DEC 5/Gold price fell by a strong $30.20 to $1767.50//Silver fell by 89 cents to $22.21 in an obvious raid trying to quell gold/silver’s rise!! We experienced another 750 contract Exchange for Risk transfer of silver contracts in an obvious fraud//COVID updates//COVID updates on China//Apple//Dr Paul Alexander//vaccine impact//vaccine impact//slay news//updates on Russia’s advance in Ukraine//swamp stories for you tonight..

118 C MACQUARIE FUT 5 132 C SG AMERICAS 1 190 H BMO CAPITAL 2 332 H STANDARD CHARTE 7 435 H SCOTIA CAPITAL 4 624 H BOFA SECURITIES 4 657 C MORGAN STANLEY 43 661 C JP MORGAN 28 700 C UBS 2 800 C MAREX SPEC 10

TOTAL: 53 53

MONTH TO DATE: 11,981DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

GOLD: NUMBER OF NOTICES FILED FOR DEC. CONTRACT: 53 NOTICES FOR 5300 OZ or .1648 TONNES

total notices so far: 11,981 contracts for 1,198,100 oz (37.265 tonnes)

SILVER NOTICES: 91 NOTICE(S) FILED FOR 455,000 OZ/

total number of notices filed so far this month 2776 for 13,880,000 oz

END

GLD

WITH GOLD DOWN xxx

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//BIG CHANGES IN GOLD INVENTORY AT THE GLD: /////HUGE CHANGES IN GLD INVENTORY: A WITHDRAWAL OF 1.45 TONNES INTO THE GLD//

INVENTORY RESTS AT TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP $.000

AT THE SLV// :/SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF OF 0.553 MILLION OZ INTO THE SLV

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 471.923 MILLION OZ (THIS IS ALSO A CRIME SCENE@!!!!

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A STRONG SIZED 429 CONTRACTS TO 126,227 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THE LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR CONSIDERABLE $0.47 GAIN IN SILVER PRICING AT THE COMEX ON FRIDAY. OUR SHORTERS/HFT WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.47 AND WERE UNSUCCESSFUL IN KNOCKING ANY SPEC LONGS, AS WE HAD A HUGE SIZED GAIN IN OUR TWO EXCHANGES OF 1010 CONTRACTS AS WELL AS ANOTHER EXCHANGE FOR RISK TRANSFER OF 750 CONTRACTS. WE HAD A ZERO ATTEMPTED SPEC SHORT COVERINGS OF THEIR SHORTFALL. .WE PROBABLY HAD ZERO SPEC SHORT ADDITIONS AS THE PRICE OF THE METAL WAS ROSE STRONGLY. // OUR BANKERS CONTINUE TO BE PURCHASERS OF NET COMEX LONGS. BUT THEY ALSO SUPPLIED THE NECESSARY SHORT CONTRACTS>>> HUGE NUMBER OF NEWBIE SPEC LONGS ADDED TO THEIR POSITIONS CAUSING ADDITIONAL MISERY TO OUR SHORTERS.

WE MUST HAVE HAD: A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 23 .24. MILLION OZ FOLLOWED BY TODAY;S QUEUE JUMP of 395,,000 /// / // V) SMALL SIZED COMEX OI LOSS/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL_545

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS DEC. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF DEC:

TOTAL CONTRACTS for 3 days, total 2760 contracts: OR 13.8 MILLION OZ PER DAY. (920 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 13.80 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 13.80 MILLION OZ INITIAL

RESULT: WE HAD A GOOD SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 429 DESPITE OUR STRONG $0.47 GAIN IN SILVER PRICING AT THE COMEX// FRIDAY.,. THE CME NOTIFIED US THAT WE HAD A GIGANTIC SIZED EFP ISSUANCE CONTRACTS: 1010 CONTRACTS ISSUED FOR MAR AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR DEC OF 23.24 MILLION OZ FOLLOWED BY TODAY:S 395,000 QUEUE JUMP / .. WE HAVE A HUGE SIZED GAIN OF 1439 OI CONTRACTS ON THE TWO EXCHANGES FOR 7.19 MILLION OZ.. THE SILVER SHORTS ARE NOW TRAPPED AS THEY ARE HAVING CONSIDERABLE DIFFICULTY IN COVERING THOSE SHORTS.

WE HAD 91 NOTICE(S) FILED TODAY FOR 455,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A STRONG SIZED 5462 CONTRACTS TO 436,240 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: ADDED 545 CONTRACTS.

.

THE STRONG SIZED DECREASE IN COMEX OI CAME WITH OUR LOSS IN PRICE. WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR DEC. AT 58.86 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY:S QUEUE JUMP of 205 contracts or 20,500 oz//(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S WILL CONTINUE UNTIL MONTH’S END) (EFP is the transfer of contracts immediately to London for potential gold deliveries originating from London)

YET ALL OF..THIS HAPPENED WITH OUR LOSS PRICE OF $1.80 WITH RESPECT TO FRIDAY’S TRADING

WE HAD A FAIR SIZED GAIN OF 2173 OI CONTRACTS (6.79 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 3279 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 436,240.

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2183 CONTRACTS WITH 5462 CONTRACTS DECREASED AT THE COMEX (SHORT SPECULATORS FAILING TO GET OUT OF THEIR MESS) AND 3279EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 2183 CONTRACTS OR 6.78 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3723 CONTRACTS) ACCOMPANYING THE STRONG SIZED LOSS IN COMEX OI (5462) TOTAL LOSS IN THE TWO EXCHANGES 2183 CONTRACTS. WE NO DOUBT HAD 1) ATTEMPTED BUT FAILED SPECULATOR SHORT COVERINGS// CONTINUED GOOD BANKER ADDITIONS BUT THEY ALSO SUPPLIED THE NECESSARY PAPER SHORT. WE HAD LIMITED SHORT SPEC ADDITIONS/// // MINOR NEWBIE SPEC ADDITIONS ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR DEC. AT 58.86 TONNES FOLLOWED BY TODAY’S QUEUE JUMP of 20,500 oz// //NEW STANDING 54.57 TONNES///3) ZERO LONG LIQUIDATION //// //.,4) STRONG SIZED COMEX OPEN INTEREST LOSS 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

DEC

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF DEC :

12,138 CONTRACTS OR 1,213,800 OZ OR 37.754 TONNES 3 TRADING DAY(S) AND THUS AVERAGING: 4046 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 3 TRADING DAY(S) IN TONNES:37.754 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 37,54/3550 x 100% TONNES 1.05% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 37.54 tonnes Initial

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW NON ACTIVE FRONT MONTH OF NOV. WE ARE NOW INTO THE SPREADING OPERATION OF BOTH SILVER AND GOLD (WILL BE SMALL AS SPREADERS DO NOT PAY ATTENTION TO NOVEMBER)

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF OCT HEADING TOWARDS THE NON ACTIVE DELIVERY MONTH OF NOV., FOR BOTH GOLD AND SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A GOOD SIZED 429 CONTRACTS OI TO 126,227 AND FURTHER FROM OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 1010 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 1010 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1010 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 116 CONTRACTS AND ADD TO THE 1010 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE SIZED GAIN OF 1434 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 7.19MILLION OZ//

OCCURRED WITH OUR GAIN IN PRICE OF $0.47….. OUR SPEC SHORTS HAVE NOWHERE TO HIDE!

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold/silver commentaries

6. Commodity commentaries//

7/CRYPTOCURRENCIES/BITCOIN ETC

3. ASIAN AFFAIRS

i)MONDAY MORNING//SUNDAY NIGHT

SHANGHAI CLOSED DOWN 18,19 PTS OR 0.58% //Hang Sang CLOSED DOWN 53,12 OR 0.29% /The Nikkei closed DOWN 30.80 OR 0.11% //Australia’s all ordinaries CLOSED UP 0.21% /Chinese yuan (ONSHORE) closed DOWN TO 7.1151//OFFSHORE CHINESE YUAN DOWN 7.1257// /Oil DOWN TO 82.31 dollars per barrel for WTI and BRENT AT 95.14 / Stocks in Europe OPENED ALL GREEN. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A GOOD SIZED 5462 CONTRACTS UP TO 436,240 DESPITE THE TINY FALL IN PRICE..$1.80

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE -ACTIVE DELIVERY MONTH OF DEC… THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 3279 EFP CONTRACTS WERE ISSUED: ;: , . 0 FEB: 3279 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 2183 CONTRACTS IN THAT 3279 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A STRONG SIZED COMEX OI LOSS OF 5462 CONTRACTS..AND THIS FAIR SIZED LOSS ON OUR TWO EXCHANGES HAPPENED DESPITE OUR SMALL LOSS IN PRICE OF GOLD $1.80. WE ARE WITNESSING MINOR SPEC SHORTS COVERINGS OF THEIR SHORTFALL. BANKERS CONTINUE AS NET BUYERS OF COMEX GOLD CONTRACTS AS THEY HAVE BEEN NET LONG FOR THE PAST FEW MONTHS. WE ALSO HAD HUGE ADDITIONAL NEWBIE SPECS GOING LONG. IT LOOKS LIKE OUR SPEC SHORTS ARE IN DEEP TROUBLE AS THEY CANNOT GET OUT OF THEIR MASSIVE SHORTFALL.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING DEC (54.57)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL (TOTAL SO FAR THIS YEAR 591.535 TONNES)

Dec. 54.57tonnes

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $1.80 AND WERE UNSUCCESSFUL IN KNOCKING OFF SOME SPECULATOR LONGS AS WE HAD A FAIR LOSS OF 2183 CONTRACTS ON OUR TWO EXCHANGES >. WE HAD NEGLIGIBLE SPEC SHORT ADDITIONS AND CONSIDERABLE SPEC SHORT COVERINGS.. WE HAD A FAIR SIZED LOSS ON OUR TWO EXCHANGES OF 2,183 CONTRACTS.// WE HAVE LOST A TOTAL OI OF 6.79 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR DEC. (54.57TONNES)…THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE OF $1.80

WE HAD +1540 CONTRACTS COMEX TRADES ADDED TO. THESE WERE ADDED AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 3723 CONTRACTS OR 372,300 OZ OR 16.580 TONNES

Estimated gold volume 178,646// poor//

final gold volumes/yesterday 192,595/ poor

INITIAL STANDINGS FOR DECEMBER 2022 COMEX GOLD //DEC 5

Total monthly oz gold served (contracts) so far this month

11,981 notices 1,1981,00 37.265 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

xxx oz

total dealer deposit 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits nil oz

customer withdrawals:1

i) Out of Brinks: 8198.500 oz

Total withdrawals: 8198.500 oz

total in tonnes: 0.05 tonnes

Adjustments: 0/

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR DECEMBER.

For the front month of DECEMBER we have an oi of 5629 contracts having LOST 220 contracts

We had 425 contracts served on Friday, so we gained 205 contracts or an additional 20,500 oz will stand for gold at the COMEX. We will gain in gold tonnage from this day forth.

The comex is running out of physical gold to serve our good friends over in London

JANUARY GAINED 40 contracts to stand at 1522

February LOST 5574 contacts down to 371,791

We had 425 notice(s) filed today for 42,500 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 53 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 28 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the DEC. /2022. contract month,

we take the total number of notices filed so far for the month (11,981x 100 oz , to which we add the difference between the open interest for the front month of (DEC. 5629 CONTRACTS) minus the number of notices served upon today 53 x 100 oz per contract equals 1,754,500OZ OR 54.57TONNES the number of TONNES standing in this active month of DEC.

thus the INITIAL standings for gold for the DEC contract month:

No of notices filed so far (11,981 x 100 oz+ (5629 OI for the front month minus the number of notices served upon today (53} x 100 oz} which equals 1,754,500oz standing OR 54.57 TONNES in this active delivery month of DEC..

TOTAL COMEX GOLD STANDING: 54.56 TONNES (A POOR STANDING//COMEX RUNNING OUT OF PHYSICAL TO SERVE UPON OUR LONGS.

To calculate the number of silver ounces that will stand for delivery in DEC. we take the total number of notices filed for the month so far at 2776 x 5,000 oz = 13,880,000 oz

to which we add the difference between the open interest for the front month of DEC( 2184) and the number of notices served upon today 91 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the DEC./2022 contract month: 2776(notices served so far) x 5000 oz + OI for front month of DEC (2184) – number of notices served upon today (91)x 50070 oz of silver standing for the DEC. contract month equates 24.345 million oz. We will gain in silver oz standing from this day forth. Also we had another criminal element to our silver oz standing: an addition of 750 EFR contract transfers which are “Exchange for risk” settlements. I do not want to bore you but needless to say they are not physical transfers so are criminal in nature. There has been 1250 Exchange for Risk contracts settled these past two days for 6.25 million oz. Thus total delivery: 30.595 million oz.

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

NOV 14/WITH GOLD UP $7.30: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD///INVENTORY RESTS AT 910.12 TONNES

NOV 11/WITH GOLD UP $15.25//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.19 TONNES INTO THE GLD////INVENTORY RESTS AT 911.57 TONNES

NOV 10/WITH GOLD UP $40.75: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 908.38 TONNES

NOV 9/WITH GOLD DOWN $2.00: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.89 TONNES INTO THE GLD////INVENTORY RESTS AT 908.38 TONNES

NOV 8/WITH GOLD UP $34.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.47 TONNES FROM THE GLD//: INVENTORY RESTS AT 905.49 TONNES

NOV 7/WITH GOLD UP $2.95: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.63 TONNES FROM THE GLD//INVENTORY RESTS AT 906.96. TONNES

NOV 4/WITH GOLD UP $44.45 TO $1673.30: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.48 TONNES FROMTHE GLD////INVENTORY RESTS AT 911.59 TONNES.

NOV 3/WITH GOLD DOWN $18.30 TO $1628.85: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.05 TONNES FROM THE GLD////INVENTORY RESTS AT 915.07 TONNES

NOV 2/WITH GOLD UP 55 CENTS TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD///INVENTORY RESTS AT 919.12 TONNES.

NOV 1/WITH GOLD UP $9.20 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.02 TONNES FORM THE GLD../INVENTORY RESTS AT 920.57 TONNES

OCT 31/WITH GOLD DOWN $4.00; BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD//INVENTORY RESTS AT 922.59. TONNES//

OCT28/WITH GOLD DOWN $19.70 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.19 TONNES FROM THE GLD..///INVENTORY RESTS AT 925.20 TONNES

OCT 27/WITH GOLD DOWN $3.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.39 TONNES

OCT 26/WITH GOLD UP $11.65 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.39 TONNES

OCT 25/WITH GOLD UP $3.85: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 928.39 TONNES

OCT 24/WITH GOLD DOWN $1.80 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.89 TONNES FROM THE GLD////INVENTORY RESTS AT 928.10 TONNES

OCT 21/WITH GOLD UP $19.10: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 930.99 TONNES

OCT 20/WITH GOLD UP $2.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 6.08 TONNES FROM THE GLD///INVENTORY RESTS AT 932.73 TONNES

OCT 19/WITH GOLD DOWN $20.65:: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD////INVENTORY RESTS AT 938.81 TONNES

OCT 18/WITH GOLD DOWN $7.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 939.10 TONNES

OCT 17/WITH GOLD UP $14.55: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.28 TONNES FROM THE GLD///INVENTORY RESTS AT 941.13 TONNES

OCT 14/WITH GOLD DOWN $26.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FROM THE GLD///INVENTORY RESTS AT 944.31 TONNES

OCT 13/WITH GOLD DOWN $0.40 TODAY: A DEPOSIT OF 1.16 TONNES INTO THE GLD// CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 945.47 TONNES

OCT 12/WITH GOLD UP $4.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 944.31 TONNES

OCT 11/WITH GOLD UP $10.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 944.31 TONNES

OCT 10//WITH GOLD DOWN $33.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 944.31 TONNES

OCT 7/WITH GOLD DOWN $10.70: NO CHANGES IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 946.34 TONNES

OCT 6/WITH GOLD UP $.70 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.45 TONNES INTO THE GLD//INVENTORY RESTS AT 946.34 TONNES

OCT 4/WITH GOLD UP $28.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.19 TONNES INTO THE GLD//INVENTORY RESTS AT 942.89 TONNES

OCT 3.WITH GOLD UP $29.30 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD AND A BIG SURPRISE: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD////INVENTORY RESTS AT 939.70 TONNES

GLD INVENTORY: 910.12 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

NOV 19

NOV 14/WITH SILVER UP 41 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 471.923 MILLION OZ//

NOV 11/WITH SILVER DOWN 2 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 553,000 OZ FROM THE SLV///INVENTORY RESTS AT 471.923 MILLION OZ//

NOV 10/WITH SILVER UP 39 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 368,000 OZ INTO THE SLV///INVENTORY RESTS AT 472.476 MILLION OZ//

NOV 9/WITH SILVER DOWN 10 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV/; A WITHDRAWAL OF 3.821 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 472.108 MILLION OZ//

NOV 8/WITH SILVER UP 48 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.751 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 475.929 MILLION OZ//

NOV 7/WITH SILVER UP 12 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 477.678 MILLION OZ//

NOV 4/WITH SILVER UP $1.31 TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.972 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 477.678 MILLION OZ//

NOV 3.WITH SILVER DOWN 16 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 566,000 OZ FROM THE SLV////INVENTORY RESTS AT 482.650 MILLION OZ//

NOV 2/WITH SILVER DOWN 9 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 92,000 OZ FROM THE SLV////INVENTORY RESTS AT 483.216 MILLION OZ//

NOV 1/WITH SILVER UP 53 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 415,000 OZ FORM THE SLV////INVENTORY RESTS AT 483.308 MILLION OZ

OCT 31: WITH SILVER FLAT: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .644 MILLION OZ FROM THE SLV/INVENTORY RESTS AT 483.723 MILLION OZ//

OCT 28/WITH SILVER DOWN 35 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 276,000 OZ INTO THE SLV////INVENTORY RESTS AT 484.367 MILLION OZ//

OCT 27/WITH SILVER UP 3 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE S: A WITHDRAWAL OF 2.579 MILLION OZ FROMTHE SLV/////INVENTORY RESTS AT 484.091 MILLION OZ//

OCT 26/WITH SILVER UP 11 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.013 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 486.670 MILLION OZ./.

OCT 25/WITH SILVER UP 17 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.083 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 487.683 MILLION OZ/

OCT 24/WITH SILVER UP 6 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .553 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 485.610 MILLION OZ//

OCT 21/WITH SILVER UP 43 CENTS: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .46 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 486.163MILLION OZ//

OCT 20/WITH SILVER UP 33 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .921 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 485.703 MILLION OZ//

OCT 19/WITH SILVER DOWN 27 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.105 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 486.624 MILLION OZ///

OCT 18/WITH SILVER DOWN 5 CENTS:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.658 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 487.729 MILLION OZ///

OCT 17/WITH SILVER UP 53 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.151 MILLION OZ INTO THE SLV////INVENTORY REST AT 486.071 MILLION OZ//

OCT 14/WITH SILVER DOWN 77 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.211 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 484.920 MILLION OZ//

OCT 13/WITH SILVER DOWN 2 CENTS TODAY: BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.513 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 482.709 MILLION OZ//

Oct 12/WITH SILVER DOWN 18 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.196 MILLION OZ

OCT 11/WITH SILVER DOWN 11 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.066 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 478.196 MILLION OZ

OCT 10//WITH SILVER DOWN 65 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 473.130 MILLION OZ/

OCT 7/WITH SILVER DOWN 37 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.447 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 473.130 MILLION OZ/

OCT 6/WITH SILVER UP 11 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY: A WITHDRAWAL OF 5.3 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 475.617 MILLION OZ//

OCT 4WITH SILVER UP $.51 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ

OCT 3/WITH SILVER UP $1.46 : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ//

CLOSING INVENTORY 471.923 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff

2 Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz//Rickards:

Von Greyerz: In The End The Dollar Goes To Zero & The US Defaults

With US and Global debt exploding prior to both assets and debt imploding, let us look at the disastrous consequences for the US and the world.

Debt explosion leading to the currency becoming worthless has happened in history for as long as there has been some form of money whether we talk about 3rd century Rome, 18th century France or 20th century Weimar Republic and many many more.

So here we are again, another monetary era and another guaranteed collapse as von Mises said:

“There is no means of avoiding the final collapse of a boom brought about by credit expansion”

This disastrous borrowed prosperity, with ZERO ability to repay the surging debt, will lead to one of the three consequences below:

1. THE US$ GOES TO ZERO

2. A US DEFAULT

3. BOTH OF THE ABOVE

The most likely outcome is number 3 in my view. The dollar will go to ZERO and the US will default. The same will happen to most countries.

I outline the consequences for the world at the end of his article.

Many people say that the US can never default. That is of course absolute nonsense.

If a country prints worthless debt that nobody will buy in a currency that no one wants to hold, the country has definitely defaulted whatever spin they put on it.

In the next few years, not just US but all sovereign debt will only have one buyer which is the country that issues the debt. And every time a sovereign state buys its own debt, it has to issue more worthless debt that nobody will touch with a barge pole.

Printing more money to pay for previous sins has never worked and never will.

And this is how money dies, just like it has throughout history.

The current monetary era started with the foundation of the Fed in 1913 and the acceleration of debt and currency debasement since 1971 when Nixon closed the gold window. With just over 100 years into this era, it is now approaching the end, like they all do.

Global currencies are already down 97-99% since 1971 and we can now expect the final 1-3% decline for all money to become virtually worthless. This is of course nothing new in history since every single currency has always gone to ZERO. We must of course remember that the final 1-3% move means a 100% fall from today. The final collapse is always the quickest so it could easily happen in the next 2-5 years.

DEBT, DEBT AND MORE DEBT

Let’s look at how it has all evolved.

Although US debt has increased virtually every year since 1930, the acceleration started in the late 1960s and 1970s. With gold backing the dollar and therefore most currencies UNTIL 1971, the ability to borrow more money was restricted without depleting the gold reserves.

Since the gold standard prevented Nixon to print money and buy votes to stay in power, he conveniently got rid of those shackles “temporarily” as he declared on August 15, 1971. Politicians don’t change. Powell and Lagarde recently called the increase in inflation “transitory” but in spite of their bogus prediction, inflation has continued to rise.

Since 1971 total US debt has gone up 53X with GDP only up 22X as the graph below shows:

As the widening Gap between Debt and GDP in the graph above shows, it now takes ever more debt to achieve increases in GDP. So without printing worthless money, REAL GDP would show a decline.

So this is what our politicians are doing, buying votes and creating fake growth through printed money. This gives the voter the illusion of increased income and wealth. Sadly he doesn’t grasp that the illusory increase in living standard is all based on debt and devalued money.

Let’s also look at US Federal Debt:

Since Reagan became president in 1981, US federal debt has on average doubled every 8 years. Thus when Trump inherited the $20 trillion debt from Obama in 2017, I forecast that the debt would double by 2025 to $40t. That still looks like a valid projection but with the economic problems I expect, a $50t debt by 2025-6 cannot be excluded.

So presidents know they can buy the love of the people by running chronic deficits and printing money to make up for the difference.

But if we look at the graph above again, it shows that debt has gone up 35X since 1981 but that tax revenue has only increased 8X from $0.6t to $4.9t.

How can any sane person believe that with debt going up 4.5X faster than tax revenue that the debt can ever be repaid.

Even worse, with US interest payments on the debt surging from around 0% to probably 5% by 2025 the interest on the debt will climb to $2 trillion or circa 30% of the annual budget.

So with higher interest rates, higher deficits and rising inflation the scene is set for a high or hyper-inflationary period in the next few years.

FED PIVOT?

So virtually every observer believes that the Fed (and ECB) will not just stop raising interest rates but pivot and lower them again.

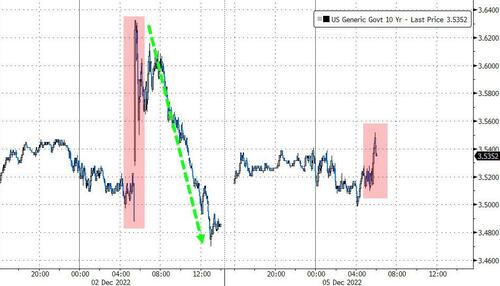

In my view this will not happen except for possibly very short term. The 40 year interest rate downtrend finished in 2020 and the world is unlikely to see low or negative rates for many years or decades. High inflation and high rates will continue for years. But as we see in the 40 year chart of the 10 year US treasury below, there will be many corrections in the coming uptrend.

US MONEY SUPPLY GROWING AT 74% ANNUALISED

Between August 1971 and August 2019 US money supply grew at 6.1% p.a.

In August 2019, the hangover from the 2006-9 Great Financial Crisis hit the financial system again resulting in major support actions from the Fed and other central banks.

So the fresh problems emerged before Covid and before Ukraine. But those two new crises obviously exacerbated the systemic problems that had been put on ice for 10 years. This led to massive money printing and M1 in the US no longer increased at 6% annually but at a hyperinflationary 74% p.a. as the graph below shows.

$25 TRILLION GLOBAL LIQUIDITY/DEBT INCREASE AT ZERO COST

Central banks are always wrong and always behind the curve. They kept short term rates at zero or negative for over a decade. From 2009 to 2019 the balance sheets of major central banks increased by $13t. But then from Aug 2019 to 2022 an explosion in central bank debt took place, expanding their balance sheets $23t from $13t to $36t. All the same reasons that I discuss in the paragraph above regarding US money supply are obviously also valid for global debt expansion.

There is nothing like free money! The banks created this money at ZERO cost. They did no work and nor did they produce any goods or services. All they needed to do was to press a button. And with interest rates at zero or negative, many central banks were actually receiving interest from the lenders.

What a beautiful Ponzi scheme. CBs print/borrow money and then they are paid for the pleasure of borrowing this money. Any private swindler launching such a scheme like Ponzi or Madoff would spend the rest of his life in prison but the bankers are praised for “saving” the system.

What virtually no individual understands is that this free money then enters the financial system as having a real intrinsic value. As with all Ponzi schemes, the current financial system will collapse too as the holders of the fake paper money realise that the money is worthless and that the emperor is totally naked.

Within the next five years or so, the triangle is likely to be inverted with central bank gold as the foundation at the bottom. But instead of gold being only 0.1% of global liabilities, it will be as much as maybe 20%. That 200x revaluation of gold will be a combination of the value of global assets and liabilities collapsing and gold rising.

Personally I don’t believe in a lasting formal reset with a new currency system backed by gold. I cannot see the three major gold producers/holders China, Russia and India agreeing with the US on a revaluation. It is also questionable if the US has anywhere near the 8,000 tonnes of gold they are declaring. Also, China and Russia probably have considerably more gold than they are declaring.

Instead, after the fake paper market in gold has collapsed, the price must be based on supply and demand of unencumbered physical gold or Free Gold. But that can only happen after the current financial system based on fake money, debt and derivatives no longer functions.

CONSEQUENCES

But before that, the world must pay for the excesses of the last 50 years. The consequences will be dire as we are facing a major cataclysm or disorderly reset which will involve:

DEBT DEFAULTS – SOVEREIGN, CORPORATE & PRIVATE

BURSTING OF EPIC BUBBLES IN STOCKS, BONDS & PROPERTY

MAJOR GEOPOLITICAL CONFLICTS WITH NO DESIRE FOR PEACE

SECULAR FALL OF LIVING STANDARDS DUE TO HIGHER COST OF ENERGY & ENERGY SHORTAGES

FOOD SHORTAGES LEADING TO MAJOR FAMINE AND CIVIL UNREST

POLITICAL AND ECONOMIC INSTABILITY & CORRUPTION

NO COUNTRY WILL AFFORD SOCIAL SECURITY OR PENSIONS

INFLATION HYPERINFLATION AND LATER DEFLATIONARY IMPLOSION

I sincerely hope that these predictions will not take place. Because if they do, everyone will suffer dramatically for an extended period. No one, rich or poor will avoid these problems.

But what I am saying is that the risk of a major catastrophe has never been higher in history, whenever it actually happens.

Physical gold and silver will not save you but clearly be the best financial insurance you can hold.

Most important is a support system of family and friends. Remember also that in addition to family and friends, some of the best things in life are free like nature, music, books and many hobbies.

3. Chris Powell of GATA provides to us very important physical commentaries//

Alameda’s Caroline Ellison Spotted In NY Amid Speculation She Is About To Roll On SBF After Hiring Iconic Clinton Lawyer

MONDAY, DEC 05, 2022 – 05:11 AM

As Sam Bankman-Fried enters day six of his whirlwind media tour in which he makes one or more daily appearances – against the advice of his lawyers – in hopes of convincing someone that he was too dumb to be a criminal mastermind with billions in crypto in cold storage and in bank accounts in Dubai and Singapore (luckily all his wire transfers can be traced), also known as the Simple Jack defense…

… the weakest link in SBF’s defense was just spotted in a New York coffee shop, amid speculation she is preparing to blow up SBF’s entire defense strategy.

According to Autism Capital, the former CEO of Alameda Capital (which as a reminder was ground zero of the FTX implosion after it blew up $8 billion in FTX client funds on trades gone horribly wrong), Caroline Ellison, was spotted at 8:15am this morning at the Ground Support Coffee on West Broad in SoHo Manhattan. This, as AC notes, “would mean she is not in Hong Kong and is in NY not in custody.”

A statement from a barista at the coffee shop confirmed that it was in fact Caroline.

Why does this matter? Because while the prominent Democrat donor, who reportedly is “responsible for Biden being in office” and who – at least according to Musk – donated over $1 billion to democrats…

… continues his deluded daily media appearances while casually throwing his former alleged lover, co-worker and penthouse-mate, Caroline – and pretty much all other co-workers – under the bus by claiming he has no idea how $8 billion in FTX client funds just vaporized in SBF’s personal hedge fund, Alameda (implying that only Alameda’s CEO, Ellison, was responsible for the theft and fraud) Caroline is two-steps ahead of SBF and is already cooperating with members of the DOJ, and specifically the SDNY, which we previously reported is probing the collapse of FTX.

Subsequent reports have only reinforced this rumor, and the latest is that Ellison is being represented by DC law firm, WilmerHale…

… best known for its Government Affairs Department Chair, Jamie Gorelick, who was the former No. 2 ranking member in the Clinton Justice Department, and in a recent interview, she referred to Garland as her “wingman.”

If indeed Ellison is working the Feds while currying favor with SBF’s former closest friends, the days of Bankman-Fried – who may or may not soon commit Epsteincide – outside of a prison cell are numbered.

As for SBF, who is still wasting his time “uhhhm“-ing and “like“-ing across various interviews hoping to demonstrate to the world – and his future jurors – just how bloody stupid he really was…

… and blaming it all on messy accounting, poor risk management, and of course, Caroline Ellison – not his premeditated fraud of course – even the CEO of Coinbase is no longer buying his relentless bullshit, saying earlier that no matter how “messy you accounting is (or how rich you are) – you’re definitely going to notice if you find an extra $8B to spend” adding that “even the most gullible person should not believe Sam’s claim that this was an accounting error” (here he is referring to Bill Ackman, of course), and correctly concluded that “it’s stolen customer money used in his hedge fund, plain and simple.”

All that’s missing is the definitive proof, and if the above rumors are correct, Caroline Ellison is in the process of, or already has provided it to the Feds. Which incidentally, may explain why SBF’s “I am Simple Ja-ja-ja-jack, i’m so-so-so-sorry” tour just came to a crashing halt, when late on Sunday, the commingling masterming told Maxine Waters he won’t be voluntarily appearing before Congress – where any lie is a perjury – on the 13th (or ever for that matter).

end

Earth To Reporters: Why Is No One Asking SBF What Happened To The $3.3 Billion He Borrowed?

Disgraced crypto chief Sam Bankman-Fried has been talking to reporters, including at the New York Times (the famed Andrew Ross Sorkin Dealbook interview), the Financial Times, and the Wall Street Journal. Despite the fact that it’s generally seen as a very bad idea to say anything about your past conduct when you are a litigation target, and likely for a criminal case, and SBF has said his lawyers are opposed to talking to the press, SBF is nevertheless swanning about on his media tour.

Even though SBF got a bit of pushback from Sorkin on the question of co-mingling of funds when SBF tried playing, “Oh it was sort of allowed and anyway things were a mess,” he and other reporters didn’t probe very hard once they got his next layer of excuses: “Oh I didn’t mean to do anything bad, I don’t have access to records any more and my memory is fuzzy, and I really didn’t have anything to do with Alameda.”

Core to Bankman-Fried’s account of how FTX ended up with a roughly $8bn shortfall of client assets was excessive lending by the exchange to Alameda, which ploughed the money into venture capital investments and doomed bets on digital tokens.

Bankman-Fried deflected the FT’s questions about the excessive borrowing and soured investments that ultimately sank Alameda, blowing a hole in FTX’s finances, and would not be drawn on the legal consequences he may face. He said he deliberately avoided getting involved in Alameda’s trading and risk management to avoid conflicts with his position as chief executive of FTX, and neglected to monitor the risk they posed to the exchange.

Got that? $8 billion hole at the hedge fund Alamada. We are supposed to believe that the was the result of FTX lending to Alamada and then Alameda doing stoopid things that burned up a lot of dough. Oh, and even though SBF is responsible for (at best) crappy controls at FTX that allowed Alameda, we are also supposed to believe SBF’s claims that he was not involved in what was happening at Alameda.

Aside from the wee problem that SBF owned 90% of Alameda and had its detailed financial information as recently as March, Alameda made $3.3 billion of loans to SBF, $1 billion as a personal loan, and $2.3 billion to a 100% SBF-controlled entity, Paper Bird, that is outside the FTX-Alameda bankruptcy.

So Alameda made $4.1 billion in loans to cronies, mainly SBF, and we are to believe that SBF had nothing to do with that?

I am at a loss for the failure to purse the question of what happened to the $3.3 billion SBF borrowed. This is already in the public domain. Yes, no doubt more will be revealed as the bankruptcy process winds forward. But help me. This is not hard.

Mark Karpelès compiled an FTX entity list, which confirms that Paper Bird is a “top” company, which is consistent with SBF being its sole shareholder. The bankruptcy filing states that Paper Bird owned 75% of FTX International.1 However, that does not make it part of the FTX bankruptcy. In fact, Paper Bird filed for its own bankruptcy, the same date at FTX did, with separate counsel: Adam Landis of Landis Roth & Cobb while the lead attorney for FTX is James Bromley of Sullivan & Cromwell.

Notice we have not heard anything about these lavish loans in SBF’s “Oh poor confused me and I feel sorry for all my chump victims too.” Since SBF seems unduly eager to try to ‘splain himself, it would improve appearances in the eyes of public opinion and perhaps later a court, if he could honesty say, “I scrounged up what I could liquidate readily and used to to try to save the company.” If that had happened, that would also mean any investor recoveries, however meager, were due in part to SBF trying to shore up his enterprise.

I have seen no claim in the press or the bankruptcy filing that SBF either did or expressed willingness to put his own money into FTX when it was collapsing. The failure of SBF to spend any of his own funds to salvage his empire no doubt contributed to its demise. If he’d put up say $3 billion of the $8 billion supposedly needed, there is a remote possibility that his napkin-doodle balance sheet would have been forgiven: “If SBF is willing to stake that much of his personal money on the odds that he can rescue FTX, there must be some real value in there despite the mess.”

And it would not be hard for a merely mildly dogged interviewer to press SBF on this topic: “You took $1 billion in personal loans from Alameda. When did that happen? You said in your Financial Times lunch earlier this year and then more recently that you had only $100,000 in bank. So where did the $999,900,000 or more go? Was it invested in real estate? Gambled away?”

Remember, he can’t play “I don’t remember” and act like he can’t get the information. This was personal money, under his control, and he still has unimpeded access to those records. The reporter could follow up: “If you don’t remember, could check your personal accounts and get back to us?” And if he demurs again, drive the knife in: “This will probably come out in court anyhow since the creditors will be looking into fraudulent conveyance. So this isn’t something you will be able to hide.”

Then an interviewer could follow a parallel line of questioning with Paper Bird. There SBF might give bafflegab about venture investments or crypto speculation, so if I were a member of the press, I’d start with the personal loan first since he has much less wriggle room there. Not being able to explain what happened to $1 billion, which is the route SBF is likely to take, is not a good look.

Separately, yours truly is becoming slightly more optimistic that SBF might wind up facing a real prosecution, as opposed to one designed to find as little as possible. From the Wall Street Journal:

In Cyprus, the country’s securities regulator is complaining that Mr. Ray’s decision to place FTX in bankruptcy has stymied investigations and is preventing European customers from getting their money back…In Turkey, authorities have seized the assets of FTX’s local subsidiary, an affront to Mr. Ray’s efforts to sweep FTX’s assets into the chapter 11 process in Delaware….

On Nov. 28, the chairman of the Cyprus Securities and Exchange Commission voiced concern about the bankruptcy process in a letter to Mr. Ray, a copy of which was seen by the Journal. FTX’s European arm, FTX EU Ltd., was licensed in Cyprus, allowing the crypto exchange to offer services elsewhere in the European Union’s single market….

The Cyprus securities regulator has ordered the company to return the money to customers, but the company has been unable to comply because its bank accounts are frozen by the chapter 11 process, the chairman said.

Mr. Theocharides also reminded Mr. Ray “that unlawful use of clients funds might constitute a criminal offense.”…

Trouble might also be brewing for Mr. Ray in Turkey, where regulators have already decided to take control of FTX’s domestic subsidiary’s winding-down. On Nov. 19, Mr. Ray said FTX had identified a number of subsidiaries with valuable franchises that could be sold to raise cash for the company’s creditors. One of them was FTX’s wholly owned Turkish subsidiary, FTX Turkey Teknoloji Ve Ticaret AS, where the company had found nearly $3.1 million in assets when it filed for bankruptcy, according to court papers.

Four days later, though, the financial crimes board of Turkey’s Treasury Ministry said it had confiscated the assets of FTX Turkey on suspicion that customer deposits were transferred or taken abroad through fraudulent transactions and that nonexistent crypto assets were sold to customers. Istanbul’s chief prosecutor began a criminal investigation into Mr. Bankman-Fried and other people associated with FTX, the ministry said.

So far, the Cyprus regulator is just whining, but his criminal offense remark is arguably a shot at Ray, not just SBF. By contrast, Türkiye is saddling up. And remember, as SBF keeps running his mouth and the bankruptcy court unearths more information, they will soon have plenty of promising material.

Both Cyprus and Türkiye have bilateral extradition treaties with the US. Federal prosecutors and regulators hate being upstaged by state counterparts; that’s why state enforcement actions regularly have the effect of rousing formerly somnambulant authorities.

It would be staggeringly embarrassing for the Department of Justice to make no filing against SBF or only a very weak and limited one, and then have jurisdictions seen as less than upstanding (that’s why SBF chose them, after all) making forceful cases that SBF had violated their laws. That pressure, which at least from Türkiye seems to be genuine, will force the DoJ to do more than dial its investigation of SBF in.

Many more to come

(zerohedge)

Three Arrows Capital Liquidators Seek $30 Million From Sale Of “Much Wow” Superyacht

SATURDAY, DEC 03, 2022 – 08:00 PM

The crypto industry continues to “pick up the pieces” after its epic collapse over the last 6 months, culminating in the implosion of FTX last month.

Three Arrows Capital, another firm that went under due to the plunging price of bitcoin, is in the process of being liquidated. Those in charge of dispersing of its assets are now looking to raise $30 million from the sale of a superyacht called “Much Wow”.

We first wrote that the yacht was being considered for sale in the bankruptcy this summer.

On Friday, a filing in the U.S. Bankruptcy Court in the Southern District of New York by the company’s liquidator, Teneo, confirmed that it had recovered $35.6 million in cash, $2.8 million from forced redemptions and “over 60” different crypto tokens and NFTs, Coingape reported.

Teneo is also seeking $30 million from the sale of the yacht, which is said to be worth $50 million. According to the report, founders of 3AC used company funds to purchase the yacht, but never made its final payment.

The yacht is currently “in insolvency proceedings in the Cayman Islands”, the report says.

Company founder Kyle Davies recently “criticized liquidators for refusing to engage with them constructively,” the report continues. Teneo has spoken out and said that they Davies and founder Zhu Su are delaying the return of funds to creditors.

The founders are in Bali and Dubai, respectively, and their U.S. citizenship is “unclear”, making it difficult to subpoena them. Read more here….ONSHORE YUAN: CLOSED DOWN 7.1151

OFFSHORE YUAN: 7.1257

SHANGHAI CLOSED DOWN 18.19 PTS OR 0.58%

HANG SANG CLOSED DOWN 53.12 OR 0.29%

2. Nikkei closed DOWN 30.80 PTS OR 0.11%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX UP TO 106.36 Euro RISES TO 1.0382

3b Japan 10 YR bond yield: RISES TO. +.242!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 140.28/JAPANESE YEN COLLAPSING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: UP-// OFF- SHORE: UP

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.0755%***/Italian 10 Yr bond yield FALLS to 3.908%*** /SPAIN 10 YR BOND YIELD FALLS TO 3.084…** DANGEROUS//

3i Greek 10 year bond yield FALLS TO 4.312//

3j Gold at $1764.00//silver at: 21.23 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 19/100 roubles/dollar; ROUBLE AT 60.34//

3m oil into the 82 dollar handle for WTI and 945 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 139.99 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9514–as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9867well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

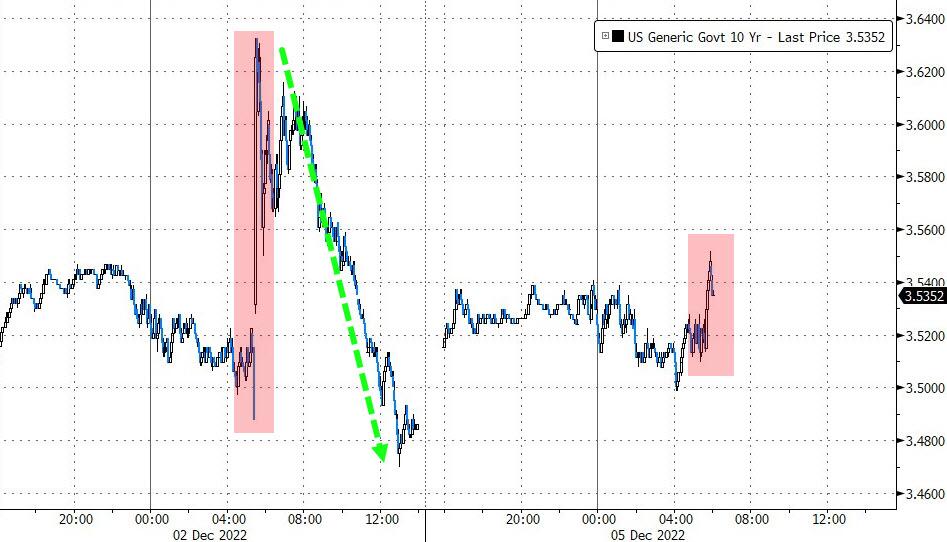

USA 10 YR BOND YIELD: 3.810% UP 4 BASIS PTS…GETTING DANGEROUS

USA 30 YR BOND YIELD: 3.908% UP 2 BASIS PTS//

USA DOLLAR VS TURKISH LIRA: 18,62…

GREAT BRITAIN/10 YEAR YIELD: 3.2974%

end

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

AND NOW NEWSQUAWK (EUROPE/REPORT)

i)MONDAY MORNING// SUNDAY NIGHT

SHANGHAI CLOSED DOWN 18,19 PTS OR 0.58% //Hang Sang CLOSED DOWN 53,12 OR 0.29% /The Nikkei closed DOWN 30.80 OR 0.11% //Australia’s all ordinaries CLOSED UP 0.21% /Chinese yuan (ONSHORE) closed DOWN TO 7.1151//OFFSHORE CHINESE YUAN DOWN 7.1257// /Oil DOWN TO 82.31 dollars per barrel for WTI and BRENT AT 95.14 / Stocks in Europe OPENED ALL GREEN. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

2 a./NORTH KOREA/ SOUTH KOREA/

///NORTH KOREA/SOUTH KOREA/

end

2B JAPAN

JAPAN

END

3c CHINA

CHINA/ECONOMY/APPLE

Apple’s retreat from China is acclerating

(zerohedge)

Apple Accelerating Supply Chain Retreat From China After iPhone Factory Chaos

SUNDAY, DEC 04, 2022 – 12:00 AM

Apple Inc’s massive exposure to Chinese manufacturing has left it with production shortfalls of iPhones due to Beijing’s harsh virus containment policies and unrest at a major factory in central China operated by Foxconn. A new report shows the iPhone maker’s retreat from China is accelerating.

WSJ said Apple is “telling suppliers to plan more actively for assembling Apple products elsewhere in Asia, particularly India and Vietnam, they say, and looking to reduce dependence on Taiwanese assemblers led by Foxconn.”

Apple’s supply chain data indicates China is the iPhone maker’s primary location. Market research firm Counterpoint Research recently noted 85% of the Pro lineup of iPhones is made in Foxconn’s giant city-within-a-city factory in Zhengzhou.

“Apple no longer feels comfortable having so much of its business tied up in one place, according to analysts and people in the Apple supply chain,” WSJ noted.

“In the past, people didn’t pay attention to concentration risks.

“Free trade was the norm and things were very predictable. Now we’ve entered a new world,” Alan Yeung, a former US executive for Foxconn, said.

People familiar with Apple’s supply chain said that not all production would be shifted outside China. However, the remaining production in China will draw on a larger pool of assemblers, not just Foxconn. They said Luxshare Precision Industry Co. and Wingtech Technology Co. are two companies in line to receive more business from Apple.

As for the shift out of China, people involved in the discussions said Apple is telling manufacturing partners to look at other countries.

However, Apple has spent decades interweaving its supply chains within China, and change won’t come overnight.

“Finding all the pieces to build at the scale Apple needs is not easy,” said Kate Whitehead, a former Apple operations manager who now owns her own supply-chain consulting firm.

Ming-chi Kuo, an analyst at TF International Securities who follows the supply chain, said Apple’s longer-term objective is to ship 40% to 45% of iPhones from India. And suppliers said Vietnam could soon be a significant player in manufacturing other Apple products such as AirPods, smartwatches, and laptops.

The bigger trend is the fracturing of the global supply chain. US firms realize China’s zero Covid policy and shutdowns, along with heightened geopolitical risk across the region, are bad for business and recently outlined in the American Chamber of Commerce in Shanghai’s latest survey of US firms in China found a near doubling of respondents over the past year that are slashing investment.

end

CHINA?COVID

Wuhan Whistleblower: Former EcoHealth VP Says Covid “Man Made”, Escaped From Lab

Just hours after we find out that the Hunter Biden laptop not only wasn’t “Russian disinformation”, but rather was being actively covered up by social media, another “conspiracy theory” that wound up costing tons of honest truth seekers their social media accounts (including Zero Hedge, who was first to talk about the lab leakall the way back in February 2020), is inching closer toward being validated as reality.

That’s because a scientist who formerly worked at the Wuhan Institute of Virology has now gone on record and has said that COVID was “man-made” and leaked from the lab.

The claims are according to the Post, who cited The Sun, who was provided a copy of the scientist’s forthcoming book.

The gravity of the allegations, which I have written about at length over the last year, would make the global Covid-19 pandemic cover up among the most stunning lies ever perpetrated on modern humanity.

The whistleblower, epidemiologist Andrew Huff, called the lab leak the “biggest US intelligence failure since 9/11″. He detailed his allegations in his book “The Truth About Wuhan”.

Get 50% off: If you enjoy this article, would like to support my work, I would love to have you as a subscriber and can offer you 50% off for life: Get 50% off forever

Huff is the former vice president of EcoHealth Alliance, which studied coronaviruses at the Wuhan Institute of Virology. He worked for the company from 2014 to 2016 and, per the Post:

…said that the non-profit helped the Wuhan lab put together the “best existing methods to engineer bat coronaviruses to attack other species” for many years.

“Foreign laboratories did not have the adequate control measures in place for ensuring proper biosafety, biosecurity, and risk management, ultimately resulting in the lab leak at the Wuhan Institute of Virology,” he wrote in his book.

Huff wrote: “China knew from day one that this was a genetically engineered agent. The US government is to blame for the transfer of dangerous biotechnology to the Chinese.

“I was terrified by what I saw. We were just handing them bioweapon technology.”

Fringe Finance has been covering the idea of a lab leak since the blog’s inception and we have long maintained that a leak from the lab was the most obvious explanation for Covid.

Now the question becomes: who will be held accountable…not only for the leak but for the campaign against those who asked honest questions about the lab for the last 3 years?

And what other “conspiracy theories” will we soon find out are closer to truth?

As protests continue to rage throughout China over the regime’s harsh COVID-19 policies, and the police respond with notable force, a bipartisan group of U.S. senators has sent a sharply worded letter to Beijing’s ambassador to Washington, Qin Gang, warning of “grave consequences for the U.S.-China relationship” if the communist regime carries out a crackdown reminiscent of the Tiananmen Square massacre of 1989.

One of the lead signers, Sen. Dan Sullivan (R-Alaska), said in a statement accompanying the letter’s publication on Dec. 1 that the world’s response to Beijing’s efforts to quell the protests has been “tepid at best.” Hence Sullivan and the other signers saw a need to speak out and warn Beijing about what would happen if it failed to respect the right of citizens to signal their opposition to the severe COVID policies that have deprived millions of Chinese of freedom of movement.

The letter emphasizes the nonviolent character of the protests going on in China, implying that any abusive and violent conduct on the part of the regime’s forces will be illegal and unethical.

“We are following the current peaceful protests in China over your government’s policies very carefully. We are also closely watching the Chinese Communist Party’s (CCP) reaction to them,” the letter states.

The letter goes on to remind Ambassador Gang about the notorious events of June 1989, which drew worldwide condemnation and became a synonym for excessive force on the part of an authoritarian regime.

“In 1989, the Chinese Communist Party and People’s Liberation Army undertook a violent crackdown on peacefully protesting Chinese students, killing hundreds, if not thousands,” the letter states, before issuing a stark warning.

“We caution the CCP in the strongest possible terms not to once again undertake a violent crackdown on peaceful Chinese protestors who simply want more freedom. If that happens, we believe there will be grave consequences for the U.S.-China relationship, causing extraordinary damage to it,” the letter concludes.

Brussels Bailing Out Ukraine Will Ruin Europe For Generations, Hungary’s Orban Warns TYLER DURDEN

SUNDAY, DEC 04, 2022 – 02:35 PM

Hungarian Prime Minister Victor Orbán warned on Friday that European policies advocating for mass joint borrowing among EU member states to continue funding Ukraine’s resistance to the Russian invasion will have devastating consequences.

The Hungarian leader told “Good morning, Hungary!” that EU sanctions on Russian energy are bound to fail, and that “not only our children, but also our grandchildren will suffer the consequences” of a mass borrowing scheme proposed by the EU, adding that potentially insolvent states will require support as well.

Orban reiterated Hungary’s opposition, and suggested that agreements to support Ukraine should be at the national level via bilateral agreements between individual countries, ReMixreports.

He highlighted that Ukraine has now found itself in a situation whereby it is incapable of functioning as an independent nation because of the ongoing conflict, and while it needs help from its neighbors and allies in the short-term, it is not for Brussels to speak on behalf of all member states.

What’s more, Orban believes that any further sanctions on Russian gas or nuclear energy would have “tragic consequences,” and argued that Hungary should be exempt from such a decision.

“We are facing a difficult winter, Ukraine is in an increasingly difficult situation, Russia is suffering difficulties, but its revenues from energy carriers are at their peak, so the policy of sanctions has not achieved its goal,” he said, explaining that while Hungary won’t be subject to an upcoming ban on European imports of Russian oil, it will still be affected by the “price-inflating effect of the sanctions.”

“We have always achieved our own national goals in the negotiations on sanctions, so we are participating in the discussion of the ninth package with good hopes,” Orban concluded, while noting that the “pressure is constant,” and that Hungary must “constantly fight to protect our interests.”

end

Switzerland, Facing an Unprecedented Power Shortage, Contemplates a Partial Ban on the Use of Electric Vehicles

Godfrey Bloom on Twitter: “I’m afraid the game is over.” / Twitter

5.//UKRAINE/RUSSIA

Airbases Deep Inside Russia Rocked By Explosions; New Wave Of Airstrikes Pummel Ukraine

MONDAY, DEC 05, 2022 – 04:45 PM

Monday saw another major escalation in the Ukraine war as Russian media reported that explosions rocked two air bases in Russia, suggesting Ukrainian forces could be seeking to launch missiles deep into Russian territory, though the exact cause or type of weapon behind the explosions are unknown. It could also possibly be another “sabotage attack” such that was previously seen in the Crimea.

One of the Russian bases struck reportedly hosts nuclear-capable strategic bombers being utilized in airstrikes on Ukrainian energy infrastructure. The Associated Press details in the aftermath of the blasts, “Russian state RIA Novosti news agency said three servicemen were killed and six others injured, and a plane was damaged, early Monday when a fuel truck exploded at an air base in Ryazan, in western Russia.”

The report underscored that “The base houses long-range flight tankers that serve to refuel bombers in the air.” The other base that was hit is being identified as in the Saratov region. The Saratov base lies some 600 kilometers east of Ukraine, so both the bases are relatively deep inside Russian territory.

Moscow meanwhile has taken quick, decisive action – once again launching a barrage of major airstrikes on Ukrainian cities, targeting particularly energy infrastructure as part of the stated purpose of degrading Ukraine’s power supply going into winter. For days Ukrainian officials have been warning the population to brace for new major attacks.

Air raid alert sirens sounded Monday across the country. “The enemy is again attacking the territory of Ukraine with missiles!” Kyrylo Tymoshenko, an official with the Ukrainian president’s office, wrote on Telegram.

Media reports referred to explosions in several parts of the country, including the cities of Odesa, Cherkasy and Kryvyi Rih. In Odesa, the local water supply company said a missile strike cut power to pumping stations, leaving the entire city without water.

Civilians are sheltering in underground places like metro stations, especially in the populous Ukrainian capital…

Ukraine has so far counted a handful of deaths from Monday’s fresh round of Russian strikes. It’s expected that power and water access in many parts will be impacted more severely given most estimates have already put the national energy grid at 40% disabled.

“Zelenskyy’s office said three rocket strikes hit the president’s hometown of Kryvyi Rih in south-central Ukraine, killing a factory worker and injuring three others,” the AP continues. “In the northeastern region of Kharkiv, a person was killed in strikes by S-300 missiles on civilian infrastructure in the town of Kupyansk, it said.”

The two Russian airbases rocked by explosions on Monday were deep inside the country, suggesting the possibility of either a long-range Ukrainian strikes or also a sabotage operation on the ground…

And further there are emerging reports that a downed rocket has been found just long the border with Moldova, suggesting like the last wave of attacks Russia is targeting ever further West in Ukraine. Likely as a result Ukraine forces will try to continue hitting targets inside Russia, also as their capability grows given they have been supplied with ever-longer range rockets from the US and NATO countries.

end

Zelensky Seeks To Ban Russian Orthodox Church In Ukraine

Ukrainian President Volodymyr Zelensky announced he is seeking to ban all religions with ties to Russia. He claims the move is needed to “guarantee spiritual independence to Ukraine.” This law will target millions of Ukrainians who identify as Russian Orthodox.

During his nightly address on Thursday, Zelensky announced he was introducing legislation that would eliminate religious organizations affiliated with Russia from operating in Ukraine. He said this will make “it impossible for religious organizations affiliated with centers of influence in the Russian Federation to operate in Ukraine.”

The Ukrainian leader said it was necessary to purge the church to preserve the country’s spiritual independence. Adding, “We will never allow anyone to build an empire inside the Ukrainian soul.” Zelensky denounced Ukrainians continuing to attend the parishes as failing to overcome “the temptation of evil.”

He claimed a series of recent raids by Kiev’s intelligence found orthodox churches which remain connected with the Moscow Patriarchate have been acting as operatives for the Kremlin. In his address, Zelensky instructed his security forces to further target Russian Orthodox parishes.

At least two-thirds of Ukrainians identify as Eastern Orthodox Christians. At one point, the majority of Ukrainians attended parishes that followed the Moscow Patriarchate.

Some recent polls say that number has dwindled to under 15%. However, the polling was only conducted in territory that was controlled by Ukrainian forces. Zelensky has vowed to return those regions to Kiev’s authority.

Dmitry Medvedev, deputy chairman of the Russian Security Council, responded by slamming Zelensky’s move as authoritarian. “The current Ukrainian authorities have openly become enemies of Christ and the Orthodox faith,” he said.

end

Perhaps on the horizon

Robert Hryniak

1:14 AM (6 hours ago)

to

Before this an form there will be much more territory given up in the Ukrainian. If for no other reason than Russia will not allow BlackRock to loot the Ukraine to line the pockets of Zelensky and his gang of thieves. And first Europe will taste a bitter winter of failed policies.

Meanwhile in America one has to deal with the delusional crowd who are not so likely to retire from their pursuit of failed hegemony expression. Such a move not handled correctly can lead to a complete loss of American hegemony in Europe over time.

When statesmen are needed few rise from the pathetic crowd.

4/12/22 By WarNews 24/7 (translayed from Greek)

A storm of reactions has been caused by the statement of the French president Emmanuel Macron about changing the security architecture in Europe. In fact, Macron emphasized that the issue was also discussed with Pre. Biden.

But what do the French mean? Will NATO forces withdraw from Eastern Europe and the Baltics as requested by Russia? Will Ukraine remain demilitarized and half a state?

However, the Ukrainian Army must be in a dire state. A few 24 hours ago the Americans stressed to Zelensky that he should negotiate and now Macron is dropping a megaton bomb.

Although the proposal will be rejected by Moscow because it no longer believes in any guarantees from the West, Macron’s public proposal nevertheless shows that the West has relented.

In more detail, French President Emmanuel Macron says he is ready to offer “guarantees” to Moscow’s “concerns” in order to put an end to the bloody war in Ukraine.

“The West will have to consider how to deal with Russia’s need for security guarantees if the Russian president agrees to negotiations to end the war in Ukraine,” the French president said on Saturday.

Macron’s message to Putin

During an interview with French TV station TF1, taped during his visit to the US and broadcast yesterday, Macron pointed out that Europe needs to prepare its future security architecture.

“There is one issue that depends on the Ukrainians, that is the border issue.

There is one issue that we need to prepare and this is what we discussed with (American) President (Joe) Biden, the security architecture in which we want to live tomorrow ,” Macron pointed out.

“This means that one of the main points to consider – as President Putin always says – is his concern that NATO is arriving at his door and the development of weapons that could threaten Russia ,” explained the French president. .

“This issue will be one of the factors for peace and therefore we have to prepare it: what are we ready to do, how will we protect our allies and member countries while offering guarantees to Russia for its own security, on the day that will come to the table” of the negotiations, Macron said.

“What is at stake in Ukraine are principles of the UN Charter: territorial integrity and national sovereignty,” the French president reminded, however, who noted that “I believe in the freedom of peoples to self-determination.”

At the same time, Macron assured that France will continue to provide weapons to Ukraine and support it.

“In the coming weeks we must help Ukraine to resist, Ukrainians to endure, continue to help them militarily, avoid escalation and intervene very specifically to protect the nuclear plants and prepare the dialogue for the day when all people will return to the table” of negotiations, Macron noted.

This week both the US and Russia said they were open in principle to talks, although Biden said he would only talk to Putin if he appeared interested in ending the war. Ukraine says negotiations will only be possible if Russia stops its offensive and withdraws its troops.

Russian Foreign Minister Sergey Lavrov said Thursday that the US and NATO’s move to focus on countering China in the Asia Pacific has led to an increase in military cooperation between Moscow and Beijing.

“We know how seriously the People’s Republic of China regards these provocations [by NATO in the South China Sea], let alone Taiwan and the Taiwan Strait. We understand that this playing with fire by NATO in that part of the world carries threats and risks for the Russian Federation,” Lavrov said at a press conference, according to TASS.Via EPA

In recent years, the US has stepped up its military presence in the South China Sea and near Taiwan, and some of its European allies have sent ships to the region, including the UK, France, and Germany.

“It’s as close to our shores and our seas as it is to Chinese territory. So, our military cooperation with the People’s Republic of China is developing. We are holding joint exercises, both counterterrorism exercises and air patrolling exercises,” Lavrov said.

NATO has identified China as a “challenge” to the alliance and has said it should forge stronger relationships with countries in the Asia Pacific, including Australia, South Korea, Japan, and India. Building new alliances in the region is a key aspect of the US strategy against China, as outlined by the Biden administration’s Indo-Pacific Strategy.

Lavrov said that the US and NATO are trying to create an “explosive situation” in the Asia Pacific and pointed to the AUKUS military pact between the US, Britain, and Australia. Under AUKUS, Australia is expected to receive technology to develop nuclear-powered submarines, and the US will expand its military presence in Australia.

China has previously warned that the Biden administration’s efforts to build alliances in the Asia Pacific could lead to a Ukraine-style “tragedy” in the region. “The United States has tried to create regional tension and provoke confrontation by pushing forward the Indo-Pacific strategy,” Chinese Foreign Minister Wang Yi said back in April.

The increasing military cooperation between Russia and China is a natural reaction to the similar pressure they are facing from the West. In a sign of the growing ties, Russian and Chinese bombers flew a joint patrol over the western Pacific on Wednesday.

end

Russia upgrades its software so they can defend the HIMARS missiles from the USA

special thanks to Robert H for providing this to us

(courtesy RT)

Russian troops get upgrade against HIMARS – RIA

Moscow’s forces have obtained software to easily tackle US-made missiles, a military commander has claimed