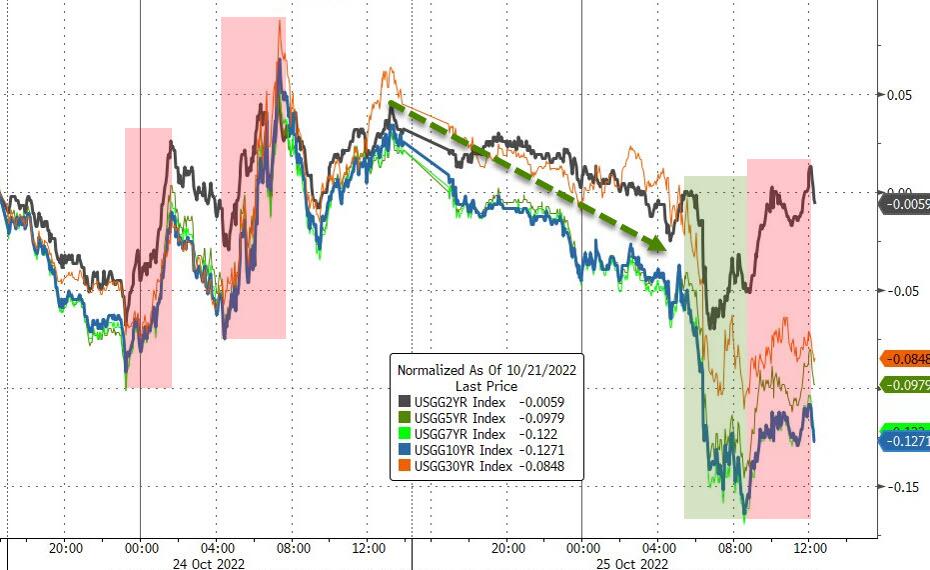

On a related subject, we wondered in yesterday’s EMR whether the WSJ article on Friday would mark the 6th attempt this year to try to pre-empt a Fed pivot after Friday’s reaction to the story. The reality is though that there hasn’t been enough follow-through in US rates pricing yesterday for this to yet qualify as a 6th attempt. In fact, we saw a part reversal of Friday’s move yesterday. Indeed, even with a monster rally in UK bonds, US rates edged back up with 2 and 10yr yields +4.5bps and +3.2bps, respectively. Implied rates from the December 2022 – July 2023 Fed contracts increased c.+2-6bps. In Asia, 2yr and 10yr UST are back -1.2bps and -4bps lower, respectively, though.

Gilts have been the standout rates mover over the last 24 hours though with 2yr and 10yrs around -37bps and -31bps lower yesterday as Rishi Sunak’s path to PM was cleared by all others dropping out. 2yr notes had their largest gain in nearly 30 years. Sunak will be formally appointed today. The rates repricing has also tempered expectations of BoE hikes beyond the next couple of meetings, amid hopes for greater fiscal discipline, with the June 23 contract falling 21bps. For further reference, from morning trading just before the mini-budget on September 23rd, 2yr, 10yr and 30yr gilts are now -15.1bps, +24.8bps and -1.5bps, respectively, with GBP c.1% higher. A massive round trip. Interestingly, 10yr UST and 10yr Bunds are +51bps and +40bps over the exact same period, so Gilts have outperformed.

Although US rates haven’t followed through on Friday’s price action, European equivalents followed Gilts and perhaps reacted to weak PMIs (more below) and the UK move more. 10yr Bunds (-8.4bps), OATs (-11.0bps) and BTPs -16.4bps rallied hard. 2yr yields also declined (-4.2bps in Germany, -4.3bps in France and -12.2 in Italy) ahead of the ECB’s meeting on Thursday.

US stocks carried on their recent bounce, shrugging off weak PMIs there too, with the S&P 500 (+1.19%) and Dow Jones (+1.34%) finishing in the green for the day amid gains in health care (+1.91%), IT (+1.38%) and staples (+1.79%). Only two sectors ended up with losses on the day – real estate (-0.1%) and materials (-0.62%) – and 82% of S&P 500 members were in the green. News of Tesla (-1.49%) lowering prices on its cars sold in China amid competitive pressures weighed on the Nasdaq (+0.86%) as well. Watch out for an upcoming 48-hour blitz of tech earnings with 20% of the S&P 500 market cap reporting across 5 names. We have Microsoft, Alphabet (after hours today), Meta (tomorrow) and Apple and Amazon (Thursday).

European equities also rallied amid a -15% fall in European natural gas prices to a below the 100 euro mark for the first time since June amid milder weather (not on my weekend break away!!) and good storage metrics. Indeed, “next hour” delivery TTF gas contracts briefly traded in negative territory yesterday having been over €300 in late August. With storage nearly full and the weather warm, there is very limited immediate delivery demand. This doesn’t change the medium-term problems but for now there’s a glut of near-term gas. The Stoxx 600 rallied +1.40%, led by utilities (+2.68%) and IT (+2.20%), with no sector in the red on the day. Bourses of Spain (IBEX +1.79%) and Italy (FTSE MIB +1.93%) were the relative outperformance but the DAX (+1.58%) and CAC 40 (+1.59%) also posted solid gains.

That’s it for the good news as the global flash PMIs painted a rather bleak picture on both sides of the Atlantic. Perhaps the most glaring miss was that for the US, with the manufacturing gauge (49.9) sliding into contractionary territory for the first time since June 2020 from September’s 52.0 reading and way off the 51.0 median estimate on Bloomberg. The services PMI reading disappointed even more, falling to 46.6 from 49.3 and defying expectations of a mild rebound to 49.5. Adding to the gloom, the employment component of the index fell to 49.4 from 52.2 and business expectations contracted to 57.4 (vs 66.7), the lowest since June and September of 2020, respectively. A silver lining came from a fall in input prices in the manufacturing PMI (63.9 vs 65.2), the lowest level since November 2020, although the measure crept higher for services (68.5 vs 67.7). Overall, this meant a fourth month in a row of being in contractionary theory for the composite.