GLAD TO BE BACK!!//NOW BRINGING TO YOU THE FULL REPORT.

GOLD PRICE CLOSE: UP $4.05 at $1789,55

SILVER PRICE CLOSE: UP 0.34 to $22.75

Access prices: closes : 4: 15 PM

Gold ACCESS CLOSE 1789.15

Silver ACCESS CLOSE: 23.05

Bitcoin morning price:, 16,815 DOWN 95 DOLLARS FROM TUESDAY

Bitcoin: afternoon price: $17,229 UP 319

Platinum price closing $1010.30

Palladium price; closing 1937.25

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2430.15 DOWN $9.53 CDN dollars per oz

BRITISH GOLD: 1461.76 DOWN 1.87 pounds per oz

EURO GOLD: 1694,80 down 5,25 euros per oz

DONATE

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: DECEMBER 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,785.500000000 USD

INTENT DATE: 12/07/2022 DELIVERY DATE: 12/09/2022

FIRM ORG FIRM NAME ISSUED STOPPED

118 C MACQUARIE FUT 7

132 C SG AMERICAS 1

332 H STANDARD CHARTE 8

435 H SCOTIA CAPITAL 5

624 H BOFA SECURITIES 18

657 C MORGAN STANLEY 3

661 C JP MORGAN 75 36

700 C UBS 2

905 C ADM 1

TOTAL: 78 78

COMEX//NOTICES FILED re JPMorgan 36/78

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

GOLD: NUMBER OF NOTICES FILED FOR DEC. CONTRACT: 78 NOTICES FOR 7800 OZ or 0/2426 TONNES

total notices so far: 12,500 contracts for 1,250,000 oz (38.880 tonnes)

SILVER NOTICES: 19 NOTICE(S) FILED FOR 95,000 OZ/

total number of notices filed so far this month 2965 for 14,825,000 oz

END

GLD

WITH GOLD $4.05

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//BIG CHANGES IN GOLD INVENTORY AT THE GLD: /////HUGE CHANGES IN GLD INVENTORY: A WITHDRAWAL OF 1.45 TONNES INTO THE GLD//

INVENTORY RESTS AT TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP $.34

AT THE SLV// :/HUGE CHANGES IN SILVER INVENTORY AT THE SLV THESE PAST 3 WEEKS! A GAIN OF 44.777 MILLION OZ

INTO THE SLV

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 516.7 MILLION OZ (THIS IS ALSO A CRIME SCENE@!!!!

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A STRONG SIZED 709 CONTRACTS TO 123,267 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THE GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR CONSIDERABLE $0.62 GAIN IN SILVER PRICING AT THE COMEX ON WEDNESDAY. OUR SHORTERS/HFT WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.62 AND WERE UNSUCCESSFUL IN KNOCKING ANY SPEC LONGS, AS WE HAD A HUGE SIZED GAIN IN OUR TWO EXCHANGES OF 1607 CONTRACTS AS WELL ( EXCHANGE FOR RISK TRANSFER OF 0 CONTRACT)S. WE HAD A ZERO ATTEMPTED SPEC SHORT COVERINGS OF THEIR SHORTFALL. .WE PROBABLY HAD ZERO SOME SHORT ADDITIONS AS THE PRICE OF THE METAL WAS ROSE STRONGLY. // OUR BANKERS CONTINUE TO BE PURCHASERS OF NET COMEX LONGS. BUT THEY ALSO SUPPLIED THE NECESSARY SHORT CONTRACTS>>> HUGE NUMBER OF NEWBIE SPEC LONGS ADDED TO THEIR POSITIONS CAUSING ADDITIONAL MISERY TO OUR SHORTERS.

WE MUST HAVE HAD:

A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 23 .24. MILLION OZ FOLLOWED BY TODAY;S QUEUE JUMP of 3,000 OZ /// / // V) HUGE SIZED COMEX OI GAIN/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL–193

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS DEC. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF DEC:

TOTAL CONTRACTS for 8 days, total 4385 contracts: OR 21.925 MILLION OZ PER DAY. (923 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 21.925 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 21.925 MILLION OZ INITIAL

RESULT: WE HAD A STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 709 WITH OUR STRONG $0.62 GAIN IN SILVER PRICING AT THE COMEX// WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE CONTRACTS: 705 CONTRACTS ISSUED FOR MAR AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR DEC OF 23.24 MILLION OZ FOLLOWED BY TODAY:S 3,000 QUEUE JUMP //NEW STANDING 24.990 MILLION OZ + EFR = 35.490 MILLION OZ. .. WE HAVE A HUGE SIZED GAIN OF 1607 OI CONTRACTS ON THE TWO EXCHANGES FOR 8.035 MILLION OZ.. THE SILVER SHORTS ARE NOW TRAPPED AS THEY ARE HAVING CONSIDERABLE DIFFICULTY IN COVERING THOSE SHORTS.

WE HAD 19 NOTICE(S) FILED TODAY FOR 95,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A SMALL SIZED 544 CONTRACTS TO 422,644 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 84 CONTRACTS.

.

THE SMALL SIZED INCREASE IN COMEX OI CAME WITH OUR STRONG GAIN IN PRICE. WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR DEC. AT 58.86 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY:S QUEUE JUMP of 96 contracts or 9600 oz//(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S WILL CONTINUE UNTIL MONTH’S END) (EFP is the transfer of contracts immediately to London for potential gold deliveries originating from London). NEW STANDING 59.269 TONNES

YET ALL OF..THIS HAPPENED WITH OUR GAIN PRICE OF $15.25 WITH RESPECT TO WEDNESDAY’S TRADING

WE HAD A FAIR SIZED GAIN OF 2696 OI CONTRACTS (8.3856 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2152 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 422,728

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2696 CONTRACTS WITH 544 CONTRACTS INCREASED AT THE COMEX (SHORT SPECULATORS FAILING TO GET OUT OF THEIR MESS) AND 2152 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 2780 CONTRACTS OR 8.646 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2152 CONTRACTS) ACCOMPANYING THE SMALL SIZED GAIN IN COMEX OI (544) TOTAL GAIN IN THE TWO EXCHANGES 2696 CONTRACTS. WE NO DOUBT HAD 1) ATTEMPTED BUT FAILED SPECULATOR SHORT COVERINGS// CONTINUED GOOD BANKER ADDITIONS BUT THEY ALSO SUPPLIED THE NECESSARY PAPER SHORT. WE HAD LIMITED SHORT SPEC ADDITIONS/// // SOME MINOR NEWBIE SPEC ADDITIONS ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR DEC. AT 58.86 TONNES FOLLOWED BY TODAY’S QUEUE JUMP of 9600 oz// //NEW STANDING 59.269 TONNES///3) ZERO LONG LIQUIDATION //// //.,4) SMALL SIZED COMEX OPEN INTEREST GAIN 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

DEC

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF DEC :

16,328 CONTRACTS OR 1,632,800 OZ OR 50.786 TONNES 8 TRADING DAY(S) AND THUS AVERAGING: 2041 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 8 TRADING DAY(S) IN TONNES:50.786 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 50.786/3550 x 100% TONNES 1.43% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 50.876 tonnes Initial

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW NON ACTIVE FRONT MONTH OF NOV. WE ARE NOW INTO THE SPREADING OPERATION OF BOTH SILVER AND GOLD (WILL BE SMALL AS SPREADERS DO NOT PAY ATTENTION TO NOVEMBER)

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF OCT HEADING TOWARDS THE NON ACTIVE DELIVERY MONTH OF NOV., FOR BOTH GOLD AND SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A STRONG SIZED 709 CONTRACTS OI TO 123,267 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 705 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 705 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 705 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 902 CONTRACTS AND ADD TO THE 705 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE SIZED GAIN OF 1414 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 7.070 MILLION OZ//

OCCURRED WITH OUR GAIN IN PRICE OF $0.62….. OUR SPEC SHORTS HAVE NOWHERE TO HIDE!

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold/silver commentaries

6. Commodity commentaries//

7/CRYPTOCURRENCIES/BITCOIN ETC

3. ASIAN AFFAIRS

i)THURSDAY MORNING//WEDNESDAY NIGHT

SHANGHAI CLOSED DOWN 2.27 PTS OR 0.07% //Hang Sang CLOSED UP 635.41 OR 3.33% /The Nikkei closed DOWN 111.97 OR 0.40% //Australia’s all ordinaries CLOSED DOWN 0.72% /Chinese yuan (ONSHORE) closed UP TO 6.9742//OFFSHORE CHINESE YUAN UP TO 6.9748// /Oil DOWN TO 72.41 dollars per barrel for WTI and BRENT AT 77.71 / Stocks in Europe OPENED ALL RED. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A SMALL SIZED 544 CONTRACTS UP TO 422,644 WITH OUR THE HUGE GAIN IN PRICE..$15.25

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE -ACTIVE DELIVERY MONTH OF DEC… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2152 EFP CONTRACTS WERE ISSUED: ;: , . 0 FEB: 2152 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 2696 CONTRACTS IN THAT 2152 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A SMALL SIZED COMEX OI GAIN OF 544 CONTRACTS..AND THIS FAIR SIZED GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR HUGE GAIN IN PRICE OF GOLD $15.25. WE ARE WITNESSING SOME SPEC SHORTS ADDITIONS TO THEIR SHORTFALL. BANKERS CONTINUE AS NET BUYERS OF COMEX GOLD CONTRACTS AS THEY HAVE BEEN NET LONG FOR THE PAST FEW MONTHS. WE ALSO HAD HUGE NEWBIE SPECS ADDITIONS.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING DEC (59.269)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL (TOTAL SO FAR THIS YEAR 591.535 TONNES)

Dec. 59.269 tonnes

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $15.25 AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS AS WE HAD A FAIR GAIN OF 2152 CONTRACTS ON OUR TWO EXCHANGES >. WE HAD SOME SPEC SHORT ADDITIONS AND ZERO SPEC SHORT COVERINGS.. // WE HAVE LOST A TOTAL OI OF 23.58 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR DEC. (54.57 TONNES), following our queue jump of 9600 oz//new standing 59.269 tonnes…THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE OF $15.25

WE HAD – 193 CONTRACTS COMEX TRADES REMOVED FROM OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET gain ON THE TWO EXCHANGES 2696 CONTRACTS OR 269600 OZ OR 8.3856 TONNES

Estimated gold volume 111,485// poor//

final gold volumes/yesterday 162,437/ poor

INITIAL STANDINGS FOR DECEMBER 2022 COMEX GOLD //DEC 8

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 514.410 oz Brinks 16kilobars brinks |

| Deposit to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz | nil. oz Manfra |

| No of oz served (contracts) today | 78 notice(s) 7800 OZ 0.2426 TONNES |

| No of oz to be served (notices) | 6550 contracts 65500 oz 20.388 TONNES |

| Total monthly oz gold served (contracts) so far this month | 12,500 notices 1,250,000 38.880 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

i)Dealer deposits: 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits nil oz

customer withdrawals:1

i) Out of Brinks: 514.410 oz (16 kilobars)

Total withdrawals: 514.41 oz

total in tonnes: 0.0012 tonnes

Adjustments: 1 customer to dealer

HSBC 41,973.453 oz/

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR DECEMBER.

For the front month of DECEMBER we have an oi of 6633 contracts having GAINED 89 contracts

We had 7 contracts served on Wednesday, so we gained 98 contracts or an additional 9600 oz will stand for gold at the COMEX. We will gain in gold tonnage from this day forth.

The comex is running out of physical gold to serve our good friends over in London

JANUARY lost 84 contracts to stand at 1402

February gained 431 contacts up to 356,934

We had 78 notice(s) filed today for 7,800 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 72 notices were issued from their client or customer account. The total of all issuance by all participants equate to 78 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 36 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the DEC. /2022. contract month,

we take the total number of notices filed so far for the month (12,500 x 100 oz , to which we add the difference between the open interest for the front month of (DEC. 6633 CONTRACTS) minus the number of notices served upon today 7 x 100 oz per contract equals 1,905,500 OZ OR 59.269 TONNES the number of TONNES standing in this active month of DEC.

thus the INITIAL standings for gold for the DEC contract month:

No of notices filed so far (12,500 x 100 oz+ (x6633 OI for the front month minus the number of notices served upon today (78} x 100 oz} which equals 1,905,500 oz standing OR 59.269 TONNES in this active delivery month of DEC..

TOTAL COMEX GOLD STANDING: 59.269 TONNES (A POOR STANDING//COMEX RUNNING OUT OF PHYSICAL TO SERVE UPON OUR LONGS.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

we had one adjustment of 110,631.591 oz Brinks

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,036,256.155 OZ 63.33 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 23,428,354,984 OZ

TOTAL REGISTERED GOLD: 11,714,505.523 OZ (364.37 tonnes)..dropping fast

TOTAL OF ALL ELIGIBLE GOLD: 11,783,849.462 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 9,678,249 OZ (REG GOLD- PLEDGED GOLD) 301.034 tonnes//rapidly declining

END

SILVER/COMEX

DEC 8//INITIAL DEC. SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 702,214.800 oz Brinks CNT INT.DELAWARE |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 599,198.980 oz CNT |

| No of oz served today (contracts) | 19 CONTRACT(S) (95,000 OZ) |

| No of oz to be served (notices) | 2033 contracts (10,165,000 oz) |

| Total monthly oz silver served (contracts) | 2965 contracts (14,825,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 1 deposits into the customer account

ii) Into CNT: 599,198.981 oz

Total deposits: 599,198.981 oz

JPMorgan has a total silver weight: 150.796 million oz/298.915 million =50.45% of comex .//dropping fast

Comex withdrawals:

i) Out of Brinks 1,024.03 oz

ii) Out of Int Delaware: 101,192.070oz

iii) Out of CNT: 599.998.700 oz

Total withdrawals; 702,214.800 oz

adjustments: dealer to customer

i)HSBC; 49,436.500 oz

ii) Out of JPM<: 10,159.200 oz

and customer and dealer

Brinks 856,168.810 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 33,845 MILLION OZ (declining rapidly).TOTAL REG + ELIG. 299.915MILLION OZ (also declining)

CALCULATION OF SILVER OZ STANDING FOR SEPT

silver open interest data:

FRONT MONTH OF DEC OI: 2052 CONTRACTS HAVING LOST 25 CONTRACT(S.)

WE HAD 31 NOTICES FILED ON WEDNESDAY. SO WE GAINED 6 CONTRACTS OR 30,000 oz

JANUARY SAW A LOSS OF 82 CONTRACTS DOWN TO 1694 CONTACTS.

FEB> LOST 153 CONTRACTS TO 98 CONTRACTS

March GAINED 707 contracts UP to 108,293 contracts

TOTAL NUMBER OF NOTICES FILED FOR TODAY:19 for 95,000 oz

Comex volumes:45,933// est. volume today// poor

Comex volume: confirmed yesterday: 54.394 contracts ( fair)

To calculate the number of silver ounces that will stand for delivery in DEC. we take the total number of notices filed for the month so far at 2965 x 5,000 oz = 14,825,000 oz

to which we add the difference between the open interest for the front month of DEC( 1052) and the number of notices served upon today 19 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the DEC./2022 contract month: 2965(notices served so far) x 5000 oz + OI for front month of DEC (2052 – number of notices served upon today (19)x 50070 oz of silver standing for the DEC. contract month equates 24.990 million oz. We will gain in silver oz standing from this day forth. Also we have another criminal element to our silver oz standing, the use of Exchange for Risk/ Today an addition of 0 EFR contract transfers which are “Exchange for risk” settlements. I do not want to bore you but needless to say they are not physical transfers so are criminal in nature. There has been 2100 Exchange for Risk contracts settled these past 5 days for 10.500 million oz. Thus total delivery: 35.49 million oz.

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

Comex volumes:72,569// est. volume today// good

Comex volume: confirmed yesterday: 79,442 contracts ( good)

END

GLD AND SLV INVENTORY LEVELS

Dec 8/WITH GOLD UP $4.05, OVER THE PAST 3 WEEKS WE LOST 2.04 TONNES//INVENTORY RESTS AT 908.09 TONNES

NOV 14/WITH GOLD UP $7.30: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD///INVENTORY RESTS AT 910.12 TONNES

NOV 11/WITH GOLD UP $15.25//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.19 TONNES INTO THE GLD////INVENTORY RESTS AT 911.57 TONNES

NOV 10/WITH GOLD UP $40.75: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 908.38 TONNES

NOV 9/WITH GOLD DOWN $2.00: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.89 TONNES INTO THE GLD////INVENTORY RESTS AT 908.38 TONNES

NOV 8/WITH GOLD UP $34.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.47 TONNES FROM THE GLD//: INVENTORY RESTS AT 905.49 TONNES

NOV 7/WITH GOLD UP $2.95: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.63 TONNES FROM THE GLD//INVENTORY RESTS AT 906.96. TONNES

NOV 4/WITH GOLD UP $44.45 TO $1673.30: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.48 TONNES FROMTHE GLD////INVENTORY RESTS AT 911.59 TONNES.

NOV 3/WITH GOLD DOWN $18.30 TO $1628.85: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.05 TONNES FROM THE GLD////INVENTORY RESTS AT 915.07 TONNES

NOV 2/WITH GOLD UP 55 CENTS TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD///INVENTORY RESTS AT 919.12 TONNES.

NOV 1/WITH GOLD UP $9.20 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.02 TONNES FORM THE GLD../INVENTORY RESTS AT 920.57 TONNES

OCT 31/WITH GOLD DOWN $4.00; BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD//INVENTORY RESTS AT 922.59. TONNES//

OCT28/WITH GOLD DOWN $19.70 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.19 TONNES FROM THE GLD..///INVENTORY RESTS AT 925.20 TONNES

OCT 27/WITH GOLD DOWN $3.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.39 TONNES

OCT 26/WITH GOLD UP $11.65 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.39 TONNES

OCT 25/WITH GOLD UP $3.85: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 928.39 TONNES

OCT 24/WITH GOLD DOWN $1.80 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.89 TONNES FROM THE GLD////INVENTORY RESTS AT 928.10 TONNES

OCT 21/WITH GOLD UP $19.10: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 930.99 TONNES

OCT 20/WITH GOLD UP $2.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 6.08 TONNES FROM THE GLD///INVENTORY RESTS AT 932.73 TONNES

OCT 19/WITH GOLD DOWN $20.65:: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD////INVENTORY RESTS AT 938.81 TONNES

OCT 18/WITH GOLD DOWN $7.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 939.10 TONNES

OCT 17/WITH GOLD UP $14.55: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.28 TONNES FROM THE GLD///INVENTORY RESTS AT 941.13 TONNES

OCT 14/WITH GOLD DOWN $26.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FROM THE GLD///INVENTORY RESTS AT 944.31 TONNES

OCT 13/WITH GOLD DOWN $0.40 TODAY: A DEPOSIT OF 1.16 TONNES INTO THE GLD// CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 945.47 TONNES

OCT 12/WITH GOLD UP $4.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 944.31 TONNES

OCT 11/WITH GOLD UP $10.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 944.31 TONNES

OCT 10//WITH GOLD DOWN $33.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 944.31 TONNES

OCT 7/WITH GOLD DOWN $10.70: NO CHANGES IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 946.34 TONNES

OCT 6/WITH GOLD UP $.70 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.45 TONNES INTO THE GLD//INVENTORY RESTS AT 946.34 TONNES

OCT 4/WITH GOLD UP $28.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.19 TONNES INTO THE GLD//INVENTORY RESTS AT 942.89 TONNES

OCT 3.WITH GOLD UP $29.30 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD AND A BIG SURPRISE: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD////INVENTORY RESTS AT 939.70 TONNES

GLD INVENTORY: 908.09 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

DEC 8/WITH SILVER RISING 34 CENTS TODAY: OVER THE PAST 3 WEEKS, WE HAVE GAINED A STRONG: 44.777 MILLION OZ/INVENTORY RESTS AT 516.700 MILION OZ.

NOV 14/WITH SILVER UP 41 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 471.923 MILLION OZ//

NOV 11/WITH SILVER DOWN 2 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 553,000 OZ FROM THE SLV///INVENTORY RESTS AT 471.923 MILLION OZ//

NOV 10/WITH SILVER UP 39 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 368,000 OZ INTO THE SLV///INVENTORY RESTS AT 472.476 MILLION OZ//

NOV 9/WITH SILVER DOWN 10 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV/; A WITHDRAWAL OF 3.821 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 472.108 MILLION OZ//

NOV 8/WITH SILVER UP 48 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.751 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 475.929 MILLION OZ//

NOV 7/WITH SILVER UP 12 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 477.678 MILLION OZ//

NOV 4/WITH SILVER UP $1.31 TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.972 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 477.678 MILLION OZ//

NOV 3.WITH SILVER DOWN 16 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 566,000 OZ FROM THE SLV////INVENTORY RESTS AT 482.650 MILLION OZ//

NOV 2/WITH SILVER DOWN 9 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 92,000 OZ FROM THE SLV////INVENTORY RESTS AT 483.216 MILLION OZ//

NOV 1/WITH SILVER UP 53 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 415,000 OZ FORM THE SLV////INVENTORY RESTS AT 483.308 MILLION OZ

OCT 31: WITH SILVER FLAT: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .644 MILLION OZ FROM THE SLV/INVENTORY RESTS AT 483.723 MILLION OZ//

OCT 28/WITH SILVER DOWN 35 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 276,000 OZ INTO THE SLV////INVENTORY RESTS AT 484.367 MILLION OZ//

OCT 27/WITH SILVER UP 3 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE S: A WITHDRAWAL OF 2.579 MILLION OZ FROMTHE SLV/////INVENTORY RESTS AT 484.091 MILLION OZ//

OCT 26/WITH SILVER UP 11 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.013 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 486.670 MILLION OZ./.

OCT 25/WITH SILVER UP 17 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.083 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 487.683 MILLION OZ/

OCT 24/WITH SILVER UP 6 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .553 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 485.610 MILLION OZ//

OCT 21/WITH SILVER UP 43 CENTS: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .46 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 486.163MILLION OZ//

OCT 20/WITH SILVER UP 33 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .921 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 485.703 MILLION OZ//

OCT 19/WITH SILVER DOWN 27 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.105 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 486.624 MILLION OZ///

OCT 18/WITH SILVER DOWN 5 CENTS:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.658 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 487.729 MILLION OZ///

OCT 17/WITH SILVER UP 53 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.151 MILLION OZ INTO THE SLV////INVENTORY REST AT 486.071 MILLION OZ//

OCT 14/WITH SILVER DOWN 77 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.211 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 484.920 MILLION OZ//

OCT 13/WITH SILVER DOWN 2 CENTS TODAY: BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.513 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 482.709 MILLION OZ//

Oct 12/WITH SILVER DOWN 18 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.196 MILLION OZ

OCT 11/WITH SILVER DOWN 11 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.066 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 478.196 MILLION OZ

OCT 10//WITH SILVER DOWN 65 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 473.130 MILLION OZ/

OCT 7/WITH SILVER DOWN 37 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.447 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 473.130 MILLION OZ/

OCT 6/WITH SILVER UP 11 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY: A WITHDRAWAL OF 5.3 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 475.617 MILLION OZ//

OCT 4WITH SILVER UP $.51 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ

OCT 3/WITH SILVER UP $1.46 : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ//

CLOSING INVENTORY 515.000 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff

Peter Schiff: The Markets Are Worried About The Wrong Fed Mistake

THURSDAY, DEC 08, 2022 – 09:25 AM

Stocks have struggled in recent days due to some better-than-expected economic data and more hawkish talk from Fed officials. This has revived fears that the Federal Reserve could make a mistake and raise rates too high and keep them there too long, sparking a recession. In his podcast, Peter Schiff said the markets are worried about the wrong mistake.

Peter said he thinks there is still a chance that St. Nick will show up with a Santa Clause rally in stocks.

I don’t expect this rally to have too much behind it, meaning I don’t look for much in the way of upside. But I do think there’s a good chance we’re going to do another short squeeze before the next leg lower, which I think will happen in January, if not even before the end of December. So, to the extent that we get the Santa Claus rally, you don’t want to buy it. In fact, you don’t even want to buy in anticipation of the rally, because it may not even happen, and you’re going to be left with coal in your stockings.”

Peter said the market reaction to Jerome Powell’s recent speech got him thinking about the possibility of a Santa Claus rally. The markets ignored Powell’s hawkish talk about interest rates going higher and staying there longer and focused totally on the prospect of a smaller rate hike in December. But in the last few days, several Fed members have repeated Powell’s messaging about having to go higher for longer.

Also, there was some better-than-expected economic news. The ISM services index came in higher than expected along with factory orders in October. It was something of a one-two punch. As soon as the data came out, the S&P Futures sold off sharply. Gold also charted a big drop.

The market perception is that this stronger-than-expected economic data will prevent the Fed from recognizing that the inflation threat has subsided. That will lead to the Fed making a mistake and raising rates too much and leaving them too high for too long, causing an unnecessary recession.

All of this is scaring the stock market. But the reality is we’re already in recession, and we don’t have a strong economy.”

Peter said of course we’ll occasionally get data that is stronger than expected. But most of the data has been weaker than expected. And a lot of the strong data — for instance, the non-farm payroll report — is only superficially strong. When you dig beneath the surface, you find a different story.

Don’t accept the numbers at face value. Dig a little deeper and look at what’s actually happening. Because if you do that with the jobs numbers as I’ve been doing on this podcast, the jobs market isn’t strong. The jobs market is weak.”

Peter emphasized that the risk everybody is worried about is the wrong risk.

It’s not that the Fed is going to raise rates too much. It’s that they’re not going to raise them enough. It’s that they’re going to pivot too quickly. It’s not that the Fed is going to mistakenly believe that the economy is strong and then overestimate how high inflation will be. It’s the weak economy that’s going to cause inflation to be higher. Because as the economy weakens, production will decline, but money printing will expand. In fact, at some point, the Fed will pivot in response to a much weaker economy than it expected, and that’s when the dollar is really going to tank, and that’s when consumer prices are really going to take off.”

Peter said the inflation that we’re experiencing now will kick into a much higher gear during the next economic downturn.

Everybody just assumes that when the economy weakens, so too will inflation. No. The weakening economy is going to strengthen inflation because inflation is the expansion of the money supply. And the weaker the economy gets, the more the Fed is going to expand the money supply to try to stimulate it. And as the return of quantitative easing causes a mass exodus out of the US dollar from foreign central banks and private holders, then the falling dollar is going to push consumer prices up dramatically.”

The weakening dollar will also cause the trade deficit to widen, putting downward pressure on GDP, and creating a self-perpetuating spiral of inflation and economic weakness.

2 Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz//Rickards:

LAWRIE WILLIAMS: China’s November gold demand slips even further

The latest gold withdrawal figures for November from the Shanghai Gold Exchange (SGE) suggest that the downturn we have been seeing in Chinese gold retail gold demand in recent months is not only continuing, but getting worse. This is probably an indication that the spate of Covid- related lockdowns that have prompted anti-government demonstrations in a number of population centres are perhaps having even more of an impact on the Chinese economy than many Western observers had even realised. Perhaps the recently announced relaxations will put demand back on track again in time for the Chinese New Year celebrations which next year falls on January 22nd and is a Rabbit year.

As can be seen from the month-by-month comparison table above, it now looks as though 2022 SGE gold withdrawals are now going to fall comfortably behind those for 2021, and hugely below the peak years from 2013 to 2017 when they totalled over 2,000 tonnes annually. However China will still retain its place as the world’s dominant gold consumer – and there remains the suspicion that the nation’s central bank continues to buy substantial amounts of gold for its reserves without reporting these purchases to the International Monetary Fund, although it has recently been reported that it has announced the purchase of a 32 tonne boost to its gold reserves last month! It is reckoned to be able to surreptitiously add to its reserves as the nation almost certainly remains the world’s No.1 gold producer from its own gold mines and from byproduct gold from its custom base metal smelting and refining industry and is thought to export none of this domestically-produced bullion. It could be adding upwards of 300 tonnes of gold a year to reserves from these sources without these statistics impacting the globally assessed figures.

The Chinese people certainly have a propensity to buy gold for savings and for gifting, and indeed have been encouraged to do so, but as we noted above, disposable incomes have almost certainly been hit by Covid-related lockdowns in key industrial areas with many workers confined to their homes and unable to get to their places of work. The downturns in Western economies also, which have been the key export markets for Chinese manufactured goods, have also reduced substantially due to belt tightening, and this is already becoming evident in global trade statistics. All this will be impacting Chinese corporate profits and individual earnings adversely, and will likely continue to do so as global economies attempt to weather the current recessionary trends.

Overall we now anticipate Chinese retail gold demand falling to perhaps as low as around 1,600 tonnes this year, or possibly even lower, in 2023. The country will still remain the world’s largest gold consumer, but India is playing catch-up again and may not be far behind in the years ahead if China’s economic growth continues to falter.

08 Dec 2022

3. Chris Powell of GATA provides to us very important physical commentaries//

GOLD/SILVER

(GATA) Robert Lambourne: BIS gold swaps reverse sharply upward as metal’s price rises

By Robert Lambourne

Wednesday, December 7, 2022

On November 10 my most recent commentary on the gold swaps of the Bank for International Settlements noted that “after 12 years in the gold swap business, the BIS seems to have just about gotten out”:

It goes to show how wrong you can be, since the bank’s November statement of account, just published —

https://www.bis.org/banking/balsheet/statofacc221130.pdf< /B>

can be used to estimate that the bank’s gold swaps, which had declined to an estimated 7 tonnes as of October 31, have risen sharply to an estimated 105 tonnes as of November 30. This is the BIS’ highest level of estimated swaps since June 30 this year.

Perhaps the BIS is taking instructions from manic- depressive gold price suppressors, and, if so, it would be reminiscent of an old nursery rhyme, slightly altered here:

Oh, the grand old BIS.

It had ten thousand swaps.

It marked them up to the top of the market

And it marked them down again.

And when they were up, they were up,

And when they were down, they were down,

And when they were only halfway up,

They were neither up nor down.

On a more serious note, it is clear from Table B below that the level of BIS swaps had been significantly higher in the first half of the year and the October total was easily the lowest in more than four years. Even the much-increased level of swaps estimated for November is still far below the average level seen in the first half of 2022.

Perhaps the key point to re-emphasize is that the BIS has been an active trader of significant volumes of gold swaps on a regular basis for at least 12 years, and the recent data indicates that this strong volume of trading is continuing, with 98 tonnes of swapped gold taken from commercial banks in November and deposited in gold sight accounts at central banks that work closely with the BIS.

Maybe this increase was simply an emergency act by the BIS to procure swapped gold, since November saw a strong increase in the gold price to $1,773 at November 30 from $1,633 at October 31.

The BIS half-year report at September 30, 2022, also has been published recently, and while it offers no direct comment on the use of gold swaps, its disclosures include confirmation of three things: first, that the BIS still holds 102 tonnes of its own gold; second, that very little of its activities in derivatives (presumably including gold swaps) are with major central banks and hence are almost certainly with commercia l bullion banks; and third, the gold in the BIS’ sight accounts is predominantly held by major central banks that are considered to be related parties.

Table A below highlights the level of gold swaps reported in the annual reports of the BIS all the way back to 2010, when the bank’s use of gold swaps appears to have begun. At only one year-end since then, in March 2016, has the swap level been lower than it is was in October 2022.

So it still seems possible that the assertions made by some commentators, for example —

https://www.gata.org/node/22300

— about “gold leases and swaps” levels at the BIS falling because of the application of “Basel III” regulations about unallocated gold are correct and remain relevant.

The estimates made here do not include leases, so I can offer no comment on them, but it is still clear that the dominant recent trend at the BIS is a reduction in gold swaps, where th e BIS takes swapped gold from bullion banks and deposits it in sight accounts with major central banks. The next few months will reveal more about the direction of the BIS’ gold swaps.

It remains highly unlikely that more information about the swaps will be released by the BIS, because, to date, apart from the bank’s disclosures in accounting notes, there has been no direct comment issued on gold swaps in the bank’s financial reports since the reference made 12 years ago and highlighted below.

… Historical context

The BIS rarely comments publicly on its gold activities, but its first use of gold swaps was considered important enough to cause the bank to give some background information to the Financial Times for an article published July 29, 2010, coinciding with publication of the bank’s 2009-10 annual report.

The general manager of the BIS at the time, Jaime Caruana, said the gold swaps were “regular commercial activities” for the bank, and he confirmed that they were carried out with commercial banks and so did not involve central banks. It also seems highly likely that the BIS’ remaining swaps are still all made with commercial banks, because the BIS annual report has never disclosed a gold swap between the BIS and a major central bank.

The swap transactions potentially have created a mismatch at the BIS, which may end up being long unallocated gold (the gold held in BIS sight accounts at major central banks) and short allocated gold (the gold required to be returned to swap counterparties). This possible mismatch has not been reported by the BIS.

The gold banking activities of the BIS have been a regular part of the services it offers to central banks since the bank’s establishment 90 years ago. The first annual report of the BIS explains these activities in some detail:

http://www.bis.org/publ/arpdf/archive/ar1931_en.p df

A June 2008 presentation made by the BIS to potential central bank members at its headquarters in Basel, Switzerland, noted that the bank’s services to its members include secret interventions in the gold and foreign exchange markets:

https://www.gata.org/node/11012

The use of gold swaps to take gold held by commercial banks and then deposit it in gold sight accounts held in the name of the BIS at major central banks doesnt appear ever to have been as large a part of the BIS gold banking business as it has been in recent years, although the recent declines suggest this is changing.

As of March 31, 2010, excluding gold owned by the BIS, there were 1,706 tonnes held in gold sight accounts at major central banks in the name of the BIS, of which 346 tonnes or 20% were sourced from gold swaps from commercial banks.

If the BIS was adopting the level of disclosures made by publicly held companies, such as commercial banks, some explanation of these changes probably would have been required by the accounting regulators. This irony may not be lost on those dealing with regulatory activities at the BIS. Presumably the shrinkage of the BIS’ gold banking business shows that even central banks now prefer to hold their own gold or hold it in earmarked form — that is, as allocated gold.

A review of Table B below highlights recent BIS activity with gold swaps, and despite the recent declines, the recent positions estimated from the BIS monthly statements remained large especially in early 2022 and the volume of trading has been significant.

No explanation for this continuing use of swaps has been published by the BIS. Indeed, no comment on the bank’s use of gold swaps has been offered since 2010.

This gold is supplied by bullion banks via the swaps to the BIS. The gold is then deposited in BIS gold sight accounts (unallocated gold accounts) at major central banks such a s the Federal Reserve.

The reasons for this activity have never been fully explained by the BIS and various conjectures have been made as to why the BIS is facilitating it. One conjecture is that the swaps are a mechanism for central banks to recover gold secretly supplied by them to cover shortfalls in the gold markets. The use of the BIS to facilitate this trade suggests a desire to conceal the rationale for the transactions.

As can be seen in Table A below, the BIS has used gold swaps extensively since its financial year 2009-10. No use of swaps is reported in the bank’s annual reports for at least 10 years prior to the year ended March 2010.

The February 2021 estimate of the bank’s gold swaps (552 tonnes) was higher than any level of swaps reported by the BIS at its March year-end since March 2010. The swaps reported at March 2021 were at the highest year-end level reported, as is clear from Table A.

—–

Table A Swaps reported in BIS annual reports

March 2010: 346 tonnes.

March 2011: 409 tonnes.

March 2012: 355 tonnes.

March 2013: 404 tonnes.

March 2014: 236 tonnes.

March 2015: 47 tonnes.

March 2016: 0 tonnes.

March 2017: 438 tonnes.

March 2018: 361 tonnes.

March 2019: 175 tonnes

March 2020: 326 tonnes

March 2021: 490 tonnes

March 2022: 358 tonnes

—–

The table below reports the estimated swap levels since August 2018. It can be seen that the BIS is actively trading gold swaps and other gold derivatives, with changes from month to month reported in excess of 100 tonnes in this period.

/4. OTHER PHYSICAL SILVER/GOLD COMMENTARIES

Ep. 102 Live from the Vault

Why 27th December is so important for physical gold and silver

In this week’s episode of Live from the Vault, Andrew Maguire underlines the inevitable paper market unwinding following Basel III compliance, as the COMEX is forced to compete with an increasingly global physical marketplace.

The London wholesaler exposes the speculators that will be left tricked with undeliverable short positions, waking up into what will likely be a bid-only market.

6/CRYPTOCURRENCIES/BITCOIN ETC

This will drive more citizens to to the Nigerian crypto

(zerohedge)

Nigeria Limits ATM Withdrawals To $45 Per Day To Force Govt-Controlled Digital Payments

THURSDAY, DEC 08, 2022 – 06:55 AM

A staggering number of Nigerians love Bitcoin, but hate government cryptocurrency (CBDCs).

In April, leading cryptocurrency exchange KuCoin noted that 35% of the adult population in Nigeria – roughly 34 million adults aged 18-60, own bitcoin or other cryptocurrencies. But when it came to the country’s Central Bank Digital Currency (CBDC), the eNaira, it was a massive failure.

According to Bloomberg, only 1 in 200 Nigerians use the eNaira – despite government implemented discounts and other incentives, implemented as desperate measures to increase adoption.

Now, the government is looking to boost digital payments by limiting ATM withdrawals to just 20,000 naira, or roughly US$45 per day, Bloomberg reports, citing a circular sent to lenders on Tuesday. The previous withdrawal limit was 150,000 naira (US$350).

Weekly cash withdrawals from banks are now limited (without fee) to 100,000 naira (US$225) for individuals, and 500,000 naira (US$1,125) for corporations. Any amount above this will incur a fee of 5% and 10% respectively.

The action is the latest in a string of central bank orders aimed at limiting the use of cash and expand digital currencies to help improve access to banking. In Nigeria’s largely informal economy, cash outside banks represents 85% of currency in circulation and almost 40 million adults are without a bank account.

The central bank last month announced plans to issue redesigned high value notes from mid-December to mop up excess cash and it’s given residents until the end of January to turn in their old notes. The bank also plans to mint more of the eNaira digital currency, which was launched last year but has faced slow adoption. -Bloomberg

What’s more, new rules which will take effect Jan. 9 will ban the cashing of checks above 50,000 naira (US$112) over-the-counter, and 10 million naira (US$22,480) through the banking systems. Point-of-sale cash withdrawals have been capped at 20,000 naira ($45).

Meanwhile, banks are only allowed to load their ATMs with 200 naira denominations and under, while individuals and corporations will be allowed to cash a maximum of 5 million and 10 million naira respectively if there are “compelling circumstances not exceeding once a month,” and which will be subject to enhanced due diligence along with processing fees, according to the central bank. Such withdrawals will also require the approval of a bank CEO.

“Customers should be encouraged to use alternative channels—Internet banking, mobile banking apps, USSD, cards, POS, eNaira to conduct their banking transactions,” said the central bank on Tuesday.

end

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings THURSDAY morning 7:30 AM

ONSHORE YUAN: UP TO 6.9742

OFFSHORE YUAN: 7.6948

SHANGHAI CLOSED DOWN 2.27 PTS OR 0.07%

HANG SANG CLOSED UP 635.41 OR 3.33%

2. Nikkei closed DOWN 111.97 PTS OR 0.40%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX UP TO 105.27 Euro FALLS TO 1.0504

3b Japan 10 YR bond yield: RISES TO. +.249!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 136.84/JAPANESE YEN COLLAPSING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE YUAN: UP-// OFF- SHORE: UP

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +1.781%***/Italian 10 Yr bond yield FALLS to 3.622%*** /SPAIN 10 YR BOND YIELD FALLS TO 2.777…** DANGEROUS//

3i Greek 10 year bond yield FALLS TO 3.689//

3j Gold at $1785.00//silver at: 22.75 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 19/100 roubles/dollar; ROUBLE AT 62.63//

3m oil into the 72 dollar handle for WTI and 77 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 136.84 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9416– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9896well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.442% UP 3 BASIS PTS…GETTING DANGEROUS

USA 30 YR BOND YIELD: 3.425% UP 1 BASIS PTS//

USA DOLLAR VS TURKISH LIRA: 18,64…

GREAT BRITAIN/10 YEAR YIELD: 3.075%

end

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

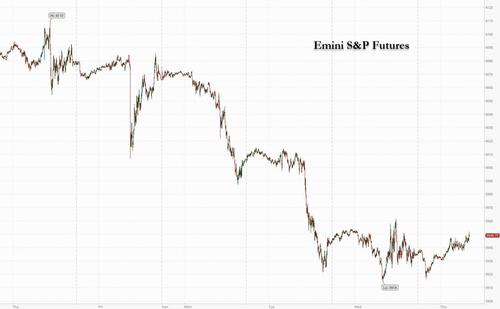

Futures Rebound After Worst Losing Streak In 2 Months SBFs $1.3 Trillion In Value

THURSDAY, DEC 08, 2022 – 08:09 AM

A blistering rout in US stocks, which saw US markets drop on 8 of the past 9 days and when the S&P 500 lost about $1.3 trillion in market capitalization in the past five days on fears of a staunchly hawkish Federal Reserve amid signs of a resilient economy, was set to pause on Thursday. Contracts on the S&P 500 were up 0.3% by 7:45 a.m. ET following the longest daily losing streak for the index in nearly two months. Nasdaq 100 futures were up 0.2%. Treasuries halted a rally that had sent the 10-year yield to an almost three-month low as investors braced for an economic downturn. The benchmark added three basis points to yield 3.44%, while a gauge of the dollar was little changed.

Among notable movers in premarket trading, Carvana was set to rebound after yesterday’s record 43% plunge as the online car dealer consults with lawyers and bankers regarding options for managing its debt load. Relmada Therapeutics shares are in focus after the failure of its study of an experimental antidepressant. Exxon rose 1.4% premarket after the US E&P giant and cash(flow) cow announced it would expand its stock buyback program by $20BN to $50BN by the end of 2024. Here are some other other notable premarket movers:

- Rent the Runway rises 16% after reporting third- quarter results that beat estimates as its number of active subscribers rose 15% year-on-year. The fashion retailer increased its annual revenue outlook and forecast a positive adjusted Ebitda margin for the year.

- Shares of US-listed Chinese internet firms and casinos that operate in Macau gain in premarket trading on more signs that China is accelerating the pivot away from its zero-tolerance stance on Covid.

- Alibaba +3.7%, Baidu +4%, Bilibili +11%, Li Auto +5.4%, Las Vegas Sands +4.3%, Melco Resorts +8.5%

- Carvana shares jump 7.6% in premarket trading, set to rebound after yesterday’s record 43% plunge as the online car dealer consults with lawyers and bankers regarding options for managing its debt load.

- Relmada’s shares tumbled 40% in US after-hours trading on Wednesday. The failure of the company’s study of an experimental antidepressant was disappointing, though not surprising, analysts said, with some reassessing the possibility of success in upcoming studies.

- Watch Principal Financial stock after it was downgraded to underperform from neutral at Credit Suisse on valuation grounds, with the broker preferring the investment manager’s peer Voya.

- Keep an eye on JPMorgan as Piper Sandler begins coverage on the stock at overweight, saying that the “big four” banks have a unique position leading the industry, with a critical presence in basically all areas of the financial system.

- Watch defense stocks after Citigroup said it is “locked in” on the sector for the next decade, with a more “nuanced” view on the outlook for commercial aerospace. It reinstates General Dynamics, Leidos, Lockheed Martin and Science Applications with buy ratings.

The rally in US stocks since mid-October which propelled the S&P to 4,100 as of Dec 1 and above the 200DMA, has stalled recently as stronger-than-expected economic data suggested the Fed could keep tightening its policy at an aggressive pace (spoiler alert: it won’t). Investors are now looking for clues from the latest inflation data on Tuesday and the Fed’s policy decision on Wednesday.

“The risk-off sentiment more widely on stock markets this week remains hard to kick into touch,” said Susannah Streeter, senior investment and markets analyst at Hargreaves Lansdown. The outlook for next year also remains uncertain, with Citigroup Inc. strategists becoming the latest to warn of weakness in equity markets amid a risk to corporate earnings. The MSCI USA index is now implying 4% earnings-per-share growth next year, close to the analyst consensus but far from Citi’s expectation of a 3% contraction, strategists led by Robert Buckland wrote in a note.

“The recent rally means US equities no longer price an EPS contraction, which seems too optimistic,” the Citi strategists wrote. Technical indicators, meanwhile, suggest stock volatility could rise next week. Measures of 30-day implied and realized volatility in the S&P 500 Index started to move closer together in recent sessions, a sign of rising anxiety after the benchmark failed to break through its 2022 downtrend and the key 200-day moving average.

Strategists from Morgan Stanley to JPMorgan have warned investors against piling back into risk on hopes the Fed is getting close to pivoting to easier policy. Translation: buy, buy, buy.

“Presumably if the Fed is pivoting this time around, it’s not for a good reason. It’s a deteriorating fundamental picture,” Joyce Chang, chair of global research at JPMorgan, said in an interview with Bloomberg TV Thursday, forgetting that that “not good reason” could very well be the ongoing devastation in risk assets. “I mean, is that really a reason to be buying risk? I think it’s premature to say that there is a Fed pivot.” No, it’s not.

Traders now await Friday’s US producer price report and the Consumer Price Index print to get a read on how effective Fed policy has been to quell inflation, and whether the central bank will be able to notch down its aggressive campaign.

Back to markets, where European stocks extended a four-day slide, with property and telecommunications firms pacing declines even as energy companies and miners gained. That said, stocks have almost erased all initial losses. Euro Stoxx 50 is little changed. CAC 40 outperforms peers, adding 0.1%, IBEX lags, dropping 0.5%. Here are some other notable European movers:

- Derichebourg rises as much as 14%, biggest intraday gain since February 2021, after the French waste-management company reported revenue for the year that beat the average analyst estimate

- IAG rises as much as 2.1% and Wizz Air as much as 7.4% after Bank of America upgraded both stocks to buy. Lufthansa climbs as much as 1.4% after BofA upgraded to neutral, while EasyJet falls as much as 3.8% after being double-downgraded to underperform

- Vertu Motors rises as much as 6.6% after announcing the acquisition of Helston Garages Group for a total of £117m

- Balfour Beatty gains as much as 3.9%, touching the highest since Sept. 16, with analysts flagging another buyback announcement and a solid outlook from the construction and infrastructure group

- Frasers Group falls as much as 8.1%, the most since Nov. 14, after the Sports Direct and House of Fraser owner reported sales around 4% below RBC expectations after a softer performance in international retail.

- Stadler Rail drops as much as 5.6% as Credit Suisse trims its price target on the train manufacturer, anticipating pressure on profitability.

- Volkswagen falls as much as 1.7% and is among the worst performers on the SXAP autos index after Exane cut its rating on the company’s preference shares to underperform from neutral, citing margin pressures.

- ASML declines as much as 1.6% after Bloomberg News reported that the Netherlands is planning new controls on exports of chipmaking equipment, potentially barring companies from selling gear capable of manufacturing 14- nanometer or more advanced chips

Asian stocks rose, led by a jump in Chinese equities on increasing expectations for reopening, helping investors dispel worries about a possible global economic recession. The MSCI Asia Pacific Index rose as much as 0.6%, driven by gains in Chinese tech names including Tencent and Alibaba. The gauge erased an earlier drop of as much as 0.5% in another day of volatile trading amid thin volumes. Hong Kong’s Hang Seng Index surged more than 3%, rebounding from Wednesday’s selloff, after a report that the city is seeking to further ease Covid-related rules. Investors have been bullish on Chinese equities of late, with JPMorgan saying that earnings downgrades are “very close to the bottom”.

The positive views have helped lift sentiment on Asia broadly, with Nomura upgrading its outlook for Hong Kong and South Korea stocks. Still, even with Thursday’s gain, the MSCI Asia equity measure is on track for its first weekly loss since the end of October as investors lock in profits after a five-week surge. “Asian investors should use this volatility as an opportunity to raise exposure,” Nomura strategists including Chetan Seth wrote in a report. “Recessions in the US/Europe in 2023 mean that a growing Asia will likely be the outperformer, with softer USD/Asia the additional kicker.”

Markets with heavy dependence on global demand for their manufactured goods, such as Taiwan and South Korea, posted notable losses while the key benchmark in Indonesia, a raw materials exporter sank as much as 2%. Japan’s stock gauge also dropped led lower by its tech and auto exporters, following US shares lower as Treasuries signaled growing concern about a recession next year. The Topix dropped 0.3% to 1,941.50 as of market close Tokyo time, while the Nikkei 225 declined 0.4% to 27,574.43. Sony Group contributed the most to the Topix’s decline, decreasing 1.9%. Out of 2,164 stocks in the index, 728 rose and 1,292 fell, while 144 were unchanged. “There’s a gradual increase in the view that the economy will probably deteriorate considerably next year,” said Takeru Ogihara, chief strategist at Asset Management One

Australian stocks also extended their losing streak as banks and miners drag: the S&P/ASX 200 index fell 0.8% to close at 7,175.50, marking three consecutive sessions of losses. Bank and materials shares contributed the most to the benchmark’s retreat. Downer EDI was the biggest decliner after cutting its earnings guidance and flagging accounting irregularities. In New Zealand, the S&P/NZX 50 index was little changed at 11,617.14.

In FX, the Bloomberg Dollar Spot Index was flat after temporarily swinging to a loss in early European hours and then modest gains. The dollar strengthened against most of its Group-of-10 peers, though trading was largely confined to narrow ranges.

- The euro was steady around $1.05. Bunds twist- flattened as the 2-year yield rose by 2bps and the 30-year yield fell by 1bp. Money-market wagers on ECB tightening increase very slightly ahead of a slew of speeches, including President Lagarde

- The pound was the worst G-10 performer, while the gilt curve bull-steepened as money markets eased BOE tightening wagers, pricing less than one-point of rate hikes by February for the first time since Nov. 11 ahead of next week’s policy meeting. Thursday marks the Bank of England’s final active QT bond sales of this year, though sales of gilts purchased as part of its recent emergency support measures will continue

- The yen traded heavy after Japan unexpectedly reported a current-account deficit

In rates, Treasuries fell across the curve, apart from the 30-year tenor, which inched up. Declines were most pronounced in the belly, where yields rose about 4bps. The belly of the curve underperformed, with 5- to 7-year yields are cheaper by as much as 3.5bp on outright basis. Long-end outperforms, with yields slightly richer on the day, leaving 5s30s spread flattest since Oct. 20. Few events scheduled during US session. Treasury 10-year yields around 3.45%, cheaper by 2bps on the day and lagging bunds, gilts by 2bp and 1bp; 2s10s spread around -83bp and steeper by 1.5bp on the session after reaching new cycle low -85.2bp Wednesday. Gilts 10-year yield reverses earlier moves as money markets pare BOE rate-hike bets, seeing less than 100bps by Feb. Bunds 10-year yield edges lower while within Wednesday’s range.

In commodities, oil rises after a four-day drop; WTI jumped more than 3% to rise above $74 following news there was an outage at the Keystone pipeline. Spot gold falls roughly $3 to trade near $1,784/oz. Most base metals trade in the green.

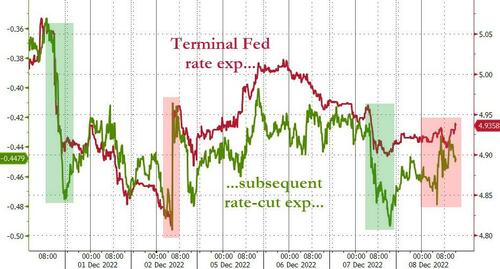

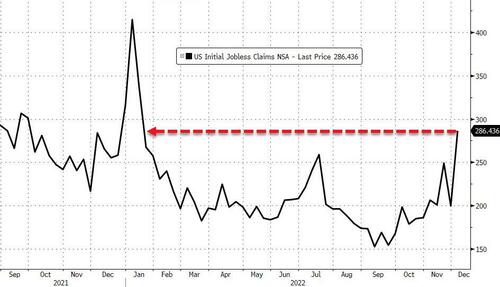

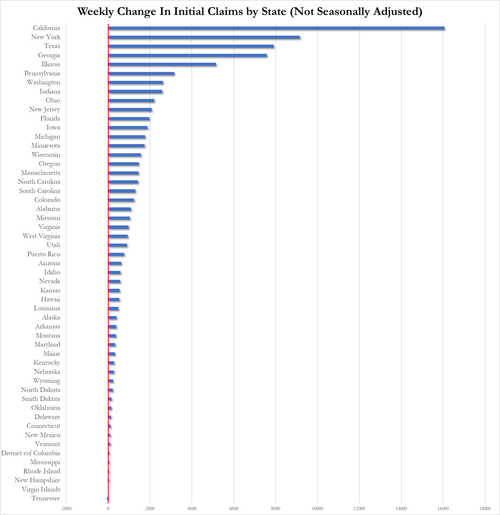

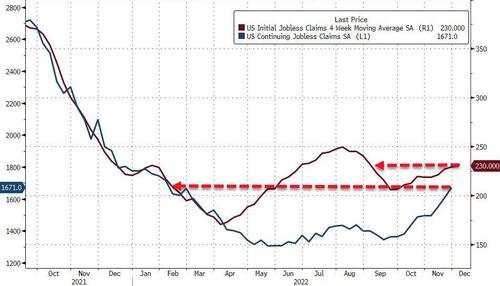

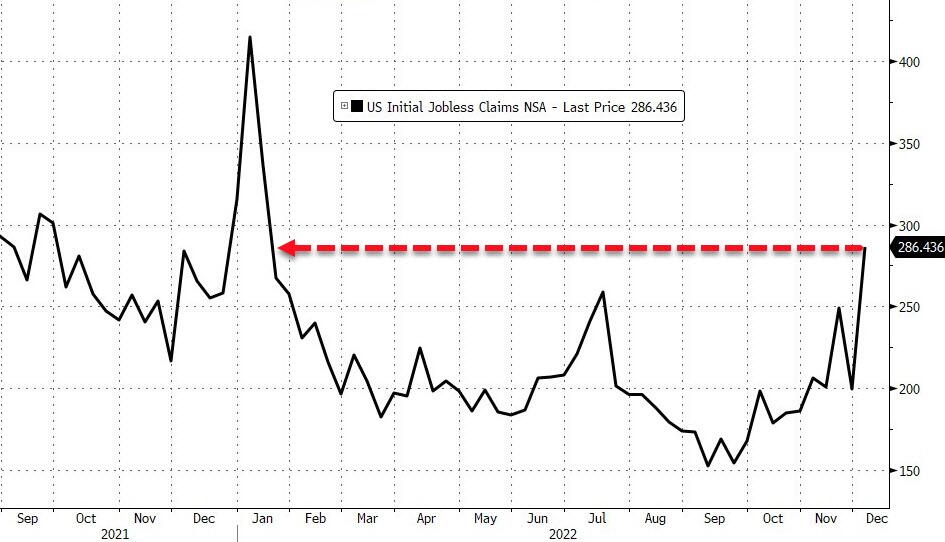

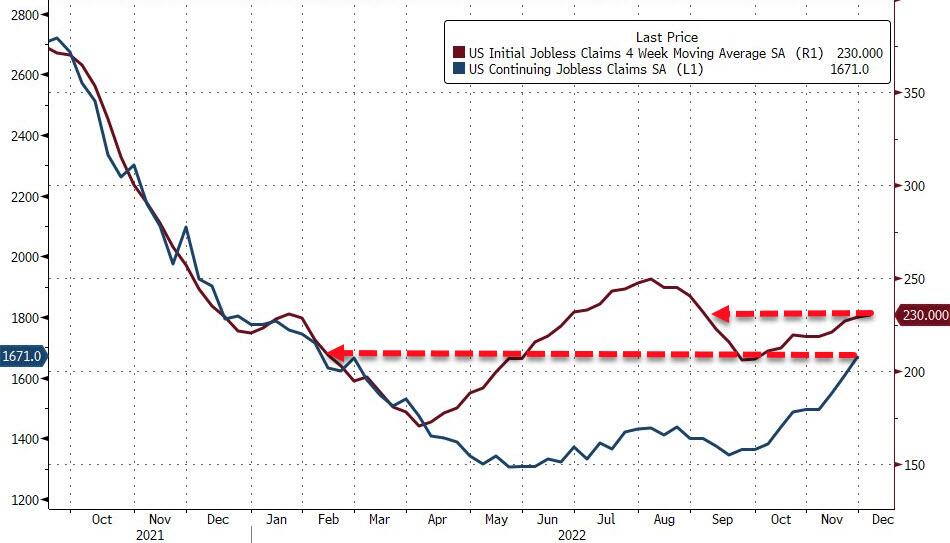

To the day ahead now, and central bank speakers include ECB President Lagarde, and the ECB’s de Cos and Villeroy. Data releases include the weekly initial jobless claims from the US. Finally, earnings releases include Costco and Broadcom.

Market Snapshot

- S&P 500 futures up 0.1% to 3,941.25

- STOXX Europe 600 down 0.1% to 435.59

- MXAP up 0.4% to 156.61

- MXAPJ up 0.9% to 511.06

- Nikkei down 0.4% to 27,574.43

- Topix down 0.3% to 1,941.50

- Hang Seng Index up 3.4% to 19,450.23

- Shanghai Composite little changed at 3,197.35

- Sensex up 0.2% to 62,517.40

- Australia S&P/ASX 200 down 0.7% to 7,175.55

- Kospi down 0.5% to 2,371.08

- German 10Y yield down 0.2% to 1.79%

- Euro down 0.1% to $1.0495

- Brent Futures up 1.0% to $77.94/bbl

- Gold spot down 0.2% to $1,783.29

- U.S. Dollar Index up 0.20% to 105.31

Top Overnight News from Bloomberg

- Europe’s governments are expected to sell more new debt in the bond market next year — upwards of €500 billion on a net basis — than anytime this century. And bond investors, scarred by the same inflation surge that the ECB is trying to squelch, aren’t in the mood to tolerate fiscal largesse right now

- The term structures in the major currencies are now in full inversion mode as the one-week tenor captures the last round of risk events for the year. They now envelope the monetary policy meetings by the Federal Reserve, the European Central Bank, the Bank of England, the Swiss National Bank and Norges Bank, as well as the US CPI report for November

- The UK’s pace of hiring and pay growth slowed in November as companies concerned about the UK economy tipping into recession became more reluctant to take on permanent staff, according to a survey

- Australian Treasurer Jim Chalmers said an independent review of the Reserve Bank will help guide his decision next year on whether to reappoint Governor Philip Lowe, whose term expires in September

- Chinese authorities may further soften their stance on property policies at its key economic meeting next week after the Communist Party’s top decision-making body said it will seek a turnaround in the economy for 2023, according to people familiar with the matter

- With China’s Covid Zero policy rapidly dismantled, the threat of economic disruption remains high. Infections are likely to surge, forcing workers to stay home, businesses may run out of supplies, restaurants could be emptied of customers and hospitals will fill up

- Japanese life insurers sold a record amount of foreign bonds last month, preliminary portfolio flow data from the nation’s Ministry of Finance show

A more detailed summary of overnight news courtesy of Newsquawk

APAC stocks traded cautiously after the lacklustre handover from Wall St where the major indices were subdued as participants digested deflationary data and Russian President Putin’s nuclear rhetoric. ASX 200 was led lower by underperformance in the energy sector after oil prices recently slipped to a YTD low and with sentiment not helped by a monthly contraction in both export and imports, as well as the failure of takeover talks between Link Administration and suitor Dye & Durham. Nikkei 225 traded negatively amid reports that the government is to propose a JPY 1tln tax income increase to fund national defence, while data releases were uninspiring as it surprisingly showed the first Current Account deficit since June and although Q3 GDP was revised higher, it remained in negative territory. Hang Seng and Shanghai Comp were mixed with the Hong Kong benchmark buoyed by strength in casino names on the reopening play as Hong Kong is said to be considering easing COVID testing rules for arrivals and may repeal the outdoor mask rule, while the mainland is indecisive amid trade-related headwinds with the Netherlands planning curbs on tech exports to China under an agreement with the US.

Top Asian News

- China is said to be mulling further property market easing measures at next week’s economic meeting, according to Bloomberg sources.

- Macau to relax COVID test rules for Chinese visitors, according to Bloomberg.

- Hong Kong reports 14.4k COVID cases (prev. 11.9k); Hong Kong government says social distancing measures are set to remain in place.

- Japanese PM Kishida said no planning to increase income tax for defense spending.

- Hong Kong Shortens Covid Isolation, Eases Testing for Travelers

- China Car Sales Drop as Covid Lockdowns Kept Buyers at Home

- GoTo Assures Investors It Has Enough Cash to Reach Profitability

European bourses and US futures reside in narrow ranges are essentially pivoting the unchanged mark; Euro Stoxx 50 +0.1, ES +0.1. In Europe, the sectoral breakdown is mixed/lower with no overarching bias emerging. Chinese November Retail Passenger Vehicle Sales -9.5% Y/Y (prev. +6.9% Y/Y in Oct), according to PCA; Tesla (TSLA) exports 37.8k China-made vehicles in November (54.5k in October). Elon Musk’s bankers are reportedly considering providing new margin loans backed by Tesla (TSLA) shares to replace some high-interest debt to acquire Twitter, via Bloomberg citing sources.

Top European News

- UK PM Sunak refused to rule out a ban on strikes by emergency services and said he will do what is needed to keep the public safe during ongoing industrial action as he threatens tougher laws, according to Sky News.

- UK’s Unite union said around 146 members will begin strike action at Petrofac’s (PFC LN) Repsol (REP) installation on December 8th and 9th over pay and working terms, while 76 members at BP (BP/ LN) installations are to strike over working rotation, according to Reuters.

- European Natural Gas Prices Surge as Winter Blast Stokes Demand

- ASML Analysts See Limited Impact From Potential Dutch Curbs

- BAT Says US Consumers Are Switching to Cheaper Cigarettes

FX

- DXY has managed to regroup amid a initial retreat in USTs; though, the index remains around the mid-point of 105.04-105.42 ranges.

- Action which has modestly dented peers across the board, particularly GBP and JPY below and above 1.22 and 137.00 respectively.

- Antipodeans and the EUR are the relative ‘outperformer’, though they are essentially unchanged vs USD

- PBoC set USD/CNY mid-point at 6.9606 vs exp. 6.9603 (prev. 6.9975)

Fixed Income

- EGBs & their UK counterpart have, despite initial pressure, staged a firm rally to a test/eclipse of Wednesdays peaks amid the latest rhetoric from Russia.

- However, USTs have been unable to keep up with this and are still softer to the tune of 10 ticks, with yields firmer across the curve as such; currently, action is most pronounced in the belly.

- German Federal Constitutional Court has rejected the request for temporary injunction on 2021 supplementary budget; decision related to govt credit authorisation of EUR 60bln for climate funds.

Commodities

- Crude benchmarks are consolidating after yesterday’s mid-week pressure, though the rebound this morning is limited and rangebound.

- Spot gold is, once again, sideways around the USD 1775/oz mark while base metals glean some support from the latest touting of Chinese economic measures.

- Former Peruvian President Castillo was detained and is accused of rebellion.

- Commodities trader Trafigura more than doubled net profits in 2022 vs 2021.

Crypto

- US federal prosecutors are investigating whether Sam Bankman-Fried and his hedge fund orchestrated trades that led to the collapse of two cryptocurrencies in May, according to NYT.

- It was initially reported that US House Finance Services Chair Waters doesn’t plan to subpoena Sam Bankman-Fried to testify at the hearing on FTX’s collapse, although Waters later denied the report.

- US SEC has investigations under way focusing on exchanges including Coinbase (COIN) and the U.S. businesses of Binance and FTX, according to WSJ sources.

Geopolitics

- German Chancellor Scholz said the risk of Russia using nuclear weapons has decreased, according to Funke Media.

- Russian Deputy Foreign Minister Ryabkov says if the US deploys medium-range missiles in Asia/Europe then Russia’s approach to the moratorium will changed, via Reuters; adds, Russia’s nuclear deterrence forces are on full alert, according to Al Jazeera.

- Taiwan Defence Ministry said 9 Chinese air force planes crossed the Taiwan Strait median line during the past 24 hours, according to Reuters.

- US, Japan, and South Korea nuclear representatives meeting in Indonesia on the 12th and 13th December over North Korea, Via Yonhap.

US Event Calendar

- 08:30: Nov. Continuing Claims, est. 1.62m, prior 1.61m

- 08:30: Dec. Initial Jobless Claims, est. 230,000, prior 225,000

DB’s Jim Reid concludes the overnight wrap