OCT 24/GOLD CLOSED DOWN $1.80 TO $1649.70//SILVER CLOSED UP 6 CENTS TO $19.23//PLATINUM WAS DOWN $12.35 TO $922.25//PALLADIUM WAS DOWN $48,50 TO $1969.75//COVID UPDATES//DR PAUL ALEXANDER//VACCINE IMPACT//VACCINE INJURIES//UK UPDATES: SUNAK THE LIKELY PRIME MINISTER//CHINESE MARKETS TUMBLE ON THE CERITIFICATION OF XI’S 3RD TERM WITH MORE STRINGENT REFORMS//JAPAN CENTRAL BANK INTERVENS AGAIN WITH 50 BILLIONS WORTH OF YEN PURCHASES AND THIS FAILS AGAIN//LOOKS LIKE 26 MILLION BRITS WILL ENTER ENERGY POVERTY//BOLEN: AN EXCELLENT COMMENTARY SUGGESTING WHY THE ECB AND THEIR CENTRAL BANKS ARE IN TROUBLE//MASSIVE MISSILE STRIKES HIT MAJOR UKRAINE CITIES THROWING THEM INTO DARKNESS/AMERICAN EXPRESS PLACES HUGE AMOUNT INTO BAD LOSS PROVISIONS INDICATING EVEN THE WEALTHY ARE SUFFERING//HUGE DOWNFALL IN BOTH THE USA PMI’S //SWAMP STORIES FOR YOU TONIGHT///

323 C HSBC 6 435 H SCOTIA CAPITAL 130 657 C MORGAN STANLEY 9 661 C JP MORGAN 13 732 C RBC CAP MARKETS 17 880 C CITIGROUP 109 905 C ADM 6

TOTAL: 145 145 MONTH TO DATE: 23,303

JPMORGAN STOPPED 13/145

GOLD: NUMBER OF NOTICES FILED FOR OCT CONTRACT: 145 NOTICES FOR 14,500 OZ or 0.45101 TONNES

total notices so far: 23,303 contracts for 2,330,300 oz (72.480 tonnes)

SILVER NOTICES: 6 NOTICE(S) FILED FOR 30,000 OZ/

total number of notices filed so far this month 450 : for 2,250,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD DOWN $1.80

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//BIG CHANGES IN GOLD INVENTORY AT THE GLD: /////A WITHDRAWAL OF 2.89 TONNES INTO THE GLD//

INVENTORY RESTS AT 928.10 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP 6 CENTS

AT THE SLV// :/BIG CHANGES IN SILVER INVENTORY AT THE SLV//: A SMALL WITHDRAWAL OF .563 MILLION OZ INTO THE SLV

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 485.610 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A STRONG SIZED 782 CONTRACTS TO 138,208 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THE STRONG GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR $0.43 GAIN IN SILVER PRICING AT THE COMEX ON FRIDAY. OUR BANKERS/HFT WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.43)., AND UNSUCCESSFUL IN KNOCKING OFF ANY SPEC LONGS, AS WE HAD A HUGE GAIN IN OUR TWO EXCHANGE OF 1101 CONTRACTS. HUGE NUMBERS OF SPECS CONTINUE TO ADD TO THEIR SHORTFALLS FROM WHICH OUR BANKERS CONTINUE TO BE PURCHASERS OF NET COMEX LONGS. SOME SPEC LONGS ADDED TO THEIR POSITIONS

WE MUST HAVE HAD: I) ZERO SPECULATOR SHORT COVERINGS BUT CONSIDERABLE SHORT ADDITIONS ////CONTINUED BANKER OI COMEX ADDITIONS /// SOME NEWBIE SPEC LONG ADDITIONS. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A SMALL ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 1.580 MILLION OZ FOLLOWING AN 5,000 OZ QUEUE. JUMP / // V) STRONG SIZED COMEX OI GAIN/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: +21

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS OCT. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF OCT:

TOTAL CONTRACTS for 18 days, total 55,880 contracts: 27.940 million oz OR 1.522MILLION OZ PER DAY. (310 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 27.940 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 27.940 MILLION OZ INITIAL

RESULT: WE HAD A STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 782 WITH OUR $0.43 GAIN IN SILVER PRICING AT THE COMEX// THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE CONTRACTS: 340 CONTRACTS ISSUED FOR DEC AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR OCT. OF 1.580 MILLION OZ FOLLOWED BY TODAY’S 5,000 QUEUE JUMP .. WE HAD A HUGE SIZED GAIN OF 1101 OI CONTRACTS ON THE TWO EXCHANGES FOR 5.505 MILLION OZ..

WE HAD 6 NOTICE(S) FILED TODAY FOR 30,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A FAIR SIZED 2896 CONTRACTS TO 441,151 AND FURTHER FROM TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. WE WILL PROBABLY SEE THE COMEX OI FALL TO AROUND 380,000 AS OUR SPECS GET ANNIHILATED.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED -220 CONTRACTS.

.

THE FAIR SIZED DECREASE IN COMEX OI CAME DESPITE OUR STRONG GAIN IN PRICE OF $19.10//COMEX GOLD TRADING/FRIDAY // CONSIDERABLE SPECULATOR SHORT COVERINGS ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE./. WE HAD ZERO LONG LIQUIDATION AND MINOR SPEC SHORT ADDITIONS BUT MAJOR SPEC SHORT COVERINGS. // CONTINUED ADDITIONS TO OUR BANKER LONGS!! THE COMEX WILL BLOW UP AS THE SPECS CANNOT DELIVER GOLD TO OUR BANKER LONGS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR OCT. AT 66.099 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE. JUMP OF 15,800 OZ//NEW STANDING 73.679TONNES (QUEUE JUMPING = EXERCISING LONDON BASED EFP’S WILL CONTINUE UNTIL MONTH’S END)

YET ALL OF..THIS HAPPENED WITH OUR GAIN IN PRICE OF $19.10 WITH RESPECT TO THURSDAY’S TRADING

WE HAD A TINY SIZED GAIN OF 82 OI CONTRACTS 0.255 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2978 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 441,371

IN ESSENCE WE HAVE A TINY SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 82 CONTRACTS WITH 2896 CONTRACTS DECREASED AT THE COMEX AND 2978 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 82 CONTRACTS OR 0.255 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2978) ACCOMPANYING THE FAIR SIZED LOSS IN COMEX OI (2896): TOTAL GAIN IN THE TWO EXCHANGES 82 CONTRACTS. WE NO DOUBT HAD 1) STRONG SPECULATOR SHORT ADDITIONS// CONTINUED GOOD BANKER ADDITIONS/// CONSIDERABLE SPEC SHORT COVERINGS// STRONG NEWBIE SPEC ADDITIONS ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR OCT. AT 66.099 TONNES FOLLOWED BY TODAY’S 15,800 OZ QUEUE. JUMP ///NEW STANDING 73.679 TONNES//. 3) ZERO LONG LIQUIDATION //// //.,4) FAIR SIZED COMEX OPEN INTEREST LOSS 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

OCT

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF OCT. :

43,544 CONTRACTS OR 4,354,400 OZ OR 135.440 TONNES 18 TRADING DAY(S) AND THUS AVERAGING: 2419 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 18 TRADING DAY(S) IN TONNES: 135.44 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 135.44/3550 x 100% TONNES 3.83% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 135.44 TONNES INITIAL ( MUCH SMALLER THAN LAST MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW NON ACTIVE FRONT MONTH OF NOV. WE ARE NOW INTO THE SPREADING OPERATION OF BOTH SILVER AND GOLD (WILL BE SMALL AS SPREADERS DO NOT PAY ATTENTION TO NOVEMBER)

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF OCT HEADING TOWARDS THE NON ACTIVE DELIVERY MONTH OF NOV., FOR BOTH GOLD AND SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A STRONG SIZED 782 CONTRACT OI TO 138,187 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 340 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 340 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 340 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 761 CONTRACTS AND ADD TO THE 340 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE SIZED GAIN OF 1122 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 5.610 MILLION OZ//

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)MONDAY MORNING// SUNDAY NIGHT

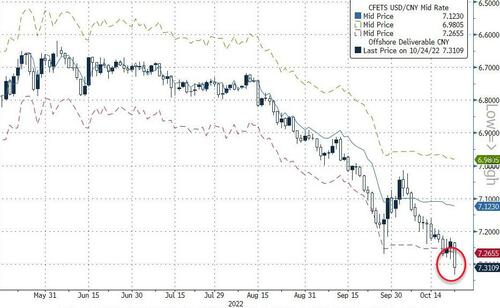

SHANGHAI CLOSED DOWN 61.37 PTS OR 2.03% //Hang Seng CLOSED DOWN 1,030.43 OR 6.36% /The Nikkei closed UP 84.32PTS OR 0.31% //Australia’s all ordinaires CLOSED UP 1.54% /Chinese yuan (ONSHORE) closed DOWN TO 7.2626 //OFFSHORE CHINESE YUAN DOWN 7.3184// /Oil DOWN TO 84,08 dollars per barrel for WTI and BRENT AT 92.69 / Stocks in Europe OPENED ALL GREEN. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 2896 CONTRACTS TO 441,151 AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS SMALL COMEX INCREASE OCCURRED WITH OUR RISE IN PRICE OF $19.10 IN GOLD PRICING FRIDAY’S COMEX TRADING. WE ALSO HAD A FAIR SIZED EFP (2978 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO MASSIVELY SHORT AND NOW THEY ARE DESPERATELY TRYING TO COVER THEIR FOLLY.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF OCT.. THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2978EFP CONTRACTS WERE ISSUED: ;: , . 0 DEC : 2978 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2978 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A SMALL SIZED TOTAL OF 82 CONTRACTS IN THAT 2978LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED COMEX OI LOSS OF 2896 CONTRACTS..AND THIS TINY SIZED GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR HUGE GAIN IN PRICE OF GOLD $19.10//WE HAD SOME SPEC SHORTS ADDITIONS, WITH BANKERS AS BUYERS OF COMEX GOLD CONTRACTS. WE ALSO HAD SOME ADDITIONAL NEWBIE SPECS GOING LONG WITH NEWS OF ADDITIONAL DOLLARS SENT TO THE SWISS NATIONAL BANK.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING OCT (73.699),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 73.669 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $19.10) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS// SPEC SHORTS ADDED TO THEIR POSITIONS AS WE HAD A TINY SIZED TOTAL GAIN ON OUR TWO EXCHANGES OF 302 CONTRACTS // WE HAVE REGISTERED A FAIR GAIN OF 0.2550 PAPER TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR OCT. (73.699 TONNES)…THIS WAS ACCOMPLISHED WITH OUR RISE IN PRICE OF $19.10

WE HAD -220 CONTRACTS COMEX TRADES REMOVED. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 82 CONTRACTS OR 8200 OZ OR 0.255 TONNES

Total monthly oz gold served (contracts) so far this month

23,303 notices 2,330,300 72.48 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

xxx oz

total dealer deposit 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 1

i)Into Brinks: 104.789 IZ

total deposits 104.789 oz

customer withdrawals:2

i) Out of Manfra: 14.789 IZ

ii) Out of Brinks 113,258.856 OZ

total: 113,258.856 oz

total in tonnes: 3.52 tonnes

Adjustments: 4// dealer to customer

i)hsbc: 3472.308 oz

ii) Out of Brinks 34,144.362 oz

iii) Out of JPMorgan: 2314.872 oz

iv) Out of Malca: 24,402.609 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR OCT.

For the front month of OCT we have an oi of 530 contracts having LOST 550 contracts . We had 708 contracts

filed on FRIDAY, so we GAINED A STRONG 158 contracts or an additional 15,800 oz will stand in this active delivery month of Oct. From this point

we should gain in total gold standing through to the end of Oct.( This is queue jumping and in reality it is the exercising of London based EFP;s for gold at the comex)

November GAINED 63 contracts to stand at 3630 (WE ARE GOING TO HAVE AN EXTRAORDINARILY LARGE NOV.GOLD DELIVERY)

December LOST 4822 contracts up to 358,480

We had 145 notice(s) filed today for 14,500 oz FOR THE OCT. 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 145 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 13 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the OCT /2022. contract month,

we take the total number of notices filed so far for the month (23,303) x 100 oz , to which we add the difference between the open interest for the front month of (OCT 530 CONTRACTS) minus the number of notices served upon today 145 x 100 oz per contract equals 2,368,800 OZ OR 73.679 TONNES the number of TONNES standing in this active month of OCT.

thus the INITIAL standings for gold for the OCT contract month:

No of notices filed so far (23,303) x 100 oz+ (530) OI for the front month minus the number of notices served upon today (145} x 100 oz} which equals 2,368,800 oz standing OR 73.699 TONNES in this NON active delivery month of OCTOBER.

TOTAL COMEX GOLD STANDING: 73.699 TONNES (A HUMONGOUS STANDING FOR OCT (GENERALLY THE POOREST DELIVERY MONTHS FOR AN ACTIVE MONTH)

WE WILL INCREASE IN GOLD TONNAGE STANDING FROM THIS DAY FORTH UNTIL THE END OF THE MONTH.

SOMEBODY IS AFTER A HUGE AMOUNT OF GOLD. THE EFPS ARE NOW BEING USED TO TAKE GOLD FROM THE COMEX. THUS THE AMOUNT OF GOLD STANDING FOR SEPT. WILL RISE EXPONENTIALLY.

To calculate the number of silver ounces that will stand for delivery in OCT we take the total number of notices filed for the month so far at 450 x 5,000 oz = 2,250,000 oz

to which we add the difference between the open interest for the front month of OCT(239) and the number of notices served upon today 6 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the OCT./2022 contract month: 450 (notices served so far) x 5000 oz + OI for front month of OCT (239) – number of notices served upon today (6) x 5000 oz of silver standing for the OCT contract month equates 3,415,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

OCT 24/WITH GOLD DOWN $1.80 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.89 TONNES FROM THE GLD////INVENTORY RESTS AT 928.10 TONNES

OCT 21/WITH GOLD UP $19.10: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 930.99 TONNES

OCT 20/WITH GOLD UP $2.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 6.08 TONNES FROM THE GLD///INVENTORY RESTS AT 932.73 TONNES

OCT 19/WITH GOLD DOWN $20.65:: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD////INVENTORY RESTS AT 938.81 TONNES

OCT 18/WITH GOLD DOWN $7.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 939.10 TONNES

OCT 17/WITH GOLD UP $14.55: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.28 TONNES FROM THE GLD///INVENTORY RESTS AT 941.13 TONNES

OCT 14/WITH GOLD DOWN $26.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FROM THE GLD///INVENTORY RESTS AT 944.31 TONNES

OCT 13/WITH GOLD DOWN $0.40 TODAY: A DEPOSIT OF 1.16 TONNES INTO THE GLD// CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 945.47 TONNES

OCT 12/WITH GOLD UP $4.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 944.31 TONNES

OCT 11/WITH GOLD UP $10.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 944.31 TONNES

OCT 10//WITH GOLD DOWN $33.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 944.31 TONNES

OCT 7/WITH GOLD DOWN $10.70: NO CHANGES IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 946.34 TONNES

OCT 6/WITH GOLD UP $.70 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.45 TONNES INTO THE GLD//INVENTORY RESTS AT 946.34 TONNES

OCT 4/WITH GOLD UP $28.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.19 TONNES INTO THE GLD//INVENTORY RESTS AT 942.89 TONNES

OCT 3.WITH GOLD UP $29.30 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD AND A BIG SURPRISE: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD////INVENTORY RESTS AT 939.70 TONNES

SEPT 30 WITH GOLD UP $3.75 TODAY : BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.01 TONNES FROM THE GLD////INVENTORY RESTS AT 941.15 TONNES

SEPT 29/WITH GOLD DOWN $.85 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.3 TONNES INTO THE GLD//INVENTORY RESTS AT 943.16 TONNES

SEPT 28/WITH GOLD UP $32.30: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FORM THE GLD////INVENTORY RESTS AT 940.549 TONNES

SEPT 27/WITH GOLD UP $1.75: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.76 TONNES FROM THE GLD////INVENTORY RESTS AT 943.47 TONNES

SEPT 26/WITH GOLD DOWN $17.15: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD////INVENTORY RESTS AT 947.23 TONNES

SEPT 23/WITH GOLD DOWN $24.60: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWALOF 2.03 TONNES FORM THE GLD//INVENTORY RESTS AT 950.13 TONNES

SEPT 22/WITH GOLD UP $5.20; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 952.16 TONNES

SEPT 21/WITH GOLD UP $4.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.79 TONNES FROM THE GLD///INVENTORY RESTS AT 952.16 TONNES

SEPT 20/WITH GOLD DOWN $6.65; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD////INVENTORY RESTS AT 957.95 TONNES

SEPT 19/WITH GOLD DOWN $4.80: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONES FROM THE GLD//INVENTORY RESTS AT 960.85 TONNES

SEPT 16.WITH GOLD UP $5.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT 1,45 TONNES INTO THE GLD//INVENTORY RESTS AT 962.01 TONNES

SEPT 15/WITH GOLD DOWN $30.20: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.35 TONNES FROM THE GLD.//INVENTORY RESTS AT 960.56 TONNES

SEPT 14/WITH GOLD DOWN $7.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY REST AT 962.88 TONNES

GLD INVENTORY: 928.10 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

OCT 24/WITH SILVER UP 6 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .553 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 485.610 MILLION OZ//

OCT 21/WITH SILVER UP 43 CENTS: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .46 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 486.163MILLION OZ//

OCT 20/WITH SILVER UP 33 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .921 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 485.703 MILLION OZ//

OCT 19/WITH SILVER DOWN 27 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: AWITHDRAWAL OF 1.105 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 486.624 MILLION OZ///

OCT 18/WITH SILVER DOWN 5 CENTS:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.658 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 487.729 MILLION OZ///

OCT 17/WITH SILVER UP 53 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.151 MILLION OZ INTO THE SLV////INVENTORY REST AT 486.071 MILLION OZ//

OCT 14/WITH SILVER DOWN 77 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.211 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 484.920 MILLION OZ//

OCT 13/WITH SILVER DOWN 2 CENTS TODAY: BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.513 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 482.709 MILLION OZ//

Oct 12/WITH SILVER DOWN 18 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.196 MILLION OZ

OCT 11/WITH SILVER DOWN 11 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.066 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 478.196 MILLION OZ

OCT 10//WITH SILVER DOWN 65 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 473.130 MILLION OZ/

OCT 7/WITH SILVER DOWN 37 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.447 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 473.130 MILLION OZ/

OCT 6/WITH SILVER UP 11 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY: A WITHDRAWAL OF 5.3 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 475.617 MILLION OZ//

OCT 4WITH SILVER UP $.51 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ

OCT 3/WITH SILVER UP $1.46 : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ//

SEPT 30/WITH SILVER UP 31 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.013 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ//

SEPT 29/WITH SILVER DOWN 15 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV//A WITHDRAWAL OF 645,000 OZ FROM THE SLV//INVENTORY RESTS AT 479.904 MILLION OZ//

SEPT 28/WITH SILVER UP $.52 TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 645,000 OZ FROM THE SLV.//INVENTORY RESTS AT 480.549 MILLION OZ//

SEPT 27/WITH SILVER DOWN 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 481.194 MILLION OZ

SEPT 26/WITH SILVER DOWN 43 CENTS : BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 737.000 OZ FROM THE SLV////INVENTORY RESTS AT 481.194 MILLION OZ//

SEPT 23/WITH SILVER DOWN 68 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .507 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 481.931 MILLION

SEPT 22/WITH SILVER UP 10 CENTS TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .691 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 481.424 MILLION OZ/

SEPT 21/WITH SILVER UP 33 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.902 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 482.115 MILLION OZ//

SEPT 20/WITH SILVER DOWN 18 CENTS/HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.475 MILLION OZ//INVENTORY RESTS AT 479.213 MILLION OZ//

SEPT 19/WITH SILVER DOWN 2 CENTS TODAY: GIGANTIC CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 8.108 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 477.738 MILLION OZ

SEPT 16/WITH SILVER UP 8 CENTS TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.58 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 469.63 MILLION OZ//

SEPT 15/WITH SILVER DOWN $.25 TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.151 MILLION OZ INTO THE SLV/////INVENTORY RESTS AT 467.050 MILLION OZ//

SEPT 14/WITH SILVER UP $0.06 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.899 MILLION OZ/

Bernanke rolled out quantitative easing to rescue the economy in the wake of the 2008 financial crisis. At the time, he swore it was a temporary emergency measure and that the Fed would eventually sell all of the bonds it was accumulating on its balance sheet. He insisted that it was not a debt monetization scheme.

Of course, it was a debt monetization scheme.

After a half-hearted effort to shrink the balance sheet a decade after the Great Recession, the Fed abandoned the effort as soon as the stock market tanked at the end of 2018. It went right back to QE and then launched QE infinity to deal with the government’s response to the pandemic.

As Peter Schiff has been saying, the inflation problem of today started decades ago and Bernanke was one of the chief culprits. As Ron Paul put it, “Honoring Bernanke for his advice on what government should do when banks fail is like giving a fire safety award to an arsonist.”

Former Federal Reserve Chairman Ben Bernanke is a 2022 recipient of the Nobel Prize in economics for his writings on how government should respond to bank failures. Honoring Bernanke for his advice on what government should do when banks fail is like giving a fire safety award to an arsonist.

Bernanke was Fed chairman when the housing bubble, created by his predecessor Alan Greenspan in the wake of the bursting of Greenspan’s tech bubble and the 9-11 attacks, exploded. When the housing market collapsed, Bernanke worked with Congress and the Bush administration to bail out big banks and Wall Street firms.

In the years following the meltdown, the Bernanke-led Fed tried to “stimulate” the economy via massive money creation, near-zero interest rates, and “quantitative easing,” where the Fed injects liquidity into the market via purchases of financial assets including Treasury bonds.

The Fed’s post-meltdown policies produced sluggish growth at best while laying the groundwork for the next bust. A sign that the next crash was around the corner came in September of 2019 when the Federal Reserve began pumping billions of dollars a day into the “repurchasing” market, which banks use to make overnight loans to each other, in order to keep that market’s interest rates from rising above the Fed’s target rate. The covid lockdowns then gave the Fed an excuse to push interest rates to zero and massively expand quantitative easing.

The Fed’s actions are the prime culprit behind the price inflation plaguing America’s economy. The Fed has responded to the price inflation by increasing interest rates, although rates remain much lower than they would be in a free market. The fact that even these relatively small increases helped push the fragile economy into recession shows the instability of our debt-based economic system.

Bernanke, and Congress, should have responded to the meltdown by letting the recession that followed the meltdown run its course. This is the only way the economy can adjust to the market distortions caused when the Fed increases the money supply and lowers interest rates.

Those who worry that this “don’t do something, just stand there” approach would inflict long-term economic pain on the American people should consider the economic depression of 1920. During this depression, the Fed refrained from trying to “stimulate” the economy, and Congress actually cut spending. The result was the downturn was quickly over. Sadly, the lessons of 1920 are largely ignored by mainstream economic historians.

In response to my questioning at a Financial Services Committee hearing, then-Fed Chairman Ben Bernanke admitted he did not consider gold to be money. Of course, gold and other precious metals are money because individuals have selected them whenever they had the freedom to choose a currency. One reason for this is that precious metals are uniquely suited to serve as a stable unit of account. In contrast, government rulers have favored fiat money precisely because it can never serve as an honest unit of account due to its value being constantly manipulated by central bankers. This is often done at the behest of power-hungry politicians.

Therefore, under a fiat monetary system we cannot know the true value of goods and services. This is why to create a sound economy that provides prosperity we should audit then end the fed.

END

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

LAWRIE WILLIAMS: Could the U.S. or any other country go back to a gold standard

We hear from time to time some economist or politician suggesting that his/her country introduce a gold backing for their country’s currency to stabilise it, although there are few countries where this would have much, if any, global impact. But one country where this would have a huge effect, and where the idea is raised from time to time, before usually being written off as totally impractical, is the U.S. – the last country which did in fact have an effective currency tie to gold until President Nixon closed the so-called gold window back in 1971.

The subject of the U.S. re-introducing a Gold Standard has yet again come to the fore with U.S. Representative Alex Mooney proposing on October 9th to repeg the dollar to gold with the Gold Standard Restoration Act – HR 9157. The proposed Act notes among other things that: The U.S. dollar has lost more than 30 percent of its purchasing power since 2000, and 97 percent of its purchasing power since the passage of the Federal Reserve Act in 1913….The American economy needs a stable dollar, fixed exchange rates, and money supply controlled by the market not the government … The Gold Standard would put control of the money supply with the market instead of the Federal Reserve, discourage excessive deficit spending, and encourages the balancing of Federal budgets, inter alia.

As with any such proposal there are a huge number of pros and cons revolving around pricing and implementation, many of which would most likely make the whole idea totally unrealistic. As presented the Act would involve the U.S. Treasury Secretary defining the value of the dollar in terms of a fixed weight of gold at the closing price of gold on a specific day within 30 months after the date of the Act’s enactment. It would have to make Federal Reserve notes redeemable for and exchangeable with gold at this fixed price and create mechanisms that facilitate such redemptions and exchanges between banks and the public.

Adhering to the restrictions implicit in the implementation of a true gold standard would be virtually impossible in this day and age of deficit financing and government debt, while the pricing of gold implicit in the Act would be the straw that breaks the camel’s back. As implied in the Mooney proposals letting the markets set the fixed price could be suicidal and lead to an enormous run on the nation’s gold holdings which would, in our opinion at least, lead to their complete decline. However, if that particular suggestion were to be ignored and the gold price set high enough to dissuade withdrawals, this would be totally unacceptable to the large proportion of the nations of the world which hold little or no gold in their reserves.

The overall arguments revolve around which is perceived as a better route to follow: the fiat currency one as at present where the potential for printing more and more dollars to finance economic profligacy can be seen as unlimited, or the far more restrictive economic controls under a gold standard system. Both have their adherents, although the fiat currency system is winning out for the time being and it is hard to see any return to an alternative.

Proponents of the Gold Standard will point to statistics suggesting that U.S. annual growth was higher when it was in place, average incomes grew faster, national debt was far lower and managed better with trade deficits being far better controlled. Defence spending would also have been far better kept in check preventing some U.S. global military involvements – although whether this should be considered a pro or con probably depends on one’s political leanings.

On the other side of the coin it is felt that gold price volatility can not provide the kind of performance necessary to maintain economic stability. It would limit the ability of the Government or the Federal Reserve to help the economy out of recessions and depressions, and to address unemployment should such problems arise. This volatility is said to be responsible for leading to periodic deflations and recessions affecting the overall economy. In potentially restricting defence spending it could adversely impact the country’s security and ability to defend itself.

Currently it seems that the majority of prominent economists are strongly, and vocally, against any return to a Gold Standard. Indeed the Britannica ProCon.org website quotes Anil K. Kashyap, PhD, Professor of Economics and Finance at the University of Chicago, as stating, “Love of the Gold Standard implies macroeconomic illiteracy.”

Thus it seems that the latest submission to U.S. Congress regarding a return to a Gold Standard is, like its predecessors, doomed to failure. Any such proposal is also unlikely to find any traction elsewhere in the world, although the introduction of a gold standard in any other country other than China would probably have little global relevance.

24 Oct 2022

END

3.Chris Powell of GATA provides to us very important physical commentaries

For those of you who missed this on Friday, I urge you to watch Andrew’s tape

(Andrew Maguire/GATA)

GLD and SLV are ‘illusions’ as metal drains away, Maguire says

Submitted by admin on Sat, 2022-10-22 19:31Section: Daily Dispatches

7:31p ET Saturday, October 22, 2022

Dear Friend of GATA and Gold:

In this week’s episode of Kinesis Money’s “Live from the Vault” program, London metals trader Andrew Maguire calls the exchange-traded gold and silver funds GLD and SLV “purely illusions.”

The gap between futures prices and prices of real metal has become so extreme, Maguire says, that little real metal is available at the futures price and the New York Commodities Exchange is quickly being drained of real metal.

The “Live from the Vault” episode is 44 minutes long and can be viewed at YouTube here:

CHRIS POWELL, Secretary/Treasurer Gold Anti-Trust Action Committee Inc. CPowell@GATA.org

end

Base metals especially copper is very tight and this belies the price drop

Submitted by admin on Sun, 2022-10-23 11:17Section: Daily Dispatches

By Yvonne Yue Li and James Attwood Bloomberg News Thursday, October 20, 2022

Copper prices don’t reflect a “strikingly tight” physical market, according to the world’s largest publicly-traded producer of the metal used in everything from computer chips to electric vehicles.

Macroeconomic headwinds have pushed copper futures down almost 30% from a peak in March, despite brisk demand and shrinking inventories that are nearing historical lows.

It’s “striking how negative financial markets feel about this market and yet the physical market is so tight,” said Richard Adkerson, chief executive officer of Freeport-McMoRan Inc.

“We’re not seeing customers scaling back orders. Customers are really fighting to get products,” Adkerson said Thursday during a conference call with analysts after the miner reported adjusted third-quarter per-share profit that exceeded estimates.

Egypt is set to introduce a new currency and this new currency might be based on gold

(Reuters)

Egypt’s new currency gauge might be based on gold, central bank boss says

Submitted by admin on Sun, 2022-10-23 20:28Section: Daily Dispatches

Egypt to develop New Currency Indicator to Wean People Off U.S. Dollar

By Patrick Werr, Mahmoud Murad, and Nayera Abdallah Reuters Sunday, October 23, 1011

CAIRO — Egypt will develop a new currency indicator partly to wean people off the idea that the Egyptian pound should be pegged to the U.S. dollar, the new central bank governor said today.

Hassan Abdalla, appointed in August, told an economic conference that the central bank was also working to introduce currency hedging and had already finished futures contracts as it revamps its currency trading system.

The indicator would be based on a basket of several currencies and possibly gold, he said.

“It is for the sake of the idea of pegging — and I’m not talking about the price, I’m speaking about the idea,” he said. “America is not my major trading partner. I don’t know why people are always fixated on the dollar.

“Part of our success will be in changing the culture and idea that we are pegged. We want to be seen against every currency.” …

US Has Only 25 Days of Diesel Supply; Shortage Could Cripple Economy

The United States is down to 25 days of diesel supply as a top White House official declared the stockpile levels to be “unacceptably low.”

Data provided by the Energy Information Administration (EIA) show that diesel stockpiles are at their lowest level for October in records that date back to 1993, according to a Bloomberg News analysis. EIA data show that the United States, as of Oct. 14, has 25.4 days of supply—down from 34.2 days of supply four weeks prior.

National Economic Council Director Brian Deese, a top adviser to President Joe Biden, told Bloomberg News last week that current diesel levels are “unacceptably” low and that “all options are on the table” to increase supplies.

The diesel crunch comes just over two weeks before the November 2022 midterm elections and will likely drive up prices even more. Diesel is the fuel used by freight trains and commonly used by long-haul truckers to transport goods and food.

“Most of the products we use are transported by trucks and trains with diesel engines, and most construction, farming, and military vehicles and equipment also have diesel engines,” the EIA’s website states. “As a transportation fuel, diesel fuel offers a wide range of performance, efficiency, and safety features. Diesel fuel also has a greater energy density than other liquid fuels, so it provides more useful energy per unit of volume.”

Prices, meanwhile, remain relatively elevated, according to AAA data. The average price for a gallon of diesel stands at around $5.33 nationwide, or up nearly $2 since the same time in 2021, the data shows.

Wholesale diesel prices at the New York spot market spiked last week to more than $200 per barrel.

It comes as the Biden administration recently announced it would release another 15 million barrels of oil from the U.S. Strategic Petroleum Reserve, part of the 180 million Biden authorized in March, that Republicans say is a bid to keep Democrats politically afloat ahead of the midterms. But Biden and his allies say that it’s not a political tactic, and the administration says it will refill the reserve when prices drop to $67–$72 per barrel.

“The United States government is going to purchase oil to refill the Strategic Petroleum Reserve when prices fall to $70 a barrel,” Biden said on Oct. 19. “And that means oil companies can invest to ramp up production now, with confidence they’ll be able to sell their oil to us at that price in the future: $70.”

The move came after the International Organization of the Petroleum Exporting Countries Plus (OPEC+) announced that it would cut oil production.

“Now, after draining our emergency reserves to a 40-year low, Democrats want billions more of taxpayer dollars to refill the [Strategic Petroleum Reserve] at more than double the price,” Sen. John Barrasso (R-Wyo.) told the New York Post last week. “This is a direct attack on every single American struggling to fill their tanks and heat their homes.”

Jack Phillips is a breaking news reporter at The Epoch Times based in New York.

end

COMMODITIES IN GENERAL/

END

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings MONDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 7.2626

OFFSHORE YUAN: 7.3184

SHANGHAI CLOSED DOWN 61.37 PTS OR 2.04%

HANG SENG CLOSED DOWN 1030.43 OR 6.36%

2. Nikkei closed UP 84.32 PTS OR 0.31%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX DOWN TO 112.34/Euro FALLS TO 0.98143

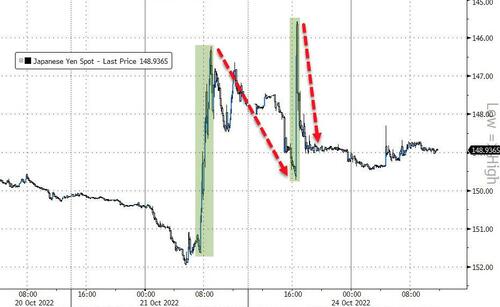

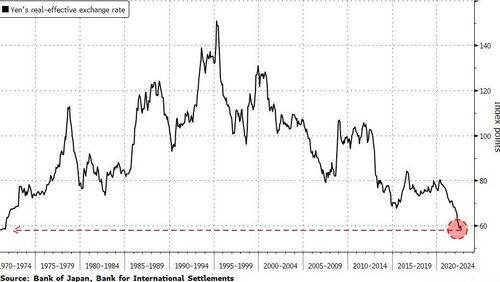

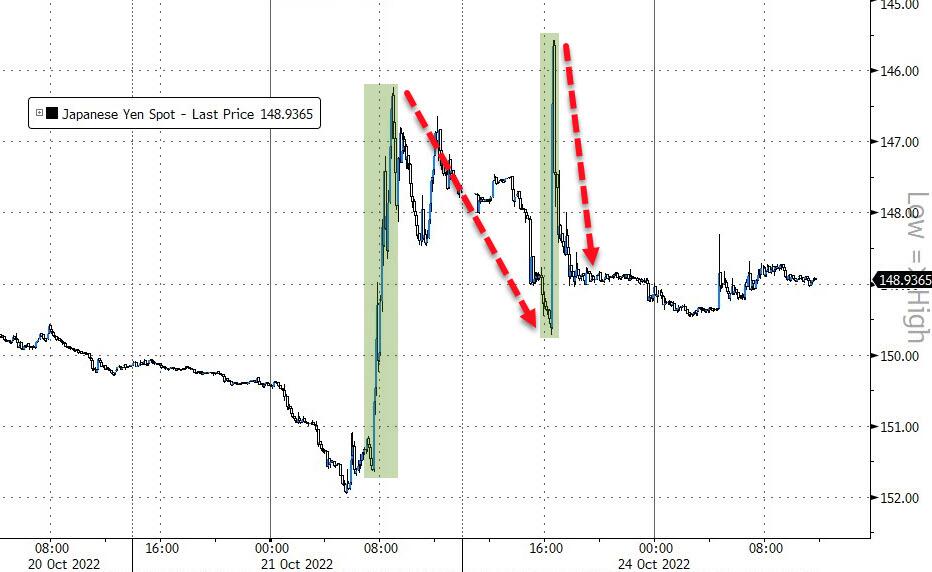

3b Japan 10 YR bond yield: RISES TO. +.249/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 149.25/JAPANESE YEN COLLAPSING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: DOWN -// OFF- SHORE: DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.3000%***/Italian 10 Yr bond yield FALLS to 4.554%*** /SPAIN 10 YR BOND YIELD FALLS TO 3.41%…** DANGEROUS//

3i Greek 10 year bond yield FALLS TO 4.83//

3j Gold at $1649.35//silver at: 19.21 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 22/100 roubles/dollar; ROUBLE AT 61.07//

3m oil into the 84 dollar handle for WTI and 92 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 149.35DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 1.0026–as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9853well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.156% DOWN 6 BASIS PTS…GETTING DANGEROUS

USA 30 YR BOND YIELD: 4.289% DOWN 2 BASIS PTS//

USA DOLLAR VS TURKISH LIRA: 18,61…GETTTING DANGEROUS

GREAT BRITAIN/10 YEAR YIELD: 3.8415%

end

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE

US Futures Stabilize After Rollercoaster Session As Yuan, Chinese Stocks Crater

MONDAY, OCT 24, 2022 – 08:12 AM

US stock futures steadied following a rollercoaster move earlier in the session and after Friday’s sharp rally as traders assessed moves by Chinese President Xi Jinping to tighten his grip on the nation’s leadership while keeping an eye on macro data now that the Fed is in a chatterbox blackout. Contracts on the S&P 500 edged 0.7% higher at 7:30a.m. in New York after earlier rising as much as 1.3% and dropping 0.7%, while the yield on the 10-year Treasury slipped for a second session. Nasdaq 100 futures were up 0.4% after bouncing between gains and losses earlier. Both underlying gauges are coming off their best week since June, and are entering the busiest week of the earnings season with 46% of the S&P 500’s market cap due to announce third-quarter results.

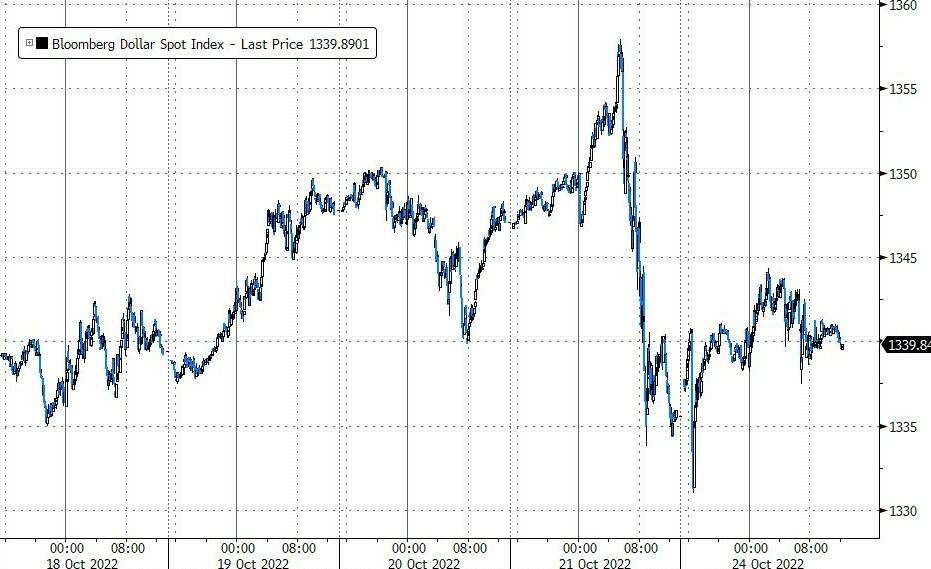

A gauge of the dollar’s strength rose sharply unwinding some of Friday’s losses, supported by a risk-off mood sparked by a rout across Chinese markets which saw the Hang Seng plunge 6.4%, the biggest one day drop since 2008!

The offshore yen resumed its decline, tumbling by 1.3% – the biggest one-day slide since August 20019, to a record of 7.31, while the pound outperformed on bets for fiscal caution from the next UK prime minister.

“Market sentiment could remain cautious near-term on China, on concerns of a shift of focus toward more state control versus a market-driven approach under the new leadership team,” said Xiaojia Zhi, the chief China economist at Credit Agricole CIB. “The exit path from zero-Covid is not yet clear.”

Chinese economic data that was delayed last week and published Monday showed a mixed recovery, with unemployment rising and retail sales weakening despite a pickup in growth. Yet Xi’s Covid-zero campaign looks likely to continue to drag on the economy and there has been speculation that his “common prosperity” goal may even lead to property and inheritance taxes.

“It’s clear demand is slowing but so far we’ve seen pockets of tech like software, cloud computing still being quite resilient,” said Laura Cooper, a senior investment strategist at BlackRock International Ltd., on Bloomberg TV. “We will be watching for any signs of cracks coming through that could put a dent to some of these earnings expectations.”

In premarket trading, US-listed Chinese stocks tumbled, dragged lower by major internet and EV names including Alibaba, Baidu and Li Auto, which closed down more than 11%; search company Baidu was 12% lower while food delivery firm Meituan tanked more than 14%. The moves come after Chinese President Xi Jinping paved the way for an unprecedented third term as leader and packed the Politburo standing committee with loyalists. Tesla shares dropped after the company cut prices in China, reversing hikes imposed earlier this year.US stock futures steadied after Friday’s rally as traders assessed moves by Chinese President Xi Jinping to tighten his grip on the nation’s leadership. Other notable premarket movers:

US-listed Macau casino stocks are also down, declining along with Chinese ADRs. Las Vegas Sands (LVS US) -7.9%, Wynn Resorts (WYNN US) -6.8%, Melco Resorts (MLCO US) -8.6%

FedEx (FDX US) declines 1.9% in premarket trading after it was cut to equal-weight from overweight at Wells Fargo on concern that the revenue implications are not yet “fully captured” as the company pivots from growth and toward efficiency.

Keep an eye on Williams-Sonoma (WSM US) stock as it was downgraded to underperform from hold at Jefferies, with broker saying it sees the home furnishing store operator underperforming ahead of a softer macroeconomic environment.

Watch NXP Semiconductors (NXPI US) and Analog Devices (ADI US) shares as they were downgraded at Barclays, with the brokerage saying it expects cuts in the analog chip sector in the coming year and recommended “rotating out of the sub-sector sooner rather than later.”

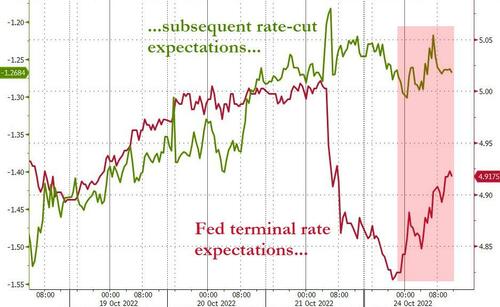

US investors have begun looking beyond the Federal Reserve’s ongoing tightening to a stage when it may begin to slow rate hikes. St. Louis Fed President James Bullard and his San Francisco counterpart Mary Daly made it clear they expect discussion at the November meeting to include debate on how high to raise rates and when to ease the pace.

At the same time, Morgan Stanley’s Michael Wilson expects stocks to grind higher as markets transition to expectations of falling inflation and lower interest rates. The strategist, who correctly predicted this year’s slump, sees the S&P 500 Index bouncing as much as 15% if it breaches its 200-week moving average of 3,605 points, about 4% below Friday’s close. A similar view is held by Stifel Nicolaus & Co. strategists, who said in a separate note they see the benchmark rallying to 4,300 points in the next 6 months.

“With the back end of the bond market offering real value for the first time since early 2021, rates are poised to come in,” Wilson in a note on Monday. “Such a move could provide the necessary fuel for the next leg of the tactical rally in stocks until we get full capitulation on 2023 earnings estimates, something we think may take a few more months.”

By contrast, Goldman Sachs Inc. strategists led by David Kostin are more cautious, seeing rising rates and slowing US growth hurting cyclicals and tech stocks. They recommend being overweight defensive sectors, as well as energy.

In Europe, the Stoxx Europe 600 Index held an advance of about 1.3%. Media, utilities and travel are the strongest-performing sectors in Europe while miners and energy lag. IBEX outperforms peers, adding 0.9%, FTSE 100 lags, dropping 0.4% after Boris Johnson pulled out of the race to lead the UK’s ruling Conservative Party, placing Rishi Sunak closer to becoming the next prime minister. A 12% slump in Prosus NV shares amid the China concerns pushed the technology sector into the red, while basic resources and energy stocks weighed on the benchmark amid lower commodity prices. Michelin shares rose as much as 3.7% in Paris trading and are the day’s top performers on the Stoxx 600 Automobiles & Parts Index, with the French tiremaker set to give a quarterly sales update on Tuesday. Here are the biggest European movers:

Pearson shares jump as much as 7.8%, reaching the highest since January 2019, after the publishing and education company reported a 7% increase in underlying revenue in the first nine months of the year.

Indivior gains as much as 7.6%, the most since February, after Morgan Stanley upgrades to overweight from equal-weight, describing the stock as a “value, growth and margin expansion story.”

Auto Trader rises as much as 4.3% after announcing the disposal of Webzone Ltd. Peel Hunt upgrades to buy from hold, saying the sale shows the company’s “dedication to its key market.”

Temenos climbs as much as 8.2%, the most intraday since mid-June, after Dealreporter reported that Goldman Sachs and Citi are sounding out interest in the buyout of the Swiss banking software developer.

Prosus falls as much as 14% in Amsterdam and parent Naspers sinks as much as 14% in Johannesburg, with both declines the sharpest since March. Naspers holds a 28% stake in Tencent, which plunged in Hong Kong trading following President Xi Jinping’s move to stack his leadership ranks with loyalists.

Galp drops as much as 6.1% after reporting third-quarter profit that missed the average analyst estimate.

Philips falls as much as 4.5% to the lowest since 2011 after saying it would cut 4,000 jobs as part of a EU300 million cost-saving package, which analysts say may imply liquidity problems for the Dutch medical technology firm.

Asian stocks fell, dragged by Chinese shares as President Xi Jinping’s move to tighten his leadership deepened investor worries, offsetting advances in Australia, South Korea and Japan. The MSCI Asia Pacific Index erased an earlier gain to drop as much as 1.2%, with Internet giants Tencent and Alibaba the biggest drags. A selloff in Chinese stocks deepened in afternoon trading, as the Hang Seng plunged by more than 6%, its biggest drop since Lehman while the Hang Seng Tech Index crashed 9.7% to the lowest since February 2016, after Xi filled China’s most powerful bodies with close allies while securing a precedent-breaking third term. He installed six trusted associates alongside him on the Politburo’s supreme Standing Committee and put his former chief of staff Li Qiang in line for the premiership.

Investors remained jittery as a leadership reshuffle highlighted Xi’s unquestioned grip over the ruling party, with allies set to take up key economic posts. An early loosening of Covid restrictions seemed less likely, while a set of long-delayed economic data showed a mixed recovery, further damping market sentiment.

“The latest rally underlines our view that markets will remain volatile, and investors should prepare for large moves in both directions,” said Mark Haefele, chief investment officer at UBS Global Wealth Management. “Incremental improvements in inflation or labor market data, indications of economic resilience, any softening of language from the Fed, has the potential to drive a market bounce, as we have seen in recent days.”

“Markets may be hoping now that the leadership transition is finalized, the focus will turn to the economy and mending the property sector,” said Marvin Chen, a strategist at Bloomberg Intelligence, adding that property investment is still a weak spot for the economy. “Still, these may take time. We may not see much change to Covid policies in the near term.” The declines in Chinese shares contrasted with the upbeat mood elsewhere in Asia, buoyed by declines in US Treasury yields and Federal Reserve officials’ indications of a potential slowing of rate hikes. Markets were closed for holidays in Singapore, India, Malaysia, Thailand and New Zealand

In FX, the Bloomberg Dollar Spot Index rose, paring some of Friday’s losses and the greenback was steady or higher against all of its Group-of-10 peers.

The pound jumped and gilts led Treasuries and European bonds higher as investors bet that Rishi Sunak would bring more stability to the country’s financial markets. Initial moves were however tempered, and the pound inched lower, sliding back under 1.13 after earlier rallying by as much as 0.9% to $1.1409.

China’s offshore yuan led the decline in most emerging Asian currencies as traders assessed the impact of President Xi Jinping’s consolidation of power. Indonesia’s rupiah outperformed peers, supported by higher nickel prices. China’s onshore yuan weakened to a 14-year low while stocks headed for their biggest daily plunge in Hong Kong since the 2008 global financial crisis. Market setbacks following the reshuffle highlighted President Xi Jinping’s unquestioned grip over the ruling party and showed deep disappointment over a likely continuation of policies staked on Covid Zero and state- driven companies.

The euro retreated after earlier rising to more than a two-week high of $0.9899. Eurozone composite PMI fell to 47.1 in October; economists had expected 47.6

The yen fell by more than 1%, to trade above 149 per dollar, after earlier surging to as much as 145.56 after suspected interventions by Japanese authorities

Australian dollar declined against all of its G-10 peers after the Reserve Bank said it isn’t yet worried about the risk of imported inflation from a falling currency. Reports of fresh Covid restrictions in Guangzhou helped fuel a drop in China stocks and the yuan, pushing the Aussie even lower

In rates, Treasuries trade off best levels of the session, although intermediate and long-end yields remain richer by 5bp-6bp. Gilts lead a global bond market rally, with front-end yields down nearly 40bp after Rishi Sunak emerged as the frontrunner to become new UK Prime Minister. 10-year TSY yields trade around 4.15%, richer by ~7bp on the day, trailing gilts by 18bp, bunds by 4bp in the sector; US 2s10s is ~5bp flatter on the day while gilt curve steepens. Treasuries extended their late-Friday rally during Monday’s Asia session, adding to a move sparked by comments from Fed’s Daly, who said policy makers should start planning for a reduction in the size of interest-rate increases, and a WSJ article predicting they will debate the size of future hikes in November. According to Bloomberg, dollar issuance slate includes OKB $1b 3Y and Cades 3Y; $20b of new bond sales are expected this week as companies emerge from earnings blackout periods; banks including JPMorgan Chase & Co., Citigroup Inc., Goldman Sachs Group Inc. and Bank of America Corp. could all come to market soon.

Commodities were clipped as the USD rebounded and recessionary concerns mount (again); crude benchmarks are hampered on such factors, though similarly to US equity futures have recently eased off lows. Specifically, WTI and Brent benchmarks post downside of circa. USD 1.00/bbl compared to losses just shy of USD 2.00/bbl at worst. Both precious and base metals are broadly speaking under pressure; currently, Gold is impaired by circa. USD 10/oz and has been pushed back below the 10-DMA at USD 1650/oz. QatarEnergy head said the Co. is open to discussing working with Shell (SHEL LN) in all energy sectors, via Reuters.

Looking at today’s calendar, we get the US October PMIs, and September Chicago Fed national activity index, we also get PMI updates from Japan, UK, Germany, France and the Eurozone.

Market Snapshot

S&P 500 futures up 0.7% to 3,792

STOXX Europe 600 up 0.5% to 398.32

MXAP down 1.1% to 134.36

MXAPJ down 2.0% to 431.12

Nikkei up 0.3% to 26,974.90

Topix up 0.3% to 1,887.19

Hang Seng Index down 6.4% to 15,180.69

Shanghai Composite down 2.0% to 2,977.56

Sensex up 0.2% to 59,307.15

Australia S&P/ASX 200 up 1.5% to 6,779.36

Kospi up 1.0% to 2,236.16

German 10Y yield down 0.2% at 2.41%

Euro down 0.3% to $0.9831

Brent Futures down 1.8% to $91.86/bbl

Gold spot down 0.6% to $1,647.67

U.S. Dollar Index up 0.25% to 112.29

Top Overnight News from Bloomberg

A sense of exasperation swept across Chinese markets as President Xi Jinping moved to stack his leadership ranks with loyalists, with stocks capping their worst day in Hong Kong since the 2008 global financial crisis and the yuan weakening to a 14-year low

The ECB is priming another hefty hike in interest rates this week as the attention increasingly switches to how high it will eventually push

Japan’s government will set out its expectation that the central bank watches the impact of moves in financial markets while emphasizing the two sides’ cooperation on policy, according to a draft of an upcoming stimulus plan obtained by Bloomberg

Most of Japan’s currency intervention, confirmed and suspected, took place outside of regular trading hours, with the exception of probable action Monday — unlike moves in 2010 and 2011 to weaken the yen. In contrast to that period, the government has only stated it intervened once, with the reluctance to do so seen as an additional tool to deter speculators

Much of continental Europe is poised for an unusually warm end to the month, with Paris seeing temperatures more common on a summer day than well into the heating season

A more detailed look at global markets courtesy of Newsquawk

Asia-Pacififc stocks traded mixed after the initial optimism from Wall Street on Friday began to fade. ASX 200 was boosted by its commodities sector as the rise in underlying metals supported mining names in the region. Nikkei 225 was also firmer but lagged behind peers (ex-China) following the touted FX intervention on Friday and again on Monday. KOSPI was led by gains in its IT names, but the region felt some jitters following an exchange of fire between North and South Korea after a North Korean boat crossed the South Korean maritime border. Shanghai Comp. initially traded flat after Chinese President Xi secured an unprecedented third term as the party leader, as expected. Chinese President Xi also suggested China’s economy has high resilience and sufficient potential. The index also saw some brief upside after China released a myriad of delayed economic data, with Q3 GDP Y/Y topping forecasts and Trade Balance printing a larger surplus than expected, whilst exports also increased more than forecast, although these gains pared back. Hang Seng buckled as Xi’s leadership overhaul could prove to result in prolonged oversight and less autonomy for Hong Kong, with the Hang Seng Tech Index slumping over 5% and Alibaba, Tencent, JD.com, Baidu and Meituan shedding as much as 7-10%.

Asia Data Recap

Chinese GDP (Q3) Y/Y 3.9% (Exp. 3.3%, Prev. 0.4%); Q/Q 3.9% (Exp. 3.5%, Prev. -2.6%)

China suspended in-person schooling and dining-in at restaurants in a district in Guangzhou, “stoking concerns about the potential for disruption in the southern Chinese manufacturing hub that’s home to about 19mln people”, Bloomberg reported.

PBoC injected CNY 10bln via 7-day reverse repos at a maintained rate 2.00% for a daily injection of CNY 8bln.

Japan’s Top Currency Diplomat Kanda will not comment on whether they intervened in FX markets and said there is no change in stance that “we are ready to take action 24/7” and will continue to take appropriate action, via Reuters. Japan’s Top Currency Diplomat Kanda offered no comments on intervention on Monday morning.

Japanese Finance Minister Suzuki said no comment on FX intervention; currently trying to confront speculators; monitoring FX with a high sense of urgency.

USD/JPY drop on Monday likely due to intervention, according to market participants cited by Reuters.

Japanese government urges the BoJ to remain vigilant to the impact of sharp market moves, according to a draft document cited by Reuters.

The Japanese government and the BoJ decided to intervene in FX on Friday by buying the Yen and selling the Dollar, according to Nikkei sources citing sources.

Japan’s FX intervention on October 21st is estimated at JPY 5.4-5.5tln, according to market sources and calculations cited by Reuters.

BoJ Governor Kuroda said CPI growth beyond next FY likely to fall below 2%, will continue to put all effort into achieving price target along with rise in wages.

Japanese gov’t expects the BoJ to watch the impact of market moves, via Bloomberg citing a document; to collaborate closely with the BoJ on the policy mix; Finance Minister will not comment on FX intervention.

Japan is to ease rules in relation to brokerages offering investment advice, according to reports citing Nikkei.

Japanese Economy Minister Yamagiwa is planning to step down, according to NHK.

South Korea is to expand its corporate-bond buying program, according to the finance minister cited by Reuters.

RBA’s Kent reiterated the Board expects to increase interest rates further in the period ahead; size and timing of rate increases in Australia will depend on incoming data.

European bourses are mixed, though are well off lows, as initial strength faded following the open amid renewed USD strength and as PMIs flash ongoing recessionary/inflationary concerns. Sectors are a touch mixed amid the above action, Energy remains the standout laggard amid the complex’s broader price action. US futures have managed to make their way back to being essentially unchanged on the session, as the initial bout of underperformance eases as US participants enter the fray pre-PMIs.

Top European News

UK’s Boris Johnson has pulled out of the Conservative Party leadership contest, according to The Times’ Swinford. UK’s Boris Johnson and Rishi Sunak failed to strike a deal in talks on Saturday, according to the Times.

UK leadership candidate Rishi Sunak so far received support from 147 MPs vs 24 for Penny Mordaunt. The deadline to reach the 100 threshold is at 14:00BST/09:00EDT on Monday.

UK leadership candidate Penny Mordaunt will stay in the race as she reportedly sees a route to 100 nominations now Boris Johnson is out, according to sources cited by Bloomberg’s Wickham.

UK Chancellor Hunt backs Rishi Sunak for PM, via The Telegraph.

UK Chancellor Hunt is said to be mulling up to GBP 20bln of tax rises in the October 31st budget, according to The Telegraph. The October 31st fiscal statement could be delayed after PM Truss’ resignation, according to the FT.

UK Chancellor Hunt is expected to extend the current freeze in income tax and allowances into the next parliament, according to FT citing sources.

BoE’s Mann said bond purchases for financial stability were targeted and temporary, and the start of bond selling on Nov 1st shows the BoE does not feel like its hands are tied. Mann said it is the BoE’s job to address financial stability risks.

Moody’s affirmed UK’s rating at Aa3; revised outlook to “Negative” from “Stable.

FX

Dollar regroups after Friday’s reversal on less hawkish Fed dynamic and reports of Japanese intervention, DXY above 112.500 at best vs 111.760 low.

Sterling underpinned ahead of deadline in race to be next UK PM with Sunak hot favourite to succeed, Cable holding within 1.1400-1.1300 range.

Yen reverses from peaks as official buying momentum wanes, USD/JPY up to 149.70 from sub-145.50 at one stage.

Aussie underperforms ahead of Budget that is expected to see growth forecast downgraded, AUD/USD under 0.6300 and Kiwi down in sympathy on NZ Labour Day as NZD/USD declines through 0.5700.

Offshore Yuan below 7.3000 vs Buck as China tightens COVID restrictions in key southern manufacturing hub.

Euro fades from a fraction below 0.9900 towards 0.9800 after broadly weak PMIs and amidst heavy option expiry interest.

PBoC set USD/CNY mid-point at 7.1230 vs exp. 7.1173 (prev. 7.1186); weakest fix since June 1st 2020.

Commodities

Commodities clipped as the USD regains poise and recessionary concerns mount; crude benchmarks are hampered on such factors, though similarly to US equity futures have recently eased off lows.

Specifically, WTI and Brent benchmarks post downside of circa. USD 1.00/bbl compared to losses just shy of USD 2.00/bbl at worst.

Both precious and base metals are broadly speaking under pressure; currently, Gold is impaired by circa. USD 10/oz and has been pushed back below the 10-DMA at USD 1650/oz.

QatarEnergy head said the Co. is open to discussing working with Shell (SHEL LN) in all energy sectors, via Reuters.

China sold 100% of wheat offered at auction of state reserves on Oct 19th, according to Reuters citing the traded centre; sold at an average price of CNY 2,829/t.

CCP National Congress

Chinese President Xi secured an unprecedented third term as Chinese Communist Party (CCP) leader, as expected.

The CCP amended its constitution to include “two establishes” and “two safeguards” to “cement” Xi Jinping’s status as the core of the party, according to Reuters.

Chinese President Xi is to head the communist party’s central commission for discipline inspection, according to state media.

The new CCP Politburo Standing Committee includes Li Qang, Li Xi, Ding Xuexiang, Cai Qi, Zhao Leji, Wang Huning, according to state media. The new Central Committee (comprising of 171 alternate members) does not include Liu He, Han Zheng, Sun Chunlan, Yi Gang, Guo Shuoing,

Chinese President Xi said China’s economy has high resilience, sufficient potential and has room for manoeuvre. Xi said China will open its doors even wider. Xi said China must ensure the CCP continues to be the backbone people can lean on, according to state media.

Geopolitics

Russian Defence Minister held phone calls with the US Pentagon Chief, UK Defence Minister, and the French Armed Forces Minister, according to Interfax and Reuters.

French Armed Forces Minister has confirmed Russian Defence Minister told him Russia fears that Ukraine may use a “dirty bomb” on Russian territory. Russia’s Shoigu warns of ‘uncontrolled escalation’ in Ukraine conflict, via Reuters.

Ukraine’s Foreign Minister spoke with US Defence Secretary Blinken and said they both agreed the Russian rhetoric on “dirty bombs” is aimed at creating a pretext for a false flag operation. They also discussed further practical steps to boost Ukraine’s air defense.

Russian forces continued to target Ukraine’s energy and military infrastructure over the weekend, according to the Russia Defence Ministry cited by Interfax.

Russian authorities said two pilots died in a military plane crash into a residential building in Irkutsk, Russia, according to Interfax.

Russian Deputy Foreign Minister said Russia completely reject any demilitarized zones in the vicinity of the Zaporozhye station, Via Al Jazeera.

Russia continues to use Iranian uncrewed aerial vehicles (UAVs) against targets throughout Ukraine, according to the UK Ministry of Defence.

US Event Calendar

08:30: Sept. Chicago Fed Nat Activity Index, est. -0.10, prior 0

09:45: Oct. S&P Global US Manufacturing PM, est. 51.0, prior 52.0

09:45: Oct. S&P Global US Composite PMI, est. 49.2, prior 49.5

09:45: Oct. S&P Global US Services PMI, est. 49.5, prior 49.3

DB’s Jim Reid concludes the overnight wrap

Morning from the middle of a forest in Center Parcs. We’ve had a biblical amount of rain, flash flooding in the resort and a weekend of over excitable children. We’re off to a safari park today where monkeys jump on your car. Only 24 hours before I can escape on a plane to New York.

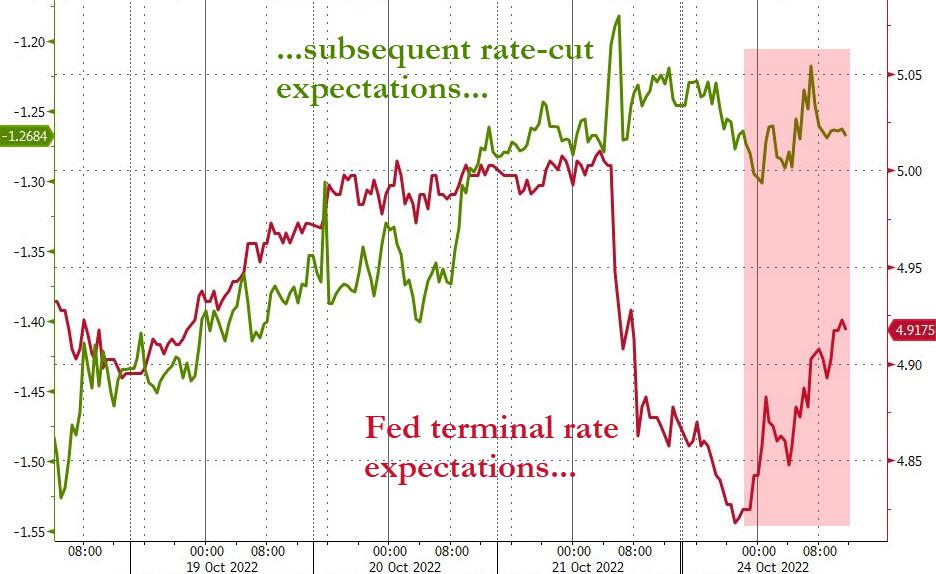

As we start a new week where we’re now in the Fed blackout period ahead of next week’s FOMC, we’re perhaps starting the 6th attempt this year at the Fed pivot trade. This only started on Friday as well-connected Nick Timiraos (WSJ) suggested that while a 75bps hike at the Fed’s next meeting was set to go ahead, officials were also likely to discuss “whether and how to signal plans to approve a smaller increase in December.” Whether this gets any further than the previous failed attempts to reprice markets only time will tell but with markets pricing in a terminal rate of over 5% prior to this, at least this is the first one that starts from anything vaguely resembling a realistic starting point given where inflation is. San Fran Fed President Daly also said on Friday that the Fed should start planning for a shift down in the pace of hikes but added that they are not there yet.

The news helped price -8.0bps less Fed tightening by year-end on Friday, whilst also triggering a significant one-day decline in the 2yr Treasury yield of -13.8bps (-16bps post Timiraos). In turn the S&P 500 completed its strongest weekly performance since June, advancing +4.74% (+2.37% Friday). Futures are +0.3% this morning. The longer end rallied 12bps off the highs but was only -1.2bps on Friday as the same article discussed how the Fed could also signal a higher dot plot for 2023. Net net this left the biggest curve steepening since the pandemic (-12.2bps) which given that its not a huge move shows how massively flatter the curve has been since then. This morning in Asia 2 and 10yr yields are -4.3bps and -6.7bps lower respectively and this continuing the momentum from Friday.

In the cold light of day (and it’s cold and dark in the forests of Center Parcs this morning), these more dovish stories are all plausible but between next week’s FOMC and the December equivalent we have CPI and NFP twice. So plenty of cold or hot water to flow under the bridge before then. On balance there are few signs at the moment that core inflation is about to see a rapid about turn and the Fed will be data dependent so it’ll be impossible to have high conviction on what they do next without a strong view on the data.

Before we examine the week ahead we should note that overall the 10yr yield ended last week up by +19.8bps (-1.2bps Friday), which marked its 12th consecutive weekly rise, and is also its longest run since 1984 when Paul Volcker was Fed Chair. So we need to put things into some perspective.

In light of all this maybe the most interesting data this week comes on Friday with the Q3 employment cost index (DB at +1.1% vs. +1.3% last month) and the September personal income (+0.1% vs. +0.3%) and consumption (+0.3% vs. +0.4%) report, including the core PCE deflator (+0.58% vs. +0.56%). With respect to core PCE, our economists expect the Fed’s preferred measure of inflation to rise by 40bps to 5.3%. Our economists highlight that as the median forecast for 2022 core PCE inflation in the Fed’s Summary of Economic Projections from the September 21st meeting was 4.5%, it’s going to be tough to signal a downshift in December.

Elsewhere this week the main highlights are the ECB (Thursday) and the BoJ (Friday) decisions and a huge round of earnings with big Tech the highlight. We’ll also have a new UK Prime Minister by Friday with a possibility we may have one after today’s ultra compressed rounds of Parliamentary votes. After Boris Johnson pulled out late last night it is possible that only tactical voting will stop ex-Chancellor Sunak being declared PM tonight. We’ll also see US Q3 GDP (Thursday) and flash PMIs in the US and Europe (today) and October CPIs and GDP for many European countries (Friday). There are other data which are in the day by day guide at the end as usual for a Monday but let’s take a brief look at the highlights outside the already discussed PCE. The ECB’s decision on Thursday will be a big event with our European economists expecting another +75bps hike (72.3bp priced in), followed by +75bps in December (c.62bps priced in), +50bps in February (c.38bps priced), and +25bps in March, reaching a terminal rate of 3%. The press conference as ever will be a focal point and there’ll be lots of attention on technical things surrounding TLTROs and excess reserves. For more on the options here see our fixed income strategists blog from Friday here.